Boston Slides t

23

Boston Chicken Case

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Boston Slides t

Boston Chicken Case

Case Overview Rapidly growing restaurant chain is one of the hottest names on Wall Street

Sales and earnings show consistent growth

But a small number of detractors argue that the strategy is flawed and the accounting numbers are misleading

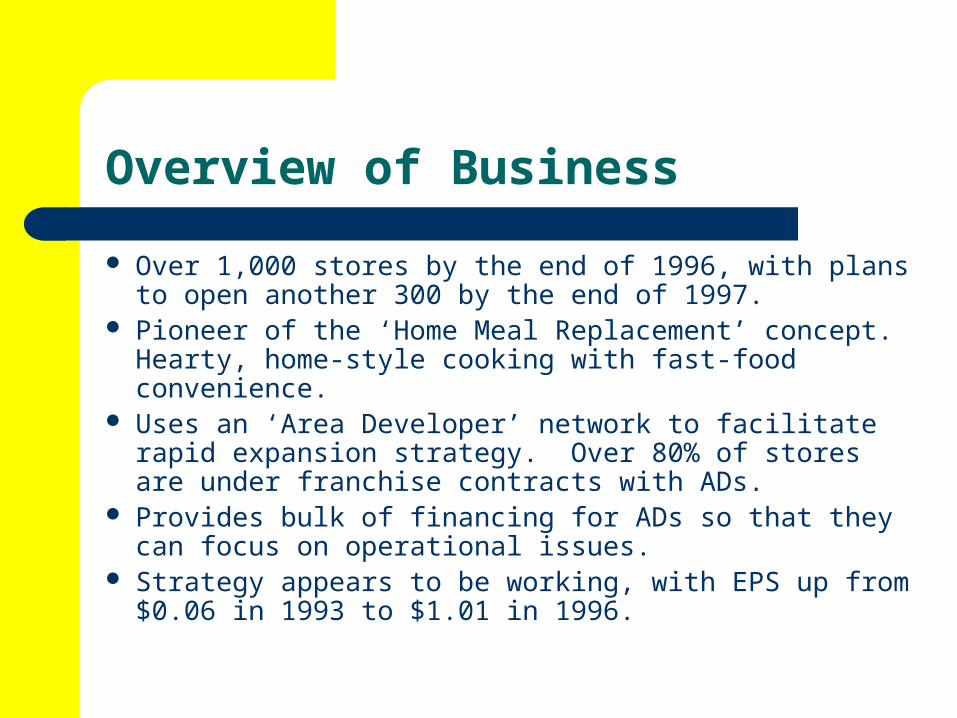

Overview of Business Over 1,000 stores by the end of 1996, with plans to open another 300 by the end of 1997.

Pioneer of the ‘Home Meal Replacement’ concept. Hearty, home-style cooking with fast-food convenience.

Uses an ‘Area Developer’ network to facilitate rapid expansion strategy. Over 80% of stores are under franchise contracts with ADs.

Provides bulk of financing for ADs so that they can focus on operational issues.

Strategy appears to be working, with EPS up from $0.06 in 1993 to $1.01 in 1996.

What is the Key Line of Business? The balance sheet suggests that most of the assets are tied up in the financing business

The income statement suggests that most of the revenues and earnings are generated by the franchise business

