Bank of England Quarterly Bulletin Summer 2006

145

Bank of England Volume 46 Number 2 Quarterly Bulletin Summer 2006

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Bank of England Quarterly Bulletin Summer 2006

Bank of England Volume 46 Number 2

QuarterlyBulletinSummer 2006

i

Foreword

Every three months, the Bank of England publishes economic research and marketreports in its Quarterly Bulletin. This quarter, the Bulletin explores the relationshipbetween house prices and consumer spending. It also examines companies’ motivesfor investing in inventories. And, as usual, it reviews the latest movements in sterlingfinancial markets.

House prices and consumer spending have often moved together in the past. But asthe Monetary Policy Committee has noted in the Inflation Report and the Minutes ofpast policy meetings, the relationship between the housing market and spending ismore subtle than is often supposed. It depends on causal links, such as the impact ofhouse prices on the amount that people can borrow to finance spending. And itdepends on common influences that affect both house prices and consumption, suchas people’s expectations about their future income.

This relationship is explored in House prices and consumer spending, by Andrew Benito,Jamie Thompson, Matt Waldron and Rob Wood. The authors explain how the strengthof the links between the housing market and spending can vary over time. Causallinks are affected by factors such as the amount of housing equity that householdsalready have available and the extent to which credit constraints are inhibitingspending. The reasons why house prices move are also important. Sometimescommon factors drive changes in both house prices and consumer spending. Atother times, house prices may shift on account of developments that are of limitedsignificance for spending. In general, the implications of a rise in house pricestherefore rest on why the rise has occurred.

In the past few years, house prices and consumption have moved together less closely.One explanation is that the causal links between the housing market and spendinghave weakened. An alternative hypothesis is that recent fluctuations in house priceshave not been the result of movements in common influences like expected income,but reflect a different set of factors that have had a more limited impact on consumerspending. The article concludes that both explanations have played a part in therecent weakening of the association between house prices and consumer spending.

Investment in inventories accounts for a much smaller proportion of total spendingthan consumption. But it is much more volatile, and fluctuations in inventories oftenhave a noticeable impact on GDP growth. Investing in inventories, by Rob Elder andJohn Tsoukalas, examines companies’ motives for holding inventories and assesses theimpact of inventory investment on the volatility of output. It also considers thecontribution of changing stock management behaviour to the stability of the UKeconomy in recent years.

The regular Markets and operations article describes financial market developmentssince the previous Bulletin. In May, there was a pickup in financial market volatilityand substantial falls in some asset prices, particularly in commodity and equitymarkets. In common with other countries, UK short-term and long-term interest rates

ii

Bank of England Quarterly Bulletin: Summer 2006

increased over the review period, while the effective exchange rate for sterlingappreciated. But despite the rise in interest rates and falls in equity prices, creditspreads did not widen significantly. This suggests that any repricing of risk has beenlimited only to certain asset classes. Finally, the article records the introduction, on18 May, of fundamental reforms to the way that the Bank implements the MPC’sinterest rate decisions in the sterling money markets. The changes are designed tokeep overnight interest rates in line with the official Bank rate and also to improve themanagement of banking system liquidity in both normal and stressed times.

Charles BeanChief Economist and Executive Director for Monetary Policy, Bank of England.

This edition of the Quarterly Bulletin also includes:

� Cost-benefit analysis of monetary and financial statistics (by Andrew Holder). Data collected by the Bank of England from UK banks are used in compiling a range of economic statistics that contribute to meeting the inflation target and maintaining financial stability. But data collection inevitably imposes some costs on those supplying the information. This article describes a cost-benefit analysis framework that has been developed to help balance the demands on data suppliers with the needs of users;

� Public attitudes to inflation (by Colin Ellis). Over the past six and a half years, GfK NOP has carried out surveys of public attitudes to inflation on behalf of the Bank of England. This article analyses the results of the surveys from May 2005 to February 2006, a period in which there was an increase in public perceptions of past inflation as well as expectations of future inflation;

� The Centre for Central Banking Studies (by Gill Hammond). The Centre for Central Banking Studies at the Bank of England organises seminars, workshops and conferences in London and abroad. These are attended by central bankers from all over the world. This article describes the Centre’s origins and current activities; and

� A review of the work of the London Foreign Exchange Joint Standing Committee in 2005. The Foreign Exchange Joint Standing Committee was established in 1973, under the auspices of the Bank of England, as a forum for bankers and brokers to discuss broad market issues. This note reviews thework undertaken by the Committee during 2005.

Research work published by the Bank is intended to contribute to debate, anddoes not necessarily reflect the views of the Bank or of MPC members.

Bank of England Quarterly BulletinSummer 2006

Recent economic and financial developments

Markets and operations 125Box on equity variance swaps 127Box on forward rates and economists’ expectations 129Box on using option prices to derive a probability distribution for the sterling exchange rate index 130Box on hedging inflation exposures by swap dealers 133Box on decomposing changes in annuity rates 134Box on the work of the Securities Lending and Repo Committee 136

Research and analysis

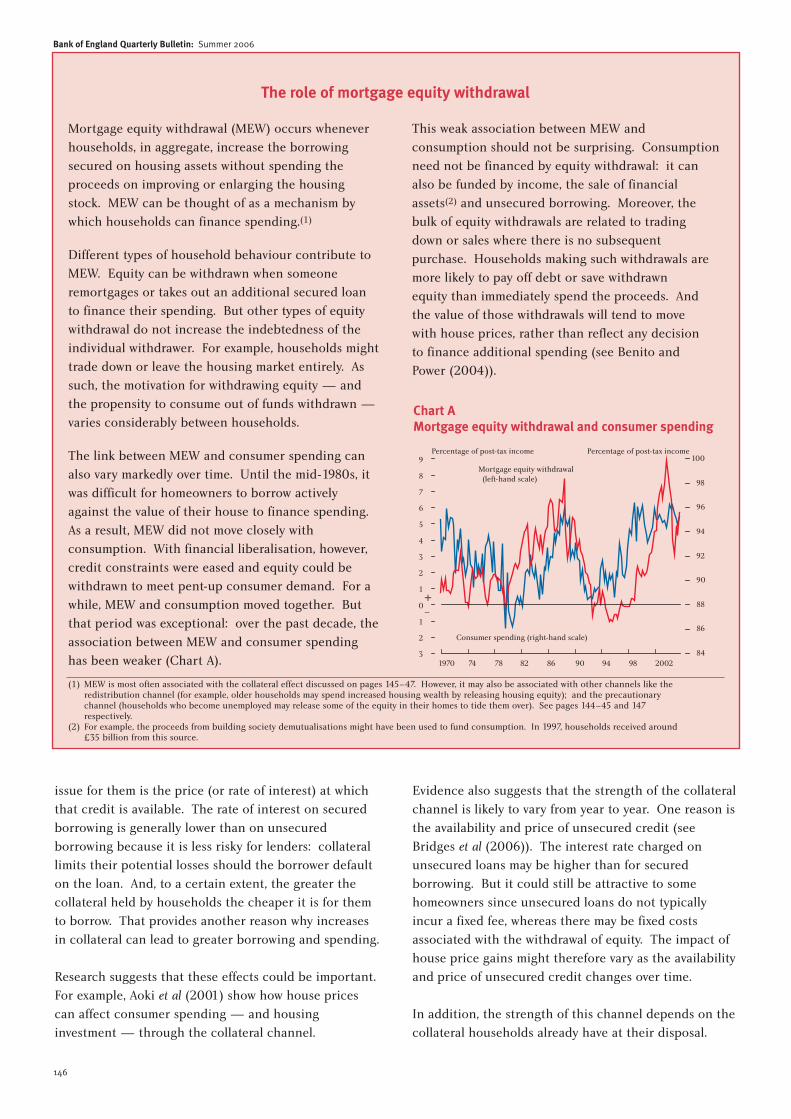

House prices and consumer spending 142Box on how important are the different channels from house prices to consumer spending? 145Box on the role of mortgage equity withdrawal 146Box on estimating the role of housing 151

Investing in inventories 155

Cost-benefit analysis of monetary and financial statistics 161Box on cost-benefit analysis in other institutions 163Box on case study: review of information collected on the industrialcomposition of banks’ business with UK residents (forms AD and AL) 167

Summaries of recent Bank of England working papersDefined benefit company pensions and corporate valuations: simulation and empirical evidence from the United Kingdom 170UK monetary regimes and macroeconomic stylised facts 171Affine term structure models for the foreign exchange risk premium 172Switching costs in the market for personal current accounts: some evidencefor the United Kingdom 173Resolving banking crises — an analysis of policy options 174How does the down-payment constraint affect the UK housing market? 175

Productivity growth, adjustment costs and variable factor utilisation: the UK case 176Sterling implications of a US current account reversal 177Optimal monetary policy in a regime-switching economy: the response to abrupt shifts in exchange rate dynamics 178Optimal monetary policy in Markov-switching models with rationalexpectations agents 179Optimal discretionary policy in rational expectations models with regime switching 180

Reports

Public attitudes to inflation 181Box on the Bank of England/GfK NOP survey on Inflation Attitudes 182

The Centre for Central Banking Studies 190

A review of the work of the London Foreign Exchange Joint Standing Committee in 2005 196

