Emerging Marginal Field Segment In The Nigerian Oil Industry: Operational and Financial Issues

37

Emerging Marginal Field Segment In The Nigerian Oil Industry: Operational and Financial Issues Amos Gagar, B.Sc , ACA, MBA. Business Finance Manager, Production Onshore The Shell Petroleum Development Company Port Harcourt 1 The Institute of Chartered Accountants of Nigeria (ICAN)

-

Upload

independent -

Category

Documents

-

view

3 -

download

0

Transcript of Emerging Marginal Field Segment In The Nigerian Oil Industry: Operational and Financial Issues

Emerging Marginal Field Segment In The Nigerian Oil Industry: Operational and

Financial Issues

Amos Gagar, B.Sc , ACA, MBA.

Business Finance Manager, Production Onshore

The Shell Petroleum Development Company

Port Harcourt 1

The Institute of Chartered Accountants of Nigeria (ICAN)

Disclaimer

The information on which this presentation is based derives from presenter’s experience, knowledge, research and data from public sources.

The opinions expressed and interpretations offered are those of the presenter and its acknowledged sources and have been reached following careful review.

However, the oil & gas business is characterized by much uncertainty, therefore all comments and conclusions should be taken in that light.

Accordingly, ICAN or its presenters do not accept any liability for any reliance which may placed on this presentation.

2

Objectives

At the end of this session, participants should be able to:

• Identify the Opportunities in the Emerging Marginal Field Sector

• Explain the Financing Issues in the Sector

3

Contents

• Overview of Nigerian Oil & Gas Industry

• Overview of marginal fields

• Legislative requirements

• Marginal field development programme

• Financing opportunities

• Case Study – Marginal field

4

Overview of the Nigerian Oil industryHistory/Current Status

• Oil was discovered in Nigeria in 1956 at Oloibiri in the Niger Delta

• Production has risen from 5,100 bpd in 1958 to about 2.5m bpd at end 2011

• Development strategies are aimed at increasing production to 4m bpd

• Proved crude oil reserves at 37.2 billion barrels (Source: BP Statistical Review of World Energy June 2013)

• Proved reserves of natural gas at 182.5 trillion cubic feet (Tcf) (Source: BP Statistical Review

of World Energy June 2013)

• Nigeria still flares about 25% of the natural gas it produces and re-injects

12% to enhance oil recovery

• Uncertainty around policy to end gas flaring

• National Gas Master Plan

• Nigeria Oil & Gas Industry Content Development (NOGICD) Act 2010

• Proposed Petroleum Industry Bill

5

Overview of the Nigerian Oil industry

The Regulatory Framework

• The regulatory framework of the industry is embodied in several legislations, regulations, guidelines and policies.

• These cover four broad areas:- Vesting rights- Technical/operational- Fiscal- Environmental

• These are administered by:- The Department of Petroleum Resources (DPR)- The Federal Inland Revenue Service- Environmental Protection Agencies and Ministry of Environment- Nigerian National Petroleum Corporation

6

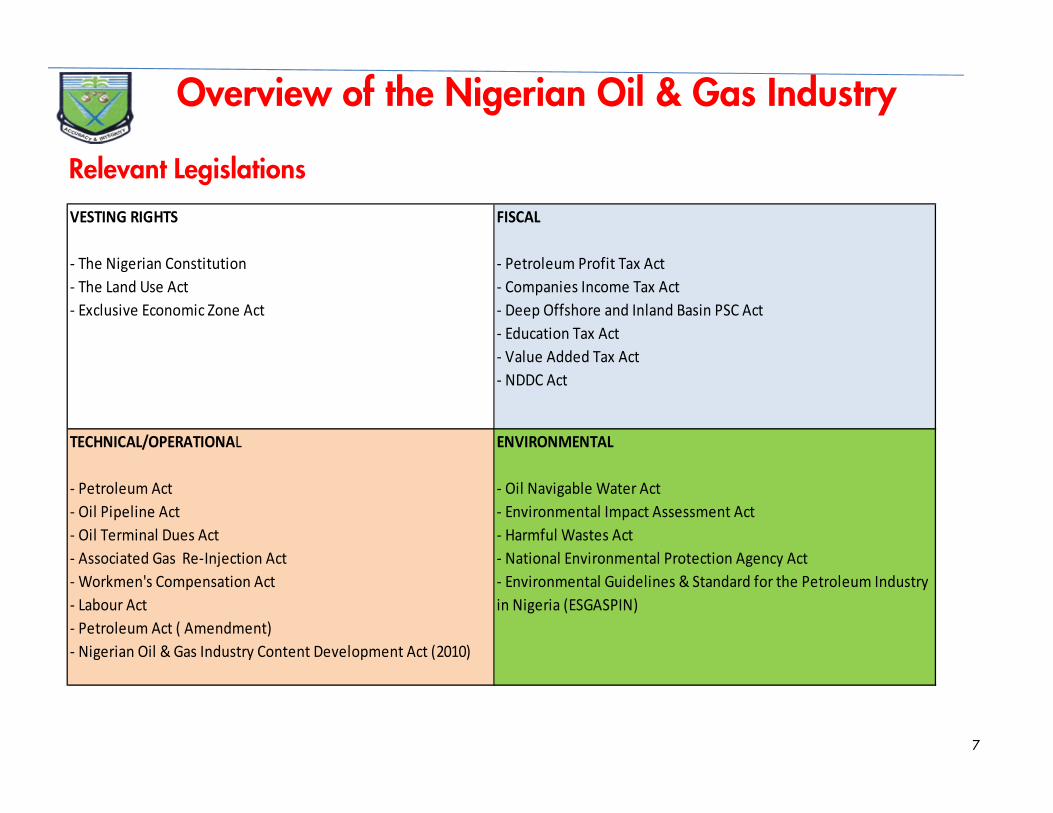

Relevant Legislations

Overview of the Nigerian Oil & Gas Industry

7

VESTING RIGHTS

- The Nigerian Constitution

- The Land Use Act

- Exclusive Economic Zone Act

FISCAL

- Petroleum Profit Tax Act

- Companies Income Tax Act

- Deep Offshore and Inland Basin PSC Act

- Education Tax Act

- Value Added Tax Act

- NDDC Act

TECHNICAL/OPERATIONAL

- Petroleum Act

- Oil Pipeline Act

- Oil Terminal Dues Act

- Associated Gas Re-Injection Act

- Workmen's Compensation Act

- Labour Act

- Petroleum Act ( Amendment)

- Nigerian Oil & Gas Industry Content Development Act (2010)

ENVIRONMENTAL

- Oil Navigable Water Act

- Environmental Impact Assessment Act

- Harmful Wastes Act

- National Environmental Protection Agency Act

- Environmental Guidelines & Standard for the Petroleum Industry

in Nigeria (ESGASPIN)

Oil & Gas Activities can be broadly split into: Upstream, Downstream and lately Midstream.

• Upstream Activities involve the acquisition of mineral interest in properties, exploration (prospecting), development and production of crude oil and gas.

• Downstream Activities involve transporting, refining, distribution and marketing of refined petroleum products, gas and derivatives.

• Midstream Activities involve liquefaction or conversion of natural gas into Natural Gas Liquids (NGL) and Liquefied Natural Gas (LNG).

