Document de référence - Altran

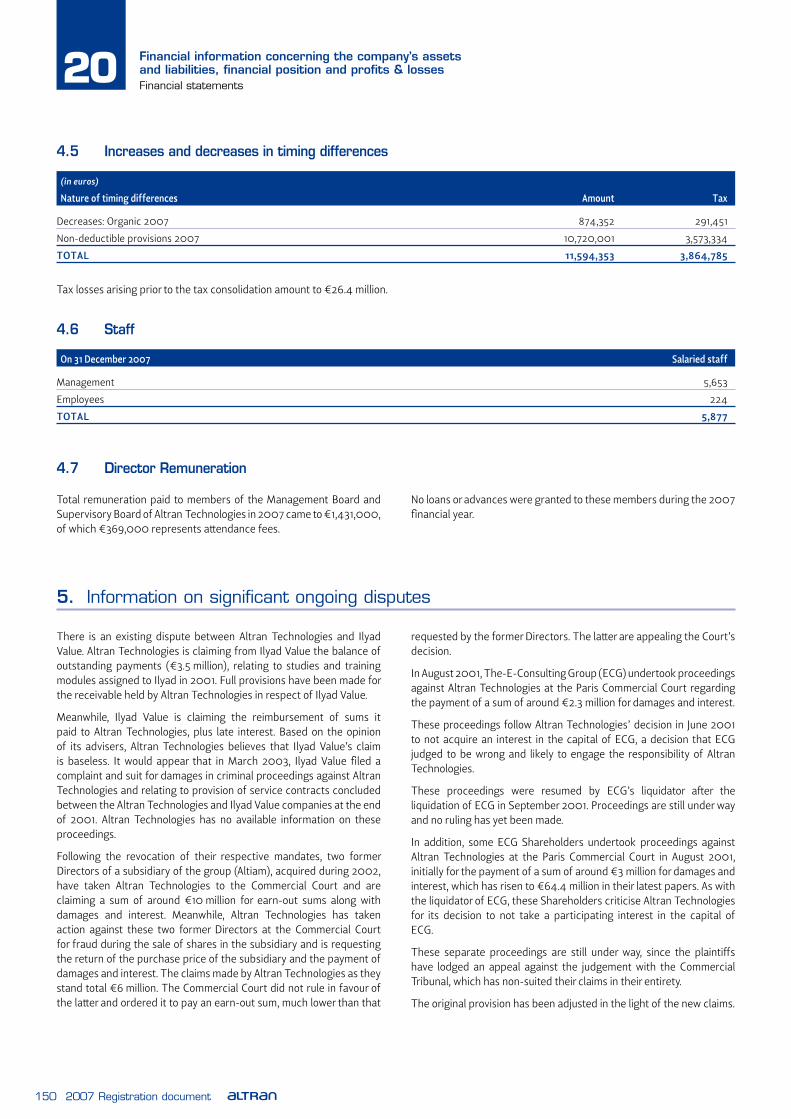

192

Registration Document 2007

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Document de référence - Altran

Registration Document 2007

Persons Responsible 5

Statutory Auditors 7

Selected fi nancial information 9

Risk factors 11

Information about Altran 13

Information about the company’s businesses 15

Organizational chart 19

Property, plant, and equipment 21

Operating and fi nancial review 23

Capital resources 61

Research and development 63

Trend information 65

Forecasts 67

Administrative, management, and supervisory bodies 69

Remuneration and benefi ts 71

Management Board and Supervisory Board practices 73

Employees 75

Major Shareholders 77

Related-party transactions 83

Financial information concerning the company’s assets and liabilities, fi nancial position and profi ts & losses 85

Additional information 161

Material contracts 167

Third-party information, expert statements, and declarations of interest 169

Documents available to the public 171

Information on holdings 173

APPENDIX

Appendix 1Internal controls 175

Appendix 22007 environmentaland labour report 183

Appendix 3Statutory Auditor’s reports 185

6

7

8

9

10

11

12

13

5

4

3

2

1 17

18

19

20

21

22

23

24

25

A1

A2

A3

14

15

16

32007 Registration document

2007 Registration document

Pursuant to article 28 of European Commission Regulation (EC) no. 809/2004, the following information is referenced in this document:

a business report, the consolidated and individual company fi nancial statements and Statutory Auditors’ reports on these fi nancial statements,

and the Statutory Auditors’ report on regulated agreements covered by article L.226-10 of the French Commercial Code and entered into by

Altran Technologies S.A. in 2005; these reports are given on pages 60 to 150 of the registration document fi led with the AMF on 29 May 2006

under number D.06-0488; and

a business report, the consolidated and individual company fi nancial statements and Statutory Auditors’ reports on these fi nancial statements,

and the Statutory Auditors’ report on regulated agreements covered by article L.226-10 of the French Commercial Code and entered into by

Altran Technologies S.A. in 2004; these reports are given on pages 36 to 150 (inclusive) of the registration document fi led with the AMF on

14 June 2005 under number R.05-091.

These documents are available on the AMF website (www.amf-france.org) and on the issuer’s website (www.altran.com).

•

•

This 2007 registration document was fi led with the French fi nancial markets authority (AMF) on 23 April 2008 in accordance with

article 212-13 of the AMF General Regulations. This registration document may be used to support a fi nancial transaction if accompanied

by a prospectus approved by the AMF.

This is a non-binding free translation into English of the original French text and is provided solely for the convenience of English

speaking users.

4 2007 Registration document

52007 Registration document

Statement by the person responsible for the 2007 registration document

I declare, after taking all reasonable measures for this purpose and

to the best of my knowledge, that the information contained in this

registration document is in accordance with the facts and makes no

omission likely to affect its impact.

I declare that to the best of my knowledge, the fi nancial statements

were prepared according to generally accepted accounting principles

and give a true and fair view of the assets and liabilities, earnings,

and fi nancial position of the company and all entities in its scope of

consolidation, and that the management report in chapter 9 gives a

faithful summary of the businesses, earnings, fi nancial position, and

main risks and uncertainties of the company and all entities in its scope

of consolidation.

I have obtained a completion letter from the Statutory Auditors in

which they state that they have audited the information relating to

the fi nancial position and the fi nancial statements presented in this

registration document and in the document as a whole.

The Statutory Auditors’ reports on the consolidated and individual

company fi nancial statements for the fi scal year ended 31 December

2007 are given in appendix 3 of this registration document and contain

no qualifi cations or observations.

Without qualifying their opinion on these fi nancial statements, the

Statutory Auditors, in their report on the fi nancial statements for

the fi scal year ended 31 December 2006, which is included in this

document for reference and in the 2006 Registration document fi led

with the AMF on 7 June 2007 under number D.07-0561, draw attention

on:

note 6 to the fi nancial statements, “Major litigation and contingent

liabilities”; and

measures taken to strengthen the company’s internal controls and

accounting information system as discussed in the Supervisory

Board Chairman’s report prepared in accordance with the last

paragraph of article L.225-68 of the French Commercial Code.

Without qualifying their opinion on these fi nancial statements, the

Statutory Auditors, in their report on the fi nancial statements for the

fi scal year ended 31 December 2006, which is included in this document

for reference and in the 2006 Registration document fi led with the

AMF on 7 June 2007 under number D.07-0561, draw attention to:

note 5 to the fi nancial statements, “Information on major ongoing

litigation”;

•

•

•

note 4.8 to the fi nancial statements on the accounting impact of

mergers completed during the fi scal year; and

measures taken to strengthen the company’s internal controls and

accounting information system as discussed in the Supervisory

Board Chairman’s report prepared in accordance with the last

paragraph of article L.225-68 of the French Commercial Code.

Without qualifying their opinion on these fi nancial statements, the

Statutory Auditors, in their report on the fi nancial statements for the

fi scal year ended 31 December 2005, which is included in this document

for reference and in the 2005 Registration document fi led with the

AMF on 29 May 2006 under number D.06-0488, draw attention to:

note 6 to the fi nancial statements, “Monitoring of signifi cant legal

disputes and possible liabilities”; and

measures taken to strengthen the company’s internal controls and

accounting information system as discussed in the Supervisory

Board Chairman’s report prepared in accordance with the last

paragraph of article L.225-68 of the French Commercial Code; and

note 4.11 to the fi nancial statements, “Net fi nancial indebtedness”,

which discusses the effects of the company’s adoption on 1 January

2005 of IAS 32 on the balance sheet presentation and net fi nancial

income.

Without qualifying their opinion on these fi nancial statements, the

Statutory Auditors, in their report on the fi nancial statements for the

fi scal year ended 31 December 2005, which is included in this document

for reference and in the 2005 Registration document fi led with the

AMF on 29 May 2006 under number D.06-0488, draw attention to:

note 2.12 to the fi nancial statements, “Provisions for contingencies

and charges”;

note 2.16 to the fi nancial statements, “Signifi cant outstanding legal

disputes”;

note 2.1 to the fi nancial statements which discusses the change

in accounting method effective 1 January 2005 on provisions for

retirement obligations recognised using the preferential method

set forth in Recommendation 2003-R01 of the French National

Accounting Board (CNC); and

measures taken to strengthen the company’s internal controls and

accounting information system as discussed in the Supervisory

Board Chairman’s report prepared in accordance with the last

paragraph of article L.225-68 of the French Commercial Code.

