Effects of Corporate Governance on Insider Trading

24

Transcript of Effects of Corporate Governance on Insider Trading

Prime Journal of Business Administration and Management (BAM) ISSN: 2251-1261. Vol. 3(10), pp. 1202-1224, October 18

th, 2013

www.primejournal.org/BAM © Prime Journals

Full Length Research Paper

Effects of corporate governance on insider trading A case of listed companies on Nairobi securities exchange

Eric Opiyo

Jomo Kenyatta University of Agriculture and Technology, Kenya.

Accepted 16th August, 2013

Corporate governance has dominated policy agenda in developed market economies for more than a decade and it is gradually warming its way to the top of the policy agenda on the African continent. The Nairobi Securities Exchange (formerly Nairobi Stock Exchange) (NSE) is the principal stock exchange of Kenya. Trading is done through the Electronic Trading System (ETS) which was commissioned in 2006. The main objective of this study was to determine the effects of corporate governance on insider trading guided by the following specific objectives: to assess the effect of board size as corporate governance attribute on insider trading; to examine the effects of board independence as corporate governance attribute on insider trading; to investigate the impact of institutional ownership on insider trading; and determine the effects of ownership concentration on insider trading. The researcher applied a descriptive research design. The target population of this study consisted of 59 firms listed companies on Nairobi Securities Exchange. The researcher sampled 29 participants from the listed 55 companies at the NSE. The sample composed of 50% of the total population. Primary data was collected using a questionnaire and analyzed using statistical package for social sciences (SPSS). The study concludes that corporate governance affects insider trading based on the findings that board size, board independence, institutional ownership and ownership concentration affected insider trading in the organization to a very great extent. The study recommends that public listed companies should practice good corporate governance approach that aims at performing the main function of separating the firm's principals and agents as well as management from the board to eliminate insider trading. Key words: Corporate governance, insider trading, board of directors, Nairobi security exchange,, board size, board independence, institutional ownership, ownership concentration. INTRODUCTION Background of the Study Abor (2007) defines corporate governance as the system by which companies are directed and controlled. It also refers to as the way in which corporations are handled by corporate boards and officers. Corporate governance has, in more recent years, become one of the most commonly used terms in the modern corporation. Corporate governance helps in defining the relation between the company and its general environment, the social and political systems in which it operates. Corporate governance is linked to economic performance. The way management and control are organized affects the company„s performance and it‟s long run competitiveness. It determines the conditions for

access to capital markets and the degree of investors‟ confidence (Brownbridge, 2007).

Insider trading involves the purchase or sale of securities, puts, calls or other options based on material non-public information. It occurs when someone possesses superior information that could influence the stock price of his company and uses this information to trade profitably with the stocks of his company. The trading may be deemed “insider” if those involved have any beneficial interest (direct or indirect) in the securities or options regardless of whose name is actually on the paperwork. Tipping is included under the umbrella of insider trading if inside information is revealed to outside individuals in order to enable said individuals to trade in

1203 Prim. J. Bus. Admin. Manage. the securities based on undisclosed information (Perry, 1991).To be guilty of insider trading or tipping, the accused must have breached a duty to someone in the acquisition of material non-public information that leads to a securities transaction. The breach of duty alone does not constitute a violation of the statutes used to prosecute insider trading. The breach of duty must be accompanied by some type of deception or manipulation (Perry, 1991).

Obviously, trading based on insider information is a matter of interest conflict between insiders and other stakeholders. This study investigates whether corporate governance contributes affects insider trading. It pinpoints the role of the board of directors, as a main corporate governance mechanism, in monitoring the trades by insiders and specifically investigates the impact of board independence, board size, ownership concentration as well as institutional ownership in limiting information-driven insider trades.

Several studies have shown that corporate governance affects insider trading. For Instance, Elder and Kim (2010) examined the relation between transparency-related governance attributes and liquidity in the U.S. stock market, and found out that corporate governance improves financial and operational transparency that decreases insider trading associated with information asymmetries. Their findings showed that firms with better governance structure exhibit narrower spreads and lower probability of information-based trading.

Similarly, Loukill and Yousfi (2010) presented evidence of the effects of corporate governance on information asymmetry information and stock liquidity in the Tunisian Stock Market during the period 1998-2007. They found out that some attributes of corporate governance such as effective board of directors (board independence) and low ownership concentration improved stock liquidity because they reduced insider trading caused due to information asymmetry. Eng and Mak (2003) studied the effect of ownership structure and board composition (being corporate governance attributes) on voluntary disclosure for firms listed on the Singapore Stock Exchange over the period of 1991-1995. They found a positive association between government ownership and voluntary disclosure, while both the number of outside directors and managerial ownership influenced disclosure behavior negatively.

Kanagaretnam et al. (2007) examined the impact of corporate governance measures, such as the board independence, board structure and board activity and ownership, on information asymmetry that breeds insider trading. He found out that corporate governance attributes of board independence, board structure (size) as well as shareholders level of ownership affected insider trading. Further studies by Charoenwong et al. (2010) indicated that the relationship between corporate governance (as measured by discipline, transparency, independence, accountability, responsibilities, fairness, and social awareness) affected insider trading.

In general, prior studies have found that a higher proportion of institutional ownership was associated with improved corporate governance which had the effect of eliminating insider trading (Healy et al., 1999; Noe, 2002 and Starks, 2000).

Developing countries, of which Kenya is no exception, have increasingly written and embraced the concept of good corporate governance, because of its ability to impact positively on sustainable growth. For instance, Jebet (2001), has written on the corporate governance structures prevalent in public listed companies in Kenya while Muka (2010) has written about the relationship between corporate governance and ownership structures of firms listed at the Nairobi Stock Exchange where he states that the ownership levels of a company characterized by low ownership levels have an inverse effect on insider trading. This paper, aims at partly filling the gap between studies conducted on area of insider trading and corporate governance, by postulating that effective corporate governance helps mitigate insider trading. Nairobi Securities Exchange The Nairobi Securities Exchange (formerly Nairobi Stock Exchange) (NSE) is the principal stock exchange of Kenya. It began in 1954 as an overseas stock exchange while Kenya was still a British colony with permission of the London Stock Exchange. The NSE is a member of the African Stock Exchanges Association. It is Africa's fourth largest stock exchange in terms of trading volumes, and fifth in terms of market capitalization as a percentage of Gross Domestic Product (GDP). The Exchange works in cooperation with the Uganda Securities Exchange and the Dar es Salaam Stock Exchange, including the cross listing of various equities. The NSE's offices and trading floor are located at the Nation Centre along Kimathi Street in Nairobi, Kenya. Trading is done through the Electronic Trading System (ETS) which was commissioned in 2006. A Wide Area Network (WAN) platform was implemented in 2007 and this eradicated the need for brokers to send their staff (dealers) to the trading floor to conduct business. Trading is now mainly conducted from the brokers' offices through the WAN. However, brokers under certain circumstances can still conduct trading from the floor of the NSE (www.nse.co.ke).

Two indices are popularly used to measure performance. The NSE 20-Share Index has been in use since 1964 and measures the performance of 20 blue-chip companies with strong fundamentals and which have consistently returned positive financial results. In 2008, the NSE All Share Index (NASI) was introduced as an alternative index. Its measure is an overall indicator of market performance. The Index incorporates all the traded shares of the day. Its attention is therefore on the overall market capitalization rather than the price movements of select counters. The Nairobi Stock

Exchange comprises approximately 55 listed companies with a daily trading volume of over United States Dollar (USD) 5 million and a total market capitalization of approximately USD 15 billion. Aside from equities, Government and corporate bonds are also traded on the Nairobi Stock Exchange. Automated bond trading started in November 2009 with the KES 25 billion KenGen bond. Average bond daily trading is USD 60m.

Trading hours are from 09:00 to 15:00. Delivery and settlement is done scrip less via an electronic Central Depository System (CDS) which was installed in 2005. Settlement is currently T+4, but moving to T+3, on a delivery-vs.-payment basis. The daily price movement for any security in a single trading session shall not be more than 10% except during major corporate announcements. The Nairobi Stock Exchange in 2006 introduced an Automated Trading System (ATS) which ensures that orders are matched automatically and are executed on a first come/first serve basis. The ATS has now been linked to the Central Bank of Kenya and the CDS thereby allowing electronic trading of Government bonds. Short selling and same day turn-around trades are not permitted. Aggregate foreign ownership limit of NSE listed companies is 75%. Almost all NSE listed companies are open to additional foreign investment, including multinational subsidiaries (www.nse.co.ke). Statement of the problem Abor (2007) defines corporate governance as the system by which companies are directed and controlled. Insider trading on the other hand, occurs when someone possesses superior information that could influence the stock price of his company and uses this information to trade profitably with the stocks of his company (Dooley, 1980).

While there are numerous firm characteristics that reflect good corporate governance, major concern is on how boards can effectively apply the same to eliminate insider trading. Several studies have explored the relation between corporate governance and insider trading. Eng and Mak (2003) studied the effect of ownership structure and board composition (being corporate governance attributes) on voluntary disclosure for firms listed on the Singapore Stock Exchange over the period of 1991-1995. They found a positive association between government ownership and voluntary disclosure, while both the number of outside directors and managerial ownership influenced disclosure behavior negatively. Elder and Kim (2010) examined the relation between transparency-related governance attributes and liquidity in the U.S. stock market, and found out that corporate governance improves financial and operational transparency that decreases insider trading associated with information asymmetries.

Similarly, Loukill and Yousfi (2010) presented evidence of the effects of corporate governance on information asymmetry information and stock liquidity in the Tunisian Stock Market during the period 1998-2007. They found out

Opiyo 1204 that some attributes of corporate governance such as effective board of directors (board independence) and low ownership concentration improved stock liquidity because they reduced insider trading caused due to information asymmetry.

