News spillovers from the Greek debt crisis: Impact on the Eurozone financial sector

Upload

imc-fh-kremsCategory

view

0download

0

I

Does Argentina represent a convincing

model for sovereign default in regard to

Greece and the Eurozone?

Possible mechanisms and lessons learned

BACHELOR PAPER 1

submitted at the

IMC Fachhochschule Krems

(University of Applied Sciences)

Bachelor Programme

„Export-Oriented Management“

by

Michael PFEIFFER

Area of emphasis/focus/special field: International Law

Coach: Univ.-Ass. (prae doc) Mag. Jane Alice Hofbauer, LL.M.

Submitted on: 29.11.2013

Statutory declaration

“I declare in lieu of an oath that I have written this bachelor thesis myself

and that I have not used any sources or resources other than stated for its

preparation. I further declare that I have clearly indicated all direct and

indirect quotations. This bachelor thesis has not been submitted elsewhere

for examination purposes.”

Date: 20.11.2013 Signature

I

Abstract

The following paper is concerned with the topic of sovereign state defaults and

focuses especially on the Argentine default of 2001. As it was one of the most

severe crises and as there have been two debt restructurings it can be concluded

that something can be learned from it to improve proceedings of future defaults.

The author wanted to compare the Argentine case with the current Greek crisis

and try to find similarities between them. Finally he wanted to highlight the most

important lessons learned in order to avoid too many losses for the actual

European crisis. As Greece is part of an International Monetary Union the most

critical issue is that it is very difficult to use currency devaluation as a solution for

its crisis as this would be a sign of failure for the whole European Integration

Process.

II

Abstract

Diese wissenschaftliche Arbeit handelt von Staatsinsolvenzen und behandelt

speziell den argentinischen Staatsbankrott im Jahr 2001. Da dieser einer der

schwerwiegendsten war und es zwei Umschuldungsverfahren gab kann man

davon ausgehen, dass etwas davon gelernt werden kann und dadurch die

Vorgänge zukünfiger Insolvenzen verbessert werden können. Der Autor wollte den

argentinischen mit dem aktuellen griechischen Fall vergleichen und versuchte,

Ähnlichkeiten herauszufinden. Schließlich beleuchtet er die wichtigsten

Erfahrungen der argentinischen Krise, die man für die griechische Krise umsetzen

könnte, um schwerwiegende Verluste eindämmen zu können. Da Griechenland zu

einer internationalen Währungsunion gehört, ist es eher schwieriger,

Währungsabwertung als eine Lösung für die Krise zu verwenden, da dies einen

Misserfolg des europäischen Integrationsprozessses darstellen würde.

III

Table of Content

1. List of Abbreviations ........................................................................................ 1

2. List of figures .................................................................................................... 2

3. Introduction ....................................................................................................... 3

a. State sovereignty and general situation ...................................................... 3

b. Why comparing Argentina to Greece .......... Error! Bookmark not defined.

4. Argentine default .............................................................................................. 5

a. Pre-default situation: strategies and measures .......................................... 5

b. Post-default situation: Argentina’s debt restructuring strategy .................... 7

i. Debt structure ......................................................................................... 7

ii. “Pesification”: currency devaluation ........................................................ 8

iii. “Canje”: The bond exchange in 2005 and the “Lock Law” ...................... 8

iv. ICSID and bilateral investment treaties ................................................ 10

v. Bond exchange in 2010 ........................................................................ 10

vi. Situation since 2010 ............................................................................. 11

vii. Outlook ................................................................................................. 11

5. Eurozone crisis: Greek debt problems ......................................................... 13

a. Greek Pre-crisis: Causes .......................................................................... 13

b. Danger of a Greek default ........................................................................ 14

i. Bailout loans and rescue packages ...................................................... 14

ii. Credit-default swaps ............................................................................. 15

6. Comparison of Argentina and Greece: lessons learned ............................. 17

a. Lacking of a plan for investment on long-term key drivers ........................ 17

b. Lender of a last resort: IMF and ECB ....................................................... 18

c. Devaluation of currency: Greek exit of European Union? ......................... 18

7. Conclusion ...................................................................................................... 21

8. Bibliography .................................................................................................... 23

1

1. List of Abbreviations

BIT Bilateral Investment Treaty

CAC Collective Action Clauses

CDS Credit Default Swap

ECB European Central Bank

EU European Union

GDP Gross Domestic Product

ICSID International Center for Settlement of Investment Disputes

IMF International Monetary Fund

SDRM Sovereign Debt Restructuring Mechanism

SEC Securities and Exchange Commission

UN United Nations

US United States (of America)

PDI Past Due Interest

2

2. List of figures

Figure 1 Percentage of debt owed by Argentina ................................................ 8

Figure 2 Countries with the most to lose if Greece defaults ............................. 15

3

3. Introduction

To find appropriate answers to the research question the author used secondary

literature such as books, academic journals or online articles.

a. State sovereignty and general situation

Managing defaults on sovereign debt always was a sophisticated venture and is

an important topic in need of further discussion in order to develop universal and

efficient regulations and models. Regarding sovereign debt, the question under

which conditions it generally exists arises. States borrow for different reasons in

non- and pro-cyclical times from private and official foreign lenders to boost their

economies and insure against bad times. In case of a default (i.e. if a state cannot

pay back its debts) in many cases a state receives money from the IMF and the

World Bank and those institutions get their money from their member states, in

turn from the tax payers (Panizza, Sturzenegger, & Zettelmeyer, 2009, p. 669).

