Corporate versus independent new ventures: Resource, strategy, and performance differences

20

ELSEVIER CORPORATE VERSUS INDEPENDENT NEW VENTURES: RESOURCE, STRATEGY, AND PERFORMANCE DIFFERENCES RODNEY C. SHRADER University of Alberta MARK SIMON Oakland University This study examines differences between independent ventures (IVs), EXECUTIVE which are established by individual entrepreneurs, and corporate ven- SUIlIclI~ARY tures ( CVs), which are controlled by larger companies. It focuses on dif- ferences between these ventures related to the resources, strategies, and performance of firms in the computer and communications equipment manufacturing industries. Thus, the findings increase the understanding of the different challenges faced by each venture type and provide insight into how each venture type should be managed. The study finds that managers of CVs and IVs emphasized different resources and strategies. Specifically, CVs emphasized the following resources: internal capital sources, proprietary knowl- edge, and marketing expertise. IVs emphasized external capital sources, technical expertise, and development of brand identification. They also differed in their strategies; IVs pursued greater stra- tegic breadth, more customer service, and focused more on specialty products. The findings that CVs had less strategic breadth was surprising in that CVs emphasized resources, such as internal capital sources, which could make pursuing broad strategies more feasible for CVs. It is possible that some CVs do not pursue broad strategies because they may be "infringing upon someone else's turp' within the corporation and thus may be discouraged. Address correspondence to Rodney C. Shrader, Department of Organizational Analysis, Faculty of Business, University of Alberta, Edmonton, Alberta, Canada T6G 2R6. The authors thank Tricia McDougall for making significant contributions to this project. In addition, they thank Jeff Covin, Ben Oviatt, Allen Amason, and two anonymous reviewers for their helpful comments on previous versions of the article. Journal of Business Venturing 12, 47-66 © 1997 Elsevier Science Inc. 655 Avenue of the Americas, New York. NY 10010 0883-9026/97/$17.00 PII S0883-9026(96)00053-5

-

Upload

independent -

Category

Documents

-

view

3 -

download

0

Transcript of Corporate versus independent new ventures: Resource, strategy, and performance differences

ELSEVIER

CORPORATE VERSUS

INDEPENDENT NEW

VENTURES: RESOURCE,

STRATEGY, AND

PERFORMANCE

DIFFERENCES

RODNEY C. SHRADER University o f Alberta

MARK SIMON Oakland University

This study examines differences between independent ventures (IVs), EXECUTIVE which are established by individual entrepreneurs, and corporate ven- S U I l I c l I ~ A R Y tures ( CVs), which are controlled by larger companies. It focuses on dif-

ferences between these ventures related to the resources, strategies, and performance of firms in the computer and communications equipment manufacturing industries. Thus, the findings increase the understanding

o f the different challenges faced by each venture type and provide insight into how each venture type should be managed.

The study finds that managers of CVs and IVs emphasized different resources and strategies. Specifically, CVs emphasized the following resources: internal capital sources, proprietary knowl- edge, and marketing expertise. IVs emphasized external capital sources, technical expertise, and development of brand identification. They also differed in their strategies; IVs pursued greater stra- tegic breadth, more customer service, and focused more on specialty products. The findings that CVs had less strategic breadth was surprising in that CVs emphasized resources, such as internal capital sources, which could make pursuing broad strategies more feasible for CVs. It is possible that some CVs do not pursue broad strategies because they may be "infringing upon someone else's turp' within the corporation and thus may be discouraged.

Address correspondence to Rodney C. Shrader, Department of Organizational Analysis, Faculty of Business, University of Alberta, Edmonton, Alberta, Canada T6G 2R6.

The authors thank Tricia McDougall for making significant contributions to this project. In addition, they thank Jeff Covin, Ben Oviatt, Allen Amason, and two anonymous reviewers for their helpful comments on previous versions of the article.

Journal of Business Venturing 12, 47-66 © 1997 Elsevier Science Inc. 655 Avenue of the Americas, New York. NY 10010

0883-9026/97/$17.00 PII S0883-9026(96)00053-5

48 R.C. SHRADER AND M. SIMON

In spite o f finding significant strategy and resource differences, the study found that IVs and CVs did not differ in performance and that resources were not directly related to performance. Based on the concept o f equifinality, it follows that both venture types can be equally successful, even if they follow different roads to success. Success may be less a function of the different resources IVs and CVs have and more a function of what strategies the firms choose based upon their re- sources.

Strategy variables did relate to performance: a low cost strategy lowered performance regard- less o f venture type and the influence o fan aggressive strategy (i.e., wide strategic breadth) on perfor- mance depended upon venture origin. Managers pursuing a low cost strategy may have had lower performance if they became penny wise and pound foolish, missing opportunities in their efforts' to lower costs. This suggests that regardless o f venture type, managers o f new ventures in these industries and perhaps in other volatile industries may need to be opportunistic.

This study indicates that pursuing broad strategies increased the performance of IVs and de- creased the performance of CVs. This finding was surprising in that CVs had greater resources, which one might think would lead to successful implementation of aggressive strategies. In securing enough resources to pursue aggressive strategies from their parents, CVs may lose the freedom of action they need to cope with the dynamism of high technology industries. This suggests that manag- ers o f CVs within the computer and communications equipment manufacturing industries should either not pursue broad strategies, or if pursuing broad strategy, they should maintain their flexibil- ity. In contrast, IVs that pursued broad strategies achieved higher performance, indicating that per- haps IVs, unencumbered by the bureaucracy that characterizes CVs, may be able to pursue aggres- sive strategies while simultaneously maintaining flexibility.

Thus, this study offers IV and CV managers several valuable insights. First, it argues that man- agers o f each type of venture may need to pursue different strategies to increase venture performance and make optimal use of their unique resources. Furthermore, it suggests that CV managers encoun- ter difficulties in applying resources to strategies and not in accessing resources. Whereas political obstacles may occur, CV managers may primarily encounter these difficulties when trying to imple- ment strategies rather than when accumulating resources from the parent, suggesting a pitfall that managers o f CVs and their parents need to avoid. Although this study has indicated that both ven- ture types can be equally successful, it suggests that they may face different obstacles and follow different roads to success. © 1997 Elsevier Science Inc.

I N T R O D U C T I O N

According to classical theories of entrepreneurship, the role of an entrepreneur is to marshal the resources necessary to start a new venture and then to effectively deploy those resources. Acquisition of resources has been called a primary function of the en- trepreneur, and both tangible and intangible resources have been linked to new venture performance (e.g., Roure and Maidique 1986; Schoonhoven, Eisenhardt, and Lyman 1990; Stuart and Abetti 1987; Sykes 1986). Resource acquisition is particularly impor- tant for new ventures, because the poverty of resources that characterizes new ventures frequently leads to their demise (Laitinen 1992). Furthermore, a fundamental premise of resource-based theory is that different resources lead to the selection of different strategies, and these resources can influence strategy effectiveness (Barney 1991; Chan- dler and Hanks 1994; Penrose 1959). Because resources have been linked to choices of strategy and strategy has been clearly linked to the performance of new ventures (Chandler and Hanks 1994; McDougall et al. 1992; Romanelli 1987; Sandberg 1984; Sandberg and Hofer 1987), it follows that the resources of new ventures may influence their performance. Consequently, the new venture literature is replete with studies ex-

CORPORATE VERSUS INDEPENDENT NEW VENTURES 49

amining sources of resources for new ventures, including venture capital, network rela- tionships, or sponsorship by corporate parents.

