Culture and accounting practices in Turkey

23

Electronic copy available at: http://ssrn.com/abstract=1370782 Culture and accounting practices in Turkey Saeed Askary* School of Accounting, College of Business Administration, Abu Dhabi University, Abu Dhabi Email: [email protected] *Corresponding author Hassan Yazdifar Sheffield University Management School, The University of Sheffield, 9 Mappin Street, Sheffield, S1 4DT, UK Email: [email protected] Davood Askarany Faculty of Business and Economics, Tamaki Campus, The University of Auckland, Auckland, New Zealand Email: [email protected] Abstract: This paper examines the effects of cultural values on accounting practices in Turkey by applying Gray’s theory (Gray, 1988) of socio-cultural factors on accounting values and practices. We compared the model of accounting with accounting-profession authority, the quality and uniformity of financial disclosures, and accounting measurements in present Turkey. This country is a unique case among developing countries because of its specific geopolitical and cultural features. Our results confirm Gray’s theory that high uncertainty avoidance and low individualism are positively associated with high conservative accounting measurements. In addition, the study confirms that the highest power distance, uncertainty avoidance, and the lower individualism are positively associated with accounting uniformity. However, large power distance, high uncertainty avoidance, and collectivisms negatively affect professionalism and financial disclosures. Keywords: culture; financial disclosures; measurements; professionalism; Turkey; uniformity. Reference to this paper should be made as follows: Askary, S., Yazdifar, H. and Askarany, D. (2008) ‘Culture and accounting practices in Turkey’, International Journal of Accounting, Auditing and Performance Evaluation, Vol. 5, No. 1, pp.66–88. Biographical notes: Saeed Askary is an Assistant Professor of accounting in the College of Business Administration at the Abu Dhabi University. His recent research with Marc Olynyk has been selected among the top 10 articles by the international compendium award-winning articles selected by the PAIB Committee of IFAC as a part of IFAC annual Articles of Merit award programme. He has published papers in Managerial Auditing Journal, Asian Review of Accounting and Australian Accounting Review. 111 2 3 4 5 6 7 8 9 1011 1 2 3 4 5 6 7 8 9 2011 1 2 3 4 5 6 7 8 9 30 1 2 3 4 5 6 7 8 9 40 1 2 3 4 5 6 711 8 66 Int. J. Accounting, Auditing and Performance Evaluation, Vol. 5, No. 1, 2008 Copyright © 2008 Inderscience Enterprises Ltd.

Transcript of Culture and accounting practices in Turkey

Electronic copy available at: http://ssrn.com/abstract=1370782

Culture and accounting practices in Turkey

Saeed Askary*School of Accounting, College of Business Administration,

Abu Dhabi University, Abu Dhabi

Email: [email protected]

*Corresponding author

Hassan YazdifarSheffield University Management School, The University of Sheffield,

9 Mappin Street, Sheffield, S1 4DT, UK

Email: [email protected]

Davood AskaranyFaculty of Business and Economics, Tamaki Campus,

The University of Auckland, Auckland, New Zealand

Email: [email protected]

Abstract: This paper examines the effects of cultural values on accountingpractices in Turkey by applying Gray’s theory (Gray, 1988) of socio-culturalfactors on accounting values and practices. We compared the model ofaccounting with accounting-profession authority, the quality and uniformityof financial disclosures, and accounting measurements in present Turkey.This country is a unique case among developing countries because of itsspecific geopolitical and cultural features. Our results confirm Gray’s theorythat high uncertainty avoidance and low individualism are positively associatedwith high conservative accounting measurements. In addition, the studyconfirms that the highest power distance, uncertainty avoidance, and thelower individualism are positively associated with accounting uniformity.However, large power distance, high uncertainty avoidance, and collectivismsnegatively affect professionalism and financial disclosures.

Keywords: culture; financial disclosures; measurements; professionalism;Turkey; uniformity.

Reference to this paper should be made as follows: Askary, S., Yazdifar, H.and Askarany, D. (2008) ‘Culture and accounting practices in Turkey’,International Journal of Accounting, Auditing and Performance Evaluation,Vol. 5, No. 1, pp.66–88.

Biographical notes: Saeed Askary is an Assistant Professor of accountingin the College of Business Administration at the Abu Dhabi University.His recent research with Marc Olynyk has been selected among the top 10articles by the international compendium award-winning articles selected bythe PAIB Committee of IFAC as a part of IFAC annual Articles of Meritaward programme. He has published papers in Managerial Auditing Journal,Asian Review of Accounting and Australian Accounting Review.

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

66 Int. J. Accounting, Auditing and Performance Evaluation, Vol. 5, No. 1, 2008

Copyright © 2008 Inderscience Enterprises Ltd.

Electronic copy available at: http://ssrn.com/abstract=1370782

Culture and accounting practices in Turkey 67

Hassan Yazdifar is a Lecturer in accounting at Sheffield UniversityManagement School. Prior to joining Sheffield in 2001, he taught at theUniversity of Manchester. He has taught accounting in wide range ofundergraduate and postgraduate courses, and has supervised a number ofdoctoral students in accounting in developing countries. His recentpublications have been published in Critical Perspectives on Accounting,Journal of Accounting, Business, & Management and International Journalof Business and Systems Research.

Davood Askarany is a Lecturer in accounting in the business school at AucklandUniversity. He teaches different sorts of accounting subjects, includingFinancial Decision Support, Performance Measurement and ManagementControl and Cost Accounting Systems. He has published research papersin Critical Perspectives on Accounting, International Journal of Businessand Systems Research, Journal of Accounting, Business & Management,and Journal of Issues in Informing Science and Information Technology.

1 Introduction

Cultural diversities are perceived to shape accounting system practices within national

borders and are more likely to prevent unified accounting practices globally (Archambault

and Archambault, 2003; Chanchani and Willett, 2004; Doupnik and Salter, 1995,

Hamid et al., 1993; Radebaugh and Gray, 2002; Salter and Niswander, 1995). The cultural

environment is a likely causal factor of different national accounting practices in

accordance with differing national cultures (e.g. Belkaoui, 1990, 1996; Doupnik and

Salter, 1995; Fechner and Kilgore, 1994; Gray, 1988; Hamid et al., 1993; Perera, 1989,

1994; Perera and Mathews, 1990; Zarzeski, 1996). The cultural environment is generally

acknowledged to be a national (or regional) system comprising language, religion, morals,

values, attitudes, law, education, politics, social organisation, technology, and material

culture. The effect of these cultural elements on accounting is therefore likely to be

exceedingly complex.

According to Perera (1989), each accounting system is a product of its specific culture

and environment. Mueller et al. (1994; p.1) have also noted, ‘Accounting is shaped by the

environment in which it operates’. In other words, different patterns of accounting are

associated with a range of cultural factors such as societal values, religion, political

systems, and historical background. Culture is a powerful influence underlying human

behaviour and social values, and its impact on accounting practices can not be

underestimated.

The main objective of this study is to test Gray’s (1988) hypotheses with respect

to cultural influences on accounting practices in Turkey. This is a developing country with

a geographical boundary that has been classified over the years as either being part

of South-Eastern Europe, South-Western Asia or the Middle East. The western portion of

Turkey, called Bosporu, is claimed to be a part of the European geopolitics. Turkey has a

total population of around 70 million, comprising a majority of Sunni Muslim, and has

a growth rate of 2% p.a. This country is a republic and its legal system is mainly drawn

from Continental Europe (The World Fact Book, 2005).

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

An investigation into the effects of cultural values on accounting practices in Turkey

is complex. Turkey’s national societal values are influenced by Islamic values such as

Islamic customs, rituals, and beliefs. However, the country has adopted a largely secular

approach to governance. The language of Turkey has been recognised as a major barrier

for international investors because they may not be able to understand and interpret the

annual reports of the country’s listed companies, which are in Turkey’s native language.

Turkey has voiced its intention since 1959 to join the European Economic Community

(EEC) to gain the advantage of better economic development. However, the process is

under review by the European Economic Commission while the Turkish government

takes major steps to align the national socio-political policies with European requirements.

Turkey’s relationship with the European Union influences the form and content of the

financial information of Turkish listed companies.

It is also notable that the country has suffered a high inflation crisis for many

years, which has had significant impacts on the currency. This has resulted in a number

of problems for professional accountants in being able to measure the value of

certain assets and net profits. Accordingly, a study to investigate the effects of culture

on accounting practices in a complex economic and geopolitical environment should

assist in the development of accounting practices in Turkey.

Our study contributes to the knowledge of international financial accounting by

understanding the impact of national culture on professionalism, financial disclosures,

measurement of accounting elements, and enforcement of accounting standards. The

results of this study may be of interest to researchers in international accounting

studies area, regulators and policy makers, such as the International Federation of

Accountants (IFAC), international investors, domestic and international business

analysts, and global organisations such as the Organisation for Economic Co-operation

and Development (OECD).

The structure of the paper is organised as follows. First, the history of accounting is

reviewed followed by an understanding of accounting practices from differing cultural

perspectives. Then, the hypotheses of the study are developed followed by the analysis.

Finally, the results, conclusion, and limitations of the study are presented.

2 Accounting in Turkey

The first legal requirement influencing accounting development in Turkey was the

Commercial Law of 1850 (adopted from French Commercial Code and practice); and

‘the impact of French accounting on Turkish Accounting Practices was significant’

as a result of the adoption (Simga-Mugan, 1995, p.341). The Law that had strong

influences on the profession until 1960 was a translation of the French Commercial

Code (ibid). After the First World War and the establishment of the Turkish Republic,

accounting practices were influenced by the development of the second Commercial

Code Law 826, which was largely adopted from German Commercial law. The influence

of German accounting endured until the 1960s due to close ties between the two

governments (Cooke and Curuk, 1996). After 1960, however, the accounting system

shifted to an adoption of the US model of accounting.

