Staff College, Bengaluru

102

11.11.2021

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Staff College, Bengaluru

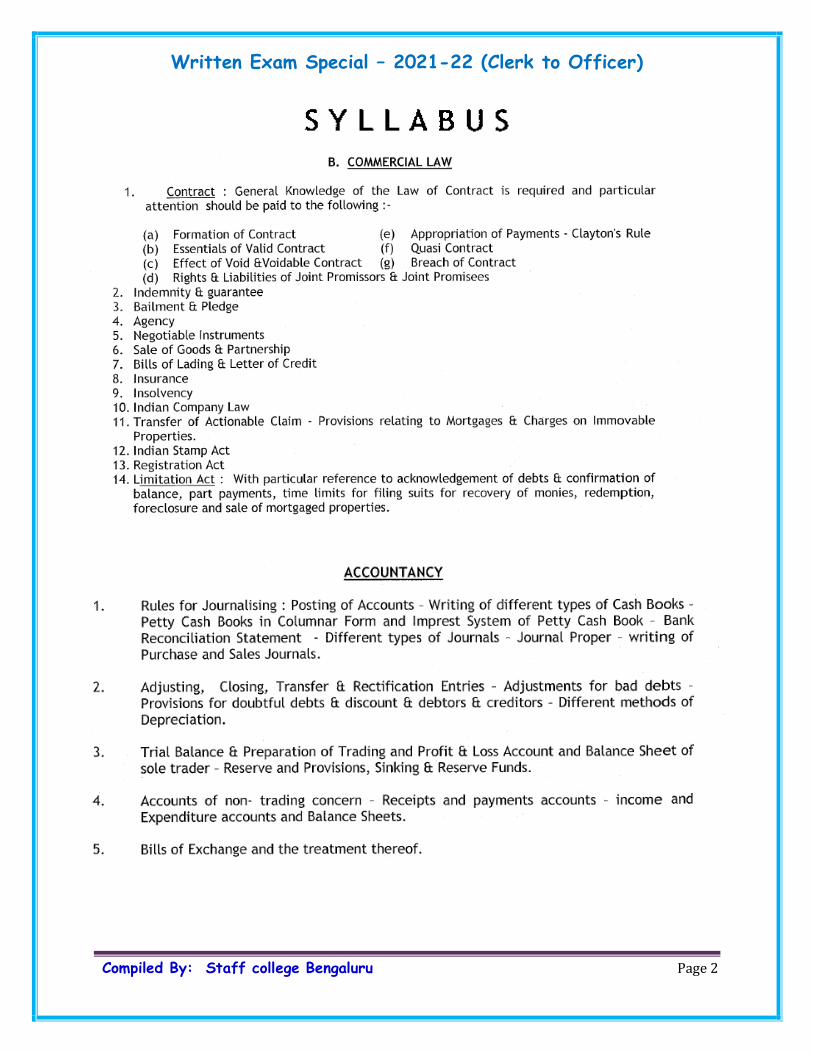

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 1

Promopedia 2021-22

Staff College, Bengaluru

Disclaimer: This is purely a voluntary effort for dissemination of knowledge and enabling people to prepare for

promotion test. Best efforts have been put to provide the accurate and updated information. However, the

users are requested to refer relevant circulars and policies of our Bank for further clarity –

11.11.2021

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 2

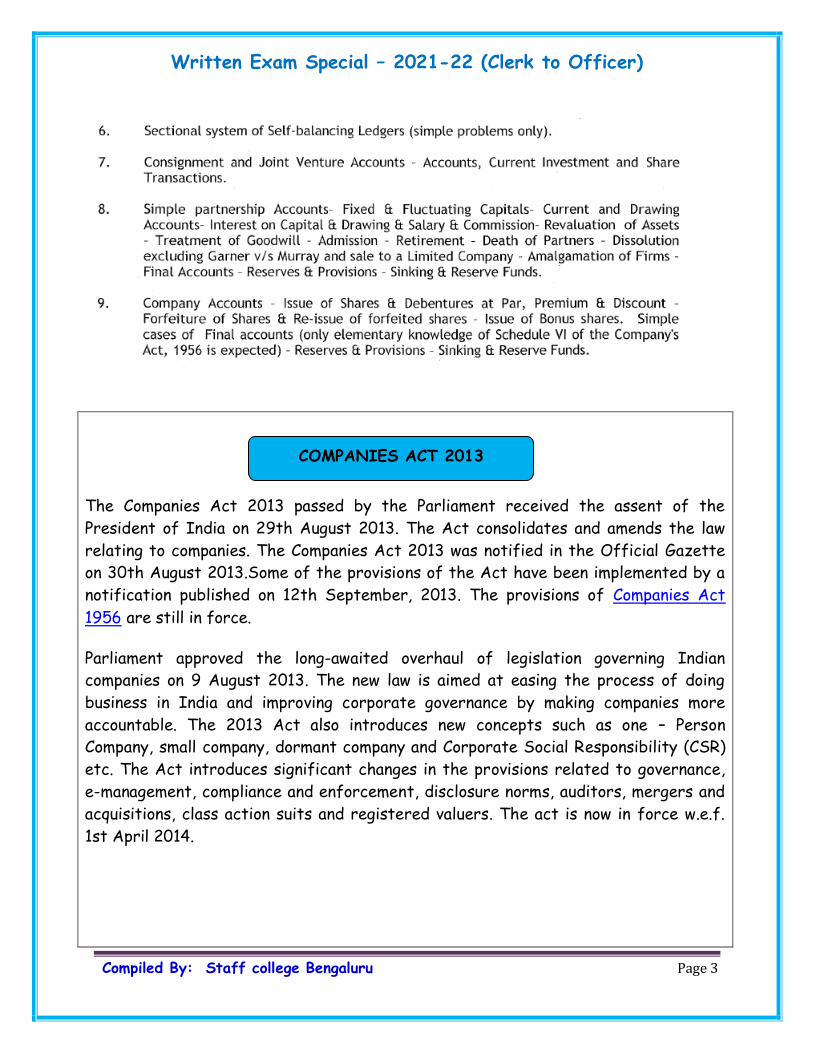

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 3

The Companies Act 2013 passed by the Parliament received the assent of the

President of India on 29th August 2013. The Act consolidates and amends the law

relating to companies. The Companies Act 2013 was notified in the Official Gazette

on 30th August 2013.Some of the provisions of the Act have been implemented by a

notification published on 12th September, 2013. The provisions of Companies Act

1956 are still in force.

Parliament approved the long-awaited overhaul of legislation governing Indian

companies on 9 August 2013. The new law is aimed at easing the process of doing

business in India and improving corporate governance by making companies more

accountable. The 2013 Act also introduces new concepts such as one – Person

Company, small company, dormant company and Corporate Social Responsibility (CSR)

etc. The Act introduces significant changes in the provisions related to governance,

e-management, compliance and enforcement, disclosure norms, auditors, mergers and

acquisitions, class action suits and registered valuers. The act is now in force w.e.f.

1st April 2014.

COMPANIES ACT 2013

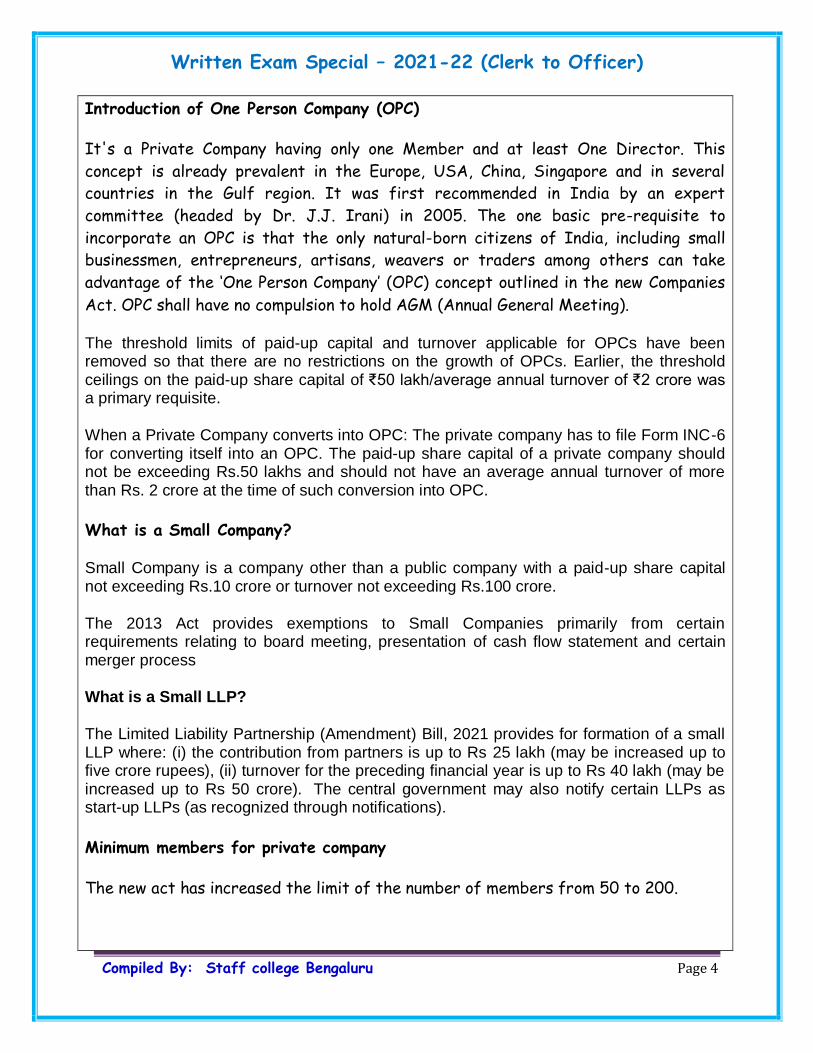

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 4

Introduction of One Person Company (OPC)

It's a Private Company having only one Member and at least One Director. This

concept is already prevalent in the Europe, USA, China, Singapore and in several

countries in the Gulf region. It was first recommended in India by an expert

committee (headed by Dr. J.J. Irani) in 2005. The one basic pre-requisite to

incorporate an OPC is that the only natural-born citizens of India, including small

businessmen, entrepreneurs, artisans, weavers or traders among others can take

advantage of the ‘One Person Company’ (OPC) concept outlined in the new Companies

Act. OPC shall have no compulsion to hold AGM (Annual General Meeting).

