Basic concept in cost - Dnyansagar Arts & Commerce College

25

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA PROF. MUBINA ATTARI www.dacc.edu.in UNIT:1 Basic concept in cost Q:1) Explain single cost unit and composite cost unit with example. Q:2) Explain the advantages of cost accounting. Q:3) Explain the term cost, costing and cost accounting Q:4) Difference between costing and cost Accountancy. Q:5) Write a short note on: 1) Cost Unit and Cost Centre. 2) Limitation of Financial Accounting. 3) Objective of Cost Accounting. 4) Difference between costing and cost Accountancy.

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Basic concept in cost - Dnyansagar Arts & Commerce College

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

UNIT:1

Basic concept in cost

Q:1) Explain single cost unit and composite cost unit with example. Q:2) Explain the advantages of cost accounting. Q:3) Explain the term cost, costing and cost accounting Q:4) Difference between costing and cost Accountancy. Q:5) Write a short note on:

1) Cost Unit and Cost Centre. 2) Limitation of Financial Accounting. 3) Objective of Cost Accounting. 4) Difference between costing and cost Accountancy.

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

UNIT:2

Elements of cost and Cost Sheet

Q:1) Explain Prime cost with example. Q:2) Explain classification of cost on the basis of controllability. Q:3) Write a short note on elements of cost. Q:4) Difference between Fixed cost and Variable cost. Q:5) Explain Sunk cost, opportunity cost with suitable example. Practical Question: Q:1) The accounts of Yash Manufacturing Company for the year ended December, 2013 show the following particulars: Factory office salaries 6,500 General office salaries 12,000 Carriage outward 4,300 Carriage on purchases 7,100 Bad Debts 6,500 Repairs of Plant and Machinery 4400 Rates, Taxes and Insurance Factory 8500 Office 2,000 Sales 450000 Stock of Materials 31stDecember,2012 62,800 31stDecember,2013 48,000 Income Tax 1,500 Material Purchased 1,85,000 Travelling Expenses 2,100 Travellers Salaries 8,800 Productive Wages 1,26,000 Depreciation Plant and Machinery 6000 Furniture 300 Directors Fees 6,500 Gas and Water Factory 1,200 Office 400 Dividend 10,000

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

Prepare cost sheet giving the following information: (a) Material Consumed (b) Prime Cost (c) Factory Cost (d) Cost of Production (e) Total Cost (f) Net Profit. Q:2) The following details have been obtained from the cost records of 4. Neelkamal Ltd., Pune for the year ended 31st March, 2014:

Stock of operating materials as on 1-4-2016 30,000 Wages paid to Direct Workers 55,000 Interim Dividend paid 12,000 Purchases of Raw Materials 87,000 Heating and lighting 36,000 Counting House Salaries 20,000 Carriage on purchase of Raw Materials 3,000 Commission on Sales 5,000 Wages Payables 5,000 Technical Director’s Fees 10,000 Stock of operating materials as on 31-3-2015 40,000 Showroom Expenses 7,000 Establishment Cost 12,000 Share Transfer Fees 2,000 Expenses of Testing Labs 4,000 Branch Office Expenses 8,000 Aftersales Service Expenses 8,000 Selling Price 250000

Prepare cost sheet showing : (i) Cost of Raw Material consumed (ii) Prime Cost (iii) Works Cost (iv) Cost of Production (v) Total Cost (vi) Profit or Loss. Q:3) From the following information prepare a statement of cost relating to Murphy Traders Mumbai for the year ended 31st March 2017

Cost of Direct Materials 2,00,000 Sales 4,00,000 Direct wages 1,00,000 Office Indirect Materials 5,000 Cost of special patterns 40,000 Postage and Telegrams 2,000 Factory rent and insurance 5,000