Speeches and papers

Uncertainty, the implementation of monetary policy, and themanagement of riskSpeech by Paul Tucker, Executive Director for Markets and a member of the Monetary Policy Committee,

to the Association of Corporate Treasurers in Newport on 19 May 2006 202

Reflections on operating inflation targetingSpeech by Paul Tucker, Executive Director for Markets and a member of the Monetary Policy Committee,

delivered at the Chicago Graduate School of Business on 25 May 2006 212

Cost pressures and the UK inflation outlookSpeech by Kate Barker, member of the Monetary Policy Committee, delivered at the CBI West Midlands

Economic Dinner in Birmingham on 21 March 2006 225

The UK current account deficit and all thatSpeech by Stephen Nickell, member of the Monetary Policy Committee, delivered on 25 April 2006 231

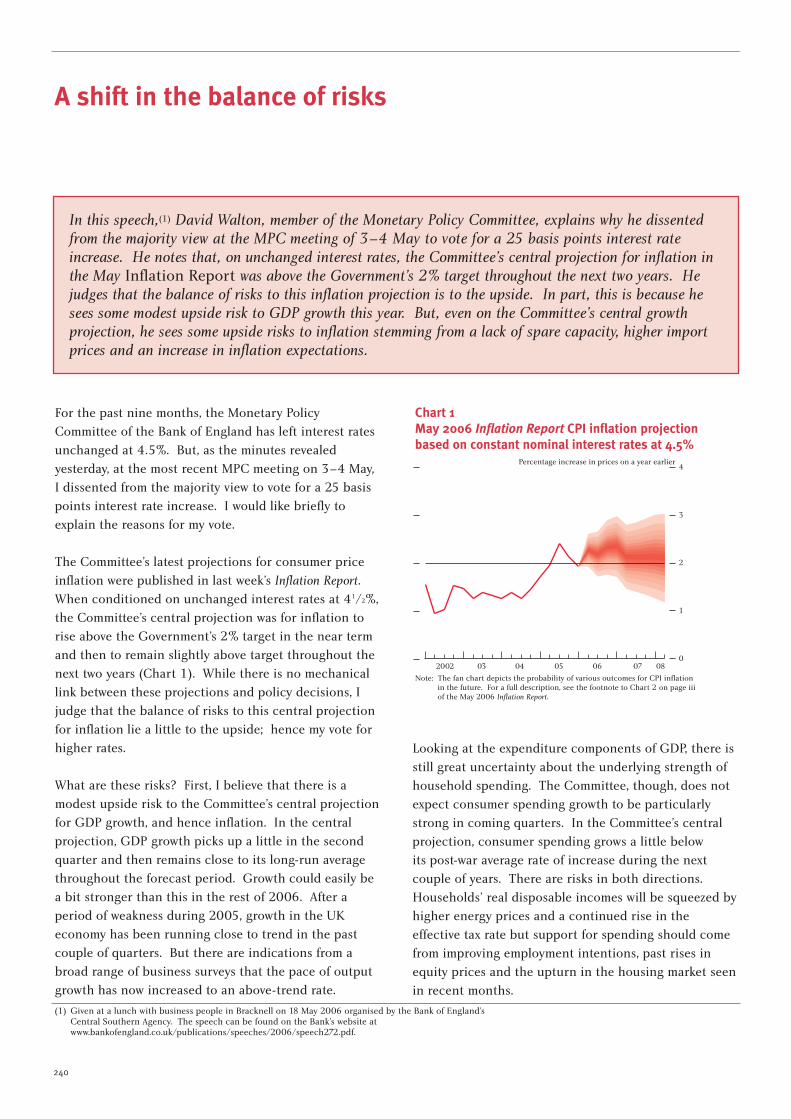

A shift in the balance of risksSpeech by David Walton, member of the Monetary Policy Committee, given at a lunch organised by

the Bank of England’s Central Southern Agency on 18 May 2006 240

What do we now know about currency unions?Paper by Michael Artis, George Fellow, Bank of England, presenting the text of an inaugural lecture

given at the Bank of England in December 2005 in memory of John Flemming 243

The contents page, with links to the articles in PDF, is available atwww.bankofengland.co.uk/publications/quarterlybulletin/index.htm. Authors of articles can be contacted at [email protected] speeches contained in the Bulletin can be found atwww.bankofengland.co.uk/publications/speeches/index.htm.Except where otherwise stated, the source of the data used in charts and tables is the Bank ofEngland or the Office for National Statistics (ONS) and all data, apart from financial marketsdata, are seasonally adjusted.

Volume 46 Number 2

125

During May, sterling markets were caught up in a global increase in asset price volatility. Commodities,equities and emerging market asset prices fell sharply.

These developments might have reflected a reappraisal of the global macroeconomic outlook. Butconsensus projections for economic growth in the major industrialised countries remained firm and there were few signs of slowing in corporate profitgrowth.

Some market commentators have highlighted a possiblerise in global inflationary pressures as a reason for theasset price adjustment. Others have attributed it tochanges in investors’ perceptions of risk. According tocontacts, some speculative investors have reducedtheir positions. Higher asset price volatility may haveadded to perceptions of somewhat greater risk, forexample, through increased Value-at-Risk measures oftraders’ positions.

Equity markets

In the United Kingdom, the rise in financial marketvolatility was manifested in a sharp fall in equity indices.The FTSE All-Share declined 5.4% from its recent peakon 21 April, and around 1% over the period as a whole(Chart 1). Mid-cap stocks fell by more in mid-May,although the FTSE 250 ended the period more than 8%higher than at the start of 2006. At the same time,expected future volatility implied by option pricesincreased, especially at short horizons (Chart 2).

Long-term sterling real interest rates rose, which otherthings being equal might have been expected toreduce equity prices via higher discount rates.But whereas long-term real interest rates increasedfairly steadily over the period, the equity price fallswere sudden and concentrated toward the end of theperiod.

The equity price falls could have been amplified byhedging of some over-the-counter equity derivatives.

Markets and operations

This article reviews developments since the Spring Quarterly Bulletin in sterling financial markets,UK market structure and the Bank’s official operations.(1)

� Volatility picked up in a number of asset markets towards the end of the period. In particular,emerging market asset prices and some commodity prices fell sharply. This seemed to reflect anadjustment in investors’ perceptions of risk, at least in these markets.

� There was a more moderate pickup in volatility in sterling interest rate markets. Short-term nominalsterling interest rates rose over the period as a whole.

� Long-term nominal sterling rates also increased, on account of higher real rates and a pickup ininflation expectations and/or inflation risk premia. The rise in real rates was common acrosscurrencies.

� Despite higher interest rates and lower equity prices, corporate bond spreads did not widen much.

� The Bank implemented fundamental reforms to modernise its operations in the sterling moneymarkets.

(1) This article focuses on sterling markets. The period under review in this article is 17 February (the data cut-off for theprevious Quarterly Bulletin) to 26 May.

126

Bank of England Quarterly Bulletin: Summer 2006

For example, as explained in the box on page 127,hedging of equity variance swaps might have added tovolatility. The pay-off from a variance swap is typicallycomputed using closing prices, so a trader’s overallposition may not be known until late in the day. As aresult, hedging may be delayed until just before themarket closes. This may have been the case on 17 Maywhen the FTSE 100 index fell sharply in late trading(Chart 3). However, some market contacts believe thisamplification effect was modest.

Commodities

Realised and implied volatility also rose sharply in somecommodity markets, especially industrial and precious

metals (Chart 4). At the same time, the prices ofsome commodities fell sharply, following a period ofrapid rises.

These earlier rises might have reflected pension fundsincreasing their exposure to commodities with the aimof increasing asset diversification and/or boostingoverall returns. This has been facilitated by newinvestment vehicles such as exchange-traded funds(ETFs), commodity indices, and more sophisticatedbespoke structured products. For example, the firstsilver ETF, launched in April 2006, accumulated anamount equivalent to more than 5% of total globalinventories of silver in its first week of trading. Greaterinvolvement of speculative investors might also havecontributed to recent volatility.

Chart 2FTSE 100 equity index implied volatility(a)

Jan. May Sep. Jan. May Sep. Jan.

Per cent

2005

26 May 2006

06

17 February 2006

07

6

8

10

12

14

16

18

20

0

Sources: Bank of England and Euronext.liffe.

(a) The solid line shows three-month (constant maturity) implied volatility. The dots indicate three-month volatility, three, six and nine months ahead respectively.

Chart 1UK and international equity indices

90

100

110

120

130

140

150

160

170

Jan. Mar. May July Sep. Nov. Jan. Mar. May

FTSE All-Share

FTSE 100MSCI World(b)

MSCI Emerging Markets(a)

Indices: 3 Jan. 2005 = 100

06

17 February

2005

FTSE 250

Sources: Bloomberg, Morgan Stanley Capital International Inc. (MSCI) and Bank calculations.

(a) The MSCI Emerging Markets index is a capitalisation-weighted index that monitors the performance of stocks in emerging markets.

(b) The MSCI World index is a capitalisation-weighted index that monitors the performance of stocks from around the world.

Chart 4Three-month implied volatilities on selected commodity indices

0

10

20

30

40

50

60

Jan. Mar. May July Sep. Nov. Jan. Mar. May2005 06

Copper

Aluminium

Per cent

17 February

Oil

Gold

Sources: Bloomberg, COMEX, NYMEX and Bank calculations.

