Asia Pacific Daily - 26 July 2019 - Bursa Marketplace

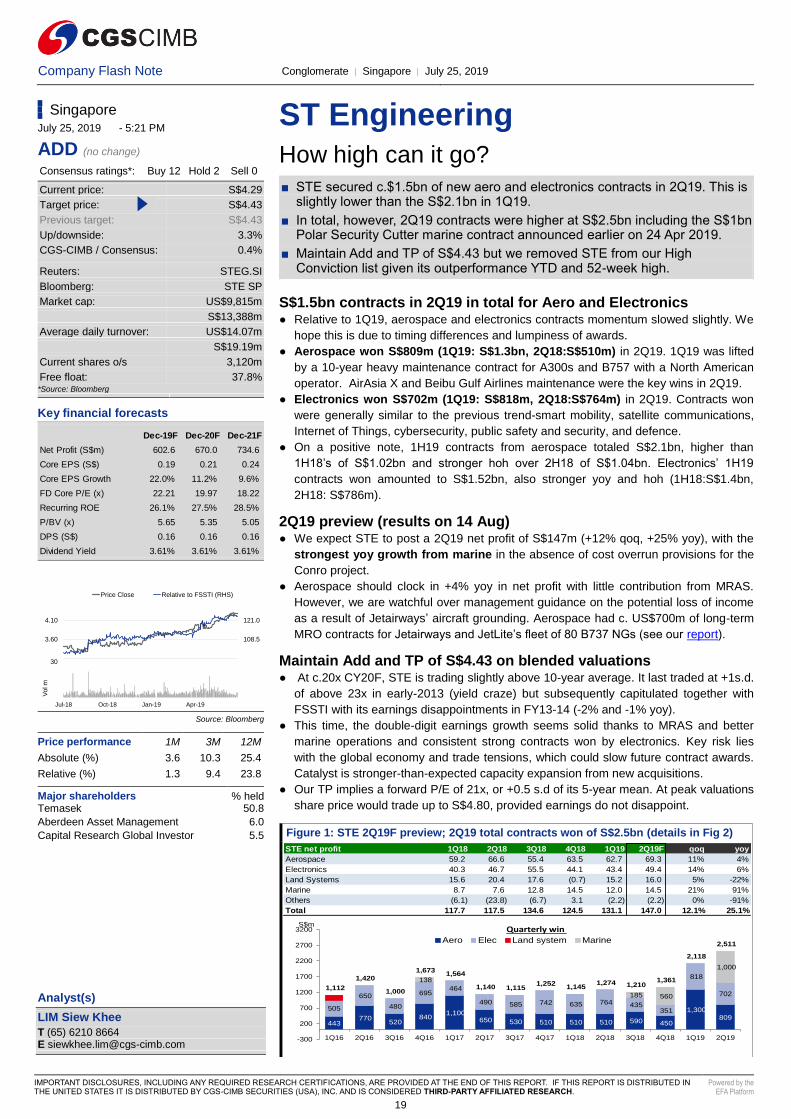

29

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CGS-CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH. Powered by the EFA Platform Asia Pacific Daily - 26 July 2019 Equity Research Reports… ▌China/Hong Kong Property - Overall (NEUTRAL) - 10% earnings growth expected for 1H19 | P2 ——————————————————————————————————————————————————————————————————————————————————————— ▌India Asian Paints Limited (HOLD, tp:Rs1,520.00▲) - Fairly priced; maintain Hold | P3 Mahindra & Mahindra Fin. (ADD, tp:Rs400.00▼) - Economic slowdown hurts asset quality | P4 Shriram Transport Finance (ADD, tp:Rs1,350.00▼) - Growth drops – asset quality largely … | P5 SKF India Ltd (ADD, tp:Rs2,150.00▼) - 1QFY20: Steady quarter | P6 Tata Motors (ADD, tp:Rs277.00) - JLR volatility concerns | P7 ——————————————————————————————————————————————————————————————————————————————————————— ▌Indonesia Bank Central Asia (HOLD, tp:Rp28,500.00) - 1H19 results: Strong PPOP offset by higher … | P8 ——————————————————————————————————————————————————————————————————————————————————————— ▌South Korea Korea Shipbuilding & Offshore (ADD, tp:W170,000.00▼) - Good earnings, weak sentiment | P9 LG Household & Health Care Ltd (ADD, tp:W1,500,000.00) - 2Q19 review: virtue of ... | P10 Mando Corporation (ADD▲, tp:W40,000.00▲) - Self-driving outside China | P11 NAVER (HOLD▲, tp:W140,000.00▲) - Positive on Naver Pay’s spinoff | P12 SK Hynix (ADD, tp:W95,000.00▲) - Moving in the right direction for a recovery | P13 ——————————————————————————————————————————————————————————————————————————————————————— ▌Malaysia Axis REIT (HOLD, tp:RM1.95) - Narrowing down its acquisition prospects | P14 CapitaLand Malaysia Mall Trust (HOLD, tp:RM1.03▼) - Prolonged impact from rental ... | P15 Pavilion REIT (HOLD, tp:RM1.91▲) - Working on DA MEN’s gradual turnaround | P16 ——————————————————————————————————————————————————————————————————————————————————————— ▌Singapore Cache Logistics Trust (HOLD, tp:S$0.76▼) - Looking for a better 3Q | P17 Mapletree Commercial Trust (ADD, tp:S$2.24) - A good start | P18 ST Engineering (ADD, tp:S$4.43) - How high can it go? | P19 Thai Beverage (ADD, tp:S$0.96▲) - NDR takeaways: Solidifying its presence | P20 ——————————————————————————————————————————————————————————————————————————————————————— ▌Thailand Carabao Group (ADD, tp:THB80.00▲) - More energy to run | P21 KCE Electronics (REDUCE, tp:THB13.60▼) - Strong earnings rebound not in sight | P22 Recent CGS-CIMB Research Ideas —————————————————————————————————— KRW: Technology Components 23/07 Diverging prospects for LGI & BH ———— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— —— THB: Hotels 17/7 NCPO legalisation will boost room supply ———— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— —— CHN: Universal Scientific Industrial 16/07 Finding the golden child ———— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— —— MAL: Rubber Gloves 12/07 Golden gloves ———— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— —— KRW: Navigating South Korea: Technology Components 10/07 Integration is key for future display tech ———— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— —— Regional Equity Research Contact ————————————————————————————————— Bertram LAI Head of Research T: (852) 2532 1111 E: [email protected] ———— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— ——— — Show Style "View Doc Map"

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Asia Pacific Daily - 26 July 2019 - Bursa Marketplace

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CGS-CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Asia Pacific Daily - 26 July 2019 Equity Research Reports…

▌China/Hong Kong Property - Overall (NEUTRAL) - 10% earnings growth expected for 1H19 | P2 ———————————————————————————————————————————————————————————————————————————————————————

▌India Asian Paints Limited (HOLD, tp:Rs1,520.00▲) - Fairly priced; maintain Hold | P3

Mahindra & Mahindra Fin. (ADD, tp:Rs400.00▼) - Economic slowdown hurts asset quality | P4 Shriram Transport Finance (ADD, tp:Rs1,350.00▼) - Growth drops – asset quality largely … | P5

SKF India Ltd (ADD, tp:Rs2,150.00▼) - 1QFY20: Steady quarter | P6

Tata Motors (ADD, tp:Rs277.00) - JLR volatility concerns | P7 ———————————————————————————————————————————————————————————————————————————————————————

▌Indonesia

Bank Central Asia (HOLD, tp:Rp28,500.00) - 1H19 results: Strong PPOP offset by higher … | P8 ———————————————————————————————————————————————————————————————————————————————————————

▌South Korea Korea Shipbuilding & Offshore (ADD, tp:W170,000.00▼) - Good earnings, weak sentiment | P9 LG Household & Health Care Ltd (ADD, tp:W1,500,000.00) - 2Q19 review: virtue of ... | P10

Mando Corporation (ADD▲, tp:W40,000.00▲) - Self-driving outside China | P11 NAVER (HOLD▲, tp:W140,000.00▲) - Positive on Naver Pay’s spinoff | P12

SK Hynix (ADD, tp:W95,000.00▲) - Moving in the right direction for a recovery | P13 ———————————————————————————————————————————————————————————————————————————————————————

▌Malaysia Axis REIT (HOLD, tp:RM1.95) - Narrowing down its acquisition prospects | P14

CapitaLand Malaysia Mall Trust (HOLD, tp:RM1.03▼) - Prolonged impact from rental ... | P15 Pavilion REIT (HOLD, tp:RM1.91▲) - Working on DA MEN’s gradual turnaround | P16 ———————————————————————————————————————————————————————————————————————————————————————

▌Singapore Cache Logistics Trust (HOLD, tp:S$0.76▼) - Looking for a better 3Q | P17 Mapletree Commercial Trust (ADD, tp:S$2.24) - A good start | P18

ST Engineering (ADD, tp:S$4.43) - How high can it go? | P19 Thai Beverage (ADD, tp:S$0.96▲) - NDR takeaways: Solidifying its presence | P20 ———————————————————————————————————————————————————————————————————————————————————————

▌Thailand Carabao Group (ADD, tp:THB80.00▲) - More energy to run | P21 KCE Electronics (REDUCE, tp:THB13.60▼) - Strong earnings rebound not in sight | P22

Sources: CIMB. COMPANY REPORTS

Recent CGS-CIMB Research Ideas ——————————————————————————————————

KRW: Technology Components 23/07 Diverging prospects for LGI & BH —————————————————————————————————————————————————————————————————————————————————

THB: Hotels 17/7

NCPO legalisation will boost room supply —————————————————————————————————————————————————————————————————————————————————

CHN: Universal Scientific Industrial 16/07

Finding the golden child —————————————————————————————————————————————————————————————————————————————————

MAL: Rubber Gloves 12/07 Golden gloves —————————————————————————————————————————————————————————————————————————————————

KRW: Navigating South Korea: Technology

Components 10/07 Integration is key for future display tech —————————————————————————————————————————————————————————————————————————————————

Regional Equity Research Contact ————————————————————————————————— Bertram LAI

Head of Research T: (852) 2532 1111 E: [email protected]

———————————————————————————————————————————————————————————————————————————————————

Show Style "View Doc Map"

Sector Note Property │ China │ July 25, 2019

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CGS-CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Property - Overall 10% earnings growth expected for 1H19

■ We estimate that 20 developers under our universe to deliver earnings growth of about 10% for 1H19, primarily driven by revenue growth.

■ Results for Aoyuan, Logan, Sunac, Shimao, Longfor could be strong while Agile, CR Land, Sino Ocean’s results may be weaker-than-expected.

■ We like Longfor among large-caps and prefer Shimao, CIFI and RF among mid-cap. Meanwhile, Times is our preferred choice for Greater Bay Area.

We estimate developers’ earnings increased about 10% for 1H19 Chinese developers will announce their 1H19 results in Aug (refer to Figs 5-6 for specific

dates and NDRs that we will host). For the 20 developers we cover, we estimate their

core earnings increased by 10% yoy on average, primarily driven by solid revenue growth

offset in part by some gross margin contraction. Earnings for Sunac, Aoyuan, Logan,

KWG, Longfor, Greentown, Shimao and Times are likely to stand out with 20-70% yoy

growth while earnings for Sino-Ocean, Evergrande, Agile, SZI and CR Land could be

lower-than-expected due to their high base last year or weak execution capability.

Gross margin to contract 2.1% pts to 31.4% on average Driven by higher land costs of projects to be recognised, the 1H19 gross margin of

developers should have contracted by an average of 2.1% pts to 31.4%. Agile, CR Land,

Sunac and Sino Ocean likely saw larger contractions of 3.5-15.6% pts in 1H19 on a high

margin in 1H18 or recognition of some projects with relatively low margins this year.

Net gearing remained manageable We estimate developers’ net gearing to increase slightly to about 81% in 1H19 from 76%

at end-2018. We think that the levels are manageable as we expect developers should be

able to increase their contracted sales by more than 10% this year. Meanwhile, we have

some concerns on Sunac, as we expect its net gearing could balloon to about 220% in

1H19 from 170% from end-2018 on its aggressive landbanking.

To see developers contracted sales increase by 15% for FY19 Developers registered 10% growth in 1H19 contracted sales on average. Shimao, CIFI,

Aoyuan, Yuzhou, Sino-Ocean and SZI stood out with growth of 32-49% yoy. Given more

project launches, a lower base in 2H18 and a relatively looser mortgage policy, we expect

developers’ sales momentum to accelerate in 2H19. In 1H19, developers had achieved

about 46% of full-year targets for FY19 and we estimate that they should be able to

increase their contracted sales by 15% for FY19.

Stay Neutral; top picks are Longfor, Shimoa, RF, CIFI and Times We like Longfor for large-cap on its decent earnings growth and strong balance sheet and

like Shimao, CIFI and RF for their attractive valuations. We also like Times for its high

exposure to the Greater Bay Area. Key risks include slower-than-expected economic

growth in China and potential policy tightening due to strong property markets.

Figure 1: Summary of 1H19 results preview

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

China

Neutral (no change)

Highlighted Companies

Longfor Group ADD, TP HK$40.00, HK$30.60 close

Longfor has benefited significantly from its proactive landbanking in China’s top tier cities. We forecast strong rental income growth of 20-25% p.a. in FY19-21F and a decent dividend yield of 4.6% in FY19F.

Shimao Property ADD, TP HK$28.00, HK$22.25 close

We like Shimao for its above-average sales and earnings growth over FY18-20F. It trades at a 44% discount to NAV and 6x FY19F P/E, which looks quite attractive for a quality mid-cap stock.

