city of midlothian, texas - annual operating budget fy 21-22

Upload

khangminh22Category

view

0download

0

City of DickinsonRegular Meeting of City Commission

Presiding Officer: President of Commission

(Vice President in absence of President) Meeting subject to current COVID-19 Federal Guidelines

Tuesday, December 21, 2021

4:30 PM

City Hall – 99 2nd St E, Dickinson, ND 58601

Opening of Meeting

Call to Order

Roll Call

President: Scott Decker

Vice President: Jason Fridrich

Commissioners: Nikki Wolla

Suzi Sobolik

John Odermann

MemoA.

Order of Business: Consideration for Approval1.

Consent Agenda2.

Approval of meeting minutes dated December 7, 2021 ( Enc.)A.Approval of Accounts Payable & Checkbook (Enc.)B.

Link for viewing Commission Meeting - This link will not be live until approximately 4:20 p.m. on December 21, 2021

https://dickinsongov.com/2021/12/21/city-commission-meeting-information-december-21-2021/

Persons who desire to be heard under Section 9 "Public Comments not on Agenda" may call in at (701) 456-7006 at 5:00 p.m.

Next Resolution No: 34-2021 Next Ordinance No: 1742

Agenda

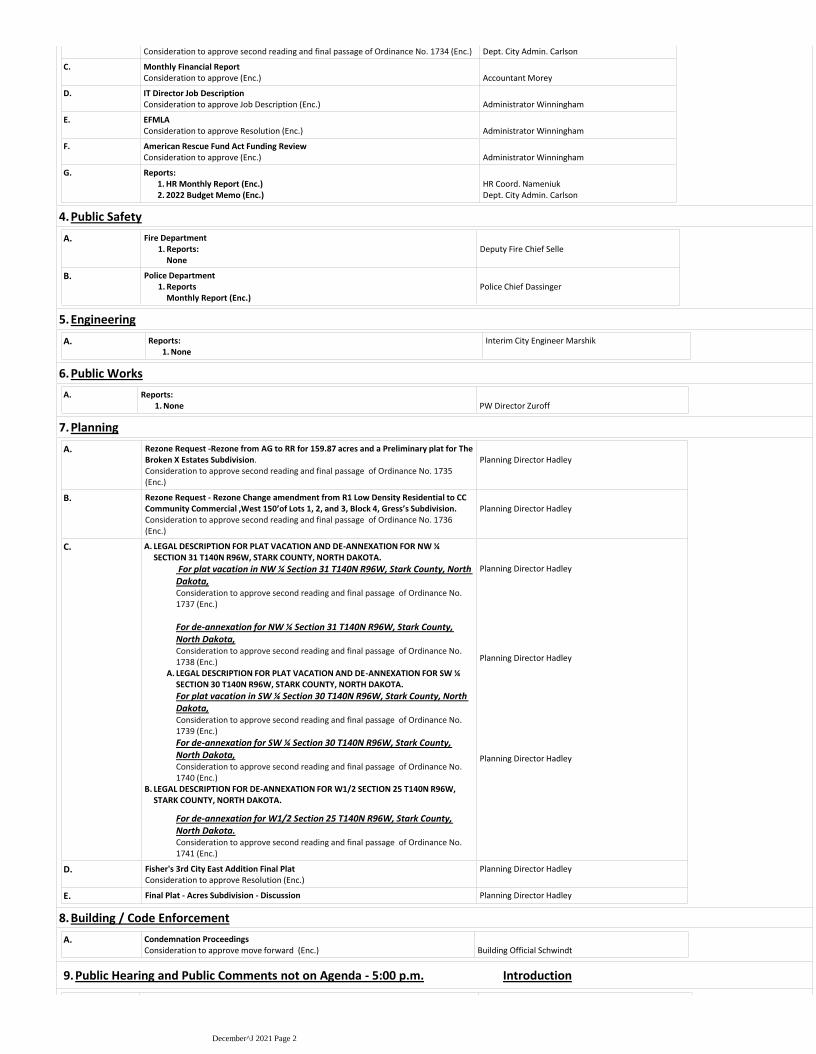

Administration / Finance 3.

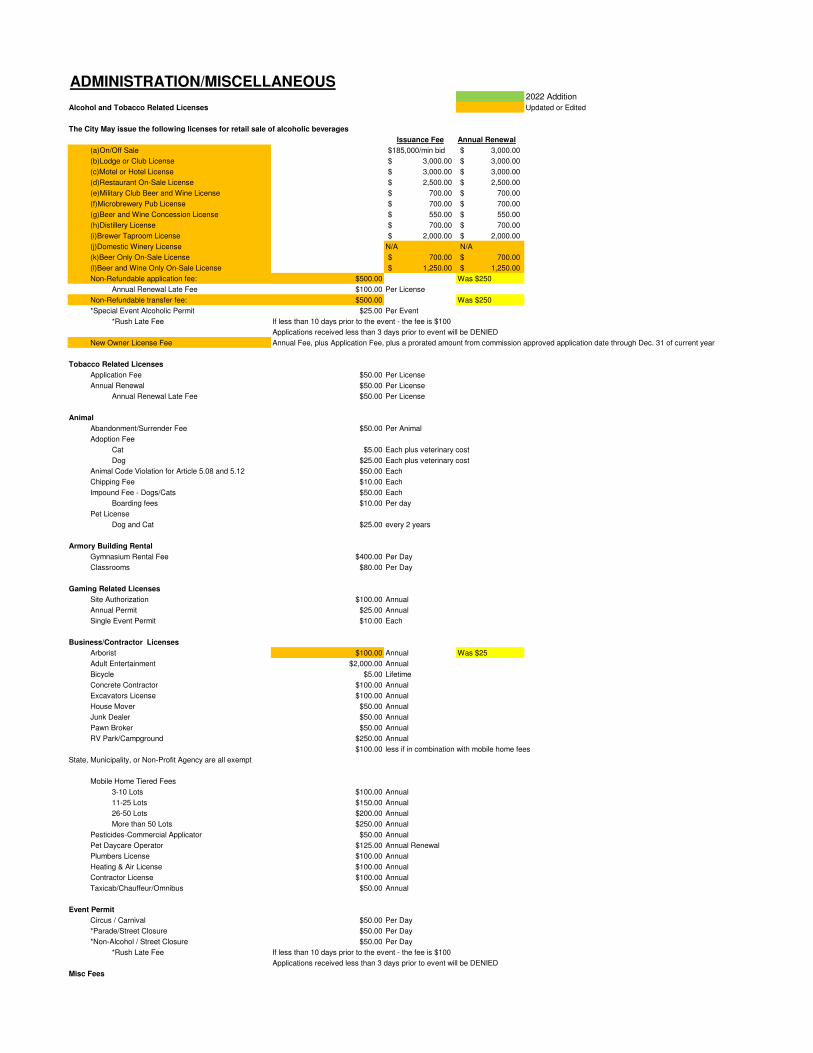

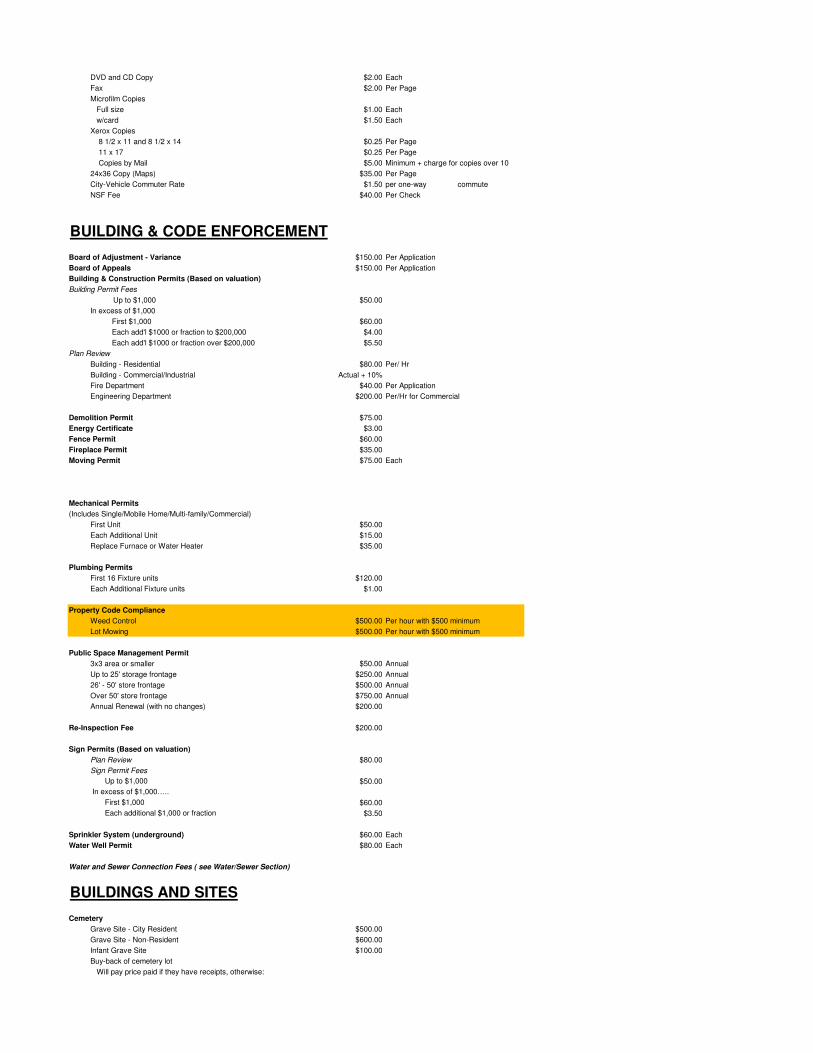

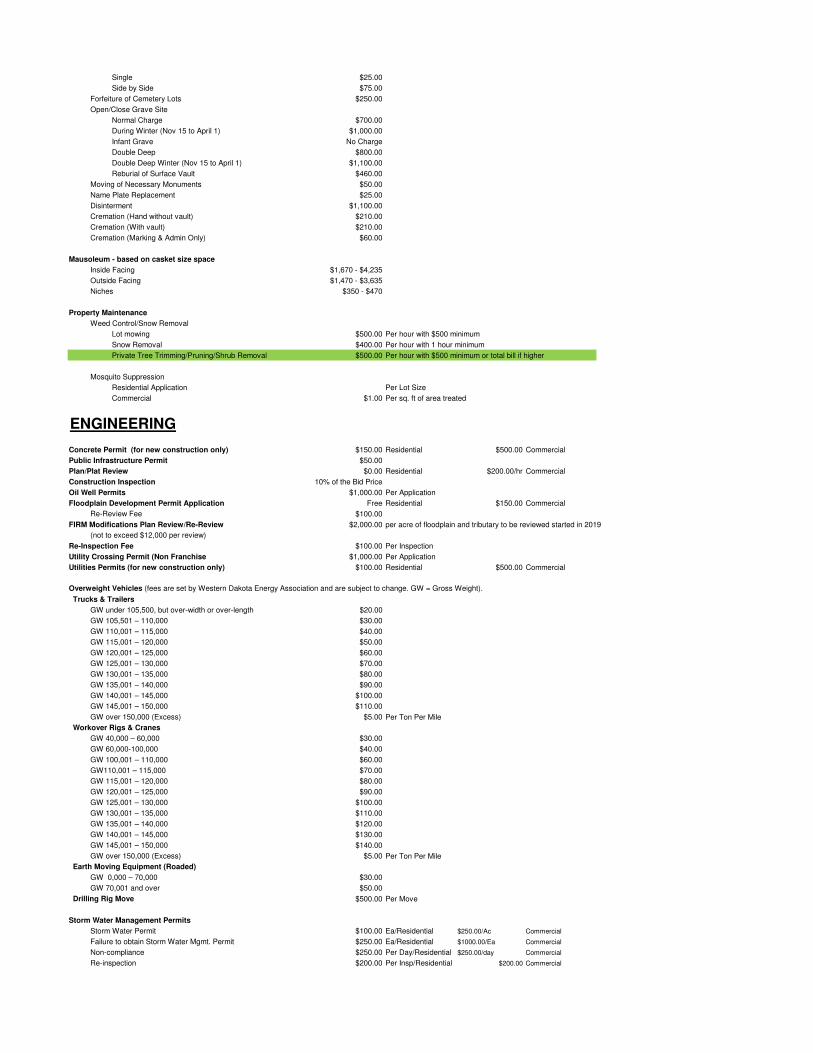

A. 2022 Fee ScheduleConsideration to approve Resolution (Enc.) Dept. City Admin. Carlson

B. Future Fund Consideration to approve second reading and final passage of Ordinance No. 1734 (Enc.) Dept. City Admin. Carlson

12-21-2021 - CCM - Printable

December^J 2021 Page 1

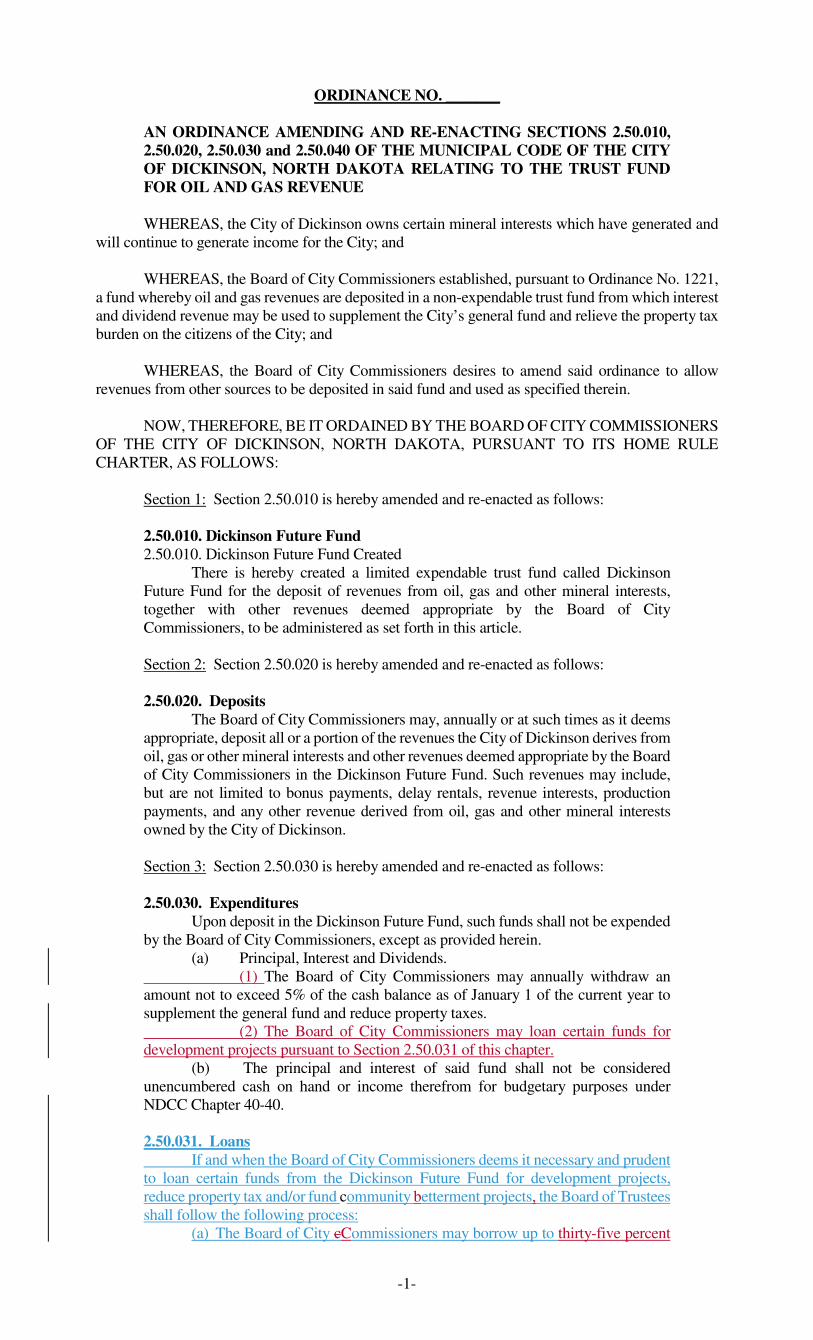

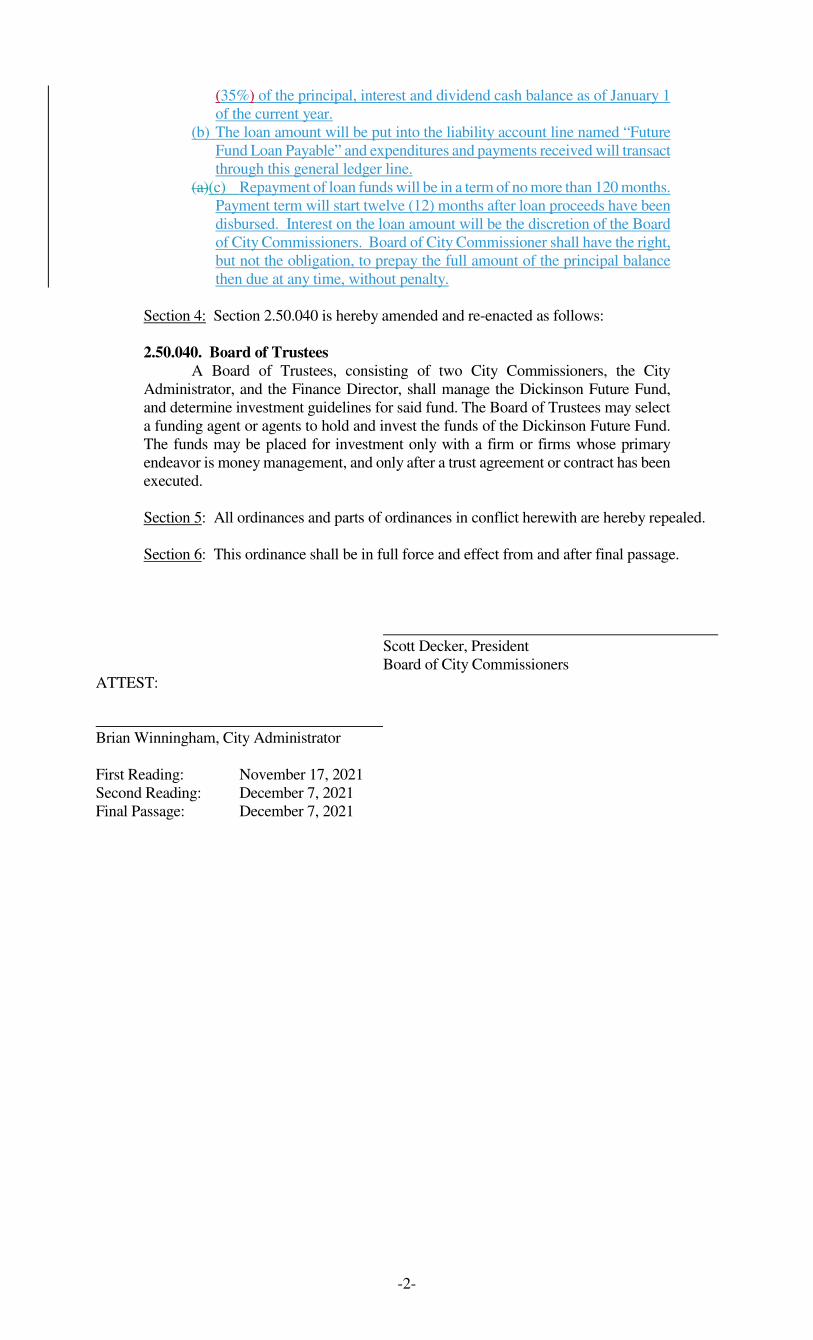

Consideration to approve second reading and final passage of Ordinance No. 1734 (Enc.) Dept. City Admin. Carlson