The most difficult issue to deal with depicts the immunity which follows from

sovereignty of states. Originated from the Roman law and now stated as

international law in the UN charta article 2 number 1 for sovereign states “Par in

parem non habet imperium/jurisdictionem” signifies that legal unities on the same

level are independent from each other and cannot enforce jurisdictional power

upon each other (Liebs, & Lehmann, 2007, p. 168). Although in the 19th century

governments replied to defaults with military intervention, since 1945 “the use of

military intervention to produce debt repayment is excluded on the basis of the

prohibition of the use of force contained in Article 2 (4) of the Charter of the United

Nations” (Schier, 2007, p. 18).

After the Second World War and due to globalization a few common practices

about this topic emerged and sovereign immunity is not used anymore as a

“bulletproof” shield for sovereign debtors against foreign creditors (Panizza, 2009,

p. 653). The motivation for paying back debt to external lenders most notably lies

in the fear of getting excluded from the international financial market in the future

which constitutes more costly or, concerning the volume, less borrowing

opportunities, hence less investment potential and as a result disturbed growth

(De Paoli, Hoggarth, & Saporta, 2006, p. 2-6). But empirical research on the latest

4

defaults has shown that there is no fundamental impact of exclusion from the

international capital market and in addition to that neither any crucial disadvantage

like sanctions or less exports in the long-term (Panizza et al., 2009, p. 688).

However, through research and practice some suggestions arose for how to deal

with state insolvencies. But up to now no unique scheme or mechanism exists that

could be applied by any state for a convenient and fast management of the default

(De Jonge, 2013, p. 4).

In 2001 the first deputy managing director of the IMF Anne Krueger suggested

a SDRM, Sovereign Debt Restructuring Mechanism, but the US vetoed the

proposal in 2003. Anyway, she made it possible that politicians discuss the

possibility of such a mechanism more frequently in order to set up a stable

international financial framework (Schier, 2007, p. 28).

b. Comparison of Argentina to Greece

The author of this paper is going to compare the Argentine and Eurozone debt

crises as in Europe “the sovereign crisis has many policy and institutional aspects

in common with the Argentine crisis that culminated in default in 2001” (Valiante,

2011, p. 1). The focus especially will be on Greece since it is the European

country that accumulated the highest sovereign debt and has the most difficulties

concerning this topic. After taking a closer look at all the proceedings and

mechanisms done and suggested, the author tries to formulate inferences from the

Argentine case which could be applicable for the Eurozone. Furthermore, the

author wants to add the view of the creditor whether an investment in Argentine or

Greek bonds was riskier.

5

4. Argentine default

The latest Argentine crisis lasted from 1998 to 2002 (there was already a crisis

before from 1974 until 1990, but this paper focuses on the most current debt

crisis). The fixed exchange rate of the Argentine peso to the US dollar, the high

borrowing from the former Argentine president Carlos Menem and finally reduced

tax revenues at the same time led to an increasing state budget deficit. Domingo

Cavallo, the former Economy minister pegged the peso to the US dollar in order to

fight hyperinflation. But unfortunately Brazil devalued its currency at that time so

that Brazilian exports became cheaper than Argentine ones and foreigners rather

imported goods from Brazil than from Argentina. Due to the high borrowing of

Carlos Menem the interest rates went up and credits became too expensive for

domestic businesses. Less business activity and privatizations led to less tax

income for the government (Time.com, 2001). In late December 2001 Argentina

decided to default on a high amount of external debt (US$ 132 billion) due to not

being able to repay it anymore at a predetermined date (Telegraph.co.uk, 2001).

a. Pre-default situation: strategies and measures

Due to a disastrous economic situation in the 1980s in Argentina and the fact of

not being able anymore to keep a healthy government budget equilibrium, inflation

has risen to an annual level of 2600%. Hyperinflation hit the country in the years

1989 and 1990 and it was time to implement reforms in order to stop the

uncontrollable disadvantageous situation, e.g. stronger laws to avoid tax evasions

or more facilitated international trade. One major reform has been the convertibility

law through which the government pegged the Argentine peso legally to the US

dollar on a one to one proportion to make inflationary governmental deficit

financing impossible. This undertaking depicts the most extreme mode of a fixed

exchange rate. Therefore the Argentine government had to accumulate foreign

currency reserves, at least at the beginning. From that point onwards the domestic

money supply could only be altered if there are sufficient reserves on the

international market available – this imposed restrictions on the flexibility of the

monetary policy (Pedro Pou, 2000).

6

Furthermore, in July of 2001 a Zero Deficit Law was introduced. The

consequence was a 13% cut in pensions and salaries to come closer to the aim of

having no deficit. With this bill the government wanted to regain market confidence

in order to increase foreign investment (Voice of America, 2009). In the second

half of 2001 the government was able to reduce all expenditures by 14.8%

compared to the previous year and in the years 1998, 1999 and 2001 tax reforms

were implemented in order to improve tax revenues. The previous set

governmental targets have not been reached but an IMF policy memorandum in

the year 2000 was met (Molina, 2004, p. 115).

Afterwards the IMF provided help to Argentina in form of loans to support the

fiscal liquidity. But all the austerity measures and helping loans from the IMF were

not sufficient to cover the burden of the permanently increasing interest payments

on the overall deficit. From 1993 until 2001 they increased by 249% (Molina, 2004,

p. 12). Generally said, “The dramatic effect of debt servicing in generating

deterioration of the fiscal balance has three primary causes: First, an accelerated

increase in total public debt, second, an increase in interest rates on existing debt,

and third, a spike in the government’s cost of borrowing.” (Bradbury, 2008, p. 17).

The Argentine average cost of borrowing in international capital markets

incremented by 50.6% from 1999 to the year of 2001 (Molina, 2004, p. 161).

Being in such a precarious situation was not enough. Some external shocks

made it even harder for the economy of Argentina to grow: The global recession, a

rising US dollar, the bursting tech bubble and the terms of trade shock from the

Brazilian real. Because of the restricted money policy Argentina was not able to

handle those external shocks and started into a vicious cycle (Bradbury, 2008, p.