Chart 3Change in FTSE 100 on 17 May

3.5

3.0

2.5

2.0

1.5

1.0

0.5

0.0

8.00 10.00 12.00 14.00 16.00Time

Per cent

–

Source: Bloomberg.

Markets and operations

127

Variance swaps are instruments that allow investorsto trade and hedge the volatility of asset prices. Atmaturity, the pay-off of the swap is equal to thedifference between the realised variance in theunderlying asset price over the life of the swap andthe pre-agreed ‘strike’ variance (Chart A).

Variance swaps provide a straightforward exposureto asset price volatility. To obtain a similarexposure using a ‘vanilla’ option would be morecomplicated because it is exposed to both thevolatility and the level of the underlying asset price.Moreover, the sensitivity of the price of a vanillaoption to changes in volatility depends upon thelevel of the underlying asset price. By contrast, avariance swap can provide a more stable exposureto volatility as its value does not depend directly onthe price of the underlying asset.

Pricing and hedging

In principle, a variance swap is straightforward toprice because its pay-off can be replicated with anappropriately weighted portfolio of vanillaoptions across a range of strike prices. Such aportfolio also provides a good hedge for a positionin a variance swap. But to ensure that thisportfolio remains a good hedge over time, it needsto be adjusted dynamically to neutralise the effecton its value of any changes in the underlying assetprice. This is typically achieved by buying orselling an appropriate amount of the underlyingasset, and is known as ‘delta-hedging’; theso-called delta measures the sensitivity of anoption price to changes in the price of theunderlying asset.

In practice, even a delta-hedged portfolio of vanillaoptions is not a perfect hedge for a position in a

variance swap. First, an investor seeking to hedge aposition in a variance swap may be restricted ifoptions across a wide range of strike prices are notactively traded and/or if the cost of constructingthe ideal hedge is prohibitive.

Second, the investor is exposed to so-called ‘jumprisk’, ie the risk of sharp discontinuous jumps inthe underlying asset price. The theoretical hedgeassumes the underlying asset price evolvesaccording to a continuous process. In the presenceof jumps, there may be a mismatch between theimpact on the variance swap and the hedge. Forexample, a jump downward in the underlying assetprice would cause an investor hedging a longposition in a variance swap with a short position ina portfolio of options to realise an overall loss —the gain on the swap would be less than the loss onthe hedge.

Variance swaps and recent moves in equity indices

Some contacts have suggested that delta-hedgingcould have amplified recent falls in equity indices.More specifically, it has been reported that sometraders, including hedge funds, sold a largeamount of equity index variance swaps over thepast year or so, as a way of maintaining returns inan environment of generally low financial marketvolatility. The counterpart was that equityderivative dealers bought volatility, which theymay have hedged by selling vanilla equity options.

Selling vanilla options leaves a dealer ‘shortgamma’. Gamma measures the sensitivity of thedelta to changes in the price of the underlyingasset. Being ‘short gamma’ means that todelta-hedge a position, an investor should sell theunderlying asset as its price declines.(1) For smallprice falls, only small adjustments are required forthe position to remain delta-neutral. But whenprice moves are large, as was the case on some daysduring the review period, more material changesmay be required. In turn, the additional sellingpressure exerted by the hedges may amplify theinitial price falls.

Equity variance swaps

(1) For more information on ‘short-gamma’ option positions see the box entitled ‘Market dynamics and optionsselling’, Bank of England Financial Stability Review, June 2005, pages 60–61.

Chart AIllustrative variance swap

CounterpartyA

CounterpartyB

[Realised variance] x [notional]

[Strike variance] x [notional]

128

Bank of England Quarterly Bulletin: Summer 2006

Short-term interest rates

Alongside the sharp rise in financial market volatility,short-term market interest rates in most developedeconomies declined towards the end of the period(Chart 5). Nonetheless, over the period as a whole,forward rates implied by short sterling futurescontracts had increased. That occurred against abackground of rising short-term market interest rates inthe other major currencies and reflected furtherevidence of the continuing strength of globalmacroeconomic conditions and some signs of a slightpickup in inflationary pressure.

On 26 May, the profile for forward sterling interest rates(derived from instruments that settle on Libor) impliedthat, broadly, the market expected two 25 basis pointincreases in the official Bank rate over the next two years(Chart 6).

In contrast to information from financial markets, theMay Reuters survey of UK economists’ expectationssuggested that the majority of economists expected theofficial Bank rate to remain at 4.5% until at least theend of 2007. As explained in the box on page 129, thereare several possible reasons for the divergence betweeneconomists’ expectations and market-based forwardrates.

Measures of uncertainty surrounding short-term sterlinginterest rates increased over the period, and the skew ofthe implied distribution of future sterling interest ratesbecame less negative (Chart 7). Early in the reviewperiod, market participants had assigned a higherprobability to a large downward move in short-term

interest rates than a comparable upward move. By theend of May, option prices suggested a roughly balancedprobability that sterling forward rates would rise or fall.

Exchange rates

Accompanying higher short-term sterling market interestrates, the sterling effective exchange rate index (ERI)rose by around 2% over the period, with most of theappreciation occurring towards the end of the reviewperiod (Chart 8). This largely reflected an increase inthe value of sterling against the dollar of around 61/2%.

The dollar also depreciated against other currencies —its ERI fell by around 5%. Most of the fall occurred inthe final month of the review period and, in particular,following the publication of a G7 communiqué in late

Chart 5Cumulative changes in June 2007 interest rate futurescontracts since 17 February

20

10

0

10

20

30

40

50

60

70

80

Feb. Mar. Apr. May

Basis points

US dollar

Euro

Yen

Sterling

2006

+

–

Sources: Bloomberg and Euronext.liffe.

Chart 6Sterling official and forward market interest ratesplus survey expectations

3.00

3.25

3.50

3.75

4.00

4.25

4.50

4.75

5.00

5.25

5.50

2003 04 05 06 07 08

Official Bank rate

26 May bank liability curve(a)

May survey of economists’ forecasts(b)

February survey of economists’ forecasts(b)

17 February bank liability curve(a)

Per cent

0.00

Sources: Bank of England, Bloomberg, Euronext.liffe and Reuters.

(a) One-day nominal forward rates implied by a curve fitted to a combination of instruments that settle on Libor.

(b) Survey expectations based on mean of end-of-quarter forecasts.

Chart 7Six-month implied volatility and skew from interestrate options

25

30

35

40

45

50

55

60

65

Jan. Mar. May July Sep. Nov. Jan. Mar. May0.9

0.8

0.7

0.6

0.5

0.4

0.3

0.2

0.1

0.0

0.1

0.2Basis points

Implied volatility (left-hand scale)

Skew (right-hand scale)

2005

17 February

06

+

–

Sources: Bank of England and Euronext.liffe.

April, which called for greater exchange rate flexibility inemerging economies, and especially China, to helpreduce global imbalances.

Information from option prices suggests thatuncertainty about the future level of the major dollarbilateral exchange rates increased slightly, particularlyfrom early May onwards (Chart 9). But despite a rise inimplied dollar-sterling volatility, based on techniquesexplained in the box on pages 130–31, the derivedimplied volatility for the sterling ERI fell slightly overrecent months.

Moreover, the same information from option pricessuggested that even if the dollar were to fall by a further10% against the euro, the mean expectation was for arelatively small change in the sterling ERI. This reflects

Markets and operations

129

Chart 8Cumulative change in sterling exchange rates

96

98

100

102

104

106

108

110

Jan. Feb. Mar. Apr. May

17 Feb. 2006 = 100

2006

$ per £

€ per £

£ ERI

17 February

¥ per £

Source: Bloomberg.

Forward rates and economists’expectations

In general, market-based sterling forward rates tend totrack closely the mean expectation for the futureofficial Bank rate from surveys of economists (Chart A).Since 2000, the average gap between the series hasbeen only 6 basis points. In early May, the gap was60 basis points, equivalent to nearly two standarddeviations from the mean.

There are several possible reasons for the unusuallylarge divergence observed recently, although theirrelative importance is unclear. First, economists mayhave had different views from financial marketparticipants about the economic outlook and hencethe path for future interest rates.

Second, the two groups may update expectations atdifferent times. Financial market prices typicallyadjust quickly in response to new information, whereasthe economists surveyed may update their forecastsless regularly. This might imply a tendency for themarket-based measure to lead mean surveyexpectations, for which there is some evidence,particularly during 2003 and 2004 H1.

Third, unlike survey expectations, market rates arelikely to incorporate term premia that compensateinvestors for the uncertainty surrounding the path offuture short-term interest rates.

Chart ASurvey expectations and sterling forward interestrates(a)

Per cent

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

2000 01 02 03 04 05 06

Market-based forward rates

Reuters’ survey

0.0

Sources: Bank of England, Bloomberg, Euronext.liffe and Reuters.

(a) Breaks in each series occur where the data refer to a different calendar year. Thechart shows mean interest rate expectations for the end of the full calendar yearfollowing the survey date. Forward interest rates are taken from the Bank’sinterbank liability curve, with rates adjusted downwards by a moving average ofthe spread between six-month Libor rates and six-month GC repo rates toaccount crudely for the credit risk implicit in Libor rates.