Theorists have argued that new ventures sponsored by parent companies (hereafter called corporate ventures or CVs) and newly started entrepreneurial companies (here- after called independent ventures or IVs) vary systematically in their ability to gather and utilize resources and may therefore select different strategies and exhibit different performance levels (Knight 1989; Lambkin 1988; Lambkin and Day 1989; Miller and Camp 1985). Specifically, theory suggests that lack of organizational legitimacy creates a liability of newness that may make it difficult for IV managers to obtain resources. In contrast, CV managers may have access to a relative wealth of resources from their corporate sponsors.

Thus, these theories suggest that venture origin is an important source of resource differences, and by extension, a source of differences in strategies and performance. Yet, despite theorists' assertions that the two types of ventures systematically differ, many researchers have treated new ventures as homogeneous and have combined both types of ventures within single studies, thereby potentially masking important relation- ships among resources, strategy, and performance.

Because it is thought that CVs and IVs differ systematically, several scholars have requested studies determining whether findings from CV studies apply to IVs (Bigga- dike 1979; Lambkin 1988; Lambkin and Day 1989; Miller and Camp 1985). Despite these requests and the compelling theoretical reasons for comparing these two types of ven- tures, no previous study has been reported that compares the resources, strategies, and performance of the two venture types. This exploratory study helps fill this void in the literature and addresses four research questions: (1) Do IVs and CVs emphasize differ- ent resources and, if so, which resources? (2) Do IVs and CVs pursue different strategies and, if so, which strategies? (3) Do IVs and CVs differ in performance and, if so, how? (4) Do the relationships of resources and strategies to performance differ between IVs and CVs and, if so, how?

L I T E R A T U R E R E V I E W A N D H Y P O T H E S E S

The literature reviewed later indicates that there are important differences between IVs and CVs, regarding their resources, strategies, and financial performance. Although the superiority of IV performance is accepted by some (Weiss 1981), the literature makes a clear case that both types possess some key advantages. Table 1 summarizes literature regarding differences between IVs and CVs. The majority of this literature is either theoretical or includes a sample composed entirely of one type or the other.

Resource Differences

Firm resources include all assets, capabilities, organizational processes, firm attributes, information, knowledge, etc. controlled by a firm that enable the firm to conceive and implement strategies that improve efficiency and effectiveness (Barney 1991; Daft 1983). According to resource-based theory, firm resources are the strengths that firms can use to derive and implement their strategies (Barney 1991, Porter 1981). Specifically, researchers have suggested several categories of resources that may be used to achieve a firm's goals, including financial, human, organizational, and technological resources (Chandler and Hanks 1994; Hofer and Schendel 1978). Because there are almost lim-

50 R.C. SHRADER AND M. SIMON

T A B L E 1 Characteristics of Independent and Corpora te New Ventures

Capital • CVs frequently have access to more capital. The retained earnings or depreciation charges of the

corporate parent may allow them to move into new markets (Hines 1957). • CVs can frequently obtain outside capital more cheaply than other newcomers (Heflebower 1951;

Hines 1957). • CVs funds are provided through politicized budgetary processes (Burgelman and Sayles 1986). • IVs supported by venture capital firms may have a longer term commitment of funds. Often the

timing of case inflows is consistent with the business development process (Fast 1981). Controls • CVs have multiple review levels (Sykes 1986). • CV sponsors impose tight cost controls and strict, relatively short-term quantitative targets

(Burgelman and Sayles 1986). • IV managers have a great deal of autonomy (Fast 1981; Sykes 1986; MacMillan et al. 1986). • IVs do not suffer from bureaucratic inertia (Stocking and Watkins 1951). • IVs have simple, centralized structures, allowing for quick action (Griener 1972). Managerial Motivations • CV managers often view venture assignments as unwelcome (Fast 1981). • CV managers must balance a variety of political and corporate objectives that pull the venture manager

in different directions (Fast 1981). • CV managers are often evaluated on how closely they adhere to a plan (Weiss 1981). • IV founders are oriented toward the ends achieved because they are compensated based on venture

performance (Weiss 1981). • IV founders must make a success of the venture because they do not have the luxury to stay in business

with high and continued losses (Weiss 1981). • IVs have clear and definite objectives (Fast 1981). Personnel and Functional Orientation • CVs have easier access to executives from diverse functional areas (Hines 1957). • CVs emphasize the marketing function (Knight 1989). • IVs top management teams are more likely to be dominated by personnel with technological backgrounds

(Knight 1989). • IVs may have greater access to entrepreneurial managers (Knight 1989). Assets Provided by CVs' Parents • CVs may be able to gain from parents' brand reputations or trademarks (Caves and Porter 1977;

Hines 1957). • CVs, through the existing facilities of parents, may have access to effective distribution systems and

dealers at a low cost (Burgelman and Sayles 1986; Caves and Porter 1977; Hines 1957). • CVs may be able to exert more control over input suppliers through entry by vertical integration

(Caves and Porter 1977). • CVs may be able to access the underutilized capacity of parents, thus gaining economies of scale

(Caves and Porter 1977; Hines 1957).

i t less ways to c o n c e i v e o f f i rm r e s o u r c e s , this s t udy focuse s o n r e s o u r c e s tha t r e p r e s e n t

t h e c a t e g o r i e s a b o v e tha t a r e m o s t r e l e v a n t to t h e i ndus t r i e s s a m p l e d ( c o m p u t e r a n d

c o m m u n i c a t i o n s e q u i p m e n t m a n u f a c t u r i n g ) , t ha t a r e e m p h a s i z e d in t he l i t e r a t u r e as

i m p o r t a n t to p e r f o r m a n c e , a n d tha t c o u l d e i t h e r be a c q u i r e d f r o m a c o r p o r a t e p a r e n t

o r d e v e l o p e d i n d e p e n d e n t l y . Th i s c o n c e p t u a l i z a t i o n o f r e s o u r c e s is a p p r o p r i a t e g i v e n

t h e e x p l o r a t o r y n a t u r e o f t he s tudy. Speci f ica l ly , t h e s tudy focuse s on cap i t a l sou rces ,

p a t e n t s a n d p r o p r i e t a r y k n o w l e d g e , m a r k e t i n g a n d t e c h n i c a l e x p e r t i s e , a n d b r a n d

n a m e iden t i f i ca t ion .

In h igh t e c h n o l o g y indus t r i e s , n e w v e n t u r e s a r e f r e q u e n t l y e s t a b l i s h e d to b r i n g n e w

t e c h n o l o g i e s to t h e m a r k e t . T h e r e f o r e , w i th in t h e i ndus t r i e s s tud ied , p r o p r i e t a r y k n o w l -

e d g e a n d m a r k e t i n g e x p e r t i s e a r e c ruc ia l r e s o u r c e s fo r n e w v e n t u r e s . T h e i m p o r t a n c e o f t h e s e r e s o u r c e s to n e w v e n t u r e s has b e e n wel l r e c o g n i z e d w i t h i n t h e e n t r e p r e n e u r s h i p

CORPORATE VERSUS INDEPENDENT NEW VENTURES 51

literature (e.g., Doutriaux 1992; Roure and Maidique 1986; Schoonhoven et al. 1990; Stuart and Abetti 1987; Sykes 1986). These resources allow new ventures to differentiate themselves from competitors, identify opportunities, and create new products.

Because a high rate of technological evolution and product introduction increases consumer uncertainty about product performance, a company's reputation can have an important impact on its ability to introduce new products, so brand identification will be a valuable resource. The importance of brand identification as a resource for new ventures has also been highlighted within the new venture literature (e.g., Lambkin 1988; Miller et al. 1991; Tsai et al. 1991).

On a more general level, undercapitalization is perhaps the greatest challenge fac- ing all new ventures and is a major cause of company failures. Access to capital reflects an important financial resource that is crucial to success, regardless of the industry being examined. Therefore, access to capital has been examined by several new venture re- searchers (Van de Ven et al. 1984; Roberts and Hauptman 1987; Duchesneau and Gar- tner 1990; Doutriaux 1992).

