MONTHLY M&A INSIDER - Abvcap

67

MONTHLY M&A INSIDER A MERGERMARKET REPORT ON GLOBAL M&A ACTIVITY OCTOBER 2012 EDITION

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of MONTHLY M&A INSIDER - Abvcap

MONTHLY M&A INSIDERA MERGERMARKET REPORT ON GLOBAL M&A ACTIVITY

OCTOBER 2012

EDITION

MONTHLY M&A INSIDERMERGERMARKET

GLOBAL OVERVIEW 01

AMERICAS: LATIN AMERICA 09

NORTH AMERICA 18

ASIA-PACIFIC 29

EUROPE 41

MIDDLE EAST & AFRICA 52

ABOUT MERRILL CORPORATION 62

www.mergermarket.comPart of The Mergermarket Group

CONTENTS

80 StrandLondon, WC2R 0RLUnited Kingdom

t: +44 (0)20 7059 6100f: +44 (0)20 7059 [email protected]

11 West 19th Street 2nd fl.New York, NY 10011USA

t: +1 212 686-5606f: +1 212 [email protected]

Suite 2401-3Grand Millennium Plaza181 Queen’s Road, CentralHong Kong

t: +852 2158 9700f: +852 2158 [email protected]

Monthly M&A Insider

GLOBAL OVERVIEW

01

Robust deal values in North America

Casting a look to regional activity, North America stands out as a global bright spot: while Q3 has seen a decline in overall M&A, aggregate deal value climbed to the highest level since the first quarter of last year at US$235.7bn. Even in the private equity arena – a space hard hit by the slowdown of the past year – buyout and exit values witnessed healthy year-on-year increases. It appears that fewer, higher-value deals are boosting dealmaking among both financial and strategic investors.

Certainly, this recent trend is evident in the consumer sector – particularly in relation to North American Kraft Foods’ spinoff of its snacks business. The deal, valued at US$26bn, ranks as the largest North American transaction in the quarter and forms part of a string of spinoffs by international food groups over the past year.

In the consumer sector itself, the spinoff comprised 74% of North American consumer deal value, and contributed heavily to the sector’s eight-fold increase in deal value between Q3 2011 and Q3 2012. With 16.6% of global M&A value, the consumer sector outstripped a number of other industries to become Q3’s second biggest in North America – in comparison, the space accounted for just 2% of global deal value in Q3 2011.

A growing appetite for Consumer dealsWhile the Kraft demerger accounts for the bulk of consumer activity in North America, there are a number of other recent, high-value consumer deals that have come to market across the globe. For instance, TCC Assets announced in September its US$10bn acquisition of Fraser & Neave (F&N),

a Singapore-based conglomerate with extensive food and brewing operations. In a related transaction, Dutch brewer Heineken moved to acquire a majority stake in Asia-Pacific Breweries (APB) for US$6.6bn in July – indeed, as F&N holds a 40% stake in APB, Heineken’s move may well have made F&N a more attractive target for TCC.

Turning to deals in the pipeline, Richard Schulze, who owns a 20.3% stake of Best Buy Co Inc, voiced his plans to take the company private – a move with a projected value of US$6.2bn.

OutlookTraditionally, after the seasonal slowdown in the summer holiday period, M&A activity picks up in the final quarter of the year, with a particularly strong showing in December. Admittedly, the early weeks of the fourth quarter have not inspired much confidence. It was widely expected that the US$45bn merger of BAE Systems and EADS – the defence sector’s biggest deal in a decade – would trigger a rush of deal-making in the industry. But with the deal failing, these hopes have been dashed.

Yet with corporate reorganisation taking place among some of the world’s largest consumer groups and other strategic investors expanding into emerging markets to seize new opportunities through M&A, it shows that despite the climate of slowed deal-making and general economic malaise, there remain opportunities for growth.

GLOBAL OVERVIEW

GLOBAL M&A ACTIVITY DISAPPOINTED IN Q3 WITH DEAL VOLUME FALLING BY 16% FROM 3,203 IN Q3 2011 TO 2,679 IN Q3 2012. DEAL VALUE PAINTS A SIMILAR PICTURE, DROPPING BY A FIFTH FROM US$579BN TO US$461BN OVER THE SAME PERIOD.

Head of Research: Elias Latsis

Editor: Gwen Ceton

For advertising opportunities contact:

Erik Wickman

Tel: + (1) 212 686-3329 [email protected]

Global overview: Kristina Thompson and Fabio Lopes

Latin America: Jennifer Ruiz

North America: Urna Chakraborty and Ashley Klepach

Asia-Pacific: Raza Hussain

Europe: Peter Kruk & Kirsty Wilson

Middle East & Africa: Darragh Riordan & Silvia Paparello

Monthly M&A Insider 02

GLOBAL OVERVIEW

LEAGUE TABLES

Monthly M&A Insider

Ranking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2012 Q1-Q3 2011 Company name Value (US$bn)

Deal count Value (US$bn)

Value change (%)

1 1 Goldman Sachs 377,755 220 467,150 -19.1%

2 3 Morgan Stanley 331,661 188 357,517 -7.2%

3 2 JPMorgan 295,608 161 372,174 -20.6%

4 9 Deutsche Bank 256,118 139 213,890 19.7%

5 6 Barclays 254,610 137 249,164 2.2%

6 7 Citigroup 233,166 118 243,254 -4.1%

7 4 Credit Suisse 226,178 131 299,405 -24.5%

8 5 Bank of America Merrill Lynch 178,746 116 250,474 -28.6%

9 12 Rothschild 144,412 166 108,572 33.0%

10 14 Nomura Holdings 135,877 91 72,644 87.0%

11 10 UBS Investment Bank 117,619 110 170,795 -31.1%

12 8 Lazard 113,179 135 216,762 -47.8%

13 13 BNP Paribas 86,908 44 72,823 19.3%

14 18 RBC Capital Markets 79,913 105 54,139 47.6%

15 11 HSBC 46,764 45 111,492 -58.1%

16 20 Jefferies & Company 41,425 78 38,353 8.0%

17 40 BMO Capital Markets 41,190 32 22,882 80.0%

18 58 Greenhill & Co 40,773 31 12,087 237.3%

19 15 Evercore Partners 37,510 59 66,624 -43.7%

20 16 SG 37,299 40 60,181 -38.0%Source: mergermarket

The financial adviser league tables by value and volume have been run from 01-Jan-12 to 30-Sep-12. The tables cover all sectors and are based on the geography of either the target, bidder or seller being Global.

TOP 20 FINANCIAL ADVISERS – GLOBAL

VALUE

Ranking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2012 Q1-Q3 2011 Company name Value (US$bn)

Deal count Deal count Deal count change

1 1 Goldman Sachs 377,755 220 251 -31

2 3 Morgan Stanley 331,661 188 198 -10

3 6 Rothschild 144,412 166 173 -7

4 5 JPMorgan 295,608 161 183 -22

5 13 Deutsche Bank 256,118 139 143 -4

6 15 Barclays 254,610 137 108 29

7 4 PwC 13,529 136 194 -58

8 12 Lazard 113,179 135 145 -10

9 8 Credit Suisse 226,178 131 165 -34

10 11 Deloitte 11,156 130 147 -17

11 2 KPMG 14,278 122 207 -85

12 14 Citigroup 233,166 118 124 -6

13 7 Bank of America Merrill Lynch 178,746 116 170 -54

14 9 UBS Investment Bank 117,619 110 163 -53

15 18 RBC Capital Markets 79,913 105 84 21

16 17 Nomura Holdings 135,877 91 89 2

17 10 Ernst & Young 11,441 90 163 -73

18 16 Jefferies & Company 41,425 78 94 -16

19 19 M&A International 1,378 75 80 -5

20 24 Houlihan Lokey 13,164 69 64 5Source: mergermarket

TOP 20 FINANCIAL ADVISERS – GLOBAL

VOLUME

Monthly M&A Insider 03

GLOBAL OVERVIEW

Ranking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2012 Q1-Q3 2011 Company name Value (US$bn)

Deal count Deal count Deal count change

1 1 DLA Piper 34,041 206 259 -53

2 3 Jones Day 87,333 204 229 -25

3 2 Latham & Watkins 126,483 192 232 -40

4 8 Kirkland & Ellis 90,859 186 196 -10

5 4 Linklaters 151,048 166 205 -39

6 7 Clifford Chance 219,543 152 196 -44

7 5 Baker & McKenzie 53,283 149 198 -49

8 10 Skadden Arps Slate Meagher & Flom 190,993 143 169 -26

9 9 Allen & Overy 76,250 137 189 -52

10 6 Freshfields Bruckhaus Deringer 205,564 131 196 -65

11 15 White & Case 95,043 122 115 7

12 13 Weil Gotshal & Manges 98,470 118 133 -15

13 11 CMS 9,174 110 161 -51

14 12 Hogan Lovells 46,225 101 152 -51

15 18 Sullivan & Cromwell 126,419 87 106 -19

16 17 Ashurst 31,911 86 107 -21

17 14 Simpson Thacher & Bartlett 103,593 83 116 -33

18 26 Paul Hastings 13,932 78 87 -9

19 21 Cleary Gottlieb Steen & Hamilton 120,576 77 97 -20

20 32 Stikeman Elliott 51,063 77 75 2Source: mergermarket

The legal adviser league tables by value and volume have been run from 01-Jan-12 to 30-Sep-12 and include lapsed and withdrawn deals. The tables cover all sectors and are based on the geography of either the target, bidder or seller being Global.

TOP 20 LEGAL ADVISERS – GLOBAL

VOLUME

Ranking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2012 Q1-Q3 2011 Company name Value (US$bn)

Deal count Value (US$bn)

Value change (%)

1 16 Clifford Chance 219,543 152 96,240 128.1%

2 7 Freshfields Bruckhaus Deringer 205,564 131 204,391 0.6%

3 3 Skadden Arps Slate Meagher & Flom 190,993 143 233,530 -18.2%

4 5 Linklaters 151,048 166 213,931 -29.4%

5 9 Latham & Watkins 126,483 192 195,603 -35.3%

6 1 Sullivan & Cromwell 126,419 87 318,424 -60.3%

7 11 Cleary Gottlieb Steen & Hamilton 120,576 77 166,396 -27.5%

8 14 Davis Polk & Wardwell 104,111 75 116,746 -10.8%

9 2 Simpson Thacher & Bartlett 103,593 83 295,246 -64.9%

10 13 Weil Gotshal & Manges 98,470 118 116,904 -15.8%

11 23 White & Case 95,043 122 67,604 40.6%

12 66 King & Wood Mallesons 91,176 61 24,487 272.3%

13 20 Kirkland & Ellis 90,859 186 74,507 21.9%

14 4 Wachtell, Lipton, Rosen & Katz 87,526 43 225,418 -61.2%

15 17 Jones Day 87,333 204 93,855 -6.9%

16 12 Allen & Overy 76,250 137 161,672 -52.8%

17 10 Cravath Swaine & Moore 74,670 34 167,170 -55.3%

18 19 Blake, Cassels & Graydon 72,479 76 79,845 -9.2%

19 8 Shearman & Sterling 66,622 74 199,800 -66.7%

20 21 Baker & McKenzie 53,283 149 72,206 -26.2%Source: mergermarket

TOP 20 LEGAL ADVISERS – GLOBAL

VALUE

LEAGUE TABLES

Monthly M&A Insider 04

GLOBAL OVERVIEW

LEAGUE TABLES

VALUE

VALUE

Rank

Q1-Q3 2012 Company name Value (US$m)

