Bulletin No. 2011-22 May 31, 2011 HIGHLIGHTS OF ... - IRS

44

Bulletin No. 2011-22 May 31, 2011 HIGHLIGHTS OF THIS ISSUE These synopses are intended only as aids to the reader in identifying the subject matter covered. They may not be relied upon as authoritative interpretations. INCOME TAX Notice 2011–40, page 806. Renewable electricity production, refined coal produc- tion, and Indian coal production; calendar year 2011 inflation adjustment factors and reference prices. This notice announces the calendar year 2011 inflation adjustment factors and reference prices for the renewable electricity pro- duction credit, refined coal production credit, and Indian coal production credit under section 45 of the Code. Rev. Proc. 2011–32, page 835. 2012 inflation adjusted amounts for Health Savings Ac- counts. This procedure provides the 2012 inflation adjusted amounts for Health Savings Accounts (HSAs) under section 223 of the Code. ADMINISTRATIVE Rev. Proc. 2011–31, page 808. Publication 4810, Specifications for Filing Form 8955–SSA, Registration Statement Identifying Separated Participants with Deferred Vested Benefits, Electronically, contains information to file Form 8955–SSA through the IRS FIRE (Filing Information Returns Electronically) system. Announcement 2011–31, page 836. This document contains a correction to final regulations (T.D. 9518, 2011–17 I.R.B. 710) providing guidance to specified tax return preparers who prepare and file individual income tax returns using magnetic media under section 6011(e)(3) of the Code. Announcement 2011–32, page 836. This announcement corrects the nonacquiescence to Robin- son Knife Manufacturing Company and Subsidiaries v. Commissioner, 600 F. 3d 121 (2d Cir. 2010), published in I.R.B. 2011–9. Finding Lists begin on page ii. Index for January through May begins on page v.

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Bulletin No. 2011-22 May 31, 2011 HIGHLIGHTS OF ... - IRS

Bulletin No. 2011-22May 31, 2011

HIGHLIGHTSOF THIS ISSUEThese synopses are intended only as aids to the reader inidentifying the subject matter covered. They may not berelied upon as authoritative interpretations.

INCOME TAX

Notice 2011–40, page 806.Renewable electricity production, refined coal produc-tion, and Indian coal production; calendar year 2011inflation adjustment factors and reference prices. Thisnotice announces the calendar year 2011 inflation adjustmentfactors and reference prices for the renewable electricity pro-duction credit, refined coal production credit, and Indian coalproduction credit under section 45 of the Code.

Rev. Proc. 2011–32, page 835.2012 inflation adjusted amounts for Health Savings Ac-counts. This procedure provides the 2012 inflation adjustedamounts for Health Savings Accounts (HSAs) under section223 of the Code.

ADMINISTRATIVE

Rev. Proc. 2011–31, page 808.Publication 4810, Specifications for Filing Form 8955–SSA,Registration Statement Identifying Separated Participants withDeferred Vested Benefits, Electronically, contains informationto file Form 8955–SSA through the IRS FIRE (Filing InformationReturns Electronically) system.

Announcement 2011–31, page 836.This document contains a correction to final regulations(T.D. 9518, 2011–17 I.R.B. 710) providing guidance tospecified tax return preparers who prepare and file individualincome tax returns using magnetic media under section6011(e)(3) of the Code.

Announcement 2011–32, page 836.This announcement corrects the nonacquiescence to Robin-son Knife Manufacturing Company and Subsidiaries v.Commissioner, 600 F. 3d 121 (2d Cir. 2010), published inI.R.B. 2011–9.

Finding Lists begin on page ii.Index for January through May begins on page v.

The IRS MissionProvide America’s taxpayers top-quality service by helpingthem understand and meet their tax responsibilities and en-

force the law with integrity and fairness to all.

IntroductionThe Internal Revenue Bulletin is the authoritative instrument ofthe Commissioner of Internal Revenue for announcing officialrulings and procedures of the Internal Revenue Service and forpublishing Treasury Decisions, Executive Orders, Tax Conven-tions, legislation, court decisions, and other items of generalinterest. It is published weekly and may be obtained from theSuperintendent of Documents on a subscription basis. Bulletincontents are compiled semiannually into Cumulative Bulletins,which are sold on a single-copy basis.

It is the policy of the Service to publish in the Bulletin all sub-stantive rulings necessary to promote a uniform application ofthe tax laws, including all rulings that supersede, revoke, mod-ify, or amend any of those previously published in the Bulletin.All published rulings apply retroactively unless otherwise indi-cated. Procedures relating solely to matters of internal man-agement are not published; however, statements of internalpractices and procedures that affect the rights and duties oftaxpayers are published.

Revenue rulings represent the conclusions of the Service on theapplication of the law to the pivotal facts stated in the revenueruling. In those based on positions taken in rulings to taxpayersor technical advice to Service field offices, identifying detailsand information of a confidential nature are deleted to preventunwarranted invasions of privacy and to comply with statutoryrequirements.

Rulings and procedures reported in the Bulletin do not have theforce and effect of Treasury Department Regulations, but theymay be used as precedents. Unpublished rulings will not berelied on, used, or cited as precedents by Service personnel inthe disposition of other cases. In applying published rulings andprocedures, the effect of subsequent legislation, regulations,

court decisions, rulings, and procedures must be considered,and Service personnel and others concerned are cautionedagainst reaching the same conclusions in other cases unlessthe facts and circumstances are substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code.This part includes rulings and decisions based on provisions ofthe Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation.This part is divided into two subparts as follows: Subpart A,Tax Conventions and Other Related Items, and Subpart B, Leg-islation and Related Committee Reports.

Part III.—Administrative, Procedural, and Miscellaneous.To the extent practicable, pertinent cross references to thesesubjects are contained in the other Parts and Subparts. Alsoincluded in this part are Bank Secrecy Act Administrative Rul-ings. Bank Secrecy Act Administrative Rulings are issued bythe Department of the Treasury’s Office of the Assistant Secre-tary (Enforcement).

Part IV.—Items of General Interest.This part includes notices of proposed rulemakings, disbar-ment and suspension lists, and announcements.

The last Bulletin for each month includes a cumulative indexfor the matters published during the preceding months. Thesemonthly indexes are cumulated on a semiannual basis, and arepublished in the last Bulletin of each semiannual period.

The contents of this publication are not copyrighted and may be reprinted freely. A citation of the Internal Revenue Bulletin as the source would be appropriate.

For sale by the Superintendent of Documents, U.S. Government Printing Office, Washington, DC 20402.

May 31, 2011 2011–22 I.R.B.

Part III. Administrative, Procedural, and MiscellaneousCredit for RenewableElectricity Production,Refined Coal Production,and Indian Coal Production,and Publication of InflationAdjustment Factors andReference Prices for CalendarYear 2011

Notice 2011–40

This notice publishes the inflation ad-justment factors and reference prices forcalendar year 2011 for the renewable elec-tricity production credit, the refined coalproduction credit, and the Indian coal pro-duction credit under section 45 of the In-ternal Revenue Code. The 2011 inflationadjustment factors and reference prices areused in determining the availability of thecredits. The 2011 inflation adjustment fac-tors and reference prices apply to calendaryear 2011 sales of kilowatt-hours of elec-tricity produced in the United States or apossession thereof from qualified energyresources and to calendar year 2011 salesof refined coal and Indian coal produced inthe United States or a possession thereof.

BACKGROUND

Section 45(a) provides that the renew-able electricity production credit for anytax year is an amount equal to the prod-uct of 1.5 cents multiplied by the kilowatthours of specified electricity produced bythe taxpayer and sold to an unrelated per-son during the tax year. This electricitymust be produced from qualified energyresources and at a qualified facility duringthe 10-year period beginning on the datethe facility was originally placed in ser-vice.

Section 45(b)(1) provides that theamount of the credit determined under sec-tion 45(a) is reduced by an amount whichbears the same ratio to the amount of thecredit as (A) the amount by which the ref-erence price for the calendar year in whichthe sale occurs exceeds 8 cents, bears to(B) 3 cents. Under section 45(b)(2), the1.5 cent amount in section 45(a), the 8 centamount in section 45(b)(1), the $4.375amount in section 45(e)(8)(A), and in sec-tion 45(e)(8)(B)(i), the $2.00 amount in

section 45(e)(8)(D)(ii)(I), the referenceprice of fuel used as feedstock (withinthe meaning of section 45(c)(7)(A)) in2002 are each adjusted by multiplying theamount by the inflation adjustment factorfor the calendar year in which the saleoccurs. If any amount as increased underthe preceding sentence is not a multipleof 0.1 cent, the amount is rounded to thenearest multiple of 0.1 cent.

Section 45(c)(1) defines qualifiedenergy resources as wind, closed-loopbiomass, open-loop biomass, geother-mal energy, solar energy, small irrigationpower, municipal solid waste, qualifiedhydropower production, marine and hy-drokinetic renewable energy.

Section 45(d)(1) defines a qualified fa-cility using wind to produce electricity asany facility owned by the taxpayer that isoriginally placed in service after Decem-ber 31, 1993, and before January 1, 2013.See section 45(e)(7) for rules relating tothe inapplicability of the credit to electric-ity sold to utilities under certain contracts.

