Credit as insurance in agrarian economies

17

Journal of Development Economics 31 (1989) 37-53. North-Holland CREDIT AS INSURANCE IN AGRARIAN ECONOMIES Mukesh ESWARAN and Ashok KOTWAL* The University of British Columbia, Vancouver, B.C., Canada V6T 1 WS Received April 1987, final version received December 1987 This paper examines consumption credit as an insurance mechanism in agrarian economies. It explains the more rapid adoption of new technology in the Green Revolution by large farmers who had greater access to consumption credit. The paper also demonstrates how the emergence and expansion of consumption credit markets, by mitigating the need for hoarding in order to meet consumption contingencies, enhances growth by encouraging investment. 1. Introduction There is increasing awareness in development economics of the key role played by the availability of credit in agricultural development. Credit, needed to finance either intermediate inputs or fixed capital, is regarded as a crucial determinant of growth and technological innovation. A substantial part of the total agricultural credit taken by farmers or farm-workers in poor countries, however, tends to be for consumption purposes [Roth (1983, p. 21)]. Should such consumption credit be regarded as a drain on the productive potential of the economy? At first glance, the answer seems to be in the affirmative; it is the usual trade-off in development economics - consumption today versus consumption tomorrow. The purpose of this paper is to present the case that consumption credit serves the role of insurance in agrarian economies and as such directly influences the risk behaviour of farmers which, in turn, affects production decisions such as the level of investment and technological innovation. ‘Risk aversion’ is one of the central themes of the literature on peasant behaviour. Roumasset (1973), Breman (1974) and Scott (1976), among others, have discussed various customs and institutions such as village insurance and patron-client relationships which protect the rural poor from ‘subsistence crises’. A method of protection, common across many countries and time *This research was supported by the Social Sciences and Humanities Research Council of Canada. We would also like to thank two anonymous referees for helpful comments. 0304-3878/89/$3.50 0 1989, Elsevier Science Publishers B.V. (North-Holland)

Transcript of Credit as insurance in agrarian economies

Journal of Development Economics 31 (1989) 37-53. North-Holland

CREDIT AS INSURANCE IN AGRARIAN ECONOMIES

Mukesh ESWARAN and Ashok KOTWAL* The University of British Columbia, Vancouver, B.C., Canada V6T 1 WS

Received April 1987, final version received December 1987

This paper examines consumption credit as an insurance mechanism in agrarian economies. It explains the more rapid adoption of new technology in the Green Revolution by large farmers who had greater access to consumption credit. The paper also demonstrates how the emergence and expansion of consumption credit markets, by mitigating the need for hoarding in order to meet consumption contingencies, enhances growth by encouraging investment.

1. Introduction

There is increasing awareness in development economics of the key role played by the availability of credit in agricultural development. Credit, needed to finance either intermediate inputs or fixed capital, is regarded as a crucial determinant of growth and technological innovation. A substantial part of the total agricultural credit taken by farmers or farm-workers in poor countries, however, tends to be for consumption purposes [Roth (1983, p. 21)]. Should such consumption credit be regarded as a drain on the productive potential of the economy? At first glance, the answer seems to be in the affirmative; it is the usual trade-off in development economics - consumption today versus consumption tomorrow. The purpose of this paper is to present the case that consumption credit serves the role of insurance in agrarian economies and as such directly influences the risk behaviour of farmers which, in turn, affects production decisions such as the level of investment and technological innovation.

‘Risk aversion’ is one of the central themes of the literature on peasant behaviour. Roumasset (1973), Breman (1974) and Scott (1976), among others, have discussed various customs and institutions such as village insurance and patron-client relationships which protect the rural poor from ‘subsistence crises’. A method of protection, common across many countries and time

*This research was supported by the Social Sciences and Humanities Research Council of Canada. We would also like to thank two anonymous referees for helpful comments.

0304-3878/89/$3.50 0 1989, Elsevier Science Publishers B.V. (North-Holland)

38 M. Eswaran and A. Kotwal, Credit as insurance in agrarian economies

periods, is to offer the poor a consumption credit service. In bad years the poor borrow and in good years they pay back. Depending upon the agrarian structure of the village, it may be a poor farmer borrowing from a rich farmer or a tenant borrowing from his landlord. A bad year may result from a production contingency such as bad weather or from a consumption contingency such as a family illness. The latter may be uncorrelated across the village population, and, if so, people could even borrow from other members of the same income class.

The theme implicit in all this is that an individual’s perception of the risk associated with a decision is closely related to the possible consumption downswing resulting from the decision. Consumption credit can serve the role of insurance due to the intertemporal nature of risk-bearing. Some decisions, such as whether to adopt new technology, involve a choice between two sequences of gambles (or, two random income streams) rather than between two single gambles. Moreover, the outcome of even a single gamble can be spread over many periods. Risk-averse individuals, character- ized by concave von Neumann-Morgenstern utility functions, would prefer a more .uniform distribution of consumption over time. This is what consump- tion credit makes possible: in situations involving uncertain income streams, it enables risks-pooling across time. It is in this sense that consumption credit plays the role of insurance.