The restaurant operating business is the least important

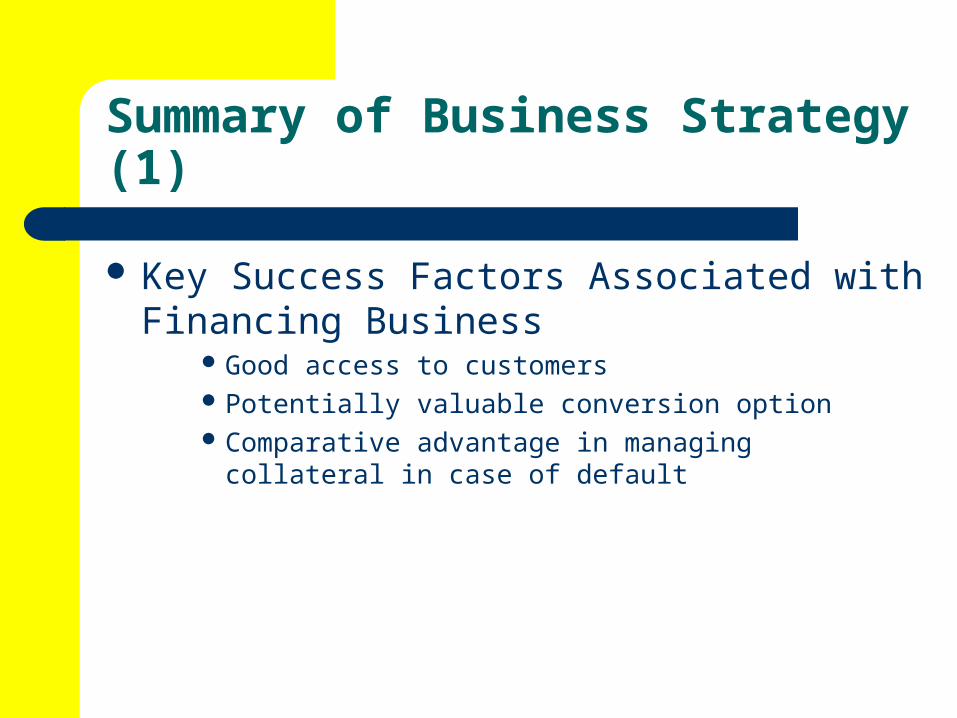

Summary of Business Strategy (1)

Key Success Factors Associated with Financing Business

Good access to customersPotentially valuable conversion optionComparative advantage in managing collateral in case of default

Summary of Business Strategy (2)

Key Risks Associated with Financing Business

Credit Risk Concentrated with a small number of ADs who are all in the same line of business

Poor interest rate spreadLow leverageRegulatory and legal risks

Summary of Business Strategy (3)

Key Success Factors Associated with Franchise Business

Premium franchise fees and royaltiesAD network promotes rapid and systematic penetration of target markets

‘Boston Market’ brand nameADs have ready access to additional capital at low cost

Summary of Business Strategy (4)

Key Risks Associated with Franchise Business

Initial franchise fees dry up as growth slows

ADs could go broke and would then be unable to continue to pay royalty and franchise fee payments

Summary of Business Strategy (5)

Key Success Factors Associated with Restaurant Business

Fist mover advantage in ‘Home Meal Replacement’ concept

‘Boston Market’ brand name

Summary of Business Strategy (6)

Key Risks Associated with Restaurant Business

Competition– KFC starts selling rotisserie chicken, fluffy mash potato etc.

– Supermarkets start selling rotisserie chickenHome Meal Replacement concept is not viable

Overall Evaluation of Boston Chicken’s Business Strategy Financing business is lackluster, but has important synergies for franchising business. Credit risk is a big concern here.

Franchise business looks great, so long as franchisees can keep paying bills.

Restaurant business looks horrible and is making substantial losses and sucking up huge amounts of cash (refer to AD losses on p. 6).

Overall Evaluation of Boston Chicken’s Business Strategy (cont.)BUT: ADs can only pay Boston Chicken so long as Boston Chicken lends cash to ADs. Boston Chicken can only lend cash to ADs as long as it raises cash from capital markets. It can only raise cash from capital markets if its financial performance looks healthy.

How long can this go on if we can’t make money selling chicken?

Why does accounting make financial performance of Boston Chicken look healthy?

Quality Issues with Boston Chicken’s Earnings Two issues:

The poor performance of the franchised stores is not reflected in Boston Chicken’s earnings. This is an important issue, because Boston Chicken is bankrolling these stores.

A large portion of 1996 earnings came from the $38,163 ‘Gain on issuance of subsidiary’s stock’.

Earnings Restatement There are two ways to account for the poor performance of the franchised stores:

A ‘pro forma’ consolidation of the franchised stores’ operating results. From an economic perspective, Boston Chicken bears the risks and rewards of ownership of these stores. Note that because they provide financing in the form of debt, consolidation is not required by GAAP.