In 1930, the accounting and auditing profession was recognised indirectly by the

new republican State Law No. 1580. This situation lasted until 1942 when the Expert

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

68 S. Askary, H. Yazdifar and D. Askarany

Culture and accounting practices in Turkey 69

Accountant’s Association of Turkey (EAAT) was established to develop the accounting

and auditing profession. Since 1940, the MOF (Ministry of Finance) has been appointing

public accountants in order to inspect and audit the work of some of the large firms

in major cities. The profession attempted to be legally recognised as an independent

profession through the tax procedures law of 1950, but that was not successful.

Following the establishment of the MOF in 1945, the first taxation law was developed

by an expert group of local accounting firms, representing the overall accounting

profession and having the expertise to handle the accounting issues for taxation purposes

(Simga-Mugan, 1995). However, the MOF continued to control accounting and auditing

practices by the board of inspectors, account experts, and tax auditors. In 1956, the

Commercial Code of Turkey was passed. The Code assured legitimacy of transactions and

a right of recognition of the accounting profession indirectly. In summary, the accounting

profession in Turkey was under statutory controls until 1974.

One of the milestones for professional accounting development was in 1974, when two

important events occurred. First, a uniform chart of accounts was developed by the MOF

and the second event was when Turkey became a member of the International Financial

Reporting Standards (IFRS) committee. The MOF established a uniform chart of accounts

and accounting principles, to be effective from 1 January 1994 (Simga-Mugan, 1995),

for two reasons. First, a mandatory policy was to be followed by all companies and

secondly it facilitated an enforcement of a set of accounting rules (ibid., p.36).

Capital market research indicates that professional accounting associations can

positively affect the capital markets because reliable and relevant accounting information

facilitates functioning of an efficient capital market. In 1981, capital market rules,

enforced by Law Code 2499, developed the necessary rules to establish the Istanbul Stock

Exchange (ISE), which started functioning in 1986 (Simga-Mugan, 1995) The Capital

Market Board (CMB), however, was established officially in 1989 and was authorised

to be the official capital market regulatory body. It had seven board members appointed

by a council of ministers for 6 years.

The Union of Certified Public Accountants and Sworn-in Certified Public Accountants

of Turkey – acronym in Turkish, TURMOB – was formed by law 3568. This union

was to be effective for 3 years after the ISE establishment, as an official association of

the profession – with participation from the Chambers of Independent Accountants,

the Certified Public Accountants and the Sworn-in Certified Public Accountants

(Demirag, 1993). TURMOB became the sole authority to award professional licenses

for members, smiliar to the AICPA in issuing CPA certificates for its members.

The The Turkish Accounting and Auditing Standards Board (TAASB), which

issued 19 Accounting Standards published by TURMOB until January 2002, was

formed to develop a set of formal accounting and auditing standards in February 1994.

These standards were not widely used by Turkish companies. TAASB was renamed

the Turkish Accounting Standard Board (TASB) in April 2002. The new standards

are substantially similar to the IFRSs. Table 1 summarises all important historical

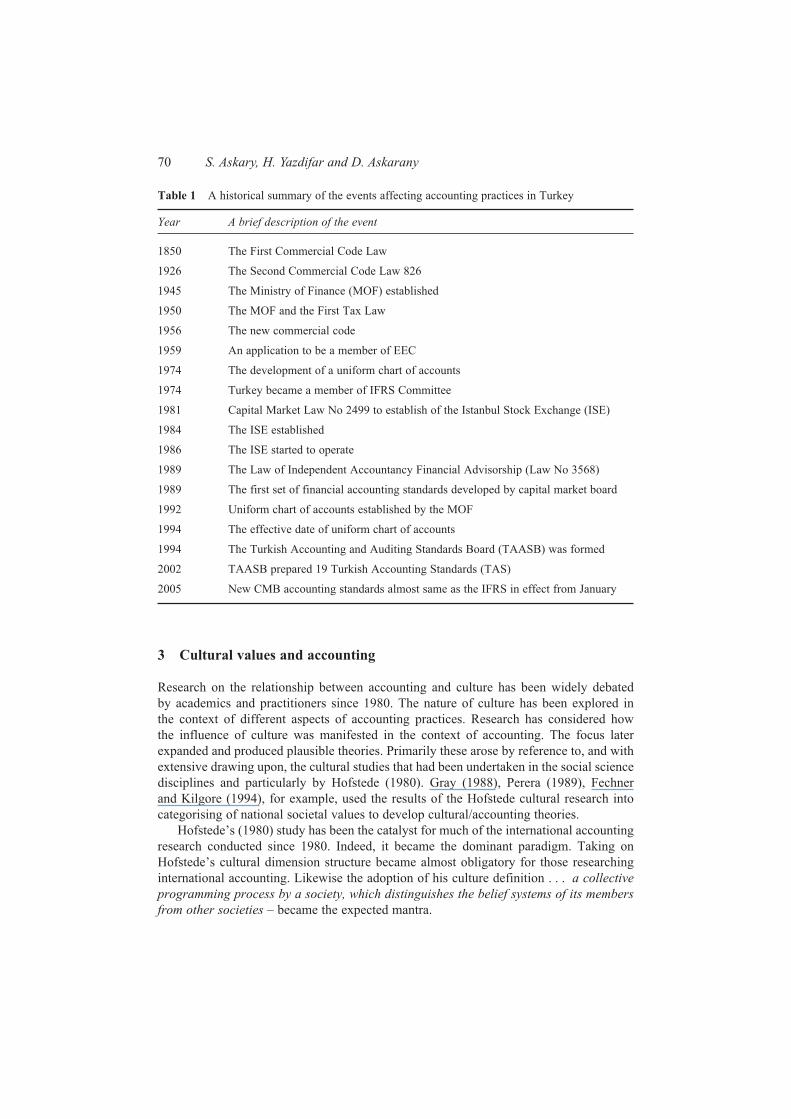

events affecting the accounting and auditing profession.

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

3 Cultural values and accounting

Research on the relationship between accounting and culture has been widely debated

by academics and practitioners since 1980. The nature of culture has been explored in

the context of different aspects of accounting practices. Research has considered how

the influence of culture was manifested in the context of accounting. The focus later

expanded and produced plausible theories. Primarily these arose by reference to, and with

extensive drawing upon, the cultural studies that had been undertaken in the social science

disciplines and particularly by Hofstede (1980). Gray (1988), Perera (1989), Fechner

and Kilgore (1994), for example, used the results of the Hofstede cultural research into

categorising of national societal values to develop cultural/accounting theories.

Hofstede’s (1980) study has been the catalyst for much of the international accounting

research conducted since 1980. Indeed, it became the dominant paradigm. Taking on

Hofstede’s cultural dimension structure became almost obligatory for those researching

international accounting. Likewise the adoption of his culture definition . . . a collectiveprogramming process by a society, which distinguishes the belief systems of its membersfrom other societies – became the expected mantra.

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

70 S. Askary, H. Yazdifar and D. Askarany

Table 1 A historical summary of the events affecting accounting practices in Turkey

Year A brief description of the event

1850 The First Commercial Code Law

1926 The Second Commercial Code Law 826

1945 The Ministry of Finance (MOF) established

1950 The MOF and the First Tax Law

1956 The new commercial code

1959 An application to be a member of EEC

1974 The development of a uniform chart of accounts

1974 Turkey became a member of IFRS Committee

1981 Capital Market Law No 2499 to establish of the Istanbul Stock Exchange (ISE)

1984 The ISE established

1986 The ISE started to operate

1989 The Law of Independent Accountancy Financial Advisorship (Law No 3568)

1989 The first set of financial accounting standards developed by capital market board

1992 Uniform chart of accounts established by the MOF

1994 The effective date of uniform chart of accounts

1994 The Turkish Accounting and Auditing Standards Board (TAASB) was formed

2002 TAASB prepared 19 Turkish Accounting Standards (TAS)

2005 New CMB accounting standards almost same as the IFRS in effect from January

Culture and accounting practices in Turkey 71

Hofstede (1980) specified four characteristics of culture: individualism, powerdistance, uncertainty avoidance, and masculinity. It is to be noted that Hofstede’s

study has enjoyed considerable attention by different disciplines. Indeed, it has been

cited in nearly 600 studies between 1981 and 1992 (Sudarwan and Fogarty, 1996).

Thus, its use in the context of accounting research is quite justified. It is understandable

therefore that accounting researchers have followed suite and sought authority for

their culture/accounting theories in Hofstede.

Individualism pertains to societies in which the ties between individuals are loose:

everyone is expected to look after himself or herself and his or her immediate family.

Collectivism as its opposite pertains to societies in which people from birth onwards

are integrated into strong, cohesive groups, which throughout people’s lifetimes continue

to protect them in exchange for unquestioning loyalty (Hofstede, 1997, p.51).

Power distance can therefore be defined as the extent to which the less powerfulmembers of institutions and organisations within a country expect and accept thatpower is distributed unequally. ‘Institutions’ are the basic elements of society like

the family, school, and the community; and ‘organisations’ are the places where people

work (Hofstede, 1997, p.28).

Uncertainty avoidance can therefore be defined as the extent to which the memberof a culture feels threatened by uncertain or unknown situations. This feeling is, among

other things, expressed through nervous stress and in a need for predictability: a need for

written and unwritten rules’ (Hofstede, 1997, p.113).