•

•

•

•

•

•

•

•

•

1Persons Responsible

6 2007 Registration document

Persons Responsible1Persons responsible for financial information

Without qualifying their opinion on these fi nancial statements, the

Statutory Auditors, in their report on the fi nancial statements for

the fi scal year ended 31 December 2004, which is included in this

document for reference and in the 2004 Registration document fi led

with the AMF on 14 June 2005 under number R.05-091, draw attention

to the following items in Notes 3.2, 4.12, 5.4, 5.5.1., and 5.5.2. to the

fi nancial statements:

changes in the internal controls environment (note 3.2);

segment information (note 4.12);

ongoing legal and regulatory proceedings (notes 5.4 and 5.5.1); and

the company’s corporate governance system (note 5.5.2).

•

•

•

•

Without qualifying their opinion on these fi nancial statements, the

Statutory Auditors, in their report on the fi nancial statements for the

fi scal year ended 31 December 2004, which is included in this document

for reference and in the 2004 Registration document fi led with the

AMF on 14 June 2005 under number R.05-091, draw attention to the

following items in notes 2.13, 2.15, and 2.16 to the fi nancial statements:

changes in the internal controls environment (note 2.13);

ongoing legal and regulatory proceedings (note 2.15); and

the company’s corporate governance system (note 2.16).

Yves de Chaisemartin – Chairman of the Management Board

•

•

•

Persons responsible for fi nancial information

Éric Albrand

Member of the Management Board

+33 (0)1 46 17 49 69

comfi @altran.com

Laurent Dubois

Head of Investor Relations

+33 (0)1 46 17 49 69

comfi @altran.com

72007 Registration document

Permanent external auditors

The permanent external auditors are members of the Versailles

Regional Statutory Auditors Commission (Compagnie Régionale de

Versailles).

Mazars & Guérard

Represented by Guy Isimat-Mirin and Jean-Luc Barlet

Tour Exaltis – 61 Rue Henri-Regnault

92075 La Défense Cedex

France

Initial appointment date: 29 June 2005

Mandate expiration date: Annual General Meeting held in 2008

to approve the fi nancial statements for the fi scal year ended

31 December 2007

A proposal will be made at the next Annual General Meeting to renew

Mazars & Guérard’s term for another six fi scal years, until the close of

the Annual General Meeting held to approve the fi nancial statements

for the fi scal year ending 31 December 2013.

Deloitte & Associés

Represented by Henri Lejetté

185 Avenue Charles-De-Gaulle

92524 Neuilly-sur-Seine Cedex

France

Initial appointment date: 28 June 2004

Mandate expiration date: Annual General Meeting held in 2010

to approve the fi nancial statements for the fi scal year ending

31 December 2009

2 Statutory Auditors

Substitute external auditors

The substitute external auditors are members of the Versailles Regional

Statutory Auditors Commission (Compagnie Régionale de Versailles).

Jean-Louis Lebrun

Tour Exaltis – 61 Rue Henri-Regnault

92075 La Défense Cedex

France

Initial appointment date: 29 June 2005

Mandat e expiration date: Annual General Meeting held in 2008

to approve the fi nancial statements for the fi scal year ended

31 December 2007

A proposal will be made at the next Annual General Meeting to renew

Jean-Louis Lebrun’s term for another six fi scal years, until the close of

the Annual General Meeting held to approve the fi nancial statements

for the fi scal year ending 31 December 2013.

BEAS

7-9 Villa Houssay

92524 Neuilly-sur-Seine Cedex

France

Initial appointment date: 28 June 2004

Mandate expiration date: Annual General Meeting held in 2010

to approve the fi nancial statements for the fi scal year ending

31 December 2009

8 2007 Registration document

92007 Registration document

2007 sales rose 6.4% to €1,591.4 million compared with €1,495.4 million in 2006.

(in million euros) 31/12/2006 H1 2007 H2 2007 31/12/2007

Sales 1,495.4 789.5 801.9 1,591.4

Current operating income 76.0 38.7 60.7 99.4

As % of sales 5.1% 4.9% 7.6% 6.2%

Non-recurring operating income (14.7) (1.7) (13.2) (14.9)

Goodwill amortisation (15.9) (12.5) (1.4) (13.9)

Operating income 45.4 24.4 46.2 70.6

As % of sales 3.0% 3.1% 5.8% 4.4%

Cost of net financial debt (23.1) (13) (16.0) (29.0)

Other financial income and expenses (3.0) (1.1) (1.1) (2.2)

Income tax charge (15.8) (15) (3.0) (18.0)

Net profit/(loss) 3.7 (4.7) 26.2 21.5

Minority interests (0.1) 0.2 (0.1) 0.1

NET PROFIT/(LOSS) ATTRIBUTABLE TO THE GROUP 3.8 (4.5) 26.1 21.6

Current operating income increased to €99.4 million in 2007 compared

with €76 million in 2006, resulting in a 6.2% current operating margin

in 2007. The current operating margin rose from 4.9% in the fi rst half

of 2007 to 7.6% in the second half of 2007.

Operating income came out at €70.6 million in 2007 (compared

with €45.4 million in 2006) after accounting for the negative impact

of non-recurring items of €14.9 million and €13.9 million in goodwill

impairment.

Cost of net fi nancial debt (-€29.0 million) is in line with group debt.

Net profi t attributable to the group totalled €21.6 million in 2007

compared with €3.8 million in 2006.

Group net debt under IFRS dropped to €359.5 million at 31 December

2007 from €379.9 million at 31 December 2006. The €77.7 million

reduction in group net debt in the second half of 2007 was due

to strong cash fl ow generation. This was the result of the group’s

improved operating margin and a reduction in DSO to 90 days at

31 December 2007.

Cost reduction plan

Increased efforts to reduce indirect costs were refl ected in a 1.2% drop

of the indirect cost rate, in 2007, which accounted for 26.3% of group

sales at 31 December 2007.

Refi nancing

Given the fi nancing agreement signed on 16 April 2008 with a banking

pool made up of four banks (see chapter 4 “Risk factors” of this

registration document for details), the scheduled increased use of

factoring, cash fl ow generation expected in 2008 and cash held at

group level, the group should have suffi cient fi nancial resources to

repay the convertible bond due on 1 January 2009.

Furthermore, as set out in detail in section 20.6 “Interim and other

fi nancial information” below, the company has announced its plans

to carry out a capital increase for a maximum of €130 million by

31 July 2008, which will enable it to strengthen its equity and

position the group to boost its development via targeted acquisitions.

3Selected fi nancial information

10 2007 Registration document

Selected fi nancial information3

Outlook

Altran aims to keep up with the market momentum despite an uncertain

macroeconomic environment. The trends seen at the end of 2007

have continued through into 2008.

In 2008 the group will pursue efforts to reduce its indirect costs and

aims to trend towards 20% of sales mid-term.

In particular, Altran will strive to maintain DSO at the current level.

112007 Registration document

The company’s risk factors are discussed in the management report in section 9.5 “Risks” on pages 35 -39 of this registration document.

4 Risk factors

12 2007 Registration document

132007 Registration document

5.1 Company history and development

5 Information about Altran

5.1.1 Company name

Altran Technologies S.A.

5.1.2 Place of registration and registration number

Paris Trade and Companies Register no. 702 012 956

Siret Number 702 012 956 00042

NAF code 742C

5.1.3 Date of incorporation and lifetime

Altran Technologies S.A. was created on 14 February 1970. Its life

extends until 14 February 2045, unless the company is dissolved

before this date or its life is extended beyond this date by law or by the

company’s Articles of Association.

5.1.4 Domicile, legal form, and governing legislation

Registered office: 58 Boulevard Gouvion-Saint-Cyr, 75017 Paris,

France.

Administrative headquarters: 2 Rue Paul Vaillant Couturier, 92300

Levallois-Perret, France.

Legal form: French public limited company with a Management Board

and Supervisory Board.

Governing legislation: French law including the French Commercial

Code and subsequent legislation concerning commercial businesses.

5.1 COMPANY HISTORY AND DEVELOPMENT 13

5.1.1 Company name 13

5.1.2 Place of registration and registration number 13

5.1.3 Date of incorporation and lifetime 13

5.1.4 Domicile, legal form, and governing legislation 13

5.2 INVESTMENTS 14

5.2.1 Principal investments 14

5.2.2 Principal future investments decided by management 14

14 2007 Registration document

Information about Altran5Investments

5.2 Investments

5.2.1 Principal investments

The signifi cant changes in 2007 to the company’s scope of

consolidation are as follows:

the merger of two companies in Belgium and six in Switzerland;

the sale of USM Endecar in Spain, which resulted in a €1,854 thousand

charge in the fi rst half (comprised of a €2,394 thousand divestment

loss, €222 thousand of related fees, and a €792 thousand provision

reversal);

the liquidation of the Cygnite subsidiary in the UK, which resulted in

an €8,000 charge; and

the creation of six new subsidiaries.

•

•

•

•

The company sold The Johnsson group in the US in July 2007; the

liquidation was fi nalised at the end of the year. The Johnsson group

generated €8,057 million of revenue in 2006. This sale was recognised

in the 2007 half-year fi nancial statements, most notably through a

€7 million goodwill impairment related to the process of selling the

business.

In the third quarter of 2007, Altran exercised its option to purchase the

75% it did not own of Arthur D. Little’s Korean subsidiary, Arthur D. Little

Yuhan Hoesa; an option which Altran acquired in July 2004. Altran

is now the full owner of Arthur D. Little Yuhan Hosea, which added

€2.8 million to the company’s overall revenue in the second half of

2007.

