bengaluru-jul-sep-2016.pdf - Magicbricks.com

56

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of bengaluru-jul-sep-2016.pdf - Magicbricks.com

FOREWORDMild tapering of inflation and a normal monsoon finally paved the way for lowering of REPO rate by 25 basis points, taking it to its lowest level in the last 5 years. The continued fall in both imports and exports, coupled with tepid investment demand has led RBI to pass on the cut. The Y-o-Y GDP growth rate also slowed down from 7.9% in the JFM quarter to 7.1% this quarter. The expected rise in oil prices from next year is also a major concern for the economy, which imports most of the oil it needs. High NPAs in the banking sector and construction delays in infrastructure and real estate also remain as major concerns.

However, the economy remains strong despite headwinds facing the world economy and geopolitical turmoil across Asia and Europe. The Manufacturing Purchasing Managers’ Index (PMI) is still above 52 level and GDP growth forecasts till 2020 by various multilateral agencies, remain above 7%. The lowering of Repo rate is expected to bring down both project finance as well as home loan costs, lowering the overall cost of buying a house.

The inevitable implementation of Real Estate Regulation and Development (RERA) Act, 2016 has led developers to hasten the delivery of their projects. This trend was clearly evident in the quarterly average prices data of Under Construction (UC) vs Ready-to-Move-in (RM) stock, where the premium commanded by RM properties came down due to increase in RM stock, as a portion of UC projects were delivered over the quarter.

RERA is a step in the right direction but will bear fruit only in 2-3 years, and till then the Indian real estate sector remains in turbulent waters, and its health can only be gauged through inferential means like pricing and inflation in the sector.

Price, as an end-product of interaction between the underlying demand and supply elements, incorporates all the sector related imperfections like delays and surge/dearth of transactions. Its trend also serves as a guidance to fiscal decision making by the government and RBI and investment decision making by private equity funds and retail home buyers.

Real estate in every city is heterogeneous and each locality and project can be mapped to different budget segments and geographies. Each budget segment and geography corresponds to a certain share of supply and consumer preference in the market.

Towards this end, Magicbricks presents a holistic price Index for each of the 14 major cities in India. The City Index reflects the price movement across localities, geographies and budget segments in the city. This bottom-up approach helps to identify factors affecting demand-supply dynamics of the city.

Analysis of City Indices over a 3-year period shows that Navi Mumbai had the highest gain of 18%, while New Delhi continued to face tough market with a 21% decline.

Regionally, Western India performed the best with 8.9% average gain, followed by South with 7.6% increment. North India saw an average decline of 7.4%, while Kolkata had the same average price as eleven quarters ago. It is important to note that any gains made are eroded when benchmarked against inflation in economy, in the study period.

Another important sign of our times is the 8% premium commanded by the Ready-to-Move-in (RM) properties over the Under Construction (UC) properties at a pan-India level. This ratio was at 5.1% eleven quarters ago and is a reflection of the falling consumer confidence in timely delivery of projects.

These are changing times and we would love to hear from you. Do write to us at [email protected] and share yours views on this report and how we could make PropIndex even better.

Sudhir Pai CEO, Magicbricks.com

METHODOLOGYRealistic price discovery has been the biggest problem area in the Indian real estate market. As consumers and industry struggle to arrive at a realistic benchmark pricing to assess the true value of their individual units, Magicbricks, as the largest repository of residential property listings, brings you the trusted Indian Apartment Price Index in a new and easy to use format. Mirroring the Indian Real Estate scenario, this price index presents an animated representation of the real estate market.

Magicbricks publishes the quarter-on-quarter inflation and deflation trends of the residential real estate prices in India. It collects real estate demand-supply data on a daily basis for more than 100 cities in India, of which, the fourteen top cities are selected for computing the National Property Price Index.

The National Property Price Index and its constituent indices are subjected to a series of stringent steps.

Each quarter, Magicbricks measures the individual property level price changes, which are then aggregated at the locality level. While comparing the average pricing figures for the current quarter and comparing with the previous one, quarterly price changes are calculated. These price changes are further aggregated at the city level and even further at an all-India level.

As the top receiver and aggregator of residential demand, Magicbricks’ data provides consumers with realistic benchmarks to the assess true property pricing. Where demand exceeds supply, consumers have no chance of negotiating values.

However, where demand is far lower than supply, buyers can look for more options and therefore, negotiate

pricing. If, on the other hand, you are a seller looking for benchmark pricing, you will effect the fastest sale if your asking values are close to the buyer’s paying power.

There are various co-relations of demand and the overall real estate market as well as its future potential. Not only is demand a preceding indicator to supply, it is also a fairly good indicator of actual transaction activity in the region.

We have aggregated the 14 cities covered under the report into various localities. While calculating the city level property pricing indicator, we have applied demand as weight to each locality. This weight is equal to the locality’s share of the demand being contributed to the city’s total demand. As a consequence, the locality receiving higher demand for residential units will be given a higher weightage. Following that, each city’s price movement is calculated by aggregating the price movements of individual localities, according to their individual weightages.

In terms of checks and balances towards making the data and analysis more robust and objective, we have made sure that superfluous information does not deviate the desired results. Hence, we have applied checks and balances at the locality level listing data collection and aggregation.

A statistical technique called “Inter-Quartile Range” (IQR) has been used to ensure that unintentional input deviations of house size and price figures, which may distort the actual value of the house and corrupt the analysis, are addressed. The technique aims to remove the outlier data sets, while securing the correct values.

The Interquartile Range technique works through measuring variability of each data set, while dividing the data set into quartiles. The technique measures the value of data points on the first and third quartiles of the data and calculates the difference between the two.

This range, called ‘IQR’, gives the effective extent of data set, while removing the first 25% and the last 25%. Subsequently, a test is applied to each of the values in the data set. If a particular data lies within an IQR of the first and third quartile values, then that data is considered part of the data set, otherwise not. The set of listing values of each locality are statistically cleaned.

Magicbricks, on an average, covers more than 500 localities for Tier-I cities of India. Yet for the sake of analysis, we take only those localities where the recipient demand is at least 0.05% of the city’s total demand. Only localities with at least 50 actively traded properties have been included in the analysis. Following that process, we shortlisted various localities which in some sense, impact the pricing dynamics of the city.

We then calculate the average prices of the city for the quarter, while applying demand weights to the average prices of each locality. These average prices at the city level are further aggregated to the final outcome of the ‘National Price Index’.

The difference in Under Construction and Ready-to-Move-in property has been assessed and included in the report. Rental yield and affordability too has been addressed for the top 10 localities by supply in every city. These are critical tools which well used can help with realistic price discovery.

GLOSSARY & DEFINITIONS1. City Property Index :This is a composite index which is a function of supply of properties as well as

the average capital appreciation/drop in various localities of the city in the quarter. The City Index is the weighted average of the average rate per square foot in that locality and the supply of properties from that locality. Localities with higher supply of properties will have a bigger impact on the Index.

2. Price trend basis budget segments: To better understand the city’s price trend, the localities have been divided into budget segments basis their capital value (Rs/sq ft). We have tracked the weighted average price for each budget segment for a 2+ year period from quarter ending September 2013 to quarter ending September 2016.

Subsequently, the movement of the localities in each price segment is mapped to derive respective short term and long term price change trends. The number of budget segments vary according to the city characteristics.

3. Zone wise distribution of localities: The various localities in the cities are all geographically divided into five key regions: Northern, Southern, Eastern, Western and Central. The localities are analyzed at the local zonal level to better understand the effect of the various drivers of price and demand, which are active mostly at the zonal level rather than at the city level.

4. Zone wise distribution of property budget segments: To better understand how each of the city zones contribute to the city’s supply, and how they are able to provide housing at various price points, the supply is distributed into budget segments across various geographic zones. For instance, if a zone has most of its supply in the premium budget segment, then it naturally becomes a premium destination within the city. The price changes within the various budget segments are also analyzed at the zonal level to go to the depths of the price changes across the city and to easily contribute the price changes to local factors.

5. Capital Value Tables (given in Annexures): This shows the actual range of prices within which properties are available in each locality in the quarter. Prices are shown in Rupees per square foot basis, these are the prevailing rates for properties in each locality.

6. Price trend – Top 10 localities by consumer preference: This section presents the price trend of the Top 10 localities in the city by consumer preference. These localities have the highest consumer focus and assessment of price trend in these localities assists in understanding the prevalent and future price trend in the city.

