Corporate tax avoidance, shareholder dividend tax policy, and ...

Upload

baruch-cunyCategory

view

0download

0

Chapter I:2

Determination of Tax

Discussion Questions

I:2-1 a. Gross income is income from taxable sources. Form1040 combines the results of computations made on severalseparate schedules. For example, income from a proprietorship isreported on Schedule C where gross income from the business isreduced by related expenses. Only the net income or losscomputed on Schedule C is carried to Form 1040. This isprocedurally convenient but means gross income is not shown onForm 1040.

b. Gross income is relevant to certain tax determinations.For example, whether a person is required to file a tax return isbased on the amount of the individual’s gross income. As theamount does not necessarily appear on any tax return, it may benecessary to separately make the computation in order todetermine whether a dependency exemption is available.

pp. I:2-2 through I:2-5.

I:2-2 The term "income" includes all income from whateversource derived based either on principles of economics oraccounting. Gross income refers only to income from taxablesources. p. I:2-3.

I:2-3 a. A deduction is an amount that is subtracted fromincome, while a credit is an amount that is subtracted from thetax itself.

b. In general, a $10 credit is worth more than a $10deduction because the credit results in a direct dollar fordollar tax savings. The savings from a deduction depends on thetax bracket that applies to the taxpayer.

c. If a refundable credit exceeds the taxpayer's taxliability, the taxpayer will receive a refund equal to the

ScholarStockI:2-1

excess. In the case of nonrefundable credits the taxpayer willnot receive a refund, but may be entitled to a carryover orcarryback. pp. I:2-4 through I:2-6.

I:2-4 All dependents (1) must have social security numbersreported on the taxpayer’s return, (2) must meet a citizenship test, (3) cannot normally file ajoint return, and (4) cannot claim others as dependents.Qualifying children must (1) be the taxpayer’s child or sibling,(2) be under 18, a full-time student under 24, or disabled, (3)live with the taxpayer, and (4) not be self-supporting. Otherdependents must (1) be related to the taxpayer, (2) have grossincome less than the amount of the personal exemption, and (3)receive over one-half of their support from the taxpayer. pp.I:2-12 through I:2-17.

I:2-5 a. Support includes amounts spent for food, clothing,shelter, medical and dental care, education, and the like.Support does not include the value of services rendered by thetaxpayer for the dependent nor does it include a scholarshipreceived by a son or daughter of the taxpayer.

b. Yes. When several individuals contribute to the supportof another, it is possible for members of the group to sign amultiple support agreement that enables one member of the groupto claim the dependency exemption. Also, in the case of divorcedcouples, the parent with custody for over half of the yearreceives the dependency exemption even if that parent did notprovide more than 50% of the child's support. Similarly, in thecase of written agreement, the dependency exemption can be givento the noncustodial parent even if that parent provided 50% orless of the child's support.

c. The value of an automobile given to an individual mayrepresent support for that individual. The automobile must begiven to the individual and must be used exclusively by theindividual. pp. I:2-15 through I:2-18.

I:2-6 A taxpayer will use a rate schedule instead of a taxtable if taxable income exceeds the maximum in the tax table

ScholarStockI:2-2

(currently $100,000) or if the taxpayer is using a special taxcomputation method such as short-year computation. p. I:2-20.

I:2-7 a. In general, it is the taxpayer's gross income thatdetermines whether the individual must file a return. Thespecific dollar amounts are listed in the text. Certainindividuals must file even if they have less than the specifiedgross income amounts. These include taxpayers who receiveadvance payments of the earned income credit and taxpayers with$400 or more of self-employment income. Dependent individualsmust file if they have either (1) unearned income over $1,000 or(2) total gross income in excess of the standard deduction.

b. Taxpayers who owe no tax because of deductions or otherreasons must still file a return if they have gross income inexcess of the filing requirement amounts. p. I:2-33.

I:2-8 Home mortgage interest and real property taxes areitemized deductions. As a result those expenses alone oftenexceed the standard deduction enabling a homeowner to itemize.Renters typically do not have these deductions and the standarddeduction may be greater than itemized deductions. p. I:2-10.

I:2-9 If the threshold were “50% or more” two individuals whoprovided equal amounts of support for another person could bothclaim a dependency exemption for that individual. By specifying“over 50%” only one individual can meet the requirement. Amultiple support agreement could be used by two individuals whoprovide equal amounts of support to allow one of the two to claima dependency exemption. p. I:2-15.

I:2-10 The normal due date for individuals and partnerships isApril 15. The normal due date for calendar year corporations isMarch 15. The normal due date is delayed to the next day that isnot a Saturday, Sunday or holiday. p. I:2-34.

I:2-11 Automatic extensions of six months are available toindividuals and corporations. Partnerships are permitted

ScholarStockI:2-3

automatic extensions of five months. Any tax that may be owedmust be paid with the application for an extension. p. I:2-34.

I:2-12 Yes. In general, the source of income is not important.It is the use that is important. An exception does exist for achild's scholarship. Parents do not have to consider a child'sscholarship when determining whether they provide over half ofthe child's support. p. I:2-15.

I:2-13 It can be, but as was noted in the preceding answer,parents may ignore a child's scholarship in deciding whether theyprovide over half of the child's support.I:2-14 The purpose of the multiple support agreement is toallow one member of a group to claim a dependency exemption whenthe members together contribute more than 50% of the support ofanother person and each member of the group contributes over 10%.The multiple support agreement results in an exception to therequirement that the taxpayer alone must provide over one-half ofthe dependent's support. p. I:2-17.

I:2-15 In general, the parent with custody for the greaterpart of the year receives the exemption. The noncustodial parentis entitled to the dependency exemption only if requireddocumentation provides that the noncustodial parent is to receivethe exemption. p. I:2-17.

I:2-16 In general, a couple must be married on the last day ofthe tax year in order to file a joint return. In addition, thehusband and wife must have the same tax year. Also, if one spouseis a nonresident alien then that spouse must agree to include hisor her income on the return. pp. I:2-19 and I:2-21.

I:2-17 The phrase "maintain a household" means to pay overone-half of the costs of the household. These costs includeproperty taxes, mortgage interest, rent, utility charges, upkeepand repairs, property insurance and food consumed on thepremises. Such costs do not include clothing, education, medical

ScholarStockI:2-4

treatment, vacations, life insurance and transportation. p. I:2-22.

I:2-18 A married person, if otherwise qualified can claimhead-of-household status if he or she is married to a nonresidentalien or if he or she qualifies as an abandoned spouse. To be anabandoned spouse, the taxpayer must have lived apart from his orspouse for the last six months of the year and maintain ahousehold for a qualifying child in which they both live. pp.I:2-22 and I:2-23.

I:2-19 a. A C Corporation is taxed on its income. In otherwords, it is taxed as a separate entity. An S Corporation isnormally not taxed on its income. Instead, its income flowsthrough and is reported by the shareholders. Each shareholderreports his or her share of the income even if it is not actuallydistributed.

b. Some corporations are ineligible for making an Scorporation election. Others may choose the C corporationbecause of lower corporate tax rates on taxable income up to$75,000. Other considerations not discussed in Chapter 2 includefringe benefits, the need to retain earnings in the business anddividend policy. pp. I:2-26 and I:2-27.

I:2-20 Up to $50,000 of income earned by a C corporation istaxed at 15%. If an individual with a significant amount ofother income operates a new business as a proprietorship, thatincome is taxed at the owner’s marginal tax rate, which will behigher than 15%. Thus, the current tax can be reduced if thecorporate form is used and income is retained in the corporation.This advantage is lost if the corporation distributes the income.New businesses often need to retain income for expansion. p. I:2-27.

ScholarStockI:2-5

I:2-21 a. The major categories of property excluded fromcapital asset status are:

• Inventory• Trade receivables• Certain properties created by the efforts of the

taxpayer• Depreciable business property and business land• Certain government publications.

b. Yes. A net long-term capital gain is taxed at 15% (0%in the case of an individual taxpayer who is in the 10% or 15%tax bracket and 20% in the case of an individual in the 39.6% taxbracket). Short-term capital gains are taxed much like otherincome.

c. The availability of favorable tax rates for long-termgains is one implication of capital asset classification.Another is the limitation on the amount of capital loss that canbe deducted from other income. At the present time only $3,000of net capital loss can be deducted from other income by anindividual taxpayer in any year. p. I:2-30.

d. Individual taxpayers first deduct (or offset) capitallosses from capital gains. If a net capital loss results, only$3,000 of the net capital loss can be deducted from other income.Net capital losses in excess of $3,000 are be carried over tofuture years. p. I:2-30.

I:2-22 Yes. By waiting the taxpayer can convert the short-termgain to a long-term gain taxed at a maximum rate of 20%. Thelong-term rate will be available if the taxpayer holds theproperty over 12 months. The taxpayer should, however, take intoconsideration other nontax factors such as whether the value ofthe asset may decline during the extended holding period. p.I:2-30.

I:2-23 a. Shifting income means moving it from one taxreturn to another. Splitting income means creating additionaltaxable entities (such as corporations) so as to spread incomebetween more taxpayers.

ScholarStockI:2-6

b. Different taxpayers are in different tax brackets. Asa result, taxes can be saved by shifting income from a taxpayerwho is in a high tax bracket to a taxpayer who is in a lower taxbracket.

c. The tax on the unearned income of a minor (i.e., thekiddie tax) was created to reduce the opportunity to reduce taxesby shifting income from parents who are in high tax brackets tochildren who have little or no other income and would, therefore,normally be in a low tax bracket. pp. I:2-30 and I:2-31.