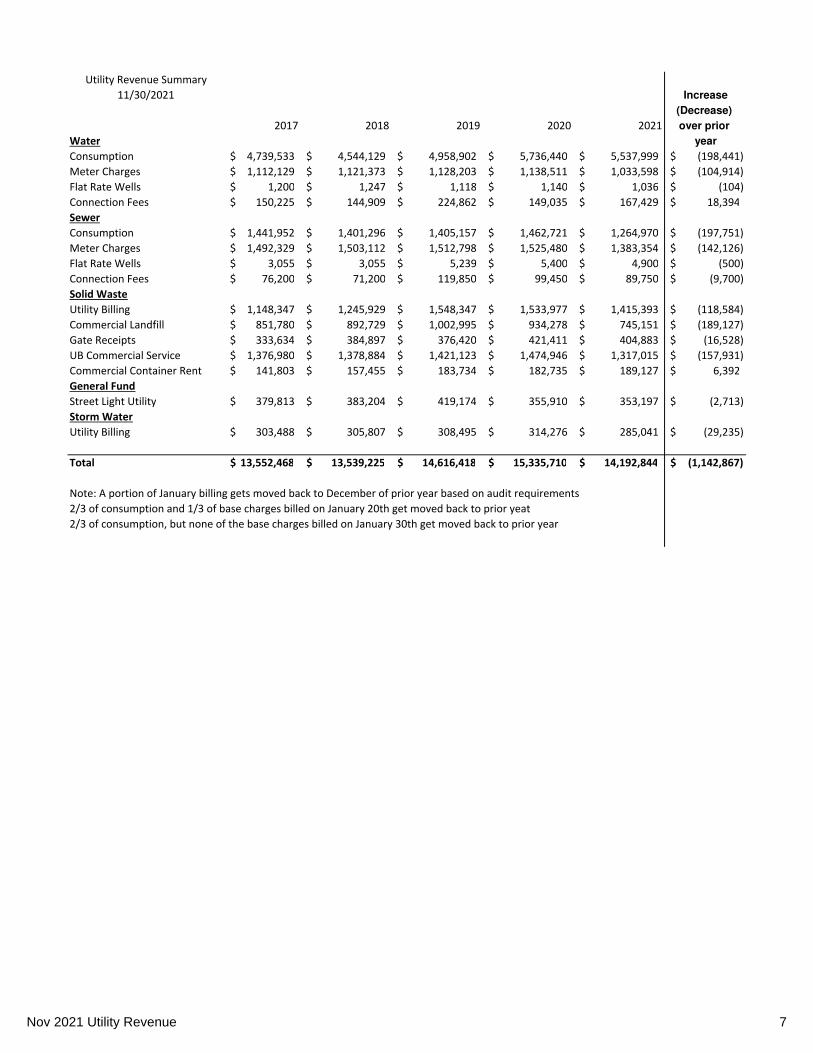

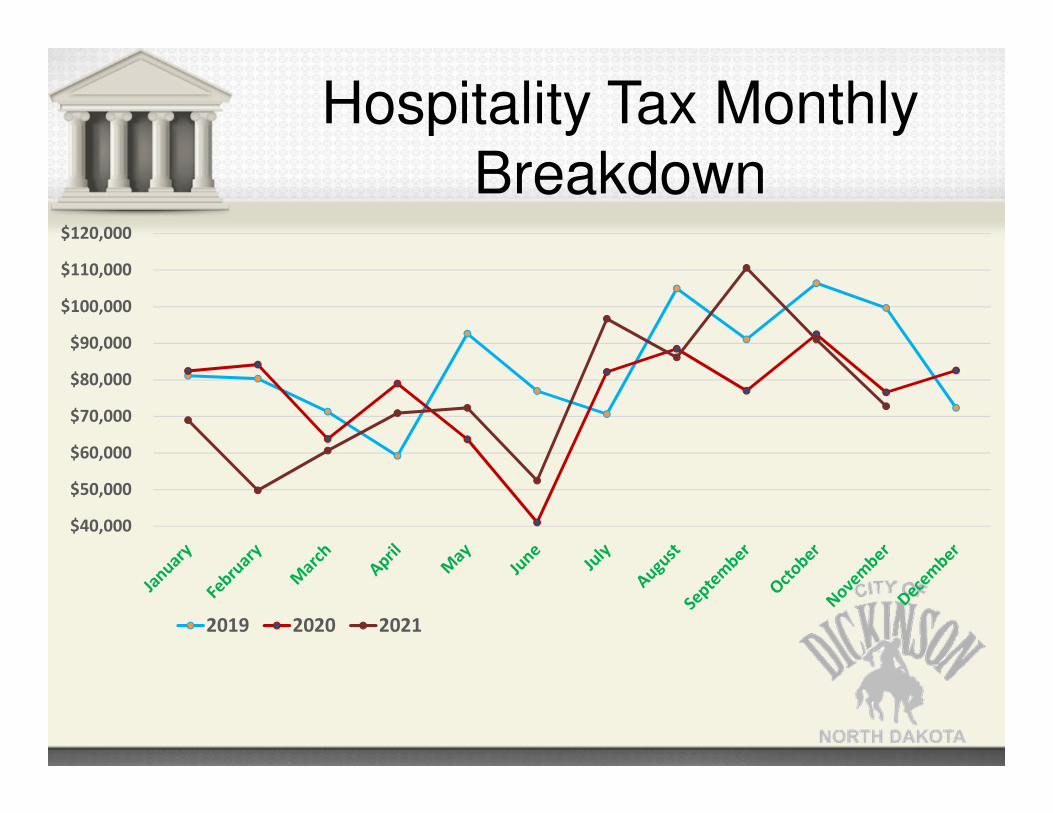

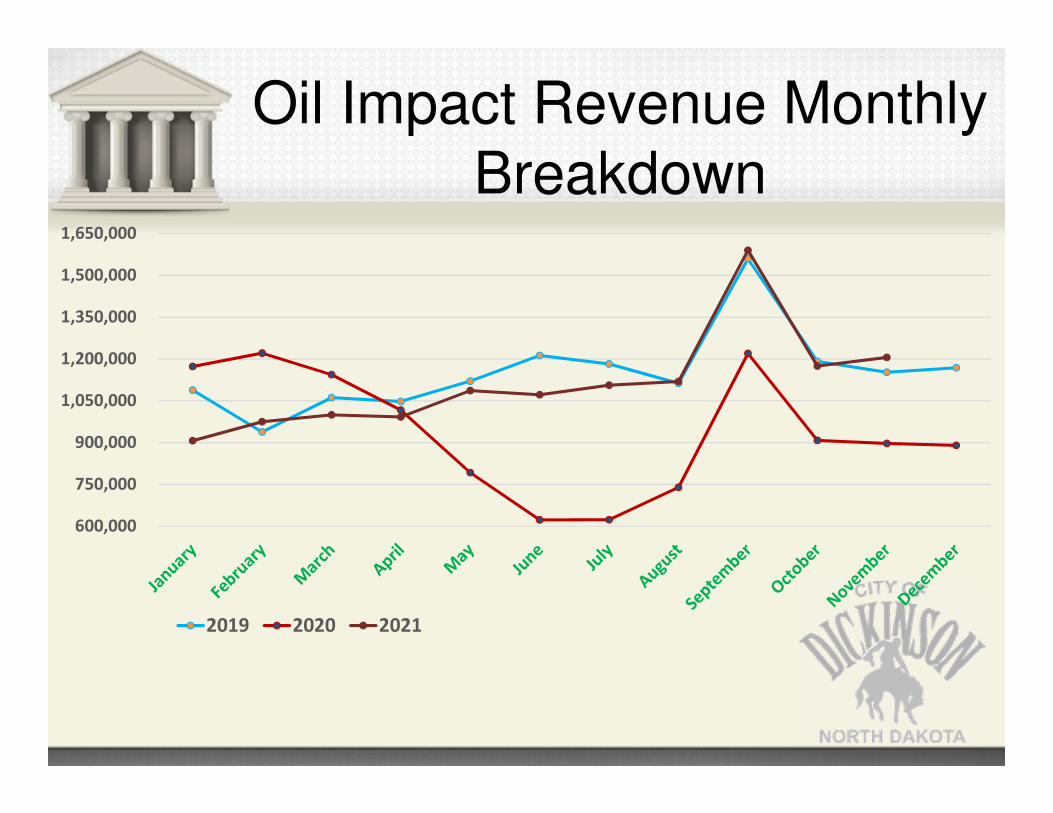

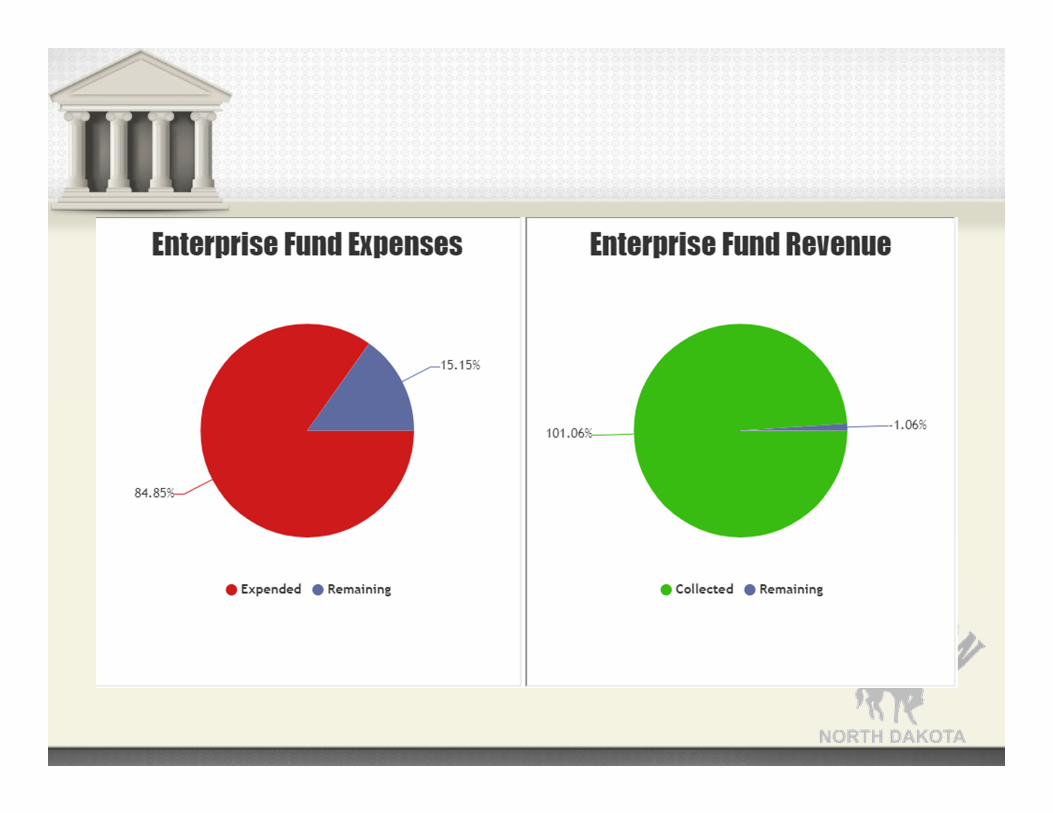

C. Monthly Financial ReportConsideration to approve (Enc.) Accountant Morey

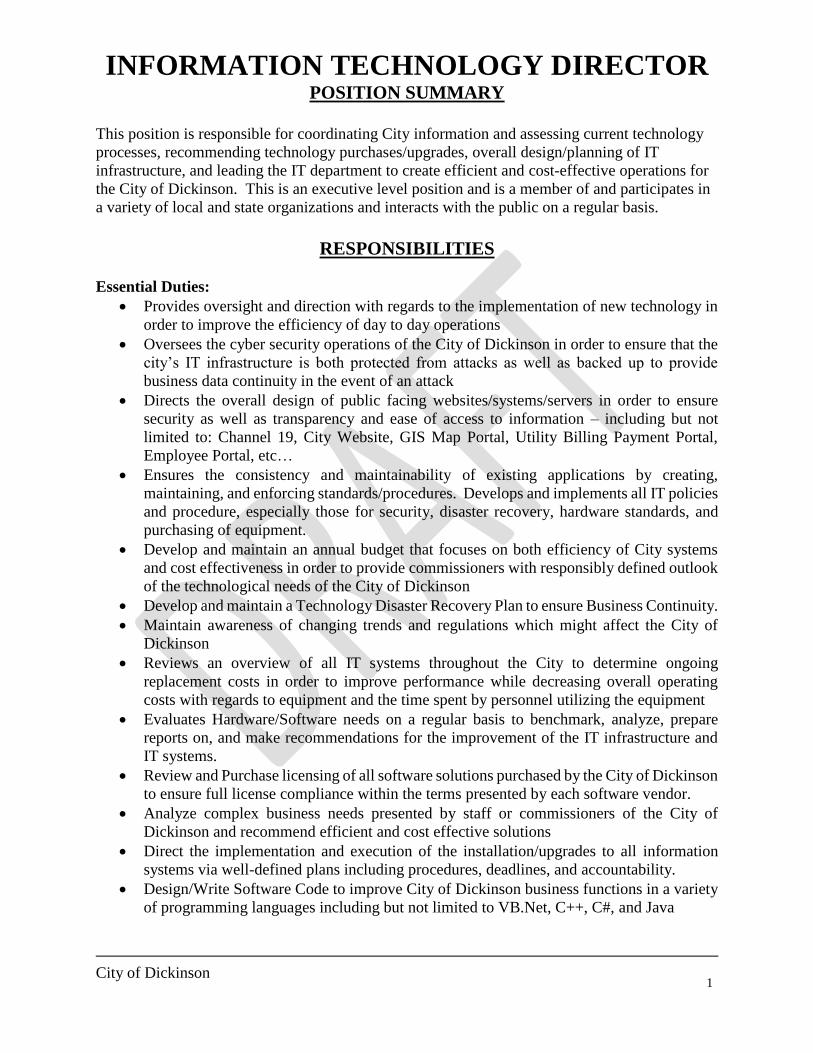

D. IT Director Job DescriptionConsideration to approve Job Description (Enc.) Administrator Winningham

E. EFMLA Consideration to approve Resolution (Enc.) Administrator Winningham

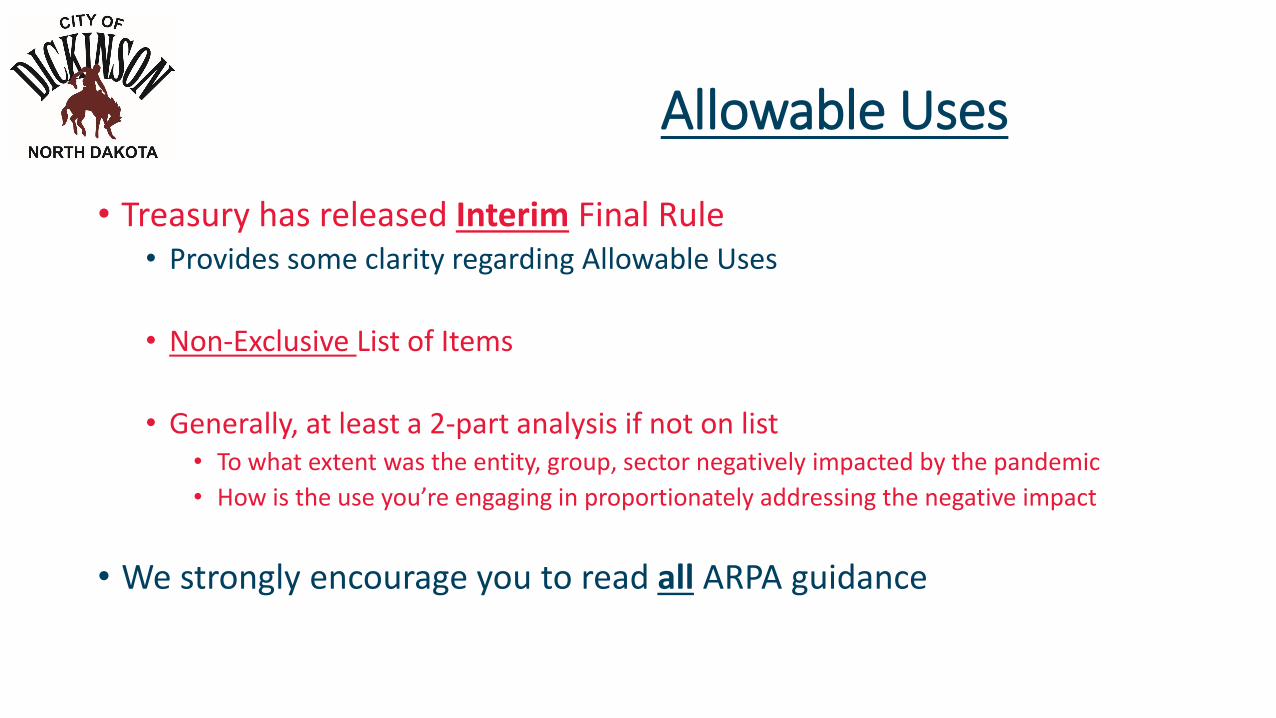

F. American Rescue Fund Act Funding Review Consideration to approve (Enc.) Administrator Winningham

G.HR Monthly Report (Enc.)1.2022 Budget Memo (Enc.)2.

Reports:HR Coord. NameniukDept. City Admin. Carlson

Public Safety4.

A.Reports:1.None

Fire Department Deputy Fire Chief Selle

B.Reports1.Monthly Report (Enc.)

Police DepartmentPolice Chief Dassinger

Engineering5.

A.None1.

Reports: Interim City Engineer Marshik

Public Works6.

A.None1.

Reports:PW Director Zuroff

Planning7.

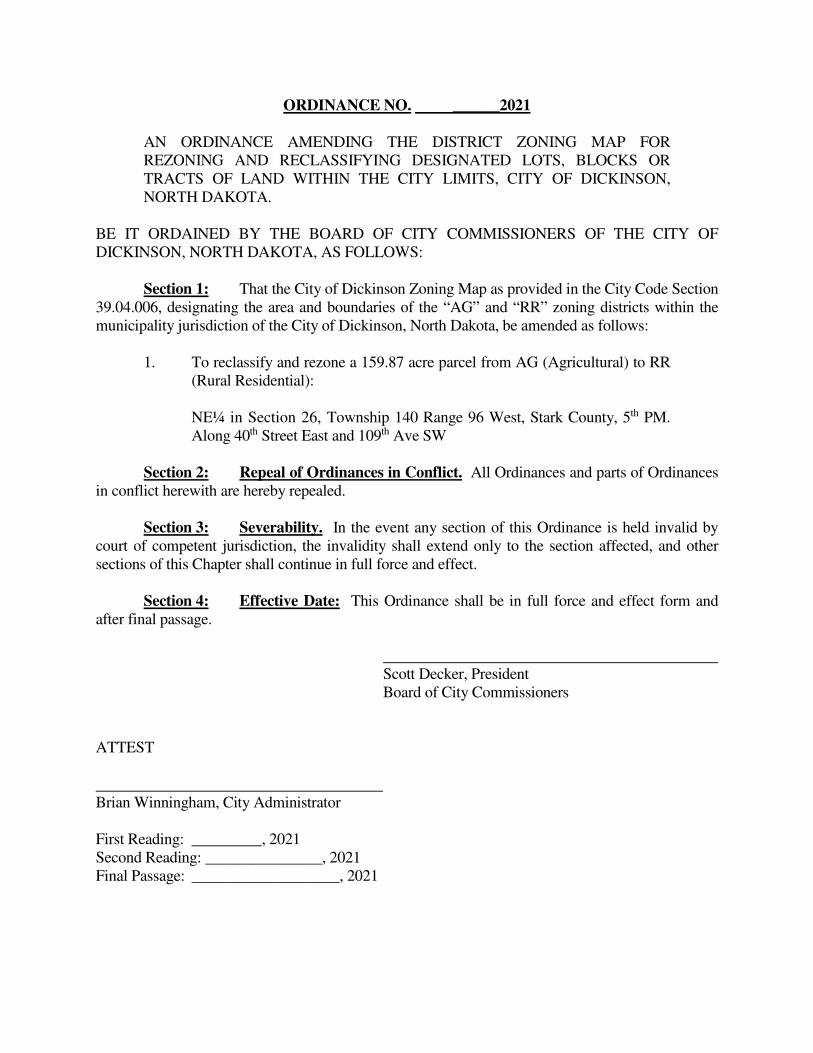

A. Rezone Request -Rezone from AG to RR for 159.87 acres and a Preliminary plat for The Broken X Estates Subdivision. Consideration to approve second reading and final passage of Ordinance No. 1735 (Enc.)

Planning Director Hadley

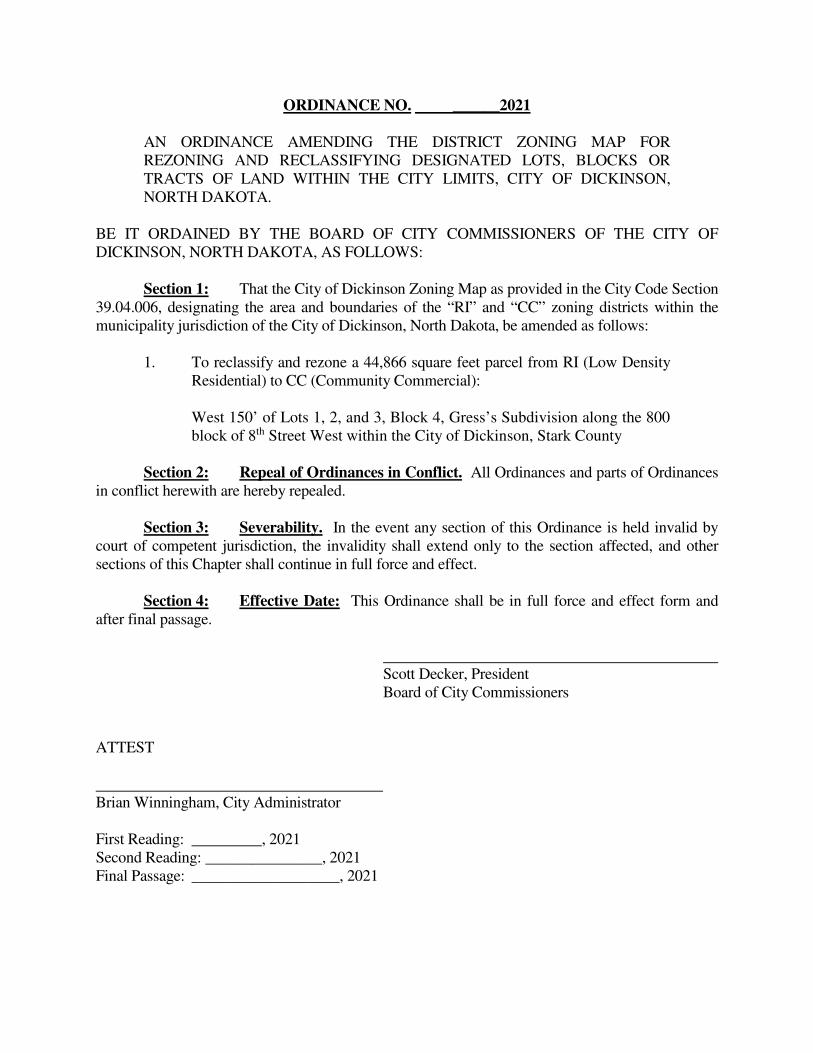

B. Rezone Request - Rezone Change amendment from R1 Low Density Residential to CC Community Commercial ,West 150’of Lots 1, 2, and 3, Block 4, Gress’s Subdivision.Consideration to approve second reading and final passage of Ordinance No. 1736 (Enc.)

Planning Director Hadley

C.

For plat vacation in NW ¼ Section 31 T140N R96W, Stark County, North Dakota,Consideration to approve second reading and final passage of Ordinance No. 1737 (Enc.)

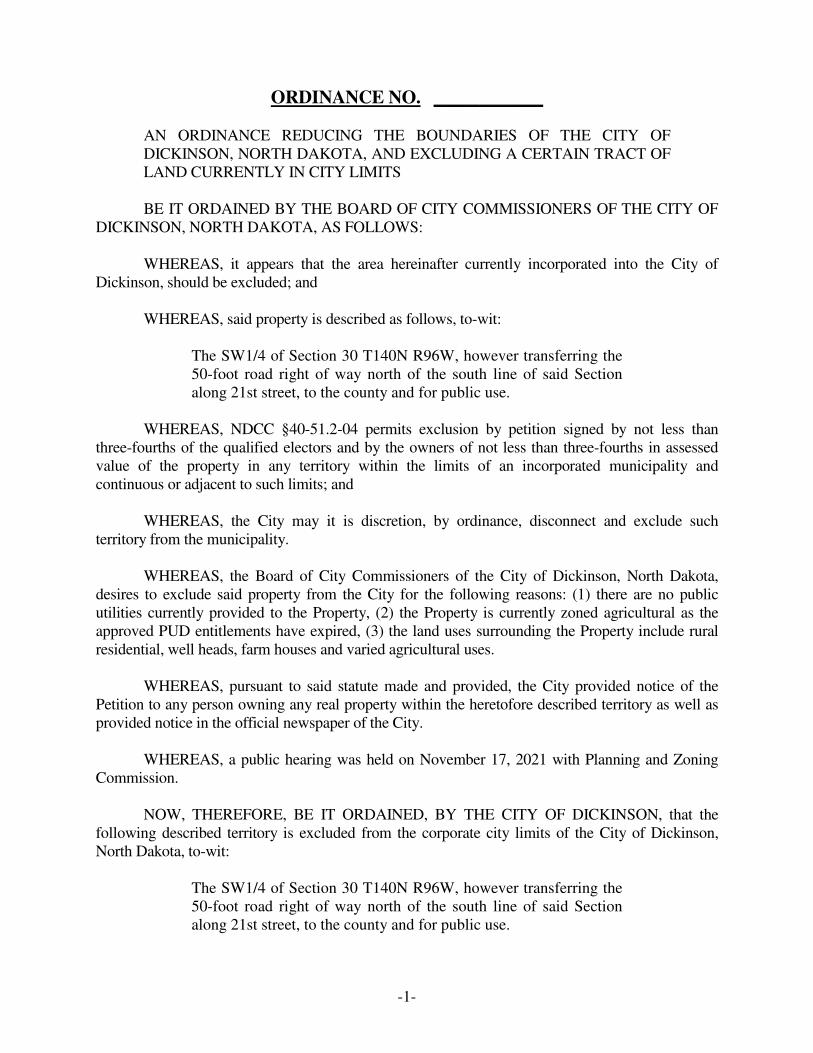

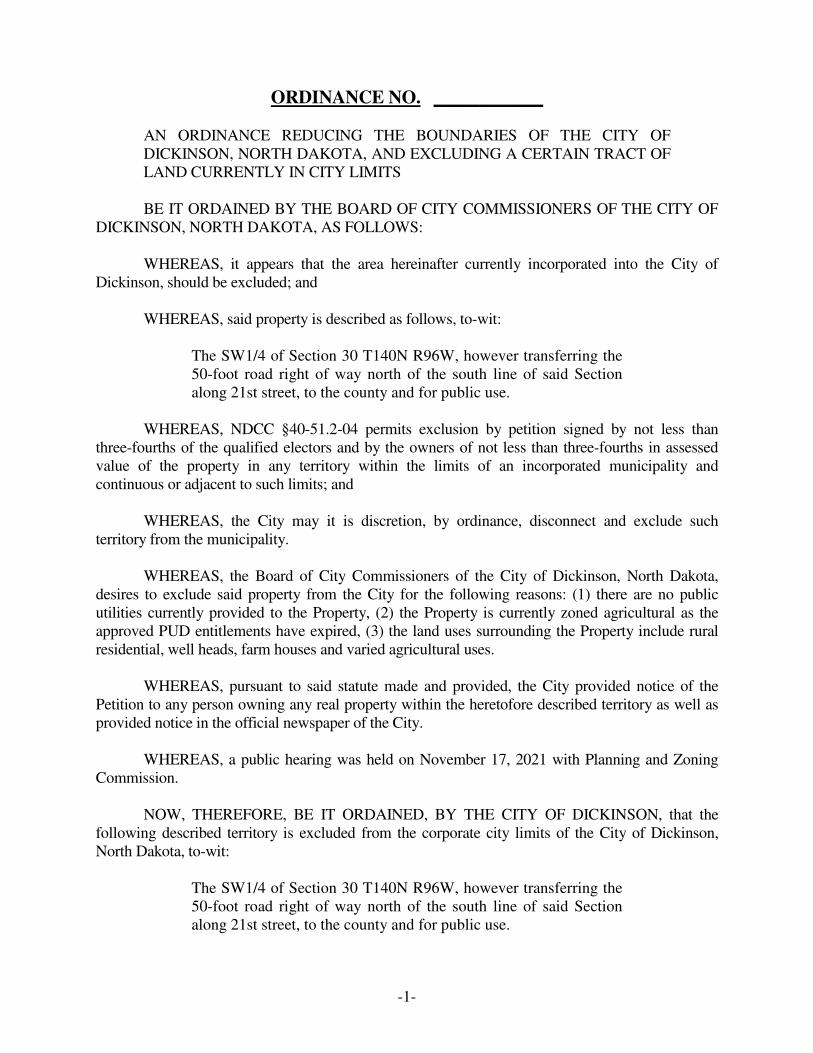

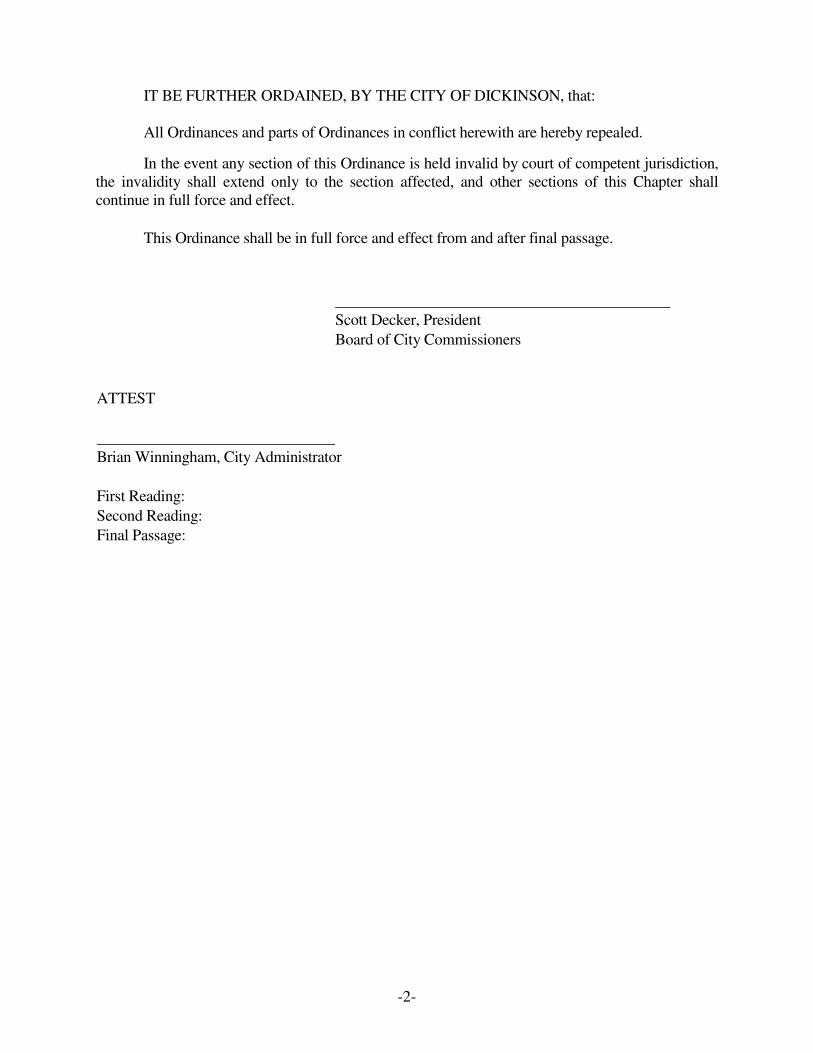

For de-annexation for NW ¼ Section 31 T140N R96W, Stark County, North Dakota,Consideration to approve second reading and final passage of Ordinance No. 1738 (Enc.)LEGAL DESCRIPTION FOR PLAT VACATION AND DE-ANNEXATION FOR SW ¼ SECTION 30 T140N R96W, STARK COUNTY, NORTH DAKOTA.

A.

For plat vacation in SW ¼ Section 30 T140N R96W, Stark County, North Dakota,Consideration to approve second reading and final passage of Ordinance No. 1739 (Enc.)

