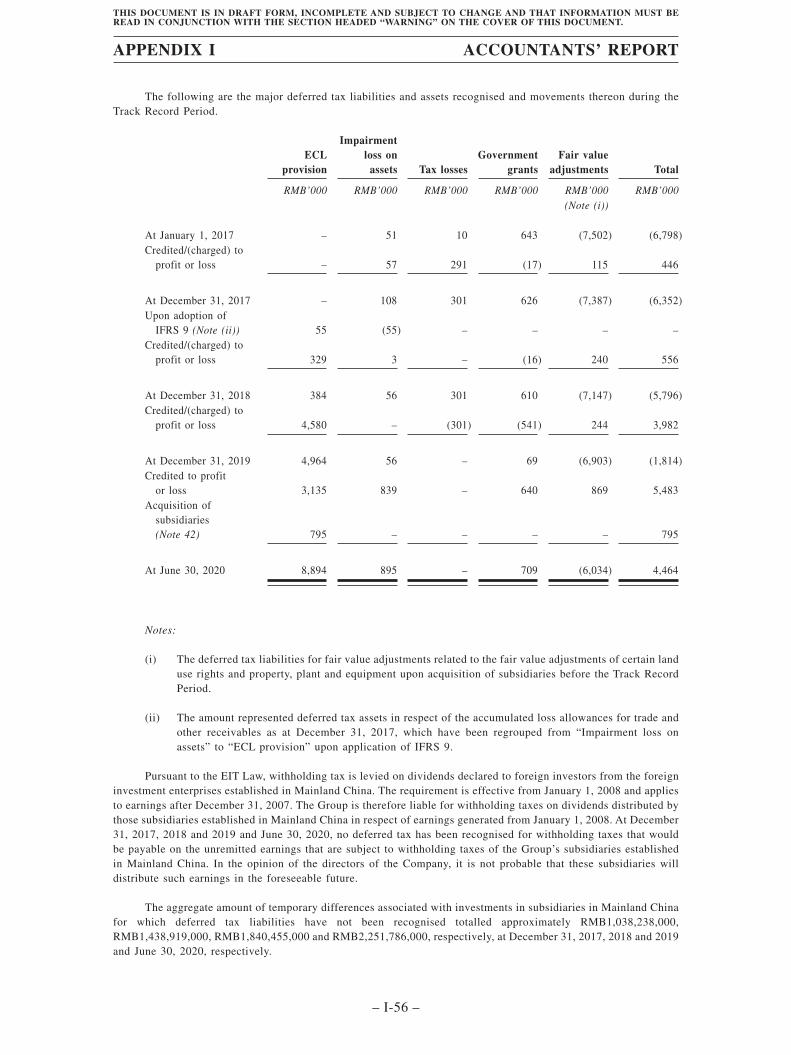

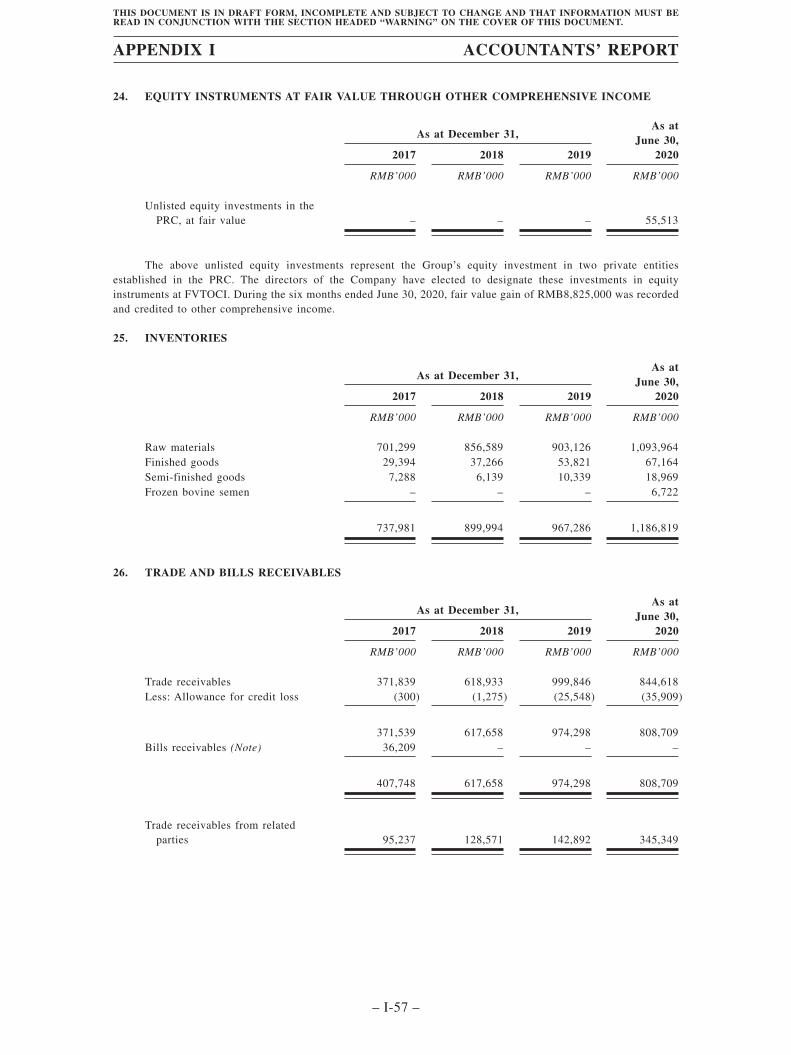

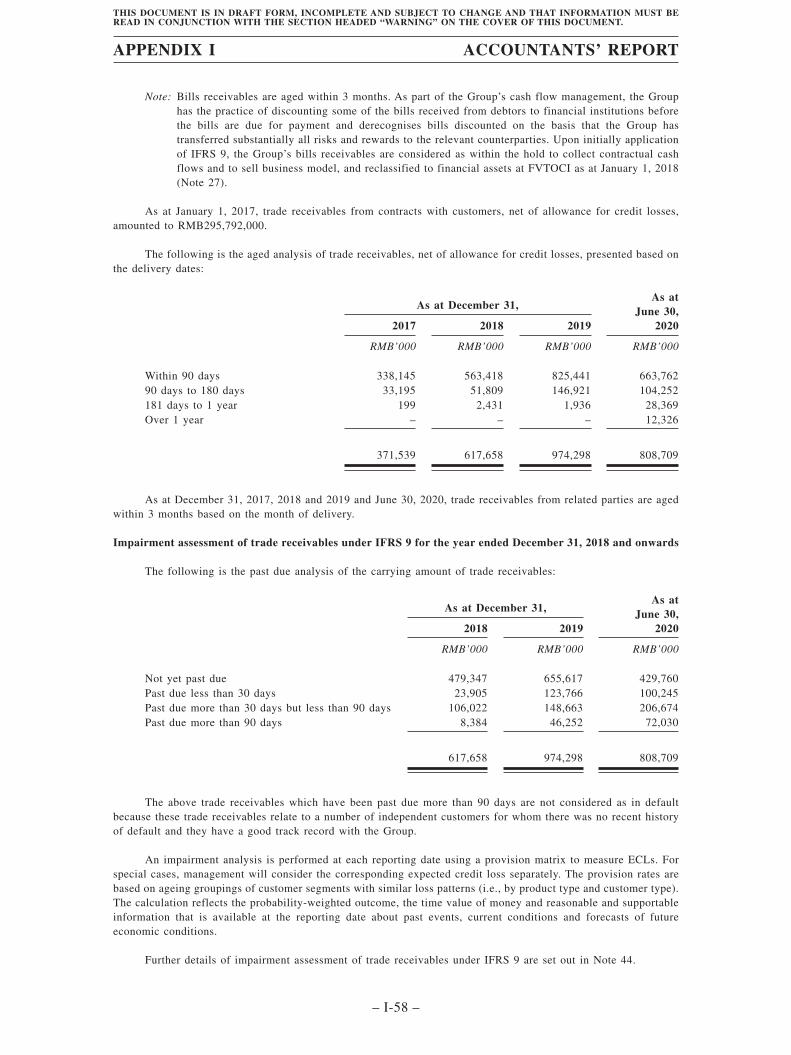

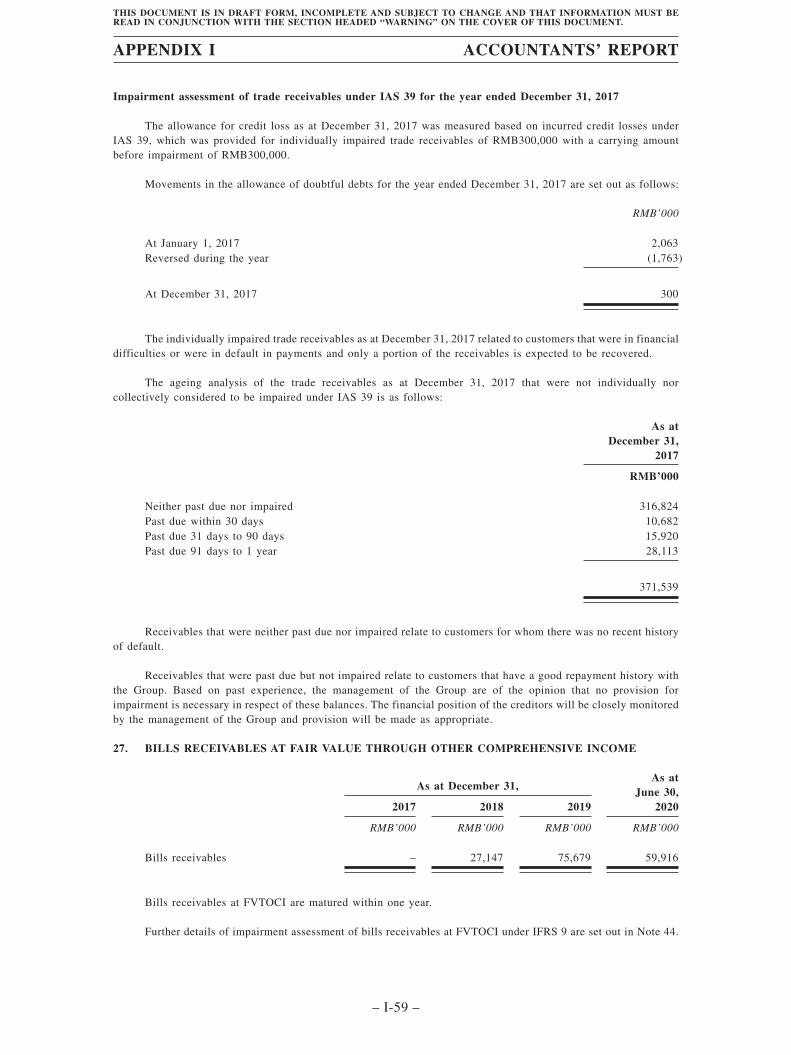

APPENDIX I ACCOUNTANTS' REPORT - AASTOCKS.com

167

The following is the text of a report set out on pages 1 to [167], prepared for the purpose of inclusion in this Document, received from the Company’s reporting accountants, Deloitte Touche Tohmatsu, Certified Public Accountants, Hong Kong. ACCOUNTANTS’ REPORT ON HISTORICAL FINANCIAL INFORMATION TO THE DIRECTORS OF CHINA YOURAN DAIRY GROUP LIMITED AND [REDACTED] Introduction We report on the historical financial information of China Youran Dairy Group Limited (the “Company”) and its subsidiaries (together, the “Group”) set out on pages I-[4] to I-[167] which comprises the combined statements of financial position of the Group as at December 31, 2017, 2018 and 2019 and June 30, 2020, and the combined statements of profit or loss and other comprehensive income, the combined statements of changes in equity and the combined statements of cash flows of the Group for each of the three years ended December 31, 2019 and the six months ended June 30, 2020 (the “Track Record Period”) and a summary of significant accounting policies and other explanatory information (together, the “Historical Financial Information”). The Historical Financial Information set