DNYANSAGAR ARTS AND COMMERCE COLLEGE

63

DNYANSAGAR ARTS AND COMMERCE COLLEGE SUBJECT: FINANCIAL ACCOUNTING SUBJECT CODE: 102 BY PROF. : MUBINA ATTARI

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of DNYANSAGAR ARTS AND COMMERCE COLLEGE

DNYANSAGAR ARTS AND COMMERCE COLLEGE

SUBJECT: FINANCIAL ACCOUNTING

SUBJECT CODE: 102

BY PROF. : MUBINA ATTARI

SYLLABUS1.Basic concept of financial accounting.

2.piecemeal distriBution of cash.

3.single entry system.

4.gst

ACCOUNTING CONCEPTS, CONVENTIONS AND PRINCIPLES AND AN OVERVIEW OF EMERGING TRENDS IN ACCOUNTING

• (A)Accounting Concepts, Conventions and Principles

1. Money Measurement

2. 2. Business Entity

3. 3. Dual Aspect

4. 4. Periodicity Concept

5. 5. Realization Concept

6. 6. Matching Concept

7. 7. Accrual / Cash Concept

8. 8. Consistency Concept

9. 9. Conservatism Principle

10. 10. Materiality Concept

11. 11. Going Concern Concept

12. 12. Historical Cost Concept

• (B)Emerging Trends in Accounting

• 1.Inflation Accounting

• 2. Creative Accounting

• 3. Environmental Accounting

• 4. Human Resource Accounting

• 5. Forensic Accounting

INFLATION ACCOUNTING

What is Inflation?

Inflation means an upward change in the prices of goods & services of general consumption.

is due tothe fall in total supply of goods and services. imbalance in total supply of goods & services.changes in general prices of basic commodities.

NEED FOR INFLATION ACCOUNTING?

Traditional accounting based on historical cost fails to

match current revenue against costs that are current

costs of purchases or depreciation are shown at historical costs, and are much below current levels

NEED FOR INFLATION ACCOUNTING?

Traditional accounting based on historical cost fails tomatch current revenue against costs that are currentstate profit realistically

as costs of purchases, depreciation are understated, reported profits are high

NEED FOR INFLATION ACCOUNTING?

Traditional accounting based on historical cost fails to-match current revenue against costs that are current- state profit realistically- provide adequate depreciation for replacement of assets

depreciation is calculated on book value of assets that are way below their current market price.

CONCLUSION

Methods of Inflation Accounting are criticized as

They are subjectiveThey are based on estimation

They are not free from flaws

Discussion on this subject gained momentum with the rise in the price levels and the tempo died down with the fall in inflation.

METHODS OF INFLATION ACCOUNTING

Current Purchasing Power (CPP)

Current Value Systems

Current Cost Accounting

Replacement Cost Accounting Method

METHODS OF INFLATION ACCOUNTING

Current Purchasing Power (CPP)

Conversion Factor = Price index at the time of conversionPrice at the date of conversion

CPP Value= Conversion Amount or Historical Value x conversion factoer

ADVANTAGES Realistic view.

Basis of Depreciation

Check on payment of dividend out of capital

True and fair Balance-sheet.

Reasonable comparison of profitability.

Check on Mis-leading Deeds

Wrong matching concepts

DISADVANTAGES Depreciation.

Replacement of Fixed Assets

Situation in Deflation

Theoretical Concept.

