Measuring Vaccine Confidence: Introducing a Global Vaccine Confidence Index

Upload

khangminh22Category

view

0download

0

Annual Report

2017

Confidence In Tomorrow

Confidence In Tomorrow

His Highness Sheikh Tamim bin Hamad Al-ThaniEmir of the State of Qatar

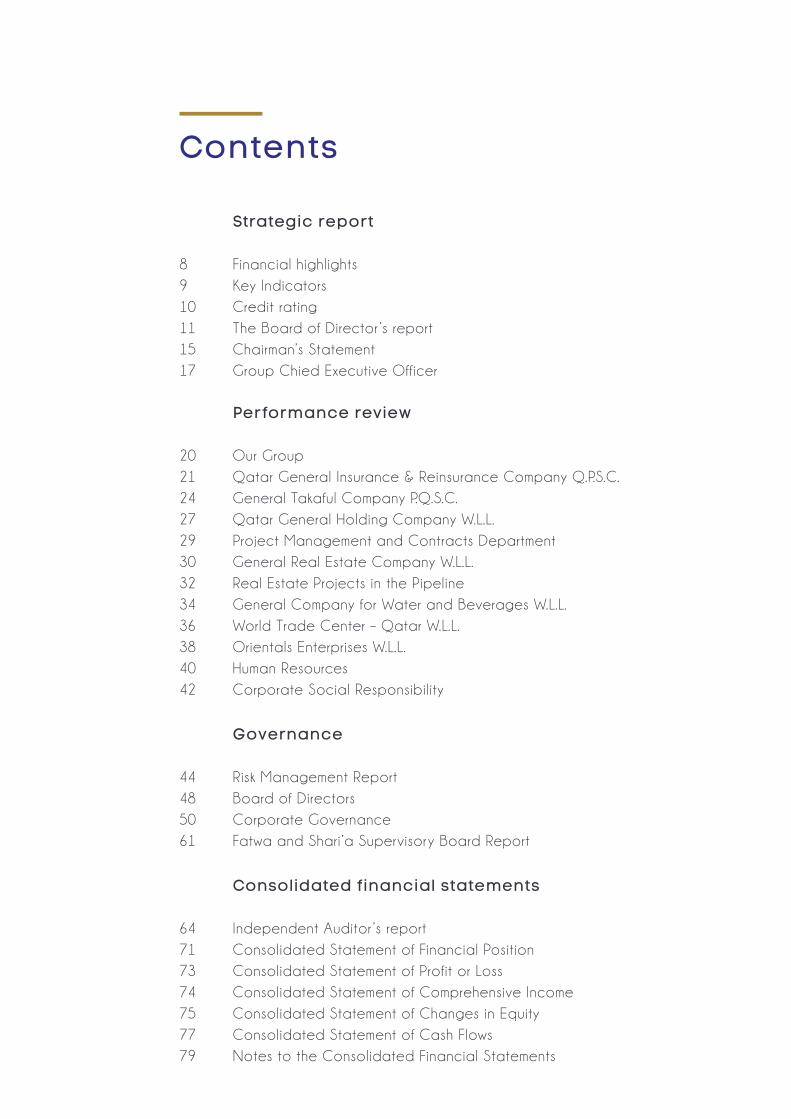

Strategic report

Financial highlights

Key Indicators

Credit rating

The Board of Director ’s report

Chairman’s Statement

Group Chied Executive Officer

8

9

10

11

15

17

Performance review

Our Group

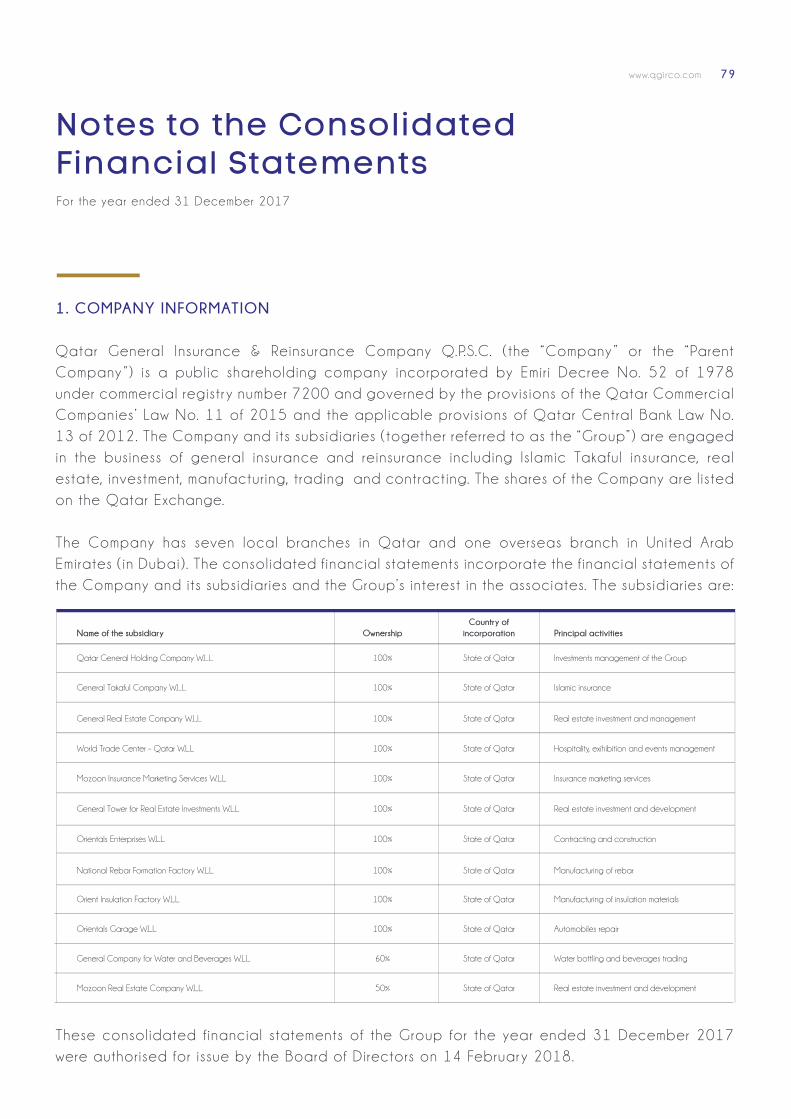

Qatar General Insurance & Reinsurance Company Q.P.S.C.

General Takaful Company P.Q.S.C.

Qatar General Holding Company W.L.L.

Project Management and Contracts Department

General Real Estate Company W.L.L.

Real Estate Projects in the Pipeline

General Company for Water and Beverages W.L.L.

World Trade Center – Qatar W.L.L.

Orientals Enterprises W.L.L.

