CRITICAL SUCCESS FACTORS IN E-BANKING: AN INDIAN PERSPECTIVE

15

IRJMST Vol 5 Issue 9 [Year 2014] ISSN 2250 – 1959 (0nline) 2348 – 9367 (Print) International Research Journal of Management Science & Technology http://www.irjmst.com Page 38 CRITICAL SUCCESS FACTORS IN E-BANKING: AN INDIAN PERSPECTIVE Mrs. Megha Singh Institute of Management Studies & Research, Maharishi Dayanand University, Rohtak, Haryana Abstract Tap, click and swipe-these are the new sounds of money. Modern technology is fast replacing paper with computer files, bank tellers with automated teller machines (ATMs) and file cabinets with server racks , and banks too have come a long way from the old days of manually recording transactions in registers and tallying them up at the end of the day. Now, customer can do multiple things from the comforts of home or office with e-Banking - a one stop solution for all banking needs. This study aims to present the factors which are critical for the success of e-banking in India. The top three factors critical for success of e-banking included: cost and promotion; security and privacy; ease of use. Apart from these banks need to pay attention towards enhancing of its services and developing simpler websites with useful content. Keywords: e-banking, e-commerce, critical success factors, Indian banks. Introduction The business of banking is changing around the globe due to four main reasons- integration of global financial markets, development of technologies, and universalisation of banking operations and diversification on non- banking activities. The physical boundaries that kept banking service providers away from customers seem to be diluting. Even the customers today want freedom from these physical barriers. The hassle of visiting branches during their own working hours, place constraints, waiting in long queues are some of the daily problems which adds to the requirement a virtual mobile service- an easy accessible delivery channel. In the last decade, a major lifestyle trend that has emerged is increasing use of e-commerce applications (Pekka, Suvi, Tommi, 2008). Due to this trend, e-commerce adoption is increasing. Customers have started understanding the benefits of this trend lately. One of the majorly boosted applications of e- commerce is Internet banking (IB) or Online banking or Electronic banking (e-banking). These terms are used interchangeably. E banking is an umbrella term for the process by which a customer may perform banking transactions electronically without visiting a brick-and-mortar institution (Insely, Al- Abed & Fleming, 2003). In the words of (Robert & paul, 2011) e banking is simple usage of banking

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of CRITICAL SUCCESS FACTORS IN E-BANKING: AN INDIAN PERSPECTIVE

IRJMST Vol 5 Issue 9 [Year 2014] ISSN 2250 – 1959 (0nline) 2348 – 9367 (Print)

International Research Journal of Management Science & Technology http://www.irjmst.com Page 38

CRITICAL SUCCESS FACTORS IN E-BANKING: AN INDIAN PERSPECTIVE

Mrs. Megha Singh

Institute of Management Studies & Research,

Maharishi Dayanand University, Rohtak, Haryana

Abstract

Tap, click and swipe-these are the new sounds of money. Modern technology is fast replacing paper

with computer files, bank tellers with automated teller machines (ATMs) and file cabinets with server

racks , and banks too have come a long way from the old days of manually recording transactions in

registers and tallying them up at the end of the day. Now, customer can do multiple things from the

comforts of home or office with e-Banking - a one stop solution for all banking needs. This study aims

to present the factors which are critical for the success of e-banking in India. The top three factors

critical for success of e-banking included: cost and promotion; security and privacy; ease of use. Apart

from these banks need to pay attention towards enhancing of its services and developing simpler

websites with useful content.

Keywords: e-banking, e-commerce, critical success factors, Indian banks.

Introduction

The business of banking is changing around the globe due to four main reasons- integration of global

financial markets, development of technologies, and universalisation of banking operations and

diversification on non- banking activities. The physical boundaries that kept banking service providers

away from customers seem to be diluting. Even the customers today want freedom from these physical

barriers. The hassle of visiting branches during their own working hours, place constraints, waiting in

long queues are some of the daily problems which adds to the requirement a virtual mobile service- an

easy accessible delivery channel.

In the last decade, a major lifestyle trend that has emerged is increasing use of e-commerce applications

(Pekka, Suvi, Tommi, 2008). Due to this trend, e-commerce adoption is increasing. Customers have

started understanding the benefits of this trend lately. One of the majorly boosted applications of e-

commerce is Internet banking (IB) or Online banking or Electronic banking (e-banking). These terms

are used interchangeably. E banking is an umbrella term for the process by which a customer may

perform banking transactions electronically without visiting a brick-and-mortar institution (Insely, Al-

Abed & Fleming, 2003). In the words of (Robert & paul, 2011) e banking is simple usage of banking

IRJMST Vol 5 Issue 9 [Year 2014] ISSN 2250 – 1959 (0nline) 2348 – 9367 (Print)

International Research Journal of Management Science & Technology http://www.irjmst.com Page 39

facilities or making banking transactions through internet using electronic devices. (Nsouli &

Schaechter, 2002)

Banks should not consider this channel as a technical issue but a vital contact point for customers.

Customers are showing a favoring attitude towards e banking due to its convenience (Linchtenstein &

Williamson, 2006), trust, security, privacy lesser costs ( Dixit & Datta, 2010; Michal & Tomasz, 2009;

Wai, 2008; Shorabi, Yee & Nathan, 2012) and many other advantages.

Despite of its advantages, people show reluctance towards it. The technologies of E banking are already

very advanced, especially in the USA (Kolodinsky, Hogarth and Hilgert, 2004; Wan, Luk and Chow,

2005). However, E-banking, or virtual banking in general, cannot entirely replace other more traditional

channels (Wan, Luk and Chow, 2005). In late 1999, bank customers using online banking were less than

1% (Hawkins, 2002). It is the challenge for the bank to increase the awareness and usefulness of the E-

banking, beside the traditional-based banking services.

Even, many of the businesses that are piling onto the Internet may totally misunderstand what this

medium is all about (Willcocks, Graeser and Lester, 1998). In the Information technology area

significant importance has been placed on perceived usefulness as a significant contributor to attitudes

and thus adoption of new technology (Fenech and OCass, 2001).