The company’s earn-out programme and assumptions for future

payouts are discussed in note 7 to the consolidated fi nancial statements,

“Off-balance sheet commitments”.

Companies acquired over the past five fiscal years

2003 2004 2005 2006 2007

Company Country Company Country Company Country Company Country Company Country

Aktiva VIP

Holding Netherlands

Little

acquisition

Co Hong

Kong and

Little

acquisition

Co Singapore

Hong

Kong and

Singapore

Hilson Moran

Italie Italy

CQ

Consulting

GmbH Austria Little Brazil Brazil

ADL Yuhan

Hosea Korea

C Quential

SRL Italy

Consultores

CA Venezuela

The following table lists the amount paid for these acquisitions each year (initial payment plus earn-out).

(in million euros) 2004 2005 2006 2007

17.6 22.7 41.1 9.4

5.2.2 Principal future investments decided by management

Altran plans to invest in the following in 2008 in order to support its

transformation:

IT system upgrades (ERPs, networks, etc.);•

tools for employee communication and collaboration (company

intranet, knowledge management software, etc.); and

a streamlining of the company’s brands.

•

•

152007 Registration document

6.1 Main businesses

6Information about the company’s businesses

Altran aims to support its customers throughout the life cycle of

a product or a service, from design or manufacturing through to

production process optimization. Altran consultants have a wide range

of skills covering just about every fi eld of engineering.

From the time the company was founded, Altran has been committed

to helping customers plan and implement important strategy, research,

and technology projects. Altran consultants play an active role in all

phases of product or service development’s life cycle.

The cornerstone of Altran’s high-quality service is its skills in mastering

a technology, and transferring that technology from one industry to

another. This unique approach to technological innovation, coupled

with an ability to break down complex procedures into manageable

steps, have prompted customers to select Altran as a preferred

partner. With the help of Altran consultants, customers can transform

innovation from a modern-day challenge to a strategic driver and

source of differentiation. Altran’s customers realise that in today’s

fast-paced markets, innovation is essential to securing a sustainable

competitive advantage.

Indeed, innovation is at the heart of Altran’s customers’ strategies,

as it will enable them to penetrate new markets and fuel continued

business growth.

Sales by business

6.1 MAIN BUSINESSES 15

6.2 MAIN MARKETS 16

6.2.1 Technology and R&D consulting 16

6.2.2 Organisation and information systems consulting 17

6.2.3 Strategy and management consulting 17

6.3 COMPETITION 18

16 2007 Registration document

Information about the company’s businesses6Main markets

6.2 Main markets

Altran operates in the following three markets:

technology and R&D consulting;

organisation and information systems consulting; and

strategy and management consulting.

6.2.1 Technology and R&D consulting

The market for technology and R&D consulting services was estimated

to be around €55 billion in the US and Europe in 2005, based on a 2005

Altran Positioning Study carried out by Pierre Audoin Consultants. This

means that the technology consulting market is now approximately the

same size as that for management consulting.

Sources: Altran Global Strategic Marketing and 2005 Altran Positioning Study by Pierre Audoin Consultants.

Altran is the leading technology consulting fi rm in Europe in terms

of revenue. Nevertheless, the European market remains highly

fragmented; the ten biggest players in Europe’s three main countries

(Germany, France, and the UK) have only a 30%-40% market

share. Altran’s market share was approximately 9.8% in France and

1.5%-5% in other European countries in 2005, according to Altran

Global Strategic Marketing.

•

•

•

Technology consulting market in Western Europe in 2005

Sources: Altran Global Strategic Marketing and 2005 Altran Positioning Study by Pierre Audoin Consultants.

The technology consulting market should expand substantially in

France and the rest of Europe over the next few years, driven by the

following factors:

heavier R&D spending, since Western European countries invest a

lower percentage of their GDP in R&D and European manufacturers

realize that they must catch-up and slash their time-to-market if

they are to remain competitive; and

a greater reliance on R&D outsourcing. While the long-term

outsourcing rate is diffi cult to estimate, it currently stands at less

than 15% of total R&D spending in Europe (according to Pierre Audoin

Consultants). This percentage will undoubtedly rise – although

probably not to the levels seen for IT services outsourcing.

The technology consulting market is highly fragmented, but should

undergo consolidation in the coming years as a result of:

pressure from customers seeking industrial partnerships with

R&D consultants, as customers cut their number of suppliers and

standardize their procurement processes;

a shift in customer demand towards more content-focused,

packaged solutions which are diffi cult for consultants offering a

single service to provide;

a growing need for fi xed-price services requiring increasingly

technical knowledge, which pushes out small players providing only

technical support; and

globalization, which means that consultants must be able to provide

international services to customer sites around the world.

•

•

•

•

•

•

172007 Registration document

Information about the company’s businesses 6Main markets

6.2.2 Organisation and information systems consulting

Approximately one-third of Altran’s revenue is generated by

organisation and information systems consulting. This market is more

structured than the technology consulting market, although Altran

has a smaller market share. The market for these services in Europe,

excluding outsourcing, is around €45 billion per year.

Altran does not intend to offer all the services typically provided by

large IT fi rms; rather, it has decided to focus on niche markets in the

IT space (SAP, application testing, etc.) where Altran already has a solid

reputation.

The software and services market grew 6.5% in France in 2006,

based on data from Syntec Informatique. This market has expanded

3-4 times faster than GDP and 1.5-2 times faster than corporate

investment spending. Much of this growth can be attributed to

business transformation projects, and the market should continue to

be supported by a wave of M&A activity. Consulting and applications

maintenance (especially third-party application maintenance) are the

market’s main drivers.

Growth has been particularly marked in the fi nancial sector, where

spending on these services jumped 8%, followed closely by the public

sector.

The organisation and information systems consulting market has

exceptional long-term growth potential as a result of expanding

business needs, a strong trend towards IT outsourcing, and repeated

technological advancements which open the doors to new uses and

fi elds of application.

6.2.3 Strategy and management consulting

Altran’s strategy and management consulting is carried out primarily

through its Arthur D. Little subsidiary, which was purchased during

an LMBO in 2002. Altran acquired all of Arthur D. Little’s operations

outside the US during this LMBO, as well as the global brand name.

The strategy and management consulting market has mushroomed

since 2005, driven by a fl urry of M&A deals in several sectors. This

market is estimated at approximately €50 billion a year in the US

and Europe, and is expected to grow 5%-7% over the next few years

(according to Kennedy Information Research group and Pierre Audoin

Consultants).

Altran’s services focus on a limited number of practices in order to take

advantage of Arthur D. Little’s robust skills in these areas on a global

level. The company has decided to target Arthur D. Little’s international

business development on fi ve industries, including healthcare, energy,

and automotive.

18 2007 Registration document

Information about the company’s businesses6Competition

6.3 Competition

Altran is the leading technology and R&D consulting fi rm in Europe. Its

competitors vary depending on the type of consulting project; these

competitors include:

strategy and/or management consultancies (particularly in terms

of Arthur D. Little’s competitors);

IT services companies;

engineering fi rms specialised in a specifi c fi eld (e.g., environmental,

mechanical, or acoustical engineering); and

listed or unlisted companies offering similar services (e.g., Alten,

AssystemBrime, and SII).

•

•

•

•

However, none of these competitors have Altran’s geographic footprint,

nor do they have skills in such a wide array of industries or technologies.

Altran’s ability to leverage its international network, provide services in

many countries, and combine state-of-the-art knowledge in several

fi elds is a key differentiating factor – and one that can help Altran’s

customers succeed as they cross new borders.

Altran recently restructured its technology consulting business in

France. The business is now grouped by vertical industry, making its

services more clear to customers. The following table gives an overview

of Altran’s main technology consulting markets in Europe.

France United Kingdom Germany

Market size in 2005 €4.0 billion €4.0 billion €4.4 billion

Top sectors

Aerospace

Automotive

Energy*

Telecoms

Aerospace

Energy*

Telecoms

Public sector

Automotive

Industrial engineering

Energy*

Aerospace

Top three competitors

Altran

Assystem

Alten

Atkins

BAE Systems

QinetiQ

Siemens

T-Systems

ESG

Trends

Consolidation, globalization, fewer suppliers,

more powerful purchasing departments

* Utilities, chemicals, and environmental industries.

Sources: Altran Global Strategic Marketing and 2005 Altran Positioning Study by Pierre Audoin Consultants.

192007 Registration document

A list of companies included in Altran’s scope of consolidation is given

in section 20.3, in note 2 to the consolidated fi nancial statements,

“Scope of consolidation”. Recent changes to this scope are discussed

in section 5.2.1 “Principal investments”.

The company does not have any commitments to purchase minority

interests.

The following paragraphs discuss the payments made between the

parent company and its subsidiaries.

Management fees and subcontracted administrative services

Altran Technologies, the parent company, pays for support functions

(communications, human resources, accounting, legal and tax affairs,

etc.), and bills the costs for these services to its French subsidiaries and

foreign holding companies. These bills, which consist of management

fees and subcontracted administrative services, are calculated using

cost-plus accounting and divided among the subsidiaries and foreign

holding companies based on the revenue generated and resources

used.

The parent company billed its subsidiaries and foreign holding

companies a total of €34.7 million for support functions in fi scal 2007.

Support functions paid for by the parent company and not re-billed

amounted to €28.9 million for the year.