General Expenses 3,400 Managers Salary (3/4 factory and 1/4 office) 10000

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

Outstanding chargeable exp. 2,000 Carriage outwards 2,500 Interest on loan 2,150 Printing and stationery 500 Factory Indirect wages 3,000 Selling on cost 4,000 Travelling salesman’s salary 4,000 Factory indirect material 1,000 Royalties 8,000 General works overheads 2,000 Bad debts written off 1,000

Also calculate the percentage of profit earned to sales. Q:4) The following information has been obtained from the records of Amol Co. Ltd., Nashik for the year ended 31-3-2010 :

Stock on 1-4-2009 : – Raw Materials 30,000 Work-in-Progress 12,000 Finished Goods 60,000 Stock on 31-3-2010 Raw Materials 25,000 Work-in-Progress 15,000 Finished Goods 55,000 Productive Wages 2,00,000 Depreciation on Machinery 44,000 Direct Chargeable Expenses 30,000 Factory Rent 48,000 Director’s Fees 15,000 Selling Overheads 20,000 General Expenses 10,000 Printing and Stationery 5,000 Sales 9,00,000 Underwriting Commission 10,000 Purchases of Raw Materials 4,50,000

Prepare a Statement of Cost showing: (a) Cost of Materials Consumed (b) Prime Cost (c) Factory Cost (d) Cost of Production (e) Cost of Goods Sold (f) Cost of Sales (g) Profit

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

Q:5) Pranav Industries has supplied you the following information for the month January, 2012:

Materials (Raw) purchased 25,900 Stock of Materials an 1st January 18,720 Bad Debts 1,000 Travellers Salary and Commission 1,078 Depreciation on Office Furniture 42 Factory Rent 1,190 Productive Wages (Direct) 17,640 Director’s Fees 840 General expenses 476 Gas and Water (Production) 168 Travelling Expenses of Sales Staff 294 Sales 75,000 Manager’s Salary (2 / 3 factory, 1 / 3 office) 1,500 Depreciation on Plant and Machinery 1,820 Discount allowed 406 Repairs to Plant and Machinery 623 Carriage Outward 602 Direct Expenses 1,001 Rent, Rates, Taxes (Office) 280 Gas and Water (Office) 56 Stock of Material (Raw) on 31 January 792

You are asked to calculate: (a) Prime Cost (b) Factory Cost (c) Cost of Production (d) Total Cost (e) Net Profit Q:6) Prepare a cost sheet of the following data relating to the manufacture of Jeans: Number of Jeans manufactured during the month 1,000 Direct materials consumed 20,000 Direct labour 8,000 Indirect labour (in factory) 2,500 Supervision costs (in factory) 1,000 Factory premises rent 1,600 Factory lighting 600 Oil for machines 100 Depreciation of machines 500 Office overheads 8,000 Office salaries 2,000

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

Misc. office expenses 1,000 Selling and distribution overheads 6,000 Note: A profit margin of 20% on the total cost of goods is expected on the sale of Jeans. Q:7) From the following information for the month of January, prepare a Cost Sheet to show the following components : (a) Prime Cost, (b) Factory Cost, (c) Cost of Production, (d) Total Cost. Direct material 57,000 Direct wages 28,500 Factory rent and rates 2,500 Office rent and rates 500 Plant repairs and maintenance 1,000 Plant depreciation 1,250 Factory heating and lighting 400 Factory manager’s salary 2,000 Office salaries 1,600 Director’s remuneration 1,500 Telephone and postage 200 Printing and stationery 100 Legal charges 150 Advertisement 1,500 Salesmen’s salaries 2,500 Showroom rent 500 Sales 1,16,000 Q:8) The Bangalore Ltd. supplies you the following information and requires you to prepare a cost sheet. Stock of raw materials on 1st Sept., 2013 75,000 Stock of raw materials on 30th Sept., 2013 91,500 Direct wages 52,500 Indirect wages 2,750 Sales 2,00,000 Work-in-progress on 1st Sept 2013 28,000 Work-in-progress on 30th Sept 2013 35,000 Purchases of raw materials 66,000 Factory rent, rates and power 15,000 Depreciation of plant and machinery 3,500 Expenses on purchases 1,500 Carriage outward 2,500 Advertising 3,500

