EM 009 854 - ERIC

286

ED 062 807 TITLE INSTITUTION SPCNS AGENCY PUB DATE NOTE EDRS PRICE DESCRIPTORS IDENTIFIERS DOCUMENT RESUME EM 009 854 Case Studies of Auditing in a Comi:uter-Based Systems Environment. General Accounting Office, Washington, D.C. Comptroller General of the U.S., Washington, D.C. Jun 71 286p. MF-$0.65 HC-$9.87 *Accounting; *Business Administration; *Computer Oriented Programs; Computer Prograns; *Computers; Data Processing; *Federal Government; Information Processing *Auditing ABSTRACT In response to a growing need for effective and efficient means for auditing computer-based systense a number of studies dealing primarily with batch-processing tyEe computer operations have been conducted to explore the impact cf computers on auditing activities in the Federal Government. This report first presents some statistical data on computers in the Federal Government, and then summarizes the result:, of the studies in three sections. The faxst section covers those studies dealing with internal auditing of computer-based systems and attempts to determine whether effective independent reviews and appraisals are being made. The next section covers system documentation to determine whether current and complete documentation is maintained; the final section examines the use of computer techniques to audit computer-based systems to assist other Government auditing organizations in checking computer-based systems. Extensive appendices provide more detailed information on auditing procedures. (Auttior/SH)

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of EM 009 854 - ERIC

ED 062 807

TITLE

INSTITUTIONSPCNS AGENCYPUB DATENOTE

EDRS PRICEDESCRIPTORS

IDENTIFIERS

DOCUMENT RESUME

EM 009 854

Case Studies of Auditing in a Comi:uter-Based SystemsEnvironment.General Accounting Office, Washington, D.C.Comptroller General of the U.S., Washington, D.C.Jun 71286p.

MF-$0.65 HC-$9.87*Accounting; *Business Administration; *ComputerOriented Programs; Computer Prograns; *Computers;Data Processing; *Federal Government; InformationProcessing*Auditing

ABSTRACTIn response to a growing need for effective and

efficient means for auditing computer-based systense a number ofstudies dealing primarily with batch-processing tyEe computeroperations have been conducted to explore the impact cf computers onauditing activities in the Federal Government. This report firstpresents some statistical data on computers in the FederalGovernment, and then summarizes the result:, of the studies in threesections. The faxst section covers those studies dealing withinternal auditing of computer-based systems and attempts to determinewhether effective independent reviews and appraisals are being made.The next section covers system documentation to determine whethercurrent and complete documentation is maintained; the final sectionexamines the use of computer techniques to audit computer-basedsystems to assist other Government auditing organizations in checkingcomputer-based systems. Extensive appendices provide more detailedinformation on auditing procedures. (Auttior/SH)

.7.4

1

A 01CCOU\

U.S. DEPARTMENT OF HEALTH.EDUCATION & WELFAREOFFICE OF EDUCATION

THIS DOCUMENT HAS BEEN REPRO-DUCED EXACTLY AS RECEIVED FROMTHE PERSON OR ORGANIZATION ORIG-INATING IT POINTS OF VIEW OR OPIN-IONS STATED DO NOT NECESSARILYREPRESENT OFFICIAL OFFICE OF EDU-CATION POSITION OR POLICY.

CASE STUDIES OF AUDITINGIN A COMPUTER-BASED

SYSTEMS ENVIRONMENT

CASE STUDIES OF AUDITING

IN A COMPUTER-BASED SYSTEMS ENVIRONMENT

UNITED STATES GENERAL ACCOUNTING OFFICE

1971

NOTE

Tlie GAO Office of Policy and Special

Studies coordinated preparation of this

study. As of July 1, 1971, tilt.: functions

of this office were realigned. Therefore

inquiries concerning the study should be

addresseJ to the Division of Financial

and General Management Studies.

3

COMPTROLLER GENERAL OF THE UNITED STATESWASHINGTON. D.C. 20548

B-115369 FOREWORD

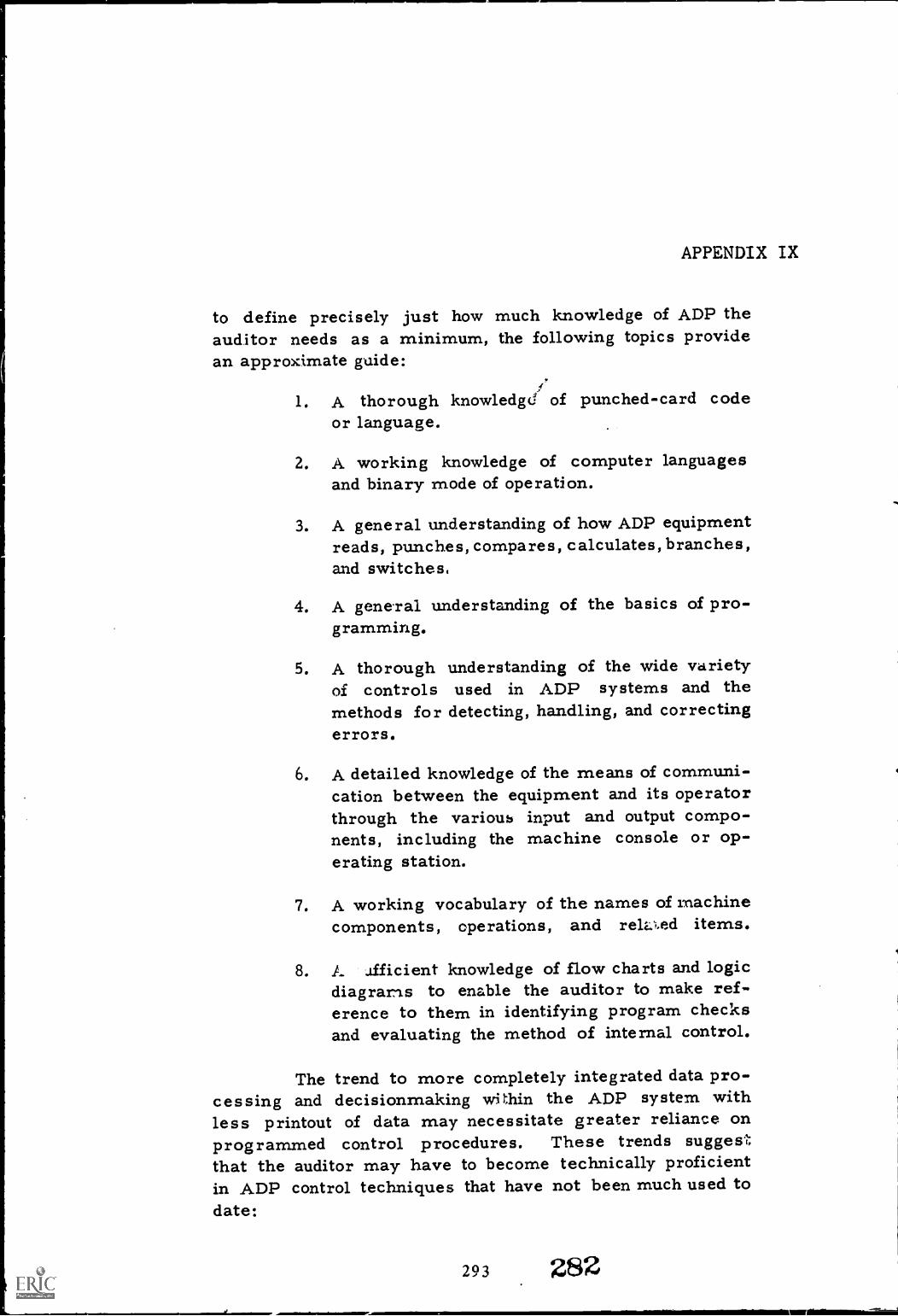

In response to the growing need for effective and efficient meansfor auditing computer-based systems, the General Accounting Office hasconducted a number of studies to explore the impact of computers onauditing activities in the Federal Government. These studies have dealtprimarily with batch-processing-type computer operations or those sys-tems that require input data to be coded and collected into groups orbatches for processing. Particular attention was devoted to:

Internal auditing of computer-based systems--to determine whethereffective independent reviews and appraisals are being mane.

System documentationto determine whether current and completedocumentation is maintained.

The use of computer techniques to audit computer-based systems--to assist other Government auditing organizations in auditingcomputer-based systems.

This report summarizes the results of these studies. Because ofthe importance of internal controls, a previously prepared review guidefor evaluating internal controls in automatic data processing systems isincluded as appendix IX. From an audit standpoint, the auditor must al-ways consider the control framework in which computer processing iscarried out.

As additional studies of more sophisticated real-time computeroperations are completed, we plan to publish aciditional information onthis important subject.

June 1971

Comptroller Generalof the United States

50TH ANNIVERSARY 1921-1971

CHAPTER

1

2

Contents

STATISTICS ON COMPUTERS IN THE FEDERAL GOV-

,Paige

ERNMENT 1

SUMMARY OF OBSERVATIONS 5

Internal audit of ADP systems 5

Documentation of ADP systemsComputer-auditing techniques 6

3 NEED TO ESTABLISH EFFECTIVE INTERNAL AUDITOF ADP SYSTEMS 7

Scope of internal auditing 9

Change in audit approach required 9

Benefits of computer-auditing techniques 11

Additional training required 14

Conclusions 15

4 NEED FOR COMPREHENSIVE ADP DOCU1ENTATION 17

What documentation is 18

ADP documentation for Federal agencies 18

Need for increased management surveil-lance of ADP documentation practices 21

Conclusions 21

5 COMPUTER-AUDITING TECHNIQUES 23

Generalized computer audit programs 25

Custom-designed computer audit programs 28

Test decks 30Review and analysis of selected computer

programs 33

Conclusions 34

APPENDIX

Restatement of certain principles and stall-dards relating to executive agency account-ing systems 39

II Review guide for Federal agency accountingsystems, section 18--automatic data process-