For de-annexation for SW ¼ Section 30 T140N R96W, Stark County, North Dakota,Consideration to approve second reading and final passage of Ordinance No. 1740 (Enc.)

LEGAL DESCRIPTION FOR PLAT VACATION AND DE-ANNEXATION FOR NW ¼ SECTION 31 T140N R96W, STARK COUNTY, NORTH DAKOTA.

A.

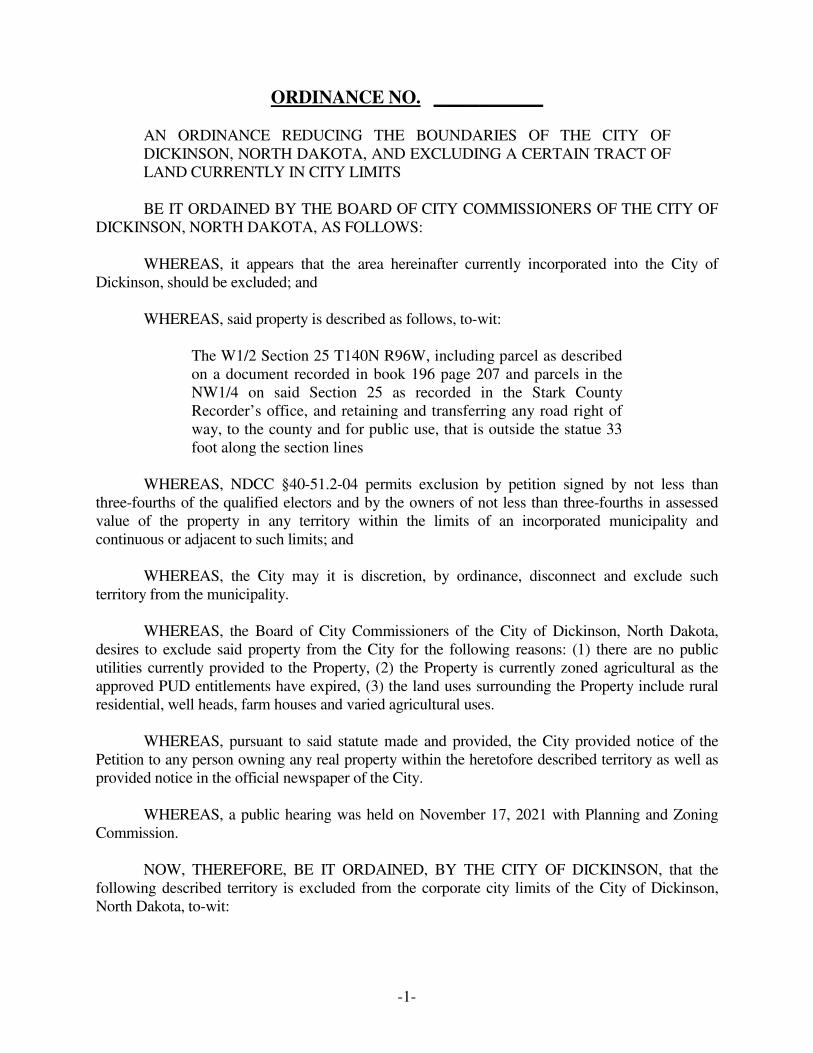

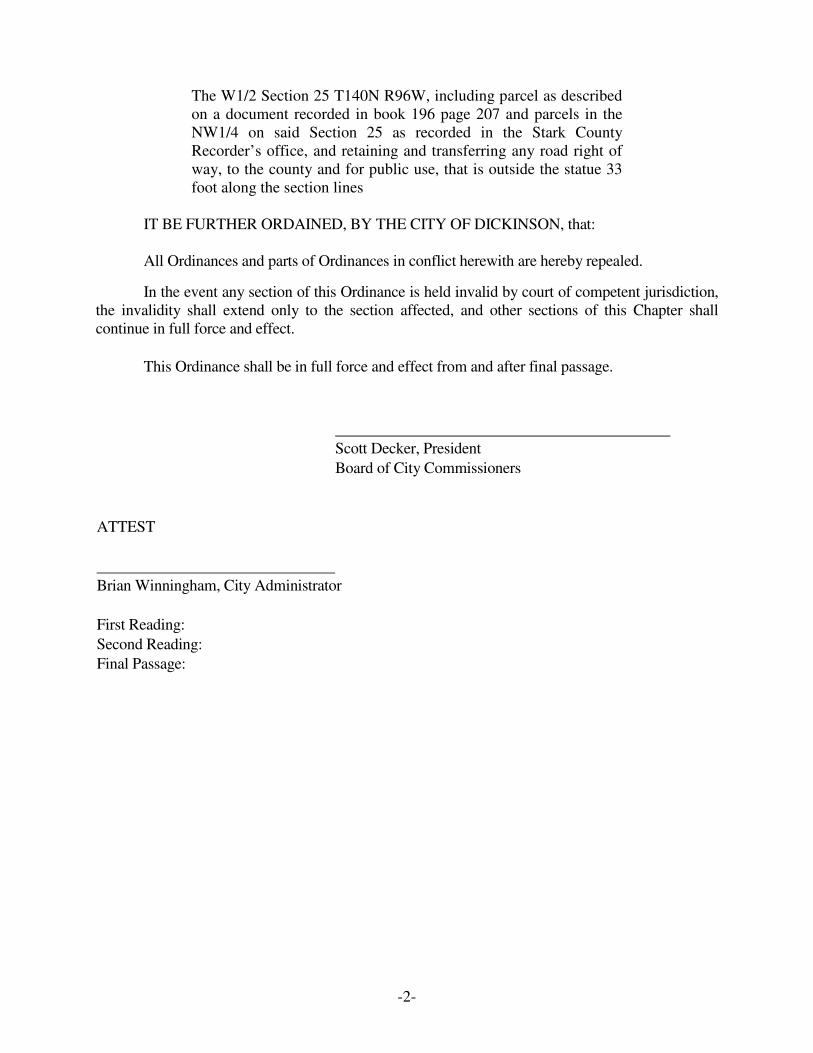

For de-annexation for W1/2 Section 25 T140N R96W, Stark County, North Dakota.Consideration to approve second reading and final passage of Ordinance No. 1741 (Enc.)

LEGAL DESCRIPTION FOR DE-ANNEXATION FOR W1/2 SECTION 25 T140N R96W, STARK COUNTY, NORTH DAKOTA.

B.

Planning Director Hadley

Planning Director Hadley

Planning Director Hadley

D. Fisher's 3rd City East Addition Final PlatConsideration to approve Resolution (Enc.)

Planning Director Hadley

E. Final Plat - Acres Subdivision - Discussion Planning Director Hadley

Building / Code Enforcement8.

A. Condemnation Proceedings Consideration to approve move forward (Enc.) Building Official Schwindt

Public Hearing and Public Comments not on Agenda - 5:00 p.m.9. Introduction

5:00 p.m. Swearing in of Police Officers - Jesse Kubik & Steven Knapp Police Chief Dassinger

December^J 2021 Page 2

Commission 10.

5:00 p.m. Swearing in of Police Officers - Jesse Kubik & Steven Knapp Police Chief Dassinger

5:05 p.m. Homeless Coalition Presentation Commissioner Odermann

5:10p.m. Public Comments not on Agenda President Decker

Adjournment

December^J 2021 Page 3

1

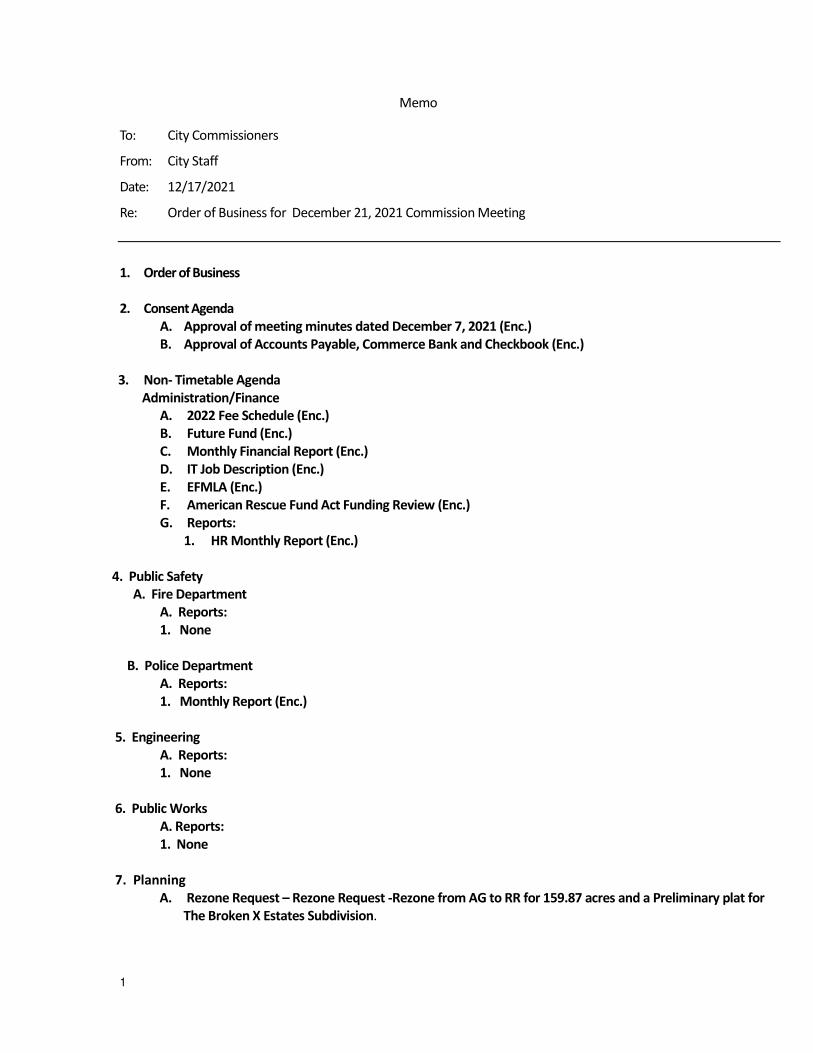

Memo

To: City Commissioners

From: City Staff

Date: 12/17/2021

Re: Order of Business for December 21, 2021 Commission Meeting

1. Order of Business

2. Consent Agenda

A. Approval of meeting minutes dated December 7, 2021 (Enc.)

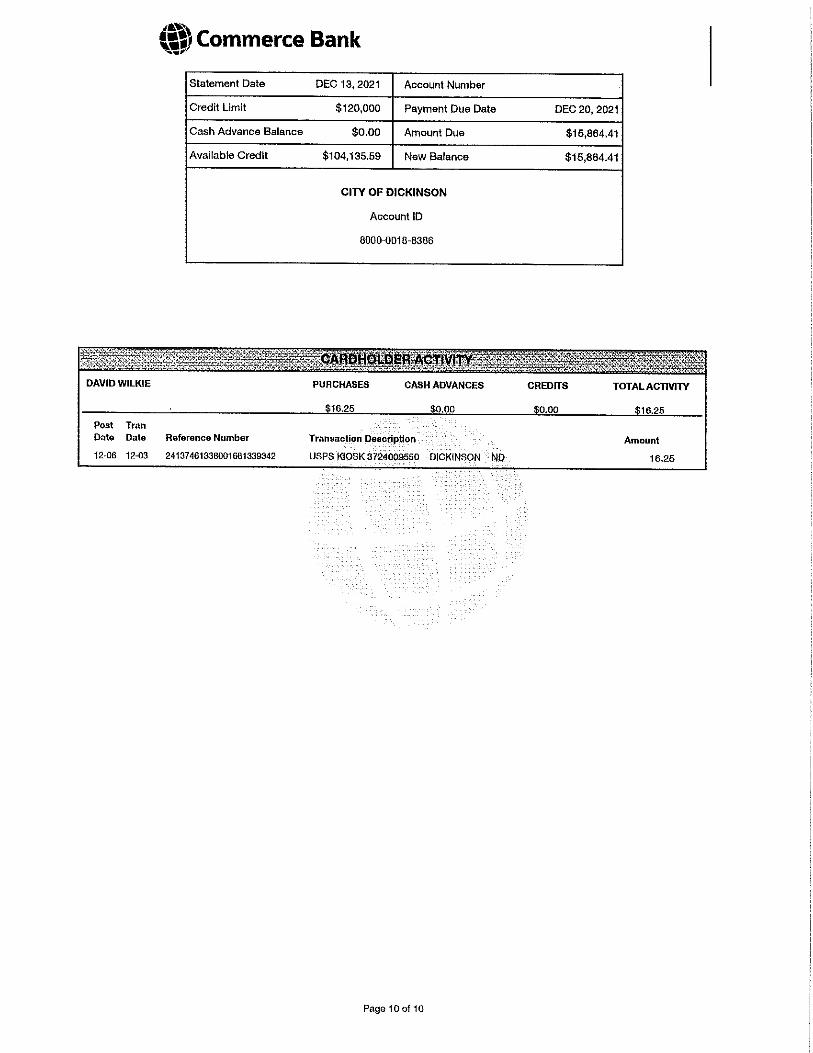

B. Approval of Accounts Payable, Commerce Bank and Checkbook (Enc.)

3. Non- Timetable Agenda

Administration/Finance

A. 2022 Fee Schedule (Enc.)

B. Future Fund (Enc.)

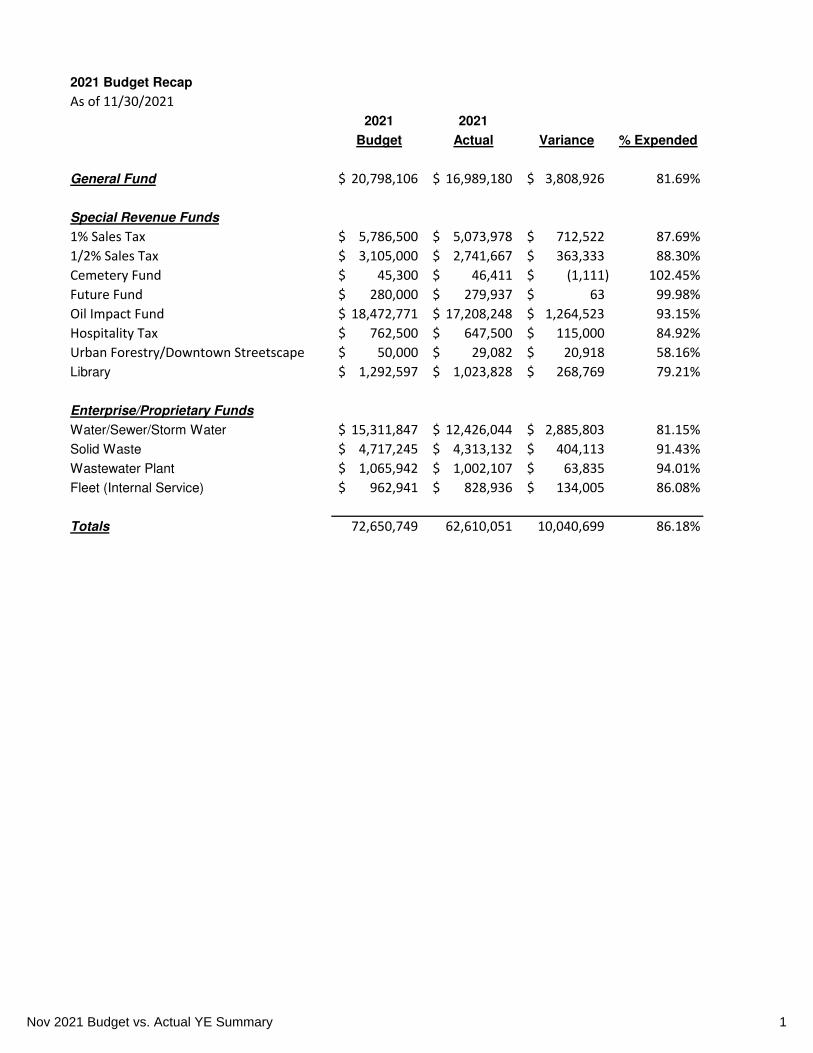

C. Monthly Financial Report (Enc.)

D. IT Job Description (Enc.)

E. EFMLA (Enc.)

F. American Rescue Fund Act Funding Review (Enc.)

G. Reports:

1. HR Monthly Report (Enc.)

4. Public Safety

A. Fire Department

A. Reports:

1. None

B. Police Department

A. Reports:

1. Monthly Report (Enc.)

5. Engineering

A. Reports:

1. None

6. Public Works

A. Reports:

1. None

7. Planning

A. Rezone Request – Rezone Request -Rezone from AG to RR for 159.87 acres and a Preliminary plat for

The Broken X Estates Subdivision.

Page 2

Item 7-A- Ordinance # 1735; REZONE REQUEST - To consider the second reading of Rezone request REZ-

009-21 for a zone change from Agricultural to Rural Residential for 159.87 acres, located in the NE ¼, all in

Section 26, Township 140 North, Range 96 W, along 109th Avenue SW, and 40th Street East, City of

Dickinson ETZ, Stark County, North Dakota. Zone Change approval. The Planning Commission conducted

a public hearing on this item during the November 17, 2021 meeting and no opposition heard. Staff and

the Planning Commission would both recommend approval of the second reading of Ordinance # 1735 as

presented.

Motion: I move the City Commission approve the second reading of Ordinance # 1735; as presented, the

proposed Zone Change is compliant with the City of Dickinson City Code and Comprehensive Plan and as

being in the best interest of the general public health, safety, and welfare.

B. Rezone Request - Rezone Change amendment from R1 Low Density Residential to CC Community

Commercial ,West 150’of Lots 1, 2, and 3, Block 4, Gress’s Subdivision.

Item 7-B-Ordinance #1736; REZONE REQUEST - To consider the second reading of Rezone request- REZ-

008-21, for a zone change from R1 Single Family to CC Community Commercial for 44,866 square foot

parcel, known as; W 150’ Lots 1, 2, and 3, Block 4, Gress’s Subdivision, along the 800 block of 8th Street SW,

within the City of Dickinson, Stark County, North Dakota. The request is in conformance with the city FLUM

map. The Planning Commission conducted a public hearing on this item during the November 17, 2021

meeting and no opposition heard. Staff and the Planning Commission would both recommend approval

of the second reading of Ordinance # 1736 as presented.

Motion: I move the City Commission approve the second reading of Ordinance # 1736; as presented, the

proposed Zone Change is compliant with the City of Dickinson City Code and Comprehensive Plan and as

being in the best interest of the general public health, safety, and welfare.

C. LEGAL DESCRIPTION FOR PLAT VACATION AND DE-ANNEXATION FOR NW ¼ SECTION 31 T140N

R96W, STARK COUNTY, NORTH DAKOTA.

Item 7 C-A-Ordinance #1737; EXCEPTIONS/EXCLUSIONS/PLAT VACATION REQUEST -To consider the

second readings of a Plat vacation request from the property owner located in the following area

currently within the City Limits of the City of Dickinson, Stark County, North Dakota:

PARCEL A. LEGAL DESCRIPTION FOR PLAT VACATION AND EXCLUSION FOR NW ¼ SECTION 31 T140N

R96W, STARK COUNTY, NORTH DAKOTA.

For plat vacation in NW ¼ Section 31 T140N R96W, Stark County, North Dakota,

The Pinecrest Parkway Street right of way, Lot 2 of Block 6, and Lot 5 of Block 2 in Pinecrest

(Subdivision), that is in the NW1/4 Section 31 T140N R96W, however retaining to the City, the 80 foot

wide, dedicated Pinecrest Parkway, street right of way along the south line of Lot 4 of Block 2 of

Pinecrest (Subdivision), the 50-foot road right of way, as described on document number 3133521 as

recorded at the Stark County Recorder’s Office and retaining the 50-foot road right of way, the south

of the north line of said Section 31 along 21st street, for the county and for public use. . The Planning

Commission conducted a public hearing on this item during the November 17, 2021 meeting and no

opposition heard. Staff and the Planning Commission would both recommend approval of the second

reading of Ordinance # 1737 as presented.

Page 3

Motion: I move the City Commission approve the second reading of Ordinance # 1737; as presented,

the proposed plat vacation is compliant with the City of Dickinson City Code and Comprehensive Plan

and as being in the best interest of the general public health, safety, and welfare.

For exclusion; same as parcel as above, Ordinance #1738:

for NW ¼ Section 31 T140N R96W, Stark County, North Dakota,

The NW1/4 Section 31 T140N R96W, except and retaining into the city all portions of Lot 4 Block 2 and

Lot 1, Block 6 in Pinecrest (Subdivision), also retaining into the City, the 80 foot wide, dedicated

Pinecrest Parkway, street right of way along the south line of Lot 4 of Block 2 of Pinecrest (Subdivision),

the 50-foot road right of way, as described on document number 3133521 as recorded at the Stark

County Recorder’s Office and retaining the 50-foot road right of way, the south of the north line of

said Section 31 along 21st street, for the county and for public use. The Planning Commission

conducted a public hearing on this item during the November 17, 2021 meeting and no opposition

heard. Staff and the Planning Commission would both recommend approval of the second reading of

Ordinance # 1738 as presented.

Motion: I move the City Commission approve the second reading of Ordinance # 1738; as presented,

the proposed exclusion is compliant with the City of Dickinson City Code and Comprehensive Plan and

as being in the best interest of the general public health, safety, and welfare.

Parcel B: LEGAL DESCRIPTION FOR PLAT VACATION AND EXCLUSION FOR SW ¼ SECTION 30 T140N

R96W, STARK COUNTY, NORTH DAKOTA.

For plat vacation in SW ¼ Section 30 T140N R96W, Stark County, North Dakota, Ordinance #1739

The Westwood Circle Street right of way, Lots 1, 2, 3 and 4 of Block 1 in Pinecrest (Subdivision), in the

SW1/4 Section 30 T140N R96W, however retaining the 50-foot road right of way north of the south

line of said Section 31 along 21st street, for the county and for public use. The Planning Commission

conducted a public hearing on this item during the November 17, 2021 meeting and no opposition

heard. Staff and the Planning Commission would both recommend approval of the second reading of

Ordinance # 1739 as presented.

Motion: I move the City Commission approve the second reading of Ordinance # 1739; as presented,

the proposed plat vacation is compliant with the City of Dickinson City Code and Comprehensive Plan

and as being in the best interest of the general public health, safety, and welfare.

For exclusion; the same parcel as above for SW ¼ Section 30 T140N R96W, Stark County, North

Dakota, Ordinance #1740

The Westwood Circle Street right of way, Lots 1, 2, 3 and 4 of Block 1 in Pinecrest (Subdivision), in the

SW1/4 Section 30 T140N R96W, however retaining the 50-foot road right of way north of the south

Page 4

line of said Section 31 along 21st street, for the county and for public use. The Planning Commission

conducted a public hearing on this item during the November 17, 2021 meeting and no opposition

heard. Staff and the Planning Commission would both recommend approval of the exclusion and

second reading of Ordinance # 1740 as presented

Motion: I move the City Commission approve the second reading of Ordinance # 1740; as presented,

the proposed exclusion is compliant with the City of Dickinson City Code and Comprehensive Plan and

as being in the best interest of the general public health, safety, and welfare.

Parcel C: LEGAL DESCRIPTION FOR EXCLUSION FOR W1/2 SECTION 25 T140N R96W, STARK COUNTY,

NORTH DAKOTA.

For exclusion for W1/2 Section 25 T140N R96W, Stark County, North Dakota. Ordinance #1741

The W1/2 Section 25 T140N R96W, including parcel as described on a document recorded in book 196

page 207 and parcels in the NW1/4 on said Section 25 as recorded in the Stark County Recorder’s

office, and retaining and transferring any road right of way, to the county and for public use, that is

outside the statue 33 foot along the section lines. The Planning Commission conducted a public

hearing on this item during the November 17, 2021 meeting and no opposition heard. Staff and the

Planning Commission would both recommend approval of the first reading of Ordinance # 1741 as

presented.

Motion: I move the City Commission approve the second reading of Ordinance # 1741; as presented,

the proposed exclusion is compliant with the City of Dickinson City Code and Comprehensive Plan and

as being in the best interest of the general public health, safety, and welfare.

