Effective management of sea cucumber fisheries and the ...

182

A study of sea cucumber fisheries and bêchedemer production in the western South Pacific Effective management of sea cucumber fisheries and the bêche-de-mer trade in Melanesia: bringing the industry under rational control Final Report April 2013 A report prepared by Nautilus Consultants on behalf of the Secretariat of the Pacific Community

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Effective management of sea cucumber fisheries and the ...

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Effective management of sea cucumber fisheries and the bêche-de-mer trade in Melanesia: bringing the industry under rational control

Final Report

April 2013

A report prepared by Nautilus Consultants

on behalf of the Secretariat of the Pacific Community

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Team Leader and lead author Crick Carleton Co-‐authors John Hambrey Hugh Govan Paul Medley in-‐country correspondents Jeff Kinch (PNG) Len Rodwell (SOL) Francis Hickey (VAN) Ravinesh Ram (FIJ) Poasi Ngaluafe (TON)

Nautilus Consultants Ltd

www.nautilus-‐consulants.co.uk crick@nautilus-‐consultants.co.uk

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Contents

Executive Summary ......................................................................................................................... v

1 Introduction ........................................................................................................................... 1

1.1 Context .................................................................................................................................. 1

1.2 The study brief ....................................................................................................................... 2

1.3 Report layout ......................................................................................................................... 3

2 An introduction to the sea cucumber industry ........................................................................ 4

3 Analysing regional BdM production ........................................................................................ 9

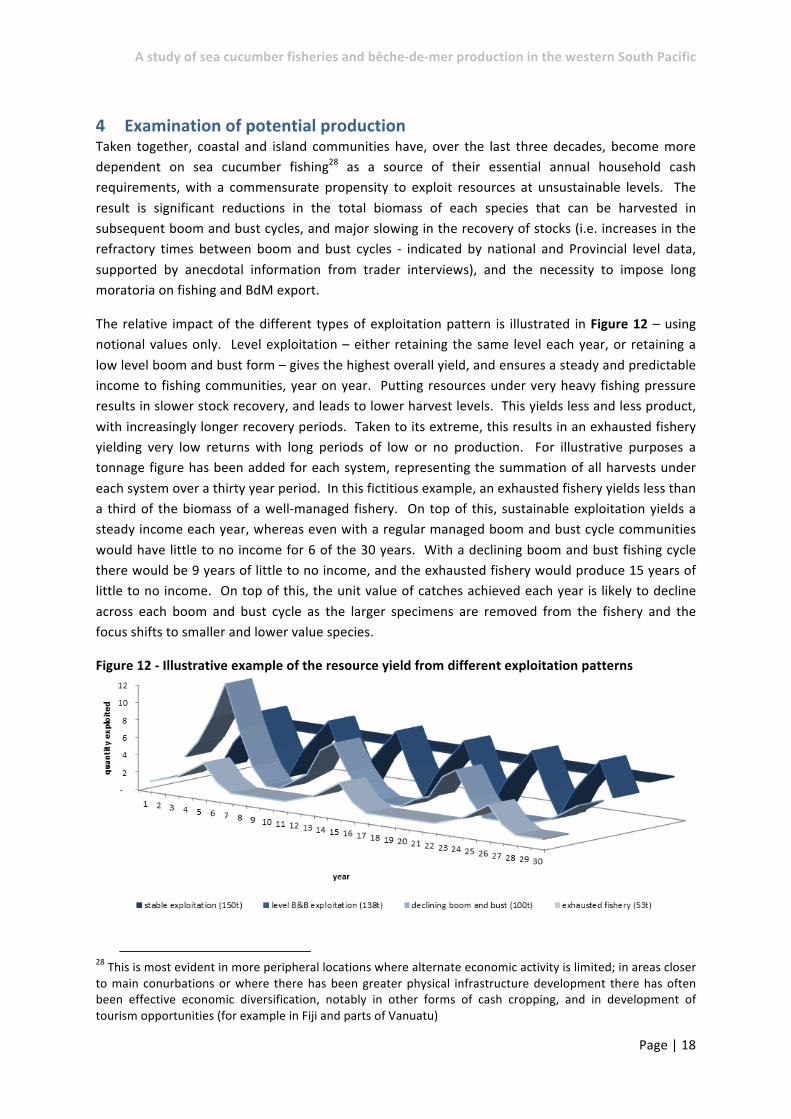

4 Examination of potential production ..................................................................................... 18

5 Approaches to the management of sea cucumber fisheries ................................................... 24

5.1 Status and pressures ............................................................................................................ 24

5.2 Management response ........................................................................................................ 24

5.3 Stock assessment ................................................................................................................. 26

5.4 Regulations and potential harvest control rules (HCRs) ...................................................... 27

5.5 Broader measures ................................................................................................................ 30

5.6 Implementation ................................................................................................................... 30

6 Fiscal, economic and trade measures ..................................................................................... 32

6.1 Informing policy ................................................................................................................... 32

6.2 Resource access ................................................................................................................... 35

6.3 Production and export caps ................................................................................................. 38

6.4 Cost recovery and economic incentives .............................................................................. 40

6.5 Monitoring, control and surveillance, and measures to discourage IUU fishing and trade 43

7 A sea cucumber / BdM sector management framework ........................................................ 45

7.1 Sea cucumber management experience ............................................................................. 45

7.2 Reinforcing management through trade information ......................................................... 47

7.3 Establishing precautionary export caps and, by extension, target catches ......................... 48

7.4 Management framework conclusions and recommendations ............................................ 49

8 Opportunities for regional cooperation ................................................................................. 54

9 References ............................................................................................................................ 56

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Annex 1 – Country BdM sector profiles Annex 2 – Country trade and data systems Appendices

Appendix 01 Terms of Reference Appendix 02 Field work schedule Appendix 03 List of interviewees Appendix 04 Common names Appendix 05 BdM prices Appendix 06 Evolution of BdM prices Appendix 07 Key characteristics of BdM Appendix 08 Country exports Appendix 09 Illustration of valuation of BdM exports under different assumptions Appendix 10 Indices of encounterability Appendix 11 15 yr average production by Province by species Appendix 12 15 yr average species mix Appendix 13 15 yr average wet weight Appendix 14 Shallow water areas and other provincial stats Appendix 15 15 yr average value Appendix 16 Main species, by value, per province Appendix 17 Prelim stock assessment Appendix 18 Priority roles for CBRM Appendix 19 Description of processing and trade structure Appendix 20 Overview of BdM industry Appendix 21 Sources of quantitative information on species, volume and values

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | v

Executive Summary

The bêche-‐de-‐mer (BdM) industry Coastal and island communities in many of the Pacific Islands Countries and Territories (PICTs) derive significant cash income from the harvesting of sea cucumber and its transformation to bêche-‐de-‐mer (BdM). These dried products are consolidated in-‐country by BdM traders who export consignments to the main Asian market entrepôts.

Demand for BdM continues to grow in line with the growth of China’s and other Asian economies, but supplies cannot keep pace with this demand, and a “boom and bust” pattern of exploitation is no longer appropriate to the needs of this market. With tens of thousands of isolated coastal and island households dependent on this trade for a significant proportion of their regular cash income requirement there is also a strong political rationale to improved management of these fisheries and this trade.

The study This study is focused on the BdM industries in four Melanesian countries and one Polynesian country – Papua New Guinea (PNG), the Solomon Islands (SOL), Vanuatu (VAN), Fiji (FIJ) and Tonga (TON). The study is part of an initiative by ACIAR1 implemented by SPC2, and responds to concerns raised by Melanesian country leaders through the Melanesian Spearhead Group (MSG), and more broadly by the Heads of Fisheries of PICTs through the SPC.

The South Pacific BdM trade is a multi-‐million dollar marine product trade; in capture fishery terms second only to the significantly larger tuna trade. There is wide recognition that the persistent over-‐exploitation of sea cucumber resources is substantially depressing the overall potential of this trade. This situation is being further exacerbated by a lack of transparency in the management and practice of this trade and, where moratoria have been imposed, to significant Illegal, Unreported and Unregulated (IUU) fishing and trading activity. This has provided fertile ground for petit corruption, and where moratoria are in place has required very significant increases in the resources that governments have had to deploy to keep a lid on illegal activity.

Accordingly this study is in the form of a scoping study to identify courses of action that can be taken forward. Its focus is five-‐fold:

• Profiling of the current and historic structure, operation and scale of sea cucumber harvesting and BdM production and export in the five countries under study;

• Estimation of the scale of revenues being foregone as a result of persistent over-‐exploitation and the “boom and bust” nature of these fisheries;

• Identification of fiscal and trade tools that could be used to better control the production and trade of BdM;

1 The Australian Centre for International Agricultural Research 2 The Secretariat of the Pacific Community

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | vi

• Identification of how management regimes could be strengthened to encourage the greater sustainable exploitation of these fragile resources and to boost income to peripheral coastal and island communities; and

• Identification of the potential for regional cooperation3 in strengthening management and increasing the revenues that can be derived from these fisheries and the trade in BdM.