Kanagaretnam et al. (2007) examined the impact of corporate governance measures, such as the board independence, board structure and board activity and ownership, on information asymmetry that breeds insider trading. The study was conducted around quarterly earnings announcements for the June and September quarters of the year 2000 made by firms whose stock were listed on the NYSE. Kanagaretnam, Lobo and Whalen (2007) found out that corporate governance attributes of board independence, board structure (size) as well as shareholders level of ownership affected insider trading. Further, prior studies find that a higher proportion of institutional ownership was associated with improved corporate governance which had the effect of eliminating insider trading (Healy et al., 1999; Noe, 2002 and Starks, 2000).

However, despite the array of literature in corporate governance and how it affects insider trading, most public listed companies in Kenya have not yet fully embraced corporate governance principles. This has resulted to weak corporate governance mechanisms amongst the boards of public listed companies which have significantly increased the probability of opportunistic insider trading while posing a great challenge to investors (Colley et al., 2003). For instance, most listed firms that have bigger board size prevent company‟s boards from being more effective at carrying out their fiduciary duty while boards which are non- independent are not successful in monitoring insider activity (Colley et al., 2003; Shleifer and Vishny's 1997). In addition, most listed firms that have a low/medium level of institutional ownership are associated with weak corporate governance that can cause stock market underperformance (Healy et al., 1999; Noe, 2002; Core et al. (2006).

The implication of these challenges is that investors (both prospective and actual shareholders) who consider that such unfair practices occur in a particular market may accordingly lose confidence in the market and put their money elsewhere (Barry, 1989) or alternatively withdraw from the market (Hudson, 2008).

Related prior research locally has examined corporate governance attributes and practices of different firms. For instance, Jebet (2001), has written on the corporate governance structures prevalent in public listed companies in Kenya; Kitonga (2002) has written on the need for corporate governance audit in Kenya; and Muka (2010) has written about the relationship between corporate governance and ownership structures of firms listed at the Nairobi Stock Exchange. Objectives of the study General objective The main objective of this study was to determine the effects

1205 Prim. J. Bus. Admin. Manage. of corporate governance on insider trading.

Specific objectives - To assess the effect of board size as corporate governance attribute on insider trading. - To examine the effects of board independence as corporate governance attribute on insider trading. - To investigate the impact of institutional ownership on insider trading. - To determine the effects of ownership concentration on insider trading. Research questions - In what ways does board size affect insider trading? - To what extent does board independence affect insider trading? - How does institutional ownership impact on insider trading? - In what ways does ownership concentration affect insider trading? Justification of the study The study was helpful to the following stakeholders: - The management of listed companies at the Nairobi Securities Exchange who found the study invaluable in making decisions regarding corporate governance and insider trading. The management personnel were able to know the effects of corporate governance on insider trading that can play a bigger role in shaping their operations. - The corporate governance practitioners also got an insight on the effects of corporate governance on insider trading. This helped them in developing policies on how to mitigate the challenges. - The researchers and academic community could also use this study as a stepping stone for further studies on listed companies on Nairobi Securities Exchange. The students and academics were going to use this study as a basis for discussions on the effects of corporate governance on insider trading. - The centre for corporate governance found the study useful as a basis of formulating policies, which can be effectively implemented for better and easier regulation of institutions in Kenya. Limitation of the Study The researcher foresaw a challenge in securing the employees of listed companies on Nairobi Securities Exchange precious time considering their busy working schedules. However, the researcher made proper arrangements with employees to avail time for the study and filling of the questionnaire after working hours as well as motivating the employees on the value of the study. The researcher exercised utmost patience and care and in view of this, by making every effort in acquiring sufficient data from respondents.

Further it was foreseen that, the respondents were likely to be reluctant in giving information fearing that the

information asked may be used to intimidate them or reflect a negative image about them or the organization. In this regard, the researcher handled the problem by carrying with her an introduction letter from the University and assured them that the information they gave was going to be treated with utmost confidentially and was to be used purely for academic purposes. Scope of the study The focus of this study was a select sample of listed companies on Nairobi Securities Exchange. LITERATURE REVIEW This section discusses the literature review of the study. The purpose of literature review is to explore on the existing and available information covered by different researchers on a given topic. The literature was reviewed from journals, reference books, working papers, periodicals and reports. The review of literature focuses on the conceptual framework of the study and also provides empirical review, summary and research gaps of the study. Insider trading and the role of corporate governance The underlying question is whether good corporate governance mitigates opportunistic insider trading. Rozanov (2008) investigated whether corporate governance affected the decision to use non-public information when trading. He conditioned the empirical tests on trading as well as the do not model the determinants of a trade taking place. While this approach limited the scope of inferences that could be drawn from the analysis, the focus of the study was to distinguish opportunistic from non-opportunistic transactions for those insiders who did trade as opposed to those who explored the propensity of corporate insiders to trade in corporate stock in general. He defined opportunistic insider trading as trade was corporate stock by corporate insiders that is motivated by non-public information and argued that while such trading was undertaken by the insiders for their own financial gain, it potentially imposed significant costs on the firm and the outside shareholders.

Although there is an unresolved debate amongst economists and jurists weighing the social costs and benefits of insider trading (Bainbridge, 2001; Haddock, 2002), corporations have an interest in restricting information-based insider trading for several reasons. First, the informational asymmetry associated with insider transactions imposes a direct adverse-selection cost on outside investors and thereby decreases liquidity (Manove, 1989; Chung and Li, 2003). Second, such insider trading decreases confidence in the capital markets among investors who hold the fundamental view that insider trading is inconsistent with principles of fairness or that inside information is the sole property of the corporation (Bainbridge, 2001). Diminished confidence has the potential to increase the cost of capital and thus lower the value of a firm.

Finally, current U.S. laws and regulations expressly prohibit trade in corporate stock that is based on material non-public information. Hence, information-based insider trading raises the risk of litigation, of losing key leadership, and of sending a negative signal about the firm's compliance and internal control systems. These arguments must be weighed against the opposing view that information-based insider trading benefits investors. Milton Friedman stated, "You want more insiders trading, not less" (Harris, 2003). Information-based insider trading contributes to the efficient pricing of securities by conveying non-public information to the capital markets (Manne, 1966; Carlton and Fischel, 1983). For example, corporations often face the need to withhold certain strategic information from the public, and information-based insider trading allows for this non-public information to be impounded in stock prices while keeping the information itself private (Manne, 1966).

Although insider trading does not usually represent a significant fraction of the trading volume, insider trades have been shown to impact prices, suggesting that the private information does get impounded in prices (Keown and Pinkerton, 1981; Meulbrock, 1992).

The study notwithstanding the ambiguity regarding the trade-off between the informational costs and benefits of information-based insider trading, he assumed that the costs of such trading outweigh the benefits from the perspective of a corporation, and thus, corporations have an interest in restriction such trade. This assumption was consistent with the legal and regulatory reforms that have been implemented in the U.S. and abroad to prevent information-based insider trading. Thus, he referred to such insider trading as opportunistic.

Despite the potential negative impact of opportunistic insider trading on outside shareholders, there was evidence suggesting that corporate insiders engage in such trading. Academic research continued to document that corporate insiders earn abnormal profits on trade in corporate stock, and at the same time, capital market regulators and participants express concern over the prevalence and magnitude of transactions based on non-public information (Ortega and Sheer, 2007). Despite improvements in the scope and enforcement of insider- trading laws and regulations since the Securities Exchange Act of 1934, the unabated concern expressed by capital market regulators and participants regarding information-based insider trading suggests prior efforts are insufficient at curtailing the opportunistic use of private information in the trade of corporate stock.

This then led me to investigate whether good corporate governance, complementing legal and market mechanisms, could help to mitigate opportunistic insider trading by corporate executives. There was reason to expect that good corporate governance can reduce opportunistic insider trading. The modern public company is characterized by a separation of ownership and control (Berle and Means, 1932). Agency theory suggests that in

Opiyo 1206 the presence of information asymmetry, managers are able to exercise self-interest at the cost of other shareholders (Jensen and Meckling, 1976). Opportunistic insider trading is such an agency problem when corporate executives profit from the trading at a potential cost to outside shareholders. Under the neoclassical view of the firm, a critical role for corporate governance is to maximize shareholder welfare by mitigating agency costs and protecting outside investors from opportunistic managerial behavior (Fama and Jensen, 1983). In fact, prior literature in finance and accounting showed that good corporate governance did mitigate agency costs associated with the separation of ownership and control (Shleifer and Vishny, 1997; Bushman and Smith, 2004).

There are a few factors that worked against finding evidence of a relation between corporate governance and insider trading. A key challenge in analyzing the impact of corporate governance on insider trading was being able to distinguish opportunistic insider transactions from trades which were not based on private information. Doing so was critical because corporate governance was unlikely to mitigate non-opportunistic insider transactions. Yet, trade in corporate stock by corporate insiders is unavoidable, particularly at firms that employ equity-based compensation.

Failure to identify opportunistic insider trading was not the only reason to expect that no relation between corporate governance and insider trading is found. A potential concern was that even if good corporate governance in general reduced opportunistic insider trading, one could find no relation with the particular governance characteristics. Larcker et al. (2007) argued that many of the governance measures used in prior research have a very modest level of reliability and construct validity. Another concern arises out of the view that corporate governance is largely irrelevant.

