China-USA Business Review (ISSN 1537-1514) Vol.14, No.3, 2015

60

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of China-USA Business Review (ISSN 1537-1514) Vol.14, No.3, 2015

China-USA

Business Review

Volume 14, Number 3, March 2015 (Serial Number 141)

David

David Publishing Company

www.davidpublisher.com

PublishingDavid

Publication Information:

China-USA Business Review (ISSN 1537-1514) is published monthly in hard copy and online by David Publishing

Company located at 1840 Industrial Drive, Suite 160, Libertyville, IL 60048, USA.

Aims and Scope:

China-USA Business Review, a monthly professional academic journal, covers all sorts of researches on Economic

Research, Management Theory and Practice, Experts Forum, Macro or Micro Analysis, Economical Studies of Theory

and Practice, Finance and Finance Management, Strategic Management, and Human Resource Management, and other

latest findings and achievements from experts and scholars all over the world.

Editorial Board Members:

Kathleen G. Rust (USA)

Moses N. Kiggundu (Canada)

Helena Maria Baptista Alves (Portugal)

Marcello Signorelli (Italy)

Doaa Mohamed Salman (Egypt)

Amitabh Deo Kodwani (Poland)

Lorena Blasco-Arcas (Spain)

Yutaka Kurihara (Japan)

Shelly SHEN (China)

Salvatore Romanazzi (Italy)

Saeb Farhan Al Ganideh (Jordan)

GEORGE ASPRIDIS (Greece)

Agnieszka Izabela Baruk (Poland)

Goran Kutnjak (Croatia)

Elenica Pjero (Albania) Kazuhiro TAKEYASU (Japan)

Mary RÉDEI (Hungary)

Bonny TU (China)

Manuscripts and correspondence are invited for publication. You can submit your papers via Web Submission, or

E-mail to [email protected], [email protected]. Submission guidelines and Web

Submission system are available at http://www.davidpublisher.com.

Editorial Office:

1840 Industrial Drive, Suite 160, Libertyville, IL 60048, USA E-mail: [email protected]

Copyright©2015 by David Publishing Company and individual contributors. All rights reserved. David Publishing

Company holds the exclusive copyright of all the contents of this journal. In accordance with the international

convention, no part of this journal may be reproduced or transmitted by any media or publishing organs (including

various websites) without the written permission of the copyright holder. Otherwise, any conduct would be

considered as the violation of the copyright. The contents of this journal are available for any citation, however, all

the citations should be clearly indicated with the title of this journal, serial number and the name of the author.

Abstracted / Indexed in:

Database of EBSCO, Massachusetts, USA

Ulrich’s Periodicals Directory, USA

ProQuest/CSA Social Science Collection, PAIS, USA

Cabell's Directory of Publishing Opportunities, USA

Summon Serials Solutions, USA

ProQuest

Google Scholar

Chinese Database of CEPS, OCLC

ProQuest Asian Business and Reference

Index Copernicus, Poland

Qualis/Capes index, Brazil

NSD/DBH, Norway

Universe Digital Library S/B, ProQuest, Malaysia

Chinese Scientific Journals Database, China

GetCITED, Canada

CiteFactor, USA

Polish Scholarly Bibliography (PBN), Poland

SCRIBD (Digital Library), USA

PubMed, USA

Open Academic Journals Index (OAJI), Russian

Electronic Journals Library (EZB), Germany

Journals Impact Factor (JIF) (0.5)

NewJour, USA

InnoSpace, USA

Publicon Science Index, USA

Scholarsteer, USA

Turkish Education Index, Turkey

Universal Impact factor, USA

BASE, Germany

WorldCat, USA

Subscription Information:

Print $640 Online $480 Print and Online $800

David Publishing Company, 1840 Industrial Drive, Suite 160, Libertyville, IL 60048, USA

Tel: +1-323-984-7526, 323-410-1082 Fax: +1-323-984-7374, 323-908-0457

E-mail: [email protected] Digital Cooperative Company: www.bookan.com.cn

David Publishing Company

www.davidpublisher.com

DAVID PUBLISHING

D

China-USA Business Review

Volume 14, Number 3, March 2015 (Serial Number 141)

Contents

Economics

Concept of Transaction Costs and Its Influence on the Development of Offshore Outsourcing 117

Elżbieta Marcinkowska

The Level of the Financial Inclusion in the African Countries and in the World Group Regions 129

Kokou Adalessossi

Management

Policy, Legal, and Institutional Frameworks for PPP Implementation in Development Process:

Stakeholders’ Perspective 143

Teshome Tafesse

Knowledge Management Strategies in Public Sector—Case Study 159

Salwa Alhamoudi

China-USA Business Review, March 2015, Vol. 14, No. 3, 117-128

doi: 10.17265/1537-1514/2015.03.001

Concept of Transaction Costs and Its Influence on the

Development of Offshore Outsourcing

Elżbieta Marcinkowska

AGH University of Science and Technology, Krakow, Poland

The theory of transaction costs is one of the major and most important trends of new institutional economics. It is

concerned with selecting the most effective method of regulating transactions. The analysis of transaction costs

requires a new look at the concept of hierarchy and market in a company. Whether companies pursue actions inside

a company or whether they transfer them to a specialised supplier is determined by a comparison of both solutions,

including comparison of their transaction costs. Companies implement solutions which are characterised by lower

transaction costs. The article presents the concept of transaction costs and its impact on the development of

outsourcing, in particular, one of its varieties, offshore outsourcing.

Keywords: outsourcing, offshore outsourcing, transaction costs, effectiveness, Poland

Introduction

The transaction costs reflect expenditures incurred in order to reduce uncertainty, namely costs of

searching, gathering, and processing information, as well as costs related to selecting a supplier, drawing up a

contract, and coordinating the course of its implementation. These costs accompany every transaction

concluded in the modern economy. Until recently, transaction costs of actions implemented in internal

structures of a company were lower than those related to implementation of activities by the market. This

situation has completely changed in the last two decades. New conditions of operations of companies related to

the process of globalisation and rapid technological development lead to modern business models being shaped.

Outsourcing is such a phenomenon in the contemporary management of a company. For many years, this

concept has been establishing its position in theory and practice of management. Outsourcing still evolves by

offering new solutions in terms of operations of an organisation. As far as the transfer of tasks outside the

company is concerned, they are transferred to outsourcing companies operating on the domestic market

(outsourcing) and those available abroad (offshoring). Why do companies transfer certain areas of their

previous activity outside so willingly? This is a result of changes in transaction costs. The suppliers of

outsourcing services perform these actions cheaper than companies on their own.

The purpose of this article is an attempt to outline the influence of transaction costs on the development of

offshore outsourcing. The article presents the method of determining the effectiveness of offshore outsourcing

and the problem of measuring transaction costs. At the end of the article, the development of offshore

Elżbieta Marcinkowska, Ph.D., assistant professor of management, Department of Economics, Finance and Environmental

Management, Faculty of Management, AGH University of Science and Technology, Krakow, Poland.

Correspondence concerning this article should be addressed to Elżbieta Marcinkowska, AGH Faculty of Management,

Gramatyka 10, 30-067 Krakow, Poland. E-mail: [email protected].

DAVID PUBLISHING

D

INFLUENCE ON THE DEVELOPMENT OF OFFSHORE OUTSOURCING

118

outsourcing in Poland, which became an important place for offshore investments, is presented.

Offshore Outsourcing—Definitional Approach

The concept of outsourcing consists in sectioning selected functions (tasks) beyond a company and

transferring them for implementation to specialised outsourcing companies. The definition of outsourcing is

broad and ambiguous in world literature. The author presenting the idea of outsourcing highlights its various

aspects. Lei and Hitt (1995) defined outsourcing as transferring production to external suppliers. Perry (1997)

emphasised the role of employment in the concept of outsourcing. Tasks which used to be performed by the

employees of a company are transferred to be performed by the employees of an external company. Sharpe

(1997) stressed the definition of outsourcing that functions which are not basic competences of a company are

subject to sectioning. Gilley and Rasheed (2000) defined outsourcing as something that was originally

delivered internally or could have been delivered internally, but the decision to order it on the outside has been

made. A broader definition of outsourcing was provided by Lysons and Gillinham (2003), who specified this

concept as the strategic use of resources to perform activities traditionally handled by internal staff and their

resources. This is a managerial strategy consisting in separating certain support functions from the

organisational structure and entrusting specialised external organisations with implementing them. This is

providing a third party with permanent managerial liability for performing a service specified in the contract.