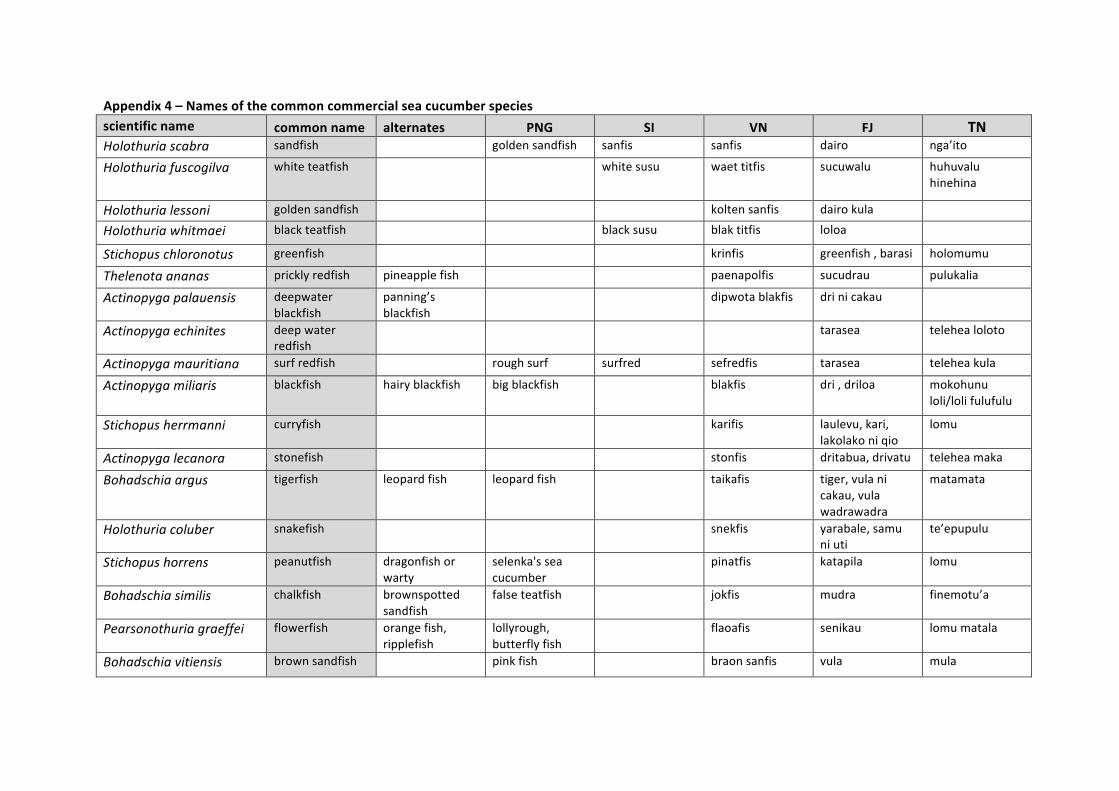

Production Sea cucumbers comprise a large and diverse group of organisms that are found in most marine environments, and are typically deposit feeders, extracting biological nutrients coating sediment or other surfaces; some are plankton feeders. Of 1400 species known to science some 60 species are widely traded from Pacific waters. Some 35 of these species of sea cucumber are found in the waters of Melanesia, of which 21 species make up over 90 per cent of the volume of trade of BdM from this area, and eight of these species make up over seventy-‐five per cent of the value of such trade – and at a more local level, usually three or four of these species make up three-‐quarters of value.

Different sea cucumber species command quite different prices, and the combination of the state of exploitation of the local resource and the value of BdM derived from that resource dictates fishing patterns and effort, with fishers tending to focus on the most cost-‐effective resource / species at any given time. The two main fishing methods are reef gleaning and free diving. It is the free divers that have greater control over the direction of their effort; reef gleaning activity – whether for shellfish, sea cucumber or octopus, etc. – is much less discriminate.

We have compiled export data from each of the countries, providing a long-‐run series for BdM exports as a generic category and shorter-‐run series for exports by species. Where data have allowed, we have also compiled production series by species by Province or District.

Figure 1: Exports of BdM from the five countries under study, 1986 to 2012, tonnes dried weight

Source: Fisheries Department statistics -‐ PNG, SOL, VAN, FIJ, TON – summarised in Appendix 8

3 With a particular focus on the member countries of the Melanesian Spearhead Group (MSG)

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | vii

From the available data it is clear that in a general sense the recent BdM trade developed dramatically from a low level across the 1970s to an early first peak in the late 1980s. This was followed by a distinct fall-‐off in production, followed by a second peak in the late 1990s, early 2000s. Nesting below these overall trends are the independent “boom and bust” cycles of the local fisheries, none of which are exactly the same.

Taken together, in 2006, regional (the five countries under study) exports of BdM were about 930 t, representing a current buy-‐in value of some USD 15.8 million. In subsequent years the fisheries of PNG, the Solomon Islands and Vanuatu were closed to allow stock recovery, and to compensate for previous excessive harvests. The Tonga fishery was opened, but was all but exhausted by the end of 2012. The Fiji fishery has remained open, but harvests have been well below those achieved in the 1980s and 1990s. In the years 2007 to 2012, the five countries under study actually exported an average of some 600 t of BdM per year, whereas under precautionary management we suggest this could have been closer to 1,000 t per year, and with a significantly higher value.

Peak production is not a very good indication of production capacity. Instead we have taken a fifteen year average as being more representative (illustrated). We have also sought to determine a “signature” species mix by given area – based on statistical data, where available, but otherwise extrapolated from quantitative and anecdotal evidence.

Figure 2 -‐ Consolidated 15-‐year (1996-‐2012) average export volume, by species (t BdM dried weight) & estimated current in-‐country purchase value (USD millions) for the five countries under study

Source: national Fishery Department statistics

Note – value is the price paid by an exporter to a producer for finished product

We have also estimated the current value of a harvest of this scale and species mix at the prices typically paid by in-‐country traders for finished dried product. Summed across the fifteen year time

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | viii

series, but using current purchase prices4, this translates into notional revenue generation of some USD 160 million5.

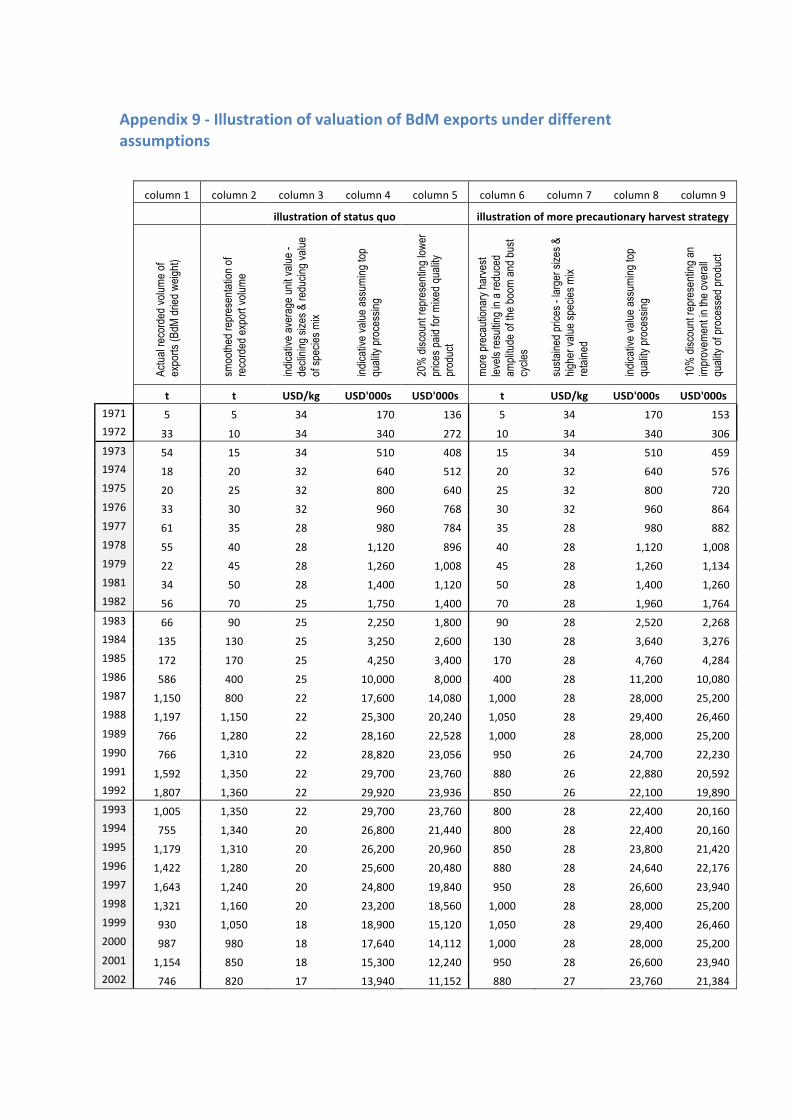

We estimate that if these resources had been managed on a more precautionary basis that moved exploitation away from the “boom and bust” cycle, medium-‐run revenues derived from the BdM trade would be as much as double those that have been achieved -‐ up to USD 330 million at current values. This is based on the reversing of various characteristics that plague current production:

• Serial over-‐exploitation of resources means that the stocks of each species are below the size of stock that would yield Maximum Sustainable Yield (MSY) and/or Maximum Economic Yield (MEY) – which is likely to impact negatively on reproduction and stock recruitment, and thus on stock biomass

• Because fishers focus on harvesting the largest individuals of each species available to them, and most stocks have been over-‐exploited, there is a preponderance of smaller sized individuals in the populations of each species – a truncated population structure – which translates into lower value BdM

• Because greater fishing effort tends to be focused on these higher value species, and the stocks of these species are not given sufficient time to recover, the average size of individuals available tends to steadily decrease over time – a shift in modal value to a smaller size – and thus command lower values

• As the availability of high value species decreases, so effort on lower value species increases – as a result the relative value of BdM exports tends to decrease over time as the mix of species sold tends towards lower value species

• Process management and the general quality of BdM processing are not good; greater care and attention is given to processing the high value species such as white teatfish and sandfish, but overall up to 30 per cent of value is lost due to poor processing.

In the medium term it is projected that more precautionary management would result in sea cucumber harvests and BdM production equivalent to the average of recent harvests, but this would be achieved each and every year, the mix would shift towards higher value species, and the value of individual BdM would be improved because more sea cucumbers would be harvested at larger sizes. In addition, if greater care and attention were paid to the quality of processing, a further uplift in value of between 10 and 20 per cent could be achieved (i.e. in practice it would not be possible to reverse all losses due to poor processing).

In the longer term, better management of each species stock will allow the rebuilding of stocks at the local level, and this in turn will allow larger volumes of each species to be harvested on a sustainable basis.

Under a “boom and bust” exploitation system revenues from sea cucumber harvesting go up and down between years, and are normally accompanied by serial over-‐exploitation. Accordingly revenues to the communities go up and down and are unpredictable. In most of the countries under study this has resulted in fisheries having to be closed for multiple years (5-‐10 years) – when

4 Prices derived from price data provided by traders interviewed, from their price lists, and from government 5 Reflecting changes over time in terms of species mix and average size of animals harvested as fisheries follow the boom and bust cycle

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | ix

communities receive no BdM revenues at all. Under a sustainable management regime, revenues are maintained year on year.

The overall recommendation arising from the study is that every effort should be made to move from a “boom and bust” basis of exploitation to a more precautionary and sustainable steady state pattern of exploitation. This requires that stocks be allowed to recover, and that any subsequent exploitation needs to be at more precautionary levels. The following actions are proposed to achieve this.

Improving control and enforcement Current management regimes include many relevant and appropriate controls, but application is inconsistent, and thus ineffective (either stakeholders are not aware of the standards they should be upholding, or the ruling standards are not enforced). As a result, monitoring systems do not yield the data that could better inform the appropriate harvest levels. The failure to utilise available data for management purposes means that the data is under-‐valued, and thus less effort is used to collect it and to ensure that it is accurate. And even where data is good, it is not acted upon. A failure to control the levels of exploitation, or to set exploitation levels at sustainable levels, has resulted in persistent over-‐exploitation, which in turn has resulted in the necessity of closing fisheries to allow the stocks to recover. Where fisheries have been closed, the intended impact of such action has been undermined by substantial increases in IUU fishing and export. A number of actions are proposed to reverse these conditions.

