Corporation as a Crucial Ally Against Corruption

14

Corporation as a Crucial Ally Against Corruption Reyes Caldero ´n Jose´ Luis A ´ lvarez-Arce Silvia Mayoral ABSTRACT. Manuscript type Empirical. Research question/ issue This paper aims to contribute to an improved theoretical and empirical understanding of the role that corporation has to play in anticorruption efforts. Research findings/insights Using cross-country data from three dat- abases (Bribe Payers Index, Corruption Perceptions In- dex, and Doing Business) we found that pro-bribery Investment Climate conditions in host countries are not related to the payments of bribes by multinational com- panies when these corporations operate abroad. Theoreti- cal/academic implications After describing the conceptual and policy framework that surrounds the discussion on the role played by firms in anticorruption, we present the current debate regarding the effectiveness of international bribery control instruments, with the World Bank-GAC (2006–2008) report as a basis. Both literature and policy seem to be divided into two main, although not mutually exclusive, positions: one demands improvements in Investment Climate conditions from a joint public–pri- vate consensus led by international agencies; the other one supports the effectiveness of self-regulation by firms, independent of Investment Climate improvements. The study provides empirical support to the idea that a better Investment Climate is not enough for reducing corrup- tion. Practitioner/policy implications This study offers insights to policy makers interested in promoting the involvement of corporations in the fight against corruption. KEY WORDS: Bribe Payers Index, corporation, cor- ruption, Corruption Perceived Index, doing business, investment climate, World Bank Governance and Anti- corruption report Introduction This paper aims to contribute to an improved understanding of the role played by corporations in economic corruption, with the current World Bank Governance and Anticorruption report (WB-GAC, 2006–2008) as a basis. With this purpose, we first provide a description of the conceptual and policy framework, and an overview of the current debate surrounding the issue. Economic corruption refers to a public official distributing commodities or allocating resources who views his/her office as a private source of gains (Jain, 2001; Rose-Ackerman, 1999). Bribery, which results from demand – the bribe taker – and supply – the bribe giver, is best understood and combated if both sides are simultaneously dealt with (Bertok, 1999). Even this being the case, for decades, policy and research primarily addressed the demand side, while the supply side, usually associated with mul- tinational corporations (MNCs) depicted as the innocent party, received little attention (Beets, 2005; MacMurray, 2006; Vogl, 1998). We explain why some factors, like the increasing costs and risks of corruption (Aidt, 2003), pressures from stakeholders (Waddock et al., 2002), and poor anticorruption performance (Veron et al., 2006), are gradually expanding the focus from demand to demand–supply factors (Sung, 2005). In this new scenario the corporation is called to participate as a ‘‘crucial ally’’ (WB-GAC, 2006–2008, p. ii) and a ‘‘key pillar of integrity’’ (UN, 2004, p. 83). Reyes Caldero ´n is Associate Dean of the School of Economics and Business Administration at the University of Navarra. Jose´ Luis A ´ lvarez-Arce is Professor of Economics at the School of Economics and Business Administration at the University of Navarra. Silvia Mayoral is Professor of Statistics at the School of Eco- nomics and Business Administration at the University of Navarra. Journal of Business Ethics (2009) 87:319–332 Ó Springer 2008 DOI 10.1007/s10551-008-9796-y

Transcript of Corporation as a Crucial Ally Against Corruption

Corporation as a Crucial Ally Against

Corruption

Reyes CalderonJose Luis Alvarez-Arce

Silvia Mayoral

ABSTRACT. Manuscript type Empirical. Research question/

issue This paper aims to contribute to an improved

theoretical and empirical understanding of the role that

corporation has to play in anticorruption efforts. Research

findings/insights Using cross-country data from three dat-

abases (Bribe Payers Index, Corruption Perceptions In-

dex, and Doing Business) we found that pro-bribery

Investment Climate conditions in host countries are not

related to the payments of bribes by multinational com-

panies when these corporations operate abroad. Theoreti-

cal/academic implications After describing the conceptual

and policy framework that surrounds the discussion on

the role played by firms in anticorruption, we present the

current debate regarding the effectiveness of international

bribery control instruments, with the World Bank-GAC

(2006–2008) report as a basis. Both literature and policy

seem to be divided into two main, although not mutually

exclusive, positions: one demands improvements in

Investment Climate conditions from a joint public–pri-

vate consensus led by international agencies; the other

one supports the effectiveness of self-regulation by firms,

independent of Investment Climate improvements. The

study provides empirical support to the idea that a better

Investment Climate is not enough for reducing corrup-

tion. Practitioner/policy implications This study offers

insights to policy makers interested in promoting the

involvement of corporations in the fight against

corruption.

KEY WORDS: Bribe Payers Index, corporation, cor-

ruption, Corruption Perceived Index, doing business,

investment climate, World Bank Governance and Anti-

corruption report

Introduction

This paper aims to contribute to an improved

understanding of the role played by corporations in

economic corruption, with the current World Bank

Governance and Anticorruption report (WB-GAC,

2006–2008) as a basis. With this purpose, we first

provide a description of the conceptual and policy

framework, and an overview of the current debate

surrounding the issue.

Economic corruption refers to a public official

distributing commodities or allocating resources

who views his/her office as a private source of gains

(Jain, 2001; Rose-Ackerman, 1999). Bribery, which

results from demand – the bribe taker – and supply –

the bribe giver, is best understood and combated if

both sides are simultaneously dealt with (Bertok,

1999). Even this being the case, for decades, policy

and research primarily addressed the demand side,

while the supply side, usually associated with mul-

tinational corporations (MNCs) depicted as the

innocent party, received little attention (Beets, 2005;

MacMurray, 2006; Vogl, 1998).

We explain why some factors, like the increasing

costs and risks of corruption (Aidt, 2003), pressures

from stakeholders (Waddock et al., 2002), and poor

anticorruption performance (Veron et al., 2006), are

gradually expanding the focus from demand to

demand–supply factors (Sung, 2005). In this new

scenario the corporation is called to participate as a

‘‘crucial ally’’ (WB-GAC, 2006–2008, p. ii) and a

‘‘key pillar of integrity’’ (UN, 2004, p. 83).

Reyes Calderon is Associate Dean of the School of Economics

and Business Administration at the University of Navarra.

Jose Luis Alvarez-Arce is Professor of Economics at the School of

Economics and Business Administration at the University of

Navarra.

Silvia Mayoral is Professor of Statistics at the School of Eco-

nomics and Business Administration at the University of

Navarra.

Journal of Business Ethics (2009) 87:319–332 � Springer 2008DOI 10.1007/s10551-008-9796-y

Subsequently, we examine the current debate,

which is raising many related questions regarding the

selection and implementation of international brib-

ery control instruments: Can societies rely on

individual company policies or on industry self-

regulation? Are other means such as laws or statutes

needed? Must the public sector lead the process?

At the forefront of this debate we find two vari-

ables: the firm’s vulnerability to the investment cli-

mate’s (IC) characteristics and the leadership of the

joint public–private coalition for reform. Both have

divided literature and policy in two main, but not

mutually exclusive, positions. One demands a join

public–private consensus led by international agen-

cies, and IC improvement as a precondition. The

other supports the effectiveness of self-regulation,

and its independence of IC improvement.1

We offer some empirical evidence on the issue.

Using the ‘‘Bribe Payers Index’’ (BPI), the ‘‘Cor-

ruption Perception Index’’ (CPI) by Transparency

International (TI), and the ‘‘Doing-Business’’ (DB)

database by the World Bank (WB), we test the

correlation between the propensity of MNCs to pay

bribes when operating abroad and the pro-bribery

IC conditions in host countries. Our results suggest a

low significance of IC factors in bribe-taking

behavior at the country level. Therefore, we con-

clude that the improvement of IC is not enough to

reduce bribery.