Human Resources

Corporate Social Responsibility

20

21

24

27

29

30

32

34

36

38

40

42

Governance

Risk Management Report

Board of Directors

Corporate Governance

Fatwa and Shari ’a Supervisor y Board Report

44

48

50

61

Consolidated financial statements

Independent Auditor ’s report

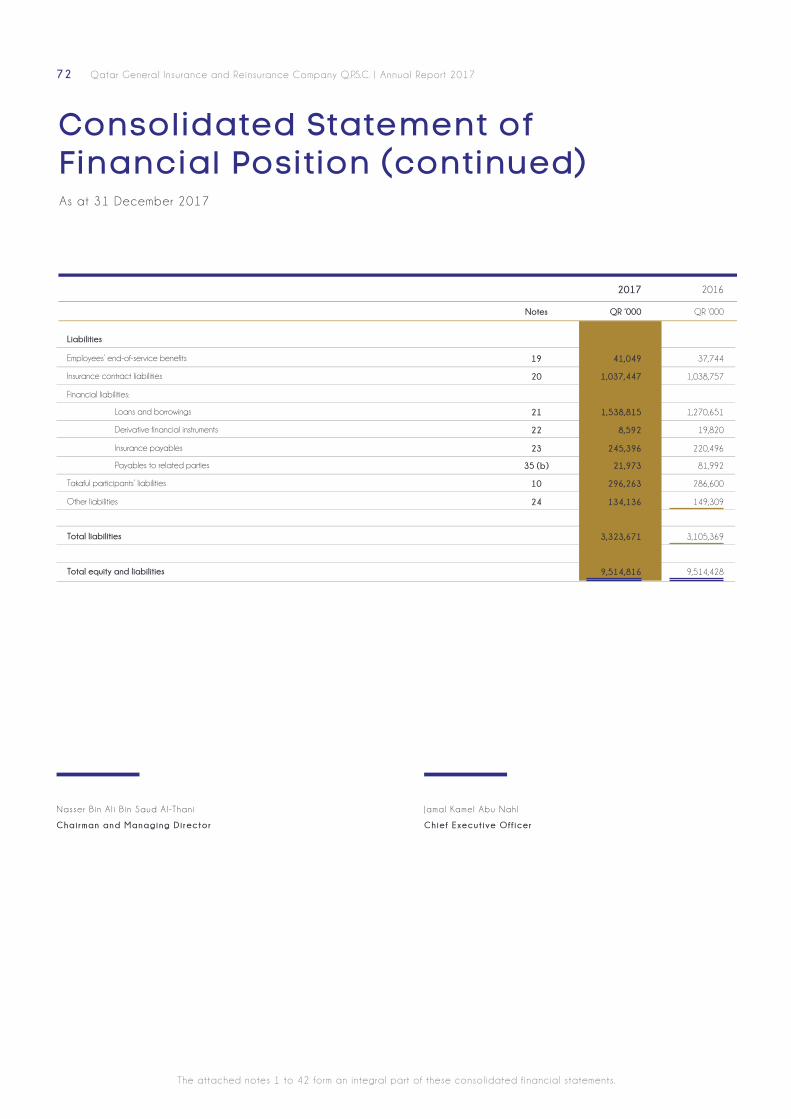

Consolidated Statement of Financial Position

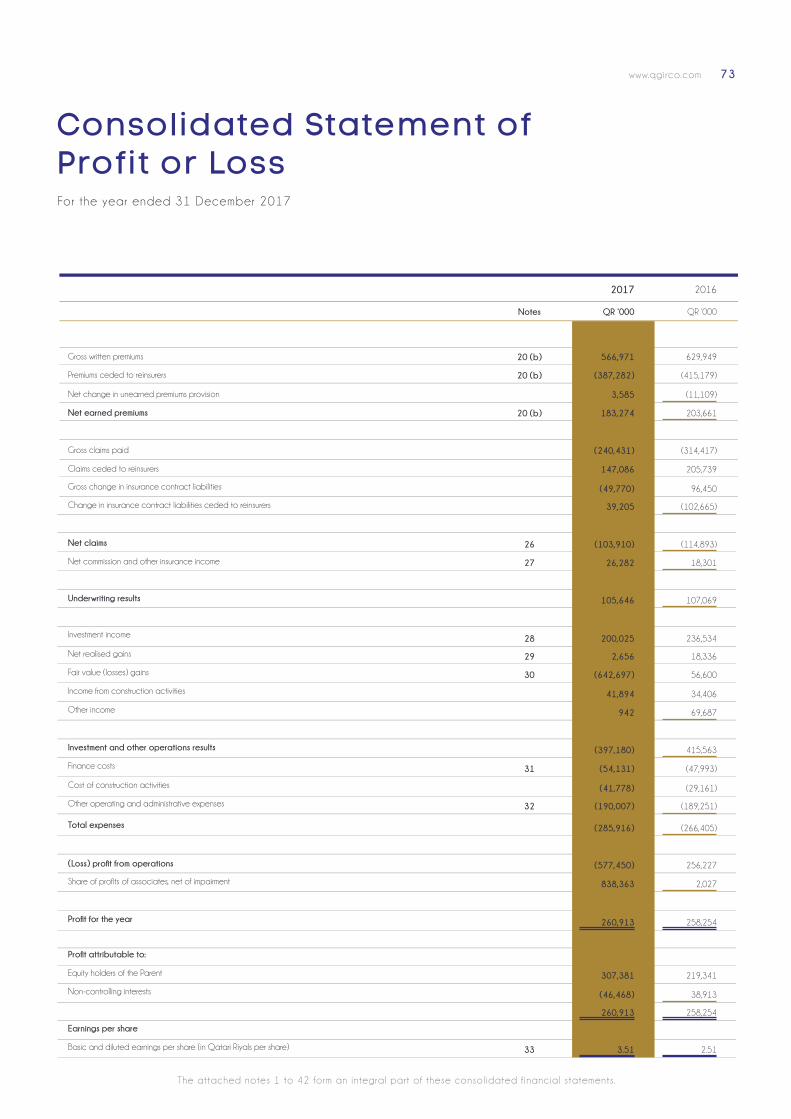

Consolidated Statement of Profit or Loss

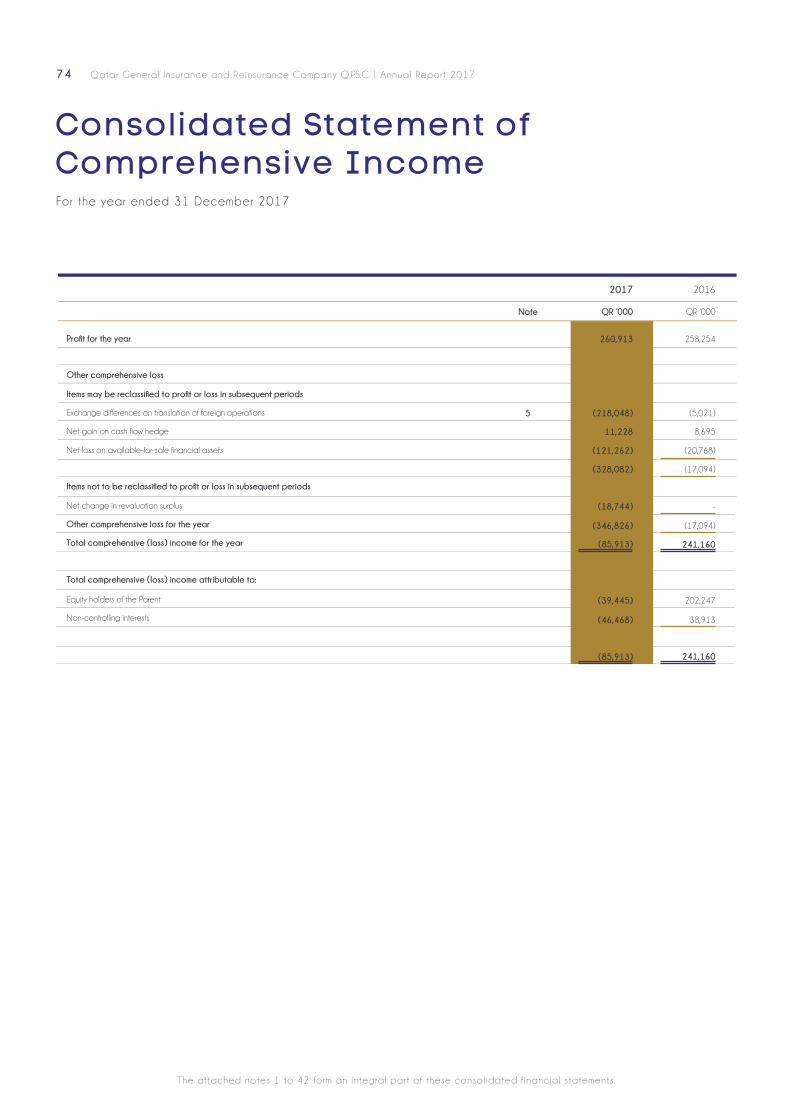

Consolidated Statement of Comprehensive Income

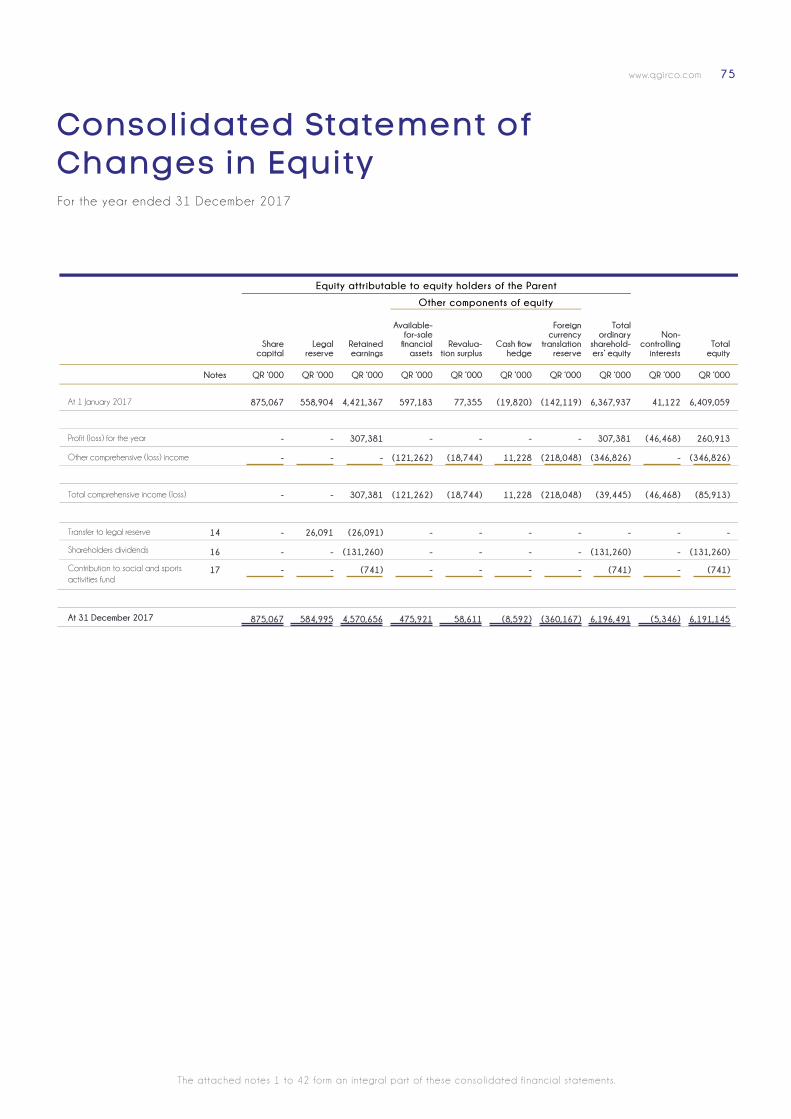

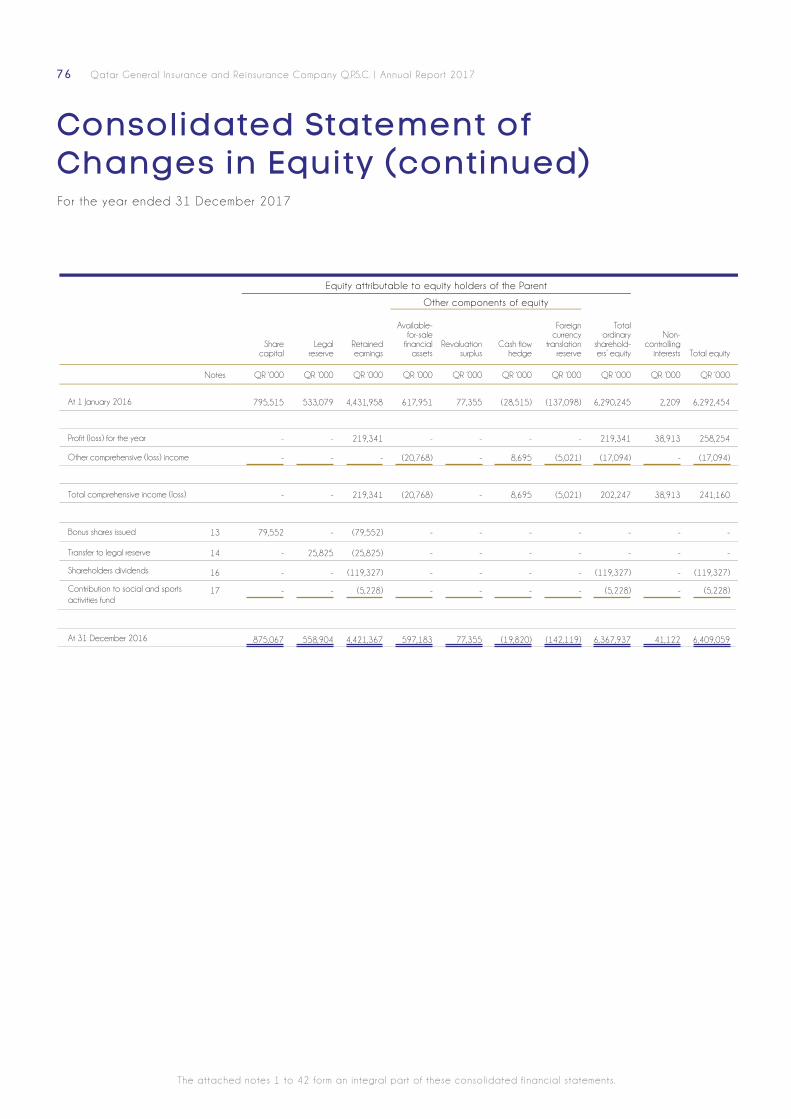

Consolidated Statement of Changes in Equity

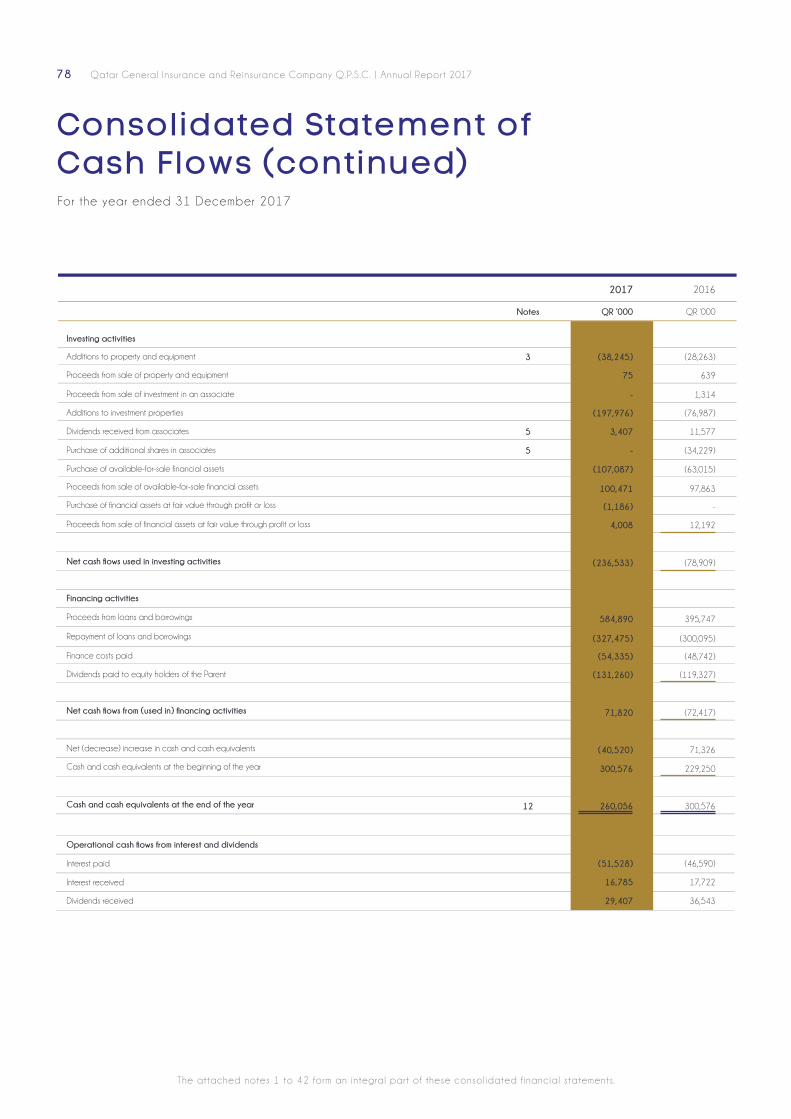

Consolidated Statement of Cash Flows

Notes to the Consolidated Financial Statements

64

71

73

74

75

77

79

Contents

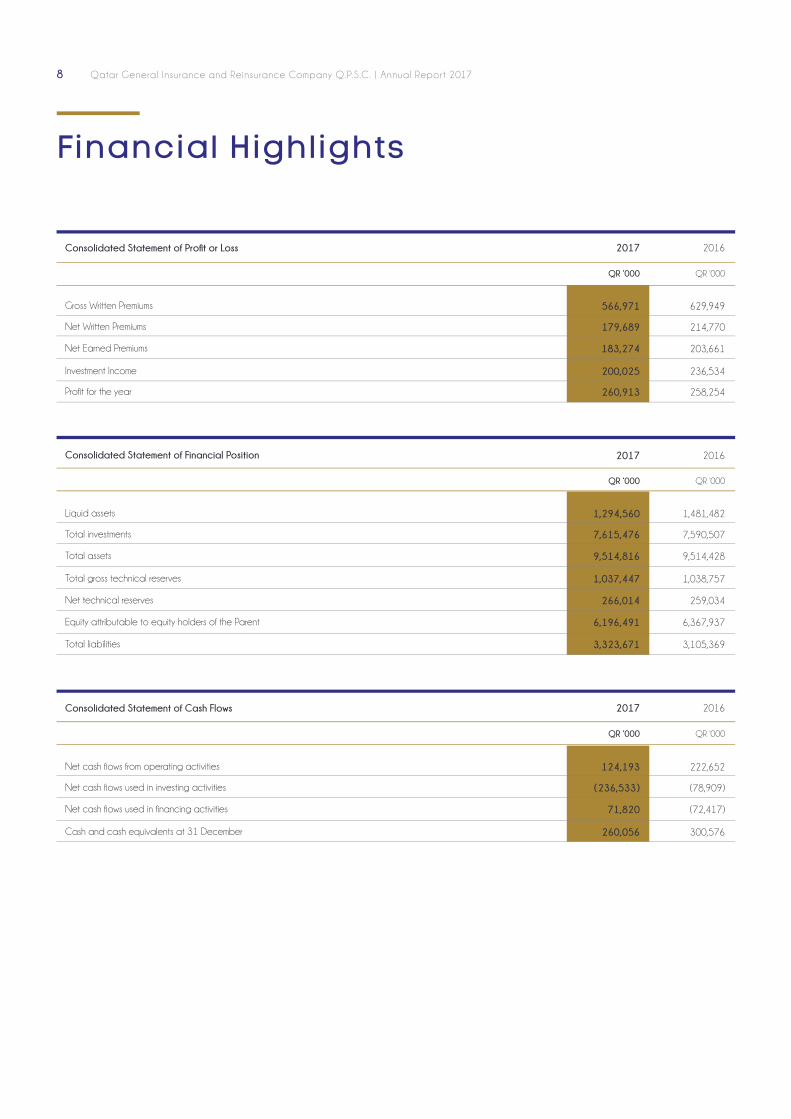

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 20178 9www.qgirco.com

QR ‘000QR ‘000

20162017Consolidated Statement of Financial Position

Consolidated Statement of Profit or Loss

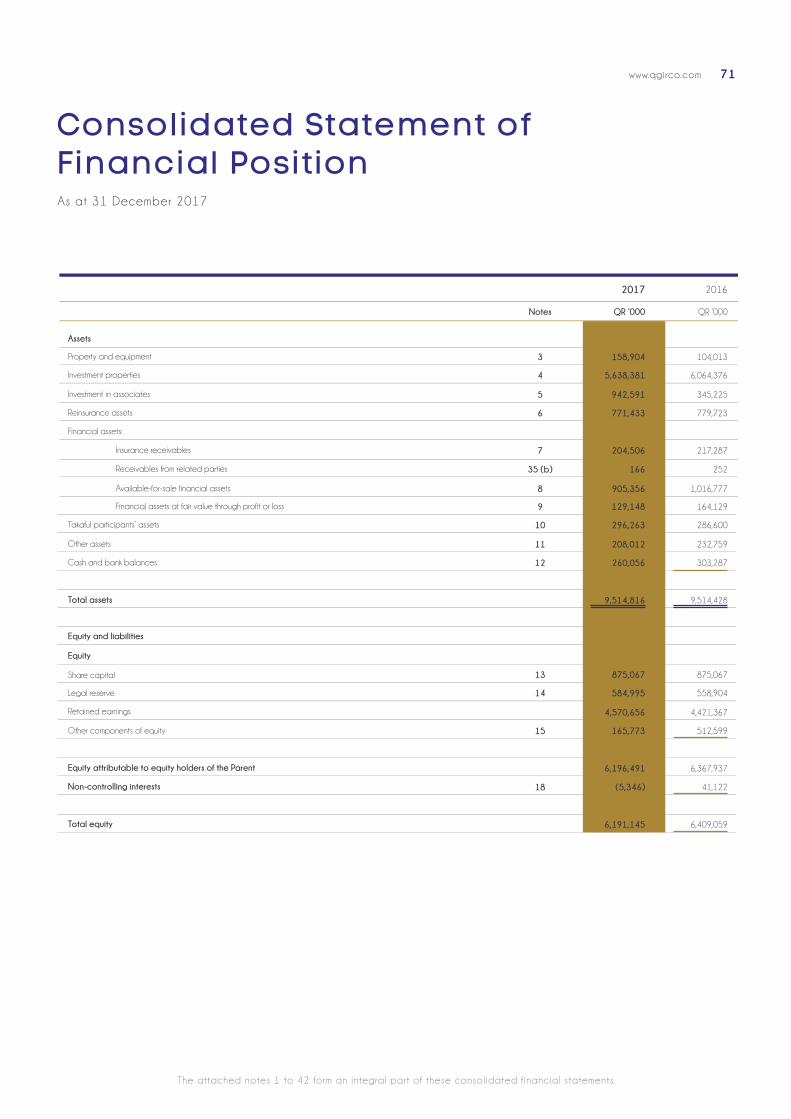

Liquid assets

Total investments

Total assets

Total gross technical reserves

Net technical reserves

Equity attributable to equity holders of the Parent

1,294,560

7,615,476

9,514,816

1,037,447

266,014

6,196,491

3,323,671

1,481,482

7,590,507

9,514,428

1,038,757

259,034

6,367,937

3,105,369Total liabilities

QR ‘000QR ‘000

20162017Consolidated Statement of Cash Flows

Net cash flows from operating activities

Net cash flows used in investing activities

Net cash flows used in financing activities

124,193

(236,533)

71,820

260,056

222,652

(78,909)

(72,417)

300,576Cash and cash equivalents at 31 December

QR ‘000QR ‘000

20162017

566,971Gross Written Premiums

179,689Net Written Premiums

183,274Net Earned Premiums

200,025Investment Income

260,913Profit for the year

629,949

214,770

203,661

236,534

258,254

Financial Highlights

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 20178 9www.qgirco.com

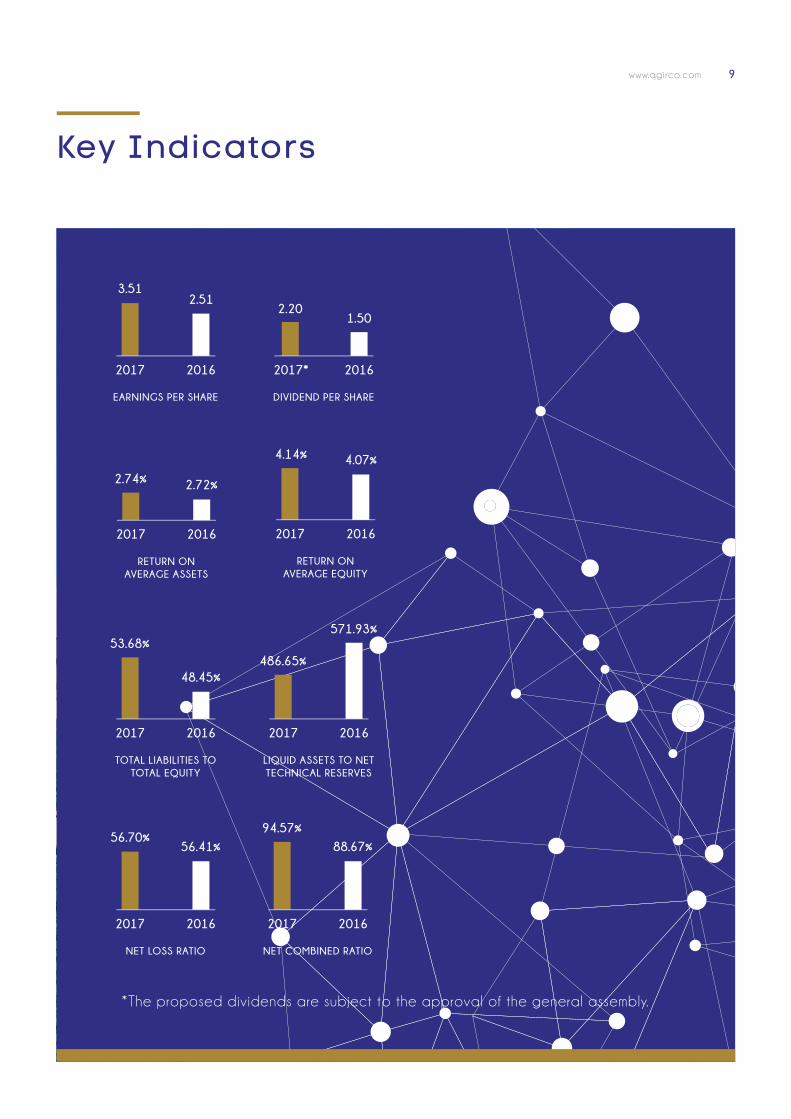

Key Indicators

2.51

EARNINGS PER SHARE

20162017

3.51

1.50

DIVIDEND PER SHARE

