CANADIAN CASES ON THE LAW OF INSURANCE

166

CANADIAN CASES ON THE LAW OF INSURANCE Fourth Series/Quatri` eme s´ erie Recueil de jurisprudence en droit des affaires VOLUME 97 (Cited 97 C.C.L.I. (4th)) EDITORS-IN-CHIEF/R ´ EDACTEURS EN CHEF Won J. Kim, B.A., LL.B. Kim Orr Barristers P.C. Toronto, Ontario QUEBEC EDITOR/R ´ EDACTEUR POUR LE QU ´ EBEC Jean-Fran¸ cois Lamoureux, LL.L. Robinson Sheppard Shapiro Montr´ eal, Qu´ ebec CARSWELL EDITORIAL STAFF/R ´ EDACTION DE CARSWELL Jeffrey D. Mitchell, B.A., M.A. Director, Editorial Production and Manufacturing Ken Murphy, B.A.(HON.), LL.B. Product Development Manager Julia Fischer, B.A.(HON.), LL.B. Sharon Yale, M.A., LL.B. Acting Supervisor, Legal Writing Supervisor, Legal Writing Mike MacInnes, B.A.(HON.), LL.B. Lisa Rao, B.SC., LL.B. Lead Legal Writer Senior Legal Writer Jocelyn Cleary, B.A.(HON.), LL.B. Stephanie Hanna, B.A., M.A., LL.B. Legal Writer Legal Writer Chauncey Glass, B.A., LL.B. Martin-Fran¸ cois Parent, LL.B., LL.M., Legal Writer DEA (PARIS II) Bilingual Legal Writer Heather Niziol, B.A. Content Editor

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of CANADIAN CASES ON THE LAW OF INSURANCE

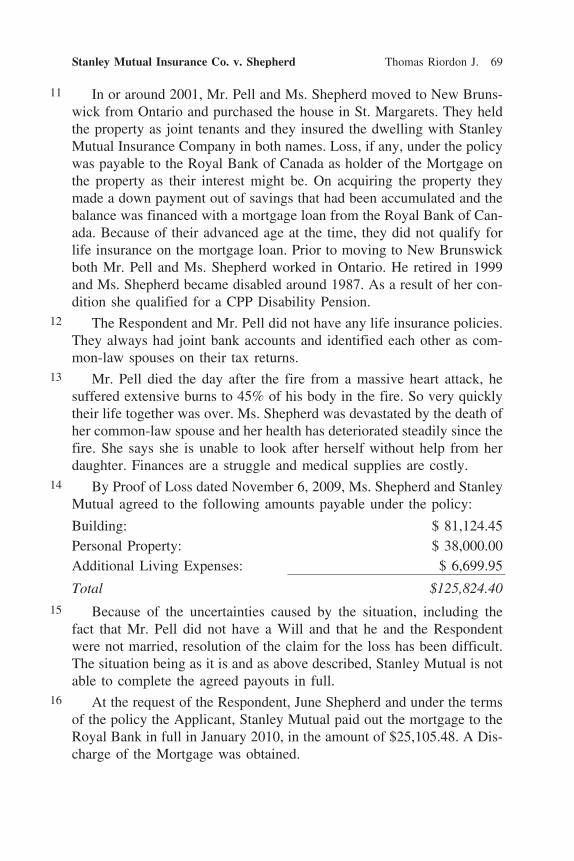

CANADIAN CASESON THE LAW OF

INSURANCEFourth Series/Quatrieme serie

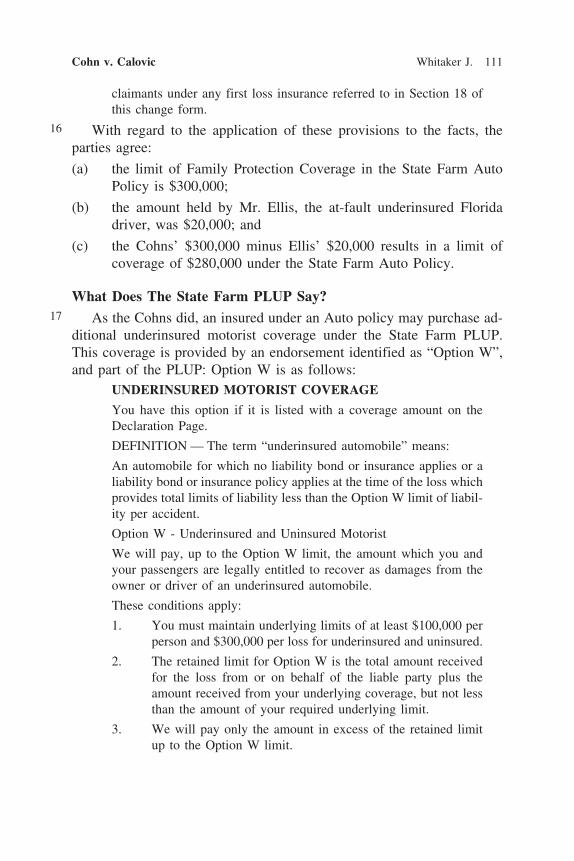

Recueil de jurisprudenceen droit des affaires

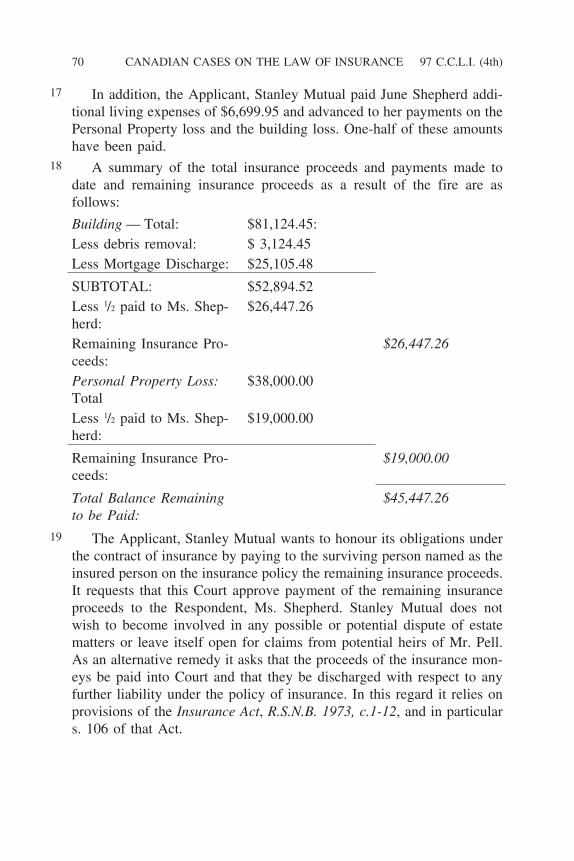

VOLUME 97(Cited 97 C.C.L.I. (4th))

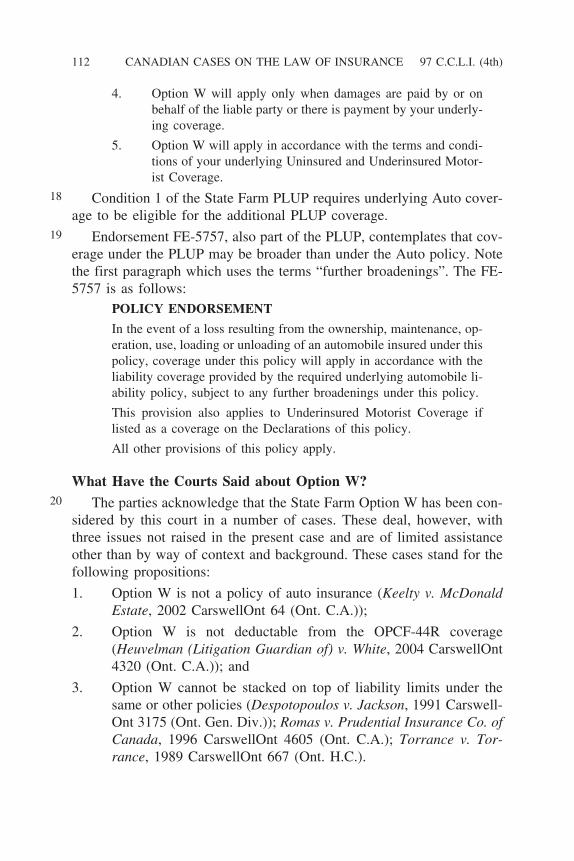

EDITORS-IN-CHIEF/REDACTEURS EN CHEFWon J. Kim, B.A., LL.B.

Kim Orr Barristers P.C.Toronto, Ontario

QUEBEC EDITOR/REDACTEUR POUR LE QUEBECJean-Francois Lamoureux, LL.L.

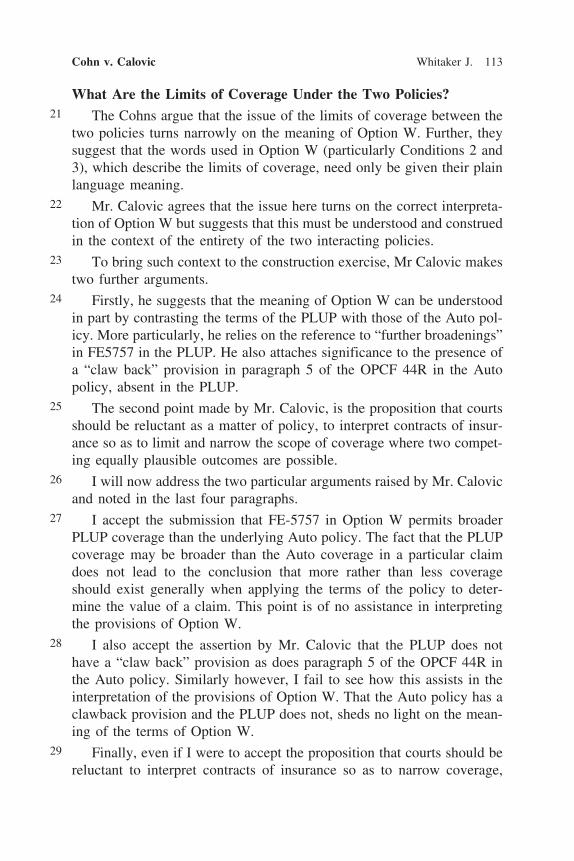

Robinson Sheppard ShapiroMontreal, Quebec

CARSWELL EDITORIAL STAFF/REDACTION DE CARSWELLJeffrey D. Mitchell, B.A., M.A.