Among others, proponents of the managerial power theory have argued that existing control mechanisms, including corporate governance, do not prevent managers from exercising self- interest at a cost to shareholders (Weisbach, 2007). Core et al. (2006) reexamined the argument that weak corporate governance causes stock market underperformance. Gompers et al., (2003) found evidence that did not support the hypothesis. Instead, the authors concluded that period-specific returns or differences in expected returns likely explained the documented abnormal returns for good governance firms. To the extent that good corporate governance does not prevent managers from engaging in opportunistic behavior in general, it is not any more likely to have an impact on opportunistic insider trading. Theoretical framework Agency theory Agency theory identifies the relationship where one party, the principle, delegates work to another, the agent

1207 Prim. J. Bus. Admin. Manage. (Mallin, 2010). The principal-agent model regards the central problem of corporate governance as self-interested managerial behaviour in a universal principal-agent relationship. Agency problems arise when the agent does not share the principal's objectives. Furthermore, the separation of ownership and control increases the power of professional managers and leaves them free to pursue their own aims and serve their own interests at the expense of shareholders (Berle and Means, 1932).

This separation is however, linked and governed through proper “agency relationship” at various levels, among others “between shareholders and boards of directors, between boards and senior management, between senior and subordinate levels of management” (Hayes and Abernathy, 1980). In such a principal-agent relationship, there is always “inherent potential for conflicts within a firm because the economic incentives faced by the agents are often different from those faced by the principals. According to International Swaps and Derivatives Association (ISDA 2002), all companies are exposed to agency problems, and to some extent develop action plans to deal with them. Stakeholders’ theories There are two main theories of stakeholder governance: the abuse of executive power model and the stakeholder model. Current Anglo-American corporate governance arrangements vest excessive power in the hands of management who may abuse it to serve their own interest at the expense of shareholders and society as a whole (Hutton, 1995). Supporters of such a view argue that the current institutional restraints on managerial behavior, such as non-executive directors, the audit process, the threat of takeover, are simply inadequate to prevent managers abusing corporate power. Shareholders protected by liquid asset markets are uninterested in all but the most substantial of abuses. Perhaps the most fundamental challenge to the orthodoxy is the stakeholder model, with its central proposition is that a wider objective function of the firm is more equitable and more socially efficient than one confined to shareholder wealth. Stewardship theory of management Davis et al. (1997) developed the stewardship theory of management as a counter strategy to agency theory. Stewardship theory of management and agency theory have both focused on the leadership philosophies adopted by the owner‟s of an organization. It grew out of the seminal work by Donaldson and Davis (1989, 1991) and was developed as a model where senior executives act as stewards for the organization and in the best interests of the principals. The model of man in stewardship theory is based upon the assumption that the manager will make decisions in the best interest of the organization, putting collectivist options above self-

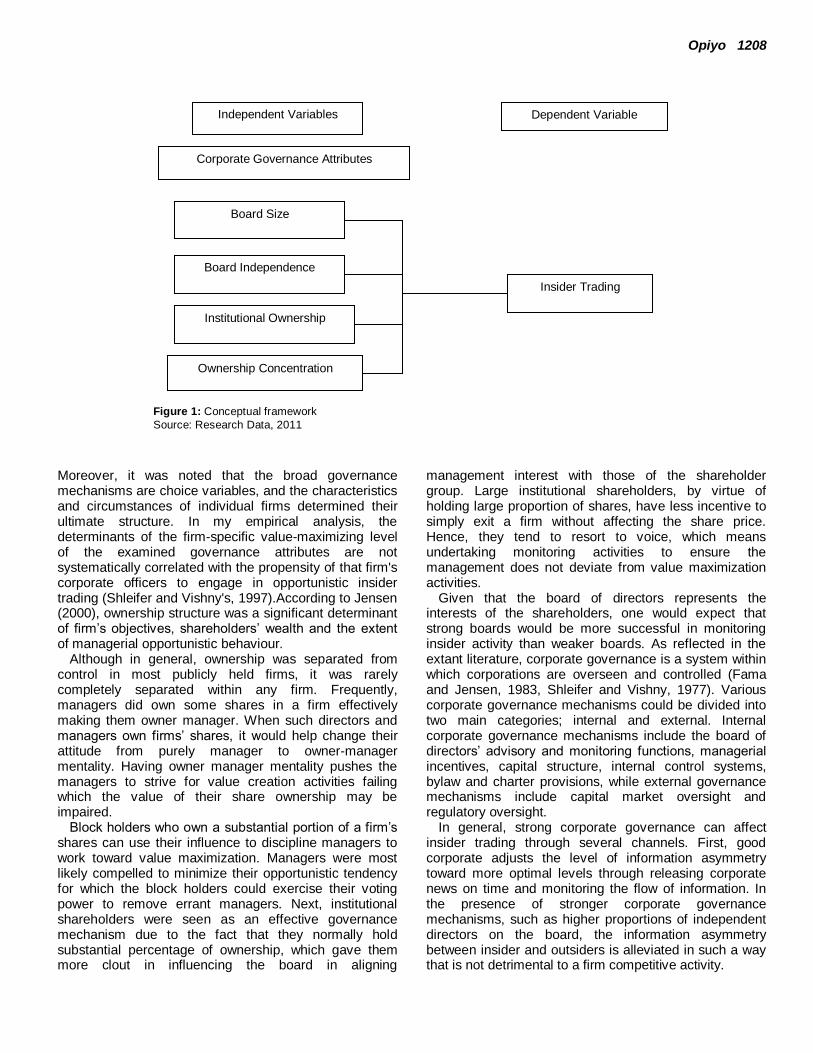

servicing options. This type of person is motivated by doing what‟s right for the organization, because she believes that she will ultimately benefit when the organization thrives. The steward manager maximizes the performance of the organization, working under the premise that both the steward and the principal benefit from a strong organization (Mallin, 2010). Conceptual framework A conceptual Framework is a basic structure that consists of certain abstract blocks which represent the observational, the experiential and the analytical/ synthetically aspects of a process or system being conceived. It is a set of broad ideas and principles taken from relevant fields of enquiry and used to structure a subsequent presentation. It is a research tool intended to assist a researcher to develop awareness and understanding of the situation under scrutiny and to communicate. The interconnection of these blocks completes the framework for certain expected outcomes. A variable is a measurable characteristic that assumes different values among subjects (Dodge, 2003). Figure 1 is a conceptual framework that guided this research. The corporate board and the ownership structure Shleifer and Vishny's (1997) viewed corporate governance as a means by which the suppliers of finance to corporations assured themselves of getting the expected return on their investment. While there were numerous firm characteristics that did reflect good corporate governance, major concern was on two dimensions of the corporate board and two dimensions of the corporate ownership structure. Through their role in monitoring corporate executives, the board and the shareholders were arguably among the most fundamental components of corporate governance. Certain characteristics of the board and of the ownership structure had been found to reflect more effective monitoring, and use these characteristics as measures of good corporate governance.

The choice to focus the empirical analysis on these broad dimensions of corporate governance as opposed to narrower control mechanisms, such as company policies on insider trading, involves several trade-offs. On the one hand, broad corporate governance encompasses numerous objectives, of which mitigating opportunistic insider trading is only one, and is thus relatively less exposed to potential endogeneity. For example, narrow control mechanisms were likely implemented in response to a specific issue, rendering the direction of causality and the predicted sign of the relation between the corporate governance mechanism and opportunistic insider trading unclear, as in early sociological studies of law enforcement and crime. On the other hand, since broad corporate governance attributes were not specifically tailored to mitigate opportunistic insider trading, finding a relation may prove difficult.

Opiyo 1208

Board Size

Board Independence

Institutional Ownership

Ownership Concentration

Insider Trading

Corporate Governance Attributes

Dependent Variable Independent Variables

Figure 1: Conceptual framework

Source: Research Data, 2011

Moreover, it was noted that the broad governance mechanisms are choice variables, and the characteristics and circumstances of individual firms determined their ultimate structure. In my empirical analysis, the determinants of the firm-specific value-maximizing level of the examined governance attributes are not systematically correlated with the propensity of that firm's corporate officers to engage in opportunistic insider trading (Shleifer and Vishny's, 1997).According to Jensen (2000), ownership structure was a significant determinant of firm‟s objectives, shareholders‟ wealth and the extent of managerial opportunistic behaviour.

Although in general, ownership was separated from control in most publicly held firms, it was rarely completely separated within any firm. Frequently, managers did own some shares in a firm effectively making them owner manager. When such directors and managers own firms‟ shares, it would help change their attitude from purely manager to owner-manager mentality. Having owner manager mentality pushes the managers to strive for value creation activities failing which the value of their share ownership may be impaired.

Block holders who own a substantial portion of a firm‟s shares can use their influence to discipline managers to work toward value maximization. Managers were most likely compelled to minimize their opportunistic tendency for which the block holders could exercise their voting power to remove errant managers. Next, institutional shareholders were seen as an effective governance mechanism due to the fact that they normally hold substantial percentage of ownership, which gave them more clout in influencing the board in aligning

management interest with those of the shareholder group. Large institutional shareholders, by virtue of holding large proportion of shares, have less incentive to simply exit a firm without affecting the share price. Hence, they tend to resort to voice, which means undertaking monitoring activities to ensure the management does not deviate from value maximization activities.

Given that the board of directors represents the interests of the shareholders, one would expect that strong boards would be more successful in monitoring insider activity than weaker boards. As reflected in the extant literature, corporate governance is a system within which corporations are overseen and controlled (Fama and Jensen, 1983, Shleifer and Vishny, 1977). Various corporate governance mechanisms could be divided into two main categories; internal and external. Internal corporate governance mechanisms include the board of directors‟ advisory and monitoring functions, managerial incentives, capital structure, internal control systems, bylaw and charter provisions, while external governance mechanisms include capital market oversight and regulatory oversight.

In general, strong corporate governance can affect insider trading through several channels. First, good corporate adjusts the level of information asymmetry toward more optimal levels through releasing corporate news on time and monitoring the flow of information. In the presence of stronger corporate governance mechanisms, such as higher proportions of independent directors on the board, the information asymmetry between insider and outsiders is alleviated in such a way that is not detrimental to a firm competitive activity.

