Does Turkish Energy Policy Effectively Address Security of Supply Issues?

25

DOES TURKISH ENERGY POLICY EFFECTIVELY ADDRESS SECURITY OF SUPPLY ISSUES? EMRAH CAN ∗ [email protected] ABSTRACT: Security of oil and gas supplies is one of the main energy policy concerns for Turkey just as it is for many other net energy importing countries in the current high oil price era. The risks associated with security of supply, in other words supply disruptions, could be mitigated by long and short term policy measures. Given the fact that oil and gas are such a vital input in the country’s economy, energy is also a part of foreign policy making. After the Cold War years, Turkey has come to the fore as the most stable pipeline transit country for the hydrocarbon resources of the FSU countries in the Caspian Sea region, and the Middle East. Therefore, recently built oil and gas pipelines might be the best solution for Turkey’s long-run supply security problems. Turkey has already been linked with nearly all of the producer countries in its region and the capacity of those pipelines might even increase with the planned new pipelines which would further diversify the sources and reduce the risk of supply disruptions. Increasing the critical oil stocks to the IEA’s required standards and investing in underground gas storage facilities in three different regions of the country would serve as the short term supply security measure. This paper considers these long and short term strategies for Turkey in a bid to address the challenges of energy supply security. ∗ The author graduated from Istanbul Technical University with BSc degree in Geology in 1990. He also received his MSc degree in Geophysics from Texas A&M University in 1996. He is a MSc student at the CEPMLP. He is currently employed by the Turkish Petroleum Corporation (TPAO). 1

-

Upload

independent -

Category

Documents

-

view

4 -

download

0

Transcript of Does Turkish Energy Policy Effectively Address Security of Supply Issues?

DOES TURKISH ENERGY POLICY EFFECTIVELY ADDRESS SECURITY

OF SUPPLY ISSUES?

EMRAH CAN∗

ABSTRACT: Security of oil and gas supplies is one of the main energy policy concerns for Turkey just as it is for many other net energy importing countries in the current high oil price era. The risks associated with security of supply, in other words supply disruptions, could be mitigated by long and short term policy measures. Given the fact that oil and gas are such a vital input in the country’s economy, energy is also a part of foreign policy making. After the Cold War years, Turkey has come to the fore as the most stable pipeline transit country for the hydrocarbon resources of the FSU countries in the Caspian Sea region, and the Middle East. Therefore, recently built oil and gas pipelines might be the best solution for Turkey’s long-run supply security problems. Turkey has already been linked with nearly all of the producer countries in its region and the capacity of those pipelines might even increase with the planned new pipelines which would further diversify the sources and reduce the risk of supply disruptions. Increasing the critical oil stocks to the IEA’s required standards and investing in underground gas storage facilities in three different regions of the country would serve as the short term supply security measure. This paper considers these long and short term strategies for Turkey in a bid to address the challenges of energy supply security.

∗ The author graduated from Istanbul Technical University with BSc degree in Geology in 1990. He also received his MSc degree in Geophysics from Texas A&M University in 1996. He is a MSc student at the CEPMLP. He is currently employed by the Turkish Petroleum Corporation (TPAO).

1

ABBREVIATIONS

BOTAS Boru Hatlari ile Petrol Tasimaciligi Anonim Sirketi – Turkish State

Pipeline Company

BTC Baku-Tbilisi-Ceyhan

DTM Dis Ticaret Mustesarligi – Undersecretariat of Foreign Trade

EIA Energy Information Administration

E&P Exploration and Production

ER Emergency Response

EU European Union

FSU Former Soviet Union

GDP Gross Domestic Product

IAEA International Atomic Energy Agency

IEA International Energy Agency

IEP International Energy Program

LNG Liquefied Natural Gas

OECD Organisation for Economic Cooperation and Development

TCGP Trans-Caspian Gas Pipeline

TEIAS Turkiye Elektrik Isletmeleri Anonim Sirketi – Turkish State Electricity

Transmission Company

ToP Take-or-Pay

TPAO Turkiye Petrolleri Anonim Ortakligi – Turkish State Oil Company

2

1. INTRODUCTION

Even though the energy policies of oil and gas importing countries have been

addressing supply security issues in various action plans for the diversification of fuel

mix and supply sources since the first oil shock, this has not been central in Turkey’s

energy policy agenda with increasing import, depending primarily on Russia since

oil prices began to rise in 2003.

Turkey’s reliance on oil and gas imports has been steadily increasing (Figure-1), and,

in order to meet its growing demand, emphasis of the energy policy has largely been

on the supply side1. However, does the current energy policy of Turkey reflect the

above reality and efficiently address security issues related particularly to oil and gas

supplies in the high oil price era?

Figure-1. Indigenous production-import balance for (a) crude oil and (b) gas Turkey's Oil Supply

(1971-2004)

0%

20%

40%

60%

80%

100%

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

years

perc

enta

ge (%

)

Indigenous Production Imports Turkey's Gas Supply

(1987-2004)

0%

20%

40%

60%

80%

100%

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

years

perc

enta

ge (%

)

Indigenous Production Imports (a) Crude oil (b) Natural gas

Source: IEA Website

Numerous definitions can be found for ‘security of supply’ which generally

underlines sustained availability of energy sources, particularly oil and gas, in

1 IEA, Energy Policies of IEA Countries - Turkey 2005 Review 12 (2005).

3

adequate amounts at affordable prices2. In the light of this description, maximisation

of domestic supplies may be seen as the most ideal option if, of course, a country is

endowed with such energy sources. Indigenous sources, in other words self

sufficiency, would guarantee such supply security to an extent, at least by reducing

import dependency.

The high priority of the current Turkish energy policy is to increase the level of

energy supply security as it is the case for almost every net oil and gas importing

country. In this regard, Turkey has recently announced several policy measures3

which specifically address the security of oil and gas supply issue:

• Diversify energy sources and exporting countries.

• Benefit from the high potential of being the ‘energy corridor’ at the optimum

level.