Section 45(d)(2)(A) defines a qualifiedfacility using closed-loop biomass to pro-duce electricity as any facility (i) ownedby the taxpayer that is originally placed inservice after December 31, 1992, and be-fore January 1, 2014, or (ii) owned by thetaxpayer which before January 1, 2014, isoriginally placed in service and modifiedto use closed-loop biomass to co-fire withcoal, with other biomass, or with both, butonly if the modification is approved un-der the Biomass Power for Rural Develop-ment Programs or is part of a pilot projectof the Commodity Credit Corporation asdescribed in 65 Fed. Reg. 63052. Sec-tion 45(d)(2)(C) provides that in the caseof a qualified facility described in section45(d)(2)(A)(ii), (i) the 10-year period re-ferred to in section 45(a) is treated as be-ginning no earlier than the date of enact-ment of section 45(d)(2)(B)(i); and (ii) ifthe owner of the facility is not the producerof the electricity, the person eligible for thecredit allowable under section 45(a) is thelessee or the operator of the facility.

Section 45(d)(3)(A) defines a quali-fied facility using open-loop biomass toproduce electricity as any facility ownedby the taxpayer which (i) in the caseof a facility using agricultural livestock

waste nutrients, (I) is originally placedin service after the date of enactmentof section 45(d)(3)(A)(i)(I) and beforeJanuary 1, 2014, and (II) the nameplatecapacity rating of which is not less than150 kilowatts; and (ii) in the case of anyother facility, is originally placed in servicebefore January 1, 2014. In the case of anyfacility described in section 45(d)(3)(A), ifthe owner of the facility is not the producerof the electricity, section 45(d)(3)(C)provides that the person eligible for thecredit allowable under section 45(a) is thelessee or the operator of the facility.

Section 45(d)(4) defines a qualified fa-cility using geothermal or solar energy toproduce electricity as any facility ownedby the taxpayer which is originally placedin service after the date of enactment ofsection 45(d)(4) and before January 1,2014 (January 1, 2006, in the case of afacility using solar energy). A qualifiedfacility using geothermal or solar energydoes not include any property described insection 48(a)(3) the basis of which is takeninto account by the taxpayer for purposesof determining the energy credit undersection 48.

Section 45(d)(5) defines a qualified fa-cility using small irrigation power to pro-duce electricity as any facility owned bythe taxpayer which is originally placed inservice after the date of enactment of sec-tion 45(d)(5) and before October 22, 2008.

Section 45(d)(6) defines a qualified fa-cility using gas derived from the biodegra-dation of municipal solid waste to produceelectricity as any facility owned by the tax-payer which is originally placed in ser-vice after the date of enactment of section45(d)(6) and before January 1, 2014.

Section 45(d)(7) defines a qualified fa-cility (other than a facility described inparagraph (6)) that burns municipal solidwaste to produce electricity as any facil-ity owned by the taxpayer which is orig-inally placed in service after the date ofenactment of section 45(d)(7) and beforeJanuary 1, 2014. A qualified facility burn-ing municipal solid waste includes a newunit placed in service in connection with afacility placed in service on or before thedate of enactment of section 45(d)(7), butonly to the extent of the increased amount

2011–22 I.R.B. 806 May 31, 2011

of electricity produced at the facility byreason of such new unit.

Section 45(d)(8) provides in the caseof a facility that produces refined coal,the term “refined coal production facility”means (i) with respect to a facility produc-ing steel industry fuel, any facility (or anymodification to a facility) which is placedin service before January 1, 2010, and (ii)with respect to any other facility producingrefined coal, and facility placed in serviceafter the date of the enactment of the Amer-ican Jobs Creation Act of 2004 and beforeJanuary 1, 2010.

Section 45(d)(9) defines a qualifiedfacility producing qualified hydroelectricproduction described in section 45(c)(8)as (A) any facility producing incremen-tal hydropower production, but only tothe extent of its incremental hydropowerproduction attributable to efficiency im-provements or additions to capacity de-scribed in section 45(c)(8)(B) placed inservice after the date of enactment of sec-tion 45(d)(9) and before January 1, 2014,and (B) any other facility placed in ser-vice after the date of enactment of section45(d)(9) and before January 1, 2014. Sec-tion 45(d)(9)(C) provides that in the caseof a qualified facility described in section45(d)(9)(A), the 10-year period referred toin section 45(a) is treated as beginning onthe date the efficiency improvements oradditions to capacity are placed in service.

Section 45(d)(10) provides in the caseof a facility that produces Indian coal,the term “Indian coal production facility”means a facility which is placed in servicebefore January 1, 2009.

Section 45(d)(11) provides in the caseof a facility producing electricity from ma-rine and hydrokinetic renewable energy,the term “qualified facility” means anyfacility owned by the taxpayer which (i)has a nameplate capacity rating of at least150 kilowatts, and (ii) which is originallyplaced in service on or after the date ofthe enactment of this paragraph and beforeJanuary 1, 2012.

Section 45(e)(8)(A) provides that therefined coal production credit is an amountequal to $4.375 per ton of qualified re-fined coal (i) produced by the taxpayer at arefined coal production facility during the10-year period beginning on the date thefacility was originally placed in service,and (ii) sold by the taxpayer (I) to an unre-lated person and (II) during the 10-year pe-

riod and the tax year. Section 45(e)(8)(B)provides that the amount of credit deter-mined under section 45(e)(8)(A) is re-duced by an amount which bears the sameratio to the amount of the increase as (i)the amount by which the reference price offuel used as feedstock (within the meaningof section 45(c)(7)(A)) for the calendaryear in which the sale occurs exceeds anamount equal to 1.7 multiplied by the ref-erence price for such fuel in 2002, bearsto (ii) $8.75. Section 45(e)(8)(D)(ii)(I)provides that in the case of a taxpayer whoproduces steel industry fuel, subparagraph(A) shall be applied by substituting “2.00per barrel-of-oil equivalent” for $4.375per ton.” Section 45(e)(8)(D)(ii)(II) pro-vides that in lieu of the 10-year periodreferred to in clauses (i) and (ii)(II) of sub-paragraph (A), the credit period shall bethe period beginning in the later of the datesuch facility was originally placed-in-ser-vice, or October 1, 2008, and ending onthe later of December 31, 2009, or thedate which is 1 year after the date suchfacility or the modifications described inclause (iii) were placed in service. Section45(e)(8)(D)(ii)(III) provides that subpara-graph (B) (dealing with the phaseout ofthe credit) will not apply.

Section 45(e)(10)(A) provides in thecase of a producer of Indian coal, the creditdetermined under section 45 for any tax-able year shall be increased by an amountequal to the applicable dollar amount perton of Indian coal (i) produced by the tax-payer at an Indian coal production facilityduring the 7-year period beginning on Jan-uary 1, 2006, and (ii) sold by the taxpayer(I) to an unrelated person, and (II) duringsuch 7-year period and such taxable year.

Section 45(e)(10)(B)(i) defines “ap-plicable dollar amount” for any taxableyear as (I) $1.50 in the case of calendaryears 2006 through 2009, and (II) $2.00 inthe case of calendar years beginning after2009.

Section 45(e)(2)(A) requires the Secre-tary to determine and publish in the Fed-eral Register each calendar year the infla-tion adjustment factor and the referenceprice for the calendar year. The inflationadjustment factors and the reference pricesfor the 2011 calendar year were publishedin the Federal Register on April 19, 2011(75 Fed. Reg. 21947).

Section 45(e)(2)(B) defines the infla-tion adjustment factor for a calendar year

as the fraction the numerator of which isthe GDP implicit price deflator for the pre-ceding calendar year and the denominatorof which is the GDP implicit price defla-tor for the calendar year 1992. The term“GDP implicit price deflator” means themost recent revision of the implicit pricedeflator for the gross domestic product ascomputed and published by the Depart-ment of Commerce before March 15 of thecalendar year.

Section 45(e)(2)(C) provides that thereference price is the Secretary’s determi-nation of the annual average contract priceper kilowatt hour of electricity generatedfrom the same qualified energy resourceand sold in the previous year in the UnitedStates. Only contracts entered into af-ter December 31, 1989, are taken into ac-count.

Under section 45(e)(8)(C), the deter-mination of the reference price for fuelused as feedstock within the meaning ofsection 45(c)(7)(A) is made according torules similar to the rules under section45(e)(2)(C).

Under section 45(e)(10)(B)(ii), in thecase of any calendar year after 2006,each of the dollar amounts under section45(e)(10)(B)(i) shall be equal to the prod-uct of such dollar amount and the inflationadjustment factor determined under sec-tion 45(e)(2)(B) for the calendar year,except that section 45(e)(2)(B) shall beapplied by substituting 2005 for 1992.

