ESR Cayman Limited - :: HKEX :: HKEXnews ::

1060

ESR Cayman Limited Stock Code: 1821 (Incorporated in the Cayman Islands with limited liability) Joint Sponsors Joint Global Coordinators and Joint Bookrunners Joint Bookrunners GLOBAL OFFERING (in alphabetical order)

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of ESR Cayman Limited - :: HKEX :: HKEXnews ::

ESR Cayman Limited

ESR C

ayman Lim

ited

ESR Cayman Limited

Stock Code: 1821

(Incorporated in the Cayman Islands with limited liability)

Joint Sponsors

Joint Global Coordinators and Joint Bookrunners

Joint Bookrunners

GLOBAL OFFERING

(in alphabetical order)

IMPORTANT

If you are in any doubt about any of the contents of this Prospectus, you should seek independent professionaladvice.

ESR Cayman Limited(Incorporated in the Cayman Islands with limited liability)

GLOBAL OFFERINGNumber of Offer Shares under the Global Offering : 653,680,000 Offer Shares (comprising 280,140,000 New

Shares and 373,540,000 Sale Shares, and subject to theOffer Size Adjustment Option and the Over-allotmentOption)

Number of Hong Kong Public Offer Shares : 34,700,000 New Shares (subject to reallocation and theOffer Size Adjustment Option)

Number of International Placing Shares : 618,980,000 Offer Shares (comprising 245,440,000 NewShares and 373,540,000 Sale Shares, and subject toreallocation, the Offer Size Adjustment Option and theOver-allotment Option)

Maximum Offer Price:(subject to a Downward Offer Price Adjustment)

: HK$17.40 per Offer Share, plus brokerage of 1%, SFCtransaction levy of 0.0027% and Stock Exchange tradingfee of 0.005% (payable in full on application in HongKong dollars and subject to refund) (If the Offer Price isset at 10% below the bottom end of the indicative OfferPrice range after making a Downward Offer PriceAdjustment, the Offer Price will be HK$14.58 per OfferShare)

Nominal value: : US$0.001 per ShareStock code: : 1821

Joint Sponsors

Joint Global Coordinators and Joint Bookrunners

Joint Bookrunners(in alphabetical order)

Hong Kong Exchanges and Clearing Limited, The Stock Exchange of Hong Kong Limited and Hong Kong Securities Clearing Company Limited take noresponsibility for the contents of this Prospectus, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever forany loss howsoever arising from or in reliance upon the whole or any part of the contents of this Prospectus.

A copy of this Prospectus, having attached thereto the documents specified in the section headed “Documents Delivered to the Registrar of Companies inHong Kong and Available for Inspection” in Appendix IX to this Prospectus, has been registered by the Registrar of Companies in Hong Kong as required bySection 342C of the Companies (Winding Up and Miscellaneous Provisions) Ordinance (Cap.32). The Securities and Futures Commission and the Registrar ofCompanies in Hong Kong take no responsibility for the contents of this Prospectus or any other documents referred to above.

The Offer Price is expected to be determined by agreement between the Joint Global Coordinators (for themselves and on behalf of the Underwriters) andour Company (for ourselves and on behalf of the Selling Shareholders) on or around Friday, October 25, 2019 and, in any event, on or before Thursday,October 31, 2019. The Offer Price will not be more than HK$17.40 per Offer Share and is expected to be not less than HK$16.20 per Offer Share (subject to aDownward Offer Price Adjustment), unless otherwise announced.

If, for any reason, our Company (for ourselves and on behalf of the Selling Shareholders) and the Joint Global Coordinators (for themselves and on behalfof the Underwriters) are unable to reach agreement on the Offer Price on or before Thursday, October 31, 2019, the Global Offering will not proceed and willlapse.

The Joint Global Coordinators (for themselves and on behalf of the Underwriters) may, where considered appropriate, and with the consent of ourCompany, reduce the number of Offer Shares and/or the indicative Offer Price range stated in this Prospectus which is HK$16.20 to HK$17.40 at any time on orprior to the morning of the last day for lodging applications under the Hong Kong Public Offering. In such case, notices of the reduction in the number of OfferShares and/or the indicative Offer Price range will be published in the South China Morning Post (in English) and the Hong Kong Economic Times (in Chinese)as soon as practicable following the decision to make such reduction, and in any event not later than the morning of the last day for lodging applications under theHong Kong Public Offering. Such notices will also be available on the website of the Stock Exchange at www.hkexnews.hk and on the website of our Companyat www.esr.com. Further details are set forth in the sections headed “Structure of the Global Offering” and “How to Apply for Hong Kong Public Offer Shares”in this Prospectus.

Prior to making an investment decision, prospective investors should consider carefully all of the information set out in this Prospectus, including the riskfactors set out in the section headed “Risk Factors” in this Prospectus.

The obligations of the Hong Kong Underwriters under the Hong Kong Underwriting Agreement are subject to termination by the Joint GlobalCoordinators (for themselves and on behalf of the Underwriters) if certain grounds arise prior to 8:00 a.m. on the Listing Date. Such grounds are set out in thesection headed “Underwriting” in this Prospectus. It is important that you refer to that section for further details.

The Offer Shares have not been and will not be registered under the U.S. Securities Act or any state securities laws in the United States and may not beoffered, sold, pledged or transferred within the United States, except that Offer Shares may be offered, sold or delivered within the United States to QIBs inreliance on Rule 144A under the U.S. Securities Act or other exemption(s) from registration under the U.S. Securities Act or outside the United States in relianceon Regulation S under the U.S. Securities Act.

October 22, 2019

EXPECTED TIMETABLE(1)

If there is any change in the following expected timetable of the Global Offering, we will issue anannouncement in Hong Kong to be published on the websites of the Stock Exchange at www.hkexnews.hk andour Company at www.esr.com.

Hong Kong Public Offering commences and WHITE and YELLOWApplication Forms available from . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

9:00 a.m. on Tuesday,October 22, 2019

Latest time for completing electronic applications under the White FormeIPO service through the designated website at www.eipo.com.hk(2) . . . .

11:30 a.m. on Friday, October 25,2019

Application lists open(3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11:45 a.m. on Friday, October 25,2019

Latest time for (a) lodging WHITE and YELLOW Application Forms,(b) completing payment for White Form eIPO applications by effectinginternet banking transfer(s) or PPS payment transfer(s) and (c) givingelectronic application instructions to HKSCC . . . . . . . . . . . . . . . . . . . .

12:00 noon on Friday,October 25, 2019

Application lists close(3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12:00 noon on Friday,October 25, 2019

Expected Price Determination Date . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Friday, October 25, 2019

(1) Where applicable, announcement of the Offer Price being set belowthe bottom end of the indicative Offer Price range after making aDownward Offer Price Adjustment (see the section headed “Structureof the Global Offering—Pricing and Allocation”) on the website of theStock Exchange at www.hkexnews.hk and the Company’s website atwww.esr.com on or before . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Thursday, October 31, 2019

(2) Announcement of the Offer Price, the level of indications of interest inthe International Placing, the level of applications in the Hong KongPublic Offering and the basis of allocations of the Hong Kong PublicOffer Shares to be published in the South China Morning Post (inEnglish) and the Hong Kong Economic Times (in Chinese) on orbefore . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Thursday, October 31, 2019

(3) Results of allocations in the Hong Kong Public Offering to beavailable through a variety of channels as described in the sectionheaded “How to Apply for Hong Kong Public Offer Shares—Publication of Results” in this Prospectus from . . . . . . . . . . . . . . . . . . . Thursday, October 31, 2019

(4) Announcement containing (2) and (3) above to be published on thewebsites of the Company and the Stock Exchange at www.esr.comand www.hkexnews.hk from . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Thursday, October 31, 2019

Results of allocations for the Hong Kong Public Offering will be availableat www.iporesults.com.hk (alternatively: Englishhttps://www.eipo.com.hk/en/Allotment; Chinesehttps://www.eipo.com.hk/zh-hk/Allotment) with a “search by ID”function from . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Thursday, October 31, 2019

Dispatch of Share certificates and White Form e-Refund paymentinstructions/refund checks on or before(4) . . . . . . . . . . . . . . . . . . . . . . . . . . Thursday, October 31, 2019

Dealings in the Shares on the Stock Exchange expected to commence on . . Friday, November 1, 2019

Notes:(1) All dates and times refer to Hong Kong dates and times.(2) You will not be permitted to submit your application under the White Form eIPO service through the designated website at

www.eipo.com.hk after 11:30 a.m. on the last day for submitting applications. If you have already submitted your application andobtained a payment reference number from the designated website prior to 11:30 a.m., you will be permitted to continue the applicationprocess (by completing payment of the application monies) until 12:00 noon on the last day for submitting applications, when theapplication lists close.

i

EXPECTED TIMETABLE(1)

(3) If there is/are a “black” rainstorm warning signal, a tropical cyclone warning signal number 8 or above and/or Extreme Conditions inforce in Hong Kong at any time between 9:00 a.m. and 12:00 noon on Friday, October 25, 2019, the application lists will not open andclose on that day. See the section headed “How to Apply for Hong Kong Public Offer Shares” in this Prospectus.

(4) The Share certificates will only become valid at 8:00 a.m. on the Listing Date, which is expected to be Friday, November 1, 2019,provided that the Global Offering has become unconditional in all respects at or before that time. Investors who trade Shares on the basisof publicly available allocation details or prior to the receipt of the Share certificates or prior to the Share certificates becoming valid doso entirely at their own risk.

For details of the structure of the Global Offering, including its conditions, and the proceduresfor applications for Hong Kong Public Offer Shares, see the sections headed “Structure of the GlobalOffering” and “How to Apply for Hong Kong Public Offer Shares” in this Prospectus, respectively.

If the Global Offering does not become unconditional or is terminated in accordance with itsterms, the Global Offering will not proceed. In such a case, the Company will make an announcementas soon as practicable thereafter.

ii

CONTENTS

IMPORTANT NOTICE TO PROSPECTIVE INVESTORS

This Prospectus is issued by us solely in connection with the Hong Kong Public Offering andthe Hong Kong Public Offer Shares and does not constitute an offer to sell or a solicitation of anoffer to buy any security other than the Hong Kong Public Offer Shares offered by this Prospectuspursuant to the Hong Kong Public Offering. This Prospectus may not be used for the purpose of, anddoes not constitute, an offer or invitation in any other jurisdiction or in any other circumstances. Noaction has been taken to permit a public offering of the Offer Shares in any jurisdiction other thanHong Kong and no action has been taken to permit the distribution of this Prospectus in anyjurisdiction other than Hong Kong. The distribution of this Prospectus and the offering of the OfferShares in other jurisdictions are subject to restrictions and may not be made except as permittedunder the applicable securities laws of such jurisdictions pursuant to registration with orauthorization by the relevant securities regulatory authorities or an exemption therefrom.

You should rely only on the information contained in this Prospectus and the ApplicationForms to make your investment decision. We have not authorized anyone to provide you withinformation that is different from what is contained in this Prospectus. Any information orrepresentation not made in this Prospectus must not be relied on by you as having been authorizedby us or any of the Relevant Persons.

