Basics of Livelihood Plan Preparation

54

Transcript of Basics of Livelihood Plan Preparation

Resource Centre, SPADE52, Garfa Main Road, Kolkata- 700 075

Ph: 033 2418 5452, 2418 6171

Income Enhancement Plan PreparationA Handbook for the Livelihood Facilitators

Income Enhancement Plan Preparation : A Handbook for the Livelihood Facilitators

First Edition : May, 2010Second Revised Edition : January, 2014

Copyright : Publisher(None of the parts of this Book could be published or utilized commercially without written permission of the Publisher)

Published by : Resource Centre, SPADE52, Garfa Main Road, Kolkata-700075, Ph: 033 24185452, 24186171,Email: [email protected],Website: www.spadewb.in

Printer: Mudrakar, 18A, Radhanath Mullick Lane, Kolkata - 700012Email: [email protected]

Since the last decade, SPADE – as a leading Capacity Building Institution, is providing Livelihood Promotion and Facilitation supports to the rural as well as urban poor in West Bengal and beyond through securing support from agencies like NABARD, Panchayat & Rural Development Department, Women Development Undertaking besides the local and International NGOs. In fact, Institution Building and Livelihood Promotion have became the major focus of SPADE and besides facilitating the poor in preparing their Income Enhancement Plans, SPADE is also providing Hand Holding Support in implementation of such Plans, providing Skill Training on selected trades, capacitating the Community Resource Persons in such activities, facilitating Linkage Development with different Government Departments and organising Exposure Visits for small and micro entrepreneurs so as to empower the poor women economically and socially

Income Enhancement Plan (IEP) is basically an innovative tool that has been developed by SPADE to facilitate the members of Self Help Groups (SHGs) to identify suitable trades or activities for themselves with minimal external intervention or influence. This step by step user-friendly tool had already been used by some thousands of SHG members in rural areas and Thrift & Credit Group members of urban areas. In many cases, the SHG members have reported an impressive growth of their income. In fact, preparation of IEP enables the SHG members to think critically before initiating a particular Income Generating Activity and thus helps them to make informed choices – choices based on some valid criteria or good reason.

Introduction

During the process of preparing Income Enhancement Plans, the SHG members would get ample scope to understand: What is the information required? What are the costs involved? What kind of supports or assistances is required? Where or to whom to contact for securing such supports? Thus, a comprehensive business outlook will get developed that will further be fine tuned through conducting local market or Haat Survey. Hence, the process has an in-built mechanism of assuring an ideal blending of conceptual learning and the scope for application of the concepts learned.

One of the interesting features of IEP is that it can not only accommodate the existing Income Generating Activities of the SHG members but also can supplement them so as to make them more profitable. This is so because the tool had been developed in consonance with the reality that poor people earn from a variety of sources and alongside adopts a number of measures to save expenditure.

As a tool IEP is equally effective for both on-farm and off-farm activities. Also, it can be applied across the different business types, viz., Production-oriented, trading or Service-oriented. Thus, it can not be denied that IEP is a highly flexible tool that assists the poor to make their own choice on the basis of some valid reasons.

Thus, we have reasons to believe that the present Handbook shall be of immense help for the Livelihood Facilitators, Federation Leaders, Community Resource Persons and NGO Workers who are actually involved in the task of promoting livelihood for the poor. We hope that the users shall properly follow the methodology described.

The Handbook had been developed by Anubrata Datta. Rajkumar Laskar and Dr. Dipak Bara Panda had also assisted him through providing some invaluable inputs. I am thankful to all of them who have directly or indirectly cooperated in bringing out the publication in time.

With Best Wishes,Baidya Nath PaulGeneral SecretarySPADE

Chapter 1 : About “Jibika”

1.1 What is “Jibika”

1.2 Distinctive features of “Jibika”

1.3 Objectives of this guidebook

1.4 Role of the Facilitators1.5 Methodology ---- at a glance

Chapter 2 : Area and Group

2.1 Selection of area

2.2 Rapport build-up with the area

2.3 Collecting primary data on SHGs

2.4 Information on members2.5 Rapport build-up with the SHGs

Chapter 3: Quick Rating

3.1 What is Quick Rating and why is it necessary

3.2 What steps to take to make a Quick Rating

3.3 Methodology for a Quick Rating

3.4 Making a Quick Rating and giving the certificate

3.5 Analysing the results of a Quick Rating3.6 Training according to the gaps identified of the group

1

1

1

22

4-6

4

4

5

66

7-14

7

8

10

10

1213

1-3

Content

3.7 Planning and training to fill the gaps

3.8 Follow up of training

Chapter 4 : Introduction of Income Enhancement Plan Preparation (IEPP)

4.1 Why should we plan for livelihood

4.2 Different types of generating activities

4.3 Various stages of IEPP

4.4 Fixed costs and variable/recurring costs4.5 Feasibility analysis

Chapter 5 : Implementation of Income Enhancement Plans

5.1 Various stages of IEPP

5.2 Implementation of IEPs

Annexure 1 : Detailed Methodology of Quick Rating

Annexure 2 : Feasibility Analysis

Annexure 3A : Income Enhancement Plan Preparation -- Production

Annexure 3B : Income Enhancement Process ---- Trading

Annexure 3C : Income Enhancement Process ---- Service

Annexure 4 : Information collected on sellers and buyers for feasibility analysis

Annexure 5A : Information sheet

Annexure 5B : Individual Member's Income Enhancement Plan

Annexure 6 : Consolidation of IEPs (Micro Credit Plan) of SHGs

13

14

15-21

15

15

16

1821

22-24

22

˛ 24

25

37

40

41

42

43

43

45

46

1

1.1. What is 'Jibika'?

1.2. Distinctive features of 'Jibika'

Jibika is the acronym of Income Enhancement Plan Preparation. The word 'Jibika' is built with the three initial letters

of 'Jibika Bikash Karyakram'. In English it is known as Income Enhancement Process. This is a continuous process.

Members of an SHG or TCG, who are either individually or together with other members of a group might get involved

or are already involved in a particular livelihood activity; need to have certain basic information at every stage, on the

various requirements of the business or trade. These are as follows:

Probable fixed and recurring costs,

The technical hitches or complications which may arise subsequently,

Who could be approached for assistance and who would be responsible for which job

Devising a project proposal with all this necessary information is generally called as Income Enhancement

Process or 'Jibika' in short.

The methodology of using team work to enhance the present income status

The process is participatory in nature

It helps the members to become self sufficient in developing their programme by utilising their own practical knowledge and experience

It teaches members to modify and improve the present livelihood and plan for a better job or, trade

The economic activity or, plan is better understood with pictures and flow chart

Members are in a position to clearly realise their own roles and those of others.

l

l

l

l

l

l

l

l

l

l

About 'Jibika'Chapter 1:

1.3. Objectives of this guidebook

1.4. Responsibilities of Facilitators

Facilitators assist the SHG members in designing the income enhancement plans and thus they are in need of technical

help themselves; this handbook serves the purpose of capacity building of the facilitators to make 'Jibika' a successful

programme.