Deal count

1 The Carlyle Group 15,495 20

2 BC Partners 10,721 4

3 Blackstone Group 8,741 14

4 Apollo Global Management 7,924 3

5 Access Industries 7,482 2

6 Riverstone Holdings 7,350 2

7 Arcus Infrastructure Partners 5,633 1

8 GS Capital Partners 4,754 5

9 Advent International 4,649 5

10 Global Infrastructure Partners 4,489 3

11 Macquarie Group 4,435 4

12 CVC Capital Partners 4,174 6

13 Bain Capital 4,141 6

14 EQT Partners 3,414 7

15 Thomas H Lee Partners 3,090 2Source: mergermarket

Rank

Q1-Q3 2012 Company name Value (US$m)

Deal count

1 GS Capital Partners 9,890 4

2 Hellman & Friedman 8,000 4

3 Kohlberg Kravis Roberts & Co 7,903 4

4 Oaktree Capital Group 7,199 4

5 General Atlantic 7,107 4

6 Macquarie Group 6,971 8

7 The Carlyle Group 6,653 8

8 Quadrangle Group 6,579 1

9 CVC Capital Partners 6,448 4

10 Permira 5,889 2

11 Novator Partners 5,806 1

12 Weston Presidio Capital 5,290 2

13 Madison Dearborn Partners 4,728 2

14 EnCap Investments 3,850 2

15 Apollo Global Management 3,776 4Source: mergermarket

VOLUME

VOLUME

Rank

Q1-Q3 2012 Company name Value (US$m)

Deal count

1 The Carlyle Group 15,495 20

2 Blackstone Group 8,741 14

3 AXA Private Equity 1,816 12

4 Kohlberg Kravis Roberts & Co 2,858 11

5 The Riverside Company 0 10

6 Lloyds TSB Development Capital 396 9

7 HIG Capital 47 8

8 EQT Partners 3,414 7

9 Vista Equity Partners 2,501 7

10 Warburg Pincus 1,638 7

11 Oaktree Capital Group 572 7

12 CVC Capital Partners 4,174 6

13 Bain Capital 4,141 6

14 Partners Group Holding 1,690 6

15 Sun Capital Partners 585 6Source: mergermarket

Rank

Q1-Q3 2012 Company name Value (US$m)

Deal count

1 Intel Capital 1,531 12

2 Draper Fisher Jurvetson 1,948 11

3 3i Group 1,122 11

4 Battery Ventures 830 9

5 The Riverside Company 70 9

6 Macquarie Group 6,971 8

7 The Carlyle Group 6,653 8

8 Sun Capital Partners 98 8

9 Benchmark Capital 1,619 6

10 Atlas Venture 1,571 6

11 Softbank Capital Partners 869 6

12 TA Associates 738 6

13 Kleiner, Perkins, Caufield & Byers 3,679 5

14 Polaris Venture Partners 1,514 5

15 Bessemer Venture Partners 873 5Source: mergermarket

ACTIVITY TABLE OF PRIVATE EQUITY FIRMS ON GLOBAL BUYOUTS

ACTIVITY TABLE OF PRIVATE EQUITY FIRMS ON GLOBAL EXITS

The private equity buyout activity tables by value and volume are based on private equity firms advising the bidder on buyout deals where the dominant geography of the target company is Global. The tables by value and volume have been run from 01-Jan-12 to 30-Sep-12 and exclude lapsed and withdrawn deals.

The private equity exit activity tables by value and volume are based on private equity firms advising the vendor on exit deals where the dominant geography of the target company is Global. The tables by value and volume have been run from 01-Jan-12 to 30-Sep-12 and exclude lapsed and withdrawn deals.

Monthly M&A Insider 05

GLOBAL OVERVIEW

TREND GRAPHS

GLOBAL M&A QUARTERLY TREND

0

200

400

600

800

1,000

1,200

1,400

Q312*

Q212

Q112

Q411

Q311

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Valu

e (U

S$bn

)

Total value Mid-market value

Num

ber of deals

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Total volume Mid-market volume

0

50

100

150

200

250

300

350

400

Q312*

Q212

Q112

Q411

Q311

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Valu

e (U

S$bn

)

Buyout value Exit value

Num

ber of deals

Buyout volume Exit volume

0

100

200

300

400

500

600

700

800

900

GLOBAL M&A ANNUAL TREND GLOBAL M&A ANNUAL PRIVATE EQUITY TREND

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4000

YTD 2012*201120102009200820072006

Valu

e (U

S$bn

)

Total value Mid-market value

Num

ber of deals

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Total volume Mid-market volume

0

100

200

300

400

500

600

700

800

900

YTD 2012*201120102009200820072006

Valu

e (U

S$bn

)

Buyout value Exit value

Num

ber of deals

Buyout volume Exit volume

0

500

1,000

1,500

2,000

2,500

3,000

3,500

GLOBAL M&A QUARTERLY PRIVATE EQUITY TREND

Monthly M&A Insider 06

GLOBAL OVERVIEW

TREND GRAPHS

GLOBAL M&A SECTOR BREAKDOWN Q3 2012

GLOBAL GEOGRAPHIC BREAKDOWN Q3 2012

VALUE

VALUE

VOLUME

VOLUME

5.9%

16.6%

2.9% 1.8%1.0%

1.7%

7.6%

8.0%

20.0%

16.5%

16.2%

Industrials & Chemicals

TMT

Consumer

Business Services

Energy, Mining & Utilities

Financial Services

Pharma, Medical & Biotech

Leisure

Construction

Transportation

Real Estate

Agriculture

Defence

0.1%

1.7%

1.8%2.7%

51.4%

21.8%

22.3% Asia-Pacific

Europe

North America

Middle East & Africa

Central & South America

10.2%

12.5%

1.6%

0.3%1.0%

3.4%3.7%

7.2%

3.8%

8.0%

20.3%

15.1%

13.1%

Industrials & Chemicals

TMT

Consumer

Business Services

Energy, Mining & Utilities

Financial Services

Pharma, Medical & Biotech

Leisure

Construction

Transportation

Real Estate

Agriculture

Defence

4.2%2.4%

33.3%

38.5%

21.5% Asia-Pacific

Europe

North America

Middle East & Africa

Central & South America

Monthly M&A Insider 07

GLOBAL OVERVIEW

TREND GRAPHS

GLOBAL M&A DEAL SIZE BREAKDOWN

VALUE VOLUME

0

10

20

30

40

50

60

70

80

90

100

2012*201120102009200820072006

42.3%

16.8%

20.8%

7.5%

12.6%

39.8%

16.9%

23.0%

7.9%

12.5%

42.0%

15.3%

19.3%

8.9%

14.5%

40.6%

16.5%

20.5%

7.9%

14.5%

27.3%

20.6%

27.6%

9.5%

14.9%

29.8%

19.3%

26.2%

10.2%

14.5%

28.5%

19.3%

28.0%

10.8%

13.5%

<US$250m or undisclosed value

US$251m-US$500m

US$501m-US$2,000m

US$2,001m-US$5,000m

>US$5,001m

Perc

enta

ge

80

82

84

86

88

90

92

94

96

98

100

2012*201120102009200820072006

<US$250m or undisclosed value

US$251m-US$500m

US$501m-US$2,000m

US$2,001m-US$5,000m

>US$5,001m

1.2%

5.0%

4.7%

88.3%

1.3%

5.5%

5.1%

87.4%

0.6%

0.9%

3.9%

4.6%

90.1%

1.0%

3.8%

3.9%

90.9%

89.2%

4.5%

4.7%

1.1%

0.4%

1.1%

4.7%

4.8%

88.8%

0.7% 0.7% 0.5%

1.1%

5.0%

5.3%

88.1%

0.5%0.5%

Perc

enta

ge

SECTOR ANALYSISGLOBAL SECTOR ANALYSISSector Q3 2012 Q3 2011 % change

Value ($m) Mrk share Deal count Value ($m) Mrk share Deal count value volume

Energy, Mining & Utilities 92,020 19.9% 272 112,348 19.4% 288 -18% -6%

Industrials & Chemicals 76,058 16.5% 544 105,397 18.2% 660 -28% -18%

Consumer 76,565 16.6% 350 50,769 8.8% 423 51% -17%

Financial Services 34,951 7.6% 213 76,005 13.1% 292 -54% -27%

Pharma, Medical & Biotech 36,672 7.9% 194 60,182 10.4% 243 -39% -20%

Technology 57,735 12.5% 308 36,456 6.3% 328 58% -6%

Business Services 27,316 5.9% 334 31,627 5.5% 400 -14% -17%

Media 16,966 3.7% 96 6,495 1.1% 112 161% -14%

Transportation 13,277 2.9% 90 12,511 2.2% 96 6% -6%

Real Estate 8,303 1.8% 42 23,326 4.0% 63 -64% -33%

Leisure 7,914 1.7% 101 8,649 1.5% 104 -8% -3%

Telecommunications 506 0.1% 100 47,682 8.2% 36 -99% 178%

Defence 4,803 1.0% 9 115 0.0% 8 4077% 13%

Construction 7,920 1.7% 100 6,304 1.1% 119 26% -16%

Agriculture 506 0.1% 26 1,558 0.3% 32 -68% -19%

Total 461,512 2,779 579,424 3,204 -20% -13%

datasite.com

M E R R I L L D A T A S I T E ®

Maximize your deal’s potential with aMerrill DataSite virtual data room.

Every day, dealmakers all over the world use virtual data rooms from Merrill DataSite® to drive deals to asuccessful conclusion. Why? Because Merrill DataSite makes it easy to present your deal to buyers any-where around the world, and it’s fully supported by an expert and experienced project management team.Invite interested parties to review your deal’s due diligence information online, via a secure virtual dataroom, hosted by Merrill DataSite.

It’s faster. It’s less expensive. It’s more convenient. It captures buyers’ actual due diligence activities onlineand provides you with valuable intelligence to help negotiate a successful deal.

To find out more, or to arrange a demonstration of our VDR solution, call +1 888 867 0309, email usat [email protected], or visit www.datasite.com today.

In today’s uncertain marketwhat is the best way to presentour company’s assetsto bring the deal to asuccessfulclose?”Wrap up your dealwith Merrill DataSite®.