I:2-24 a. Both the husband and wife are liable foradditional taxes on a joint return. An exception exists for theso-called innocent spouse. To utilize the innocent spouseprovision, the tax must be attributable to erroneous items of theother spouse. In addition, the innocent spouse cannot have knownor had reason to know of the error, and must elect relief withintwo years after the IRS begins collection activities. Further,it must be inequitable to hold the innocent spouse liable for theunderstatement.

b. In the event of underpayment of taxes on a joint returnthe IRS can look to either spouse to collect the taxes. pp. I:2-32 and I:2-33.

I:2-25 Couples may change from joint returns to separatereturns only prior to the due date for the return. Couples maychange from separate returns to a joint return within three yearsof the due date including extensions. pp. I:2-32 and I:2-33.Issue Identification Questions

I:2-26 The main issue is whether Yung can claim a dependencyexemption for his nephew. The nephew must be a U.S. resident inorder to qualify. Normally, this requires that a person have avisa as a permanent resident, but a dependency exemption has beenpermitted when special circumstances were present. For example,the Tax Court allowed an exemption when it considered the lengthof the dependent's stay, the individual's intent, and thepresence of substantial assets in the U.S. [Carmen R. Escobar, 68TC 304 (1977)]. The nephew's desire to stay and the desire of

ScholarStockI:2-7

other members of the family to move here could all be factorsthat are considered in determine whether the nephew is aresident. p. I:2-13.

I:2-27 The primary tax issue is whether they should file ajoint return. Filing jointly could produce a tax savings becausemore income will be taxed at the low 10% and 15% rates. Carmen,however, should carefully consider whether Carlos is disclosingall of his income. If not, she may be liable for additionaltaxes, interest, and penalties resulting from the unreportedincome. The innocent spouse rules may not protect her. She isnot required to know with certainty Carlos' income in order to beliable. The fact that Carmen is "surprised" that Carlos' incomeis so low suggests that she has reason to know that there isunreported income. p. I:2-32.

I:2-28 The primary tax issue is the filing status for bothBill and Jane. Both can file as single taxpayers because theywere divorced prior to the end of the tax year. To file as ahead of household a taxpayer must pay more than one-half of thecosts of maintaining a household (as one's home) in which adependent relative lives for more than one-half of the year. Inthe case of divorce, the child need not be a dependent of thecustodial spouse. The facts in this question are similar to W.E.Grace v. CIR, 25 AFTR 2d 70-328, 70-1 USTC ¶ 9149 (5th Cir.,1970) and Levon P. Biolchin v. CIR, 26 AFTR 2d 70-5727, 70-2 USTC¶ 9674 (7th Cir., 1970) where the courts disregarded the factthat the taxpayer owned the house and denied head of householdstatus. Jane should also fail to quality for head of householdstatus because she did not pay more than one-half of the costs ofmaintaining the household. Secondary issues concern the treatmentof child support payments and whether the furnishing of homeexpenses can be treated as alimony. pp. I:2-22 and I:2-23.

ScholarStockI:2-8

Problems

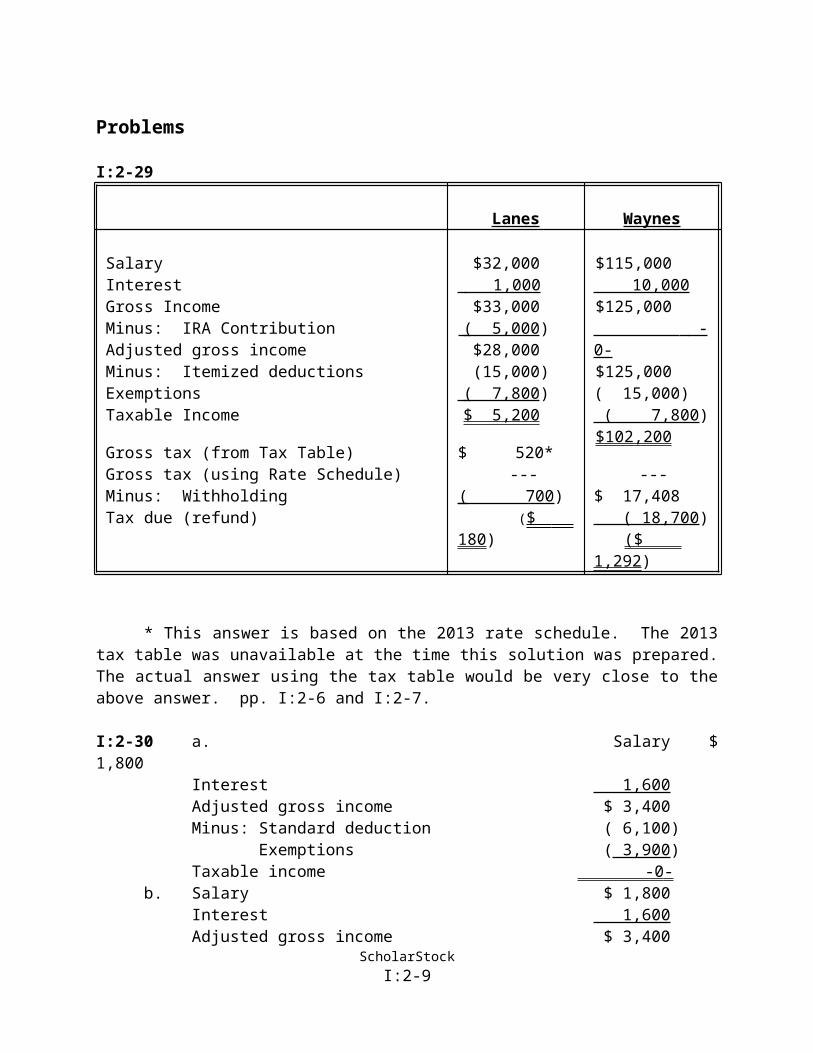

I:2-29

Lanes Waynes

SalaryInterestGross IncomeMinus: IRA ContributionAdjusted gross incomeMinus: Itemized deductionsExemptionsTaxable Income

Gross tax (from Tax Table)Gross tax (using Rate Schedule)Minus: WithholdingTax due (refund)

$32,000 1,000 $33,000

( 5,000 )$28,000(15,000)

( 7,800 )$ 5,200

$ 520*---

( 700 ) ($ 180)

$115,000 10,000$125,000 - 0-$125,000( 15,000) ( 7,800)$102,200

---$ 17,408 ( 18,700) ($ 1,292)

* This answer is based on the 2013 rate schedule. The 2013tax table was unavailable at the time this solution was prepared.The actual answer using the tax table would be very close to theabove answer. pp. I:2-6 and I:2-7.

I:2-30 a. Salary $1,800

Interest 1,600Adjusted gross income $ 3,400Minus: Standard deduction ( 6,100) Exemptions ( 3,900)Taxable income -0 -

b. Salary $ 1,800Interest 1,600Adjusted gross income $ 3,400

ScholarStockI:2-9

Minus: Standard deduction ($1,800 + $350) ( 2,150) Exemption -0 -

Taxable income $ 1,250

pp. I:2-11 and I:2-12.

ScholarStockI:2-10

I:2-31 a. Adjusted gross income$36,000

Minus: Standard deduction (12,200)Exemptions ( 7,800 )Taxable income $16,000

b. Salary (Carl) $14,000Minus: Itemized deductions -0-Exemption ( 3,900 )Taxable income $10,100

Salary (Carol) $22,000Minus: Itemized deductions ( 8,500)Exemption ( 3,900)Taxable income $ 9,600

Note: Because Carol claimed itemized deductions on her return,Carl must also itemize. Both could have claimed a standarddeduction of $6,100 (total of $12,200), so combined they lostdeductions of $3,700 ($12,200–$8,500) by itemizing deductions.

p. I:2-31.

I:2-32 a. Salary and interest$19,100

Minus: Standard deduction (12,200)Exemptions ( 7,800)Taxable income

- 0 -

Gross tax $- 0 -

b. Salary $ 18,000Minus: Standard deduction ( 6,100)Exemption ( 3,900)Taxable income $ 8,000

Gross tax $ 800 ScholarStockI:2-11

Note that Hal would also be required to file a separate returnand pay a tax of $10 based upon taxable income of $100 ($1,100interest - $1,000 standard deduction).

c. Hal and Ruth should not file a joint return. Theparents will have to pay an additional $1,092 in taxes, while Haland Ruth only save $810 [($800 + $10) - $0] by filing a jointreturn.

I:2-33 a. Brian may not be claimed as a dependent becausehis gross income exceeds $3,900 (2013). Brian is not aqualifying child because he is over age 23. He is not an otherdependent because he fails the gross income test.

b. No effect. Brian’s student status is irrelevantbecause he is over age 23. Thus, Wes and Tina may not claimBrian in this case.

c. Sherry may be claimed as a dependent by Wes and Tina asshe is considered a qualifying child. She meets the four testsof relationship, age, abode, and support. Her gross income is notrelevant.

d. Under these facts, Sherry would not be eligible to beclaimed as a dependent because she doesn’t qualify as aqualifying child. Under the other dependent test, the grossincome test may not be waived, as she is not a full-time studentand is over age 18.

e. Granny may not be claimed as a dependent as she failsthe gross income test. Her interest from the U.S. bonds exceeds$3,900 and no exception applies. If Granny’s interest had beenless than $3,900, she would have qualified, as Social Security isnot included in her gross income.

pp. I:2-14 through I:2-18.