In India, the scenario of e-banking is on the wave. Customers are performing several e-banking

functions such as inter-account fund transfers, third party payments, opening deposit accounts, ordering

cheque books and demand drafts, paying utility bills, applying for loans and credit cards online, getting

account statements etc without are visiting a branch. According to Reserve Bank of India data, during

2011-12, the volume of online fund transfers through National Electronic Fund Transfer (NEFT) and

Real Time Gross Settlement System (RTGS) grew by 71 % and 11.7% respectively. In a recent

interview, Chanda Kochhar, MD & CEO of ICICI bank said that only 15 % of the transactions on an

average take place through the branches. “The rest is happening outside”, she added.

Hence, it is inevitable for the banks to skip the analysis of increasing significance of e-banking.

This paper is aimed at learning all the critical success factors (CSFs) to a bank in its e-banking

success. The study is based on Indian banks and customers, for there has been little literature

on the same. Moreover with the increasing risk acceptance by consumers in regard to internet-

based services (Linchtenstein & Williamson, 2006) and the growing importance of offering

deep levels of consumer support for such services, the study gains gravity.

Literature Review

This section reviews the studies that have been carried so far in the e-banking context. The

explosion of internet based electronic application in the recent years (Liao & Cheung, 2003)

has created highly competitive market conditions for bank providers (Beckett, Hever &

Howcraft, 2000). Nevertheless, it has also created opportunities for them. Most of the banks

IRJMST Vol 5 Issue 9 [Year 2014] ISSN 2250 – 1959 (0nline) 2348 – 9367 (Print)

International Research Journal of Management Science & Technology http://www.irjmst.com Page 40

are using Information Technology as a vital tool to stay aggressive against other competitors in

the market . Banking technology helps increase customer satisfaction, customer loyalty,

improvised growth and performance of banks (Tater, Tanwar & Murai, 2011).This clearly

enhances the demand to get a better understanding of „what‟ factors (Critical success factors)

an e- banking customer considers to be important.

Critical success factor (CSF) refers to the aspect or component or an ingredient that is must

for an organization to survive in the highly competitive environment and achieve its goal. It is

this cause which is necessary for achieving the victory of a company or an organization. In the

words of (Boylon & Zmud, 1984) as cited by Wikipedia, "Critical success factors are those few

things that must go well to ensure success for a manager or an organization, and, therefore,

they represent those managerial or enterprise area, that must be given special and continual

attention to bring about high performance. CSFs include issues vital to an organization's

current operating activities and to its future success." D. Ronald Daniel of McKinsey &

Company gave the theory of “success factors” in 1961which was further polished as critical

success factors by Rockart between 1979 and 1981. The explanation of Critical Success

Factors by (Rockart, 1979) is used for this paper. Various CSFs pointed out by earlier

researchers have been complied for the study.

I. Customized products/ services

A product or service customized in accordance with the expectation and preference of

the customer is an important factor (Liao et al., 2008). Navigating from one website to

another makes customers irate. The findings of a study by (Lichtenstein & Williamson,

2006) pointed out that convenience is the main motivator for customers to bank on

internet. (Jayawardhena & Foley, 2000) suggested that with the changes brought by the

internet, banks must continually invent new products and also make existing products

suitable for online delivery.

II. Perceived Risk & Trust

As pointed by (Polatoglu and Ekin, 2001), consumer adoption of e banking services , as

well as customer satisfaction, is affected by perceived risk. Uncertainty Gives birth to

perceived risk. Many researchers like, (Black et al., 2001; Rotchanakitumnuai and

Spence, 2003; Singh, 2004; Lee et al., 2005 and Gerrard et al., 2006) have found the

negative relationship between the level of perceived risk and attitude towards e-

banking. Trustworthiness is another vital variable towards customer risk perceptions &

attitude on banking services (Sonja , Rita, 2008; Yeoh & Benjamin, 2011). A research

work based on theory of planned behavior (Ajen, 1985) and diffusion of innovation

theory (Rogers, 1985) revealed that attitudinal and perceived behavior control factors

rather than social influence, play a vital role in influencing the intention to adopt internet

banking(Tan & Teo, 2000). Also, customer trust if reflected by their confidence to bank‟s

competency in providing reliable and secure e-banking. (Suan & Han, 2002) found trust

IRJMST Vol 5 Issue 9 [Year 2014] ISSN 2250 – 1959 (0nline) 2348 – 9367 (Print)

International Research Journal of Management Science & Technology http://www.irjmst.com Page 41

as valuable factor using web based survey, while (Rexha et al., 2003) obtained same

results in Singapore.

III. Security & Privacy concerns

The technology-related frauds in the banking sector are adding huge to the losses

(Singh, 2013). A study by (Fitzergerald, 2004) concluded that security is one of the

major concern area for which people do not adopt e-banking. It is highly essential to

protect customers‟ data and provide safe transaction s preventing frauds (Enos, 2001;

Turban et al., 2000; Regan & Macaluso, 2000). On surveying UK customers, (White &

Nteli, 2004) found that they ranked security as most important attribute of internet

banking service quality. In Saudi Arabia as well, „Security‟ is the biggest concern for

customers when conducting financial transactions (Sohail & Shaikh, 2007). In another

study by (Aladwani, 2001), potential customers ranked internet security and privacy as

important future challenges banks are facing. While making a financial transaction

online, personal & financial information can be intercepted and used of fraudulent

purposes. Greater concerns are involved in online investing than traditional trading;

users need to have a feeling of security which is still a major hindrance to e-commerce

growth (Lee & Turban, 2002). In their study 200 adult consumers (age above 35) (Dixit

& Datta, 2010) revealed that inspite of security and privacy concern, adult customers

are willing to adopt online banking if the banks provides them necessary guidance.

IV. Simpler websites

Confusing web pages and complex steps discourages adult customers to use online

banking (Mattila et al., 2003). Perceived difficulty in using computers combined with the

lack of personal service in e-banking was found to be the main barriers of Internet

banking adoption among mature customers (Mattila et al., 2003). Moreover, older

people prefer websites involving knotty software and hyperlinks (Cleaver, 1999). The

functions involving simple and clear navigation function are appreciated.

Result based analysis of data relating to nearly 200 respondents , in Mauritius,

(Padachi, Rojid & Seetanah, 2008) indicated that the most significant factor influencing

adoption of internet banking was ease of use.

