Economic Overview of Insurance

36

Contents Introduction................................................... Risk and Insurance............................................. Types of Risks................................................. Methods of Handling Risk....................................... Benefits of Insurance.......................................... Market Imperfections........................................... Imperfections in Insurance Market.............................. Market Power................................................... Demand for Insurance.......................................... Supply for Insurance.......................................... Pricing of Insurance.......................................... Benefits and Costs of Insurance............................... Factors Affecting Insurance Consumption....................... Conclusion.................................................... Bibliography..................................................

-

Upload

independent -

Category

Documents

-

view

6 -

download

0

Transcript of Economic Overview of Insurance

Contents

Introduction...................................................

Risk and Insurance.............................................

Types of Risks.................................................

Methods of Handling Risk.......................................

Benefits of Insurance..........................................

Market Imperfections...........................................

Imperfections in Insurance Market..............................

Market Power...................................................

Demand for Insurance..........................................

Supply for Insurance..........................................

Pricing of Insurance..........................................

Benefits and Costs of Insurance...............................

Factors Affecting Insurance Consumption.......................

Conclusion....................................................

Bibliography..................................................

IntroductionInsurance is an arrangement by which a company or the state

undertakes to provide a guarantee of compensation for

specified loss, damage, illness, or death in return for

payment of a specified premium. It is the equitable transfer

of the risk of a loss, from one entity to another in exchange

for payment. It is a form of risk management primarily used

to hedge against the risk of a contingent, uncertain loss.

Risk arises out of uncertainty. If a person is able to

identify his/her loss then there cannot be any risk and

insurance without any risk is null and void. Insurance is the

tool for risk management. Economics underpins all business

activities, with insurance business being no exception.

Economics plays a pivotal role in operating and regulating the

insurance business. Therefore it is very important to

understand the economic environment that shapes the insurance

sector.

Any risk that can be quantified can potentially be insured.

Specific kinds of risk that may give rise to claims are known

as perils. An insurance policy will set out in detail which

perils are covered by the policy and which are not. Below are

non-exhaustive lists of the many different types of insurance

that exist. A single policy may cover risks in one or more of

the categories set out below. For example, vehicle

insurance would typically cover both the property risk (theft

or damage to the vehicle) and the liability risk (legal claims

arising from an accident). A home insurance policy in the

1 | P a g e

United States typically includes coverage for damage to the

home and the owner's belongings, certain legal claims against

the owner, and even a small amount of coverage for medical

expenses of guests who are injured on the owner's property.

Business insurance can take a number of different forms, such

as the various kinds of professional liability insurance, also

called professional indemnity (PI), which are discussed below

under that name; and the business owner's policy (BOP), which

packages into one policy many of the kinds of coverage that a

business owner needs, in a way analogous to how homeowners'

insurance packages the coverage that a homeowner needs.

Risk and InsuranceInsurance is basically a form of risk management primarily

undergone for hedging the risk of a contingent loss in the

near future. The probability of risk can be hedged by

undergoing into some insurance. It is defined as the equitable

transfer of risk of loss from one entity to another in

exchange for a premium. Premium is an amount paid periodically

to the insurer by the insured for covering his risk. For

taking this risk, the insurer charges an amount called the

premium. The premium is a function of a number of variables

like age, type of employment, medical conditions, etc. The

actuaries are entrusted with the responsibility of2 | P a g e

ascertaining the correct premium of an insured. The premium

paying frequency can be different. It can be paid in monthly,

quarterly, semiannually, annually or in a single premium. The

company that sells the insurance policy is termed as the

insurer.

The primary function of insurance is risk spreading. It is a

co-operative device to spread the loss caused by a particular

risk over a number of persons who are exposed to it and who

agree to ensure themselves against that risk.

Risk arises out of uncertainty. There may be possibilities of

an outcome being different from that of the expected. A risk

and uncertainty are two different concepts. Risk is

essentially the level of possibility that an action or

activity will lead to lead to a loss or to an undesired

outcome. The risk may even pay off and not lead to a loss, it

may lead to a gain. Uncertainty, on the other hand, is

unpredictable. It has too many unknown variables which do not

even allow one to estimate as to what is going to happen. Risk

is insurable, while uncertainty is not. Risks become insurable

when past data makes it possible to predict or draw inference

of what will happen in the future, which is important to

future. These techniques are based around the probability

theory and the law of large numbers.

Types of RisksWith regards insurability, there are basically two categories

of risks;

Dynamic Risk

3 | P a g e

Speculative (dynamic) risk is a situation in which either

profit or loss is possible. Examples of speculative risks

are betting on a horse race, investing in stocks/bonds and

real estate. In the business level, in the daily conduct

of its affairs, every business establishment

faces decisions that entail an element of risk. The

decision to venture into a new market, purchase new

equipment, diversify on the existing product line, expand

or contract areas of operations, commit more to

advertising, borrow additional capital, etc., carry risks

inherent to the business. Speculative risk is not

insurable.