• Participate in every single transportation stage of the oil and natural gas

projects related to the Caspian Sea and the Middle East regions.

• Increase the capacity of strategic oil and natural gas underground storage

facilities.

• Increase fuel flexibility in order to provide usage of alternative energy

sources in power generation.

As a matter of fact, the above supply-side of the energy policy4 has not considerably

changed compared to earlier policies in the past 10 years5. The attention was also on

diversifying energy sources to avoid import dependency, being a pipeline transit

country for Caspian resources to European markets, as well as increasing domestic

energy sources. This policy is consistent with the European Union’s (EU) concerns

where Turkey is mentioned in the Green Paper as a transit country which is an 2 Skinner, R. and Arnott, R., the Oil Supply and Demand Context for Security of Oil Supply to the EU from the GCC Countries 23-24 (2005). 3 Author’s translation of the speech of Hilmi Guler, Turkish Energy and Natural Resources Minister, in addressing Turkish energy policy during the annual parliamentary budget planning meetings, http://www.enerji.gov.tr/belge/butce2006.doc (last accessed on April 20, 2006) - in Turkish. 4 Only the oil and gas security of supply related policy tools are mentioned here in a rearranged order in the scope of this research paper. 5 Presentation by S. Burcu Ozdamar, ‘Turkey’s Policies on Security of Energy Supply’ for the European Commission Workshop on the Internal Market for Gas November 7-8, 2002 Brussels, http://europa.eu.int/comm/energy/gas/workshop_2002/doc/candidate_countries/turkey_security_supply.pdf (last accessed on April 20, 2006).

4

essential element for the full exploitation of the resources of the Caspian Sea, as well

as the southern Mediterranean, to improve energy security by diversifying geographic

sources of supplies6.

Even though almost any energy policy measure can be fashionably attributed to and

easily justified for ‘security’, simple pair of energy security indicators7 (IAEA, 2005;

13), namely ‘imports’ and ‘stocks of critical fuel’ would be the focus of this research

paper in order to assess the energy policy of Turkey. Since energy policy is a very

complex subject, this paper does not have an intention to offer a solution or policy

advice, it rather attempts to draw the borderlines for the supply-side energy policy.

When looking at the issue of security of supply, regardless of how it is defined, an

energy policy should adequately address the following elements to be successful8.

• Trade relationships

• Continuing investment in the energy supply chain

• Physical disruption of supply

• Functionality of sectors in physical disruption

These policy elements may also provide a backdrop for discussing the Turkish energy

policy with regard to ‘security of oil and gas supplies’ in different time spans.

This research paper concludes that Turkey has been pursuing an energy policy which

is greatly interlinked to its foreign policy under which the long-term supply security

issues are addressed with the big pipeline projects. Furthermore, the short-term supply

security issues are handled in accordance with the International Energy Agency’s

(IEA)9 Emergency Response (ER) measures.

2. SECURITY INDICATORS

6 European Commission, Towards a European Strategy for the Security of Energy Supply 24 (2000). 7 IAEA, Energy Indicators for Sustainable Development: Guidelines and Methodologies 13 (2005) 8 See Skinner and Arnott, supra 28. 9 This international organisation was founded by the member countries of the Organisation for Economic Co-operation and Development (OECD) after the first oil shock to monitor the energy markets and to act as energy policy advisor.

5

Any questioning about Turkey’s energy policy towards security of oil and gas

.1. IMPORT DEPENDENCE

his indicator may be the most publicised and most debated security issue for a

port dependency could be looked at on two different levels: fuel type and source,

igure-2. Domestic final energy consumption by fuel type in the period of 1960-2003

supplies should begin by introducing some statistics related with this industry. The

data from several different sources have been compiled to present the picture about

Turkey’s present oil and gas supply situation. These, however, will be looked at in a

perspective of the country’s import dependency and fuel stocks, as the two main

supply security indicators.

2

T

consumer country in general. However, for a net importing country like Turkey,

where, in 2004, its domestic oil production accounted for only 9.5% of its final crude

oil consumption, and the natural gas production met only 3% of its domestic natural

gas demand, this subject becomes even more vital for its economy (Figure-2).

Im

which basically means exporting country. First of all, oil account for 44.3% of

Turkey’s final energy consumption, whereas it is 11.1% for gas10 (Figure-2).

F

Final Energy Consumption by Fuel Type

0%

20%

40%

60%

80%

100%

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

years

perc

enta

ge, %

Oil Coal Electricity Natural Gas Combustible Renewables and Residulas Geothermal Solar/Wind

Source: IEA Website 10 57.45% of imported natural gas is used in electricity generation in 2005 (data source: BOTAS).

6

Turkey imports 90.5% of its oil needs mostly from Russia and the Middle East

igure-3a. Crude oil imports by country of origin in the period of 1978-2004

countries (Figure-3a, 3b and 4).

F

Turkey's Crude Oil Imports by Country of Origin

0%

20%

40%

60%

80%

100%

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

years

perc

enta

ge, %

Iran Saudi Arabia Iraq Libya Russia Other Middle East Other Africa Non Specified/Others

Source: IEA Website Figure-3b. Changes in the import dependency to the main oil suppliers in the period of 1996-2004

7

Turkey's Oil Import Dependency

0%

5%

10%

15%

20%

25%

30%

35%

40%

1996

1997

1998

1999

2000

2001

2002

2003

2004

years

perc

enta

ge, %

Russia Iran Libya Saudi Arabia Iraq

Source: IEA Website Figure-4. Crude oil imports by country of origin for (a) end 2004 and (b) January-October 2005

Russia28%

Iran24%

Libya21%

Saudi Arabia14%

Iraq6%

Others7%

Russia31%

Iran27%

Libya19%

Saudi Arabia15%

Iraq5%

Others3%

(a) End-2004 (b) January-October 2005

Source: IEA and DTM Websites

Besides increasing dependence on Russian oil supplies in recent years, Turkey has

also become over-dependent on Russian gas, especially for power generation since

1987. (Figure-5). Between 1987 and 1993, Russia was the sole natural gas supplier.