7. Price trend basis construction status: This Index looks at the movement in prices of Under Construction (UC) and Ready-to-Move-in (RM) properties across localities in the city. It is a weighted price index where weight is assigned to each locality basis its share in the consumer preference in the city.

What is the PropIndex?

The PropIndex gives you locality-wise property values in two forms – as locality price ranges for sale and rent in the annexure to every city with additional information on whether it has gone up or down in the quarter, and what is the rental yield in that locality. These prices are based on the listed prices of properties for sale or rent on the website www.magicbricks.com. This helps you to understand the average locality price ranges and to assess whether the price of the property for sale or rent that you are assessing, lies within the average price ranges in the locality. In a market where data or information is hard to come by, this data helps you to assess whether you are being quoted rational values for the property you are considering.

Why do I get locality sale and rent prices and how do I use them?

When you buy a property you must know what the average locality prices are. When you buy property directly from the developer, the price per sq ft is the value you pay. Then there are additional preferred location charges (PLC) such as vastu related, view related or floor related. When you buy from the secondary market or from an individual seller, the price is determined basis a notional value of the property. The sale values in the PropIndex help you to establish the price you should demand if you are a seller or what you should pay if you are a buyer. Rental values, similarly, are the average values that are listed on the website. They serve as benchmarks of the expected rental prices in the locality.

What is rental yield and why is it significant?

If you pay a certain price for a property, there is an amount you earn per annum as rent. When the rental income is expressed as a percentage of the property value, it is rental yield. It is a good yardstick to compute which property to select as a Buy to Let investment.

Why is it called a Property Index and not Property values?

Magicbricks has a very large number of listings. The number per locality depends on market conditions and how many consumers or brokers or developers choose to post their properties for sale or rent. When we are computing values at the locality or city levels we do not want any one locality to skew the index value of the city. As a result when any one or more localities have more than usual or less than usual number of listings, using the ratio of price to number of listings helps to even out unusual spikes or troughs in the data. This gives you unbiased city or locality averages.

How do I use an index number?

Magicbricks Index was computed first in 2011. The values in the year 2011 have been used as the base value and is assumed to be 100. When the value is below that

base number, the index is said to have fallen. When it is more than that number, the index is said to have gone up. This gives users like you, who are interested in property markets, an idea of how the property market in your city has performed vis-à-vis other cities. When the economic conditions are good and the builder is actively developing and the consumer is actively buying, the index value rises above 100. When markets are flat due to lack of economic activity and therefore developer and consumer disinterest, the index values remain at 100 or drop below that.

Very high index values shows a lot of investor activity and therefore severe peaking of property values. As an end user you should avoid buying when there is intense buying and speculative activity. That however, is a good time for you to sell as high property prices will give you good returns on your investment. When the index value comes down dramatically, the chances are that you will not get good returns as a seller. But if you find the property that you like in this cycle, it is a good time to negotiate the best values and buy as the chances are that there will be fewer buyers in the market. Since the PropIndex is now 5-years old, a look at how the index values have moved over the years gives you a good idea of how the market has performed in different quarters. If you are interested in how property markets have performed across a period of time, the PropIndex values give you a fair idea of the movement.

Do I get any specific Advice that helps my property decisions?

Magicbricks has a team of data scientists and researchers who are constantly studying the property markets and values to get the trends. In the past two quarters, for instance, they have noticed that ready-to-move-in property has been significantly more expensive than under construction property. This probably indicates that consumers do not want to buy property that is not complete and has chances of delayed delivery and prefer to spend more to buy property that they can purchase and move into. This is useful to you as a buyer and alerts you to general trends of other buyers.

What is the editorial and how is it useful to me?

The editorial team of Magicbricks constantly assesses the property market developments and factors such as infrastructure announcements and transport corridor development, to figure out how they can impact values of residential real estate in your city. In each edition of PropIndex they assess what all has happened in the quarter and how it will impact the value of the property that you are interested in. This analysis gives you an idea of the issues you should consider when buying property in that city.

How do I use the different sections of the PropIndex?

The key takeaways are useful in getting an overview of the property market in your city. The geographical distribution of localities allows you to assess in which areas property is available for sale. The distribution of properties by capital value allows you to freeze the price segment where you are likely to get the type of property you are looking for. The budget wise price change helps to compute how the price range that you are looking for has been performing. If values have been rising in your budget of interest you may have to hurry up with your property decision if you are an end user. If it has dropped, figure out if there is a problem in that category. This exercise has been done for each part of the city. The price trend by construction basis tells you which the best stage is at which you should enter the property market. The price changes basis construction status takes this analysis a step forward. Read it carefully and you will be able to assess exactly when you should enter the market as a buyer and as an investor.

What is the Corridor of Growth?

Magicbricks has figured that the bulk of new property in any city is developed along a few transport corridors leading out of the city. These have been identified and studied for stock, price rise, current status, future potential and its physical and social infrastructure such as water, power, sewerage and drainage facilities, transport links, schools, colleges, hospitals and entertainment centres in the vicinity. Advice has been given on the basis of rental and buyer’s demand, the best configurations to buy – 2, 3 and 4BHK, past and future estimated price trends and also how it figures in the master plan of the city. News updates of each corridor allows you to understand the drivers of those corridors.

HOW TO USE THE PROPINDEX

Jayashree Kurup, Head content

In line with general lack of activity in the residential market, the National Property Index remained stagnant at the same level

as in the last quarter, with prices falling by a marginal 0.12%. This is in continuation of the inactivity seen in the last many quarters.

NPI is the weighted average of consumer preference share of 14 cities and their individual City Index value.

On a quarterly level, South was the only region which inched up substantially in terms of prices from the last quarter while North fell the most. Although it cannot be said with certainty that prices have hit rock bottom and will not fall any further, any downward movement, going forward, will be restricted.

On a three year scale, Western India has done better than all other regions, with its cities having 8.9% price increment, on an average.

The worst performer was the North region, where prices fell by more than 7% in the last three years. The second best gains were witnessed in Southern India, where prices moved up by 7.6% over the same period.

In terms of historical price change, Navi Mumbai was the best performer with a significant 18% increment over the last three years, followed by Hyderabad and Pune, which had a 10% gain each. Thane stood fourth with a 9% gain, while Bengaluru and Ahmedabad had a 7% gain each. Next were Mumbai and Chennai with a 5% gain each.

Gains of lower than 5% were witnessed only in the North and Eastern regions, with Noida and Greater Noida showing the maximum gain in Delhi-NCR of just 4% each. Both, Gurgaon from Delhi-NCR and Kolkata from the Eastern region, had the same price in the Jul-Sep

2016 quarter, as three years ago. Only two of the top 14 cities considered for PropIndex saw a price decline in the last three years and both belonged to Delhi-NCR. While prices in Ghaziabad fell by 6%, New Delhi performed the worst, with a whopping 21% fall in prices.

In terms of quarterly change, Hyderabad performed the best with a 2.8% increase over the last quarter, followed by Bengaluru at 2.0% and Navi Mumbai at 1.2%. Overall, the Southern region was the best performer, with Chennai also giving a 0.7% price increment and standing fourth in the top 14 cities.

In terms of worst performers, four cities saw price drop, with the highest drop in Greater Noida of 1.7%, followed by Noida witnessing a drop of 1.2%. Mumbai and New Delhi were the other two cities noting a price drop, amounting to 0.8% and 0.7%, respectively.

VOL 6, ISSUE 2; JUL-SEP, FY 2016-17 propindex.magicbricks.com

[Jul-Sep 2016]

[Buyers looking for an exit]

The realty sector in India has been tepid for the past few years with low transaction volumes and stagnant price level. Weak

economic scenario, perceived high price level and lack of consumer confidence in the developers with respect to project completion led to transaction volumes reducing drastically.

Magicbricks research shows that consumers are willing to pay more for Ready-to-Move-in (RM) options as compared to under-construction (UC) properties. They’re willing to pay a premium on completed projects rather than expose themselves to delivery risk. Project delay leads to consumers having to bear additional financial burden of paying rent over and above applicable home loan instalments for an extended period. All this has made consumers wary of putting money in Under-Construction projects.

This is reflected in the price differential between Under Construction (UC) and Ready-to-Move-in (RM) properties. Magicbricks tracks the weighted average price for UC and RM properties on a pan-India basis covering 14 cities. It compares the 3 year trend from Sep 2013 to Sep 2016 where Sept 2013 has been taken as the base. It also shows the premium (discount) of RM properties over UC properties.

