The Presence of Non..;Ec Multinationals in European Industry

Geoffrey Jones

Control, Performance, and KnowledgeTransfers in Large Multinationals:

Unilever in the United States, 1945-1980

This article considers key issues relating to the organizationand performance of large multinational firms in the post-Second World War period. Although foreign direct invest-ment is defined by ownership and control, in practice thenature of that "control" is far from straightforward. The issueof control is examined, as is the related question of the "sticki-ness" of knowledge within large international firms. The dis-cussion draws on a case study of the Anglo-Dutch consumergoods manufacturer Unilever, which has been one of the larg-est direct investors in the United States in the twentieth cen-tury. After 1945 Unilever's once successful business in theUnited States began to decline, yet the parent company main-tained an arms-length relationship with its U.S. affiliates,refusing to intervene in their management. Although Unilever"owned" large U.S. businesses, the question of whether it"controlled" them was more debatable.

Some of the central issues related to the organization and performanceof multinationals after the Second World War can be illustrated by

studying the case of Unilever in the United States. Since Unilever'screation in 1929 by a merger of British and Dutch soap and margarinecompanies, it has ranked as one of Europe's, and the world's, largestconsumer-goods companies.1 Its sales of $45,679 million in 2000

GEOFFREY JONES is professor of business administration at Harvard Business School.This article draws extensively on the confidential business records held by Unilever PLC

and Unilever N.V., and the author would like to thank Unilever for permission to cite them. Apreliminary version of this article benefited from the insightful comments of Mira Wilkins,the members of the Business History Seminar at Harvard Business School, and three anony-mous referees. I am grateful for the research assistance of Lina Galvez-Mufioz and PeterMiskell. Anne-Marie Kuijlaars undertook some of the initial research on the early history ofLever Brothers and T. J. Lipton.

1 Charles Wilson, The History of Unilever, 3 vols. (London, 1954,1968); Alfred D. ChandlerJr., Scale and Scope (Cambridge, Mass, 1990), 378-89.

Business History Review 76 (Autumn 2002): 435-478 . © 2002 by The Pres-ident and Fellows of Harvard College.

Geoffrey Jones / 436

ranked it fifty-fourth by revenues in the Fortune 500 list of largestcompanies for that year.

Unilever was an organizational curiosity in that, since 1929, it hasbeen headed by two separate British and Dutch companies—UnileverLtd. (PLC after 1981), and Unilever N.V.—with different sets of share-holders but identical boards of directors. An "Equalization Agreement"provided that the two companies should at all times pay dividends ofequivalent value in sterling and guilders. There were two head offices—in London and Rotterdam—and two chairmen. Until 1996 the "chiefexecutive" role was performed by a three-person Special Committeeconsisting of the two chairmen and one other director.

Beneath the two parent companies a large number of operatingcompanies were active in individual countries. They had many names,often reflecting predecessor firms or companies that had been ac-quired. Among them were Lever; Van den Bergh & Jurgens; Gibbs;Batchelors; Langnese; and Sunlicht. The name "Unilever" was not usedin operating companies or in brand names. Lever Brothers and T. J.Lipton were the two postwar U.S. affiliates. These national operatingcompanies were allocated to either Ltd./PLC or N.V. for historical orother reasons. Lever Brothers was transferred to N.V. in 1937, and until1987 (when PLC was given a 25 percent shareholding) Unilever's busi-ness in the United States was wholly owned by N.V. Unilever's business,as a result, counted as part of Dutch foreign direct investment (FDI) inthe country. Unilever and its Anglo-Dutch twin Royal Dutch Shellformed major elements in the historically large Dutch FDI in theUnited States.2 However, the fact that all dividends were remitted toN.V. in the Netherlands did not mean that the head office in Rotterdamexclusively managed the U.S. affiliates. The Special Committee had bothDutch and British members, and directors and functional departmentswere based in both countries and had managerial responsibilities with-out regard for the formality of N.V. or Ltd./PLC ownership. Thus, whileownership lay in the Netherlands, managerial control was Anglo-Dutch.

The organizational complexity was compounded by Unilever's wideportfolio of products and by the changes in these products over time.Edible fats, such as margarine, and soap and detergents were the his-torical origins of Unilever's business, but decades of diversificationresulted in other activities. By the 1950s, Unilever manufactured con-venience foods, such as frozen foods and soup, ice cream, meat prod-ucts, and tea and other drinks. It manufactured personal care products,including toothpaste, shampoo, hairsprays, and deodorants. The oils

2 Roger van Hoesel and Rajneesh Narula, eds., Multinational Enterprises from the Neth-erlands (London, 1999), especially ch. 8.

Unilever in the United States, 1945-1980 / 437

and fats business also led Unilever into specialty chemicals and animalfeeds. In Europe, its food business spanned all stages of the industry,from fishing fleets to retail shops. Among its range of ancillary serviceswere shipping, paper, packaging, plastics, and advertising and marketresearch. Unilever also owned a trading company, called the United Af-rica Company, which began by importing and exporting into WestAfrica but, beginning in the 1950s, turned to investing heavily in localmanufacturing, especially brewing and textiles. The United AfricaCompany employed around 70,000 people in the 1970s and was thelargest modern business enterprise in West Africa.3 Unilever's totalemployment was over 350,000 in the mid-1970s, or around seventimes larger than that of Procter & Gamble (hereafter P&G), its mainrival in the U.S. detergent and toothpaste markets.

An early multinational investor, by the postwar decades Unileverpossessed extensive manufacturing and trading businesses throughoutEurope, North and South America, Africa, Asia, and Australia. Unileverwas one of the oldest and largest foreign multinationals in the UnitedStates. William Lever, founder of the British predecessor of Unilever,first visited the United States in 1888 and by the turn of the century hadthree manufacturing plants in Cambridge, Massachusetts, Philadel-phia, and Vicksburg, Mississippi.4 The subsequent growth of the busi-ness, which was by no means linear, will be reviewed below, but it wasalways one of the largest foreign investors in the United States. In 1981,a ranking by sales revenues in Forbes put it in twelfth place.5

Unilever's longevity as an inward investor provides an opportunityto explore in depth a puzzle about inward FDI in the United States. Fora number of reasons, including its size, resources, free-market econ-omy, and proclivity toward trade protectionism, the United States hasalways been a major host economy for foreign firms. It has certainlybeen the world's largest host since the 1970s, and probably was before1914 also.6 Given that most theories of the multinational enterprisesuggest that foreign firms possess an "advantage" when they invest in aforeign market, it might be expected that they would earn higher re-turns than their domestic competitors.7 This seems to be the general

3D. K. Fieldhouse, Merchant Capital and Economic Decolonization—The United AfricaCompany 1929-1987 (Oxford, U.K., 1994).

4Mira Wilkins, The History of Foreign Investment in the United States to 1914 (Cam-bridge, Mass., 1989), 340-2.

5 "The 100 Largest Foreign Investments in the US," Forbes (6 July 1981).6Mira Wilkins, "Comparative Hosts," Business History 36, no. 1 (1994); Geoffrey Jones,

The Evolution of International Business (London, 1996).7 The concept of "advantage" originated with the pioneering contribution of Stephen

Hymer and is a basic component of the eclectic paradigm developed by John H. Dunning.See Dunning, Multinational Enterprises and the Global Economy (Wokingham, U.K., 1992).

Geoffrey Jones / 438

case, but perhaps not for the United States. Considerable anecdotal evi-dence exists that many foreign firms have experienced significant andsustained problems in the United States, though it is also possible tocounter such reports with case studies of sustained success.8

During the 1990s a series of aggregate studies using tax and otherdata pointed toward foreign firms earning lower financial returns thantheir domestic equivalents in the United States.9 One explanation forthis phenomenon might be transfer pricing, but this has proved hard toverify empirically. The industry mix is another possibility, but recentstudies have suggested this is not a major factor. More significant influ-ences appear to be market share position—in general, as a foreign-owned firm's market share rose, the gap between its return on assetsand those for United States-owned companies decreased—and age ofthe affiliate, with the return on assets of foreign firms rising with theirdegree of newness.10 Related to the age effect, there is also the strong,but difficult to quantify, possibility that foreign firms experienced man-agement problems because of idiosyncratic features of the U.S. econ-omy, including not only its size but also the regulatory system and"business culture." The case of Unilever is instructive in investigatingthese matters, including the issue of whether managing in the UnitedStates was particularly hard, even for a company with experience inmanaging large-scale businesses in some of the world's more challeng-ing political, economic, and financial locations, like Brazil, India, Nige-ria, and Turkey.

Finally, the story of Unilever in the United States provides rich newempirical evidence on critical issues relating to the functioning of mul-tinationals and their impact. It raises the issue of what is meant by"control" within multinationals. Management and control are at theheart of definitions of multinationals and foreign direct investment (asopposed to portfolio investment), yet these are by no means straight-forward concepts. A great deal of the theory of multinationals relates tothe benefits—or otherwise—of controlling transactions within a firmrather than using market arrangements. In turn, transaction-cost theorypostulates that intangibles like knowledge and information can often betransferred more efficiently and effectively within a firm than between

8 Geoffrey Jones and Lina Galvez-Munoz, eds., Foreign Multinationals in the UnitedStates (London, 2001).

9 H. Grubert, T. Goodspeed, and D. Swenson, "Explaining the Low Taxable Income ofForeign-Controlled Companies in the United States," in A. Giovannini, R. Glenn Hubbard,and J. Slemrod, eds., Studies in International Taxation (Chicago, 1993); R. J. Mataloni, "AnExamination of the Low Rates of Return of Foreign-Owned US Companies," Survey of Cur-rent Business (2000): 55-73.