LATIN AM

ERICA

LATIN AMERICAA MERGERMARKET M&A REPORT ON

Monthly M&A Insider 09

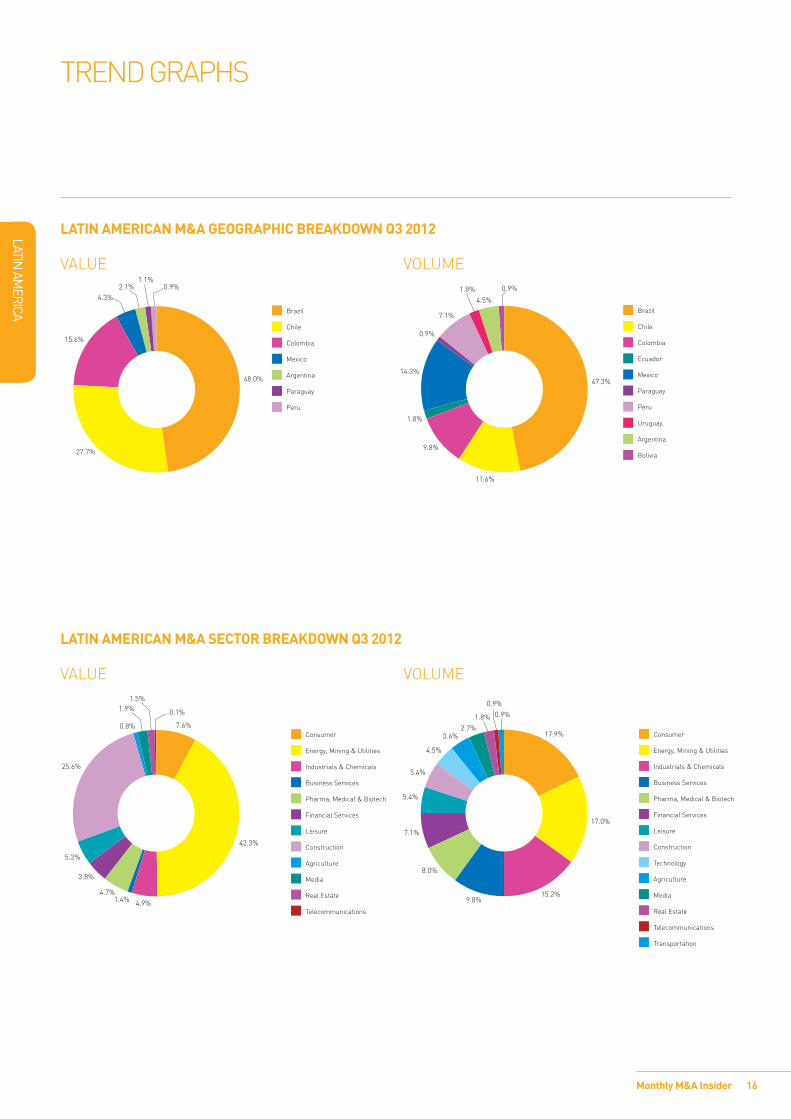

Brazil, Mexico, and Chile with the largest market share As expected, Brazil, with 247 deals worth US$37.9bn in the first three quarters of 2012, or a 47.3% market share of the Latin American M&A, was the most active country in the region. The largest deal in the year-to-date for Brazil remains the acquisition of a 44.4% stake in Redecard, a provider of credit card payment processing services, by Itau Unibanco for a deal value of US$5.2bn. The transaction was announced in February 2012.

Mexico was the second most active Latin American country in the first three quarters of the year, attaining a 29.2% share of deal value with 40 deals worth US$23.4bn. Such a large combined deal value was mainly due to the acquisition of a 49.7% stake in Grupo Modelo, a beer brewing company, by Anheuser-Busch. This transaction, which was valued at US$20.1bn, took place at the very end of June 2012.

Chile came in third with 38 deals and a US$7.1bn deal value representing an 8.8% market share in the region. Corporacion Nacional del Cobre de Chile’s acquisition of a 24.5% stake in Anglo American Sur SA, a copper mining and smelting company, for US$1.7bn was the largest in Chile in the year-to-date.

Consumer was the most active sector in the year-to-date, followed by Energy, Mining & UtilitiesIn the first three quarters of the year, the Consumer sector, which saw 27 deals worth US$29.1bn, was the most active sector in Latin America with a 36.3% market share by deal value. During the comparable period last year it was Telecommunications that dominated the Latin American M&A market, with 11 deals valued at US$32.6bn, or a 32% market share by deal value. Similarly to last year’s values for Telecommunications, which can mainly be attributed to a few extremely large deals, the Consumer sector has had unusually high investments thus far this year.

The largest deal in this sector in the year-to-date was the already mentioned acquisition of Grupo Modelo. The second largest deal was the acquisition of a 41.6% stake in Cerveceria Nacional Dominicana, the Dominican Republic beverage company, by Ambev Brasil Bebidas, the Brazil based manufacturer of soft drinks and alcoholic beverages, for US$1bn. The third largest deal happened to be the acquisition of another beverage company, Chile-based Embotelladoras Coca Cola Polar, by Embotelladora Andina for US$956m.

The Energy, Mining & Utilities sector attained a 23.6% market share by deal value in the year-to-date, with 74 deals valued at US$19bn. The largest transaction in the sector was the acquisition of a 60.1% stake in Cia de Gas de Sao Paulo, the Brazil-based energy company, by Cosan SA Industria e Comercio for US$2.6bn.

LATIN AMERICAN M&A ACTIVITY IN Q3 2012 SAW 112 DEALS WORTH US$13.4BN, THE LOWEST DEAL VALUE SINCE Q1 2009, WHICH HAD 101 DEALS VALUED AT US$12.1BN. THE TOP DEAL FOR Q3 2012 WAS THE ACQUISITION OF OBRASCON HUARTE LAIN BRASIL, THE BRAZIL-BASED CONSTRUCTION COMPANY, BY ABERTIS INFRAESTRUCTURAS SA AND BROOKFIELD INFRASTRUCTURE PARTNERS LP FOR US$2.7BN. IT WAS FOLLOWED BY THE ACQUISITION OF A 75% STAKE IN PROMIGAS SA ESP, THE COLOMBIA-BASED OPERATOR OF NATURAL GAS TRANSMISSION AND DISTRIBUTION SYSTEMS, BY CORPORACION FINANCIERA COLOMBIANA SA FOR US$1.9BN.

10

LATIN AM

ERICA

Monthly M&A Insider

Deal summary

Announced: 06-Aug-12 Deal Value: US$2,763m

Brookfield Infrastructure Partners LP and Abertis Infraestructuras, SA has agreed to acquire a 60% stake in Obrascon Huarte Lain Brasil SA from OHL Concesiones SA.

TERMS:• Abertis will issue 81.48m shares, representing a 10% of

its total outstanding shares, as an equity consideration to OHL Brazil.

• An assumed concessions liability of ¤504.1m of OHL.

• A cash consideration of ¤10.7m (US$13.3m).

• The implied equity value of the transaction is approximately ¤2,197.6m.

• The offer provides a discount of 7.8% based on OHL Brazil closing share price of BRL17.6 (US$8.58) on 07-Aug-12.

• The offer provides a discount of 10.9% based on OHL Brazil closing share price of BRL16.22 (US$8.88) on 06-Jul-12.

RATIONALE: • The acquisition is in line with Abertis’ expansion strategy.

• The acquisition will increase the concessions portfolio managed by Abertis and Brookfield.

• The acquisition will enable Brookfield to generate stable cash flow.

POST DEAL DETAILS: • Brookfield and Abertis will launch a tender offer to

acquire the remaining 40% stake in OHL Brazil.

• Brookfield Infrastructure expects to initially invest approximately US$250m in OHL Brazil.

• OHL Brasil will own a 15% stake in Abertis.

EXPECTED COMPLETION: • The transaction is expected to close in the fourth quarter

of 2012.

CONDITIONS:• Subject to customary closing conditions.

• Subject to approval from regulatory authorities.

• Subject to third party consents.

• Subject to Obrascon Huarte Lain Brasil SA shareholders’ approval.

BACKGROUND: • On 06-Aug-12, a joint venture was formed

between Brookfield and Abertis to acquire a 60% stake in OHL Brazil.

• Brookfield Infrastructure and its institutional partners would own 49% of the joint venture and Abertis would own the remaining 51% in the joint venture.

• Earlier OHL Brazil held a 5% stake in Abertis.

DEAL OF THE QUARTER

11

LATIN AM

ERICA

Monthly M&A Insider

DEAL OF THE QUARTER

Target

Obrascon Huarte Lain Brasil SA

Headquarters: Rua Joaquim Floriano, 913 - 6 FloorItaim BibiSao PauloBrazil

Sector: Construction

Description: Brazil based company engaged highway operator and construction

Bidder

Abertis Infraestructure Partners SA

Headquarters: Avinguda del Parc Logistic 12-20Barcelona 08040Spain

Sector: Construction

Description: Spain based company engaged in the management of mobility and telecommunications infrastructures

Brookfield Infrastructure Partners LP

Headquarters: Canada

Sector: Construction

Description: Canada based operator of infrastructure assets

Advisers

Target/Seller Bidder

Financial Banco BTG Pactual JPMorgan

Financial SG

Legal Clifford Chance (Advising JPMorgan);Lefosse Advogados; Linklaters

Legal Freshfields Bruckhaus Deringer;Machado Meyer Sandacz e Opice

Exit multiples – Y/E 31-Dec-11 Premium analysis

Multiples Value (US$m) Offer price per share (US$) -

Revenue 2.6x 18,655 1 day before -7.79%

EBITDA 7.1x 3,324 1 month before -10.87%

EBIT 8.9x 2,960 1 day after -7.32%

Earnings 2.5x 1,839 Pre-rumour -5.66%

12

LATIN AM

ERICA

Monthly M&A Insider

TOP 10 LATIN AMERICAN ANNOUNCED DEALS OF Q3 2012Announced Bidder company Target company Target dominant

sectorSeller company Exit multiples (x) Bid premia

1-day before

Deal value

(US$m)Revenue EBITDA P/E

6-Aug-12 Abertis Infraestructuras SA; and Brookfield Infrastructure Partners LP

Obrascon Huarte Lain Brasil SA (60% stake)

Construction OHL Concesiones SA 2.6 7.1 2.5 -7.8% 2,763

24-Jul-12 Corporacion Financiera Colombiana SA

Promigas SA ESP (75.03% stake)

Energy, Mining & Utilities

20.2 39.1 19.3 -13.5% 1,908

23-Aug-12 Corporacion Nacional del Cobre de Chile

Anglo American Sur SA (24.5% stake)

Energy, Mining & Utilities

Anglo American Plc - - - - 1,700

23-Aug-12 Mitsui & Co Ltd; and Corporacion Nacional del Cobre de Chile

Anglo American Sur SA (5% stake)

Energy, Mining & Utilities

Anglo American Plc; and Mitsubishi Corporation

- - - - 1,100

02-Jul-12 Public Sector Pension Investment Board

Isolux Infrastructure SA (undisclosed stake)

Construction Grupo Isolux Corsan SA - - - - 630

08-Aug-12 Royal DSM NV Tortuga Companhia Zootecnica Agraria

Pharma, Medical & Biotech

- - - - 575

19-Jul-12 Consortium led by LarrainVial SA

Repsol Butano Chile Industrials & Chemicals

Repsol SA - - - - 540

05-Jul-12 STR Projetos e Participacoes Ltda

STR Projetos e Participacoes em Recursos Naturais SA (9% stake)

Energy, Mining & Utilities

Banco BTG Pactual SA - - - - 367

11-Jul-12 Australia Acquisition Corp Ferrous Resources do Brasil Ltda (9.7% Stake); and Asian Coast Development (Canada) Limited (65.4% Stake)

Leisure Harbinger Capital Partners

- - - - 350

13-Sep-12 The Carlyle Group LLC Tok & Stok Ltda (60% stake)

Consumer 1.2 - - - 345

Based on announced deals, including lapsed and withdrawn bids Based on dominant geography of target company being Latin AmericaData correct as of 09-Oct-12

Source: mergermarket

TOP DEALS

13

LATIN AM

ERICA

Monthly M&A Insider

The financial adviser league tables by value and volume have been run from 01-Jan-12 to 30-Sep-12. The tables cover all sectors and are based on the geography of either the target, bidder or seller being Latin American.

VALUERanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2012 Q1-Q3 2011 Company name Value (US$m)

Deal count Value (US$bn)

Value change (%)

1 12 JPMorgan 36,158 13 9,630 275%

2 17 Lazard 30,177 11 7,035 329%

3 19 Deutsche Bank 27,725 10 5,172 436%

4 10 Barclays 26,604 4 14,780 80.0%

5 15 Bank of America Merrill Lynch 25,039 10 7,573 231%

6 8 Morgan Stanley 23,244 6 15,235 52.6%

7 2 Banco Itau BBA 21,361 29 26,761 -20.2%

8 1 Banco BTG Pactual 18,826 31 35,751 -47.3%

9 6 Goldman Sachs 17,652 17 19,470 -9.3%

10 7 Citigroup 15,121 9 15,735 -3.9%

11 3 Banco Bradesco BBI 14,126 16 24,973 -43.4%

12 5 Rothschild 12,657 16 20,391 -37.9%

13 4 Credit Suisse 11,095 19 23,178 -52.1%

14 11 Santander Global Banking and Markets 6,068 8 14,170 -57.2%

15 16 Banco Espirito Santo de Investimento 5,783 5 7,192 -19.6%

16 42 BR Partners 5,700 8 509 1019%

17 14 UBS Investment Bank 4,022 8 7,950 -49.4%

18 - ABN AMRO Bank 3,456 1 - -

19 - SG 2,763 1 - -

20 13 HSBC 2,115 4 8,916 -76.3%Source: mergermarket

TOP 20 FINANCIAL ADVISERS – LATIN AMERICA

VOLUMERanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2012 Q1-Q3 2011 Company name Value (US$m)

Deal count Deal count Deal count change

1 1 Banco BTG Pactual 18,826 31 26 5

2 2 Banco Itau BBA 21,361 29 25 4

3 3 Credit Suisse 11,095 19 22 -3

4 4 Goldman Sachs 17,652 17 19 -2

5 5 Banco Bradesco BBI 14,126 16 17 -1

6 9 Rothschild 12,657 16 11 5

7 14 JPMorgan 36,158 13 7 6

8 19 Lazard 30,177 11 5 6

9 25 Deutsche Bank 27,725 10 4 6

10 17 Bank of America Merrill Lynch 25,039 10 6 4

11 8 Citigroup 15,121 9 13 -4

12 7 Santander Global Banking and Markets 6,068 8 14 -6

13 10 BR Partners 5,700 8 11 -3

14 16 UBS Investment Bank 4,022 8 6 2

15 20 Vinci Partners 153 7 5 2

16 6 Morgan Stanley 23,244 6 14 -8

17 11 Banco Espirito Santo de Investimento 5,783 5 10 -5

18 18 Barclays 26,604 4 5 -1

19 23 HSBC 2,115 4 4 0

20 - Ernst & Young 57 4 - -Source: mergermarket

TOP 20 FINANCIAL ADVISERS – LATIN AMERICA

LEAGUE TABLES

14

LATIN AM

ERICA

Monthly M&A Insider

The legal adviser league tables by value and volume have been run from 01-Jan-12 to 30-Sep-12 and include lapsed and withdrawn deals. The tables cover all sectors and are based on the geography of either the target, bidder or seller being Latin American.

LEAGUE TABLES

VOLUMERanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2012 Q1-Q3 2011 Company name Value (US$m)

Deal count Deal count Deal count change

1 2 Machado Meyer Sendacz e Opice 9,740 41 34 7

2 1 Pinheiro Neto Advogados 3,339 32 39 -7

3 6 Souza, Cescon, Barrieu & Flesch Advogados 7,194 24 19 5

4 3 Mattos Filho, Veiga Filho, Marrey Jr. e Quiroga Advogados 17,020 21 27 -6

5 4 Barbosa, Mussnich & Aragao 4,644 20 25 -5

6 21 Lefosse Advogados 8,102 15 9 6

7 20 Veirano Advogados 873 15 10 5

8 30 Azevedo Sette Advogados 1,466 14 5 9

9 44 Linklaters 6,547 12 3 9

10 16 Gomez-Pinzon Zuleta 1,055 12 11 1

11 5 Tozzini Freire Teixeira e Silva Advogados 937 12 21 -9

12 7 Baker & McKenzie 2,553 11 17 -6

13 12 Estudio Muniz, Ramirez, Perez-Taiman & Olaya Abogados 1,104 11 13 -2

14 17 Skadden Arps Slate Meagher & Flom 31,122 10 10 0

15 8 Clifford Chance 27,741 10 14 -4

16 23 Jones Day 5,819 10 7 3

17 19 Prieto & Carrizosa 1,047 9 10 -1

18 10 Rodrigo Elias & Medrano 732 9 13 -4

19 18 Sullivan & Cromwell 24,161 8 10 -2

20 57 Uria Menendez 6,368 8 2 6Source: mergermarket

TOP 20 LEGAL ADVISERS – LATIN AMERICA

VALUERanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2012 Q1-Q3 2011 Company name Value (US$m)

Deal count Value (US$bn)

Value change (%)

1 3 Skadden Arps Slate Meagher & Flom 31,122 10 17,783 75.0%

2 6 Clifford Chance 27,741 10 14,430 92.2%

3 54 Freshfields Bruckhaus Deringer 25,517 3 884 2787%

4 4 Sullivan & Cromwell 24,161 8 17,452 38.4%

5 - Alston & Bird 20,805 3 - -

6 55 Creel, Garcia-Cuellar, Aiza y Enriquez 20,466 4 844 2325%

7 155 Greenberg Traurig 20,120 5 39 51490%

8 56 Mijares, Angoitia, Cortes y Fuentes 20,100 3 819 2354%

9 17 Cravath Swaine & Moore 20,100 1 6,535 208%

10 19 Mattos Filho, Veiga Filho, Marrey Jr. e Quiroga Advogados 17,020 21 6,458 164%

11 14 Shearman & Sterling 10,069 7 7,887 27.7%

12 5 Machado Meyer Sendacz e Opice 9,740 41 16,222 -40.0%

13 31 Lefosse Advogados 8,102 15 2,503 224%

14 9 Souza, Cescon, Barrieu & Flesch Advogados 7,194 24 10,922 -34.1%

15 11 Cleary Gottlieb Steen & Hamilton 7,022 5 9,819 -28.5%

16 47 Linklaters 6,547 12 1,092 500%

17 40 Uria Menendez 6,368 8 1,414 350%

18 8 Simpson Thacher & Bartlett 6,097 4 11,621 -47.5%

19 69 Jones Day 5,819 10 658 784%

20 - Bredin Prat 5,427 1 - -Source: mergermarket

TOP 20 LEGAL ADVISERS – LATIN AMERICA

15

LATIN AM

ERICA

Monthly M&A Insider

TREND GRAPHS

0

10

20

30

40

50

60

70

Q312*

Q212

Q112

Q411

Q311

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Total value Mid-market value

Num

ber of dealsValu

e (U

S$bn

)

0

20

40

60

80

100

120

140

160

180

Total volume Mid-market volume

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Q312*

Q212

Q112

Q411

Q311

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Valu

e (U

S$m

)

Buyout value Exit value

Num

ber of deals

Buyout volume Exit volume

0

2

4

6

8

10

12

14

16

18

0

20

40

60

80

100

120

140

160

180

YTD 2012*201120102009200820072006

Total value Mid-market value

Num

ber of dealsValu

e (U

S$bn

)

0

100

200

300

400

500

600

700

Total volume Mid-market volume

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

YTD 2012*201120102009200820072006

Valu

e (U

S$m

)