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

Office rent and taxes 2,500 Travellers wages and commission 6,500 Stock of finished goods on 1st Sept., 2013 54,000 Stock of finished goods on 30th Sept., 2013 31,000 Q:9) From the following information prepare a cost sheet to show : (a) Prime cost; (b) Works cost; (c) Cost of production ; (d) Cost of sales; and (e) Profit. Raw materials purchased 32,250 Carriage on purchases 850 Direct wages 18,450 Factory overhead 2,750 Selling overhead 2,450 Office overhead 1,850 Sales 75,000 Sale of factory scrap 250 Opening stock of finished goods 9,750 Closing stock of finished goods 11,100 Q:10) A manufacturer has shown an amount of RS 19,310 in his books as ‘Establishment’ which really include the following expenses: Interest on debentures 1,200 Agents’ commission 6,750 Warehouse wages 1,800 Warehouse repairs 1,500 Lighting of office 70 Office salaries 1,130 Director’s remuneration 1,400 Travelling expenses of salesmen 1,760 Rent, rates and insurance of warehouse 310 Rent, rates and insurance of office 230 Lighting of warehouse 270 Printing and stationery 1,500 Trade magazines 70 Donations 150 Bank charges 100 Cash discount allowed 770 Bad debts 300

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

From the above information prepare a statement showing in separate total: (a) Selling expenses, (c) Administration expenses. (b) Distribution expenses, (d) Expenses which you would exclude from costs sheet. Q:11 Pranav Industries has supplied you the following information for the month January, 2012 : Materials (Raw) purchased 25,900 Stock of Materials an 1st January 18,720 Bad Debts 1,000 Travellers Salary and Commission 1,078 Depreciation on Office Furniture 42 Factory Rent 1,190 Productive Wages (Direct) 17,640 Director’s Fees 840 General Expenses 476 Gas and Water (Production) 168 Travelling Expenses of Sales Staff 294 Sales 75,000 Manager’s Salary (2 / 3 factory, 1 / 3 office) 1,500 Depreciation on Plant and Machinery 1,820 Discount allowed 406 Repairs to Plant and Machinery 623 Carriage Outward 602 Direct Expenses 1,001 Rent, Rates, Taxes (Office) 280 Gas and Water (Office) 56 Stock of Material (Raw) on 31 January 792 You are asked to calculate: (a) Prime Cost (b) Factory Cost (c) Cost of Production (d) Total Cost (e) Net Profit Q:12) The following information was available from the records of M/s. Usha Ltd. during the year ended 31st March, 2010 : Opening Stock of Raw Materials 65,000 Material Purchased 2,60,000 Cost of Free Samples 10,000 Productive Wages 1,60,000 Factory Rent, Rates and Insurance 12,000 Staff Salaries 7,000 Establishment Charges 4,500 Gas and Water 1,500

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

Opening Stock of Work-in-progress 10,000 Closing Stock of Work-in-progress 7,000 Opening Stock of Finished Goods 15,000 Closing Stock of Finished Goods 5,000 Sales 5,60,000 Manager’s Salary 15,000 Royalties 10,000 Closing Stock of Raw Materials 50,000 Donations 5,000 Interest on Loans 1,000 Gift Tax 500 Carriage Inwards 5,000 Loss on Sale of Machinery 1,000 Direct Expenses 10,000 Bad Debts 10,000 R.D.D. 5,000 Property Tax 500 The Manager devotes two third of his time for factory. Prepare Cost Sheets. Q:13) The following information has been obtained from the records of Amol Co. Ltd., Nashik for the year ended 31-3-2010 : Stock on 1-4-2009 : Raw Materials 30,000 Work-in-Progress 12,000 Finished Goods 60,000 Stock on 31-3-2010 : Raw Materials 25,000 Work-in-Progress 15,000 Finished Goods 55,000 Productive Wages 2,00,000 Depreciation on Machinery 44,000 Direct Chargeable Expenses 30,000 Factory Rent 48,000 Director’s Fees 15,000 Selling Overheads 20,000 General Expenses 10,000 Printing and Stationery 5,000 Sales 9,00,000 Underwriting Commission 10,000