out on pages I-[4] to I-[167] forms an integral part of this report, which has been prepared for inclusion in the document of the Company dated [●] (the “Document”) in connection with the [REDACTED] of The Stock Exchange of Hong Kong Limited (the “Stock Exchange”). Directors’ responsibility for the Historical Financial Information The directors of the Company are responsible for the preparation of the Historical Financial Information that gives a true and fair view in accordance with the basis of preparation and presentation set out in Note 2 to the Historical Financial Information, and for such internal control as the directors of the Company determine is necessary to enable the preparation of the Historical Financial Information that is free from material misstatement, whether due to fraud or error. Reporting accountants’ responsibility Our responsibility is to express an opinion on the Historical Financial Information and to report our opinion to you. We conducted our work in accordance with Hong Kong Standard on Investment Circular Reporting Engagements 200 “Accountants’ Reports on Historical Financial Information in Investment Circulars” issued by the Hong Kong Institute of Certified Public Accountants (the “HKICPA”). This standard requires that we comply with ethical standards and plan and perform our work to obtain reasonable assurance about whether the Historical Financial Information is free from material misstatement. APPENDIX I ACCOUNTANTS’ REPORT – I-1 – THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BE READ IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of APPENDIX I ACCOUNTANTS' REPORT - AASTOCKS.com

The following is the text of a report set out on pages 1 to [167], prepared for the purposeof inclusion in this Document, received from the Company’s reporting accountants, DeloitteTouche Tohmatsu, Certified Public Accountants, Hong Kong.

ACCOUNTANTS’ REPORT ON HISTORICAL FINANCIAL INFORMATION TO THEDIRECTORS OF CHINA YOURAN DAIRY GROUP LIMITED AND [REDACTED]

Introduction

We report on the historical financial information of China Youran Dairy Group Limited(the “Company”) and its subsidiaries (together, the “Group”) set out on pages I-[4] to I-[167]which comprises the combined statements of financial position of the Group as at December31, 2017, 2018 and 2019 and June 30, 2020, and the combined statements of profit or loss andother comprehensive income, the combined statements of changes in equity and the combinedstatements of cash flows of the Group for each of the three years ended December 31, 2019 andthe six months ended June 30, 2020 (the “Track Record Period”) and a summary of significantaccounting policies and other explanatory information (together, the “Historical FinancialInformation”).