10 R. J. Mataloni, "An Examination of the Low Rates of Return."

Unilever in the United States, 1945-1980 / 439

independent firms. There are several reasons for this, including the factthat much knowledge is tacit. Indeed, it is well established that sharingtechnology and communicating knowledge within a firm are neithereasy nor costless, though there have not been many empirical studies ofsuch intrafirm transfers.11 Orjan Solvell and Udo Zander have recentlygone so far as to claim that multinationals are "not particularly wellequipped to continuously transfer technological knowledge acrossnational borders" and that their "contribution to the international dif-fusion of knowledge transfers has been overestimated."12 This studyof Unilever in the United States provides compelling new evidence onthis issue.

Lever Brothers in the United States:Building and Losing Competitive Advantage

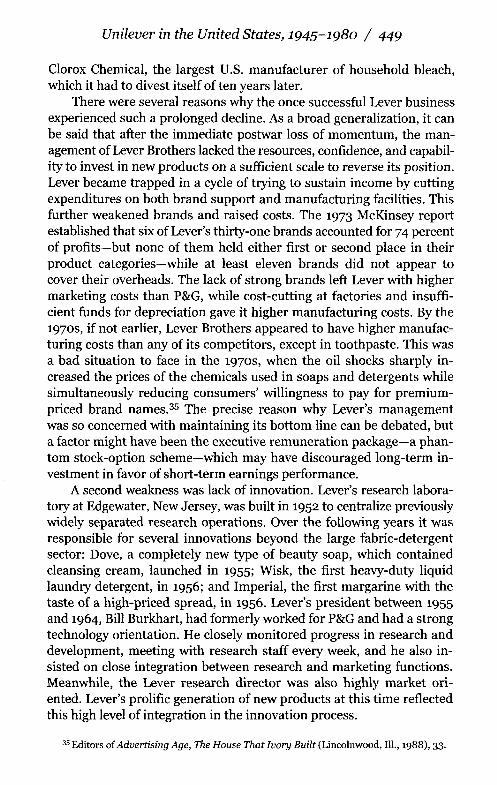

Lever Brothers, Unilever's first and major affiliate, was remarkablysuccessful in interwar America. After a slow start, especially because of"the obstinate refusal of the American housewife to appreciate SunlightSoap," Lever's main soap brand in the United Kingdom, the LeverBrothers business in the United States began to grow rapidly under anew president, Francis A. Countway, an American appointed in 1912.13

Sales rose from $843,466 in 1913, to $12.5 million in 1920, to $18.9million in 1925. Lever was the first to alert American consumersto the menace of "BO," "Undie Odor," and "Dishpan Hands," and tomarket the cures in the form of Lifebuoy and Lux Flakes. By the endof the 1930s sales exceeded $90 million, and in 1946 they reached$150 million.

By the interwar years soap had a firmly oligopolistic market struc-ture in the United States. It formed part of the consumer chemicalsindustry, which sold branded and packaged goods supported by heavyadvertising expenditure. In soap, there were also substantial through-put economies, which encouraged concentration. P&G was, to applyAlfred D. Chandler's terminology, "the first mover"; among the main

11S. Ghoshal and C. A. Bartlett, "Creation, Adoption, and Diffusion of Innovation by Sub-sidiaries of Multinational Corporations," Journal of International Business Studies 19 (Fall1988): 365-88; U. Zander and B. Kogut, "Knowledge and the Speed of the Transfer and Imi-tation of Organizational Capabilities," Organizational Science 6 (Jan.-Feb. 1995): 76-92;A. K. Gupta and V. Govindarajan, "Knowledge Flows within Multinational Corporations,"Strategic Management Journal 21 (April 2000): 473—96.

12 0. Solvell and I. Zander, "International Diffusion of Knowledge: Innovating Mecha-nisms and the Role of the MNE," in Alfred D. Chandler Jr. et al., The Dynamic Firm (NewYork, 1998), 402.

13 Wilson, History of Unilever, 1, 204.

Geoffrey Jones / 440

"Lorelei, now thatLifebuoy smells so goodand stops B.O. so long,

Why doesn'teverybody use it?"

"'Causehasn't smelted it,

Let's give 'cm aFREE cake!"

. • Mfehnv'i nalitinr rtcr I. Iton! Stenuid Ijnelrl i,s«< b«n

»M • kwily row fngnncr! Tto<n l»I Ttal'i

pmoahnthalluu.aurvHciitaibI u a dv> Pucil,,, .tap » «

•ha. Bra eui'l arr .t. > r feel It-

„ .0I Vra fool ihe bill. »,ai pluawtl

SIEVE Mri LOKiHi i "BIG TOWN'1;Over StaHw WCBS-nEvtwy Than., 9:» P.M. •.

SET ! G e l N e w l ifebuoy _No Strings Attached!

MaMb.«d«bHtojWirstor."

TBISlUCELAK SIZE u n i F I t VBSBI

TAKE IT TO VOCB ST9BBI

Advertisement for Lifebuoy appearing in New York News in 1951. Lever Brothers inventedthe concept of Body Odor (BO) in the interwar years, and then proceeded to cure it with Life-buoy Soap. (Photograph courtesy Ad'Access On-Line Project-Ad #BHO994, John W. HartmanCenter for Sales, Advertising & Marketing History, Duke University Rare Book, Manuscript,and Special Collections Library, http://scriptorium.lib.duke.edu/adaccess/. Permissiongranted by Unilever.)

followers were Colgate and Palmolive-Peet, which merged in 1928.Neither P&G nor Colgate Palmolive diversified greatly beyond soap,though P&G's research took it into cooking oils before 1914 and intoshampoos in the 1930s. Lever made up the third member of the oligopoly.The three firms together controlled about 80 percent of the U.S. soap

Unilever in the United States, 1945-1980 / 441

market in the 1930s.14 By the interwar years, this oligopolistic rivalrywas extended overseas. Colgate was an active foreign investor, whilein 1930 P&G—previously confined to the United States and Canada-acquired a British soap business, which it proceeded to expand, seri-ously eroding Unilever's market share.15

The soap and related markets in the United States had a number ofcharacteristics. Although P&G had established a preponderant marketshare, shares were strongly contested. Entry, other than by acquisition,was already not really an option by the interwar years, so competitiontook the form of fierce rivalry between incumbent firms with a long ex-perience of one another. During the 1920s and the first half of the1930s, Lever made substantial progress against P&G. Lever's sales inthe United States as a percentage of P&G's sales rose from 14.8 percentbetween 1924 and 1926 to reach almost 50 percent in 1933. In 1930P&G suggested purchasing Lever in the United States as part of a worlddivision of markets, but the offer was declined.16 Lever's success peakedin the early 1930s. Using published figures, Lever estimated its profit asa percentage of capital employed at 26 percent between 1930 and 1932,compared with P&G's 12 percent.

Countway's greatest contribution was in marketing. During thewar, Countway put Lever's resources behind Lux soapflakes, promotedas a fine soap that would not damage delicate fabrics just at a timewhen women's wear was shifting from cotton and lisle to silk and finefabrics. The campaign featured a variety of tactics, including washingdemonstrations at department stores. In 1919 Countway launchedRinso soap powder, coinciding with the advent of the washing machine.In the same year, Lever's agreement with a New York agent to sell itssoap everywhere beyond New England was abandoned and a new salesorganization was established. Finally, in the mid-i92os, Countwaylaunched, against the advice of the British parent company, a whitesoap, called "Lux Toilet Soap." J. Walter Thompson was hired to de-velop a marketing and advertising campaign stressing the glamour ofthe new product, with very successful results.17 Lever's share of the U.S.

14 Chandler, Scale and Scope, ch. 5; Thomas K. McCraw, American Business, 1920-1980:How It Worked (Wheeling, 111., 2000), ch. 3.

15 Wilson, The History of Unilever, vol. 2, 344; Chandler, Scale and Scope, 385-8; Geof-frey Jones, "Foreign Multinationals and British Industry before 1945," Economic History Re-view 41, no. 3 (1988): 429-53.

16 "History of Lever Brothers USA, 1912—1952," Unilever Economics and Statistics De-partment, 18 Dec. 1953, Unilever Historical Archives London (UAL). The archives containtwo unpublished draft chapters on the history of Unilever in the United States (dated Janu-ary 1990). The author would like to thank Unilever PLC and N.V. for permission to read thisdraft, which draws heavily on confidential interviews with former executives.

17 Kathy Peiss, "On Beauty and the History of Business," in Beauty and Business, ed.Philip Scranton (New York, 2001), 15.

