Copyright 2015-16 - CalCPA

113

Individual Tax Planning Topics Karen Brosi, EA, CFP

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Copyright 2015-16 - CalCPA

Copyri

ght 2

015-1

6

Individual Tax Planning Topics Karen Brosi, EA, CFP

Copyri

ght 2

015-1

6

Notice to Readers

CalCPA Education Foundation programs and publications are designed to provide CPAs and financial professionals current, accurate information concerning the subject matter covered. However, the CalCPA Education Foundation gives no assurance that such information is comprehensive in its coverage of a subject matter or that it is suitable in dealing with specific client problems or business-related circumstances. Accordingly, information published or provided by the CalCPA Education Foundation should not be relied upon as a substitute for independent research to original sources of authority. The CalCPA Education Foundation does not render any accounting, legal or other professional advice, nor does it have any responsibility for updating or revising any programs or publications which it may present, distribute or sponsor. CPE Credit Policies Course, Conference, Onsite—The California Board of Accountancy (CBA) grants one CPE credit hour for each 50 minutes of class time. To qualify for CPE, a program must be at least 50 minutes in length. The CBA tracks CPE in 25-minute segments after the first 50 minutes. For each additional 25-minute segment completed, 0.5 CPE credit hours will be granted. To accurately track participation, registrants are required to legibly sign your name on the official sign-in sheet prior to the start of the event. If you arrive late, you must note your arrival time on the sign-in sheet. If you need to leave early, you must initial and note your departure time on the sign-in sheet to receive partial credit. The CBA requires CPE providers to closely monitor attendance during CPE. If you are not in the room during a portion of the CPE event, you will not receive credit. Your official record of attendance for the event is available via the My Events section of the website within one week. The host provider must retain the record of attendance, written educational goals and specific learning objectives, as well as a syllabus, which provides a general outline instructional objective and a summary of topics for the course for a period of five years. A copy of the educational goals, learning objectives, and course syllabus shall be made available to the CBA upon request. Webcast—For webcast participants to receive credit, three times every hour, you will be required to respond to an attendance question that appears on the screen. If viewing the webcast as part of a group, the group leader is required to answer the attendance questions on behalf of all participants. Group attendance is verified and documented by the group attendance form the day of the event. The CalCPA Education Foundation archives attendance records as required by the CBA to verify your CPE attendance in the event your CPE records are audited. Webcast are broadcast via the internet to those individuals who have registered for the webcast. The CalCPA Education Foundation takes all reasonable efforts to maintain the camera on the speaker, but does on occasion pan across the audience while following a speaker around the room. Furthermore, as the broadcast requires the use of microphones and other devices to amplify the speaker to both the live and webcast audience, an attendee’s voice may be broadcast during the webcast and, no attendee should have an expectation of privacy as to potentially being identifiable in the webcast. Self-Study—An online exam is included with your purchase. After studying the materials, to take the exam please go to www.calcpa.org/MySelfStudy. You may be asked to log in. Once you have logged in, find this product and click “Take Exam.” You will have a total of (3) attempts to take the final exam. Once you have completed the online final exam, you will be notified if you have passed or failed. To pass, you need a minimum passing grade of 70% (except for California regulatory review courses where the minimum passing grade is 90% as specified in Reg. Sec. 87.9(3)). You will be able to download your certificate of completion documenting the number of CPE credits earned for the course through your CPE Tracker at www.calcpa.org/CPE_Tracker. Please monitor the time it takes to complete the course. Record your total time and your comments about the course on the evaluation e-mailed to you. In accordance with the Standards of the National Association of State Boards of Accountancy (NASBA), one credit hour is granted for each 50 minutes of interactive self-study completed. Recommended credit hours are included in each course description. However, state boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Self-study courses must be completed by one year from date of purchase. If you have any problems or questions using your online course, please e-mail [email protected]. If you move before completing this course, please contact Member Services at (800) 922-5272 with your new address. Materials Terms and Conditions—CalCPA Education Foundation program materials, both hardcopy and electronic, are protected by U.S. copyright law. Materials are provided only for use by the participant registered for the program. You agree that you will not sell, distribute, transmit, or otherwise transfer all or any portions of the content of program materials without written permission from the author(s). Please contact the CalCPA Education Foundation course materials coordinator at [email protected] or (650) 522-3208 to obtain permission. eBook FAQs—Visit www.calcpa.org/ebooks to view frequently asked questions. Be sure to save your annotations made throughout the course. The CalCPA Education Foundation Guarantee—If any continuing education product fails to meet your expectations, or if you are not satisfied for any reason, you may return it within 30 days for an exchange or refund. (Shipping and handling fees are nonrefundable). Call Member Services at (800) 922-5272 for return instructions.

Copyright © 2015 Karen Brosi, EA, CFP

No copyright claimed in U.S. Government materials.

ITXP _________________________________________________________________________________________________________www.calcpa.org (800) 922-5272 rev 03/2015

Copyri

ght 2

015-1

6

CalCPA Education Foundation www.calcpa.org (800) 922-5272

This page intentionally left blank.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning i

Individual Tax Planning Topics

WHAT IS TAX PLANNING? ......................................................................................... 1

WHERE TO LOOK FOR PLANNING OPPORTUNITIES ........................................................... 1 Change in Marital Status ............................................................................................ 1 Change in Family Structure ........................................................................................ 1 Change in Earned Income .......................................................................................... 1 Change in Assets ......................................................................................................... 1 Change in Health ........................................................................................................ 1

THE STRUCTURE OF THE TAX PLANNING ENGAGEMENT .................................................. 2 A Word About Software .............................................................................................. 3 Gathering the Data ..................................................................................................... 4 Projecting for the Year................................................................................................ 4

FILING STATUS .............................................................................................................. 5

COMMON LAW MARRIAGE STATUS ................................................................................. 5 Common Law Marriage Jurisdictions ........................................................................ 6

SAME-SEX MARRIAGES ................................................................................................... 7 Same-Sex Marriage States in the US .......................................................................... 7

THE DEFENSE OF MARRIAGE ACT (DOMA) .................................................................... 7 SUPREME COURT HEARS ARGUMENTS ON THE CONSTITUTIONALITY OF DOMA ............ 8

The 2015 Supreme Court Cases .................................................................................. 9 Community/Separate Property.................................................................................... 9 IRS Reverses Decision Regarding Community Property .......................................... 10 Confusion Reigns ...................................................................................................... 11

DEPENDENTS.................................................................................................................. 11

GROSS INCOME ........................................................................................................... 12

WAGES .......................................................................................................................... 12 Employee or Independent Contractor? ..................................................................... 12 Maximizing Deferrals ............................................................................................... 14

INTEREST AND DIVIDENDS ............................................................................................. 14 Tax-Exempt Interest .................................................................................................. 14 Obligations That Are Not Bonds ............................................................................... 15 Registration Requirement ......................................................................................... 15 Indian Tribal Government ........................................................................................ 15 Tax-Exempt Bonds Purchased at Original Issue Discount ....................................... 15 Tax-Exempt Bonds Purchased at Market Discount .................................................. 15 Planning with Tax-Exempts ...................................................................................... 15

DIVIDENDS ..................................................................................................................... 16 Dividends & JGTRRA 2003 ...................................................................................... 16 Mutual Funds ............................................................................................................ 16 Tax-Efficient Funds ................................................................................................... 17

CAPITAL GAINS.............................................................................................................. 18 Harvesting Losses ..................................................................................................... 18 The 2015 Planning Opportunity – Harvesting Gains ............................................... 19