23).

Concerning the issuing of sovereign bonds it became very popular to put them

standardized on the international market after the famous Brady deals were issued

during the crisis in the 1980s. Bond financing became the main instrument

although the bonds are most of the times denominated in foreign currency, e.g. the

US dollar. The danger of that method emerges when the domestic currency

devaluates which is also known as exchange rate risk. Already 95.6% of the

7

Argentine public debt was foreign currency in the year 2000 (Argentine Ministry of

Economy, 2000).

After the end of the convertibility regime Argentina exchanged voluntary debt

in 2001 to extend the maturities of the bonds. But this only increased the overall

interest payments and debt burden. Not even a $40 billion injection by the IMF,

called “blindaje”, could help to stabilize the country’s finances. In order to make the

Argentine economy sustainable, the authorities implemented the “corralito”, a

restriction for the citizens to withdraw money from domestic banks and to keep the

money in the country. At the end of 2001 however, the country finally defaulted

and suspended a high portion of its debt (Bradbury, 2008, p. 29).

b. Post-default situation: Argentina’s debt restructuring strategy

In case of a default a country follows a procedure in order to solve the financial

crisis and to continue growth. This procedure includes adjusting policy

modifications, getting financial aid from the IMF and implementing debt

restructuring in order to regain trust and get again access to the international

capital market.

i. Debt structure

Argentina’s debt portfolio consists of performing debt, non-performing debt not to

be restructured and non-performing debt to be restructured. The focus of the

restructuring process lies on the non-performing debt to be restructured. It

includes the Principal value of all debt and the PDI, Past Due Interest which

means interest accrued or accruing and not paid up to now. The performing debt

consists of debt to international financial institutions, bonds to indemnify the losses

of the “pesification” (will be explained later on in this paper) and the loans that

were part of the voluntary exchange described above in the previous section. The

reason for classifying those as performing debt, i.e. debt to be paid full and as a

first choice within other creditors, is because those creditors were helping the

country actively to improve its financial situation. Furthermore, if Argentina would

not pay foremost attention to debt owed to international institutions it would be

banned from any external capital (Hornbeck, 2004, p. 6).

8

The non-performing categories are designed to write off debt. The state of the

debt not to be restructured is uncertain and consists of a small amount owed to

countries or commercial banks. The focus lies on the non-performing debt to be

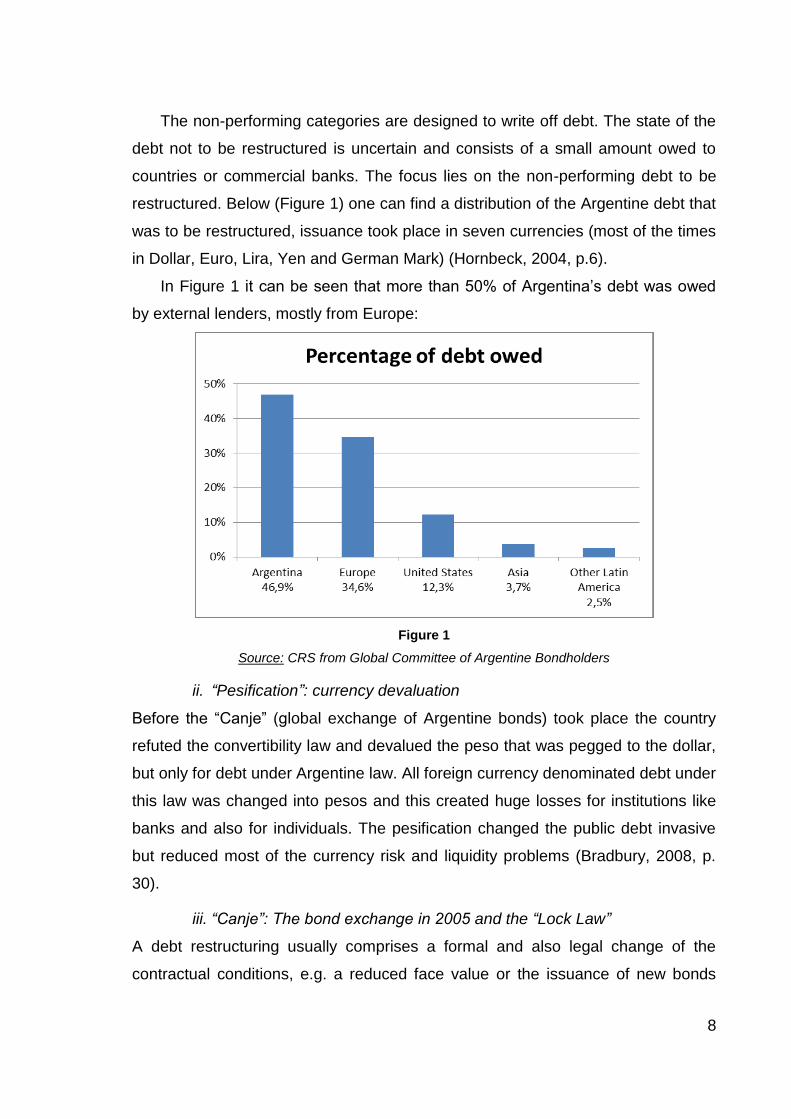

restructured. Below (Figure 1) one can find a distribution of the Argentine debt that

was to be restructured, issuance took place in seven currencies (most of the times

in Dollar, Euro, Lira, Yen and German Mark) (Hornbeck, 2004, p.6).