The structure of this paper is as follows. We

first provide the theoretical framework, describing

factors that explain the growing interest in the

supply side of corruption. Then, we carry out a

critical description of WB-GAC, emphasizing the

roles assigned to IC and corporation. After that,

we discuss the debate and main positions regarding

the selection and implementation of antibribery

instruments. In the last section, we describe the

empirical analysis and show our results. Findings

are then discussed, and the final section examines

some limitations of our analysis as well as possible

venues for future research.

The supply side of anticorruption efforts

Most research and conventions on anticorruption

adopt demand-pull perspectives (MacMurray, 2006;

Sung, 2005; Vogl, 1998). Although observers vouch

for the generalization and extension of bribery –

$1 trillion in 2003 (WBI, 2004) – with the corpo-

ration ranked as the most corrupt institution in

countries like Hong Kong and the Netherlands

(Transparency International, 2004), strategies have

largely neglected the role played by bribe givers.

With few exceptions – the ‘‘Foreign Corrupt

Practices Act’’ (FCPA, 1977) and the OECD’s

‘‘Convention on Combating Bribery of Foreign

Public Officials in International Business Transac-

tion’’ (OECD, 1997), which will be discussed

afterward – all countries criminalize and punish

corrupt officials, while sanctions for paying bribes

remain rare (Rose-Ackerman, 2002). The insistence

on addressing the demand side was based on two

elements: the supposed efficiency of demand-pull

instruments, and all the problems associated with

attempting to regulate the supply side.

The demand-side perspective is built on one key

assumption: there is a systemic failure, symptom of

the state’s fundamental weaknesses, which can be

efficiently combated by different means: ethical

development in the public sector’s infrastructure

(Bertok, 1999); better legislative actions and law

enforcement (Dollar and Levin, 2006); stronger and

more effective public institutions (Huang and Wei,

2006); accountability and transparency requirements

(Everett et al., 2007); and privatization and decen-

tralization (Caselli and Morelli, 2004). Authors add

the positive impact of government on wealth pro-

motion (Husted, 1999), the reduction of inequality

(You and Khagram, 2005), the control of extractive

industries (O’Higgins, 2006), and the support of an

anticorruption culture (Sanyal, 2005).

This spirit is clearly seen in the Inter-American

Convention against Corruption (1996), whose preamble

proposes ‘‘especially…action against persons who

commit acts of corruption in the performance of

public functions.’’

When focusing on supply-side instruments,

however, some difficulties emerge. One of these is

the likelihood of a ‘‘race to the bottom’’ effect in

cross-country competition for doing and attracting

business. While some countries impose strict laws on

domestic firms competing for offshore business,

others are reluctant. The US Department of State

claims that, due to this factor, between 1994 and

2001, American business lost 400 major contracts

(Sung, 2005).

320 Reyes Calderon et al.

On the other hand, the corporation is constituted

as a legal person, for whom only dissuasive non-

criminal sanctions are applicable (OECD, 1997,

art. 3). Moreover, the literature shows strong tech-

nical problems related with data and aggregation,

due to the heterogeneity of the supply (Dollar et al.,

2005). These factors explain why only one main

instrument – the disallowing of the tax deductibility

of bribes – has obtained consensus.

However, a new sensibility seems to be emerging.

All the involved agents now agree that corporations

have a main role to play in promoting transparency

and curbing corruption. The WB-GAC names the

corporation a ‘‘crucial ally against corruption’’ and

the UN (2004, p. 84) considers it as a ‘‘key pillar of

integrity.’’

Poor results of anticorruption efforts explain this

new view. After two decades of emphasis on

demand-side elements, corruption has not dissipated

and improvements have mostly stagnated (Veron

et al., 2006). Policymakers and academia have finally

become convinced that ‘‘governments alone cannot

contain corruption’’ (UN, 2004, p. 17). ‘‘Traditional

public sector intervention is not enough in tackling

challenges. Wider engagement with the domestic

private sector and MNCs is required’’ (WB-GAC,

2006–2008, introduction).

Impelled by stakeholder pressures and the per-

ceived costs and risks, the corporation has accepted

its new role. Bribery and corruption are nowadays

among the great issues on corporate governance’s

agenda (Elkington, 2006). Although corrupt prac-

tices can be beneficial for some individual firms,

corruption increases costs and risks for the whole. In

contrast with free markets and quality institutions,

corruption increases transaction and doing-business

costs (Pantzalis et al., 2008). With insecure property

rights, high risk of expropriation, and low reliability

of contract enforcement, the number and size of

firms (Beck et al., 2005), foreign investment

(Mauro, 1995), profit per firm (Ades and Di Tella,

1997), long-term performance (Baucus and Baucus,

1998), and quality of produced goods (Nwabuzor,

2005) are reduced.

Gjessing and Syse (2007) signal that investors

recognize the additional risk, and attempt to ensure

the corporation has sufficient internal controls while

top management supports and implements relevant

anticorruption rules. Enron and its sequels have

reinforced the main hypothesis: it is in the best

interest of the private sector to apply self-imposed

anticorruption measures (Howlett and Rayner,

2006).

Additionally, in light of a wide range of events

linked to labor, health, and safety rights (Belcher,

2002) and environmental concerns (Elkington,

2006), broad discussions have emerged to address the

role of the corporation in society, its ethical stan-

dards, corporate governance practices, and manage-

ment decisions systems (Bonn and Fisher, 2005). As

a result, primary and external stakeholders around

the world compel companies ‘‘to respond in a more

responsible and transparent way to environmental

pressures’’ (Waddock et al., 2002, p. 132). Due to

growing evidence of rampant consequences of

bribery on development, poverty, inequality, and

human suffering,2 anticorruption has become a ‘‘hot

issue.’’

The new framework: WB-GAC (2006-08)

Some evidence of change may be perceived in the

‘‘new generation’’ of anticorruption strategies

(Coleman and Perl, 1999), such as the WB-GAC. In

comparison to past reports – FCPA (1977) and

OECD (1997), which simply conceptualized the

corporation as the agent who pays bribes – the WB-

GAC includes a multidisciplinary approach, focusing

on governance and IC.

FCPA (1977), which makes extraterritorial brib-

ery explicitly illegal for US companies and creates

requirements for greater transparency, and OECD

(1997), an attempt to extend sanctions around the

world, present three main coincidences:

– Both try to legally avoid corrupt behavior. Like

Rose-Ackerman (2002), they consider that a

firms’ main argument to reject corruption is

their status as a legal person operating at the state’

suffrage. Attitudes or values, which have been

essential in countries like Hong Kong, are lar-

gely neglected.

– While both welcome the contribution of compa-

nies, the role of self-regulation and private codes

is left unaddressed.

Corporation as a Crucial Ally Against Corruption 321

– Both recognize the role that governments play

in the prevention of bribe solicitation, but

neglect the analysis of the IC’s impact.

Contrarily, the WB-GAC (a) refuses the

monopoly of legal focus, admitting that champions

of reform may be found inside and outside the

executive branch of government, including the

business community; (b) names the corporation a

‘‘crucial ally’’; and (c) focuses especially on the

improvement of the IC.

Addressing the private sector, the WB-GAC

(2006–2008, pp. 12–14) begins describing the

divergence of incentives. In the middle and long-

term, corruption increases vulnerability and

uncertainty for firms, and has a detrimental impact

on their dynamism and growth. Consequently,

MNCs have a strong incentive to reject venal

officials as strategic partners. But in the short-term,

corruption creates lucrative opportunities with low

risk for unethical corporations. Many private busi-

nesses, ‘‘including some from developed countries,

themselves engage in corrupt practices’’ (WB-

GAC, 2006–2008, p. 12).

If integrity and incentives were always positively

correlated, debate would be superfluous (Rose-

Ackerman, 2002). However, divergences affect firm

behavior. Thus, in order to deter the last type of

behavior and to fuel the first, the WB-GAC estab-

lishes three type of actions.

