Do Wealth Creating Mergers and Acquisitions Really Hurt Bidder Shareholders?

63

1 Do Wealth Creating Mergers and Acquisitions Really Hurt Acquirer Shareholders? * Ron Masulis † , Peter L. Swan ‡ and Brett Tobiansky § , School of Banking and Finance, Australian School of Business, UNSW Draft: June 16, 2011 ABSTRACT We examine the expected economic benefits of mergers and acquisitions. We conclude that both signaling and revelation biases are responsible for the commonly reported finding that on average takeovers are harmful to acquirer shareholder wealth. After accounting for these two biases that lead to a price fall on announcement of 18.9% ($563.9 million), we demonstrate that acquirers generally benefit from takeovers with an average 81% share of the economic gains from the transaction. By studying bids that fail for exogenous reasons, which are largely free of signaling and revelation biases, we confirm the neoclassical view that takeovers are positive NPV projects for a typical acquirer, which produce a sizeable return on capital of 21% to the acquirer ($626.6 million) and 21.2% ($772.2 million) to the combined acquirer-target. This conclusion is based on two important findings. First, on a failed acquisition announcement, the combined acquirer and target value on average falls, where both target and acquirer suffer significant negative abnormal returns. Second, acquirers share in a significant portion of the economic benefits of a successful acquisition, reflected in a significantly positive relationship between acquirer and target stock returns utilizing a 60-day initial bid announcement window and a 100-day period following the termination announcement. Over the same window, exogenously failed cash bidders significantly underperform successful cash bidders by 10.7% and exogenously failed stock bidders significantly underperform successful stock bidders by a further 15.5% making a total differential of 26.2%. Moreover, in the long term, stock-funded targets typically only receive half the premium of cash targets. Key Words: M&A, takeover bids, acquisition benefits, acquirer gains, acquisition synergies, failed bids. JEL Codes: G34, G14 * We thank Ken Ahern and Emir Hrnjic for constructive comments. Also, participants at Financial Intermediation Research Society (FIRS) Conference, Sydney 2011. Eugene Chua, Nick Orlic, and Ewe Helmes provided assistance earlier on. † Email: [email protected]. ‡ Contact author. Department of Banking and Finance, ASB, UNSW Sydney NSW 2052 Australia. Tel: +61 (0) 2 9385 5871. Email: [email protected]. § Email: [email protected].

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of Do Wealth Creating Mergers and Acquisitions Really Hurt Bidder Shareholders?

1

Do Wealth Creating Mergers and Acquisitions Really Hurt Acquirer Shareholders?*

Ron Masulis†, Peter L. Swan

‡ and Brett Tobiansky

§,

School of Banking and Finance, Australian School of Business, UNSW

Draft: June 16, 2011

ABSTRACT

We examine the expected economic benefits of mergers and acquisitions. We conclude that

both signaling and revelation biases are responsible for the commonly reported finding that

on average takeovers are harmful to acquirer shareholder wealth. After accounting for these

two biases that lead to a price fall on announcement of 18.9% ($563.9 million), we

demonstrate that acquirers generally benefit from takeovers with an average 81% share of the

economic gains from the transaction. By studying bids that fail for exogenous reasons, which

are largely free of signaling and revelation biases, we confirm the neoclassical view that

takeovers are positive NPV projects for a typical acquirer, which produce a sizeable return on

capital of 21% to the acquirer ($626.6 million) and 21.2% ($772.2 million) to the combined

acquirer-target. This conclusion is based on two important findings. First, on a failed

acquisition announcement, the combined acquirer and target value on average falls, where

both target and acquirer suffer significant negative abnormal returns. Second, acquirers share

in a significant portion of the economic benefits of a successful acquisition, reflected in a

significantly positive relationship between acquirer and target stock returns utilizing a 60-day

initial bid announcement window and a 100-day period following the termination

announcement. Over the same window, exogenously failed cash bidders significantly

underperform successful cash bidders by 10.7% and exogenously failed stock bidders

significantly underperform successful stock bidders by a further 15.5% making a total

differential of 26.2%. Moreover, in the long term, stock-funded targets typically only receive

half the premium of cash targets.

Key Words: M&A, takeover bids, acquisition benefits, acquirer gains, acquisition synergies,

failed bids.

JEL Codes: G34, G14

*

We thank Ken Ahern and Emir Hrnjic for constructive comments. Also, participants at Financial

Intermediation Research Society (FIRS) Conference, Sydney 2011. Eugene Chua, Nick Orlic, and Ewe Helmes

provided assistance earlier on. † Email: [email protected].

‡ Contact author. Department of Banking and Finance, ASB, UNSW Sydney NSW 2052 Australia. Tel: +61 (0)

2 9385 5871. Email: [email protected]. § Email: [email protected].

2

Do Wealth Creating Mergers and Acquisitions Really Hurt Acquirer Shareholders?

Draft: June 16, 2011

ABSTRACT

We examine the expected economic benefits of mergers and acquisitions. We conclude that

both signaling and revelation biases are responsible for the commonly reported finding that

on average takeovers are harmful to acquirer shareholder wealth. After accounting for these

two biases that lead to a price fall on announcement of 18.9% ($563.9 million), we

demonstrate that acquirers generally benefit from takeovers with an average 81% share of the

economic gains from the transaction. By studying bids that fail for exogenous reasons, which

are largely free of signaling and revelation biases, we confirm the neoclassical view that

takeovers are positive NPV projects for a typical acquirer, which produce a sizeable return on

capital of 21% to the acquirer ($626.6 million) and 21.2% ($772.2 million) to the combined

acquirer-target. This conclusion is based on two important findings. First, on a failed

acquisition announcement, the combined acquirer and target value on average falls, where

both target and acquirer suffer significant negative abnormal returns. Second, acquirers share

in a significant portion of the economic benefits of a successful acquisition, reflected in a

significantly positive relationship between acquirer and target stock returns utilizing a 60-day

initial bid announcement window and a 100-day period following the termination

announcement. Over the same window, exogenously failed cash bidders significantly

underperform successful cash bidders by 10.7% and exogenously failed stock bidders

significantly underperform successful stock bidders by a further 15.5% making a total

differential of 26.2%. Moreover, in the long term, stock-funded targets typically only receive

half the premium of cash targets.

Key Words: M&A, takeover bids, acquisition benefits, acquirer gains, acquisition synergies,

failed bids.

JEL Codes: G34, G14

3

1. INTRODUCTION

Many studies document that acquirers systematically destroy shareholder wealth in

mergers and acquisitions (M&As), while targets benefit at their expense.5 Moeller,

Schlingemann, and Stulz (2005) find that shareholders of acquiring firms over the 1998-2001

period lose 12 cents per dollar on takeover announcement and an incredible $240 billion in

dollar terms. In their survey, Betton, Eckbo, and Thorburn (2008) find a significantly

negative abnormal return of -2.21 percent for large stock bidders of public targets, which

shrinks to -0.3 percent for large cash bidders of public targets. Small stock bidders

approximately break-even, while small cash bidders gain 3.06 percent. Thus, if one sets a

zero NPV as the floor return to the bidder in an auction market, only small bidders, not large

bidders where most of the investment is, satisfy this rationality criterion. Bayazitova, Kahl,

and Valkanov (2011) find that these large acquirers (mega-mergers) account for 43% of all

merger outlays. Apparent value-destroying deals representing large negative NPV projects do

not represent some minor backwater in which irrationality flourishes. Strangely, in view of its

wealth-destructive properties, M&A activity plays a significant role in the global economy,

constituting $2.1 trillion in the US in just one year alone, or 15% of GDP (see Bao and

Edmans (2011)).

The virtually universal finding that acquiring shareholders do not gain from M&A activity

features in practically every major textbook (see, for example, Ross, Westerfield, and Jordan

(2008, p. 835) or Copeland, Weston, and Shastri (2005, p. 778)). The overall synergistic

benefits made up of the net change in the value of the bidder and target on takeover

announcement are marginally positive, where acquirer shareholders are distinct losers, while

target shareholders are clear winners.

These virtually universal findings stand in stark contrast to what may be termed the neo-

classical theory of M&A (see Ahern and Weston (2007)) which asserts the profit motive of

the acquirer will naturally drive the ownership of assets to their highest value use. It follows

from this motivation that the initiator (acquirer and its shareholders) will benefit from such

wealth-enhancing transactions, rather than suffer losses. Thus, if there are changes in

technology due (say) to innovation, regulatory changes, or shifts in demand for goods and

5 For an early example of a study showing that acquirer value falls at the time of takeover announcement see

Dodd (1980). Betton, Eckbo, and Thorburn (2008, Table 6) summarize 16 relatively recent large-sample studies

of acquirer returns. Most report sizeable takeover samples in which the bidder‟s share price reaction is negative.

4

services such that the existing ownership of assets is no longer optimal, M&A activity should

occur to redistribute the ownership and control of assets from a target to a bidder so as to

enhance the overall value of the merged firms, resulting in improved utilization of the

combined firm‟s assets.

In this paper and consistent with neoclassical theory, we show that there is no foundation

for the belief that, even where target shareholders benefit, this typically comes at a

considerable cost to acquirer shareholders. To the contrary, we demonstrate that not only are

the net economic benefits of M&A large, but they are typically shared between acquirer and

target. In fact, an acquirer on average gains the lion‟s share from a typical acquisition,

capturing a 81% share or US$626.6 million of the associated total economic benefits, which

average US$772.2 million. These gains are not obvious to researchers since making a bid also

releases bad news about a bidder‟s value, which reduces its equity capitalization by $563.9

million or 18.9%. While this loss in value is offset by the prospective benefits of a typical

M&A bid, the net effect implies little change in a bidder‟s equity value.

Most recently, behavioral financial economists have focused on the use of the acquirer‟s

own stock, rather than cash as the means of payment for the target (e.g., Shleifer and Vishny

(2003) and Dong, Hirshleifer, Richardson, and Teoh (2006)). It is argued that managers of

acquirers may use their firms‟ relatively overvalued stock to benefit their own shareholders at

the expense of target shareholders, with no combined economic gain to bidders and targets,

but potentially huge losses to society as a whole.