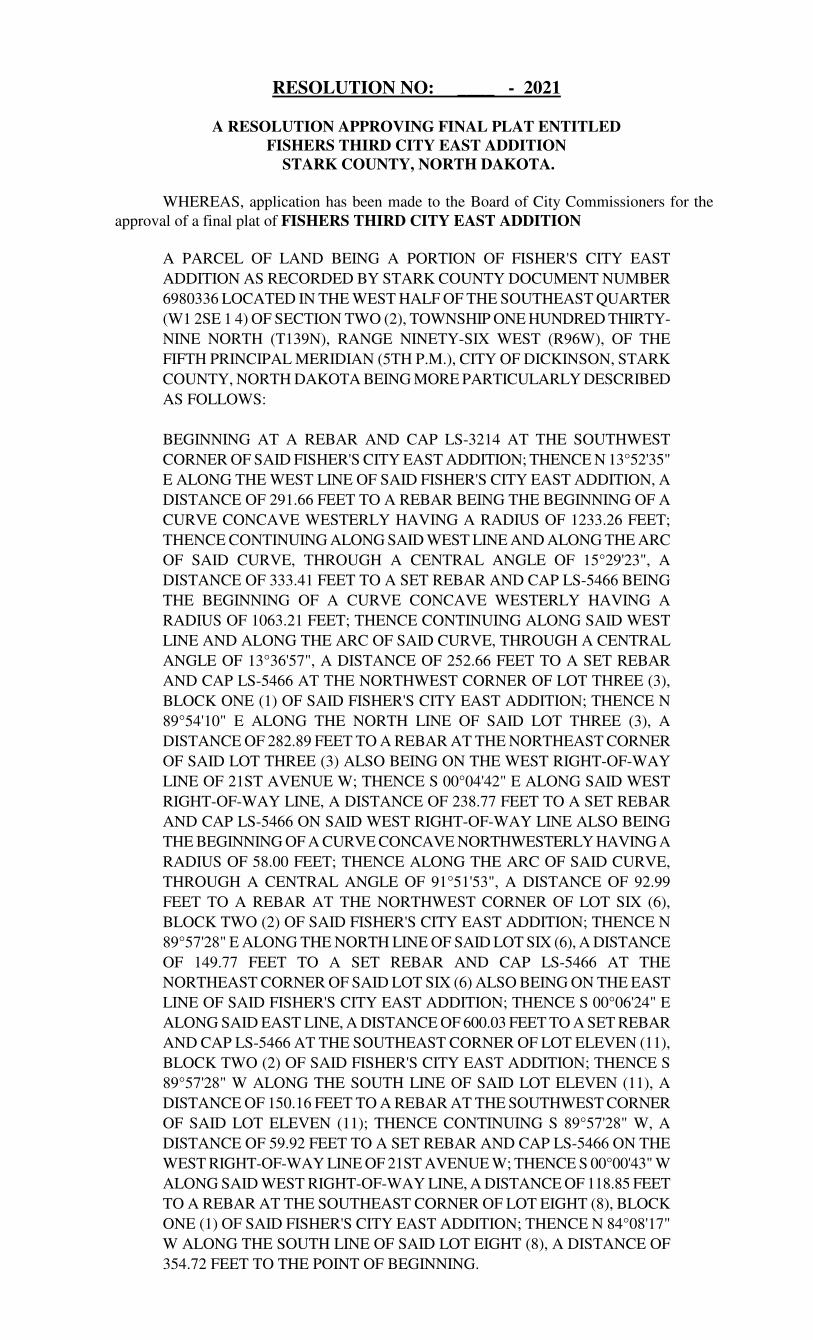

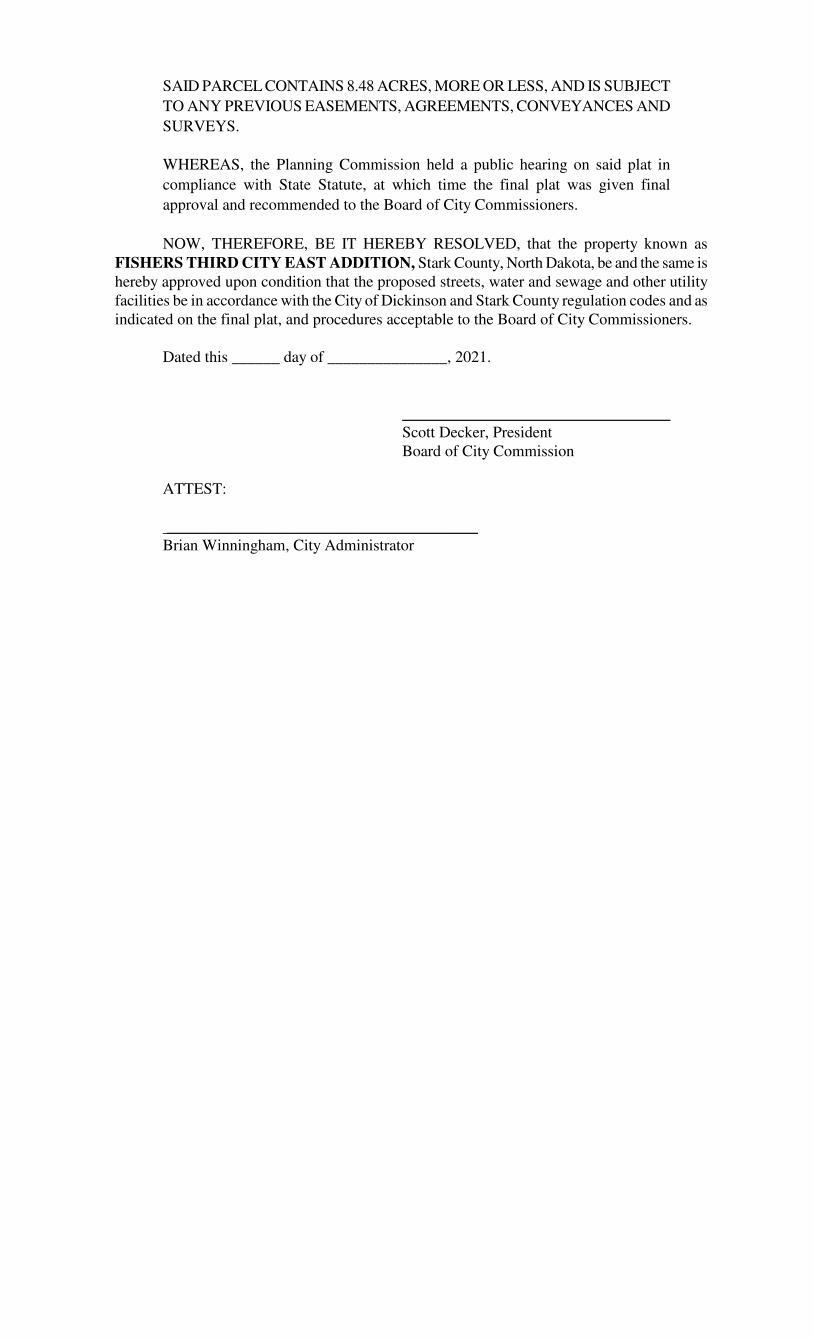

D. Fisher’s 3rd City East Addition Final Plat (Enc.)

Item 7 D-To consider Resolution # ______ for FLP-009-2021, Final Plat for Fisher’s 3rd City East

Addition, as a replat of Lots 3-8, Block 1, and Lots 6-11, Block 2 of Fisher’s East Addition which

includes the vacation of a portion of 21st Avenue East, and some existing easements to create Fisher’s

3rd City East Addition including 2 General Commercially zoned lots on 8.36 acres. The Planning

Commission considered this item on the December 15, 2021 planning agenda with no opposition.

The Planning Commission and Staff would recommend approval of Resolution #______ as

presented.

Motion: I move the City Commission approve Resolution #_______; as presented, the proposed final

plat is compliant with the City of Dickinson City Code and Comprehensive Plan and as being in the

best interest of the general public health, safety, and welfare.

E. Final Plat – Acres Subdivision – Discussion (Enc.)

Item 7 E-The Acres Subdivision was approved via Resolution #33-2021 at a previous City Commission

meeting based on the removal of a no-access easement along the existing property to the east of

Page 5

the proposed public roadway as indicated on the map/slide. Staff felt that it would amount to a

takings of property rights unless that property owner signed off on the request. The property owner

hasn’t signed off on the request and the applicant agreed to remove the easement so it could move

forward in the process. This easement was added on to the plat a few days before the planning

commission meeting and staff isn’t sure that everyone involved acknowledged the change. It was a

deviation from the submittal that was advertised for the planning hearing. The adjacent neighbor

has not responded to the applicant and staff has invited him to the previous city commission meeting

to hear the discussion via a mailed agenda. Staff has sent a certified notice to the owner to attend

this meeting (Dec.21st) and provide input. During the last City Commission meeting (Dec. 7th) it was

agreed that notice would be given and that the developer would reach out to the owner and the

commission would discuss once again. Staff would still support the initial recommendation of

removal of the no access easement as initially recommended, or obtain agreement from the

adjacent owner, or have the applicant amend the plat so the public right-of-way isn’t adjacent to the

existing property. Legal, Engineering, and Planning Staff are all in agreement with this continued

recommendation based on limiting the liability to the City and averting a possible future takings of

property rights claim.

8. Building/Code Enforcement

A. Repots:

1. Condemnation Proceedings Presentation (Enc.)

9. Public Hearing and Public Issues of City Concern Not On Agenda Commission

A. Swearing in of Officers – Jesse Kubik and Steven Knapp

B. Homeless Coalition Presentation

C. Public Comments not on Agenda

10. Commission

REGULAR MEETING DICKINSON CITY COMMISSION December 7, 2021

I. CALL TO ORDER

President Scott Decker called the meeting to order at 4:30 PM.

II. ROLL CALL

Present were: President Scott Decker, Vice President Jason Fridrich,

Commissioners Suzi Sobolik, John Odermann and Nikki Wolla

Absent: None

1. ORDER OF BUSINESS

MOTION BY: Jason Fridrich SECONDED BY: Nikki Wolla

To approve the December 7, 2021 Order of Business as presented.

DISPOSITION: Roll call vote…Aye 5, Nay 0, Absent 0

Motion declared duly passed

2. CONSENT AGENDA

MOTION BY: Nikki Wolla SECONDED BY: Suzi Sobolik

A. Approval of meeting minutes dated November 16, 2021.

B. Approval of Accounts Payable and Checkbook.

C. Approval of 2022 Tobacco Licenses

DISPOSITION: Roll call vote…Aye 5, Nay 0, Absent 0

Motion declared duly passed

3. ADMINISTRATION/FINANCE

A. Chapter 13 Revisions

City Attorney Christina Wenko presents for a second reading Chapter 13 revisions. She states these changes are related to the Fire Department transitioning from volunteer firefighters to part time firefighters. Ms. Wenko states there have been no changes since the first reading and recommends approval. MOTION BY: John Odermann SECONDED BY: Jason Fridrich

To approve second reading and final passage of Ordinance No. 1731.

ORDINANCE NO. 1731

AN ORDINANCE AMENDED AND RE-ENACTING SECTION 13.12.02010

AND REPEALING SECTIONS 13.12.02040 AND 13.12.02130 OF THE CITY

CODE OF THE CITY OF DICKINSON, NORTH DAKOTA, RELATING TO

ARTICLE 13.12 - FIRE DEPARTMENT

DISPOSITION: Roll call vote…Aye 5, Nay 0, Absent 0 Motion declared duly passed

B. Chapter 32 Revisions

City Attorney Christina Wenko presents for a second reading Chapter 32 revisions. She states these changes are related to the Fire Department transitioning from volunteer firefighters to part time firefighters. Ms. Wenko states there have been no changes since the first reading and recommends approval. MOTION BY: Nikki Wolla SECONDED BY: Jason Fridrich

To approve second reading and final passage of Ordinance No. 1732.

ORDINANCE NO. 1732

AN ORDINANCE AMENDED AND RE-ENACTING SECTION 32.16,

32.16.010, 32.16.020, 32.16.040, 32.16.080, 32.16.150, 32.16.150 OF THE CITY

CODE OF THE CITY OF DICKINSON, NORTH DAKOTA, RELATING TO

ARTICLE 32.16 – DICKINSON VOLUNTEER FIRE DEPARTMENT

PENSION PLAN

DISPOSITION: Roll call vote…Aye 5, Nay 0, Absent 0

Motion declared duly passed

C. Vanguard Contract Amendment

City Assessor Joe Hirschfeld presents a Vanguard contract amendment. Mr. Hirschfeld states Vanguard is having issues with staffing, therefore would like to change the scope of work for 2022. Mr. Hirschfeld states Vanguard would inspect properties that have had some changes to them otherwise properties that have had no changes would not be inspected. Assessor Hirschfeld feels the city should consider this option and to keep Vanguard on schedule. Assessor Hirschfeld states the contract would decrease by about $99,000. MOTION BY: Jason Fridrich SECONDED BY: John Odermann

Approve Vanguard Contract Amendment.

DISPOSITION: Roll call vote…Aye 5, Nay 0, Absent 0

Motion declared duly passed

D. Chapter 4 Revisions

City Attorney Christina Wenko presents Chapter 4 for a second reading. She recaps some of the liquor license ordinance changes. The changes do not contain additional license for convenience stores to sell beer nor wine based on a vote from the Commissioners last meeting. There is some clarification of restaurants having gaming licenses and she has added no electronic gaming unless a designated bar area premises. She states there has been a change to special events as only Class A liquor licenses can have special event permits. Ms. Wenko states this ordinance will take affect on 1/1/2022. There was some question on whether a special event could be held if extended to parking lots of facilities. Police Chief Dustin Dassinger states only on rare occasions where other then a Class A license would be allowed off premises. Restaurant such as Blue 42 has been allowed to take their license off premises but this will not be allowed in the future. Commissioner Jason Fridrich states if Players would hold an event in their parking lot, the City should consider. Police Chief Dustin Dassinger state this is more of a concern should they move their license off of the premises. MOTION BY: Jason Fridrich SECONDED BY: Nikki Wolla

To approve second reading and final passage of Ordinance No. 1733.

ORDINANCE NO. 1733

AN ORDINANCE AMENDING AND RE-ENACTING SECTIONS 4.04.010,

4.08.030, 4.08.060, 4.08.070, 4.08.075, 4.08.170, 4.08.180, 4.08.200, 4.08.230,

4.08.240, 4.08.270, 4.08.280 AND ENACTING SECTION 4.08.065 OF

ARTICLE 4 OF THE MUNICIPAL CODE OF THE CITY OF DICKINSON,

NORTH DAKOTA, RELATING TO ALCOHOLIC BEVERAGES

DISPOSITION: Roll call vote…Aye 5, Nay 0, Absent 0

Motion declared duly passed

E. 2022 Liquor License Renewals

City Administrator Brian Winningham presents the 40+ liquor license renewals for 2022. He states they have been reviewed by staff and recommend approval. He states there are 18 Commercial On-Sale/Off-Sale liquor licenses and Mr. Winningham discusses two of them for more awareness but potential to deny application. Administrator Winningham discusses the Rock which essentially has two locations for the Rock. He states there is a

tenant in between the two areas that the Rock is designating as a bar. This has been approved in the past with some conditions. Mr. Winningham would like for the Commissioner to be aware of this and questions to see whether this license is status quo or to have two separate licenses for two locations. There have been no complaints. President Scott Decker states the second portion is only used for special events. Police Chief Dustin Dassinger states the city has required them to have a special event when utilizing the corner bar. This has not been done on a routine basis. Commissioner Jason Fridrich discusses the past license holders of Army’s and the liquor store behind them. He feels this one has been approved in the past as it is considered contiguous as it is still under one roof. He remembers no issues with this license. City Administrator Brian Winningham states the City came last year about the delineation and feels they covered this pretty clearly with no revisions. He states there are some issues with the Elks and gaming device. Mr. Winningham states the City is going to notify the Elks to remove the gaming device that sits in the front entrance of the Elks as it is near minors. If they do not accept this request then the license will not be able to be renewed. Commissioner Jason Fridrich states it was his understanding that no minors were allowed on high top tables. If they designate high tops to only 21+ there would be no issues. City Attorney Christina Wenko states she cannot speak if this was actually done. The gaming is right around the corners and there is concern obviously of having access to anyone under the age 21 and not having them spaced out and this is the City’s concern. City Administrator Brian Winningham states it is staff recommendation that the City will work with the Elks to remove the gaming from the front door. If staff follows up then the license can be approved. Police Chief Dustin Dassinger states the City needs to be consistent and the City would ask the same from the Elks as the City did from Phat Fish. Commissioner Suzi Sobolik feels the standards have to be the same across the board. City Attorney Christina Wenko states the City has addressed the code and gaming. She states in order to be consistent and the city required separate spaces for gaming then the city should continue to be consistent in their requirements. Commissioner John Odermann questions what the solution would be to the Elks. He does not see any delineation in the gaming at all. He feels the Elks have done something that the city is uncomfortable with. Police Chief Dustin Dassinger would like to see some type of hard delineation and where minors would not have access to the gaming devices. City Administrator Brian Winningham states the Police Department will be working with the businesses in question and review the separation of gaming from the restaurant. The City will come forward with a report on the Elks and St. Anthony Clubs. MOTION BY: Jason Fridrich SECONDED BY: Nikki Wolla

Approve the 2022 Liquor Licenses as presented.

DISPOSITION: Roll call vote…Aye 5, Nay 0, Absent 0

Motion declared duly passed

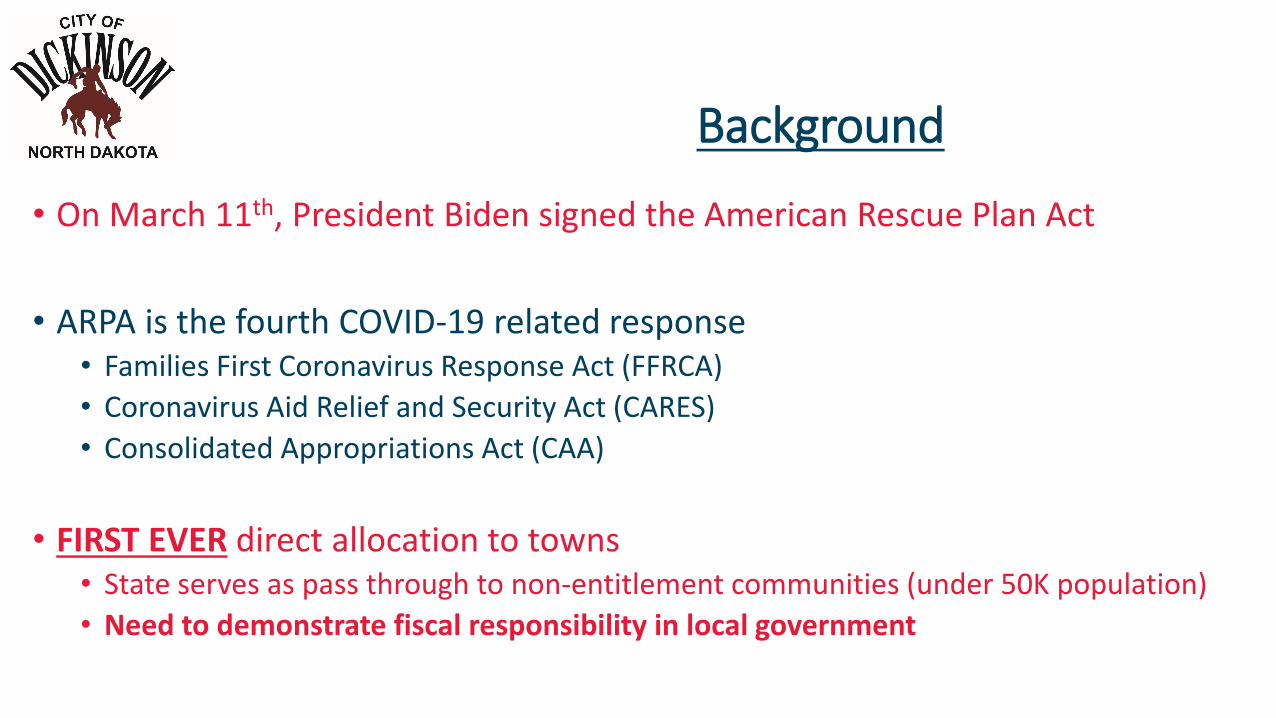

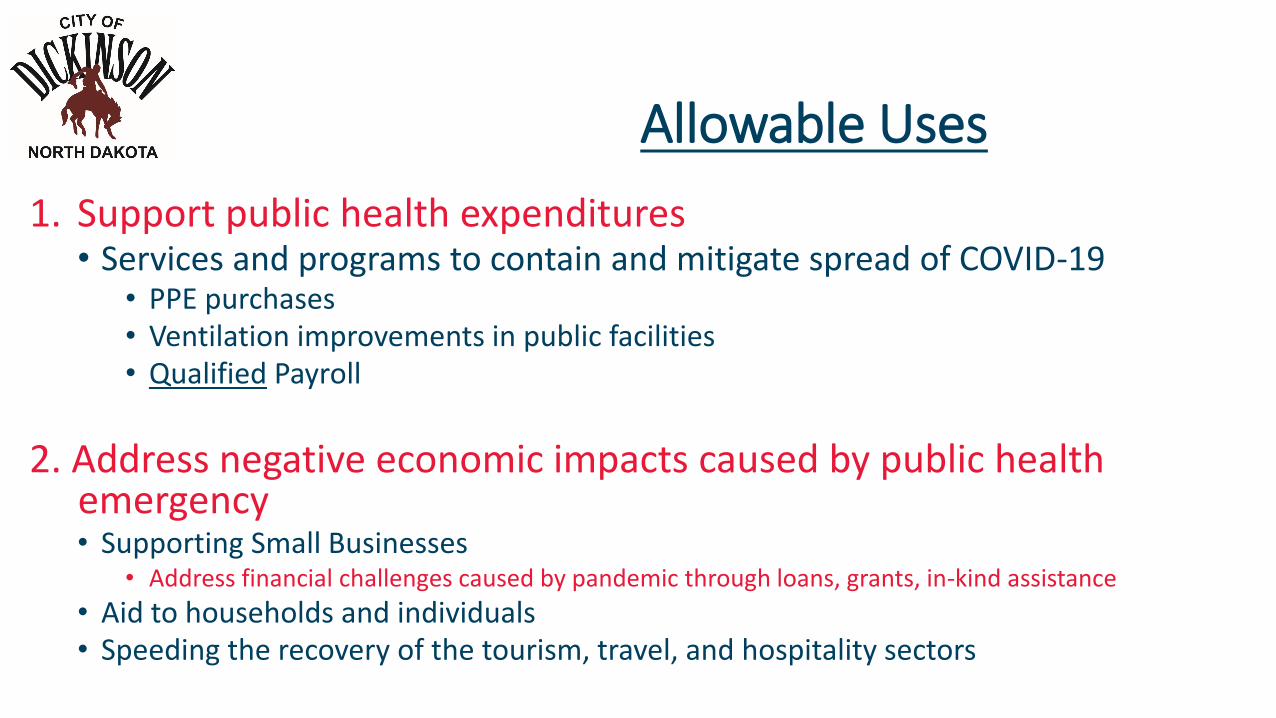

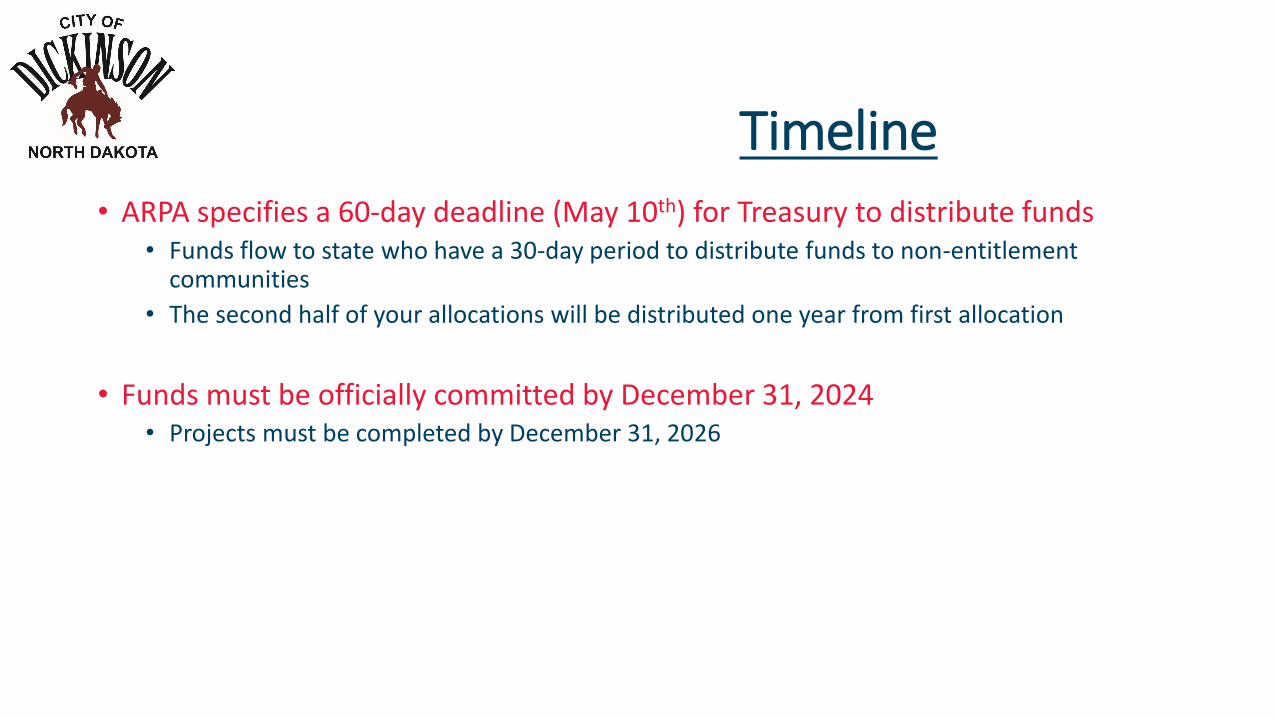

F. American Rescue Fund Act Funding Review

City Administrator Brian Winningham reviews the Cares Act Funding. He discusses the eligible uses for the Cares Act funds. He states it came as a general fund amount. He states the fund has now allowed the city to reduce oil revenue transfer to zero. There is $3.4 million that can be appropriately used. He suggests that the city pay the obligated money