Offshoring is a concept in company management which has become more and more significant in recent

years. Business entities decide to transfer production activities abroad in order to achieve specific corporate

goals. Subject literature often fails to distinguish between offshoring and outsourcing and uses the two concepts

interchangeably. This is an incorrect approach. Outsourcing is a practice of separating by companies’ certain

activities from their own organizational structure and transferring them to outside entities, to other business

partners based in the same country. Offshoring leads to a separation of selected services and transferring them

for implementation to companies based in a different country.

Offshoring is defined as a process as a result of that services are executed on the territory of another

country. This process may be provided by the company internally (captive offshoring) or by a foreign business

partner (offshore outsourcing). This leads to the differentiation of two basic types of offshoring:

Captive offshoring is a process as a result of which the company forms a branch abroad or an equity

related company. This allows the company to retain complete control over the transferred production or service

processes;

Offshore outsourcing is a process consisting of transferring selected production or service activities to an

external company, non-equity related, conducting business activities in another country.

Another classification of offshoring is based on the criterion of location of the offshoring company. The

following forms of offshoring should be then distinguished: offshore, nearshoring, and farshoring. Nearshoring

is defined as cooperation among entities in markets which are geographically and culturally close. Offshore is

the cooperation among entities in markets which are remote in geographical terms, but close in cultural and

economic ones. Farshoring is a market which is geographically, culturally, and economically remote.

As it has been already mentioned, offshoring is a concept in business management successfully

implemented all around the world. Companies adopting offshoring seek mainly the following benefits:

the possibility opportunity to focus on primary activities;

improvement in the quality of provided services, resulting from the work of highly-qualified employees;

INFLUENCE ON THE DEVELOPMENT OF OFFSHORE OUTSOURCING

119

improvement in competitiveness or gaining a competitive advantage;

introduction of innovative solutions;

greater customer satisfaction (Marcinkowska, 2013).

The development of offshoring commenced successfully many years ago, when international companies

transferred their production services abroad. Various industry branches, in particular, the clothing industry (e.g.,

Puma and Nike) and the automotive industry (e.g., Porsche and Daimler—Chrysler), transferred their

production to the Far East as well as to Central and Eastern Europe. The next widely used offshoring service

was the IT service. The share of service offshoring has been growing for several years. Typical business

functions became of a dominant significance in offshoring services. Offshoring companies began to create

service centers on a global scale in order to efficiently and effectively handle their customers. Offshoring

entities operating in the international market include:

shared service centers (SSC);

business process outsourcing (BPO);

information technology outsourcing (ITO);

research & development (R&D);

call centers (CC).

Such a wide service offer on the international level requires offshoring entities to employ workers with

varied competencies and qualifications. Some offshoring services are typical of a repeated nature and do not

require specialized knowledge. However, highly-specialized services based on knowledge (knowledge process

offshoring—KPO) are becoming more and more significant in offshoring activities. The implementation of

these services requires employees to have high qualifications, experience, and knowledge.

Theoretical Perspective of Transaction Costs

The problem of transaction costs in business management was introduced by a Nobel Prize winner, Coase

(1937), in his article The Nature of Firm. Coase (1937) raised a question about the purposefulness of the

existence of companies. He began his discussion on this topic with a definition of market system. The market

system is the coordination of business activity through a system of prices. The fact that market coordination

requires sustaining costs is of fundamental significance. Coase (1937) distinguished the costs of the operation

of the market mechanism and the costs of organizing transactions inside the company. Each transaction

concluded in economy is accompanied by transaction costs. The author was of the opinion that as long as the

costs of organizing transactions within companies were lower than the costs of purchasing this service on the

market or contracting it to another company, companies would increase their size, expanding their

organizational structure. Coase (1937) stated that companies were established in order to decrease the costs of

transactions, and thus he assumed that the internal implementation of actions was cheaper than their

implementation by the market, which was confirmed by the economic practice of that time. For a few decades,

the companies expanded their structure, creating new departments, units, and etc.. They implemented their

functions on their own, using their own material, capital, and human potential.

Even at the beginning of the 1990s, another Nobel Prize winner, dealing with transaction costs,

Williamson believed that the implementation of actions within the company was more profitable than

contracting them outside. This resulted from the fact that transaction costs of actions implemented outside were

still higher than the savings which companies achieved by delegating them to suppliers. Subsequent decades

INFLUENCE ON THE DEVELOPMENT OF OFFSHORE OUTSOURCING

120

brought changes in transaction costs and the implementation of actions outside became more effective from the

implementation in one’s own organizational structure.

What are transaction costs? To answer this question, this paper has to introduce the notion of transaction.

Transaction is the basic unit of economic analysis. Transaction takes place when goods or services go through

technically specified limits. One sphere of activity ends and another one begins (Williamson, 1985).

Transaction does not only imply market exchange, but also includes other acts of exchange within the

organization.

The notion of contract is associated with the transaction. This is a transaction with a clearly outlined

structure, not always a formal one. Furubotn and Richter (1997, p. 53) defined a contract as a “bilateral

transaction, in which both parties agree as to their certain obligations. Apart from the parties’ agreement

concerning their relations (planning relations), the existence of legal sanctions (enforceable by law) is regarded

as a characteristic feature of the contract”. Each contract involves costs related to its handling, regardless of

whether or not it is internalized within the organization or proceeds as a market transaction. The method in

which the contract is managed is selected on the basis of the criterion of minimizing transaction costs and this

is the basic assumption of the economics of transaction costs. Therefore, it can assume that transaction costs are

the costs of the operation of the socio-economic system; they reflect the expenditures incurred as a result of all

possible types of concluded transactions.

It can express transaction costs as a function of three components: specific nature of assets, frequency, and

uncertainty (Williamson, 1998).

The specific nature of assets results, essentially from their high value, rareness, and the lack of substitutes

and idiosyncrasy. Specific assets are those which may not be easily transferred for other applications and also

cannot be easily replaced, e.g., the specific nature of tangible assets, the specific nature of human assets, the

specific nature of location, and the specific nature of the intended use of assets. If the transaction is

characterized by specific assets, the effect is the growth in the complexity of contracts concluded between

market entities and, as a result, growth in transaction costs. The second significant factor affecting the amount

of transaction costs is uncertainty, presented in two dimensions as the uncertainty of the external environment

and behavioral uncertainty. When companies conclude transactions, they are not able to take into account all

factors which may affect their course. The occurrence of new facts leads to the renegotiation of contracts and

this, in turn, leads to the growth in transaction costs. The last factor determining the level of transaction costs is

frequency, which is less frequently displayed in the literature on the subject. According to Williamson (1985,

1998), if transactions are characterized by high frequency, companies are more willing to use vertical

integration.

According to the theory of transaction costs, the basic management function is to limit costs related to the

coordination of the implementation of a given transaction, namely the selection of such a structure of managing

transactions inside the company, so that the costs of coordination are as low as possible. Transaction costs are

saved by connecting transactions of various attributes with management structures in a diverse manner.

Theoretically, this paper may distinguish two extreme methods of regulating transactions: market regulation

and administrative (hierarchical) regulation. Between the two extremes which are the market and the hierarchy,

there is a spectrum of methods for conducting transactions. The effectiveness of particular forms of regulations

depends on the previously characterized transaction attributes, namely on the specific nature of assets, the

frequency of transactions and the uncertainty.

INFLUENCE ON THE DEVELOPMENT OF OFFSHORE OUTSOURCING

121

Combining management structures with transaction attributes serves the purposes of effectiveness.

Transaction costs are saved by connecting transactions of various attributes with management structures in a

diverse manner. It is assumed that the amount of transaction costs determines the adopted solution. If these

costs are at a low level, companies decide to transfer their activities to the market, many transactions are

concluded, based on the market mechanism. When transaction costs are high, companies avoid or limit the

number of transactions on the market and execute actions in their own organizational structures. As mentioned

earlier, there are situations when transaction costs are high, regardless of whether the transactions are

conducted on the market or internally in a company. Then, companies choose to function in the so-called

hybrid forms. These are intermediate solutions between the market and the internal hierarchy (for instance the

network).

Measurement of Transaction Costs

As it has already been mentioned, a weakness of transaction cost theory is the problem with measurement

of these costs. It is difficult to determine the exact level of transaction costs. Calculations of these costs are to a

large extent based on assumptions, since a part of these costs are costs that will occur in the future (estimates).

However, this is not a premise to disregard measurement of transaction costs. If the basic reason for using

offshoring is to reduce costs of business operations, failure to measure transaction costs may result in a failure

of offshoring. Underestimation of transaction costs with assessment of offshoring effectiveness affects the

increase in risk. The risk of offshoring increases due to shortcomings in preparation of the separation process

(at every stage of preparation of the course of the process, transaction costs should be calculated). An example

of increase in the risk of offshoring is, e.g., increase in the price of services provided by foreign suppliers. At

the stage of preparation of the contract, a company should secure itself against possible unfavourable situation.

