Corporate Governance and Market Liquidity: An Empirical Analysis

31

Electronic copy available at: http://ssrn.com/abstract=1929116 Electronic copy available at: http://ssrn.com/abstract=1929116 Corporate Governance and Market Liquidity: An Empirical Analysis Pawan Jain Doctoral Student The University of Memphis Christine Jiang Professor of Finance The University of Memphis Mohamed Mekhaimer Doctoral Student The University of Memphis This Draft: 16 September 2011

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Corporate Governance and Market Liquidity: An Empirical Analysis

Electronic copy available at: http://ssrn.com/abstract=1929116Electronic copy available at: http://ssrn.com/abstract=1929116

Corporate Governance and Market Liquidity:

An Empirical Analysis

Pawan Jain Doctoral Student

The University of Memphis

Christine Jiang Professor of Finance

The University of Memphis

Mohamed Mekhaimer Doctoral Student

The University of Memphis

This Draft: 16 September 2011

Electronic copy available at: http://ssrn.com/abstract=1929116Electronic copy available at: http://ssrn.com/abstract=1929116

Introduction

Corporate governance deals with the set of mechanisms designed to mitigate the agency

problem that arise from the separation of ownership and control in a firm. It provides different

ways in which investors or suppliers of finance assure that the agents or managers act for their

investors’ ultimate benefits (Shlelifer and Vishny, 1997, La porta et al 2000, Lin et al 2009).

Corporate governance is important as it influences firm valuation (Gomper, Ishii, and Metrick

2003, Danies 2001, Morck and Yang 2001 and Bhagat and Bolton 2008), capital structure

(Skaife et al 2004, Novaes and zingales 1999), and liquidity (Goh, et al 2008, Chung et al 2010).

In this paper we provide a comprehensive analysis of the various channels through which

the corporate governance impacts the stock market liquidity of a firm. Liquidity is a very

important aspect of financial markets. Kyle (1985) notes that ‘‘Liquidity encompasses a number

of transactional properties of markets, including tightness, depth, and resiliency” (p. 1316).

Liquid market provide block holders with the mechanism by which they can easily to intervene

more effectively to correct managers’ actions (Maug, 1998), control management compensations

(Holmstrom and Tirole, 1993), decrease the information asymmetry of stock price through

stimulating trades of informed investors (Subrahmanyam and Titman, 2001; Khanna and Sonti,

2004)and lessen executives opportunism (Edmans, 2009; Admati and Pfleiderer, 2009).

Prior studies examined how external corporate governance (e.g., the institutional

ownership, analyst following, legal/regulatory environments and markets for corporate control)

and internal corporate governance (e.g. managerial compensation, director independence and

charter provisions) affect firm value, cost of capital, stock returns and liquidity. In this paper we

provide a comprehensive analysis of three different layers of corporate governance namely

external, internal and the intersection between both layers and their effect on market liquidity.

Electronic copy available at: http://ssrn.com/abstract=1929116Electronic copy available at: http://ssrn.com/abstract=1929116

The relationship between the corporate governance and liquidity is not unique to our paper

(seeGoh, et al 2008, chung et al 2010, Dumitrescu 2010).However, to the best of our knowledge

this paper provides the first empirical test based on the cumulative as well as the individual effect

of three different layers of corporate governance on market liquidity.

The results show a significant positive relation between liquidity (measured by quoted

spread, Amihud illiquidity and turnover) and Acharya, et al, (2010) internal monitoring as

measured by the relative age difference between CEO and top subordinates’ managers. Results

are robust across the whole sample of both NYSE/AMEX firms and NASDAQ firms with

respect to different liquidity measures. The results is consistent with Acharya et al (2010), in the

sense that subordinates managers, who cares about firm’s future, act in more public spirited to

compete for the next CEO position. In addition, we find the coefficients on G-Index are

significantly negative for the quoted spread and Amihud illiquidity for the individual and

combined samples of NYSE/AMEX and NASDAQ firms. The results also show that external

governance, as measured by the number of block holder and the number of analyst following,

has a significant positive relationship with the different measures of liquidity. This result is

consistent with the conclusions in Coffee (1991) and Bhide (1993), who found that more liquid

shares may encourage block holders to sell their shares if they are not happy with the firm

performance. The results are robust for a pooled analysis of the incremental effect of the three

different layers of monitoring discussed before.

Acharya, Myers and Rajan (2010), depart from the traditional view of governance by

introducing internal governance model. The main distinction in their model is that they see the

firm as a composition of diverse agents with different horizons, different interests and different

opportunities for misappropriation and growth and the best way to administer the agency cost

and the diverse ways of managing the firm is the internal governance.

Acharya, et al. (2011) argues that subordinate managers are important stakeholders in the

firm, who care about its future. Because of their power to withdraw their contributions to the

firm, these stakeholders can force the CEO to act in a more public-spirited and far-sighted way,

even if the CEO acts in his or her own short-term self interest and shareholders are dispersed and

powerless. The authors further states that the Three ingredients go into producing the firm’s cash

flow include the firm’s capital stock; the CEO’s ability to manage the firm, which depends on his

skill and firm-specific knowledge; and the young subordinate manager’s effort, which allows her

to learn and prepare for promotion. Hence, Acharya et al. (2011) model (see also Prendergast

(1993)) suggests that the rewards to learning may be prospective control rents from promotion in

the firm, which, in turn, make employees far more effective in exerting internal governance.

However, they do not do this by asserting “voice” in Hirschman’s terminology (probably an easy

way to get fired), but by reducing effort. None of this needs any coordination on the part of

employees or any appeal to the board of directors, nor does it require external governance.

There are various theoretical models that examine the potential trade-off between

liquidity and control. Coffee (1991) argues that large investors have increasingly supported

measures that improve internal corporate governance because such measures also improve stock

market liquidity (which makes their exit less costly). Bhide (1993) holds that high stock market

liquidity discourages internal monitoring (by active stockholders) and the benefits of market

liquidity must be weighed against the cost of impaired shareholder activism.

In contrast, Faure-Grimaud and Gromb (2004) show that information generated by liquid

markets increases the large shareholder’s incentive to undertake value-enhancing activities, such

as monitoring. Using an alternative definition of liquidity (i.e., the ability to trade anonymously)

several authors also show that liquidity increases the incentive to monitor by lowering the cost of

acquiring large positions (see Kahn and Winton (1998), Maug (2002), and Noe (2002)).

More recently, Chung, Elder and Kim (2011) analyzed the relationship between internal

corporate governance (based on governance index) and stock market liquidity. They find that

firms with better corporate governance have narrower spread and higher market quality index.

Goh, Ng and Yong (2008) also study the effect of internal governance (based on the institutional

ownership and board independence) through mediating factors on the market liquidity. However,

considering the model presented by Acharya et al (2010), we argue that Chung et al 2010 and

Goh et al 2008 measures of internal liquidity do not truly measures the construct.

Prior literature shows that external corporate governance is linked to various capital

market consequences. We use two widely accepted external corporate governance measures

found in previous literature- the number of block holders and analyst coverage. There are various

incentives for the block holders to engage inactivities that will increase firm value and enhance

its performance in the capital market. The most important one is theirown stake in the firm. Since

the block holder participates in a value increase in proportion to his equity stake, a larger stake

increases the benefit to him from the firm value being high (Faure-Grimaud and Gromb, 2004).

The view that large shareholders affect firm value is indeed widespread (Shleifer and Vishny,

1997). They alleviate the free-rider problem pervasive in firms with passive dispersed investors,

unable or unwilling to affect the firm's operations, that is, outsiders. The market for corporate

control can provide some discipline, but it is hard to see it as effective in controlling operational

decisions (Acharya, Myers and Rajan, 2010). Institutional holding reflect the extent of external

monitoring imposed by the outsiders to reduce the agency cost and divergence among investors

and firm managers benefits.

The effect of analyst coverage on the firm behavior has two competing effects

(Knyazeva, 2007). The first perspective argues that the analyst have incentive to build their own

reputation to increase the compensation. To achieve a better reputation and higher compensation,

they try to obtain private information to reduce the information asymmetry among market

participants. Lang, Lins and Miller (2003) reported that analyst are more likely to follow poor

governed firms and the value of analyst coverage is much higher in the countries with weak

investor rights protection. While the second perspective considers firms that are widely followed

by analysts may be pressured to adopt better corporate governance (Chung, et. al., 2011). Also,

there exist possible behavioral biases in analyst coverage such as herding, anti-herding,

investment banking affiliation and optimism (Clarke and Subramanian 2006, Hong et al 2000).

Kenyazeva (2007) reported that analyst following serve as a partial substitute for the corporate

governance mechanisms.

Poor governanceimplies poor financial and operational transparency (Chung, et al, 2011),

which increases information asymmetries between insiders and outside investors (e.g., outside

owners and liquidityproviders), as well as among outside investors. Poor transparency insulates

management,which can expropriate firm value through shirking,empire building, risk aversion,

and perquisites [see Gompers, Ishii, and Metrick (2003) and Bebchuk,Cohen, and Ferrell

(2005)]. Diamond (1985) shows that such information asymmetries betweenmanagement and

traders increase the latter’s incentive to acquire private information, leading to

greaterheterogeneity among trader beliefs and larger speculative positions among informed

traders. Liquidityproviders may therefore post wider spreads and smaller depths for stocks of

poorly governed companiesbecause they face greater adverse selection problems in these stocks

(Glosten and Milgrom, 1985).

Theory therefore suggests that poor corporate governance may impair stock market

liquidity tothe extent that poor governance is associated with low transparency and poor investor

protection. In thisbroad context, we examine the effect of corporate governance on liquidity.We

present a comprehensive empirical analysis of the relationship between corporate governance

and monitoring. We propose 3 levels of corporate governance: pure internal, internal/external

and pure external and analyze how each level affects stock market liquidity. Monitoring is costly

and hence, any organizational structure that promotes internal monitoring would be very

beneficial for the institutional investors or block holders and will improve the efficiency of the

capital markets. Also, internal governance can be effective when there is a breakdown of external

governance.

Corporate Governance Measures

An index of corporate governance that is relevant for stock market liquidity requires data

on governance standards that would, in theory, improve financial/operational transparency and

investor protection. Existing metrics of corporate governance are not completely adequate in this

regard. We intend to use the following three measures of corporate governance.

Internal Governance

Relative Age of top executives to CEO: The Relative age difference is the average

difference between the CEO’s ageand subordinate managers’ ages in each company.If the CEO

believes that undertaking future-oriented actions will increase current cash flows, and thus his

welfare, then she would require key stakeholders like customers and employees (see Hirschman

(1970), Titman (1984)) to be interested in the future, even if the CEO is not. Customers are,

however, typically at a distance, and leaving aside the purchase of high-value durable goods, are

unlikely to be appropriately informed or concerned about a seller’s future health. This then

leaves employees, particularly early- or mid-career managers, as the stakeholders most

concerned, informed, and able to act against short-sighted CEOs (Acharya, et al, 2010).