INFLATION ADJUSTMENT FACTORSAND REFERENCE PRICES

The inflation adjustment factor forcalendar year 2011 for qualified energyresources and refined coal is 1.4459. Theinflation adjustment factor for Indian coalis 1.1066. The reference price for calendaryear 2011 for facilities producing electric-ity from wind (based upon informationprovided by the Department of Energy)is 4.68 cents per kilowatt hour. The ref-erence prices for fuel used as feedstockwithin the meaning of section 45(c)(7)(A),relating to refined coal production (basedupon information provided by the Depart-ment of Energy) are $31.90 per ton forcalendar year 2002 and $55.66 per ton forcalendar year 2011. The reference pricesfor facilities producing electricity fromclosed-loop biomass, open-loop biomass,geothermal energy, solar energy, small

May 31, 2011 807 2011–22 I.R.B.

irrigation power, municipal solid waste,qualified hydropower production, marineand hydrokinetic energy have not beendetermined for calendar year 2011.

PHASE-OUT CALCULATION

Because the 2011 reference price forelectricity produced from wind does notexceed 8 cents multiplied by the infla-tion adjustment factor, the phaseout of thecredit provided in section 45(b)(1) doesnot apply to such electricity sold duringcalendar year 2011. Because the 2011 ref-erence price of fuel used as feedstock forrefined coal does not exceed the $31.90reference price of such fuel in 2002 mul-tiplied by the inflation adjustment factorand 1.7, the phaseout of credit provided insection 45(e)(8)(B) does not apply to re-fined coal sold during calendar year 2011.Further, for electricity produced fromclosed-loop biomass, open-loop biomass,geothermal energy, solar energy, smallirrigation power, municipal solid waste,qualified hydropower production, marineand hydrokinetic energy, the phaseout ofcredit provided in section 45(b)(1) doesnot apply to such electricity sold duringcalendar year 2011.

CREDIT AMOUNT BY QUALIFIEDENERGY RESOURCE AND FACILITY,REFINED COAL, AND INDIAN COAL

As required by section 45(b)(2), the1.5 cent amount in section 45(a)(1), the8 cent amount in section 45(b)(1), the$4.375 amount in section 45(e)(8)(A) andthe $2.00 amount in § 45(e)(8)(D) areeach adjusted by multiplying such amountby the inflation adjustment factor for thecalendar year in which the sale occurs. Ifany amount as increased under the pre-ceding sentence is not a multiple of 0.1cent, such amount is rounded to the near-est multiple of 0.1 cent. In the case ofelectricity produced in open-loop biomassfacilities, small irrigation power facilities,landfill gas facilities, trash combustionfacilities, qualified hydropower facili-ties, marine and hydrokinetic renewableenergy, section 45(b)(4)(A) requires theamount in effect under section 45(a)(1)(before rounding to the nearest 0.1 cent)to be reduced by one-half. Under the cal-culation required by section 45(b)(2), thecredit for renewable electricity productionfor calendar year 2011 under section 45(a)is 2.2 cents per kilowatt hour on the saleof electricity produced from the qualifiedenergy resources of wind, closed-loop

biomass, geothermal energy, and solar en-ergy, and 1.1 cent per kilowatt hour on thesale of electricity produced in open-loopbiomass facilities, small irrigation powerfacilities, landfill gas facilities, trash com-bustion facilities, qualified hydropowerfacilities, marine and hydrokinetic energyfacilities. Under the calculation requiredby section 45(b)(2), the credit for refinedcoal production for calendar year 2009under section 45(e)(8)(A) is $6.33 perton on the sale of qualified refined coal.The credit for steel industry fuel is $2.89per barrel-of-oil equivalent of steel indus-try fuel sold. The credit for Indian coalproduction for calendar year 2011 undersection 45(e)(10)(B) is $2.20 per ton onthe sale of Indian coal.

DRAFTING AND CONTACTINFORMATION

The principal author of this notice isPhilip Tiegerman of the Office of As-sociate Chief Counsel (Passthroughsand Special Industries). For further in-formation regarding this notice contactMr. Tiegerman at (202) 622–3110 (not atoll-free call).

Following is a list of related instructions and forms for filing Form 8955–SSA, Annual Registration Statement IdentifyingSeparated Participants with Deferred Vested Benefits, electronically:

• Current Instructions for Form 8955–SSA, Annual Registration Statement Identifying Separated Participants with De-ferred Vested Benefits

• Form 4419 — Application for Filing Information Returns Electronically

The Internal Revenue Service (IRS), Information Returns Branch (IRB) encourages filers to make copies of the blank forms in theback of this publication for future use. These forms can also be obtained by calling 1–800–TAX–FORM (1–800–829–3676). You canalso download forms and publications from the IRS web site at IRS.gov.

IMPORTANT NOTE:

The Filing Information Returns Electronically (FIRE) system will be down December 16, 2011 through January 2, 2012,for programming updates. It is not operational during this time for submissions.

Use this Revenue Procedure to prepare the current plan year and prior plan year information returns for submission to InternalRevenue Service (IRS) electronically.

This Revenue Procedure may not be revised every year. Updates will be printed as needed in the Internal Revenue Bulletin.General Instructions for Form 8955–SSA are revised every year. Be sure to consult current instructions when preparing Form8955–SSA.

2011–22 I.R.B. 808 May 31, 2011

Rev. Proc. 2011–31

TABLE OF CONTENTS

Part A. General

SEC. 1. PURPOSE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 810

SEC. 2. WHERE TO FILE AND HOW TO CONTACT THE IRS, INFORMATION RETURNS BRANCH (IRB) . . . . . . . . . . . . . . . . . . 810

SEC. 3. FORM 4419, APPLICATION FOR FILING INFORMATION RETURNS ELECTRONICALLY(FIRE). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 811

SEC. 4. DUE DATES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 812

SEC. 5. AMENDED RETURNS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 812

SEC. 6. DEFINITION OF TERMS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 812

SEC. 7. STATE ABBREVIATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 813

SEC. 8. FOREIGN COUNTRY CODES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 814

Part B. Electronic Filing Specifications

SEC. 1. GENERAL. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 816

SEC. 2. ELECTRONIC FILING APPROVAL PROCEDURE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 817

SEC. 3. TEST FILES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 817

SEC. 4. ELECTRONIC SUBMISSIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 818

SEC. 5. PIN REQUIREMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 818

SEC. 6. ELECTRONIC FILING SPECIFICATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 818

SEC. 7. CONNECTING TO THE FIRE SYSTEM. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 818

SEC. 8. COMMON SUBMISSION ERRORS AND PROBLEMS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 820

Part C. Record Format Specifications and Record Layouts

SEC. 1. TRANSMITTER “T” RECORD. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 821

SEC. 2. SPONSOR “S” RECORD . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 825

SEC. 3. ADMINISTRATOR “A” RECORD . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 828

SEC. 4. PARTICIPANT “P” RECORD . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 831

SEC. 5. END OF TRANSMISSION “F” RECORD . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 833

Part A. General

Revenue Procedures are generally revised periodically to reflect legislative and form changes. Comments concerning this RevenueProcedure, or suggestions for making it more helpful, can be addressed to:

Internal Revenue ServiceInformation Reporting Program230 Murall Drive, Mail Stop 4360Kearneysville, WV 25430

May 31, 2011 809 2011–22 I.R.B.

Sec. 1. Purpose

.01 The purpose of this Revenue Procedure is to provide the specifications for filing Form 8955–SSA, Annual Registration State-ment Identifying Separated Participants with Deferred Vested Benefits, with Internal Revenue Service/Information Returns Branch(IRS/IRB) electronically through the FIRE (Filing Information Returns Electronically) System. This Revenue Procedure must be usedto prepare current and prior year information returns filed beginning January 1, 2011, and received by FIRE by December 31,2011.

.02 Electronic reporting of Form 8955–SSA eliminates the need to submit paper documents to the IRS. CAUTION: Do not sendCopies of the paper forms to IRS for any forms filed electronically. This will result in duplicate filing.

.03 Generally, the box names on the paper Form 8955–SSA correspond with the fields used to file electronically; however, ifdiscrepancies occur, the instructions in this Revenue Procedure govern.

.04 Refer to Part A, Sec.6, for definitions of terms used in this publication.

.05 The following instructions and publications provide more detailed filing procedures for certain information returns:(a) Instructions for Form 8955–SSA, Annual Registration Statement Identifying Separated Participants with Deferred Vested

Benefits.(b) Publication 3609, Filing Information Returns Electronically (FIRE)

Sec. 2. Where To File and How to Contact the IRS, Information Returns Branch (IRB)

.01 All information returns filed electronically are processed at IRS/IRB. General inquiries concerning the filing of 8955–SSAForms should be sent to the following address:

Internal Revenue ServiceInformation Returns BranchAttn: 8955–SSA Reporting230 Murall Drive, Mail Stop 4360Kearneysville, WV 25430

.02 To request an extension to file Form 8955–SSA, submit a Form 5558, Application for Extension of Time to File Certain Em-ployee Plan Returns, before the due date of the Form 8955–SSA to the following address:

Internal Revenue Service CenterOgden, UT 84201–0024

.03 The telephone numbers for electronic filing inquiries are:

Information Returns Branch Centralized Call Site1–866–455–7438 or

Outside the U.S. 304–263–8700e-mail at [email protected]

304–579–4827 — TDD(Telecommunication Device for the Deaf)

Fax MachineWithin the U.S. — 877–477–0572Outside the U.S. — 304–579–4105

Electronic Filing — FIRE Systemhttp://fire.irs.gov

Tax Exempt/Government Entities (TE/GE) Helpline1–877–829–5500

TO OBTAIN FORMS:1–800–TAX–FORM (1–800–829–3676)

IRS.gov — IRS Web Site access to forms and publications

.04 The current Instructions for Form 8955–SSA have been included in Publication 4810 for your convenience.