1209 Prim. J. Bus. Admin. Manage. Information asymmetry between insiders and outsiders provides the biggest incentive for insiders to trade based on their non-public information ( Hertzel et al, 2002, Durnev and Nain, 2007). The information asymmetry increases around earning announcements and serves as a source of private information for insiders (Skinner, 1991; Kim and Verrecchia, 1994).

Several studies suggested a positive association between insider-trading profits and information asymmetry (Rogers and Stocken, 2005; Huddart et al., 2007). Frankel and Li (2004) found that higher financial statement in formativeness and more precise analyst investigations reduced the association between insider trades and subsequent stock returns. Second, the strength of corporate governance mechanisms increased the cost of information-driven trades for insiders since such trades are more likely to be detected and disciplined by the board of directors. Each of these scenarios would be very costly to the insider in terms of any penalty or reputation damage. Insider trading regulations were more effective in deterring information-driven insider trading in the presence of stronger corporate governance mechanisms and therefore every measure to mitigate insider trading based on nonpublic information should emphasize empowering corporate governance mechanisms. Especially, it is postulated that stronger boards reduce the incidence of insider trading and profitability of insider trades. Thus, it was expected that in corporations with strong boards, there were be fewer trades by insiders and when those trades did occur, they would be less profitable than trades in companies with weak board Board size From a legal perspective, the board of directors is the first and foremost body responsible for governing the affairs of a corporation because directors have a fiduciary duty to look after the best interests of the shareholders. In general, conventional corporate governance wisdom suggests that smaller boards and more independent boards are more effective at carrying out this fiduciary duty (Colley et al., 2003). Smaller boards were more likely to consist of individuals for a specific reason and were more likely to build internal trust and act decisively (Lipton and Lorsch, 1992; Jensen, 1993). Some evidence in the literature was consistent with these views. For example, smaller boards were associated with higher equity valuations (Huther, 1997; Eisenberg et al., 1998). However, Yermack (1996), among others, showed that larger boards lead to more effective monitoring. Klein (2002b) argues that board monitoring increases in board size because the responsibilities can be distributed over a greater number of monitors.

Consistent with this alternative view, Adams and Mehran (2002) found that board size was positively associated with banking firm performance. Anderson et al. (2004) found that the cost of debt is considered jointly,

the evidence suggests that there are costs to having boards that are either too large or too small and the relation between board size and effective monitoring is likely to be non-monotonic. Not surprisingly, some studies found mixed results when using board size as a proxy for governance and others omitted board size from the analysis. For example, Karamanou and Vafeas (2005) found mixed evidence on the association between board size and the quality of financial disclosures, while Ajinkya et al. (2005) did not consider board size in their analysis of variation in disclosure quality.

Moreover, optimal board size was likely determined by firm- and industry-specific characteristics. In a study examining the evolution of board structure during the 10 years following a firm's IPO, Boone et al. (2007) found that board size increases in the size of the firm, was associated with the firm's competitive environment, and unlike board independence, reflects a trade-off between firm-specific benefits and costs of monitoring.

In order to capture the complex relation between board size and effective monitoring, Rozanov (2008) measured board size as the absolute value of the deviation of the number of directors serving on the firm's corporate board from the median number of directors serving on the corporate boards in the firm's industry, size quintile, and year. To the extent that this median captures an optimum, the greater the deviation from this median, the less effective is the monitoring by the board. The board size measure operationalizes this prediction, which is based on evidence in prior research as outlined above. Then expect board size to be positively associated with my measure of opportunistic insider trading. To my knowledge, such a measure has not been used in prior research. Board independence Board independence was another attribute that had been linked to effective governance. Independent boards were more likely to protect the interests of shareholders against managerial opportunism than boards that consist predominantly of corporate insiders and affiliates. Prior research has argued that directors benefit from prestige, reputation, learning opportunities, and networking by serving on a corporate board (Fama and Jensen, 1983). Outside directors who did not monitor corporate executives effectively were more likely to lose these benefits than those who did. Gilson (1989) found that directors were held accountable for corporate failures as evidenced through greater board turnover following such events.

Similarly, Srinivasan (2005), found that accounting restatements increase the likelihood that an outside director will lose his or her position on the restating firm's corporate board as well as directorships at other firms. Consistent with this view, prior research showed that boards with a higher fraction of outside directors were more effective at mitigating agency problems. For

example, Weisbach (1988) found that independent boards were more likely to remove poorly performing Chief Executive Officer (CEOs). Robenstein and Wyatt (1990) found that board independence was associated with greater appreciation in shareholder wealth. Several studies found out that greater board independence was associated with a lower likelihood of accounting fraud (Farber, 2003) and lower levels of earnings management (Klein, 2002a; Peasnell et al., 2005).

Likewise, Ajinkya et al. (2005) found that management guidance was less optimistically biased, more accurate, and more precise when the issuing firm had a greater fraction of outside directors. More broadly, Sengupta (2004) found that firms with more independent boards were more likely to release quarterly earning earlier.

The presence of independent directors on a board was found to be an important factor in the board‟s monitoring function (Rosenstein and Wyatt, 1990). Arguably, boards dominated by outsiders were in a better position to monitor and control managers (Dunn, 1987). In fact, independent directors were more highly motivated than inside directors in monitoring management since the weight of their external benefits, such as reputation, were much higher than their benefits accrued from the firm (Fama and Jensen; Srinivasan, 2005).

Several studies suggested that independent boards were more successful in management‟s compliance with accounting rules and produced more accurate financial statements (Farber, 2004; Sengupta, 2004). In an example of market reaction toward independent directors, Worrell et al. (1993) showed that outsider appointments were perceived by the market as being beneficial immediately, while insider appointments caused a wait-and-see reaction. Consequently, if outside directors enhanced monitoring of managers; their presence would be associated with lower abuse of insider information by the management.

A few studies questioned the benefits of board independence. These studies suggested that information asymmetry and fear of litigation would reduce the ability of outside directors to control opportunistic managerial behavior (Drymiotes, 2007). Moreover, outside directors could be appointed by and have allegiance to the management and board culture in general discourages conflict, rendering the effects of board independence weak or non-existent (Bushman et al., 2004; Larcker et al., 2007). However, the broader consensus in the literature, supported by analytical papers that derive optimal board structure (Harris and Raviv, 2006), was that while outside directors on the board could potentially lead to information loss, they were more likely to reduce agency costs.

As with board size, it was examined whether Board Independence, measured as the number of outside directors divided by the total number of directors serving on the corporate board, was associated with opportunistic insider trading. To the extent that more independent

Opiyo 1210 boards helped to attenuate opportunistic insider trading, it was expected that board independence to be negatively associated with measure of opportunistic insider trading. Institutional ownership Notwithstanding the function of the board, some shareholders choose to actively monitor the affairs of a corporation themselves. As Adam Smith noted more than two centuries ago, shareholders had a more direct incentive than directors serving on the corporate board to monitor the management. He further stated that directors of joint stock companies, however, being the managers rather of other people's money than their own, could not well be expected, that they could watch over it with the same anxious vigilance as stockholders" (Smith, 1776). Prior research documents prove that certain ownership-structure characteristics, such as the proportion of institutional holdings or the level of ownership concentration, were associated with the shareholders' willingness and ability to monitor the management.

A key argument underlying the effective corporate governance role of concentrated shareholders and institutional investors was that they have relatively more value at stake and have a greater incentive, and potentially greater means, to monitor managers. In general, prior studies found that a higher proportion of institutional ownership was associated with improved corporate governance (Healy et al., 1999; Noe, 2002). Several studies found that greater institutional ownership was associated with greater shareholder protection, increased firm value, and improved performance (Mallette and Fowler, 1992; Denis and Serrano, 1996; Gillan and Starks, 2000).

Likewise, as with firms that have greater board independence, management guidance was less optimistically biased, more accurate, and more precise for firms with greater dispersed institutional ownership (Ajinkya et al., 2005). A few studies raised concerns, about potential costs of high institutional ownership. For example, Baysinger et al. (1991) suggested that some institutional investors attempt to benefit at the cost of other shareholders. Moreover, Bushee (1998) found cross-sectional variations in the corporate governance role of different types of institutional investors.

Rozanov (2008) measured institutional ownership as the fraction of shares held by institutional investors and examine whether this governance characteristic was associated with opportunistic insider trading. If higher institutional ownership resulted in more effective monitoring, then it was expected that institutional ownership to be negatively associated with the measure of opportunistic insider trading. Ownership concentration Economic theory suggests that agency costs arise as a result of the separation of ownership and control, so to the extent that concentrated ownership, in contrast to

1211 Prim. J. Bus. Admin. Manage. diffuse ownership, reduces such separation, ownership concentration is likely to result in lower agency costs. Consistent with this view, several studies suggest that blockholders tend to actively promote long-term performance and to discipline management (Alchian and Demsetz, 1972; Shleifer and Vishny, 1986; Shleifer and Vishny, 1997).

In general, however, prior empirical evidence on the association between ownership concentration and indicators of good corporate governance, such as firm value, is somewhat mixed. Several studies found out that ownership concentration had no effect or a non-linear effect on a firm‟s value (Demsetz and Lehn, 1985; Himmelberg et al., 1999; Demsetz and Villalonga, 2001; Holderness, 2003). Nevertheless, many of these studies concluded that diffuse ownership exacerbates agency problems notwithstanding the ambiguous impact on overall firm value.

Other studies did find a positive relation between ownership concentration and firm value (Morck, Shleifer, and Vishny, 1988; McConnell and Servaes, 1990; Dittmar and Mahrt-Smith, 2007), and more direct tests of the relation between ownership concentration and monitoring of management find the association to be positive (Agrawal and Mandelker, 1990). These results were consistent with the argument that the free-rider problem makes it cost ineffective for small shareholders to act as monitors of management (Grossman and Hart, 1980).