Complicated System

Expensive Technique

Subjectivity in the valuation process

piecemeal distriBution of cash

Key Points

Surplus Capital Method

Accounting Treatment

fiXed assets

current assetsstocKs

current assets

deBtors

Bills receiVaBle

BanK Balance

cash realised

piecemeal distriBution of cash

Secured Liabilities

Taxes/ Govt. dues

Preferential Liabilities

Employees dues

Partner’s Loan Partner’s

capital

Realization expenses

Unsecured liabilities

piecemeal distriBution of cash

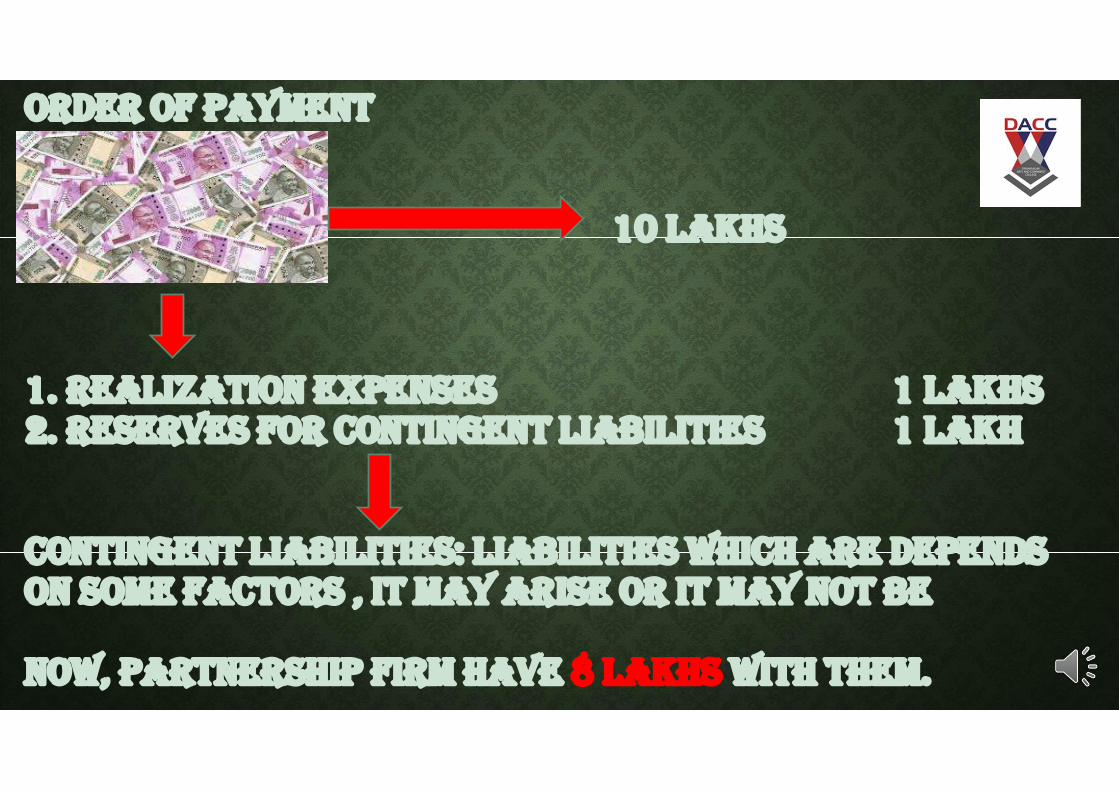

ORDER OF PAYMENT

liaBilities paid off

What is the order of payment?

order of payment

10 laKhs

1. realiZation eXpenses 1 laKhs2. reserVes for contingent liaBilities 1 laKh

contingent liaBilities: liaBilities Which are depends on some factors , it may arise or it may not Be

noW, partnership firm haVe 8 laKhs With them.

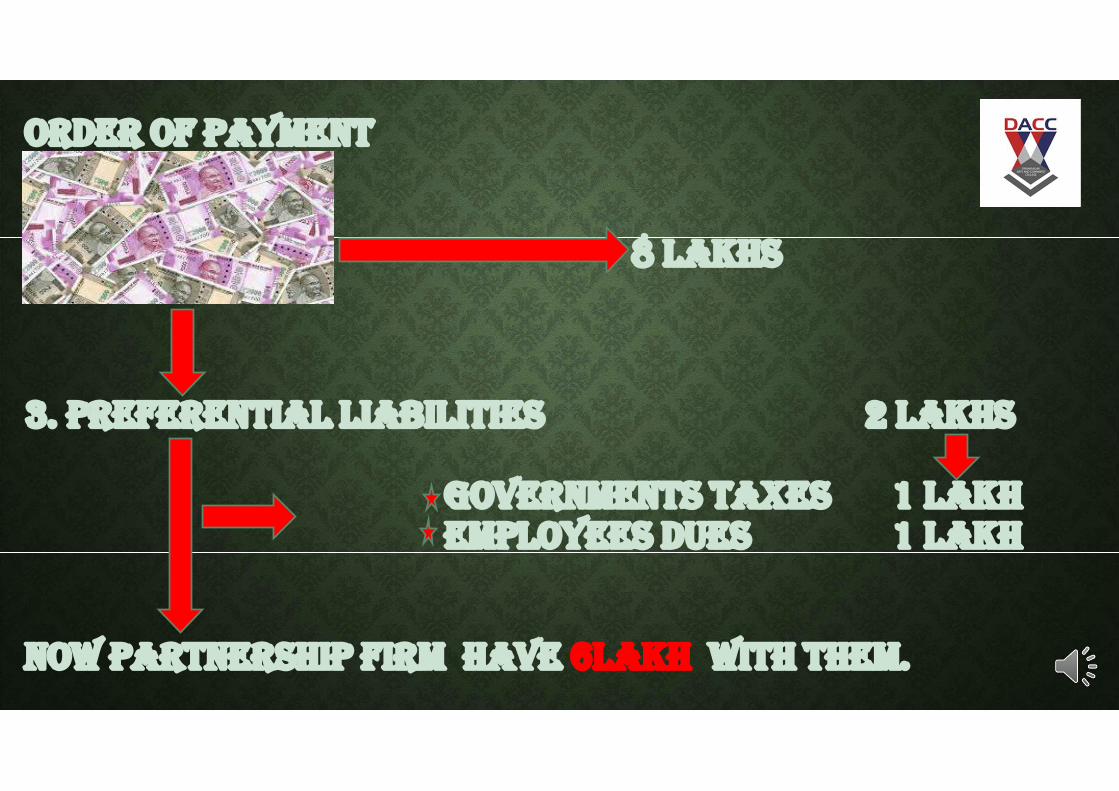

order of payment

8 laKhs

3. preferential liaBilities 2 laKhs

goVernments taXes 1 laKhemployees dues 1 laKh

noW partnership firm haVe 6laKh With them.