The desire of risk-averse agents to stabilize consumption in the face of uncertain income streams has some basic implications: it is a motivation for

saving in ‘good’ states. In an environment characterized by considerable uncertainty and subsistence level incomes, it may very well be the most important motivation for saving, giving credence to the old-fashioned idea of saving for a rainy day. If the uncertainty associated with the typical consumption or production contingency is great, a risk-averse individual is prone to save a large proportion of his income in good states for future contingencies. An apparently undesirable aspect of the environment - its riskiness - actually enhances the savings and hence the growth potential of the economy. But whether or not these higher savings are channelled into capital formation depends crucially on the feasibility of having a productive capital asset that is also liquid enough to cover a contingency. In an agrarian economy, it is difficult to come up with examples of such capital assets. Irrigation, farm animals, trees, farm machinery and implements are all illiquid assets; an attempt to convert them quickly into cash when a contingency arrives would be prohibitively expensive. If so, the act of committing savings to investment renders them unavailable for any other purpose. Even the use of savings for working capital needed to finance intermediate inputs such as fertilizer, seeds, pesticides and machinery rentals denies a farmer the consumption smoothing benefits of these funds during the crop period. As a result, in the absence of a market for consumption

M. Eswaran and A. Kotwal, Credit as insurance in agrarian economies 39

credit, he would hoard a part of his savings in ‘good’ states as a sort of

contingency fund, partly at the expense of present consumption and partly at the expense of investment.’ Clearly, the higher the level of uncertainty characterizing the environment, the higher would be the rate of hoarding and the lower would be the rate of investment. Uncertainty would thus inhibit the rate of investment and growth.

If contingencies are uncorrelated across the population, there are incen- tives for people to come up with risk-mitigating institutions such as insurance. If information on contingent claims, however, is difficult to verify, such devices are not likely to be viable. A consumption credit market would enable individuals to partially insure themselves in such circumstances. In this market, the people with good draws will lend to those with bad draws, thereby enabling each individual to pool risk across time. The funds lent out in the credit market are equivalent to the hoarding that would have taken place in the absence of the market.

An interesting and important implication of the above discussion is a theory of interest appropriate for an agrarian economy. A farmer’s desire to hoard part of his savings to cushion consumption implicitly determines the amount he would be willing to lend in the credit market. The foregone service of consumption smoothing for the loan period may be construed as the opportunity cost of the loan funds as perceived by the lender. Together with the demand side, given by the marginal efficiency of investment, it would then determine the interest rate. Even when the time rate of discount is zero, the interest rate would be positive. This view of interest rate determination is similar to Keynes’ view that interest rate is a premium on liquidity. The motive for hoarding to ward off consumption contingencies, however, is more relevant than a speculative motive in the context of an

agrarian economy. In the next section of this paper, we characterize, in the expected utility

framework, risk preferences appropriate to intertemporal decision-making. In section 3 we analyse an individual’s investment behaviour when there

exists a consumption credit market for risk-pooling. We show how the per capita investment rate decreases with the amount of uncertainty and increases with the number of participants in the consumption credit market. The emergence of the consumption credit market and its growth lowers the perceived risk-premium and consequently lowers the opportunity cost of investment, the result being a higher rate of investment. The partial insurance offered by consumption credit can thus play a positive role in inducing growth. We also argue, in this section, that the rate of interest on investment funds would be positive in this economy even in the absence of a positive rate of time preference.

In section 4, we analyse one implication of different access to consumption

‘Newberry and Stiglitz (1981) have stressed that savings can greatly reduce the cost of risk.

40 M. Eswaran and A. Kotwal, Credit as insurance in agrarian economies

credit. Since consumption credit enables risk taking, farmers with greater access to it would choose to put a greater proportion of their land under new (and hence perceived as risky) technology. This could explain the differential rates of adoption of high yielding technology during the Green Revolution in South Asia.

2. Characterization of intertemporal risk-preferences

The risk behaviour of an agent is determined not only by his preference structure but also by the availability of institutions that facilitate risk- bearing. In an intertemporal context, one such institution that is of relevance is the capital market. The conventional approach to modelling risk behav- iour in intertemporal contexts invariably assumes the existence of perfect capital markets [Dreze and Modigliani (1972), Stiglitz (1969)]. This does not allow us to separate the contribution to risk behaviour of capital markets from that of intrinsic preferences. In this section, we briefly characterize (for use in subsequent sections) risk preferences in an intertemporal context when capital markets are absent. We can then discern the effects of the introduc- tion of capital markets.

Let an individual’s (cardinal) von Neumann-Morgenstern utility function be denoted by U(c’,c’), where ci denotes consumption in period i, i= 1,2. Also let y’ denote the individual’s (random) income in period i (i= 1,2), with

yj,j=l,2 )...) n, as the possible realizations of y’. Denote by qjk the prob- ability that the individual will receive the income yf in period 1 and y: in period 2. When there are no capital markets that link the two periods, each period’s consumption will equal the realized income of that period. (This presumes, of course, that there do not exist durable commodities.) Under the expected utility hypothesis, the individual will then evaluate two-period gambles by the expected utility functional

ilki qjk u(Yj' T Yif).

Risk preferences are here characterized by the curvature properties of the utility function U(c’, c’). In particular, risk-averse preferences are character- ized by the strict (joint) concavity of U(c’,c’) in its two arguments [Blackorby, Davidson and Donaldson ( 1977)].2

In this paper, we shall assume that all individuals possess identical, risk- averse preferences. For convenience, we take it that the two-period utility function has the additively separable form:

*This result is a trivial modification of Theorem 2 of Blackorby, Davidson and Donaldson (1977).

M. Eswaran and A. Kotwal, Credit as insurance in agrarian economies 41

u(c’,c2)=u(c1)+u(c2), (2)

where u( .) is increasing and strictly concave in its argument. The assumed symmetry in c1 and c2 implies that individuals have no intrinsic time preference. In the subsequent sections we use the characterization of risk preferences that we have set forth above.