Masculinity pertains to societies in which social gender roles are clearly distinct

(i.e. men are supposed to be assertive, tough, and focused on material success whereas

women are supposed to be more modest, tender, and concerned with the quality of life):

femininity pertains to societies in which social gender roles overlap, i.e. both men

and women are supposed to be modest, tender, and concerned with the quality of life)

(Hofstede, 1997, pp.82–83).

Gray (1988) translated Hofstede’s cultural and societal values into accounting

values and posited a relation between them (Table 2). Gray’s model proposed that

all accounting policy decisions, at a national level, are made in response to cultural

values that are explicable in the terms of the Hofstede study (Salter and Niswaner, 1995).

Gray’s justification of that framework closely follows Hofstede’s explanation of

cultural dimensions. Essentially, it entailed the substitution of accounting terminology

for Hofstede’s cultural rhetoric.

Professionalism is defined as a preference by accountants for exercising individual

professional judgement in undertaking accounting tasks. (Gray, 1988). It entails the

maintenance of professional self-regulation. This stands in contrast with statutorycontrol – the imposition of force on accountants to comply with prescriptive legal

requirements with the backing of legal sanctions for non-compliance.

According to Gray (1988), high individualism and low uncertainty-avoidance and

power distance in a society mesh tightly with accounting professionalism. He explained

that ‘. . . [a] preference for independent professional judgement is consistent with a

preference for a loosely knit cultural framework where there is more emphasis on

independence, a belief in individual decisions and respect for individual endeavour.’ (p.9)

On those grounds, he reasoned that professionalism in accounting is more likely to

be accepted in a small power-distance society with a concern for the exercise of

equal rights.

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

72 S. Askary, H. Yazdifar and D. Askarany

Table 2 Matrix of relationship of accounting values with societal values

Cul

tura

l soc

ieta

l val

ues

Acco

untin

g va

lues

Prof

essi

onal

ism

Stat

utor

y co

ntro

lU

nifo

rmity

Flex

ibili

tyC

onse

rvat

ism

Opt

imis

mSe

crec

yTr

ansp

aren

cy

Indiv

idual

ism

Posi

tive

Neg

ativ

eN

egat

ive

Posi

tive

Neg

ativ

eP

osi

tive

Neg

ativ

eP

osi

tive

Coll

ecti

vis

mN

egat

ive

Posi

tive

Posi

tive

Neg

ativ

eP

osi

tive

Neg

ativ

eP

osi

tive

Neg

ativ

e

Lar

ge

pow

er

Neg

ativ

eP

osi

tive

Posi

tive

Neg

ativ

eN

/AN

/AP

osi

tive

Neg

ativ

e

dis

tance

Sm

all

pow

erP

osi

tive

Neg

ativ

eN

egat

ive

Posi

tive

N/A

N/A

Neg

ativ

eP

osi

tive

dis

tance

Str

ong

Neg

ativ

eP

osi

tive

Posi

tive

Neg

ativ

eP

osi

tive

Neg

ativ

eP

osi

tive

Neg

ativ

e

unce

rtai

nty

avoid

ance

Wea

kP

osi

tive

Neg

ativ

eN

egat

ive

Posi

tive

Neg

ativ

eP

osi

tive

Neg

ativ

eP

osi

tive

unce

rtai

nty

avoid

ance

Mas

culi

nit

y

Posi

tive

N/A

N/A

N/A

Posi

tive

Neg

ativ

eN

egat

ive

Posi

tive

Fem

inin

ity

Neg

ativ

eN

/AN

/AN

/AN

egat

ive

Posi

tive

Posi

tive

Neg

ativ

e

Sour

ce:

Rad

ebau

gh a

nd G

ray (

2002),

p.4

Culture and accounting practices in Turkey 73

Secrecy is taken in the culture/accounting debate to manifest a preference for

confidentiality. Its accounting manifestation thus lies in the restriction on the disclosure

of financial information pertinent to the assessment and evaluation of the performance

and state of business affairs. This contrasts with a more transparent, open and publicly

accountable approach (Gray, 1988). Gray’s hypotheses suggest that of the four Hofstede

values, uncertainty avoidance and individualism are the most influential in relation to

the accounting values. According to this reasoning, the positive effects of uncertainty

avoidance and power distance combine to evoke secrecy. As a consequence, it is to be

expected that small power distance and weak uncertainty avoidance may evoke positive

effects on transparency.

Enforcement in respect to accounting, in the context of the cultural debate, is a

preference for either insisting on uniform accounting practices or, its opposite, flexibility

in accordance with the perceived circumstances of individual companies (Gray, 1988).

The disclosure of financial data in general purpose financial statements is a particular

setting in which uniformity, or otherwise, is an issue (Askary, 2001).

To Gray, this accounting value dimension is very substantial because other attitudes

such as consistency and comparability are incorporated as fundamental features of

accounting principles worldwide. Gray reasoned that individualism and uncertainty

avoidance are linked closely with uniformity. Gray thereby links uniformity closely to

uncertainty avoidance, because strong uncertainty avoidance is perceived by him to be

linked with rigid codes of behaviour, law, order and written rules and regulations, which

avoid mistakes and unpredictable outcomes. As a consequence, a large power distance

society is deemed to facilitate uniformity by imposing laws and codes of a uniform

character on that society. It is to be expected then, that those countries deemed to practice

large power distance would have a large catalogue of accounting standards.

Conservatism does not take on any special meaning in the context of the accounting

/culture debate. As in the conventional focus on accounting, conservatism is a preference

for a cautious approach to measurement of accounting elements such as the monetary

amounts of assets and liabilities, revenues, expenses and the calculation of profit or loss,

calculated with uncertainty of future events in mind. In contrast, optimism can be regarded

a laissez-faire, risk-taking approach in accounting measurements. This conforms to the

culture/accounting debate context (Gray, 1988).

Gray’s explanation implies that only uncertainty avoidance can be linked closely

to conservatism. High uncertainty avoidance, in regard to measurement of profit and

the worth of assets, is consistent with highly conservative accounting values expressed

for assets in the balance sheets of companies. In addition, there is a perceived link, even

if less strong, between individualism, masculinity and conservatism. Because of an

emphasis on individual achievement and performance which is likely to be conducive

to a less conservative approach to measurement, with a view to bolstering reported

performance outcomes and inducing perceptions of what Gray (consistent with Hofstede)

considers are indicative of highly attuned masculine traits.

Doupnik and Riccio (2006) investigated ‘. . . Gray’s conservatism and secrecy

hypothesis in the context of interpreting verbal probability expression used as recognition

and disclosure thresholds in IFRSs.’ (p.254) They found that ‘Gray’s theory as applied to

the interpretation of accounting standards by individual accounting is universally valid’

and ‘differences in cultural values across countries could lead to differences in recognition

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

and disclosure decision based on those interpretations.’ (ibid.) In addition, Doupnik and

Richter (2004) supported the idea that Gray’s conservatism hypothesis extend to the

more developed Latin cultural area.

Perera (1989) added a further element to Gray’s (1988) theory by injecting the

notion of accounting values into the analysis of the development of accounting practices.

Perera’s accounting practice values were: the authority for accounting systems, the

capacity to enforce accounting uniformity, the foundation for the measurement basis,

and the boundaries for the parameters – transparency and secrecy – used in respect of

information disclosure. To Perera, there was a positive relationship between authorityand professionalism, uniformity and enforcement, conservatism and measurement,and transparency and disclosure. In addition, Perera and Matthews (1990) have

claimed that cultural dimensions of uncertainty avoidance and individualism exert

the strongest influence on accounting values (p.265), simply as a result of the positive

effects of individualism and negative effects of weak uncertainty avoidance on Gray’s

professionalism, flexibility, optimism and transparency.

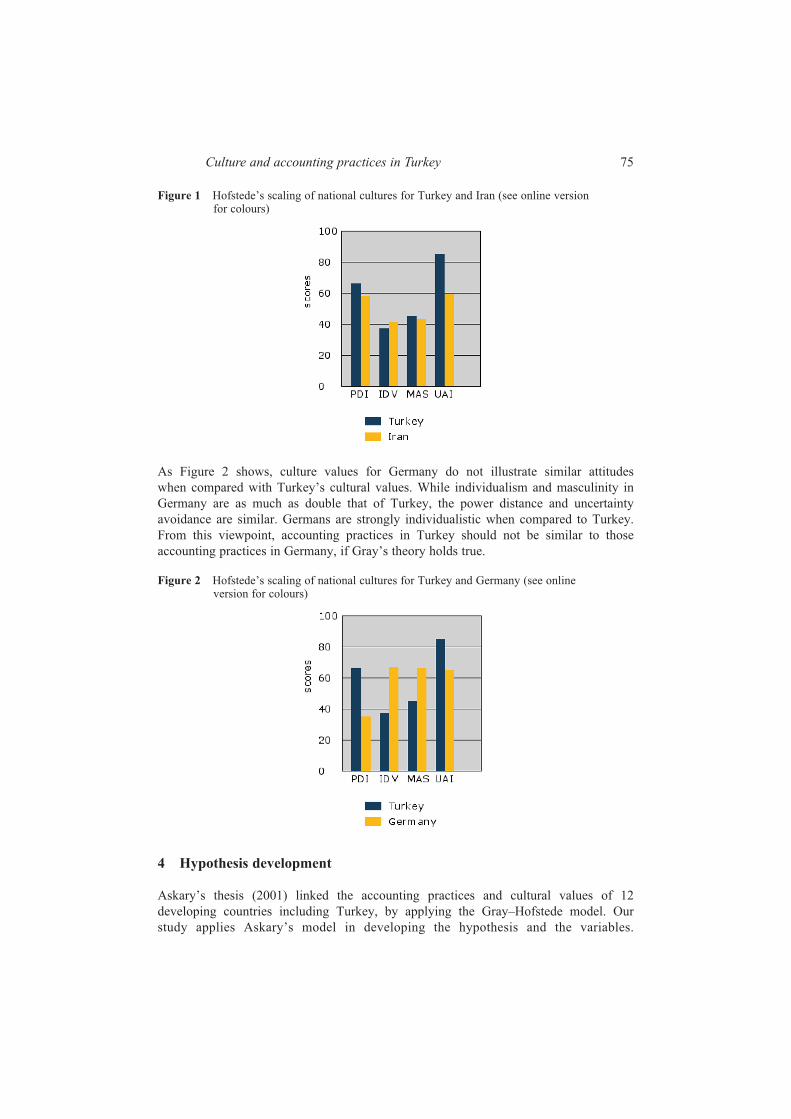

Turkey is one of the Middle Eastern countries that was studied by Hofstede (1980).