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning ii

Playing the Spread .................................................................................................... 19 Planning for Gains in 2015 and Beyond................................................................... 20 Installment Sales ....................................................................................................... 21 3.8% Medicare Tax Imposed on Net Investment Income - Starting 2013 ................ 22 What Investment Expenses Are Deductible in Computing Net Investment Income (NII)? (§1.1411-4) ..................................................................................................... 24 Can Rental Real Estate Income Be Derived in the Ordinary Course of a Trade or Business?................................................................................................................... 26 A Real Estate Professional’s Rental Income May Not Be NII .................................. 27 Planning for MAGI May Involve the Installment Sales Provision in the Future ...... 28

SOLE PROPRIETORS ........................................................................................................ 30 Bonus Depreciation Expired in 2014 ........................................................................ 30 Bonus Depreciation Chart ........................................................................................ 31 Maximum Amount and Phase-out Threshold under §179 ........................................ 31 §179 Chart ................................................................................................................ 31 Taxable Income Limitation ....................................................................................... 32 Comparing §179 and Bonus Depreciation ............................................................... 32 Section 179 is Recaptured as Ordinary Income at Sale ........................................... 32 §179 Cannot Create or Increase a Loss ................................................................... 33 Business Related Health Benefits .............................................................................. 34 IRS Changes Its Mind on Medicare Premiums as Self-Employed Health Insurance 35 Office-in-home Rules ................................................................................................ 38 Home Office Definition of “Principal Place of Business” ....................................... 38 Simplified Option for Claiming Home Office Deduction Starting with 2013 Returns................................................................................................................................... 39

PASSIVE ACTIVITIES ...................................................................................................... 41 Releasing Passive Losses .......................................................................................... 41 Self-Charged Interest ................................................................................................ 43

SOCIAL SECURITY .......................................................................................................... 44 When Should I Retire? .............................................................................................. 44 Full Retirement Age .................................................................................................. 44 Early Retirement ....................................................................................................... 45 Late Retirement ......................................................................................................... 46 How Work Affects Benefits........................................................................................ 47 What Are The Year 2015 Earnings Limits? .............................................................. 47 Work Can Increase Benefits Too .............................................................................. 48 Social Security Changes Rule Revising Withdrawal Policy ..................................... 49 Taxing Social Security Benefits ................................................................................ 49 Medicare Part B Premiums ...................................................................................... 53 Married couples ........................................................................................................ 54 Planning around Medicare Part B Premiums .......................................................... 54

ADJUSTMENTS TO INCOME ............................................................................................. 55 Qualified State Tuition Programs §529 .................................................................... 55 Coverdell Educational Savings Accounts §530 ........................................................ 57

DEDUCTION PLANNING ............................................................................................ 58

BUNCHING STRATEGIES ................................................................................................. 58

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning iii

TAX PAYMENTS ............................................................................................................. 58 MORTGAGE INTEREST .................................................................................................... 59

Secured Debt ............................................................................................................. 59 Collateral Must Be Correct ...................................................................................... 60 Choice to Treat the Debt as Not Secured by Home .................................................. 60 The “10-T” Election ................................................................................................. 61 Collateral Chart ........................................................................................................ 63 Is Acquisition Debt Allocated Per Person or Per Property? .................................... 63

CHARITABLE CONTRIBUTION PLANNING ....................................................................... 65 Donor Advised Funds ............................................................................................... 66 Charitable Remainder Trusts .................................................................................... 67 Charitably Minded IRA Owners Waiting for Extender for 2015 .............................. 68

GAMBLING LOSSES ........................................................................................................ 70 Recordkeeping Regarding Wagering Winnings and Losses (Rev. Proc. 77-29) ...... 70 Requirements to Become a Professional Gambler ................................................... 71 Professional Horse Racing Gambler Permitted to Deduct Business Expenses That Create a Loss ............................................................................................................ 71

SPECIAL INCOME AND DEDUCTION TOPICS .................................................... 74

PARENTS NEED CHILDREN’S HELP ................................................................................ 74 TAX-DEFERRED EXCHANGES ......................................................................................... 74

Basic Exchange Rules ............................................................................................... 75 Gain Recognized ....................................................................................................... 75 When is an exchange not advisable? ........................................................................ 76 The Basic Exchange .................................................................................................. 76 A More Complicated Exchange ................................................................................ 77

ALTERNATIVE MINIMUM TAX ....................................................................................... 81 The Basic Calculation ............................................................................................... 81 Which Do You Pay? .................................................................................................. 81 So Now the AMT is Fixed, Isn’t It? ........................................................................... 81 What Did it Cost to Index the AMT? ......................................................................... 82 Percentage of Taxpayers on AMT by State 2012 ...................................................... 82 Repeal? Not Without Complete Tax Reform ............................................................ 83

THE TOP 10 AMT KICKERS ........................................................................................... 83 Prepay State Income Taxes and Reduce the AMT .................................................... 86 Capital Gains and Dividends .................................................................................... 87 2014 Top of 15% Marginal Rate Bracket ................................................................. 87

KIDDIE TAX ................................................................................................................... 88 EDUCATION CREDITS ..................................................................................................... 89

American Opportunity Tax Credit And Lifetime Learning Credits §25a ................. 89

TAX RATES .................................................................................................................... 92

ELECTIONS ................................................................................................................... 92

DEDUCTIBLE IRAS ......................................................................................................... 92 NONDEDUCTIBLE IRAS HAVE NEW LIFE AFTER TIPRA ’05 ......................................... 93

Individuals of Any Income May Convert Traditional IRAs to Roth IRAs in 2010 .... 93

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning iv

CAPITALIZE CARRYING CHARGES .................................................................................. 95 INVESTMENT INTEREST .................................................................................................. 96

TAX PLANNING CHECKLIST ................................................................................... 97

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

Together with the related lecture this handout is designed to provide accurate and authoritative information about complex areas of tax law. But, the information contained in this manual may change as a result of new tax legislation, Treasury Department regulations, Internal Revenue Service or Franchise Tax Board interpretations, or judicial and state agency interpretations of existing tax law. This manual is not intended to provide legal, accounting, or other professional services and is provided with the understanding that the publisher is not engaged in rendering legal, accounting, or other professional services. This manual and related lecture should not be used as a substitute for professional advice. If legal advice or other expert assistance is required, the services of a competent tax advisor should be sought. From a Declaration of Principles jointly adopted by a Committee of the American Bar Association and a committee of Publishers and Associations.

©2015 Karen Brosi, EA, CFP®

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

This Page Intentionally Left Blank

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 1

What is Tax Planning? Tax planning could and should be a year-round process. At its most basic, tax planning involves examining alternatives related to personal and business transactions and determining the tax impact of those choices. Because decisions made in one year can impact taxes in future years, careful tax planning should always encompass multiple years.

Where to Look for Planning Opportunities Throughout the year, our clients experience changes in their personal, business and financial lives. Staying in touch, and knowing what to look for, can provide us with opportunities to help reduce taxes.