3. Consumption credit and growth

This section is designed to illustrate how the development of a capital market for consumption loans impinges on growth by facilitating risk- pooling across time. The per capita hoarding set aside to meet consumption contingencies is shown to decline as the extent of the consumption loan market increases and, as a result, more resources are released for investment purposes. It is also shown that the more uncertain the environment, the greater will be the proportion of capital set aside for consumption-smoothing and the smaller the proportion allocated to productive investments. To demonstrate these points with the greatest ease, we abstract from distri- butional considerations and assume identical agents. It must be noted, however, that such a characterization would not be inappropriate for pre- feudal subsistence economies, and also for some egalitarian village economies found today in parts of Africa and South Asia.

Consider an economy comprised of N identical agents. We assume a two- period world in which each agent’s income in the first period is z-cr or z +o (z>a>O) with equal probability and z in the second period. It will be argued later that the main results of this section are not sensitive to the simplifying assumption that there is no uncertainty in the second period. The first-period incomes of the various agents in the economy will be assumed to be uncorrelated. (We are simulating consumption contingencies by uncorrelated income contingencies.) It will be assumed that investment expenditure has to be committed prior to the realization of the state in period 1. The return on the investment is realized in the second period. We denote by Ii the investment of agent i and by r the (exogenous) rate of return on it.

After each individual’s income is realized in period 1, we assume a competitive consumption loan market develops in which agents can borrow or lend for consumption stabilization purposes. Let p denote the interest rate that prevails in this market. (This interest rate will clearly be stochastic since it depends on the proportion of agents who realize the good state as opposed to the bad one.) Let c5i denote the consumption of agent i in period t when he realizes state j in the first period (j= 1 is the bad state and j = 2 is the good state). Agent i’s second-period consumption must be related to his first- period consumption through the budget constraint

42 M. Eswaran and A. Kotwal, Credit as insurance in agrarian economies

(3)

where y, = z - g and y, = z + 6. Thus if agent i realizes state j in period 1 and if p is the prevailing interest rate in the competitive consumption loan market, he will solve

max u(ck) +(c$) s.t. (3). c:,,c:Z

(4)

Denote the solution to (4) by &(r, p, I,), t = 1,2. Now p will be endogenously determined by the market-clearing condition

that the excess demand for loans be non-positive. Let m denote the number of agents who realize the good state in period 1, S denote the set of such agents, and pz denote the equilibrium interest rate that prevails in this circumstance. Then p* must be the solution to the market-clearing condition

(5)

with &=O if the above inequality is strict. (Note that pz will depend on the investment decisions of all the agents.)

Let pAm) denote the probability that agent i realizes state j in period 1 and a total of m agents realize the good state, a probability which is clearly independent of i. This binomial probability is trivially computed.3 The expected utility of agent i is then given by

N-l

where the two summations yield agent i’s expected utility in his bad and good states, respectively. We can finally determine agent i’s investment, under the assumption of rational expectations on the distribution of p, by maximizing (6) with respect to Ii. (Note that since each agent is a price taker in the consumption loan market, he will ignore the effect of his investment choice on pi.)

To investigate the comparative static properties of the solution, we assume

3This probability is given by

p,(m) = (N-l)! 1 N

0 2 p’(m)=&)* 1 N

m!(N-l-m)! ’ 0 2

M. Eswaran and A. Kotwal, Credit as insurance in agrarian economies 43

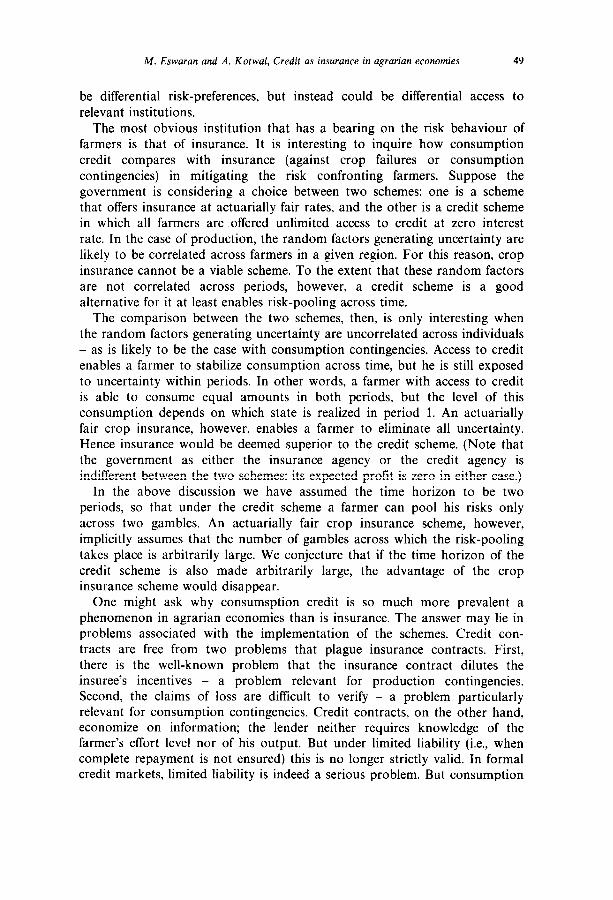

0 1 62 10 16 N

Fig. 1. Per capita investment as a function of the number of agents participating in the consumption loan market (parameter values: a = b = p = 1, z = 1, r = 0.2).

in this section of the paper that all agents have identical risk preferences represented by the von Neumann-Morgenstern utility function of the constant absolute risk aversion type:

u(c)=a-bexp(-pc), b>O, p>O. (7)

For given investment choices Ii, i= 1,2,. . . , N, we can solve analytically each agent’s problem (4) and also the market-clearing condition (5) for &,

m=O, l,..., N. The optimal investment choice of each agent - which entails the maximization of (6) with respect to Ii - has to be done numerically. Since all agents are identical, their investment choices (made ex ante) are too. The parameters that are exogenous to our model are: N (the number of agents), z and c (the mean and standard deviation, respectively, of the first period’s income), p (the index of absolute risk aversion) and r (the return on investment). Endogenous to the model are each agent’s consumption in each state and period, the investment choices, the interest rates that prevail in the consumption loan market, and the expected utilities of the agents. We present below the comparative static properties of the model. Although we present the results only for specific parameter values for reasons of space, it must be emphasized that the qualitative features of the results are robust with respect to parameter changes.