Times China Holdings Ltd ADD, TP HK$21.00, HK$14.50 close

We expect Times to be one of the biggest beneficiaries of the development plan for the Greater Bay Area, in which some 90% of its land bank is located. The stock, trading at 4.4x FY19F P/E and 6.8% yield, looks very attractive.

Summary Valuation Metrics

Insert

Analyst(s)

Raymond CHENG, CFA

T (852) 2539 1324 E [email protected]

Will CHU T (852) 2539 1327 E [email protected]

Jeffrey MAK T (852) 2539 1328 E [email protected]

P/E (x) Dec-19F Dec-20F Dec-21F

Longfor Group 9.84 8.01 6.66

Shimao Property 5.89 4.88 4.14

Times China Holdings Ltd 4.43 3.55 2.88

P/BV (x) Dec-19F Dec-20F Dec-21F

Longfor Group 1.78 1.58 1.40

Shimao Property 0.88 0.76 0.65

Times China Holdings Ltd 0.90 0.71 0.56

Dividend Yield Dec-19F Dec-20F Dec-21F

Longfor Group 4.57% 5.62% 6.76%

Shimao Property 5.59% 6.51% 7.59%

Times China Holdings Ltd 6.54% 8.16% 10.07%

Bloomberg

Net

gearing

Company Ticker 1H19F yoy chg 1H19F pts chg 1H19F yoy chg 1H19F yoy chg 1H19F

COLI 688 HK 102,719 16% 33.5% -2.3% 21,108 10% 0.44 10% 35%

CR Land 1109 HK 55,471 27% 38.0% -10.1% 7,803 7% 0.12 9% 40%

China Vanke - H 2202 HK 113,518 8% 32.8% -0.9% 12,229 17% NA NA 35%

CIFI 884 HK 21,955 19% 33.5% -0.2% 2,907 19% 0.08 20% 85%

Country Garden 2007 HK 187,886 42% 27.0% 0.5% 13,925 17% 0.20 8% 60%

Evergrande 3333 HK 285,331 -5% 35.0% -1.2% 27,234 -15% NA NA 145%

Greentown 3900 HK 35,210 5% 24.0% 5.9% 1,653 28% NA NA 110%

Guangzhou R&F 2777 HK 39,200 15% 36.0% -2.5% 4,532 10% 0.44 10% 170%

KWG 1813 HK 5,369 55% 30.8% -0.3% 2,765 41% 0.28 10% 70%

Longfor 960 HK 35,257 30% 35.0% -2.1% 4,476 20% 0.28 20% 55%

Shimao Prop 813 HK 55,342 30% 29.5% -1.5% 5,393 23% 0.55 10% 60%

Sino-Ocean 3377 HK 16,872 10% 20.0% -3.5% 1,146 -26% 0.10 -29% 80%

SOHO China 410 HK 899 6% 75.8% -0.1% 182 -6167% NA NA 45%

Sunac 1918 HK 74,532 60% 30.0% -4.1% 9,931 70% NA NA 220%

Yuzhou 1628 HK 11,461 24% 30.9% -0.6% 1,337 15% 0.13 14% 88%

Agile 3383 HK 27,837 15% 34.0% -15.6% 3,679 -9% 0.50 0% 85%

China Aoyuan 3883 HK 19,984 46% 28.3% -0.3% 1,548 44% NA NA 65%

Logan Property 3380 HK 23,998 58% 34.0% -3.0% 3,780 43% 0.26 30% 65%

SZ Investment 604 HK 10,463 -7% 35.0% 0.7% 1,232 -3% 0.07 0% 50%

Times China 1233 HK 12,572 20% 28.7% 0.5% 1,479 25% NA NA 65%

China Vanke - A* 000002 CH 120,635 14% 26.9% -0.5% 12,229 17% NA NA 35%

Average 16.2% 31.4% -2.1% 9% 8% 81%

Gross margin

Core earnings

(Rmb m)Revenue DPS

2

Company Note Building Materials │ India │ July 25, 2019

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CGS-CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Insert

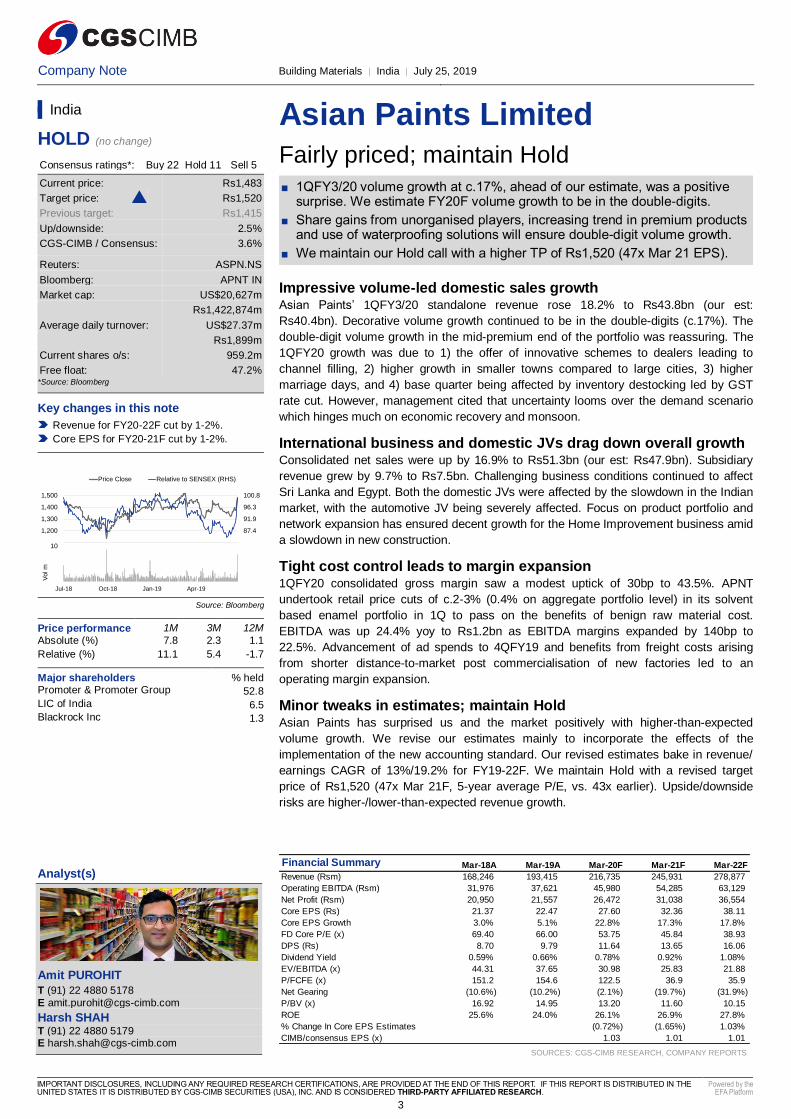

Asian Paints Limited

Fairly priced; maintain Hold

■ 1QFY3/20 volume growth at c.17%, ahead of our estimate, was a positive surprise. We estimate FY20F volume growth to be in the double-digits.

■ Share gains from unorganised players, increasing trend in premium products and use of waterproofing solutions will ensure double-digit volume growth.

■ We maintain our Hold call with a higher TP of Rs1,520 (47x Mar 21 EPS).

Impressive volume-led domestic sales growth Asian Paints’ 1QFY3/20 standalone revenue rose 18.2% to Rs43.8bn (our est:

Rs40.4bn). Decorative volume growth continued to be in the double-digits (c.17%). The

double-digit volume growth in the mid-premium end of the portfolio was reassuring. The

1QFY20 growth was due to 1) the offer of innovative schemes to dealers leading to

channel filling, 2) higher growth in smaller towns compared to large cities, 3) higher

marriage days, and 4) base quarter being affected by inventory destocking led by GST

rate cut. However, management cited that uncertainty looms over the demand scenario

which hinges much on economic recovery and monsoon.

International business and domestic JVs drag down overall growth Consolidated net sales were up by 16.9% to Rs51.3bn (our est: Rs47.9bn). Subsidiary

revenue grew by 9.7% to Rs7.5bn. Challenging business conditions continued to affect

Sri Lanka and Egypt. Both the domestic JVs were affected by the slowdown in the Indian

market, with the automotive JV being severely affected. Focus on product portfolio and

network expansion has ensured decent growth for the Home Improvement business amid

a slowdown in new construction.

Tight cost control leads to margin expansion 1QFY20 consolidated gross margin saw a modest uptick of 30bp to 43.5%. APNT

undertook retail price cuts of c.2-3% (0.4% on aggregate portfolio level) in its solvent

based enamel portfolio in 1Q to pass on the benefits of benign raw material cost.

EBITDA was up 24.4% yoy to Rs1.2bn as EBITDA margins expanded by 140bp to

22.5%. Advancement of ad spends to 4QFY19 and benefits from freight costs arising

from shorter distance-to-market post commercialisation of new factories led to an

operating margin expansion.

Minor tweaks in estimates; maintain Hold Asian Paints has surprised us and the market positively with higher-than-expected

volume growth. We revise our estimates mainly to incorporate the effects of the

implementation of the new accounting standard. Our revised estimates bake in revenue/

earnings CAGR of 13%/19.2% for FY19-22F. We maintain Hold with a revised target

price of Rs1,520 (47x Mar 21F, 5-year average P/E, vs. 43x earlier). Upside/downside

risks are higher-/lower-than-expected revenue growth.

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

India

HOLD (no change)

Consensus ratings*: Buy 22 Hold 11 Sell 5

Current price: Rs1,483

Target price: Rs1,520

Previous target: Rs1,415

Up/downside: 2.5%

CGS-CIMB / Consensus: 3.6%

Reuters: ASPN.NS

Bloomberg: APNT IN

Market cap: US$20,627m

Rs1,422,874m

Average daily turnover: US$27.37m

Rs1,899m

Current shares o/s: 959.2m

Free float: 47.2% *Source: Bloomberg

Key changes in this note

Revenue for FY20-22F cut by 1-2%.

Core EPS for FY20-21F cut by 1-2%.

Source: Bloomberg

Price performance 1M 3M 12M

Absolute (%) 7.8 2.3 1.1

Relative (%) 11.1 5.4 -1.7

Major shareholders % held Promoter & Promoter Group 52.8

LIC of India 6.5 Blackrock Inc 1.3

Insert

Analyst(s)

Amit PUROHIT

T (91) 22 4880 5178

Harsh SHAH T (91) 22 4880 5179 E [email protected]

Financial Summary Mar-18A Mar-19A Mar-20F Mar-21F Mar-22F

Revenue (Rsm) 168,246 193,415 216,735 245,931 278,877

Operating EBITDA (Rsm) 31,976 37,621 45,980 54,285 63,129

Net Profit (Rsm) 20,950 21,557 26,472 31,038 36,554

Core EPS (Rs) 21.37 22.47 27.60 32.36 38.11

Core EPS Growth 3.0% 5.1% 22.8% 17.3% 17.8%

FD Core P/E (x) 69.40 66.00 53.75 45.84 38.93

DPS (Rs) 8.70 9.79 11.64 13.65 16.06

Dividend Yield 0.59% 0.66% 0.78% 0.92% 1.08%

EV/EBITDA (x) 44.31 37.65 30.98 25.83 21.88

P/FCFE (x) 151.2 154.6 122.5 36.9 35.9

Net Gearing (10.6%) (10.2%) (2.1%) (19.7%) (31.9%)

P/BV (x) 16.92 14.95 13.20 11.60 10.15

ROE 25.6% 24.0% 26.1% 26.9% 27.8%

% Change In Core EPS Estimates (0.72%) (1.65%) 1.03%

CIMB/consensus EPS (x) 1.03 1.01 1.01

83.0

87.4

91.9

96.3

100.8

1,100

1,200

1,300

1,400

1,500

Price Close Relative to SENSEX (RHS)

5

10

Jul-18 Oct-18 Jan-19 Apr-19

Vol m

3

Company Note Finance Companies │ India │ July 25, 2019

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CGS-CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Insert Insert

Mahindra & Mahindra Finance Economic slowdown hurts asset quality

■ The disappointing 1QFY3/20 earnings were driven by a spike in GNPLs (up 150bp qoq), Rs6.2bn of provisions and a 45% spike in opex.

■ AUM growth was robust at 22% yoy but outlook is weak due to a slowdown in the economy.

■ We cut FY20-21F EPS due to higher provisions and lower loan growth estimates. Our TP is reduced to Rs400 (1.7x FY21 BV). Maintain Add.

Sharp deterioration in asset quality a key highlight of 1QFY3/20 Asset quality witnessed a sharp deterioration with headline gross NPLs increasing 150bp qoq to 7.4% in 1QFY20; consequently, credit costs rose to 3.58% vs. 2.1% in 4QFY19. Net NPLs also rose by 90bp qoq and stood at 7.4% in 1QFY20 with a PCR of 24.9%. Provisions were unexpectedly high and formed 85.5% of PPP. As per management, no additional provisions are expected unless the realisable value of disposable assets is substantially lower than expected. 1QFY20 PAT made up just 6% of our FY20F estimate.

Management guides a 15% AUM growth Management expects overall AUM/disbursement growth to weaken at ~15%/10% yoy respectively in FY20. Assets under management (AUM) growth was strong at 22% yoy in 1Q, however disbursements growth came in weak at 2.5% yoy with overall economic slowdown and poor auto demand. AUM growth was largely driven by the commercial vehicle (CV)/construction equipment (CE) segment which grew at a robust 65% yoy. The CV/CE segment comprised 19% of overall AUM vs. 18% in 4Q19.