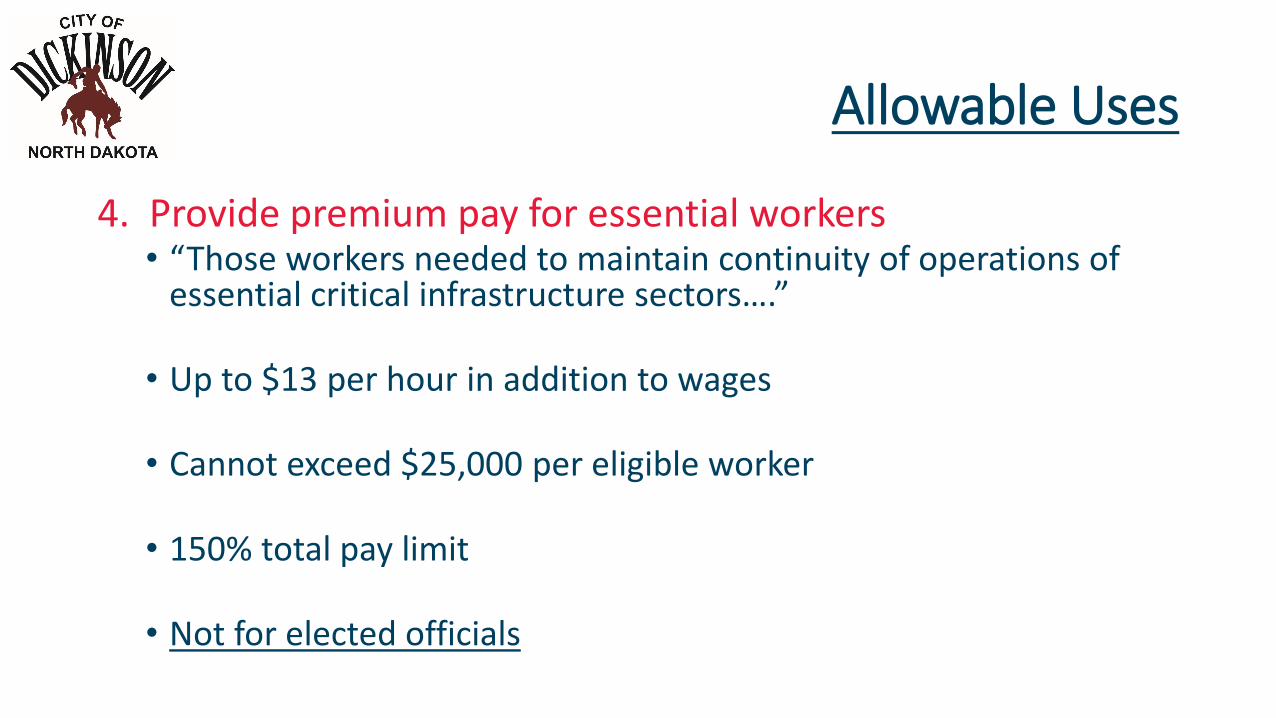

that normally the 1% sales tax pays for grants and then put the 1% sales tax funds into the general fund for the Commissioners to decide where to use these funds. He discusses briefly the premium pay for employees. He feels there should be some endurance pay for funding to city staff who were required to be working during the pandemic. He states it has been difficult to hire employees. Mr. Winningham feels citizens should receive the best quality of service and states many of the employees are faced with putting gas in our vehicle tanks. Administrator Winningham states the inflationary cost are up to 6% and it is hard to hold on to have employees be their best in this hard-economic time. He states citizens cannot go to another city to get services. There are a lot of challenges. The city of Dickinson is on a good path to pay their employees. Administrator Winningham states it would be idea that the Commissioners look at giving the employees a premium pay of 1.5 to 2% of ARPA funds. The highest amount of this pay would be $1,900. President Scott Decker states after looking at the data that Mr. Winningham had presented he would make a recommendation of what Mr. Winningham had suggested and look at paying the people whom are funded with the 1% such as the Downtown Association and others and possibly refund some license or fees paid by businesses and those businesses closed down during the pandemic. He does hear from business owners and others on how hard the employees work and he does recommend premium pay for hourly employees. This amount would be around $1,800. City Administrator Brian Winningham states the city could create a grant program and have people come forward and presenting during this process their economic impact. The city could look at this need on a case by case need. The city would set the dollar amount of up to $1,000. Commissioner Jason Fridrich questions what paying these subsidies out of the Cares Act fund would help the city out. He states the subsides are already set to come out of the taxes that the city collects. He feels the money should go to everyone in the community. He does not see how this would help the community. He feels everyone in the community has been affected in some way over Covid. He does not see the benefit of subsiding out of the other fund would benefit anyone. City Administrator Brian Winningham states the city already pays grants out of the 1% sales tax and for the commission to have more flexibility with the Cares Act the city could pay for the 1% sales tax items out of Cares and have the 1% funds to be dedicated to something else. There would be no strings attached to the 1% funds if the subsidies were paid out of the Cares Act Funds. Commissioner Jason Fridrich states the city could take $750,000 for the next three years and take a reduction in the mill levy. Commissioner Fridrich states the city cannot prove we had a deduction in revenue. He states the tax and oil revenue were down. The next priority is mental health care. City Administrator Brian Winningham states the city cannot use ARPA funds for the reduction of mill levy. He states that the city cannot show that they had a loss of revenue as the city covered the budget. The city needs to show a 1 for 1 revenue loss. The city was still able to cover the bills without revenue loss. Commissioner John Odermann feels that if the city is going to expend for the grants then they would have extra sales tax money for local control and have the flexibility. City Administrator Brian Winningham states the city could use some of these funds for premium pay. He wanted to put some work into the ARPA for trading these funds to give the Commission some flexibility. If the city uses ARPA funding for subsidies then the $750,000 goes back into the general fund to be spent as the Commission sees fit. Commissioner Jason Fridrich states if the city takes the money and pays the contracts then the money is just washed back into the pile we the city will not see the benefit down the road. He does not feel this is where the city wants to go. Commissioner Fridrich would like to see a list of where the ARPA funding went.

Commissioner Suzi Sobolik states she would like to make sure the money goes to where the city wants to spend it on. She feels if the Cares Act funds pay for the 1% sales tax subsidies then this would open up a better way to spend the city’s funding on something else. She does not want it to pay the bills that the city gets year after year. She would like for the city to be creative with it. Commissioner Jason Fridrich states whatever ARPA money and the sales tax money is going to be a separate fund so the commissioners can see on a daily basis what it is being spent on. If the city pays the subsidies out of the ARPA funding then the sales tax money needs to go to the sales tax fund account. The dollars need to be 1 for 1 in those accounts. He questions whether this will really give the city the flexibility. He feels the money should be put towards the mill levy. City Administrator Brian Winningham states the city will always be short in the mill levy on road impact. Possibly use the money for funding the roads. It is a good place for Dickinson to be but it makes it challenging that the city funds all these extra things. Subsidies are given back to the community. The city of Dickinson is in good condition.

G. Reports:

1. Dickinson Youth Commission

President Reilley Meyer updates the Commission on the Dickinson Youth Commission. President Meyer states there are 10 teenager commissioners who advise the city commission. She is grateful for the City commissioners to allow them to advise them on city events. Mr. Truman Hamburger whom is part of the Dickinson Youth Commission states they have conducted a youth survey to gauge what youth in the community would like to see and do. These events would be for teenagers from the age of 15-18. He states the youth would like to see a snow day in February and a valentine’s day dance. President Meyer and Mr. Hamburger update the commission on the Instagram for the youth commission.

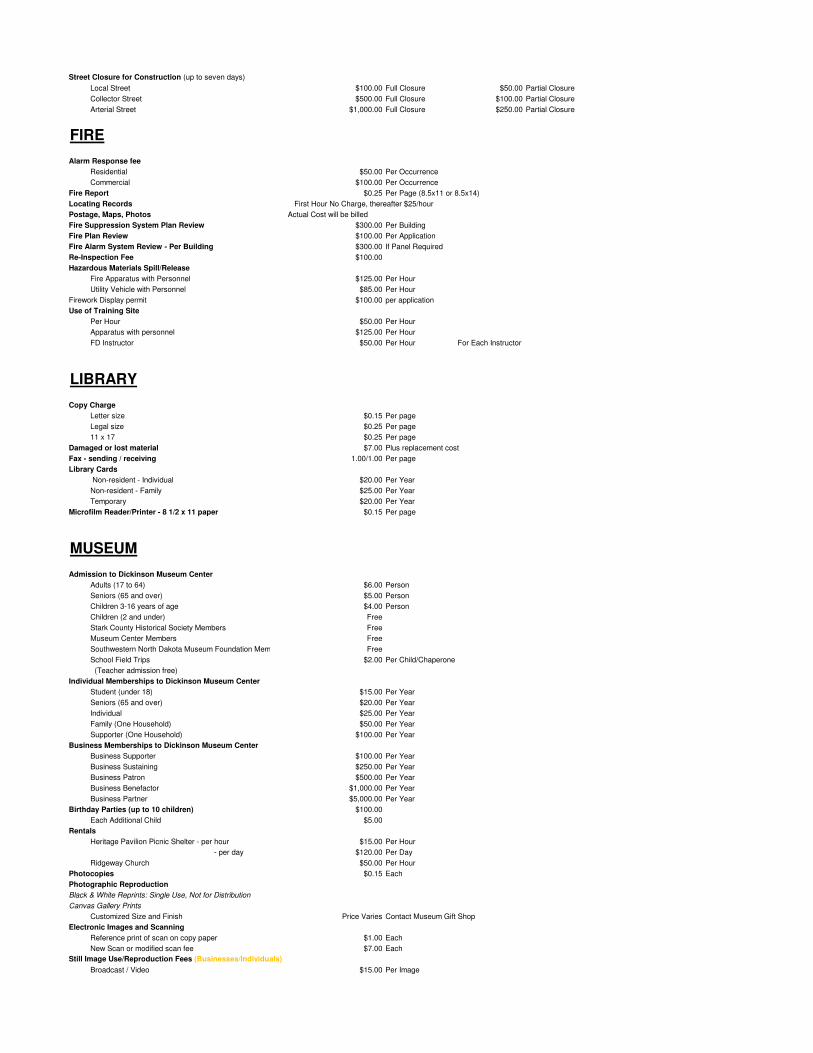

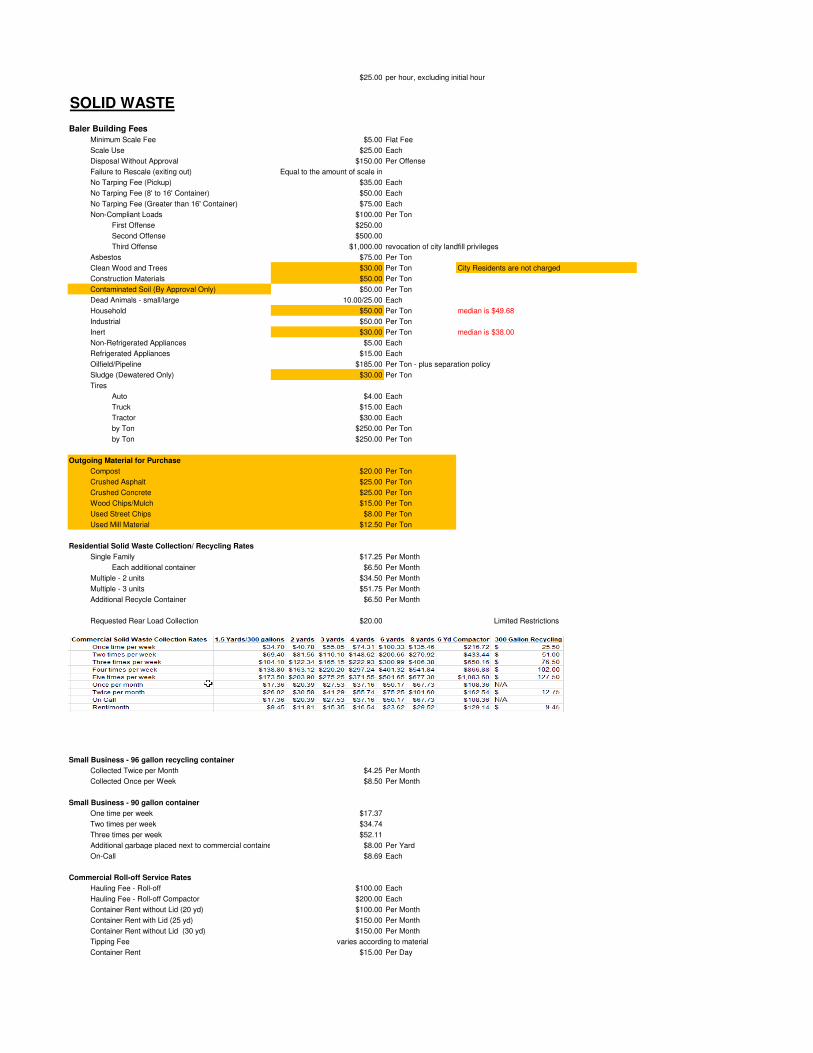

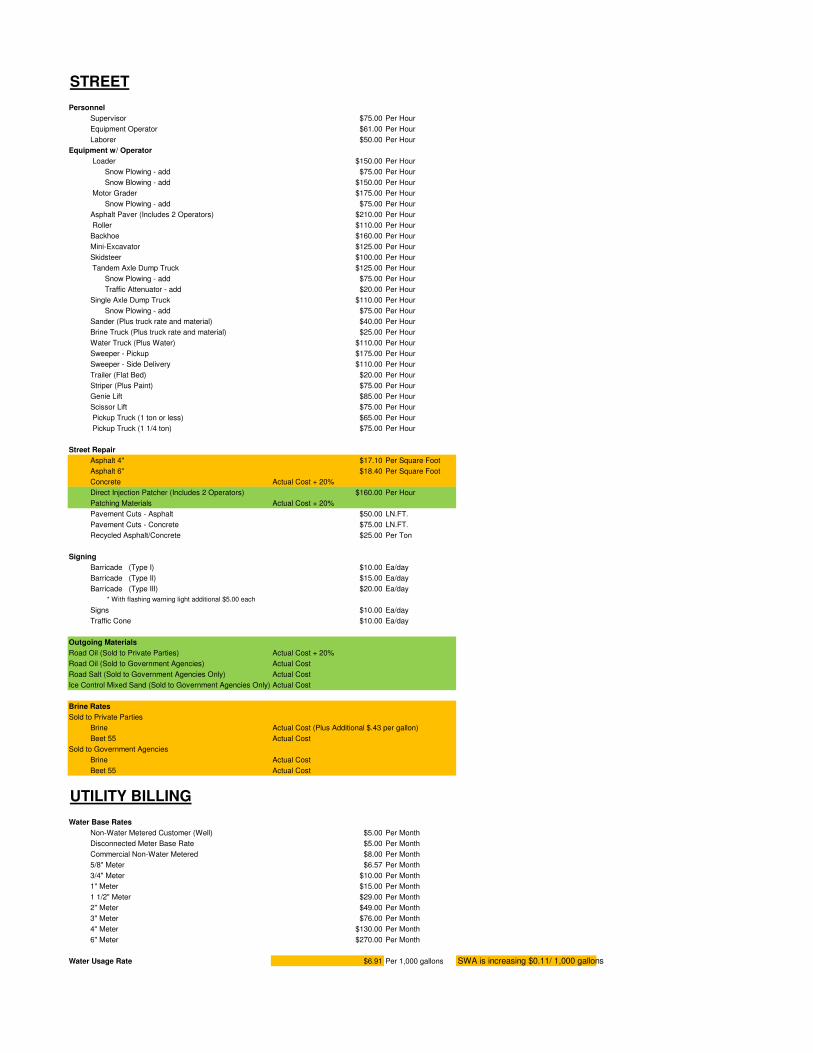

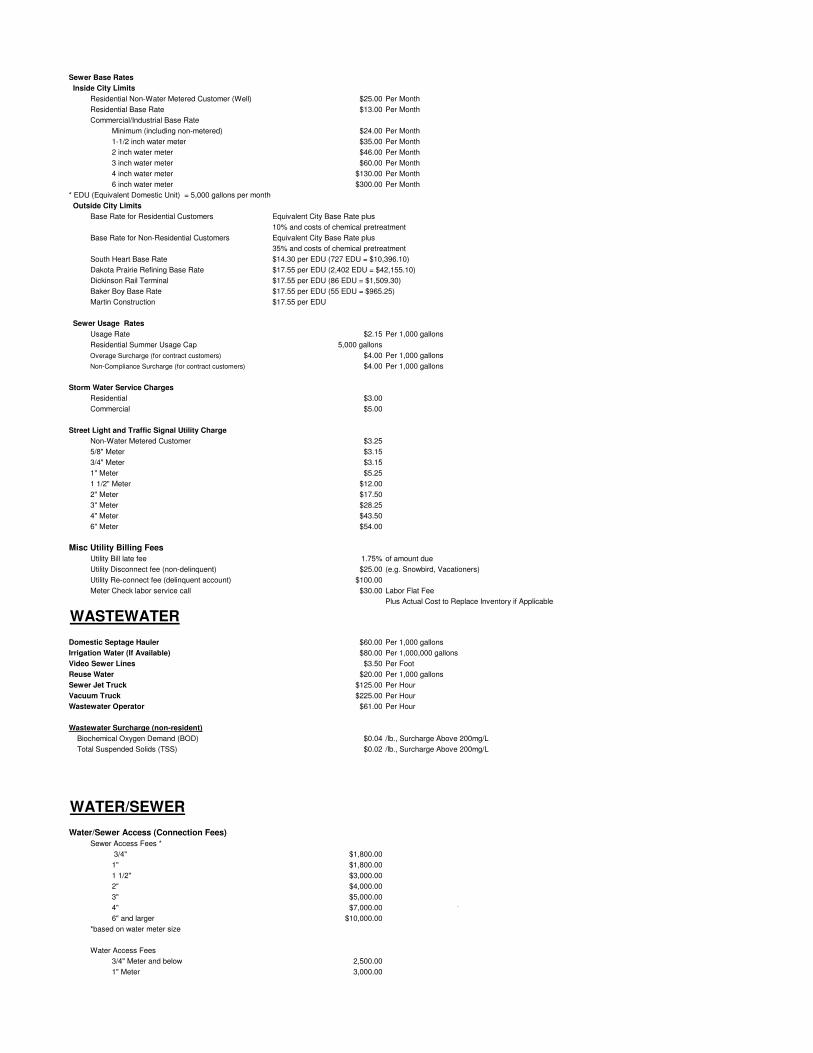

2. 2022 Fee Schedule

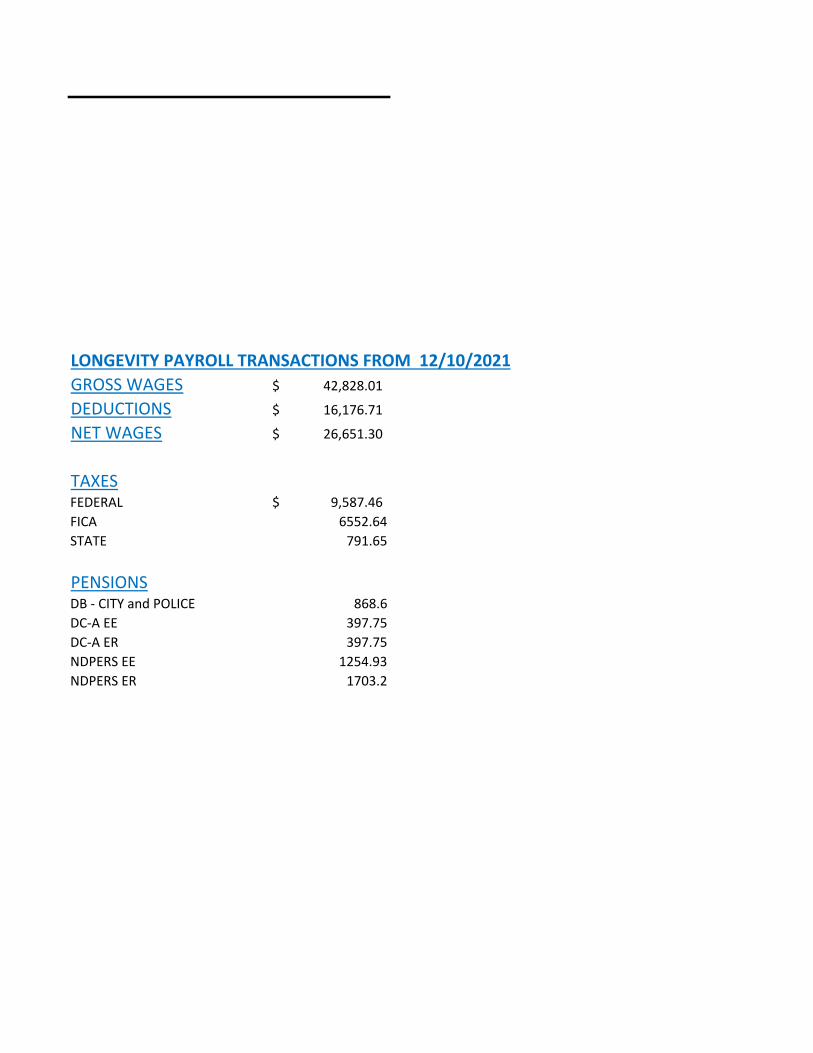

Deputy City Administrator Linda Carlson presents the 2022 Fee Schedule. She states these changes will take effect on 1/1/2022. She states there are some changes to the liquor licenses, domestic wintery, nonrefundable application fee and new owner license fee. She also states the Arborist would like to raise the Arborist business contract to $100 from $25 dollars. She also updates the Commission on the private tree trimming compliance, body cams DVD/CD’s and water usage rate changing. She states SW Water has raised .11 cents per 1000 gallons and this will be passed onto the customer. Ms. Carlson states will bring this fee schedule for approval at the next meeting.

3. 2020 Audit

Deputy City Administrator Linda Carlson presents the results of the final audit for 2020. Ms. Carlson reads the findings. She states overall the city had a good audit as it went smoothly and on time.

4. Prosecution Contract Presentation

City Attorney Christina Wenko gives an annual prosecution contract presentation. She

states currently there are 657 cases with 77 active cases. The most common case is driving

under suspension, DUI, alcohol related driving and others. She updates the commission

on the change of law with marijuana as a reduction in fines. She states the city has seen an

increase in fees collected, highest number in the city has ever collected in 10 years. She

feels stimulus money has been used for fines and fees. She discusses the trends as it shows

DUI/DUS as the majority of criminal cases. She states she works hand in hand with the

animal shelter. Attorney Wenko states the animal shelter staff do an absolute wonderful

job. City Attorney Wenko discusses the city contract with hearings and trail discussion.

She states in 2020 she was appointed as a special Assistant States Attorney in domestic

violence cases. Attorney Wenko states the contract relies heavily on Dickinson Police

Department and the city clerk’s office. She states she has read thousands of police reports

and hours of video. She has now gotten a deeper understating of what it is like to be a

Police Officer. Her perception over the last 8-9 years the police deal with individual on

their worse days and worse circumstances. Their task is that they deal with the utmost

level of professionalism. She could not be prouder of the Dickinson Police Department

officers. She states it is is hard to find people and I just consider their team an extension

of her team. She could not be prouder of them. They have the most uncanning ability to

bring humor, compassion and kindness to the public on a daily basis. She states the City

and her office have worked very well together with good communication, trust and she

look forward to working with the City in 2022.

Police Chief Dustin Dassinger thanks Ms. Wenko and her team for their professional

approach that they provide to the city of Dickinson and municipal court office and the team

effort and the city commends her for that.

President Scott Decker thanks Ms. Wenko for all her hard work.

4. PUBLIC SAFETY

A. Fire Department

1. Reports:

None

B. Police Department

1. Reports

None

5. ENGINEERING

A. 4th Avenue East Bid Consideration

Interim City Engineer Loretta Marshik presents a low bid tabulation, bid comparison and

preliminary bid abstract for 4th Avenue East. She states this location is between 21st Street

East and 26th Street East, East of Walmart. She states Northern Improvement is the only

bidder and it has come in 40% higher than the Engineer’s bid. She states the city will

receive $800,000 of the Federal Funding for this project. The city would need to pay

$426,367.80. Ms. Marshik feels the city should reject this bid and review the project to

make this project more appealing.

Commissioner Jason Fridrich states $800,000 is a small amount for federal funding for

this project.

MOTION BY: Jason Fridrich SECONDED BY: Nikki Wolla

Deny the 4th Avenue East Bid from Northern Improvement.

DISPOSITION: Roll call vote…Aye 5, Nay 0, Absent 0

Motion declared duly passed

B. East Broadway Dam – Project Alternatives

Interim City Engineer Loretta Marshik discusses alternatives for modifying the existing

East Broadway Dam. Ms. Marshik presents three alternatives to address the deficient

condition of the deteriorating dam. She states each alternative improves public safety. City

Engineer Marshik reviews the pros and cons of each option.

President Scott decker states the damn removal is the cheapest option but then there would

be no river. President Decker states a rock arch would be installed then kayaks would still

be able to use the river.

Commissioner John Odermann would like to see additional information on downstream

impacts. Commissioner Odermann feels something needs to be done but he feels additional

information is needed prior to a vote. He also would like to know what the impact will be

on downstream land owners. He feels the ripple is the best.

Commissioner Jason Fridrich feels the rock arch riffles would be nice.

Interim City Engineer Loretta Marshik states staff will visit with the consultant and maybe

move the ripple upstream so it would be a closer location to the existing park to make it

more accessible. Ms. Marshik will bring back more information on downstream.

C. Reports:

1. Extending 15th Street from State Avenue to 30th Avenue West

Interim City Engineer Loretta Marshik gives a report on the undeveloped street extending

from 15th Street from State Avenue to 30th Avenue West. This is in coordination with the

future land map.

2. Entrance Signs

Interim City Engineer Loretta Marshik discusses the six entrance signs and the vision the

Commission would like to see so an RFP can be created. She shows pictures of signs from

other cities to include the sizes, preferences, material, and others.

Deputy City Administrator Linda Carlson states $120,000 was put aside for six signs. N,

E, S, W, on T-Rex mall corner and the CVB signs were the ones that were included.

Public Works Director Gary Zuroff states when the city eliminated the banners across

highway 22 then it was discussed to have a digital sign at the T-Rex mall. He would like

to see a larger digital sign to replace the banners.

Commissioner Jason Fridrich would like to see the west sign move further to west possibly

at Fairway and west business loop from Frankie’s. Also, the east sign can move further to

the east. He feels these signs will cost more than the $120,000.

Interim City Engineer Marshik will bring back more information in regards to the signs.

3. Undeveloped Roads

Interim City Engineer Loretta Marshik states there are 14 miles of platted, undeveloped

roads, and this project could be completed with about $60 million dollars. Ms. Marshik

states most of the roadways are local. She states right now the city is asking developers to

develop them up front. They have discussed that the developer would cover the utilities

but maybe storm water would follow the roadway. The local road is 100% developer’s

responsibility but could be split for special assessments. She states the current process is

that the developer funds the costs and then the price is reflected in the lot price.

Commissioner Jason Fridrich questions whether the little roads to finish larger roads could

be federally funded.

6. PUBLIC WORKS

A. KLJ Task Order for City/Town Square Parking Lot

Public Works Director Gary Zuroff brings forward a KLJ Task Order for the city/town

square parking lot. This lot is west of the new city hall. Director Zuroff states once this

is surveyed, planned and decided on scope of project then bidding and construction of

service will be added. Director Zuroff, along with city staff recommend approval.

Director Zuroff states he is not sure of all the items that this will include which will include

additional lighting for better lighting in the parking lot.

Commissioner Nikki Wolla questions where patrons are going to park. Ms. Wolla is

wondering if we are going to limit how much parking city employees have. She states

other business employees will be parking in the same lot.

City Administrator Brian Winningham states Bravera bank has 65 parking spaces and it

will be public parking lot. No city employee will park next to the building but not limit

some of the public to park where they want to. The city is still considering the one way

on 1st on 1st. Parking is very limited in front of the building.