Not only has past research suggested that the variables above are important to new venture performance and high technology industries, they have also been frequently discussed in the theoretical literature regarding proposed differences between IVs and CVs. Although separate empirical studies of IVs and CVs have frequently examined these resources (e.g., Chandler and Hanks 1994; Laitinen 1992; Lambkin 1988; Miller et al. 1991; Ramachandran and Ramanarayan 1993; Williams et al. 1991), no study has directly compared these resources across venture types.

Because CVs may be able to acquire resources from their parents, it is expected that CVs and IVs will emphasize different resources. Theoretical literature indicates that a primary resource difference between IVs and CVs is the manner in which they are funded. Whereas CVs are funded by existing companies and may be subsidized by their parents' other operations (Hines 1957), IVs do not have this advantage. They must seek capital from external sources. Although financial losses in CVs can often be under- written by their parents, IVs seldom have the luxury to stay in business with high and continued losses (Weiss 1981). Frequently, this means that undercapitalized IVs fail or are acquired.

Besides funding, CVs may also have access to other resources previously accrued by their parents, including brand names, marketing skills, trademarks, and other intangible assets (Burgelman and Sayles 1986; Caves and Porter 1977; Hines 1957). In general, whereas CVs may have access to their parents' resources, IVs are often constrained by severe resource limitations (Laitinen 1992). For example, whereas CVs can often rely on their parents' images, 1Vs need to develop their own brand identification. In some cases, it is the resources provided by a parent company that make it possible for a CV to enter a given market (e.g., Bevan 1974). In sum, the existing new venture and strategic management literatures provide the theoretical basis for the study's first set of hypothe- ses;

HI: IVs and CVs will emphasize different resources.

Ilia: IVs will place greater emphasis on external capital sources.

Hlb: CVs will place greater emphasis on use of patents and proprietary knowledge.

Hlc: CVs will place greater emphasis on marketing expertise.

Hid: IVs will place greater emphasis on developing brand ID.

52 R.C. SHRADER AND M. SIMON

Strategy Differences Given possible resource differences, IVs and CVs may select different strategies. Spe- cifically, the study will explore three strategic directions a new venture can take: breadth of market entry, emphasis on low cost, and emphasis on specific means of differentiation. These three strategy elements provide a framework for understanding how firms com- pete (Porter 1980). This framework was chosen because it has a prominent place in strategy literature, having been referenced in almost half of the 'articles published in Strategic Management Journal to date.

Early entrepreneurship literature, which did not distinguish between the two ven- ture types, advised new ventures to pursue "niche" strategies to avoid direct competition with large firms and to pursue opportunities too small to be of interest to large, economy- of-scale oriented firms (e.g., Vesper 1980). Others have advised that new ventures differ- entiate their product offering by concentrating on specialized products and providing high levels of customer service, selling to market segments where customization and high levels of customer service create unique advantages (Cohn and Lindberg 1972).

In contrast to these recommendations, Biggadike's (1979) widely cited study found that successful CVs entered with aggressive share objectives and invested and marketed accordingly. Although Biggadike's (1979) results refuted "prevailing wisdom," it is im- portant to note his sample was composed entirely of CVs. Therefore, early research suggesting that new ventures pursue niche strategies may apply to IVs, but not to CVs.

It is plausible that the more limited resources of IVs prohibit such large-scale entry. CV access to parent resources, such as excess capacity, established brand name, and established distribution channels, may allow them to achieve broad market entry and resulting economies of scale (Hines 1957). Because of scarce resources, many IVs must avoid head-to-head competition. Therefore, IVs may enter niche markets offering dif- ferentiated products at either the upper or lower end, providing specialty products and/ or high levels of customer service at premium prices, or designing low priced products for low income niches (Cohn and Lindberg 1972; Hines 1957).

An additional force driving strategy in CVs is the fact that CV funds are commonly provided through a politicized budgetary process (Burgelman and Sayles 1986), which often results in the imposition of tight cost controls and strict quantitative targets on CVs. Consequently, it is reasonable to assume that in addition to broader entry strate- gies, CVs will also place greater emphasis on low cost production. In summary, the dispa- rate resources of these two venture types is expected, in part, to lead to the pursuit of different strategies.

H2: IVs and CVs will pursue different strategies.

H2a: CVs will place greater emphasis on broad entry strategies.

H2b: IVs will place greater emphasis on specialty products.

H2c: IVs will place greater emphasis on customer service.

H2d: CVs will place greater emphasis on concern for low cost.

Performance Differences

If CVs and IVs indeed emphasize different resources and strategies, the question re- mains as to whether these differences will in turn lead to performance differences. Re- searchers have emphasized two distinct perspectives when comparing the relative ad-

CORPORATE VERSUS INDEPENDENT NEW VENTURES 53

vantages of CVs and IVs, both of which have only been partially tested. Earlier researchers stressed CVs access to sponsors' resources, believing that these resources would generate superior financial performance (Caves and Porter 1977; Hines 1957). These researchers mentioned several specific advantages that could increase venture performance, including access to sponsors' distribution systems, dealers, brand reputa- tions, and trademarks. They believed these resources would provide advantages for CVs in the marketplace. In addition to marketplace advantages, they believed that CVs would gain greater access to capital, because of their parents' strong financial positions. Furthermore, early researchers suggested that CVs might be able to gain cost advan- tages by using parents' excess capacity, thus gaining economies of scale (Caves and Por- ter 1977; Hines 1957). The superior resources of CVs leads to the following hypothesis:

H3a: CVs will exhibit higher performance than IVs.

Although the advantages of CVs have been accepted by some, their ability to produce superior performance has been challenged by others (Fast 1981; Weiss 1981). Some re- searchers believe that the highly political process of accessing corporate resources might decrease venture autonomy (Burgelman and Sayles 1986). It has also been suggested that IV managers may be more motivated than CV managers, who often feel pulled in several directions and frequently resent assignment to new ventures (Fast 1981; Knight 1989). Additionally, IV managers may be more motivated because often their whole livelihood depends on their ventures' financial performance and growth. The literature implies that the advantages of autonomy and managerial motivation held by IVs have a greater impact on performance than the resources typically associated with CVs. It is not so much resources themselves, but the way resources are combined and utilized that affects performance (Hamel and Prahalad 1993; McGrath et al. 1994; Penrose 1959). Therefore, greater autonomy and managerial performance may lead to greater ability to exploit resources and, consequently, to superior performance.

Although limited, empirical evidence suggests that IVs will outperform CVs. Weiss (1981) found that a sample of venture capital-funded IVs outperformed CVs. It is not known, however, if this is true of a more generic class of IVs. Van de Ven and his col- leagues (1984) found that IVs exhibited higher performance than CVs, although the difference was not statistically significant, perhaps due to the study's small sample size (12 ventures). Thus theory and some empirical evidence suggest the following compet- ing hypothesis to H3a above:

H3b: IVs will exhibit higher performance than CVs.

As important as determining whether one type of venture exhibits higher performance than the other is determining whether factors that influence performance vary by ven- ture type. Resource-based theory suggests that strategies that build on a venture's re- sources are likely to improve firm performance. This suggests that CVs and IVs not only choose different strategies, but also that those strategies affect venture performance differently. This also suggests, as previously argued, that it is not so much resources themselves that affect performance, but the way resources are combined and utilized (Hamel and Prahalad 1993; McGrath et al. 1994; Penrose 1959).

