CMD-SLIDESHOW.pdf - Covivio

106

CAPITAL MARKETS DAY DECEMBER 13 TH

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of CMD-SLIDESHOW.pdf - Covivio

CAPITAL MARKETS DAY

DECEMBER 13TH

AGENDA OF THE DAY

2

09:00 – 12:00

12:00 – 13:30

13:30 – 17:00

Presentation

Lunch

Asset tour

I. A DIVERSIFIED PORTFOLIO READY FOR GROWTHChristophe Kullmann, CEO

II. AN AMBITIOUS & WELL-RECOGNIZED ESG STRATEGYYves Marque, CCO

III. EUROPEAN OFFICES

A. ROUNDTABLETristan Cazin, Deputy General Secretary, Expertise France / Enrico Vanin, CEO Italy, AON / Virginie Grolleau, Journalist, Challenges

B. COVIVIO OFFICES STRATEGYOlivier Estève, Deputy CEO / Alexei Dal Pastro, CEO Italy / Marielle Seegmuller, Head of Operations

IV. HOTELS

A. ACCOR’S VISIONMaud Bailly, CEO Southern Europe, Accor

B. COVIVIO HOTELS STRATEGYTugdual Millet, CEO Hotels

V. RESIDENTIAL GERMANYDr Daniel Frey, CEO Residential

VI. KEY TAKEAWAYS

3

4

13

23

24

25

69

70

71

86

102

SUMMARY

I. A DIVERSIFIED PORTFOLIO READY FOR GROWTH

Symbiosis – Milan

5

COVIVIO TODAY: € 17BN DIVERSIFIED PORTFOLIO WITH BEST-IN-CLASS PLATFORMS IN EACH ASSET CLASS

A diversified REIT

58%Offices in

France, Italy

& Germany

15%Hotels

in Europe

27%Residential

in Germany

A European portfolio

Germany

39%

France

39%

Italy

16%Others in Europe

6%

€17bn(€26bn 100%)

1.6msqm of offices

~40,800apartments

45,500Hotel rooms

Figures as of Q3 2021

95%Average occupancy

rate

7YearsWALB

6

SUSTAINED ASSET ROTATION, VALUE CREATION & DELEVERAGING…

- € 6bn+ € 7bn

Portfolio value

End-2015

Cash

disposals CapexAcquisitions

Value

Creation

Portfolio value

H1 2021

+ € 2bn

+ € 3bn

€17 bn(GS)

€11 bn(GS)

45% LTV

<40% LTV1 policy

-5pts LTV

END OF 2015 TODAY

1. 41% in H1 2021

7

… FOR A BETTER-QUALITY PORTFOLIO (1/2)

Offices

62%

Non-

strategic

5%

Hotels

13%

Offices

58%

Hotels

15%

German

Resi.

27%

€ 11bn € 17bn

German Resi.

20%

END OF 2015 TODAY

Increase in German residential exposure

Offices reinforced in city-centers in Paris, Milan and Berlin

Hotels focused on major European destinations

Exit of non-strategic activities

8

… FOR A BETTER-QUALITY PORTFOLIO (2/2)

93%Of the portfolio in

top locations*

88%Green assets

72%

Better Assets

locations…

END OF 2015

… And more

sustainable portfolio

Of the portfolio in

top locations

35%Green

assets

TODAY

* Offices: large European cities; Hotels: top touristic destinations; Residential: city-centers of Berlin, Dresden, Leipzig, Hamburg and large cities of NRW

9

REAL ESTATE IS CHANGING, SO ARE WEAT THE FOREFRONT OF THE INDUSTRY THANKS TO CONSTANT AGILITY & INNOVATION

Climate change is a priority

Ability to operate working spaces

Client-centricity

Launch in 2017 of Wellio, our flexible workspace offer

8 sites in operation as of today, one new opening planned in 2022 (Via Unione Milan)

- 40%Target2010-2030

All-in-one offer for our office clients with a wide-range of services

Design thinking process to involve all key stakeholders

Wide range of services for our residential clients: electricity purchase, services for senior…

- 20%Reduction in carbon emissions 2010-2020

70%

75%

80%

85%

90%

95%

100%

2015 2016 2017 2018 2019 2020 Q3 2021

100

105

110

115

120

125

130

135

140

2015 2016 2017 2018 2019 2020 H1 2021

10

BEST-IN-CLASS PLATFORMS IN EACH OF OUR MARKETS

CRITICAL SIZE IN

EACH PRODUCTSTRONG PERFORMANCE OVER THE YEARS

Amongst the largest REITs in

each asset class

TOP 5Office platform in Europe

TOP 5German residential

platform

#1Hotel platform in Europe

Occupancy rate

96.7%average

occupancy rate

Cumulated LfL Value change

+4.4%CAGR

FY15 – H1 21

On a 100 basis

7.1 years average WALT

CAP 18 PARIS, 90,000 m²

11

SCALO MILAN, 70,000 m²EUROMED MARSEILLE, 125,000 m²

NOEME BORDEAUX, 46,500 m²DUCA D’AOSTA MILAN, 2,500 m²MONTE TITANO MILAN, 6,000 m²

Development of new districts: our expertise makes us a natural partner for cities & neighborhoods

Ability to maximize the value of an asset by changing its use, e.g., from office to residential or hotel

COMPLEMENTARITYSTRUCTURAL TREND OF AGILITY BETWEEN ASSET CLASSES

ALEXANDERPLATZ BERLIN, 60,000 m²

INFLOR&SENS FONTENAY-SOUS-BOIS, 20,900 m²

8.7 € 10.0 € 11.0 €

12.0 € 2,900 €

3,580 €

4,520 €

5,140 €

2,500 €

3,000 €

3,500 €

4,000 €

4,500 €

5,000 €

5,500 €

8.0 € 9.0 €

10.0 € 11.0 € 12.0 € 13.0 € 14.0 € 15.0 € 16.0 €

2015 2016 2017 2018 2019 2020 2021

12

MAIN TRENDS IN OUR ASSET CLASSES

€790 €780 €800 €810€870 €900 €930

3.25% 3.00% 3.00% 2.70%

2015 2016 2017 2018 2019 2020 2021

Paris prime rents Paris prime yield

Fly to quality sustaining rents and values in top locationsOFFICES

Strong rebound in the activity when restrictions easeHOTELS

Steady imbalance between supply and demandGERMAN

RESIDENTIALAverage asking rents in Berlin Portfolio asking price in Berlin

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Covivio Hotels variable revenues 2019 2020 2021

250 bpsSpread to

Bund 10Y

290 bpsSpread to

Bund 10Y

Scalo di Porta Romana – Milan

II. AN AMBITIOUS & WELL-RECOGNIZED ESG STRATEGY

Cité Numérique - Bordeaux

14

OUR PURPOSE, THE BACKBONE OF OUR ESG STRATEGYBUILD SUSTAINABLE RELATIONSHIPS & WELL-BEING

SUSTAINABLE

BUILDINGS

1

WELL-BEING

OF OUR

END-USERS

2

DEVELOPING OUR

TALENTS

3

HIGH

GOVERNANCE

STANDARDS

4

THAIS LEVALLOIS, 5,600 m²

15

SUSTAINABLE BUILDINGS

Buildings generate nearly

40% of annual CO2 emissions

Our responsibility is strong as we have

the power and the means to foster carbon reduction across

the value chain

Thus, we decided since 2018 to set a carbon

reduction target on all scopes, including

construction & refurbishment in our scope 3

1

2

3

CONSTRUCTION

ACCOUNTS FOR

OF OUR TOTAL EMISSIONS

>50%

AMBITIOUS CARBON REDUCTION TARGETS (1/2)1

16

50

75

100

2010 2015 2020 2025 2030

TARGET ACROSS ALL SCOPES

NET ZERO BY 2030SCOPES 1 & 2

TARGET ON SCOPE 3 REDUCTIONALIGNED WITH WELL BELOW 2°C TRAJECTORY

Decrease by 63% our emissions vs. 2010

Compensate the remaining part of our emissions

-40%

Build in a more sustainable way

Help tenants to reduce their emissions

(kgCO2 / m² / year)

All scopes

All products

Construction + operation

Target

- 40%

End of 2020

- 20%

CARBON TRAJECTORY

SUSTAINABLE BUILDINGSAMBITIOUS CARBON REDUCTION TARGETS (2/2)1

17

>50% of our new development projects are existing buildingsrestructuration, with a target of zero net artificialization17,550 tCO2e saved on Silex² by restructuring vs. demolishingthe existing tower

Most of our new office development projects will be certifiedBBCA or equivalent (>75% in France and >50% outside)

Development with the CSTB(1) of European standards for life-cycle analysis

New tools to measure our performance

Target by 2030 to supply with renewable energy 100% of ouroffice and hotels assets directly managed (61% at end-2020)