Public Works Director Gary Zuroff states the parking lot west of the building has had some

milling and temporary striping for the winter. This parking lot will add quite a bit of

designated area. There are some temporary lights.

MOTION BY: Jason Fridrich SECONDED BY: Nikki Wolla

To approve the KLJ Task Order for City/Town Square Parking Lot.

DISPOSITION: Roll call vote…Aye 5, Nay 0, Absent 0

Motion declared duly passed

B. Reports:

1. City Hall Update

Operations Manager Dave Clem updates the Commissioners on the progress and the cost

of the new city hall. He discusses change orders and the subfloor repairs. He states the

security glass is installed and the commission room is coming along very well with the

podium and others. The carpet is installed into the commission room. Operations

Manager Clem does encourage everyone to go over and look at the progress.

7. PLANNING

A. Final Plat – Acres Subdivision

City Administrator Brian Winningham states the Acres Subdivision final plat should have

had a bit more conversation last commission meeting, therefore, he has brought this

forward for discussion. He states the plat was approved but the developers are questioning

why it was not approved with a non-access easement. Commissioner Winningham wants

to have the full commissioners view.

Planning Director Walter Hadley states Acres Subdivision requested to put a non-access

easement into the area to restrict access to the public road on the final plat. Mr. Hadley

states Engineering, Legal and the Planning Staff agree that this not the prudent thing to do

as it is restricting the neighbors use of their lot. He states the neighbor probably did not

ask for this public road to be built in this area. He feels there are alternates for this.

A different plat was approved at the Planning and Zoning meeting. The plat with the non-

access easement was brought to the city the morning of the meeting and was not able to

be attached into the packets.

Interim City Engineer Loretta Marshik states the plat that the city does not agree with that

not been in the packet as it came later than required for the packets. Ms. Marshik states

hard copies were handed out at the meeting.

City Attorney Christina Wenko states that visiting with the engineering firm there was a

concern for the private entry for an adjoining land owner. She states there were concerns

of the notice and due process to adjacent landowner as the plat was handed out and brought

to the meeting on the date. She states the given easement would burden the adjacent land

owner. She states this new plat was assessing an easement against this property without

compensation, acknowledgement and others. The city is concerned about the easement on

the second plat that was presented.

Andrew Shrank whom represents Acres Subdivision questions who has authority in the

ETZ. He states the plat owners had submitted a plat with changes to the right away

connection. They had also added a non-access line on the revised plat. He states the main

reason for the non-access line as the county does not maintain the road. He states Venture

is going to pay 100% for the road. The adjourning neighbor does not participate in the

cost. Mr. Shrank states the adjoining neighbor was at the meeting and did not have any

concerns. Mr. Shrank feels the acres subdivision is going to create an HOA to remove the

snow. There is no restriction on that he gets free maintenance and access. Venture does

not feel this would be fair to them if this would occur to build a road with no participation

from the neighbor.

Aaron Grinsteinner states the adjourning neighbor does not currently have access today

and Venture does not feel it is fair for him to use the road without cost. We are trying to

take away a right that we are giving him. Mr. Grinsteinner does not feel they are infringing

upon his right.

Andrew Shrank has reached out to the landowner and he has agreed to a 1’access and not

has not heard anything back from the landowner. He states that the landowner does not

intent to develop his land. He states it is a substantial investment for this developer. Mr.

Shrank states it was discussed at the planning and zoning meeting with a recommendation

of approval with a non-access line. Staff was recommending approval at that time. It was

the understanding with a non-access line.

City Attorney Christina Wenko states the commission could rescind their motion. She

states her concern is while it was discussed she is not sure that the information in the packet

was correct. She is not sure if commissioners understand exactly what is taking place. She

states what was asked of the city is to create an easement that does affect the property

owner and the property. She feels there are better options such as compensation. She states

there is not enough due process of what is happening. Ms. Wenko states there is still

concern that potentially would be able to vacate and have planning and zoning all of them

understanding.

Commissioner Jason Fridrich questions why this did not come up at planning and zoning

meeting and why no one has brought it up that this could put the city in jeopardy.

City Attorney Christina Wenko states the information was not thoroughly vetted as it was

handed out that morning. This causes concern to have a non-access easement and to place

that conversation in an a very open context could be very difficult to understand. Ms.

Wenko states that Mr. Shrank understood where the city was coming from. The city is not

going to pick winners and losers and a fair decision needs to be made with everyone in full

understanding of what is being requested. This might be the best option for December.

She states city staff is open to discussing the issue with Venture Homes. She states this

issue needs to be resolved prior to moving forward. She states the situation for

conversation with due process and having a conversation and discussion with the adjacent

landowner needs to occur. There needs to be an agreement.

Andrew Shrank suggests a development agreement. He also suggestions platting 79’ and

leave one tract of land and Venture will own it until the adjoining land owner purchases

that from HOA for an x amount of dollars. If this helps alleviate these concerns or speeds

up the process. He states the non-conforming lot questionable. He states Venture will

have a 1’ private property owned by Venture commercial until they have a due payment

process for that property. Mr. Shrank will work with the city.

City Attorney Christina Wenko states the agreement would have to go to the county first

and then come to the city. Ms. Wenko states this issue will need to be ironed out by the

county also. The best situation right now is to decide whether you want to rescind the

motion and go back to P&Z or what has been approved can move forward and work with

staff.

Commissioner John Odermann does not see why it would go back to P&Z. Commission

could rescind the motion this evening and approve a plat with a non-access easement this

evening.

President Scott Decker states if the commissioner is willing to take on a non-access

easement.

City Attorney Christina Wenko states this could be rescinded to table the item. Ms. Wenko

is all about due process and notes the adjoining land owner needs to fully understand what

this plat does to his property. A certified letter needs to be sent to the land owner.

No action has been taken on this issue.

8. BUILDING/CODE ENFORCEMENT

A. Reports

1. Condemnation Proceedings Presentation

City Attorney Christina Wenko states Mr. Blaine Dukart will be giving an overview of

some of the concerns that the city has with property of condemnation. She states following

a formal hearing type process for each property that will come before the commission at a

later date.

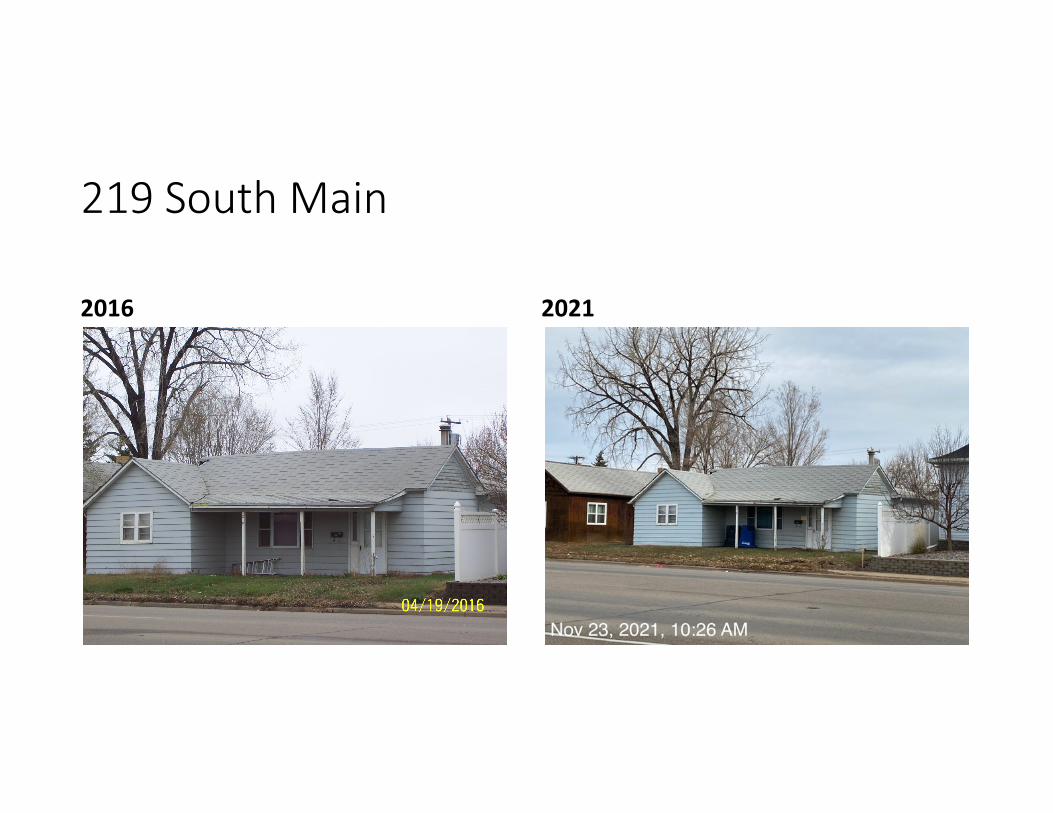

Bldg. Inspector I Blaine Dukart has brought before the commission the properties at 243

2nd Street SW, 219 South Main and 1520 West Villard. He updates the commissioners on

the conditions such as dilapidation, collapsible, deteriorated and others. He states how

poor of a condition these properties are in and states the city does not see any other possible

way to rectify these issues unless they go through the condemnation process.

City Attorney Christina Wenko states the city will schedule a time to have the

condemnation and demolishing a building and an information meeting along with a special

meeting will be scheduled and more in depth discussion can be had on these properties.

9. PUBLIC HEARING AND PUBLIC COMMENTS NOT ON AGENDA – 5:00 P.M.

A. Public Hearing – Future Fund

Deputy City Administrator Linda Carlson presents an ordinance to allow a loan from the Future Fund. She states there was clear and explicit language added to this ordinance to come into compliance with its expenditure. She states the Board of City Commissioner may loan certain funds. She has not received any comments, suggestions or changes. Commissioner John Odermann thanks Deputy City Administrator Linda Carlson for all her work on the ordinance. President Scott Decker opens the public hearing at 5:09 p.m. Hearing no public comment, the public hearing was closed at 5:11 p.m. and the following motion was made.

MOTION BY: John Odermann SECONDED BY: Suzi Sobolik

To approve first reading of Ordinance No. 1734.

ORDINANCE NO. 1734

AN ORDINANCE AMENDING AND RE-ENACTING SECTIONS 2.50.010,

2.50.020, 2.50.030 and 2.50.040 OF THE MUNICIPAL CODE OF THE CITY

OF DICKINSON, NORTH DAKOTA RELATING TO THE TRUST FUND

FOR OIL AND GAS REVENUE

DISPOSITION: Roll call vote…Aye 5, Nay 0, Absent 0 Motion declared duly passed

B. Dickinson Hockey Club Presentation

Mr. Chad Groll from the Dickinson Hockey Club presents to the City Commissioners the trend of hockey and the need for another sheet of ice. It is estimated to have 571 participants for hockey this season. He states that if Dickinson would get another sheet of ice then they would rank in the upper range as compared to western ND clubs. Mr. Groll

states hockey is the largest youth sporting activity utilized by children. He states the benefit of a third sheet of ice would be availability, affordability, social aspect and would eliminate early and late practices, year-round ice, additional ice and others. He reviewed potential locations and states the timeline is sooner than later. Commissioner Jason Fridrich asks for the Hockey Club to include the City to the interested parties when creating this third sheet of ice. C. Public Hearing – Rezone Request – Rezone Change Amendment from AG to RR

for 159.87 acres and a Preliminary plat for The Broken X Estates Subdivision. Planning Director Walter Hadley presents the rezoning request for Broken X Estates Subdivision. The Zone Change approval will allow the Broken X subdivision to move forward beyond the preliminary plat stage, to extend to 109th Avenue SW. He states there was no opposition and staff would recommend approval. President Scott Decker opens the public hearing up at 5:46 p.m. Hearing no public comments, the public hearing was closed at 5:49 p.m. and the following motion was made.

MOTION BY: Jason Fridrich SECONDED BY: Nikki Wolla

To approve first reading of Ordinance No. 1735.

ORDINANCE NO. 1735

AN ORDINANCE AMENDING THE DISTRICT ZONING MAP FOR

REZONING AND RECLASSIFYING DESIGNATED LOTS, BLOCKS OR

TRACTS OF LAND WITHIN THE CITY LIMITS, CITY OF DICKINSON,

NORTH DAKOTA.

DISPOSITION: Roll call vote…Aye 5, Nay 0, Absent 0 Motion declared duly passed

D. Public Hearing - Rezone Request - Rezone Change amendment from R1 Low

Density Residential to CC Community Commercial ,West 150’of Lots 1, 2, and 3,

Block 4, Gress’s Subdivision.

Planning Director Walter Hadley presents a zone change from R1 Single Family to CC

Community Commercial for 44,866 square foot parcel in Lots 1, 2, and 3, Block 4, Gress’s

Subdivision, along the 800 block of 8th Street SW. This request is in conformance with the

city FLUM map. No opposition was heard and staff recommends approval.

President Scott Decker opens the public hearing up at 5:50 p.m. Hearing no public comments, the public hearing was closed at 5:52 p.m. and the following motion was made.

MOTION BY: Suzi Sobolik SECONDED BY: Nikki Wolla

To approve first reading of Ordinance No. 1736.

ORDINANCE NO. 1736

AN ORDINANCE AMENDING THE DISTRICT ZONING MAP FOR

REZONING AND RECLASSIFYING DESIGNATED LOTS, BLOCKS OR

TRACTS OF LAND WITHIN THE CITY LIMITS, CITY OF DICKINSON,

NORTH DAKOTA.

DISPOSITION: Roll call vote…Aye 5, Nay 0, Absent 0 Motion declared duly passed

E. PUBLIC HEARING - LEGAL DESCRIPTION FOR PLAT VACATION AND

DE-ANNEXATION FOR NW ¼ SECTION 31 T140N R96W, STARK COUNTY,

NORTH DAKOTA.

Planning Director Walter Hadley presents an exclusion for Frenzel along which is a de-annexation for a final plat for Pinecrest. The city has received no opposition.

President Scott Decker opens the public hearing up at 5:54 p.m. Hearing no public comments, the public hearing was closed at 5:55 p.m. and the following motion was made.

For plat vacation in NW ¼ Section 31 T140N R96W, Stark County, North Dakota, MOTION BY: Jason Fridrich SECONDED BY: Nikki Wolla

To approve first reading of Ordinance No. 1737.

ORDINANCE NO. 1737

AN ORDINANCE VACATING A FINAL PLAT ENTITLED

STARK COUNTY, NORTH DAKOTA

DISPOSITION: Roll call vote…Aye 5, Nay 0, Absent 0 Motion declared duly passed

For de-annexation for NW ¼ Section 31 T140N R96W, Stark County, North

Dakota,

MOTION BY: Jason Fridrich SECONDED BY: Nikki Wolla

To approve first reading of Ordinance No. 1738

ORDINANCE NO. 1738

AN ORDINANCE REDUCING THE BOUNDARIES OF THE CITY OF

DICKINSON, NORTH DAKOTA, AND EXCLUDING A CERTAIN TRACT

OF LAND CURRENTLY IN CITY LIMITS

DISPOSITION: Roll call vote…Aye 5, Nay 0, Absent 0 Motion declared duly passed

F. LEGAL DESCRIPTION FOR PLAT VACATION AND DE-ANNEXATION

FOR SW ¼ SECTION 30 T140N R96W, STARK COUNTY, NORTH DAKOTA.

Planning Director Walter Hadley presents a plat vacation for the Westwood Circle Street

right of way, Lots 1, 2, 3 and 4 of Block 1 in Pinecrest (Subdivision). This is retaining the 50-foot road right of way north of the south line of said Section 31 along 21st street, for the county and for public use. There have been no public comments and staff recommends approval.

President Scott Decker opens the public hearing up at 6:00 p.m. Hearing no public comments, the public hearing was closed at 6:01 p.m. and the following motion was made.

For plat vacation in SW ¼ Section 30 T140N R96W, Stark County, North Dakota, MOTION BY: Nikki Wolla SECONDED BY: Jason Fridrich

To approve first reading of Ordinance No. 1739.

ORDINANCE NO. 1739

AN ORDINANCE VACATING A FINAL PLAT ENTITLED

STARK COUNTY, NORTH DAKOTA

DISPOSITION: Roll call vote…Aye 5, Nay 0, Absent 0 Motion declared duly passed

For de-annexation for SW ¼ Section 30 T140N R96W, Stark County, North

Dakota, MOTION BY: Suzi Sobolik SECONDED BY: Jason Fridrich

To approve first reading of Ordinance No. 1740

ORDINANCE NO. 1740

AN ORDINANCE REDUCING THE BOUNDARIES OF THE CITY OF

DICKINSON, NORTH DAKOTA, AND EXCLUDING A CERTAIN TRACT

OF LAND CURRENTLY IN CITY LIMITS

DISPOSITION: Roll call vote…Aye 5, Nay 0, Absent 0 Motion declared duly passed

G. LEGAL DESCRIPTION FOR DE-ANNEXATION FOR W1/2 SECTION 25

T140N R96W, STARK COUNTY, NORTH DAKOTA.

Planning Director Walter Hadley presents a de-annexation for W1/2 Section 25 T140N R96W. The Planning Commission heard no opposition. Staff and the Planning Commission would both recommend approval of the first reading of Ordinance # 1741 as presented. He states there are six homes in this area that are currently served by the city garbage servicers. Also, public works does some plowing in this area. Planning Director Hadley states the county is well aware of this transition.

City Administrator Brian Winningham states the city will notify these customers that they will need to move their collections from city to county. The City will also notify the county that they will no longer be doing snow removal in this area. Administrator Winningham states the city will give them a 60-day notice.

President Scott Decker opens the public hearing up at 6:06 p.m. Hearing no public comments, the public hearing was closed at 6:07 p.m. and the following motion was made.

For de-annexation for W1/2 Section 25 T140N R96W, Stark County, North

Dakota.

MOTION BY: Jason Fridrich SECONDED BY: Nikki Wolla

To approve first reading of Ordinance No. 1741

ORDINANCE NO. 1741

AN ORDINANCE REDUCING THE BOUNDARIES OF THE CITY OF

DICKINSON, NORTH DAKOTA, AND EXCLUDING A CERTAIN TRACT

OF LAND CURRENTLY IN CITY LIMITS

DISPOSITION: Roll call vote…Aye 5, Nay 0, Absent 0 Motion declared duly passed

D. Public Comments not on Agenda

Mr. Andrew Mejia whom is the President of St. Joseph’s Plaza on 7th Street West would

like to discuss the one way and would like to request that the City consider making 7th

Street West a one-way street again. He states this street is very busy and feels it would be

a benefit to the community to have a one-way street.

Public Works Director Gary Zuroff states Mr. Mejia should coordinate with City Engineer

Marshik and look at the one way again. He states once it became a two-way street the city

looked at angle parking and made it parallel.

Interim City Engineer Loretta Marshik state there was some agreement for when St.

Joseph’s Plaza had enough businesses in it then the city would look at going back to a one

lane street. She feels the plaza has reached the threshold to revert back to the one-way

street. She feels the parking on this street could be utilized. She states some stripping at

the intersection and signage could be done.

Planning Director Walter Hadley states in a special use permit stated when the hospital

achieved 50% occupancy then it was the applicant’s responsibility to put the one way back

in. He will review this SUP.

10. COMMISSION

Commissioner John Odermann feels there are a number of items that are on the agenda this

evening that could have been on the work session. He feels sadly that the staff was

misguided and short sided. He does not believe a developer needs to wait until 9:00 p.m.

to discuss an issue. Commissioner Odermann feels some items are better suited for a work

session. Commissioner Odermann feels this was unfortunate and not respectful of city

staff nor their expertise. He feels there are number of items that should be on the work

session. He feels this evening that the city wasted the publics time.

President Scott Decker states he felt bad when he didn’t introduce himself nor did he

introduce the bell ringer at the tree lighting Fire Chief Jeremy Presnell as the weather was

so cold.

ADJOURNMENT

MOTION BY: Jason Fridrich SECONDED BY: Nikki Wolla

Adjournment of the meeting 9:35 P.M.

DISPOSITION: Roll call vote… Aye 5, Nay 0, Absent 0

Motion declared duly passed.

OFFICIAL MINUTES PREPARED BY:

Rita Binstock, Assistant to City Administrator

APPROVED BY:

Brian Winningham, City Administrator

Scott Decker, President

Board of City Commissioners

Date: December 21, 2021

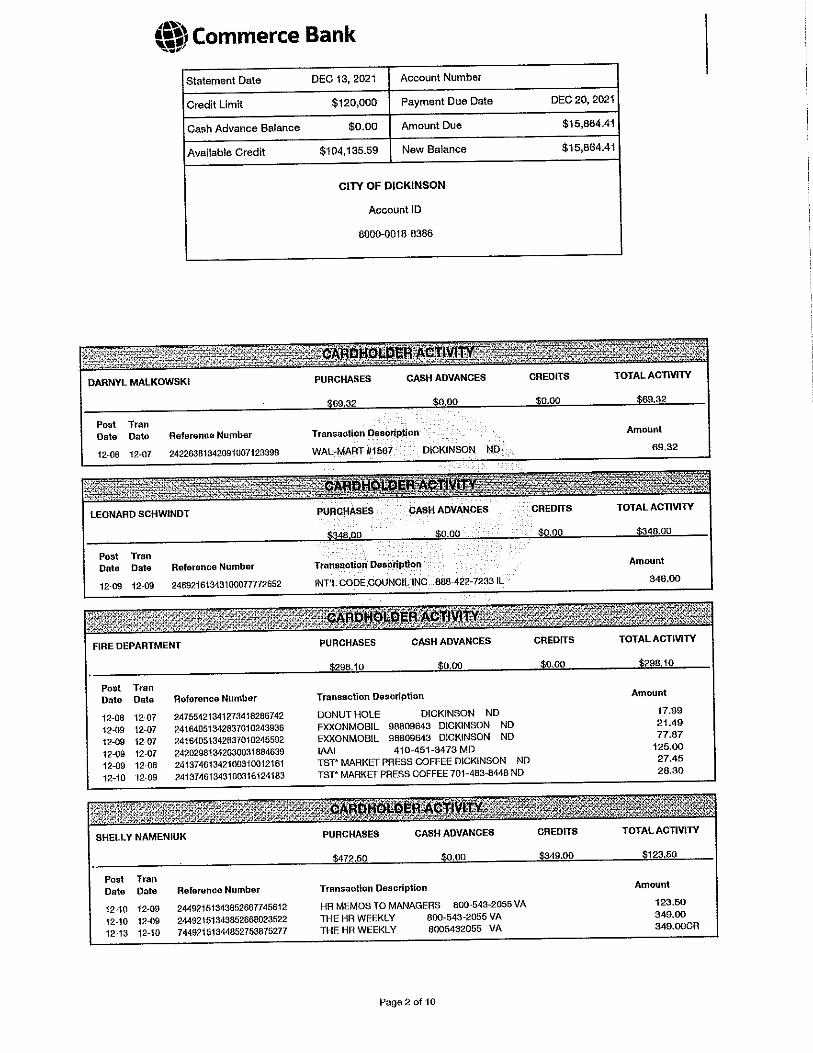

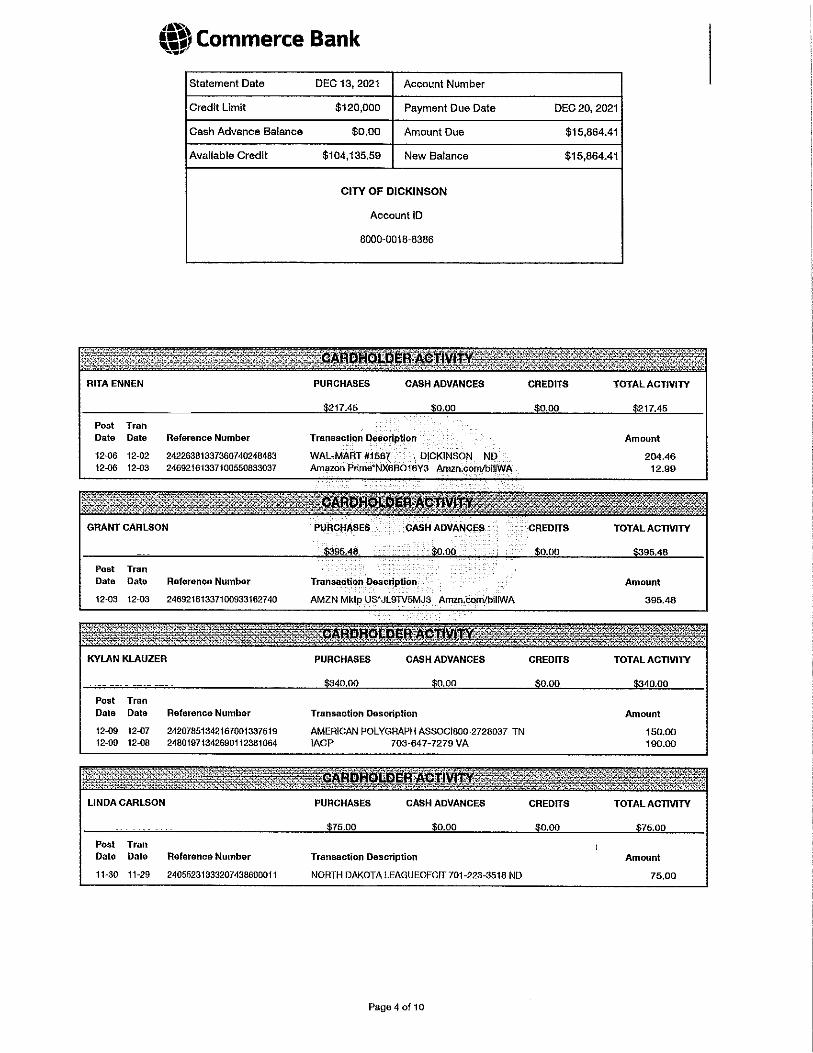

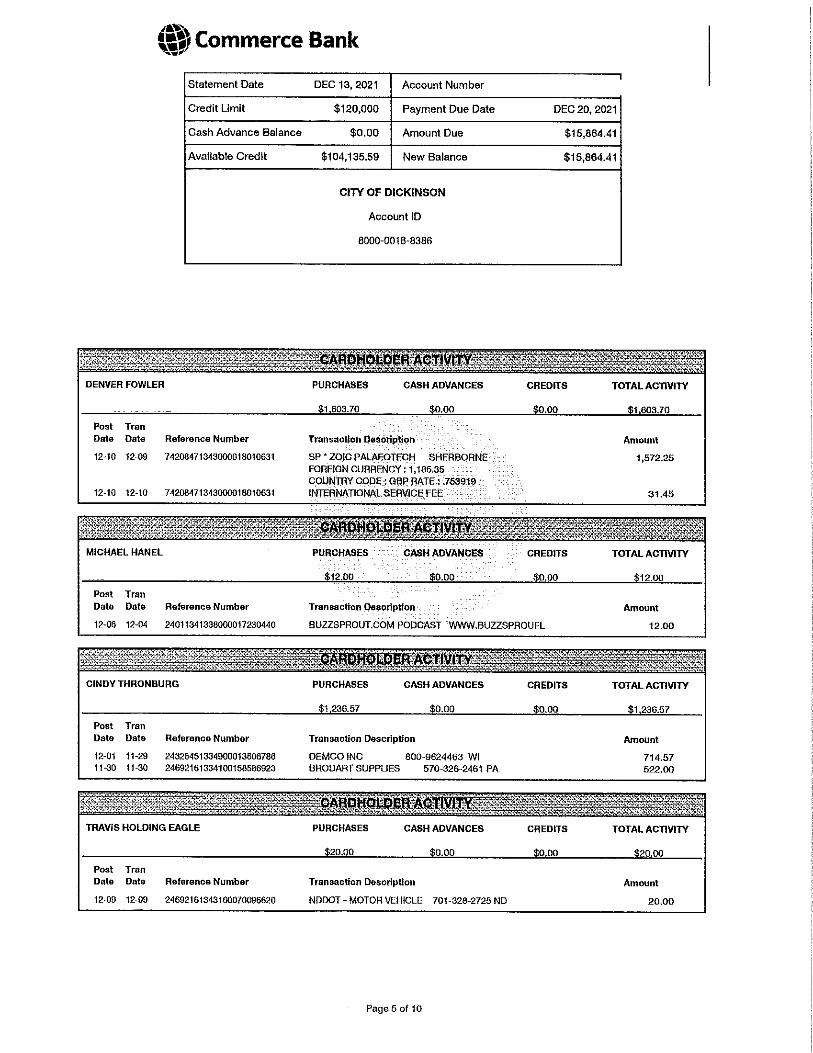

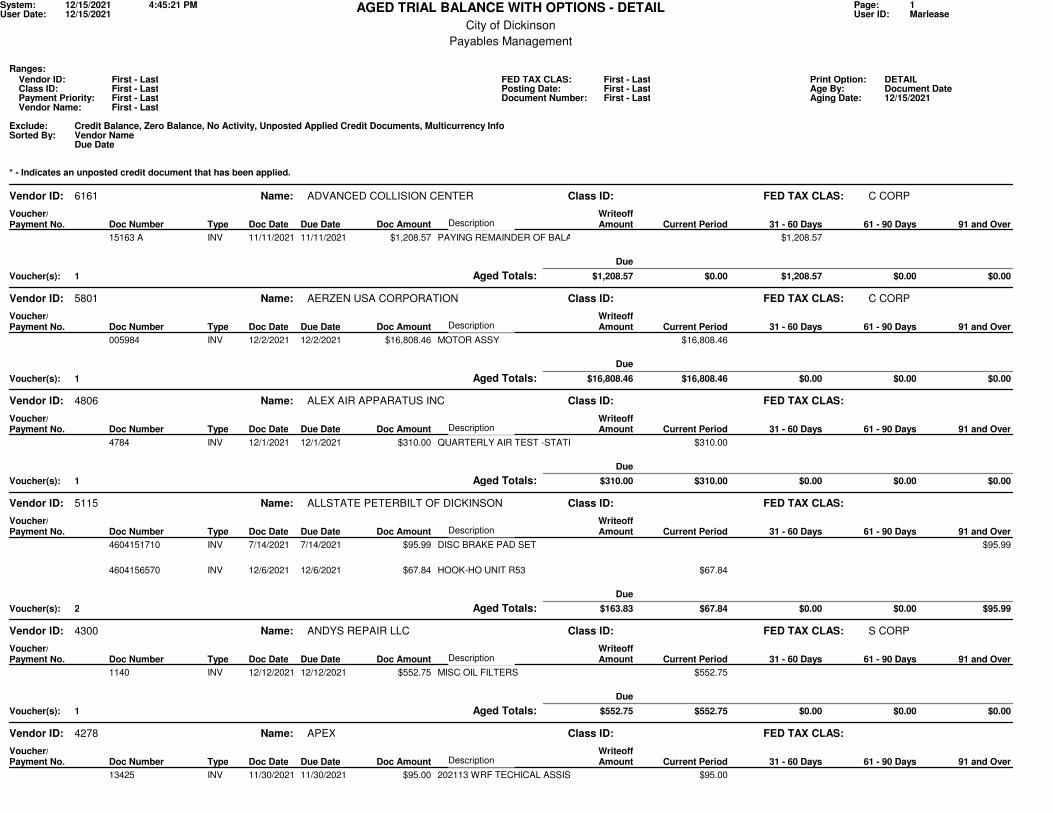

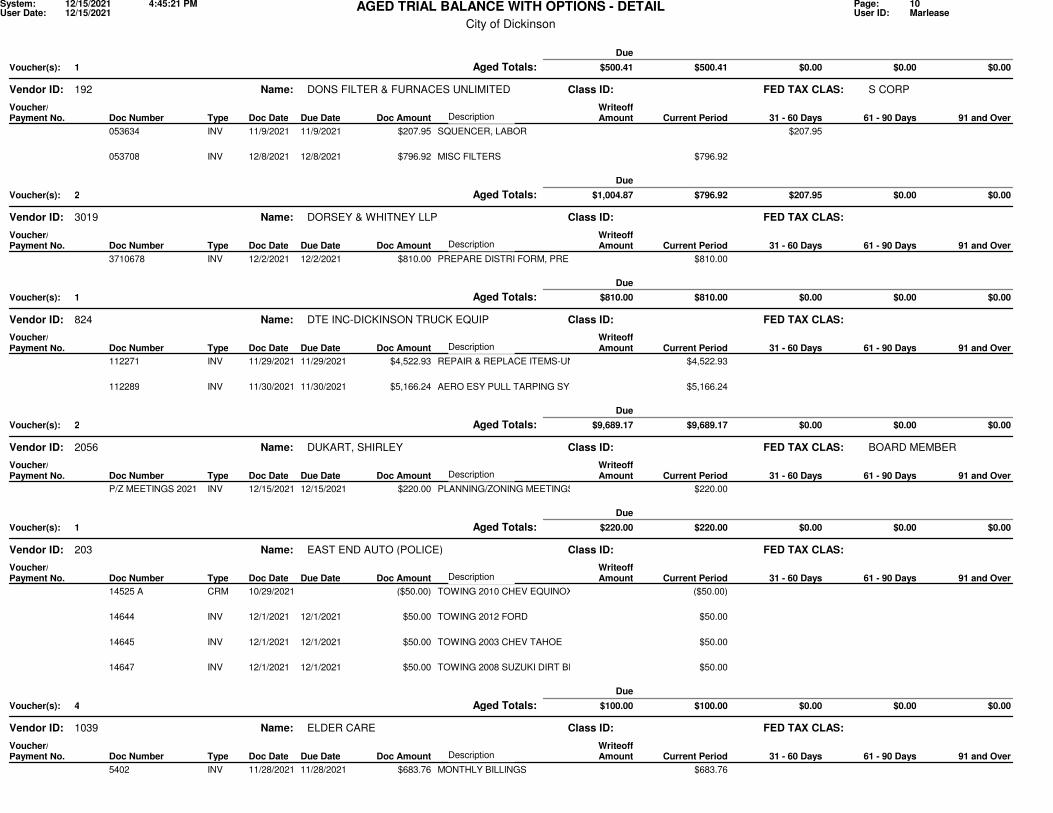

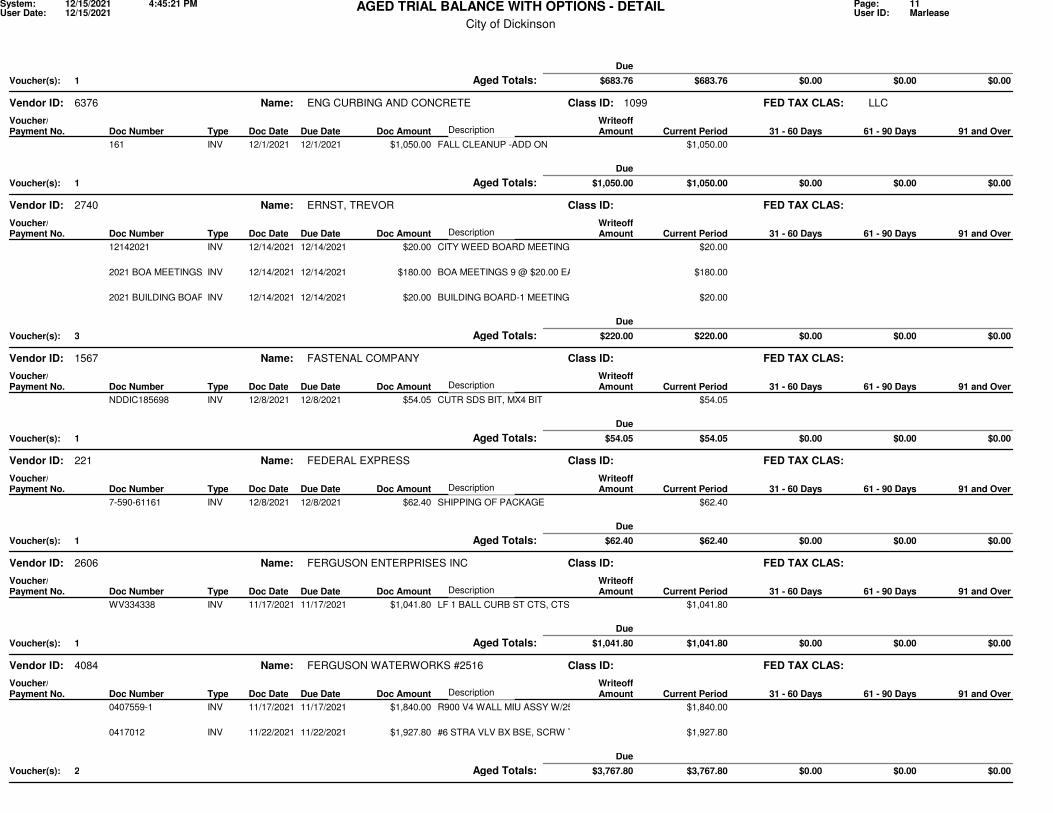

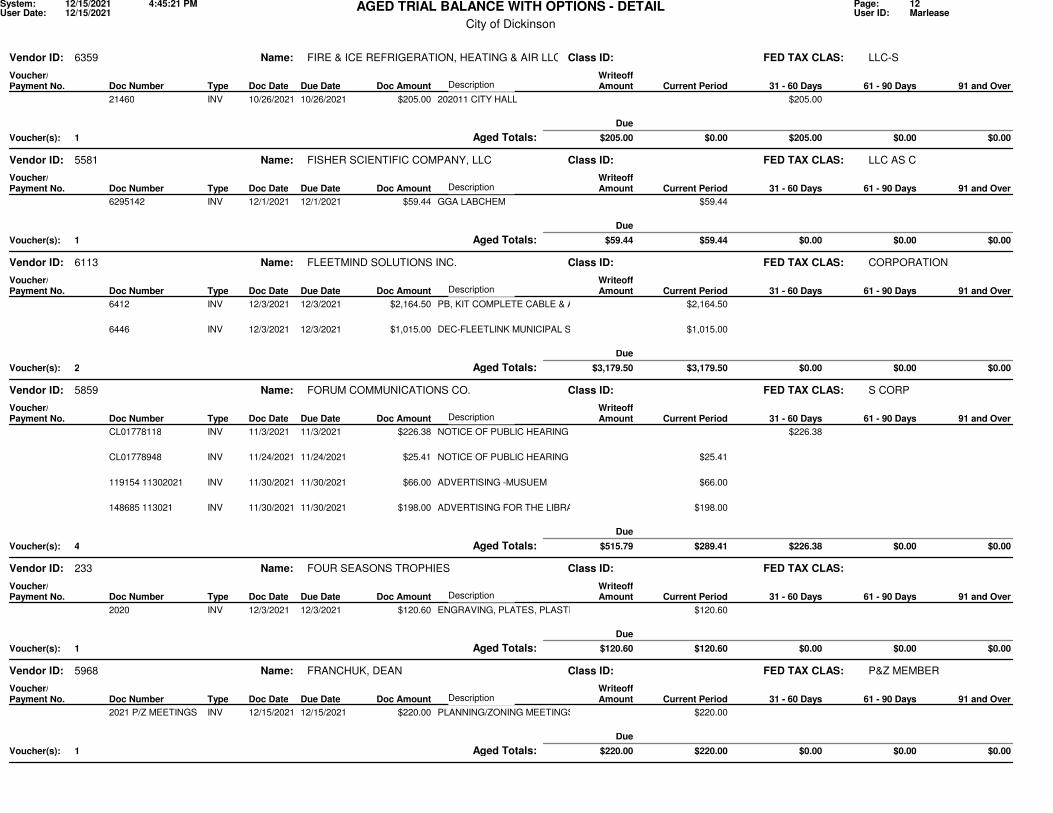

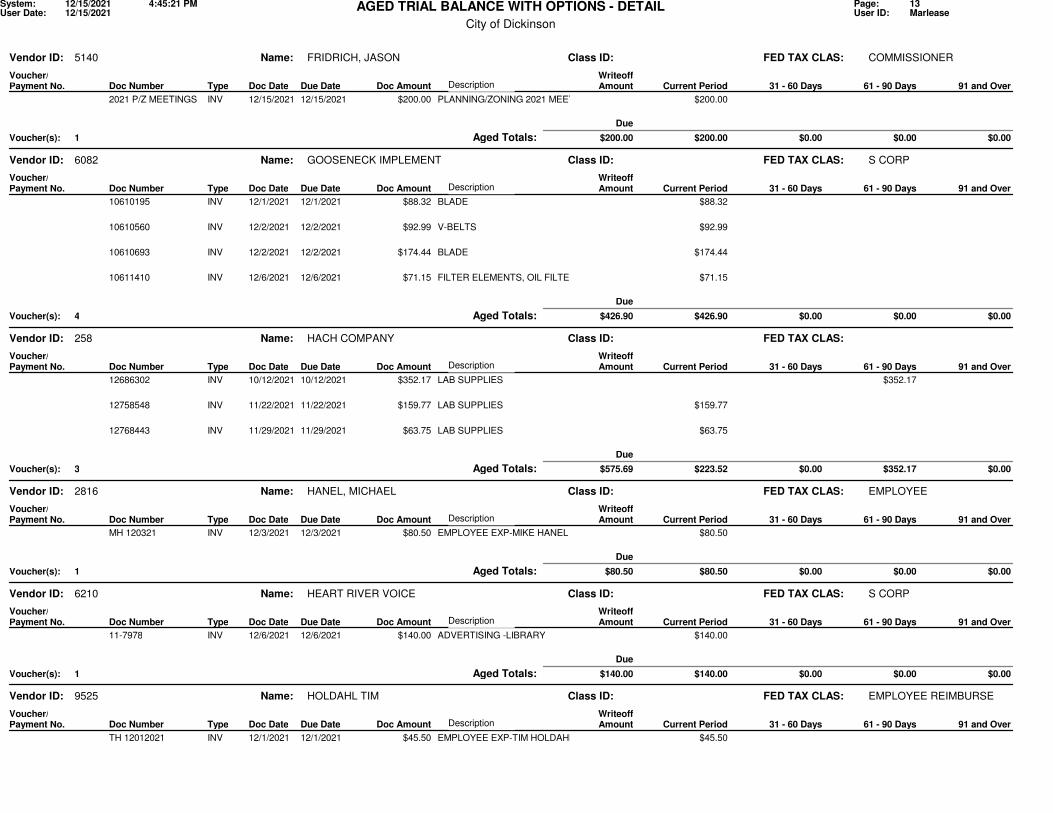

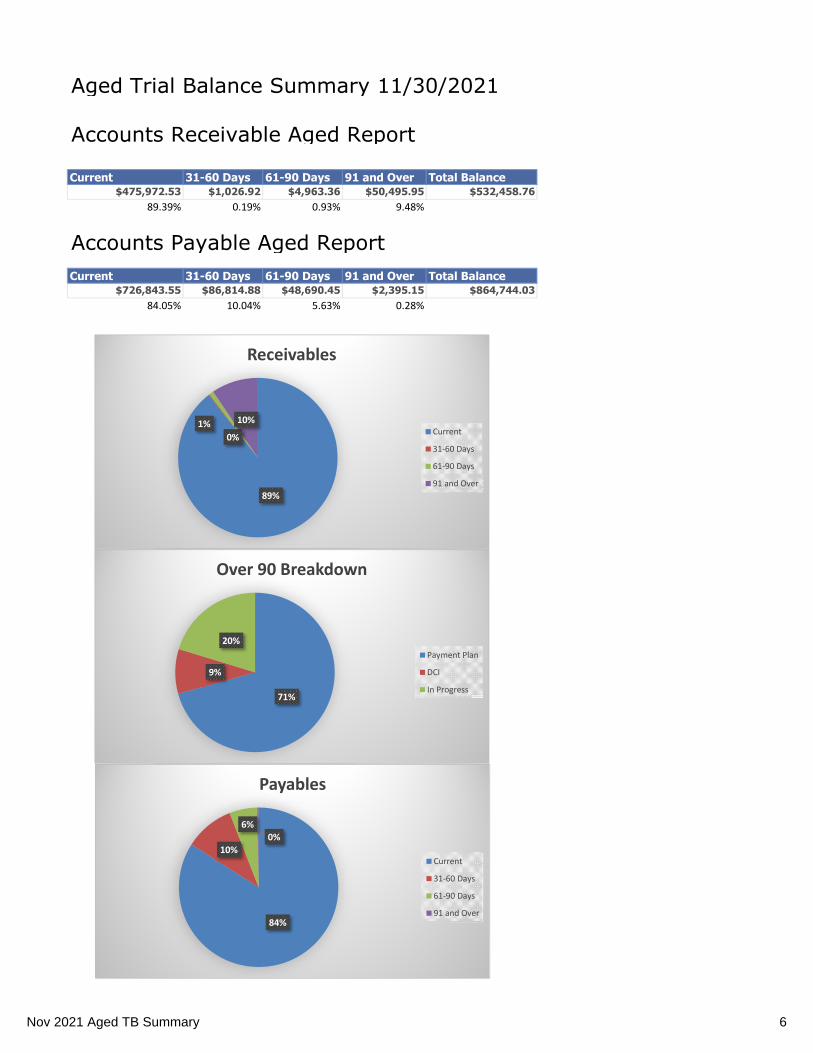

Payables Management

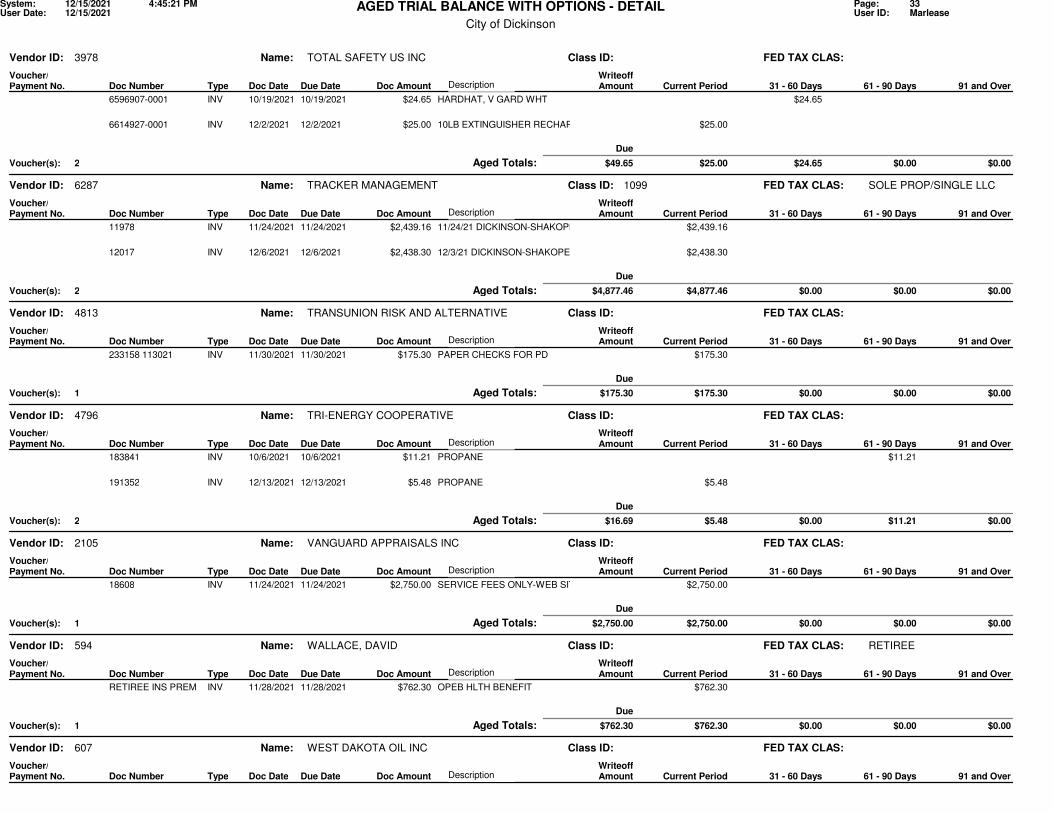

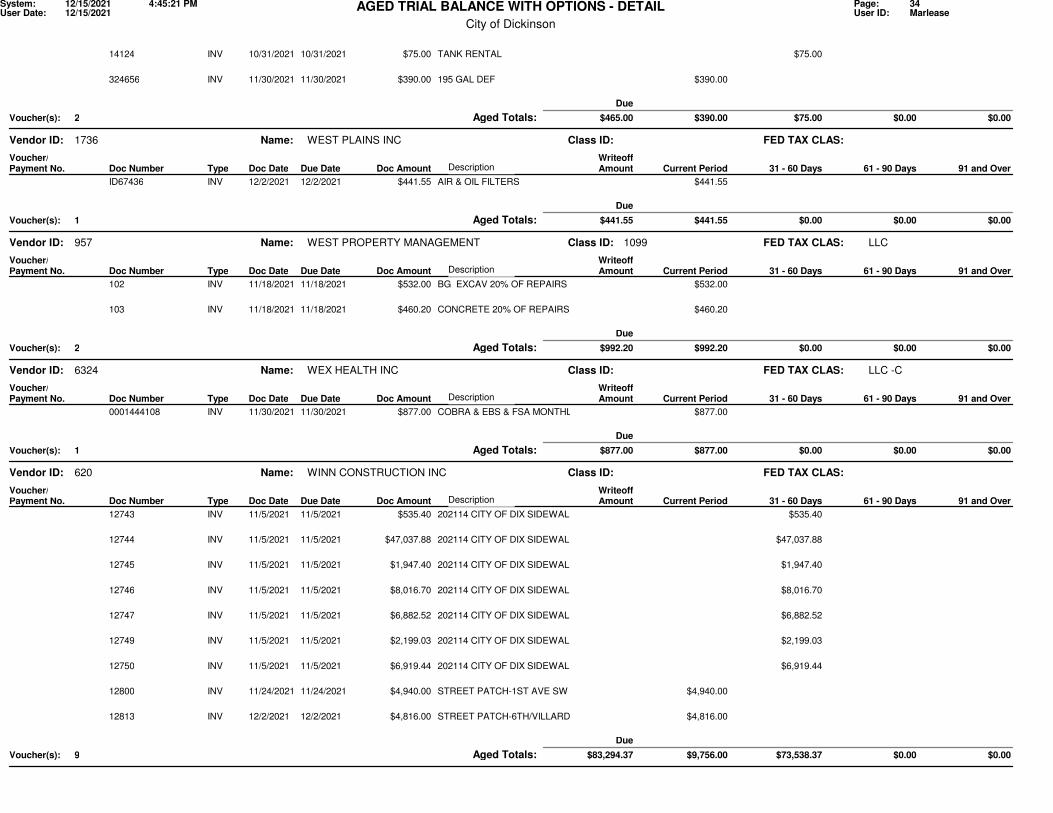

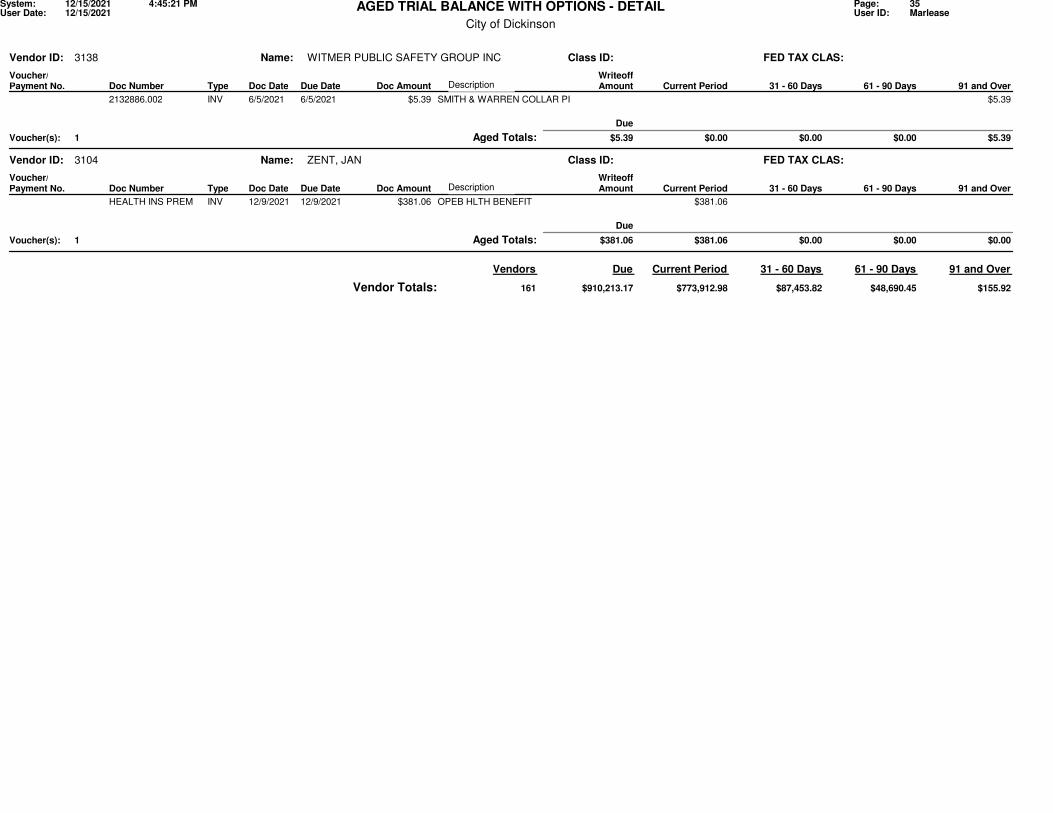

City of Dickinson

AGED TRIAL BALANCE WITH OPTIONS - DETAIL

First - Last

First - Last

First - LastFirst - Last

First - LastFirst - LastFirst - Last

Document Date

Vendor NameDue Date

Sorted By:

Aging Date:

Vendor ID:

Vendor Name:

Class ID:

Ranges:FED TAX CLAS:

Payment Priority: Document Number:Age By:

Credit Balance, Zero Balance, No Activity, Unposted Applied Credit Documents, Multicurrency Info

12/15/2021 4:45:21 PM12/15/2021

DETAILPosting Date:

Print Option:

Exclude:

12/15/2021

Page: 1User ID: Marlease

System:User Date:

* - Indicates an unposted credit document that has been applied.