Although previous studies have not directly examined how the strategy-perfor- mance relationship varies by origin, some tentatively suggest that different strategies enhance the performance of corporate and independent ventures. For example, Stuart and Abetti's (1987) study, made up primarily of IVs, indicated a focus strategy enhanced

54 R.C. SHRADER AND M. SIMON

performance. In contrast, Biggadike's (1979) study suggested that more aggressive entry improved the performance of CVs. Using their original sample, a later study of Stuart Abetti (1990) indicated that a low cost emphasis increased IV performance. Miller and Camp (1985), however, determined that emphasizing low cost did not aid CVs. Whereas the studies above tentatively indicate that venture origin influences the strategy-perfor- mance relationship, CVs and IVs need to be compared more directly. Thus, resource- based theory and past findings suggest:

H4: The performance of new ventures will be significantly related to the strategies they pursue, and the relationship between strategy and performance will differ by venture origin.

METHOD Sample and Data To test the study's hypotheses data were analyzed for a matched sample of 30 CVs and 30 IVs. Methods used to collect data and match ventures are described later. First, data were collected from 250 new ventures--companies that existed for eight years or fewer (Biggadike 1979; Miller and Camp 1985)--in the computer and communications equip- ment manufacturing industries. The computer and communication equipment manufac- turing industries were selected because they include both venture types, and because they are widely regarded as growth industries, presenting the opportunity for companies to pursue an array of different strategies and subsequently to achieve a wide range of performance.

A mail survey, which had been validated in a pilot study, was used to collect data. A survey was the most appropriate means of collecting data, because secondary sources did not contain detailed information regarding companies' resources, strategies, and performance. This paucity of data stems from the nature of the data sought, as well as the newness of the companies. Privately owned IVs do not publish annual reports, and data on CVs are often subsumed into the sponsors' reports. The survey targeted heads of ventures, because they typically possess the most comprehensive knowledge of their organizations and strategies (Hambrick 1981).

Responding firms were checked for representativeness with both Biggadike's (1979) PIMS sample of CVs and the Dun & Bradstreet (D&B) data base, primarily composed of IVs. When compared with Biggadike's sample of CVs, there was a marked similarity between the two samples in market share objectives. When compared with the population of D&B new ventures for industries included in the study, chi-square analysis confirmed that survey respondents did not significantly differ (p > .05 level) from the D&B sample on firm size or firm geographical location. Thus, the sample does not appear to exhibit any size or location bias when compared with the general popula- tion of D&B new ventures in these industries. In an additional effort to guard against nonrespondent bias, a follow-up telephone survey of 23 nonrespondents was conducted. There were no significant differences in any of the basic characteristics describing nonre- spondents and the participants.

Following the key informant approach espoused by Huber and Power (1985), data were gathered from the owner, CEO, president, or board chairperson of each firm. The top manager is arguably the best qualified person to provide strategy-related informa- tion (Hambrick 1981). However, to help assess the reliability of the items on the survey

CORPORATE VERSUS INDEPENDENT NEW VENTURES 55

instrument, a second respondent was solicited from 50 companies randomly selected from the group of firms originally surveyed. Second respondents were also top execu- tives in their companies. For the items used in this study, Pearson correlation coefficients between first and second respondents averaged 0.45 and were statistically significant (p < .05). In addition, t-tests indicated that first and second responses were not signifi- cantly different on any of the measures.

Respondents indicated that seven of these companies originated as joint ventures. To avoid confounding the results, these seven companies were eliminated from the study, leaving 243 companies, which included 35 CVs and 208 IVs. The ventures within the sample, however, were significantly different in their age (CV mean age was 5.11 years; IV mean age was 3.79 years) and size (CV mean size was 91.86 employees; IV mean size was 24.14 employees). Furthermore, preliminary analyses suggested that firm age and size significantly affected the relationships explored in this study. Controlling for age is particularly important, because new ventures pass through a progression of distinct stages, often shifting their emphasis, strategies, and skills as they evolve (Kazan- jian and Drazin 1990). As new ventures amass resources, their emphasis on specific re- sources and strategies may change. Age is especially important given the extremely high percentage growth new ventures can experience in a relatively short period of time. Age was measured by subtracting the venture's year of origin from the year of the survey. Company size may also systematically influence other variables of interest (Cooper et al. 1989), and thus should be controlled. Company size was measured by the number of employees. The most effective way to control for these variables was to use them as the criteria for selecting matched pairs of CVs and IVs. After eliminating ventures for which no acceptable match could be found, the matching procedure resulted in a sample consisting of 30 IVs and 30 CVs.

Measures

Data were collected about venture type, resources, strategy, and performance, as well as company age and size.

Venture Type

Managers were asked to classify their companies as newly started entrepreneurial com- panies (IVs), as subsidiaries or business units of established companies (CVs), or as joint ventures.

Resource and Strategy Variables

Table 2 presents the list of variables used in the study and their means and standard deviations for both IVs and CVs. On the questionnaire, all resource and strategy items were operationalized on a 7-point bipolar scale, and each manager was asked to indicate on the scale his or her company's emphasis on that resource or strategy item. These scales were anchored at each end by opposite extremes, and responses in the middle of the scale indicated that neither extreme was emphasized. For example, at the ex- tremes of one strategy item were "providing minimal or no customer service" and "pro- viding high levels of customer service."

Five bipolar survey items were used to measure the strategic breadth of each ven-

56 R.C. SHRADER AND M. SIMON

TABLE 2 Variable Means and Standard Deviations (unstandardized)

Independent Venture Corporate Venture n = 30 n = 30

Mean (SD) Mean (SD)

Resource variables Internal/External capital sources 4.67 (2.68) 2.50 (1.98) Proprietary knowledge 3.83 (2.31) 5.03 (1.67) Technical/marketingexpertise 2.07 (1.44) 3.67 (2.22) Brand lD 6.07 (1.48) 5.03 (1.77)

Strategy variables Strategic breadth 4.58 (1.37) 3.71 (1.44) Specialty/commodity products 1.26 (0.52) 1.87 (1.07)

Customer service 6.53 (1.20) 5.63 (1.75) Low cost concern 3.43 (2.22) 3.93 (1.74)

Performance variables Adjusted sales growth 7.67 (11.66) 1.43 (2.28) Adjusted ROS -0.84 (0.33) -1.14 (0.61)

Variables for matching pairs Company age 3.73 (1.44) 3.83 (1.95) Company size (employees) 34.27 (44.94) 32.04 (35.27)

ture. These items were (1) range of products, (2) broadness of markets, (3) number of market segments, (4) number of customers, and (5) number of distribution channels. The coefficient alpha of the five items was 0.75. Consequently, the strategic breadth measure appears to have an acceptable level of reliability (Nunnally 1967). An individ- ual venture's strategic breadth score was computed as the mean score on the five strate- gic breadth items.

Performance Both objective and subjective measures of two different performance variables were studied: growth in sales and return on sales (ROS). To help control for the effects of environmental influences that could directly impact performance, each measure was calculated in terms of how a company performed relative to the norms of its primary industry segment. The sample included firms with primary operations in seven different standard industrial classification codes (SICs). Archival data were gathered to compute mean performance within each of the seven SICs (Dun & Bradstreet 1985). Adjusted sales growth over a three-year period was computed by first calculating the company's sales growth rate, then subtracting the segment mean growth rate as follows (((company salesvear 3 - company saleswar 0/company salesy~ar 1 ) - ((segment saleswar 3 - segment salesvear 1)/segment saleswar 1))). Adjusted ROS was calculated by subtracting the seg- ment mean ROS from the companies' self-reported ROS. Subjective measures of sales growth and ROS asked managers to evaluate their firms' performance in these areas relative to the average performance of firms in their industries, asking them to check the quintile that best represented their company's performance.