Director, Editorial Production and Manufacturing

Ken Murphy, B.A. (HON.), LL.B.

Product Development Manager

Julia Fischer, B.A. (HON.), LL.B. Sharon Yale, M.A., LL.B.

Acting Supervisor, Legal Writing Supervisor, Legal Writing

Mike MacInnes, B.A. (HON.), LL.B. Lisa Rao, B.SC., LL.B.

Lead Legal Writer Senior Legal Writer

Jocelyn Cleary, B.A. (HON.), LL.B. Stephanie Hanna, B.A., M.A., LL.B.

Legal Writer Legal Writer

Chauncey Glass, B.A., LL.B. Martin-Francois Parent, LL.B., LL.M.,Legal Writer DEA (PARIS II)

Bilingual Legal Writer

Heather Niziol, B.A.

Content Editor

CANADIAN CASES ON THE LAW OF INSURANCE, a national series of Recueil de jurisprudence canadienne en droit des assurances, une serie

topical law reports, is published 12 times per year. Subscription rate $337.00 nationale de recueils de jurisprudence specialisee, est publie 12 fois par an-

per bound volume including parts. Indexed: Carswell’s Index to Canadian nee. L’abonnement est de 337 $ par volume relie incluant les fascicules. In-

Legal Literature. dexation: Index a la documentation juridique au Canada de Carswell.

Editorial Offices are also located at the following address: 430 rue St. Pierre, Le bureau de la redaction est situe a Montreal — 430, rue St. Pierre, Mon-

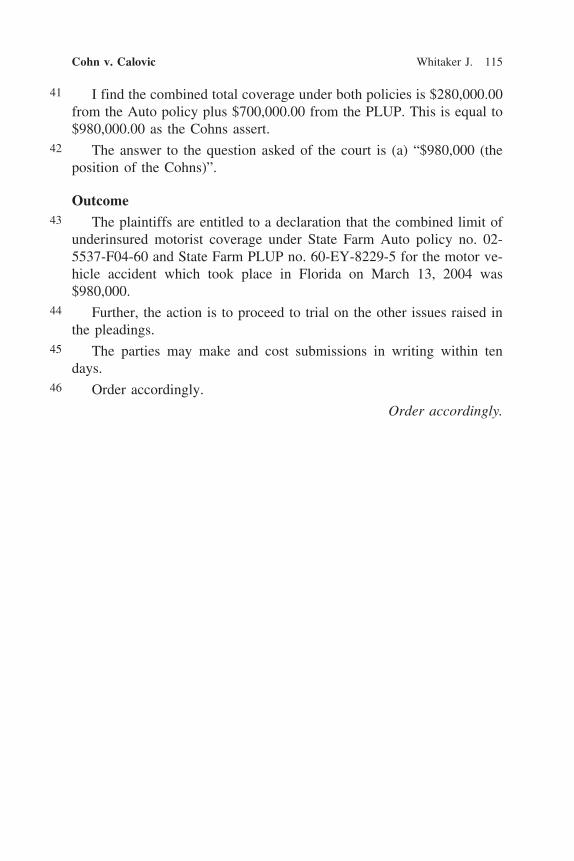

Montreal, Quebec, H2Y 2M5. treal, Quebec, H2Y 2M5.

________ ________

© 2011 Thomson Reuters Canada Limited © 2011 Thomson Reuters Canada Limitee

NOTICE AND DISCLAIMER: All rights reserved. No part of this publica- MISE EN GARDE ET AVIS D’EXONERATION DE RESPON-

tion may be reproduced, stored in a retrieval system, or transmitted, in any SABILITE : Tous droits reserves. Il est interdit de reproduire, memoriser sur

form or by any means, electronic, mechanical, photocopying, recording or un systeme d’extraction de donnees ou de transmettre, sous quelque forme ou

otherwise, without the prior written consent of the publisher (Carswell). par quelque moyen que ce soit, electronique ou mecanique, photocopie, enre-

gistrement ou autre, tout ou partie de la presente publication, a moins d’en

avoir prealablement obtenu l’autorisation ecrite de l’editeur, Carswell.A licence, however, is hereby given by the publisher:

Cependant, l’editeur concede, par le present document, une licence :

(a) to a lawyer to make a copy of any part of this publication to give to a a) a un avocat, pour reproduire quelque partie de cette publication pour

judge or other presiding officer or to other parties in making legal submis- remettre a un juge ou un autre officier-president ou aux autres parties dans

sions in judicial proceedings; une instance judiciaire;

b) a un juge ou un autre officier-president, pour produire quelque partie de

(b) to a judge or other presiding officer to produce any part of this publication cette publication dans une instance judiciaire; ou

in judicial proceedings; orc) a quiconque, pour reproduire quelque partie de cette publication dans le

cadre de deliberations parlementaires.

(c) to anyone to reproduce any part of this publication for the purposes of« Instance judiciaire » comprend une instance devant une cour, un tribunal ou

parliamentary proceedings.une personne ayant l’autorite de decider sur toute chose affectant les droits ou

les responsabilities d’une personne.

“Judicial proceedings” include proceedings before any court, tribunal or per-Ni Carswell ni aucune des autres personnes ayant participe a la realisation et

son having authority to decide any matter affecting a person’s legal rights ora la distribution de la presente publication ne fournissent quelque garantie

liabilities.que ce soit relativement a l’exactitude ou au caractere actuel de celle-ci. Il est

entendu que la presente publication est offerte sous la reserve expresse que ni

Carswell and all persons involved in the preparation and sale of this publica- Carswell, ni le ou les auteurs de cette publication, ni aucune des autres per-

tion disclaim any warranty as to accuracy or currency of the publication. This sonnes ayant participe a son elaboration n’assument quelque responsabilite

publication is provided on the understanding and basis that none of Carswell, que ce soit relativement a l’exactitude ou au caractere actuel de son contenu

the author/s or other persons involved in the creation of this publication shall ou au resultat de toute action prise sur la foi de l’information qu’elle

be responsible for the accuracy or currency of the contents, or for the results renferme, ou ne peuvent etre tenus responsables de toute erreur qui pourrait

of any action taken on the basis of the information contained in this publica- s’y etre glissee ou de toute omission.

tion, or for any errors or omissions contained herein.La participation d’une personne a la presente publication ne peut en aucun

cas etre consideree comme constituant la formulation, par celle-ci, d’un avis

No one involved in this publication is attempting herein to render legal, ac- juridique ou comptable ou de tout autre avis professionnel. Si vous avez

counting, or other professional advice. If legal advice or other expert assis- besoin d’un avis juridique ou d’un autre avis professionnel, vous devez

tance is required, the services of a competent professional should be sought. retenir les services d’un avocat ou d’un autre professionnel. Les analyses

The analysis contained herein should in no way be construed as being either comprises dans les presentes ne doivent etre interpretees d’aucune facon

official or unofficial policy of any governmental body. comme etant des politiques officielles ou non officielles de quelque organ-

isme gouvernemental que ce soit.

8 The paper used in this publication meets the minimum requirements of 8 Le papier utilise dans cette publication satisfait aux exigences minimales

American National Standard for Information Sciences — Permanence of Pa- de l’American National Standard for Information Sciences — Permanence of

per for Printed Library Materials, ANSI Z39.48-1984. Paper for Printed Library Materials, ANSI Z39.48-1984.

ISSN 0824-2585 ISBN 978-0-7798-0434-4

Printed in Canada by Thomson Reuters

CARSWELL, A DIVISION OF THOMSON REUTERS CANADA LIMITED

One Corporate Plaza Customer Relations2075 Kennedy Road Toronto 1-416-609-3800Toronto, Ontario Elsewhere in Canada/U.S. 1-800-387-5164M1T 3V4 Fax 1-416-298-5082

www.carswell.comE-mail www.carswell.com/email

CANADIAN CASESON THE LAW OF

INSURANCEFourth Series/Quatrieme serie

Recueil de jurisprudence canadienne en droit des assurances

[Indexed as: Saskatchewan Government Insurance v. Becker]

Saskatchewan Government Insurance, Appellant and EmiliaBecker and Automobile Injury Appeal Commission,

Respondents

Saskatchewan Court of Appeal

Docket: 1735

2011 SKCA 24

Richards, Smith, Ottenbreit JJ.A.

Heard: January 18, 2011

Judgment: February 23, 2011

Insurance –––– Automobile insurance — Government automobile insuranceplans — Entitlement to coverage — Miscellaneous issues.

Insurance –––– Automobile insurance — Government automobile insuranceplans — Removal of right of action –––– Insured, then 11 years old, sufferedbrain injury and motor disabilities in school bus accident — Representative ofinsurer felt that it would be benefit for insured to have parent involved in hercare — From October 2006 to September 2007 insured’s mother took unpaidleave from her full-time employment to look after insured — In September2007, mother negotiated with her employer to work at 35 percent of her formersalary, allowing her to work around insured’s appointments — Insurer reim-bursed mother for income lost up to fall of 2007 when insured was expected toreturn to school full time; insurer considered this to be ex gratia payment author-ized by s. 206 of Automobile Accident Insurance Act — Insurer notified motherthat it would discontinue payment at beginning of school year (decision let-ter) — Insured appealed to appeal commission seeking payment for differencebetween mother’s salary prior to collision and what she earned at reducedhours — Insurer wrote to mother claiming to withdraw decision letter and madeoffer to settle on ex gratia basis, provided that appeal be withdrawn and finalrelease be executed — At hearing, mother stated that she had not accepted set-tlement and wanted appeal to continue; insurer argued that decision letter had

CANADIAN CASES ON THE LAW OF INSURANCE 97 C.C.L.I. (4th)2

been withdrawn and therefore right of appeal no longer existed — Commissionheld that appeal was that of insured and could not be discontinued without herconsent and ordered insurer to make payment for net wage loss — Insurer ap-pealed — Appeal dismissed — Offer letter was clearly not unconditional agree-ment to settle; it required signed release and payment was on ex gratia basis —Acceptance of offer would have left insured with no basis for further claim, hadfurther need for her mother’s extended care become necessary — Mootness ofissue does not necessarily deprive adjudicator of jurisdiction over appeal, but ismatter of discretion — It was within commission’s jurisdiction to hear matterdespite settlement offer.