20162017*

2.20

TOTAL LIABILITIES TO TOTAL EQUITY

20162017

48.45%

53.68%

LIQUID ASSETS TO NET TECHNICAL RESERVES

20162017

571.93%

486.65%

RETURN ON AVERAGE ASSETS

20162017

2.74% 2.72%

RETURN ON AVERAGE EQUITY

20162017

4.07%4.14%

NET COMBINED RATIO

20162017

88.67%

94.57%

NET LOSS RATIO

20162017

56.70%56.41%

*The proposed dividends are subject to the approval of the general assembly.

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201710 11www.qgirco.com

Credit Rating

For the fifth consecutive year, QGIRCO has

maintained its strength rating and issuer credit

rating. Product diversification, strong risk-

adjusted capitalisation, and enhanced risk

management capabilities have underpinned

the company ’s stable per formance.

Our Group maintains a ver y strong capital

position that continues to support our excellent

financial strength rating (A-, A.M. Best).

Our balance sheet strength remains at the

strongest level, supported by robust operating

per formance and appropriate enterprise risk

management. Our attention to risk exposure

and frequent analysis of our situation has been

enhanced with improved systems spanning

across the Group, ensuring we maintain

sufficient liquidity to meet our insurance and

non-insurance liabilities.

FINANCIAL STRENGTH RATING

A - (Excellent)

ISSUER CREDIT RATING

a -

OUTLOOK FOR BOTH RATINGS

STABLE

Capital Strength

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201710 11www.qgirco.com

The Board of Director’s Report

Our performance

While many companies are stil l suffering the

impact of the prevailing unfavourable market

conditions of the past year, 2017 year also

came burdened with its own challenges to many

companies in the State of Qatar. Nevertheless,

and despite of these exceptional times, we

have succeeded through our robust capital

base and diversified investments portfolio, to

support our Group in meeting its strategy and

consequently per forming well during such a

year. I am pleased to report that QGIRCO has

achieved a net profit of QR 261 million for the

year ended 31 December 2017 (compared

to QR 258 million for the year ended 31

December 2016).