However, they do not do this by asserting “voice” in Hirschman’s terminology (probably an easy

way to get fired), but by reducing effort. None of this needs any coordination on the part of

employees or any appeal to the board of directors, nor does it require external governance.

CEO Tenure: The tenure is measured number of years CEO holds her office.The longer

the tenure, the more influence the CEO can have on directors and internal pay practices (Core,

Holthausen, and Larcker (1999); Cyert, Kang, and Kumar (2002); and Harford and Lie (2007))

Internal/External Monitoring

We use the governance index created by Gomper et al (2003) as a measure of

internal/external monitoring (GIM hereafter). The 24 governance standards provided by

Gompers et al (2003) can be influenced by both, the insiders and outsiders. For e.g. standard

related to the independence of the audit committee (to capture the extent to whichgovernance

may improve financial and operational transparency as well as protect shareholder interests) can

be changed either by the firm insiders or by outside investors. The GIM index is commonly used

in to measure corporate governance (Chung et al 2011, Bhagat and Bolton 2008, Venkatachalam

2005). The index construction is straightforward: for every firm (GIM) add one point for every

provision that restricts shareholder rights. The 24 governance standards are equally weighted in

the index construction.

External Monitoring:

Number of block holders: Since the block holder participates in a value increase in

proportion to his equity stake, a larger stake increases the benefit to him from the firm value

being high (Faure-Grimaud and Gromb, 2004). The view that large shareholders affect firm

value is indeed widespread (Shleifer and Vishny, 1997). We also have used the number of

analyst following to proxy the external governance of the firm. Lang, Lins and Miller (2003)

reported that analyst are more likely to follow poor governed firms and Kenyazeva (2007)

reported that analyst following serve as a partial substitute for the corporate governance

mechanisms.

Liquidity Measures

Liquidity is difficult to define and even more difficult to estimate. Kyle (1985) notes that

‘‘liquidity is a slippery and elusive concept, in part because it encompasses a number of

transactional properties of markets, these include tightness, depth, and resiliency,’’ (p. 1316).

Empirical liquidity definitions span direct trading costs (tightness), measured by the bid–ask

spread (quoted or effective), to indirect trading costs (depth and resiliency), measured by price

impact. The literature provides a menu of measures and proxies to consider for estimating

liquidity.

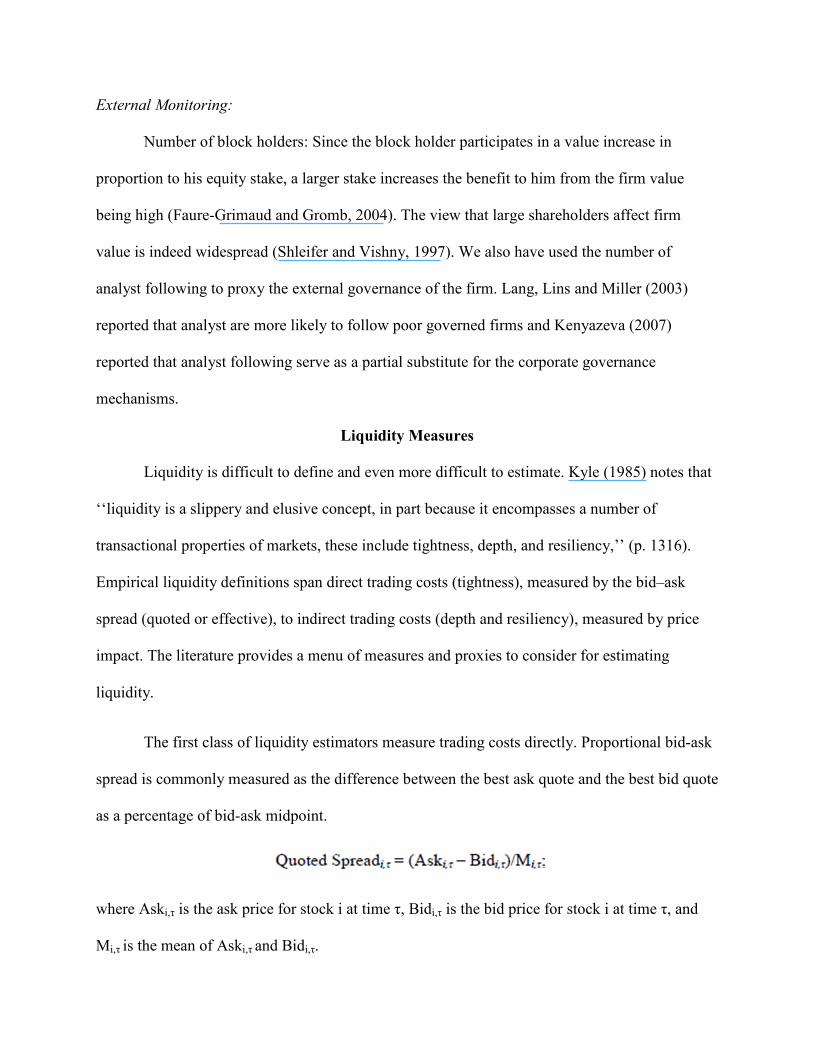

The first class of liquidity estimators measure trading costs directly. Proportional bid-ask

spread is commonly measured as the difference between the best ask quote and the best bid quote

as a percentage of bid-ask midpoint.

where Aski,τ is the ask price for stock i at time τ, Bidi,τ is the bid price for stock i at time τ, and

Mi,τ is the mean of Aski,τ and Bidi,τ.

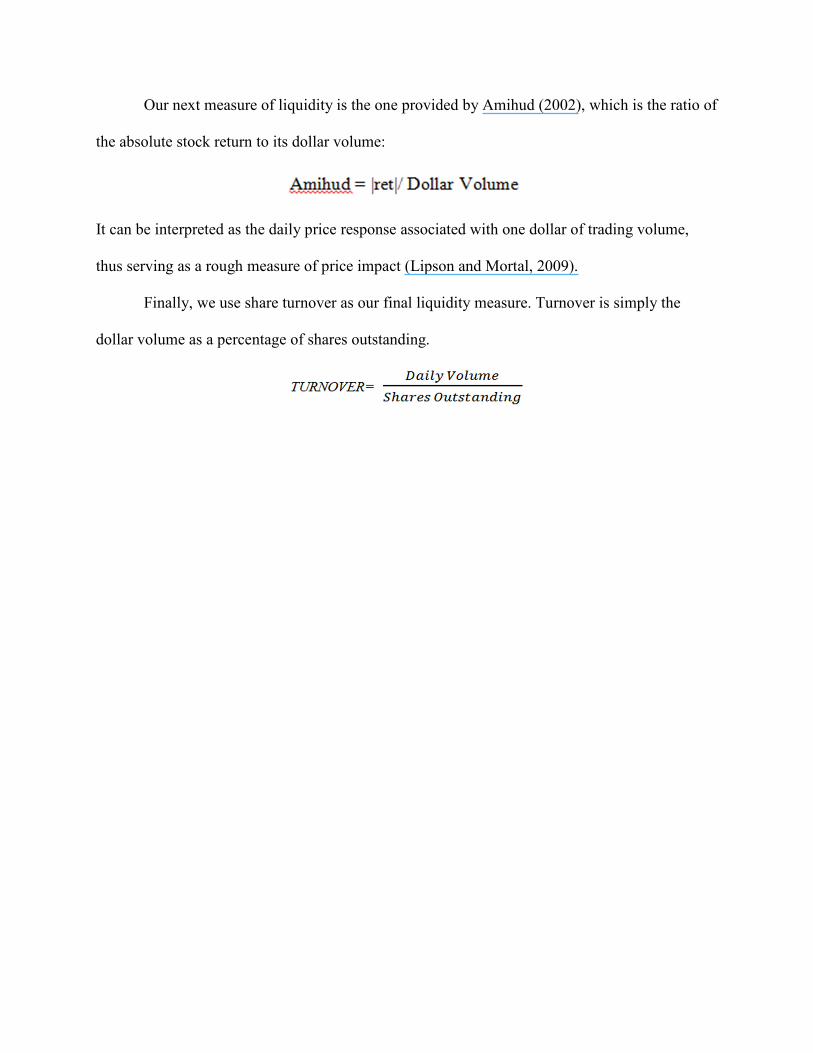

Our next measure of liquidity is the one provided by Amihud (2002), which is the ratio of

the absolute stock return to its dollar volume:

It can be interpreted as the daily price response associated with one dollar of trading volume,

thus serving as a rough measure of price impact (Lipson and Mortal, 2009).

Finally, we use share turnover as our final liquidity measure. Turnover is simply the

dollar volume as a percentage of shares outstanding.

Data sources

Our sample includes 6 years of data on all firms listed on NYSE, AMEX and Nasdaq for

the period 1996 to 2001. Stock prices, closing bid and ask prices, trading volume, shares

outstanding, exchange information are provided from the Center for Research in Stock Prices

(CRSP) database. The Data on number of analyst following is extracted from the Institutional

Brokers' Estimate System (I/B/E/S) dataset while the number of Institutional owners is provided

by the Blockholders database. Block holder’s data is available only for 1996-2001 period. Risk

metrics database provide the GIM index or the Governance index (G-Index). Finally, we obtain

financial and accounting data such as total assets, intangible assets, dividend information, and R

& D expenses from Compustat database. The trading data included some trades with zero trading

prices and bid and ask quotes for the locked and crossed markets (bid price less than/equal to ask

price). These observations are removed from the final sample and the cleaned data included

observations for 14,475 firm years, with 5007 being NYSE/AMEX firm years and the remaining

9,468 being the Nasdaq firm years.