Insurance –––– Automobile insurance — Government automobile insuranceplans — Practice and procedure in matters involving government insur-ers –––– Jurisdiction of Appeal Commission — Insured, then 11 years old, suf-fered brain injury and motor disabilities in school bus accident — Representa-tive of insurer felt that it would be benefit for insured to have parent involved inher care — From October 2006 to September 2007 insured’s mother took unpaidleave from her full-time employment to look after insured — In September2007, mother negotiated with her employer to work at 35 percent of her formersalary, allowing her to work around insured’s appointments — Insurer reim-bursed mother for income lost up to fall of 2007 when insured was expected toreturn to school full time; insurer considered this to be ex gratia payment author-ized by s. 206 of Automobile Accident Insurance Act — Insurer notified motherthat it would discontinue payment at beginning of school year (decision let-ter) — Insured appealed to appeal commission, seeking payment for differencebetween mother’s salary prior to collision and what she earned at reducedhours — Insurer wrote to mother claiming to withdraw decision letter and madeoffer to settle on ex gratia basis, provided that appeal be withdrawn and finalrelease be executed — At hearing, mother stated that she had not accepted set-tlement and wanted appeal to continue; insurer argued that decision letter hadbeen withdrawn and therefore right of appeal no longer existed — Commissionheld that appeal was that of insured and could not be discontinued without herconsent and ordered insurer to make payment for net wage loss — Insurer ap-pealed — Appeal dismissed — Offer letter was clearly not unconditional agree-ment to settle; it required signed release and payment was on ex gratia basis —Acceptance of offer would have left insured with no basis for further claim, hadfurther need for her mother’s extended care become necessary — Mootness ofissue does not necessarily deprive adjudicator of jurisdiction over appeal, but ismatter of discretion — It was within commission’s jurisdiction to hear matterdespite settlement offer.

Cases considered by Smith J.A.:

Borowski v. Canada (Attorney General) (1989), [1989] 3 W.W.R. 97, [1989] 1S.C.R. 342, 57 D.L.R. (4th) 231, 92 N.R. 110, 75 Sask. R. 82, 47 C.C.C.

Saskatchewan Government Insurance v. Becker Smith J.A. 3

(3d) 1, 33 C.P.C. (2d) 105, 38 C.R.R. 232, 1989 CarswellSask 241, 1989CarswellSask 465, [1989] S.C.J. No. 14 (S.C.C.) — considered

Statutes considered:

Automobile Accident Insurance Act, R.S.S. 1978, c. A-35Generally — referred tos. 112(2) — considereds. 189(1) — referred tos. 193(7)(b) — considereds. 194(1) — pursuant tos. 206 — considered

Regulations considered:

Automobile Accident Insurance Act, R.S.S. 1978, c. A-35Personal Injury Benefits Regulations, R.R.S., c. A-35, Reg. 3

s. 12(e)(ii) — considereds. 12(e)(iii) — considered

APPEAL by government insurer from decision of appeal commission orderinginsurer to reimburse insured’s mother for lost wages.

Robert G. Kennedy, Q.C., for AppellantSharon H. Pratchler, Q.C., for Automobile Injury Appeal Commission

Smith J.A.:

I Introduction1 This appeal is brought by Saskatchewan Government Insurance

(“SGI”) from a decision of the Automobile Injury Appeal Commission,pursuant to s. 194(1) of The Automobile Accident Insurance Act, R.S.S.1978, c. A-35, which permits an appeal to this Court on a question oflaw. The appellant argues that the Appeal Commission lacked jurisdic-tion to hear the appeal, or, alternatively, lost jurisdiction when the appealbecame moot, or, alternatively, lacked jurisdiction to award recovery asit did, rather than referring the matter back to SGI. The Appeal Commis-sion appeared on the appeal to make submissions solely in relation to itsjurisdiction. The respondent, Emilia Becker, relied on the submissions ofthe Appeal Commission.

II Background Facts2 On October 17, 2006 the respondent Emilia Becker, then 11 years

old, was an unrestrained passenger in a school bus that failed to yield the

CANADIAN CASES ON THE LAW OF INSURANCE 97 C.C.L.I. (4th)4

right of way, struck another vehicle and rolled. She was unconscious atthe scene of the accident and was initially diagnosed with a concussion.When she did not progress as expected, follow-up tests disclosed a mod-erate brain injury. She also suffered multiple abrasions and bruising, apunctured lung and a fractured thumb which healed uneventfully. Shewas entitled to personal injury benefits pursuant to The Automobile Acci-dent Insurance Act. Heather Becker and Mark Becker are her parents.

3 In November 2006, Emilia returned to school for one hour a day, pro-gressing to two hours a day by Christmas. In January and for part ofFebruary 2007, she returned to school full time. However, she exper-ienced dizziness, severe headaches, difficulty with concentration andmemory, was irritable and suffered extreme fatigue, often falling asleepat school. She also suffered motor disabilities including difficulty inwalking up the stairs, an inability to run or to ride her bicycle. Prior tothe accident she had been an excellent student and also excelled in anumber of physical activities including ballet, jazz and tap dancing at acompetitive level.

4 In February 2007, Dr. Nanson, a neuropsychologist recommendedthat Emilia attend school for half days, in the mornings only, because hersymptoms were made worse by fatigue. Dr. Nanson recommended thatshe be at home in the afternoon with parental supervision to nap and rest,and reduce the risk of falls when she was dizzy. Other medical reportsfiled with SGI discussed the role of parental involvement in careful mon-itoring of Emilia’s activities to avoid problems of fatigue, monitor hersymptoms, and to supervise regular therapy to relearn the motor andmental skills she had lost.

5 It was intended that Emilia would return to school full time in Sep-tember 2007, but in the summer of 2007 she was referred to the Chil-dren’s Program at Wascana Rehabilitation Centre that would continue toJanuary 23, 2008, to deal with continuing cognitive difficulties in motorplanning and perceptual skills that were affecting her gross and fine mo-tor skills. It is a policy of the Program for a parent to be in attendancewhen a child is at therapy in the Children’s program. It was not consid-ered to be appropriate for Emilia to be looked after by a babysitter forthis purpose.

6 Sharon Hoiland, SGI injury representative, was responsible for Emi-lia’s claim during this period. She felt that it would be a benefit for Emi-lia to have a parent involved in her care. The family lived on a farm andEmilia’s age, symptoms and behavioural difficulties made it difficult to

Saskatchewan Government Insurance v. Becker Smith J.A. 5

employ alternative care for her. Between October 2006 and September2007 Heather Becker took an unpaid leave from her full time employ-ment to look after Emilia and her two siblings, all of whom had beeninjured in the same accident. In September 2007 Heather Becker negoti-ated a contract with her employer to work at 35% of her former full timewage, allowing her to work around Emilia’s schedule of appointments,lunch time, after school and other times when Emilia was tired, confusedor had severe headache.

7 There is no express provision in the Act authorizing reimbursement ofthe parent of an injured insured minor who takes off work to care for theinjured child for lost wages, although SGI has a written policy permittingrecovery of lost income of a parent for up to 21 days when an injuredchild is hospitalized and in acute care. In the instant case, however, SGIaccepted the view of medical advisors and school officials that HeatherBecker’s presence was beneficial to Emilia’s treatment and recovery anddecided to reimburse her for the income lost for almost a year up to thefall of 2007 when Emilia was expected to return to school full time. SGIconsidered this to be an ex gratia payment, authorized by s. 206 of theAct, on the basis that parental income recovery is not a “legislatedbenefit”.

8 Section 206 of the Act provides as follows: 206 If the insurer considers that the payment of a claimant’s claim isin the interest of the insurer and the better administration of this Part,the insurer may authorize an ex gratia payment to be made to thatclaimant.

9 When almost a year had expired, SGI considered it had gone as far asit could go on an ex gratia basis, and notified Mark and Heather Becker,by letter dated August 20, 2007 that it would discontinue payment at thebeginning of the school year. This letter commented:

....As our office has pointed out in the past, salary for parents is onlycovered when the patient is in acute care. Our office did agree tocontinue Heather’s salary to provide time for alternate arrangements.As this has continued for 10 months, our office will be discontinuingthis payment upon the beginning of the school year.

10 This letter did not include notice of a claimant’s right to ask for medi-ation or to appeal the insurer’s decision as is required of a letter respect-ing the claimant’s entitlement to benefits by s. 189(1) of the Act. A more

CANADIAN CASES ON THE LAW OF INSURANCE 97 C.C.L.I. (4th)6

formal decision letter was, however, provided on November 28, 2007.This letter, addressed to Heather Becker, provided, in part, as follows:

As you are aware our office did cover your full salary up to and in-cluding September 7, 2007.

As of this date our office is prepared to cover your salary for timerequired to miss to attend Emilia’s medical appointments. We are notin a position to cover your salary for any other time missed. I under-stand the school is prepared to provide taxi service for Emilia to at-tend band.

As we have previously discussed there is no legislation provision toprovide funding for your salary, but our office will provide you theappeal option for this decision.

If you don’t agree with the decision made regarding the benefits,please let me know. You can ask me to have my supervisor call youto discuss the decision.

You also have the right to apply for an appeal of our decision on thebenefits.

The letter then set out the procedure for filing an appeal. In neither of theletters did SGI suggest that it had determined that it was no longer neces-sary or desirable for Heather Becker to take time off work to look afterthe care and rehabilitation of Emilia.

11 An appeal to the Appeal Commission was brought in Emilia’s name.The appeal indicated: “We are applying for SGI to pay the differencebetween what Heather’s salary was prior to the collision and what sheearned at her reduced hours for the dates: September 5, 2007 - January24, 2008.”

III The Procedure Before the Appeal Commission12 At the appeal hearing, SGI was represented by counsel but the Beck-

ers were not. Before the Appeal Commission, SGI submitted that thepayments made to reimburse Heather Becker’s lost income (referred toby SGI as “income replacement benefits”) were gratuitous and not pro-vided for by the Act. It pointed out that the Commission cannot order itto make an ex gratia payment and argued that it must therefore dismissthe appeal. The Commission ruled that it would reserve its decision onthat issue and hear evidence on the merits of the claim, since all partiesand witnesses were already before it. At the conclusion of the hearing,the Commission requested that SGI provide a copy of its Acquired BrainInjury Guidelines. After reviewing the guidelines and the legislation, it

Saskatchewan Government Insurance v. Becker Smith J.A. 7

asked the parties to reconvene to answer questions about Emilia’s entitle-ment to rehabilitation benefits.