Centralized cash management

The parent company manages cash for all its entities through a cash

management subsidiary, GMTS, which covers subsidiary overdrafts

and pays interest on cash surpluses on a daily basis.

Dividends

Altran Technologies, the parent company, receives dividends from its

direct subsidiaries.

7 Organizational chart

20 2007 Registration document

Organizational chart7

Simplifi ed organizational chart

Altran Technologies SA owned 100% of Altran International BV when it was founded in 1997, but in 1997 sold a 5% stake to a former manager with

whom Altran is in legal proceedings.

212007 Registration document

8.1 Signifi cant property, plant, and equipment

8Property, plant, and equipment

Altran has a policy of leasing its business premises, although it owns

buildings with a combined value of €8.5 million in France, Italy, the

UK, and Venezuela. No property is owned either directly or indirectly

by Altran managers, nor is leased to Altran or an Altran subsidiary.

8.2 Environmental issues

Not material.

8.3 Brands and patents

Altran’s customers are the sole owners of new products and technology

developed with the help of Altran consultants. Altran has one subsidiary

that carries out development work and fi les patents exclusively

for Altran.

Altran owns all its brands.

8.1 SIGNIFICANT PROPERTY, PLANT, AND EQUIPMENT 21

8.2 ENVIRONMENTAL ISSUES 21

8.3 BRANDS AND PATENTS 21

22 2007 Registration document

232007 Registration document

9 Operating and fi nancial review

9.1 SIGNIFICANT EVENTS 24

9.1.1 Corporate governance 24

9.1.2 Changes in scope of consolidation 24

9.1.3 AMF’s Enforcement Committee Decision 24

9.1.4 2007/2009 Operational efficiency plan 24

9.1.5 The operational merger in Paris of Altran Consulting & Information Services (CIS) and Altran Telecoms, Electronics & Media (TEM). 25

9.1.6 Issuance of a new stock option plan and bonus share plan for employees 25

9.1.7 Refinancing 25

9.2 SITUATION OF THE COMPANIES INCLUDED IN THE CONSOLIDATION SCOPE 26

9.3 SEGMENT REPORTING 30

9.4 ACTIVITIES OF ALTRAN TECHNOLOGIES S.A. AND ITS MAIN SUBSIDIARIES 34

9.5 RISKS 35

9.6 RESEARCH AND DEVELOPMENT 39

9.7 FORESEEABLE FUTURE TRENDS AND OUTLOOK 40

9.8 SUBSEQUENT EVENTS 40

9.9 ALTRAN TECHNOLOGIES S.A.’S COMPANY FINANCIAL STATEMENTS AND ALLOCATION OF EARNINGS 41

9.10 SUBSIDIARIES AND EQUITY HOLDINGS 41

9.11 INFORMATION ON THE SHARE CAPITAL, CROSS-SHAREHOLDINGS, TREASURY SHARES 41

9.12 CONTROLLING COMPANIES AND THEIR OWNERSHIP INTEREST IN ALTRAN TECHNOLOGIES 41

9.13 TRANSACTIONS CARRIED OUT DURING THE YEAR SUBJECT TO ARTICLE L.621-18-2 OF THE FRENCH MONETARY AND FINANCIAL CODE AND ARTICLE 222-15-3 OF THE AUTORITÉ DES MARCHÉS FINANCIERS’ GENERAL REGULATION 42

9.14 SHARE BUYBACKS 42

9.15 INFORMATION ON THE CALCULATION METHODS AND EFFECTS OF ADJUSTMENTS TO THE CONVERSION BASIS FOR BONDS AND THE SUBSCRIPTION OR PURCHASE OF SECURITIES CONVERTIBLE OR EXCHANGEABLE INTO SHARES 42

9.16 EMPLOYEE SHARE OWNERSHIP 43

9.17 STOCK OPTIONS 43

9.18 COMPANY MANAGEMENT – CORPORATE OFFICERS 46

9.18.1 Composition of the Supervisory and Management Boards 46

9.18.2 Compensation of corporate officers 58

9.19 COMMITMENTS MADE BY THE COMPANY TO ITS CORPORATE OFFICERS 60

9.20 ADDITIONAL INFORMATION 60

24 2007 Registration document

Operating and fi nancial review9Significant events

9.1 Signifi cant events

9.1.1 Corporate governance

The Management Board is comprised of two members:

Mr Yves de Chaisemartin, Chairman;

Mr Eric Albrand.

They were appointed by the Supervisory Board on 11 January 2007,

for a period of two years, in compliance with Altran Technologies’ by-

laws.

The Supervisory Board is currently comprised of the following

members:

Mr Dominique de Calan, Chairman;

Mr Michel Sénamaud, Vice-Chairman;

Mr Roger Alibault;

Mr Jacques-Etienne de T’Serclaes, Member of the Supervisory

Board and Chairman of the Audit Committee, appointed on 5 March

2007 with effect from 30 March 2007.

Their term of offi ce expires at the end of the Annual General Meeting

held to approve the fi nancial statements for the year ended 31 December

2008.

Mrs Guylaine Saucier resigned from the Supervisory Board on

15 February 2007.

9.1.2 Changes in scope of consolidation

During 2007 the group completed several transactions affecting its

scope of consolidation including:

Acquisitions

Since it became part of the group on 1 August 2007, Hilson Moran Italia

has generated sales totalling €1.4 million.

An option to purchase 75% of the share capital of the Korean subsidiary

Arthur D. Little Yuhan Hosea was exercised in August 2007. The

sales contribution of this company in the second half of 2007 was

€2.8 million.

Disposals

The US company The Johnsson group was sold on 2 July 2007 prior

to liquidation. 2006 sales totalled €12.6 million. The consequences of

this disposal were accounted for in the 2007 half yearly results, namely

the partial impairment of goodwill linked to the disposal of this activity,

with a negative impact of €7 million.

•

•

•

•

•

•

USM Endecar in Spain was sold on 5 February 2007. This company’s

sales totalled €2 million in 2006. This disposal had a net negative

impact of €1.9 million in the fi rst half of 2007 (including -€2.4 million

in capital losses arising from the deconsolidation, -€0.2 million in fees

linked to the transaction and +€0.8 million in reversal of provisions).

Mergers & liquidations

Within the framework of the group’s effort to streamline its scope of

consolidation Altran carried out a number of mergers and liquidations

in Switzerland, France, the United States, Belgium and the United

Kingdom.

Creations

The group created 6 new subsidiaries in 2007, namely to support the

geographical diversifi cation of the US subsidiary CSI.

9.1.3 AMF’s Enforcement Committee Decision

On 31 May 2007, Altran group was informed of the AMF’s Enforcement

Committee Decision relating to the accounting periods ending

31 December 2001 and 30 June 2002, imposing an administrative

penalty of €1.5 million. The Committee imposed a fi ne on the company

for the misconduct of its former managers who have all now left the

group. This decision does not take into account the Rapporteur’s

conclusions which recommended far more moderate fi nes. This

decision penalises all of Altran’s current Shareholders for past actions.

Altran has appealed against this decision. Nonetheless, the fi nancial

penalty has been paid in full.

9.1.4 2007/2009 Operational efficiency plan

At the Shareholders’ Annual General Meeting held on 29 June 2007,

Altran announced an operational effi ciency plan for 2007/2009 in an

aim to improve group performance and signifi cantly reduce its indirect

costs.

The objective is to cut indirect costs by at least three percentage points

by 2009 reducing them to 25% of sales. In the medium term the group

aims to bring indirect costs down towards the industry average of 20%

of sales.

The fi rst measures taken in collaboration with a consulting fi rm

covered:

sales effi ciency: reviewing the group’s sales organisation in terms

of costs and effi ciency;

•

252007 Registration document

Operating and fi nancial review 9Significant events

purchasing: reviewing the steps taken to implement a group

purchasing policy;

WCR: reviewing performance in terms of working capital

management;

support functions France: analysing the organisation and

performance of the support functions France;

international support functions: analysing the organisation and

performance of international support functions.

This plan is also supported by actions taken pursuant to the former

performance plan presented in 2005:

positive effect of investments already made (IT, property,

purchasing);

the group’s structure has been gradually simplifi ed since 2006 and

the number of companies has been reduced by a third;

the budget process has been reviewed; authorisation to incur

additional expenses is now subject to growth achievement;

full commitment to the execution of this plan is requested from

country managers.

9.1.5 The operational merger in Paris of Altran Consulting & Information Services (CIS) and Altran Telecoms, Electronics & Media (TEM).

Over the past few months the group has noted that both Information

Systems and Telecommunications have experienced strong growth in

France and that it is becoming harder to defi ne the frontier between

these two large markets.

•

•

•

•

•

•

•

•

Therefore the group has decided to merge these two businesses in

Paris, opening up opportunities to:

create a new and unmatched Telecommunications offer for our CIS

clients, mainly in the Bank and Insurance sector in which we are a

key player;

to expand our Information Systems offer for our TEM customers.

The group has also appointed a new management team to boost

creativity and increase shared offers between these two activities.

The skills and size of the Altran CIS Paris and Altran TEM teams will

make this new merged business the driving force behind creating the

group’s value added offer.

9.1.6 Issuance of a new stock option plan and bonus share plan for employees

On 20 December 2007, the group issued 2,589,830 stock options and

818,740 bonus shares to 2,191 employees. This plan represents 2.9% of

the company’s share capital.