8

Overview of Oil & Gas Operations

Categorisation of Oil & Gas Activities

Legislative Requirements

The Legislative considerations and actions to support marginal fields operations are:

(1) The specific laws to be enforced include:

– Petroleum Act 1969

– Petroleum (Amendment) Act 1996 (the legal framework that established the ''Marginal Fields'' programme)

– Petroleum Profits Tax Act

– Nigerian Oil & Gas Industry Local Content Act 2010

(2) Guidelines for the Farm-out and Operation of Marginal Fields 2013

(2013 Guidelines)

(3) Passage of pending legislation - the Petroleum Industry Bill

9

Overview of Marginal fields What is marginal field?

“any field that has reserves booked and reported annually to the DPR and has remained un-produced for a period of over 10 years” (DPR)

Marginal fields are fields capable of producing less than 10,000 barrels per day (bpd) but have been acquired by the Federal Government from multinational oil companies who had abandoned them, due to low reserves and productivity as well as higher overhead costs.

Characteristics of marginal fields

• Not considered by license holders for development because of assumed

marginal economics under prevailing fiscal terms.

• At least one exploratory well drilled and has been reported as an oil and

gas discovery for more than 10 years.

• With crude oil characteristics different from other streams which cannot be

produced through conventional methods or current technology.10

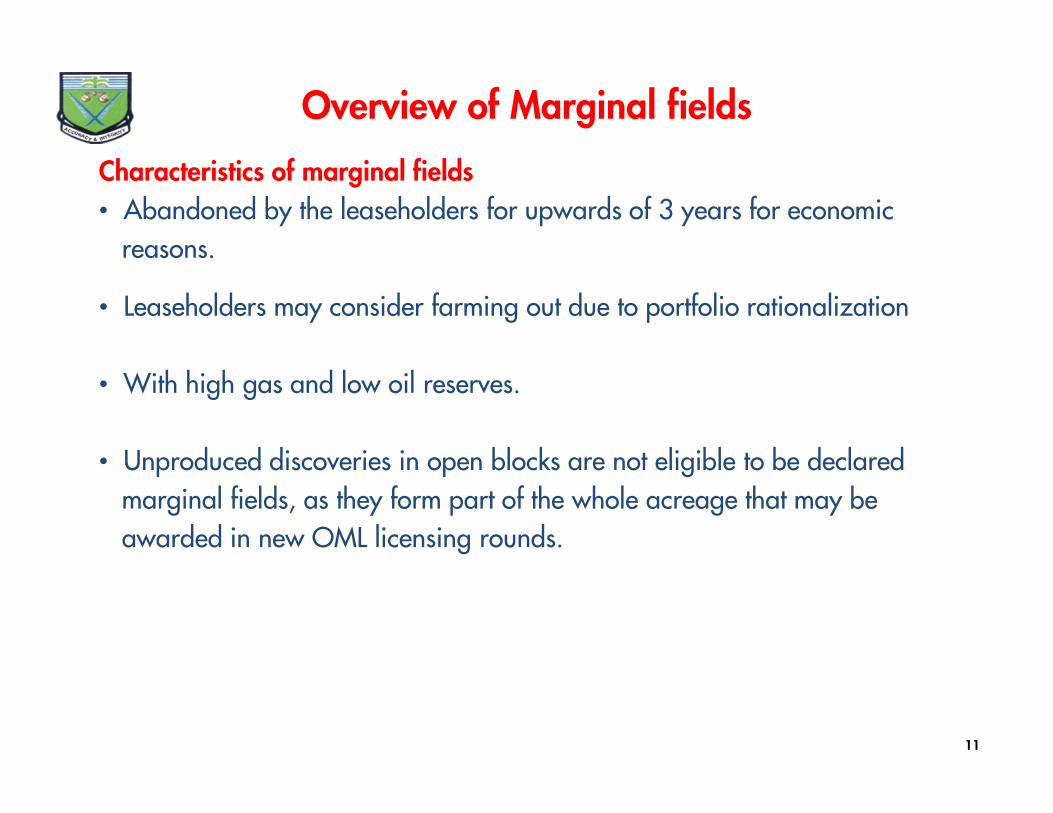

Overview of Marginal fields

Characteristics of marginal fields

• Abandoned by the leaseholders for upwards of 3 years for economic

reasons.

• Leaseholders may consider farming out due to portfolio rationalization

• With high gas and low oil reserves.

• Unproduced discoveries in open blocks are not eligible to be declared

marginal fields, as they form part of the whole acreage that may be

awarded in new OML licensing rounds.

11

Overview of Marginal fields

12

Marginal Field

Farm Out

Agreement

FARMOR

Overiding Royalty

Graduated rates - Oil

Zero Rate - Gas

Assignment

of Interest

Evacuation of

Farmee’s

Petroleum

FARMEE

Government

Participation

Joint

Operating

Agreement

Re-Definition of

Farm Out Area

Environmental

Baseline

Survey

Key Elements of Marginal Field Operations

Termination

Abandonment

Security

Insurance

The Marginal Field Development Programme

• Expanding the scope of indigenous participation in Nigeria’s oil industry

- diversifying the sources of investment and inflow of funds

- festering technological transfer and local content development

- gainfully engage the pool of high level technically competent Nigerians

- enhancing employment opportunities especially with host communities

• Increasing the oil and gas base through aggressive exploration

• Providing opportunities for portfolio rationalisation

• Discourage continuous holding of undeveloped fields by International Oil companies

• Expanding production output capacity

• Promoting common usage of assets/facilities to ensure optimum utilisation of available excess capacities

13

281 298

202

OML64

OML66

OML111

118

302

304

474

307

OML103

OML98

OML96

204

201

205206

902

135

228

907

207

208

234235

231236

452

203

230

OML52

OML51

OML50

OML55

OML54

OML53

OML49

303

308

301

305 306

913

910

912

901

911

905

908

903 904

906

909

OML57

OML58

OML59

OML56OML60

OML62

OML61

OML63

OML45

OML19

OML16OML27

OML24

OML41

OML4

OML33

OML36

OML21

OML39

OML20

OML25

OML26

OML23

OML7

OML40

OML14

OML31

OML32

OML5

OML22

OML43OML42

OML28

OML34

OML29

OML18

OML1

OML46

OML30

OML35

OML17

OML13

OML38

OML11

FORCADOS

BONNY

Lagos

Port Harcourt

Warri

OML 132

247

OML 127

250

249

293 294

284

291 295

252

292

286

279

285

246

OML 130

OML 133

214

321 323

OML 134

OML 125

244

OML 121

OML 120

310

OML 113

320

215

OML 129OML 128

OML 131

248

318

242

256

251

324

223

222

221

OML 135

OML 118

322

245

JDZ 06

JDZ 03

JDZ 02JDZ 01

JDZ 04 JDZ 05

326

258

257262261

255 260

269268

264

271270

346345 265 267266

273272

331330

329

328

254253

336335

334333

344343342341

340339338337

317

312

319

314313

327

259

325

311

315

332

233

289 471

OPL226

OML224

229

91

OML11298

90225

75

74

453

454

241

238

458

OML91

OML89

OML90

OML95

OML83OML84

OML85

OML86

OML88

OML69

OML68

94

OML67OML70

OML101

OML100

OML99

OML102472

OML71

OML81

OML77

OML79

OML72OML74

BRASS

Monipulo

Amalgam

Asaries

Aries

Crescent

Opic

Shell

Elf

Mareena

Addax

Lamont

Chevron

Seawolf

NorthEast Petro.