Fig. 1 displays the per capita investment undertaken as a function of the

44 M. Eswaran and A. Kotwal, Credit as insurance in agrarian economies

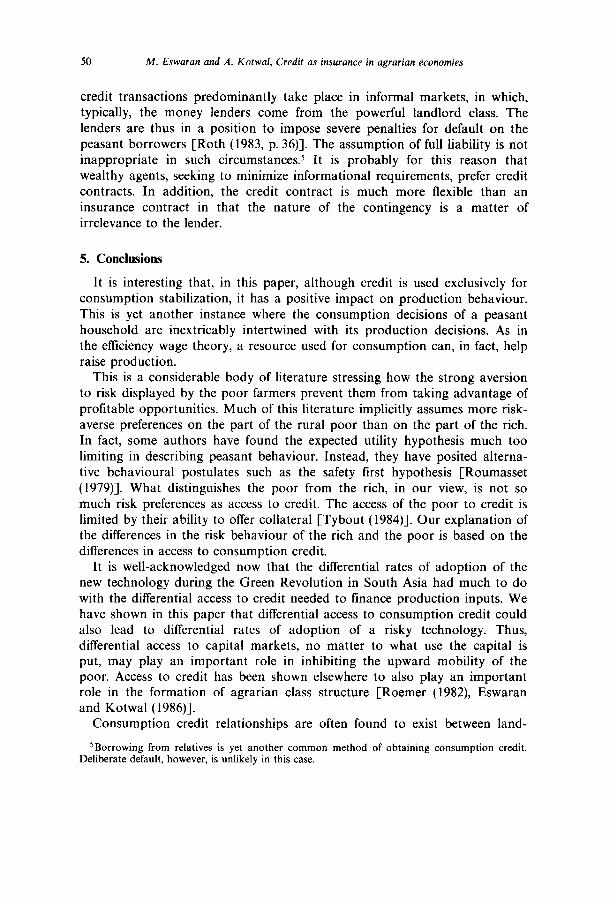

01 I 0 0.5 o

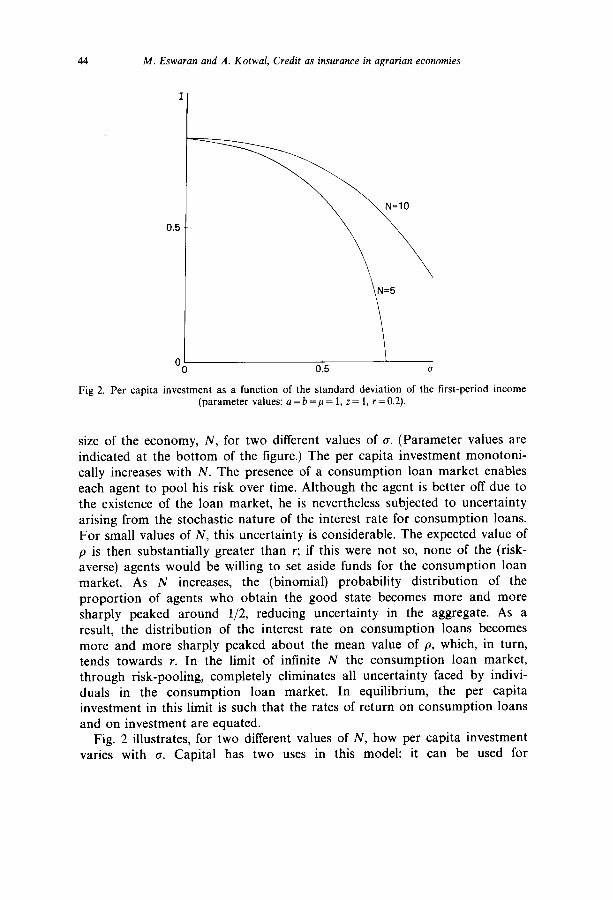

Fig 2. Per capita investment as a function of the standard deviation of the first-period income (parameter values: a=b=p= 1, z= 1, r=0.2).

size of the economy, N, for two different values of O. (Parameter values are indicated at the bottom of the figure.) The per capita investment monotoni- cally increases with N. The presence of a consumption loan market enables each agent to pool his risk over time. Although the agent is better off due to the existence of the loan market, he is nevertheless subjected to uncertainty arising from the stochastic nature of the interest rate for consumption loans. For small values of N, this uncertainty is considerable. The expected value of p is then substantially greater than r; if this were not so, none of the (risk- averse) agents would be willing to set aside funds for the consumption loan market. As N increases, the (binomial) probability distribution of the proportion of agents who obtain the good state becomes more and more sharply peaked around l/2, reducing uncertainty in the aggregate. As a result, the distribution of the interest rate on consumption loans becomes more and more sharply peaked about the mean value of p, which, in turn, tends towards r. In the limit of infinite N the consumption loan market, through risk-pooling, completely eliminates all uncertainty faced by indivi- duals in the consumption loan market. In equilibrium, the per capita investment in this limit is such that the rates of return on consumption loans and on investment are equated.