Promote the use of renewable energies

Low carbon construction

88%of our portfolio

is green-certified

Favor refurbishment &

fight urban sprawling

SUSTAINABLE BUILDINGS5 STRATEGIC PRIORITIES TO REACH OUR CARBON AMBITIONS

Responsible

supply chain

1

Mobilizing our suppliers & clients since 2011to decarbonize our activity

100%target by 2025

(1) Centre Scientifique et Technique du Bâtiment

18

GENERATE WELL-BEING

100%

OFFER MORE SERVICES

award

Independent survey updated every year

among 26 German residential companies,

including ~1,400 tenants surveyed

German Residential - Hamburg

Picnic with tenants to inform on energy modernization works

#1 of our new office developments projects with a well-being certification

of core office & residential buildings with a wide range of services by 2025

100%

Fairest

IN THE FOCUS MONEY SURVEY 2020

Landlord

WELL-BEING OF OUR END-USERS

#2

2

19

Independent survey carried

out every 2 years by Kantar

Average turnover over the last 5 years

Among the lowest in our industry

In the Executive Committee

Of our employees choose Covivio shares

for their incentives bonus

Ex-Aequo

mentorship

program

Leadership

program

European

Graduate program

Training week

95%

Optimism in the future of Covivio

83%

Employee satisfaction

8%

>80%

42%

36%

Women in management

position

DEVELOPING OUR TALENTS3

20

DEVELOPING OUR TALENTSABILITY TO ATTRACT & RETAIN TALENTS FOR LONG-LASTING CAREERS3

Chief Transformation

& IT Officer - Europe

General Secretary

German residential

Financial manager

Germany

▪ Graduated from ESCP-Europe

business school in 2012

▪ Joined Covivio in 2014 as a

portfolio analyst in France

▪ Moved to Germany in 2017 as

financial manager

▪ Promoted in 2021 to General

Secretary of the German

Residential business

▪ Graduated from HEC Paris in 2018

▪ Joined Covivio as a young

graduate in 2018 as an

investment analyst in France

▪ Moved to Germany in 2020 to

lead the set-up of the JV of

Alexanderplatz project

▪ Promoted to portfolio manager

for German Offices in 2021

▪ Graduated from HEC Paris 2010

▪ Joined Covivio as a young

graduate in 2010 as M&A analyst

▪ From 2012-2015: worked on pan-

European topics as a special

advisor to the CEO

▪ Led the portfolio management

team in France Offices

▪ Since 2018, now leading

Transformation and IT projects

across Europe. Member of the

EXCOM

Head of transactions

& special projects - Italy

▪ Graduated from Bocconi in 2010

▪ Joined Covivio in 2016 as asset

manager

▪ Participant in Covivio’s European

Leadership Program in 2018

▪ Promoted to Head of Transactions

& special projects in 2019

Laurie GOUDALLIER

Arnaud BREMENT

Francesco BARBIERI

Sandra LEMAÎTRE

21

Delfin (since 2007)

27%

Crédit Agricole Assurances (since 2005)

8%

ACM (since 2003)

8%Covea (since 2003)

7%

Free-float

50%

97%Say-on-Pay approval rate on average

HIGH GOVERNANCE STANDARDS

Separate chairman & CEO

40% women members (vs. 10% in 2011)

60% independent members (vs. 40% in 2011)

Strong experience with diversity of skills

ESG incentives in management remuneration

ESG Committee

Stakeholder committee

Be

st

pra

cti

ce

s b

oa

rd

co

mp

os

itio

n

Ta

ck

lin

g E

SG

at

ev

ery

lev

els

4

22

WELL-RECOGNIZED ESG PERFORMANCE

83/100Sector leader

Top 10 worldwide across sectors

AAA rating Best possible rating

Among the leaders

90/100Global sector leader

Negligible riskBest possible rating

62nd worldwide (15,000 companies)

A1+Best possible rating

Sector leader

B- ratingPrime universe since 2015

81/100Platinium

Top 1% worldwide

#1Companies with revenues >500 M€

Since 2014

III. EUROPEAN OFFICESA. ROUNDTABLE

B. COVIVIO OFFICES STRATEGY

Gobelins – Paris 5th

24

ROUNDTABLE

Virginie Grolleau

Journalist

Moderator

Deputy General Secretary

Tristan Cazin

CEO Italy

Enrico Vanin

III. EUROPEAN OFFICESA. ROUNDTABLE

B. COVIVIO OFFICES STRATEGY

MAIN TRENDS IN OFFICE MARKETS

COVIVIO’S OFFICES PORTFOLIO

CORE ASSETS

MANAGE-TO-CORE ASSETS

DEVELOPMENT PIPELINE

TRANSFORMATION INTO RESIDENTIAL

OFFICES STRATEGIC ROADMAP

Gobelins – Paris 5th

26

LEASING MARKETS ARE RECOVERING ACROSS EUROPE…

10-year averageSources: BNPP RE, JLL, Savills

0

100,000

200,000

300,000

400,000

500,000

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

GREATER PARIS TOP 5 GERMAN CITIES MILAN

vs 2020

+ 21%

vs 2020

+ 10%

vs 2020

+ 26%

4.5%

5.2%

2.6%

4.7%

7.7%

3.6%

Paris

Milan

Berlin

Munich

Frankfurt

Hamburg

27

… WITH A POLARIZATION TOWARDS WELL-LOCATED GRADE-A ASSETS…

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021E

Grand Paris Milan Berlin Munich Francfort Hambourg

Vacancy rates have increased in all markets since the beginning of the crisis… … but structural lack of offer in

city-centers continues

Vacancy rate in inner-cities at Q3 2021

Prime rents increased in Paris (+6%)

and in Germany’s top cities (+4% on

average) & Milan (+3%) since the

beginning of the crisis

Sources: BNPP RE, JLL, Savills

125,000 m²118,800 m²

113,300 m²

126,500 m²

114,500 m²

72,500 m²

159,000 m²

2015 2016 2017 2018 2019 2020 2021

28

… AS DEMONSTRATED BY OUR OWN 2021 RECORD YEAR

159,000 M² LET OR PRE-LET TO TOP TENANTS

11 years average new lease duration

2021

New lettings

50,000 m²Pre-letting

86,000 m²Sold to end-user

23,000 m²

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

29

INVESTORS’ INTEREST REMAIN STRONG…

FLY-TO-QUALITY IS DRIVING DOWN PRIME YIELDS… … BUT RISK PREMIUM REMAINS VERY HIGH

Sources: BNPP RE, JLL, Savills

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

4.50%

2.70%

1.35%

2.70%

Prime yield in Paris Risk premium of Paris prime yield vs. OAT 10-year

Q1 2020 Q2-Q4 2020 H1 2021

30

… AS DEMONSTRATED BY OUR DISPOSAL VOLUME

Italian non-core assets, 113 M€

Milan Cernaia, 94 M€

Marseille Astrolabe, 44 M€

Nanterre Respiro, 83 M€

Issy-les-Moulineaux EDO, 133 M€

Lyon 288 & Lille Helios, 94 M€

€148m4.1% margin

€703m7.0% margin

Data in group share

€1.1 BN OFFICES NEW DISPOSAL AGREEMENTS

SINCE EARLY 2020

€1.1bn5.2% margin

FY 2020 Q3

✓ Target 100% of our offices <5’ from metro/train station by 2025

31

ACCELERATION OF TRENDS IN OFFICES

Generalization of work-from-home (c. 2 days/w on average for jobs that can be done remotely). But the office is more than ever strategic for

companies to attract & retain talents as well as foster creativity & innovation. It must also reflect the ESG ambitions of companies

✓ Target 100% of our properties with a dedicated service offer

✓ Flex-office offer with our network of Wellio sites

✓ Strong differentiation with our All-in-One offer to accompany clients

✓ Implementing our design thinking process

✓ Target 100% of our offices green certified by 2025 (86% to date)

✓ Target 100% of our development with a WELL certification

ESG

QUALITY,

SERVICES &

FLEXIBILITY

LOCATION

32

OUR COMPETITIVE EDGE: DESIGN THINKING & ALL-IN-ONE OFFER

CAPEX

+0,5 b€(-0,3 b€ GS)

CORSO ITALIA11,600 m²

CB 2168,000 m²

GOBELINS4,400 m²

MONCEAU10,800 m²

VIA DANTE4,700 m²

SOPOP31,300 m²

DESIGN THINKING ALL-IN-ONE

DESIGN THINKING ALL-IN-ONE

DESIGN THINKING

DESIGN THINKING ALL-IN-ONE

ALL-IN-ONE

DESIGN THINKING ALL-IN-ONE

SILEX²30,900 m²

DESIGN THINKING ALL-IN-ONE

III. EUROPEAN OFFICESA. ROUNDTABLE

B. COVIVIO OFFICES STRATEGY

MAIN TRENDS IN OFFICE MARKETS

COVIVIO’S OFFICES PORTFOLIO

CORE ASSETS

MANAGE-TO-CORE ASSETS

DEVELOPMENT PIPELINE

TRANSFORMATION INTO RESIDENTIAL

OFFICES STRATEGIC ROADMAP

Gobelins – Paris 5th

34

A €10 BN PORTFOLIO FOCUSED ON CITY-CENTERS & ATTRACTIVE BUSINESS DISTRICTS

Figures as at June 30, 2021 and restated from assets under preliminaries

58%

51% Paris & Neuilly/Levallois

37% Greater Paris

12% Major regional cities

€5.7bn

27%91% Milan excl. Telecom Italia€2.6bn

15% 100% Top 7 German cities€1.5bn

35

STRATEGIC SCORING OF OUR OFFICE PORTFOLIO IN LIGHT OF MARKETS’ EVOLUTIONS

Manage-to-core(72% let, 4.1-year WALB)

Development pipeline

Transformation into residential

52%

6% 1% Non-core

€10bnOFFICES

PORTFOLIO1

1. Excluding €0.2m assets under preliminary

Core(96% let, 6.7-year WALB)

16%

21%

4%Telecom Italia

(100% let, 10-year WALB)

III. EUROPEAN OFFICESA. ROUNDTABLE

B. COVIVIO OFFICES STRATEGY

MAIN TRENDS IN OFFICE MARKETS

COVIVIO’S OFFICES PORTFOLIO

CORE ASSETS

MANAGE-TO-CORE ASSETS

DEVELOPMENT PIPELINE

TRANSFORMATION INTO RESIDENTIAL

OFFICES STRATEGIC ROADMAP

Gobelins – Paris 5th

37

CORE ASSETS: €5.1 BN (52%)

€5.1bnCORE

PORTFOLIO

High occupancy (96%)

Long WALB (6.7 years)