In Figure 1 it can be seen that more than 50% of Argentina’s debt was owed

by external lenders, mostly from Europe:

Figure 1

Source: CRS from Global Committee of Argentine Bondholders

ii. “Pesification”: currency devaluation

Before the “Canje” (global exchange of Argentine bonds) took place the country

refuted the convertibility law and devalued the peso that was pegged to the dollar,

but only for debt under Argentine law. All foreign currency denominated debt under

this law was changed into pesos and this created huge losses for institutions like

banks and also for individuals. The pesification changed the public debt invasive

but reduced most of the currency risk and liquidity problems (Bradbury, 2008, p.

30).

iii. “Canje”: The bond exchange in 2005 and the “Lock Law”

A debt restructuring usually comprises a formal and also legal change of the

contractual conditions, e.g. a reduced face value or the issuance of new bonds

9

with longer maturities and less interest. In the process the IMF usually takes an

assisting position as a third party between debtors and creditors. Argentina was

negotiating from 2002 until 2005. The country wanted to write down a large

amount of the debt owed by private entities and postpone action on IMF and Paris

Club debt (the Paris Club consists of 19 member countries with most of the

biggest economies worldwide). Finally, Argentina came up with a unilateral

decision. Together with the SEC (Securities and Exchange Commission) it offered

bond exchanges to private entities, codified with the “Ley Cerrojo” (Lock Law) that

prohibited the government to offer better future bond exchanges or reopen them.

This led to a higher participation of creditors as it was ensured that they would not

be better off if they would have waited for better future offers (Hornbeck, 2013, p.

8). Three options were unilaterally presented by Argentina: discount and par

bonds with reference to international law and quasi-par bonds governed by

Argentine law.

All options include the new collective action clauses which means that an offer

normally only needs 75% approval from the creditors to apply to all of them.

Discount bonds were the result of the reduction of bonds by 63% and

denominated in US dollars. Par bonds were also denominated in US dollar but

without a discount, only with longer maturities. Quasi-par bonds were denominated

in pesos with very long maturities (Hornbeck, 2004, p. 12-13). Additionally GDP-

linked warrants were added to some bonds in order to make them more lucrative.

GDP-linked warrants act like shares and are dependent of the GDP of a country. I

the GDP rises higher than expected the country has to pay yield to the beneficiary

of the warrant (Hornbeck, 2010, p. 16).

In January 2005 the face value of debt was $81.8 billion and the PDI (Past

Due Interest) amounted $20.8 billion and Argentina began with its debt exchange.

Although the general opinion of the creditors was negatively towards the offer from

Argentina $62.3 billion of the $81.8 billion were exchanged to $35.2 billion. This

constituted approximately 76% of the whole debt. However, Argentina did not find

a solution together with the Paris Club creditors and the IMF for the remaining debt

and the PDI. But in 2006 it repaid the whole IMF debt in order to have less

pressure from the institution (Hornbeck, 2013, p. 9).

10

iv. ICSID and bilateral investment treaties

Until the Argentine sovereign debt crisis took place holdout litigation1 was only

limited to national courts. But 170,000 Italian bondholders of the Task Force

Argentina bondholder association filed a claim against Argentina as an ICSID2

(International Center for Settlement of Investment Disputes) arbitration in 2006

which was the first of that kind. The case is commonly known as “Ablacat and

others vs. The Argentine Republic” and the Global Committee of Argentina

Bondholders coordinated this arbitration (Waibel, 207, p. 711). More than 40 of all

the cases pending before ICSID are against the Republic of Argentina and many

investors see their rights violated that are part of Argentina’s BITs (Bilateral

Investment Treaties). The reason to choose ICSID rather than national courts is

because ICSID awards have much more power than just national ones. But it is

anyway still possible that the enforcement of ICSID awards cannot be fulfilled due

to immunity of sovereigns (Waibel, 2007, p. 711). E.g. Argentina mentioned the

NPM provision (Non-precluded measures) which allows the state to follow actions

that are not complying with the bilateral investment treaty because of the

protection of public order (Burke-White, 2008, p. 3).

v. Bond exchange in 2010

In 2010 Argentina had three incentives to undergo a new bond exchange with the

rest of its debt ($29 billion dollar to private entities and $6.3 billion to countries of

the Paris Club): it is and was dependent from international capital markets, ad hoc

financing was becoming more difficult and current market conditions encouraged

the placement of debt (short time before the Eurozone crisis). At the end of April in

2010 it was possible to make an offer due to the support of the president Cristina

Fernández Kirchner, the temporarily suspension of the “Lock Law” and an

approval from the SEC. 67.7% were exchanged and $6 billion of debt unsolicited.

In total, 91.3% of the debt was exchanged by that time. But problems regarding

the default still remained because of the remaining debt. Litigations and

attachment orders hindered the country of issuing any new international bonds.

This remaining debt consisted of 11.2$ billion owed by holdouts worldwide and

1 Holdouts are creditors who take not part in the bond exchange and try to get all their money back through litigation

2 ICSID is an independent organization and was founded by the World Bank in 1965. ICSID tries to help to arbitrate

investment disputes between countries and wants to support international investments.

11

$6.3 billion owed by Paris Club countries. There has been one out of 3 ways for

Argentina to choose: do nothing with the holdouts and wait for the result of the

courts, settle with holdouts or plan a third swap to cover all remaining holdouts.

Argentina followed the first way of waiting but current court rulings could make it

difficult for the country to proceed with that strategy (Hornbeck, 2013, p. 7-8).

vi. Situation since 2010

As the holdout bondholders (those who do not agree with the collective bond

exchange and try to get their whole money back on their own) do not get paid

anything compared to the bondholders who exchanged the debt, this inequality is

currently challenged in court as an illegal issue because of the “pari passu” (equal

treatment) provision of bond contracts.