Geoffrey Jones / 442

soap market rose from around 2 percent in the early 1920s to 8.5 per-cent in 1932.18 Brands were built up by spending heavily on advertising.As a percentage of sales, advertising averaged 25 percent between 1921and 1933, thereby funding a series of noteworthy campaigns conceivedby J. Walter Thompson. This rate of spending was made possible by thelow price of oils and fats in the decade and by plowing back profitsrather than remitting great dividends. By 1929 Unilever had received$12.2 million from its U.S. business since the time of its start, butthereafter the company reaped benefits, for between 1930 and 1950 cu-mulative dividends were $50 million.19

After 1933 Lever encountered tougher competition in soap fromP&G, though Lever's share of the total U.S. soap market grew to 11 per-cent in 1938. P&G launched a line of synthetic detergents, includingDreft, in 1933, and came out with Drene, a liquid shampoo, in 1934;both were more effective than solid soap in areas of hard water. How-ever, such products had "teething problems," and their impact on theU.S. market was limited until the war. Countway challenged P&G inanother area by entering branded shortening in 1936 with Spry. Thisalso was launched with a massive marketing campaign to attack P&G'sCrisco shortening, which had been on sale since 1912.20 The attack be-gan with a nationwide giveaway of one-pound cans, and the result was"impressive."21 By 1939 Spry's sales had reached 75 percent of Crisco's,but the resulting price war meant that Lever made no profit on the prod-uct until 1941. Lever's sales in general reached as high as 43 percent ofP&G's during the early 1940s, and the company further diversified withthe purchase of the toothpaste company Pepsodent in 1944. Expansioninto margarine followed with the purchase of a Chicago firm in 1948.

The postwar years proved very disappointing for Lever Brothers,for a number of partly related reasons. Countway, on his retirement in1946, was replaced by the president of Pepsodent, the thirty-four-year-old Charles Luckman, who was credited with the "discovery" of BobHope in 1937 when the comedian was used for an advertisement. Count-way was a classic "one man band," whose skills in marketing were notmatched by much interest in organization building. He never gavemuch thought to succession, but he liked Luckman.22 This proved amisjudgment. With his appointment by President Truman to head a food

18 Wilson, History of Unilever, vol. 1, 284-7 ; "History of Lever Brothers USA, 1912-1952," UAL.

19 Memo on Lever Brothers, c. 1964, UAL.20 The classic case study of the launch and marketing of Crisco is by Susan Strasser, Satis-

faction Guaranteed (New York, 1989).21 McCraw, American Business, 47-8.22 Special C o m m i t t e e Minu te s , 3 Aug. 1944, UAL.

Unilever in the United States, 1945-1980 / 443

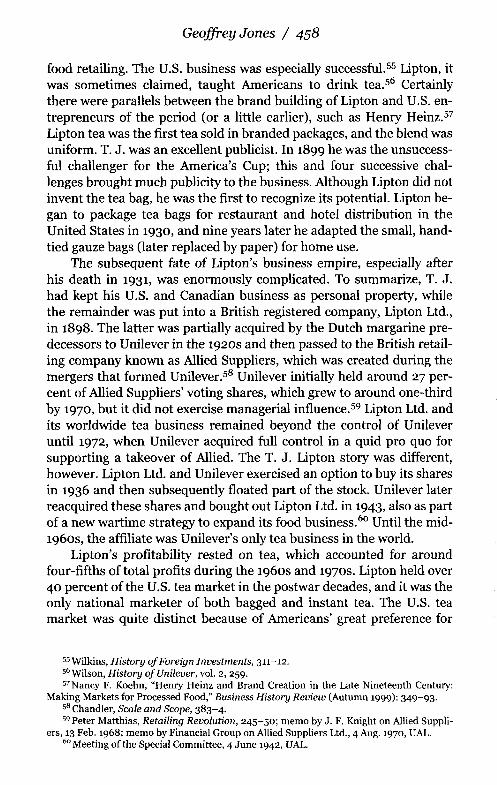

program in Europe at the same time, Luckman became preoccupiedwith matters outside Lever for a significant portion of his term, thoughperhaps not to a sufficient degree. Convinced that Lever's managementwas too old and inbred, he dismissed about 15 percent of the work forcesoon after taking office, and he completed the transformation by mov-ing the head office from Boston to New York, taking only around one-tenth of the existing executives with him.23 The head office, constructedin Cambridge by Lever in 1938, was subsequently acquired by MIT andbecame the Sloan Building.

Luckman's move, which was supported by a firm of managementconsultants, the Fry Organization of Business Management Experts,was justified on the grounds that the building in Cambridge was notlarge enough, that it would be easier to find the right personnel in NewYork, and that Lever would benefit by being closer to the large adver-tising agencies in the city.24 There were also rumors that Luckman,who was Jewish, was uncomfortable with what he perceived as wide-spread anti-Semitism in Boston at that time. The cost of building theNew York Park Avenue headquarters, which became established as a"classic" of the new postwar skyscraper, rose steadily from $3.5 mil-lion to $6 million. Luckman had trained as an architect at the Univer-sity of Illinois, and he was very involved in the design of the pioneeringNew York office.

While these events unfolded, P&G introduced a heavy-duty syn-thetic detergent called "Tide," which swept the market. By 1949 one outof four Americans did their laundry with Tide.25 Tide represented atechnological discontinuity in cleaning, which changed the nature ofthe market. It quickly surpassed Ivory Soap as P&G's flagship brand,and it set a new pattern, whereby P&G invested heavily in research tobuild a succession of premium consumer brands.

Lever Brothers lagged in the development of synthetics and had towithdraw its competitor product, Surf. By 1949 Lever was losing sales,which in constant dollars were more or less the same as in 1945. Lever'sperformance, shown in Table 1, can be contrasted with that of P&G,shown in Table 2. (Both tables give figures in nominal and constantdollars.) The failure in synthetics was not Luckman's fault, as their de-velopment was underestimated by Unilever. The Second World Warheld up research work on synthetics and delayed the establishment of

23 Luckman's autobiography presents his case for this episode. See Charles Luckman,Twice in a Lifetime: From Soap to Skyscrapers (New York, 1988), 202, 230-40.

24 George Fry a n d Associates , "Repor t on Relocat ion of H e a d q u a r t e r s , " A H K 2117, Uni -lever Historical Archives R o t t e r d a m (UAR).

25 Spencer Klaw, "The Soap Wars," Fortune (June 1963).

Geoffrey Jones / 444

Lever House, in New York City on Park Avenue between 53rd and 54th Streets, 1952. De-signed by the architectural firm Skidmore, Owings & Merrill, it set the standard for the glass-and-steel office towers in the United States that followed. (Photograph courtesy of theGottscho-Schleisner Collection, Library of Congress.)

production facilities in Europe.26 Unilever may have had a special diffi-culty because of its close research links with the German chemical com-pany I. G. Farben, which was broken up by the Allies after the end ofthe war.27 In the United States, Countway argued that nobody wouldbuy synthetic detergents. The total disruption of the company at this

26 P. A. R. Puplett, Synthetic Detergents (London, 1957), 59-60.271 owe this point to Ben Wubs.

Unilever in the United States, 1945-1980 / 445

Table 1Sales and Net Profits of Lever Brothers, 1945-1980

($ million and constant $ 1982-84 = 100)

Year

194519461947194819491950195119521953195419551956195719581959196019611962196319641965196619671968196919701971197219731974197519761977197819791980

Sales

150150220260200———

215235250282346383410389410413415437456434443454488525521527566669747753780861957

1,036

NetProfits

57

147

- 7———

- 4- 3

636

101511111013151569

1259

11136

1011124

- 1 1- 7

- 1 7

ConstantSales

833769986

1,079840———

805873933

1,0371,2311,3251,4091,3141,3711,3671,3561,4091,4431,3391,3261,3041,3291,3531,2861,2611,2751,3571,3871,3231,2871,3181,3221,257

ConstantNet Profit

28366329

- 2 9———

- 1 5- 1 1

22112135523737334242471827341423273116202021

7- 1 7- 1 0- 2 1

Geoffrey Jones / 446

Table 2Sales and Net Profits of P&G, 1945-1980

($ million and constant $ 1982-84 = 100)

Year

194519461947194819491950195119521953195419551956195719581959156019611962196319641965196619671968196919701971197219731974197519761977197819791980

Sales

342310534724697632861818850911966

1,0381,1561,2951,3691,4411,5421,6191,6541,9142,0592,2432,4392,5432,7072,9793,1783,5143,9074,9126,0826,5137,2848,1009,329

10,772

NetProfits

20214765296151424252575968738298

107109116131133149174202187212238276302317334401461512577643

ConstantSales

1,9001,5902,3953,0042,9292,6223,3113,0863,1833,3873,6043,8164,1144,4814,7044,8685,1575,3615,4056,1746,5376,9237,3027,3077,3767,6797,8478,4078,7999,963

11,30511,44612,02012,42312,85013,073

ConstantNet Profit

111108211270122253196158157193231217242253282331358361379423422460521580510546588660680643621704761785795780

19611972

1977

1914

12.5

4443

50

Unilever in the United States, 1945-1980 / 447

Table 3Shares of North American Market Detergents, 1961-1977

(in percent)

Date Lever P&G Colgate

101412

Source: Unilever Archives London (UAL). The 1961 figures refer to the United Statesonly. The other figures include Canada.