We take pride in our ability to retain and

strengthen our notable and strong position in

the insurance industr y and marketplace in the

State of Qatar with gross written premiums of

QR 796 million (including Takaful businesses)

at the end of the year, (compared to QR 838

million for the year 2016), which is regarded

as a good achievement, given the severe

impact of the competitive international prices

on insurance premiums.

In terms of Investment returns, the Group has

achieved QR 200 million for the year ended 31

December 2017 (compared to QR 237 million

for the year 2016). As for the total assets it

amounted to QR 9.5 billion and a total equity

of QR 6.2 billion as at 31 December 2017.

The Board of Directors proposes distributing

cash dividends to the shareholders at the

rate of 22% of the nominal value of the share

(equivalent to QR 2.2 per share), and adopting

the Company ’s balance sheet and Profit &

Loss account for the financial year ended 31

December 2017.

We are honoured to reveal that the Company ’s

financial strength and credit rating remains

stable, as affirmed by A.M. Best Credit Rating

Agency by granting the Company a Financial

Strength Rating (FSR) of “A-“ (Excellent) and a

Long-Term Issuer Credit Rating (Long-Term ICR)

of “a-“, with stable outlook for both ratings.

Diversification towards Group’s prosperity

Within the Company ’s strategic approach of

business diversification, arrangements are in

place to enter the medical insurance industr y

Dear Esteemed Shareholders,

May peace, mercy and blessings Be Upon You

With great honour, we present to you our Company ’s Annual Report for the financial year

ended 31 December 2017. This Report sets out a general overview of the Group’s Companies

per formance, objectives and goals for the forthcoming year.

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201712 13www.qgirco.com

being a milestone of the insurance industr y, and

are currently engaged in finalising the related

platform and relevant procedures.

Resolutions promoting growth

Driven by the Company ’s best interests, the

Board of Directors has adopted many significant

resolutions designed to promote the aspired

vigorous growth and development of our Group

through developing the Company owned plots

of land while taking into consideration the

development priorities of these lands.

It is worth noting that the Company has acquired

a number of plots in the Manateq area, and

currently work is under way on its development in

the near future, God willing, to the benefit of the

Company, thereby emphasising the Company ’s

contribution in advancing the robust national

economy in the State of Qatar.

On the other hand, the Water and Beverages’

factor y construction has been completed and

is expected to start operation and production

by the month of April 2018.

Nurturing and developing our staff to sustain progress

Training and developing our staff has been

our investment throughout the year 2017,

whilst working on enhancing their professional

expertise aiming to offer them a better

professional career development prospects.

During 2017, our Program known as NEXTGEN

which is specifically designed for new graduates

has marked the appointment of a number of

young graduates to join our technical teams

across the various departments of the Company.

As to Qatarisation, we were keen to align our

strategy along with Qatar ’s National Vision

2030, and we dedicated considerable

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201712 13www.qgirco.com

efforts towards developing and creating

a distinctive and competent workforce. The

Company supports the career development of

Qatari youth by encouraging them to pursue

the completion of all levels of education

whether inside or outside the State of Qatar,

in addition to providing a vital internal training,

and training courses such as Business English

Language and Personal Skills Services for

insurance, Sales and Customer Services, and

training on the Information and Communication

Systems.

Besides, the Upper Management of the

Company is committed towards implementing

and monitoring its Qatarisation Strategy, and

increasing the Qatari cadres in the Company, in

order to be among the top ranked Companies

as to Qatarisation ratios across the State of

Qatar.

Focus remains on risks

Our team has been keen to implement the

requirements stipulated in the Executive

Instructions for Insurance and the Principles

of Corporate Governance issued by Qatar

Central Bank. As well, they ensured complying

with the national and international regulations.

Yet, we remain ready to comply with all

regulator y framework amendments, whilst our

team strives to take the lead in adopting

upcoming improvements to the best interest

of our client base. We pursue by our strong

Governance Framework to maintain an ongoing

per formance development, while keenly working

to meet all local and international regulator y

and statutor y requirements.

As a part of the solid Governance Framework,

we continue complying with the Group’s

adopted manual with respect to transacting

with related parties. Such a relation is built

upon the principles of transparency and full

disclosure for all transactions and partnerships

with the related parties, such as Al-Sari

Trading Company, Group of Nest Investments

(Holding) Limited, Group of Trust International

Companies, North Africa Energy Company and

Falcon Ready Mix Company. In this respect,

we would like to note that all such transactions

with related parties in the region that were

conducted under the Board’s guidance for

the ultimate benefit of the Company have

yielded rewarding proceeds to our Company.

The Company was able to establish a strong

presence in the region led by its investments in

Algeria that resulted in a productive outcome

to the Company ’s benefit.

Dear valued Shareholders

We extend our thanks and gratitude to the

valued Shareholders and to our loyal customers

for their great support and confidence. We

would like to specially express our appreciation

to the Group’s staff and to Senior Management

for their efforts and dedication towards the

prosperity and vision realising of the Group.

Finally, and on behalf of the Board of Directors I

am honoured to raise our sincere appreciation

and gratitude to His Highness the Emir Sheikh

Tamim Bin Hamad Bin Khalifa Al-Thani, may

God protect him, and his wise government for

the continuous support and patronage and

sincere endeavours towards building a solid

and robust economy for the State of Qatar.

Nasser Bin Ali Bin Saud Al-ThaniChairman of the Board

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201714 15www.qgirco.com

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201714 15www.qgirco.com

Chairman’s Statement

A year of new opportunities

We are a strong and confident nation. It is

this power ful strategic leadership that has

shown us, throughout our histor y, that with every

challenge comes an even stronger opportunity.

2017 presented our Group, like many others,

with challenges that needed to be assessed,

considered and consequently overcome; and

as a Group we certainly achieved this. However

it is pertinent to remind ourselves that it is our

years of strong governance, our confident

approach to investment, and our proven ability

to adapt and change to the growing needs of

our countr y, that has supported us once again

in delivering results that are strong and steady,

all things considered.

Made in Qatar

Throughout the year our Government continued

to initiate projects to support the realisation

of the Qatar National Vision 2030 including

the Single Window initiative for industrial

investment. This focus and development of

local products and services, along with a rising

trend of ‘Made in Qatar ’ products have seen

the domestic industr y grow, having an overall

positive effect on businesses such as ourselves.

As such, and as part of our overall long-term

strategy, we continue to develop our Group

of companies to produce their own ‘Made in

Qatar ’ products, such as our soon to launch,

Al Rawda water, from our General Company For

Water & Beverages.

We are proud to be an established Qatari

company, remaining steadfast and strong.

We continue to contribute to Qatar National

Vision 2030, remaining robust and relevant to

the growing needs of our countr y.

Nasser Bin Ali Bin Saud Al-Thani Chairman and Managing Director

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201716 17www.qgirco.com

Our people

Qatarisation remains an integral part of our

Group’s human resources strategy and we

continually look for opportunities to nurture

the distinctive talent of our Qatari colleagues

as they strive towards leadership positions

across our Group. We aim to support them

grow throughout our organisation and beyond,

becoming strong corporate figures within the

business community.

Outlook

We remain optimistic for the future. Our strategic

approach, which is translated into our ever yday

business, is aligned across the Group to support

overall strength and growth. Economic outlook

stil l indicates a strong economy and we are

committed to developing all areas of our

businesses to support the growth aspirations of

our Group and our Countr y.

I would like to express my gratitude and

appreciation to all of our stakeholders for their

continued support. We will remain true to our

strategy and strive to achieve our long-term

aspirations. To the Board of Directors, I thank you

for your commitment, stewardship and strategic

direction. To our loyal team, your commitment,

focus and energy is appreciated by all. Finally,

for our strong guidance and leadership I thank

Qatar Central Bank. Your unwavering support

for our Group within our Countr y is treasured.

Finally, and on behalf of the Board of Directors

I am honored to raise our sincere appreciation

and gratitude to His Highness the Emir Sheikh

Tamim Bin Hamad Bin Khalifa Al Thani, may God

protect him, and his wise government for the

continuous support and patronage and sincere

endeavors towards building a solid and robust

economy for the State of Qatar.

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201716 17www.qgirco.com

Group Chief Executive Officer

Review of the year

2017 saw a series of unprecedented events

that substantiates our attitude to risk and the

Group’s strategy to diversify products and

services while working in synergy with each

other.

Although a challenging year, our per formance

was stable. The cash dividend per share of

QR 2.2 for 2017 recommended by the Board

demonstrates our strong financial health.

Changing landscape

Large infrastructure projects continued, and as

a Group with strong insurance products (Qatar

General Insurance and Reinsurance and

General Takaful) and construction expertise

(Orientals Enterprises), we are blessed to

be able to contribute to these significant

developments at many levels. General Tower

is one such iconic development, which signifies

our commitment to Qatar ’s evolution, creating

modern, state-of-the-art offices for business

lease.

Additionally, we saw the completion of General

Takaful ’s new head office on C Ring Road by

Orientals Enterprises. An iconic building that

showcases our commitment to providing best

in class Takaful products and services to our

growing customer base.

This year proved challenging for many businesses

in Qatar. We overcame many extraordinary

circumstances, yet utilised our strength in the

marketplace to seek new opportunities for

sustainable growth

Ghazi Abu Nahl Group Chief Executive Officer

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201718 19www.qgirco.com

Greater efficiency for greater growth

During the year, we focused on improving

customer experiences which is vital to enabling

us to distinguish our services from our competitors.

Improving our communication and processes

enables our Group to grow customer loyalty,

increase positive referrals and enjoy a higher

success rate at cross-selling. We constantly

remind ourselves and all of our team that we

are one Group and it is our duty to provide an

excellent level of care and attention to details

to all our customers across all channels.

I am proud to share with you that A.M. Best has

reaffirmed to Qatar General Insurance and

Reinsurance Company (Q.P.S.C) its Financial

Strength Rating (FSR) of “A-” (Excellent) and

the Long-Term Issuer Credit Rating (Long-

Term ICR) of “a-” with stable outlook for both

ratings. These ratings reflect QGIRCO’s strong

risk-adjusted capitalisation, improving risk

management capabilities and track record of

solid operating per formance.

Outlook

We are a legacy in Qatar; a Group of

companies that has grown with the countr y

and its people. Despite a challenging year,

we are confident that we and our countr y are

at the beginning of a new journey of growth.

Our countr y and government have worked

incredibly hard to drive forward our nation’s

ability to become self-sufficient. Government

initiatives are promoting ‘Made in Qatar ’

products and services over imports and

supporting entrepreneurs to establish strong

and sustainable businesses at home.

We will continue to seek out new opportunities

across our Group, working hard to develop our

companies range of products.

positive achievements

2017

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201718 19www.qgirco.com

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201720 21www.qgirco.com

Our Group

QATAR GENERAL HOLDING

COMPANY W.L.L.

GENERAL TAKAFUL

COMPANY P.Q.S.C.

GENERAL REAL ESTATE

COMPANY W.L.L.

WORLD TRADE CENTER

QATAR W.L.L.

MOZOON INSURANCE

MARKETING SERVICES W.L.L.

GENERAL TOWER FOR REAL

ESTATE INVESTMENTS W.L.L.

ORIENTALS ENTERPRISES W.L.L.

GENERAL COMPANY FOR WATER

AND BEVERAGES W.L.L.

MOZOON REAL ESTATE

COMPANY W.L.L.

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201720 21www.qgirco.com

Qatar General Insurance & Reinsurance Company Q.P.S.C.

Proud of our long-standing reputation as a

trusted provider, Qatar General Insurance &

Reinsurance Company (QGIRCO) provides

individuals, families and businesses with

innovative insurance solutions.