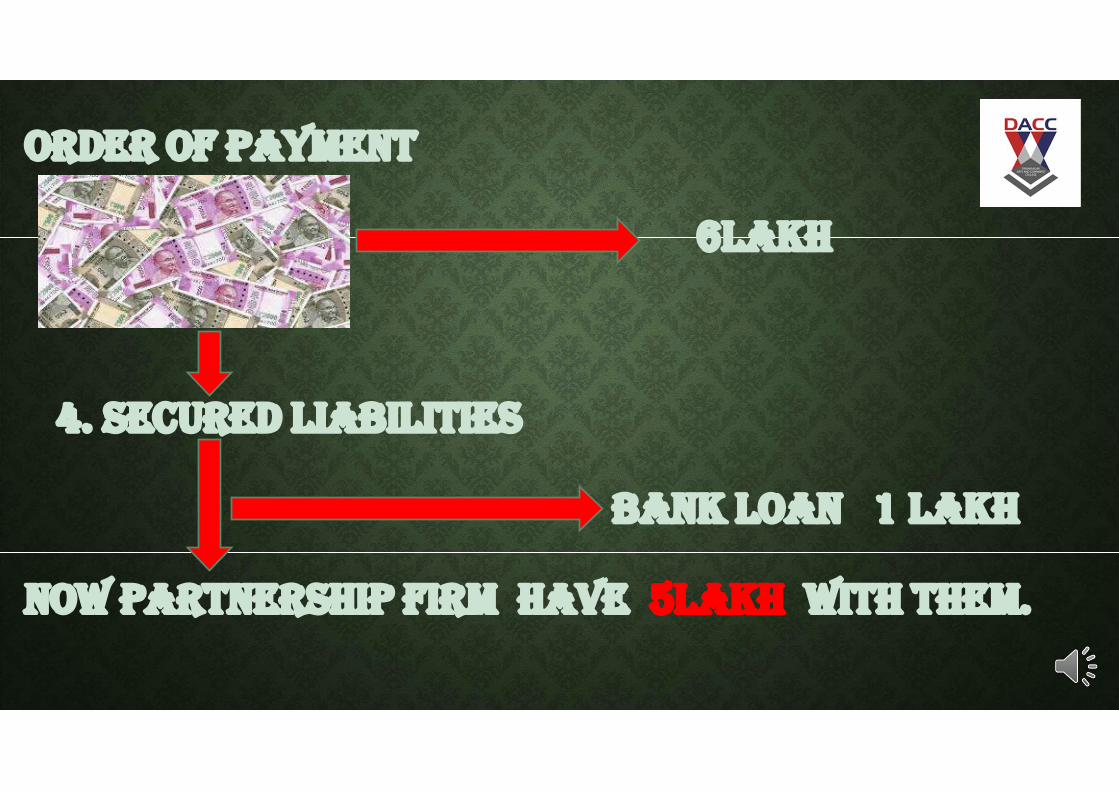

order of payment

6laKh

4. secured liaBilities

BanK loan 1 laKh

noW partnership firm haVe 5laKh With them.

order of payment

5laKh

5. unsecured liaBilities

creditors 1 laKhBills payaBle 1 laKhm/s a’s loan 1 laKh

noW partnership firm haVe 2laKh With them.

2 laKh

6 . partners capital

a’s capital B’s capital

1 laKh 1 laKh

FOLLOWING INFORMATION IS GIVEN IN THE QUESTION

1.CASH RECEIVED FROM THE SALE OF ASSETS.

2.DATE OF CASH REALIZATION

3.LIABILITIES PAID OFF.

4.PROFIT SHARING RATIOS.( ASSUMED EQUAL IF NOT GIVEN)

Balance sheet as on 31st march 2020Liabilities Assets

Capital Accounts 60000 Building 100000A 20000 Machinery 30000B 20000 Debtors 20000C 20000 Cash 50000Government Dues 10000Creditors 20000Secured Bank loan 90000

200000 200000

A, B, and C share profits and losses in equal ratio. Their balance sheet as on 31 st march is as follows.

CONTINUE.........THE FIRM WAS DISSOLVED AND IT WAS AGREED THAT THE NET REALIZATION SHOULD BE DISTRIBUTED IN THEIR DUE ORDER AT THE END OF EACH CALENDAR MONTH. THE GRADUAL REALIZATIONS WERE AS FOLLOWS:REALIZATION EXPENSES WAS RS 20000DATE AMOUNTAPRIL RS 50000MAY RS 75000JUNE RS 50000

PREPARE THE STATEMENT SHOWING ORDER OF PAYMENT.