Pure or Static Risk:

The second category of risk is known as pure or static

risk. Pure (static) risk is a situation in which there are

only the possibilities of loss or no loss, as oppose to

loss or profit with speculative risk. The only outcome of

pure risks are adverse (in a loss) or neutral (with no

loss), never beneficial. Examples of pure risks include

premature death, occupational disability, catastrophic

medical expenses, and damage to property due to fire,

lightning, flood etc.

Methods of Handling Risk1. Risk Avoidance:

A risk management technique whereby risk of loss is

prevented in its entirety by not engaging in activities

that present the risk. For example, a construction firm

4 | P a g e

may decide not to take on environmental remediation

projects to avoid the risks associated with this type of

work. Of course, all stocks cannot be avoided. By

avoiding risk, one may be avoiding many opportunities of

life.

2. Risk Distribution:

It implies the spreading of risk over a number of

individuals so that the resultant gain or loss can be

shared among them.

3. Risk Combination:

It is linked to the law of large numbers. Two persons

agreeing to share each other’s’ risk bring no substantial

advantage. Combining individual exposure units in large

numbers reduces uncertainty as predictions to the outcome

of pure risks can be made with acceptable accuracy.

4. Risk Transfer:

The most effective way to handle risk is to transfer it

so that the loss is borne by another party. Insurance is

the most common method of transferring risk from an

individual or group to an insurance company. There is no

reduction in risk, but it will transfer the risk from the

insured to the insurer.

5. Hedging:

Hedging implies making an investment to reduce the risk

of adverse price movements in an asset. Normally, a hedge

5 | P a g e

consists of taking an offsetting position in a related

security, such as a futures contract.

6. Self- Insurance:

It is the handling of the unavoidable risk internally by

creating funds, out of which the losses will eventually

be met.

Benefits of InsuranceInsurance is another major method that most people,

businesses, and other organizations can use to transfer pure

risks by paying a premium to an insurance company in exchange

for a payment of a possible large loss. By using the law of

large numbers, an insurance company can estimate quiet

reliably the amount of loss for a given number of customers

within a specific time. An insurance company can pay for

losses because it pools and invests the premiums of many

subscribers to pay the few who will suffer significant losses.

Speculative risks are not insurable. Major benefits of

insurance as stated by Life Insurance Council are-

Risk Cover:

Life today is full of uncertainties; in this scenario

Life Insurance ensures that your loved ones continue to

enjoy a good quality of life against any unforeseen

event.

Planning for life stage needs:

Life Insurance not only provides for financial support

in the event of untimely death but also acts as a long

term investment. You can meet your goals, be it your

children's education, their marriage, building your dream

6 | P a g e

home or planning a relaxed retired life, according to

your life stage and risk appetite. Traditional life

insurance policies i.e. traditional endowment plans,

offer in-built guarantees and defined maturity benefits

through variety of product options such as Money Back,

Guaranteed Cash Values, Guaranteed Maturity Values.

Protection against rising health expenses:

Life Insurers through riders or standalone health

insurance plans offer the benefits of protection against

critical diseases and hospitalization expenses. This

benefit has assumed critical importance given the

increasing incidence of lifestyle diseases and escalating

medical costs.

Builds the habit of thrift:

Life Insurance is a long-term contract whereas

policyholder, you have to pay a fixed amount at a defined

periodicity. This builds the habit of long-term savings.

Regular savings over a long period ensures that a decent

corpus is built to meet financial needs at various life

stages.

Safe and profitable long-term investment:

Life Insurance is a highly regulated sector. IRDA, the

regulatory body, through various rules and regulations

ensures that the safety of the policyholder's money is

the primary responsibility of all stakeholders. Life

Insurance being a long-term savings instrument, also

7 | P a g e

ensures that the life insurers focus on returns over a

long-term and do not take risky investment decisions for

short term gains.

Assured income through annuities:

Life Insurance is one of the best instruments for

retirement planning. The money saved during the earning

life span is utilized to provide a steady source of

income during the retired phase of life.

Protection plus savings over a long term:

Since traditional policies are viewed both by the

distributors as well as the customers as a long term

commitment; these policies help the policyholders meet

the dual need of protection and long term wealth creation

efficiently.

Growth through dividends:

Traditional policies offer an opportunity to participate

in the economic growth without taking the investment

risk. The investment income is distributed among the

policyholders through annual announcement of

dividends/bonus.

Facility of loans without affecting the policy benefits:

Policyholders have the option of taking loan against the

policy. This helps you meet your unplanned life stage

needs without adversely affecting the benefits of the

policy they have bought.

Tax Benefits:

Insurance plans provide attractive tax-benefits for both

at the time of entry and exit under most of the plans.

8 | P a g e

Mortgage Redemption:

Insurance acts as an effective tool to cover mortgages

and loans taken by the policyholders so that, in case of

any unforeseen event, the burden of repayment does not

fall on the bereaved family.