Another important element of accurate measurement of transaction costs results from the fact that most

often, these measurable transaction costs are definitely higher in the case of offshoring than in the case of

implementation inside the organizational structure of the company. An important factor will be the amount of

total transaction costs. The total value of transaction costs should affect the decision on offshoring. What is

equally important, practice proves that total transaction costs are dominated by those with variable cost nature.

If these are variable costs, then people, as managers, can affect their amount and respond to changes in variable

costs relatively quickly.

Companies that perform measurement of transaction costs do it within the information system of the

company, both in financial accounting system and in the managerial accounting system. The main tool used for

that purpose is, obviously, the cost account. Managers must have information on whether the transaction costs

are higher within the market or within the organization. A particular role, when estimating transaction costs,

can be played by the tools of management accounting, such as activity-based costing and balanced scorecard.

Caring about achieving the objectives of contracting, management structures are adjusted to transaction

conditions. These structures vary between one another in the capacity for an effective reaction to interferences.

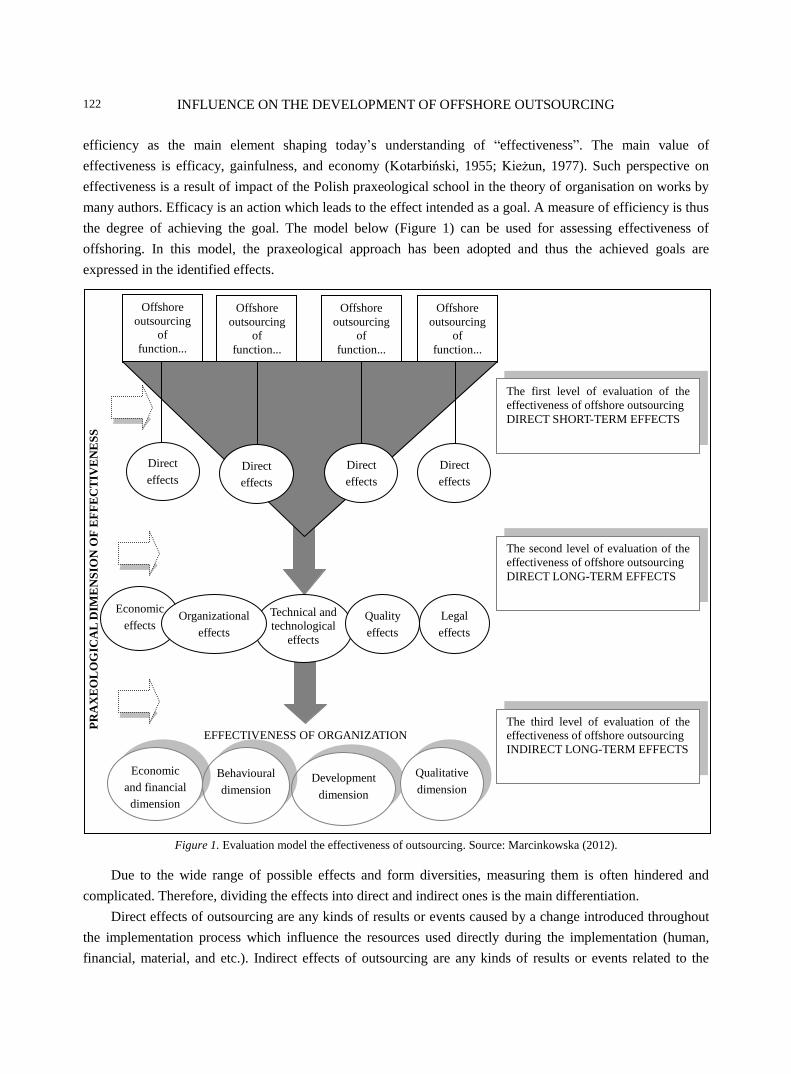

Effectiveness of Offshore Outsourcing

Effectiveness is not a clear notion. Literature often mentions terms with similar meaning, like efficacy,

productivity, profitability, or economy. An important publication, containing a comprehensive analysis of the

notion of effectiveness is the work by Holstein-Beck (1987) entitled Sketches About Work. The author presents

INFLUENCE ON THE DEVELOPMENT OF OFFSHORE OUTSOURCING

122

efficiency as the main element shaping today’s understanding of “effectiveness”. The main value of

effectiveness is efficacy, gainfulness, and economy (Kotarbiński, 1955; Kieżun, 1977). Such perspective on

effectiveness is a result of impact of the Polish praxeological school in the theory of organisation on works by

many authors. Efficacy is an action which leads to the effect intended as a goal. A measure of efficiency is thus

the degree of achieving the goal. The model below (Figure 1) can be used for assessing effectiveness of

offshoring. In this model, the praxeological approach has been adopted and thus the achieved goals are

expressed in the identified effects.

Figure 1. Evaluation model the effectiveness of outsourcing. Source: Marcinkowska (2012).

Due to the wide range of possible effects and form diversities, measuring them is often hindered and

complicated. Therefore, dividing the effects into direct and indirect ones is the main differentiation.

Direct effects of outsourcing are any kinds of results or events caused by a change introduced throughout

the implementation process which influence the resources used directly during the implementation (human,

financial, material, and etc.). Indirect effects of outsourcing are any kinds of results or events related to the

Development

dimension

Offshore

outsourcing

of

function...

Offshore

outsourcing

of

function...

Offshore

outsourcing

of

function...

Offshore

outsourcing

of

function...

The third level of evaluation of the

effectiveness of offshore outsourcing

INDIRECT LONG-TERM EFFECTS

The first level of evaluation of the

effectiveness of offshore outsourcing

DIRECT SHORT-TERM EFFECTS

The second level of evaluation of the

effectiveness of offshore outsourcing

DIRECT LONG-TERM EFFECTS

Qualitative

dimension

Behavioural

dimension

Economic

and financial

dimension

Direct

effects

Direct

effects

Direct

effects

Economic

effects

EFFECTIVENESS OF ORGANIZATION

Technical and

technological

effects

Legal

effects

Quality

effects

PR

AX

EO

LO

GIC

AL

DIM

EN

SIO

N O

F E

FF

EC

TIV

EN

ES

S

Direct

effects

Organizational

effects

INFLUENCE ON THE DEVELOPMENT OF OFFSHORE OUTSOURCING

123

implementation of outsourcing which are identified in different areas of activity of an organisation. Based on

the assumed occurrence criteria of effects, a three-stage evaluation leading to a complete analysis of the

effectiveness of outsourcing may be performed.

In Table 1 below, proposes measures assess the effectiveness of offshore outsourcing.

Table 1

Effectiveness of Offshore Outsourcing

Efficiency of

offshore

outsourcing

Effectiveness of offshore processes (services)

Direct short-term effects Direct long-term effects

Dimension Measures of assessment Dimension Measures of assessment

economic

organizational

technical and

technological

qualitative

legal

other

cost reduction

number of reduced

workplaces

number of

complaints

economic

organizational

technical and

technological

qualitative

legal

other

investment outlays

level

work effectiveness,

know-how of

employees,

number of conflicts

time of their

solution

Effectiveness of organization

Operational effectiveness Strategic effectiveness

Effects: cost reduction, growth in work efficiency,

shortening production and service cycles, increase in

profit, simplification of the organizational structure,

and etc.

Effects: new products, new markets, new

technologies, introduced innovations, focus on basic

activity, and etc.

Source: Prepared by the author.

Effects of separation and transfer for implementation under offshoring are identified in two planes: the

effectiveness of offshore operations and the organizational effectiveness of offshoring. The main differentiation

is the division into direct effects (short-term and long-term). Direct effects are any kinds of results or events

caused by the change introduced into the implementation of the functions (action/service). Indirect effects are

identified results of offshoring having impact on the whole organization. In the proposed model for assessment

of effectiveness, several dimensions of effectiveness have been adopted, such as economic, organizational,

technical and technological, qualitative, and legal dimension. Each dimension can be attributed to measures

reflecting degree of achievement of goals for which offshoring has been used. These dimensions of

effectiveness might not only be used in the assessment of the separated function itself and direct effects that it

yields, but also can be used to assess the effect of offshoring on effectiveness of the whole company. These

effects are indirect and they can be additionally divided into operational and strategic effects.