Combating illegal activity

Recommendation 167 -‐ As a matter of management objective, sea cucumber fisheries and BdM supply chains should be managed in such a way as to preclude the need to close a fishery; closing a fishery incurs significant additional monitoring, control and surveillance (MCS) costs, and forces the trade underground.

Recommendation 2 -‐ Use of Underwater Breathing Apparatus (UBA) gear should continue to be outlawed, and management resources should be focused on achieving full compliance with this; the primary target of such fishing is white teatfish, and opportunities for identifying UBA caught white teatfish through the supply chain (on the basis of local intelligence) should be explored.

Data

Recommendation 3 -‐ As part of efforts to remove the conditions where illegal activity and petit corruption can thrive, each country should make clear and unambiguous annual declarations on industry performance over the preceding period, and on government expectations and regulatory / administrative framework governing industry performance for the subsequent period.

6 Note: in the following, a couple of recommendations are repeated under different section heads so as to maintain the logic of arguments presented 7 Note: a word search on “Recommendation X” will take the reader to the point in the report where the issue is discussed in more detail

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | x

Recommendation 4 -‐ It is normally a condition of export, buyer and processor licenses that data should be provided to fishery managers to assist in management; these conditions should be enforced and systematically collected, collated and analysed.

Recommendation 5 -‐ Data collected by Customs and Fisheries Departments should, within the limits of the law and commercial confidentiality, be shared one with the other.

Recommendation 6 -‐ Data provision should as a minimum link to the Province of harvest.

Recommendation 7 -‐ Export packing lists should nominate the species and average size of product in each bag, and this should be verified by sample weighings at point of inspection prior to shipment; these data to be used to monitor changes in the size distribution of species harvested and exported and for use in assessing stock condition and strength.

Cost recovery

Recommendation 8 -‐ A valid commercial invoice, nominating fob value8 per species and product size / quality should be required as part of export documentation, and subject to verification – it is this value that is used in the calculation of an export levy9.

Recommendation 9 -‐ Exporters should also routinely provide Fisheries Departments, in confidence, with a schedule of prices used in the purchase of finished BdM from buyers and fishermen – this provides an alternate basis for calculation of an export levy.

Recommendation 10 -‐ The cost of a BdM export license should be raised significantly to better reflect the value of this trade, recoup some of the costs of management, to discourage small-‐scale operators, and to discourage the practice of patronage within the sector10.

Recommendation 11 -‐ The eligibility criteria for export licenses should be narrowed and deepened to exclude operations where the risk of non-‐compliance is high – including greater scrutiny of the integrity and background of the principals and partners of the business owners.

Recommendation 12 -‐ The primary (i.e. excluding small-‐scale household and village based consolidators) BdM buyers and processors operating at a Provincial level should be required to hold a buyer / processor license, a condition of which requires the provision of monthly species based throughput data, including details of source fishery (already a requirement of license in some countries, already specified in database structures, but not consistently collated).

Management framework: the need for an adaptive management system The BdM Management Plans that are already in operation, and the revisions currently in draft, form a sound and coherent basis to sector management. Weaknesses in dissemination and compliance

8 The price at which the importer has agreed to buy the product from the exporter, expressed as fob (Free On Board) price 9 Note that revenues derived from export levies are channelled to general government revenues rather than to fisheries management 10 A corollary of this is that licensing authorities need to be more inquisitive as to where company funding comes from, and who controls (makes the decisions in) the company

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | xi

are evident, but the main shortcoming is the absence of any clear mechanism for adaptive management – decisions for future action that respond to the evidence from the effects of past action.

Central to this is the fact that managers do not have the wherewithal to assess stock size – only whether a particular resource is thought to be under-‐ or over-‐exploited. This greatly limits the advice they can give. The pragmatic response is thus to use a combination of tools that encourage conservative behaviour and moderate exploitation on the basis of the observed impacts of past behaviour, but more needs to be done in this area.

The following are the four key elements required in an effective management system for sea cucumber:

1. Engagement of resource users in contributing to the setting of overall national harvest targets and standard regulations; and developing and agreeing local harvest control rules in broad conformity with these national targets.

2. Incentives and disincentives to promote compliance at all levels, including thorough inspections and economic incentives at the point of export.

3. Information relating to the implementation of harvest control rules, and the impact on the stock, effectively monitored and analysed at local, provincial and national (export) level; and fed back into the management process.

4. Agreed response mechanisms at national and local level should data analysis suggest stock decline or improvement.

While some of these elements appear in existing national plans and frameworks, few countries have all of these elements in place.

Local harvest control rules might include, as well as implementation of existing minimum size restrictions, a restricted harvesting season, and protected areas / no-‐fishing zones or some combination of these; national / provincial harvest limits and rules might include provincial or national annual production / export quotas.

Incentives might include peer pressure at the local level, fines / confiscation of product at intermediate trade and export level, and graduated export levies, with higher rates for more valuable / vulnerable species.

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | xii

Stock status monitoring using trade data11 (an approach successfully explored as part of this study-‐ see Appendix 17) will be crucial to monitoring success and adjusting harvest control rules in an effective and timely manner in response to improved or declining stock health.

Gaining agreement on response mechanisms prior to their implementation should greatly facilitate implementation and reduce opportunities for corruption.

Recommendation 13 –Each government should ensure that all four key elements for an effective management system are in place and serve as the backbone for national sea cucumber management strategies and plans.

Recommendation 14 – Where engagement with stakeholders has not already been done a process of engagement should be undertaken to a) share understanding of the value of BdM and potential returns from a well-‐managed fishery; b) discuss the need for, and key elements of, an effective management system; c) agree on local harvest control rules compatible with those established at national level.

Information flow and data transfer

Recommendation 15 – As a contribution to improved transparency and public disclosure, government should prepare and publish (in English and relevant local languages) an annual compendium on BdM sector rules, performance, and expectations, and make this readily available to traders, intermediaries, fishermen, community leaders – using a wide range of media and dissemination routes.

Recommendation 16 -‐ Whilst it is recognised that the capacity of Provincial administrations to support industry management is limited, it is important that they play their part – through licensing, through data collation and analysis, and through industry contact; to this end, all principal Province based buyers / processors should be licensed, and license conditions should include the provision of monthly purchase information.

Recommendation 17 -‐ Compliance with Provincial quotas should be monitored through data provided at point of export, supported by purchase data provided at national and Provincial levels as conditions of license.

Recommendation 18 -‐ Fishing communities will necessarily be responsible for managing local sea cucumber exploitation, and should be supported in this task with the

11 More conventional species-‐based stock assessment modelling is difficult for sea cucumbers, since details of spatial distribution, growth rate and recruitment are not readily available. In the absence of conventional stock assessment modelling there is no clear consensus on stock recovery rates and what might constitute precautionary levels of fishing mortality. Whilst fishery independent surveys of resource density are widely used to assess under-‐ or over-‐exploitation, they cannot be readily converted to estimates of biomass (which would require multiplication of density figures by habitat area, but sea cucumber distribution is not narrowly limited by habitat type). Test modelling of production time-‐series data (export data), using a bio-‐economics sub-‐model to estimate likely changes in the underlying fishing effort, suggests that estimates of MSY and key stock management reference points can be derived, the impacts of different Harvest Control Rules (HCRs) can be assessed, and this information can provide a useful addition to any adaptive management regime.

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | xiii

development and dissemination of simple questionnaires12 (for measuring changes in average size of sea cucumbers, and capturing other stock status information – on a qualitative and quantitative basis).

Estimation of stock status and precautionary export caps that limit exploitation

Unfortunately, most stocks of sea cucumber in most parts of the countries under study are considered to be over-‐exploited -‐ hence the situation where it has been necessary to put in place moratoria across the region. As yet there is no tried and tested management system that can deliver long-‐term sustainable exploitation of this mixed species resource. The main reasons for this are that this a very valuable but also open access fishery, there are next to no barriers to entry to the fishery, it is difficult to define stocks (not least it is difficult to model and predict stock recruitment), it is difficult to measure stock condition, and it is difficult to predict the impact of management measures on future stock condition. Management using a handful of sensible measures as part of an adaptive management regime is the responsible and only way to proceed. Taking into consideration the need to sustain coastal livelihoods (of which earnings from sea cucumber harvesting are particularly important) and to make the most of market conditions, continuing to support a boom and bust harvesting regime is not a responsible action. What is required is that harvesting (and thus exporting) levels are substantially reduced -‐ as a means of re-‐building stocks, and then exploiting at long-‐term sustainable levels. It is thus essential that upper limits are placed on how much of each species is harvested and exported as part of any adaptive management regime. Until such time as the setting of such limits can be based on sound and verifiable scientific assessment, precautionary caps need to be established – we would argue at the national and provincial levels – based on best available information.

Recommendation 19 -‐ We are of the view that national per species precautionary export caps, monitored at the point of export, should be established as a means of moderating fishing and purchasing behaviour that leads to instances of local over-‐exploitation of resources; whilst it is recognised that not all the requisite sources of information are currently available, these caps should be set through a process of stakeholder engagement, and based on historical export levels, evidence of under-‐ / over-‐exploitation, stock modelling, examination of the impact of different HCRs, and changes in the size composition of harvests; these should form an integral part of an adaptive management regime; since a number of these data sources are not currently available, further work will be required to develop the necessary information on which export caps can be determined.

Recommendation 20 – Bearing in mind that most stocks are currently in poor, over-‐exploited condition, stock recovery strategies13 need to be put in place in each country – typically a combination of a period of fishery closure, followed by the setting of graded precautionary export caps that contribute to any stock recovery strategy – and bearing in

12 Some question the benefits of form-‐filling and data collation at the community level – arguing that this acts as a disincentive to improved community based management; there are, however, simple qualitative and quantitative techniques that can be readily incorporated into existing community management systems (see for example Kinch 2004 & Friedman et al 2008); we suggest that these should be developed and tested as part of a distinct applied research thread. 13 These need to be established through a process of dialogue between government and trade and fishing stakeholders, particularly given known current weaknesses in consensus as to how to assess stock strength and condition

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | xiv

mind that relatively little is known about the stock recovery time needed for different species under different circumstances14.

Recommendation 21 – We are of the view that the same processes of setting precautionary export caps should be extended to the Provincial level; these can become more science-‐based as the capacity of government to inspect and monitor trade and exports improves and as information on the status of stocks improves.