Strong value resiliency

& liquidity

Selective disposals to

finance new acquisitions

and development capex

€3.1bn (60%)in city-centers

€2.0bn (40%)in top-business districts

Via Amedei

Citygate,

FrankfurtWellio Gare de Lyon, Paris Wellio Montmartre, Paris Steel, Paris

Marquette, Toulouse

Wellio Gobelins, Paris

Wellio Via Dante, MilanCarré Suffren, Paris

Wellio Miromesnil, Paris Thais, LevalloisVia Amedei, Milan

38

CORE ASSETS IN THE CITY-CENTERSIN PARIS, MILAN, TOP GERMAN CITIES & FRENCH REGIONAL CITIES

Selected examples of our portfolio

€3.1bnmarket value

96%Occupancy

6 yearsWALB

89%green assets

98%<5 min

from metro

SILEX², THE NEW PRIME REFERENCE IN LYON CBD

30,900 m²

5.8%Yield-on-cost

92%Occupancy

9 yearsWALB

LOCATED in front of

Part-Dieu train

station in Lyon

CBD, the asset was

acquired in 2001

DELIVERED in July 2021

and 92% occupied to date

HIGH LEVEL of

services + Wellio

flexible space

The RESTRUCTURATION

of the asset started in 2017

and the project was shared

(50%) with our long-term

partner ACM

€85mBudget (group share)

>40%Value creation

39

40

PARIS PERCIER, TROPHY ASSET IN PARIS CBD WITH STRONG REVERSIONARY POTENTIAL

8,500 m²+30%

reversionary potential

100%Occupancy

2 yearsWALB

LOCATED in the 8th

arrondissement

Asset ACQUIRED

by Covivio in 2009

HEADQUARTER

of Chloé

STRONG RENT increase in

Paris CBD market due to strong

supply & demand imbalance

leading to significant

reversionary potential

41

TORRI GARIBALDI, BUSINESS CENTER IN MILAN

44,700 m²>20%

reversionary potential

100%Occupancy

PRIME ASSET

renovated in 2011 on

top of Milan Garibaldi

train station in Porta

Nuova

7 yearsWALB

Strong

REVERSIONARY

POTENTIAL that

materialized in 2021

with the reletting of

2,400 m² with +40%

rent reversionMULTI-LET towers

(14 tenants)

41

Thalès campus, Vélizy-Meudon The Sign, Milan

Symbiosis A&B, Milan

Ecole Ducasse,

Vélizy-Meudon

Frankfurt Airport

CenterFlow, Montrouge

Sunsquare, Munich

Symbiosis School, Milan

Dassault campus, Vélizy-Meudon

Eiffage campus, Vélizy-Meudon

42

CORE ASSETS IN TOP BUSINESS DISTRICTSATTRACTIVE LOCATIONS & LONG-TERM LEASES

Selected examples of our portfolio – ~70%

of our core assets in top business districts

€2.0bnmarket value

96%Occupancy

8 yearsWALB

84%green assets

76%<5 min from metro

(88% excluding Symbiosis)

43

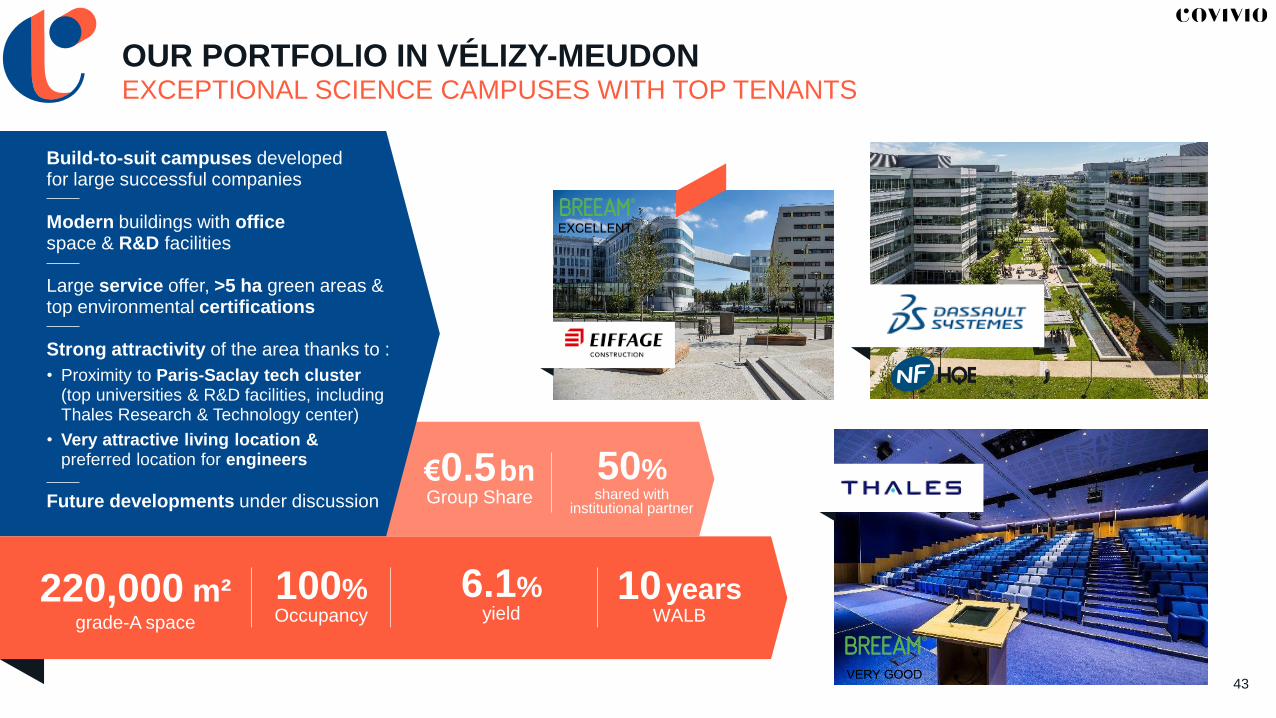

OUR PORTFOLIO IN VÉLIZY-MEUDONEXCEPTIONAL SCIENCE CAMPUSES WITH TOP TENANTS

220,000 m²grade-A space

50%shared with

institutional partner

100%Occupancy

10yearsWALB

6.1%yield

€0.5bnGroup Share

Build-to-suit campuses developed for large successful companies

Modern buildings with officespace & R&D facilities

Large service offer, >5 ha green areas & top environmental certifications

Strong attractivity of the area thanks to :

• Proximity to Paris-Saclay tech cluster (top universities & R&D facilities, including Thales Research & Technology center)

• Very attractive living location & preferred location for engineers

Future developments under discussion

44

SYMBIOSISTHE CREATION OF A BRAND-NEW BUSINESS DISTRICT

46,800 m²grade-A space

+79,000 m²

further developments

96%Occupancy

10yearsWALB

5.6%yield

€330mGroup Share

1st delivery in 2018, with Fastweb pre-

letting 100% of Symbiosis AB

2nd delivery in 2020, with ICS Milan pre-letting 100% of the building

3rd delivery in 2021, Symbiosis D, 92% pre-let to LVMH, Orsero and Boehringer Ingelheim

2021: launch of Symbiosis G+H, 100% pre-let to Moncler, and of Symbiosis F (build-to-sell agreement with SNAM)

Pursuit of the development of the area, with the development of Symbiosis C+E, and the development of Scalo di Porta Romana (70,000 m², starting in 2023)

+30%Rent growth since start of

the project

Symbiosis A+B, 20,500 m² ICS International school, 7,900 m²

Symbiosis D, 18,500 m²

W

Romolo

45

THE SIGN MILANANOTHER EVIDENCE OF OUR ABILITY TO DEVELOP TOP BUSINESS DISTRICTS

27,000 m²grade-A space

+14,000 m² further

developments

96%Occupancy

9yearsWALB

6.0%yield

€150mGroup Share

High accessibility, 5 min walk from

nearest metro station

27 000 m² office space delivered in 2020 and 2021

Offices fully let to top tenants (AON & NTT Data) with long-term lease

High environmental performance: The Sign A obtained in 2021 the highest LEED score in Europe

School

Construction of a built-to-suit and completely

independent office building

12,400 m²

10-year WALB

€64m budget

7.0% yield-on-cost

The Sign D

Delivery Q3 2024

The Sign A

Delivered in

March 2020

The Sign B+C

Delivered in April

2021

III. EUROPEAN OFFICESA. ROUNDTABLE

B. COVIVIO OFFICES STRATEGY

MAIN TRENDS IN OFFICE MARKETS

COVIVIO’S OFFICES PORTFOLIO

CORE ASSETS

MANAGE-TO-CORE ASSETS

DEVELOPMENT PIPELINE

TRANSFORMATION INTO RESIDENTIAL

OFFICES STRATEGIC ROADMAP

Gobelins – Paris 5th

47

MANAGE-TO-CORE ASSETS: €1.6 BN (16%)

€1.6bnMANAGE-TO-CORE

PORTFOLIO

€20mpotential rents

28% average vacancy

4.1 years WALB

Good fundamentalsAttractive location (83%

<5 min to metro)

In established business

districts

Asset management

initiatives to turn them

into core assets

48

INCREASE OCCUPANCY: €20M RENTS POTENTIAL

La Défense – CB 2168,100 m² – Occ. 83%

Boulogne – Grenier7,800 m² – Occ. 41%

Orly – Belaïa23,600 m² – Occ. 58%

Milan – Marostica8,600 m² – Occ. 83%

Milan – Innovazione19,800 m² – Occ. 83%

Châtillon – IRO25,600 m² – Occ. 25%

Düsseldorf – HerzogT.55,700 m² – Occ. 51%

Hamburg – Zeughaus38,600 m² – Occ. 81%

Munich – Eight D.17,600 m² – Occ. 26%

60%OF TOTAL OFFICES

VACANCY

€20MPOTENTIAL

ANNUALIZED

RENTS

ASSET MANAGEMENT&Ca. €50mREFURBISHMENT CAPEX

49

HERZOGTERRASSEN

TODAY TOMORROW

A VIBRANT BUSINESS CENTER IN THE HEART OF DÜSSELDORF

WALB

4.6 years

OCCUPANCY

51%SURFACE

55,700 m²

49% vacancy following

WeWork’s lease

cancellation

Capex program should have

been performed by WeWork

to upgrade the spaces

€20mCAPEX IN 2022

New building concept

Refurbished common areas

Five stars service offer

7 000m² rooftop terraces

Improve the energy efficiency

Owned at

75%

<5% of our office

portfolio

Surface (m²)

