Distortions to Agricultural Incentives in Asia

606

DISTORTIONS TO AGRICULTURAL INCENTIVES IN ASIA Editors Kym Anderson • Will Martin

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Distortions to Agricultural Incentives in Asia

DISTORTIONSTO AGRICULTURAL

INCENTIVES INASIA

EditorsKym Anderson • Will Martin

Distortions toAgriculturalIncentives in

Asia

Washington, D.C.

Distortions toAgriculturalIncentives in

Asia

Kym Andersonand Will Martin, Editors

© 2009 The International Bank for Reconstruction and Development / The World Bank1818 H Street NWWashington DC 20433Telephone: 202-473-1000Internet: www.worldbank.orgE-mail: [email protected]

All rights reserved.

1 2 3 4 12 11 10 09

This volume is a product of the staff of the International Bank for Reconstruction and Development / The WorldBank. The findings, interpretations, and conclusions expressed in this volume do not necessarily reflect the views ofthe Executive Directors of The World Bank or the governments they represent.

The World Bank does not guarantee the accuracy of the data included in this work. The boundaries, colors,denominations, and other information shown on any map in this work do not imply any judgement on the part ofThe World Bank concerning the legal status of any territory or the endorsement or acceptance of such boundaries.

Rights and PermissionsThe material in this publication is copyrighted. Copying and/or transmitting portions or all of this work without per-mission may be a violation of applicable law. The International Bank for Reconstruction and Development / TheWorld Bank encourages dissemination of its work and will normally grant permission to reproduce portions of thework promptly.

For permission to photocopy or reprint any part of this work, please send a request with complete informationto the Copyright Clearance Center Inc., 222 Rosewood Drive, Danvers, MA 01923, USA; telephone: 978-750-8400;fax: 978-750-4470; Internet: www.copyright.com.

All other queries on rights and licenses, including subsidiary rights, should be addressed to the Office of the Pub-lisher, The World Bank, 1818 H Street NW, Washington, DC 20433, USA; fax: 202-522-2422; e-mail:[email protected].

Cover design: Tomoko Hirata/World Bank.Cover photo: © Tran Thi Hoa/World Bank Photo Library.

ISBN: 978-0-8213-7662-1eISBN: 978-0-8213-7663-8DOI: 10.1596/978-0-8213-7662-1

Library of Congress Cataloging-in-Publication DataDistortions to agricultural incentives in Asia / edited by Kym Anderson and Will Martin.

p. cm.Includes bibliographical references and index.ISBN 978-0-8213-7662-1 — ISBN 978-0-8213-7663-8 (electronic)1. Agriculture—Economic aspects—Asia. 2. Agriculture and state—Asia. 3. Agriculture—Taxation—Asia. 4.

Agricultural subsidies—Asia. I. Anderson, Kym. II. Martin, Will, 1953- HD2056.Z8D57 2008338.1'85—dc22

2008029534

Dedication

To the authors of the country case studies and their assistants, especially for generating the time series of distortion estimates

that underpin the chapters, and, in particular, to Yujiro Hayami for his insights and advice during this project

and his related and influential work on Asia over several decades.

CONTENTS

Foreword xvii

Acknowledgments xxi

Contributors xxiii

Abbreviations xxvii

Map: The Focus Economies of Asia xxviii

PART I INTRODUCTION 1

1 Introduction and Summary 3Kym Anderson and Will Martin

PART II NORTHEAST ASIA 83

2 Republic of Korea and Taiwan, China 85 Masayoshi Honma and Yujiro Hayami

3 China 117Jikun Huang, Scott Rozelle, Will Martin, and Yu Liu

PART III SOUTHEAST ASIA 163

4 Indonesia 165George Fane and Peter Warr

5 Malaysia 197Prema-Chandra Athukorala and Wai-Heng Loke

6 The Philippines 223Cristina David, Ponciano Intal, and Arsenio M. Balisacan

vii

7 Thailand 255Peter Warr and Archanun Kohpaiboon

8 Vietnam 281Prema-Chandra Athukorala, Pham Lan Huong, andVo Tri Thanh

PART IV SOUTH ASIA 303

9 Bangladesh 305Nazneen Ahmed, Zaid Bakht, Paul A. Dorosh, and Quazi Shahabuddin

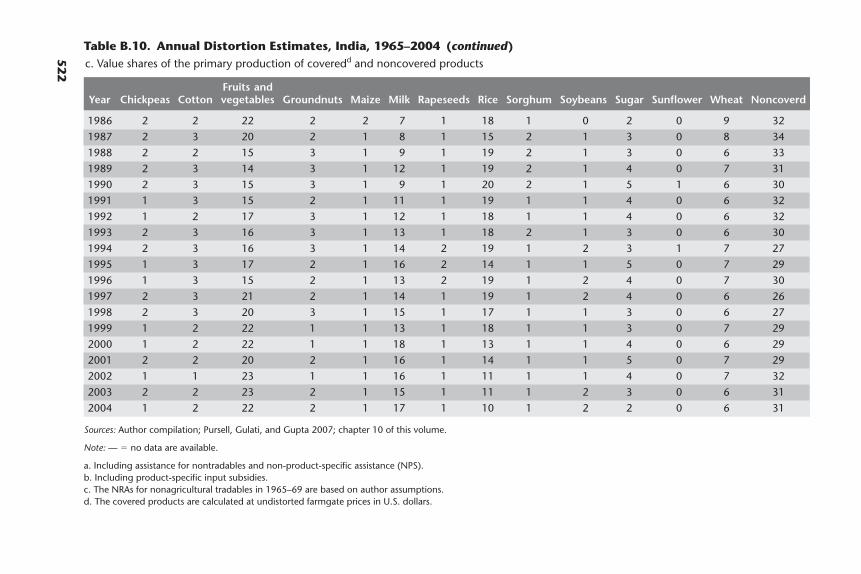

10 India 339Garry Pursell, Ashok Gulati, and Kanupriya Gupta

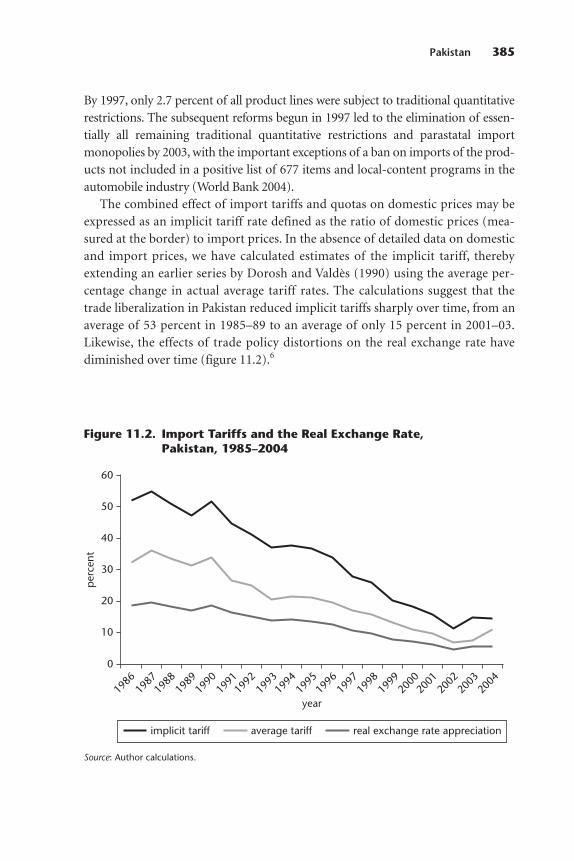

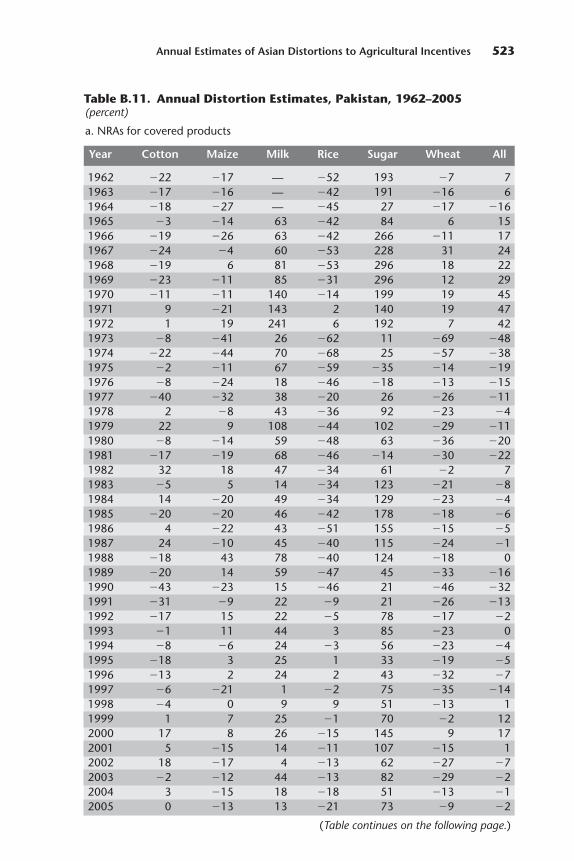

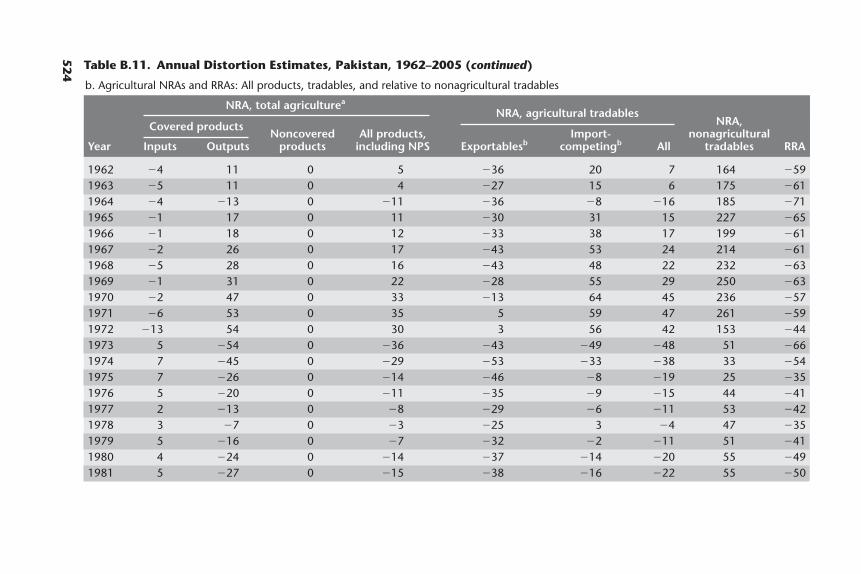

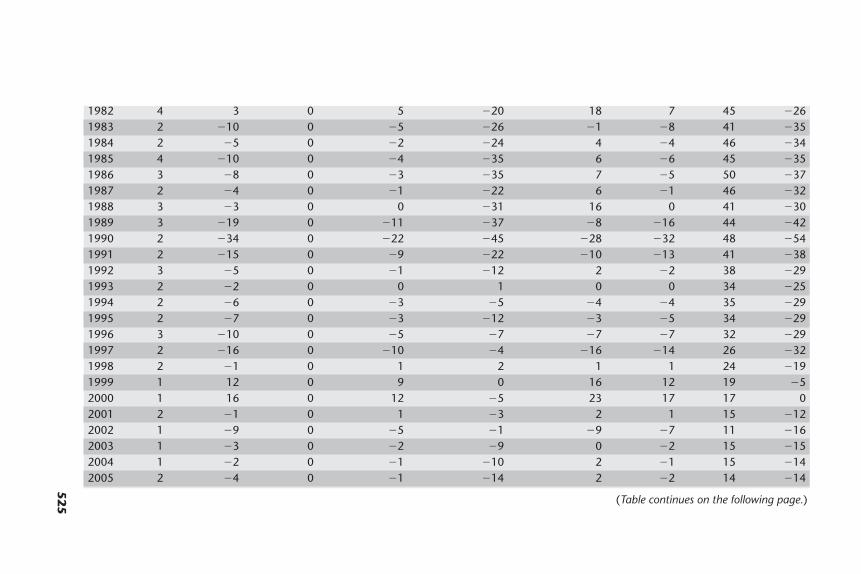

11 Pakistan 379Paul A. Dorosh and Abdul Salam

12 Sri Lanka 409Jayatilleke Bandara and Sisira Jayasuriya

Appendix A: Methodology for MeasuringDistortions to Agricultural Incentives 441Kym Anderson, Marianne Kurzweil, Will Martin,Damiano Sandri, and Ernesto Valenzuela

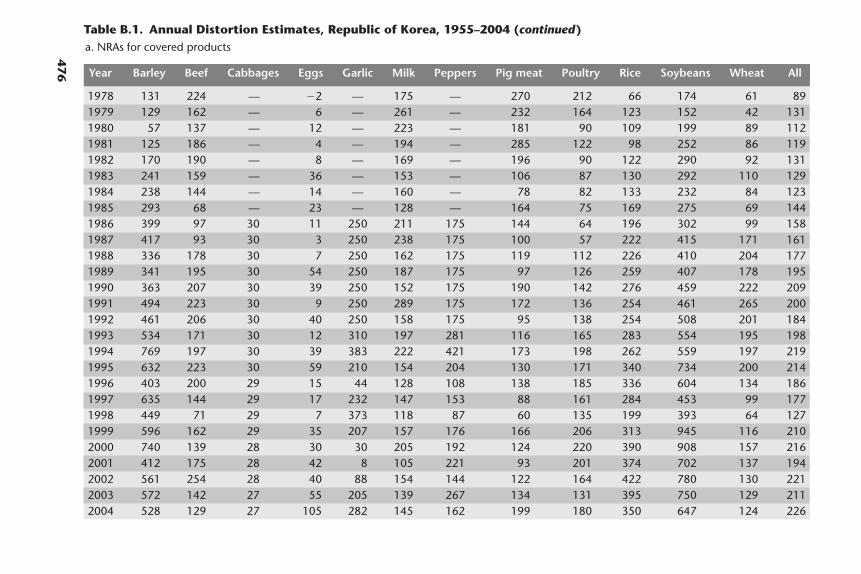

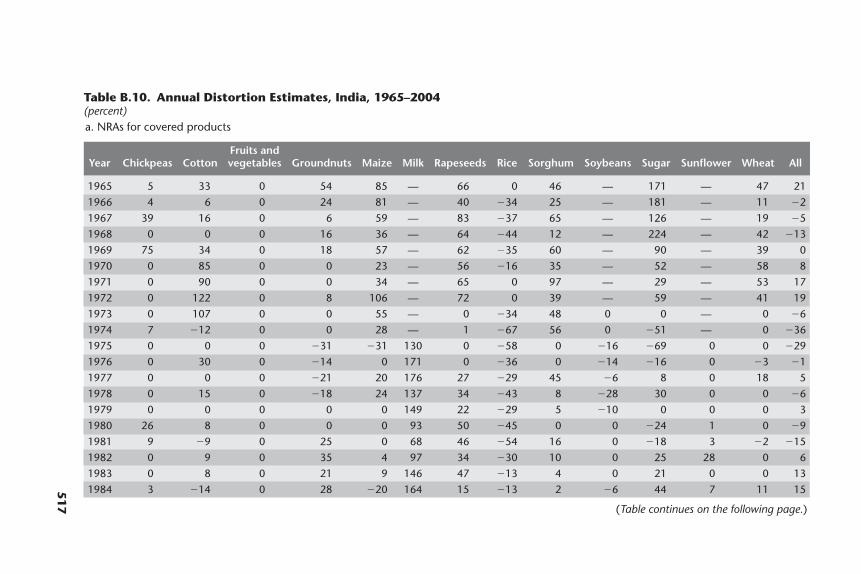

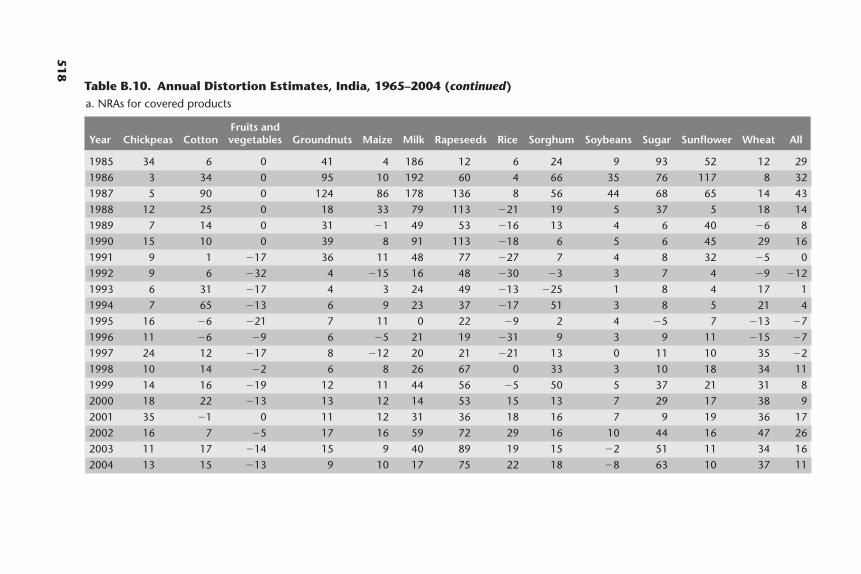

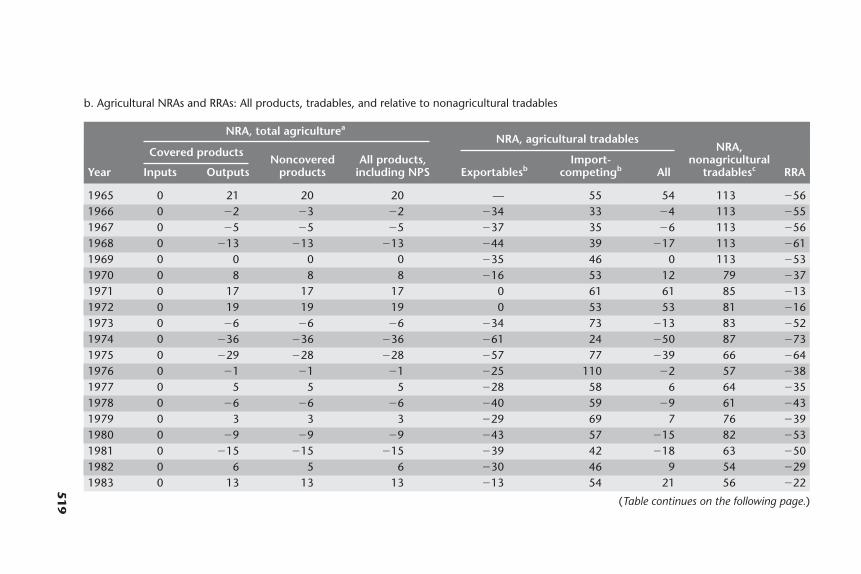

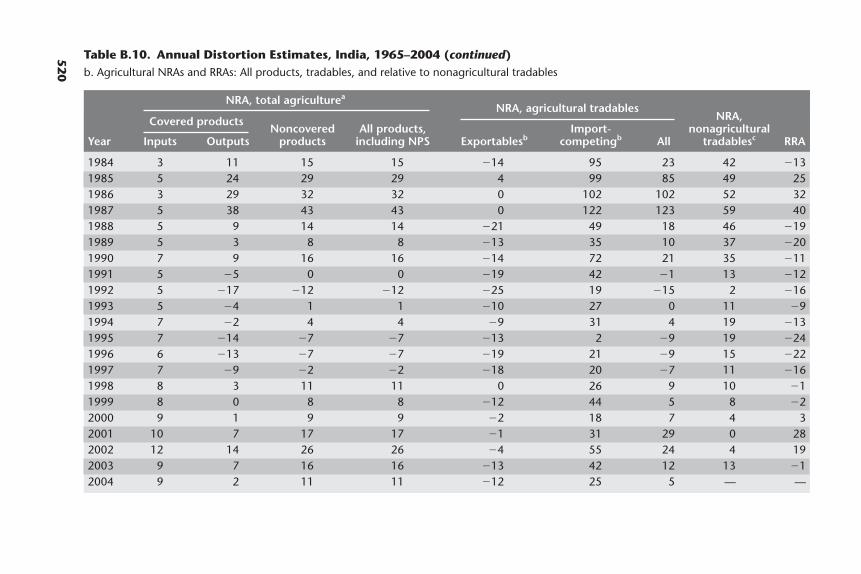

Appendix B: Annual Estimates of AsianDistortions to Agricultural Incentives 473Ernesto Valenzuela, Marianne Kurzweil, Johanna Croser, Signe Nelgen, and Kym Anderson

Index 563

Figures1.1 Index of Real Per Capita GDP, Asia Relative to the United States,

1950–2006 111.2 NRAs in Agriculture, Asian Focus Economies, 1980–84

and 2000–04 281.3 NRAs, by Product, Asian Focus Economies, 1980–84

and 2000–04 291.4 NRAs for Rice, Milk, and Sugar, Asian Focus Economies,

1980–84 and 2000–04 301.5 NRAs for Exportable, Import-Competing, and All Agricultural

Products, Asian Focus Economies, 1955–2004 331.6 NRAs for Agricultural and Nonagricultural Tradables and the RRA,

Asian Focus Economies, 1955–2004 51

viii Contents

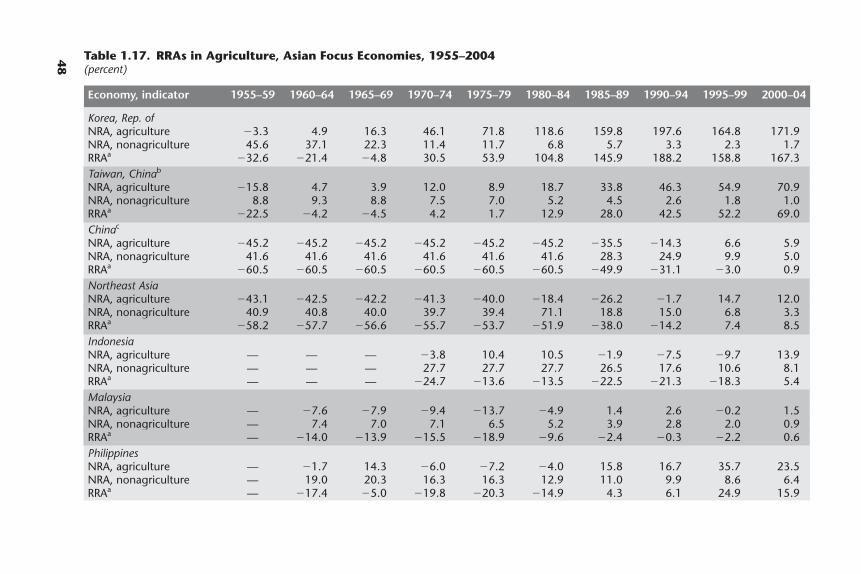

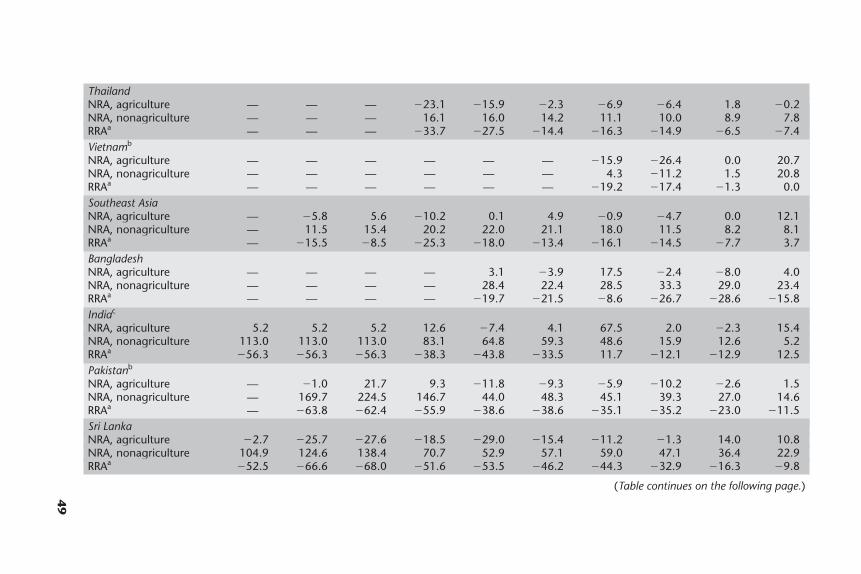

1.7 RRAs in Agriculture, Asian Focus Economies, 1980–84and 2000–04 52

1.8 NRAs and RRAs, China and India, 1965–2004 531.9 NRAs and RRAs, Africa, Asia, and Latin America, 1965–2004 541.10 Income Distribution, Asian Subregions and the World, 2000 551.11 Regressions of Real GDP Per Capita and Agricultural NRAs

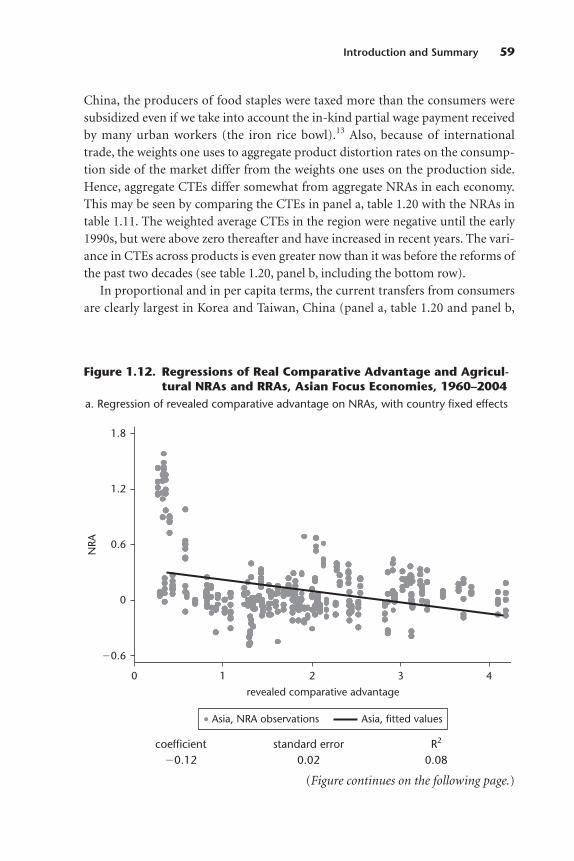

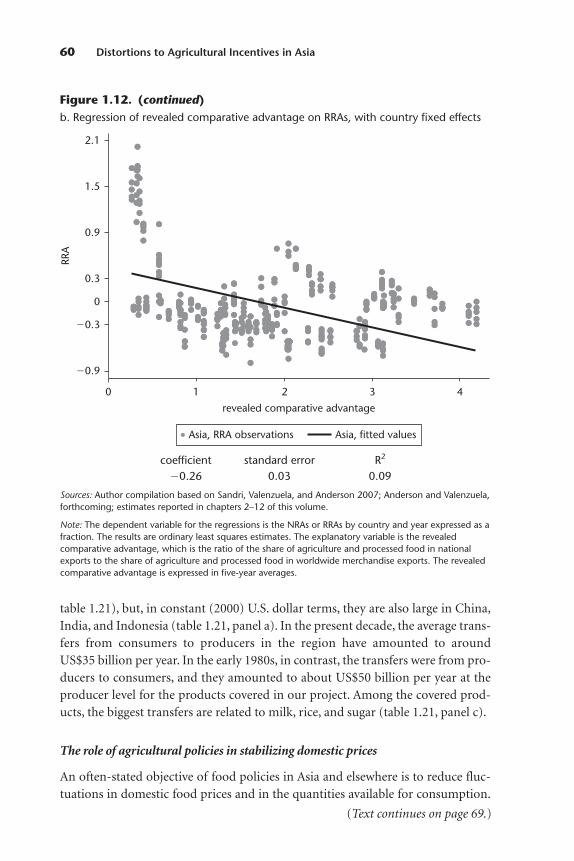

and RRAs, Asian Focus Economies, 1955–2005 581.12 Regressions of Real Comparative Advantage and Agricultural

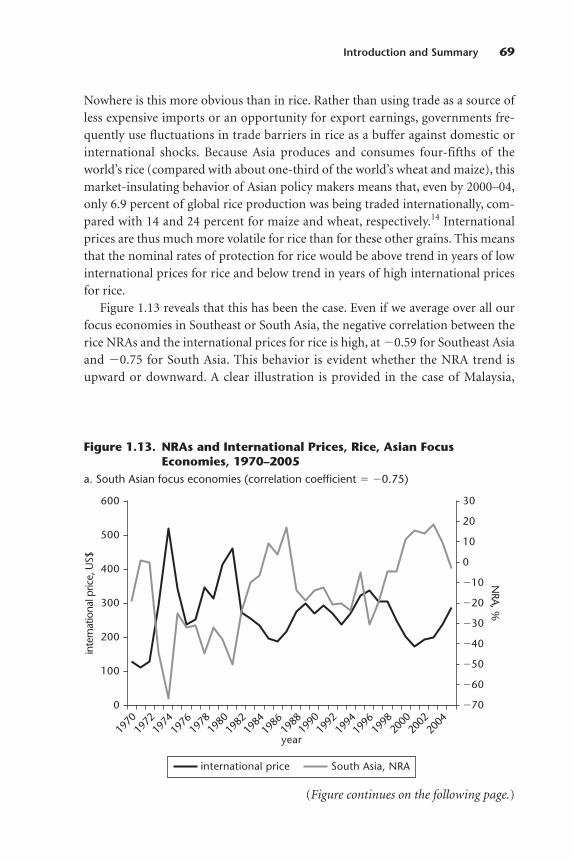

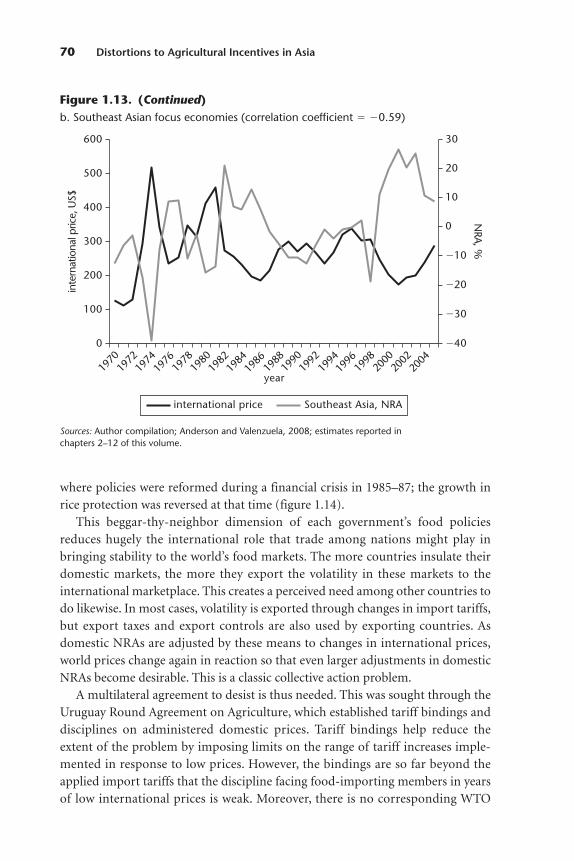

NRAs and RRAs, Asian Focus Economies, 1960–2004 591.13 NRAs and International Prices, Rice, Asian Focus Economies,

1970–2005 691.14 NRAs for Rice, Malaysia, 1960–2004 711.15 RRAs and TBIs in Agriculture, Asian Focus Economies,

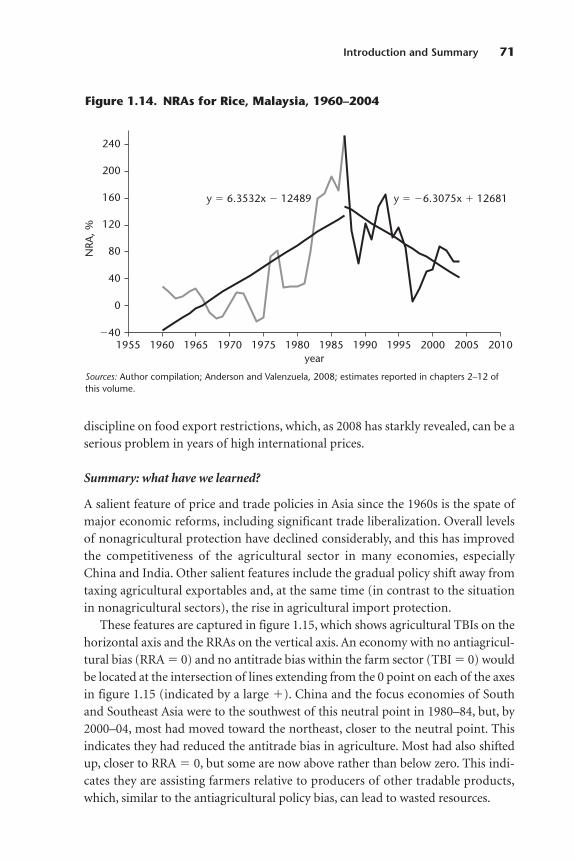

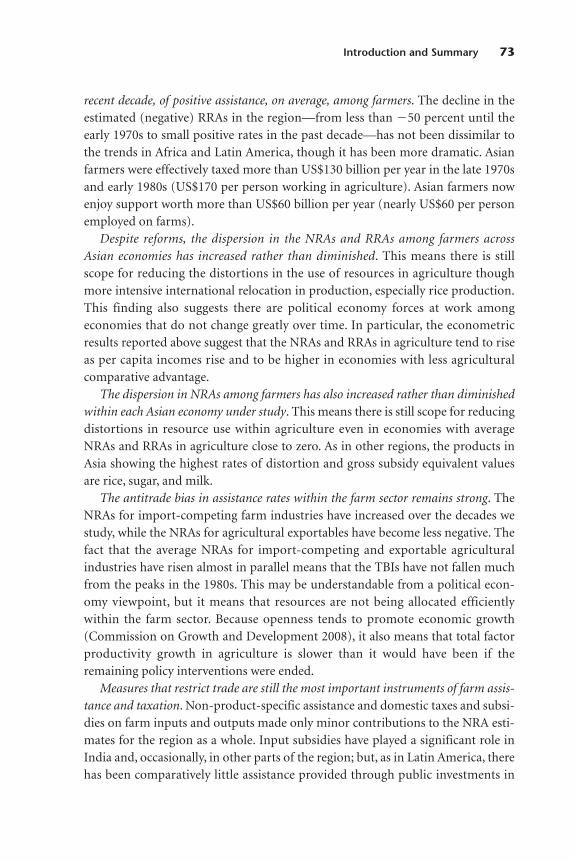

1980–84 and 2000–04 721.16 RRAs and Real Per Capita GDP, India, Japan, and

Northeast Asian Focus Economies, 1955–2005 751.17 NRAs for China, Japan, and the Republic of Korea and

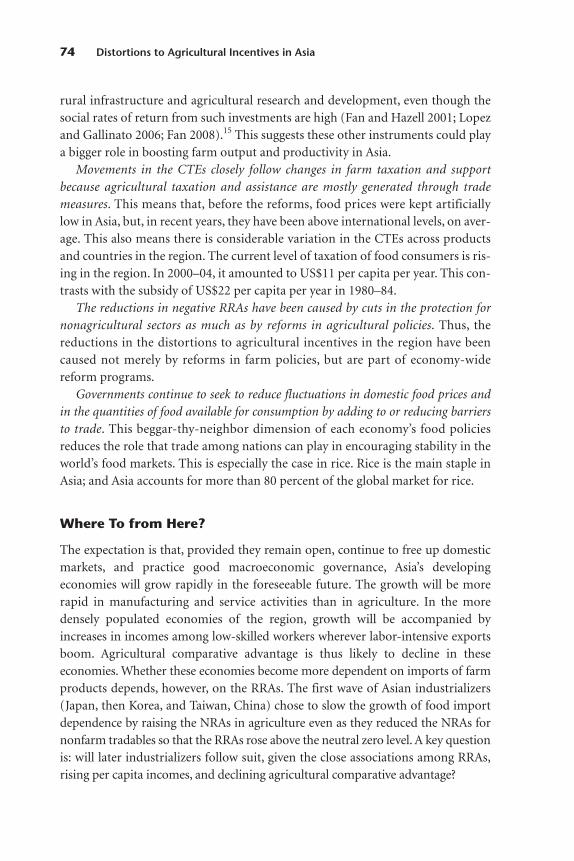

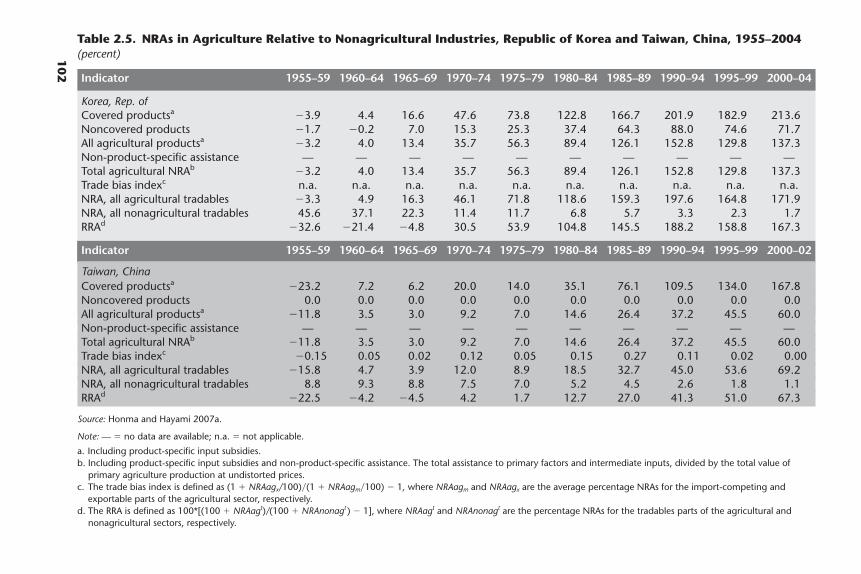

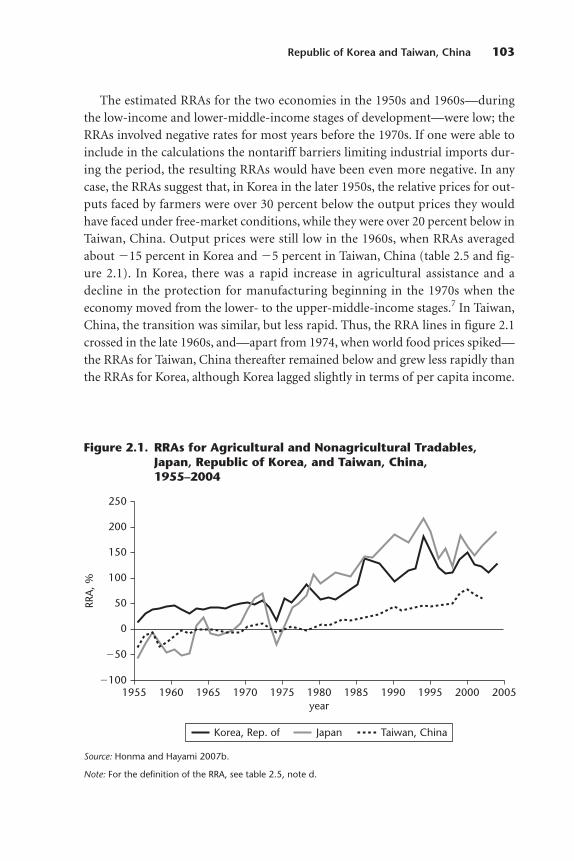

GATT/WTO Accession, 1955–2005 762.1 RRAs for Agricultural and Nonagricultural Tradables,