Change in Marital Status

Marriage Divorce Unmarried Life Partners Death of Spouse

Change in Family Structure

Birth of child Adoption Loss of dependency exemption Birth of a grandchild

Change in Earned Income

New employment/return to work Loss of job Change from employee to

independent contractor (and vice versa)

Bonus/stock options Deferred compensation

Qualified plan contributions Control timing of income collection

and expenses Retirement

Change in Assets

Acquisition of personal residence Sale of personal residence Extraordinary capital losses Extraordinary capital gains Sale of business activity Sale of passive activity Inheritance Gifts made

Change in Health

Disability Long-term care Funding extraordinary medical

expenses

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 2

The Structure of the Tax Planning Engagement Tax planning is an estimate of the tax impact of certain transactions on the individual’s tax situation. It is important that your clients recognize the approximate nature of the planning process and that they understand that, no matter how complex, projections are meant to be estimates demonstrating the relative tax consequences of planning assumptions. Nevertheless, it is equally important that we, as tax professionals, provide sound planning techniques with strict attention to the intricacies of the tax code and regulations.

Caution! Pencil to paper tax estimates are a sure-fire way to test the efficacy of your E&O insurance.

Limitations on itemized deductions, phase-outs of personal exemptions, five different capital gains rates, passive loss limitations, and the Alternative Minimum Tax are just a few of the factors that make it impossible to produce effectively a manual tax calculation. Moreover, rarely can we isolate the tax on any single item of income or expense without examining it within the context of the client’s entire tax picture.

Example. Sharon and Vern are contemplating selling some appreciated stock with a long-term capital gain of $100,000. They are California residents (marginal tax rate = 9.3%), and in 2014 they had Adjusted Gross Income of $200,000 consisting of $195,000 wages and $5,000 interest. They paid $7,000 property taxes and $30,000 mortgage interest. Assuming other income and expenses will be the same as last year, they want you to tell them how much they should set aside for taxes from the stock sale.

Is your answer $24,300?

Answer: Let’s hope not! Vern and Sharon will actually owe an additional $28,100 from the $100,000 long-term capital gains. Here’s how: Without Capital Gain

2015 With Capital Gain

2015 Income: Wages 195,000 195,000Interest and Dividends 5,000 5,000Capital Gains & Losses 100,000Adjusted Gross Income 200,000 300,000Itemized Deductions: Taxes 16,961 16,961Interest Expense 30,000 30,000 Total Itemized 46,961 46,961Personal Exemptions 8,000 8,000Total Deductions from AGI 54,961 54,961Taxable Income 145,039 245,039

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 3

Without Capital Gain 2015

With Capital Gain 2015

Regular Tax: Schedule or Table Tax 27,847 56,392Alternative Capital Gain Tax 0 42,847Appropriate Regular Tax 27,847 42,847Net Alternative Minimum Tax 0 1,891Medicare Investment Income Tax 0 1,900Total Federal Taxes 27,847 46,638CA State Tax 9,961 19,261Total Taxes 37,808 65,899

A Word About Software

Most of the major tax preparation software makers now also provide some form of planning software. These can be very convenient in that they allow you to transfer prior year data into the projection year and then make changes as appropriate. As an alternative, you can purchase a variety of stand-alone planning software that ranges in price as well as complexity. Some of these allow you to import data from your preparation software, some do not. Like preparation software, the choice of planning and projection software is an individual one and should be driven by the amount of planning work you perform and the nature and complexity of the work. A few popular stand-alone packages:

BNA Income Tax Planner with 50 States www.bnasoftware.com

CFS Tax Tools www.taxtools.com

Back to Basics www.btb-tax.com

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 4

Gathering the Data

The first step in any planning engagement is to gather as much data as necessary to produce a realistic estimate of tax liability. In most cases, you will not have the kind of detailed forensic information you normally gather to produce a tax return. Remember, planning is a process of estimating, making assumptions, and comparing alternatives. Prior Years’ Returns. If this is a new client, always collect the last two years’ tax returns. These will provide you with carry over amounts, as well as a benchmark for safe harbors. Current Year Income Sources. Year-to-date pay stubs are an absolute must for any planning engagement. In addition, don’t forget to ask about any bonuses or other extraordinary pay that may not be reflected on the pay stubs or may be payable later in the year. For business income, obtain a year-to-date profit and loss report and an estimate of projected revenues and expenses for the remainder of the year. Don’t forget to include depreciation and any other non-cash expenses in your projection. Investment income (i.e., interest, dividends and capital gains distributions) can be obtained from current bank statements and broker reports. Unless there has been a significant change (large investment or withdrawal) you may simply determine that this income is SALY (same as last year!). Realized capital gains and loss reports are often included with the client’s monthly statements from brokers and investment advisors. Online traders will need to provide an estimate of year-to-date gains and losses. Stock option holders can obtain reports from their companies of options exercised, ESPP shares purchased, and options available for exercise. Determine if passive activities, partnership and S-Corporation income, and retirement plan distributions are the same or altered for the current year. Social Security recipients are sent a notice of the amount of their annual benefits at the beginning of each year. Current Year Deductions. Unless the taxpayer has refinanced or bought or sold a home, mortgage interest expenses will drop slightly and property taxes will rise slightly for the current year. In the case of a purchase, sale, or refinance, obtain the escrow closing statement. Determine if medical and charitable expenses will remain the same or if the taxpayer made extraordinary payments in the prior year or anticipates doing so in the current year. Find out the amount of state income taxes paid for the previous year in the current year and any state estimate paid in January for the prior year.

Projecting for the Year

Depending upon when in the tax year you are providing planning services, you may need to project out certain items of income and expense. Because we always want our clients to remember that a projection is not a tax return, we often round off certain projected amounts.

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 5

Filing Status The definition of marriage is changing across the country. Generally, whether a taxpayer is married for Federal income tax purposes is determined by reference to the laws of the State of the taxpayer’s marital domicile. There have been several cases on this point:

Sullivan v. Commissioner, 256 F.2d 664 (4th Cir. 1958), affg. 29 T.C. 71 (1957); Dunn v. Commissioner, 70 T.C. 361, 366 (1978), affd. without published opinion

601 F.2d 599 (3d Cir. 1979); Lee v. Commissioner, 64 T.C. 552, 556-559 (1975), affd. 550 F.2d 1201 (9th Cir.

1977)

But recent years have shown that while the courts continue to rely on state law for determining marriage in common-law states, states’ rights do not prevail when the state recognizes same-sex marriages. The result can be a different filing status for federal tax purposes and for state purposes.

Common Law Marriage Status Texan Hatem Elsayed originally filed his 2004 return as a single, unmarried man. Later, on audit, he changed his story claiming he and his sweety pie Irma Angelica Cueto were married by common law at the end of 2004 (though he actually married her in separate civil and religious ceremonies in March of 2005). IRS balked at his newfound assertion, declining his plea for joint filing status. The Tax Court, looking to state (Texas) law, also choose not to recognize his assertion of common law marriage (Hatem Elsayed v. Comm., TCS 2009-81). Texas law acknowledges common law marriage if three conditions are met: (1) the parties must agree to marry; (2) they must live together in Texas; and (3) they must represent to others that a marriage exists. The court ruled that Hatem and Angelica handily met the first two tests, but failed the third because: (a) Hatem purchased a house in 2004 utilized as their personal residence in his name only; (b) he did not add her to the utility bills or his bank account until 2005; (c) she did not change her driver’s license to her married name until 2005; (d) they did not register their marriage at the county courthouse, as was available under Texas law; (e) he filed his Form 1040 under single filing status in 2004; and (f) he only raised the issue of common law marriage after his return was audited.

Planning. According to www.findlaw.com, twelve states currently recognize common law marriage established within their state boundaries, and another four states recognize certain prior established, “grandfathered in” common law marriages.