We show the findings, that acquirer shareholders and, particularly, large acquirer

shareholders, do not gain from takeovers and may be worse off, is due to a fundamental

“revelation bias” in the standard event study methodology used to identify synergistic gains

and, to assess whether acquirer shareholders are victims of manager-shareholder agency

problems.

First, acquirer managers rewarded for short-term performance often instigate a “signaling

bias” by deliberately timing the “good news” of the bid announcement to coincide with the

release of bad news such as unmet earnings targets (see Bhagat, Dong, Hirshleifer, and Noah

(2005)). This common practice, documented in the Wall Street Journal, 1998, p. C1,

confounds the information about an acquisition‟s value to a bidder that is capitalized into the

bidder‟s stock price on the acquisition announcement, and results in a downward revaluation

of a bidder‟s stand-alone value.

5

Second, the bid itself typically releases bad news about an acquirer, even when there is no

motive to distort the market‟s perception of company value. For example, it may reveal

serious empire-building tendencies of incumbent management, or management perception

that the bidder has run out of profitable internal growth opportunities (see Fuller, Netter, and

Stegemoller (2002), and Hietala, Kaplan, and Robinson (2003)). Shleifer and Vishny‟s (2003)

market timing explanation for stock bids when the stock is relatively overvalued falls into the

same category.

Third, the acquirer may already have a long history of generally successful bids, such that

a new acquisition announcement is no surprise to the market, which leads to a close to zero

market reaction even to a beneficial acquisition. Serial acquirers such as General Electric,

Cisco, GlaxoSmithKline and Capital One for example are possible examples in this activity.6

Fourth, for reasons relating to conflicts between existing and new shareholders put

forward by Myers and Majluf (1984), stock financed acquisitions represent new equity issues

that by their very nature can represent bad news about the stock‟s true value since stock may

be preferred to retained earnings and debt when it is overvalued.

Finally, the initial bidder announcement return could be downward-biased because of the

likelihood of failure, perhaps because of the subsequent entry of competing bidders. Bhagat,

Dong, Hirshleifer, and Noah (2005) introduce the probability scaling method (PSM) that uses

post-bid data to factor in the probability of a successful bid and the intervention method (IM)

to take account of the likelihood of competing bids. They show that both of these methods

increase the perceived value of the takeover and reduce the likelihood of finding that the

bidder is overpaying for the target. Hence, release of information that is extraneous from the

critical question of whether an acquisition will create bidder shareholder value poses a severe

problem from the perspective of traditional M&A event study methodology. The PSM and

IM methods tackle only limited dimensions of this complex problem.

Our study builds on the well-known contribution by Shleifer and Vishny (2003) that put

forward a conditionality explanation for stock acquisition offers as opposed to cash bids.

Acquiring shareholders may gain and target shareholders correspondingly lose from the

resulting swap of the firm‟s own equity for the target‟s relatively underpriced equity. Hence,

the issuance of stock bids is endogenous in this arbitrage operation and is conditional on

management discovering that their stock is overpriced relative to the targets. This mechanism

6 The point made here about expectations and share price reaction is quite distinct from the considerable

empirical literature on whether serial acquirers are successful or not.

6

is a major contributor to the “revelation bias” that occurs on a bid announcement as it signals

that the offer‟s acquisition currency, bidder stock, is relatively overvalued. Stock price falls

on announcement of a stock financed bid, not because it is a bad bid, lacking synergies and

likely to destroy shareholder wealth, but because this is a strong signal that the stock is

currently relatively overvalued, much like the signal released by a seasoned equity offer

announcement.7 Here, decisions to issue equity by a stock offer are conditional on some

value-destruction occurring within the firm itself that reveals itself to the market along with

the offer to the target or, less plausibly, that target shares are undervalued.

The most recent contribution to this literature is a study by Savor and Lu (2009) who

restrict their analysis to acquirers only. They find that withdraw stock bids suffer a more

severe value reduction than those that are not withdrawn. They interpret this finding to be due

to the unsuccessful bidders inability to swap their overvalued equity for fairly valued target

equity and conclude that, indeed, stock acquirers realize sizable benefits from successful bids.

In our analysis, we include the market responses of matched targets following bid failures to

show that value reduction occurs because failed bidders are unable to realize the synergistic

benefits associated with their bids, with both bidders and targets losing value as a

consequence. Both Shleifer and Vishny (2003) and Savor and Lu (2009) assume a complete

absence of synergistic gain, but since neither investigates the price changes in the associated

targets, their argument remains only partially tested. Since firms with relatively overvalued

equity are likely to have insufficient internal growth prospects, it makes sense for such firms

to concentrate on external growth prospects achieved via synergistic gains.

Our contribution is related to the fact that failed bids are subject to a much weaker

“revelation bias” relative to new bids, and this is especially true for stock bids. The bidder

stock price following the initial bid already reflects the endogenous valuation error of

announcing a stock bid due to perceived relative overvaluation, managerial empire-building

incentives, evidence of weak internal growth prospects, and all other revelation problems. By

contrast, the induced change in a stock bidder‟s value following an offer withdrawal

represents a much cleaner experiment than the market reaction to the initial bid

7 Seasoned equity issues by overvalued but mature firms are rare but nonetheless have statistically significant

effects in terms of explaining the probability of an SEO (see DeAngelo, DeAngelo, and Stulz (2010)). This

rarity could be explained in part by the likelihood that investors see through the ploy and thus underprice the

offering. Conditionality problems also plague event study analysis of stock splits, as well as stock-based

takeover announcements and seasoned equity issues. Stock splits generally occur only following stock price run-

ups. Hence, an event study of stock splits will show considerable value-enhancement whereas in reality none

has occurred (see Brown, Goetzmann, and Ross (1995)).

7

announcement. This is especially the case where a bid has failed for exogenous reasons

unrelated to the existing value of the bidder or the target. Unlike Savor and Lu (2009), by

matching our bids with their targets, we show that both bidder and target are subject to large

losses in value on bid withdrawal due to exogenous failure, consistent with both being subject

to loss of synergistic benefits. The more the target falls, the more the bidder falls, and vice

versa, indicating that the bidder as well as the target suffers a loss of synergistic benefits.

Thus our fundamental insight is that when failed bidders are matched with their associated

failed targets and the reason for deal failure is exogenously triggered, then it is possible to

impute the share of gains received by the bidder when the deal succeeds.

We find that studying failed bids yields a great deal more insight than conventional

approaches concerned largely with successful bids. With failed bids, one can observe the

subsequent long-term history of both the bidder and target, whereas with successful bids one

cannot generally observe either individual firm post-acquisition, as they are combined

entities. Thus, failed bids are a huge and largely untapped mine of new information about the

fundamental causes and consequences of mergers and acquisitions.

In this study, we overcome the problems in the existing empirical literature by devising a

new approach to assessing the economic benefits of the M&A offers by using successful and

failed takeover deals in our sample of both bidders and targets. Moreover, as a means of

increasing our analysis of matched bidders and targets when the bid fails, we compile a much

larger database of mergers and acquisitions over four countries: Australia, Canada, the United

Kingdom and the United States, compared with conventional studies that focus on a single

country.8 Using our new database, we take a novel approach to analyzing the gains and

distribution of the synergistic benefits in mergers and acquisitions between bidder and target.

Following Savor and Lu‟s (2009) approach of studying bidders in M&A offers that are

cancelled for exogenous reasons, we extend this concept to analyze target firms and a

matched sample, where requisite financial information about both an acquirer and a target of

an offer is available for our offer sample. Utilizing this large sample, we incorporated new

variables into our cross-sectional regression models, which include indicators of failed offers

and exogenously failed offers and acquirer and target reactions to their counterparty‟s

abnormal announcement returns.

8 We are not the first to consider acquisitions outside of the United States. For example, Netter, Stegemoller, and

Wintoki (2011) examine a comprehensive set of mergers and acquisitions.

8

Our central line of reasoning is as follows. One would assume that a rational economic

motivation for a bidder to enter into a merger and acquisition transaction would be the ability

to invest in a positive net present value investment and thus, return excess abnormal returns

to their long-term shareholders. This view is in line with the findings of Schlingemann

(1994), Cooney and Kalay (1993), and Lang et al. (1991). Hence, we seek to investigate

whether mergers and acquisitions are positive NPV investments for acquirers using either

cash or stock financing and yield genuine economic gains and do not simply transfer wealth

(theft!) from target shareholders in the case of stock bids.

Our research question follows from the above reasoning, which examines whether the

pursuit of synergistic economic benefits serves as the primary motive for acquiring firms

participating in merger and acquisitions. We find support for our first hypothesis that (HI) on

the announcement of a failure of a merger, the combined value of the acquirer and target fall.

Having shown that synergistic benefits do exist for the combined firm, we then evaluate our

second hypothesis that (HII) acquirers gain a significant share of the synergistic benefits

created on announcement of a merger or acquisition.

We conduct our analysis in two stages. First, using our entire sample of 2,963 acquirers

and 4,606 targets, we conduct an investigation into the abnormal returns around: (i) the initial

announcement of a merger or acquisition, and (ii) the announcement date that the merger and

acquisition either succeeds or fails with certainty. Specifically we find a mean stock price

run-up and announcement return for acquirers of two percent and −1 percent respectively,

representing an approximate net gain to acquirers on announcement of one percent. This

result is consistent with evidence from Ahern and Sosyura (2011) suggesting that stock

acquirers release a string of positive announcements in the lead up to a merger or acquisition

announcement, thereby boosting their share price. In their sample, merger talks begin on

average 64.5 days prior to the public announcement. Consistent with the findings of Andrade,

Stafford and Mitchell (2001), we find that acquirer and target abnormal returns over a five-

day window are −1.05 percent and 19.22 percent, respectively. Hence, our sample replicates

the standard finding using conventional methodology that acquisitions are destructive of

acquirer value, thus earning (apparent) negative synergies. We find that the combined firm

announcement returns appreciate on the initial offer announcement (2.67 percent) and fall on

the announcement of an offer failure (−1.82 percent). Thus, this evidence yields strong

support for the existence of overall synergistic gains in our sample, consistent with

Hypothesis I and the findings of many prior empirical studies.