Recommendation 22 -‐ To facilitate setting of precautionary export caps, and ultimately science-‐based exploitation targets, each country should start with revisiting review of the availability and accuracy of data on harvest / production (building on the information already collated as part of this study, plus the results of dive surveys, and information from fishing communities and BdM buyers and traders).

Recommendation 23 -‐ More precautionary export caps should be set for the higher value species, many of which tend to be slower growing15 or longer lived, and have been subjected to higher, more focused and more persistent fishing effort.

Recommendation 24 -‐ In most Provinces and countries three or four sea cucumber species dominate the value of local production, suggesting that the monitoring of stock status, determination of MSY, and implementation of quota ceilings and harvest control rules should focus first on these species – top of this list are sandfish, white-‐teatfish and lolly fish16; these core species should form the focus of initial follow-‐on research work.

Recommendation 25 -‐ Confidence in the estimation of stock status and reference points could be strengthened using additional information on changes in the average size or the size mix of harvests / Provincial production – which can be derived from the sampling of export shipments, and also by capturing community based information through completion of simple fisher survey questionnaires.

Recommendation 26 -‐ Confidence in the estimation of stock status and reference points could also be strengthened using information on the areas of different habitats existing within each Province – building on the valuable work already developed within the Reefbase Pacific project and the Millennium Coral Reef Mapping project; this is not, and should not be treated as, a precise process – instead the focus of research should be on finding simple but effective ways of using habitat area data as a means of supporting stock assessments / biomass estimates.

Recommendation 27 – Minimum size limits are in place in all countries studied, but Harvest Control Rules (HCRs) should be developed to encourage fishers to shift effort onto other species once the average size of animals falls below a given threshold (a threshold

14 There is evidence that some stocks can recover over relatively short periods of time (5 to 10 years), whilst in some instances it is evident that stocks still have not recovered after several decades (Battaglene & Bell 2004) – much undoubtedly depends on spawning densities, larval settlement patterns, and levels of recruitment to commercially exploited populations 15 The highest value species, sandfish, is known to be relatively fast-‐growing 16 Note that in terms of trade records, a number of species may be erroneously lumped together as lollyfish

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | xv

well above the legal minimum size limits); examination of the impact of such rules can be explored using appropriate modelling (see footnote 10 & Appendix 16).

Recommendation 28 -‐ It would be helpful to explore if different harvest control rules could be developed for each of free diving and reef gleaning fishing methods.

Compliance and managing supply chain risk

Recommendation 29 -‐ Regular meetings should be convened between government, industry and fishermen to discuss sector management and performance; this appears to be a rarity at present.

Recommendation 30 – As a means of controlling fishing effort, fishing communities should be encouraged to limit fishing to short periods of time only (a matter of days or weeks per year), and probably distinguishing between free diving and reef gleaning fisheries; to avoid a free-‐for-‐all, closed seasons should also be set at the national level, but these can revisited as part of the adaptive management regime.

Recommendation 31 -‐ Given that BdM fishing, processing and trade will be proscribed for at least part of any year, care will need to be taken to discourage the licensing of opportunist BdM export businesses that simply shift from one national jurisdiction to another as stocks are exhausted, and instead favour those businesses that are there for the long-‐haul – committed to a process of co-‐management.

Recommendation 32 -‐ Use of UBA gear should continue to be outlawed for sea cucumber harvesting, and control resources focused on achieving full compliance with this17; the primary target of such fishing is white teatfish and opportunities for identifying UBA caught white teatfish through the supply chain should be explored (relying mainly on following up on local intelligence on the use of illegal gear).

Opportunities for regional cooperation Trade in BdM is an international business, with product sourced from all over the globe; but at the centre of this trade are a relatively small number of wholesale importers concentrated in locations such as Hong Kong, Guangzhou, Singapore and parts of Malaysia. Exporters in different countries are in touch with each other – directly and via their importing customers – and share knowledge and experience. In addition, funding of buying and exporting operations is often provided by the main importers, who thus have considerable knowledge of and involvement in these businesses, and who may encourage joint ownership of operations in different countries.

In managing this trade and these fisheries, governments operate at a disadvantage if they do not understand the structure and operation of this business, and if they do not also share information with other producer countries in similar situations to their own.

Extending this argument further, it is evident that many of the problems facing the industry are in part the result of or compounded by unnecessary secrecy with regard to the scale and performance

17 It should be noted that UBA gear is legally allowed to be used for collecting fish and invertebrates for the aquarium trade

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | xvi

of this sector, with regard to the geographical distribution of production, and in identifying those who are licensed to operate within the sector. This situation should be changed.

Recommendation 33 -‐ Most investigations into the functional dimensions of this trade, including statistical research, and liaison with the governments of importing countries, should be undertaken on a regional rather country by country basis, and the results of research that are not commercially sensitive should be routinely shared across the region.

Recommendation 34 -‐ Governments of producing countries should share information on the who owns (nominated in company law), manages (who deals with day-‐to-‐day practice, sales negotiation, and quality control – a matter of practice) and funds (shareholders, source of loans and source of working capital / advance payments) the BdM trading companies that they are licensing and which operate in their respective territories; to do otherwise is to operate at a distinct disadvantage, particularly in the areas of enforcement and compliance.

Recommendation 35 -‐ Governments should make much more effort to ensure that provision of a valid commercial invoice forms a necessary part of Customs clearance procedures, that the veracity of the prices quoted is confirmed (i.e. that the prices quoted are a genuine market price agreed between buyer and seller, and that transfer prices are not being used); the veracity of prices has particular importance given that in many (but not all) businesses it is the importer that is providing the working capital for BdM supply chain networks in-‐country (a system that offers considerable potential for transfer pricing).

Recommendation 36 -‐ Governments should be much more open in reporting on sector performance, and such information should be consolidated in an annual regional report.

Recommendation 37 – Countries need to take a closer and clearer look at the distribution of economic benefits from the BdM trade to the producing country and its people – focusing more on who benefits financially from BdM exports (focusing on sources of working capital, transfer pricing, distribution of profits), and how participants in the supply chain benefit from the business (the proportions of value that go to coastal / rural households, numbers of intermediaries, and who benefits from adding value); a degree of regional cooperation in such research is to be encouraged, as is in the setting of relevant policies.

Recommendation 38 -‐ It is not evident that the Pacific Islands and their BdM businesses are making the most of their position in what is now a sellers’ market; there needs to be more focused research into the market for BdM, with a focus on who the dominant buyers are, what changes are underway in the structure of the industry, and in particular what changes are occurring at the retail and catering end of the business (ease of use, product form, species preference, market diversification); in the first instance this information should be shared in so far as commercial confidentiality allows, so that it can be used to better inform trade policy.

Recommendation 39 -‐ Existing research suggests that up to 30 per cent of potential product value is lost due to poor BdM processing; efforts need to be made to reduce this

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | xvii

economic loss, through focused training of processor households and, where feasible, more centralised processing (at village and provincial levels), and increased focus on process control; any such intervention should be coordinated at a regional level [see Appendix 19].

Box 1 -‐ Research priorities

r Develop Bayesian18 statistical treatment of PNG species export data to arrive at better modelling of sea cucumber stocks and MSY estimates, and the impact of different types of HCR on stock conditions

r Develop rule of thumb guidelines for village communities on improved management of sea cucumber resources – (i) focused on free-‐diving fisheries, and (ii) focused on reef gleaning fisheries; not only covers crude mapping of resource disposition, seasonality, etc., but how to develop and apply local HCRs, how to determine size of animals, and how to trigger the move-‐on rule

r Research the structure of the trade in Hong Kong and Guangzhou – including prices, company structures, and trade financing

r Research changes in preferences of catering and retailing sectors – species preferences by region, size preference, emergence of new product forms (part-‐dried, pre-‐prepared, boil-‐in-‐the-‐bag, frozen)

r Get to grips with why salt is not used in western Melanesia

r Develop more detailed stock models and management advice for most important species – white teatfish, black teatfish, lolly, snakefish, red surf fish

r Extend habitat maps of Melanesian countries to enable more detailed biomass estimates linking density survey data with biomass per species

r Develop a simple prompt sheet and accompanying methodology for determining when a move-‐on rule should be applied in sea cucumber harvesting management (combines crude resource mapping, quantitative or subjective capture of changes in size distribution of harvests of main species, and interpretation of responses to prompt sheet)

r Prepare best practice BdM inspection and data capture guidelines for Fisheries and Customs Officers

18 Bayesian statistics -‐ statistical methods that assign probabilities or distributions to events or parameters based on experience or best guesses before experimentation and data collection, and that apply Bayes' theorem to revise the probabilities and distributions after obtaining experimental data

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | xviii

Box 2 -‐ Action plan

r Measures to aid stock recovery in each country – mainly moratoria, but also how to manage exploitation and export when moratoria lifted, or in the absence of moratoria (e.g. Fiji) – requires national meetings between managers, scientists, fishermen and traders to discuss a tabled proposal

r Drafting and publishing – within the next twelve months -‐ of national BdM sector performance reports, based on a common contents sheet and format across the MSG (if not further) – based on and extending the data amassed within this consultancy; the purpose of this exercise is to show the historical and current scale, structure and activity of this sector across the value chain -‐ fishing communities, intermediaries, traders; needs governments to compile, analyse, and, where appropriate, to tidy up, historic data sets

r Establishment of national and provincial interim export caps – by species – for each country, based on historical export record, density surveys, and discussions between managers, fishermen and trade

r Compile a regional database of all companies involved in BdM exporting (name, corporate form, capitalisation, when export licenses held, record of volume and value of BdM exported), including details of affiliations and associates of owners, advisors and managers, source of funding (balance of advances from importers, shareholding, borrowings, working capital)

r Regularisation of the data capture, data recording, and data sharing protocols operated by relevant Fisheries Departments and Customs Departments – requires representatives of both departments in each country to sit down and work through what is possible and what is not possible

r Customs and Fisheries Departments to review and upgrade the protocols for pre-‐shipment inspections, data capture (of purchases, packing lists, manifests, inspections) – leading to drafting and publication of a best practice manual

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | 1

1 Introduction

1.1 Context

Sea cucumber fisheries are the second most valuable capture-‐based (after tuna) export fishery in the South Pacific, yet their sustainable management has proved an intractable problem over the years. In years of peak exploitation, production has been valued at over USD 50 million, but in poor years the value has been only a small fraction of this. With better management, combined with today’s higher prices, the fishery could be worth more – but this potential wealth and income to coastal and island communities is being lost due to persistent over-‐fishing and the wild swings in productivity that over-‐exploitation causes.