Chart 9Three-month implied volatility from foreign exchange options

5

6

7

8

9

10

11Per cent

17 February

Jan. Mar. May July Sep. Nov. Jan. Mar. May2005 06

Sterling/dollar

Sterling/euro

Sterling ERI(a)

Dollar/euro

40

Sources: Bank of England and British Bankers’ Association.

(a) Based on a simplified sterling ERI as discussed in the box on pages 130–31.

130

Bank of England Quarterly Bulletin: Summer 2006

Foreign currency option prices contain informationabout market participants’ expectations of futuremovements in exchange rates. This box outlines atechnique that uses option prices to gaugeexpectations about the future path of the sterlingexchange rate index (ERI).(1)

A ‘simplified’ sterling ERI probability distribution

As there is no actively traded market in options onthe sterling ERI, the risks to the future value of theindex cannot be inferred directly. An indirectapproach is to model the probability distribution ofa ‘simplified’ sterling ERI based solely on the pricesof options on euro-sterling and dollar-sterling, whichare the key bilateral exchange rates in the sterlingERI.(2)

A statistical tool (known as a copula function) can beused to map the euro-sterling and dollar-sterlingimplied distributions onto a joint distribution. Theprocess by which this is done can be explained in thefollowing steps:

Step one — Use option prices to estimate(risk-neutral) probability distributions foreuro-sterling and dollar-sterling.(3) Then construct ajoint distribution using (arbitrary) initial values forthe copula function parameters.

Step two — From this joint distribution, back out theimplied marginal distribution for the euro-dollarexchange rate and compare it with a distributionestimated directly from euro-dollar option prices.

Step three — Update the parameters of the copulafunction so that they reduce the difference betweenthe directly and indirectly inferred distributions foreuro-dollar.

Step four — Repeat steps two and three until thedifference between the two euro-dollar distributionsis negligible.

An example of the resulting joint distribution for theeuro-sterling and dollar-sterling exchange rates isshown in Chart A.

From the joint distribution, an estimate of the impliedprobability distribution for the simplified sterling ERIcan be constructed. More specifically, using weightsof 0.7 for euro-sterling and 0.3 for dollar-sterling, it ispossible to back out an implied probabilitydistribution for the sterling ERI.(4) Chart B shows the

Using option prices to derive a probability distributionfor the sterling exchange rate index

Chart AJoint probability distribution

1.20 1.25 1.30 1.35 1.40 1.45 1.50 1.55 1.60 1.65

1.61.71.81.92.02.12.2

0

2

4

6

8

10

12

14

16

18

$ per £

€ per £

Probability

Source: Bank calculations.

(1) For a more in-depth discussion of this topic see Hurd, M, Salmon, M and Schleicher, C (2005), ‘Using copulas to construct bivariate foreign exchangedistributions with an application to the sterling exchange rate index’, CEPR Discussion Paper no. 5114.

(2) The euro-sterling exchange rate has a weight of around 55% and the dollar-sterling exchange rate a weight of around 20% in the sterling ERI.(3) For more details on risk-neutral distributions see Clews, R, Panigirtzoglou, N and Proudman, J (2000), ‘Recent developments in extracting information from

options markets’, Bank of England Quarterly Bulletin, February, pages 50–60.(4) These weights were found by regressing euro-sterling and dollar-sterling against the overall ERI index.

Chart BTwelve-month sterling ERI probability distribution

0

1

2

3

4

5

6

7

8

9

10

75 80 85 90 95 100 105 110 115 120 125

Probability, per cent(a)

Index level

Source: Bank calculations.

(a) Probability of the sterling ERI being within ±0.5 index points of any given level. For example, the probability of the ERI being at 100 (between 99.50 and 100.50 in a year’s time was around 9%.

Markets and operations

131

distribution of the twelve-month ahead sterling ERIon 26 May 2006.

Given the probability distribution for the sterling ERI,it is possible to construct synthetic measures ofimplied volatility and risk-reversal statistics. Chart 9in the main text shows that the implied volatility ofthe sterling ERI has declined a little over recentmonths. And, as shown in Chart C, the probabilitydistribution has recently become less negativelyskewed — on 26 May the perceived risks to thesterling ERI were broadly balanced.

Estimating conditional probabilities

Another use of the joint distribution is to calculateconditional probabilities. For example, it is possibleto construct an implied distribution for the sterlingERI over the next twelve months given an assumedchange in the euro-dollar exchange rate.

Chart D shows an aerial view of the joint probabilitydistribution for the simplified sterling ERI shown inChart A. Essentially, a conditional distribution takesa vertical ‘slice’ of the joint distribution.(5) Thelocation of the ‘slice’ is determined by thecombination of dollar-sterling and euro-sterlingexchange rates that are consistent with the assumedfall in the euro-dollar exchange rate. The diagonallines in Chart D correspond to the locations of theconditional distributions (or ‘slices’) for a 10% or

20% appreciation (+) or depreciation (-) of the dollarversus the euro.

Chart E shows the conditional distributions for thesterling ERI in the event of a 10% fall/rise in thevalue of the dollar against the euro at thetwelve-month horizon, as well as the unconditionaldistribution. At face value, the distributions indicatethat option market participants perceived that evenrelatively large bilateral movements in the value of thedollar against the euro would tend have a relativelymodest impact on the probability distribution of the(‘simplified’) sterling ERI.

Chart CTwelve-month ‘synthetic’ risk reversal for the sterling ERI

0.3

0.2

0.1

0.0

0.1

0.2

0.3

2002 03 04 05 06

Percentage points

+

–

Sources: Bank of England and British Bankers’ Association.

Chart DContour ‘map’ of joint probability distribution

€ per £

$ p

er £

1.1 1.2 1.3 1.4 1.5 1.6 1.7

1.4

1.6

1.8

2.0

2.2

2.4

+20%

+10%

-20%-10%

Source: Bank calculations.

(5) More precisely, the conditional probabilities are calculated by applying Bayes’ Law. See Hurd, Salmon and Schleicher (2005) for more details.

Chart ETwelve-month unconditional and conditionalsterling ERI probability distributions(a)

0

1

2

3

4

5

6

7

8

9

10

75 80 85 90 95 100 105 110 115 120 125

Conditional on a 10% rise in the dollar versus the euro

Conditional on a 10% fall in the dollar versus the euro

Unconditional

Probability, per cent

Index level

Source: Bank calculations.

(a) Probability of the sterling ERI being within ±0.5 index points of any given level.

132

an expected appreciation of sterling against the dollarroughly offsetting an anticipated depreciation in sterlingagainst the euro. And the risks around that conditionalprojection appeared to be broadly balanced (Chart E inthe box on pages 130–31).

Long-term interest rates

Looking along the yield curve, sterling nominal forwardrates rose (Chart 10). Out to around a five-year horizon,that predominantly reflected an increase in inflationexpectations and/or inflation risk premia. Some marketcontacts reported that the move was consistent with thepossibility of higher energy and commodity pricesfeeding through into consumer price inflation.

Sterling real forward rates rose across the curve. Muchof the rise was in line with international long-term realrates, which increased steadily from mid-January untilmid-May (Chart 11). However, towards the end of thereview period long real forward rates fell slightly,perhaps reflecting some ‘flight to quality’ as financialmarket volatility rose and equity indices fell.

The increase in real forward rates over the period partlyreversed the steady falls observed during the previoustwo years.(1) But just as it was difficult to be categoricalabout what had pushed them lower, so it is hard to becertain about the reasons for the recent rise.

It is possible that a change in sentiment among bondinvestors may have pushed up term premia onlong-dated bonds over the review period. However,

implied volatilities derived from long-datedswaptions prices provided little evidence of a sharppickup in uncertainty surrounding long-term interestrates.

Alternatively, sterling long real forward rates may havebeen influenced by the rise in short-term market interestrates. In principle, long real forward rates should berelated to the equilibrium real interest rate, which islikely to be fairly stable over time. But over the past fewyears, movements in long-term real and short-termnominal interest rates have been highly correlated(Chart 12). One possible explanation is that marketparticipants might have been updating their beliefsabout the long-run equilibrium real rate based onobserved moves in short-term rates.

Chart 10Changes in sterling forward curves since 17 February(a)

20

10

0

10

20

30

40

50

60

70

80Basis points

0 5 10 15 20 25

Inflation

Nominal

Real

Years ahead

+

–

(a) Instantaneous forward rates derived from the Bank’s government liability curves.

(1) Previous Bulletins have identified several possible explanations for the gradual drift down in long real forward rates,which began in late 2003. For example, see page 6 of the Spring 2006 Quarterly Bulletin.

Chart 11International nine-year real forward rates(a)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan. Apr. July Oct. Jan. Apr. July Oct. Jan. Apr.

17 February

US dollar

Euro

Sterling

2004 05 06

Per cent

(a) Real component of euro rates implied by nominal government bond yields less inflation swap rates. Sterling and dollar real rates derived from the Bank’s government liability curves.

