CHAPTER 14 - Bahattin Buyuksahin

115

Bond Prices and Yields CHAPTER 14

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of CHAPTER 14 - Bahattin Buyuksahin

Bond Prices and Yields

CHAPTER 14

BOND CHARACTERISTICS

Face or par value

Coupon rate

Zero coupon bond

Compounding and payments

Accrued Interest

Indenture

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 2

DIFFERENT ISSUERS OF BONDS

U.S. Treasury Notes and Bonds

Corporations Municipalities International Governments and Corporations Innovative Bonds Floaters and Inverse Floaters Asset-Backed Catastrophe

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 3

FIGURE 14.1 LISTING OF TREASURY

ISSUES

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 4

FIGURE 14.2 LISTING OF CORPORATE

BONDS

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 5

PROVISIONS OF BONDS

Secured or unsecured

Call provision

Convertible provision

Put provision (putable bonds)

Floating rate bonds

Preferred Stock

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 6

CONVERTIBLE BONDS

Give bondholders an option to exchange each bond for a specified nb of

shares of common stock

Conversion ratio

= number of shares per convertible bond

Market conversion value

= conversion ratio * current market value per share

Conversion premium

= bond value - conversion value

intuitively: extra amount to pay so as to become a shareholder

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 7

CONVERSION EXAMPLE

Burroughs Corporation

7 ¼% Due 8-1-2010

--------------------------------------------------------------------------

Agency rating (Moody’s/S&P) A3/A-

Conversion ratio 12.882

Market price of convertible 102

Market price of common stock $ 66.00

Dividend per share-common $ 2.60

Call price (first call: 8-1-1990) 106

Estimated floor price $ 66.50

-------------------------------------------------------------------------

(a) Market conversion value?

(b) Conversion premium per common share?

(c) Current yield-convertible?

(d) Dividend yield-common?

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 8

CONVERSION EXAMPLE

(a) Market conversion price = value if converted into stock

= market price of common stock x conversion ratio

= 12.882 x $66 = $850.21

(b) Conversion premium = Bond price – value if converted into stock

= $1020 – (12.882 x $66) = $1020 - $850.21 = $169.79

Thus, the conversion premium per share = ($169.79/12.882) = $13.18

(c) Current yield = (coupon/price) = ($72.50/$1020) = 0.0711 = 7.11%

(d) Dividend yield on common = (dividend per share/price) = ($2.60/$66) = 3.94%

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 9

INNOVATION IN THE BOND MARKET

Inverse Floaters

Asset-Backed Bonds

Catastrophe Bonds

Indexed Bonds

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 10

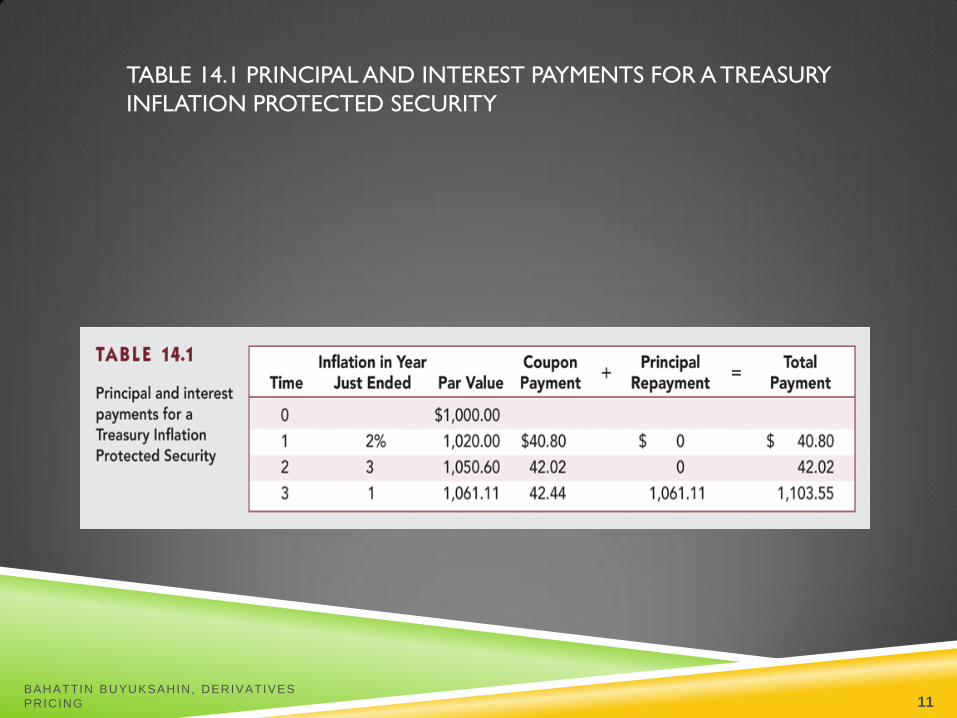

TABLE 14.1 PRINCIPAL AND INTEREST PAYMENTS FOR A TREASURY

INFLATION PROTECTED SECURITY

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 11

BOND PRICES AND YIELDS

Time value of money and bond pricing

Time to maturity and risk

Yield to maturity

vs. yield to call

vs. realized compound yield

Determinants of YTM

risk, maturity, holding period, etc.

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 12

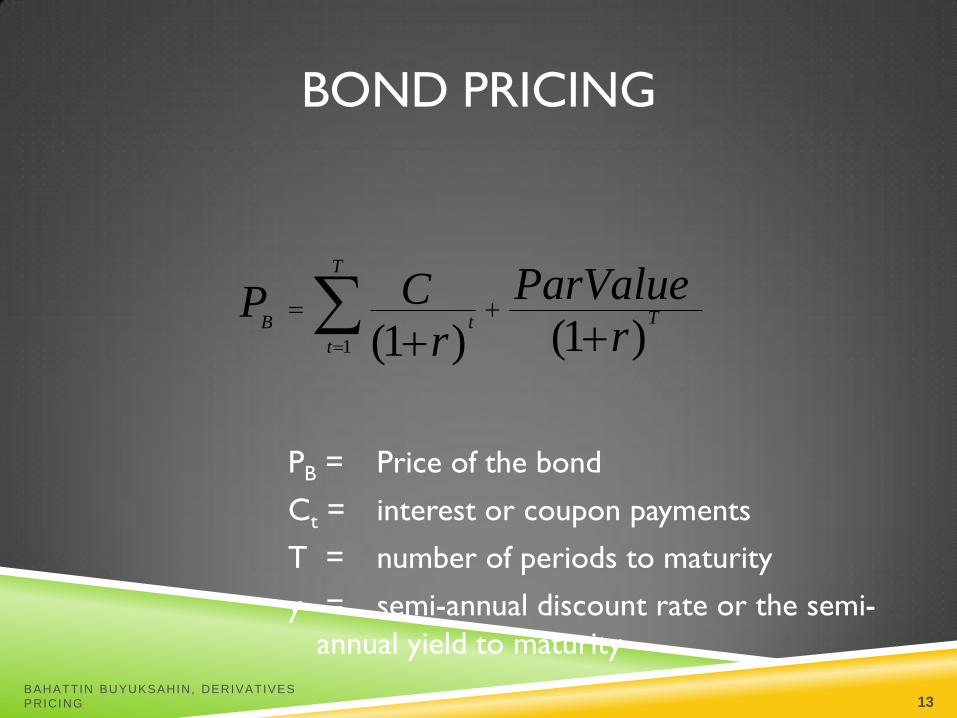

BOND PRICING

1 (1 )(1 )

T

TB t

t

ParValueCPrr

PB = Price of the bond

Ct = interest or coupon payments

T = number of periods to maturity

y = semi-annual discount rate or the semi-

annual yield to maturity

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 13

Ct = 40 (SA)

P = 1000

T = 20 periods

r = 3% (SA)

PRICE: 10-YR, 8% COUPON, FACE =

$1,000

77.148,1$

)03.1(

1000

03.1

140

20

20

1

P

Pt

t

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 14

BOND PRICING

Equation:

P = PV(annuity) + PV(final payment)

=

Example: Ct = $40; Par = $1,000; disc. rate = 4%; T=60 )1()1(1 r

Par

r

couponT

T

tt

000,1$06.95$94.904$)04.01(

000,1$

)04.01(

40$60

60

1

t

tP

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 15

BOND PRICES AND YIELDS

Prices and Yields (required rates of return)

have an inverse relationship

When yields get very high the value of the

bond will be very low

When yields approach zero, the value of the

bond approaches the sum of the cash flows

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 16

PRICES VS. YIELDS

P yield

intuition

convexity

Fig 14.3

intuition: yield P price impact

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 17

FIGURE 14.3 THE INVERSE RELATIONSHIP

BETWEEN BOND PRICES AND YIELDS

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 18

TABLE 14.2 BOND PRICES AT DIFFERENT

INTEREST RATES (8% COUPON BOND,

COUPONS PAID SEMIANNUALLY)

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 19

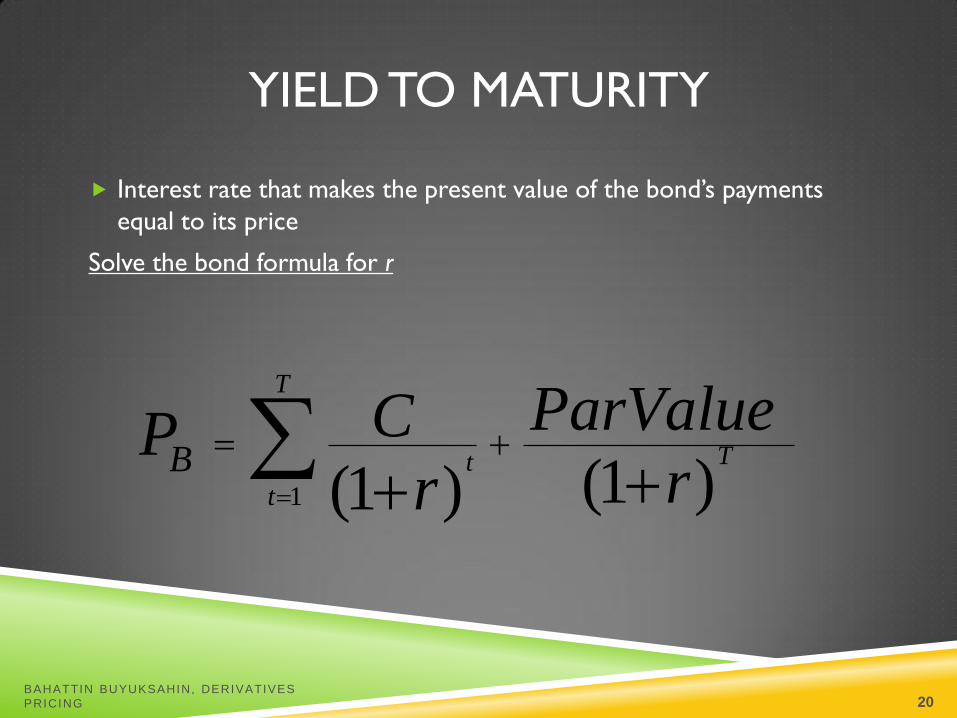

YIELD TO MATURITY

Interest rate that makes the present value of the bond’s payments

equal to its price

Solve the bond formula for r

1 (1 )(1 )