Rozanov (2008) evaluated the relation between ownership concentration, as a proxy for good corporate governance, and opportunistic insider trading. Ownership concentration was measured as the fraction of shares held by all beneficial owners of more than 5 percent of the company's common stock. If higher ownership concentration reduced the ability of corporate officers to engage in opportunistic insider trading, then it was expected that ownership concentration to be negatively associated with the measure of opportunistic insider trading.

This section focused on review of literature, theoretical review, empirical review, section summary and research gaps of the study. It also laid out the conceptual framework which was a basic structure that consists of certain abstract blocks which represented the observational, the experiential and the analytical/ synthetically aspects of a process or system being conceived.

Furthermore, this section pointed out the inherent effects of corporate governance on insider trading by writing literature and advancing on the various independent variables to wit board size, institutional ownership, board independence and ownership concentration against the dependent variable which is insider trading. For the Capital Market in Kenya to grow, it requires the elimination of information asymmetries that lead to insiders raking in millions to the detriment of the ordinary investors (Hansen, 2003).Further the Capital

Markets Authority must ensure that, investors in the market are protected since, the bedrock of any market is market integrity and investor confidence.

Such protection includes incorporating strong licensing standards and swift but effective disciplinary sanctions for errant parties in instances of malpractices. It is however important to note that regulation should seek to strike a balance between catering for the protection of investors and at the same time provide the market with freedom to innovate and develop (Hudson, 2008). METHODOLOGY This section discusses the design and methodology that was used in the research study. This entailed the methods and procedures that assist the researcher in identifying the sources of data, the sampling method to be used, the sampling design and sample size. It further showed the data collection methods that were used, techniques, instruments and procedures. Research design A research design is defined as an overall plan for research undertaking .The researcher applied a descriptive and inference research design. Descriptive research involves field survey where the researcher goes to the population of interest to ask certain issues about the problem under the study. The design was used to obtain information concerning the current status of the phenomena to describe what existed, with respect to variables or conditions in a situation (Mugenda and Mugenda, 2003). Target population Target population is that population that which the research wishes to generates the study (Mugenda and Mugenda, 2003). The target population of this study consisted of 55 listed companies at the Nairobi Securities Exchange. Sampling frame The sampling frame comprised of a comprehensive list of all the sampling units from which a sample could be selected. A sampling frame is required to define the universe (population). The frame (data sources) could be a list from households, establishments, and industries with detailed addresses, products produced and/or consumption, expenditure, revenue data, and so on. Sampling size and sampling techniques According to Babbie (1995) sampling procedure is the process of selecting a number of individuals for a study in such a way that the selected individuals represent the larger group from which they were selected, while a sample is a set of individuals selected to participate in a study (Mugenda and Mugenda, 2003). Cooper and Schindler (2003) argue that if well chosen, samples of about 10% of a population can often give good reliability.

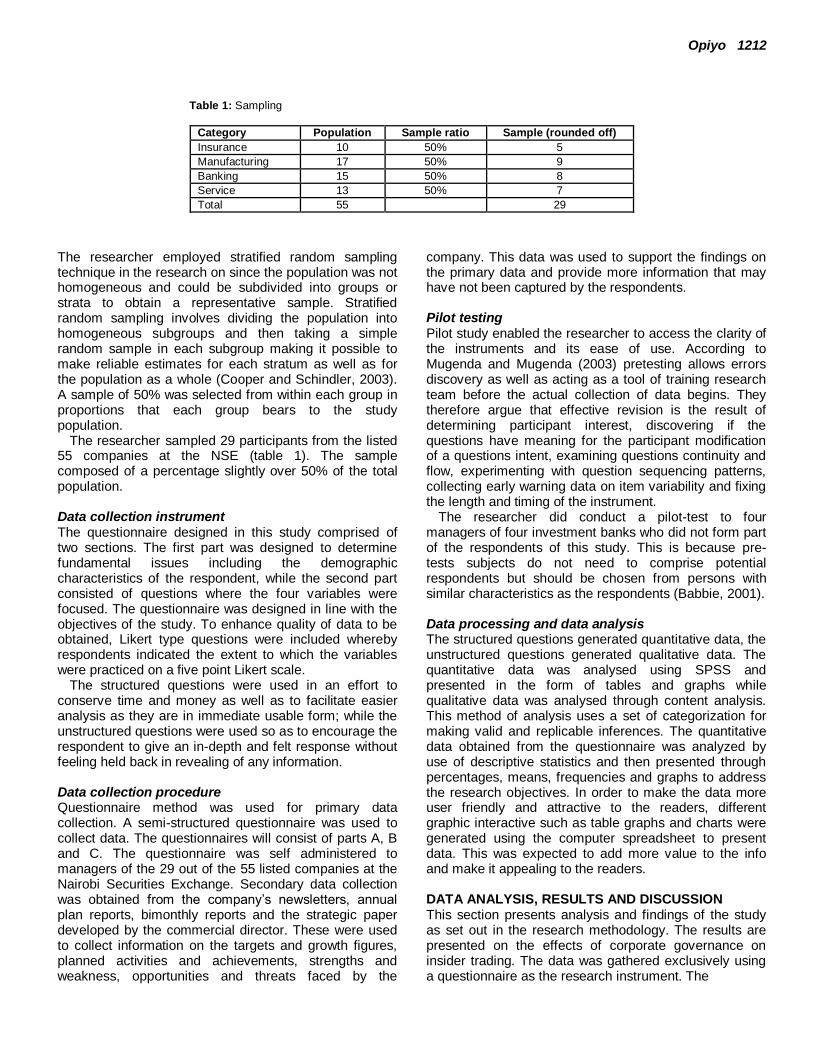

Opiyo 1212

Table 1: Sampling

Category Population Sample ratio Sample (rounded off)

Insurance 10 50% 5

Manufacturing 17 50% 9

Banking 15 50% 8

Service 13 50% 7

Total 55 29

The researcher employed stratified random sampling technique in the research on since the population was not homogeneous and could be subdivided into groups or strata to obtain a representative sample. Stratified random sampling involves dividing the population into homogeneous subgroups and then taking a simple random sample in each subgroup making it possible to make reliable estimates for each stratum as well as for the population as a whole (Cooper and Schindler, 2003). A sample of 50% was selected from within each group in proportions that each group bears to the study population.

The researcher sampled 29 participants from the listed 55 companies at the NSE (table 1). The sample composed of a percentage slightly over 50% of the total population. Data collection instrument The questionnaire designed in this study comprised of two sections. The first part was designed to determine fundamental issues including the demographic characteristics of the respondent, while the second part consisted of questions where the four variables were focused. The questionnaire was designed in line with the objectives of the study. To enhance quality of data to be obtained, Likert type questions were included whereby respondents indicated the extent to which the variables were practiced on a five point Likert scale.

The structured questions were used in an effort to conserve time and money as well as to facilitate easier analysis as they are in immediate usable form; while the unstructured questions were used so as to encourage the respondent to give an in-depth and felt response without feeling held back in revealing of any information. Data collection procedure Questionnaire method was used for primary data collection. A semi-structured questionnaire was used to collect data. The questionnaires will consist of parts A, B and C. The questionnaire was self administered to managers of the 29 out of the 55 listed companies at the Nairobi Securities Exchange. Secondary data collection was obtained from the company‟s newsletters, annual plan reports, bimonthly reports and the strategic paper developed by the commercial director. These were used to collect information on the targets and growth figures, planned activities and achievements, strengths and weakness, opportunities and threats faced by the

company. This data was used to support the findings on the primary data and provide more information that may have not been captured by the respondents. Pilot testing Pilot study enabled the researcher to access the clarity of the instruments and its ease of use. According to Mugenda and Mugenda (2003) pretesting allows errors discovery as well as acting as a tool of training research team before the actual collection of data begins. They therefore argue that effective revision is the result of determining participant interest, discovering if the questions have meaning for the participant modification of a questions intent, examining questions continuity and flow, experimenting with question sequencing patterns, collecting early warning data on item variability and fixing the length and timing of the instrument.

The researcher did conduct a pilot-test to four managers of four investment banks who did not form part of the respondents of this study. This is because pre-tests subjects do not need to comprise potential respondents but should be chosen from persons with similar characteristics as the respondents (Babbie, 2001). Data processing and data analysis The structured questions generated quantitative data, the unstructured questions generated qualitative data. The quantitative data was analysed using SPSS and presented in the form of tables and graphs while qualitative data was analysed through content analysis. This method of analysis uses a set of categorization for making valid and replicable inferences. The quantitative data obtained from the questionnaire was analyzed by use of descriptive statistics and then presented through percentages, means, frequencies and graphs to address the research objectives. In order to make the data more user friendly and attractive to the readers, different graphic interactive such as table graphs and charts were generated using the computer spreadsheet to present data. This was expected to add more value to the info and make it appealing to the readers. DATA ANALYSIS, RESULTS AND DISCUSSION This section presents analysis and findings of the study as set out in the research methodology. The results are presented on the effects of corporate governance on insider trading. The data was gathered exclusively using a questionnaire as the research instrument. The