The threshold limits of paid-up capital and turnover applicable for OPCs have been removed so that there are no restrictions on the growth of OPCs. Earlier, the threshold ceilings on the paid-up share capital of ₹50 lakh/average annual turnover of ₹2 crore was a primary requisite.

When a Private Company converts into OPC: The private company has to file Form INC-6 for converting itself into an OPC. The paid-up share capital of a private company should not be exceeding Rs.50 lakhs and should not have an average annual turnover of more than Rs. 2 crore at the time of such conversion into OPC.

What is a Small Company?

Small Company is a company other than a public company with a paid-up share capital not exceeding Rs.10 crore or turnover not exceeding Rs.100 crore.

The 2013 Act provides exemptions to Small Companies primarily from certain requirements relating to board meeting, presentation of cash flow statement and certain merger process

What is a Small LLP?

The Limited Liability Partnership (Amendment) Bill, 2021 provides for formation of a small LLP where: (i) the contribution from partners is up to Rs 25 lakh (may be increased up to five crore rupees), (ii) turnover for the preceding financial year is up to Rs 40 lakh (may be increased up to Rs 50 crore). The central government may also notify certain LLPs as start-up LLPs (as recognized through notifications).

Minimum members for private company

The new act has increased the limit of the number of members from 50 to 200.

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 5

Immediate changes in stationery

The letterhead, bills or invoices, quotations, emails, publications & notifications,

letters or other official communications, should bear the full name of contact person,

address of company’s registered office, Corporate Identity Number ( CIN No. which

is a 21 digit number allotted by Government), Telephone number, fax number, Email

id, contact website (if any).

Memorandum of Association & Article of Association

Memorandum of Association (also known as Charter of the Company or document of

outdoor management) specifies relationship of the company with outside world.

Articles of Association (document of indoor management) lays down the regulations

for carrying the objects, activities and management of its internal affairs as defined

in its Memorandum of Association.

Commencement of business

Companies (public/private company) registered under Companies Act 2013 needs to

file the following with the Registrar of Companies (ROC) in order to commence their

business –

1. A declaration by the director in prescribed form stating that the subscribers/

promoters to the memorandum have paid the value of shares agreed to be

taken by them

2. A confirmation that the company has filed a verification of its registered

office with the Registrar of Companies (ROC)

In the case of a company requiring registration from any sectoral regulators such as

RBI, SEBI etc., approval from such regulator shall be required prior to starting the

business.

Financial Year

The Companies Act 1956 Act provided companies to elect financial year. The

Companies Act 2013 Act eliminates the existing flexibility in having a financial year

different than 31 March. The 2013 Act provides that the financial year for all

companies should end on 31 March, with certain exceptions approved by the National

Company Law Tribunal. Companies should align the financial year to 31 March within

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 6

two years from 01 April 2014.

Eligibility age to become Managing Director or whole time Director

The eligibility criterion for the age limit has been revised to 21 years as against the

existing requirement of 25 years.

Number of directorships held by an individual

- Section 165 provides that a person cannot have directorships (including alternate

directorships) in more than 20 (twenty) companies, including ten (ten) public

companies. It provides a transition period of one year from 1 April 2014 to comply

with this requirement

Board of Directors and Disqualifications for appointment of director

- The 2013 Act requires that the company shall have a maximum of 15 (fifteen)

directors (earlier it was 12) and appointing more than 15 (fifteen) directors will

require special resolution by shareholders.

Further, it requires appointment of at least one woman director on the board for

prescribed class of companies. It also requires that company should have at least 1

(one) resident director i.e. who has stayed in India for a total period of not less than

182 (hundred and eighty two days) in the previous calendar year.

All existing directors must have Directors Identification Number (DIN) allotted by

central government. Directors who already have DIN need not take any action.

However, Directors not having DIN should initiate the process of getting DIN

allotted to him and inform the respective companies on which he is a director. The

Company, in turn, has to inform the registrar of companies (ROC).

Independent Directors

- The 2013 Act defines the term "Independent Director". In case of listed

companies, one third of the board of directors should be independent directors.

There is a transition period of 1 (one) year form 01 April 2014 to comply with this

requirement. The 2013 Act also provides additional qualifications/ restrictions for

independent directors as compared to the 1956 Act.

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 7

Section 150 enables manner of selection of independent directors and maintenance of

databank of independent directors and enables their selection out of data bank

maintained by a prescribed body

Resident Director:

Every Company must have atleast one director who has stayed in India for a total

period of 182 days or more in previous calendar year. For existing companies, the

compliance need to be made before 31st March 2015.

Loans to director

– The Company cannot advance any kind of loan / guarantee / security to any director,

Director of holding company, his / her partner/s, his/ her relative/s, Firm in which he

or his relative is partner, private limited in which he is director or member or any

bodies corporate whose 25% or more of total voting power or Board of Directors is

controlled by him.

Appointment of managing director, whole time director or manager [section 196

of 2013 Act]

- The re-appointment of a managerial person cannot be made earlier than one year

before the expiry of the term instead of two years as per the existing provision of

section 317 of the 1956 Act. However, the term for which managerial personnel can

be appointed remains as five years. Further, the 2013 Act lifts the upper bar for age

limit and thus an individual above the age of 70 years can be appointed as key

managerial personnel by passing a special resolution.

Key Managerial Personnel (KMP)

- The Provisions relating to appointment of KMP includes (i) the Chief Executive

Officer (CEO) or the managing director (MD) or the manager (ii) the company

secretary (iii) the whole-time director; (iv) the Chief Financial Officer (CFO); and (v)

such other officer as may be prescribed is applicable only for Public Limited

Companies having paid up capital more than 10 crore and Private Limited Companies

are exempted from appointment of KMPs.

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 8

Attending Board Meetings

- As per section 167 of the Act, a Director shall vacate his/her office if he/she

absents himself from all the meetings of the Board of Directors held during a period

of 12 (twelve months) with or without seeking leave of absence of the Board. Simply

speaking, attending at least one Board Meeting by a director in a year is a must else

he has to vacate his/her office.

Board meetings

- Atleast 7 days notice to be given for Board Meeting. The Board need to meet

atleast 4 times within a year. There should not be a gap of more than 120 days

between two consecutive meetings.

Appointment of Statutory Auditors

- Every Listed company can appoint an individual auditor for 5 years and a firm of

auditors for 10 years. This period of 5 / 10 years commences from the date of their

appointment. Therefore, those companies who have reappointed their statutory

auditors for more than 5 / 10 years, have to appoint another auditor in their Annual

General Meeting for year 2014.

Other specialized services which cannot be provided by Statutory Auditors

- The Statutory Auditor of the Company cannot give following specialized services

directly or indirectly to the company –

a. Accounting and book keeping services

b. Internal audit

c. Design and implementation of any financial information system

d. Actuarial services

e. Investment advisory services

f. Investment banking services

g. Rendering of outsourced financial services

h. Management and/or any other services as may be prescribed

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 9

Corporate Social Responsibility (CSR)

The company has to constitute a CSR committee of the Board and 2% of the average

net profits of the last three financial years are to be mandatorily spent on CSR

activities by an Indian company if any of the following criteria is met:

Net worth of Rs.500 crores or

Turnover of Rs. 1000 crores or more or

Net profit of Rs. 5 crores or more

Contributing to Incubators, which has been notified by the Government of India, is

eligible for spending under CSR. This is a prosperous time for incubators and

entrepreneurs and can really change the entrepreneurial eco system in India.

Financial statements

- Financial Statements are now defined under the Act as comprising of the following.