Fig. 2 illustrates, for two different values of N, how per capita investment varies with 0. Capital has two uses in this model: it can be used for

M. Eswaran and A. Kotwal, Credit as insurance in agrarian economies 45

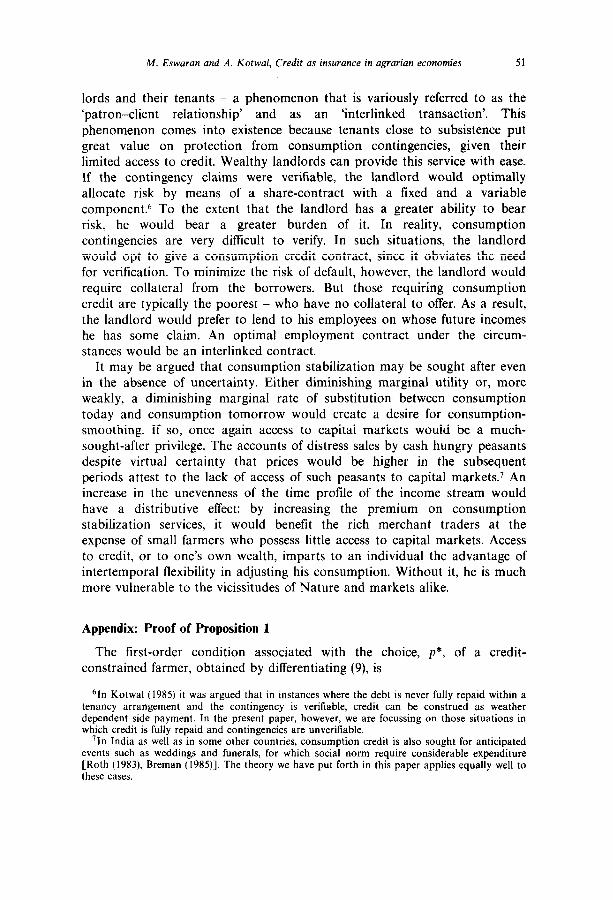

0.5 --

Supply of

investment funds

1 0 1 .o 2.0

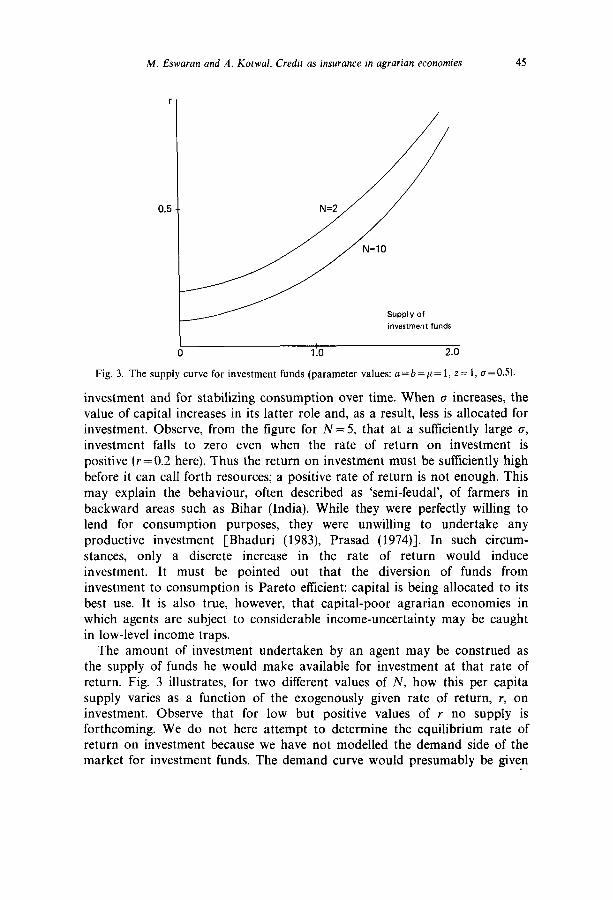

Fig. 3. The supply curve for investment funds (parameter values: a = b = p = 1, z = 1, 0 = 0.5).

investment and for stabilizing consumption over time. When rs increases, the value of capital increases in its latter role and, as a result, less is allocated for investment. Observe, from the figure for N= 5, that at a sufficiently large CJ, investment falls to zero even when the rate of return on investment is positive (r=0.2 here). Thus the return on investment must be sufficiently high before it can call forth resources; a positive rate of return is not enough. This may explain the behaviour, often described as ‘semi-feudal’, of farmers in backward areas such as Bihar (India). While they were perfectly willing to lend for consumption purposes, they were unwilling to undertake any productive investment [Bhaduri (1983), Prasad (1974)]. In such circum- stances, only a discrete increase in the rate of return would induce investment. It must be pointed out that the diversion of funds from investment to consumption is Pareto efficient: capital is being allocated to its best use. It is also true, however, that capital-poor agrarian economies in which agents are subject to considerable income-uncertainty may be caught in low-level income traps.

The amount of investment undertaken by an agent may be construed as the supply of funds he would make available for investment at that rate of return. Fig. 3 illustrates, for two different values of N, how this per capita supply varies as a function of the exogenously given rate of return, I, on investment. Observe that for low but positive values of I no supply is forthcoming. We do not here attempt to determine the equilibrium rate of return on investment because we have not modelled the demand side of the market for investment funds. The demand curve would presumably be given

46 M. Eswaran and A. Kotwal, Credit as insurance in agrarian economies

by a downward sloping marginal efficiency of investent schedule. The point to note here, however, is that the equilibrium interest rate on investment funds would necessarily be positive - even in the absence of any time preference. (Recall that our two-period utility function did not embody any time preference.) In this story, the service provided by capital in consumption-smoothing is the opportunity cost of funds allocated for investment.