Different bondholder groups are following different litigation and settlement

policies. Institutional funds just negotiate for the best terms because litigation is

too expensive for them. Individual or retail investors set their bonds pretty early off

in the secondary markets. Hedge funds buy the discounted bonds and try to sue

for full recovery as some of them have special knowledge and therefore higher

success rates in that field (Hornbeck, 2013, p. 8). When there are just a few

holdouts left the chance of getting full repayment is even higher and especially

United States federal courts increased the pressure on Argentina (Miller und

Thomas, 2006, p. 1497).

One issue was a disposal of attachment orders on assets held by the central

bank of Argentina in the Federal Reserve Bank of New York, but those were

immune from attachment as this is stated in US law and an attachment could

follow a large withdrawal of reserves. Another issue is the pari passu provision of

bond contracts where claims found success in US courts. This is a difficult

situation for Argentina and under this judgment the country would need to default

on the exchanged debt. A suggestion was to reopen the previous bond exchange

for the holdouts but the issue still remains unresolved (Hornbeck, 2013, p. 13).

vii. Outlook

A question about which policies for an external creditor could be most effective for

resolving the debt issue arises. For example the US prohibited any financing or

issuing of new loans to Argentina. Only loans that benefit the very poor are

12

allowed (US Department of State, 2010/2013). As it is very hard to enforce

sovereigns as it was stated in the introduction bondholders had no success after

costly litigation processes. However, the biggest success has been the

introduction of the collective action clauses in sovereign debt contracts in the US,

which was already norm in the British law. They are now standard in the market

and if the majority of the creditors decides something the rest of them has to obey

the same like the majority (Hornbeck, 2013, p. 16).

13

5. Eurozone crisis: Greek debt problems

The Eurozone crisis came to light in 2009 as the newly elected Greek government

revealed the real numbers of their budget deficit and debt burden (from deficit-

GDP ratio of 6.7% to 12.7%). Tax evasion and overspending have been the key

factors that led to this precarious Greek financial situation after having faced the

burden of the global financial crisis. Public sector wages grew above average and

Greece also accumulated high debts because of hosting the Olympic Games in

2004. In May 2010 the Greek government received help from international

institutions as it was not anymore able to pay its creditors their money back at

agreed conditions ($73 billion in total) (Belkin, Weiss, Nelson, & Mix, 2012, p. 1).

In order to facilitate and accelerate the process of future debt restructurings

following has been decided recently for the whole Eurozone (Economic and

Financial Committee, 2013):

“In accordance with the ESM Treaty (Paragraph 3 of Article 12) the model CAC (Collective Action Clauses) will become mandatory in all new euro area government securities with maturity above one year issued on or after 1 January 2013, and not 1 July 2013, as previously contemplated.”

Through the implementation of the Collective Action Clauses into the sovereign

bond contracts it will be easier in future when it comes to restructuring after

sovereign debts as only a majority vote is needed to enforce a negotiated bond

exchange for all creditors.

a. Greek Pre-crisis: Causes

Within the European Union it was agreed on a deficit-GDP ratio threshold of 3%

but Greece could not fulfill this target as its expenditures overtook its revenues.

Generally said it was difficult for Greece to “maintain fiscal discipline” as tax

evasion and costly public systems (Greece had one of the most generous pension

systems) were part of the country’s problems. Moreover Greece’s international

competitiveness declined vastly as wages rose and production decreased at the

same time.

14

Since Greece joined the European Monetary Union it got easier access to

cheaper credit as external investors saw Greece acting under the rules of the

European Central Bank. An accumulation of a high level of debt was following.

Furthermore the Stability and Growth Pact which upon was agreed in 1997 did not

find its way to Greece.

b. Danger of a Greek default

After installing austerity measures and receiving financial assistance from the IMF

there has been also the suggestion of exiting the Eurozone and implementing the

country’s former currency, the drachme, again. This would increase its exports and

help to regain economic growth but the European and Greek leaders generally

don’t want to follow this strategy. Future borrowing costs would be higher for

Greece. But if the problem of the budget deficit cannot be solved with austerity

measures and financial assistance Greece has to default (Nelson, & Belkin, & Mix,

2010, p. 10).

i. Bailout loans and rescue packages

In May 2010 Greece received its first bailout loan from the EU (€80 billion) and the

IMF (€30 billion) of €110 billion with a 3 year maturity and interest rate of 5.5%.

Furthermore it was obliged to follow austerity measures which awoke plenty of

protests in Greece. But this loan did not help a lot since in May 2011 it was clear

that the country could not reach its fiscal aims (Ian Traynor, The Guardian, 2011).

Greece would have defaulted in July 2011 if it would not have got additional

€12 billion from the EU and IMF – therefore the country had to cut spending over

the next 5 years by €28 billion (BBC News, 2011). After extensions of maturities

and a reduction in the interest rate to 3.5% for the loans a second package of

€109 billion was agreed upon (and a rescue package of the newly created

European Financial Stability Facility) and it was accepted to write off Greek debt

by 50% (€100 billion) (Euro Summit Statement, 2011). In December 2011 the

debt-GDP ratio was 9% and the austerity measures followed a smaller deficit

before interest payments. But therefore the recession worsened and in 2011 the

GDP decreased by 7.1% and unemployment rose to 48.1% in 2011(Eurostat,

2012, p. 1).

15

Some economists argued it would be better for Greece to leave the euro and

implement its own currency but this would bring not only advantages like higher

exports but also disadvantages like hyperinflation. In October 2011 the EU

decided to offer an orderly default to Greece in combination with a €130 billion

loan with new austerity measures (BBC News, 2012).