Table 3 shows the Hofstede scale of socio-cultural values in Turkey. Turkey is classified

relatively low on individualism and masculinity, but higher on power distance and

uncertainty avoidance.

The scores for uncertainty avoidance and power distance are relatively high, consistent

with the fact that these societies have highly rule-oriented laws and controls. These

cultures are more likely to cause significant downward mobility of its citizens. By

combining the two dimensions, it creates a situation where leaders have virtually ultimate

power and authority, and the rules, laws and regulations developed by those in power,

reinforce their own leadership and control.

We compare the Hofstede scales for Turkey, Germany, and Iran. Iran is a Muslim

country and Turkey’s close neighbour and they share many common socio-cultural values.

Germany is a European country and has many historical and political relationships with

Turkey. Iran has high uncertainty avoidance and power distance which are almost similar

to Turkey. This indicates – at the time of the survey in 1972 – that Iran had a moderate

application of these two Hofstede dimensions when compared with other countries.

However, with the over-throw of the Shah in January of 1979, and the subsequent turning

toward Islamic values, the current Hofstede dimensions for Iran should be closer to

Muslim countries in terms of higher uncertainty avoidance and power distance rankings.

Iran’s highest dimension ranking was uncertainty avoidance at 59, which indicates the

society’s low level of tolerance for uncertainty, compared to Turkey’s ranking of 85.

Figure 1 compares Iran and Turkey in Hofstede’s study.

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

74 S. Askary, H. Yazdifar and D. Askarany

Table 3 Hofstede’s scaling of national cultures for Turkey

Individualism Power distance Uncertainty avoidance MasculinityIndex Rank Index Rank Index Rank Index Rank

37 24 66 34–35 85 34–35 45 20–21

Low Low High High High High Low Low

Culture and accounting practices in Turkey 75

As Figure 2 shows, culture values for Germany do not illustrate similar attitudes

when compared with Turkey’s cultural values. While individualism and masculinity in

Germany are as much as double that of Turkey, the power distance and uncertainty

avoidance are similar. Germans are strongly individualistic when compared to Turkey.

From this viewpoint, accounting practices in Turkey should not be similar to those

accounting practices in Germany, if Gray’s theory holds true.

4 Hypothesis development

Askary’s thesis (2001) linked the accounting practices and cultural values of 12

developing countries including Turkey, by applying the Gray–Hofstede model. Our

study applies Askary’s model in developing the hypothesis and the variables.

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

Figure 1 Hofstede’s scaling of national cultures for Turkey and Iran (see online versionfor colours)

Figure 2 Hofstede’s scaling of national cultures for Turkey and Germany (see onlineversion for colours)

According to Gray (1988), accounting practices in Turkey should have the attributes

originating from its specific cultural values. We use the Hofstede study of Turkish

cultural attributes and Gray’s hypotheses to determine how accounting practices in

Turkey are affected as a result of the Turkish cultural values. These values can be seen to

affect the accounting practices (AP) in Turkey as formulated in Table 2. The relationship

between the accounting-function and cultural values can be represented as follows:

AP = f(PD, UA, MAS, IND), where PD, UA, MAS, and IND indicate power distance,

uncertainty avoidance, masculinity, and individualism respectively. APs, as Perera (1989)

explained, are demonstrated in four different aspects: accounting authority, disclosure,

enforcement, and measurement. A brief explanation of each aspect is presented below.

4.1 Accounting authorityWhen accounting values orient towards statutory controls, then accounting practices

are governed more by legal requirements and less by the application of professional judgement.

Professionalism requires that only professional accounting bodies as a unique group, make

judgements regarding accounting practices, such as, asset and income measurements or

valuations as well as various aspects of disclosures of financial information for different users.

By referring to Haniffa and Cooke’s (2002) study, Table 4 represents the relationship

between Hofstede’s societal values and Gray’s hypotheses regarding accounting

professionalism.

Table 4 is a result of consolidation of Tables 2 and 3. It is a combination of the

Hofstede (1980) scales and Gray’s (1988) hypotheses about accounting authority in

Turkey which is expected to have more statutory controls and less professionalism.

If this initial prediction for the accounting authority holds good, then the first

hypothesis of this study is:

Hypothesis 1: in Turkey, professional bodies are under a statutory control domain

rather than professionalism.

4.2 Accounting disclosureDisclosure in the Gray model is concerned with transparency or secrecy. Transparency is

a preference to unveil comprehensive financial information about different elements of

financial statements and for a broad range of users. Secrecy represented a preference for

a cautious approach to disclosing financial information as a result of the influence of

management on both the quantity and quality of information presented to outside users.

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

76 S. Askary, H. Yazdifar and D. Askarany

Table 4 Cultural values and Gray’s hypothesis of accounting professionalism in Turkey

Hofstede societal values Turkey’s values The predicted accounting value under Gray’s theory

Power distance High High statutory control

Masculinity Low

Uncertainty avoidance High

Individualism Low

Culture and accounting practices in Turkey 77

The Hofstede–Gray model of financial-information disclosures in Turkey reveals a

low level of transparency, in other words, high secrecy, as Table 5 illustrates.

If we consider Table 5 to be an initial prediction of financial disclosures in Turkey,

then the following hypothesis is plausible:

Hypothesis 2: listed companies in Turkey are secret rather than transparent in

disclosing financial information.

4.3 Accounting enforcementUniformity, as defined by Gray (1988, p.8), is a preference for applying similar

accounting practices within companies and for the consistent use of such practices

over time periods. This definition covers two dimensions. First, there is inter-temporal

consistency in accounting practices and; second, the uniformity in application of accounting

policies and procedures.

Similar to previous tables, Table 6 is derived from the Gray’s (1988) study, showing

the normative accounting enforcement in Turkey, that is, a desire for a uniform approach

in applying accounting methods because of high power distance and uncertainty avoidance

and low individualism.

If we assume Table 6 to be an initial predictor about accounting enforcement in Turkey,

then the following hypothesis should be testable:

Hypothesis 3: listed companies in Turkey are uniform rather than flexible in applying

diverse accounting methods.

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

Table 6 Cultural values and Gray’s hypothesis of uniformity in Turkey

Hofstede societal values Turkey’s values The predicted accounting value under Gray’s theory

Power distance High High uniformity

Masculinity Low

Uncertainty avoidance High

Individualism Low

Source: Tables 1 and 2

Table 5 Cultural values and Gray’s hypothesis of financial disclosures in Turkey

Hofstede societal values Turkey’s values The predicted accounting value under Gray’s theory

Power distance High High secrecy

Masculinity Low

Uncertainty avoidance High

Individualism Low

Source: Tables 1 and 2

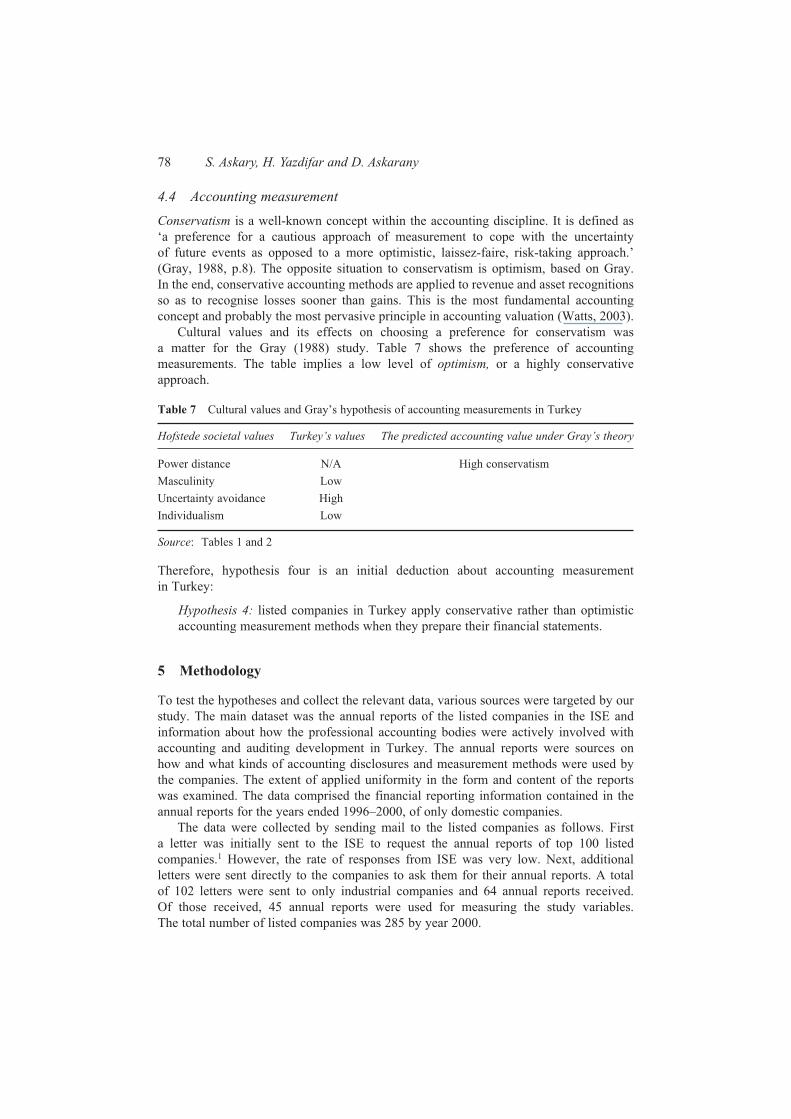

4.4 Accounting measurementConservatism is a well-known concept within the accounting discipline. It is defined as

‘a preference for a cautious approach of measurement to cope with the uncertainty

of future events as opposed to a more optimistic, laissez-faire, risk-taking approach.’