1. Actions from government to private sector. The

report recognizes the main role played by the

IC and indicates that some IC features make

firms vulnerable to corruption in host coun-

tries. Thus, it proposes to help governments

to ‘‘eliminate excessive red tape and non-

transparent regulations, reduce monopolistic

practices, transparently and competitively pri-

vatize state-owned business and banks, facili-

tate the entry of small and medium

enterprises’’ (WBG, 2006, p. 12).

2. Actions that encourage a joint public–private coali-

tion for reforms. A public leadership coalition,

with ‘‘the International Financial Corpora-

tion and Multilateral Investment Guarantee

Agency working directly with the private

sector to introduce ethical corporate prac-

tices’’ (WBG, 2006, p. 12).

3. Public sanctions. Measures to raise the cost to busi-

nesses that continue to engage in corruption.

The WB-GAC is already in force. Its term, com-

mencing in 2006, is proving itself to be long and

problematic. It has included a WBG-IMF forum,

internal and external feedback, and consultation with

governments, donor agencies, etc. The last version

(October 2007) will likely be definitively approved

in 2008.

Some factors related with IC and firms have been

in dispute. For example, while in the last version

transparency continues to be demanded, references

to red tape and monopolistic practices have disap-

peared and national conditions have come to the

forefront: each country ‘‘will have explicit gover-

nance indicators to monitor for positive change’’ (p.

18). In fact, a critical question remains: must the IC’s

improvement and rigorous international monitoring

be correlated? Can corporation collaboration be re-

quired without assuring the collaboration of host

countries? A second conflictive factor is the reform-

leading agent. In the cited feedback, some countries

have refused the multilateral approach in an attempt

to minimize the business sector’s contribution, as the

next comment shows: ‘‘The private sector have

vested interests of their own (‘‘money-making’’),

and this will hamper aid effectiveness to a great

deal…’’ [Respondent type: Government; Region:

South Asia].

The debate around mechanisms

The new generation of anticorruption effort is built

on the involvement of both private and public ac-

tors, which, being not mutually exclusive, must

cautiously work to develop measures that harmonize

law, social and national interests, self-regulation,

firm freedom, etc. (Jordan et al., 2006).

In the achievement of the ultimate objective – the

reduction of bribery through a mix of supply–

demand instruments – discussions have focused on

two different elements:

(a) Who must lead the effort of developing initia-

tives, defining standards, adopting rules that

force corporations toward integrity, and moni-

toring important exporters and producers?

322 Reyes Calderon et al.

(b) The obligatory character of removing

impediments that make corporations victims

of their environment.

In relation with these questions, we identify two

positions: the bribery environment position, which

requires IC improvements and a joint public–private

consensus led by international agencies, and the bribe

giver position, which defends the effectiveness of the

corporation’s self-regulation, independent of IC

improvement.

The bribery environment position

This position maintains that an individual official

may not change pro-bribery IC elements; neither is

an individual corporation able to impact the national

culture and law (Schechter, 2007). While legal

deterrence through legal sanctions may be needed to

succeed (Sung, 2005; Zhang, 2007), or ‘‘practices are

so ingrained in a culture that there seems to be

neither need nor realistic opportunity for change

overnight’’ (Gjessing and Syse, 2007, p. 431), any

substantial progress requires the collaboration be-

tween the global corporation and the host countries

(Potts and Matuszewski, 2004). This is in conformity

with Bethoux et al. (2007), who find that business

codes attempt to prohibit bribery, referring to types

of conduct that violate public regulations and law.

This position underlines that public–private col-

laboration could require the acceptance of external

actors such as international agencies. Following the

US example, all the developed European and

American exporting countries have introduced

domestic legislation following OECD (1997), and

even UN (2004) conventions. Many former bribery-

tolerant industrialized countries (i.e., France and

Germany) have rectified and now reject the tax-

deductibility of bribes.

However, commitment cannot be measured by

simple participation in conventions. While the US is

engaged in combating bribery even if corrupt IC in

host countries remains unchanged, the political will of

other countries has not been as strong. SenGupta

(2006) shows that the US has brought action against 35

foreign bribery cases since 1998, France only three,

and Germany just one case. In the UK, there have

been no prosecutions since 2002. This demonstrates

that public–private collaboration, though necessary, is

not a sufficient condition to prevent corruption.

In the search for explanations, and aligned with

recent literature, the vulnerability of the firm to IC

conditions is often signaled. In the literature, IC is

referred to as the set of present or expected institu-

tional, policy, and regulatory environmental factors

that may influence the returns and risks of a corpo-

ration’s investment (Dollar et al., 2005). IC depends

on infrastructures and institutions, macro-economic

or governance factors.

The research on bribery has put more attention on

how the governance block [property rights’ protec-

tion, transaction costs, coercion, bureaucracy harass-

ment, poor governance, and corruption (Batra et al.,

2002)] affects firm performance, and on the status of

bias caused by the mobility of firms across regions and

countries. But results are inconclusive, correlations

tend to be unclear, and data must be interpreted with

caution. For instance, while Dollar et al. (2005) find a

robust link between financial services and firm per-

formance, they do not find that general measures of

corruption or poor government explain differences in

outcomes across countries, contrary to the results

presented by Batra et al. (2002).

However, the literature continues to emphasize

the vulnerability of the firm (Demirguc-Kunt et al.,

2006). Authors consider it unjustifiably harsh to

prosecute or denounce an individual firm for paying

bribes in countries whose IC factors prevent the

corporation from not engaging in corruption (Col-

lins and UhlenBruck, 2004; Wu, 2006) and oblige

such activity for self-protection (Posner, 1998). For

instance, Peng and Bajona (2008) report that most of

the Chinese state-owned enterprises are insolvent.

As a result, this position supports a combined fight

against poor governance and bribe-taking, led by

international agencies.

The Bribe giver position

The alternative position suggests that ‘‘the structural

characteristic of bribe-accepting countries may not be

the most crucial determinant of bribery’’ (Vogl, 1998,

p. 30). If this is true, corporate corruption is not a

conflict of interest between the corporation and the host gov-

ernment, but rather a conflict of the corporation with itself,

which must be combated through integrity.

Corporation as a Crucial Ally Against Corruption 323

Cadbury (2000) supports that corruption can be

most directly contained by raising standards of cor-

porate governance and, contrary to Rose-Ackerman

(2002), argues that decisions of a single institution or

corporation can have considerable economic and

social consequences. At the root of this idea, we find

the hypothesis that voluntary principles and stan-

dards of conduct may be economically viable,

operationally feasible, and socially profitable (Sethi,

2005).

Vincke and Heimann (2003) emphasize that a

broad practical consensus in the business community

is crucial. Cragg (2005) signals that there is a

remarkable consensus across a broad range of state-

ments and codes about those aspects that require

regulation or standard settings, and also in the values

involved. The critical question is how to address

practices embedded in corporate structure (Bonn

and Fisher, 2005).

The WB-GAC suggests that practices emanate

from public sector to private sector. Because the

nations’ capacity to regulate commerce has been

attenuated by globalization, the report demands a

‘‘broad consensus’’ led by international agencies and

national governments.

On the contrary, Mungui-Pippidi (2006) argues

that the government cannot solve the problem be-

cause it is itself the problem by definition, and

proposes the self-regulation of business. Hopkin and

Rodrıguez-Pose (2007) find that the degree of reg-

ulation of private business activity is the strongest

predictor of corruption. Private sector organizations

(for instance, Combating Extortion and Bribery (2005)

from the International Chamber of Commerce)

declare that the success of rules depends on their

voluntary acceptance and on self-regulation by

business enterprises, which suggests the erosion of

states’ regulatory capacity.