Regardless of the pipeline gas supplies from Iran and LNG from Algeria and Nigeria,

Turkey currently imports majority of its gas demand from Russia accounting for

8

63.62% of the total import volume via two different pipeline routes11 (Table-1 and

Figure-6).

11 The Western pipeline route via Ukraine, Moldova, Romania, Bulgaria and the Blue Stream directly under the Black Sea.

9

Figure-5. Electricity generation by fuel type12 in the thermal plants in the period of

1940-2004

Electricy Generation by Fuel Typein Thermal Power Plants

0%

20%

40%

60%

80%

100%19

40

1944

1948

1952

1956

1960

1964

1968

1972

1976

1980

1984

1988

1992

1996

2000

2004

years

perc

enta

ge, %

Coal Oil Natural Gas Renewables/Residues

Source: TEIAS Website

Table-1. Natural gas export dependency as of end-2005

Exporting

Country Dependency

Russia (pipeline) 63.62%

Iran (pipeline) 17.08%

Algeria (LNG) 15.22%

Nigeria (LNG) 4.07%

Source: BOTAS Website

12 Imported coal is included in the total share of coal.

10

Figure-6. Natural gas imports by country of origin in the period 1987-200513

Turkey's Natural Gas Imports

0%

20%

40%

60%

80%

100%

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

years

perc

enta

ge (%

)

Spot LNGNigeria LNGAlgeria LNGQatar LNGIranBlue StreamRussiaAustralia

Source: IEA and BOTAS Websites

The high level of both oil and gas import dependency evidently increases Turkey’s

vulnerability to supply disruptions of these resources. This problem would be, of

course, more severe in case of loosing supplies from the major supplier countries.

However, when the oil and gas import volumes are looked at in totality, Russia is the

most critical country on which Turkey depends. Simply from the definition of

dependence, supply disruptions from Russia, along with its geo-political influence,

would be the highest on the Turkish energy market compared to the other supplier

countries.

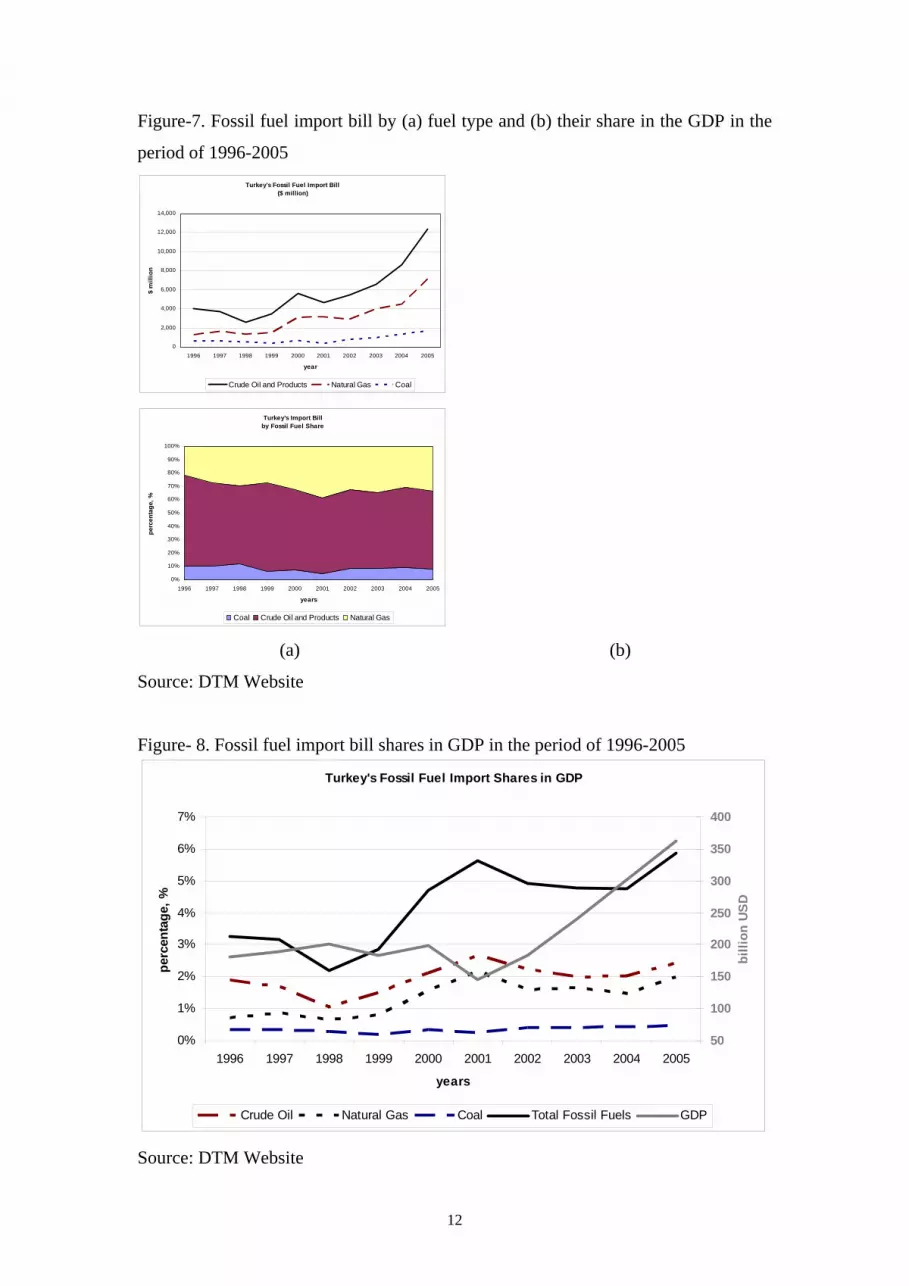

From an economical point of view, Turkey’s fossil-fuel imports account for 5.9% of

its gross domestic product (GDP) (Figure-7 and 8). Rising price levels of these fuels

would adversely affect the balance of payments of the country. A $1 increase in oil

price would increase Turkey’s oil import bill by approximately $170 million. When

other commodities are also taken into account in relation to the oil supplies, such a

small price increase would bring an additional burden of nearly $400 million on the

total energy cost14.