Buyout value Exit value

Num

ber of deals

Buyout volume Exit volume

0

5

10

15

20

25

30

35

40

45

50

LATIN AMERICAN M&A QUARTERLY TREND

LATIN AMERICAN M&A ANNUAL TREND LATIN AMERICAN M&A ANNUAL PRIVATE EQUITY TREND

LATIN AMERICAN M&A QUARTERLY PRIVATE EQUITY TREND

16

LATIN AM

ERICA

Monthly M&A Insider

TREND GRAPHS

LATIN AMERICAN M&A GEOGRAPHIC BREAKDOWN Q3 2012

VALUE VOLUME

15.6%

27.7%

2.1%1.1%

0.9%

48.0%

4.3%

Brazil

Chile

Colombia

Mexico

Argentina

Paraguay

Peru

47.3%

11.6%

14.3%

1.8%

9.8%

0.9%

7.1%

1.8%4.5%

0.9%

Brazil

Chile

Colombia

Ecuador

Mexico

Paraguay

Peru

Uruguay

Argentina

Bolivia

LATIN AMERICAN M&A SECTOR BREAKDOWN Q3 2012

VALUE VOLUME

7.6%

4.9%

5.3%

3.8%

4.7%1.4%

42.3%

25.6%

1.5%

0.1%1.9%

0.8%Consumer

Energy, Mining & Utilities

Industrials & Chemicals

Business Services

Pharma, Medical & Biotech

Financial Services

Leisure

Construction

Agriculture

Media

Real Estate

Telecommunications

17.9%

17.0%

15.2%9.8%

8.0%

4.5%

2.7%3.6%

0.9%0.9%

1.8%

7.1%

5.4%

5.4%

Consumer

Energy, Mining & Utilities

Industrials & Chemicals

Business Services

Pharma, Medical & Biotech

Financial Services

Leisure

Construction

Technology

Agriculture

Media

Real Estate

Telecommunications

Transportation

17

LATIN AM

ERICA

Monthly M&A Insider

LATIN AMERICAN M&A DEAL SIZE BREAKDOWN

VALUE VOLUME

0

10

20

30

40

50

60

70

80

90

100

2012*201120102009200820072006

<US$250m or undisclosed value

US$251m-US$500m

US$501m-US$2,000m

US$2,001m-US$5,000m

>US$5,001m

12.7%

10.3%

21.8%

8.3%

46.9%

25.2%

15.6%

32.4%

10.7%

16.2%

14.6%

10.0%

24.5%

20.3%

30.6%

14.8%

10.1%

36.6%

29.3%

9.2%

39.6%

19.2%

24.9%

6.9%

9.4%14.5%

10.7%

27.5%

18.4%

28.9%

14.0%

14.1%

3.5%

32.3%

36.1%

Perc

enta

ge

20

30

40

50

60

70

80

90

100

2012*201120102009200820072006

1.0%

5.4%

7.4%

85.1%

0.2%

5.5%

6.2%

87.5%

0.6%

4.7%

5.3%

88.2%

0.3%

6.9%

5.4%

85.7% 82.3%

6.3%

8.1%

1.2%1.0% 0.7% 1.2% 1.8% 2.0%

6.0%

5.8%

86.3%

0.8% 0.5%

Perc

enta

ge

1.1%

7.7%

6.9%

84.6%

<US$250m or undisclosed value

US$251m-US$500m

US$501m-US$2,000m

US$2,001m-US$5,000m

>US$5,001m

0.3%

TREND GRAPHS

LATIN AMERICAN SECTOR ANALYSISSector Q3 2012 Q3 2011 % change

Value ($m) Mrk share Deal count Value ($m) Mrk share Deal count Value Volume

Energy, Mining & Utilities 5,696 42.3% 19 4,133 9.3% 15 38% 27%

Industrials & Chemicals 659 4.9% 17 1,166 2.6% 28 -43% -39%

Consumer 1,020 7.6% 20 6,160 13.8% 31 -83% -35%

Financial Services 516 3.8% 8 6,199 13.9% 11 -92% -27%

Pharma, Medical & Biotech 626 4.7% 9 891 2.0% 10 -30% -10%

Technology 5 0.0% 5 811 1.8% 9 -99% -44%

Business Services 192 1.4% 11 1,483 3.3% 18 -87% -39%

Media 250 1.9% 3 0 0.0% 2 0% 50%

Transportation 0 0.0% 1 836 1.9% 4 -100% -75%

Real Estate 202 1.5% 2 874 2.0% 7 -77% -71%

Leisure 711 5.3% 6 134 0.3% 4 431% 50%

Telecommunications 12 0.1% 1 21,010 47.1% 5 0% 100%

Defence 0 0.0% 0 0 0.0% 0 100% 0%

Construction 3,447 25.6% 6 165 0.4% 4 100% 50%

Agriculture 114 0.8% 4 774 1.7% 8 -85% -50%

Total 13,450 112 44,636 156 -70% -28%

SECTOR ANALYSIS

NORTH AM

ERICA

A MERGERMARKET M&A REPORT ON

18Monthly M&A Insider

NORTH AMERICA

Q3 2012 HIGHEST PERFORMING QUARTER SINCE Q1 2011 Q3 2012 ENDED ON A HIGH NOTE WITH 879 DEALS COLLECTIVELY VALUED AT US$235.7BN, THE HIGHEST VALUE SINCE Q1 2011 (US$263BN). THIS WAS A 12.7% INCREASE IN VALUE FROM Q3 2011, BUT A 10.8% DECREASE IN VOLUME (US$209.2BN WITH 985 DEALS). THE HIGHEST PERFORMING QUARTER IN THE YEAR-TO-DATE, Q3 2012, REPRESENTS 39.7% OF TOTAL NORTH AMERICAN M&A IN THE YEAR-TO-DATE. BOTH BUYOUTS AND EXITS DECREASED IN VOLUME FOR Q3 FROM THE LAST QUARTER BY 15.2% AND 8.9% RESPECTIVELY.

Energy, Mining and Utilities dominated top deals for the third quarterThe Energy, Mining and Utilities sector secured three of the top 10 deal spots with the acquisition of Nexen Inc by China National Offshore Oil Corporation Ltd for US$17.6bn, which was the second largest deal of the month, and two other acquisitions worth over US$5bn. Due to the large value of deals for this quarter, Energy, Mining and Utilities represented 24.5% of all North American M&A by value.

Consumer sector sees strong growth in SeptemberFor the last month of the quarter, the Consumer sector saw an increase of 717% from Q3 2011 with 78 deals worth US$35.3bn. The largest deal for this quarter was also in the Consumer sector, with the US$26.3bn spin-off of Kraft Foods Inc’s North American grocery business, Kraft Foods Group Inc, to the shareholders of Kraft Foods. This growth brought the Consumer sector’s market share in the year-to-date to 15% by value, a 13% increase from the comparable period last year.

Goldman Sachs tops financial advisers league tablesWith 136 deals worth US$223bn, Goldman Sachs climbed to the top spot on mergermarket’s league tables for financial advisers in both value and volume. This represented an 18.7% increase in value for the investment bank.

19

NORTH AM

ERICA

Monthly M&A Insider

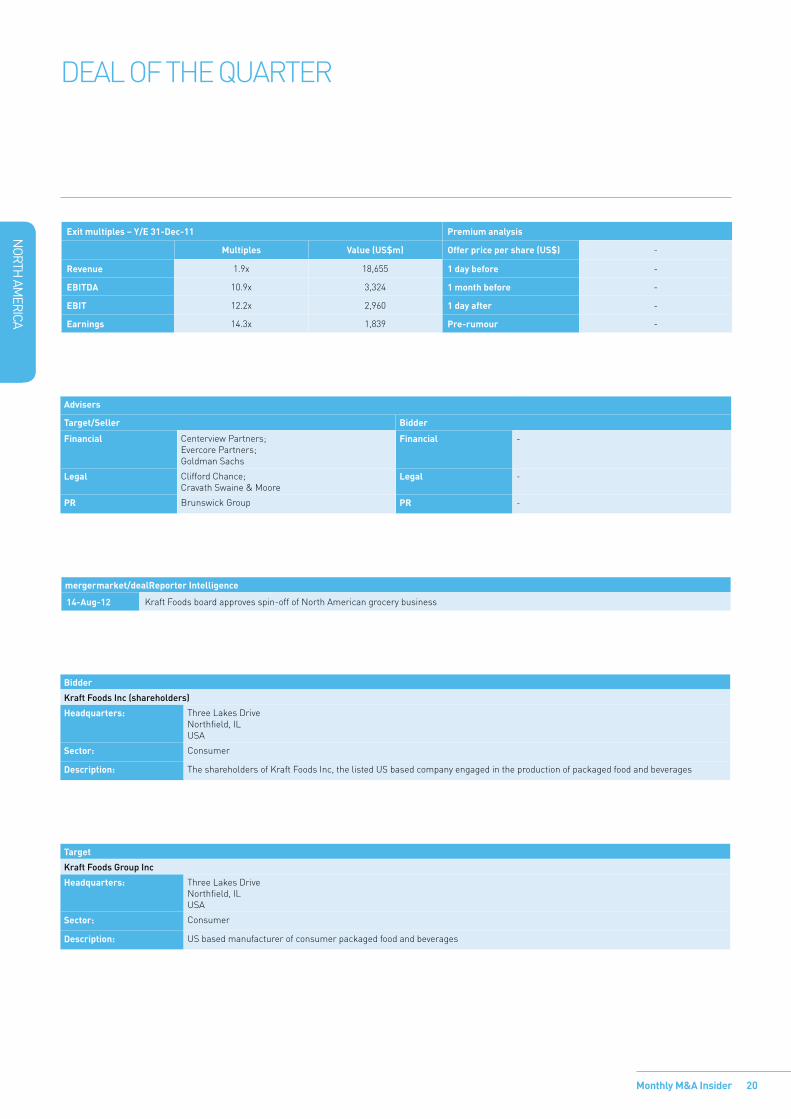

DEAL OF THE QUARTER

Deal summary

Announced: 14-Aug-12 Deal Value: US$26,294m

Kraft Foods Inc has agreed to spin off its North American grocery business, Kraft Foods Group Inc, to the shareholders of Kraft Foods.

TERMS:• Kraft Foods’ shareholders will receive one share of Kraft

Foods Group for every three shares of Kraft Foods held.

• The distribution will be made in book-entry form, and no physical share certificates will be issued.

• In addition, no fractional Kraft Foods Group shares will be issued. All fractional shares will be aggregated and sold in the open market. The cash proceeds from such sales will be distributed to the shareholders who would have otherwise received fractional shares. Such cash distributions, unlike the distribution of shares, will be taxable.

POST DEAL DETAILS:• Kraft Foods Group will be listed on NASDAQ Global Select

Market, under the symbol “KRFT”.

• Kraft Foods will change its name to Mondelez International Inc and its ticker symbol to “MDLZ”.

EXPECTED COMPLETION: • Kraft Foods Group is expected to commence trading

on 02-Oct-12.

CONDITIONS:• Customary closing conditions.

BACKGROUND: • Kraft Foods’ Board of Directors has approved

the transaction.

UPDATE 01-OCT-12:• Kraft Foods have completed the spin-off of its North

American grocery business. Kraft Foods has changed its name to Mondelez International. Kraft Foods Group shares will begin trading on NASDAQ on 02-Oct-12, under the ticker symbol “KRFT”.

UPDATE 02-OCT-12:• Kraft Foods Group has started trading on NASDAQ at the

opening price of US$44.45.

20

NORTH AM

ERICA

Monthly M&A Insider

DEAL OF THE QUARTER

Bidder

Kraft Foods Inc (shareholders)

Headquarters: Three Lakes DriveNorthfield, ILUSA

Sector: Consumer

Description: The shareholders of Kraft Foods Inc, the listed US based company engaged in the production of packaged food and beverages

Target

Kraft Foods Group Inc

Headquarters: Three Lakes DriveNorthfield, ILUSA

Sector: Consumer

Description: US based manufacturer of consumer packaged food and beverages

Advisers

Target/Seller Bidder

Financial Centerview Partners;Evercore Partners;Goldman Sachs

Financial -

Legal Clifford Chance;Cravath Swaine & Moore

Legal -

PR Brunswick Group PR -

mergermarket/dealReporter Intelligence

14-Aug-12 Kraft Foods board approves spin-off of North American grocery business

Exit multiples – Y/E 31-Dec-11 Premium analysis

Multiples Value (US$m) Offer price per share (US$) -

Revenue 1.9x 18,655 1 day before -

EBITDA 10.9x 3,324 1 month before -

EBIT 12.2x 2,960 1 day after -

Earnings 14.3x 1,839 Pre-rumour -

21

NORTH AM

ERICA

Monthly M&A Insider

TOP DEALS & EXPECTED DEALS

TOP 10 NORTH AMERICAN ANNOUNCED DEALS OF Q3 2012Announced Bidder company Target company Target dominant

sectorSeller company Exit multiples (x) Bid premia

1-day before

Deal value(US$m)Revenue EBITDA P/E

14-Aug-12 Kraft Foods Inc (shareholders)

Kraft Foods Group Inc Consumer Mondelez International Inc

1.9 10.9 14.3 - 26,294

23-Jul-12 China National Offshore Oil Corporation Ltd

Nexen Inc Energy, Mining & Utilities

2.7 4.5 22.2 61.2% 17,654

18-Jul-12 BC Partners Limited; and Canada Pension Plan Investment Board

Suddenlink Communications

Telecommunications GS Capital Partners; Oaktree Capital Group; and Quadrangle Group

3.4 8.9 - - 6,579

06-Aug-12 Kinder Morgan Energy Partners LP

El Paso Natural Gas Company (50% stake); and Tennessee Gas Pipeline Company LLC

Energy, Mining & Utilities

Kinder Morgan Inc - - - - 6,220

20-Aug-12 Aetna Inc Coventry Health Care Inc Pharma, Medical & Biotech

0.5 5.7 11.4 20.3% 5,702

10-Sep-12 Plains Exploration & Production Company

BP plc (Outer Continental Shelf of the Gulf of Mexico assets)

Energy, Mining & Utilities

BP Plc - - - - 5,550

30-Aug-12 The Carlyle Group LLC DuPont Performance Coatings

Industrials & Chemicals

E I du Pont de Nemours and Company

1.1 - - - 4,900

09-Jul-12 WellPoint Inc Amerigroup Corporation Pharma, Medical & Biotech

0.7 8.6 24.1 43.0% 4,558

30-Jul-12 Chicago Bridge & Iron Company NV

The Shaw Group Inc Industrials & Chemicals

- - - 72.3% 4,249

01-Jul-12 Linde AG Lincare Holdings Inc Pharma, Medical & Biotech

2.3 9.4 21.5 22.0% 4,245

Based on announced deals, including lapsed and withdrawn bids Based on dominant geography of target company being North America (US + Canada) Data correct as of 08-Oct-12

Source: mergermarket

22

NORTH AM

ERICA

Monthly M&A Insider

Situation Target company Sector Potential bidder company

Financial adviser to bidder (B); target (T); seller (S)

Seller company

Market cap/ est. value (US$m)

Comments

Expected Deal Best Buy Co Inc Consumer Richard Schulze

Goldman Sachs (B) 6,286 Richard Schulze, the 20.3% shareholder of Best Buy Co Inc, the listed US based retailer of electronics, has announced that he plans to take the company private for US$24 to US$26 per share. On 24-Jul-12, Best Buy engaged Goldman Sachs to explore defensive measures.