Spreads declined driven by fall in yields Management highlighted that liquidity remains comfortable despite uncertainty in the credit market. Management said asset liability management (ALM) is comfortable in the near term. Overall spreads contracted 50bp qoq in 1QFY20 with sequential dip in yields of 40bp and stands at 14.2%. Cost of funds were flat qoq at 6.6%.

Sharp spike in opex also led to tepid PPP Net interest income for the quarter grew at 17.5% yoy. Overall PAT was down 74.6% at Rs6.84bn due to higher opex and provisions made during the quarter. Management highlighted high opex growth of 45% yoy was on account of higher employee expenses and depreciation. The cost-to-income ratio was at 43.6% in 1QFY20 vs. 41.6% in 4QFY19. Provisions formed 85.5% of operating profit, dragging the credit cost to 3.58% vs. 2.11% in 1QFY19.

Cut FY20F/21F EPS by 17.6%/12.8%; maintain Add Given the current weak economic scenario and overall auto sales, we expect loan growth to be sluggish with largely stable spreads in the medium term. As such, we cut our earnings by 17.6%/12.8% for FY20F/21F and reduce our TP to Rs400 (Rs540 previously), based on 1.7x FY21F P/BV at the company level and Rs50 for its housing subsidiary. However, we keep our Add call as valuations are attractive at 1.3x FY21F P/BV. Key risks are lower-than-expected AUM growth and weak asset quality. Potential catalysts are strong loan growth and improving asset quality.

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

India

ADD (no change)

Consensus ratings*: Buy 27 Hold 3 Sell 6

Current price: Rs304.5

Target price: Rs400.0

Previous target: Rs540.0

Up/downside: 31.4%

CGS-CIMB / Consensus: -17.4%

Reuters: MMFS.NS

Bloomberg: MMFS IN

Market cap: US$2,727m

Rs188,079m

Average daily turnover: US$13.26m

Rs920.7m

Current shares o/s: 614.9m

Free float: 48.8% *Source: Bloomberg

Key changes in this note

FY20F core EPS decreased by 17.6%.

FY21F core EPS decreased by 12.8%.

FY22F numbers introduced

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) -21.8 -29.8 -36.9

Relative (%) -18.5 -26.7 -39.7

Major shareholders % held Mahindra & Mahindra 51.2 LIC 3.1 UTI FUNDS MANAGEMENT 2.2

Insert

Analyst(s)

Dhiren SHAH

T (91) 22 4880 5170 E [email protected]

Siddharth TELI T (91) 22 4880 5158 E [email protected]

Saili CHHEDA T (91) 22 4880 5184 E [email protected]

Financial Summary Mar-18A Mar-19A Mar-20F Mar-21F Mar-22F

Net Interest Income (Rsm) 35,025 46,700 51,803 62,065 72,010

Total Non-Interest Income (Rsm) 1,660 1,953 2,148 2,363 2,600

Operating Revenue (Rsm) 36,686 48,653 53,950 64,428 74,611

Total Provision Charges (Rsm) (5,681) (6,352) (8,599) (9,208) (10,681)

Net Profit (Rsm) 10,761 15,571 15,067 19,082 21,807

Core EPS (Rs) 18.25 25.33 24.50 31.03 35.46

Core EPS Growth 157% 39% (3%) 27% 14%

FD Core P/E (x) 16.69 12.02 12.42 9.81 8.58

DPS (Rs) 2.00 3.50 3.50 3.50 3.50

Dividend Yield 0.66% 1.15% 1.15% 1.15% 1.15%

BVPS (Rs) 156.6 177.4 197.8 224.8 256.1

P/BV (x) 1.94 1.72 1.54 1.35 1.19

ROE 13.3% 15.2% 13.1% 14.7% 14.8%

% Change In Core EPS Estimates (17.6%) (12.8%)

CIMB/consensus EPS (x) 0.78 0.81 0.90

55.0

67.0

79.0

91.0

103.0

115.0

280

330

380

430

480

530

Price Close Relative to SENSEX (RHS)

10

20

30

Jul-18 Oct-18 Jan-19 Apr-19

Vol m

4

Company Note Finance Companies │ India │ July 25, 2019

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CGS-CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Insert Insert

Shriram Transport Finance Growth drops – asset quality largely stable

■ Overall economic slowdown and weak auto sector demand dragged AUM growth to 5.8% yoy in 1QFY3/20. Disbursements fell 8.4% yoy.

■ Slight deterioration in GNPLs/NNPLs which inched up 15/48bp qoq. Coverage ratio declined 2.6% pts qoq to 31.8% in 1Q.

■ We trim our FY20/21F EPS by 4.9/0.2% to factor in slightly lower asset growth and higher provisions. Maintain Add.

Modest AUM growth due to weak economic sentiment Overall AUM growth was modest at 5.8% yoy in 1QFY20. Disbursements for the quarter were down 8.4% yoy. Management highlighted that overall disbursements were down in the first month of the quarter (election impact), which led to the tepid disbursement growth in 1QFY20 (down 8.4%). New vehicle disbursements dipped 54% yoy while old vehicle disbursements grew 2.8% yoy. Management guided for overall growth of 10/15% yoy for disbursements/AUM in FY20F.

Asset quality deteriorates marginally Overall 1QFY20 gross NPL (Gross Stage 3) ratio under IndAS was higher qoq, at 8.52% vs. 8.37% in 4QFY19 with gross NPLs up 3.5% qoq to Rs89.3bn. Stage 3 coverage ratio declined qoq and stood at 31.8% in 1QFY20 vs. 34.4% in 4QFY19, while stage 1 & 2 provisions stood at 2.88% vs. 2.76% in 4QFY19. Management expects credit quality to remain largely stable unless the economic outlook weakens significantly – we factor in average credit costs at ~2.2% through FY22F.

Overall margins declined 6bp sequentially Overall NIMs for the quarter stood at 7.16% and were down 6bp sequentially – higher balance sheet liquidity was one of the key reasons for the decline in NIMs. Yields expanded by 42bp qoq in 1Q which was offset by a 40bp increase in cost of funds; yield/cost of funds came in at 15.2/9.1% respectively. We believe the increase in yields is attributable to a change in mix from new vehicle to old vehicle lending. We expect NIMs to largely stabilise at current levels unless system liquidity worsens further.

Operating performance largely in line 1QFY20 net profit rose 10.7% yoy to Rs63.4bn and PPOP was up 9.75% yoy. 1QFY20 net profit formed 22% of our full-year forecast. NII grew 8% yoy on account of higher cost of funds. Overall opex growth was 2.7% yoy, with cost-to-income ratio at 22.4% vs. 22.1% in 4QFY19. Credit costs were higher than expected, with a deterioration in asset quality to 2.13% in 1Q vs. 2.07% in 4Q.

Valuations attractive We expect an improvement in AUM growth with stable spreads in the medium term. However, given the weak economic outlook, we trim our FY20/21F EPS by 4.9/0.2%. The stock is trading at attractive valuations of 1x FY21F P/BV with ROEs of ~17%. Retain Add with a lower TP of Rs1,350 (Rs1,400 previously) which translates into 1.4x FY20F P/BV based on GGM. Prolonged low AUM growth and higher slippages are key risks.

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

India

ADD (no change)

Consensus ratings*: Buy 31 Hold 6 Sell 2

Current price: Rs925.4

Target price: Rs1,350

Previous target: Rs1,400

Up/downside: 45.9%

CGS-CIMB / Consensus: 4.1%

Reuters: SRTR.NS

Bloomberg: SHTF IN

Market cap: US$3,044m

Rs209,946m

Average daily turnover: US$32.04m

Rs2,227m

Current shares o/s: 226.9m

Free float: 73.9% *Source: Bloomberg

Key changes in this note

FY20F core EPS decreased by 4.9%.

FY21F core EPS decreased by 0.2%.

FY22F numbers introduced.

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) -17 -21.7 -26.9

Relative (%) -13.7 -18.6 -29.7

Major shareholders % held Shriram Capital ltd 26.1 HDFC Trustee Company LTD 3.3 Sanlam Life Insurance Ltd 3.0

Insert

Analyst(s)

Siddharth TELI

T (91) 22 4880 5158 E [email protected]

Dhiren SHAH T (91) 22 4880 5170 E [email protected]

Saili CHHEDA T (91) 22 4880 5184 E [email protected]

Financial Summary Mar-18A Mar-19F Mar-20F Mar-21F Mar-22F

Net Interest Income (Rsm) 68,248 78,730 84,645 99,127 111,427

Total Non-Interest Income (Rsm) 3,079 1,614 1,822 1,975 2,184

Operating Revenue (Rsm) 71,326 80,344 86,467 101,103 113,611

Total Provision Charges (Rsm) (17,223) (23,823) (25,727) (29,091) (32,467)

Net Profit (Rsm) 24,605 25,640 27,172 32,722 36,443

Core EPS (Rs) 108.4 113.0 119.7 144.2 160.6

Core EPS Growth 95.7% 4.2% 6.0% 20.4% 11.4%

FD Core P/E (x) 8.53 8.19 7.73 6.42 5.76

DPS (Rs) 11.00 12.00 13.00 13.00 12.00

Dividend Yield 1.19% 1.30% 1.40% 1.40% 1.30%

BVPS (Rs) 598 698 802 931 1,078

P/BV (x) 1.55 1.33 1.15 0.99 0.86

ROE 19.7% 17.4% 16.0% 16.6% 16.0%

% Change In Core EPS Estimates (4.89%) (0.22%)

CIMB/consensus EPS (x) 0.97 1.02 0.97

65.0

81.7

98.3

115.0

870

1,070

1,270

1,470

Price Close Relative to SENSEX (RHS)

10

20

30

40

Jul-18 Oct-18 Jan-19 Apr-19

Vo

l m

5

Company Note Industrial Machinery │ India │ July 25, 2019

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CGS-CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Insert Insert

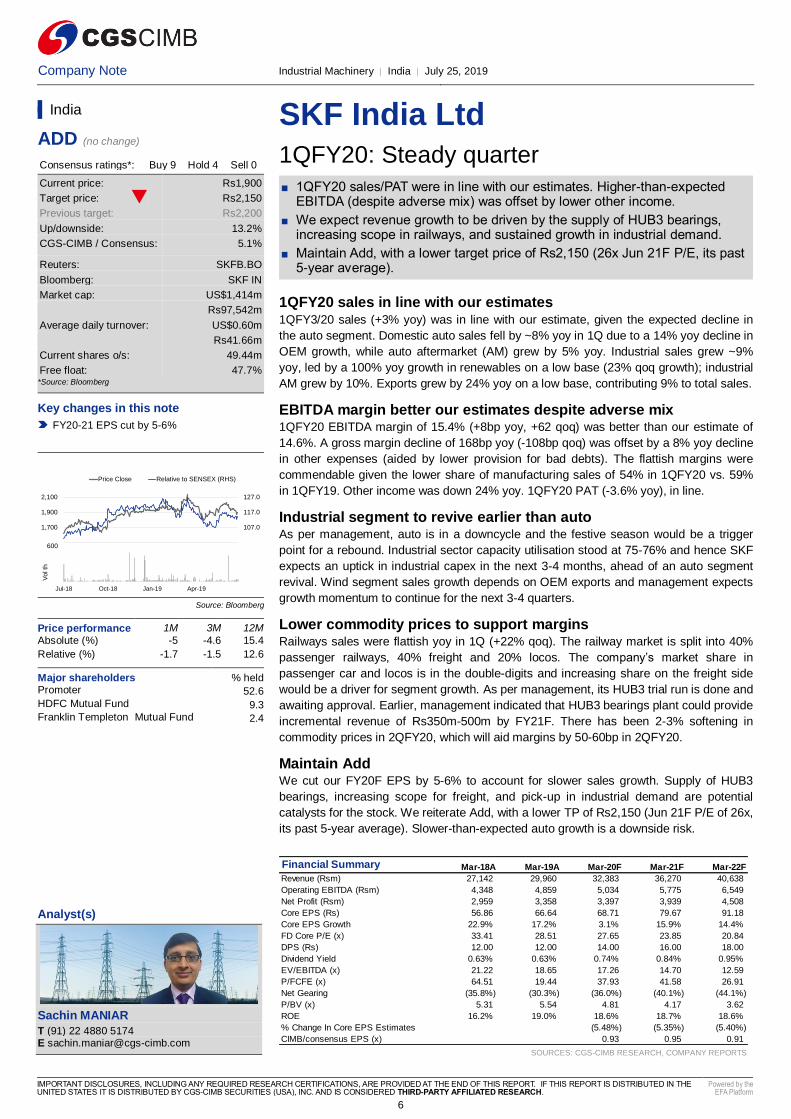

SKF India Ltd

1QFY20: Steady quarter

■ 1QFY20 sales/PAT were in line with our estimates. Higher-than-expected EBITDA (despite adverse mix) was offset by lower other income.

■ We expect revenue growth to be driven by the supply of HUB3 bearings, increasing scope in railways, and sustained growth in industrial demand.

■ Maintain Add, with a lower target price of Rs2,150 (26x Jun 21F P/E, its past 5-year average).

1QFY20 sales in line with our estimates 1QFY3/20 sales (+3% yoy) was in line with our estimate, given the expected decline in

the auto segment. Domestic auto sales fell by ~8% yoy in 1Q due to a 14% yoy decline in

OEM growth, while auto aftermarket (AM) grew by 5% yoy. Industrial sales grew ~9%

yoy, led by a 100% yoy growth in renewables on a low base (23% qoq growth); industrial

AM grew by 10%. Exports grew by 24% yoy on a low base, contributing 9% to total sales.