ing (ADP) 43

APPENDIX Page

III

IV

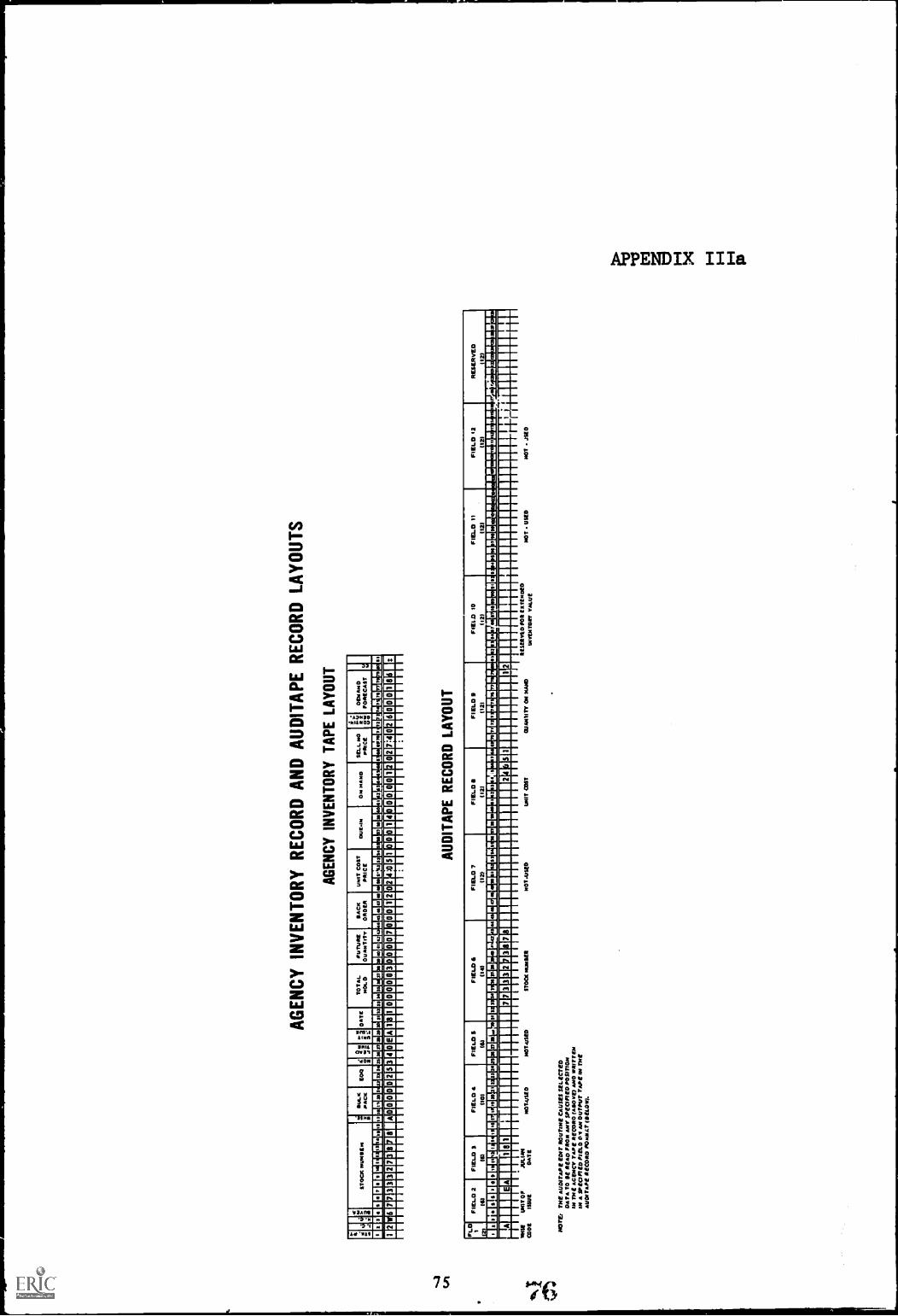

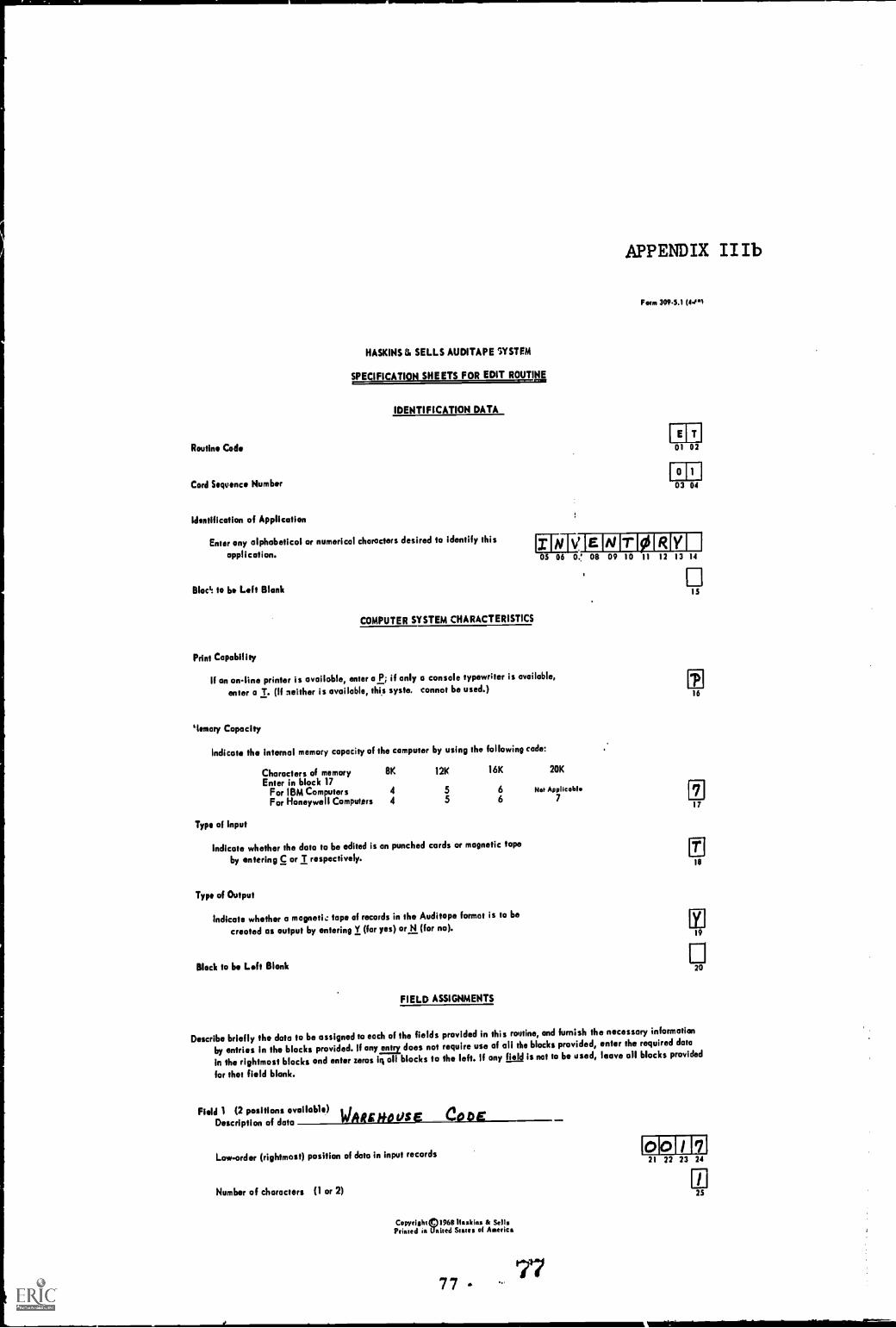

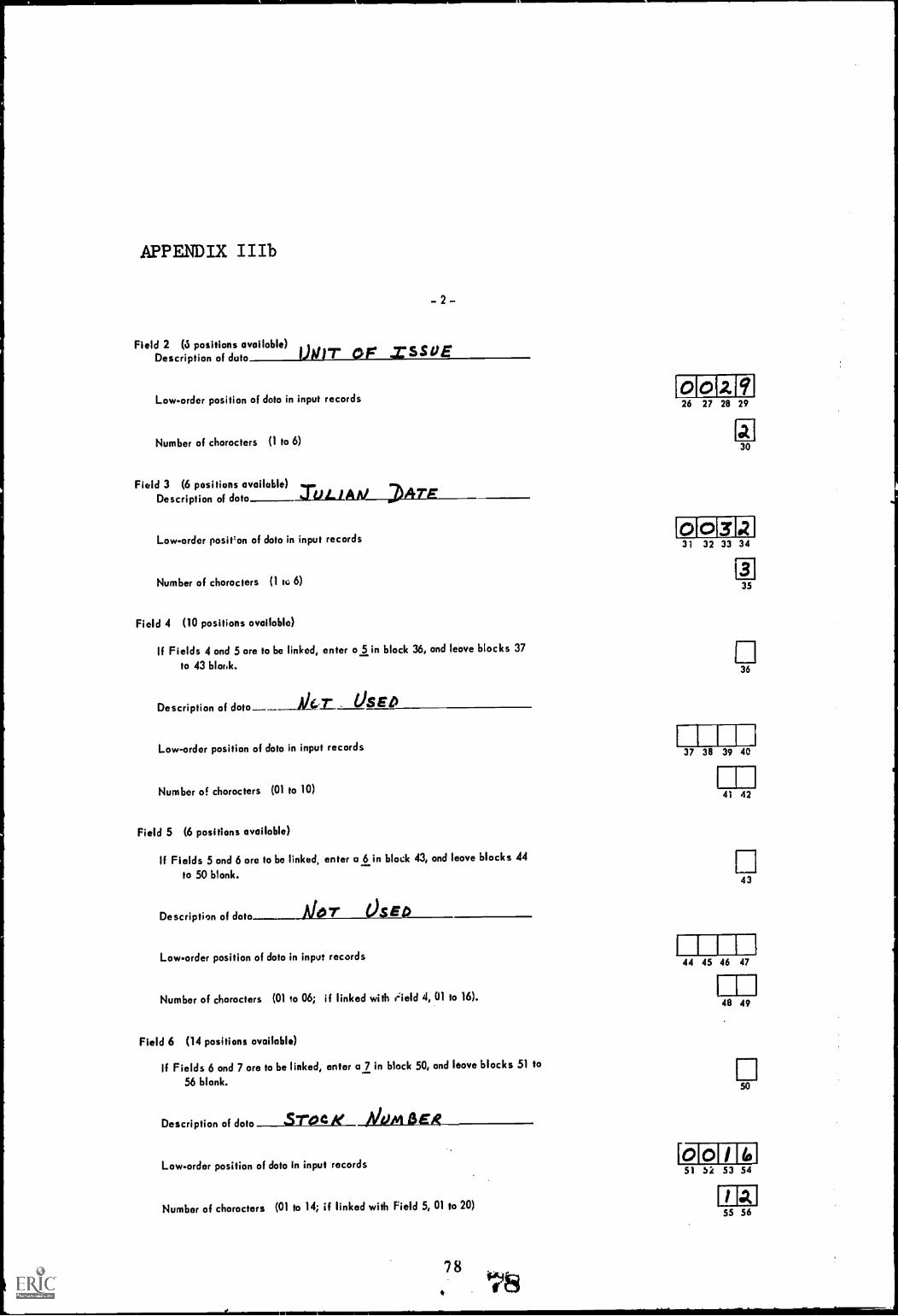

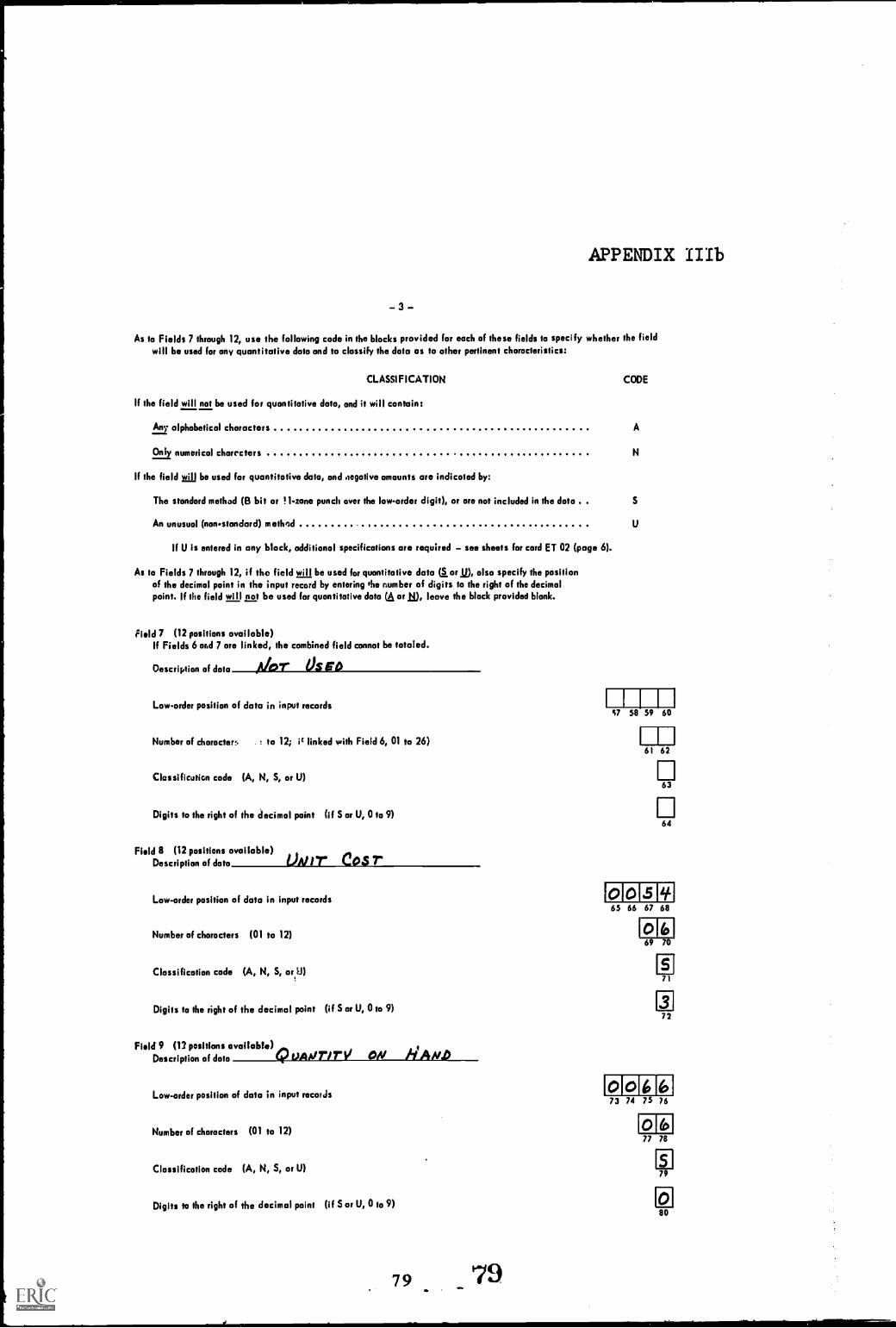

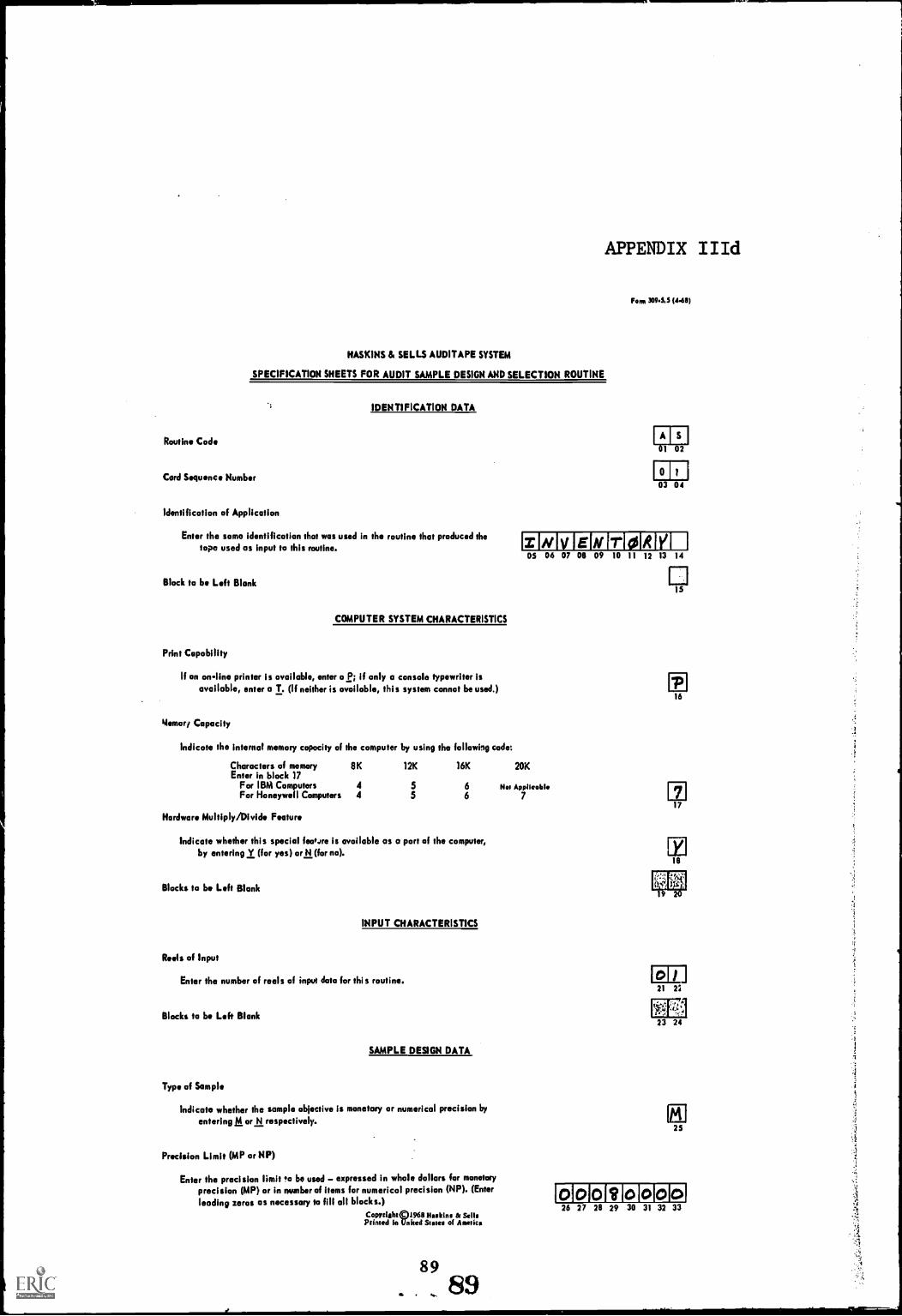

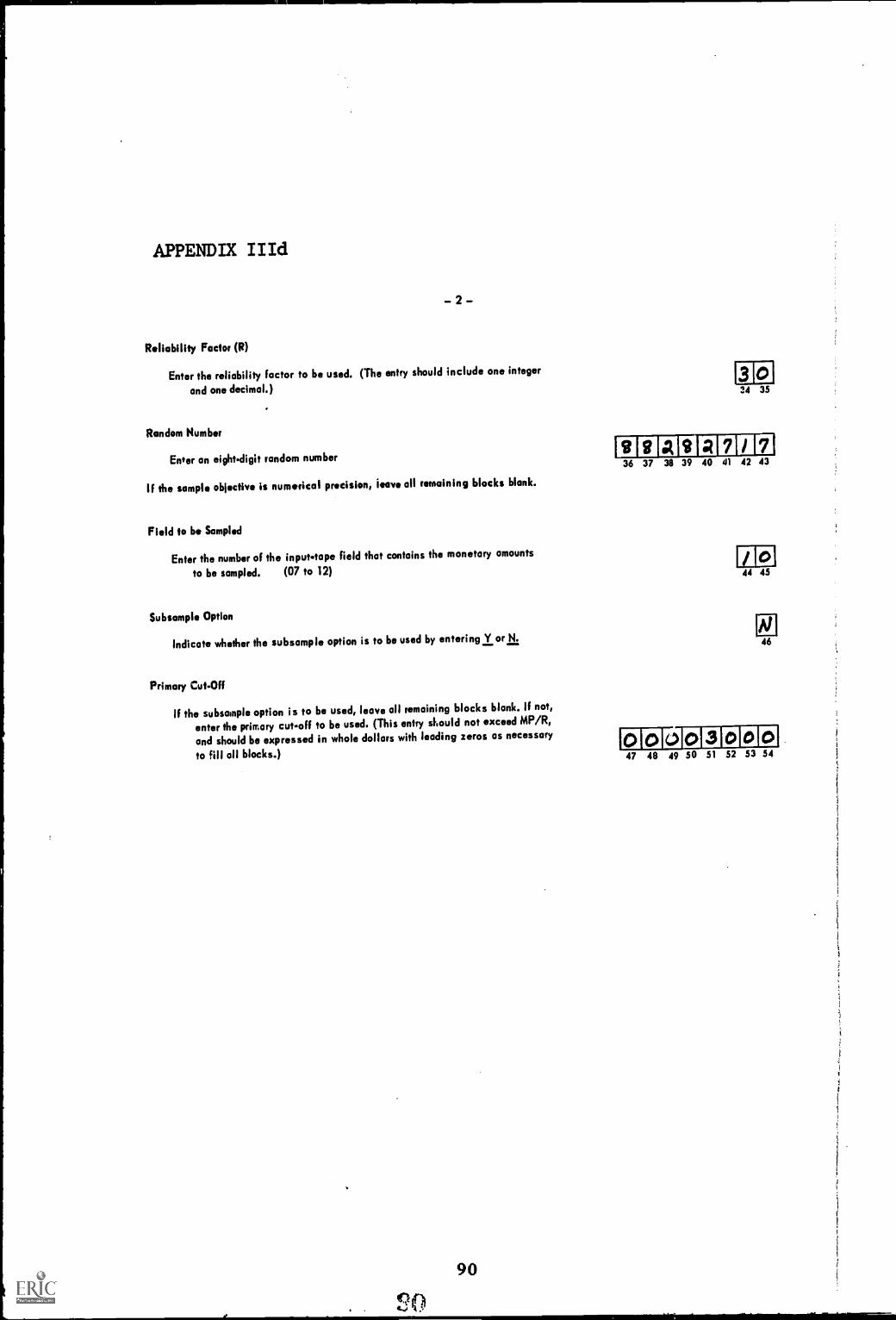

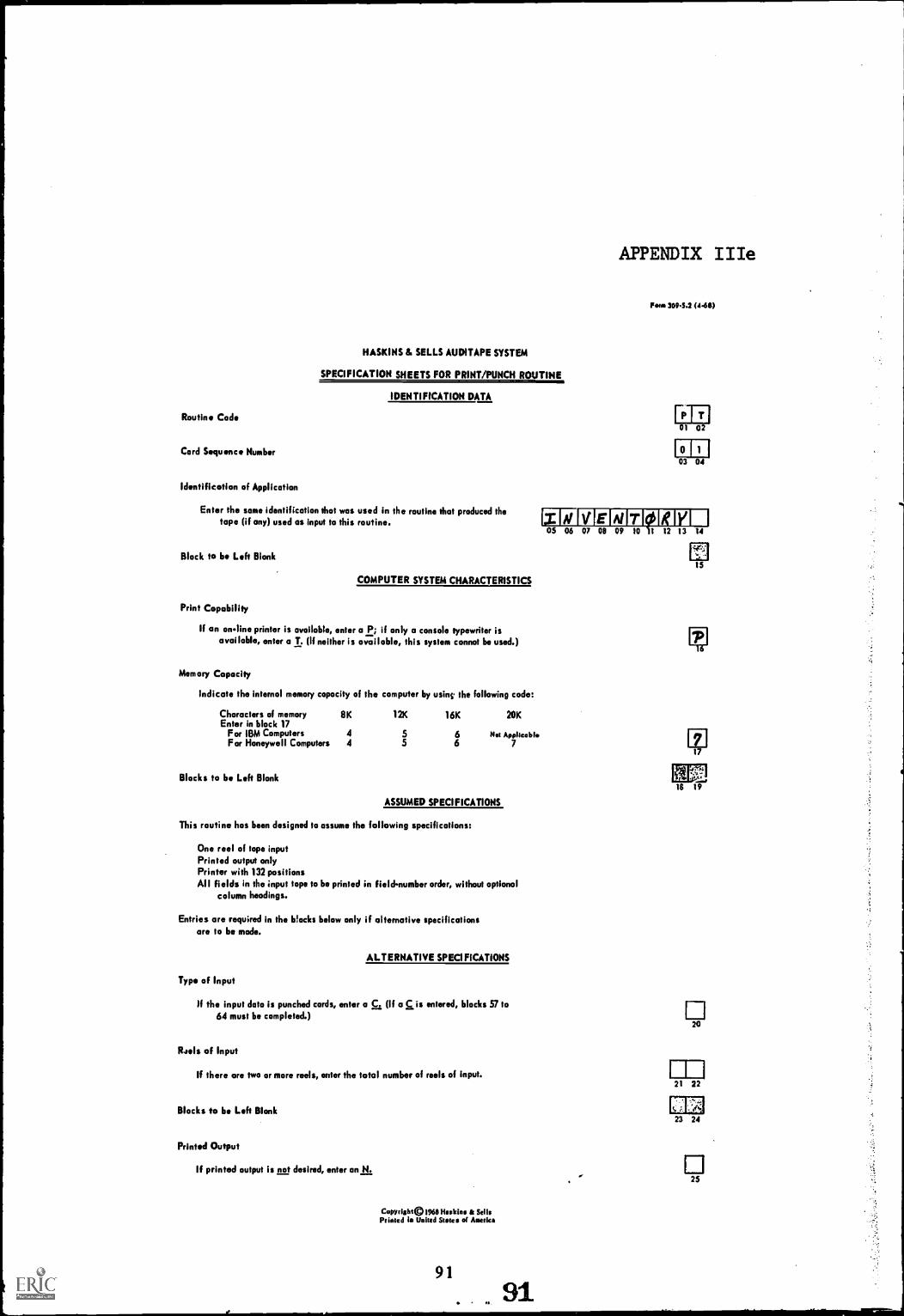

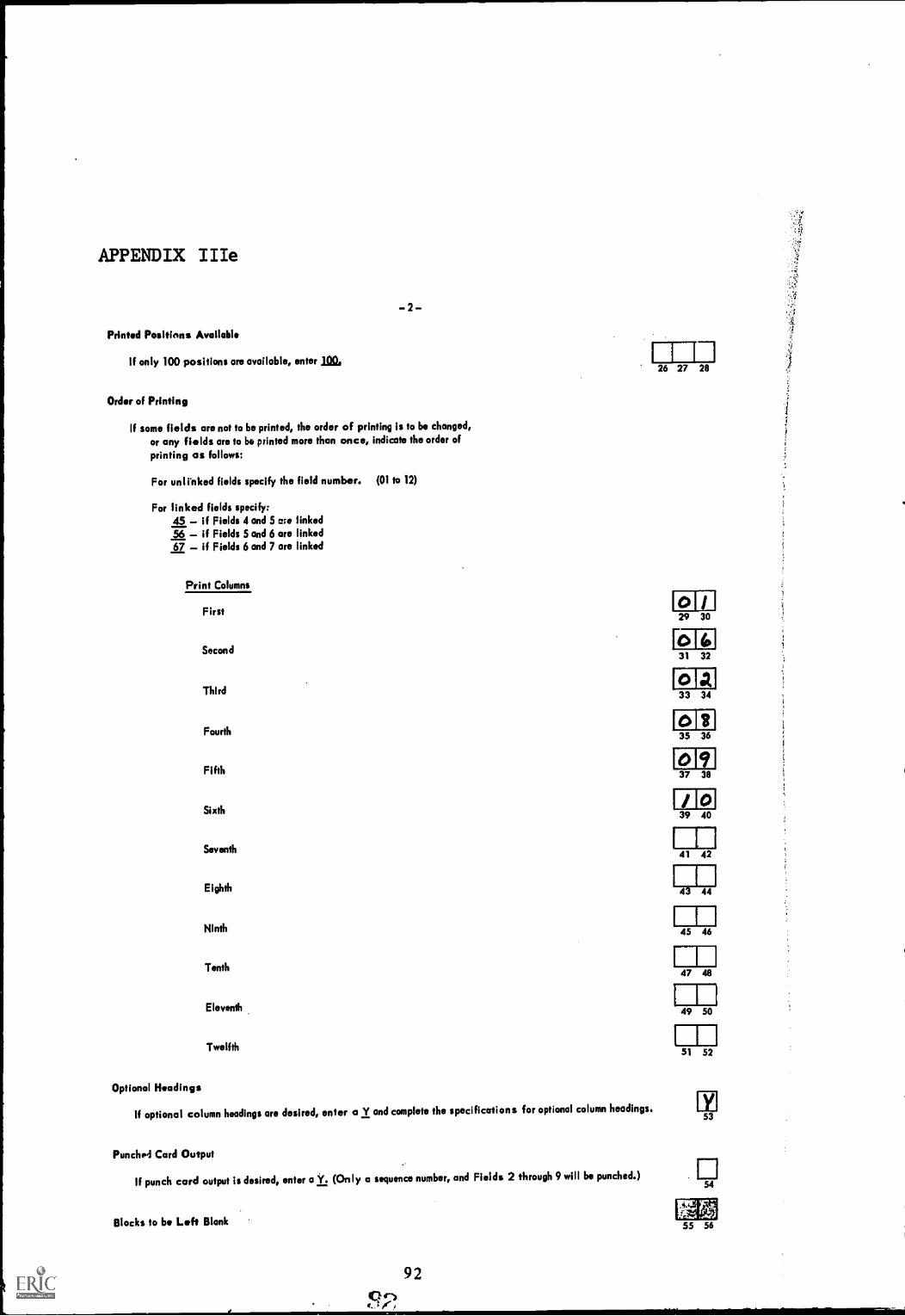

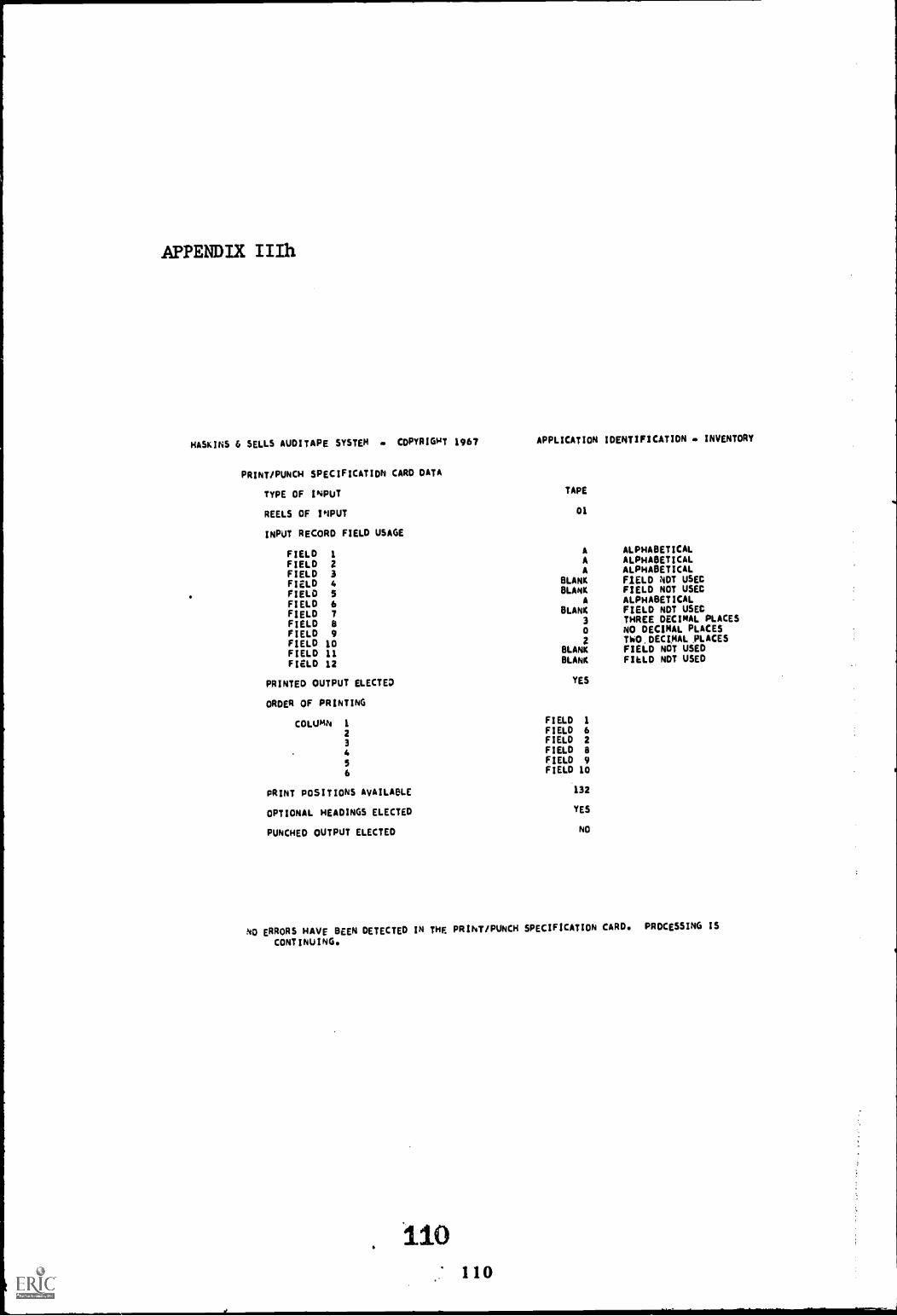