(Gray, 1988, p.8). The opposite situation to conservatism is optimism, based on Gray.

In the end, conservative accounting methods are applied to revenue and asset recognitions

so as to recognise losses sooner than gains. This is the most fundamental accounting

concept and probably the most pervasive principle in accounting valuation (Watts, 2003).

Cultural values and its effects on choosing a preference for conservatism was

a matter for the Gray (1988) study. Table 7 shows the preference of accounting

measurements. The table implies a low level of optimism, or a highly conservative

approach.

Therefore, hypothesis four is an initial deduction about accounting measurement

in Turkey:

Hypothesis 4: listed companies in Turkey apply conservative rather than optimistic

accounting measurement methods when they prepare their financial statements.

5 Methodology

To test the hypotheses and collect the relevant data, various sources were targeted by our

study. The main dataset was the annual reports of the listed companies in the ISE and

information about how the professional accounting bodies were actively involved with

accounting and auditing development in Turkey. The annual reports were sources on

how and what kinds of accounting disclosures and measurement methods were used by

the companies. The extent of applied uniformity in the form and content of the reports

was examined. The data comprised the financial reporting information contained in the

annual reports for the years ended 1996–2000, of only domestic companies.

The data were collected by sending mail to the listed companies as follows. First

a letter was initially sent to the ISE to request the annual reports of top 100 listed

companies.1 However, the rate of responses from ISE was very low. Next, additional

letters were sent directly to the companies to ask them for their annual reports. A total

of 102 letters were sent to only industrial companies and 64 annual reports received.

Of those received, 45 annual reports were used for measuring the study variables.

The total number of listed companies was 285 by year 2000.

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

78 S. Askary, H. Yazdifar and D. Askarany

Table 7 Cultural values and Gray’s hypothesis of accounting measurements in Turkey

Hofstede societal values Turkey’s values The predicted accounting value under Gray’s theory

Power distance N/A High conservatism

Masculinity Low

Uncertainty avoidance High

Individualism Low

Source: Tables 1 and 2

Culture and accounting practices in Turkey 79

In addition to the contents of annual reports, the study also focused on other aspects

such as information about the accounting and auditing standards setting process, the

professional bodies, and how the members were involved in developing and implementing

the accounting and auditing regulations. Accordingly, further letters were sent to all

professional bodies asking them for any information helpful for the purposes of this study.

Finally, we used all the information available on the webpages of Turkish and non-Turkish

weblogs which was considered to be helpful for the purpose of the study. The rest of

the section is divided into four subsections, each section deals with the variables for testing

of the four hypotheses of the study.

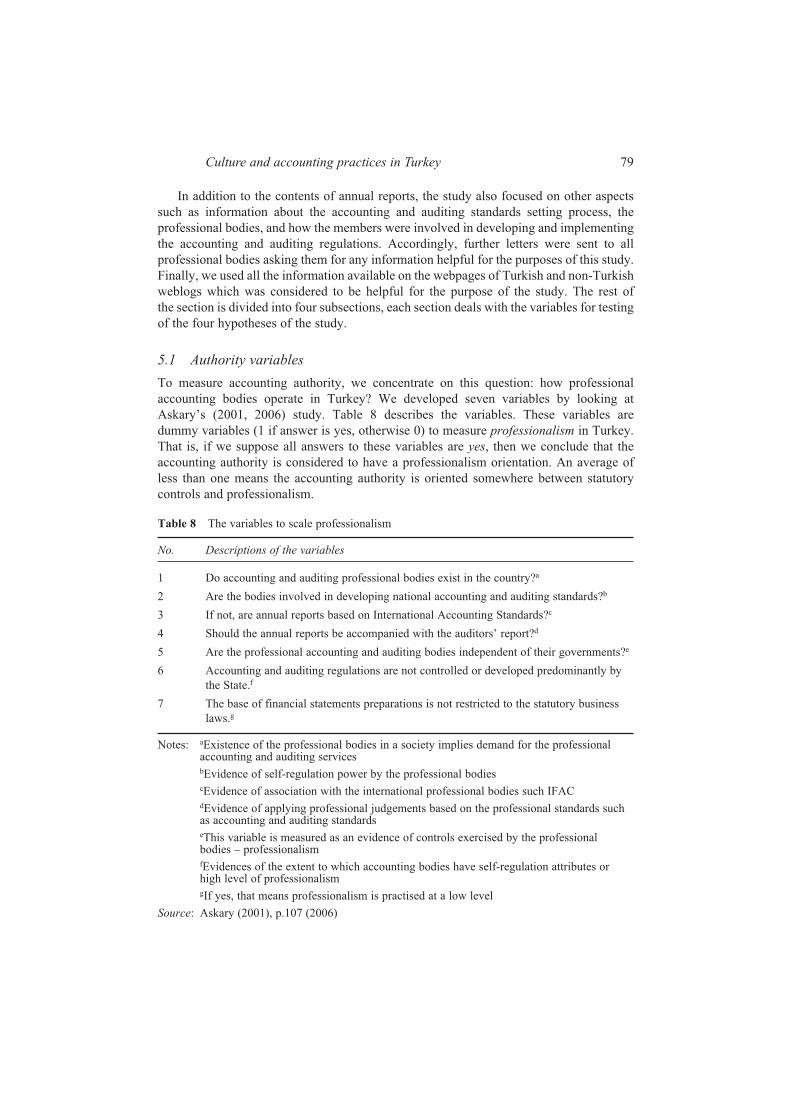

5.1 Authority variablesTo measure accounting authority, we concentrate on this question: how professional

accounting bodies operate in Turkey? We developed seven variables by looking at

Askary’s (2001, 2006) study. Table 8 describes the variables. These variables are

dummy variables (1 if answer is yes, otherwise 0) to measure professionalism in Turkey.

That is, if we suppose all answers to these variables are yes, then we conclude that the

accounting authority is considered to have a professionalism orientation. An average of

less than one means the accounting authority is oriented somewhere between statutory

controls and professionalism.

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

Table 8 The variables to scale professionalism

No. Descriptions of the variables

1 Do accounting and auditing professional bodies exist in the country?a

2 Are the bodies involved in developing national accounting and auditing standards?b

3 If not, are annual reports based on International Accounting Standards?c

4 Should the annual reports be accompanied with the auditors’ report?d

5 Are the professional accounting and auditing bodies independent of their governments?e

6 Accounting and auditing regulations are not controlled or developed predominantly by

the State.f

7 The base of financial statements preparations is not restricted to the statutory business

laws.g

Notes: aExistence of the professional bodies in a society implies demand for the professionalaccounting and auditing servicesbEvidence of self-regulation power by the professional bodiescEvidence of association with the international professional bodies such IFACdEvidence of applying professional judgements based on the professional standards suchas accounting and auditing standardseThis variable is measured as an evidence of controls exercised by the professionalbodies – professionalismfEvidences of the extent to which accounting bodies have self-regulation attributes orhigh level of professionalismgIf yes, that means professionalism is practised at a low level

Source: Askary (2001), p.107 (2006)

According to Askary (2001, 2006), the first variable measures how important for a

society is to have accounting and auditing professional bodies? The existence of the bodies

is an initial step in examining the development of professionalism of accountants

and auditors. The second variable determines the degree of the professional bodies’

involvement in developing accounting and auditing standards. If, for example, the

government totally controls the standard-setting development, then professionalism

would be at the lowest level. The third variable is about national accounting and auditing

standards. To have national accounting and auditing standards or adopting IASs consider

as 1 otherwise 0. Variable four is about how professional judgements are applied to

the financial statements by members of accounting bodies. The fifth and sixth variables

measure professional independence in term of developing the professional standards for

members. The last variable measures the extent to which financial report preparation

reflects the requirements of business law (statutory control) or reflects established

accounting standards.

5.2 Financial-disclosure variablesDisclosures of financial information by listed companies to the public, as required

by organisations such as SEC, leading the capital markets to higher efficiency, are

another accounting practice to be linked to cultural values in Gray’s (1998) model.

An accumulated body of literature on compliance with IFRSs exists; for example

see Dumontier and Raffournier (1998); Murphy (1999); Street and Bryant (2000); and

Street and Gray (2001). For the purposes of this study, a disclosure index is taken from

the study of Askary (2001) and Askary and Jackling (2005). Using a dummy variable

approach, for every item disclosed in the financial statements of listed companies the

value is one, otherwise zero. To reduce subjectivity in determining the applicable items,

first the entire annual report was read to determine its applicability. In addition, all of

the reports were initially read and coded by one person for consistency.