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

Purchases of Raw Materials 4,50,000 Prepare a Statement of Cost showing : (a) Cost of Materials Consumed (b) Prime Cost (c) Factory Cost (d) Cost of Production (e) Cost of Goods Sold (f) Cost of Sales (g) Profit

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

UNIT:3 OVERHEADS

Q:1 Explain classification of overheads in detail.

Q:2 Difference between fixed overhead and variable overhead. Q:3 Explain the Allocation and Apportionment of the overheads. State the difference between Allocation and Apportionment of overheads

Q:4 Explain “All overheads are cost but all cost are not overheads”.

Practical Questions Q:1) The Modern Company is divided into four departments: A, B and C are producing departments, and D is a service department. The actual costs for a period are as follows: Rent Rs.1000 Repairs to Plant Rs.600 Supervision Rs.1500 Fire Insurance in respect of Stock Rs.500 Depreciation of Plant Rs.450 Power Rs.900 Light Rs.120 Employers’ liability for insurance Rs.150 The following information is available in respect of the four departments Dept. A Dept. B Dept. C Dept. D Area (sq.mtrs) 1,500 1,100 900 500 Number of Employees 20 15 10 5 Total Wages (Rs.) 6,000 4,000 3,000 2,000 Value of Plant (Rs.) 24,000 18,000 12,000 6,000 Value of stock (Rs.) 15,000 9,000 6,000 – H.P. of Plant 24 18 12 6 Apportion the costs to the various departments on the most equitable basis Q:2) A will Ltd. has two production departments A, B and one service department S. The actual costs for a period are as follows:

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

Q:3) Finolex Co. Ltd. has three production departments and four service departments. The expenses of these departments as per primary distribution summary were as follows:

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

The following information is also available in respect of production departments:

Apportion the cost of various service departments to the production departments.

Q:4) A manufacturing company has two production departments X and Y, and three service departments, Stores, Time-keeping and Maintenance. The departmental distribution summary showed the following expenses for March 1998:

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

Q:5) The following information is supplied from the costing records of a company : Rent 4000 Maintenance 2400 Depreciation 1800 Lighting 400 Insurance 2000 Employer's contribution to Provident Fund 600 Energy, 3600 Supervision 6000