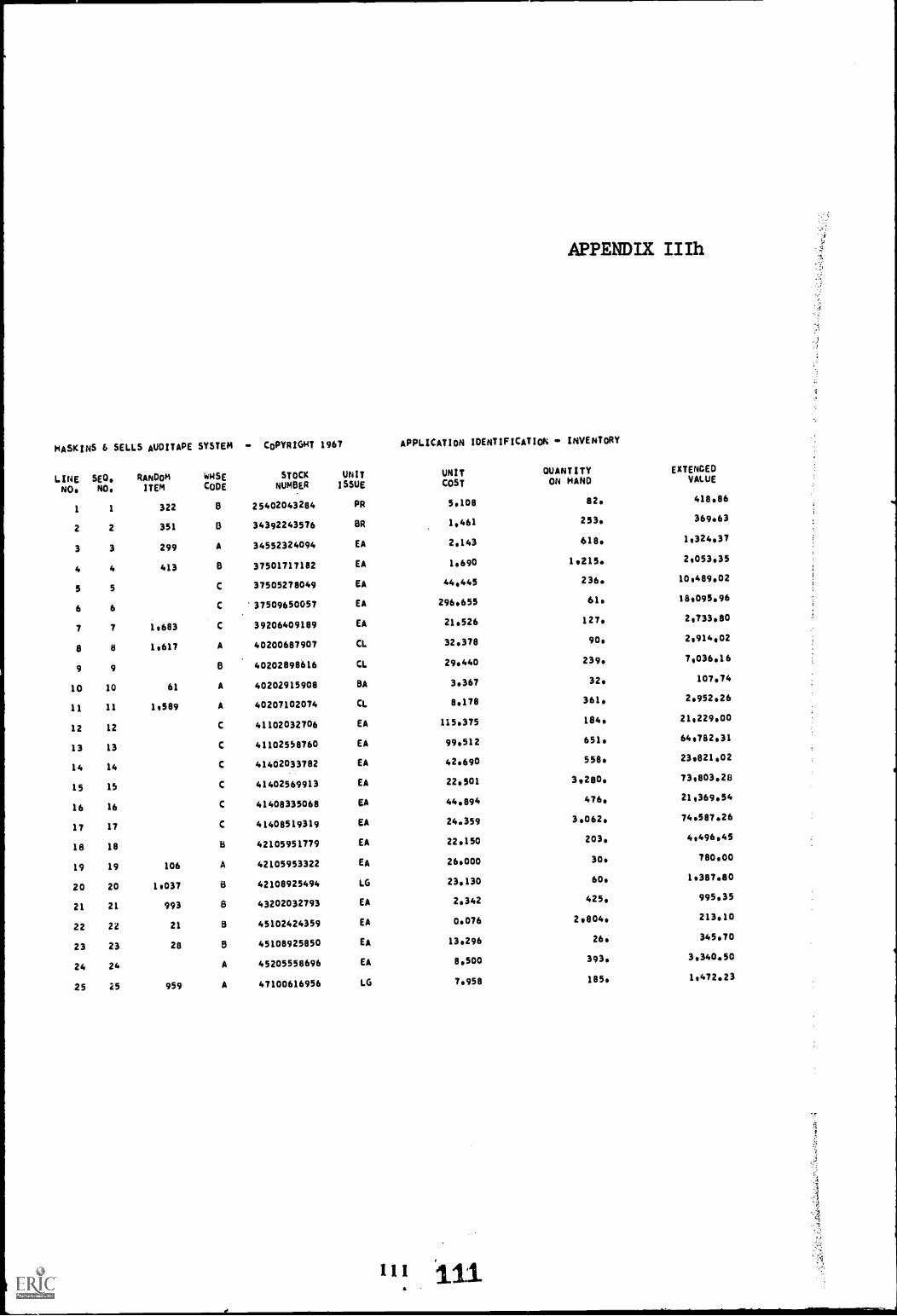

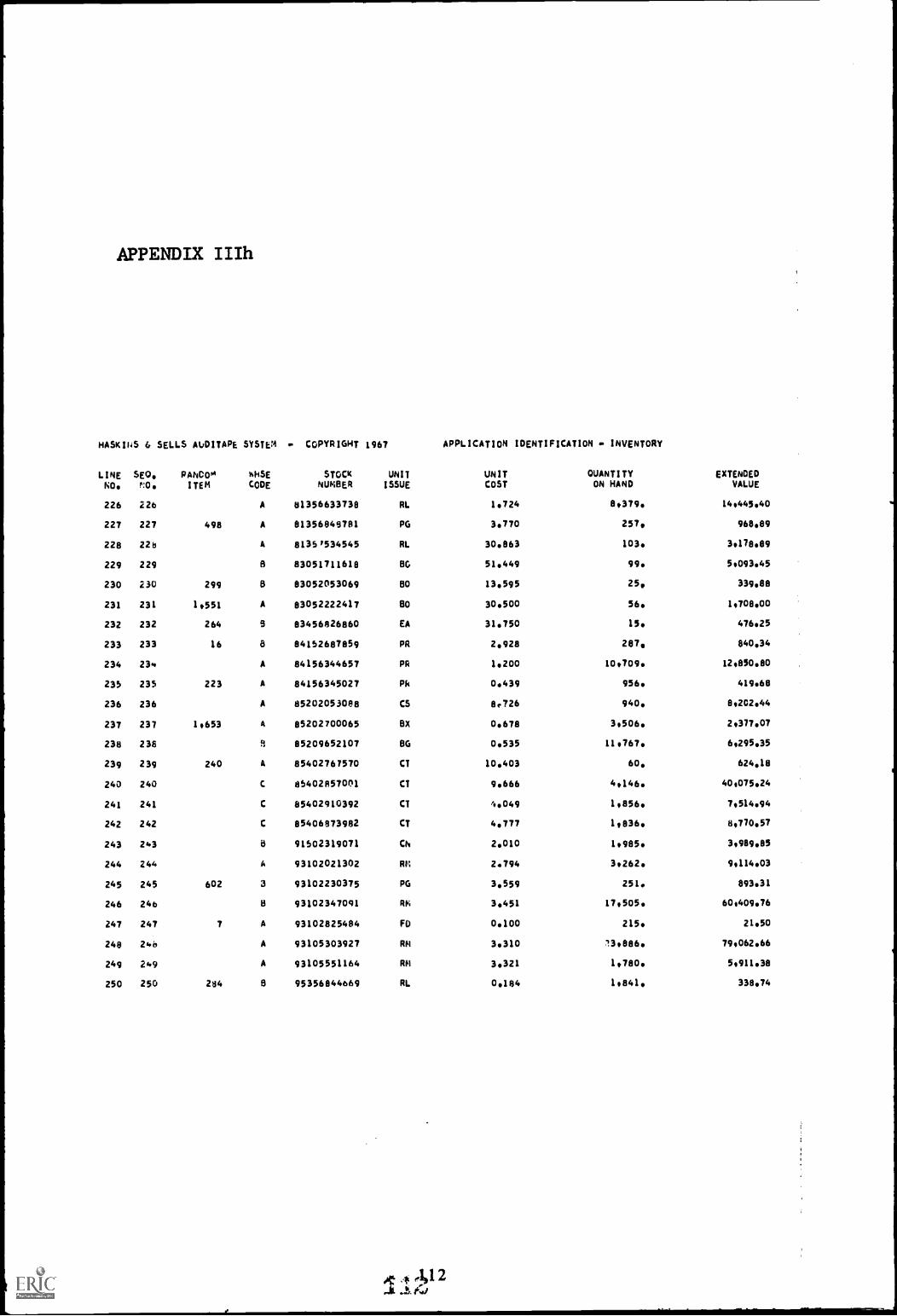

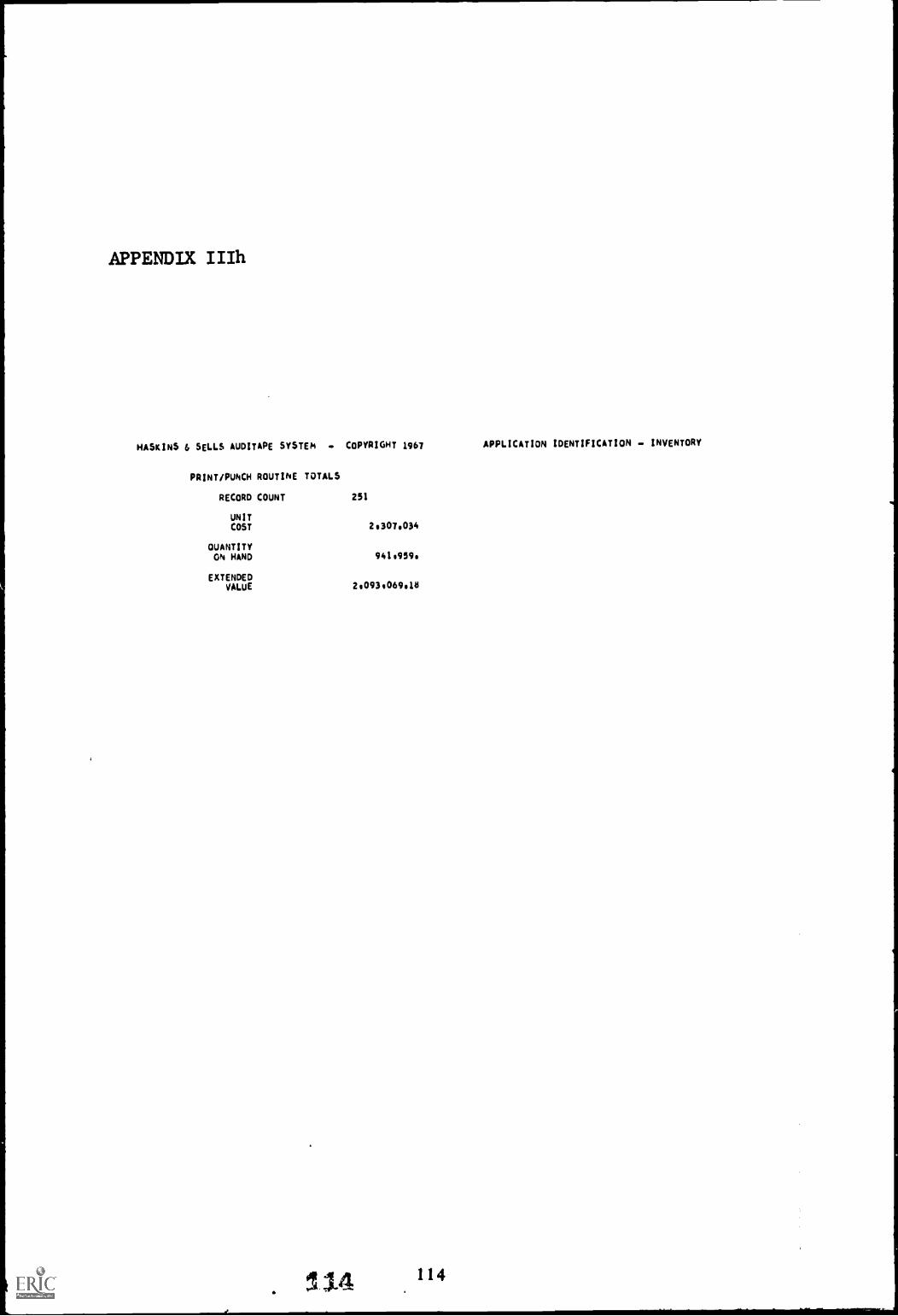

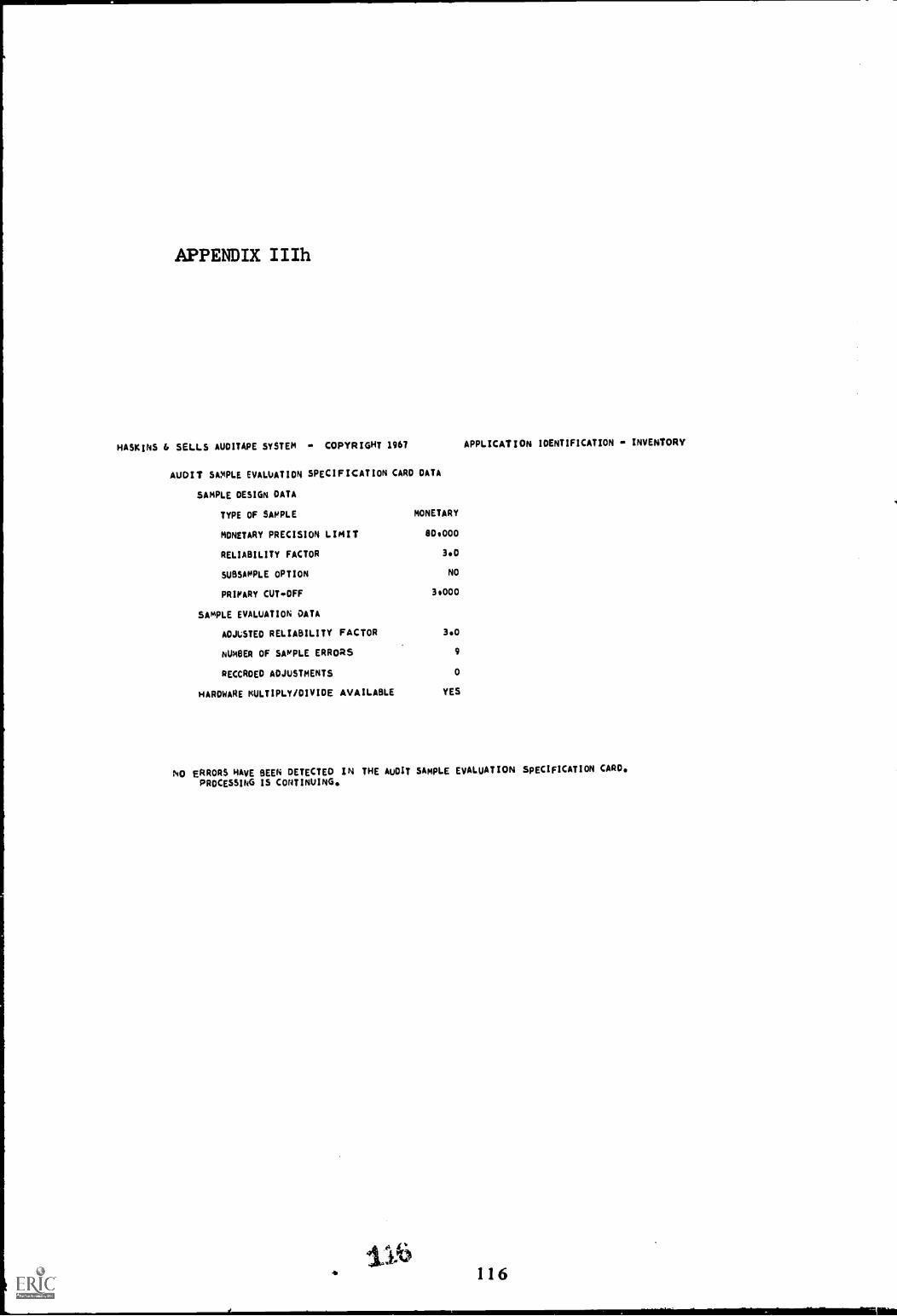

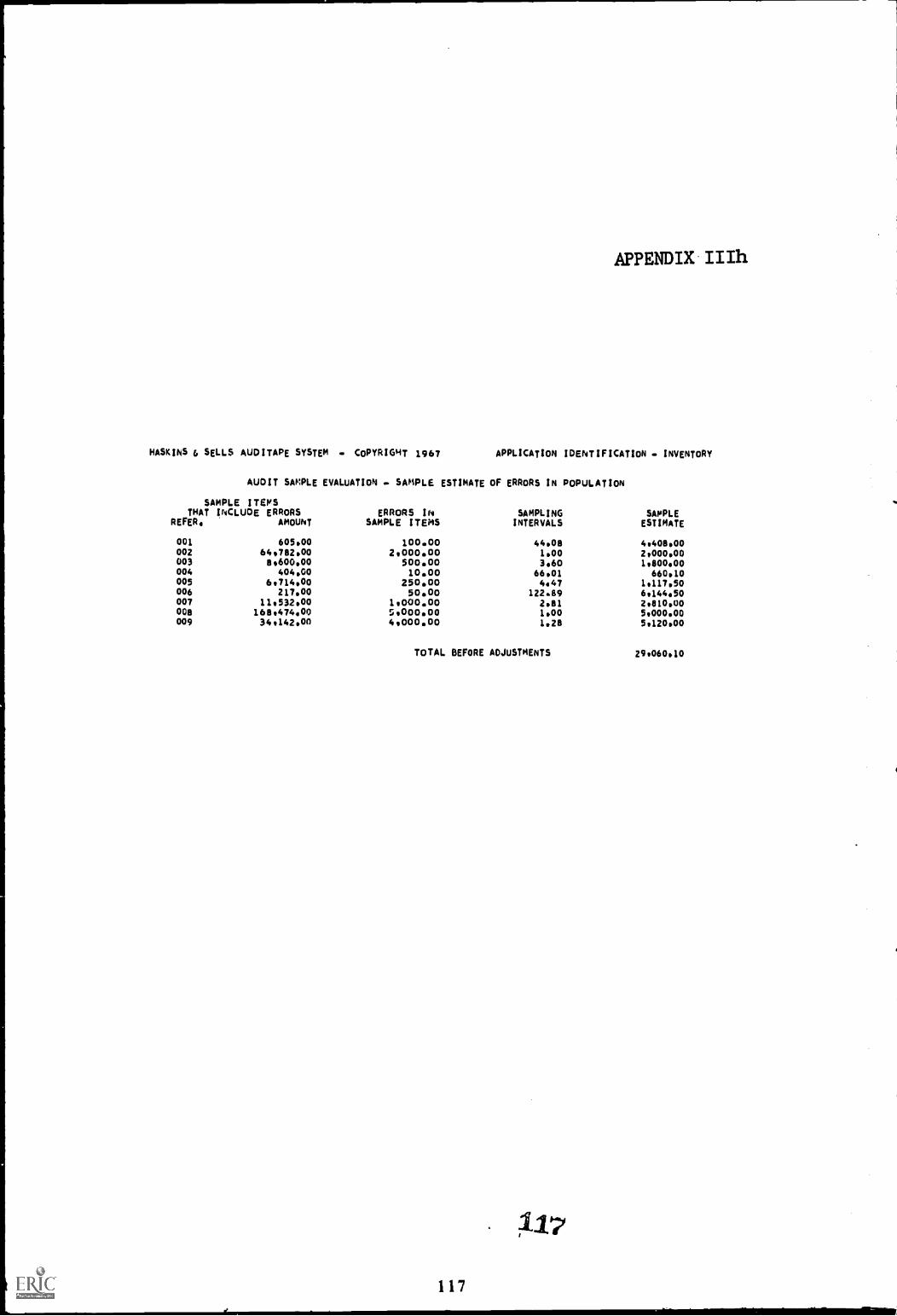

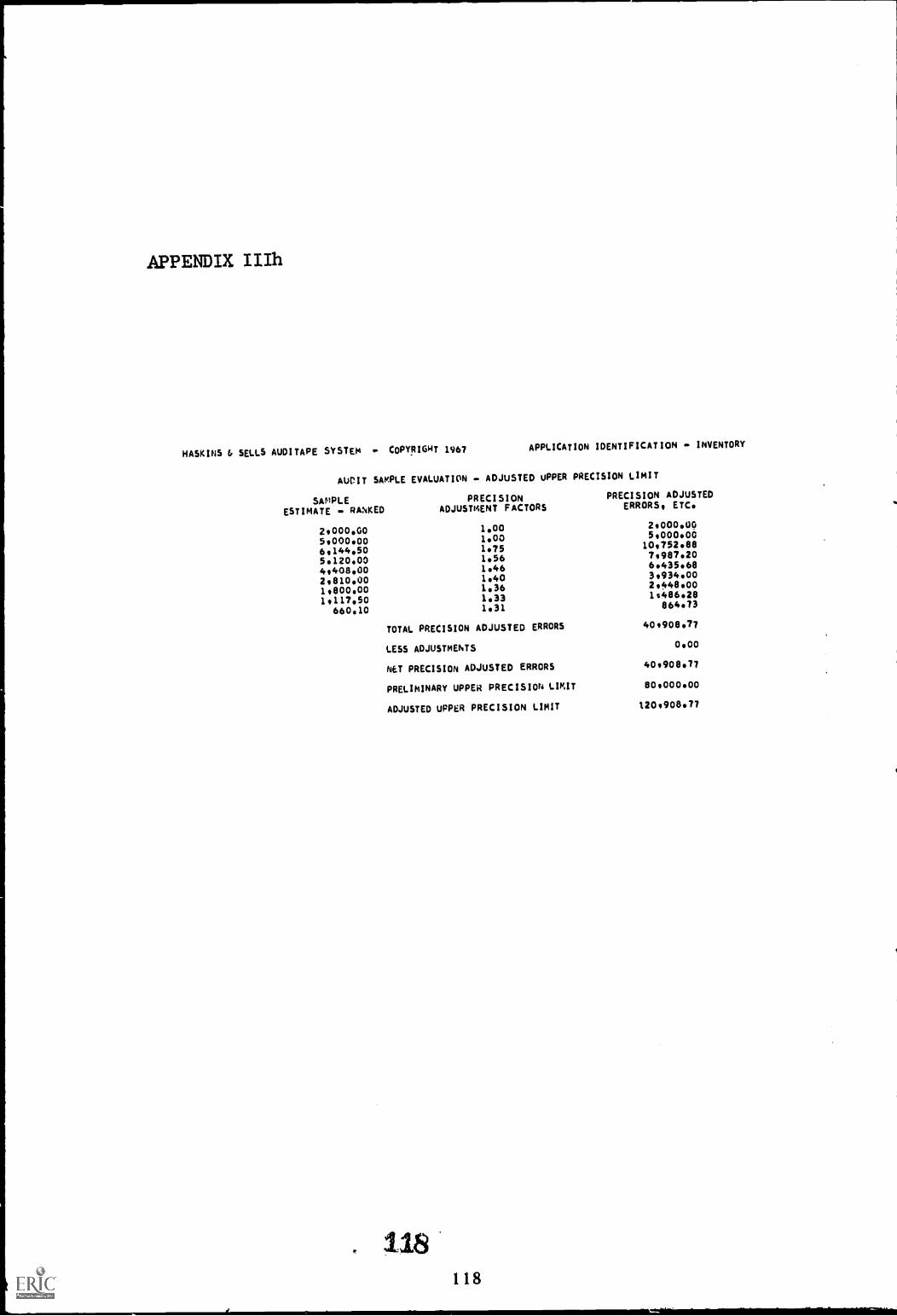

Illustrative example of an inventory auditapplication using Haskins & Sells AuditapeSystem on a Honeywell 1250 computer 61