V. Cost factor

Bank charges and the internet costs have been major hindrances among customers in

adoption of internet banking. (Wong, 2005) developed a theoretical model linking

customer satisfaction and switching costs to customer retention. The model has two

main features. First, it examines the main direct effects of customer satisfaction and

switching costs on customer retention. Second, the model examines the moderating

role of switching costs on the relationship between customer satisfaction and customer

retention. The empirical research was based on data collected by an Internet survey of

adopters of Internet banking service in Hong Kong. Results from statistical analyses

IRJMST Vol 5 Issue 9 [Year 2014] ISSN 2250 – 1959 (0nline) 2348 – 9367 (Print)

International Research Journal of Management Science & Technology http://www.irjmst.com Page 42

showed that both customer satisfaction and switching costs have strong positive direct

effects on customer retention. These analyses also confirm the moderating role of

switching costs on the relationship between customer satisfaction and customer

retention.

To win the loyalty of the customers, service has to be cheaper than the alternatives

(Cronin, 1998). Transaction costs economics theory suggests people will choose the

cheaper method between electronic banking and traditional services to transact (Huang,

2002) (Simpson, 2002). Nevertheless, to encourage this new phenomenon banks are

offering lower fees and better rates on deposits and loans while using e-banking (Michal

& Tomasz, 2009).

VI. Content of Websites

Rich content on websites always prove useful while attracting the increasing number of

website visitors (Stamoulis, 2000). Banks‟ website has lot of information about its

corporate profile, products, payments, special services, new offers, categorical pages

etc. Banks have to make sure that the content displayed does not create a negative

impact on the visitor. It has to valuable, organized, easily accessible and to the point.

The 24- hr interaction facility provided by most of the bank websites has also supported

the success of e-banking (Franco & Klein, 1999). Infact, the data that is collected

through the interaction can be very helpful in analyzing the customers‟ preferences,

requirements as well as expectations. This in turn would be a big support for the

marketing teams.

VII. Organizational flexibility

Undoubtedly, „understanding the customer‟ remains the major success factor in e-

banking (Shah & Siddiqui, 2006). But the internal factors to an organization do create a

high impact on the customers. A research work by (Vafaie, 2009) at Iran studied the

effect of organizational factors by dividing them in three categories- strategic factors,

operational factors and tactical factors. He found that organizational flexibility, systems

integration, systematic change management and support from top management be

considered by organizations for e-banking success. Banks have to engage themselves

in substantial adjustments with respect to their organization. The target of e-commerce

strategy should be the integration of channels of e-banking with other service delivery

channels in order to reap maximum benefits (Shah & Siddiqui, 2006). Lack of top

management support was found to be an inhibiting factor in the adoption of electronic

commerce applications by the banks in the Arab Gulf region (Khalfan , AlRAfae, Al-

Hajery, 2006).

After surveying 145 respondents in China, the factors of leadership, strategy and

organisation management were pointed as success factors in e-banking (Huang & Li,

2008)

IRJMST Vol 5 Issue 9 [Year 2014] ISSN 2250 – 1959 (0nline) 2348 – 9367 (Print)

International Research Journal of Management Science & Technology http://www.irjmst.com Page 43

VIII. Other Factors

(La Rose et al., 2001) studied the effect of habit strength in an individual decision to use

internet. People who are addicted/ habitual in using the internet find it comfortable in

adopting internet.

At times previous experience or imitation factors also act as great influencers (Limayen

& Hut, 2003). Another work by (Shi & Zanton, 2010) examined irrational imitation factors

underlying adoption of internet banking. It tested 173 internet users and found that

outcome-based and frequency based imitations are significant determinants of Internet

banking adoption.

Methodology

The Questionnaire and the Variables

As per the objectives of the study and content available through literature, a structured questionnaire was

prepared. It had two sections: demographic information of the respondent and e-banking success factors.

The first section collected the demographic information of the respondents mainly age, gender,

educational qualification, profession, etc. This information seeks to explain the homogeneity of the

respondents while deciding critical success factors of e-banking.

In the second section of the questionnaire, respondents were asked to rate the relative importance of the

28 factors which contribute to the success of e-banking. They were measured on a five point Likert-type

scale of importance ranging from 1 (not important at all) to 5 (very important). The list was based on

previous similar studies (Thwaites & Vere, 1995; Almossawi, 2001; Gerrard & Cunningham, 2001).

Sample and Data Collection

The sample of the study was selected from the general banking customers of Rohtak city, Haryana. A

non-probability convenience sampling method was chosen taking a sample of 285 customers, given the

exploratory nature of the study. The filling of questionnaires was carried April – May 2014.

Approximately 20 minutes were given to fill the responses

From the 285 questionnaires distributed, 262 were returned, out of which 246 were deemed usable (valid

and completed), yielding giving an excellent response rate of 86.31 percent. Such a response rate was

considered sufficient for statistical reliability and generalisability (Tabachnick and Fidell, 2001). The

high response rate was attributed to self administered approach undertaken during collection of data.

Results

Demographics of Respondents

IRJMST Vol 5 Issue 9 [Year 2014] ISSN 2250 – 1959 (0nline) 2348 – 9367 (Print)

International Research Journal of Management Science & Technology http://www.irjmst.com Page 44