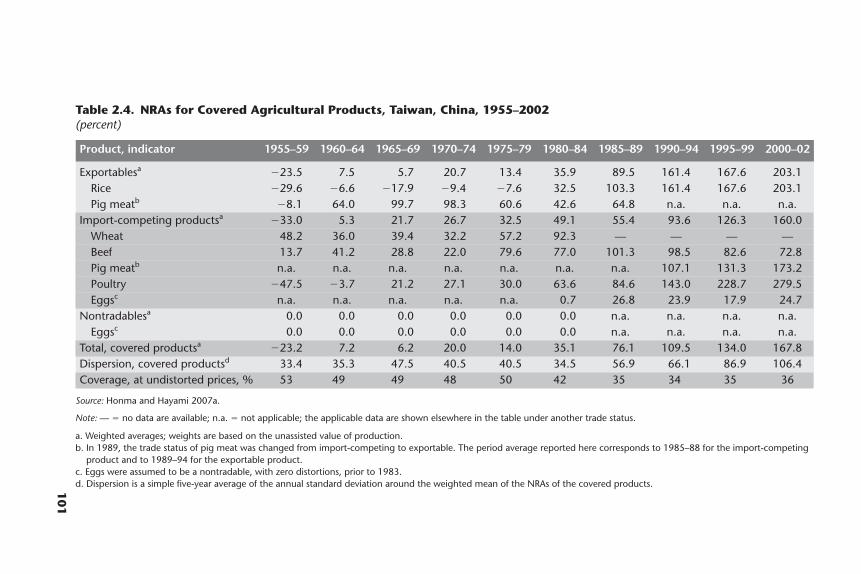

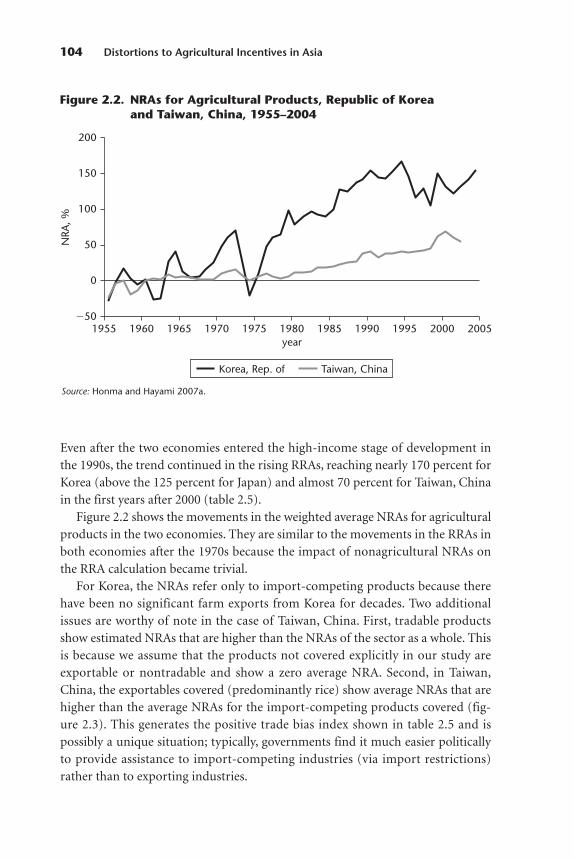

Japan, Republic of Korea, and Taiwan, China, 1955–2004 1032.2 NRAs for Agricultural Products, Republic of Korea and

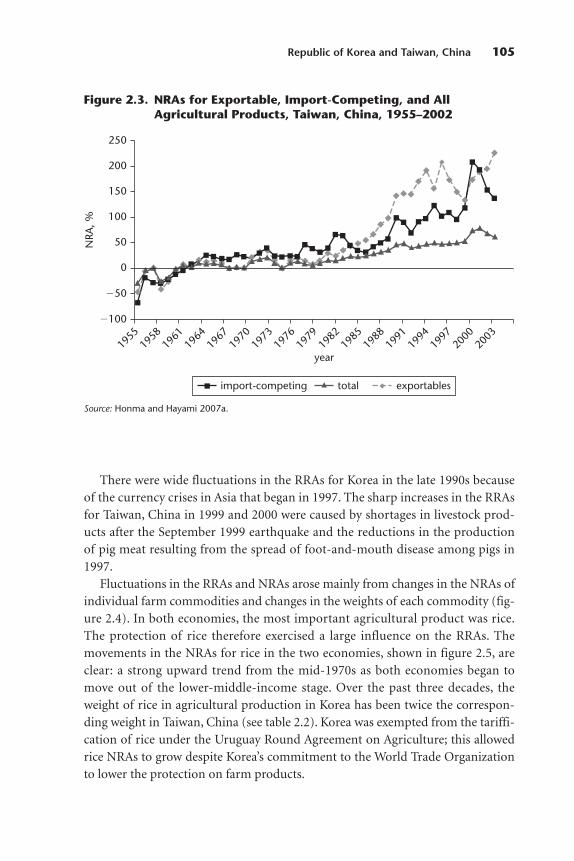

Taiwan, China, 1955–2004 1042.3 NRAs for Exportable, Import-Competing, and All Agricultural

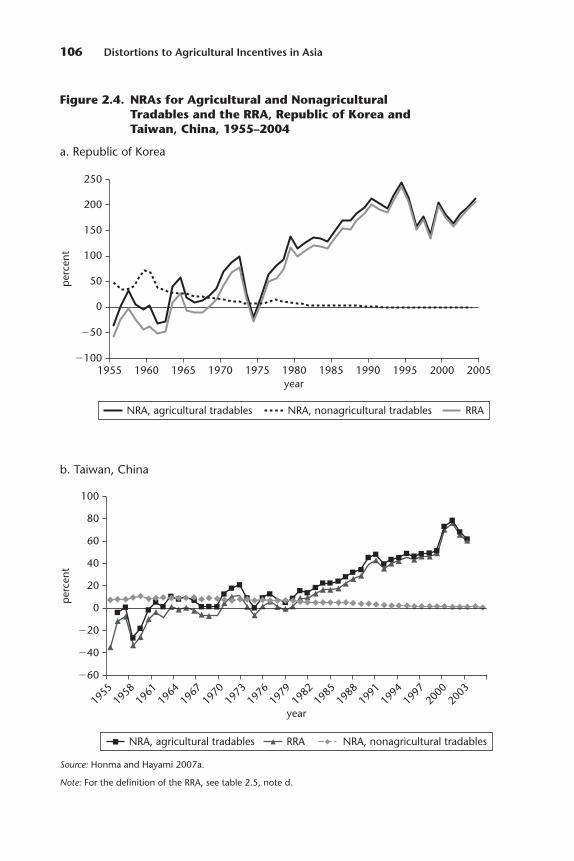

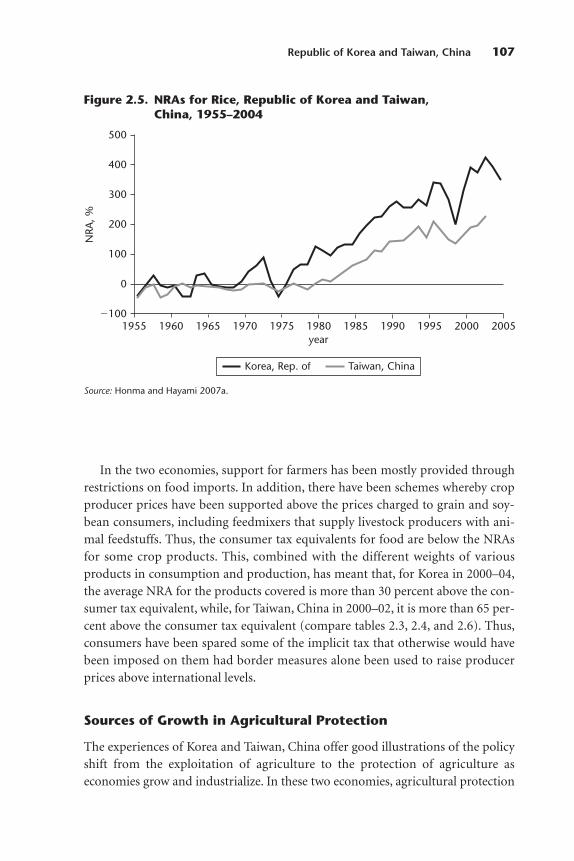

Products, Taiwan, China, 1955–2002 1052.4 NRAs for Agricultural and Nonagricultural Tradables and

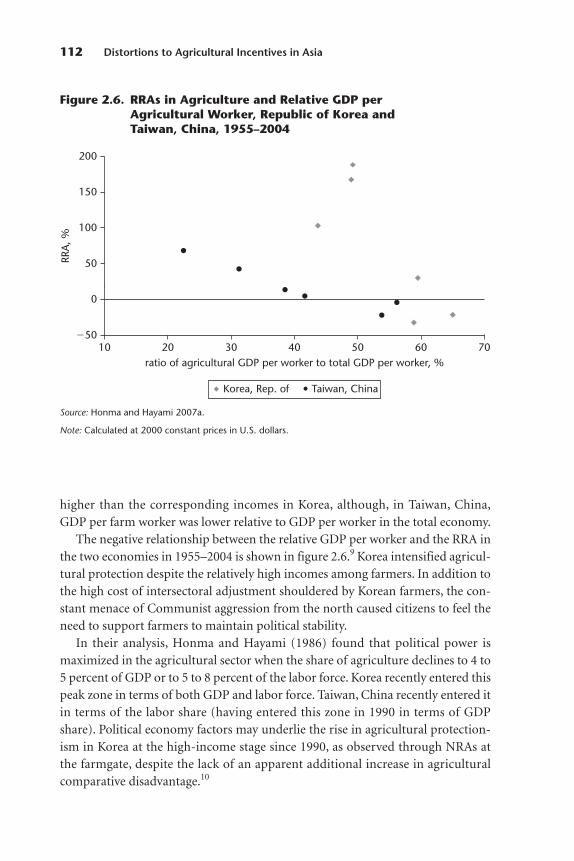

the RRA, Republic of Korea and Taiwan, China, 1955–2004 1062.5 NRAs for Rice, Republic of Korea and Taiwan, China, 1955–2004 1072.6 RRAs in Agriculture and Relative GDP per Agricultural Worker,

Republic of Korea and Taiwan, China, 1955–2004 1123.1 Agricultural Trade Balance, by Factor Intensity, China, 1985–2002 1283.2 The Domestic Market for Foreign Currency, China 1413.3 NRAs for Exportable, Import-Competing, and All Agricultural

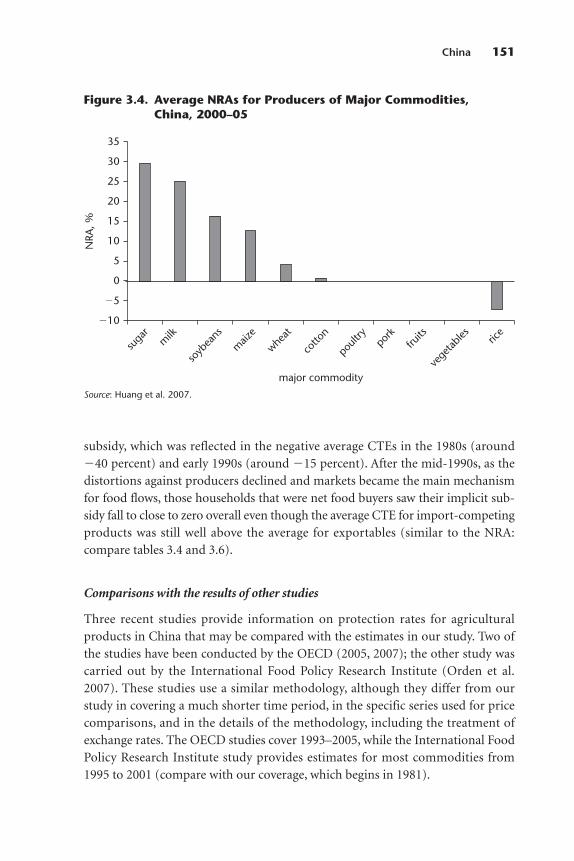

Products, China, 1981–2004 1493.4 Average NRAs for Producers of Major Commodities,

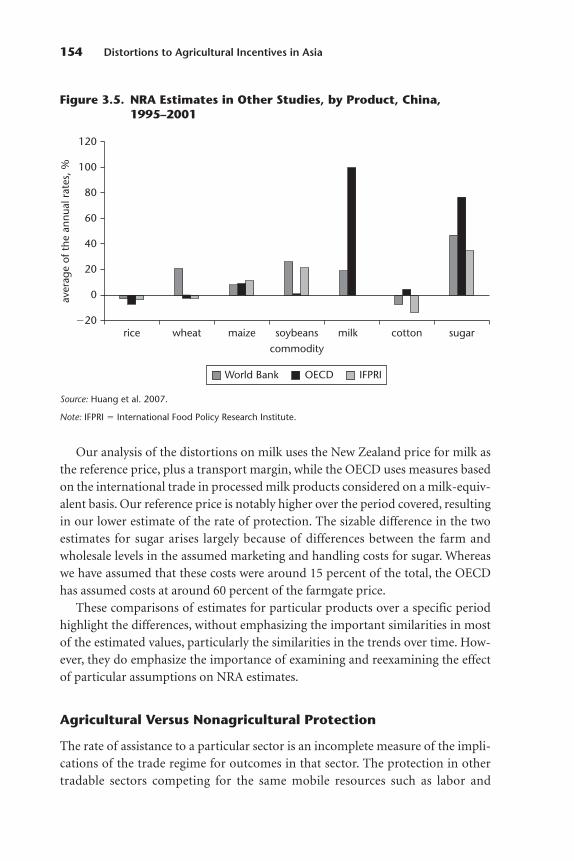

China, 2000–05 1513.5 NRA Estimates in Other Studies, by Product, China, 1995–2001 1543.6 NRAs for Agricultural and Nonagricultural Tradables and

the RRA, China, 1981–2004 1554.1 Border and Domestic Prices of Import-Competing Products

Relative to the GDP Deflator, Rice and Urea Fertilizer,Indonesia, 1975–2005 174

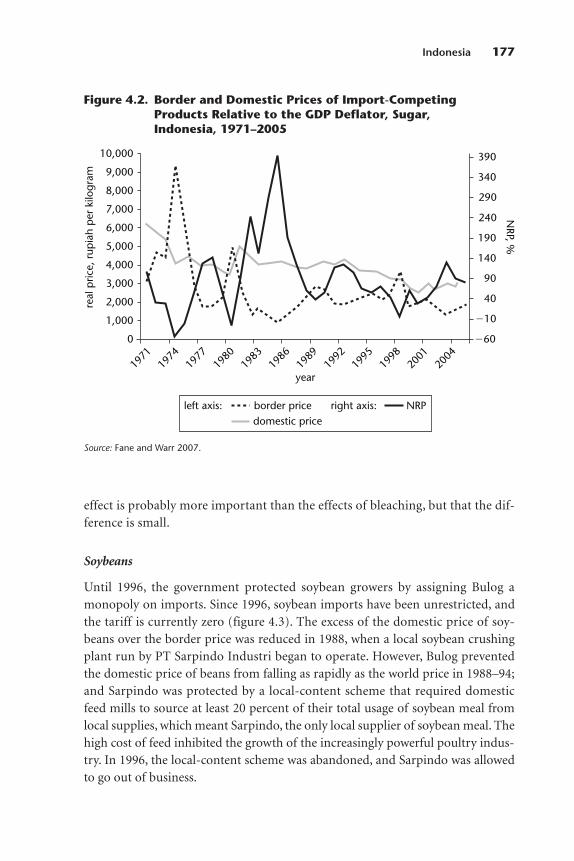

4.2 Border and Domestic Prices of Import-Competing ProductsRelative to the GDP Deflator, Sugar, Indonesia, 1971–2005 177

Contents ix

4.3 Border and Domestic Prices of Import-Competing ProductsRelative to the GDP Deflator, Soybeans, Indonesia, 1970–2005 178