T

Tt

t

BParValueCP

rr

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 20

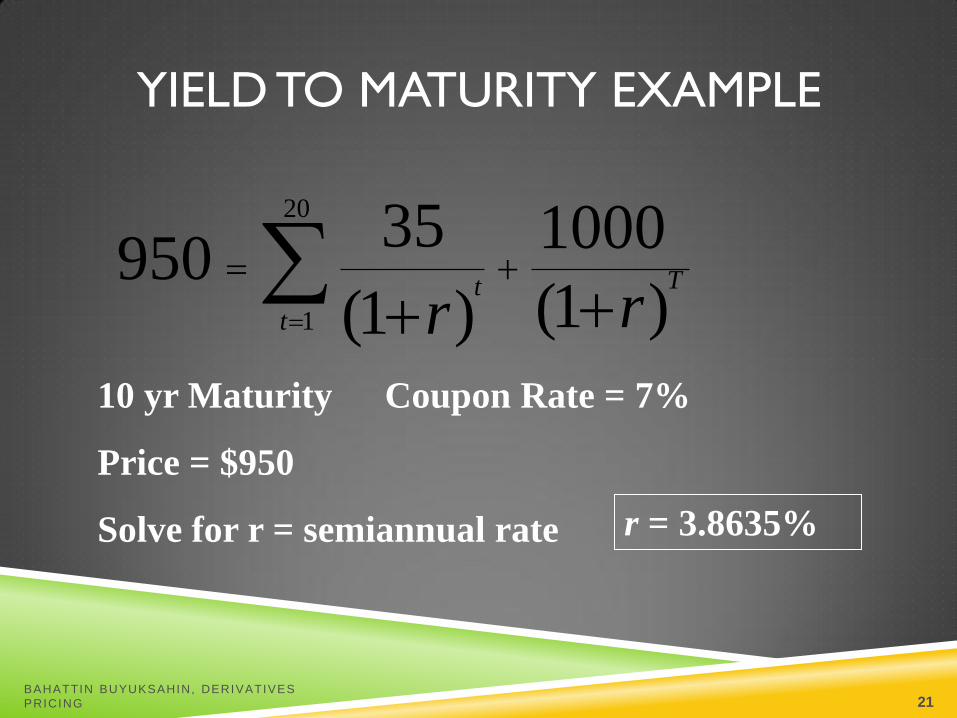

YIELD TO MATURITY EXAMPLE

)1(

1000

)1(

35950

20

1 rrT

t

t

10 yr Maturity Coupon Rate = 7%

Price = $950

Solve for r = semiannual rate r = 3.8635%

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 21

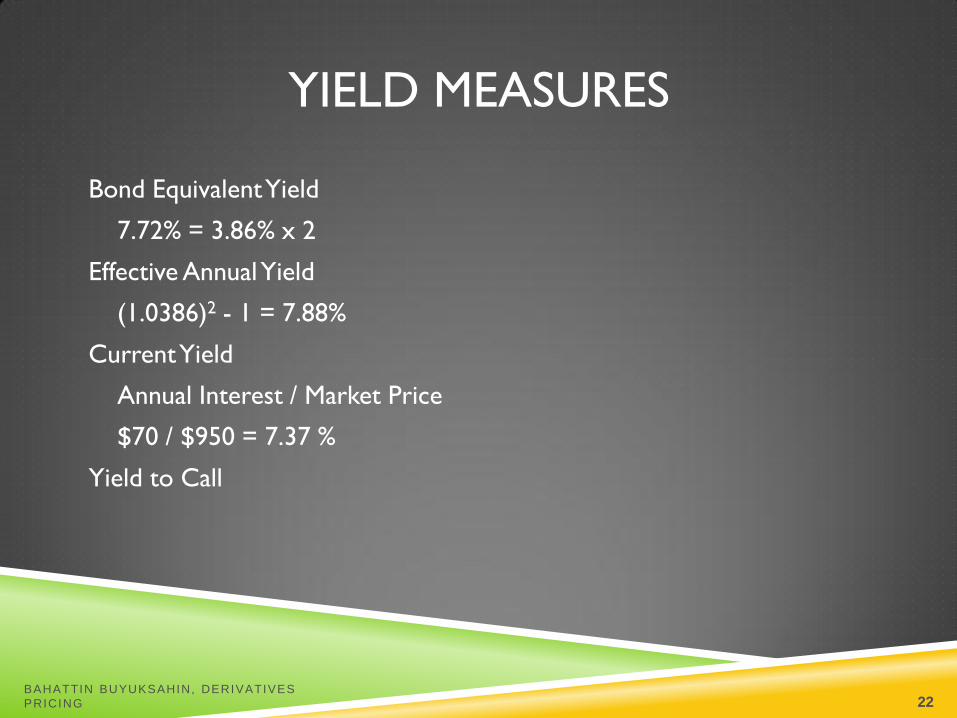

YIELD MEASURES

Bond Equivalent Yield

7.72% = 3.86% x 2

Effective Annual Yield

(1.0386)2 - 1 = 7.88%

Current Yield

Annual Interest / Market Price

$70 / $950 = 7.37 %

Yield to Call

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 22

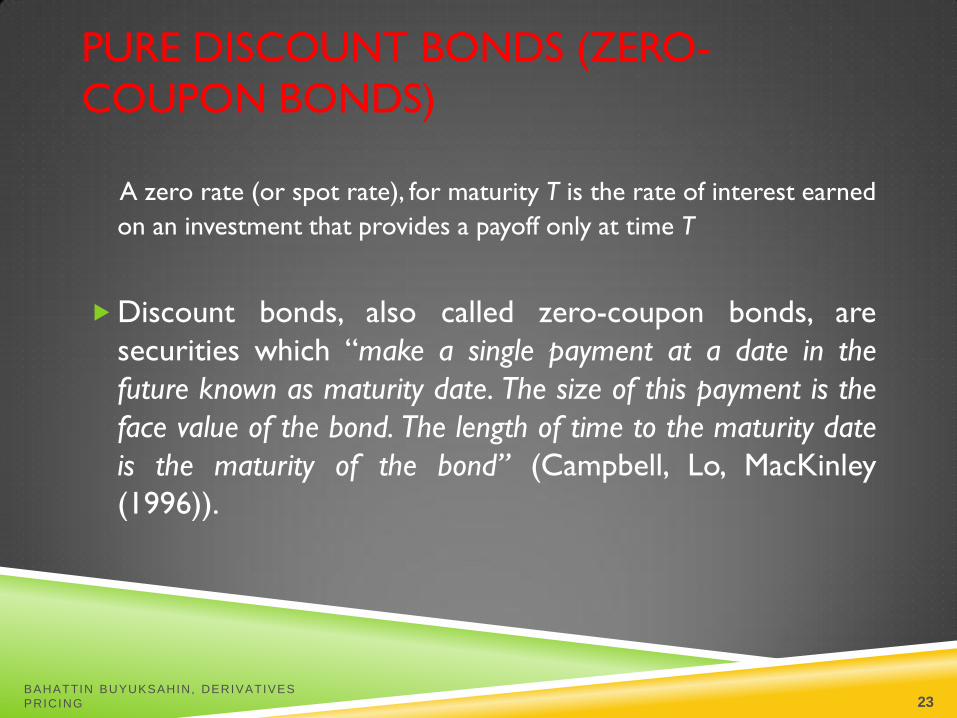

PURE DISCOUNT BONDS (ZERO-

COUPON BONDS)

A zero rate (or spot rate), for maturity T is the rate of interest earned

on an investment that provides a payoff only at time T

Discount bonds, also called zero-coupon bonds, are

securities which “make a single payment at a date in the

future known as maturity date. The size of this payment is the

face value of the bond. The length of time to the maturity date

is the maturity of the bond” (Campbell, Lo, MacKinley

(1996)).

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 23

PURE DISCOUNT BOND

The promised cash payment on a pure discount bond is called its face

value or par value. Yield (interest rate) on a pure discount bond is the

annualized rate of return to investors who buy it and hold it until it

matures.

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 24

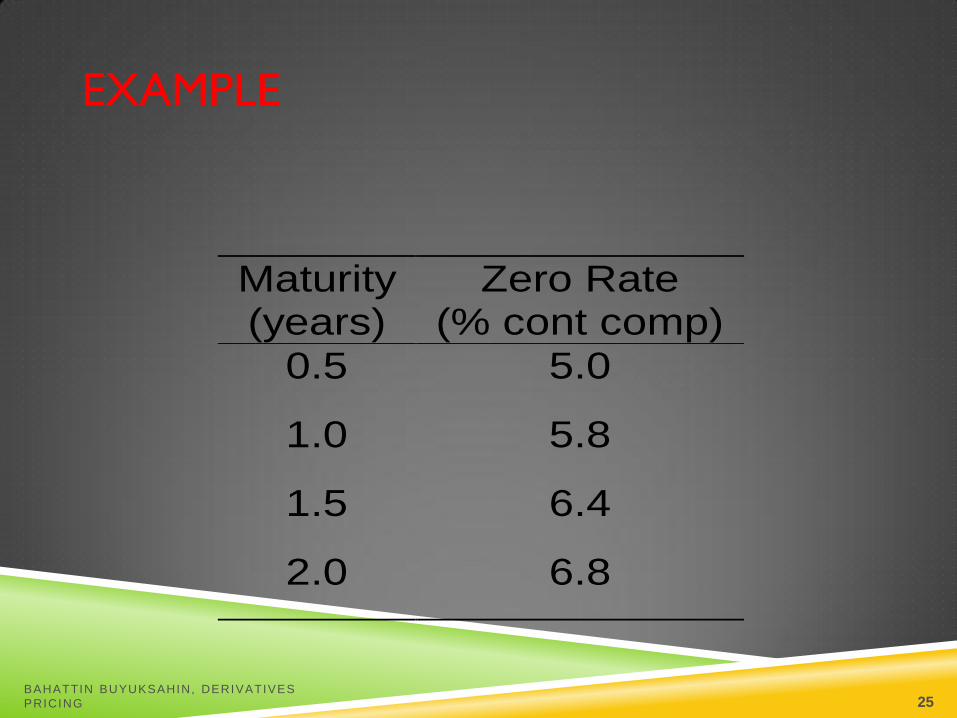

EXAMPLE

Maturity(years)

Zero Rate(% cont comp)

0.5 5.0

1.0 5.8

1.5 6.4

2.0 6.8

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 25

BOND PRICING

To calculate the cash price of a bond we discount

each cash flow at the appropriate zero rate

The theoretical price of a two-year bond

providing a 6% coupon semiannually is

3 3 3

103 98 39

0 05 0 5 0 058 1 0 0 064 1 5

0 068 2 0

e e e

e

. . . . . .

. . .

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 26

BOND YIELD

The bond yield is the discount rate that makes the present value of the cash flows on the bond equal to the market price of the bond

Suppose that the market price of the bond in our example equals its theoretical price of 98.39

The bond yield is given by solving

to get y = 0.0676 or 6.76%.

3 3 3 103 98 390 5 1 0 1 5 2 0e e e ey y y y . . . . .

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 27

PAR YIELD

The par yield for a certain maturity is the coupon

rate that causes the bond price to equal its face

value.