Our national level index for tracking prices of RM and UC properties shows that at a pan India level, RM properties command an average 8% premium over UC properties. This level of premium for RM properties has held for the last three quarters.

Analysis of actively traded properties on Magicbricks shows that when it comes to RM properties, an overwhelming number of options are in the resale segment. At a pan-

India level, 69% of RM properties are in the resale bracket while balance 31% are offers of fresh booking or ‘New Properties’. The graph gives the share of resale and new properties for each of the 14 cities analysed.

The predominance of resale options under RM properties category indicates that many buyers who had made purchase from an investment perspective are looking to exit their investment. With end-users looking for RM options to protect themselves from project completion risk, it is likely that many investors with RM properties see this as the best opportunity to liquidate their asset(s).

Most of the investors looking to exit at this point are unlikely to make any gains. In many cases, when the return is indexed to inflation, the return might actually be negative. This is because the prices have either been stagnant or have seen insignificant increment over the last few years. The following graph shows percentage change in the City Price Index for 14 cities from Sep 2013 to Sep 2016.

As is evident from the graph, the weighted average price across most cities has seen marginal increment over the last three years. In case of cities like Delhi and Ghaziabad, the price levels have declined. In all other cases, when the price increment is indexed to inflation, there is an implicit price decline.

Regional wise analysis of the ratio of ‘New’ and ‘Resale’ options under RM segment shows that

propindex.magicbricks.com VOL6, ISSUE 2; JUL-SEP, FY 2016-1702

markets which historically had high investor to end-user ratio have corresponding higher percentage of ‘Resale’ options in this segment.

Major North Indian markets like Gurgaon and Noida, which have seen large scale residential development, have 80% or higher ‘resale’ options in the RM segment. Similarly, all Western Indian cities have a high share of such options in the RM category. Opposite phenomenon was seen in case of all South Indian cities – Bengaluru, Chennai and Hyderabad. These markets have had high end-user participation and this reflects in the ratio of ‘New’ and ‘Resale’ options. Both these options have almost equal share in the RM segment in these cities.

These statistics also indicate that supply in markets with high ‘resale’ versus ‘new’ options in the RM category was in excess to demand at the given price points.

Market ImpactPresence of a large number of resale options puts pressure on the market in multiple ways:

l First, these resale options add to the unsold inventory available with developers, thereby exacerbating an already difficult scenario

l Large number of resale options in Ready-to-Move-in projects take the demand away

from Under-Construction projects. One set of inventory is getting sold multiple times while another set with the developers remains unsold. This is adding to delay in completion of projects as developers are not keen to complete projects where unsold inventory is on a higher side

l In the prevailing market scenario, large resale inventory also impacts the price level in a project as well as overall market. Price quote in the resale market is lower than the builder’s price and this impacts saleability of the unsold inventory with the developer. Further, the developer cannot increase the price and out-price his inventory vis-à-vis resale options

l New project launches also have to be sensitive to the prevailing price in the resale segment in their price segment

ConclusionIdeally, transaction activity in the resale segment gives depth to the primary segment. It allows investors to book profit and unlock their capital. However, in the present scenario where transaction activity is low and consumers are looking for Ready-to-Move-in options, the resale segment is likely to do better than the primary market and continue to put pressure on the primary market.

Given the large percentage of resale properties available in the market, this situation is likely to persist in short to medium term.

VOL6, ISSUE 2; JUL-SEP, FY 2016-17 propindex.magicbricks.com03

BENGALURU propindex.magicbricks.com VOL6, ISSUE 2; JUL-SEP, FY 2016-1704

[PROPINDEX - BENGALURU][Key Takeaways]

Maintaining real estate symmetry

Bengaluru market is trying hard to balance its real estate equilibrium. On one hand, the authorities are undertaking strict

measures to streamline practices. These include restriction on new construction projects, demolition drives, mandate for sewage plants, etc. On the other hand, easing out of STP norms, addition of new Karnataka cities, etc have till now maintained the balance.

The High Court told BBMP and BDA to not allow new construction projects near Bellandur Lake. This came into spotlight when some builders tried to flout rules by seeking consent for establishment without attaining approvals from civic agencies like BBMP, BMRDA and BDA.

In a similar transgression, NGT and state govt barred construction activity within 75 metres of the periphery of water bodies and also set

limits for buildings near feeder canals. The Karnataka’s Environment Impact Assessment Authority has put on hold the environmental clearance for 10 mega construction projects, including large residential projects, for alleged encroachment of lakes and drains.

This move might lead to an increase in property prices. According to some builders and consultants, project cost will go up by around 30% as developers will have to redesign the projects and also keep paying interest on bank loan. Further, builders will also pay govt charges for re-approval of their project plans.

On to the good spate of events, BWSSB relaxed STP norms and focussed buildings on larger sites. All sites measuring 21,527 sq ft housing flats or apartments and non-domestic buildings should have STPs. The water board came up

with STP norms following rap from pollution control board and courts over pollution of Bellandur and Varthur Lakes, both bearing the brunt of sewage inflow.

The state govt has revised the Karnataka Land Revenue Rules (1966) which regularizes constructions up to a distance of 18-km from the periphery of BBMP limits. Illegal constructions which have not followed rules can now pay Rs 10,000 for an illegal structure and get a ‘legal’ tag. The move was undertaken as demolition wasn’t a prudent option. The only issue was its timing - now or next year in the run up to the assembly polls. The government expects crores of rupees through this move.

Government policies are important in shaping the future of any sector. Hopefully, Bengaluru is on the right track.

Magicbricks Bureau

EDITORIAL

The City Index saw a rise of 2% over the last quarter. More localities saw price increase than price decline

In the Jul-Sep 2016 quarter 68% localities saw an average price increase of 3.2% while balance 38% localities saw 3.7% price decline

Price movement across all but one budget segment has been positive with price movement ranging from -1.1% in the Rs 3,000-4,000 per sq ft segment to 4.2% in the above Rs 9,000 per sq ft budget segment. This shows an overall gain in the Jul-Sep 2016 quarter

Positive price movement across the city was on account of price increment across all the major high

consumer preference localities like Whitefield, Sarjapur Road, Marathahalli and Bannerghatta Main Road

Eastern zone, which accounts for more than 40% share of consumer preference and supply in the secondary market, saw a marginal price increment of 0.7%. This zone consists of important localities like Whitefield and Sarjapur Road

The North zone, which is centred on Hebbal Junction, had a marginal increment. The South zone consisting of localities such as Electronic City also witnessed a marginal average price increment of 1.6% in the quarter

While West zone also saw marginal price increment, the overall level in the Central zone remained stagnant

Analysis across 94 localities in Bengaluru shows that on an average, RM properties were 4.9% more expensive than UC properties in the Jul-Sep 2016 period

The average difference in prices has increased from the Apr-Jun 2016 quarter. While the weighted average price of RM properties was Rs 5,266 per sq ft, the same for UC properties was Rs 5,020 per sqft

The average price of both RM and UC properties has increased over the last quarter by 1.1% and 1.8%, respectively

VOL6, ISSUE 2; JUL-SEP, FY 2016-17 propindex.magicbricks.com BENGALURU05

Properties distribution by capital value (Rs/sq ft)Apr-Jun 2016 to Jul-Sep 2016

This graph shows the distribution of actively traded properties by their capital values. Bengaluru is a price sensitive market with most of the supply (65%) in the Rs 3,000–5,000 per sq ft category

The higher mid-segment of Rs 5,000-6,000 per sq ft category comes second and has a healthy share of 28%. The premium and luxury segments in the Rs 6,000-9,000 per sq ft and above Rs 9,000 per sq ft form a small share

Price movement in the Bengaluru market is predominantly defined by the lower and mid budget segments. The geographical spread of budget segments show that East zone has more even spread of budget segments while in the South zone, the lower budget segments are seen to dominate

In the Northern part of Bengaluru city it was noted that properties were in the mid to higher budget segments.

