Effects of Corporate Governance Practices on the Growth of Pension Schemes in Kenya

93

THE EFFECTS OF CORPORATE GOVERNANCE PRACTICES ON THE GROWTH OF PENSION SCHEMES IN KENYA BY LAMECK OKEYO D53/OL/22116/2011 A Research Project Submitted to the School of Business, Department of Business Administration in Partial Fulfillment of the Requirement for the award of Master of Business Administration of Kenyatta University

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Effects of Corporate Governance Practices on the Growth of Pension Schemes in Kenya

THE EFFECTS OF CORPORATE GOVERNANCE PRACTICES ON

THE GROWTH OF PENSION SCHEMES IN KENYA

BY

LAMECK OKEYO

D53/OL/22116/2011

A Research Project Submitted to the School of

Business, Department of Business Administration

in Partial Fulfillment of the Requirement for the

award of Master of Business Administration of

Kenyatta University

NOVEMBER, 2013

DECLARATION

This research Project is my original work and has not

been presented for a degree in any other university or

for any other award.

Signature……………………………………………Date…………………………

Lameck Okeyo

D53/OL/22116/2011

This Project has been submitted for examination with my

approval as the university supervisor.

Signature……………………………………………Date…………………………

Dr. Stephen Muathe (PhD),

Department of Business Administration,

School of Business, Kenyatta University.

This Project has been approved for examination by the

chairman of the department.

Signature……………………………………………Date…………………………

The Chairman,

ii

Department of Business Administration,

School of Business, Kenyatta University.

DEDICATION

I would like to dedicate this project to my parents whose

love for education encouraged and saw me through the

educational system to university level.

I would also wish to dedicate this research project to my

family members. Their prayers and support was a great

encouragement to me in the entire research process.

iii

ACKNOWLEDGEMENT

I would like to acknowledge with gratitude my supervisor

namely; Dr. S. Muathe (PhD) for his tireless assistance

and supervision during my research work and preparation

of the project. I also acknowledge my classmates for the

support with ideas that contributed to the success of

this project.

iv

I would also like to thank the librarians at the Kenyatta

University Library for their support with the books used

for literature review and other valuable information that

they provided to aid in the completion of this project.

Above all, I thank God Almighty for taking me

through my studies and the research work so for.

v

TABLE OF CONTENTS

TITLE

PAGE .....................................................

..........................................................

i

Declaration................................................ii

Dedication................................................iii

Acknowledgement............................................iv

Table of Contents...........................................v

List of Figures...........................................vii

List of Tables...........................................viii

Abbreviations and Acronyms................................ix

Operational Definition of Terms...........................x

Abstract...................................................xii

CHAPTER ONE: INTRODUCTION..................................1

1.1 Background to the study...........................1

1.2 Statement of the Problem..........................3

1.3 Objectives of the Study...........................3

1.4 Research Questions................................4

1.5 Significance of the Study.........................5

1.6 Scope of the Study................................5

1.7 Limitations of the Study..........................5

CHAPTER TWO:LITERATURE REVIEW..............................7

2.1. Introduction.....................................7

2.2 Theoretical Review................................7

2.3 Empirical Review..................................8

2.4 Summary of the Review and Research Gaps..........15

vi

2.5 Conceptual Framework.............................15

CHAPTER THREE:RESEARCH METHODOLOGY.......................17

3.1 Introduction.....................................17

3.2 Research Design..................................17

3.3 Target Population................................17

3.4 Sampling Techniques..............................17

3.5 Data Collection Instruments......................18

3.6 Data Collection Techniques.......................20

3.7 Data Processing and Analysis.....................20

CHAPTER FOUR:RESEARCH FINDINGS AND DISCUSSIONS..........22

4.1 Introduction.....................................22

4.2 Analysis of the Response Rate and Demographic

Information..........................................22

4.3 Risk Based Internal Control......................24

4.4 Financial Management Systems.....................26

4.5 Regulatory Framework Compliance..................29

4.6 Record Management Systems........................30

4.7 Competencies of the Management Body..............32

4.8 Growth of the Pension Schemes....................35CHAPTER FIVE: SUMMARY, CONCLUSION AND RECOMMENDATIONS.......39

5.1 Introduction.....................................39

5.2 Summary..........................................39

5.3 Conclusion.......................................41

5.4 Recommendations..................................42

5.5 Suggestions for Further Research.................43

REFERENCES.................................................44

APPENDICES.................................................46

Appendix I: Questionnaire cover letter...............46

vii

Appendix II: Questionnaire..........................47

LIST OF FIGURES

Figure 2.1: The Conceptual Framework...................16

Figure 4.1: Effectiveness of Financial Management Systems

.......................................................28

Figure 4.2: Management Team Training Adequacy.........34

Figure 4.3: Overall Growth of the Pension Schemes......35

Figure 4.4: Satisfaction with the Growth of the Pension

Schemes................................................36

viii

LIST OF TABLES

Table 3.1: Reliability Assessment......................20

Table 4.1: Analysis of the Study Response Rate.........22

Table 4.2: Analysis of the Demographic Information.....23

ix

Table 4.3: Analysis of Risk based Internal Control

Aspects................................................25

Table 4.4: Analysis of Financial Management Systems of

the Pension Schemes....................................27

Table 4.5: Pension Schemes’ Compliance to the Regulatory

Framework..............................................29

Table 4.6: Analysis of the Record Management System

Issues.................................................31

Table 4.7: Results of the Analysis of Management Body

Competencies...........................................33

Table 4.8: Results of the Pearson Correlation Analysis. 37

x

ABBREVIATIONS AND ACRONYMS

GDP : Gross Domestic Product

IOPS : Institute for Pension Supervisors

IFPS : Institute for Pension Supervisors

NCVO : National Council for Voluntary

Organisations

OECD : Organisation for Economic Co-operation and

Development

RBA : Retirement Benefits Authority

UK : United Kingdom

USA : United States of America

SPSS : Statistical Package for Social Sciences

xi

OPERATIONAL DEFINITION OF TERMS

Growth: This is the process of measuring

an enterprise's success. Business

growth can be achieved either by

boosting the top line or revenue of

the business with greater sales or

service income, or by increasing the

bottom line or profitability of

the operation by minimizing

costs.

xii

Governance: This is the systems and

processes concerned with

ensuring the overall direction,

effectiveness, supervision and accountability

of an organisation.

Corporate Governance: This is where the

governance provides the

structure through which the objectives of the

company are set, and the means of

attaining those objectives

and monitoring performance are

determined.

Risk-Management Frameworks: This is as the process -

effected by an

organisation’s board of trustees, management

and other personnel - designed to

provide reasonable assurance

regarding the achievement of

objectives in terms of: effectiveness and

efficiency of operations; reliability of

financial reporting; and

xiii

compliance with laws and

regulations.

Financial Management System: This is the process of

managing an

organization’s financial resources so that it

can meet its objectives.

Budget: This is a financial or business

plan that indicates incomes of a

business firm and apportioned

expenditure to cater for the

operations over a given period

of time.

xiv

ABSTRACT

Pension funds are the principal sources of retirementincome for millions of people in the world. Pensionschemes contribute significantly to the reduction in old-age poverty since a large proportion of the incomes ofretirees is derived from their previous pensionarrangements. In addition, retirement income accounts for68% of the total income of retirees in Kenya hence animportant contributor to the gross domestic product (GDP)of country. However, the pension schemes in Kenya havebeen characterized by rampant mismanagement andmisappropriation of funds that have led tounderperformance. In addition, the effectiveness of theapplication of the corporate governance practices havebeen blamed for failure of many pension schemes to meettheir financial obligations and overall mismanagement ofthe schemes. In addition, most pension schemes in Kenyaare grossly under-funded and this has a negative effecton their growth. This study sought to assess the effectsof corporate governance practices on the growth ofpension schemes in Kenya. The study design wasdescriptive research design. The target population

xv

included all the 1216 Pensions Schemes registered byRetirement Benefits Authority (RBA) in Kenya. Systematicrandom sampling method was used to draw a sample of 122respondents (which represents 10% of the targetpopulation) from the Pensions Schemes registered by RBA.Semi- structured questionnaires was administered to therespondents. The data was analyzed by generatingdescriptive statistics such as percentages, frequencies,means and standard deviation. In addition, inferentialstatistics were also utilized. Key inferential statisticsutilized was Pearson correlation analysis. This was usedto establish the relation between the dependent and theindependent variables of study. Statistical Package forSocial Sciences (SPSS) aided in the statistical analysisof quantitative data. Data was presented using tables,charts and bar graphs. The findings showed that themembers of the pension schemes receive inaccurateinformation which led to inappropriate decisions, latepayment of contributions was also evident which led todelay or inaccuracies in payment of benefits. Inaddition, the existing IT system was found to beinsufficient to handle the financial transactionseffectively. This study recommends that the pensionschemes invest in an efficient financial managementsystems that will effectively safeguard the members’contribution. In addition, the management needs to put inplace a good and efficient IT system that is sufficientto handle all the financial transactions effectively.

xvi

CHAPTER ONE

INTRODUCTION

1.1 Background to the Study

Globally, retirement income is an extremely important

component of every individual's life cycle. The

retirement income comes from one of the four key pillars

of support in old age: unfunded state pensions (that is,

transfers from the current working population via the tax

system), funded private pensions (that is, from savings

accumulated in private sector pension schemes), direct

private savings, and post-retirement work. For most

people in developed countries, the key sources of

retirement income are state and private pension schemes.

Good governance of the pension scheme is there crucial if

the pension schemes are to deliver their duty to their

contributors/members (World Bank, 2009).

The National Council for Voluntary Organisations (NCVO)

(2005) defines governance as ‘the systems and processes

concerned with ensuring the overall direction,

effectiveness, supervision and accountability of an

organisation. Governance involves the governing body of

the scheme; however nearly every scheme activity involves

the governing body to some extent. In the corporate

governance context the Organisation for Economic Co-

operation and Development (OECD) states that governance

1

provides the structure through which the objectives of

the company are set, and the means of attaining those

objectives and monitoring performance are determined

(OECD, 2004).

Global indices indicate that pension assets are important

to any economy. According to Alliance Global Investors

(2007), pension assets in Australia amount to AU$

1trillion (equivalent to 20% of the GDP), while in

Belgium pension assets amounted to 140 billion Euro in

2004. In 2003, the pension assets of Canada were worth

CAD 1.3 trillion (30% of the GDP), while in China pension

assets amounted to RMB 714 billion (24% of GDP) for same

year. The contribution of pension assets to the GDP of

the United Kingdom reached 14% (GDP 1.9 trillion) in

2003, while in the United States of America, the pension

assets had a value of US$ 14.5 trillion (37.7% of all

household financial assets). Closer to home, namely in

Kenya and South Africa, the pension assets had a value of

KSH 130 billion in 2006, which accounted for 30% of the

GDP (RBA 2007) and ZAR 1098 billion in 2004 (Alliance

Global Investors 2007) respectively. Pension funds are

therefore important contributors to the GDPs of countries

and should consequently be managed effectively.

Old age poverty rates are increasing in the 21st Century.

The Institute for Pension Supervisors (IFPS) (2008a)

estimates the old age poverty rates at 30.6% in Ireland,

2

26.9% in Australia, 23.6% in USA, 22% in Japan, 10.3% in

UK, 9.9% in German, 8.8% in France and 56% in Kenya with

other African countries recording much higher rates.

Research shows that old age poverty arises because 85% of

the World’s population over 65 years have no retirement

benefit at all (Holzman and Hinz 2001; Stewart and Yermo

2008).