AmalgamIpec

NPDC

CNPC

Mobil

Paclantic Summit Summit

Nigerian Bitumen

Devine

James Pet.

Texaco GeneralOil

Conoil

Shell

Shell

Dubri

Elf

Shell

Revoked

Shell

ShellShell

Shell

Revoked

Solgas

Addax

Sunlink

Orient

MLM

Addax

Queen PC

Peak

CavenQueen PC

Elf

Elf

Elf

Agip

Agip

Agip

Agip

Mobil

Mobil

Obekpa

Texaco

CNPC

Clearwaters

Summit

Revoked

Chevron

ChevronChevron

Elf

Ipec

Express

Atlas

Conoil

Chevron

NigerDelta

Revoked

Chevron

Chevron

Shell

227

NPDC

NPDC

NPDC

Texaco

Texaco

Texaco

Texaco

Shell

Shell

Shell

Shell

Shell

Shell

Shell

ShellShell

Shell

Shell

Shell

Shell

Shell

Shell

Shell

Shell

Revoked

Shell

Elf

Addax

Mobil

Elf

Chevron

Chevron

Shell

Chevron

Pan Ocean

Shell

Amni

Shell

Agip

Revoked4000m

3000m

2000m

1000m

200m

OML 122

Revoked

Revoked

JDZ 10

JDZ 09

JDZ 07JDZ 08

JDZ 11

Nigeria Concession Map (Untapped Opportunities for Marginal Field Operators)

±

Abo

Okodo

OyoEwoBosi

EnguleUdoro

Oberan

Obeje

Bobo

ErinmiBoi

Nsiko

Aparo

Bonga SW

Bonga N

Bonga

Egere

Iroko

Uge

Onigun

Bilabri

OrobriPreye

Kiniun

Okpoi

Ikija

Agbami

Dou

EkoliAtabila

Pina

Bilah

Sehki

Gbigiri

Adaka

EtanAkpo

Ebitemi

KuroEgina

Preowei

Egina

S. Obo

Tari

Okpok Ine

Usan

Ukot

Efere

Zabazaba

Ngolo

Ajamabri

Ikubio

ForupaAziama

Oko

0 25 50 75 100 Km

Shallow Offshore

Peak [60%] (40% Shell)OML122

J. D.Z : Joint Development Zone

(Nigeria 60%, Sao Tome 40%)

03 Anadarko [51%] (15% Addax, 10% ERHC,10% DNO/EER,10% Equinox/PetroChina,4% Ophir/Broadlink)

04 Addax [47.3%] (17.7% ERHC, 20% Conoil,10% Hercules, 5% Godsonic)

02Sinopec [43.34%] (14.33% Addax, 7.33% ERHC,

9% Equator, 13.5% ONGC2.5% Hartman, 5% Foby,5% Momo).

05ICC/OEC [75%] (15% ERHC,

10% Sahara/Denham/Wood)

06 ERHC [15%] (85% Filthim-Huzod)

Chevron [51%] (40% ExxonMobil,9% Dangote/Energy Equity)

01

08 Sinopec [100%]

Chevron [100%]

Chevron [35%] (10% Oil & Gas, 5% SASOL50% NNPC)

Chevron [50%] (35% Shell8.625% Petrobras6.375% ConocoPhillips)

Chevron [20%] (50% NNPC, 20% Total

10% Heritage)

Conoco- [47.5%] (47.5% ExxonMobil Phillips 5% Medal)

Chevron [32%] (20% Famfa Oil8% Petrobras, 40% NNPC)

Shell [55%] (20% ExxonMobil12.5% Total, 12.5% Agip)

Shell [100%]

Agip [50.19%] (49.81% Shell)

Agip [90%] (10% NPDC)

Exxon- [20%] (20% ChevronMobil 20% ConocoPhillips

20% Occidental15% NPDC, 5% SASOL)

Yinka [40%] (25% SyntroleumFolawiyo 12.5% Providence Res.

12.5% Challenger Minerals10% Energy Equity Res.)

Exxon- [56.25%] (43.75% Shell) Mobil

Statoil [53.85%] (46.15% Chevron)

Total [20%] (60% Noreast 20% ConocoPhillips)

Conoco- [28.8%] (50% NNPCPhillips 10% Zebbra

11.2% ExxonMobil)

Conoco- [33%] (27% ShellPhillips 20% NPDC

20% Chevron)

Shell [40%] (10% Dajo Oil, 50% NNPC)

Agip [40%] 60% Allied

Total [20%] (30% Chevron30% ExxonMobil20% Nexen)

Total [24%] (45% CNOOC, 16% Petrobras,15% South Atlantic)

Devon [37.5%] (25% Pioneer(Ocean E.) 12.5% Spinnacker

20% Sonangol, 5% NPDC)

Total [90%] (10% NPDC)

Total [60%] (40% Chevron)

Optimum [100%]

Devon [37.5%] (37.5% Anadarko(Ocean E.) 25% NPDC)

KNOC/KEPCo/ [60%] (30% Equator/ONGC Daewoo 10% LCV)

Deep Offshore

321323

OML118OML135

245

322

OML125OML134

244

OML120OML121

OML113

OML133

214

OML128OML129

OML 132

249

250

OML127

247

OML131

318

248

215

221

222

223

OML130

242

256

Pioneer [51%] (31.85% Oranto17.15% Orandi)

320

251

310

LEGEND%s from various Public Domain Sources

Petrobras [37.5%] (25% Statoil37.5% ExxonMobil

324

Petrobras [35%] (35% Statoil30% ASK)

315

BG [40%] (60% Sahara Energy/Mustang/Deen/NEO)

286

BG [40%] (60% Sahara)332

OMEL [40%] (60% LCV)279

OMEL [90%] (10% LCV)285

INC [100%]

Transcorp [100%]

252292

295

Oando [50% ] ( 50% Stella/Ashburt, Cosy Energy &Trans Energy)

325

Conoil [100%]257

ECL [%] ( % NNPC, % Petroplus)

Agip/Lotus [100%]284

Addax [72.5%] (27.5% Starcrest)291

OMEL [%] (% EMO)

CPC/Starcrest [100%]294

REVOKED LICENCES

297

OMEL [100%]293

15

• The collective reserves of the marginal fields total approximately 1.3 billion barrels.

• Sixty-six out of 70 pre-qualified indigenous companies placed bids on Nigeria's 24 marginal oil fields in 2003. A committee, comprising representatives of the DPR and the lease holders of the marginal fields (NNPC and its joint venture partners) evaluated the bids.

• 24 marginal fields were awarded to 31 indigenous companies in what constituted the first round of such exercise.

• Winners paid signature bonus of $150,000 per field.

• Two other fields (Okwok and Ebok fields) were awarded on a discretionary basis to Oriental Energy to compensate the company for losing part of its OML 115 to Equatorial Guinea due boundary adjustments.