I:2-34 a. Carole and John can claim David and Kristen thisyear. Jack is not a qualifying child (over age 18 and not afull-time student) and is not another relative because his grossincome exceeds $3,900. David can be claimed as a dependentbecause he is considered a qualifying child. He meets the four

ScholarStockI:2-12

tests of relationship, age, abode, and support. Gross income isnot considered for the qualifying child test. Kristen also is aqualifying child and can be claimed as a dependent.

b. In this case, Jack would be considered a qualifyingchild as he now meets the age test (under age 24 and a full-timestudent). Carole and John can claim Jack as a dependent.

c. In this case, Jack would not be a qualifying childbecause he fails the age test. However, he is a qualifyingrelative as he meets the relationship, gross income, and supporttests. His gross income is less than $3,900 in 2013.

d. If David was a part-time student, he would not beeither a qualifying child or qualifying relative. With respectto the qualifying child test, David fails the age test as he is apart-time student. As to the qualifying relative test, Davidfails the gross income test.

e. David would not be a dependent as he fails the supporttest for both the qualifying child and qualifying relative tests.pp. I:2-14 through I:2-18.

I:2-35 a. Robert cannot claim Jane as a dependent. Jane isnot his qualifying child as she fails the age, abode, andpresumably the support test. The facts in the problem do notspecify how the $26,000 ($11,000 + $15,000) of support isallocated between Jane and her two children. But this isirrelevant as she fails the age and abode tests. Jane also failsthe qualifying relative test because she has too much grossincome.

b. Jane can claim her children as dependents. Robertapparently provides over one-half of their support, but that isirrelevant as they are Jane’s “qualifying children.” The supportrequirement only says that the children cannot be self-supporting.

c. Jane is entitled to the child credit for each of hertwo children. Even if Robert were eligible to claim dependencyexemptions for the children, he would not benefit from the childcredit because of his income. pp. I:2-14 through I:2-18.

ScholarStockI:2-13

I:2-36 Based on the facts given, Juan cannot claim eitherMaria or Norma as dependents. He can claim Jose only if writtendocumentation exists.

Maria cannot be claimed as a dependent as she provides overone-half of her own support.

Although Juan provides more than one-half of Jose’s support,Jose lives with Linda. Absent required documentation, Linda isentitled to the dependency exemption. If Linda signs a completedForm 8332, Juan can claim the exemption.

Norma is not a “qualifying child” for either her father orJose as she lives with neither. Further, she is a part-timestudent. She does not qualify as a “qualifying relative” becauseshe has too much gross income. pp. I:2-14 through I:2-18.

I:2-37 a. Either Mario or Elaine. Caroline cannot becauseshe is unrelated to Anna, and Doug cannot because he providesless than 10% of Anna's support.

b. Elaine must agree in writing to the arrangement.c. No. Head-of-household status cannot be based on a

dependency exemption obtained as the result of a multiple supportagreement.

d. No. Old-age allowances are not available fordependents. Old-age allowances increase the amount of thestandard deduction. pp. I:2-14 through I:2-18.

I:2-38 a. Joan, the custodial spouse, receives both thedependency exemption and child credit.

b. No. p. I:2-17.

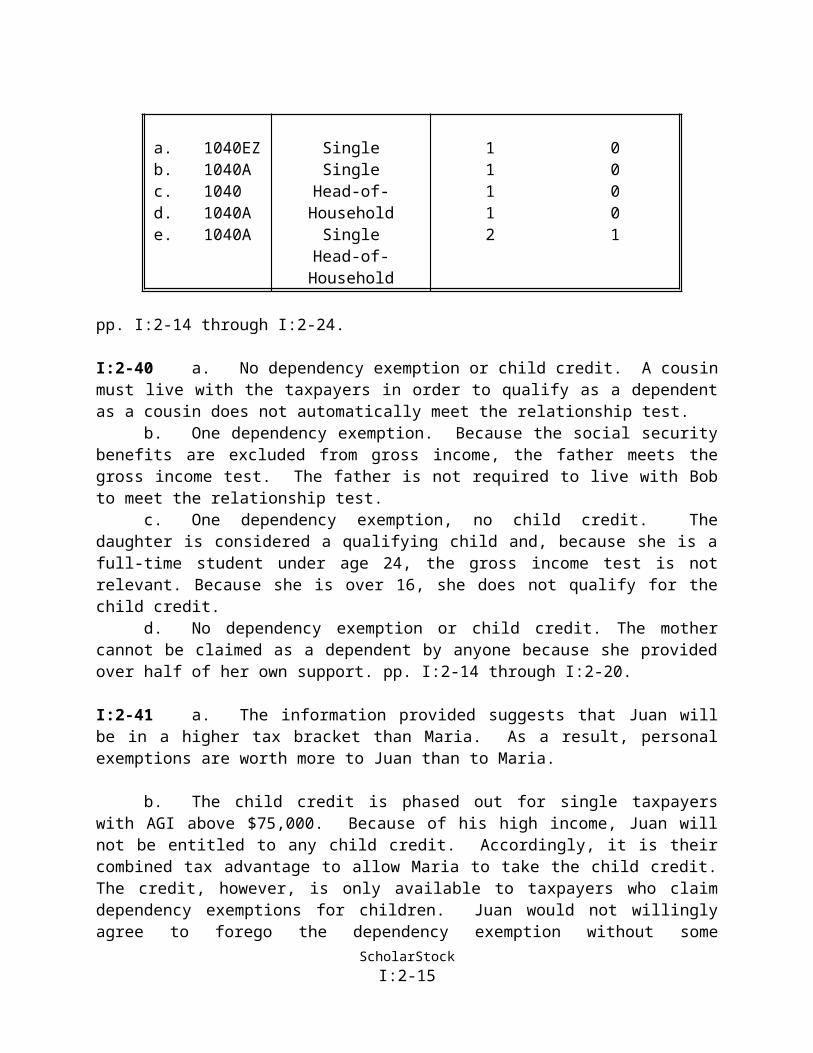

I:2-39

Form Filing Status Exemptions Child Credit

ScholarStockI:2-14

a. 1040EZb. 1040Ac. 1040d. 1040Ae. 1040A

SingleSingleHead-of-HouseholdSingleHead-of-Household

11112

00001

pp. I:2-14 through I:2-24.

I:2-40 a. No dependency exemption or child credit. A cousinmust live with the taxpayers in order to qualify as a dependentas a cousin does not automatically meet the relationship test.

b. One dependency exemption. Because the social securitybenefits are excluded from gross income, the father meets thegross income test. The father is not required to live with Bobto meet the relationship test.

c. One dependency exemption, no child credit. Thedaughter is considered a qualifying child and, because she is afull-time student under age 24, the gross income test is notrelevant. Because she is over 16, she does not qualify for thechild credit.

d. No dependency exemption or child credit. The mothercannot be claimed as a dependent by anyone because she providedover half of her own support. pp. I:2-14 through I:2-20.

I:2-41 a. The information provided suggests that Juan willbe in a higher tax bracket than Maria. As a result, personalexemptions are worth more to Juan than to Maria.

b. The child credit is phased out for single taxpayerswith AGI above $75,000. Because of his high income, Juan willnot be entitled to any child credit. Accordingly, it is theircombined tax advantage to allow Maria to take the child credit.The credit, however, is only available to taxpayers who claimdependency exemptions for children. Juan would not willinglyagree to forego the dependency exemption without some

ScholarStockI:2-15

consideration. The tax savings received by Maria from thedependency exemptions and the child credit should be consideredwhen the amount of child support is being determined

c. As the custodial parent, Maria is entitled to file as ahead-of-household. This is true even if she does not claim thedependency exemption or child credit. Juan will file as a singletaxpayer. pp. I:2-18 and I:2-19.

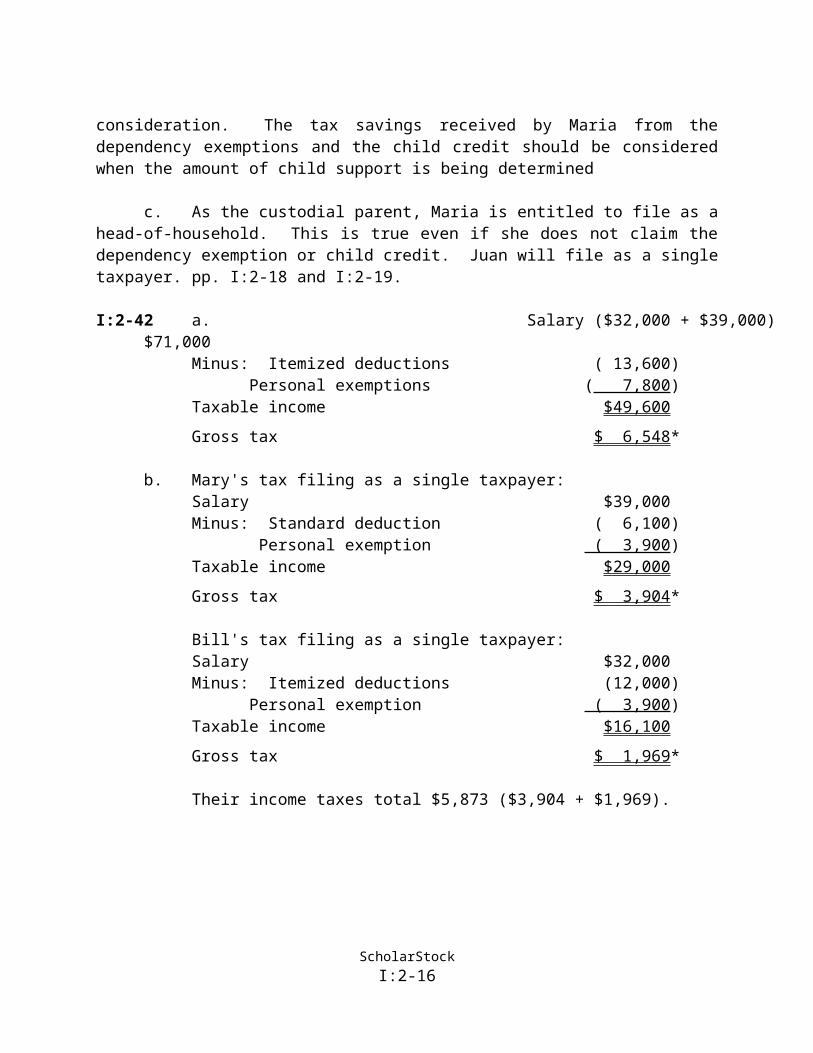

I:2-42 a. Salary ($32,000 + $39,000)$71,000

Minus: Itemized deductions ( 13,600) Personal exemptions ( 7,800)

Taxable income $49,600Gross tax $ 6,548*

b. Mary's tax filing as a single taxpayer:Salary $39,000Minus: Standard deduction ( 6,100)

Personal exemption ( 3,900)Taxable income $29,000Gross tax $ 3,904*

Bill's tax filing as a single taxpayer:Salary $32,000Minus: Itemized deductions (12,000)

Personal exemption ( 3,900)Taxable income $16,100Gross tax $ 1,969*

Their income taxes total $5,873 ($3,904 + $1,969).