Public principles and discourses are not enough

to develop values such as integrity, as they must

be actively supported by managers (Valentine et

al., 2006). This requires the rewarding of appro-

priate business conduct, the facilitation of the

relationship between the organization and its

employees, and the punishment of unacceptable

acts (Trevino, 1986).

Only businesses themselves may offer credible

strategies to foster integrity. If the acceptable

behavioral model varies within a given nation, the

corporation’s integrity loses credibility. If ethical

belief significantly fluctuates among cultures, integ-

rity is dead. Williamson (1975) suggests that man-

agers use norms, habits, and routines in order to

develop the voluntary acceptance of self-restraint

with regard to opportunism. Nevertheless, oppor-

tunistic actions by employees are facilitated if top

management is perceived as being unethical (Koh

and Boo, 2001). Facilitating or authorizing subor-

dinates’ bribery while remaining ignorant of the

details encourages actions that employees themselves

would consider immoral in personal/organizational

life (Rose-Ackerman, 2002). If, through this disso-

nant behavior, deceit is institutionalized, a harmful

effect upon the organization has been accepted

(Asforth and Anand, 2003).

Discrepancies between both positions have been

analyzed as arising from (a) the role assigned to IC

and (b) the leadership of reform. In order to provide

empirical evidence for this debate, we test the

influence of the first factor. Specifically, we test how

the inclination of foreign MNCs to pay bribes cor-

relates to pro-bribery conditions of the IC in host

countries.

Data, methodology, and findings

Data

To conduct our empirical study, we rely on three

datasets on corruption (CPI), bribery (BPI), and IC

(DB). TI’s CPI measures perceived corruption in

different countries on a scale from 0 (highly corrupt)

to 10 (highly clean). Although the literature suggests

some methodological problems, the CPI provides

probably the best measure currently available for a

worldwide ranking (Seligson, 2006).

In 2006 TI published its last BPI, the third of a

series, after its 2001 and 1999 reports. The BPI ranks

leading exporting countries in terms of the degree to

which international companies with their head-

quarters in those countries are likely to pay bribes to

public officials abroad. The index is a score between

0 (bribes are habitual) to 10 (bribes never occur). We

take the list of countries ranked in the BPI as our

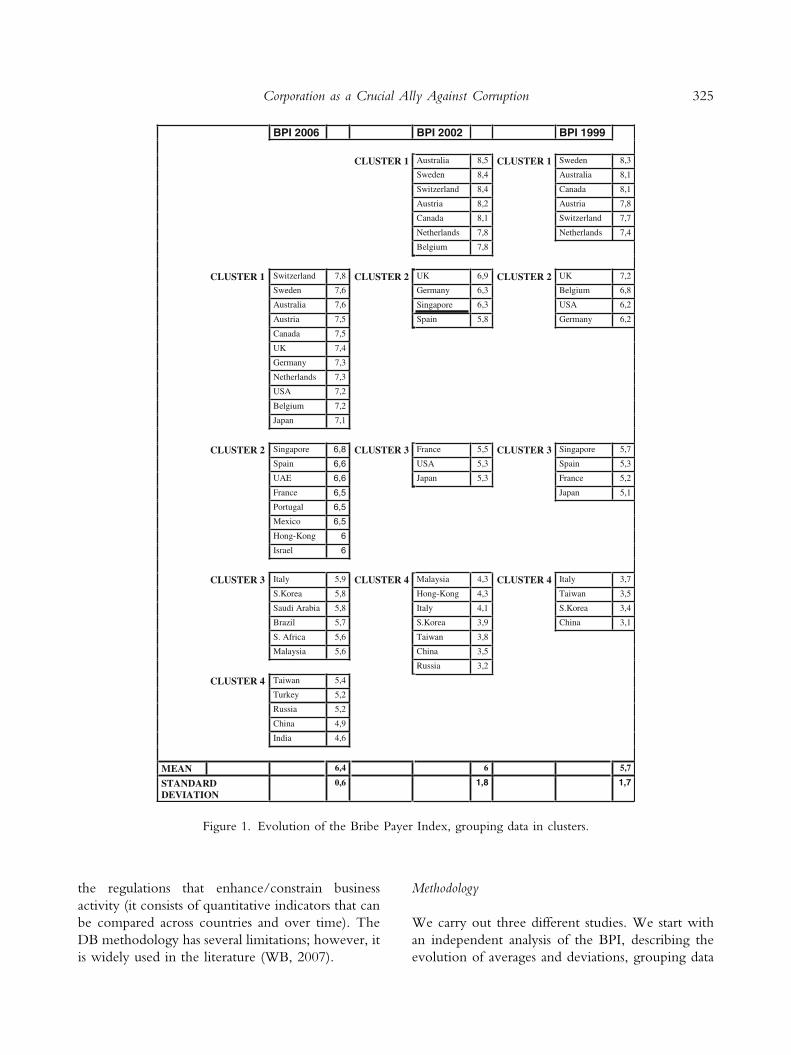

study sample (Figure 1).

Finally, we use the Doing Business (DB) database,

a series of annual reports published by the WB on

324 Reyes Calderon et al.

the regulations that enhance/constrain business

activity (it consists of quantitative indicators that can

be compared across countries and over time). The

DB methodology has several limitations; however, it

is widely used in the literature (WB, 2007).

Methodology

We carry out three different studies. We start with

an independent analysis of the BPI, describing the

evolution of averages and deviations, grouping data

BPI 2006 BPI 2002 BPI 1999

CLUSTER 1 Australia 8,5 CLUSTER 1 Sweden 8,3

Sweden 8,4 Australia 8,1

Switzerland 8,4 Canada 8,1

Austria 8,2 Austria 7,8

Canada 8,1 Switzerland 7,7

Netherlands 7,8 Netherlands 7,4

Belgium 7,8

CLUSTER 1 Switzerland 7,8 CLUSTER 2 UK 6,9 CLUSTER 2 UK 7,2

Sweden 7,6 Germany 6,3 Belgium 6,8

Australia 7,6 Singapore 6,3 USA 6,2

Austria 7,5 Spain 5,8 Germany 6,2

Canada 7,5

UK 7,4

Germany 7,3

Netherlands 7,3

USA 7,2

Belgium 7,2

Japan 7,1

CLUSTER 2 Singapore 6,8 CLUSTER 3 France 5,5 CLUSTER 3 Singapore 5,7

Spain 6,6 USA 5,3 Spain 5,3

UAE 6,6 Japan 5,3 France 5,2

France 6,5 Japan 5,1

Portugal 6,5

Mexico 6,5

Hong-Kong 6

Israel 6

CLUSTER 3 Italy 5,9 CLUSTER 4 Malaysia 4,3 CLUSTER 4 Italy 3,7

S.Korea 5,8 Hong-Kong 4,3 Taiwan 3,5

Saudi Arabia 5,8 Italy 4,1 S.Korea 3,4

Brazil 5,7 S.Korea 3,9 China 3,1

S. Africa 5,6 Taiwan 3,8

Malaysia 5,6 China 3,5

Russia 3,2

CLUSTER 4 Taiwan 5,4

Turkey 5,2

Russia 5,2

China 4,9

India 4,6

MEAN 7,564,6

STANDARD DEVIATION

0,6 1,8 1,7

Figure 1. Evolution of the Bribe Payer Index, grouping data in clusters.

Corporation as a Crucial Ally Against Corruption 325

into clusters in each period, and examining if the

evolution of the BPI and CPI is correlated. Data are

segmented in four clusters of countries, following TI

methodology.

Secondly, in order to measure differences be-

tween domestic and guest behavior, we define the

following variable:

DIFðtÞ ¼ CPIðtÞ � BPIðtÞ

which provides us with a proxy of the loss of busi-

ness transparency in international transactions. We

analyze DIF (2006) in a general perspective, testing

the hypothesis DIF = 0. We repeat the exercise in a

geographical division of DIF – Africa, Newly Inde-

pendent States, Low Income, Middle East, Asia-Pa-

cific, Europe, OECD and America – following the

BPI (2006) criteria, in order to study possible re-

gional differences. We also compare DIF means by

regions through an Analysis of Variance (Anova).