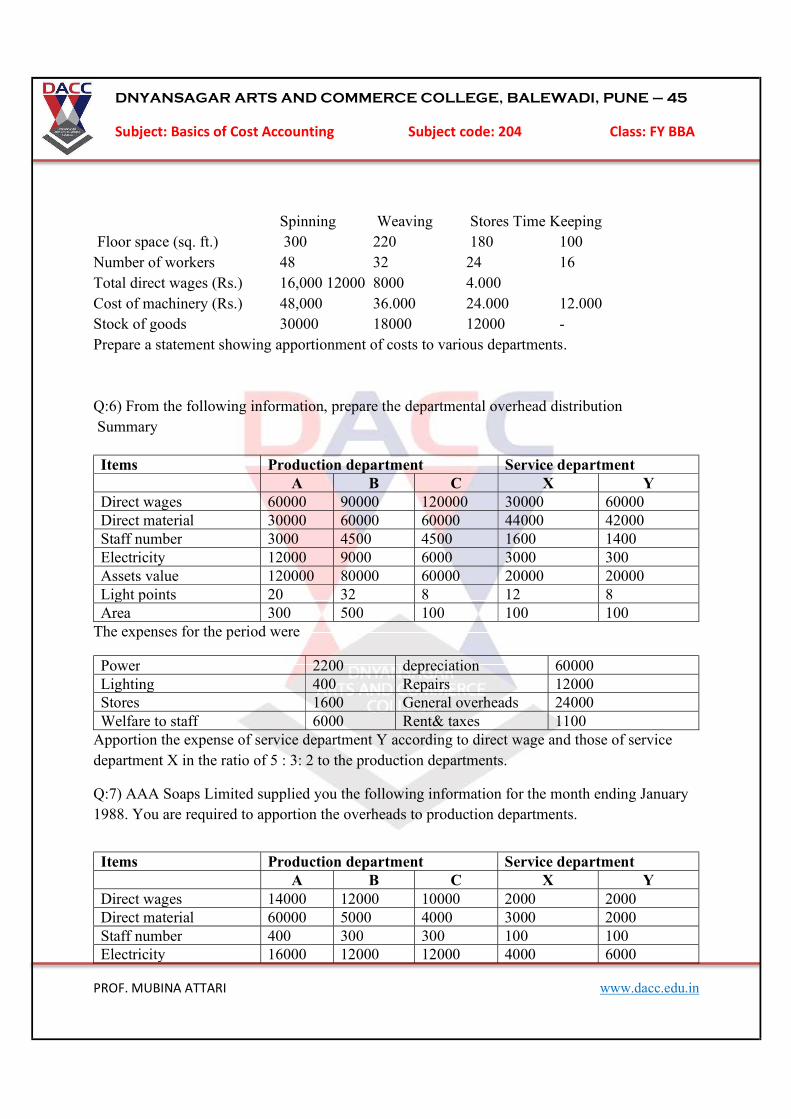

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

Spinning Weaving Stores Time Keeping

Floor space (sq. ft.) 300 220 180 100 Number of workers 48 32 24 16 Total direct wages (Rs.) 16,000 12000 8000 4.000 Cost of machinery (Rs.) 48,000 36.000 24.000 12.000 Stock of goods 30000 18000 12000 - Prepare a statement showing apportionment of costs to various departments. Q:6) From the following information, prepare the departmental overhead distribution Summary

The expenses for the period were

Power 2200 depreciation 60000 Lighting 400 Repairs 12000 Stores 1600 General overheads 24000 Welfare to staff 6000 Rent& taxes 1100

Apportion the expense of service department Y according to direct wage and those of service department X in the ratio of 5 : 3: 2 to the production departments.

Q:7) AAA Soaps Limited supplied you the following information for the month ending January 1988. You are required to apportion the overheads to production departments.

Items Production department Service department A B C X Y Direct wages 60000 90000 120000 30000 60000 Direct material 30000 60000 60000 44000 42000 Staff number 3000 4500 4500 1600 1400 Electricity 12000 9000 6000 3000 300 Assets value 120000 80000 60000 20000 20000 Light points 20 32 8 12 8 Area 300 500 100 100 100

Items Production department Service department A B C X Y Direct wages 14000 12000 10000 2000 2000 Direct material 60000 5000 4000 3000 2000 Staff number 400 300 300 100 100 Electricity 16000 12000 12000 4000 6000

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

The expenses for the period were

Power 3000 depreciation 12000 Lighting 40000 Repairs 2400 Stores 80 General overheads 20000 Welfare to staff 6000 Rent& taxes 1200

Apportion the expenses of Department X in the ratio of 4 : 3 : 3 and that of the Department Y in proportion to direct wages to Department A, B & C respectively.

Q:8) A company has three production departments and two service departments, and for a period the departmental distribution summary has the following totals

Q:9) You are supplied with the following information and required to work out the production hour rate recovery of overhead in departments A, B and C reapportioning service department expenses by simultaneous equation method as well as by repeated distribution method:

Assets value 100000 60000 40000 20000 20000 Light points 20 30 30 10 10 Area 1600 1200 1200 400 400

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

Q:10) You are supplied with the following information of Ravalgoan Ltd. Ranjangaon, for the year ended 31-3-2017, from which work out the production hour rate of recovery of overheads in Depts. ‘A’, ‘B’ and ‘C’.