EBITDA margin better our estimates despite adverse mix 1QFY20 EBITDA margin of 15.4% (+8bp yoy, +62 qoq) was better than our estimate of

14.6%. A gross margin decline of 168bp yoy (-108bp qoq) was offset by a 8% yoy decline

in other expenses (aided by lower provision for bad debts). The flattish margins were

commendable given the lower share of manufacturing sales of 54% in 1QFY20 vs. 59%

in 1QFY19. Other income was down 24% yoy. 1QFY20 PAT (-3.6% yoy), in line.

Industrial segment to revive earlier than auto As per management, auto is in a downcycle and the festive season would be a trigger

point for a rebound. Industrial sector capacity utilisation stood at 75-76% and hence SKF

expects an uptick in industrial capex in the next 3-4 months, ahead of an auto segment

revival. Wind segment sales growth depends on OEM exports and management expects

growth momentum to continue for the next 3-4 quarters.

Lower commodity prices to support margins Railways sales were flattish yoy in 1Q (+22% qoq). The railway market is split into 40%

passenger railways, 40% freight and 20% locos. The company’s market share in

passenger car and locos is in the double-digits and increasing share on the freight side

would be a driver for segment growth. As per management, its HUB3 trial run is done and

awaiting approval. Earlier, management indicated that HUB3 bearings plant could provide

incremental revenue of Rs350m-500m by FY21F. There has been 2-3% softening in

commodity prices in 2QFY20, which will aid margins by 50-60bp in 2QFY20.

Maintain Add We cut our FY20F EPS by 5-6% to account for slower sales growth. Supply of HUB3

bearings, increasing scope for freight, and pick-up in industrial demand are potential

catalysts for the stock. We reiterate Add, with a lower TP of Rs2,150 (Jun 21F P/E of 26x,

its past 5-year average). Slower-than-expected auto growth is a downside risk.

[Add FP Header] [Add FP BodyText]

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

India

ADD (no change)

Consensus ratings*: Buy 9 Hold 4 Sell 0

Current price: Rs1,900

Target price: Rs2,150

Previous target: Rs2,200

Up/downside: 13.2%

CGS-CIMB / Consensus: 5.1%

Reuters: SKFB.BO

Bloomberg: SKF IN

Market cap: US$1,414m

Rs97,542m

Average daily turnover: US$0.60m

Rs41.66m

Current shares o/s: 49.44m

Free float: 47.7% *Source: Bloomberg

Key changes in this note

FY20-21 EPS cut by 5-6%

Source: Bloomberg

Price performance 1M 3M 12M

Absolute (%) -5 -4.6 15.4

Relative (%) -1.7 -1.5 12.6

Major shareholders % held Promoter 52.6

HDFC Mutual Fund 9.3 Franklin Templeton Mutual Fund 2.4

Insert

Analyst(s)

Sachin MANIAR

T (91) 22 4880 5174 E [email protected]

Financial Summary Mar-18A Mar-19A Mar-20F Mar-21F Mar-22F

Revenue (Rsm) 27,142 29,960 32,383 36,270 40,638

Operating EBITDA (Rsm) 4,348 4,859 5,034 5,775 6,549

Net Profit (Rsm) 2,959 3,358 3,397 3,939 4,508

Core EPS (Rs) 56.86 66.64 68.71 79.67 91.18

Core EPS Growth 22.9% 17.2% 3.1% 15.9% 14.4%

FD Core P/E (x) 33.41 28.51 27.65 23.85 20.84

DPS (Rs) 12.00 12.00 14.00 16.00 18.00

Dividend Yield 0.63% 0.63% 0.74% 0.84% 0.95%

EV/EBITDA (x) 21.22 18.65 17.26 14.70 12.59

P/FCFE (x) 64.51 19.44 37.93 41.58 26.91

Net Gearing (35.8%) (30.3%) (36.0%) (40.1%) (44.1%)

P/BV (x) 5.31 5.54 4.81 4.17 3.62

ROE 16.2% 19.0% 18.6% 18.7% 18.6%

% Change In Core EPS Estimates (5.48%) (5.35%) (5.40%)

CIMB/consensus EPS (x) 0.93 0.95 0.91

97.0

107.0

117.0

127.0

1,500

1,700

1,900

2,100

Price Close Relative to SENSEX (RHS)

200

400

600

Jul-18 Oct-18 Jan-19 Apr-19

Vo

l th

6

Company Flash Note Autos │ India │ July 26, 2019

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CGS-CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Insert Insert

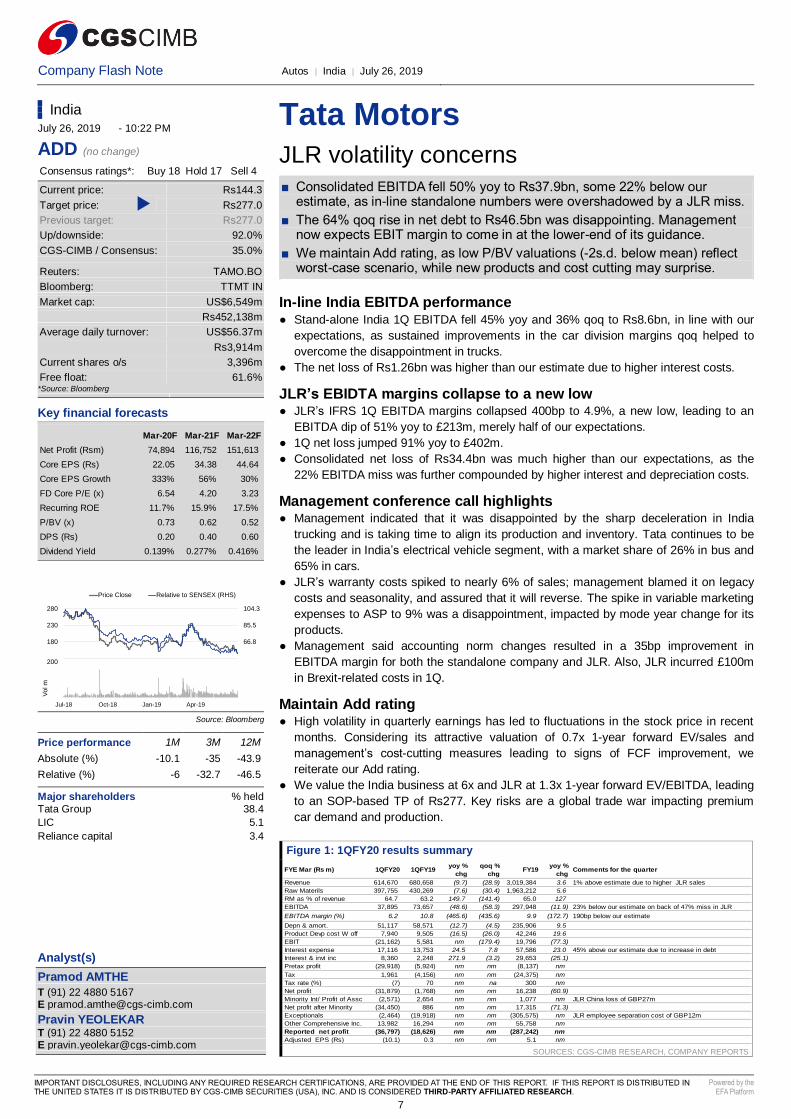

Tata Motors

JLR volatility concerns

■ Consolidated EBITDA fell 50% yoy to Rs37.9bn, some 22% below our estimate, as in-line standalone numbers were overshadowed by a JLR miss.

■ The 64% qoq rise in net debt to Rs46.5bn was disappointing. Management now expects EBIT margin to come in at the lower-end of its guidance.

■ We maintain Add rating, as low P/BV valuations (-2s.d. below mean) reflect worst-case scenario, while new products and cost cutting may surprise.

In-line India EBITDA performance ● Stand-alone India 1Q EBITDA fell 45% yoy and 36% qoq to Rs8.6bn, in line with our

expectations, as sustained improvements in the car division margins qoq helped to

overcome the disappointment in trucks.

● The net loss of Rs1.26bn was higher than our estimate due to higher interest costs.

JLR’s EBIDTA margins collapse to a new low ● JLR’s IFRS 1Q EBITDA margins collapsed 400bp to 4.9%, a new low, leading to an

EBITDA dip of 51% yoy to £213m, merely half of our expectations.

● 1Q net loss jumped 91% yoy to £402m.

● Consolidated net loss of Rs34.4bn was much higher than our expectations, as the

22% EBITDA miss was further compounded by higher interest and depreciation costs.

Management conference call highlights ● Management indicated that it was disappointed by the sharp deceleration in India

trucking and is taking time to align its production and inventory. Tata continues to be

the leader in India’s electrical vehicle segment, with a market share of 26% in bus and

65% in cars.

● JLR’s warranty costs spiked to nearly 6% of sales; management blamed it on legacy

costs and seasonality, and assured that it will reverse. The spike in variable marketing

expenses to ASP to 9% was a disappointment, impacted by mode year change for its

products.

● Management said accounting norm changes resulted in a 35bp improvement in

EBITDA margin for both the standalone company and JLR. Also, JLR incurred £100m

in Brexit-related costs in 1Q.

Maintain Add rating ● High volatility in quarterly earnings has led to fluctuations in the stock price in recent

months. Considering its attractive valuation of 0.7x 1-year forward EV/sales and

management’s cost-cutting measures leading to signs of FCF improvement, we

reiterate our Add rating.

● We value the India business at 6x and JLR at 1.3x 1-year forward EV/EBITDA, leading

to an SOP-based TP of Rs277. Key risks are a global trade war impacting premium

car demand and production.

Figure 1: 1QFY20 results summary

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

FYE Mar (Rs m) 1QFY20 1QFY19 yoy %

chg

qoq %

chg FY19

yoy %

chg Comments for the quarter

Revenue 614,670 680,658 (9.7) (28.9) 3,019,384 3.6 1% above estimate due to higher JLR sales

Raw Materils 397,755 430,269 (7.6) (30.4) 1,963,212 5.6

RM as % of revenue 64.7 63.2 149.7 (141.4) 65.0 127

EBITDA 37,895 73,657 (48.6) (58.3) 297,948 (11.9) 23% below our estimate on back of 47% miss in JLR

EBITDA margin (%) 6.2 10.8 (465.6) (435.6) 9.9 (172.7) 190bp below our estimate

Depn & amort. 51,117 58,571 (12.7) (4.5) 235,906 9.5

Product Devp cost W off 7,940 9,505 (16.5) (26.0) 42,246 19.6

EBIT (21,162) 5,581 nm (179.4) 19,796 (77.3)

Interest expense 17,116 13,753 24.5 7.8 57,586 23.0 45% above our estimate due to increase in debt

Interest & invt inc 8,360 2,248 271.9 (3.2) 29,653 (25.1)

Pretax profit (29,918) (5,924) nm nm (8,137) nm

Tax 1,961 (4,156) nm nm (24,375) nm

Tax rate (%) (7) 70 nm na 300 nm

Net profit (31,879) (1,768) nm nm 16,238 (60.9)

Minority Int/ Profit of Assc (2,571) 2,654 nm nm 1,077 nm JLR China loss of GBP27m

Net profit after Minority (34,450) 886 nm nm 17,315 (71.3)

Exceptionals (2,464) (19,918) nm nm (305,575) nm JLR employee separation cost of GBP12m

Other Comprehensive Inc. 13,982 16,294 nm nm 55,758 nm

Reported net profit (36,797) (18,626) nm nm (287,242) nm

Adjusted EPS (Rs) (10.1) 0.3 nm nm 5.1 nm

India

July 26, 2019 - 10:22 PM

ADD (no change) Consensus ratings*: Buy 18 Hold 17 Sell 4

Current price: Rs144.3

Target price: Rs277.0

Previous target: Rs277.0

Up/downside: 92.0%

CGS-CIMB / Consensus: 35.0%

Reuters: TAMO.BO

Bloomberg: TTMT IN

Market cap: US$6,549m

Rs452,138m

Average daily turnover: US$56.37m

Rs3,914m

Current shares o/s 3,396m

Free float: 61.6% *Source: Bloomberg

Key financial forecasts

Source: Bloomberg

Price performance 1M 3M 12M

Absolute (%) -10.1 -35 -43.9

Relative (%) -6 -32.7 -46.5

Major shareholders % held

Tata Group 38.4

LIC 5.1

Reliance capital 3.4

Insert

Analyst(s)

Pramod AMTHE

T (91) 22 4880 5167 E [email protected]

Pravin YEOLEKAR T (91) 22 4880 5152 E [email protected]

Mar-20F Mar-21F Mar-22F

Net Profit (Rsm) 74,894 116,752 151,613

Core EPS (Rs) 22.05 34.38 44.64

Core EPS Growth 333% 56% 30%

FD Core P/E (x) 6.54 4.20 3.23

Recurring ROE 11.7% 15.9% 17.5%

P/BV (x) 0.73 0.62 0.52

DPS (Rs) 0.20 0.40 0.60

Dividend Yield 0.139% 0.277% 0.416%

48.0

66.8

85.5

104.3

130

180

230

280

Price Close Relative to SENSEX (RHS)

50

100

150

200

Jul-18 Oct-18 Jan-19 Apr-19

Vol m

7

Company Note Banks │ Indonesia │ July 25, 2019

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CGS-CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Insert Insert