In the Sub-Saharan Africa, less than 10% of the

population has a contributory pension arrangement to help

them save for their retirement (Palacios and Pallares-

Miralles 2000). Pension schemes contribute significantly

to the reduction in old-age poverty since a large

proportion of the incomes of retirees is derived from

their previous pension arrangements (Kakwani, Sun and

Hinz, 2006). According to the Alliance Global Investors

(2007), 75% of the elderly population relies on pension

income in South Africa while 82% of the retirees depend

on pension income in the East African countries. Pension

fund arrangements should therefore be encouraged to

enable the general population to save for retirement and

consequently reduce the old-age poverty levels.

In the Kenyan financial markets, pension fund industry is

a significant source of capital (Omondi, 2008). According

to Omondi, pension funds invested a sum of Ksh. 223

billion in the Kenyan financial sector in 2007 of which

Ksh. 77 billion (22% of the outstanding domestic debt)

3

was invested in government securities. Kakwani, et al

(2006) reported that retirement income accounts for 68%

of the total income of retirees in Kenya. Pensions

therefore play an important role in breaking

intergenerational poverty cycles and thus increase the

life expectancy of the elderly generation (Help Age

International 2006; Keizi, 2007). Pension funds are thus

significant institutional investors and must therefore be

managed efficiently to ensure they play their rightful

role in the country’s economy.

1.2 Statement of the Problem

Pension schemes play an important role in breaking

intergenerational poverty cycles and thus increase the

life expectancy of the elderly generation (Help Age

International 2006; Keizi, 2007). According to Brunner,

Hinz and Rocha (2008), the pension schemes in Kenya have

been characterized by rampant mismanagement and

misappropriation of funds that led to underperformance.

This has ultimately contributed to the low growth of the

pension schemes. In addition, the management strategies

employed by the Kenyan fund managers have been questioned

which points to the efficiency in application of

corporate governance practices in the pension schemes.According to RBA (2010) most of the pension schemes in Kenya

are grossly under-funded while others have poor investment

strategies resulting to lack of prudence in the investment

of pensioner’s funds. In addition, the gross financial

inefficiency that characterized most pension schemes in

4

Kenya have resulted to higher costs of operation, low

returns on investment and in extreme cases to the demise of

the funds (Bikker and Dreu, 2009). Low investment returns

and the closure of pension funds reduce the latter’s

contribution to the GDPs of countries.

While previous empirical reports (Keizi, 2006; Rajan,

2003; Barrientos, 2007) have emphasized on the reasons

for low coverage and suggestions to increase the coverage

of pension schemes, they fail to explore the

effectiveness of corporate governance practices and their

effects on the growth of pension schemes in Kenya. This

poses a knowledge gap which this study sought to fill.

1.3 Objectives of the Study

1.3.1 Broad objective

The broad objective of the study was to assess the

effects of corporate governance practices on the growth

of Pension Schemes in Kenya.

1.3.2 Specific Objectives

The study will address the following specific objectives;

5

i. To assess the effects of risk based internal control

on the growth of Pension Schemes in Kenya.

ii. To establish how the existing financial management

systems affect the growth of Pension Schemes in

Kenya.

iii. To establish the competencies of the management body

and its influence on the growth of Pension Schemes in

Kenya.

iv. To assess of the effects of the existing record

management systems on the growth of Pension Schemes

in Kenya.

v. To establish the extent to which compliance to the

existing regulatory framework affect the growth of

Pension Schemes in Kenya.

1.4 Research Questions

The study will seek to answer the following research

questions:

i. How does risk based internal control influence the

growth of Pension Schemes in Kenya?

ii. How do the existing financial management systems

affect the growth of Pension Schemes in Kenya?

6

iii. How do the competencies of the management body

influence the growth of Pension Schemes in Kenya?

iv. What are the effects of the existing record

management systems on the growth of Pension Schemes

in Kenya?

v. How does the compliance to the existing regulatory

framework affect the growth of Pension Schemes in

Kenya?

1.5 Significance of the Study

This study is useful to the Retirement Benefits Authority

since the recommendations made if adopted will help to

strengthen the governance of pension schemes and enhance

compliance to the set laws.

The pension schemes management may also benefit from this

study since the recommendations made will help in

designing strategy to enhance good governance as well as

increase the pension schemes growth and compliance with

the set rules and regulation.

The government will get policy direction in relation to

the pension sector from this study. It will be easy for

government policy makers to determine the next policy

requirements if the industry is to remain relatively

trouble free.

7

Researchers, scholars and academicians interested to

research further in areas of the pension schemes and

retirement benefits will also benefit from the results of

this study.

1.6 Scope of the Study

This study was limited to registered pension schemes in

Kenya. There are 1216 Pension schemes registered by RBA

in Kenya. The researcher sampled these Pension schemes

whereby one respondent from the sampled firms was

targeted. The respondents were the trustees, top manager

or senior supervisor of the Pension schemes who have key

information on the internal governance of the pension

scheme.

1.7 Limitations of the Study

The study was faced by the limitation of concealment of

information by the respondents. This was mitigated by

obtaining an introductory letter from the university as

well as a research permit detailing the purpose of the

study. The study was also faced by the limitation of

accessing the respondents since the study targeted the

trustees and/or top management who are mainly busy due to

their involvements in the running of the pension schemes.

To address this problem, the researcher purposively

sampled pension schemes whose senior managements and

trustees was available and were willingly accepting to

respond in the study. Therefore, those who were on annual

leave or out of office on official assignments or not

8

easily accessible due to the nature of their job

schedules were not included in the sample. In addition,

the researcher booked appointments with the concerned

respondents to increase the response rate.

9

CHAPTER TWO

LITERATURE REVIEW

2.1. Introduction

The purpose of the literature review is to set

the study subject in a broader context through

investigation of the relevant literature and other

sources. The chapter presents a review of the related

literature on the subject under study as presented by

various researchers, scholars, analysts and authors. The

review covers issues on global perspective on the growth

of pension schemes; risk based internal control of

pension schemes, financial management systems of pension

schemes, pension schemes compliance to regulatory

framework, record management systems of pension schemes,

competencies of managerial team of the pension schemes

and conceptual framework.

2.2 Theoretical Review

This study was based on theory of social security.

2.2.1 Theory of Social Security

The origins of social security theory are difficult to

pinpoint, but debates frequently return to Ancient Greece

(Steven, 2008). The theory posits that social elements

influence human nature. Human beings tend to feel secure

when they are institutionalized or organised into a

10

functional groups from which they can derive certain

benefits or satisfactions (Macionis, John and Plummer,

2005). This theory can be used to explain the operations

and pooling together of resources in pension schemes. The

key essence of a pension scheme is to bring together

individual little resources into a pool which can benefit

the members at old age. In many countries, social

security accounts for a large fraction of the government

budget. This is so, given that at any point in time, the

number of beneficiaries of the social security is smaller

than the number of contributors. If the size of social

security is larger, the greater is the proportion of

elderly people in the population, and the greater is the

inequality of pre-tax income within each generation.

Contemporary social protection financing systems face

three major challenges. They are said to be ill-equipped

to deal with the ageing of the population and with

globalization, and the financial burden placed on

contributors and taxpayers in all countries is said to

have reached the limits of affordability. According to

World Labour Report (2000), ageing - often misrepresented

as the key challenge for the financing of formal social

transfer systems - will pose a major problem if rapidly

ageing societies cannot contain overall social

dependency. However, dependency could be reduced

substantially through increased retirement ages and

greater labour force participation of women. An ageing

11

society need not face any crisis, as long as it is able

to provide jobs for its ageing workforce. After decades

of heavy investment in health care through social

protection, people should remain fit and healthy until

later in life and should be able to work longer. In

addition, modern and more flexible lifetime working

patterns should be able to accommodate employment

patterns needed by parents and older workers.

2.3 Empirical Review

According to OECD (2009), Pension schemes have grown

strongly in recent years in many OECD countries as well

as in emerging markets, both relative to GDP and compared

to banks. The rapid growth of pension funds in many

countries, and the stimulus they are providing to the

growth of capital markets, both suggest that their

activities as financial intermediaries merit considerable

attention. According to Bodie and Davis (2000), pension

funds’ growth is an important component since they

complement, and hence stimulate development of capital

markets, while acting as substitutes for banks.

Since withdrawal of funds is usually restricted or

forbidden, pension funds have long term liabilities,

allowing holding of high risk and high return

instruments. Accordingly, monies are intermediated by

pension funds into a variety of financial assets, which

include corporate equities, government bonds, real

estate, corporate debt (in the form of loans or bonds),

12

securitized loans, foreign holdings and money market

instruments and deposits as forms of liquidity (IOPS,

2007).

Davis (2005) defined Pension funds as forms of

institutional investor, which collect pool and invest

funds contributed by sponsors and beneficiaries to

provide for the future pension entitlements of

beneficiaries. They thus provide means for individuals to

accumulate saving over their working life so as to

finance their consumption needs in retirement, either by

means of a lump sum or by provision of an annuity, while

also supplying funds to end-users such as corporations,

other households (via securitized loans) or governments

for investment or consumption.

According to OECD (2009), pooling and diversification is

a fundamental characteristic of pension funds, given

their size and consequent economies of scale. In this

context, it is important to note that mutually

reinforcing development of securitization of individual

assets (such as loans), which has provided a ready supply

of assets in which pension funds may invest instead of

banks holding them on their balance sheets. In addition,

IOPS (2007) notes that participation costs to market

activity may also be of major importance in determining

the demand for services of pension funds.

13

According to Allen and Santomero (2008), pension schemes

have continued to grow because participation costs

complements that of transactions costs, and low

transactions costs. The basic idea is that there is a

fixed cost to learning about a company, and also an

ongoing cost to being active in the market and remaining

up-to-date, which may discourage individuals from holding

sufficient shares for adequate diversification.

Furthermore, the skills needed to undertake risk

management may be too costly for individuals to acquire

(Davis, 2005).

2.3.1 Risk based Internal Control of Pension Schemes

OECD guidelines outline requirements regarding the risk-

management systems of pension funds. According to OECD

(2004), Pension entities should have adequate risk

control mechanisms in place to address investment,

operational and governance risks, as well as internal

reporting and auditing mechanism. In addition, the OECD’s

Guidelines for Pension Fund Governance (OECD 2009)

address risk-based internal controls as part of the

governance mechanisms. According to OECD’s Guidelines,

there should be appropriate controls in place to ensure

that all persons and entities with operational and

oversight responsibilities act in accordance with the

objectives set out in the pension entity's by-laws,

statutes, contract, or trust instrument, or in documents

associated with any of these, and that they comply with

14

the law. Risk-management frameworks process does not

involve just one policy or procedure performed at a

certain point of time but should be continually operating

at all levels of the organisation, and involve all staff.

According to IOPS (2007), key part of a risk-based

approach to pension supervision involves the supervisory

authority transitioning from checking detailed compliance

requirements for the cooperation of pension funds to

reviewing the internal decision-making processes and

bodies of these funds. One of the main objectives of

risk-based supervision is to ensure sound risk management

at the institutional level taking into account both the

quality of risk management and the accuracy of the risk

assessment. Risk-based supervision allows much of the

responsibility for risk management to rest with the

individual pension fund companies themselves, while the

supervisory agency verifies the quality of the fund’s

risk management processes and adapts its regulatory

stance in response (OECD, 2009).

Brunner, Hinz and Rocha (2008) argues that some of the

decline in assets recently experienced by pension funds

around the world may well have been avoided through

stronger risk- management frameworks, as some funds

appear to have been exposed to instruments whose risk

profiles they did not fully understand. A sound risk

framework for pension funds is essential for their

15

prudent operation and the stability of the financial

system as a whole (Retirement Benefits Authority, 2003).

2.3.2 Financial Management Systems of Pension Schemes

Financial management system encompasses the two core

processes of finance operations and resource management

operations including management decisions. Financial

management encompasses accounting and financial

reporting, forecasting and budgeting (OECD, 2004).

Garbutt (1976) describes accounting as a discipline

concerned with the recording, analysis, and forecasting

of income and wealth of business and other activities.