The map shows the geographical spread of localities considered for calculating the City Price Index. These localities have been grouped together to understand the zone wise price trend in the city

With the exception of Whitefield, Bengaluru has grown radially along and off all the main arterial roads emanating from the city. Major growth axis includes Sarjapur Road in the East, Old Madras Road in the North-East, NH-7 and New Airport Road in the North, Tumkur Road in the North-West, Mysore Road in the South-West, Banerghatta Road in the South and Electronic City in the South-East along Hosur Road

Localities in the East zone shown on the map account for 50% share of consumer preference in the city. Whitefield and Sarjapur Road are the two leading localities in this zone

Geographical distribution of localitiesCity has grown in a radial manner

BENGALURU propindex.magicbricks.com VOL6, ISSUE 2; JUL-SEP, FY 2016-1706

The City Index for Bengaluru reflects the price movement across 94 prominent localities. These have been chosen using the twin criterion of share in overall consumer preference as well as share of actively traded properties. The weight

assigned to each is its share of consumer preference in the city. This makes for a comprehensive Index which covers localities with high consumer preference as well as high number of actively traded properties in the secondary market

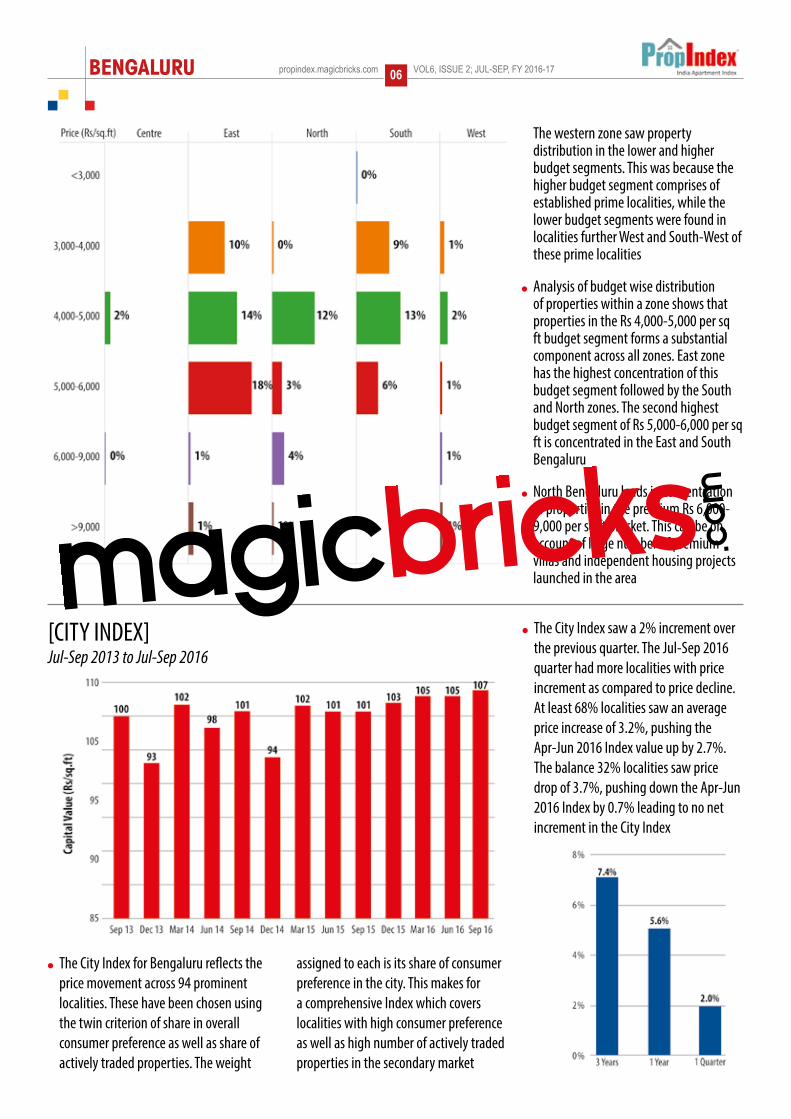

The City Index saw a 2% increment over the previous quarter. The Jul-Sep 2016 quarter had more localities with price increment as compared to price decline. At least 68% localities saw an average price increase of 3.2%, pushing the Apr-Jun 2016 Index value up by 2.7%. The balance 32% localities saw price drop of 3.7%, pushing down the Apr-Jun 2016 Index by 0.7% leading to no net increment in the City Index

The western zone saw property distribution in the lower and higher budget segments. This was because the higher budget segment comprises of established prime localities, while the lower budget segments were found in localities further West and South-West of these prime localities

Analysis of budget wise distribution of properties within a zone shows that properties in the Rs 4,000-5,000 per sq ft budget segment forms a substantial component across all zones. East zone has the highest concentration of this budget segment followed by the South and North zones. The second highest budget segment of Rs 5,000-6,000 per sq ft is concentrated in the East and South Bengaluru

North Bengaluru leads in concentration of properties in the premium Rs 6,000-9,000 per sq ft bracket. This can be on account of large number of premium villas and independent housing projects launched in the area

[CITY INDEX]Jul-Sep 2013 to Jul-Sep 2016

VOL6, ISSUE 2; JUL-SEP, FY 2016-17 propindex.magicbricks.com BENGALURU07

Budget wise price changeApr-Jun 2016 to Jul-Sep 2016

To understand the contribution of various budget segments and localities in the Index movement, we have grouped 94 localities under the Index, into budget segments on the basis of their capital values. A further micro picture of price movement is presented by looking at price change across different geographies and their constituent budget segments

Price movement across all but one budget segment has been positive with price movement ranging from -1.1% in Rs 3,000-4,000 per sq ft segment to 4.2% in the above Rs 9,000 per sq ft budget segment. This shows that Bengaluru overall gained in prices in the Jul-Sep 2016 quarter

The price trend in a given budget segment was more or less mirrored across different geographical zones

Price movement across zones:

South Price increment was witnessed across all

budget segments in the zone

The highest price increment was in the less than Rs 3,000 per sq ft segment with 5% increase. This was followed by 2.3% increment in the Rs 5,000-6,000 per sq ft and 1.5% increment in the Rs 3,000-4,000 per sq ft price brackets

High consumer preference localities across different budget segments such as Electronic City and Bannerghatta Road saw price increment

East There was a price increment in four out of

the five budget segments in the zone

In the largest budget segment in the zone by share of supply (Rs 5,000-6,000 per sq ft), there was a price increment of 1.8%. This was on account of price increment noted in high demand localities like Whitefield

The next highest supply segment of Rs 4,000-5,000 per sq ft also saw a marginal gain of 1.6%. Prominent

Geographic and budget wise price changeApr-Jun 2016 to Jul-Sep 2016

BENGALURU propindex.magicbricks.com VOL6, ISSUE 2; JUL-SEP, FY 2016-1708

localities like Sarjapur Road and Varthur in this segment saw price increment

The premium segment witnessed the highest movement. Both Koramangala and Indiranagar in the Rs 6,000-9,000 per sq ft bracket saw increment

North Of the five budget segments present in

North Bengaluru, three saw price rise

Most localities in the important Rs 4,000-5,000 per sq ft segment saw a price increase leading to overall 1.6% rise in this budget segment. Next highest supply segment of Rs 6,000-9,000 per sq ft saw a price decline of 1.9% as important localities like Sanjay Nagar and Yashwantpur saw a price decline

Another prominent locality in the zone, Hebbal, saw a price increment of 2.5% in this quarter

Centre Localities in the Central zone saw price

increment across all prominent budget segments

Price change – Top localities by consumer preferenceApr-Jun 2016 to Jul-Sep 2016

Price trend basis construction statusJul-Sep 2013 to Jul-Sep 2016

VOL6, ISSUE 2; JUL-SEP, FY 2016-17 propindex.magicbricks.com BENGALURU09

Price change basis construction status Top localities by consumer preference in Jul-Sep 2016 period

The graph shows the trend in the prices of ‘Ready-to-Move-in’ properties (RM) and Under Construction (UC) properties. Analysis across 94 localities in Bengaluru shows that on an average, RM properties were 4.9% more expensive than UC properties in the Jul-Sep 2016 period

The average difference in prices has increased from the Apr-Jun 2016 quarter. While the weighted average price of RM

properties was Rs 5,266 per sq ft, the average price for UC properties was Rs 5,020 per sq ft

The average price of both RM and UC properties has increased over the last quarter by 1.1% and 1.8%, respectively

In terms of price increase, Under Construction properties posted a price increment of 11% over the Sep 2013

to Sep 2016 period, while the price of Ready-to-Move-in properties declined by 1%. The price decline in case of RM properties decreased due to slight price increase over the last quarter

As the graph below shows, the price of both RM and UC properties has increased in the Jul-Sep 2016 quarter across most of the top 10 localities by consumer preference in the zone