2011–22 I.R.B. 810 May 31, 2011

.05 Requests for paper Form 8955–SSA should be made by calling the IRS number 1–800–TAX–FORM (1–800–829–3676) orvia the IRS Web Site at IRS.gov/formspubs. File paper forms, schedules, statements, and attachments at the following address:Department of the Treasury, Internal Revenue Service Center, Ogden, UT 84201–0027.

.06 Filers should not contact IRS/IRB if they have received a penalty notice and need additional information or are requesting anabatement of the penalty. A penalty notice contains an IRS representative’s name and/or telephone number for contact purposes; or,the filer may be instructed to respond in writing to the address provided. IRS/IRB does not issue penalty notices and does not havethe authority to abate penalties. For penalty information, refer to the Penalty section of the current Instructions for Form 8955–SSA.

.07 Electronic Products and Services Support, Information Returns Branch, Customer Service Section (IRB/CSS), answers elec-tronic, paper filing, and tax law questions from the payer community relating to the correct preparation and filing of business informa-tion returns (Forms 1096, 1097, 1098, 1099, 5498, 8027, and W–2G). IRB/CSS also answers questions relating to the electronicfiling of Forms 8955–SSA. Call 1–800–455–7438 for specific information on 8955–SSA filing. Filers with inquiries regarding taxlaw issues and paper filing of Form 8955–SSA should call the TE/GE Help Line at 877–829–5500. Inquiries dealing with backupwithholding and reasonable cause requirements due to missing and incorrect taxpayer identification numbers are also addressed byIRB/CSS. Assistance is available year-round to payers, transmitters, and employers nationwide, Monday through Friday, 8:30 a.m.to 4:30 p.m. Eastern Time, by calling 1–866–455–7438 or via e-mail at [email protected]. Do not include Social Security Numbers(SSNs) or Employer Identification Numbers (EINs) in e-mail correspondence. Electronic mail is not secure and the information couldbe compromised. The Telecommunications Device for the Deaf (TDD) toll number is 304–579–4827. Call as soon as questions ariseto avoid the busy filing seasons. Recipients of information returns (payees) should continue to contact 1–800–829–1040 with anyquestions on how to report the information returns data on their tax returns.

Sec. 3. Form 4419, Application for Filing Information Returns Electronically (FIRE)

.01 Transmitters (See Part A, Section 6 for definition) are required to submit Form 4419, Application for Filing Information ReturnsElectronically (FIRE), to request authorization to file Form 8955–SSA with IRS/IRB. A single Form 4419 may be filed. IRS/IRBencourages transmitters who file for multiple plan administrators to submit one application and to use the assigned Transmitter ControlCode (TCC) for all. Form 4419 may be faxed to IRS/IRB within the U.S. at 877–477–0572 or outside the U.S. at 304–579–4105.Plan administrators may also choose to submit Form 8955–SSA on paper.

Note: EXCEPTIONS — In order to file additional form types, a different TCC must be assigned. Submit another Form 4419for filing Forms 1097, 1098, 1099, 3921, 3922, 5498 and W–2G, Form 1042–S, and Form 8027. See the back of Form 4419 fordetailed instructions.

.02 Form 4419 may be submitted anytime during the year; however, it must be submitted to IRS/IRB at least 30 days before thedue date of the return(s) for current year processing. This will allow IRS/IRB the minimum amount of time necessary to process andrespond to applications.

.03 Electronically filed returns may not be submitted to IRS/IRB until the application has been approved. Please read the in-structions on the back of Form 4419 carefully. A Form 4419 is included in Publication 4810 for the filer’s use. This form may bephotocopied. Additional forms may be obtained by calling 1–800–TAX–FORM (1–800–829–3676). The form is also available atIRS.gov.

.04 Upon approval, a five-character alpha/numeric Transmitter Control Code (TCC) beginning with the digit “6”, to be used onlyfor Form 8955–SSA, will be assigned and included in an approval letter. The TCC must be coded in the Transmitter “T” Record. Ifa transmitter uses more than one TCC to file, each TCC must be reported on a separate electronic transmission.

.05 If any of the information (name, TIN or address) on the Form 4419 changes, please notify IRS/IRB in writing so the IRS/IRBdatabase can be updated. The transmitter should include the TCC in all correspondence.

.06 Please make sure you submit your electronic files using the correct TCC. The FIRE System creates a filename that includes theTCC and a four-digit sequence number. All files submitted through the FIRE System will have a unique filename assigned.

.07 If a plan administrator’s files are prepared by a service bureau, it may not be necessary to submit an application to obtain aTCC. Some service bureaus will produce files, code their own TCC on the file, and send it to IRS/IRB for the plan administrator.Other service bureaus will prepare electronic files for the plan administrator to submit directly to IRS/IRB. These service bureaus mayrequire the plan administrators to obtain a TCC to be coded in the Transmitter “T” Record. The plan administrator should contacttheir service bureaus for further information.

.08 Once a transmitter is approved to file electronically, it is not necessary to reapply each year unless:(a) The plan administrator has discontinued filing electronically for two consecutive years; the plan administrator’s TCC may

have been reassigned by IRS/IRB. Plan administrators who are aware that the TCC assigned will no longer be used arerequested to notify IRS/IRB so these numbers may be reassigned; or

(b) The plan administrator’s electronic files were transmitted in the past by a service bureau using the service bureau’s TCC,but now the plan administrator has computer equipment compatible with that of IRS/IRB and wishes to prepare his or herown files. The plan administrator must request a TCC by filing Form 4419.

May 31, 2011 811 2011–22 I.R.B.

.09 One Form 4419 may be submitted per TIN. If a single transmitter needs to transmit more than 9,999 files in a single calendaryear, contact IRS/IRB toll-fee at 866–455–7438. Only one TCC will be issued per TIN unless the filer has checked the applicationfor the following forms in addition to the Form 8955–SSA: Forms 1097, 1098, 1099, 3921, 3922, 5498, W–2G, 8027 and 1042–S. Aseparate TCC will be assigned for these forms.

.10 Approval to file does not imply endorsement by IRS/IRB of any computer software or of the quality of tax preparation servicesprovided by a service bureau or software vendor.

Sec. 4. Due Dates

.01 The due dates for filing paper returns with IRS also applies to electronic filing of Form 8955–SSA.

.02 Form 8955–SSA filed electronically must be submitted to IRS/IRB on or before the due date. The due date for Form 8955–SSAis the end of the 7th month after the end of the plan year.

.03 An extension may be requested by filing Form 5558 before the due date of the Form 8955–SSA. Mail Form 5558 to InternalRevenue Service Center, Ogden, UT, 84201–0024. If an automatic extension is granted, the extended due date is the 15th day of the3rd month following the last day of the plan year.

.04 If any due date falls on a Saturday, Sunday or legal holiday, the return or statement is considered timely if filed or furnished onthe next day that is not a Saturday, Sunday, or legal holiday.

Sec. 5. Amended Returns

.01 If you filed a Form 8955–SSA with the IRS/IRB and later discovered an error with the filing after IRS/IRB accepted your file;you must send an amended 8955–SSA.

.02 Amended returns should be filed as soon as possible. When a record is incorrect, all fields on that record must be completedwith the correct information. Resubmit the entire file again with the amended returns.

.03 Prior year data, original and amended returns, must be filed according to the requirements of this Revenue Procedure. Ifsubmitting prior year amended returns, use the record format for the current year and submit in a separate transmission. However, usethe actual year designation of the amended return in Field Positions 2–5 of the “T” Record. A separate electronic transmission mustbe made for each plan year.

.04 All paper returns, whether original or amended, must be filed with Department of the Treasury Service Center, Internal RevenueService, Ogden, UT 84201–0024.

Sec. 6. Definition of Terms

Element Description

Amended Return An amended return is an information return submitted by thetransmitter to amend an information return that was previouslysubmitted to and processed by IRS/IRB, but containederroneous information.

Employer Identification Number (EIN) A nine-digit number assigned by IRS for Federal tax reportingpurposes.

Electronic Filing Submission of information returns electronically via theInternet. See Part B of this publication for specific informationon electronic filing.

File For purposes of this Revenue Procedure, a file consists of oneTransmitter “T” Record at the beginning of the file, a Sponsor“S” Record, followed by the Administrator “A” Record, andParticipant “P” Record (s) ending with the last record on thefile, and the End of Transmission “F“ Record. Nothing shouldbe reported after the End of Transmission “F” Record.

Filer Person (may be plan administrator, plan sponsor and/ortransmitter) submitting information returns to IRS.