9

The second stage of our analysis utilizes a series of cross-sectional regression models to

investigate the creation, and subsequent loss of synergistic benefits. Using an innovative

method of examining synergistic benefits, we split our analysis into three subsections. The

first subsection analyses the creation of synergistic benefits using an event study of an initial

announcement of a merger or acquisition. We improve on existing methodology by extending

the event window to include a 60-day period preceding the initial announcement to capture

any price run-up, potentially due to proprietary information leaks, and define the dependent

variable to be equal to this run-up plus the five-day window around the offer announcement.

We find that for long-horizon models of target abnormal returns, the market predicts offer

failures and exogenously failed bids, where targets of these bids earn significantly lower

returns leading up to and on the initial offer announcement. Additionally, we find a

significant positive relationship between acquirer and target returns, hence finding leading

support for Hypotheses I and II.

How can we rule out reverse causation - that the deal failed because the target found a way

to trigger deal failure after it correctly anticipates poor future acquirer performance? This

might occur when the target obtains information about acquirer overvaluation from its due

diligence investigation. We rule out this otherwise plausible story by also incorporating the

target‟s reaction to the announcement of deal failure when examining bidder abnormal

returns and vice versa when examining target abnormal returns around the same

announcement. Were the reverse causality story true, both the bidder and target would

decline in value together due to release of bad news about the bidder until the endogenous

collapse of the bid. The bidder would then continue to fall in value as it could no longer

receive the benefit of the relatively underpriced target, but the target‟s stock would shoot up

in value as it is now free of the yoke of being tied to the overvalued bidder. We do not find

evidence consistent with this scenario. In fact, we find quite the opposite. The values of both

the target and bidder continue to fall pari passu together for the next 100 days, consistent

with a mutual loss of synergistic benefits.

As noted by Fuller, Netter and Stegemoller (2002) and Hietala, Kaplan and Robinson

(2003), information is released on the M&A offer announcement. The takeover

announcement reveals information about the stand-alone value of the bidder and target in

addition to any potential synergies arising from the combination of the two firms, and

distribution of these gains between target and acquirer. Due to this complication in measuring

synergistic gains on the initial announcement of an acquisition, we study the loss of

synergistic benefits on the announcement of a failure of an acquisition. We find evidence in

10

favor of negative abnormal returns to acquirers, targets, and the hypothetical combined firm

on the announcement of failed bids.

A third form of analysis involves investigating the relationship of the expected synergistic

benefits found in a long-horizon study of acquisition wealth creation, and the subsequent

losses of these synergistic benefits. Measuring abnormal returns commencing 60 days prior

the initial announcement until 100 days post the date participants know whether the bid is

successful or fails, we find strong evidence for the existence of synergistic benefits for

acquirers, supporting Hypothesis II. Specifically, we find that failed cash bidders

significantly underperform successful cash bidders by approximately 10.7 percent and failed

stock bidders underperform successful stock bidders by a further 15.5 percent in bids that fail

for exogenous reasons. Additionally, we find that failed target stock prices in stock bids fall

back to their pre-bid levels, which is the reverse of the predictions made by Savor and Lu

(2009). We also find that after 100 days following deal outcome successful stock bidders do

only about half as well (relative return of -13.3%) as successful cash bidders. This

substantially subtracts from the target‟s premium and synergistic share.

According to the market timing hypothesis, acquirers purchasing targets use relatively

overvalued equity as currency. One would expect that on the news of bid failure, long-term

target shareholders would react positively, which is the exact opposite of our findings. We

agree that bidders with overvalued stock use their shares as currency. Our point is that the

market is not entirely fooled. The terms on which targets accept bidder stock reflects to some

extent the bidder overvaluation and collective synergistic gains so that the target price can

only fall on deal failure, not rise as proponents of no synergistic gains predict. Additionally,

we find strong positive correlations between acquirer and target announcement return,

suggesting that there is a strong complementarity and sharing of synergistic gains between

acquirer and target shareholders. This complementarity is inconsistent with the Roll (1986)

hubris hypothesis, which predicts a more positive bidder stock return (with a larger target

price fall) following a bid failure announcement reflecting a reversal of a bidder‟s stock price

discount for its expected overpayment for the target. It is also inconsistent with the Shleifer

and Vishny (2003) and Savor and Lu (2009) “theft” explanation as the bidder price falls and

target must rise in response to deal failure and the unwinding of the “theft” of the target‟s

relatively undervalued equity, according to this explanation.

Our study makes at least two valuable contributions to the literature. First, we propose a

new approach to examining the synergistic benefits in merger and acquisitions. Our evidence

suggests that looking at failed bids provides an additional opportunity to more clearly identify

11

the gains in mergers and acquisition by studying the unexpected loss of these expected gains.

Second, we show the possibility of improvements to current methodology by including the

acquirer price run-up as a dependent variable when studying acquirer and target returns in

M&A. This price run-up is significantly negatively correlated with the unexpected losses

incurred if the bid subsequently fails typically many months hence. Remarkably, it is not only

correlated with the fall in the price of the bidder, but also with the target with the impact on

the target only slightly smaller in magnitude. This is to be expected if there is sharing of the

synergistic gains, with on-going private negotiations occurring between bidder and target

during the run-up period.

We structure the study as follows. Section 2 reviews existing literature and develop a

contextual basis for our key hypotheses. Hypotheses are further constructed in Section 3.

Section 4 describes our data sources, acquisition sample and empirical methods. Section 5

contains the empirical work and discusses the results, Section 6 presents our estimates as to

how synergistic gains are shared and Section 7 concludes.

2. LITERATURE REVIEW

Real synergy involves combining assets in the form of positive net present value (NPV)

projects, creating positive excess (abnormal) returns to an acquirer‟s long-term shareholders.

By contrast, Roll (1986) posits the hubris hypothesis that at least some managers over-bid for

targets due to errors in valuing synergies, leading to no overall value improvement. These

inefficient investments can also be due to agency problems such as empire-motivated

managers not acting in shareholder interests.

Jennings and Mazzeo (1991) conclude that bidders learn nothing from the share price

reaction to a bid. Thus, a negative share price reaction does not make deal completion less

likely. Luo (2005) disagrees with the earlier finding, utilizing a larger deal set and different

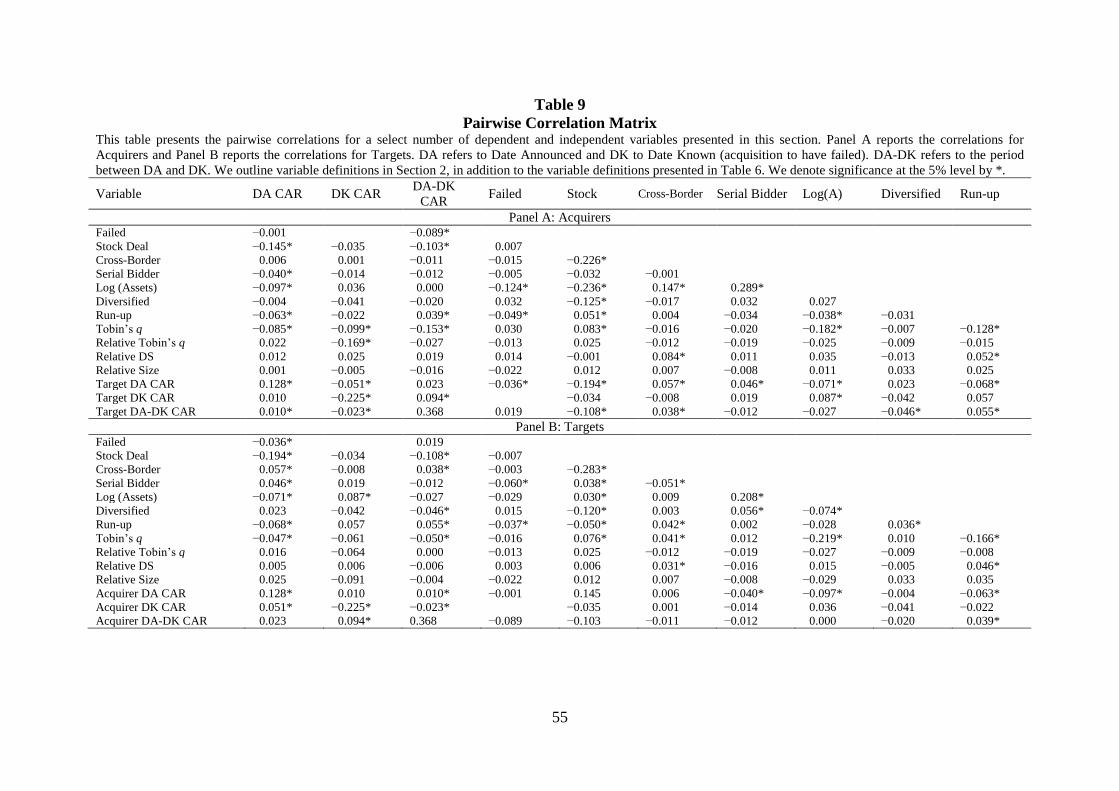

methodology and set of tests. We find that the pairwise correlation coefficient between the

cumulative abnormal returns (CARs) of the bidder over the five-day window is uncorrelated

with bid outcome in agreement with Jennings and Mazzeo (1991). When we add in a full set

of controls, the market is able to predict failure of the sample inclusive of endogenously

failed bids but not exogenously failed bids. Failure significance disappears even for

endogenous sample inclusive of the run-up period after maintaining the full set of controls.

Hence, the full market reaction to the bid does not appear to predict bid failure, suggesting

that the presumed inside information is not affected by the reaction of outside investors. This

12

evidence is consistent with our finding that the market reaction to the bid announcement does

not say a great deal about likely synergistic gains accruing to the bidder. We do find,

however, a significant negative correlation between the target announcement CAR and bid

failure that disappears when a full set of controls is included. Once we take account of the

target‟s price run-up and thus the information leakage, the market appears able to predict deal

failure for targets, but not for bidders. This is not so surprising when one considers that the

target event is much cleaner as it is not so contaminated by the revelation of bad news about

the bidder.