Analysis MANOVA was used to test for differences between IVs and CVs in resources, strate- gies, and performance. MANOVA measures differences in a set of continuous depen-

CORPORATE VERSUS INDEPENDENT NEW VENTURES 57

dent variables (in this case, resources, strategies, and performance) based on a categori- cal predictor variable (in this case, venture origin), while controlling experiment-wide error rate. In addition, when groups of equal size are used, MANOVA is robust with respect to violations of its underlying assumptions (Hair et al. 1992). Therefore, MANOVA offers important advantages for a study using matched pairs design. Subse- quent to the MANOVA test, post hoc ANOVAs were used to examine specific variable differences between IVs and CVs.

Before conducting regression analyses, correlations between independent vari- ables were examined, and SAS multicollinearity diagnostics were used to determine that there were no serious problems with multicollinearity among the variables to be tested. Although resources were not hypothesized to have a direct relationship with venture performance, regression analyses were used to rule out that possibility before subsequently using regression analyses to examine the relationship between strategy and performance (ROS and sales growth). In order to determine whether the impact of resources and strategies on performance differed by venture type, a dichotomous variable indicating venture origin (coded 0 for IVs and i for CVs) was included in each regression model, then interactions between venture origin and the other independent variables were examined. With this technique, analyses were based on the 55 firms for which performance data were available (five firms did not respond to items requesting performance data), which provided a ratio of more than six observations per indepen- dent variable, exceeding the minimum recommended for regression procedures (Hair et al. 1992). This technique was used to test four models. In two models, ROS or sales growth was the dependent variable, and resources, origin, and interactions of resources with origin were predictor variables. In the other two models, ROS or sales growth was the dependent variable, and strategies, origin, and interactions of strategies with origin were predictor variables.

RESULTS

MANOVA results indicated that there were highly significant differences between IVs and CVs with respect to the resources (F = 15.904;p < .001) and strategies (F = 6.4911; p < .001) they emphasized. However, IVs and CVs did not differ in performance (F = 1.25; p > .28). Results of post hoc ANOVA tests are reported in Table 3 and described later. The means in Table 2 indicate which type of venture rated higher on a given variable.

Differences in Resources

ANOVA results (Table 3) indicated that, as hypothesized, IVs placed greater emphasis than CVs on external capital sources and development of brand ID, whereas CVs placed greater emphasis on the use of patents and proprietary knowledge, and marketing ex- pertise. Therefore, Hypothesis 1 and its subhypotheses were all supported in this sample.

Differences in Strategy

ANOVA results (Table 3) also indicated that IVs and CVs indeed emphasized different strategies. As hypothesized, IVs placed greater emphasis on customer service and spe-

58 R.C. SHRADER AND M. SIMON

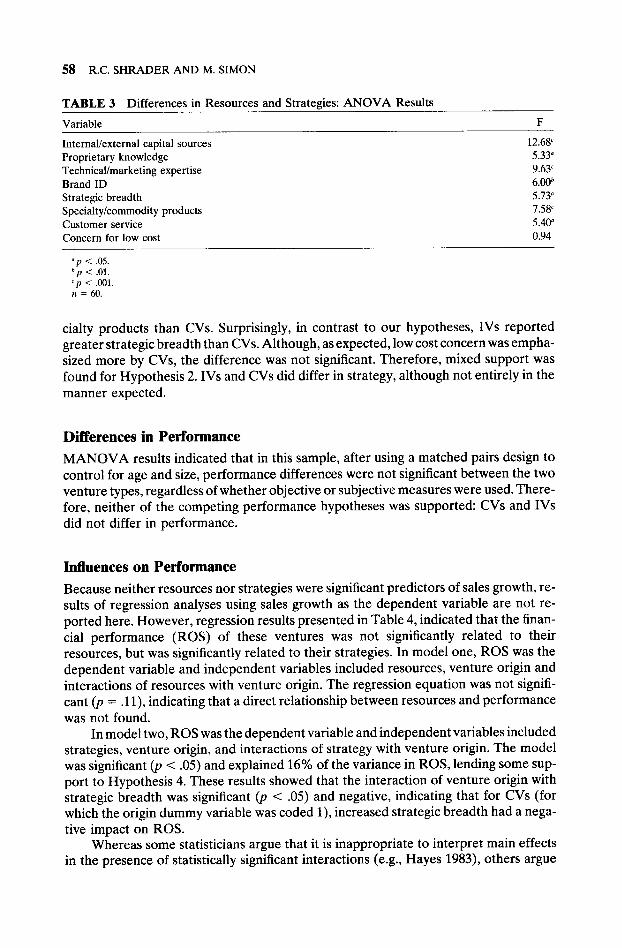

TABLE 3 Differences in Resources and Strategies: ANOVA Results

Var i ab l e F

In t e rna l / ex t e rna l cap i ta l sources 12.68 c

P r o p r i e t a r y k n o w l e d g e 5.33 °

T e c h n i c a l / m a r k e t i n g exper t i se 9.63 c

Brand ID 6.0tY'

S t ra teg ic b r e a d t h 5.73" Spec i a l t y / commodi ty p roduc t s 7.58 C

C u s t o m e r service 5.41Y

C o n c e r n for low cost 0.94

"p < .05. b p < .01. ' p < .001. n = 60.

cialty products than CVs. Surprisingly, in contrast to our hypotheses, IVs reported greater strategic breadth than CVs. Although, as expected, low cost concern was empha- sized more by CVs, the difference was not significant. Therefore, mixed support was found for Hypothesis 2. IVs and CVs did differ in strategy, although not entirely in the manner expected.

Differences in Performance

MANOVA results indicated that in this sample, after using a matched pairs design to control for age and size, performance differences were not significant between the two venture types, regardless of whether objective or subjective measures were used. There- fore, neither of the competing performance hypotheses was supported: CVs and IVs did not differ in performance.

Influences on Performance

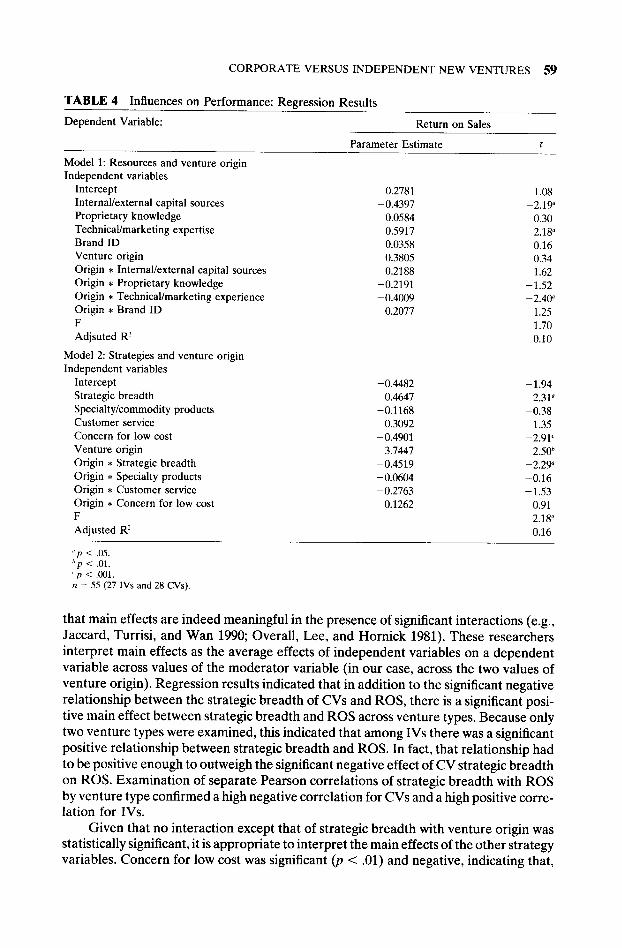

Because neither resources nor strategies were significant predictors of sales growth, re- sults of regression analyses using sales growth as the dependent variable are not re- ported here. However, regression results presented in Table 4, indicated that the finan- cial performance (ROS) of these ventures was not significantly related to their resources, but was significantly related to their strategies. In model one, ROS was the dependent variable and independent variables included resources, venture origin and interactions of resources with venture origin. The regression equation was not signifi- cant (p = .11), indicating that a direct relationship between resources and performance was not found.