Information Return The vehicle for a plan administrator to submit requiredinformation concerning recipients to IRS.

2011–22 I.R.B. 812 May 31, 2011

Element Description

Participant Generally, for these purposes, any individual entitled to receivebenefits under a plan.

Plan Administrator The person designated by the plan, or in the absence of adesignation, as either (1) the employer (in the case of theplan maintained by a single employer) or (2) the association,committee, or joint board of trustees who maintain the plan (incase of a plan maintained by more than one employer).

Record A record contains specific information for the filing of Form8955–SSA. Records include the Transmitter “T” Record, theSponsor “S” Record, the plan Administrator “A” Record,the Participant “P” Record and the “F” End of TransmissionRecord. All records are a fixed length of 750 positions.

Service Bureau Person or organization with whom the plan administrator hasa contract to prepare and/or submit information return files toIRS/IRB. A parent company submitting data for a subsidiary isnot considered a service bureau.

Social Security Number (SSN) A nine-digit number assigned by Social Security Administrationto an individual for wage and tax reporting purposes.

Special Character Any character that is not a numeric, an alpha, or a blank.

Sponsor Refers to the sponsor of the plan, generally is one of thefollowing (1) the employer (in case of a plan maintained bya single employer), (2) the employee organization (in caseof a plan maintained by an employee organization), or (3)the association, committee, or joint board of trustees of theparties who maintain the plan (in the case of a plan maintainedjointly by one or more employers and one or more employeeorganizations, or by two or more employers).

Taxpayer Identification Number(TIN) Refers to either an Employer Identification Number (EIN) or aSocial Security Number (SSN).

Transmitter Refers to the person or organization submitting file(s)electronically. The transmitter may be the plan administrator oragent of the plan administrator.

Transmitter Control Code (TCC) A five-character alpha/numeric number assigned by IRS/IRBto the transmitter prior to filing electronically. An applicationForm 4419 must be filed with IRS/IRB to receive this number.This number is inserted in the Transmitter “T” Record (fieldpositions 16–20) of the file and must be present before the filecan be processed. Transmitter Control Codes assigned to Form8955–SSA transmitters will always begin with “6”.

Vendor Vendors include service bureaus that produce informationreturn files electronically for plan administrators. Vendors alsoinclude companies that provide software for those who wish toproduce their own electronic files.

Sec. 7. State Abbreviations

.01 The following table provides state and U.S. territory abbreviations that are to be used when developing the state code portionof address fields.

May 31, 2011 813 2011–22 I.R.B.

State Code State Code State Code

Alabama AL Kansas KS No. Mariana Islands MPAlaska AK Kentucky KY Ohio OHAmerican Samoa AS Louisiana LA Oklahoma OKArizona AZ Maine ME Oregon ORArkansas AR Maryland MD Pennsylvania PACalifornia CA Massachusetts MA Puerto Rico PRColorado CO Michigan MI Rhode Island RIConnecticut CT Minnesota MN South Carolina SCDelaware DE Mississippi MS South Dakota SDDistrict of Columbia DC Missouri MO Tennessee TNFederated States of Micronesia FM Montana MT Texas TXFlorida FL Nebraska NE Utah UTGeorgia GA Nevada NV Vermont VTGuam GU New Hampshire NH Virginia VAHawaii HI New Jersey NJ U.S. Virgin Islands VIIdaho ID New Mexico NM Washington WAIllinois IL New York NY West Virginia WVIndiana IN North Carolina NC Wisconsin WIIowa IA North Dakota ND Wyoming WY

.02 When reporting APO/FPO addresses use the following format:

EXAMPLE:

Recipient Payee Name PVT Willard J. DoeRecipient Mailing Address Company F, PSC Box 100

167 Infantry REGTRecipient Payee City APO (or FPO)Recipient Payee State AE, AA, or AP*Recipient Payee ZIP Code 098010100

*AE is the designation for ZIP codes beginning with 090–098, AA for ZIP code 340, and AP for ZIPcodes 962–966.

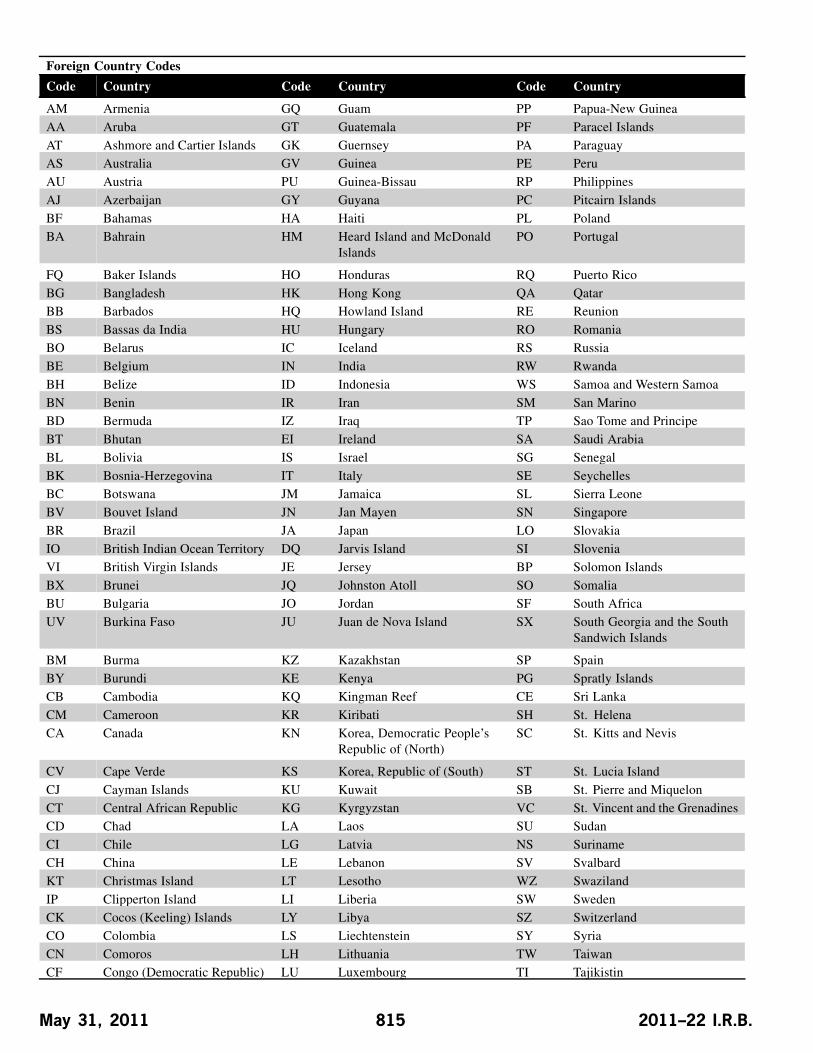

Sec. 8. Foreign Country Codes

.01 The following table provides the Foreign Country Codes that are to be used when developing the country code portion ofaddress fields.

Foreign Country Codes

Code Country Code Country Code Country

AF Afghanistan GZ Gaza Strip NE NiueAL Albania GG Georgia NF Norfolk IslandAG Algeria GM Germany CQ Northern Mariana IslandAQ American Samoa GH Ghana NO NorwayAN Andorra GI Gibraltar MU OmanAO Angola GO Glorioso Islands OC Other CountriesAV Anguilla GR Greece PK PakistanAY Antarctica GL Greenland LQ Palmyra AtollAC Antigua and Barbuda GJ Grenada PS PalauAR Argentina GP Guadeloupe PM Panama

2011–22 I.R.B. 814 May 31, 2011

Foreign Country Codes

Code Country Code Country Code Country

AM Armenia GQ Guam PP Papua-New GuineaAA Aruba GT Guatemala PF Paracel IslandsAT Ashmore and Cartier Islands GK Guernsey PA ParaguayAS Australia GV Guinea PE PeruAU Austria PU Guinea-Bissau RP PhilippinesAJ Azerbaijan GY Guyana PC Pitcairn IslandsBF Bahamas HA Haiti PL PolandBA Bahrain HM Heard Island and McDonald

IslandsPO Portugal

FQ Baker Islands HO Honduras RQ Puerto RicoBG Bangladesh HK Hong Kong QA QatarBB Barbados HQ Howland Island RE ReunionBS Bassas da India HU Hungary RO RomaniaBO Belarus IC Iceland RS RussiaBE Belgium IN India RW RwandaBH Belize ID Indonesia WS Samoa and Western SamoaBN Benin IR Iran SM San MarinoBD Bermuda IZ Iraq TP Sao Tome and PrincipeBT Bhutan EI Ireland SA Saudi ArabiaBL Bolivia IS Israel SG SenegalBK Bosnia-Herzegovina IT Italy SE SeychellesBC Botswana JM Jamaica SL Sierra LeoneBV Bouvet Island JN Jan Mayen SN SingaporeBR Brazil JA Japan LO SlovakiaIO British Indian Ocean Territory DQ Jarvis Island SI SloveniaVI British Virgin Islands JE Jersey BP Solomon IslandsBX Brunei JQ Johnston Atoll SO SomaliaBU Bulgaria JO Jordan SF South AfricaUV Burkina Faso JU Juan de Nova Island SX South Georgia and the South

Sandwich Islands

BM Burma KZ Kazakhstan SP SpainBY Burundi KE Kenya PG Spratly IslandsCB Cambodia KQ Kingman Reef CE Sri LankaCM Cameroon KR Kiribati SH St. HelenaCA Canada KN Korea, Democratic People’s

Republic of (North)SC St. Kitts and Nevis

CV Cape Verde KS Korea, Republic of (South) ST St. Lucia IslandCJ Cayman Islands KU Kuwait SB St. Pierre and MiquelonCT Central African Republic KG Kyrgyzstan VC St. Vincent and the GrenadinesCD Chad LA Laos SU SudanCI Chile LG Latvia NS SurinameCH China LE Lebanon SV SvalbardKT Christmas Island LT Lesotho WZ SwazilandIP Clipperton Island LI Liberia SW SwedenCK Cocos (Keeling) Islands LY Libya SZ SwitzerlandCO Colombia LS Liechtenstein SY SyriaCN Comoros LH Lithuania TW TaiwanCF Congo (Democratic Republic) LU Luxembourg TI Tajikistin

May 31, 2011 815 2011–22 I.R.B.