Bank of England Quarterly Bulletin: Summer 2006

Chart 12Comovement of one-year nominal forward rates withten-year nominal, real and inflation forward rates(a)(b)

0.2

0.0

0.2

0.4

0.6

0.8

1997 98 99 2000 01 02 03 04 05 06

Nominal

Inflation

Real

+

–

(a) Instantaneous forward rates derived from the Bank’s government liability curve.(b) Coefficient from 260-day rolling regression of changes in ten-year nominal, real

and inflation forwards on one-year nominal forward rates.

133

Despite the rise in long real forward rates, thesterling curve remained inverted. As discussed inprevious Bulletins, the inversion may indicate continuedrobust demand, relative to available supply, forlong-maturity index-linked bonds from defined-benefitpension funds.

Over the review period, there were announcements bythe UK Debt Management Office and by the UKPensions Regulator (summarised on pages 135),which had the potential to affect the balance ofanticipated supply of, and demand for, long-datedgilts. However, there were no obvious significantreactions in implied forward rates around the time ofthe announcements.

In addition to demand for long-dated gilts fromdefined-benefit pension funds, defined-contributionpension schemes may add to demand for long-datedgilts if scheme members purchase annuities onretirement and the annuity-provider then hedges itsexposure in the bond market. The relationship betweenannuity prices and long-term interest rates is describedin the box on this page.

Previous Bulletins have also noted that a large part ofthe demand for ultra-long dated sterling assets hasbeen in the form of interest rate or inflation swapstailored to match the future liabilities of pension funds.The providers of such swaps subsequently haveexposure to inflation risk. Some ways in which theymight seek to hedge this risk are outlined in the box onthis page.

Credit markets and the search for yield

Despite the rise in long-term interest rates and falls inequity and other prices, spreads on sterling-denominatedcorporate bonds ended the period narrower, althoughthey did widen a little around the middle of May(Chart 13).

Elsewhere, there was some evidence of a slight repricingof risk. For example, spreads on emerging marketcorporate debt widened by around 50 basis pointsduring May, although they still remained quite close tohistorical lows recorded earlier in the year. Primaryissuance also slowed in some corporate credit markets,and a few initial public offerings (IPOs) were postponed.But more generally, credit conditions did not appear tohave changed significantly in the wake of the recentpickup in financial market volatility.

Hedging inflation exposuresby swap dealers

Dealers providing inflation swaps can hedge theirexposure by isolating the inflation-linked cash flowson index-linked bonds using so-called asset swaps.

More specifically, having entered an inflation swaptransaction, a dealer can convert fixed payments intofloating (Libor-linked) payments using an interest rateswap (Chart A). The dealer can then borrow cash, onwhich it pays floating (Libor-linked) payments, which itinvests in an index-linked bond to provideinflation-linked cash flows. Dealers may enter intoasset swaps themselves or receive inflation-linked cashflows from hedge funds that undertake the asset swap.To the extent that these hedge funds are locatedoverseas, this highlights the need for care ininterpreting statistics on the location of gilt holdings,as the interest rate and inflation risk exposures on thegilts may have been transferred to a different locationthrough the swap market.

Dealers can sometimes find hedges for theirinflation-linked exposures in other parts of theirbusiness, such as making inflation-linked loans tocompanies, private finance initiative (PFI) projects orcommercial property leases, although they may stillneed to retain exposures until they can find a suitablehedge. Alternatively, they can use non-governmentsterling-denominated inflation-linked bonds, issuanceof which picked up recently. Over the review period,more than £1 billion of bonds linked to PFI projectswere issued. There has also been a steady stream ofindex-linked bond issuance from utilities companiesand other corporates, for example retailers.

Chart AHedging using an inflation-linked bond asset swap

INFLATIONSWAP

INTERESTRATE SWAP

INFLATION-LINKEDBOND

(Purchased usingborrowed funds)

DEALER

Provides inflationswap to pension fund

Hedges cash flowsvia index-linked

asset swap

Floating inflation-linked cash flows

Fixed cash flows

Floating Libor-linked cash flows

Markets and operations

134

Bank of England Quarterly Bulletin: Summer 2006

On retirement, an individual with a defined-contribution

(DC) pension scheme will usually purchase an annuity, to

provide a future income stream.(1) Providers of annuities

typically purchase bonds in order to hedge this exposure,

implying a link between bond yields and annuity rates.

In recent years, annuity rates have fallen steadily, and at the

end of 2005 had reached the lowest levels observed in

several decades (around 7%). In part, these falls reflected

declines in long-term interest rates (Chart A). However,

annuity prices are determined by a number of factors.

Annuity rates fall as discount rates fall; as life expectancy

increases; and as the ‘mark-up factor’ (ie the expected

compensation to the annuity provider) rises.

To see how these factors can affect annuity rates, it is

informative to consider a simple model of fixed annuities

with the price of an annuity equal to the present value of

the expected future cash flows paid to the pensioner

(adjusted to provide some expected profit to the annuity

provider). Using the Bank’s government liability yield

curves, together with mortality data from the ONS,(2) it is

possible to decompose changes in annuity rates into

changes in these underlying components (Chart B).

Approximately 35% of the decline in annuity rates since

1985 can be attributed to a fall in breakeven inflation, with

the largest falls following Bank operational independence in

1997. A further 27% of the decline is attributed to lower

real interest rates. Twenty nine per cent of the decline

reflects increased life expectancy, while the remainder

appears to be attributable to an increase in the mark-up

factor, estimated here as a residual.

One explanation for the rise in the mark-up is that annuity

providers may have become more risk-averse as a result of

unanticipated upward revisions to life expectancy.

Increased life expectancy and a higher mark-up factor are

likely to reduce pensioners’ expected retirement income. In

response, DC scheme members may choose to increase their

age of retirement and/or increase their pension saving.

Lower inflation expectations do not neccessarily reduce the

expected real retirement income of DC scheme members. At

the same time, lower real interest rates should only reduce

expected real retirement income if they are perceived to be

permanent. And to some extent this effect may be offset by

a rise in the value of these members’ pension funds. For

example, a simple dividend discount model of equity prices

would predict a rise in the value of equities when real

interest rates fall.

Decomposing changes in annuity rates

(1) Although there are a variety of annuity products on the market, this box focuses on a simple annuity that provides a fixed nominal payment each period untildeath, with a five-year guarantee, purchased by a male who retires aged 65.

(2) These data provide estimated survival probabilities for the general population. The analysis also assumes that changes in general population life expectancyproxy changes in the life expectancy of the annuity holder.

Chart ASterling annuity and long-term interest ratessince 1957

0

2

4

6

8

10

12

14

16

18

20

1960 65 70 75 80 85 90 95 2000 05

Annuity rate — male aged 65

Long spot rate(a)

Per cent

Sources: Bank of England, Edmond Cannon (Bristol University), GlobalFinancialData.com, William Burrows Annuities.

(a) 21/2% consol yield until 1980 then 15-year spot rate. Spot rates derived from theBank’s government liability curve.

Chart BContributions to cumulative changes in annuityrates (1985–05)(a)

8

7

6

5

4

3

2

1

0

1

1985 87 89 91 93 95 97 99 2001 03 05

Percentage pointsAnnuity mark-up factor

Real interest rateBreakeven inflationLife expectancy

Annuity rate

+

–

Sources: Bank of England, Edmond Cannon (Bristol University), GlobalFinancialData.com, ONS, William Burrows Annuities and Bankcalculations.

(a) Decomposition is a linear approximation of a non-linear relationship. As a result, the components of the chart do not sum exactly to the observed annuity rate.

Against a generally benign global macroeconomicbackdrop, it is perhaps too early to tell whether therecent increase in financial market volatility and thegradual withdrawal of monetary accommodation isprompting a widespread repricing of risk.

Anecdotal evidence suggests that some marketparticipants, especially hedge funds and others in thespeculative community, have either reappraised theamount of financial risk associated with particular assetclasses or reassessed their overall attitude towards risk.However, there are as yet few signs that other investorswith longer investment horizons (for example pensionfunds and insurance companies) have significantlyincreased their required compensation for taking onrisk.

Moreover, a number of the key elements of the ‘searchfor yield’ — described in previous Bulletins and in theBank’s recent Financial Stability Reviews — would appearto have remained largely intact over recent months. Inparticular, the repackaging of credit risk throughcollateralised debt obligations backed by assets such asleveraged loans, commercial real estate loans, homeequity loans and investment-grade bonds continuedapace. And credit conditions for leveraged buyouts ofcompanies remained favourable.

Developments in market structure

Over the review period, there were two significantdevelopments affecting the supply of and demand forlong-dated sterling-denominated bonds. In addition, theBank launched fundamental reforms to modernise theway in which the MPC’s interest rate decisions areimplemented in the sterling money markets. The box on

pages 136–37 describes the work of the SecuritiesLending and Repo Committee over the past year.

DMO funding remit

On 22 March, HM Treasury announced the UK DebtManagement Office (DMO) financing remit for the2006–07 financial year. It stated that, of a totalplanned £63 billion of gilt issuance, there would be aminimum core programme of £53 billion comprising atleast £10 billion in short conventional gilts (up to sevenyears’ maturity), £10 billion in medium conventionalgilts (7 to 15 years), £17 billion in long conventionalgilts (over 15 years) and £16 billion in index-linked gilts.As well as the core programme, a £10 billion programmeof supplementary issuance was introduced to allow theDMO to respond to changes in market conditions andthe pattern of demand for gilts within the financial year.The supplementary issuance will be allocated on aquarterly basis, with the first quarter’s £2.5 billion shareallocated to long conventional gilts. The secondquarter’s share, announced on 31 May, will be split bythe DMO between £1.25 billion of long conventionalgilts and £1.25 billion of index-linked gilts.