4.4 Border and Domestic Prices of Import-Competing ProductsRelative to the GDP Deflator, Maize, Indonesia, 1969–2005 179

4.5 Border and Domestic Prices of Export Crops Relative to the GDP Deflator, Indonesia, 1967–2005 181

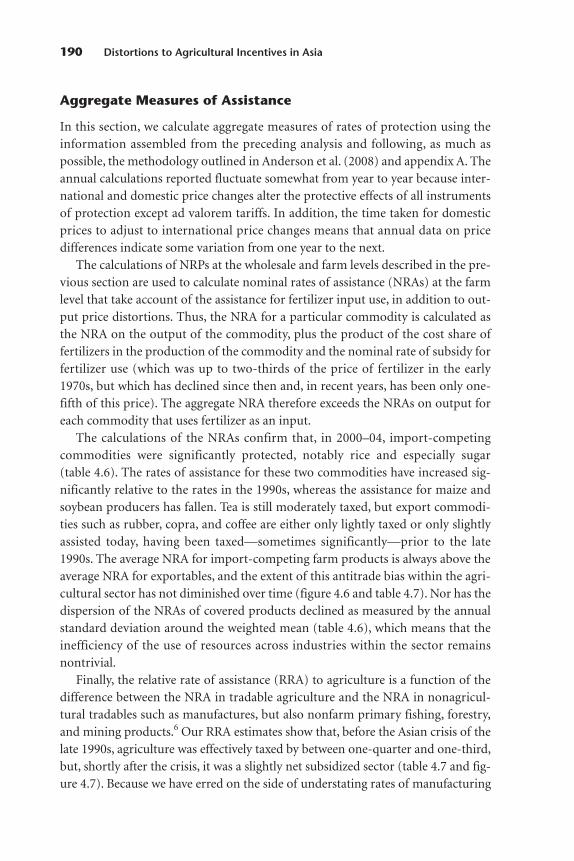

4.6 NRAs for Exportable, Import-Competing, and All Agricultural Products, Indonesia, 1970–2004 192

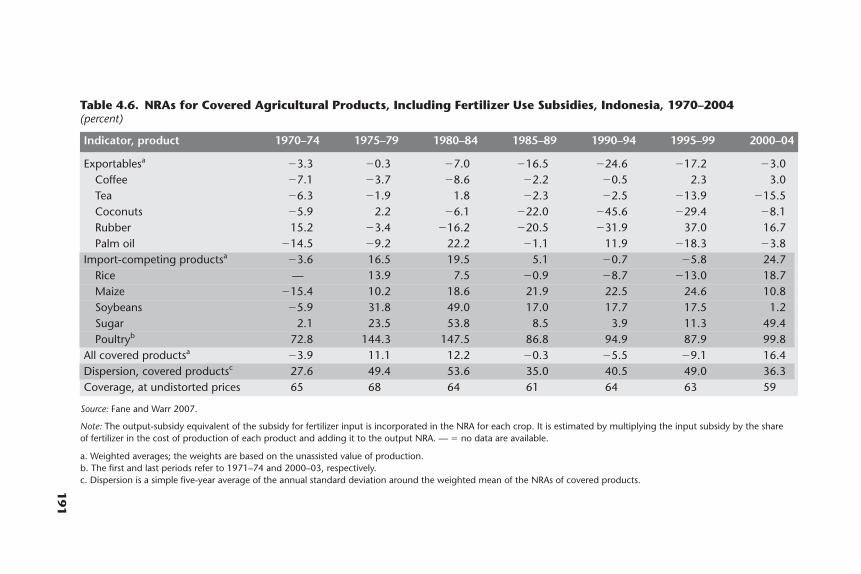

4.7 NRAs for Agricultural and Nonagricultural Tradables andthe RRA, Indonesia, 1970–2004 194

5.1 Commodity Composition of Agricultural GDP, Malaysia,1965–2005 200

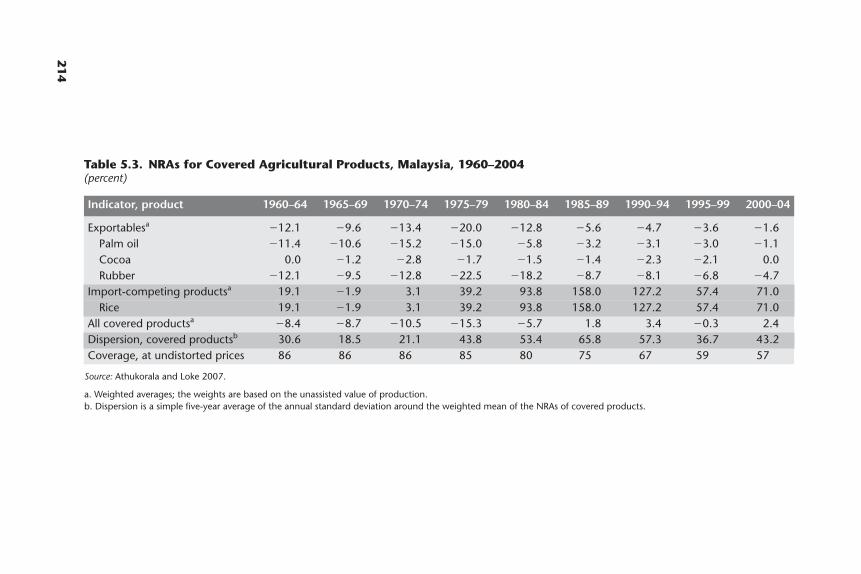

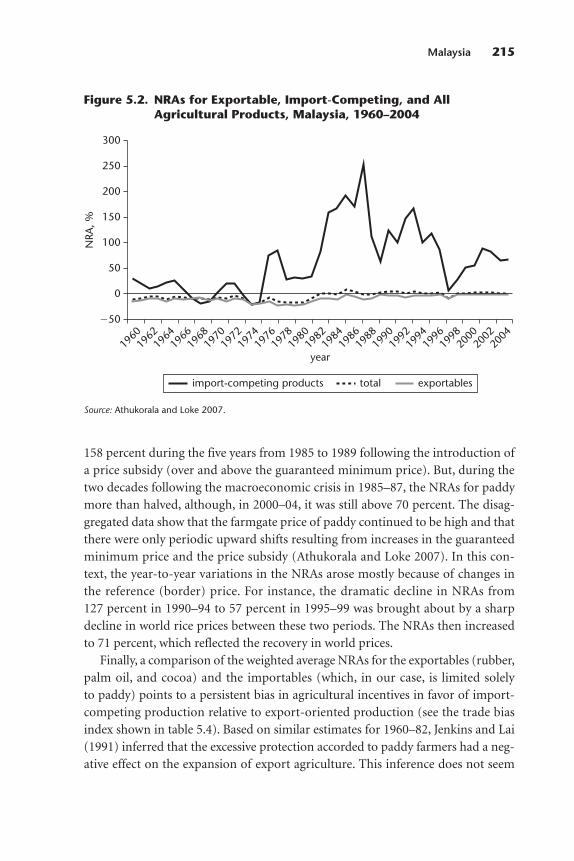

5.2 NRAs for Exportable, Import-Competing, and All Agricultural Products, Malaysia, 1960–2004 215

5.3 NRAs for Agricultural and Nonagricultural Tradables andthe RRA, Malaysia, 1960–2004 217

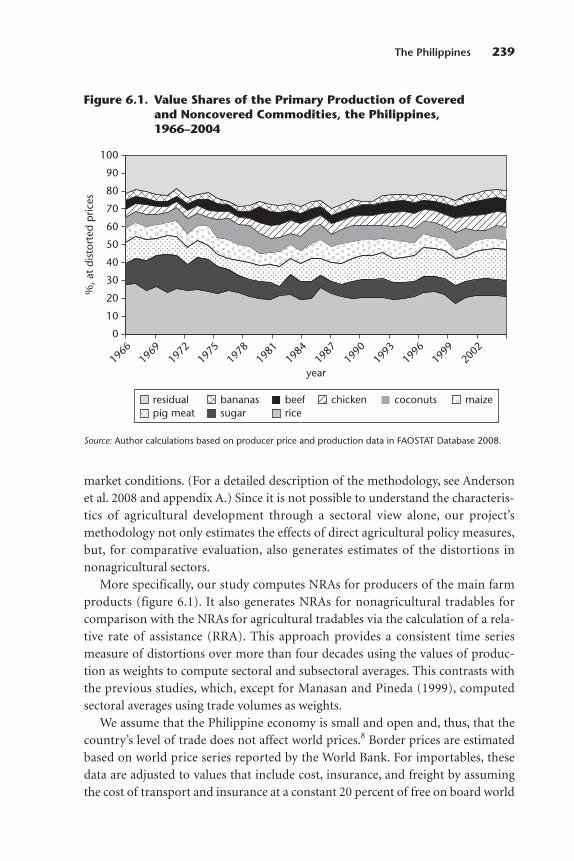

6.1 Value Shares of the Primary Production of Covered andNoncovered Commodities, the Philippines, 1966–2004 239

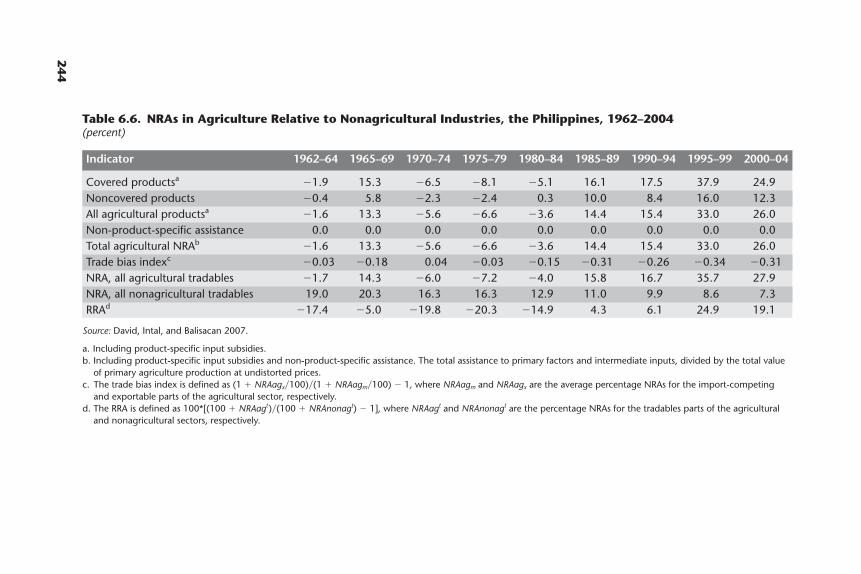

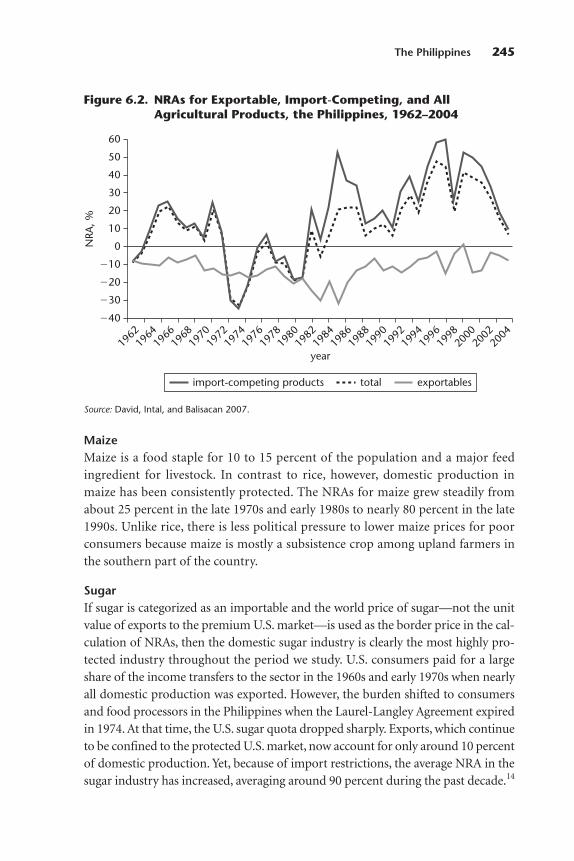

6.2 NRAs for Exportable, Import-Competing, and All Agricultural Products, the Philippines, 1962–2004 245

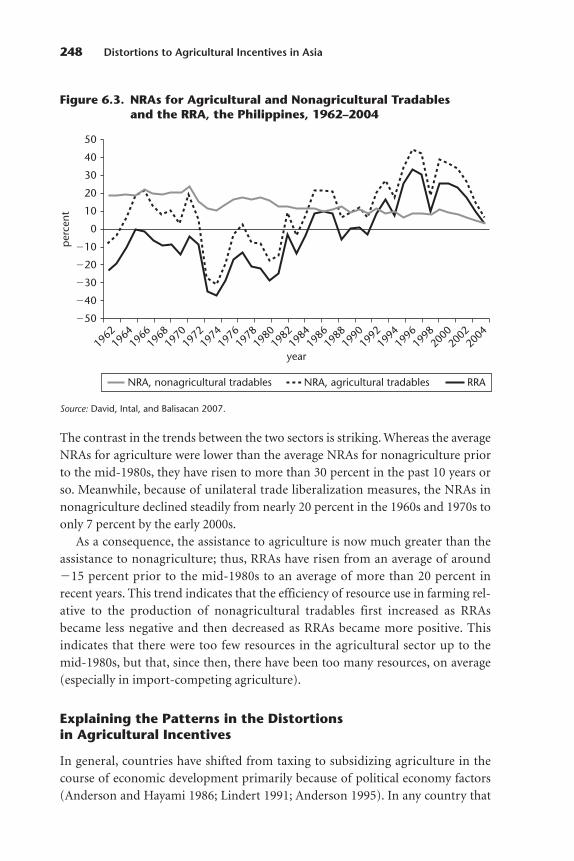

6.3 NRAs for Agricultural and Nonagricultural Tradables andthe RRA, the Philippines, 1962–2004 248

7.1 Price Comparisons and NRPs at Wholesale, Rice, Thailand,1968–2005 262

7.2 Price Comparisons and NRPs at Wholesale, Maize, Thailand,1968–2005 263

7.3 Price Comparisons and NRPs at Wholesale, Cassava, Thailand,1969–2004 264

7.4 Price Comparisons and NRPs at Wholesale, Soybeans, Thailand,1984–2005 265

7.5 Ratios, Consumer Prices to Border Prices and Miller Prices toGrower Prices, Sugar, Thailand, 1968–2005 266

7.6 Price Comparisons and NRPs at Wholesale, Sugar, Thailand,1968–2005 267

7.7 Price Comparisons and NRPs at Wholesale, Palm Oil, Thailand,1995–2004 267

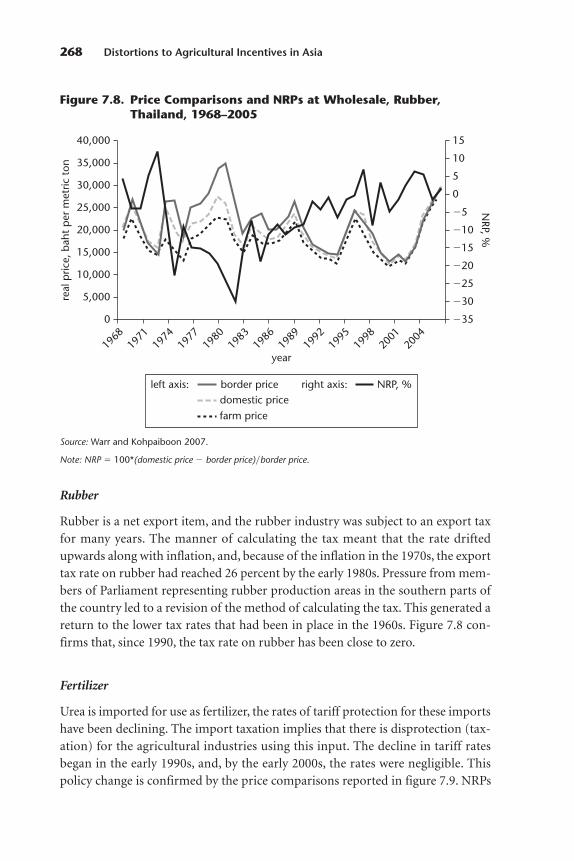

7.8 Price Comparisons and NRPs at Wholesale, Rubber, Thailand,1968–2005 268

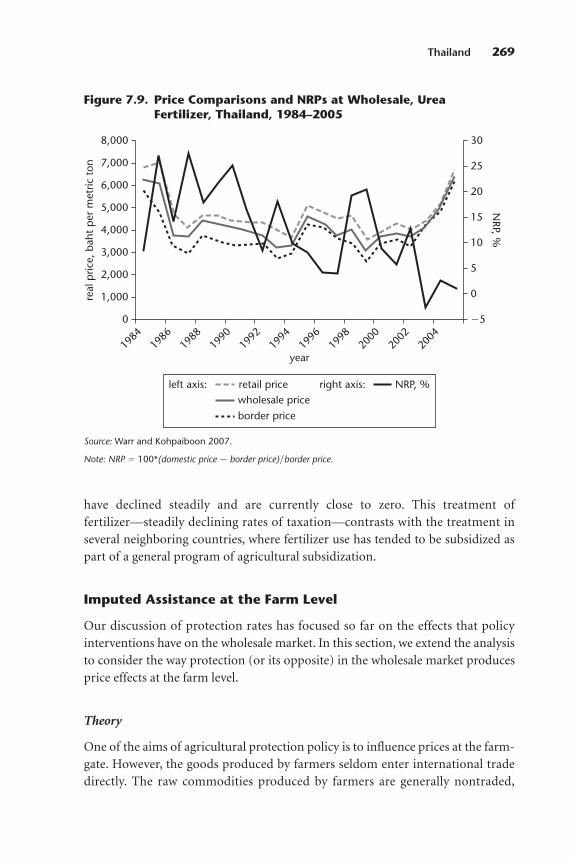

7.9 Price Comparisons and NRPs at Wholesale, Urea Fertilizer,Thailand, 1984–2005 269

7.10 NRAs for Agricultural and Nonagricultural Tradables andthe RRA, Thailand, 1970–2004 277

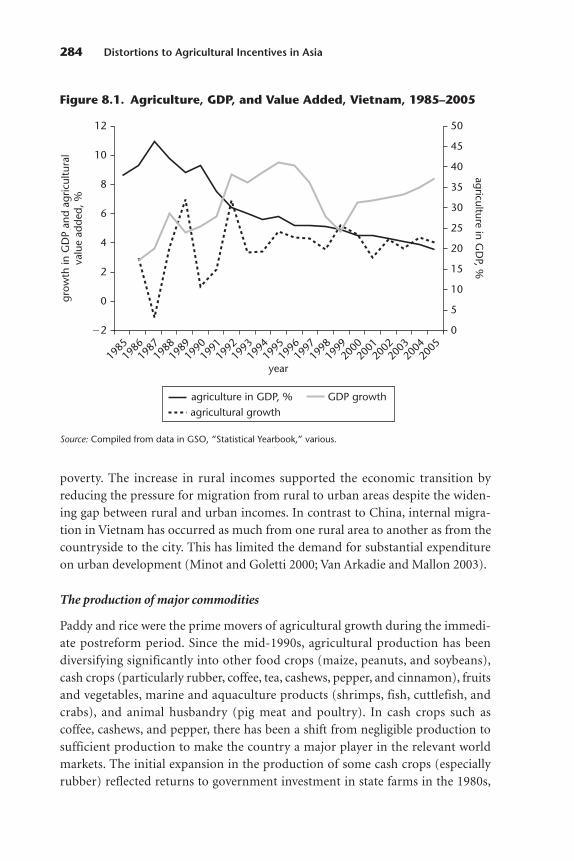

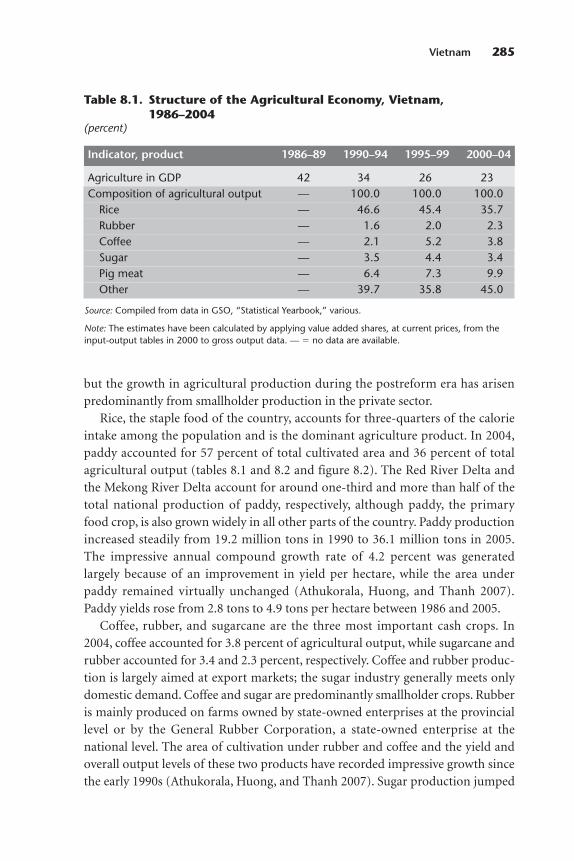

8.1 Agriculture, GDP, and Value Added, Vietnam, 1985–2005 284

x Contents

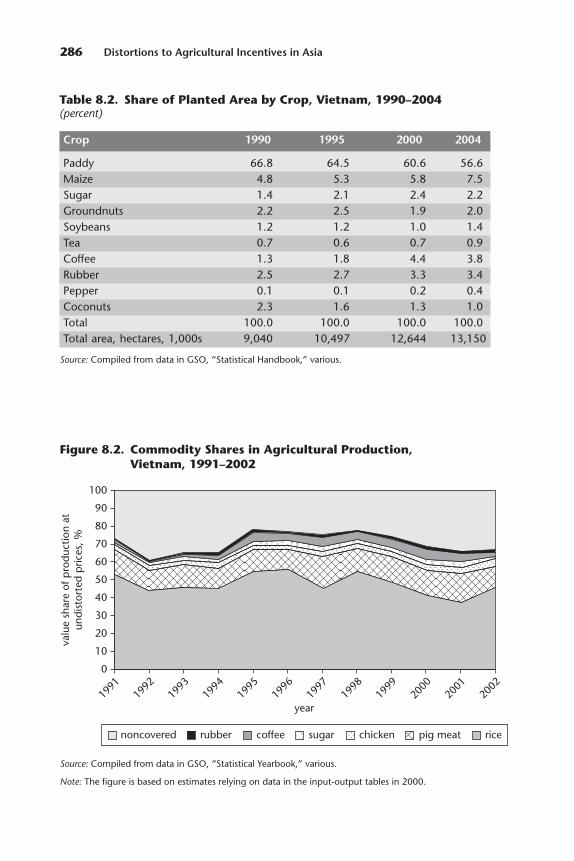

8.2 Commodity Shares in Agricultural Production, Vietnam,1991–2002 286

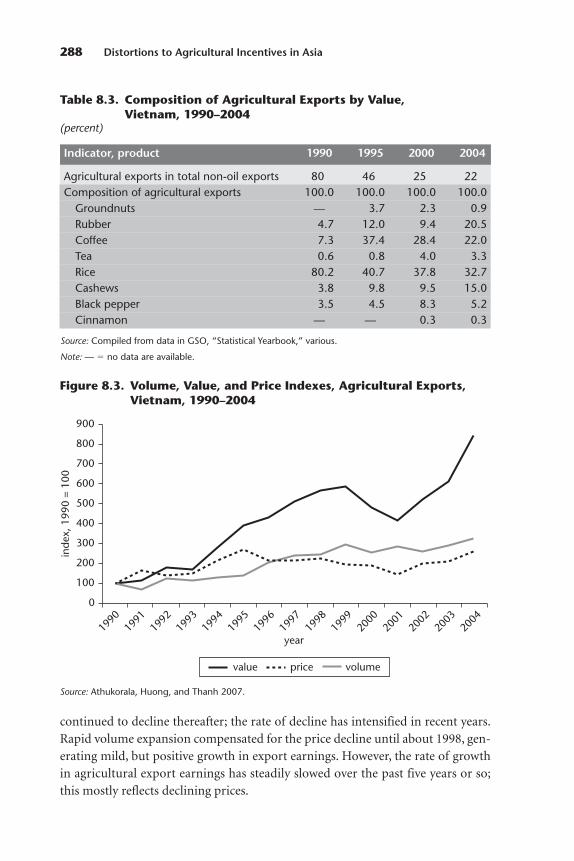

8.3 Volume, Value, and Price Indexes, Agricultural Exports,Vietnam, 1990–2004 288

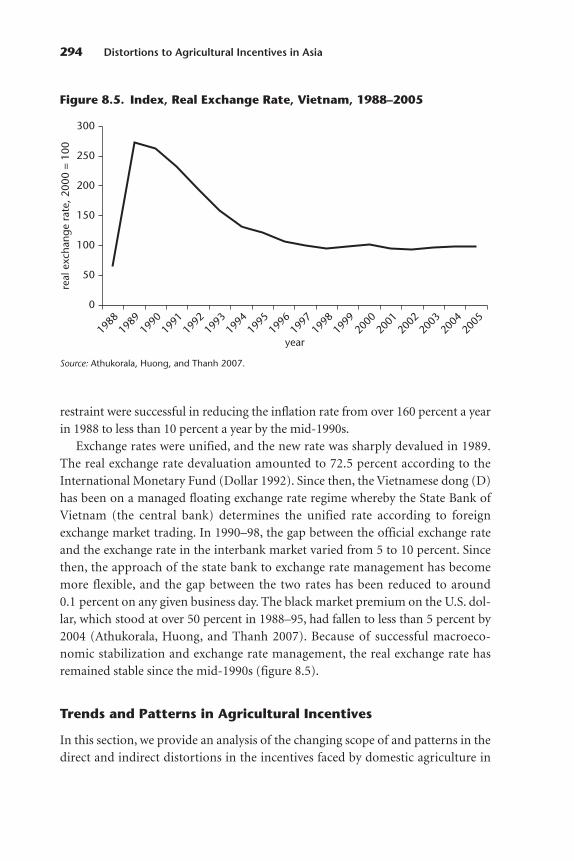

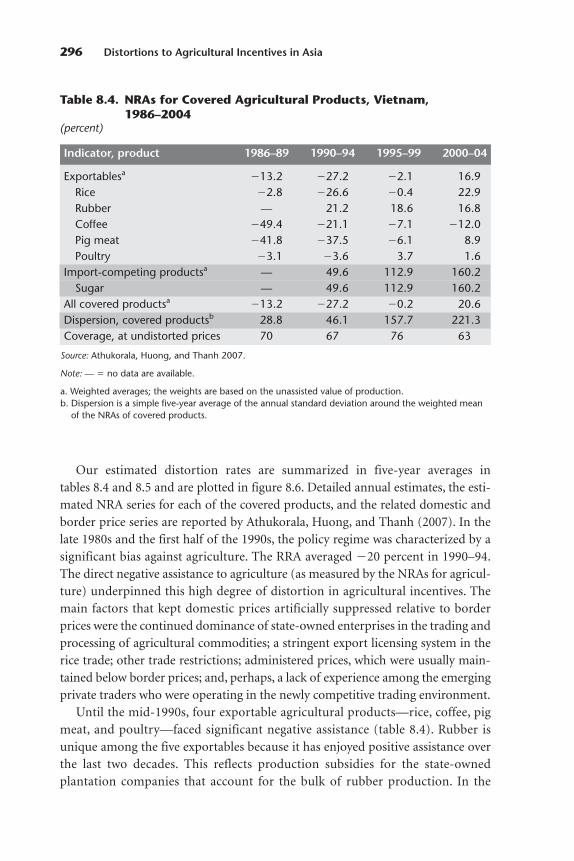

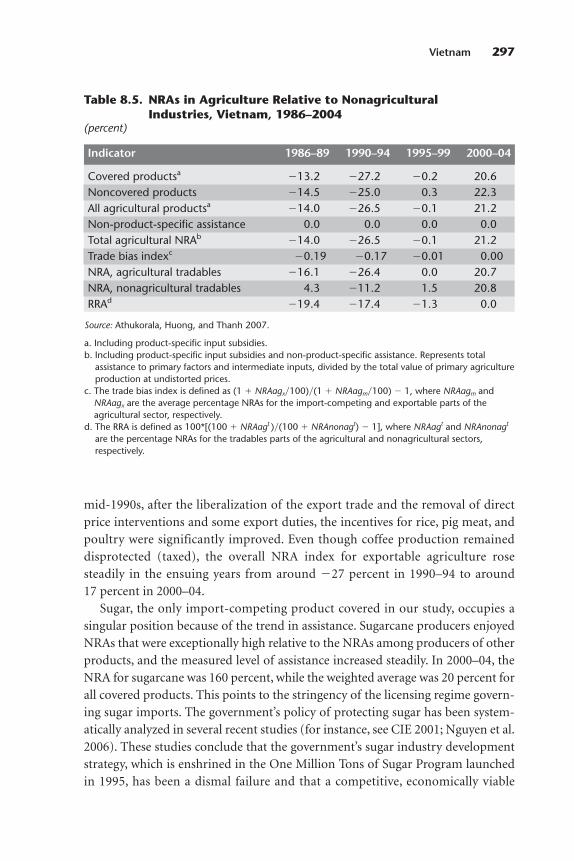

8.4 Weighted Average Import Duties, Vietnam, 1990–2004 2928.5 Index, Real Exchange Rate, Vietnam, 1988–2005 2948.6 NRAs for Agricultural and Nonagricultural Tradables and

the RRA, Vietnam, 1986–2004 2989.1 Commodity Shares in Agricultural Production,

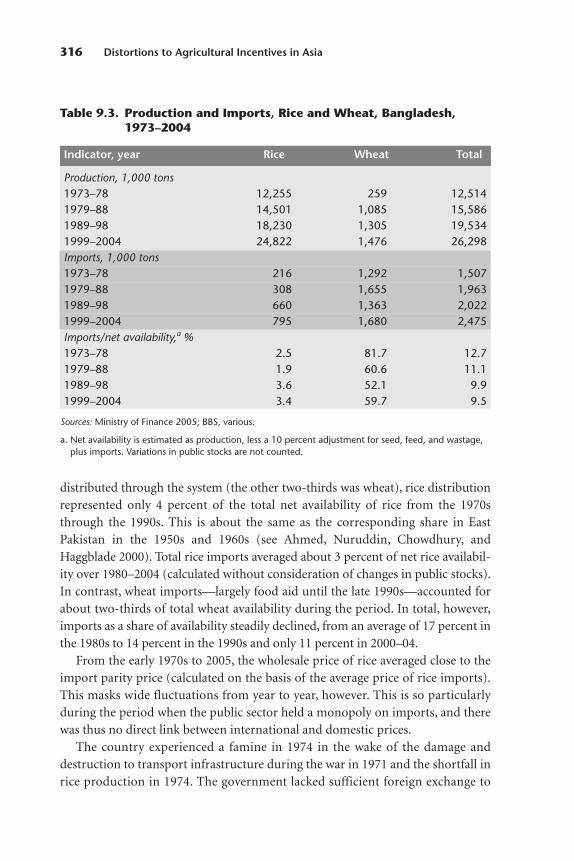

Bangladesh, 1971–2003 3159.2 NRAs and Border Prices, Rice, Bangladesh, 1974–2004 3179.3 Prices and Private Sector Imports, Rice, Bangladesh, 1997–2007 3199.4 NRAs for Exportable, Import-Competing, and All Agricultural

Products, Bangladesh, 1974–2004 3269.5 NRAs for Agricultural and Nonagricultural Tradables and

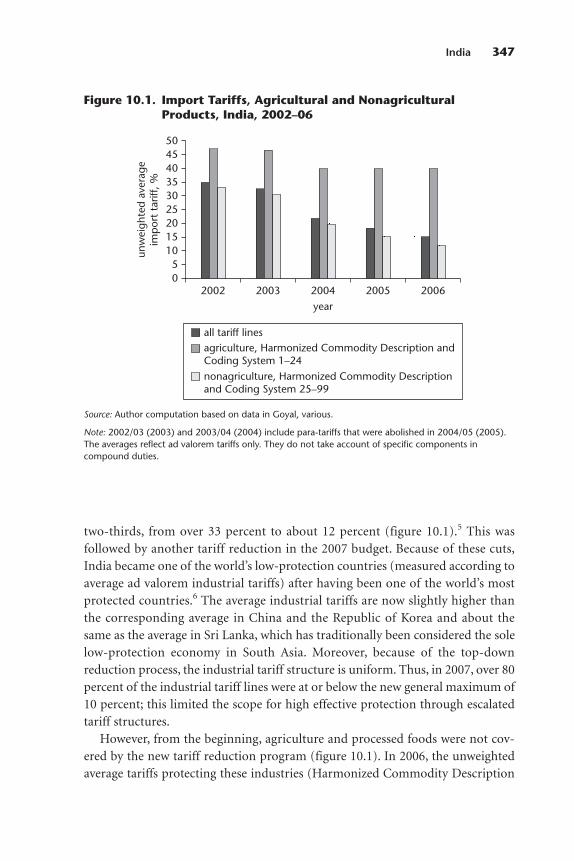

the RRA, Bangladesh, 1974–2004 32810.1 Import Tariffs, Agricultural and Nonagricultural Products, India,

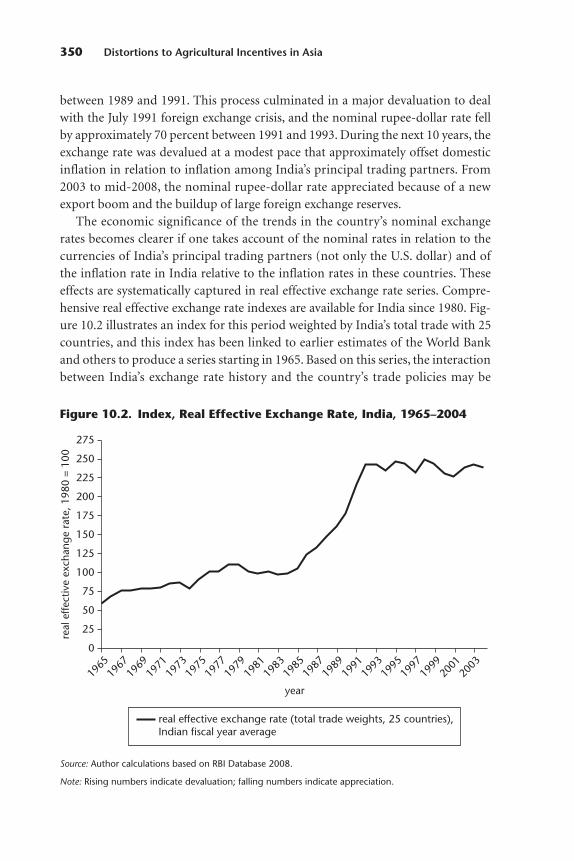

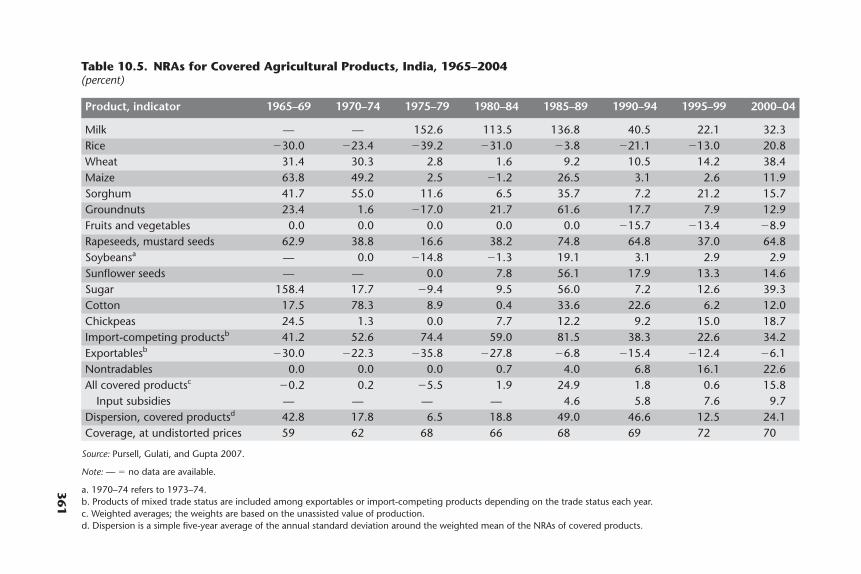

2002–06 34710.2 Index, Real Effective Exchange Rate, India, 1965–2004 35010.3 NRAs for Exportable, Import-Competing, and All Agricultural

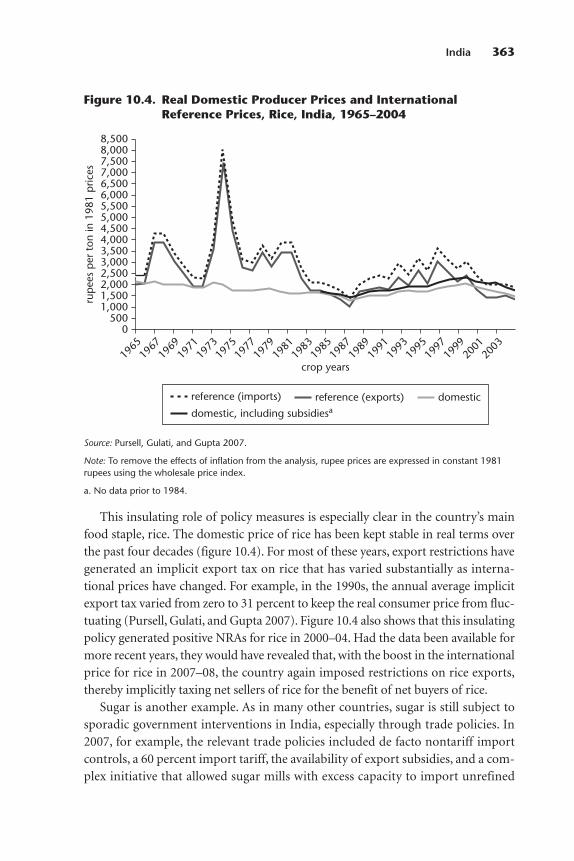

Products, India, 1965–2004 36010.4 Real Domestic Producer Prices and International

Reference Prices, Rice, India, 1965–2004 36310.5 NRAs for Agricultural and Nonagricultural Tradables and

the RRA, India, 1965–2004 36611.1 Commodity Shares in Agricultural Production, Pakistan,

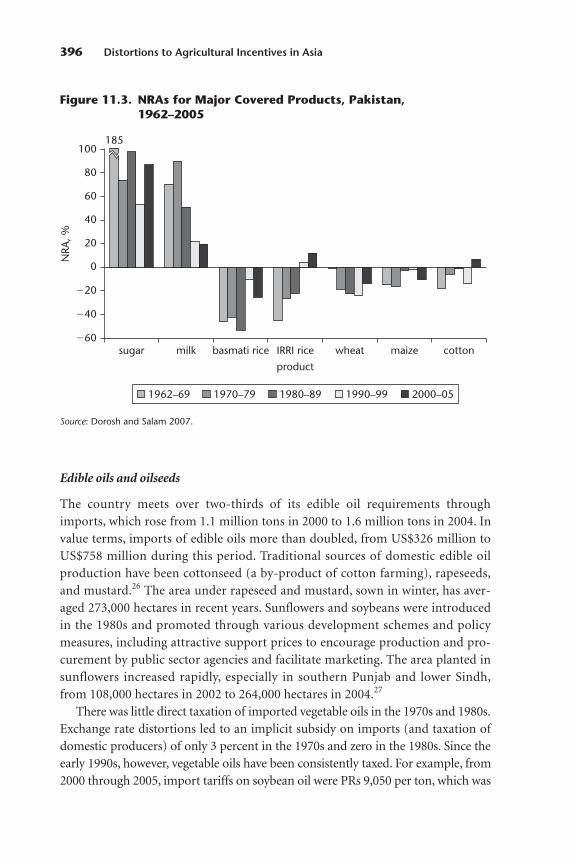

1965–2005 38111.2 Import Tariffs and the Real Exchange Rate, Pakistan, 1985–2004 38511.3 NRAs for Major Covered Products, Pakistan, 1962–2005 39611.4 NRAs for Exportable, Import-Competing, and All Agricultural

Products, Pakistan, 1973–2005 39811.5 NRAs for Agricultural and Nonagricultural Tradables and

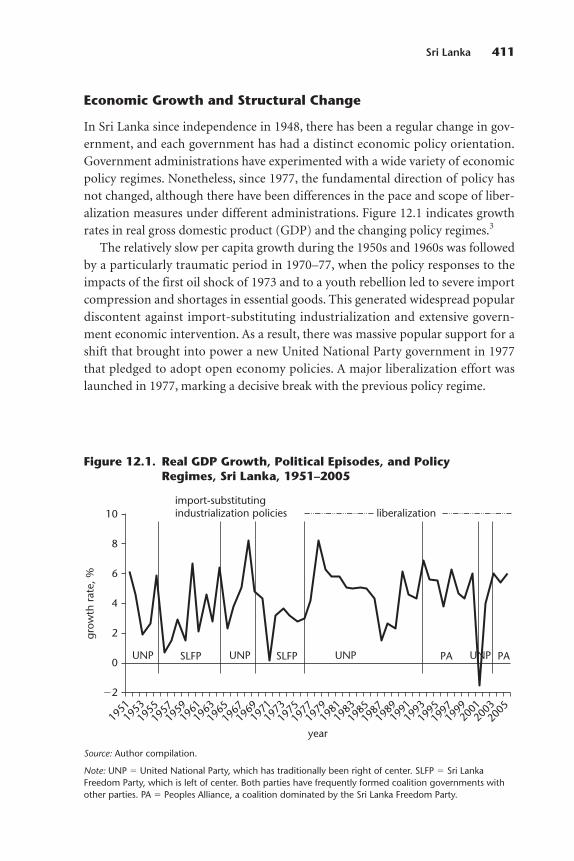

the RRA, Pakistan, 1973–2005 40112.1 Real GDP Growth, Political Episodes, and Policy Regimes,

Sri Lanka, 1951–2005 41112.2 Agriculture in GDP and Exports, Sri Lanka, 1950–2005 41412.3 Commodity Shares in Agricultural Production, Sri Lanka,

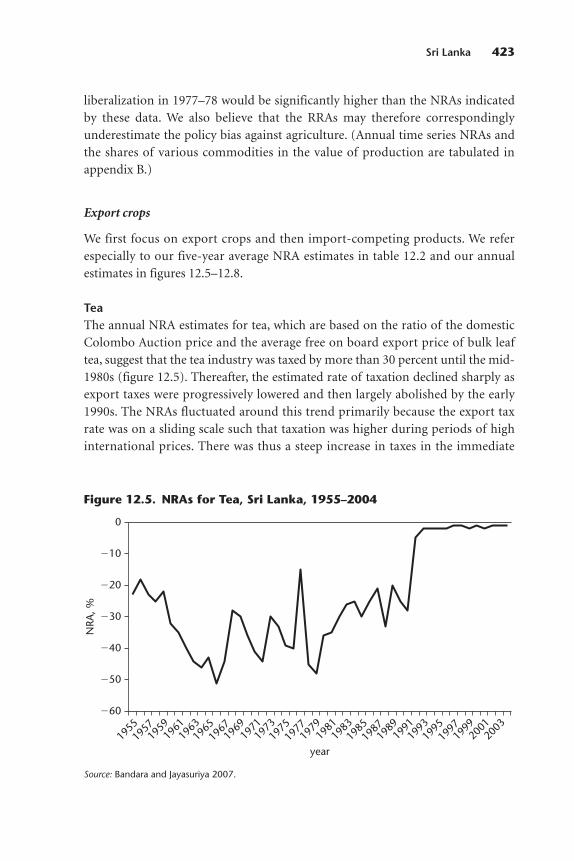

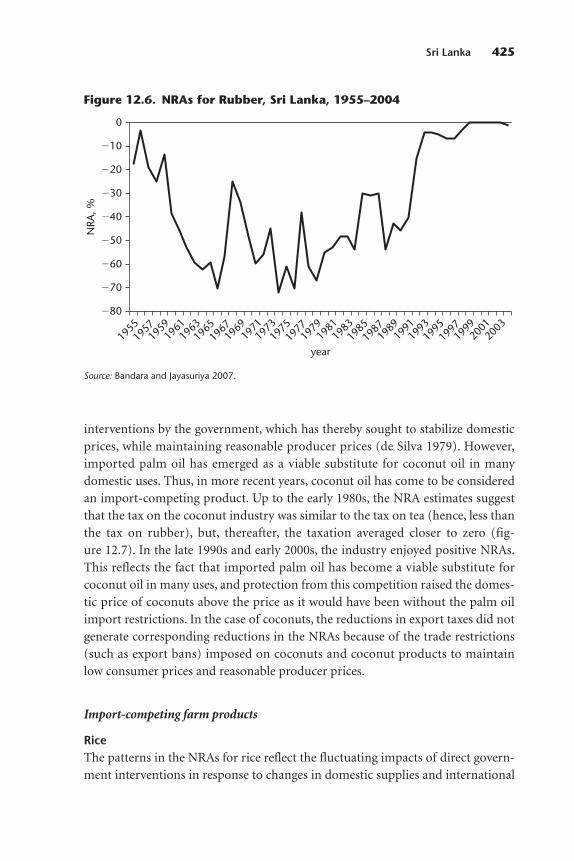

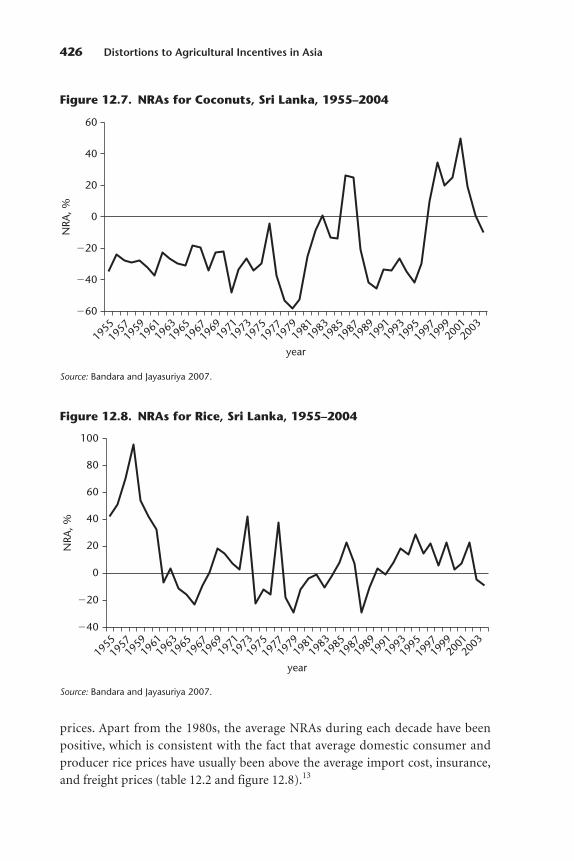

1966–2004 41412.4 Fertilizer Subsidy, Sri Lanka, 1962–2007 41912.5 NRAs for Tea, Sri Lanka, 1955–2004 42312.6 NRAs for Rubber, Sri Lanka, 1955–2004 42512.7 NRAs for Coconuts, Sri Lanka, 1955–2004 42612.8 NRAs for Rice, Sri Lanka, 1955–2004 426

Contents xi

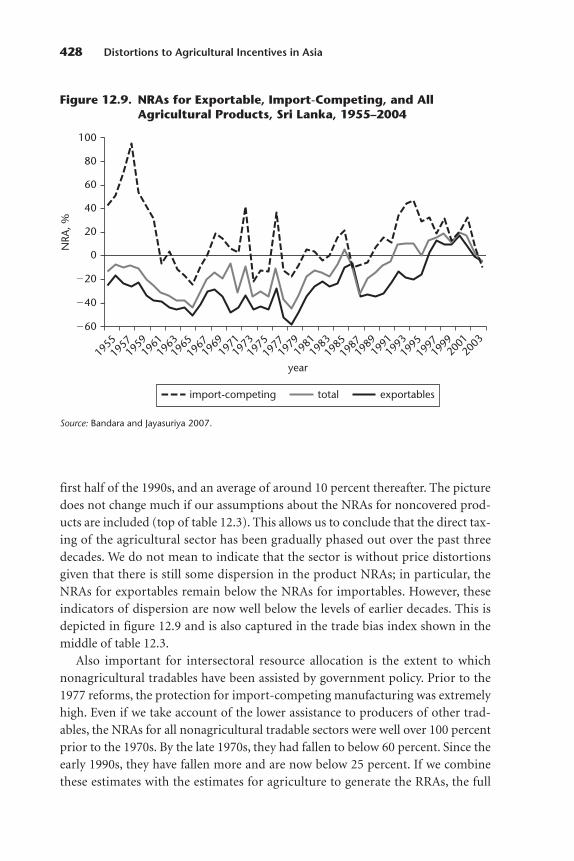

12.9 NRAs for Exportable, Import-Competing, and All Agricultural Products, Sri Lanka, 1955–2004 428

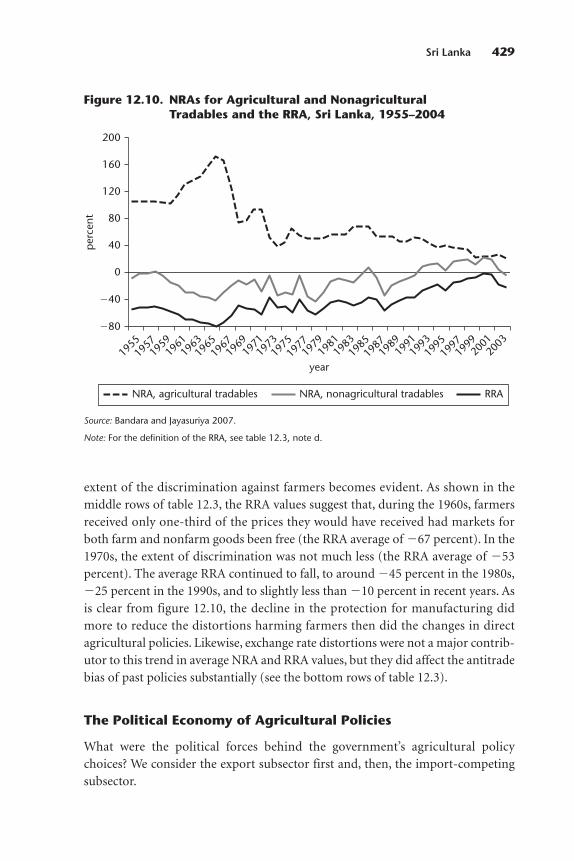

12.10 NRAs for Agricultural and Nonagricultural Tradables andthe RRA, Sri Lanka, 1955–2004 429

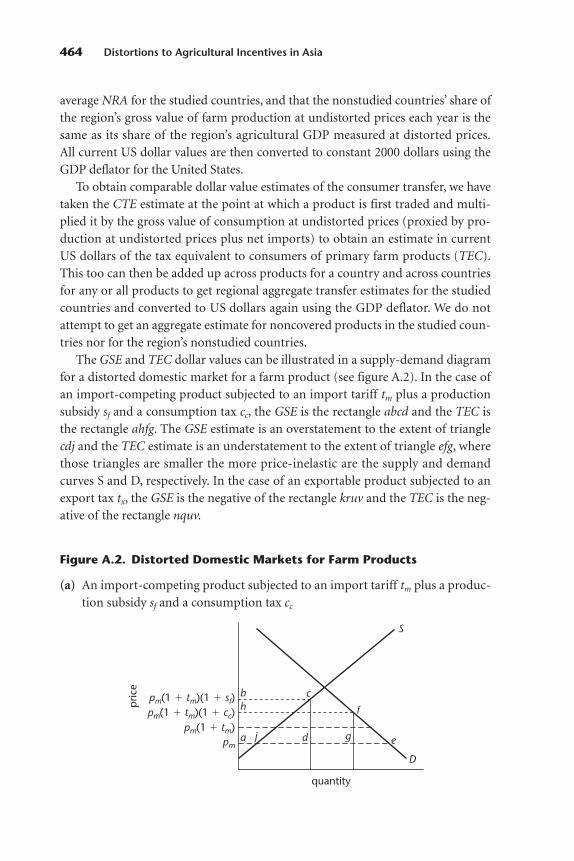

A.1 A Distorted Domestic Market for Foreign Currency 445A.2 Distorted Domestic Markets for Farm Products 464

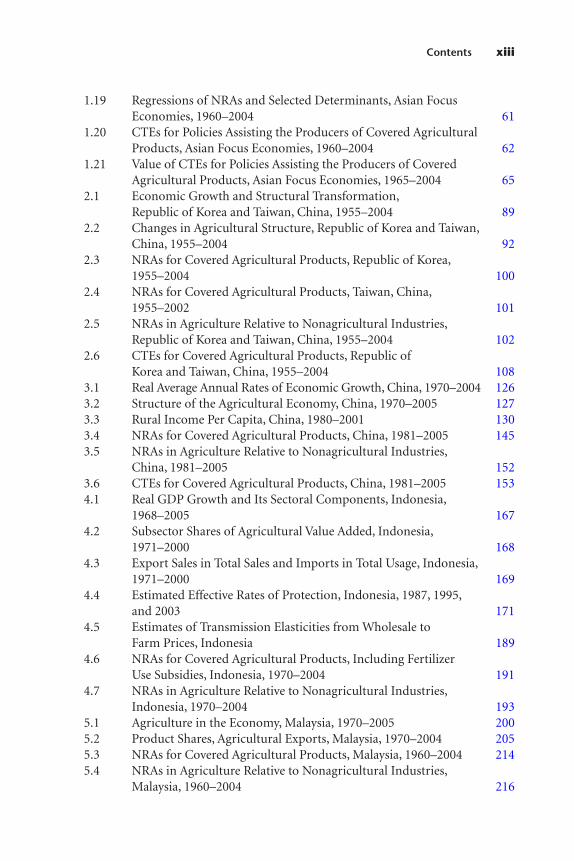

Tables1.1 Key Economic and Trade Indicators, Asian Focus Economies,

2000–04 61.2 Poverty Levels in Asia, 1981–2004 81.3 Real Growth in GDP and Exports, Asian Focus Economies,

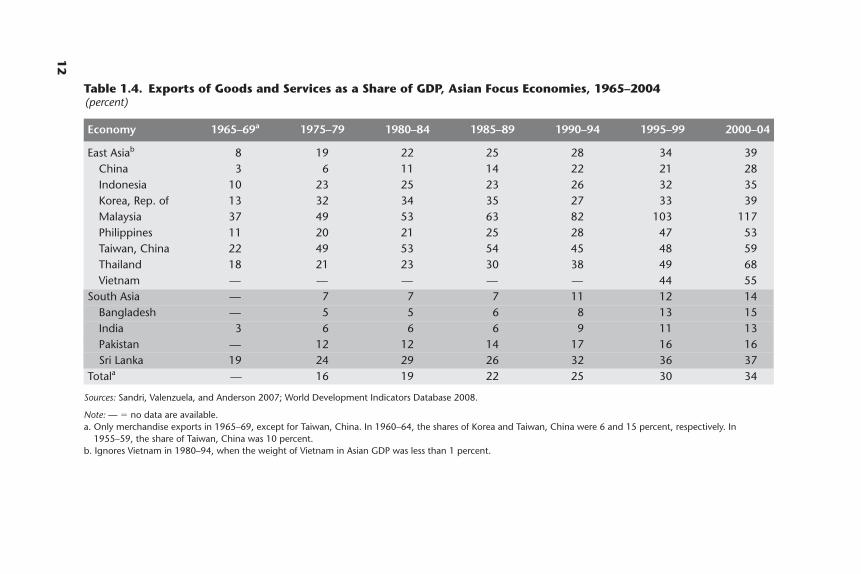

1980–2004 101.4 Exports of Goods and Services as a Share of GDP, Asian Focus

Economies, 1965–2004 121.5 Share of Nonfood Manufactures in World Exports, Asian Focus

Economies, 1990–2006 131.6 Sectoral Shares of GDP, Asian Focus Economies, 1965–2004 141.7 Agriculture’s Share in Employment, Asian Focus Economies,