Foreign Country Codes

Code Country Code Country Code Country

CW Cook Islands MC Macau TZ TanzaniaCR Coral Sea Islands MK Macedonia TH ThailandVP Corsica MA Madagascar TO TogoCS Costa Rica MI Malawi TL TokelauIV Cote D’Ivoire (Ivory Coast) MY Malaysia TN TongaHR Croatia MV Maldives TD Trinidad and TobagoCU Cuba ML Mali TE Tromelin IslandCY Cyprus MT Malta TS TunisiaEZ Czech Republic IM Man, Isle of TU TurkeyDA Denmark RM Marshall Islands TX TurkmenistanDJ Djibouti MB Martinique TK Turks and Caicos IslandsDO Dominica MR Mauritania TV TuvaluDR Dominican Republic MP Mauritius UG UgandaTT East Timor MF Mayotte UP UkraineEC Ecuador MX Mexico TC United Arab EmiratesEG Egypt MQ Midway Islands UK United Kingdom (England,

Northern Ireland, Scotland,and Wales)

ES El Salvador MD Moldova UC Unknown CountryEK Equatorial Guinea MN Monaco UY UruguayER Eritrea MG Mongolia UZ UzbekistanEN Estonia MH Montserrat NH VanuatuET Ethiopia MO Morocco VT Vatican CityEU Europa Island MZ Mozambique VE VenezuelaFK Falkland Islands (Islas

Malvinas)WA Namibia VM Vietnam

FO Faroe Islands NR Nauru VQ Virgin IslandsFM Federated States of Micronesia BQ Navassa Island WQ Wake IslandFJ Fiji NP Nepal WF Wallis and FutunaFI Finland NL Netherlands WE West BankFR France NT Netherlands Antilles WI Western SaharaFG French Guinea NC New Caledonia YM Yemen (Aden)FP French Polynesia NZ New Zealand YO Yugoslavia

FS French Southern and AntarcticLands

NU Nicaragua ZA Zambia

GB Gabon NG Niger ZI ZimbabweGA The Gambia NI Nigeria

Part B. Electronic Filing Specifications

Note 1: The FIRE System DOES NOT provide fill-in forms. Filers must program files according to the Record Layout Speci-fications contained in this publication. For a list of software providers, log on to IRS.gov and go to the Approved IRS e-file forBusiness Providers link.

Note 2: The FIRE System may be down every Wednesday from 2:00 a.m. to 5:00 a.m. ET for maintenance.

Sec. 1. General

.01 Filing Forms 8955–SSA through the FIRE (Filing Information Returns Electronically) System (originals and amended) is themethod of filing for plan administrators who wish to file electronically instead of filing on paper.

2011–22 I.R.B. 816 May 31, 2011

.02 All electronic filing of information returns are received at IRS/IRB via the FIRE System. To connect to the FIRE System, pointyour browser to http://fire.irs.gov.

The system is designed to support the electronic filing of information returns only..03 The electronic filing of information returns is not affiliated with any other IRS electronic filing programs.Filers must obtain separate approval to participate in each program. Only inquiries concerning electronic filing of information

returns should be directed to IRS/IRB..04 Files submitted to IRS/IRB electronically must be in standard ASCII code. Do not send paper forms with the same information

as electronically submitted files. This would create duplicate reporting..05 Current and prior year data must be submitted in separate electronic transmissions. Each plan year must be a separate electronic

file..06 Filers who have prepared their information returns in advance of the due date can submit their file any time after the plan year

ends..07 Plan administrators should retain a copy of the information returns filed with IRS/IRB or have the ability to reconstruct the

data for at least 3 years from the due date of the returns..08 See Part C, Record Format Specifications and Record Layouts, for the proper record format.

Sec. 2. Electronic Filing Approval Procedure

.01 Filers must obtain a Transmitter Control Code (TCC) prior to submitting files electronically. Refer to Part A, Sec. 3, forinformation on how to obtain a TCC.

.02 Once a TCC is obtained, electronic filers create their own user ID, password and PIN (Personal Identification Number) and donot need prior or special approval. See Part B, Sec. 5, for more information on the PIN.

.03 If a filer is submitting files for more than one TCC, it is not necessary to create a separate User ID and password for each TCC.

.04 For all passwords, it is the user’s responsibility to remember the password and not allow the password to be compromised.Passwords are user created at first logon and must be 8 alpha/numerics containing at least 1 uppercase, 1 lowercase, and 1 numeric.However, filers who forget their password or PIN, can call 1–866–455–7438 for assistance. The FIRE System will require users tochange their passwords periodically. Users can change their passwords at any time from the Main Menu. Prior passwords cannot beused.

Sec. 3. Test Files

.01 Filers are not required to submit a test file; however, the submission of a test file is encouraged for all new electronic filers totest hardware and software. Generally, testing is available between November 1 and February 15. To connect to the FIRE test System,point your browser to http://fire.test.irs.gov.

.02 IRS/IRB encourages first time electronic filers to submit a test.

.03 The test file must consist of a sample of each type of record:(a) Transmitter “T” Record (all fields marked required must include transmitter information)(b) Sponsor “S” Record(c) Administrator “A” Record(d) Multiple Participant “P” Records (at least 11 “P” Records per each “T” Record)(e) End of Transmission “F” Record (See Part C for record formats.)

.04 Use the Test Indicator “T” in Field Position 28 of the “T” Record to show this is a test file.

.05 IRS/IRB will check the file to ensure it meets the specifications of this Revenue Procedure.For current filers, sending a test file will provide the opportunity to ensure their software reflects any programming changes..06 Filers who encounter problems while transmitting the electronic test file can contact IRS/IRB at 1–866–455–7438 for assistance..07 Within 5 days after your file has been sent, you will be notified via e-mail as to the acceptability of your file if you provide a

valid e-mail address on the “Verify Your Filing Information” screen. If you are using e-mail filtering software, configure your softwareto accept e-mail from [email protected] and [email protected]. If the file is bad, the filer must return to http://fire.irs.gov to determinewhat the errors are in the file by clicking on CHECK FILE STATUS.

If your results indicate:(a) “Good” — Your test file is good for Federal reporting.(b) “Bad” — This means that your test file contained errors. Click on the filename for a list of the errors. If you want to send

another test file, send it as a test (not as an original or amended).(c) “Not Yet Processed” — The file has been received, but we do not have results available yet. Please allow another day for

results.

May 31, 2011 817 2011–22 I.R.B.

Sec. 4. Electronic Submissions

.01 Electronically filed information may be submitted to IRS/IRB 24 hours a day, 7 days a week. Technical assistance is availableMonday through Friday between 8:30 a.m. and 4:30 p.m. ET by calling 1–866–455–7438.

.02 The FIRE System will be down from 2 p.m. ET December 16, 2011, through January 2, 2012. This allows IRS/IRB toupdate its system to reflect current year changes. In addition, the FIRE System may be down every Wednesday from 2:00 a.m. to5:00 a.m. ET for maintenance.

.03 If you are sending files larger than 10,000 records electronically, data compression is encouraged. Your file size can not exceed2.5 million records. WinZip and PKZIP are the only acceptable compression packages. IRS/IRB cannot accept self-extracting zip filesor compressed files containing multiple files. The time required to transmit information returns electronically will vary dependingupon the type of connection to the Internet and if data compression is used. The time required to transmit a file can be reduced upto 95 percent by using compression.

.04 Transmitters may create files using self assigned filename(s). Files submitted electronically will be assigned a new uniquefilename by the FIRE System. The filename assigned by the FIRE System will consist of submission type (TEST, ORIG [original],and AMEN [amended]), the filer’s TCC and a four-digit sequence number. The sequence number will be incremented for every filesent. For example, if it is your first original file for the calendar year and your TCC is 66666, the IRS assigned filename would beORIG.66666.0001. Record the file name. This information will be needed by IRS/IRB to identify the file, if assistance is required.