The pensions regulator’s approach to funding ofdefined-benefit pension schemes

On 4 May, the Pensions Regulator announced how itwould regulate the funding of defined-benefit (DB)pension schemes, following a consultation exercise thatbegan in October 2005. The main points noted bymarket commentators were: the increased emphasis onSection 179 and FRS17/IAS19 valuations for deficitmeasurements (which discount liabilities using marketinterest rates), rather than valuations on a buyoutbasis (which is the payment required by an insurer totake on the liabilities); that triggers should not beseen as standards or targets against which DB schemeswould be measured; and that there would be norequirement for schemes sponsored by companies ingood financial health to change their investmentstrategy.

Money market reform

The new framework for the implementation of UKmonetary policy launched by the Bank on 18 May hasfour objectives:

� Overnight market interest rates to be in line withthe official Bank rate, so that there is a flat moneymarket yield curve, consistent with the official

135

Chart 13Option-adjusted corporate bond spreads

200

250

300

350

400

450

500

550

600

Jan. May Sep. Jan. May Sep. Jan. May

40

50

60

70

80

90

100

Sterling high-yield (right-hand scale)

Global emerging market corporate (right-hand scale)

Sterling investment-grade (left-hand scale)

2004 05 06

Basis points Basis points

17 February

00

Source: Merrill Lynch.

Markets and operations

136

Bank of England Quarterly Bulletin: Summer 2006

The Securities Lending and Repo Committee (SLRC),chaired by the Bank, was formed in 1990. It providesa forum for discussion of market, infrastructure andlegal developments in securities lending and repomarkets and, where appropriate, makesrecommendations to market participants and relevantauthorities. It typically meets quarterly andcomprises representatives from repo and securitieslending practitioners, trade associations,infrastructure providers and UK authorities (the FSA,DMO and HM Revenue and Customs). SLRCmembership has recently been widened to ensure abroader representation of market practitioners andtrade associations. The minutes of SLRC meetings areavailable on the Bank’s website.(1)

Over the past year, the SLRC has discussed proposedchanges to the infrastructure supporting the UKsecurities lending and repo markets, including:

� Euroclear’s consultation on securities financing on itsfuture Single Platform, to which it is planned thatthe current national central securitiesdepositories in the Euroclear group (includingCREST in the United Kingdom) will migrate.SLRC members emphasised that the SinglePlatform should include the best features of thecurrent national systems, including CREST. Inparticular, delivery-by-value (DBV), or somethinganalogous, should be available on the newplatform to enable bundles of securities to befinanced overnight, or for a longer period, in astraightforward way. Relatedly, the Bank hasbeen pressing for any DBV facility to be not justovernight, as at present in CREST, but also toinclude provision for term transactions toremain ‘intact’ during the day in order to reducethe intraday liquidity required to unwind DBVsat the start of each day.

� LCH.Clearnet gilt DBV repo clearing project,scheduled to be introduced in 2006, which aimsto introduce the benefits of a centralcounterparty, including netting, for reposagainst bundles of gilts selected using the DBVservice offered in CREST. In particular, SLRC

members have discussed the proposed standardsize (shape) for trades sent to LCH for clearing,favouring no compulsory size on the basis thatfailed trades were rare in the gilt DBV market.

The SLRC’s market participant members have alsodiscussed the impact of proposed regulatory changesaffecting securities lending and repo markets, inparticular two new EU directives:

� The Transparency Directive, due forimplementation in January 2007, and inparticular its requirements regardingnotification of interests in shares in securitieslending transactions. SLRC practitionermembers had raised concerns about the limitedvalue of this information and the potentialreporting burden on securities lending marketparticipants. SLRC has discussed further howthese requirements might be implemented in away that meets the requirements of the Directivewhile being workable and cost-effective formarket participants.

� The Market in Financial Instruments Directive(MiFID), due for implementation in November2007. It seems that MiFID’s implications forrepo and securities lending will be limited; forexample, the best execution requirement will notapply to repo and security lending transactionsconducted between Eligible Counterparties (over90% of the total securities lending market). TheCommittee has also discussed whetheradditional reporting requirements to the FSAwould apply to securities lending and repo.

The SLRC has worked to improve understanding ofthe securities lending and repo markets and explaintheir important role at the heart of the modernfinancial system. For example, the Committee hascontributed to debates about how lenders of sharescan meet their corporate governance responsibilities.To this end, in conjunction with a number of tradeassociations representing the various participants inthe market and the London Stock Exchange, the SLRChas sponsored two publications:

The work of the Securities Lending and Repo Committee

(1) www.bankofengland.co.uk/markets/gilts/slrc.htm.

Markets and operations

137

� An Introduction to Securities Lending, which aimsto describe the modern markets for anon-expert; and

� Securities Lending and Corporate Governance.

Both publications are available on the SLRC pages onthe Bank of England website.(1)

One important function of the SLRC is to maintainvoluntary codes of market conduct for the gilt repo,securities lending and equity repo markets. TheSecurities Borrowing and Lending Code and the UKAnnex to the Code were first published in December2000 and updated in December 2004. The Gilt andEquity Repo Codes are currently being updated andnew versions should be issued later in 2006 or early2007.

Other issues recently discussed by the SLRC included:

� Basel II requirements, in particular relating to thedisclosure of underlying principals in securitiesloans. Except where borrowing is undertakenthrough what is classed as a ‘centralcounterparty’, this requirement will requireborrowers to identify the individual lenders ofsecurities and to identify what collateral is beingallocated to the lender.

� The ESCB/CESR(2) standards on clearing andsettlement, which aim to promote the safety andefficiency of European clearing and settlementsystems and to create a level playing fieldthrough the provision of a harmonisedregulatory framework. Standards relevant tosecurities lending include a dedicatedstandard on securities lending and a standardon risk controls to address participants’failures to settle. The finalisation andsubsequent implementation of the ESCB/CESRstandards will continue to be monitored bySLRC.

� Amendments to the FSA rules to allow securitieslending through Euroclear’s automated lendingprogramme by UK insurance companies.Securities lending is ‘approved’ if certainconditions are met concerning the assets lent,the counterparty and the collateral provided.Approval means the securities lent are stilltreated as being the lending company’s assetsfor solvency purposes.

� The 2003 Giovannini group report on EUcross-border clearing and settlement arrangements,setting out a process to overcome 15 barriers toefficiency. Current issues include work underway to harmonise national rules relating tocorporate actions processing, which could havean impact on securities lending.

An SLRC subgroup, comprising trade associationrepresentatives and legal advisers, is responsible forobtaining legal opinions on the effectiveness of theclose-out netting provisions in the Global MasterSecurities Lending Agreement (GMSLA), the OverseasSecurities Lender’s Agreement (OSLA) and the MasterGilt Edged Stock Lending Agreement (GESLA) underdifferent jurisdictions around the world. UKauthorised firms are required to obtain these legalopinions in order to support the reporting ofsecurities lending exposures to the FSA (on a netbasis) for capital adequacy purposes.

Recently the subgroup has been discussing thepotential to harmonise this exercise in gathering legalopinion with the similar process organised by theInternational Capital Markets Association (ICMA) andThe Bond Market Association (TBMA) for repotransactions under the Global Master RepoAgreement (GMRA). That would probably yield costsavings and efficiency gains for participating firms.Further work will be carried out to finalise the format,timing and funding of combined opinions, as well asestablishing the appropriate committee structures toreview them.

(1) Available at www.bankofengland.co.uk/markets/gilts/securitieslending.pdf andwww.bankofengland.co.uk/markets/gilts/skgjun05.pdf.

(2) European System of Central Banks/Committee of European Securities Regulators.

138

Bank of England Quarterly Bulletin: Summer 2006

Bank rate, out to the next MPC decision date, withvery limited day-to-day or intraday volatility inmarket interest rates at maturities out to thathorizon.

� An efficient, safe and flexible framework forbanking system liquidity management — both incompetitive money markets and, whereappropriate, using central bank money — inroutine and stressed, or otherwise extraordinary,conditions.

� A simple, straightforward and transparentoperational framework.

� Competitive and fair sterling money markets.

The framework is based on a system of voluntaryremunerated reserves with a period-averagemaintenance requirement, together with standingborrowing and deposit facilities available on demandthroughout the banking day to a wide range ofcommercial banks.

Reserve accounts are current accounts with the Bankthat are remunerated at the official Bank rate decided bythe MPC. Banks target average balances with the Bankover the periods between the MPC’s monthly interestrate decisions rather than having to ‘square up’ at closeof business every day, making it easier for them tomanage day-to-day cash flows. In the interests ofsimplicity, it has therefore been possible to discontinuetwo facilities previously used by banks to manage theirend-of-day payments flows.

Specifically, the Bank of England Late Transfer Scheme(BELTS) End-of-Day Transfer Scheme (EoDTS) facilitiesended on 17 May. There is, however, still a short windowfor settlement banks to make payments to each otherafter the payment system has closed on the last day ofeach maintenance period (when banks need to achievetheir average reserve targets). This is in addition to theovernight standing facilities.