ORDER OF PAYMENTMONTH AMOUNT LIABILITIES PAID OFFAPRIL 50000 1. REALIZATION EXPENSES 20000

(20000)

30000 2. GOVERNMENT DUES 10000

(10000)

20000 3. SECURED BANK LOAN 20000

(20000) (90000-20000)= 70000

0

MAY 75000 1. SECURED BANK LOAN 70000

(70000)

5000 2. CREDITORS 5000(20000-5000)= 15000

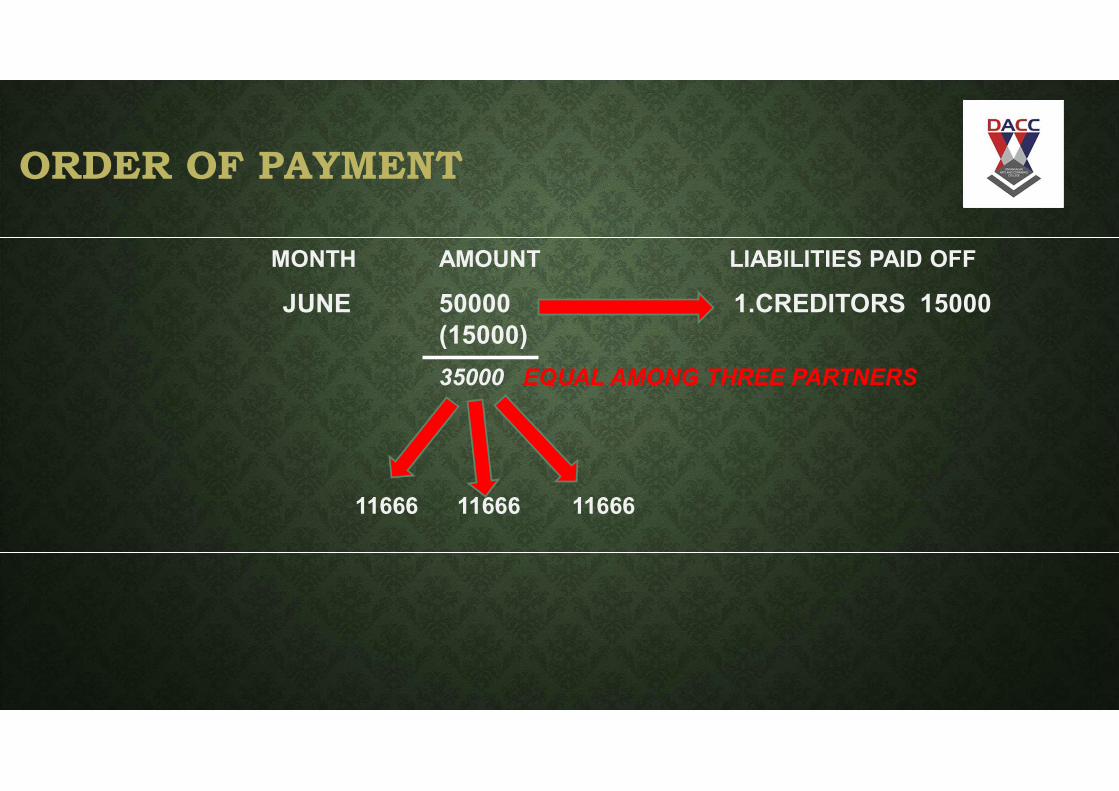

ORDER OF PAYMENT

MONTH AMOUNT LIABILITIES PAID OFF

JUNE 50000 1.CREDITORS 15000(15000)