Sensitisation of group members on the methodology of Income Enhancement Process or, 'Jibika

Preparation of plans of individual members

Consolidating all the individual plans of the members at the group level

Building linkages with banks and other line departments for mobilising necessary assistance

l

l

l

l

1. Area selection Communicating with SHGs,Clusters etc.

2. Rapport building with localities Awareness Campaign with “Jibika” leaflets

3. Collecting primary information on the local Gathering primary information from the SHG register of SHGs with information of the area the Gram Panchayat and filling up Chart-1 with the same

4. Collecting information about the individual members Filling up Chart-2

5. Establishing regular contacts through the facilitatorsEstablishing contact and interacting with the SHGs

1.5.Methodology - at a glance

Steps Ways in which steps are to be taken

2

6. Getting ready for the Quick Rating by fixing Bringing out a half-page leaflet which is area specificvenue, date and time. and subject based and filling up Chart-3 for collecting

necessary information required for Quick Rating.

7. Quick Rating and giving Certificates (certificates Quick Rating ( Chart-4)will be awarded to the groups getting A and B. Strategies for groups who get C will be decided upon later).

8. Functioning for analysis of the results of Quick Description of specific weaknesses both area and groupRating and removing the gaps of the groups specific (Chart - 5,6,7) and training program based on(planning and training, with necessary assessment Specific weaknesses (Chart-8,9) according to progress made)

9. Follow up of training program Chart-10

10. Increased awareness level on “Jibika” fixing up Modules, leaflets and flow chart (production oriented,venue, date and time for next meeting service and trade specific), distribution of IEP formats

(Chart-11A,11B,11C and12 , Annexure-3A,3B,3C)

11. Survey of Hat and other markets Annexure-4

12. Accepting advise to implement project plans, Responsibilities accepted according to work planfixing responsibilities for implementation, and arranging for monitoringmonitoring and evaluation

[ ]

To form a preliminary idea watch the videodeveloped by SHG Promotional Forum

'Setu Bandhan'

3

2.1 Selection of Area

2.2. Rapport build-up in the Area

In case the donor agency makes the area selection we have nothing to comment on it, but if we have the option to

identify and select an area, we should be alert on certain matters. There should be a fair scope of creating rapport with

the Panchayet, Banks and Government departments and other Non-Governmental Organisations. SHGs in those areas

should be of a good standard and the members should have an entrepreneurial attitude. The above mentioned criteria

will be the deciding factor in the success of 'Jibika'.

It is essential to develop an understanding with the people of our project area. Even though we shall build up rapport

with the whole populace, we shall put stress on building cordial relations with the following ones:

Panchayet Pradhan, Panchayet Members, officials of Panchayat and especially who entrusted with the

responsibility of SHG affairs and ofcourse the Community Resource Persons (CRPs).

Local Self Help Promoting Institutions (SHPIs) or NGOs

Local opinion leaders particularly those who are enthusiastic about the empowerment of women

The officials of the local bank

The office bearers and members of SHGs, Clusters and Federations

Leaflets have to be prepared stating what we wish to do, why and where. As a result, the people of the area will have a

clear understanding of what we are actually going to do. Common people also can easily remember the same. Here we

present a sample of the leaflet. According to requirement this leaflet could be modified and enlarged.

l

l

l

l

l

Chapter 2: The Area and the Group

4

Boost your income with 'Jibika'

You have formed an SHG or are a member of an SHG, but have failed to make yourself or others self- reliant. There was much espectation during the formation of the group, now the feeling is of dejection. But don't be disappointed. With the help of 'Jibika' you can advance towards self-reliance.

Members, either individually or together with a few others are planning to be engaged or are already engaged in a business or trade. They really need to collect information on the basic requirements at various stages of the trade, the probable amount of fixed or recurring costs involved, complications or problems, which may surface, whom to approach for various kinds of assistance and who among the group would be responsible for coordinating with them; 'Jibika' is there to assist you to plan well in advance by providing guidance. Years of experience has proved that 'Jibika' methodology is quite successful in income enhancement. We invite you to avail of this opportunity for implementing the income enhancement plans.

Matter of the leaflet:

2.3. Collection of Primary Information on the SHGs (including area-related information):l

l

Why is collecting primary information vital?Collection of primary information on the existing SHGs in the area where we are supposed to work with the SHGs is

essential. We shall come to know about the exact status of the groups from these data and it is impossible to move

forward without them.

Where will the information be available?To get this information we must first visit the GP office, where the SHG register would be of immense help. Banks are

another great source of information on SHGs. Here is a format on the subject of the information to be collected.

5

Name of District: Name of Block:Serial Name of Name No. of SHG Name of Name and Remarks

No. Gram of SHGs members Mouza/ Gram Tel. No. of

Panchayat Samsad office bearer

Chart-1 Format for collecting primary information on local SHGs

2.4 Information on Members:

The required format for collecting information of members is shown here:

Chart -2: Individual Information schedule of Members:

2.5 Building rapport with the SHGs:

Its better, if communication has already been in vogue with other SHGs. Otherwise, arrangements will have to be made for an open session of interaction with the groups. In this session, we have to be honest and transparent while talking to all present about the objectives of our work. We must ensure that the SHG members feel comfortable with our facilitators.

District: Block: G.P. Name of SHG: ˛

Name of the Member

Serial no

Age

Caste

AP

L / B

PL

Fam

ily Occupation

Gross M

onthly Incom

e of family(in R

s)

Present O

ccupation of M

ember

Average m

onthly incom

e(in Rs)

Special skill, if any

Willing to get involved

in new occupation

If so, why

What kind of assistance

required

6

3.1 What is Quick Rating and why is it Important?Quick Rating is a process of determining the strengths and weaknesses of the Self Help Groups to get loans from the Banks, Federations and other Financial Institutions before assisting in the livelihood related activities of the members of the groups. This rating is done within a short span of time by applying a special method named Panchasutra. The methodology of this rating process is a quite distinctive one. The principal objective of Quick Rating is to determine whether the members of a particular SHG are capable of running a trade successfully with loans from financial institutions.

Quick Rating is a process whereby the eligibility and competency of an SHG are assessed. Generally rating of a SHG is done at definite (e.g., 6 months / 1 year) intervals. To decide the merit or relevance of a particular issue, some corresponding indicators are identified and each indicator is given a score. The sum of the scores obtained against the various indicators is considered to be the outcome of the particular evaluation.