68,000

Occupancy

83%

WALB

4years

CB21 – REPOSITIONING AN EMBLEMATIC ASSET IN LA DÉFENSE

1st Business district in Europe

Metro line at the foot of the building1

Improve interior design and

services offer

ca. €15m Capex

Ideal location… …in a volatile market

Complete repositioning in 2020-2021

Price repositioning

€480/m² From

€410/m²To &

5,000 m² let over last 18 months

La Défense vacancy rate

4.0%

6.0% 6.6%

10.7%9.1%

5.5%3.4%

9.2%

14.0%

08 09 10 11 12 13 14 15 16 17 18 19 20 Q3 21

€19m €17m

€2m

€11m

€8m

€37m

€20m

€15m

€8m

€4m

€4m

2022 2023 2024

51

LEASE EXPIRIES: LIMITED CHALLENGES

CORE

€14M ALREADY SECURED

RESIDENTIAL

DEVELOPMENT

OFFICE

REDEVELOPMENT

MANAGE-TO-CORE MANAGE-TO-CORE

AVERAGE YEARLY

EXPIRIES

<1%OF COVIVIO’S

ANNUALIZED RENTS

LEASES EXPIRIES SCHEDULE

III. EUROPEAN OFFICESA. ROUNDTABLE

B. COVIVIO OFFICES STRATEGY

MAIN TRENDS IN OFFICE MARKETS

COVIVIO’S OFFICES PORTFOLIO

CORE ASSETS

MANAGE-TO-CORE ASSETS

DEVELOPMENT PIPELINE

TRANSFORMATION INTO RESIDENTIAL

OFFICES STRATEGIC ROADMAP

Gobelins – Paris 5th

53

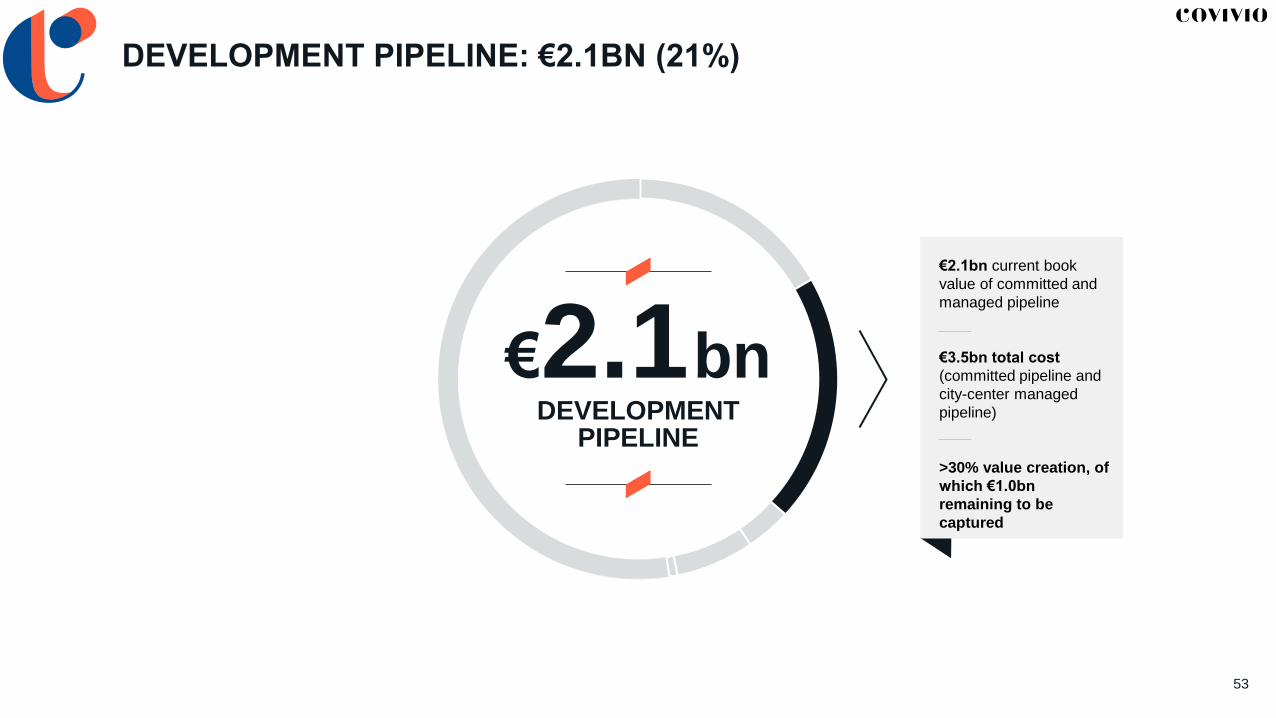

DEVELOPMENT PIPELINE: €2.1BN (21%)

€2.1bnDEVELOPMENT

PIPELINE

€2.1bn current book

value of committed and

managed pipeline

€3.5bn total cost

(committed pipeline and

city-center managed

pipeline)

>30% value creation, of

which €1.0bn

remaining to be

captured

AN OUTSTANDING TRACK RECORD

€1.4bnBUDGET

SINCE 2017

32PROJECTS

DELIVERED

96%AVERAGE

OCCUPANCY RATE

12 MONTHS AFTER

DELIVERY

~30%VALUE

CREATION

97%LET

2021: 110,000 M² DELIVERED

The Sign A Milan,

9,300 m², 2020

Art&Co Paris,

13,400 m², 2017

Wellio Gobelins Paris,

4,500 m², 2021

Flow Montrouge,

23,600 m², 2021

Principe Amedeo Milan,

6,500 m², 2019

Thais Levallois,

5,500 m², 2017

Euromed Center Marseille,

24,000 m², 2017

Toulouse Marquette,

11,000 m², 2018

Wellio Via Dante Milan,

4,700 m², 2020

Cité Numérique Bordeaux,

19,200 m², 2019

55

INVESTING IN EUROPEAN MAJOR CITIES

€1.8bnTotal budget GS€0.8bn remaining capex

PARIS

BERLINMILAN

Grands Boulevards

Voltaire

AlisN2 Streambuilding

Madrid

Goujon

Anjou

SOPOP

Keller

Bobillot

Raspail

CAP 18

Jemmapes

Centre

Porta Nuova

Semi-centre

ScaloThe Sign D

Corso Italia

Unione

Symbiosis

Vitae

Spree

Centre

Fringe

Subcentres

City

LOFTALXP

Plano

COMMITTED PIPELINE

€540mValue creation €380m remaining to be booked

€1.7bnTotal budget GS€1.1bn remaining capex

MANAGED PIPELINE IN CITY-CENTERS

€0.6bnValue creation

Other French committed assets:

Velizy campus, Lyon Sévgné, Bordeaux Jardin de l’Ars

Committed assets

Managed assets

Committed assets

Managed assets

Committed assets

Managed assets

The Sign D, 14,000 m², 92% pre-

let

Q2 2024

Bordeaux Ars, 19,200 m²

51% pre-let

56

INVESTING IN THE CITY-CENTERS & TOP BUSINESS DISTRICTS€1.8bn budget | €540m value creation (€380m remaining to be captured)

82% IN CITY-CENTERS 18% IN TOP BUSINESS DISTRICTS

Paris Goujon, 8,600 m²

60% pre-let

Paris SoPop, 31,300 m²

33% pre-let

Levallois Alis, 19,800 m²Paris N2, 15,600 m²Paris Madrid, 5,850 m²

100% pre-let

Berlin ALXP, 60,000 m²

Berlin LOFT, 7,600 m²

Symbiosis G+H, 38,000 m², 100%

pre-let

Vitae, 10,000 m², 18% pre-let

Dassault extension, Paris region,

27,500 m², 100% pre-letUnione Milan, 4,500 m²

100% pre-let

Paris Anjou, 9,300 m²

Exclusivity talks

Q2 2024

Q1 2022 Q2 2022 Q2 2023

Q3 2022 Q2 2023

Q3 2024

Q1 2024

Q2 2024 Q4 2025

Q1 2022

Q2 2022

Q4 2023

€1.5bn

Total Costs

4.6%

Yield

€450m

Value Creation

€300m to book

22%

Pre-let

€0.3bn

Total Costs

6.7%

Yield

€90m

Value Creation

€80m to book

88%

Pre-letCorso Italia, 11,600m²

Q3 2023

60% pre-let to Roland Berger

and an executive search

company

57

INVESTING IN CITY-CENTERSPARIS CBD GOUJON PROJECT CASE STUDY

€189MTOTAL BUDGET

4.0%YIELD

>40%VALUE CREATION

KEY

INDICATORS

2018

2021

2019

2022

Delivery of the new building with

average target rent at ~€900/m²

Start of the renovation works

Acquisition of a 1930s typical

Parisian building

PARIS CBD

TROPHY ASSET

8,600 M² SURFACE

58

INVESTING IN CITY-CENTERSLOFT: MIXED-USE PROJECT IN BERLIN’S TRENDY AREA

7,600M² MIXED-USE PROPERTY

TRENDY LOCATION

STATE OF THE ART

20% Residential

80% Offices

Attractive & lively neighborhood of Berlin (Moabit).