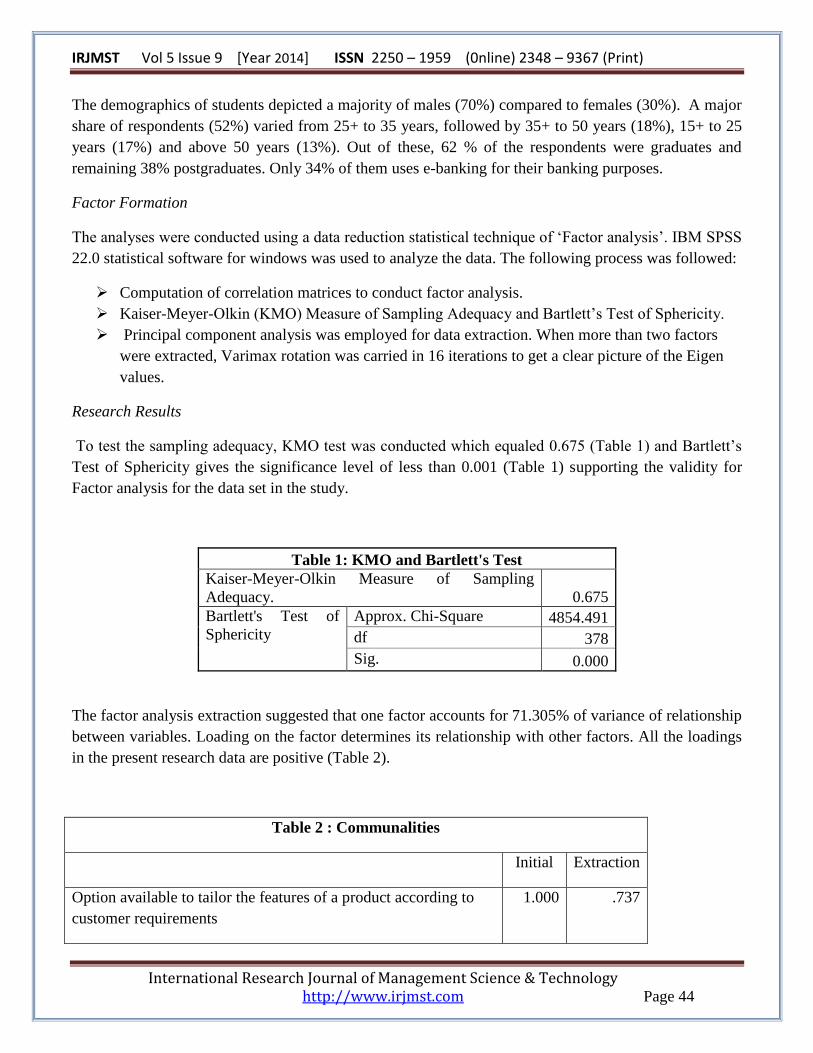

The demographics of students depicted a majority of males (70%) compared to females (30%). A major

share of respondents (52%) varied from 25+ to 35 years, followed by 35+ to 50 years (18%), 15+ to 25

years (17%) and above 50 years (13%). Out of these, 62 % of the respondents were graduates and

remaining 38% postgraduates. Only 34% of them uses e-banking for their banking purposes.

Factor Formation

The analyses were conducted using a data reduction statistical technique of „Factor analysis‟. IBM SPSS

22.0 statistical software for windows was used to analyze the data. The following process was followed:

Computation of correlation matrices to conduct factor analysis.

Kaiser-Meyer-Olkin (KMO) Measure of Sampling Adequacy and Bartlett‟s Test of Sphericity.

Principal component analysis was employed for data extraction. When more than two factors

were extracted, Varimax rotation was carried in 16 iterations to get a clear picture of the Eigen

values.

Research Results

To test the sampling adequacy, KMO test was conducted which equaled 0.675 (Table 1) and Bartlett‟s

Test of Sphericity gives the significance level of less than 0.001 (Table 1) supporting the validity for

Factor analysis for the data set in the study.

Table 1: KMO and Bartlett's Test

Kaiser-Meyer-Olkin Measure of Sampling

Adequacy. 0.675

Bartlett's Test of

Sphericity

Approx. Chi-Square 4854.491

df 378

Sig. 0.000

The factor analysis extraction suggested that one factor accounts for 71.305% of variance of relationship

between variables. Loading on the factor determines its relationship with other factors. All the loadings

in the present research data are positive (Table 2).

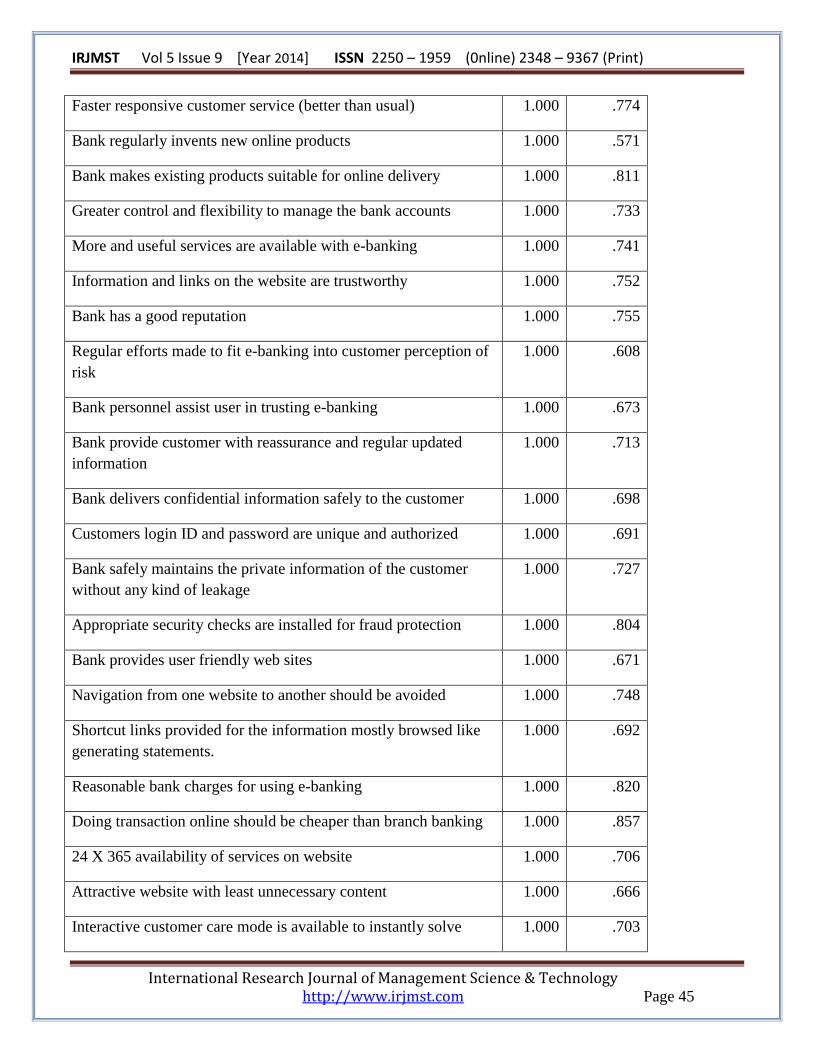

Table 2 : Communalities

Initial Extraction

Option available to tailor the features of a product according to

customer requirements

1.000 .737

IRJMST Vol 5 Issue 9 [Year 2014] ISSN 2250 – 1959 (0nline) 2348 – 9367 (Print)

International Research Journal of Management Science & Technology http://www.irjmst.com Page 45

Faster responsive customer service (better than usual) 1.000 .774

Bank regularly invents new online products 1.000 .571

Bank makes existing products suitable for online delivery 1.000 .811

Greater control and flexibility to manage the bank accounts 1.000 .733

More and useful services are available with e-banking 1.000 .741

Information and links on the website are trustworthy 1.000 .752

Bank has a good reputation 1.000 .755

Regular efforts made to fit e-banking into customer perception of

risk

1.000 .608

Bank personnel assist user in trusting e-banking 1.000 .673

Bank provide customer with reassurance and regular updated

information

1.000 .713

Bank delivers confidential information safely to the customer 1.000 .698

Customers login ID and password are unique and authorized 1.000 .691

Bank safely maintains the private information of the customer

without any kind of leakage

1.000 .727

Appropriate security checks are installed for fraud protection 1.000 .804

Bank provides user friendly web sites 1.000 .671

Navigation from one website to another should be avoided 1.000 .748

Shortcut links provided for the information mostly browsed like

generating statements.