Schlingemann (1994) conducts a study of 623 cash takeovers during the period

1984−1998. He concludes that retained-earning sourced cash transactions positively relate to

bidder announcement abnormal returns. He attributes this finding to firms using internally

generated cash to invest in positive NPV investments (Cooney and Kalay (1993)).9 The

results of the study are also consistent with Lang et al. (1991) who hypotheses that managers

at times have incentives to waste excess free cash flows in wealth destroying investments.

Martynova and Renneboog (2009) conclude that transactions financed by internally generated

funds underperform those financed with debt. Lang et al. (1991) also identifies a relationship

between Tobin‟s q and investment policy such that that high q firms, compared to low q

firms, are more likely to have positive NPV projects. Hence, low q firms should on average

pay out their excess cash, rather than invest in poor acquisition prospects.

Grinblatt and Titman (2002) suggest, “the stock returns of the bidder at the time of the

announcement of the bid may tell us more about how the market is reassessing the bidder‟s

business than it does about the value of the acquisition”.10

Similarly, Hietala, Kaplan and

Robinson (2003) note that the announcement of takeovers reveals information about the

stand-alone value of the bidder and target, any potential synergies arising from the

combination, and the distribution of gains between the target and acquirer. Additionally, they

state that it is often not possible to infer the respective synergies, overpayment, and

distribution of gains simply from the change in the market price of the bidder and target. Our

model hopes to fill this gap by including a failed sample where the bid has failed for

exogenous reasons. Thus, an unexpected offer failure provides valuable additional evidence

about the value of an offer captured in the forgone economic gains of the offer.

9 Cooney and Kalay (1993) adopt the innovative methodology of including negative NPV projects into the

financing decision, shows that the new issue of equity to finance projects can signal an exceptional valuable

project, where the market may react positively to the news. This is contrary to the prediction by Myers and

Majluf (1984) where they believe that the market will never react positively to new issue of equity. 10

Grinblatt and Titman (2002, p. 708).

13

A negative share price reaction to offer withdrawal announcements for targets should

indicate the size of the loss of synergistic benefits (Bradley, Desai, and Kim (1983) and

Samuelson and Rosenthal (1986)). Bradley et al. (1983) find that after an offer withdrawal

the target‟s share fall back over an extended time-period toward its previous pre-offer levels,

as it becomes clear that no subsequent acquisition bid is likely. Comparatively, those targets

that receive subsequent offers experience additional increases in share price. Bradley‟s (1980)

study of 100 percent cash offers shows that bidders experience severe negative reactions to

offer failure, compared to positive reactions for successful offers.

Savor and Lu (2009) incorporate failed bid announcements into their sample. They

interpret the larger reduction in share price for failed stock offers, compared with successful,

as an inability to swap overvalued equity for more fairly-valued target equity. A more

plausible explanation is the inability of failed bidders to attain anticipated synergistic

benefits. Savor and Lu also point out that failed cash bids do not suffer such a loss in value

and continue to perform relatively well compared to failed stock bids. We agree but our

explanation is entirely different: stock bids by their nature, with high relative Tobin‟s q and

high-priced equity indicative of bidder relative managerial advantage, achieve far higher

synergistic gain. Hence, the loss on exogenous deal failure is also far higher. Their

supposition of no synergistic gain for stock bids predicts the exact opposite of their finding:

their failed stock bids should do much better than failed cash bids as the former suffer no loss

of embodied synergistic gain by assumption.

An important part of Savor and Lu„s approach is their solution to the endogeneity problem

that arises from the inclusion of failed bids. Bidders with overvalued stock have greater

incentives to propose stock as the mode of payment rather than cash. This complicates

matters as the bid may fail due to target shareholders discovering the acquirer‟s

overvaluation. Savor and Lu solve this endogeneity issue by attempting to create an

“exogenous failed subsample” where mergers fail for exogenous reasons outside of the

control of the bidder or target, and thus are unrelated to the acquirer‟s or target‟s valuation.

M&A researchers rarely use the technique of failed acquirers in their analysis.

A natural extension of the Savor and Lu approach is to focus on target reactions to bid

failure. If the market-timing theory is correct and no synergistic benefits exist, then rational

target shareholders should expect that a bidder‟s stock to be relatively overvalued. If this

happens systematically over time then in anticipation of future acquirer price falls, the price

of the target may fall below the notional cash value of the equivalent acquirer stock even

though the acquisition seems very likely to go ahead. Thus, upon the announcement of the

14

stock bid failure, the target share price could go up if the target‟s price has significantly fallen

for this reason. Alternatively, it may drop slightly representing only a fraction of the notional

value of the bid. In contrast, this study postulates that synergistic gains exist. Hence, upon the

offer failure announcement, we expect to see a fall in the combined value of the acquirer and

target equity capitalization due to a loss of jointly shared synergistic gains. More specifically,

we do not expect to see a target‟s share price rise because shareholders are no longer to

receive burdensome stock that may be rapidly falling in value. Instead, we expect the bidder

stock price to fall in a complementary fashion to the fall in target price, due to a shared loss in

synergistic benefit.

Ahern (2011) finds that in terms of dollar gains, targets do not do a geat deal better than

acquirers that tend to be much larger. Moreover, in vertical acquisitions a target‟s relative

scarcity and product market dependence help explain its share of total merger gains. Cai,

Song, and Walkling (2011) present evidence to show that some bids come as more of a

surprise to the market than others. In particular, the first bid in an industry has both greater

surprise and a higher return than subsequent bids. They conclude that, after accounting for

anticipation, bidding activity generates wealth. Malmendier, Opp, and Saidi (2011) find that

targets react much more favorably to cash bids than do stock bids on a deal failure

announcement utilizing a relatively short 25-day window. They suppose that cash targets are

initially undervalued so that by paying in cash rather that stock, the bidder captures the entire

gain. We find no difference in the way stock and cash bids react negatively to deal failure

with a much longer event window post the deal outcome news. It is true that we find stock

financed targets return to their pre-bid levels within the 100-day window following a deal

failure announcement and cash financed targets do not. Hence, we believe that failed targets

of cash bids remain in play for longer, even though Malmendier, Opp, and Saidi (2011) find

no evidence that they do subsequently become targets.

Dimopoulos and Sacchetto (2011) structurally estimate preemptive bidding and target

resistance based on an extension of Fishman‟s (1988) theoetical model. They show that only

rarely is there a second bidder, meaning that most initial bids are preemptive. Their

simulations imply that the initial bidder‟s valuation of the target is 97% of the pre-bid value

and potential rivals far lower at only 58%. This means that prospective synergistic gains are

likely to be the monopoly of just one bidder and the main barrier to the bidder extracting

most of the gains is target resistance. Our findings are the first to justify the high initial bidder

valuations that are otherwise unexplained by their modelling. Furthermore, in their

framework, deals fail endogenously because synergsitic gains are insufficient to overcome

15

target resistance. Thus, endogenously failed deals yield fewer synergistic benefits than

exogenously failed deals, which is precisely what we find with our sample of endogenously

and exogenously failed deals.

3. Hypothesis Development and Construction

3.a Hypothesis Development

As outlined above, despite a comprehensive body of research documenting the

performance of firms around acquisition announcements and the motives behind these

takeovers, there are serious limitations with these methodologies due to revelation and other

biases. We will analyze the short and long-term impacts of M&A offer failures. From this

analysis, we seek to fill some important gaps in our understanding of the motives for mergers

and acquisitions and in the process, to improve on the interpretation of M&A announcement

effects. We first assess whether the pursuit of synergistic benefits is a plausible motive for

bidders to make takeover offers.

Hypothesis I:

In our analysis, we include failed and exogenously failed takeover bids. In doing so, we

overcome the revelation bias issue posed by Hietala, Kaplan and Robinson (2003), where the

announcement of a takeover reveals information about the stand-alone value of the bidder

and target and their businesses, in addition to any potential synergies arising from the

combination of the two firms. Based on the existing literature and empirical evidence, we

propose the following hypothesis:

HI: On the announcement of the failure of a merger and acquisition offer, the combined

value of the acquirer and target will fall.

We foresee that this result will prove robust to a variety of samples, methodological

approaches, and estimation techniques, revealing that on an M&A offer failure there is a

decline in the combined acquirer and target equity capitalization, and hence a loss in

synergistic benefits.

16

Hypothesis II:

We hypothesis that:

HII: Acquirer shareholders gain a significant share of the synergistic benefits created on

the announcement of a merger and acquisition and, similarly, lose a significant

amount on failure of the bid.

To assess the validity of this proposition, we employ both event study analysis and cross

sectional regression models to analyze the returns around initial bid announcements and

failure announcements. We seek to assess whether bidders gain a significant share of the

expected synergistic benefits on announcement of an M&A offer. To test this proposition, we

examine whether on the announcement of a bid failure, bidder stocks lose their expected

portion of the synergistic benefits created at the bid announcement.

4. DATA AND METHODOLOGY

4.a Sample Construction

This study focuses on initial merger and acquisition offers and possible later withdrawals

announcements. We study merger and acquisition offers for public targets from four major

“Anglo” developed economies: Australia, Canada, the United Kingdom and the United

States, mainly to increase sample size particularly for the “failed offer” sample. Our study is

the first to combine data on matched acquirers and targets from a number of Anglo countries

with quite similar competitive tender offer rules. The core data used in this study represents

merger and acquisition characteristics, which comes from the Securities Data Corporation‟s

(SDC) Platinum Global and US Mergers and Acquisitions database. We examine initial bids

announced between January−1, 1985 and December 31, 2009 and obtain the following

information on from the SDC Platinum database: (i) the identities of the parties involved in

the transaction, (ii) whether the deal was consummated, (iii) the deal‟s mode of payment, (iv)

any toehold the acquirer or target held in each other prior to the offer, (v) the initial offer

announcement date, (vi) the announcement date of offer consummation or withdrawal, (vii)

offer characteristics, (viii) the industry and nation of the acquiring and target firms.