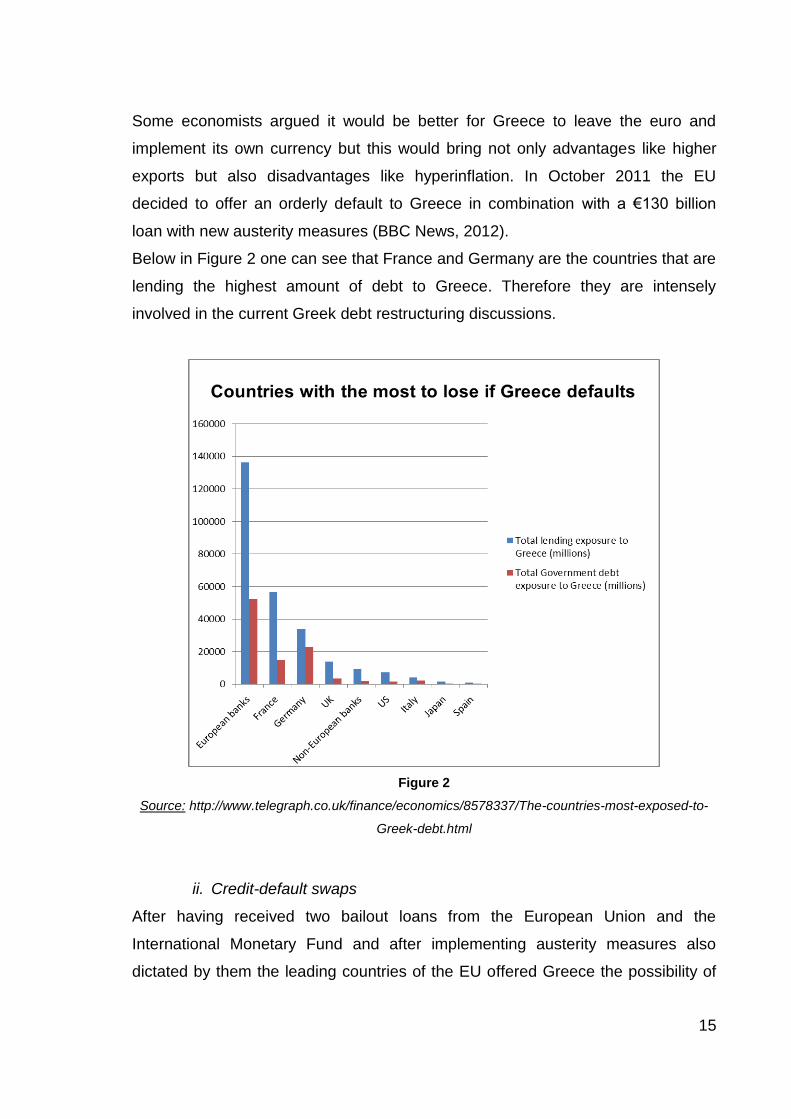

Below in Figure 2 one can see that France and Germany are the countries that are

lending the highest amount of debt to Greece. Therefore they are intensely

involved in the current Greek debt restructuring discussions.

Figure 2

Source: http://www.telegraph.co.uk/finance/economics/8578337/The-countries-most-exposed-to-

Greek-debt.html

ii. Credit-default swaps

After having received two bailout loans from the European Union and the

International Monetary Fund and after implementing austerity measures also

dictated by them the leading countries of the EU offered Greece the possibility of

16

undergoing an orderly default in combination with new austerity implications (BBC

News, 2012). An orderly default is a controlled preemptively engineered default.

Greek bonds were issued under the collective action clause and after the

majority of private holders of Greek debt agreed in 2012 on exchanging the bonds

the bonds became less worth with low interest rate for every creditor. Those bonds

are the first ones with credit-default swaps. This indicates an “insurance against

bad debts” to make them more attractive to the international creditors (Economist,

2012).

17

6. Comparison of Argentina and Greece: lessons learned

After 10 years from its default Argentina still did not manage to get back into the

global credit market. The consequences are huge and there has to happen a lot

until it will be considered as a serious country again. As Greece depicts the next

default model in international financial markets politicians can learn from the

Argentine model, although it is a quite different country and not part of a monetary

union like Greece (Valiante, 2011, p. 1).

Greece is highly likely hit worse than Argentina as its deficit was 10.5% of the

GDP in 2010 – Argentina’s only was 3.2% during the default. Greece also had a

debt-GDP ratio of 150% and Argentina only 54% (Newbery, & Barrionuevo, The

New York Times, 2011).

Concerning the devaluation of the peso (“pesification”) in Argentina there exist

different opinions about if it would be a wise decision for Greece or not to exit the

European monetary union as well. Fact is that the tool of devaluating its own

sovereign currency was a big help for Argentina to fight the economic downturn.

Another issue to consider is that the payback to the IMF was more important than

it would have been to private bondholders in the Argentine case. The most

important lesson Argentina can teach Greece is the danger of fatalism: Everything

can be changed and it is crucial that the people do not give up hope. Greece has

to implement major strategies to improve its competitiveness and long-term growth

prospects (Newbery, & Marrionuevo, the New York Times, 2011).

A big difference between those 2 cases is that the procedures and decisions in

Europe take much longer than they took in Argentina. As there was and still is the

perception that Europe will rescue Greece until the bitter end, the events in

Greece can be seen as a “slow motion” version of the events in Argentina

(Cavallo, 2011).

a. Lacking of a plan for investment on long-term key drivers

The case of Argentina has taught the financial world that austerity implementations

cannot be done when there is a lack of a plan for long-term growth. Making wrong

fiscal and monetary decisions never gives a country the chance of getting off a

vicious cycle. The IMF involved in the Argentine and Greek case is not to be seen

18

as an institution that supports long term growth but more as an institution that

helps to improve short-term liquidity or to make it possible again for a certain

amount of time. It should rather make conditions on monetary policy than

prescribe conditioned austerity measures. The World Bank and the European

Union should focus more on long-term growth for the country (Valiante, 2011, p.