13 ‘Blue Stream’ is graphed separately due to the fact that this pipeline directly delivers gas to Turkey without going through any transit country. 14 The year 2006 program, p. 34, http://ekutup.dpt.gov.tr/program/2006.pdf ( last accessed on April 19, 2006) – in Turkish.

11

Figure-7. Fossil fuel import bill by (a) fuel type and (b) their share in the GDP in the

period of 1996-2005 Turkey's Fossil Fuel Import Bill

($ million)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

year

$ m

illio

n

Crude Oil and Products Natural Gas Coal Turkey's Import Bill

by Fossil Fuel Share

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

years

perc

enta

ge, %

Coal Crude Oil and Products Natural Gas (a) (b)

Source: DTM Website Figure- 8. Fossil fuel import bill shares in GDP in the period of 1996-2005

Turkey's Fossil Fuel Import Shares in GDP

0%

1%

2%

3%

4%

5%

6%

7%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

years

perc

enta

ge, %

50

100

150

200

250

300

350

400

billi

on U

SD

Crude Oil Natural Gas Coal Total Fossil Fuels GDP

Source: DTM Website

12

Figure-9. Total crude oil imports against the oil price15 in the period of 1986-2005

Monthly Crude Oil Imports

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

mill

ion

tonn

es

0

10

20

30

40

50

60

70

$/bb

ls

Crude Oil Imports Oil Price

Source: DTM Website

Obviously, such dependence on imported oil and natural gas which are the major

sources of energy in Turkey exposes the economy to price fluctuations as well

(Figure-9). The imported oil volumes are inversely related to the oil price levels. In

other words, when the oil price increases, the import level decreases to avoid higher

import bills on the balance sheet.

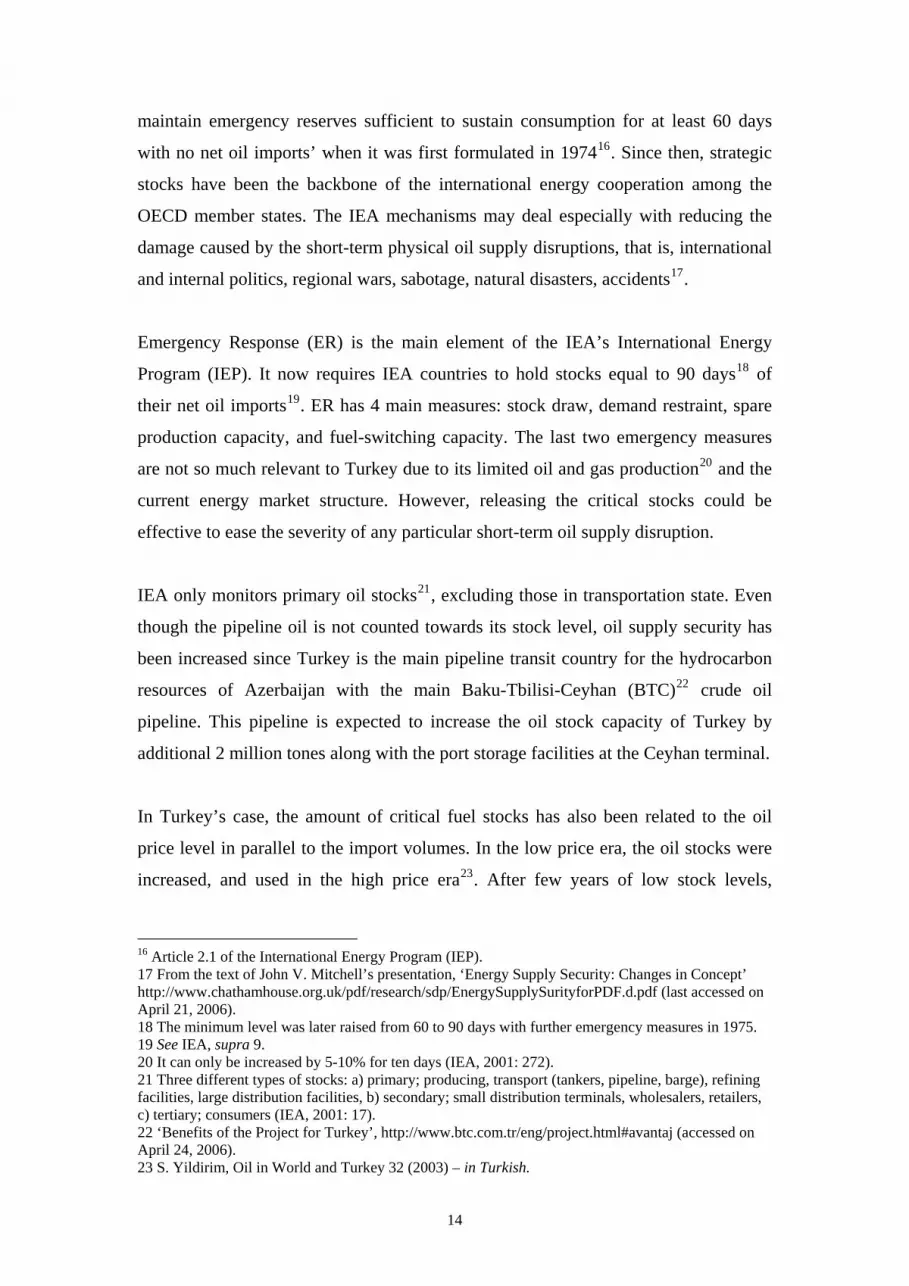

2.2. CRITICAL FUEL STOCKS

As a founding member of the OECD, Turkey has been pursuing an energy policy to

meet the IEA fuel stock obligations. The IEA’s initial stockholding obligation was ‘to

15 This oil price actually reflects the cost of the crude oil imports per barrels to the country, not any other particular reference market price.