Expected Deal Monster Worldwide Inc Technology Undisclosed bidder

Stone Key Partners (T); Bank of American Merrill Lynch (T)

986 On 01-Mar-12, Monster Worldwide Inc, the listed US based provider of employment services, announced that its Board of Directors was reviewing strategic alternatives for the company. Monster Worldwide has retained Stone Key Partners and Bank of American Merrill Lynch as financial advisors for the review.

Expected Deal Digital Generation Systems Inc

Business Services

Undisclosed bidder

Goldman Sachs (T) 318 On 16-Jul-12, Digital Generation Systems Inc, the listed US based provider of digital technology services, announced that its Board of Directors was looking into strategic alternatives for the company. The company has engaged Goldman Sachs in connection with the matter.

Expected Deal Winnebago Industries Inc Industrials & Chemicals

North Street Capital

263 On 18-May-12, Winnebago Industries Inc, the listed US based manufacturer of recreation vehicles, received an unsolicited proposal from North Street Capital, the US based private equity firm. As a part of the offer, North Street Capital would acquire Winnebago Industries for US$11.00 per share.

Expected deals based on confirmed announcements by companies involved Data correct as of 08-Oct-12

PIPELINE OF NORTH AMERICAN EXPECTED DEALS

TOP DEALS & EXPECTED DEALS

23

NORTH AM

ERICA

Monthly M&A Insider

Ranking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2012 Q1-Q3 2011 Company name Value (US$bn)

Deal count Value (US$bn)

Value change (%)

1 2 Goldman Sachs 222,999 136 187,886 18.7%

2 1 JPMorgan 135,918 96 190,897 -28.8%

3 6 Barclays 122,790 100 125,356 -2.0%

4 3 Morgan Stanley 122,663 94 161,290 -23.9%

5 5 Bank of America Merrill Lynch 121,341 83 129,695 -6.4%

6 4 Credit Suisse 116,980 77 138,082 -15.3%

7 9 Deutsche Bank 108,119 73 80,038 35.1%

8 8 Citigroup 103,662 67 83,065 24.8%

9 12 RBC Capital Markets 71,696 92 29,223 145.3%

10 11 Evercore Partners 61,431 49 51,916 18.3%

11 17 Centerview Partners 53,318 12 17,887 198.1%

12 7 Lazard 47,875 76 108,334 -55.8%

13 10 UBS Investment Bank 47,202 50 78,495 -39.9%

14 19 BMO Capital Markets 41,260 32 17,591 134.6%

15 13 Jefferies & Company 39,962 67 28,744 39.0%

16 18 Rothschild 38,839 48 17,745 118.9%

17 41 Greenhill & Co 34,122 22 5,328 540.4%

18 16 Wells Fargo Securities 24,712 39 19,703 25.4%

19 22 Nomura Holdings 23,994 14 15,248 57.4%

20 62 Rabobank 23,516 9 1,874 1154.9%Source: mergermarket

The financial adviser league tables by value and volume have been run from 01-Jan-12 to 30-Sep-12. The tables cover all sectors and are based on the geography of either the target, bidder or seller being US or Canadian.

TOP 20 FINANCIAL ADVISERS – NORTH AMERICA

LEAGUE TABLES

Ranking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2012 Q1-Q3 2011 Company name Value (US$bn)

Deal count Deal count Deal count change

1 1 Goldman Sachs 222,999 136 109 27

2 9 Barclays 122,790 100 54 46

3 4 JPMorgan 135,918 96 78 18

4 3 Morgan Stanley 122,663 94 82 12

5 11 RBC Capital Markets 71,696 92 48 44

6 2 Bank of America Merrill Lynch 121,341 83 89 -6

7 6 Credit Suisse 116,980 77 65 12

8 12 Lazard 47,875 76 44 32

9 10 Deutsche Bank 108,119 73 48 25

10 8 Citigroup 103,662 67 59 8

11 7 Jefferies & Company 39,962 67 61 6

12 13 Houlihan Lokey 8,311 63 41 22

13 5 UBS Investment Bank 47,202 50 66 -16

14 20 Evercore Partners 61,431 49 25 24

15 14 Rothschild 38,839 48 37 11

16 16 Raymond James & Associates 3,073 44 29 15

17 23 Moelis & Company 18,721 43 22 21

18 26 William Blair & Company 4,593 41 22 19

19 33 Wells Fargo Securities 24,712 39 15 24

20 27 Keefe, Bruyette & Woods 2,343 38 21 17Source: mergermarket

TOP 20 FINANCIAL ADVISERS – NORTH AMERICA

VALUE

VOLUME

24

NORTH AM

ERICA

Monthly M&A Insider

Ranking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2012 Q1-Q3 2011 Company name Value (US$bn)

Deal count Deal count Deal count change

1 2 Kirkland & Ellis 86,729 177 119 58

2 3 Jones Day 71,304 167 104 63

3 1 Latham & Watkins 111,664 157 122 35

4 5 DLA Piper 25,394 122 83 39

5 4 Skadden Arps Slate Meagher & Flom 134,122 104 85 19

6 8 Weil Gotshal & Manges 77,727 95 69 26

7 6 Simpson Thacher & Bartlett 94,466 76 79 -3

8 41 Vinson & Elkins 46,945 73 33 40

9 17 Stikeman Elliott 48,289 72 50 22

10 7 Sullivan & Cromwell 76,036 70 69 1

11 12 Blake, Cassels & Graydon 64,013 69 57 12

12 21 Morgan Lewis & Bockius 9,823 68 45 23

13 13 Davis Polk & Wardwell 98,135 64 53 11

14 60 White & Case 57,489 62 23 39

15 42 Morrison & Foerster 40,264 62 32 30

16 19 Baker & McKenzie 23,771 61 46 15

17 22 Greenberg Traurig 18,799 59 44 15

18 32 Paul Hastings 10,954 57 39 18

19 11 Hogan Lovells 16,087 52 58 -6

20 9 Wilson Sonsini Goodrich & Rosati 11,035 52 65 -13Source: mergermarket

The legal adviser league tables by value and volume have been run from 01-Jan-12 to 30-Sep-12 and include lapsed and withdrawn deals. The tables cover all sectors and are based on the geography of either the target, bidder or seller being US or Canadian.

TOP 20 LEGAL ADVISERS – NORTH AMERICA

LEAGUE TABLES

Ranking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2012 Q1-Q3 2011 Company name Value (US$bn)

Deal count Value (US$bn)

Value change (%)

1 7 Skadden Arps Slate Meagher & Flom 134,122 104 115,283 16.3%

2 4 Latham & Watkins 111,664 157 131,978 -15.4%

3 12 Davis Polk & Wardwell 98,135 64 75,350 30.2%

4 2 Simpson Thacher & Bartlett 94,466 76 178,911 -47.2%

5 20 Kirkland & Ellis 86,729 177 49,541 75.1%

6 3 Wachtell, Lipton, Rosen & Katz 86,583 42 156,351 -44.6%

7 9 Cleary Gottlieb Steen & Hamilton 81,526 43 104,675 -22.1%

8 10 Weil Gotshal & Manges 77,727 95 89,044 -12.7%

9 1 Sullivan & Cromwell 76,036 70 181,584 -58.1%

10 44 Clifford Chance 72,109 38 21,116 241.5%

11 19 Jones Day 71,304 167 58,209 22%

12 15 Blake, Cassels & Graydon 64,013 69 61,351 4.3%

13 35 White & Case 57,489 62 24,688 132.9%

14 8 Cravath Swaine & Moore 53,633 30 107,070 -49.9%

15 6 Shearman & Sterling 50,636 49 117,439 -56.9%

16 117 Bracewell & Giuliani 50,099 27 3,598 1292.4%

17 25 Stikeman Elliott 48,289 72 29,699 62.6%

18 33 Vinson & Elkins 46,945 73 25,269 85.8%

19 16 Freshfields Bruckhaus Deringer 45,261 46 61,106 -25.9%

20 28 Gibson Dunn & Crutcher 43,114 45 28,223 52.8%Source: mergermarket

TOP 20 LEGAL ADVISERS – NORTH AMERICA

VALUE

VOLUME

25

NORTH AM

ERICA

Monthly M&A Insider

LEAGUE TABLES

VALUE

VALUE

Rank

Q1-Q3 2012 Company name Value (US$m)

Deal count

1 The Carlyle Group 15,495 20

2 GS Capital Partners 11,333 6

3 BC Partners 10,039 2

4 Blackstone Group 8,980 15

5 Apollo Global Management 7,924 2

6 Access Industries 7,482 2

7 Riverstone Holdings 7,350 2

8 Advent International 7,339 6

9 Oaktree Capital Group 7,151 8

10 Quadrangle Group 6,579 1

11 Hellman & Friedman 6,027 4

12 Madison Dearborn Partners 5,146 5

13 TPG Capital 4,370 7

14 Bain Capital 4,141 5

15 Global Infrastructure Partners 3,188 2Source: mergermarket

Rank

Q1-Q3 2012 Company name Value (US$m)

Deal count

1 GS Capital Partners 10,620 7

2 The Carlyle Group 10,195 10

3 Kohlberg Kravis Roberts & Co 10,114 9

4 Hellman & Friedman 9,727 5

5 CVC Capital Partners 7,448 5

6 Oaktree Capital Group 6,579 5

7 BC Partners 6,579 1

8 Quadrangle Group 6,579 1

9 General Atlantic 6,567 7

10 Madison Dearborn Partners 6,191 5

11 Advent International 6,166 5

12 Bain Capital 6,075 7

13 Permira 5,500 2

14 Weston Presidio Capital 5,290 2

15 TPG Capital 4,218 5Source: mergermarket

VOLUME

VOLUME

Rank

Q1-Q3 2012 Company name Value (US$m)

Deal count

1 The Carlyle Group 15,495 20

2 Blackstone Group 8,980 15

3 The Riverside Company 0 13

4 Kohlberg Kravis Roberts & Co 2,858 11

5 Sun Capital Partners 569 10

6 Oaktree Capital Group 7,151 8

7 Warburg Pincus 2,313 8

8 Audax Private Equity Group 124 8

9 H.I.G. Capital 47 8

10 TPG Capital 4,370 7

11 Vista Equity Partners 2,501 7

12 GS Capital Partners 11,333 6

13 Advent International 7,339 6

14 Wynnchurch Capital 169 6

15 Arsenal Capital Partners 161 6Source: mergermarket

Rank

Q1-Q3 2012 Company name Value (US$m)

Deal count

1 Draper Fisher Jurvetson 1,948 12

2 The Carlyle Group 10,195 10

3 Battery Ventures 830 10

4 Kohlberg Kravis Roberts & Co 10,114 9

5 Intel Capital 1,127 9

6 Audax Private Equity Group 124 9

7 Sun Capital Partners 98 9

8 Kleiner, Perkins, Caufield & Byers 3,962 8

9 TA Associates 931 8

10 The Riverside Company 70 8

11 GS Capital Partners 10,620 7

12 General Atlantic 6,567 7

13 Bain Capital 6,075 7

14 Benchmark Capital 1,619 6

15 Bessemer Venture Partners 1,056 6Source: mergermarket

ACTIVITY TABLE OF PRIVATE EQUITY FIRMS ON NORTH AMERICAN BUYOUTS

ACTIVITY TABLE OF PRIVATE EQUITY FIRMS ON NORTH AMERICAN EXITS

The private equity buyout activity tables by value and volume are based on private equity firms advising the bidder on buyout deals where the dominant geography of the target company is US or Canadian. The tables by value and volume have been run from 01-Jan-12 to 30-Sep-12 and exclude lapsed and withdrawn deals.