The indicators generally being used in this rating are as follows:---1. a) Number of regular meetings held

b) Members' attendance at the meetings2. On time deposit of savings by members3. Internal lending within the group4. On time loan repayment by members

5. Maintenance and up-dated posting of books of accounts

To be very specific, Quick Rating is important to know the status of SHGs prior to starting livelihood related activities

for the SHG's members. The following information is generated through Quick Rating:-

What is the present status of the SHG

l

Chapter 3: Quick Rating

7

l

l

l

l

What are the main problems of the SHG

How the said problems could be resolved

a) A meeting has to be organised with all the members of the SHG at a fixed venue, date and time, with emphasis on

the location or venue, which is convenient for everyone.

b) The members will have to be informed about the Quick Rating at least a week before the fixed date.

c) At the time of Quick Rating the presence of all the members of the SHG is a must

d) Members will have to be requested to bring all the documents lying with them, for example -- (1) Individual

Passbooks (2) Minutes Book/Meeting Register, (3) Savings Ledger, (4) Loan Ledger, (5)Bank Passbook and (5)

Cash Book etc. will have to be brought at the venue of the meeting

e) The members must be informed about the time required at the meeting, i.e., 2 – 3 hrs -- well in advance

f) Seating arrangements must be made for all the members at the venue

The fact that a Quick Rating is going to be performed - must be made known well in advance to:-The office bearers of the SHG

The facilitators or organisations involved in nurturing the SHG

3.2 What are the steps for conducting Quick Rating correctly :-

8

Recognize the status of your Self Help Group

You have formed the Self Help Group over a long period, yet you can not avail of any loans or any other

advantages. But have you tried finding out, why you are unable to get these? Is your group really strong, or

quite shaky? Have you identified the present standard of your group? Through the process of Quick Rating

you will come to know the actual status of your group. Banks carry out the necessary tests with certain

parameters for grading purposes. Before such grading is conducted by the bank, you better know the status

of your group with the help of Quick Rating. Quick Rating process will identify the exact weaknesses or,

gaps present in your group. You will get the opportunity to fill up the gaps or get rid of the

underperformances of your group. When you have removed the weaknesses of your group apply for Bank

Grading. If weaknesses remain in the group, then there is a high possibility of failing in the Bank Grading

process which is quite strict in nature. To find out the gaps or, weaknesses, Quick Rating is therefore

essential. It increases the acceptability of the SHG to the Banks and other supportive financial institutions.

A leaflet will have to be developed for convenience of group and the format of the leaflet is shown here :-

Matter of the Leaflet:

Name of the District Name of Block

Serial Name of Mouza / Name of Name of Telephone Date of Time of Venue ofno Gram Sansad SHG group leader number Quick Rating Quick Rating Quick Rating

Chart – 3: Plan of Mouza or, Gram Sansad based Quick Rating

9

3.3. Methodology of Quick Rating:

Generally the activities of the past six months of a group are assessed to perform Quick Rating of that group. The indicators of Quick Rating are as follows……..

Indicator Value

No. of regular meetings 10

Attendance of members at the meetings 10

On time deposit of savings by members 20

Internal lending 20

On time loan repayment by members 20

Maintenance and up-dated posting of Books of Accounts 20

1. a)

b)

2.

3.

4.

5.

To measure the indicators stated above a systematic review will have to be done of the following registers:-

1. Minutes Book/Meeting Register 2. Attendance Register

3. Savings Ledger 4. Loan Ledger

5. Bank Passbook 6. Individual Pass-book7. Written Bye- laws of the group 8. Cash Book

The methodology of Quick Rating is illustrated in detail in Annexure – 1A

Grade A and B will be awarded on the basis of obtained marks. Based on the certification appropriate measures will be taken by the facilitators, Cluster and Banks. Granting of Grade:- C depending upon the marks obtained by the SHG will have to be considered after assessing the situation.

3.4. Quick Rating and Certification:

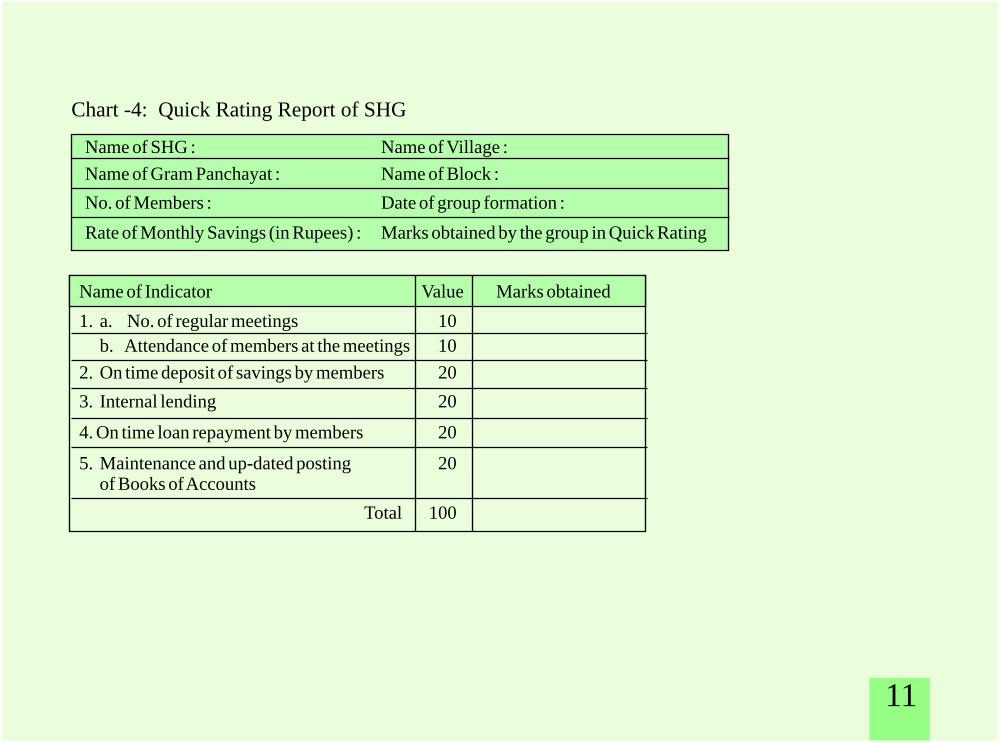

10

Name of Indicator Value Marks obtained

a. No. of regular meetings

b. Attendance of members at the meetings

On time deposit of savings by members

Internal lending

On time loan repayment by members

Maintenance and up-dated posting of Books of Accounts

Total

˛

1. 10

10

2. 20

3. 20

4. 20

5. 20

100

Chart -4: Quick Rating Report of SHG

Name of SHG : Name of Village :

Name of Gram Panchayat : Name of Block :

No. of Members : Date of group formation :

Rate of Monthly Savings (in Rupees) : Marks obtained by the group in Quick Rating

11

Observations of the Evaluator:

Sl No. Weaknesses of the SHG Strategies to be adopted forelimination of weaknesses of the SHG

Date of Quick Rating Signature of Evaluator

3.5. Analysing the results of Quick Rating:Use the following formats

Chart – 5 : Gram Samsad or Area wise Review Report of Quick Rating

Chart – 6: Classification of Self Help Groups on the basis of Quick Rating

District Block

Gram Total No. Total No. of Grade-A Grade-B Grade-C Unsuccessful RemarksPanchayat of SHGs Members

Name of District Name of Block Name of Gram Panchayat

Date of Reporting Evaluator's Signature

Sl. Name of Date of Meeting Attendance Savings Internal Loan On time Marks Remarks No. SHG Quick Lending Disbursement Repayment Obtained

Rating of Loan

12

3.6. Training Program based on gaps of SHG:

Identify the gaps of SHGs with the help of Quick Rating and take necessary measures and also arrange for requisite training of the said SHGs.

Chart – 7: Description of identified weaknesses/gaps of SHGs as per Block based on Quick Rating

Sl. No. Name of Block Indicators Gaps/ Weaknesses

To eliminate weaknesses and gaps of SHGs, necessary provisions should be made for appropriate planning and hand-holding training programs, necessary discussions in an extensive manner. Work must be done .according to progress achieved gradually.