Table 9 shows a description of seven variables adopted from the Askary (2001)

and Askary and Jackling (2005) studies. The only difference is related to variable 2 which

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

80 S. Askary, H. Yazdifar and D. Askarany

Table 9 Financial disclosure variables

No. Descriptions of the variables

1 Willingness of firms to be open (transparent) to the public

2 Disclosures of fundamental accounting assumption and general information about entitya

3 Disclosures required by IFAC for Balance sheet

4 Disclosures required by IFAC for Profit and Loss Statement

5 Disclosures required by IFAC for Cash flow statement

6 Disclosures required by IFAC for accounting policies

7 Disclosures of notes to financial statements as required by IFAC

Note: aAs these requirements are necessitated by IFRS 1, item 13, 5 items 7 and 9, andIFRS 14, item 9

Source: Askary and Jacking (2005), p.54

Culture and accounting practices in Turkey 81

is a mix of both variable 2 and 3 in the Askary (2001) and Askary and Jackling (2005)

studies. That is ‘disclosure of fundamental accounting assumption’ and ‘general

information about entity’ is mixed into single variable 2 as ‘disclosure of fundamental

accounting assumption and general information about entity’. All other assumptions

used by Askary and Askary and Jackling were valid for this study.

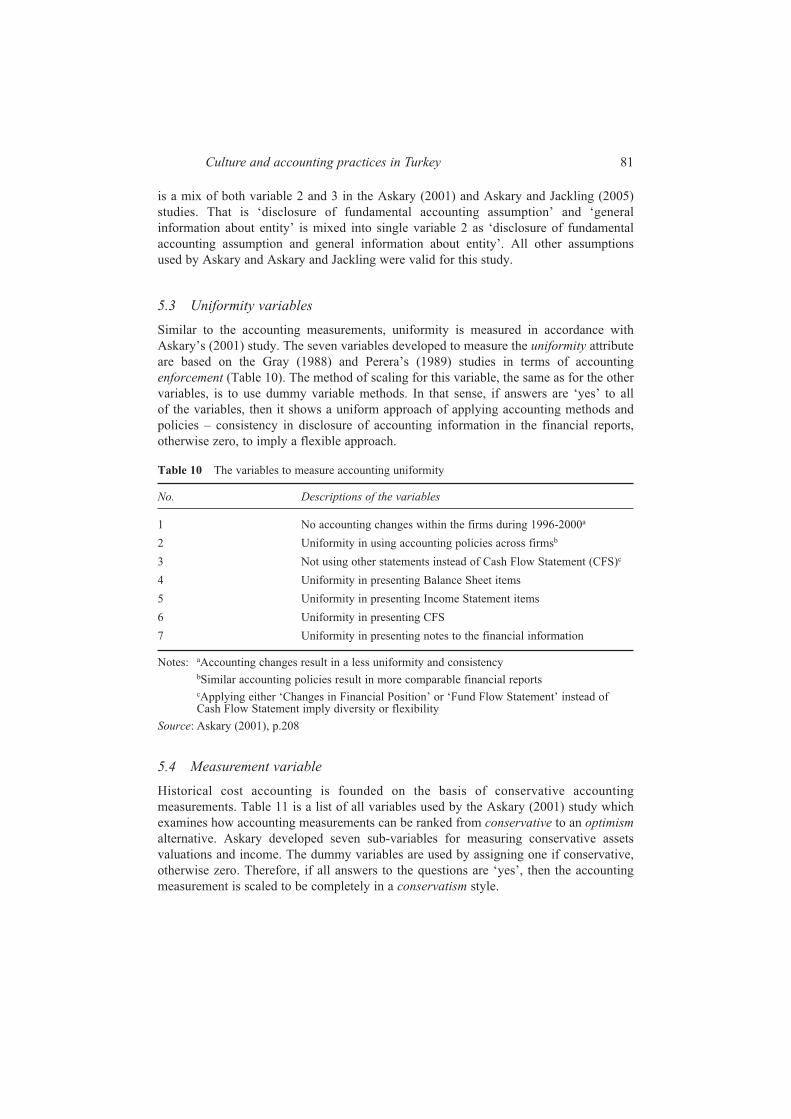

5.3 Uniformity variablesSimilar to the accounting measurements, uniformity is measured in accordance with

Askary’s (2001) study. The seven variables developed to measure the uniformity attribute

are based on the Gray (1988) and Perera’s (1989) studies in terms of accounting

enforcement (Table 10). The method of scaling for this variable, the same as for the other

variables, is to use dummy variable methods. In that sense, if answers are ‘yes’ to all

of the variables, then it shows a uniform approach of applying accounting methods and

policies – consistency in disclosure of accounting information in the financial reports,

otherwise zero, to imply a flexible approach.

5.4 Measurement variableHistorical cost accounting is founded on the basis of conservative accounting

measurements. Table 11 is a list of all variables used by the Askary (2001) study which

examines how accounting measurements can be ranked from conservative to an optimismalternative. Askary developed seven sub-variables for measuring conservative assets

valuations and income. The dummy variables are used by assigning one if conservative,

otherwise zero. Therefore, if all answers to the questions are ‘yes’, then the accounting

measurement is scaled to be completely in a conservatism style.

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

Table 10 The variables to measure accounting uniformity

No. Descriptions of the variables

1 No accounting changes within the firms during 1996-2000a

2 Uniformity in using accounting policies across firmsb

3 Not using other statements instead of Cash Flow Statement (CFS)c

4 Uniformity in presenting Balance Sheet items

5 Uniformity in presenting Income Statement items

6 Uniformity in presenting CFS

7 Uniformity in presenting notes to the financial information

Notes: aAccounting changes result in a less uniformity and consistencybSimilar accounting policies result in more comparable financial reportscApplying either ‘Changes in Financial Position’ or ‘Fund Flow Statement’ instead ofCash Flow Statement imply diversity or flexibility

Source: Askary (2001), p.208

6 Results

Table 12 summarises all actual averages of the seven variables applied respectively to

each accounting practice as follows.

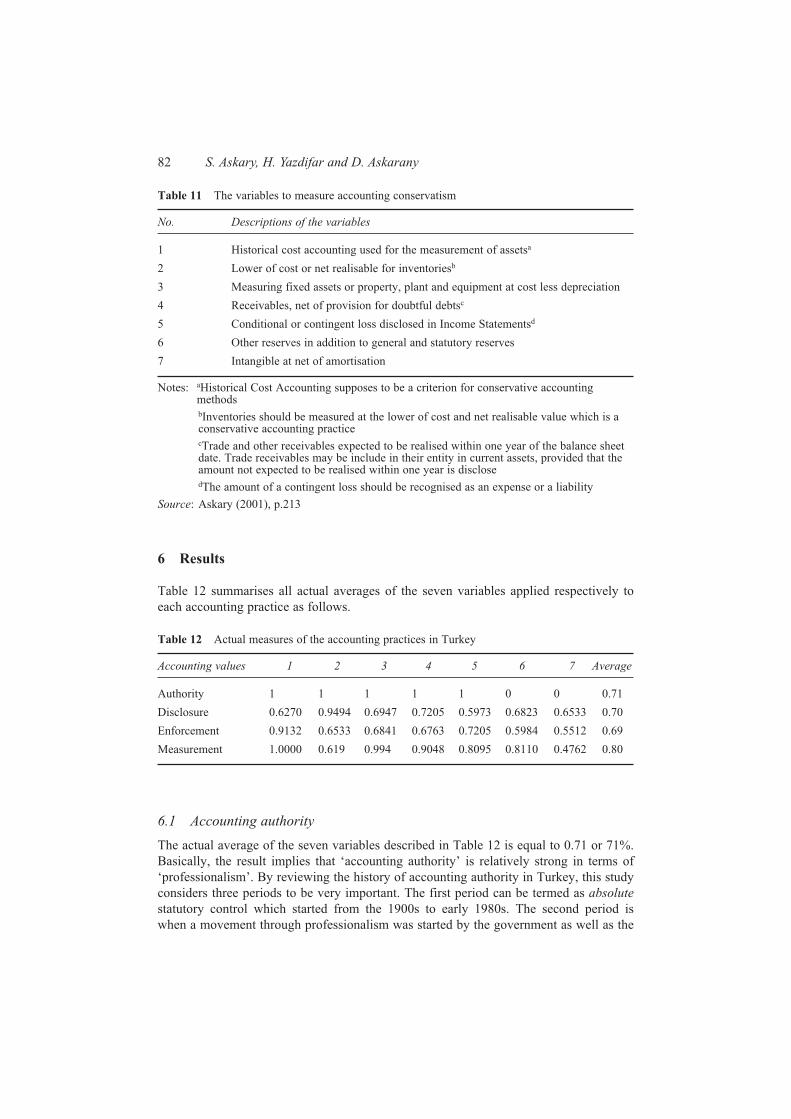

6.1 Accounting authorityThe actual average of the seven variables described in Table 12 is equal to 0.71 or 71%.

Basically, the result implies that ‘accounting authority’ is relatively strong in terms of

‘professionalism’. By reviewing the history of accounting authority in Turkey, this study

considers three periods to be very important. The first period can be termed as absolutestatutory control which started from the 1900s to early 1980s. The second period is

when a movement through professionalism was started by the government as well as the