35000 EQUAL AMONG THREE PARTNERS

11666 11666 11666

distriBution of cash among the partners

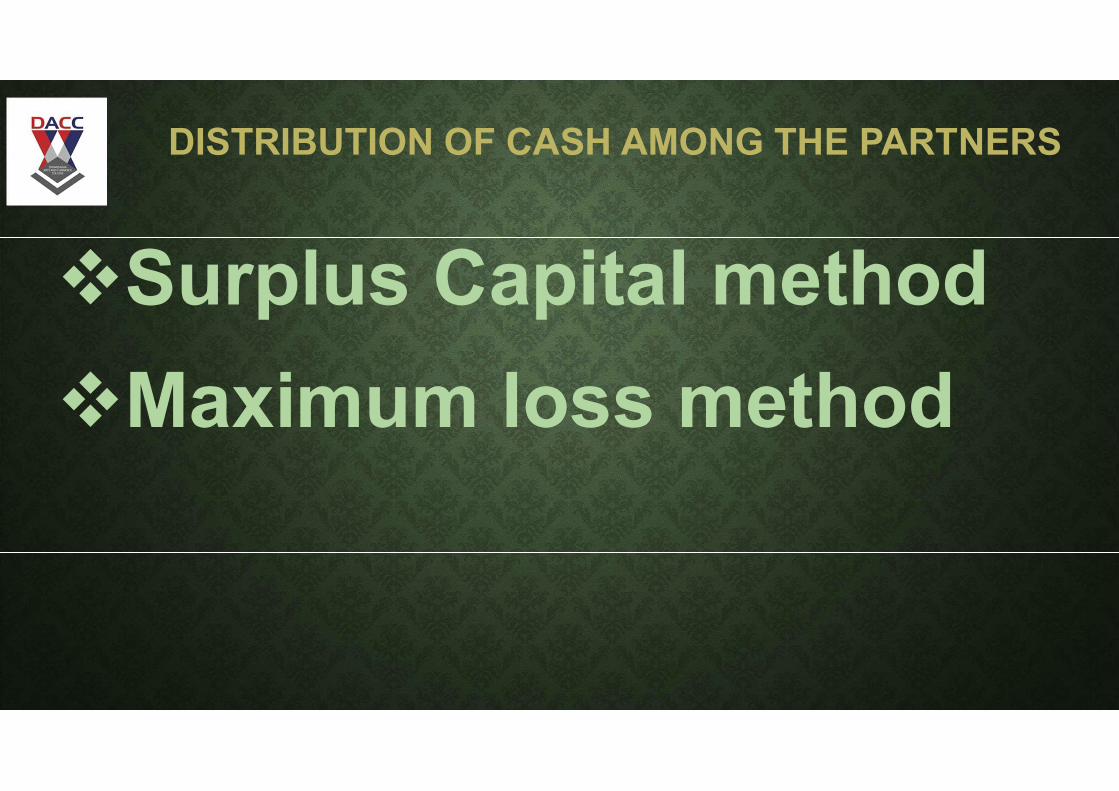

DISTRIBUTION OF CASH AMONG THE PARTNERS

Surplus Capital method

Maximum loss method

SURPLUS CAPITAL METHOD

Prepare statement of excess capital: This statement is prepared in order to make the capital of partners equal so that all the partners are on same ground.

INFORMATION REQUIRED IN PREPARATION OF STATEMENT OF SURPLUS CAPITAL.

1.CAPITAL BALANCES OF PARTNERS.

2.PROFIT SHARING RATIO.

Practical Question

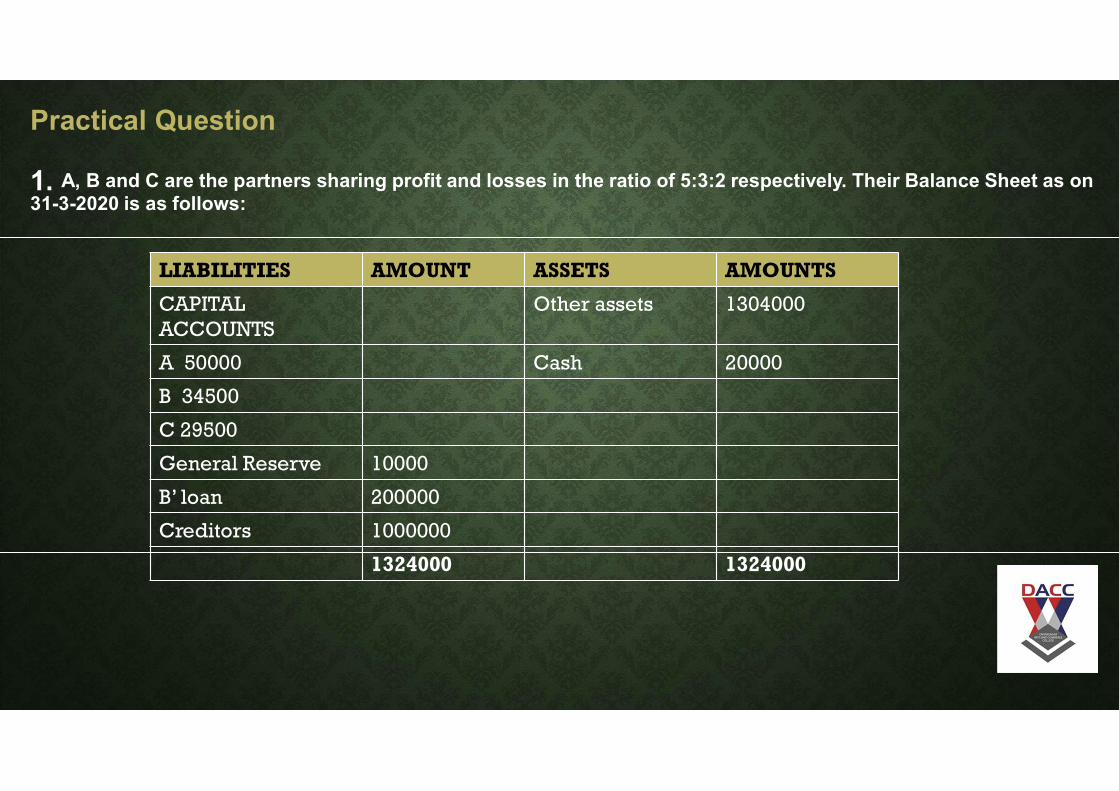

1. A, B and C are the partners sharing profit and losses in the ratio of 3:2:1 respectively. Their Balance Sheet as on 31-3-2020 is as follows:

The partnership firm dissolved and the assets are realized as follows:Instalments AmountFirst realization 10000Second realization 15000Third realization 24000

Show distribution of cash as per excess capital method.