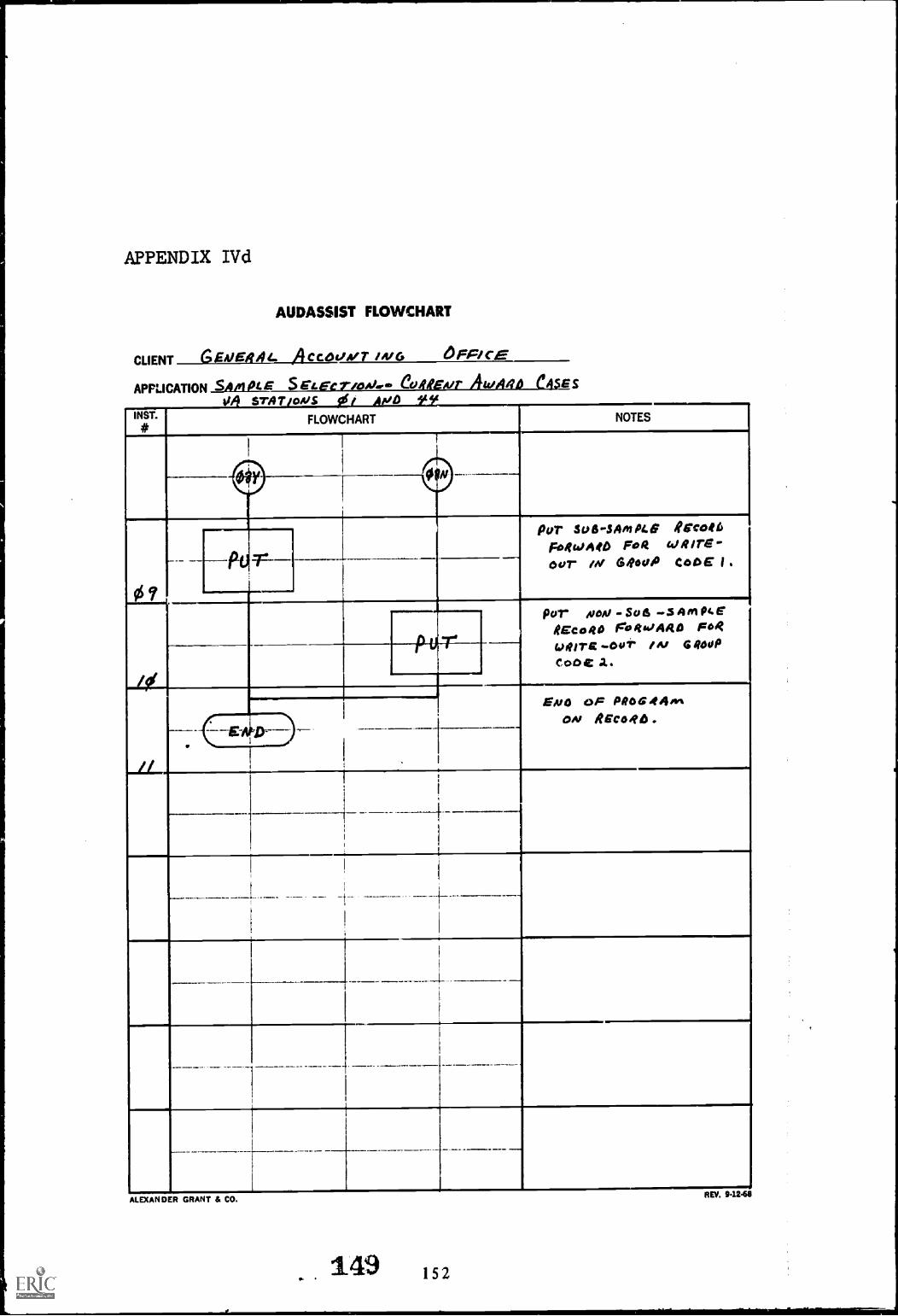

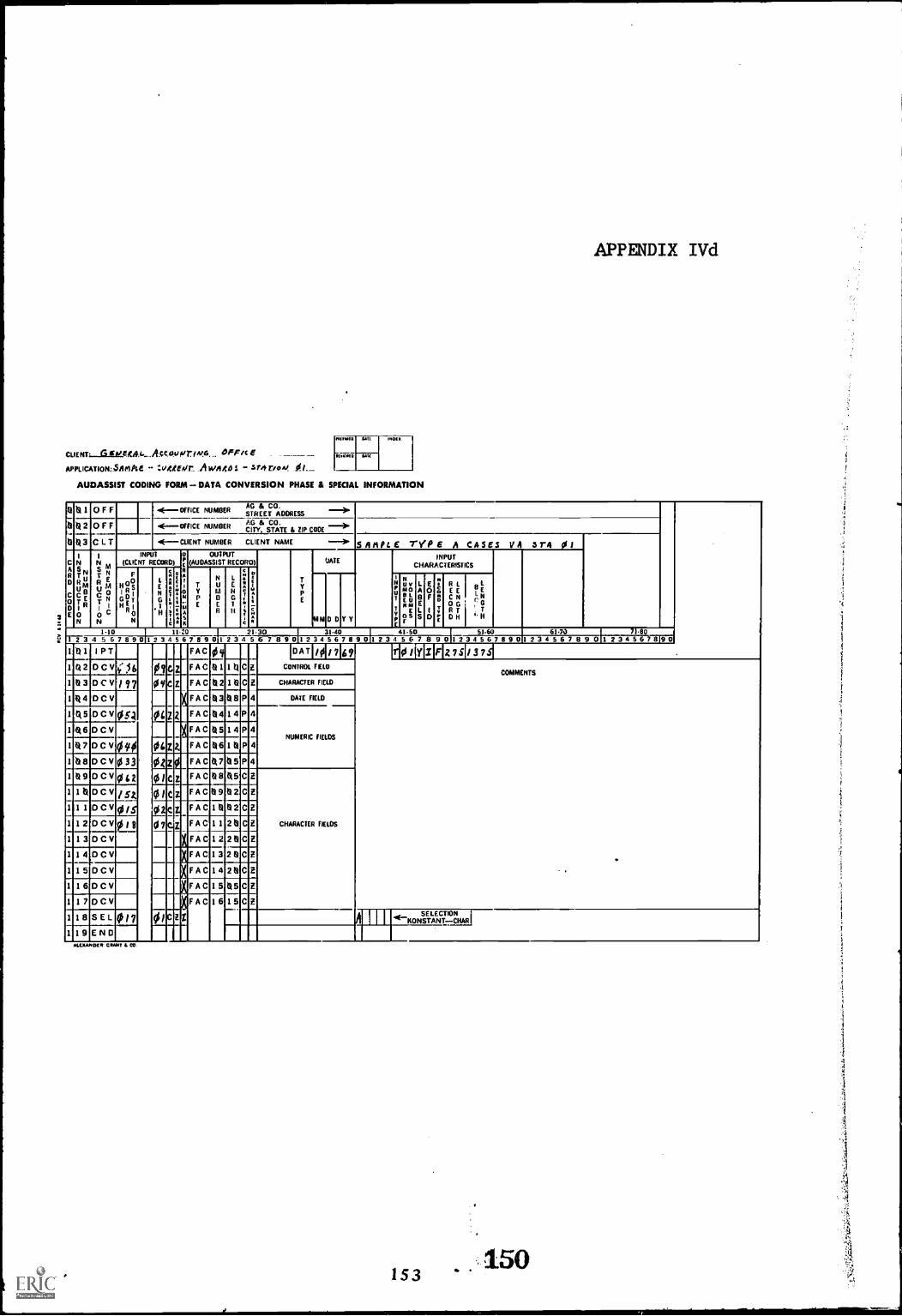

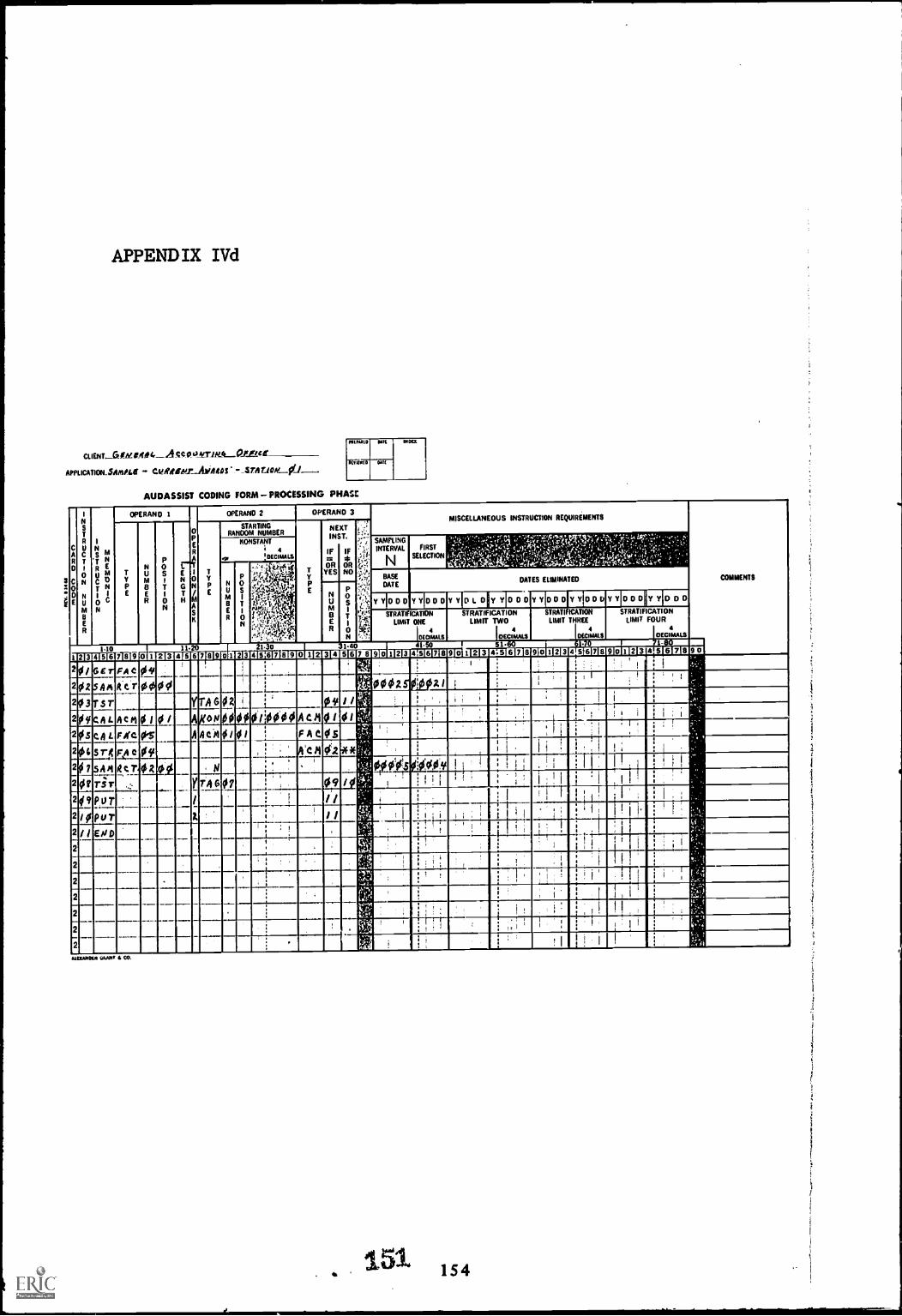

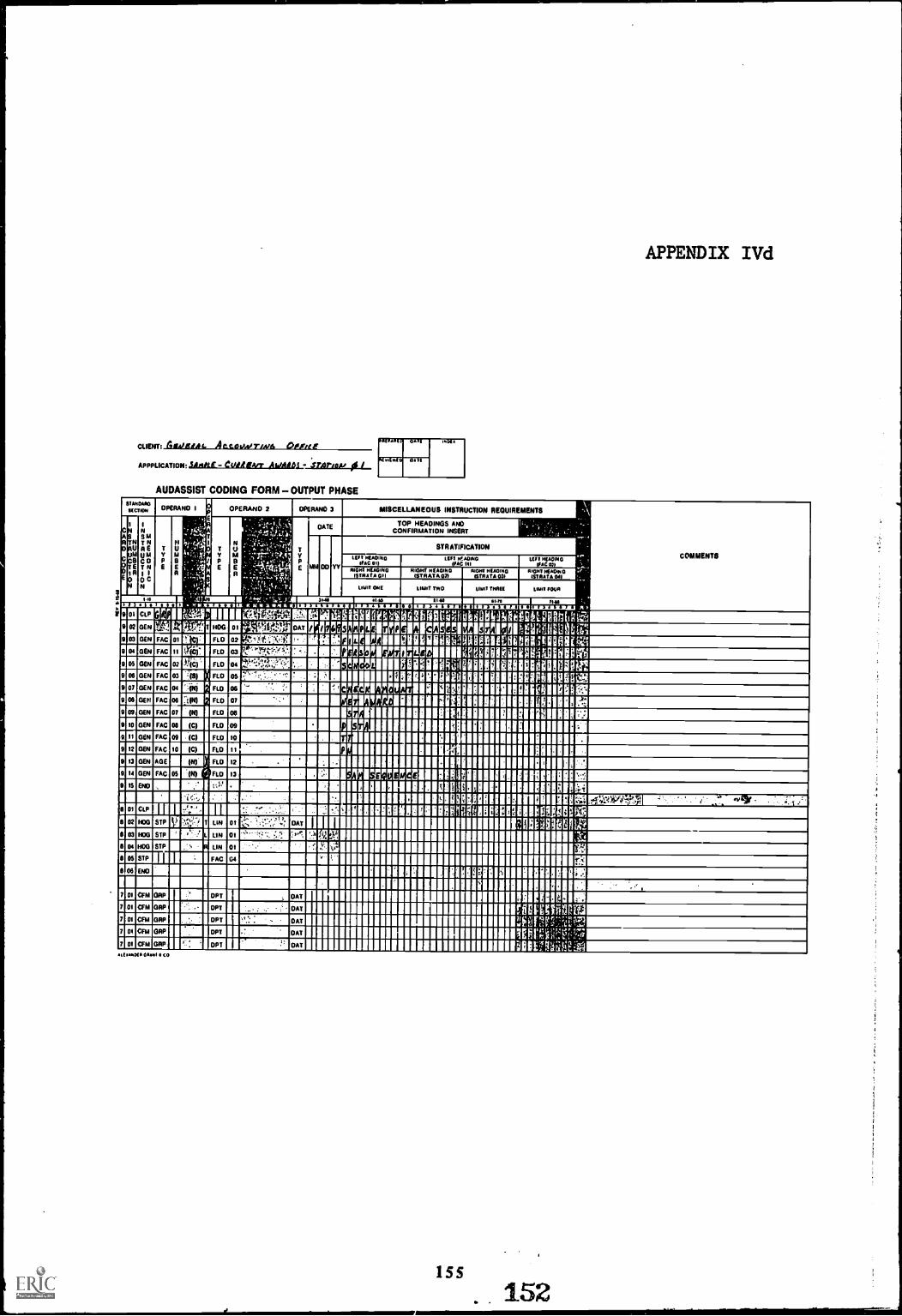

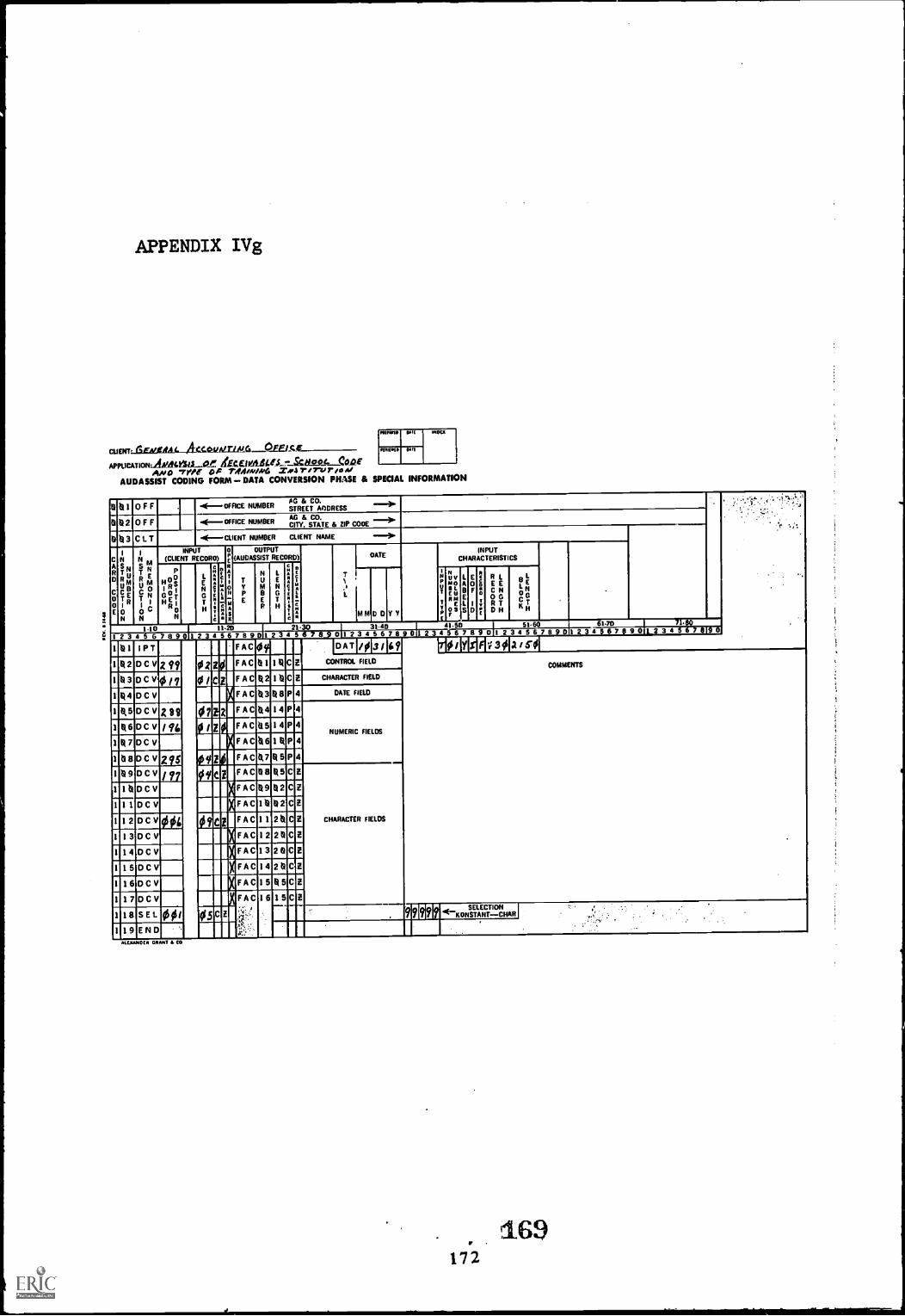

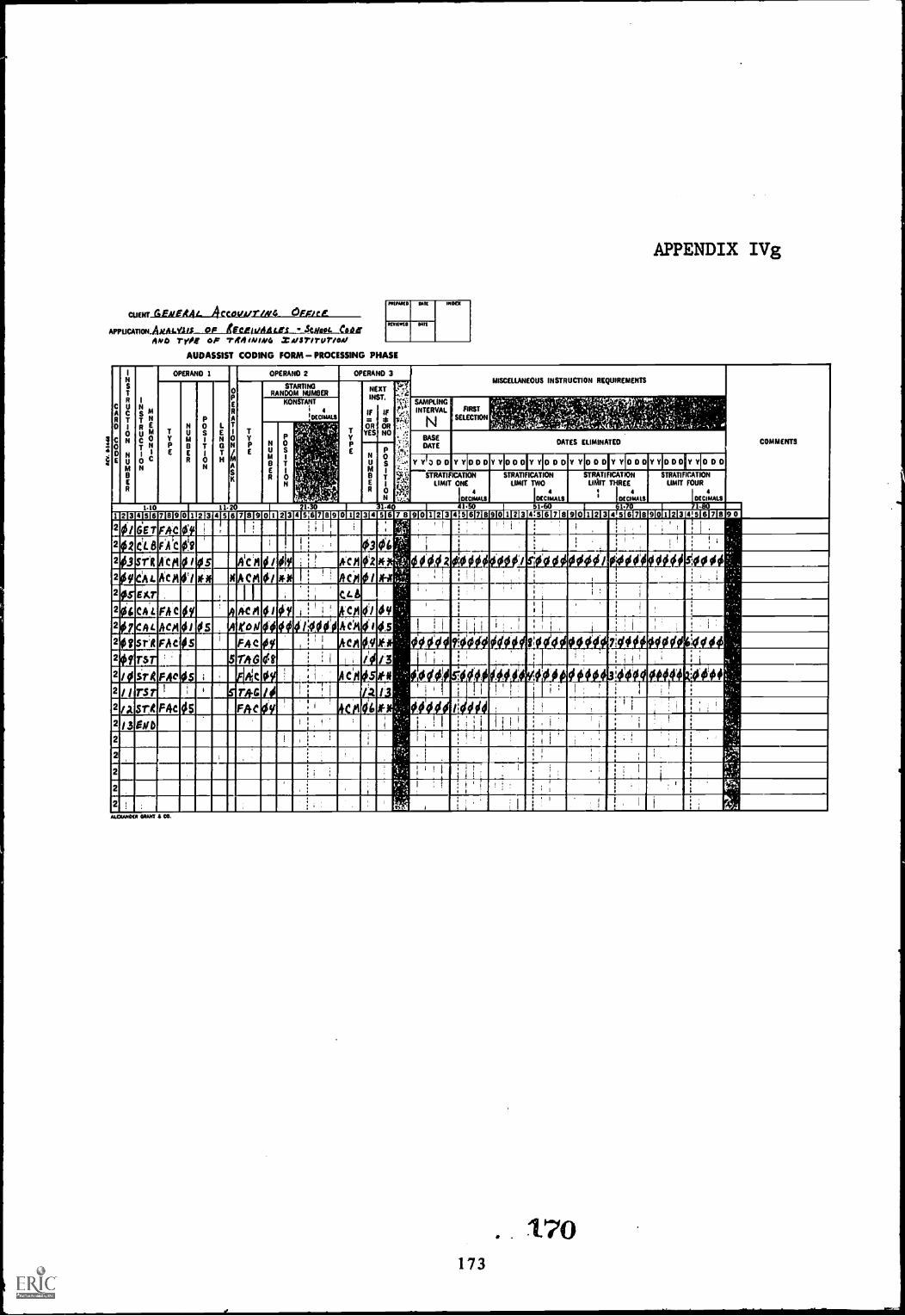

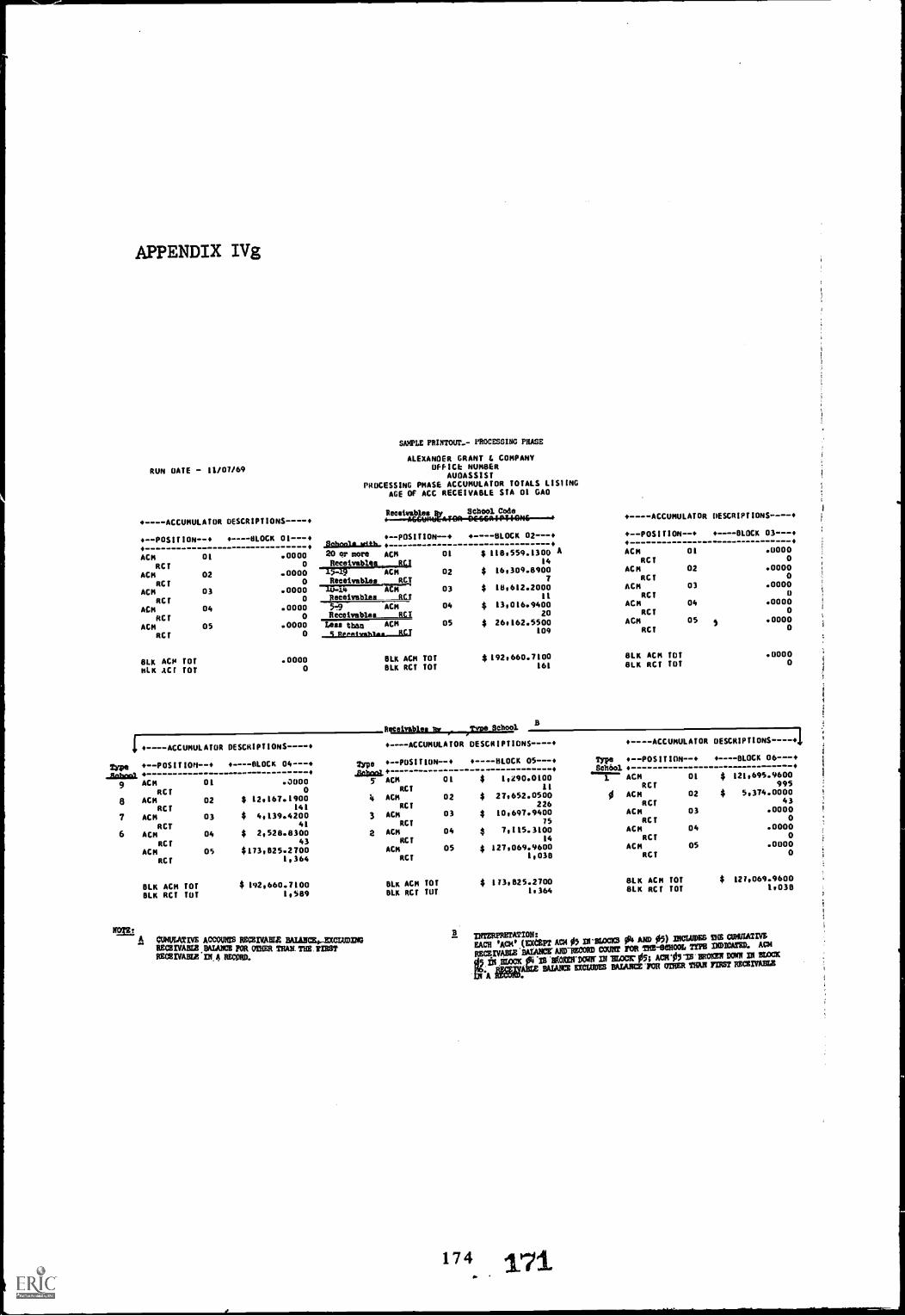

Case study on use of Alexander Grant & Com-pany's Audassist System in a review ofVeterans Administration educational assis-tance payments 121

V Test decking at the Federal Crop InsuranceCorporation 175

VI Case study--review of selected computer ap-plications at the Federal Housing Adminis-tration 185

VII Custom-designed computer matdh routine foran IBM 1401 computer 229

VIII Use of test files for comprehensive systemtesting at the Veterans AdministrationCenter, Philadelphia, Pennsylvania

IX Review guide for evaluating internal con-trols in automatic data processing sys-tems