Market ImperfectionsMarket imperfections generally mean any deviations from the

assumptions of perfect competition. Many of the assumptions in

a perfectly competitive model are implicit rather than

explicit. Below is a description of the different types of

imperfections and distortions. Different types of distortions

are- Monopoly, Duopoly and Oligopoly.

Monopoly, Duopoly and Oligopoly:

Perhaps the most straightforward deviation from perfect

competition occurs when there are a relatively small number of

firms operating in an industry. At the extreme, one firm

produces for the entire market, in which case the firm is

referred to as a monopoly. A monopoly has the ability to

affect both its output and the price that prevails in the

market. A. duopoly consists of two firms operating in a

market. An oligopoly represents more than two firms in a

market but less than the many, many firms assumed in a

perfectly competitive market. The key distinction between an

oligopoly and perfect competition is that oligopoly firms have

some degree of influence over the price that prevails in the

market. In other words, each oligopoly firm is large enough,

relative to the size of the market, and changes in its output

9 | P a g e

cause a change in the equilibrium price prevalent in the

market.

Another key feature of these imperfectly competitive markets

is that the firms within them make positive economic profits.

The profits, however, are not sufficient to encourage entry of

new firms into the market. In other words, free entry in

response to profit is not allowed. The typical method of

justifying this is by assuming that there are relatively high

fixed costs. High fixed costs in turn imply increasing returns

to scale. Thus, most monopoly and oligopoly models assume some

form of imperfect competition.

Imperfections in Insurance MarketCompetition not only leads to economic efficiency, it provides

an automatic mechanism for fulfilling consumer needs and. for

creating a greater variety of choices. Additionally,

competition compels the insurers to improve their products and

services, thus further benefiting the b conditions are buyers.

The following necessary for a perfectly competitive insurance

market:

1. A sufficiently large number of buyers and sellers

such that no one buyer or seller or group of them

can influence the market.

2. Sellers have freedom of entry into and exit from the

market.

3. Sellers produce identical products.

10 | P a g e

4. Buyers and sellers are well informed about the

products.

A market that is workably competitive functions well and

provides most of the benefits of perfect competition. Markets

characterized by workable competition generally have low entry

and exit barriers, numerous buyers and sellers, good

information, governmental transparency, and the absence of

artificial restrictions on competition. The markets for

numerous products satisfy these conditions sufficiently such

that little government intervention is required for the market

to function well. For an insurance market to be workably

competitive, however, rather substantial government

intervention is ordinarily necessary because of the important

imperfections that exist in such markets. Because of these

market imperfections, government intervention into key areas

is required to ensure healthy competition and good

performance.