A provision for bad debts on the notes receivable. Since the franchised stores are losing money with no evidence of a turnaround, a generous allowance would seem appropriate – say 10% of new originations. This would be consistent with GAAP, but the absence of prior defaults gives Boston Chicken and the auditors leeway to book no provision for bad debts.

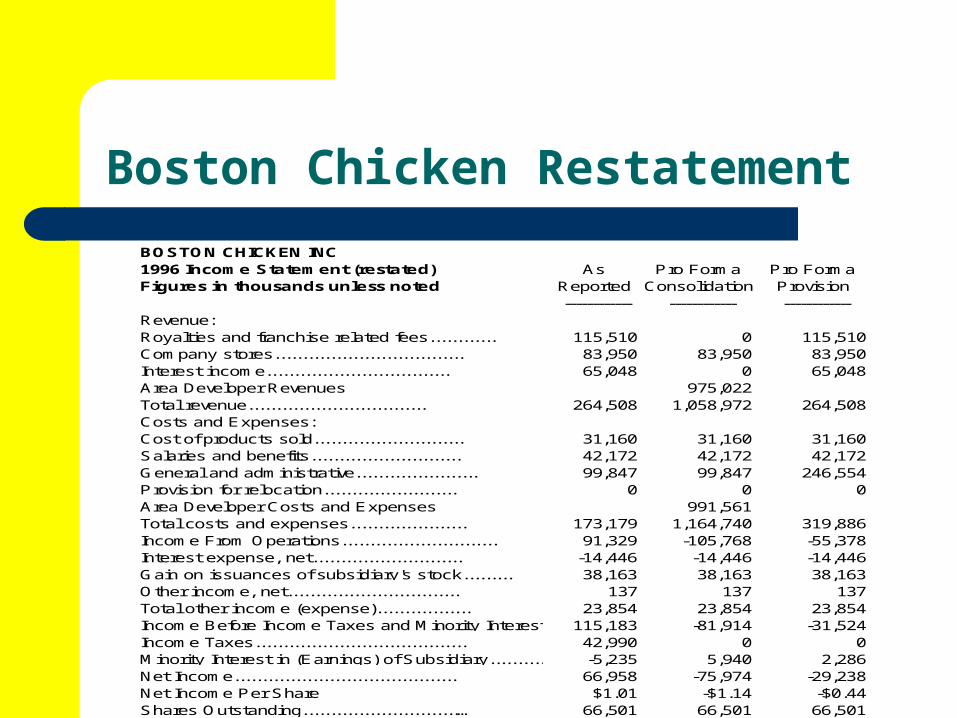

Boston Chicken RestatementBOSTON CHICKEN INC1996 Incom e Statem ent (restated) As Pro Form a Pro Form aFigures in thousands unless noted Reported Consolidation Provision

------------ ------------ ------------Revenue:Royalties and franchise related fees............ 115,510 0 115,510Com pany stores.................................. 83,950 83,950 83,950Interest incom e................................. 65,048 0 65,048Area Developer Revenues 975,022Total revenue................................ 264,508 1,058,972 264,508Costs and Expenses:Cost of products sold........................... 31,160 31,160 31,160Salaries and benefits........................... 42,172 42,172 42,172General and adm inistrative...................... 99,847 99,847 246,554Provision for relocation........................ 0 0 0Area Developer Costs and Expenses 991,561Total costs and expenses..................... 173,179 1,164,740 319,886Incom e From Operations............................ 91,329 -105,768 -55,378Interest expense, net........................... -14,446 -14,446 -14,446Gain on issuances of subsidiary's stock......... 38,163 38,163 38,163Other incom e, net............................... 137 137 137Total other incom e (expense)................. 23,854 23,854 23,854Incom e Before Incom e Taxes and M inority Interest..........................115,183 -81,914 -31,524Incom e Taxes...................................... 42,990 0 0M inority Interest in (Earnings) of Subsidiary..................................-5,235 5,940 2,286Net Incom e........................................ 66,958 -75,974 -29,238Net Incom e Per Share $1.01 -$1.14 -$0.44Shares Outstanding............................… 66,501 66,501 66,501