ScholarStockI:2-16

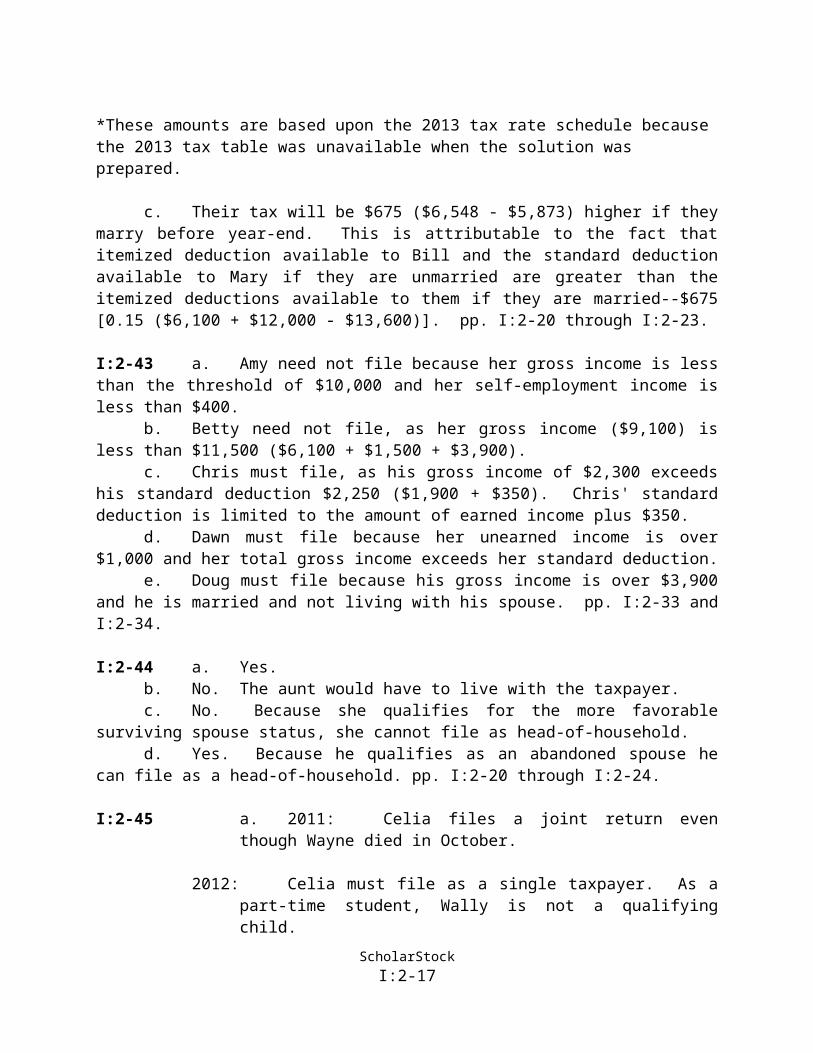

*These amounts are based upon the 2013 tax rate schedule because the 2013 tax table was unavailable when the solution was prepared.

c. Their tax will be $675 ($6,548 - $5,873) higher if theymarry before year-end. This is attributable to the fact thatitemized deduction available to Bill and the standard deductionavailable to Mary if they are unmarried are greater than theitemized deductions available to them if they are married--$675[0.15 ($6,100 + $12,000 - $13,600)]. pp. I:2-20 through I:2-23.

I:2-43 a. Amy need not file because her gross income is lessthan the threshold of $10,000 and her self-employment income isless than $400.

b. Betty need not file, as her gross income ($9,100) isless than $11,500 ($6,100 + $1,500 + $3,900).

c. Chris must file, as his gross income of $2,300 exceedshis standard deduction $2,250 ($1,900 + $350). Chris' standarddeduction is limited to the amount of earned income plus $350.

d. Dawn must file because her unearned income is over$1,000 and her total gross income exceeds her standard deduction.

e. Doug must file because his gross income is over $3,900and he is married and not living with his spouse. pp. I:2-33 andI:2-34.

I:2-44 a. Yes.b. No. The aunt would have to live with the taxpayer.c. No. Because she qualifies for the more favorable

surviving spouse status, she cannot file as head-of-household.d. Yes. Because he qualifies as an abandoned spouse he

can file as a head-of-household. pp. I:2-20 through I:2-24.

I:2-45 a. 2011: Celia files a joint return eventhough Wayne died in October.

2012: Celia must file as a single taxpayer. As apart-time student, Wally is not a qualifyingchild.

ScholarStockI:2-17

2013: Same as 2012.

2014: Same as 2012.b. Single. Juanita does not qualify for head-of-household

status because Josh is not a “qualifying child.” He is over 17and is not a full-time student.

c. Gertrude may use the head-of-household filing status.Even though she is still legally married, she meets the tests foran abandoned spouse. She lived apart from her spouse for thelast six months of the taxable year and paid over one-half thecost of maintaining a household for her dependent son. pp. I:2-21 through I:2-23.

Note to Instructor: A good exercise is to ask the class how thisproblem would change if Wally were a full-time student rather than part-time. Celia would qualify as a surviving spouse in 2012 and 2013 and a single taxpayer in 2014.

ScholarStockI:2-18

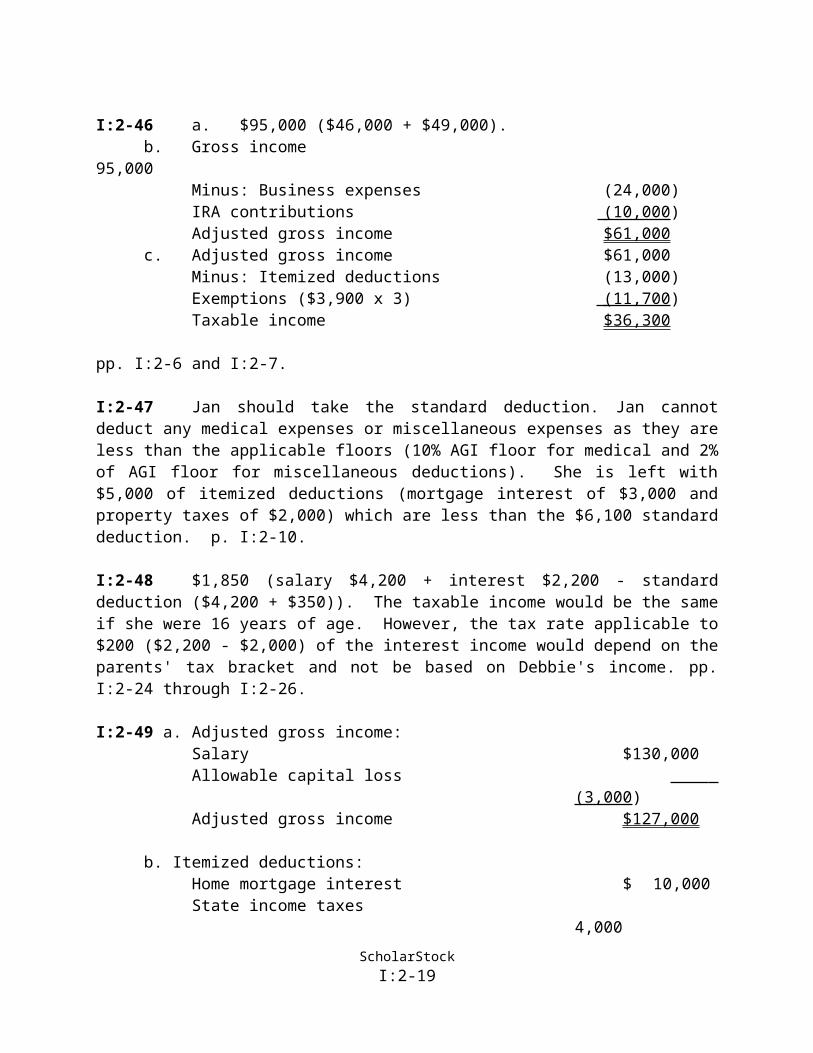

I:2-46 a. $95,000 ($46,000 + $49,000).b. Gross income

95,000Minus: Business expenses (24,000)IRA contributions (10,000 )Adjusted gross income $61,000

c. Adjusted gross income $61,000Minus: Itemized deductions (13,000)Exemptions ($3,900 x 3) (11,700 )Taxable income $36,300

pp. I:2-6 and I:2-7.