1.000 .692

Reasonable bank charges for using e-banking 1.000 .820

Doing transaction online should be cheaper than branch banking 1.000 .857

24 X 365 availability of services on website 1.000 .706

Attractive website with least unnecessary content 1.000 .666

Interactive customer care mode is available to instantly solve 1.000 .703

IRJMST Vol 5 Issue 9 [Year 2014] ISSN 2250 – 1959 (0nline) 2348 – 9367 (Print)

International Research Journal of Management Science & Technology http://www.irjmst.com Page 46

queries

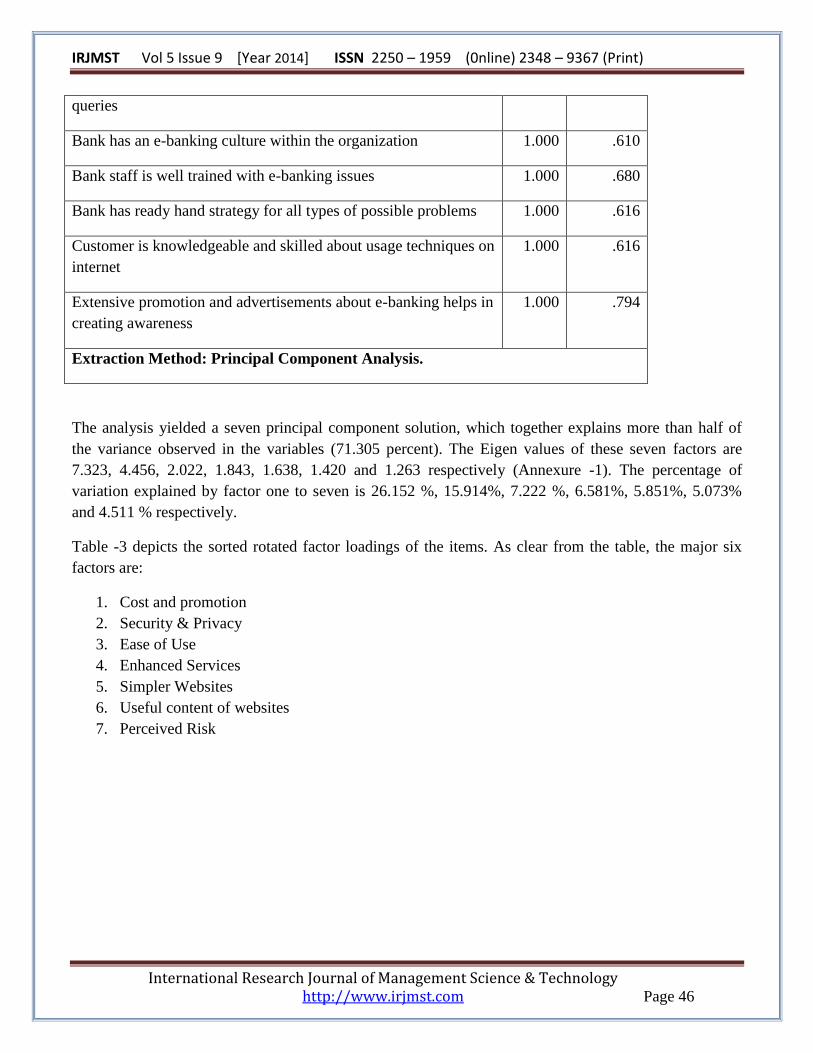

Bank has an e-banking culture within the organization 1.000 .610

Bank staff is well trained with e-banking issues 1.000 .680

Bank has ready hand strategy for all types of possible problems 1.000 .616

Customer is knowledgeable and skilled about usage techniques on

internet

1.000 .616

Extensive promotion and advertisements about e-banking helps in

creating awareness

1.000 .794

Extraction Method: Principal Component Analysis.

The analysis yielded a seven principal component solution, which together explains more than half of

the variance observed in the variables (71.305 percent). The Eigen values of these seven factors are