Transaction Costs and Development of Offshore Outsourcing in Poland

The theoretical assumptions of the concept of transaction costs are applied in economic practice. An

example of the application of the theory of transaction costs in economic life is outsourcing. This concept

involves a transfer of certain activities (functions) outside the company’s structure and realizing them by

specialized external companies. In the last two decades, companies all around the world and in Poland more

and more often use outsourcing. In the first phase of outsourcing popularity, companies decided to transfer

additional functions, often referred to as peripheral, in the company. These were functions which were not

complex, which did not require the involvement of specific resources for their implementation. However, with

time, apart from additional functions, companies widened the scope of separations covering also functions

INFLUENCE ON THE DEVELOPMENT OF OFFSHORE OUTSOURCING

124

critical for the company. Companies transferred such areas of activity as production, tests, development, and

customer service to external suppliers.

The impact of changes in transaction costs may be noticed in a certain variety of outsourcing referred to as

offshore outsourcing. This is a form of outsourcing, in which tasks are transferred abroad.

The market of offshoring services has been growing for many years. Figure 2 presents the value of

offshoring transactions concluded all over the world in the years from 2004 to 2009.

Figure 2. Global market for offshore outsourcing of services from 2004 to 2009 (USD billion). Source: Prepared by

the author; United Nations Conference on Trade and Development (2009).

A sudden growth in separations of activity and their transfer to other countries results from the change in

transaction costs. The main drivers of that change are development of information technologies and

globalization.

As a result of the development of new information technologies, especially the internet, the costs of

communication decreased, as well as the costs related to searching for information and suppliers. But these are

not the only benefits resulting from the application of new technologies in the field of IT. Companies use

modern technologies to collect and send data all around the world. They do it cheaply and safely.

Globalization has also affected the decrease in transaction costs to a significant degree. Conducting

transactions “with the whole world” emphasized numerous differences in the area of shaping prices, costs, and

conditions in which production is implemented. Globalization has also showed cultural differences in

organizations. Companies very quickly responded to these differences and moved transactions, where the

conditions for their implementation were more attractive.

As it has already been mentioned, companies transfer selected actions to offshoring suppliers for

implementation. Actions related to IT and BPO, but only these, are most often separated. They transfer

production, tests, development, and other functions considered basic to suppliers.

Even at the beginning of the 1980s, such companies as Adidas or Puma used to employ thousands of

workers in Germany who manufactured sports shoes. Today, these companies do not have a single factory.

They contracted the whole production of shoes and clothes to partners in the Far East and Southeast Europe.

Nike submitted key elements of production to offshore outsourcing, focusing on unique activity, such as

research and development and post-production actions (distribution, sales, and marketing). Argyle Diamonds,

one of the largest manufacturers of diamonds in the world, went even further. It outsourced all mining and

35

51 65

76

93 96

0

20

40

60

80

100

120

2004 2005 2006 2007 2008 2009

INFLUENCE ON THE DEVELOPMENT OF OFFSHORE OUTSOURCING

125

distribution operations, conducting on its own only actions related to the separation and sorting of diamonds.

Similarly, the company Apple Computers submitted 70% of its production and other essential elements, e.g.

designing and part of marketing activities to outsourcing in order to focus on the production of unique parts,

such as Apple DOS (disk operating systems) and systems supporting macro software which are unique for

Apple products, and therefore key (Quinn & Hilmmer, 1994).

Production activities in the automotive industry are also no longer basic competences for the

manufacturers of vehicles. Production is an action of a low specific nature. Supplier specialized only in

production appeared on the market. The company Porsche decided to completely subject the production of the

model US Boxer to outsource to the company Velmet from Finland. Porsche focuses on engineering, marketing,

and controlling suppliers. Daimler Chrysler, a vehicle manufacturer, transferred the management of his supplier

portfolio to Andersen Consulting in the form of outsourcing.

Offshore outsourcing has also become strong in the electronic and telecommunication industry. A new

situation has emerged in the electronic industry and this situation is slowly being transferred onto the whole

industry. Large renowned companies with strong brands transfer production to companies with a network of

production sites all around the world. It turns out that these companies have higher skills in manufacturing than

their clients. Even though they are unknown to the general public, these companies form a new industry which

is referred to as contract manufacturing industry. Large contract manufacturers (Solectron and Celestica)

implement orders from the largest competitors. The assembly belts of Flextronics (100 sites in 30 countries,

including Poland) handle mobile phones from the companies Sony Ericsson, Nokia, and Alcatel (Polish Press

Agency, 2002).

The dominant reason why companies resign from the domestic market and move the implementation of

tasks to the global market is the possibility to reduce costs. This cost reduction results mainly from the access

to cheap workforce. When China, India, Brazil, and Mexico entered the global market, they gave the

opportunity to employ more than one billion low-qualified employees.

Searching for savings in costs on the global market, the potential of developing countries has also been

noticed. These potential results from having qualified employees whose employment costs are still lower

than in highly-developed countries. Such an attractive labor market with educated employees is, above all,

Poland and the remaining countries of Central-Eastern Europe. For many years, the employees support a

Western European companies doing for them services in the field of finance, accounting, tax, customer service,

and etc..

The attractiveness of offshore outsourcing services location is confirmed by report results. The report

entitled Offshoring Opportunities Amid Economic Turbulence presented a list of the most attractive offshore

outsourcing locations in the world. Table 2 presents leaders of provided offshoring services. The order in which

the countries have been presented results from the investment attractiveness index level which is shaped by

such parameters as low costs including taxes, infrastructure, quality and availability of employees, and business

environment.

Transferring various actions abroad, where the costs of their implementation are definitely lower, affects

the economic performance and the competitiveness of companies. The low costs of wages, low taxes, and

political-economic stability determine the fact that India, China, and Malaysia have been leaders of the ranking

for several years. Poland is also gaining a stronger and stronger position on the map of attractive locations.

Within two years, Poland moved up in the ranking from the 38th place to the 24th place.

INFLUENCE ON THE DEVELOPMENT OF OFFSHORE OUTSOURCING

126

Table 2

Global Services Location Index 2009 and 2011

Rank 2011 Country Rank 2009/change in ranking

1 India 1 (0)

2 China 2 (0)

3 Malaysia 3 (0)

4 Egypt 6 (+2)

5 Indonesia 5 (0)

6 Mexico 11 (+5)

7 Thailand 4 (-3)

8 Vietnam 10 (+2)

9 Philippines 7 (-2)

10 Chile 8 (-2)

11 Estonia 18 (+5)

12 Brazil 12 (0)

13 Latvia 22 (+14)

14 Lithuania 21 (+7)

24 Poland 38 (+15)

Source: Prepared by the author; A. T. Kearney Global Services Location Index (2009, 2011).

Poland is the Central and Eastern European leader in the sector of modern business services. This country

has more than 470 business services centers with foreign capital which employ more than 128 thousand

employees. Additionally, the employment in this sector is systematically growing every year by 20%. Poland’s

attractiveness on the map of offshoring investment projects results mainly from a very well qualified and cheap

workforce. Offshoring centers located here offer both BPO and KPO services. Employees need to have

specialized knowledge and education, very often technical, in order to provide this type of services, especially

those based on knowledge.

Strong centers of advanced business services in Poland include large cities, such as Krakow, Warsaw,

Poznan, Wroclaw, and Lodz. These cities are not selected as business service centers by accident. These are

cities in which thousands of young people learn in universities. Those who are well educated and who know

foreign languages will easily find employment in business service centers. An educated personnel is the basic

factor for which foreign investors open their centers in Poland. Poland’s policy of supporting the sector of

modern services is also of significance. Investors may obtain tax allowances when investing in Special

Economic Zones. After meeting specific conditions (Polish Information and Foreign Investment Agency), they

may obtain direct budget subsidies for their investment projects. R&D activity enjoys a special interest and

support from governmental authorities in the form of subsidies (Marcinkowska, 2013).

Polish attractiveness stems from the growing importance soft factors when companies select a country.

Over 40% of companies include soft factors when selecting a country (Figure 3).

Cost reduction remains the overarching objective of offshoring. But location criteria goes beyond

benchmarking of hard facts and is influenced by soft factors, such as following competitors, promotion by

target countries, and internal lobbying by a foreign affiliate (Figure 4).

The business services sector is one of the priority sectors of the economic policy in Poland. The polish

investment incentive policy gives special preferences for this sector. Key investment incentives for the business

services sector are:

INFLUENCE ON THE DEVELOPMENT OF OFFSHORE OUTSOURCING

127

tax reliefs on Special Economic Zone (CIT tax exemption);

direct budget subsidies for new investment/employment;

support for R&D activities.

Figure 3. Approach for country selection—Soft factors. Source: Prepared by the author; United Nations Conference on

Trade and Development (2004).

Figure 4. Soft factors. Source: Prepared by the author; United Nations Conference on Trade and Development (2004).