Marginal Fields in Nigeria

Marginal fields in Nigeria

� Ogbele field, which was negotiated prior to the introduction of the MFDPand is operated by Niger Delta Petroleum Resources Limited (“NDPR”),came on stream in 2005.

� Otakikpo and Ubima fields were awarded to Green Energy Limited andAllgrace Energy Limited respectively in 2010. The award also included acommitment to develop a small – scale gas utilization project within 30months of the commencement of production.

� The MFD also gives the leaseholders the right to award ‘’marginal’’ fieldswithin their concessions to willing ‘’farmees’’ provided such rights areexercised with the consent of the President.

I16

Marginal fields in Nigeria

Current status of Marginal Fields in Nigeria (1):

• Marginal Fields grew Nigeria's reserves by 302.6million barrels as atApril 2013 from 141 million barrels in 2004 ( Source: DPR Aug 2013)

• Production now up to 60,000 bopd and 100 mmscf/d for gas (Source: DPR, Mar

2013)

• Breaking new grounds, integrating the value through crude oilproduction, monetisation of gas and small scale refining

• Deployment of new technologies.

• Equipped to better manage local communities.

I17

Marginal fields in Nigeria

8 of the 28 marginal fields assigned and licensed have come on stream

at Feb 2013 after 10 years. They include:

18

Field Marginal Field Operator (Bopd/MMscf)

Umusagede Midwestern Oil & Gas Plc 14,000

Asuokpu/Umutu Platform Petroleum Limited 2,100

Ibigwe Walter Smith Petroman Oil Limited 4,335

Umusati/Igbuku Pillar Oil Limited 2,700

Obodugwa/Obodeti Energia Company Limited 3,500

Ajapa Britannia U) 5,000

Qua Ibo Frontier Oil 35 MMscf/d

Okwok/Ebok Oriental Energy ??

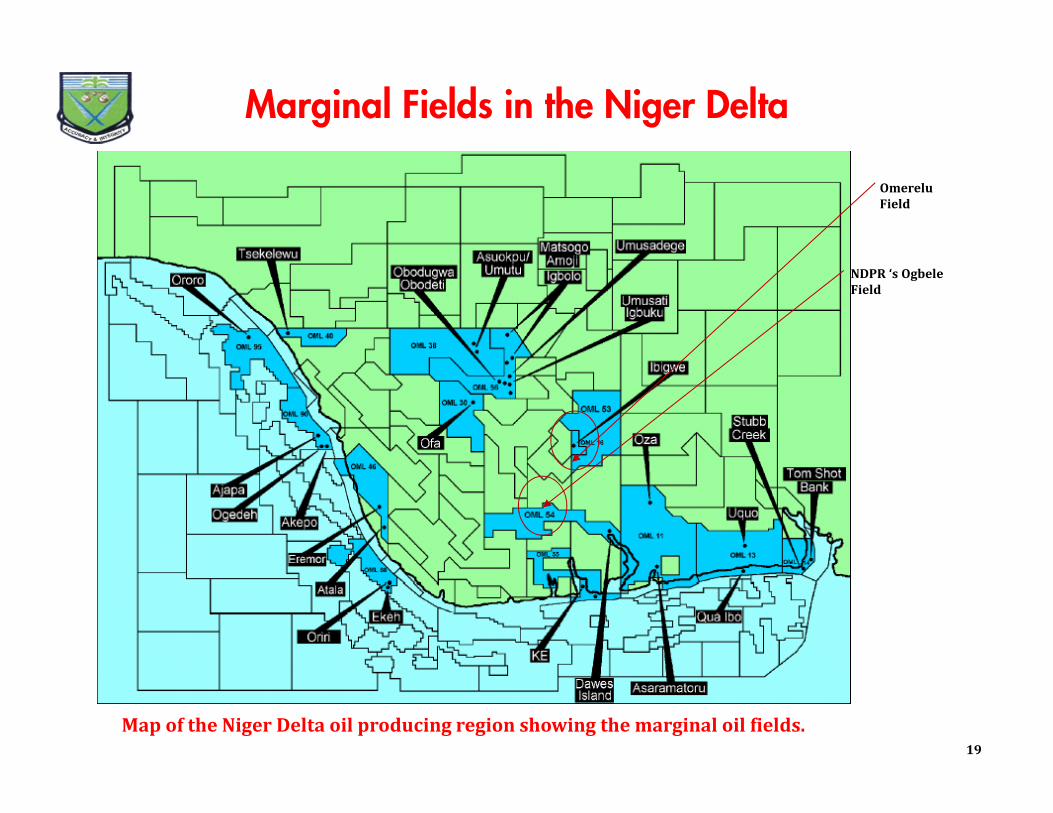

19Map of the Niger Delta oil producing region showing the marginal oil fields.

NDPR ‘s Ogbele

Field

Marginal Fields in the Niger Delta

19

Omerelu

Field

Marginal fields in Nigeria

Current status of Marginal Fields in Nigeria (2):

Slow development of marginal fields as result of the following

• Difficulty of obtaining funds for field development purposes

• The non bankability of some of the assets

• Lack of technical expertise, failure on a rig for example can wipe out acompany's finances

• The Federal Government's imposition of partners on the operators duringthe award of the marginal field licence was a major flaw

• Partnership issues - many awardees ended up in litigations with technicalpartners

• Investment climate - hostile, deficiency in trust, transparency,collaboration and alliances