Page

EXPECTED TIMETABLE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . i

CONTENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iii

SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

DEFINITIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

FORWARD-LOOKING STATEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

WAIVERS AND CONSENT FROM STRICT COMPLIANCE WITH THE LISTING RULES ANDEXEMPTIONS FROM COMPANIES (WINDING UP AND MISCELLANEOUS PROVISIONS)ORDINANCE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 114

INFORMATION ABOUT THIS PROSPECTUS AND THE GLOBAL OFFERING . . . . . . . . . . . . . . . . 126

DIRECTORS AND PARTIES INVOLVED IN THE GLOBAL OFFERING . . . . . . . . . . . . . . . . . . . . . . 131

CORPORATE INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 137

HISTORY, DEVELOPMENT AND CORPORATE STRUCTURE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 139

BUSINESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 165

RELATIONSHIP WITH WARBURG PINCUS X . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 222

DIRECTORS AND SENIOR MANAGEMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 224

SHARE CAPITAL . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 235

SUBSTANTIAL SHAREHOLDERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 238

FINANCIAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 240

FUTURE PLANS AND USE OF PROCEEDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 329

iii

CONTENTS

Page

CORNERSTONE INVESTOR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 331

UNDERWRITING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 334

STRUCTURE OF THE GLOBAL OFFERING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 348

HOW TO APPLY FOR HONG KONG PUBLIC OFFER SHARES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 360

APPENDIX I ACCOUNTANTS’ REPORT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . I-1

APPENDIX II-A AUDITED FINANCIAL STATEMENTS ON PROPERTYLINK FOR THE THREEYEARS ENDED 30 JUNE 2018 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . II-A-1

APPENDIX II-B AUDITED FINANCIAL STATEMENTS ON PROPERTYLINK FOR THEPERIOD FROM 1 JULY 2018 TO 20 MARCH 2019 . . . . . . . . . . . . . . . . . . . . . . . . . II-B-1

APPENDIX III UNAUDITED PRO FORMA FINANCIAL INFORMATION . . . . . . . . . . . . . . . . . . III-1

APPENDIX IV INDUSTRY OVERVIEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . IV-1

APPENDIX V REGULATORY OVERVIEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . V-1

APPENDIX VI PROPERTY VALUATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . VI-1

APPENDIX VII SUMMARY OF THE CONSTITUTION OF OUR COMPANY AND CAYMANCOMPANIES LAW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . VII-1

APPENDIX VIII STATUTORY AND GENERAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . VIII-1

APPENDIX IX DOCUMENTS DELIVERED TO THE REGISTRAR OF COMPANIES INHONG KONG AND AVAILABLE FOR INSPECTION . . . . . . . . . . . . . . . . . . . . . . IX-1

iv

SUMMARY

This summary aims to give you an overview of the information contained in this Prospectus.As it is a summary, it does not contain all of the information that may be important to you. Youshould read the whole Prospectus before you decide whether to invest in the Offer Shares. There arerisks associated with any investment. Some of the particular risks in investing in the Offer Shares areset out in the section headed “Risk Factors” in this Prospectus. You should read that sectioncarefully in full before you decide whether to invest in the Offer Shares.

OUR MISSION

We aim to build modern logistics infrastructure for 21st century commerce across APAC. Weendeavor to offer tenants modern, state-of-the-art logistics facilities and solutions, and provideinvestors with exposure to a dynamic sector in the fast-growing APAC region.

OVERVIEW

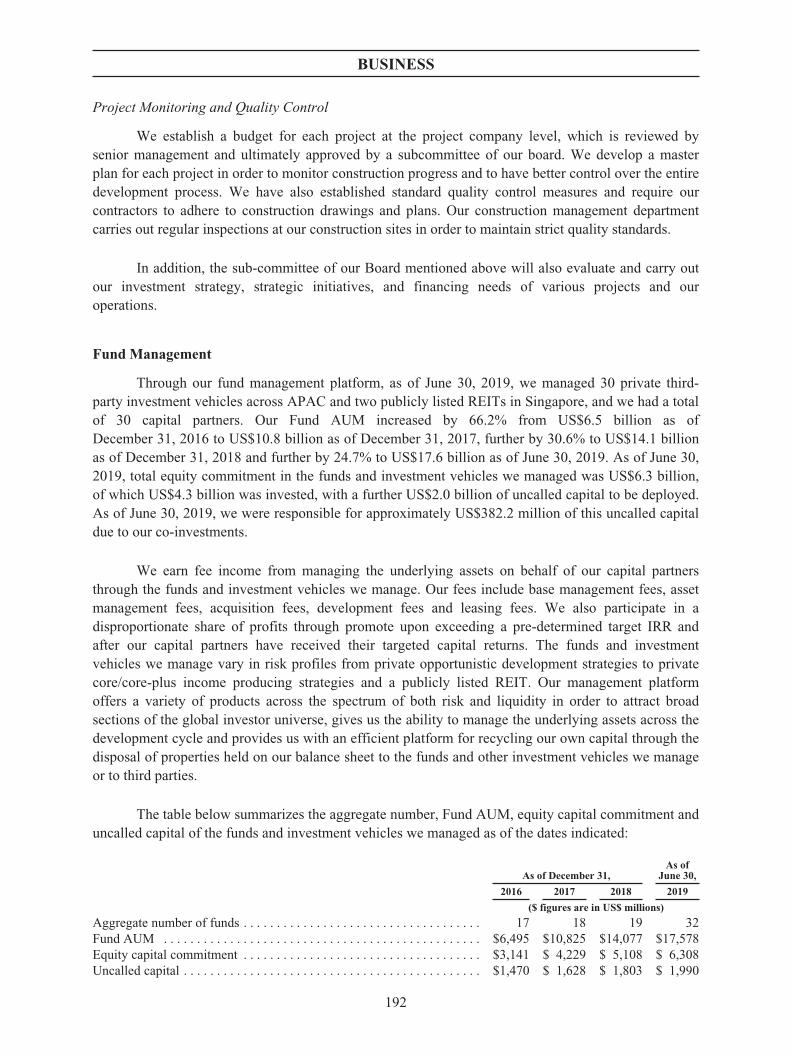

We are the largest APAC focused logistics real estate platform by GFA and by value of thePortfolio Assets and have the largest development pipeline in aggregate across the major APACmarkets as measured by GFA from July 1, 2019 to December 31, 2020, according to the JLL Report.We develop and manage modern logistics facilities that cater to e-commerce companies, 3PLproviders, bricks-and-mortar retailers, manufacturers, cold-chain logistics providers and others inAPAC as logistics infrastructure continues to evolve for the modern economy. We focus solely onAPAC, which comprised over 3.6 billion people (around 50% of the global population) and overUS$28.6 trillion of GDP (over 33% of the global GDP) in 2018, according to the JLL Report. Wecurrently operate in the PRC, Japan, South Korea, Singapore, Australia and India markets thatrepresent close to 90% of GDP in APAC in 2018, according to the JLL Report. We have grownsignificantly during the Track Record Period. Our revenue grew by 58.5% from US$96.7 million in2016 to US$153.3 million in 2017, and further grew by 65.8% to US$254.1 million in 2018. Ourrevenue grew by 66.3% from US$93.7 million for the six months ended June 30, 2018 to US$155.8million for the six months ended June 30, 2019. Our management fee income, a key component of ourrevenue, grew significantly from US$46.5 million in 2016 to US$94.3 million in 2017, and further toUS$135.6 million in 2018, driven by robust growth in our Fund AUM. Our management fee incomegrew from US$59.0 million for the six months ended June 30, 2018 to US$61.8 million for the sixmonths ended June 30, 2019. Our net profit grew by 91.6% from US$104.8 million in 2016 toUS$200.8 million in 2017, and further grew by 6.0% to US$212.9 million in 2018. Our net profit grewby 32.0% from US$63.7 million for the six months ended June 30, 2018 to US$84.1 million for the sixmonths ended June 30, 2019. During the Track Record Period, the majority of our profit was derivedfrom fair value gains on investment properties and share of profits and losses of joint ventures andassociates, which together amounted to US$142.9 million, US$232.2 million, US$237.8 million,US$61.0 million and US$121.9 million in 2016, 2017 and 2018 and for the six months ended June 30,2018 and 2019, respectively.

We hold a portfolio of logistics properties on our balance sheet and manage a broad range offunds and investment vehicles that invest in logistics properties at various stages of the property lifecycle across APAC. As of June 30, 2019, we managed 30 private third-party pooled investmentvehicles, with over US$6.3 billion in total equity commitments, and two REITs listed on the SGX-STwith aggregate appraised carrying value of approximately US$2.9 billion. As of June 30, 2019, ourAUM was approximately US$20.2 billion (of which US$2.7 billion was on our balance sheet) and

1

SUMMARY

comprised approximately 8.5 million sq.m of GFA of completed properties, approximately 4.4 millionsq.m of GFA of properties under construction (which we expect to be completed over the next two tofive years and the size of which is expected to be more than half of the GFA of our current completedproperties) and approximately 2.4 million sq.m of GFA to be built on land held for future development,adding up to over 15.3 million sq.m of GFA in total. GFA on land held for future development refers tototal estimated GFA upon completion based on the Company’s construction plans. See the sectionheaded “Business—Property Operations—Classification of the Portfolio Assets” in this Prospectus forfurther details.

We develop logistics real estate primarily in Tier 1 and 1.5 cities in APAC, targeting strategiclocations near key logistics hubs, major seaports, airports, transportation hubs and industrial zones inthe PRC, Japan, South Korea, Singapore, Australia and India, which are the markets we believe willdrive future growth across APAC. The majority of the tenants in the Portfolio Assets service domesticconsumption in APAC. According to the JLL Report, APAC’s substantial middle class populationcoupled with rapid economic growth and rising income levels are expected to support risingconsumption levels in the region. Private consumption in China, Japan, South Korea, Singapore,Australia and India is forecasted to grow at a CAGR of 8.1% between 2019 and 2023, approximatelytwo times the anticipated 4.0% growth in the US during the same period. As of June 30, 2019,e-commerce and 3PL tenants made up approximately 48.5% of the tenant base of the Portfolio Assetsby leased area. In 2016, 2017 and 2018 and for the six months ended June 30, 2019, rental revenuesfrom e-commerce and 3PL tenants in our balance sheet properties amounted to 82.6%, 76.7%, 63.5%and 41.0% of our total rental revenues, respectively. The decrease in the proportion of rental revenuesfrom e-commerce and 3PL tenants in the six months ended June 30, 2019 was due to our acquisition ofPropertylink, the property portfolio of which had a higher percentage of traditional logistics andindustrial tenants, as well as the disposal of certain balance sheet properties to NCI Core Fund, themajority of which were occupied by e-commerce tenants.

With our APAC-focused business model, we grew significantly during the Track Record Periodthrough organic growth and strategic merger and acquisition (“M&A”), increasing our AUM fromUS$7.4 billion as of December 31, 2016, to US$12.0 billion as of December 31, 2017, toapproximately US$16.0 billion as of December 31, 2018 and further to US$20.2 billion as of June 30,2019. We have also attracted investments from three out of the top six real estate capital providersglobally based on IP&E Real Assets’ top 100 ranking of the world’s largest real estate investors in2018. We were ranked #29 in the world in PERE’s “Fab 50”, the flagship ranking of the private realestate world’s top managers (by total annual fundraising amount) in 2018. Our total consolidatedbalance sheet assets, which include our investment properties, investments in joint ventures, andfinancial assets at fair value, grew by 45.4% from US$2,101.5 million as of December 31, 2016 toUS$3,054.9 million as of December 31, 2017, and further grew by 45.1% to US$4,431.6 million as ofDecember 31, 2018 and 34.2% to US$5,946.0 million as of June 30, 2019.