Proper schedule of training should be formed to reduce gaps and weaknesses of SHGs.

Chart – 8: Capacity Building Training Program

Name of Month Name of Trainer

Block G.P. Gram Date of Venue of No. of Number of Participants RemarksSamsad Training Training SHGs

3.7. Training, participatory discussions, particular planning is required to eliminate weaknesses and action must be taken according to progress achieved.

Members Others Total

13

Chart – 9: Assessment Chart of Training Program

District Block G.P. Gram SamsadSl. Name of Name of SHG Initial Present RemarksNo. Trainer Status Status

Training programs should be regular, need based and continuous. To assess the training programs an appropriate format should be used. A sample format is illustrated here…

Chart – 10: Evaluation of Training Program

District Block Gram Panchayat

Contents/ Sub-contents Understood Not understood Remarks

3.8.: Follow up of Training Program

14

4.1. What are the needs for planning for 'Jibika'?

4.2. Various types of Income Generating Activities

1. To bridge the gap between imagination and reality

2. To become successful in the initiative of enterprise and income enhancement

3. Participating critically in enterprise selection and project planning for its successful implementation

4. Before commencing an income generating enterprise one should be aware of the essential primary activities involved, viz., where to go, who are the people to meet, what are the inputs and materials required, how to get those resources, rates, costs involved, where's the market to sell products, expected profit margin from trading of the same etc, All this is necessary to be to achieve the desired success..

5. Everyone should have a clear idea about how much capital is required at different phases and how much profit could be generated in a certain period of time.

6. Income enhancement process should be followed to increase profit and there should always be an effort to reduce the margin of losses, if any.

7. It is mandatory to present a Micro Credit Plan to Banks and other financial institutions to avail of loans for business and the IEP helps one to put into words the said plan for Banks etc.

8. IEP is essential not only to get subsidy or, loans from Banks etc, but also for successfully putting into practice a sustainable income generating activity.

The members of Self Help Groups could be associated with three broad categories of income generating activities.

These are as follows:

Chapter 4: Introduction of Income Enhancement Process (IEPP)

15

l

l

l

l

l

l

l

l

l

Production: Raw materials are purchased from the market and passed through several processes and

converted to produce a finished product which is then sold in the market to earn profit, for example, paddy

cultivation, goat rearing, pisciculture, jam making, weaving of towel etc.

Trading: Buying and selling of any particular product on a continuous basis to earn profit is known as trading,

for example grocery shop, clothing outlet, fertiliser or pesticide selling etc.

Service: There is another sector which is different from the businesses of producing or trading of anything

which you can see or touch, i.e., service, where you serve the consumer in a specific manner. Such as band

party, van/rickshaw driving, CD shop, beauty-parlour etc.

1. Inputs:Once purchased or built, these can be utilised for quite a long time.

There is no direct relation between the quantity of inputs with that of the produce or finished product.

In course of the production processes there are no fixed or tangible changes with the inputs. Such as in case of goat rearing, the inputs are the rope used to tie up the goats, water container, goat shelter etc. which is used over and over again.

2. Raw Materials:Repeated procurement of raw materials is a must for production.

The quantity of finished goods are directly proportionate to the quantity of raw materials.

There is a tangible change of raw materials in production processes and raw material is converted into a part of the new produce, e.g. in case of goat rearing, raw materials are kids, grower feed, medicines, grass etc. Raw material is converted into functional produce and is illustrated here:

4.3. Various Stages of IEPP

16

Income generating activities Inputs Raw Materials

House Diary Tying Rope, Fodder, Water Container, Calves, Cereal, Grass, MedicineCowshed

Tailoring Sewing Machine, Scissors, Tape, Chair Thread, Cloth, Machine Oil

˚

3. Production Process or Value Addition:Production or value addition is a process which involves several steps.

In this process capital and labour is mixed with the raw materials procured from market.

As a result a new product is produced which is both usable and marketable.

e.g., molasses created from sugarcane.

4. Marketing:Generally marketing is defined as anticipation of buyer's demand, producing or procuring merchandise accordingly, fixing the right price of the said merchandise or service and earning a profit by the sale of the same.

Prerequisites of right kind of marketing:Who are the prospective customers? What should be the quality and price of the product- which is of utmost importance to these customers? What are the quality factors they look for in a product?

Find out the exact nature of their demands?

l

l

l

l

l

17

Find out the target group whose demands are to be fulfilled

Find out how to fulfil those particular demands

Find out who are your competitors in the market and gather information on the quality and pricing of their products or services

Find out how to improve the quality of your products or services

What kind of infrastructure is required for marketing (Permanent shop, electricity / water connection, furniture etc.)?

Will you sell the products yourself or, through wholesale distributors?

Will you sell your products from home/ local market / hats / nearby town?

Is transport available there to reach the market and how much expensive is it?

Try to figure out the exact nature of demand of the product, duration of the demand, target group and also quantify the demand level in the market

You need to know when the rates of your products go up, find out the reasons behind it

More than a few forms of expenditures are associated with initiating a new enterprise or to continue with an established one. Proper accounting of all the expenditures associated with the business must be done in order to keep a track on the profit and/or loss made by the enterprise. Otherwise it would be difficult to keep the business operational. The expenditures associated with business are divided into two major heads:

Fixed Costs: There are certain expenses which occur only once to begin or run the businesses. These have no or little relation with the production or sale in the business and are known as fixed costs. With the increase in volume of

l

l

l

l

l

l

l

l

l

l

4.4. Fixed Costs and Recurring/Variable Costs:

18

production or more sales, there shall be no change in the fixed expenditures. That is why, in the beginning, if production could be raised, per unit cost of production with respect to fixed expenditure will be minimised.

Recurring/Variable Costs: The expenditures made repeatedly or quite often are called recurring expenditures. Recurring expenditures also change with the variation in production or sales. Recurring expenditures could be daily/weekly/monthly ones, or as per the business cycle. Fixed and recurring expenditures are illustrated here:

Income Generating Activities Fixed Cost Recurring Cost

Goatery Shed, Food bowl, Water container, Rope, Cereal, Medicine, Transport,Hessian Cloth, Cost of Goat Selling expenses

Pisciculture Fishing Net, Basket, Pong, Lime, Cost of Fish Spawn,Bucket Selling expenses

˛ ˛

19

Please discuss amongst yourselves to decide which are fixed costs and which are recurring costs from the chart shown here;

Identification of fixed and recurring costs: Goat rearing

The different expenditures are listed here. To identify the fixed and recurring costs please tick (ü) in the right box.

Items Fixed Cost Recurring Cost

Hessian Cloth

Cost of Goat

Subscription for market committee

Rope

Water container

Grower feed

Medicines

Medicines

Cost of shed

Insurance charges

Food for seller

Transport

Food bowl

˛

20

l

l

l

l

l

l

l

Total expenditures:In case of IEP the sum of fixed costs and recurring costs over a certain period of time is the amount of total investment or expenditure.

Net Profit:A part of the fixed costs and recurring costs are deducted from gross turnover to calculate the surplus and this surplus amount is the net profit. The formula is thus: Net Profit=Gross turnover less Recurring costs less Interest loan less Depreciation.