Market demand currently exceeds global supplies, and prices, particularly of the more sought after species of sea cucumber are on the rise. Far from strengthening the position of sea cucumber fishers, the lure of easy money, combined with pressure on the local trade from the main importers, is encouraging poor practices and poor management, which is making the situation worse. In four of the five countries forming the focus of this study, sea cucumber fisheries are or have been closed for between five and ten years at a time to allow recovery. Yet even before they are reopened, inappropriate manoeuvrings by business people and civic leaders has or is undermining the recovery efforts, and stocks are due to plummet again – and will take still longer to recover to harvestable levels than the last time.

It could be argued that this is simply “business as usual” – a valuable renewable resource is rising in value, and a range of people, from peripheral small-‐scale fishing communities to business people and politicians, seeking to make a quick profit from this unfolding opportunity. But there are five elements to the current circumstances surrounding this fishery and trade that are particularly disturbing:

• The stocks are so run down that in each boom and bust cycle they yield less than half the volume of product than they used to, and this yield falls further with every new cycle19.

• Sea cucumbers play an important role in maintaining the health of many marine habitats, cleaning and aerating expanses of mud, sand and reef; where they are absent or in low numbers, ecosystem structure and function is altered, changes in the structure of reef communities can occur and overall productivity (of food fish and shellfish) is compromised, the physical protection of the shore line afforded by reef systems is reduced, and the nutrient recycling capacity of these environmental complexes is impaired.

• The high value now placed on prime sea cucumber product is encouraging fishers and their households to focus on this activity at the expense of subsistence and other revenue generating activities, and encouraging their greater dependence on imported foodstuffs and other household items – requiring that they earn still more from harvesting sea cucumbers.

• The market makers, particularly import businesses in Hong Kong and mainland China (centred on Guangzhou), have searched the globe for new sources of product and, in each case, local fishers have been encouraged to harvest as much of the resource as possible, resulting in stock collapse; the market makers are struggling to find the new sources of

19 Prior to the 1990s, exploitation in the 1800s and 1900s involved extracting as much as possible over a short period (the equivalent of clear-‐felling a forest) and then allowing long periods for recovery; from the 1990s onwards, stocks have still been over-‐exploited, but there has been no effective recovery period

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | 2

supply they require, and so we are entering a period when the rate of increase in the volume of global supplies will steadily fall – simply moving on to new sources of supply is now an untenable business strategy over the medium-‐term.

• The extent to which those involved in sea cucumber trading can make substantial short-‐term profit in return for very limited investment and at low risk, combined with lax or non-‐existent control on exploitation and trade, and an absence of transparency, supports corrupt practices and illegal activity as a range of influential players seek to opportunistically profit from these circumstances; it has not been, and is still not, in the interests of these traders and other players to regularise the sea cucumber business and to bring it under more considered and responsible management.

These are corrosive influences with effects and impacts that go far beyond the sea cucumber industry:

• the heightened role that the income from sea cucumber fishing and processing is having in the local coastal and island economies in rural locations across the South Pacific is undermining efforts towards more responsible management;

• it is also challenging the traditional authority and decision-‐making processes of community leaders, and in some instances is altering attitudes towards subsistence farming and fishing;

• the lack of transparency and incidents of petit corruption are undermining public trust in government institutions, policy, politicians and the rule of law.

Bringing the sea cucumber industry under responsible and sustainable management is of the utmost importance. The key elements of such management are well known – but it is the practicalities of putting them in place that is problematic; not just how to do it, but how to monitor and enforce it. A key difficulty is the matter of how to break or moderate the “boom and bust” cycle that is so typical of this industry. But the changing dynamics of the industry is also of some relevance. A more considered, strategic and coordinated approach to managing this supply could greatly strengthen this position, to the distinct benefit of national economies and rural coastal and island communities. These form the focus of this study.

1.2 The study brief

It is intended that this study raise the profile of sea cucumber fisheries in Papua New Guinea, the Solomon Islands, Fiji, Vanuatu and Tonga, by highlighting the potential economic returns from a sustainable fishery, and the wealth lost through inadequate management. The study is part of an initiative by ACIAR managed by SPC, and builds on long-‐term work undertaken by SPC, and combines this with inputs and resources from its member countries, other technical organisations, and individual experts.

The aim of the initiative is to launch more effective approaches to the management of sea cucumber fisheries in the region with an initial focus on Melanesia. The current study is to provide the foundation for a programme of future work – guided by field work, drawing on other information and experience, and building on and adding to the considerable published research record. The study is to identify economic measures that can be used at the national level to promote sustainable management of the resource and generate revenue to support monitoring and enforcement action. It is also to determine areas in which collaboration between neighbouring island countries could strengthen management and enhance economic returns.

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | 3

The study Terms of Reference were endorsed in late April 2012 at a meeting of the Fisheries Technical Advisory Committee of the Melanesian Spearhead Group (MSG) and again at an informal consultation with the Heads of Fisheries in June 2012 (which recommended the inclusion of Tonga in the research). The Terms of Reference for the study are shown as Appendix 1 to this report.

1.3 Report layout The report is laid out in seven main sections, supported by country profiles (Annexes 1 & 2), and twenty-‐one data appendices. The first section, Chapter 2, provides a brief overview of the sea cucumber and bêche-‐de-‐mer industry so as to allow better interpretation of subsequent analysis. Chapter 3 draws on the available data to quantify and describe historic production. And this forms the basis of analysis described in Chapter 4 to as to the levels of production that could be achieved under more conservative and sustainable management. Chapter 5 examines the different approaches to the management of sea cucumber fisheries. Chapter 6 looks at the fiscal and economic measures that could be put in place to better manage and control production – combining fiscal, regulatory and enforcement measures – systems that are, in general, independent of the specific BdM industry management strategy applied, and which complement other stock / fishery management approaches. In Chapter 7 we examine what might constitute an improved framework for BdM management incorporating elements of fishery, supply chain and trade management. In Chapter 8 we look briefly at opportunities for regional initiatives and cooperation that could strengthen sector management and boost market revenues.

References cited in the text and appendices are listed in Chapter 9.

Annex 1 provides thumbnail sketches of the BdM industry in each country. Annex 2 focuses on the inter-‐relationship between geography and industry structure, data sources and sector scale, and how the industry is managed.

Supporting this analysis and discussion is a substantial range of Appendices (1-‐21). The underlying data used in the analysis is presented in appendices, together with descriptions of the key characteristics of the various species of sea cucumber that figure most significantly in this trade.

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | 4

2 An introduction to the sea cucumber industry Bêche-‐de-‐mer (BdM) is the trade name for dried sea cucumber. Used as a generic term it refers to the cooked and dried form of some 60 commercially traded species of sea cucumber. Sea cucumbers are a group of soft-‐bodied sand and reef living detritus feeders most commonly found in relatively shallow marine environments down to depths of some 30m.

As the price of bêche-‐de-‐mer has increased over the years the product has taken on the characteristics of a delicacy, and is now commonly served as a centre-‐piece in ceremonial meals – for Chinese New Year, weddings, and formal occasions. It is also used as an ingredient in other dishes, and it is used in powder form as an ingredient in Chinese medicines.

Different species of sea cucumbers inhabit a wide range of habitats and niches present across the coastal shallows and reef systems – from mud substrates through sand, to coral debris to the insides, tops and outer sides of reef systems. Those existing on particulate substrates ingest and clean particles of any biological material – and by recycling this substrate they play a particularly important role in aerating and turning-‐over this material. Those on harder substrates tend to cycle particulate matter found on the hard surfaces and in crevices, and again play a significant role in maintaining the health and vitality of reef systems.

Whilst 35 sea cucumber species are traded across Melanesia, our examination of production and export records suggests that 21 species make up more than 90 per cent of production volume, and eight of these species make up over three quarters of production value (see Appendix 4). Production and trade in sea cucumber and bêche-‐de-‐mer is typically reported in generic terms, and most commonly in terms of product weight – i.e. dried (less than 5 per cent moisture content) bêche-‐de-‐mer. When expressed in value terms it is widely recognised that bêche-‐de-‐mer made from different species command different prices, but inconsistencies in the recording of harvests, production and trade by species means that such value differentiation is not typically transcribed to quantification of overall BdM production. This creates the illusion of homogeneity, when in fact the fisheries and supply chains are much more complex.

Some of the most valuable sea cucumber species can be found, in a healthy population, at densities of 10 to 30 per hectare – e.g. white teatfish, prickly redfish and surf redfish – whereas lower value species can be found at several hundred or indeed several thousand per hectare, e.g. snakefish and lolly fish (see Appendix 7). The former species will be typically harvested by free divers (diving to depths of some 20m), whereas the latter are more commonly harvested through shallow water gleaning (walking the reefs at low tide). Specimens found in deeper water are sometimes harvested using “bombs” – basically a weighted barbed spike on a cord that is dropped from the surface to impale a sea cucumber. Some fishers use scuba or hookah gear to harvest sea cucumbers, allowing fishers to stay longer underwater, and to work at greater depths. This type of fishing is widely discouraged, and is illegal in Melanesian countries20. Not only is it extremely dangerous (deaths and paralysis from diving accidents are common), but it results in the harvesting of much larger proportions of mature adults of any given species – and adversely impacts spawning and stock recovery.

20 Though Fiji has in recent years issued a limited number of licenses for the harvesting of sea cucumber using UBA gear

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | 5

Sea cucumber harvesting most typically follows a “boom and bust” pattern of exploitation. But the more heavily a stock is fished, the longer it takes for it to recover to healthy levels (and sometimes stocks can take several decades to recover, if they recover at all). If a stock is fished down again before it has fully recovered, then the harvested volume and average size of animals harvested is diminished. Underpinning this relationship is the fact that most sea cucumbers are broadcast spawners, with a pelagic larval stage where animals are carried by sea currents for up to 20 days (i.e. there is a limit to how far currents can carry these larvae from source) before settling on suitable (often shallow water) substrate. Stock recovery is dependent on their being a sufficient concentration of spawning adults present, that larvae find suitable substrate to settle on, and that a sufficient proportion of young survive long enough to recruit to the adult and commercially exploited population. This means that populations are particularly susceptible to local extinction due to over-‐fishing, and because many of the islands covered in this study are separated by very deep waters, recruitment from one shallow water area to another across such stretches of open ocean are all but impossible.