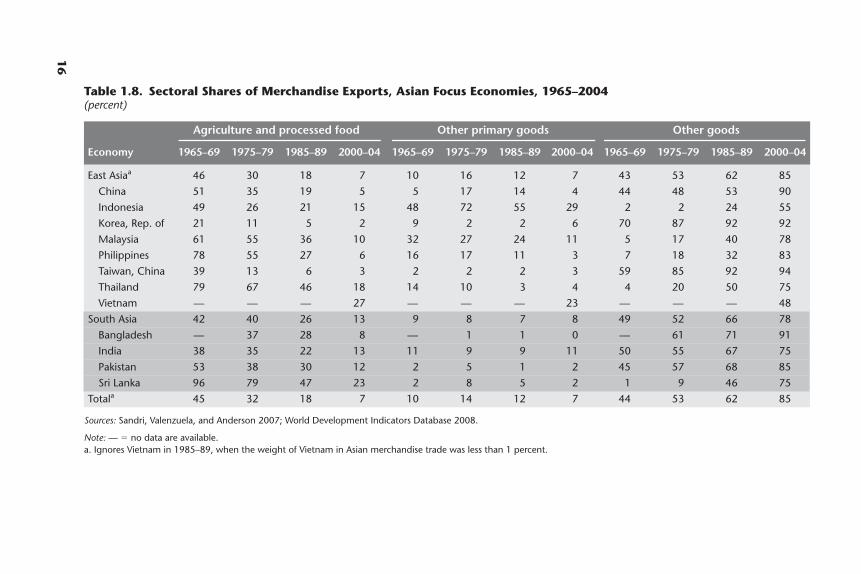

1965–2004 151.8 Sectoral Shares of Merchandise Exports, Asian Focus Economies,

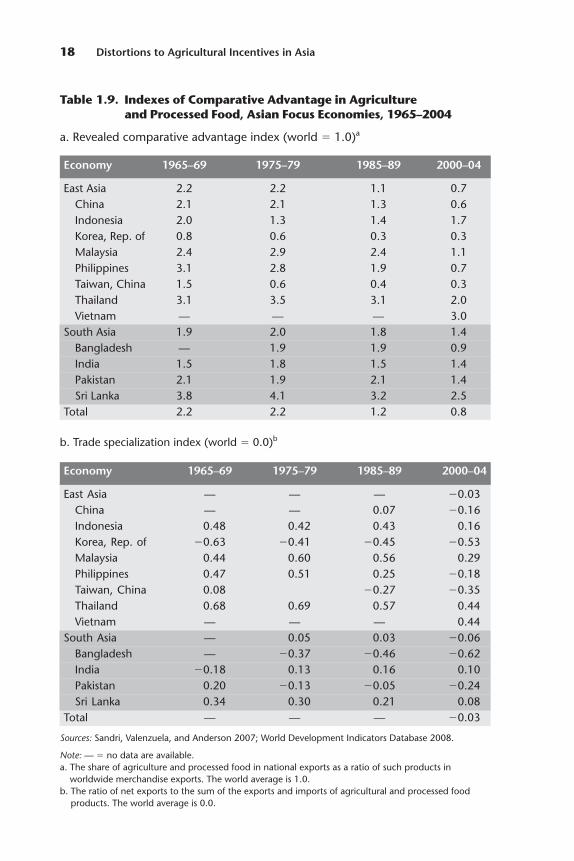

1965–2004 161.9 Indexes of Comparative Advantage in Agriculture and

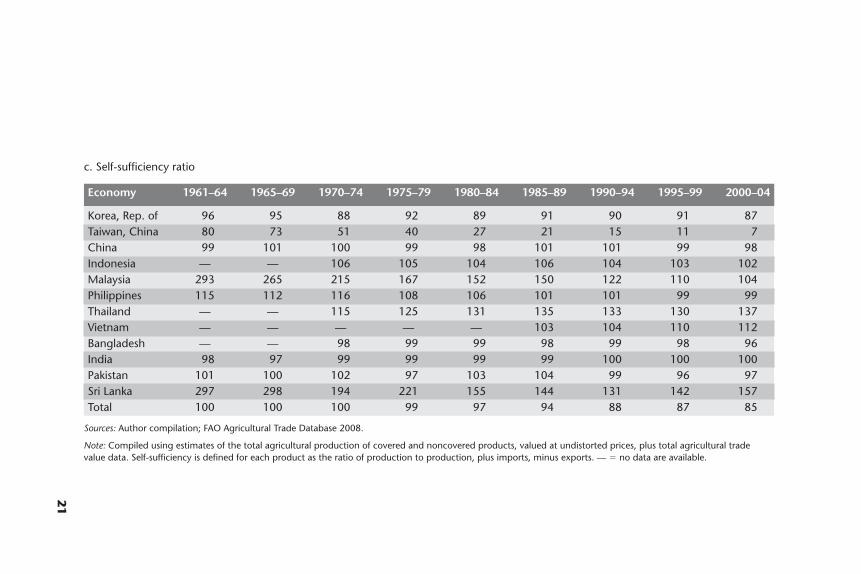

Processed Food, Asian Focus Economies, 1965–2004 181.10 Export Orientation, Import Dependence, and Self-Sufficiency

in Primary Agricultural Production, Asian Focus Economies,1961–2004 19

1.11 NRAs for Agricultural Products, Asian Focus Economies, 1955–2004 27

1.12 NRA Dispersion across Covered Agricultural Products,Asian Focus Economies, 1955–2004 32

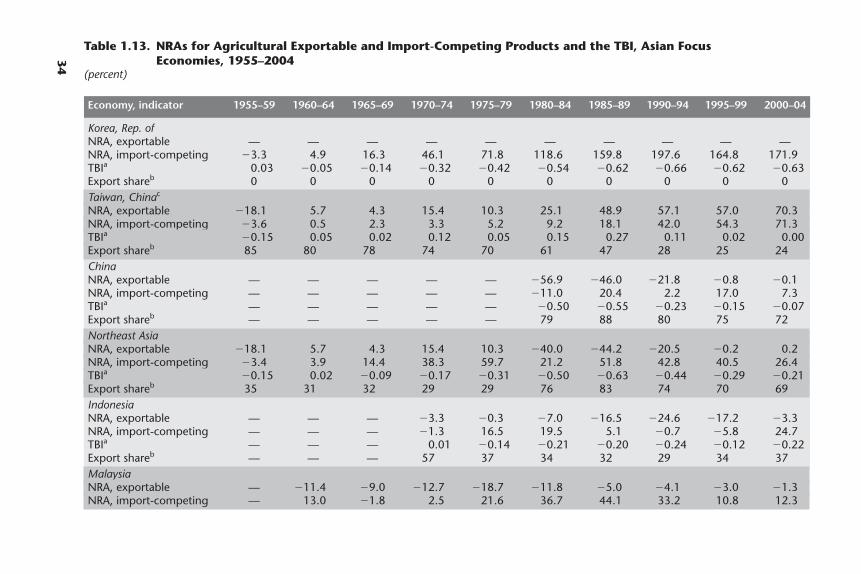

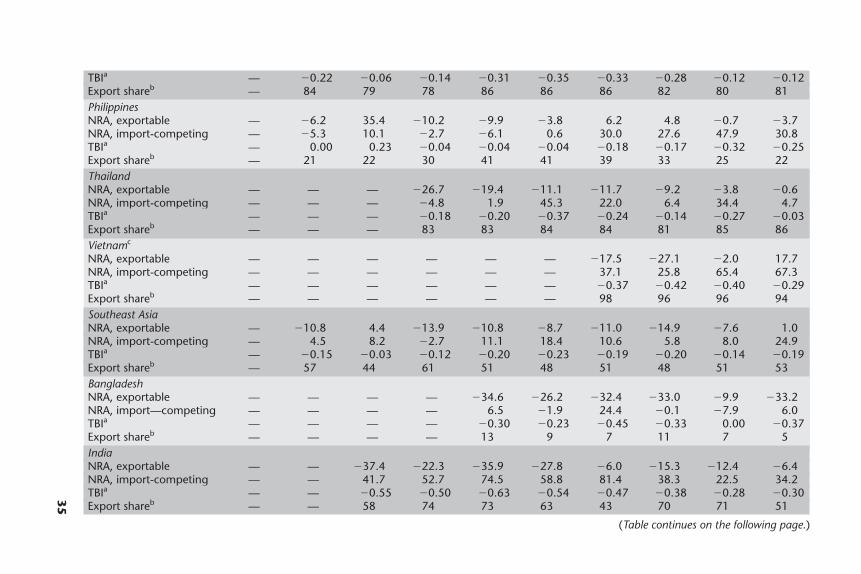

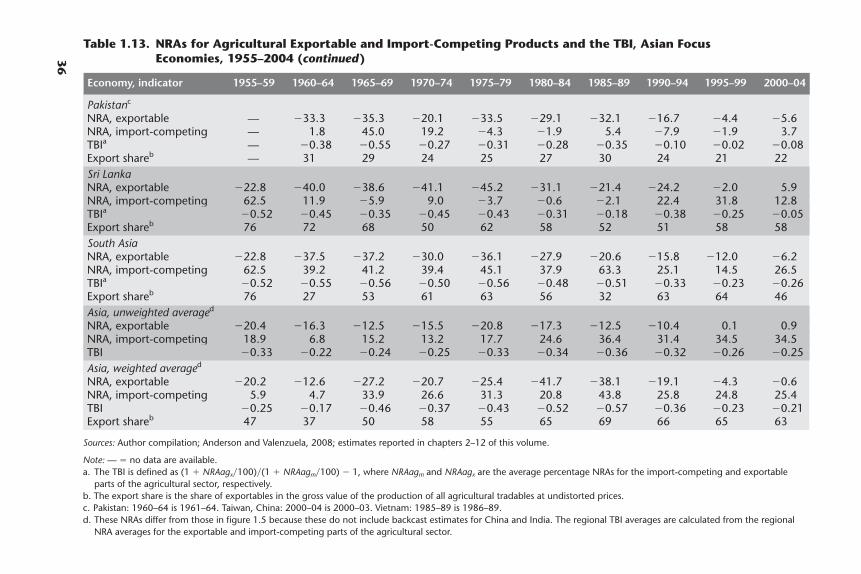

1.13 NRAs for Agricultural Exportable and Import-CompetingProducts and the TBI, Asian Focus Economies, 1955–2004 34

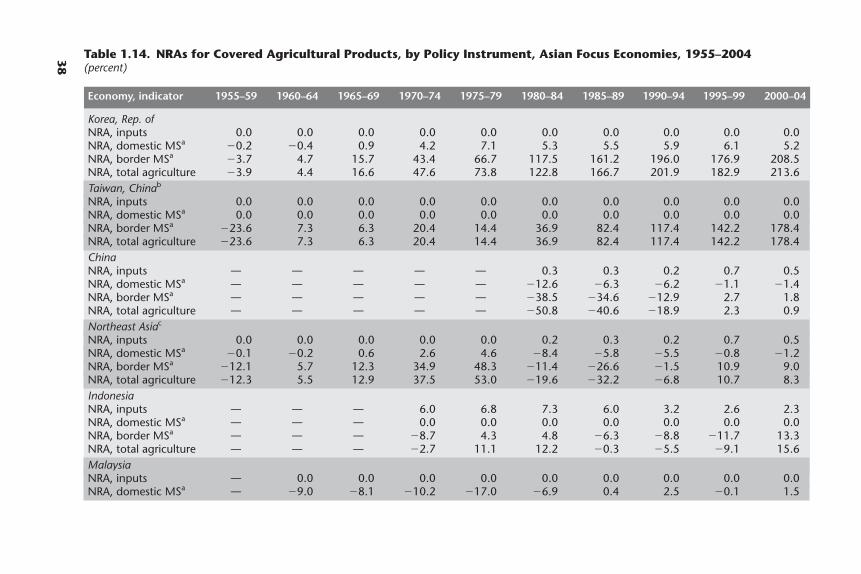

1.14 NRAs for Covered Agricultural Products, by Policy Instrument,Asian Focus Economies, 1955–2004 38

1.15 Gross Subsidy Equivalents of Agricultural Assistance,Total and Per Farmworker, Asian Focus Economies, 1955–2004 41

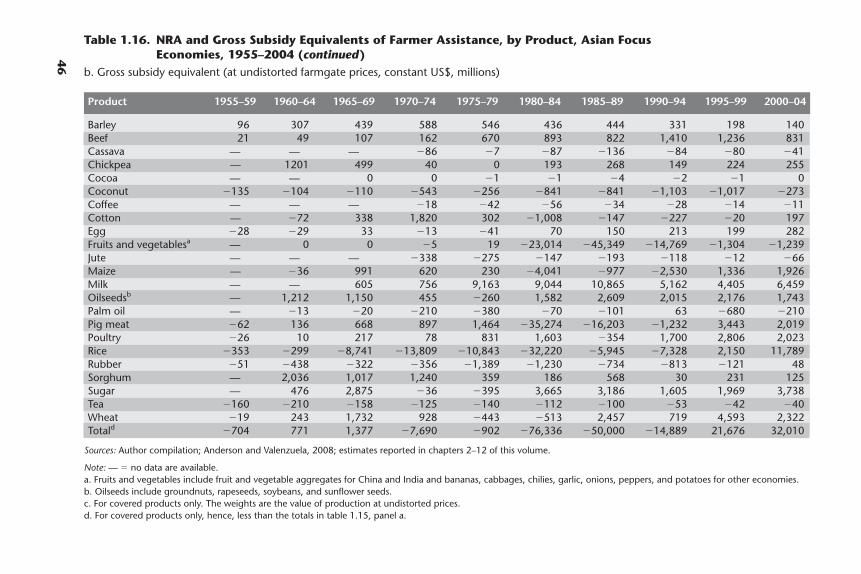

1.16 NRA and Gross Subsidy Equivalents of Farmer Assistance,by Product, Asian Focus Economies, 1955–2004 45

1.17 RRAs in Agriculture, Asian Focus Economies, 1955–2004 481.18 Relative Per Capita Income, Agricultural Comparative Advantage,

and NRAs and RRAs for Agricultural Tradables, Asian FocusEconomies, 2000–04 57

xii Contents

1.19 Regressions of NRAs and Selected Determinants, Asian FocusEconomies, 1960–2004 61

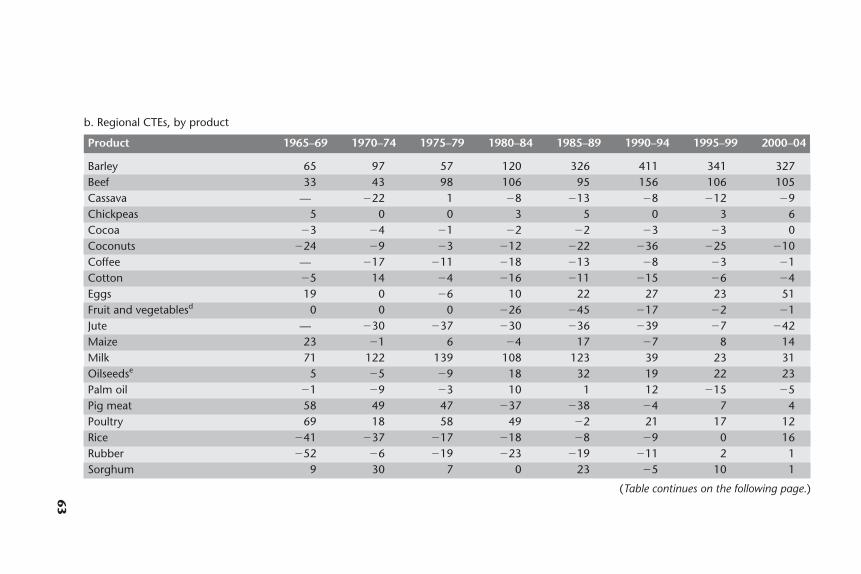

1.20 CTEs for Policies Assisting the Producers of Covered Agricultural Products, Asian Focus Economies, 1960–2004 62

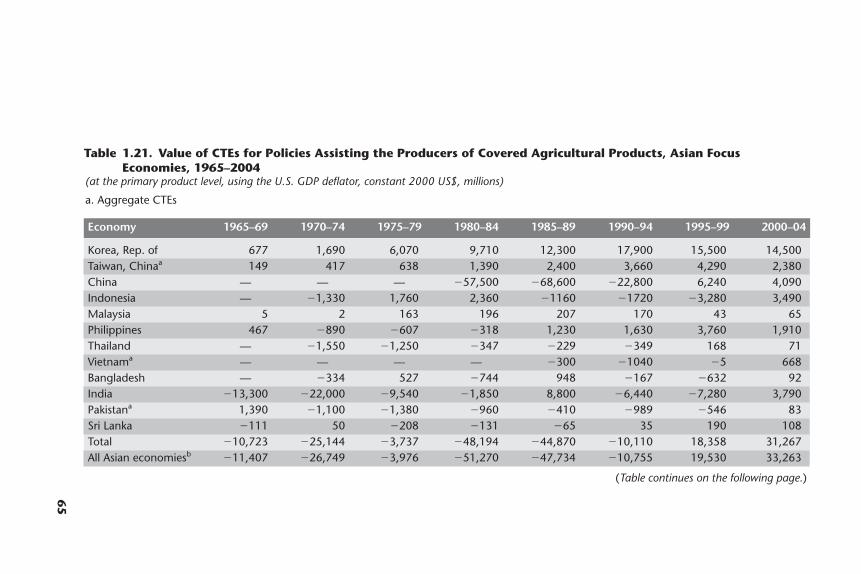

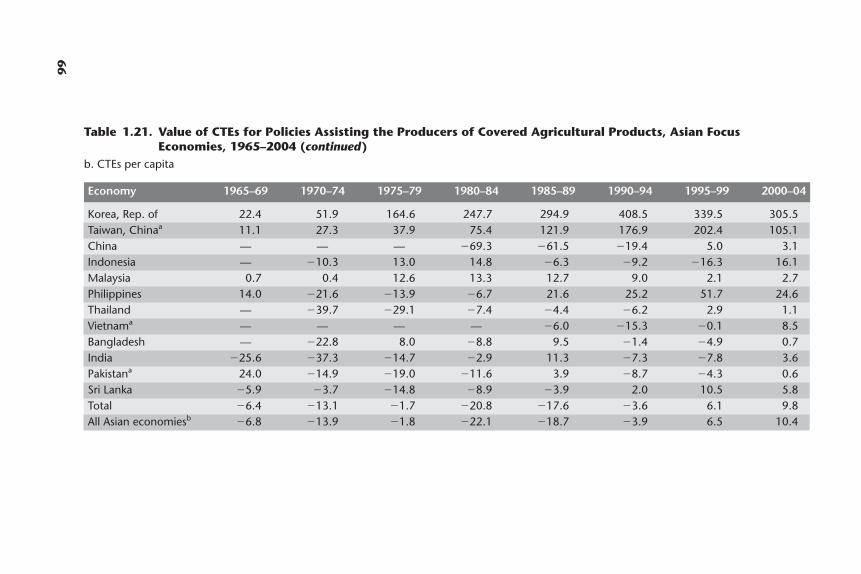

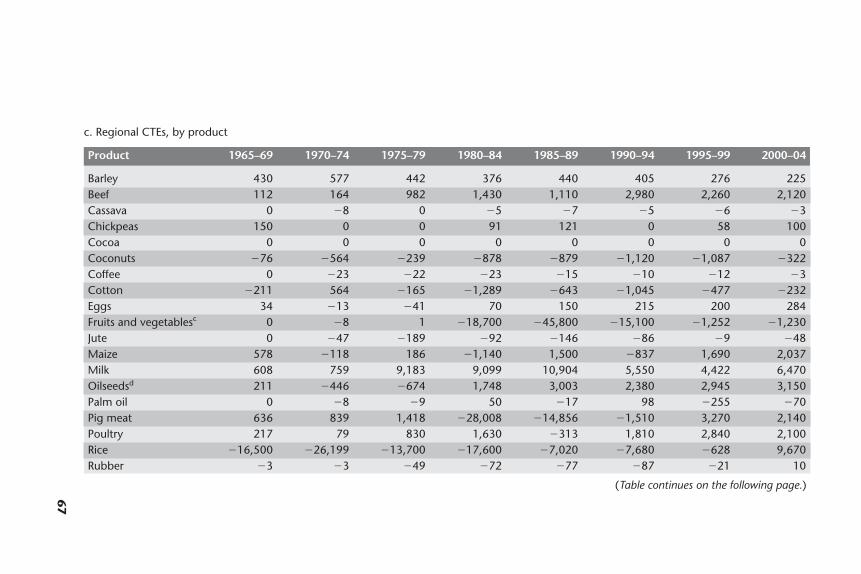

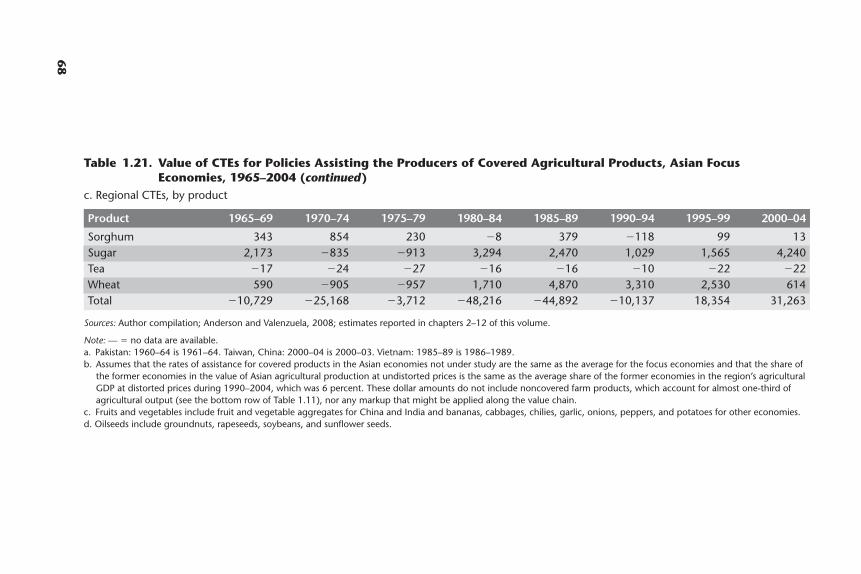

1.21 Value of CTEs for Policies Assisting the Producers of Covered Agricultural Products, Asian Focus Economies, 1965–2004 65

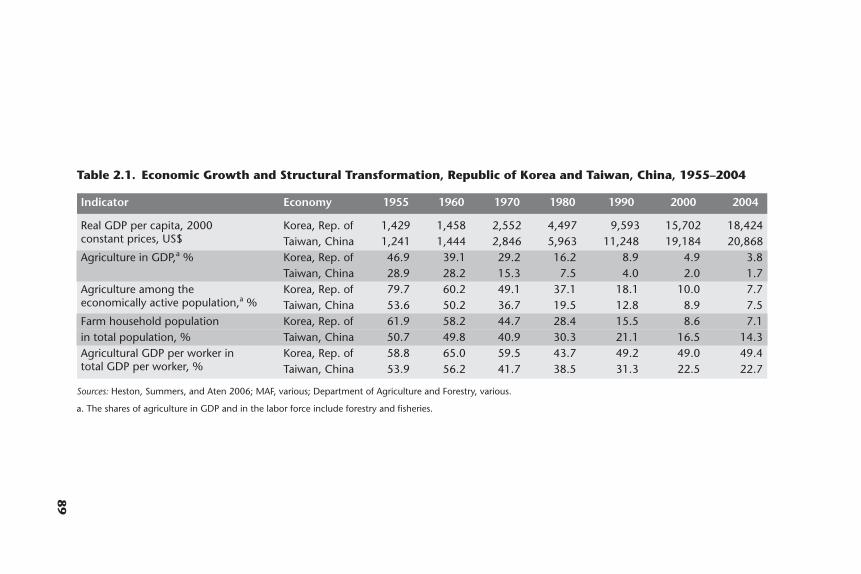

2.1 Economic Growth and Structural Transformation,Republic of Korea and Taiwan, China, 1955–2004 89

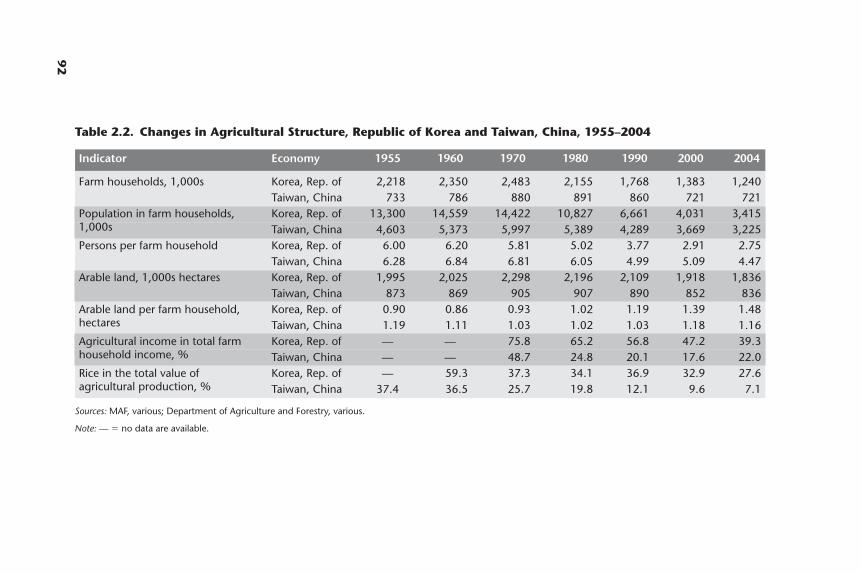

2.2 Changes in Agricultural Structure, Republic of Korea and Taiwan,China, 1955–2004 92

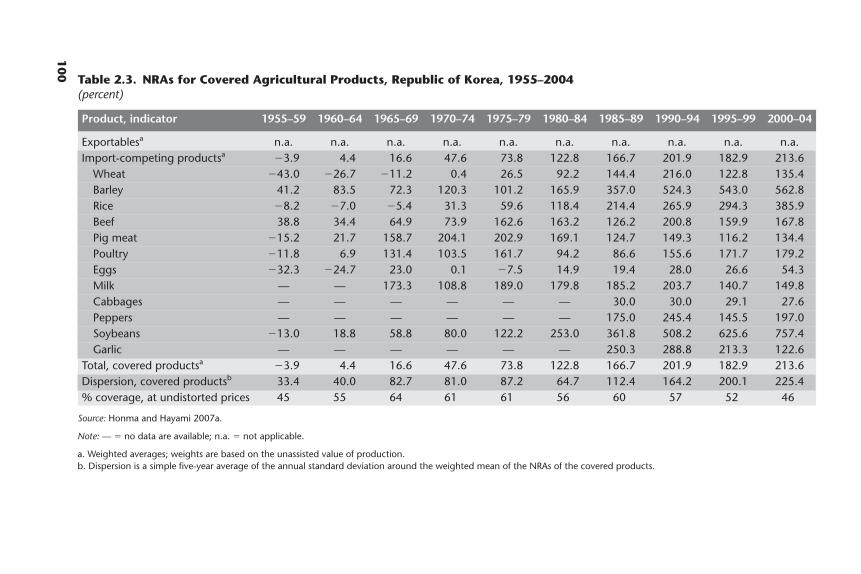

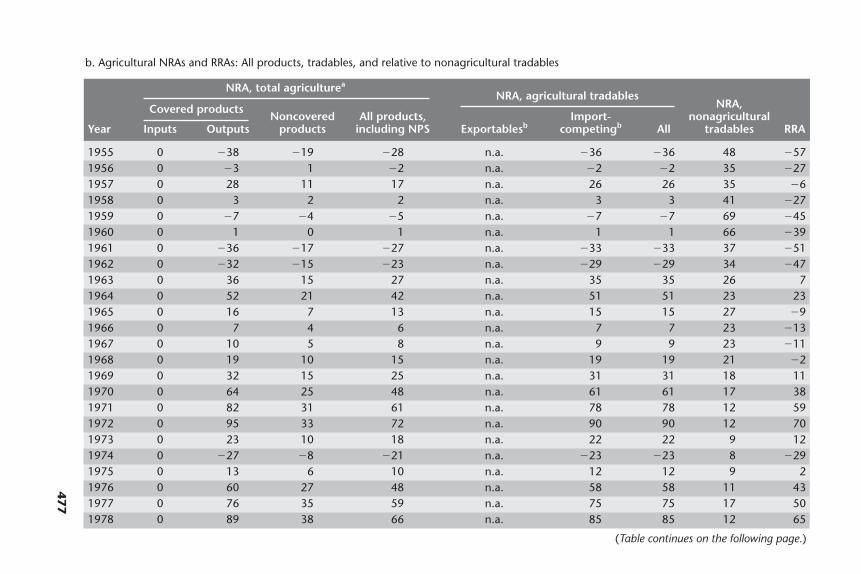

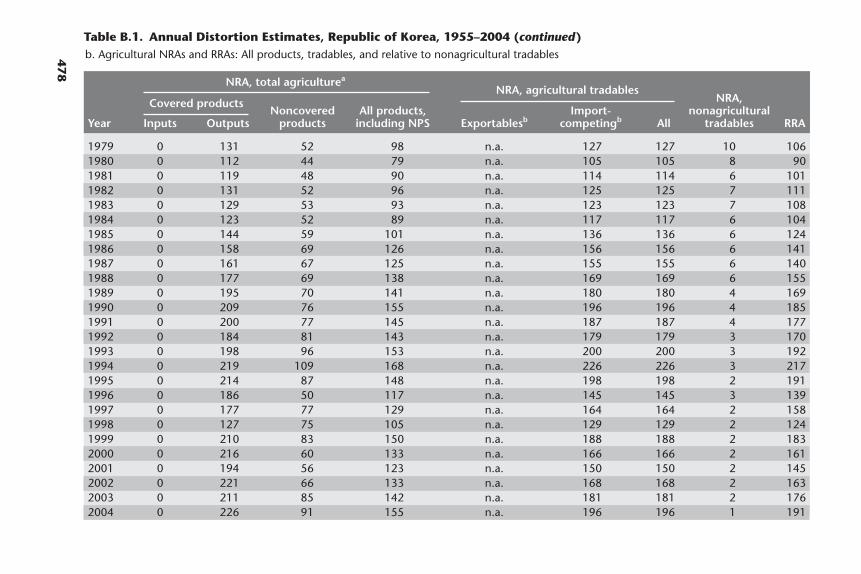

2.3 NRAs for Covered Agricultural Products, Republic of Korea,1955–2004 100

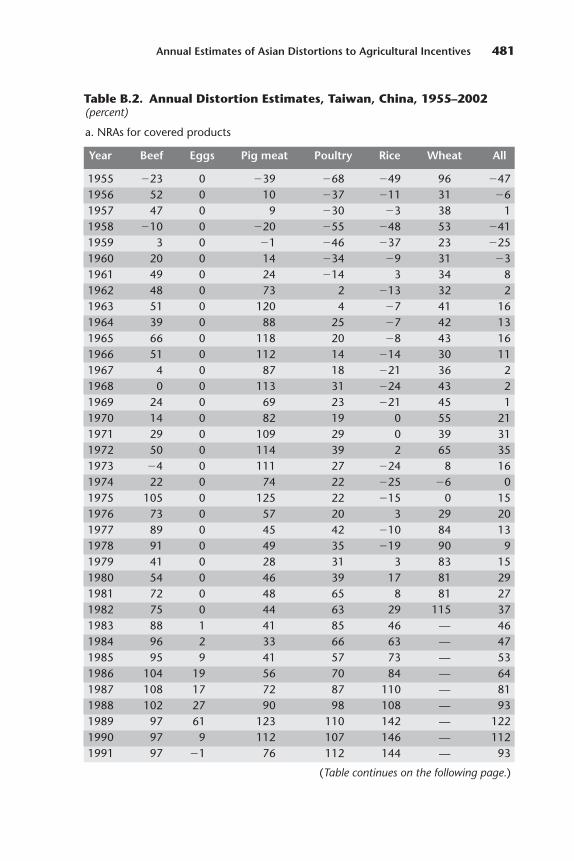

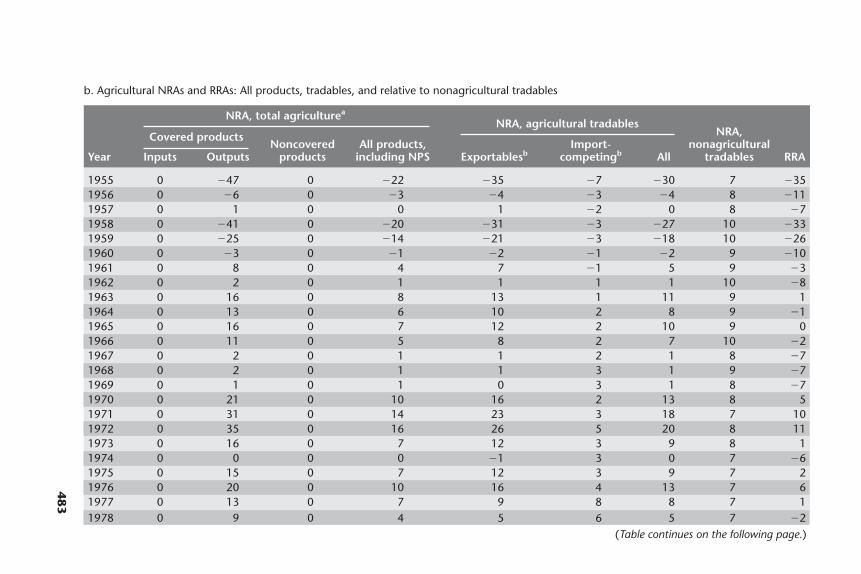

2.4 NRAs for Covered Agricultural Products, Taiwan, China,1955–2002 101

2.5 NRAs in Agriculture Relative to Nonagricultural Industries,Republic of Korea and Taiwan, China, 1955–2004 102

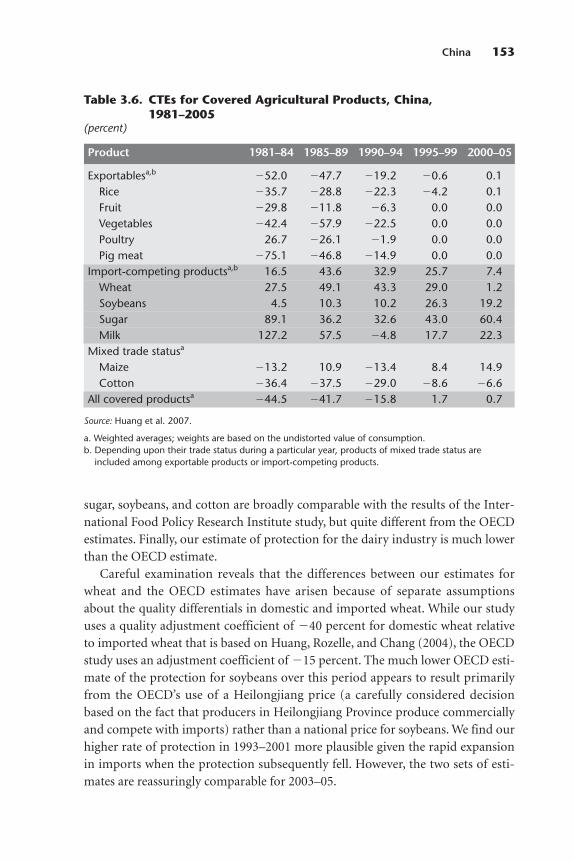

2.6 CTEs for Covered Agricultural Products, Republic ofKorea and Taiwan, China, 1955–2004 108

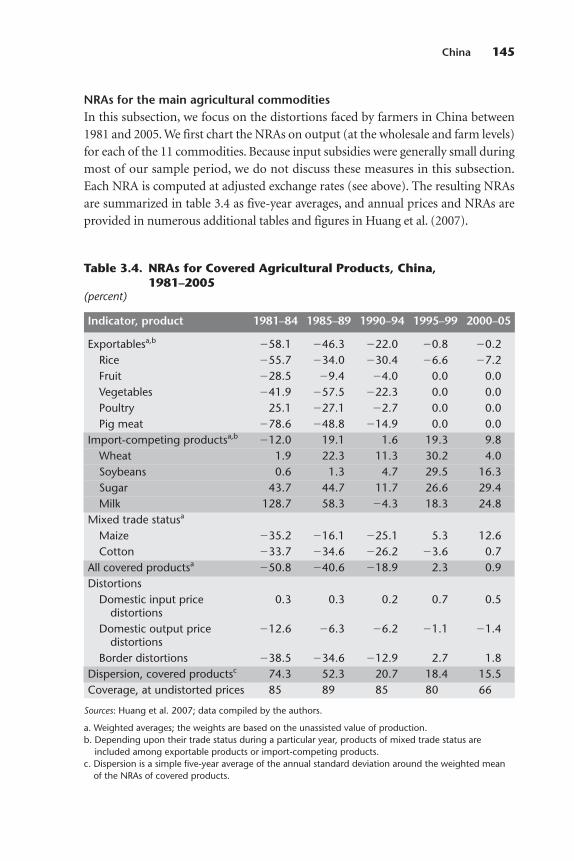

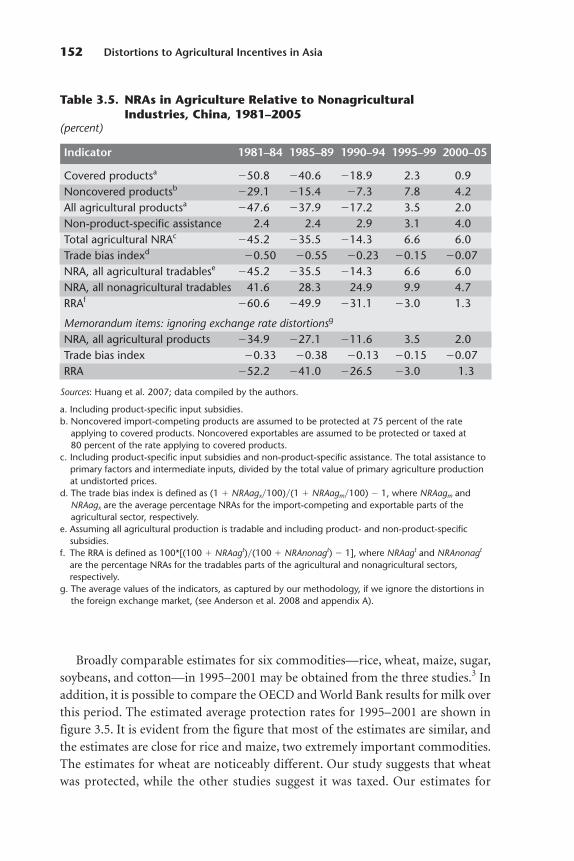

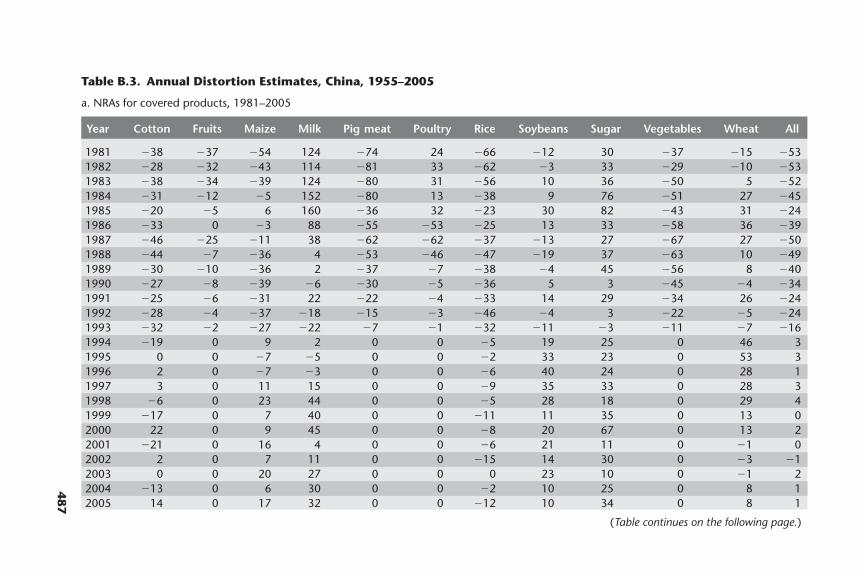

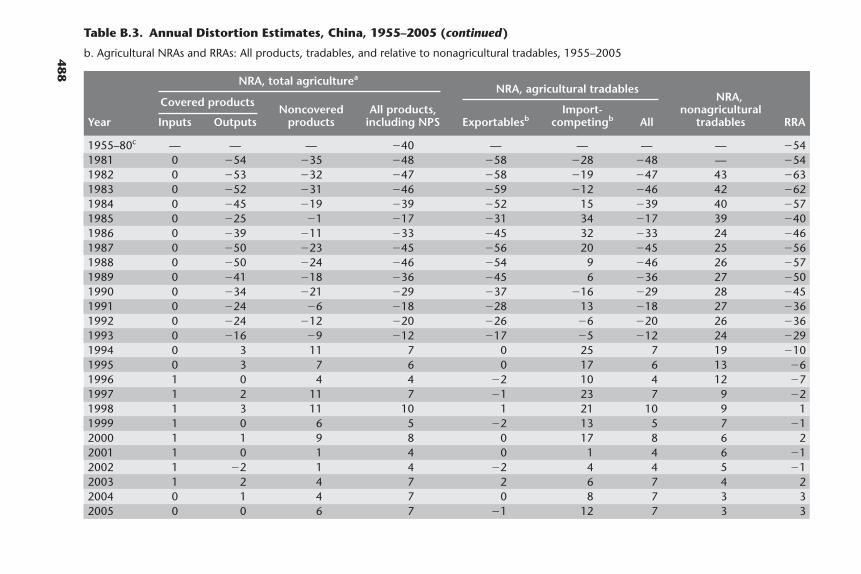

3.1 Real Average Annual Rates of Economic Growth, China, 1970–2004 1263.2 Structure of the Agricultural Economy, China, 1970–2005 1273.3 Rural Income Per Capita, China, 1980–2001 1303.4 NRAs for Covered Agricultural Products, China, 1981–2005 1453.5 NRAs in Agriculture Relative to Nonagricultural Industries,