9.1.7 Refinancing

Given the fi nancing agreement signed on 16 April 2008 with a banking

pool made up of four banks (see section 9.5.1 “Liquidity risk”), the

scheduled increased use of factoring, cash fl ow generation expected

in 2008 and cash held at group level, the group should have suffi cient

fi nancial resources to repay the convertible bond due on 1 January

2009.

Furthermore, the company has announced its plan to carry out a

capital increase for a maximum of €130 million by 31 July 2008, which

will enable it to strengthen its equity and position the group to boost its

development via targeted acquisitions.

•

•

26 2007 Registration document

Operating and fi nancial review9Situation of the companies included in the consolidation scope

9.2 Situation of the companies included in the consolidation scope

(in million euros)

December 2007 December 2006

(12 months) (12 months)

Sales 1,591 1,495

Other revenue 2 3

TOTAL REVENUE 1,593 1,498

CURRENT OPERATING INCOME AND EXPENSES 99 76

Other non-recurring operating income and expenses (15) (15)

Goodwill impairment (14) (16)

OPERATING INCOME 71 45

Cost of net financial debt (29) (23)

Other financial income 6 5

Other financial expenses 9 8

Income tax (18) (16)

Share of net profit/(loss) from associated companies

NET PROFIT/(LOSS) BEFORE RESULTS OF DISCONTINUED AND HELD-FOR-SALE 22 4

NET PROFIT/(LOSS) AFTER TAX OF DISCONTINUED AND HELD-FOR-SALE

NET PROFIT/(LOSS) 22 4

Minority interests

NET PROFIT/(LOSS) ATTRIBUTABLE TO THE GROUP 22 4

Earnings per share (in euros) 0,18 0,03

Diluted earnings per share (in euros) 0,18 0,03

Current operating income (excluding non recurrent items) totalled

€99.4 million, implying a current operating margin of 6.2% up 1.1%

compared with 2006. This improved performance is due to strong

momentum in the second half of 2007 and is due to the combination

of four factors:

Technologies and Innovation (TI) in France returned to profi t. The

current operating margin in France came out at 5.9% in the second

half of 2007 compared with -0.1% in the fi rst half;

•

the Northern zone performed well, sustaining growth close to 10%

and containing wage increases;

the Southern zone driven by Spain (+9.5% growth between

the second half of 2007 and the second half of 2006) where

restructuring measures programmed in 2008 should support

recovery further;

the group’s holding company contributed to income optimisation

by reducing costs, refl ecting sustained efforts to streamline the

group’s central support functions.

•

•

•

272007 Registration document

Operating and fi nancial review 9Situation of the companies included in the consolidation scope

(in million euros) 2007 H2 2007 H1 2007 2006 H2 2006 H1 2006

Turnover 1,591 802 789 1,495 749 746

Gross margin 518 263 255 487 236 251

% 32.5% 32.8% 32.3% 32.6% 31.5% 33.6%

General fees (418) (202) (216) (411) (209) (202)

% (26.3)% (25.2)% (27.4)% (27.5)% (27.9)% (27.1)%

CURRENT OPERATING INCOME 99 61 39 76 27 49

% 6.2% 7.6% 4.9% 5.1% 3.6% 6.5%

Gross margin remained stable between 2006 and 2007 (32.5% vs.

32.6%), whilst overheads were reduced by 1.2%. The overhead rate

after consolidation adjustments dropped from 27.5% in 2006 to 26.3%

in 2007 (note that reported data indicated an overhead rate down

from 28.1% in 2006 to 26.4% in 2007).

Current operating margin came out at 7.6% for the second half of 2007

up from 4.9% in the fi rst half.

Goodwill impairment of €13.9 million was recorded in 2007 including

€12.2 million for the fi rst half and €1.7 million for the second half.

group fi nancial loss (-€31.2 million) is in line with group debt.

Net income totalled €21.6 million in 2007.

Sales

2007 sales totalled €1,591.4 million up 6.4% compared with 2006, i.e.

a €96 million increase. This growth rate takes into account the -0.6%

negative impact of currency movements and the -0.4% negative scope

effect.

This increase in group sales refl ects strong performance in the

Northern zone, a return to growth in France and in the Southern zone

in the second half of the year.

International activities were supported by strong performance in the

Benelux countries, Sweden, Germany and the UK, particularly in the

fi rst half of 2007. In the second half growth was mainly driven by Italy

and Spain.

In France, growth was strengthened by the reorganisation of

Consulting & Information Services (CIS) and Technologies & Innovation

(TI) activities, adding transparency to operational organisation and

enabling improved effi ciency. TI France showed strong sales growth,

particularly in the fourth quarter where the group gained market

share.

At group level, the main growth drivers are increased resources

(73%) and tariffs (18%). Increased resources were most evident in the

Northern zone, whereas tariffs rose mainly in the Southern zone (Italy,

Spain) and in Germany. These three countries represent 26.5% of total

sales and 37% of growth.

The positive impact of these two drivers was heightened by a +0.5%

increase in the billing rate, up from 84.1% to 84.6%.

Expenses

Current operating expenses showed a mixed trend over the year, but

overall sales outgrew expenses.

Taking each half-year separately:

in the fi rst half of 2007, with the exception of TI France, none

of the geographical areas managed to pass on wage increases

to customers, resulting in a tighter margin; the relative weight of

payroll expenses as a percentage of sales rose 1.5%, from 69% to

70.6%;

however, in the second half of 2007 sales grew (+7%) at a faster

pace than payroll expenses (+2.4%), as a result of the recovery of

TI France. Overall, there is a clear reduction in payroll expenses as a

percentage of sales (-3 percentage points).

•

•

(in million euros) 2007 2006 2007 vs 2006

Turnover 1,591 1,495 6.4%

Staff costs 1,096 1,042 5.3%

% Turnover 68.9% 69.7% (0.8) pt

(in million euros)

2007

H2

2007

H1

2006

H2

2006

H1

H2 2007

vs H2 2006

H1 2007

vs H1 2006

Turnover 802 789 749 746 7.0% 5.8%

Staff costs* 539 557 527* 515 2.4% 8.2%

% Turnover 67.3% 70.6% 70.3% 69.0% (3.0) pts 1.5 pt

* In this table the €512.4 million in payroll expenses reported for 2006. do not include stock options and employee benefits for €14.4 million which are included in the notes in the registration document.

28 2007 Registration document

Operating and fi nancial review9Situation of the companies included in the consolidation scope

External expenses

(in million euros) 2007 2006 2007 vs 2006

Total external charges 344 320 7.5%

% Turnover 21.6% 21.4% 0.2 pt

Sub-contracting 111 96 15.3%

% Turnover 7.0% 6.4% 0.5 pt

BC Red. 4 4 6.8%

% Turnover 0.2% 0.2% 0.0 pt

Simple rentals and external expenses 58 54 8.0%

% Turnover 3.6% 3.6% 0.1 pt

Training 10 9 6.1%

% Turnover 0.6% 0.6% 0.0 pt

External services and fees 46 49 (7.3)%

% Turnover 2.9% 3.3% (0.4) pt

Transportation and travels 75 68 9.4%

% Turnover 4.7% 4.6% 0.1 pt

Other purchases and outside services 41 40 3.4%

% Turnover 2.6% 2.7% (0.1) pt

(in million euros) H2 2007 H1 2007 H2 2006 H1 2006

H2 2007 vs

H2 2006

H1 2007 vs

H1 2006

Total external charges 174 170 161 159 8.5% 6.4%

% Turnover 21.7% 21.5% 21.4% 21.4% 0.3 pt 0.1 pt

Sub-contracting 57 53 48 48 19.8% 10.7%

% Turnover 7.2% 6.7% 6.4% 6.4% 0.8 pt 0.3 pt

BC red. 2 2 2 2 18.7% (3.9)%

% Turnover 0.2% 0.2% 0.2% 0.2% 0.0 pt 0.0 pt

Simple rentals and external expenses 30 28 27 27 11.1% 4.9%

% Turnover 3.7% 3.6% 3.5% 3.6% 0.1 pt 0.0 pt

Training 5 5 5 4 (6.9)% 23.3%

% Turnover 0.6% 0.6% 0.7% 0.5% (0.1) pt 0.1 pt

External services and fees 23 23 24 26 (5.2)% (9.3)%

% Turnover 2.8% 2.9% 3.2% 3.4% (0.4) pt (0.5) pt

Transportation and travel 38 37 34 35 12.9% 6.0%

% Turnover 4.7% 4.7% 4.5% 4.7% 0.2 pt 0.0 pt

Other purchases and outside services 20 21 22 18 (8.1)% 17.2%

% Turnover 2.5% 2.7% 2.9% 2.4% (0.4) pt 0.3 pt

External expenses rose by 7.5%, up €23.9 million, due to a hike in

subcontracting expenses (+15.3%, i.e. 0.5% of sales at €14.6 million)

which account for 61% of this increase.

The Northern zone, which represents 87.5% of the total increase in

group external expenses, saw a 20.8% increase in subcontracting to

overcome staff shortages in a number of countries. CIS France also

contributed to this increase (+46.1% rise in subcontracting), particularly

in the second half of the year.

“Travel expenses” (+9.4%) and “Operating leases” (+8%) explain the

remainder of the increase in external expenses. These items increased

across all geographic zones, with the exception of France where

operating lease expenses dropped 1.2%, due to the reorganisation

carried out at the end of 2006.

Due to continued efforts the group reduced fees, by 7.3% i.e. by

€3.6 million.