17

Where possible stock returns, firm size and accounting data, are obtained from the

CRSP/Compustat merged database. Due to the limited coverage in the CRSP/Compustat

merged database of international stocks, we used Datastream to collect stock returns, firm

size and accounting data. Since Datastream has limited financial statement coverage, we also

relied on Aspect Huntley, ORBIS and SDC Platinum to obtain the missing accounting

information.

The M&A sample criteria are as follows.

(i) The target is a public listed firm that is incorporated in Australia, Canada, the

United Kingdom or the United States.

(ii) The acquirer is a publicly listed firm.

(iii) The deal can be clearly classified as successfully completed or a failure.

(iv) The bidder seeks to acquire more than 50 percent of the target firm shares in order

to gain control and holds less than 50 percent of its shares beforehand.

(v) The deal value must be greater than one million dollars.11

(vi) The method of payment used in the bid must be solely cash or stock.

(vii) The firm‟s stock is actively traded and its stock price and market value must be

readily available from either CRSP or Datastream.

(viii) The firm‟s annual financial statement information must be available from

CRSP/Compustat Merged Database, Datastream, Aspect Huntley‟s FinAnalysis,

ORBIS or SDC Platinum.

(ix) Deal value must represent five percent or more of a bidder‟s equity capitalization

to insure that the deal has a material impact on a bidder‟s stock price.

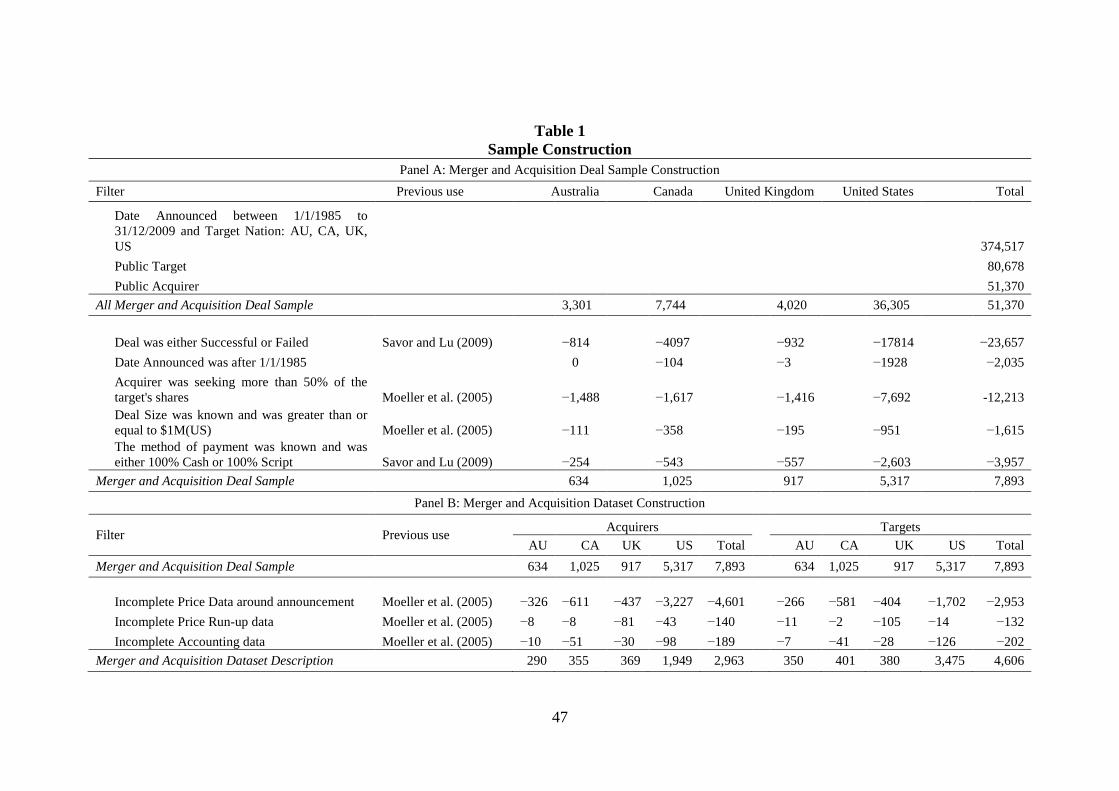

The final sample includes 3,147 acquirers and 4,793 targets firms. Table 1 reports the

reduction in the sample as we impose additional sample criteria. We start with raw data

collected from SDC Platinum and in the end obtain our final sample shown in Table 1, Panel

A. We finally require the bidder and target firms to have stock price and accounting data

available, which yields our final dataset described in Table1, Panel B.

<<Insert Table1 about here>>

11

Deal value is defined in US$ as the consideration paid by the acquirer for the target, excluding fees and

expenses.

18

The four-country selection allows us to analyze the motives for cross-border acquisitions

and to analyze merger and acquisition activity outside the US, as well as to substantially

expand our sample size. Along with the usual sample criteria, we required that bidders seek

more than 50 percent of target shares since at this level of ownership an acquirer will

typically have full control over the target. We also find that setting an absolute cut-off on the

method of payment of either 100 percent cash or 100 percent stock, does not significantly

reduce the sample size.12

The final sample consists of 2,963 acquirers, 4,606 targets and 1,941 deals where data is

available for both acquirer and target. Figure 1 describes the time-series distribution of the

sample and the US dollar amount of stock bids relative to cash bids in each year. The figure

first shows that that we have more targets than acquirers with the required data and even

fewer deals where we have data for both bidder and target. Second, we identify the

frequencies of stock and cash financed deals in the sample. Stock based deals become more

popular than cash financed deals in the 1990s, which corresponds to the 1990s merger and

acquisition boom. The merger boom of the second half of the 1990s is noteworthy for the

largely stock financed transactions. Table 2 presents the sample distribution of completed and

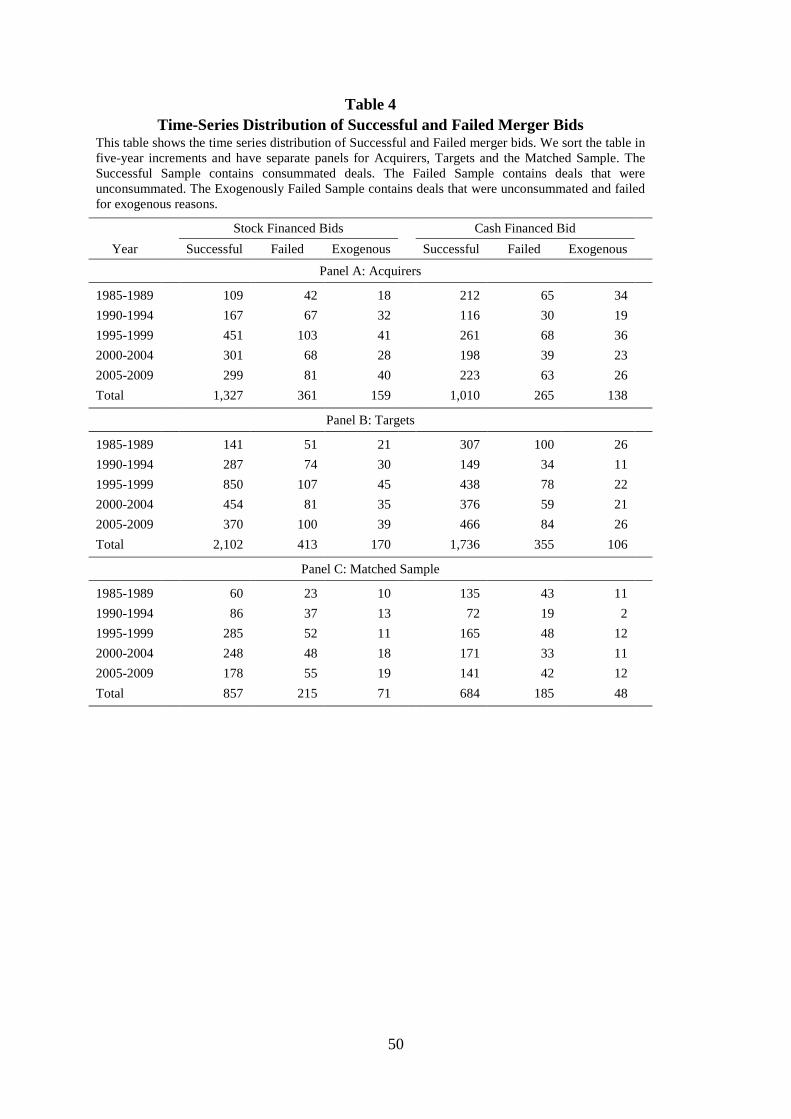

failed bids, by country and by stock and cash financed deals.

<<Insert Figure 1 and Table 2 about here>>

According to Shleifer and Vishny‟s (2003) market-timing hypothesis, overvalued firms

have a relatively greater incentive to make stock acquisitions. Hence, an acquiring firm may

use mispricing of their stock to swap their overvalued equity for relatively less overvalued

target equity. This is very similar to the adverse selection in the Myers and Majluf (1986)

model of stock offers. Thus, the acquirer is using its overvalued stock to purchase a target‟s

assets at a discount. This hypothesis corresponds to the evidence presented in Figure 1, where

we see that the stock market and merger booms of the 1990s corresponds to an increasing use

of stock over cash as an acquisition currency. An announcement of an equity-finance merger

and acquisition may signal that the acquiring firm is mispriced and overvalued. Accordingly,

one expects on this negative signal of overvaluation that the acquirer‟s stock should fall in

value. Hence, if synergies exist from combining two firms, then on the offer announcement

they will co-mingle with the negative signal. This makes it difficult to isolate the synergy

12

A table of bids lost by imposing the 100 percent cash or stock requirement is available on request.

19

effect when studying the distribution of returns on the announcements of M&A deals. Thus,

we construct a sample of failed bids caused by exogenous factors, where the bids fail for

reasons extraneous to the valuation or decisions of the acquirer or target.