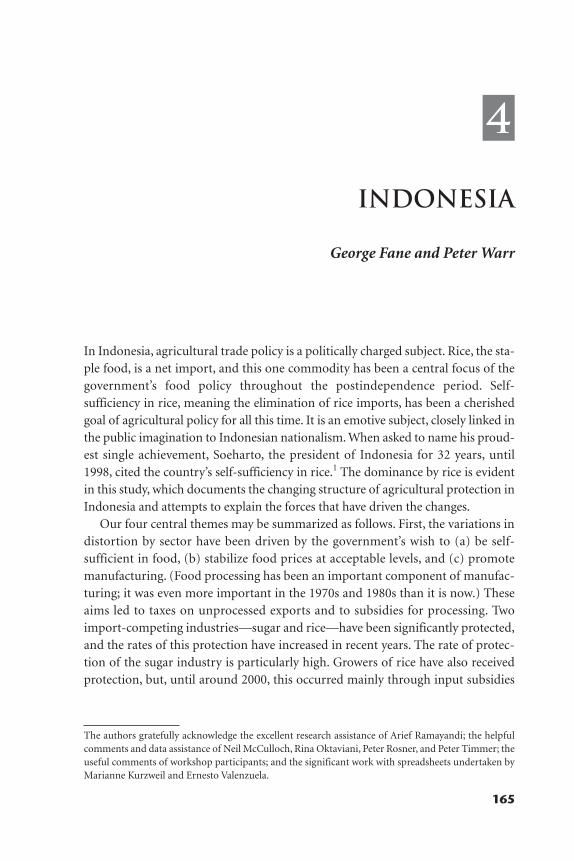

China, 1981–2005 1523.6 CTEs for Covered Agricultural Products, China, 1981–2005 1534.1 Real GDP Growth and Its Sectoral Components, Indonesia,

1968–2005 1674.2 Subsector Shares of Agricultural Value Added, Indonesia,

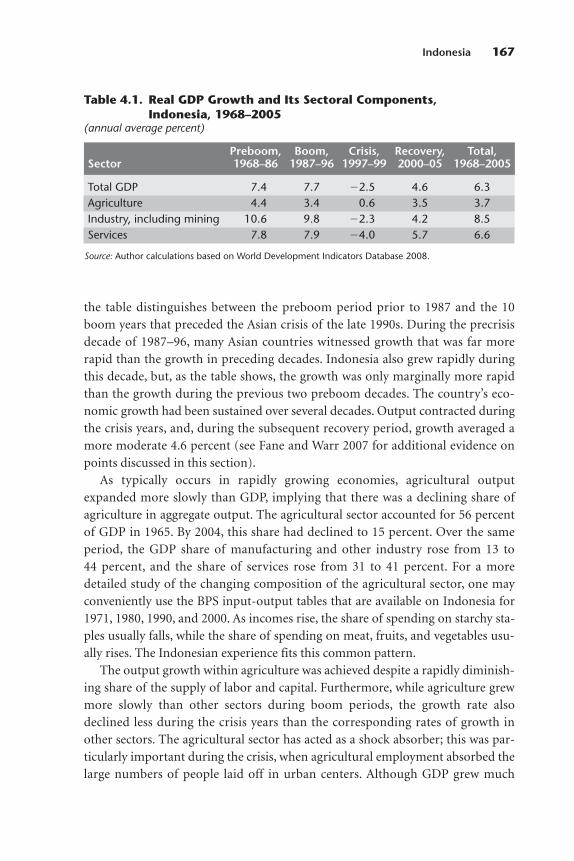

1971–2000 1684.3 Export Sales in Total Sales and Imports in Total Usage, Indonesia,

1971–2000 1694.4 Estimated Effective Rates of Protection, Indonesia, 1987, 1995,

and 2003 1714.5 Estimates of Transmission Elasticities from Wholesale to

Farm Prices, Indonesia 1894.6 NRAs for Covered Agricultural Products, Including Fertilizer

Use Subsidies, Indonesia, 1970–2004 1914.7 NRAs in Agriculture Relative to Nonagricultural Industries,

Indonesia, 1970–2004 1935.1 Agriculture in the Economy, Malaysia, 1970–2005 2005.2 Product Shares, Agricultural Exports, Malaysia, 1970–2004 2055.3 NRAs for Covered Agricultural Products, Malaysia, 1960–2004 2145.4 NRAs in Agriculture Relative to Nonagricultural Industries,

Malaysia, 1960–2004 216

Contents xiii

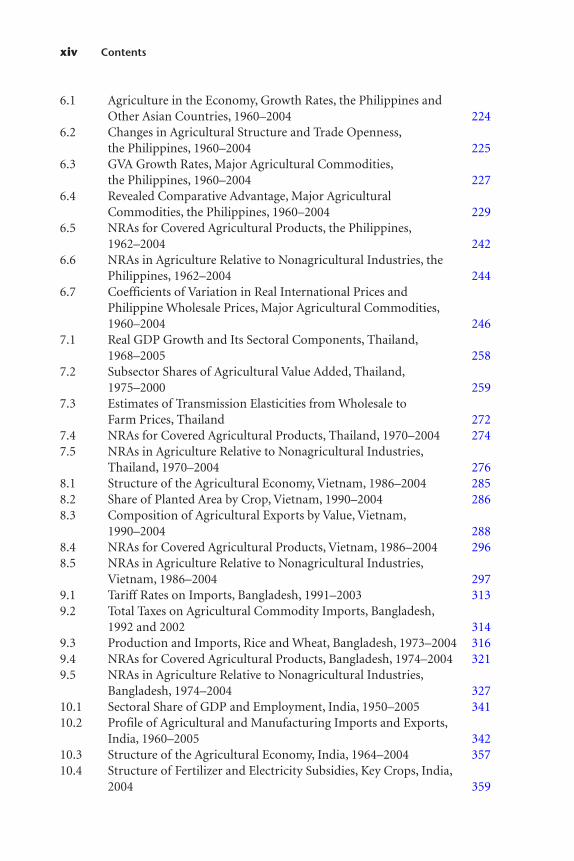

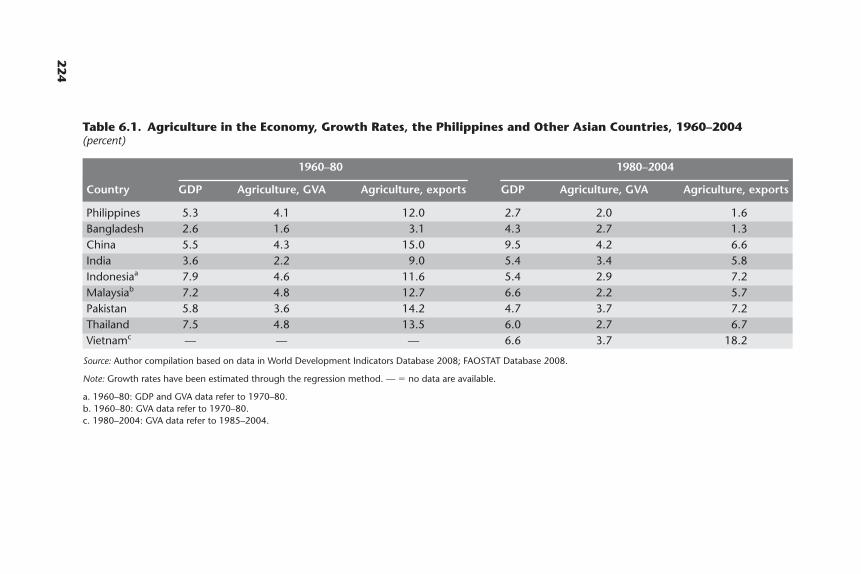

6.1 Agriculture in the Economy, Growth Rates, the Philippines andOther Asian Countries, 1960–2004 224

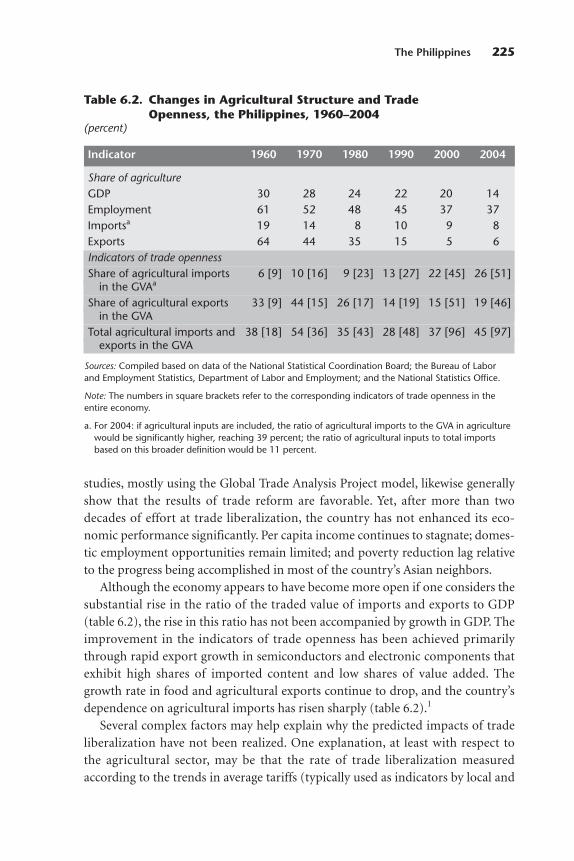

6.2 Changes in Agricultural Structure and Trade Openness,the Philippines, 1960–2004 225

6.3 GVA Growth Rates, Major Agricultural Commodities,the Philippines, 1960–2004 227

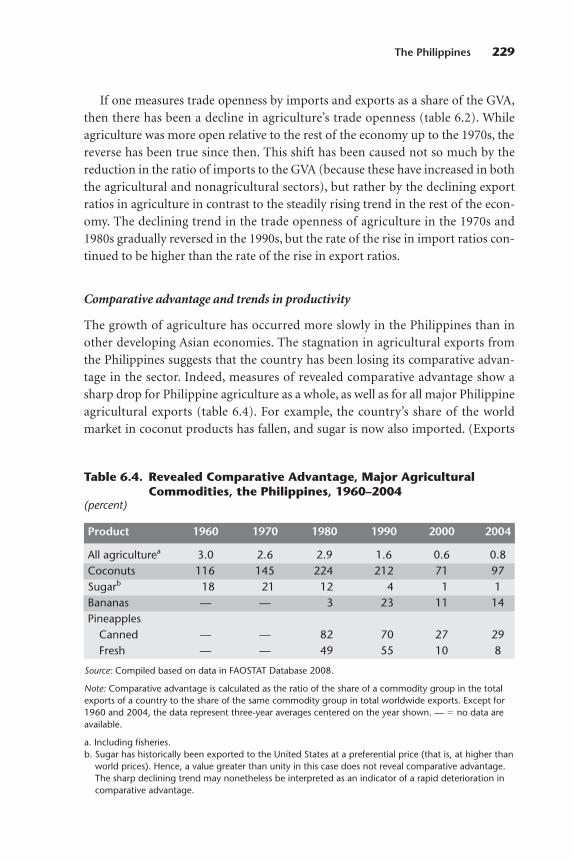

6.4 Revealed Comparative Advantage, Major AgriculturalCommodities, the Philippines, 1960–2004 229

6.5 NRAs for Covered Agricultural Products, the Philippines,1962–2004 242

6.6 NRAs in Agriculture Relative to Nonagricultural Industries, the Philippines, 1962–2004 244

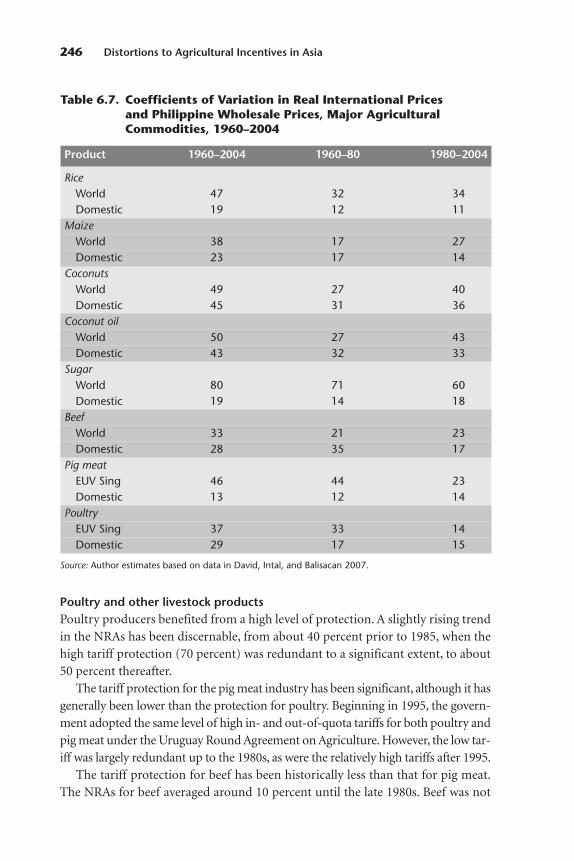

6.7 Coefficients of Variation in Real International Prices andPhilippine Wholesale Prices, Major Agricultural Commodities,1960–2004 246

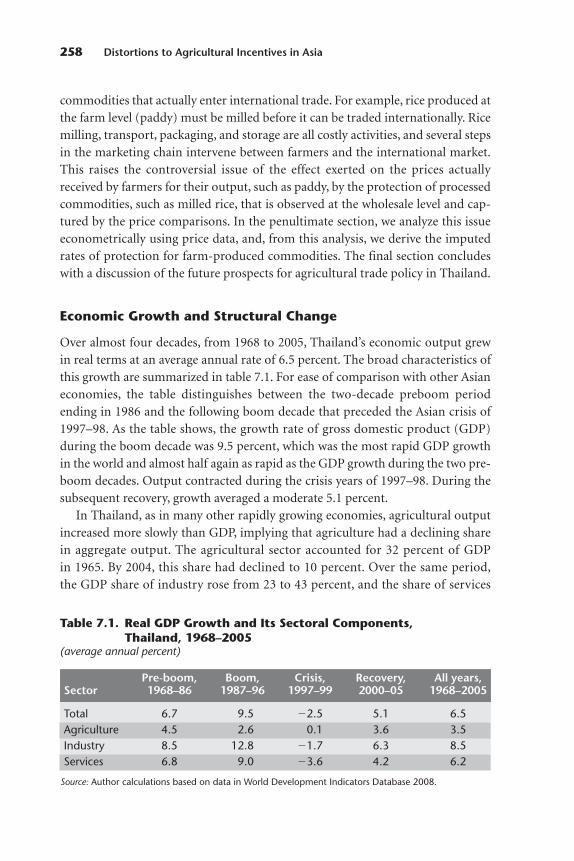

7.1 Real GDP Growth and Its Sectoral Components, Thailand,1968–2005 258

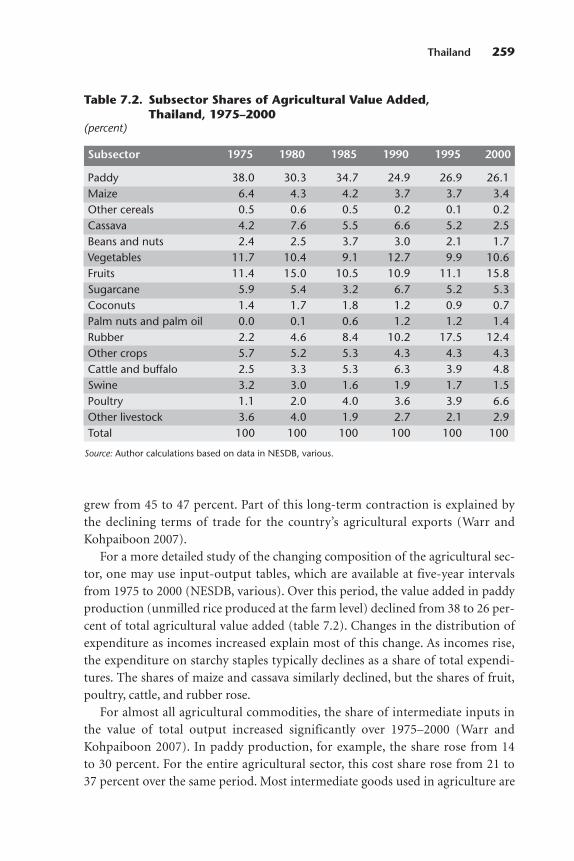

7.2 Subsector Shares of Agricultural Value Added, Thailand,1975–2000 259

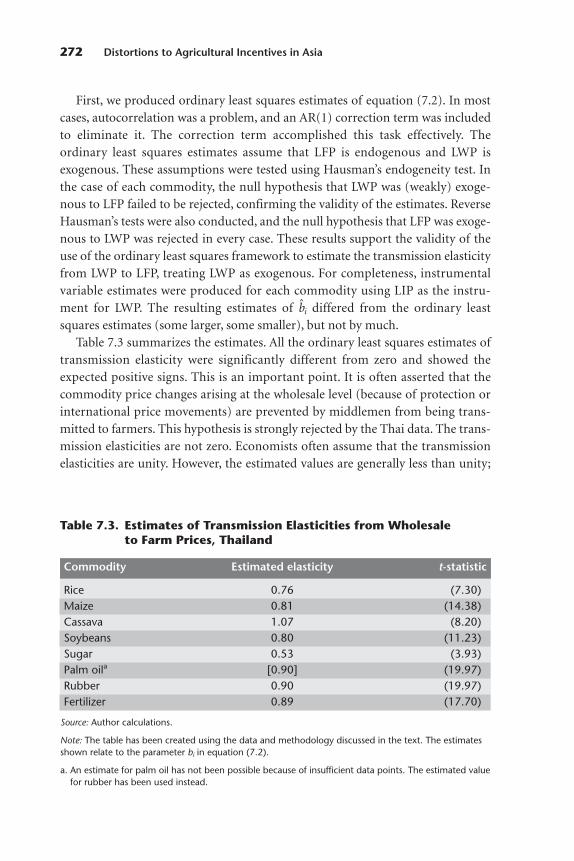

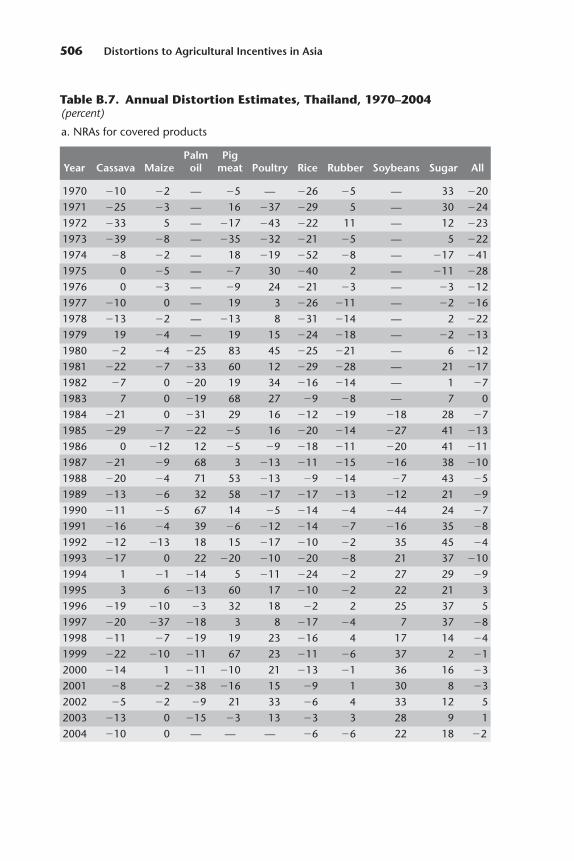

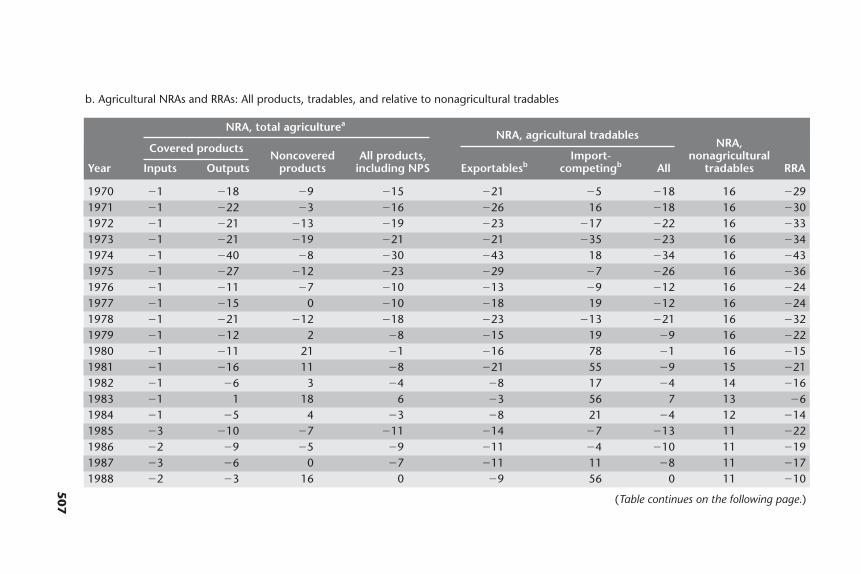

7.3 Estimates of Transmission Elasticities from Wholesale toFarm Prices, Thailand 272

7.4 NRAs for Covered Agricultural Products, Thailand, 1970–2004 2747.5 NRAs in Agriculture Relative to Nonagricultural Industries,

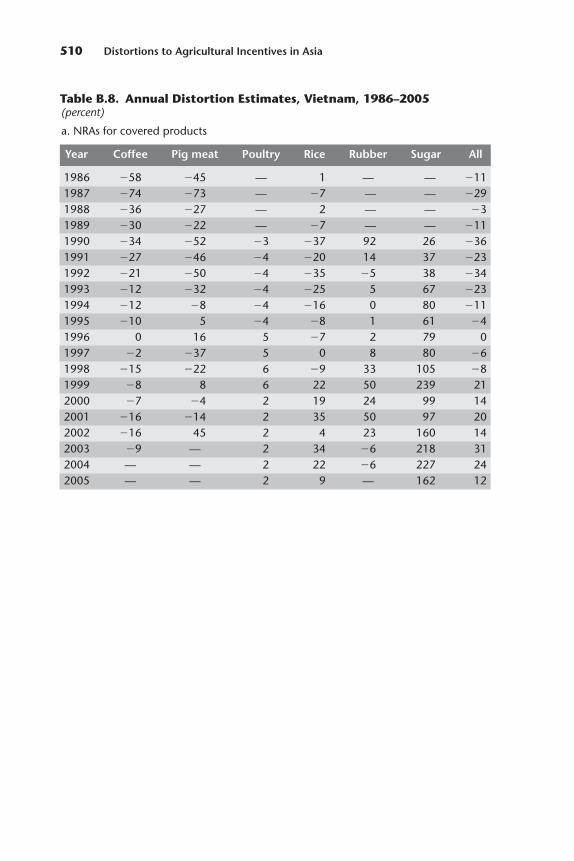

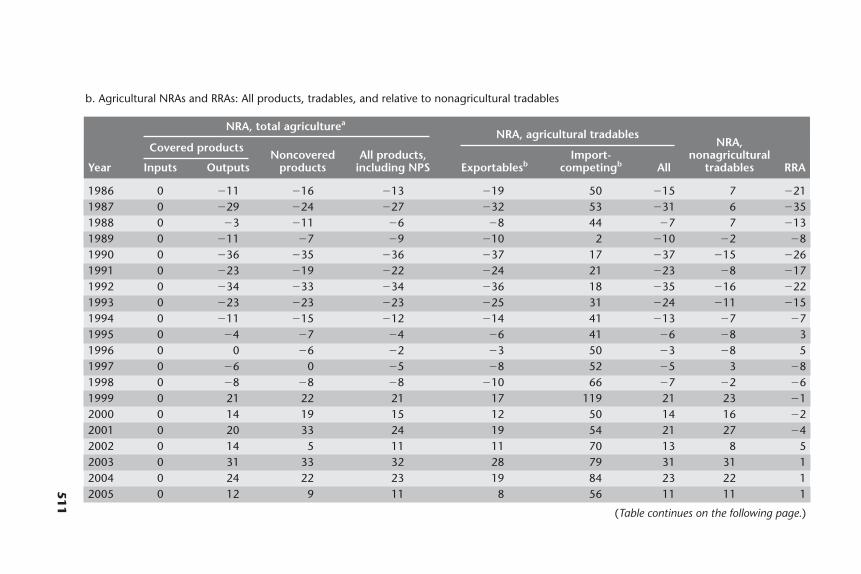

Thailand, 1970–2004 2768.1 Structure of the Agricultural Economy, Vietnam, 1986–2004 2858.2 Share of Planted Area by Crop, Vietnam, 1990–2004 2868.3 Composition of Agricultural Exports by Value, Vietnam,

1990–2004 2888.4 NRAs for Covered Agricultural Products, Vietnam, 1986–2004 2968.5 NRAs in Agriculture Relative to Nonagricultural Industries,

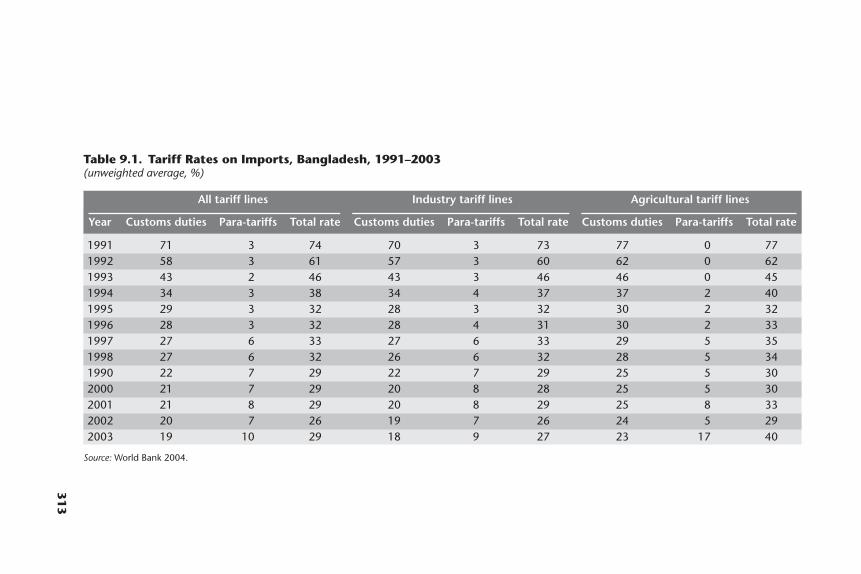

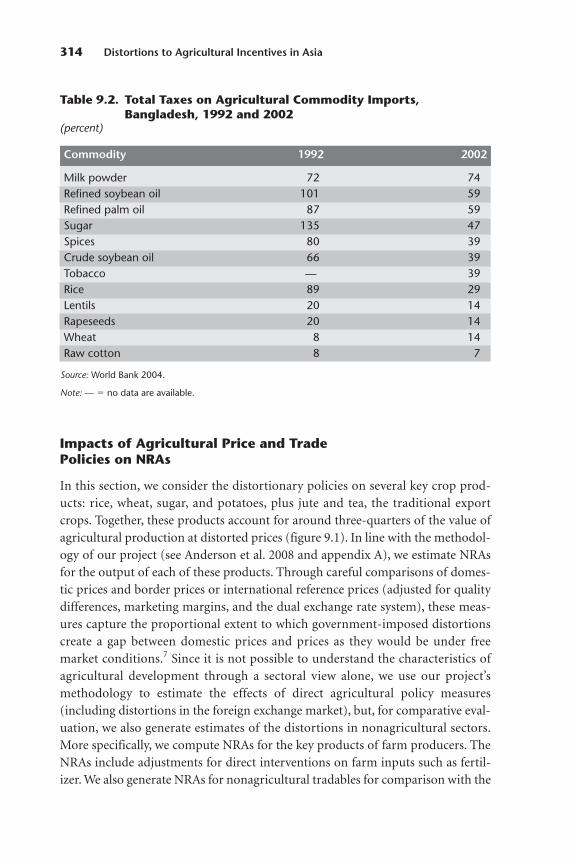

Vietnam, 1986–2004 2979.1 Tariff Rates on Imports, Bangladesh, 1991–2003 3139.2 Total Taxes on Agricultural Commodity Imports, Bangladesh,

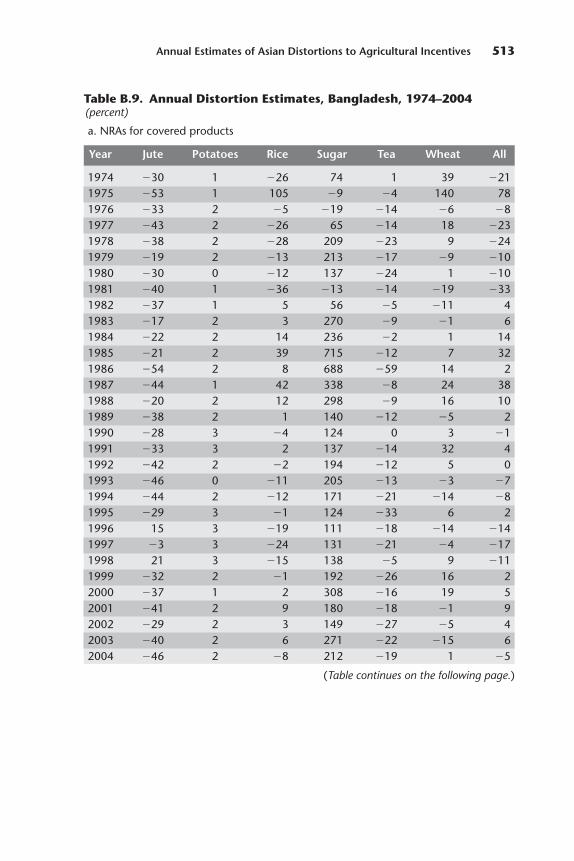

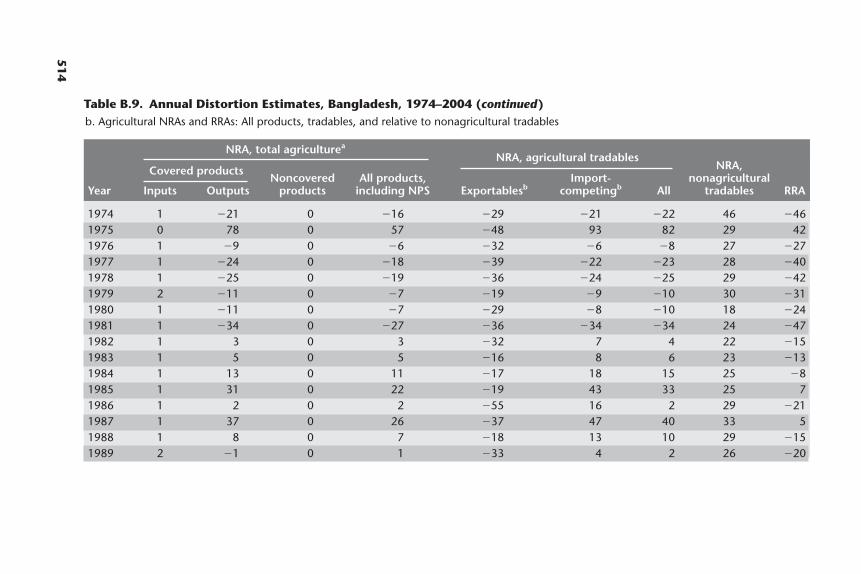

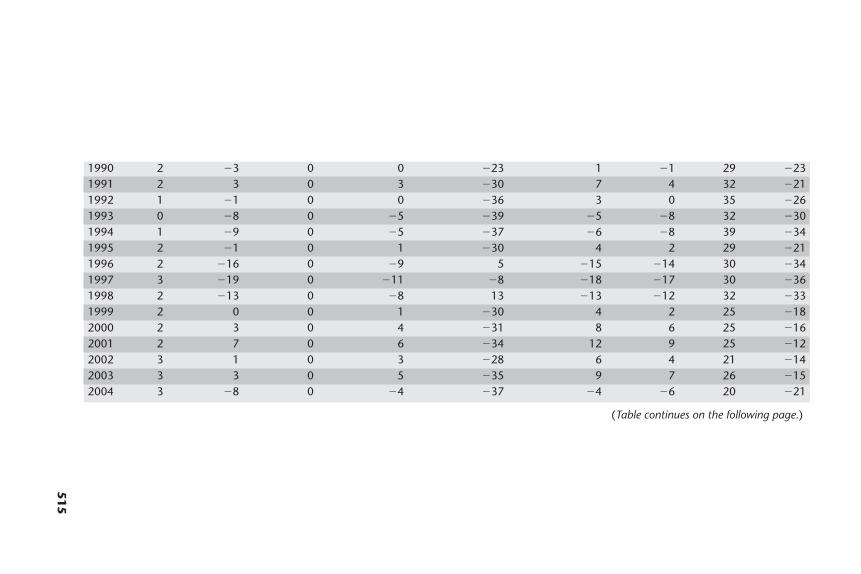

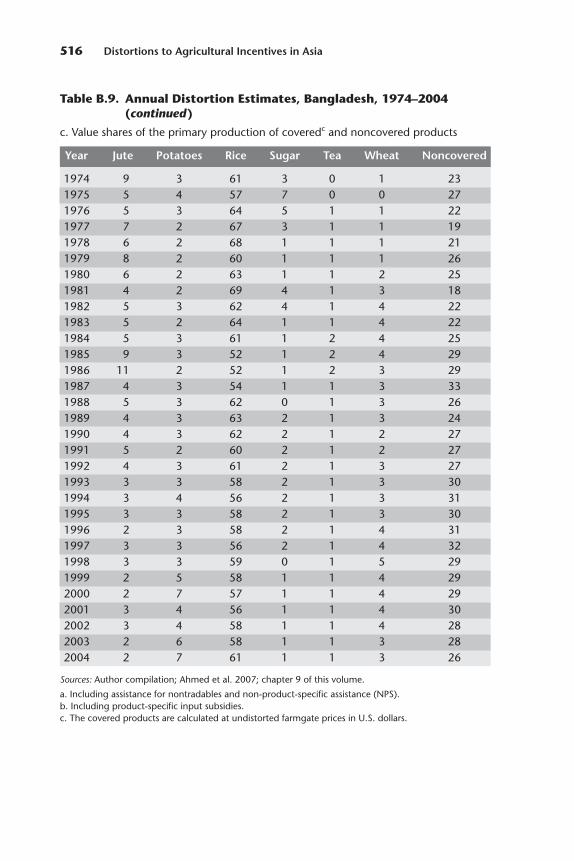

1992 and 2002 3149.3 Production and Imports, Rice and Wheat, Bangladesh, 1973–2004 3169.4 NRAs for Covered Agricultural Products, Bangladesh, 1974–2004 3219.5 NRAs in Agriculture Relative to Nonagricultural Industries,