Results

Descriptive Statistics

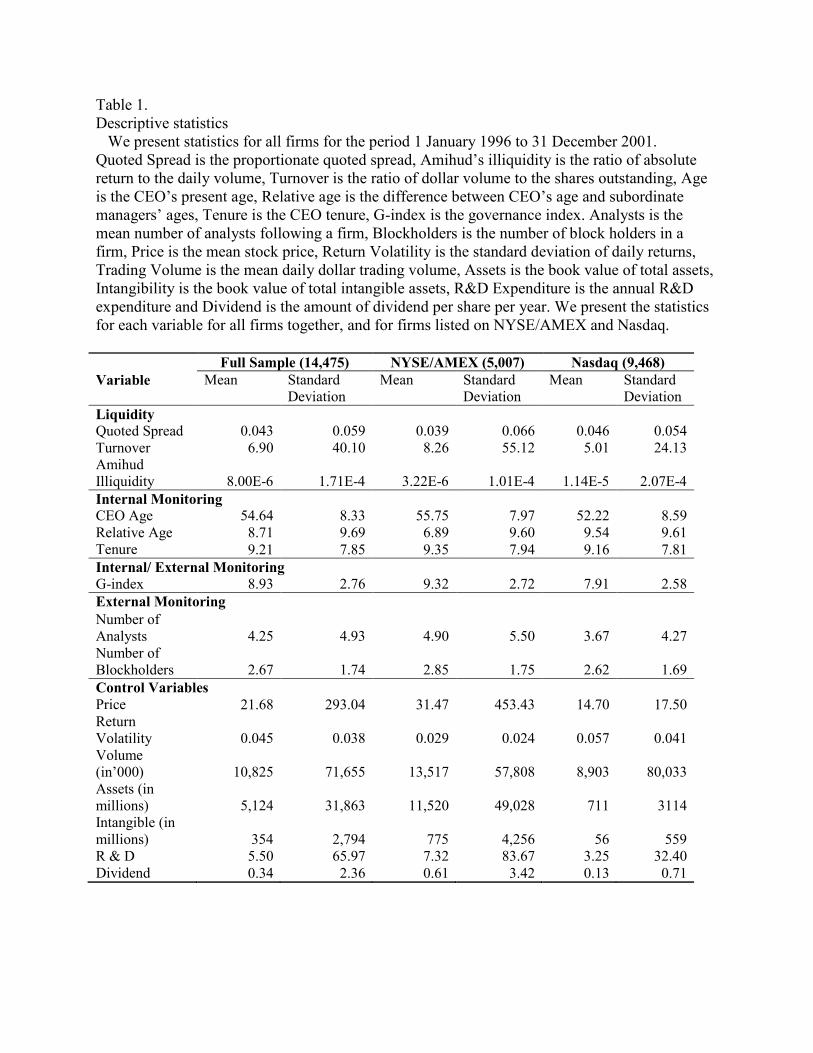

Table 1 reports the descriptive statistics on Governance- Index (g-index), liquidity

measures, CEO age and other stock and CEO attributes for the sample firms included in the

study. Given the differences in both the market structure and the governance standards for

listing, we report our results separately for NYSE/AMEX and NASDAQ firms as well. For the

NYSE/AMEX firms in our sample, the mean value of g-index is 9.32, while for Nasdaq firms the

mean g-index is 7.91, indicating that, on average, Nasdaq firms meet about one-third of the

governance standards. Average age of a CEO of a typical firm is about 55 years and a CEO

typically holds the office for 9.21 years. The average age and tenure for CEO of NYSE/AMEX

firms is higher than the Nasdaq firms. The average age gap between the CEO and subordinate

managers is 6.89 years for NYSE/AMEX firms which is much lower than the mean age gap of

9.54 years for Nasdaq firms. Hence, based on the argument presented by Acharya et al. (2011),

the internal governance should be more visible in Nasdaq firms than the NYSE/AMEX firms.

The descriptive statistics also show that NYSE/AMEX firms in our sample tend to be

larger in size as measured by total assets, have greater trading volume, and exhibit lower return

volatility than NASDAQ firms. NYSE/AMEX firms tend to be more liquid with lower quoted

spreads and exhibit smaller Amihud illiquidity than NASDAQ firms. In addition, NYSE/AMEX

firms are followed by more analysts, and exhibit higher institutional ownership. For example, the

mean number of analysts (4.90) for the NYSE/AMEX sample is significantly greater than the

corresponding figure (3.67) for the NASDAQ sample. Total intangible assets, R&D expenditure

and dividend yield are much larger for the NYSE/AMEX firms in comparison with the Nasdaq

firms.

Regression Results

In this section, we examine how our liquidity measures are related to corporate

governance after controlling for other possible determinants of stock market liquidity.

To examine the relation between liquidity and corporate governance, we regress the

liquidity measures: quoted spreads, Amihud’s illiquidity and turnover, on the different layers of

monitoring and a number of control variables using the pooled cross-sectional and time-series

data. Prior studies show that a significant portion of cross-sectional and time-series variation in

spreads can be explained by select stock attributes such as dollar trading volume, share price,

return volatility and dividend yield (McInish and Wood, 1992; Chung, Van Ness, and Van Ness,

1999; and Stoll, 2000). To isolate the effect of corporate governance on liquidity, we include

stock price (in log), return volatility, dollar trading volume (in log) and dividend yield in the

regression model as control variables.

We note that level of monitoring and our measures of market liquidity could be

spuriously correlated because they are related to a common set of variables. Including the

variables that are related to both level of monitoring and market liquidity in the regression model

reduces the possibility that any estimated relation between level of monitoring and market

liquidity is spurious. For example, larger firms may simultaneously exhibit better governance

structure due to higher investor interest and lower spreads due to smaller adverse selection risks

(e.g., more information is available on largerfirms). To examine whether corporate governance

has an independent, direct impact on liquidity, we include firm size (as measured by the book

value of total assets) in the regression model.

For the same reason, we also include asset tangibility and R&D expenditure as additional

control variables. Asset tangibility could reduce asymmetric information problems as payoffs on

tangible assets’ are easier to observe. In contrast, high R&D intensity may increase asymmetric

information problems because payoffs from R&D are difficult to predict.

Based on these considerations, we estimate the following regression model for our study

sample ofNYSE/AMEX firms, NASDAQ firms, and the combined sample of NYSE/AMEX and

NASDAQ firms, respectively:

Quoted Spreadi,tor Amihud illiquidityi,t or Turnoveri,t= β0 + β1Level of Monitoringi,t +

β2Log(Pricei,t) + β3Return Volatilityi,t+ β4Log(Trading Volumei,t) + β5Log(Assetsi,t)(1)+

β6AssetIntangibilityi,t+ β7R&D Expenditurei,t+ β8DividendYieldi,t + εi,t;

where Quoted Spreadi,t is the proportionate quoted percentage spread of stock i in year t,

Amihudilliquidityi,t is return per dollar volume, Turnoveri,t is average daily volume per share

outstanding, Level of Monitoring is internal governance (measured by CEO’s age relative to

subordinate managers’ age, CEO age and CEO tenure) for the first regression, internal/external

governance (G-Indexi,t) for the second regression, external governance (measured by number of

block holders and number of analysts following) for the third regression, Pricei,t is the mean

stock price, Return Volatilityi,t is the standard deviation of daily returns, Trading Volumei,t is the

mean daily dollar trading volume, Assetsi,t is the book value of total assets, Intangibilityi,tis the

book value of total intangible assets, DividendYieldi,t is the ratio of dividend paid per share to the

share price, and εi,t is the error term. We calculate t-statistics using White’s (1980) standard

errors and report them in parentheses.

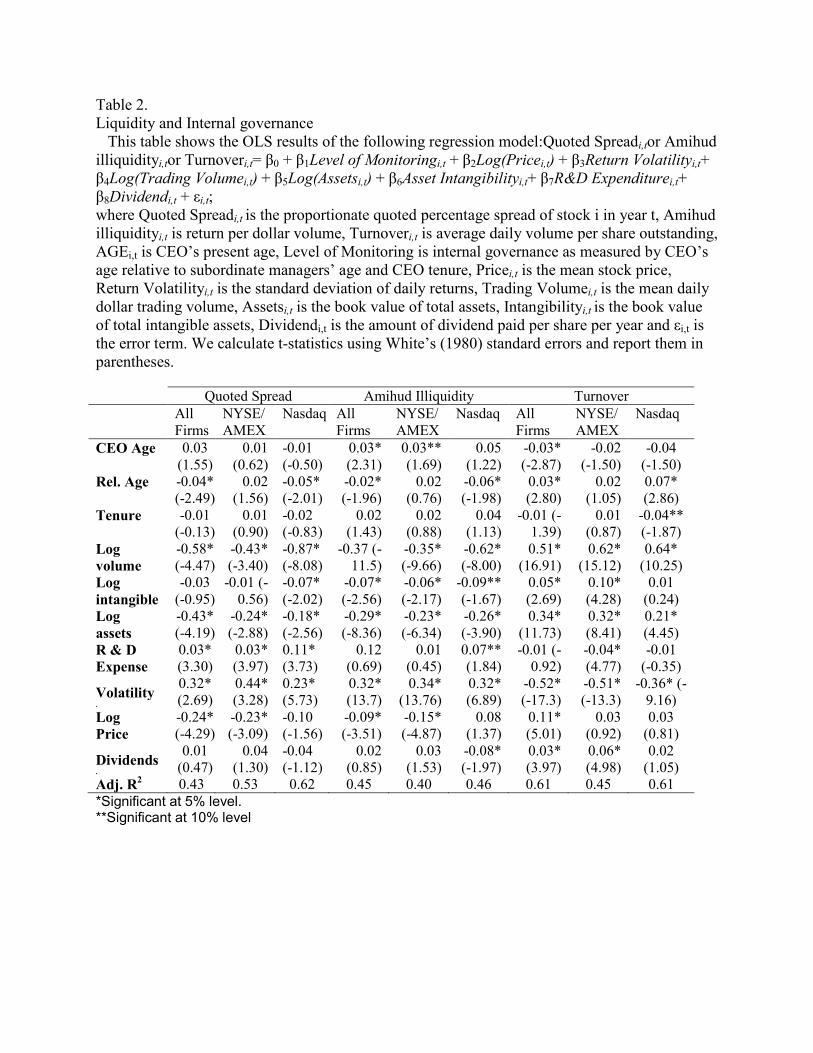

Internal monitoring and liquidity

Table 2 summarizes the results explaining the relationship between liquidity and internal

governance as measured by the difference between CEO’s age and subordinate manager’s ages

(Relative age). The results show that the coefficients on relative age in the quoted spread model,

Amihud illiquidity model are all negative and significant for NASDAQ firms, and the combined

sample of NYSE/AMEX and NASDAQ firms. We obtain qualitatively similar results for the

turnover. Hence, the larger the age difference between the CEO and subordinate managers, the

higher is the firm’s liquidity. Our regression models capture a large fraction of the variation in

liquidity as shown by the high R2 value for the regressions.

Consistent with the finding of prior research, liquidity is significantly and positively

related to log price, firm size, asset intangibility and return volatility, and negatively to trading

volume in both markets. R & D expenses are negatively related to liquidity and this result is

consistent with Chung et al. (2011). High R&D expenditure may increase asymmetric

information problems because payoffs from R&D are difficult to predict.

These results are remarkably robust across our sample of both NYSE/AMEX firms and

NASDAQ firms and with respect to different variable measurement methods. Our empirical

results thus far support the hypothesis that better internal corporate governance is associated with

higher stock market liquidity.