Cost of net fi nancial debt

Cost of net fi nancial debt corresponds mainly to fi nancial income

arising from the investment of cash and cash equivalents less fi nancial

expenses.

The latter include primarily interest due on the convertible bond (2009

OCEANE), credit lines and trade receivables due.

Cost of net fi nancial debt rose €5.9 million in 2007. This is mainly due

to a rise in short-term interest rates.

292007 Registration document

Operating and fi nancial review 9Situation of the companies included in the consolidation scope

Income tax

Income tax expenses totalled €18.0 million in 2007 compared with

€15.8 million in 2006. This increase is primarily due to the group’s

improved profi tability.

The effective tax rate dropped from 45% to 34% due to a better

recognition of deferred tax assets against tax losses and to lower

additional taxes in Germany (“Gewerbesteuer”) and in Italy (“IRAP”).

Cash fl ow

Cash fl ow statement for the years ending 31 December 2007 and 31 December 2006:

(in million euros)

2007

12 months

2006

12 months

Change

2006/2007

Net financial debt at opening (1 January) (338.7) (301.5) (37.2)

Net cash flow generated by business activities 53.5 9.7 43.8

Net cash flow generated by investment activities (27.6) (71.8) 44.1

Net cash flows before financing operations 25.9 (62.0) 87.9

Exchange rate impact and others (1.6) (0.6) (1.0)

Impact of capital increase (Spring) 25.4 (25.4)

Net financial debt at closing (31 December) (314.4) (338.7) 24.3

Net cash fl ow generated by operating activities

Net cash fl ow generated by operating activities rose sharply

from €9.7 million at 31 December 2006 to €53.5 million at

31 December 2007. This is mainly due to:

increased cash fl ow (+€30 million);

improved working capital requirements (+€32 million), mainly

linked to better recovery of trade receivables;

an increase in taxes paid (-€13 million).

•

•

•

Net cash used in investment activities

Net cash used in investment activities in the year ending

31 December 2007 totalled €27.6 million compared with €71.8 million

at 31 December 2006. This is due to:

lower earn-out payments (-€32 million), as the majority of the

earn-out contracts have now expired;

an asset renewal programme which is reduced compared with that

of 2006, which was affected by fi ttings purchased as part of the

group’s relocation in 2006 (-€12 million).

•

•

Group net debt

Net fi nancial debt is the difference between total fi nancial liabilities and cash and cash equivalents.

(in million euros) 31/12/2007 31/12/2006 Change

2009 Convertible 197.9 197.9 -

Medium-term credit line 30.7 62.4 (31.6)

Short-term credit line 263.4 204.7 58.7

of which factoring 196.1 159.0 37.1

Total financial debt 492.0 464.9 27.0

Cash and cash equivalents 177.6 126.2 51.4

Net financial debt 314.4 338.7 (24.4)

Employee profit sharing 10.9 14.1 (3.2)

Accrued interests 34.2 27.1 7.2

Net debt 359.5 379.9 (20.4)

30 2007 Registration document

Operating and fi nancial review9Segment reporting

The group’s net debt has been reduced by €20.4 million to

€359.5 million at 31 December 2007 (compared with €379.9 million at

31 December 2006).

Cash and cash equivalents totalled €177.6 million at 31 December 2007

compared with €126.2 million at 31 December 2006.

Change in number of staff

31/12/2005 30/06/2006 31/12/2006 30/06/2007 30/12/2007

Total workforce at the end of period 16,152 16,488 17,057 17,167 17,502

H2 2005 H1 2006 H2 2006 H1 2007 H2 2007

Average workforce during the period 16,202 16,313 16,808 17,072 17,189

At 31 December 2007, the group employed 17,502 people compared

with 17,057 at the end of 2006. This increase of 445 employees, 75%

of which were hired in the second half of the year, provides a solid basis

for growth in 2008.

The recruitment of consultants continued at an upbeat pace

(5,117 hired in 2007 compared with 4,947 in 2006 excluding disposals)

to support business growth, particularly in the Northern zone,

CIS France and Italy. The balance of 170 offsets the 0.3% increase

in consultant turnover (29.3% in 2007 compared with 29% in 2006).

For France TI, priority was given in the fi rst half of the year to reducing

the inter-contract rate and improving the billing rate. This cut staff

turnover by almost 5% (24.8% in 2007 compared with 29.6% in 2006)

while maintaining resources similar to 2006 (4,963 in 2007 compared

with 4,976 in 2006). Recruitments in France rose sharply in the second

half of the year (58% of recruitments were made in H2 2007 compared

with 53% in H2 2006), which explains the increase in the headcount in

the second half of 2007 compared with the fi rst half of 2007.

9.3 Segment reporting

In accordance with IAS 14 “Segment reporting”, the primary reporting

segment corresponds to geographical segments and the secondary

reporting segment to business segments.

Altran ’s geographical segments:

France;

Northern zone: Germany, Austria, Benelux, Ireland, East European

countries, United Kingdom, Sweden, Switzerland;

Southern zone: Andorra, Brazil, Spain, Italy, Portugal, Venezuela;

•

•

•

Rest of the world: North America, Asia.

Business segments:

Technologies & Innovation;

Consulting & Information Services;

Strategy and Management consulting;

Other.

•

•

•

•

•

Sales by geographical area

Breakdown of sales by geographical area:

(in million euros)

2007 2006

Sector total

Inter-sector

eliminations

Total

revenues % revenues

Total

revenues % revenues Change

France 694 21 673 42.3% 642 42.9% 4.8%

North 533 18 515 32.4% 467 31.3% 10.2%

South 310 5 305 19.2% 284 19.0% 7.5%

Rest of the world 103 4 99 6.2% 102 6.8% (3.6)%

TOTAL 1,641 (49) 1,591 100.0% 1,495 100.0% 6.4%

312007 Registration document

Operating and fi nancial review 9Segment reporting

Sales for 2007 totalled €1,591 million up 6.4% compared with 2006,

i.e. an increase of €96 million.

The contribution to group sales of the Northern zone, the group’s most

profi table area, increased 1.1%, while France’s contribution decreased

(-0.6%) along with the Rest of the world (-0.6%). The Southern zone’s

contribution rose 0.2%, due to strong activity in the second half of

2007.

Breakdown of sales by country:

(in thousands euros)

YTD

2007

%

revenues H2 2007

%

revenues H1 2007

%

revenues

YTD

2006

%

revenues H2 2006

%

revenues H1 2006

%

revenues

2007

vs

2006

France 672,819 42.3% 340,289 42.4% 332,530 42.1% 641,929 42.9% 315,745 42.2% 326,184 43.7% 4.8%

Germany 154,302 9.7% 79,740 9.9% 74,562 9.4% 139,046 9.3% 72,185 9.6% 66,862 9.0% 11.0%

Austria/PECO 7,615 0.5% 4,303 0.5% 3,312 0.4% 6,355 0.4% 3,281 0.4% 3,074 0.4% 19.8%

Great-Britain/Ireland 130,430 8.2% 63,663 7.9% 66,767 8.5% 117,445 7.9% 62,663 8.4% 54,783 7.3% 11.1%

Benelux 153,618 9.7% 75,686 9.4% 77,932 9.9% 131,170 8.8% 69,133 9.2% 62,037 8.3% 17.1%

Switzerland 29,482 1.9% 13,714 1.7% 15,768 2.0% 40,620 2.7% 20,591 2.7% 20,029 2.7% (27.4)%

Sweden 39,314 2.5% 19,598 2.4% 19,716 2.5% 32,661 2.2% 15,753 2.1% 16,908 2.3% 20.4%

Romania 59 0.0% 37 0.0% 21 0.0% 0 0.0% 0 0.0% 0 0.0%

Italy 156,179 9.8% 79,658 9.9% 76,521 9.7% 141,581 9.5% 70,028 9.3% 71,554 9.6% 10.3%

Spain 111,480 7.0% 56,361 7.0% 55,120 7.0% 106,016 7.1% 51,492 6.9% 54,524 7.3% 5.2%

Portugal 18,584 1.2% 9,169 1.1% 9,415 1.2% 19,065 1.3% 9,670 1.3% 9,395 1.3% (2.5)%

Brazil/Venezuela 18,799 1.2% 9,269 1.2% 9,530 1.2% 17,080 1.1% 8,685 1.2% 8,395 1.1% 10.1%

ASIA 26,022 1.6% 16,607 2.1% 9,414 1.2% 16,819 1.1% 7,175 1.0% 9,644 1.3% 54.7%

USA 72,653 4.6% 33,787 4.2% 38,866 4.9% 85,561 5.7% 43,061 5.7% 42,501 5.7% (15.1)%

TOTAL 1,591,356 100.0% 801,881 100.0% 789,475 100.0% 1,495,350 100.0% 749,461 100.0% 745,890 100.0% 6.4%

In 2006, non-group sales (€467,3 million) were presented after intersegment eliminations, in contrast to the notes in the registration document.

Following the trend seen in 2006, sales growth (+6.4%) was generated

by Northern European countries in 2007, led by Sweden (+20.4%)

followed by the Benelux countries (+17.1%), the UK (+11.1%) and

Germany (+11%).

However, some of the Southern countries also reported double digit

growth between the second half of 2007 and the second half of 2006,

such as Italy (+10.3%), and Brazil (+10.1%) with Spain following closely

behind (+9.5%).

France, and more specifi cally the TI business, which until now had

shown negative growth, reported a 4.8% increase between 2006 and

2007.