Pro Forma Consolidation ComputationsRestated Revenue = Reported Revenue + Revenue of Boston Market

Financed Area Developers + Revenue of ENBC Financed Area Developers – Revenue Received by Boston Chicken from Area Developers

= 264,508 + 865,082 + 109,940 – 115,510 – 65,048= 1,058,972Restated Costs and Expenses = Reported Costs and Expenses + Expenses of Boston

Market Financed Area Developers + Expenses of ENBC Financed Area Developers – Expenses Paid by Area Developers to Boston Chicken

= 173,179 + (865,082+156,505) + (109,940+40,592) –115,510 – 65,048

= 1,164,740

Pro Forma Consolidation Computations (continued)Restated Income Taxes

Income taxes are set to zero, as Boston Chicken is making pre-tax losses, and it is not reasonably certain that they will be able to offset the losses against future income.

Restated Minority InterestThis is recomputed by assuming that the minority stockholders have the same proportionate interest in pre-tax incomeas reported % interest = -5,235/(115,183-42,990) = -7.25%restated minority interest = -7.25% of -81,914 = 5,940

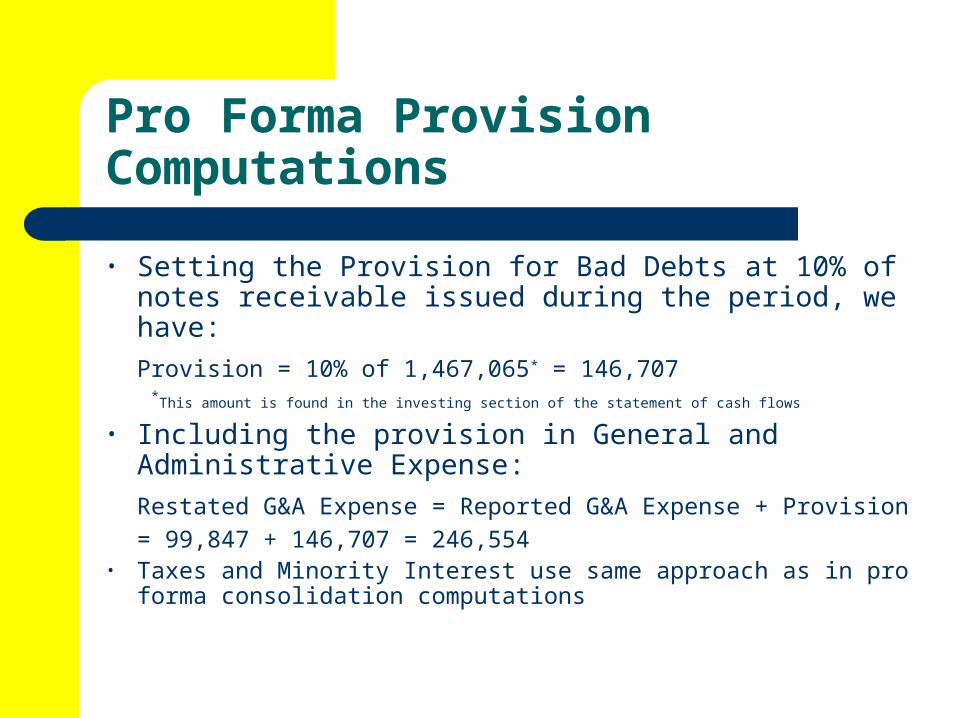

Pro Forma Provision Computations • Setting the Provision for Bad Debts at 10% of notes receivable issued during the period, we have:Provision = 10% of 1,467,065* = 146,707 *This amount is found in the investing section of the statement of cash flows

• Including the provision in General and Administrative Expense:Restated G&A Expense = Reported G&A Expense + Provision= 99,847 + 146,707 = 246,554

• Taxes and Minority Interest use same approach as in pro forma consolidation computations

Future Events That Will Cause Problems to Surface Capital markets recognize problems with business strategy and refuse to provide additional capital on favorable terms