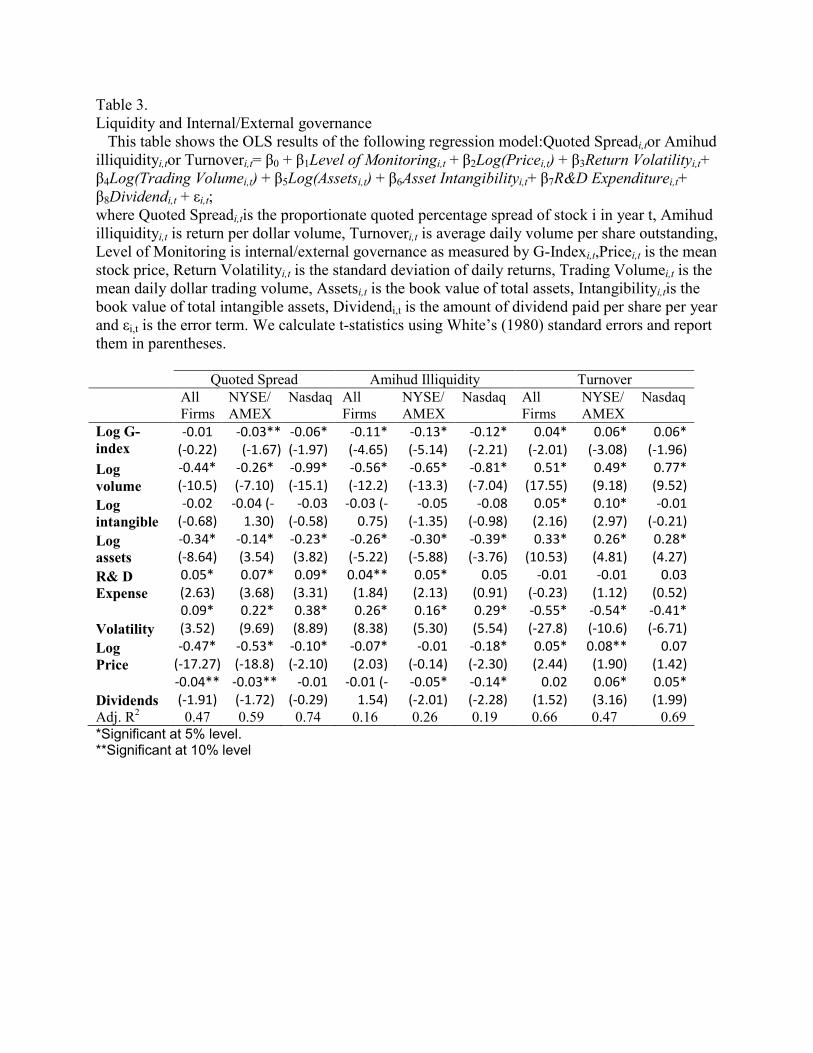

Internal/external monitoring and liquidity

Table 3 summarizes the results explaining the relationship between liquidity and

internal/external governance as measured by the Gompers, Ishii and Metrick (2003) (g-index).

The results show that the coefficients on G-index in the quoted spread model, and Amihud

illiquidity model are all negative and significant for NYSE/AMEX firms, NASDAQ firms, and

the combined sample of NYSE/AMEX and NASDAQ firms. We obtain qualitatively similar

results for the turnover. Our regression models capture a large fraction of the variation in

liquidity, with the R2of greater than 0.65 for the Nasdaq firms. Hence, the higher the G-index,

the higher is the stock market liquidity. The results on control variable are consistent with prior

literature.

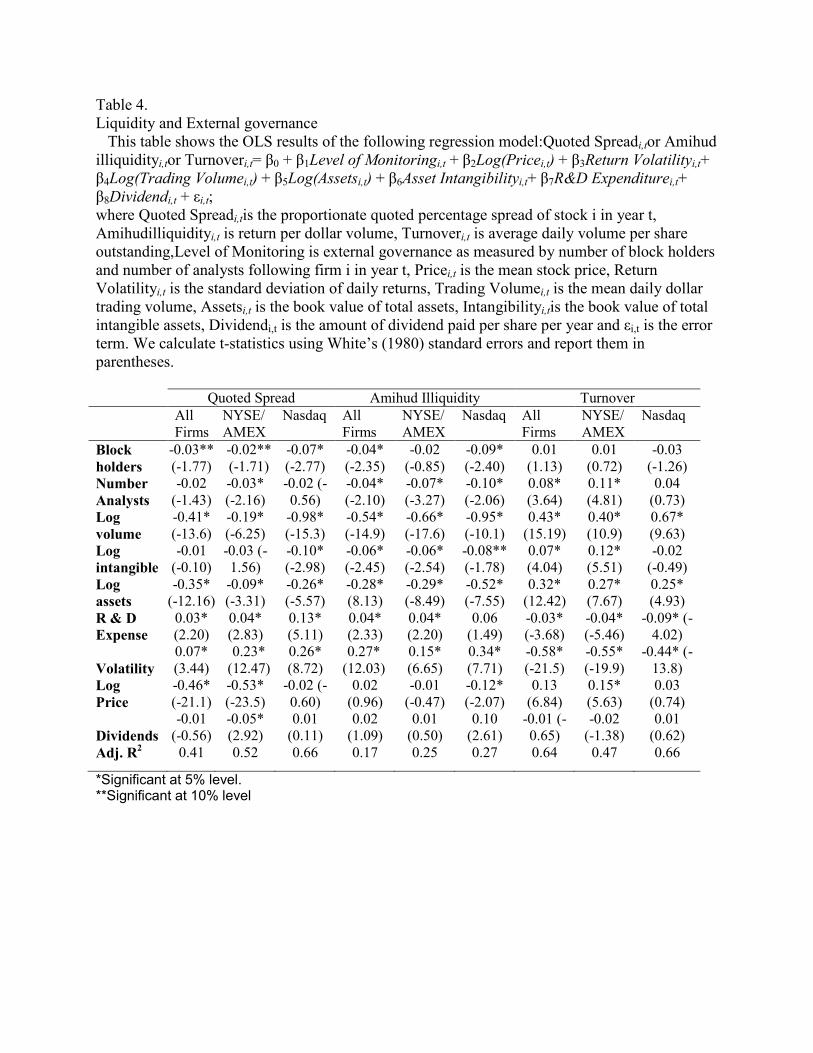

External monitoring and liquidity

Table 4 summarizes the results explaining the relationship between liquidity and external

governance as measured by the number of block holders and number of analysts following. The

results show that the coefficients on block holders and number of analysts following in the

quoted spread model, and Amihud illiquidity model are mostly negative and significant for

NYSE/AMEX firms, NASDAQ firms, and the combined sample of NYSE/AMEX and

NASDAQ firms. Results are not significant for the number of block holders for turnover model.

The results on control variable are consistent with prior literature. Our empirical results thus far

support the hypothesis that better external corporate governance is associated with higher stock

market liquidity.

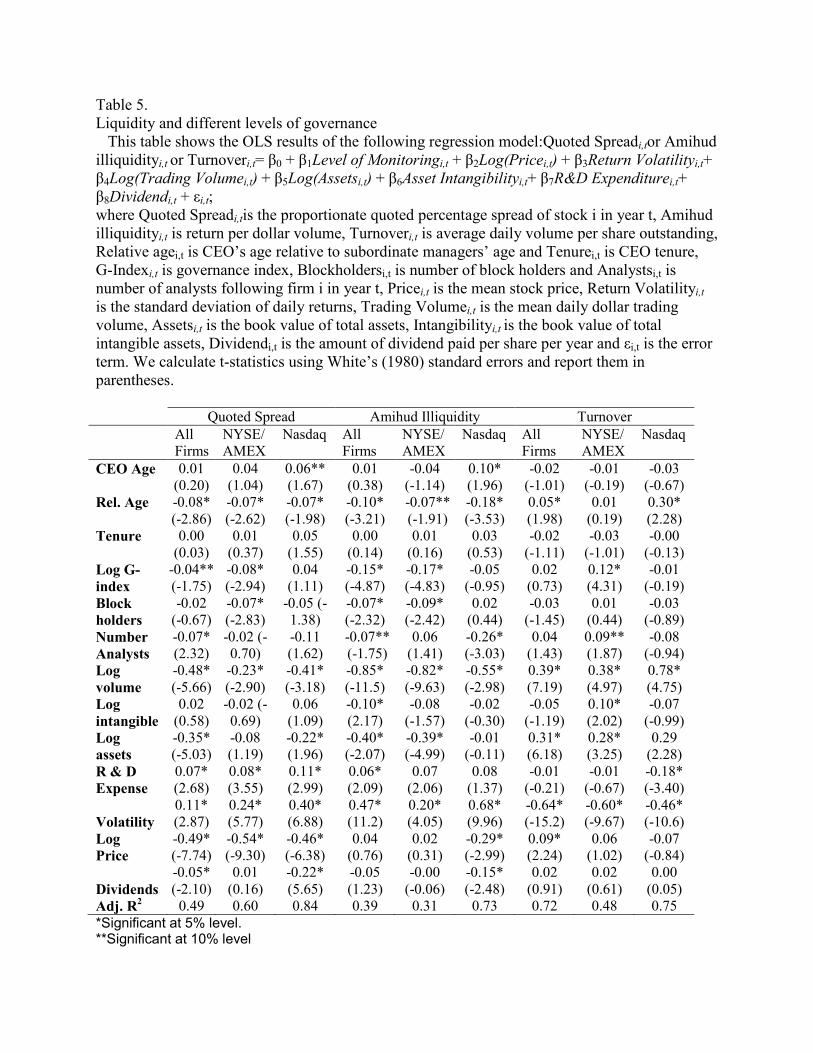

Liquidity and different levels of monitoring

For our final analysis, we run a pooled regression by including all three layers of

monitoring in one regression model. We analyze the incremental effect of different layers of

monitoring on liquidity. Results from this analysis are summarized in table 5. CEO age is

significantly negatively related to liquidity as measured by quoted spread or Amihud’s

illiquidity. Our measure of internal monitoring, relative age difference between CEO and

subordinate managers is significantly positively related to liquidity, even after controlling for the

other measure of corporate governance. This result is robust across different model specifications

and across firms listed on NYSE/AMEX or Nasdaq.

We also find a significantly positive relationship between liquidity and both, the

internal/external governance (G-index) and the external governance (number of block holders)

for NYSE/AMEX firms.

Based on these results we can conclude that better corporate governance is associated

with higher liquidity. We also find that internal governance significantly impacts stock market

liquidity beyond the traditional governance measures.