I:2-47 Jan should take the standard deduction. Jan cannotdeduct any medical expenses or miscellaneous expenses as they areless than the applicable floors (10% AGI floor for medical and 2%of AGI floor for miscellaneous deductions). She is left with$5,000 of itemized deductions (mortgage interest of $3,000 andproperty taxes of $2,000) which are less than the $6,100 standarddeduction. p. I:2-10.

I:2-48 $1,850 (salary $4,200 + interest $2,200 - standarddeduction ($4,200 + $350)). The taxable income would be the sameif she were 16 years of age. However, the tax rate applicable to$200 ($2,200 - $2,000) of the interest income would depend on theparents' tax bracket and not be based on Debbie's income. pp.I:2-24 through I:2-26.

I:2-49 a. Adjusted gross income:Salary $130,000Allowable capital loss

(3,000)Adjusted gross income $127,000

b. Itemized deductions:Home mortgage interest $ 10,000State income taxes

4,000ScholarStockI:2-19

Charitable contributions 5,000

Itemized deductions $ 19,000

c. Personal exemptions (4) $ 15,600

d. Taxable incomeAdjusted gross income $127,000Itemized deductions

(19,000) Personal exemptions

(15,600)Taxable income $ 92,400

ScholarStockI:2-20

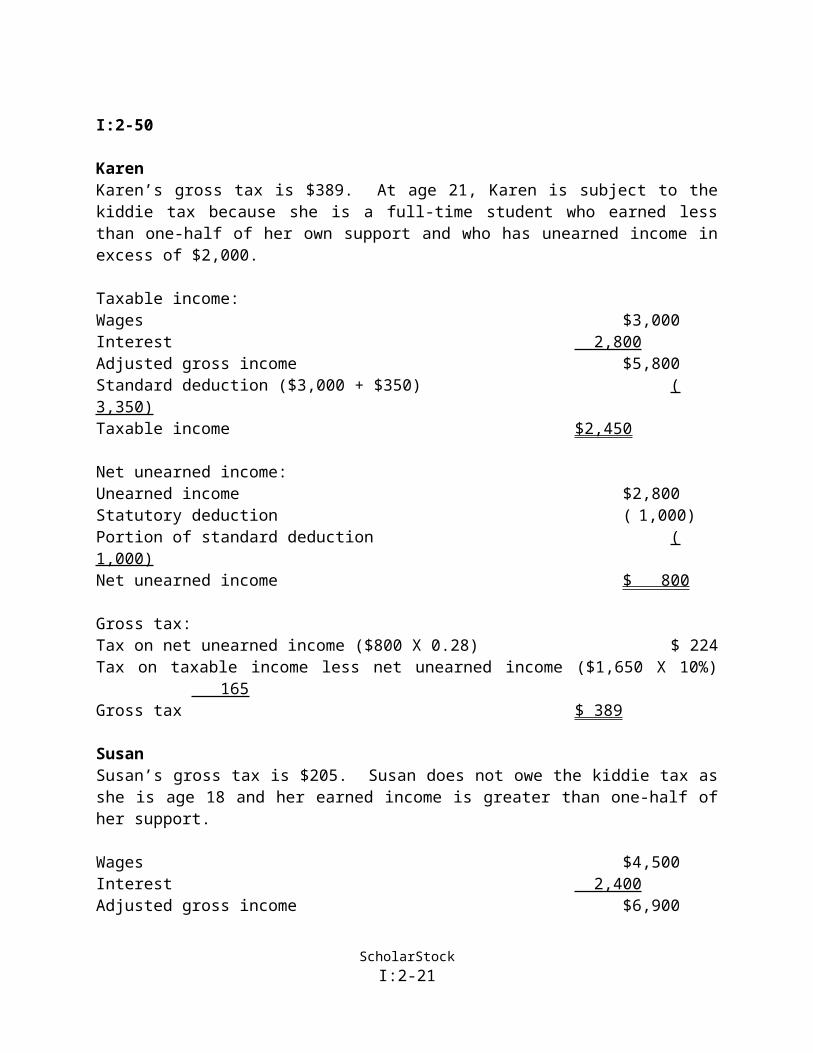

I:2-50

KarenKaren’s gross tax is $389. At age 21, Karen is subject to thekiddie tax because she is a full-time student who earned lessthan one-half of her own support and who has unearned income inexcess of $2,000.

Taxable income:Wages $3,000Interest 2,800Adjusted gross income $5,800Standard deduction ($3,000 + $350) (3,350)Taxable income $2,450

Net unearned income:Unearned income $2,800Statutory deduction ( 1,000)Portion of standard deduction (1,000)Net unearned income $ 800

Gross tax:Tax on net unearned income ($800 X 0.28) $ 224Tax on taxable income less net unearned income ($1,650 X 10%)

165Gross tax $ 389

SusanSusan’s gross tax is $205. Susan does not owe the kiddie tax asshe is age 18 and her earned income is greater than one-half ofher support.

Wages $4,500Interest 2,400Adjusted gross income $6,900

ScholarStockI:2-21

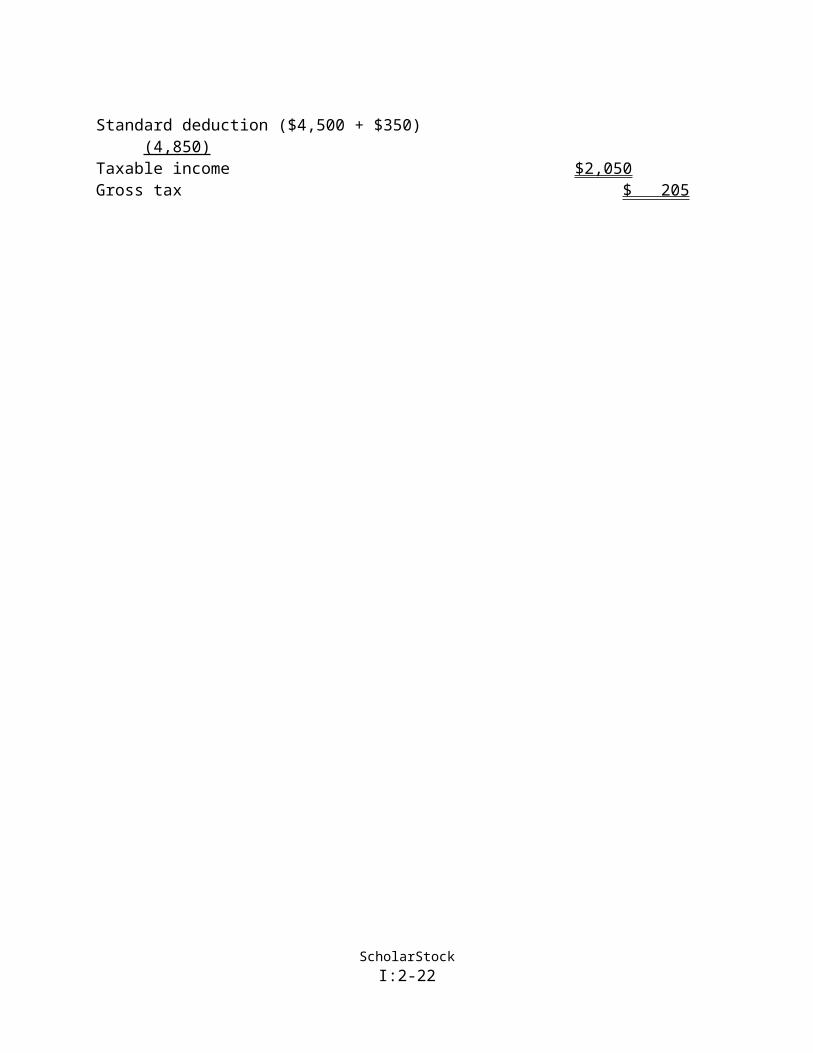

Standard deduction ($4,500 + $350)(4,850)

Taxable income $2,050Gross tax $ 205

ScholarStockI:2-22

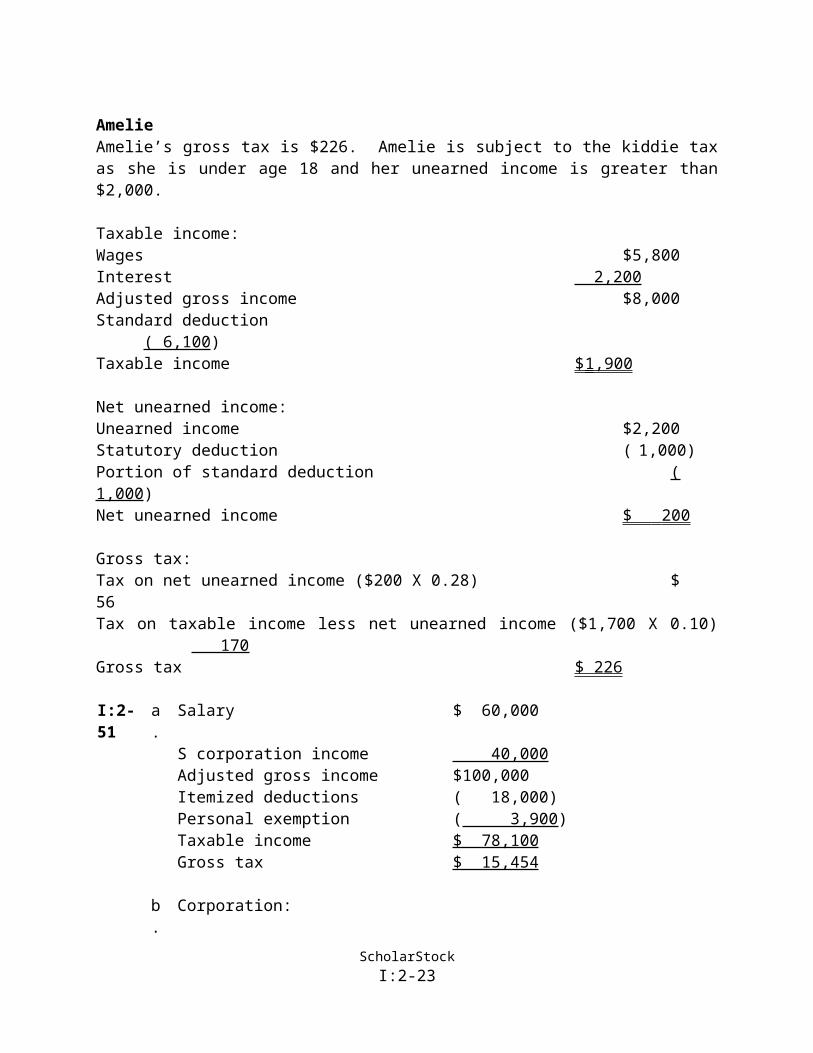

AmelieAmelie’s gross tax is $226. Amelie is subject to the kiddie taxas she is under age 18 and her unearned income is greater than$2,000.