Overview

2017’s growth strategy has been strong and

steady, as we continued to focus our efforts on

writing profitable business. We have sought to

achieve this through diversifying our channels

of distribution, enhancing our existing products,

and implementing strong processes targeted

at improving our business retention ratios which

is the main driver to the growth strategy.

Putting the customer first

Our customers are our priority and it is the

method through which we service them that

encourages them to remain true and loyal to

our company. We have worked hard to create

a stronger omni-channel experience for our

customers, ensuring that, whichever method

they choose to engage with us, they receive

the same level of care and dedication.

To support this customer-first approach, we

welcomed local graduates from our NEXTGEN

programme to be part of our dedicated

Customer Service Unit (CSU). Led by a team

of experienced managers, our newly-expanded

team enables us to improve communication

with our valued customers in order to be ready

for the upcoming changes, especially in the

medical insurance..

Our insurance strategy this year has been

focused on sustainable and profitable growth,

retaining loyal customers and at the same time

developing products that cater to the needs

of the growing local business community.

Jamal Abu Nahl Chief executive officer - Insurance

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201722 23www.qgirco.com

Furthermore, the new dedicated CSU supports

customer retention through better notification

and awareness of policy renewal dates. As well

as being contacted through SMS and email,

customers are now contacted by personal

phone call from our dedicated CSU team and

able to renew their policy instantly over the

phone. This marks a huge removal of a ‘barrier

to renewal ’ for our customers and provides

them with the additional, hands on service they

desire from a leading insurance provider. This

new service has had a significantly positive

effect on our retention rate – we want our

customers to come to us and stay with us, and

now we’re making that even easier.

In collaboration with our Human Resources

department, we have also invested in training

and development of our brokers and branch

staff, upskill ing them to be able to offer

knowledgeable and internationally qualified

support and guidance to our customers.

Boosting business through partnerships and rewards

This year, we launched our motor, travel,

personal accident and household insurance

through the Ahlibank branch network. These

products, now available in 16 branches across

Qatar vastly increases our reach.

Growing and promoting Personal and SME

The rise of factories and local SMEs due to

the single window initiatives supported by

ministries and government agencies has

opened a new window of opportunity for our

insurance business. Our products, services

and overarching knowledge help provide the

trusted financial protection these businesses

need in their early stage establishment and as

they move forward to operating safe, efficient

and productive businesses.

Enhancing efficiency and improving margins

Customers expect fast service, with enquiries

and claims to be dealt with swiftly. Internal

digital transformation has enabled us to

provide breakthrough per formance via

improved efficiency and back-office processes

to enhance the speed that claims are dealt

w i th .

Outlook

Despite unusual market conditions the near to

medium-term outlook remains positive. We will

continue to target profitable local business for

positive growth. Additionally, we remain focused

on further strengthening internal processes

to build on the strong claims handing and

customer retention success we have seen in

2017.

Above all, we will continue to develop and

grow with our countr y, concentrating our

efforts on the Qatar National Vision 2030

and supporting the realisation of a strong,

sustainable, diversified economy.

Qatar National Vision

2030

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201722 23www.qgirco.com

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201724 25www.qgirco.com

General Takaful Company P.Q.S.C.

Established in 2008, General Takaful Company

became one of the leading providers of Takaful

products and major player in Takaful market

in Qatar. Our mission is to enable individuals

and corporations to manage financial risk. We

provide Islamic insurance products and services

tailored to fit with the frequently changing risk

exposures faced by our customers. We build

value for our investors and partners through

the strength of cooperation based on Takaful

principles.

Overview

Keeping in mind our long-term strategy, we

continue to realign our products to suit

today ’s challenging markets and taking into

considerations the requirements of Shari ’a

principles. Overall business per formance has

shown improvement despite the challenging

geopolitical situation. We witnessed a 10%

increase in gross written premiums comparing

to last year - Gross Written Premium for year

ending 31 December 2017 was QR 229 million.

During 2017, we invested heavily in human

capital, expanding our team to ensure we are

fully equipped to grow non-motor business and

improve claim controls. We expect to see returns

on this investment throughout 2018 and beyond,

as well as achieve our objective of diversifying

our product portfolio and continuing to reduce

our exposure to Third Party Motor Insurance.

Bringing innovation into our services

An efficient claims management process delivers

happy customers as well as reducing overall

costs of settlement. During the year we worked

Service excellence is our specialty and concern

while achieving our targets of expansion and

diversification.

Majed AkelGeneral Manager

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201724 25www.qgirco.com

strategic location and sizeable development,

close to business and many residential areas

raises our profile and offers customers further

convenience.

Relocation to the new Head Office is planned

for early 2018. The new modern three-stor y

building provides the company with more room

for its expanded workforce while enabling

us to promote our ambitious and enhancing

convenience to our customers. General Takaful

Company will occupy around one third of

the building and the other two thirds will be

rented out which supports the diversification of

investment income of the Company.

This relocation will also enable us to expand

our branch network, with our vacated head

office set to be transformed into a new branch

occupied by our Family Takaful department. This

expansion allows us to focus on the mandatory

medical insurance that will be implemented

soon in Qatar.

Outlook

2017 brought positive achievements to the

company, and we will continue to build upon

this momentum and focus our efforts on growth.

The foundations that have been laid over the

past few years to diversify our portfolio have

enabled us to deepen our corporate customer

relationships across our product range.

Motor insurance remains a key part of our

business and we will continue to develop and

diversify these products and processes to fulfi l

the needs of our customers.

We expect 2018 to be a positive year for

General Takaful. Our aim is to continuously

be one of the preferred provider of Islamic

Insurance and the best Takaful risk carrier in

Qatar.

towards more effective use of technology to

manage claims through phone applications

and our website, as well as re-engineering the

back office process. We are currently working

to open a new payment gateway and obtain

online premiums for personal products which

will definitely boost our sales. This is in addition

to enhancement of current mobile application

and services through our website.

Additionally, the claims department was

restructured for swifter processing and better

control, with strong governance and oversight

at the centre of this initiative. Overall a tangible

difference has been recognised internally as

well as by our expanding customer base.

Enhanced product portfolio

General Takaful has experienced growth over

the past few years and is recognised as a key

player in the domestic market, with Motor as

the main driver. We have strived to develop

our motor products to better suit our customers ’

needs through improved add-on services for

individual and corporate customers.

Continuing from 2016, we have expedited our

sales diversification strategy, focusing more on

non-motor insurance. Our branch network now

offers non-motor products, with our employees

well training to manage individual and

corporate customer enquiries on our full range

of products, with a particular focus on life and

engineering business. As part of this direction

we have increased our engineering portfolio

due to the long-term relationships we have

forged with local construction and engineering

companies since our establishment.

Expanding our reach across Qatar

This year, work completed on the iconic

General Takaful Head Office located on the

C-Ring, in the heart of downtown Doha. This

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201726 27www.qgirco.com

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201726 27www.qgirco.com

Qatar General Holding Company W.L.L

As to what we do at Qatar General Holding

Company level, we manage the Group’s

investment portfolio, providing a strong and

stable financial foundation aiming to best serve

our client needs and meet our shareholders

expectations. The company holds major

participations in a number of key companies

which contribute significantly to Qatar ’s

economic growth and employment creation.

Qatar General Holding is proud of its role and

involvement in the development of a number of

land mark projects in Qatar.

The politically imposed crisis since June 2017

significantly impacted Qatar ’s economy at its

inception, as foreign capital panicked and

started exiting the domestic economy. Many

of the countr y ’s businesses were affected by

this uncertainty and drop of confidence and

capital outflow. However, the initial shock was

easily absorbed thanks to the smart moves

taken by the Government to step in and fil l this

created gap. Liquidity was quickly reinjected

in the economy, and Government incentives

introduced to encourage entrepreneurs to

set up new businesses to replace imports and

create a more or less self sufficient economy.

Following the embargo against the State of

Qatar, the Company embarked on a plan to

radically reduce its exposure to the governments

and private entities of the boycotting countries.

Also, additional actions were taken to increase:

(1) fixed deposits in Qatari Riyals and (2)

investments in USD fixed income securities within

the developing countries of South East Asia

due to the strong economic fundamentals of

such countries and the encouraging yields.

To the surprise of the whole world, The State

of Qatar was able (thanks to its Rational

Leadership) to bypass with high merits, the

negative impacts resulting from the unjust

blockade imposed since June 2017.

This was possible due to its enlightened

Leadership, the flexibility of applied policies,

and the steadfastness and readiness of its

economic structure. We remain confident

and trust our readiness to overcome these

extraordinary circumstances. We are optimistic

about the future being prosperous, both at our

company and the State of Qatar levels.

Abdallah BarrageDeputy Chief Executive Officer - investments

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201728 29www.qgirco.com

Furthermore, strategic investments in local

companies listed on the Qatar Stock Exchange

(QSE) were maintained, as the decline in the

QSE Index was considered to be a knee-

jerk reaction to the crisis. The fundamentals

of the economy in Qatar are solid , resilient

and capable to offset the short-term negative

implications of the crisis.

Finally, even though the reduction in rental

rates have affected the yield on our property

portfolio , real estate developments pertaining

to the construction of four hotels in Doha

were kept on track, to be ready for FIFA 2022.

Also, the aim of turning our other strategically

located land plots in and around Doha into

income producing properties remained intact.

Outlook

Our endeavors remain driven by Qatar

National Vision 2030, which aims at supporting

and diversifying the Local economic base while

contributing towards overall economic growth

and employment creation.

Our commitment to Qatar remains strong as this

is our base and the market that we know best,

with the most expected rewards in the medium

term without running any currency risks.

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201728 29www.qgirco.com

Project Management and Contracts Department

Great achievements are realised with proper

planning and good management, and this is

what the Project Management Department is

targeting.

Hani AkkawiGeneral Manager

The Group witnessed over recent years, major

diversification in its business activity by venturing

into the field of Real Estate Development. One

of the Group’s most prestigious projects is the

Mozoon Towers in the West Bay Area in Doha,

a hospitality project consisting of Marriott,

Oberoi and Retaj branded hotel rooms and

serviced apartments considered an added

landmark to the Countr y and coming on the

heels of an earlier development The World

Trade Center another landmark in the corniche

area.

To keep pace with the positive development

in Real Estate Market and recognising the

critical need to communicate and co-ordinate

work across departments and outsourced

consultancy and contracting services it was

decided to establish under the Qatar General

Holding a Project Management and Contracts

Department to manage the consultancy and

construction contracts of the Projects being

developed by the Group with a futuristic

vision to transform the PMC Department to an

engineering office specialised in engineering

contracts and project management.

At its core, Project Management focuses on the

planning and control of all activities involved

in delivering the desired end result of any

Project under development. It uses various

tools to measure accomplishments, cost and

time control, track project tasks, reduce risks

and increase the chances of success.

Often, a triangle, commonly called the “ triple

constraint ”, is used to summarize project

management. The three most important factors

are time, cost and scope. These form the

vertices with quality as the central theme.

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201730 31www.qgirco.com

General Real Estate Company W.L.L.

Established in 2008 as a wholly-owned

subsidiar y of Qatar General Holding Company,

General Real Estate Company (GRECO)

includes a diversified mix of major projects,

residential, offices, commercial, leisure and

lifestyle and industrial developments. GRECO

provides a full-range of services for in-house

and third parties which include project, facilities,

property and hospitality management.

Overview

Our real estate portfolio is aligned to our

investment strategy with strong attention to our

local market: our market value is QR 5.638

million with a focus on real estate investment

within the State of Qatar.

Throughout 2017 our focus has been on

Mozoon Towers which will be followed by Salwa

road project in 2018 and Al Wakra project in

2019.

During the year, Lusail Water front project

successfully received building approval and

construction is expected to start in Q2 2018.

Development of Mozoon Towers is making good

progress, with skeleton construction underway

with our own sister company, Orientals Enterprises

W.L.L. We are pleased to report that that we

are set to reach our estimated completion

date, Q4 2020, which increases Qatar ’s ability

to accommodate the anticipated rise in visitor

numbers the countr y is expecting to see over

the next 5 years.