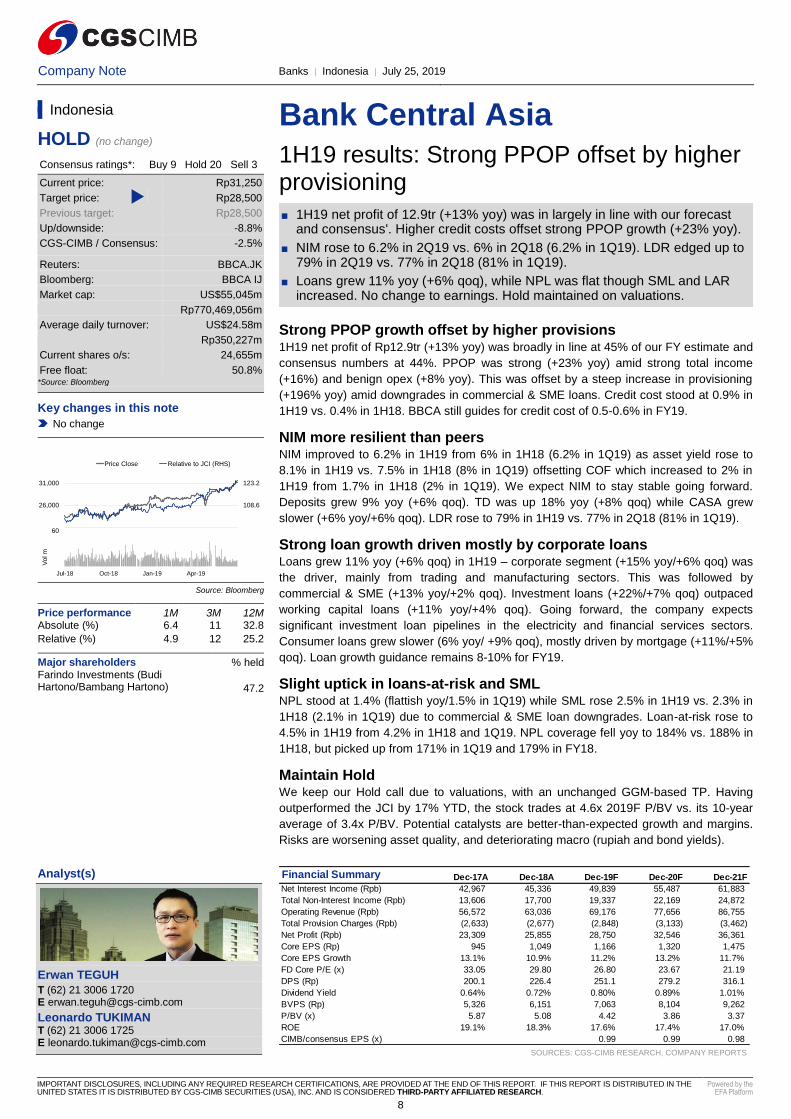

Bank Central Asia 1H19 results: Strong PPOP offset by higher provisioning

■ 1H19 net profit of 12.9tr (+13% yoy) was in largely in line with our forecast and consensus'. Higher credit costs offset strong PPOP growth (+23% yoy).

■ NIM rose to 6.2% in 2Q19 vs. 6% in 2Q18 (6.2% in 1Q19). LDR edged up to 79% in 2Q19 vs. 77% in 2Q18 (81% in 1Q19).

■ Loans grew 11% yoy (+6% qoq), while NPL was flat though SML and LAR increased. No change to earnings. Hold maintained on valuations.

Strong PPOP growth offset by higher provisions 1H19 net profit of Rp12.9tr (+13% yoy) was broadly in line at 45% of our FY estimate and

consensus numbers at 44%. PPOP was strong (+23% yoy) amid strong total income

(+16%) and benign opex (+8% yoy). This was offset by a steep increase in provisioning

(+196% yoy) amid downgrades in commercial & SME loans. Credit cost stood at 0.9% in

1H19 vs. 0.4% in 1H18. BBCA still guides for credit cost of 0.5-0.6% in FY19.

NIM more resilient than peers NIM improved to 6.2% in 1H19 from 6% in 1H18 (6.2% in 1Q19) as asset yield rose to

8.1% in 1H19 vs. 7.5% in 1H18 (8% in 1Q19) offsetting COF which increased to 2% in

1H19 from 1.7% in 1H18 (2% in 1Q19). We expect NIM to stay stable going forward.

Deposits grew 9% yoy (+6% qoq). TD was up 18% yoy (+8% qoq) while CASA grew

slower (+6% yoy/+6% qoq). LDR rose to 79% in 1H19 vs. 77% in 2Q18 (81% in 1Q19).

Strong loan growth driven mostly by corporate loans Loans grew 11% yoy (+6% qoq) in 1H19 – corporate segment (+15% yoy/+6% qoq) was

the driver, mainly from trading and manufacturing sectors. This was followed by

commercial & SME (+13% yoy/+2% qoq). Investment loans (+22%/+7% qoq) outpaced

working capital loans (+11% yoy/+4% qoq). Going forward, the company expects

significant investment loan pipelines in the electricity and financial services sectors.

Consumer loans grew slower (6% yoy/ +9% qoq), mostly driven by mortgage (+11%/+5%

qoq). Loan growth guidance remains 8-10% for FY19.

Slight uptick in loans-at-risk and SML NPL stood at 1.4% (flattish yoy/1.5% in 1Q19) while SML rose 2.5% in 1H19 vs. 2.3% in

1H18 (2.1% in 1Q19) due to commercial & SME loan downgrades. Loan-at-risk rose to

4.5% in 1H19 from 4.2% in 1H18 and 1Q19. NPL coverage fell yoy to 184% vs. 188% in

1H18, but picked up from 171% in 1Q19 and 179% in FY18.

Maintain Hold We keep our Hold call due to valuations, with an unchanged GGM-based TP. Having

outperformed the JCI by 17% YTD, the stock trades at 4.6x 2019F P/BV vs. its 10-year

average of 3.4x P/BV. Potential catalysts are better-than-expected growth and margins.

Risks are worsening asset quality, and deteriorating macro (rupiah and bond yields).

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Indonesia

HOLD (no change)

Consensus ratings*: Buy 9 Hold 20 Sell 3

Current price: Rp31,250

Target price: Rp28,500

Previous target: Rp28,500

Up/downside: -8.8%

CGS-CIMB / Consensus: -2.5%

Reuters: BBCA.JK

Bloomberg: BBCA IJ

Market cap: US$55,045m

Rp770,469,056m

Average daily turnover: US$24.58m

Rp350,227m

Current shares o/s: 24,655m

Free float: 50.8% *Source: Bloomberg

Key changes in this note

No change

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) 6.4 11 32.8

Relative (%) 4.9 12 25.2

Major shareholders % held Farindo Investments (Budi Hartono/Bambang Hartono) 47.2

Insert

Analyst(s)

Erwan TEGUH

T (62) 21 3006 1720 E [email protected]

Leonardo TUKIMAN T (62) 21 3006 1725 E [email protected]

Financial Summary Dec-17A Dec-18A Dec-19F Dec-20F Dec-21F

Net Interest Income (Rpb) 42,967 45,336 49,839 55,487 61,883

Total Non-Interest Income (Rpb) 13,606 17,700 19,337 22,169 24,872

Operating Revenue (Rpb) 56,572 63,036 69,176 77,656 86,755

Total Provision Charges (Rpb) (2,633) (2,677) (2,848) (3,133) (3,462)

Net Profit (Rpb) 23,309 25,855 28,750 32,546 36,361

Core EPS (Rp) 945 1,049 1,166 1,320 1,475

Core EPS Growth 13.1% 10.9% 11.2% 13.2% 11.7%

FD Core P/E (x) 33.05 29.80 26.80 23.67 21.19

DPS (Rp) 200.1 226.4 251.1 279.2 316.1

Dividend Yield 0.64% 0.72% 0.80% 0.89% 1.01%

BVPS (Rp) 5,326 6,151 7,063 8,104 9,262

P/BV (x) 5.87 5.08 4.42 3.86 3.37

ROE 19.1% 18.3% 17.6% 17.4% 17.0%

CIMB/consensus EPS (x) 0.99 0.99 0.98

94.0

108.6

123.2

21,000

26,000

31,000

Price Close Relative to JCI (RHS)

20

40

60

Jul-18 Oct-18 Jan-19 Apr-19

Vo

l m

8

Company Note Shipbuilding │ South Korea │ July 25, 2019

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CGS-CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

HIGH

CONVICTION

Insert Insert

Korea Shipbuilding & Offshore Good earnings, weak sentiment

■ 2Q19 EBIT was in line with our forecast, thanks to 1) 25% yoy sales growth, 2) product mix improvement, 3) a weak Won and 4) lower steel prices.

■ The management reaffirmed strong order enquiries and maintained its shipbuilding order target for FY19F (US$8bn parent-base).

■ KSO has successfully raised prices for LNGC orders that suffered delayed option exercise YTD. We expect further newbuild price hike in 2H19F.

■ SOP-based target price cut to W170,000 to reflect the weak sentiment.

2Q19 turns around as expected KSO’s W55bn 2Q19 EBIT was broadly in line with our forecast (W60bn) and way above

Bloomberg consensus (W7bn), buoyed by: 1) 25% yoy revenue growth; 2) product mix

improvement (36% of sales represented by LNGC); 3) a weak Won; and 4) lower steel

prices. Shipbuilding division posted 44% yoy revenue growth with 4% OPM, offsetting the

W31bn loss at the offshore/plant division. Net profit surprise (W202bn) was driven by a

one-off taxation write-back following KSO’s intermediate holding company transition.

Shipbuilding order target intact Despite the weak order run rate YTD, the management reaffirmed strong order enquiries

and maintained its FY19F shipbuilding order target (US$8bn parent-base). KSO is upbeat

on potential order wins across LPGC, very-large-crude-carriers (VLCC) and ad-hoc

LNGC (e.g. those dedicated to spot market demand, apart from the mega-orders

expected from Qatar/Mozambique) in Jul-Aug. KSO does not see competition with China

as a threat for LNG-marine-fuel containers, as China banks no longer offer 0% down-

payment scheme in their ship finance terms.

Priority still on LNGC price hike We were relieved by the company’s confirmation that it has raised prices for the delayed

option exercise of LNGCs already ordered (10 units), which were impacted by the US-

China trade tensions, as these are allegedly tied to charter contracts to China, i.e. which

has newly emerged as the no.1 importer of LNG globally. Given the constrained yard

capacity for LNGC globally, we see minimal risk of KSO locking in orders at a higher

price range of US$190m-195m ahead (i.e. only a few delivery slots left for FY22F while

slots for FY23-24F look set to be guaranteed by orders from Qatar/Mozambique in

4Q19F-1Q20F).

Add: Wait for sentiment recovery Given the robust earnings growth, we see the recent correction as overdone. However,

our SOP TP is trimmed to W170,000 with a lower 10x target EV/EBITDA multiple (on par

with Airbus), as we reflect slower order run-rate and dampened industrial sector

sentiment due to the trade war, weak macros (EU) and political unrest (Iran). We foresee

an inflection point with LNGC order recommencement, while Japan’s potential reluctance

to approve KSO’s merger with DSME remains the key downside risk to our call.

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

South Korea

ADD (no change)

Consensus ratings*: Buy 27 Hold 2 Sell 1

Current price: W102,500

Target price: W170,000

Previous target: W200,000

Up/downside: 65.9%

CGS-CIMB / Consensus: 5.0%

Reuters: 009540.KS

Bloomberg: 009540 KS

Market cap: US$6,159m

W7,254,245m

Average daily turnover: US$18.26m

W22,136m

Current shares o/s: 70.77m

Free float: 57.8% *Source: Bloomberg

Key changes in this note

FY19F EPS raised by 93%.