2

SUMMARY

Below is a summary of the Portfolio Assets we directly owned as of June 30, 2019:

CountryNumber ofproperties(1)

GFA ofcompleted

properties(2)(3)

GFA ofproperties

underconstruction(3)

GFA on landheld forfuture

development(3)

(sqm in thousands)

The PRC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27 1,105.4 842.4 657.4Greater Shanghai . . . . . . . . . . . . . . . . . . . . . . . . . . . 8 516.1 403.3 245.6Greater Beijing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5 253.7 — 147.8Greater Guangzhou . . . . . . . . . . . . . . . . . . . . . . . . . . 6 238.6 — 107.9Others . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8 96.9 439.1 156.2

Japan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 — 575.0 300.0Tokyo . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 — 575.0 300.0

Australia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41(4) 481.7 35.9 —(4)

New South Wales . . . . . . . . . . . . . . . . . . . . . . . . . . . 15 158.6 18.4 —Queensland . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10 80.5 — —Victoria . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13 214.9 17.5 —Western Australia . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 27.6 — —

India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 — 116.5 229.9Mumbai . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 — 116.5 199.3Kolkata . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 — — 30.7

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75 1,587.1 1,569.7 1,187.3

Notes:(1) Includes completed properties, properties under construction and GFA on land held for future development.(2) Includes both stabilized and pre-stabilized completed properties. “Stabilized properties” refer to completed properties: (i) for which

construction or acquisition had been completed for more than 12 months; or (ii) reached an occupancy rate of 93% or higher. “Pre-stabilized properties” refer to completed properties: (i) for which construction or acquisition had been completed for less than 12 months;or (ii) with an occupancy rate of less than 93%.

(3) For the definitions of “completed properties,” “properties under construction,” and “GFA on land held for future development,” see thesection headed “Business—Property Operations—Classification of the Portfolio Assets” in this Prospectus.

(4) We also own four parcels of land in Australia to be developed in the future, and are currently in the process of formulating theconstruction plans and as such have not included the number of properties or the GFA figures to be built on such land.

As of June 30, 2019, the portion of the Portfolio Assets that we held on our balance sheet wasvalued at US$2.7 billion.

3

SUMMARY

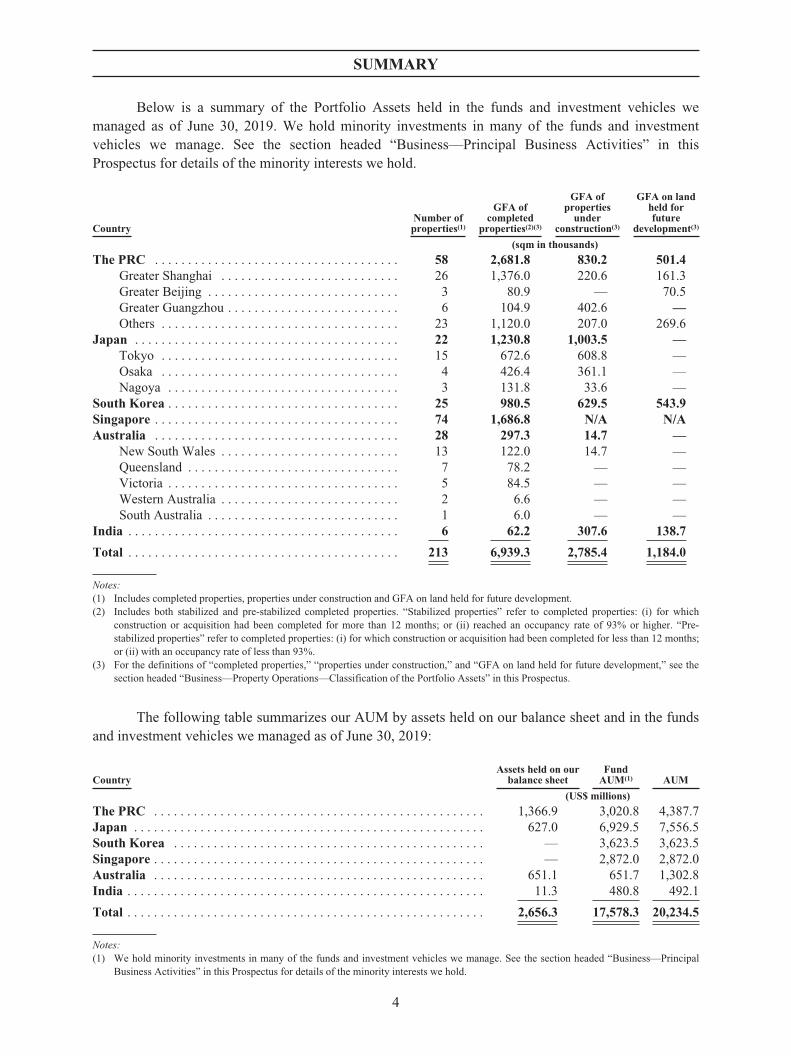

Below is a summary of the Portfolio Assets held in the funds and investment vehicles wemanaged as of June 30, 2019. We hold minority investments in many of the funds and investmentvehicles we manage. See the section headed “Business—Principal Business Activities” in thisProspectus for details of the minority interests we hold.

CountryNumber ofproperties(1)

GFA ofcompleted

properties(2)(3)

GFA ofproperties

underconstruction(3)

GFA on landheld forfuture

development(3)

(sqm in thousands)

The PRC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58 2,681.8 830.2 501.4Greater Shanghai . . . . . . . . . . . . . . . . . . . . . . . . . . . 26 1,376.0 220.6 161.3Greater Beijing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 80.9 — 70.5Greater Guangzhou . . . . . . . . . . . . . . . . . . . . . . . . . . 6 104.9 402.6 —Others . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23 1,120.0 207.0 269.6

Japan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22 1,230.8 1,003.5 —Tokyo . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15 672.6 608.8 —Osaka . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 426.4 361.1 —Nagoya . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 131.8 33.6 —

South Korea . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25 980.5 629.5 543.9Singapore . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74 1,686.8 N/A N/AAustralia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28 297.3 14.7 —

New South Wales . . . . . . . . . . . . . . . . . . . . . . . . . . . 13 122.0 14.7 —Queensland . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 78.2 — —Victoria . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5 84.5 — —Western Australia . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 6.6 — —South Australia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 6.0 — —

India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 62.2 307.6 138.7

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 213 6,939.3 2,785.4 1,184.0

Notes:(1) Includes completed properties, properties under construction and GFA on land held for future development.(2) Includes both stabilized and pre-stabilized completed properties. “Stabilized properties” refer to completed properties: (i) for which

construction or acquisition had been completed for more than 12 months; or (ii) reached an occupancy rate of 93% or higher. “Pre-stabilized properties” refer to completed properties: (i) for which construction or acquisition had been completed for less than 12 months;or (ii) with an occupancy rate of less than 93%.

(3) For the definitions of “completed properties,” “properties under construction,” and “GFA on land held for future development,” see thesection headed “Business—Property Operations—Classification of the Portfolio Assets” in this Prospectus.

The following table summarizes our AUM by assets held on our balance sheet and in the fundsand investment vehicles we managed as of June 30, 2019:

CountryAssets held on our

balance sheetFundAUM(1) AUM

(US$ millions)

The PRC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,366.9 3,020.8 4,387.7Japan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 627.0 6,929.5 7,556.5South Korea . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — 3,623.5 3,623.5Singapore . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — 2,872.0 2,872.0Australia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 651.1 651.7 1,302.8India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.3 480.8 492.1

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,656.3 17,578.3 20,234.5

Notes:(1) We hold minority investments in many of the funds and investment vehicles we manage. See the section headed “Business—Principal

Business Activities” in this Prospectus for details of the minority interests we hold.