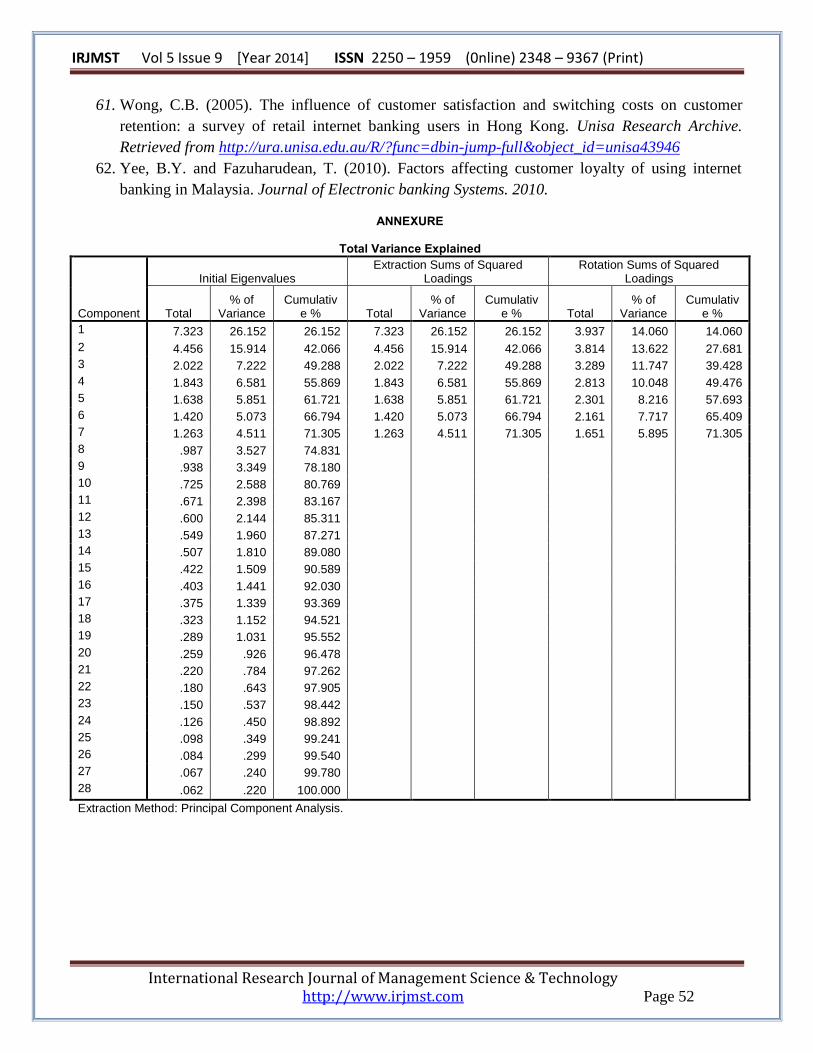

7.323, 4.456, 2.022, 1.843, 1.638, 1.420 and 1.263 respectively (Annexure -1). The percentage of

variation explained by factor one to seven is 26.152 %, 15.914%, 7.222 %, 6.581%, 5.851%, 5.073%

and 4.511 % respectively.

Table -3 depicts the sorted rotated factor loadings of the items. As clear from the table, the major six

factors are:

1. Cost and promotion

2. Security & Privacy

3. Ease of Use

4. Enhanced Services

5. Simpler Websites

6. Useful content of websites

7. Perceived Risk

IRJMST Vol 5 Issue 9 [Year 2014] ISSN 2250 – 1959 (0nline) 2348 – 9367 (Print)

International Research Journal of Management Science & Technology http://www.irjmst.com Page 47

Table 3: Rotated Component Matrix

Factor Label Variables Factor

Loadings

1 Cost And

Promotion

Bank has a good reputation .814

Bank personnel assist user in trusting e-banking .571

Reasonable bank charges for using e-banking .847

Doing transaction online should be cheaper than

branch banking .854

Extensive promotion and advertisements about e-

banking helps in creating awareness .716

2 Security &

Privacy

Option available to tailor the features of a product

according to customer requirements .775

Faster responsive customer service (better than usual) .733

Bank safely maintains the private information of the

customer without any kind of leakage .800

Appropriate security checks are installed for fraud

protection .687

Shortcut links provided for the information mostly

browsed like generating statements. .533

Bank delivers confidential information safely to the

customer .781

3 Ease of Use

More and useful services are available with e-banking .768

Information and links on the website are trustworthy .777

Navigation from one website to another should be

avoided .653

Bank has ready hand strategy for all types of possible

problems .458

4 Enhanced

Services

Bank regularly invents new online products .575

24 X 365 availability of services on website .562

Interactive customer care mode is available to

instantly solve queries .623

Bank staff is well trained with e-banking issues .542

5 Simpler

Websites

Bank makes existing products suitable for online

delivery .762

Greater control and flexibility to manage the bank

accounts .694

Bank provides user friendly web sites .552

6

Useful

Content On

Websites

Attractive website with least unnecessary content .764

Customer is knowledgeable and skilled about usage

techniques on internet .685

7 Perceived

Risk

Regular efforts made to fit e-banking into customer

perception of risk .706

Customers login ID and password are unique and

authorized .571

IRJMST Vol 5 Issue 9 [Year 2014] ISSN 2250 – 1959 (0nline) 2348 – 9367 (Print)

International Research Journal of Management Science & Technology http://www.irjmst.com Page 48

Conclusion

In today‟s ever advancing technological world, customers are attracted toward the latest technological

equipments. The future banking customers i.e. present students rate the hi-tech services of mobile

banking and e banking highly important.

The customers‟ attitude towards service industry has changed. Their demanding approach towards

banking services should be taken as a wakeup call for all those who are working in sleep mode. People

don‟t have time to visit every place for their smallest needs. A businessman or serviceman would never

cancel his meeting to merely go to bank for fund transfer. All a customer wants is an excellent e-banking

service with reasonable cost. Even the undergraduate students place high importance of e-banking

service (Singh, 2014)

The study supports the fact customers are more concerned about the cost. They need a cheaper service

with regular assistance from the bank personnel. No less importance has been played to the security

issue. This comes second in line after cost and promotion factor. People are adapting more to the e-

banking service. To win the them, all banks need to do is to make sure that the confidential information

is delivered safely and privately to the customer and install appropriate security checks for fraud

protection.

Even though security and privacy feature are the norms of websites, banks need to equip themselves

with a ready hand strategy to deal with all type of problems that may occur. Simultaneously, new online

product is always as a big attraction. Well trained staff can assist the user with the new things and gain

their trust. Simpler the better. A user friendly website with greater control and flexibility is next critical

success factor. A knowledgeable customer who is informed about the internet is easy to convince.

Hence, regular efforts should be made to fit e-banking in customers‟ perception.

Hence, the banks should keep in mind the above discussed critical factors for success of e-banking.

Scope for further Research

On a closing note, this should be noted that this research has been carried on a specific region and

chosen people and thus do not represent banking customers as a whole. The results holds good in its

limited time frame and sample. It would be interesting to applicability of findings in other states or

countries.

References

1. Aladwani, M. Adel (2001). Online banking: a field study of drivers, development challenges, and

expectations. International Journal of Information Management, 213-225.

2. Almossawi, M. (2001). Bank selection criteria employed by college students in Bahrain: An

empirical analysis. International Journal of Bank Marketing, 19(3), 115-125.

3. Beckett, A., Hewer, P., & Howcroft, B. (2000). An exposition of consumer behaviour in the

financial services industry. The International Journal of Bank Marketing. 18(1).

IRJMST Vol 5 Issue 9 [Year 2014] ISSN 2250 – 1959 (0nline) 2348 – 9367 (Print)

International Research Journal of Management Science & Technology http://www.irjmst.com Page 49

4. Black, N.J., Lockett, A., Winklhofer, H. and Ennew, C. (2001). The adoption of internet

financial services: a qualitative study. International Journal of Retail & Distribution

Management, 29 (8), 390-398.