The averaging mechanism for reserves allows banks torun their balances at the Bank up or down in responseto changes in market interest rates. Arbitrage shouldsmooth overnight market interest rates so that they do

not deviate materially from the rate expected to prevailon the final day of the monthly maintenance period.And on the final day of the maintenance period, thestanding facilities perform a rate-setting function,setting a narrower ±25 basis points corridor for marketrates.

The standing facilities provide liquidity insurance tofinancial institutions. A wide range of banks andbuilding societies can borrow (against collateral) from,or deposit money with, the Bank in unlimited amounts.Except on the final day, the penalty rates are ±100 basispoints (around the official Bank rate).

The Bank has also changed its open market operations(OMOs). The purpose of OMOs is to finance banknotesin circulation and ensure that the banking system canachieve its aggregate reserves target over themaintenance period. The Bank’s short-term OMOs havechanged to weekly repo operations for one-weekmaturity. A routine overnight fine-tuning operation isconducted on the final day of the maintenance period.

To reduce the size of the weekly short-term OMOs,monthly long-term repo OMOs were introduced inJanuary 2006. These provide financing at market rates,at maturities of three, six, nine and twelve months. TheBank also plans to purchase conventional gilts andhigh-quality foreign currency bonds swapped intofixed-rate sterling to back the enduring part of thebanknote issue;(1) further details will be announcedfollowing consultation with OMO counterparties, andliaison with the DMO.

The Bank’s new framework is set out in more detail inits ‘Red Book’ issued on 15 May.(2)

Bank of England official operations

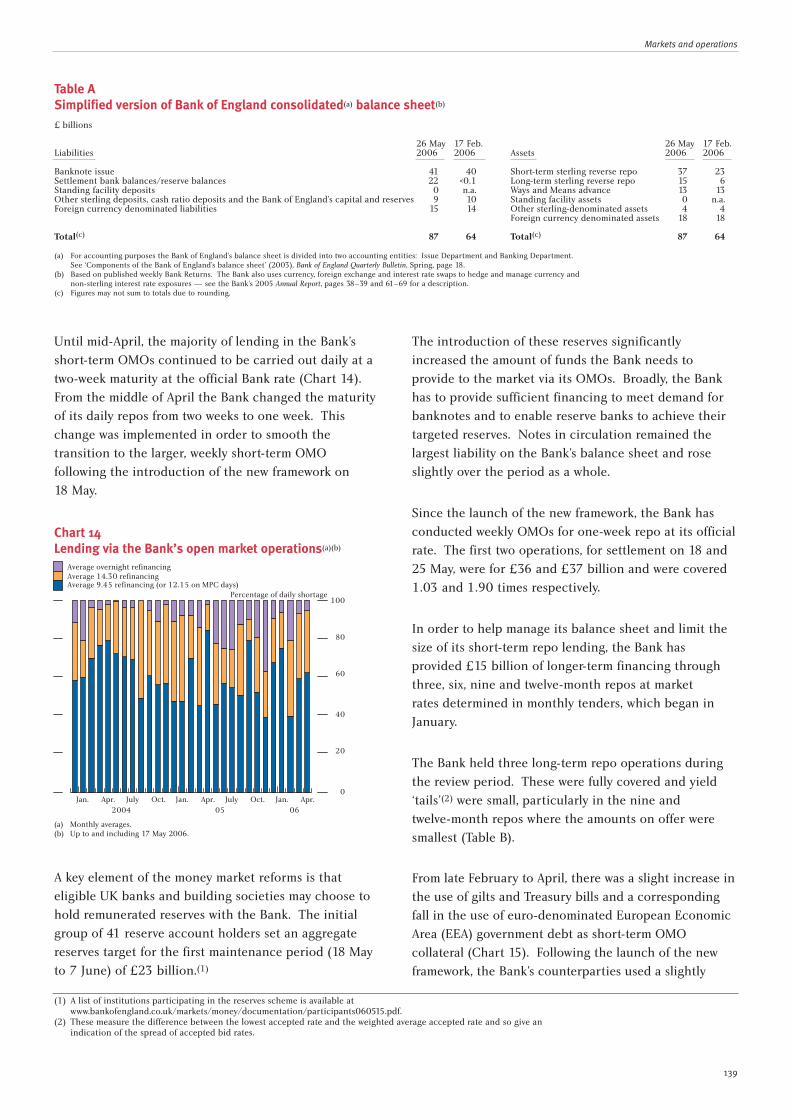

Changes in the sterling components of the Bank ofEngland balance sheet

The size of the sterling components of the Bank’sbalance sheet grew following the reforms to the Bank’ssterling monetary operations (Table A). To reflectbetter the structure of the balance sheet following thelaunch of the new framework, the Bank has revised theweekly Bank Return published on its website.(3)

(1) A joint statement by the Bank and the DMO was issued on 15 May and is available atwww.bankofengland.co.uk/markets/money/documentation/boe_dmo.pdf.

(2) ‘The Framework for the Bank of England’s Operations in the Sterling Money Markets’ is available atwww.bankofengland.co.uk/markets/money/publications/redbook0506.pdf.

(3) Available at www.bankofengland.co.uk/publications/bankreturn/index.htm.

Markets and operations

139

Until mid-April, the majority of lending in the Bank’sshort-term OMOs continued to be carried out daily at atwo-week maturity at the official Bank rate (Chart 14).From the middle of April the Bank changed the maturityof its daily repos from two weeks to one week. Thischange was implemented in order to smooth thetransition to the larger, weekly short-term OMOfollowing the introduction of the new framework on18 May.

A key element of the money market reforms is thateligible UK banks and building societies may choose tohold remunerated reserves with the Bank. The initialgroup of 41 reserve account holders set an aggregatereserves target for the first maintenance period (18 Mayto 7 June) of £23 billion.(1)

The introduction of these reserves significantlyincreased the amount of funds the Bank needs toprovide to the market via its OMOs. Broadly, the Bankhas to provide sufficient financing to meet demand forbanknotes and to enable reserve banks to achieve theirtargeted reserves. Notes in circulation remained thelargest liability on the Bank’s balance sheet and roseslightly over the period as a whole.

Since the launch of the new framework, the Bank hasconducted weekly OMOs for one-week repo at its officialrate. The first two operations, for settlement on 18 and25 May, were for £36 and £37 billion and were covered1.03 and 1.90 times respectively.

In order to help manage its balance sheet and limit thesize of its short-term repo lending, the Bank hasprovided £15 billion of longer-term financing throughthree, six, nine and twelve-month repos at marketrates determined in monthly tenders, which began inJanuary.

The Bank held three long-term repo operations duringthe review period. These were fully covered and yield‘tails’(2) were small, particularly in the nine andtwelve-month repos where the amounts on offer weresmallest (Table B).

From late February to April, there was a slight increase inthe use of gilts and Treasury bills and a correspondingfall in the use of euro-denominated European EconomicArea (EEA) government debt as short-term OMOcollateral (Chart 15). Following the launch of the newframework, the Bank’s counterparties used a slightly

Table ASimplified version of Bank of England consolidated(a) balance sheet(b)

£ billions

26 May 17 Feb. 26 May 17 Feb.Liabilities 2006 2006 Assets 2006 2006

Banknote issue 41 40 Short-term sterling reverse repo 37 23Settlement bank balances/reserve balances 22 <0.1 Long-term sterling reverse repo 15 6Standing facility deposits 0 n.a. Ways and Means advance 13 13Other sterling deposits, cash ratio deposits and the Bank of England’s capital and reserves 9 10 Standing facility assets 0 n.a.Foreign currency denominated liabilities 15 14 Other sterling-denominated assets 4 4

Foreign currency denominated assets 18 18

Total(c) 87 64 Total(c) 87 64

(a) For accounting purposes the Bank of England’s balance sheet is divided into two accounting entities: Issue Department and Banking Department. See ‘Components of the Bank of England’s balance sheet’ (2003), Bank of England Quarterly Bulletin, Spring, page 18.

(b) Based on published weekly Bank Returns. The Bank also uses currency, foreign exchange and interest rate swaps to hedge and manage currency and non-sterling interest rate exposures — see the Bank’s 2005 Annual Report, pages 38–39 and 61–69 for a description.

(c) Figures may not sum to totals due to rounding.

Chart 14Lending via the Bank’s open market operations(a)(b)

0

20

40

60

80

100

Jan.2004

Apr. July Oct. Jan.05

Apr. July Oct. Jan.06

Apr.

Percentage of daily shortage

Average overnight refinancingAverage 14.30 refinancing Average 9.45 refinancing (or 12.15 on MPC days)

(a) Monthly averages.(b) Up to and including 17 May 2006.

(1) A list of institutions participating in the reserves scheme is available atwww.bankofengland.co.uk/markets/money/documentation/participants060515.pdf.

(2) These measure the difference between the lowest accepted rate and the weighted average accepted rate and so give anindication of the spread of accepted bid rates.

140

higher proportion of gilts in short-term OMOs than inthe period running up to the reforms. In the longer-termrepo operations, counterparties used a slightly largerproportion of euro-collateral relative to that used in theshort-term operations. Contacts suggested that this wasmainly due to cost considerations.