Why feasibility analysis of a project is necessary:

Before the commencement of a particular income generating activity, the SHG members ought to analyse the feasibility of the same if it's really to be useful in the preparation of the project proposal. If this could be done – the project would be a sustainable and a profitable one. The process or method of analysing an income generating activity before it has commenced, to validate its appropriateness is generally known as feasibility analysis. If the feasibility analysis is done well before the commencement of the project, certain advantages are there, viz,

Certain most necessary precautionary measures and alternative arrangements are identified and undertaken to reduce the risks associated with the implementation of the project

Out of a bunch of projects the most viable one is chosen carefully for implementation

The project could be anticipated, if the members of the SHGs are skilled enough to properly utilise the funds received from Banks/SHGs

It can also be conceptualised whether or not the members of SHGs would be able to implement the project successfully and refund the loans taken for the same project.

It could be ascertained If the project would be a profitable one.

Feasibility Analysis is illustrated in Annexure -2

4.5. Feasibility Analysis:

21

5.1. Different stages of IEPP and how to get it done:

l

l

l

Members are sensitised on the introductory concepts of various forms of income generating activities. Then with

the help of pictorial charts, all the activities related to the particular activity is explained to the members.

Annexure -3A, B, C).

Information are provided with the drawings on various problems related to the trade -- how the difficulties

develop, how to reach out for help and information related to income and expenditures

We have to keep in mind that in the case of 'Jibika' planning the steps mentioned above are very important. With

the help of these we can have a first-hand knowledge of all the nitty-gritties of 'Jibika' and we also become aware

of what are the requirements for that particular work or, trade, the possible expenditures, who could be of help in

case of need etc. Suppose we think of fish seedlings for pisciculture. Members should know whether locally

available items are better or whether those are apt to die prematurely. Members should be aware of all the pros and

cons of the matter. All the members of the family should be involved in this exercise from the beginning. This is

because; in many cases family members are associated with all the financial activities.

The market survey for the said income generating activities shall have to be carried out(Annexure-4).Whatever

be the IEP plan, market survey is very crucial for production, trade or, service. For an IEP the information on

Chapter 5: Implementation of Income Enhancement Plan Preparation (IEPP)

22

market or hat, functional time in a week, management of market, general footfall at the hat or market is essential.

What are the products or service available largely here; to what extent is there demand? How is the demand for

other products and are the buyers unable to get those products? If so, why? All these information can be made

available from the market or hat. These would be of immense value to the SHG members pursuing an IEP.

Market is directly or indirectly related to any form of income generating activities. It might be related to

marketing of the finished goods, procurement of raw materials, production, the requirements related to

production or necessary technology etc

These formats are to be filled up after completion of market survey. Ensure the participation of family members.

Knowledgeable persons in the trade should be included in the discussion in an open manner. The formats should

be filled up in such participatory manner. This should be the first draft of members' income enhancement plans.

The format should be filled up based on all available information. An example is shown on Muri making

(Annexure -5A, B).

Based on these plans, a consolidated Micro Credit Plan (MCP) is prepared for all the members of the SHG. The

amount of loan required, type of training required, type of assistance to be made available from a certain sector --

everything should be there in this plan. With this MCP; Banks, Panchayat, other line departments and NGOs

should be approached for possible assistance. The SHG can take all necessary steps including discussions with

the Community Resource Persons and Clusters with the help of this draft plan (Annexure- 6).

l

l

l

23

˛

District Block

G.P. Mouza / Sansad

Name of SHG Date of MCP

Serial Name of Principal Availability of Duration ResponsibleNo Trade Responsibility assistance from persons

Once the MCP is ready, find out the necessary assistance required by members. Roles and responsibilities

are to be allocated among the members. Everyone has to accomplish the responsibilities assigned to her

maintaining coordination amongst all to succeed as a closely knit team.

A plan has to be made compiling all the group activities at the Cluster of NGO level to figure out the necessary support and monitoring mechanism to be adopted

Systematic monitoring is essential for a flawless implementation of IEPP. The facilitator will prepare a format of his/her own for the purpose of monitoring.

5.2 Implementation of the IEPP:

l

l

l

Consolidation of all the assistance required by the members of the SHG and linkage with various departments are to be done in the way shown here in the Chart below:-

24

1. a. Number of regular meetings held:

The Minutes Book/Meeting Register of the SHG is to be checked to measure this indicator. The Minutes Book

indicates how many meetings were held in the past six months. The actual number of meetings scheduled to be held in

the last six months as per the bye-laws of the SHG has to be found out from the members. Hence, a calculation has to be

done of the number of meetings scheduled to be held and the actual number of meetings held in the past six months to

find out the Meeting Indicator of the period.

For instance, suppose Nibedita Group was scheduled to have (as per the bye-laws of Group) 4X6=24 No. of meetings

in the past six months.

The Real Picture:

January February March April May June Total no of meetings held

3 4 2 3 3 2 17

Formula:

Total number of regular meetings held

Total no of meetings scheduled

The numerical value of meeting indicator of Nibedita SHG is 7.08 in the last six months

It is to be remembered that this issue cannot be raised in any special or, emergency meeting.

«

× 10 = × 10 = 7.081724

Annexure – 1: Detailed methodology of Quick Rating

25

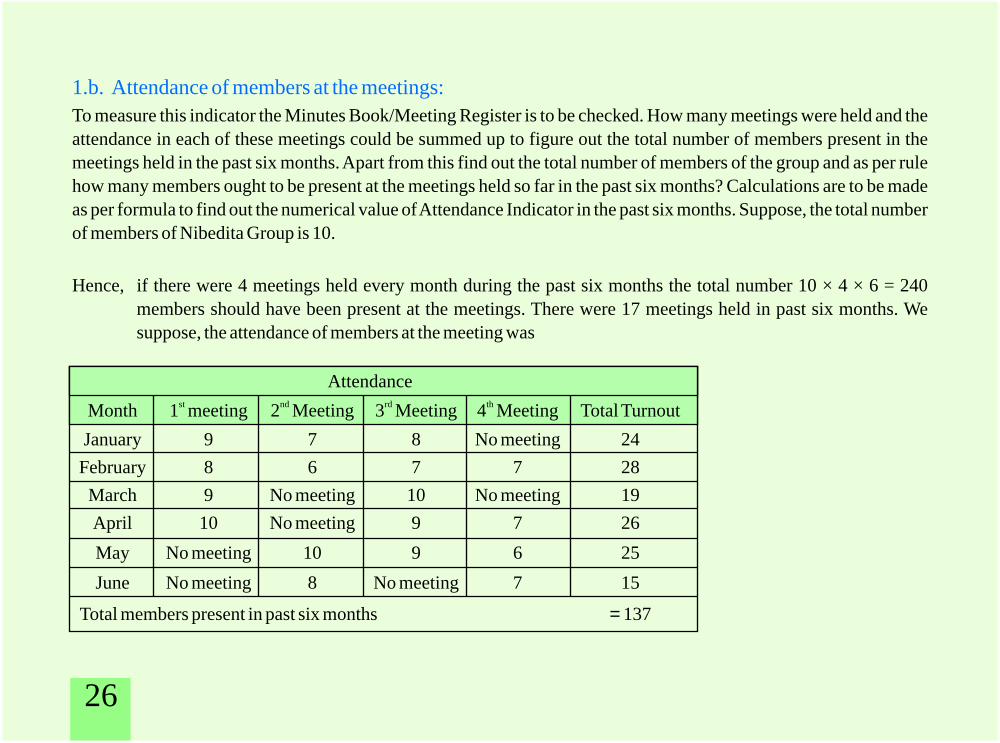

1.b. Attendance of members at the meetings:

To measure this indicator the Minutes Book/Meeting Register is to be checked. How many meetings were held and the

attendance in each of these meetings could be summed up to figure out the total number of members present in the

meetings held in the past six months. Apart from this find out the total number of members of the group and as per rule

how many members ought to be present at the meetings held so far in the past six months? Calculations are to be made

as per formula to find out the numerical value of Attendance Indicator in the past six months. Suppose, the total number

of members of Nibedita Group is 10.