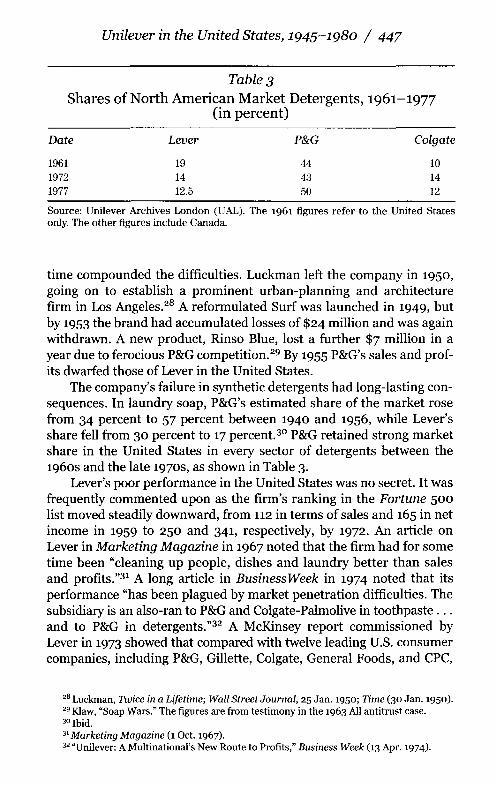

time compounded the difficulties. Luckman left the company in 1950,going on to establish a prominent urban-planning and architecturefirm in Los Angeles.28 A reformulated Surf was launched in 1949, butby 1953 the brand had accumulated losses of $24 million and was againwithdrawn. A new product, Rinso Blue, lost a further $7 million in ayear due to ferocious P&G competition.29 By 1955 P&G's sales and prof-its dwarfed those of Lever in the United States.

The company's failure in synthetic detergents had long-lasting con-sequences. In laundry soap, P&G's estimated share of the market rosefrom 34 percent to 57 percent between 1940 and 1956, while Lever'sshare fell from 30 percent to 17 percent.30 P&G retained strong marketshare in the United States in every sector of detergents between the1960s and the late 1970s, as shown in Table 3.

Lever's poor performance in the United States was no secret. It wasfrequently commented upon as the firm's ranking in the Fortune 500list moved steadily downward, from 112 in terms of sales and 165 in netincome in 1959 to 250 and 341, respectively, by 1972. An article onLever in Marketing Magazine in 1967 noted that the firm had for sometime been "cleaning up people, dishes and laundry better than salesand profits."31 A long article in BusinessWeek in 1974 noted that itsperformance "has been plagued by market penetration difficulties. Thesubsidiary is an also-ran to P&G and Colgate-Palmolive in toothpaste . . .and to P&G in detergents."32 A McKinsey report commissioned byLever in 1973 showed that compared with twelve leading U.S. consumercompanies, including P&G, Gillette, Colgate, General Foods, and CPC,

2 8 Luckman, Twice in a Lifetime; Wall Street Journal, 25 Jan . 1950; Time (30 Jan . 1950).29 Klaw, "Soap Wars ." The figures are from test imony in the 1963 All ant i t rus t case.3° Ibid.31 Marketing Magazine (1 Oct. 1967).32 "Unilever: A Mul t ina t iona l ' s N e w Route to Profits," Business Week (13 Apr . 1974).

Geoffrey Jones / 448

-2.00

-4.00

Figure l. Return on sales of Lever Brothers and P&G, 1945-1980 (in percent).

Lever ranked last in sales growth, return on assets, and return on salesbetween 1963 and 1973.33 (Figure 1 shows Lever's long-term poor per-formance compared with P&G's, measured in terms of return on sales.)Unilever's postwar difficulties in the United States were colorfully de-scribed in an article published in Fortune in May 1986, which notedthat the "world's biggest packaged goods company was a laughing stockin the world's biggest market." For forty years, the article continued,P&G had "easily won 45% to 50% of the market for just about anyhousehold product worth mentioning. Lever slumped to being an occa-sionally money-losing also-ran. In such products as deodorants, sham-poos, ice cream, and other frozen products, Unilever ranks no 1 or 2 onthe planet but is practically invisible in the United States."34

These decades before 1970 were notably successful for Lever'sgreat competitor, P&G, which diversified its product range, often ex-ploiting scope economies. Sales per unit volume doubled every decadeat the company. During the 1950s, P&G successfully entered the tooth-paste market and also paper products with the acquisition of CharminPaper in 1957. In classic P&G fashion, expertise was accumulated byacquisition, followed by internal development and learning. Twelveyears after the Charmin acquisition, Pampers disposable diapers werelaunched nationally. P&G essentially developed its products within thefirm in this period. It made no acquisitions between 1963 and 1980,mainly because of regulatory constraints imposed after antitrust ac-tions were brought against it after the company's acquisition in 1957 of

33 McKinsey & Co. to Thomas S. Carroll, 15 J a n . 1974, UAL.34 "Unilever Fights Back in the US," Fortune (26 May 1986).

Unilever in the United States, 1945-1980 / 449

Clorox Chemical, the largest U.S. manufacturer of household bleach,which it had to divest itself of ten years later.

There were several reasons why the once successful Lever businessexperienced such a prolonged decline. As a broad generalization, it canbe said that after the immediate postwar loss of momentum, the man-agement of Lever Brothers lacked the resources, confidence, and capabil-ity to invest in new products on a sufficient scale to reverse its position.Lever became trapped in a cycle of trying to sustain income by cuttingexpenditures on both brand support and manufacturing facilities. Thisfurther weakened brands and raised costs. The 1973 McKinsey reportestablished that six of Lever's thirty-one brands accounted for 74 percentof profits—but none of them held either first or second place in theirproduct categories—while at least eleven brands did not appear tocover their overheads. The lack of strong brands left Lever with highermarketing costs than P&G, while cost-cutting at factories and insuffi-cient funds for depreciation gave it higher manufacturing costs. By the1970s, if not earlier, Lever Brothers appeared to have higher manufac-turing costs than any of its competitors, except in toothpaste. This wasa bad situation to face in the 1970s, when the oil shocks sharply in-creased the prices of the chemicals used in soaps and detergents whilesimultaneously reducing consumers' willingness to pay for premium-priced brand names.35 The precise reason why Lever's managementwas so concerned with maintaining its bottom line can be debated, buta factor might have been the executive remuneration package—a phan-tom stock-option scheme—which may have discouraged long-term in-vestment in favor of short-term earnings performance.

A second weakness was lack of innovation. Lever's research labora-tory at Edgewater, New Jersey, was built in 1952 to centralize previouslywidely separated research operations. Over the following years it wasresponsible for several innovations beyond the large fabric-detergentsector: Dove, a completely new type of beauty soap, which containedcleansing cream, launched in 1955; Wisk, the first heavy-duty liquidlaundry detergent, in 1956; and Imperial, the first margarine with thetaste of a high-priced spread, in 1956. Lever's president between 1955and 1964, Bill Burkhart, had formerly worked for P&G and had a strongtechnology orientation. He closely monitored progress in research anddevelopment, meeting with research staff every week, and he also in-sisted on close integration between research and marketing functions.Meanwhile, the Lever research director was also highly market ori-ented. Lever's prolific generation of new products at this time reflectedthis high level of integration in the innovation process.

35 Editors of Advertising Age, The House That Ivory Built (Lincolnwood, 111., 1988), 33.

Geoffrey Jones / 450

After 1964 Burkhart's successors were drawn from the finance ormarketing sectors and were much less interested in long-term productdevelopment. Innovation at Lever Brothers slowed. The general patternwas that P&G innovated and Lever responded by trying to achieve in-cremental improvements in packaging and areas peripheral to productdevelopment.36 During the 1970s, spending on innovation was cut to apoint that research activity consisted of little more than the defense ofexisting businesses by combating regulatory initiatives and focusing oncost-saving activities. There were problems as well with the organiza-tion and quality of Lever's management. Through the postwar years,the basic organizational structure remained a unitary one, leaving se-nior managers responsible for a span of products from soap to tooth-paste to margarine and syrup. Detergents were the dominant product,attracting the best people, or at least the best people who wanted towork for Lever.37 Not surprisingly, a 1973 McKinsey report recom-mended the creation of three main product divisions.38 However, thecompany did not establish full divisions until 1980.

Within this context, the different product areas had somewhat dif-ferent experiences. Lever Brothers was primarily identified with deter-gents, which made up about 40 percent of its sales in the mid-1960s. In1957 Lever finally got into synthetics with the purchase of the All brandfrom Monsanto, leading to some improvement in market share at thecost of an antitrust suit, but P&G's market leadership was left un-scathed. P&G's market share in core product areas provided it withhigh profit margins and a solid base of earnings and cash generation.P&G's cash flow from detergents funded its diversification into otherproducts and its spending on innovation. Lever struggled throughthe 1970s to hold second place against Colgate. Its few new productlaunches only succeeded in taking volume from its existing businesses,and its market share drifted downward until the end of the 1970s. TheLever strategy was in effect to concentrate on the fringe products thatmade money, like Wisk, and soap bars, like Lifebuoy, Lux, and Dove,leaving the mainstream fabric-detergent business to P&G. In soap bars,Lever held 27 percent of the market in i960 and 17 percent in 1979, butthey only composed 13 percent and 7 percent, respectively, of the totalU.S. detergent market. Dove itself was adversely affected by the launchof Dove Liquid for dishwashing in 1965, which did not sell, forcingLever to cut its price. Dove ended up as a brand for a discount dish-

36 Memo concerning Unilever research in relation to the American business, M. Mum-ford, 20 July 1964, Special Committee Support ing Documents ; McKinsey Report, 1973, UAL.