5 min walk from the metro

Full refurbishment & roof extension (+900 m²)

Loft-style offices designed to foster creativity & well-being

1,000m² green oasis

€40MTOTAL BUDGET

5.2%YIELD

>35%VALUE CREATION

KEY

INDICATORS

City-center projects to be

launched in the short-term

[ 2022 – 2023 ]

59

MANAGED PIPELINE: FURTHER VALUE CREATION

Landbanks in top business districts

City-center projects to be

launched in the mid-term

[ 2024 – 2025 ]

Potential commitment subject to

significant pre-let

City-centers: €1.7 bn budget / €0.6 bn value creation

68%€0.2bn current book

value

32%€0.4bn current book

value

220,000 m²

CAP 18, ~90,000 m² mixed-use project in

Paris

Scalo, ~70,000 m² project in Milan

Exclusivity talks for a new 35,000 m² development

Land bank

Land bank

60

MANAGED PIPELINESCALO PORTA ROMANA: COVIVIO INVESTING IN MILAN’S URBAN REGENERATION

>50%of green areas

North-

South

connectio

ns

Olympic Village

(Coima)

High Line

Public Park

Residenti

al Area

(Coima)

Prada

Area

Resid

entia

l

Are

a

(Coim

a)

LODI TIBB

SYMBIOSIS

Elevated

squareCovivio

Plot

70,000 m² €500mTOTAL BUDGET

>30%VALUE CREATION

▪ One of the greatest urban regeneration project of the next decades for Milan, after

Symbiosis last delivery in 2023

▪ Strategic plot with strong potential connecting Symbiosis to the city center

▪ Excellent accessibility (Porta Romana train station and M3 LODI), and future main hub

of the new CIRCLE LINE that will cross the city from South, towards East and North

2022

Approval of the masterplan

& acquisition of the land Delivery

Beginning

of works

2023 2025

2026

2027

III. EUROPEAN OFFICESA. ROUNDTABLE

B. COVIVIO OFFICES STRATEGY

MAIN TRENDS IN OFFICE MARKETS

COVIVIO’S OFFICES PORTFOLIO

CORE ASSETS

MANAGE-TO-CORE ASSETS

DEVELOPMENT PIPELINE

TRANSFORMATION INTO RESIDENTIAL

OFFICES STRATEGIC ROADMAP

Gobelins – Paris 5th

62

TRANSFORMATION INTO RESIDENTIAL: €0.4BN (4%)

€0.4bnOFFICES-TO-RESIDENTIAL

86% occupancy

1.6-year WALB

2,100 unitso/w

(1,545 units committed

at end-2021)

€415mtotal budget

(€256m committed at

end-2021)

>10% margin

63

BEFORE 2020: €0.1BN ASSETS TO BE TRANSFORMED INTO RESIDENTIAL

Bordeaux Lac project: from 11,000 m² office building into a new 46,500 m² residential district

▪ December 2004: sale-and-leaseback with IBM for its

regional HQ (11,000 m²) for €7m

▪ Between 2004 and 2018: urban transformation of the area

▪ July 2018: release of IBM

▪ 2020: building permit and start of the works of 46,500 m²

of traditional housing, coliving and senior housing

▪ Budget: €120m

▪ Target margin: >10%

20242004

Some of our office assets are located in areas that became secondary

office markets but highly attractive residential areas over the course of

10+ years

➔ Transforming into residential to take advantage

of market shifts

€0.1bnbook value

Residential transformation pipeline before 2020

(committed + managed)

Rueil Vinci: new strategy following stressed office market

▪ 2016: acquisition of Vinci HQ in Rueil (36,000 m²)

for 129 M€ and 7.75% yield (~10 M€ annual rent)

▪ Strategic review of the project to change from 100% office

to mixed-use office/residential

▪ Current book value: ~3,200 €/m²

▪ New housing price: ~10,000 €/m²

64

SINCE THE COVID CRISIS: +€0.3BN ADDITIONAL ASSETS TO BE TRANSFORMED INTO RESIDENTIAL

▪ Vacant or soon-to-be vacant assets in stressed office markets

marked by excessive immediate & future offer

▪ However, these assets are located in attractive areas of Paris’ inner

ring or major regional cities ➔ residential strategy to de-risk the

asset & defend the value

98% OCCUPANCY 1.6-YEAR WALB

3,700Units

+1,600 units since 2020

€1.1bntotal budget

+0.7bnsince 2020

>10% target

margin

€0.4bnbook value

+€0.3bn since 2020

Updated residential transformation pipeline

Today Tomorrow

65

GROWING RESIDENTIAL PIPELINE IN THE COMING YEARS, DRIVING UP DEVELOPMENT MARGINS

2,800UNITS*

200,000M²

80% IN GREATER

PARIS€44m

€256m

€374m

2020 2021 2022

205units

1,545units

x7

€256m / 100,000 m² pipeline in France at end 2021

1,985units

Deliveries2021 & 2022100% sold

>2022

BEYOND

Total of 5,000 units to be developed over the next ~7 years

Ramp-up of development margin to reach ~10-15 M€ per year from 2022 until ~2028

* Including 1,200 units from mixed-use projects

66

UNLOCKING VALUE IN RESIDENTIAL TRANSFORMATION

Set-up of a dedicated

team since 2017

A team of 15 people with diverse

skills

✓Structuring

✓Engineering

✓Commercialization

GLA: from 2,500 m² to 1,900 m²

Total budget: €11m

Margin: 11%

Nice Brancolar, 265 units Fontenay-sous-Bois, 250 units

Meudon Bellevue, XXX units St-Germain-en-Laye, 24 units

GLA: from 1,830 m² to 2,000 m²

Total budget: €12m

Target margin: 12%

GLA: from 13,800 m² to 18,000 m²

Total budget: €85m

Target margin: 10%

GLA: from 5,600 m² to 17,700 m²*

Total budget: €32m (Group Share)

Target margin: 10%

Meudon Bellevue, 26 units

Delivery

2022

Delivery

2024

Delivery

2026

Delivery

2024

III. EUROPEAN OFFICESA. ROUNDTABLE

B. COVIVIO OFFICES STRATEGY

MAIN TRENDS IN OFFICE MARKETS

COVIVIO’S OFFICES PORTFOLIO

CORE ASSETS

MANAGE-TO-CORE ASSETS

DEVELOPMENT PIPELINE

TRANSFORMATION INTO RESIDENTIAL

OFFICES STRATEGIC ROADMAP

Gobelins – Paris 5th

68

STRATEGIC ROADMAP IN OFFICES

€20m annualized rents

3

4

INCREASE OCCUPANCY ON MANAGE-TO-CORE ASSETS

ACCELERATE OUR ASSET ROTATION STRATEGY

INVEST IN THE DEVELOPMENT PIPELINE

ACCELERATE OFFICE INTO RESIDENTIAL TRANSFORMATION

Focusing on core mature assets to

crystalize value creation & finance the pipeline

€1.0bn value creation

remaining to be captured

€10-15m average margin per

year at maturity

1

2

IV. HOTELSA. ACCOR’S VISION

B. COVIVIO HOTELS STRATEGY

HOTEL MARKET

A PORTFOLIO WELL PLACED TO BENEFIT FROM THE RECOVERY

GROWTH OPPORTUNITIES

Mercure – Boulogne

70

ACCOR’S VISION OF THE FUTURE OF HOSPITALITY

Maud Bailly

CEO Southern Europe

IV. HOTELSA. ACCOR’S VISION

B. COVIVIO HOTELS STRATEGY

HOTEL MARKET

A PORTFOLIO WELL PLACED TO BENEFIT FROM THE RECOVERY

GROWTH OPPORTUNITIES

Mercure – Boulogne

72

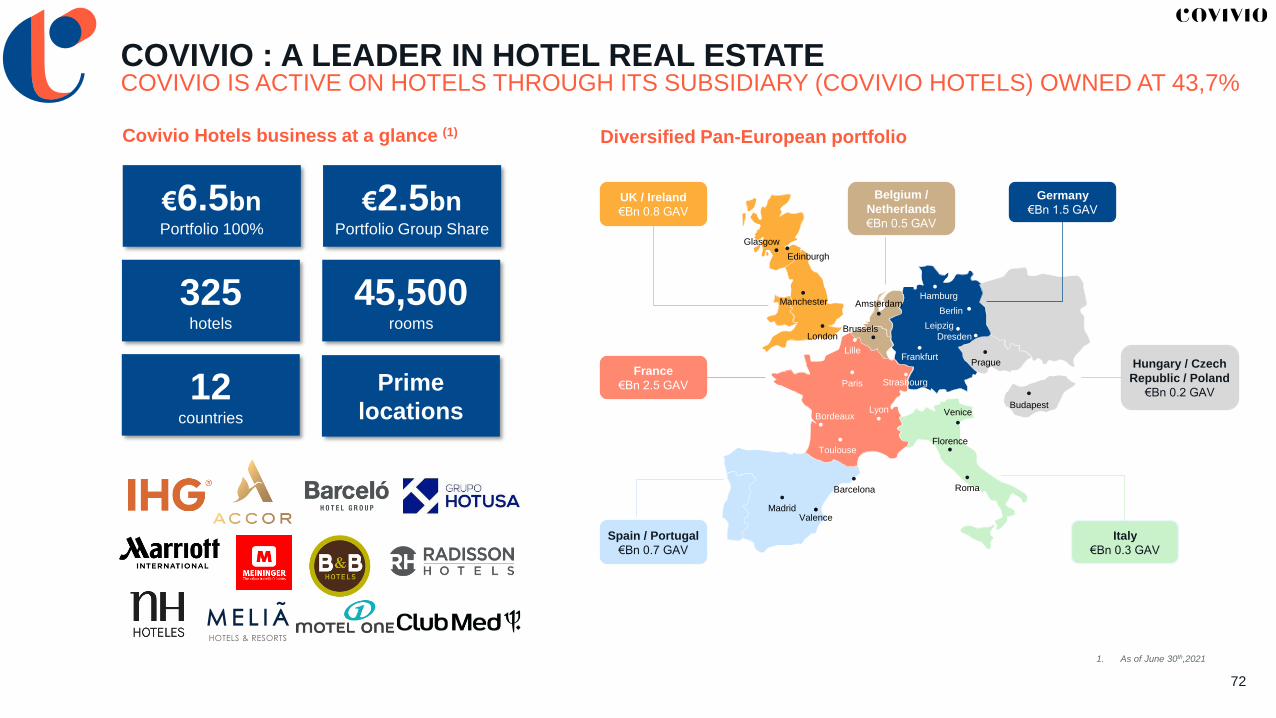

COVIVIO : A LEADER IN HOTEL REAL ESTATECOVIVIO IS ACTIVE ON HOTELS THROUGH ITS SUBSIDIARY (COVIVIO HOTELS) OWNED AT 43,7%