Conclusions

The changes that have occurred in transaction costs in the past two decades have influenced the

development of offshore outsourcing. Enterprises are looking for the best fit business models for your needs.

Companies decide to transfer the implementation of previous tasks outside the company’s structure.

Outsourcing is a method that reduces transaction cost. Domestic outsourcing and offshore outsourcing are

booming. Moving business processes abroad proves to be an effective solution for multinational companies.

41%

59%

Influence of soft factors

Influence of hard factors:

costs, skills, time zone, and etc.

0% 10% 20% 30% 40% 50% 60%

Experience with target country

Promotion by target country officials

Internal lobbying by a foraign affiliate

Offer of a business partner

Political situation

Following competitor's best practice

INFLUENCE ON THE DEVELOPMENT OF OFFSHORE OUTSOURCING

128

That’s why today Poland becomes obvious location for business processes for companies from Europe and the

USA. Company managements make initial decisions on the separation of certain actions on the basis of the

conducted cost benefit analysis, which is possible to obtain as a result of introduced changes. The first hint for

the separation is a surplus of benefits over costs obtained as a result of the analysis. This means that the costs of

implementation outside are lower than the costs of implementation within a company. However, this result

should not decide the separation. The generated benefits should also cover the transaction costs. It should be

born in mind that there is a real problem with the quantification of transaction costs. They may take the form of

financial costs and benefits, as well as qualitative costs and benefits. Therefore, the effectiveness of outsourcing

is of a praxeological dimension. This specific nature of transaction costs and the difficulty to measure them

affect the fact that many companies probably do not take them into account in the process of offshore

outsourcing analysis.

References

A. T. Kearney Global Services Location Index. (2009). The shifting geography of offshoring. Retrieved from

http://www.atkearney.com/documents/10192/fda82529-b60a-4fae-8d92-22cfd69b95b3

A. T. Kearney Global Services Location Index. (2011). Offshoring opportunities amid economic turbulence. Retrieved from

http://www.atkearney.com/documents/10192/f062cfd8-ee98-4312-ae4f-0439afc10880

Coase, R. (1937). The nature of the firm. Economica, 4, 386-405.

Furubotn, E. G., & Richter, R. (1997). Institutions and economic theory: The contribution of the new institutional economics. Ann

Arbor: The University of Michigan Press.

Gilley, M. K., & Rasheed, A. (2000). Making more by doing less: An analysis of outsourcing. Journal of Management, 26,

763-790.

Holstein-Beck, M. (1987). Szkice o pracy (Sketches about work). Warszawa: Książka i Wiedza.

Kieżun, W. (1977). Podstawy organizacji i zarzadzania (Principles of organization and management). Warszawa: Książka i

Wiedza.

Kotarbiński, T. (1955). Traktat o dobrej robocie (Treatise on good job). Łódź: Ossolineum.

Lei, D., & Hitt, M. (1995). Strategic restructuring and outsourcing: The effect of mergers and acquisitions and LBOs on building

firm skills and capabilities. Journal of Management, 21, 835-859.

Lysons, M., & Gillinham, M. (2003). Purchasing and supply chain management. Essex: Financial Times/Prentice Hall.

Marcinkowska, E. (2012). Outsourcing w zarządzaniu szpitalem publicznym (Outsourcing in management of public hospital).

Warszawa: ABC a Wolters Kluwer business.

Marcinkowska, E. (2013). Offshoring for business services in Poland. Proceedings from virtual multidisciplinary conference,

Quaesti, Zilina.

Perry, C. (1997). Outsourcing and union power. Journal of Labour Research, 18, 521-534.

Polish Press Agency. (2002). Przekazywanie produkcji wykonawcom kontraktowym (Transfer of production to contractors

contract). Management in the World, 3, 42-46.

Quinn, J. B., & Hilmmer, F. (1994). Strategic outsourcing. Sloan Management Review, 35, 43-55.

Sharpe, M. (1997). Outsourcing, organizational competitiveness, and work. Journal of Labour Research, 18, 535-549.

United Nations Conference on Trade and Development. (2004). Service offshoring takes off in Europa—In search of improved

competitiveness. Retrieved from http://unctad.org/sections/press/docs/SurveyOffshoring_en.pdf

United Nations Conference on Trade and Development. (2009). Information economy report. Trends and outlook in turbulent

times. Retrieved from http://unctad.org/en/Docs/ier2009_en.pdf

Williamson, O. E. (1985). The economic institutions of capitalism. New York: Simon and Schuster.

Williamson, O. E. (1998). Ekonomiczne instytucje kapitalizmu (The economic institutions of capitalism). Warsaw: PWN.

China-USA Business Review, March 2015, Vol. 14, No. 3, 129-142

doi: 10.17265/1537-1514/2015.03.002

The Level of the Financial Inclusion in the African Countries

and in the World Group Regions

Kokou Adalessossi

Akdeniz University, Antalya, Turkey

One key component of inclusive development is financial inclusion, an area in which Africa has been lagging

behind unlike other continents. At most, one adult out of four in Africa has access to an account in a formal

financial institution. The objective of this study is to find out the level of the financial inclusion among 41 African

countries on one hand and the level of the financial inclusion among the world six group regions on the other hand. To

find out which country or which group region has a higher level or a lower level in the financial inclusion, according

to some indicators, such as account at a formal financial institution, access to formal accounts, use of formal accounts,

mobile payments, savings, credits patterns, and insurance decision as underlined in the literature review that the latter

constituted the principal indicators for inclusive financing, an appropriate and reliable statistical method has been

used, such as cluster analysis. The data set was the secondary data taken from the World Bank website; the first data

published by the World Bank in 2012 on the global financial inclusion concerning 148 countries in the world. The

empirical results from this study reveal that most of African countries with lower levels are low-income countries and

those with higher levels remain largely of middle-income countries. Among the world group regions, only

Sub-Saharan African region has the low level in five of the seven indicators used in this research, when compared

with the other group regions. This study will awaken most African countries including the Sub-Saharan African

region to develop strategies to enhance their level in the future in order to reduce poverty and to strengthen their

financial system which leads to economic growth.

Keywords: African countries, financial inclusion, World Bank, indicators, cluster analysis

Introduction

Africa is now the world’s second fastest growing region after Asia, with annual GDP growth rates in

excess of 5% over the last decade (Thouraya & Faye, 2013). Despite this growth, the Arab Spring events

showed that good economic growth in the continent has not translated into shared prosperity and better

livelihoods for the majority. Growth has to be inclusive to be socially and politically sustainable. One key

component of inclusive development is financial inclusion, an area in which Africa has been lagging behind

other continents. Less than one adult out of four in Africa has access to an account at a formal financial

institution. Broadening access to financial services will mobilize greater household savings, marshal capital for

investment, expand the class of entrepreneurs, and enable more people to invest in themselves and their families.

Kokou Adalessossi, Ph.D. student researcher in finance, Faculty of Economics and Business Administration Sciences, Business

Administration Department, Akdeniz University, Antalya, Turkey.

Correspondence concerning this article should be addressed to Kokou Adalessossi, Akdeniz University, Dumlupinar Bulvari,

07058 Kampus, Antalya, Turkey. Tel: +905078510893. E-mail: [email protected].

DAVID PUBLISHING

D

FINANCIAL INCLUSION IN THE AFRICAN COUNTRIES

130

In recent decades, access to financial services has been dramatically improved in African countries

(Thouraya & Faye, 2013). More financial services, especially credit, are now provided to individuals and

enterprises. New technologies, such as mobile money, have also helped broaden access to financial services,

including savings and payment products. Yet, until recently, in Africa and elsewhere, little was known about

the reach of the financial sector—the extent of financial inclusion and the degree to which disadvantaged

groups, such as the poor, women, and youth, are excluded from formal financial systems. Financial services are

increasingly being seen as important to poverty reduction and achievement of the millennium development

goals. By borrowing, saving, or buying insurance, the poor can plan for their future beyond the short term.

They can build up assets and invest in education and health. Financial services can help them cope in times of

need and hardship. Beyond this, access to financial services can promote social inclusion and build

self-confidence and empowerment, in particular among women.

Access to financial services plays a critical part in development by facilitating economic growth and

reducing income inequality. Inclusive financial systems allow poor people to smooth their consumption and

insure themselves against economic vulnerabilities, from illness and accidents to theft and unemployment.

Financial access enables poor people to save and borrow—allowing them to build their assets, to invest in

education and entrepreneurial ventures, and thus to improve their livelihoods. While significant progress has

been made in expanding access to financial services by the poor, there is still more to be done. It is estimated

that more than 2.7 billion people in developing countries (World Bank, 2008), particularly Africa

countries—the majority of adults—are still excluded from the financial services market.