All firms require finances to do their routine

(administrative), business transactions and investment

purposes. Garbutt (1976) further argues that a good

financial system should comprehensively cover all

operations of the organization. It should include

internal control measures that ensure resources use is

consistent with the policies; resources are safeguarded

against loss and misuse; and reliable data are obtained,

maintained, and disclosed in reports.

According to OECD (2004), appropriate internal controls

should be applied to all system inputs, processing, and

outputs. Organisations should have an efficient financial

system to ensure that the financial information generated

is timely and relevant to support management decision,

16

support budget formulation and execution functions and

monitor the system to ensure integrity of financial data.

Budgets are important for planning and control purposes.

Garbutt (1976) further describes a budget as a financial

or business plan that indicates incomes of a business

firm and apportioned expenditure to cater for the

operations over a given period of time.

Managers are supposed to adhere to the financial plan and

its one tool used for evaluation of business performance

in terms achieving set objectives while keeping within

the financial plan. Governance regulations should require

that pension funds have appropriate controls in place to

ensure that all persons or entities with operational and

oversight responsibilities act in the best interest of

plan members and beneficiaries.

2.3.3 Pension Schemes’ Compliance to Regulatory Framework

According to OECD (2004), Governance regulations have not

always been present in all countries. Most often, they

have been introduced as a response to cases of fraud or

misappropriation of pension assets. In the United

Kingdom, for example, the decision to enhance the

responsibility of trustees over pension fund management

and to increase their independence vis-à-vis employers

was mainly a response to the Maxwell scandal, in which

the Maxwell companies’ main pension fund lost a large

part of its assets as a result of lending to and

17

investment in insolvent companies linked to the late

Robert Maxwell. Similarly, the fiduciary standards

introduced by the 1974 ERISA law in the United States

were largely in response to various unhappy episodes of

fraud in pension fund management and of plan insolvency

caused by the bankruptcy of the plan sponsor.

In Kenya, the retirement benefits Act was enacted in the

year 1996 and the retirement benefits authority

established in 1997. Ever since the RBA has attempted to

reign in the players in the pensions sector by coming up

with a number of rules, regulations and requirements. The

members of the industry have been under pressure to

comply with these requirements (Retirement Benefits

Authority, 2003). The Retirement Benefits Act requires

each retirement benefits scheme to seek the services of a

registered fund manager. The manager, for the purposes of

the Retirement Benefits Act, is a company whose business

includes undertaking, pursuant to a contract or other

arrangement, the management of the funds and other assets

of a scheme fund for purposes of investment; providing

consultancy services on the investment of scheme funds;

and reporting or disseminating information concerning the

assets available for investment of scheme funds. The

managers must be licensed by the Retirement Benefits

Authority on an annual basis in order to carry out fund

management of pension scheme assets (RBA, 2009).

18

Governance regulations need to be designed under the

guidance of the overriding objective that pension funds

are set up to serve as a secure source of funds for

retirement benefits. The governance structure should

ensure an appropriate division of operational and

oversight responsibilities, and the accountability and

suitability of those with such responsibilities (Brunner,

Hinz and Rocha, 2008).

Pension entities are established in accordance to

statutes, by-laws, contract, or trust instrument. These

documents, sometimes together with associated material,

should define the legal form of the pension entity as

well as its internal governance structure and main

objectives. The main objectives of the pension entity

will vary depending on the type of plan that they

support. In defined contribution plans, the main

objective of the pension entity may be to invest the

pension assets in order to maximize risk-adjusted

returns. In defined benefit plans, the pension entity may

have several objectives, such as ensuring an adequate

match between the pension plan assets and its liabilities

and paying benefits upon the death or retirement of plan

members (RBA, 2009).

According to World Bank (1994), poor regulatory framework

has contributed to governance issues resulting to

contribution evasion among contributors. Some analysts

19

have considered contribution evasion to be primarily a

problem of defined benefit schemes with the replacement

of those schemes by defined contribution schemes solving

the problem.

A study done in Chile reporting compliance of 95 percent

(Chamorro 1992) is certainly, however, considerably

overstates compliance. In any case, the percentage of

workers in Chile not participating in the defined

contribution system is roughly equal to those not

participating in the defined benefit system it replaced.

Experience in Uruguay, Colombia and Peru also indicates

that switching to a defined contribution system from a

defined benefit system does not solve the problem of

contribution evasion. In all these countries, roughly

half of the workforce participates in the mandatory

defined contribution system (Burkhauser and Turner,

1995).

2.3.4 Record Management Systems of Pension Schemes

According to RBA (2009) a proper record management system

should be a fundamental daily activity of any pension

scheme and is relevant throughout a scheme’s lifecycle.

Incomplete and inaccurate records and poor financial

management controls can place significant risk on the

security of scheme assets. For example, it could result

in the over payment of benefits or misappropriation of

funds. According to Njoroge (2003), poor records can also

lead to increased costs at key events, for example scheme

20

buy outs, and these extra costs will fall either on

employers or reduce member benefits.

According to World Bank (2005), the risks associated with

inaccurate data, for example incorrect benefit

calculations, can have short and long-term implications

for schemes and beneficiaries. Therefore, throughout a

scheme’s lifecycle, trustees need to ensure that accurate

and complete membership data and records are maintained.

This includes basic information such as a member’s date

of birth, date of retirement, National Insurance number

etc.

Trustees must be confident that controls ensure data is

accurately recorded, regularly reviewed and all data

fields are complete. Inaccurate records could lead to the

wrong value being placed on benefits. This may have

consequences for calculating technical provisions,

benefits, and the levy. These may in turn have harmful

consequences for the employer.

According to RBA (2009) a framework to evaluate data

should be designed to provide an indication of whether

record-keeping needs further consideration in the context

of risks; measurement of data accuracy is not an end in

itself. Where trustees are aware of or have identified

data deficiencies they should develop a continuous

improvement strategy in relation to scheme records.

Trustees should also produce a data improvement plan,

21

covering a reasonable time frame, with specific data

improvement deliverables which can be monitored and

tracked.

2.3.5 Competencies of Managerial Team of the Pension

Schemes

Managerial competencies are critical in ensuring good

administration and effective governance of pension

schemes. According to Njoroge (2003), the management of

the pension schemes has always been the employers of the

pensioner/contributors of the Pension schemes. This

brings in conflict of interest in the management of

pension scheme funds.

In Kenya, the employer is always the sponsor of the fund.

This implies that the employer is responsible for the

appointment of auditor, and actuaries, including the

trustees. This gives employers access to funds of the

scheme. This has always rendered the scheme to abuse by

the employer. This has led to a situation whereby the

pension scheme is not able to meet its obligations to the

pensioners. Effective corporate governance ensures that

legislative and regulatory requirements are met, that the

provisions of the trust deed and rules are complied with,

and that members receive the level of benefits and

service to which they are entitled (Burkhauser and

Turner, 1995).

22

According to the Retirement Benefits Authority (2003),

every pension fund should have a competent governing body

or administrator vested with the power to administer the

pension fund and who is ultimately responsible for

ensuring the adherence to the terms of the arrangement

and the protection of the best interest of plan members

and beneficiaries. The responsibilities of the governing

body should be consistent with the overriding objective

of a pension fund which is to serve as a secure source of

retirement income.

According to World Bank (1994), mechanisms are needed to

ensure that the pension funds are managed by competent

personnel. The internal staff as well as the external

service providers (such as those providing consultancy,

actuarial analysis, asset management, and other services

for the pension entity) should have the required

qualification for effective management of the pension

funds.

Risks to members from poor governance are often higher

during periods of change to the employer(s), for example

during mergers, takeovers or insolvencies. At such times

the focus may be on other areas of the business, so it is

important to have competent trustees who will ensure that

members’ records are preserved and their interests

safeguarded at these times (Ngai, 2009).

23

2.4 Summary of the Review and Research Gaps

This chapter has reviewed literature on corporate

governance of the pension schemes both locally and

internationally. The review has shown that good

governance practices contribute significantly to the

success of pension schemes in both private and public

sector. The challenge has been to institutionalize

reforms and introduce best governance practices that will

guarantee effective management and ultimately promote the

growth of pension schemes in Kenya. However, many pension

schemes are grossly mismanaged while others are under-

financed hence not able to meet their financial

obligation (RBA 2009). Studies on pension schemes in

Kenya have focused on increasing the membership,

efficiency of the funds and institutionalization of

reforms but have failed to address issues of corporate

governance practice and their effects on the growth. This

posses a knowledge gap which this study sought to fill.

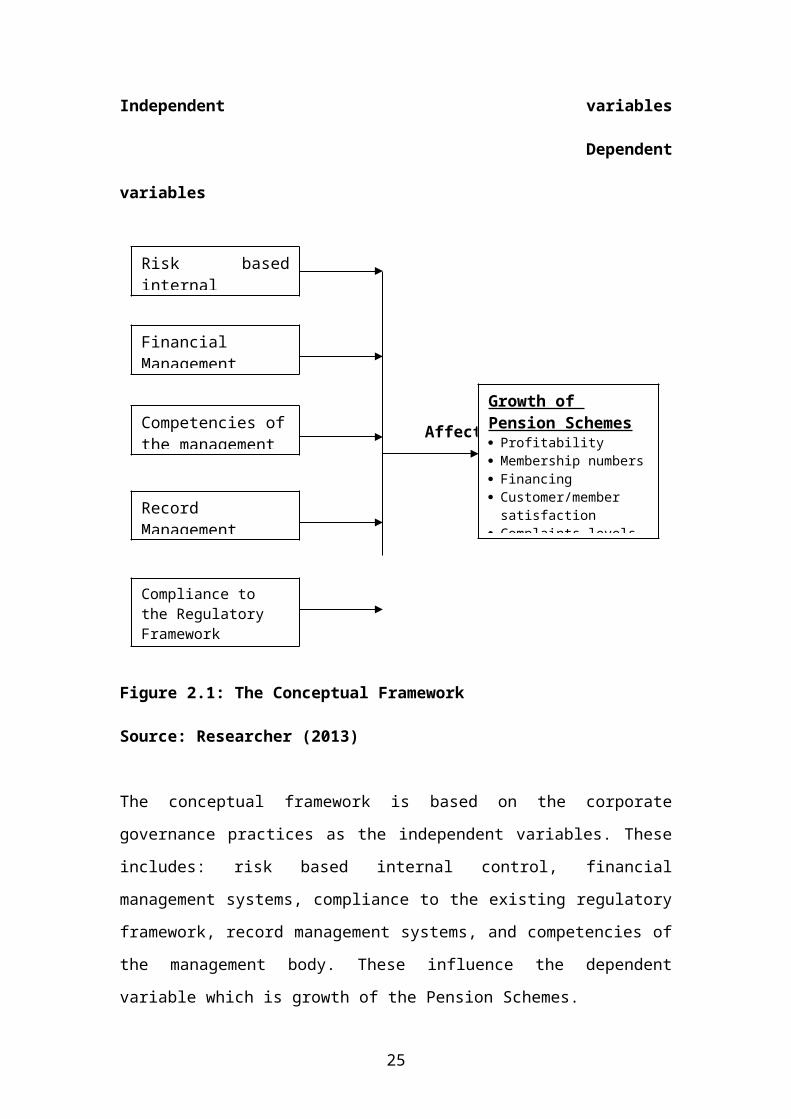

2.5 Conceptual Framework

Figure 2.1 shows the conceptualization of the

relationship between the dependent and the independent

variables.

24

Independent variables

Dependent

variables

Affects

Figure 2.1: The Conceptual Framework

Source: Researcher (2013)

The conceptual framework is based on the corporate

governance practices as the independent variables. These

includes: risk based internal control, financial

management systems, compliance to the existing regulatory

framework, record management systems, and competencies of

the management body. These influence the dependent

variable which is growth of the Pension Schemes.