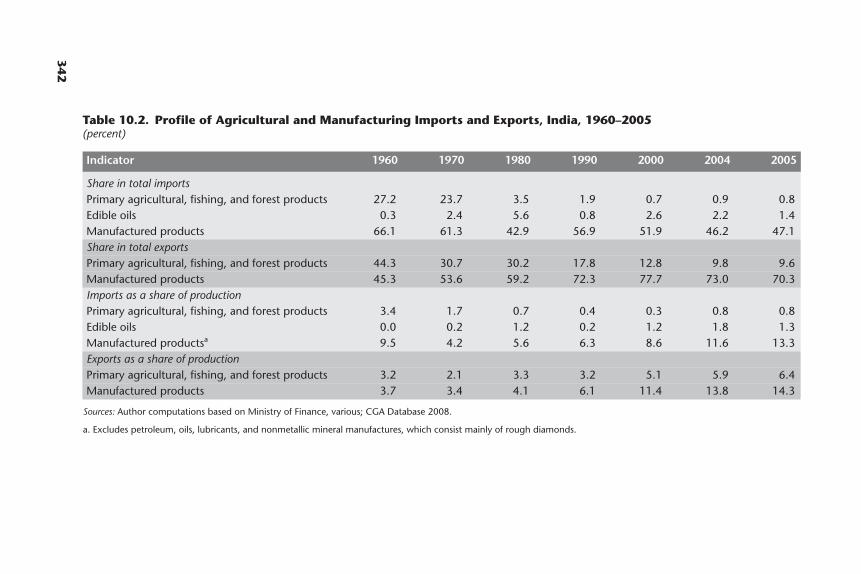

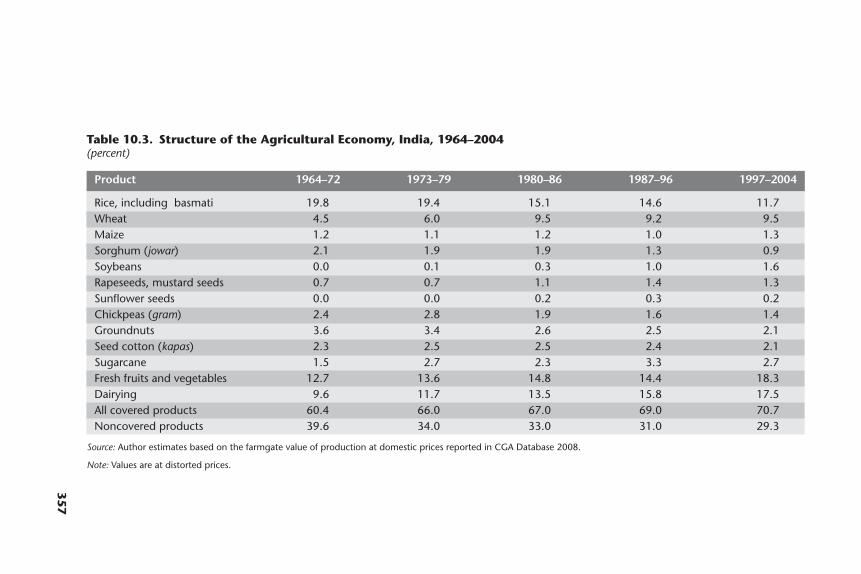

Bangladesh, 1974–2004 32710.1 Sectoral Share of GDP and Employment, India, 1950–2005 34110.2 Profile of Agricultural and Manufacturing Imports and Exports,

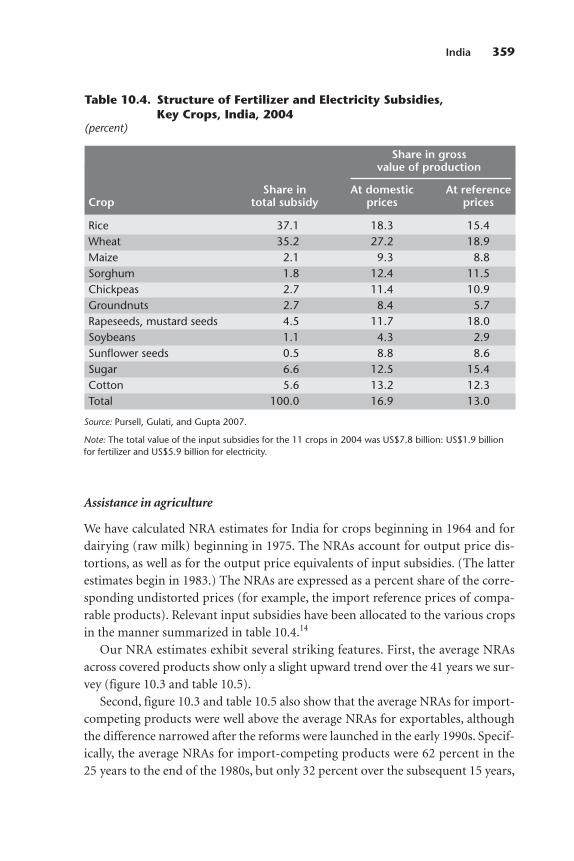

India, 1960–2005 34210.3 Structure of the Agricultural Economy, India, 1964–2004 35710.4 Structure of Fertilizer and Electricity Subsidies, Key Crops, India,

2004 359

xiv Contents

10.5 NRAs for Covered Agricultural Products, India, 1965–2004 36110.6 NRAs in Agriculture Relative to Nonagricultural Industries, India,

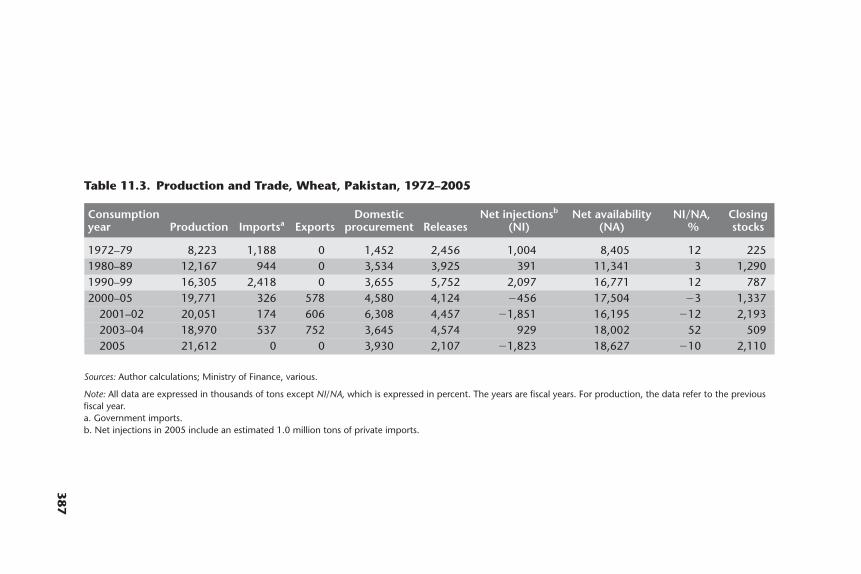

1965–2004 36210.7 Self-Sufficiency Ratios, Selected Food Products, India, 1961–2004 36511.1 Agriculture in the Economy, Pakistan, 1965–2004 38011.2 Structure of the Agricultural Economy, Major Crops, Pakistan,

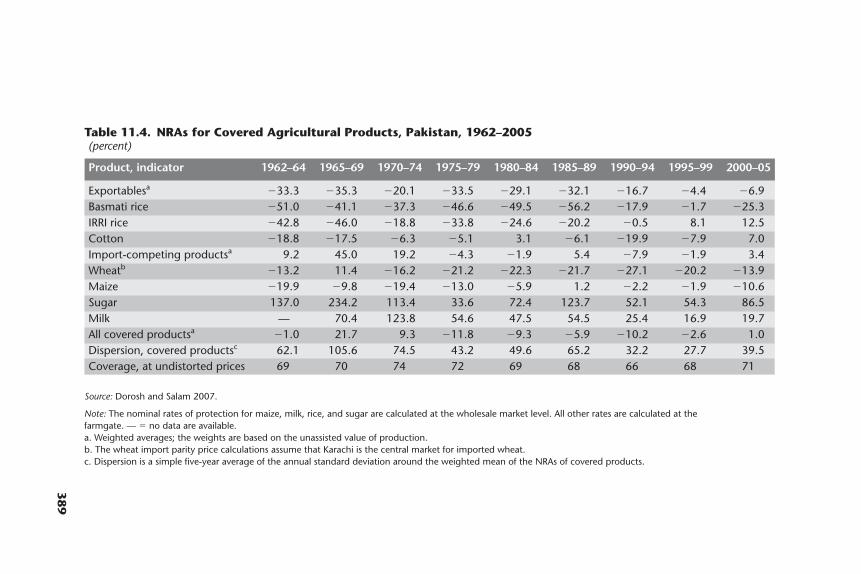

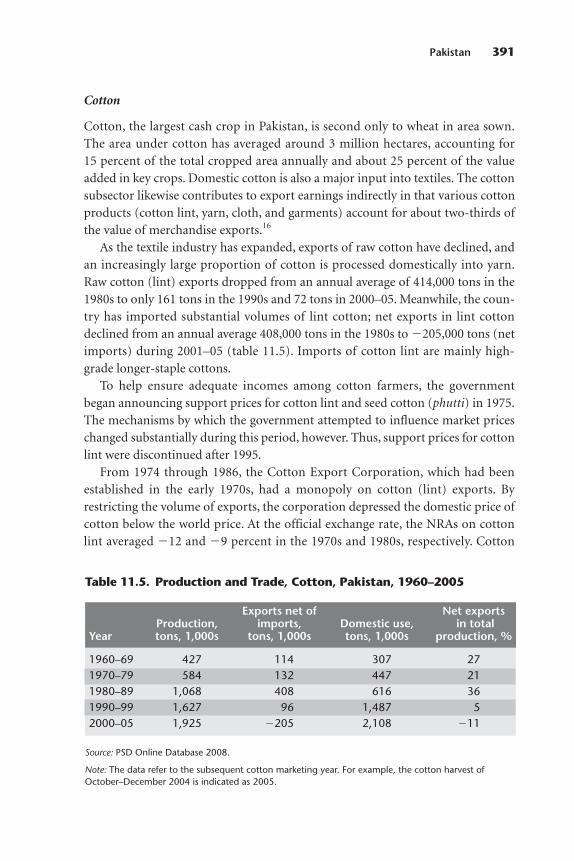

2004–06 38311.3 Production and Trade, Wheat, Pakistan, 1972–2005 38711.4 NRAs for Covered Agricultural Products, Pakistan, 1962–2005 38911.5 Production and Trade, Cotton, Pakistan, 1960–2005 39111.6 NRAs in Agriculture Relative to Nonagricultural Industries,

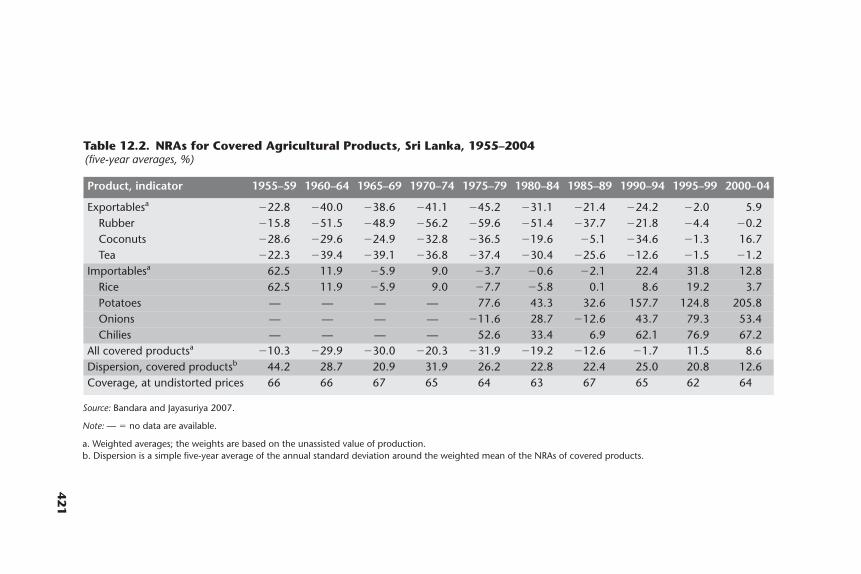

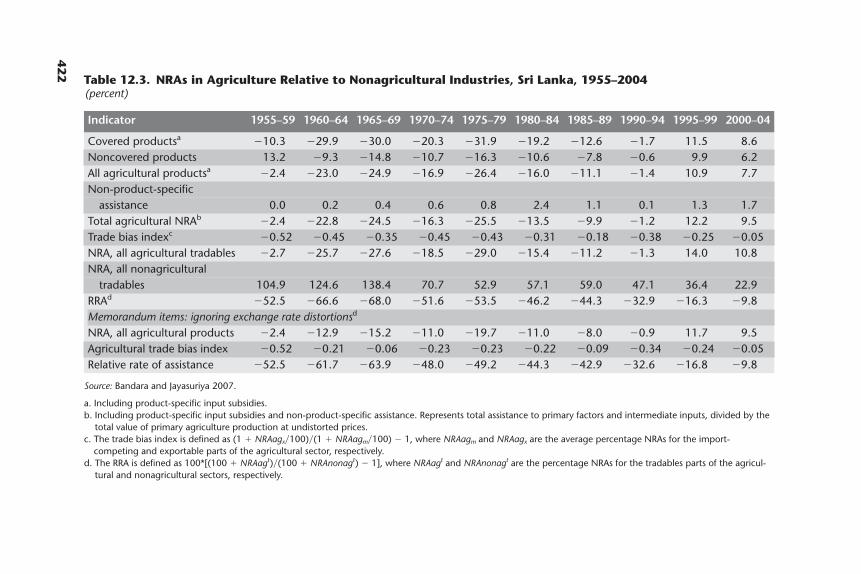

Pakistan, 1962–2005 40012.1 Agriculture in the Economy, Sri Lanka, 1950–2005 41312.2 NRAs for Covered Agricultural Products, Sri Lanka, 1955–2004 42112.3 NRAs in Agriculture Relative to Nonagricultural Industries,

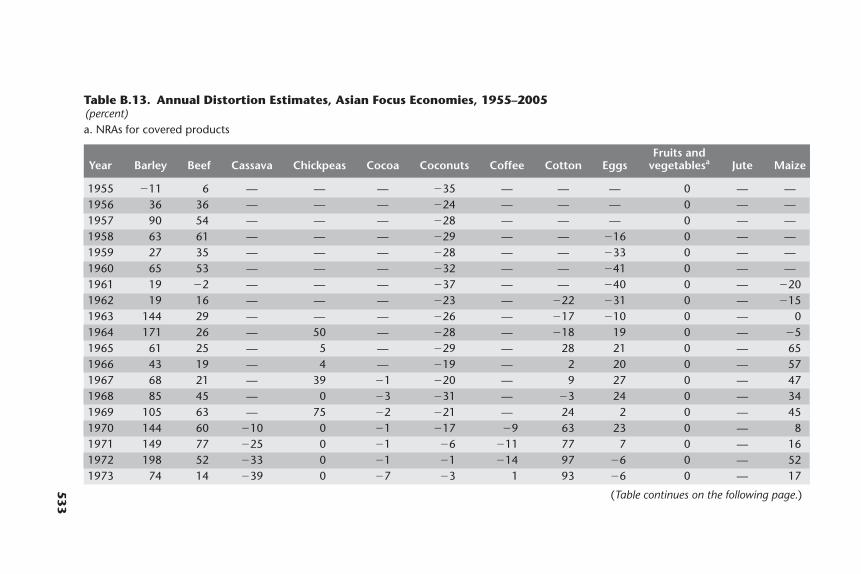

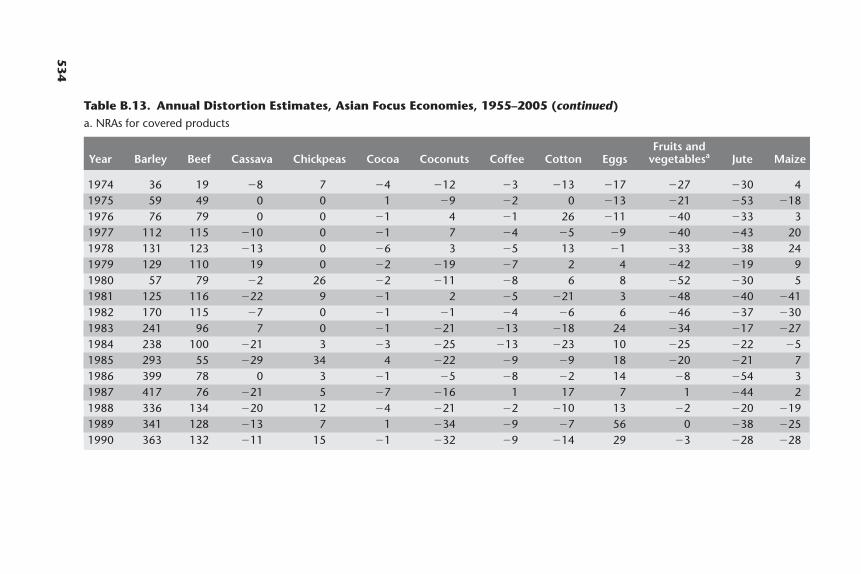

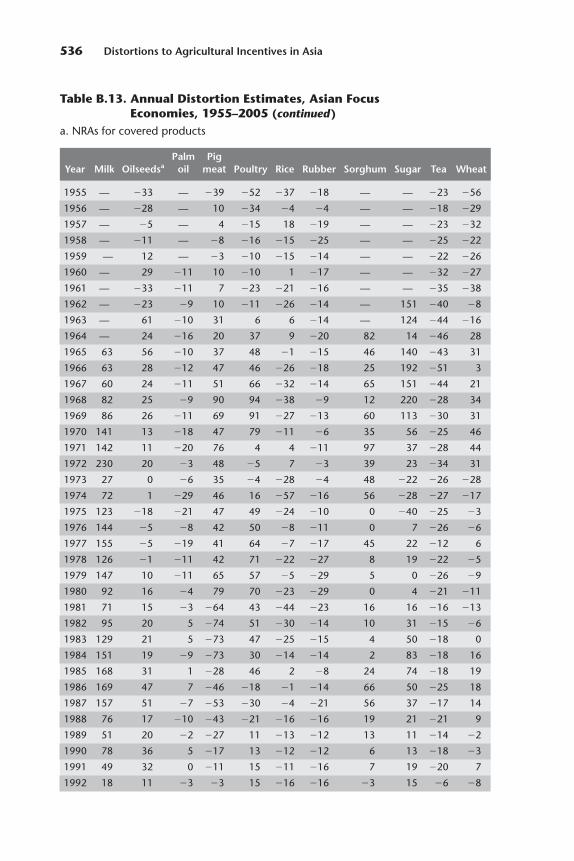

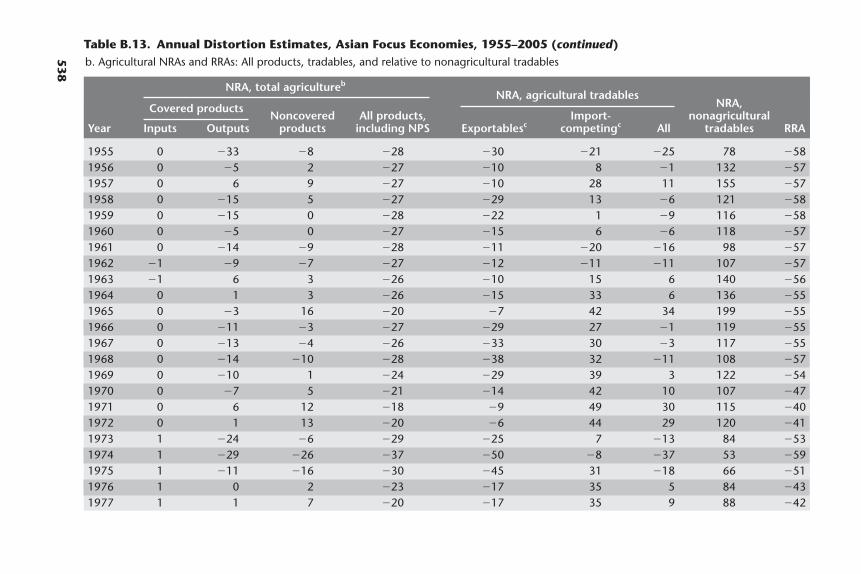

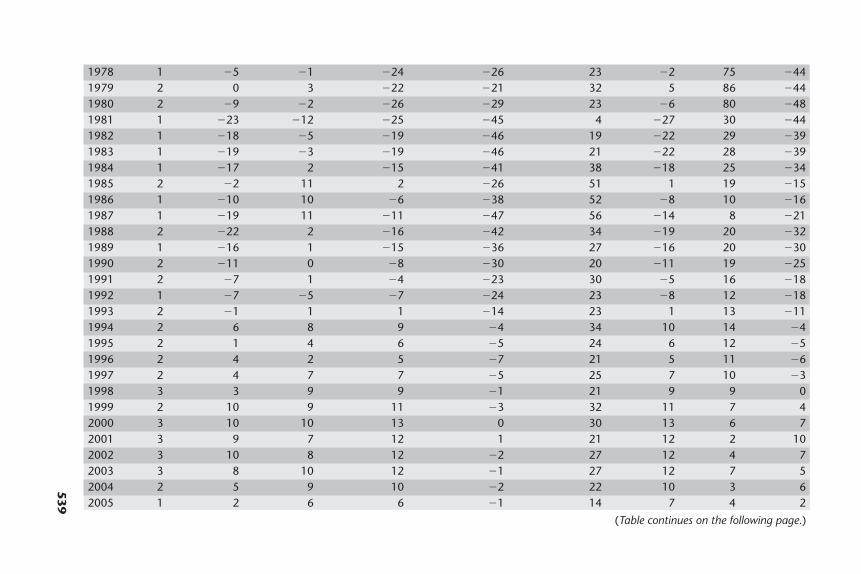

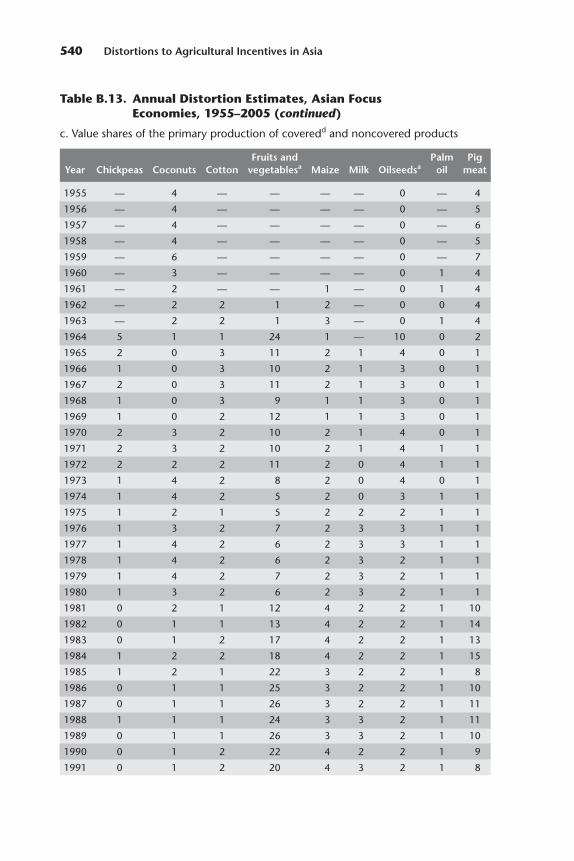

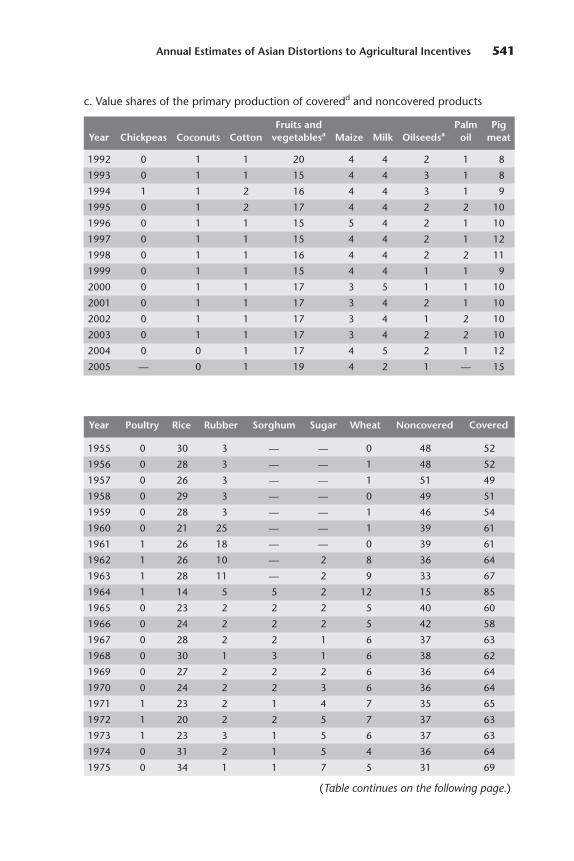

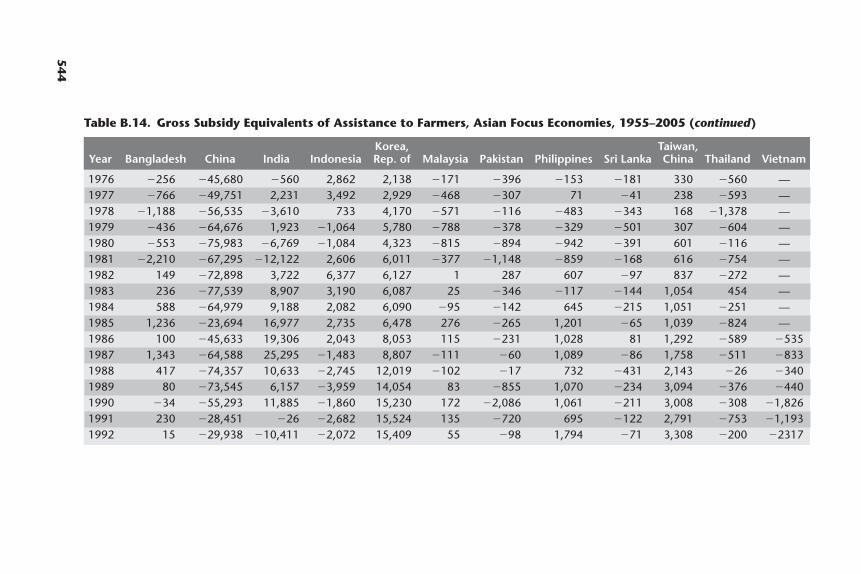

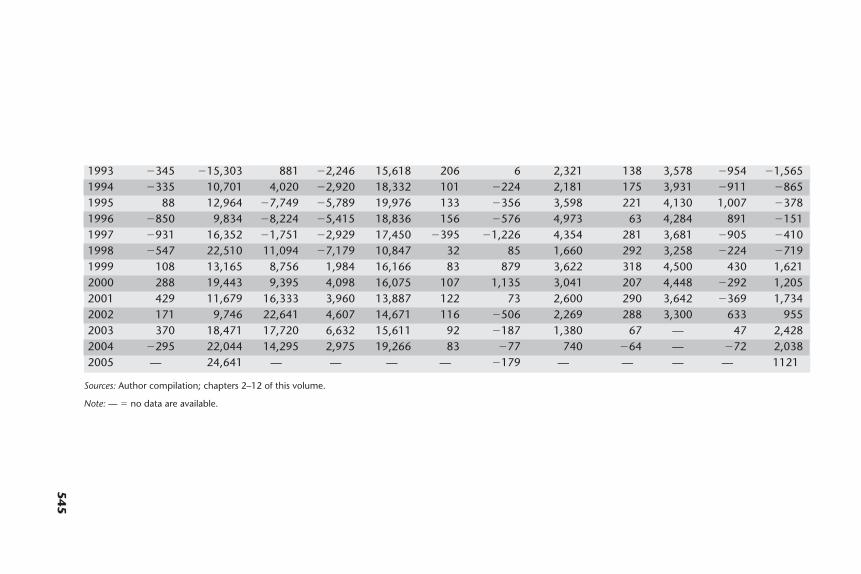

Sri Lanka, 1955–2004 422B.1 Annual Distortion Estimates, Republic of Korea, 1955–2004 475B.2 Annual Distortion Estimates, Taiwan, China, 1955–2002 481B.3 Annual Distortion Estimates, China, 1955–2005 487B.4 Annual Distortion Estimates, Indonesia, 1970–2004 490B.5 Annual Distortion Estimates, Malaysia, 1960–2004 496B.6 Annual Distortion Estimates, the Philippines, 1962–2004 502B.7 Annual Distortion Estimates, Thailand, 1970–2004 506B.8 Annual Distortion Estimates, Vietnam, 1986–2005 510B.9 Annual Distortion Estimates, Bangladesh, 1974–2004 513B.10 Annual Distortion Estimates, India, 1965–2004 517B.11 Annual Distortion Estimates, Pakistan, 1962–2005 523B.12 Annual Distortion Estimates, Sri Lanka, 1955–2004 527B.13 Annual Distortion Estimates, Asian Focus Economies, 1955–2005 533B.14 Gross Subsidy Equivalents of Assistance to Farmers, Asian Focus

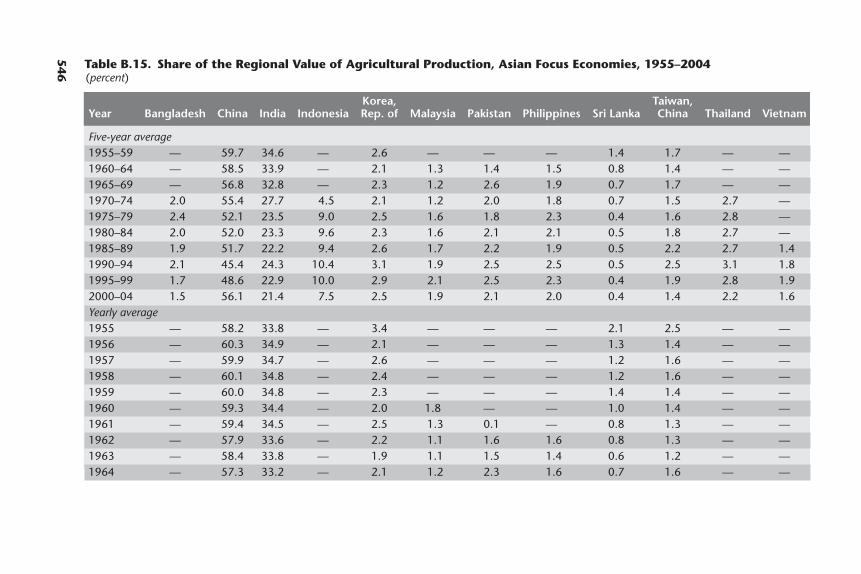

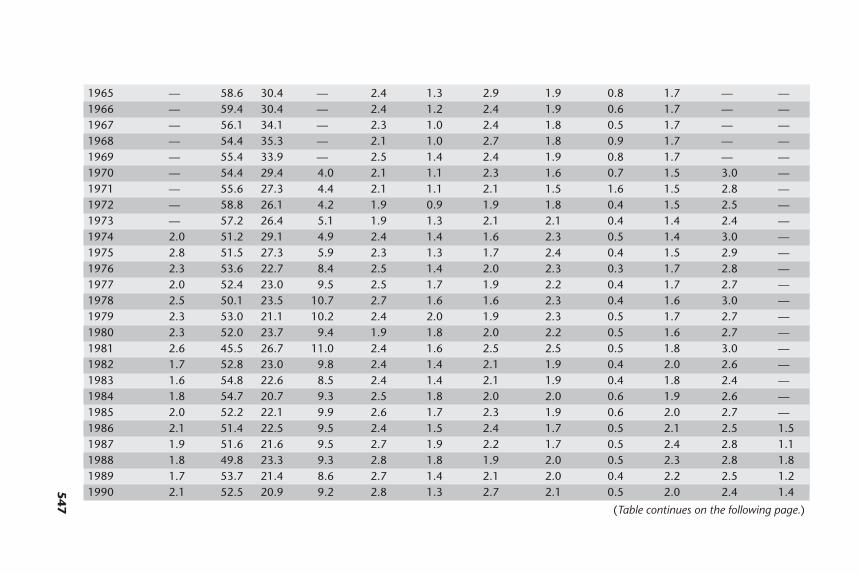

Economies, 1955–2005 543B.15 Share of the Regional Value of Agricultural Production,

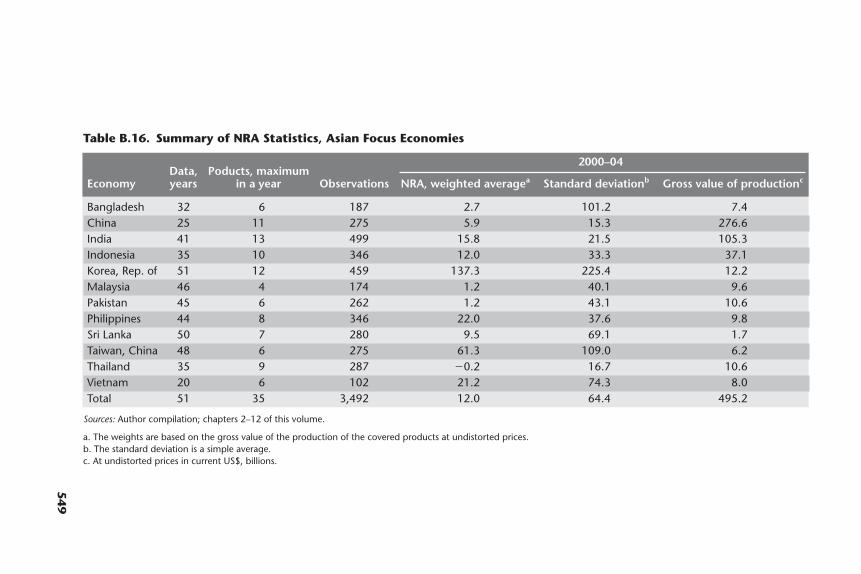

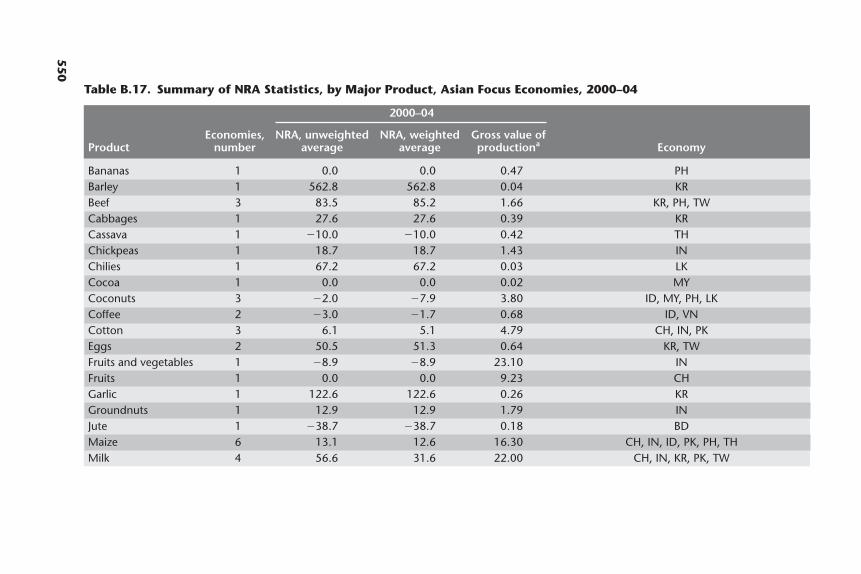

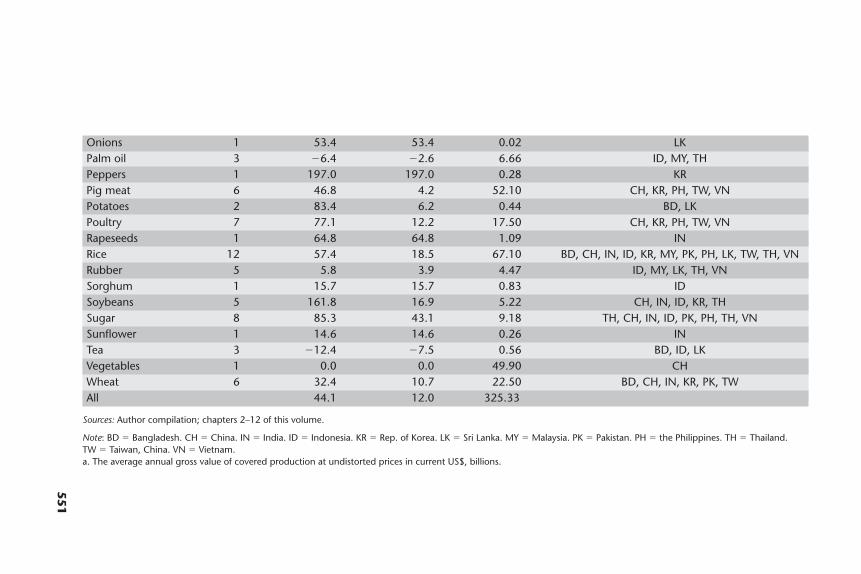

Asian Focus Economies, 1955–2004 546B.16 Summary of NRA Statistics, Asian Focus Economies 549B.17 Summary of NRA Statistics, by Major Product, Asian Focus