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 6

Common Law Marriage Jurisdictions

Jurisdictions Where Common Law Marriage May Be Established Currently

Alabama

Must agree to be husband and wife, have the mental capacity to enter into and understand such an agreement and consummate the marital relationship

Colorado Proven cohabitation and reputation for being married

District of Columbia

Explicit intent to be married and cohabitation

Iowa Intent and agreement to be married, continuous cohabitation and the couples’ public declarations they are husband and wife

Kansas Mental capacity to marry, agreement to be married at the present time and represent to the public they are married

New Hampshire Must have the mental capacity to marry, agreement to be married at the present time and represent to public they are married

Montana Capacity to consent to marriage, agreement to be married, cohabitation and have a reputation of being married

Oklahoma Must be competent, agree to enter into a marriage relationship and cohabitate

Rhode Island A man and woman have a serious intent to be married and engage in conduct that leads to a reasonable belief in the community they are married

South Carolina If a man and woman intend for others to believe they are married, a common law marriage may be established

Texas Agree to be married, cohabitate and represent to others (including sign a form provided by the county clerk) that they are married

Utah Sign a form provided by the county clerk, agree to be married, cohabitate, represent to others that they are married and sign a form provided by the county clerk

Jurisdictions Recognizing Prior Established, “Grandfathered In“ Common Law Marriages

Georgia Recognizes common law marriages entered into before January 1, 1997

Idaho Recognizes common law marriages entered into before January 1, 1996

Ohio Recognizes common law marriages entered into prior to October 10, 1991

Pennsylvania Recognizes common law marriages entered into prior to January 1, 2005

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 7

Planning. An important question to ask is whether a state that does not itself recognize common law marriage (e.g., Louisiana) will recognize the common law marriage recognized by another state (e.g., Texas). The answer to this question will, of course, vary by state. Some states, even though they do not themselves have statutes providing for common law marriages, will recognize a common law marriage if it is established and valid in a state recognizing common law marriage.

Same-Sex Marriages On June 26, 2013, the US Supreme Court ruled Section 3 of the 1996 Defense of Marriage Act (DOMA) unconstitutional. In rendering its decision, the Court changed the way same-sex married couples will be treated under federal tax law.

Planning. While the IRS now acknowledges same-sex unions for federal tax purposes, state tax planning in non-recognition states has become more complex.

Same-Sex Marriage States in the US

Massachusetts Connecticut California Iowa Vermont New Hampshire District of Columbia New York Maine Washington Maryland Rhode Island Delaware Minnesota Hawaii Illinois New Jersey New Mexico Oregon

Pennsylvania Indiana Oklahoma Utah Virginia Wisconsin Colorado Nevada West Virginia North Carolina Idaho Alaska Arizona Wyoming Kansas Montana South Carolina Alabama * Florida

* On Mar. 3, 2015, the Alabama Supreme Court ordered the state’s 68 probate judges to stop issuing marriage licenses to same-sex couples, despite an earlier federal court ruling that struck down the state’s gay marriage ban, and the US Supreme Court’s decision to allow same-sex marriages to proceed in the state. The state Supreme Court gave probate judges five days to respond if they do not feel they have to follow the order.

The Defense of Marriage Act (DOMA) The Defense of Marriage Act is a United States federal law signed into law by President Bill Clinton on September 21, 1996, whereby the federal government defines marriage as

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 8

a legal union between one man and one woman. Under the law, also known as DOMA, no state (or other political subdivision within the United States) may be required to recognize as a marriage a same-sex relationship considered a marriage in another state. The law passed both houses of Congress by large majorities. Section 3, which prevents the federal government from recognizing the validity of same-sex marriages, has been found unconstitutional in eight federal courts, including the First and Second Circuit Courts of Appeals.

Supreme Court Hears Arguments on the Constitutionality of DOMA On March 27, 2013, the US Supreme Court heard oral arguments in Windsor v. United States. In 1963 Edie Windsor met her late spouse, Thea Spyer, in New York City. Shortly thereafter, Windsor and Spyer entered into a committed relationship and lived together in New York. In 1993, Windsor and Spyer registered as domestic partners in New York City, as soon as that option became available. In 2007, as Spyer’s health began to deteriorate due to her multiple sclerosis and heart condition, Windsor and Spyer decided to get married in Canada where gays and lesbians are permitted to marry. Spyer died in February 2009. According to her last will and testament, Spyer’s estate passed for Windsor’s benefit. Because of the operation of DOMA, Windsor did not qualify for the unlimited marital deduction under §2056(a) and was required to pay $363,053 in federal estate tax on Spyer’s estate, which Windsor paid in her capacity as executor of the estate. On November 9, 2010, Windsor commenced suit, seeking a refund of the federal estate tax levied on Spyer’s estate and a declaration that section 3 of DOMA violates the Equal Protection Clause of the Fifth Amendment of the US Constitution. The Bipartisan Legal Advisory Group of the U.S. House of Representatives (BLAG) moved to intervene to defend the constitutionality of the statute. BLAG’s motion was granted on June 2, 2011. In rendering its decision on June 6, 2012, the US District Court Southern District of New York held in favor of Ms. Windsor that section 3 of DOMA is unconstitutional as applied to her and awarded judgment in the amount of the full amount of estate tax paid, plus interest. On October 18, 2012, the Second Circuit Court of Appeals upheld the lower court’s ruling and on December 7, 2012 the Supreme Court agreed to hear the case. The Court is expected to rule in June, 2013. On March 27, 2013, the US Supreme Court heard oral arguments in Windsor v. United States and on June 26, 2013 ruled Section 3 of DOMA is unconstitutional. In the 5-4 decision Justice Anthony Kennedy, writing for the majority, explained “that the principal purpose and the necessary effect of this law are to demean those persons who are in a lawful same-sex marriage. This requires the Court to hold, as it now does, that DOMA is unconstitutional as a deprivation of the liberty of the person protected by the Fifth Amendment of the Constitution.”

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 9

The 2015 Supreme Court Cases

Since June 2013, there have been 65 rulings in favor of marriage for same-sex couples. In spring 2015, the question of whether same-sex couples everywhere can marry had its day before the nation’s highest court. In January 2015, the Court granted review of cases from four states - Kentucky, Michigan, Ohio and Tennessee – and an oral argument was held on April 28. A decision should be announced by the end of June 2015. This followed an earlier decision in October 2014 when the Court denied petitions in five marriage cases, thereby allowing court-mandated marriages to take effect in 11 states. Nearly 72 percent of Americans live in a state that grants marriage to same-sex couples. There are now just 13 states without same-sex marriage recognition.

Community/Separate Property

Community property is the total of the following property acquired and earnings received:

By a registered domestic partner (RDP) during a registered domestic partnership while domiciled in a community property state.

By an RDP that is not separate property. Each RDP owns one-half of all community property.

Separate property is:

All property owned separately by an RDP before entering into a registered domestic partnership.

All property acquired separately after entering into a registered domestic partnership, such as gifts, inheritances, and property purchased with separate funds.

Money earned while domiciled in a separate property state. All property declared separate property in a valid agreement entered into before or

after registration of the domestic partnership. Community income is all income from community property, wages, salaries, and other compensation for personal services of either RDP while in a registered domestic partnership. Community income is divided equally between RDPs . Under California law community status ends in any of the following situations:

Upon the death of either RDP. When the decree of dissolution or termination of registered domestic partnership

becomes final. When RDPs separate with no immediate intention of reconciliation.

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 10

Income from separate property is income of the RDP who owns the property. When filing separate returns, the domicile of the RDP who earns the income determines the division of income between the RDPs. For income tax purposes, the income of RDPs domiciled in a community property state may be community income or separate income. When RDPs file separate returns, each RDP reports the following:

One-half of the community income All of his or her separate income.