Infrastructure, master developments, property

and sports and leisure venues continue to be

a focus of our Countr y in line with the Qatar

National Vision 2030: this investment into our

countr y ’s future has been extremely beneficial

for our company.

Emad eldin Mousa Qenibi Acting General Manager

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201730 31www.qgirco.com

Managing these towers and welcoming

overseas guests to Qatar will be Oberoi (Tower

A, Hotel). Marriott (Tower B, Hotel and Tower

D, serviced apartments) and Retaj (Tower C,

serviced apartments.

Outlook

We are positive about our countr y ’s and our

company ’s long-term outlook and growth. Qatar

continues to seek new avenues to diversify

its economy, with tourism and sporting events

playing major roles in this overall strategy. As

such, there continues to be a strong demand for

property development throughout the countr y.

Our mission remain to convert more non-income

producing holdings to income-producing

property, when the opportunity arises for

a greater return of investment. We seek to

achieve a reasonable return on investment

while maintaining a diversified portfolio and

balanced capital investment.

2018 is also the year we seek to invest more

resources and capital into Facility Management,

which is growing in demand as new offices and

event spaces continue to open in Qatar. We

currently undertake this role for the World Trade

Centre and are eager to enhance our service

offering.

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201732 33www.qgirco.com

Real Estate Projects in the Pipeline

MOZOON TOWERS | WEST BAY

The project comprises of 4 Towers, with 5 basements floors,

podium on ground, 1st and 2nd floor (varies for each tower). All

carparks are in the ground and basements with a total of 2,252

carparks. This one of a kind building complex will showcase

terraces in the sky, with variable stepped-height 4-towers.

The four-tower complex includes boutiques, cafe, restaurants,

ballrooms, laundry, spa, club house and external pool. Mozoon

Towers is set to introduce an innovative contemporary concept

in high-rise residential developments. Good quality daylight, as

well as various views to the surroundings can be enjoyed from

the inside.

FOX HILLS ZONE -H DEVELOPMENT | LUSAIL

The Project will be located at 22 Plots at Fox Hills District in

Lusail. The 22 plots shall be designed as offices with retail

areas at the ground floor / residential units/ hotels as per the

usage regulations of Lusail with complete amenities, services,

parking spaces and landscape areas. With a Total Plot area

of 62,909 sq.m.

FOXHILLS –MU/C07 COMMERCIAL DEVELOPMENT | LUSAIL

The Project Development has a Plot Area of 2,939.42

sq.m. and total B.U.A of 14,551.91 M2 and is situated at

Foxhills District, Lusail Area and shall be built into RETAIL

(864m2)+RESIDENTIAL(1/14BR and 2/34BR), services, parking

spaces (93 Carparks) and landscape as per land use.

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201732 33www.qgirco.com

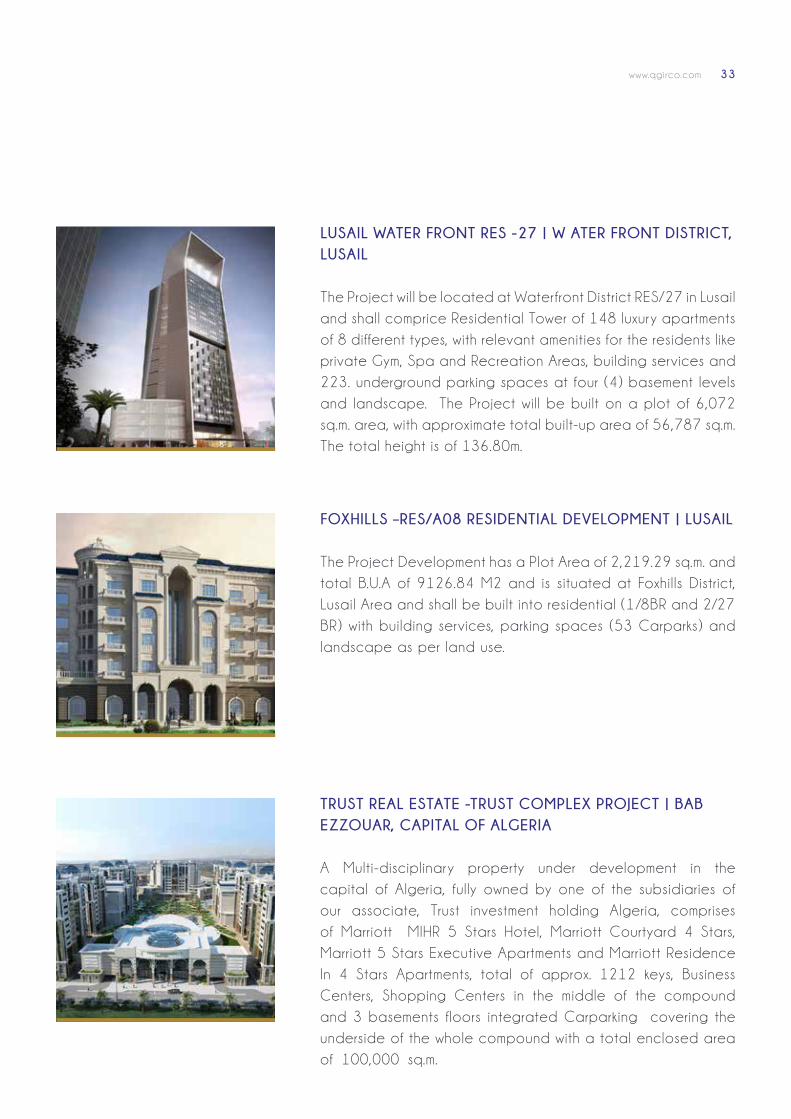

LUSAIL WATER FRONT RES -27 | W ATER FRONT DISTRICT, LUSAIL

The Project will be located at Water front District RES/27 in Lusail

and shall comprice Residential Tower of 148 luxur y apartments

of 8 different types, with relevant amenities for the residents like

private Gym, Spa and Recreation Areas, building services and

223. underground parking spaces at four (4) basement levels

and landscape. The Project will be built on a plot of 6,072

sq.m. area, with approximate total built-up area of 56,787 sq.m.

The total height is of 136.80m.

FOXHILLS –RES/A08 RESIDENTIAL DEVELOPMENT | LUSAIL

The Project Development has a Plot Area of 2,219.29 sq.m. and

total B.U.A of 9126.84 M2 and is situated at Foxhills District,

Lusail Area and shall be built into residential (1/8BR and 2/27

BR) with building services, parking spaces (53 Carparks) and

landscape as per land use.

TRUST REAL ESTATE -TRUST COMPLEX PROJECT | BAB EZZOUAR, CAPITAL OF ALGERIA

A Multi-disciplinar y property under development in the

capital of Algeria, fully owned by one of the subsidiaries of

our associate, Trust investment holding Algeria, comprises

of Marriott MIHR 5 Stars Hotel, Marriott Courtyard 4 Stars,

Marriott 5 Stars Executive Apartments and Marriott Residence

In 4 Stars Apartments, total of approx. 1212 keys, Business

Centers, Shopping Centers in the middle of the compound

and 3 basements floors integrated Carparking covering the

underside of the whole compound with a total enclosed area

of 100,000 sq.m.

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201734 35www.qgirco.com

General Company for Water and Beverages W.L.L.

Over the past three years, we endeavoured

to complete the build of our mineral water

factor y. We have managed to achieve this,

despite the blockade which began in June,

installing the latest machiner y equipped to

the highest technological level, and ensuring

that we have the best raw materials, bottling

and packaging materials to go to market. We

have also worked hard to meet the conditions

and specifications stipulated by the civil

defence and other government authorities. All

the necessar y licenses have been obtained to

launch production at the beginning of 2018.

During the second quarter of 2018, we shall

start the testing phase for 30 (thirty) days to

ensure we attain the laborator y results needed

to provide safe, great tasting water. Al Rawda

Water products will contain a balanced

combination of minerals and salts necessar y for

human body, and contain a low percentage of

Sodium of no more than 0.4%.

Alternatively, we have finalised our sales and

marketing plan in order to cover the whole

footprint of the countr y, where Al Rawda

Water will be made available through various

distribution channels

Our strategy is to succeed in the current

competitive economic environment and meet

local demand by utilising high quality materials

and the latest state-of-the-art technology.

Maher AkelGeneral Manager

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201734 35www.qgirco.com

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201736 37www.qgirco.com

World Trade Center - Qatar W.L.L.

The World Trade Center - Qatar W.L.L. (WTC

Qatar) is part of the World Trade Center

Association which consists of 332 centres in

116 countries around the world that promotes

and facilitates trade and investment between

Qatari and international companies. Our

mission is to introduce trading partners to the

Qatari market through events and exhibitions.

Overview

In 2017, our focus remained on reaching out

to other nations to create and build upon

trading and investment partnerships. Part of this

work included collaborating with 18 African

embassies to ensure that the African Fair will be

successful event for all parties involved.

WTC Qatar were also proud to attend the

48th World Trade Center Association General

Assembly 2017 held in Las Vegas, USA,

connecting and strengthening our relationships

with hundreds of people from around the globe.

During the year we worked in close collaboration

with Qatar ’s Chamber of Commerce and Industr y,

and Qatar Development Bank, participating

in events alongside local dignitaries and

ambassadors to actively promote Qatar ’s

strong economic position. We also attended

many business match-making events to meet

with overseas delegations who visited Qatar

to collaborate with businesses here.

Outlook

During 2017, WTC Qatar made seamless

efforts with the embassies of the Association

of Southeast Asian Nations (ASEAN) to action

We continue to work as a cooperative chain,

linking Qatari businesses to international

traders. 2017 saw us forging mutually beneficial

relationships with countries through their local

embassies, and attending events that raised

our countr y ’s profile around the world.

Eng. Sadallah Elsaid General Manager

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201736 37www.qgirco.com

our plans for a future ASEAN exhibition. This

work is gathering pace and we look forward to

sharing more news of this event. We also actively

participated in events and activities that

demonstrated the solutions and opportunities

we can offer to new partners.

In April 2018 WTC Qatar will be attending the

49th WTCA General Assembly at Leeuwarden,

Netherlands, to build business opportunities

and strengthen the WTCA network enables us

to enhance relationship and demonstrate the

progressive nature of our countr y ’s initiatives.

We look forward to bringing another array of

busines-link opportunties to Qatar throughout

the coming year that will further support the

mission of the World Trade Centers Association,

WTC Qatar and the Qatar National Vision

2030.

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201738 39www.qgirco.com

Orientals Enterprises W.L.L.

Established in 1999, Oriental Enterprises has

become a leading construction company. From

providing a wide range of products including

rebar and insulation materials to construction

management services, deploying a big team of

more than 600 professionals across residential,

commercial and industrial medium-to-large

scale projects.

Overview

Orientals Enterprises has proved to be an

added value to the Group. Since its acquisition

in 2015, it has enabled the Group to gain

substantial savings via reduced construction

materials and local transportation costs. These

reduced overheads, enabled the Group to

improve the cost of projects, and compete

within the local and regional markets while

increasing future profit margins.

Stability and continuous development was the

principle adopted by the Company during

2017. During the year, we saw completion

of the new General Takaful Headquarters, a

three-stor y office building that will be utilized

for growth and reach across Qatar. We also

managed to expedite the execution of the

construction concrete works contract in Mozoon

Towers located in West Bay, and completed

the expansion of National Rebar Fabrication

Factor y.

We have also heavily invested in human

capital, increasing our talent pool by 20% to

improve the quality of our services and enables

the Group to engage in larger projects. This

expansion allows us to reach our goals of

raising brand awareness and improve our

experience and expertise.

We have faith in a bright future. We have

actively contributed to the Group’s success,

developing major projects that enable our

company to gain recognition and build a

positive reputation in the region and around

the world while driving the realization of Qatar

National Vision.

Eng. Raghib Jalabi General Manager

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201738 39www.qgirco.com

Outlook

Buoyed by government ’s commitment

and investment in major infrastructure and

landmark projects, we look forward to the

future development of Qatar ’s architectural

landscape, which provides favorable

conditions for us to grow.