In model two, ROS was the dependent variable and independent variables included strategies, venture origin, and interactions of strategy with venture origin. The model was significant (p < .05) and explained 16% of the variance in ROS, lending some sup- port to Hypothesis 4. These results showed that the interaction of venture origin with strategic breadth was significant (p < .05) and negative, indicating that for CVs (for which the origin dummy variable was coded 1), increased strategic breadth had a nega- tive impact on ROS.

Whereas some statisticians argue that it is inappropriate to interpret main effects in the presence of statistically significant interactions (e.g., Hayes 1983), others argue

C O R P O R A T E V E R S U S I N D E P E N D E N T N E W V E N T U R E S 5 9

T A B L E 4 Influences on Performance: Regression Results

Dependent Variable: Return on Sales

Parameter Estimate t

Model 1: Resources and venture origin Independent variables

Intercept 0.2781 1.08 Internal/external capital sources - 0 . 4 3 9 7 - 2 . 1 9 °

Proprietary knowledge 0.0584 0.30

Technical/marketing expertise 0.5917 2.18 ~

Brand I D 0 .0358 0.16

Venture origin 0.3805 0.34

Origin • Internal/external capital sources 0.2188 1.62

Origin • Proprietary knowledge - 0 . 2 1 9 1 - 1 . 5 2

Origin • Technical/marketing experience - 0 . 4 0 0 9 - 2 . 4 0 ~

Origin • Brand I D 0 .2077 1.25

F 1.70 Adjsuted R 2 0.10

Model 2: Strategies and venture origin Independent variables

Intercept - 0 . 4 4 8 2 - 1.94

Strategic breadth 0.4647 2.31 a

Specialty/commodity products - 0 . 1 1 6 8 - 0 . 3 8

Customer service 0.3092 1.35

Concern for low cost - 0 . 4 9 0 1 - 2 . 9 V

Venture origin 3.7447 2.5@

Origin • Strategic breadth - 0 . 4 5 1 9 - 2 . 2 9 ~

Origin • Specialty products - 0 . 0 6 0 4 - 0 . 1 6

Origin • Customer service - 0 . 2 7 6 3 - 1 . 5 3

Origin • Concern for low cost 0.1262 0.91

F 2.18 ° Adjusted R 2 0.16

"p < .05. p < .01.

' p < .001. n = 55 (27 IVs and 28 CVs).

that main effects are indeed meaningful in the presence of significant interactions (e.g., Jaccard, Turrisi, and Wan 1990; Overall, Lee, and Hornick 1981). These researchers interpret main effects as the average effects of independent variables on a dependent variable across values of the moderator variable (in our case, across the two values of venture origin). Regression results indicated that in addition to the significant negative relationship between the strategic breadth of CVs and ROS, there is a significant posi- tive main effect between strategic breadth and ROS across venture types. Because only two venture types were examined, this indicated that among IVs there was a significant positive relationship between strategic breadth and ROS. In fact, that relationship had to be positive enough to outweigh the significant negative effect of CV strategic breadth on ROS. Examination of separate Pearson correlations of strategic breadth with ROS by venture type confirmed a high negative correlation for CVs and a high positive corre- lation for IVs.

Given that no interaction except that of strategic breadth with venture origin was statistically significant, it is appropriate to interpret the main effects of the other strategy variables. Concern for low cost was significant (p < .01) and negative, indicating that,

60 R.C. SHRADER AND M. SIMON

for both venture types, concern for low cost was negatively related to ROS. Examination of separate Pearson correlations supported this finding.

DISCUSSION This study sought to determine differences in two types of ventures. Specifically, IVs and CVs were compared across three major areas: resources, strategies, and perfor- mance. As predicted in HI, results indicated that IVs and CVs emphasized very different resources. However, the results offered mixed support for H2. Although there were important differences in the strategies pursued by the two types, some expected differ- ences were not found, and other differences were not in the direction anticipated. No support was found for either of the competing performance hypotheses (H3a and H3b); the venture types did not differ significantly in performance. Finally, limited support also was found for H4; performance was related to strategy and the association between strategy and performance did vary by venture type.

The fact that CVs placed greater emphasis on internal capital sources, proprietary knowledge, and marketing expertise, while placing less emphasis on development of brand identification, suggests that CVs may be able to share the resources of their corpo- rate parents. The findings that IVs placed greater emphasis on external capital sources and development of brand identification are consistent with the expectations of Weiss (1981). The determination that CVs emphasized marketing expertise more than IVs is consistent with Knight's (1989) findings. The finding that CVs emphasized proprietary knowledge is not surprising, given that many CVs may have been established to com- mercialize technology and to encourage innovation (Kanter et al. 1991).

A fundamental premise of strategic management theory is that differing resources may lead to the selection of different strategies (Barney 1991; Daft 1983). Specific hypotheses regarding strategies for this study were predicated upon hypothesized re- source differences. Although resources differed in the manners expected, strategies did not in all cases.

Most notably, CVs did not emphasize strategic breadth more than IVs, but vice versa. One explanation for this result is that although CVs might have some superior resources, they may be limited in strategic options due to political obstacles. Turning resources into action may become difficult. For CVs, pursuing strategic breadth may mean "infringing upon someone else's turf" within the corporation and thus may be discouraged. This finding helps to shed some light on the common assertion that CVs may be impaired by political obstacles. Whereas previous research has argued that CVs may not be able to obtain resources from their corporate parents, this research suggests that CVs can obtain resources but may be hampered in the efforts to deploy these re- s o u r c e s .

As expected, IVs were more likely to emphasize customer service and specialty products. These emphases provide the means for IVs to differentiate themselves and pursue the focus-type strategies that several researchers (Lambkin and Day 1989; Coo- per et al. 1986) have suggested are sometimes appropriate. Also as expected, CVs did exhibit more concern for low cost, but the difference between CVs and IVs was not significant. In fact both venture types leaned toward low cost emphasis. Perhaps this result indicates that whereas CVs are pressured by budgetary constraints to emphasize low costs (Burgelman and Sayles 1986), IVs are pressured by the harsh reality of limited resources to emphasize low costs.

CORPORATE VERSUS INDEPENDENT NEW VENTURES 61

Although CVs and IVs did emphasize different resources and strategies, it is nota- ble that the firms in this sample did not differ significantly in performance. There were reasons to expect that either type might outperform the other. If CVs had access to superior resources it was expected that they would demonstrate higher performance than IVs (H3a). Contrarily, the greater autonomy and managerial motivation among IVs was expected to enhance their performance (H3b), but these hypotheses were not supported.

Based on the concept of equifinality, it follows that both venture types can be equally successful, even if they follow different roads to success. Or conversely, based on the challenges faced by all new ventures and their often poor performance (Laitinen 1992), both venture types might also have equal opportunity to perform poorly. These views are not without support from the literature. Although few direct comparisons of IV and CV performance have been made, various studies indicate that within each group there is a wide range of performance (e.g., Biggadike 1979; Keeley and Roure 1990; Miller and Camp 1985; Sandberg and Hofer 1987). Because the literature (summarized in Table 1) makes a clear case that both venture types possess key advantages, it is un- clear whether one group should outperform the other. It is logical to assume that those firms within each group that exploit their advantages judiciously can perform well, whereas others within their groups may not.