It must be noted that the uncertainty in the first period is simulating a consumption contingency during the gestation period of the investment. If there were uncertainty in the future also (i.e., after the investment returns accrue) a risk-averse agent would certainly save more from the first-period income. These increased savings, however, would not be channelled entirely into investment: the possibility of a consumption contingency within the gestation period would induce agents to hoard some of the savings. The main point of this section, therefore, is not sensitive to the presence or absence of uncertainty in the second period.

It may also be noted that for tractability we have assumed a two-period utility function to be additively separable, and the single-period utility function to be of constant absolute risk-aversion variety. The fact that the results are in accord with intuition suggest their robustness with respect to these assumptions.

4. Consumption credit, insurance and adoption of technology

An important implication of the thesis that consumption credit plays the role of insurance is that the farmers who have access to consumption credit may be emboldened to adopt new technology. Unfamiliarity with the new technology may mean greater fluctuations (or greater uncertainty) in the level of output. But as long as a farmer can distribute a possible downswing over future periods he is more willing to adopt new technology. This may be one explanation why rich farmers have been found to adopt new technology much more readily than small and marginal farmers in South Asia.

Suppose each farmer has one unit of land which he can cultivate using an old technology or a new one. The old technology yields a deterministic output of x per unit of land cultivated. The new technology yields, per unit of cultivated area, an uncertain output of z+ CJ or z-r~ (z >a>O) with equal probability in the first period, and a certain output of z in the second period. The uncertainty associated with the new technology in the first period captures the realistic feature of the absence of know-how on the part of farmers using the technology for the first time. We shall assume that the expected output of the new technology exceeds the certain income generated by the old technology, i.e., that z >x. In order to ensure that there is a non- trivial trade-off between risk and return across the two technologies, we assume that z-cr<x, i.e., that the realization of the output in the poorer

M. Eswaran and A. Kotwal, Credit as insurance in agrarian economies 47

state of the new technology falls short of the certain output that would have obtained with the old one.

The farmer has to decide what proportion of his one unit of land he will cultivate with the new technology. Let p denote this proportion. For tractability, we shall assume that this proportion is determined and commit- ted in the beginning of the first period and remains the same as in the next period.4

The focus of our attention here is on how access to consumption credit impinges on the choice of technology. So we shall assume that a farmer can borrow up to a maximum of B in period 1, to be returned in period 2. Credit rationing is a pervasive phenomenon in the less-developed countries [Binswanger and Sillers (1983), Tybout (1984), Rudra (1982)]; we accept that as our basic premise here and work out its implications in the present context. The credit ceiling differs across farmers - presumably depending upon the amount of collateral they can offer. Since the interest rate plays no essential role in this section, we shall assume it to be zero.

Let us first consider the decision problem of a farmer who is not constrained by his credit ceiling at all, i.e., he can borrow more than he would choose to. Given the strict concavity of the utility function u( .), the farmer would completely smooth out his consumption across the two periods; he would borrow or save so that he consumes identical amounts in the two periods. The income in the second period is pz + (1 -p)x. If the poor state is realized in the first period, the income in that period is p(z-o) +( 1 -p)x. The farmer will then borrow pa/2 in the first period and consume [pz + ( I- p)x - pa/21 in each of the two periods. If the good state is realized in period 1, the farmer would save pa/2 in the first period and consume [pz +( 1 -p)x +pa/2] in each of the two periods. The only remain- ing decision confronting the farmer is the choice of p. This he will choose so as to maximize the two-period expected utility:

maxu[pz+(l-p)x-pa/2]+u[pz+(l-p)x+pa/2]. P

(8)

Since the objective function in (8) is strictly concave in p, the solution to the above problem is unique. Let p denote this unique solution.

A farmer who is unconstrained in his access to consumption credit, would borrow, in the poor state of period 1, an amount B=pa/2. Any farmer whose credit ceiling, B, exceeds B would thus choose to cultivate a proportion p of his land with the new technology. Farmers with credit ceilings less than B will necessarily be credit-constrained. A farmer with B<B will consume [pz+( 1 -p)x-ppa+B] in period 1 and [pz+( 1 -p)x-L?] in period 2 if the

4A logical procedure might be to set p= 1 in the second period since there is no uncertainty in this period. This, however, would complicate the algebra without adding anything of substance.

48 M. Eswaran and A. Kotwal, Credit as insurance in agrarian economies

poor state is realized in period 1. If the good state is realized in period 1 then, as before, he would save pa/2 in the first period and consume [pz + (1 -p)x + pa/21 in both periods. Thus the optimization problem facing a credit-constrained farmer is

max+{u[pz+(l-p)x-pa+B]+u[Pz+(l-P)x-Bl}

+u[pz+(1-p)x+pu/2]. (9)

Let p*(B) denote the (unique) solution to the optimization problem stated in

(9). The following proposition records how p*(B) changes with B.

Proposition 1. If the consumption credit available to a credit-constrained farmer is increased, he will cultivate a greater proportion of his land with the new technology.

Proof. See appendix.