Inclusive financing is especially likely to benefit disadvantaged groups, such as women, youth, and rural

communities. For all these reasons, financial inclusion has gained prominence in recent years as a policy

objective to improve the lives of the poor. Financial inclusion or inclusive financing is the delivery of financial

services at affordable costs to sections of disadvantaged and low-income segments of society, in contrast to

financial exclusion where those services are not available or affordable. Adults of an estimated 2.5 billion

working-age globally have no access to the types of formal financial services delivered by regulated financial

institutions (World Bank, 2012), for example, in Sub-Saharan Africa, only 24% of adults have a bank account

even though African formal financial sector has grown in recent years. It is argued that as banking services are in

the nature of public good, the availability of banking and payment services to the entire population without

discrimination is the prime objective of financial inclusion public policy.

The aim of this study is to find out their level in the inclusive financing in one side among 41 African

countries and measure the level of the financial inclusion among the world six group regions in the second side.

This is to show that, according to some indicators, which country and group region has a high level in financing

inclusion. After touching by finger which the literature review has said about in the second section, this paper will

move on the data and methodology of the research in the third section. The empirical results analysis and

discussions are in the fourth section before concluding at the end.

Literature Review

Conceptual Framework of Financial Inclusion

Committee on financial inclusion defines financial inclusion as delivery of financial services at an

affordable cost to vast sections of disadvantaged and low-income groups (Government of India, 2008).

Unrestrained access to public goods and services is the essential condition of an open and efficient society. This

FINANCIAL INCLUSION IN THE AFRICAN COUNTRIES

131

view is reiterated in the definition “the process of ensuring access to timely and adequate credit and financial

services to vulnerable groups at an affordable cost” (Kamath, 2007, pp. 1334-1335). As banking services are in

the nature of public good, it is essential that availability of banking and payment services to the entire

population without discrimination should be the prime objective of the public policy. The international

definitions of financial inclusion have been viewed in much wider perspective (Leeladhar, 2005). The

definitions of financial inclusion emphasize several dimensions (Sharma, 2008), e.g., accessibility, suitability,

availability, and usage of the financial system. These dimensions together build an inclusive financial system.

Another issue that needs to be taken care of is whether to measure access or usage. Because in transaction

banking and insurance, it can be found that people do not use it, even if they have access to it. Access

dimension implies mere access to services, while usage dimension is a broader term requiring examination of

aspects like access, suitability, availability, and actual usage.

World Bank

World Bank also distinguishes between those who are formally served (have access to financial services

from a bank and/or other formal providers) and those who are financially served (include people who use

informal providers). In contrast to the other work described above, the term “financially excluded” is only used

to describe those who have no access at all (World Bank, 2005). This study considers only the formal sector

which includes all legally endorsed financial services. The definitions of financial inclusion vary across the

geographic regions decided by the concomitant economic development. This study focuses on financial

inclusion with respect to the poorest of the poor and emphasizing a wider connotation of the term “financial

services” than defining it in a narrow perspective of owning a savings account with a bank. The definition of

several aspects of the term propounded by several authors, committees, and commissions is reviewed here to

arrive at an acceptable working definition.

Definitions of financial inclusion in literature tend to vary on dimensions, such as breadth, focus, and

degree of exclusion (Reserve Bank of India, 2009). The breadth dimension is the broadest of all definitions

which defines financial inclusion, as a consequence of social inclusion which prevents the poor and the

disadvantaged from gaining access to the mainstream financial system. Some of the definitions of financial

inclusion reiterating this view are as follows. Financial inclusion infers accessibility and usage of financial

services from formal service providers. United Nations (2006) defined financially inclusion as the financial

sector that provides access to credit for all bankable people and firms, to insurance for all insurable people and

firms, and to savings and payments services for everyone. Inclusive finance does not require that everyone who

is eligible uses each of the services, but he should be able to choose to use them if desired. The degree

dimension is the narrowest of all and defines financial exclusion as exclusion from usage of particular sources

of credit and other financial services, including insurance, bill payment services, and accessible and appropriate

deposit accounts. World Bank (2005) described exclusion as a phenomenon with access to key areas, such as

transaction banking, savings, credit, and insurance.

For the purpose of the study, this definition has been accepted as the bench mark. Though all services

including credit, savings, and insurance offered by the banks and other financial institutions are taken as the

benchmark, more weight age is given to credit segment. Financial inclusion may be interpreted as the ability of

every individual to access basic financial services which include savings, loans, and insurance in a manner that

is reasonably convenient and flexible in terms of access and design; and reliable in the sense that savings will

FINANCIAL INCLUSION IN THE AFRICAN COUNTRIES

132

be safe and that insurance claim will be paid with certainty (Mor & Ananth, 2007). Indeed, having a current

account/savings account on its own cannot be regarded as an accurate indicator of financial inclusion (Chatrath

& Vallabh, 2006).

Financial inclusion is characterized primarily as either general access to loans or access to savings

accounts (Arunachalam, 2008). Very few risk management and vulnerability reducing products are available to

small holder producers. Financial inclusion cannot only be restricted merely to opening savings accounts and/or

providing credit for consumption/consumer spending, but should also encompass delivering financial products

tailor-made to cope with the fluctuating earning pattern of the poor. Rogaly (1999) defined financial exclusion

in the perspective of exclusion from particular sources of credit and other financial services (including

insurance, bill payment services, and accessible and appropriate deposit accounts).

The review of literature suggests that most of the definitions are context specific, originating from country

specific problems related to financial exclusion with regard to the respective of socio-economic dimensions

which assumes importance in the public policy perspective. On the basis of the above review, the following

working definition has been accepted with regard to financial inclusion throughout the study

Financial inclusion may be interpreted through poor households’ access to basic financial services from

formal and semiformal service providers which include savings, loans, insurance, and other financial services

in a manner that is reasonably convenient and flexible in terms of access and design. In this perspective, the

study attempts to measure financial inclusion as a composite one that takes into consideration access to

transaction banking, savings, credit, and insurance:

Transaction banking: It refers to access to bank’s financial services other than savings, credit, and

insurance;

Savings: Lesser savings leads to lesser capital formation implying lesser development. Not having a

savings account can lead to financial exclusion;

Credit: It is the most valid indicator for assessing the status of financial inclusion. Though other indicators

are measured, credit access and indebtedness of a family determine the level of well being achieved. Credit

measured as a sole measure of financial inclusion can also be useful, because it may provide status of the

stakeholder considering aspects like source, cost of borrowing, adequacy, proximity, and etc.;

Insurance: Insurance provides coverage to the accidents/emergencies arising in a society affecting human

lives, assets, or livelihoods. Recent developments have increased popularity and access to insurance. Also

government has enacted insurance policies for the benefit of sea faring fishers. Insurance inclusion is measured

as sub element in the financial inclusion designating appropriate weights.

Data and Research Methods

Data

The data set of this study was taken from the global index database covering 148 economies that includes

41 African countries (Demirgüç-Kunt & Klapper, 2012). This data was published in 2012 by the World Bank

on its website titled The Global Financial Inclusion using indicators, such as formal bank accounts, payments

behavior, savings patterns, credit patterns, and insurance decisions. This data provides country-level indicators

of financial inclusion summarized for all adults and disaggregated by key demographic characteristics—gender,

age, education, income, and rural or urban residence.

This research chose 41 African countries, according to the World Bank’s available data for countries and

FINANCIAL INCLUSION IN THE AFRICAN COUNTRIES

133

the six regions: East Asia and Pacific (grouping nine countries), Europe and Central Asia (grouping 24

countries), Latin America and the Caribbean (grouping 19 countries), Middle East and North Africa (grouping

12 countries), South Asia (grouping six countries), and Sub-Saharan Africa (grouping 36 country).

Research Methods

To perform this study, the appropriate and reliable statistical method used is the method of two-step

clusters analysis. It enables identifying groups of individual or objects that are similar to each other, but

different from individuals in other group. This method will help to classify the countries into two groups and

will show which of them belongs to first group and the second group.

The limit of this study is that all the African countries (54) did not take part in this study. Indeed, it will

be very good that all the African countries took part with a view to gauging the level of all countries in

inclusive financing. But due to the World Bank group classification, only 41 African countries data were

accounted for.

Method of Cluster

Classification and clustering have become an increasingly popular method of multivariate analysis over

the past two decades and they have become a vast amount of published material. Since there is no journal

devoted exclusively to cluster analysis as a general topic and it has been used in many (Scoltock, 1982) fields

of study, the novice user is faced with the daunting prospect of searching through a multitude of journals for

appropriate references. It has already been suggested that cluster analysis techniques have been applied to data

from numerous and diverse fields of study. In his review, Anderberg (1973) attributed the diversity to a mixture

of professional jealousy, relative isolation among the fields and genuine differences of viewpoint. Porter (1998),

who is the most frequently cited advocate and analyst of cluster policy, defined clusters as geographic

concentrations of interconnected companies and institutions in a particular field, linked by commonalities and

complementarities.