Particular Total A B C D F Factory Rent 12000 2400 4800 2000 2000 800 General overheads 3600 100 2100 800 300 300 Indirect Materials 5900 1200 2000 1000 1300 400 Machinery Depreciation 5000 250 1600 200 500 200

Electric lighting 4000 800 2000 500 400 300 Total 30500 7000 12500 4500 4500 2000 Estimated Working hrs 1750 3000 1125 -------- ---------

Expenses of Service Depts. ‘D’ and ‘E’ are to be apportioned as per Simultaneous Equation Method as under.

Particular A B C D E Service Dept D 30% 40% 20% -- 10% Service Dept E 10% 20% 50% 20% --

Q:11) You are supplied with the following information and required to work out the hourly rate of recovery of overhead in departments A, B and C reapportioning service departments expenses by repeated distribution method. Rent and rates 5,000 General lighting 600

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

Indirect Wages 1,500 Power 1,500 Depreciation of Machinery 10,000 Sundries 10,000 The following further details are available :

Particulars Production Dept Service Dept Total A B C D E Floor Space 10000 2000 2500 3000 2000 500 Light points 60 10 15 20 10 5 Direct wages 10000 3000 2000 3000 1500 500 HP of machine 150 60 30 50 10 -- Value of machine 250000 60000 80000 100000 5000 5000

Working hrs --- 6226 4028 4066 --- -- The expenses of D and E are allocated as follows :

A B C D E D 20% 30% 40% -- 10% E 40% 20% 30% 10% --

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

UNIT:4

Contact and Process Cost and Methods of Costing

Q:1) Write a short notes on:

(a) Process Costing (b) Contract Costing (c) Abnormal Gain (d) Normal Loss (e) Types of Contracts (f) Work certified and work uncertified

Q:2) Explain with the example in which industry process costing is used?

Q:3) Difference between joint product and by product?

Practical Questions (Contract Costing)

Q:1) Morwal Builders, Pune undertook several large contracts. The following are the particulars relating to Contract No. 22 for the year ended 31st March 2017:

Material issued from storehouse 90,000

Material purchased 40,000

Material transferred from Contract No. 27 25,000

Materials returned to storehouse 500

Material at site on 31-3-2017 1,000

Plant purchased and installed at site 72,000

Freight and installation charges of plant 8,000

Operating wages 1,22,000

Process labour outstandings 5,000

Other direct expenses 12,000

Operating expenses payable 2,000

Establishment on cost 27,000

Office expenses accrued 1,500

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

Work uncertified 6,000

Contract price 16,00,000

Cash received from contractee 3,20,000

(represented full amount of work certified less 20% as retention money)

Provide depreciation on plant @ 10% p.a. as per reducing balance method. You are required to prepare Contract Account and Contractee’s Account.

Q:2) Amey Builders Pune is engaged on two contracts during the year 2016-17. The following particulars are available on 31st March, 2017 in respect to contract A. Contract Price 6,00,000 Material issued to contract 1,60,000 Material returned to stores 4,000 Material on site on 31-3-2017 22,000 Material transferred to contract B 9,000 Direct Labour 1,40,000 Chargeable Expenses Outstanding 6,000 Wages Payable 2,000 Direct Expenses 60,000 Hire of Special Machinery 10,000 Administration Overheads 25,000. Plant installed at site at cost 75,000 Cost of contract not yet certified 23,000 Plant installation charges 5,000 Value of work certified 4,20,000 Value of plan on 31-3-2017 65,000 Cash received from contractee 3,78,000 You are required to prepare Contract A account for the year ended 31st March, 2017 Q:3) Reliable Constructions Ltd., Pune undertook a 5. contract of ` 8,00,000 for the construction of a Sports Gymkhana on 1st April, 2014. The following information is taken up from the Contract Ledger as on 31-3-2015 : Material directly issued from stores 1,30,000 Material purchased 70,000 Scrap Material sold 8,000 Material transferred to other contract 10,000 Materials in hand on site 11,000 Materials returned to stores 6,000