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

82 S. Askary, H. Yazdifar and D. Askarany

Table 11 The variables to measure accounting conservatism

No. Descriptions of the variables

1 Historical cost accounting used for the measurement of assetsa

2 Lower of cost or net realisable for inventoriesb

3 Measuring fixed assets or property, plant and equipment at cost less depreciation

4 Receivables, net of provision for doubtful debtsc

5 Conditional or contingent loss disclosed in Income Statementsd

6 Other reserves in addition to general and statutory reserves

7 Intangible at net of amortisation

Notes: aHistorical Cost Accounting supposes to be a criterion for conservative accountingmethodsbInventories should be measured at the lower of cost and net realisable value which is aconservative accounting practicecTrade and other receivables expected to be realised within one year of the balance sheetdate. Trade receivables may be include in their entity in current assets, provided that theamount not expected to be realised within one year is disclosedThe amount of a contingent loss should be recognised as an expense or a liability

Source: Askary (2001), p.213

Table 12 Actual measures of the accounting practices in Turkey

Accounting values 1 2 3 4 5 6 7 Average

Authority 1 1 1 1 1 0 0 0.71

Disclosure 0.6270 0.9494 0.6947 0.7205 0.5973 0.6823 0.6533 0.70

Enforcement 0.9132 0.6533 0.6841 0.6763 0.7205 0.5984 0.5512 0.69

Measurement 1.0000 0.619 0.994 0.9048 0.8095 0.8110 0.4762 0.80

Culture and accounting practices in Turkey 83

professional bodies, which occurred from 1980 to 1990. And finally the third period

started with the movement toward an enhanced improvement in accounting

professionalism from the 1990s until now. From this viewpoint then, the result of the

study for professionalism is valid due to the conformity of our variables measured with

the recent movements toward professionalism over past years.

The variables 6 and 7 with 0 scales represent a statutory-control feature of the

accounting practice in Turkey, and the variables 1–5 show entirely professionalism.

Thus, by looking at the figure, one can conclude that accounting authority in Turkey

tends toward professionalism. Therefore, Hypothesis 1 is rejected by the results and

Gray’s theory in regard to this accounting practice is not acceptable for Turkey. In order

words, large power distance and high uncertainty avoidance as well as collectivism

does not affect professionalism in Turkey. One possible reason for this is the recent

movements by the accounting profession and the government in Turkey towards the

harmonisation of accounting reporting practices with International Financial Accounting

Standards.

6.2 Financial disclosuresMost research applying Gray’s secrecy/transparency hypothesis has concentrated on the

relationship between cultural values and disclosures represented in corporate financial

reports (Baydoun and Gray, 1990; Belkaoui, 1997; Gray and Vint, 1995; Harrison and

McKinnon, 1986; Hope, 2002; Jaggi and Low, 2000; Zarzeski, 1996). Transparency is all

about quality disclosure of financial information as well as a willingness to be open to

users on a timely basis. The willingness attitude of managers of the listed companies in

Turkey depends on their attitude toward providing the public with full financial disclosure.

Variable 1 is measured by considering the fact of how the companies, have an overall

desire to be open to disclosing their financial information to the public. Due to the fact that

we did not have an answer to the question from a reliable source or a past study, we

measured the sub-variable by dividing the number of requested-letters sent to the

companies (102 letters) by the number of annual reports received from them (64 annual

reports), that is, 62.7% and an indication of a mid tendency towards transparency in

respect of being open to users.

Other variables, as shown in Table 12, are ordered from the low average to high and

depicted in Figure 3. This figure illustrates that variable 5 and 2 are two limits of financial

disclosures in terms of low and high transparency. Variables 2 and 7 have the highest

degree of transparency and variables 1, 7, 6, and 3 have an average close to the total

average of the variables for transparency – 0.70 or 70%. Thus, Hypothesis 2 is rejected by

the actual average of the study and Gray’s theory in predicting financial disclosure in

Turkey does not apply. In order words, large power distance and high uncertainty

avoidance as well as collectivism cannot affect financial disclosures in Turkey. Consistent

with variable 1, the possible reason for this is the adoption of the International Financial

Accounting Standards for Turkey’s national accounting and auditing standards.

6.3 EnforcementThe results show that accounting enforcement has a preference toward a uniform approach

in presenting financial information and consistency in applying accounting methods for

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

the period 1996–2000. The results are also consistent with the background of accounting

in Turkey: the tax procedures code and the uniform chart of accounts prescribe

homogeneous accounting practices within the listed companies through prescribing a code

of accounts and a format for the presentation of financial statements. These formats are

obligatory for all companies as prescribed by government through the MOF, particularly

for tax purposes.

Figure 4 confirms that variables 7 and 1 hold the lowest and highest level uniformity.

Variable 7 – no accounting changes within the firms during 1996–2000 – has the lowest

average which may relate to high uncertainty avoidance. Variables 2–4 have close

averages and are located between the averages of variables 6 and 5. As a result, the study

– in term of accounting enforcement – confirms Hypothesis 3 and verifies that high power

distance and uncertainty avoidance and low individualism are positively associated with

accounting uniformity. Thus, Gray’s hypothesis is confirmed by the results of the study.

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

84 S. Askary, H. Yazdifar and D. Askarany

Figure 3 The limit of transparency in accounting disclosures in Turkey

Figure 4 The limit of uniformity in accounting enforcement in Turkey

Culture and accounting practices in Turkey 85

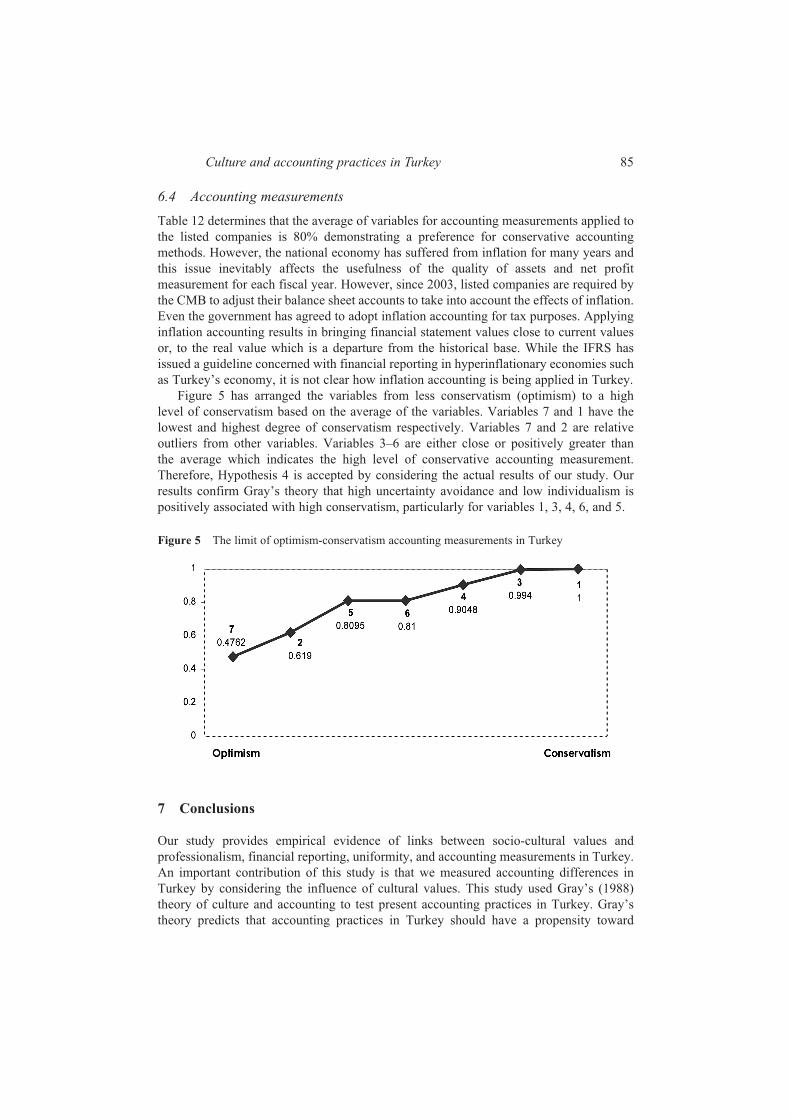

6.4 Accounting measurementsTable 12 determines that the average of variables for accounting measurements applied to

the listed companies is 80% demonstrating a preference for conservative accounting

methods. However, the national economy has suffered from inflation for many years and

this issue inevitably affects the usefulness of the quality of assets and net profit

measurement for each fiscal year. However, since 2003, listed companies are required by

the CMB to adjust their balance sheet accounts to take into account the effects of inflation.

Even the government has agreed to adopt inflation accounting for tax purposes. Applying

inflation accounting results in bringing financial statement values close to current values

or, to the real value which is a departure from the historical base. While the IFRS has

issued a guideline concerned with financial reporting in hyperinflationary economies such

as Turkey’s economy, it is not clear how inflation accounting is being applied in Turkey.

Figure 5 has arranged the variables from less conservatism (optimism) to a high

level of conservatism based on the average of the variables. Variables 7 and 1 have the

lowest and highest degree of conservatism respectively. Variables 7 and 2 are relative

outliers from other variables. Variables 3–6 are either close or positively greater than

the average which indicates the high level of conservative accounting measurement.

Therefore, Hypothesis 4 is accepted by considering the actual results of our study. Our

results confirm Gray’s theory that high uncertainty avoidance and low individualism is

positively associated with high conservatism, particularly for variables 1, 3, 4, 6, and 5.

7 Conclusions

Our study provides empirical evidence of links between socio-cultural values and

professionalism, financial reporting, uniformity, and accounting measurements in Turkey.