A clearer understanding of why the performance of CVs and IVs did not differ was found by looking at how resources and strategies relate to the performance of each type. Findings indicated that resources were not significantly related to the performance of either type, indicating that the relationship between resources and performance is not direct. It is not the resources themselves that translate into performance, but how those resources are leveraged (Hamel and Prahalad 1993). If political obstacles con- strain the strategic options of CVs, superior resources cannot translate into superior performance. Additionally, if CVs are required to use existing resources of their parent, those resources could actually become liabilities for the CVs. For example, if CVs are compelled to use the existing technologies of their parents, that constrains the CVs' choices of technologies, thereby limiting their abilities to innovate. In addition, the avail- ability of slack resources of the parent can often lead CVs to escalation of commitment, i.e., to continue courses of action despite negative outcomes (Garud and Van de Ven 1992). Thus, because of the cushion of slack resources, CVs may be sheltered from the pressures that would force IVs to either enhance their performance or go out of business.

Whereas resources were not directly related to firm performance, results indicated that strategy did directly influence performance. For both venture types, concern for low costs was strongly negatively related to financial performance, giving credence to the common wisdom that new ventures should compete on the basis of differentiation, not on the basis of low cost (Cohn and Lindberg 1972; Vesper 1980). Moreover, when new ventures emphasize concern for low costs, it may be at the expense of missed oppor- tunities.

In addition to finding that CVs placed less emphasis on strategic breadth than IVs, results also indicated that for CVs, increased strategic breath had a negative impact on their performance. This adds further support to the argument that CVs that pursue broad entry strategies may encounter political obstacles in doing so. Thus, financial per- formance might be reduced because internal competition hinders CVs' ability to deploy resources effectively.

In discussing the finding that increased strategic breadth was negatively related to

62 R.C. SHRADER AND M. SIMON

the performance of CVs, it is important to note that this finding is in contrast with Big- gadike's (1979) finding that among CVs, strategic breadth was positively related to firm performance. However, it should be noted that Biggadike's sample consisted of firms from a wide variety of industries, and the sample used here consisted entirely of new ventures in two closely related industry segments, thereby providing greater control for industry effects. These contradictory findings suggest that perhaps in some industries, increased strategic breadth increases CV performance, whereas in other industries the opposite is true. The industries examined in this study are highly volatile and are charac- terized by high rates of technological change, requiring that firms maintain the flexibility to respond rapidly to change. CVs that have acquired through a highly politicized pro- cess the relatively larger amounts of resources needed to pursue broad strategies may find it difficult to change strategic directions in response to external change, thus affect- ing subsequent performance.

Implications This research has both supported and refuted previous literature, which may have im- portant implications for practitioners and future researchers. Perhaps the strongest im- plication of this study is the finding that although CVs appeared to have access to supe- rior resources through their parents, these resource differences did not translate into higher performance for CVs. These results may indicate that CVs do not use their par- ents' resources to create strategic advantages. This appears consistent with Burgelman and Sayles's (1986) admonition that to enhance CV performance, CVs should be given more autonomy and managed more like IVs. Whereas managers of CVs may benefit from having the option of using their parents' resources, they should not be compelled to use these resources if it is at the expense of pursuing other opportunities.

On the other hand, although IVs are thought to have more autonomy and freedom of action, leading them to be more entrepreneurial, these characteristics (though not directly tested within the scope of this study) did not appear to translate into higher performance for IVs. Although IVs may have more autonomy, they may be severely constrained by resource limitations. This suggests that IVs may need to investigate ways to gain access to more substantial resources, such as through social networks.

In contrast to the negative relationship between strategic breadth and performance for CVs, results indicated that among IVs, strategic breadth was positively related to performance. These results indicate that perhaps IVs, unencumbered by the bureau- cracy that characterizes CVs, may be able to pursue aggressive strategies while simulta- neously maintaining the flexibility that enhances performance in volatile industries.

Results of the study also indicated that emphasizing concern for low costs was nega- tively related to the performance of both venture types. Therefore, managers of both CVs and IVs should be cautioned not to be penny wise and pound foolish, as striving to lower costs may result in missed opportunities in volatile industries such at those studied here.

Future Research Directions This study has sought to advance the literature by being the first to concurrently look at resources, strategies, and performance in the context of new ventures. However, given the study's exploratory nature, several areas of future research are suggested. Whereas

CORPORATE VERSUS INDEPENDENT NEW VENTURES 63

the companies in this study were in promising industries for entry by new ventures, the findings should not be indiscriminately generalized to other industries. Future research should consider whether the relationships found here are also found in other industries. For example, future research should explore the specific circumstances under which strategic breadth increases the performance of CVs and circumstances under which stra- tegic breadth decreases the performance of CVs. Furthermore, whereas variables in this study were selected based upon their relevance to existing literature and to the indus- tries studied, use of more comprehensive strategy measures and existing typologies may be the next logical step. In addition, studies of new ventures in other industries would shed light on the importance of specific resources and strategies to different industries. For example, within the volatile industry segments studied here, developing brand name recognition, producing specialty products, and providing high levels of customer service were emphasized by both CVs and IVs and may represent key success factors for all companies in these segments, therefore limiting the strategic choice of firms in these industries.

Whereas greater understanding of different types of ventures was gained by explor- ing differences in ventures' resources, strategies, and performance, the results indicate the need to explicitly examine several process variables that may provide more definitive answers to questions like: how can IVs acquire needed resources and how can CVs gain more freedom to act? Also, future research should explore how environmental influ- ences affect the strategic choices of CVs and IVs differently. Because in the current research these groups did have access to different resources but did not perform differ- ently, perhaps there are environmental determinants of strategy that influenced both groups.

C O N C L U S I O N

This research served as an important first step in contrasting two types of ventures and has thereby provided another answer to Cooper's (1993) call for comparative studies of new ventures by type. In doing so, it has confirmed some preexisting beliefs and chal- lenged others. The results of this study confirm theories that CVs and IVs systematically differ in the resources they emphasize. Whereas previous research has argued that polit- ical obstacles may inhibit CVs' access to their parent companies' resources, this study suggests that parents may share resources but may constrain ventures when translating those resources into strategies. The study also found that neither venture type outper- formed the other and that strategies, and not resources, directly related to performance. Thus, the leverage of existing resources may be more important than the possession of any given resource. Finally, this study indicated that CVs and IVs indeed differed systematically, and thus these new ventures should not be viewed as a homoge- neous group.

REFERENCES

Barney, J. 1991. Firm resources and sustained competitive advantage. Journal of Manage- ment 1:99-120.

Bevan, A. 1974. U.K. potato crisp industry, 1960-72: A study of new entry competition. Journal of Industrial Economics 22:281-297.

Biggadike, E.R. 1979. The risky business of diversification. Harvard Business Review 57:103-111.

64 R.C. SHRADER AND M. SIMON

Burgelman, R., and Sayles, L. 1986. Inside Corporate Innovation. New York: The Free Press. Caves, R.E., and Porter, M.E. 1977. From entry barriers to mobility barriers: Conjectural deci-

sions and continued deterrence to new competition. Quarterly Journal of Economics 91:241-261.

Chandler, G.N., and Hanks, S.H. 1994. Market attractiveness, resource-based capabilities, ven- ture strategies, and venture performance. Journal of Business Venturing 9:331-349.

Cohn, T., and Lindberg, R. 1972. How Management Is Different in Small Companies. New York: American Management Association.

Cooper, A.C. 1993. Challenges in predicting new firm performance. Journal of Business Ventur- ing 8:241-253.