All companies (except one person Company, small company and dormant company)are

now mandatorily required to maintain the following, which may not include the cash

flow statement) –

A balance sheet as at the end of the financial year

A profit and loss account / an income and expenditure account for the financial

year, as the case may be

Cash flow statement for the financial year

A statement of changes in equity (if applicable)

Any explanatory note annexed to, or forming part of, any document referred

to in sub-clause (i) to sub-clause (iv)

As per sec-2(h) of Indian Contract Act, a contract is AN AGREEMENT ENFORCEABLE

BY LAW. ALL CONTRACTS ARE AGREEMENTS, BUT ALL AGREEMENTS ARE NOT CONTRACTS

Agreements can become contracts, if they are made by free consent of parties

competent to contract, for a lawful consideration, with a lawful object and are

not expressly declared as void

An agreement is combination of lawful offer and unconditional acceptance

Indian Contract Act

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 10

Minority, lunacy, insolvency, purdahnashin etc. makes persons incompetent to

contract

No consideration, no contract. Consideration is give & take benefit for both

parties

Undue influence, coercion and fraud takes away the free consent factor

As per sec-2(g). anything unenforceable by law is void

When the modalities of an agreement is such that it can be either valid or void

as per the option of parties, it can be termed as a voidable contract

Both void and voidable contracts may be unenforceable, but not illegal

Offer and acceptance are two sides of the coin called agreement

Offer and invitation to offer are not one and the same. An invitation to offer

is to responded by lawful offers

Offer is the intention to create legal relationships, not for fun

Communication of offer either written or oral is necessary

Cross offers/counter offers are not encouraged

Offers can be distinguished as standing, open, continuing, specific or general

Acceptance must be communicated to the offeror

Acceptance must be absolute and unqualified and made during the validity of

offer

As per sec-6, an offer can be revoked by notice/ by lapse of time/ by failure

to fulfill a condition/by death or insanity of the offeror

As per sec-5, an acceptance can be revoked at any time before sending

communication to the offeror

Consideration is the most essential element of a valid contract. It may be past,

present or future. It may be an act or abstinence or promise in exchange as

reciprocation of both parties. It may not be adequate except for illegal &

fraudulent purposes. It should not lead to illegal, immoral or acts opposing

public policy (sec-23)

As per section 39, actual breach of contract takes place on non-performance

on the due date. Anticipatory breach of contract may take place before the

due date

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 11

Law Related To Appropriation Of Payments

When the debtor owes several distinct debts to a creditor, and he makes some

payment which is not enough to cover the payment of all the debts in full; the

question arises as to which particular debt the payment proceeds to be

appropriated/applied. The rule of appropriation as per contract act are as

follows:

When the debtor indicates a choice to apply the amount to a particular debt,

the creditor has to follow it faithfully. In case, the creditor does not want it,

he must not accept the payment at all (sec-59)

When a debtor fails to make any indication of his intention for appropriation,

then the creditor has a right to appropriate the amount to any actually due and

lawful debt. Even, a time barred debt is lawfully due (sec-60)

In case, neither debtor nor creditor makes any indication for appropriation,

then the payment shall be applied/appropriated in discharge of debts in order

of time. Here, the oldest one is to be discharged first of all, even though time

barred. THE FAMOUS CLAYTON’S RULE IS REFERRED HERE (SEC-61)

QUASI CONTRACTS deal with certain relations resembling those created by a

contract. However, this may not be always a valid contract. The basis and legal

sanction here suggest that no one should have unjust benefit at the cost of the

other party(AIR 1990)

Some examples of quasi contracts are: (sec-68 to 72)

Claims for necessaries supplied to a person incompetent to contract

Reimbursement of money paid, due by another

Obligation of a person enjoying benefits of non-gratuitous Act( not

free/charity)

Responsibility of finder of lost goods

Liability of a person getting benefit under mistake or coercion

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 12

1.INDEMNITY:

Sec 124 of Indian Contract Act define Contract of Indemnity as” A contract

by which one party promises to save the other from loss caused to him by the

conduct of the promisor himself, or by the conduct of any other person”. Thus,

in this case the Indemnifier (one who gives indemnity) undertakes through the

contract of indemnity that he would make good the loss incurred by the

Indemnified (in whose favour the indemnity is given) on account of his own

conduct or conduct of a third person.

In Banks we generally take Indemnity Bond while issuing duplicate DD or

duplicate Deposit Receipt etc.

We also obtain counter-Indemnity from the borrowers wherever we issue

Letter of Guarantee. Through this counter Indemnity, borrower undertakes to

indemnify the bank.

2. GUARANTEE:

2.1. As per Sec.126 of Indian Contract Act 1872,”it is a contract to perform the

promise or discharge the obligation of a third person in case of his default”. There

are three parties to a contract of Guarantee i.e. Principal Debtor (borrower), Surety

(Guarantor) and Creditor (Bank). Guarantor’s liability arises on default made by the

principal debtor.

2.2. A Guarantee may be specific or continuing one. Guarantee issued for a specific

single transaction is called “specific guarantee”. When a guarantee extends to a

serious of transactions it is called a “continuing guarantee “(Sec.129). Normally the

guarantee obtained by the bank for the loan given is a continuing guarantee.

2.3. Guarantees are also further classified into Performance Guarantee, Financial

Guarantee, and Deferred Payment Guarantee.

INDEMNITY/ GUARANTEE

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 13

2.4. The liability of the guarantor is co-extensive with that of principal debtor

(borrower) (u/s 128).

2.5. Consideration for Guarantee:

Anything done or any promise made to the principal debtor is sufficient consideration

to the surety for giving the guarantee (Sec 127) and law does not require any

separate consideration to be given to the guarantor for a valid contract of guarantee.

3. GUARANTEE BY TWO OR MORE PERSONS:

3.1. Two or more persons can undertake a “joint liability” or a “joint and several

liability”. Guarantee taken by the Bank is usually is with “joint and several liability”

clause. All the joint sureties should sign the guarantee document. Those who have not

signed the guarantee shall not be liable for the guarantee. Further, even the

guarantee may not be enforceable even against those who signed the guarantee, if

the other guarantors have not signed

4. GUARANTEE BY PARTNERSHIP FIRM:

4.1. Where the partnership firm is giving the guarantee, all the partners should sign

the guarantee on behalf of the firm to bind the firm, unless providing guarantee is a

normal business of the firm. In case partners are giving their personal guarantee for

the loan taken by the firm, then they have to sign the guarantee in their personal

capacity (without the firm’s seal).

5. GUARANTEE BY A LIMITED COMPANY:

5.1. A limited Company can give a guarantee if the Memorandum of Association and

Articles of Association expressly permit for giving such guarantee. A Board

resolution to be passed for giving the guarantee and authorizing specific persons to

execute the guarantee. Common seal is required to be affixed in presence of

directors/executives authorized in the board resolution/AOA.

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 14

6. DETERMINATION OF LIABILITY:

The liability of the guarantor stands determined (crystallization) on happening of any

of the following events:

6.1. Revocation of Guarantee:

When the continuing guarantee is revoked, guarator’s liability stands determined and

he is liable for the balance in the account as on the date of receipt of notice by bank

6.2. Death of Guarantor:

Death of surety results in revocation of gurantee as to future transactions. Deceased

guarantor’s asset is liable for the balance in the account as on date of receipt of the

news of death by the bank. On getting the information of death, bank should stop

further credits in the account (so as to avoid application of Clayton’s Rule). If Bank

decides to continue operation, account is to be first ruled off (either by opening new

account in Finacle or with one simultaneous credit and debit entry in the same

account to reflect “ruling off”) and also an undertaking to be obtained from the legal

heirs of the deceased guarantor that they are liable for the balance in the account

on the day the Bank has the notice of death of the guarantor.

7. LIMITATION FOR GUARANTEE:

Limitation against the guarantor starts from the date demand is made on the

guarantor. It is advised that branches are to obtain composite DBC signed by

borrower and the guarantor to extend the limitation period against the guarantor

also due to conflicting judgments of various High Courts on extending limitation

against the guarantor’s liability. However, now it is the settled law that the limitation

against the guarantor starts from the date of demand made on him. However,

branches to continue to take guarantor’s signature on the composite DBC.

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 15

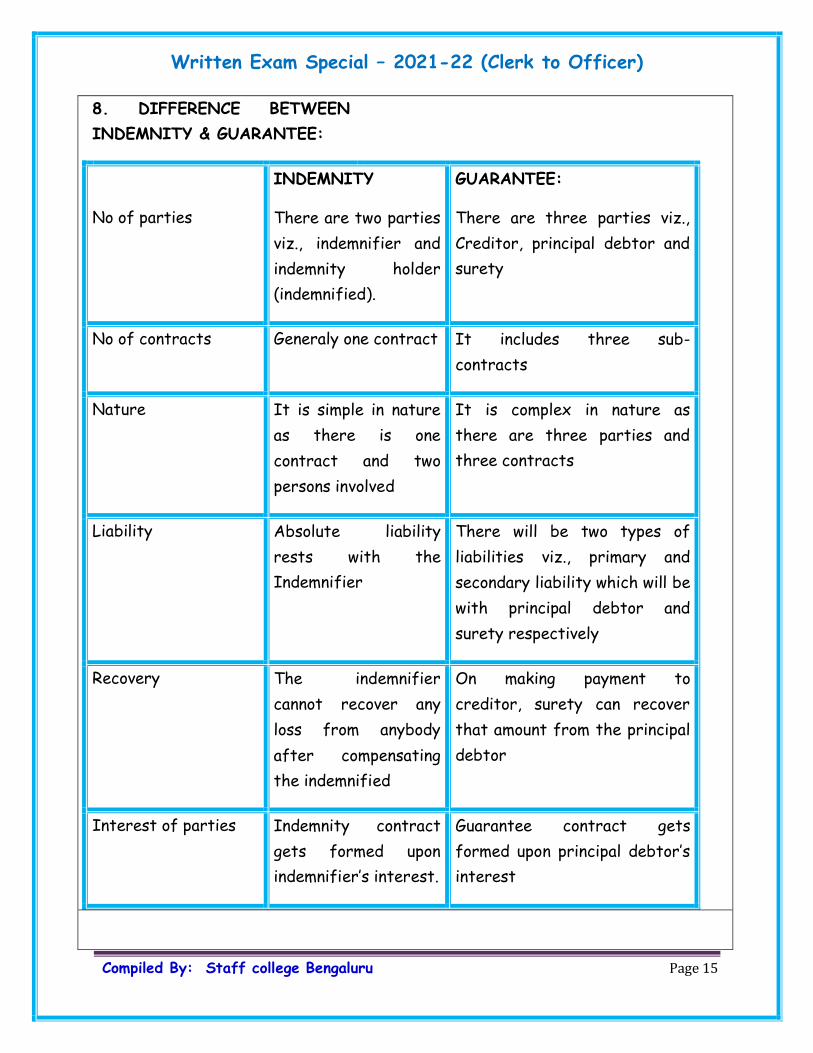

8. DIFFERENCE BETWEEN

INDEMNITY & GUARANTEE:

No of parties

INDEMNITY

There are two parties

viz., indemnifier and

indemnity holder

(indemnified).