13

maintain emergency reserves sufficient to sustain consumption for at least 60 days

with no net oil imports’ when it was first formulated in 197416. Since then, strategic

stocks have been the backbone of the international energy cooperation among the

OECD member states. The IEA mechanisms may deal especially with reducing the

damage caused by the short-term physical oil supply disruptions, that is, international

and internal politics, regional wars, sabotage, natural disasters, accidents17.

Emergency Response (ER) is the main element of the IEA’s International Energy

Program (IEP). It now requires IEA countries to hold stocks equal to 90 days18 of

their net oil imports19. ER has 4 main measures: stock draw, demand restraint, spare

production capacity, and fuel-switching capacity. The last two emergency measures

are not so much relevant to Turkey due to its limited oil and gas production20 and the

current energy market structure. However, releasing the critical stocks could be

effective to ease the severity of any particular short-term oil supply disruption.

IEA only monitors primary oil stocks21, excluding those in transportation state. Even

though the pipeline oil is not counted towards its stock level, oil supply security has

been increased since Turkey is the main pipeline transit country for the hydrocarbon

resources of Azerbaijan with the main Baku-Tbilisi-Ceyhan (BTC)22 crude oil

pipeline. This pipeline is expected to increase the oil stock capacity of Turkey by

additional 2 million tones along with the port storage facilities at the Ceyhan terminal.

In Turkey’s case, the amount of critical fuel stocks has also been related to the oil

price level in parallel to the import volumes. In the low price era, the oil stocks were

increased, and used in the high price era23. After few years of low stock levels,

16 Article 2.1 of the International Energy Program (IEP). 17 From the text of John V. Mitchell’s presentation, ‘Energy Supply Security: Changes in Concept’ http://www.chathamhouse.org.uk/pdf/research/sdp/EnergySupplySurityforPDF.d.pdf (last accessed on April 21, 2006). 18 The minimum level was later raised from 60 to 90 days with further emergency measures in 1975. 19 See IEA, supra 9. 20 It can only be increased by 5-10% for ten days (IEA, 2001: 272). 21 Three different types of stocks: a) primary; producing, transport (tankers, pipeline, barge), refining facilities, large distribution facilities, b) secondary; small distribution terminals, wholesalers, retailers, c) tertiary; consumers (IEA, 2001: 17). 22 ‘Benefits of the Project for Turkey’, http://www.btc.com.tr/eng/project.html#avantaj (accessed on April 24, 2006). 23 S. Yildirim, Oil in World and Turkey 32 (2003) – in Turkish.

14

Turkey has continually met its obligation since 1 January 2004 in the IEA standards

(Figure-10).

Critical fuel stocks of Turkey are held by the companies in the industry. The law

imposes a penalty on oil companies in case of non-fulfillment of stockholding

requirements24. Besides overall stock level, National Protection Law No. 79, together

with the National Security Act, provides the government with a broad range of

authority to control the oil sector to obtain voluntary action immediately and also ‘to

implement different types of demand restrained programs which include energy-

saving campaigns, compulsory measure, delivery quotas of gasoline, and rationing25.

Such measures would primarily be the response of Turkey in case of an emergency,

since quantity of available critical fuel stocks would generally be limited.

Figure-10. Critical fuel stock level in the period of 1978-2004

Crude Oil Stock Level

0

1,000

2,000

3,000

4,000

5,000

6,000

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

years

1000

tonn

es

0

5

10

15

20

25

30

mill

ion

tonn

es

Crude Oil Stocks Crude Oil Imports

Source: IEA Website

The lead time for demand restrained measures other than rationing schemes is

estimated about one month from the preparation and decision making to first

24 See IEA, supra 24. 25 Ibid, 269-270.

15

measurable effect26. The administrative procedures were proved to fully function

during the first Gulf War as an indication of the establishment and proper functioning

of the ER system27.

IEA does not require its member countries to hold natural gas stocks since its storage

is considerably more expensive, and at the same time geologically and logistically far

less effective than oil stocks. However, Turkey has been investing in natural gas

underground storage facilities ‘in order to regulate the seasonal, daily and hourly

fluctuations in consumption’, as well as to meet any potential natural gas supply

shortage in the future28. Two depleted gas fields in the Thrace Basin are expected to

be operational by the end of April 200629, one salt dome structure in the central

Anatolia will be in use by 2010 and another salt structure in the southern Anatolia are

under study30.

4. ENERGY POLICY

Energy policy has to be consistent in a number of separate aims which, at times, may

be in conflict with one another. These main concerns can be summarised as: security

of supply, competitiveness, environmental protection and social aims31. As a net

importer of energy with a growing reliance on external suppliers, security of supply

has risen in importance for Turkey relative to environmental issues, competitiveness

and social aims.

The essential idea of what determines security of oil supply had been expressed by

Winston Churchill in his often-quoted declaration: “On no one quality, on no one

process, on no one country, on no one route, and on no one field must we be

dependent. Safety and certainty in oil lie in variety and variety alone.” Thus variety,

26 The whole process includes preparation, decision making, implementation, full operation. 27 See IEA, supra 272. 28 BOTAS, ‘The Natural Gas Underground Storage Project’ http://www.botas.gov.tr/eng/projects/allprojects/underground.asp (last accessed on April 23, 2006). 29 TPAO, Silivri Dogal Gaz Depolama Projesi, http://www.tpao.gov.tr/winter2005/bg-tr/alt/silivri.htm (last accessed on April, 2006) – in Turkish. 30 BOTAS, 2001 Annual Report, http://www.botas.gov.tr/raporlar/Botas/projeler.htm (last accessed on April 23, 2006). 31 The Royal Academy of Engineering (RAE), Inquiry into Energy Policy - Security of Supply 1 (2001).