Our long-term vision remains focused on

contributing in Qatar National Vision,

contributing to medium-to-large scale

developments that enable our countr y to

diversify its economy and improve the prosperity

of our society.

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201740 41www.qgirco.com

Human Resources

Driving our success

Our staff are our most valuable resource, helping

us to achieve our goals and growth aspirations

as well as gain a competitive advantage

through strong customer interactions. We

strive to be an employer of choice, providing

a collaborative and cooperative environment

that nurtures future leaders.

Throughout 2017 we invested in training and

development, working to enhance our in-house

expertise and enabling our employees to enjoy

career development and progression.

Promoting Qatarisation

We have aligned our strategies with Qatar

National Vision 2030 and we are dedicated

to the development and creation of a strong

Qatari workforce. We work closely with the

Ministr y of Labor to find suitable Qatari

recruits and nurture their education for career

progression. We provide vital in-house training,

providing courses such as English language for

business, insurance, sales and customer service

soft skil ls and ICT training.

Succession planning

We have a robust HR vision and structure in

place to ensure that we provide vital coaching

leardership and teambuilding training to

managers and future leaders. Our succession

planning enables us to identify managers and

leaders and help them acquire the technical

skills to progress.

We’re only as strong as our people. Investment

in our talent pool drives our business forward

and enables us to remain an employer of

cho ice.

Jassim Mohamed Yousef Al KawariGroup Admin and H.R. Manager

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201740 41www.qgirco.com

The NEXTGEN Programme

This year, our graduate NEXTGEN Programme

saw the recruitment of many young professionals

into our company where they have joined our

team. This customised training programme

enables us to find and develop our leaders of

the future. We give bright ambitious graduates

a structured training plan that helps them to

learn specialist insurance skills.

Career fairs

During 2017 we participated in career fairs

across Qatar, promoting our company to

graduates while raising awareness of the

insurance industr y ’s key contribution to the

financial services sector and the overall

economic growth of our countr y.

Promoting women and equal opportunities in the workplace

We recognise the valuable skills and importance

of women in the workplace and implement

strategies to bring more female employees

onboard. The current percentage of women

employees is 31%, which is continuously growing.

We are extremely proud of Deepa

Chandrashekar QGIRCO’s acting Chief

Financial Officer who achieved second place

at the MENA CFO Excellence Awards 2017

in the category of Woman in Finance Qatar.

Developed in partnership with ACCA, this

award was given in recognition of Deepa’s

career achievements, success and leadership.

In March 2013, Deepa founded an informal

forum in Qatar in association with the Associate

of Chartered Certified Accountants, UK. Under

her leadership, the forum conducted two

successful events during 2014 and 2016. The

forum represents of over 120 women in Qatar

working in the finance sector and has received

support from the Big 4 and other professional

associations such as ACCA, CMA and IIA.

Professional exams and qualifications

We offer our employees the chance to further

their skil l set and gain professional recognition

for their expertise.

Chartered Insurance Institute (CII) exams

We continue to promote and encourage our

employees to gain these highly acclaimed

internationally-recognised qualifications, which

enable them to gain in depth financial services

knowledge. Investing in these qualifications

enable us to build competencies and trust in

services.

Recognised as an approved employer

We are an ACCA approved employer and

listed on the professional accounting body ’s

website. This recognition and enables us

to boost our reputation as an employer of

choice and showcases our commitment to high

standards. The listing is viewed by people

seeking employment opportunities and helps us

to attract the ver y best talent from around the

world.

Deepa ChandrashekarActing Chief Financial Officer

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201742 43www.qgirco.com

Corporate Social Responsibility

Committed to our country and community

We are proud of the progress we have achieved

in Qatar thus far, forming strong foundations

for a bright future that will boost society, our

architectural landscape and our community.

The Qatar National Vision 2030 drives our CSR

strategy which seeks to have a positive social,

cultural, environmental and economic impact.

As a leading organisation, we are aware of our

role in encouraging and promoting corporate

social responsibility throughout our countr y. We

are keen to participate in sports and social

activities and inspire staff to take part in sports

and awareness initiatives that bring people

together and support making healthy lifestyle

changes.

In 2017, QGIRCO organised and hosted

the fifth local insurance companies Futsal

Tournament. This event was a chance for

colleagues across the industr y to socialise and

compete in a fun atmosphere. This competition

received high participation and its organisation

was applauded by both the media and the

participating delegations. QGIRCO also

participated in the National Sports Day by

holding sports activities for the staff and their

families at Al Arabi Sports Club- a healthy and

social day enjoyed by all.

Recognition for our contribution

QGIRCO was honoured to receive the CSR

Leadership Award 2017, in recognition of

the contribution Qatar General Insurance

and Reinsurance Company has made to its

community. The Ceremony, hosted by Qatar

University, also marked the launch of the CSR

We are aware of the important role that we play

as a leading corporation in Qatar in setting a

good example for others to follow and adding

value to our society.

Marwan Azar Group Head of Marketing and Corporate Communication Department

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201742 43www.qgirco.com

Report, ‘The National Book ’ – Qatar 2016. This

award was presented by Dr. Hasan Al Derham,

President of Qatar University and received

by Group Head of Marketing and Corporate

Communication Department, Marwan Azar. This

award highlighted how large companies are

playing an effective role in promoting social

awareness.

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201744 45www.qgirco.com

Risk Management Report

Actuarial and Risk Management

(a) The Governance Framework

QGIRCO has implemented, and continues

to strengthen a formalised enterprise risk

management (ERM). Among the key elements

of the ERM framework is the adoption of

detailed risk management procedures, and the

implementation of a risk-based asset liability

matching framework as well as the development

of an economic capital model that is used as a

tool for strategic decision-making.

The Group’s risk management policies are

approved by the Board of Directors and they

define the Group’s identification of risk and

its interpretation. Within its risk management

framework, the Group maintains a varied limit

structure to ensure the appropriate quality

and diversification of assets, and to align

underwriting and reinsurance strategy to the

corporate goals in a manner consistent with its

risk appetite. The following illustrate the Group’s

commitment to enhancing and improving risk

management:

— The Risk Management and Actuarial

Department oversees the ongoing process

of identifying, documenting and managing

the key risks the organization is facing. The

department, in coordination with the various

group entities and functions, per forms

regular risk reviews across the group, in

order to maintain an up to date picture of

the group’s exposure to risk.

— To manage the business continuity risks

arising from the group’s key operations, the

risk management department is responsible

for maintaining an up to date Business

Continuity Plan. The department launched

a Business Continuity Plan update project

in Q4 2017 which is expected to be

completed during Q1 2018.

— The Group utilizes a modern risk management

platform (GRC) from leading business

solutions provider SAP. The platform serves

as a repositor y and reporting tool for the

group’s risk database.

— The Group has an active Board Risk

Management Committee which oversees

the risk management activities of the Group.

The committee consists of three board

members, abides by the board approved

charter, meets regularly and takes an active

role in the implementation and embedding

of risk management across the organization.

Following the company ’s Annual General

Assembly held in March 2017, the Board

of Directors appointed new directors and

chairman for the Board Risk Management

Committee. In addition, the Board of

Directors approved the amended committee

charter to comply with all applicable laws

and regulations, providing additional

duties and responsibilities to the committee.

The committee held four meetings during

2017 and provided the Board with key

information regarding the group’s exposure

to risk.

— With the implementation of a Business

Intelligence Platform across the insurance

operations including its subsidiar y General

Takaful, the company has enhanced access

to critical information related to its exposure

to insurance risk.

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201744 45www.qgirco.com

— The recently introduced (2016) regulator y

framework (QCB Executive Instructions) by

the Qatar Central Bank introduced risk-

based capital requirements for all insurance

companies operating in Qatar. Qatar

General Insurance & Reinsurance Company

continues to maintain a ver y high solvency

ratio at 240% as of Q3 2017 as per QCB’s risk

capital model (minimum 150%). In addition,

the company has established a committee

at the senior management level to manage

the compliance and regulator y risks arising

from the QCB Executive Instructions related

to corporate governance.

— The Group is committed to maintaining

full compliance with all applicable Anti

Money Laundering laws and regulations.

To strengthen its AML framework, the group

plans to implement an AML software within

2018.

— Following the events of June 6, 2017 and

the blockade imposed on the state of

Qatar by U.A.E., Saudi Arabia, Bahrain

and Egypt, the group has taken immediate

actions to control its risk exposure to these

four countries.

The Group went through the rating review

process with the rating agency A.M. Best, which

reaffirmed its financial strength rating of A-

(Excellent) with a stable outlook, reflecting the

Group’s ver y strong risk adjusted capitalisation,

operating per formance and enhanced

enterprise risk management (ERM) capabilities.

(b) Capital management objectives, policies and approach

The Group’s approach to managing capital

involves managing assets, liabilities and risks

in a coordinated way, assessing shortfalls

between available and required capital levels

(by each regulated entity) on a regular basis

and taking appropriate actions to enhance

the capital position of the Group in the light

of changes in economic conditions and risk

characteristics.

In managing the risks that affect the Group’s

capital position we have established several

capital management objectives, policies and

approaches, including the following:

— Setting target risk-adjusted rates of return,

which are aligned to per formance objectives

and ensure that the Group is focused on

the creation of value for shareholders

— To maintain the required level of stability of

the Group thereby providing a degree of

security to policyholders

— To retain financial flexibility by maintaining

strong liquidity and access to a range of

capital markets

— To align the profile of assets and liabilities

taking account of risks inherent in the

business

— To maintain financial strength to support

new business growth and to satisfy the

requirements of the policyholders, regulators

and stakeholders

(c) Regulatory Framework

Regulators are primarily interested in protecting

the rights of policyholders and monitor them

closely to ensure that the Group is satisfactorily

managing affairs for their benefit. At the same

time, regulators are also interested in ensuring

that the Group maintains an appropriate

solvency position to meet unforeseen liabilities

arising from economic shocks or natural

disasters.

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201746 47www.qgirco.com

The operations of the Group are subject to

regulator y requirements within the jurisdictions

in which it operates and such regulations

prescribe approval and monitoring of activities

and impose certain restrictive provisions to

minimise the risk of default and insolvency of

insurance companies. All regulated entities

within the Group act in accordance with their

regulator y requirements.