Financial Management

Risk basedinternal

Competencies ofthe management

Record Management

Growth of Pension Schemes Profitability Membership numbers Financing Customer/membersatisfaction

Complaints levels

Compliance to the Regulatory Framework

25

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 Introduction

This chapter details the methodological approaches and

procedures that were used in conducting this study. The

key sections discussed in this chapter include; the

research design, the target population, the sampling

techniques, data collection instruments, sample size and

the techniques used in data analysis.

3.2 Research Design

The study adopted a descriptive research design.

Descriptive research includes surveys and fact-finding

enquiries of different kinds. The major purpose of

descriptive research design is the description of the

state of affairs as it exists at present (Kothari, 2004).

The researcher applied this design to investigate the

current situation in relation to the effects of corporate

26

governance practices on the growth of Pension Schemes in

Kenya.

3.3 Target Population

According to Mugenda and Mugenda (2003), a target

population refers to all the members of a population to

which the researcher wishes to generalize the results of

the research. The target population for this study

included all the 1216 pension schemes registered by the

Retirement Benefits Authority (RBA) by June 2013. The

respondents were the trustees, the top management and/or

senior supervisor of the pension schemes. The trustees,

the top management and/or senior supervisor were selected

because they are responsible for implementation of

corporate governance practices, management of the pension

schemes as well as ensuring compliance with the statutory

requirements as defined by the relevant legal statutes.

3.4 Sampling Techniques

A list of all the 1216 registered pension schemes in

Kenya was obtained which assisted in the sampling

process. Systematic random sampling was used to select

the target pension schemes. This technique was

appropriate because it gives all pension schemes equal

probability of being chosen and hence reduce biases.

According to Kothari (2003), an optimum sample is the one

that fulfills the requirements of efficiency,

representativeness, reliability and flexibility. This

sample should be in a range of 10%-30%. A sample of 10%

27

of all the registered pension schemes was drawn from the

target population to satisfy these requirements of

optimality and representativeness.

3.4.1 Sampling Frame

Based on the 10% sampling percentage as earlier

described, a sample size of 122 respondents (That is; 10%

of 1216 registered pension schemes) was obtained. One

respondent, that is, the trustees, the top manager or

senior supervisor from each of sampled schemes were

targeted. Using systematic random sampling, the first

pension scheme was selected from the list of registered

pension schemes, then the others were selected at an

interval of ten (10th pension scheme) until the sample

size of 122 respondents was achieved.

3.5 Data Collection Instruments

The study utilized both primary and secondary data.

Primary data was collected by use of questionnaires that

was administered to the trustees or senior management of

the sampled Pension Schemes. The questionnaire consisted

of both open-ended and closed questions covering issues

on all the variables of study. The open-ended questions

permitted free responses from the respondents, without

providing or suggesting any structure for the replies.

The closed ended questions enabled the responses of the

respondents to be limited to stated alternatives. These

28

alternatives were designed in such a way as to be simple

for the respondents to understand. The questionnaires was

administered through drop and pick method. The secondary

data was collected from the RBA publications, pension

schemes publications, journals and peer reviews.

3.5.1 Validity of the Instruments

Research instrument was pre-tested using a selected

sample of the target population in order to establish its

validity and the level of suitability. The procedure that

was used in pre-testing was similar to that which was

used in the actual study only that the sample was small

(about 1% of the target population=12 pension schemes).

This pre-testing was necessary because it helped to

detect wrong questions, little space, unclear direction

and clustered questions. Also the vague questions were

revealed and these were properly rephrased.

3.5.2 Reliability of the Instruments

Reliability measures the internal consistency of the

inter-item of the research instrument used in the study.

In this study, the Cronbach alpha reliability coefficient

for the pre-tested questionnaires was computed for all

the variables of the study. Cronbach’s alpha reliability

coefficient normally ranges between 0 and 1. The closer

Cronbach’s alpha coefficient is to 1.0 the greater the

29

internal consistency of the items, hence the higher the

reliability of the study instruments.

The purpose of reliability assessment was to assess the

internal consistency of the data collected by the

research questionnaire. In order to measure this,

Cronbach Alpha (α) was computed for each of the variable

to assess the reliability of the data collected.

According to Leedy and Ormrod (2003), a Cronbach Alpha

value greater than 0.6 is regarded satisfactory for

reliability assessment.

Table 3.1: Reliability Assessment

Independent Variables of Study

Variables

Cronbach Alpha (α)

Values

30

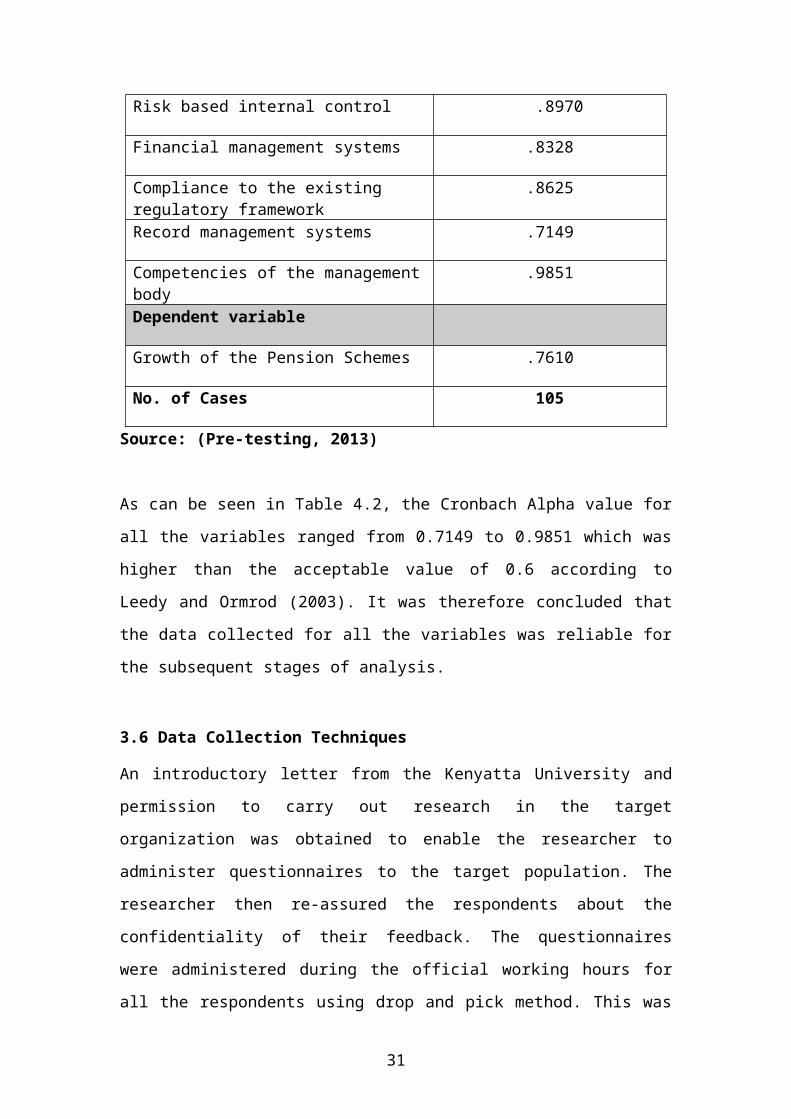

Risk based internal control .8970

Financial management systems .8328

Compliance to the existing regulatory framework

.8625

Record management systems .7149

Competencies of the managementbody

.9851

Dependent variable

Growth of the Pension Schemes .7610

No. of Cases 105

Source: (Pre-testing, 2013)

As can be seen in Table 4.2, the Cronbach Alpha value for

all the variables ranged from 0.7149 to 0.9851 which was

higher than the acceptable value of 0.6 according to

Leedy and Ormrod (2003). It was therefore concluded that

the data collected for all the variables was reliable for

the subsequent stages of analysis.

3.6 Data Collection Techniques

An introductory letter from the Kenyatta University and

permission to carry out research in the target

organization was obtained to enable the researcher to

administer questionnaires to the target population. The

researcher then re-assured the respondents about the

confidentiality of their feedback. The questionnaires

were administered during the official working hours for

all the respondents using drop and pick method. This was

31

necessary to increase the response rate. The data

collection was scheduled to take one month.

3.7 Data Processing and Analysis

The collected data was checked, edited and coded as soon

as the questionnaires were returned. Analysis of the raw

data was then done using statistical package for social

sciences (SPSS) to make statistical inferences. Both

descriptive and inferential statistical techniques were

utilized. The descriptive statistics used included;

frequencies, means, standard deviations, percentages

while the inferential statistics included; Pearson

correlation analysis. In addition, the qualitative data

was analyzed using content analysis techniques. The data

was presented through the use of tables, bar charts and

pie charts.

32

CHAPTER FOUR

RESEARCH FINDINGS AND DISCUSSIONS

4.1 Introduction

This chapter contains the data analysis, results and the

interpretations. The chapter is organised based on the

objectives of the study. Both descriptive statistics such

as Mean, Percentages, Frequencies, Standard Deviation as

well as inferential statistics such as Pearson

Correlation analysis were utilized.

4.2 Analysis of the Response Rate and Demographic

Information

4.2.1 Analysis of the Response Rate

The study targeted the pension schemes registered by RBA

in Kenya and the response rate achieved in the study is

as shown in Table 4.1.

33

Table 4.1: Analysis of the Study Response Rate

Responses Values Percentages

Administered

questionnaires

122 100.0%

Unusable, unreturned & disqualified questionnaires

17 13.9%

Completed usable

questionnaires

105 86.1%

Source: (Survey Data, 2013)

As can be seen in Table 4.1, a total of 122

questionnaires were administered to the respondents,

resulting in an 86.1% final response rate. Out of these,

17 questionnaires representing 13.9% were disqualified

due to incompletion, not being returned or those

unwillingly to participate in the study. The analysis of

the results is thus based on 105 questionnaires. Sekaran

(2003) is of the view that a minimum sample size of 30 to

a maximum of 500 is sufficient and acceptable for a

scientific investigation. During data cleansing and

verification process of this study, the questionnaires

with omissions and errors were disregarded as can be seen

in Table 4.1. The data cleansing and verification

procedure ensured that all quality standards were met

(Kerlinger, 2004).

4.2.2 Analysis of Demographic Information

34

The study sought to establish the background information

of the sampled respondents. Key attributes investigated

included: Gender, highest level of education, type of the

pension scheme and respondents’ designation

Table 4.2: Analysis of the Demographic Information

DemographicInformation

Categories

Frequen

cy (n)

Percent

age

(%)

Gender Male 75 71.4Female 30 28.6

Highest level of

education

College 4 3.8Undergraduat

e

44 41.9

Post

graduate

57 54.3

Type of the Pension

Scheme

Public

Sector

50 47.6

Private

sector

55 52.4

Respondents

designation

Trustee 51 48.6Top

management

40 38.1

supervisors 14 13.3Overall Total (N) 105 100.0

Source: (Survey Data, 2013)

35

The findings show that majority of the respondents

(71.4%) were male while 28.6% were female. Majority of

the respondents were degree holders with Post Graduate

accounting for 54.3% while Undergraduate accounted for

41.9%. The findings further show that most Pension

Schemes sampled were in Private sector (52.4%) with

public sector accounting for 47.6%. in addition, the

findings show that most respondents were Trustees (48.6%)

with top management and supervisors accounting for 38.1%

and 13.3% respectively. This information is shown in

Table 4.2.