ADP

FHA

GAO

VA

ABBREVIATIONS

Automatic Data Processing

Federal Housing Administration

General Accounting Office

Veterans Administration

237

251

CHAPTER 1

STATISTICS ON COMPUTERS IN THE FEDERAL GOVERNMENT

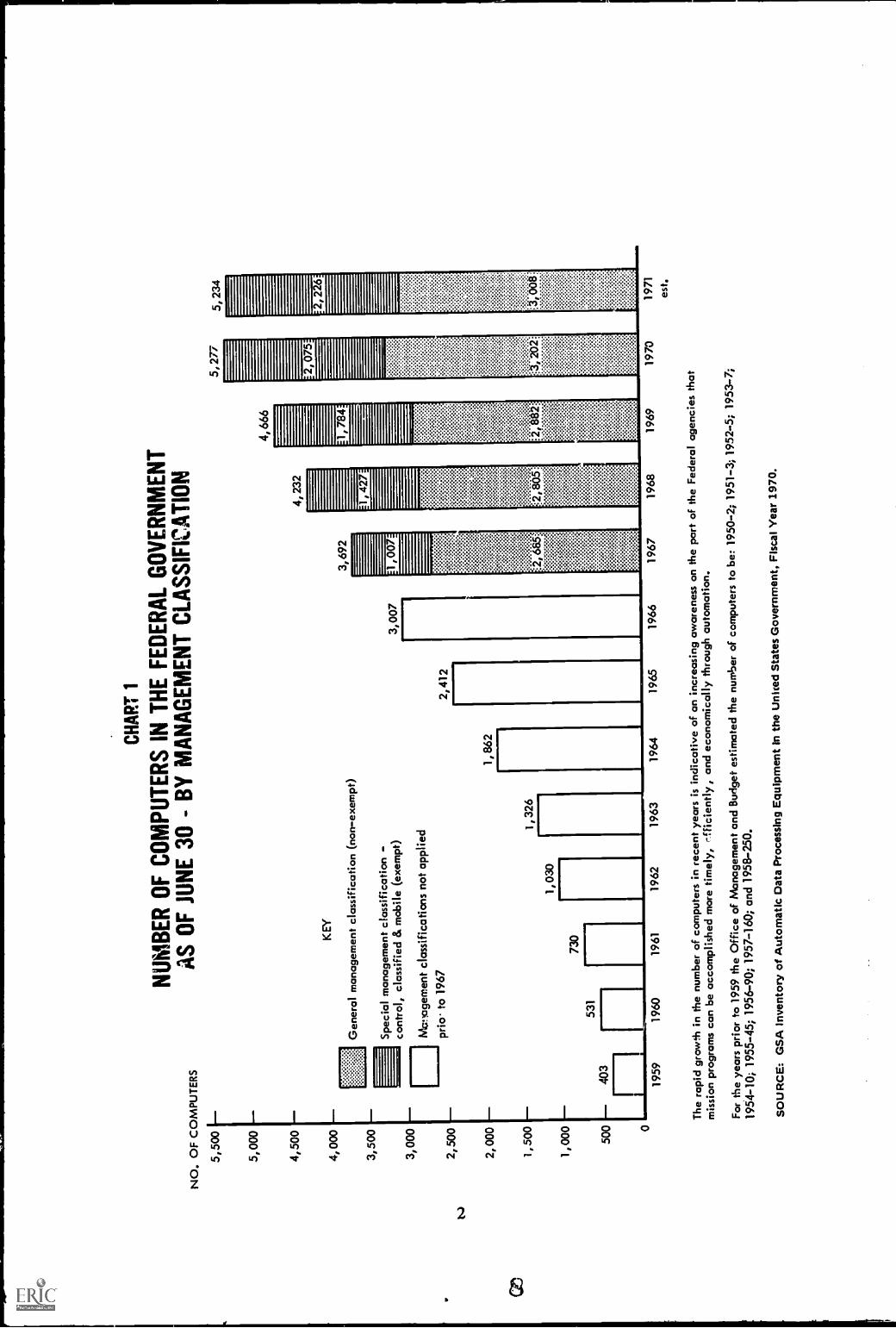

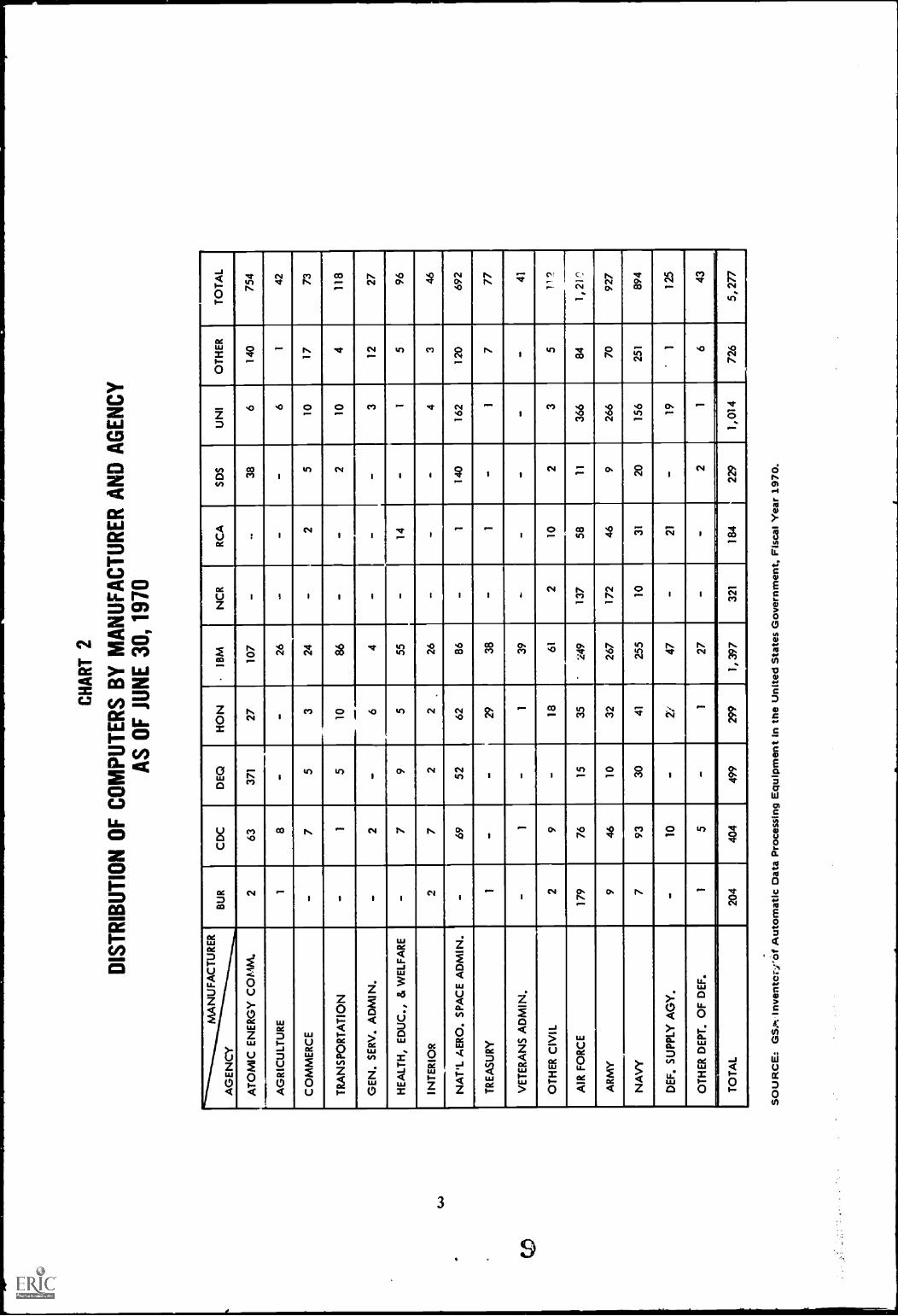

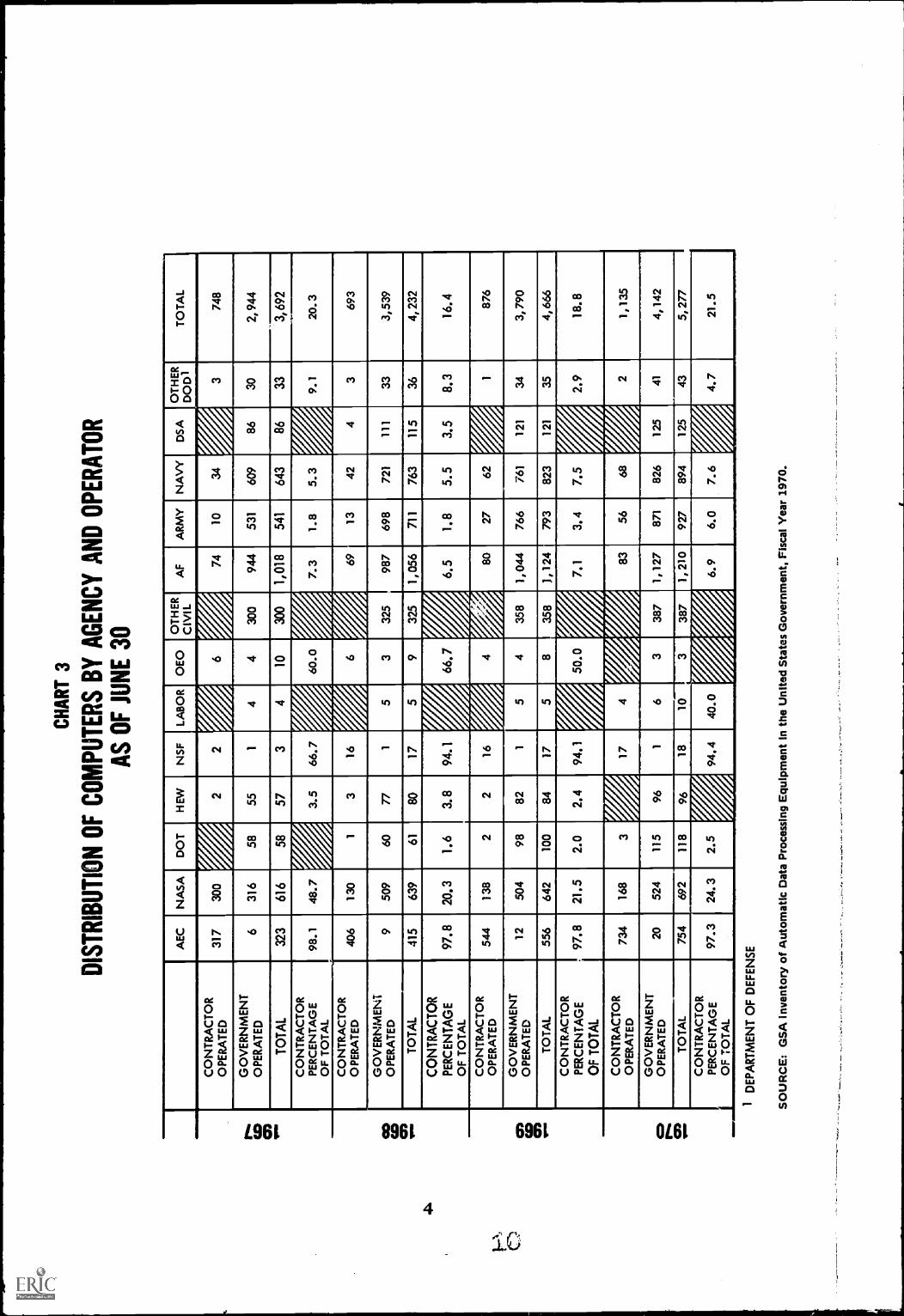

The use of computers in the Federal Government hasgrown rapidly in the past decade. The following charts pro-vide a quick picture of the growth of computer use and thedistribution of computers by manufacturer and by agency.For example, over 5,200 computers, exclusive of analog andother computers built or modified to special Governmentdesign specifications, were installed in the Federa Govern-ment by 1970. Only 10 years prior there were as few as 531.

Billions of dollars have been invested in the develop-ment and use of computers and computer-related devices.The annual Federal Government expenditures for the purchaseand use of automatic data processing (ADP) equipment is notreadily avOlable. In congressional hearings conducted inJuly 1970,' these expenditures were estimated between $4 bil-lion and $6 billion.

Computer uses extend into almost every phase, both ad-ministrative ard technical, of Government operations. Theelectronic computer has come to be regarded as a major andvital resource for accomplishing the primary program respon-sibilities of many Government agencies. Therefore specialmanagement and audit attention is warranted to ensure thatthis resource is used efficiently and effectivtly.

1Hearing before the Subcommittee on Economy in Government ofthe Joint Economic Committee, Ninety-first Congress, secondsession, dated July 1, 1970, pages 17 and 18.

1

NO

. OF

CO

MP

UT

ER

S

5,50

0

5,00

0

4,50

0

4,00

0

3,50

0

3,00

0

2,50

0

2,00

0

1,50

0

1,00

0

500 0

CH

AR

T 1

NU

MB

ER

OF

CO

MP

UT

ER

S IN

TH

E F

ED

ER

AL

GO

VE

RN

ME

NT

AS

OF

JU

NE

30

- B

Y M

AN

AG

EM

EN

TC

LAS

SIF

ICA

TIO

N

KE

Y

Gen

eral

man

agem

ent c

lass

ifica

tion

(non

-exe

mpt

)

Spe

cial

man

agem

ent c

lass

ifica

tion

cont

rol,

clas

sifie

d &

mob

ile (

exem

pt)

ivi,a

gem

ent c

lass

ifica

tions

not

app

lied

pric

y to

196

7

531

403

1959

1,03

0

730

1,32

6

1,86

2

2,41

2

3,00

7

3,69

2

1:1,

007=

4,23

2

1,42

7=

,665 :,

4,66

6

784

:-2,

.882

;

5,27

7

2,07

5=

5,23

4

2,22

6

3,00

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

est.

The

rap

id g

row

th in

the

num

ber

of c

ompu

ters

in r

ecen

t yea

rs is

indi

cativ

eof

an

incr

easi

ng a

war

enes

s on

the

part

of t

he F

eder

al a

genc

ies

that

mis

sion

pro

gram

s ca

n be

acc

ompl

ishe

d m

ore

timel

y, r

fFic

ient

ly,

and

econ

omic

ally

thro

ugh

auto

mat

ion.

For

the

year

s pr

ior

to 1

959

the

Offi

ce o

f Man

agem

ent a

nd B

udge

test

imat

ed th

e nu

mbe

r of

com

pute

rs to

be:

195

0-2;

195

1-3;

195

2-5;

195

3-7;

1954

-10;

195

5-45

; 195

6-90

; 195

7-16

0; a

nd 1

958-

250.

SO

UR

CE

: GS

A In

vent

ory

of A

utom

atic

Dat

a P

roce

ssin

g E

quip

men

tin

the

Uni

ted

Sta

tes

Gov

ernm

ent,

Fis

cal Y

ear

1970

.

CH

AR

T 2

DIS

TR

IBU

TIO

N O

F C

OM

PU

TE

RS

BY

MA

NU

FA

CT

UR

ER

AN

D A

GE

NC

YA

S O

F J

UN

E 3

01 1

970

MA

NU

FA

CT

UR

ER

AG

EN

CY

BU

RC

DC

DE

QH

ON

IBM

NC

RR

CA

SD

SU

N!

OT

HE

RT

OT

AL

AT

OM

IC E

NE

RG

Y C

OM

M.

263

371

2710

7-

-38

614

075

4

AG

RIC

ULT

UR

E1

8-

-26

--

-6

142

CO

MM

ER

CE

-7

53

24-

25

1017

73

TR

AN

SP

OR

TA

TIO

N-

15

1086

--

210

411

8

GE

N. S

ER

V. A

DM

IN.

-2

-6

4-

--

312

27

HE

ALT

H, E

DU

C.,

8 W

ELF

AR

E-

79

555

-14

-1

596

INT

ER

IOR

17

22

26-

--

43

46

NA

T'L

AE

RO

. SP

AC

E A

DM

IN.

-69

5262

86-

114

016

212

069

2

TR

EA

SU

RY

1-

-29

38-

1-

I7

77

VE

TE

RA

NS

AD

MIN

.-

1-

139

--

--

-41

OT

HE

R C

IVIL

29

-18

612

102

35

112

AIR

FO

RC

E17

976

1535

''4

4913

758

1136

684

1,21

?

AR

MY

946

1032

267

172

469

266

7092

7

NA

VY

793

3041

255

1031

2015

625

189

4

DE

F. S

UP

PLY

AG

Y.

-10

-71

47-

21-

191

125

OT

HE

R D

EP

T. O

F D

EF

.1

5-

127

--

21

643

TO

TA

L20

440

449

929

91,

397

321

184

229

1,01

472

65,

277

SO

UR

CE

: GS

.tb. i

nven

tor:

la A

utom

atic

Dat

a P

roce

ssin

g E

quip

men

t in

the

Uni

ted

Sta

tes

Gov

ernm

ent,

Fis

cal Y

ear

1970

.

4:6

CH

AR

T 3

DIS

TR

IBU

TIO

N O

F C

OM

PU

TE

RS

BY

AG

EN

CY

AN

D O

PE

RA

TO

R

AS

OF

JU

NE

30

AE

CN

AS

AD

OT

HE

WN

SF

LAB

OR

0E0

OT

HE

RC

IVIL

AF

AR

MY

NA

VY

DS

AO

TH

ER

DO

D1

TO

TA

L

r...

CD

CD 1- .

CO

NT

RA

CT

OR

OP

ER

AT

ED

317

300

42

2/

6..,

7410

34A

374

8

GO

VE

RN

ME

NT

OP

ER

AT

ED

316

5855

14

430

094

453

160

986

302,

944

TO

TA

L32

361

658

573

10

60. 0

300

,'/- r1,

018

7. 3

541

1. 8

643

.,5.

3

86

i33 9. 1

3,69

2C

ON

TR

AC

TO

RP

ER

CE

NT

AG

EO

F T

OT

AL

98. 1

48. 7

3.5

66. 7

GO

CC 0, .....

CO

NT

RA

CT

OR

OP

ER

AT

ED

406

130

13

16

,

6/4

69

.

1342

43

693

GO

VE

RN

ME

NT

OP

ER

AT

ED

950

960

771

53

325

987

698

721

111

333,

539

TO

TA

L41

563

961

8017

59

325

1,05

671

176

311

536

4,23

2C

ON

TR

AC

TO

RP

ER

CE

NT

AG

EO

F T

OT

AL

97. 8

20.3

1.6

3.8

94.1

v66

. 7V

,/,.

6. 5

1. 8

5. 5

3. 5

8. 3

16. 4

0, CO

CO

CO

NT

RA

CT

OR

OP

ER

AT

ED

544

138

22

164

/7, ,

8027

62V

187

6

GO

VE

RN

ME

NT

OP

ER

AT

ED

1250

498

821

54

358

1, 0

4476

676

112

134

3, 7

90

TO

TA

L55

664

210

084

175

835

81,

124

793

823

121

354,

666

CO

NT

RA

CT

OR

PE

RC

EN

TA

GE

OF

TO

TA

L97

.821

.52.

02.

494

.150

.0ef

7.1

3.4

7.5/

2.9

18.8

4=0 r co _.

....

CO

NT

RA

CT

OR

OP

ER

AT

ED

734

168

3'

417

4f n

A83

56a

42

1, 1

35

GO

VE

RN

ME

NT

OP

ER

AT

ED

2052

411

596

16

338

71,

127

-

871

,

826

125

414,

142

TO

TA

L75

469

211

896

1810

338

71,

210

927

894

125

435,

277

CO

NT

RA

CT

OR

,P

ER

CE

NT

AG

E

1O

F T

OT

AL

97. 3

24. 3

2.5

94. 4

40. 0

j A6

9 -6.

07.

6/

j ,4. 7

21. 5

1D

EP

AR

TM

EN

T O

F D

EF

EN

SE

SO

UR

CE

: GS

A i

nven

tory

of A

utom

atic

Dat

a P

roce

ssin

g E

quip

men

t in

the

Uni

ted

Sta

tes

Gov

ernm

ent,

Fis

cal Y

ear

1970

.

CHAPTER 2

SUMMARY OF OBSERVATIONS

INTERNAL AUDIT OF ADP SYSTEMS

In individual Federal agencies, internal audit coverage

of agency computer operations varies from comprehensive sys-

tem testing to practically no work at all. Although some

internal audit groups recently have shown increased interest,

in the past, auditors have tended to shy away from compre-

hensive reviews of computer-based systems. Even though com-

puter systems are becoming increasingly an integral part of

agency management and control, independent reviews and ap-

praisals are generally not made to assist managers in es-

tablishing effective controls over complex computer systems.

The General Accounting Office (GAO) believes that it

is important for an independent group to review and evaluate

agency computer operations, especially those systems whichaffect agency management and control operations, as well as,

those systems which involve the disbursement of billions of

dollars every year. In the absence of independent evalua-

tions of computer-based systems, the computer operation is

vulnerable to undetected error, misuse, and possibly fraud.

GAO believes that Federal agency managers should require

internal auditors, or a similar group, to devote more atten-

tion to computer systems than currently is being done.

DOCUMENTATION OF ADP SYSTEMS

A related problem centers on the fact that most Federal

agencies have not developed or implemented agencywide doc-

umentation standards for computer-based systems. In general,

documentation being produced is incomplete and inadequate.

Documentation may be used by management not only to monitor

and control the computer facility resources of an organiza-

tion but also as a check on performance and compliance withestablished goals and standards for such resources. Conse-

quently, GAO believes that Government-wide documentatica

standards should be developed and promulgated by the execu-

tive branch to guide all Federal agencies in maintaining an

adequate level of system documentation. GAO believes also

that the heads of Federal agencies, as an interim measure

5

ti

`14

A

pending adoption of Federal standards by the executivebranch, shauld take necessary action to ensure that their

computer systems documentation meets the standards listed

in this report. (See pp. 18 to 21.)

COMPUTER-AUDITING TECHNIQUES

New computer-auditing techniques have been developed

to assist the auditor in reviewing computer systems and

computer-generated records. These techniques permit the

auditor to use the computer's speed and accuracy to

--search files and select data for examination,--make special analyses or summarizations of data,

--perform computations,--identify unusual transactions, and--test check processing accuracy.

Several techniques used successfully by GAO include general.

ized computer audit programs, customAesigned computer au-dit programs, test decks, and detailed reviews of selected

computer programs. Chapter 5 contains a discussion of eachtechnique and a reference to case studies for the reader

interested in further study.

6

CHAPTER 3

NEED TO ESTABLISH EFFECTIVE

INTERNAL AUDIT OF ADP SYSTEMS

Internal audit coverage has not kept pace with the

computerizatron of agency operations. Few of the departments

and agencies that we visited during GAO's study indicated

that the internal audit staffs review operational ADP sys-

tems on a regular basis. Some audit staffs do very little

work, or no work at all, on these computerized systems.Reviews of computer systems normally are not made unlessthe computer operation is an integral part of an accounting,

supply, or some other function that is being audited.

Internal audit staffs generally have not reviewed ADPsystems to determine whether they meet original objectivesor whether they are operating efficiently and effectively.Although there has been an increase in internal audit inter-est and involvement with computer systems late in 1970 andearly in 1971, GAO believes that this effort must be in-creased and the scope of coverage broadened. It is impor-tant for internal audit staffs to understand, review, andevaluate agency ADP operations. In the absence of an inde-pendent review and appraisal of such a major part of anagency operation, GAO believes also that the adequacy ofinternal controls and safeguards over ADP operations aresubject to question.