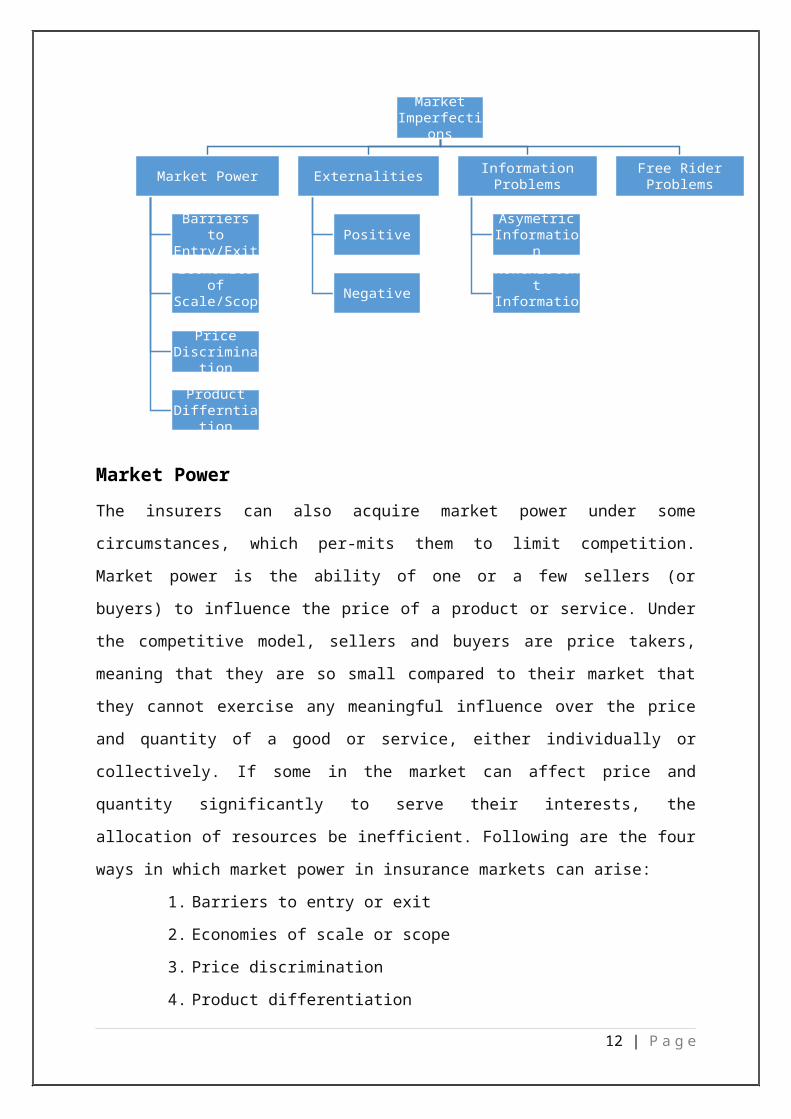

The existence of imperfections in insurance markets explains

and justifies innumerable insurer practices and operations, as

well as most insurance regulations. Nonetheless, the four

broad categories shown in the following diagram-

11 | P a g e

Market PowerThe insurers can also acquire market power under some

circumstances, which per-mits them to limit competition.

Market power is the ability of one or a few sellers (or

buyers) to influence the price of a product or service. Under

the competitive model, sellers and buyers are price takers,

meaning that they are so small compared to their market that

they cannot exercise any meaningful influence over the price

and quantity of a good or service, either individually or

collectively. If some in the market can affect price and

quantity significantly to serve their interests, the

allocation of resources be inefficient. Following are the four

ways in which market power in insurance markets can arise:

1. Barriers to entry or exit

2. Economies of scale or scope

3. Price discrimination

4. Product differentiation

12 | P a g e

Market Imperfecti

ons

Market Power

Barriers to

Entry/ExitEconomies

of Scale/Scop

ePrice

Discrimination

Product Differntia

tion

Externalities

Positive

Negative

Information Problems

Asymetric Informatio

nNonexisten

t Informatio

n

Free Rider Problems

Barriers to Entry or Exit:

The suppliers have market power if a market has barriers to

entry or to exit. The governments often put restrictions on

entry or exit for various reasons. There are entry barriers in

all countries in the form of licensing requirements and

minimum capital requirements. But exit barriers are

comparatively exceptional worldwide.

Technically, national licensing requirements are entry

barriers, although they are justified on consumer protection

grounds. Some entry restrictions are appropriate to ensure

that the insurers are financially sound and their owners and

managers are honest and competent. However, some governments

go beyond this legitimate objective and will not grant a new

license unless a market need to do so is established. Other

countries will not grant new licenses under any circumstances

or will require local equity participation. Transparency in

the licensing process is less than desired in many markets due

to the presence of numerous unwritten rules. Reasonable

freedom of entry does not exist in many of the world's

insurance markets. Several countries prohibit or severely

limit the creation of new national insurers, and many erect

substantial entry barriers to foreign insurers, although the

trend is towards more liberal markets.

Economies of Scale or Scope:

13 | P a g e

Market power can originate from a firm enjoying economies of

scale or scope. The economies of scale characterize a

production process in which an increase in the scale of the

firm causes a decrease in the long run average cost of each

unit. The economies of scope are conceptually similar to

economies of scale. Whereas the economies of scale primarily

refer to efficiencies associated with supply-side changes,

such as increasing or decreasing the scale of production of a

single product type, the economies of scope refer to

efficiencies primarily associated with demand-side changes,

such as increasing or decreasing the scope of marketing and

distribution of different types of products.

Studies on insurance scale economies generally find increasing

returns to scale for small to moderate size firms, and either

constant, moderately increasing or decreasing returns for

larger firms. Thus, market power because of scale economies

might be minimal in insurance, with no compelling evidence of

a natural monopoly.

Whether an insurer possesses market power from scale or scope

economies depends upon its size relative to its market, rather

than its absolute size. A small firm in a small market may

have market power. A big insurer in an international may have

very little such power.

Price Discrimination:

It occurs when a firm charges different price to different

group of consumers for identical goods or services, for

14 | P a g e

reasons not associated with cost. The insurers often attempt

price discrimination, although regulatory requirements may

prevent this strategy. The insurance regulators become

concerned about price discrimination when the insurer's

underlying loss experience or expenses do not justify price

differences on otherwise identical policies.

Product Differentiation:

Distinction/Differentiation in the looks of a product may be

done to make the product more attractive by contrasting its

unique qualities with other competing products. Successful

product differentiation creates a competitive advantage for

the seller, as customers view these products as unique or

superior. If an insurer can differentiate its products from

those of its competitors in the minds of its customers, it

gains market power and can secure higher profits. Product

differentiation exists when buyers prefer one firm's products

to those of its rivals. Product differentiation is good from

the customer point of view also, as it can lead to enhanced

consumer choice and to continuous product improvement. But the

regulators are often concerned if the effect of product

differentiation is to mislead purchasers.

Externalities:

Externalities represent economic actions, which have effects

external to the market in which the action is taken.