In our example we solve

g)compoundin s.a.(with 876get to

1002

100

222

0.2068.0

5.1064.00.1058.05.005.0

.c=

ec

ec

ec

ec

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 28

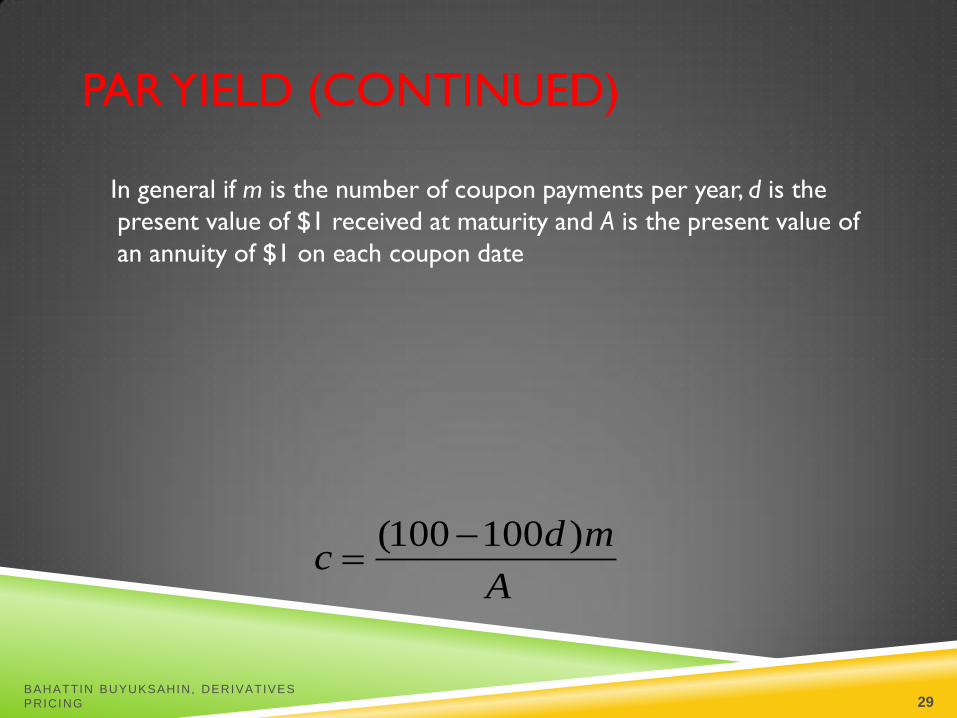

PAR YIELD (CONTINUED)

In general if m is the number of coupon payments per year, d is the

present value of $1 received at maturity and A is the present value of

an annuity of $1 on each coupon date

A

mdc

)100100(

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 29

BOOTSTRAP METHOD TO CALCULATE

DISCOUNT FACTOR

A discount function is a set of discount factors, where each discount

factor is just a present value multiplier. For example, d(1.0) is the

present value of $1 dollar received in one year. The key idea is that each

d(x) can be solved as one variable under one equation because we

already solved for shorter-term discount factors.

The most popular approach is to use bootstrap method

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 30

BOOTSTRAP : EXAMPLE

Face (par) value $1,000

Years to Maturity 0.5 1 1.5 2 2.5 3

Bond Price $980 $990 $990 $980 $970 $960

Coupon Rate 0.00% 4.00% 5.00% 5.00% 5.00% 6.00%

Discount function 0.9800 0.9514 0.9187 0.8866 0.8552 0.7983

FV Cash Flows

Years 0.5 $1,000 $20 $25 $25 $25 $30

DF 0.9800 0.9800 0.9800 0.9800 0.9800 0.9800

1 $1,020 $25 $25 $25 $30

DF 0.9514 0.9514 0.9514 0.9514 0.9514

1.5 $1,025 $25 $25 $30

DF 0.9187 0.9187 0.9187 0.9187

2 $1,025 $25 $30

DF 0.8866 0.8866 0.8866

2.5 $1,025 $30

DF 0.8552 0.8552

3 $1,030

0.7983

d(.5) is present value of $1 in six month

d(1) is present value of $1 in one year

$980=d(.5)*($1000 in six month)

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 31

DISCOUNT FACTOR

0.6000

0.6500

0.7000

0.7500

0.8000

0.8500

0.9000

0.9500

1.0000

1 2 3 4 5 6 7

D

i

s

c

o

u

n

t

F

a

c

t

o

r

Years to Maturity

Discount function

as a set of discount factor

Discount function

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 32

DETERMINING TREASURY ZERO

RATES

Face (par) value $1,000

Years to Maturity 0.25 0.5 1 1.5 2

Bond Price $975 $949 $900 $960 $1,016

Coupon Rate 0.00% 0.00% 0.00% 8.00% 12.00%

Discount function 0.9750 0.9490 0.9000 0.8520 0.8056

Zero Rates 10.127% 10.469% 10.536% 10.681% 10.808%

FV Cash Flows

Years 0.25 $1,000 $0 $0 $0 $0

DF 0.9750 0.9800 0.9800 0.9800 0.9800

0.5 $1,000 $0 $40 $60

DF 0.9490 0.9490 0.9490 0.9490

1 $1,000 $40 $60

DF 0.9000 0.9000 0.9000

1.5 $1,040 $60

DF 0.8520 0.8520

2 $1,060

DF 0.8056

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 33

TREASURY ZERO RATE CURVE

9.6%

9.8%

10.0%

10.2%

10.4%

10.6%

10.8%

11.0%

1 2 3 4 5

I

n

t

e

r

e

s

t

R

a

t

e

Maturity (years)