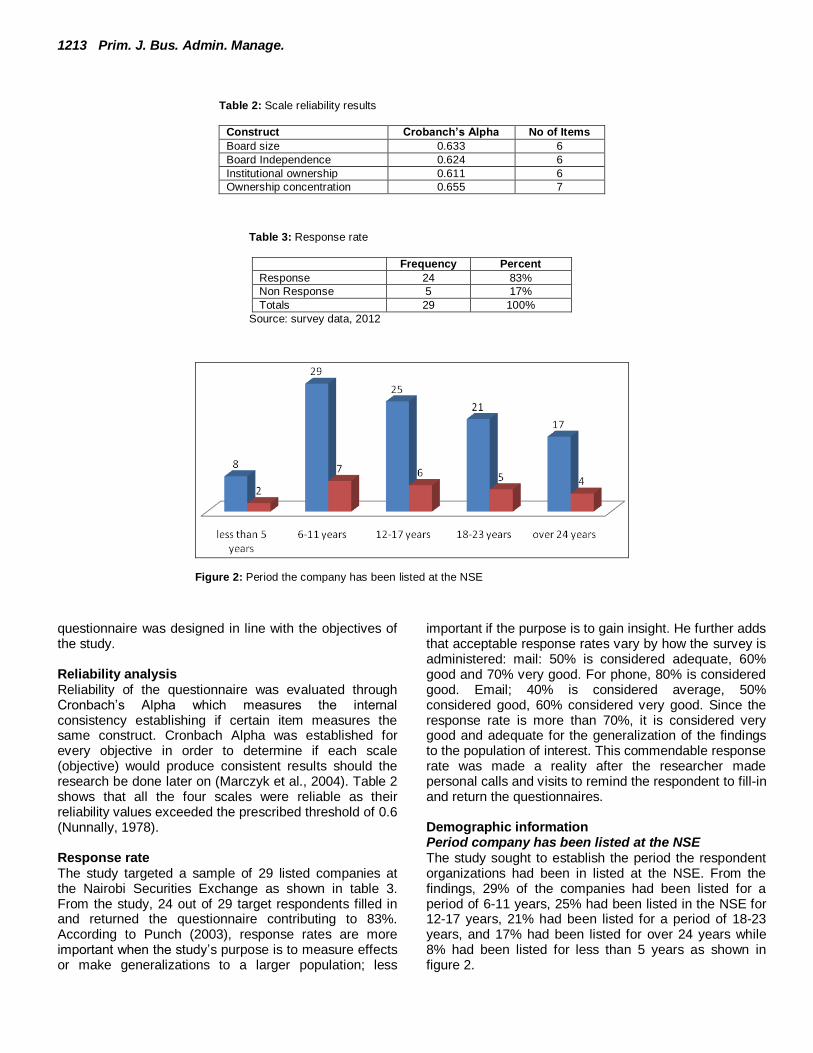

1213 Prim. J. Bus. Admin. Manage.

Table 2: Scale reliability results

Construct Crobanch’s Alpha No of Items

Board size 0.633 6

Board Independence 0.624 6

Institutional ownership 0.611 6

Ownership concentration 0.655 7

Table 3: Response rate

Frequency Percent

Response 24 83%

Non Response 5 17%

Totals 29 100%

Source: survey data, 2012

Figure 2: Period the company has been listed at the NSE

questionnaire was designed in line with the objectives of the study. Reliability analysis Reliability of the questionnaire was evaluated through Cronbach‟s Alpha which measures the internal consistency establishing if certain item measures the same construct. Cronbach Alpha was established for every objective in order to determine if each scale (objective) would produce consistent results should the research be done later on (Marczyk et al., 2004). Table 2 shows that all the four scales were reliable as their reliability values exceeded the prescribed threshold of 0.6 (Nunnally, 1978). Response rate The study targeted a sample of 29 listed companies at the Nairobi Securities Exchange as shown in table 3. From the study, 24 out of 29 target respondents filled in and returned the questionnaire contributing to 83%. According to Punch (2003), response rates are more important when the study‟s purpose is to measure effects or make generalizations to a larger population; less

important if the purpose is to gain insight. He further adds that acceptable response rates vary by how the survey is administered: mail: 50% is considered adequate, 60% good and 70% very good. For phone, 80% is considered good. Email; 40% is considered average, 50% considered good, 60% considered very good. Since the response rate is more than 70%, it is considered very good and adequate for the generalization of the findings to the population of interest. This commendable response rate was made a reality after the researcher made personal calls and visits to remind the respondent to fill-in and return the questionnaires. Demographic information Period company has been listed at the NSE The study sought to establish the period the respondent organizations had been in listed at the NSE. From the findings, 29% of the companies had been listed for a period of 6-11 years, 25% had been listed in the NSE for 12-17 years, 21% had been listed for a period of 18-23 years, and 17% had been listed for over 24 years while 8% had been listed for less than 5 years as shown in figure 2.

Opiyo 1214

Figure 3: Type of organization

Figure 4: Years in operation

Type of organization The study sought to find the type of organizations listed in the NSE. According to the findings, 38% of the listed companies were found to be in the manufacturing industry, 25% were in the banking industry, and 21% were in the service industry. 17% of the companies were in the insurance industry as indicated in figure 3. Years in operation In relation to the years in operation, the study findings established that most (42%) of the listed companies had been in operation for 22-32 years, 29% were found to have operated for 11-21 years,17% of the listed companies had operated for over 33 years and 13% had been in operation for 1-10 years as indicated in figure 4. Corporate Governance Effect of corporate governance on insider trading The study also sought to establish whether corporate governance affected insider trading of listed companies in

Figure 5: Effect of corporate governance on insider trading

the NSE. From the findings, majority (92%) of the companies indicated that corporate governance affected insider trading while 8% indicated otherwise as illustrated in the figure 5.

1215 Prim. J. Bus. Admin. Manage.

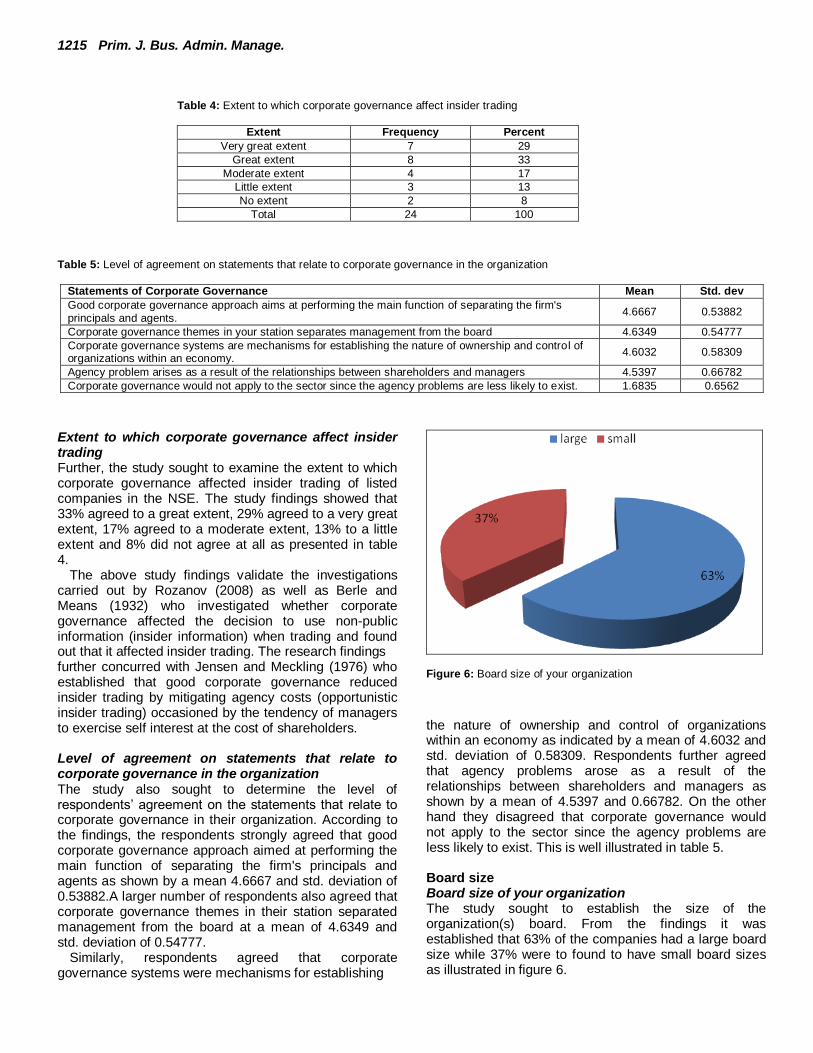

Table 4: Extent to which corporate governance affect insider trading

Extent Frequency Percent

Very great extent 7 29

Great extent 8 33

Moderate extent 4 17

Little extent 3 13

No extent 2 8

Total 24 100

Table 5: Level of agreement on statements that relate to corporate governance in the organization

Statements of Corporate Governance Mean Std. dev

Good corporate governance approach aims at performing the main function of separating the firm's principals and agents.

4.6667 0.53882

Corporate governance themes in your station separates management from the board 4.6349 0.54777

Corporate governance systems are mechanisms for establishing the nature of ownership and control of organizations within an economy.

4.6032 0.58309

Agency problem arises as a result of the relationships between shareholders and managers 4.5397 0.66782

Corporate governance would not apply to the sector since the agency problems are less likely to exist. 1.6835 0.6562

Extent to which corporate governance affect insider trading Further, the study sought to examine the extent to which corporate governance affected insider trading of listed companies in the NSE. The study findings showed that 33% agreed to a great extent, 29% agreed to a very great extent, 17% agreed to a moderate extent, 13% to a little extent and 8% did not agree at all as presented in table 4.

The above study findings validate the investigations carried out by Rozanov (2008) as well as Berle and Means (1932) who investigated whether corporate governance affected the decision to use non-public information (insider information) when trading and found out that it affected insider trading. The research findings further concurred with Jensen and Meckling (1976) who established that good corporate governance reduced insider trading by mitigating agency costs (opportunistic insider trading) occasioned by the tendency of managers to exercise self interest at the cost of shareholders. Level of agreement on statements that relate to corporate governance in the organization The study also sought to determine the level of respondents‟ agreement on the statements that relate to corporate governance in their organization. According to the findings, the respondents strongly agreed that good corporate governance approach aimed at performing the main function of separating the firm's principals and agents as shown by a mean 4.6667 and std. deviation of 0.53882.A larger number of respondents also agreed that corporate governance themes in their station separated management from the board at a mean of 4.6349 and std. deviation of 0.54777.