GUARANTEE:

There are three parties viz.,

Creditor, principal debtor and

surety

No of contracts Generaly one contract It includes three sub-

contracts

Nature It is simple in nature

as there is one

contract and two

persons involved

It is complex in nature as

there are three parties and

three contracts

Liability Absolute liability

rests with the

Indemnifier

There will be two types of

liabilities viz., primary and

secondary liability which will be

with principal debtor and

surety respectively

Recovery The indemnifier

cannot recover any

loss from anybody

after compensating

the indemnified

On making payment to

creditor, surety can recover

that amount from the principal

debtor

Interest of parties Indemnity contract

gets formed upon

indemnifier’s interest.

Guarantee contract gets

formed upon principal debtor’s

interest

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 16

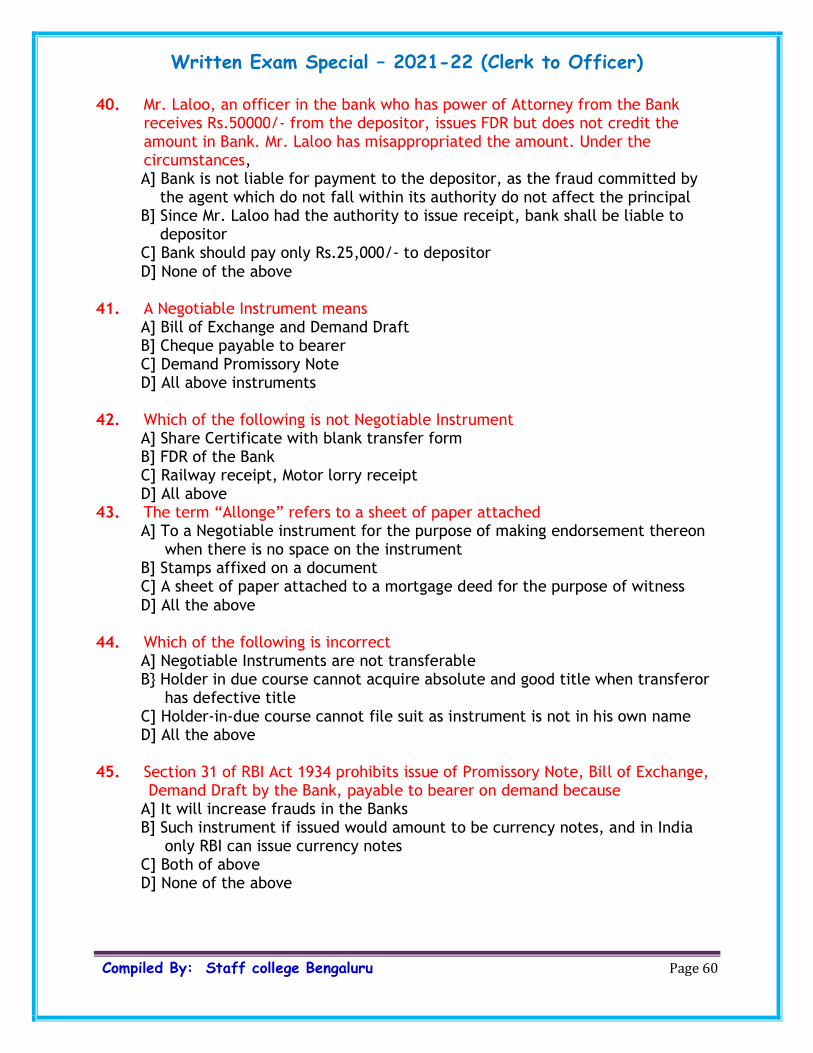

As per sec-13, a negotiable instrument means and includes a promissory note, a

bill of exchange or a cheque

The special of this instrument is that the right, title and interest can be

transferred all at a time from one person to another by mere delivery and

sometimes by endorsement & delivery. The transferee of the negotiable

instrument, who takes it in good faith and for consideration gets a good title

even though the title of the transferor is defective(sec-9)

As per sec-4, a promissory note must be writing and signed by the maker, must

be an unconditional undertaking to pay, it must be payable in money only in

certain amount and the payee must be certain person

As per sec-5, a bill of exchange is an instrument in writing, contains an

unconditional order, directing a certain person to pay a certain sum of money,

only to or the order of a certain person or the bearer of the instrument

Parties in a bill of exchange include drawer, drawee, payee, acceptor, drawee in

case of need

As per sec-6, a cheque is a bill of exchange drawn on a specified banker and

not expressed to be payable otherwise than on demand

A promissory note cannot be made payable to the maker himself

A bill of exchange can be accepted before payment and enjoys days of grace

As per sec-31 of RBI Act which supersedes the N.I. Act prohibits issue of

bearer promissory note and bill of exchange

Crossing is a special feature applicable only to Cheques

Noting and protest are features applicable to bill of exchange

Any negotiable instrument made or drawn and payable in India or drawn in

India on a person resident in India is called as inland instrument

Foreign instrument is one which is not an inland instrument. Examples are:

promissory note made in India payable at London, made in London payable at

Bangalore, bill of exchange drawn in India and payable in Paris, bill drawn in

New York payable at Mumbai.

NEGOTIABLE INSTRUMENTS ACT

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 17

NI Act amended in 2018, included an amount of Interim compensation payable by

the drawer to the complainant during the court proceeding that can be up to 20% of

the amount of cheque.

A contract of sale of goods is a contract whereby the seller transfers or

agrees to transfer the property in the goods to the buyer for a price( sec-4 of

the Act )

Where under a contract of sale, the property in the goods is transferred from

the seller to the buyer, the contract is called as a SALE. But when the

transfer of property in the goods is to take place at a future time or subject

to some conditions thereafter to be fulfilled, the contract is called AN

AGREEMENT TO SELL

AN AGREEMENT TO SELL BECOMES A SALE WHEN THE TIME ELAPSES OR

THE CONDITIONS ARE FULFILLED SUBJECT TO WHICH THE PROPERTY

IN THE GOODS IS TO BE TRANSFERRED

Goods form the subject matter of Sale and include all kinds of movable

property other than actionable claims and money. It also includes stocks and

shares, growing crops, grass & things attached to or forming part of the land

Goods may be existing, future or contingent. The price in a contract of sale

must be expressed in terms of money only

When the price is not determined specifically, the buyer must pay the seller a

reasonable price (sec-9 )

A stipulation in a contract of sale with reference to goods sold/to be sold may

be a condition or a warranty (sec-12.1)

A CONDITION is a stipulation essential to the main purpose of the contract.

Its violation gives a right to the buyer to cancel/refuse the contract

A WAARANTY is a stipulation collateral to the main purpose of the contract.

Its violation gives rise to a claim for damages, but not a right to reject the

goods and treat the contract as refused/cancelled

Sale of Goods Act

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 18

In a contract of sale, there is an implied warranty that 1. The buyer shall have

and enjoy quiet possession of the goods 2. The goods are free from any charge

or encumbrance in favor of any third party

CAVEAT EMPTOR means LET THE BUYER BE AWARE and thus a privilege

available to seller. However, this privilege shall not be available when 1. Implied

warranty is there 2. The buyer gives a choice and depends solely on the seller’s

skill/judgment 3. There is practice in trade to deny this privilege 4. there is a

fraud committed by seller

The general rule of law is that only the owner of the goods or any person

specifically authorized by him can sell the goods. If any other person sells

it, the title of the buyer will not be better than that of the unauthorized

seller

Some exceptions to the above rule are: 1. Sale by a mercantile agent 2. Sale

under the implied authority of the owner 3. Sale by one of the several joint

owners 4. Sale by a seller in possession of goods under a voidable contract 5.

Sale by a seller in possession after sale 6. Sale by a buyer in possession after

having bought or agreed to buy the goods 7. Sale by an UNPAID SELLER

The rights of an unpaid seller are:

Lien of unpaid goods

Stoppage of goods in transit

Withholding delivery of unpaid goods

Re-sale of unpaid goods

Suit against the buyer for unrealized price

Suit against the buyer for damages

Refusal/cancellation/repudiation of the contract made earlier with the buyer

Suit for realization of interest as time value for money

A bill of lading is a document which acknowledges receipt of goods delivered to

a general ship for carriage of goods and is negotiable

It contains the terms & conditions of the carriage of goods, which have been

agreed upon by parties

BILLS OF LADING

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 19

It is also a document of title to goods described therein. Bill of Lading 3

originals will be issued by the carrier

In case of a bill of lading, the transferee, even though he acquires it bona fide

and for value; takes it subject to all the defects in the title of the transferor

A clean bill of lading is one not indicating any defects in packing but a claused

bill of lading contains some qualifying remarks about quality of packing

When goods are to be carried partly by sea and partly by land; it is called

through multi modal bill of lading

In a received bill of lading, the ship owner only acknowledges the receipt of

goods for shipment in a particular ship without mention of time of shipment.