Zero Rates given by the bootstrap method

Zero Rates

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 34

FIGURE 14.4 BOND PRICES: CALLABLE AND

STRAIGHT DEBT

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 35

EXAMPLE 14.4 YIELD TO CALL

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 36

REALIZED YIELD VERSUS YTM

Reinvestment Assumptions

Holding Period Return

Changes in rates affect returns

Reinvestment of coupon payments

Change in price of the bond

BAHATTIN BUYUKSAHIN, DERIVATIVES

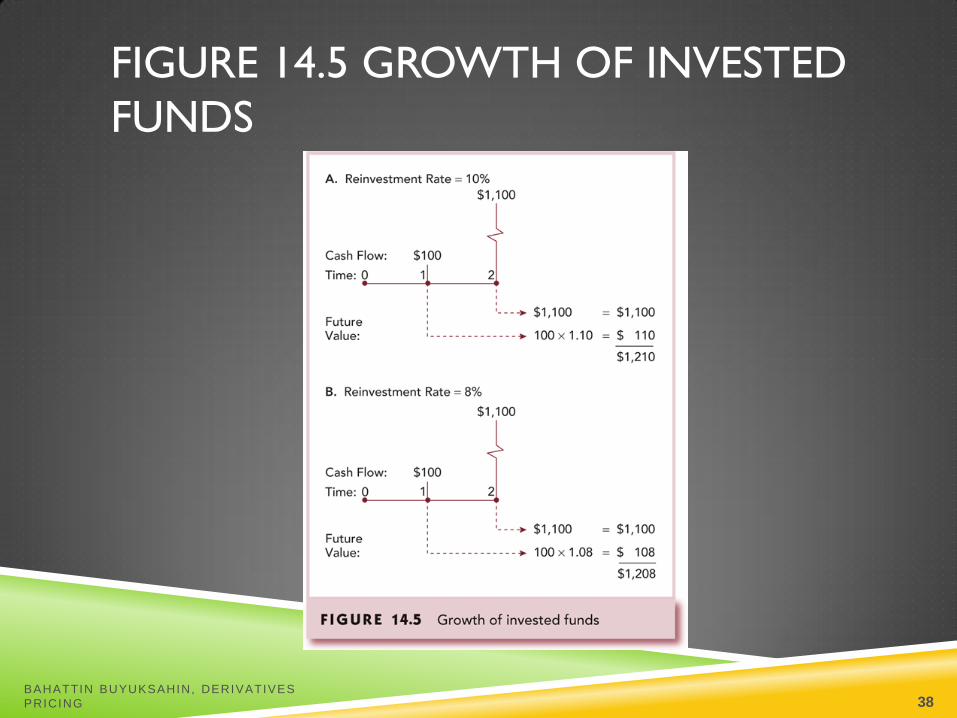

PRICING 37

FIGURE 14.5 GROWTH OF INVESTED

FUNDS

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 38

FIGURE 14.6 PRICES OVER TIME OF 30-YEAR MATURITY, 6.5%

COUPON BONDS

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 39

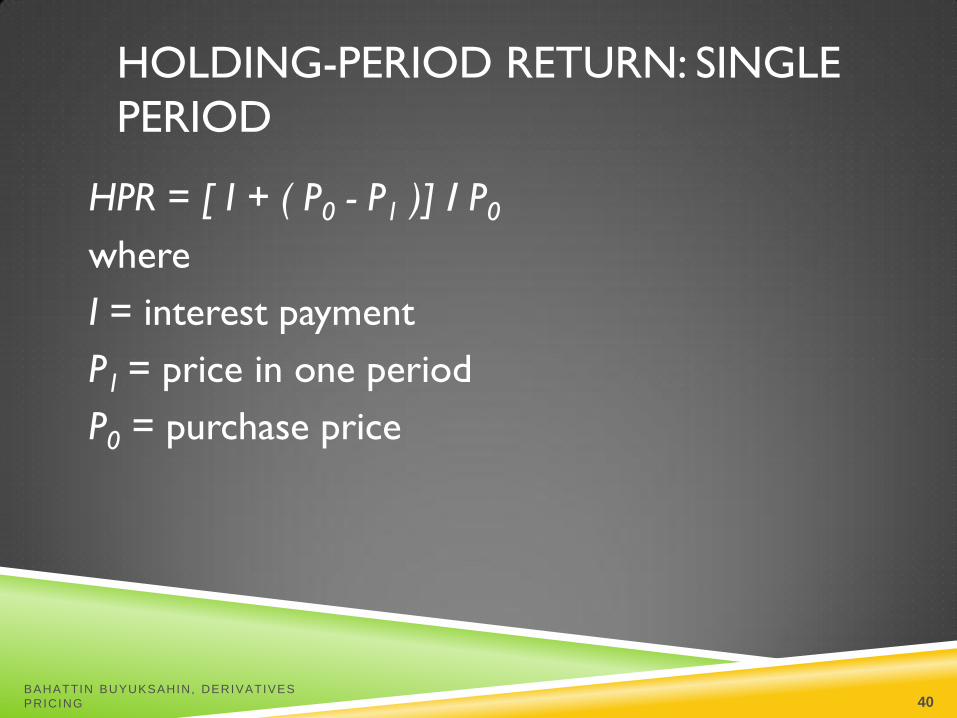

HOLDING-PERIOD RETURN: SINGLE

PERIOD

HPR = [ I + ( P0 - P1 )] / P0

where

I = interest payment

P1 = price in one period

P0 = purchase price

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 40

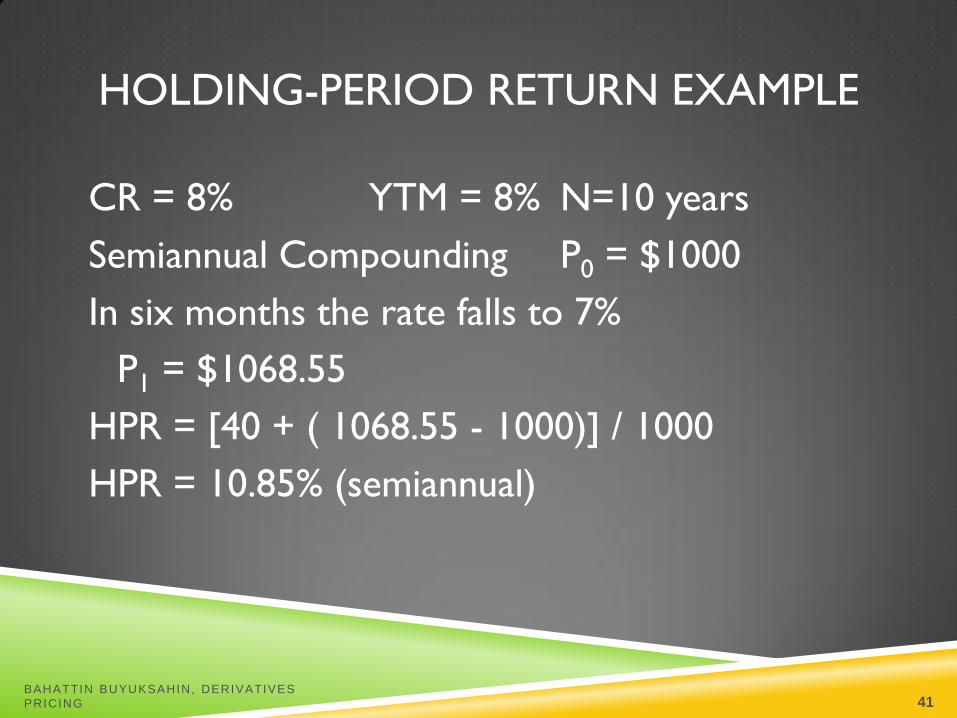

HOLDING-PERIOD RETURN EXAMPLE

CR = 8% YTM = 8% N=10 years

Semiannual Compounding P0 = $1000

In six months the rate falls to 7%

P1 = $1068.55

HPR = [40 + ( 1068.55 - 1000)] / 1000

HPR = 10.85% (semiannual)

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 41

FIGURE 14.7 THE PRICE OF A 30-YEAR ZERO-COUPON BOND OVER TIME

AT A YIELD TO MATURITY OF 10%

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 42

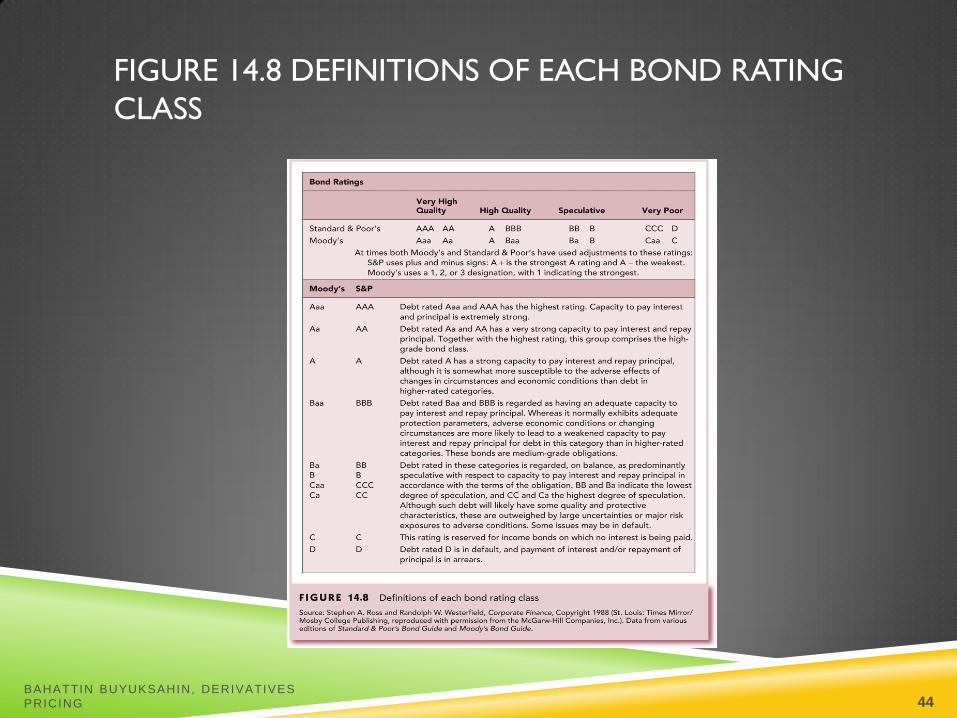

DEFAULT RISK AND RATINGS

Rating companies Moody’s Investor Service

Standard & Poor’s

Fitch

Rating Categories Investment grade

Speculative grade/Junk Bonds

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 43

FIGURE 14.8 DEFINITIONS OF EACH BOND RATING

CLASS

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 44

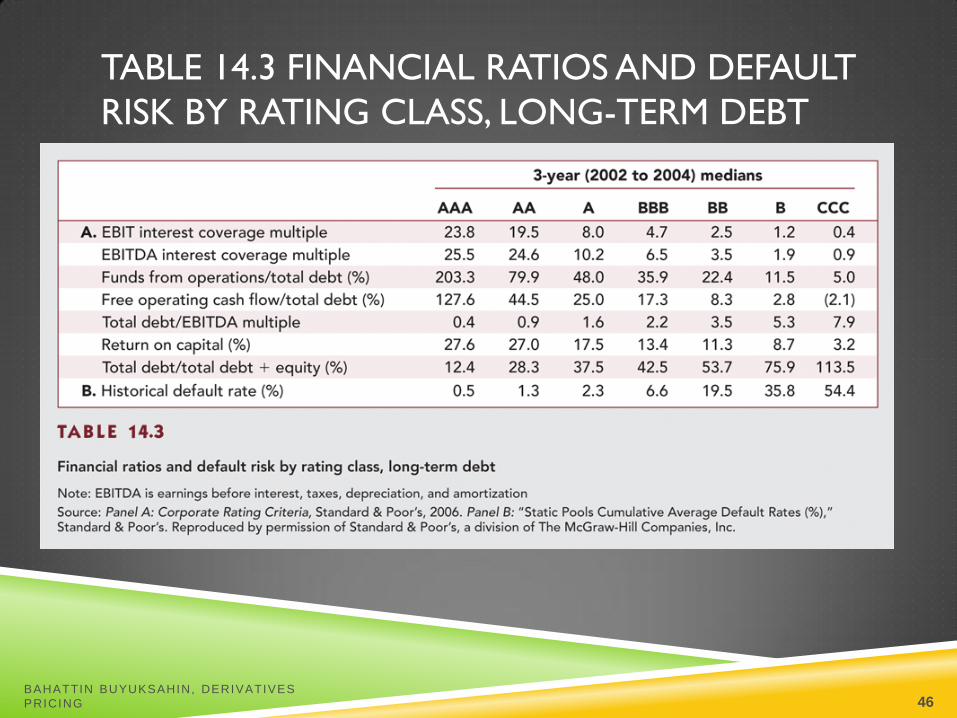

FACTORS USED BY RATING

COMPANIES

Coverage ratios

Leverage ratios

Liquidity ratios

Profitability ratios

Cash flow to debt

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 45

TABLE 14.3 FINANCIAL RATIOS AND DEFAULT

RISK BY RATING CLASS, LONG-TERM DEBT

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 46

FIGURE 14.9 DISCRIMINANT ANALYSIS

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 47

PROTECTION AGAINST DEFAULT

Sinking funds

Subordination of future debt

Dividend restrictions

Collateral

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 48

FIGURE 14.10 CALLABLE BOND ISSUED

BY MOBIL

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 49

DEFAULT RISK AND YIELD

Risk structure of interest rates

Default premiums

Yields compared to ratings

Yield spreads over business cycles

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 50

FIGURE 14.11 YIELDS ON LONG-TERM

BONDS, 1954 – 2006

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 51

CREDIT RISK AND COLLATERALIZED DEBT

OBLIGATIONS (CDOS)

Major mechanism to reallocate credit risk in

the fixed-income markets

Structured Investment Vehicle (SIV) often

used to create the CDO

Mortgage-backed CDOs were an

investment disaster in 2007

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 52

FIGURE 14.12 COLLATERALIZED DEBT

OBLIGATIONS

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 53

CHAPTER 15

The Term Structure of Interest Rates

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 54

OVERVIEW OF TERM STRUCTURE

Information on expected future short term

rates can be implied from the yield curve

The yield curve is a graph that displays the

relationship between yield and maturity

Three major theories are proposed to explain

the observed yield curve

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 55

FIGURE 15.1 TREASURY YIELD CURVES

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 56

BOND PRICING

Yields on different maturity bonds are not all

equal

Need to consider each bond cash flow as a

stand-alone zero-coupon bond when valuing

coupon bonds

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 57

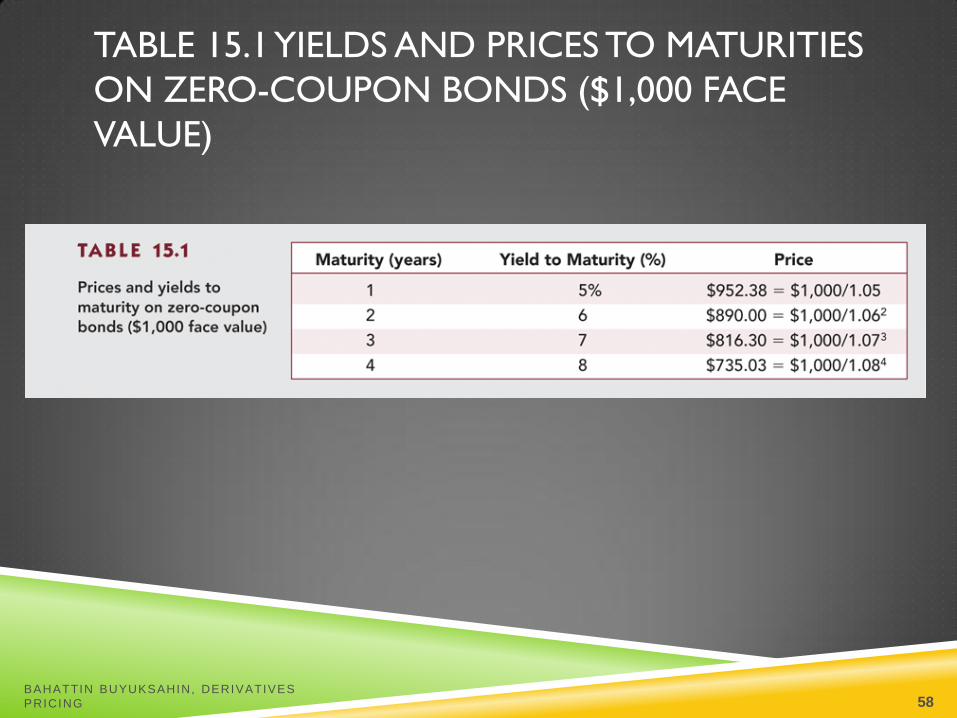

TABLE 15.1 YIELDS AND PRICES TO MATURITIES

ON ZERO-COUPON BONDS ($1,000 FACE

VALUE)

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 58

YIELD CURVE UNDER CERTAINTY

An upward sloping yield curve is evidence that short-term rates are going to be higher next year

When next year’s short rate is greater than this year’s short rate, the average of the two rates is higher than today’s rate