• Misalignment between marginal field development aspirations andimplementation

20

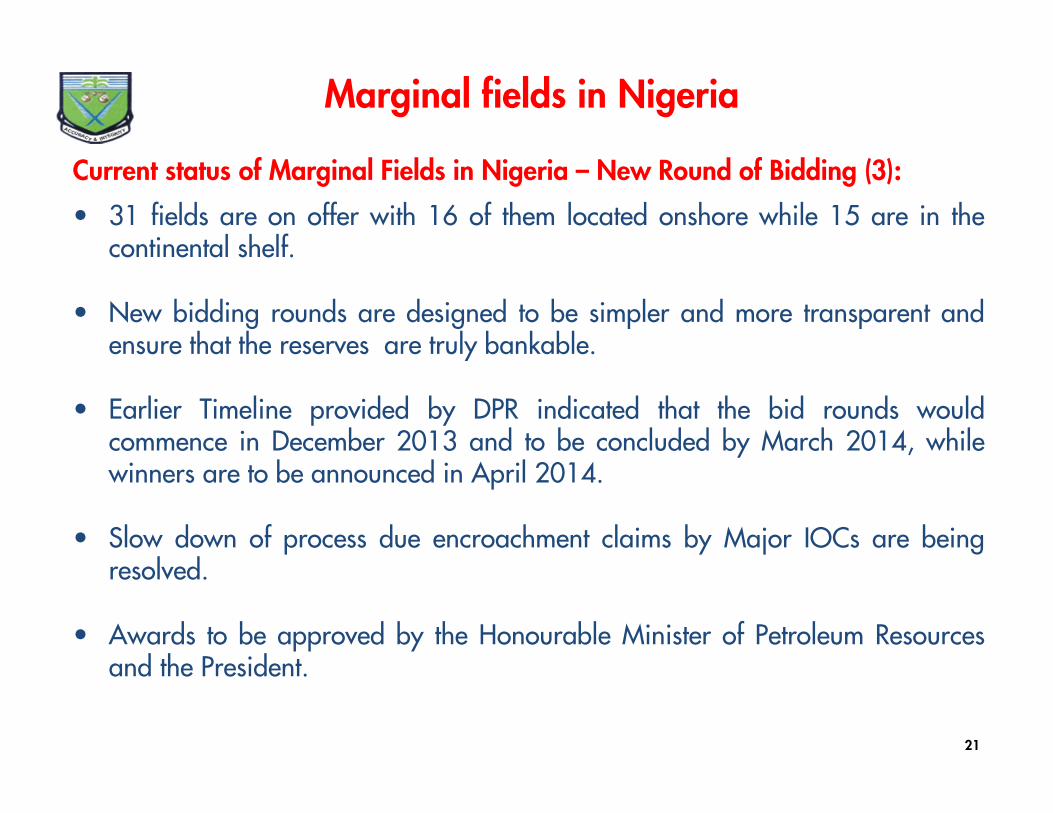

Marginal fields in Nigeria

Current status of Marginal Fields in Nigeria – New Round of Bidding (3):

• 31 fields are on offer with 16 of them located onshore while 15 are in thecontinental shelf.

• New bidding rounds are designed to be simpler and more transparent andensure that the reserves are truly bankable.

• Earlier Timeline provided by DPR indicated that the bid rounds wouldcommence in December 2013 and to be concluded by March 2014, whilewinners are to be announced in April 2014.

• Slow down of process due encroachment claims by Major IOCs are beingresolved.

• Awards to be approved by the Honourable Minister of Petroleum Resourcesand the President.

21

22

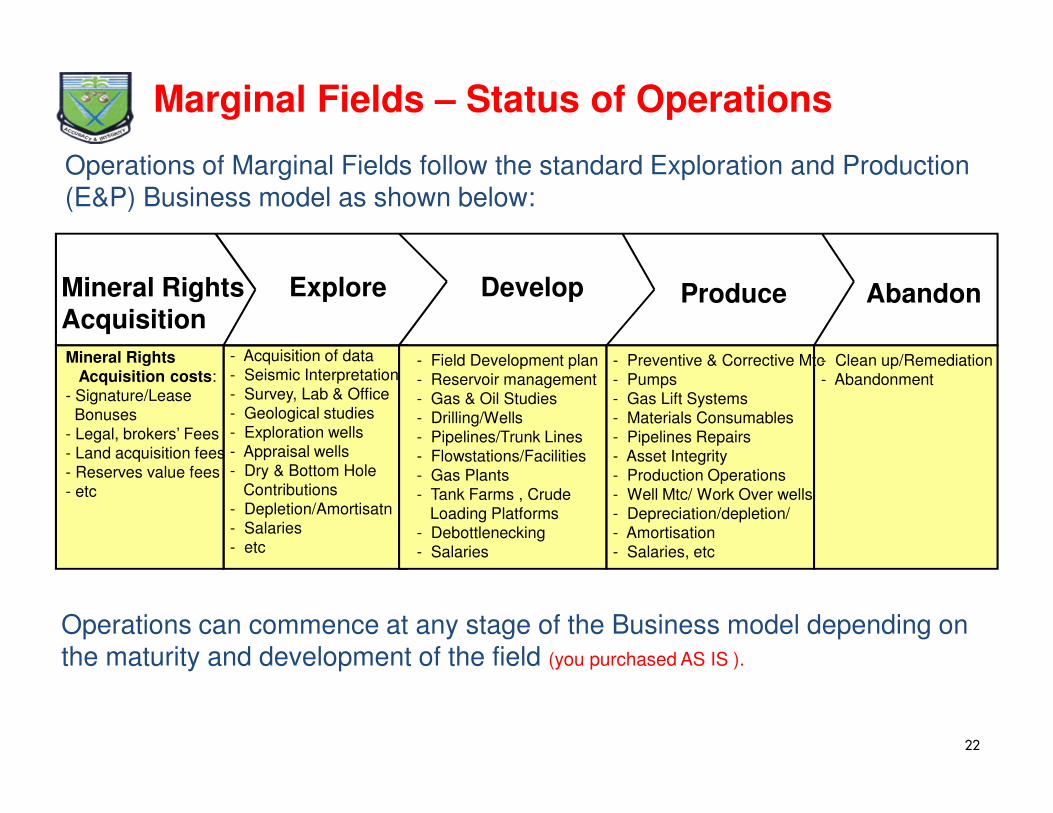

Marginal Fields – Status of Operations

Operations of Marginal Fields follow the standard Exploration and Production (E&P) Business model as shown below:

Explore ProduceDevelop Abandon

- Acquisition of data

- Seismic Interpretation

- Survey, Lab & Office

- Geological studies

- Exploration wells

- Appraisal wells

- Dry & Bottom Hole

Contributions

- Depletion/Amortisatn

- Salaries

- etc

- Field Development plan

- Reservoir management

- Gas & Oil Studies

- Drilling/Wells

- Pipelines/Trunk Lines

- Flowstations/Facilities

- Gas Plants

- Tank Farms , Crude

Loading Platforms

- Debottlenecking

- Salaries

- Preventive & Corrective Mtc

- Pumps

- Gas Lift Systems

- Materials Consumables

- Pipelines Repairs

- Asset Integrity

- Production Operations

- Well Mtc/ Work Over wells

- Depreciation/depletion/

- Amortisation

- Salaries, etc

- Clean up/Remediation

- Abandonment

Mineral Rights Acquisition

Mineral Rights Acquisition costs:

- Signature/Lease

Bonuses

- Legal, brokers’ Fees

- Land acquisition fees

- Reserves value fees

- etc

Operations can commence at any stage of the Business model depending on the maturity and development of the field (you purchased AS IS ).

Financing opportunities

General consideration

• Oil and gas industry is large capital intensive that requires enormous

resources for its finance, management and operations

• The inability of local banks in Nigeria and south of Sahara to finance

massive oil and gas projects

• Long Gestation Period (exploration, development & production)

• Consortium borrowing/lending

• International financial institutions (World Bank, International Finance

Corporation, African Development Bank, Africa Finance Corporation,

JP Morgan, Goldman Sachs)

• Strengthen linkages between key sectors of the economy (financial sector,

Power)

• Technology intensive, skilled personnel and strives on sanctity of contracts

23

24

Financing Opportunities

Financing Options

• Joint Venture Arrangement (Operator)

• Production Sharing Contracts (PSC)

• Carry Arrangements/Project Specific Financing

• Service Contracts

25

Joint Venture Arrangement – Operator

• Co-owns the license

• Operations funded by cash calls

• Profit shared in proportion of participating interest

• Approvals are a joint management decision

Un-incorporated Joint Venture: Governed by A Joint Operating Agreement (JoA).The assets and their operations are owned and controlled by the investors according to the terms of the agreement.