The private equity exit activity tables by value and volume are based on private equity firms advising the vendor on exit deals where the dominant geography of the target company is US or Canadian. The tables by value and volume have been run from 01-Jan-12 to 30-Sep-12 and exclude lapsed and withdrawn deals.

26

NORTH AM

ERICA

Monthly M&A Insider

TREND GRAPHS

NORTH AMERICAN M&A QUARTERLY TREND

0

100

200

300

400

500

600

Q312*

Q212

Q112

Q411

Q311

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Valu

e (U

S$bn

)

Total value Mid-market value

Num

ber of deals

0

200

400

600

800

1,000

1,200

1,400

1,600

Total volume Mid-market volume

0

50

100

150

200

250

Q312*

Q212

Q112

Q411

Q311

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Valu

e (U

S$bn

)

Buyout value Exit value

Num

ber of deals

Buyout volume Exit volume

0

50

100

150

200

250

300

350

NORTH AMERICAN M&A ANNUAL TREND NORTH AMERICAN M&A ANNUAL PRIVATE EQUITY TREND

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

YTD 2012*201120102009200820072006

Total value Mid-market value

Num

ber of dealsValu

e (U

S$bn

)

0

1,000

2,000

3,000

4,000

5,000

6,000

Total volume Mid-market volume

0

50

100

150

200

250

300

350

400

450

500

YTD 2012*201120102009200820072006

Valu

e (U

S$bn

)

Buyout value Exit value

Num

ber of deals

Buyout volume Exit volume

0

200

400

600

800

1,000

1,200

NORTH AMERICAN M&A QUARTERLY PRIVATE EQUITY TREND

27

NORTH AM

ERICA

Monthly M&A Insider

TREND GRAPHS

NORTH AMERICAN M&A SECTOR BREAKDOWN Q3 2012

VALUE VOLUME

6.5%

24.5%

13.6%

15.0%

12.2%

6.8%

4.7%

3.4%

2.0%

1.9%

1.9%

5.1%

1.6% 0.7%

Industrials & Chemicals

Financial Services

Energy, Mining & Utilities

Consumer

Pharma, Medical & Biotech

Technology

Business Services

Media

Telecommunications

Defence

Real Estate

Transportation

Leisure

Construction

10.8%

8.9%

11.9%

13.0%

14.2%

0.9%0.7%

0.9% 2.6% 2.3%0.5%

4.6%

2.2%

9.1%

17.5% Industrials & Chemicals

Financial Services

Energy, Mining & Utilities

Consumer

Pharma, Medical & Biotech

Technology

Business Services

Media

Telecommunications

Defence

Real Estate

Transportation

Leisure

Construction

Agriculture

NORTH AMERICAN M&A DEAL SIZE BREAKDOWN

VALUE VOLUME

0

10

20

30

40

50

60

70

80

90

100

2012*201120102009200820072006

<US$250m or undisclosed value

US$251m-US$500m

US$501m-US$2,000m

US$2,001m-US$5,000m

>US$5,001m

52.8%

14.7%

16.8%

6.2%

9.5%

43.5%

18.8%

21.5%

6.5%

9.6%

49.1%

14.0%

17.4%

7.3%

12.2%

58.8%

13.3%

13.2%

5.5%

9.2% 12.6%

9.7%

27.7%

18.0%

32.0%36.9%

21.4%

21.0%

8.9%

11.8%

24.3%

25.1%

29.9%

9.3%

11.4%

Perc

enta

ge

75

80

85

90

95

100

2012*201120102009200820072006

1.1%

1.5%

5.3%

5.3%

86.9%

1.1%

1.8%

6.2%

5.3%

85.6%

0.9%

3.7%

4.1%

90.6%

1.0%

3.4%

3.8%

91.0%

87.4%

5.3%

5.6%

1.1% 1.4%

4.9%

5.3%

87.6%

0.7% 0.7% 0.6% 0.7%

1.6%

6.4%

5.5%

85.9%

0.6%

<US$250m or undisclosed value

US$251m-US$500m

US$501m-US$2,000m

US$2,001m-US$5,000m

>US$5,001m

Perc

enta

ge

28

NORTH AM

ERICA

Monthly M&A Insider

NORTH AMERICAN SECTOR ANALYSISSector Q3 2012 Q3 2011 % change

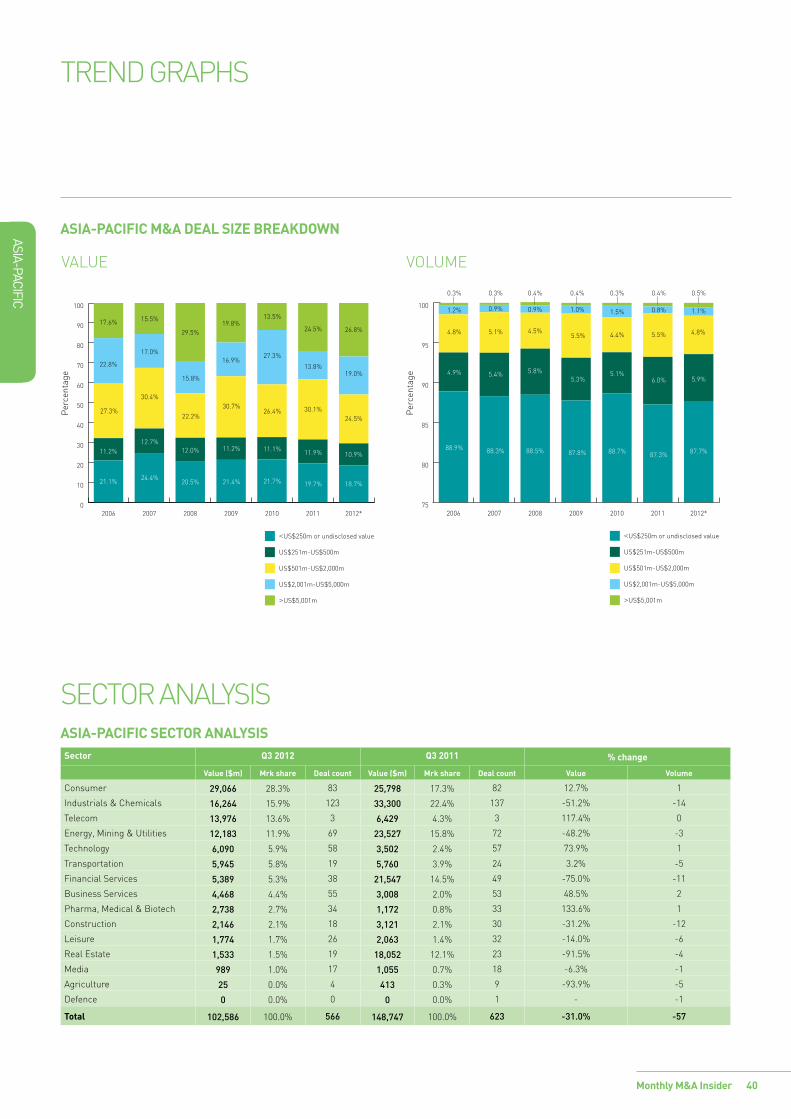

Value ($m) Mrk share Deal count Value ($m) Mrk share Deal count Value Volume

Energy, Mining & Utilities 57,785 24.5% 95 36,363 17.4% 85 59% 12%

Industrials & Chemicals 32,085 13.6% 154 47,517 22.7% 188 -32% -18%

Consumer 35,331 15.0% 78 4,325 2.1% 90 717% -13%

Financial Services 15,381 6.5% 80 9,843 4.7% 114 56% -30%

Pharma, Medical & Biotech 28,711 12.2% 105 53,277 25.5% 112 -46% -6%

Technology 15,985 6.8% 114 17,106 8.2% 149 -7% -23%

Business Services 11,975 5.1% 125 17,271 8.3% 131 -31% -5%

Media 11,166 4.7% 40 2,552 1.2% 32 338% 25%

Transportation 4,497 1.9% 23 1,653 0.8% 15 172% 53%

Real Estate 4,543 1.9% 8 927 0.4% 5 390% 60%

Leisure 3,731 1.6% 20 1,693 0.8% 22 120% -9%

Telecommunications 8,070 3.4% 8 15,947 7.6% 13 -49% -38%

Defence 4,803 2.0% 6 86 0.0% 4 5485% 50%

Construction 1,621 0.7% 19 670 0.3% 23 142% -17%

Agriculture 0 0.0% 4 0 0.0% 2 - 100%

Total 235,684 879 209,230 985 13% -11%

SECTOR ANALYSIS

ASIA-PACIFIC

A MERGERMARKET M&A REPORT ON

Monthly M&A Insider 29

ASIA-PACIFIC

Asia regaining its sheen?Growing economic uncertainties, coupled with a general slowdown in economic growth have put the brakes on large deals across the globe. The Asia-Pacific region, however, has bucked the downward trend. Deals worth over US$5bn have grown as a proportion of total deal value for two successive years to hit 25.6%, the highest level since 2008. Private equity buyout and exit deal values have also grown for the past two quarters, which may be interpreted as a vote of confidence in Asia’s growth prospects. While fears of a slowdown in the region’s export-oriented economies continue to linger, these rises attest to the faith acquirers have placed in the region. Rising incomes, along with favourable demographics and sluggish growth in other regions are likely to cement Asia’s status as the focal point of global M&A activity in the near future.

Unabated Japanese outbound activityIndia’s Infrastructure sector received a big shot in the arm in the shape of the Japanese government’s acquisition of a US$4.5bn stake in the Delhi Mumbai Industrial Corridor. The project, slated to cost US$90bn, will rely heavily on low-interest loans and technical assistance from the Japanese government. This increased assertiveness on the part of Japanese bidders is also underscored by the fact that three of the top 10 largest deals featuring Asian companies involved Japanese bidders. Japanese corporations have embarked on a relentless drive to snap up stable, high profile counterparts in developed countries and gain headway in other emerging economies as they grapple with a mature home market. This is also borne out by phenomenal growth in overseas acquisitions by Japanese firms, which hit an all-time high last year and have attained 82% of that level during the first three quarters of 2012.

Chinese outbound activityChinese bidders accounted for two of the largest outbound deals to emanate from the region. Li Ka Shing’s tryst with

British utilities continued after he sought to add Wales & West Utilities to the Northumbrian Water Group he snapped up last year. The desire to secure high, stable yields will prompt Asian bidders to scour the developed world for utility providers. More striking, however, was CNOOC’s bid for oil major Nexen. It represented the largest ever bid for a foreign corporation to emerge from China at a time when Chinese state-owned enterprises are being scrutinised by the US government and regulatory bodies. The timing of the acquisition is even more significant, as it comes before leadership transitions in both China and the US. State-owned corporations in China have been loath to make big forays in foreign markets in light of the disastrous US$3bn investment in Blackstone by CIC in 2007. Thus, making such a large bid amid political and economic uncertainties reflects China’s desire to maintain high economic growth at all costs. This is also lent credence by the fact that Chinese outbound activity reversed three successive quarters of decline to post a total of US$28.1bn, the highest quarterly tally since 2004.