LIABILITIES AMOUNT ASSETS AMOUNTS

CAPITAL ACCOUNTS

ASSETS 80000

A 30000

B 30000

C 20000 80000

80000 80000

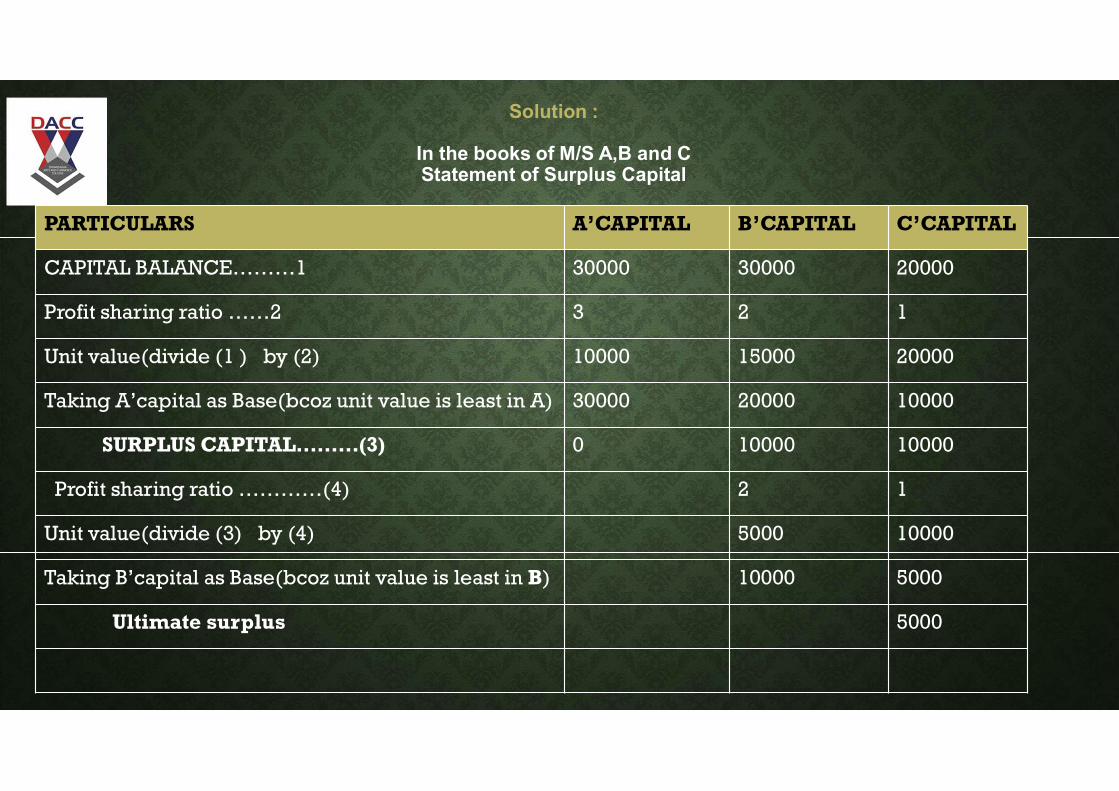

Solution :

In the books of M/S A,B and C Statement of Surplus Capital

PARTICULARS A’CAPITAL B’CAPITAL C’CAPITAL

CAPITAL BALANCE………1 30000 30000 20000

Profit sharing ratio ……2 3 2 1

Unit value(divide (1 ) by (2) 10000 15000 20000

Taking A’capital as Base(bcoz unit value is least in A) 30000 20000 10000

SURPLUS CAPITAL………(3) 0 10000 10000

Profit sharing ratio …………(4) 2 1

Unit value(divide (3) by (4) 5000 10000

Taking B’capital as Base(bcoz unit value is least in B) 10000 5000

Ultimate surplus 5000

STATEMENT SHOWING PIECEMEAL DISTRIBUTION OF CASHParticular Cash A’capital B’capital C’capital

Balances Due 30000 30000 20000

First Realisation 11000

Paid to C’capital (5000) (5000)

Amount left after 1st realisation 6000

Paid to B and C ( 2:1 ) (4000) (2000)

0

Second realization 15000

Paid to B and C (9000) (6000) (3000)