Sales in Switzerland (-27.4%) and the United States (-15.1%;

-9.9% excluding changes in scope of consolidation) dropped

signifi cantly in 2007.

Net income by geographic zone

Northern zone

North

(in million euros) YTD 2007 H2 2007 H1 2007 YTD 2006 H2 2006 H1 2006 2007 vs 2006

Turnover, non-group 533.3 266.9 266.4 485.8 253.7 232.1 9.8%

Total operating income 533.9 267.3 266.6 486.1 253.9 232.2 9.8%

Total operating expenses (473.0) (237.7) (235.3) (428.0) (222.9) (205.2) 10.5%

Current operating income 60.9 29.6 31.3 58.1 31.0 27.1 4.8%

% Current operating income 11.4% 11.1% 11.7% 12.0% 12.2% 11.7% (0.5) pt

Operating income 58.5 27.3 31.2 59.3 33.1 26.2 (1.3)%

% Operating income 11.0% 10.2% 11.7% 12.2% 13.0% 11.3% (1.2) pt

In 2006, non-group sales (€467,3 million) were presented after intersegment eliminations, in contrast to the notes in the registration document.

32 2007 Registration document

Operating and fi nancial review9Segment reporting

The Northern zone reported sales growth of 9.8%, and alone, accounts

for almost 50% of group growth, i.e. €47.5 million.

The group has now started refocusing on two key East European

countries offering the most business development potential, namely

Slovakia and the Czech Republic.

The growth of this very dynamic area was driven by an increase in

resources, despite a tougher recruitment environment particularly in

the Netherlands (-3.7% vs 2006).

However, a good improvement in the invoicing rate (+0.5 point) did not

offset lower tariffs.

Operating expenses outpaced sales (+10.5%), reducing the current

operating margin by -0.5 point. The strong improvement in business

activity entailed the need for increased resources leading the

Northern zone to make considerable use of subcontracting. Indeed,

subcontractors alone accounted for almost half of the increase in

external expenses (+48.4%).

Wage increases were contained due to close monitoring of the

consultant turnover rate (+2.3 points vs. 2006). Sales outgrew payroll

expenses (+9.3%).

Operating income is down 1.3%, due to the non-recurrence of €7 million

in operating income recorded in 2006.

Southern zone

South

(in million euros) YTD 2007 H2 2007 H1 2007 YTD 2006 H2 2006 H1 2006 2007 vs 2006

Turnover, non-group 310.3 157.0 153.4 287.9 141.9 146.0 7.8%

Total operating income 310.6 157.0 153.7 288.4 142.1 146.4 7.7%

Total operating expenses (289.3) (145.9) (143.4) (274.3) (140.2) (134.1) 5.4%

Current operating income 21.4 11.1 10.3 14.1 1.9 12.2 51.4%

% Current operating income 6.9% 7.1% 6.7% 4.9% 1.3% 8.4% 2.0 pts

Operating income 12.7 7.8 4.8 6.1 (1.2) 7.3 106.6%

% Operating income 4.1% 5.0% 3.1% 2.1% (0.8)% 5.0% 2.0 pts

In 2006, non-group sales (€283.7 million) were presented after intersegment eliminations. in contrast to the notes in the registration document.

Southern zone sales rose 7.8% up €22.4 million vs. 2006, accounting

for 23% of group growth.

This improvement is due for 54.5% to higher tariffs, particularly in

Spain, and for 31.7% to increased resources, mainly in Italy. The positive

impact of higher tariffs is compounded by the fact that the invoicing

rate remained stable at -0.2 point vs. 2006.

In contrast to the Northern zone, operating expenses for the Southern

zone rose less than sales (+5.4%), resulting in a 2% improvement in

current operating margin in 2007. Higher payroll expenses (+8%)

accounted for 97% of this increase and refl ect strong wage infl ation.

Subcontracting expenses in the Southern zone, which account for

41.2% of external expenses, increased less than group subcontracting

expenses (+6.8% vs +15.3%), mainly due to Italy where recruitments

were still robust (+10.8% vs 2006) despite a tight employment

market.

Operating income was affected by goodwill impairment (-€3.8 million)

and non-recurring items (-€4.9 million).

France

France

YTD 2007 H2 2007 H1 2007 YTD 2006 H2 2006 H1 2006 2007 vs 2006

Turnover, non-group 694.0 351.1 342.9 659.1 324.6 334.6 5.3%

Total operating income 694.9 351.8 343.1 661.4 326.5 334.9 5.1%

Total operating expenses (674.4) (331.1) (343.3) (658.6) (331.6) (327.0) 2.4%

Current operating income 20.6 20.8 (0.2) 2.9 (5.1) 7.9 615.3%

% Current operating income 3.0% 5.9% (0.1)% 0.4% (1.6)% 2.4% 2.5 pts

Operating income 11.1 12.6 (1.5) (16.8) (15.8) (1.0) 166.1%

% Operating income 1.6% 3.6% (0.4)% (2.6)% (4.9)% (0.3)% 4.2 pts

In 2006, non-group sales (€641,9 million) were presented after intersegment eliminations, in contrast to the notes in the registration document.

332007 Registration document

Operating and fi nancial review 9Segment reporting

More than 36% of group growth, i.e. €34.9 million is generated by

France, where sales grew 5.3% in 2007. Sales in France were up +8.2%

compared with the second half of 2006, as opposed to last year’s

negative growth -1.6% in H2 2006 vs. H2 2005.

France has returned to growth as a result of restructuring carried out

at the end of 2006.

As a result of a targeted reduction in the inter-contract rate, the

Technology & Innovation business is driven by an improved invoicing

rate up 3% (accounting for almost 45% of sales increase in France),

together with robust recruitments (+10%) and a lower consultant

turnover rate (4.8%).

Growth in Consulting & Information Services is due to increased

resources (+6.2%; i.e. 32.7% of the increase in sales). Recruitment

diffi culties (-5.4% vs 2006) and an increase in the consultant turnover

(4.1%) led the group to use subcontractors extensively.

Furthermore, the recovery felt in France is compounded by slightly

higher tariffs.

The increase seen in operating expenses (2.4%) was lower than that

of sales, resulting in a 2.5% improvement in the current operating

margin, as opposed to the trend seen in the fi rst half. The sharp rise

in subcontracting expenses incurred by the CIS business (+46.1% in

France, accounting for 64.1% of the rise in operating expenses) was

partly offset by lower fees (-15.3%) and a reduction in “Other purchases

and external services” (-9.7%).

France includes operating activities and the group holding activities

which group together management and cross-functional services. The

group holding central services costs totalled €28.9 million in 2007

(€19 million in H1 and €9.9 million in H2) compared with €41.8 million

in 2006, mainly due to lower expenses in the second half of 2007.

Operational profi tability in France (excluding central service costs)

came out at 7.1% in 2007 (5.5% in the fi rst half and 8.7% in the second

half) compared with 6.7% in 2006. This refl ects improved growth due

to an increased invoicing rate and contained overheads.

Rest of the world

Rest of the world

(in million euros) YTD 2007 H2 2007 H1 2007 YTD 2006 H2 2006 H1 2006 2007 vs 2006

Turnover, non-group 103.0 52.4 50.6 105.8 52.1 53.7 (2.6)%

Total operating income 103.3 52.7 50.6 105.6 52.0 53.7 (2.2)%

Total operating expenses (106.8) (53.5) (53.2) (104.5) (52.5) (52.0) 2.1%

Current operating income (3.5) (0.9) (2.6) 1.1 (0.5) 1.6 (419.0)%

% Current operating income (3.4)% (1.6)% (5.2)% 1.0% (1.0)% 3.0% (4.4) pts

Operating income (11.7) (1.7) (10.1) (2.8) (2.5) (0.3) (315.4)%

% Operating income (11.4)% (3.2)% (19.9)% (2.7)% (4.8)% (0.6)% (8.7) pts

In 2006, non-group sales (€102,4 million) were presented after intersegment eliminations, in contrast to the notes in the registration document.

Sales in this region (Asia and the United States) dropped 2.6%, mainly

because of the United States. Indeed, in the US, the group saw a

signifi cant slowdown in the business generated by the implementation

of Sarbanes-Oxley (SOX) and experienced diffi culties in the energy

sector. The invoicing rate in the United States dropped 9 points on a

comparable basis of consolidation.

Steps have been taken to offset the decline in activity at the US

subsidiary CSI, by developing the SOX activity in Japan.

This region’s foreign exchange impact, largely due to fl uctuations in

the US dollar, accounts for more than 85% of the group’ exchange rate

impact.

Operating expenses rose 2.1%, up €2.3 million, despite signifi cant

reductions in headcount, mainly at CSI. Personnel costs dropped 15.8%

between the second half of 2006 and the fi rst half of 2007. External

expenses were reduced by 3% between 2007 and 2006.

Operating income was mainly impacted by goodwill impairment

(€8.7 million).

34 2007 Registration document

Operating and fi nancial review9Activities of Altran Technologies S.A. and its main subsidiaries

9.4 Activities of Altran Technologies S.A. and its main subsidiaries

The table below presents the group’s 10 main companies.