In this study, GAO observed that the degree to which

auditors were involved in evaluating computer systems varied

from comprehensive system testing, including a check of

every computer program change, to almost no work at all.

For example, the resident system auditors at the Veterans

AdmLnistration (VA) Center in Philadelphia use a permanent

test file to perform comprehensive testing of the VA insur-

ance program. The test file is used on a continuing basis

to establish the validity and accuracy of operating com-

puter programs. Every change is checked and certified be-

fore it goes "live." A detailed discussion of the VA's

test file is included in appendix VIII.

7

.y!

At the other extreme, we found that internal auditorsperform almost no work at all on their agency's ADP opera-tions. At one agency the internal auditors advised us thatthey make no reviews of the computer systems; instead, theyaudit around the computer. Management officials relied ontesting procedures that simply verified the consistency ofprocessing plus other quality control checks that, in ouropinion, constituted neither a complete nor independent re-view. Furthermore, documentation or written descriptionsnecessary for understanding how the computer system operatedgenerally were incomplete or not current. Under these con-ditions, we believe that a system is extremely vulnerable toerror or misuse. GAO views the achievement of efficient,economical, and effective operations as a basic agency man-agement responsibility. Because computers are used inachieving these goals, management officials must assurethemselves as to the adequacy of the controls over computeroperations, especiallz in view of the multibillion-dollaroperations handled through computers.

One of the essential tools of management, complementingall other elements of management control, is the internalaudit function. The Congress, through the Budget and Ac-counting Procedures Act of 1950, requires that the head ofeach agency establish and maintain systems of internal con-trol designed to provide effective control over and account-ability for all funds, property, and other assets for whichthe agency is responsible, including appropriate internalaudit. For many years GAO emOasized the importance ofstrong internal audit systems.' To provide necessary con-trols over computer operations, we believe that the scope ofinternal audit coverage should be expanded to include reviewsand evaluation of all agency computer systems.

1General Accounting Office Policy and Procedures Manual forGuidance of Federal Agencies, title 3, chapter 11--InternalAuditing.

Internal Auditing in Federal Agencies, United States Gen-eral Accounting Office, pamphlet dated October 1968.

GAO Views on Internal Auditing in the Federal Agencies,United States General Accounting Office, booklet dated 1970.

SCOPE OF INTERNAL AUDITING

To be of maximum usefulness, internal auditing shouldextend to all agency activities and related management con-trols. Its scope should not be restricted.

In the specific area of data processing, the internalauditor's coverage should include both new systems underdevelopment and those in operation. For example, the auditorshould be consulted in the development, design, and testingof ADP systems to help ensure that adevate controls are es-tablished and adequate audit trails are provided in the sys-tem to avoid costly changes after a new system has been in-stalled. For systems already in operation, the auditorshould continuously monitor the computer operation and per-form necessary appraisals to determine whether an effectiveand reliable system is functioning.

CHANGE IN AUDIT APPROACH REQUIRED

To perform an effective review and appraisal of certainsophisticated ADP systems, a change in the audit approachis required.

The advent of the computer has not changed the gener-ally accepted auditing standard that the auditor must studyand evaluate the existing internal controls as an integralpart of his audit work. In the non-ADP environment, theauditor has historically been able to see and follow theflow of transactions through the system. A visible audittrail has been the key to this approach. In an ADP environ-ment, however, some of the characteristics of today' s moresophisticated computer systems make this approach impracti-cal, if not,impossible. The visible audit trail no longerexists in some systems. For example, the computer systemmay

--rearrange input data and perform calculations inter-

nally,

--store data on magnetic tapes, disks, and drums for

later use,

9

--print out summary ..nformation which bears no visiblerelationghip to the original input data, and

- -use equipment and computer programs that contain con-t7:631 and edit procedures which operate interna4y.

In sophisticated computer systems where more and more

of the controls and decisions are incorporated within the

computer, the audit approach must concentrate on ADP con-

trols. The audit must establish whether ADP controls are

adequate to ensure that acceptable input results in reliable

output. This kind of environment exposes the auditor to

types of controls, languages, and conceptual problems which

differ fram those prrmiously encountered.

To meet these changing needs, ADP audit nanuals or

guides, internal control questionnaires, and other computer-

auditing techniques have been developed to assist in the re-

view of computer systems. Because it is not feasible to

prepare a detailed audit program that will be uniformly ap-

plicable to all computer systems, review guides can be used.

.GAO has prepared a review guide for use in evaluating inter-

nal controls in ADP systems.1 It includes background in-

formation on ADP controls and a questionnaire for use in re-

viewing them. Another guide is the recently developed ADP

review guide for Federal agency accounting systems,.2 parts

of which are equally applicable to any data processing op-

eration.

Along with changeg in the audit approach, new tools for

auditing computer records also have been developed. Theyinclude generalized retrieval programs which permit the userto retrieve, summarize, calculate, sample, and print out

1Review Guide for Evaluating Internal Controls in AutomaticData Processing Systems, United States General Accounting

Office, 1968. (See app. IX.)

2Review Guide for Federal Agency Accounting Systems, United

States General Accounting Office. (See ADP section--app.

II.)

10

16

computerized information. Other techniques that are not

new, such as test decks and custom-designed computer audit

programs are used also. All of these computer-auditing

tools or techniques have proven to be beneficial under cer-

tain circumstances. Chapter 5 includes a more detailed

discussion of computer-auditing techniques.

BENEFITS OF COMPUTER-AUDITING TECHNIQUES

Reviews and evaluations of computer systems usingcomputer-auditing techniques do provide tangible benefits

for both auditor and management. Aside from the important

control factor provided by an independent review, some of

the benefits are

--more confidence in system output,

- -more efficient operations, and- -cost savings.

Several examples that illustrate these benefits are dis-

cussed below. In each example the computer itself was used

to perform much of the actual detailed audit work.

1. GAO conducts an annual audit of the Federal HousingAdministration (FHA) financial statements. The au-

dit involves FHA's computerized mortgage insurance

program under which lending institutions are in-sured against loss in financing first mortgages onvarious types of housing. The computer systems ac-

count for over 4-1/2-million mortgages.

As the procedures and controls were transferred to

the computer, it became more difficult for the audi-

tor to use the traditional audit approach, i.e.,

checking output to input. Summary informationprinted out by the computer could not readily be

traced back to the original input data, the tremen-

dous volume of transactions limited the scope of the

manual audit, and the auditor did not understandfully what was going on inside the computer.

To overcome these problems the audit approach was

modified to include a review and evaluation of ADP

procedures and controls. A review of computer sys-

tems documentation including the related coding of

ii

11

of selected computer programs and the processing of

selected input data through auditor controlled ver-

sions of agency computer programs were unique fea-

tures of the new review approach. The reasoning

here is that if the auditorknows exactly how the

computer processes input data and that adequate

internal controls exist, he can rely on system out-put. By using this approach the auditor; in effect,tests the computer system that generates the data

being audited.

The results of this approach pravided the auditor,for the first time, with a detailed understandingof what actually was taking place within the compu-ter. By virtue of this knowledge, the auditor hadincreased confidence in the information and totalsgenerated by the computer system. Appendix VI con-tains a more detailed description of the audit ap-proach used in the FHA audit.

2. The Air Force determines its procurement and repairneeds for reparable-type stock items through a com-puterized reparable requirement system. The require-ments computations are lengthy and complex--eachcomputation involves about 5,000 mathematical calcu-lations. The auditor had the problem of determiningthe effect, if any, that different input data had onfinal computed requirements. GAO first manuallytried to recompute the requirements. Each manualrecomputation required 1 to 1-1/2 days to complete,and even then, the auditors were not able to dupli-cate accurately the machine process because of themathematical complexity and the Sheer volume of cal-culations. The auditors could not be sure that theresults of their computations were correct.

As an alternative the auditors explored the possibil-ity of using Air Force computers to recompute re-quirements. A plan was worked out with Air Forceofficials who agreed to write a computer programthat wauld permit the auditor to make changes in theinput data. After appropriate changes were made,Air Force officials reran the requirements computa-tions with the same files used to run the original

1 2

1st

computations. Because these recomputations were madeon Air Force computers with Air Force programs, therewas no question that Air Force procedures had beenfollowed. The auditors were able to get accurate re-quirements computations that.were acceptable to theAir Force and from which it was possible to deter-mine the effect of changes in input data.

Use of the computer in this review

--saved 300 man-days that would have been needed to re-calculate requirements computations manually and

--provided the auditor with a greater degree of assur-ance and confidence in results of the work.

The next examples illustrate that an auditor, with mini-mal computer knowledge and armed with a relatively easy touse computer audit retrieval program, can use the speed ofthe computer to quickly and efficiently obtain needed infor-mation either for audit use or management needs. In eadhexample below, direct cost savings were achieved in termsof time saved to do the work.

1. Agency payroll information was maintained on compu-ter tape. The auetor needed to extract selectedinformation for audit verification at six differentfield locations. The auditor extracted and printedthe information in an easy to use format by using ageneralized computer audit retrieval program. Theseneatly printed listings were then mailed to the ap-propriate field location for audit verification.11.e auditor estimated that he had saved 15 man-daysthat otherwise would have been necessary to manuallyselect and list the necessary information on sepa-rate schedules.

2. Agency stock records were maintained on computertape. As part of an audit, a generalized computeraudit retrieval program was used to

--extend the dollar value of 42,000 stock items,

1 3

--obtain record counts and dollar amounts of

several different types of stock items, and

--select statistical samples of stock items fordetailed audit verification.

The auditor estimated that the computer had savedhim 30 man-days to perform this work.

3. A large system designed to operate and control con-tainerized freight shipments was maintained on com-puters. The auditor needed to extract informationfrom a large file to evaluate controls and container-use factors. He used a generalized computer auditretrieval program to extract information on typesof shipments necessary for

--review of perishable and nonperiShable ship-ments from selected locations,

--review of container shipments to and from se-lected locations,

--computation of percentagGs of cubic feet useof all shipments of containers by Variousshippers,

--summarization of container shipments by portof discharge, and

--review of distribution of nonperishable ship-ments by weight and number of pallets foreach container.

The auditor estimated that he had saved 50 man-days byusing the computer to extract needed information.

ADDITIONAL TRAINING REQUIRED

To work effectively in a computer environment, the au-ditor must get additional training in computer technologyand develop new computer-auditing skills. For example, if

he is expected to evaluate a highly complex data processingsystem, he must acquire a detailed understanding of the com-puter operation, in addition to, a thorough knowledge ofagency procedures. The necessary proficiency in evaluatingcomputer operations can be obtained through formal training,individual study of computer technology, and most importantof all, actual on-the-job experience.

Management also has a responsibility to extend its un-derstanding of computer operations. To be able to satisfy

itself that an ADP system is effective and functioning prop-

erly, management ought to have a basic knowledge of the con-

cepts and principles of data processing. Without this know-

ledge, management will surrender its decisionmaking role in-

volving agency use of comyuters to technically oriented data

processing persons who may be unskilled in managerial methods.

CONCLUSIONS

The increasing use of computers in Gavernment and thetrend toward more sophisticated and complex systems have

important implications for auditors. GAO believes that the

scope and techniques of auditing in the ADP environment must

be expanded. The auditor must become proficient in computertechnology to an extent necessary to evaluate computer opera-

tions. Prime consideration needs to be given to trainingand the use of advanced techniques.

GAO believes also that an independent review and evalu-

ation of agency computer systems is a must. To be effective,

the review group should be independent of daily computer op-

erations and should report to a high-level management offi-

cial. It seems logical that the internal audit groups

should make these evaluations. An adequate evaluation of

any complex ADP system requires both a detailed understand-

ing of computer operations and a thorough knowledge of agency

procedures. By "living with" the agency system, internal

auditors are in the most favorable position to acquire the

necessary know-how and keep it up to date. They are also in

a position to monitor the computer's operation continuously.

In general, GAO believes further that internal auditors

must develop and extend their activities to include reviews

and evaluations of data processing systems. In the absence

of these independent evaluations, the computer operation ismore vulnerable to undetected error, misuse, and iiossiblyfraud. To help strengthen controls and safeguards overagency computer operations, GAO believes that Federal agencymanagers should require internal audit or a similar group todevote more attention to computer systems than currently isbeing done.

1 6

CHAPTER 4

NEED FOR COMPREHENSIVE ADP DOCUMENTATION

During fiscal years 1966 through 1969, the FederalGovernment devoted over 100,000 man-years to the analysis,design, and programming of ADP systems. The investment ofFederal resources in these systems continues to expand, andthe related costs are becoming increasingly significant.As part of our study, we looked into the practices used byFederal agencies to document computer systems and identi-fied what we consi.der to be the minimum documentation ele-ments necessary to ensure that all essential information isproperly preserved and available for management and opera-tional use.

This study encompassed Federal departments and agen-cies utilizing about 97 percent of the ADP equipment beingoperated in Government. Discussions were held with high-level officials at twelve departments and agencies, sixteenbureaus, and thirteen ADP installations. At the thirteenADP installations we visited, we examined into standardsand procedures, along with the documentation created forover 300 scientific and business computer programs.

Briefly, it was found that most Federal agencies havenot developed or implemented agencywide documentation stan-dcicds or guidelines, and that, generally, the documentationprluced was incomplete and inadequate. This can result in

serious consequences. The cost of poor or outdated infor-mation--in terms of inefficient and uncoordinated opera-tions, wasted man-hours, r\Aundant efforts, and disillu-sioned users--usually is not apparent immediately from ashort-range viewpoint. The available evidence bears outthat, from an overall long-range standpoint, however, aninefficient operation is often characterized by a lack ofgood documentation.

1 7

WHAT DOCUMENTATION IS

The term "documentation" generally is used to denote

a collection of documents or information on a given sub-

ject.1 As used in this report, however, it refers specifi-

cally to the information that is recorded during the de-

sign, development, and maintenance of computer applica-

tions, to explain ail pertinent aspects of a data process-

ing system--including purposes, methods, logic, relation-

ships, capabilities, and limitations.

Documentation should be created as an integral part of

the development process. As such, it may t used by man-

agement not only to monitor and control an organization's

resources, but also as a method of measuring performance

and compliance with established goals and standards. Conse-

quently, documentation policies and procedures within the

Federal Government need to be stated clearly, systemati-cally communicated, and designed to promote the carrying

out of authorized activities efficiently and effectively.

At present, adequate documentation is unusual among Federal

agencies.

ADP DOCUMENTATION FOR FEDERAL AGENCIES

On November 25, 1970, the Comptroller General issued a

restatement of certain requirements relating tg executive

agency accounting systems. These requirements include the

following types of documentation deemed necessary for GAO

approval of proposed mechanized and automated accounting

systems.

1American National Standard Vocabulary for Information

Processing, Armerican National Standards Institute, Inc.,

(ANSI), 1970 issue.

2General Accounting Office Policy and Procedures Manual,

title 2, section 27.5, part 6 as revised by Comptroller

General letter B-114365(2) dated November 25, 1970. (See

app. I.)

11a. The planned use of ADP and other mechanicalequipment including the following:

(1) A statement of objectives pertaining tothe use of automation and the degree towhich the system will be automated.

(2) An overall narrative description and ac-companying flow chart of the general flowof information through the system. Thisshould tie in with the general descrip-tion of the accounting system.

(3) A description of the equipment configura-tion and capabilities, and the computerlanguage(s) which will be utilized inprogramming the processing operations.Where specific equipment has not been se-lected, the description should include astatement of the general equipment re-quirements for processing and storage andassociated peripheral operations, and astatement of the primary computer lan-guage to be used.

"b. The design specifications which describe thelogic of the proposed ADP system, including

(1) Flow charts showing the sequence of oper-ations to be performed by each proposedcomputer run.

(2) For each proposed computer program, abrief description of the functions to beperformed, processing frequency, type ofinput, and the resulting product(s).

(3) Descriptions of the physical characteris-tics of the data elements to be containedin the transaction records and data files,including the media (punched card, mag-netic ttipe, etc.) to be used.

19

25

(4) Descriptions of controls to be provided

over data

(a) inputs, including the types and pur-

poses of edit and other purification

or validation routines;

(b) processing, including the plan for

back-up operations;

(c) storage, including the plans for re-construction of the data files; and

(d) outputs.

(5) Identification of audit trails in the au-tomated system with special attentiongiven to systems in which conventionalaudit trails *** will be obscured in the

processing operations and alternativeprocedures will be necessary."

Although this list was promulgated as a requirement

prerequisite to GAO approval of automated Federal account-

ing systems designs, it may also serve as a minimum docu-

mentation level during the development phase of any ADP

system and will provide a reasonable level of documentation

for a general understanding of overall system design. Addi-

tional detail, however, is required for operational sys-

tems, including:

1. Operator instructions (or run book) showing program

loading procedures, processing schedules, peripheral

equipment used, tapes needed, and error conditions

and procedures.

2. Instructions showing how input data is prepared for

processing, scheduled preparation dates, and valid-

ity checks.

3. Source listings with appropriate comments and ex-

planations.

4. Data processing center organization information,

including organizational components, responsibili-

ties, controls, and emergency operating procedures.

20

Nows

5. Test data and results including documentationthe data used to test syStem performance, thecedures used, descriptions of test cases, andresults of tests, including samples when approate.

of

pro-the

pri-

Although GAO believes that these documentation elements should be required as a minimuth, they do not necessarily represent the full scope of information that shoube recorded within a documentation package. Additionaldata may be necessary for many systems, depending upon sufactors as the degree of management control required, sys-tem complexity and purpose, and reliability requirements.In every case, documentation is adequate only as (1) it iskept current and complete and (2) it communicates easilyand logically all important facts and relationships tothose who need them.

Id

NEED FOR INCREASED MANAGEMENT SURVEILLANCEOF ADP DOCUMENTATION PRACTICES

Where agency management has made the decision to uti-lize computers, the technologies of information handling,communications, controls, and related developments in in-formation theory are generally applied in ways that havesignificantly changed methods of operations. These changescall for improvements in the management process also. Newmanagerial techniques must be incorporated that will ade-quately insure a proper level of control over the use ofGovernment resources.

CONCLUSIONS

GWO believes that system documentation is a basic pre-requesite to improved managerial capacity. Consequently,Government-wide documentation standards should be developedand promulgated by the executive branch to guide all Federalagencies in maintaining an adequate level of system docu-mentation. As an interim measure pending adoption of Fed-eral standards by the executive branch, Federal agenciesshould critically examine existing docunentation practicesas a fundamental step toward improving the effectivenessof their computer operations. This effort should include

21

27

the development of uniform agency documentation standards

and procedures that meet the minimum levels described above

and periodic reviews of agency practices.

22

CHAPTER 5

CCHPUTER-AUDITING TECHNIQUES

In today's ADP environment, auditors can use computer-auditing techniques to conduct independent reviews and im-prove responsiveness to management needs by using new toolsand techniques that were not previously available. Auditorstrained in computer-oriented techniques can use the computerto do detailed clerical-type auditing work. These tech-niques also can be used to assist in the review and evalua-tion of computerized systems including the internal controlsunique to this new environment.

The computer can perform quickly and accurately manyof the detailed and tadious tasks involved in auditing. Forexample, the computer can

--seardh files and select data for examination,

--check the accuracy of analyses and summarizations,

--create flow charts for portrayal of systems,

- -prepare special analyses or repor?-.3 for managementor audit needs, and

- -check the performance of computer programs.

There are undoubtedly many other uses to which the com-puter can be put. They are limited only by the resourceful-ness of the user.

To evaluate computerized systems, an understanding ofnew types of controls not encountered in manual systems isnecessary. These new controls are associated with computerhardware, computer programs, ADP operations, and organiza-tions. For example, hardware controls are available to pre-vent accidental destruction of data on magnetic tapes, com-puters are programmed to count records and develop controltotals, procedures are established to assure that computeroperators mount proper magnetic tapes for each operation,and manuals and written procedures are prepared to ensureadequate communication.

23

29

AB suggested by the above examples, the auditor is

faced with a different situation when working in an ADP en-

vironment. Computer-auditing techniques are needed. Sev-

eral of those used successfully by GAO are:

--Generalized corn uter audit rograms. These consist

of a series of prewritten computer programs that can

be linked together and used by an auditor. Such

names as Audassist, Auditape, CARS, Easytrieve, and

STRATA fall under this heading. There are others.

--Custom designed compu,:er audit programs. These gen-

erally include computer programs written especially

for a specific audit purpose.

--Test decks. These include test decks, test files, or

test documents.

--Reviews of selected computer programs. These involve

a review of programming documentation and the related

coding of the computer program.

It should be remembered that in most cases no single

audit technique will suffice. Instead, a combination is re-

quired to satisfy the auditors' needs. Professional judgment

and the element of risk still govern the extent of testing.

A, more detailed discussion of computer-assisted-auditingtechniques with references to appropriate case studies is

included below. Arrangements for use of different computer

audit packages can be made with the developer.

2 4

GENERALIZED COMPUTER AUDIT PROGRAMS

A. most important development in recent years that hasprovided auditors with an efficient and effective means ofauditing records maintained by computers is the generalizedcomputer audit program. These programs or systems permitthe auditor to retrieve a wide variety of information fromcomputerized records and to perform different auditing pro-cedures.

A generalized computer audit program usually consistsof a series of prewritten computer programs that easily canbe linked together and readily adapted by the auditor tothe requirements of a specific audit situation. Some of theuses include:

--Search and retrieve. The auditor can search a largefile of records at computer speeds and identify andretrieve items that have audit significance.

- -Selection of samples. The computer can be instructedto select samples using any one of several systematicrandom-sampling techniques, or to calculate and se-lect a sample necessary to satisfy desired statisti-cal confidence levels.

- -Mathematical computations. The basic mathematicaloperations of addition, subtraction, multiplication,and division can be performed at computer speeds.

--File comparison, merges, and sorts. Input files canbe merged or sorted in almost any sequence desired.Files can be compared with an option to print outeither matched or unmatched records.

--Summarizing and reporting. Large volumes of data inmachine-readable form can be easily and quickly sum-marized to satisfy audit requirements.

--Printing and punching. Desired output can be punchedinto cards or printed in almost any desired orderwith descriptive headings over columns of data.

25

31

These generalized programs examine and manipulate the

output produced by a data processing system. They have not

been designed to examine agency programs. Instead, they

merely perform on an automated basis the same type of cleri-

cal work that has characterized much audit work in the past.

Substantial amounts of audit time can be saved by using

a generalized program, especially if it is used on a recur-

rent basis on the same audit application. Even if first-

time savings cannot be achieved, the automated approach may

result in benefits such as better audit coverage, better

documentetion, and a better understanding of the agency com-

puter system. In some cases the generalized programs permit

the auditor to retrieve data which, as a practical matter,

could not have been obtained manually.

There are a number of generalized computer audit pro-

grams. Most of the public accounting firms, as well as

some private firms have developed such programs. GAO has

not reviewed all the generalized programs, and it is beyond

the scope of this report to comment on their differences.

A partial listing follows.