Amount left after 2nd realisation 6000

Paid to A, B and C in 3:2:1 (6000) 3000 2000 1000

0

Third realization 24000

Paid to A, B and C in 3:2:1 (24000) 12000 8000 4000

Realization Loss 15000 10000 5000

Practical Question

1. A, B and C are the partners sharing profit and losses in the ratio of 5:3:2 respectively. Their Balance Sheet as on 31-3-2020 is as follows:

LIABILITIES AMOUNT ASSETS AMOUNTS

CAPITAL ACCOUNTS

Other assets 1304000

A 50000 Cash 20000

B 34500

C 29500

General Reserve 10000

B’ loan 200000

Creditors 1000000

1324000 1324000

There is a bill for Rs 4000 due to on 1st

April 2020 under discount. Other Assets realized as follows:

1st

April 2020: 885000, 1st

May 2020:300000, 1st

June2020:8000, 1st

July 2020:5000 , 1st

August 2020 : 10000

The expenses of realization were expected to be 5000 but ultimately amounted to be 4000 only and were paid on 1

stAugust. The acceptor

of the bill under discount met the bill on to due date .Prepare a statement showing monthly distribution of cash according to Surplus capital method.

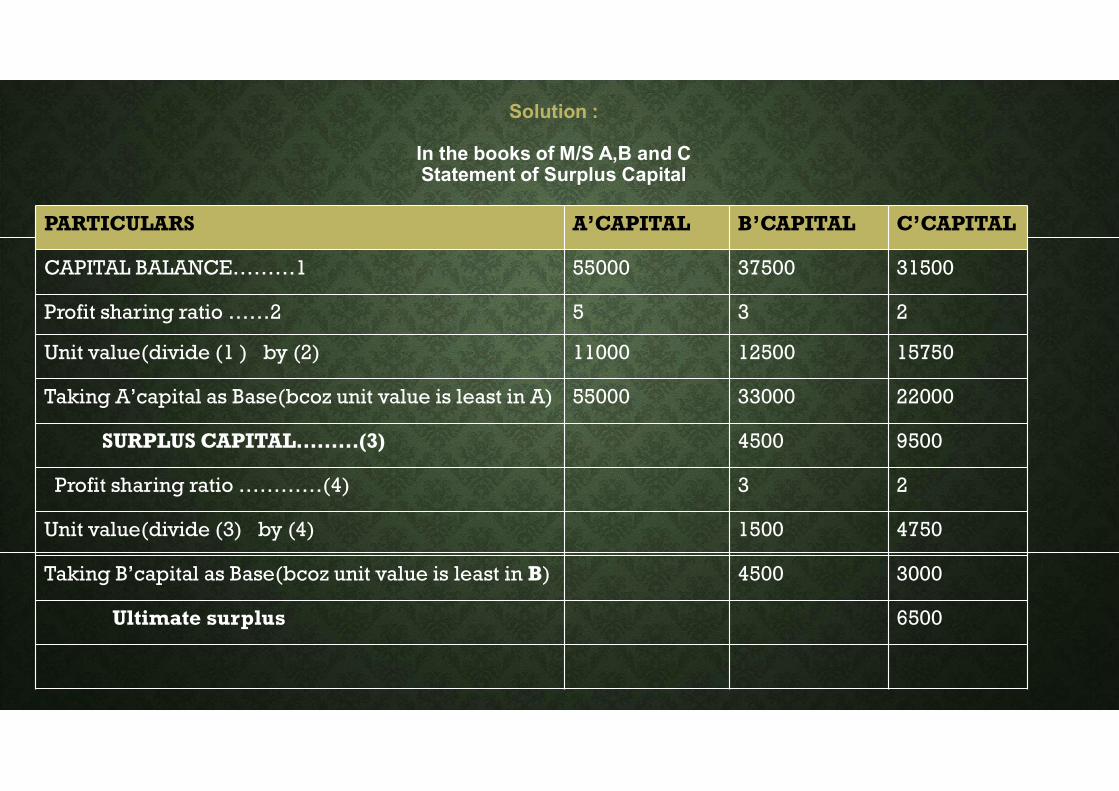

Solution :

In the books of M/S A,B and C Statement of Surplus Capital

PARTICULARS A’CAPITAL B’CAPITAL C’CAPITAL

CAPITAL BALANCE………1 55000 37500 31500

Profit sharing ratio ……2 5 3 2

Unit value(divide (1 ) by (2) 11000 12500 15750

Taking A’capital as Base(bcoz unit value is least in A) 55000 33000 22000

SURPLUS CAPITAL………(3) 4500 9500

Profit sharing ratio …………(4) 3 2

Unit value(divide (3) by (4) 1500 4750

Taking B’capital as Base(bcoz unit value is least in B) 4500 3000

Ultimate surplus 6500

STATEMENT SHOWING PIECEMEAL DISTRIBUTION OF CASHParticular Cash A’capital B’capital C’capital