13 SGI replied that the Commission had no jurisdiction to adjudicate thisissue, since the payments made had, in its view, been ex gratia, andasked for the questions the Commission had to be put in writing. TheCommission complied, asking the parties to make submissions as towhether Emilia was entitled to benefits such as custodial care from hermother under s. 112(2) of the Act, and the Acquired Brain Injury Guide-lines and, as to whether, on the assumption that SGI thought compensat-ing the mother for her lost income while caring for her daughter waseither necessary or advisable, it had reasonably terminated that benefit.The Commission indicated it was prepared to receive submissions inwriting on these points.

14 Section 112(2) of the Act provides as follows: (2) Subject to the regulations, the insurer may take any measure itconsiders necessary or advisable to contribute to the rehabilitation ofan insured, to lessen a disability resulting from bodily injury and tofacilitate the insured’s recovery from the accident.

15 At this point, rather than make submissions to the Commission, onSeptember 23, SGI wrote to Heather and Mark Becker making a formaloffer to settle the matter by paying the lost wages claimed, provided thatEmilia withdraw her appeal and that Heather and Mark Becker execute a“Final Release” in relation to any economic loss arising from these cir-cumstances. This was followed up on October 31, 2008, in a letter ad-dressed to Emilia, as follows:

After further consideration, we have decided to withdraw our deci-sion letter dated November 28, 2007 (the “Decision Letter”) andmake the payment you have requested. As you well know the Deci-sion Letter was the basis of your appeal. As such, the withdrawal ofthe Decision Letter has the legal effect of rendering your appealmoot. Further, in our view, the Appeal Commission now has nofoundation to adjudicate this matter and no further jurisdiction.

We are enclosing a cheque in the amount of $10,838.62 which is thedifference between your mother’s full-time net salary in 2006 at thetime of the collision and her new contract at 35 percent minus pay-ments made by SGI for your mother accompanying yourself to medi-cal appointments, plus pre-judgment interest in the amount of$357.78 from September 17, 2007, to present.

We understand you may have out of pocket expenses related to yourappeal and would ask that you please advise us as to these costs and

CANADIAN CASES ON THE LAW OF INSURANCE 97 C.C.L.I. (4th)8

provide back-up documentation so that we may reimburse you thesame to the legislated cap of $2,500.

In order to be clear this payment is made ex gratia.

Please note, it is our intention to appear at the next scheduled date forthe appeal only and solely to advise the Appeal Commission of theactions we have taken.

SGI also wrote to the Commission, reiterating its position that the Com-mission was without jurisdiction to pursue the enquiries it had raised.

16 The hearing reconvened on November 6, 2008. At this point, SGItook the position that the November 2007 decision letter had been “with-drawn”, by the letter of October 31, 2008, the payment requested hadbeen made, and the right of appeal no longer existed. Emilia and herparents stated that they had not accepted SGI’s settlement (no paymenthad in fact been made) and wanted the appeal to continue. Emilia, inparticular, stated that she believed the appeal was not just about money,but about the entitlement to the benefit, and she wanted the appeal tocontinue for the benefit for other families who might face similarsituations.

17 The Commission ruled that it was seized with the matter and wouldcontinue, giving leave to the parties to make further submissions on thenew jurisdictional point, relating to SGI’s purported withdrawal of its de-cision letter. SGI expressly declined to make any submissions as towhether s. 112(2) and the regulations entitled Emilia to the benefitclaimed. Rather, it relied on its submission that the matter was now mootand the Commission had no jurisdiction to render a decision.

III The Decision of the Commission18 On the question of whether the appeal had been rendered moot by

SGI’s purported withdrawal of its letter of decision and offer of settle-ment, the Commission took the view that the appeal was that of the in-sured, and could not be discontinued without the insured’s consent.

19 In relation to the question of whether the Commission lacked jurisdic-tion over the matter because the payments in question were ex gratia, theCommission began with the following observation:

[56] We start from the premise that no-fault benefits are a statutoryinsurance scheme funded by insureds, and we think it follows thatSGI cannot spend those monies except in accordance with the statu-tory scheme. If SGI is routinely making payments for a process orthing then it must be the money is being spent within the statutory

Saskatchewan Government Insurance v. Becker Smith J.A. 9

scheme or SGI is spending money on a regular basis for which it isnot authorized. In other words, you can’t spend money you are notauthorized to spend. SGI may, of course, make payments under s.210 at its sole and unfettered discretion but if it is using ex gratiapayments on a regular basis then, in our view, it means there is some-thing wrong with the legislation or else the interpretation of it. [2009SKAIA 006]

20 Noting its disappointment that SGI had declined to make any submis-sions on the interplay between the written acquired brain injury policy,the Act, and Emilia’s entitlement to rehabilitation benefits under the Act,the Commission then went on to analyze these aspects of the compensa-tion scheme, focusing on s. 112(2) of the Act, set out above, and s. 12(e)of the Personal Injury Benefits Regulations, which provides for funding:

(ii) to lessen the insured’s disability; and

(iii) to facilitate the insured’s recovery from an accident to improve hisor her earning capacity and level of independence.

21 Concluding that these provisions, properly interpreted, could coverincome replacement benefits for a parent of a brain injured child, wherethe parent’s presence was considered necessary or advisable to lessen theAppellant’s disability and facilitate her recovery, the Commission con-cluded as follows:

[61] The question we now must ask is whether the mother’s care wasnecessary or advisable to lessen the Appellant’s disability and facili-tate her recovery and “... to improve...her earning capacity and levelof independence”. Considering those words generally and broadly soas to have application to a young child, we interpret “improve herearning capacity” as being a long term effect. Based on the medicalreports and assessments filed respecting the Appellant’s abilities andprogress, the testimony of the occupational therapist and educator,and the parents, we are satisfied that the care the Appellant’s motherprovided was both necessary and advisable from the date of the acci-dent and gradually decreasing to when the Appellant finished therapyat WRC Children’s Program. SGI too thought the mother’s care wasnecessary and/or advisable because it funded it for almost a year.Leaving aside the question of whether it is a so-called legislated ben-efit, the only disagreement was when the payment should terminate.

[62] SGI terminated payment of the mother’s wage loss when theAppellant returned to school full-time in the fall of 2007. The Appel-lant however was just starting rehabilitative therapy WRC Children’sProgram and there was substantial evidence the Appellant still re-quired supervisory and parental care with school, tasks of daily living

CANADIAN CASES ON THE LAW OF INSURANCE 97 C.C.L.I. (4th)10

and mobility. At first blush it might seem reasonable to terminatefunding when the Appellant returned to school full time, but we con-clude that it wasn’t reasonable given she had just started rehabilita-tion therapy for documented cognitive and mobility problems.

[63] Children, fortunately, tend to be resilient in recovering from in-juries, including brain injuries. This does not mean that they shouldnot get proper treatment, or that such treatment should be compro-mised because a parent is not available to maximize treatment goals,or to sound a warning if the treatment goes awry. We do not require“Cadillac” treatment: we do insist on reasonable and effective treat-ment. For children, this will require parental participation at a reason-able level. The mother’s decision to work part time during this criti-cal period was principled, responsible, and both necessary andadvisable to facilitate her daughter’s recovery.

22 The Commission concluded that funding for Emilia’s mother’s netwage loss for the period September 7, 2007 to January 23, 2008 was notreasonably terminated and ordered SGI to make that payment togetherwith pre-judgment interest.

IV Analysis23 The appeal raises three issues, all questions of law for which the ap-

pellate standard of review is correctness:

1. Did the committee err in continuing to entertain the appeal in spiteof SGI’s letters of September 23 and October 31, 2008?

2. Did the Committee err in concluding that the Act and Regulations,properly interpreted, were broad enough to authorize payment ofthe benefit in question in appropriate circumstances?

3. Assuming that the first two questions are answered in the nega-tive, did the Commission have jurisdiction to make an award pur-suant to s. 112(2) rather than referring this matter back to SGI?

24 It is our view that the Commission did not err in the exercise of itsjurisdiction and that the appeal should be dismissed.

25 SGI’s letters of September 23 and October 31, 2008 were clearly notan unconditional agreement to settle the issues raised on the appeal. Thefirst required Heather and Mark Becker to sign a release and the latterwas expressed to be solely on the basis of an ex gratia payment. Accept-ance of this offer would have left the insured with no basis for any fur-ther claim had further need for her mother’s extended care become nec-essary. Further, the settlement was clearly not accepted by Emilia or her

Saskatchewan Government Insurance v. Becker Smith J.A. 11

parents, who wanted this issue determined. Finally, mootness of an issuedoes not necessarily deprive an adjudicator of jurisdiction over an ap-peal, but is a matter of discretion. The appellant relies on Borowski v.Canada (Attorney General), [1989] 1 S.C.R. 342 (S.C.C.), but this deci-sion simply stands for the proposition that a court, as an incident of con-trol over its procedure, has discretion to decline to adjudicate a questionthat has become moot. In the instant case, the Commission clearly ac-cepted Emilia’s decision to continue the appeal to determine the point ofprinciple at issue. It was within the Commission’s jurisdiction to hearthis matter despite SGI’s settlement offer.

26 The issue of statutory interpretation raises two subsidiary issues thatshould be addressed. The first is that the appellant argues that in deter-mining the entitlement to this benefit pursuant to s. 112(2) of the Act, theCommission unilaterally “changed the appeal” from one concerning “in-come replacement” to one concerning rehabilitation benefits.

27 This argument should be soundly rejected. SGI’s characterization ofthis benefit as an ex gratia payment of “income replacement” was ex-actly what was at issue in this appeal. Nothing in the notice of appeal tothe Commission confines the issue in this way. It was, in my view,clearly within the Commission’s jurisdiction to determine whether thischaracterization of the benefit was correct in the course of determiningthe appellant’s entitlement to continuation of the benefit.

28 Secondly, the appellant argues that the Commission strayed from in-terpreting the Act, and decided, instead, on the basis of what it thoughtthe Act ought to provide. I do not agree with this interpretation of whatthe Commission did. The point made by the Commission was that thefact that SGI felt compelled to fall back on ex gratia payments to coverpayments deemed necessary or desirable for the rehabilitation of an in-sured suggested that SGI had failed to give a proper interpretation to theAct. This, in my view, is a sound point. Section 206 authorizes paymentsto be made in the interest of the insurer, for the better administration ofthe Act. Clearly this would, for example, authorize SGI to expend fundsto settle contentious but doubtful claims, for example to avoid the costsand risks of litigation. The widespread use of this provision, however,simply to fund benefits for an insured not otherwise authorized by thelegislation seems questionable, and the sense that such benefits ought, asa matter of logic, to be provided, invites a more careful scrutiny of thelegislation to determine whether it does, in fact, authorize such benefits.