(d) Asset Liability Management (ALM) Framework

Financial risks arise from open positions in

interest rate, currency and equity products, all

of which are exposed to general and specific

market movements. We have been following a

few simple premises under our practicing ALM:

— Match assets to the liabilities arising from

insurance contracts by reference to the

type of benefits payable to policyholders

— Ensure in each period sufficient cash flow

is available to meet liabilities arising from

insurance contracts and any other sources

Corporate Governance

STRONG

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201746 47www.qgirco.com

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201748 49www.qgirco.com

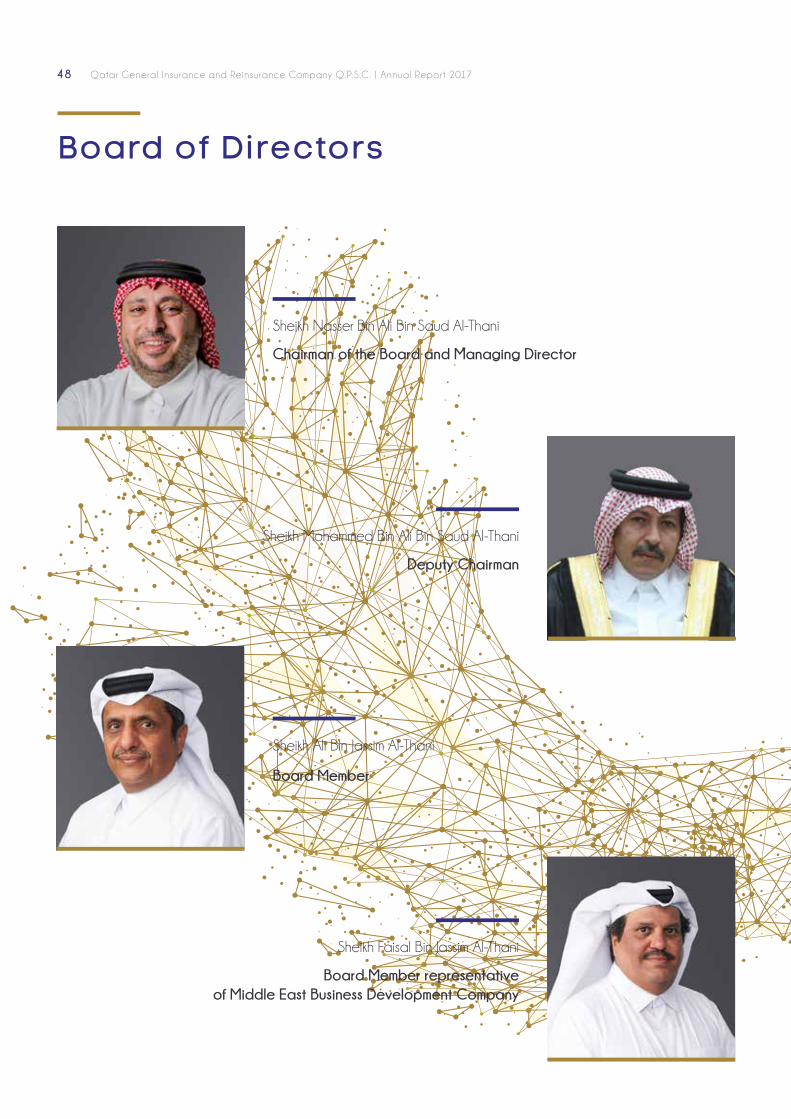

Board of Directors

Sheikh Nasser Bin Ali Bin Saud Al-Thani

Chairman of the Board and Managing Director

Sheikh Mohammed Bin Ali Bin Saud Al-Thani

Deputy Chairman

Sheikh Ali Bin Jassim Al-Thani

Board Member

Sheikh Faisal Bin Jassim Al-Thani

Board Member representative of Middle East Business Development Company

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201748 49www.qgirco.com

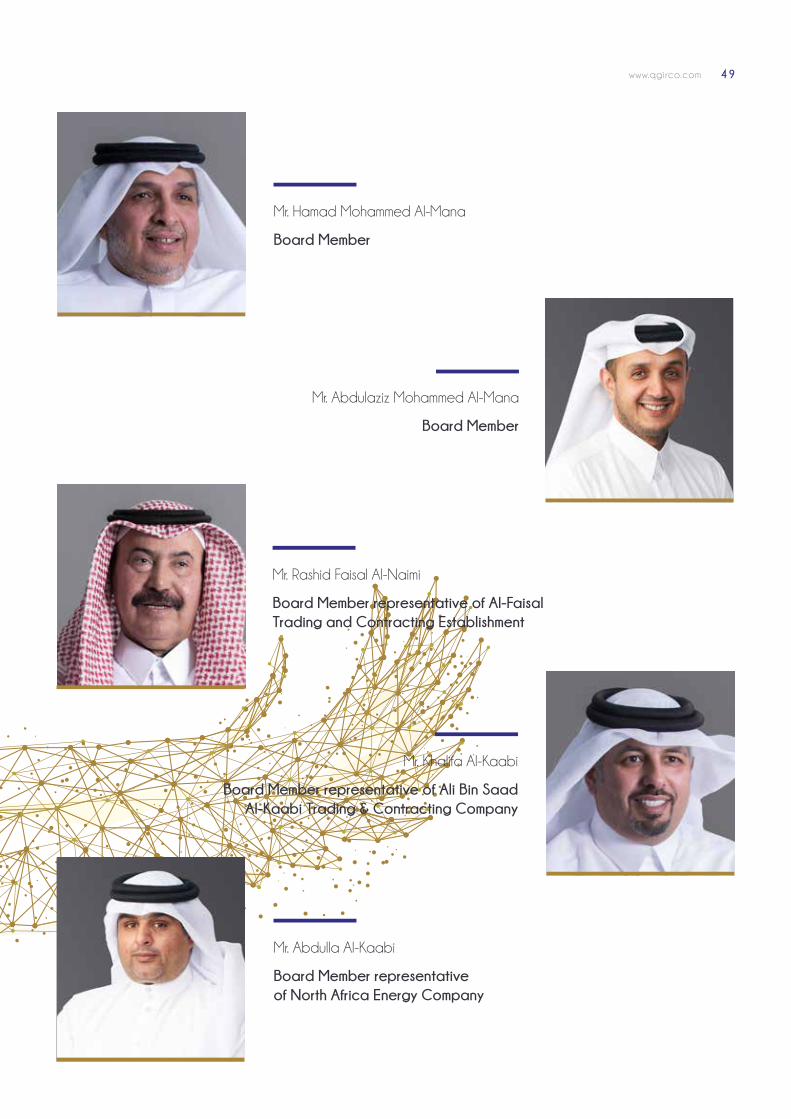

Mr. Abdulla Al-Kaabi

Board Member representative of North Africa Energy Company

Mr. Khalifa Al-Kaabi

Board Member representative of Ali Bin Saad Al-Kaabi Trading & Contracting Company

Mr. Rashid Faisal Al-Naimi

Board Member representative of Al-Faisal Trading and Contracting Establishment

Mr. Abdulaziz Mohammed Al-Mana

Board Member

Mr. Hamad Mohammed Al-Mana

Board Member

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201750 51www.qgirco.com

Corporate Governance

Company Profile:

Qatar General Insurance and Reinsurance

Company Q.P.S.C. (the “Company ”) is a public

joint-stock company, founded in 1979 under

the provisions of the Joint-Stock Companies

Regulation Law of 1961 as amended by

Commercial Companies Law No. (5) of 2002

which in turn was amended by the Commercial

Companies Law No.11 of 2015, to conduct all

types of insurance and reinsurance business

(except life insurance) and for capital and

property investment. The Company ’s paid up

capital is QR 875,067,030 (Qatari Riyals

Eight Hundred Seventy Five Million Sixty Seven

Thousand Thirty) divided into 87,506,703

shares (Eighty-Seven Million Five Hundred Six

Thousand Seven Hundred and Three shares).

Board of Directors:

The Company is managed by a Board of

Directors composed of nine members, who

possess the necessar y expertise for the

Company ’s business. Under the Company ’s

Memorandum and Articles of Association, the

Board of Directors (the “Board”) is collectively

responsible for the Company ’s management

and per formance, for developing the overall

comprehensive strategy of the Company and

the required policies and procedures, including

credit and investment policies, whether directly

or through the Board Committees to implement

the key business plans and provide the required

administrative and supervisor y guidance and

the effective control of the Company.

The members of the Board are elected

through the General Assembly of Shareholders

in accordance with the provisions of the

Company ’s Memorandum and Articles of

Association, Qatar ’s Commercial Companies

Law, QFMA’s regulations and as per the

provisions of the law of Qatar Central Bank,

in addition to fulfi l l ing any other requirements

stipulated in the applicable laws and

regulations. It is noteworthy that it is observed

to have one third of the Board members as

independent and experienced members.

The Board of Directors is composed of nine

members, serving for a three-year renewable

term. The current Board was elected by the

Shareholders for a period of three years (2017-

2019) at the Ordinary and Extraordinary

General Assembly held on 21 March 2017,

in which it was resolved that the number of

the Board members to be increased from 8

to 9 members and to amend the Company ’s

Articles of Association accordingly. The Board

members have the required experience and

knowledge to per form their duties particularly

in the financial and economic sectors.

The Board’s Charter:

The Board per forms its duties and responsibilities

in accordance with the Charter of the Board of

Directors, developed as per the form annexed

to the Corporate Governance Code, defining

the Board’s tasks, duties and responsibilities,

the duties of its members, the composition of

the Board and its Committees. The Charter

also defines the voting and decision-making

mechanism and generally the Board’s role in

leading the Company in accordance with the

requirements of the Company ’s Memorandum

and Articles of Association, QFMA’s regulations,

the Commercial Companies Law, Qatar Central

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201750 51www.qgirco.com

Bank Law and the Executive Instructions issued

pursuant to it. The Board Charter is made

available to the public through the Company ’s

website, which is one of the key requirements

of Corporate Governance principles aimed to

develop Corporate functioning. This Charter is

in the process of being amended to comply

with the provisions of the new Commercial

Companies Law No.11 of 2015, the Insurance

Executive Instructions and the Governance

Principles for Insurance Companies issued by

Qatar Central Bank and the new Governance

Code.

The Board’s Tasks and Responsibilities:

1. The Board is responsible for the management

of the Company, and the development

and supervision of implementation by the

Company ’s Executive Management of

the key business plans, comprehensive

strategies and main objectives. Subject to

the competence of the General Assembly,

the Board shall assume all the authorities

and powers necessar y for the management

of the Company and shall discharge its

duties as set out in all the applicable laws

and regulations and the Company ’s Articles

of Association and by-laws. The Board

shall remain responsible for all the Board

Committees.

2. The Board shall carr y out and per form its

duties prudently, in good faith with a view

to the best interests of the Company and its

resolutions shall be based upon adequate

information from the Executive Management

or any other reliable source.

3. The Board shall ensure providing its

members with a full and prompt access to

Company related information, documents

and records via the Board Committees. The

Company ’s Executive Management shall

provide the Board and its Committees with

all requested documents and information.

4. Among Board’s functions is to develop

and adopt the Company ’s management

and organisational structuring, the policies

(financial, accounting, internal audit, etc.),

strategies and systems especially the Risk

Management system and the Internal

Administrative system; the definition of

tasks, functions, duties and responsibilities;

the formation of the Committees and the

definition of their functions; the nomination

of the Company ’s External Auditor based

on competency and efficiency; and

determining the Auditor ’s fees for the

Company ’s General Assembly.

5. The Board members shall ensure the

attendance of the Nomination and

Remuneration Committee members, the Audit

Committee members, the Internal Auditors

and representatives of the External Auditors

the Company ’s General Assembly Meeting.

6. The Board shall design a training programme

for newly appointed Board members to

ensure that, members upon election shall

have an adequate understanding of the

Company ’s functions and operations and

that they are fully aware of their respective

responsibilities.

7. The Board members shall assume

responsibility for having an appropriate

understanding of their functions and duties,

and for educating themselves in financial,

business and industr y practices as well as

the Company ’s operations and functions.

In this respect, the Board shall adopt an

appropriate formal training to enhance

Board members’ skil ls and knowledge.

8. The Board shall at all times keep its members

aware of the latest developments in the

area of Governance and best practices

relating thereto. The Board may delegate

the same to the Audit Committee or the

Qatar General Insurance and Reinsurance Company Q.P.S .C. | Annual Repor t 201752 53www.qgirco.com

Governance Committee or any other body

as it deems appropriate.

9. The Company ’s Articles of Association shall

include clear procedures for the tasks,

authorities and powers of the Board, the

terms and conditions of membership and

isolation terms in the event of failing to attend

the Board meetings, and other Company

provisions related to the Board. The Board

shall also assume all the other functions,

duties and responsibilities prescribed in the

relevant laws and regulations.

10. The Board shall prepare an Annual Report

that includes a comprehensive assessment

of the Company ’s per formance and results

of its activities during the year.

The Board shall have the broadest powers to

manage the Company ’s affairs; set, develop

and adopt future plans and strategic objectives

and policies; approve, supervise and regularly

review the Internal Control systems. The Board

shall approve the appointment, determine

the remuneration and review the per formance

of Executive Managers; and shall review the

overall per formance of the Company based on

the recommendations of the Nomination and

Remuneration Committee.

The Board shall also bear the overall

responsibility for the Company ’s compliance

with the applicable related laws, the Company ’s

Memorandum and Articles of Association. It

shall be also responsible for protecting the

Company from illegal business or practices,

ensuring the Company ’s adherence to the

provisions of the Corporate Governance code

and the provisions of Qatar Central Bank ’s