Area developers will be forced to default if they receive no new loans from Boston Chicken

OR Boston Chicken will have to covert the area developer loans to equity and begin to consolidate their losses

Auditors recognize poor performance of area developers is likely to continue and require a provision to be charged against notes receivable

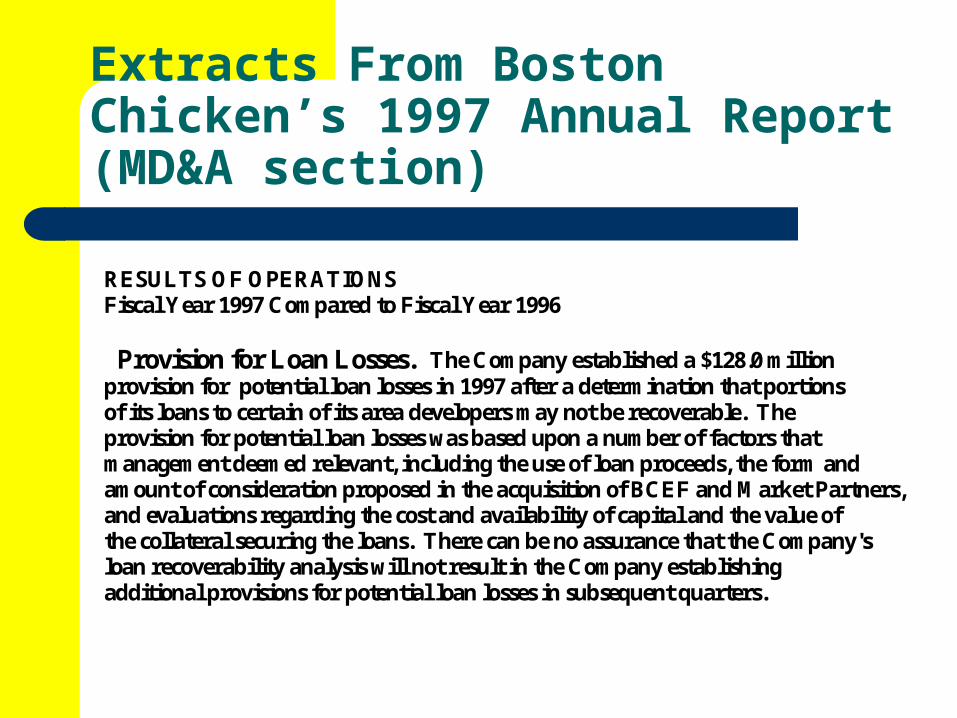

Extracts From Boston Chicken’s 1997 Annual Report (MD&A section)

RESULTS OF OPERATIONS Fiscal Year 1997 Com pared to Fiscal Year 1996 General and Adm inistrative. Included in general and adm inistrative expenses for 1997 were special charges of $120.0 m illion prim arily for asset write-downs and provisions associated with the Com pany's strategic redirection and the m oratorium on new store developm ent. Also included in general and adm inistrative expenses for 1997 were special charges of $15.5 m illion incurred by ENBC prim arily in connection with its transition to a com pany-owned system . Included in general and adm inistrative expenses for 1996 were special charges of $38.0 m illion for asset write-downs and a provision to purchase certain store equipm ent from Boston M arket area developers. Absent these item s, general and adm inistrative expenses increased $95.2 m illion or 154% for 1997 com pared to 1996. The increases in general and adm inistrative expenses, exclusive of the special charges, included $61.5 m illion associated with operating a larger Com pany store base and $23.0 m illion of greater depreciation and am ortization expense resulting prim arily from the acquisition of Com pany stores and ENBC's conversion to a com pany-owned system .

Extracts From Boston Chicken’s 1997 Annual Report (MD&A section)

RESULTS O F OPERATIONS Fiscal Year 1997 Com pared to Fiscal Year 1996 Provision for Loan Losses. The Com pany established a $128.0 m illion provision for potential loan losses in 1997 after a determ ination that portions of its loans to certain of its area developers m ay not be recoverable. The provision for potential loan losses was based upon a num ber of factors that m anagem ent deem ed relevant, including the use of loan proceeds, the form and am ount of consideration proposed in the acquisition of BCEF and M arket Partners, and evaluations regarding the cost and availability of capital and the value of the collateral securing the loans. There can be no assurance that the Com pany's loan recoverability analysis will not result in the Com pany establishing additional provisions for potential loan losses in subsequent quarters.