Acharya, et al. (2011) argues that subordinate managers are important stakeholders in the

firm, who care about its future. Because of their power to withdraw their contributions to the

firm, these stakeholders can force the CEO to act in a more public-spirited and far-sighted way,

even if the CEO acts in his or her own short-term self interest and shareholders are dispersed and

powerless. The authors further states that the Three ingredients go into producing the firm’s cash

flow include the firm’s capital stock; the CEO’s ability to manage the firm, which depends on his

skill and firm-specific knowledge; and the young subordinate manager’s effort, which allows her

to learn and prepare for promotion. Hence, Acharya et al. (2011) model (see also Prendergast

(1993)) suggests that the rewards to learning may be prospective control rents from promotion in

the firm, which, in turn, make employees far more effective in exerting internal governance.

Based on the above argument, we can hypothesize that the relationship between internal

monitoring, as measured by difference between CEO’s age and Subordinate managers’ ages, and

liquidity should be visible for firms that emphasizes internal promotions.

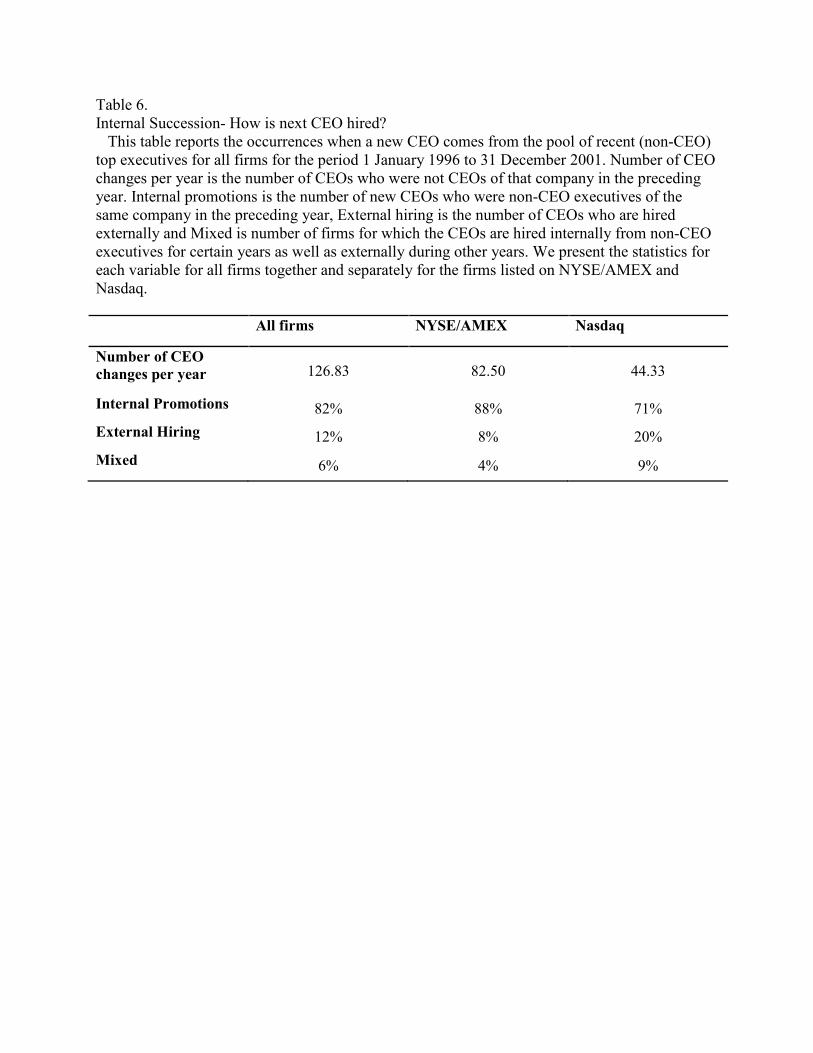

To test the above hypothesis, we analyze a subsample of the firms for which the

information about the internal promotions or external hiring could be extracted. To derive the

internal promotion information, we compare the names of new CEO with the already existing

pool of subordinated managers and if we find a match, that firm is considered to be emphasizing

internal promotions. We also compare the date when there is a change in CEO with the date the

new CEO joins the firm. If the two dates are identical, the firm is classified as the one hiring the

CEO externally.

Table 6 presents the descriptive statistics about the number of CEO changes for a given

firm and how the new CEO is hired. The statistics show that about 82% of the new CEOs are

appointed from the top non-CEO executives in the firm in the previous year. Larger

NYSE/AMEX firms emphasize more on internal promotions than the smaller Nasdaq firms. So,

if the level of internal promotions is the driving force behind the relative age difference and

liquidity relationship, then the relative age-liquidity relationship should be stronger for the

NYSE/AMEX firms but that is not observed in the results summarized in earlier sections.

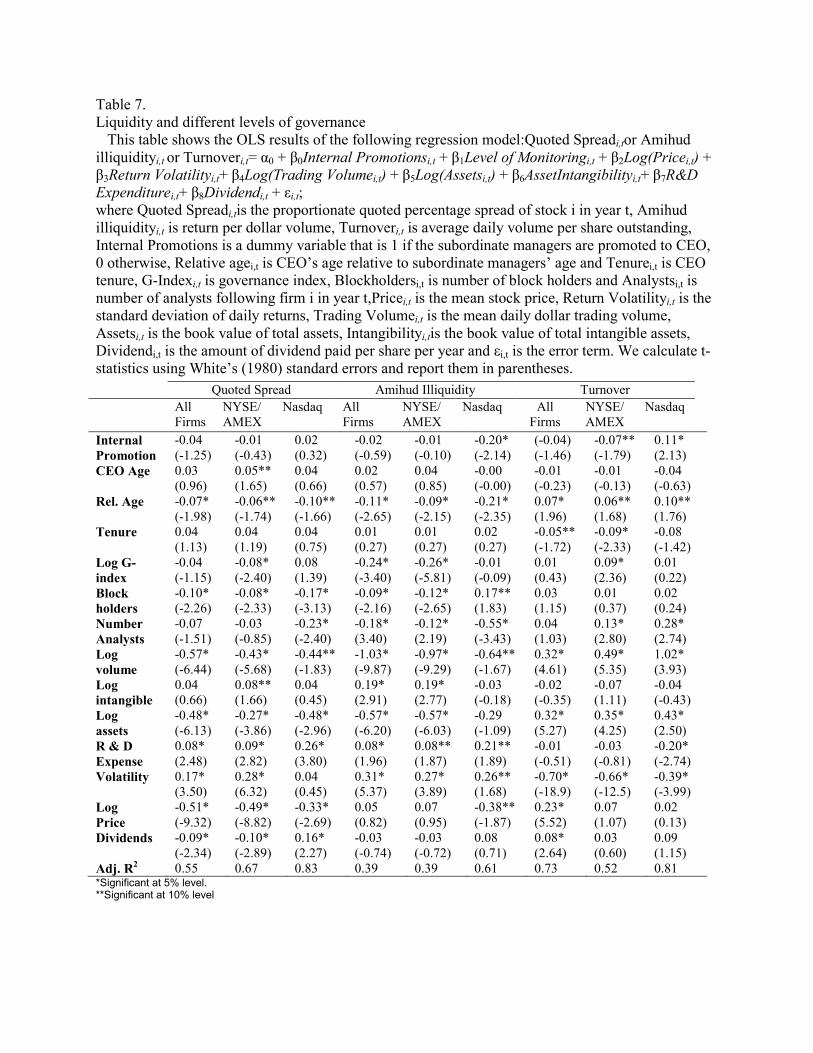

Liquidity and different levels of monitoring

For our final analysis, we run a pooled regression by including data on internal

promotions and all three layers of monitoring in one regression model. If the level of internal

promotions is the driving force behind the relative age difference and liquidity relationship, then

we should observe a significantly positive coefficient for the internal promotion variable. Results

from this analysis are summarized in table 7. First thing to note is that the relative age difference

between CEO and subordinate managers is significantly positively related to liquidity, even after

controlling for the other measure of corporate governance and level of internal promotions. This

result is robust across different model specifications and across firms listed on NYSE/AMEX or

Nasdaq.

Level of internal promotions is not significant predictor for most of the quoted spreads

and Amihud illiquidity regression models. Level of internal promotions is significantly positively

related to the liquidity for smaller Nasdaq firms. For NYSE/AMEX firms for turnover model we

get counter-intuitive results, we find that level of internal promotions is negatively related to

liquidity.

We also find a significantly positive relationship between liquidity and both, the

internal/external governance (G-index) and the external governance (number of block holders)

for NYSE/AMEX firms.

Based on these results we can conclude that better corporate governance is associated

with higher liquidity. The most robust result across all regression models is that internal

governance significantly positively impacts stock market liquidity beyond the traditional

governance measures. This relationship holds even after controlling for level of internal

promotions.

Robustness tests

We re-analyze the results by deleting the banking and utility firms and firms with stock

price less than $5, we find similar results as reported in the previous sections. However, results

for internal monitoring were weaker for the turnover model.

We reanalyze the model using the maximum likelihood estimation technique and the

results were qualitatively similar to the ones reported in the previous section using the regular

OLS estimation method

Conclusion

Companies with good corporate governance are likely to have liquid secondary markets

for their shares because good governance improves financial and operational transparency, which

ultimatelyreduces information asymmetries between the insiders and outside owners/liquidity

providers. Liquidity providers are therefore likely to post smaller spreads and larger depths for

stocks of these companies.Whether these effects on liquidity are discernable and economically

significant is an empirical question,and our study addresses this question. We also analyze if the

existence of internal monitoring, as defined by Acharya et al. (2011), serves as a self-disciplining

mechanism and improves the stock market liquidity.

Our empirical results show that companies with better corporate governance generally

have greater stock market liquidity as measured by narrower quoted spreads, lower Amihud

illiquidity, and higher turnover. Our results are robust to alternative estimation methods, across

different markets, and different measures of liquidity. Although the results of our study suggest

that good governance could enhance firm value through its effect on stock market liquidity,

whether companies choose to adopt additional governance standards remains a question. As

suggested by Aggarwal et al. (2008), governance standards may be selected bythe controlling

shareholder to maximize his private value of the firm. The controlling shareholder’s decision of

whether to adopt additional governance standards therefore involves weighing the benefits of

greater liquidity and lower cost of equity capital against the cost associated with, for example,

the diminished ability of the controlling shareholder to expropriate firm value. Hence, we look at

the different layers of monitoring to understand if the self-governing mechanism as proposed by

Acharya et al. (2011) impacts liquidity.

Our results document that, all things being equal, firms with larger age difference

between CEO and subordinate managers are more liquid than others. The relationship between

the level of internal monitoring and liquidity holds even after controlling for the level of

internal/external monitoring (governance index) and the level of external monitoring (number of

block holders and number of analysts following). In this perspective, a firm should hire younger

subordinate managers, which in turn, lowers the cost of external and internal/external monitoring

and improves the stock market liquidity.