Late transfer schemes

The relatively low level of flows in the end-of-dayschemes continued (Chart 16). Average daily paymentsin the Bank of England Late Transfer Scheme (BELTS)were less than £50 million on average, while averagedaily flows in the End-of-Day Transfer Scheme (EoDTS)were generally less than £150 million. As reported

above, these facilities are not needed in the modernisedsystem and have been withdrawn.

Changes in the foreign-currency components of theBank of England balance sheet

As part of the new monetary regime introduced in 1997,the Bank has been able to hold its own foreign exchangereserves. These, and other assets used to facilitateparticipation in the euro area’s TARGET payment system,are financed by issuing foreign-currency securities.

On 28 March 2006, the Bank auctioned €1 billion ofthe 2009 note as part of its euro-denominated notesprogramme; the first €2 billion tranche had beenauctioned on 24 January 2006. Cover in the auction ofthe second tranche was 2.8 and the average acceptedyield was 3.393%, approximately 13.2 basis points belowthe euro swaps curve at the time. This was the secondand final auction of the 2009 note and increased thevalue outstanding in the market to €3 billion. The totalnominal value of Bank euro notes outstanding in themarket rose to €7 billion.

On 24 April, the Bank of England announced it wouldissue no further euro bills, with the April 2006 euro billauction being the last in the series. The final euro billwill mature on 12 October 2006.

Employment of the Bank of England’s capital

As set out in previous Bulletins, the Bank holds aninvestment portfolio of gilts (currently around£2 billion) and other high-quality sterling-denominateddebt securities (currently £1.1 billion) of approximately

Bank of England Quarterly Bulletin: Summer 2006

Chart 15Instruments used as OMO collateral in short-termoperations(a)

Gilts and Treasury bills Euro-denominated EEA securitiesEligible bank bills Bank of England euro billsSterling-denominated EEA securities

0

20

40

60

80

100

Jan.2004

Apr. July Oct. Jan.05

Apr. July Oct. Jan.06

Apr.

Per cent

(a) Monthly averages.

Chart 16Bank of England Late Transfer Scheme and End-of-Day Transfer Scheme(a)(b)

Bank of England Late Transfer Scheme

£ millions

0

50

100

150

200

250

300

350

400

450

Jan.2004

May Sep. Jan.05

May Sep. Jan.06

May

End-of-Day Transfer Scheme

(a) Monthly averages.(b) Up to 17 May 2006.

Table BLong-term repo operations

Three-month Six-month Nine-month Twelve-month

14 March 2006On offer (£ millions) 2,850 750 400 200Cover 2.67 5.12 3.25 5.15Weighted average rate(a) 4.417 4.457 4.515 4.565Highest accepted rate(a) 4.430 4.460 4.515 4.565Lowest accepted rate(a) 4.410 4.455 4.455 4.565Tail(b) (basis points) 0.7 0.2 0 0

18 April 2006On offer (£ millions) 2,850 750 400 200Cover 2.34 3.35 3.25 3.75Weighted average rate(a) 4.468 4.513 4.575 4.64Highest accepted rate(a) 4.48 4.515 4.575 4.64Lowest accepted rate(a) 4.46 4.505 4.575 4.64Tail(b) (basis points) 0.8 0.8 0 0

16 May 2006On offer (£ millions) 2,850 750 400 200Cover 3.16 2.48 2.31 4Weighted average rate(a) 4.548 4.65 4.755 4.845Highest accepted rate(a) 4.57 4.65 4.755 4.845Lowest accepted rate(a) 4.541 4.65 4.755 4.845Tail(b) (basis points) 0.7 0 0 0

(a) Per cent.(b) The yield tail measures the difference between the weighted average accepted bid rate

and the lowest accepted rate.

141

the same size as its capital and reserves and aggregatecash ratio deposits with the Bank. These investmentsare generally held to maturity. Over the current reviewperiod, gilt purchases were made in accordance with thepublished screen announcements: £37.6 million of4.75% 2020 in March, £37.6 million of 4.75% 2015 inApril and £37.6 million of 5% 2014 in May. A screenannouncement on 1 June 2006 detailed the purchasesto be made over the following three months.

Markets and operations

142

Introduction

In a famous experiment, Pavlov showed how a pastassociation between two events could be mistaken for acausal link between the two. In his experiment, a bellwas rung as his dogs were provided with food. Overtime, the dogs learned to associate the two, believingthat the ringing of a bell would be accompanied by thearrival of food. Of course, that was not necessarily thecase. It is an example of the fact that correlation is notcausation.

A similar point applies to the interpretation ofcorrelations among many macroeconomic time series.The link between consumer spending and house pricesis a good example. The two series have tended to movetogether in the past. In part, that is because houseprice movements can cause changes in spending. Butthe correlation also reflects the influence of commonfactors, like expectations of future income, that affectboth house prices and consumption.

More recently, the empirical association between houseprices and spending has waned (Chart 1). That mightreflect a weakening in the causal links between them.Or it could be the case that, in contrast with the past,recent fluctuations in house prices have not been drivenby common factors like expected income. Instead, adifferent set of factors might have been important. Theycould have boosted house prices, but had a more limitedimpact on consumer spending. This illustrates that theimplications of a rise in house prices for consumerspending depend on why house prices have risen.

This article starts by discussing the common factors andcausal links that lie behind the association between

house prices and consumer spending. It then examineshow changes in the strength of these different channels,and the impact of other influences, might account forthe apparent weakness of that relationship in recentyears. Throughout the article, a common theme is thatthe linkages between house prices and consumerspending are more subtle — and rather less stable overtime — than is often supposed.

What explains the past empirical association?

Common factors

There are a number of factors that affect both houseprices and consumer spending. For example, areduction in interest rates, an increase in people’s accessto credit, and an improvement in income expectationswould all tend to boost demand for consumer goods and

House prices and consumer spending

This article explores the complex relationship between house prices and consumer spending. It explainsthat the strength of the relationship can vary considerably over time. And it highlights the key roles thatboth common factors and causal links have played in the weakening association between house pricesand consumer spending in recent years.

By Andrew Benito, Jamie Thompson, Matt Waldron and Rob Wood of the Bank’s Monetary Analysisarea.

Chart 1Real house prices(a) and consumer spending

6

4

2

0

2

4

6

8

10

12

1971 76 81 86 91 96 2001 0630

20

10

0

10

20

30

40Percentage change on a year earlier Percentage change on a year earlier

Consumer spending (right-hand scale)

Real house prices (left-hand scale)

+

_ +

_

Sources: Nationwide and ONS.

(a) Nationwide house price index deflated by the consumer expenditure deflator.

House prices and consumer spending

143

services, as well as demand for housing. In such cases,there might appear to be a direct relationship betweenhigher house price inflation and higher consumerspending growth. But, in reality, both outcomes aredriven by a common influence.

The key common factor is probably expected income(see King (1990) and Attanasio and Weber (1994)). Ifthere is an increase in the income households expect toearn in the future, that would lead them to plan higherspending — both now and in the years ahead.Households would demand more consumer goods andservices, and their demand for housing would rise too.The increase in future expected income would thereforelead to a rise in both consumer spending and houseprices.

Evidence suggests that income expectations have attimes played an important role in the comovementbetween house prices and consumer spending. Forexample, changes in income expectations should affectthe behaviour of renters as well as homeowners. So ifincome expectations had played a key role, we mightexpect the spending of renters to have moved with houseprices — even though they do not own a home. Basedon evidence from household surveys, that appears tohave been the case (Chart 2).

Similarly, if income expectations have been important,then house price movements would tend to be moreclosely related to the spending of the young than theold. Younger households have more years of work ahead

of them and should benefit most from a general rise inthe wages that people expect to earn in future. Chart 3 shows that the spending of younger householdsdid indeed appear to move more closely with risinghouse prices in the late 1980s and late 1990s, as well aswith the fall in house prices in the early 1990s. As thebox on page 145 explains, however, some studies havealso pointed to a strong link between house prices andthe spending of older households. So evidence on thespending behaviour of different age groups is not clear-cut.

House prices and household wealth

Wealth and consumer spending are closely linked. Theamount that a household can spend over its lifetime islimited by the wealth it can accumulate. And, in general,a household is likely to respond to an increase in wealthby spending more both now and in the future.

As a result, it is often supposed that house pricesinfluence consumer spending because housing is amajor part of households’ wealth. Housing accounts foraround 40% of total household assets. More people ownhomes than shares (see Banks and Smith (2000)). And,for many households, housing is the most valuable assetthey own (see Barwell et al (2006)).

But, in reality, the link between house prices andaggregate wealth cannot explain the historicalassociation between house prices and consumerspending (see Aoki et al (2001)). That is because of akey characteristic of housing.

Chart 2House prices and consumer spending by tenure group

6

3

0

3

6

9

12

1977 81 85 89 93 97 2001

Renters’ spending

Homeowners’ spending

House prices Percentage changes on a year earlier(a)

+

–

Chart 3House prices and consumer spending by age group

6

3

0

3

6

9

12

1977 81 85 89 93 97 2001

Under 35s’ spending

35–60s’ spending

Over 60s’ spending

House pricesPercentage changes on a year earlier(a)

-

+