Externalities can arise either out of the production processes

(production externalities) or out of the consumption

15 | P a g e

activities (consumption externalities). The external effects

can either be beneficial (positive externalities) or

detrimental (negative externalities) to others. Typically

because the external effects occur to someone other than the

producer or consumer. They do not take the effects into

account while making their production or consumption

decisions. Nature of Externalities The conditions described

earlier for a perfectly competitive market presume that all

costs of production are fully included in each firm's costs.

This is not always true. The producers can impose positive and

negative spread out effects on others.

Positive production externalities occur when:

1. Production has a beneficial effect in other markets

in the economy.

2. Consumption has a beneficial effect in other markets

in the economy.

Negative production externalities occur when:

1. Production has a detrimental effect in other markets

in the economy.

2. Consumption has a detrimental effect in other

markets in the economy.

The purely competitive economic model does not accommodate

externalities easily because the prices of goods and services

that carry externalities fail to reflect the true benefits and

costs of such goods and services. The problem lies with

allowing competitive markets to deal freely with goods and

services that carry externalities.

16 | P a g e

1. With negative externalities, too many goods or

services will be produced or consumed, the price

will be too low, and too little effort and resources

will be devoted to correcting or reducing the

externality.

2. Conversely, with positive externalities, too few

goods or services will be produced, the price will

be too high, and too little will be devoted to

enhancing the externality.

Externalities and Insurance:

In life and health insurance, both negative and positive

externalities exist. Health insurance related fraud is the

most significant negative externality. Another extreme example

of a negative externality related to life insurance is when a

murder is committed in an effort to collect the death

proceeds.

Positive externalities also exist in insurance. For example,

the insurers h • e very rarely sought protection under

intellectual property law for their product and service

innovations. Consequently, tendency may exist for firms to

engage less in such development than they would otherwise. Free rider problems:

The collectively consumed goods and services that are desired

by the public are called public goods. Public goods have two

defining characteristics - non-rivalry and non-excludability.

17 | P a g e

Non-rivalry means that the consumption or use of a good by one

consumer does not diminish the usefulness of the good for

another. Non-excludability means that once the good is

provided, it is exceedingly costly to exclude non-paying

customers from using it. The main problem posed by public

goods is the difficulty of a free market to get people to pay

for them.

Public goods provide a very important example of market

failure, in which market-like behavior of individual gain-

seeking does not produce efficient results. The production of

public goods results in positive externalities, which are not

remunerated. Because no private organization can reap all the

benefits of a public good that they have produced, there will

be insufficient incentives to produce it voluntarily. The

consumers can take advantage of public goods without

contributing sufficiently to their creation. This is called

the free rider problem (because consumer's contributions will

be small but not zero).

Free Rider and Insurance Free rider problems also exist in

insurance. Insurance-related free rider problems arise when

individuals know that if they suffer any losses then there are

others who will make good of such losses. Thus, if an

individual knows that he/she will receive free emergency

medical care, he will have less incentive to purchase any

personal health insurance. The characteristics of a public

good are incorporated in the insurance regulation, thereby

benefiting the individuals and firms even if they pay little

or nothing for it.

18 | P a g e

Information problems:

A critically important assumption of the competitive model is

that both buyers and sellers are well informed. Information

problems abound in insurance, and are arguably the industry's

most important market imperfection.

Insurance is a complex business with buyers having superior .r

information to sellers in certain instances (e.g., the buyers

have better be relative risk when they apply for insurance)

and vice versa in others (e.g., the insurer knows more about

its financial condition than does the buyer). Asymmetric

information problems exist when one party to a transaction has

the relevant information that the other does not have.

The nature of the insurance transaction involves a contract

that makes a present promise of the future performance upon

the occurrence of the stipulated events. Individuals and

businesses purchase policies in good faith, relying on the

integrity of the insurance company and its representatives.

Assuming that the insured could be induced to take an interest

in the financial condition of their insurers, few are

sufficiently knowledgeable to do so without any assistance.

Insurance is necessarily a technical and complicated subject,

and the true financial condition of an insurance company can

be determined only by expert examination. Also, some

individuals may have difficulty in understanding the complex19 | P a g e

nature of insurance contracts. These statements are less

applicable for sophisticated buyers, such as large businesses,

than for individuals.

Information problems for insurance customers provide the

rationale for the great majority of insurance regulations. The

insurers and their representatives have little incentive to

disclose adverse information to potential customers. Doing so

hurts sales. The government seeks to rectify the unequal

positions between insurance buyer and seller by mandating

certain disclosures for the insurers, by monitoring the

insurer's financial condition, by regulating the insurer's

marketing practices, and through other means.