BENGALURU propindex.magicbricks.com VOL6, ISSUE 2; JUL-SEP, FY 2016-1710

Capital values

Banashankari 4274-6863 12000-19000 3.3%Banaswadi 3434-5723 13000-20000 4.3%Bannerghatta Main Road 3464-5949 12000-20000 4.00%Basaveshvara Nagar 8698-15632 12000-19000 1.4%Bellandur 4365-7104 15000-22000 4.2%Bommanahalli 3341-4790 12000-20000 4.6%Brookefield 4327-6601 14000-21000 4.1%BTM Layout 3799-6652 14000-21000 3.8%BTM Layout Stage 2 3893-6985 15000-21000 3.8%C V Raman Nagar 3376-6358 13000-20000 4.6%Electronic City 2810-4937 10000-17000 4.3%Electronic City Phase 1 3309-5491 11000-17000 4.2%Electronic City Phase 2 2573-4298 9000-15000 4.00%Frazer Town 5750-9953 18000-26000 3.2%Hebbal 4509-7819 12000-20000 3.1%Hennur Main Road 4188-6516 12000-21000 3.8%Hoodi 3197-5250 13000-20000 4.4%Horamavu 3197-5270 11000-16000 4.1%HRBR Layout 7540-13146 13000-24000 2.1%Indira Nagar 5058-9595 18000-30000 4.4%ITPL 3829-6306 13000-21000 4.1%Jayanagar 5476-9753 16000-25000 3.3%JP Nagar 3679-6592 13000-21000 3.9%JP Nagar Phase 7 3602-6858 14000-21000 4.2%K R Puram 3125-5176 11000-17000 4.1%Kadugodi 3494-5080 10000-16000 3.8%Kaggadasapura 3194-4908 12000-18000 4.5%Kanakapura Road 3760-6183 9000-15000 2.9%Kasavanahalli 3717-5917 14000-21000 4.2%Kasturi Nagar 7174-11301 14000-22000 2.2%Koramangala 6860-11457 19000-31000 3.3%Kundalahalli 3854-6156 14000-21000 4.5%Mahadevapura 3654-6116 14000-22000 4.6%Malleshwaram 9809-13807 20000-31000 2.7%Marathahalli 4002-6704 15000-23000 4.2%Marathahalli-Sarjapur ORR 5396-7353 17000-24000 4.00%Old Airport Road 4838-8542 16000-26000 4.00%Panathur 3952-5874 13000-20000 4.5%Rajaji Nagar 9007-14526 19000-34000 2.6%Rajarajeshwari Nagar 3219-5149 10000-14000 3.6%Ramamurthy Nagar 3217-5023 11000-16000 4.4%RT Nagar 3681-6396 11000-18000 3.5%Sahakara Nagar 4351-7091 11000-18000 3.2%Sanjay Nagar 4476-8069 13000-21000 3.7%Sarjapur Road 4026-6875 15000-24000 4.4%Thanisandra 3961-6031 11000-18000 3.5%Varthur 3209-5351 12000-18000 4.5%Vidyaranyapura 2859-4676 9000-14000 3.8%Whitefield 3677-6259 13000-21000 4.2%Yelahanka 3672-5662 10000-16000 3.1%Yeshwantpur 5500-8345 15000-24000 3.2%

LOCALITY CAPITAL RENTAL YIELD

Corridor Description and RatingAreas Included: Electronics City, Hosur Road, Huskur, Chandapura, Bommasandra, Kudlu, Bommanahalli and Hosa Road

Fig 1: Map of the corridor

E L E C T R O N I C C I T Y

Corridor of growth (COG)13

Properties available in the corridor

The corridor offers a wide range of properties with majority of them in the Rs 20-40 lakh price segment.

Considering the corridor has a high population of employees working in the IT/ITES sector,

the demand is highest (63%) for 2BHK units. Interestingly Fig 3 shows that 53% of the property in this corridor is ready-to-move-in. This means it is a buyer’s market as many developers would be ready to dispose the

ready-to-move-in inventory. The corridor has an almost uniform rate throughout until Electronics City but a few premium apartments close to Central Silk Board are quoting upwards of Rs 1 crore for a 2BHK unit.

About the Corridor

Electronics City Corridor, located in South Bengaluru, is the largest electronics park in India spread across an area of 350 acre

in Anekal Taluk. Unlike other corridors which are radial, this is a linear growth corridor with residential and commercial hubs on either side of Hosur Road.

Currently the corridor is connected to rest of Bengaluru through the 4-lane tolled elevated expressway opened in 2010 from Madivala (Central Silk Board) to Electronics City and the BMIC-NICE Corridor which connects Electronics City to Bannerghatta Road, Kanakapura Road, Mysore Road and Tumkur Road. The corridor can also be accessed from the Sarjapur Road Corridor through the Outer Ring Road (ORR) or Haralur Road which connects at Jail Road (Naganathapura) or through the SH-35, also known as Sarjapur-Attibele Road.

As part of Metro Phase-II a new line will be added to the existing green line which will connect from Jayadeva Hospital Junction to Bommasandra. This will cover most of the areas on the Electronics City Corridor and as

per current estimates should be completed by 2020. Heavy traffic logging on the Central Silk Board Circle has now prompted the authorities to also include this corridor as part of the Phase-III Metro work and RITES (a design consultancy firm) has been entrusted the work to conduct feasibility studies to link the metro through this corridor to connect to North Bengaluru. The Central Silk Board to Hebbal Line will be parallel to the ORR and cover areas such as Sarjapur Road, Marathahalli and Mahadevpura.

The proposed PRR which starts from Hosur Road, an 8-lane expressway, will provide an arterial connection to Tumkur Road and will allow heavy traffic coming from Mumbai, Pune, Chennai etc to bypass the city.

The proposed Neo Mall and the Hiranandani Mall are currently progressing at a slow pace. Although the area has a floating population of almost 1.5 lakh professionals, the social infrastructure is yet to catch up as residential communities have just started functioning in most parts of the corridor. Unlike other

corridors that are mostly under BBMP jurisdiction, here different parts of the corridor are under different authorities such as BBMP, Gram Panchayats, ELCITA and BMRDA-Anekal Planning Authority.

Although the area boasts of a good expressway and a NICE corridor to connect to the rest of Bengaluru, Central Silk Board which is the most nodal point connecting this corridor to the Peripheral Business District (PBD) and the Central Business District (CBD), still faces lot of traffic congestion throughout the day.

This has been a key factor for investors holding back from investing in this corridor. Social infrastructure is yet to catch up as well as there are no good malls or shopping centers in this corridor currently. Problems with maintenance of the localities are attributed to the fact that most of them are under the ambit of the Gram Panchayats which are not well equipped to handle the issues of large communities coming up in this corridor.

Overall Connectivity Social Infrastructure Security/Water

Fig 2: Distribution of properties by price Fig 3: Distribution of properties by delivery status Fig 4: Distribution of properties by bedroom configuration

Corridor of growth (COG)14

Within the corridor, the locality with the highest rental demand is surrounding Electronics City. The area

has the highest demand of about 46% as it is close to work locations such as the Electronics

City Phase-I, Velankanni Tech Park, Infosys and Wipro campus. Hosa Road commands the highest rental, as of now, with an average rental value of Rs 24,000 per month for a 2BHK house.

Electronics City Corridor has almost constant average rental yields in all localities, which is around 4%. As one moves away from the corridor towards Hosur, property prices and rental demand starts reducing.

As explained, prices in the corridor move north as one moves towards the Central Silk Board. So an investor will get better value for money in areas beyond Chandapura where prices are affordable and developers are offering good area for the money invested. Typically Rs 40 lakh which will buy a 1BHK unit near the start of Hosur Road will be able to buy a 2BHK unit

closer to Bommasandra or Chandapura. As one moves south of Attibele, it is observed that the floor area/built-up area of apartments are larger and there are 2BHK units with super built-up area of even 1600 sq ft. The corridor is affordable as one moves to interior areas such as Iggalur on Chandapura-Anekal Road where a 1BHK unit costs about Rs 14 lakh.