Extracts From Boston Chicken’s 1997 Annual Report (MD&A section)

RESULTS OF OPERATIONS Fiscal Year 1997 Com pared to Fiscal Year 1996 Losses of Boston Chicken, Inc.'s Area Developers. Since October 1997, the Com pany has recognized, in a single line item on its statem ent of operations, the net losses of the area developers in which BCEF and M arket Partners have preferred equity interests. Such losses, which aggregated $49.4 m illion, include $42.0 m illion of special charges and non-cash charges taken by these area developers, which prim arily relate to store closures. Such am ount represents the net losses (reduced by the am ount of royalties, franchise and related fees and interest not recognized by the Com pany) of the area developers com m encing from the date the Com pany announced its intent to acquire BCEF and M arket Partners in October 1997. The Com pany will continue to recognize the area developer net losses in a single line item on its statem ent of operations until it has acquired a m ajority equity interest in such area developers through conversion of its convertible loans to such area developers or other acquisition by the Com pany of such area developers. Upon acquisition of a m ajority equity interest in an area developer, the Com pany will then consolidate such area developer's results of operations in its financial statem ents.

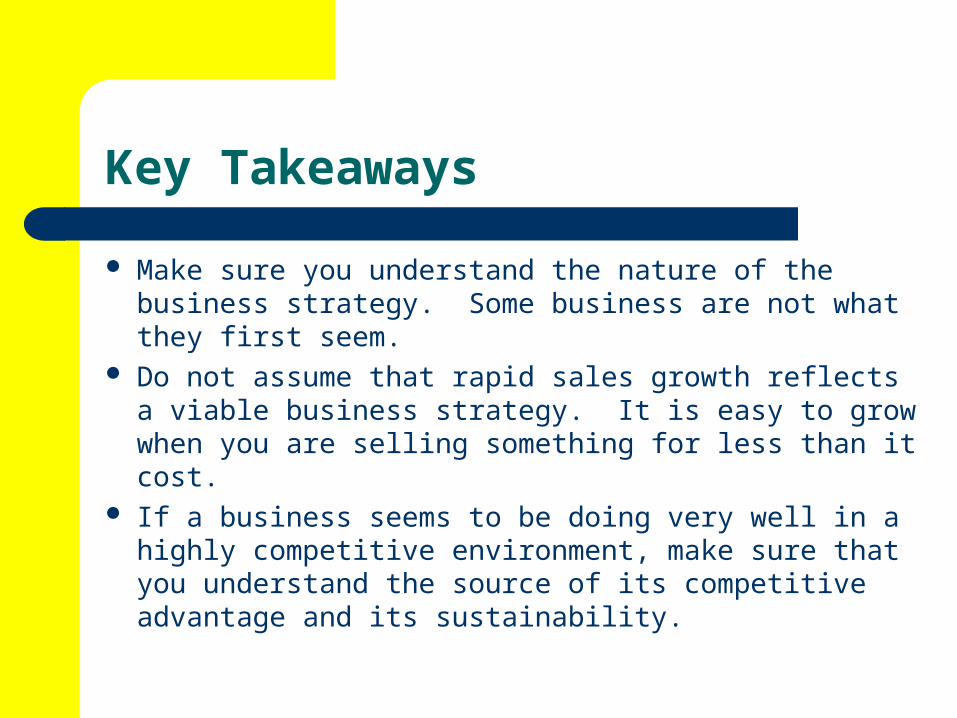

Key Takeaways Make sure you understand the nature of the business strategy. Some business are not what they first seem.

Do not assume that rapid sales growth reflects a viable business strategy. It is easy to grow when you are selling something for less than it cost.

If a business seems to be doing very well in a highly competitive environment, make sure that you understand the source of its competitive advantage and its sustainability.