Because insurance is a financial future-delivery product tied

closely to public interest, the governments judge this

information imbalance between buyers and sellers to warrant

substantial oversight of the financial condition of the

insurers. The widely accepted view is that the public,

especially poorly informed consumers must be protected. In

many aspects of insurance processes, neither the buyer nor the

seller has complete information because the desired

information simply does not exist. The insurers cannot know

the future. Environmental factors, such as the economy,

inflation, new laws and regulations, and changing consumer

attitudes and preferences, present great uncertainty to both

the insurance buyers and sellers. Asymmetric information and

other factors can lead to principal-agent problems in the

insurance markets. Such problems arise, for instance, when the

policyholders have difficulty in monitoring and controlling

20 | P a g e

the behavior of their insurer. The insurer might incur

additional financial risk that is hazardous to its

policyholders' interests or fail to meet its obligations to

the policyholders. If the insurer becomes insolvent or refuses

to pay claims, the policyholders may find it very costly or

impossible to recover funds or force the insurer to fulfill

its obligations. Unequal resources and bargaining power

between the insurer and an individual policyholder can

exacerbate the problem. Because of these problems and other

market imperfections, private insurers will not supply every

type of insurance that the consumers demand. The insurers may

perceive excessive adverse selection or moral hazard problems

or they may be unable to diversify their loss exposures.

Nonexistent Information:

The desired information does not exist in many aspects of the

insurance processes. As a result neither the buyer nor the

seller has complete information. In insurance contracts, both

the insurers and the individuals face uncertainty as it

promises future delivery and the price is set before the cost

of production (claims and expenses). The insurers cannot know

the future. Similarly, individuals cannot have complete

knowledge about the consequences of their present and future

choices. Nonexistent and asymmetric information problems are

also responsible for individuals who are so completely ill-

informed unable to know their own best interests.

21 | P a g e

Demand for InsuranceBefore studying in detail about the demand for insurance, it

is better to know about the demand for goods. The quantity

demanded of a good is a function of:

1. Price of the goods

2. Price of the other good

3. Consumer incomes

4. Consumer tastes

These are the only factors that influence demand. The demand

for insurance comes from the need for the financial safety

achieved through risk transfer. An individual by taking an

insurance cover protects his own and his dependent's financial

interests against the losses caused by the occurrence of pure

risks. The determinants of demand are expressed in a short-

hand form below, followed by an initial interpretation.

Dn = f (Pn, Pog, Y, T)

where,

Dn = Demand for any normal product or

service

Pn = Price of the goods

Pog = Price of the other goods

Y = Consumer incomes

T = Consumer tastes

The determinants of demand are applied to insurance.

22 | P a g e

There is an inverse relationship between price and demand. As

far as insurance is concerned, it is useful to focus attention

on the utility analysis of choice involving risk (developed by

Friedman and Savage). The consumers vary in their attitude to

risk–risk averters, risk neutrals, and risk preferrers. Risk

aversion is a common human characteristic well evidenced by

the existence of the insurance industry. A risk averter

prefers a certain premium that may exceed loss expectancy to

unknown losses. Persons unprepared to pay premium exceeding

loss expectancy are called risk neutrals. Risk preferrers seek

out risky situations and would gamble by not paying even as

much as for the loss expectancy of an equivalent amount. Also,

as an individual buys more insurance, his security increases,

and there is, thus, diminishing marginal utility from

additional purchases.

The demand varies directly with the price of a substitute. An

increase in return on the bank deposits may result in the

business abandoning the savings-based life assurance. An

increase in price of those substitutes can be expected to

increase the demand for insurance. The price of complements

for insurance is inversely related to the demand for

insurance. For instance, a fall in the price of cars increases

the demand for car insurance. When real income increases, the

demand for insurance will increase because:

1. To protect the increased standard of living there

will be a higher demand for insurance.

23 | P a g e

2. Higher levels of income increase the ability to

save, leading to an increased demand for saving-

based life assurance.

3. Higher real incomes are associated with economic

growth, which increases investment in business with

corresponding increase in the demand for insurance.

Tastes and preferences are linked to attitudes ranging from

risk aversion to risk preference. Attitude, according to

Friedman and Savage, could change as wealth increases. A

wealthy person could at certain levels of income become a risk

preferer instead of being an averter.

Price Elasticity of Demand for Insurance:

The prices will affect the elasticity of demand for insurance

as it happens in the case of other products. In the cases of

compulsory classes of insurance, market demand would be

perfectly inelastic. On the other hand, in the cases of non-

com-pulsory classes of insurance, market demand would be more

and more elastic. In reality, as there are no close

substitutes available for insurance, the market demand for

insurance is relatively inelastic. But in case of life

insurance, where it takes a form of savings, there are close

substitutes available. The countries where social insurance is

not available, there may not be any close substitute for life

insurance, particularly for lower and middle-income groups.

Income Elasticity of Demand for Insurance:

In case of increase in incomes, the demand for life insurance

and property insurance will also increase. Demand for more

24 | P a g e

consumption and leisure goods will increase the demand for

personal insurances. But in under-developed poor countries,

even increase in income may not increase such demand for

insurance, as they will absorb their additional income in

satisfying their consumption.