2

2 1 2

1

22 1 2

(1 ) (1 ) (1 )

1 (1 ) (1 )

y r x r

y r x r

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 59

FIGURE 15.2 TWO 2-YEAR INVESTMENT

PROGRAMS

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 60

FIGURE 15.3 SHORT RATES VERSUS

SPOT RATES

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 61

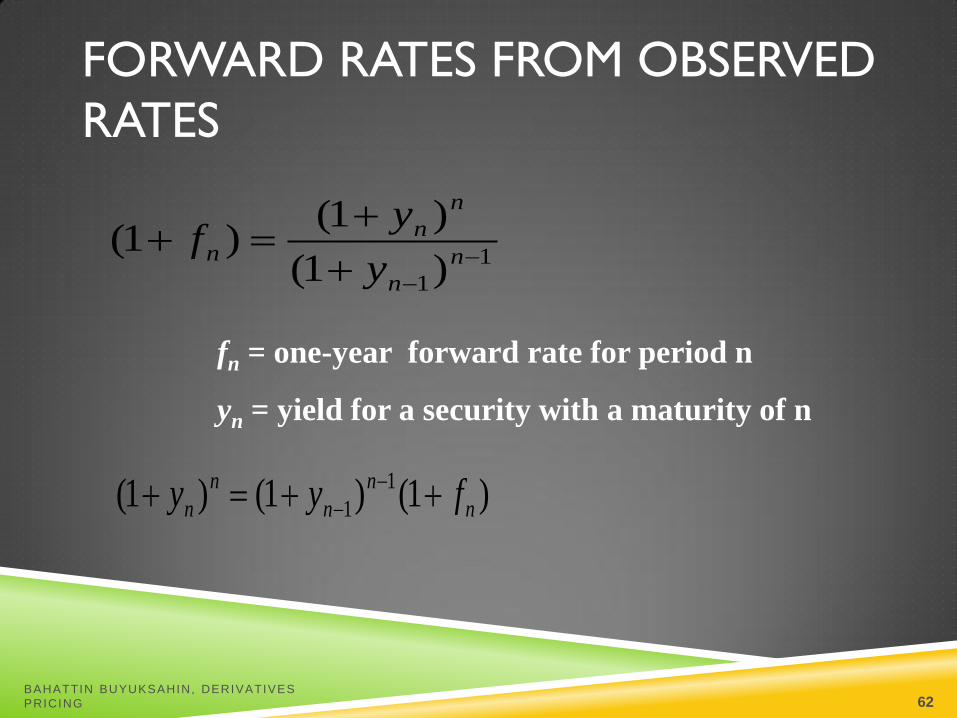

1

1)1(

)1()1(

n

n

n

nn

y

yf

fn = one-year forward rate for period n

yn = yield for a security with a maturity of n

)1()1()1( 1

1 n

n

n

n

n fyy

FORWARD RATES FROM OBSERVED

RATES

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 62

EXAMPLE 15.4 FORWARD RATES

4 yr = 8.00% 3yr = 7.00% fn = ?

(1.08)4 = (1.07)3 (1+fn)

(1.3605) / (1.2250) = (1+fn)

fn = .1106 or 11.06%

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 63

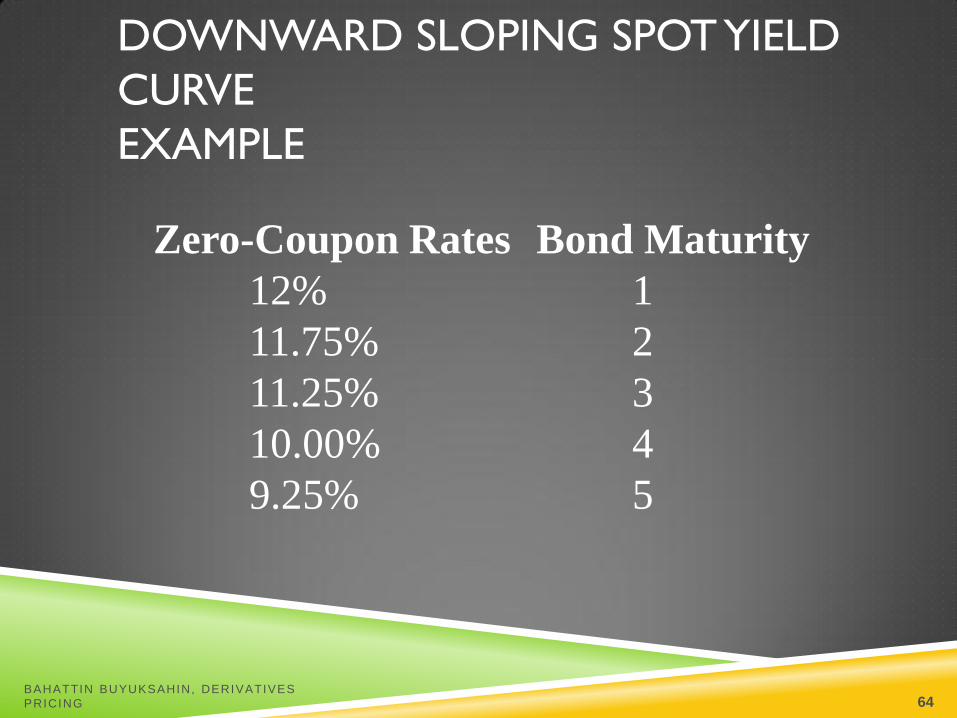

DOWNWARD SLOPING SPOT YIELD

CURVE

EXAMPLE

Zero-Coupon Rates Bond Maturity

12% 1

11.75% 2

11.25% 3

10.00% 4

9.25% 5

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 64

FORWARD RATES FOR DOWNWARD SLOPING

Y C EXAMPLE

1yr Forward Rates

1yr [(1.1175)2 / 1.12] - 1 = 0.115006

2yrs [(1.1125)3 / (1.1175)2] - 1 = 0.102567

3yrs [(1.1)4 / (1.1125)3] - 1 = 0.063336

4yrs [(1.0925)5 / (1.1)4] - 1 = 0.063008

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 65

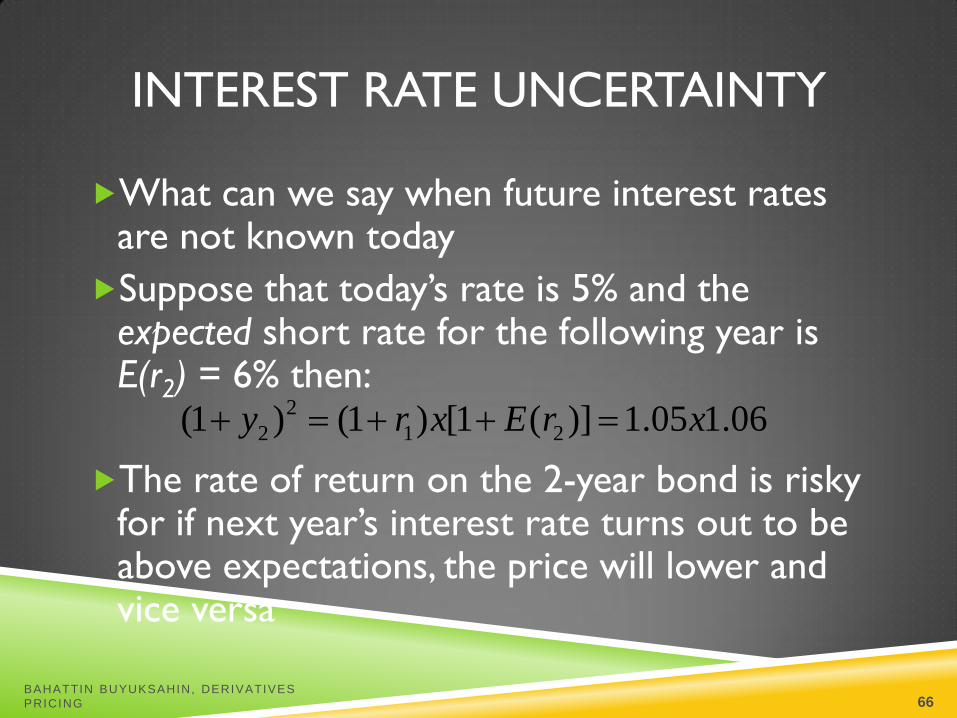

INTEREST RATE UNCERTAINTY

What can we say when future interest rates are not known today

Suppose that today’s rate is 5% and the expected short rate for the following year is E(r2) = 6% then:

The rate of return on the 2-year bond is risky for if next year’s interest rate turns out to be above expectations, the price will lower and vice versa

2

2 1 2(1 ) (1 ) [1 ( )] 1.05 1.06y r x E r x

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 66

INTEREST RATE UNCERTAINTY

CONTINUED

Investors require a risk premium to hold a

longer-term bond

This liquidity premium compensates short-

term investors for the uncertainty about

future prices

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 67

TERM STRUCTURE OF INTEREST RATES

The term structure of interest rates (or yield curve) is the relationship of

the yield to maturity against bond term (maturity).

Typical shapes are: increasing (normal), decreasing, humped and flat.

Yield

Maturity

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 68

UPWARD VS DOWNWARD SLOPING

YIELD CURVE

For an upward sloping yield curve:

Fwd Rate > Zero Rate > Par Yield

For a downward sloping yield curve

Par Yield > Zero Rate > Fwd Rate

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 69

THEORIES OF THE TERM STRUCTURE

A number of theory have been proposed: Expectation

Hypothesis, Liquidity Preference Theory, Preferred Habitats

Theory, Segmentation Hypothesis.

Fabozzi (1998): Pure Expectation Hypothesis, Liquidity

Preference Theory, Preferred Habitats Theory are different

forms of the expectation theory ==> two major theories:

expectation theory and market segmentation theory.

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 70

THEORIES OF THE TERM STRUCTURE OF INTEREST

RATES (1)

The Pure Expectation Hypothesis: Implied forward rates are unbiased expectations of future spot rates ==> a rising term structure indicate that market expects short-term rates to rise in the future; a flat term structure reflects expectations that the future short term structure will be constant; and so on; Hicks (1937). Problems: It neglects the risks inherent in investing in bonds: if forward rates were perfect predictors of future interest rates then the future prices of bonds will be known with certainty.

The Liquidity Preference Theory (Keynes): Given that there is uncertainty, long bonds should have higher returns than short bonds ==> we should expect a risk premium arising out from investors liquidity preferences. It is consistent with the empirical results that yield curves are upward sloping ==> positive risk premium.

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 71

THEORIES OF THE TERM STRUCTURE OF INTEREST

RATES (2)

The Preferred Habitat Theory: It adopts the view that the term structure is

composed by two components: Expectations plus risk premium (=

liquidity preference theory). However, the risk premium might be

negative as well as positive to induce market participants to shift out of

their preferred habitat (Modigliani & Sutch (1966)).

The Segmentation Hypothesis (Culbertson (1957)): It also recognises that

investors have preferred habitat (= preferred habitat theory) ==>

individuals have strong maturity preferences ==> there need be no

relationship between bonds with different maturities ==> bonds with

different maturities are traded in different markets.