16

or diversity of supply in fuels and their sources is more than anything else the essence

of security of supply. The transport sector’s high dependency on oil and the electricity

generation sector’s dependency on natural gas leave Turkey not much choice in

diversifying neither of these primary energy sources in the short term (Table-2). Even

though overall domestic consumption of petroleum products has fallen fractionally

over the last two decades, this has been mostly due to fuel switching from oil to gas

for electricity generation. The underlying trend for the transportation sector’s oil

consumption is still rising. However, it could be more relevant to discuss any options

in the scope of demand-side management.

Table-2. Sectoral oil and gas consumption in 2003

Sectors Oil Gas Transportation 97.29% 1.71% Agriculture 77.21% 7.16% Industry 31.08% 27.26% Commercial and Public Services 19.48% 29.50%

Residential 17.63% 38.74% Source: IEA Website

By the end of the Cold War, the concept of energy supply security had changed in the

national and international political and economic contexts. However, supply

disruption still remains as the main threat. Turkey has been gaining a very strong

position as a pipeline transit country since the break-up of the Soviet Union in 1991.

Therefore, the E&P and pipeline projects from the Caspian Basin have rapidly come

to the fore in the energy policy agenda of Turkey (Table-3) and they have been seen

as ‘the ultimate thing to improve energy supply security’32. In general, the potential to

diversify by origin for gas is more limited than that for oil because the supply routes

for gas are dedicated specific pipelines.

Table-3. Operational and planned Oil and Gas pipelines from the Caspian Sea region

Crude Oil Pipelines:

32 From the PowerPoint presentation by Mithad Rende, ‘Turkey’s Energy Strategy’, TUROGE Caspian & Black Sea Oil & Gas Conference 2005, http://www.bemltd.com/pages/documents/MithatRende.ppt#12 (last accessed on April19, 2006).

17

Baku-Tbilisi-Ceyhan (BTC)

Azerbaijan-Georgia-Turkey

Trans-Caspian (Kazakhstan Twin Pipelines)

Aqtau (Western Kazakhstan, on Caspian coast) to Baku; could extend to Ceyhan

Natural Gas Pipelines:

Baku-Erzurum (SCP)

Baku (Azerbaijan) via Tbilisi (Georgia) to Erzurum (Turkey), linking with Turkish natural gas pipeline system

Trans-Caspian Gas Pipeline (TCGP)

Turkmenbashy (Turkmenistan) via Baku and Tbilisi to Erzurum, linking with Turkish natural gas pipeline system

Source: EIA33

Turkey has been pursuing an energy policy in coherence with the IEA’s

recommendations since 1974. However, IEA’s main policy measures have been

mainly focused on the domestic energy markets, their liberalisation and regulation,

energy efficiency and environment since mid-1980s when the state controlled

economy was replaced with liberal economy34. Turkey has broken up its large

nationalised utilities in the petroleum and electricity sectors through the free market

economy since then. Liberalisation is still underway.

In the IEA’s 2001 review35, upstream security of supply related energy policy

recommendations to Turkey were only about giving priority to new oil and gas

pipeline projects and seeking to ensure further supplies for these pipelines36. The

2005 recommendations addressing Turkey’s security of supply issues, can simply be

highlighted as the continuation of the promotion of gas transit routes and encouraging

the petroleum industry to bypass Turkish Straits due to increased oil tanker traffic in

the Dardanelles and Bosporus straits 37. As a matter of fact, the Turkish energy policy

33 http://www.eia.doe.gov/emeu/cabs/caspgrph.html (last accessed on April 24, 2006). 34 O.A. Yilmaz and T. Uslu, Energy policies of Turkey during the period 1923–2003 (in press) 35 http://www.iea.org/textbase/nppdf/free/2000/turkey2001.pdf (accessed on April 20, 2006). 36 See IEA (2005), supra 8. 37 Ibid 18.

18

reflects all of these long-term recommendations. For example, a look at the BTC

pipeline reveals a number of benefits for the supply security of Turkey namely38:

• Turkey would be able to purchase Azeri oil at a discounted price due to

transit fees and operations services payments.

• 200 billion barrels of crude oil and 18 trillion m3 would flow through

Turkey

• Environmental risks associated with tanker traffic through the congested

Turkish Straits will be mitigated.

Since none of the projections regarding the future demand and supply levels in the

world energy markets are definite, and may change due to various alterations, a

meaningful and realistic assessment of Turkey’s policy options closely based on its

regional position as in the case of the above listed pipeline projects, is essential.

Russia is the main oil and gas supplier of Turkey and this energy trade relationship, in

other words dependency, may remain unchanged for a long time or even increase

since Russia is one of the biggest oil and gas producers in the world with vast

reserves. In a case of severe supply disruption from Russia, Turkey will lose 30% of

its oil imports and 65% of its gas imports. Besides having two separate gas pipelines,

the Western route and the Blue Stream, Russia is still interested in increasing its gas

export capacity to Turkey in a bid to reach to the European gas markets, and Israel

with an additional crude oil pipeline from the Black Sea to the Mediterranean coast39.

Russia’s intensions, of course, could be expected to further increase the already hot

debate about being ‘too dependent’ first on Russian gas and then its oil. However, this

could be easily diverted by flexible terms of contracts between the two countries.

Besides existing and planned pipeline projects from Russia and the Caspian Sea

region, Turkey currently has another twin crude oil pipeline from Iraq, and several

additional gas pipelines are planned to be built from Iraq and Egypt to supply oil and

38 ‘Benefits of the Project for Turkey’, http://www.btc.com.tr/eng/project.html#avantaj (accessed on April 24, 2006). 39 ‘Putin talks up Turkey gas pipeline’, BBC Monitoring - Energy, November 18, 2005.