Cross-Elasticity of Demand for Insurance:

The changes in demand for insurance are due to changes in the

prices of other goods and services. This cross-elasticity of

demand for insurance will have a negative value, especially in

case of endowment policies where the saving element is more

because a person may invest his savings in highly productive

investments rather than in life insurance. This type of cross-

elasticity affects only the new business and not the existing

business because of the costs involved in transferring the

existing policies or surrendering them. This cross-elasticity

may not affect as far as the general insurance business is

concerned. The Government also influences the demand for

insurance. Taxation, inflation, compulsory insurance, and

regulatory changes are the various means through which the

Government practices its influence on the demand for

insurance.

Supply for InsuranceBefore studying in detail about the supply for insurance, it

is better to know about the supply for goods. The quantity

supplied of a good is a function of:

1. Price of the goods

25 | P a g e

2. The (opportunity) cost of resources needed to

produce the goods

3. The technology available to produce the goods

These are the main factors that influence supply. But there

are some other determinants of supply, such as government laws

and prices of other goods. The determinants of supply are

expressed in a short-hand form below, followed by an initial

interpretation.

Sn = f (Pn, Fc, Th)

where, Sn = Supply for any or service

Pn = Price of the goods

Fc = Cost

Th = Technology

The determinants of supply are applied to insurance.

Being a labour-intensive industry, an insurance company is in

a privileged position to enjoy the very low level of fixed

costs. The variable costs vary in proportion to the actual

business undertaken. Therefore, the insurer may be able to

reach at a break-even point at quiet a lower level so that

beyond this level the business tenders maximum profits. The

break-even point indicates that at a particular level of the

business, the total costs are equal to the total revenue. In

case of capital-intensive industry, this break-even point will

be at a substantially higher level, as compared to a labour-

intensive industry, due to the high level of fixed costs. In

the case of insurance business, uncertainty of the insurer's

26 | P a g e

costs arises, as claims are the biggest single component of

total costs. The uncertainty faced by an insurer can minimize

by means of reinsurance, combining large numbers, selectivity

in underwriting, and effective claims handling. The insurance

market is such that it offers more incentives to the new

entrant. The insurance industry has to come up with different

plans of insurance to cater to different sections of the

people so as to meet their widely differing requirements.

Pricing of InsuranceIn industry, generally, price is determined through the

interaction of supply and demand. The insurance industry is

not perfectly competitive, therefore, price is not determined

by the interaction of supply and demand. Insurance premium is

the price for the insurance service. Premium is the monetary

consideration payable by the insured to the insurer for the

insurance granted under the policy.

Premium = Risk Premium + Expenses + Fluctuations Loading +

Profit

1. Risk Premium:

It is the product of probability of the event and average

loss expectancy.

2. Expenses:

Costs can be broken down into average fixed and average

variable costs. Claims, a significant cost, are included

in average variable costs and, therefore, in risk

27 | P a g e

premium. Other variable costs include commission, which

is collected by the insurer as an integral part of the

premium and paid to the intermediary. Fixed costs are

allocated when direct, i.e., the result of the resources

used entirely in the supply of a particular class of

insurance.

3. Fluctuations Loading:

A reasonable provision must be made for fluctuations in

both experience and contingencies.

4. Profit:

A reasonable provision must be made for a margin for

profit. The amount depends on the business objectives,

extent of competition, and perhaps, effect on investment

income as well as demand. Non-price competition is one of

the features in insurance. It is the competition among

industries that choose to differentiate their products

through non-price means such as service quality, physical

evidence and celebrity endorsement. Product

differentiation, sales promotion and advertising, and

special schemes for selected groups are the examples.

Benefits and Costs of InsuranceEconomic and Social Benefits of Insurance:

Following are the major economic and social benefits of

insurance:

1. Indemnity for loss

28 | P a g e

2. Less worries and fear

3. Source of investment funds

4. Loss prevention

5. Enhancement of credit

Indemnification for Loss:

As the principle of indemnity is applicable to insurance,

therefore, families and individuals are restored to their

earlier financial position after a loss occurs.

Indemnification provides financial security to families and

business firms, and hence is the most important benefit of

insurance.

Less Worries and Fear:

Insurance helps to reduce the worry and fear before and after

a loss. If insurance is there, the family feels secured and

enjoys greater peace of mind as they know that they are

covered in case any loss occurs and worry less after a loss

occurs as the insurer will pay for the loss.

Source of Investment Funds:

Insurance companies are collecting premium in advance and

funds, which are not immediately needed, are invested in

various sectors of a society such as hospitals and housing

development. These investments help to promote economic growth

and full employment.

Loss Prevention:

29 | P a g e

Insurance companies that provide social and economic benefits

implement various loss prevention programmes.

Enhancement of Credit:

Insurance increases a person's credit risk as it provides a

guaranteed assurance that the loan will be repaid. The

financial institution as a col-lateral security accepts

insurance.