4.b Exogenous Failed Bids: Sample Construction

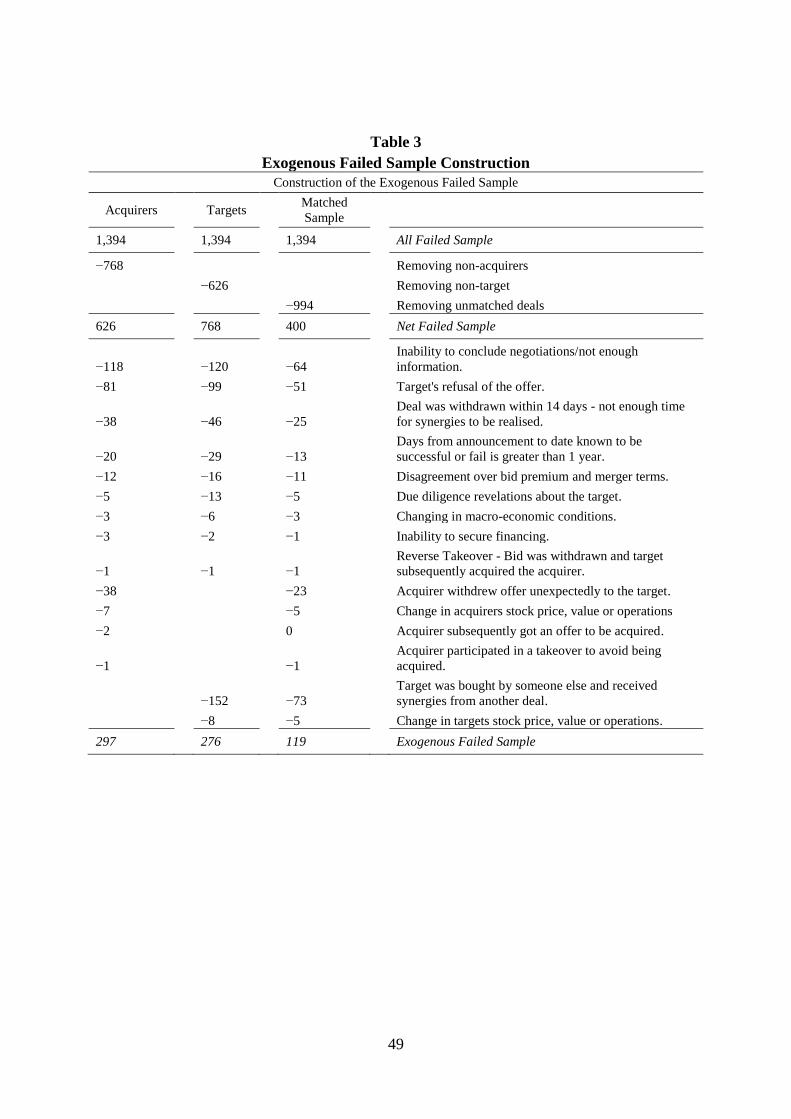

We follow a method similar to Savor and Lu (2009) to construct a sample of exogenously

induced merger and acquisition bid failures, shown in Table 3. As postulated in the market-

timing theory, there is a positive relationship between a firm‟s overvaluation and the

probability of a stock-based acquisition when bids fail due to target shareholder recognition

that a bidder‟s equity is overvalued. Empirically, on the initial announcements of stock-based

deals, bidder returns significantly underperform cash-based deals.

<<Insert Table 3 about here>>

To account properly for loss of expected synergies, we must first be sure that expected

synergies are associated with the acquisition announcement. We know that a variety of

important pieces of information are released with the initial bid announcement. The

announcement reveals information about the stand-alone values of the bidder and target, the

expected synergies arising from the combination, as well as the distribution of the expected

synergies between target and bidder shareholders. Thus, we must exclude bids where the

offer is doomed to fail from the beginning, or failed because of any revelations concerning

bidder or target valuation. Thus, we construct an exogenously caused offer failure sample,

which reduces our “failed bid sample” by more than 50 percent

Our methodology differs slightly from Savor and Lu (2009) because we include target

firms and a matched sample (where we have both acquirer and target firms in our sample).

Therefore, we determine what is exogenous in context of the three different sample

categories. The goal of the exogenous sample is to keep only deals that fail unexpectedly and

for reasons that are outside of the two firms control, which in a semi-strong form efficient

market means that new information was not previously priced by the market. Ideally, we

want to study bids that trigger market capitalization of a bid‟s expected synergies on its initial

announcement date, which is subsequently lost on the bid‟s announced failure. It is critical

that the withdrawal news does not co-mingle with signals concerning revision in the bidder‟s

20

valuation. For this reason, acquirer and target samples differ from each other. Additionally,

the matched sample must only contain acquirers and targets in exogenously failed deals.

The subsample of exogenously failed acquirers contains deals that failed due to regulatory

disapproval, competing offers, and unexpected target developments. Likewise, the

exogenous subsample for targets contains bids that failed due to regulatory disapproval,

unexpected acquirer developments and competing offers such that the initial offer to the

target firm remained unconsummated. Finally, for the matched-sample, the merger must have

failed due to reasons outside the control of the acquirer and target, such as regulatory

disapproval and competing offers. This extends Savor and Lu (2009) approach which finds

that mergers are beneficial to acquiring firm shareholders. They compare post-event returns

to find that successful acquirers on average outperform failed acquirers. Our methodology

differs from theirs because we allow for a more plausible alternative explanation for this

performance difference, namely the loss of synergistic benefits on the failure of the deal, and

not because of the loss of the opportunity to buy the target with overvalued bidder stock.

Furthermore, we extend their “exogenous failed” sample to include targets so as to improve

our power to distinguish between the conflicting hypotheses.

The information sources used to determine why a takeover failed differs slightly from

Savor and Lu (2009). Due to the difference in size of the number of failed bids in their study,

355 for their sample compared to 1,394 in our sample, we use a variety of information

sources to determine the reasons for bid failures. We investigate every failed deal using the

combined resources of Factiva, LexisNexis, news articles from Google, and the synopsis and

deal history provided by SDC Platinum. We find a similar success rate to Savor and Lu

(2009) in being able to explain the cause for bid failures.

The process of constructing the exogenously failed sample begins with the “All Failed

Bid” sample and then we divide the failed bid sample into acquiring and target firms and a

third category in which both the bidder and the bidder‟s actual target remain to form a

matched sample. We arrange the “endogenous” reasons why deals failed by whether they are

(i) common to both acquirer and target, (ii) common only to acquirers and (iii) common only

to targets so as to leave only acquirers, targets and matched pairs of acquirer-target

companies where both the acquirer‟s bid and the target failed for exogenous reasons and

where information is complete on both parties.

Thus, we first exclude bids where there is insufficient information due to an indeterminate

cause for the bid failure, resulting in a more decisive exogenous sample with known reasons

for failure. Second, we exclude deals where there is a flat rejection of an acquirer‟s offer, or

21

where the deal failed within a very short period, i.e., 14 days, in which case we believe no

synergies would have manifested themselves into the share prices of the acquirer or target

during that period. Similarly, we exclude deals where the deal failed after one year following

the bid‟s initial announcement, because of a low probability that the stock returns over this

long time period solely reflected the information about the changes in the bid and its likely

outcome.

In addition, we exclude bids where there are disagreements over the bid premium and

merger terms. We also exclude bids where the bid failed due to revelations about the target

valuation, changes in macro-economic conditions or an inability to secure financing, as these

cases have valuation implications beyond the loss of the synergistic benefits of the proposed

bid. The end-point of this exclusion process is the collection of remaining deals that failed for

exogenous reasons unrelated to valuation changes. Ideally, we want the firms remaining in

the sample not to have a permanent fall in value due to anything other than the loss of an

acquisition‟s synergistic benefits. Thus, there will be some cases where an acquirer will lose

synergistic benefits and a target will not or vice-versa. For example, the acquirer loses the

chance to consummate the deal due to a successful competing bid, so that the target is still

acquired. Consequently, the acquirer loses the deal‟s expected synergies, while the target

realizes its share of the synergies through the takeover premium of the successful competing

bidder. Table 4 displays the time-series distribution of successful and failed acquisition bids

in our final sample that we term the All Failed sample, inclusive of consummated bids.

<<Insert Table 4 about here>>

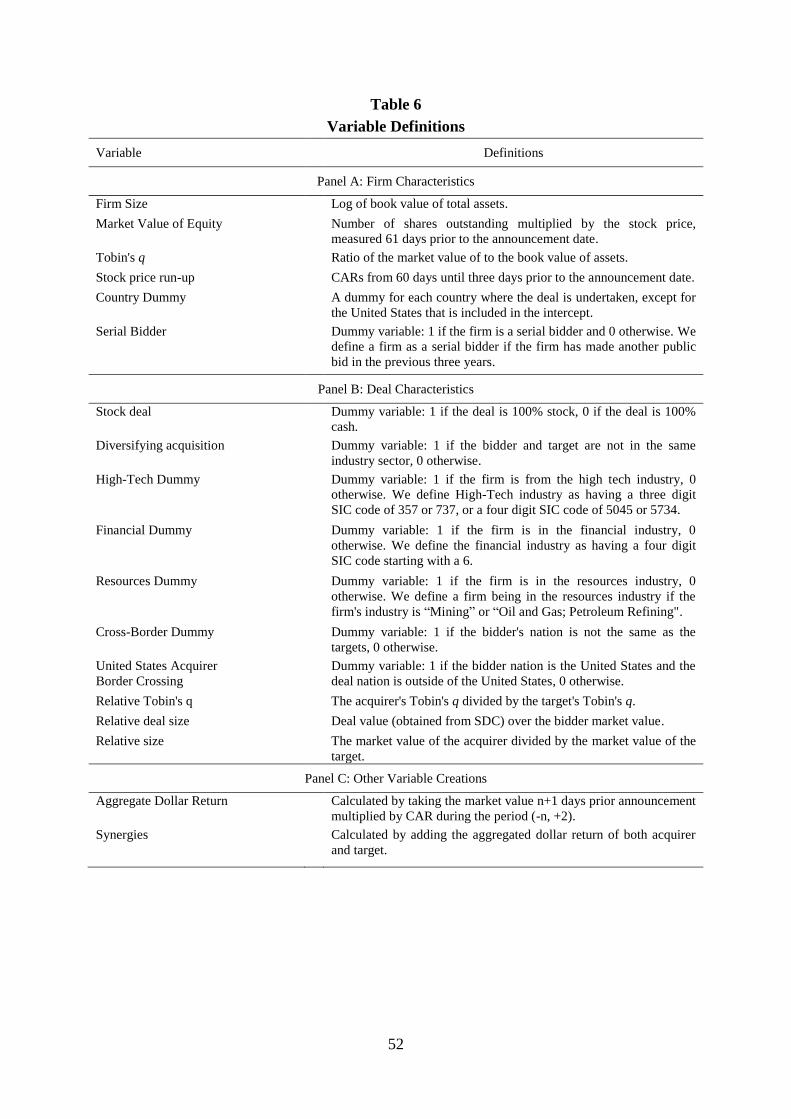

4.c Variable Construction

In this subsection, we discuss variable definitions.