Finally, we add an aggregate index of five regu-

latory areas from the DB database: (1) starting a

business: regulations associated with the number,

time, and cost of procedures for starting a business,

including licenses and legal registration (Djankov

et al., 2002; Klapper et al., 2006); (2) lack of access

to credit (Black and Strahan, 2002); (3) employment

law (Botero et al., 2004); (4) tax disadvantage (Fis-

man and Svensson, 2007); and (5) bankruptcy pro-

cess and other investor protection systems (Lee et al.,

2007). Despite the problems caused by aggregation,3

this index permits us to explore how constraints on

doing business are associated with DIF.

Findings

From that analysis, we get the following results.

Propensity to pay bribes

As the BPI (2006) report emphasizes, there is a ‘‘con-

siderable propensity for companies of all nationalities to

bribe when operating abroad.’’ Even the best-per-

forming nation – Switzerland (7.81) – is far from 10.

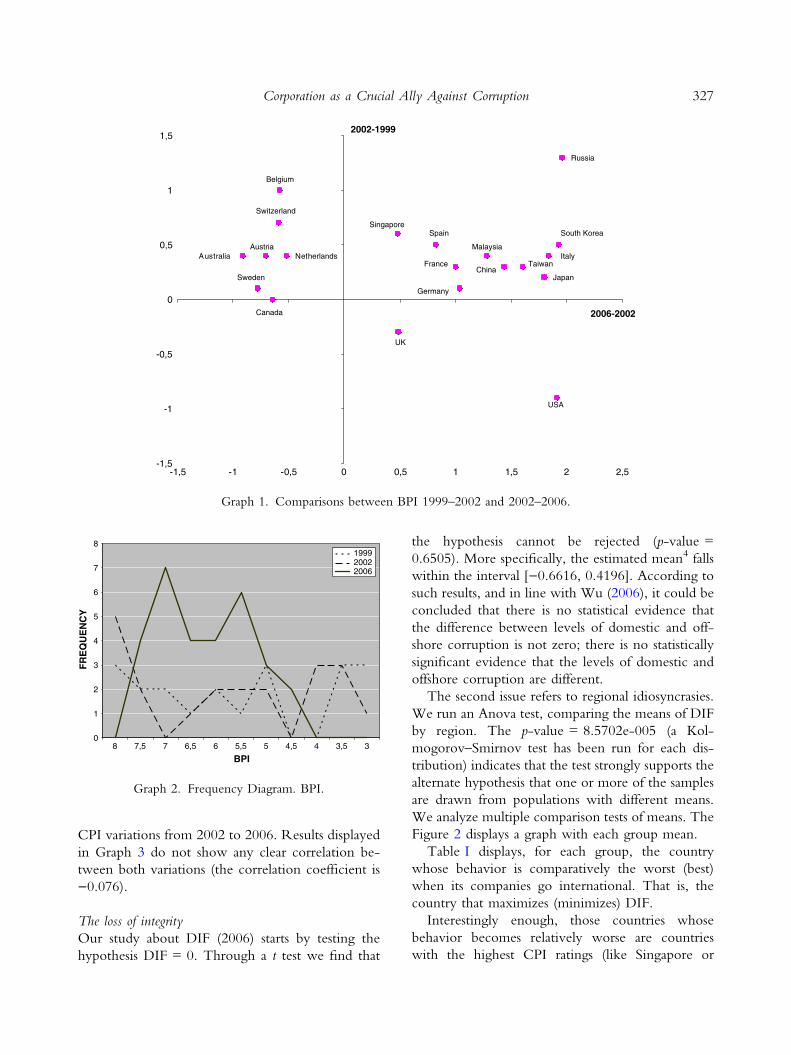

Figure 1 describes theBPI evolution in the four clusters.

From the data, some interesting issues emerge:

a. The global average of BPI ratings has im-

proved from 5.7 in 1999 to 6.4 in 2006.

b. The average has significantly improved in

three of the four clusters. That is especially

true for the last one: 3.4 in 1999 and 5.0 in

2006. Businesses from developing and in

transition countries, such as China, Russia,

or South Korea, are increasingly putting

effort in improving transparency and integrity.

c. The worst evolution comes from the first

cluster, which includes countries on the top

of the ranking. While the average score

weakly increased, coinciding with the enact-

ment of the OECD Convention (the good

behavior of countries like Belgium or Spain

compensates for the poor behavior of USA

and UK), results worsened in the period

2002–2006, with a loss of 0.7 points. Inter-

estingly enough, those countries with the

worst behavior in the first period obtained

much better scores in 2006: the score of

USA increased two points and Japan regis-

tered one of the biggest improvements, from

5.3 to 7.1.

Graph 1 shows the comparisons of the BPI evolu-

tion in both periods of time.

d. Another positive feature is the density of the

first quadrant: a big number of countries im-

proved in both periods. The negative coun-

terpart can be found in the second quadrant

with some of the most transparent economies

in the world such as Switzerland or Sweden.

The peculiar behavior of the UK and USA is

reflected in the fourth quadrant.

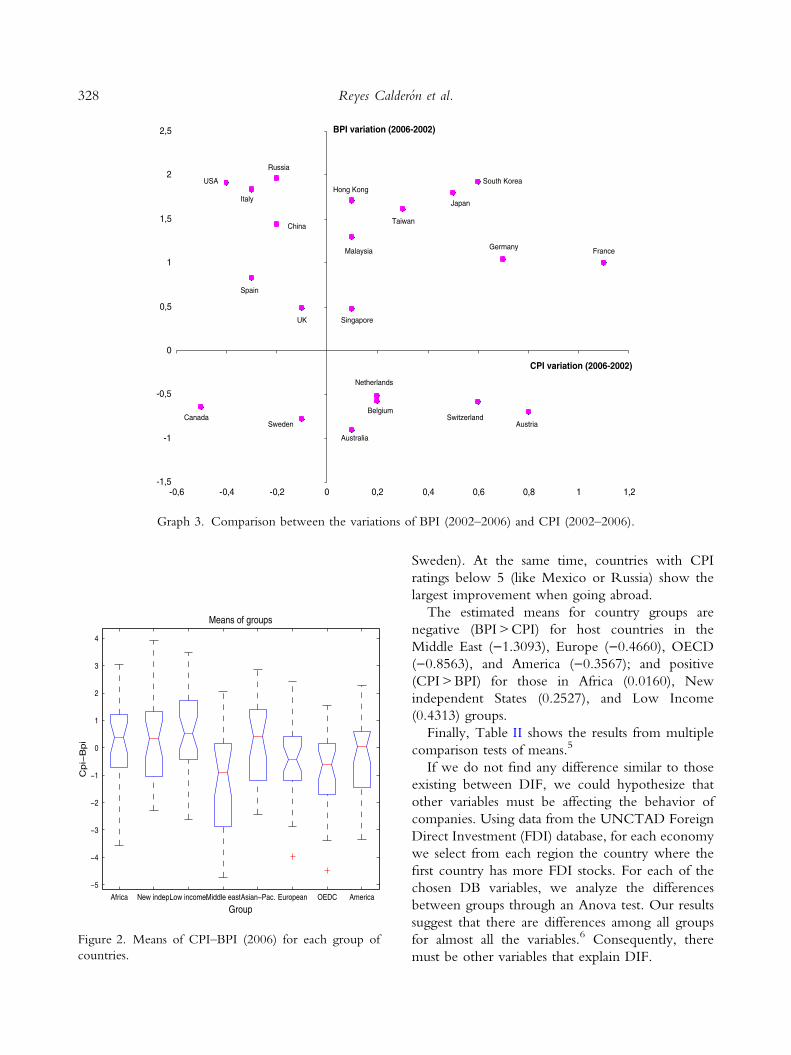

e. We also highlight how deviations from the

mean become smaller over time. Graph 2

shows an illustrative frequency diagram of

BPI. Changes slowly initiated in 2002, and

accelerated in the last period, signaling a clear

trend toward concentration, which could

well respond to a homogenization related to

globalization. Distances between the best and

the worst BPI rating were 62.65% in 1999

and 36.74% in 2006 (the standard deviation

dropped from 1.7 to 0.6).