An important contribution of this study is that we measured accounting differences in

Turkey by considering the influence of cultural values. This study used Gray’s (1988)

theory of culture and accounting to test present accounting practices in Turkey. Gray’s

theory predicts that accounting practices in Turkey should have a propensity toward

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

Figure 5 The limit of optimism-conservatism accounting measurements in Turkey

statutory controls in accounting authority, secrecy in regard to disclosing financial

statements, and using uniform but conservative accounting methods in measuring

financial statement elements. Our results confirm Gray’s prediction of uniformity

in applying accounting methods and applying conservative measurements; however, the

actual results signified opposite attributes for professionalism for accounting authority and

transparency in disclosures of financial information.

Our results confirm Gray’s theory that high uncertainty avoidance and low

individualism is positively associated with high conservatism. In addition, the study – in

terms of accounting enforcement – confirms Hypothesis 3 and verifies that the highest

power distance and uncertainty avoidance and lowest individualism are positively

associated with accounting uniformity. However, large power distance and high

uncertainty avoidance as well as collectivism do not affect professionalism and financial

disclosures in Turkey. Our results on the accounting practices in Turkey are consistent

with the results from Askary (2001, 2006) and Askary and Jackling (2005).

It seems then that the influence of culture on the accounting profession in Turkey has

diminished as a result of Turkey’s drive to become part of the EU. First of all, there is a

conflict between some of the Turkish national or cultural values and European demands.

In addition, the convergence of accounting practices to the EU style minimises the effect

of national culture in Turkey which is a developing country and the only Muslim nation

in Europe which departs from the typical European culture. Thus, Turkish cultural values

should demonstrate conformity with the commissioners of the EU directives if the country

wants to become a fully-fledged accepted member of the EU.

There are some limitations of this study. Firstly, the findings should be interpreted

with some caution, particularly in terms of the generalisation of results. Secondly, the

study did not perform further statistical tests. Thirdly, the study used the Hofstede (1980)

study that has been widely used by more than 600 studies (Askary, 2001). However,

Hofstede’s theory has been criticised by Baskerville (2003).

References

Archambault, J.J. and Archambault, M.E. (2003) ‘A multinational test of determinations ofcorporate disclosure’, The International Journal of Accounting, Vol. 38, pp.173–194.

Askary, S. (2001) ‘The influence of Islamic culture on the accounting values and practices ofMuslim countries’, Doctoral Dissertation, The University of Newcastle, Newcastle,Australia.

Askary, S. (2006) ‘Accounting Professionalism – a cultural perspective of developing countries’,Managerial Auditing Journal, Vol. 21, Nos. 1/2, pp.102–111.

Askary, S. and Jackling, B. (2005) ‘Corporate financial disclosure practices in Asian and MiddleEast Countries’, Asian Review of Accounting, Vol. 13, No. 1, pp.45–72.

Baskerville, R.F. (2003) ‘Hofstede never studied culture’, Accounting, Organizations and Society,Vol. 28, No. 1 (14), pp.1–14.

Baydoun, N. and Gray, R. (1990) ‘Financial accounting and reporting in the Lebanon: anexploratory study of accounting in hyperinflationary conditions’, Research in Third WorldAccounting, Vol. 1, pp.227–262.

Belkaoui, A. (1990) Judgment in International Accounting: A Theory of Cognition, Cultures,Language, and Contracts, New York: Quorum Books.

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

86 S. Askary, H. Yazdifar and D. Askarany

Culture and accounting practices in Turkey 87

Belkaoui, A.R. (1996) ‘Political, financial, and economic risks and accounting disclosurerequirements of global stock exchanges’, Research in Accounting Regulation, Vol. 10,pp.179–191.

Belkaoui, A.R. (1997) The Nature and Determinants of Disclosure Adequacy: An InternationalPerspective, New York: Quorum Books.

Chanchani, S. and Willett, R. (2004) ‘An empirical assessment of Gray’s accounting valueconstructs’, International Journal of Accounting, Vol. 39, No. 2, pp.125–154.

Cooke, T.E. and Curuk, T. (1996) ‘Accounting in Turkey with reference to the particular problemsof lease transactions’, The European Accounting Review, Vol. 5, No. 2, pp.339–359.

Demirag, I.S. (1993) ‘Development of Turkish capitalism and accounting regulation in Turkey’,Research in Third World Accounting, Vol. 2, pp.97–120.

Doupnik, T.S. and Salter, S.B. (1995) ‘External environment, culture and accounting practices: apreliminary test of a general model of international accounting development’, The InternationalJournal of Accounting, Vol. 30, pp.189–207.

Doupnik, T.S. and Richter, M. (2004) ‘The impact of culture on the interpretation of ‘in-context’verbal probability expression’, Journal of International Accounting Research, Vol. 3. pp.1–20.

Doupnik, T.S. and Riccio E.L. (2006) ‘The influence of conservatism and secrecy on theinterpretation of verbal probability expression in the Anglo and Latin cultural areas’,The International Journal of Accounting, Vol. 41, pp.237–261.

Dumontier, P. and Raffournier, B. (1998) Why firms comply voluntarily with IFRS: an empiricalanalysis with Swiss data’, Journal of International Financial Management and Accounting,Vol. 9, No. 3, pp.216–245.

Fechner, H.H.E. and Kilgore, A. (1994) ‘The influence of cultural factors on accounting practice’,The International Journal of Accounting, Vol. 29, pp.265–277.

Gray, S.J. (1988) ‘Towards a theory of cultural influence on the development of accounting systemsinternationally’, Abacus, Vol. 24, No. 1, pp.1–15.

Gray, S.J. and Vint, H.M. (1995) ‘The impact of culture on accounting disclosures: someinternational evidence’, Asia-Pacific Journal of Accounting, pp.33–43.

Hamid, S., Craig, R. and Clarke, F. (1993) ‘Religion: a confounding cultural element in theinternational harmonization of accounting?’, Abacus, Vol. 29, No. 2, pp.131–148.

Haniffa, R.M. and Cooke, T.F. (2002) ‘Culture, corporate governance and disclosure in Malaysiancorporations’, Abacus, Vol. 38, No. 3, pp.317–349.

Harrison, G.L. and McKinnon, J.L. (1986) ‘Cultural and accounting change: a new perspective oncorporate reporting regulation and accounting policy formulation’, Accounting, Organizationsand Society, Vol. 11, No. 3, pp.233–252.

Hofstede, G. (1997) Cultures and Organizations; Software of Mind, New York: McGraw-Hill.

Hofstede, G. (1980) Culture’s Consequences: International Differences in Work-related Values,Beverly Hills, California, USA: Sage Publications.

Hope, O.K. (2002) ‘Firm-level disclosures and the relative roles of culture and legal origin’,Journal of International Financial Management and Accounting, Vol. 14, pp.218–248.

Jaggi, B. and Low, P.Y. (2000) ‘Impact of culture, market forces, and legal system on financialdisclosures’, The International Journal of Accounting, Vol. 35, pp.495–519.

Mueller, G.G., Gernon, H. and Meek, G. (1994) Accounting: An International Perspective,New York: Business One Irwin.

Murphy, A. (1999) ‘Firm characteristics of Swiss companies that utilize International AccountingStandards’, The International Journal of Accounting, Vol. 34, No. 1, pp.121–131.

Perera, H. (1994) ‘Culture and international accounting: some thoughts on research issues andprospects’, Advances in International Accounting, Vol. 7, pp.267–285.

Perera, M.H.B. (1989) ‘Towards a framework to analyse the impact of culture on accounting’,The International Journal of Accounting, Vol. 4, No. 1, pp.42–56.

111

2

3

4

5

6

7

8

9

1011

1

2

3

4

5

6

7

8

9

2011

1

2

3

4

5

6

7

8

9

30

1

2

3

4

5

6

7

8

9

40

1

2

3

4

5

6

711

8

Perera, M.H.B. and Mathews, M.R. (1990) ‘The cultural relativity of accounting and internationalpatterns of social accounting’, Advances in International Accounting, Vol. 3, pp.215–251.

Radebaugh, L.H. and Gray, S.J. (2002) International Accounting and Multinational Enterprises,5th edn., New York: John Wiley and Sons.

Salter, S. and Niswaner, R. (1995) ‘Cultural influence on the development of accounting systemsinternationality: a test of Gray’s (1988) theory’, Journal of International Business Studies,Vol. 26, No. 2, pp.379–398.

Simga-Mugan, C. (1995) ‘Accounting in Turkey’, The European Accounting Review, Vol. 4,No. 2, pp.351–371.

Street, D.L. and Bryant, S.M. (2000) ‘Disclosure level and compliance with IASs: a comparison ofcompanies with and without US listings and filings’, The International Journal of Accounting,Vol. 35, No. 3, pp.305–329.

Street, D.L. and Gray, S.J. (2001) Observance of International Accounting Standards: FactorsExplaining Noncompliance, Glasgow: The Association of Chartered Certified Accountants.

Sudarwan, M. and Fogarty, T.J. (1996) ‘Culture and accounting in Indonesia: an empiricalexamination’, The International Journal of Accounting, Vol. 31, No. 4, pp.463–481.

World Fact Book (2005) Available from: http://www.cia.gov/cia/publications/factbook/.

Watts, R. (2003) ‘Conservatism in accounting Part I: explanations and implications’, AccountingHorizons, Vol. 17, No. 3, pp.207–221.

Zarzeski, M.T. (1996) ‘Spontaneous harmonization effects of culture and market forces onaccounting disclosure practices’, Accounting Horizons, Vol. 10, pp.18–37.

Note

1 By applying the statistical sampling techniques from homogenous samples, only non-financialcompanies were selected.

111

2

3