Covivio Hotels business at a glance (1) Diversified Pan-European portfolio

1. As of June 30th,2021

Paris

Madrid

Barcelona Roma

Budapest

Prague

London

Manchester

Edinburgh

Glasgow

Brussels

AmsterdamBerlin

Venice

Florence

Lyon

UK / Ireland

€Bn 0.8 GAV

Spain / Portugal

€Bn 0.7 GAV

France

€Bn 2.5 GAV

Italy

€Bn 0.3 GAV

Hungary / Czech

Republic / Poland

€Bn 0.2 GAV

Belgium /

Netherlands

€Bn 0.5 GAV

Germany

€Bn 1.5 GAV

Leipzig

Frankfurt

Bordeaux

Lille

Dresden

Hamburg

Toulouse

Strasbourg

Valence

€6.5bnPortfolio 100%

325hotels

€2.5bnPortfolio Group Share

45,500rooms

12countries

Prime

locations

IV. HOTELSA. ACCOR’S VISION

B. COVIVIO HOTELS STRATEGY

HOTEL MARKET

A PORTFOLIO WELL PLACED TO BENEFIT FROM THE RECOVERY

GROWTH OPPORTUNITIES

Mercure – Boulogne

74

DEMAND SIGNIFICANTLY INCREASED DURING H2 2021

Demand significantly increased since June 2021, driven by people’s strong desire to travel, the progress in vaccination numbers and the easing of government restrictions

During summer 2021, some touristic areas led by leisure demand even surpassed 2019 levels

As from September, the demand continued to increase, driven by business clientele in large cities. In Paris, the occupancy more than doubled between June (27%) and October (69%)

JUNE 2021 SUMMER 2021 SEPTEMBER 2021

62%58%

63%66%

63%

0%

10%

20%

30%

40%

50%

60%

70%

France Germany UK Spain Italy

June July August Sept. Oct.

69% 67%

55%

67%

57%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Paris Berlin London Madrid Rome

June July August Sept. Oct.

JUNE TO OCTOBER AVERAGE OCCUPANCY RATES

Source : MKG

75

HOTELS HAVE ALWAYS QUICKLY RECOVERED

-20%

-15%

-10%

-5%

0%

5%

10%

2001

-15%

-10%

-5%

0%

5%

10%

15%

11%

2 Source: Oxford Economics (oct. 2021)

1 Source: Oxford Economics

2006 2008 2012

2001 crisis Global financial crisis

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

6%9%

12%

2021 202220202019 2023 2024 2025

FORECASTS FOR FUTURE CUSTOMER TRAVEL

SPENDING EUROPE2

EVOLUTION OF CUSTOMER TRAVEL

SPENDING DURING PAST CRISES EUROPE1

In October 2021, B&B CEO stated that he expected 2019 performances to be reached by the end of 2021.

Expects that its Premier Inn brand will return to 2019 performances by 2022, hence one year earlier than its initial base case forecast.

OPERATOR FORECASTS

2005

2010

76

COVIVIO FULLY BENEFITS FROM THE SURGE IN ACTIVITY

ACCORINVESTVARIABLE LEASES22% OF REVENUES

OPERATING PROPERTIES23% OF REVENUES

-36%vs Q3 2019

-29% vs Oct. 2019

-26% vs Nov. 2019

OCTOBER 2021 NOVEMBER 2021

Q3 2021 RESULTS

-45%vs Q3 2019

Q3 2021 RESULTS

+192% vs Oct. 2020

+520% vs Nov. 2020

+104%vs Q3 2020

+390%vs Q3 2020

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

COVIVIO VARIABLE REVENUES

RECOVERING QUICKLY DURING H2 2021

2019 2020 2021

IV. HOTELSA. ACCOR’S VISION

B. COVIVIO HOTELS STRATEGY

HOTEL MARKET

A PORTFOLIO WELL PLACED TO BENEFIT FROM THE RECOVERY

GROWTH OPPORTUNITIES

Mercure – Boulogne

78

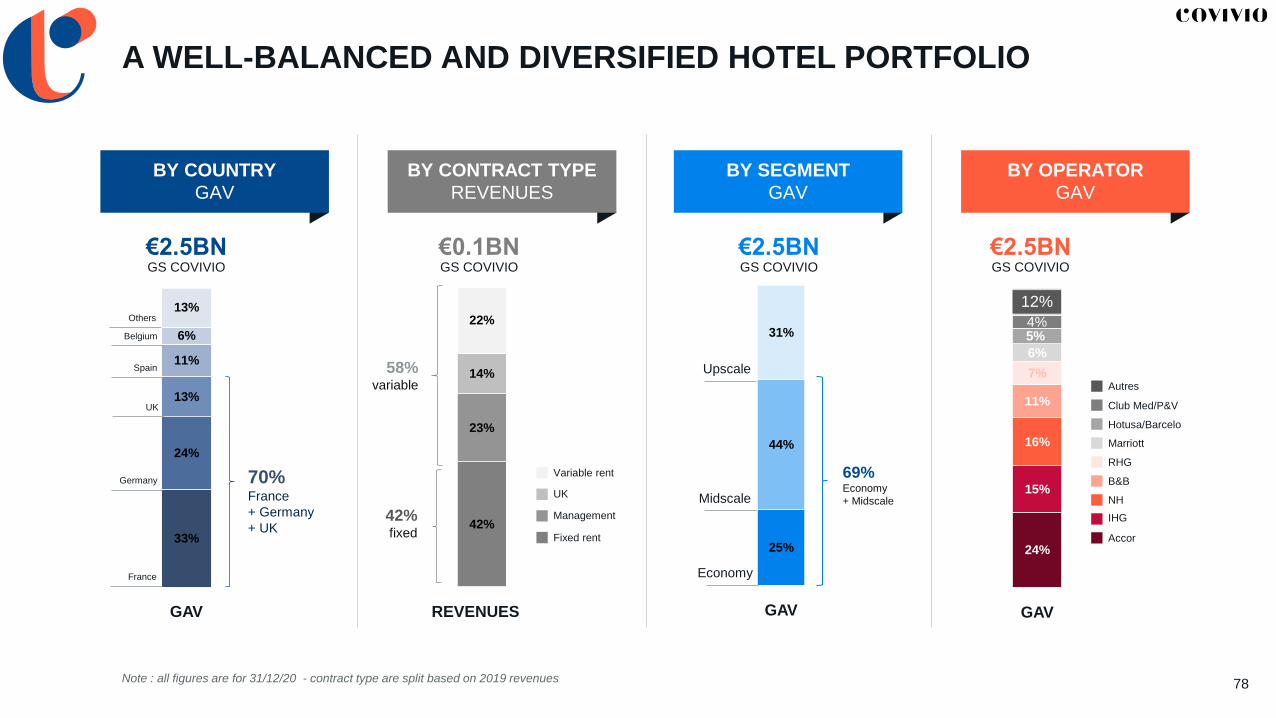

A WELL-BALANCED AND DIVERSIFIED HOTEL PORTFOLIO

€2.5BNGS COVIVIO

42% 44%

23% 20%

14% 13%

22% 22%

€0.1BNGS COVIVIO

42%fixed

58%variable

33%

24%

13%

11%

6%

13%

24%

15%

16%

11%

7%

6%

5%

12%

4%

25%

44%

31%

GAV REVENUES GAVGAV

Club Med/P&V

Hotusa/Barcelo

Autres

Accor

IHG

RHG

NH

B&B

Marriott

Others

Fixed rent

Variable rent

Management

UK

€2.5BNGS COVIVIO

€2.5BNGS COVIVIO

70%France

+ Germany

+ UK

69%Economy

+ Midscale

Note : all figures are for 31/12/20 - contract type are split based on 2019 revenues

Belgium

Spain

UK

Germany

France

Upscale

Midscale

Economy

BY COUNTRY

GAV

BY CONTRACT TYPE

REVENUES

BY SEGMENT

GAV

BY OPERATOR

GAV

79

LEASED ASSETS (42%) WITH SUSTAINABLE OPERATIONS

STRATEGIC HOTELS FOR OUR PARTNERS

Limited cash& earnings impact from covid negotiations(collection rate 2020/2021 92%1)

c.60%Sustainable average

effort rate

x

8.8/10Average Booking.com

location grade

TOTAL ASSETS

No change in long term lease structure & level

(1) >70% incl. rent free & deferred rent

80

ASSETS WITH VARIABLE REVENUES (58%) ARE WELL-POSITIONED FOR THE RECOVERY

FRANCE & GERMANY UNITED KINGDOM

CONTRACT STRUCTURE

% OF HOTEL REVENUES(based on 2019)

KEY DRIVERS

FOR RECOVERY

1

2

% of regional clientele(Domestic + Europe)

% of Leisure clientele

Mostlyindividual regional clients traveling for leisure

83%

56%

78%

59%

44% 14%

FULLY VARIABLE LEASE with MAC clause

81

85% OF THE GAV WITH A RESILIENT, OR HIGHLY RESILIENT CUSTOMER BASECUSTOMER MIX OF OUR HOTELS: LEISURE VS. BUSINESS, DOMESTIC VS. INTERNATIONAL

14%

54%

32%

A WELL POSITIONED

PORTFOLIO FOR RECOVERY

Higher

dependency

Fixed

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

% Leisure

% Domestic

Variable (incl. operated properties)

23 HOTELS

14% OF GAV

1

1

23

178 HOTELS

54% OF GAV

2 124 HOTELS

32% OF GAV

3

Highly resilient

Resilient

Higher dependency on International and/or business

Resilient

Highly

resilient

Overallportfolio

4%

57%

29%

Variablerevenuesportfolio

Bubble size = GAV

IV. HOTELSA. ACCOR’S VISION

B. COVIVIO HOTELS STRATEGY

HOTEL MARKET

A PORTFOLIO WELL PLACED TO BENEFIT FROM THE RECOVERY

GROWTH OPPORTUNITIES

Mercure – Boulogne

INTENSIVE ASSET MANAGEMENT OPPORTUNITIES

FINANCING CAPEX

CHANGE OF BRAND

FLEXIBILITY TO MOVE

BETWEEN LEASE &

OPERATE

Repositioning of rooms

Lobby/ground floor improvement

Construction of extra rooms

➜ Performance and rent increase

Buy-back Opco to fully control the upgrade of the hotel

Could be done with a mix of financing capex and change of brand

➜ Increase revenues and values

Renew attractiveness of the hotel

Change customer mix

➜ Improve operating performance

Méridien Nice (operating properties)

Louvre hotelsSold the Opcos of 9 Première Classe branded hotels to B&B in 2016.Signed a new 15-year lease with B&B (MGR-based)Value creation : +4%

Change of operator in 2020 following a tender processCapex : €9m for rebranding financed by the operatorRent increase : +60%Value creation : +50%

3 WAYS TO INCREASE PROFITABILITY

83

Full renovation of rooms and common areas conducted in 2019 for €14mEBITDA impact : c.+€2,5m (+75%)Net value creation : c.+20%

Radisson Red Madrid(leased properties)

84

SUPPORT THE DEVELOPMENT OF OUR EXISTING PARTNERS

Meininger Paris porte de Vincennes

B&B Paris porte des Lilas

COVIVIO BENEFITS FROM A LARGE SPECTER OF LEADING HOTEL OPERATING PARTNERS…

…WHO CONTINUE TO GROW, AND COVIVIO STANDS AS A TRUSTWORTHY PARTNER TO ACCOMPANY THEM ON NEW PROJECTS

New partnership in 2020 on 8 upscale

hotels in Italy, Hungary, Czech Republic

and France

Dec 2019 : opening with Covivio of three

new hotels in Poland.