IRS Reverses Decision Regarding Community Property

As mentioned above, federal tax law does not recognize civil unions or RDPs for purposes of filing status. While RDPs must use a married filing status (MFJ or MFS) for their state tax returns, these taxpayers must continue to use whatever single status (Single or Head of Household) is appropriate for federal income tax purposes. IRC §61(a)(1) provides that gross income means all income from whatever source derived including compensation for services such as fees, commissions, fringe benefits, and similar items. Federal tax law generally respects state property law characterizations and definitions (U.S. v. Mitchell, 403 U.S. 190 (1971), Burnet v. Harmel, 287 U.S. 103 (1932)). In Poe v. Seaborn, 282 U.S. 101 (1930), the Supreme Court held that for federal income tax purposes a wife owned an undivided one-half interest in the income earned by her husband in Washington, a community property state, and was liable for federal income tax on that one-half interest. Accordingly, the Court concluded that husband and wife must each report one-half of the community income on his or her separate return regardless of which spouse earned the income. United States v. Malcolm, 282 U.S. 792 (1931), applied the rule of Poe v. Seaborn to California's community property law. Community property laws developed in the context of marriage and originally applied only to the property rights and obligations of spouses. The laws operated to give each spouse an equal interest in each community asset, regardless of which spouse is the holder of record (d'Elia v. d'Elia, 58 Cal. App. 4 th 415 (1997)). By 2007, California had extended full community property treatment to registered domestic partners. Washington extended this coverage in 2009 as did Nevada and Wisconsin. On May 5, 2010, the Office of Chief Counsel issued CCA 201021050 regarding the treatment of community property for RDPs on their federal income tax returns. Applying the principle that federal law respects state law property characterizations, the federal tax treatment of community property should apply to RDPs. Consequently, for tax years beginning after December 31, 2006, a California registered domestic partner must report one-half of the community income, whether received in the form of

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 11

compensation for personal services or income from property, on his or her federal income tax return. The CCA went on to stipulate, however, that for tax years beginning before June 1, 2010, registered domestic partners may, but are not required to, amend their returns to report income in accordance with this CCA. Further, in CCA 201021048 the IRS stipulated that one-half of the credit for income tax withholding should be allocated to each RDP. Reg. §1.31-1(a) provides that the recipient of the income is the person subject to the tax imposed under the income tax provisions upon the wages from which the tax was withheld. In an example, the regulation states that if a husband and wife domiciled in a community property state file separate returns, each reporting for income tax purposes one half of the wages received by the husband, each spouse is entitled to one half of the credit allowable for the tax withheld at source with respect to such wages. Because an RDP is the recipient of half of the community property income, he/she is entitled to half of the amount withheld as a credit against the income tax imposed on the income. The requirement under state law to treat a taxpayer’s earnings as community property, and thus half of a taxpayer’s earnings as vested in his/her partner, does not result in a transfer of property by the taxpayer to his/her partner for federal gift tax purposes under IRC §2501.

Confusion Reigns

Even with IRS’s updates to Publication 555 Community Property and the new Form 8958, practitioners and taxpayers alike have questions about what is and isn’t community property.

Dependents With two exceptions, if a child may be claimed as a qualifying child by 2 or more taxpayers for a taxable year, such individual shall be treated as the qualifying child of the taxpayer who is a parent of the individual, or if not a parent, the taxpayer with the highest adjusted gross income for such taxable year (§152(c)(4)(A)(i) & (ii)). Exception #1. When both parents claim a qualifying child, the child shall be treated as the qualifying child of the parent with whom the child resided for the longest period of time during the taxable year, or if the child resides with both parents for the same amount of time during such taxable year, the parent with the highest adjusted gross income.(§152(c)(4)(B)(i) & (ii)).

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 12

Example. Although never married, Matt and Sara live together with their one biological child, Jack. Therefore, Jack is the qualifying child for both. As Sara’s AGI is higher than Matt’s AGI, starting in 2009, Matt cannot claim Jack as a qualifying child on his return, unless they mutually decide, between themselves, who will claim Jack and, thereby, avoid the tie-breaking rules. Planning. This change may reduce the opportunity to claim an EIC by requiring that the qualified child be claimed on the return of the highest paid (unmarried) parent. Exception #2. Starting in 2009, if the parents of an individual may claim such individual as a qualifying child but no parent claims the individual, such individual may be claimed as the qualifying child of another taxpayer but only if the adjusted gross income of such taxpayer is higher than the highest adjusted gross income of any parent of the individual (§152(c)(4)(C)). Planning. If the child or individual fails to meet the five requirements to be considered a qualifying child, the individual may still be claimed as a “qualifying relative” if he or she meets those requirements.

Gross Income

Wages IRS Asks Workers to Identify Employers Who Misclassify (IR-2007-203).

Employee or Independent Contractor?

Want to cut worker/independent-contractor’s SE tax in half? IRS blesses a new option! Instead of reporting compensation on the employee/worker’s W-2, some businesses treat the worker as an independent contractor to save on payroll taxes (i.e., 7.65% FICA tax) and report the compensation on Form 1099-MISC. The worker then reports this amount on Schedule C, resulting in the worker paying self-employment (SE) taxes at a 15.3% rate on the net earnings. Some workers complain they should have been treated as employees instead of an independent contractors and therefore should only be required to contribute 7.65% FICA instead of the 15.3% SE tax (5.65% vs. 13.3% for 2012). Starting with the 2007 tax year, the IRS allows the worker to file Form 8919, Uncollected Social Security and Medicare Tax on Wages, instead of filing Schedule SE (Form 1040), Self-Employment Tax, if they meet at least one of seven criteria (e.g., reason codes) as enumerated below. Previously, misclassified workers were required to file Form 4137, Social Security and Medicare Tax on Unreported Tip Income, for this purpose, a form that will still be used by certain tipped employees to report social security and Medicare taxes on allocated tips and tips not reported to their employers.

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 13

Example. The 2014 FICA wage base is $117,000. The self-employed’s maximum SE tax for OASDI is $14,500 whereas the employee’s maximum OASDI FICA tax is half that, $7,250, resulting in an annual $7,250 savings! This option can create a substantial tax savings for the qualified worker. Planning. By filing Form 8919, the worker’s social security and Medicare taxes will be credited to the worker’s social security record. In other words, the worker will get the same credit as if filing as self-employed – at half the cost. Four requirements to file Form 8919. The worker may file Form 8919 if all of the following apply:

The worker performed services for a firm; The firm did not withhold the worker’s share of social security and Medicare

taxes from the worker’s pay; The worker’s pay from the firm was not for services as an independent contractor;

and One or more of the reasons listed below under reason codes apply to the worker.

Reason codes. When treated by the employer as an independent contractor, the worker should indicate on Form 8919 one of six reasons why he/she determines he/she should have been treated as an employee. If none of the first six reason codes apply, but the worker still believes he/she should have been treated as an employee, the worker should enter reason code G, and file Form SS-8 on or before filing the worker’s tax return.

A. Worker filed Form SS-8 and received a determination letter stating that the worker was an employee of the firm.

B. The worker was designated as a “section 530 employee” by the employer or by the IRS prior to January 1, 1997.

C. The worker received other correspondence from the IRS stating the worker was an employee.

D. The worker was previously treated as an employee by the firm and was performing services in a substantially similar capacity and under substantially similar direction and control. (The worker must also enter reason code G.)

E. Any co-workers, performing substantially similar services under substantially similar direction and control, were treated as employees. (The worker must also enter reason code G.)