Sales Price Covered Area ( Lacs) (Sq.ft)

1 BHK 13-98 500-1000

2 BHK 13-200 500-1977

3 BHK 17-300 650-3800

4 BHK and Above 52-226 1872-3735

Best sectors to invest in a home Based on rental demand in sectors

Table 1: Sizes and prices of flats available for various room configurations

Based on home buying demand in sectors

Fig 5: Top 10 localities by consumer for renting a house

Fig 6: Top 10 localities by consumer for buying a house

Best bedroom configurations to buy Preferred buying and renting options

Buying Renting Total (BHKs) Total (BHKs)

1 BHK 3% 2%

2 BHK 48% 52%

3 BHK 47% 43%

4 BHK and Above 2% 3%

Table 2: Demand distribution for buying and renting

In the case of demand for home buying, Electronics City has the highest share. The next highest demand is in Electronics

City Phase-1. Most of the people working in Electronics City prefer to stay here

and it is also a sought-after location by investors who can expect good rental returns of 4-5%. Bommanahalli which is close to both Electronics City as well as Sarjapur Road Corridor through the HSR

Layout and to Bannerghatta Road through Devarachikkanahalli commands the highest price. Since it is close to Central Silk Board and is located before the elevated expressway there is good demand from people.

It is observed from the given tables that for rent 2BHK apartments are the most preferred. The buying is also prefrerred

for 2BHK segment. According to the table, 48% consumers are preferring to buy 2BHK category as the demnd is high there. From a sale perspective, both 2 and 3BHK units have the same demand in this corridor. About 52%

people looking to rent are considering 2BHK units. In fact, the 3BHK units are the second most preferered localities in the corridor. Here, 47% people prefer 3BHK segment currently. The demand for ultra-luxury apartments and villas above 4BHK is only about 2-3% for renting and buying.

Price changes and future prospects Historic Price movement

6 monthly change Yearly change

6% 14%

Table 3: Historical Price changes

Electronic City has seen that property prices have risen over the last one year at a steady rate. It is also one of the few

corridors that have actually seen a price rise over the last one year in Bengaluru. It is also seen that price rise has been higher in areas closer to Central Silk board where new projects have been launched in the affordable and mid segment budget category.

The trend is in confirmation to what has been seen in other areas of Bengaluru as well where prices have remained stagnant in the luxury and premium segment and the mid segment has seen highest consumer demand as well as price appreciation. Most of the people looking for property in these areas are typically employees in the IT/ITES companies in this corridor and are keener to purchase 2-3 BHKs in the mid segment price range

Fig 7: Historical Price changes of corridor

Corridor of growth (COG)15

Corridor Average Price Rs/sqft

Price movement for top localities by Consumer Preference

The last quarter has witnessed the prices moving up for three of the five localities with high consumer demand. Bommanahalli and Electronic City which have seen maximum number of new launches

in the locality has also seen a steady appreciation of greater than 4% in the last quarter. Also over the last quarter about 1600+ units were completed and ready for possession in this corridor which has contributed to the increase in the price.

Although significant number of top localities witnessed price increases this quarter, this has been against the continual drop in the average prices of localities in the last two years and the current rise in prices does not follow a long term trend.

Fig 8: Price changes in top localities by consumer demand

Master Plan

It is observed that large tracts of the corridor are designated for industrial and high technology segments. Closer to Central Silk Board, on either

side of Hosur Road there are large areas earmarked for residential and mixed residential use. The corridor is guided by three different planning agencies such as ELCITA (Electronics City Industrial Township Association), BBMP and BMRDA - Anekal. In South Bengaluru, the corridor has acute water shortage, but projects such as KSWN (Karnataka State Water Network) in partnership with IT companies in the vicinity aiming at de-sludging the lakes in Doddathoguru and efficient ground water management have shown good results.

Fig 9: Land use of various localities in the corridor

Corridor of growth (COG)16

Infrastructure Updatesl As part of Metro Phase-II, a new line will

be added to the existing green line which will connect Jayadeva Hospital Junction to Bommasandra. This will cover most of the areas on the Electronics City Corridor and as per current estimates should be completed by 2020. Heavy traffic logging on the Central Silk Board Circle has now prompted the authorities to include this corridor also as part of the Phase-III Metro work and RITES (a design consultancy firm) has been entrusted the work to conduct feasibility studies to link the metro through this corridor to connect to North Bengaluru. The Central Silk Board to Hebbal Line will be parallel to the ORR and cover areas such as Sarjapur Road, Marathahalli and Mahadevpura

l The 8-lane PRR - Peripheral Ring Road - connects Hosur Road to Tumkur Road and passes through the Old Madras Road, KR Puram and Bellary Road. This will provide seamless connectivity and allow vehicles from plying to Mumbai, Pune etc from Chennai and South Tamil Nadu to byepass the city.

A recent visit to the corridor revealed that there is a lot of activity happening in terms of residential spaces coming up. Electronics City has traditionally been an area with a high concentration of office spaces. So, most people working there prefer to stay in BTM Layout, Begur Road and other localities in the Bannerghatta Road Corridor although these areas are far from Electronics City. Central Silk Board continues to be a major traffic bottleneck

and all plans to ease traffic at this junction have proved futile. Other than Hosur Main Road, other roads are not well maintained as the three agenices responsible for maintaining the roads are always at loggerheads with each other.

There are a few malls which have been in the construction stage for a long time but the progress has been very slow and there is no sign of completion in the next 3-4 years. Water scarcity has been a major problem in this corridor and there are many apartment complexes that are ready-to-move-in but people are not occupying as the monthly maintenance charges are very high, considering that most of them are serviced only by tanker supplied water.

Why you should invest on Hosur Road?

Hosur Road, one of the main roads in Bengaluru, is known for its connectivity within the city, to the established suburbs and also to the other cities in Tamil Nadu. Several factors make this location a highly active area for realestate development and investment. One of the primary reasons to live in Hosur Road is its emergence as the centre for residential, commercial and retail establishments. Living in proximity to the retail spaces such as hyper-markets, malls and convenience stores, has been constantly garnering attention of buyers. The demand for housing is growing in Hosur Road and buyers are getting healthy returns. It might be a good time to invest in the area to earn good returns and enjoy a high-end lifestyle.

n Source: Magicbricks Bureau

Cyient sets up SMEC’s global design center in Bengaluru

Cyient has announced that it has inaugurated a new global design center at Cyient’s Electronic City campus in Bangalore for an Australian consultancy firm, SMEC. It is an IT firm already operating in the city. The center will commence operations from July 2016. The facility that is built and operated by Cyient is SMEC’s first offshore design center. The centre will support SMEC’s global design work primarily around civil and structural, including building information modelling (BIM). SMEC caters to varied sectors including transport, energy, water, environment, health, education, and government advisory.

n Source: The Times of India

Bengaluru demands more apartments

Electronic City is a fast emerging locality in Bengaluru. In fact, it is preferred by the home buyers immensely. The area has majority of young buyers looking for investible options. Whitefield, Sarjapur Road, Bannerghatta Road, Rajarajeshwari Nagar, KR Puram, Marathahalli and Kanakapura Road are some of the other preferred choices among city buyers. But, the home buyers are showing keen interests for investing in the locality. Further, the reason for growth in demand in the electronic city is enhanced metro network and improving social infrastructure such as there are schools, restaurants, and other basic amenities.

n Source: Magicbricks Bureau

Hosur Road - An emerging retail hub

The primary driver for the emergence of Hosur Road as a commercial, residential and retail centre is its efficient connectivity to Electronics City as well as established suburbs of the city. Hosur Road connects the Outer Ring Road (ORR) to the NICE Ring Road, which provides easy connectivity to other IT hubs, such as Whitefield, and also to the airport. Hosur Road, one of the first IT belts in the city, has, over time, turned into one such micro-market with retail growth pacing up to match the requirements of the people. Moreover, the area has sufficient land at competitive rates, civic infrastructure and favourable government initiatives.

n Source: The Times of India

IN NEWS

Corridor of growth (COG)17

Corridor Description and RatingAreas Included: Bannerghatta Road, Gottigere, Jigani, Hulimavu, Koppa, Begur, Begur-Koppa Road, Kalkere, Kothnur and JP Nagar 9th Phase

Fig 1: Map of the corridor

B A N N E R G H AT TA R O A D

Corridor of growth (COG)19

Properties available in the corridor

The corridor offers a wide range of properties in price segments from affordable to premium. Although 40%

properties fall in the category of Rs 40-60 lakh, almost 44% properties in the corridor are in

the premium and luxury segments. This is due to the fact that most of the people buying property in this corridor are those who want to stay close to the CBD areas but want properties at more affordable prices than CBD prices. Fig 4

shows that 52% properties in the corridor are 2BHK units and 43% are 3BHK units. Most of the available supply in this corridor is catering to both these segments. Interestingly Fig 3 shows that 60% of the property in this corridor

About the Corridor

Bannerghatta Road, which extends from Jayadeva Hospital Circle to Bannerghatta National Park is located

in South Bengaluru. This is a completely residential corridor that has a lot of demand from residents looking to live close to Central Bengaluru. A linear corridor which stretches for a length of about 28-km and has localities on both sides of the Bannerghatta Road. It is close to some of the costliest residential areas in Bengaluru such as Jayanagar, JP Nagar and BTM Layout.