Financing Opportunities

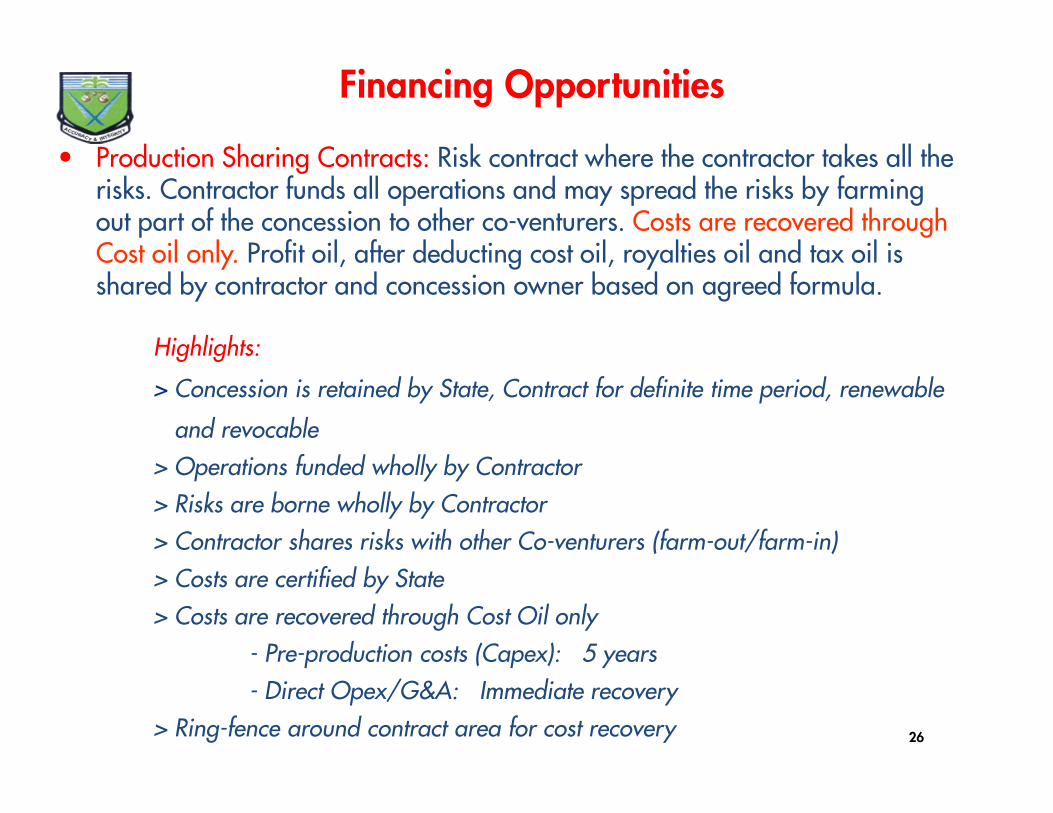

26

• Production Sharing Contracts: Risk contract where the contractor takes all the risks. Contractor funds all operations and may spread the risks by farming out part of the concession to other co-venturers. Costs are recovered through Cost oil only. Profit oil, after deducting cost oil, royalties oil and tax oil is shared by contractor and concession owner based on agreed formula.

Highlights:

> Concession is retained by State, Contract for definite time period, renewable

and revocable

> Operations funded wholly by Contractor

> Risks are borne wholly by Contractor

> Contractor shares risks with other Co-venturers (farm-out/farm-in)

> Costs are certified by State

> Costs are recovered through Cost Oil only

- Pre-production costs (Capex): 5 years

- Direct Opex/G&A: Immediate recovery

> Ring-fence around contract area for cost recovery

Financing Opportunities

27

Carry ArrangementsArrangement where partners in a JV relationship agree to ‘carry’ one of the partners for a specific project in the E&P Operations. Carrying partners are rewarded through agreed formula as follows:

• Equity Oil• Carry Oil• Shared Oil

The carrying partner is required to keep records showing:- Tangible Carry Capital Costs- Intangible Carry Capital Costs- Carry Capital Costs amortized- Carry Tax Relief- Carry Oil Received- Shared Oil Value Received- Residue Carry expenditure

Financing Opportunities

28

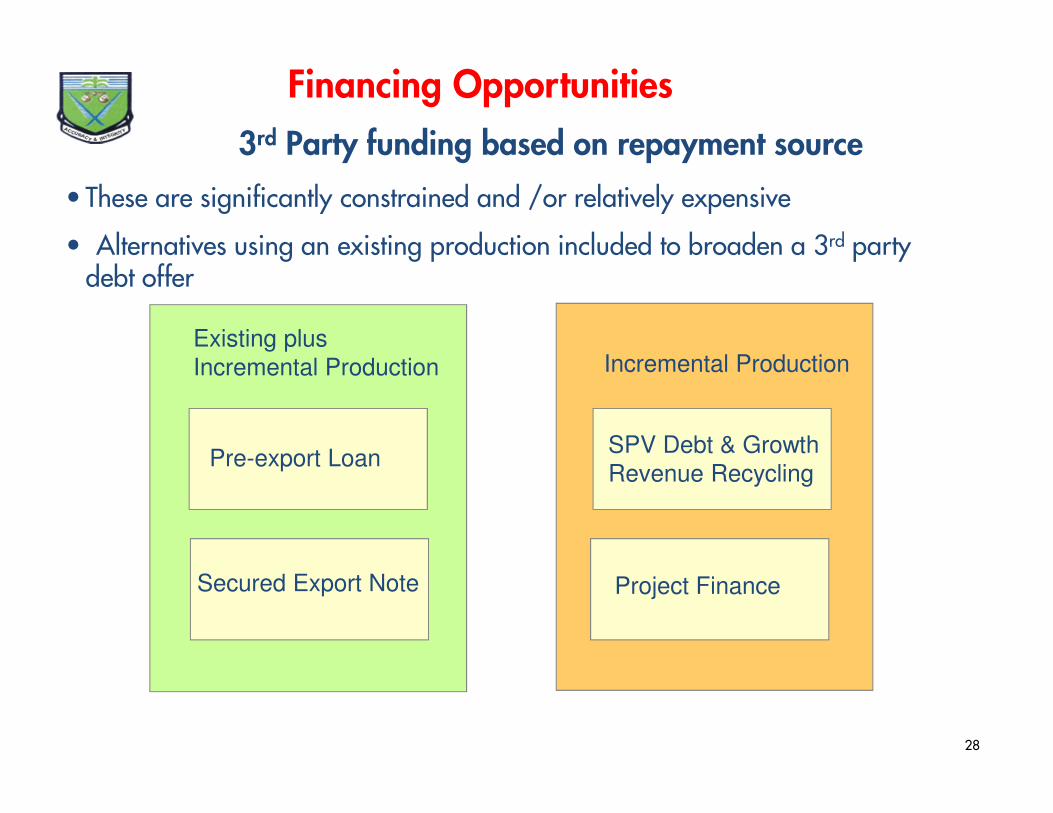

3rd Party funding based on repayment source

Existing plus

Incremental Production Incremental Production

Pre-export Loan

Secured Export Note Project Finance

SPV Debt & Growth

Revenue Recycling

• These are significantly constrained and /or relatively expensive

• Alternatives using an existing production included to broaden a 3rd party debt offer