F. Any co-workers, performing substantially similar services under substantially similar direction and control, filed Form SS-8 for the firm and received a determination that they were employees. (The worker must also enter reason code G.)

G. The worker filed Form SS-8 with the IRS and has not received a reply.

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 14

Planning. Risk of filing Form 8919 may result in job loss! Along with the reason code, the worker must list the firm’s name and the firm’s federal identification number. If the worker enters reason codes D, E, F, or G, the worker or the firm that paid the worker may be contacted by the IRS for additional information. Additionally, the use of these reason codes is not a guarantee that the IRS will agree with the worker’s status determination. If the IRS does not agree that the worker is an employee, the worker will probably be billed for the additional tax, penalties, and interest resulting from the change to this worker status.

Maximizing Deferrals

In the tax planner’s bag of tricks, this is about the only idea for reducing tax that doesn’t involve giving someone else the money. Today most people don’t have a traditional pension, so saving for retirement is everyone’s responsibility. And using a 401(k) deferral makes saving tax deferred. Here are a few planning tips for wage earners looking to maximize their deferral program:

1. Strive to defer the maximum. For 2014 that’s $17,500 for everyone. Individuals age 50 and older can defer an additional $5,500.

2. Take full advantage of company match. If an individual can’t defer the maximum dollar amount for the year, at least contribute enough to receive the full amount the company will match. And try to stay until fully vested in the company’s match.

3. Consider Roth 401(k). Although this alternative gives up current deduction for salary deferred, it plans for a bigger payoff later when distributions are entirely tax free. Presumably, the taxpayer may be in a higher tax bracket later.

4. Don’t take the money out. Even if the individual changes jobs, and most will do so several times over the course of their careers, keep 401(k) funds tax deferred. Choices often include, leaving the plan with the former employer, rolling into and IRA or transferring to a new company’s plan.

5. Manage the investments within the plan. Retirement plan assets should be as carefully managed as outside investments, even though they may have a longer investment time profile.

Interest and Dividends

Tax-Exempt Interest

Interest on a bond used to finance government operations generally is not taxable if the bond is issued by a state, the District of Columbia, a U.S. possession, or any of their political subdivisions (§103). Political subdivisions include:

Port authorities,

Toll road commissions,

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 15

Utility services authorities,

Community redevelopment agencies, and

Qualified volunteer fire departments (for certain obligations issued after 1980).

There are other requirements for tax-exempt bonds. See IRC §§141-150 and the related regulations. Obligations That Are Not Bonds Interest on a state or local government obligation may be tax exempt even if the obligation is not a bond. For example, interest on a debt evidenced only by an ordinary written agreement of purchase and sale may be tax exempt. Also, interest paid by an insurer on default by the state or political subdivision may be tax exempt.

Registration Requirement

A bond issued after June 30, 1983, generally must be in registered form for the interest to be tax exempt (§149(a)).

Indian Tribal Government

Bonds issued after 1982 by an Indian tribal government are treated as issued by a state. Interest on these bonds is generally tax exempt if the bonds are part of an issue of which substantially all of the proceeds are to be used in the exercise of any essential government function. However, interest on private activity bonds (other than certain bonds for tribal manufacturing facilities) is taxable (§7871(a)(4)).

Tax-Exempt Bonds Purchased at Original Issue Discount

Original issue discount (OID) on tax-exempt state or local government bonds is treated as tax-exempt interest (§1272(a)(2)(A)).

Tax-Exempt Bonds Purchased at Market Discount

Market discount on a tax-exempt bond is not tax-exempt (§1276(a)(1)). If a taxpayer bought the bond after April 30, 1993, you can choose to accrue the market discount over the period he/she owns the bond and include it in income currently, as taxable interest. If you do not make that choice, or if the taxpayer bought the bond before May 1, 1993, any gain from market discount is taxable when he/she disposes of the bond.

Planning with Tax-Exempts

Investing in tax-exempt bonds and/or mutual funds can produce tax advantages for the right investors. Caution! Remember that tax-exempt income is not included in AGI for purposes of determining the limitation on itemized deductions or the phase-out of personal exemptions. In addition, tax-exempt income is not part of net investment income or AGI

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 16

for the 3.8% Medicare surtax. For taxpayers with AGI in excess of the thresholds, the rate of return on a taxable investment will need to be higher.

Example. Rob and Denise have adjusted gross income in 2014 of $250,000. They receive $3,500 in tax-exempt interest income from a $100,000 investment earning 3.5%. Their taxable income of $187,600 places them in the 28% marginal rate bracket. Under a basic calculation, it would appear that if they invested in a taxable fund returning 4.86%, they would net the same after-tax cash flow. However, because of the limitations, their actual results are:

Federal income tax with $4,860 taxable income $41,735 Federal income tax with $3,500 tax-exempt income 39,982 Tax savings 1,753

After-tax yield on taxable investment ($4,860 - $1,753 tax) $3,107

Dividends Ordinary (taxable) dividends are the most common type of distribution from a corporation. They are paid out of the earnings and profits of a corporation and are ordinary income to the taxpayer (§316(a); Reg. §1.316-1).

Dividends & JGTRRA 2003

Dividends received by an individual shareholder from domestic corporations are taxed at the same rates that apply to net capital gains originally through 2008, extended to 2010 by TIPRA 2005, extended through 2012 by TRA 2010 and made permanent by ATRA 2012. This treatment applies for purposes of both the regular tax and the Alternative Minimum Tax. Thus, under these provisions, dividends are taxed at rates of 0% and 15% through 2012, and at rates of 0%, 15% and 20% beginning in 2013. Although dividends are taxed at capital gain rates and the calculation of that tax is done on the federal Schedule D, dividends may not be offset by capital losses.

Tax Rates on Qualifying Dividends 10% & 15% Bracket 25% - 35% Bracket 39.6% Bracket 2003 – 2007 5% 15% N/A 2008 – 2012 0% 15% N/A 2013 and later 0% 15% 20% Mutual Funds Mutual funds can cause tax headaches because investors have no control over when and how much their funds realize in gains. Fund managers buy and sell securities for fund investors, often without taking tax considerations into account. Mutual funds must pass along to their shareholders any realized capital gains that are not offset by realized losses

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 17

by the end of their accounting year. That is particularly painful if you have just purchased the fund, because you are paying taxes for gains you didn't get.

Example. Sharon invested $250 in Fund D on Monday. The fund’s Net Asset

Value (NAV) was $25, so she was able to buy 10 shares. If the fund made a $5-per-share distribution on Tuesday (which means Sharon was handed a $50 distribution) and she reinvested, her investment is still worth the same $250 because the fund’s NAV would have decreased with the distribution:

Monday 10.0 shares @ $25 = $250

Tuesday 12.5 shares @ $20 = $250

The trouble is, Sharon now owes taxes on that $50 distribution. We’ll assume that the distribution is made up entirely of long-term gains and is therefore taxed at 15%. That would translate into a $7.50 tax bill for Sharon.

If Sharon immediately sold the fund, the whole thing would be a wash, as the capital gains would be offset by a capital loss. But we’re guessing that if Sharon just invested in the fund, she wasn't planning to turn around and sell it right away.

Funds occasionally can add insult to injury by paying out a large capital-gains distribution in a year in which the fund lost money. In other words, investors can lose money in a fund and still have to pay taxes. In 2000, for example, many specialty-technology funds made big capital gains distributions, even though almost all of them were in the red for the year. Although the funds lost money during the year, they sold some stocks bought at lower prices and had to pay out capital gains as a result. Technology fund investors lost money to both the market and Uncle Sam that year.