But on board bill of lading is better and preferred one as it contains the actual

date of loading on Board

As per UNIFORM CUSTOMS & PRACTICES ON DOCUMENTARY CREDIT, a

Letter of Credit is “ any arrangement, however named or described, whereby a

Bank(Issuing bank) acting at the request and in accordance with the

instructions of a customer(the applicant of credit) is to make payment to or to

the order of a third party(the beneficiary) or is to pay, accept or negotiate

bills of exchange(drafts) drawn by the beneficiary or authorities, such

payments to be made or such drafts to be paid, accepted or negotiated by

another Bank; against stipulated documents and compliance with stipulated

terms & conditions.”

Parties to a letter of credit are: the Applicant, The Issuing Bank, The

beneficiary, The Advising Bank, the confirming Bank and the nominated Bank

authorized to negotiate the Letter of Credit

Types of Letter of Credit are irrevocable, confirmed, unconfirmed, red clause,

Green Clause, revolving, transferable, back to back

AS PER SUPREME COURT VERSION: “A LETTER OF CREDIT IS

INDEPENDENT OF AN UNQUALIFIED CONTRACT OF SALE OR

UNDERLYING TRANSACTION. THE AUTONOMY OF AN IRREVOCABLE

LETTER OF CREDIT IS ENTITLED TO PROTECTION. AS A RULE, COURTS

REFRAIN FROM INTERFERING WITH THAT AUTONOMY.”

“THE issuing Bank has to pay under the letter of credit WHEN THE DOCUMENTS

ARE PRESENTED exactly as per LC terms

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 20

IT is a contract whereby one person, called as the INSURER, ASSURER OR

UNDERWRITER undertakes(indemnifies) to make good the loss of another

called THE INSURD OR ASSURED by payment of money to him on the

happening of a specified event

The consideration for which the insurer undertakes to indemnify the assured

is called PREMIUM

The instrument in which the contract of insurance is generally described is

called THE POLICY. The policy itself is not the contract. It is the evidence of

contract

The thing or property insured is called the subject matter of insurance

and the interest of the assured in the subject matter is called insurable

interest

PERILS INSURED AGAINST IS THE LOSS ARISING FROM UNCERTAIN

EVENTS OR CASUALTIES IN FORM OF DESTRUCTION/DAMAGE TO

PROPERTY OR DEATH/DISABLEMENT OF A PERSON.

FUNDAMENTAL ELEMENTS OF INSURANCE:

1. IT must have all essential elements of a valid contract

2. It is a contract of malafide i.e. of utmost good faith. A mis-statement or

withholding of any material information is fatal to the contract of insurance

3. It is a contract of indemnity. The assured is paid for the actual loss not

exceeding the amount of policy

4. The assured must be so situated with regard to things insured that he would

benefit from its existence and suffer loss from its destruction

5. The assured can recover the loss only if it is caused by any of the perils

insured against

6. If for any reason the risk is not run, the consideration fails and the insurer

must return the premium

The Law of Insurance

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 21

7. In the event of any mishap to the insured property, if the assured fails to take

all necessary steps to mitigate the loss; the insurer can avoid the payment of

loss which is attributable to the assured’s negligence

8. Where there are two or more insurances on one risk, the principle of

contribution applies between different insures

9. The insurer who has agreed to indemnify the assured on making good for loss,

is entitled to succeed to all ways and means by which the assured might have

protected himself against the loss. THIS IS CALLED AS THE DOCTRINE

OF SUBROGATION

If an insurer has insured a venture in which the risk involved is beyond his

capacity, he may insure the same risk either wholly or partially with other

insurers. This facility is called RE-INSURANCE and can be resorted to in all

kinds of insurance

Where the assured insures the same risk with two or more independent

insurers and the total sum insured exceeds the actual value of subject matter,

the assured is said to be OVER INSURED BY DOUBLE INSURANCE. But, in

case of loss, the assured cannot recover more than the actual amount of loss

This is because, a contract of insurance (other than life and personal accident

insurance) is a contract of indemnity

Insurance ombudsman handles all grievance regarding insurance policies and

has the authority to handle claims up to Rs. 30 lakhs.

The law relating to Insolvency of a debtor is contained in two statutes: the

PRESIDENCY TOWNS INSOLVENCY ACT, 1909 APPLYING TO the

presidency towns of Bombay, Calcutta and Madras; while the PROVINCIAL

INSOLVENCY ACT, 1920 applies to rest of India

INSOLVENCY

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 22

The two main aspects of insolvency act are: 1. To protect the embarrassed

debtor from harassment by his creditors and 2. To ensure an expeditious but

equitable distribution of his assets amongst the creditors

A person can be adjudged insolvent only if he is a debtor and has committed an

act of insolvency

An act of insolvency is something done or suffered by a debtor which gives

jurisdiction to the Insolvency Court to adjudge him as insolvent

A debtor commits an act of insolvency in each of the following cases:

1. If he transfers his property or any part thereof with intention to defeat or

delay his creditors

2. Any whole or part transfer of his property, which would be void under any

law in force as a proof of fraudulent preference in the pre-insolvency stage

3. If he departs or remain out of India with an intention to defeat or delay his

creditors

4. Departs from his dwelling house or usual place of business or otherwise

absents himself

5. Secludes himself so as to deprive his creditors of the means of

communicating with him

6. If any of his properties sold or attached for a period of not less than

21days in execution of the decree of any court for payment of money

7. If he petitions to be adjudged insolvent or he is imprisoned in execution of

the decree of any court for payment of money

8. If he has given notice to any of his creditors to the effect that he has

suspended or is about to suspend payment of his debt

9. If an insolvency notice issued against him remains unsatisfied

Stages in insolvency proceedings include a. presentment of insolvency petition

b. appointment of interim receiver c. order of adjudication and d. discharge of

insolvent

The following debts of the insolvent are called preferential debts and paid in

priority over the other debts of the insolvent:

All debts due to the Govt. or any local authority like municipal taxes, land

revenue, water tax etc

Salaries and wages due to any low paid clerk/servant or laborers in respect of

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 23

services rendered during four months before the presentation of the

insolvency petition

Rent due to landlord not exceeding one month

All preferential debts as above, rank equally among themselves and are paid in

full when property is sufficient to meet them. When property is insufficient, it

is distributed in equal proportions

INSOLVENCY AND BANKRUPTCY CODE-2016

The code has come in to force w e f 1.12.2016)( IC No 766/02.01.2017)

Definitions

1. Insolvency:

A state of being unable to pay the money owed by a person or company on time.

2. Bankruptcy:

It is the legal status of a person or other entity that cannot repay the debts it owes

to creditors. Bankruptcy is imposed by a court order, initiated by the debtor

(In this chapter, we refer Bankruptcy to Individuals & and insolvency and liquidation

to Companies)

Scope of IBC 2016

Insolvency and Bankruptcy code (IBC 2016) is a consolidated law which deals with:

1. Reorganization

2. Restructuring

3. Insolvency

4. Winding up or dissolution

4. Provides rights apart from SARFAESIA and DRT

5. Provisions regarding Insolvency and Liquidation of companies have been put in

force on 1.12.2016

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 24

6. The provisions in the Insolvency Code in respect of insolvency resolution and

Bankruptcy for individuals and partnership firms have been notified and made

effective from 1-12-2019 only for personal guarantors of corporate debtors

(not for other individual and partnership firms)

Process and Eligibility

In the process:

7. First step is insolvency resolution

8. Second step is liquidation of the company

9. Eligibility criterion: Dues of Rs. 1 crore and more

Insolvency Resolution Process - Steps

Application is filed with NCLT (National Company Law Tribunal) for IRP

(Insolvency Resolution Process)

1 Banks will furnish all details of borrower

2 Submit proof of default

3 Recommend the name of IRP(Insolvency resolution professionals

licensed by IBBI)

• NCLT appoints the IRP, makes a public announcement of 180 days moratorium.

The Corporate Insolvency Resolution Process (CIRP) shall mandatorily be

completed within a period of 330 days from the insolvency commencement date,

including any extension of the period of corporate insolvency resolution process

granted under section 12 of Insolvency Code.