Acquirer and Target Returns

We measure market reactions to bid announcement and failure dates using cumulative

abnormal returns (CARS) defined over a specified event window around the announcement

dates, where returns are adjusted for market-wide effects using a one-factor market model,

, ,i t i i m t tR R . (1)

22

The one-factor market model is estimated using daily stock returns, Ri,t, over the pre-

announcement period [−250, −30]. Daily market returns, Rm,t, are defined as value-weighted

stock indices construct from listed stocks on the major stock exchanges in each country. For

Australian firms, we use the All Ordinaries Index taken from SIRCA database; for the US,

we use the CRSP Value Weighted Index; and for other countries, we use local value-

weighted market index taken from Datastream.13

Stock i‟s abnormal return, ARi,t, is defined

as the stock‟s raw return minus the estimated one-factor market model:

, , ,i t i t i tAR R E R , (2)

where ,i tE R is estimated from the one factor market model shown in equation (1) and t is

from the first day of the event window until the last day, n. The cumulative abnormal return

(CAR) is defined as:

1

,n

t

t

CAR t n AR

. (3)

For comparison purposes, we use the CRSP Equal-Weighted Index as the equal-weighted

benchmark for all firms in our sample. There are many concerns when modeling and

interpreting abnormal returns around short- and long-term event studies. Studies of gains and

losses in mergers and acquisitions for short-term events have typically taken the three-day

CAR (Betton et al. (2008), Moeller, Schlingemann and Stulz (2005), and Savor and Lu

(2009)), and five-day CAR (Masulis, Wang and Xie (2007) and Fuller, Netter and

Stegemoller (2002)) windows around the initial acquisition announcement dates. Fuller et al.

(2002) find that for a random sample of 500 acquisitions from 1990 to 2000, the

announcement dates provided by SDC are correct for 92.6 percent of the sample.

Additionally, they find that for the remaining 7.4 percent SDC is incorrect by no more than

two trading days. For this reason, we employ a five-day event window around announcement

date, instead of a three-day event period.

Table 5 presents the summary statistics of the five-day CAR of both acquirers and targets

around the announcements of mergers and acquisitions. The results in the table are consistent

with existing empirical research on takeover announcement effects. We find that targets earn

significantly positive abnormal returns (20.9 percent) around M&A announcements, while

acquirers earn on average negative returns (−0.8 percent). The results are as expected and

appear to be contrary to Hypothesis II, which predicts that acquirers share a significant

portion of the synergistic benefits created by an M&A transaction. Interestingly, we find that 13

All Indices account for dividends.

23

targets of subsequently failed bids earn lower announcement returns. This observation holds

for targets of both the failed bid and exogenous failed bid samples. Bidders in the exogenous

failed bid sample suffer more severe negative returns (−1.2 percent) than the combination of

successful and failed bidders (−0.8 percent). In Panel−C, we show results for our hypothetical

combined bidder and target firm created from our matched sample. We see that all our

subsamples exhibit positive combined returns for takeover announcements. This finding

provides some initial evidence in favor of Hypothesis I and suggests that not only do

synergistic benefits exist, but they are observable in takeover announcements.

<<Insert Table 5 about here>>

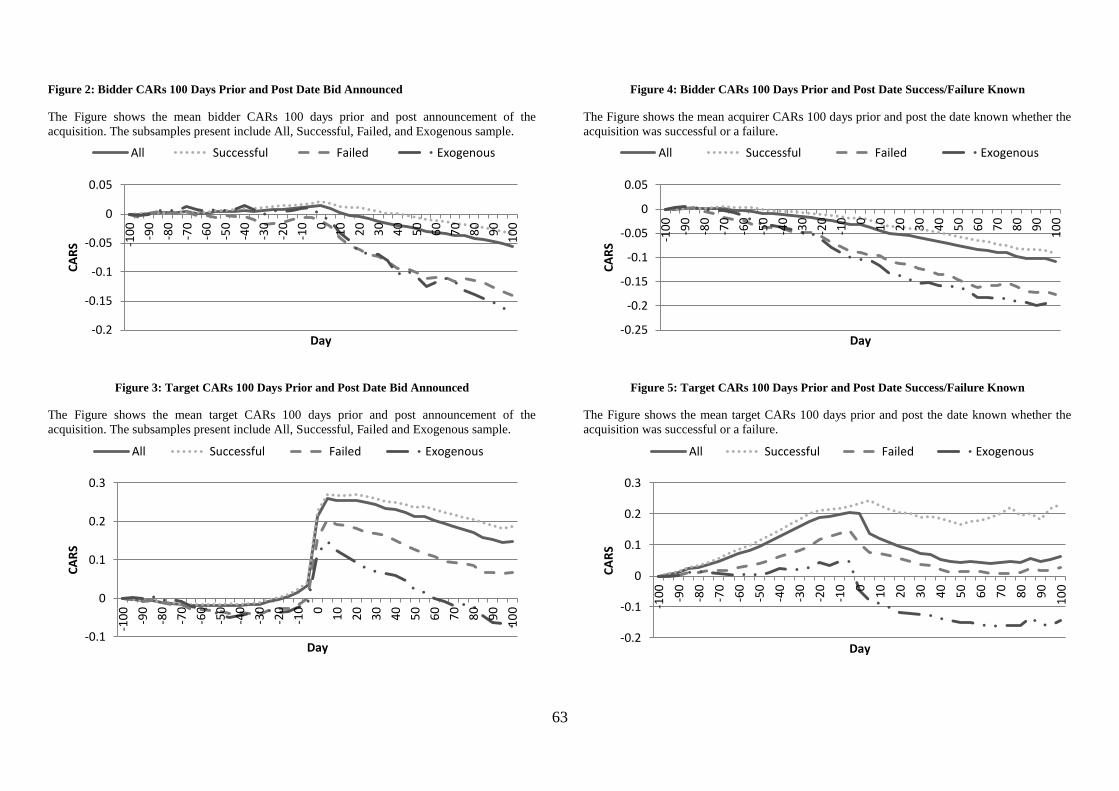

Figures 2 and 3, respectively, plot average bidder and target cumulative abnormal returns

over 100 trading days before and after the bid announcement, measured in five-day

increments. Similarly, Figures 4 and 5 plot average acquirer and target cumulative returns

around the date when the market learns that the acquisition either is approved or fails. We

further separate the figures into subsamples of all firms (All), those acquisitions that were

successful (Successful), those that failed (Failed), and those that failed for exogenous reasons

(Exogenous). The effect of the announcements on targets is particularly evident in both the

initial announcement of the acquisition, creation of synergies and, secondly, on the

announcement of bid failure, loss of synergistic benefits. On the announcement, targets in our

sample earn on average abnormal returns of approximately 20 percent. Targets on bids that

subsequently fail earn significantly lower returns than targets that are successfully completed.

This is evidence that the market has some ability to predict which bids are likely to fail. Thus,

returns may only reflect an expected gain, conditional on the deal value and its likely

completion, and not the full value of the synergistic gains. This finding is consistent with

methodology employed by Bhagat et al. (2005), where they rescale returns using probability

scaling and intervention methods.

<< Insert Figures 2, 3, 4 and 5 about here>>

Plots of bidder returns in Figures 2 and 4 are consistent with the existing literature and

empirical findings, which report negligible returns and sometimes losses for acquirers around

acquisition announcements. In addition, Figure 4 is consistent with the findings of Savor and

24

Lu (2009) that acquirers in failed bids underperform acquirers in consummated bids over a

longer post-acquisition horizon. Thus, our results show that acquirers gain from takeovers

but, so far, we do not know why they realize gains.

There are two main methodological approaches in long-horizon event studies:

characteristic-based matching approach, also known as the BHAR (Buy-Hold Abnormal

Returns) and the Jensen‟s alpha approach, otherwise known as the calendar-time portfolio

approach (see Eckbo, Masulis and Norli (2000) and Fama (1998)). While the question of

which is the best model of returns for long-horizon event studies is yet to be resolved,14

in

this study we employ the BHARs to calculate the long-term abnormal returns and compare

the long-term performance of successful and failed acquirer and target firm pairs. With the

calendar-time approach, we face a similar obstacle to that of Savor and Lu (2009). They find

it difficult to implement due to the limited number of firms in their exogenously failed bid

sub-sample. The diversity of countries that our targets and acquirers come from exacerbates

this difficulty. Hence, this makes it extremely difficult to find an adequate number of firms

with similar size and book to market factors to implement the calendar time approach.

Researchers commonly utilize CARs in short-term event studies, but they find numerous

flaws to using them in longer-term studies: (i) CARs bear little resemblance to the returns

accrued by a long-term investor, and (ii) the process of aggregating short-term abnormal

returns over a longer time-period is likely to result in the emergence of spurious upward or

downward drift due to market microstructure issues, according to Conrad and Kaul (1993).

They also point out that accumulating single-period returns over longer time-periods assumes

portfolio rebalancing each period. Hence, the appropriate performance measure should be

buy-and-hold returns over longer intervals. However, in measuring CARs for the period

between announcement and failure dates, we hope to obtain a better understanding of the

stock returns around the two announcement dates and between these two announcements.