.05 If a file submitted timely is bad, the filer will have up to 60 days from the day the file was transmitted to submit an acceptableoriginal file. If an acceptable original file is not received within 60 days, the plan administrator could be subject to late filing orincomplete return penalties.

Sec. 5. PIN Requirements

.01 The user will be prompted to create a PIN consisting of 10 numeric characters when establishing their initial User ID name andpassword.

.02 The PIN is required each time an ORIGINAL or AMENDED file is sent electronically and serves as permission to release thefile. It is not needed for a TEST file. An authorized agent may enter their PIN; however, the plan administrator is responsible for theaccuracy of the returns. The plan administrator will be liable for penalties for failure to comply with filing requirements. If you forgetyour PIN, please call 1–866–455–7438 for assistance.

.03 If the file is good, it is released for mainline processing.

Sec. 6. Electronic Filing Specifications

.01 The FIRE System is designed exclusively for the filing of Forms 8955–SSA, 1042–S, 1097, 1098, 1099, 3921, 3922, 5498,8027, 8935 and W–2G.

.02 A transmitter must have a TCC (see Part A, Sec. 3) before a file can be transmitted.

.03 After 5 business days, the results of the electronic transmission will be e-mailed if provided an accurate e-mail address on the“Verify Your Filing Information” screen. If you are using e-mail filtering software, configure your software to accept e-mail [email protected] and [email protected]. If after receiving the e-mail it indicates that the file is bad, filers must log into the FIRESystem and go to the CHECK FILE STATUS area of the FIRE System to determine what the errors are in the file.

Sec. 7. Connecting to the FIRE System

.01 Before connecting, have the TCC and TIN available.

.02 Filers should turn off pop-up blocking software before transmitting their files.

.03 The browser must support the security standards listed below.

.04 The browser must be set to receive “cookies.” Cookies are used to preserve the User ID status.

.05 Point the browser to http://fire.irs.gov to connect to the FIRE System.

.06 FIRE Internet Security Technical Standards are:

HTTP 1.1 Specification (http://www.w3.org/Protocols/rfc2616/rfc2616.txt)

SSL 3.0 or TLS 1.0. SSL and TLS are implemented using SHA and RSA 1024 bits during the asymmetric handshake.

SSL 3.0 Specifications (http://wp/netscape.com/eng/ssl3)

TLS 1.0 Specifications (http://www.ief.org/rfc/rfc2246.txt)

2011–22 I.R.B. 818 May 31, 2011

The filer can use one of the following encryption algorithms, listed in order of priority, using SSL or TLS:

AES 256-bit (FIPS–197)

AES 128-bit (FIPS–197)

TDES 168-bit (FIPS–46–3)

First time connection to the FIRE System If you have logged on previously, skip to Subsequent Connections to the FIRESystem.)

Click “Create New Account.”Fill out the registration form and click “Submit.”Create your User IDCreate and verify your password (the password is user created and must be 8 alpha/numericcharacters, containing at least 1 uppercase, 1 lowercase and 1 numeric. It cannot contain the UserID). FIRE will require you to change the password periodically.Click “Create.”If you receive the message “Account Created,” click “OK.”Create and verify your 10-digit self-assigned PIN (Personal Identification Number).Click “Submit.”If you receive the message “Your PIN has been successfully created!,” click “OK.”Read the bulletin(s) and/or “Click here to continue.”

Subsequent connections to the FIRE System

Click “Log On.”Enter your User ID.Enter your password (the password is case sensitive).Read the bulletin(s) and/or “Click here to continue.”

Uploading your file to the FIRE System

At Menu Options:Click “Send Information Returns.”Enter your TCC.Enter your TIN.Click “Submit.”

The system will then display the company name, address, city, state, ZIP code, telephonenumber, contact and e-mail address. This information will be used to e-mail the transmitterregarding their transmission. Update as appropriate and/or Click “Accept.”

Note: Please ensure that the e-mail address is accurate so that the correct person receivesthe e-mail and it does not return to us undeliverable. If you are using SPAM filteringsoftware, configure it to allow an e-mail from [email protected] and [email protected].

Click one of the following:Original FileAmended FileTest File

Enter your 10-digit PIN (You are not prompted for this if a test is being sent).Click “Submit”.Click “Browse” to locate the file and open it.Click “Upload”.

When the upload is complete, the screen will display the total bytes received and tell you the name of the file you justuploaded. Print this page and keep it for your records.

If you have more files to upload for that TCC:Click “File Another?”; otherwise,Click “Main Menu”.

May 31, 2011 819 2011–22 I.R.B.

It is your responsibility to check the acceptability of your file; therefore, be sure to check back into the system in 5business days using the CHECK FILE STATUS option.

Checking your FILE STATUS

If the correct e-mail address was provided on the “Verify Your Filing Information” screen when the file was sent, an e-mail willbe sent regarding your FILE STATUS. If the results in the e-mail indicate “Good, Released” and you agree with the “Count ofParticipants”, then you are finished with this file. If you have any other results, please follow the instructions below.

At the Main Menu:Click “Check File Status.”Enter your TCC.Enter your TIN.Click “Search.”

If “Results” indicate:“Good, Released” — File has been released to our mainline processing.

“Good, Released with Error Status” — File has been released but containsminor errors.

“Bad” — Click on filename to view error message(s). Correct the errors andtimely resubmit the file as an “original”.

“Not yet processed” — File has been received, but we do not have resultsavailable yet. Please check back in a few days.

Click on the desired file for a detailed report of your transmission.When you are finished, click on Main Menu.Click “Log Out.”Close your Web Browser.

Sec. 8. Common Submission Errors and Problems

IRS/IRB encourages filers to verify the format and content of each type of record to ensure the accuracy of the data. This maybe important for those filers who have either had their files prepared by a service bureau or who have purchased software packages.Filers who engage a service bureau to transmit files on their behalf should be careful not to report duplicate data. This sectionlists some of the problems most frequently encountered with electronic files submitted to IRS/IRB. These problems may result inIRS/IRB rejecting files as “Bad”.

.01 Your electronic file appears to be incomplete. The count of participant records in the P-RECORD-COUNT field of the End ofTransmission “F” Record does not equal the number of Participant “P” records in your file.

.02 Your electronic file appears to be incomplete. The count of all records in the FILE-RECORD-COUNT field of the End ofTransmission “F” Record does not equal the number of records in your file.

.03 You submitted a test file to the production system. If the file you submitted wasn’t a test file, please Correct the TEST-FILE-INDon the Transmitter “T” Record. If you submitted a test file to the production system in error, you don’t need to do anything; the filewill be deleted if a corrected file isn’t received in 60 days.

.04 You submitted a file with more than one Transmitter “T” Record. Each file submitted through FIRE can contain only oneTransmitter “T” Record.

.05 You submitted a file with more than one Sponsor “S” Record. Each file submitted through FIRE can contain only one Sponsor“S” Record.

.06 You submitted a file with more than one Administrator “A” Record. Each file submitted through FIRE can contain only oneAdministrator “A” Record.

.07 You submitted a file with more than one End of Transmission “F” Record. Each file submitted through FIRE can contain onlyone End of Transmission “F” Record.

.08 You submitted a file with records which appear to be from different filings. (The Plan Year Begin Date, Plan Year End Date,Sponsor EIN, and Plan Number are not the same on every record in your file.)

.09 Your filing contained too many participants to be submitted in a single FIRE file, so it was included in multiple FIRE files andone of these FIRE files had an error. All of the FIRE files related to this single filing must be corrected and resubmitted (even if therewas an error in only one of the files).

2011–22 I.R.B. 820 May 31, 2011

.10 Your filing did not include a Sponsor EIN in positions 18–26 of the Sponsor “S” Record.

.11 Your filing included a non-numeric Sponsor EIN in positions 18–26 of the Sponsor “S” Record.

.12 Your filing did not include a Sponsor Name in positions 74–143 of the Sponsor “S” Record.

.13 Your filing did not include a Sponsor Address in positions 249–400 of the Sponsor “S” Record.

.14 Your filing included a non-numeric Plan Number in positions 27–29 of the Sponsor “S” Record. The Plan Number should be001–999.

.15 Your filing did not include a Plan Name in positions 411–550 of the Sponsor “S” Record.

.16 We have already received a filing with the same Sponsor EIN, Plan Number, and Plan Year Ending Date. If your file wassubmitted to correct a previous error but is being submitted more than 60 days after you were notified of the error, or if this file wasmeant to amend a previously submitted filing, please make sure that it is identified as an amended return (AMENDED-IND = “1”in position 34 of the Sponsor “S” Record. If your file was submitted in error (it was a duplicate filing), or if this is not a duplicatereturn and you did not previously submit a filing with the same Sponsor EIN, Plan Number, and Plan Year Ending Date, please contactIRS/IRB.

.17 The count of total participants reported on Form 8955–SSA (Line 3) in positions 568–575 of the Sponsor “S” Record does notequal the count of Participant “P” Records received. If the filing was too large to be submitted on a single FIRE file, Form 8955–SSALine 3 should be the total reported in all of the associated FIRE files.