19

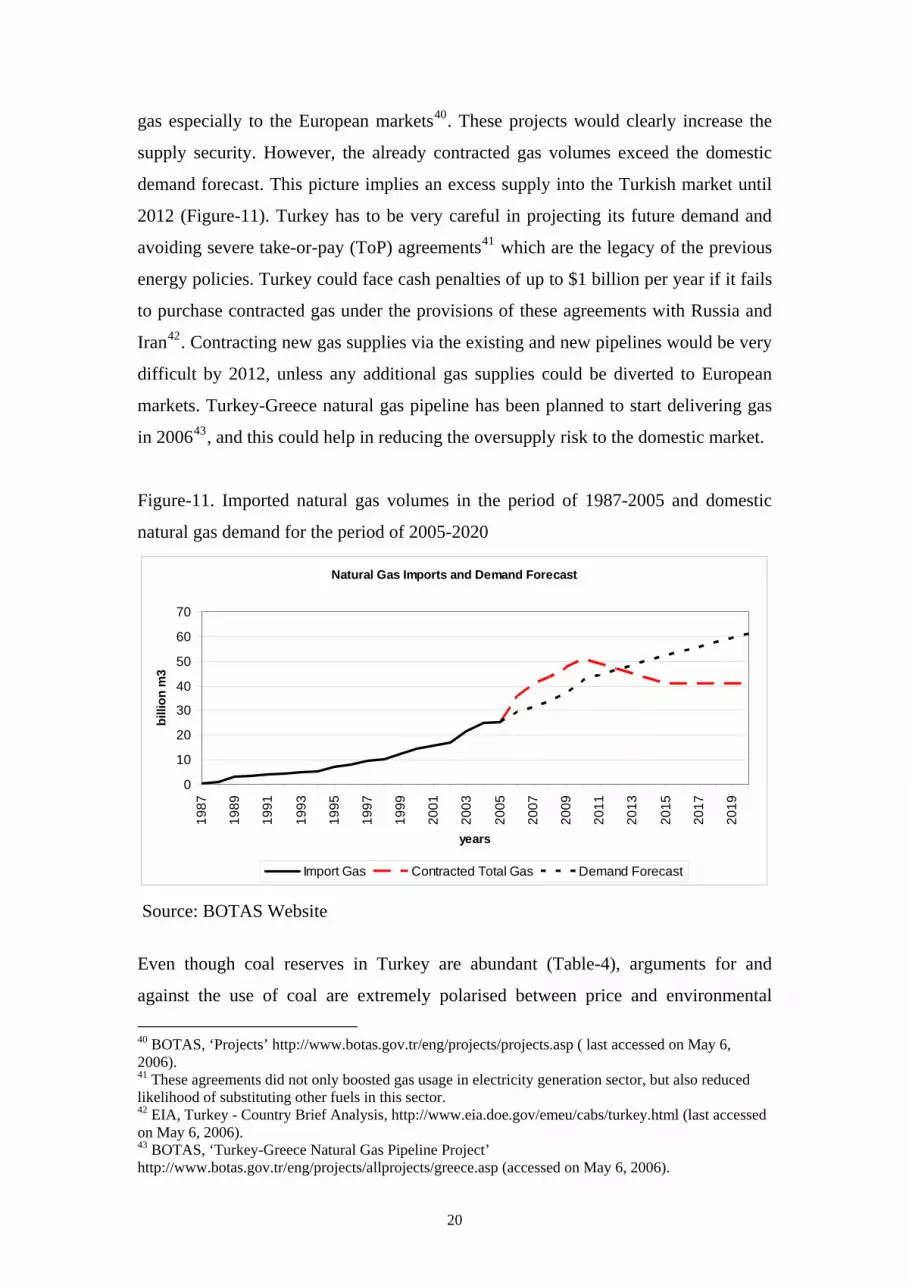

gas especially to the European markets40. These projects would clearly increase the

supply security. However, the already contracted gas volumes exceed the domestic

demand forecast. This picture implies an excess supply into the Turkish market until

2012 (Figure-11). Turkey has to be very careful in projecting its future demand and

avoiding severe take-or-pay (ToP) agreements41 which are the legacy of the previous

energy policies. Turkey could face cash penalties of up to $1 billion per year if it fails

to purchase contracted gas under the provisions of these agreements with Russia and

Iran42. Contracting new gas supplies via the existing and new pipelines would be very

difficult by 2012, unless any additional gas supplies could be diverted to European

markets. Turkey-Greece natural gas pipeline has been planned to start delivering gas

in 200643, and this could help in reducing the oversupply risk to the domestic market.

Figure-11. Imported natural gas volumes in the period of 1987-2005 and domestic

natural gas demand for the period of 2005-2020

Natural Gas Imports and Demand Forecast

0

10

20

30

40

50

60

70

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

years

billi

on m

3

Import Gas Contracted Total Gas Demand Forecast

Source: BOTAS Website

Even though coal reserves in Turkey are abundant (Table-4), arguments for and

against the use of coal are extremely polarised between price and environmental 40 BOTAS, ‘Projects’ http://www.botas.gov.tr/eng/projects/projects.asp ( last accessed on May 6, 2006). 41 These agreements did not only boosted gas usage in electricity generation sector, but also reduced likelihood of substituting other fuels in this sector. 42 EIA, Turkey - Country Brief Analysis, http://www.eia.doe.gov/emeu/cabs/turkey.html (last accessed on May 6, 2006). 43 BOTAS, ‘Turkey-Greece Natural Gas Pipeline Project’ http://www.botas.gov.tr/eng/projects/allprojects/greece.asp (accessed on May 6, 2006).

20

issues. The reasons for subsidising coal production range well beyond security of

supply and centre on the socio-economic needs of the coal producing areas in Turkey.

Given this perspective, the fuel mix is not based on economic considerations, but

rather political decisions in the government’s energy policies. The maintenance of

such an indigenous energy supply and at the same time avoidance of its permanent

closure is another dimension for the coal production sector. The security of coal

supply is usually overshadowed by the environmental externalities of its usage.

Actually, coal was first largely replaced by natural gas for electricity generation and

household heating for this reason44, and then the replacement has further increased

due to the ToP import contracts for the natural gas.