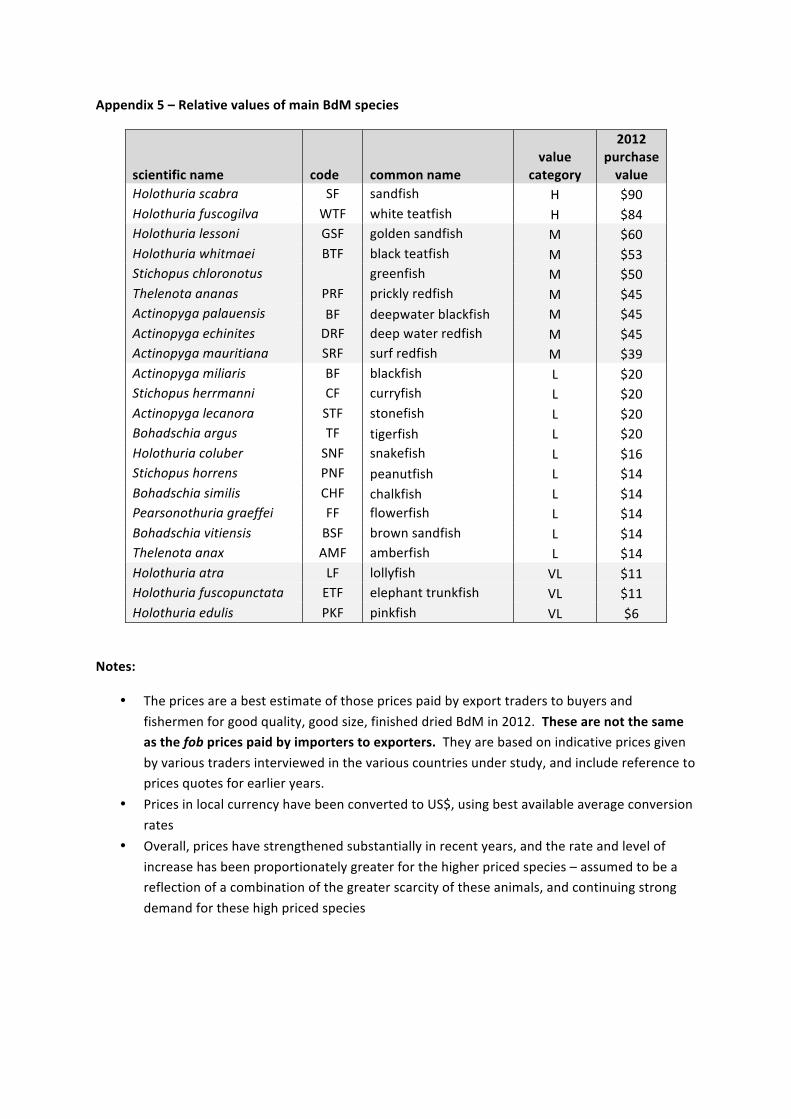

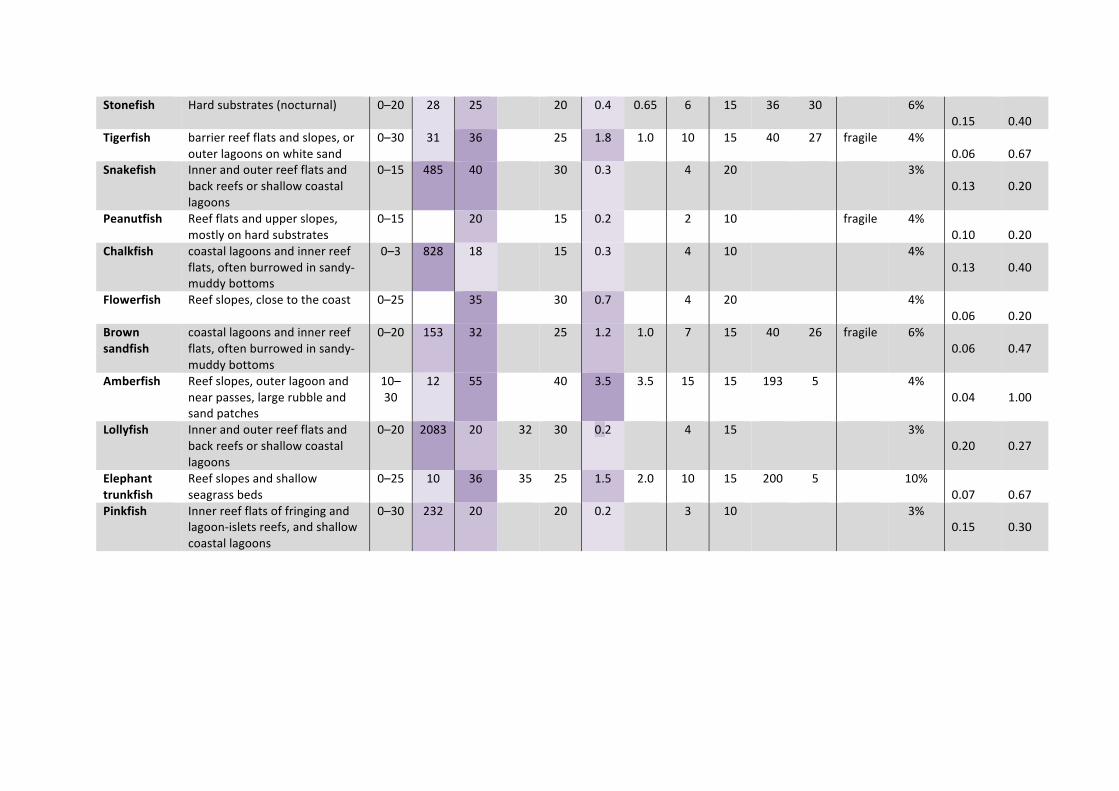

Table 1 – the main sea cucumber species traded in the Western Central Pacific

code common name scientific name

purchase price USD/kg dried1

value grp2

av. t/yr BdM3

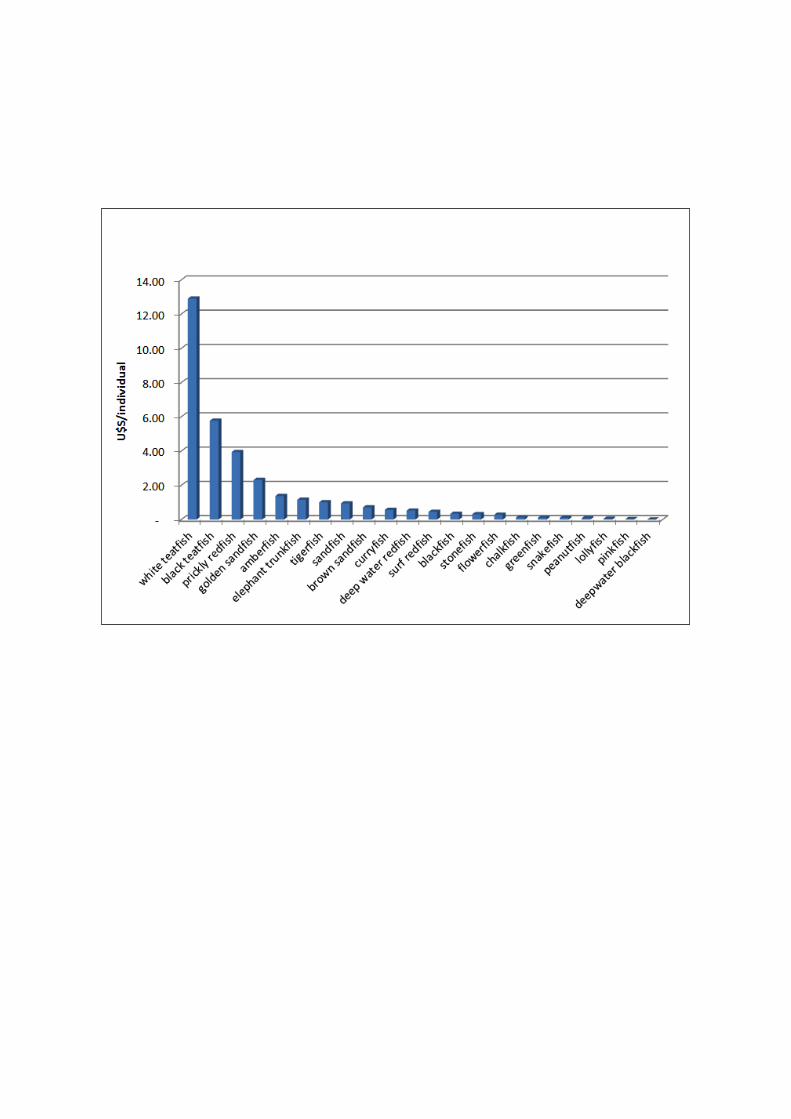

SF sandfish Holothuria scabra $90 H 70 WTF white teatfish Holothuria fuscogilva $84 H 159 GSF golden sandfish Holothuria lessoni + $60 M -‐ BTF black teatfish Holothuria whitmaei $53 M 29 GF greenfish Stichopus chloronotus $50 M 19 PRF prickly redfish / pineapple fish Thelenota ananas $45 M 30 BF deepwater blackfish / Panning’s blackfish Actinopyga palauensis $45 M 1 DRF deep water redfish Actinopyga echinites $45 M 8 SRF surf redfish Actinopyga mauritiana $39 M 45 BF blackfish / hairy blackfish Actinopyga miliaris $20 L 26 CF curryfish Stichopus herrmanni $20 L 53 STF stonefish Actinopyga lecanora $20 L 18 TF tigerfish / leopard fish Bohadschia argus $20 L 74 SNF snakefish Holothuria coluber $16 L 86 PNF peanutfish / dragonfish / warty Stichopus horrens $14 L 7 CHF chalkfish / brownspotted sandfish Bohadschia similis * $14 L 48 BSF brown sandfish Bohadschia vitiensis * $14 L 3 FF flowerfish / orange fish / ripple fish Pearsonothuria graeffei $14 L 97 AMF amberfish Thelenota anax $14 L 48 LF lollyfish / reef lolly fish Holothuria atra $11 VL 182 ETF elephant trunkfish Holothuria fuscopunctata $11 VL 42 PKF pinkfish Holothuria edulis $6 VL 18 Notes

1 the estimated price at which A-‐grade dried product was bought from producers (Appendices 5 & 6) 2 product grouped by price bracket – H high; M medium; L low; VL very low

3 the average amount of dried product of each species exported each year, based on production over 15 years (incorporating periods when fisheries closed), 1996 to 2012

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | 6

+ Golden sandfish has previously been classified as H. scabra var. versicolor but has recently been re-‐classified as a separate species (Kinch et al 2008) * species with taxonomy due to be reviewed (Kinch et al 2008) – B. similis now renamed B. marmorata (Uthicke et al 2010)