Taxable income:Wages $5,800Interest 2,200Adjusted gross income $8,000Standard deduction

( 6,100)Taxable income $ 1,900

Net unearned income:Unearned income $2,200Statutory deduction ( 1,000)Portion of standard deduction (1,000)Net unearned income $ 200

Gross tax:Tax on net unearned income ($200 X 0.28) $56Tax on taxable income less net unearned income ($1,700 X 0.10)

170Gross tax $ 226

I:2-51

a.

Salary $ 60,000

S corporation income 40,000 Adjusted gross income $100,000Itemized deductions ( 18,000)Personal exemption ( 3,900)Taxable income $ 78,100 Gross tax $ 15,454

b.

Corporation:

ScholarStockI:2-23

Taxable income $ 40,000 Gross tax (0.15 x $40,000) $ 6,000

Individual:Salary $ 60,000Dividend ($40,000 - $6,000) 34,000 Adjusted gross income $ 94,000Itemized deductions ( 18,000)Personal exemption ( 3,900 )Taxable income $ 72,100 Gross tax $ 10,554 Total tax ($6,000 +$10,554)

$ 16,554

*The individual’s gross tax is the total of the tax onthe dividend income and the tax on the remaining income.The tax on the dividend income of $34,000 is $5,100(0.15 x $34,000). The tax on the remaining income of$38,100 ($72,100 - $34,000) is $5,454 computed using therate schedule for single taxpayers.

c.

The answer to part a is unchanged as the shareholder istaxed on the S corporation’s income regardless ofwhether it is distributed. In part b, the corporation’stax is the same, $6,000, but the shareholder is onlytaxed on the salary of $60,000.Adjusted gross income $ 60,000Itemized deductions ( 18,000)Personal exemption ( 3,900)Taxable income $ 38,100 Gross tax $ 5,454 Total tax ($6,000 + $5,454) $ 11,454

The shareholder will be taxed on the corporation’sundistributed income if it is paid out as a dividend ina future year.

pp. I:2-26 through I:2-29.ScholarStockI:2-24

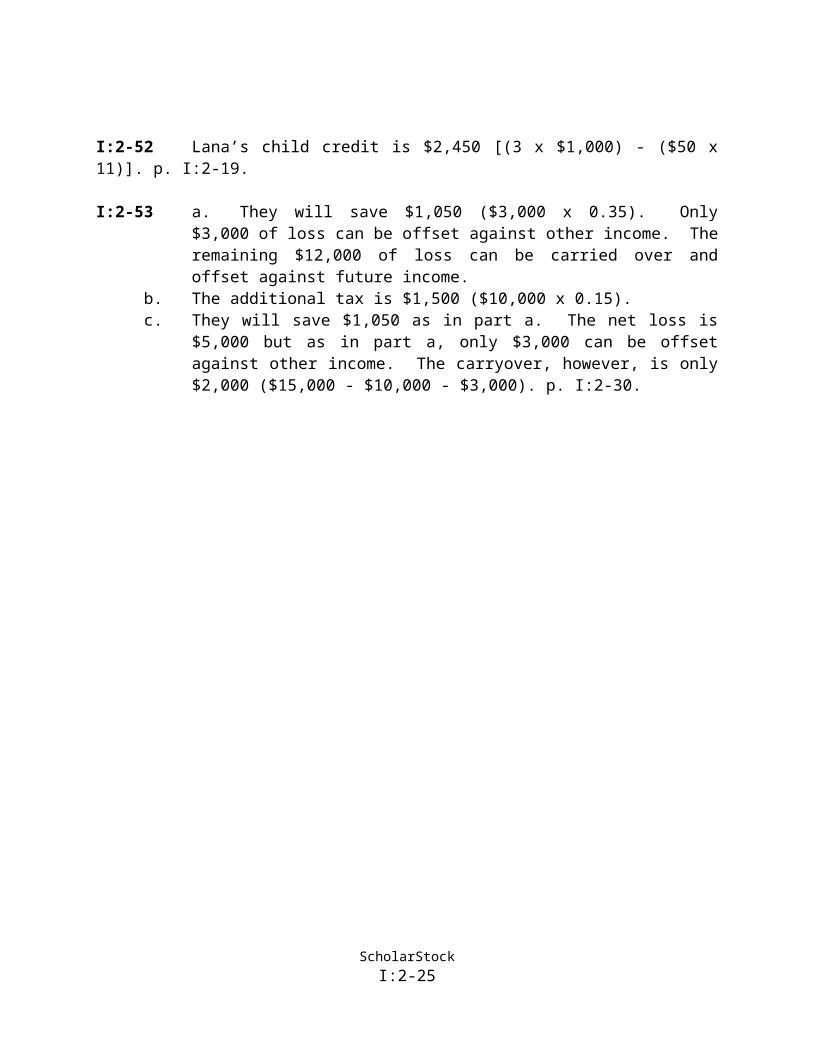

I:2-52 Lana’s child credit is $2,450 [(3 x $1,000) - ($50 x11)]. p. I:2-19.

I:2-53 a. They will save $1,050 ($3,000 x 0.35). Only$3,000 of loss can be offset against other income. Theremaining $12,000 of loss can be carried over andoffset against future income.

b. The additional tax is $1,500 ($10,000 x 0.15).c. They will save $1,050 as in part a. The net loss is

$5,000 but as in part a, only $3,000 can be offsetagainst other income. The carryover, however, is only$2,000 ($15,000 - $10,000 - $3,000). p. I:2-30.

ScholarStockI:2-25

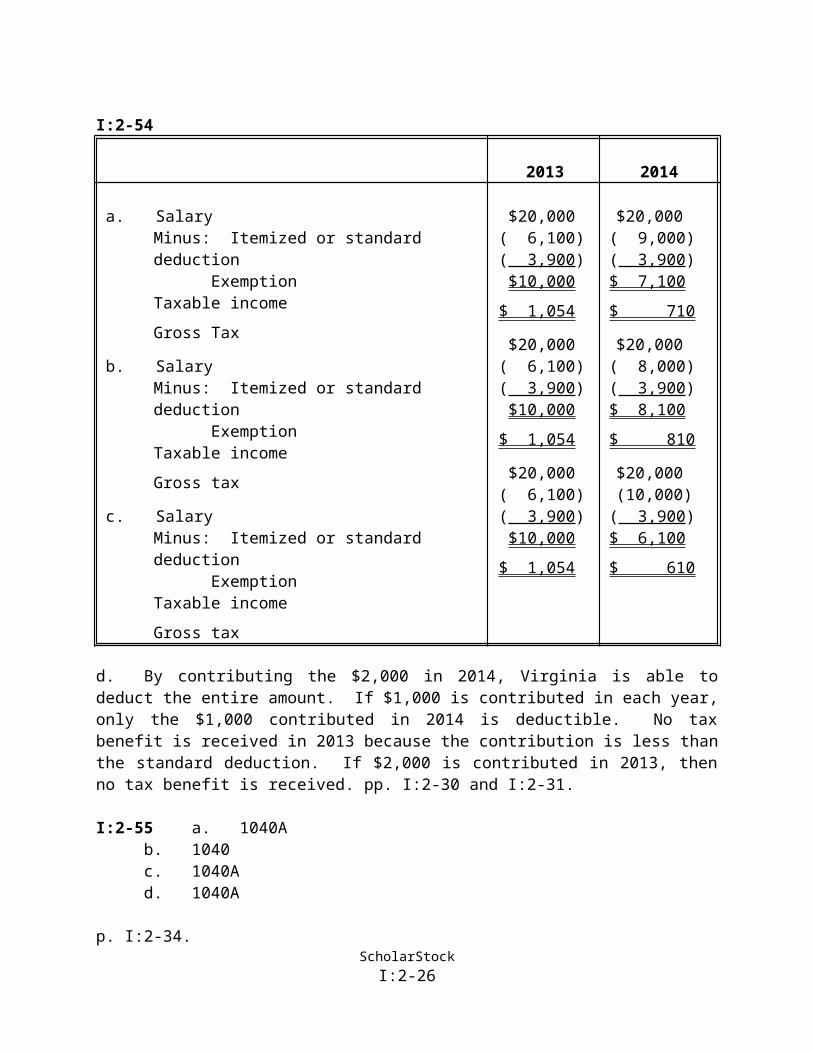

I:2-54

2013 2014

a. SalaryMinus: Itemized or standard deduction

ExemptionTaxable incomeGross Tax

b. SalaryMinus: Itemized or standard deduction

ExemptionTaxable incomeGross tax

c. SalaryMinus: Itemized or standard deduction

ExemptionTaxable incomeGross tax

$20,000( 6,100)( 3,900)$10,000

$ 1,054

$20,000( 6,100)( 3,900)$10,000

$ 1,054

$20,000( 6,100)( 3,900)$10,000

$ 1,054

$20,000( 9,000)( 3,900)$ 7,100$ 710

$20,000( 8,000)( 3,900)$ 8,100$ 810

$20,000(10,000)( 3,900)$ 6,100$ 610

d. By contributing the $2,000 in 2014, Virginia is able todeduct the entire amount. If $1,000 is contributed in each year,only the $1,000 contributed in 2014 is deductible. No taxbenefit is received in 2013 because the contribution is less thanthe standard deduction. If $2,000 is contributed in 2013, thenno tax benefit is received. pp. I:2-30 and I:2-31.