Balances Due 50000 34500 29500

General Reserve 5000 3000 2000

First Realisation

Paid to C’capital

Amount left after 1st realisation

Paid to B and C ( 2:1 )

Second realization

Paid to B and C

Amount left after 2nd realisation

Paid to A, B and C in 3:2:1

Third realization

Paid to A, B and C in 3:2:1

Realization Loss

practical proBlem

After paying off the liabilities the assets of M/S P,Q,R and Co. realized as follows:First realization 02/10/2020 14000Second Realization 25-11-2020 18000Third Realization 31-12-2020 30000Fourth Realization 23-01-2020 30000

The Capital account of the partner P, Q, R showed credit balance of 10000, 40000, 60000 respectively. The partner shared the profit of the business in the ratio of 3:2:1Prepare a statement showing distribution of cash as per Maximum Loss Method.

UNIT3: ACCOUNTS FROM INCOMPLETE RECORDS

Key points

Meaning

Features

Conversion of Single Entry into double entry

Practical Prblems

INTRODUCTION

It is not necessary to a small business to maintain books of accounts under double entry system

They are usually happy with the minimum information

Thus, they are adopting a different method which is came to known as single entry system of accounting

MEANING

It is also known as incomplete accounting system

An accounting system which is not based on double entry system is known as single entry system of accounting

Such system maintains only personal accounts and cash book

Expenses and incomes are reflected in the cash book, where as personal accounts reflects the position of debtors and creditors

It usually follows cash basis of accounting

FEATURES

Maintained by small business organisationsMaintenance of cash bookOnly personal accounts are keptCollection of information from original

documentsLack of uniformityDifficulty in preparation of final accounts

SINGLE ENTRY V/S DOUBLEENTRY

Both debit and credit aspects of all transactions are recorded

Various subsidiary books aremaintained

Ledger contains personal, real and nominal accounts

Preparation Trial Balance ispossible

Trial Balance, Profit/Loss A/c and Balance Sheet are prepared in a scientific manner

It is a mixture of double entry, one entry and noentry

No subsidiary books, except

• cash book is maintained

Ledger contains personal accounts only

Preparation Trial Balance is not possible

Only rough estimates of profit or loss statement affairs is made

Double Entry System Single Entry System

ADVANTAGES

Quick and easy to maintainDoes not require employing a qualified

accountantExtremely useful for small business

organisationsEconomical

DISADVANTAGES

Trial balance cannot be preparedArithmetical accuracy cannot be guaranteedIncomplete and unrealistic result of tradingNot possible to prepare balance sheetDifficult to detect errors and fraudImproper valuation of assets and liabilitiesChance for mixing business and personal

transactions of ownersExternal agencies cannot use financial

information

GST

• Goods and service tax (GST) is a comprehensive tax levy onmanufacture, sale and consumption of goods and service at anational level.

• Gst is a tax on goods and services with value addition at eachstage.

• Gst will include many state and central level indirecttaxes.

• It overcomes drawback present tax system

WHY DOES INDIA NEEDGST

• GST is being introduced majorly due to 2 reason

1. The current indirect tax structure is full of uncertainties due tomultiple rates.

2. Due to multiple rates there are multiple forms.

• GST the tax complexity in the prevailing tax regime.

TAX STRUCTURE IN INDIA

• Direct Tax :

e.g.: Income Tax, Corporate Tax, Wealth Tax

• Indirect Tax :

e.g.: Excise duty, custom duty, Service Tax, Octrai Tax,VAT.

3

TAX STRUCTURE UNDER GST

SGST

IGST

• Stands for Central GST• Tax collected by Central Government• Applicable on supplies within the state

• Stands for State GST• Tax collected by State Government• Applicable on supplies within the state

• Stands for Integrated GST• Tax collected is shared between Centre and State• Applicable on interstate and import transactions

UTGST• Stands for Union Territory GST• Tax collected by Union Territory• Applicable on supplies within the Union Territory

CGST

5

UNDERSTANDING CGST, SGST, UTGST &IGST

Foreign TerritoryState 1

Union territory without legislatureState 2

5

6

FEATURES OF CONSTITUTION AMENDMENTACT

Concurrent jurisdiction for levy & collection of GST by the Centre (CGST) and theStates (SGST)

Centre to levy and collect IGST on supplies in the course of inter-State trade orcommerceincluding imports

Compensation for loss of revenue to States for five years

GST on petroleum crude, high speed diesel, motor spirit (commonly known aspetrol), natural gas & aviation turbine fuel to be levied from a later date onrecommendations of Council

6

SHORT COMINGS IN CURRENT TAXSYSTEM

Tax Cascading (Tax on Tax)

Complexity

Taxation at Manufacturing Level

Exclusion of Services

Tax Evasion

Corruption

BENEFITS OFGST

Transparent Tax System

Uniform Tax system Across India

Reduce TaxEvasion

Export will be more competitive