Tax-Efficient Funds

How do you find tax-wise funds? According to John Waggoner, a personal finance columnist for USA Today, the simplest way is to look for funds sold as “tax-managed” funds. The top performers for the past five years are comprised of many international or small-company funds. That's because both categories have fared well since 2001. But you don't have to restrict yourself to the subset of self-described tax-managed funds. You can find funds that are tax-efficient without bragging about it. The best indicator of a tax-efficient fund is one that has been tax-efficient in the past, says Jim Peterson, vice president at Charles Schwab, the discount brokerage. Morningstar's tax-cost ratio is one measure of that. Lower is better. A ratio of 1 means that the fund gave up an average of 1 percentage point to taxes over time. You can find a fund's tax-cost ratio at www.morningstar.com.

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 18

Index funds, particularly large-company index funds, also tend to be tax-efficient. The funds simply track a stock index, such as the Standard & Poor's 500-stock index. These funds tend to trade infrequently. Funds that are most likely to hit you with a big tax bill have a few things in common:

New manager. If the fund manager left, it's likely that the new manager will rearrange the portfolio. That can result in an above-average gains distribution.

New management. If the fund is merged into another fund, the old fund's

holdings could be liquidated — which might also produce a big payout.

Capital Gains The traditional method of capital gains planning involved offsetting gains by “harvesting” losses before year end. Although 2008 and 2009 market performance resulted in extraordinary capital losses for many clients, more recent results brings us back to this traditional process.

Harvesting Losses

Offset capital gains by selling other capital assets at a loss. Look for assets inherited in 1998 through 2000 when market values may have been substantially higher. Other sources of capital losses: Worthless stock. Stocks, stock rights and bonds that became worthless during the tax

year are treated as though they were sold on the last day of the tax year (§165(g)). Use this date in determining the holding period for worthless securities. Report as either long-term or short-term on Schedule D and print “worthless” in the column for sale price.

Example. Joe bought 100 shares of Schwartz, Inc on May 1, 2000, for a total price of $1,000. On April 1, 2015 Schwartz ceased doing business, and the company was liquidated. Shareholders of Schwartz received no consideration for their shares. Joe reports a long-term capital loss on his 2015 return for $1,000. To prove total worthlessness, investors need to prove that the securities truly have zero value. For instance, a company declared bankruptcy, stopped doing business and is insolvent. If the company's shares are still trading - even at pennies per share - they're not considered worthless, and no deduction will be granted. Nor can you claim a deduction for a partially worthless corporate bond. Selling shares that are traded on the so-called pink sheets can be tricky business for individual investors you'll likely have to turn to a full-service brokerage to execute that trade. If that seems too costly or unwieldy, you might be tempted to hang on to those

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 19

shares until they do become worthless. If that’s the case, look for news that can bolster your claim of worthlessness. Taxpayers may file a claim for a credit or refund due (Form 1040X, Amended U.S. Individual Income Tax Return) to amend a return for the year a security became worthless. Amended returns may be filed within 7 years from the date the original return for that year had to be filed, or 2 years from the date the tax was paid, whichever is later. Repositioning Portfolio. For clients using modern portfolio theory models for their

asset allocations, selling off securities with accumulated losses may be an opportunity to reposition their portfolios and reduce taxable capital gains.

The 2015 Planning Opportunity – Harvesting Gains

For many clients, the bad news bear markets of 2008 and 2009 can provide an opportunity to sell assets that they have been reticent to dispose of because of large built-in gains. As tax professionals, each of us probably has at least one client with capital losses that could exceed his or her lifetime. Remember that 35 year old taxpayer with a $135,000 capital loss carryover will have to live to be 80 to use up that loss in $3,000 annual increments. Where do we help them find the gains – and perhaps – tax-free income? Sell gifted assets with very low cost basis Sell appreciated second home/vacation homes Sell collectibles – These can also avoid 28% capital gains rate if losses offset Take taxable boot in an exchange Sell negative basis limited partnership interests to generate phantom income –

make sure it will be capital gain and not ordinary income! Accelerate installment sale collections Sell personal residence that has gain in excess of the Section 121 exclusion

Playing the Spread

The spread between ordinary income tax rates and the long-term capital gains tax for all taxpayers has increased for sales after May 5, 2003 through December 31, 2012. The previous spread between the highest income tax brackets was 18.6 percent (38.6% less 20%). Even though marginal rates were lowered under the 2003 law, the spread increased to 20 percent (35% less 15%). As a result, keeping an eye on holding period is extremely important from a tax planning perspective. Of course, other financial considerations, including risk and market volatility, must be weighed in the balance. Nevertheless, some value may be lost while netting an after-tax gain for waiting-out the holding period.

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 20

Example. Vern is holding 1,000 shares of Tax Inc. currently valued at $50 per share. Vern originally purchased the shares June 10, 2014, at $10 per share. If Vern sells the shares today, May 19, 2015, he’ll recognize a short-term capital gain of $40,000. Vern is in the highest tax marginal bracket, and he’ll pay roughly $14,000 tax on the gain. Vern nets $36,000 ($50,000 proceeds less $14,000 tax) after-tax on the sale.

If Vern decides to wait until June 11, 2015, to sell the shares, he risks a downturn in the value of the stock. But suppose the stock drops 10% in value during the month. Vern sells the shares for $45,000 and pays long-term capital gains at the rate of 15%, or approximately $5,250. In this case, Vern nets $39,750 after-tax on the sale.

Planning for Gains in 2015 and Beyond

For a higher-income taxpayer, it’s tough to plan to have a very low income year for just one year, but on January 1, 2013, Congress extended and made permanent the lower capital gains rates enacted in 2003. This may give more taxpayers the chance to receive some capital gains “tax-free.”

In order to take advantage of this opportunity, the amount of ordinary income in a taxpayer’s total taxable income must be less than the upper threshold for the 15% marginal tax bracket for his or her filing status. Then, the amount of taxable income within the limit that is made up of qualified dividends and/or long-term capital gains will be taxed at 0%.

Example. Karen, a single taxpayer, has taxable income in 2015 of $100,000. Of this amount, $25,000 is ordinary and $75,000 is long-term capital gains. Using the top of the 15% marginal rate bracket for 2015, $12,450 ($37,450 – 25,000) of Karen’s capital gains will be taxed at 0%. The remaining $62,550 will be taxed at 15%.

Strategies for reducing taxable income include: Defer receipt of income where taxpayer can control payment sources Take a sabbatical or unpaid leave Invest in tax-free income producing assets Invest for appreciation rather than current income Bunch deductible expenses Prepay deductible expenses to the extent allowable Perform deferred maintenance and repairs on rental properties generating taxable

income Maximize Section 179 expensing for new business assets acquired If possible under RMD guidelines, reduce distributions from retirement plans

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 21

Installment Sales

When a taxpayer sells property and some or all of the payments for sale are to be paid in the future, the transaction generally is called an installment sale. When installment reporting of the gain is available, it is an important financing and tax planning option for both the seller and the buyer.

Why use the installment method? To spread the taxable gain over multiple years. A taxpayer who sells property on the installment plan is allowed to have a pro-rata portion of the total gain taxed as each installment is actually received. Thus, the seller, instead of paying the whole tax in the year of the sale, may spread the tax on the gain over the period during which the installments are received. Benefits of an Installment Sale: Taking payments over time may facilitate the sale and improve the price.

Deferring long-term capital gain may provide the opportunity to offset it with a loss realized in the future.