Financing Opportunities

29

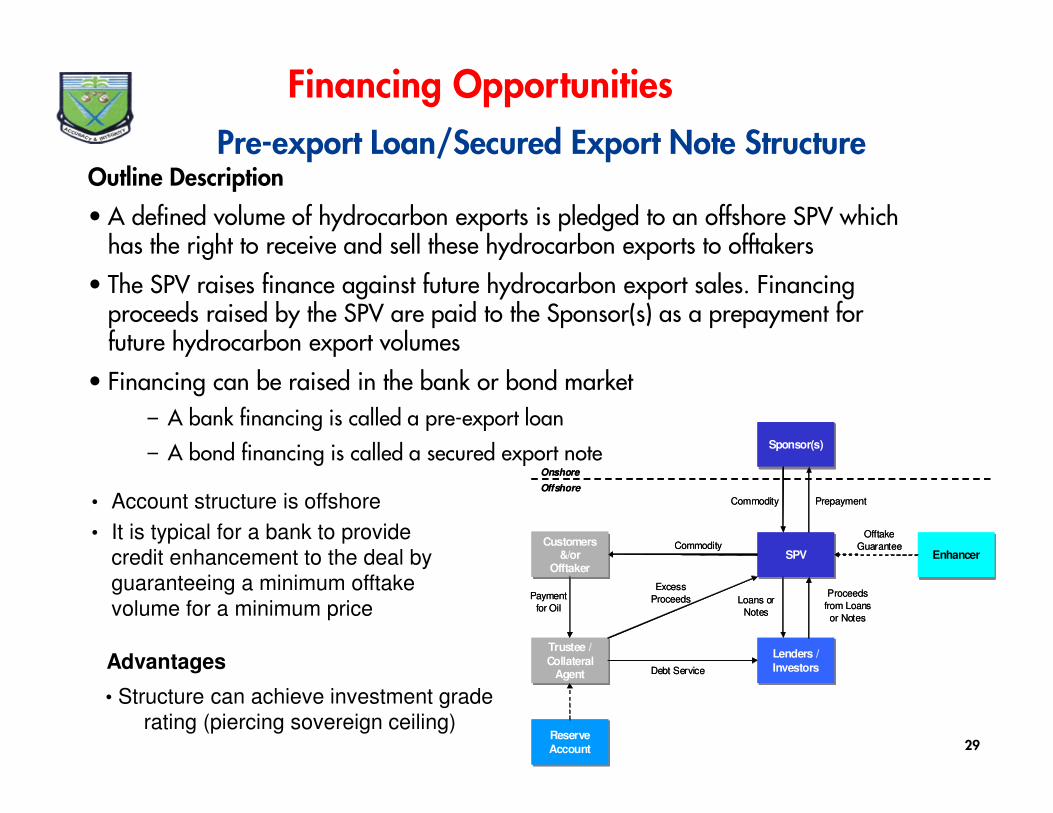

Pre-export Loan/Secured Export Note Structure Outline Description

• A defined volume of hydrocarbon exports is pledged to an offshore SPV which has the right to receive and sell these hydrocarbon exports to offtakers

• The SPV raises finance against future hydrocarbon export sales. Financing proceeds raised by the SPV are paid to the Sponsor(s) as a prepayment for future hydrocarbon export volumes

• Financing can be raised in the bank or bond market

– A bank financing is called a pre-export loan

– A bond financing is called a secured export note Sponsor(s)Sponsor(s)

SPVSPV

Lenders / Investors

Lenders /

Investors

Customers &/or

Offtaker

Customers &/or

Offtaker

Trustee / Collateral

Agent

Trustee /

Collateral Agent

Reserve Account

Reserve Account

EnhancerEnhancer

Onshore

Offshore

Payment

for OilLoans or

Notes

Proceeds

from Loans

or Notes

Excess

Proceeds

Debt Service

Offtake

Guarantee

Commodity Prepayment

Commodity

Sponsor(s)Sponsor(s)

SPVSPV

Lenders / Investors

Lenders /

Investors

Customers &/or

Offtaker

Customers &/or

Offtaker

Trustee / Collateral

Agent

Trustee /

Collateral Agent

Reserve Account

Reserve Account

EnhancerEnhancer

Onshore

Offshore

Payment

for OilLoans or

Notes

Proceeds

from Loans

or Notes

Excess

Proceeds

Debt Service

Offtake

Guarantee

Commodity Prepayment

Commodity

• Account structure is offshore

• It is typical for a bank to provide

credit enhancement to the deal by

guaranteeing a minimum offtake

volume for a minimum price

Advantages

• Structure can achieve investment grade

rating (piercing sovereign ceiling)

Financing Opportunities

30

• Service Contracts: Right granted by a principal to a company (agent) to explore and produce oil & gas. In some countries, mineral rights are vested in the state while in others, individuals hold the rights.

Funding is by the principal. Company gets a fee for its services.

There could be variant of service contracts where the service fee is linked to the profit (Risk Service Contracts)

Highlights:

> Concession is retained by principal

> Operations funded wholly by principal

> Risks & Rewards are borne wholly by principal

> Agent gets agreed fee for his services

Financing Opportunities

Case study – Marginal field Operations

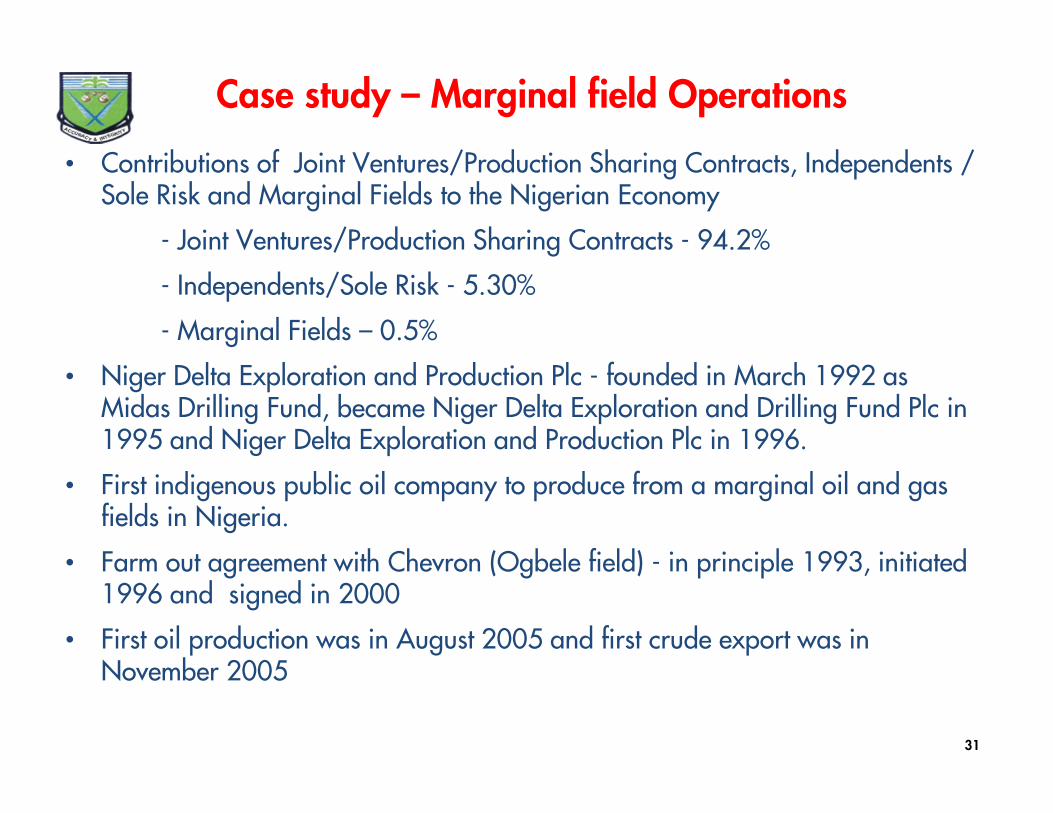

• Contributions of Joint Ventures/Production Sharing Contracts, Independents / Sole Risk and Marginal Fields to the Nigerian Economy

- Joint Ventures/Production Sharing Contracts - 94.2%

- Independents/Sole Risk - 5.30%

- Marginal Fields – 0.5%

• Niger Delta Exploration and Production Plc - founded in March 1992 as Midas Drilling Fund, became Niger Delta Exploration and Drilling Fund Plc in 1995 and Niger Delta Exploration and Production Plc in 1996.