• IRP will take control of the management of the company, collects all

information for determining the financial position of the company

Within 180/330 days lenders to submit the Resolution Plan to IRP, involving

strategy for running the company, payment of other creditors etc. (Requires

approval of 66% of secured/unsecured creditors) No legal action can be taken

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 25

during the moratorium period

The approved plan will be placed before NCLT

Once approved, implemented by IRP, and binding on all stake holders

1. If Resolution Plan is unsuccessful, NCLT orders liquidation

2. Liquidator will be appointed by NCLT, who completes the process of

distribution

Important bodies under IBC 2016

IBBI: Insolvency and Bankruptcy Board of India

1. Acts as a Regulator for the process

2. Maintains the list of Resolution professionals

3. Constituted by Govt. of India

NCLT and NCLAT: National Company Law Tribunal and National Company Law

appellate Tribunal

Action Points

1. Branches to examine each NPA account of companies and file application

before NCLT in consultation with Law Officer and the Advocate

2. To take approval from controlling office to invite expression of interest from

Insolvency Resolution Professionals (3 quotation to be obtained)

3. After proper background check, recommend the Resolution Professional to

NCLT

Powers of liquidator under IBC 2016

1. Receives and verifies creditors’ claims

2. Takes control and custody of assets

3. Evaluates the assets and property

4. Protects the assets and runs the business till assets sold

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 26

5. Distributes the sale proceeds among the creditors and stake holders, as per

order mentioned by IBC

Order of distribution of proceeds under IBC 2016

In order of preference:

1. Costs and fee of the IRP and Liquidator

2. Workmen dues for 2 years preceding the date of liquidation and debts

payable to secured creditors in equal proportion

3. Wages and dues of the employees preceding 1 year

4. Debts payable to unsecured creditors

5. Government Tax Dues and unpaid secured creditors in equal proportion

6. Other remaining debts and dues

7. Preference share holders

8. Equity share holders

Bank’s Options:

Bank may opt not to surrender the securities to the liquidator, in that case, in the

order of preference as “Secured Creditors” Bank will not be having a preference

In this case, Bank will proceed against the secured assets in its own way by

completing legal action (SARFAESIA or DRT) after the moratorium and realize the

assets.

Fast Track Insolvency Resolution Process:

The Regulations and the fast track resolution process are applicable to the following

categories of corporate debtors.

a. a small company as defined under the Companies Act, 2013.

b. a Startup (other than the partnership firm).

c. an unlisted company with total assets, as reported in the financial statement of the

immediately preceding financial year, not exceeding rupees one crore.

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 27

The process to be completed within 90 days with an additional grace period of 45

days i.e. maximum period of 135 days (Extension is granted only if 75% of the

committee of creditors agree for it)

Our Bank guidelines say that we should prefer not to surrender the securities to the

liquidator.

1. Actionable claims include claims as to UNSECURED DEBTS or as to beneficial

interest in movable property. Examples are: money due for goods sold, the right to

claim benefit of a contract for purchase of goods, a claim to money under

insurance policy, a claim to rent falling due in future, a claim to recover arrears of

maintenance, a Muslim widow’s claim for unpaid dower(share of deceased husband’s

property) and a negotiable instrument

2. The transfer of an actionable claim whether with or without consideration is to be

affected only by execution of an instrument in writing signed by the transferor.

An oral transfer is invalid. The written document need not be registered

3. All rights and remedies of the transferor shifted to the transferee after

execution of the instrument

4. The transferee of an actionable claim after execution of documents, may sue or

institute proceedings in his own name without the transferor’s consent

MORTGAGES AND CHARGES

As per sec-100 of Transfer of Property Act: where immovable property is

offered as security by one party to another for payment of money in a

contract other than MORTGAGE, the lender is said to have a charge on the

property

All mortgages are charges, but all charges are not mortgages

Mortgage is a transfer of an interest in a specific immovable property, but

charge only creates a right

A mortgage is good against a subsequent transferee, whereas charge is only

good against a subsequent transferee with notice of charge

A charge may be created by act of parties or operation of law, but the

ACTIONABLE

CLAIMS

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 28

mortgage can be created by act of parties only

Generally, there is no personal liability to pay in a charge, whereas it is very

much there in a mortgage

A charge created by operation of law does not require registration, while a

simple mortgage requires registration

Mortgage relates to specified property, while charge may related to

unspecified property too

LIEN is a CHARGE by operation of law

The law relating to the stamping of documents is governed by Indian Stamp Act.,

1899 and the respective State Stamp Acts. Under Indian Constitution, the rate of

stamp duty in respect of 10 different documents is included in the Central List. The

items are Promissory Note, Bill of Exchange, Receipt, Cheque, Bill of Lading, Policy of

insurance, Transfer of shares, Debentures, Proxies, Receipts. (“Cheque” is totally

exempt from stamp duty). In respect of these items accordingly the stamp duty

rates are determined by Parliament and the Central Government. As regards all other

instruments stamp duty rates are determined by the appropriate State Governments

and Legislatures. Accordingly these items are contained in the State Stamp Act. In

some of the State Stamp Act, they have included also the provisions of Indian Stamp

Act and the Rates of stamp Duty applicable for those instruments covered by the

Central Act.

DUE STAMPING:

In order to be enforceable in a court of law, any instrument, which is required

to be stamped, has to be “duly stamped".

The words "due Stamping" as per stamp Act means stamped with appropriate

stamp and stamps of requisite value is used for the same.

Documents which are unstamped or insufficiently stamped or bear a wrong

stamp will be inadmissible in evidence.

Indian Stamp Act

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 29

STAMP DUTY HOW PAYABLE:

The stamp duties which are payable under the Stamp Act are to be paid by

means of stamps according to the provisions of the Stamp Act or where no

such provisions are applicable according to the Rules made by the state

Governments.

These rules may include provisions regarding the description and number of the

stamps to be used or as in the case of promissory notes and bills of exchange

the size of the paper on which the instruments are to be written etc.

MODES OF STAMPING:

The stamp duty for the purpose of Stamp Act is to be paid by means of either

adhesive stamps or impressed stamps.

The impressed stamps are otherwise called non-judicial stamp papers. In most

of the States the impressed stamps are substituted with special adhesive

stamps.

Such Special Adhesive stamps can be cancelled by the officials of the Bank

(Branch Manager or Officer handling the documents/stamps) as provided in

the respective State Act.

The following instruments to be stamped with adhesive stamps: (a) Receipts

(b) Bills of Exchange and promissory notes drawn or made outside India (c)

Entry as an advocate, vakil or attorney or on the rolls of the High Court (d)

Notarial acts and (e) Transfer by endorsement of shares in any incorporated

company or other Body Corporate.

Whenever special adhesive stamps are not available, the instrument can be

typed and executed on non-judicial stamp paper of requisite value. Where non-

judicial stamp papers are used, care should be taken to ensure that each non-

judicial stamp paper is typed or written in hand with at least some portion of

the matter.

The printed document duly signed by the executants has to be attached to the

stamp paper bearing portion of the printed material duly typed/handwritten

and duly signed by the executants in such a way that the printed document

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 30

becomes an integral part of the stamp paper.

The executants should also authenticate the cancelled portion in the printed

document, by signing along the cancelled portion.

In respect of documents which do not require registration with the Registrar

of Assurances, the typing of document on non-judicial stamp paper can be on

both sides of the paper.

Many States have now introduced E-Stamping system. These E-stamp papers

have to be used in the similar way a non-judicial stamp paper is used.

WHERE DOCUMENT IS TO BE EXECUTED AT TWO OR MORE PLACES:

The document should be properly and adequately stamped at the place where it

is first executed as per the stamp duty applicable to that State.

Then the document is to be forwarded to the other place/State for execution.

If the stamp duty payable in this State is more than the duty paid in the first

State, then the difference of the stamp duty should be paid in the second

state either by purchasing non-judicial stamp or special adhesive stamp or e-

stamping as the case may be. A noting also should be made on this additional

stamp duty paid “this stamp paper form part of ........(name of the document)

dated ......... and signature of the executants should be obtained on this stamp.

When document is executed at different places, the executants should put the

date of execution below their signature. The Bank officer getting the

documents executed should also put a noting on a separate paper having got the

document executed in the different place mentioning the name of the

executants, place, date etc.

TIME OF STAMPING

In terms of Section 17 of Indian Stamp Act, instruments executed in India are

required to be duly stamped before or at the time of execution.

Documents executed out of India :

The documents executed outside India have to be stamped with proper stamp

duty as may be applicable in the place in India where it is received.

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 31

In the case of documents other than the Bill of Exchange and Promissory Note,

the instrument has to be stamped within 3 months from the date of receipt of

the said documents in India.

In the case of Usance Bills of Exchange, they have to be stamped by the first

holder in India before presentation of the same for acceptance or for payment

and in the case of Promissory Notes before he endorses transfers or

negotiates the same in India.

Documents executed out of India are required to be stamped with Indian

stamps, despite the fact of them bearing foreign stamps.

CANCELLATION OF STAMPS:

1. The duty of cancelling the adhesive stamps on instruments is on the party

affixing it, and failing that, on whoever executed the instruments.

2. In terms of Section 12 of the Stamp Act, any instrument bearing an adhesive

stamp which has not been cancelled so that it can be used again, shall so far as

such stamp is concerned be deemed to be unstamped.

3. As regards revenue stamps, it has to be cancelled by the executant under his

full signature. As regards special adhesive stamps, it depends on the

respective State Stamp Rules. In certain States, it has to be affixed and

cancelled only at the respective Stamp Depot.

4. With regard to the correct procedure for cancellation of stamps, the

respective Nodal Regional Offices/Zonal Offices have to issue suitable

guidelines to the branches under their jurisdiction.

5. The person affixing any adhesive stamp to an instrument chargeable with duty

shall cancel the stamp on or before execution so that it cannot be used again.

A person may cancel an adhesive stamp by writing on or across the stamp his

name or initials or the name or initials of the firm or company with the date of

so writing or any other effectual manner so that the stamps cannot be used

again.

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 32

6. Instruments stamped with impressed stamps should be written in such a

manner that the stamp appears on the face of the instrument and it cannot be

used for or applied to any other instrument. Only one instrument can be

written on the same stamp paper.