I:2-55 a. 1040Ab. 1040c. 1040Ad. 1040A

p. I:2-34.ScholarStockI:2-26

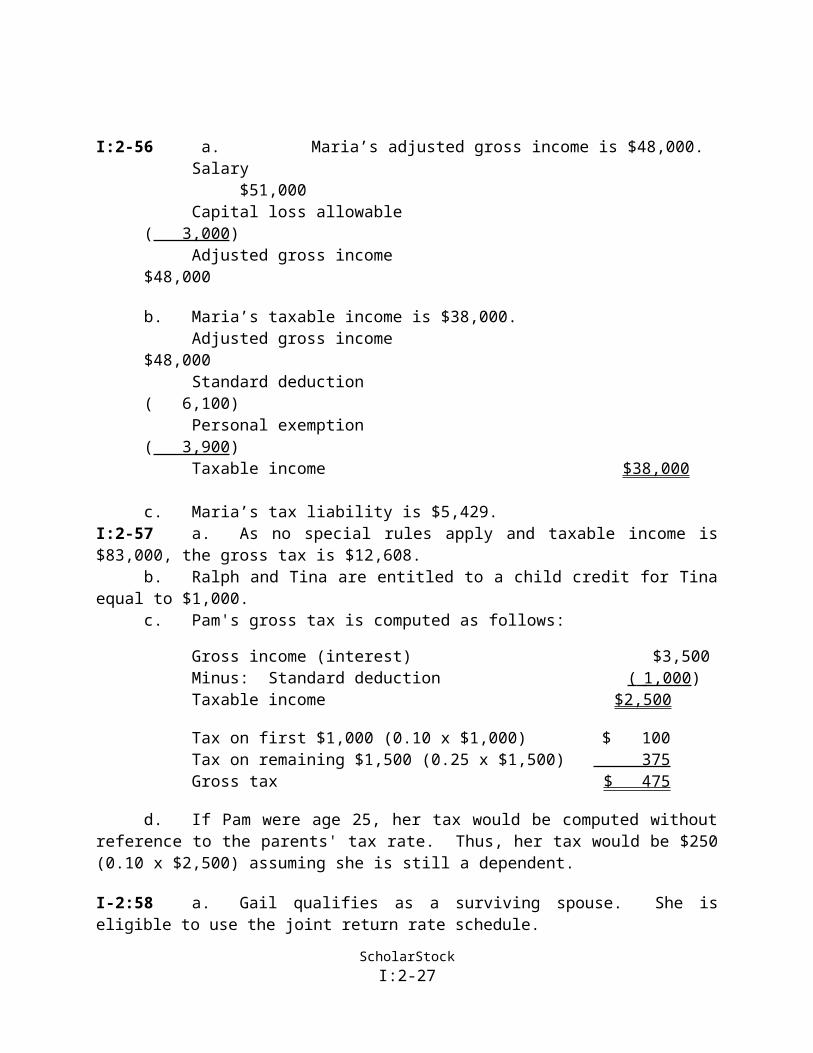

I:2-56 a. Maria’s adjusted gross income is $48,000.Salary

$51,000Capital loss allowable

( 3,000)Adjusted gross income

$48,000

b. Maria’s taxable income is $38,000.Adjusted gross income

$48,000Standard deduction

( 6,100)Personal exemption

( 3,900)Taxable income $38,000

c. Maria’s tax liability is $5,429.I:2-57 a. As no special rules apply and taxable income is$83,000, the gross tax is $12,608.

b. Ralph and Tina are entitled to a child credit for Tinaequal to $1,000.

c. Pam's gross tax is computed as follows:

Gross income (interest) $3,500Minus: Standard deduction ( 1,000 )Taxable income $2,500

Tax on first $1,000 (0.10 x $1,000) $ 100Tax on remaining $1,500 (0.25 x $1,500) 375Gross tax $ 475

d. If Pam were age 25, her tax would be computed withoutreference to the parents' tax rate. Thus, her tax would be $250(0.10 x $2,500) assuming she is still a dependent.

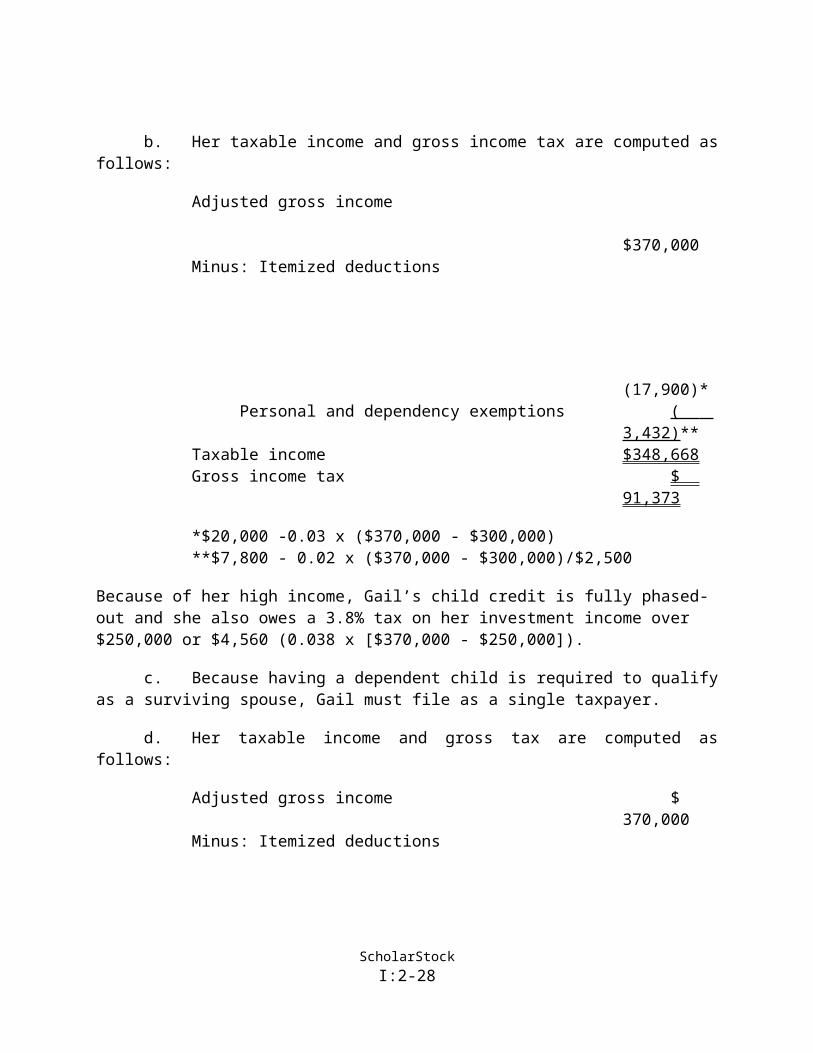

I-2:58 a. Gail qualifies as a surviving spouse. She iseligible to use the joint return rate schedule.

ScholarStockI:2-27

b. Her taxable income and gross income tax are computed asfollows:

Adjusted gross income

$370,000Minus: Itemized deductions

(17,900)*

Personal and dependency exemptions ( 3,432)**

Taxable income $348,668Gross income tax $

91,373

*$20,000 -0.03 x ($370,000 - $300,000)**$7,800 - 0.02 x ($370,000 - $300,000)/$2,500

Because of her high income, Gail’s child credit is fully phased-out and she also owes a 3.8% tax on her investment income over $250,000 or $4,560 (0.038 x [$370,000 - $250,000]).

c. Because having a dependent child is required to qualifyas a surviving spouse, Gail must file as a single taxpayer.

d. Her taxable income and gross tax are computed asfollows:

Adjusted gross income $

370,000Minus: Itemized deductions

ScholarStockI:2-28

(16,400)*Personal exemption

( 156)**

Taxable income $353,444Gross income tax

$100,767

*$20,000 -0.03 x ($370,000 - $250,000)**$3,900 - 0.02 x ($370,000 - $250,000)/$2,500

As noted in part b, she owes the additional on her investment income, in this case, over $200,000 because she is a single taxpayer.

pp. I:2-10, I:2-18, and I:2-30.Tax Strategy Problems

I:2-59 The tax liability under the three alternatives iscomputed as below:

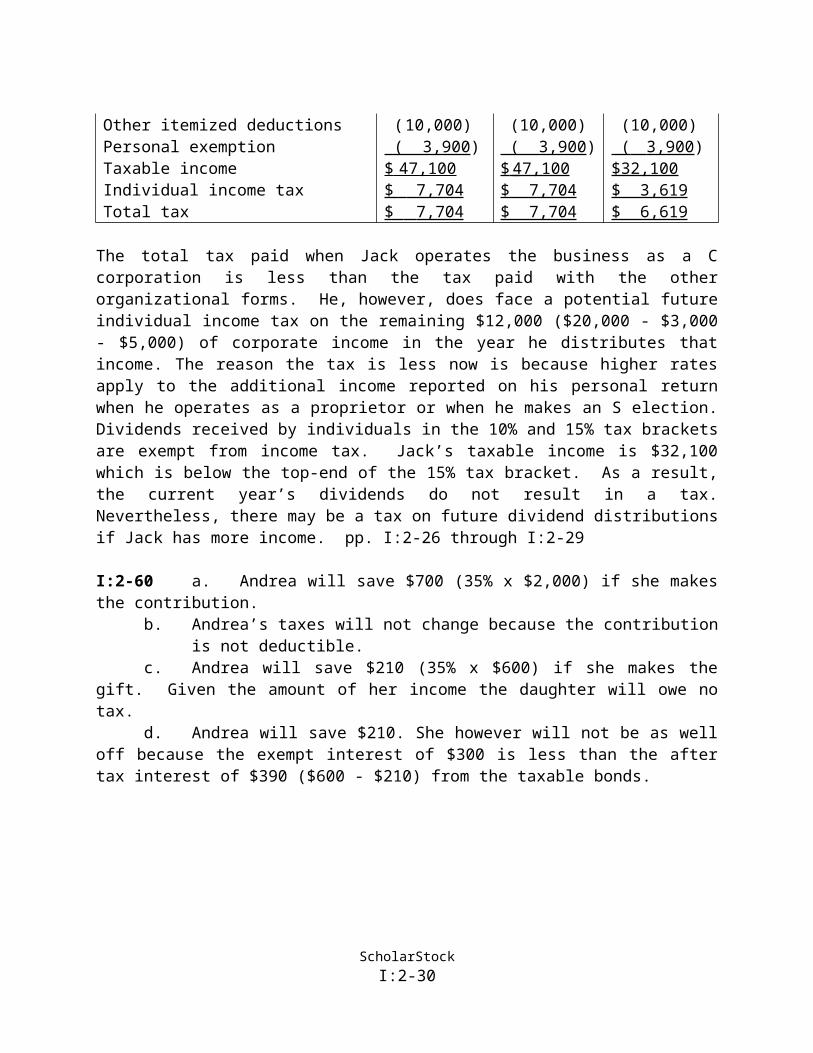

Business income Proprietorship

SCorporation

CCorporation

Operating income $ 60,000 $60,000 $60,000Compensation paid to Jack _______ ( 40,000 ) ( 40,000 )Net $ 60,000 $20,000 $20,000Corporate income tax $ 3,000

Jack’s incomeBusiness income $ 60,000 $20,000Compensation 40,000 $40,000Dividends 5,000Other income 1,000 1,000 1,000Adjusted Gross Income $ 61,000 $61,000 $46,000

ScholarStockI:2-29

Other itemized deductions ( 10,000) (10,000) (10,000)Personal exemption ( 3,900) ( 3,900) ( 3,900 )Taxable income $ 47,100 $ 47,100 $32,100Individual income tax $ 7,704 $ 7,704 $ 3,619Total tax $ 7,704 $ 7,704 $ 6,619

The total tax paid when Jack operates the business as a Ccorporation is less than the tax paid with the otherorganizational forms. He, however, does face a potential futureindividual income tax on the remaining $12,000 ($20,000 - $3,000- $5,000) of corporate income in the year he distributes thatincome. The reason the tax is less now is because higher ratesapply to the additional income reported on his personal returnwhen he operates as a proprietor or when he makes an S election.Dividends received by individuals in the 10% and 15% tax bracketsare exempt from income tax. Jack’s taxable income is $32,100which is below the top-end of the 15% tax bracket. As a result,the current year’s dividends do not result in a tax.Nevertheless, there may be a tax on future dividend distributionsif Jack has more income. pp. I:2-26 through I:2-29

I:2-60 a. Andrea will save $700 (35% x $2,000) if she makesthe contribution.

b. Andrea’s taxes will not change because the contributionis not deductible.

c. Andrea will save $210 (35% x $600) if she makes thegift. Given the amount of her income the daughter will owe notax.

d. Andrea will save $210. She however will not be as welloff because the exempt interest of $300 is less than the aftertax interest of $390 ($600 - $210) from the taxable bonds.

ScholarStockI:2-30

Tax Form/Return Preparation Problems

I:2-61 (See Instructor’s Resource Manual)

I:2-62 (See Instructor’s Resource Manual)

I:2-63 (See Instructor’s Resource Manual)

Case Study Problems

I:2-64 This question has some interesting implications. Oneproblem relates to the sale of the loss property. Bala and Anncan only deduct $3,000 of the capital loss from ordinary incomeeach year. As a result, it would take ten years to use up theloss unless they realize a capital gain against which to offsetthe loss. Although a $3,000 capital loss offsets income thatwould otherwise be taxed at 35% it takes a long time to use upthe loss. If Bala and Ann sell both of the parcels they own theywill realize a net loss of $8,000 which will be used up in thecurrent and next two years even if they realize no additionalgains. Further, the $8,000 net loss will offset income thatwould otherwise be taxed at 35%.

Because of her age, Kim is currently subject to the “kiddietax”, which means that most of her capital gain will be taxed ather parents’ rate (15% for capital gains). By waiting to sellher land when she is no longer subject to the kiddie tax, shewill be able to use her standard deduction to offset part of thegain and the remainder may be taxed at a low rate (perhaps 15% orless if capital gains are taxed at preferential rates in futureyears). p. I:2-28.

I:2-65 As Larry and Sue were married at the end of the year,they can file either a joint income tax return or two separatereturns. On the surface there is not much difference between thetax liability on a joint return versus separate returns. Theimportant issue here is the fact that Sue believes that Larry maybe under-reporting tip income. If they file a joint return, Suemay be liable for the joint tax liability including penalties

ScholarStockI:2-31

that may result from under-reporting. There is an innocentspouse provision, but one condition for claiming innocent spousestatus is that the taxpayer did not know and had no reason toknow that there was under-reporting. As Sue is suspicious of herhusband, she should file a separate return to protect herselffrom possible tax liability associated with unreported income.pp. I:2-29 and I:2-30.

Tax Research Problems

I:2-66 Since the stepdaughter and her family do not live withEd, they must be related to him in order to qualify as hisdependents. Clearly, the stepdaughter meets this test.Stepdaughters are specifically listed in Sec. 152(a)(2) asrelatives. Further, Reg. Sec. 1.152-2(d) states that arelationship "once existing will not terminate by divorce ordeath of a spouse."

On the other hand, Ed is not related to the stepdaughter'shusband. Stepson-in-laws are not listed in Sec. 152(a). The TaxCourt in Desio Barbetti [9 T.C. 1097 (1947)] held that the term"grandchildren" does not include step-grandchildren, and thatneither stepchild nor son-in-law covers stepson-in-laws. Currentlaw refers to step-children and their descendants which suggeststhat the child is eligible to be claimed as a dependent.I:2-67 The full exemption deduction for a dependent isavailable even though the dependent is born or dies during theyear. In Rev. Rul. 73-156, 1973-1 C.B. 58 the IRS ruled that anexemption may be claimed if state or local law treats the childas having been born alive, and this is evidenced by an officialdocument such as a birth or death certificate. If the child hadno social security number the IRS instructs taxpayers to enter“DIED” in place of the social security number on Form 1040.

I:2-68 Although Larry may not meet the technical definition of"blind" when he wears the new contact lens, the fact that he canonly wear the lens for brief times means that he cannot depend onhaving the advantage of improved sight. Therefore, the Tax Courtin Emanuel Hollman, 38 T.C. 251 (1963) granted an extra personal

ScholarStockI:2-32

exemption for blindness permitted under prior law. It seemslikely that the same rule would be available to taxpayers todayclaiming the additional standard deduction amount available toblind taxpayers under current law.

“What Would You Do In This Situation?” Solution

Ch. I:2, p. I:2-28. What Would You Do In This Situation?

A married person has the option of filing a joint return oras a married person filing separately. Whether a person ismarried depends on the laws of the state of residence. Theabandoned spouse rules provide an exception, but the rules onlyapply if the taxpayer maintains a household for a dependentchild. This case does not indicate that Jane has a child.

State laws establish conditions that must be met for amissing person to be declared legally dead. Typically, a missingperson cannot be declared legally dead for seven years. Duringthe interim, a guardian can be appointed to handle the affairs ofthe missing person. This all taken together indicates that Janeis still classified as a married person for tax purposes.

The IRS has ruled that a spouse who is appointed guardian mayelect to file a joint return with his or her missing spouse (Rev.Rul. 55-387, 1955-1 CB 131). The joint return would enable Jane totake advantage of the lower rate schedule, claim an additionalpersonal exemption, and utilize a larger standard deduction.Before she could file a joint return, Jane would have to beappointed as Jim's guardian.

Choosing to file a joint return does have some risks. Janedoes not know how much income Jim has or whether he is evenalive. Should she file a joint return, the innocent spouseprovision probably would protect Jane from tax on any income thatJim may be earning.

One unusual aspect of the situation is that the IRS may knowScholarStockI:2-33

of her husband's status. This is because the IRS would have anyreturn that Jim is filing and have information on any income thatis being reported under his social security number on 1099's andW-2's. The IRS is prohibited from giving out information ontaxpayers including where they live. As a result, it is unclearwhat the IRS would do with the information should Jane file ajoint return.

Jane could file for a divorce. If the divorce were grantedbefore year end, Jane would file as a single taxpayer. Also, ifJim is declared legally dead Jane will file as a single taxpayer.

ScholarStockI:2-34

Copyright © 2022 FDOKUMEN

![* tax c u t]](https://static.fdokumen.com/doc/165x107/631a284e0255356abc089143/-tax-c-u-t.jpg)