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) -15.6 -16 4

Relative (%) -13.4 -10.7 12.7

Major shareholders % held Hyundai Heavy Industries Holdings 31.0 National Pension Service 9.4 KCC Corp 6.6

Insert

Analyst(s)

KJ HWANG

T (82) 2 6730 6123 E [email protected]

Alex PARK T (82) 2 6730 6131 E [email protected]

Financial Summary Dec-17A Dec-18A Dec-19F Dec-20F Dec-21F

Revenue (Wb) 15,469 13,120 14,572 16,309 18,519

Operating EBITDA (Wb) 601 (128) 632 1,042 1,438

Net Profit (Wb) 2,458 (489) 322 794 1,149

Normalised EPS (W) 37,059 (7,675) 4,544 11,221 16,234

Normalised EPS Growth 417% (121%) 147% 45%

FD Normalised P/E (x) 2.77 NA 22.56 9.14 6.31

DPS (W) - - - - -

Dividend Yield 0% 0% 0% 0% 0%

EV/EBITDA (x) 17.72 NA 13.64 7.63 4.91

P/FCFE (x) 5.68 54.07 19.60 15.30 10.57

Net Gearing 22.2% 13.5% 4.6% 0.1% (5.2%)

P/BV (x) 0.52 0.61 0.62 0.58 0.53

ROE 18.2% (4.3%) 2.7% 6.5% 8.8%

% Change In Normalised EPS Estimates 92.9% 0.0% (0.0%)

Normalised EPS/consensus EPS (x) 306.5 3.7 2.8

94.0

117.3

140.7

164.0

94,000

114,000

134,000

154,000

Price Close Relative to KOSPI (RHS)

1

1

2

2

Jul-18 Oct-18 Jan-19 Apr-19

Vo

l m

9

Company Flash Note Personal Products │ South Korea │ July 25, 2019

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CGS-CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Insert Insert

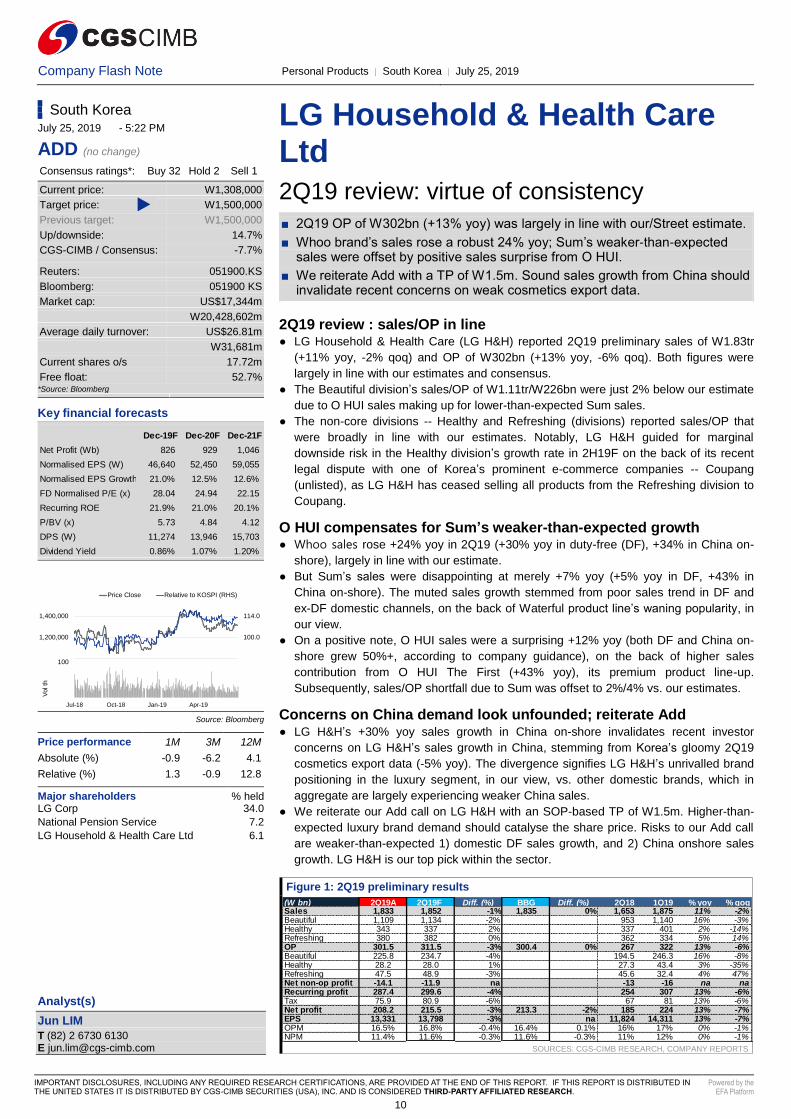

LG Household & Health Care Ltd 2Q19 review: virtue of consistency

■ 2Q19 OP of W302bn (+13% yoy) was largely in line with our/Street estimate.

■ Whoo brand’s sales rose a robust 24% yoy; Sum’s weaker-than-expected sales were offset by positive sales surprise from O HUI.

■ We reiterate Add with a TP of W1.5m. Sound sales growth from China should invalidate recent concerns on weak cosmetics export data.

2Q19 review : sales/OP in line ● LG Household & Health Care (LG H&H) reported 2Q19 preliminary sales of W1.83tr

(+11% yoy, -2% qoq) and OP of W302bn (+13% yoy, -6% qoq). Both figures were

largely in line with our estimates and consensus.

● The Beautiful division’s sales/OP of W1.11tr/W226bn were just 2% below our estimate

due to O HUI sales making up for lower-than-expected Sum sales.

● The non-core divisions -- Healthy and Refreshing (divisions) reported sales/OP that

were broadly in line with our estimates. Notably, LG H&H guided for marginal

downside risk in the Healthy division’s growth rate in 2H19F on the back of its recent

legal dispute with one of Korea’s prominent e-commerce companies -- Coupang

(unlisted), as LG H&H has ceased selling all products from the Refreshing division to

Coupang.

O HUI compensates for Sum’s weaker-than-expected growth ● Whoo sales rose +24% yoy in 2Q19 (+30% yoy in duty-free (DF), +34% in China on-

shore), largely in line with our estimate.

● But Sum’s sales were disappointing at merely +7% yoy (+5% yoy in DF, +43% in

China on-shore). The muted sales growth stemmed from poor sales trend in DF and

ex-DF domestic channels, on the back of Waterful product line’s waning popularity, in

our view.

● On a positive note, O HUI sales were a surprising +12% yoy (both DF and China on-

shore grew 50%+, according to company guidance), on the back of higher sales

contribution from O HUI The First (+43% yoy), its premium product line-up.

Subsequently, sales/OP shortfall due to Sum was offset to 2%/4% vs. our estimates.

Concerns on China demand look unfounded; reiterate Add ● LG H&H’s +30% yoy sales growth in China on-shore invalidates recent investor

concerns on LG H&H’s sales growth in China, stemming from Korea’s gloomy 2Q19

cosmetics export data (-5% yoy). The divergence signifies LG H&H’s unrivalled brand

positioning in the luxury segment, in our view, vs. other domestic brands, which in

aggregate are largely experiencing weaker China sales.

● We reiterate our Add call on LG H&H with an SOP-based TP of W1.5m. Higher-than-

expected luxury brand demand should catalyse the share price. Risks to our Add call

are weaker-than-expected 1) domestic DF sales growth, and 2) China onshore sales

growth. LG H&H is our top pick within the sector.

Figure 1: 2Q19 preliminary results

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

(W bn) 2Q19A 2Q19F Diff. (%) BBG Diff. (%) 2Q18 1Q19 % yoy % qoqSales 1,833 1,852 -1% 1,835 0% 1,653 1,875 11% -2%Beautiful 1,109 1,134 -2% 953 1,140 16% -3%Healthy 343 337 2% 337 401 2% -14%Refreshing 380 382 0% 362 334 5% 14%OP 301.5 311.5 -3% 300.4 0% 267 322 13% -6%Beautiful 225.8 234.7 -4% 194.5 246.3 16% -8%Healthy 28.2 28.0 1% 27.3 43.4 3% -35%Refreshing 47.5 48.9 -3% 45.6 32.4 4% 47%Net non-op profit -14.1 -11.9 na -13 -16 na naRecurring profit 287.4 299.6 -4% 254 307 13% -6%Tax 75.9 80.9 -6% 67 81 13% -6%Net profit 208.2 215.5 -3% 213.3 -2% 185 224 13% -7%EPS 13,331 13,798 -3% na 11,824 14,311 13% -7%OPM 16.5% 16.8% -0.4% 16.4% 0.1% 16% 17% 0% -1%NPM 11.4% 11.6% -0.3% 11.6% -0.3% 11% 12% 0% -1%

South Korea July 25, 2019 - 5:22 PM

ADD (no change) Consensus ratings*: Buy 32 Hold 2 Sell 1

Current price: W1,308,000

Target price: W1,500,000

Previous target: W1,500,000

Up/downside: 14.7%

CGS-CIMB / Consensus: -7.7%

Reuters: 051900.KS

Bloomberg: 051900 KS

Market cap: US$17,344m

W20,428,602m

Average daily turnover: US$26.81m

W31,681m

Current shares o/s 17.72m

Free float: 52.7% *Source: Bloomberg

Key financial forecasts

Source: Bloomberg

Price performance 1M 3M 12M

Absolute (%) -0.9 -6.2 4.1

Relative (%) 1.3 -0.9 12.8

Major shareholders % held LG Corp 34.0

National Pension Service 7.2

LG Household & Health Care Ltd 6.1

Insert

Analyst(s)

Jun LIM

T (82) 2 6730 6130 E [email protected]

Dec-19F Dec-20F Dec-21F

Net Profit (Wb) 826 929 1,046

Normalised EPS (W) 46,640 52,450 59,055

Normalised EPS Growth 21.0% 12.5% 12.6%

FD Normalised P/E (x) 28.04 24.94 22.15

Recurring ROE 21.9% 21.0% 20.1%

P/BV (x) 5.73 4.84 4.12

DPS (W) 11,274 13,946 15,703

Dividend Yield 0.86% 1.07% 1.20%

86.0

100.0

114.0

1,000,000

1,200,000

1,400,000

Price Close Relative to KOSPI (RHS)

50

100

Jul-18 Oct-18 Jan-19 Apr-19

Vo

l th

10

Company Note Auto Parts │ South Korea │ July 25, 2019

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CGS-CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Insert Insert

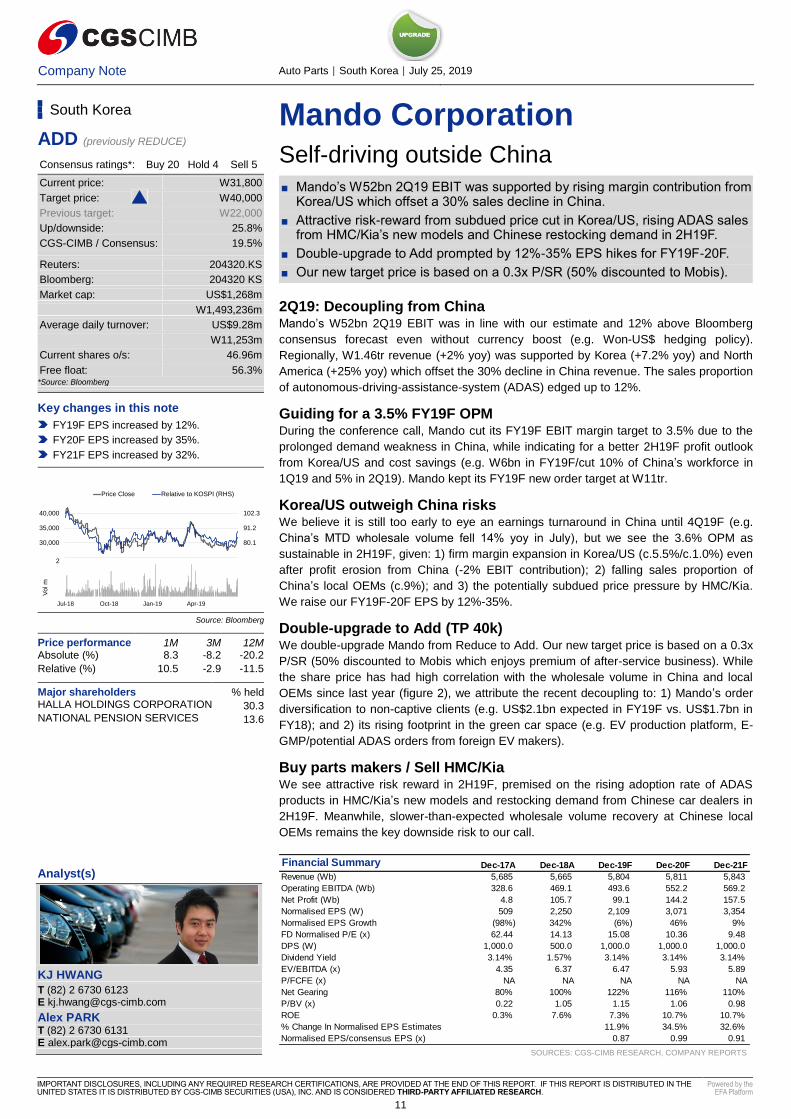

Mando Corporation Self-driving outside China

■ Mando’s W52bn 2Q19 EBIT was supported by rising margin contribution from Korea/US which offset a 30% sales decline in China.

■ Attractive risk-reward from subdued price cut in Korea/US, rising ADAS sales from HMC/Kia’s new models and Chinese restocking demand in 2H19F.

■ Double-upgrade to Add prompted by 12%-35% EPS hikes for FY19F-20F.

■ Our new target price is based on a 0.3x P/SR (50% discounted to Mobis).

2Q19: Decoupling from China Mando’s W52bn 2Q19 EBIT was in line with our estimate and 12% above Bloomberg

consensus forecast even without currency boost (e.g. Won-US$ hedging policy).

Regionally, W1.46tr revenue (+2% yoy) was supported by Korea (+7.2% yoy) and North

America (+25% yoy) which offset the 30% decline in China revenue. The sales proportion

of autonomous-driving-assistance-system (ADAS) edged up to 12%.

Guiding for a 3.5% FY19F OPM During the conference call, Mando cut its FY19F EBIT margin target to 3.5% due to the

prolonged demand weakness in China, while indicating for a better 2H19F profit outlook

from Korea/US and cost savings (e.g. W6bn in FY19F/cut 10% of China’s workforce in

1Q19 and 5% in 2Q19). Mando kept its FY19F new order target at W11tr.

Korea/US outweigh China risks We believe it is still too early to eye an earnings turnaround in China until 4Q19F (e.g.

China’s MTD wholesale volume fell 14% yoy in July), but we see the 3.6% OPM as

sustainable in 2H19F, given: 1) firm margin expansion in Korea/US (c.5.5%/c.1.0%) even

after profit erosion from China (-2% EBIT contribution); 2) falling sales proportion of

China’s local OEMs (c.9%); and 3) the potentially subdued price pressure by HMC/Kia.

We raise our FY19F-20F EPS by 12%-35%.

Double-upgrade to Add (TP 40k) We double-upgrade Mando from Reduce to Add. Our new target price is based on a 0.3x

P/SR (50% discounted to Mobis which enjoys premium of after-service business). While

the share price has had high correlation with the wholesale volume in China and local

OEMs since last year (figure 2), we attribute the recent decoupling to: 1) Mando’s order

diversification to non-captive clients (e.g. US$2.1bn expected in FY19F vs. US$1.7bn in

FY18); and 2) its rising footprint in the green car space (e.g. EV production platform, E-

GMP/potential ADAS orders from foreign EV makers).