Similarly, respondents agreed that corporate governance systems were mechanisms for establishing

Figure 6: Board size of your organization

the nature of ownership and control of organizations within an economy as indicated by a mean of 4.6032 and std. deviation of 0.58309. Respondents further agreed that agency problems arose as a result of the relationships between shareholders and managers as shown by a mean of 4.5397 and 0.66782. On the other hand they disagreed that corporate governance would not apply to the sector since the agency problems are less likely to exist. This is well illustrated in table 5. Board size Board size of your organization The study sought to establish the size of the organization(s) board. From the findings it was established that 63% of the companies had a large board size while 37% were to found to have small board sizes as illustrated in figure 6.

Figure 7: Effect of board size on insider trading

Table 6: Extent to which the board size affects insider trading

Extent Frequency Percent

Very great extent 7 29

Great extent 9 38

Moderate extent 5 21

Little extent 2 8

No extent 1 4

Total 24 100

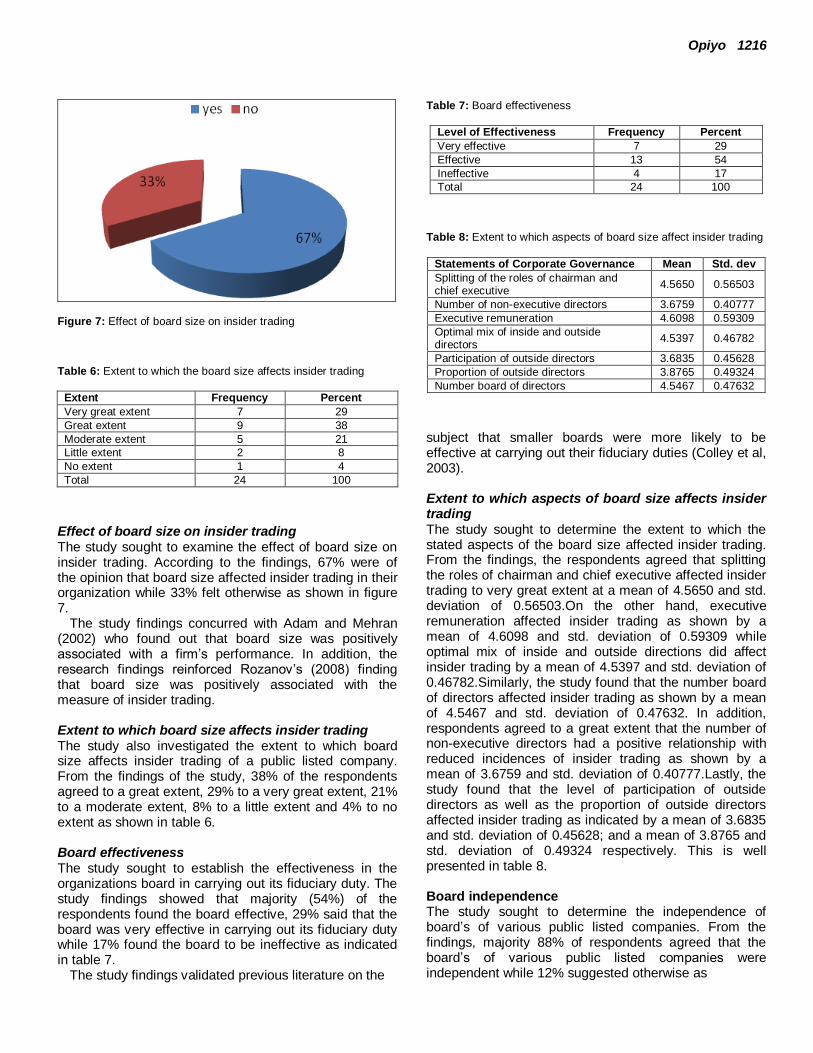

Effect of board size on insider trading The study sought to examine the effect of board size on insider trading. According to the findings, 67% were of the opinion that board size affected insider trading in their organization while 33% felt otherwise as shown in figure 7.

The study findings concurred with Adam and Mehran (2002) who found out that board size was positively associated with a firm‟s performance. In addition, the research findings reinforced Rozanov‟s (2008) finding that board size was positively associated with the measure of insider trading. Extent to which board size affects insider trading The study also investigated the extent to which board size affects insider trading of a public listed company. From the findings of the study, 38% of the respondents agreed to a great extent, 29% to a very great extent, 21% to a moderate extent, 8% to a little extent and 4% to no extent as shown in table 6. Board effectiveness The study sought to establish the effectiveness in the organizations board in carrying out its fiduciary duty. The study findings showed that majority (54%) of the respondents found the board effective, 29% said that the board was very effective in carrying out its fiduciary duty while 17% found the board to be ineffective as indicated in table 7.

The study findings validated previous literature on the

Opiyo 1216 Table 7: Board effectiveness

Level of Effectiveness Frequency Percent

Very effective 7 29

Effective 13 54

Ineffective 4 17

Total 24 100

Table 8: Extent to which aspects of board size affect insider trading

Statements of Corporate Governance Mean Std. dev

Splitting of the roles of chairman and chief executive

4.5650 0.56503

Number of non-executive directors 3.6759 0.40777

Executive remuneration 4.6098 0.59309

Optimal mix of inside and outside directors

4.5397 0.46782

Participation of outside directors 3.6835 0.45628

Proportion of outside directors 3.8765 0.49324

Number board of directors 4.5467 0.47632

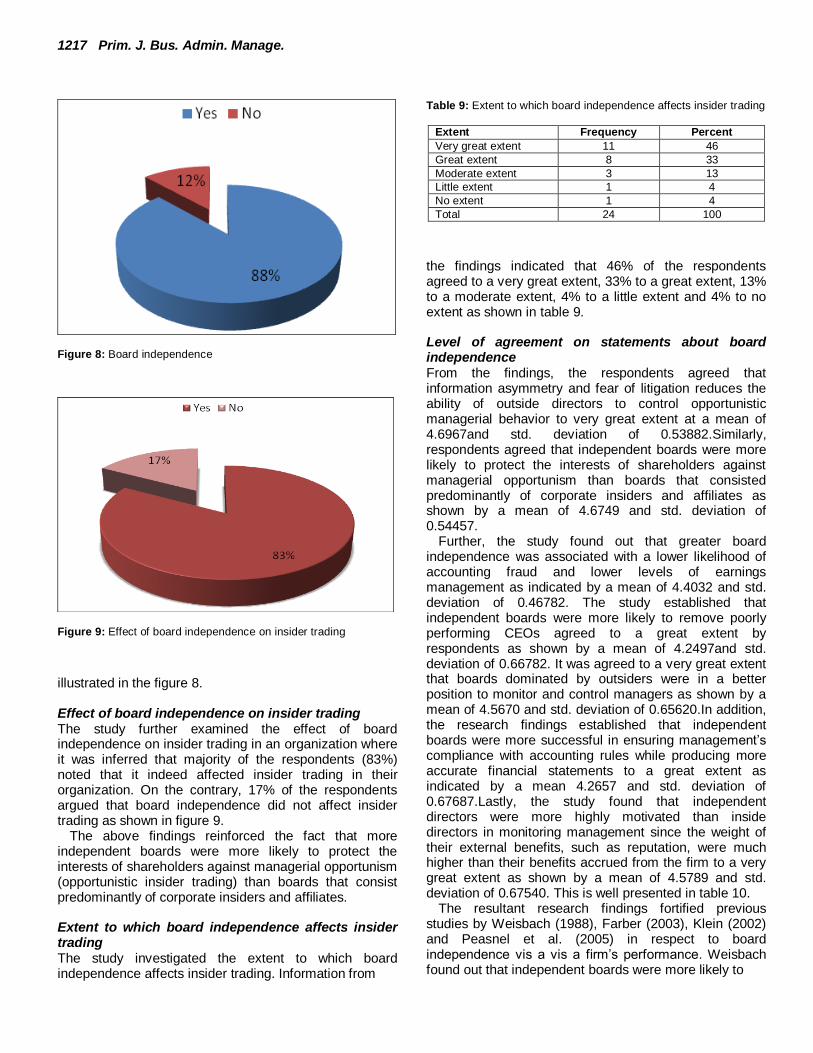

subject that smaller boards were more likely to be effective at carrying out their fiduciary duties (Colley et al, 2003). Extent to which aspects of board size affects insider trading The study sought to determine the extent to which the stated aspects of the board size affected insider trading. From the findings, the respondents agreed that splitting the roles of chairman and chief executive affected insider trading to very great extent at a mean of 4.5650 and std. deviation of 0.56503.On the other hand, executive remuneration affected insider trading as shown by a mean of 4.6098 and std. deviation of 0.59309 while optimal mix of inside and outside directions did affect insider trading by a mean of 4.5397 and std. deviation of 0.46782.Similarly, the study found that the number board of directors affected insider trading as shown by a mean of 4.5467 and std. deviation of 0.47632. In addition, respondents agreed to a great extent that the number of non-executive directors had a positive relationship with reduced incidences of insider trading as shown by a mean of 3.6759 and std. deviation of 0.40777.Lastly, the study found that the level of participation of outside directors as well as the proportion of outside directors affected insider trading as indicated by a mean of 3.6835 and std. deviation of 0.45628; and a mean of 3.8765 and std. deviation of 0.49324 respectively. This is well presented in table 8. Board independence The study sought to determine the independence of board‟s of various public listed companies. From the findings, majority 88% of respondents agreed that the board‟s of various public listed companies were independent while 12% suggested otherwise as

1217 Prim. J. Bus. Admin. Manage.

Figure 8: Board independence

Figure 9: Effect of board independence on insider trading

illustrated in the figure 8. Effect of board independence on insider trading The study further examined the effect of board independence on insider trading in an organization where it was inferred that majority of the respondents (83%) noted that it indeed affected insider trading in their organization. On the contrary, 17% of the respondents argued that board independence did not affect insider trading as shown in figure 9.