Hence, if there were 4 meetings held every month during the past six months the total number

members should have been present at the meetings. There were 17 meetings held in past six months. We

suppose, the attendance of members at the meeting was

Attendancest nd rd thMonth 1 meeting 2 Meeting 3 Meeting 4 Meeting Total Turnout

January 9 7 8 No meeting 24

February 8 6 7 7 28

March 9 No meeting 10 No meeting 19

April 10 No meeting 9 7 26

May No meeting 10 9 6 25

June No meeting 8 No meeting 7 15

Total members present in past six months 137

10 × 4 6 = 240

=

×

26

Formula:

Total number of members present

Total number of members should have been present

Attendance indicator of Nibedita SHG in the last six months is 5.7

The measurement of this indicator Savings Ledger and Bank passbook of the SHG must be checked. If necessary the

Cash Book might also be checked. Find out the total number of members and the scheduled monthly savings amount of

each member every month. There we come to know the total amount of savings deposit each month. For instance, no of

members is 10 and monthly savings deposit is Rs. 30/- for each member every month, then savings deposit every

month should be 10 30=300/- and total amount of savings in six months should be 300 6 = 1800/- and Bank Pass

Book should reflect the same amount in the past six months.

For instance, suppose each of the 10 members of Nibedita group deposits 30/- each month and the monthly amount is

300/-.. Then in six months the amount should be 300 6=1800/-

Savings deposited in last six months:

January February March April May June Total

«

× ×

×

300 240 330 300 270 300 1740

2. On time deposit of savings by members:

× 10 = × 10 = 5.7137240

27

Formula:

Total amount of on time payment of savings

Total amount planned to be saved

The savings deposit indicator of Nibedita SHG is 19

To measure this indicator one has to check the internal lending part of the Loan Ledger and Cash Book. We have to find

out the velocity of internal lending. Let us find out the amount of loan disbursed in the first six months, and then we

must check the group corpus in the last six months. Now we see, Group corpus = total savings + bank interest + interest

on loan received from members + collection of penalties + other incomes of the SHG. Bank loan is not added here.

Average corpus of the group in the last six months has to be calculated. That means, (Opening corpus at the beginning

of 6 months + Closing corpus on the last day of 6 months period) 2 = Average corpus of the group.

Now we have to calculate the exact value of internal lending Indicator by using the formula.

For instance, we suppose the savings of Nibedita SHG till date is 3600/- + bank interest 25/- + interest on internal

lending 150/- = Group corpus 3775/-. Till date internal loan disbursed is 2000/- . Suppose the opening

corpus of the group 6 months back was 1975/- . Hence the average corpus= (1975+3775) 2 = 2875/- .

«

÷

÷

3. Internal Lending :

× 20 = × 20 = 19.3317401800

28

Formula:

Total Amount of internal loan

Average corpus

According to formula we get the numerical value which is equivalent to the loan disbursed out of corpus.

Standardisation will be based on this value.

A. Over 1.5 times

B. Between 1 – 1.5 times

C. Between 0.5 – 0.9

D. Less than 0.5

The internal lending indicator of Nibedita SHG is 5.

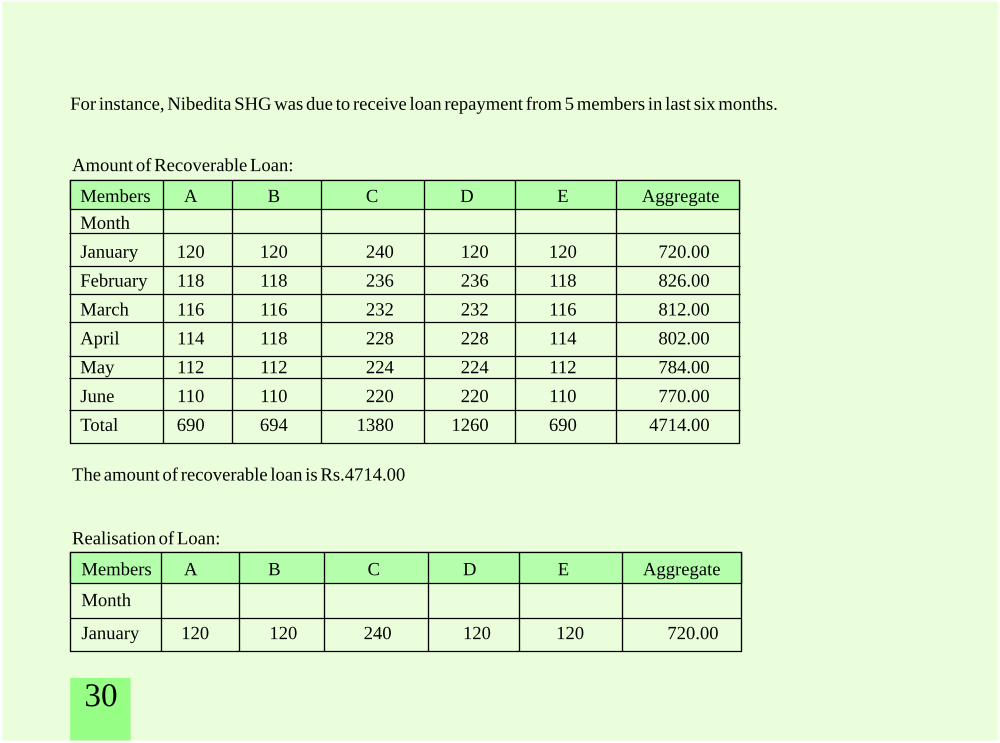

To measure this indicator we need to check the Loan Ledger, members Passbook and Cash Book. The number of

members granted loan and the amount due from each of them in the last 6 months must be ascertained. The recoverable

loan amount of the SHG in the last 6 months must also be known. The total amount of loan repaid by the members in the

same period must also be checked. Then the value of on-time loan repayment indicator can be deduced.

20

10

5

0

«

4. On Time Loan Repayment:

2000

2875= = 0.69

29

For instance, Nibedita SHG was due to receive loan repayment from 5 members in last six months.