37 Visit t o Nor th America, Sir Ernest Woodroofe's Report to the Board, 5 Oct. 1973, Con-ference of Directors Files, UAL.

38 McKinsey Report , 1973.

Unilever in the United States, 1945-1980 / 451

Table 4Unilever, P&G, and Colgate Trading Margins in

U.S. Detergents, 1962-1978

Date

1962-661967-7119721978

Unilever

7.33.371

P&G

15.113.91515

Colgate

1.41.822

Source: Detergents World Strategic Plan (July 1973); Corporate Strategy Advisory Com-mittee, "Background Paper: Detergents" (17 June 1983), ES 83173, Unilever ArchivesRotterdam (UAR).

washing liquid and a premium soap, and neither flourished until Dovebeauty soap was relaunched in 1979 with a medical marketing programclaiming that dermatologists had confirmed that it irritated skin lessthan other soaps. Over time Lever's falling market share became seri-ous. By the 1970s Lever's level of sales meant that it lacked the volumeto support its five detergent factories.

So far as Unilever could tell, its margins were consistently dwarfedby those earned by P&G in the U.S. market, though not by Colgate untilthe late 1970s. Table 4 gives Unilever's estimates of trading margins-profits as a percentage of sales—on detergents in the United States. TheP&G and Colgate figures were informed guesses, but the overall pictureseems clear.

Unilever as a whole had a problem with P&G during these years.Unilever was always a larger company worldwide than P&G, its portfolioof products was far wider, and it was active in many more countries.39

Beginning in the 1950s, Unilever's European business lost marketshare to the American company. Worldwide, Unilever's most profitabledetergent business operated outside North America and Europe. InAustralia, South Africa, Brazil, India, and many developing countries,Unilever held large market shares in detergents. During the 1970s, Bra-zil was Unilever's most profitable detergent business in the world. P&Ghad only a limited presence in such markets, arguably because—in thewords of one study—the firm was "comfortable only in advanced coun-tries."40 Certainly P&G does not seem to have been comfortable in de-veloping nations marked by high inflation and political instability,whereas Unilever was able to do well in these countries.

39 In 1950 Unilever's sales were $2 ,087 million and P&G's were $861 million. In 2 0 0 0Unilever's sales were $43 ,680 million and P&G's were $38,125 million.

40 The House that Ivory Built, 2 0 3 .

Geoffrey Jones / 452

Unilever's difficulties in competing against P&G in developed mar-kets had several causes. P&G's powerful position in the U.S. market en-abled it to take full advantage of scale economies and was very profit-able. Meanwhile, in Europe P&G was able to enter the market withnewer and fewer plants and brands than Unilever, which was burdenedby its historical legacy of factories and brands in every country. At thesame time, P&G's centralization enabled it to transfer brands like Tide,Fairy, and Crest, developed first in the United States, to European affil-iates. Unilever's decentralized structure made product transfers and in-novation generally a slower process. Although Unilever as a wholespent proportionally as much as P&G on research and came up withmany innovations, it persistently lagged in the launch of new detergentproducts.41

The two companies functioned in different fashions. P&G usedtechnology to deliver product benefits that consumers valued, and itwas notably centralized in its Cincinnati head office. Unilever's detergentbusiness had been developed by a Liverpool-based wholesaler, who em-phasized understanding the differences in markets and providingchoice. Unilever strongly believed in local autonomy for its affiliates.There were considerable differences in marketing management be-tween the two firms also. P&G's brand management system, developedafter 1931, was said to be partially inspired by observations of the chaosresulting from the competition between Unilever's brands in Europeduring the early 1930s. Unilever only adopted the brand-managementsystem sometime in the early 1960s, and even then the company's man-agers normally handled several brands. Unilever's decentralizationresulted in its having far too many brands, whereas P&G put more re-sources behind a limited number of "power brands." There was a markedcultural difference also. Nonperforming managers quickly left P&G.42

At Unilever, the prevailing culture before the 1980s was variously de-scribed as "clubby" or "cozy." A manager who was not very good mightnot be promoted, but some task would be found to enable him tocontinue working within the firm. As decisions were reached by con-sensus, it often took a long time to make them.

The "personal care" business was different from detergents. It rep-resented around 30 percent of Lever's sales in the mid-1960s. The cate-gory of personal care is amorphous, spanning products from toothpasteand shampoos to deodorants, skin creams, and perfumery. These prod-ucts thus had very different characteristics. While some had similaritiesto detergents, in the prestige end of cosmetics and perfumery, brand

41 "P&G in Nor th America, 1985," Misc. Competi tors : P&G, UAL.42 The House that Ivory Built, 88-9.

Unilever in the United States, 1945-1980 / 453

images built up over long periods were decisive. The prosperous post-war U.S. market provided an excellent environment for the growth ofsuch products, and these decades saw a rapid growth of firms likeAvon, Estee Lauder, Revlon, Max Factor, Elizabeth Arden, and Chese-brough Ponds.43 Unilever estimates suggested that North America ac-counted for nearly one-half of the total world personal care market inthe 1950s and 1960s. Following the purchase of Pepsodent, Lever'smain entry in the personal care business in the United States wastoothpaste. During the late 1940s, Colgate had established leadershipwith a market share of more than 40 percent. P&G entered the tooth-paste industry in 1953, and in 1956 launched Crest, the first anticavitiesproduct. Crest took off after the ADA's endorsement in i960, replacingColgate as the largest single brand in 1962. It took a market share ofover 35 percent in the United States for most of the 1970s, and proved along-lasting success.44

In the toothpaste market, Lever's fortunes fluctuated. For over adecade it relied on the Pepsodent brand, but in 1958 Lever introduceda new product after buying the rights from a New York inventor for amethod of making toothpaste come out of a tube striped like a candystick. "Stripe" was not entirely cosmetic, as it contained fluoride andmade therapeutic claims, but it was the novel appearance of the tooth-paste that set it apart. However, the timing of the launch in the UnitedStates was unfortunate, as it just preceded the American Dental Associ-ation's endorsement of Crest. Stripe's market share reached 8 percentin its second year and then declined. There were also technical failures:the toothpaste in one of three cases did not appear striped as it emergedfrom the tube.45 During the 1960s, Lever's toothpaste business lan-guished, in contrast to the achievements of the U.K. company, Beechams,which introduced Macleans, with its brand image of "whiteness," to theU.S. cosmetic market in 1962. In the mid-1960s Lever's total marketshare was down to 9 percent, behind P&G, Colgate, and even Beechams.

The Lever response was again to avoid a head-on clash with P&G.As Crest dominated the so-called therapeutic sector of the market,Lever focused on cosmetic products (around a third of the market). In1970 Lever launched a new gel, called "Close-Up," which it based on

43 For accounts of the growth of this industry in the United States, see especially KathyPeiss, Hope in a Jar (New York, 1998), and Philip Scranton, ed., Beauty and Business (NewYork, 2001). Nancy F. Koehn, Brand New (Boston, 2001) , has a chapter on the growth ofEst6e Lauder; and Richard S. Tedlow, Giants of Enterprise (New York, 2001) , discusses t heearly history of Revlon.

44 Salomon Brothers, P&G—The Ultra Consumer Products Company (New York:Salomon Brothers, 1995).

45 Report on Visit to USA, by H. M. Threlfall, March-Apr i l 1961, UAR.

Geoffrey Jones / 454

mmMew-flavor

ftpeodent!

sifKPKis&iWedcnf» flavorpnierced our new one, bandsAwn! To our surprise, fctrft m t ieroqt /or d/ What*s more, ftfamoia univerifty prowl P »̂~oodenf s ORAL DETERGENTgiv«i you the CIMMSI IMU of•II te«line toothj«at«! Pep«»dent is tn»anteed by LeverBrothen Company to pleaseyour whole family—or yourmoney bade

K M O K N f f e OML DETCAQSNT gives y»> the

CUANSSTTUTU' YSHTOHB proof i. tt>e

Clean Mooth Taste Hours

Advertisement for Pepsodent from New York Times, 1954. Lever Brothers diversified intotoothpaste with the purchase of the Pepsodent Company in 1944. This was Lever's onlytoothpaste brand in the United States until "Stripe" was launched in 1958. (Photograph cour-tesy Ad* Access On-Line Project-Ad #BH225i, John W. Hartman Center for Sales, Advertis-ing & Marketing History, Duke University Rare Book, Manuscript, and Special CollectionsLibrary, http://scriptorium.lib.duke.edu/adaccess/. Permission granted by Unilever.)