CANADIAN CASES ON THE LAW OF INSURANCE 97 C.C.L.I. (4th)12

29 Section 112(2), on the other hand, by its clear wording gives SGI anextremely broad discretion to make payments considered necessary oradvisable to contribute to the rehabilitation of an insured. In my view, theAppeal Commission did not err in concluding that, where a parent’s pres-ence is considered necessary or advisable for the proper recovery or re-habilitation of a child who suffered an acquired brain injury, this provi-sion is broad enough to authorize funding necessary to make thatpresence possible. I agree with the Commission that in appropriate cir-cumstances, this could include replacement of lost income to make itpossible for the parent to be available to the child. As the Commissionrightly pointed out, SGI clearly had considered Heather Becker’s pres-ence to be necessary or desirable, a determination supported by the medi-cal and other evidence, and it did not contest the point that circumstanceshad not changed to render it unnecessary at the time the funding wasdiscontinued.

30 I would conclude that the Appeal Commission did not err in its inter-pretation of the Act and the Regulations.

31 Finally, it is my view that the Commission had jurisdiction to orderthe payment of this benefit to the insured rather than refer the matterback to SGI to exercise its discretion under s. 112(2). Section 193(7)(b)expressly authorizes the Appeal Commission to “make any decision thatthe insurer is authorized to make pursuant to this Part.” SGI declined tomake any submissions as to whether the payments should be made pur-suant to s. 112(2) and did not otherwise contest the insured’s contentionthat the circumstances that justified the initial payment had not changedfor the period of the claim. In these circumstances it was not necessaryfor the Appeal Commission to refer the matter back to SGI.

32 The appeal is dismissed with costs to the Appeal Commission.

Richards J.A.:

I concur

Smith J.A.(for Ottenbreit J.A.):

I concur

Appeal dismissed.

Gablehouse v. Borza 13

[Indexed as: Gablehouse v. Borza]

Richard Darrell Gablehouse, Respondent (Plaintiff) and DerrickDodge (1980) Ltd., Appellant (Defendant) and Ryan J. Borzaand Borza Inspections Ltd., Not a Party to the Appeal (Third

Parties)

Alberta Court of Appeal

Docket: Edmonton Appeal 1003-0204-AC

2011 ABCA 102

Jean Cote, Clifton O’Brien, Patricia Rowbotham JJ.A.

Heard: March 29, 2011

Judgment: March 29, 2011

Written reasons: March 31, 2011

Insurance –––– Automobile insurance — Extent of risk — Terms of art —Miscellaneous terms –––– Van leased by business was involved in automobileaccident — Plaintiff driver of other vehicle commenced action for damages forpersonal injuries sustained in accident — Driver of van was convicted underHighway Traffic Act — Business mailed cheque as part of buy out optionshortly before accident — Cheque was received after collision — On hearing, itwas determined that title had not passed from lessor to business, and that bothlessor and business were owner of vehicle for insurance purposes — Lessor ap-pealed — Appeal dismissed — Clause of lease stated that title to van would beregistered in lessor until company notified otherwise, and it never did so beforecollision — Option and bill of sale were conditional on full payment, which wasnever tendered.

Cases considered:

Alas v. Solis (2003), 2003 ABCA 137, 2003 CarswellAlta 617, 14 Alta. L.R.(4th) 1, 226 D.L.R. (4th) 744, 39 M.V.R. (4th) 294, [2003] 9 W.W.R. 623,327 A.R. 192, 296 W.A.C. 192, [2003] A.J. No. 497 (Alta. C.A.) —considered

Archdekin v. McDonald (1912), 1 D.L.R. 664, 1 W.W.R. 1014, 1912 Car-swellMan 207 (Man. K.B.) — referred to

Delory v. Guyett (1919), 47 O.L.R. 137, 52 D.L.R. 506 (Ont. C.A.) —distinguished

Hansraj v. Ao (2004), 354 A.R. 91, 329 W.A.C. 91, 2004 ABCA 223, 2004CarswellAlta 849, 34 Alta. L.R. (4th) 199, [2005] 4 W.W.R. 669, [2004]A.J. No. 734 (Alta. C.A.) — followed

CANADIAN CASES ON THE LAW OF INSURANCE 97 C.C.L.I. (4th)14

Hayduk v. Pidoborozny (1972), [1972] 4 W.W.R. 522, 29 D.L.R. (3d) 8, 1972CarswellAlta 55, [1972] S.C.R. 879, 1972 CarswellAlta 141 (S.C.C.) —considered

Kruse v. Fallows (1921), [1921] 2 W.W.R. 210, 16 Alta. L.R. 384, 59 D.L.R.169, 1921 CarswellAlta 25 (Alta. S.C. (App. Div.)) — referred to

Saskatchewan River Bungalows Ltd. v. Maritime Life Assurance Co. (1992), 92D.L.R. (4th) 372, 10 C.C.L.I. (2d) 278, [1992] I.L.R. 1-2895, 127 A.R. 43,20 W.A.C. 43, 1992 CarswellAlta 382 (Alta. C.A.) — referred to

Saskatchewan River Bungalows Ltd. v. Maritime Life Assurance Co. (1994),[1994] 2 S.C.R. 490, 1994 CarswellAlta 744, [1994] 7 W.W.R. 37, 20 Alta.L.R. (3d) 296, 168 N.R. 381, (sub nom. Maritime Life Assurance Co. v.Saskatchewan River Bungalows Ltd.) [1994] I.L.R. 1-3077, 155 A.R. 321,73 W.A.C. 321, 115 D.L.R. (4th) 478, 23 C.C.L.I. (2d) 161, 1994 Carswell-Alta 769, [1994] S.C.J. No. 59, EYB 1994-66952 (S.C.C.) — referred to

Statutes considered:

Currency Act, R.S.C. 1985, c. C-52s. 8 — referred to

Sale of Goods Act, R.S.A. 2000, c. S-2Generally — referred tos. 19 — considereds. 20(2) — considered

Traffic Safety Act, R.S.A. 2000, c. T-6Generally — referred to

APPEAL by lessor from judgment reported at Gablehouse v. Borza (2010), 72B.L.R. (4th) 198, 98 M.V.R. (5th) 253, 28 Alta. L.R. (5th) 152, 2010 ABQB294, 2010 CarswellAlta 1022, 485 A.R. 364 (Alta. Q.B.), regarding determina-tion of ownership of vehicle for insurance purposes.

K.P. Feehan, Q.C., A.E. Jarman, for Respondent / PlaintiffJ.L. Cairns, for Appellant / Defendant

Per curiam (orally):

1 Legislatures in Canada have long recognized the terrible power ofmotor vehicles to kill, maim and destroy in a moment’s inadvertence.Their toll now surpasses most diseases and wars. Our Legislature there-fore enacts a scheme for reliable compensation for those injuries. Thescheme interlocks and includes:

1. Vicarious and joint and several liability of drivers, owners, andemployees to pay compensation;

Gablehouse v. Borza Per curiam 15

2. Compulsory registration of vehicles, their owners, and their ad-dresses, and

3. Compulsory liability insurance of vehicle owners.

All three are necessary to let most innocent collision victims or theirfamilies actually collect compensation. See Hansraj v. Ao (2004), 354A.R. 91 (Alta. C.A.) (para. 114).

2 At 7:15 a.m. one morning, the respondent Gablehouse was driving onthe outskirts of Edmonton, when a van crossed the centre line and hit therespondent’s sedan head on. The respondent was severely injured, in-cluding fractures of his thigh bone and pelvis, producing much pain andongoing disability.

3 The time limit for suing was two years. Shortly before it expired, therespondent sued the van’s driver, the driver’s employer, and theowner/lessor of the van (the appellant). Two people were named on thevan’s registration certificate: the appellant and the employer (Extracts, p.A157). The respondent claimed for ongoing loss of income and cost offuture care.

4 The appellant admitted that it was the lessor of the van, but deniedthat it was still the owner of the van.

5 Just before the trial date, all parties in the suit limited its issues toone. They asked the Court to rule on that one issue in special chambers.The question is whether the lease by the appellant to the employer wasstill in force at the time of the collision, and whether the appellant lessorwas still the owner or deemed owner of the van. A Pierringer settlementalso agreed that the driver and employer were negligent and responsiblefor the collision, and would pay the injured respondent $1,000,000. Iffound still the van owner, the appellant lessor agreed then to pay an addi-tional $900,000 to the respondent.

6 The chambers judge decided (2010 ABQB 294 (Alta. Q.B.)) that thelessor was still the owner and vicariously liable (for the additional$900,000). The appellant lessor appeals.

7 The initial lease by the appellant to the employer originally wouldhave expired long before the collision. Then it was extended, to expiretwo days after the collision. The lessee employer forgot to renew its un-dertaking to insure the van.

8 The lease provided that title and registration would remain in the les-sor appellant (Extracts, p.A124, cl. 13).

CANADIAN CASES ON THE LAW OF INSURANCE 97 C.C.L.I. (4th)16

9 The lease contained an option: the lessee employer could buy the van.(A later letter fixed the option price.) The lessee employer mailed acheque two days before the accident purporting to exercise that option;but there were two flaws:

(a) the cheque was not received until after the collision, and

(b) the lessee employer never made the last monthly lease payment,due about three weeks before the collision. Yet the option to buywas exercisable only if the “Lessee is not in default”. (Extracts, p.A124, cl. 6)

10 After the collision, the appellant lessor prepared a bill of sale to trans-fer title to the lessee employer, and signed it. But the bill of sale ex-pressly stated that ownership would remain with the lessor “until allsums owing are paid” (Extracts, p. A153, cl. 4). The lessee employernever signed the bill of sale.

11 At the time of the collision, the lessor of the van, publicly registeredas such with the government, was the appellant lessor. The lessee em-ployer was also shown as “registrant”.

12 Had title to the van passed before the collision? The appellant reliesheavily on the Sale of Goods Act, but it gives somewhat limited assis-tance. For transfer of ownership of specific or ascertained deliverablegoods, the Act requires both a contract, and intent of the parties about thetime that title is to be transferred. The intent is to be ascertained from theterms of the contract, the parties’ conduct, and the circumstances of thecase (s. 19). Absent a different intention, the time of transfer sometimesis the time of contracting even if the payment or delivery is postponed (s.20(2)). But that subsection is confined to unconditional contracts. Thiscontract was expressly conditional on payment.