Consumer sector regaining favour? The consumer sector notched up US$29.1bn-worth of deals this quarter, the highest quarterly haul ever for the region on mergermarket’s record. This mind-boggling figure was attained courtesy of competing bids for Asia-Pacific Breweries. Heineken’s determination to acquire the target came in the wake of attempts to expand its footprint in one of the fastest growing consumer regions in the world. It also underscored the fiscal clout of Asian bidders vis-a-vis their counterparts in more developed economies. As the region continues to develop, Asian corporations from outside China and Japan continue to amass substantial resources, which they will use to deter competitors from encroaching on their turf and making inroads in other fast-growing parts markets. In this respect, this tug-of-war between Heineken and Thai billionaire Charoen Sirivadhanabhakdi may set the template for future interactions between firms from developed and emerging economies who have their sights on the same targets.

M&A ACTIVITY IN THE ASIA-PACIFIC REGION DURING THE THIRD QUARTER OF THE YEAR WITNESSED A SLIGHT DECREASE, BUT FARED REMARKABLY WELL CONSIDERING THE GLOOMY OUTLOOK FOR OTHER REGIONS. A TOTAL OF 566 DEALS WORTH US$102.6BN WERE RECORDED IN THE REGION BETWEEN JULY AND SEPTEMBER, A TALLY VIRTUALLY UNCHANGED BY VALUE AND 10% LOWER BY VOLUME COMPARED TO THE PREVIOUS QUARTER. A RAFT OF SIGNIFICANT ACQUISITIONS WAS ANNOUNCED DURING THIS PERIOD, DEALS WHICH MAY BE THE HARBINGER OF FUTURE M&A ACTIVITY IN THE REGION.

30

ASIA-PACIFIC

Monthly M&A Insider

DEAL OF THE QUARTER

Deal summary

Announced: 23-Jul-12 Deal value: US$17,654m

Nexen Inc(NXY), an Alberta corporation, has signed a definitive agreement to be acquired by CNOOC (883), a Beijing corporation. The board of directors of both companies have approved the merger.

TERMS:• The offer provides a premium of 62% based on NXY’s

closing share price on 20-Jul-12 of US$17.06.

• The implied equity value of the transaction is approx. US$14,556.74m.

• If approved by the holders of preferred shares in a separate class vote, CNOOC Limited will acquire the outstanding preferred shares of Nexen for a purchase price of CAD26.00 (US$27.5) per share in cash, plus any dividends accrued but unpaid at the time of closing.

• If a superior offer were to emerge for NXY, the company would be required to give CNOOC at least four business days to make adjustments to its current offer before NXY’s board of directors could effect a change of recommendation of the deal.

FINANCING• The transaction will be funded by CNOOC Limited’s

existing cash resources and external financing.

TERMINATION/INDUCEMENT FEE• US$425m, or 3% based on the implied equity value of the

deal. The per-share increase required to cover this fee in a superior offer would be US$0.8. A Reverse Termination Fee of US$425m will be payable by CNOOC to NXY in the event the Arrangement Agreement is terminated solely as a result of the PRC Approvals having not been obtained.

RATIONALE• The acquisition of Nexen enhances CNOOC Limited’s

presence in Canada, Nigeria and the Gulf of Mexico, adds a significant presence in the UK North Sea and diversifies CNOOC Limited’s growth platform.

POST DEAL DETAILS• CNOOC Limited plans to establish Calgary as the head

office of its North and Central American operations. This head office will be responsible for operating and growing Nexen’s assets in North and South America, Europe and West Africa and CNOOC Limited’s portfolio in Canada, the US and Central America.

• CNOOC Limited intends to retain Nexen’s current management team and employees.

• CNOOC Limited intends to list its common shares on the TSX.

EXPECTED COMPLETION• The transaction is expected to close in the fourth quarter

of 2012.

CONDITIONS• HSR (USA).

• CA (Canada).

• ICA (Canada).

• CFIUS (USA).

• EU (Europe).

• MOFCOM (China).

• NDRC (China).

• SASAC (China).

• OFT (UK).

• Competition Commission (UK).

• NXY EGM (Two thirds of affirmative vote required to approve).

UPDATE:• Awaits update.

31

ASIA-PACIFIC

Monthly M&A Insider

DEAL OF THE QUARTER

mergermarket/dealReporter Intelligence

23-Jul-12 Nexen to be acquired by CNOOC for US$15.1bn

24-Jul-12 Nexen/CNOOC deal subject to review under Investment Canada Act, Minister Paradis confirms

24-Jul-12 CNOOC has no plan to spin-off overseas assets into separate listing

24-Jul-12 CNOOC does not see regulatory hurdles in US for Nexen deal

25-Jul-12 Nexen: CNOOC considering bond offering to fund its offer

29-Jul-12 CNOOC may borrow billions of US dollars in 2013 to fund Nexen’s bid

31-Jul-12 CNOOC merger with Nexen faces opposition from US lawmaker Ed Markey over royalties

02-Aug-12 CNOOC to raise bridge and long-term loans from overseas lenders to back Nexen bid

07-Aug-12 CNOOC to pay LIBOR +150bp on bridge loan to support Nexen bid

10-Aug-12 CNOOC to delay dispatch of circular in relation to Nexen bid to a date on or before 13 December

24-Aug-12 Govt of Canada will weigh issues such as public sentiment, reciprocity as it considers whether or not to allow CNOOC to buy Nexen

03-Sep-12 CNOOC to raise US$10bn via bank loans and bonds to finance Nexen deal

11-Sep-12 CNOOC secures US$5bn - US$6bn one-year loan for Nexen bid

12-Sep-12 CNOOC submits formal application with Committee of Foreign Investment to review Nexen takeover bid

19-Sep-12 Govt of Canada's junior finance minister receives lots of negative feedback over CNOOC's bid for Nexen

21-Sep-12 Nexen shareholders approve plan of arrangement with CNOOC Limited and CNOOC Canada Holding Ltd

26-Sep-12 Top oil sector execs largely support CNOOC-Nexen deal but still want govt to implement rules to protect Canadian ownership of large oil sands entities

27-Sep-12 U.S. Congress members want Obama administration to force CNOOC to divest five Gulf of Mexico leases before getting approval to buy Nexen

10-Oct-12 New Democratic Party of Canada formally rejects CNOOC's bid for Nexen

Advisers

Target/Seller Bidder

Financial Goldman Sachs; RBC Capital Markets; Sumitomo Mitsui Financial Group

Financial BMO Capital Markets; Citigroup

Legal Blake, Cassels & Graydon; Osler Hoskin & Harcourt; Paul Weiss Rifkind Wharton & Garrison

Legal Cleary Gottlieb Steen & Hamilton; Davis Polk & Wardwell; Herbert Smith; Morrison & Foerster; Stikeman Elliott

PR - PR Pelham Bell Pottinger

Exit multiples – Y/E 31-Mar-12 Premium analysis

Multiples Value (US$m) Offer price per share (US$) 27.5

Revenue 2.7 6,469 1 day before 17.06

EBITDA 4.5 3,940 1 month before 15.83

EBIT 8.7 2,027 1 day after 26

Earnings 22.2 697 Pre-rumour -

32

ASIA-PACIFIC

Monthly M&A Insider

DEAL OF THE QUARTER

Bidder

China National Offshore Oil Corporation Ltd

Headquarters: No 25 Chaoyangmenbei Main StreetDongcheng DistrictBeijing, China

Sector: Energy

Description: China based company engaged in the exploration, development, production and sales of crude oil and natural gas and other petroleum products

Target

Nexen Inc

Headquarters: 801 7th Avenue S WCalgary T2P 3P7Alberta, Canada

Sector: Energy; Chemicals and materials

Description: Canada based energy company engaged in oil and gas, Syncrude, energy marketing and chemicals business

33Monthly M&A Insider

ASIA-PACIFIC

TOP 10 ASIA-PACIFIC ANNOUNCED DEALS OF Q3 2012Announced Bidder company Target company Target dominant

sectorSeller company Exit multiples (x) Bid premia

1-day beforeDeal value

(US$m)Revenue EBITDA P/E

23-Jul-12 Nexen Inc China National Offshore Oil Corporation Ltd

Energy, Mining & Utilities

2.7 4.5 22.2 61.2% 17,654

22-Aug-12 China Telecommunication Corporation (certain CDMA Network assets)

China Telecom Corporation Limited

Telecom China Telecommunications Corporation

4.6 8.9 (loss) n/a 13,307

13-Sep-12 Fraser & Neave Limited (69.64% stake)

TCC Group Consumer 2.7 13.4 21.5 4.3% 10,134

20-Jul-12 Asia Pacific Breweries Limited (58.1% stake)

Heineken NV Consumer 4.9 21.3 46.8 27.4% 6,593

23-Aug-12 Delhi Mumbai Industrial Corridor Development Corporation Limited (26% stake)

Government of Japan; and Japan Bank for International Cooperation

Transportation - - - n/a 4,500

12-Jul-12 Aegis Group Plc Dentsu Inc Media 2.9 15.2 36.9 48.0% 4,345

20-Jul-12 Hebei Shougang Qian'an Iron and Steel Co Ltd

Beijing Shougang Co Ltd

Industrial and Chemicals

Shougang Group Corporation

0.9 9.9 23.5 n/a 4,168

29-Aug-12 Goodman Global Inc Daikin Industries Ltd Industrial and Chemicals

Hellman & Friedman LLC 1.8 - - n/a 3,700

26-Jul-12 CFAO SA (29.8% stake) Toyota Tsusho Corporation

Business Services

PPR SA 0.8 8.5 19.0 -0.8% 3,189

25-Jul-12 Wales & West Utilities Limited

Cheung Kong Infrastructure Holdings Limited; Power Assets Holdings Limited ; Li Ka Shing Foundation Limited; and Cheung Kong (Holdings) Limited

Energy, Mining & Utilities

Industry Funds Management Pty Ltd; Canada Pension Plan Investment Board; Macquarie Group Limited; AMP Capital Investors Limited; and Codan Trust Company Limited

5.6 14.3 (loss) n/a 3,030

Based on announced deals, including lapsed and withdrawn bids Based on dominant geography of target company being Asia-Pacific Data correct as of 09-Oct-12

Source: mergermarket

TOP DEALS & EXPECTED DEALS

34

ASIA-PACIFIC

Monthly M&A Insider

Situation Target company Sector Potential bidder company Financial adviser to bidder (B); target (T); seller (S)

Seller company

Market cap/ est. value (US$m)

Comments

Expected deal 7 Days Group Holdings Limited

Leisure The Carlyle Group LLC; Sequoia Capital China; and Mr Boquan He (Private Investor)

590 7 Days Group Holdings Limited received an offer from the consortium led by Carlyle Group and Sequoia Capital China estimated to US$4.233 per share and US$12.7 per ADS in Sep 2012.

Expected deal Focus Media Holding Ltd Media FaountainVest Partners; The Carlyle Group LLC; CITIC Capital Partners; CDH Investments; and China Everbright Limited