Audassist

AUDEX

Auditape

Auditpak

Auditronic 16

AY Audit/ManagementSystem

CARS

tj'fir.2

Alexander Grant & CompanyCertified Public Accountants

Arthur Andersen & Co.Certified Public Accountants

Haskins & SellsCertified Public Accountants

Lybrand, Ross Bros. , & MontgomeryCertified Public Accountants

Ernst & ErnstCertified Public Accountants

Arthur Young & Co.Certified Public Accountants

Computer Audit Systems, Inc.725 Park AvenueEast Orange, New Jersey

26

Computer File Price Waterhouse & Co.Analyzer Certified Public Accountants

Easytrieve/300

SCORE

STRATA

System 2170

Computer Audit Corporation1320 Fenwick LaneSilver Spring, Maryland

Atlantic Software, Inc.5th and Chestnut StreetsPhiladelphia, Pennsylvania

Touche Ross & Co.Certified Public Accountants

Peat, Marwick, Mitchell & Co.Certified Public Accountants

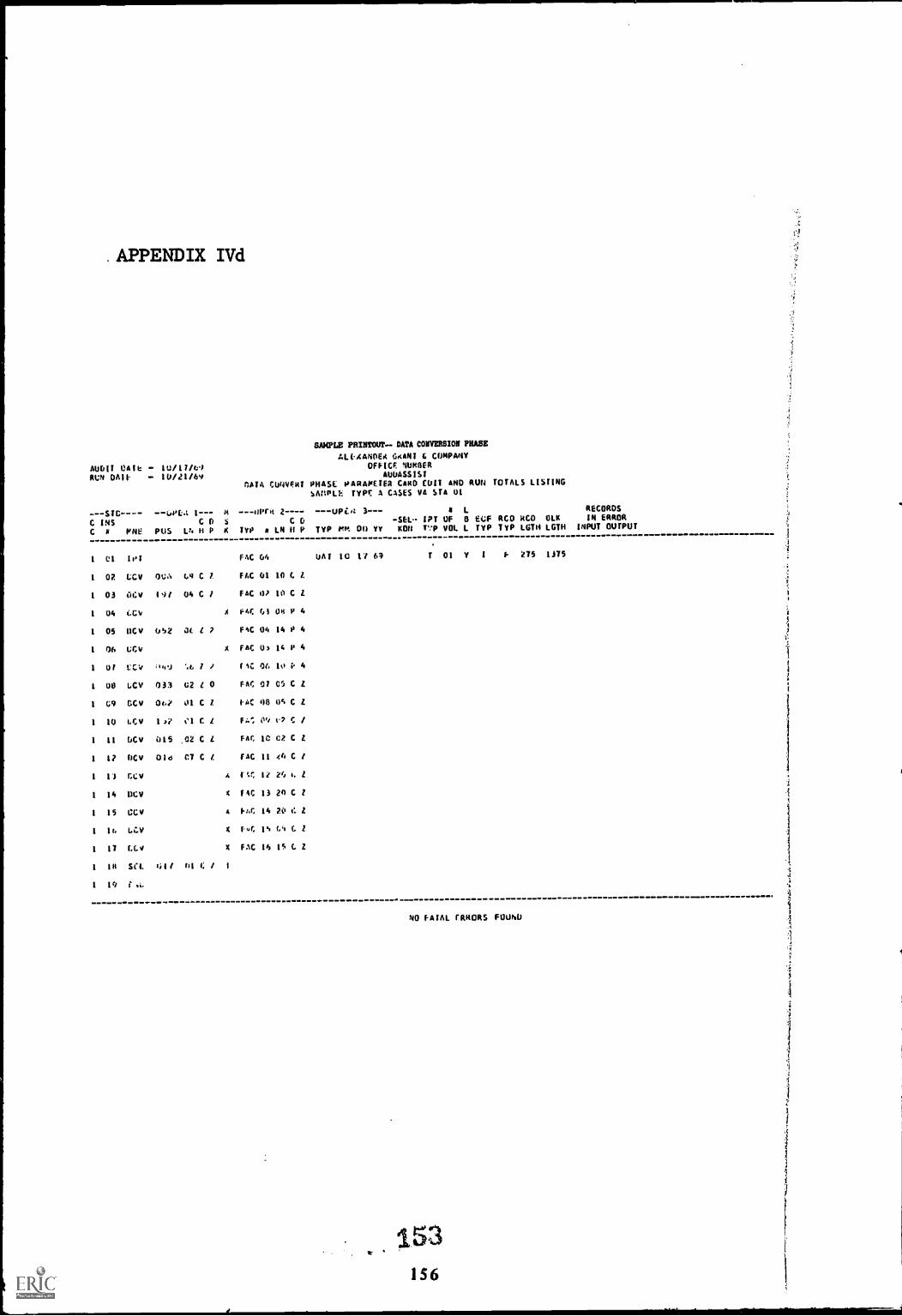

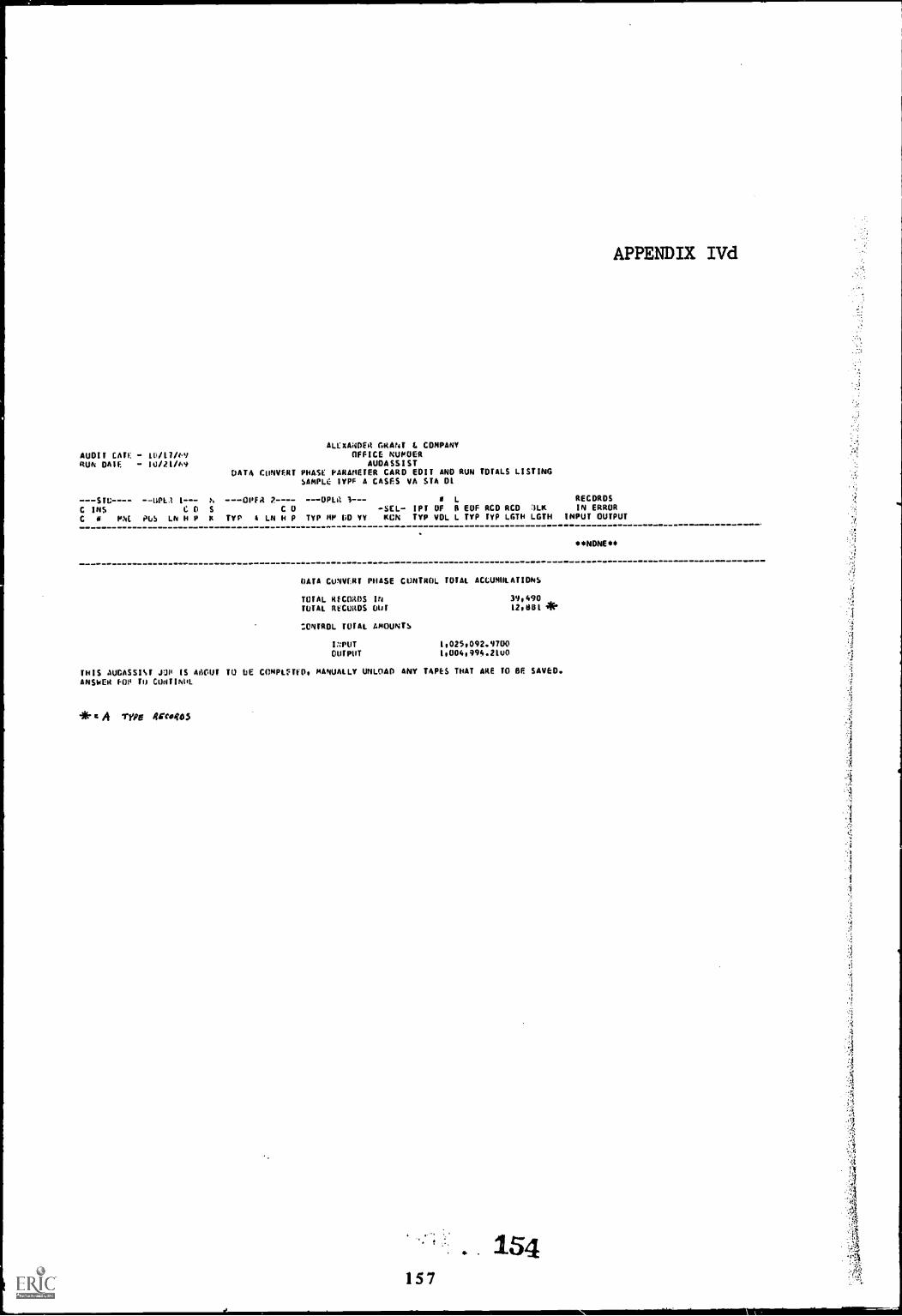

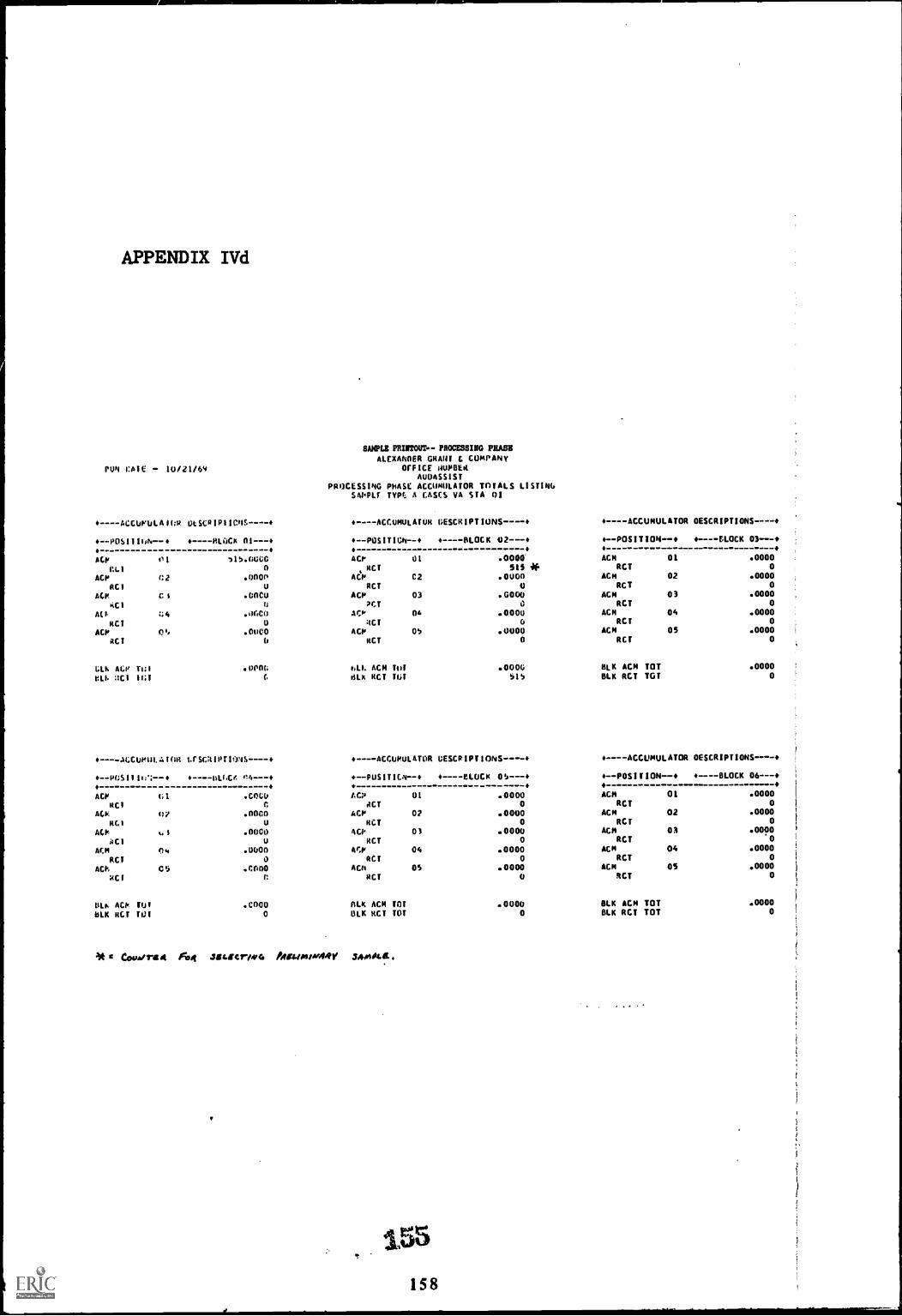

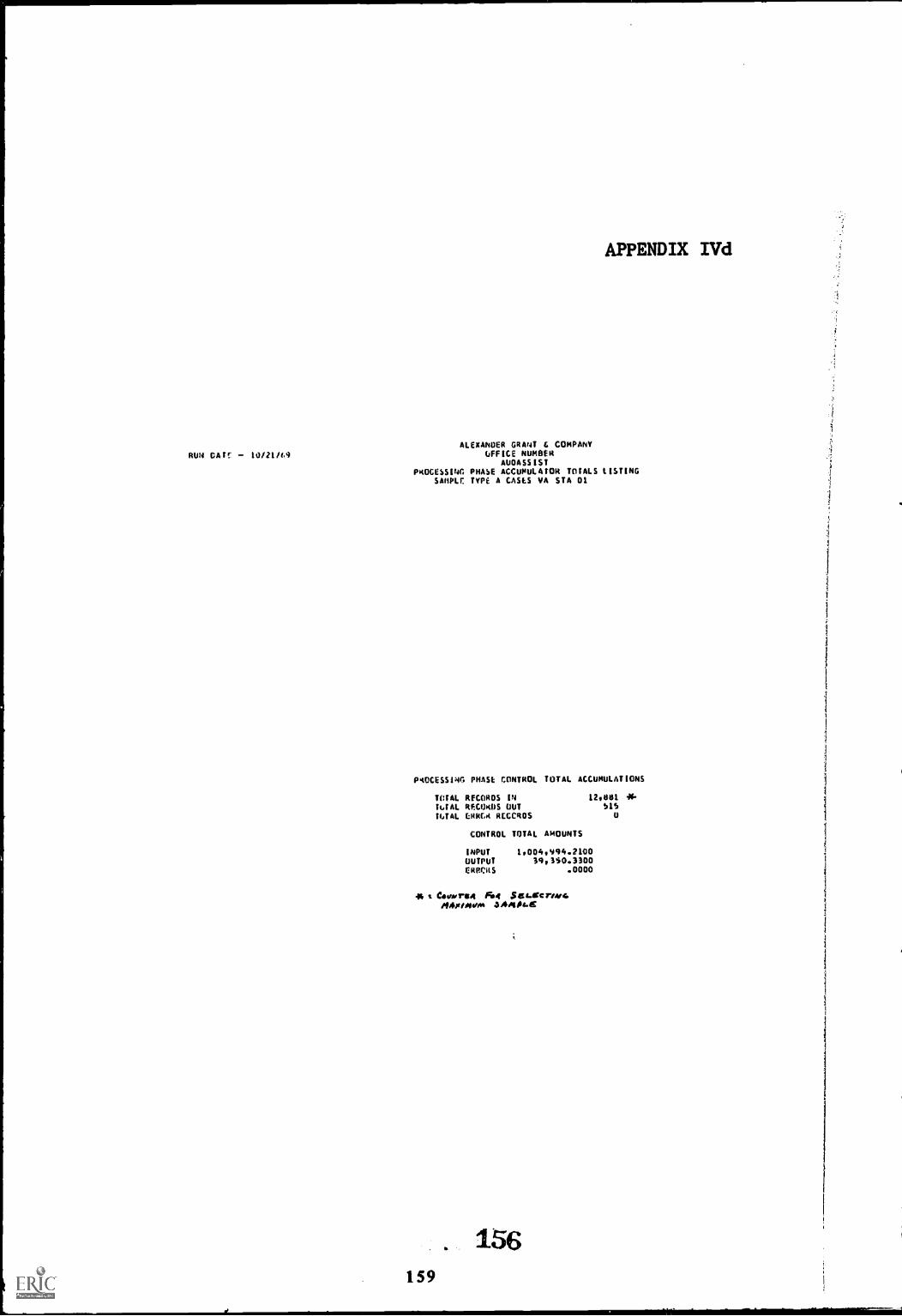

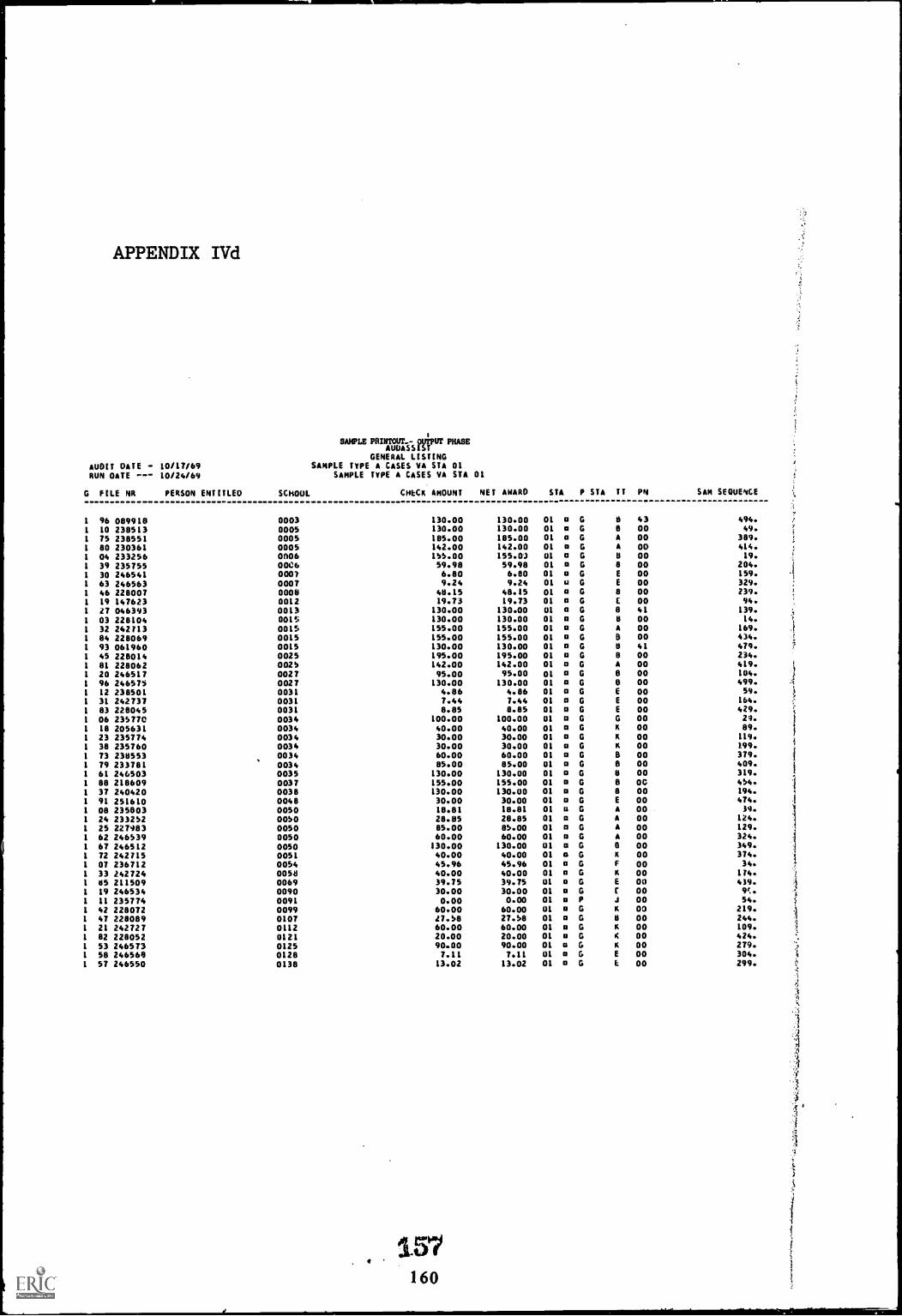

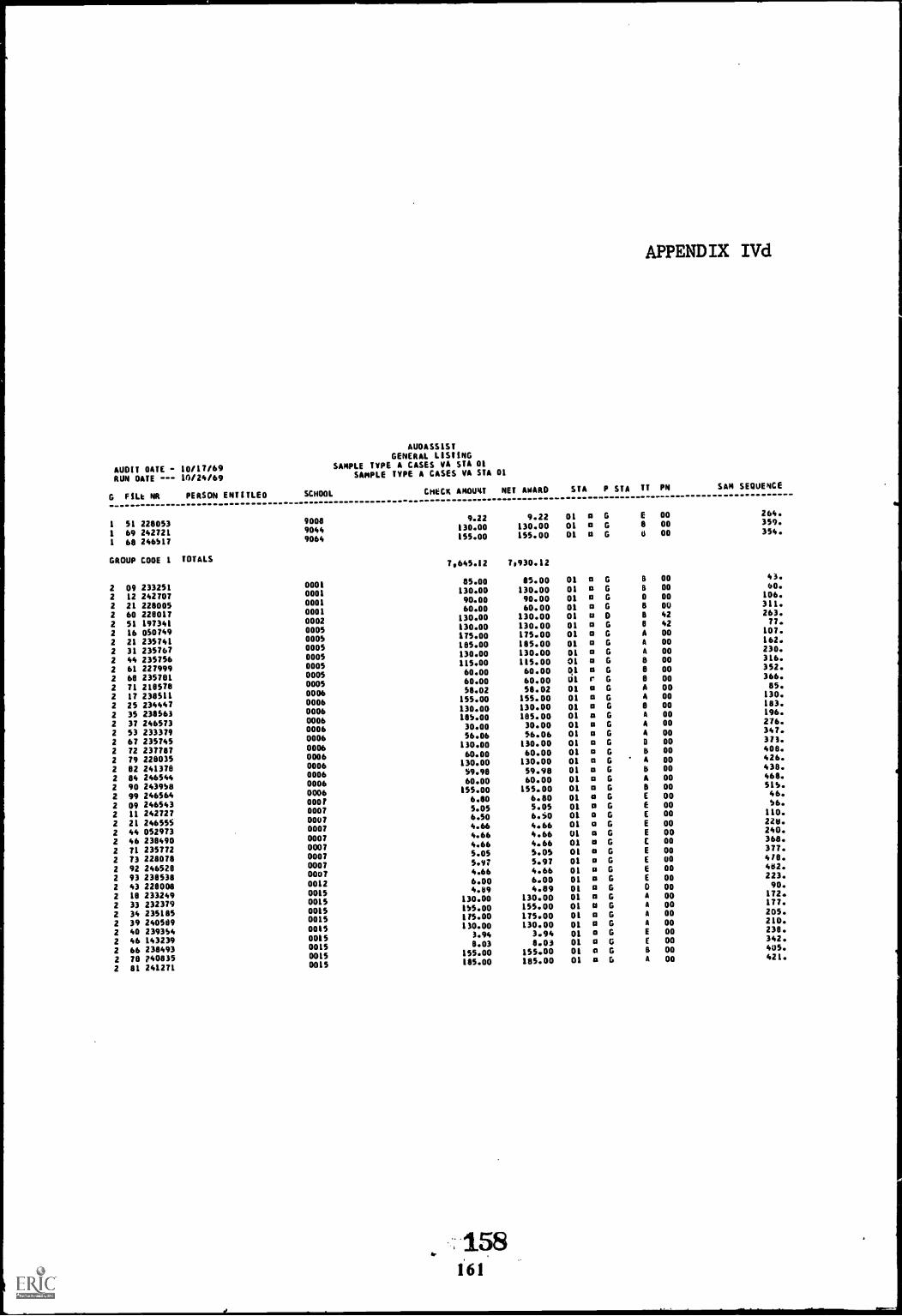

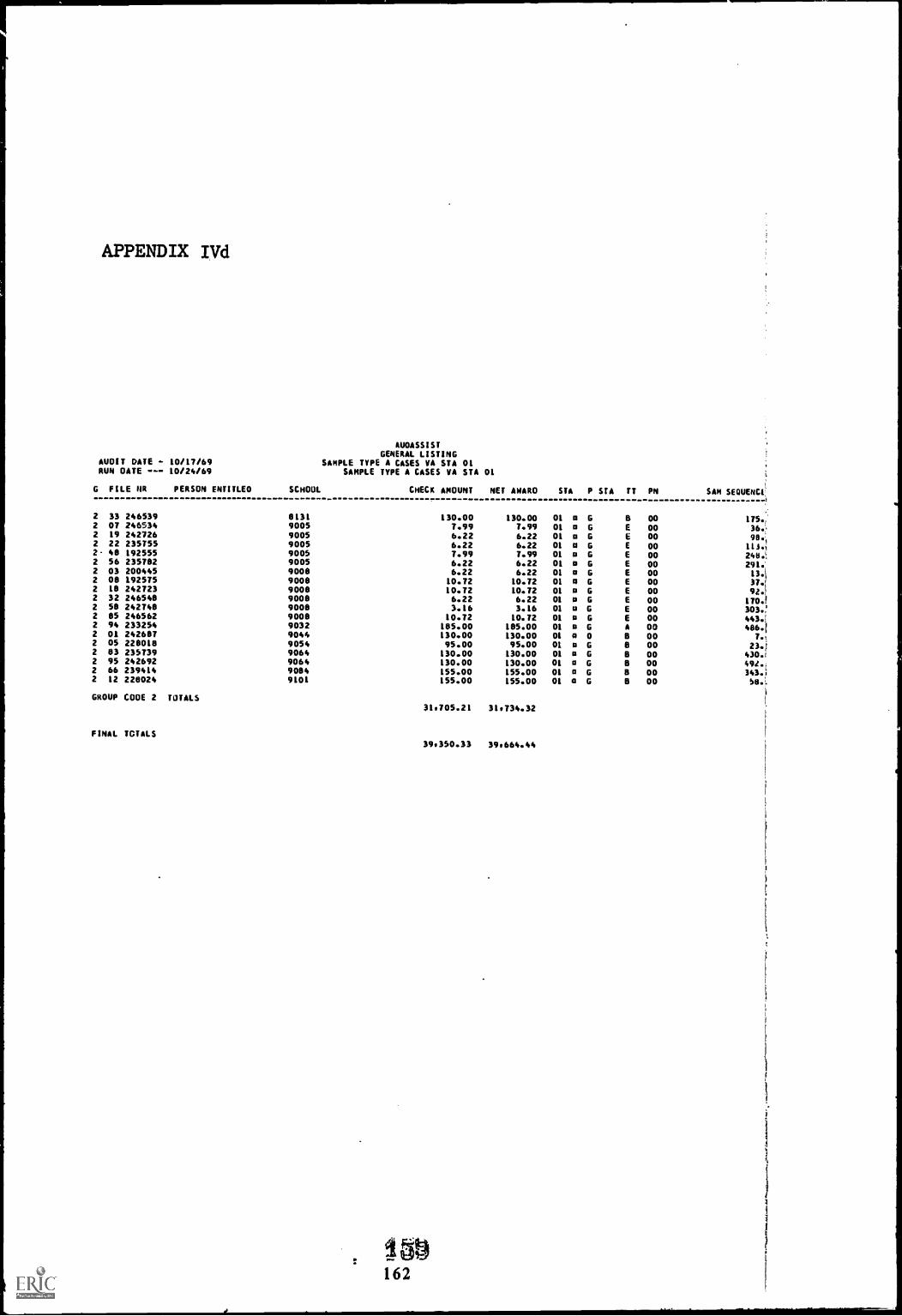

Detailed descriptions and illustrations of the use ofHaskins & Sells Audatape System and Alexander Grant & Com-pany's Audassist are included in appendix III and IV. Theseillustrations demonstrate some of the capabilities of thegeneralized computer audit program for the reader interestedin further study.

The generalized computer audit program has great poten-tial for saving audit time and enhancing the auditors'knowledge of computers. It should be considered a valuabletool to assist the auditor or manager in examining recordsmaintained by computers.

27

33

CUSTOM-DESIGNED COMPUTER AUDIT PROGRAMS

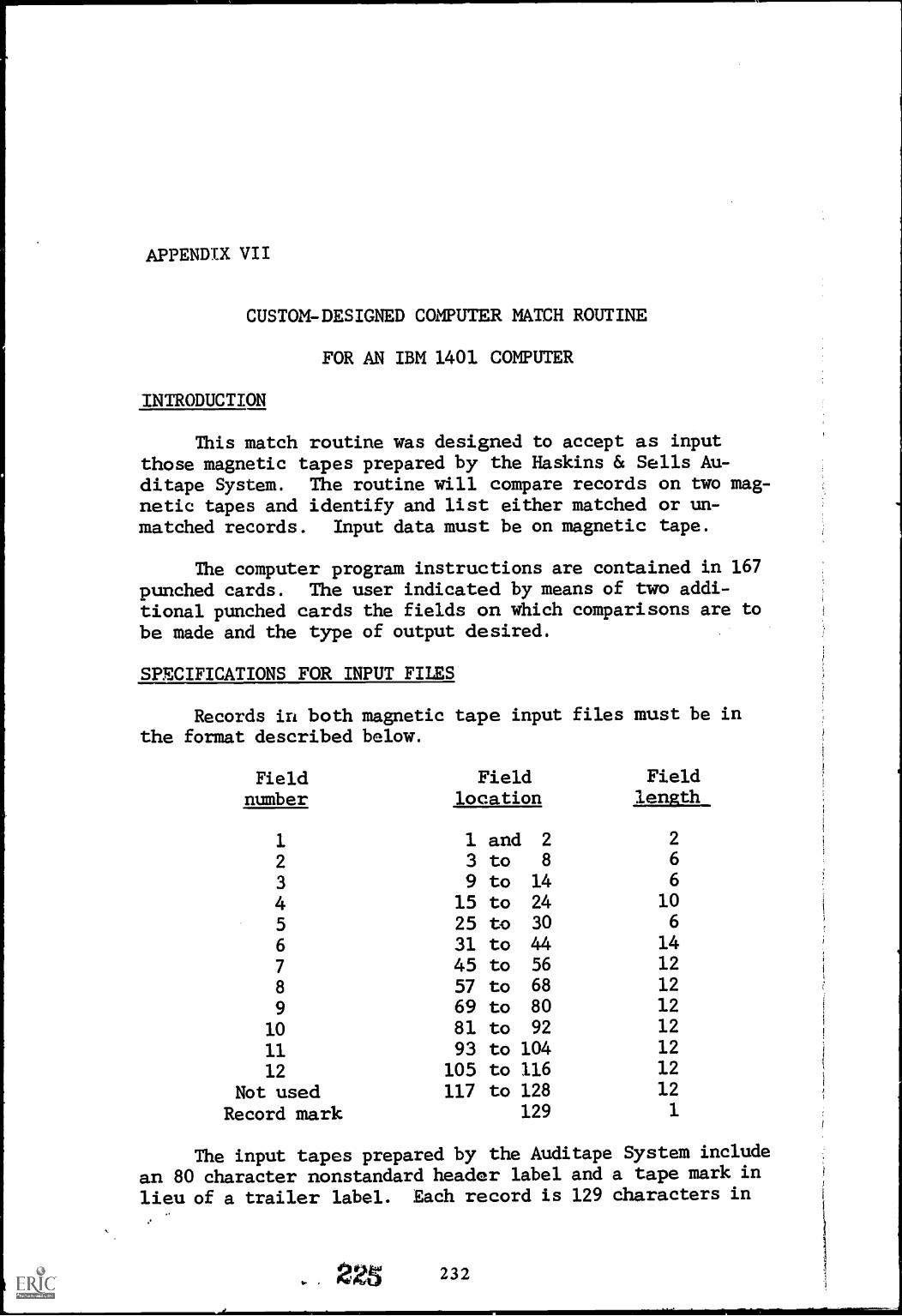

A custom-designed computer audit program is defined

here as a computer program especially written either by or

for an auditor to accomplish a specific audit objective.

In contrast to a generalized computer audit program which

can be used on a variety of records or computers, the

custom-designed program normally works only on the system

or computer for which it was designed.

Oftentimes the need for a custom-designed program de-

velops when the auditor encounters an audit situation for

which a generalized program is unsuited. A decision to

custom design such a program requires careful consideration

of the costs and benefits. In comparison with an already

existing generalized program, development of a custom pro-

gram for a one-shot application is relatively expensive.

It takes time and costs money to design, write, test, and

debug a computer program.

Other practical considerations also are involved. If

programs are prepared by someone other than the auditor,

the auditor must establish the validity of the programs for

his independent purpose. If programs are prepared by the

auditor, he obviously must have a working knowledge of

several programming languages. Either case requires a

working knowledge of computer hardware and several program-

ming languages which is not now a universal skill of audi-

tors.

Once the decision is made that the value of a custom-

designed program justifies the cost of development, it soon

becomes apparent that such a program has several unique ad-

vantages. For example:

--The program can be tailored to fit the exact needs

of the auditor, as opposed to satisfying a need using

limited capabilities of a generalized program.

--On a recurring audit, it may be possible to use the

same program again with only minor modifications or

updating.

28

--Although not a major consideration for a one-shotapplication, the custom program probably will runmore quickly and efficiently than a generalized pro--gram.

To date, development and use of custom-designed com-puter audit programs in GAO has not been extensive. Onerather small computer program designed to compare recordson two magnetic tapes and to identify and list eithermatched or unmatched records is described in appendix VII.More complex and sophisticated examples of custom-designingnew programs and customizing existing computer programs areincluded as part of a case study in appendix VI.

TEST DECKS

A test deck is a set of dummy transactions created to

test the procedures and controls in a computer program. Theconcept originated with computer programming persons who

used test decks in debugging computer programs. Auditors

adopted the technique to determine exactly how different

types of transactions are handled by the data processing

system.

Auditors can use test decks to

--test computer programs to verify the existence andeffectiveness of program controls, and

--verify computational operations or program process,ing.

Test decks can be processed against live current files,

in which case special precautions must be taken to safeguard

agency records, or test decks can be processed against du-plicate or simulated files. A comparison of the results of

processing test data with predetermined results will indi-

cate whether the program is functioning as described. Theseresults merely verify that the system is, or is not, func-

tioning properly at a point in time--file accuracy cannotbe validated with test decks. If test decking does indicate

a program error or the possibility that files are inaccurate,additional audit work is required to determine the cause and

impact.

A clear understanding of the data processing system andits relationship to the audit objectives is necessary todevelop an effective test deck. The types of transactionsto be included in the test requires careful considerationif the auditor is to test the programs fully. He must con-

sider all of thE significant data variations.

The auditor can select the types of test transactionsby reviewing and analyzing test decks used by programmersin debuggina the program or by analyzing system documenta-

tion. A combination of the two methods is usually best.

30

The test deck should include transactions to test proc-essing or handling of

--valid conditions,- -erroneous data,--missing transactions,--illogical conditions, and--validation checks.

In many cases it is impractical to develop a test deckto test every possible combination of conditions. Judggentand the element of risk govern the extent of testing.

Advantages

1. Versatility--test decks can be designed for any pro-gram, system, or equipment.

2. Positive resultsresults are irrefutable if thetest is made with a production program.

3. Ease in understanding resultseither the test proc-esses correctly or incorrectly.

Disadvantages

1. Design difficultythe auditor must understand thefunctioning of the system to develop an adequatetest deck.

2. Inflexibility--a test deck is valid for a single ap-plication or program for which it was designed.

3. Maintenance required--the test deck must be updatedto incorporate program or system changes.

4. Error identificationtest deck processing pointsout errors, not the cause or impact.

5. Error detectionthere is only a limited chance ofdetecting an invalid condition if a program has beenaltered to manipulate a specific account or amount.

Under certain conditions, test decks can be a highly

effective audit tool. For example, GAO uses test decks in

the audit of the Federal Crop Insurance Corporation. A de-

tailed discussion is included in appendix V.

An important use of the test-decking procedure is being

made at the Veterans Administration (VA) Center in Philadel-

phia, Pennsylvania. The resident systems auditors have

used test decking for a number of years to perform compre-

hensive testing of VA insurance programs. This application

is important because

--the permanent test file designed for and used on a

continuing basis enables the auditors to meet their

responsibility for certifying to the validity and

accuracy of the computer programs and

--a group, independent of daily computer operations,provides management with an independent review and

appraisal of the computer system operation.

A discussion of the VA's test-decking procedures is in-

cluded in appendix VIII.

REVIEW AND ANALYSIS OFSELECTED COMPUTER PROGRAMS

In sophisticated computer systems, the computer per-forms a significant amount of internal processing. For ex-ample, input data may be highly summarized making it im-possible, or at best impractical, to trace transactionsthrough the system or to associate input with output. In

this environment the audit approach must concentrate on ADPprocedures and controls since it is no longer practical totrace transactions through the system.

If an auditor is to evaluate a computerized operationor to rely on its output, he must understand and test thecomputer system. New types of controls, different termi-nology, and different conceptual problems are involved inthis environment. In some cases, the auditor may not feelqualified to perform the required analysis. He may wish toconsult with a computer-auditing specialist or other techni-cally qualified persons.

One approach to auditing these sophisticated computersystems is described below. A combined team effort betweenauditors and computer specialists is required. A unique ifnot controversial procedure is included. It is the reviewand analysis of selected computer programs encompassing notonly the analysis of programming documentation but the re-lated coding of the program. The methodology for perform-ing such a review includes the following steps.

--Analyze the computer application or system on thebasis of a review of documentation and interviewswith agency employees. How does the system work?

--Review internal controls surrounding the computer-based system and also the related internal controlsover actual processing. Are internal controls ad-equate?

--Analyze selected computer programs including relatedcoding of the program. Is the system functioning inconformity with representations contained in systemdocumentation? Will it produce accurate and ac-ceptable output?

33

39

--Evaluate results of the above systems review. How

and to what extent should the system be tested?

--Modify existing agency computer programs or prepare

new programs that will produce output needed by the

auditor to test the system.

--Test the system. Establish the consistency of pro-

cessing and verify source data entering the system.

One method of establishing the consistency of pro-

cessing is to reprocess selected input data through

auditor controlled vexsions of agency computer prow

grams and compare the auditors' results with the

agency's results. Other routines can be incorporated

in the auditor-controlled programs that will concur-

rently accumulate totals or select and print records

for verifying source data.

A review such as that described above could not be

performed by an auditor unskilled in the computer arts. Acombined team effort between auditors and computer special-