4

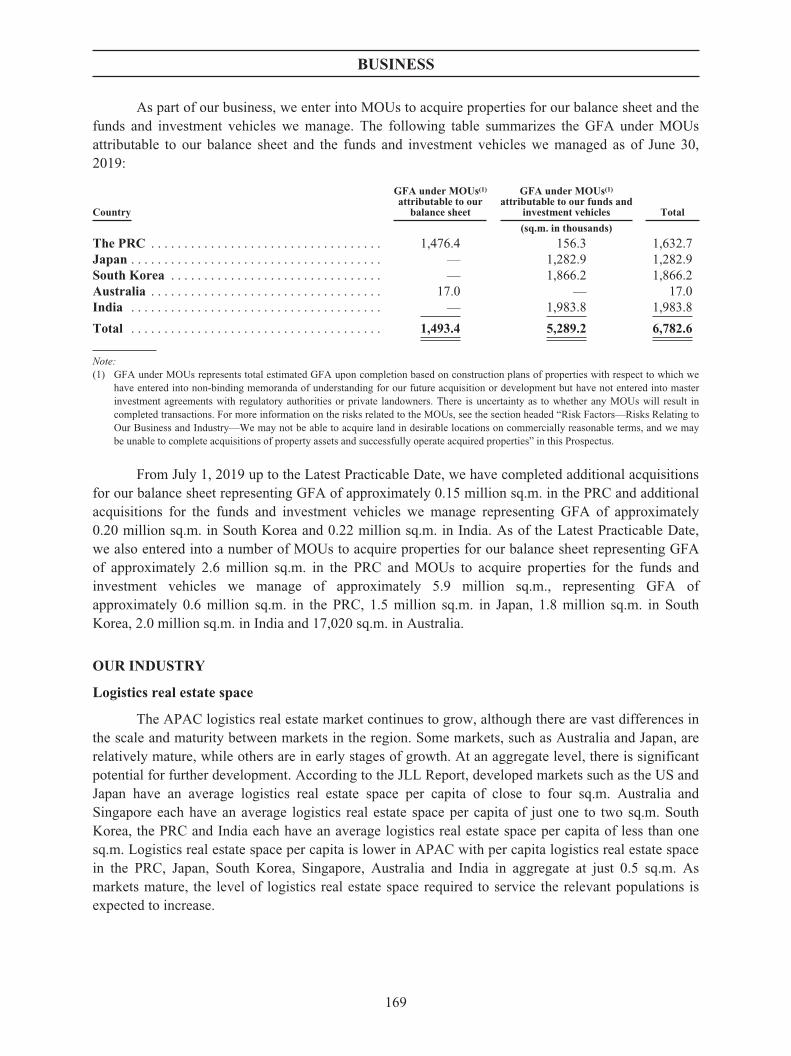

SUMMARY

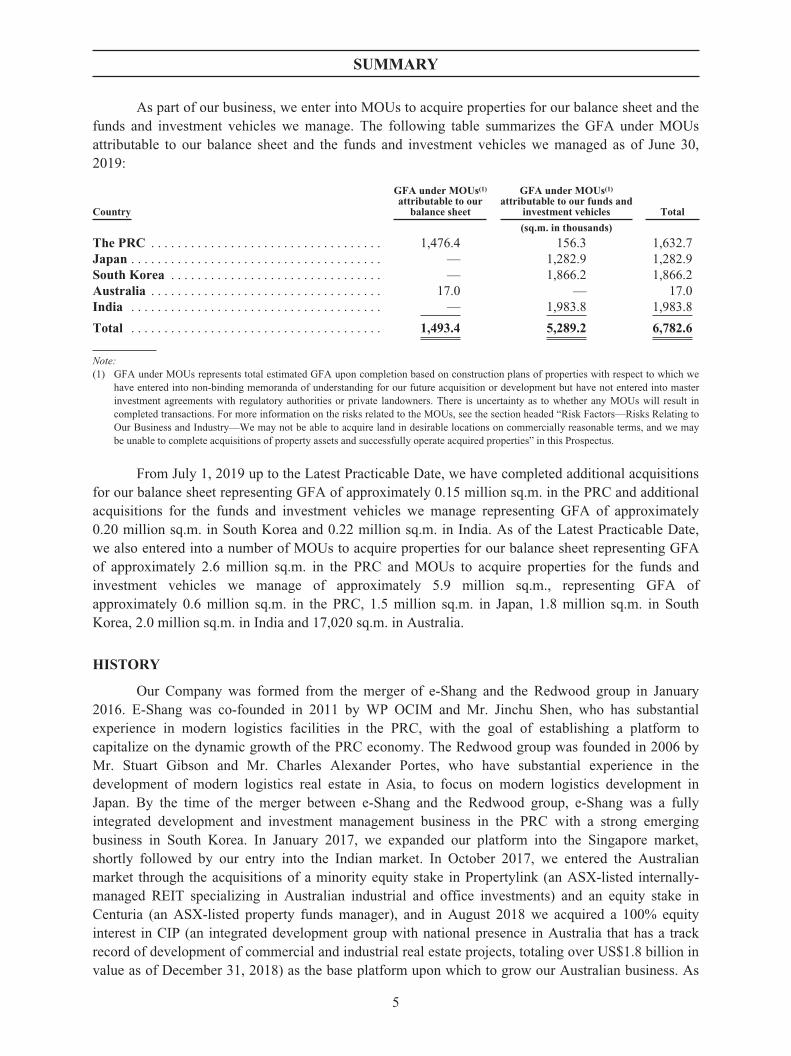

As part of our business, we enter into MOUs to acquire properties for our balance sheet and thefunds and investment vehicles we manage. The following table summarizes the GFA under MOUsattributable to our balance sheet and the funds and investment vehicles we managed as of June 30,2019:

Country

GFA under MOUs(1)attributable to our

balance sheet

GFA under MOUs(1)attributable to our funds and

investment vehicles Total

(sq.m. in thousands)

The PRC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,476.4 156.3 1,632.7Japan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — 1,282.9 1,282.9South Korea . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — 1,866.2 1,866.2Australia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17.0 — 17.0India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — 1,983.8 1,983.8

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,493.4 5,289.2 6,782.6

Note:(1) GFA under MOUs represents total estimated GFA upon completion based on construction plans of properties with respect to which we

have entered into non-binding memoranda of understanding for our future acquisition or development but have not entered into masterinvestment agreements with regulatory authorities or private landowners. There is uncertainty as to whether any MOUs will result incompleted transactions. For more information on the risks related to the MOUs, see the section headed “Risk Factors—Risks Relating toOur Business and Industry—We may not be able to acquire land in desirable locations on commercially reasonable terms, and we maybe unable to complete acquisitions of property assets and successfully operate acquired properties” in this Prospectus.

From July 1, 2019 up to the Latest Practicable Date, we have completed additional acquisitionsfor our balance sheet representing GFA of approximately 0.15 million sq.m. in the PRC and additionalacquisitions for the funds and investment vehicles we manage representing GFA of approximately0.20 million sq.m. in South Korea and 0.22 million sq.m. in India. As of the Latest Practicable Date,we also entered into a number of MOUs to acquire properties for our balance sheet representing GFAof approximately 2.6 million sq.m. in the PRC and MOUs to acquire properties for the funds andinvestment vehicles we manage of approximately 5.9 million sq.m., representing GFA ofapproximately 0.6 million sq.m. in the PRC, 1.5 million sq.m. in Japan, 1.8 million sq.m. in SouthKorea, 2.0 million sq.m. in India and 17,020 sq.m. in Australia.

HISTORY

Our Company was formed from the merger of e-Shang and the Redwood group in January2016. E-Shang was co-founded in 2011 by WP OCIM and Mr. Jinchu Shen, who has substantialexperience in modern logistics facilities in the PRC, with the goal of establishing a platform tocapitalize on the dynamic growth of the PRC economy. The Redwood group was founded in 2006 byMr. Stuart Gibson and Mr. Charles Alexander Portes, who have substantial experience in thedevelopment of modern logistics real estate in Asia, to focus on modern logistics development inJapan. By the time of the merger between e-Shang and the Redwood group, e-Shang was a fullyintegrated development and investment management business in the PRC with a strong emergingbusiness in South Korea. In January 2017, we expanded our platform into the Singapore market,shortly followed by our entry into the Indian market. In October 2017, we entered the Australianmarket through the acquisitions of a minority equity stake in Propertylink (an ASX-listed internally-managed REIT specializing in Australian industrial and office investments) and an equity stake inCenturia (an ASX-listed property funds manager), and in August 2018 we acquired a 100% equityinterest in CIP (an integrated development group with national presence in Australia that has a trackrecord of development of commercial and industrial real estate projects, totaling over US$1.8 billion invalue as of December 31, 2018) as the base platform upon which to grow our Australian business. As

5

SUMMARY

of June 30, 2019, we owned a 14.8% stake in Centuria. In April 2019, we completed our acquisition ofPropertylink. See the section headed “Business—The Propertylink Acquisition” in this Prospectus forfurther information.

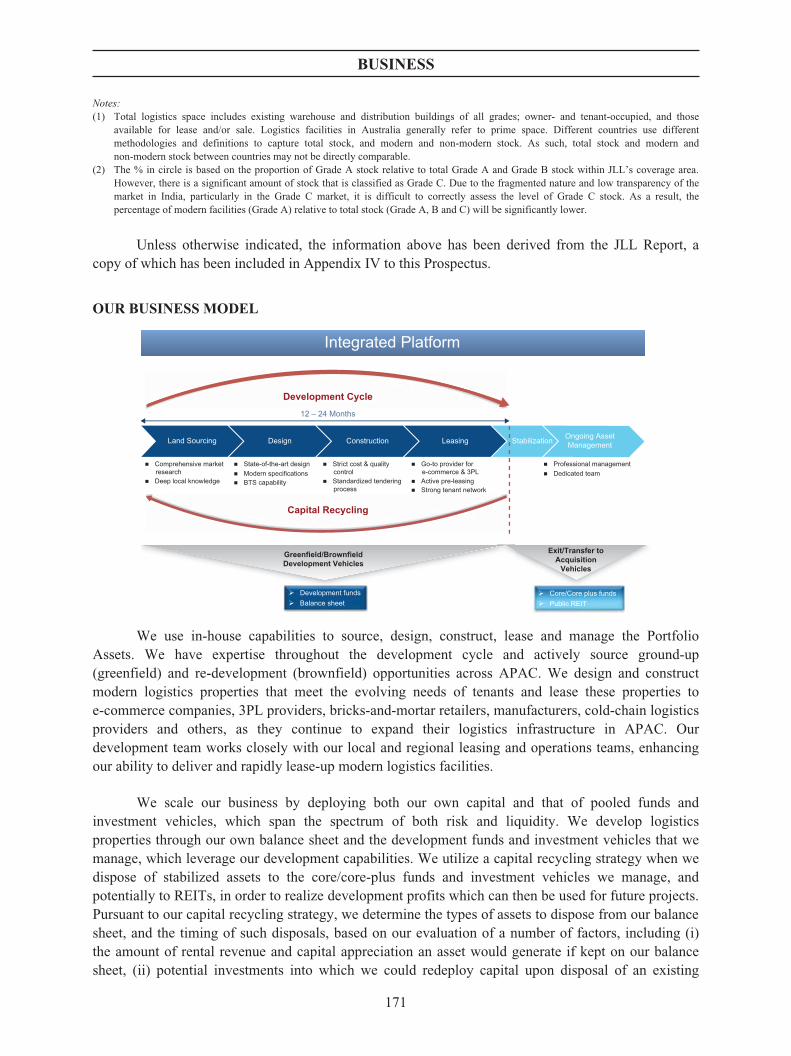

OUR BUSINESS MODEL

Development Cycle

Capital Recycling

12 – 24 Months

Land Sourcing

� Comprehensive marketresearch

� Deep local knowledge

� State-of-the-art design� Modern specifications� BTS capability

� Strict cost & qualitycontrol

� Standardized tenderingprocess

� Go-to provider fore-commerce & 3PL

� Active pre-leasing� Strong tenant network

� Professional management� Dedicated team

Integrated Platform

Development Cycle

Capital Recycling

� Core/Core plus funds� Public REIT

� Development funds� Balance sheet

Design Construction Leasing Ongoing AssetManagementStabilization

Greenfield/BrownfieldDevelopment Vehicles

Exit/Transfer toAcquisition

Vehicles

We use in-house capabilities to source, design, construct, lease and manage the PortfolioAssets. We have expertise throughout the development cycle and actively source ground-up(greenfield) and re-development (brownfield) opportunities across APAC. We design and constructmodern logistics properties that meet the evolving needs of tenants and lease these properties toe-commerce companies, 3PL providers, bricks-and-mortar retailers, manufacturers, cold-chain logisticsproviders and others, as they continue to expand their logistics infrastructure in APAC. Ourdevelopment team works closely with our local and regional leasing and operations teams, enhancingour ability to deliver and rapidly lease-up modern logistics facilities.

We scale our business by deploying both our own capital and that of pooled funds andinvestment vehicles, which span the spectrum of both risk and liquidity. We develop logisticsproperties through our own balance sheet and the development funds and investment vehicles that wemanage, which leverage our development capabilities. We utilize a capital recycling strategy when wedispose of stabilized assets to the core/core-plus funds and investment vehicles we manage, andpotentially to REITs, in order to realize development profits which can then be used for future projects.During the Track Record Period, we disposed of a total of 12 completed properties in the PRC with anaggregate value of approximately US$572.4 million from our balance sheet, and a total of sixcompleted properties with an aggregate value of approximately US$959.0 million from a developmentfund that we manage, in both cases, to certain of the core funds that we manage where we maintain aninterest in the assets through our fund interests and continue to collect recurring fees. In June 2019, weeffected the transfer of 50% of the interest in a logistics property in Japan at a purchase price ofJPY4,395.0 million (approximately US$40.5 million), which was held jointly by two of ourdevelopment funds, to a new private REIT in Japan which we recently established. Going forward weintend to continue effecting disposals of properties when appropriate to funds and investment vehicleswe manage, such as certain properties held by Propertylink. Pursuant to our capital recycling strategy,

6

SUMMARY

we determine the types of assets to dispose from our balance sheet, and the timing of such disposals,based on our evaluation of a number of factors, including (i) the amount of rental revenue and capitalappreciation an asset would generate if kept on our balance sheet, (ii) potential investments into whichwe could redeploy capital upon disposal of an existing asset, (iii) the fees that we could generate froman asset if it were held in a fund or investment vehicle we manage, and (iv) the investment mandates ofour funds and investment vehicles. We generally consider the disposal of a property once it has beencompleted, and we prioritize the disposal of our balance sheet properties to the funds and investmentvehicles we manage in order to manage assets for the long term where our fund mandates permit. Weretain the option to dispose of assets to third-parties if we deem it appropriate to do so. The synergiesbetween our development and core/core-plus funds and investment vehicles give us the opportunity tomanage the underlying assets throughout their useful lives and build recurring revenue streams. Wecan acquire, develop and own assets that fit our capital partners’ risk-reward profiles and still captureopportunities using our own balance sheet which may not fall within the investment criteria of thefunds and investment vehicles we manage. The flexibility of this dual approach helps us avoid a timeconsuming search for a co-investor on each individual project and provides future capital partners withvisibility over the assets on our balance sheet that might form a fund or investment vehicle.