Based on these results we can conclude that better corporate governance is associated

with higher liquidity. The most robust result across all regression models is that internal

governance significantly positively impacts stock market liquidity beyond the traditional

governance measures. Acharya et al. (2011) assert that the level of internal promotions is the

driving force behind the relative age difference and liquidity relationship. We do not find support

for this assertion rather for NYSE/AMEX firms we find contradicting evidence. Future research

can focus on explaining the channel through which internal governance affects liquidity.

Table 1. Descriptive statistics We present statistics for all firms for the period 1 January 1996 to 31 December 2001. Quoted Spread is the proportionate quoted spread, Amihud’s illiquidity is the ratio of absolute return to the daily volume, Turnover is the ratio of dollar volume to the shares outstanding, Age is the CEO’s present age, Relative age is the difference between CEO’s age and subordinate managers’ ages, Tenure is the CEO tenure, G-index is the governance index. Analysts is the mean number of analysts following a firm, Blockholders is the number of block holders in a firm, Price is the mean stock price, Return Volatility is the standard deviation of daily returns, Trading Volume is the mean daily dollar trading volume, Assets is the book value of total assets, Intangibility is the book value of total intangible assets, R&D Expenditure is the annual R&D expenditure and Dividend is the amount of dividend per share per year. We present the statistics for each variable for all firms together, and for firms listed on NYSE/AMEX and Nasdaq.

Full Sample (14,475) NYSE/AMEX (5,007) Nasdaq (9,468)

Variable Mean Standard Deviation

Mean Standard Deviation

Mean Standard Deviation

Liquidity Quoted Spread 0.043 0.059 0.039 0.066 0.046 0.054 Turnover 6.90 40.10 8.26 55.12 5.01 24.13 Amihud Illiquidity 8.00E-6 1.71E-4 3.22E-6 1.01E-4 1.14E-5 2.07E-4

Internal Monitoring CEO Age 54.64 8.33 55.75 7.97 52.22 8.59 Relative Age 8.71 9.69 6.89 9.60 9.54 9.61 Tenure 9.21 7.85 9.35 7.94 9.16 7.81

Internal/ External Monitoring G-index 8.93 2.76 9.32 2.72 7.91 2.58

External Monitoring Number of Analysts 4.25 4.93 4.90 5.50 3.67 4.27 Number of Blockholders 2.67 1.74 2.85 1.75 2.62 1.69

Control Variables Price 21.68 293.04 31.47 453.43 14.70 17.50 Return Volatility 0.045 0.038 0.029 0.024 0.057 0.041 Volume (in’000) 10,825 71,655 13,517 57,808 8,903 80,033 Assets (in millions) 5,124 31,863 11,520 49,028 711 3114 Intangible (in millions) 354 2,794 775 4,256 56 559 R & D 5.50 65.97 7.32 83.67 3.25 32.40 Dividend 0.34 2.36 0.61 3.42 0.13 0.71

Table 2. Liquidity and Internal governance This table shows the OLS results of the following regression model:Quoted Spreadi,tor Amihud illiquidityi,tor Turnoveri,t= β0 + β1Level of Monitoringi,t + β2Log(Pricei,t) + β3Return Volatilityi,t+ β4Log(Trading Volumei,t) + β5Log(Assetsi,t) + β6Asset Intangibilityi,t+ β7R&D Expenditurei,t+ β8Dividendi,t + εi,t; where Quoted Spreadi,t is the proportionate quoted percentage spread of stock i in year t, Amihud illiquidityi,t is return per dollar volume, Turnoveri,t is average daily volume per share outstanding, AGEi,t is CEO’s present age, Level of Monitoring is internal governance as measured by CEO’s age relative to subordinate managers’ age and CEO tenure, Pricei,t is the mean stock price, Return Volatilityi,t is the standard deviation of daily returns, Trading Volumei,t is the mean daily dollar trading volume, Assetsi,t is the book value of total assets, Intangibilityi,t is the book value of total intangible assets, Dividendi,t is the amount of dividend paid per share per year and εi,t is the error term. We calculate t-statistics using White’s (1980) standard errors and report them in parentheses.

Quoted Spread Amihud Illiquidity Turnover

All Firms

NYSE/ AMEX

Nasdaq All Firms

NYSE/ AMEX

Nasdaq All Firms

NYSE/ AMEX

Nasdaq

CEO Age 0.03 (1.55)

0.01 (0.62)

-0.01 (-0.50)

0.03* (2.31)

0.03** (1.69)

0.05 (1.22)

-0.03* (-2.87)

-0.02 (-1.50)

-0.04 (-1.50)

Rel. Age -0.04* (-2.49)

0.02 (1.56)

-0.05* (-2.01)

-0.02* (-1.96)

0.02 (0.76)

-0.06* (-1.98)

0.03* (2.80)

0.02 (1.05)

0.07* (2.86)

Tenure -0.01 (-0.13)

0.01 (0.90)

-0.02 (-0.83)

0.02 (1.43)

0.02 (0.88)

0.04 (1.13)

-0.01 (-1.39)

0.01 (0.87)

-0.04** (-1.87)

Log

volume

-0.58* (-4.47)

-0.43* (-3.40)

-0.87* (-8.08)

-0.37 (-11.5)

-0.35* (-9.66)

-0.62* (-8.00)

0.51* (16.91)

0.62* (15.12)

0.64* (10.25)

Log

intangible

-0.03 (-0.95)

-0.01 (-0.56)

-0.07* (-2.02)

-0.07* (-2.56)

-0.06* (-2.17)

-0.09** (-1.67)

0.05* (2.69)

0.10* (4.28)

0.01 (0.24)

Log

assets

-0.43* (-4.19)

-0.24* (-2.88)

-0.18* (-2.56)

-0.29* (-8.36)

-0.23* (-6.34)

-0.26* (-3.90)

0.34* (11.73)

0.32* (8.41)

0.21* (4.45)

R & D

Expense

0.03* (3.30)

0.03* (3.97)

0.11* (3.73)

0.12 (0.69)

0.01 (0.45)

0.07** (1.84)

-0.01 (-0.92)

-0.04* (4.77)

-0.01 (-0.35)

Volatility .

0.32* (2.69)

0.44* (3.28)

0.23* (5.73)

0.32* (13.7)

0.34* (13.76)

0.32* (6.89)

-0.52* (-17.3)

-0.51* (-13.3)

-0.36* (-9.16)

Log

Price

-0.24* (-4.29)

-0.23* (-3.09)

-0.10 (-1.56)

-0.09* (-3.51)

-0.15* (-4.87)

0.08 (1.37)

0.11* (5.01)

0.03 (0.92)

0.03 (0.81)

Dividends .

0.01 (0.47)

0.04 (1.30)

-0.04 (-1.12)

0.02 (0.85)

0.03 (1.53)

-0.08* (-1.97)

0.03* (3.97)

0.06* (4.98)

0.02 (1.05)

Adj. R2 0.43 0.53 0.62 0.45 0.40 0.46 0.61 0.45 0.61

*Significant at 5% level. **Significant at 10% level

Table 3. Liquidity and Internal/External governance This table shows the OLS results of the following regression model:Quoted Spreadi,tor Amihud illiquidityi,tor Turnoveri,t= β0 + β1Level of Monitoringi,t + β2Log(Pricei,t) + β3Return Volatilityi,t+ β4Log(Trading Volumei,t) + β5Log(Assetsi,t) + β6Asset Intangibilityi,t+ β7R&D Expenditurei,t+ β8Dividendi,t + εi,t; where Quoted Spreadi,tis the proportionate quoted percentage spread of stock i in year t, Amihud illiquidityi,t is return per dollar volume, Turnoveri,t is average daily volume per share outstanding, Level of Monitoring is internal/external governance as measured by G-Indexi,t,Pricei,t is the mean stock price, Return Volatilityi,t is the standard deviation of daily returns, Trading Volumei,t is the mean daily dollar trading volume, Assetsi,t is the book value of total assets, Intangibilityi,tis the book value of total intangible assets, Dividendi,t is the amount of dividend paid per share per year and εi,t is the error term. We calculate t-statistics using White’s (1980) standard errors and report them in parentheses.

Quoted Spread Amihud Illiquidity Turnover

All Firms

NYSE/ AMEX

Nasdaq All Firms

NYSE/ AMEX

Nasdaq All Firms

NYSE/ AMEX

Nasdaq

Log G-

index

-0.01

(-0.22)

-0.03**

(-1.67)

-0.06*

(-1.97)

-0.11*

(-4.65)

-0.13*

(-5.14)

-0.12*

(-2.21)

0.04*

(-2.01)

0.06*

(-3.08)

0.06*

(-1.96)

Log

volume

-0.44*

(-10.5)

-0.26*

(-7.10)

-0.99*

(-15.1)

-0.56*

(-12.2)

-0.65*

(-13.3)

-0.81*

(-7.04)

0.51*

(17.55)

0.49*

(9.18)

0.77*

(9.52)

Log

intangible

-0.02

(-0.68)

-0.04 (-

1.30)

-0.03

(-0.58)

-0.03 (-

0.75)

-0.05

(-1.35)

-0.08

(-0.98)

0.05*

(2.16)

0.10*

(2.97)

-0.01

(-0.21)

Log

assets

-0.34*

(-8.64)

-0.14*

(3.54)

-0.23*

(3.82)

-0.26*

(-5.22)

-0.30*

(-5.88)

-0.39*

(-3.76)

0.33*

(10.53)

0.26*

(4.81)

0.28*

(4.27)

R& D

Expense

0.05*

(2.63)

0.07*

(3.68)

0.09*

(3.31)

0.04**

(1.84)

0.05*

(2.13)

0.05

(0.91)

-0.01

(-0.23)

-0.01

(1.12)

0.03

(0.52)

Volatility

0.09*

(3.52)

0.22*

(9.69)

0.38*

(8.89)

0.26*

(8.38)

0.16*

(5.30)

0.29*

(5.54)

-0.55*

(-27.8)

-0.54*

(-10.6)

-0.41*

(-6.71)

Log

Price

-0.47*

(-17.27)

-0.53*

(-18.8)

-0.10*

(-2.10)

-0.07*

(2.03)

-0.01

(-0.14)

-0.18*

(-2.30)

0.05*

(2.44)

0.08**

(1.90)

0.07

(1.42)

Dividends

-0.04**

(-1.91)

-0.03**

(-1.72)

-0.01

(-0.29)

-0.01 (-

1.54)

-0.05*

(-2.01)

-0.14*

(-2.28)

0.02

(1.52)

0.06*

(3.16)

0.05*

(1.99)

Adj. R2 0.47 0.59 0.74 0.16 0.26 0.19 0.66 0.47 0.69 *Significant at 5% level. **Significant at 10% level

Table 4. Liquidity and External governance This table shows the OLS results of the following regression model:Quoted Spreadi,tor Amihud illiquidityi,tor Turnoveri,t= β0 + β1Level of Monitoringi,t + β2Log(Pricei,t) + β3Return Volatilityi,t+ β4Log(Trading Volumei,t) + β5Log(Assetsi,t) + β6Asset Intangibilityi,t+ β7R&D Expenditurei,t+ β8Dividendi,t + εi,t; where Quoted Spreadi,tis the proportionate quoted percentage spread of stock i in year t, Amihudilliquidityi,t is return per dollar volume, Turnoveri,t is average daily volume per share outstanding,Level of Monitoring is external governance as measured by number of block holders and number of analysts following firm i in year t, Pricei,t is the mean stock price, Return Volatilityi,t is the standard deviation of daily returns, Trading Volumei,t is the mean daily dollar trading volume, Assetsi,t is the book value of total assets, Intangibilityi,tis the book value of total intangible assets, Dividendi,t is the amount of dividend paid per share per year and εi,t is the error term. We calculate t-statistics using White’s (1980) standard errors and report them in parentheses.