Costs of Insurance:

Following are the major social costs of insurance:

1. Cost of doing business

2. Fraudulent claims

3. Inflated claims

Cost of Doing Business:

An insurance company also requires economic resources, land,

labour, capital and business enterprise, for providing

insurance to the society. An expense loading is the amount

required to pay all types of expenses. These loadings are

added to the pure premium to cover the expenses incurred by

the company in their day to day operations. The cost of doing

business is one of the important costs.

Fraudulent Claims:

Submission and payment of fraudulent claims is the second cost

as it results in higher premiums to all the insured. These

costs directly fall on the society.

30 | P a g e

Inflated Claims:

Inflated claims mean that amount of claims may exceed the

actual financial loss. Here the loss may not be intentionally

caused by the insured. Inflated claims are an important social

cost as they result in higher premium to all the insured. This

cost also directly falls on the society.

Factors Affecting Insurance ConsumptionPrice and many other economic, demographic, socio-cultural and

political factors determine the consumption of life and health

insurance of each economy.

Price:

It is an important determinant of insurance demand and supply.

The prices charged by the insurers are influenced by their

cost structures, competitiveness of the particular line of

insurance, and the government tax and other policies.

Economic Environment:

Among the many economic factors that influence life and health

insurance consumption, the most important is the level of a

country's economic development.

Income:

A country's income level is the most important factor in

determining the level of national life and health insurance

consumption. Other factors affecting insurance consumption

(event risk, statutory insurance mandate by government, etc.)

31 | P a g e

being equal, the higher a country's income, the more it spends

on all types of insurances.

Inflation and Interest Rates:

Inflation and interest rates are important factors for

determining demand and supply. High inflation and the

resulting high and volatile interest rates may affect the

demand for life insurance policies. Policy owners may not

prefer longer-term policies. They may prefer shorter-term and

more liquid investment products.

Demographic Environment:

As we know, demography is the study of human population.

Therefore, changes in demographics affect insurance

consumption. High birth rate, low death rate, early marriage,

social and religious reasons, and illiteracy are some of the

reasons for increasing population. Population ageing is the

most significant result of the process known as demographic

transition. Reduction of fertility leads to a decline in the

proportion of the young in the population. Reduction in

mortality means a longer life span for individuals. Population

ageing involves a shift from high mortality/high fertility to

low mortality/low fertility, and consequently an increased

proportion of older people in the total population. India is

undergoing such a demographic transition. Increasing life

expectancy translates into a greater demand for savings-based

life insurance products, as well as for long-term care

insurance.

Education:

32 | P a g e

Literacy plays a very important role. The educational level of

the population affects insurance consumption. It is expected

that more educated people can understand the need for

insurance.

Household Structure:

The nuclear family and the extended family are the core family

forms of most of the households. The demand for insurance may

change according to the needs of double income families and

single parent families also.

Industrialization and Urbanization:

Due to industrialization, family units have become smaller.

The outcome of industrialization is urbanization. Insurance

consumption has been affected due to industrialization and

urbanization.

Social Environment:

Today, due to higher education, consumers have become more

demanding. Higher education gives rise to insurance

consumption. Education and culture are the dimensions of the

social environment that influences insurance consumption. As a

result, cultural perceptions of the role of life and health

products can vary substantially.

Political Environment:

Insurance demand is influenced by country's political and

economic stability. An unstable political environment

depresses insurance demand and, at the same time, decisions

made by insurance regulators affect insurance consumption.

33 | P a g e

ConclusionInsurance is the tool to manage risk, which arises out of

uncertainty. Due to the risk which is a common phenomenon,

insurance business is becoming so popular. As an individual or

a business person can transfer its pure risk to another

organization. As a part of the economic system, insurance

business is also affected by the regulation, operation and

practices relating to economics. Like other business

enterprises, insurance is also affected by the market

imperfections. It arises due to various reasons like market

power, externalities, information problems, free rider

problems etc. Demand, supply and pricing of the insurance are

very important aspects. Demand for the insurance products is

shaped by the factors like price of the goods, consumer

incomes, and consumer tastes etc. Thus, economic factors

affect the insurance business in a distinct manner.

34 | P a g e

Bibliography

1. Mishra K.C and Bakshi M., “Insurance Business Environment

and Insurance Company Operations” Cengage Learning India

Pvt Ltd, 2009.

2. Cain M., “Risk and Insurance: Perspectives on Fertility

and Agrarian Change in India and Bangladesh”, Population

Council, 1981.

3. Retrieved from

http://www.lifeinscouncil.org/consumers/advantages-of-

insurance.

4. Eackhoudt L. and Kimball M. “Background Risk, Prudence

and the Demand for Insurance”, University of Michigam.

5. Michael H., “Categorizing Risks in The Insurance

Industry,” Quarterly Journal of Economics, 1982.

6. CROCKER, KEITH J. and SNOW, A., “The Efficiency Effects

of Categorical Discrimination in the Insurance Industry,”

Journal of Political Economy, 1986.

35 | P a g e