4).

b. Lender of a last resort: IMF and ECB

A country that defaults or is at the brink of a default needs always a lender of last

resort. Some economists say that it is easier for Greece nowadays to have a

sufficient lender because it has the ECB but the IMF always helped out emerging

economies as a last resort as well and did so with Argentina in 2001. But in the

Argentine case the private sector was initially also involved: Private banks should

help the government to roll over Argentina’s debt in order to fulfill fiscal targets. But

those have not been fulfilled and deposits withdrawals from the local banks

followed. Afterwards the idea of a debt restructuring appeared but no one knew

how a debt restructuring should look like and this increased uncertainty as well.

The spreads of Greece have been nevertheless higher as 2001 in Argentina

because rating agencies downgraded the bonds. The Greek government does not

know how to proceed in the orderly debt restructuring process as it was the case

in Argentina as well (Cavallo, 2011).

One lesson that can be learned from Argentina is that the IMF is not willing to

take a haircut compared to commercial creditors (Newbery, & Barrionuevo, 2011).

Furthermore after Argentina paid its debt back firstly to the IMF and not to the

commercial creditors freed the government from restrictions by the IMF.

c. Devaluation of currency: Greek exit of European Union?

“A big Problem for Greece is that they have a strong currency, much stronger in

relation to their productivity” said Eric Ritondale in a New York Times Interview.

The biggest barrier for Greece in monetary policy is the common currency shared

with the rest of the countries of the European Monetary Union. Argentina’s peso

was pegged to the US dollar and the devaluation helped the country to regain

growth through exports (Newbery, & Barrionuevo, 2011).

19

The difference between Argentina and Greece concerning that issue lies in the

scope of banks’ assets/liabilities and contracts that need to be denominated. In

Argentina contracts continued to be denominated in pesos because the local

currency was not eliminated. Greece would need to devaluate all contracts and

this would lead to many bankruptcies. Moreover Greece has an international

institutional framework (Troika: IMF, ECB and EU) that Argentina missed and this

can help the country to regain its balance without any devaluation.

However, the biggest losers of a possible Greek currency devaluation would

be the ECB and its member banks and not the private households as private

deposits decreased vastly and Central bank loans rose. Private deposits are only

a small part of the total Greek funding as capital flight took place. Furthermore

Greece could restore its competitiveness more easily with currency devaluation.

Pulling off a deficit without this proven method by Argentina will need a template

never seen before (G.I., 2012).

d. Legal procedures

Concerning the negotiation process of the restructuring there are different legal

procedures available for the creditors. They don’t have to take part in the

exchange offers (those creditors are known as “holdouts”) but then they face the

risk of receiving no money at all. Generally said creditors can bring the claims for

payment before the court which is stated in the bond or before an international

court of arbitration (or e.g. ICSID). However, if a CAC is concluded in the bond

terms and conditions a creditor who does not participate in the exchange has no

success if he tries to start legal action.

10% of the Greek bonds that were restructured in 2012 were subject to

English law, the rest of the debt subject to Greek law. Initially there were no CACs

in the contracts included but the Greek government implemented them

retrospectively. Creditors with bonds under English law could have brought

forward their claims before English courts who did not implement CACs. They

most probably would have been successful.

A lot of creditors who had Argentine bonds under foreign law (e.g. Germany)

also filed claims against Argentina and tried to seize Argentine assets abroad, but

20

not very successfully. More successful were the United States concerning

enforcement of judgments regarding the Argentine default: If Argentina does not

pay back its debt it is not allowed to use New York as a financial venue

(Benninghofen, 2013).

All in all it is obvious that Greek is in a much more severe crisis than Argentina

was but it has also more help of financial institutions and organizations at disposal.

Bondholders of Greek debt under Greek law have less possibilities of filing a claim

against the government than bondholders of debt under foreign law.

21

Conclusion

As mentioned in the introduction one of the most difficult tasks in international

affairs is dealing with a sovereign that cannot pay back its debt to its external

lenders. There is no international framework for that although the European Union

together with the ECB and the IMF represent a tough framework for the Greek

crisis. A former deputy of the IMF, Anne Krueger, prepared the SDRM but was not

successful because it is really difficult to find a general procedure with which all

countries are satisfied. Resolving defaults quickly and efficiently is important for

avoiding long lasting recessions and missing growth opportunities. Therefore, it is

important to learn from each other like the Eurozone or especially Greece should

do so regarding the Argentine case.

However, one big difference between these two countries is that Greece is part of

the European integration process and therefore many decisions were made under

the influence of the European Union. A currency exit from the Eurozone leading to

devaluation and the reimplementation of the Greek drachme is no option and

would be against this integration policy. But Greece also has the ECB as a lender

of last resort that has more financial resources than the IMF which acted as a

lender of last resort for Argentina (and for Greece too, additionally to the ECB).

Furthermore Greece acts as kind of model for future Eurozone problems. Other

countries in troubles like Spain, Portugal or Ireland would follow the policies of

Greece and if it would devaluate its currency the whole Euro-integration-process

would fail.

As currency devaluation cannot be used as a strategy the decision makers

should focus on finding processes and structures for regaining long-term growth

and therefore regain the confidence of external investors. Bailout loans and rescue

packages only help to keep the short-term financial liquidity of the country and limit

the government’s flexibility as it has to obey austerity measures.

Argentina’s debt restructuring was a hard unnecessarily long-lasting fight and

in the end the country made a take it or leave it unilateral offer to its debt holders.