.18 Your filing did not include an Administrator EIN in positions 35–43 of the Administrator “A” Record.

.19 Your filing included a non-numeric Administrator EIN in positions 35–43 of the Administrator “A” Record.

.20 Your filing did not include an Administrator Address in positions 149–300 of the Administrator “A” Record.

.21 Your filing had plan participant record(s) which contained data but did not have a valid entry code.

.22 Your filing had plan participant record(s) on which you indicated an Entry Code of “A” or “B” in box 7a, however you didn’tprovide all of the remaining data for Lines 7(b) through 7(g) in positions 44–131 of the Participant “P” record.

.23 Your filing had plan participant record(s) on which you indicated an Entry Code of “D”, however you didn’t provide all of theremaining data for Lines 7(b) and 7(c) in positions 44–99 of the Participant “P” record.

.24 Your filing had plan participant record(s) on which you indicated an Entry Code of “C”, however you didn’t provide all of theremaining data for Lines 7(b) (positions 44–52), 7(c) (positions 53–99), 7(h) (positions 132–140), and 7(i) (positions 141–143) in theParticipant “P” Record.

.25 SPAM filters are not set to receive e-mail from [email protected] and [email protected]. If you want to receive e-mailsconcerning your files, processing results, reminders and notices, set your SPAM filter to receive e-mail from [email protected] [email protected].

.26 An incorrect e-mail address was provided. When the “Verify Your Filing Information” screen is displayed, make sure yourcorrect e-mail address is listed. If not, please update with the correct e-mail address.

.27 The transmitter does not check the FIRE System to determine why the file is bad. The results of your file transfer are postedto the FIRE System within five business days. If the correct e-mail address was provided on the “Verify Your Filing Information”screen when the file was sent, an e-mail will be sent regarding your FILE STATUS. If you have any other results, please follow theinstructions in the Check File Status option. If the file contains errors, you can get an online listing of the errors. Date received andnumber of payee records are also displayed.

.28 The transmitter compresses several files into one. Only compress one file at a time. For example, if you have 10 uncompressedfiles to send, compress each file separately and send 10 separate compressed files.

.29 The file is formatted as EBCDIC. All files submitted electronically must be in standard ASCII code.

.30 An incorrect file is not replaced timely. If your file is bad, correct the file and timely resubmit as an original.

.31 The transmitter sends a file and CHECK FILE STATUS indicates that the file is good, but the transmitter wants to send anamended file to replace the original file. Once a file has been transmitted, you cannot send another file unless CHECK FILE STATUSindicates the file is bad (5 business days after file was transmitted). If you do not want us to process the file, you must first contact us1–866–455–7438 to see if this is a possibility.

Part C. Record Format Specifications and Record Layouts

Sec. 1. Transmitter “T” Record

.01 This record identifies the entity preparing and transmitting the file. The transmitter and the plan administrator may be the same,but they need not be.

.02 The first record of a file MUST be a Transmitter “T” Record. The “T” Record must appear on each electronic file; otherwise,the file will be rejected.

.03 The “T” Record is a fixed length of 750 positions.

.04 All alpha characters entered in the “T” Record must be upper case.

May 31, 2011 821 2011–22 I.R.B.

Note 1: For all fields marked “Required”, the transmitter must provide the information described under Description andRemarks. If required fields are not completed in accordance with these instructions, IRS will contact you to request a newfile. For those fields not marked “Required”, a transmitter must allow for the field, but may be instructed to enter blanks orzeroes in the indicated field position(s) and for the indicated length. All records have a fixed length of 750 positions. Refer tothe Instructions for Form 8955–SSA for additional filing information.

Record Name: Transmitter “T” Record

FieldPositions Field Title Length Description and Remarks

1 Record Type 1 Required. Enter “T”.

2–5 Plan Year 4 Required. Enter 2011. If reporting prior year data, report the year which applies(2010, 2009, etc.) and set the Prior Year Indicator in field position 6.

6 Blank 1 Enter a blank.

7–15 Transmitter’s TIN 9 Required. Enter the nine-digit Taxpayer Identification Number of thetransmitter. Do NOT enter blanks, hyphens or alpha characters. An EINconsisting of all the same digits (e.g., 111111111) is not acceptable.

16–20 Transmitter ControlCode (TCC)

5 Required. Enter the five-character alpha/numeric Transmitter Control Codeassigned by IRS/IRB.

21–27 Reserved 7 Enter blanks.

28 Test FileIndicator

1 Required for test files only. Enter a “T” if this is a test file; otherwise, enterblank.

29 Foreign EntityIndicator

1 Enter a “1” (one) if the transmitter is a foreign entity; otherwise, enter a blank.

30–69 Transmitter’s Name 40 Required. Enter the name of the transmitter in the manner in which it is usedin normal business. Left justify the information and fill unused positions withblanks.

70–109 Transmitter’s Name(Continuation)

40 Required. Enter any additional information that may be part of the name. Leftjustify the information and fill unused positions with blanks.

110–149 Company Name 40 Required. Enter the name of the company to be associated with the addresswhere correspondence should be sent. Left justify the information and fillunused positions with blanks.

150–189 Company Name(Continuation)

40 Enter any additional information that may be part of the name. Left justify theinformation and fill unused positions with blanks.

190–229 Company MailingAddress

40 Required. Enter the mailing address where correspondence should be sent. Leftjustify the information and fill unused positions with blanks.

Note: Any correspondence relating to problem electronic files will be sent to this address.

For U.S. addresses, the administrator’s city, state, and ZIP Code must be reported as a 40, 2, and 9-position field, respectively.Filers must adhere to the correct format for the city, state, and ZIP Code.

For foreign addresses, filers may use the administrator’s city, state, and ZIP Code as a continuous 51-position field. Enterinformation in the following order: city, province or state, postal code, and the name of the country. When reporting a foreignaddress, the Foreign Entity Indicator in position 29 must contain a “1” (one).

230–269 CompanyCity

40 Required. Enter the city, town, or post office where correspondence should besent. Left justify the information and fill unused positions with blanks.

270–271 CompanyState Code

2 Required. Enter the valid U.S. Postal Service state code abbreviation. SeePart A, Sec. 7.

2011–22 I.R.B. 822 May 31, 2011

Record Name: Transmitter “T” Record

FieldPositions Field Title Length Description and Remarks

272–280 CompanyZIP Code

9 Required. Enter the valid nine-digit ZIP assigned by the U.S. Postal Service. Ifonly the first five-digits are known, left justify the information and fill unusedpositions with blanks.

281–303 Reserved 23 Enter blanks.

304–343 Contact Name 40 Required. Enter the name of the person to be Contacted if IRS/IRB encountersproblems with the file or transmission. Left justify the information and fillunused positions with blanks.

344–358 Contact TelephoneNumber

15 Enter the telephone number of the person to contact regarding electronic files.Omit hyphens. If no extension is available, left justify the information and fillunused positions with blanks. For example, the IRS/IRB Customer ServiceSection phone number of 866–455–7438 with an extension of 52345 wouldbe 866455743852345.

359–408 Contact EmailAddress

50 Required if available. Enter the e-mail address of the person to contactregarding electronic files. Left-justify the information. If no e-mail address isavailable, enter blanks.

409–517 Reserved 109 Enter blanks.

518 Vendor Indicator 1 Required. Enter the appropriate code from the table below to indicate if yoursoftware was provided by a vendor or produced in-house.

Indicator Usage

V Your software was purchased from avendor or other source.

I Your software was produced byin-house programmers.

Note: In-house programmer is defined as an employee or a hired contract programmer. If your software is producedin-house, the following Vendor information fields are not required.

519–558 Vendor Name 40 Required. Enter the name of the company from whom you purchased yoursoftware. Left justify the information and fill unused positions with blanks.

For U.S. addresses, the vendor city, state, and ZIP Code must be reported as a 40, 2, and 9-position field, respectively. Filersmust adhere to the correct format for the administrator’s city, state, and ZIP Code.

For foreign addresses, filers may use the administrator’s city, state, and ZIP Code as a continuous 51-position field. Enterinformation in the following order: city, province or state, postal code, and the name of the country.

559–598 Vendor MailingAddress

40 Required. Enter the mailing address. Left justify the information and fill unusedpositions with blanks.

599–638 Vendor City 40 Required. Enter the city, town, or post office. Left justify the information andfill unused positions with blanks.

639–640 Vendor State 2 Required. Enter the valid U.S. Postal Service state abbreviation. Refer to thechart of valid state codes in Part A, Sec. 7.

641–649 Vendor ZIP Code 9 Required. Enter the valid nine-digit ZIP Code assigned by the U.S. PostalService. If only the first five-digits are known, left justify the information andfill unused positions with blanks.

650–689 Vendor Contact Name 40 Required. Enter the name of the person who can be contacted concerning anysoftware questions.

690–704 Vendor ContactPhone Number &Extension

15 Required. Enter the telephone number of the person to contact concerningsoftware questions. Omit hyphens. If no extension is available, left justify theinformation and fill unused positions with blanks.