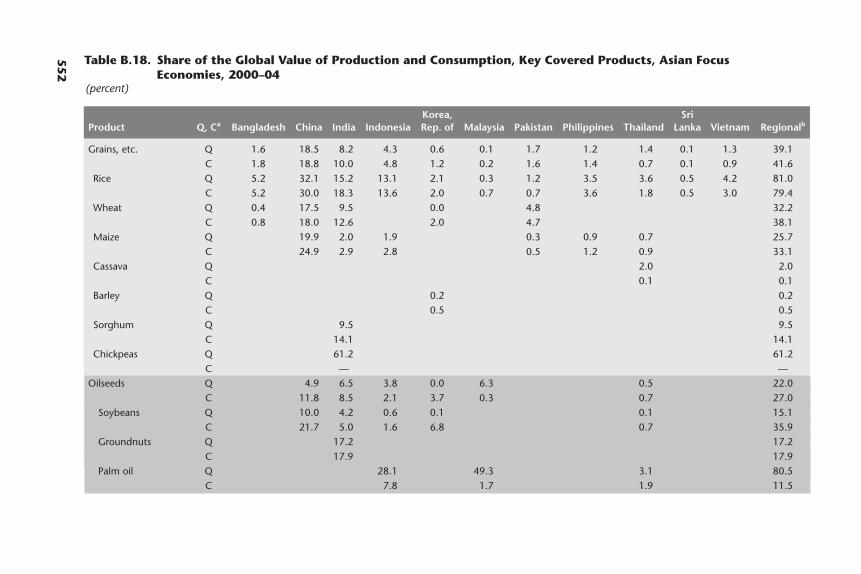

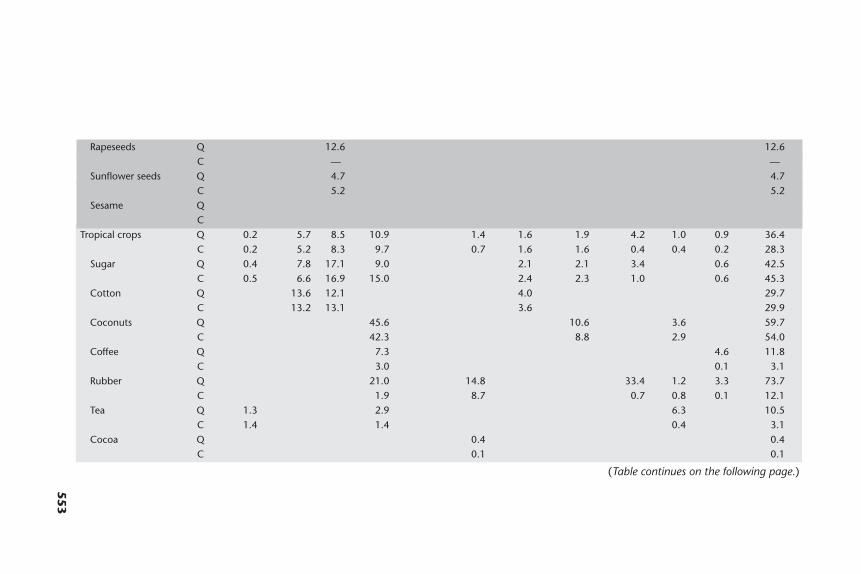

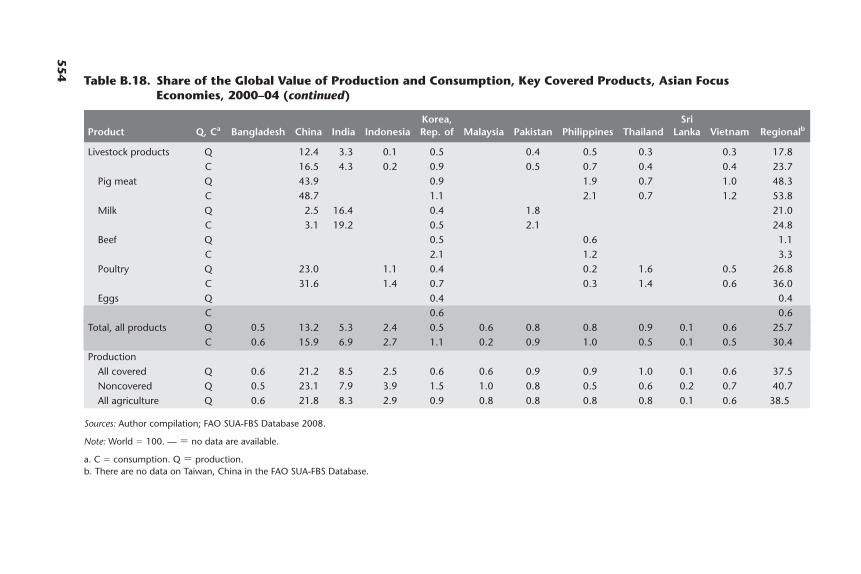

Economies, 2000–04 550B.18 Share of the Global Value of Production and Consumption,

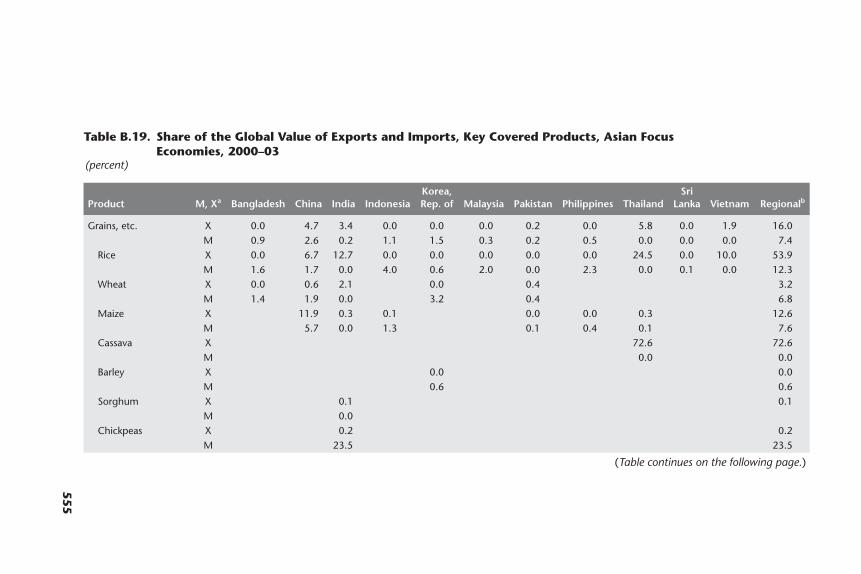

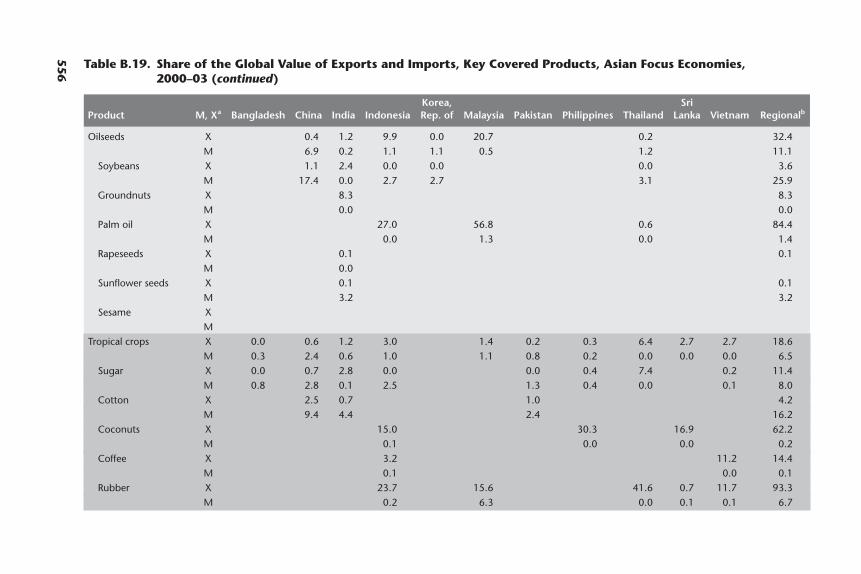

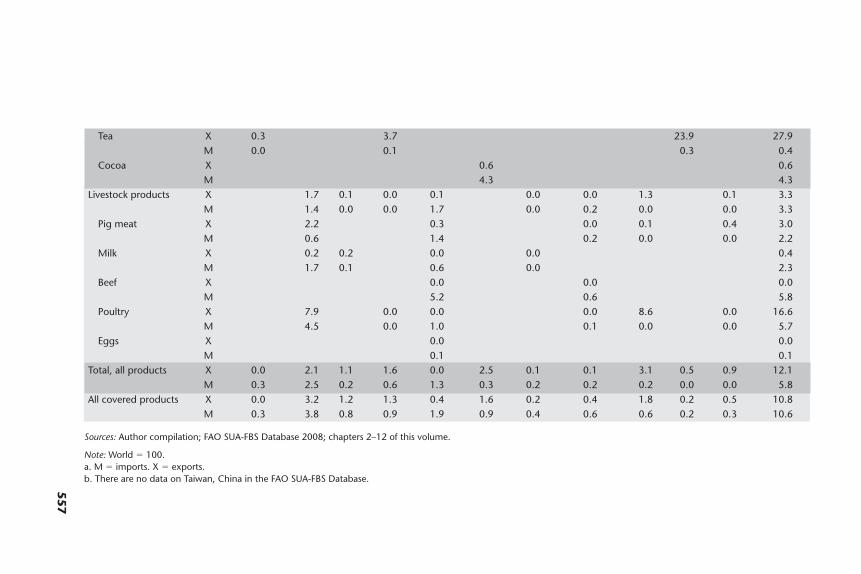

Key Covered Products, Asian Focus Economies, 2000–04 552B.19 Share of the Global Value of Exports and Imports, Key Covered

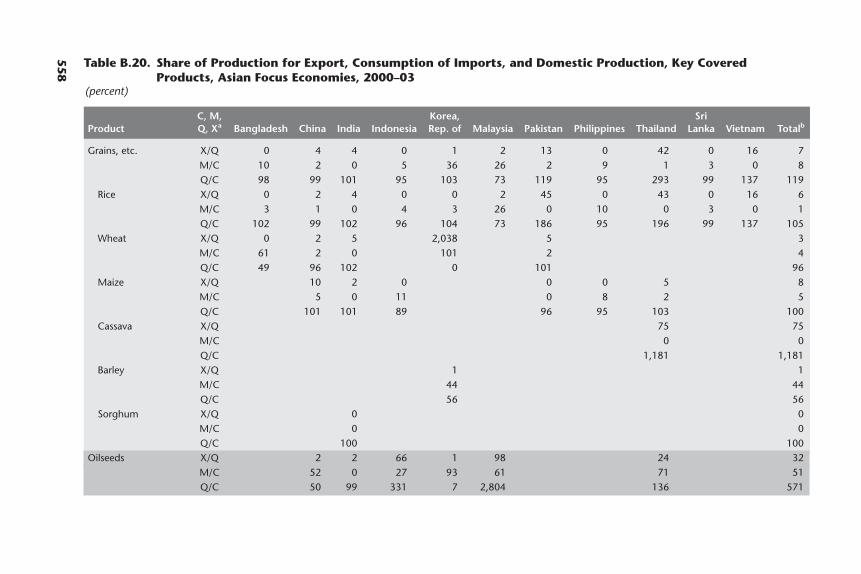

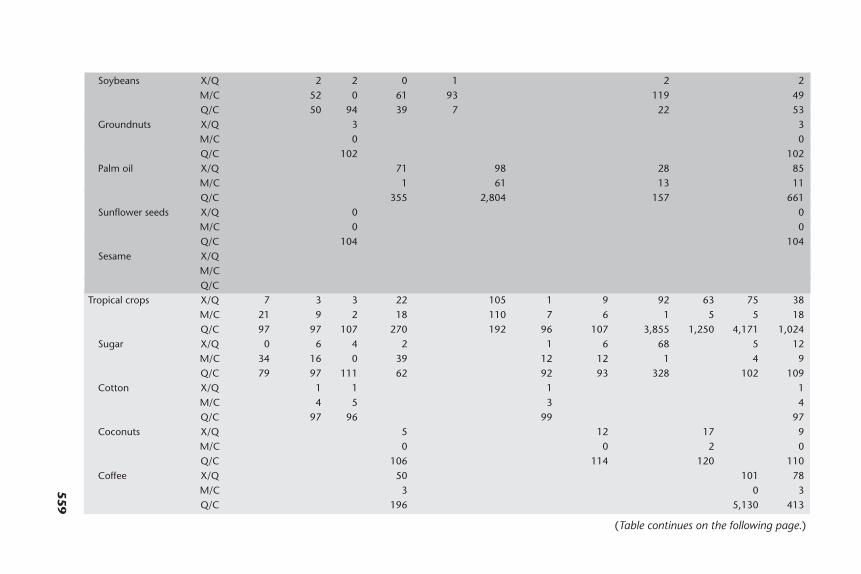

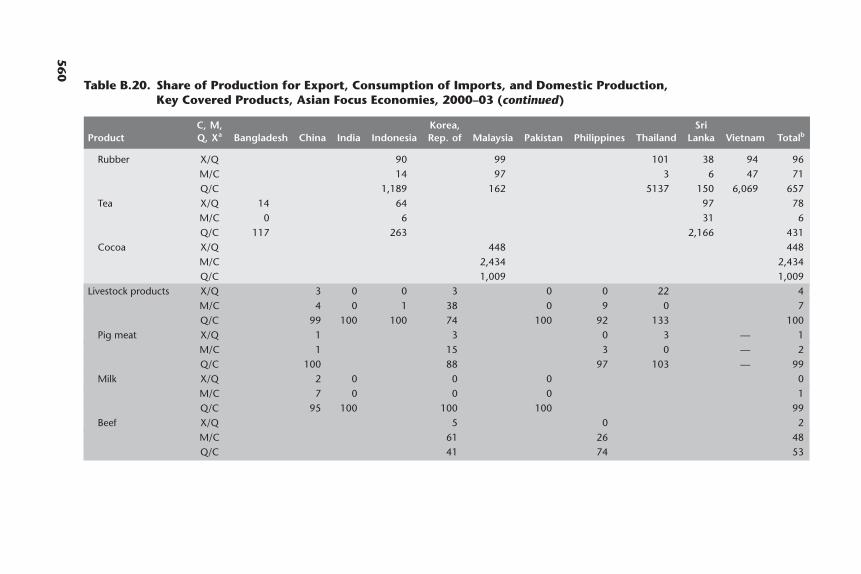

Products, Asian Focus Economies, 2000–03 555B.20 Share of Production for Export, Consumption of Imports, and

Domestic Production, Key Covered Products, Asian Focus Economies, 2000–03 558

Contents xv

Three-quarters of the world’s poorest households depend on farming for theirlivelihoods, and the majority live in Asia where 81 percent of the poor (morethan 900 million people earn less than US$1.25/day) are engaged directly or indi-rectly in agriculture. During the 1960s and 1970s, many developing countrieshad in place pro-urban and anti-agricultural policies, while many high-incomecountries restricted agricultural imports and subsidized their farmers. Althoughprogress has been made over the past two decades to reduce those policy biases,particularly the anti-agricultural bias in Asia, the extent of reform has not beensystematically quantified. Nor has it been clear how many trade- and welfare-reducing price distortions remain in Asian agriculture, both within and betweencountries, and whether later developing countries have followed Japan and theRepublic of Korea in replacing past anti-agricultural policies with not a neutralregime but a pro-agricultural set of policies—which could be just as wasteful ofnational resources.

To help fill this lacuna, the World Bank launched a major research project in2006 aimed at quantifying the changing extent of distortions to agricultural incen-tives over recent decades. This volume is one of a series of four regional books thatsummarizes the findings. By including all the large Asian economies as case studies,no less than 95 percent of Asian GDP and agricultural output is covered.

These estimates are used to help address questions such as the following:Where is there still a policy bias against agricultural production? To what extenthas there been overshooting in the sense that some developing-country farmersare now being protected from import competition? What are the political andeconomic forces behind the more successful reformers, and how do these forcescompare with those in less successful countries where major distortions in agri-cultural incentives remain? How important have domestic political forces been in

FOREWORD

xvii

bringing about reform, compared with international forces? What explains thecross-commodity pattern of distortions within the agricultural sector of eachcountry? What policy lessons and trade implications can be drawn from these dif-fering experiences with a view to ensuring better growth-enhancing and poverty-reducing outcomes in other still-distorted developing countries during theirreforms in the future?

In Asia more than anywhere else, the reforms have been truly transformational.The world’s most populous nations, China and India, have been among the mostambitious in raising incentives for farmers, albeit from a very low base in eachcase. Vietnam also has undertaken major and rapid reforms, while in other South-east Asian economies the reforms have been more gradual (or nonexistent in thecases of Myanmar and the Democratic People’s Republic of Korea, but they werenot able to be included as case studies because of lack of access to data). Mean-while, the Republic of Korea has moved from taxing agriculture relative to othertradable sectors in the 1950s to increasingly protecting it beginning in the 1970s.This development has raised concerns that other emerging economies may followsuit and pursue the same agricultural protection growth path of more-advancedeconomies.

The new empirical indicators summarized in these case studies provide astrong evidence-based foundation for assessing the successes and failures of poli-cies of the past and for evaluating policy options for the years ahead. The analyti-cal narratives reveal that the reforms to agricultural price and trade policies weresometimes undertaken unilaterally. In other cases, they were also partly inresponse to international pressures such as the Uruguay Round (for example, theRepublic of Korea), commitments required for accession to the World TradeOrganization (WTO) (for example, China), and structural adjustment loan con-ditionality by international financial institutions (for example, the Philippines inthe 1980s).

The study is timely because the WTO is in the midst of the Doha round of mul-tilateral trade negotiations, and agricultural policy reform is one of the most con-tentious issues in those talks. Hopefully China and South and Southeast Asiancountries will not make use of the legal wiggle room they have allowed themselvesin their WTO bindings and follow Japan and the Republic of Korea into high agri-cultural protection. It might be argued, on one hand, that a laissez-faire strategycould increase rural-urban inequality and poverty and thereby generate socialunrest. On the other hand, policies that lead to high prices for staple foods, in par-ticular, involve potentially serious risks for the urban and rural poor who are netbuyers of food in developing countries. Available evidence suggests that problemsof rural-urban poverty gaps have been alleviated in parts of Asia by some of themore-mobile members of farm households finding full- or part-time work off the

xviii Foreword

farm and repatriating part of their higher earnings back to those remaining infarm households. Efficient ways of assisting any left-behind groups of poor (non-farm as well as farm) households include public investment measures that havehigh social payoffs, such as in basic education and health and in rural infrastruc-ture, as well as in agricultural research and development. As argued in the WorldBank’s World Development Report 2008, the latter also provide more sustainableand more equitable ways of securing domestic food supplies than artificiallypropping up prices.

Justin Yifu LinSenior Vice President and Chief Economist

The World Bank

Foreword xix

ACKNOWLEDGMENTS

xxi

This book provides an overview of the evolution of the distortions to agriculturalincentives caused by price and trade policies in the World Bank–defined regionsof East Asia and South Asia. The volume includes an introduction and summarychapter and commissioned studies of three Northeast Asian, five Southeast Asian,and four South Asian economies. The chapters are followed by two appendixes.The first appendix describes the methodology we have used to measure the nom-inal and relative rates of assistance for farmers and the taxes and subsidies on foodconsumption. The second appendix provides summaries of our annual estimatesof these rates of assistance across the focus economies. Together, the 12 economieswe study account for no less than 95 percent of the region’s agricultural valueadded, farm households, total population, and total gross domestic product.

To the authors of the case studies, who are listed on the following pages, we areextremely grateful for the dedicated way in which they have delivered far morethan we could have reasonably expected. We are particularly grateful to YujiroHayami for his insights and advice during this project and his influential, relatedwork over several decades. Staff at the World Bank’s East Asia and Pacific Depart-ment and South Asia Department have provided generous and insightful adviceand assistance throughout the project. This has included participation in twoBank-wide seminars that provided helpful suggestions on the draft studies. Weoffer thanks likewise to the World Bank directors in the focus economies, whoexamined and cleared the working paper versions of each chapter. We have simi-larly benefited from the feedback provided by many participants at workshopsand conferences in which drafts have been presented over the past year or so.Johanna Croser, Francesca de Nicola, Esteban Jara, Marianne Kurzweil, Signe Nelgen, Damiano Sandri, and Ernesto Valenzuela have generously assisted in

compiling material for the opening overview chapter, and Johanna Croser andMarie Damania assisted in copyediting the case study chapters.

We wish to extend our thanks to the Organisation for Economic Co-operationand Development and the International Food Policy Research Institute for sharingmethodological insights, and also to the members of the project’s Senior AdvisoryBoard, who have provided sage advice and much encouragement throughout theplanning and implementation stages. The board is comprised of Yujiro Hayami,Bernard Hoekman, Anne Krueger, John Nash, Johan Swinnen, Stefan Tangermann,Alberto Valdés, Alan Winters, and, until his untimely death in 2008, Bruce Gardner.

Our thanks go also to the Development Research Group and to the Trust Fundsof the governments of Ireland, Japan, the Netherlands, and the United Kingdomfor financial assistance. This support has made it possible for this set of economiesto be included as part of a wider study that also encompasses more than 30 otherdeveloping countries, 18 economies in transition from central planning, and 20high-income countries. Three companion volumes examine case studies of otheremerging economies in a similar way and for a similar time period (back to themid-1950s or early 1960s, except for the transition economies). Also published bythe World Bank in 2008 or 2009, they cover Africa (coedited by Kym Andersonand Will Masters), Latin America (coedited by Kym Anderson and AlbertoValdés), and Europe’s transition economies (coedited by Kym Anderson andJohan Swinnen). A global overview volume edited by Kym Anderson will be pub-lished in 2009.

Kym Anderson and Will MartinNovember 2008

xxii Acknowledgments

Nazneen Ahmed is a research fellow at the Bangladesh Institute of DevelopmentStudies, Ministry of Planning in Dhaka, Bangladesh.

Kym Anderson is George Gollin Professor of Economics at the University of Adelaide and a fellow of the Center for Economic Policy Research, London. During2004–07, he was on an extended sabbatical as lead economist (trade policy) in theDevelopment Research Group of the World Bank in Washington, DC.

Prema-Chandra Athukorala is professor of economics in the Research School ofPacific and Asian Studies at the Australian National University in Canberra.

Arsenio M. Balisacan is professor of agricultural economics and director of theSoutheast Asian Regional Center for Graduate Study and Research in Agriculturein Los Baños, Laguna, the Philippines.

Zaid Bakht is research director at the Bangladesh Institute of Development Stud-ies, Ministry of Planning in Dhaka, Bangladesh.

Jayatilleke Bandara is associate professor of economics at Griffith University inBrisbane, Australia.

Johanna Croser has been a consultant with this project and is a PhD student in theDepartment of Economics of the University of British Columbia in Vancouver,Canada.

Cristina David is a senior research fellow at the Philippine Institute for Develop-ment Studies in Makati City, the Philippines.

xxiii

CONTRIBUTORS

Paul A. Dorosh is a senior rural development economist at the Agriculture andRural Development Department (South Asia Agriculture and Rural DevelopmentGroup) at the World Bank in Washington, DC.

George Fane is an adjunct professor of economics in the Research School of Pacificand Asian Studies, Australian National University in Canberra.

Ashok Gulati is the Asian Director for the International Food Policy ResearchInstitute in New Delhi. Previously, he headed the institute’s Markets, Trade, andInstitutions Division.

Kanupriya Gupta is a senior research analyst with the International Food PolicyResearch Institute in New Delhi.

Yujiro Hayami is chairman of the graduate faculty of the Foundation forAdvanced Studies on International Development. He is also visiting professor inthe National Graduate Institute of Policy Studies, Tokyo.

Masayoshi Honma is professor of agricultural and resource economics at the University of Tokyo. He is also a member of the Board of Trustees of the Interna-tional Food Policy Research Institute in Washington, DC.

Jikun Huang is director and professor, Center for Chinese Agricultural Policy, Chinese Academy of Sciences in Beijing.

Pham Lan Huong is a researcher with the Central Institute of Economic Manage-ment in Hanoi, Vietnam.

Ponciano Intal is professor and director, Angelo King Institute for Economic andBusiness Studies, De La Salle University in Manila.

Sisira Jayasuriya was director, Asian Economics Center and associate professor inthe Department of Economics, University of Melbourne at the time of the studyand is now professor of economics at La Trobe University (Bundoora) in Victoria,Australia.

Archanun Kohpaiboon is lecturer in the economics department of ThammasatUniversity in Bangkok.

Marianne Kurzweil is a young professional at the African Development Bank inTunis. During 2006–07, she was consultant with this project at the DevelopmentResearch Group at the World Bank in Washington, DC.

xxiv Contributors

Yu Liu is researcher at the Center for Chinese Agricultural Policy, Chinese Acad-emy of Sciences in Beijing.

Wai-Heng Loke is lecturer at the Department of Economics, Faculty of Economicsand Administration at the University of Malaya in Kuala Lumpur, Malaysia.

Will Martin is lead economist in the Development Research Group at the WorldBank in Washington, DC. He specializes in trade and agricultural policy issuesglobally, especially in Asia.

Signe Nelgen has been a consultant with this project and is a PhD student in theSchool of Economics of the University of Adelaide in Australia.

Garry Pursell is visiting fellow at the Australia South Asia Research Center, Australian National University in Canberra. Previously, he was with the SouthAsia Department of the World Bank.

Scott Rozelle holds the Helen Farnsworth Endowed Professorship and is senior fellow and professor at the Freeman Spogli Institute for International Studies atStanford University in Stanford, California.

Abdul Salam is professor of economics at the Federal Urdu University and is for-mer chairman of the Agricultural Prices Commission in Islamabad, Pakistan.

Damiano Sandri is a PhD candidate in economics at Johns Hopkins University inBaltimore, Maryland. During 2006–07, he was a consultant with this project at theDevelopment Research Group at the World Bank in Washington, DC.

Quazi Shahabuddin is director general of the Bangladesh Institute of Develop-ment Studies, Ministry of Planning in Dhaka, Bangladesh.

Vo Tri Thanh is a researcher with the Central Institute of Economic Managementin Hanoi, Vietnam.

Ernesto Valenzuela is lecturer in economics and research fellow at the University ofAdelaide in Australia. During 2005–07, he was consultant at the DevelopmentResearch Group of the World Bank in Washington, DC.

Peter Warr is the John Crawford Professor of Agricultural Economics and found-ing Director of the Poverty Research Centre in the Division of Economics,Research School of Pacific and Asian Studies at the Australian National Universityin Canberra.

Contributors xxv

CTE consumer tax equivalentGDP gross domestic productGVA gross value addedIMF International Monetary FundNRA nominal rate of assistanceNRP nominal rate of protectionNTB nontariff barrierOECD Organisation for Economic Co-operation and DevelopmentRRA relative rate of assistanceTBI trade bias indexWTO World Trade Organization

Note: All dollar amounts are U.S. dollars (US$) unless otherwise indicated.

xxvii

ABBREVIATIONS

PHILIPPINES

CHINA

TAIWAN,CHINA

REP. OFKOREA

MALAYSIA

VIETNAMTHAILAND

INDIA

SRILANKA

PAKISTAN

BANGLADESH

INDONESIA

IBRD 36674DECEMBER 2008

This map was produced by the Map Design Unit of The World Bank. The boundaries, colors, denominations and any other informationshown on this map do not imply, on the part of The World BankGroup, any judgment on the legal status of any territory, or anyendorsement or acceptance of such boundaries.

0 500 1000 Kilometers

0 500 1000 Miles

The Focus Economies of Asia

Part III

INTRODUCTION

Farm earnings in developing countries have often been depressed by a pro-urban,antiagricultural bias in government policies. Progress has been made since the1980s in reducing the policy bias in many countries, however. In some cases, thechanges have been modest and intermittent, but, in China and, to a lesser extent,India, they have been transformational. Many trade-reducing price distortionsnonetheless remain within the agricultural sector in low- and middle-incomeeconomies, including in Asia. This is important for the majority of households inthe world because 45 percent of the global workforce is employed in agriculture,and 75 percent of the world’s poorest households depend directly or indirectly onfarming for livelihoods. It is even more important in Asia’s developing economies,where 60 percent of the workforce and 81 percent of the poor (625 million peopleeach earning less than US$1 a day) are engaged in agriculture (World Bank 2007;Chen and Ravallion 2007).

This study is part of a global research project seeking to understand the chang-ing scope and impact of the policy bias against agriculture and the reasons behindagricultural policy reforms in Africa, Europe’s transition economies, Latin Amer-ica and the Caribbean, and Asia.1 One purpose of the project is to obtain quanti-tative indicators of the effects of recent policy interventions. A second objective isto gain a deeper understanding of the political economy of trends in the distor-tions in agricultural incentives in various national settings. The third goal is to usethis deeper understanding to explore the prospects for reducing the distortions inagricultural incentives and discover the likely implications for agricultural com-petitiveness, equality, and poverty reduction in many countries, large and small.

3

1

INTRODUCTIONAND SUMMARY

Kym Anderson and Will Martin

The compilation of new annual time series estimates of the protection and tax-ation of farmers over the past half century is a core component of the first stage ofour research project. These estimates are used to help address questions such asthe following: Where is the policy bias against agricultural production? To whatextent has there been overshooting in that some food producers are now beingprotected from import competition in developing countries in much the sameway they were protected in Europe and Japan during earlier periods of industrial-ization? What are the political economy forces behind successful reforms in somecountries? How do they compare with the forces in other countries where reformsare less successful and major distortions in agricultural incentives remain? Overthe past two decades, how important have domestic political forces been in gener-ating reform relative to forces operating in earlier decades or international forces,such as loan conditionality, rounds of multilateral trade negotiations in the WorldTrade Organization (WTO), regional integration agreements, accession to theWTO, and the globalization of supermarkets and other firms along the valuechain? What has caused the patterns of distortion within the agricultural sectorsof individual countries? What policy lessons and trade implications may be drawnfrom these differing experiences so that we may seek to ensure growth-enhancingand poverty-reducing outcomes, including less overshooting and fewer protec-tionist regimes, during future reforms in still-distorted developing economies inAsia and elsewhere?

Our study is timely for at least four reasons. First, the WTO is in the midst of theDoha Round of multilateral trade negotiations, and agricultural policy reform isone of the most contentious issues in these talks. Second, countries are also seekingto position themselves favorably in preferential trade negotiations in the wake ofother forces in globalization, including revolutions in information, communica-tions, agricultural biotechnology, and supermarketing. Third, poorer countries andtheir development partners are striving to achieve the United Nations MillenniumDevelopment Goals by 2015, including the prime goals of alleviating hunger andreducing poverty. Fourth, the outputs of our study are timely also because worldfood prices spiked at high levels in 2008, and governments in some developingcountries, in their panic to deal with the inevitable protests from consumers, havereacted in ways that are not optimal. Spikes have occurred in the past, most notablyin 1973–74, and lessons on appropriate policy responses may be drawn from theexperiences then. The empirical estimates reported in our study reveal that govern-ments in Asia have differed in their responses to such shocks, although this is lessthe case of rice, the region’s main staple.

This study on Asia is based on a sample of 12 developing economies. Weexclude Japan, which has been a high-income country throughout our reviewperiod and, so, is analyzed separately as part of the high-income group in the

4 Distortions to Agricultural Incentives in Asia

project’s global overview volume. In Northeast Asia, we include China,the Republic of Korea (hereafter referred to as Korea), and Taiwan, China. InSoutheast Asia, we include the five large economies of Indonesia, Malaysia, thePhilippines, Thailand, and Vietnam, and, in South Asia, we include the fourlargest economies: Bangladesh, India, Pakistan, and Sri Lanka. In 2000–04, theseeconomies (all of them now WTO members) accounted for more than 95 per-cent of Asia’s agricultural value added, total farm households, total population,and total gross domestic product (GDP).2 The distortion estimates are providedfor as many years as data permit over the past five decades (an average of42 years), and they are presented for an average of eight crop and livestock prod-ucts per economy, which, in aggregate, amounts to about 70 percent of the grossvalue of agricultural production in each of these economies. The time series andcountry coverage in our study greatly exceed the data and country coverage of ear-lier studies, including Anderson and Hayami (1986); Krueger, Schiff, and Valdés(1991); Orden et al. (2007); and the Organisation for Economic Co-operationand Development (OECD 2007). The product coverage is broader in each of ourcase studies than in all earlier case studies other than the study by the OECD(2007).3

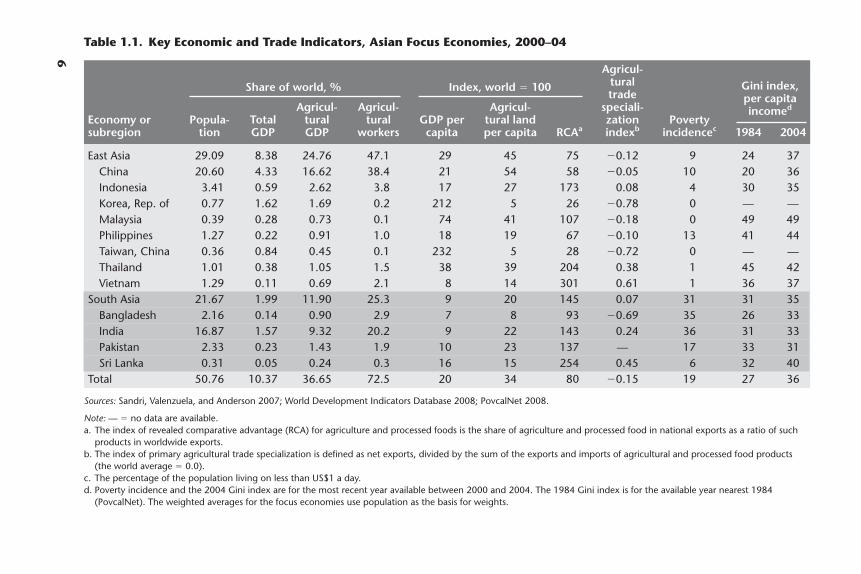

The key characteristics of these economies—accounting in 2000–04 for only10 percent of worldwide GDP, but 37 percent of global agricultural value added,51 percent of the world’s population, and 73 percent of the world’s farmers—areshown in table 1.1. The table reveals the considerable diversity within the regionin development, relative resource endowments, comparative advantage, trade spe-cialization, and the incidence of poverty and income inequality. These economiesthus provide a rich sample for comparative study.

Per capita incomes in Bangladesh, India, and Vietnam are barely 8 percentof the world average. In Indonesia, the Philippines, and Sri Lanka, they arearound 16 percent. In China, they are over 25 percent. In Thailand, they aremore than 30 percent. In Malaysia, they are about 75 percent of the world aver-age. Korea and Taiwan, China appear exceptional in that average per capitaincomes are currently twice the global average; however, in the 1950s, at thestart of the period of our study, these two economies were among the poorest inthe world.

Korea and Taiwan, China are also exceptional in the per capita endowment ofagricultural land; they have only around 5 percent of the world average endow-ment ratio. Bangladesh has a little more, followed by Sri Lanka and the Philip-pines. Even India, Indonesia, and Pakistan have only about 25 percent of theglobal average endowment, while Malaysia and Thailand have about 40 percent,and China, over 50 percent.4 Thus, these Asian economies are not relatively wellendowed with cropland or pastureland; on a per capita basis, the region has only

Introduction and Summary 5

6

Table 1.1. Key Economic and Trade Indicators, Asian Focus Economies, 2000–04

Sources: Sandri, Valenzuela, and Anderson 2007; World Development Indicators Database 2008; PovcalNet 2008.

Note: — � no data are available.a. The index of revealed comparative advantage (RCA) for agriculture and processed foods is the share of agriculture and processed food in national exports as a ratio of such

products in worldwide exports.b. The index of primary agricultural trade specialization is defined as net exports, divided by the sum of the exports and imports of agricultural and processed food products

(the world average � 0.0).c. The percentage of the population living on less than US$1 a day.d. Poverty incidence and the 2004 Gini index are for the most recent year available between 2000 and 2004. The 1984 Gini index is for the available year nearest 1984

(PovcalNet). The weighted averages for the focus economies use population as the basis for weights.

Agricul-

Share of world, % Index, world � 100 tural Gini index,trade per capita

Agricul- Agricul- Agricul- speciali- incomed

Economy or Popula- Total tural tural GDP per tural land zation Povertysubregion tion GDP GDP workers capita per capita RCAa indexb incidencec 1984 2004

East Asia 29.09 8.38 24.76 47.1 29 45 75 �0.12 9 24 37China 20.60 4.33 16.62 38.4 21 54 58 �0.05 10 20 36Indonesia 3.41 0.59 2.62 3.8 17 27 173 0.08 4 30 35Korea, Rep. of 0.77 1.62 1.69 0.2 212 5 26 �0.78 0 — —Malaysia 0.39 0.28 0.73 0.1 74 41 107 �0.18 0 49 49Philippines 1.27 0.22 0.91 1.0 18 19 67 �0.10 13 41 44Taiwan, China 0.36 0.84 0.45 0.1 232 5 28 �0.72 0 — —Thailand 1.01 0.38 1.05 1.5 38 39 204 0.38 1 45 42Vietnam 1.29 0.11 0.69 2.1 8 14 301 0.61 1 36 37

South Asia 21.67 1.99 11.90 25.3 9 20 145 0.07 31 31 35Bangladesh 2.16 0.14 0.90 2.9 7 8 93 �0.69 35 26 33India 16.87 1.57 9.32 20.2 9 22 143 0.24 36 31 33Pakistan 2.33 0.23 1.43 1.9 10 23 137 — 17 33 31Sri Lanka 0.31 0.05 0.24 0.3 16 15 254 0.45 6 32 40

Total 50.76 10.37 36.65 72.5 20 34 80 �0.15 19 27 36

34 percent of the global average. This might suggest that the comparative advan-tage of the Asian economies in agricultural goods is low, were it not for the varia-tions in these economies in the level of industrial development, the quality of landand water, and the related institutional arrangements and entitlements. As aresult, the strengths of these economies in agricultural competitiveness arediverse. The differences are reflected in the index of revealed comparative advan-tage and the agricultural trade specialization index (table 1.1). A majority of ourfocus economies have an index of revealed comparative advantage well above 100,indicating the extent to which the share of agricultural and food products in aneconomy’s merchandise trade exceeds the global average share of these products.For Korea and Taiwan, China, the index is below 30, and, for China and the Philip-pines, it is around 60. The index of agricultural trade specialization measures netexports as a ratio of exports, plus imports of farm products, and, so, it is boundedbetween �1 and �1. It is positive for half of our focus economies, but is �0.7 forBangladesh, Korea, and Taiwan, China.

Income inequality has risen slightly over the past two decades, but is still lowthroughout much of the region relative to the rest of the world. In 2004, the Ginicoefficient was between 0.40 and 0.49 in Malaysia, the Philippines, Sri Lanka, andThailand and averaged between 0.31 and 0.37 in the rest of the region. The regionalaverage of 0.36 contrasts with, for example, the average of 0.52 in Latin America.Likewise, the Gini coefficient for land distribution is relatively low in Asia, at only0.41 for China and Pakistan and below 0.50 also in Bangladesh; Indonesia; Korea;Taiwan, China; and Thailand. Even in India, the coefficient for land distribution isonly 0.58, and it is 0.50 in Vietnam. However, these coefficients imply that the distri-bution of land is more equal in Asia than it is in Latin America, where the Gini coef-ficient for land distribution is above 0.70 for major countries such as Argentina andBrazil and possibly for the region as a whole (World Bank 2007). A significant pro-portion of the rural population is landless in South Asia, however; so 31 percent ofthe population of South Asia was still living on less than US$1 a day in 2004 com-pared with only 9 percent in East Asia (table 1.1).