Cooper, A.C., Woo, C.Y., and Dunkelberg, W.C. 1989. Entrepreneurship and the initial size of firms. Journal of Business Venturing 4:317-332.

Cooper, A.C., Willard, G., and Woo, C.Y. 1986. Strategies of high-performing new and small firms: A reexamination of the niche concept. Journal of Business Venturing 1:21-32.

Daft, R. 1983. Organization Theory and Design. New York: West. Doutriaux, J. 1992. Emerging high tech firms: How durable are their comparative start-up advan-

tages? Journal of Business Venturing 7:303-322. Duchesneau, D.A., and Gartner, W.D. 1990. A profile of new venture success and failure in an

emerging industry. Journal of Business Venturing 5:297-312. Dun's Census of American Business. 1985. USA: Dun and Bradstreet. Fast, N.D. 1981. Pitfalls of corporate venturing. Research Management 24:21-24. Garud, R., and Van de Ven, A.H. 1992. An empirical evaluation of the internal corporate ventur-

ing process. Strategic Management Journal 13:93-109. Griener, L.E. 1972. Evolution and revolution as organizations grow. Harvard Business Review

July-August:37-46. Hair, J., Anderson, R., Tatham, R., and Black, W. 1992. Multivariate Data Analysis with Readings.

New York: Macmillan Publishing Company. Hambrick, D.C. 1981. Strategic awareness within to management teams. Strategic Management

Journal 2:263-279. Hamel, G., and Prahalad, C.K. 1993. Strategy as stretch and leverage. Harvard Business Re-

view 71(2):75-84. Hayes, W.L. 1983. Statistics. New York: Holt, Rinehart and Winston. Heflebower, R.B. 1951. Economics of size. Journal of Business of the University of Chicago

24:258-273. Hines, H.H. 1957. Effectiveness of "entry" by already established firms. Quarterly Journal of Eco-

nomics 75:132-150. Hofer, C., and Schendel, C. 1978. Strategy Formation: Analytical Concepts. St. Paul, MN: West. Huber, G.P., and Power, J.D. 1985. Retrospective reports of strategic level managers. Strategic

Management Journal 6:171-180. Jaccard, J., Turrisi, R., Wan, C.K. 1990. Interaction Effects in Multiple Regression. Newbury Park,

CA: Sage. Kanter, R.M., Richardson, L., North, J., and Morgan, E. 1991. Engines of progress: Designing

and running entrepreneurial vehicles in established companies: The new venture process at Eastman Kodak, 1983-1989. Journal of Business Venturing 6(1):63-82.

Kazanjian, R.K., and Drazin, R. 1990. A stage contingent model of design and growth for technol- ogy based new ventures. Journal of Business Venturing 5:137-150.

Keeley, R.H., and Roure, J.B. 1990. Management, strategy, and industry structure as influences on the success of new firms: A structural model. Management Science 36(10):1256-1267.

Knight, R.M. 1989. Technological innovation in Canada: A comparison of independent entrepre- neurs and corporate innovators. Journal of Business Venturing 4(4):281-288.

Laitinen, E.K. 1992. Prediction of failure of a newly founded firm. Journal of Business Ventur- ing 7(4):323-340.

CORPORATE VERSUS INDEPENDENT NEW VENTURES 65

Lambkin, M. 1988. Order of entry and performance in new markets. Strategic Management Jour- nal 9:127-140.

Lambkin, M., and Day, G. 1989. Evolutionary processes in competitive markets: Beyond the product life cycle. Journal of Marketing 53:4-20.

MacMillan, I.C., Block, Z., and Narisimham, P.N.S. 1986. Corporate venturing: Alternatives, ob- stacles encountered, and experience effects. Journal of Business Venturing 1(2):177-192.

McDougall, P.P., Deane, R.H., and D'Souza, D. 1992. Manufacturing strategy and business origin of new venture firms in the computer and communications equipment industries. Produc- tion and Operations Management 1:53-69.

McGrath, R.G., Venkatraman, S., and MacMillan, I.C. 1994. The advantage chain: Antecedents to rents from internal corporate ventures. Journal of Business Venturing 9:351-369.

Miller, A., and Camp, B. 1985. Exploring determinants of success in corporate ventures. Journal of Business Venturing 1:87-105.

Miller, A., Spann, M.S., and Lerner, L. 1991. Competitive advantages in new corporate ventures: The impact of resource sharing and reporting level. Journal of Business Venturing 6:335-350.

Nunnally, J.C. 1967. Psychometric Theory. New York: McGraw-Hill. Overall, J.E., Lee, D.M., and Hornick, C.W. 1981. Comparisons of two strategies for analyses

of variance in nonorthogonal decisions. Psychological Bulletin 90:367-375. Penrose, E. 1959. The Theory of the Growth of Firm. New York: Wiley. Porter, M.E. 1981. The contributions of industrial organization to strategic management. Acad-

emy of Management Review 6:609-620. Porter, M.E. 1980. Competitive Strategy: Techniques for Analyzing Industries and Competitors.

New York: The Free Press. Ramachandran, K., and Ramanarayan, S. 1993. Entrepreneurial orientation and networking:

Some Indian evidence. Journal of Business Venturing 8:513-524. Roberts, E.R., and Hauptman, O. 1987. The financing threshold effect on success and failure of

biomedical and pharmaceutical start-ups. Management Science 33(3):381-394. Robinson, R.B., Jr., and Pearce, J.A., II. 1986. Product life-cycle considerations and the nature

of strategic activities in entrepreneurial firms. Journal of Business Venturing 207-224. Romanelli, E. 1987. New venture strategies in the minicomputer industry. California Management

Review 30(1). Roure, J.B., and Maidique, M.A. 1986. Linking prefunding factors and high technology venture

success: An exploratory study. Journal of Business Venturing 1:295-306. Sandberg, W. 1984. The determinants of new venture performance: Strategy, industry structures,

and entrepreneur. Doctoral dissertation, University of Georgia. Sandberg, W.R., and Hofer, C.W. 1987. Improving new venture performance: The role of strat-

egy, industry structure, and the entrepreneur. Journal of Business Venturing 2:5-28. Schoonhoven, C.B., Eisenhardt, K.M., and Lyman, K. 1990. Speeding products to market: Wait-

ing time to first product introduction in new firms. Administrative Science Quarterly 35:177-207.

Stocking, G.W., and Watkins, M.W. 1951. Monopoly and Free Enterprise. New York: Twentieth Century Fund.

Stuart, R.W., and Abetti, P.A. 1987. Start-up ventures: Towards the prediction of initial success. Journal of Business Venturing 2:215-230.

Stuart, R.W., and Abetti, P.A. 1990. Impact of entrepreneurial and management experience on early performance. Journal of Business Venturing 5:151-162.

Sykes, H.B. 1986. The anatomy of a corporate venturing program: Factors influencing success. Journal of Business Venturing 1:275-293.

Tsai, W.M., MacMillan, I.C., and Low, M.B. 1991. Effects of strategy and environment on corpo- rate venture success in industrial markets. Journal of Business Venturing 6(1):9-28.

Van de Ven, A.H., Hudson, R.M, and Schroeder, D.M. 1984. Designing new business startups:

66 R.C. SHRADER AND M. SIMON

Entrepreneurial, organizational, and ecological considerations. Journal of Management 10(1):87-107.

Vesper, K.H., 1980. New Venture Strategies. Englewood Cliffs, NJ: Prentice-Hall. Weiss, C.A. 1981. Start up businesses: A comparison of performances. Sloan Management Re-

view 23:37-53. Williams, M.L., Tsai, M., and Day, D. 1991. Intangible assets, entry strategies, and venture success

in industrial markets. Journal of Business Venturing 6:315-333.