B&B continues to grow in other European

countries (Portugal, Belgium…)

€573mPurchase price

including capex

(€248m GS)

4.7%Minimum

guaranteed yield

€24mPurchase price

for 3 assets in

Poland

(€10m GS)

6.3%Minimum

guaranteed yield

85

STRATEGIC ROADMAP IN HOTELS

Recovering €70m revenues & €200m of

values to get back to pre-Covid levels

3

BENEFIT FROM THE RECOVERY

INTENSIVE ASSET MANAGEMENT IN OUR PORTFOLIO TO DRIVE GROWTH

ACTIVE ASSET ROTATION

Refurbishment, change of operator, buyback of OpCos

Continue supporting the development of our

partners

1

2

V. RESIDENTIAL GERMANY

MARKET ENVIRONMENT

A PRIME PORTFOLIO

FURTHER GROWTH OPPORTUNITIES

Steglitz - Berlin

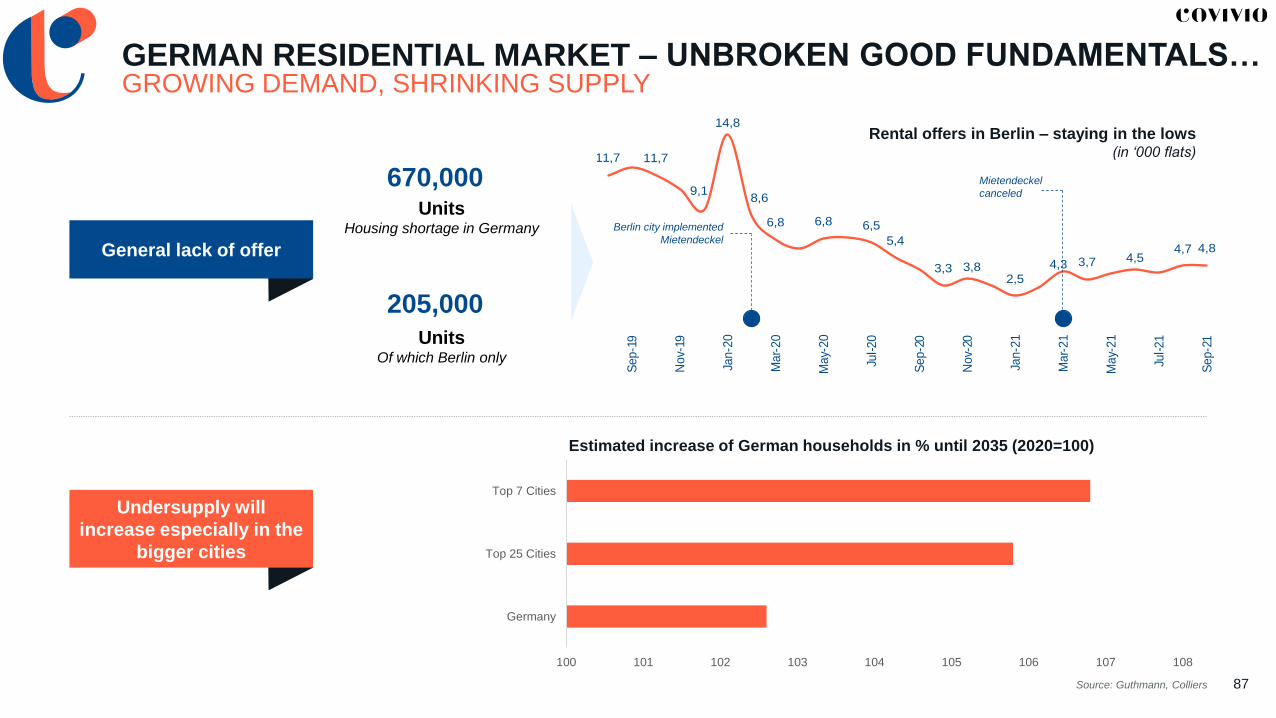

11,7 11,7

9,1

14,8

8,6

6,8 6,8 6,5

5,4

3,3 3,82,5

4,3 3,7 4,54,7 4,8

Sep-1

9

Nov-

19

Jan-2

0

Mar-

20

May-

20

Jul-20

Sep-2

0

Nov-

20

Jan-2

1

Mar-

21

May-

21

Jul-21

Sep-2

1

Rental Offers

87

GERMAN RESIDENTIAL MARKET – UNBROKEN GOOD FUNDAMENTALS…GROWING DEMAND, SHRINKING SUPPLY

Berlin city implemented

Mietendeckel

Mietendeckel

canceled

Rental offers in Berlin – staying in the lows(in ‘000 flats)

UnitsHousing shortage in Germany

670,000

UnitsOf which Berlin only

205,000

General lack of offer

Source: Guthmann, Colliers

Undersupply will

increase especially in the

bigger cities

100 101 102 103 104 105 106 107 108

Germany

Top 25 Cities

Top 7 Cities

Estimated increase of German households in % until 2035 (2020=100)

0 1000 2000 3000 4000 5000 6000 7000 8000 9000 10000

Leipzig

Köln

Düsseldorf

Stuttgart

Berlin

Hamburg

Frankfurt

Munich

2016 H1 2021

…LEADING TO CONTINUOUS VALUE INCREASE

90

100

110

120

130

140

150

160

I II III IV I II III IV I II III IV I II III IV I II III IV I II

2016 2017 2018 2019 2020 2021

House prices new buildings existing buildings

88

APARTMENTS PRICES CONTINUE TO RISE IN GERMANY… …BERLIN REACHED A MEDIAN OF €5,260/M² FOR CONDOMINIUMS

MEDIAN CONDOMINIUM PRICE IN €/M² OF THE BIG 8 CITIESHOUSING PRICE INDEX IN GERMANY (BASIS 100 IN 2015)

+11% in 2021

Source: destatis, JLL

+52%in Berlin

Covivio residential locations

in €

89

THE GERMAN INVESTMENT MARKET RECOGNIZED THE POTENTIALRESIDENTIAL INVESTMENT MARKET CONTINUES TO SOAR WITH RECORD NUMBERS

Source: BNP PARIBAS

Top A-Locations with €8.4bn investment volume in Berlin (including

Akelius transaction)

High margins possible due to big difference between bloc and

privatization values

High market activity

Investors convinced of a further positive market development

Q1–Q3: over 270 transactions thereof 33 > €100m

Q1-Q3 Investment volumes (€m)

Q4 Investment volumes (€m)

% of A-Locations

21 422

-

5 000

10 000

15 000

20 000

25 000

2016 2017 2018 2019 2020 2021

64%

47%

46% 33%41%50%

13 351

5 474

9 726

4 2757 298

6 228

In €m

RECORD RESIDENTIAL INVESTMENT VOLUME IN 2021 OF WHICH HIGH SHARE OF A-LOCATIONS

▪ Climate neutrality to be reached by 2045

▪ Promote energetic modernization with subventions both on

the new and existing buildings

90

POLITICAL ENVIRONMENT: A CLEAR PATH

2 main targets for the real-estate industry

▪ Promote construction of 400 000 units per year (and reduction

of building permit process)