5. Boynlon, A.C., and Zmud, R.W. (1984). An Assessment of Critical Success Factors. Sloan

Management Review. 25(4), 17-27.

6. Cleaver, J. (1999). Surfing for seniors. Marketing News, 33 (15).

7. Cronin, M. J. (1998) Defining Net Impact: The Realignment of Banking and Finance on the

Web, in Cronin, M. J. (Ed.) Banking and Finance on the Internet. Chapter 1, John Wiley & Sons,

New York, USA, 1-18.

8. Daniel, D. R., (1961). Management Information Crisis. Harvard Business Review, Sept.-Oct.

9. Dixit, N. & Datta, S. K., (2010). Acceptance of E banking among adult customers: An empirical

investigation in India. Journal of Internet banking and E commerce .15(2).

10. Enos, L. (2001) Report: Critical Errors in Online Banking. e-Commerce Times, April 11.

Retrieved from http://www.ecommercetimes.com/perl/story/8867.htm

11. El Sawy, O. A., Malhotra, A., Gosain, S., Young, K. M. (1999). IT-Intensive Value Innovation

in the Electronic Economy: Insights from Marshall Industries. MIS Quarterly. 23( 3),305-335.

12. Fenech, T.; and OCass, A. (2001), Internet Users Adoption of Web Retailing: User and Product

Dimensions, Journal of Product & Brand Management, Vol. 10, No. 6, pp. 361 C 381.

13. Fitzergelad, K. (2004). An Investigation into People‟s Perceptions of Online Banking.

14. Franco, S. C. and Klein, T. (1999). Online Banking Report, Piper. Jaffray Equity Research.

Retrieved from www.pjc.com/ec-ie01.asp?team=2

15. Gerrard, P., Cunningham, J.B. and Devlin, J.F. (2006). Why consumers are not using internet

banking: a qualitative study. Journal of Services Marketing, 20 (3), 160-8.

16. Hawkins, J. (2002), E-Finance and Development: Policy Issues, E-Finance for Development:

National Practices and Prospects for Future, E-Finance for Development, UN International

Conference on Financing for Development, 19 March, Monterrey, Mexico.

17. Huang, J.S. (2002). Customer Choice between Electronic and Traditional Markets: an Economic

Analysis. Proceedings of 35th

Hawaii International Conference on System Sciences (HICSS

2002), IEEE Society Press.

18. Insley, R., Al-Abed H. and Fleming T. (2003). What is the definition of e-banking? Bankeronline

.com. Retrieved from http://www.bankersonline.com/technology/gurus_tech081803d.html

19. Jayawardhena, C., Foley, P. (2000). Changes in the Banking Sector – the Case of Internet

Banking in the UK. Internet Research: Electronic Networking Applications and Policy, 10(1),

19-30.

20. Khalfan, A., AlRefae, Y., Al-Hajery, M. (2006). Factors influencing the adoption of internet

banking in Oman: a descriptive study analysis. International Journal of Financial Services

Management. 1(2-3), 155-172.

21. Kolodinsky, J.M.; Hogarth, J.M.; and Hilgert, M.A. (2004), The Adoption of Electronic Banking

Technologies by US Consumers, International Journal of Bank Marketing, Vol. 22, No. 4, pp.

238-59.

IRJMST Vol 5 Issue 9 [Year 2014] ISSN 2250 – 1959 (0nline) 2348 – 9367 (Print)

International Research Journal of Management Science & Technology http://www.irjmst.com Page 50

22. LaRose, R., Mastro, D. A., and M.S.Eastin (2001). Understanding Internet usage: A social

cognitive approach to uses and gratifications. Social Science Computer Review.19, 395-413.

23. Lee, M.K.O. and Turban, E. (2002). A trust model for consumer internet shopping. International

Journal of Electronic Commerce, 6 (1), 75-91.

24. Lee, E.K., Kwon, K.N. and Schumann, D.W. (2005). Segmenting the non-adopter category in the

diffusion of internet banking. International Journal of Bank Marketing, 23 (5), 414-37.

25. Lichtenstein, S. & Williamson, K. (2006). Understanding consumer adoption of Internet

Banking: An interpretive study in the Australian Banking Context. Journal Of Electronic

Commerce Research. 7(2), 50-66.

26. Liao, S., Shao, Y. P., Wang, H., and Chen, A. (1999). The Adoption of Virtual Banking: An

Empirical Study,” International Journal of Information Management. 19(1), 63-74.

27. Liao, Z. Cheung, T. (2002). Internet based e-banking and consumer attitude: an empirical study.

Information and Management. 39, 283-295.

28. Limayem, M. and Hurt, S. G. (2003). Force of Habit and Information Systems Usage. Journal of

the Association of Information Systems. 4(3), 65-97.

29. Mattila, M., Karjaluoto, H. and Pento, T. (2003). Internet banking adoption among adult

customers: early majority or laggards? Journal of Services Marketing, 17 (5), 514-28.

30. Michal, P. & Tomasz, P.W. (2009). Empirical analysis of internet banking adoption in Poland.

International Journal of Bank Marketing. 27(1), 32-53.

31. Nsouli, S.M. & Schaechter, A. (2002). Challenges of the “E-banking Revolution”. Finance &

Development. 39(3). Retrieved from http://www.ieo-imf.org/external/pubs/ft/fandd/2002/09/

nsouli.htm

32. Oppenheim, A. N. (1992). Questionnaire Design, Interviewing and Attitude Measurement,

Pinter, London, UK.

33. Padachi, K., Rojid, S., Seetanah B. (2002). Investigating into the factors that influence the

adoption of internet banking in Mauritius. Journal of internet Business. 5, 99-120.

34. Polatoglu, V. and Ekin, S. (2001). An empirical investigation of the Turkish consumers‟

acceptance of internet banking services. International Journal of Bank Marketing. 19 (4), 156-

65.

35. Regan, K., Macaluso, N. (2000) Report: Consumers Cool to Net Banking. e-Commerce Times,

October 3, 2000.

36. Rexha, N., Kingshott, R.P.J. and Aw A.S.S.(2003). The impact of the relational plan on adoption

of electronic banking. Journal of Services Marketing, 17(1), 53-67.

37. Robert, J.N. & Paul, H.P.Y. (2011). Crucial web usability factors of 36 industries for students: a

large scale empirical study. Electronic Commerce Research. 11, 151-180.