We also use our balance sheet to grow our business through the acquisition of private andpublic platforms in prospective growth markets. For example, in January 2017, we expanded into theSingapore market and obtained control of the ESR-REIT Manager. In April 2019, we completed ouracquisition of Propertylink in Australia. See the section headed “Business—The PropertylinkAcquisition” in this Prospectus for further information. In June 2019, we completed the SabanaManager Acquisition in Singapore. As we continue to expand the business, we have and will continueto utilize our business model to acquire local expertise and assemble business teams in each of ourmarkets of operation. See the section headed “Business—Principal Business Activities—Development” in this Prospectus for further details.

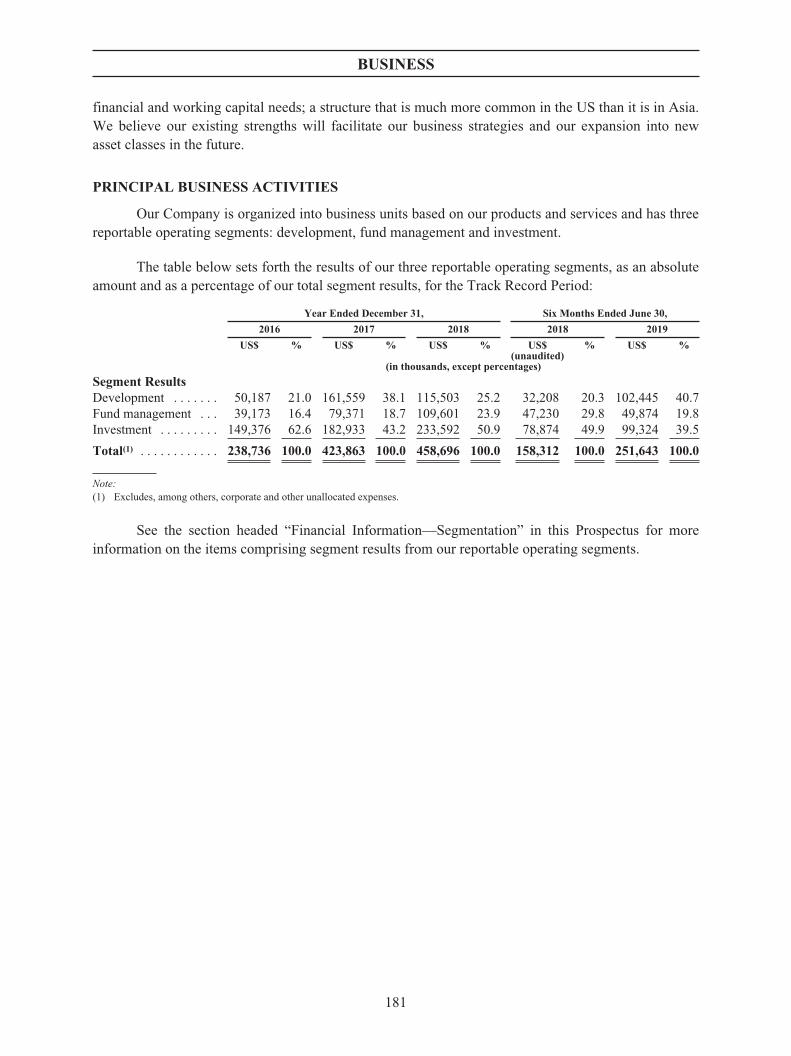

Our Company is organized into business units based on our products and services and has threereportable operating segments as follows:

Š Development. We earn development profit through the development, construction and saleof completed properties on our balance sheet. Our development profit includesconstruction income (as a result of the consolidation of CIP since August 2018), fair valuegains on investment properties under construction and gains on disposal of subsidiaries.We also derive pro rata earnings and pro rata value appreciation through the developmentactivities of the development funds and investment vehicles we manage in proportion toour co-investments in those funds and investment vehicles.

Š Fund management. We earn fee income from managing the underlying assets on behalf ofour capital partners via the funds and investment vehicles we manage. Our fees includebase management fees, asset management fees, acquisition fees, development fees andleasing fees. We also participate in a disproportionate share of profits (a “promote”) uponexceeding a pre-determined target IRR and after our capital partners have received theirtargeted capital returns.

Š Investment. Our investment segment is divided into three main categories: (i) completedproperties that we hold on our balance sheet, from which we derive rental income andappreciation in value; (ii) our co-investments in the funds and investment vehicles and thepublic REIT we manage, from which we derive dividend income, pro rata earnings and/orpro rata value appreciation; and (iii) other investments.

7

SUMMARY

Since March 2019, we consolidated the results of operations of Propertylink in our investmentand fund management segments. For further information, see the section headed “FinancialInformation—Segmentation” in this Prospectus.

As of June 30, 2019, we owned or managed: (i) completed GFA of 8.5 million sq.m; (ii) GFAunder construction of 4.4 million sq.m; and (iii) GFA on land held for future development ofapproximately 2.4 million sq.m. As of June 30, 2019, 71.5% of the Portfolio Assets in terms of GFAwere held by the funds and investment vehicles that we manage, with the rest held on our balancesheet.

COMPETITIVE STRENGTHS

We believe that the following competitive strengths contribute to our success and differentiateus from our competitors:

Š we are the largest APAC focused logistics real estate platform;

Š we have an integrated development platform with strong project sourcing and executioncapabilities, complemented by our efficient capital recycling strategy;

Š our fund management platform provides us with high margin and stable fee income largelyindependent of property values;

Š our platform is supported by a network of high-quality tenants and capital partners withwhom we have strong and long-standing relationships;

Š we have a proven ability to grow organically and to execute opportunistic M&Atransactions to expand our capabilities, broaden the scope of the Portfolio Assets, andsupport our growth in the logistics real estate industry; and

Š we are led by a strong management team and backed by reputable shareholders.

For a detailed discussion of these competitive strengths, see the section headed “Business—Competitive Strengths and Strategies—Competitive Strengths” in this Prospectus.

OUR GROWTH STRATEGIES

Our goal is to expand on our position as a leading logistics real estate and fund managementplatform in APAC. We intend to pursue the following growth strategies to achieve this goal:

Š continue to execute our integrated strategy and capitalize on the significant marketopportunities across APAC;

Š leverage our scale and geographic presence to expand into new growth markets to deepenour regional connectivity;

Š expand our fund management platform across geographies, strategies and liquidity profilesand attract new capital partners while bringing existing capital partners across markets;and

Š strategically explore and expand into adjacent businesses and investment products withinAsia.

For a detailed discussion of these strategies, see the section headed “Business—CompetitiveStrengths and Strategies—Strategies” in this Prospectus.

8

SUMMARY

CUSTOMERS

Tenants

The Portfolio Assets are leased to a broad range of large and mid-sized, multinational anddomestic tenants that require logistics and distribution facilities, including e-commerce companies,3PL providers, bricks-and-mortar retailers, manufacturers, cold-chain logistics providers and others.3PL providers serve end-users in a large variety of industries, including e-commerce, electronics, fast-moving consumer goods, retail and fast food chains, general logistics services, auto and parts,pharmaceuticals, and medical instruments and machinery. We seek to be a regional partner for ourtenants, with a goal to be the single point of contact to design and build a multi-market distributionnetwork for tenants throughout the PRC, Japan, South Korea, Singapore, Australia and India.

In 2016, 2017 and 2018 and for the six months ended June 30, 2019, rental revenue generatedfrom the single largest tenant of our balance sheet properties accounted for approximately 19.7%,12.6%, 9.3% and 9.8%, respectively, of our total revenue. For the same periods, rental revenueattributable to the five largest tenants of our balance sheet properties accounted for approximately40.7%, 25.8%, 17.4% and 13.8%, respectively, of our total revenue. Our five largest tenants for eachyear during the Track Record Period are independent third parties. In 2016 and 2017, three of our fivelargest tenants were e-commerce companies and two were bricks-and-mortar retailers. In 2018, two ofour five largest tenants were e-commerce companies, two were manufacturers and one was a bricks-and-mortar retailer. For the six months ended June 30, 2019, one of our five largest tenants was an e-commerce company, one was a bricks-and-mortar retailer and three were manufacturers.

We expect the percentage of revenue attributable to our five largest tenants to decrease in thefuture as we increase the proportion of the Portfolio Assets held in the funds and investment vehicleswe manage.

Funds and Investment Vehicles

We manage 30 funds and investment vehicles and generate revenue from the management ofthose funds and investment vehicles. In 2016, 2017 and 2018 and for the six months ended June 30,2019, revenue generated from the single largest fund we managed on the basis of management feeincome accounted for approximately 10.9%, 12.2%, 12.0% and 8.8%, respectively, of our totalrevenue. For the same periods, revenue attributable to the five largest funds and investment vehicleswe managed, all of which were development funds and investment vehicles, accounted forapproximately 34.0%, 31.5%, 27.9% and 23.8%, respectively, of our total revenue.

SUPPLIERS

Our suppliers primarily consist of construction companies, property management companies,interior designers and commercial real estate brokers. In 2016, 2017 and 2018 and for the six monthsended June 30, 2019, transaction amounts with our single largest supplier accounted for approximately16.7%, 20.3%, 10.8% and 11.3%, respectively, of our total purchase amount incurred in the period. Forthe same periods, transaction amounts with our five largest suppliers in aggregate accounted forapproximately 35.5%, 38.1%, 20.0% and 19.0%, respectively, of our total purchase amount incurred inthe period. These suppliers are mostly construction contractors. As we select contractors on a projectbasis, we do not rely on any single contractor despite the relatively high contribution of our largest orfive largest contractors/suppliers to our cost incurred in a given period. Our five largest suppliers areindependent third parties.

9

SUMMARY

COMPETITION

We face competition from other large international and domestic developers, owners andoperators of other logistics facilities and fund managers and, within any specific individual market,also from smaller and local players. We compete with other providers for locations and sites for futurelogistics facilities as well as tenants. For a discussion of the key players in the industry and regions inwhich we operate, see the JLL Report included in Appendix IV of this Prospectus.

RISK FACTORS

Our business and the Global Offering involve certain risks as set out in “Risk Factors” in thisProspectus. You should read that section in its entirety carefully before you decide to invest in ourShares. Some of the major risks we face include:

Š our business is concentrated in APAC and may be affected by regional and globaleconomic and political developments;

Š the success of our business depends on our ability to service the rising demand of thee-commerce and 3PL sectors in APAC and the sustainability of this rising demand inAPAC;

Š we operate a multinational business in APAC with a relatively short operating history andare subject to complex operational risks which may be difficult to address;

Š our business is intensely competitive;

Š the returns from investments in the Portfolio Assets could be adversely affected byfluctuations in the income generated from, and the value of, the Portfolio Assets and otherfactors, including the concentration of the Portfolio Assets in the logistics real estatesector;

Š our profitability may be affected by revaluation of the properties held on our balancesheet, as well as the properties held by the funds and investment vehicles that we manage;

Š we may not be able to secure capital resources, either through equity or debt financing, oncommercially reasonable terms, or at all;

Š we depend on our senior management team and certain key senior personnel as well asskilled employees;

Š we may face difficulties in realizing the benefits of any acquisitions and successfullyintegrating acquired businesses, including Propertylink; and

Š we may not be successful in executing our business strategy, including the expansion intonew geographical locations and adjacent businesses.