Unilever in the United States, 1945-1980 / 455

research in the United States on breath freshness. There was no compet-itor until Beechams came out with Aquafresh in 1979. P&G did not intro-duce its Crest gel until the early 1980s. Lever launched another brand,called "Aim," a few years later. Lever's share of the U.S. toothpaste mar-ket peaked at almost 24 percent in 1977, which put it alongside Colgatein second place in the market, though still behind the one-third shareheld by P&G. This did not translate into profits, however, in part be-cause advertising and marketing promotions had to be spread overLever's three brands of Pepsodent, Close-Up, and Aim.46

Lever was unable to develop a significant personal care businessbeyond toothpaste. Unilever was one of the world's largest shampoomanufacturers, and its Sunsilk was probably the world's best-sellingbrand of shampoo, but Lever Brothers only had a tiny shampoo busi-ness, whose market share peaked at 3.3 percent in 1971 before beingphased out some years later. Lever Brothers had also experiencedmisfortunes when trying to invest in postwar "permanent-wave kits,"designed to enable women to wave their own hair at home. In 1947Luckman had proposed the purchase of a firm called "Toni ColdWave" for $8 million, but this had been turned down by Unilever,which considered the fashion-related business as too risky.47 In thefollowing year, however, he was allowed to make a $1.6 million pur-chase of Rayve, a cream shampoo, and Hedy Home Permanent Wave,a wave mixture. By 1950 these ventures had recorded losses of $1.5million and held national market shares of less than 7 per cent, com-pared with the 80 percent held by Toni, which had by then been acquiredby Gillette.48

In 1947 Lever had also paid $1.4 million for Harriet Hubbard Ayerof New York. This was America's oldest cosmetic firm. It had beenstarted by an American working in late-nineteenth-century Paris andhad operations both in the United States and France. The business didnot flourish inside Lever. By 1949, losses had reached $4 million, and itwas sold in 1954, though the European operations were retained underthe control of French Unilever.49 From the 1960s on, Lever's directorsdiscussed making another acquisition in this product area, but the in-dustry was fragmented and firms were usually family owned or closelyheld. Large acquisitions were also considered impractical because ofLever's poor performance. Chesebrough Ponds, a favorite candidate as

46 "Competition in the US Toothpaste Market, 1960—1985," Unilever Economics Depart-ment Paper ES 86073, UAR.

47 Special Committee Minutes, 3 Aug. 1947, UAL.48 Special Committee Minutes, 1 July 1948, UAL; Wall Street Journal, 25 Jan . 1950.49 Wilson, The History of Unilever, vol. 3,199.

Geoffrey Jones / 456

far back as 1970, was considered at that time to be "out of reach."50 Notuntil 1986, when Unilever did acquire Chesebrough Ponds, was a majoracquisition actually carried out.

Food, which accounted for less than 15 percent of Lever turnover inthe mid-1960s and was mainly centered in margarine, was the least suc-cessful of all the product groups. Unilever was the largest margarine busi-ness in Europe and the world. Based on a cluster of research and devel-opment laboratories and factories near Rotterdam, Unilever in Europepursued, after the late 1950s, a successful strategy of splitting a homoge-neous market into a segmented one. A flow of new products and brandsemphasized both the health and indulgent dimensions of the product.

There was no sign of such dynamism in Lever Brothers. Its entryinto margarine had occurred in 1948 through the purchase of the firmof Jelke in Chicago for $4.5 million, shortly after some of the legal re-strictions on the product's manufacture and sale in the United Stateshad been removed when the federal margarine taxes were abolished.This was not a product in which P&G ever invested, and in his auto-biography Luckman blamed Unilever in Europe for the purchase. Tightregulations on margarine remained in the United States, which meantthat it could only be sold in its natural white form to preclude its beingmistaken for butter.51 The business got off to a rocky start, when itemerged that the former owner had also been engaged in the prostitutionbusiness, rapidly causing "Jelke's Good Luck Margarine" to be renamed"Good Luck Margarine." However, the introduction of Imperial marga-rine in the mid-1950s made Lever the second largest brand in the UnitedStates: with 5 percent of the market in 1965, it was just ahead of Kraft'sParkay and behind Standard Brand's Blue Bonnet, which had over 9 per-cent. However, Imperial's fortunes waned after this point, a problemworsened by the company's failed attempt to diversify. By 1980 Lever'stotal share of the U.S. margarine market was 7 percent, compared withParkay, which had 14 percent, and Blue Bonnet, which had 11 percent.

Lever's margarine business by the 1970s persistently broughtlosses. Between 1975 and 1980, its food division lost Lever $120 million.The core problem was an uncompetitive cost structure arising fromhigh production, plant overhead, and warehousing costs, and from majordiseconomies of scale, which obliged Imperial in the 1970s to sell at a pricepremium of approximately 13 percent above its major competitors.52

50 "Unilever in Nor th America. Some Financial Possibilities and Impossibilities," C. Sten-h a m , 3 Nov. 1970, UAL.

51 Luckman, Twice in a Lifetime, 219.52 Lever Brothers Company, U.S. Foods Division, Margar ine Business Proposal, Paper

7861, p repa red for Special Commit tee Meeting, 12 Dec. 1980, UAL.

Unilever in the United States, 1945-1980 / 457

Around two-thirds of production took place in Hammond, Indiana, andthe remainder in Los Angeles. Hammond's facilities were wholly obso-lete, resulting in Lever's costs being higher than its selling price. Thelack of transfer of technological and other capabilities from Unilever'sEuropean margarine business was a striking example of the "sticki-ness" of knowledge within the firm.

Lever's attempts to build a wider foods business largely floundered.In the late 1950s, Mrs. Butterworth's, a maple-flavored syrup contain-ing butter, was launched and became a modest success. Unilever wasfascinated by the rapid growth in the U.S. market for convenience foodsduring the late 1950s.53 However, little was achieved by purchases ofsmall, not especially distinctive, firms like Dinner-Redy, which sup-plied precooked sliced meat and poultry products. Lever tested themarkets for dehydrated fruits, dehydrated potatoes and peas, and pack-aged desserts, but by 1963 the company abandoned foods entirely, ex-cept for Mrs. Butterworth's syrup.54

The three decades after 1945, therefore, saw Lever Brothers lose itsonce strong market position in the United States. It had become trappedin lowly second place to P&G in detergents, had no personal care busi-ness except toothpaste, and had an unprofitable margarine business.The contrast with the successes of the interwar years was extraordinary.

T. J. Lipton: Exploiting Brand Equity in Tea and Soup

During the postwar decades, a curious feature of Unilever's U.S.business was its division into two separate businesses that maintainedremarkably little contact with each other and recorded very different fi-nancial performances. The second affiliate was the food and beveragecompany, T. J. Lipton, which in 1986 was spotlighted as only one of twoFortune 500 companies that had increased sales and income for eachof the previous thirty-five years. Lipton operated in different marketconditions than Lever. The U.S. food industry had dominant firms inparticular products, such as canned soup and canned meat, but therewas no dominant player across the sector that matched P&G or Colgate.Many food products were fragmented among numerous regional com-panies. In the U.S. tea market, Lipton was the leading firm.

T. J. Lipton originated as part of the tea group built up by SirThomas Lipton in the late nineteenth century. Around 1889 Lipton, aBritish grocer, diversified into tea trading, which expanded rapidly inmany countries except the United Kingdom, where the business remained

53 Notes o n Visit to t h e Uni ted States of Amer ica , A p r i l - M a y 1957, AHK 2118, UAR.54 Notes on Visit to the United States and Canada, 8-25 Feb. 1963, AHK 2118, UAR.

Geoffrey Jones / 458

food retailing. The U.S. business was especially successful.55 Lipton, itwas sometimes claimed, taught Americans to drink tea.56 Certainlythere were parallels between the brand building of Lipton and U.S. en-trepreneurs of the period (or a little earlier), such as Henry Heinz.57

Lipton tea was the first tea sold in branded packages, and the blend wasuniform. T. J. was an excellent publicist. In 1899 he was the unsuccess-ful challenger for the America's Cup; this and four successive chal-lenges brought much publicity to the business. Although Lipton did notinvent the tea bag, he was the first to recognize its potential. Lipton be-gan to package tea bags for restaurant and hotel distribution in theUnited States in 1930, and nine years later he adapted the small, hand-tied gauze bags Qater replaced by paper) for home use.

The subsequent fate of Lipton's business empire, especially afterhis death in 1931, was enormously complicated. To summarize, T. J.had kept his U.S. and Canadian business as personal property, whilethe remainder was put into a British registered company, Lipton Ltd.,in 1898. The latter was partially acquired by the Dutch margarine pre-decessors to Unilever in the 1920s and then passed to the British retail-ing company known as Allied Suppliers, which was created during themergers that formed Unilever.58 Unilever initially held around 27 per-cent of Allied Suppliers' voting shares, which grew to around one-thirdby 1970, but it did not exercise managerial influence.59 Lipton Ltd. andits worldwide tea business remained beyond the control of Unileveruntil 1972, when Unilever acquired full control in a quid pro quo forsupporting a takeover of Allied. The T. J. Lipton story was different,however. Lipton Ltd. and Unilever exercised an option to buy its sharesin 1936 and then subsequently floated part of the stock. Unilever laterreacquired these shares and bought out Lipton Ltd. in 1943, also as partof a new wartime strategy to expand its food business.60 Until the mid-1960s, the affiliate was Unilever's only tea business in the world.