38. Rotchanakitumnuai, S. and Spence, M. (2003). Barriers to internet banking adoption: a

quantitative study among corporate customers in Thailand. International Journal of Bank

Marketing, 21 (6/7), 312-23.

39. Rockart, J. F(1979). Chief Executives Define their Own Data Needs. Harvard Business Review.

40. Rockart, J. F. (1979)(2). Chief executives define their own data needs. Harvard Business

Review. 81-93.

IRJMST Vol 5 Issue 9 [Year 2014] ISSN 2250 – 1959 (0nline) 2348 – 9367 (Print)

International Research Journal of Management Science & Technology http://www.irjmst.com Page 51

41. Rockart, J. F. (1986). A Primer on Critical Success Factors. The Rise of Managerial Computing:

The Best of the Center for Information Systems Research, edited with Christine V. Bullen.

(Homewood, IL: Dow Jones-Irwin), 1981, OR, McGraw-Hill School Education Group (1986)

42. Rogers, E.M., Diffusion of Innovations, 4th ed., The Free Press, New York, NY, 1995.

43. Shah, M.H., Siddiqui, F. A. (2006). Organizational critical success factors in adoption of e-

banking at the Woolwich Bank. International Journal of Information Management. 26(6), 442-

456.

44. Shei, W. & Zanton, K. (2010). Why use Internet banking? An irrational imitation model.

International Journal of Banking, Accounting & Finance. 2(2), 156-175.

45. Singh, A.M. (2004). Trends in South African internet banking. Aslib Proceedings, 56 (3),187-96.

46. Singh, M. (2013). A study on the Financial frauds the the Indian Banking sector. Intercontinental

Journal of Finance Resource Research Review. 1(9), 82-95.

47. Singh, M. (2014). Selection of Commercial bank: Undergraduate students‟ perspective. Asian

Journal of Research in Banking & Finance. 4(4), 252-261.

48. Sohrabi, M., Yee, J.Y.M. & Nathan, R.J. (2013). Critical Success Factors for the Adoption of E-

banking in Malaysia. International Arab Journal of E- Technology. 3(2), 76-82.

49. Sonja, G. & Rita, F. (2008). Consumer acceptance of internet banking: the influence of internet

trust. International Journal of Bank Marketing. 26(7). 483-504.

50. Stamoulis, D. S. (2000). How Banks Fit in an Internet Commerce Business Activities Model,

Journal of Internet Banking and Commerce .5(1).

51. Suh, B. and Han, I. (2002). Effect of trust on customer acceptance of Internet banking.

Electronic Commerce Research and Applications. 1, 247-261.

52. Tabachnick, B.G. and Fidell, L.S. 1996. Using Multivariate Statistics, HarperCollins, New York

53. Tan, M. & Teo, T.S.H. (2000). Factors influencing adoption of Internet banking. Journal of the

Association for Information Systems. 1(5). [doi-10.1016/S0378-7206(01)00097-0]

54. Tater, B., Tanwar, M. and Murari, K. (2011). Customer adoption of banking technology in

Private Banks in India. The International Journal of Banking and Finance. 8(3), 73-88.

55. Thwaites, D. and Vere, L. 1995. Bank selection criteria: a student perspective. Journal of

Marketing Management, 11, 133-49.

56. Vafaie, N. (2009). Critical Success factors of organization in adoption of e banking business at

Eniac-Tech.

57. Wai, C.P. (2008). Users‟ adoption of e banking services: the Malaysian perspective. Journal of

Business and Industrial Marketing. 23(1). 59-69.

58. Wan, W.W.N.; Luk, C.L.; and Chow, C.W.C. (2005), Customers Adoption of Banking Channels

in Hong Kong, International Journal of Bank Marketing, Vol. 23, No. 3, pp. 255-272.

59. White, H. and Nteli, F. (2004). Internet banking in the UK: why are there not more customers?.

Journal of Financial Services Marketing, 9 (1), 49-56.

60. Willcocks, L.; Graeser, V.; and Lester, S. (1998), Cybernomics and IT Productivity: Not

Business at Usual?, European Management Journal, Vol. 16, No. 3, pp. 272 C 283.

IRJMST Vol 5 Issue 9 [Year 2014] ISSN 2250 – 1959 (0nline) 2348 – 9367 (Print)

International Research Journal of Management Science & Technology http://www.irjmst.com Page 52

61. Wong, C.B. (2005). The influence of customer satisfaction and switching costs on customer

retention: a survey of retail internet banking users in Hong Kong. Unisa Research Archive.

Retrieved from http://ura.unisa.edu.au/R/?func=dbin-jump-full&object_id=unisa43946

62. Yee, B.Y. and Fazuharudean, T. (2010). Factors affecting customer loyalty of using internet

banking in Malaysia. Journal of Electronic banking Systems. 2010.

ANNEXURE

Total Variance Explained

Component

Initial Eigenvalues Extraction Sums of Squared

Loadings Rotation Sums of Squared

Loadings

Total % of

Variance Cumulativ

e % Total % of

Variance Cumulativ

e % Total % of

Variance Cumulativ

e %

1 7.323 26.152 26.152 7.323 26.152 26.152 3.937 14.060 14.060

2 4.456 15.914 42.066 4.456 15.914 42.066 3.814 13.622 27.681

3 2.022 7.222 49.288 2.022 7.222 49.288 3.289 11.747 39.428

4 1.843 6.581 55.869 1.843 6.581 55.869 2.813 10.048 49.476

5 1.638 5.851 61.721 1.638 5.851 61.721 2.301 8.216 57.693

6 1.420 5.073 66.794 1.420 5.073 66.794 2.161 7.717 65.409

7 1.263 4.511 71.305 1.263 4.511 71.305 1.651 5.895 71.305

8 .987 3.527 74.831

9 .938 3.349 78.180

10 .725 2.588 80.769

11 .671 2.398 83.167

12 .600 2.144 85.311

13 .549 1.960 87.271

14 .507 1.810 89.080

15 .422 1.509 90.589

16 .403 1.441 92.030

17 .375 1.339 93.369

18 .323 1.152 94.521

19 .289 1.031 95.552

20 .259 .926 96.478

21 .220 .784 97.262

22 .180 .643 97.905

23 .150 .537 98.442

24 .126 .450 98.892

25 .098 .349 99.241

26 .084 .299 99.540

27 .067 .240 99.780

28 .062 .220 100.000

Extraction Method: Principal Component Analysis.