PROPERTY VALUATION

All of our completed investment properties and investment properties under construction wererevalued on December 31, 2016, 2017 and 2018 and June 30, 2019 (save as disclosed below) based onvaluations performed by independent professionally qualified valuers and industry specialists ininvestment property valuation, including Beijing Colliers International Real Estate Valuation Co., Ltd.,CBRE Valuation Pty Limited, Jones Lang LaSalle Advisory Services Pty Ltd and Cushman &Wakefield K.K., at fair value. In determining fair value of the Portfolio Assets, a combination of

10

SUMMARY

approaches and methods were used, including the Direct Comparison Method and Discounted CashFlow Method. A combination of valuation approaches and methods are used because suitable valuationmethods for properties may vary depending on the nature of the property and available information.For example, for a development project in very early stages where future cash flows are less certain, acomparative approach to valuation may be more reliable. On the other hand, during more mature stagesof development where projected cash flows can be determined more accurately, a discounted cash flowmethod may be more suitable. Certain investment properties recently acquired were revalued as ofJune 30, 2019 with reference to (i) their purchase price or (ii) the independent valuation performed atthe time of the acquisition. For further details on each of the valuation methods, see the section headed“Financial Information—Analysis of Selected Consolidated Statements of Financial Position Items—Investment Properties” in this Prospectus. See Note 20 to the Accountant’s Report in Appendix I tothis Prospectus for details of the key inputs used in the valuation techniques. In connection with theListing, we engaged property valuers to value our directly held investment properties in the PRC,Japan and Australia as of September 30, 2019 pursuant to the relevant requirements under the ListingRules. The text of their respective letters, summaries of valuation and the valuation certificates are setforth in Appendix VI to this Prospectus.

SUMMARY HISTORICAL FINANCIAL INFORMATION

The following is a summary of our consolidated financial information for the periods and as ofthe dates indicated. We have derived the summary from our consolidated financial information setforth in the Accountants’ Report in Appendix I to this Prospectus. The below summary should be readtogether with the consolidated financial information in Appendix I to this Prospectus, including theaccompanying notes and the information set forth in the section headed “Financial Information” in thisProspectus. Our consolidated financial information has been prepared in accordance with IFRS.

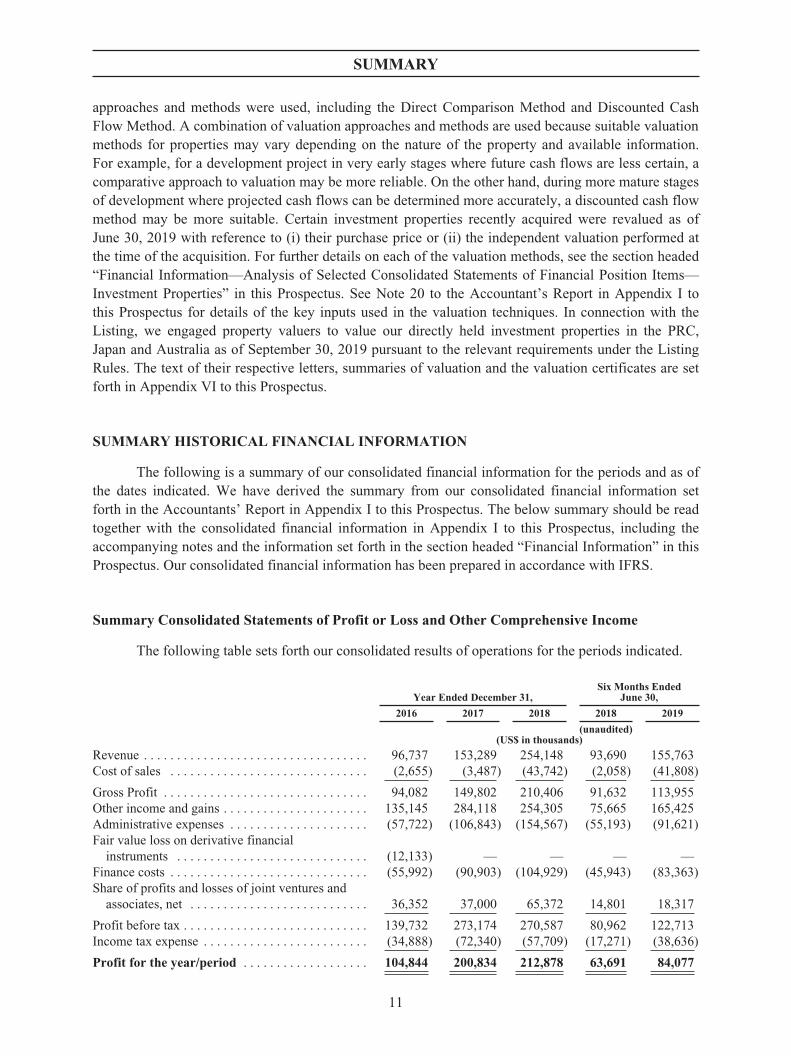

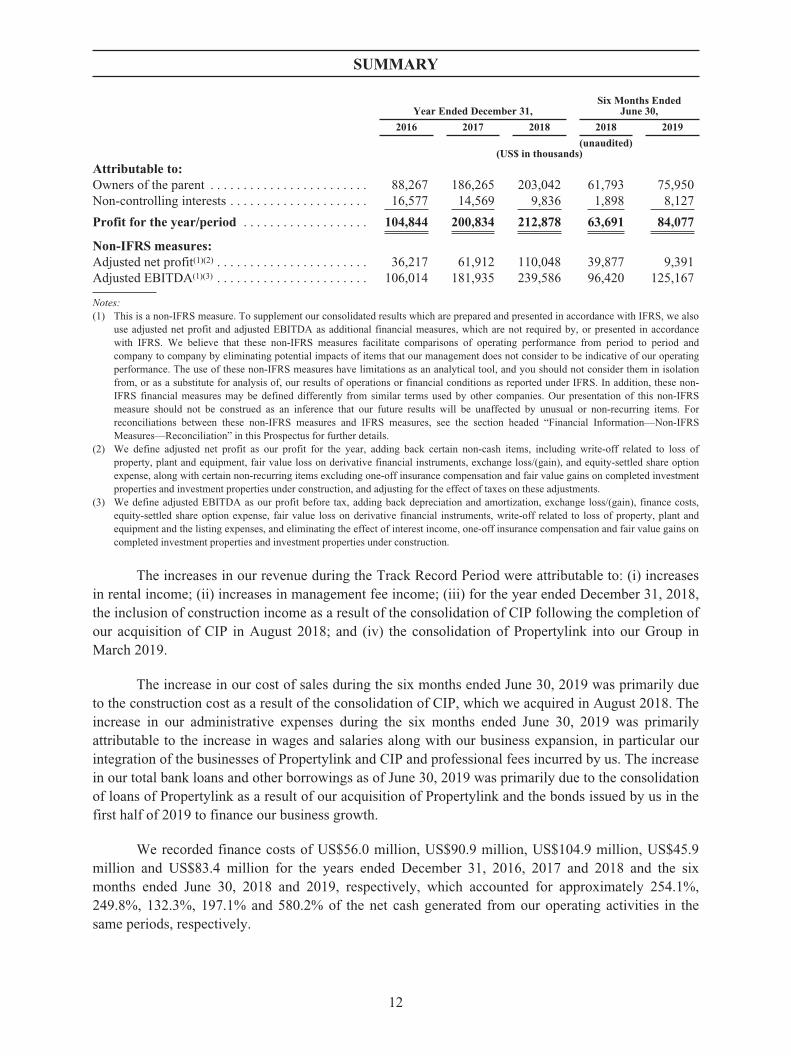

Summary Consolidated Statements of Profit or Loss and Other Comprehensive Income

The following table sets forth our consolidated results of operations for the periods indicated.

Year Ended December 31,Six Months Ended

June 30,

2016 2017 2018 2018 2019

(unaudited)(US$ in thousands)

Revenue . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96,737 153,289 254,148 93,690 155,763Cost of sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (2,655) (3,487) (43,742) (2,058) (41,808)

Gross Profit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94,082 149,802 210,406 91,632 113,955Other income and gains . . . . . . . . . . . . . . . . . . . . . . 135,145 284,118 254,305 75,665 165,425Administrative expenses . . . . . . . . . . . . . . . . . . . . . (57,722) (106,843) (154,567) (55,193) (91,621)Fair value loss on derivative financial

instruments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (12,133) — — — —Finance costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (55,992) (90,903) (104,929) (45,943) (83,363)Share of profits and losses of joint ventures and

associates, net . . . . . . . . . . . . . . . . . . . . . . . . . . . 36,352 37,000 65,372 14,801 18,317

Profit before tax . . . . . . . . . . . . . . . . . . . . . . . . . . . . 139,732 273,174 270,587 80,962 122,713Income tax expense . . . . . . . . . . . . . . . . . . . . . . . . . (34,888) (72,340) (57,709) (17,271) (38,636)

Profit for the year/period . . . . . . . . . . . . . . . . . . . 104,844 200,834 212,878 63,691 84,077

11

SUMMARY

Year Ended December 31,Six Months Ended

June 30,

2016 2017 2018 2018 2019

(unaudited)(US$ in thousands)

Attributable to:Owners of the parent . . . . . . . . . . . . . . . . . . . . . . . . 88,267 186,265 203,042 61,793 75,950Non-controlling interests . . . . . . . . . . . . . . . . . . . . . 16,577 14,569 9,836 1,898 8,127

Profit for the year/period . . . . . . . . . . . . . . . . . . . 104,844 200,834 212,878 63,691 84,077

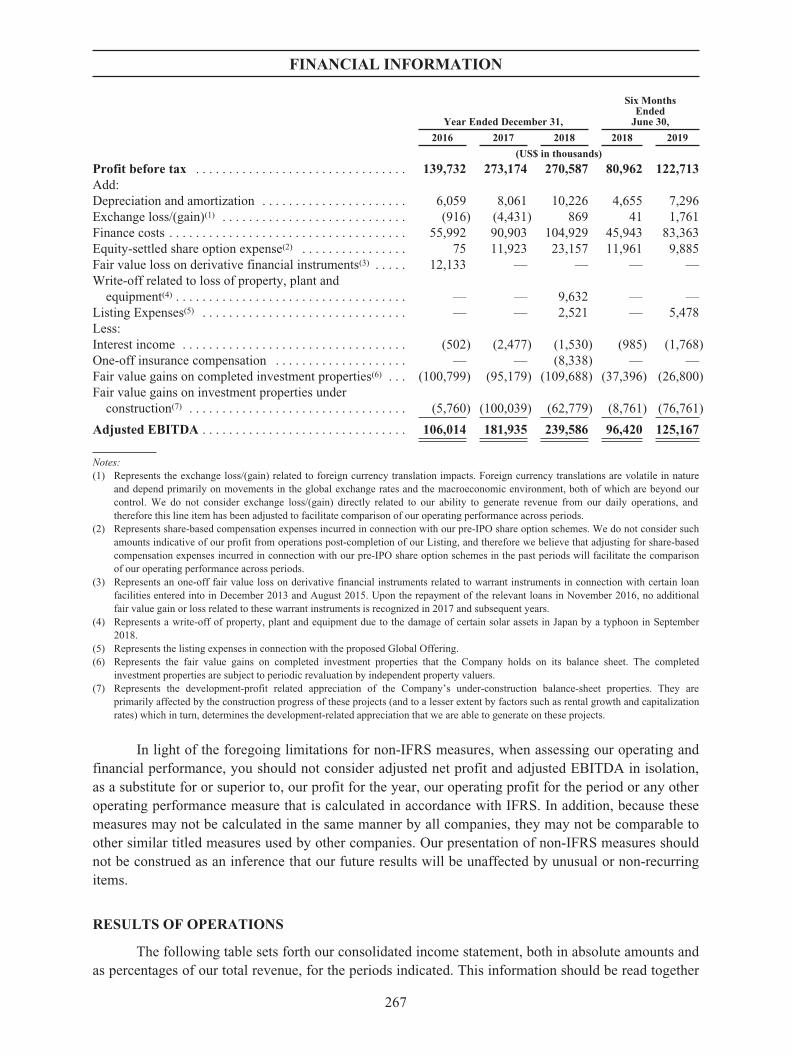

Non-IFRS measures:Adjusted net profit(1)(2) . . . . . . . . . . . . . . . . . . . . . . . 36,217 61,912 110,048 39,877 9,391Adjusted EBITDA(1)(3) . . . . . . . . . . . . . . . . . . . . . . . 106,014 181,935 239,586 96,420 125,167