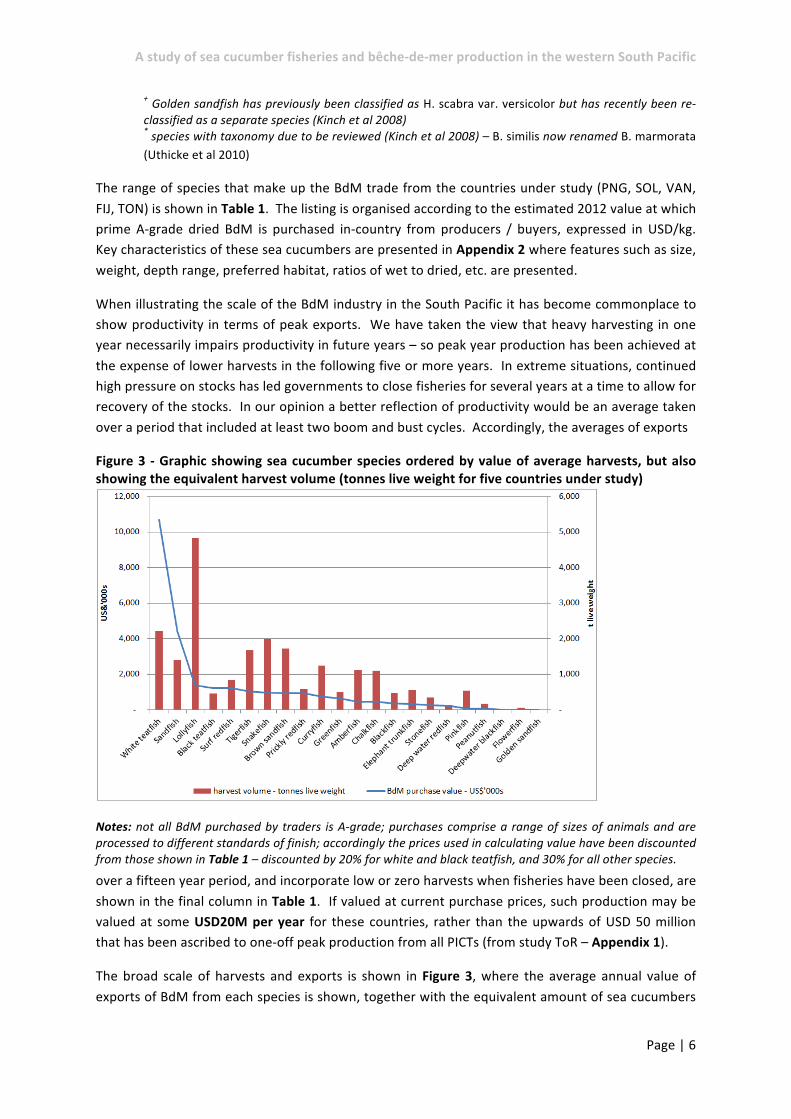

The range of species that make up the BdM trade from the countries under study (PNG, SOL, VAN, FIJ, TON) is shown in Table 1. The listing is organised according to the estimated 2012 value at which prime A-‐grade dried BdM is purchased in-‐country from producers / buyers, expressed in USD/kg. Key characteristics of these sea cucumbers are presented in Appendix 2 where features such as size, weight, depth range, preferred habitat, ratios of wet to dried, etc. are presented.

When illustrating the scale of the BdM industry in the South Pacific it has become commonplace to show productivity in terms of peak exports. We have taken the view that heavy harvesting in one year necessarily impairs productivity in future years – so peak year production has been achieved at the expense of lower harvests in the following five or more years. In extreme situations, continued high pressure on stocks has led governments to close fisheries for several years at a time to allow for recovery of the stocks. In our opinion a better reflection of productivity would be an average taken over a period that included at least two boom and bust cycles. Accordingly, the averages of exports

Figure 3 -‐ Graphic showing sea cucumber species ordered by value of average harvests, but also showing the equivalent harvest volume (tonnes live weight for five countries under study)

Notes: not all BdM purchased by traders is A-‐grade; purchases comprise a range of sizes of animals and are processed to different standards of finish; accordingly the prices used in calculating value have been discounted from those shown in Table 1 – discounted by 20% for white and black teatfish, and 30% for all other species.

over a fifteen year period, and incorporate low or zero harvests when fisheries have been closed, are shown in the final column in Table 1. If valued at current purchase prices, such production may be valued at some USD20M per year for these countries, rather than the upwards of USD 50 million that has been ascribed to one-‐off peak production from all PICTs (from study ToR – Appendix 1).

The broad scale of harvests and exports is shown in Figure 3, where the average annual value of exports of BdM from each species is shown, together with the equivalent amount of sea cucumbers

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | 7

harvested. The largest biomass harvested is of the low value lolly sea cucumber. The second highest biomass harvested is of the very high value white teatfish. Behind these are the low value snakefish, tigerfish and brown sandfish, and the very high value sandfish. This latter species is different from the other species in that its habitat preference is quite narrow – generally limited to shallow water (<20m) with fine mud and sand substrate, including seagrass beds, with high nutrient levels; they can also tolerate reduced salinity (20 ppt) for short periods and so are sometimes found in brackish water (Agudo 2006 and Preston 1993). As a result its distribution across the region is not even. Additionally, where it is found, it can be found in large numbers, and its high price tag is such that it can be very easily over-‐fished.

These figures are shown in disaggregated form (disaggregated by country and by species) in Table 2.

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | 8

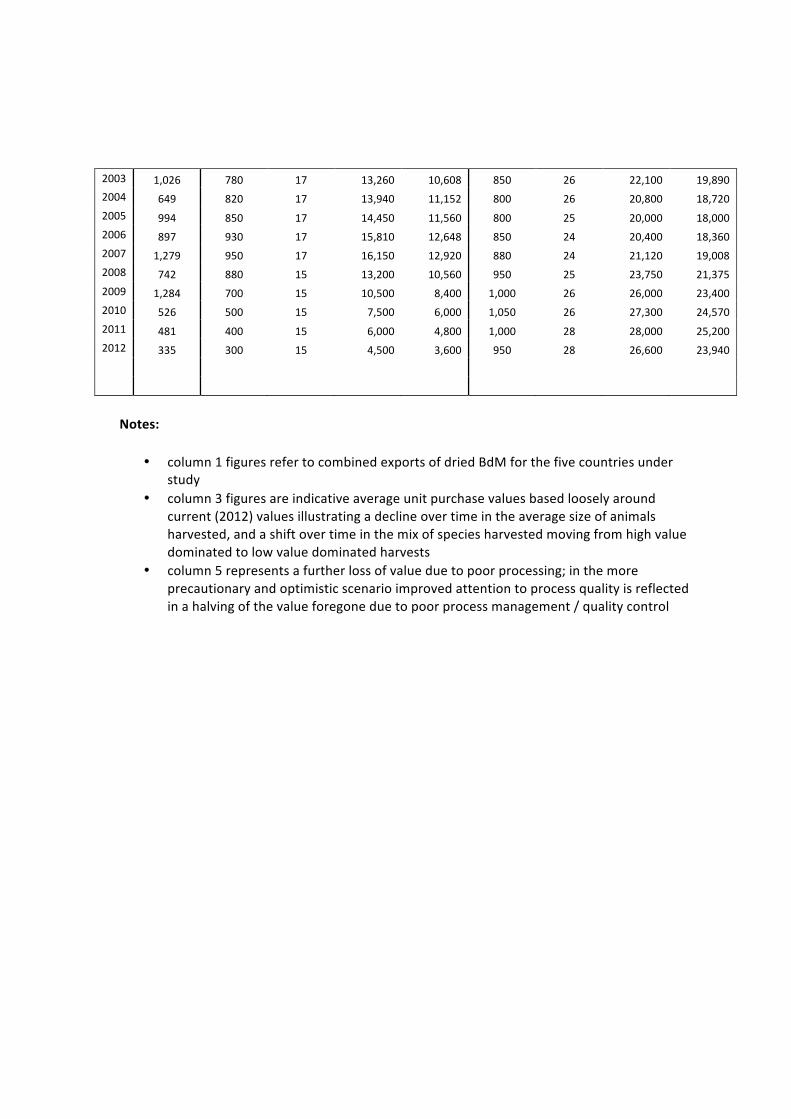

Table 2 -‐ 15 year average BDM exports per country, by species, 1998 to 2012 – expressed in tonnes of dried BdM; plus estimated current purchase value21

15 year average exports -‐ t dried BdM value at current purchase prices – USD million

PNG SOL VAN FIJ TON PNG SOL VAN FIJ TON Sandfish 75 (16%) 1 (1%) 1 (6%) -‐ 0 (0%) $3.59 $0.03 $0.03 $0.00 $0.01 White teatfish 96 (21%) 30 (18%) 1 (6%) 22 (8%) 4 (7%) $4.31 $1.37 $0.06 $0.98 $0.17 Golden sandfish -‐ -‐ -‐ -‐ -‐ $0.00 $0.00 $0.00 $0.00 $0.00 Black teatfish 11 (2%) 5 (3%) 1 (6%) 8 (3%) 2 (4%) $0.27 $0.11 $0.02 $0.20 $0.04 Greenfish 10 (2%) 0 (0%) 1 (6%) 5 (2%) 1 (2%) $0.24 $0.01 $0.02 $0.13 $0.02 Prickly redfish 23 (5%) 0 (0%) 0 (0%) 6 (2%) 1 (2%) $0.48 $0.01 $0.00 $0.13 $0.02 Deepwater blackfish -‐ 1 (1%) 0 (0%) -‐ -‐ $0.00 $0.01 $0.00 $0.00 $0.00 Deep water redfish 0 (0%) 3 (2%) 0 (0%) 3 (1%) 0 (0%) $0.00 $0.07 $0.00 $0.06 $0.00 Surf redfish 23 (5%) -‐ 3 (17%) 6 (2%) 6 (11%) $0.41 $0.00 $0.05 $0.10 $0.10 Blackfish 8 (2%) 4 (2%) 0 (0%) 10 (4%) 1 (2%) $0.07 $0.03 $0.00 $0.10 $0.01 Curryfish 36 (8%) 4 (2%) -‐ 14 (5%) 1 (2%) $0.34 $0.03 $0.00 $0.13 $0.01 Stonefish -‐ 4 (2%) -‐ 5 (2%) 3 (6%) $0.00 $0.04 $0.00 $0.05 $0.03 Tigerfish 34 (7%) 5 (3%) 1 (1%) 25 (9%) 5 (9%) $0.32 $0.05 $0.00 $0.23 $0.05 Snakefish 10 (2%) 9 (5%) 1 (1%) 44 (16%) 10 (19%) $0.07 $0.06 $0.01 $0.32 $0.07 Peanutfish -‐ 5 (3%) -‐ -‐ 0 (0%) $0.00 $0.03 $0.00 $0.00 $0.00 Chalkfish 21 (4%) 8 (5%) -‐ 14 (5%) 2 (4%) $0.13 $0.05 $0.00 $0.09 $0.01 Flowerfish 2 (0%) -‐ 0 (0%) 0 (0%) 0 (0%) $0.01 $0.00 $0.00 $0.00 $0.00 Brown sandfish 36 (8%) 23 (14%) 4 (22%) 19 (7%) 4 (7%) $0.24 $0.15 $0.02 $0.13 $0.03 Amberfish 22 (5%) 6 (4%) 0 (0%) 16 (6%) 2 (4%) $0.15 $0.04 $0.00 $0.11 $0.01 Lollyfish 32 (7%) 45 (27%) 4 (22%) 66 (24%) 10 (19%) $0.17 $0.24 $0.02 $0.34 $0.05 Elephant trunkfish 21 (4%) 7 (4%) 0 (0%) 8 (3%) 2 (4%) $0.11 $0.04 $0.00 $0.04 $0.01 Pinkfish 8 (2%) 5 (3%) 0 (0%) 3 (1%) 0 (0%) $0.02 $0.01 $0.00 $0.01 $0.00 Total 467 164 18 274 54 $10.94 $2.38 $0.26 $3.15 $0.66

average unit value of exports -‐ USD/kg dried BdM $23/kg $15/kg $14/kg $12/kg $12/kg Source: exports by species from National Department of Fisheries statistics; values from trader interviews (see Appendices 5 & 6)