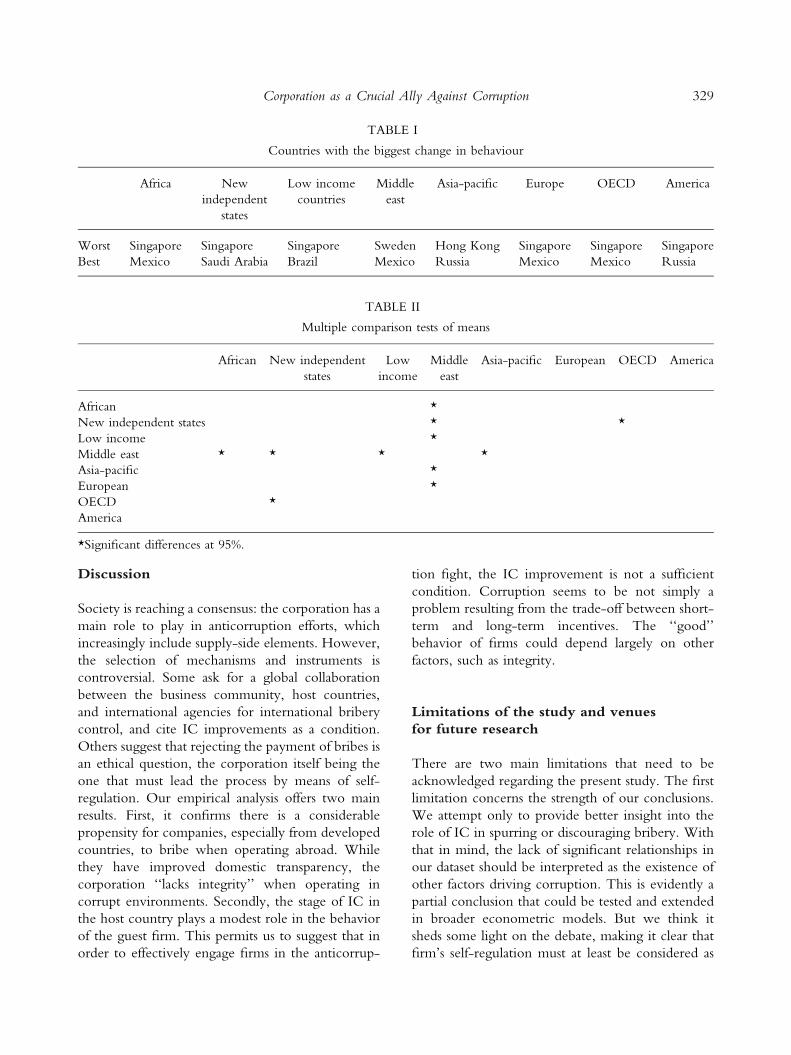

To address the possibility that BPI variations could

be the result of integrity changes in the countries of

origin and not in corporations, we compare BPI and

326 Reyes Calderon et al.

CPI variations from 2002 to 2006. Results displayed

in Graph 3 do not show any clear correlation be-

tween both variations (the correlation coefficient is

)0.076).

The loss of integrity

Our study about DIF (2006) starts by testing the

hypothesis DIF = 0. Through a t test we find that

the hypothesis cannot be rejected (p-value =

0.6505). More specifically, the estimated mean4 falls

within the interval [)0.6616, 0.4196]. According to

such results, and in line with Wu (2006), it could be

concluded that there is no statistical evidence that

the difference between levels of domestic and off-

shore corruption is not zero; there is no statistically

significant evidence that the levels of domestic and

offshore corruption are different.

The second issue refers to regional idiosyncrasies.

We run an Anova test, comparing the means of DIF

by region. The p-value = 8.5702e-005 (a Kol-

mogorov–Smirnov test has been run for each dis-

tribution) indicates that the test strongly supports the

alternate hypothesis that one or more of the samples

are drawn from populations with different means.

We analyze multiple comparison tests of means. The

Figure 2 displays a graph with each group mean.

Table I displays, for each group, the country

whose behavior is comparatively the worst (best)

when its companies go international. That is, the

country that maximizes (minimizes) DIF.

Interestingly enough, those countries whose

behavior becomes relatively worse are countries

with the highest CPI ratings (like Singapore or

-1,5

-1

-0,5

0

0,5

1

1,5

-1,5 -1 -0,5 0 0,5 1 1,5 2 2,5

Belgium

Switzerland

Australia NetherlandsAustria

Sweden

Canada

UK

USA

Russia

SingaporeSpain

France

Germany

Malaysia

ChinaTaiwan

Japan

Italy

South Korea

2006-2002

2002-1999

Graph 1. Comparisons between BPI 1999–2002 and 2002–2006.

0

1

2

3

4

5

6

7

8

8

BPI

FR

EQ

UE

NC

Y

199920022006

3,5 344,555,566,577,5

Graph 2. Frequency Diagram. BPI.

Corporation as a Crucial Ally Against Corruption 327

Sweden). At the same time, countries with CPI

ratings below 5 (like Mexico or Russia) show the

largest improvement when going abroad.

The estimated means for country groups are

negative (BPI > CPI) for host countries in the

Middle East ()1.3093), Europe ()0.4660), OECD

()0.8563), and America ()0.3567); and positive

(CPI > BPI) for those in Africa (0.0160), New

independent States (0.2527), and Low Income

(0.4313) groups.

Finally, Table II shows the results from multiple

comparison tests of means.5

If we do not find any difference similar to those

existing between DIF, we could hypothesize that

other variables must be affecting the behavior of

companies. Using data from the UNCTAD Foreign

Direct Investment (FDI) database, for each economy

we select from each region the country where the

first country has more FDI stocks. For each of the

chosen DB variables, we analyze the differences

between groups through an Anova test. Our results

suggest that there are differences among all groups

for almost all the variables.6 Consequently, there

must be other variables that explain DIF.

-1,5

-1

-0,5

0

0,5

1

1,5

2

2,5

-0,6 -0,4 -0,2 0 0,2 0,4 0,6 0,8 1 1,2

Australia

Austria

BelgiumCanada

China

FranceGermany

Hong KongItaly Japan

Malaysia

Netherlands

Russia

Singapore

South Korea

Spain

SwedenSwitzerland

Taiwan

UK

USA

CPI variation (2006-2002)

BPI variation (2006-2002)

Graph 3. Comparison between the variations of BPI (2002–2006) and CPI (2002–2006).

Africa New indep.Low income.Middle eastAsian−Pac. European OEDC America

−5

−4

−3

−2

−1

0

1

2

3

4

Cpi−

Bpi

Group

Means of groups

Figure 2. Means of CPI–BPI (2006) for each group of

countries.

328 Reyes Calderon et al.

Discussion

Society is reaching a consensus: the corporation has a

main role to play in anticorruption efforts, which

increasingly include supply-side elements. However,

the selection of mechanisms and instruments is

controversial. Some ask for a global collaboration

between the business community, host countries,

and international agencies for international bribery

control, and cite IC improvements as a condition.