13 Even if those sections did apply, there is an issue whether a differentintention or different contractual terms applied. The idea that an expen-sive vehicle would be sold on credit with no security is very improbable,as the chambers judge found. Obviously the lessee employer knew thatpayment was needed to exercise the option, as it sent a large cheque.

14 Clause 13 of the lease stated that title to the van would be registeredin the lessor appellant until that company notified otherwise, and it neverdid so before the collision.

15 The only contract for sale was the option. But it was conditional onfull payment, which was never even tendered. That is because onemonthly payment never occurred, in any form. The bill of sale similarly

Gablehouse v. Borza Per curiam 17

was conditional on full payment: it postponed transfer of title until thatapplied. Either the payout payment was too low, or the lease was not ingood standing as the option expressly required. Or both.

16 All that may well render academic whether exercise of the optioncould be effective on mailing, before receipt by the offeror (the lessor).In any event, we have seen no legal authority for payment ever beingeffective on mailing.

17 No one has found any authority saying that putting a cheque into themail is payment at that moment. The appellant cites Delory v. Guyett(1919), 52 D.L.R. 506 (Ont. C.A.), 519, but it is distinguishable, becauseit is not about postal acceptance at all. And the passage cited is a dissentcontrary to the majority view (p. 513). Contrary to the appellant’s pro-position is Saskatchewan River Bungalows Ltd. v. Maritime LifeAssurance Co. (1992), 127 A.R. 43 (Alta. C.A.) (paras. 18, 88, 89), revd.on other grds. [1994] 2 S.C.R. 490 (S.C.C.).

18 It is true that sometimes a contract can be formed by mailing an ac-ceptance of an offer. But it is trite law that merely communicating wordsof acceptance does not always suffice. Some offers can only be acceptedby performance, or some other act: Treitel, Law of Contract 37-38 (11thed. 2003) (“unilateral contracts”). That was plainly so here. (See Ex-tracts, pp. A124, cl. 6, ll. 3-7 and A135 and A142.)

19 In any event, a cheque is not legal tender: Currency Act, R.S.C. 1985,c. C-52, s. 8. See Archdekin v. McDonald (1912), 1 W.W.R. 1014 (Man.K.B.), 1016; Kruse v. Fallows (1921), 59 D.L.R. 169 (Alta. S.C. (App.Div.)), 174. And this one arrived after the collision.

20 The respondent submits that exercise of the option could only be ef-fective at the end of the lease, two days after the collision. That is argua-ble, but we need not pursue that. Nor need we opine upon the chambersjudge’s additional ground relating to insurable interest.

21 There is another freestanding bar to this appeal. There can be morethan one owner of a vehicle for liability purposes: Alas v. Solis, infra.Those who allow their names to be registered with the government asowner of a motor vehicle, are that vehicle’s “owner” for purposes of vi-carious liability under the Traffic Safety Act. (Consent to drive is not con-tested here.) That is clear from Hayduk v. Pidoborozny, [1972] S.C.R.879, 29 D.L.R. (3d) 8 (S.C.C.), which binds us. It points out that it is theregistered owner whom the statute requires to give proof of insurance (p.

CANADIAN CASES ON THE LAW OF INSURANCE 97 C.C.L.I. (4th)18

885 S.C.R.). As the Supreme Court says, the whole reason to registerowners

is to give notice to all users of the highway the identity of an indivi-dual to whom they may look as owner in the event of an accident.

In other words to see whom to sue. That refers to the integrated schemewith which these reasons opened. Even if Hayduk is read as a rebuttablepresumption, there was no rebuttal proved here.

22 The appellant was shown on the van’s registration as the leasing com-pany of the leased vehicle. That is the owner. That the lessee was alsonamed there as “registrant” does not detract from that (Extracts, p.A157). See Alas v. Solis, 2003 ABCA 137, 327 A.R. 192 (Alta. C.A.).

23 An injured person has but two years to sue, and cannot know the pri-vate dealings between the registered owner and others, so the victim’sreliance upon the registered name as owner is vital. Without that, thevictim would need an examination for discovery about all those dealingsbefore the two years expired. Discovery of records is necessary before anexamination for discovery, so in effect that would almost halve the twoyears to sue, to one year. In the long run, thus shrinking times wouldfrustrate settlement, multiply litigation, and deprive the injured of com-pensation because of peculiar private arrangements. It would reward reg-istering vehicles in the names of cat’s paws and men of straw. And itwould reward retroactive rewriting of intra-family arrangements.

24 The appeal is dismissed.25 It helps the Court if a book of extracts has a descriptive table of con-

tents; mere exhibit numbers tell little. The key document here (the lease)is reproduced in small print from a bad faxed copy. If a better copy is notavailable, the document should be retyped. We have often complainedfruitlessly of that practice.

Appeal dismissed.

Pearlman v. Atlantic Trading Co. 19

[Indexed as: Pearlman v. Atlantic Trading Co.]

David Pearlman, Appellant (Plaintiff) and Atlantic TradingCompany Ltd. and Rebecca Lee Spence, Respondents

(Defendants)

British Columbia Court of Appeal

Docket: Vancouver CA036501

2011 BCCA 183

Saunders, Smith, Hinkson JJ.A.

Heard: February 10, 2011

Judgment: April 13, 2011

Civil practice and procedure –––– Practice on appeal — Powers and dutiesof appellate court — Miscellaneous.

Civil practice and procedure –––– Costs — Costs of particular proceed-ings — Motion for judgment –––– Plaintiff was involved in motor vehicle col-lision — Plaintiff brought four actions against various parties — Actions weredismissed — Plaintiff appealed — Plaintiff was ordered to post security forcosts — Plaintiff failed to post security in time and appeal was dismissed asabandoned — Defendants brought motion to dismiss appeal — Chambers judgedismissed defendants’ motion as moot, as appeal had already been dismissed asabandoned — Chambers judge made no comment on costs in her reasons, butwhen order resulting from proceedings before her was submitted to Registry,counsel included provision that plaintiff shall pay costs of application to defend-ants — Plaintiff brought applications for review of orders of chambers judgesunder s. 9(6) of Court of Appeal Act — Applications granted in part — Order ofchambers judge varied to remove order as to costs — As situation was not gov-erned by s. 23 of Act, defendants were not entitled to costs, unless they weredealt with by chambers judge — There was no basis upon which defendantscould be considered to have succeeded before chambers judge.

Civil practice and procedure –––– Practice on appeal — Abandonment ofappeal –––– Plaintiff was involved in motor vehicle collision — Plaintiffbrought four actions against various parties — Actions were dismissed — Plain-tiff appealed — Plaintiff applied for indigent status on appeals — Applicationfor indigent status on present appeal was dismissed — Plaintiff was ordered topost security for costs — Plaintiff failed to post security and appeal was dis-missed as abandoned — Defendants brought motion to dismiss appeal — Cham-bers judge H dismissed defendants’ motion as moot, as plaintiff’s appeal hadalready been dismissed as abandoned — Plaintiff made new application for indi-

CANADIAN CASES ON THE LAW OF INSURANCE 97 C.C.L.I. (4th)20

gent status based on new evidence, which was dismissed by chambers judgeG — Plaintiff brought applications for review of chambers judges’ orders unders. 9(6) of Court of Appeal Act — Applications granted in part — Order ofchambers judge G varied to grant indigent status to plaintiff for limited purposeof permitting him to apply to reinstate his appeal — There was no basis uponwhich to interfere with substantive part of order dismissing defendants’ motionas moot on basis that appeal had been dismissed as abandoned — Plaintiff ar-gued that dismissal of his appeal as abandoned should not have occurred, asdefendants rendered matter active when they applied for dismissal pursuant toss. 10(2) and 24(2) of Act — Plaintiff’s position was not without merit — Firstground set out in leading case on granting indigent status was met with respectto narrow issue of whether plaintiff’s appeal should have been dismissed asabandoned.

Civil practice and procedure –––– Institution of proceedings — Proceedingsin forma pauperis –––– Plaintiff was involved in motor vehicle collision —Plaintiff brought four actions against various parties — Actions were dis-missed — Plaintiff appealed — Plaintiff was ordered to post security forcosts — Plaintiff failed to post security and appeal was dismissed as aban-doned — Defendants served notice of motion to dismiss appeal — Defendants’motion was dismissed by chambers judge H as moot, as appeal had already beendismissed as abandoned — Plaintiff faced significant costs as result of dismissalof appeal — Plaintiff brought unsuccessful application for order that he be de-clared indigent based on new circumstances, based on new evidence regardingcosts — Chambers judge G dismissed application — Plaintiff brought applica-tions for review of orders of chambers judges, under s. 9(6) of Court of AppealAct — Applications granted in part — Order of chambers judge varied to grantindigent status to plaintiff for limited purpose of permitting him to bring hisapplication to reinstate his appeal — As his appeal stood dismissed, plaintiffcould not achieve indigent status on main appeal, even based upon new evi-dence, unless appeal was reinstated by way of successful application pursuant tos. 25(6) of Act — Plaintiff was entitled to apply to re-instate appeal under s.25(6), and to have his application for indigent status dealt with, with respect tothat limited potential application — Plaintiff’s otherwise precarious financialcircumstances were sufficiently compromised by his exposure to payment ofcosts, that he could now be said to be within that category of persons, who, byreason of financial circumstances, could be described as indigent — Review ofdismissal of application by plaintiff to reinstate his appeal would not be com-pletely unmeritorious, and his financial circumstances were such that he mightotherwise be denied access to Court to pursue application.