Lipton's profitability rested on tea, which accounted for aroundfour-fifths of total profits during the 1960s and 1970s. Lipton held over40 percent of the U.S. tea market in the postwar decades, and it was theonly national marketer of both bagged and instant tea. The U.S. teamarket was quite distinct because of Americans' great preference for

55 Wilkins, History of Foreign Investments, 311-12.56 Wilson, History of Unilever, vol. 2, 259.57 Nancy F. Koehn, "Henry Heinz and Brand Creation in the Late Nineteenth Century:

Making Markets for Processed Food," Business History Review (Autumn 1999): 3 4 9 - 9 3 .58 Chandler, Scale and Scope, 3 8 3 - 4 .59 Peter Matthias, Retailing Revolution, 2 4 5 - 5 0 ; memo by J. F. Knight on Allied Suppli-

ers, 13 Feb. 1968; memo by Financial Group on Allied Suppliers Ltd., 4 Aug. 1970, UAL.60 Meeting of the Special Committee, 4 J u n e 1942, UAL.

Unilever in the United States, 1945-1980 / 459

convenience products and, beginning at least in the 1930s, it was alsonotable for the fact that at least three-quarters of the tea consumed wasdrunk iced. T. J. Lipton held a dominant position in the southernstates, where most of this iced tea was consumed. Tea can be regardedas a classic advertising-intensive business, in which the market sharesof long-established brands are very hard to overcome.61 The sunk costsof establishing names like T. J. Lipton as leading brands presented for-midable barriers to entry, especially as tea is a "traditional" product, inwhich reputation and heritage are critical factors in consumer choice.The Lipton tea brand provided a brand franchise of superior quality onwhich high profit margins could be earned.

The Lipton brand was exploited by line and brand extensions andsupported by technical innovation and extensive advertising. Shortlyafter the end of the war, Lipton got the exclusive U.S. rights to a devicethat became the flow-through teabag, which was introduced in 1952. Byincreasing the brewing surface of tea bags, this innovation overcamethe problems of flavor, packaging, and bag strength that had previouslyrestricted the popularity of tea bags, though their sales were seasonal inthe United States because of Americans' dislike of hot tea in summer.Lipton was rather slower to come up with innovations for instant tea,enabling Nestle's Nestea to take the largest market share in the 1960s,but in other products Lipton introduced a string of line extensions. In1966 a low-calorie iced tea was introduced, followed by Iced Tea in aCan in 1972. Later in the decade, flavored, herbal, and special blendswere developed. Flavored-leaf tea products with a storage life of twelvemonths were made possible by the development between 1974 and 1977of tea particles—or "prills"—containing encapsulated volatile flowersthat could be blended with leaf tea. This enabled the flavors to be stabi-lized in tea bags, and the flavor prills formed the basis for Lipton's fla-vored teas.62 Lipton's overall strategy was to deny entry points to pos-sible competitors by introducing flanker products whenever a reasonablemarket opportunity was shown to exist. Herbal teas were introduced in1980: the first herbal tea to be marketed through normal grocery out-lets by a major manufacturer.

In marketing, Lipton faced the problem that tea had a conserva-tive image and was often associated with the older generation. Conse-quently, a lot of money was spent promoting tea as a dynamic andyoung beverage. Building on T. J.'s yacht racing, Lipton tea commer-cials in the 1970s used sports personalities to enhance the image of

61 John Sutton, Sunk Costs and Market Structure (Cambridge, Mass, 1991).62 W. J. Beck, History of Research and Engineering in Unilever, 1911—ig86 (Rot terdam,

1996), 3,12-

Geoffrey Jones / 460

Coolest drink under the sun

NMttI«e cook you off like Upton kwdTe. ' Andthi yt>« mxb a «ft at the M M tun*!

*rw* flavor worta botfa wemfem « -you Hn no otfaonRmuwtiRM drink...pick*

you up without letting you down.Make it * h*bit anytime you fed t w n and

wtmry,*tap *nd enjoy a ftwty ft** of

Better ixaazm it's feint.'And ttoiftior tli*n moM «uomertirae d

LIPTON W ^ i ICED TEAAdvertisement for Lipton iced tea in the mid-1950s. Lipton allegedly "taught Americans todrink tea." In the post-World War II decades it held a dominant share of the iced-tea market.(Photograph courtesy of Unilever.)

tea, supplied tea to the Olympic games and sports events and, towardthe end of the decade, to the North American Soccer League.63

Lipton expanded successfully into two other products, soup andsalad dressings, which provided the nontea residual of the profits. Thesoup business came with the acquisition of Continental Foods in 1940.After the Lipton name was added to the brand, sales grew rapidly.There was also considerable innovation in soups, especially Cup-A-Soup launched in 1970-71, the first brand to solve the formidable tech-nical problems of providing a "respectable-tasting" instant soup. Dur-ing 1973, its first year of going national, Cup-A-Soup generated $36.5million in net sales and made a pretax profit of over $3 million. It helda dominant share of the U.S. instant-soup market by 1975. The launchof a Nestle competitor product, Souptime, that year dented this position,but within six years Nestle had withdrawn and Lipton emerged in the1980s as the market leader. Finally, in 1957 Lipton had purchasedWish-Bone Salad Dressing, a midwestern business that Lipton ex-panded nationally and then built up through line extensions, whichincluded low-calorie products.

63 Sundry Foods and Drink Co-ordination Marketing and Sales Directors' Visit to T. J.Lipton, Inc., April-May 1979, UAL.

Unilever in the United States, 1945-1980 / 461

Table 5 shows the performance of T. J. Lipton between 1945 and1980, and Figure 2 compares its returns on sales with those of LeverBrothers.

The obvious question is why Lipton performed so much better thanLever. The answer was not that it received outside assistance from Uni-lever, for Unilever had no business in tea outside North America untilthe 1970s. Clearly, Lipton developed considerable skills and competen-cies in its core product areas. It had a distinctive cohesive "feel," per-haps stimulated by the continuity in its top management that grew outof having only three presidents between 1939 and 1988 and by the factthat all its corporate functions, from marketing to research and devel-opment, were centralized in one complex at Englewood Cliffs, New Jer-sey. Meanwhile the high earnings from the tea business attracted acadre of good managers and a kind of confident atmosphere—the oppo-site of the spiral of decline seen at Lever.

The question that arises with Lipton is the quality of its competen-cies as a U.S. food business, quite aside from its effectiveness as an ex-ploiter of the brand name, Lipton. From the 1960s on, Lipton pursueda strategy to broaden the basis of its business by diversifying beyondtea, soup, and salad dressings into other foodstuffs. By the 1970s,other foodstuffs amounted to a third of total sales, but collectivelytheir contribution to profits was negative. A series of attempts to intro-duce new products, such as Lemon Tree Lemonade Mix and, in 1975, aburger with a soy-protein additive, did not succeed, and by 1979 Liptonhad lost about $20 million on such ventures over the previous decade.64

Diversification through acquisition proved equally problematic.The credibility of the Lipton brand name in tea and soup did not extendfurther. From 1961 onward, when it bought the ice-cream companyGood Humor, Lipton made regular acquisitions of companies in manyfood products, including noodles, cat food, spaghetti, and snacks, butalmost all were unsuccessful. Thus the Tabby cat food business, ac-quired in 1969 for $19 million, began to lose market share immediatelyafter its purchase, and by the mid-1970s it was stranded with less than3 percent of the market for gourmet cat food. Subsequently, a new catproduct, Tasty Dinners, failed entirely, and the whole business had tobe closed. The company's difficulties could be described under theheading of one general problem: Lipton's acquisitions followed the broadstrategy of identifying a regional brand that appeared to have the potentialto sell in the national market but ended up not succeeding outside theregion, as its salad dressings had once done.

64 "US Lipton. Background Material for Strategic Issues," Unilever Economics Depart-ment, Oct. 1980, UAL.

Geoffrey Jones / 462

Table 5Sales and Net Profits of T. J. Lipton, 1945-1980

($ million and constant $ 1982-84 = 100)

Year

194519461947194819491950195119521953195419551956195719581959196019611962196319641965196619671968196919701971197219731974197519761977197819791980

Sales

2327314048586269758187949496102108130140143151166193211229251276308403403437465513574617698798

NetProfits

0.510.61242233355667788911131415161718191922242831333843

ConstantSales

128138139166202240238260281301325346334332350365435464467487527596632658683711760964908886866902947945965968

ConstantNet Profits

3535715799121118191921232525253035404243444444454347454951505252

Unilever in the United States, 1945-1980 / 463

6.00

4.00

2.00 -

0.00

-2.00

-4.00

Figure 2. Return on sales of Lever Brothers and Iipton, 1945—1980 (in percent).

The most serious failure was Good Humor ice cream, whichcaught on primarily in the big cities on the East Coast in the 1960s and1970s but failed to sell in supermarkets in the form of multipacks.65

The business showed a loss in 1968 and continued to lose money everyyear until 1984. Good Humor closed down its street-vending businessin the late 1970s, and by the early 1980s had closed two of its threeplants. Total sales of Good Humor ice cream were still only $27.5 mil-lion in 1981, and they remained concentrated in New York, Chicago,Baltimore, and Washington, D.C. In effect, Lipton had a token pres-ence in the world's largest ice-cream market, where per capita con-sumption was four times the European average. This was a strange sit-uation, as Unilever had a long-established, substantial ice-creambusiness in Europe.