Others suggest that rejecting the payment of bribes is

an ethical question, the corporation itself being the

one that must lead the process by means of self-

regulation. Our empirical analysis offers two main

results. First, it confirms there is a considerable

propensity for companies, especially from developed

countries, to bribe when operating abroad. While

they have improved domestic transparency, the

corporation ‘‘lacks integrity’’ when operating in

corrupt environments. Secondly, the stage of IC in

the host country plays a modest role in the behavior

of the guest firm. This permits us to suggest that in

order to effectively engage firms in the anticorrup-

tion fight, the IC improvement is not a sufficient

condition. Corruption seems to be not simply a

problem resulting from the trade-off between short-

term and long-term incentives. The ‘‘good’’

behavior of firms could depend largely on other

factors, such as integrity.

Limitations of the study and venues

for future research

There are two main limitations that need to be

acknowledged regarding the present study. The first

limitation concerns the strength of our conclusions.

We attempt only to provide better insight into the

role of IC in spurring or discouraging bribery. With

that in mind, the lack of significant relationships in

our dataset should be interpreted as the existence of

other factors driving corruption. This is evidently a

partial conclusion that could be tested and extended

in broader econometric models. But we think it

sheds some light on the debate, making it clear that

firm’s self-regulation must at least be considered as

TABLE I

Countries with the biggest change in behaviour

Africa New

independent

states

Low income

countries

Middle

east

Asia-pacific Europe OECD America

Worst Singapore Singapore Singapore Sweden Hong Kong Singapore Singapore Singapore

Best Mexico Saudi Arabia Brazil Mexico Russia Mexico Mexico Russia

TABLE II

Multiple comparison tests of means

African New independent

states

Low

income

Middle

east

Asia-pacific European OECD America

African *

New independent states * *

Low income *

Middle east * * * *

Asia-pacific *

European *

OECD *

America

*Significant differences at 95%.

Corporation as a Crucial Ally Against Corruption 329

a potential solution to bribery and corruption

problems. Unfortunately, there are no data available

for testing the influence of self-regulation on the

degree of corruption at the country level. This

would be an interesting issue to study in the future.

The second drawback involves the dataset. In fact,

several limitations in this study come from data, since

indices like the CPI or BPI have different and seri-

ous methodological flaws (Calderon and Liu, 2003).

The CPI may suffer from an endogeneity problem; it

may be strongly influenced by factors which sup-

posedly depend on corruption (Seligson, 2006). The

CPI also has a demand-side bias (it puts the spotlight

on the bribe takers) that the BPI tries to correct

(Sampford et al., 2006). But they are still the most

widely used measures on cross-country corruption.

A final point for further research: The regions in

our study show different patterns. Studies at specific

regional levels could shed more light on how multi-

nationals become involved in bribery and corruption.

Notes

1 Good self-regulation could even promote a better

Investment Climate.2 See Calderon and Alvarez (2007) for a review.3 An important limitation must be noted: BPI is not

available at a host-country level, while DB variables are

disaggregated at that level. If we tried to aggregate the

later variables, estimates would not be reliable.4 We have run a Kolmogorov–Smirnov test (95%) to

ensure that we cannot reject the hypothesis that the

CPI – BPI variable comes from a Normal distribution.5 Since the evidence suggests the presence of differ-

ences between countries with high (CPI > 5) and low

CPI (CPI < 5), we run the same analysis separating

countries in both groups. The results are similar to

those in Table II.6 Results are available from the authors. They are not

presented as they have no further interest and because

of the number of variables and country groups.

Acknowledgments

We thank Antonio Argandona, Isabel Rodrıguez Teje-

do, Prakash Sethi, and especially two anonymous refer-

ees for their comments, which have greatly helped to

improve the paper; WBG authorities; and Luis Orgaz

from the Spanish Ministry of Economy for his hospital-

ity during the 2006 IMF/World Bank Group Annual

Meeting and the participation in the WBG-GAC

report’s development. We are grateful for the support

received from the PIUNA program of the University of

Navarra.

References

Ades, A. and R. Di Tella: 1997, ‘The New Economics of

Corruption: A Survey and Some New Results’,

Political Studies 45(3), 496–515.

Aidt, T.: 2003, ‘Economic Analysis of Corruption: A

Survey’, Economic Journal 113, 632–652.

Ashforth, B. and V. Anand: 2003, ‘The Normalization of

Corruption in Organizations’, Research in Organiza-

tional Behavior 25, 1–52.

Batra, G., D. Kaufmann and A. Stone: 2002, Voices of Firm

2000: Investment Climate and Governance Findings of the

World Business Environment Survey (World Bank,

Washington).

Baucus, M. S. and D. Baucus: 1998, ‘Paying the Piper:

An Empirical Examination of Longer-Term Financial

Consequences of Illegal Corporate Behavior’, The

Academy of Management Journal 40(1), 129–151.

Beck, T., A. Demirguc-Kunt and R. Levine: 2005, ‘Bank

Supervision and Corruption in Leanding’, Journal of

Monetary Economics 53(8), 2131–2163.

Beets, S.: 2005, ‘Understanding the Demand Side Issues

of Corruption’, Journal of Business Ethics 57, 65–81.

Belcher, A.: 2002, ‘Corporate Killing as a Corporate

Governance Issue’, Corporate Governance an International

Review 10(1), 47–54.

Bertok, J.: 1999, ‘OECD Targets Both the ‘‘Supply Side’’

and ‘‘Demand Side’’ of Corruption’, Public Personnel

Management 28(4), 673–687.

Bethoux, E., C. Didry and A. Mias: 2007, ‘What Codes of

Conduct Tell Us: Corporate Social Responsibility and

the Nature of the Multinational Corporation’, Corporate

Governance: An International Review 15(1), 77–90.

Black, S. E. and P. E. Strahan: 2002, ‘Entrepreneurship

and Bank Credit Availability’, Journal of Finance 57,

2807–2833.

Bonn, I. and J. Fisher: 2005, ‘Corporate Governance and

Business Ethics: Insights from the Strategic Planning

Experience’, Corporate Governance: An International

Review 13(6), 730–738.

Botero, J., S. Djankov, R. La Porta, F. Lopez-de-Silanes

and A. Schleifer: 2004, ‘The Regulation of Labour’,

The Quarterly Journal of Economics 119(4), 1339–1382.

330 Reyes Calderon et al.

Cadbury, A.: 2000, ‘The Corporate Governance Agenda’,

Corporate Governance, an International Review 8(1), 7–15.

Calderon, R. and J. Alvarez: 2007, Corruption, Complexity

and Governance, University of Navarra. Available at

http://www.unav.es/econom/index.php?section=170.

Calderon, C. and L. Liu: 2003, ‘The Direction of Cau-

sality Between Financial Development and Economic

Growth’, Journal of Development Economics 72(1), 321–

334.

Caselli, F. and M. Morelli: 2004, ‘Bad Politicians’, Journal

of Public Economics 88(3–4), 759–782.

Coleman, W. D. and A. Perl: 1999, ‘Internationalized

Policy Environments and Policy Network Analysis’,

Political Studies 47, 691–709.

Collins, J., and K. Uhlenbruck: 2004, ‘How Firms

Respond to Government Corruption: Insights from

India’, Academy of Management Best Paper Proceedings

(New Orleans).

Cragg, W.: 2005, Ethics Codes, Corporations and the

Challenge of Globalization (Edward Elgar, London).

Demirguc-Kunt, A., I. Love and V. Maksimovic: 2006,

‘Business Environment and the Incorporation Deci-

sion’, Journal of Banking and Finance 30, 2967–2993.

Djankov, S., R. La Porta, F. Lopez de Silanes and

A. Shleifer: 2002, ‘The Regulation of Entry’, Quarterly

Journal of Economics 117(1), 1–37.

Dollar, D., M. Hallward-Driemeier and T. Mengistae:

2005, ‘Investment Climate and Firm Performance in

Developing Economies’, Economic Development and

Cultural Change 54(1), 1–31.