21 Purchase value refers here to the price paid by the main exporters to fishermen, processors, buyer intermediaries for grade “A” fully processed BdM

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | 9

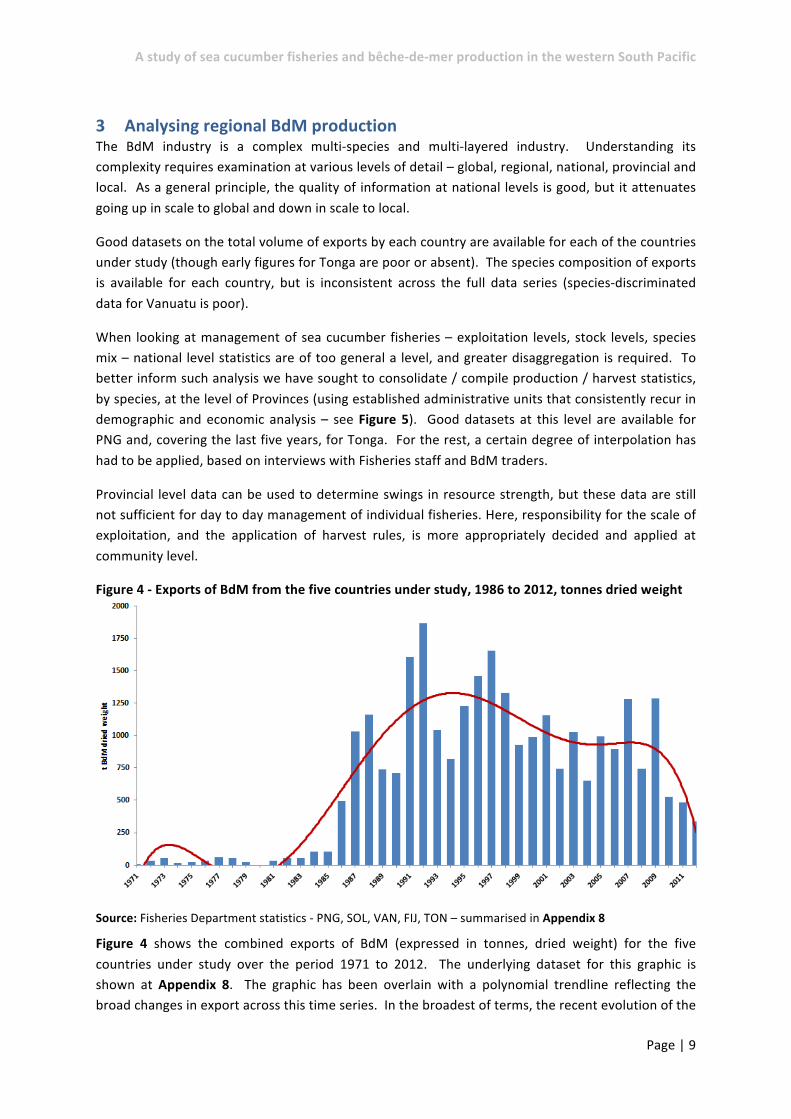

3 Analysing regional BdM production The BdM industry is a complex multi-‐species and multi-‐layered industry. Understanding its complexity requires examination at various levels of detail – global, regional, national, provincial and local. As a general principle, the quality of information at national levels is good, but it attenuates going up in scale to global and down in scale to local.

Good datasets on the total volume of exports by each country are available for each of the countries under study (though early figures for Tonga are poor or absent). The species composition of exports is available for each country, but is inconsistent across the full data series (species-‐discriminated data for Vanuatu is poor).

When looking at management of sea cucumber fisheries – exploitation levels, stock levels, species mix – national level statistics are of too general a level, and greater disaggregation is required. To better inform such analysis we have sought to consolidate / compile production / harvest statistics, by species, at the level of Provinces (using established administrative units that consistently recur in demographic and economic analysis – see Figure 5). Good datasets at this level are available for PNG and, covering the last five years, for Tonga. For the rest, a certain degree of interpolation has had to be applied, based on interviews with Fisheries staff and BdM traders.

Provincial level data can be used to determine swings in resource strength, but these data are still not sufficient for day to day management of individual fisheries. Here, responsibility for the scale of exploitation, and the application of harvest rules, is more appropriately decided and applied at community level.

Figure 4 -‐ Exports of BdM from the five countries under study, 1986 to 2012, tonnes dried weight

Source: Fisheries Department statistics -‐ PNG, SOL, VAN, FIJ, TON – summarised in Appendix 8

Figure 4 shows the combined exports of BdM (expressed in tonnes, dried weight) for the five countries under study over the period 1971 to 2012. The underlying dataset for this graphic is shown at Appendix 8. The graphic has been overlain with a polynomial trendline reflecting the broad changes in export across this time series. In the broadest of terms, the recent evolution of the

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | 10

fisheries has been low-‐level exploitation through the 1970’s, steady growth of exploitation in the 1980s reaching a peak in the early 1990s. Harvests dropped off after this but a secondary, lower level, peak was reached in the mid-‐2000s. Concerns about widespread over-‐fishing of stocks resulted in the subsequent closure of fisheries in the Solomon Islands, Vanuatu and PNG (the Tongan fishery was closed from 1997). In the late 2000s, with most fisheries subject to moratorium, regional production is being provided by Fiji and Tonga only22 – and in both these countries stocks are now thought to be over-‐exploited, and reduced fishing pressure will be required in future years to allow for stock recovery23.

The build-‐up of interest in BdM over the last 25 years can be largely ascribed to the growth of demand from China as its economy has grown and income levels have risen. As supplies from the traditional sources of BdM have reduced, so the trade has actively sought out new sources of supply – but in turn these too have been over-‐exploited (Purcell et al 2012a & To & Shea 2012). The overall result has been substantial upward pressure on market prices, typically a two to three-‐fold increase over the last seven years for lower value species, and a four or five-‐fold increase for higher value species – which in the case of the higher value species converts to very significant increases in dollar terms – purchase prices paid to local processors for finished BdM rising from USD20/kg to USD80/kg over this period. In addition to this, however, it is clear from the data that the volume of white teatfish harvested from the region has been kept high – we would suggest as a result of continued over-‐fishing of this species in response to the high prices paid, including the resorting to the illegal use of UBA gear (though given limited legality in the case of Fiji). This leads us to suggest that the disproportionate rise in prices for high value species is a result of both supply and demand factors, but with greater emphasis on changes in demand.

Such price changes are illustrated in Appendix 6. This information has been drawn together from the various product purchase price points that traders, Fisheries Departments and fishers have been able to give to the researchers. These prices refer to those prices paid by main traders / exporters for prime quality fully dried BdM. Lower prices are paid for poorly processed product, part processed product, and small sized product. A quick comparison of the trend lines added to these price points24 indicates that, not unexpectedly, the dollar increase for the higher priced species has been substantially greater than for low priced species. This is a major incentive for buyers and exporters to encourage fishermen to focus on exploiting these high value species – attractive because these are low volume high markup products. But high volume low markup products, such as lollyfish -‐ predominantly harvested through reef gleaning -‐ have particular merit from a socio-‐economic perspective. These price graphs have been used to inform the estimation of 2012 prices used in putting a value to the BdM exports. Note that these prices are not the same as export prices25 which are more difficult to establish with any confidence.

A predictable result of these very significant value increases has been that price has become the major determinant of fishing activity, with, for some, sea cucumber fishing offering much better

22 Note that New Caledonia, not included in this study, is a significant regional BdM producer and exporter 23 The Tonga fishery has been closed again as from the beginning of 2013 24 We have been able to collate a number of price points, but these are neither sufficient nor definitive, and further discussion with traders on these issues is encouraged 25 fob (free on board – equivalent to ex factory) prices agreed between exporter and importer

A study of sea cucumber fisheries and bêche-‐de-‐mer production in the western South Pacific

Page | 11

returns on effort than fishing for finfish, harvesting and processing copra, or seeking work as a casual labourer.

Over the period illustrated in Figure 4 prices have strengthened, so whilst traded volume has weakened, in dollar terms the overall value of production has broadly increased. But the mix of species harvested has shifted to lower value species, the overall volume of harvests and exports is substantially down, and for many species the average size of individuals harvested is also down. The recent scale and quality of harvests are not as good as they were, and even with “rest” periods stocks are not returning to the same levels as were found in 1980s.

Figure 5 shows the same dataset disaggregated by country. It should be noted that, towards the end of this period, a number of country fisheries have been subject to moratorium, as follows:

• the Tongan fishery was closed for ten years between 1998 and 2007; • the Solomon Islands fishery has been closed since 2006 (albeit with partial openings in

response to the hardship in some areas of the country arising from the 2007 tsunami event); • the fishery in Vanuatu has been closed since 2008; • that in PNG has been closed since 2009; • the Fijian fishery has not been closed over the last two decades of this time series.

Each closure has been a considered management response to evidence of significant over-‐exploitation of the main sea cucumber stocks.

Figure 5 -‐ Export volume of BdM, 1986-‐2012, tonnes of product (dried) weight