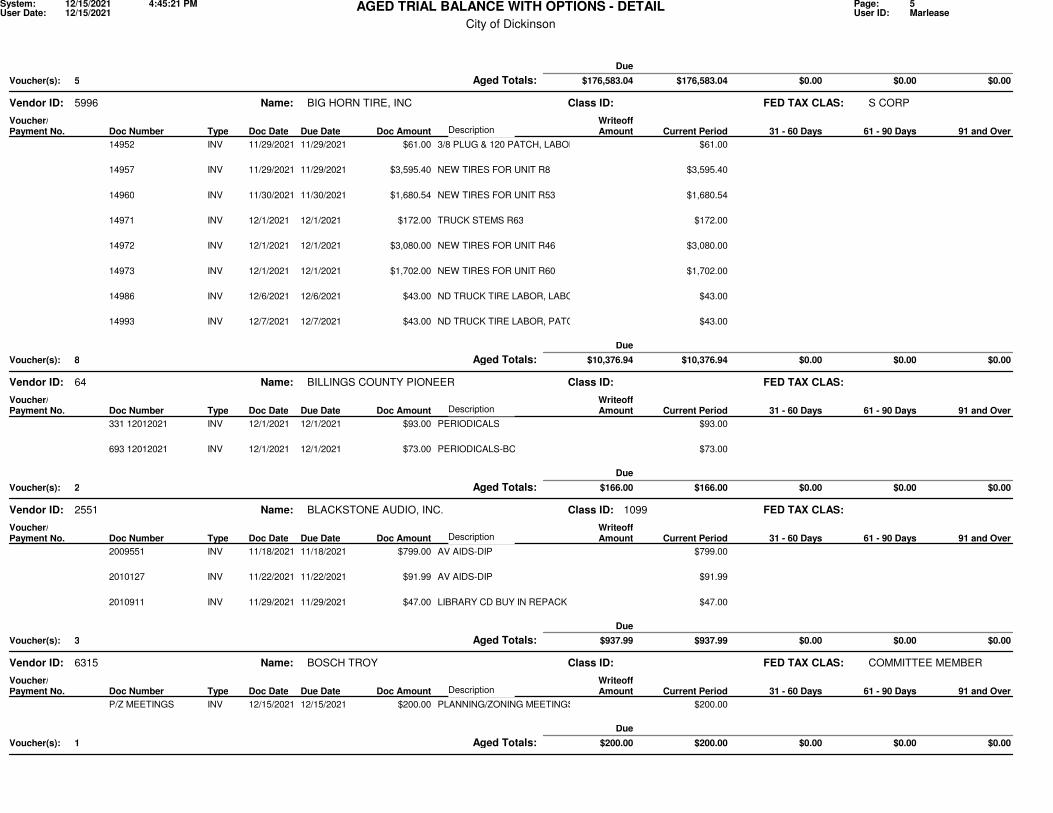

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

ADVANCED COLLISION CENTER C CORP6161 FED TAX CLAS:

Voucher/ Writeoff Description

15163 A 11/11/2021INV 11/11/2021 $1,208.57 $1,208.57 PAYING REMAINDER OF BALANCE

Aged Totals: Voucher(s):

Due

1 $1,208.57 $0.00 $1,208.57 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

AERZEN USA CORPORATION C CORP5801 FED TAX CLAS:

Voucher/ Writeoff Description

005984 12/2/2021INV 12/2/2021 $16,808.46 $16,808.46 MOTOR ASSY

Aged Totals: Voucher(s):

Due

1 $16,808.46 $16,808.46 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

ALEX AIR APPARATUS INC4806 FED TAX CLAS:

Voucher/ Writeoff Description

4784 12/1/2021INV 12/1/2021 $310.00 $310.00 QUARTERLY AIR TEST -STATIONS

Aged Totals: Voucher(s):

Due

1 $310.00 $310.00 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

ALLSTATE PETERBILT OF DICKINSON5115 FED TAX CLAS:

Voucher/ Writeoff Description

4604151710 7/14/2021INV 7/14/2021 $95.99 $95.99 DISC BRAKE PAD SET

4604156570 12/6/2021INV 12/6/2021 $67.84 $67.84 HOOK-HO UNIT R53

Aged Totals: Voucher(s):

Due

2 $163.83 $67.84 $0.00 $0.00 $95.99

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

ANDYS REPAIR LLC S CORP4300 FED TAX CLAS:

Voucher/ Writeoff Description

1140 12/12/2021INV 12/12/2021 $552.75 $552.75 MISC OIL FILTERS

Aged Totals: Voucher(s):

Due

1 $552.75 $552.75 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

APEX4278 FED TAX CLAS:

Voucher/ Writeoff Description

13425 11/30/2021INV 11/30/2021 $95.00 $95.00 202113 WRF TECHICAL ASSISTANCE

City of Dickinson

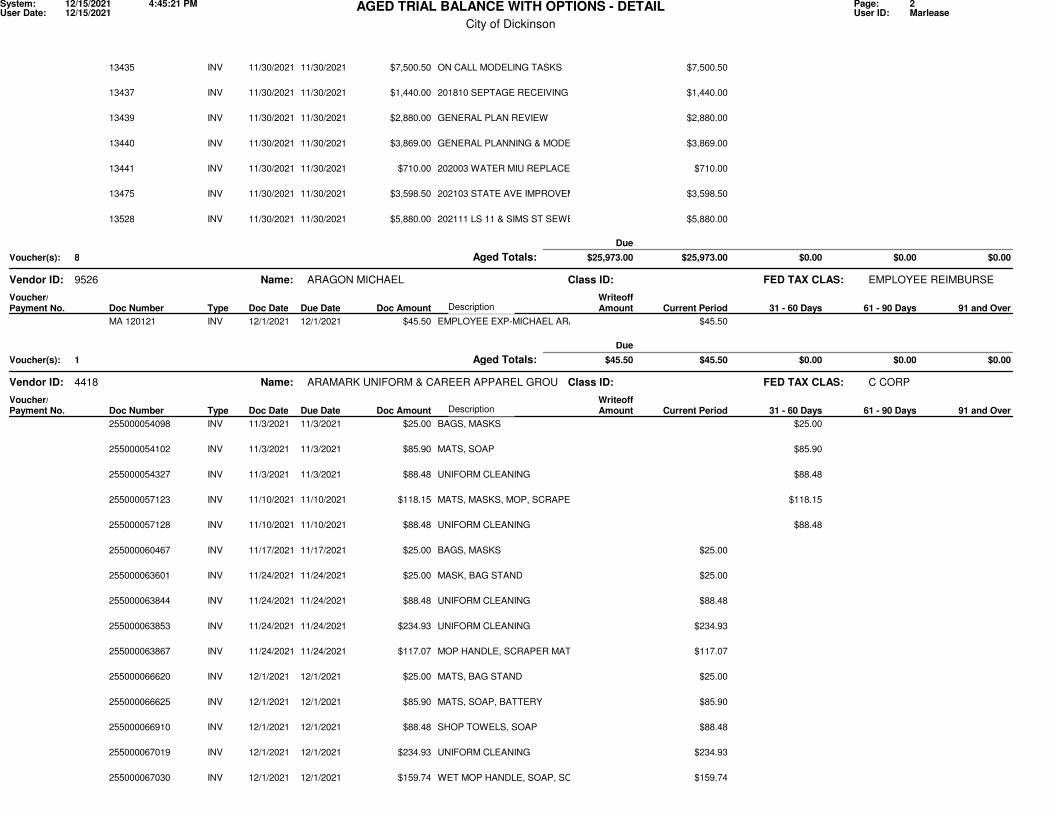

AGED TRIAL BALANCE WITH OPTIONS - DETAIL12/15/2021 4:45:21 PM Page:System: 2User Date: User ID:12/15/2021 Marlease

13435 11/30/2021INV 11/30/2021 $7,500.50 $7,500.50 ON CALL MODELING TASKS

13437 11/30/2021INV 11/30/2021 $1,440.00 $1,440.00 201810 SEPTAGE RECEIVING STATI

13439 11/30/2021INV 11/30/2021 $2,880.00 $2,880.00 GENERAL PLAN REVIEW

13440 11/30/2021INV 11/30/2021 $3,869.00 $3,869.00 GENERAL PLANNING & MODELING

13441 11/30/2021INV 11/30/2021 $710.00 $710.00 202003 WATER MIU REPLACEMENT

13475 11/30/2021INV 11/30/2021 $3,598.50 $3,598.50 202103 STATE AVE IMPROVEMENTS

13528 11/30/2021INV 11/30/2021 $5,880.00 $5,880.00 202111 LS 11 & SIMS ST SEWER

Aged Totals: Voucher(s):

Due

8 $25,973.00 $25,973.00 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

ARAGON MICHAEL EMPLOYEE REIMBURSE9526 FED TAX CLAS:

Voucher/ Writeoff Description

MA 120121 12/1/2021INV 12/1/2021 $45.50 $45.50 EMPLOYEE EXP-MICHAEL ARAGON

Aged Totals: Voucher(s):

Due

1 $45.50 $45.50 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

ARAMARK UNIFORM & CAREER APPAREL GROUP,INC

C CORP4418 FED TAX CLAS:

Voucher/ Writeoff Description

255000054098 11/3/2021INV 11/3/2021 $25.00 $25.00 BAGS, MASKS

255000054102 11/3/2021INV 11/3/2021 $85.90 $85.90 MATS, SOAP

255000054327 11/3/2021INV 11/3/2021 $88.48 $88.48 UNIFORM CLEANING

255000057123 11/10/2021INV 11/10/2021 $118.15 $118.15 MATS, MASKS, MOP, SCRAPERMAT

255000057128 11/10/2021INV 11/10/2021 $88.48 $88.48 UNIFORM CLEANING

255000060467 11/17/2021INV 11/17/2021 $25.00 $25.00 BAGS, MASKS

255000063601 11/24/2021INV 11/24/2021 $25.00 $25.00 MASK, BAG STAND

255000063844 11/24/2021INV 11/24/2021 $88.48 $88.48 UNIFORM CLEANING

255000063853 11/24/2021INV 11/24/2021 $234.93 $234.93 UNIFORM CLEANING

255000063867 11/24/2021INV 11/24/2021 $117.07 $117.07 MOP HANDLE, SCRAPER MAT,SOAP

255000066620 12/1/2021INV 12/1/2021 $25.00 $25.00 MATS, BAG STAND

255000066625 12/1/2021INV 12/1/2021 $85.90 $85.90 MATS, SOAP, BATTERY

255000066910 12/1/2021INV 12/1/2021 $88.48 $88.48 SHOP TOWELS, SOAP

255000067019 12/1/2021INV 12/1/2021 $234.93 $234.93 UNIFORM CLEANING

255000067030 12/1/2021INV 12/1/2021 $159.74 $159.74 WET MOP HANDLE, SOAP, SCRAPER

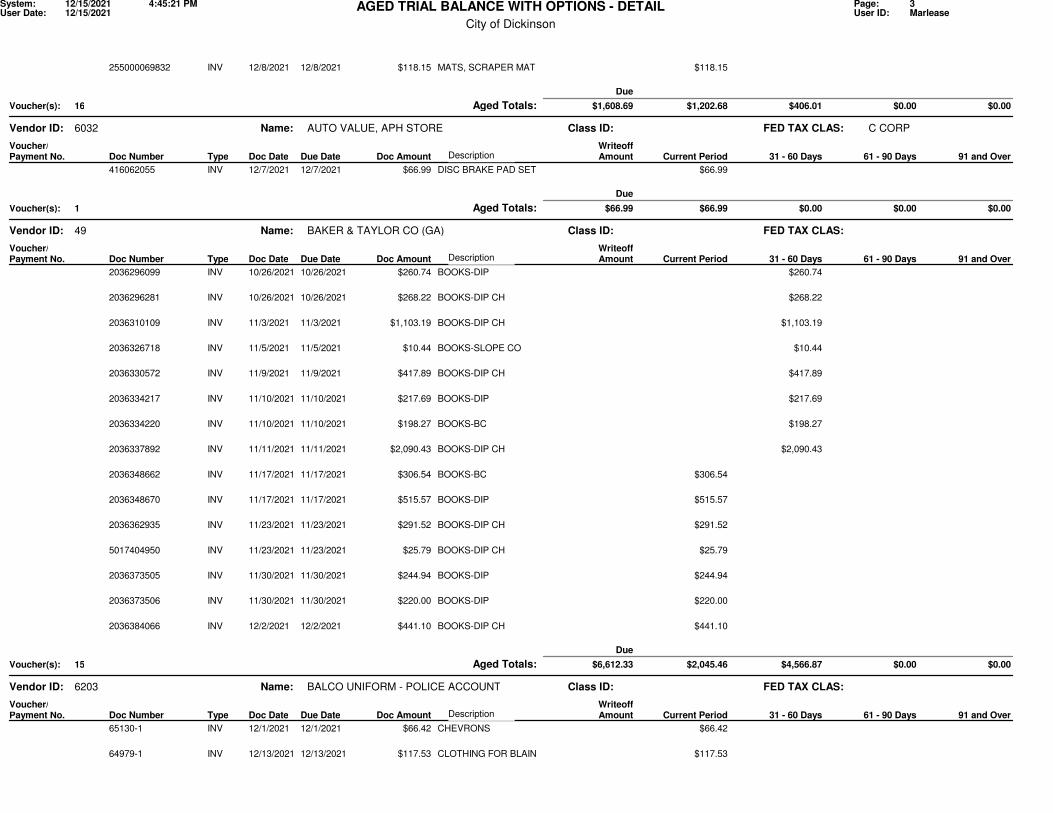

City of Dickinson

AGED TRIAL BALANCE WITH OPTIONS - DETAIL12/15/2021 4:45:21 PM Page:System: 3User Date: User ID:12/15/2021 Marlease

255000069832 12/8/2021INV 12/8/2021 $118.15 $118.15 MATS, SCRAPER MAT

Aged Totals: Voucher(s):

Due

16 $1,608.69 $1,202.68 $406.01 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

AUTO VALUE, APH STORE C CORP6032 FED TAX CLAS:

Voucher/ Writeoff Description

416062055 12/7/2021INV 12/7/2021 $66.99 $66.99 DISC BRAKE PAD SET

Aged Totals: Voucher(s):

Due

1 $66.99 $66.99 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

BAKER & TAYLOR CO (GA)49 FED TAX CLAS:

Voucher/ Writeoff Description

2036296099 10/26/2021INV 10/26/2021 $260.74 $260.74 BOOKS-DIP

2036296281 10/26/2021INV 10/26/2021 $268.22 $268.22 BOOKS-DIP CH

2036310109 11/3/2021INV 11/3/2021 $1,103.19 $1,103.19 BOOKS-DIP CH

2036326718 11/5/2021INV 11/5/2021 $10.44 $10.44 BOOKS-SLOPE CO

2036330572 11/9/2021INV 11/9/2021 $417.89 $417.89 BOOKS-DIP CH

2036334217 11/10/2021INV 11/10/2021 $217.69 $217.69 BOOKS-DIP

2036334220 11/10/2021INV 11/10/2021 $198.27 $198.27 BOOKS-BC

2036337892 11/11/2021INV 11/11/2021 $2,090.43 $2,090.43 BOOKS-DIP CH

2036348662 11/17/2021INV 11/17/2021 $306.54 $306.54 BOOKS-BC

2036348670 11/17/2021INV 11/17/2021 $515.57 $515.57 BOOKS-DIP

2036362935 11/23/2021INV 11/23/2021 $291.52 $291.52 BOOKS-DIP CH

5017404950 11/23/2021INV 11/23/2021 $25.79 $25.79 BOOKS-DIP CH

2036373505 11/30/2021INV 11/30/2021 $244.94 $244.94 BOOKS-DIP

2036373506 11/30/2021INV 11/30/2021 $220.00 $220.00 BOOKS-DIP

2036384066 12/2/2021INV 12/2/2021 $441.10 $441.10 BOOKS-DIP CH

Aged Totals: Voucher(s):

Due

15 $6,612.33 $2,045.46 $4,566.87 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

BALCO UNIFORM - POLICE ACCOUNT6203 FED TAX CLAS:

Voucher/ Writeoff Description

65130-1 12/1/2021INV 12/1/2021 $66.42 $66.42 CHEVRONS

64979-1 12/13/2021INV 12/13/2021 $117.53 $117.53 CLOTHING FOR BLAIN

City of Dickinson

AGED TRIAL BALANCE WITH OPTIONS - DETAIL12/15/2021 4:45:21 PM Page:System: 4User Date: User ID:12/15/2021 Marlease

Aged Totals: Voucher(s):

Due

2 $183.95 $183.95 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

BARES, LARRY744 FED TAX CLAS:

Voucher/ Writeoff Description

2021 BOA MEETINGS 12/14/2021INV 12/14/2021 $160.00 $160.00 BOA MEETINGS 8 @ $20.00 EACH

2021 BUILDING BOARD 12/14/2021INV 12/14/2021 $20.00 $20.00 BUILDING BOARD-1 MEETING

Aged Totals: Voucher(s):

Due

2 $180.00 $180.00 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

BARR ENGINEERING CO. C CORP6467 FED TAX CLAS:

Voucher/ Writeoff Description

34451050.01-7 12/9/2021INV 12/9/2021 $1,191.00 $1,191.00 202108 EAST BROADWAY DAM

Aged Totals: Voucher(s):

Due

1 $1,191.00 $1,191.00 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

BARROS, DEBORA EMPLOYEE54 FED TAX CLAS:

Voucher/ Writeoff Description

HEALTH INS PREMIUM 12/12/2021INV 12/12/2021 $222.01 $222.01 OPEB HLTH BENEFIT

Aged Totals: Voucher(s):

Due

1 $222.01 $222.01 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

BARROS, GREGORY EMPLOYEE/RETIREE1672 FED TAX CLAS:

Voucher/ Writeoff Description

HEALTH INS PREMIUM 12/12/2021INV 12/12/2021 $222.01 $222.01 OPEB HLTH BENEFIT

Aged Totals: Voucher(s):

Due

1 $222.01 $222.01 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

BECKER, DANA EMPLOYEE817 FED TAX CLAS:

Voucher/ Writeoff Description

HEALTH INS PREM 12/12/2021INV 12/12/2021 $159.85 $159.85 OPEB HLTH BENEFIT

Aged Totals: Voucher(s):

Due

1 $159.85 $159.85 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

BERGER ELECTRIC INC773 FED TAX CLAS:

Voucher/ Writeoff Description

202011 1 12/2/2021INV 12/2/2021 $163,620.00 $163,620.00 202011 CITY HALL

82180 12/2/2021INV 12/2/2021 $1,135.00 $1,135.00 INSTALL 5KW ELECTRIC HEATER

82244 12/8/2021INV 12/8/2021 $10,245.00 $10,245.00 WIRE CHRISTMAS STAR-RKY BUTTE

82266 12/8/2021INV 12/8/2021 $367.54 $367.54 REPR BROKEN UNDERGRD WIRE

82267 12/8/2021INV 12/8/2021 $1,215.50 $1,215.50 ADDITIONAL WORK DONE

City of Dickinson

AGED TRIAL BALANCE WITH OPTIONS - DETAIL12/15/2021 4:45:21 PM Page:System: 5User Date: User ID:12/15/2021 Marlease

Aged Totals: Voucher(s):

Due

5 $176,583.04 $176,583.04 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

BIG HORN TIRE, INC S CORP5996 FED TAX CLAS:

Voucher/ Writeoff Description

14952 11/29/2021INV 11/29/2021 $61.00 $61.00 3/8 PLUG & 120 PATCH, LABOR

14957 11/29/2021INV 11/29/2021 $3,595.40 $3,595.40 NEW TIRES FOR UNIT R8

14960 11/30/2021INV 11/30/2021 $1,680.54 $1,680.54 NEW TIRES FOR UNIT R53

14971 12/1/2021INV 12/1/2021 $172.00 $172.00 TRUCK STEMS R63

14972 12/1/2021INV 12/1/2021 $3,080.00 $3,080.00 NEW TIRES FOR UNIT R46

14973 12/1/2021INV 12/1/2021 $1,702.00 $1,702.00 NEW TIRES FOR UNIT R60

14986 12/6/2021INV 12/6/2021 $43.00 $43.00 ND TRUCK TIRE LABOR, LABOR

14993 12/7/2021INV 12/7/2021 $43.00 $43.00 ND TRUCK TIRE LABOR, PATCH

Aged Totals: Voucher(s):

Due

8 $10,376.94 $10,376.94 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

BILLINGS COUNTY PIONEER64 FED TAX CLAS:

Voucher/ Writeoff Description

331 12012021 12/1/2021INV 12/1/2021 $93.00 $93.00 PERIODICALS

693 12012021 12/1/2021INV 12/1/2021 $73.00 $73.00 PERIODICALS-BC

Aged Totals: Voucher(s):

Due

2 $166.00 $166.00 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

BLACKSTONE AUDIO, INC. 10992551 FED TAX CLAS:

Voucher/ Writeoff Description

2009551 11/18/2021INV 11/18/2021 $799.00 $799.00 AV AIDS-DIP

2010127 11/22/2021INV 11/22/2021 $91.99 $91.99 AV AIDS-DIP

2010911 11/29/2021INV 11/29/2021 $47.00 $47.00 LIBRARY CD BUY IN REPACK

Aged Totals: Voucher(s):

Due

3 $937.99 $937.99 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

BOSCH TROY COMMITTEE MEMBER6315 FED TAX CLAS:

Voucher/ Writeoff Description

P/Z MEETINGS 12/15/2021INV 12/15/2021 $200.00 $200.00 PLANNING/ZONING MEETINGS-10

Aged Totals: Voucher(s):

Due

1 $200.00 $200.00 $0.00 $0.00 $0.00

City of Dickinson

AGED TRIAL BALANCE WITH OPTIONS - DETAIL12/15/2021 4:45:21 PM Page:System: 6User Date: User ID:12/15/2021 Marlease

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

BOSS OFFICE PRODUCTS S CORP6272 FED TAX CLAS:

Voucher/ Writeoff Description

428154-1 11/29/2021INV 11/29/2021 $37.97 $37.97 BATTERY, PAPER, NOTES

430224-0 12/3/2021INV 12/3/2021 $56.97 $56.97 DESK PAD, LINER, WASTE

431235-0 12/7/2021INV 12/7/2021 $14.99 $14.99 PEN, GEL, RTR

431255-0 12/7/2021INV 12/7/2021 $129.90 $129.90 PAPER

Aged Totals: Voucher(s):

Due

4 $239.83 $239.83 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

BRAUN DISTRIBUTING4390 FED TAX CLAS:

Voucher/ Writeoff Description

33350 12/1/2021INV 12/1/2021 $6.90 $6.90 2 5 GAL SPRING WATER

33371 12/9/2021INV 12/9/2021 $18.90 $18.90 3 5 GAL SPRING WATER,RETURN

Aged Totals: Voucher(s):

Due

2 $25.80 $25.80 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

BRAVERA INSURANCE592 FED TAX CLAS:

Voucher/ Writeoff Description

13002 12/3/2021INV 12/3/2021 $41.00 $41.00 ADD JEEP, DELETE HYUNDAI

Aged Totals: Voucher(s):

Due

1 $41.00 $41.00 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

BREN, PAT2396 FED TAX CLAS:

Voucher/ Writeoff Description

12142021 12/14/2021INV 12/14/2021 $20.00 $20.00 CITY WEED BOARD MEETING-1MEET

2021 BOA MEETINGS 12/14/2021INV 12/14/2021 $200.00 $200.00 BOA MEETINGS 10 @ $20.00 EACH

2021 BUILDING BOARD 12/14/2021INV 12/14/2021 $20.00 $20.00 BUILDING BOARD-1 MEETING

Aged Totals: Voucher(s):

Due

3 $240.00 $240.00 $0.00 $0.00 $0.00

Vendor ID:

Doc Number Type Doc Amount Due Date Amount

Name:

Doc Date Current Period 91 and Over 61 - 90 Days 31 - 60 Days

Class ID:

Payment No.

BREZDEN, JEFF EMPLOYEE/RETIREE80 FED TAX CLAS:

Voucher/ Writeoff Description

HEALTH INS PREM 12/11/2021INV 12/11/2021 $399.71 $399.71 OPEB HLTH BENEFIT-50% SPOUSE