Dollar, D. and V. Levin: 2006, ‘The Increasing Selectivity

of Foreign Aid, 1984–2003’, World Development

34(12), 2034–2046.

Elkington, J.: 2006, ‘Governance for Sustainability’,

Corporate Governance: An International Review 14(6),

522–529.

Everett, J., D. Neu and A. Shiraz: 2007, ‘Accounting and

the Global Fight Against Corruption’, Accounting,

Organizations and Society 32(6), 513–542.

Fisman, R. and J. Svensson: 2007, ‘Are Corruption and

Taxation Really Harmful to Growth? Firm-Level Evi-

dence’, Journal of Development Economics 83(1), 63–75.

Gjessing, O. and H. Syse: 2007, ‘Norwegian Petroleum

Wealth and Universal Ownership’, Corporate Gover-

nance: An International Review 15(3), 427–437.

Hopkin, J. and A. Rodrıguez-Pose: 2007, ‘‘‘Grabbing

Hand’’ or ‘‘Helping Hand’’?: Corruption and the Eco-

nomic Role of the State’, Governance 20(2), 187–208.

Howlett, M. and J. Rayner: 2006, ‘Globalization and

Governance Capacity’, Governance 19(2), 251–275.

Huang, H. and S.-J. Wei: 2006, ‘Monetary Policies for

Developing Countries: The Role of Institutional Qual-

ity’, Journal of International Economics 10(1), 239–252.

Husted, B.: 1999, ‘Wealth, Culture, and Corruption’,

Journal of International Business Studies 30(2), 339–359.

Jain, A. K.: 2001, ‘Corruption. A Review’, Journal of

Economic Surveys 15(1), 71–121.

Jordan, A., R. Wurzel and A. Zito: 2006, ‘The Rise of

‘‘New’’ Policy Instruments’, Political Studies 53, 477–496.

Klapper, L., L. Laeven and R. Rajan: 2006, ‘Entry

Regulation as a Barrier to Entrepreneurship’, Journal of

Financial Economics 82, 591–629.

Koh, H. C. and E. Boo: 2001, ‘The Link Between

Organizational Ethics and Job Satisfaction: A Study of

Managers in Singapore’, Journal of Business Ethics 29,

309–324.

Lee, S.-H., M. Peng and J. Barney: 2007, ‘Bankruptcy

Law and Entrepreneurship Development: A Real

Option Perspective’, Academy of Management Review

32(1), 257–272.

MacMurray, W.: 2006, ‘Private Sector Response to the

Emerging Anti-Corruption Movement’, in S. Puri

(ed.), Development Outreach (World Bank, Washington).

Mauro, P.: 1995, ‘Corruption and Growth’, Quarterly

Journal of Economics 110(3), 681–712.

Mungui-Pippidi, A.: 2006, ‘Corruption: Diagnosis and

Treatment’, Journal of Democracy 17(3), 86–99.

Nwabuzor, A.: 2005, ‘Corruption and Development: New

Initiatives in Economic Openness and Strengthened

Rule of Law’, Journal of Business Ethics 59, 121–138.

OECD: 1997, Convention on Combating Bribery of Foreign

Public. Working Group on Bribery in International Business

Transactions (CIME) (OECD, Paris).

O’Higgins, E.: 2006, ‘Corruption, Underdevelopment,

and Extractive Industries: Addressing the Vicious

Cycle’, Business Ethics Quarterly 16(2), 235–254.

Pantzalis, C., J. Park and N. Sutton: 2008, ‘Corruption

and Valuation of Multinational Corporations’, Journal

of Empirical Finance 15(3), 387–417.

Peng, D. and C. Bajona: 2008, ‘China’s Vulnerability to

Current Crisis’, China Economic Review 19(2), 138–151.

Posner, R. A.: 1998, ‘On Creating a Legal Framework for

Economic Development’, The World Bank Research

Observer 13(1), 1–12.

Potts, S. D. and I. L. Matuszewski: 2004, ‘Ethics and

Corporate Governance’, Corporate Governance: An

International Review 12(2), 177–179.

Rose-Ackerman, S.: 1999, Corruption and Government:

Causes, Consequences, and Reform (Cambridge Univer-

sity Press, Cambridge).

Rose-Ackerman, S.: 2002, ‘‘‘Grand’’ Corruption and the

Ethics of Global Business’, Journal of Banking and

Finance 26, 1889–1918.

Sampford, C., A. Shacklock, C. Connors and F. Galtung:

2006, Measuring Corruption (Ashgate Publishing Group

Aldershot, UK).

Corporation as a Crucial Ally Against Corruption 331

Sanyal, R.: 2005, ‘Determinates of Bribery in Interna-

tional Business: The Cultural and Economic Factors’,

Journal of Business Ethics 59, 139–145.

Schechter, L.: 2007, ‘Theft, Gift-Giving and Trustwor-

thiness’, The American Economic Review 97(5), 1560–

1582.

Seligson, M. A.: 2006, ‘The Measurement and Impact of

Corruption Victimization’, World Development 34(2),

381–404.

SenGupta, R.: 2006, ‘Trouble at Home for Overseas

Bribes’, Financial Times, 2nd February 2006.

Sethi, S. P.: 2005, ‘Voluntary Codes of Conduct for

Multinational Corporations’, Journal of Business Ethics

59, 1–2.

Sung, H.: 2005, ‘Between Demand and Supply: Bribery

in International Trade’, Crime, Law, and Social Change

44, 111–131.

Transparency International: 2004, Global Corruption Bar-

ometer 2004 (Berlin, Germany).

Trevino, K. T.: 1986, ‘Ethical Decision Making in

Organizations: A Person-Situation Interaction Model’,

Academy of Management Review 11, 601–617.

United Nations: 2004, The Global Programme Against

Corruption. U.N. Anticorruption Toolkit (United Nations

Office on Drugs and Crime, New York).

Valentine, S., M. Greller and S. B. Richtermeyer: 2006,

‘Employee Job Response as a Function of Ethical

Context and Perceived Organization Support’, Journal

of Business Research 59(5), 582–588.

Veron, R., G. Williams, S. Corbridge and M. Srisvastava:

2006, ‘Corruption Decentralization? Community

Monitoring of Poverty-Alleviation Schemes in Eastern

India’, World Development 34(11), 1922–1941.

Vincke, F. and F. Heimann: 2003, Fighting Corruption. A

Corporate Practices Manual (International Chamber of

Commerce, Paris).

Vogl, F.: 1998, ‘The Supply Side of Global Bribery’,

Finance and Development 35(2), 30–33.

Waddock, S., C. Bodwell and S. G. Graves: 2002,

‘Responsibility: The New Business Imperative’,

Academy of Management Executive 16(2), 132–148.

Williamson, O.: 1975, Markets and Hierarchies, Analysis

and Antitrust Implications: A Study in the Economics of

Internal Organization (Free Press, New York).

World Bank: 2007, Doing Business 2007 (IBRD and WB,

Washington).

World Bank Group 2006-8, Strengthening Bank Group

Engagement on Governance and Anticorruption, DC2006-

0017.

Wu, S. J.: 2006, ‘Corruption and Cross-Border Invest-

ment by Multinational Firms’, Journal of Comparative

Economics 34(4), 839–856.

You, J. and S. Khagram: 2005, ‘A Comparative Study of

Inequality and Corruption’, American Journal of Sociol-

ogy 70(1), 136–157.

Zhang, Z.: 2007, ‘Legal Deterrence: The Foundation of

Corporate Governance Evidence from China’, Cor-

porate Governance: An International Review 15(5), 741–

767.

School of Economics and Business Administration,

University of Navarra,

Campus Universitario s/n.,

31080, Pamplona,

Spain

E-mail: [email protected]

E-mail: [email protected]

E-mail: [email protected]

332 Reyes Calderon et al.