Notes:(1) This is a non-IFRS measure. To supplement our consolidated results which are prepared and presented in accordance with IFRS, we also

use adjusted net profit and adjusted EBITDA as additional financial measures, which are not required by, or presented in accordancewith IFRS. We believe that these non-IFRS measures facilitate comparisons of operating performance from period to period andcompany to company by eliminating potential impacts of items that our management does not consider to be indicative of our operatingperformance. The use of these non-IFRS measures have limitations as an analytical tool, and you should not consider them in isolationfrom, or as a substitute for analysis of, our results of operations or financial conditions as reported under IFRS. In addition, these non-IFRS financial measures may be defined differently from similar terms used by other companies. Our presentation of this non-IFRSmeasure should not be construed as an inference that our future results will be unaffected by unusual or non-recurring items. Forreconciliations between these non-IFRS measures and IFRS measures, see the section headed “Financial Information—Non-IFRSMeasures—Reconciliation” in this Prospectus for further details.

(2) We define adjusted net profit as our profit for the year, adding back certain non-cash items, including write-off related to loss ofproperty, plant and equipment, fair value loss on derivative financial instruments, exchange loss/(gain), and equity-settled share optionexpense, along with certain non-recurring items excluding one-off insurance compensation and fair value gains on completed investmentproperties and investment properties under construction, and adjusting for the effect of taxes on these adjustments.

(3) We define adjusted EBITDA as our profit before tax, adding back depreciation and amortization, exchange loss/(gain), finance costs,equity-settled share option expense, fair value loss on derivative financial instruments, write-off related to loss of property, plant andequipment and the listing expenses, and eliminating the effect of interest income, one-off insurance compensation and fair value gains oncompleted investment properties and investment properties under construction.

The increases in our revenue during the Track Record Period were attributable to: (i) increasesin rental income; (ii) increases in management fee income; (iii) for the year ended December 31, 2018,the inclusion of construction income as a result of the consolidation of CIP following the completion ofour acquisition of CIP in August 2018; and (iv) the consolidation of Propertylink into our Group inMarch 2019.

The increase in our cost of sales during the six months ended June 30, 2019 was primarily dueto the construction cost as a result of the consolidation of CIP, which we acquired in August 2018. Theincrease in our administrative expenses during the six months ended June 30, 2019 was primarilyattributable to the increase in wages and salaries along with our business expansion, in particular ourintegration of the businesses of Propertylink and CIP and professional fees incurred by us. The increasein our total bank loans and other borrowings as of June 30, 2019 was primarily due to the consolidationof loans of Propertylink as a result of our acquisition of Propertylink and the bonds issued by us in thefirst half of 2019 to finance our business growth.

We recorded finance costs of US$56.0 million, US$90.9 million, US$104.9 million, US$45.9million and US$83.4 million for the years ended December 31, 2016, 2017 and 2018 and the sixmonths ended June 30, 2018 and 2019, respectively, which accounted for approximately 254.1%,249.8%, 132.3%, 197.1% and 580.2% of the net cash generated from our operating activities in thesame periods, respectively.

12

SUMMARY

Reconciliation for Non-IFRS Measures

The following tables set forth the reconciliations of our non-IFRS financial measures for theperiods indicated to the nearest measures prepared in accordance with IFRS:

Year Ended December 31,

Six MonthsEndedJune 30,

2016 2017 2018 2018 2019

(US$ in thousands)

Profit for the year/period . . . . . . . . . . . . . . . . . . . . . . . . . 104,844 200,834 212,878 63,691 84,077Add:Write-off related to loss of property, plant and

equipment(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — — 9,632 — —Fair value loss on derivative financial instruments(2) . . . . . 12,133 — — — —Exchange loss/(gain)(3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . (916) (4,431) 869 41 1,761Equity-settled share option expense(4) . . . . . . . . . . . . . . . . 75 11,923 23,157 11,961 9,885Tax effects of adjustments . . . . . . . . . . . . . . . . . . . . . . . . . . 26,640 48,804 44,317 10,341 17,229Less:One-off insurance compensation . . . . . . . . . . . . . . . . . . . . . — — (8,338) — —Fair value gains on completed investment properties(5) . . . (100,799) (95,179) (109,688) (37,396) (26,800)Fair value gains on investment properties under

construction(6) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (5,760) (100,039) (62,779) (8,761) (76,761)

Adjusted net profit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36,217 61,912 110,048 39,877 9,391

Notes:(1) Represents a write-off of property, plant and equipment due to the damage of certain solar assets in Japan by a typhoon in September

2018.(2) Represents an one-off fair value loss on derivative financial instruments related to warrant instruments in connection with certain loan

facilities entered into in December 2013 and August 2015. Upon the repayment of the relevant loans in November 2016, no additionalfair value gain or loss related to these warrant instruments is recognized in 2017 and subsequent years.

(3) Represents the exchange loss/(gain) related to foreign currency translation impacts. Foreign currency translations are volatile in natureand depend primarily on movements in the global exchange rates and the macroeconomic environment, both of which are beyond ourcontrol. We do not consider exchange loss/(gain) directly related to our ability to generate revenue from our daily operations, andtherefore this line item has been adjusted to facilitate comparison of our operating performance across periods.

(4) Represents share-based compensation expenses incurred in connection with our pre-IPO share option schemes. We do not consider suchamounts indicative of our profit from operations post-completion of our Listing, and therefore we believe that adjusting for share-basedcompensation expenses incurred in connection with our pre-IPO share option schemes in the past periods will facilitate the comparisonof our operating performance across periods.

(5) Represents the fair value gains on completed investment properties that the Company holds on its balance sheet. The completedinvestment properties are subject to periodic revaluation by independent property valuers.

(6) Represents the development-profit related appreciation of the Company’s under-construction balance-sheet properties. They areprimarily affected by the construction progress of these projects (and to a lesser extent by factors such as rental growth and capitalizationrates) which in turn, determines the development-related appreciation that we are able to generate on these projects.

13

SUMMARY

Year Ended December 31,

Six MonthsEndedJune 30,

2016 2017 2018 2018 2019

(US$ in thousands)

Profit before tax . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 139,732 273,174 270,587 80,962 122,713Add:Depreciation and amortization . . . . . . . . . . . . . . . . . . . . . . 6,059 8,061 10,226 4,655 7,296Exchange loss/(gain)(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . (916) (4,431) 869 41 1,761Finance costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55,992 90,903 104,929 45,943 83,363Equity-settled share option expense(2) . . . . . . . . . . . . . . . . 75 11,923 23,157 11,961 9,885Fair value loss on derivative financial instruments(3) . . . . . 12,133 — — — —Write-off related to loss of property, plant and

equipment(4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — — 9,632 — —Listing Expenses(5) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — — 2,521 — 5,478Less:Interest income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (502) (2,477) (1,530) (985) (1,768)One-off insurance compensation . . . . . . . . . . . . . . . . . . . . — — (8,338) — —Fair value gains on completed investment properties(6) . . . (100,799) (95,179) (109,688) (37,396) (26,800)Fair value gains on investment properties under

construction(7) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (5,760) (100,039) (62,779) (8,761) (76,761)

Adjusted EBITDA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106,014 181,935 239,586 96,420 125,167

Notes:(1) Represents the exchange loss/(gain) related to foreign currency translation impacts. Foreign currency translations are volatile in nature

and depend primarily on movements in the global exchange rates and the macroeconomic environment, both of which are beyond ourcontrol. We do not consider exchange loss/(gain) directly related to our ability to generate revenue from our daily operations, andtherefore this line item has been adjusted to facilitate comparison of our operating performance across periods.

(2) Represents share-based compensation expenses incurred in connection with our pre-IPO share option schemes. We do not consider suchamounts indicative of our profit from operations post-completion of our Listing, and therefore we believe that adjusting for share-basedcompensation expenses incurred in connection with our pre-IPO share option schemes in the past periods will facilitate the comparisonof our operating performance across periods.

(3) Represents an one-off fair value loss on derivative financial instruments related to warrant instruments in connection with certain loanfacilities entered into in December 2013 and August 2015. Upon the repayment of the relevant loans in November 2016, no additionalfair value gain or loss related to these warrant instruments is recognized in 2017 and subsequent years.

(4) Represents a write-off of property, plant and equipment due to the damage of certain solar assets in Japan by a typhoon in September2018.

(5) Represents the listing expenses in connection with the proposed Global Offering.(6) Represents the fair value gains on completed investment properties that the Company holds on its balance sheet. The completed

investment properties are subject to periodic revaluation by independent property valuers.(7) Represents the development-profit related appreciation of the Company’s under-construction balance-sheet properties. They are

primarily affected by the construction progress of these projects (and to a lesser extent by factors such as rental growth and capitalizationrates) which in turn, determines the development-related appreciation that we are able to generate on these projects.