▪ Soft rent regulation (cap of 11% increase in 3 years) for

existing tenants

Outcome of the Federal Elections

The new coalition already agreed on main targets

✓ Transformation of economy to fight climate change

✓ Innovate Germany via digitalization: infrastructure and

public administration

✓ European integration, International cooperation

✓ Promote construction and reduce administrative building

permit process by 50%

MEET THE SUPPLY AND DEMAND1

A GREENER REAL-ESTATE MARKET2

V. RESIDENTIAL GERMANY

MARKET ENVIRONMENT

A PRIME PORTFOLIO

FURTHER GROWTH OPPORTUNITIES

Mercure – Boulogne

0%

5%

10%

15%

20%

25%

-

1

1

2

2

3

3

4

4

5

5

€0.7bn

COVIVIO RESIDENTIAL PORTFOLIO HAS GROWN CONTINUOUSLY

92

SINCE 2012 SINCE H1 2021SINCE 2015 SINCE 2018

Reinforcement in German Residential + + +

Acquisitions in Fast-Growing Cities

Lauching pipeline & acquiring Land Banks

Further acquisitions & delivery of the development pipeline

Size of German residential portfolio in Group share of Covivio’s portfolio

+24% INCREASE PER YEAR SINCE 2012

€4.4bn

€3.7bn

€2.2bn9%

20%

24%

27%

%

93

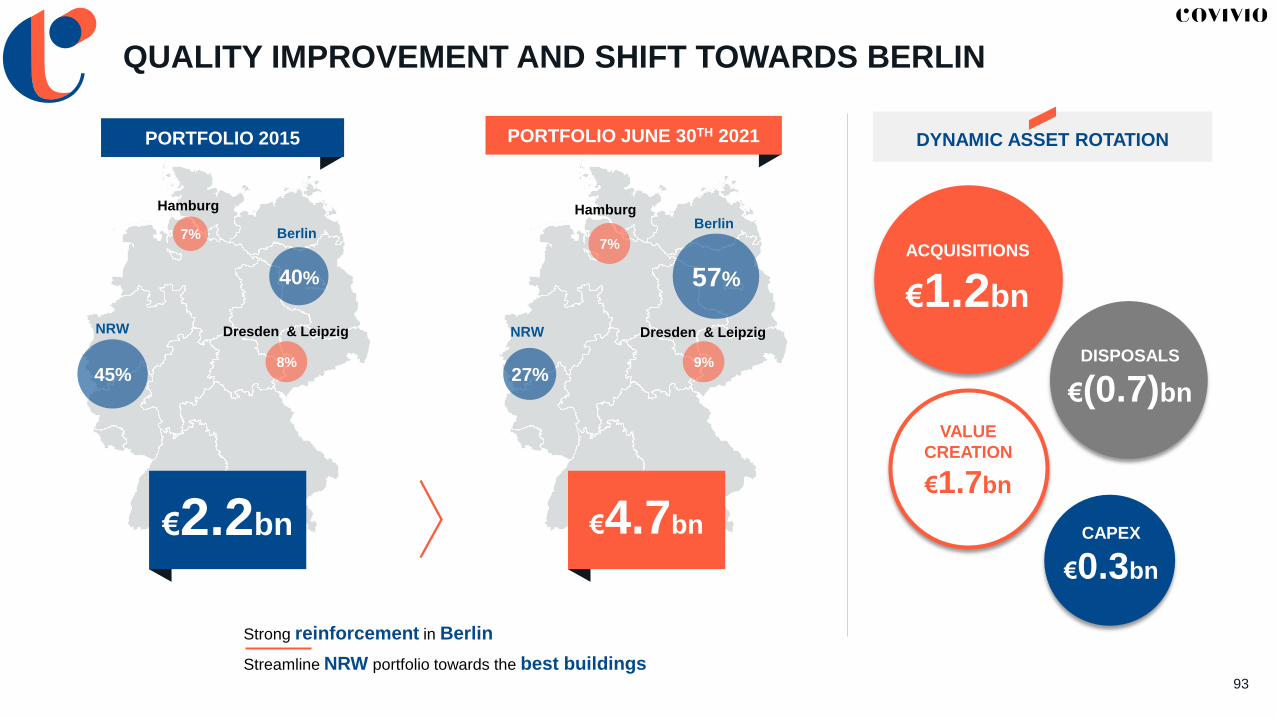

QUALITY IMPROVEMENT AND SHIFT TOWARDS BERLIN

Strong reinforcement in Berlin

Streamline NRW portfolio towards the best buildings

40%

8%

7%

45%

NRW

Hamburg

Berlin

Dresden & Leipzig NRW

HamburgBerlin

Dresden & Leipzig

9%27%

7%

€4.7bn

PORTFOLIO 2015 PORTFOLIO JUNE 30TH 2021

€2.2bn

57%

ACQUISITIONS

€1.2bn

VALUE

CREATION

€1.7bn

DISPOSALS

€(0.7)bn

CAPEX

€0.3bn

DYNAMIC ASSET ROTATION

A TEAM OF OVER 600 EMPLOYEES TO MANAGE THE WHOLE REAL-ESTATE VALUE-CHAIN

94

ACQUISITIONASSET AND PROPERTY

MANAGEMENTCRAFTMEN DEVELOPMENT DISPOSALS

€1.2bn

acquisitions since 2015

300employees managing the

whole property

management process

23service centers

Integration of a construction company to internalize maintenance and modernisation works

c.100 employees

Full integration of the development activity from

2018 with now

60 employees

In-house team and joint-venture with Best Place.

c.30 employees dedicated to

Covivio’s portfolio

95

OVERVIEW OF THE PORTFOLIO

1 in Q3 2021

2 in H1 2021

RENTAL YIELD

3.6%

PORTFOLIO 100%

€7.2 BN

PORTFOLIOGROUP SHARE

€4.7 BN

56%Berlin

8%Hamburg

9%Dresden

& Leipzig

27%NRW

% revenue in Group shareVALUE / SQM

€2,600

OCCUPANCY

99%

LFL RENTS1

+4.1%

RENT

POTENTIAL

20%

STRONG OPERATIONAL

INDICATORS

LFL VALUE2

+7.4%

€4.7bn

96

SELECTIVE ACQUISITIONS IN 2021Q1 – Q3 2021 ACQUISITIONS

100%Berlin

1 23

45

6

7

8

9

10

1112

13

14

15

16

17

18 19

7 7

All assets are divided in condominium

High growth potential

+21%

+61%

+64%

Price Rent

€13.5 /m²Average market rent

€10.2 /m²Federal rental level

€8.4 /m²Acquisition rents

€5,260 /m²Median condo. price

€3,146 /m²Acquisition price

19

~€100mNEW ACQUISITIONS1

22 assets / 626 units

46,200 m²

96.8%Occupancy rate

3.5%Acquisition yield

1. €145m at 100%

V. RESIDENTIAL GERMANY

MARKET ENVIRONMENT

A PRIME PORTFOLIO

FURTHER GROWTH OPPORTUNITIES

Mercure – Boulogne

GROWTH POTENTIAL THROUGH RENT INCREASE

98

STILL A HIGH REVERSIONNARY POTENTIAL

3 ways to capture the rent increase

AN AMBITIOUS PLAN OF

MODERNIZATION

>€50m(GS)

CAPEX

3%/year

Units

concernedRENT INCREASE DUE TO RELETTING c. 20%

of the total rent increase in 2021

RENT INCREASE DUE TO INDEXATION

RENT INCREASE DUE TO MODERNIZATIONS

c. 35%of the total rent increase in 2021

c. 45%of the total rent increase in 2021

20%Based on the current

regulation

30%Based on the market

rents without regulations

4-5%

Yield

99

GROWTH POTENTIAL THROUGH VALUE

LATEST TRANSACTIONS ALSO CONFIRMED THESE VALUES

IMPORTANT DRIVERS FOR VALUES

Shortage of housing supply

and increasing demand

High gap between bloc

and unit value

Strong investor appeal

for German residential

Still significant headroom for value growth

Sources: JLL 1 Median of existing condominiums 2 Estimates GreenStreet advisors 3as of 30/06/2021

ALREADY MORE THAN 50% OF THE PORTFOLIO IN BERLIN DIVIDED INTO CONDOMINIUM

(and 20% pending) and 20% divided in Hamburg (40% pending)

BERLIN HAMBURG

€3,200/m²Average Covivio’s value3

€4,600/m²Average Akelius price2

€3,800/m²Average Covivio’s value3

€6,250/m²Median condominium price1

+64%

+43%

+64%

+34%

€5,260/m²Median condominium price1

€5,100/m²Average Akelius price2

GROWTH POTENTIAL THROUGH DEVELOPMENT€0.7BN TOTAL PIPELINE (€1.0BN AT 100%)

BERLIN€ 530m pipeline

2,400 units

190,000 sqm

HAMBURG€ 80m pipeline

430 units

30,000 sqm

NRW€ 60m pipeline

460 units

31,000 sqm

DRESDEN &

LEIPZIG€ 5m pipeline

30 units

1,500 sqm

100

70%WITH A LETTING

STRATEGY

20%VALUE CREATION

AND

4.5% YIELD-ON-COSTS

30%WITH A SALES

STRATEGY

€50mPROMOTION MARGIN

(C. 25%)

(€75m at 100%)

€200mALREADY COMMITTED

(€300m at 100%)

All committed projects to be delivered by 2024

101

STRATEGIC ROADMAP IN RESIDENTIAL

3

4

CATCH THE REVERSIONARY POTENTIAL

EXTRACT THE RESERVE OF VALUE GROWTH

ACCELERATE OUR GROWTH IN GERMAN RESIDENTIAL

CONTINUE OUR SELECTIVE ACQUISITIONS STRATEGY

€0.7bn development pipeline with 20%

value creation on build-to-rent & 30% on

build-to-sell (~€10m/year margin on average)

€90m Berlin portfolio under

exclusivity

1

2

+20% based on the current regulation (€30m)

Over €1.3bn based on the latest market

transactions and the condominium prices

VI. KEY TAKEAWAYS

Gobelins – Paris 5th

103

COVIVIO’S STRATEGIC ROADMAP

OFFICESGERMAN RESIDENTIAL HOTELS

1

2

3

1

2

3

1

2

3

Active asset rotation, especially

for core mature assets

Continue to invest through

acquisitions & developmentsCatch the recovery

Accelerate on the development

pipeline in top locationsCapture value growth potential

Extract value through active asset

management

Accelerate the transformation into

residential to benefit from strong

housing market

Work on buildings efficiency &

capture rental reversion

Be the preferred partner for

operators’ expansion

4 Position ourselves as a leading

Real-Estate as a Service operator

GERMAN RESIDENTIAL

HOTELS

OFFICES

104

OUR GROWTH DRIVERS

Increase in occupancy and development pipeline

Acceleration of our development strategy

Continue to benefit from the recovery

€70mRental upside to get backto 2019 level

€1.0bn>30% value creation from the development pipeline remaining to be captured

€1.3bnValuation growth potential by capturing the reversion, Capex, and disposal of condominium

€0.2bnValue upside to get back to 2019 level

€20mIncreasing occupancy back to historical levels (97%)

€15mProperty development margin from transformation into residential

REVENUES VALUES

€145mRevenue growth potential

€2.5bnValue growth potential

€30mRent reversion vs federal rent (20%)

€10mDevelopment margin

Q&A

Paris

30, avenue Kléber

75116 Paris

Tel.: +33 1 58 97 50 00

CONTACT

Paul ArkwrightTel.: +33 1 58 97 51 85

www.covivio.eu

Quentin DrumareTel.: +33 1 58 97 51 94