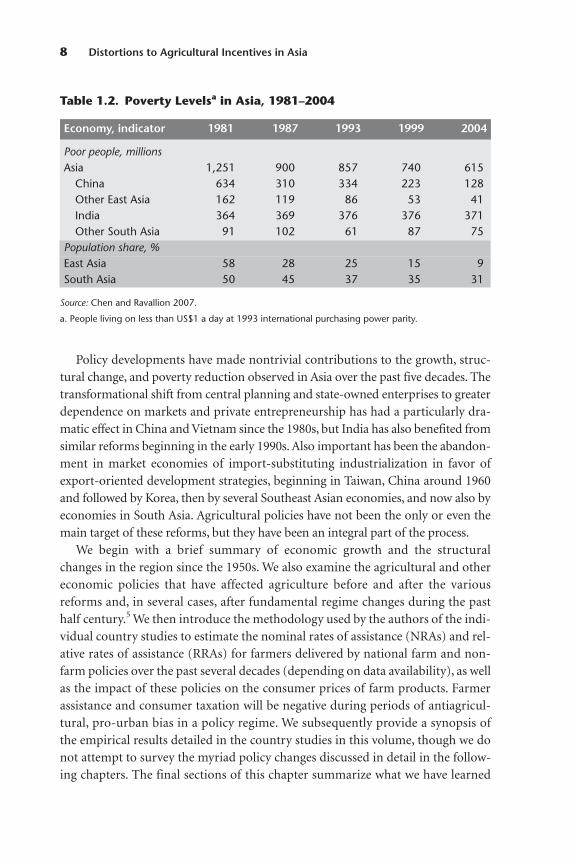

The extent of the decline in poverty in Asia has been unprecedented. The num-ber of people living on less than US$1 a day has been reduced by half since 1981(in 1993 purchasing power parity dollars). Most of the decline has occurred inEast Asia, especially China. In East Asia, the poverty rate declined from 58 percentto less than 10 percent of the population; but, even in South Asia, the proportionhas fallen from 50 to around 30 percent (table 1.2). During the 10 years to 2002,no less than 75 percent of the decline in the share of the poor among the popula-tion in Asia occurred in rural areas, and another 15 percent of the decline was gen-erated by a movement out of poverty among rural people who had migratedbecause of better opportunities in urban areas (Chen and Ravallion 2007).

Introduction and Summary 7

Policy developments have made nontrivial contributions to the growth, struc-tural change, and poverty reduction observed in Asia over the past five decades. Thetransformational shift from central planning and state-owned enterprises to greaterdependence on markets and private entrepreneurship has had a particularly dra-matic effect in China and Vietnam since the 1980s, but India has also benefited fromsimilar reforms beginning in the early 1990s. Also important has been the abandon-ment in market economies of import-substituting industrialization in favor ofexport-oriented development strategies, beginning in Taiwan, China around 1960and followed by Korea, then by several Southeast Asian economies, and now also byeconomies in South Asia. Agricultural policies have not been the only or even themain target of these reforms, but they have been an integral part of the process.

We begin with a brief summary of economic growth and the structuralchanges in the region since the 1950s. We also examine the agricultural and othereconomic policies that have affected agriculture before and after the variousreforms and, in several cases, after fundamental regime changes during the pasthalf century.5 We then introduce the methodology used by the authors of the indi-vidual country studies to estimate the nominal rates of assistance (NRAs) and rel-ative rates of assistance (RRAs) for farmers delivered by national farm and non-farm policies over the past several decades (depending on data availability), as wellas the impact of these policies on the consumer prices of farm products. Farmerassistance and consumer taxation will be negative during periods of antiagricul-tural, pro-urban bias in a policy regime. We subsequently provide a synopsis ofthe empirical results detailed in the country studies in this volume, though we donot attempt to survey the myriad policy changes discussed in detail in the follow-ing chapters. The final sections of this chapter summarize what we have learned

8 Distortions to Agricultural Incentives in Asia

Table 1.2. Poverty Levelsa in Asia, 1981–2004

Economy, indicator 1981 1987 1993 1999 2004

Poor people, millionsAsia 1,251 900 857 740 615

China 634 310 334 223 128Other East Asia 162 119 86 53 41India 364 369 376 376 371Other South Asia 91 102 61 87 75

Population share, %East Asia 58 28 25 15 9South Asia 50 45 37 35 31

Source: Chen and Ravallion 2007.

a. People living on less than US$1 a day at 1993 international purchasing power parity.

and draw out the implications of the findings for poverty, inequality, and the possible future direction of policies affecting agricultural incentives in Asia.

Growth and Structural Change

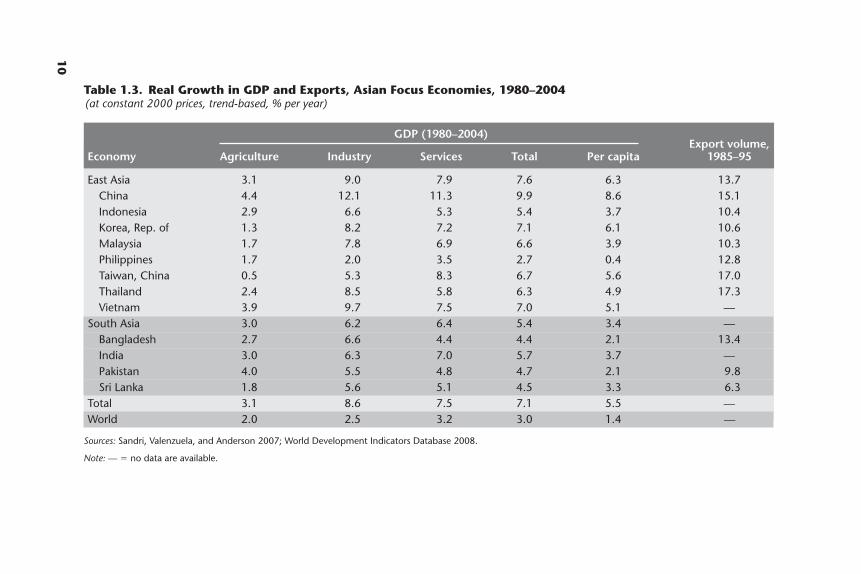

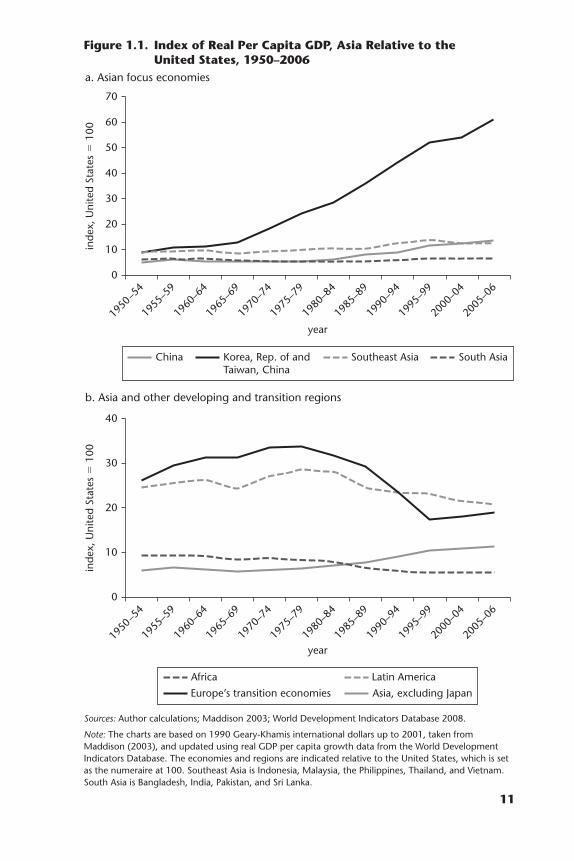

The most striking economic characteristic of the developing economies in Asia,particularly East Asia, is the rates of economic growth and industrial developmentin Korea; Taiwan, China; and elsewhere over the past three decades or more(Anderson 2008). The recent report of the Commission on Growth and Develop-ment (2008) has noted that 13 of the world’s economies have had sustainedgrowth in real per capita income of more than 7 percent for at least 25 consecutiveyears since World War II, and nine of these economies are in East Asia.6 Between1980 and 2004, per capita GDP grew 6.3 percent per year in East Asia and 3.4 per-cent per year in South Asia, while the global average was only 1.4 percent. Asia’sindustrial growth during this period was 8.6 percent per year. This compares withthe world average of 2.5 percent. Even the agricultural growth rate was more thanhalf again as high in Asia relative to the world average (3.1 percent and 2.0 percentper year, respectively; see table 1.3). As a consequence of this growth performance,per capita incomes in some Asian economies have been converging rapidly, albeitfrom a low base, toward incomes in rich countries, while other developing andtransition economies have, on average, been slipping away from the performanceof rich countries such as the United States (figure 1.1).

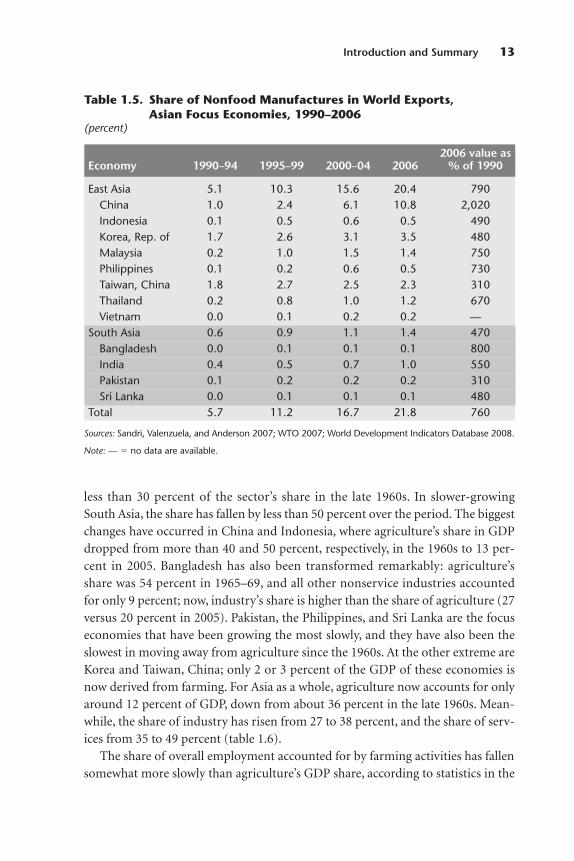

A key driver of the rapid growth and industrialization in Asia has been thedecision by many governments in the region to open up economies and abandonan import-substituting development strategy in favor of an export-orientedapproach. This shift occurred at different times in our focus economies, beginningwith Korea and Taiwan, China in the 1960s. China joined the group in the late1970s, Vietnam in the mid-1980s, and India haltingly in the early 1980s and moreconcertedly in 1991. As a result, export volumes grew at double-digit rates (lastcolumn of table 1.3). The share of exports in GDP rose steadily in the region,more than doubling in the 30 years to 2004 (table 1.4). East Asia’s share in world-wide exports of nonfood manufactures has quadrupled since 1990, thanks espe-cially to industrialization in China. China accounted for 11 percent of the world’smanufacturing exports in 2006, compared with less than 1 percent in 1990: a 20-fold increase in current U.S. dollar terms. Our other focus economies experiencedan average fivefold increase, and all the economies have contributed to the region’sgrowing share in global manufacturing exports since 1990 (table 1.5).7

Along with the export-led growth has come a dramatic restructuring of Asia’seconomies that has involved a shift from agriculture toward manufacturing andservice activities. In East Asia, the share of the agricultural sector in GDP is now

Introduction and Summary 9

10

Table 1.3. Real Growth in GDP and Exports, Asian Focus Economies, 1980–2004(at constant 2000 prices, trend-based, % per year)

GDP (1980–2004)Export volume,

Economy Agriculture Industry Services Total Per capita 1985–95

East Asia 3.1 9.0 7.9 7.6 6.3 13.7China 4.4 12.1 11.3 9.9 8.6 15.1Indonesia 2.9 6.6 5.3 5.4 3.7 10.4Korea, Rep. of 1.3 8.2 7.2 7.1 6.1 10.6Malaysia 1.7 7.8 6.9 6.6 3.9 10.3Philippines 1.7 2.0 3.5 2.7 0.4 12.8Taiwan, China 0.5 5.3 8.3 6.7 5.6 17.0Thailand 2.4 8.5 5.8 6.3 4.9 17.3Vietnam 3.9 9.7 7.5 7.0 5.1 —

South Asia 3.0 6.2 6.4 5.4 3.4 —Bangladesh 2.7 6.6 4.4 4.4 2.1 13.4India 3.0 6.3 7.0 5.7 3.7 —Pakistan 4.0 5.5 4.8 4.7 2.1 9.8Sri Lanka 1.8 5.6 5.1 4.5 3.3 6.3

Total 3.1 8.6 7.5 7.1 5.5 —World 2.0 2.5 3.2 3.0 1.4 —

Sources: Sandri, Valenzuela, and Anderson 2007; World Development Indicators Database 2008.

Note: — � no data are available.

0

10

20

30

40

50

60

70

year

inde

x, U

nite

d St

ates

� 1

00

1950

–54

1955

–59

1960

–64

1965

–69

1970

–74

1975

–79

1980

–84

1985

–89

1990

–94

1995

–99

2000

–04

2005

–06

Southeast Asia South AsiaChina Korea, Rep. of andTaiwan, China

Figure 1.1. Index of Real Per Capita GDP, Asia Relative to theUnited States, 1950–2006

a. Asian focus economies

Sources: Author calculations; Maddison 2003; World Development Indicators Database 2008.

Note: The charts are based on 1990 Geary-Khamis international dollars up to 2001, taken fromMaddison (2003), and updated using real GDP per capita growth data from the World DevelopmentIndicators Database. The economies and regions are indicated relative to the United States, which is setas the numeraire at 100. Southeast Asia is Indonesia, Malaysia, the Philippines, Thailand, and Vietnam.South Asia is Bangladesh, India, Pakistan, and Sri Lanka.

0

10

20

30

40

year

inde

x, U

nite

d St

ates

� 1

00

1950

–54

1955

–59

1960

–64

1965

–69

1970

–74

1975

–79

1980

–84

1985

–89

1990

–94

1995

–99

2000

–04

2005

–06

Europe’s transition economies Asia, excluding Japan

Africa Latin America

b. Asia and other developing and transition regions

11

12

Table 1.4. Exports of Goods and Services as a Share of GDP, Asian Focus Economies, 1965–2004(percent)

Economy 1965–69a 1975–79 1980–84 1985–89 1990–94 1995–99 2000–04

East Asiab 8 19 22 25 28 34 39China 3 6 11 14 22 21 28Indonesia 10 23 25 23 26 32 35Korea, Rep. of 13 32 34 35 27 33 39Malaysia 37 49 53 63 82 103 117Philippines 11 20 21 25 28 47 53Taiwan, China 22 49 53 54 45 48 59Thailand 18 21 23 30 38 49 68Vietnam — — — — — 44 55

South Asia — 7 7 7 11 12 14Bangladesh — 5 5 6 8 13 15India 3 6 6 6 9 11 13Pakistan — 12 12 14 17 16 16Sri Lanka 19 24 29 26 32 36 37

Totala — 16 19 22 25 30 34

Sources: Sandri, Valenzuela, and Anderson 2007; World Development Indicators Database 2008.

Note: — � no data are available.a. Only merchandise exports in 1965–69, except for Taiwan, China. In 1960–64, the shares of Korea and Taiwan, China were 6 and 15 percent, respectively. In

1955–59, the share of Taiwan, China was 10 percent.b. Ignores Vietnam in 1980–94, when the weight of Vietnam in Asian GDP was less than 1 percent.

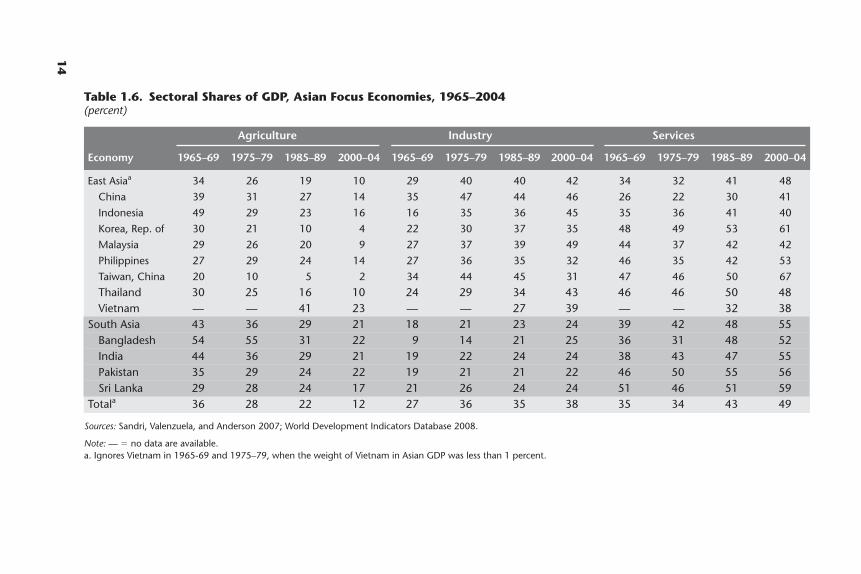

less than 30 percent of the sector’s share in the late 1960s. In slower-growingSouth Asia, the share has fallen by less than 50 percent over the period. The biggestchanges have occurred in China and Indonesia, where agriculture’s share in GDPdropped from more than 40 and 50 percent, respectively, in the 1960s to 13 per-cent in 2005. Bangladesh has also been transformed remarkably: agriculture’sshare was 54 percent in 1965–69, and all other nonservice industries accountedfor only 9 percent; now, industry’s share is higher than the share of agriculture (27versus 20 percent in 2005). Pakistan, the Philippines, and Sri Lanka are the focuseconomies that have been growing the most slowly, and they have also been theslowest in moving away from agriculture since the 1960s. At the other extreme areKorea and Taiwan, China; only 2 or 3 percent of the GDP of these economies isnow derived from farming. For Asia as a whole, agriculture now accounts for onlyaround 12 percent of GDP, down from about 36 percent in the late 1960s. Mean-while, the share of industry has risen from 27 to 38 percent, and the share of serv-ices from 35 to 49 percent (table 1.6).

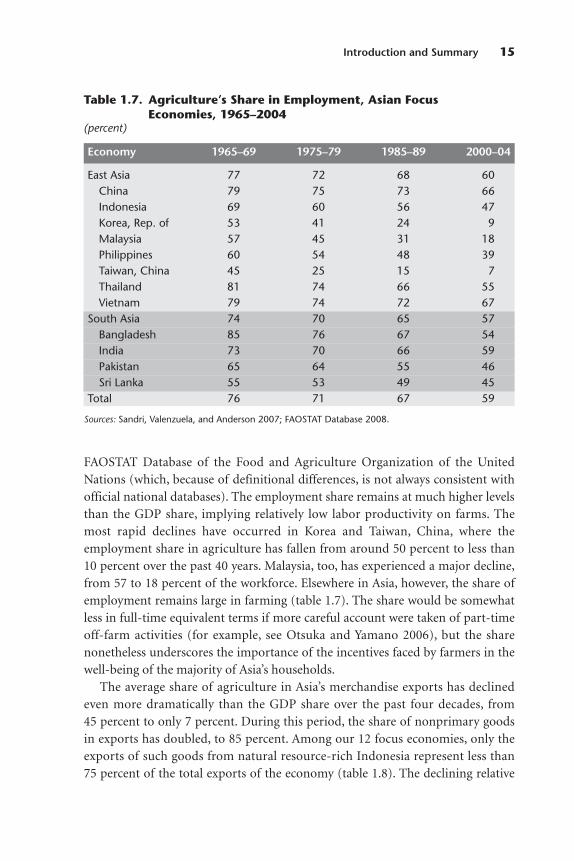

The share of overall employment accounted for by farming activities has fallensomewhat more slowly than agriculture’s GDP share, according to statistics in the

Introduction and Summary 13

Table 1.5. Share of Nonfood Manufactures in World Exports,Asian Focus Economies, 1990–2006

(percent)

2006 value asEconomy 1990–94 1995–99 2000–04 2006 % of 1990

East Asia 5.1 10.3 15.6 20.4 790China 1.0 2.4 6.1 10.8 2,020Indonesia 0.1 0.5 0.6 0.5 490Korea, Rep. of 1.7 2.6 3.1 3.5 480Malaysia 0.2 1.0 1.5 1.4 750Philippines 0.1 0.2 0.6 0.5 730Taiwan, China 1.8 2.7 2.5 2.3 310Thailand 0.2 0.8 1.0 1.2 670Vietnam 0.0 0.1 0.2 0.2 —

South Asia 0.6 0.9 1.1 1.4 470Bangladesh 0.0 0.1 0.1 0.1 800India 0.4 0.5 0.7 1.0 550Pakistan 0.1 0.2 0.2 0.2 310Sri Lanka 0.0 0.1 0.1 0.1 480

Total 5.7 11.2 16.7 21.8 760

Sources: Sandri, Valenzuela, and Anderson 2007; WTO 2007; World Development Indicators Database 2008.

Note: — � no data are available.

14

Table 1.6. Sectoral Shares of GDP, Asian Focus Economies, 1965–2004(percent)

Agriculture Industry Services

Economy 1965–69 1975–79 1985–89 2000–04 1965–69 1975–79 1985–89 2000–04 1965–69 1975–79 1985–89 2000–04

East Asiaa 34 26 19 10 29 40 40 42 34 32 41 48

China 39 31 27 14 35 47 44 46 26 22 30 41

Indonesia 49 29 23 16 16 35 36 45 35 36 41 40

Korea, Rep. of 30 21 10 4 22 30 37 35 48 49 53 61

Malaysia 29 26 20 9 27 37 39 49 44 37 42 42

Philippines 27 29 24 14 27 36 35 32 46 35 42 53

Taiwan, China 20 10 5 2 34 44 45 31 47 46 50 67

Thailand 30 25 16 10 24 29 34 43 46 46 50 48Vietnam — — 41 23 — — 27 39 — — 32 38

South Asia 43 36 29 21 18 21 23 24 39 42 48 55Bangladesh 54 55 31 22 9 14 21 25 36 31 48 52India 44 36 29 21 19 22 24 24 38 43 47 55Pakistan 35 29 24 22 19 21 21 22 46 50 55 56Sri Lanka 29 28 24 17 21 26 24 24 51 46 51 59

Totala 36 28 22 12 27 36 35 38 35 34 43 49

Sources: Sandri, Valenzuela, and Anderson 2007; World Development Indicators Database 2008.

Note: — � no data are available.a. Ignores Vietnam in 1965-69 and 1975–79, when the weight of Vietnam in Asian GDP was less than 1 percent.

FAOSTAT Database of the Food and Agriculture Organization of the UnitedNations (which, because of definitional differences, is not always consistent withofficial national databases). The employment share remains at much higher levelsthan the GDP share, implying relatively low labor productivity on farms. Themost rapid declines have occurred in Korea and Taiwan, China, where theemployment share in agriculture has fallen from around 50 percent to less than10 percent over the past 40 years. Malaysia, too, has experienced a major decline,from 57 to 18 percent of the workforce. Elsewhere in Asia, however, the share ofemployment remains large in farming (table 1.7). The share would be somewhatless in full-time equivalent terms if more careful account were taken of part-timeoff-farm activities (for example, see Otsuka and Yamano 2006), but the sharenonetheless underscores the importance of the incentives faced by farmers in thewell-being of the majority of Asia’s households.

The average share of agriculture in Asia’s merchandise exports has declinedeven more dramatically than the GDP share over the past four decades, from45 percent to only 7 percent. During this period, the share of nonprimary goodsin exports has doubled, to 85 percent. Among our 12 focus economies, only theexports of such goods from natural resource-rich Indonesia represent less than75 percent of the total exports of the economy (table 1.8). The declining relative

Introduction and Summary 15

Table 1.7. Agriculture’s Share in Employment, Asian FocusEconomies, 1965–2004

(percent)

Economy 1965–69 1975–79 1985–89 2000–04

East Asia 77 72 68 60China 79 75 73 66Indonesia 69 60 56 47Korea, Rep. of 53 41 24 9Malaysia 57 45 31 18Philippines 60 54 48 39Taiwan, China 45 25 15 7Thailand 81 74 66 55Vietnam 79 74 72 67

South Asia 74 70 65 57Bangladesh 85 76 67 54India 73 70 66 59Pakistan 65 64 55 46Sri Lanka 55 53 49 45

Total 76 71 67 59

Sources: Sandri, Valenzuela, and Anderson 2007; FAOSTAT Database 2008.

16

Table 1.8. Sectoral Shares of Merchandise Exports, Asian Focus Economies, 1965–2004(percent)

Agriculture and processed food Other primary goods Other goods

Economy 1965–69 1975–79 1985–89 2000–04 1965–69 1975–79 1985–89 2000–04 1965–69 1975–79 1985–89 2000–04

East Asiaa 46 30 18 7 10 16 12 7 43 53 62 85

China 51 35 19 5 5 17 14 4 44 48 53 90

Indonesia 49 26 21 15 48 72 55 29 2 2 24 55

Korea, Rep. of 21 11 5 2 9 2 2 6 70 87 92 92

Malaysia 61 55 36 10 32 27 24 11 5 17 40 78

Philippines 78 55 27 6 16 17 11 3 7 18 32 83

Taiwan, China 39 13 6 3 2 2 2 3 59 85 92 94

Thailand 79 67 46 18 14 10 3 4 4 20 50 75

Vietnam — — — 27 — — — 23 — — — 48

South Asia 42 40 26 13 9 8 7 8 49 52 66 78

Bangladesh — 37 28 8 — 1 1 0 — 61 71 91

India 38 35 22 13 11 9 9 11 50 55 67 75

Pakistan 53 38 30 12 2 5 1 2 45 57 68 85

Sri Lanka 96 79 47 23 2 8 5 2 1 9 46 75

Totala 45 32 18 7 10 14 12 7 44 53 62 85

Sources: Sandri, Valenzuela, and Anderson 2007; World Development Indicators Database 2008.

Note: — � no data are available.a. Ignores Vietnam in 1985–89, when the weight of Vietnam in Asian merchandise trade was less than 1 percent.

importance of farm exports has been much more rapid in Asia than in the rest ofthe world: the index of the revealed agricultural comparative advantage for Asia—defined as the share of agriculture and processed food in national exports as aratio of the share of such products in worldwide merchandise exports—has fallensince the 1980s by about two-thirds in East Asia and one-third in South Asia. Theindex of agricultural trade specialization (defined as net exports, divided by thesum of imports and exports of agricultural and processed food products) has alsofallen. The latter index, by definition, ranges from �1 to �1. It has becomeincreasingly less positive, or it has become negative in virtually all our Asian focuseconomies in recent decades (table 1.9).

This apparent decline in agricultural comparative advantage is evident in theself-sufficiency data on primary farm products. Until 30 years ago, the region wasalmost exactly 100 percent self-sufficient in farm products; but, since then, theindicator has declined to less than 85 percent. The share of farm production thatis exported has not changed much, averaging in the 4–6 percent range. However,there have been substantial changes in individual economies, including declines inMalaysia, the Philippines, Sri Lanka, and Taiwan, China and increases in China,Thailand, and Vietnam. In contrast, since the late 1970s, the share of imports inthe domestic consumption of farm products has quadrupled, to around 20 per-cent (table 1.10).

The growing dependence on imports of farm products in Asia has occurreddespite reductions in the taxation of agricultural exports and increases in the incen-tives provided to farmers through government policy reforms (discussed below).These reforms have probably contributed to poverty reduction in Asia. Using a priceindicator that is simpler than the one developed by us below, Ravallion and Chen(2007) show that the reduction in the antiagricultural bias in farm price policies hascontributed significantly to poverty reduction in China. Rural growth is also a keycontributor to the reduction in poverty in India (Ravallion and Datt 1996). One mayrevisit these and other, similar studies using the more comprehensive measures of theextent of changes in distortions to agricultural incentives summarized below. To gen-erate these measures, a common methodology has been adopted by the authors ofthe country case studies in this volume. A summary of the methodology follows, andadditional details may be found in Anderson et al. (2008) and in appendix A.

Methodology for Measuring Ratesof Assistance or Taxation

The NRA is defined as the percentage by which government policies have raised(or lowered if the NRA is less than 0) the gross returns to producers above (or below)the gross returns they would have received without government intervention. If a

Introduction and Summary 17

(Text continues on page 22.)

18 Distortions to Agricultural Incentives in Asia

b. Trade specialization index (world � 0.0)b

Economy 1965–69 1975–79 1985–89 2000–04

East Asia — — — �0.03China — — 0.07 �0.16Indonesia 0.48 0.42 0.43 0.16Korea, Rep. of �0.63 �0.41 �0.45 �0.53Malaysia 0.44 0.60 0.56 0.29Philippines 0.47 0.51 0.25 �0.18Taiwan, China 0.08 �0.27 �0.35Thailand 0.68 0.69 0.57 0.44Vietnam — — — 0.44

South Asia — 0.05 0.03 �0.06Bangladesh — �0.37 �0.46 �0.62India �0.18 0.13 0.16 0.10Pakistan 0.20 �0.13 �0.05 �0.24Sri Lanka 0.34 0.30 0.21 0.08

Total — — — �0.03

Sources: Sandri, Valenzuela, and Anderson 2007; World Development Indicators Database 2008.

Note: — � no data are available.a. The share of agriculture and processed food in national exports as a ratio of such products in

worldwide merchandise exports. The world average is 1.0.b. The ratio of net exports to the sum of the exports and imports of agricultural and processed food

products. The world average is 0.0.

Table 1.9. Indexes of Comparative Advantage in Agricultureand Processed Food, Asian Focus Economies, 1965–2004

a. Revealed comparative advantage index (world � 1.0)a

Economy 1965–69 1975–79 1985–89 2000–04

East Asia 2.2 2.2 1.1 0.7China 2.1 2.1 1.3 0.6Indonesia 2.0 1.3 1.4 1.7Korea, Rep. of 0.8 0.6 0.3 0.3Malaysia 2.4 2.9 2.4 1.1Philippines 3.1 2.8 1.9 0.7Taiwan, China 1.5 0.6 0.4 0.3Thailand 3.1 3.5 3.1 2.0Vietnam — — — 3.0

South Asia 1.9 2.0 1.8 1.4Bangladesh — 1.9 1.9 0.9India 1.5 1.8 1.5 1.4Pakistan 2.1 1.9 2.1 1.4Sri Lanka 3.8 4.1 3.2 2.5

Total 2.2 2.2 1.2 0.8

19

Table 1.10. Export Orientation, Import Dependence, and Self-Sufficiency in Primary AgriculturalProduction, Asian Focus Economies, 1961–2004

(%, at undistorted prices)

a. Exports, as a share of production

Economy 1961–64 1965–69 1970–74 1975–79 1980–84 1985–89 1990–94 1995–99 2000–04

Korea, Rep. of 0 0 0 0 0 0 0 2 1Taiwan, China 5 9 13 14 10 10 6 5 6China 2 2 2 3 5 5 7 7 7Indonesia — — 6 5 5 6 4 5 4Malaysia 70 64 54 41 35 34 19 12 9Philippines 13 11 14 8 7 2 1 1 1Thailand — — 13 20 24 26 25 25 30Vietnam — — — — — 3 4 9 11Bangladesh — — — 3 3 3 2 1 1India 1 1 1 1 1 1 1 1 2Pakistan 7 5 5 2 5 8 4 2 1Sri Lanka 68 62 44 52 36 34 24 31 39Total 3 4 4 4 4 6 6 5 5

(Table continues on the following page.)

20

Table 1.10. Export Orientation, Import Dependence, and Self-Sufficiency in Primary AgriculturalProduction, Asian Focus Economies, 1961–2004 (continued)

b. Imports, as a share of apparent consumption

Economy 1961–64 1965–69 1970–74 1975–79 1980–84 1985–89 1990–94 1995–99 2000–04

Korea, Rep. of 4 5 12 8 11 9 11 11 13Taiwan, China 24 33 56 66 76 81 86 90 93China 2 2 2 3 5 5 7 7 7Indonesia — — 0 1 1 1 1 2 2Malaysia 13 6 3 1 1 1 2 3 6Philippines 0 0 1 0 1 0 0 2 1Thailand — — 0 0 0 0 0 2 5Vietnam — — — — — 0 0 0 0Bangladesh — — — 3 4 5 3 3 5India 3 4 2 2 1 1 1 1 2Pakistan 6 5 3 5 2 5 5 6 4Sri Lanka 7 5 1 0 1 4 1 3 5Total 3 4 4 5 7 12 17 17 19

21

c. Self-sufficiency ratio

Economy 1961–64 1965–69 1970–74 1975–79 1980–84 1985–89 1990–94 1995–99 2000–04

Korea, Rep. of 96 95 88 92 89 91 90 91 87Taiwan, China 80 73 51 40 27 21 15 11 7China 99 101 100 99 98 101 101 99 98Indonesia — — 106 105 104 106 104 103 102Malaysia 293 265 215 167 152 150 122 110 104Philippines 115 112 116 108 106 101 101 99 99Thailand — — 115 125 131 135 133 130 137Vietnam — — — — — 103 104 110 112Bangladesh — — 98 99 99 98 99 98 96India 98 97 99 99 99 99 100 100 100Pakistan 101 100 102 97 103 104 99 96 97Sri Lanka 297 298 194 221 155 144 131 142 157Total 100 100 100 99 97 94 88 87 85

Sources: Author compilation; FAO Agricultural Trade Database 2008.

Note: Compiled using estimates of the total agricultural production of covered and noncovered products, valued at undistorted prices, plus total agricultural tradevalue data. Self-sufficiency is defined for each product as the ratio of production to production, plus imports, minus exports. — � no data are available.

trade measure is the sole government intervention, then the measured NRA willalso be the consumer tax equivalent (CTE) rate at that same point in the valuechain. Where there are also domestic producer or consumer taxes or subsidies, theNRA and CTE will no longer be equal, and at least one of them will be differentfrom the price distortion at the border caused by trade measures.8

NRAs and CTEs may be used for several purposes, and the purpose affects theappropriate choice of methodology. In our project, we rely on NRAs and CTEs toachieve three purposes. One purpose is to generate a comparable set of numbersacross a wide range of countries and over a long time period. This means themethodology must be both simple and somewhat flexible. Another purpose is toprovide a single number, the NRA, to indicate the total extent of transfers to orfrom farmers because of government agricultural policies and another number,the CTE, to indicate the extent of the transfers to or from consumers. The NRAand the CTE are both expressed as a percentage of the undistorted price or in dol-lar terms. This is also the purpose of the OECD’s producer and consumer supportestimates, which may be negative if the transfers from the relevant group exceedthe transfers to the relevant group. Our research project’s agricultural NRAs andCTEs are similar in spirit to the OECD estimates, but there are also important dif-ferences, which are outlined below. Our third purpose is to enable economic mod-elers to use the NRAs as producer price wedges for individual primary and lightlyprocessed agricultural products and to use the CTEs as consumer price wedges insingle-sector, multisector, and economy-wide policy simulation models by allo-cating these wedges to particular policy instruments such as trade taxes or domes-tic producer or consumer subsidies or taxes.

The NRAs are based on our estimates of assistance to individual industries.Great care has gone into generating the NRAs for each covered agricultural indus-try, particularly in countries where trade costs are high, the pass-through alongthe value chain is affected by imperfect competition, and the markets for foreigncurrency have been highly distorted to varying degrees at various times.

Most distortions in industries producing tradables arise from trade measuressuch as quantitative trade restrictions or tariffs imposed on the import cost,insurance, and freight price or export subsidies or taxes imposed on the free onboard price at the country’s border. An ad valorem tariff or export subsidy is theequivalent of a production subsidy and a consumption tax at the same rateexpressed as a percentage of the border price. For this reason, such tariffs and sub-sidies are captured in the NRAs and CTEs at the point in the value chain at whicha product is first traded. To obtain the NRAs for farmers, the authors of the coun-try studies have estimated or guessed the extent of pass-through back to the farm-gate and added any domestic farm output subsidies. To obtain the CTEs, they have

22 Distortions to Agricultural Incentives in Asia

also added any product-specific domestic consumer taxes to the distortionscaused by border measures. Note that the NRAs and CTEs differ from the OECD’sproducer and consumer support estimates in that the latter pair is expressed as apercentage of the distorted price and, hence, will be lower (for positive protectionrates) than the former pair, which is expressed as a percentage of the undistortedprice.

We have decided not to seek estimates of the more complex effective rate ofassistance even though it is, in principle, a better single partial equilibrium measureof the distortions in producer incentives. To establish these alternative estimates,we must know, for each product, the value added and various intermediate inputshares in output. These data are not available in most developing countries even fora few years, let alone for every year in the long time series that is the focus of ourstudy. Moreover, in most countries, the distortions in farm input prices are smallcompared with the distortions in farm output prices. Nonetheless, if the product-specific distortions to input costs are significant, they may be captured by estimat-ing their equivalent values in terms of a higher output price and then including thisestimate in the NRA for individual agricultural industries wherever data allow. Wealso add any non-product-specific distortions, including distortions in farm inputprices, into the estimate for the overall sectoral NRA for agriculture.

The targeted minimum product coverage of our NRA estimates is 70 percentbased on the gross value of farm production at undistorted prices. This target cov-erage is similar to the coverage of the OECD producer support estimates. Unlikethe OECD, however, we do not routinely assume that the nominal assistance forcovered products applies equally to the farm products we do not cover. This isbecause, in developing countries, agricultural policies affecting our noncoveredproducts are often different from those affecting our covered products. For exam-ple, nontradables among noncovered farm goods—often highly perishable prod-ucts or products of low value relative to the transport cost—are frequently notsubject to direct distortionary policies. We have asked the authors of the countrycase studies to provide three sets of NRA guesstimates for noncovered farm prod-ucts, one each for the import-competing, exportable, and nontradable subsectors.Weighted averages for all agricultural products have then been generated usingthe gross values of production at unassisted prices as weights. For countries thatalso provide non-product-specific agricultural subsidies or taxes—assumed to beshared on a pro rata basis between tradables and nontradables—or assistancedecoupled from production, the net assistance from these measures is then addedto the product-specific assistance to obtain NRAs for total agriculture. We applythe same procedure to obtain NRAs also for tradable agriculture for use in gener-ating RRAs (which are defined below).

Introduction and Summary 23