Amount of Recoverable Loan:

Members A B C D E Aggregate

Month

January

February

March

April

May

June

Total

The amount of recoverable loan is Rs.4714.00

Realisation of Loan:

Members A B C D E Aggregate

Month

January

120 120 240 120 120 720.00

118 118 236 236 118 826.00

116 116 232 232 116 812.00

114 118 228 228 114 802.00

112 112 224 224 112 784.00

110 110 220 220 110 770.00

690 694 1380 1260 690 4714.00

120 120 240 120 120 720.00

30

... 118 36 236 ... 390

134 116 336 232 236 1054

114 114 332 228 114 902

150 112 200 224 ... 686

110 110 150 220 112 702

628 690 1294 1260 582 4454

February

March

April

May

June

July

Formula:

Total amount of loan repaid

Total amount of recoverable loan

The acquired numerical value of on-time loan repayment is 18.89

To measure this indicator, at least 5 types of registers of the SHGs, viz. Individual Passbook, Meeting Register,

Savings Ledger, Loan Ledger and Cash Book need to be checked. Marks are allotted for each register. If the registers

are up-to-date in all respects then the Group receives full marks. If registers are not updated then the marks will be

reduced proportionately.

«

5. Maintenance and Updated posting of Books of accounts:

× 20 = × 20 = 18.894454

4714

31

Suppose the Individual Passbook, Meeting Register and Savings ledger of Nibedita SHG were updated in the last 6 months. Loan Ledger and Cash Book were not done for 1 month and 2 months respectively.

Formula:

Register Value

1. Individual Passbook 4

2. Meeting Register 4

3. Savings Ledger 4

4. Loan Ledger 4

5. Cash Book 4

Total Marks 20

In this case the marks obtained by Nibedita SHG will be

Register Marks Obtained

1. Personal Handbook 4

2. Meeting resolution register 4

3. Savings Ledger 4

4. Loan Ledger

5. Cash Book

Total Marks

«

17.99

× 4 = = 3.33

× 4 = = 2.66

2

23

3

56

46

103

83

32

Grading of SHG:

Indicator Indicator Value

1. a) Number of regular meetings held 10

b) Attendance of the members at the meeting 10

2. On time deposit of savings by members 20

3. Internal lending 20

4. On time loan repayment by members 20

5. Maintenance and up-dated posting of books of accounts 20

Total value for 5 indicators 100

Here 5 indicators have been used. Now we have to calculate the marks obtained by the group. The sum of the values of indicators is the marks obtained by group.

Marks obtained by Nibedita SHG in Quick Rating:

Indicator Indicator Value

1. a) No of regular meetings held

b) Attendance of the members at the meeting

2. On time deposit of savings by members

«

7.08

5.7

19.33

33

5

18.89

17.99

73.99

3. Internal lending

4. On time loan repayment by members

5. Maintenance and up-dated posting of books of accounts

Total

Henceforth, the following formula will have to be used to find out the grade of the SHG in Quick Rating ---

Total marks obtained Rating

80 or more A

70 – 79 B

60 – 69 C

Below 60 D

Hence, the grade of Nibedita SHG is “B”.

If there are many SHGs in a Cluster or, Federation, please prepare a list as illustrated here.

Assessment Report of SHGs:

34

Name of G.P. ...........................................................................................................................

Name of Block ........................................................... District ...............................................

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

Sl. Name of Age of SHG Members Date of Marks Grade RemarksNo. SHG (month /year) at present Rating obtained

A roll of Grades obtained by the SHGs in a Cluster / Federation

35

Name of the Evaluator: Name of Block:

Name of G.P.: District:

Format for Assessment of SHGs

Date of Q

uickR

ating

Serial N

o

Nam

e of SH

G

Address

No of m

embers

Age of S

HG

Marks obtained in Quick Rating

Rating of the

SH

G

In case ofQuick Rating

Difficulties observed

Benefits experienced

Total

Maintenance of

Accounts

On-tim

e loan repaym

ent

Internal lending

Savings

Attendance

Meetings

36

To analyse the feasibility of a certain income generating activity, one has to verify the following areas:

Technical Feasibility–

Financial Feasibility–

Commercial Feasibility–

A) Technical feasibility can be defined as to whether the infrastructure, equipment, raw

materials, production process to be utilised as described in the IEP are the right matter and sufficient for the project. At this stage more stress is exerted on the technology used for the production, raw materials, infrastructure, optimal utilisation capacity of the machines and the limits thereof etc. These are the most important matters. How the raw materials have been sourced and from where and what would be the quality of the same. How and where the machines are going to be installed, whether sufficient precautionary measures have been taken for machines etc. Supply of raw materials is to be ensured throughout and production capacity to be used fully to achieve the time frame of the project. A continuous supply of water and electricity will have to be ensured to achieve production targets. How the effluents and garbage disposal will be taken care of successfully or the pollution level will be tackled effectively, all these have to be analysed at this stage.

B) Generally the financial transactions and related issues are analysed in this phase. If the

pricing of the services or of products have been correctly done; if there is any crisis related to the working capital after the project has begun; at various stages, the amount of money to be held in as cash balance or, in Bank remaining as such – all these will have to be checked. How to curtail escalating costs, if cash in handy is enough to operate the project at various stages; if ratio of labour to production is in right proportion; whether production capacity is proportionate to the storage capacity and distribution strength. All these are analysed in financial feasibility study.

C) At this stage the commercial viability of the project is being analysed – if the project

as a business will be a profitable one. Generally the SHG members are interested in producing the items they are capable of, but they fail to realise the fact that these products must have a demand in the local market and even if

È

È

È

Annexure – 2: Analysis of Feasibility

37

there's a demand, their products may fail in the quality test. Members must realise that other products have already flooded the markets which are machine made and of better quality. For instance we may consider the making of petticoats, blouses etc. They know the tailoring job and as they have the sewing machine at home, they think it's a better option for them. But today, there are machine made better quality products coming from outside and their dress materials are falling behind. It is really difficult for them to compete in the market with their products, and there comes the question of commercial viability of a particular trade or occupation. When we discuss about commercial feasibility it's important to give stress on the following :-

If the product or service has demand in the marketIf the products would be able to compete with similar products available in the marketHow is the level of competition of the product in market and what is the pricing of competitors' products compared to oursIf the demand of local market can be fulfilled by the produce in our proposed project – i.e. if the demand in local market is of higher quantity or lower than our production capacityWhether produce from the proposed project can be sold in local market for cash or on credit. If we have to sell the products on credit then when do we get the payment and in between how we arrange for working capital

D) In this phase we try to analyse the social factors related to the project. Before the

implementation of a project one must analyse the social stigma, values, local culture and customs etc. What is the status of the member in her family, if the other family members will support her project. The status of the families in society and the way local people think, all these factors should be thought of before we initiate a project in an area. All the pros and cons of a particular project in a region must be analysed: such as the family custom, values and social stigma. These play significant roles in the success or failure of the project involving women. During the project preparation we should think if the family members and her neighbours would be of any help or create trouble for the project selected. While analysing the social probability of a certain project we should try to find out the following answers :-

Will it be necessary to travel outside the village for business related matters?

È

l

l

l

l

l

l

Social Feasibility–

38

.ä È

l

l

l

l

l

l

l

l

l

l

l

l

l

l

l

l

If objections would come from other family members?How many visits to other places will be required? And how far will a member have to travel?How much time it would take?Are there necessary public transport arrangements to travel safely?If the duties and travel will be finished by the day and she will be back at home the same day? Because it would not be possible for her to stay out of village at night.Is it necessary to take permission from any Government department or any other authority to begin a business or trade?Is license required? If so, where to visit for the purpose? What are the procedures involved? Does it require money to get license? What are the documents required?