• First indigenous public oil company to produce from a marginal oil and gas fields in Nigeria.

• Farm out agreement with Chevron (Ogbele field) - in principle 1993, initiated 1996 and signed in 2000

• First oil production was in August 2005 and first crude export was in November 2005

31

Case study – Marginal field

• Production maintained at 3,500 bpd in 2006 and got to its first 1million barrels of crude production in 2007; 3,700bpd in 2008 and peaked 8,000bpd (with average 4,333bpd) in 2009.

• Attained 5.5million barrels of crude oil production in August 2010 from Ogbele field

• Crude is evaluated through SPDC’s trunkline

• 100 mmscf/d Gas plant development in Ogbele field commenced in March 2011.

• 20km gas pipeline to NLNG, attained 6 bscf Gas supply to NLNG

• Built mini diesel Refinery ‘’Topping Plant’’ with installed capacity of 1000 barrels per day

• Strong governance framework with professional board of Directors

32

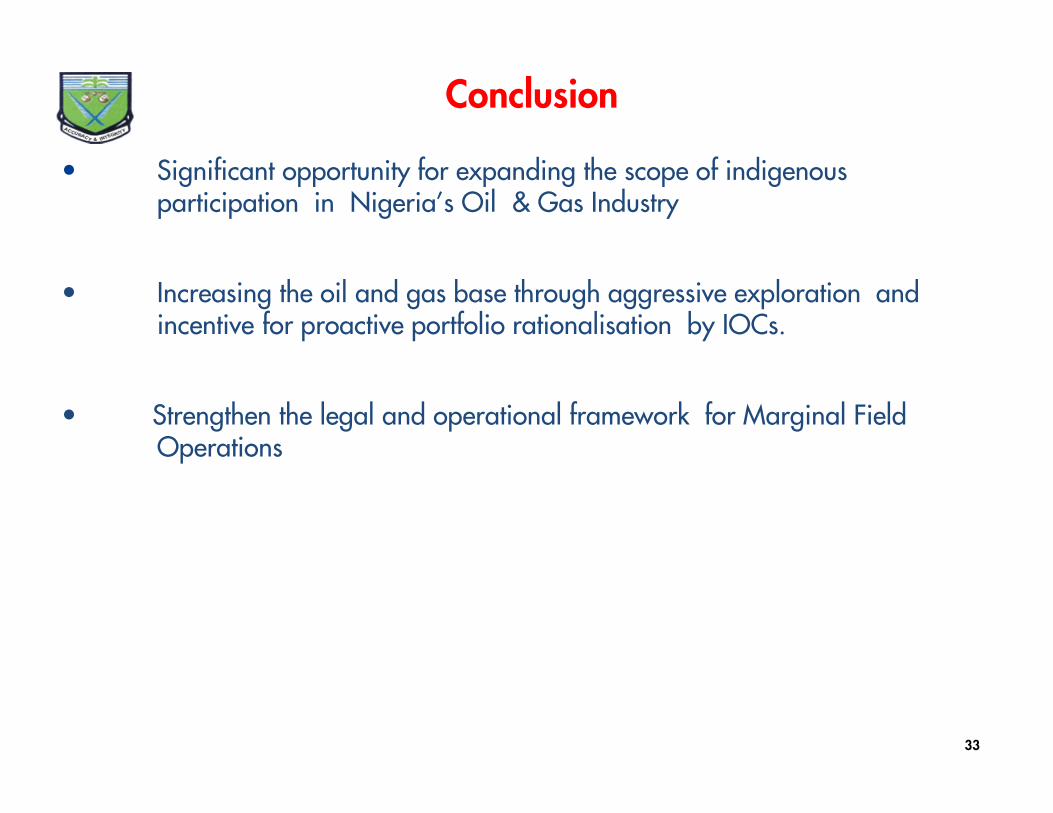

Conclusion

• Significant opportunity for expanding the scope of indigenous participation in Nigeria’s Oil & Gas Industry

• Increasing the oil and gas base through aggressive exploration and incentive for proactive portfolio rationalisation by IOCs.

• Strengthen the legal and operational framework for Marginal Field Operations

33

34

Questions! Questions!!Comments!

References

• Nigeria Vision 20: 2020 Economic Transformation Blueprint October 2009.

• Fatona, L. (2012). Marginal fields and successful growth portfolio – a presentation at the 5th Nigerian Independents Forum.

• Olorunsola, O. (2013). Marginal Fields Development In Nigeria- A Review Of Policy, Regulation, Activities And Future Outlook. Paper delivered as guest speaker at the recent official launch of NOGintelligence, Lagos.

• Energy Project Financing December 2008 A Directory of Financing Sources for Energy Projects in Developing Countries, Office of Financial Services Industries Manufacturing and Services. International Trade Administration, Department of Commerce, USA.

• Gagar, A.O., (2010). Financing Oil & Gas Projects and Risk Management. MCPE Presentation to Institute of Chartered Accountants (Ghana).

• Financing Oil & Gas Projects in Latin America & the Caribbean. Conferencia Arpel, Dessarollo Sostenible, Punta de Este, Uruguay, April 24th 2009.

• Dunkerley Joy. (1995). Financing the energy sector in developing countries. Washington. Energy Policy, Vol 23 No 11 pp. 929 – 939.

• Unuigbe Emilomo. Funding energy projects in developing countries: Is this the dawn of local lending in project finance? A Nigerian perspective.

• Hossein, R. (1996). Financing Oil and Gas Projects in Developing Countries. Oil and Gas Division World Bank’s Industry and Energy Department. Finance & Development / June 1996.

• BP Statistical Review of World Energy June 2013, Bp.com/statistical review.

36

References con’t

• Akanni, F. (2013). The Next Phase of the Marginal Field Experience. African Oil & Gas Report, The Guardian, Wednesday Sept 4, 2013.

• Talent Edge 2020: Redrafting talent strategies for the uneven recovery. Deloitte January 2012.

• Adams Gary. 2010 Deloitte Oil & Gas Conference Summary Report. Houston. Deloitte Center for Energy Solutions.

• Nigerian Oil and Gas Industry Content Development Act 2010

• Ashurst LLP (2014). Nigeria Oil and Gas: Marginal Fields

37