Quoted Spread Amihud Illiquidity Turnover

All Firms

NYSE/ AMEX

Nasdaq All Firms

NYSE/ AMEX

Nasdaq All Firms

NYSE/ AMEX

Nasdaq

Block

holders

-0.03** (-1.77)

-0.02** (-1.71)

-0.07* (-2.77)

-0.04* (-2.35)

-0.02 (-0.85)

-0.09* (-2.40)

0.01 (1.13)

0.01 (0.72)

-0.03 (-1.26)

Number

Analysts

-0.02 (-1.43)

-0.03* (-2.16)

-0.02 (-0.56)

-0.04* (-2.10)

-0.07* (-3.27)

-0.10* (-2.06)

0.08* (3.64)

0.11* (4.81)

0.04 (0.73)

Log

volume

-0.41* (-13.6)

-0.19* (-6.25)

-0.98* (-15.3)

-0.54* (-14.9)

-0.66* (-17.6)

-0.95* (-10.1)

0.43* (15.19)

0.40* (10.9)

0.67* (9.63)

Log

intangible

-0.01 (-0.10)

-0.03 (-1.56)

-0.10* (-2.98)

-0.06* (-2.45)

-0.06* (-2.54)

-0.08** (-1.78)

0.07* (4.04)

0.12* (5.51)

-0.02 (-0.49)

Log

assets

-0.35* (-12.16)

-0.09* (-3.31)

-0.26* (-5.57)

-0.28* (8.13)

-0.29* (-8.49)

-0.52* (-7.55)

0.32* (12.42)

0.27* (7.67)

0.25* (4.93)

R & D

Expense

0.03* (2.20)

0.04* (2.83)

0.13* (5.11)

0.04* (2.33)

0.04* (2.20)

0.06 (1.49)

-0.03* (-3.68)

-0.04* (-5.46)

-0.09* (-4.02)

Volatility

0.07* (3.44)

0.23* (12.47)

0.26* (8.72)

0.27* (12.03)

0.15* (6.65)

0.34* (7.71)

-0.58* (-21.5)

-0.55* (-19.9)

-0.44* (-13.8)

Log

Price

-0.46* (-21.1)

-0.53* (-23.5)

-0.02 (-0.60)

0.02 (0.96)

-0.01 (-0.47)

-0.12* (-2.07)

0.13 (6.84)

0.15* (5.63)

0.03 (0.74)

Dividends

-0.01 (-0.56)

-0.05* (2.92)

0.01 (0.11)

0.02 (1.09)

0.01 (0.50)

0.10 (2.61)

-0.01 (-0.65)

-0.02 (-1.38)

0.01 (0.62)

Adj. R2 0.41 0.52 0.66 0.17 0.25 0.27 0.64 0.47 0.66

*Significant at 5% level. **Significant at 10% level

Table 5. Liquidity and different levels of governance This table shows the OLS results of the following regression model:Quoted Spreadi,tor Amihud illiquidityi,t or Turnoveri,t= β0 + β1Level of Monitoringi,t + β2Log(Pricei,t) + β3Return Volatilityi,t+ β4Log(Trading Volumei,t) + β5Log(Assetsi,t) + β6Asset Intangibilityi,t+ β7R&D Expenditurei,t+ β8Dividendi,t + εi,t; where Quoted Spreadi,tis the proportionate quoted percentage spread of stock i in year t, Amihud illiquidityi,t is return per dollar volume, Turnoveri,t is average daily volume per share outstanding, Relative agei,t is CEO’s age relative to subordinate managers’ age and Tenurei,t is CEO tenure, G-Indexi,t is governance index, Blockholdersi,t is number of block holders and Analystsi,t is number of analysts following firm i in year t, Pricei,t is the mean stock price, Return Volatilityi,t is the standard deviation of daily returns, Trading Volumei,t is the mean daily dollar trading volume, Assetsi,t is the book value of total assets, Intangibilityi,t is the book value of total intangible assets, Dividendi,t is the amount of dividend paid per share per year and εi,t is the error term. We calculate t-statistics using White’s (1980) standard errors and report them in parentheses. Quoted Spread Amihud Illiquidity Turnover

All Firms

NYSE/ AMEX

Nasdaq All Firms

NYSE/ AMEX

Nasdaq All Firms

NYSE/ AMEX

Nasdaq

CEO Age 0.01 (0.20)

0.04 (1.04)

0.06** (1.67)

0.01 (0.38)

-0.04 (-1.14)

0.10* (1.96)

-0.02 (-1.01)

-0.01 (-0.19)

-0.03 (-0.67)

Rel. Age -0.08* (-2.86)

-0.07* (-2.62)

-0.07* (-1.98)

-0.10* (-3.21)

-0.07** (-1.91)

-0.18* (-3.53)

0.05* (1.98)

0.01 (0.19)

0.30* (2.28)

Tenure 0.00 (0.03)

0.01 (0.37)

0.05 (1.55)

0.00 (0.14)

0.01 (0.16)

0.03 (0.53)

-0.02 (-1.11)

-0.03 (-1.01)

-0.00 (-0.13)

Log G-

index

-0.04** (-1.75)

-0.08* (-2.94)

0.04 (1.11)

-0.15* (-4.87)

-0.17* (-4.83)

-0.05 (-0.95)

0.02 (0.73)

0.12* (4.31)

-0.01 (-0.19)

Block

holders

-0.02 (-0.67)

-0.07* (-2.83)

-0.05 (-1.38)

-0.07* (-2.32)

-0.09* (-2.42)

0.02 (0.44)

-0.03 (-1.45)

0.01 (0.44)

-0.03 (-0.89)

Number

Analysts

-0.07* (2.32)

-0.02 (-0.70)

-0.11 (1.62)

-0.07** (-1.75)

0.06 (1.41)

-0.26* (-3.03)

0.04 (1.43)

0.09** (1.87)

-0.08 (-0.94)

Log

volume

-0.48* (-5.66)

-0.23* (-2.90)

-0.41* (-3.18)

-0.85* (-11.5)

-0.82* (-9.63)

-0.55* (-2.98)

0.39* (7.19)

0.38* (4.97)

0.78* (4.75)

Log

intangible

0.02 (0.58)

-0.02 (-0.69)

0.06 (1.09)

-0.10* (2.17)

-0.08 (-1.57)

-0.02 (-0.30)

-0.05 (-1.19)

0.10* (2.02)

-0.07 (-0.99)

Log

assets

-0.35* (-5.03)

-0.08 (1.19)

-0.22* (1.96)

-0.40* (-2.07)

-0.39* (-4.99)

-0.01 (-0.11)

0.31* (6.18)

0.28* (3.25)

0.29 (2.28)

R & D

Expense

0.07* (2.68)

0.08* (3.55)

0.11* (2.99)

0.06* (2.09)

0.07 (2.06)

0.08 (1.37)

-0.01 (-0.21)

-0.01 (-0.67)

-0.18* (-3.40)

Volatility

0.11* (2.87)

0.24* (5.77)

0.40* (6.88)

0.47* (11.2)

0.20* (4.05)

0.68* (9.96)

-0.64* (-15.2)

-0.60* (-9.67)

-0.46* (-10.6)

Log

Price

-0.49* (-7.74)

-0.54* (-9.30)

-0.46* (-6.38)

0.04 (0.76)

0.02 (0.31)

-0.29* (-2.99)

0.09* (2.24)

0.06 (1.02)

-0.07 (-0.84)

Dividends

-0.05* (-2.10)

0.01 (0.16)

-0.22* (5.65)

-0.05 (1.23)

-0.00 (-0.06)

-0.15* (-2.48)

0.02 (0.91)

0.02 (0.61)

0.00 (0.05)

Adj. R2 0.49 0.60 0.84 0.39 0.31 0.73 0.72 0.48 0.75

*Significant at 5% level. **Significant at 10% level

Table 6. Internal Succession- How is next CEO hired? This table reports the occurrences when a new CEO comes from the pool of recent (non-CEO) top executives for all firms for the period 1 January 1996 to 31 December 2001. Number of CEO changes per year is the number of CEOs who were not CEOs of that company in the preceding year. Internal promotions is the number of new CEOs who were non-CEO executives of the same company in the preceding year, External hiring is the number of CEOs who are hired externally and Mixed is number of firms for which the CEOs are hired internally from non-CEO executives for certain years as well as externally during other years. We present the statistics for each variable for all firms together and separately for the firms listed on NYSE/AMEX and Nasdaq.

All firms NYSE/AMEX Nasdaq

Number of CEO

changes per year 126.83 82.50 44.33

Internal Promotions 82% 88% 71%

External Hiring 12% 8% 20%

Mixed 6% 4% 9%

Table 7. Liquidity and different levels of governance This table shows the OLS results of the following regression model:Quoted Spreadi,tor Amihud illiquidityi,t or Turnoveri,t= α0 + β0Internal Promotionsi,t + β1Level of Monitoringi,t + β2Log(Pricei,t) + β3Return Volatilityi,t+ β4Log(Trading Volumei,t) + β5Log(Assetsi,t) + β6AssetIntangibilityi,t+ β7R&D

Expenditurei,t+ β8Dividendi,t + εi,t; where Quoted Spreadi,tis the proportionate quoted percentage spread of stock i in year t, Amihud illiquidityi,t is return per dollar volume, Turnoveri,t is average daily volume per share outstanding, Internal Promotions is a dummy variable that is 1 if the subordinate managers are promoted to CEO, 0 otherwise, Relative agei,t is CEO’s age relative to subordinate managers’ age and Tenurei,t is CEO tenure, G-Indexi,t is governance index, Blockholdersi,t is number of block holders and Analystsi,t is number of analysts following firm i in year t,Pricei,t is the mean stock price, Return Volatilityi,t is the standard deviation of daily returns, Trading Volumei,t is the mean daily dollar trading volume, Assetsi,t is the book value of total assets, Intangibilityi,tis the book value of total intangible assets, Dividendi,t is the amount of dividend paid per share per year and εi,t is the error term. We calculate t-statistics using White’s (1980) standard errors and report them in parentheses.