14

SUMMARY

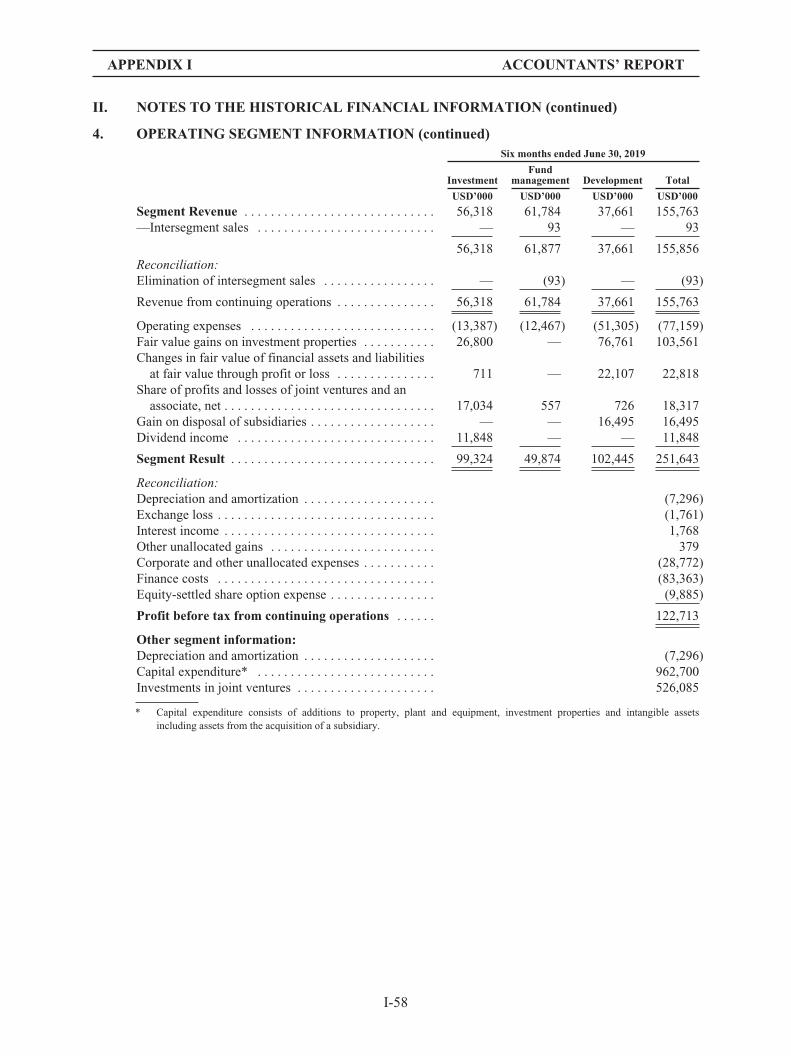

Summary Operating Segment Information

The table below sets forth the line items that comprise the segment results for each of our threereportable operating segments, which are reported and prepared based on our consolidated statement ofprofit or loss and other comprehensive income, together with a reconciliation, for the periods indicated.See the section headed “Financial Information—Segmentation” in this Prospectus for moreinformation about the line items comprising the segments.

Year Ended December 31,Six Months Ended

June 30,

2016 2017 2018 2018 2019

(unaudited)(US$ in thousands)

Development SegmentSegment revenue . . . . . . . . . . . . . . . . . . . . . . . . . . . . — — 40,665 — 37,661Fair value gains on investment properties under

construction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5,760 100,039 62,779 8,761 76,761Changes in fair value of financial assets and

liabilities at fair value through profit or loss . . . . . 23,792 8,497 31,741 16,014 22,107Share of profits and losses of joint ventures and

associates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27,151 26,505 35,200 12,059 726Gain on disposal of subsidiaries . . . . . . . . . . . . . . . . 32 38,311 2,662 — 16,495Allocable operating expenses . . . . . . . . . . . . . . . . . . (6,548) (11,793) (57,544) (4,626) (51,305)

Development segment result . . . . . . . . . . . . . . . . . . . 50,187 161,559 115,503 32,208 102,445

Fund Management SegmentSegment revenue . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46,464 94,268 135,579 59,033 61,784Share of profits and losses of joint ventures and

associates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — — — — 557Allocable operating expenses . . . . . . . . . . . . . . . . . . (7,291) (14,897) (25,978) (11,803) (12,467)

Fund management segment result . . . . . . . . . . . . . . . 39,173 79,371 109,601 47,230 49,874

Investment SegmentSegment revenue . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50,273 59,021 77,904 34,657 56,318Fair value gains on completed investment

properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100,799 95,179 109,688 37,396 26,800Changes in fair value of financial assets and

liabilities at fair value through profit or loss . . . . . 2,936 24,242 13,196 2,355 711Share of profits and losses of joint ventures and

associates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9,201 10,495 30,172 2,742 17,034Dividend income . . . . . . . . . . . . . . . . . . . . . . . . . . . . — 10,679 25,519 9,771 11,848Allocable operating expenses . . . . . . . . . . . . . . . . . . (13,833) (16,683) (22,887) (8,047) (13,387)

Investment segment result . . . . . . . . . . . . . . . . . . . . . 149,376 182,933 233,592 78,874 99,324

Total segment result . . . . . . . . . . . . . . . . . . . . . . . . 238,736 423,863 458,696 158,312 251,643

Reconciliation:Depreciation and amortization . . . . . . . . . . . . . . . . . (6,059) (8,061) (10,226) (4,655) (7,296)Exchange gain/(losses) . . . . . . . . . . . . . . . . . . . . . . . 916 4,431 (869) (41) (1,761)Interest income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 502 2,477 1,530 985 1,768Other unallocated gains . . . . . . . . . . . . . . . . . . . . . . . 408 234 7,190 653 379Corporate and other unallocated expenses(1) . . . . . . . (26,571) (46,973) (57,648) (16,388) (28,772)Finance costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (55,992) (90,903) (104,929) (45,943) (83,363)Equity-settled share option expense . . . . . . . . . . . . . (75) (11,923) (23,157) (11,961) (9,885)Fair value loss on derivative financial instrument . . (12,133) — — — —Gain on deemed partial disposal of a joint

venture . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — 29 — — —

Profit before tax from continuing operations . . . . 139,732 273,174 270,587 80,962 122,713

15

SUMMARY

Note:(1) Corporate and other unallocated expenses relate primarily to head office and corporate expenses that are not directly attributable to

operations of the reportable segments, and thus cannot be allocated to any of the reportable operating segments. They primarilycomprised professional services fees related to our financing and M&A activities, operating costs such as lease expenses andmaintenance costs which are not directly related to any business segment, and other miscellaneous expenses like bank service fees,meeting and office expenses, travel and welfare expenses and entertainment fees, which are not directly related to any of the operatingsegments. The increase in corporate and other unallocated expenses from US$26.6 million in 2016 to US$47.0 million in 2017, andfurther to US$57.7 million in 2018, and from US$16.4 million for the six months ended June 30, 2018 to US$28.8 million for the sixmonths ended June 30, 2019 was primarily led by increases in professional services fees, leasing expenses and other expenses. Weconsistently monitor the results of our operating segments excluding these unallocated expenses for the purpose of making decisionsabout resource allocation and performance assessment.

Fluctuations in fair value gains on completed investment properties and fair value gains oninvestment properties under construction could significantly affect our performance. See the sectionsheaded “Financial Information—Principal Components of Our Consolidated Statement of Profit orLoss—Other Income and Gains—Fair Value Gains on Completed Investment Properties and FairValue Gains on Investment Properties Under Construction,” “Financial Information—Segmentation—Investment Segment” and “Financial Information—Segmentation—Development Segment” in thisProspectus for further information.

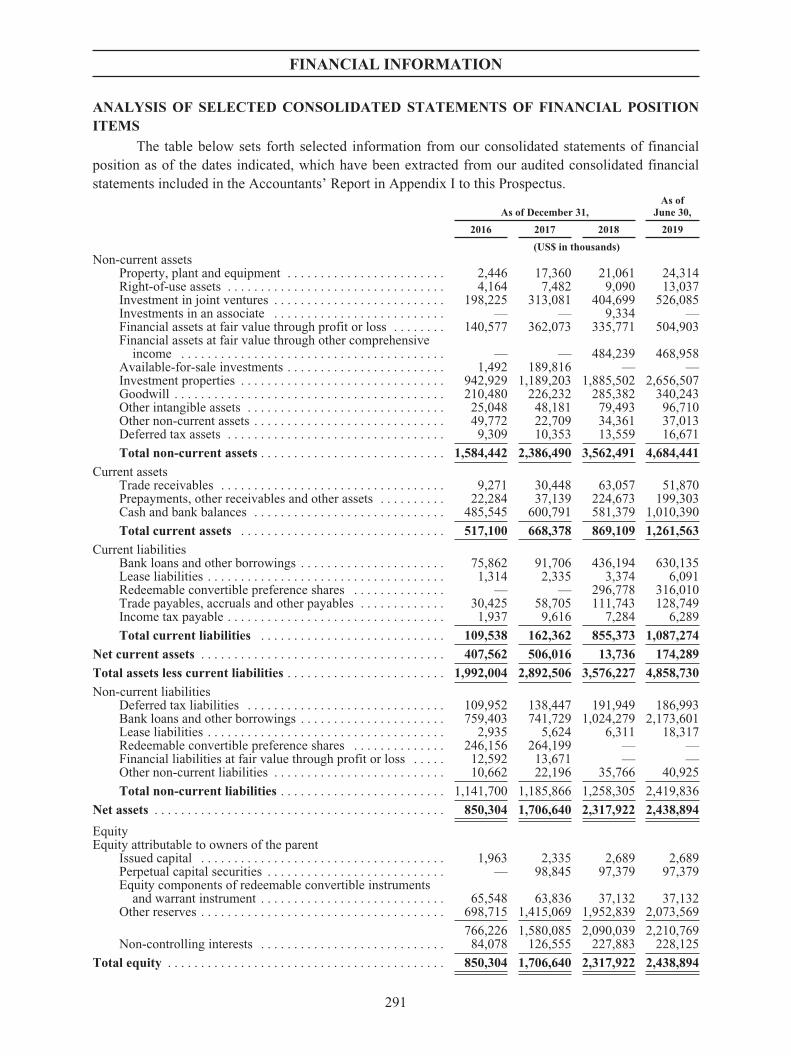

Summary Consolidated Statements of Financial Position

As of December 31,As of

June 30,

2016 2017 2018 2019

(US$ in thousands)

Non-current assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,584,442 2,386,490 3,562,491 4,684,441Current assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 517,100 668,378 869,109 1,261,563Current liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 109,538 162,362 855,373 1,087,274Net current assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 407,562 506,016 13,736 174,289Non-current liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,141,700 1,185,866 1,258,305 2,419,836Net assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 850,304 1,706,640 2,317,922 2,438,894Total Equity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 850,304 1,706,640 2,317,922 2,438,894

Summary Consolidated Statements of Cash Flows

Year Ended December 31,Six Months Ended

June 30,

2016 2017 2018 2018 2019

(unaudited)(US$ in thousands)

Net cash generated from operating activities . . . . . 22,039 36,396 79,340 23,306 14,367Net cash used in investing activities . . . . . . . . . . . . (264,271) (472,801) (786,778) (463,706) (583,970)Net cash generated from financing activities . . . . . 522,081 526,691 688,677 445,394 1,008,912Net increase/(decrease) in cash and cash

equivalents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 279,849 90,286 (18,761) 4,994 439,309Cash and cash equivalents at beginning of year . . . 144,319 411,765 526,988 526,988 502,056Effect of foreign exchange rate changes, net . . . . . (12,403) 24,937 (6,171) 372 2,254Cash and cash equivalents at end of

year/period . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 411,765 526,988 502,056 532,354 943,619

16

SUMMARY

Major Financial Ratios

The following table sets forth the major financial ratios as of, or for, the periods indicated.

As of or For the Year Ended December 31,As of or For the Six

Months Ended June 30,

2016 2017 2018 2019

Return on average equity(1) . . . . . . . . . . . . . . . . . . . . 16.7% 15.7% 10.6% N/ACurrent ratio(2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 472.1% 411.7% 101.6% 116.0%Net gearing ratio(3) . . . . . . . . . . . . . . . . . . . . . . . . . . 16.6% 7.6% 19.8% 30.2%

Notes:(1) Return on average equity is calculated using net profit divided by the average of total equity at the beginning and at the end of the year.(2) Current ratio is calculated by dividing current assets by current liabilities at the end of each year or period.(3) Net gearing ratio is calculated by dividing net debt, defined as total bank loans and other borrowings less cash and bank balances, by

total assets at the end of each year or period.

THE PROPERTYLINK ACQUISITION