Here we resolve to decide if there is a demand or, market of the

proposed product /services of our project and if so, where and how it could be sold. We do also analyse the reaction of the buyers and that of our competitors. If we do not analyse the feasibility of marketing logically, it will be extremely difficult afterwards to sell our products or services when products are ready for the market. During the market feasibility study we should look for answers to the following queries :-

Is there any demand in the market? Frequency of use? If the product is for everyone's usage or for the use of a particular section of people? Used throughout the year or during a certain period?How's the competition in market?Price or quality, what do customers look for?Where to sell the product?Who are the buyers?How the buyers decide on the quality of the product and pick and choose the sameIn present circumstances from whom are the buyers purchasing?At what price they are buying the product or service?Whether product will be sold by the SHG itself or through wholesalers?

Feasibility study of Market and Marketing–

39

Name of Project: Muri making Type of Project: Production related

Stages Information required Income Expenditure Remarks

Annexure – 3A: Income Enhancement Plan Preparation

40

Project name: Trading of Vegetables Project type: Trading

Stages Information required Income Expenditure Remarks

Annexure – 3B: Income Enhancement Plan Preparation

41

Project: Mobile Tailoring unit Project type: Service

Stages Information required Income Expenditure Remarks

Annexure – 3C: Income Enhancement Plan Preparation

42

Name of Market: Address/Location of Market:Name of G.P.: Name of Block:District :

Name of Market: Address/Location of Market:Name of G.P.: Name of Block:

Information collected on Sellers/Vendors for feasibility analysis of the productAnnexure – 4:

Remarks

Serial N

o.

Nam

e of IEP

Activity

No. of S

hops

Type of activity

Descriptionof Products

Location ofproduction

Feasibility of the activity

Low

Quantity

Am

ount(R

s)

From

own

village

From

outsidethevillage

High

Medium

Information collected on Buyers in the market for feasibility analysis:

Remarks

Serial N

o

Price of the

product

Quantity

purchased

Why do you buy from this market?

Unavailable

elsewhere

Low

Price

Good

Quality

Product

Provision

ofbargaining

Availability

of several

types of

products

Extended

durationof them

arket

43

SHG: Amader Sankalpa Swanirvar Gosthee Member: Kalyani Halder Name of Activity: Muri making

4500.00 .............1000.00 .............

225.00 ............. 60.00 .............

800.00 .............30.00 .............

400.00 .............

............. ............. 90.00 .............

200.00 .............

200.00 .............

300.00 ............. 3000.00 .............

200.00 .............195.00 .............

............. 7700

11200 7700

Information required Expenditure IncomeParticulars (Rs) Particulars (Rs)

Rice- Krishnahati BazarKhari- Bamna BazarKuron- Meerut Rice MillSalt- Barisal ParaKadai- Amtala BazarLarge Spoon- Amtala BazarDhali and Khejur Pati- Krishnahati Bazar

Labour- SelfHessian Bag- Nepalganj BazarPlastic Bag-Amtala Bazar

Sign Board- Pailan Bazar

Weighing Scale- Amtala BazarCycle- Amtala BazarWeights-AmtalaPolybags/Paper Bags – Amtala BazarSale proceeds

Total

Pictures

Annexure – 5A: Information Sheet

44

Activity:Muri making Member: Kalyani Halder Group:Amader Sankalpa SHG Village: BarishalparaG.P.:Amgachia Block: Bishnupur-1 Production scale: 1000 Kg. Rice daily (25 days in a month)

Various

Stages

Essential Information Cost Difficulties/

ProblemsAssistance required Responsibility

Fixed Cost RecurringCost

What type From whom

Input &

Raw

materials

Production

and

Value

Addition

Marketing

of

Product

Rice- Krishnahati BazarKhari- Bamna BazarKuron- Meerut Rice MillSalt- Barisal ParaKadai- Amtala BazarLarge Spoon-Amtala BazarDhali- KrishnahatiKhejur Pati-Krishnahati Bazar

Labour- SelfHessian Bag-Nepalganj BazarPlastic Bag and Rope –Amtala Bazar

Sign Board- Pailan BazarWeighing Scale- Amtala BazarCycle – Amtala BazarWeights-AmtalaPolybags / Paper Bags

Amtala Bazar

– 4500.00– 1000.00 – 225.00– 60.00

800.00 – 30.00 –

100.00 – 300.00 –

– – 90.00 – 200.00 –

200.00300.00

3000 .00

– 125.00

200.00 70.00

o ˛ o ˛ o ˛ o ˛o ˛

o ˛ o ˛ o ˛ o ˛o ˛

o o ˛ o ˛ o ˛o ˛ o ˛

o ˛ o ˛o

o o o o ˛o o o ˛

o o ˛o

o

Lack of Good Rice Self required capital quality rice wholesaler SHGNon- Loan SHG Clusteravailability of assistance Bankgood qualityrice for Muri locally

Process is Loan Bank Self

difficult in assistance SHG SHG

monsoon Space for Cluster

Lack of storage storagespace in monsoonCredit sale Loan SHG Self

Transport assistance Business SHG

problem Initiative of community Cluster

Problems of Business local market Association

PermanentShop

5220.00 5980.00

Annexure – 5B: Individual Income Enhancement Plan

- -

- -

-

Total capital: Rs. 11,200.00a) Fixed cost : Rs. 5220.00b) Recurring : Rs. 5980.00

Total Income: Sale value of Muri -- 7700.00Less Recurring costs– 5980.00Profit: 1720.00

Signature of SHG member/plannerDate

Signature of SHG office bearer with sealDate

45

SHG: Amader Swanirvar Gosthi Village: Barisalpara

G.P: Amgachia Block: Bishnupur-1 District: 24 Pargana (S)

Sl. Member Proposed Project Cost Amount of Capital (Rs) RemarksNo. Scheme

1 11200.00 1000.00 1000.00 9200.00 11200.00

2 û 7500.00 500.00 1000.00 6000.00 7500.00

3 7500.00 500.00 500.00 6500.00 7500.00

4 10000.00 1500.00 1500.00 7000.00 10000.00

5 13000.00 3000.00 1500.00 8500.00 13000.00

6 10000.00 1000.00 1000.00 8000.00 10000.00

7 7500.00 500.00 1000.00 6000.00 7500.00

8 11000.00 1500.00 1000.00 8500.00 11000.00 –

9 7500.00 500.00 1000.00 6000.00 7500.00

10 8500.00 1000.00 1000.00 6500.00 8500.00

Kalyani Halder Fried Rice –

Pratima Thaku Goatery Insurance required

Kalpana Das

Srabani Pal Poultry Insurance required

Rita Mistri Fishery Insurance required

Dipana Sil Fried Rice –

Babi Majumder Goatery Insurance required

Rita Das Grocery Shop

Rina Mondal Goatery Insurance required

Krishna Halder Jute Bag School trained

Annexure – 6: Consolidation of IEPs (Micro Credit Plan) of SHGs

Own Group Bank Total

Use ofOrganic manure

VegetableCultivation

46

Signature with seal of SHG Office Bearers :

President Secretary TreasurerDate Date Date