RATE/AMOUNT OF STAMP DUTY PAYABLE:

As stated above, the rates of stamp duty in respect of 10 documents are

determined by the Central Government. All other instruments chargeable with

stamp duty shall be as prescribed in Schedule to the respective State Stamp

Act.

For each instrument, appropriate rate/s of stamp duty is/are prescribed. The

Schedule has been subject to amendment by respective States and also the

modification in the rates of stamp duty from time to time. The State

Government has the right to reduce or remit the stamp duties in respect of

those classes of instruments falling within their purview.

Hence, Branches have to refer to their respective State Stamp Act to know

the stamp duty payable on different instruments. They can get it from the Law

Officer attached to their Regional Office.

CONSEQUENCES OF INSTRUMENTS NOT DULY STAMPED:

The instrument may be impounded i.e. ordered to be kept in the custody of law by the

competent authority in case it is not stamped or under-stamped. In the case of a

receipt, instead of impounding, a properly stamped receipt may be required at the

discretion of the Officer.

They are inadmissible in evidence nor can be acted upon or registered by an Officer

except in the following cases:

(a) On payment of penalty of 10 times the value of proper stamp duty or deficiency as

the case may be including Pro-notes and Bills of exchange.

(b) Unstamped receipt will be admitted on payment of Re. 1 as penalty.

(c) Instruments, which are not duly stamped, can be admitted in criminal proceedings.

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 33

(d) Instruments which are executed by or on behalf of the Government.

UNDER STAMPING - REMEDIES:

As per Stamp Law, the instruments attracting stamp duty if under-stamped can be

rectified by payment of penalty upto 10 times the deficiency as determined by the

Adjudicating Authority or by the Court, if the same is impounded by the Court during

judicial proceedings. While every care has to be taken to ensure that the documents

are duly stamped, if it comes to the notice of the Branch that there are under-

stamped documents, Branch concerned may send such documents to the Adjudicating

Authority for adjudication and for proper stamping with due permission from the

controlling Office.

The Collector can adjudicate such a document about the stamp duty payable or

accept the deficit stamp duty if it is brought to him within one month of execution

(Sec 32 of Stamp Act).

If any instrument is not duly stamped not being an instrument chargeable [with a

duty not exceeding ten naye paise] only or a bill of exchange or promissory note,

either by accident, mistake or urgent necessity and the same is brought before the

Collector within one year of execution, the Collector if satisfied with the reason can

collect the stamp duty/deficit stamp duty and penalty and give the necessary

endorsement (Sec 41 & 42 of Stamp Act).

INTRODUCTION: Certain documents executed while availing loan have to be registered

with various authorities. These authorities are:

a. Registrar of Assurances (Sub-Registrar/SRO)

b. Registrar of Companies (ROC)

c. CERSAI

Each of these registrations is covered under different laws. Registration with

Registrar of Assurances is covered under the Indian Registration Act (also State

Registration Acts), whereas the registration with ROC is covered under the Indian

Companies Act. Registration with CERSAI is covered under SARFAESI Act.

Registration

act:

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 34

2. REGISTRATION WITH THE SRO/REGISTRAR OF ASSURANCES

2.1. Indian Registration Act provides for registration of certain transactions with the

Authorities constituted under the Act. The Authority constituted under the Act is

called the Registrar of Assurances or popularly known as the Sub-Registry or SRO.

2.2. The purpose of this registration is that matters, which are of public interest or

transactions with individuals particularly those involving a charge over immovable

property are made known to others so that the people dealing with the property have

knowledge about the charges/ownership of the property.

2.3. The Registration Act classifies instruments into three categories (a) those

requiring compulsory registration (b) those which are optionally registerable and (c)

those which need not be registered. All those transactions affecting immovable

property, subject to certain exceptions, are required to be compulsorily registered.

2.4. The Transfer of Property Act, 1882 provides that any transfer of Immovable

property of value Rupees 100 or above are required to be carried out through a

registered instrument only i.e. a Deed duly registered with the Registrar of

Assurances. There are a few exceptions. One such exception so far as Bank

documentation is concerned is equitable mortgage (mortgage by deposit of title

deeds). Accordingly equitable mortgage is NOT required to be registered (however,

now many states EMs also require compulsorily registration like Maharashtra, Gujarat

etc.).

2.5. Many States have now made provision for registration of EM also with the

SRO. Wherever there is such provision, branches have to register the EM with SRO.

Even in those states where registration of EM is not mandatory, branches should

explore the possibility of registering the EMs

2.6. Again, as per Transfer of Property Act, transfer of or charge on movable

property is not required to be registered. Accordingly, the hypothecation

Agreements/Pledge Agreements Banks usually take from the Borrower whereby a

charge is created over the movable property are NOT required to be registered.

2.7. The period within which documents are to be registered as per Registration Act

is 4 months from the date of execution of the document. If the document is

presented for registration beyond this period it will not be accepted by the Sub-

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 35

Registry. However, owing to urgent necessity or unavoidable accident if a document is

submitted for registration after 4 months, Sub Register may accept such document

for registration within delayed period not exceeding 4 months along with a fine not

exceeding ten times the amount of registration fees (Sec 25 of Registration Act).

2.8. The documents requiring compulsory registration generally dealt with by Bankers

are Lease deeds where Banks take premises on lease for housing its Branches or for

residential purposes. In such cases the Lease deed for any period beyond 11 months is

to be compulsorily registered.

2.9. Similarly, simple mortgage deeds require compulsorily registration. Presentation

of documents for registration and also execution of documents, which require

registration, are to be done on behalf of the Bank by P.A. Holder Officers. In the

absence of PA holder in the branch, it can be done by the Branch Manager or an

Officer duly authorized by the Branch Manager.

2.10. The documents which require registration, apart from attracting stamp duty as

per provisions of the relevant stamp Act, shall also attract Registration charges as

per relevant Registration Act & Rules in vogue from time to time.

2.11. The consequences of non-registration of those documents requiring compulsory

registration are quite disastrous. As per Registration Act, a document requiring

compulsory registration if not registered shall be void and has no evidentiary value

before the court of law. Further, as per Registration Act, there is no remedy

prescribed for curing the defect of non-registration. Accordingly due care has to be

taken to get those documents requiring registration to be registered within the

stipulated time.

2.12. The documents dealt with by the bank and which require compulsory

registration with SRO are Simple Mortgage Deed and Lease Deed for more than 11

months. Though registration of Power of Attorney is not mandatory as per the

Registration Act, branches should generally insist for registered Power of Attorney

whenever it is acting upon a power of attorney.

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 36

3.REGISTRATION OF CHARGES WITH REGISTRAR OF COMPANIES

3.1. Definition of charge:

As per Section-2 (16) of the Companies Act 2013, Charge means - An

interest or lien

created on the property or assets of a company or

any of its undertakings or both as security and includes a mortgage;

3.2. Need for creating a charge on company’s assets:

3.2.1. Almost all the large and small companies depend upon share capital and

borrowed capital for financing their projects. Borrowed capital may consist of funds

raised by issuing debentures, which may be secured or unsecured, or by obtaining

financial assistance from Financial Institution or banks.

3.2.2. With a view to enable a person who intends to deal with a Company as a secured

creditor to ascertain whether the Company has already encumbered its property,

Section 77 of the Companies Act 2013 requires a company to file with the Registrar

of Companies complete particulars together with the instrument, if any, creating or

evidencing the charge or a certified copy of such instrument within 30 days of

creation of the charge.

3.3. Types of Charges to be registered:

3.3.1. As per Section 77 of the Companies Act 2013, Companies are required to

register ALL TYPES OF CHARGES with ROC within 30 days of its creation -

Charges created within or outside India,

on its property or assets or any of its undertakings,

whether tangible or otherwise, and

situated in or outside India

3.4. Time Limit for Registration of Charges:

3.4.1. The charges to be registered with ROC are to be registered within a period of

30 days of its creation, in form CHG-1.

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 37

3.4.2. After expiry of 30 days but not beyond 300 days (30 days + additional period

of 270 days), the Company may make an application to the ROC with additional fees.

3.4.3. Application to be supported by a declaration in Form CHG-10 from the CS or

Director of the Company that such belated filing will not adversely affect the rights

of any creditors of the company.

3.4.4. After Expiry of 300 days -Application for Condonation of Delay is to be made

to Regional Director in form CHG-8.

3.5. Duty of registration of charge:

3.5.1. As per Section 77 it is duty of Company to Create charge.

3.5.2. As per Section 78, if Company fails to file form for registration of charge

then, the person (Bank) in whose favour charge is created will apply to the Registrar

for registration of charge along with instrument created for charge (Form No. CHG-1

or CHG-9 as the case may be).

3.5.3. Registrar upon receipt of such application within a period of 14 days after

giving notice to the Company, unless the company itself register the charge or shows

sufficient cause why such charge should not be registered, allow such registration on

payment of such fees as may be prescribed. The person is entitled to recover from

the company the amount of fees.

3.5.4. It is not the responsibility of Person/Bank (in whose favour charge is created)

to file form. Therefore if company fails to file form for registration of charge and

Bank also not filed form then Bank will not be liable to pay any penalty.

3.5.5. However, to safeguard its interest, Bank should ensure that the registration of

charges wherever applicable is done within the specified time.

3.6. Certificate of Registration of Charge:

After filling of Creation of charge ROC will issue a certificate of registration of

charge in form CHG-2. The certificate issued by the Registrar under CHG-2 shall be

conclusive evidence that the requirements of Act and the rules made there under as

to registration of creation of charge have been complied with.