The above findings reinforced the fact that more independent boards were more likely to protect the interests of shareholders against managerial opportunism (opportunistic insider trading) than boards that consist predominantly of corporate insiders and affiliates. Extent to which board independence affects insider trading The study investigated the extent to which board independence affects insider trading. Information from

Table 9: Extent to which board independence affects insider trading

Extent Frequency Percent

Very great extent 11 46

Great extent 8 33

Moderate extent 3 13

Little extent 1 4

No extent 1 4

Total 24 100

the findings indicated that 46% of the respondents agreed to a very great extent, 33% to a great extent, 13% to a moderate extent, 4% to a little extent and 4% to no extent as shown in table 9. Level of agreement on statements about board independence From the findings, the respondents agreed that information asymmetry and fear of litigation reduces the ability of outside directors to control opportunistic managerial behavior to very great extent at a mean of 4.6967and std. deviation of 0.53882.Similarly, respondents agreed that independent boards were more likely to protect the interests of shareholders against managerial opportunism than boards that consisted predominantly of corporate insiders and affiliates as shown by a mean of 4.6749 and std. deviation of 0.54457.

Further, the study found out that greater board independence was associated with a lower likelihood of accounting fraud and lower levels of earnings management as indicated by a mean of 4.4032 and std. deviation of 0.46782. The study established that independent boards were more likely to remove poorly performing CEOs agreed to a great extent by respondents as shown by a mean of 4.2497and std. deviation of 0.66782. It was agreed to a very great extent that boards dominated by outsiders were in a better position to monitor and control managers as shown by a mean of 4.5670 and std. deviation of 0.65620.In addition, the research findings established that independent boards were more successful in ensuring management‟s compliance with accounting rules while producing more accurate financial statements to a great extent as indicated by a mean 4.2657 and std. deviation of 0.67687.Lastly, the study found that independent directors were more highly motivated than inside directors in monitoring management since the weight of their external benefits, such as reputation, were much higher than their benefits accrued from the firm to a very great extent as shown by a mean of 4.5789 and std. deviation of 0.67540. This is well presented in table 10.

The resultant research findings fortified previous studies by Weisbach (1988), Farber (2003), Klein (2002) and Peasnel et al. (2005) in respect to board independence vis a vis a firm‟s performance. Weisbach found out that independent boards were more likely to

Opiyo 1218 Table 10: Level of agreement on statements about board independence

Statements about board independence Mean Std. dev

Information asymmetry and fear of litigation may reduce the ability of outside directors to control opportunistic managerial behavior

4.6967 0.53882

Independent boards are more likely to protect the interests of shareholders against managerial opportunism than boards that consist predominantly of corporate insiders and affiliates

4.6749 0.54457

Greater board independence is associated with a lower likelihood of accounting fraud and lower levels of earnings management

4.4032 0.83309

Independent boards are more likely to remove poorly performing CEOs 4.2497 0.66782

Boards dominated by outsiders are in a better position to monitor and control managers 4.5670 0.6562

Independent boards are more successful in management‟s complying with accounting rules and produce more accurate financial statements

4.2657 0.67687

Independent directors are more highly motivated than inside directors in monitoring management since the weight of their external benefits, such as reputation, is much higher than their benefits accrued from the firm

4.5789 0.6754

Board independence is associated with greater appreciation in shareholder wealth 4.1879 0.64322

Figure 10: Institutional ownership

remove poorly performing CEO‟s, while Farber and Peasnel established that greater board independence were associated with a lower likelihood of accounting fraud, lower levels of earning management and a great appreciation in shareholder wealth.

Similarly, the study findings concurred with Fama and Jensen (1983) who asserted that outside directors (independent directors) were more highly motivated than inside directors in monitoring management since the weight of their external benefits, such as reputation and prestige were much higher than the benefits they accrued from the firm. Institutional ownership The study sought to examine the effect of institutional ownership on insider trading in the organizations. From the findings, majority 87% of respondents agreed that institutional ownership affected insider trading while a minority of 13% suggested otherwise as illustrated in the figure 10.

Table 11: Extent to which institutional ownership affect insider

trading

Extent Frequency Percent

Very great extent 10 42

Great extent 9 38

Moderate extent 3 13

Little extent 2 8

No extent 0 0

Total 24 100

Extent to which institutional ownership affect insider trading From the findings it was established that 42% of the respondents agreed to a great extent that institutional ownership affects insider trading. 38% accepted to a great extent, 13% to a moderate extent while 8% agreed to that it only affected to a little extent. None of the respondent argued that institutional ownership does not affect insider trading. As indicated in table 11.

The study findings were in line with the studies of Rozanov (2008) who had established that higher institutional ownership resulted in a more effective monitoring of management which consequently reduced opportunistic insider trading tendencies. In addition, the study findings concurred with studies conducted by Ajinkya et al (2005) who asserted that firms with greater institutional ownership (dispersed) were more likely to have management that were less optimistically biased, more accurate and precise. Level of agreement to benefits of greater institutional ownership The study also sought to investigate level of respondents‟ agreement with some stated benefits of institutional ownership to insider trading. It was inferred that the respondents agreed to a very great extent that higher institutional ownership led to greater shareholder protection as shown by a mean of 4.5670 and a std. deviation of 0.56323.

Similarly, they agreed that greater institutional

1219 Prim. J. Bus. Admin. Manage.

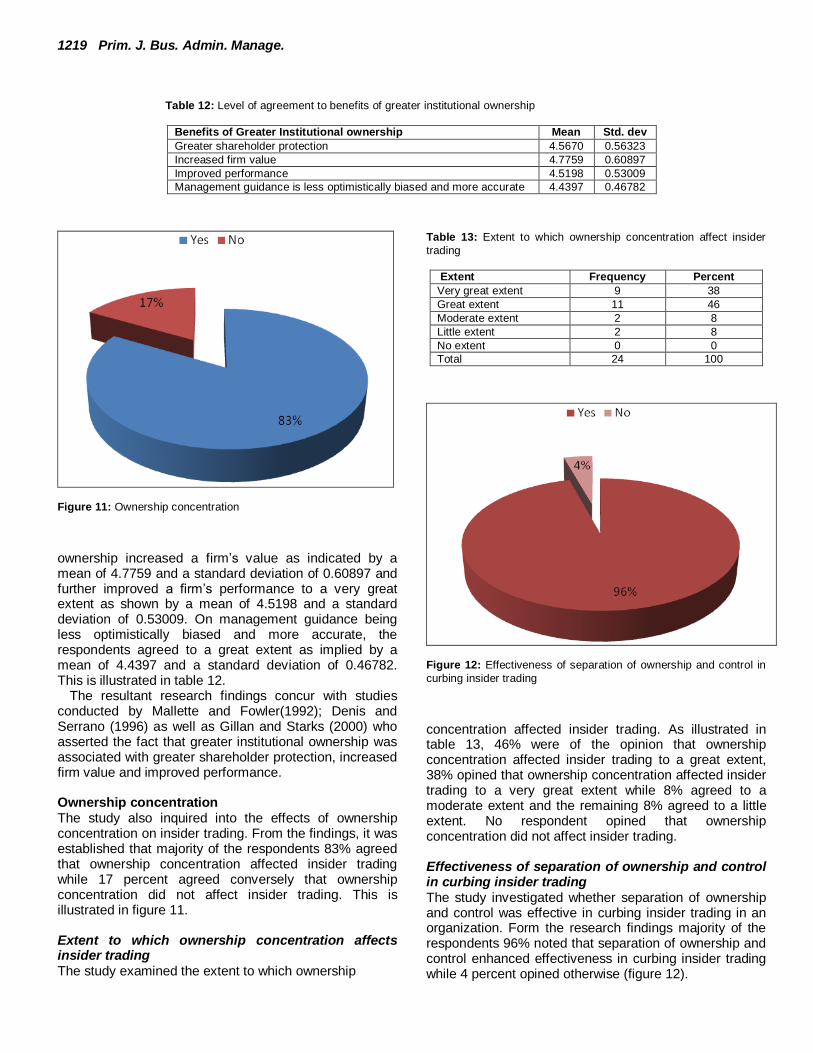

Table 12: Level of agreement to benefits of greater institutional ownership

Benefits of Greater Institutional ownership Mean Std. dev

Greater shareholder protection 4.5670 0.56323

Increased firm value 4.7759 0.60897

Improved performance 4.5198 0.53009

Management guidance is less optimistically biased and more accurate 4.4397 0.46782

Figure 11: Ownership concentration

ownership increased a firm‟s value as indicated by a mean of 4.7759 and a standard deviation of 0.60897 and further improved a firm‟s performance to a very great extent as shown by a mean of 4.5198 and a standard deviation of 0.53009. On management guidance being less optimistically biased and more accurate, the respondents agreed to a great extent as implied by a mean of 4.4397 and a standard deviation of 0.46782. This is illustrated in table 12.

The resultant research findings concur with studies conducted by Mallette and Fowler(1992); Denis and Serrano (1996) as well as Gillan and Starks (2000) who asserted the fact that greater institutional ownership was associated with greater shareholder protection, increased firm value and improved performance. Ownership concentration The study also inquired into the effects of ownership concentration on insider trading. From the findings, it was established that majority of the respondents 83% agreed that ownership concentration affected insider trading while 17 percent agreed conversely that ownership concentration did not affect insider trading. This is illustrated in figure 11. Extent to which ownership concentration affects insider trading The study examined the extent to which ownership

Table 13: Extent to which ownership concentration affect insider

trading

Extent Frequency Percent

Very great extent 9 38

Great extent 11 46

Moderate extent 2 8

Little extent 2 8

No extent 0 0

Total 24 100

Figure 12: Effectiveness of separation of ownership and control in