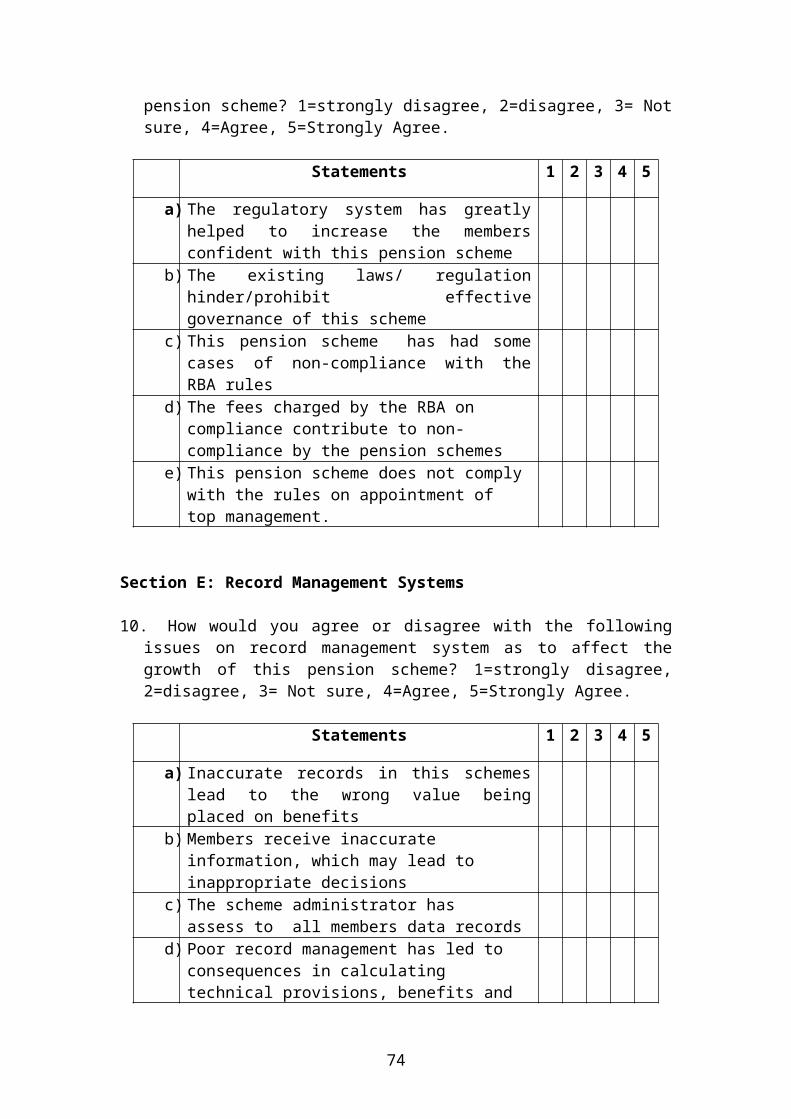

4.3 Risk Based Internal Control

The first objective of the study sought to assess the

effects of risk based internal control on the growth of

Pension Schemes in Kenya.

4.3.1 Issues on Risk based Internal Control

The respondents were presented with statements on Risk

based Internal Control issues thought to influence the

growth of the pension scheme and were required to rate

the extent to which they agreed or disagreed with the

listed statements. A five-point likert scale comprising

of strongly agree, Agree, neutral, disagree, strongly

disagree was used and the findings presented in Table

4.3.

36

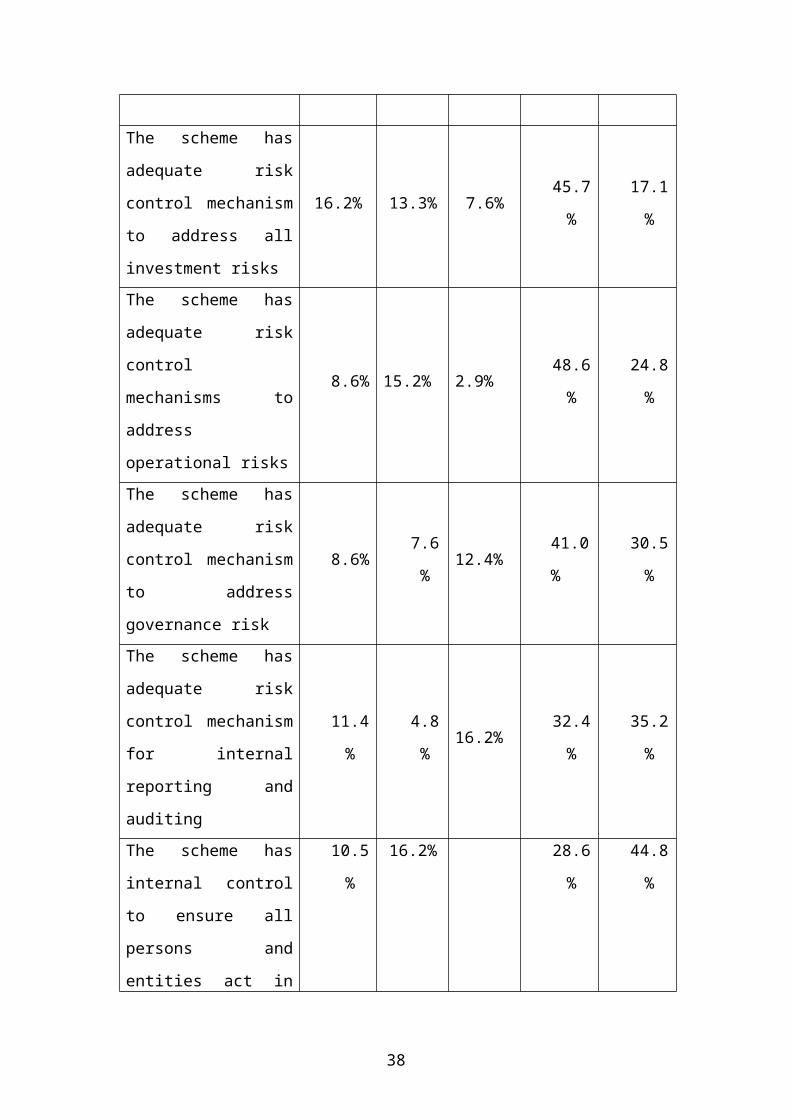

Table 4.3: Analysis of Risk based Internal Control

Aspects

Strong

ly

Disagr

ee

Disagr

ee

Not

sure Agree

Strong

ly

Agree

% % % % %

37

The scheme has

adequate risk

control mechanism

to address all

investment risks

16.2% 13.3% 7.6%45.7

%

17.1

%

The scheme has

adequate risk

control

mechanisms to

address

operational risks

8.6% 15.2% 2.9%48.6

%

24.8

%

The scheme has

adequate risk

control mechanism

to address

governance risk

8.6%7.6

%12.4%

41.0

%

30.5

%

The scheme has

adequate risk

control mechanism

for internal

reporting and

auditing

11.4

%

4.8

%16.2%

32.4

%

35.2

%

The scheme has

internal control

to ensure all

persons and

entities act in

10.5

%

16.2% 28.6

%

44.8

%

38

accordance with

the lawThe scheme has

sound framework

for stability of

pension funds

11.4

%10.5% 7.6%

35.2

%

35.2

%

Source: (Survey Data, 2013)

The findings in Table 4.3 show that most of the

respondents agreed with the following statements; The

scheme has adequate risk control mechanism to address all

investment risks, the pension scheme has adequate risk

control mechanisms to address operational risks, the

scheme has adequate risk control mechanism to address

governance risk, the scheme has adequate risk control

mechanism for internal reporting and auditing, the scheme

has internal control to ensure all persons and entities

act in accordance with the law and the scheme has sound

framework for stability of pension funds as accounted by

the 62.8%,73.4%,71.5%, 67.6%, 73.4% and 70.4% (strongly

agree and agree) cumulative responses respectively. This

shows that the pension schemes had adequate risk control

mechanisms to address operational risks, governance risk,

internal reporting and auditing. Further, the pension

schemes had internal control to ensure all persons and

entities act in accordance with the law and had sound

framework for stability of pension funds. These issues

39

promoted the growth of the pension schemes in the

country. These findings are consistent with the OECD

report (2004) which stated that pension entities should

have adequate risk control mechanisms in place to address

investment, operational and governance risks, as well as

internal reporting and auditing mechanism. In addition,

IOPS (2007) argued that key part of a risk-based approach

to pension supervision involves the supervisory authority

transitioning from checking detailed compliance

requirements for the cooperation of pension funds to

reviewing the internal decision-making processes and

bodies of these funds.

4.4 Financial Management Systems

The second objective of the study sought to establish how

the existing financial management systems affect the

growth of Pension Schemes in Kenya.

4.4.1 Financial Management Systems

The respondents were presented with statements related to

financial management systems and were required to rate

the extent to which they agreed or disagreed on how they

affected the growth of Pension Schemes in Kenya. A five-

point likert scale comprising of strongly agree, Agree,

neutral, disagree, strongly disagree was used whereby the

means and the standard deviations were computed. The key

to five point likert scale included; strongly disagree

(SD): 1.0 – 1.49, disagree (D): 1.5 – 2.49,

40

Undecided/Neutral (U): 2.5– 3.49, Agree (A): 3.5 – 4.49

and Strongly Agree (SA): 4.5 – 5. The responses were

interpreted and the findings presented in Table 4.4

below.

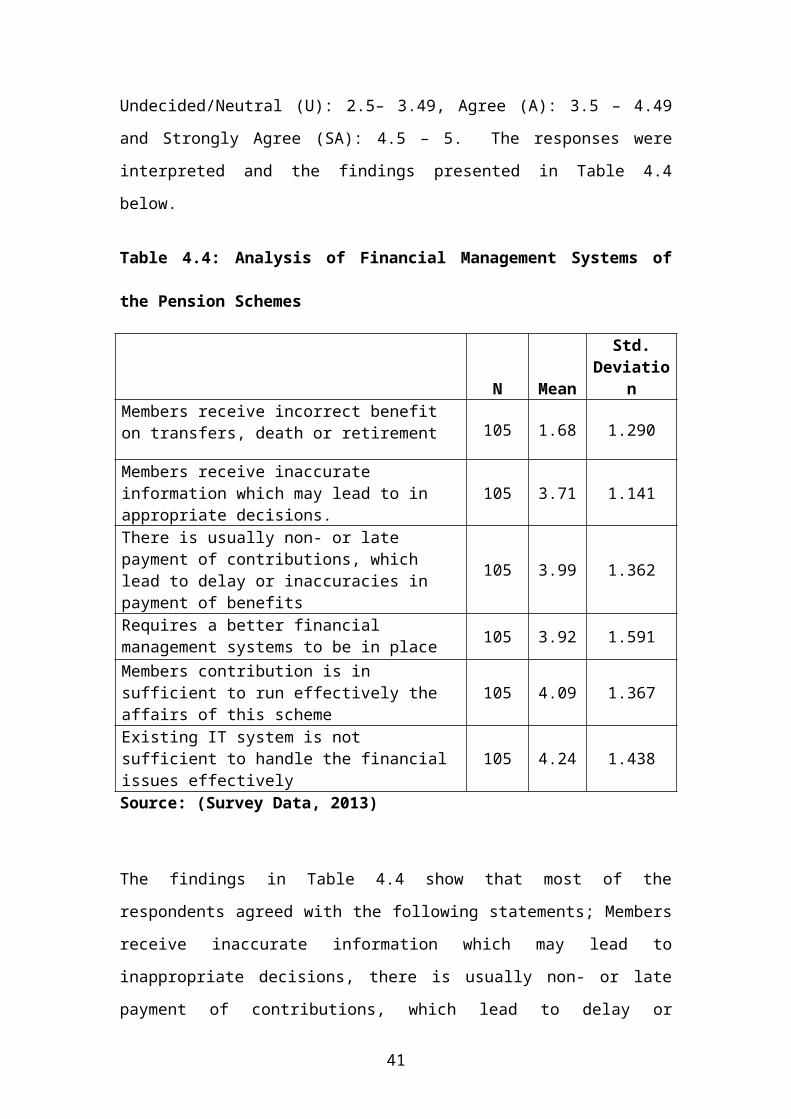

Table 4.4: Analysis of Financial Management Systems of

the Pension Schemes

N Mean

Std.Deviatio

nMembers receive incorrect benefit on transfers, death or retirement 105 1.68 1.290

Members receive inaccurate information which may lead to in appropriate decisions.