Cluster analysis classifies a set of observations into two or more mutually exclusive unknown groups

based on combinations of interval variables. The purpose of cluster analysis is to discover a system of

organizing observations, usually people and objects into groups where members of the groups share properties

in common. It is cognitively easier for people to predict behavior or properties of people or objects based on

group membership, all of whom share similar properties. It is generally cognitively difficult to deal with

individuals and predict behavior or properties based on observations of other behaviors or properties. Cluster

analysis classifies unknown groups, while discriminant function analysis classifies known groups. The procedure

for doing a discriminant function analysis is well established. There are few options, other than type of output,

that need to be specified, when doing a discriminant function analysis. Cluster analysis, while, allows many

choices about the nature of the algorithm for combining groups. Each choice may result in a different grouping

structure. There are three types of clusters: two-step cluster analysis, hierarchical cluster, and non-hierarchical

clusters (k-means cluster). In this research, two-step cluster analysis is used to classify the countries in two

groups using SPSS 13.

Definition of Variables

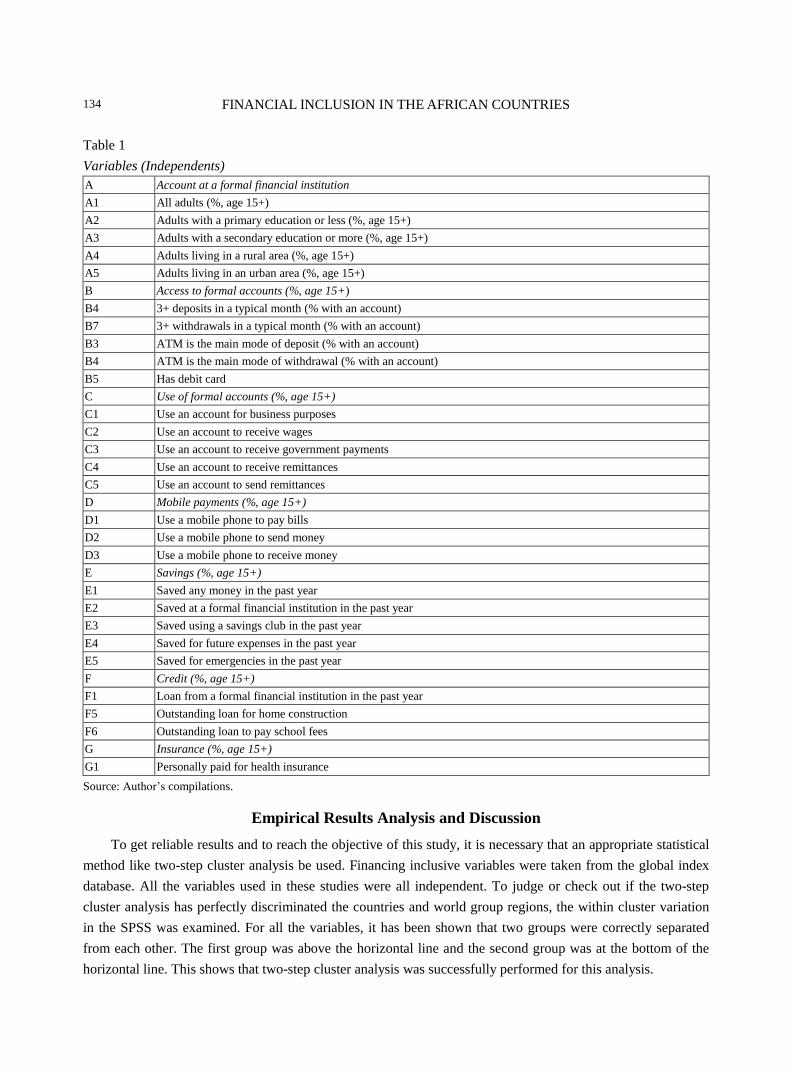

Variables used for this research are all continuous ones (independents variables). These variables are

recapitulated in the Table 1.

FINANCIAL INCLUSION IN THE AFRICAN COUNTRIES

134

Table 1

Variables (Independents)

A Account at a formal financial institution

A1 All adults (%, age 15+)

A2 Adults with a primary education or less (%, age 15+)

A3 Adults with a secondary education or more (%, age 15+)

A4 Adults living in a rural area (%, age 15+)

A5 Adults living in an urban area (%, age 15+)

B Access to formal accounts (%, age 15+)

B4 3+ deposits in a typical month (% with an account)

B7 3+ withdrawals in a typical month (% with an account)

B3 ATM is the main mode of deposit (% with an account)

B4 ATM is the main mode of withdrawal (% with an account)

B5 Has debit card

C Use of formal accounts (%, age 15+)

C1 Use an account for business purposes

C2 Use an account to receive wages

C3 Use an account to receive government payments

C4 Use an account to receive remittances

C5 Use an account to send remittances

D Mobile payments (%, age 15+)

D1 Use a mobile phone to pay bills

D2 Use a mobile phone to send money

D3 Use a mobile phone to receive money

E Savings (%, age 15+)

E1 Saved any money in the past year

E2 Saved at a formal financial institution in the past year

E3 Saved using a savings club in the past year

E4 Saved for future expenses in the past year

E5 Saved for emergencies in the past year

F Credit (%, age 15+)

F1 Loan from a formal financial institution in the past year

F5 Outstanding loan for home construction

F6 Outstanding loan to pay school fees

G Insurance (%, age 15+)

G1 Personally paid for health insurance

Source: Author’s compilations.

Empirical Results Analysis and Discussion

To get reliable results and to reach the objective of this study, it is necessary that an appropriate statistical

method like two-step cluster analysis be used. Financing inclusive variables were taken from the global index

database. All the variables used in these studies were all independent. To judge or check out if the two-step

cluster analysis has perfectly discriminated the countries and world group regions, the within cluster variation

in the SPSS was examined. For all the variables, it has been shown that two groups were correctly separated

from each other. The first group was above the horizontal line and the second group was at the bottom of the

horizontal line. This shows that two-step cluster analysis was successfully performed for this analysis.

FINANCIAL INCLUSION IN THE AFRICAN COUNTRIES

135

Table 2

Cluster Distribution/Account at Formal Financial Institution

No. % of combined % of total

Cluster 1 19 40.4% 40.4%

2 28 59.6% 59.6%

Combined 47 100.0% 100.0%

Total 47 100.0%

Source: SPSS 13.

In Table 2, the cluster distribution, when based on account at formal financial institution, shows that out of

the 47 countries and world group regions, 19 were classified in the first group (high level), whereas 28 of them

are classified in the second group (low level). It means that eight countries and world group regions have the

high level in account at formal financial institution.

Table 3

Cluster Profiles Centroids/Account at Formal Financial Institution

All adults

(%, age 15+)

Adults with a

primary education or

less (%, age 15+)

Adults with a

secondary education

or more (%, age 15+)

Adults living in a

rural area

(%, age 15+)

Adults living in an

urban area

(%, age 15+)

Mean

Std.

Deviation Mean

Std.

Deviation Mean

Std.

Deviation Mean

Std.

Deviation Mean

Std.

Deviation

Cluster 1 39.642 12.41 27.12 15.838 49.81 17.0199 32.926 16.759 49.042 17.966

2 12.289 6.432 7.343 4.253 24.014 9.866 9.9107 6.2424 20.792 10.157

Combined 23.346 16.391 15.34 14.317 34.442 18.2821 19.21 16.221 32.212 19.576

Source: SPSS 13.

Observing the cluster profiles in Table 3, when based on account at formal financial institution, it is shown

that countries and world group regions of the first group (high level) have accounted for higher value in mean

and standard deviation than those in the second group.

Table 4

Cluster Distribution/Access to Formal Account

No. % of Combined % of Total

Cluster

1 22 46.8% 46.8%

2 25 53.2% 53.2%

Combined 47 100.0% 100.0%

Total 47 100.0%

Source: SPSS 13.

The results in Table 4 show that, when based on access to formal account, out of the 47 countries and

world group regions, 19 (46.8%) were classified in the first group (high level), whereas 28 of them are

classified in the second group (low level). It means that eight countries and world group region have a high

level in account at formal financial institution.

The results from Table 5 show that the first group (high level) of countries and world group regions

compared to the second when based on access to formal account has the high value in mean and standard

deviation.