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 72

EXPECTATIONS THEORY

Observed long-term rate is a function of

today’s short-term rate and expected future

short-term rates

Long-term and short-term securities are

perfect substitutes

Forward rates that are calculated from the

yield on long-term securities are market

consensus expected future short-term rates

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 73

LIQUIDITY PREMIUM THEORY

Long-term bonds are more risky

Investors will demand a premium for the risk

associated with long-term bonds

The yield curve has an upward bias built into

the long-term rates because of the risk

premium

Forward rates contain a liquidity premium and

are not equal to expected future short-term

rates

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 74

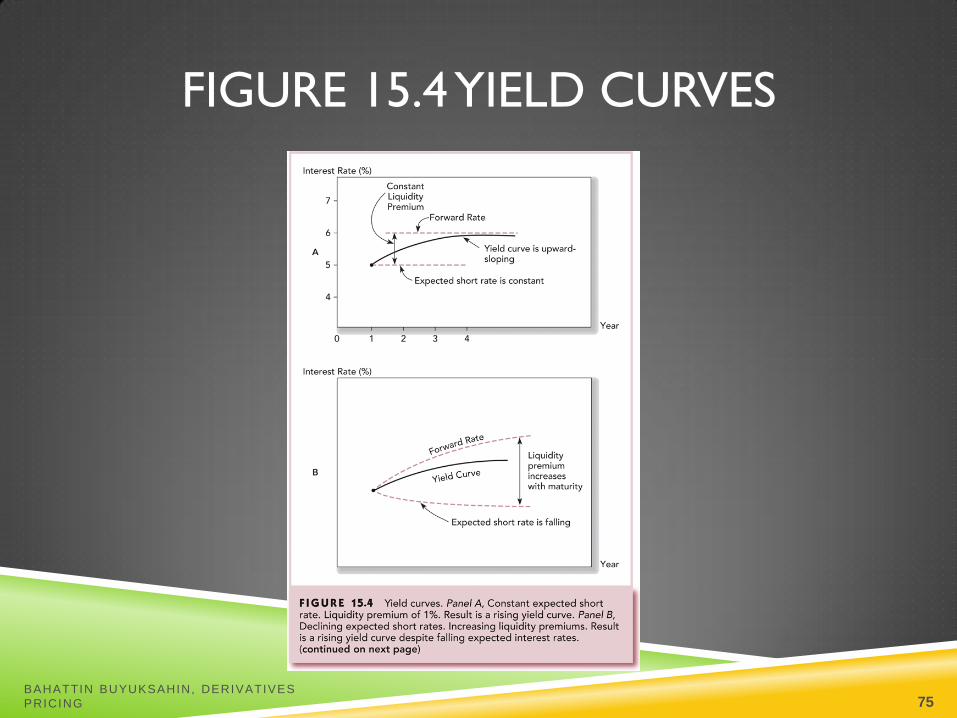

FIGURE 15.4 YIELD CURVES

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 75

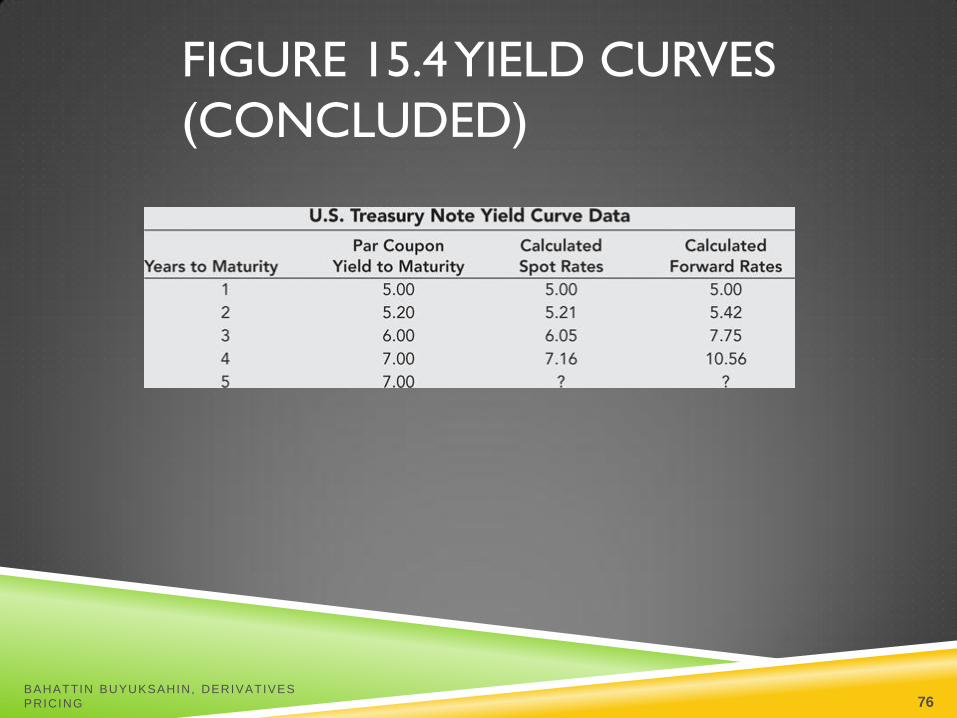

FIGURE 15.4 YIELD CURVES

(CONCLUDED)

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 76

INTERPRETING THE TERM

STRUCTURE

If the yield curve is to rise as one moves to

longer maturities

A longer maturity results in the inclusion of

a new forward rate that is higher than the

average of the previously observed rates

Reason:

Higher expectations for forward rates or

Liquidity premium

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 77

FIGURE 15.5 PRICE VOLATILITY OF LONG-TERM

TREASURY BONDS

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 78

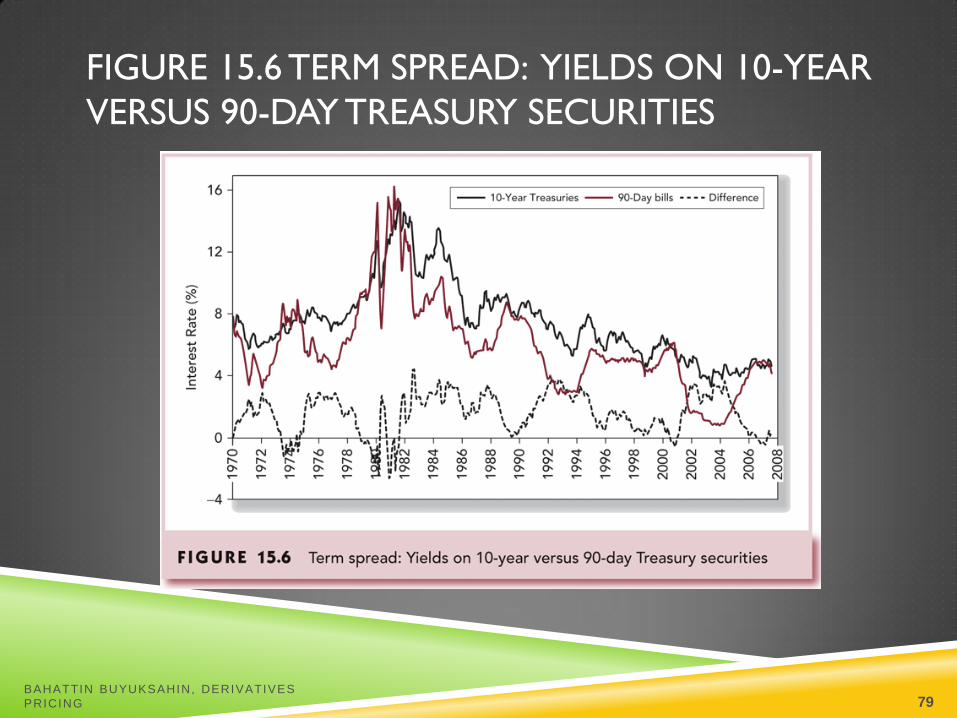

FIGURE 15.6 TERM SPREAD: YIELDS ON 10-YEAR

VERSUS 90-DAY TREASURY SECURITIES

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 79

FORWARD RATES AS FORWARD

CONTRACTS

In general, forward rates will not equal the

eventually realized short rate Still an important consideration when trying to make decisions :

Locking in loan rates

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 80

FIGURE 15.7 ENGINEERING A SYNTHETIC

FORWARD LOAN

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 81

CHAPTER 16

Managing Bond Portfolios

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 82

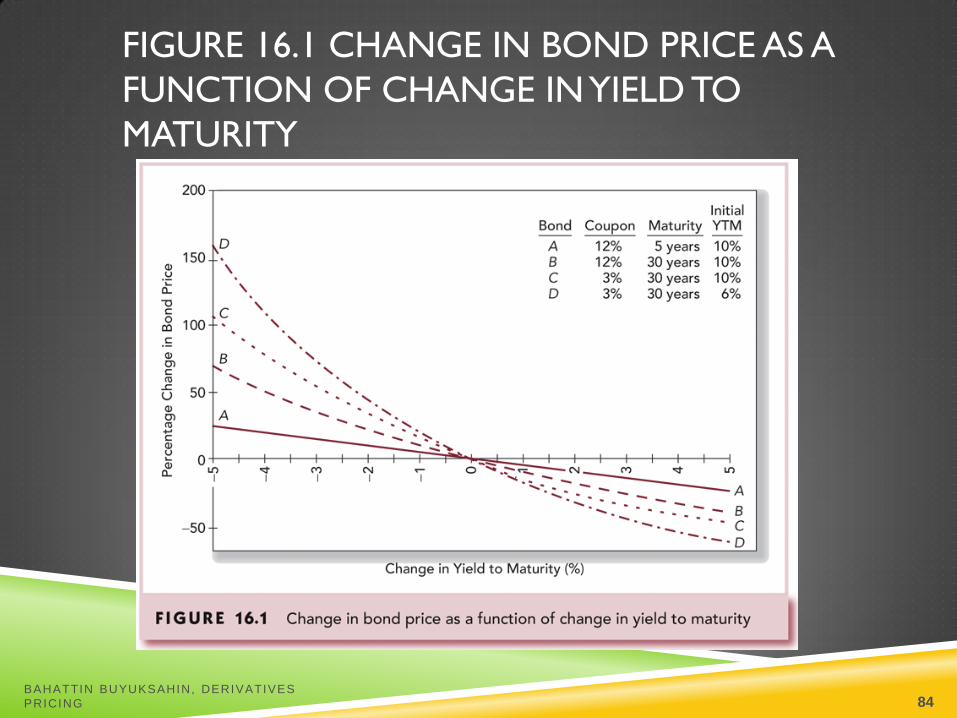

BOND PRICING RELATIONSHIPS

Inverse relationship between price and yield

An increase in a bond’s yield to maturity

results in a smaller price decline than the gain

associated with a decrease in yield

Long-term bonds tend to be more price

sensitive than short-term bonds

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 83

FIGURE 16.1 CHANGE IN BOND PRICE AS A

FUNCTION OF CHANGE IN YIELD TO

MATURITY

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 84

BOND PRICING RELATIONSHIPS

CONTINUED

As maturity increases, price sensitivity

increases at a decreasing rate

Price sensitivity is inversely related to a bond’s

coupon rate

Price sensitivity is inversely related to the yield

to maturity at which the bond is selling

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 85

TABLE 16.1 PRICES OF 8% COUPON BOND

(COUPONS PAID SEMIANNUALLY)