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 38

3.7. Modification of charge:

3.7.1. Provisions of Modification of charge are completely same as provisions of

Creation of Charge. After filling form for Modification of Charge Registrar will issue

certificate for modification of charge in form CHG-3.

3.7.2. Any modification in the terms or conditions or the extent or operation of any

charge registered under that section also requires registration.

3.7.3. The following are examples of what would constitute ‘modification’:

Security created for enhanced limit of credit facility

Further charge for the same loan or credit facility by way of additional

security on different property

Release of a part of security from the operation of the charge

Inclusion of different type of loan or credit facility within the overall limit

(provided original charge has not been registered for overall limit as such

without giving break up)

Addition of another creditor as a charge holder by modifying the original

document of charge, with or without any additional credit limit

Change in chargeable rate of interest (other than Base Rate/MCLR) (provided

these terms are mentioned in the original forms)

Change in the nature of security in respect of a charge already created (eg.

EM, SM, Hypothecation to Pledge)

Handing over title deeds by the mortgagee to another creditor for

continuation of security

Assignment of a charge

3.8. Satisfaction of charge:

3.8.1. Charge is created as security for loan or debentures or as security for some

other purpose. If the amount of loan is repaid or debentures are fully paid or other

purpose is fulfilled, there remains no necessity of the charge. This is called

satisfaction of charge.

3.8.2. As per Section 82 – Satisfaction of charge will be filed in form CHG-4 within

30 days of satisfaction of charge. If company fails to file form CHG-4 within 30 days

of satisfaction of charge, then company has to go for condonation of delay for

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 39

satisfaction of charge.

3.9. Effect of registration of charge:

3.9.1. As per Section- 81 ROC will maintain Register of Charges in respect of each

company, containing particulars of all charges registered. The Register of charges

maintained by ROC is open for inspection by any person on payment of prescribed

inspection fees.

3.9.2. Deemed Notice: Any person intending to lend moneys or who has lent money to

a company can know which of company’s assets are already charged and extent of

charge.

3.9.3. Charge binding even on subsequent purchaser: Provisions relating to charge

apply even to a subsequent purchaser, even if he had not purchased property directly

from company. The purchaser is required to make reasonable enquiries as to title of

vendor.

3.10. Effect of non-registration of charge:

3.10.1. As per Section 77(3), If charge is not registered with ROC, the charge shall

not be taken into account by the liquidator in liquidation proceedings or any other

Creditor. Mere filing of charge with Registrar would not be sufficient. It has to be

actually registered by ROC and certificate of registration should be issued.

3.10.2. However, this is so only if company is under winding up/liquidation. Otherwise,

contract or obligation for repayment of the money secured by charge is there even if

charge was not registered - Sec 77(4)

3.11. Penalty for not filing charges:

If any company contravenes any provision of this Chapter, the company shall be

punishable with fine which shall not be less than one lakh rupees but which may

extend to ten lakh rupees and every officer of the company who is in default shall be

punishable with imprisonment for a term which may extend to six months or with fine

which shall not be less than twenty-five thousand rupees but which may extend to

one lakh rupees, or with both. 10

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 40

3.12. Process of Creation or Modification of Charge:

Process of Creation/ Modification of charge is as under:-

3.12.1. Company to conduct a Board meeting to arrive at a positive decision to avail

the facility including security of Charges. In the said business of availing facility,

authority to execute necessary documents is also required to be given.

3.12.2. File extracts of the said resolution with the Registrar of Companies in form

MGT 14 within 30 days of its passing.

3.12.3. Execute necessary documents for availing the facility including the security

being given.

3.12.4. Make entries in the register of Charges maintained in form CHG-7 forthwith

after the creation/ modification/ satisfaction and get it authenticated by Director

or Secretary of the company or any person authorized by the board.

3.12.5. Submit form CHG-1 (for other than debentures) or Form CHG-9 (for

debentures including rectification) with the prerequisite fees within a period of 30

days from the date of creation/ modification of charge. After due compliance,

Registrar shall issue certificate of registration in form CHG-2, where charge is

registered under section 77(1) or 78 or in form CHG-3, where charge is registered

under section 79.

3.12.6. If CHG-1 (for other than debentures) or Form CHG-9 (for debentures

including rectification) is not being submitted within the period of 30 days, however

within the period of 300 days, prepare an application for condonation in form CHG-10

which shall be supported by a declaration by the secretary or director of the

company that delay shall not affect the rights of creditors. After due compliance,

Registrar shall issue certificate of registration in form CHG-2, where charge is

registered under section 77(1) or 78 or in form CHG-3, where charge is registered

under section 79.

3.12.7. If CHG-1 (for other than debentures) or Form CHG-9 (for debentures

including rectification) is after 300 days, prepare an application for condonation in

form CHG-8 and submit the same with Regional Director having territorial

jurisdiction over the registered office of the company under The Companies Act,

2013.

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 41

3.12.8. Pay the requisite penalty imposed by the Regional Director having territorial

jurisdiction over the registered office of the company. Normally 15 days’ time is

being given for the payment of penalty.

3.12.9. After payment of requisite penalty, submit the chalans with Regional director

office with the covering letter containing request to issue and order allowing

condonation of delay.

3.12.10. Submit the order issued by the regional director with the ROC within the

stipulated time given in the order itself in form INC 28.

3.12.11. After the approval of the form INC 28, get the form CHG-1 (for other than

debentures) or Form CHG-9 (for debentures including rectification) approved. After

due compliance, Registrar shall issue certificate of registration in form CHG-2, where

charge is registered under section 77(1) or 78 or in form CHG-3, where charge is

registered under section 79.

3.13. Process of filing Satisfaction of Charge:

Process of Satisfaction of Charge is as under:-

3.13.1. Gets the letter of satisfaction from the bank containing declaration that

there are no dues towards the facility provided.

3.13.2. Conduct a Board meeting to consider the letter of satisfaction and after

taking note of the same in the said board meeting pass the resolution containing

authorization to file form CHG-4 with letter of satisfaction as an attachment. It

must be noted that the said form CHG-4 is required to be submitted within 30 days

of satisfaction. The period of 300 days is applicable in case of creation/modification

of charges only and for satisfaction of charges, there is no relaxation of time period.

3.13.3. Make entries in the register of Charges maintained in form CHG-7 forthwith

after the satisfaction and get it authenticated by Director or Secretary of the

company or any person authorized by the board.

3.13.4. Submit form CHG-4. After due compliance, Registrar shall issue certificate of

registration of satisfaction in form CHG-5.

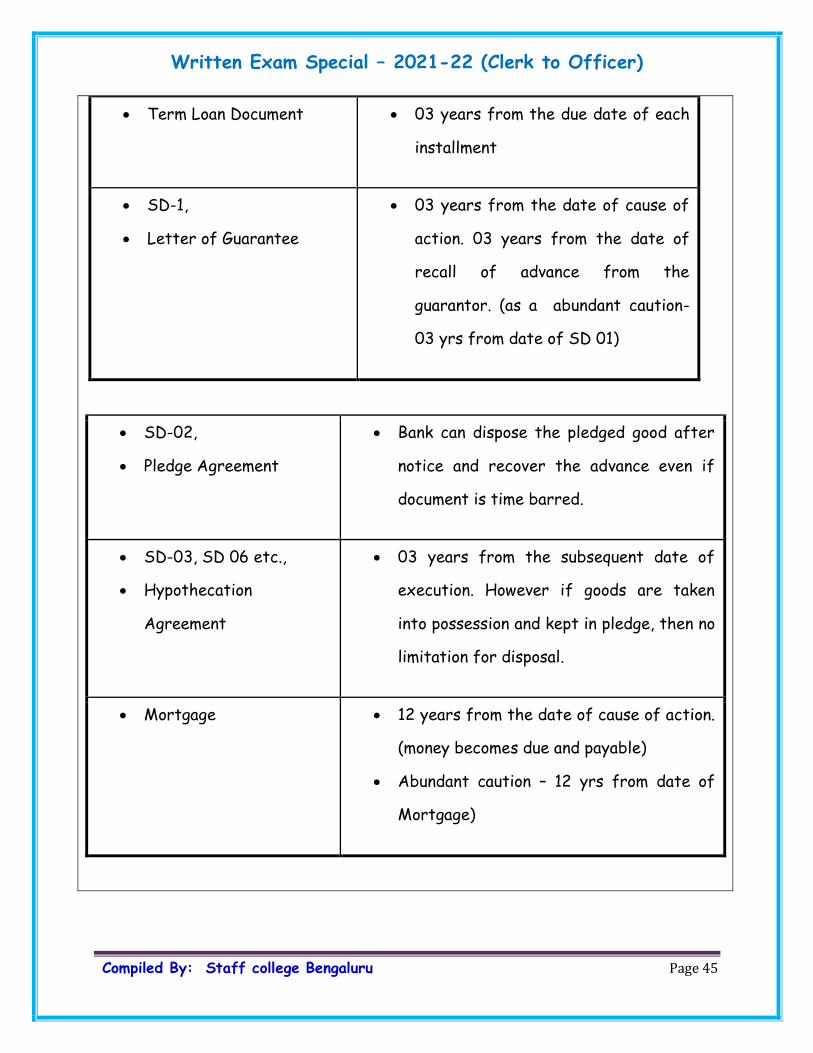

Written Exam Special – 2021-22 (Clerk to Officer)

Compiled By: Staff college Bengaluru Page 42