Turnover, non group

(i n million euros) 2007 2006 2007 vs 2006

Altran Technologies 458.2 456.4 0.4%

Altran CIS (Italie) 73.1 51.4 42.2%

Datacep 46.6 41.2 13.1%

Arthur D. Little (Allemagne) 43.2 34.8 24.3%

Altran Systèmes d’Information 39.5 42.9 (8.1)%

Axiem 38.3 22.1 73.3%

Altran Europe 37.7 29.7 26.7%

Cambridge Consultants 35.8 29.8 20.4%

Hilson Moran Partnership 35.2 25.8 36.3%

Askon Consulting group 35.1 39.9 (12.1)%

TOTAL OF THE 10 COMPANIES 842.7 774.0 8.9%

Others 748.6 721.3 3.8%

TOTAL GROUP 1,591.4 1,495.4 6.4%

Altran Technologies (TI)

In 2006, Altran Technologies absorbed 26 companies from the TI

business. Operations are now organised by geographical area Paris/

Provinces, and by business lines: Automobile, Infrastructures and

Transport/Aeronautics, Space and Defence/Telecoms, Electronics and

Media/Energy, Industrial sectors and Life Sciences/Innovation.

This reorganisation was carried out in an aim to providing better client

satisfaction. It has been successful, as TI is now backing on the track

to growth.

Altran CIS (Italy) (CIS)

On 30 June 2006, three Italian companies made an asset contribution

to Altran CIS Italy. Therefore the comparison between 2006 and 2007

is not relevant.

Altran CIS Italy groups together CIS businesses in the following markets:

banking, insurance, manufacturing, media, energy, telecoms and public

administration. Telecoms and banking represent 50% of CIS’ activity,

with a client portfolio focused on major Italian accounts. Altran CIS Italy

operates mainly in Turin, Milan, Rome and Genoa. Insurance operations

have recently been expanded to Trieste.

This activity will be merged with Altran Italy in 2008 to group all of

Altran’s Italian operations together into a single entity. The company

will be organised by markets.

Datacep (CIS)

DATACEP (CIS) is present in Paris and Lille and continued on a strong

growth path in 2007. The client base is mainly comprised of clients

from the manufacturing, energy, retail and transport industries.

Activities include technical support and information systems.

Arthur D. Little (Germany) (Strategy and management consulting)

In 2007, this company maintained the strong growth initiated in 2006.

Growth is due both to a strong economic environment in Germany,

and also to the group’s expansion into Eastern Europe. Improved

collaboration between the Central European offi ces has provided a

sound base for business development. Robust activity in automobile,

energy and fi nancial institutions together with an improved billing rate,

turned growth into profi ts in 2007.

Altran Systèmes D’Information (CIS)

This company is focused mainly on markets with high added value,

particularly in the banking and insurance industries. The company’s

operations have progressed from the fi eld of information systems

technical support to business support, and more specifi cally on the

trading fl oor. This repositioning has been detrimental to growth but

has consolidated margins and granted the group a leading position on

niche markets with high added value.

352007 Registration document

Operating and fi nancial review 9Risks

Axiem (CIS)

At the end of 2006 Axiem was absorbed by the information systems

business of the former company Altior and redirected operations

towards its Project Management Offi ce offer. This resulted in a

signifi cant improvement in tariffs. Due to this company being

consolidated in 2006, the comparison between 2006 and 2007 is not

relevant.

Altran Europe (TI)

Altran EUROPE is based in Belgium. In 2007, this company reported

26.7% growth. The company’s projects are focused in the telecoms,

media and electronic industries.

Cambridge Consultants (Other)

Cambridge Consultants is based in the United Kingdom and reported

+20.4% growth in 2007. Cambridge Consultants is active in specifi c

research and development projects in medical devices, telecoms and

the industrial sector. Cambridge Consultants is very active in the United

States and also acts as an incubator for research activities.

Hilson Moran Partnership – HMP (Other)

Based in the United Kingdom, HMP reported 36.3% growth in 2007.

HMP is active in the construction industry.

Askon Consulting group (TI)

Based in Germany, Askon Consulting group’s client base is comprised

primarily of companies in the aeronautical and automobile industries.

Due to restructuring in this sector in 2007, Askon Consulting group

reported a -12.1% decline in sales in 2007.

9.5 Risks

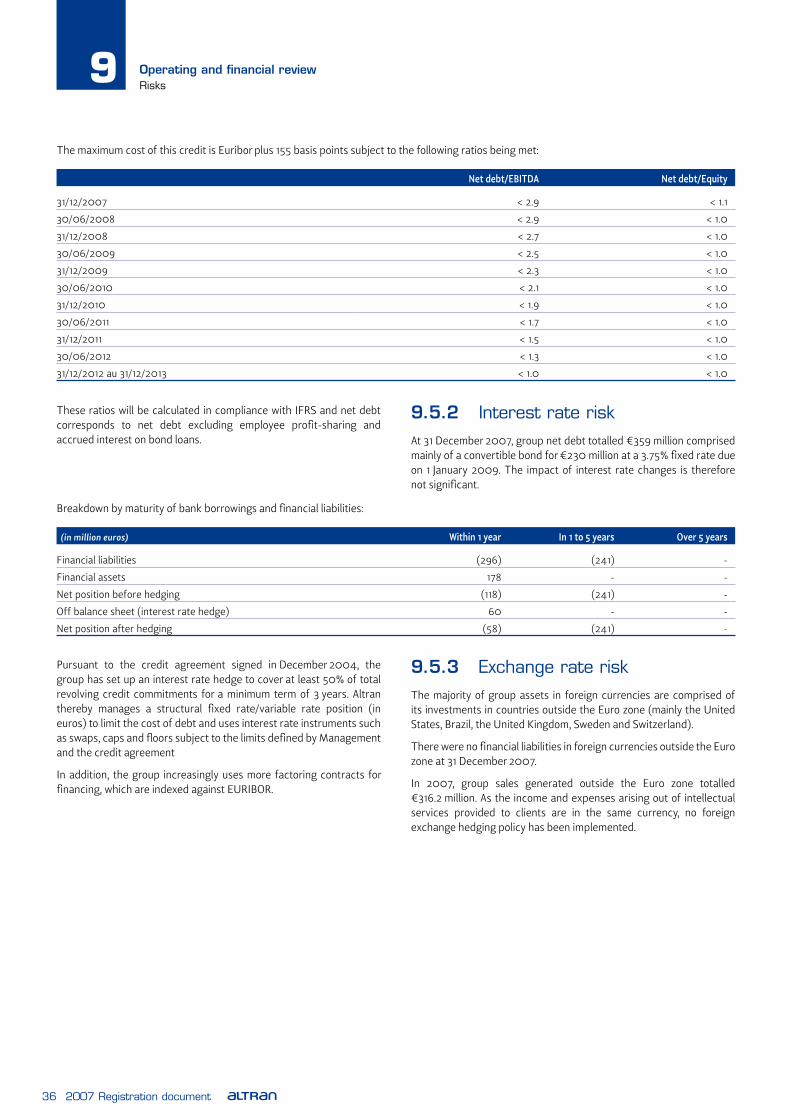

9.5.1 Liquidity risk

On 22 December 2004 the group entered into an agreement with

its three main banks (BNP Paribas, Crédit Agricole Île de France and

Société Générale) for €150 million in credit lines. At 31 December 2007

the outstanding credit totalled €59.5 million.

Group net debt totalled €359.5 million at 31 December 2007 reduced

by €20.4 million compared with 31 December 2006. Breakdown of

net debt and consolidated cash fl ow are presented on page 27 of this

registration document.

Group ratios at 31 December 2007:

Net debt to equity 0.88

Net debt/EBITDA before profit-sharing (financial leverage) 2.71

At 31 December 2007 the group did not meet its fi nancial leverage

ratio covenant which must not exceed 2.5. Altran has asked the three

banks of the banking pool (BNP Paribas, Crédit Agricole Île de France

and Société Générale) not to exercise the early redemption clause on

these lines.

Furthermore, on 17 April 2008 Altran announced that it was in the

process of signing a refi nancing agreement with a group of banks: BNP

Paribas, Crédit Agricole Île de France, Natixis and Société Générale.

This refi nancing agreement grants a 5 year credit facility of €150 million,

and includes €26 million in existing credit lines that were initially due

in 2009.

This credit facility enables Altran to refi nance debt, and in particular its

convertible bond due in January 2009.

Pursuant to this termsheet the current credit lines will be rescheduled

and the banking pool will grant an additional €126 million in medium-

term credit lines by 1 January 2009. The group will therefore be granted

access to €150 million due 5 years from the date of fi rst drawdown.

This credit line, repayable on a half-yearly basis over 5 years from the

date of fi rst drawdown is subject to the following conditions:

as from 2009, one third of consolidated net cash fl ow above

€15 million must be allocated to debt reduction (excluding any

market operations);

acquisitions in 2008 and 2009 to be limited to €10 million per year

and thereafter €40 million per year, if no operations are carried out

to strengthen equity;

in the event of a capital increase or the issue of bonds redeemable

into shares for a minimum of €100 million, Altran is authorised to

make acquisitions for an aggregated amount of €50 million per year

without prior approval from the banks.

•

•

•

36 2007 Registration document

Operating and fi nancial review9Risks

The maximum cost of this credit is Euribor plus 155 basis points subject to the following ratios being met:

Net debt/EBITDA Net debt/Equity

31/12/2007 < 2.9 < 1.1

30/06/2008 < 2.9 < 1.0

31/12/2008 < 2.7 < 1.0

30/06/2009 < 2.5 < 1.0

31/12/2009 < 2.3 < 1.0

30/06/2010 < 2.1 < 1.0

31/12/2010 < 1.9 < 1.0