*Significant at 5% level. **Significant at 10% level

Quoted Spread Amihud Illiquidity Turnover

All Firms

NYSE/ AMEX

Nasdaq All Firms

NYSE/ AMEX

Nasdaq All Firms

NYSE/ AMEX

Nasdaq

Internal

Promotion

-0.04 (-1.25)

-0.01 (-0.43)

0.02 (0.32)

-0.02 (-0.59)

-0.01 (-0.10)

-0.20* (-2.14)

(-0.04) (-1.46)

-0.07** (-1.79)

0.11* (2.13)

CEO Age 0.03 (0.96)

0.05** (1.65)

0.04 (0.66)

0.02 (0.57)

0.04 (0.85)

-0.00 (-0.00)

-0.01 (-0.23)

-0.01 (-0.13)

-0.04 (-0.63)

Rel. Age -0.07* (-1.98)

-0.06** (-1.74)

-0.10** (-1.66)

-0.11* (-2.65)

-0.09* (-2.15)

-0.21* (-2.35)

0.07* (1.96)

0.06** (1.68)

0.10** (1.76)

Tenure 0.04 (1.13)

0.04 (1.19)

0.04 (0.75)

0.01 (0.27)

0.01 (0.27)

0.02 (0.27)

-0.05** (-1.72)

-0.09* (-2.33)

-0.08 (-1.42)

Log G-

index

-0.04 (-1.15)

-0.08* (-2.40)

0.08 (1.39)

-0.24* (-3.40)

-0.26* (-5.81)

-0.01 (-0.09)

0.01 (0.43)

0.09* (2.36)

0.01 (0.22)

Block

holders

-0.10* (-2.26)

-0.08* (-2.33)

-0.17* (-3.13)

-0.09* (-2.16)

-0.12* (-2.65)

0.17** (1.83)

0.03 (1.15)

0.01 (0.37)

0.02 (0.24)

Number

Analysts

-0.07 (-1.51)

-0.03 (-0.85)

-0.23* (-2.40)

-0.18* (3.40)

-0.12* (2.19)

-0.55* (-3.43)

0.04 (1.03)

0.13* (2.80)

0.28* (2.74)

Log

volume

-0.57* (-6.44)

-0.43* (-5.68)

-0.44** (-1.83)

-1.03* (-9.87)

-0.97* (-9.29)

-0.64** (-1.67)

0.32* (4.61)

0.49* (5.35)

1.02* (3.93)

Log

intangible

0.04 (0.66)

0.08** (1.66)

0.04 (0.45)

0.19* (2.91)

0.19* (2.77)

-0.03 (-0.18)

-0.02 (-0.35)

-0.07 (1.11)

-0.04 (-0.43)

Log

assets

-0.48* (-6.13)

-0.27* (-3.86)

-0.48* (-2.96)

-0.57* (-6.20)

-0.57* (-6.03)

-0.29 (-1.09)

0.32* (5.27)

0.35* (4.25)

0.43* (2.50)

R & D

Expense

0.08* (2.48)

0.09* (2.82)

0.26* (3.80)

0.08* (1.96)

0.08** (1.87)

0.21** (1.89)

-0.01 (-0.51)

-0.03 (-0.81)

-0.20* (-2.74)

Volatility

0.17* (3.50)

0.28* (6.32)

0.04 (0.45)

0.31* (5.37)

0.27* (3.89)

0.26** (1.68)

-0.70* (-18.9)

-0.66* (-12.5)

-0.39* (-3.99)

Log

Price

-0.51* (-9.32)

-0.49* (-8.82)

-0.33* (-2.69)

0.05 (0.82)

0.07 (0.95)

-0.38** (-1.87)

0.23* (5.52)

0.07 (1.07)

0.02 (0.13)

Dividends

-0.09* (-2.34)

-0.10* (-2.89)

0.16* (2.27)

-0.03 (-0.74)

-0.03 (-0.72)

0.08 (0.71)

0.08* (2.64)

0.03 (0.60)

0.09 (1.15)

Adj. R2 0.55 0.67 0.83 0.39 0.39 0.61 0.73 0.52 0.81

References

Acharya, V., S. Myers, and R. Rajan, 2011, “The Internal Governance of Firms,” Journal of

Finance, Forthcoming.

Admati, A., Pfleiderer, P., 2009. The ‗‗wall street walk‘‘ and shareholder activism: exit as a

form of voice. Review of Financial Studies 22, 2645–2685.

Amihud, Y., 2002. Illiquidity and stock returns: cross section and time-series effects. Journal of

Financial Markets 5, 31–56.

Bebchuk, L. A., Cohen, A., 2005. The costs of entrenched boards. Journal of Financial

Economics 78,v409-433.

Bebchuk, L. A., A. Cohen, and A. Ferrell. 2005. “What Matters in Corporate Governance?”

Working Paper, Harvard Law School.

Bhide, A., 1993, The Hidden Cost of Stock Market Liquidity, Journal of Financial Economics

34, 31-51.

Chung, K.H, J. Elder, and J.C Kim. 2010. “Corporate governance and liquidity.” Journal of

Financial and Quantitative Analysis, forthcoming.

Clarke, J., Subramanian, A., 2006. Dynamic forecasting behavior by analysts: theory and

evidence. Journal of Financial Economics 80, 81-113.

Coffee, J., 1991, "Liquidity versus Control: The Institutional Investor as Corporate Monitor,"

Columbia Law Review, 91, 1277-1368

Core, J. E., R. W. Holthausen, and D. F. Larcker, 1999, Corporate governance, CEO

compensation, and firm performance, Journal of Financial Economics 51, 371-406.

Cyert, R., S. H. Kang, and P. Kumar, 2002, Corporate governance, takeovers, and top-

management compensation: Theory and evidence, Management Science 48, 453-469.

Diamond, D.W., 1985. Optimal Release of Information By Firms. Journal of Finance 40, 1071-

1094.

Kenyazera. D. 2007. “Corporate Governance, Analyst Following, and Firm Behavior”. Working

paper-New York University

Dumitrescu A. 2010. “Corporate Governance and Market Liquidity”.Working Paper SSRN

working papers.

Edmans, A., Manso, G., 2009. Governance through exit and voice: a theory of multiple

blockholders. Unpublished working paper, University of Pennsylvania—the Wharton

School and MIT Sloan School of Management.

Edmans, A., 2009. Blockholder trading, market efficiency, and managerial myopia. Journal of

Finance, forthcoming.

Faure-Grimaud, A. and Gromb, D., 2004. Public trading and private incentives, Review of

Financial Studies, 17, 985-1014.

Glosten, L., Milgrom, P.R., 1985. Bid, ask, and transaction prices in a specialist market with

heterogeneously informed agents. Journal of Financial Economics 14, 71-100.

Gompers, P., Ishii, J., Metrick, A., 2003. Corporate governance and equity prices. Quarterly

Journal of Economics 118, 107-155.

Harford, J., and K. Lie, 2007, Decoupling CEO wealth and firm performance: The case of

acquiring CEOs, Journal of Finance 62, 917-949.

Hirschman, Albert, 1970, Exit, Voice, and Loyalty: Response to Declines in Firms,

Organizations, and States, Harvard University Press, Cambridge.

Holmstro¨ m, B., Tirole, J., 1993.Market liquidity and performance monitoring. Journal of

Political Economy 101, 678–709.

Khanna, N., Sonti, R., 2004. Value creating stock manipulation: feedback effect of stock prices

on firm value. Journal of Financial Markets 7, 237–270.

Kyle, A. S., 1985, "Continuous Auctions and Insider Trading," Econometrica, 53, 1315-1335.

Kyle, A. S., and Vila J. L., 1991, "Noise Trading and Takeovers," Rand Journal of Economics,

22, 54-71.

Lang, M., Lins, K., Miller, D., 2004. Concentrated control, analyst following and valuation: Do

analysts matter most when investors are protected least? Journal of Accounting

Research42, 589-623

La Porta, R., Lopez-de-Silanes, F., Shleifer, A. and R. Vishny, 2000, Investor Protection and

Corporate Governance, Journal of Financial Economics 58, 3-27.

Landier, A., Sraer D., and Thesmar, D, 2006, Bottom-up corporate governance, Working paper,

New York University.

Lin, X., Zhang, Y., Zhu, N. 2009."Does Bank Ownership Increase Firm Value?Evidence from

China." Journal of International Money and Finance, 28, 720–737.

Lipson, M. L., and Mortal, S., 2009. Liquidity and Capital Structure, Journal of Financial

Markets 12, 611-644.

Maug, E., 1998, Large Shareholders as Monitors: Is There a Trade-Off between Liquidity and

Control?, Journal of Finance 53 (1), 65-98.

McInish, T., and R. Wood. 1992. An Analysis of Intraday Patterns in Bid/Ask Spreads for NYSE

Stocks. Journal of Finance, 47, 753-64.

Morck, R., Shleifer, A., Vishny, R., 1988. Management ownership and market valuation: an

empirical analysis. Journal of Financial Economics 20, 293–315.

Morck, Randall, F. Yang. 2001. "The Mysterious Growing Value of S&P Index Membership."

NBER Working Paper No. 8654.

Noe, T. H., 2002, "Investor Activism and Financial Market Structure," Review of Financial

Studies, 15, 289-318.

Novaes, Walter, and Luigi Zingales, 1999, Capital structure choice under a takeover threat,

University of Chicago working paper.

Shleifer, A., and Vishny, R., 1986, Large shareholders and corporate control. Journal of Political

Economy 94, 461-488.

Shleifer, A. and Vishny, R., 1997. A Survey of Corporate Governance, Journal of Finance 52 (2),

737-82.

Shleifer, A. and Vishny, R., 2003. "Stock Market Driven Acquisitions," Journal of Financial

Economics, 70, December 2003, pp. 295-311.

Stoll, H. 2000. “Friction.” Journal of Finance, 55, 1479-1514.

Subrahmanyam, A., and S. Titman, 2001 Feedback from stock prices to cash flows, Journal of

Finance 56, 2389—2413.

Titman, Sheridan, 1984, The Effect of Capital Structure on a Firm's Liquidation Decision,

Journal of Financial Economics 13, 137-151.

Van Ness, B., R. Van Ness, and R. Warr (2001). “How Well Do Adverse Selection Components

Measure Adverse Selection?” Financial Management, 30, 77-98.

White, H. 1980. “A Heteroskedasticity-Consistent Covariance Estimator and a Direct Test for

Heteroskedasticity.”Econometrica, 48, 817-838.