The above proposition demonstrates that access to consumption credit impinges in a non-trivial fashion on the extent to which risky technologies are adopted. By facilitating consumption stabilization over time, access to credit enables an individual to absorb more risk than he could in the absence of credit. This insurance aspect of credit results in differential risk-behaviour amongst agents who have identical risk-preferences but differential access to credit. This is consistent with the experimental work of Moscardi and de Janvry (1977) and Binswanger and Sillers (1983). Moscardi and de Janvry (1977), in their experimental work performed in Puebla, Mexico, provide evidence that farmers with larger land-holdings (who, we would argue, possess greater access to credit) take greater risks. They also found that farmers belonging to ‘solidarity groups’ - groups that collectively had access to credit through pooled endowments - exhibited less risk aversion. Binswanger and Sillers (1983) conducted experiments in several LDCs. They tried to elicit the risk preferences of farmers by engaging them in small gambles (which render irrelevant any credit constraint). They discovered that the risk preferences were fairly homogeneous across the sample, despite observed differences in their risk behaviour as reflected by their willingness to adopt new technology. Binswanger and Sillers attribute the differences in adoption behaviour to differences in access to production credit; larger farmers endowed with superior access adopt new technologies faster. Our result above which deals with consumption credit reinforces the Binswanger- Sillers view that the main source of differential adoption behaviour may not

M. Eswaran and A. Kotwal, Credit as insurance in agrarian economies 49

be differential risk-preferences, but instead could be differential access to relevant institutions.

The most obvious institution that has a bearing on the risk behaviour of farmers is that of insurance. It is interesting to inquire how consumption credit compares with insurance (against crop failures or consumption contingencies) in mitigating the risk confronting farmers. Suppose the government is considering a choice between two schemes: one is a scheme that offers insurance at actuarially fair rates, and the other is a credit scheme in which all farmers are offered unlimited access to credit at zero interest rate. In the case of production, the random factors generating uncertainty are likely to be correlated across farmers in a given region. For this reason, crop insurance cannot be a viable scheme. To the extent that these random factors are not correlated across periods, however, a credit scheme is a good alternative for it at least enables risk-pooling across time.

The comparison between the two schemes, then, is only interesting when the random factors generating uncertainty are uncorrelated across individuals _ as is likely to be the case with consumption contingencies. Access to credit enables a farmer to stabilize consumption across time, but he is still exposed to uncertainty within periods. In other words, a farmer with access to credit is able to consume equal amounts in both periods, but the level of this consumption depends on which state is realized in period 1. An actuarially fair crop insurance, however, enables a farmer to eliminate all uncertainty. Hence insurance would be deemed superior to the credit scheme. (Note that the government as either the insurance agency or the credit agency is indifferent between the two schemes: its expected profit is zero in either case.)

In the above discussion we have assumed the time horizon to be two periods, so that under the credit scheme a farmer can pool his risks only across two gambles. An actuarially fair crop insurance scheme, however, implicitly assumes that the number of gambles across which the risk-pooling takes place is arbitrarily large. We conjecture that if the time horizon of the credit scheme is also made arbitrarily large, the advantage of the crop insurance scheme would disappear.

One might ask why consumsption credit is so much more prevalent a phenomenon in agrarian economies than is insurance. The answer may lie in problems associated with the implementation of the schemes. Credit con- tracts are free from two problems that plague insurance contracts. First, there is the well-known problem that the insurance contract dilutes the insuree’s incentives - a problem relevant for production contingencies. Second, the claims of loss are difficult to verify - a problem particularly relevant for consumption contingencies. Credit contracts, on the other hand, economize on information; the lender neither requires knowledge of the farmer’s effort level nor of his output. But under limited liability (i.e., when complete repayment is not ensured) this is no longer strictly valid. In formal credit markets, limited liability is indeed a serious problem. But consumption

50 M. Eswaran and A. Kotwal, Credit as insurance in agrarian economies

credit transactions predominantly take place in informal markets, in which, typically, the money lenders come from the powerful landlord class. The lenders are thus in a position to impose severe penalties for default on the peasant borrowers [Roth (1983, p. 36)]. The assumption of full liability is not inappropriate in such circumstances .5 It is probably for this reason that wealthy agents, seeking to minimize informational requirements, prefer credit contracts. In addition, the credit contract is much more flexible than an insurance contract in that the nature of the contingency is a matter of irrelevance to the lender.

5. Conclusions

It is interesting that, in this paper, although credit is used exclusively for consumption stabilization, it has a positive impact on production behaviour. This is yet another instance where the consumption decisions of a peasant household are inextricably intertwined with its production decisions. As in the efficiency wage theory, a resource used for consumption can, in fact, help raise production.

This is a considerable body of literature stressing how the strong aversion to risk displayed by the poor farmers prevent them from taking advantage of profitable opportunities. Much of this literature implicitly assumes more risk- averse preferences on the part of the rural poor than on the part of the rich. In fact, some authors have found the expected utility hypothesis much too limiting in describing peasant behaviour. Instead, they have posited alterna- tive behavioural postulates such as the safety first hypothesis [Roumasset (1979)]. What distinguishes the poor from the rich, in our view, is not so much risk preferences as access to credit. The access of the poor to credit is limited by their ability to offer collateral [Tybout (1984)]. Our explanation of the differences in the risk behaviour of the rich and the poor is based on the differences in access to consumption credit.

It is well-acknowledged now that the differential rates of adoption of the new technology during the Green Revolution in South Asia had much to do with the differential access to credit needed to finance production inputs. We have shown in this paper that differential access to consumption credit could also lead to differential rates of adoption of a risky technology. Thus, differential access to capital markets, no matter to what use the capita1 is put, may play an important role in inhibiting the upward mobility of the poor. Access to credit has been shown elsewhere to also play an important role in the formation of agrarian class structure [Roemer (1982), Eswaran and Kotwal (1986)].

Consumption credit relationships are often found to exist between land-

SBorrowing from relatives is yet another common method of obtaining consumption credit. Deliberate default, however, is unlikely in this case.