ists is necessary. Obviously this approach should not be

employed as a routine one without adequate technical support

and guidance. S. D. Leidesdorf & Co., Certified Public Ac-

countants, is one firm that has developed computer audit

routines and incorporated computer program reviews in their

audits. The approach is to review the computer programsused in processing data and to combine the audit routines

within such programs. If the reviewed program is satisfac-

tory and is used in processing, the auditor can be assured

of the accuracy of processing.

GAO with the assistance of S. D. Leidesdorf & Co., in-

cluded a detailed review of selected computer programs as

part of the annual audit of FHA. A team consisting of GAO

auditors, and S. D. Leidesdorf & Co., computer systems

analysts and computer-trained auditors, did the work. Acase study on this audit approach is included in appendix

VI .

CONCLUSIONS

Computer-auditing techniques are invaluable as audit

tools whether they be generalized computer audit programs,

custom-designed programs, test decks, or computer program

34

. 40

reviews. In most cases no one audit technique will satisfythe auditors' needs. Each technique has its advantages anddisadvantages. The auditor ought to be familiar with dif-ferent techniques to select the combination that best meetsthe specific need.

35

41'

APPENDIX I

B-114-365 (2)

COMPTROLLER GENERAL OF THE UNITED STATESWASHINGTON. D.C. 20548

November 25, 1970

HEADS OF FEDERAL DEPARTMENTS AND AGENCIES

Subject: Restatement of certain principles and standardsrelating to executive agency accounting systems

We are amending our instructions regarang the development andimprovement of agency accounting systems to effectuate the changesin General Accounting Office review and approval policies announcedin my letter to you dated October 16, 1969, subject "General AccountingOffice operations with respect to executive agency accounting systems."

The changes being made are designed to provide more completeguidance in the development and approval of Federal agency accountingprinciples and standards and accounting systems designs. An advancecopy of the revised pertinent parts of section 27, entitled "Improvementof Accounting Systems," of Title 2--Accounting--of the General AccountingOffice Policy and Procedures Manual for Guidance of Federal agencies isenclosed.

Enclosure rL See GAO note.]

Comptroller Generalof the United.States

GAO note: Parts of the enclosure have been deleted.

APPENDIX I

27.5 SYSTEM DESIGN

The extent and nature of mechanization and automation

In a system employing ADP equipment, adequate documen-tation varies according to the circumstances involved butit is necessary for the success of any operation. The types

of documentation specified below are deemed to be necessaryto provide an understanding of the design of the system.Programmed instructions and operator instructions are notrequired to be submitted for approval of the accounting sys-tem design.

a. The planned use of ADP and other meg:hanical equip-

ment including the following:

(1) A statement of objectives pertaining to the useof automation and the degree to which the sys-tem will be automated.

(2) An overall narrative description and accompany-ing flow chart of the general flow of informa-tion through the system. This should tie inwith the general description of the accountingsystem.

(3) A description of the equipment configuration andcapabilities, and the computer language(s) whichwill be utilized in programming the processingoperations. Where specific equipment has notbeen selected, the description should include astatement of the general equipment requirementsfor processing and storage and associated periph-eral operations, and a statement of the primarycomputer language to be used.

b. The design specifications which describe the logicof the proposed ADP system, including

(1) Flow charts showing the sequence of operationsto be performed by each proposed computer run.

40. 44

APPENDIX I

(2) For each proposed computer program, a brief de-scription of the functions to be performed, proc-essing frequency, type of input, and the result-ing product(s).

(3) Descriptions of the physical characteristics ofthe data elements to be contained in the trans-action records and data files, including themedia (punched card, magnetic tape, etc.) to beused.

(4) Descriptions of controls to be provided overdata

(a) inputs, including the types and purposes ofedit and other purification or validationroutines;

(b) processing, including the plan for back-upoperations;

(c) storage, including the plans for reconstruc-tion of the data files; and

(d) outputs.

(5) Identification of audit trails in the automatedsystem with special attention given to systemsin which conventional audit trails (see item 7below) will be obscured in the processing opera-tions and alternative procedures will be neces-sary.

7. The internal controls to be maintained

a. A description of the manner in which financial, man-power, and property resources are controlled andsafeguarded by the regular authorization, approval,documentation, recording, reconciling, reporting,and related accounting processes.

b. An outline of controls over quantity, timeliness,reliability, and accuracy of inputs, processing, andoutputs (whether for manual, automated, or mechanical

41 45

1

APPENDIX I

systems), sufficient to demonstrate reasonable as-surance of accurate recording of transactions andreporting of their effects in the accounting periodin which they occur.

c. A statement of the basis for auditability of thesystem in terms of results of operation and currentcondition, and identification of the audit trailsthroughout the system. This includes a descriptionof the manner in which a pari:icular element of datathat exists in the files can be traced backward tothe source of the transaction that created it andforward to its position in a report.

4642

APPENDIX II

REVIEW GUIDE FOR FEDERAL AGENCY ACCOUNTING SYSTEMS

SECTION 18--AUTOMATIC DATA PROCESSING (ADP)

In a system employing ADP equipment, adequate documen-tation varies according to the circumstances involved butit is necessary for the success of any operation. The pro-cess of system design approval from the viewpoint of itsADP aspects involves the assurance that the system (1) hasadequate audit trails, (2) is adequately controlled, and(3) provides for a minimum of redundancy and duplication ofprocessing. To obtain this assurance, it is necessary togain a fairly comprehensive kncwledge of the entire systemand how it is planned to operate. The following questionsare intended to be used as a guide to determine the adequacyof ADP documentation to provide the basis for system com-prehension.

OBJECTIVES

1. Is there a statement of objectives pertaining to the useof automation?

2. Does the statement include the degree to which the ac-counting system will be automated?

a. Does it specify the functions or actions which will beautomated and those which will be manual?

b. Does it specify the relationship of the accountingsystem with other systems?

DESCRIPTION

1. Is there an overall narrative description of the automatedportion of the system?

2. Does the description tie in with the general descriptionof the accounting system?

3. Is there a flow chart of the general flow of informationthrough the automated portion of the system?

4. Is the flow chart keyed to the narrative?

43 47

APPENDIX II

5. Does the flow chart tie in with the general charts depict-

ing the major accounting processes?

6. Does the above documentation adequately provide a basis

for understanding the purposes and interrelationships of

the various computer runs?

EQUIPMENT CONFIGURATION

1. Is there a description of the equipment configuration?

a. Does the description include a statement as to the

capabilities (and limitations) of the equipment to

handle the processing of data for the accounting sys-

tem?

b. Does the description include:

(1) Computer manufacturer and model number('

(2) Size of internal memory?(3) Type and quantity of file storage devices?

(4) Type and quantity of input/output devices?

(5) Information on other peripheral devices?

2. Is there a list of the general-purpose and utility soft-

ware which is planned for use with the system?

3. Is there a statement of the primary computer language

which will be utilized in programming the processing

operations?

a. Does the statement include information on what other

language(s) will be uzeci?

b. Does it specify to what extent the other language(s)

will be used?

SYSTEM LOGIC

1. Are there flow charts which depict the sequence of oper-

ations to be performed by each proposed computer run or

process?

, 4844

APPENDIX II

2. Are these flow charts keyed to the flow of data so thatit can be traced through the various levels of detaildown to the program level?

3. Are there narrative descriptions for each proposed com-puter program?

a. Do these descriptions include:

(1) The functions to be performed?

(2) Processing frequency and relationship to cut-offdates?

(3) Types of input?

(4) The resulting product(s) (output)?

b. Are the program descriptions concise and yet suffi-ciently comprehensive to permit a clear understanding?

or.

c. Are the descriptions tied in to the computer run flowcharts mentioned in 1. above?

4. Are there descriptions of the physical characteristics(size, alpha/numeric, etc.) of the data elements to becontained in the transaction records and data files?

a. Do the descriptions clearly indicate the media (punchedcard, magnetic tape, etc.) to be used for each recordand file?

D. Are the descriptions in the form of layouts, charts,or listings?

5. Azie there adequate descriptions of controls included inthe automated system? (Refer to pp. 49 to60 for the in-ternal control check list.)

a. Are the control descriptions identifiable as to:

(1) Input, including:

(a) Types and purposes of edit routines?

45 . . 49

APPENDIX II

(b) Types and purposes of other validation or pu-

rification routines?

(2) Processing, including:

(a) Types of prognammed controls to be used?

(b) Plans for operational controls in the data

processing center?

(c) Plans for back-up operation?

(3) Storage, including:

(a) Plans for reconstruction of the data files?

(b) Plans for security of the data files?

(4) Outputs, including:

(a) Plans for error detection and control?(b) Plans for control and distribution of products?

b. Is there a list of the controls built into the equip-

ment by the manufacturer?

c. Are the controls incorporated in the manufacturer's

software (operating system) identified?

d. Is the system free of any duplication of manual and

automated controls?

(1) Are controls automated whenever feasible?

(2) Are the automated controls established as close

to the source of the data as possible and feasible?