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

Direct wages paid and payable 85,000 Direct charges 45,000 Overheads charged to contract 40,000 Subcontract Cost 9,000 Cost of Additional Work 3,400 Outstanding Direct Expenses 1,600 Plant purchased on 1-4-2014 and issued directly 80,000 Additional Depreciation on Plant 8,000 Plant transferred on 1-4-2014 to other contract 40,000 Cash received being 90% of work certified 3,60,000 Uncertified work being 8% of certified work. You are required to prepare : (i) Contract Account (ii) Contractee’s Account Q:4) The following are the particulars relating to a contract which has begun on 1st January 2014 Contract Price 5,00,000 Machinery 30,000 Materials 1,70,600 Wages 1,48,750 Direct Expenses 6,330 Cash received 3,51,000 Value of work certified 3,80,000 Outstanding wages 5,380 Uncertified work 19,000 Overheads 8,240 Material returned 1,400 Material in hand 31st Dec,2014 3,900 Value of Machinery on 31st Dec, 2014 22,000 Prepare the Contract Account for the year 2014 and show the amount of work in progress as it would appear in the Balance Sheet of the year. Q:5) A firm of building contractors began to trade on 1st April, 2010, the following was the expenditure on a contract for Rs. 4,50,000 : Material used to contract 76,500 Plant used for contract 22,500 Wages 1,21,500 Other expenses 7,500 Cash received on account up to 31st March, 2011 amounted to Rs. 1,92,000, being 80% of the work certified. Of the plant and materials charged to contract, plant costing Rs. 4,500 and materials costing Rs. 3,750 were lost. On 31st March, 2011 plant costing Rs. 3,000 was returned to stores, the cost of

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

work done but uncertified was Rs. 1,500 and material costing Rs. 3,450 were in hand. Charge 15% depreciation on plant, reserve 1/3rd profit earned and prepare Contract Account from the above particulars. Q:6) A firm of building contractor began to trade on 1-4-2016. The following was the expenditure on the contract for Rs. 4,00,000. Materials issued to contract 50,000 Plant used for contract 20,000 Wages 71,000 Other expenses 10,000 Cash received on account to 31-3-2017 amounted to 1,44,000 The work certified was 1,80,000 . Of the plant and materials charged to the contract, plant which cost 4,000/- and materials which cost 3,000 were lost. On 1-3-2017 plant which cost 3,000 was returned to stores. The cost of work done but uncertified was ` 1,500/- and material costing 2,500/- were in hand on site. Charge 15% depreciation on plant and take to the Profit and Loss Account 2 /3 of the profit received. Prepare a Contract Account, Contractee’s Account and Balance Sheet from the above particulars. Q:7) From the following information prepare Contract Accounts for the year ending 31st March, 2016. Commencement Contract A Contract B

1st April 2016 1st Oct. 2016 Contract price 75,000 60,000 Raw Material 24,400 21,600 Wages 12,000 12,400 General Charges 800 560 Plant Installed 4,000 3,200 Materials on hand 800 800 Wages Accrued 800 800 Works Certified 40,000 32,000 Work uncertified 1,200 1,600 Cash received in respect of work certified 30,000 24,000 Depreciation is to be charged on the plant @10% which was installed on the opening date of the contract in each case

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

Practical Questions (Process Costing)