Pushing gain into a future year when the current year has a NOL may allow more loss to be carried back against a previous year’s ordinary income.

Deferring gain may place the income into a lower tax-bracket year.

Example. Ralph and Cay, residents of California, sold appreciated property in 2014 with an adjusted basis of $50,000 at a sale price of $150,000. They received $75,000 on the close of the sale, and will receive the remaining $75,000 one year from the date of the close. They surrendered title on the closing date and received a note, payable with interest, for the remaining $75,000.

Without

Installment Sale

With Installment Sale 2014 2015 2014 2015 Other Ordinary Income 50,000 50,000 50,000 50,000 Interest 5,000 5,000 5,000 5,000 Capital Gains 100,000 0 50,000 50,000 Adjusted Gross Income 155,000 55,000 105,000 105,000 Itemized Deductions

Taxes 8,474 775 3,886 3,886

Standard Deduction 12,400 12,600 12,400 12,600 Personal Exemptions 7,900 8,000 7,900 8,000 Taxable Income 134,700 34,400 84,700 84,400 Federal Regular Tax 13,436 4,238 5,936 5,663 State Regular Tax 8,474 775 3,886 3,886

2-Year Total Taxes

26,923

19,371

©2015. These materials are copyrighted and may not be reproduced or distributed in whole or in part without permission of the author/CalCPA Education Foundation.

Copyri

ght 2

015-1

6

© 2015 Karen Brosi, EA, CFP® Individual Tax Planning 22

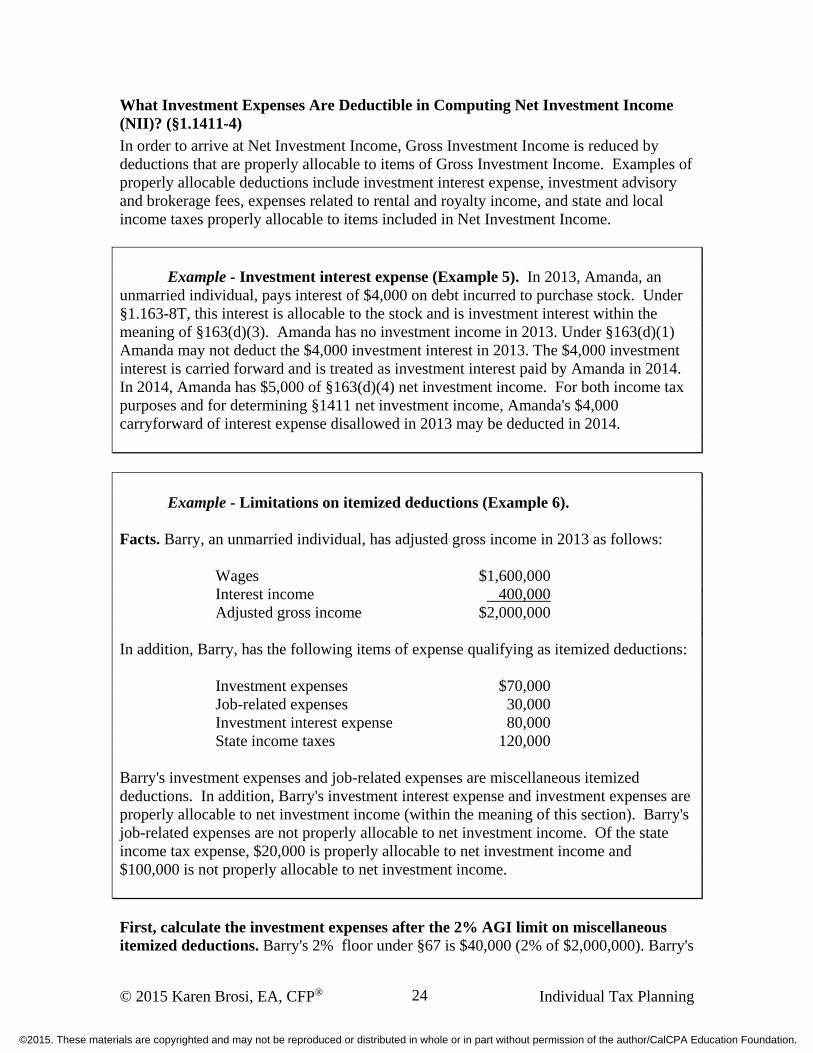

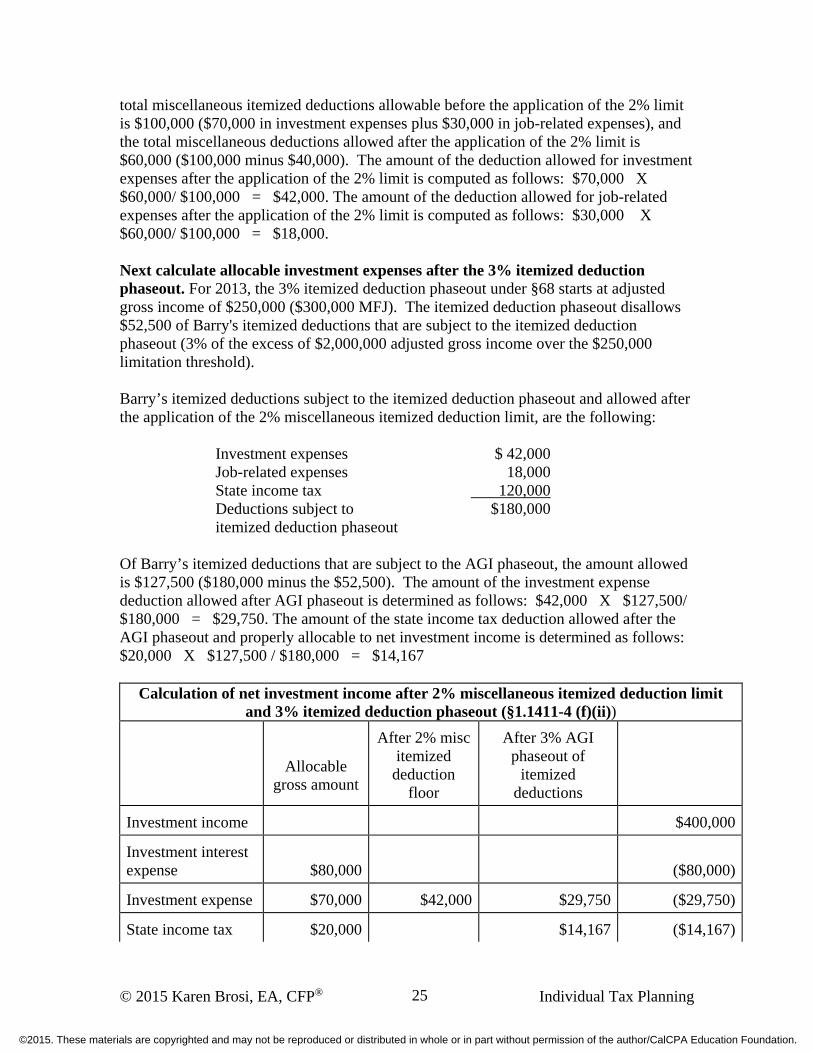

3.8% Medicare Tax Imposed on Net Investment Income - Starting 2013

Starting in 2013, a 3.8% Medicare tax is imposed on the lesser of:

an individual's net investment income for the tax year or modified AGI in excess of a floor: $250,000 for joint filers and surviving

spouses, $125,000 for a married taxpayer filing separately and $200,000 in any other case (§1411(a)(1) & (b)).