105 3.71 1.141

There is usually non- or late payment of contributions, which lead to delay or inaccuracies in payment of benefits

105 3.99 1.362

Requires a better financial management systems to be in place 105 3.92 1.591

Members contribution is in sufficient to run effectively the affairs of this scheme

105 4.09 1.367

Existing IT system is not sufficient to handle the financial issues effectively

105 4.24 1.438

Source: (Survey Data, 2013)

The findings in Table 4.4 show that most of the

respondents agreed with the following statements; Members

receive inaccurate information which may lead to

inappropriate decisions, there is usually non- or late

payment of contributions, which lead to delay or

41

inaccuracies in payment of benefits, requires better

financial management systems to be in place, members

contribution is insufficient to run effectively the

affairs of the scheme and existing IT system is not

sufficient to handle the financial issues effectively as

accounted by the means of 3.71, 3.99, 3.92, 4.09 and

4.24 respectively. The findings further show that most

respondents disagreed that members receive incorrect

benefit on transfers, death or retirement (1.68). This

shows that members of the pension scheme receive

inaccurate information which may lead to inappropriate

decisions, there is usually non- or late payment of

contributions, which lead to delay or inaccuracies in

payment of benefits, requires a better financial

management systems to be in place, members contribution

is insufficient to run effectively the affairs of the

scheme and existing IT system is not sufficient to handle

the financial issues effectively. These issues need to be

addressed since they affect negatively the growth of

pension schemes in the country. These findings were not

consistent with Garbutt (1976) who argues that a good

financial system should comprehensively cover all

operations of the organization. It should include

internal control measures that ensure resource use is

consistent with the policies; resources are safeguarded

against loss and misuse; and reliable data are obtained,

maintained, and disclosed in reports.

42

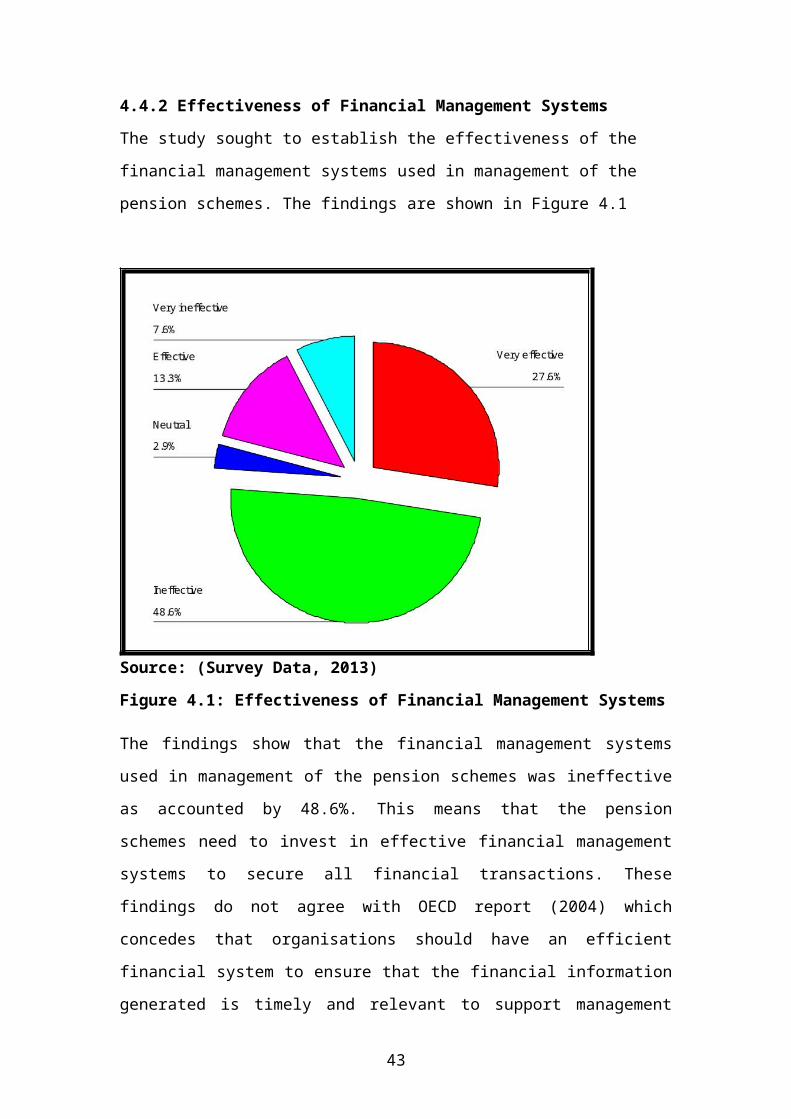

4.4.2 Effectiveness of Financial Management Systems

The study sought to establish the effectiveness of the

financial management systems used in management of the

pension schemes. The findings are shown in Figure 4.1

Source: (Survey Data, 2013)

Figure 4.1: Effectiveness of Financial Management Systems

The findings show that the financial management systems

used in management of the pension schemes was ineffective

as accounted by 48.6%. This means that the pension

schemes need to invest in effective financial management

systems to secure all financial transactions. These

findings do not agree with OECD report (2004) which

concedes that organisations should have an efficient

financial system to ensure that the financial information

generated is timely and relevant to support management

43

decision, support budget formulation and execution

functions and monitor the system to ensure integrity of

financial data.

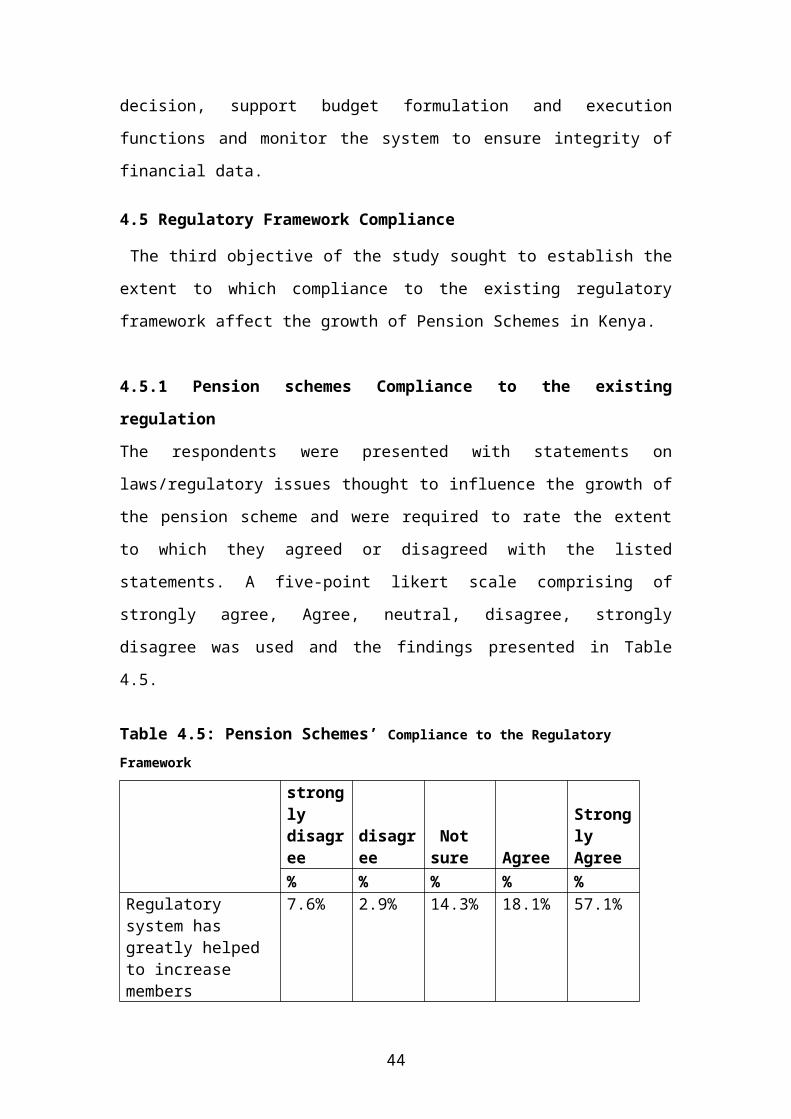

4.5 Regulatory Framework Compliance

The third objective of the study sought to establish the

extent to which compliance to the existing regulatory

framework affect the growth of Pension Schemes in Kenya.

4.5.1 Pension schemes Compliance to the existing

regulation

The respondents were presented with statements on

laws/regulatory issues thought to influence the growth of

the pension scheme and were required to rate the extent

to which they agreed or disagreed with the listed

statements. A five-point likert scale comprising of

strongly agree, Agree, neutral, disagree, strongly

disagree was used and the findings presented in Table

4.5.

Table 4.5: Pension Schemes’ Compliance to the Regulatory Framework

strongly disagree

disagree

Not sure Agree

Strongly Agree

% % % % %Regulatory system has greatly helped to increase members

7.6% 2.9% 14.3% 18.1% 57.1%

44

confident with this pension schemeExisting laws, regulation hinder prohibiteffective governance of this scheme

31.4% 37.1% 7.6% 8.6% 15.2%

pension scheme has had some cases of non-compliance withRBA rules

35.2% 20.0% 5.7% 22.9% 16.2%

Fees charged byRBA on compliance contribute to non-compliance by the schemes

32.4% 21.9% 18.1% 11.4% 16.2%

Pension scheme does not complywith the rules on appointment of top management

53.3% 23.8% 8.6% 14.3%

Source: (Survey Data, 2013)

The findings in Table 4.5 show that most of the

respondents agreed that regulatory system has greatly

helped to increase members confidence with the pension

schemes as accounted by the 75.2% (strongly agree and

agree) cumulative responses respectively. In addition,

most of the respondents disagreed with the following

statements; Existing laws, regulation hinder prohibit

effective governance of this scheme, pension scheme has

had some cases of non-compliance with RBA rules, Fees

45

charged by RBA on compliance contribute to non-compliance

by the schemes, Pension scheme does not comply with the

rules on appointment of top management accounted by the

68.5%, 55.2%, 54.3% and 77.1% (strongly disagree and

disagree) cumulative responses respectively. This shows

that the pension schemes had regulatory system which had

greatly helped to increase members confidence, Existing

laws, regulation does not prohibit effective governance

of the scheme, pension schemes had no cases of non-

compliance with RBA rules, Fees charged by RBA on

compliance did not contribute to non-compliance by the

schemes, Pension scheme complies with the rules on

appointment of top management. These were positive

attributes that play a major role in the growth of the

pension schemes. These finding agree with Brunner, Hinz

and Rocha (2008) who argued that governance regulations

need to be designed under the guidance of the overriding

objective that pension funds are set up to serve as a

secure source of funds for retirement benefits. The

governance structure should ensure an appropriate

division of operational and oversight responsibilities,

and the accountability and suitability of those with such

responsibilities. The findings also agree with RBA (2009)

that the pension entity may have several objectives, such

as ensuring an adequate match between the pension plan

assets and its liabilities and paying benefits upon the

death or retirement of plan members. The World Bank

(1994) also concedes that poor regulatory framework has

46

contributed to governance issues resulting to

contribution evasion among contributors.