The corridor witnessed an influx of people wanting to reside here during the initial IT boom in the city. The area had a good talent pool as many engineering colleges are in and around this corridor and that led to concentration of IT firms here. Most of the big IT companies have had their first offices on this road and many of them continue to hold onto these smaller spaces even though they have large office spaces in other corridors of Bengaluru. Currently the corridor is in demand as it has a well-developed social infrastructure

and is close to work locations on Sarjapur Road, Hosur Road and Electronics City.

The corridor is well connected to rest of Bengaluru by the Bannerghatta Road which connects to the CBD. The NICE Road connects the corridor to Tumkur Road, Mysore Road, Kanakapura Road and Hosur Road. The corridor is strategically located between the Hosur Road on the east and Kanakapura Road on the west, thus, providing best access to both these roads for people living here.

The corridor has the widest range of properties available in terms of affordable plots as one moves towards Jigani and Koppa to high-end ultra-luxury apartments close to JP Nagar and Jayanagar near Bannerghatta Road.

Currently the road is not covered in the Namma Metro network, but the red line that will be added soon will connect Gottigere to Nagawara. This is a 21.25-km long line that passes through Bannerghatta Main Road all the way until the Jayadeva Hospital. The project has been delayed as there is some

realignment in process. The corridor is close to the existing green metro line which passes through Puttenahalli.

The corridor has equal supply of 2 and 3BHK formats and a supply which matches the demand. There are a few luxury villa projects as one moves towards Jigani but the demand is generally low for luxury villas. Luxury and ultra-premium 3 and 4BHK units have good demand at the start of the corridor close to the IT offices and near BTM Layout and JP Nagar.

Bannerghatta Road on the corridor has the highest traffic density during peak hours and since there is no other parallel road, this is a major bottleneck. Since most of the development was during the IT boom and was done hastily, the infrastructure has not kept pace and most approach roads are narrow and choked at many intersections. Although there are large forest areas towards the Bannerghatta National Park, the road is mostly devoid of green spaces in all other areas.

Overall Connectivity Social Infrastructure Security/Water

Fig 2: Distribution of properties by price Fig 3: Distribution of properties by delivery status Fig 4: Distribution of properties by bedroom configuration

Corridor of growth (COG)20

Within the corridor, the locality with the highest rental demand is on the Bannerghatta Main Road. Overall

this is the most sought-after destination with almost 70% demand for rental

accommodation. Rental yield shows the amount of rent that can be generated from a property in a year in terms of sale price. Bannerghatta Road Corridor has an average rental yield ranging from 3-4% in all localities.

From the graph, it is evident that properties closer to Begur, Hosur Road and Gottigere, which is nearby to NICE Road, command better rental yields.

is in the ready-to-move-in category. In fact, many developers would be ready to dispose the ready-to-move-in inventory at the earliest.

As explained above prices in the corridor move north as one moves towards the CBD. So an investor will get better value for money at areas beyond Gottigere where prices are much more affordable and developers are offering

good area for the money invested. So, typically Rs 40 lakh which will buy a 1BHK unit near the start of Bannerghatta Road will be able to buy a 2BHK unit closer to Jigani. As one moves south of Kalkere, it is observed that the floor area/built-up area of apartments is larger and there are 2BHK units with super built-up area of even 1600 sq ft.

Sales Price Covered Area ( Lacs) (Sq.ft)

1 BHK 12-48 515-1000

2 BHK 17-200 600-2760

3 BHK 24-350 900-4185

4BHK and Above 51-475 1815-5000

Best sectors to invest in a home Based on rental demand in sectors

Table 1: Sizes and prices of flats available for various room configurations

Based on home buying demand in sectors

Fig 5: Top 10 localities by consumer for renting a house

Fig 6: Top 10 localities by consumer for buying a house

Best bedroom configurations to buy Preferred buying and renting options

Buying Renting Total (BHKs) Total (BHKs)

1 BHK 3% 2%

2 BHK 48% 52%

3 BHK 47% 43%

4 and Above 2% 3%

Table 2: Demand distribution for buying and renting

In the case of demand for home buying, Bannerghatta Main Road has the highest share. The next highest demand is in Begur

Road which provides good connectivity to Electronics City. People working in this area

prefer to stay here as it is very close and also has an alternate link road to Electronics City. In Bannerghatta Main Road, 2BHK properties fetch good rental returns and have limited availability. The road also has better water

facility as compared to other corridors. Most parts of the road are serviced by BWSSB (Bangalore Water and Sewerage Supply Board) and in other areas the ground water level is not too below the ground level.

It is observed from the given tables that for rent 2BHK apartments are the most preferred, but from a buy perspective, both 2

and 3BHK units have the same demand in this corridor. About 48% of the people looking to buy and 52% looking to rent are considering 2BHK units. Moreover, the demand for rent in the 2BHK segment is more than 3BHK

category. About 61% of the consumers are interested in the 2BHK units for rent and the 3BHK demand distribution for rent is 34%. The demand for ultra-luxury apartments and villas above 4BHK is only about 2-3% for buying and renting. The home buyers are preferring to buy and rent in this corridor.

Price changes and future prospects Historic Price movement

6 monthly change Yearly change

3% 6%

Table 3: Historical Price changes

Bannerghatta Main road corridor has seen an average appreciation over the last one year. It is observed property prices have

been stable in the first half of 2015 and that prices have appreciated after the 2nd quarter mainly due to the launch of two large multi storey apartment projects by Tier 1 developers in the corridor.

Overall the corridor has seen a price rise of 6% over the last one year. The demand is mostly by employees in the IT/ITES companies working in the Electronic City corridor who prefer to live in and around this corridor which has good social infrastructure.

Fig 7: Historical Price changes of corridor

Corridor of growth (COG)21

Corridor Average Price Rs/sqft

Price movement for top localities by Consumer Preference

The last quarter has witnessed the prices moving up for three out of the top localities by consumer demand. Areas such as Hulimavu and Bannerghatta, which have significant consumer interest has seen

that the prices have increased by 3-6%. In Hulimavu the price change is mainly due to a new project launched here with about 900 units in the mid segment budget and in Bannerghatta which is close to the Koppa gate and Jigani, due to a constant demand for affordable plots approved under the Anekal planning authority.

Begur and Gottigere are other two areas where a large number of properties are ready for possession and lot of investor units are up for sale. This has dragged down the prices although there is still significant consumer demand in these localities.Fig 8: Price changes in top localities by consumer demand

Master Plan

It is observed that large tracts of the corridor are designated as primary residential areas. Both sides of Bannerghatta Road has areas

earmarked for commercial development due to which prices are high on this road. Beyond Gottigere, where the NICE corridor intersects the Bannerghatta Main Road, vast areas are marked for forest and a green belt region. There are no large areas earmaked for High tech or other industrial areas. Due to this the area has seen most of the initial IT/ITES companies that setup offices here, moving to other corridors such as Electronics City and Sarjapur Road. These have large SEZ and high tech industrial areas which provide better sops to companies than operating from independent office spaces.

Fig 9: Land use of various localities in the corridor

Corridor of growth (COG)22

Infrastructure Updatesl As part of Metro Phase II, the Nagawara-

Gottigere line will link metro to this corridor. The work on this stretch has slowed down as there is some realignment at the Jayadeva hospital junction.

l There is a plan to widen the existing four lane Bannerghatta road into a six lane road but the plan has been stalled many times due to protest from residents on both sides of this stretch.

l As part of the Cauvery phase IV plan the corridor has been connected by Cauvery pipeline in most of the areas until Gottigere and many houses and apartments have

already started to get water supply as well although a tad irregular.

A recent visit to the corridor has revealed that there is a lot of activity happening in terms of residential spaces coming up. But there is a general doubt in the investor if the infrastructure in the area will keep pace with all the development in the corridor. The corridor will witness the completion of almost close to 12000 units by the end of 2016 which are main multi storey buildings. This will put more strain on the already poor infrastructure and Bannerghatta main road will be the single point of roadblock and traffic jam. Currently

there are no alternate parallel roads and people will have bear with the traffic issues. Alternate modes of transport such as metro has been going very slow and with the latest plan to reallign the metro in order to avoid disturbing the Jayadeva hospital area has added more delays to the much awaited Nagawara-Gottigere line.