Because of not having the CACs in the first offering relatively much holdouts did

not want to take part in the collective exchange and tried to get their money back

22

through litigation which produced further cost for the creditors. There is still a case

pending at the ICSID involving a group with Italian bondholders (Task Force

Argentina). Greece owes most of their debt to European banks, France and

Germany who are the main leaders in Europe. As they design the restructuring

process together with Greece the negotiation process is not that hard as it was in

Argentina. Furthermore in all Greek bonds the CAC clauses are included and

besides the GDP-linked warrants they also came up with a new type, the credit-

default-swaps, to make the exchanged bonds more attractive to the creditors.

As this case is not over yet and maybe the start of a long process this topic

stays highly interesting and will be in need of further research.

To answer the research question Argentina does only partly represent a

convincing model for the Eurozone crisis. Greece applied similar legal procedures

but more advanced ones to convince more creditors to take part in the bond

exchange.

23

7. Bibliography

Benninghofen, J. (2013). Creditor rights during sovereign debt restructuring. CMS Hasche Sigle. Downloaded on November 29th, 2013 from http://www.lexology.com/library/detail.aspx?g=48978691-f1c0-4dbb-ab9d-6647c397cc60 Cavallo, D. (2011). Looking at Greece in the Argentinean mirror. VOX. Downloaded on November 22nd, 2013 from http://www.voxeu.org/article/looking-greece-argentinean-mirror De Jonge, A. (2013). Suffolk Transnational Law Review. Boston: Suffolk. De Paoli, B., Hoggarth, G., Saporta, V. (2006). Costs of sovereign default. London: Bank of England. G.I. (2012). What Argentina tells us about Greece. The Economist. Downloaded on November 22nd, 2013 from http://www.economist.com/blogs/freeexchange/2012/02/greece-and-euro Hornbeck, J. F. (2004). Argentina’s Sovereign Debt Restructuring. CRS Report for Congress. Downloaded on November 22nd, 213 from http://ww.w.ncseonline.org/NLE/CRSreports/04Oct/RL32637.pdf Hornbeck, J. F. (2013). Argentina’s Defaulted Sovereign Debt: Dealing with the “Holdouts”. USA: Congressional Research Service. Liebs, D., Lehmann, H. (2007). Lateinische Rechtsregeln und Rechtssprichwörter. München: C. H. Beck oHG. MECON Ministry of Economy and Public Finance (2002). Economic Report. Secretariat of Economy Policy. Downloaded on November 22nd, 2013 from http://www.mecon.gov.ar/peconomica/basehome/report.html Miller, M., Thomas, D. (2006). Sovereign Debt Restructuring: The Judge, the Vultures, and Creditor Rights. Warwick: University of Warwick. Molina, F., C. (2004). Registration Statement under Schedule B of the Securities Act of 1933, The Republic of Argentina. Securities and Exchange Commission. Downloaded on November 22nd, 2013 from http://www.sec.gov/Archives/edgar/data/914021/000095012304009731/y00143a1svbza.htm Nelson, R. M., Belkin, P., Mix, D. E., Weiss, M. A. (2012). The Eurozone Crisis: Overview and Issues for Congress. USA: Congressional Research Service.

24

Panizza, U., Sturzenegger, F., Zettelmeyer, J. (2009). The Economics and Law of Sovereign Debt and Default. Journal of Economic Literature, 47 (3), 651-698. USA: American Economic Association. Pedro, P. (2000). Argentina’s Structural Reforms of the 1990s. IMF Finance & Development. Downloaded on November 22nd, 2013 from http://www.imf.org/external/pubs/ft/fandd/2000/03/pou.htm Sub-Committee on EU Sovereign Debt Markets (2012). CAC. Economic and Financial Committee Europa. Downloaded on November 22nd, 2013 from http://europa.eu/efc/sub_committee/cac/index_en.htm Traynor, I. (2011). Greek debt crisis: Eurozone ministers delay decision on €12bn lifeline. The Guardian. Downloaded on November 22nd, 2013 from http://www.theguardian.com/business/2011/jun/19/greek-debt-crisis-eurozone-ministers?intcmp=239 Unknown author (2001). Argentina’s crisis explained. Time.com. Downloaded on November 22nd, 2013 from http://content.time.com/time/world/article/0,8599,189393,00.html Unknown author (2001). Argentina to default on $132bn debts. Telegraph.co.uk. Downloaded on November 22nd, 2013 from http://www.telegraph.co.uk/finance/economics/2746711/Argentina-to-default-on-132bn-debts.html Unknown author (2012). Eurozone crisis explained. BBC News. Downloaded on November 22nd, 2013 from http://www.bbc.co.uk/news/business-13798000 Unknown author (2009). Argentine Senate Approves Zero Deficit Law 30-07-2001. Voice of America. Downloaded on November 22nd, 2013 from http://www.voanews.com/content/a-13-a-2001-07-30-22-argentine-66952417/377971.html Unknown author (2011). EU leaders pledge to do what is needed to help Greece. BBC News. Downloaded on November 22nd, 2013 from http://www.bbc.co.uk/news/world-europe-13886099 Unknown Author (2011). Euro Summit Statement. Brussels: European Union. Downloaded on November 22nd, 2013 from http://www.consilium.europa.eu/uedocs/cms_Data/docs/pressdata/en/ec/125644.pdf Unknown author (2012). Euro area unemployment rate at 10.7%. Eurostat. Downloaded on November 22nd, 2013 from http://epp.eurostat.ec.europa.eu/cache/ITY_PUBLIC/3-01032012-AP/EN/3-01032012-AP-EN.PDF

25

Valiante, D. (2011). The Eurozone Debt Crisis: From its origins to a way forward. Brussels: Centre for European Policy Studies. Waibel M. (2007). Opening Pandora’s Box: Sovereign Bonds in international arbitration. The American Journal Of International Law (711-759). Cambridge: University of Cambridge.

Copyright © 2022 FDOKUMEN