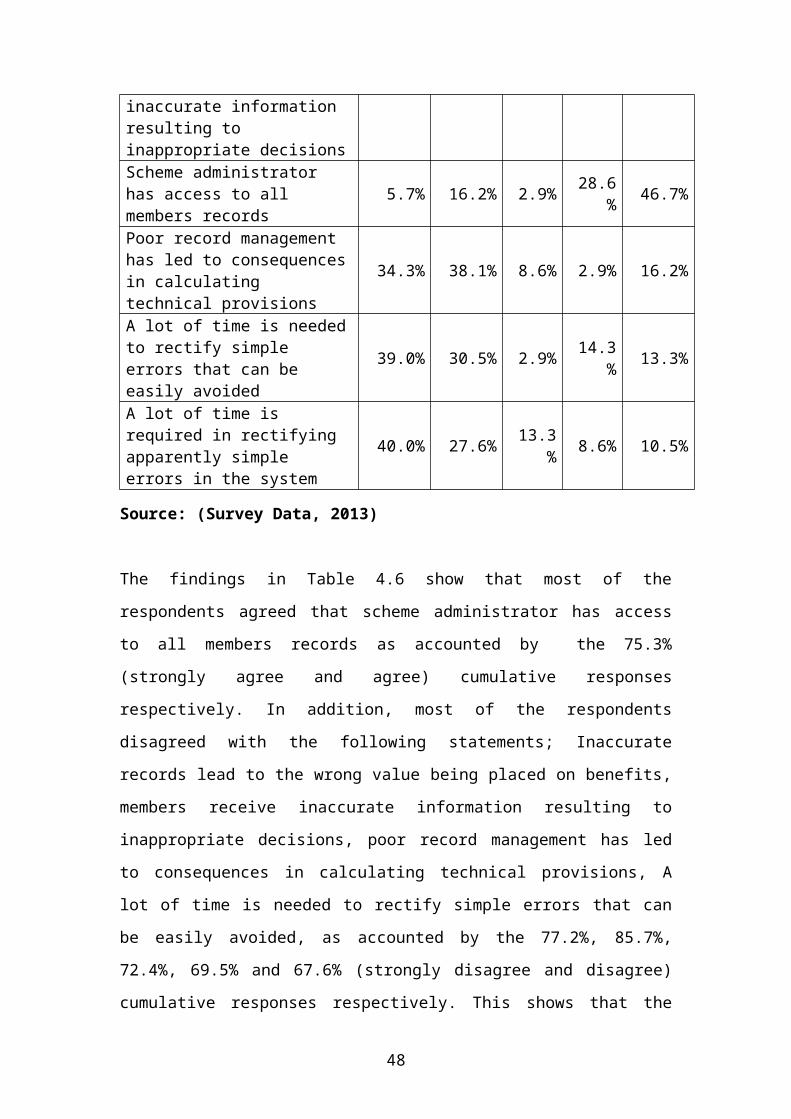

4.6 Record Management Systems

The fourth objective of the study sought to assess of the

effects of the existing record management systems on the

growth of Pension Schemes in Kenya.

4.6.1 Assessment of the Record Management System Issues

The respondents were presented with statements on record

management system issues thought to influence the growth

of the pension scheme and were required to rate the

extent to which they agreed or disagreed with the listed

statements. A five-point likert scale comprising of

strongly agree, Agree, neutral, disagree, strongly

disagree was used and the findings presented in Table

4.6.

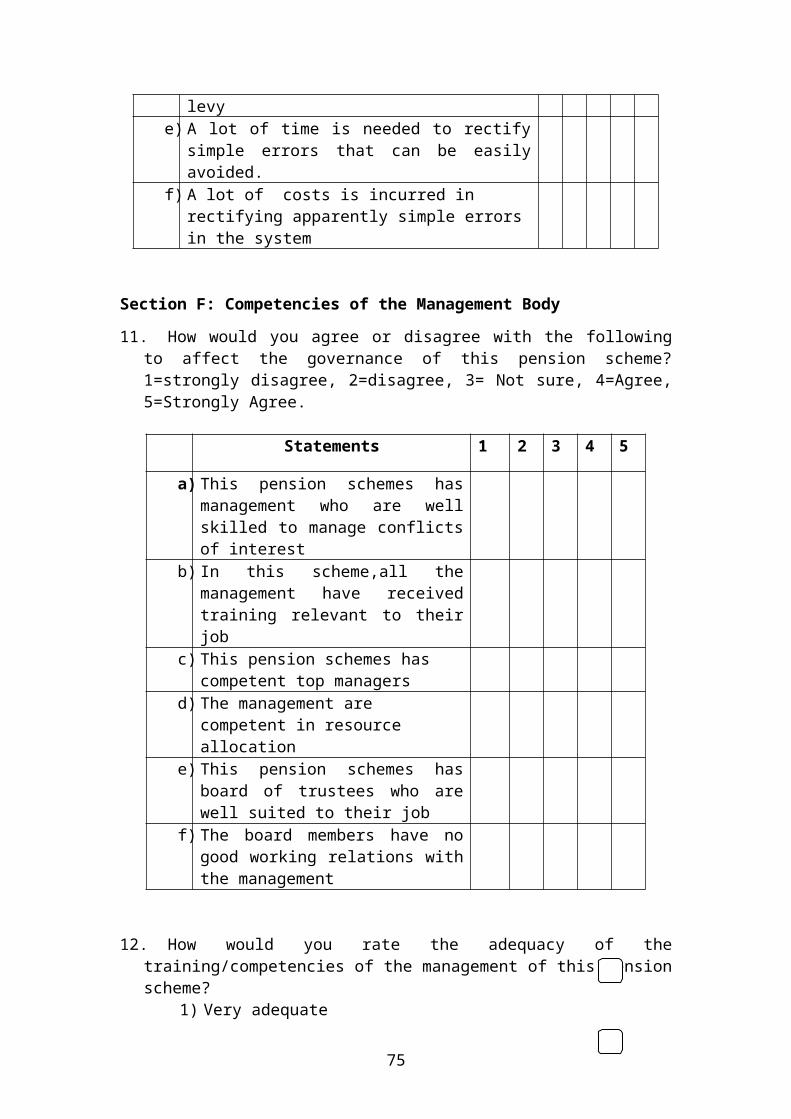

Table 4.6: Analysis of the Record Management System

Issues

Strongly

Disagree

Disagree

NotSure

Agree

Strongly

Agree% % % % %

Inaccurate records leadto the wrong value being placed on benefits

48.6% 28.6% 0.0% 8.6% 14.3%

Members receive 49.5% 36.2% 0.0% 8.6% 5.7%

47

inaccurate information resulting to inappropriate decisionsScheme administrator has access to all members records

5.7% 16.2% 2.9% 28.6% 46.7%

Poor record management has led to consequencesin calculating technical provisions

34.3% 38.1% 8.6% 2.9% 16.2%

A lot of time is neededto rectify simple errors that can be easily avoided

39.0% 30.5% 2.9% 14.3% 13.3%

A lot of time is required in rectifying apparently simple errors in the system

40.0% 27.6% 13.3% 8.6% 10.5%

Source: (Survey Data, 2013)

The findings in Table 4.6 show that most of the

respondents agreed that scheme administrator has access

to all members records as accounted by the 75.3%

(strongly agree and agree) cumulative responses

respectively. In addition, most of the respondents

disagreed with the following statements; Inaccurate

records lead to the wrong value being placed on benefits,

members receive inaccurate information resulting to

inappropriate decisions, poor record management has led

to consequences in calculating technical provisions, A

lot of time is needed to rectify simple errors that can

be easily avoided, as accounted by the 77.2%, 85.7%,

72.4%, 69.5% and 67.6% (strongly disagree and disagree)

cumulative responses respectively. This shows that the

48

pension schemes had accurate records and that wrong value

were not being placed on benefits, members receive

accurate information, proper record management hence no

consequences in calculating technical provisions, and a

lot of time was not needed to rectify simple errors. This

implies that the pension schemes had accurate and a

proper record management in place and this was

contributing to the growth of the pension schemes. These

findings agree with the RBA (2009) that proper record

management system should be a fundamental daily activity

of any pension scheme and that incomplete and inaccurate

records and poor financial management controls can place

significant risk on the security of scheme assets. For

example, it could result in the over payment of benefits

or misappropriation of funds. The findings also agrees

with Njoroge (2003) that poor records can also lead to

increased costs at key events, for example scheme buy

outs, and these extra costs will fall either on employers

or reduce member benefits. In addition, World Bank (2005)

position that the risks associated with inaccurate data,

for example incorrect benefit calculations, can have

short and long-term implications for schemes and

beneficiaries.

4.7 Competencies of the Management Body

The fifth objective of the study sought to establish the

competencies of the management body and its influence on

the growth of Pension Schemes in Kenya.

49

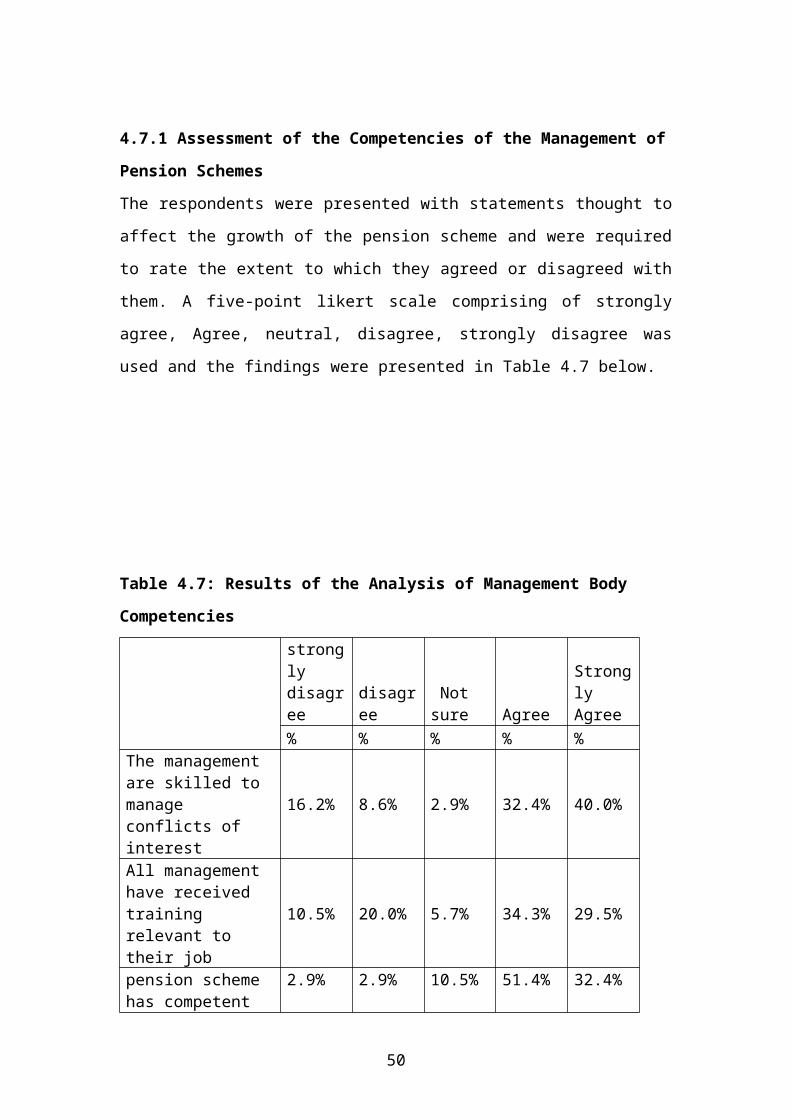

4.7.1 Assessment of the Competencies of the Management of

Pension Schemes

The respondents were presented with statements thought to

affect the growth of the pension scheme and were required

to rate the extent to which they agreed or disagreed with

them. A five-point likert scale comprising of strongly

agree, Agree, neutral, disagree, strongly disagree was

used and the findings were presented in Table 4.7 below.