Buy parts makers / Sell HMC/Kia We see attractive risk reward in 2H19F, premised on the rising adoption rate of ADAS

products in HMC/Kia’s new models and restocking demand from Chinese car dealers in

2H19F. Meanwhile, slower-than-expected wholesale volume recovery at Chinese local

OEMs remains the key downside risk to our call.

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

South Korea

ADD (previously REDUCE)

Consensus ratings*: Buy 20 Hold 4 Sell 5

Current price: W31,800

Target price: W40,000

Previous target: W22,000

Up/downside: 25.8%

CGS-CIMB / Consensus: 19.5%

Reuters: 204320.KS

Bloomberg: 204320 KS

Market cap: US$1,268m

W1,493,236m

Average daily turnover: US$9.28m

W11,253m

Current shares o/s: 46.96m

Free float: 56.3% *Source: Bloomberg

Key changes in this note

FY19F EPS increased by 12%.

FY20F EPS increased by 35%.

FY21F EPS increased by 32%.

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) 8.3 -8.2 -20.2

Relative (%) 10.5 -2.9 -11.5

Major shareholders % held HALLA HOLDINGS CORPORATION 30.3 NATIONAL PENSION SERVICES 13.6

Insert

Analyst(s)

KJ HWANG

T (82) 2 6730 6123 E [email protected]

Alex PARK T (82) 2 6730 6131 E [email protected]

Financial Summary Dec-17A Dec-18A Dec-19F Dec-20F Dec-21F

Revenue (Wb) 5,685 5,665 5,804 5,811 5,843

Operating EBITDA (Wb) 328.6 469.1 493.6 552.2 569.2

Net Profit (Wb) 4.8 105.7 99.1 144.2 157.5

Normalised EPS (W) 509 2,250 2,109 3,071 3,354

Normalised EPS Growth (98%) 342% (6%) 46% 9%

FD Normalised P/E (x) 62.44 14.13 15.08 10.36 9.48

DPS (W) 1,000.0 500.0 1,000.0 1,000.0 1,000.0

Dividend Yield 3.14% 1.57% 3.14% 3.14% 3.14%

EV/EBITDA (x) 4.35 6.37 6.47 5.93 5.89

P/FCFE (x) NA NA NA NA NA

Net Gearing 80% 100% 122% 116% 110%

P/BV (x) 0.22 1.05 1.15 1.06 0.98

ROE 0.3% 7.6% 7.3% 10.7% 10.7%

% Change In Normalised EPS Estimates 11.9% 34.5% 32.6%

Normalised EPS/consensus EPS (x) 0.87 0.99 0.91

69.0

80.1

91.2

102.3

25,000

30,000

35,000

40,000

Price Close Relative to KOSPI (RHS)

1

1

2

2

Jul-18 Oct-18 Jan-19 Apr-19

Vo

l m

11

Company Note IT Services │ South Korea │ July 25, 2019

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CGS-CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Insert Insert

NAVER Positive on Naver Pay’s spinoff

■ Naver’s 2Q19 OP of W128.3bn was below our estimates, no thanks to Line.

■ We still think LINE’s ramp-up could take more time. But strong domestic business likely dispels concerns on waning consolidated earnings in 2H19F.

■ We upgrade Naver to Hold and raise our SOP-based TP to W140k. We are positive on the Naver Pay spinoff, which could be worth over W1.5tr.

Concerns over LINE Pay’s competitiveness Due to LINE’s widening operating loss, Naver reported a weak 2Q19 consolidated OP of

W128.3bn, -48.8% yoy. This is 17.0% below our estimate and 17.2% below Bloomberg

consensus. However, the market seems to be ignoring the weak earnings as the share

price has risen by as much as 8% after the 2Q19 earnings conference call during which

management revealed plans to spin off Naver Pay into a separate entity.

Parent company’s performance was still strong Excluding LINE, Naver reported a solid parent-only OP of W322.5bn (17% yoy), in line

with our estimate. Naver’s CPM ad revenue rose +12% yoy, the first double-digit yoy

increase since 2Q18. Our Reduce call was premised on Naver’s warning of the threat

posed by YouTube and Instagram ads taking Naver’s market share. This apprehension

proved unfounded as CPM (click per mille) revenue growth improved in 1H19.

Positive on the spinoff; likely boosted by Naver Pay in 2H19 Naver’s Business Platform division, including Naver Shopping, registered substantial

revenue growth of 17% yoy in 2Q19. IT platform, including Naver Pay, recorded a 22.6%

yoy revenue growth, due to synergies with Naver’s strong commerce platform. Naver

announced that it plans to spin off Naver Pay, which will become a separate entity named

Naver Financial. Mirae Asset Daewoo (006800 KS, Not rated) will invest W500bn in the

new entity and likely become its second biggest shareholder after Naver.

Naver Financial could be worth W1.5tr We previously did not factor Pay’s equity value into Naver’s SOP valuation as the

business entity did not independently generate material income. However, after the

spinoff and external funding, new entity Naver Financial is likely to seek business

opportunities outside Naver, such as selling insurance, loans or securities. Using the peer

comparable valuation method (see fig 1), we now include the value of Naver’s stake in

Naver Financial’s in our SOP valuation, which could be worth over W1.5tr.

Upgrade to Hold with a higher TP of W140k We upgrade Naver from a Reduce to Hold and raise our SOP-based TP to W140K. We

raised FY20-21F EPS forecasts to reflect the higher-than-expected domestic ad revenue

growth rate. Upside risks are faster-than-expected profit contribution from LINE and an

increase in domestic video platform market share. Downside risk is decreasing market

share in domestic ad market in 2H19F.

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

South Korea

HOLD (previously REDUCE)

Consensus ratings*: Buy 31 Hold 3 Sell 2

Current price: W134,000

Target price: W140,000

Previous target: W100,000

Up/downside: 4.5%

CGS-CIMB / Consensus: -7.3%

Reuters: 035420.KS

Bloomberg: 035420 KS

Market cap: US$18,751m

W22,084,994m

Average daily turnover: US$40.58m

W50,361m

Current shares o/s: 164.8m

Free float: 75.0% *Source: Bloomberg

Key changes in this note

FY19F/20F Revenue increased by 2%/2%.

FY19F/20F OP increased by 10%/15%.

FY19F/20F/21F EPS increased by 2%/6%/10%.

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) 17 11.2 -10.2

Relative (%) 19.2 16.5 -1.5

Major shareholders % held National Pension Service 10.0 BlackRock Inc 5.7

Insert

Analyst(s)

Namjun LEE

T (82) 2 6730 6135 E [email protected]

Financial Summary Dec-17A Dec-18A Dec-19F Dec-20F Dec-21F

Revenue (Wb) 4,678 5,587 6,474 6,959 7,508

Operating EBITDA (Wb) 1,385 1,204 1,200 1,529 1,689

Net Profit (Wb) 772.9 648.8 521.8 657.8 720.2

Normalised EPADS (W) 4,705 3,907 3,186 3,992 4,370

Normalised EPS Growth 1.9% (17.0%) (18.4%) 25.3% 9.5%

FD Normalised P/E (x) 28.48 34.30 42.05 33.57 30.66

DPADS (W) 197.7 257.7 278.5 156.7 217.1

Dividend Yield 0.96% 0.21% 0.12% 0.16% 0.18%

EV/EBITDA (x) 13.95 16.40 16.70 12.99 11.62

P/FCFE (x) NA 16.8 NA 130.1 101.0

Net Gearing (62.2%) (51.3%) (44.6%) (44.3%) (44.3%)

P/BV (x) 4.64 4.21 4.01 3.70 3.40

ROE 18.6% 12.9% 9.8% 11.5% 11.6%

% Change In Normalised EPADS Estimates 2.2% 5.9% 10.3%

Normalised EPADS/consensus EPADS (x) 0.97 0.87 0.76

77.0

87.0

97.0

107.0

100,000

120,000

140,000

160,000

Price Close Relative to KOSPI (RHS)

1

1

2

2

Jul-18 Oct-18 Jan-19 Apr-19

Vo

l m

12

Company Note Semiconductor │ South Korea │ July 25, 2019

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CGS-CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Insert Insert

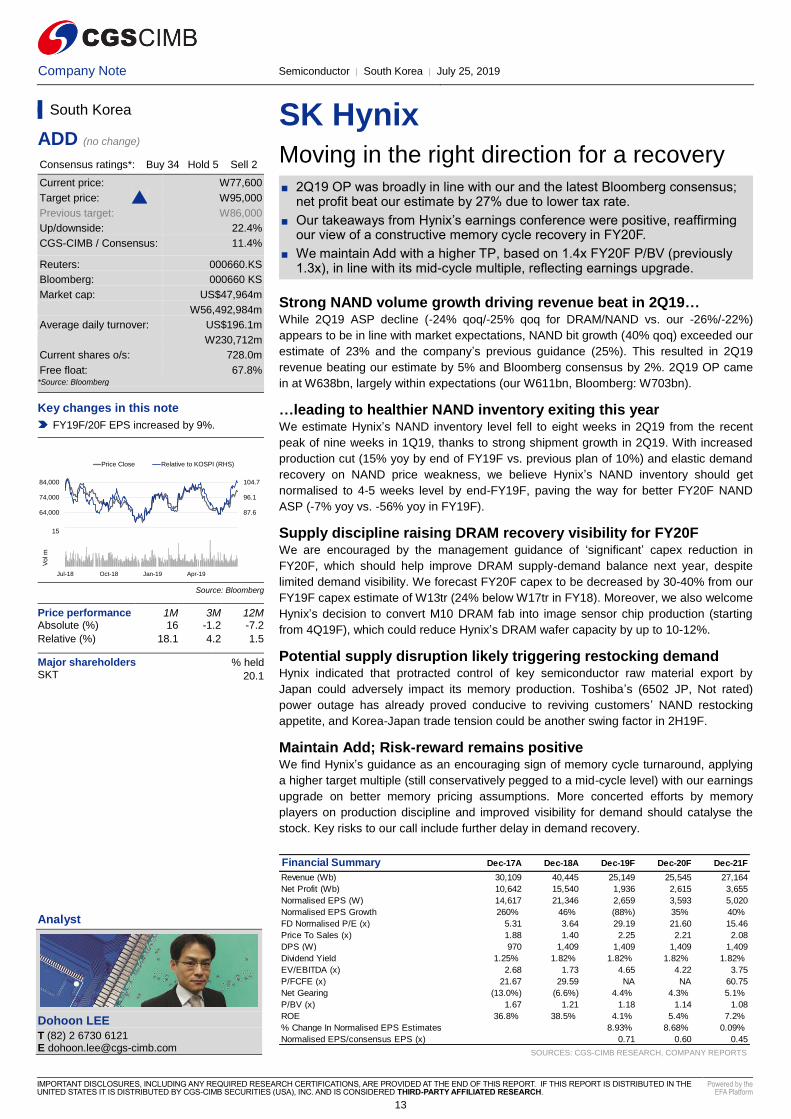

SK Hynix Moving in the right direction for a recovery

■ 2Q19 OP was broadly in line with our and the latest Bloomberg consensus; net profit beat our estimate by 27% due to lower tax rate.

■ Our takeaways from Hynix’s earnings conference were positive, reaffirming our view of a constructive memory cycle recovery in FY20F.

■ We maintain Add with a higher TP, based on 1.4x FY20F P/BV (previously 1.3x), in line with its mid-cycle multiple, reflecting earnings upgrade.

Strong NAND volume growth driving revenue beat in 2Q19… While 2Q19 ASP decline (-24% qoq/-25% qoq for DRAM/NAND vs. our -26%/-22%)

appears to be in line with market expectations, NAND bit growth (40% qoq) exceeded our

estimate of 23% and the company’s previous guidance (25%). This resulted in 2Q19

revenue beating our estimate by 5% and Bloomberg consensus by 2%. 2Q19 OP came

in at W638bn, largely within expectations (our W611bn, Bloomberg: W703bn).

…leading to healthier NAND inventory exiting this year We estimate Hynix’s NAND inventory level fell to eight weeks in 2Q19 from the recent

peak of nine weeks in 1Q19, thanks to strong shipment growth in 2Q19. With increased

production cut (15% yoy by end of FY19F vs. previous plan of 10%) and elastic demand

recovery on NAND price weakness, we believe Hynix’s NAND inventory should get

normalised to 4-5 weeks level by end-FY19F, paving the way for better FY20F NAND

ASP (-7% yoy vs. -56% yoy in FY19F).

Supply discipline raising DRAM recovery visibility for FY20F We are encouraged by the management guidance of ‘significant’ capex reduction in

FY20F, which should help improve DRAM supply-demand balance next year, despite

limited demand visibility. We forecast FY20F capex to be decreased by 30-40% from our

FY19F capex estimate of W13tr (24% below W17tr in FY18). Moreover, we also welcome

Hynix’s decision to convert M10 DRAM fab into image sensor chip production (starting

from 4Q19F), which could reduce Hynix’s DRAM wafer capacity by up to 10-12%.

Potential supply disruption likely triggering restocking demand Hynix indicated that protracted control of key semiconductor raw material export by

Japan could adversely impact its memory production. Toshiba’s (6502 JP, Not rated)

power outage has already proved conducive to reviving customers’ NAND restocking

appetite, and Korea-Japan trade tension could be another swing factor in 2H19F.