It is evident that Lipton's competencies in innovation and manage-ment were narrowly confined to a certain range of products, notablytea. It had a real problem as well with the strategy of acquiring smallcompanies, which were difficult to grow into big ones. It is evident thatLipton's management did not want to make big acquisitions or big in-vestments in product areas like ice cream. Lipton's profits from teaprovided no urgent incentive for growth through diversification; indeedthey were a positive disincentive. The Lipton brand was an excellentfranchise in the United States. Lipton could as a result earn high mar-gins over long periods, subject only to the constraint that tea competedwith many other beverages and was not a fast-growing market. The dis-advantage was that tea was too profitable for management to contem-

65 Pim Reinders, Licks, Sticks and Bricks (Rotterdam, 1999), 239.

Geoffrey Jones / 464

A display of Tabby cat food products in 1976. In 1969 T. J. Lipton acquired Usen Productsand its Tabby cat food business. This was a regional canned cat food operation, which Liptonwas unable to expand nationally. Tabby, which is no longer a Unilever brand, began to losemarket share from 1969, and by the mid-1970s it held less than 3 percent of the nationalmarket for gourmet cat food. (Photograph courtesy of Unilever.)

plate risky or large acquisitions. A former executive interviewed inBusinessWeek in 1983 put it like this: "For a long time, there was nourgency to grow. . . . The tea business was so profitable that it slowedLipton down in new products."66

Lipton, then, stood in contrast to Lever as an important source ofprofits for Unilever in the United States, and, by the mid-1970s, as theonly source of profits. However, Lipton remained a medium-sized U.S.food company. As a result, while Unilever was a world leader in icecream and frozen products, it remained wholly insignificant in theworld's largest ice-cream and frozen-products market.

Unilever and the United States:Ownership without Control

There were a number of reasons why Unilever should have beenconcerned about the performance of its business in the United States

"lipton Goes on the Offensive," Business Week, 5 Sept. 1983.

Unilever in the United States, 1945-1980 / 465

and why it should have been expected to intervene in some fashion. TheUnited States, the world's richest consumer market, was a diminishingsource of sales and profits between 1945 and the late 1970s. Whereas in1945 one-fifth of Unilever's worldwide sales came from the UnitedStates, by 1977 the proportion had shrunk to 2 percent. There was noquestion of "transfer prices" or other distortions disguising Lever's per-formance. Lever's profitability really was bad. Lever did pay dividends,but by the 1970s these were little more than Unilever received from In-donesia, far smaller than those from South Africa, and tiny comparedwith those earned by its West African trading company, the United Af-rica Company. Low profitability in the United States left Unilever relianton its European home region—a mature market hit since the 1970s byrecessions and unemployment—and politically risky emerging markets.

A second issue was that Unilever did not take advantage of the pos-sibilities for innovation that existed in the United States. The problemwas less in foods, where Lipton was a significant innovator, at least intea and soup, than elsewhere. In detergents, and perhaps even more inpersonal care products, the United States was a major source of innova-tion. Household appliances were much more widely distributed in theUnited States than in Europe, resulting in many innovations associatedwith their use. The much greater use of tumble dryers and dishwashersmeant that fabric softeners and dishwashing detergents for these appli-ances were pioneered in the United States.

Third, in an oligopolistic industry like detergents, Unilever's weak-ness in the United States could be exploited by its U.S. competitorselsewhere. By the late 1950s, Unilever's U.S. competitors were invest-ing in Europe, especially in response to European integration. Unileverwas aware of the threat but underestimated the scale of the challenge.67

In the postwar decade, Unilever had dominated the European deter-gent market, though it had significant competition from Henkel,among others. In the mid-1960s, while Unilever's share of Europeandetergents was around 28 percent, P&G had around 13 percent andHenkel and Colgate each controlled under 10 percent. By the 1980s,when market positions had stabilized, Unilever and P&G were equal,with around 20 percent.68 P&G was able to draw resources from theUnited States for use in Europe, safe from any serious challenge byLever Brothers.

In view of the consequences of the U.S. situation for Unilever'sbusiness, it is surprising that the parent company's role in the affairs ofits U.S. affiliates remained passive until the late 1970s. The manage-

67 Report by Lord Heyworth at the Directors Conference on 9 J a n . 1959, UAL.68 "Detergents Co-ordination Longer Te rm Plans," UAL.

Geoffrey Jones / 466

ments of Lever and Lipton had considerable autonomy. They reporteddirectly to Unilever's three-person Special Committee rather than com-municate through its London- and Rotterdam-based managementproduct groups, using the same conventions in which they made theirlocal reports. This meant, among other things, that the chairmen of theU.S. companies discussed and presented their results to local head-quarters, while the Special Committee looked at them after they wereconverted to the Unilever financial reporting system.69

There was remarkably little contact between personnel across theAtlantic. Visits by Unilever executives to the United States were closelyregulated and rationed on the American side. Many Unilever executiveslater remembered that, in the 1960s and 1970s, senior European man-agers in the United States would sit in waiting rooms because their U.S.counterparts were "too busy" to see them. There was minimal inter-change of personnel. In 1976 Unilever's Personnel Division noted that"the one and only place in the entire Unilever world of which PersonnelDivision had no knowledge whatsoever of the personnel arrangementsof the companies was the United States of America."70 This was a sig-nificant statement in a company that was already very advanced in de-veloping an international cadre of managers and had considerable ex-perience in sending nationals of many countries to foreign posts.

There was no real exercise of authority by London and Rotterdamover the U.S. affiliates. When the British chairman of Unilever sug-gested in 1971 that the European-based product managers become in-volved in strategy discussions in the United States, the president of Lip-ton replied that "he would not want anyone who did not know theAmerican market instructing him on how he should conduct the busi-ness."71 While Lipton's profits, if not its unsuccessful ventures into icecream and cat food, might justify such a stance, the similar attitude bythe Lever management was less explicable.

The distinctiveness of this situation needs careful definition. ManyU.S. companies operating abroad in the postwar decades had problemslike those of Unilever in the United States in establishing "control" overforeign affiliates, selecting the right nationality to manage them, and soon. Stopford and Wells's sample of 187 large U.S. multinational enter-prises (MNEs) active in the mid-1960s showed a pattern whereby firmsmoved along an organizational spectrum from autonomous subsidiariesto international divisions to global structure. The first stage reflected thefact that many U.S. firms had "stumbled into manufacturing abroad

69 Memo by Maurice Zinkin to Special Commit tee on Report ing Ar rangemen t s -Nor thAmerica, 5 Feb. 1976, UAL.

70 Minutes of t he Special Commit tee , 9 Sept. 1976, UAL.71 "Dr. Woodroofe ' s Visit to USA," Report to the Board, 17 Sept. 1971.

Unilever in the United States, 1945-1980 / 467

without much design."72 Unilever, however, by this period had a longhistory of widespread multinational businesses.

Within this general context, there were three reasons why Unilevercontinued to manage its U.S. divisions while holding them at a dis-tance. First, Unilever was a highly decentralized organization. Like al-most all European firms in the postwar decades, the legacy of interwarprotectionism, the war, and exchange controls was a decentralized or-ganizational structure that delegated to national managers a high de-gree of responsibility. As early as 1952, Unilever had begun formingproduct groups in Europe, known as "Co-ordinations," in order toavoid even a hint of P&G-style centralization. However it was not until1966 that the role of Co-ordinators, the senior executives—usuallydirectors—who headed these groups, became more than advisory, whenthey were given profit responsibility in some European countries. Itwas not until 1972, after a big McKinsey investigation, that their execu-tive authority was fully confirmed, and then only for Europe. Elsewheremanagement groups were regional rather than product based. Thereaf-ter local and consensus-style management remained a hallmark of thefirm. Indeed, Unilever believed that local responsiveness formed theheart of what would be later termed its "core competence." Such decen-tralization in Unilever and similar firms is likely to have slowed the dif-fusion of innovation, though as Sumantra Ghoshal and Christopher A.Bartlett and others have shown, the issues are complex ones.73

Second, and within this general context, there was popular belief inthe uniqueness of the United States and the superiority of its manage-ment. This was a widely held conviction in postwar Europe, where theU.S. victory in the war was generally perceived to have been based on asuperior business and political system.74 Within Unilever, the out-standing interwar success of Lever had reinforced the belief that Amer-ican managers had enormous potential. This was the strong convictionof Unilever's British chairman in the 1940s and 1950s, Geoffrey Hey-worth, who felt that British business was lagging behind that of theUnited States and had much to learn from it.75 This was the conven-tional wisdom at the time. In 1950, London's Financial Times, re-sponding to speculation that Unilever intended to exert more directcontrol over Lever Brothers, was moved to observe that "the idea of

72 John M. Stopford and Louis T. Wells, Managing the Multinational Enterprise (Lon-don, 1972), ch. 2.

73 Ghoshal and Bartlett, "Creation, Adoption, and Diffusion."74 M. Kipping and O. Byarnar, eds., The Americanization of European Business (London,

1998); J. Zeitlin and G. Herrigal, eds., Americanization and its Limits (Oxford, U.K., 2000).75 Comments by Charles Wilson, in Geoffrey Heyworth, Baron Hey worth of Oxton. A

Memoir (London, 1985).

Geoffrey Jones / 468

having absentee landlords in London and Amsterdam shaping policyfor a fiercely battling business in the United States is a sure way of help-ing Lever's competitors. . . . [T]he widest measure of home rule shouldbe given to their subsidiaries."76