Q:1) The product of Glaxo India Ltd., Goregaon passes through two processes A and B and then to finished stock. It is ascertained that in each process normally 5% of the total weight is lost and 10% is scrap which from process A and B realise RS 80 per ton and RS 200 per ton respectively. The following are the figures relating to both the processes: Prepare Process Cost Account showing cost per ton of each process. There was no stock or work in progress in any process. Q:2) Product X is obtained after it passes through three distinct processes arranged in Neelkamal Ltd. Aurangabad. You are required to prepare process account from the following information : Particulars Total Process I Process II Process III Materials 15084 5200 3960 5924 Direct wages 18000 4000 6000 8000 Production Overheads 18000 …… …………. ………… Actual output 950 840 750 Normal Loss 5 10 15 Value of scrap per units 4 8 10

1000 units @ ` 6 per unit were introduced in process I account. Production overheads are to be distributed as 100% of Direct Wages. Q:3) A product in F Ltd. passes through two distinct processes A and B. From the following information you are required to prepare Process A Account, Process B Account, Abnormal Loss Account, and Abnormal Gain Account : Particulars Process A Process B Materials(Introduced 20000unitss in process A) 30000 3000 Labour 10000 12000 Overheads 7000 9850 Normal Loss 10% 4% Scrap value of normal loss Rs 1 Per unit Rs 2 per unit Output(units) 17500 17000

There is no stock or work-in-progress in any process.

Particulars Process A Process B Materials (tons) 1000 700 Cost of material per ton 125 200 Wages 28000 10000 Manufacturing Expenses 8000 5250 Output (tons) 830 780

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

Q:4) Product Y is obtained after it passes through three distinct processes, you are required to prepare process accounts, showing the total cost and cost per unit of each process from the following information: Items Process I Process II Process III Material 5200 3960 5924 Wages 4000 6000 8000

Production overheads Rs 18,000 to be apportioned on 100% of wages. 1,000 units @ Rs 6 per unit were introduced in Process I Actual output Units Normal loss Value of Scrap per unit Process I 950 5% Rs 4 Process II 840 10% Rs 8 Process III 750 15% Rs 10

Q:5) A product passes through two processes. The output of process I become the input of Process II and the output of process II is transferred to warehouse. The quantity of raw materials introduced into Process I is 20,000 kg. at Rs. 10 per kg. The cost and output data for the month under review are as under: The company’s policy is to fix the selling price of the end product in such a way as to yield a profit of 20% on selling price. Prepare process accounts and determine the selling price per kg. of the end product. Q:6) The finished product of a factory has to pass through three process 1, 2 and 3. During August 2017 data relating to this product was as shown below :

Particulars Process1 Process 2 Process 3 Total

Basic Raw Material(10000 units) 6000 …. ………. 6000 Direct material added 8500 9500 5500 23500 Direct wages 4000 6000 12000 22000 Direct expenses 1200 930 1340 3470 Production overheads(observed as a percentages of direct wages)

16500

Particulars Process I Process II Direct Material 60000 40000 Labour 40000 30000 Production overheads 39000 40250 Normal loss 8% 5% Output 18000 17400 Loss realization Rs/ kg 2 3

DNYANSAGAR ARTS AND COMMERCE COLLEGE, BALEWADI, PUNE – 45 Subject: Basics of Cost Accounting Subject code: 204 Class: FY BBA

PROF. MUBINA ATTARI www.dacc.edu.in

Output units 9200 8700 7900 Normal loss % 10 5 10 Scrap value of normal loss per unit .20 .50 1

There was no stock at the beginning or at the end of any process. You are required to prepare :-

i) Process ‘1’ Account. ii) Process ‘2’ Account. iii) Process ‘3’ Account. iv) Abnormal Loss Account. v) Abnormal Gain Account.

Q:7) Prepare Process Accounts from the following Particulars Process X Process Y Material in tons 100 162 Cost of materials per ton 120 200 Loss in weight 2% 4% Scrap in tons 10% 10% Scrap realization per ton 100 200 Wages 20,000 30,000 Manufacturing expenses 10,000 15,000