Table-4. World’s proved lignite reserves as of 2004

Rank45 Country

Sub-bituminous and Lignite (million tonnes)

Anthracite and bituminous(million tonnes

Total (million tonnes)

Share of Total

R/P ratio

1 USA 135305 111338 246643 27.1% 245

2 Former Soviet Union (FSU) 132741 94513 227254 25.0% -

3 Russia 107922 49088 157010 17.3% - 4 China 52300 62200 114500 12.6% 59 5 Australia 39900 38600 78500 8.6% 215 6 Ukraine 17879 16274 34153 3.8% 424 7 Brazil 10113 - 10113 1.1% - 8 Germany 6556 183 6739 0.7% 32 9 Indonesia 4228 740 4968 0.5% 38 10 Turkey 3908 278 4186 0.5% 87 Source: BP Workbook 2005

Turkish energy policy also emphasizes the utilisation of underground natural gas

storage facilities to meet the seasonal demand fluctuations as well as to reduce the

supply disruption risk as a short-term security measure along with the oil stocks. First

underground gas storage project will be completed with a capacity of 1.6 billion m3

by mid-200646.

44 F. Gazel, Blue Stream: Genetic Code Depicted 55-56 (2003) – in Turkish. 45 This ranking is made according to the world lignite reserves. 46 The year 2006 program, p. 191, 207.

21

Turkey also has a substantial budget to invest in domestic upstream offshore projects,

and international E&P projects in the Caspian Basin47.

5. CONCLUSION

Turkey is not blessed with rich indigenous hydrocarbon reserves. Therefore, its

economy inevitably relies on imports from the producer countries; oil from mainly

Russia, Iran, Libya, Saudi Arabia (Figure-3b and 4), and gas from mainly Russia and

Iran (Figure-6 and Table-1). The real energy policy issue is related with how much

dependency on a particular export source should be tolerated in order to reduce both

short and long term supply related risks, rather than a particular fuel type.

After the Cold War years, Turkey’s role has been changed to an important transit

country in the last two decades from being only a consumer country. For countries

with limited energy resources but that are in key locations, there is always

considerable benefit to be gained. Therefore, Turkey’s energy policy should reflect

this new character of the country. Over dependence particularly on the Russian oil and

gas imports has been seen as one of the main supply risk element. However, its share

in total supplies could reduce after the flow of additional Azeri oil and gas via the

BTC pipeline this year and the SCP pipeline in coming years. Turkey's long-term goal

of diversifying its fuel suppliers could then be met with these projects.

On the other hand, energy policies to reduce import dependence from any major

exporter country may also reduce the competitiveness of Turkey in the other markets

of that country, an example is Turkey’s stake in the Russian construction sector.

However, creating complex economic interdependency, in other words, wide

spectrum trade relationships, through energy cooperation could lower the disruption

risks from the suppliers. Russia’s willingness to redirect its gas to Europe through

Turkey after the recent gas trade disputes with its major transit route, Ukraine, is a

very good example of this energy cooperation. This is also relevant to the other

exporting countries with existing or potential pipeline projects to Turkey like Egypt48.

The planned pipelines further diversify the sources and reduce the risk of disruption.

47 Ibid 196, 205-207. 48 ‘Turkey, Egypt can cooperate in shipment of Egyptian gas’, BBC Monitoring – Energy, April 20, 2006.

22

There is also a potential to increase the existing capacity. This policy approach, of

course would be advantageous only when the new oil and gas resources are to be

delivered to the world energy markets via Turkey. Already saturated Turkish gas

market, for example, may not be able to economically accommodate more gas.

Otherwise, over-supply would then impose an economic risk under the ToP contracts

since Turkey’s portfolio already imports more natural gas than it probably needs at

least until 2012 (Figure-11).

Given the fact that international energy cooperation has been increasing in the region

since the end of Cold War, the chances of an energy crisis leading to supply

disruption from Russia and Azerbaijan appears to be minimal in the short-term.

However, events over which it has little or no influence may make Turkey more

vulnerable to energy supply disruptions.

As a short term measure to increase the supply security, maintaining the critical fuel

stocks remain a policy tool. Besides oil stocks, Turkey’s investment in underground

gas storage facilities further reduces gas supply disruption risks.

From the perspective of security of supply being a risk related to ‘delivery of energy’,

the Turkish energy policy can be assessed as being effective in addressing supply

disruption risks in both short and long terms.

23

BIBLIOGRAPHY

Articles:

Gazel, F. (2003) ‘Blue Stream: Genetic Code Depicted’, ASAM Avrasya Dosyasi, 9

(1), pp. 53-93 – in Turkish.

Yilmaz, O.A, and Uslu, T. ‘Energy policies of Turkey during the period 1923–2003’,

Energy Policy (in press).

Reports:

European Commission (2000), ‘Towards a European Strategy for the Security of

Energy Supply’, Green Paper, Brussels.

IEA (2001) ‘Oil Supply Security: The Energy response Potential of IEA Countries in

2000’, Paris.

Stern, J. ‘The Russian-Ukrainian Gas Crises of January 2006’ Oxford Institute for

Energy Studies Report: London, UK, 2006.

The Royal Academy of Engineering (2001) Inquiry into Energy Policy - Security of

Supply, London.

Internet Sources:

IAEA (2005) ‘Energy Indicators for Sustainable Development: Guidelines and

Methodologies’, Vienna, http://www-

pub.iaea.org/MTCD/publications/PDF/Pub1222_web.pdf, ( last accessed on April 21,

2006)

IEA (2005) ‘Energy Policies of IEA Countries - Turkey 2005 Review’, Paris.

http://www.iea.org/textbase/npsum/Turkey2005SUM.pdf (last accessed on April 20,

2006)

Skinner, R. & Arnott, R. (2005) ‘The Oil Supply and Demand Context for Security of

Oil Supply to the EU from the GCC Countries’, EUROGULF project report, Oxford

24

Institute for Energy Studies, London, http://www.oxfordenergy.org/pdfs/WPM29.pdf

( last accessed on April 20, 2006)

Yıldırım, S. (2003) ‘Oil in World and Turkey’, Undersecretariat of Foreign Trade,

Ankara, http://www.dtm.gov.tr/ead/petrol/petrol-kitap.doc ( last accessed on April

22, 2006) – in Turkish.

25