All these factors combined with the movement of the IT/ITES offices to much affordable areas such as North Bengaluru and Electronic City have further reduced the attractiveness of the corridor from investment perspective.

IT, retail hubs drive growth on Bannerghatta Road

Bengaluru South witnessed the beginnings of the IT sector, with the first IT cluster at Electronics City. The Outer Ring Road (ORR) played a major role in making areas considered peripheral in early 2000 easily accessible for corporate to set up business. Bannerghatta Road, linked to the city centre through Hosur Road beginning at Vellara junction, is the main link to the IT hubs dotting the road from the Dairy Circle flyover. It also connects to Koramangala and BTM Layout, the key residential and retail belts. This has led to its turning into one of the earliest key routes of the city. This kind of development is driving growth of the area.

n Source: The Times of India

Metro rail will open up new areas

The Metro corridor has undoubtedly created a positive impact on the realty growth in its periphery. The presence of metro is making the area quite convenient to commute. The metro is well-connected to the new and upcoming areas, which is helping to attract home buyers. The impact of metro will be more visible only when the entire stretch is operational. The realty growth in these regions is witnessing more vertical development, mixed land use as well as integrated township developments. The Metro connectivity will add advantage to this connectivity from the railways and roadways.

n Source: The Times of India

Infrastructure push for Bannerghatta Road localities

The projects on the anvil to enhance connectivity will lead to more development in the vicinity. Bannerghatta Road, one of the busiest roads in the city, connects the core city areas to prominent locations

in the south such as Koramangala, JP Nagar, BTM Layout, and through NICE Road to other arterial roads and the peripheral locations. Infrastructure projects are being planned to boost development of the area. The government has invested money to widen Bannerghatta Road.

n Source: The Times of India

Affordable housing market grows in Bangalore

Infrastructure has been the most significant determinant of growth in the peripheral areas of the city. Good connectivity as well as allocation of land by the government for commercial and industrial growth led to development around 15 km away from the city centre. The next phase of development is now taking place 30 km and beyond with improvement of national highways, road widening projects and elevated expressways. It has led to the rise of the affordable housing market in the city.

n Source: Magicbricks Bureau

What makes Bannerghatta Road attractive for buyers

Bannerghatta Road has wide variety of residential offerings which support the extensive growth of the office space market. Efficient connectivity is set to fuel further growth in this belt. With its start at Hosur Main Road, Bannerghatta Road branches off and runs parallel to it. It is one of the first IT belts to develop into a flourishing catchment area with commercial, residential and social infrastructure retail, options in schooling and healthcare. Locations on Bannerghatta Road will benefit from a swift commute thanks to a new Metro line that will link Nagavara to Gottigere in Phase II.

n Source: Magicbricks Bureau

IN NEWS

Corridor of growth (COG)23

Corridor Description and RatingAreas Included: Thanisandra, Jakkur, Sahakara Nagar, Hebbal, Hennur Main Road, Yelahanka New Town, Kogilu, Nagawara and Bagalur Main Road

Fig 1: Map of the corridor

N O R T H B E N G A L U R U

Corridor of growth (COG)25

Properties available in the corridor

This is a unique corridor which offers a good number of properties in all the segments, although the share of

property in the price range of Rs 40-60 lakh is slightly higher at 25%. Since the corridor

is developing, Fig 3 shows that almost 63% of the property in the corridor is still under-construction and will take a few more years for possession. Fig 4 shows that the number of 3BHK units in the corridor is 49% which is

higher than the number of 2BHK units at 41%. This is due to the fact that since the area has large open spaces available for development, property seekers look at larger floor plans than what is offered in properties closer to the

About the Corridor

North Bengaluru Corridor extends from Hebbal Junction to Yelahanka in the north and from Thanisandra Main Road

to Bagalur Main Road. This is a radial corridor that runs along the Bellary Road but also includes areas beyond the Jakkur Military Airport, Sahakara Nagar, Hennur Main Road and Yelahanka New town.

The corridor is commonly known as North Bengaluru and is closest to the Kempegowda International Airport (KIAL). Hebbal, about 28-km away, takes about 30 minutes to reach the airport. Since it was setup recently, it has very broad, well laid out roads. Bellary Road itself is a 6-lane highway with service roads and connects Hebbal to the airport. The corridor can also be accessed through the Outer Ring Road (ORR) at the intersection of NH-7 at Hebbal and Thanisandra Main Road at HBR Layout.

Although the corridor is not part of the Namma Metro-Phase II work, it will get a new metro route – the Nagawara-Kempegowda International Airport which is a 25-km line as

part of Phase-III planning by RITES, a design consultancy agency that is tasked with making the detailed project report.

Another line which runs from Hebbal to Central Silk Board will provide access to all points on the ORR until Hosur Road. These routes are still in the planning stages and it might take a few years to even start the actual groundwork.

The proposed PRR starting from Hosur Road is an 8-lane expressway which will provide an arterial connection to Tumkur Road and allow heavy traffic coming from Mumbai, Pune, and Chennai to bypass the city. This road will pass through the corridor at Bellary Road (NH-7). The KIADB Industrial Park is currently operational while, Shell India has started its set-up on a 52-acre plot and will be operational soon. European Aerospace and Defence and Jupiter Aviation are other big companies that will soon be setting up their India operations center here. KIADB has also earmarked about 60-acre land for residential purpose in the proposed industrial park.

The corridor has the widest range of properties available in terms of affordable plots as one moves towards Bagalur and Sathanur to high-end ultra-luxury apartments close to Hebbal and Nagawara near the ORR. It is a unique corridor as it is the only one where the supply of 3BHK units at 49% is higher than the number of 2BHK units at 41%. This is mainly due to the fact that the corridor was developed recently and vast tracts of land are available for development. The demand is also high for apartments with larger floor spaces and more open areas.

Although the corridor has good infrastructure in terms of wide roads, drainage and water pipelines, it has an acute water crisis and is mostly dependent on tanker water supply for daily needs. There are a lot of residential projects that are ready-to-move-in, but currently there are not many people living here. It might take a few more years for all the social infrastructure to be set-up and make this corridor completely liveable.

Overall Connectivity Social Infrastructure Security/Water

Fig 2: Distribution of properties by price Fig 3: Distribution of properties by delivery status Fig 4: Distribution of properties by bedroom configuration

Within the corridor, the locality with the highest rental demand is Hebbal, which is a well-developed

locality and close to some of the premium areas such as RT Nagar and Sadashivnagar.

Rental yield shows the amount of rent that can be generated from a property in a year in terms of sale price. The corridor has low to average rental yields in all localities, ranging from 2-5%. From the graph it is evident that

properties which are towards North of Bellary Road such as Kogilu, have lower rental yield. Thanisandra, on the other hand, has properties which are priced high although there is not much social infrastructure here.

CBD. It is also seen that at 3%, the number of 1BHK units is very less as the corridor is not much preferred by bachelors since there are not many work locations here other than the Manyata Tech Park at Nagawara. There are a lot of luxury villa projects available here. As explained, prices in the corridor move north as one moves towards the CBD around Hebbal

and Nagawara, which are closer to BDA layouts such as HBR and HRBR. As one moves North of Bagalur, it is observed that the floor area/built-up area of apartments are larger and there are 2BHK units with super built-up area of even 1600 sq ft. The corridor also has a good supply of luxury villas with sizes in the range of 2500-11000 sq ft.

Sales Price Covered Area ( Lacs) (Sq.ft)

1 BHK 15-146 520-1200

2 BHK 19-225 575-1800

3 BHK 22-400 900-5347

4 BHK and Above 100-650 2000-6300

Best sectors to invest in a home Based on rental demand in sectors

Table 1: Sizes and prices of flats available for various room configurations

Based on home buying demand in sectors

Fig 5: Top localities by consumer for renting a house

Fig 6: Top localities by consumer for buying a house

Corridor of growth (COG)26

Best bedroom configurations to buy Preferred buying and renting options

Buying Renting Total (BHKs) Total (BHKs)

1 BHK 5% 7%

2 BHK 42% 52%

3 BHK 49% 39%

4 and Above 4% 2%

Table 2: Demand distribution for buying and renting

In the case of demand for home buying, again Hebbal has the highest share at 49% of the entire demand. It is preferred by end