Cases considered by Hinkson J.A.:

Booty v. Hutton (2009), 2009 BCCA 375, 2009 CarswellBC 2247, 275 B.C.A.C.139, 465 W.A.C. 139 (B.C. C.A. [In Chambers]) — considered

Pearlman v. Atlantic Trading Co. 21

D. (M.J.) v. D. (J.P.) (2001), 2001 BCCA 155, 2001 CarswellBC 395, 149B.C.A.C. 153, 244 W.A.C. 153 (B.C. C.A. [In Chambers]) — considered

Hannigan v. Hannigan (2006), 2006 BCCA 167, 2006 CarswellBC 828, 226B.C.A.C. 100, 373 W.A.C. 100, 33 C.P.C. (6th) 205 (B.C. C.A.) — referredto

Pearlman v. American Commerce Insurance Co. (2008), 2008 BCSC 1091,2008 CarswellBC 1718 (B.C. S.C.) — referred to

Pearlman v. American Commerce Insurance Co. (2009), 2009 BCCA 78, [2009]I.L.R. I-4809, 91 B.C.L.R. (4th) 267, 267 B.C.A.C. 27, 450 W.A.C. 27, 2009CarswellBC 387, 72 C.C.L.I. (4th) 1 (B.C. C.A.) — referred to

Pearlman v. Atlantic Trading Co. (2009), 469 W.A.C. 99, 277 B.C.A.C. 99,2009 CarswellBC 2944, 2009 BCCA 482 (B.C. C.A.) — considered

Pearlman v. Atlantic Trading Co. (2010), 492 W.A.C. 81, 291 B.C.A.C. 81,2010 BCCA 362, 2010 CarswellBC 2011 (B.C. C.A. [In Chambers]) — re-ferred to

Pearlman v. Atlantic Trading Co. (2010), 410 N.R. 391 (note), 2010 Car-swellBC 2469, 2010 CarswellBC 2470, [2010] S.C.C.A. No. 176 (S.C.C.) —referred to

Pearlman v. Atlantic Trading Co. (2010), 2010 BCCA 568, 2010 CarswellBC3690 (B.C. C.A.) — referred to

Pearlman v. Insurance Corp. of British Columbia (2007), 2007 BCCA 451,2007 CarswellBC 2293, 55 C.C.L.I. (4th) 7 (B.C. C.A. [In Chambers]) —referred to

Pearlman v. Insurance Corp. of British Columbia (2007), 2007 BCCA 464,2007 CarswellBC 2365, 55 C.C.L.I. (4th) 10 (B.C. C.A.) — referred to

Pearlman v. Insurance Corp. of British Columbia (2010), 284 B.C.A.C. 14,2010 CarswellBC 622, 2010 BCCA 49, [2010] B.C.J. No. 456 (B.C.C.A.) — considered

Trautmann v. Baker (1997), 1997 CarswellBC 501, 25 R.F.L. (4th) 341n, [1997]B.C.J. No. 452 (B.C. C.A. [In Chambers]) — considered

Statutes considered:

Court of Appeal Act, R.S.B.C. 1996, c. 77s. 9(6) — pursuant tos. 10(2) — referred tos. 23 — referred tos. 24(2) — referred tos. 25(5) — referred tos. 25(6) — referred to

Rules considered:

Court of Appeal Rules, B.C. Reg. 297/2001R. 34(1) — referred toR. 34(3) — referred to

CANADIAN CASES ON THE LAW OF INSURANCE 97 C.C.L.I. (4th)22

Rules of Court, 1990, B.C. Reg. 221/90R. 18A — referred to

APPLICATIONS by plaintiff for review of orders of chambers judges, pursuantto s. 9(6) of Court of Appeal Act.

Appellant, for himselfV. Critchley, for Respondent

Hinkson J.A.:

1 Mr. Pearlman brings two applications for review under s. 9(6) of theCourt of Appeal Act, R.S.B.C. 1996, c. 77. The first is to discharge orvary the order of Madam Justice Huddart in chambers, pronounced onNovember 19, 2010, and the second to discharge or vary the order ofMadam Justice Garson in chambers, pronounced on November 30, 2010.

2 Mr. Pearlman was involved in a motor vehicle accident on November25, 2004, when the vehicle he was driving was struck from the rear by avehicle owned by Atlantic Trading Company Ltd., and driven by Ms.Spence. Mr. Pearlman brought four actions following the accident:

(a) He sued the owner and operator of the other vehicle (the AtlanticTrading Company Ltd. and Rebecca Lee Spence), who were in-sured by ICBC;

(b) He sued his own automobile insurer, the American Commerce In-surance Company (“ACIC”);

(c) He brought a claim against his former family doctor, Dr. Stan Lu-bin; and

(d) He sued ICBC and Kelly Winn, the adjuster handling his claim.3 Mr. Pearlman advised us that he was granted indigent status in his

Supreme Court proceedings. The action in which we are asked to reviewthe orders of Huddart and Garson JJ.A. is Mr. Pearlman’s action againstAtlantic Trading Company Ltd. and Rebecca Lee Spence which was dis-missed at trial. The respondents were awarded double costs of the trialagainst Mr. Pearlman.

4 On October 29, 2008, Mr. Pearlman applied for indigent status beforeMr. Justice Chiasson in his appeal in these proceedings. That applicationwas refused, both on the ground that Mr. Pearlman had not establishedthat requiring him to pay the court fees would deprive him of the neces-saries of life and on the basis that there was no merit in his appeal. Mr.

Pearlman v. Atlantic Trading Co. Hinkson J.A. 23

Justice Chiasson also ordered Mr. Pearlman to post $5,000 of security forthe costs of the appeal on or before 19 December 2008. When that secur-ity was not posted as ordered, Madam Justice Newbury dismissed hisappeal as abandoned on February 18, 2009.

5 In his action against the ACIC, the insurer applied under Rule 18A tohave Mr. Pearlman’s action dismissed. That application was heard in Au-gust 2008, and Mr. Justice Meiklem declined to dismiss the action in itsentirety, but granted orders sought in the alternative, dismissing Mr.Pearlman’s claim for general damages in respect to injuries sustained inthe November 25, 2004 motor vehicle accident and his claim for funds toreimburse B.C. Medical Services Plan. The reasons for judgment are in-dexed as 2008 BCSC 1091 (B.C. S.C.). This Court allowed the insurer’sappeal in February 2009 and dismissed the action in its entirety (2009BCCA 78 (B.C. C.A.)).

6 The action against Dr. Lubin was tried before Madam Justice Morri-son in December 2008. She dismissed the claim. Mr. Pearlman subse-quently filed a notice of appeal, an application for leave to appeal, andsought a declaration of indigent status. On April 17, 2009, Mr. JusticeBauman, as he then was, ruled that leave to appeal was not required butdeclined to grant indigent status to Mr. Pearlman.

7 Mr. Pearlman’s claim against ICBC and Ms. Winn alleged bad faith,fraud, negligence and misrepresentation. That action was dismissed byMr. Justice Cullen on May 4, 2007.

8 Mr. Pearlman appealed the decision of Mr. Justice Cullen, and onJuly 25, 2007, brought an application for indigent status in that appealbefore Mr. Justice Hall. Mr. Justice Hall dismissed the application hold-ing that although Mr. Pearlman’s financial circumstances supported afinding of indigency, there was no possibility of success of his proposedappeal: Pearlman v. Insurance Corp. of British Columbia, 2007 BCCA451 (B.C. C.A. [In Chambers]).

9 Mr. Pearlman sought a review of Mr. Justice Hall’s order refusinghim indigent status. On September 20, 2007, (2007 BCCA 464 (B.C.C.A.)) this Court dismissed his application stating that:

[11] Mr. Pearlman was unable to persuade Mr. Justice Hall that therewas arguable error on the part of Mr. Justice Cullen. This panel canreview the chambers order only on the ground that the chambersjudge committed a legal error. We cannot substitute our discretionfor that of the chambers judge.

CANADIAN CASES ON THE LAW OF INSURANCE 97 C.C.L.I. (4th)24

10 On July 3, 2009, Madam Justice Kirkpatrick, in chambers, refusedMr. Pearlman’s application for indigent status in his appeal from the de-cision of Mr. Justice Cullen and granted the respondents’ application foran order requiring Mr. Pearlman to post security for costs of the appeal.

11 Mr. Pearlman sought a review of the decision of Madam Justice Kirk-patrick which was dismissed by this Court on both grounds set out in D.(M.J.) v. D. (J.P.), 2001 BCCA 155, 149 B.C.A.C. 153 (B.C. C.A. [InChambers]): 1) the likelihood of success of the appeal; and 2) the finan-cial position of the appellant, holding at 2010 BCCA 49 (B.C. C.A.),paras. 11-13:

[11] I am unable to apprehend any error on the part of the chambersjudge in concluding that there was no likelihood that a division ofthis Court would be persuaded to reverse the findings of the trialjudge.

[12] As to Mr. Pearlman’s financial status, the chambers judge ex-amined his financial circumstances and reached the same conclusionas the ones reached earlier by two other justices of this court. I see noerror in her conclusion that Mr. Pearlman’s financial circumstances,although constrained, are not such that he cannot pay the necessaryfiling fees as indeed he has done on other occasions. In any event, thefirst ground, that is the question of merits, is dispositive of thisapplication.

[13] In my view Mr. Pearlman’s application for indigent status failson both grounds.

12 With this description of Mr. Pearlman’s several actions and appeals, Iturn back to this case. Mr. Pearlman sought a review of the order of Mr.Justice Chiasson dismissing his application for indigent status in theseproceedings and of the order of Madam Justice Newbury dismissing hisappeal as abandoned. The review upheld the decision of Chiasson J.A.,finding in the words of Mr. Justice Frankel in 2009 BCCA 482 (B.C.C.A.), para. 13, that:

Applying that standard of review to the order declining to grant Mr.Pearlman indigent status, and ordering him to post security for costsof the appeal, no basis has been shown that justifies interfering withChiasson J.A.’s decisions. Mr. Pearlman has been unable to showthat Chiasson J.A. made any error of fact, principle, or law in comingto the conclusions that he did. In particular, it has not been shownthat any such error was committed with respect to the determinationthat it was in the interests of justice to require that security be posted.

Pearlman v. Atlantic Trading Co. Hinkson J.A. 25

It is not for a division of the Court, on a review application, to con-sider the matter de novo.

13 With respect to the order of Madam Justice Newbury, Frankel J.A.said at para. 14:

This brings me to Newbury J.A.’s order. When the matter camebefore her on February 18, 2009, the deadline for the posting of se-curity for costs had expired, and it appeared that Mr. Pearlman haddone nothing to prosecute his application to review that order. In-deed, the affidavit filed by Atlantic Trading in support of the dismis-sal application makes no mention of the then outstanding review ap-plication. On the basis of what was before her, Newbury J.A.reasonably concluded that Mr. Pearlman did not have an excuse forfailing to comply with an order of a judge of this Court.