FINANCIAL INCLUSION IN THE AFRICAN COUNTRIES

136

Table 5

Cluster Profiles Centroids/Access to Formal Account

3+ deposits in a

typical month (%

with an account)

3+ withdrawals in a

typical month (%

with an account)

ATM is the main

mode of deposit (%

with an account)

ATM is the main

mode of withdrawal

(% with an account)

Has debit card

Mean Std.

Deviation Mean

Std.

Deviation Mean

Std.

Deviation Mean

Std.

Deviation Mean

Std.

Deviation

Cluster

1 24.027 13.069 32.12 12.075 11.495 7.6781 57.423 20.1214 22.232 12.818

2 17.216 8.993 13.24 6.8037 4.816 3.8212 15.172 14.1967 4.664 3.8448

Combined 20.404 11.488 22.08 13.4692 7.943 6.7736 34.949 27.2784 12.887 12.6978

Source: SPSS 13.

Table 6

Cluster Distribution Use a Formal Account

No. % of Combined % of Total

Cluster

1 11 23.4% 23.4%

2 36 76.6% 76.6%

Combined 47 100.0% 100.0%

Total 47 100.0%

Source: SPSS 13.

The results in Table 6 show that, when based on access to formal account, out of the 47 countries and

world group regions, 11 (23.4%) were classified in the first group (high level), whereas 28 of them were

classified in the second group (low level). It means that 11 countries and world group regions have the highest

level in a formal account.

Table 7

Cluster Profiles Centroids/Use a Formal Account

Use an account for

business purposes

Use an account to

receive wages

Use an account to

receive government

payments

Use an account to

receive remittances

Use an account to

send remittances

Mean Std.

Deviation Mean

Std.

Deviation Mean

Std.

Deviation Mean

Std.

Deviation Mean

Std.

Deviation

Cluster 1 8 2.9462 17.48 5.1563 8.464 4.3202 14.809 4.3885 10.582 3.1644

2 3.514 1.843 6.786 4.569 4.494 4.1919 3.308 2.5987 2.608 1.9608

Combined 4.564 2.8561 9.289 7.718 5.423 4.7944 6 5.7924 4.474 4.0923

Source: SPSS 13.

In Table 7, it is shown that the first group has the higher value than the second group when based on a

formal account.

Table 8

Cluster Distribution in Mobile Payments

No. % of Combined % of Total

Cluster 1 8 17.0% 17.0%

2 39 83.0% 83.0%

Combined 47 100.0% 100.0%

Total 47 100.0%

Source: SPSS 13.

FINANCIAL INCLUSION IN THE AFRICAN COUNTRIES

137

The cluster distribution in Table 8 shows that out of the 47 countries and world group regions, eight were

classified in the first group, whereas 39 of them were classified in the second group. It means that eight

countries and world group regions have a high level in mobile payment (use a mobile phone to pay bills, send

money, and receive money).

Table 9

Cluster Profiles Centroids in Mobile Payments

Use a mobile phone to pay bills

Use a mobile phone to send

money

Use a mobile phone to receive

money

Mean Std. Deviation Mean Std. Deviation Mean Std. Deviation

Cluster 1 9.588 8.1341 29.588 15.4335 38.263 14.6938

2 1.736 1.7285 3.303 3.9233 5.000 5.2778

Combined 3.072 4.6296 7.777 12.1929 10.662 14.6810

Source: SPSS 13.

Table 9 shows that, trough mobile payments, the first group (high level) has the higher value in mean and

standard deviation than the second group.

Table 10

Cluster Distribution Savings

No. % of Combined % of Total

Cluster

1 18 38.3% 38.3%

2 29 61.7% 61.7%

Combined 47 100.0% 100,0%

Total 47 100.0%

Source: SPSS 13.

The cluster distribution shown in Table 10 indicates that out of the 47 countries and world group regions,

18 (38.3%) were classified in the first group, whereas 29 (61.7%) of them were classified in the second group.

It shows that 18 countries and world group regions have the high level in savings patterns.

Table 11

Cluster Profile Centroids in Savings

Saved at a formal financial institution in the

past year Saved for emergencies in the past year

Mean Std. Deviation Mean Std. Deviation

Cluster

1 18.094 5.5837 30.150 8.7424

2 5.779 3.4822 15.886 4.4545

Combined 10.496 7.4513 21.349 9.4576

Source: SPSS 13.

Table 11 shows that the countries and world group regions belonging to the first group have accounted to

higher value in mean and standard deviation, when based on savings patterns than those belonging to the

second group. Also, the examination of the “within cluster variation” in the SPSS shows that the two groups

were correctly separated from each other. The first group was above the horizontal line and the second group

was at the bottom of the horizontal line. This indicates that the two-step cluster analysis has successfully

discriminated the countries and world regions in two groups.

FINANCIAL INCLUSION IN THE AFRICAN COUNTRIES

138

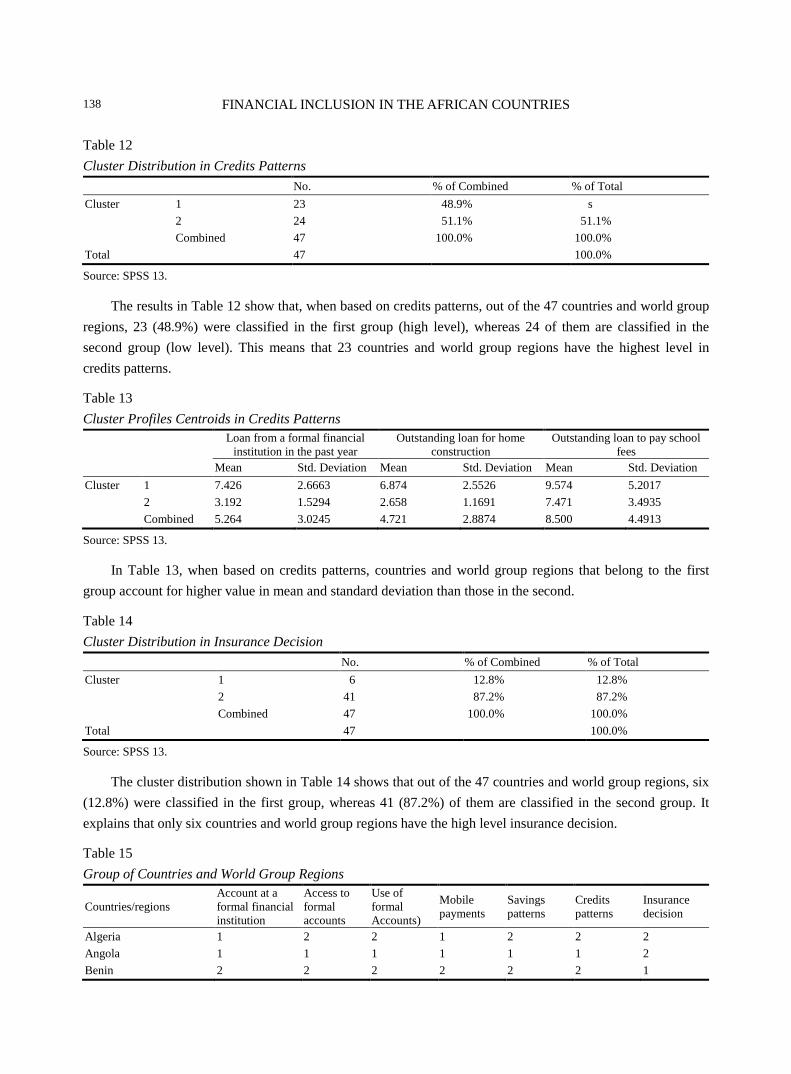

Table 12

Cluster Distribution in Credits Patterns

No. % of Combined % of Total

Cluster 1 23 48.9% s

2 24 51.1% 51.1%

Combined 47 100.0% 100.0%

Total 47 100.0%

Source: SPSS 13.

The results in Table 12 show that, when based on credits patterns, out of the 47 countries and world group

regions, 23 (48.9%) were classified in the first group (high level), whereas 24 of them are classified in the

second group (low level). This means that 23 countries and world group regions have the highest level in

credits patterns.

Table 13

Cluster Profiles Centroids in Credits Patterns

Loan from a formal financial

institution in the past year

Outstanding loan for home

construction

Outstanding loan to pay school

fees

Mean Std. Deviation Mean Std. Deviation Mean Std. Deviation

Cluster 1 7.426 2.6663 6.874 2.5526 9.574 5.2017

2 3.192 1.5294 2.658 1.1691 7.471 3.4935

Combined 5.264 3.0245 4.721 2.8874 8.500 4.4913

Source: SPSS 13.

In Table 13, when based on credits patterns, countries and world group regions that belong to the first