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 86

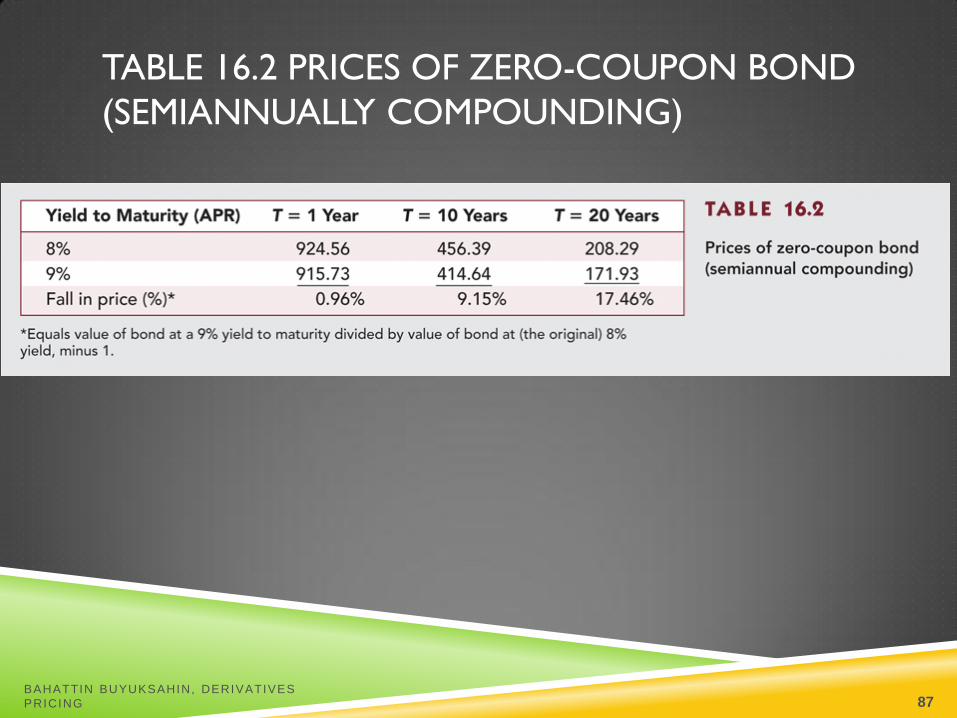

TABLE 16.2 PRICES OF ZERO-COUPON BOND

(SEMIANNUALLY COMPOUNDING)

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 87

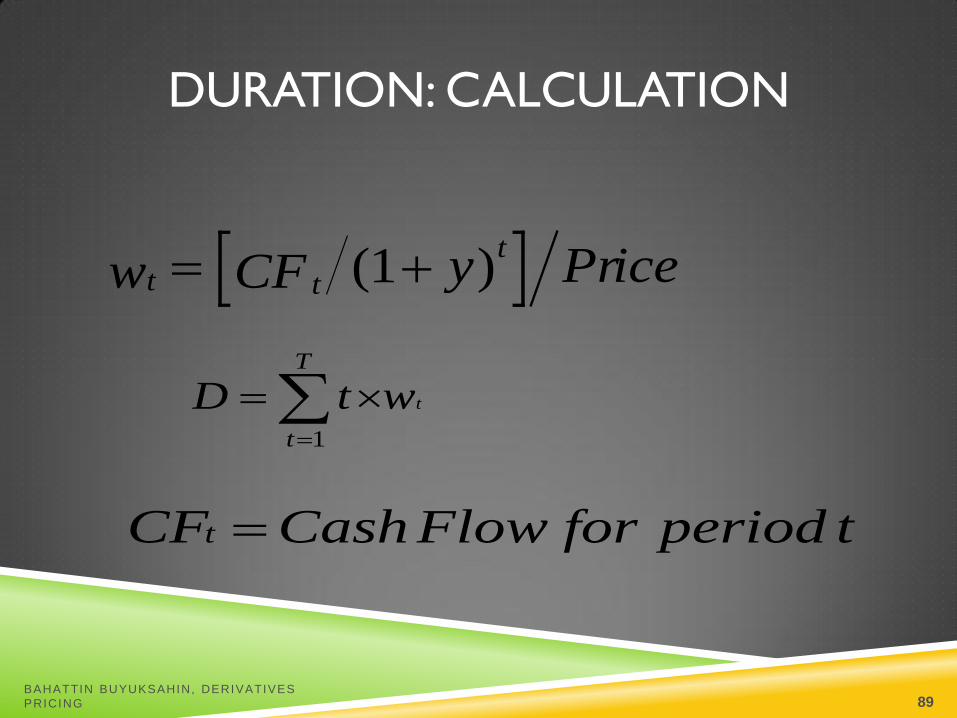

DURATION

A measure of the effective maturity of a bond

The weighted average of the times until each

payment is received, with the weights

proportional to the present value of the

payment

Duration is shorter than maturity for all bonds

except zero coupon bonds

Duration is equal to maturity for zero coupon

bonds

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 88

t t

tw CF y ice ( )1 Pr

twtDT

t

1

CF CashFlow for period tt

DURATION: CALCULATION

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 89

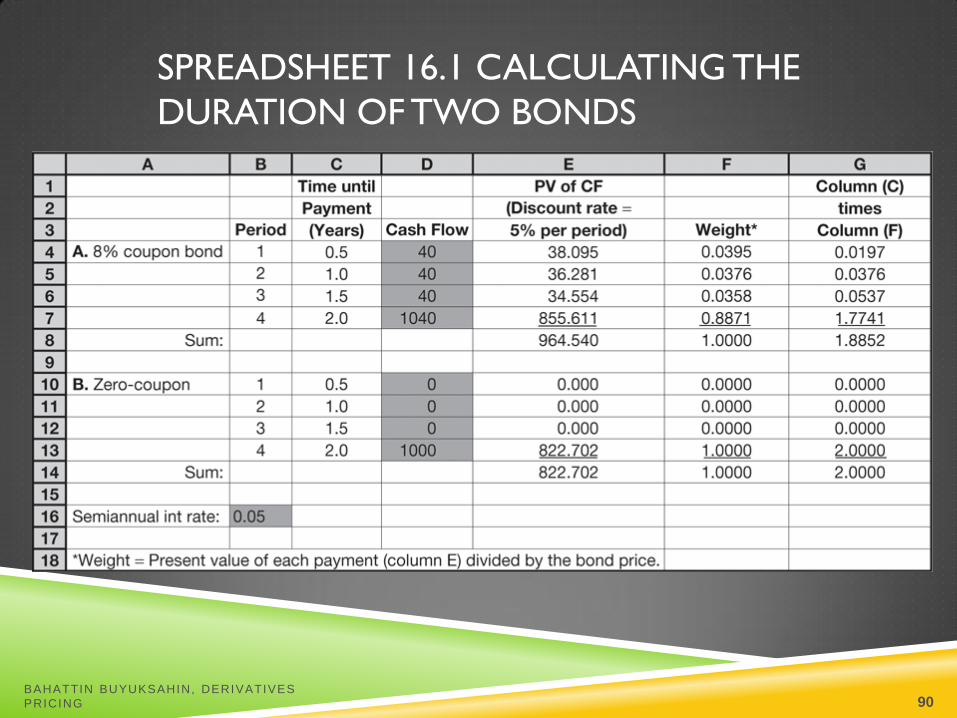

SPREADSHEET 16.1 CALCULATING THE

DURATION OF TWO BONDS

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 90

DURATION/PRICE RELATIONSHIP

Price change is proportional to duration and not

to maturity

D* = modified duration

(1 )

1

P yDx

P y

*P

D yP

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 91

RULES FOR DURATION

Rule 1 The duration of a zero-coupon bond equals its time to maturity

Rule 2 Holding maturity constant, a bond’s duration is higher when the coupon rate is lower

Rule 3 Holding the coupon rate constant, a bond’s duration generally increases with its time to maturity

Rule 4 Holding other factors constant, the duration of a coupon bond is higher when the bond’s yield to maturity is lower

Rules 5 The duration of a level perpetuity is equal to: (1+y) / y

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 92

FIGURE 16.2 BOND DURATION VERSUS

BOND MATURITY

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 93

TABLE 16.3 BOND DURATIONS (YIELD TO

MATURITY = 8% APR; SEMIANNUAL COUPONS)

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 94

CONVEXITY

The relationship between bond prices and

yields is not linear

Duration rule is a good approximation for

only small changes in bond yields

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 95

FIGURE 16.3 BOND PRICE CONVEXITY: 30-YEAR

MATURITY, 8% COUPON; INITIAL YIELD TO

MATURITY = 8%

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 96

CORRECTION FOR CONVEXITY

n

tt

t tty

CF

yPConvexity

1

2

2)(

)1()1(

1

Correction for Convexity:

21 [ ( ) ]2

PD y Convexity y

P

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 97

FIGURE 16.4 CONVEXITY OF TWO

BONDS

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 98

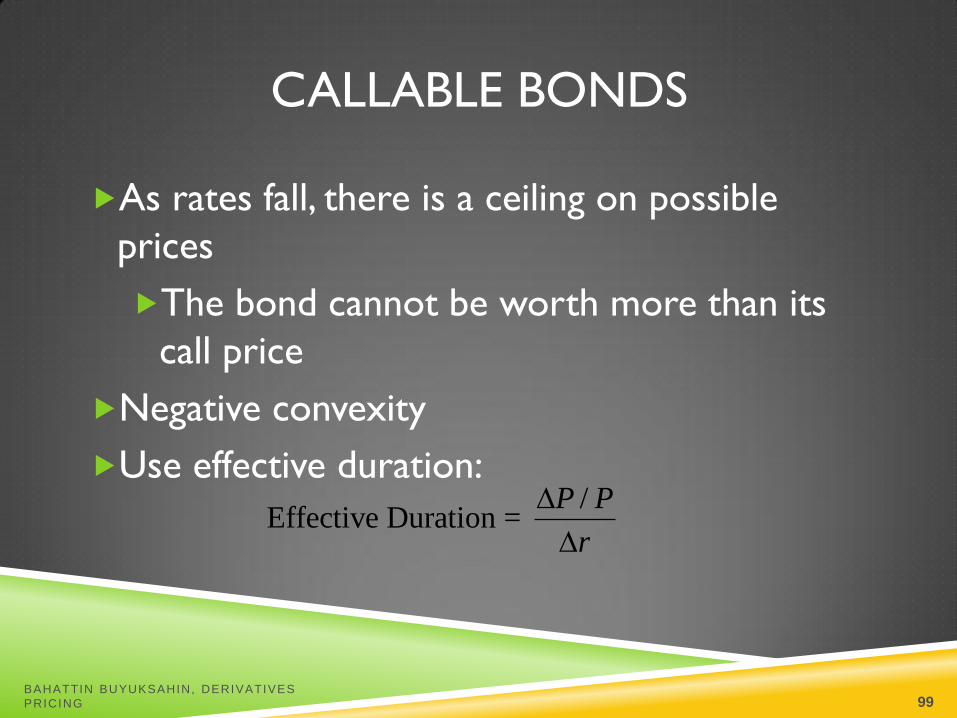

CALLABLE BONDS

As rates fall, there is a ceiling on possible

prices

The bond cannot be worth more than its

call price

Negative convexity

Use effective duration:

/

Effective Duration = P P

r

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 99

FIGURE 16.5 PRICE –YIELD CURVE FOR A

CALLABLE BOND

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 100

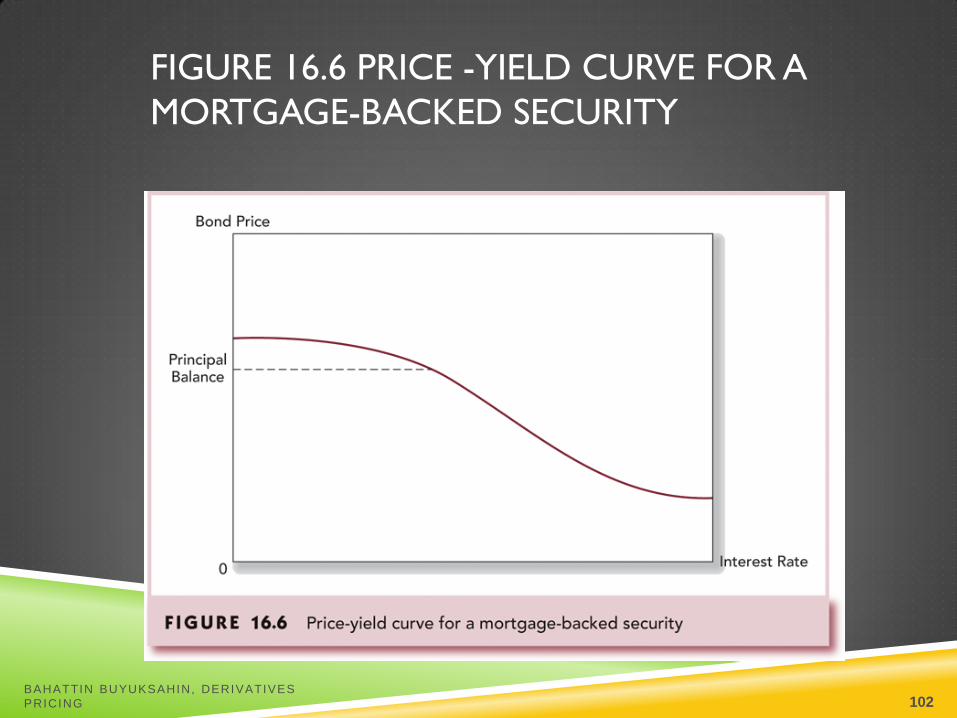

MORTGAGE-BACKED SECURITIES

Among the most successful examples of

financial engineering

Subject to negative convexity

Often sell for more than their principal

balance

Homeowners do not refinance their loans

as soon as interest rates drop

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 101

FIGURE 16.6 PRICE -YIELD CURVE FOR A

MORTGAGE-BACKED SECURITY

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 102

MORTGAGE-BACKED SECURITIES

CONTINUED

They have given rise to many derivatives

including the CMO (collateralized mortgage

obligation)

Use of tranches

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 103

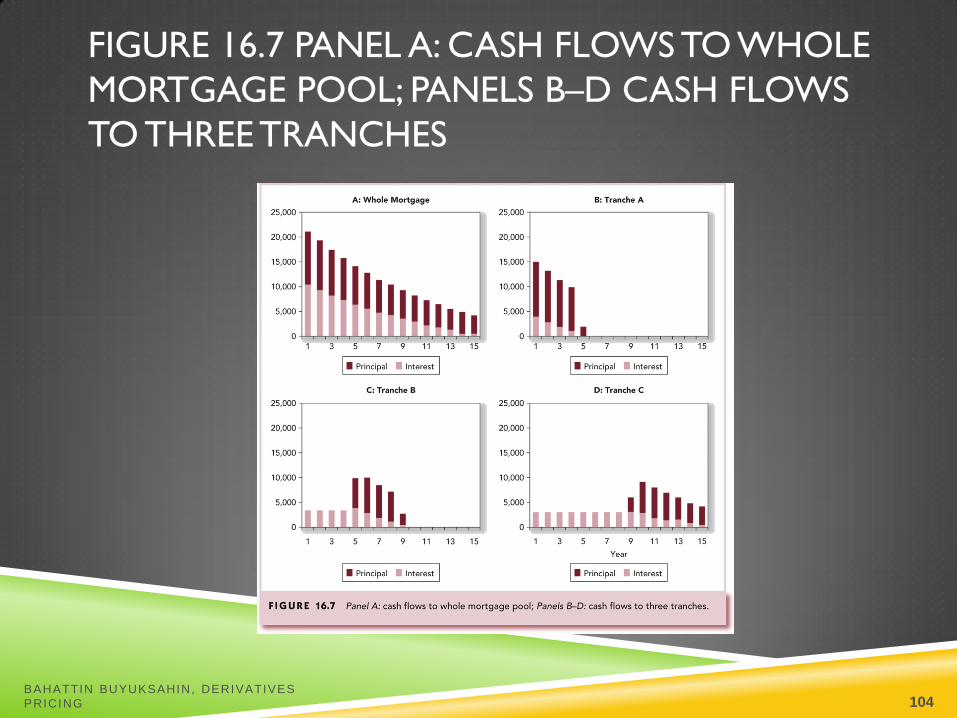

FIGURE 16.7 PANEL A: CASH FLOWS TO WHOLE

MORTGAGE POOL; PANELS B–D CASH FLOWS

TO THREE TRANCHES

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 104

PASSIVE MANAGEMENT

Bond-Index Funds

Immunization of interest rate risk:

Net worth immunization

Duration of assets = Duration of liabilities

Target date immunization

Holding Period matches Duration

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 105

FIGURE 16.8 STRATIFICATION OF BONDS INTO

CELLS

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 106

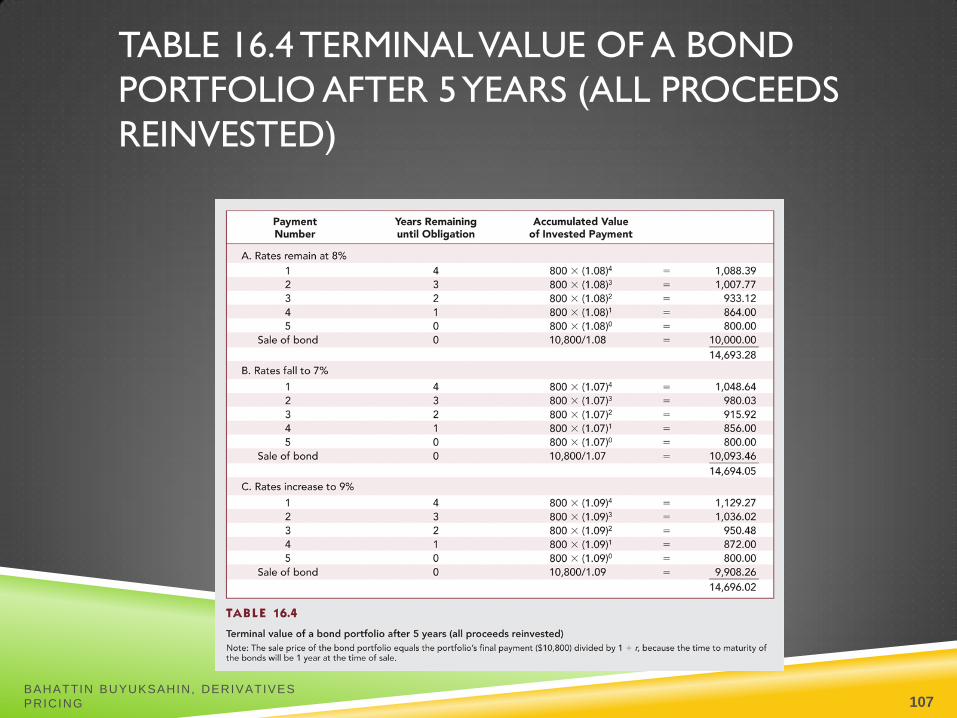

TABLE 16.4 TERMINAL VALUE OF A BOND

PORTFOLIO AFTER 5 YEARS (ALL PROCEEDS

REINVESTED)

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 107

FIGURE 16.9 GROWTH OF

INVESTED FUNDS

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 108

FIGURE 16.10 IMMUNIZATION

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 109

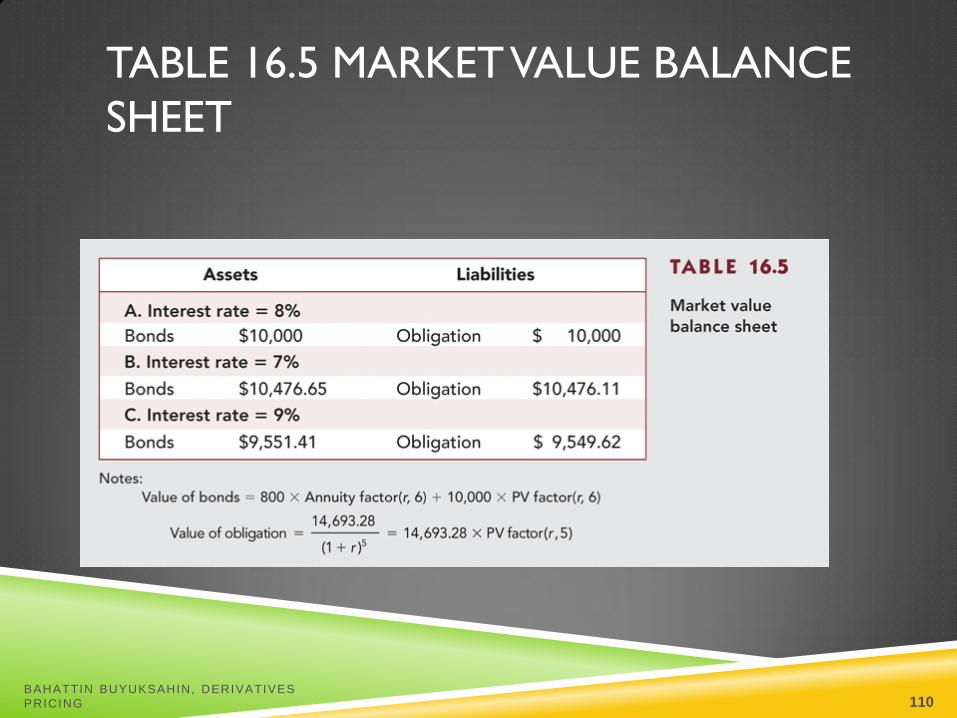

TABLE 16.5 MARKET VALUE BALANCE

SHEET

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 110

CASH FLOW MATCHING AND

DEDICATION

Automatically immunize the portfolio from

interest rate movement Cash flow and obligation exactly offset each other

i.e. Zero-coupon bond

Not widely used because of constraints

associated with bond choices

Sometimes it simply is not possible to do

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 111

ACTIVE MANAGEMENT: SWAPPING

STRATEGIES

Substitution swap

Intermarket swap

Rate anticipation swap

Pure yield pickup

Tax swap

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 112

HORIZON ANALYSIS

Select a particular holding period and predict

the yield curve at end of period

Given a bond’s time to maturity at the end of

the holding period

Its yield can be read from the predicted

yield curve and the end-of-period price can

be calculated

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 113

CONTINGENT IMMUNIZATION

A combination of active and passive management

The strategy involves active management with a floor rate of return

As long as the rate earned exceeds the floor, the portfolio is actively managed

Once the floor rate or trigger rate is reached, the portfolio is immunized

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 114

FIGURE 16.11 CONTINGENT

IMMUNIZATION

BAHATTIN BUYUKSAHIN, DERIVATIVES

PRICING 115