M. Eswaran and A. Kotwal, Credit as insurance in agrarian economies 51

lords and their tenants - a phenomenon that is variously referred to as the ‘patron-client relationship’ and as an ‘interlinked transaction’. This phenomenon comes into existence because tenants close to subsistence put great value on protection from consumption contingencies, given their limited access to credit. Wealthy landlords can provide this service with ease. If the contingency claims were verifiable, the landlord would optimally allocate risk by means of a share-contract with a fixed and a variable component6 To the extent that the landlord has a greater ability to bear risk, he would bear a greater burden of it. In reality, consumption contingencies are very difficult to verify. In such situations, the landlord would opt to give a consumption credit contract, since it obviates the need for verification. To minimize the risk of default, however, the landlord would require collateral from the borrowers. But those requiring consumption credit are typically the poorest - who have no collateral to offer. As a result, the landlord would prefer to lend to his employees on whose future incomes he has some claim. An optimal employment contract under the circum- stances would be an interlinked contract.

It may be argued that consumption stabilization may be sought after even in the absence of uncertainty. Either diminishing marginal utility or, more weakly, a diminishing marginal rate of substitution between consumption today and consumption tomorrow would create a desire for consumption- smoothing. If so, once again access to capital markets would be a much- sought-after privilege. The accounts of distress sales by cash hungry peasants despite virtual certainty that prices would be higher in the subsequent periods attest to the lack of access of such peasants to capital markets.7 An increase in the unevenness of the time profile of the income stream would have a distributive effect: by increasing the premium on consumption stabilization services, it would benefit the rich merchant traders at the expense of small farmers who possess little access to capital markets. Access to credit, or to one’s own wealth, imparts to an individual the advantage of intertemporal flexibility in adjusting his consumption. Without it, he is much more vulnerable to the vicissitudes of Nature and markets alike.

Appendix: Proof of Proposition 1

The first-order condition associated with the choice, p*, of a credit- constrained farmer, obtained by differentiating (9), is

61n Kotwal (1985) it was argued that in instances where the debt is never fully repaid within a tenancy arrangement and the contingency is verifiable, credit can be construed as weather dependent side payment. In the present paper, however, we are focussing on those situations in which credit is fully repaid and contingencies are unverifiable.

‘In India as well as in some other countries, consumption credit is also sought for anticipated events such as weddings and funerals, for which social norm require considerable expenditure [Roth (1983), Breman (1985)]. The theory we have put forth in this paper applies equally well to these cases.

52 M. Eswaran and A. Kotwal, Credit as insurance in agrarian economies

+(z-x-o)u’[p*z+(1 -pP*)x-pp*o+B]

+gz - x)u’[p*z + (1 - p*)x -B]

+(z-X+a/2)u’[p*z+(l-p*)x+p*a/2]=0, (A.1)

where primes denote derivatives. Differentiating (A.l) totally with respect to B and rearranging, we obtain

{+(z -x - o)%“[p*Z + (1 - p*)x --p*a + B]

+$z-x)%“[p*z+(l--*)x-B

+(z-x+a/2)~u”[JI*z+(l-p*)x+(p*~/2]}~

= -gz-x-cT)u”[p*z+(1 -p*)x-p*a+Lq

++(z-x)u”[p*z+(l

Since u( .) is strictly concave that

dp* E>O. Q.E.D.

-p*)x-B]. (A.9

and z-x>O>z-X-CT, it follows from (A.2)

(A.3)

References

Bhaduri, A., 1983, The economic structure of backward agriculture (Academic Press, London). Binswanger, H. and D. Sillers, 1983, Risk-aversion and credit constraints in farmers’ decision-

making: A reinterpretation, Journal of Development Studies 20, 5-21. Blackorby, C., R. Davidson and D. Donaldson, 1977, A homiletic exposition of the Expected

Utility Hypothesis, Economica 44, 351-358. Breman, J., 1974, Patronage and exploitation (University of California Press, Berkeley, CA). Breman, J., 1985, Of peasants, migrants and paupers (Oxford University Press, New Delhi). D&e, J. and F. Modigliani, 1972, Consumption decisions under uncertainty, Journal of

Economic Theory 5, 308-335. Eswaran, M. and A. Kotwal, 1986, Access to capital and agrarian production organization,

Economic Journal 96, 482498. Kotwal, A., 1985, The role of consumption credit in agricultural tenancy, Journal of Develop-

ment Economics 18, 273-295. Moscardi, E. and A. de Janvry, 1977, Attitudes toward risk among peasants: An econometric

approach, American Journal of Agricultural Economics 59, 710-716.

M. Eswaran and A. Kotwal, Credit as insurance in agrarian economies 53

Newberry, D. and J. Stiglitz, 1981, The theory of commodity price stabilization: A study if the economics of risk (Oxford University Press, New York).

Prasad, P., 1974, Reactionary role ofVusurer’s capital in rural India, Economic and Political Weekly 9, 1305-1308.

Roth, H., 1983, Indian moneylenders at work (Manohar Publishers, New Delhi). Roemer, J., 1982, The general theory of exploitation and class (Harvard University Press,

Cambridge, MA). Roumasset, J., 1973, Risk-aversion, indirect utility functions, and market failure, in: J.

Roumasset, J. Boussard and 1. Singh, eds., Risk, uncertainty and agricultural development (Agricultural Development Council, New York).

Roumasset, J., 1979, Rice and risk (California University Press, Berkeley, CA). Rudra, A., 1982, Indian agricultural economics (Allied Publishers, New Delhi). Scott, J., 1976, The moral economy of the peasant (Yale University Press, New Haven, CT). Stiglitz, J., 1969, Behaviour toward risk with many commodities, Econometrica 37, 660-667. Tybout, J., 1984, Interest controls and credit allocation in developing countries, Journal of

Money, Credit and Banking 16, 474487. von Pischke, J., D. Adams and G. Donald, eds., Rural financial markets in developing countries

(Johns Hopkins University Press, Baltimore, MD).