Table 4.7: Results of the Analysis of Management Body

Competencies

strongly disagree

disagree

Not sure Agree

Strongly Agree

% % % % %The management are skilled to manage conflicts of interest

16.2% 8.6% 2.9% 32.4% 40.0%

All management have received training relevant to their job

10.5% 20.0% 5.7% 34.3% 29.5%

pension scheme has competent

2.9% 2.9% 10.5% 51.4% 32.4%

50

top managersmanagement are competent in resource allocation

14.3% 8.6% 12.4% 36.2% 28.6%

The board of trustees are well suited to their job

2.9% 2.9% 24.8% 30.5% 39.0%

board members have no good working relations with the management

54.3% 26.7% 5.7% 5.7% 7.6%

Source: (Survey Data, 2013)

The findings in Table 4.7 show that most of the

respondents agreed with the following statements; The

management are skilled to manage conflicts of interest,

All management have received training relevant to their

job, pension scheme has competent top managers,

management are competent in resource allocation and the

board of trustees are well suited to their job as

accounted by 72.4%, 63.8%, 83.8%

64.8% and 69.5% (Strongly agree and agree) cumulative

responses respectively. The findings further show that

the respondents disagreed that board members have no

good working relations with the management as accounted

by the 81.0% (strongly disagree and disagree) cumulative

responses respectively. This show that pension schemes’

management were skilled to manage conflicts of interest,

were well trained and competent in their job especially

on resource allocation. In addition, the boards of

51

trustees were also well suited to their job and had good

working relations with the management. This was

contributing to the growth of the pension schemes in the

country.

Managerial competencies are critical in ensuring good

administration and effective governance of pension

schemes. According to Njoroge (2003), the management of

the pension schemes has always been the employers of the

pensioner/contributors of the Pension schemes. This

brings in conflict of interest in the management of

pension scheme funds. These findings are consistent with

the RBA (2003) which asserts that every pension fund

should have a competent governing body or administrator

vested with the power to administer the pension fund and

who is ultimately responsible for ensuring the adherence

to the terms of the arrangement and the protection of the

best interest of plan members and beneficiaries. In

addition, the World Bank (1994) concedes that mechanisms

are needed to ensure that the pension funds are managed

by competent personnel.

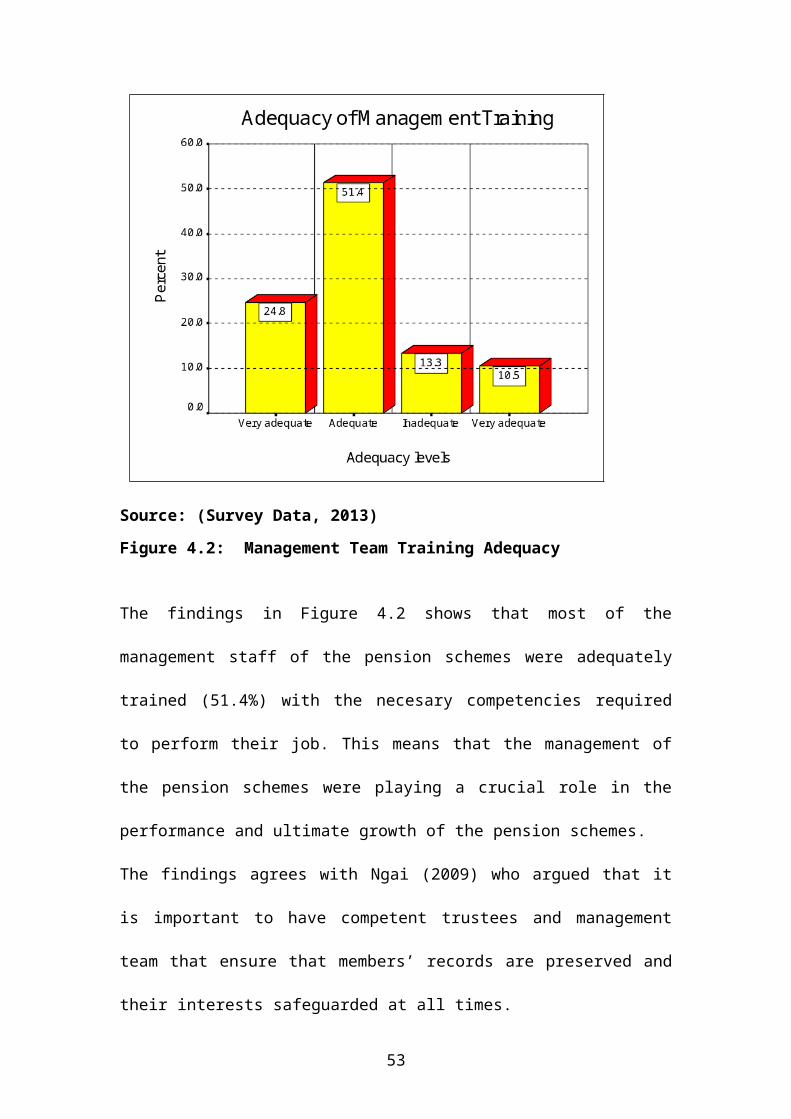

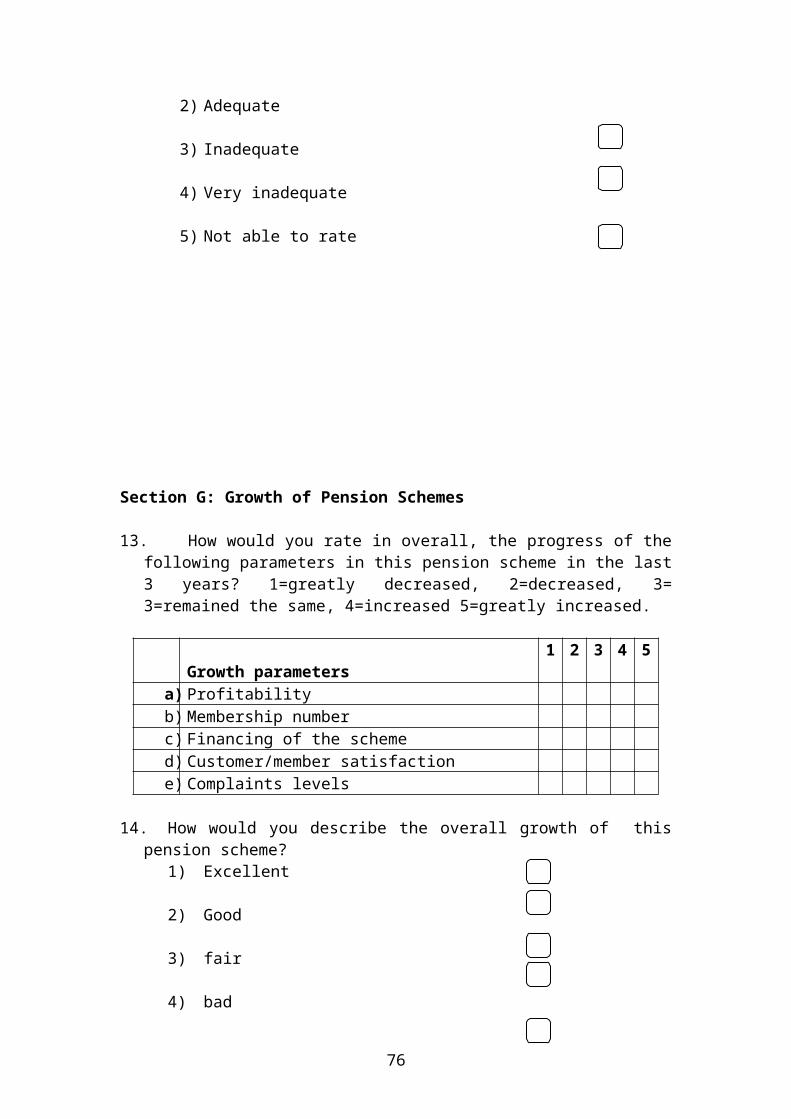

4.7.2 Adequacy of the Management Team Training

The respondents rated the adequacy of the training or the

competencies of the management of the pension scheme and

the findings were as shown in Figure 4.2.

52

Source: (Survey Data, 2013)

Figure 4.2: Management Team Training Adequacy

The findings in Figure 4.2 shows that most of the

management staff of the pension schemes were adequately

trained (51.4%) with the necesary competencies required

to perform their job. This means that the management of

the pension schemes were playing a crucial role in the

performance and ultimate growth of the pension schemes.

The findings agrees with Ngai (2009) who argued that it

is important to have competent trustees and management

team that ensure that members’ records are preserved and

their interests safeguarded at all times.

53

4.8 Growth of the Pension Schemes

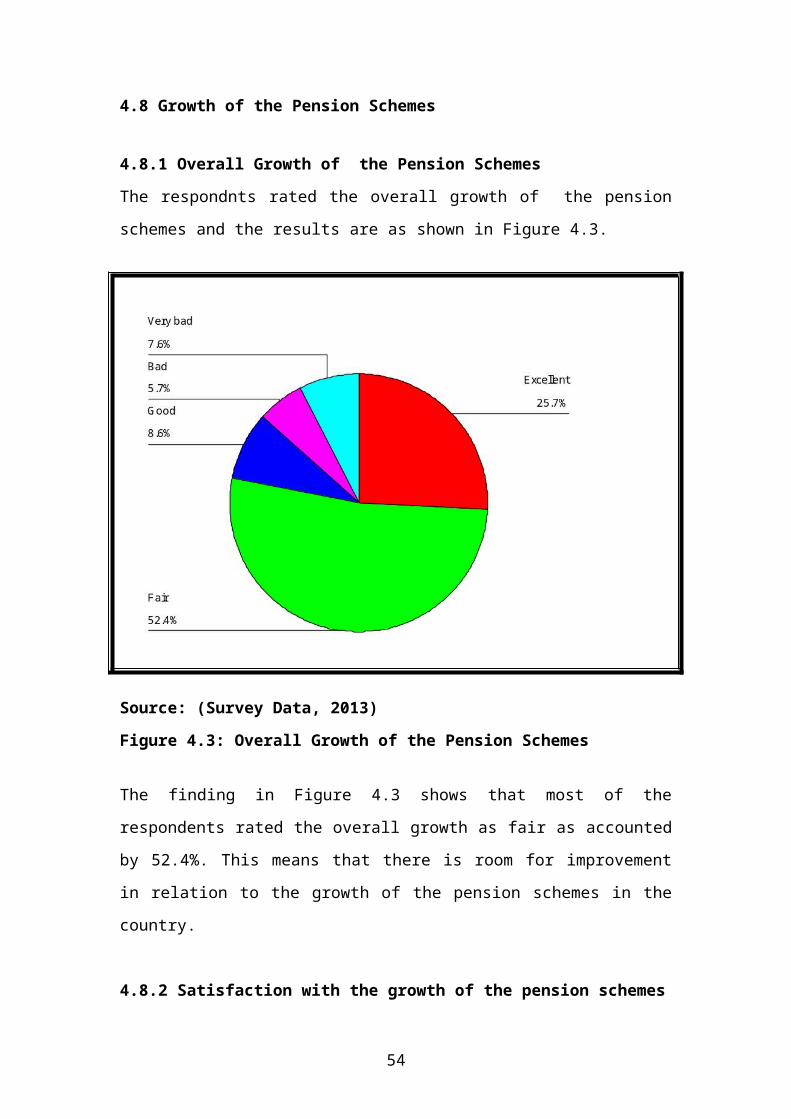

4.8.1 Overall Growth of the Pension Schemes

The respondnts rated the overall growth of the pension

schemes and the results are as shown in Figure 4.3.

Source: (Survey Data, 2013)

Figure 4.3: Overall Growth of the Pension Schemes

The finding in Figure 4.3 shows that most of the

respondents rated the overall growth as fair as accounted

by 52.4%. This means that there is room for improvement

in relation to the growth of the pension schemes in the

country.