14 Frankel J.A. found, however, at para. 18 that “the failure to have thereview application heard before either December 19, 2008, or February18, 2009, does not rest with Mr. Pearlman. Having complied with therequirements of Rule 34(1), Mr. Pearlman could reasonably expect thatthe hearing date would be set by the registrar in accordance with Rule34(3). Indeed, this view is expressed in Atlantic Trading’s counsel’s let-ter of January 28, 2009”, and concluded at paras. 21-22 that:

[21] In my view, if Newbury J.A. had been made aware of the regis-try’s failure to arrange a date for the review application in accor-dance with Rule 34(3), then she would not have proceeded with thedismissal motion. When an application is brought in accordance withthe Rules of Court, the moving party has a right to have that applica-tion dealt with as provided for in those Rules. Unlike Mr. Brown inFarmers Insurance Co. of Oregon v. Brown (at para. 10), it cannot besaid that Mr. Pearlman is the victim of his own defaults.

[22] Regardless of the lack of merit in the review application, Mr.Pearlman was entitled to have the process requirements of the Courtof Appeal Rules followed on his application. Unfortunately, that didnot occur, and he is entitled to redress. In my view, he should be putin the position he would have been in had the review applicationbeen heard prior to December 19, 2008. To that end, the order dis-missing the appeal as abandoned should be discharged, and ChiassonJ.A.’s order varied only to the extent of extending the time for theposting of security for costs of the appeal to December 1, 2009.While the December 1st date gives Mr. Pearlman more time than hewould have had to post security had his review application beenheard promptly last year, the manner in which that application washandled warrants giving him this consideration.

CANADIAN CASES ON THE LAW OF INSURANCE 97 C.C.L.I. (4th)26

15 Mr. Pearlman sought leave to appeal the decision in 2009 BCCA 482(B.C. C.A.) to the Supreme Court of Canada, but leave to appeal wasrefused ([2010] S.C.C.A. No. 176 (S.C.C.)).

16 On July 29, 2010, Mr. Justice Low declared Mr. Pearlman to be avexatious litigant and granted an order prohibiting him from bringing anymore appeals from any final orders without leave in any matters relatingto his motor vehicle accident of November 25, 2004. The decision ofLow J.A. is indexed as 2010 BCCA 362 (B.C. C.A. [In Chambers]).

17 Mr. Pearlman did nothing to advance his appeal, so on September 30,2010 the respondents served a notice of motion to dismiss the appeal. OnOctober 20, 2010, the respondents learned that the appeal had been dis-missed as abandoned pursuant to s. 25(5) of the Court of Appeal Act.When the respondent’s motion came on for hearing before Huddart J.A.in chambers on November 19, 2010, it was dismissed on the basis that itwas moot as the appeal had already been dismissed as abandoned. Inresponse to submissions from Mr. Pearlman, Madam Justice Huddartstated:

[2] Mr. Pearlman cannot file a cross-appeal of his own appeal. Whathe wants to do is re-instate his appeal. He can do that on a motion tothis Court to re-instate the appeal under s. 25(6) of the Court of Ap-peal Act. Until he does that, this appeal stands dismissed and thisapplication is moot.

18 On November 24, 2010, the appellant served an application for anorder that he be declared indigent, due to what he asserted were newcircumstances. He filed an affidavit setting out what he asserted to be thechange in his circumstances since his application before Chiasson J.A.The new application was heard and dismissed by Garson J.A. on Novem-ber 30, 2010, who found, at paras. 8-10 of her reasons that:

[8] Only a division of the court, hearing an application to vary ordischarge an order of a justice, pursuant to s. 9(6) may vary the orderof a justice. I have no jurisdiction, sitting as a justice in chambers, tovary the order of a justice. Mr. Pearlman has already sought a dis-charge or variation of Mr. Justice Chiasson’s order and that applica-tion in respect to the indigent status application was dismissed. Inany event, I am bound by the decision of Mr. Justice Chiasson.

[9] Mr. Pearlman has also filed a Notice of Application to Vary anOrder of a Justice which he attached to his application for indigentstatus. In that November 23, 2010, application he seeks an order va-rying or discharging an order of Madam Justice Huddart made on

Pearlman v. Atlantic Trading Co. Hinkson J.A. 27

November 19, 2010. As I have already said, I have no jurisdiction tohear such an application.

[10] In support of his application today, Mr. Pearlman has filed aMemorandum of Argument with about 107 pages of attachments. Iunderstand from his submissions that he considers that these docu-ments will have some bearing on the argument about the merits ofthe appeal. In particular, he drew my attention to a recently obtainedtranscript of a pre-trial conference that occurred shortly before thetrial in the within action. I have read that transcript. The remainder ofthe materials according to Mr. Critchley are medical reports and doc-uments from the trial. Mr. Pearlman has not filed an application forthe court to consider new evidence on this application. Assumingwithout deciding that such an application is available, I do not con-sider that these materials are likely to convince a court to revisit theapplication for indigent status.

19 On December 10, 2010, Mr. Justice Mackenzie, for the Court, upheldthe decision of Mr. Justice Low declaring Mr. Pearlman to be a vexatiouslitigant, and the orders flowing from that declaration: see 2010 BCCA568 (B.C. C.A.).

Analysis20 Mr. Justice Frankel addressed the standard of review on an applica-

tion to vary a chambers judge’s order on Mr. Pearlman’s earlier applica-tions at 2009 BCCA 482 (B.C. C.A.), para. 12:

The standard of review on an application to vary a chambers judge’sorder is succinctly set out in Redpath v. Redpath, 2009 BCCA 168,wherein Chiasson J.A. stated:

[3] We are guided in the exercise of this authority by theobservation of McEachern C.J.B.C. in Frew v. Roberts,[1990] B.C.J. No. 2175[44 C.P.C. (2d) 34], that a divisionof this Court should interfere with a decision of a Cham-bers judge only if it concludes the judge was wrong in thelegal sense and not merely because the division concludesthe judge incorrectly exercised discretion.

[4] Lambert J.A. further explained the test in Haldorson v.Coquitlam (City), [2000] B.C.J. No. 2532 (C.A.) [2000BCCA 672, 149 B.C.A.C. 197] as follows:

[7] It comes to this: that the review hearing isnot a hearing of the original application as if itwere a new application brought to a division ofthe court rather than to a chambers judge, but

CANADIAN CASES ON THE LAW OF INSURANCE 97 C.C.L.I. (4th)28

is instead a review of what the chambers judgedid against the test encompassed by asking:was the chambers judge wrong in law, orwrong in principle, or did the chambers judgemisconceive the facts. If the chambers judgedid not commit any of those errors, then thedivision of the court in review should notchange the order of the chambers judge.

a) The review application of the order of Madam Justice Huddart21 No basis has been shown that justifies interference with the substan-

tive part of the order of Huddart J.A. Her order did nothing more thanleave matters as they stood prior to November 19, 2010: Mr. Pearlman’sappeal stood dismissed as abandoned, and he was advised that if hewished to re-instate his appeal, he could attempt to do so by bringing amotion to re-instate the appeal under s. 25(6) of the Court of Appeal Act.There is no basis upon which this division could interfere with that as-pect of her order.

22 In her brief reasons, Madam Justice Huddart made no comment oncosts, but when the order resulting from the proceedings before her wassubmitted to the Registry, counsel included the provision that “The Ap-pellant shall pay costs of this application to the Respondents”. As thesituation is not one that is governed by s. 23 of the Court of Appeal Act,the respondents were not entitled to costs, unless they were dealt with byMadam Justice Huddart. Normally a successful party is entitled to itscosts on an application before this Court, and I can think of no basisupon which the respondents could be considered to have succeeded onthe application before Madam Justice Huddart. Counsel for the respon-dents does not oppose a variation of the order of Huddart J.A. to removethe order as to costs, and I would accede to that variation in that order.

b) The review application of the order of Madam Justice Garson23 The order of Madam Justice Garson appears to be based upon a mis-

conception of Mr. Pearlman’s application. While Garson J.A. was correctto say that as a single judge in chambers she had no jurisdiction to varythe order of another justice that is not what Mr. Pearlman’s applicationrequired, in order to succeed. Mr. Pearlman was bringing a new applica-tion, based upon a new evidence in a new affidavit, and was entitled tohave the new application considered based upon that new evidence.

Pearlman v. Atlantic Trading Co. Hinkson J.A. 29

24 As his appeal stood dismissed, Mr. Pearlman could not achieve indi-gent status on the main appeal, even based upon new evidence, unless theappeal was reinstated by way of a successful application pursuant to s.25(6) of the Court of Appeal Act. Mr. Pearlman was, however, entitled toapply to re-instate the appeal under s. 25(6) of the Court of Appeal Act,and to have his application for indigent status dealt with, with respect tothat limited potential application.

25 The test for whether this Court will reinstate an appeal that has beendismissed was set out by Mr. Justice Tysoe, in chambers, in Booty v.Hutton, 2009 BCCA 375 (B.C. C.A. [In Chambers]):

[22] As with applications for an extension of time and applications torestore an appeal to the active list, the ultimate question on applica-tions to reinstate a dismissed appeal is whether it is in the interests ofjustice to do so. The factors to be considered in assessing the inter-ests of justice on a reinstatement application include the following:

(a) the length of the delay and, in particular, whether the delayhas been inordinate;

(b) the reason for the delay and, in particular, whether the delayis excusable;

(c) whether the respondent has suffered prejudice as a result ofthe delay; and

(d) the extent of the merits of the appeal.

See Hannigan v. Hannigan, 2006 BCCA 167, 33 C.P.C. (6th) 205(B.C. C.A.) at paras. 12-13.

26 Since the hearing of Mr. Pearlman’s applications to review the ordersof Huddart and Garson JJ.A., counsel for the respondents has filed fur-ther material addressing what he argues is the lack of any merit in theappeal that Mr. Pearlman may apply to reinstate. Mr. Pearlman has re-sponded with material that he argues shows merit in that appeal.

27 It is important to recognize that the merits of the appeal that Mr.Pearlman may apply to have reinstated are not before us at this juncture.Before us, Mr. Pearlman argued that the dismissal of his appeal as aban-doned on the inactive list should not have occurred, as the respondentshad rendered the matter active when applying for the dismissal, as theydid, pursuant to ss. 10(2) and 24(2) of the Court of Appeal Act. I find thatthis position is not without some merit. I make no comment uponwhether the appeal that he wishes to reinstate has merit, as it would bepremature to do so, but as identified by Tysoe J.A., that is only one of thefactors to be considered when Mr. Pearlman’s application pursuant to s.

CANADIAN CASES ON THE LAW OF INSURANCE 97 C.C.L.I. (4th)30

25(6) of the Court of Appeal Act is heard. I conclude that the first of thetwo grounds set out in D. (M.J.) v. D. (J.P.) is met with respect to thenarrow issue of whether Mr. Pearlman’s appeal should have been dis-missed as abandoned.