The second and most popular long-run event study technique is the buy-and-hold

benchmark approach, whereby we multiplicatively compound daily returns over the event-

window and then compare these returns to a given benchmark over the same period. We then

subtract the compounded returns for the benchmark from the compounded returns of the firm,

in order to obtain the stock‟s buy-and-hold abnormal returns (BHARs). Due to the diversity

of firms from multiple countries, we do not use an equal-weighted matching portfolio as a

benchmark for the firm. Instead, we use an equal-weighted index obtained from CRSP and

14

See Kothari and Warner (2007).

25

the same value-weighted index, as mentioned above for the CARs. This methodology enables

us to compare the BHARs and CARs, facilitating a more in depth robust analysis. Using the

broader benchmarks, we also avoid any cross-correlation problems, whereby correlation

occurs in the events of the firm of interest and have material effects on one or more firms.

Calculation of buy-and-hold returns for firm i and its associated market index over a given

time interval is as follows:

,21 1

n

i i ttR r

, (4)

where iR is the long-term buy-and-hold return of firm i, and ,i tr is the return of firm i‟s stock

on day t. We use the same process to calculate returns for the market index. The

buy−and−hold abnormal returns (BHAR) for firm i become:

2,

i

n i iBHAR R BR , (5)

where2,

i

nBHARis the buy-and-hold abnormal returns between two days prior announcement

andiBR is the return of benchmark i over the same period.

15

The technique that we use to measure firm performance of companies is a relative one.

Due to the large sample size of our merger and acquisition database, we are able to include a

large sample of merger pairs where we have complete data for both acquirer and target. Thus,

we are able to compute Tobin‟s q for both acquirer and target. Shleifer and Vishny (2003)

discuss relative overvaluations, rather than absolute valuations. We adopt their basic intuition

to use a relative performance measure, rather than an absolute one. Garvey et al. (2010),

employ a similar approach to investigate the link between the likelihood of a merger and the

market mispricing. The relative valuation method we develop in this study to account for the

mispricing and valuation hypothesis is a relative Tobin‟s q. We calculate the relative Tobin‟s

q by dividing an acquirer‟s Tobin‟s q, by its target‟s Tobin‟s q as show below:

Acquirer

Target

Tobin sRelative Tobin s

Tobin s

q

. (6)

The variable definitions are given in Table 6.

<<Insert Table 6 about here>>

15

Summary information for bidders and targets on the date known announcement cumulative abnormal returns,

long-term buy-and-hold abnormal returns upon merger consummation or failure, and long-term cumulative

abnormal returns upon merger consummation or failure are available from the authors.

26

5. CROSS-SECTIONAL ANALYSIS

This section examines the cross-sectional analysis of returns to acquirers and targets

around acquisition bids and bid failure announcements. We begin with summary statistics for

our sample, followed by a cross-sectional regression analysis of abnormal returns around

these events. The cross-sectional analysis allows us to estimate the magnitude and

distribution of expected synergistic benefits created in acquisition bids. This section is split

into three parts. The first sub-section analyzes expected synergistic benefits around

acquisition bid announcement dates. The second sub-section analyzes the predictions of

Hypothesis I concerning the loss of expected synergistic gains on bid failure announcements.

The third sub-section analyzes abnormal announcement returns over a longer event window,

starting with the bid announcement until the bid outcome announcement of a bid‟s success or

failure. From this analysis, we obtain a clearer picture of whether there are expected

synergistic benefits in typical acquisition bids. This analysis also allows us to assess whether

the pursuit of synergistic benefits is a fundamental motive for acquisition bids.

If the pursuit of synergistic benefits is an important motive for acquisition bidders, then

acquirers should share in any synergistic benefits associated with a bid. It follows that bidder

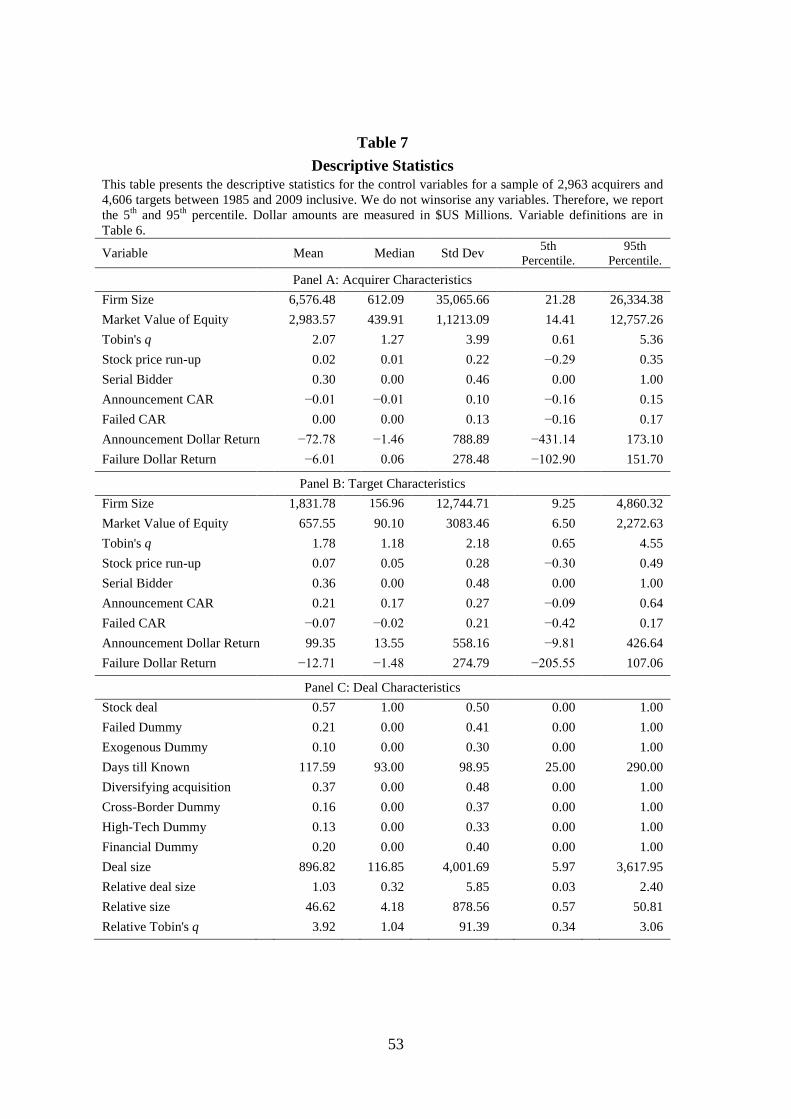

stock price reactions to acquisition bid announcements should be significantly positive. Table

7 shows that acquirers have a mean price run-up of two percent prior to the bid and a

cumulative abnormal return on the bid announcement of −1 percent. Ahern and Sosyura

(2011) suggest that acquirers release a string of positive announcements in the weeks and

months leading up to the public announcement of an acquisition, boosting their share price

and in the case of script offers, obtaining a better ratio on a stock merger swap. Therefore, if

we take account of the acquirer‟s pre-bid price run-up in measuring a bidder‟s acquisition

announcement return, then bidders realize a positive acquisition bid announcement return of

one percent. This preliminary evidence provides support for Hypothesis II: on average

acquirers realize positive returns on acquisition bid announcements, even though the gain in

percentage terms is small. While targets appear to capture the bulk of the acquisition induced

synergies since they exhibit larger announcement effects compared to bidders, this is

somewhat misleading because targets tend to be much smaller in size than bidders. Thus,

even if there is an equal division of the synergies between bidder and target, the target would

exhibit a much larger percentage gain.

<<Insert Table 7 about here>>

27

The market for corporate control literature documents strong evidence that targets receive

a substantial share of synergistic benefits associated with acquisitions, based on significant

positive market reactions to acquisition announcements. Similar to Betton et al. (2008), Panel

B presents a positive announcement CAR for target firms of 21 percent and a price run-up of

seven percent. Thus, in the 60 days prior to announcement until two days after the acquisition

announcement, the target firm enjoys an abnormal return of approximately 28 percent.

The descriptive statistics in Table 7 depict an interesting relationship between the relative

Tobin‟s q of acquirers and targets. The mean value for Tobin‟s q for acquirers and targets is

respectively 2.07 and 1.78. However, using our matched sample of acquirers and targets, we

are able to compute the relative Tobin‟s q present in a deal. Utilizing the latest accounting

figures prior to the bid and a firm‟s equity market value 61 days prior to the bid

announcement, the mean relative Tobin‟s q is 3.92, indicating that on average acquirers have

a Tobin‟s q that is approximately four times greater than that of their targets.

At one level, this may provide evidence to support Shleifer and Vishny‟s (2003) market-

timing theory and the explanation of Savor and Lu‟s (2009) of relative overvaluation of

acquirers compared to targets. This large disparity in acquirer and target Tobin‟s q figures

provides evidence to support the view that overvalued high-growth acquirers tend to purchase

relatively lower growth (and less overvalued or more undervalued) targets. Thus, Savor and

Lu‟s explanation rests on acquirers exploiting target shareholders by paying them in

(relatively) overvalued stock. We depart from the behaviorist point of view by using of

rational economic decision making to explain acquirer motives arising from slower than

expected growth prospects, which lead managers to seek external growth options, including

the pursuit of synergistic benefits through acquisitions. What Grossman and Hart (1981)

define as “allocational mergers” create synergistic benefits, where assets transfer from low-

productivity to high-productivity firms, thereby increasing the economic benefits that an asset

can produce.

Table 8 presents the announcement period and the sum of the 60-day run-up period plus

announcement abnormal returns, as well as the announcement period and the sum of the 60-

day run-up period plus announcement aggregate dollar returns for the sample used in the

cross-sectional regression. For this sample, we find similar results to the past literature (e.g.,

Andrade et al. (2001)). We find that on bid announcements bidders on average earn

negligible returns, which are sometimes losses (of –1.05 percent and –0.44 percent,

respectively). Furthermore, we see large gains to target firms on announcement date (19.22

28

percent and 27.01 percent). As hypothesized, we see large losses to both bidders (-9.34