Maintain Add; Risk-reward remains positive We find Hynix’s guidance as an encouraging sign of memory cycle turnaround, applying

a higher target multiple (still conservatively pegged to a mid-cycle level) with our earnings

upgrade on better memory pricing assumptions. More concerted efforts by memory

players on production discipline and improved visibility for demand should catalyse the

stock. Key risks to our call include further delay in demand recovery.

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

South Korea

ADD (no change)

Consensus ratings*: Buy 34 Hold 5 Sell 2

Current price: W77,600

Target price: W95,000

Previous target: W86,000

Up/downside: 22.4%

CGS-CIMB / Consensus: 11.4%

Reuters: 000660.KS

Bloomberg: 000660 KS

Market cap: US$47,964m

W56,492,984m

Average daily turnover: US$196.1m

W230,712m

Current shares o/s: 728.0m

Free float: 67.8% *Source: Bloomberg

Key changes in this note

FY19F/20F EPS increased by 9%.

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) 16 -1.2 -7.2

Relative (%) 18.1 4.2 1.5

Major shareholders % held SKT 20.1

Insert

Analyst

Dohoon LEE

T (82) 2 6730 6121 E [email protected]

Financial Summary Dec-17A Dec-18A Dec-19F Dec-20F Dec-21F

Revenue (Wb) 30,109 40,445 25,149 25,545 27,164

Net Profit (Wb) 10,642 15,540 1,936 2,615 3,655

Normalised EPS (W) 14,617 21,346 2,659 3,593 5,020

Normalised EPS Growth 260% 46% (88%) 35% 40%

FD Normalised P/E (x) 5.31 3.64 29.19 21.60 15.46

Price To Sales (x) 1.88 1.40 2.25 2.21 2.08

DPS (W) 970 1,409 1,409 1,409 1,409

Dividend Yield 1.25% 1.82% 1.82% 1.82% 1.82%

EV/EBITDA (x) 2.68 1.73 4.65 4.22 3.75

P/FCFE (x) 21.67 29.59 NA NA 60.75

Net Gearing (13.0%) (6.6%) 4.4% 4.3% 5.1%

P/BV (x) 1.67 1.21 1.18 1.14 1.08

ROE 36.8% 38.5% 4.1% 5.4% 7.2%

% Change In Normalised EPS Estimates 8.93% 8.68% 0.09%

Normalised EPS/consensus EPS (x) 0.71 0.60 0.45

79.0

87.6

96.1

104.7

54,000

64,000

74,000

84,000

Price Close Relative to KOSPI (RHS)

5

10

15

Jul-18 Oct-18 Jan-19 Apr-19

Vo

l m

13

Company Note REIT │ Malaysia │ July 26, 2019 Shariah Compliant

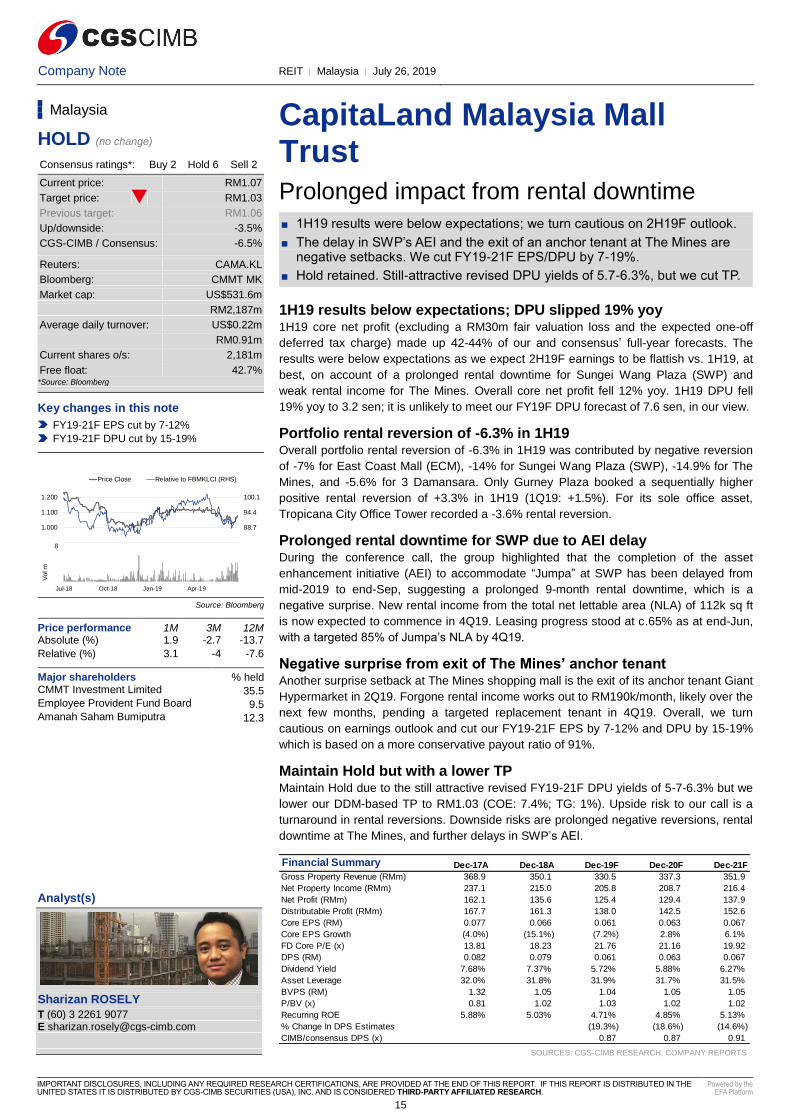

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CGS-CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Insert Insert

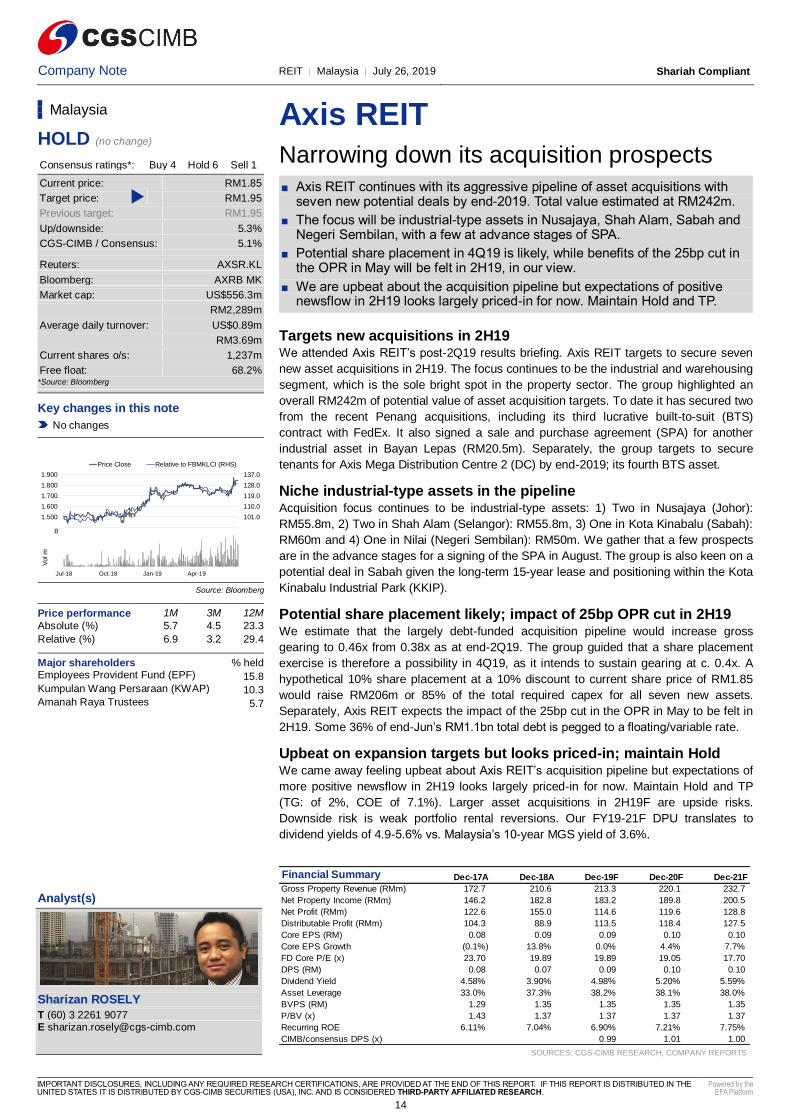

Axis REIT

Narrowing down its acquisition prospects

■ Axis REIT continues with its aggressive pipeline of asset acquisitions with seven new potential deals by end-2019. Total value estimated at RM242m.

■ The focus will be industrial-type assets in Nusajaya, Shah Alam, Sabah and Negeri Sembilan, with a few at advance stages of SPA.

■ Potential share placement in 4Q19 is likely, while benefits of the 25bp cut in the OPR in May will be felt in 2H19, in our view.

■ We are upbeat about the acquisition pipeline but expectations of positive newsflow in 2H19 looks largely priced-in for now. Maintain Hold and TP.

Targets new acquisitions in 2H19 We attended Axis REIT’s post-2Q19 results briefing. Axis REIT targets to secure seven

new asset acquisitions in 2H19. The focus continues to be the industrial and warehousing

segment, which is the sole bright spot in the property sector. The group highlighted an

overall RM242m of potential value of asset acquisition targets. To date it has secured two

from the recent Penang acquisitions, including its third lucrative built-to-suit (BTS)

contract with FedEx. It also signed a sale and purchase agreement (SPA) for another

industrial asset in Bayan Lepas (RM20.5m). Separately, the group targets to secure

tenants for Axis Mega Distribution Centre 2 (DC) by end-2019; its fourth BTS asset.

Niche industrial-type assets in the pipeline Acquisition focus continues to be industrial-type assets: 1) Two in Nusajaya (Johor):

RM55.8m, 2) Two in Shah Alam (Selangor): RM55.8m, 3) One in Kota Kinabalu (Sabah):

RM60m and 4) One in Nilai (Negeri Sembilan): RM50m. We gather that a few prospects

are in the advance stages for a signing of the SPA in August. The group is also keen on a

potential deal in Sabah given the long-term 15-year lease and positioning within the Kota

Kinabalu Industrial Park (KKIP).

Potential share placement likely; impact of 25bp OPR cut in 2H19 We estimate that the largely debt-funded acquisition pipeline would increase gross

gearing to 0.46x from 0.38x as at end-2Q19. The group guided that a share placement

exercise is therefore a possibility in 4Q19, as it intends to sustain gearing at c. 0.4x. A

hypothetical 10% share placement at a 10% discount to current share price of RM1.85

would raise RM206m or 85% of the total required capex for all seven new assets.

Separately, Axis REIT expects the impact of the 25bp cut in the OPR in May to be felt in

2H19. Some 36% of end-Jun’s RM1.1bn total debt is pegged to a floating/variable rate.

Upbeat on expansion targets but looks priced-in; maintain Hold We came away feeling upbeat about Axis REIT’s acquisition pipeline but expectations of

more positive newsflow in 2H19 looks largely priced-in for now. Maintain Hold and TP

(TG: of 2%, COE of 7.1%). Larger asset acquisitions in 2H19F are upside risks.

Downside risk is weak portfolio rental reversions. Our FY19-21F DPU translates to

dividend yields of 4.9-5.6% vs. Malaysia’s 10-year MGS yield of 3.6%.

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Malaysia

HOLD (no change)

Consensus ratings*: Buy 4 Hold 6 Sell 1

Current price: RM1.85

Target price: RM1.95

Previous target: RM1.95

Up/downside: 5.3%

CGS-CIMB / Consensus: 5.1%

Reuters: AXSR.KL

Bloomberg: AXRB MK

Market cap: US$556.3m

RM2,289m

Average daily turnover: US$0.89m

RM3.69m

Current shares o/s: 1,237m

Free float: 68.2% *Source: Bloomberg

Key changes in this note

No changes

Source: Bloomberg

Price performance 1M 3M 12M

Absolute (%) 5.7 4.5 23.3

Relative (%) 6.9 3.2 29.4

Major shareholders % held Employees Provident Fund (EPF) 15.8 Kumpulan Wang Persaraan (KWAP) 10.3 Amanah Raya Trustees 5.7

Insert

Analyst(s)

Sharizan ROSELY

T (60) 3 2261 9077 E [email protected]

Financial Summary Dec-17A Dec-18A Dec-19F Dec-20F Dec-21F

Gross Property Revenue (RMm) 172.7 210.6 213.3 220.1 232.7

Net Property Income (RMm) 146.2 182.8 183.2 189.8 200.5

Net Profit (RMm) 122.6 155.0 114.6 119.6 128.8

Distributable Profit (RMm) 104.3 88.9 113.5 118.4 127.5

Core EPS (RM) 0.08 0.09 0.09 0.10 0.10

Core EPS Growth (0.1%) 13.8% 0.0% 4.4% 7.7%

FD Core P/E (x) 23.70 19.89 19.89 19.05 17.70

DPS (RM) 0.08 0.07 0.09 0.10 0.10

Dividend Yield 4.58% 3.90% 4.98% 5.20% 5.59%

Asset Leverage 33.0% 37.3% 38.2% 38.1% 38.0%

BVPS (RM) 1.29 1.35 1.35 1.35 1.35

P/BV (x) 1.43 1.37 1.37 1.37 1.37

Recurring ROE 6.11% 7.04% 6.90% 7.21% 7.75%

CIMB/consensus DPS (x) 0.99 1.01 1.00

92.0

101.0

110.0