The Historical Financial Information set out on pages I-[4] to I-[167] forms an integralpart of this report, which has been prepared for inclusion in the document of the Companydated [●] (the “Document”) in connection with the [REDACTED] of The Stock Exchange ofHong Kong Limited (the “Stock Exchange”).

Directors’ responsibility for the Historical Financial Information

The directors of the Company are responsible for the preparation of the HistoricalFinancial Information that gives a true and fair view in accordance with the basis of preparationand presentation set out in Note 2 to the Historical Financial Information, and for such internalcontrol as the directors of the Company determine is necessary to enable the preparation of theHistorical Financial Information that is free from material misstatement, whether due to fraudor error.

Reporting accountants’ responsibility

Our responsibility is to express an opinion on the Historical Financial Information and toreport our opinion to you. We conducted our work in accordance with Hong Kong Standard onInvestment Circular Reporting Engagements 200 “Accountants’ Reports on HistoricalFinancial Information in Investment Circulars” issued by the Hong Kong Institute of CertifiedPublic Accountants (the “HKICPA”). This standard requires that we comply with ethicalstandards and plan and perform our work to obtain reasonable assurance about whether theHistorical Financial Information is free from material misstatement.

APPENDIX I ACCOUNTANTS’ REPORT

– I-1 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

Our work involved performing procedures to obtain evidence about the amounts and

disclosures in the Historical Financial Information. The procedures selected depend on the

reporting accountants’ judgment, including the assessment of risks of material misstatement of

the Historical Financial Information, whether due to fraud or error. In making those risk

assessments, the reporting accountants consider internal control relevant to the entity’s

preparation of the Historical Financial Information that gives a true and fair view in accordance

with the basis of preparation and presentation set out in Note 2 to the Historical Financial

Information in order to design procedures that are appropriate in the circumstances, but not for

the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Our

work also included evaluating the appropriateness of accounting policies used and the

reasonableness of accounting estimates made by the directors of the Company, as well as

evaluating the overall presentation of the Historical Financial Information.

We believe that the evidence we have obtained is sufficient and appropriate to provide a

basis for our opinion.

Opinion

In our opinion the Historical Financial Information gives, for the purposes of the

accountants’ report, a true and fair view of the Group’s financial position as at December 31,

2017, 2018 and 2019 and June 30, 2020, and of the Group’s financial performance and cash

flows for the Track Record Period in accordance with the basis of preparation and presentation

set out in Note 2 to the Historical Financial Information.

Review of stub period comparative financial information

We have reviewed the stub period comparative financial information of the Group which

comprises the combined statement of profit or loss and other comprehensive income, the

combined statement of changes in equity and the combined statement of cash flows of the

Group for the six months ended June 30, 2019 and other explanatory information (the “Stub

Period Comparative Financial Information”).

The directors of the Company are responsible for the preparation and presentation of the

Stub Period Comparative Financial Information in accordance with the basis of preparation and

presentation set out in Note 2 to the Historical Financial Information. Our responsibility is to

express a conclusion on the Stub Period Comparative Financial Information based on our

review. We conducted our review in accordance with Hong Kong Standard on Review

Engagements 2410 “Review of Interim Financial Information Performed by the Independent

Auditor of the Entity” issued by the HKICPA. A review consists of making inquiries, primarily

of persons responsible for financial and accounting matters, and applying analytical and other

review procedures. A review is substantially less in scope than an audit conducted in

accordance with International Standards on Auditing and consequently does not enable us to

obtain assurance that we would become aware of all significant matters that might be identified

in an audit. Accordingly, we do not express an audit opinion.

APPENDIX I ACCOUNTANTS’ REPORT

– I-2 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

Based on our review, nothing has come to our attention that causes us to believe that the

Stub Period Comparative Financial Information, for the purposes of the accountants’ report, is

not prepared, in all material respects, in accordance with the basis of preparation and

presentation set out in Note 2 to the Historical Financial Information.

Report on matters under the Rules Governing the Listing of Securities on the StockExchange and the Companies (Winding Up and Miscellaneous Provisions) Ordinance

Adjustments

The Historical Financial Information is stated after making such adjustments to the

Underlying Financial Statements as defined on page I-[4] as were considered necessary.

Dividends

We refer to Note 16 to the Historical Financial Information which states that no dividend

was declared or paid by the group entities comprising the Group in respect of the Track Record

Period and contains information about the dividend declared by the Company subsequent to the

Track Record Period.

No historical financial statements for the Company

No financial statements have been prepared for the Company since its date of

incorporation.

[Deloitte Touche Tohmatsu]Certified Public Accountants

Hong Kong

[Date]

APPENDIX I ACCOUNTANTS’ REPORT

– I-3 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

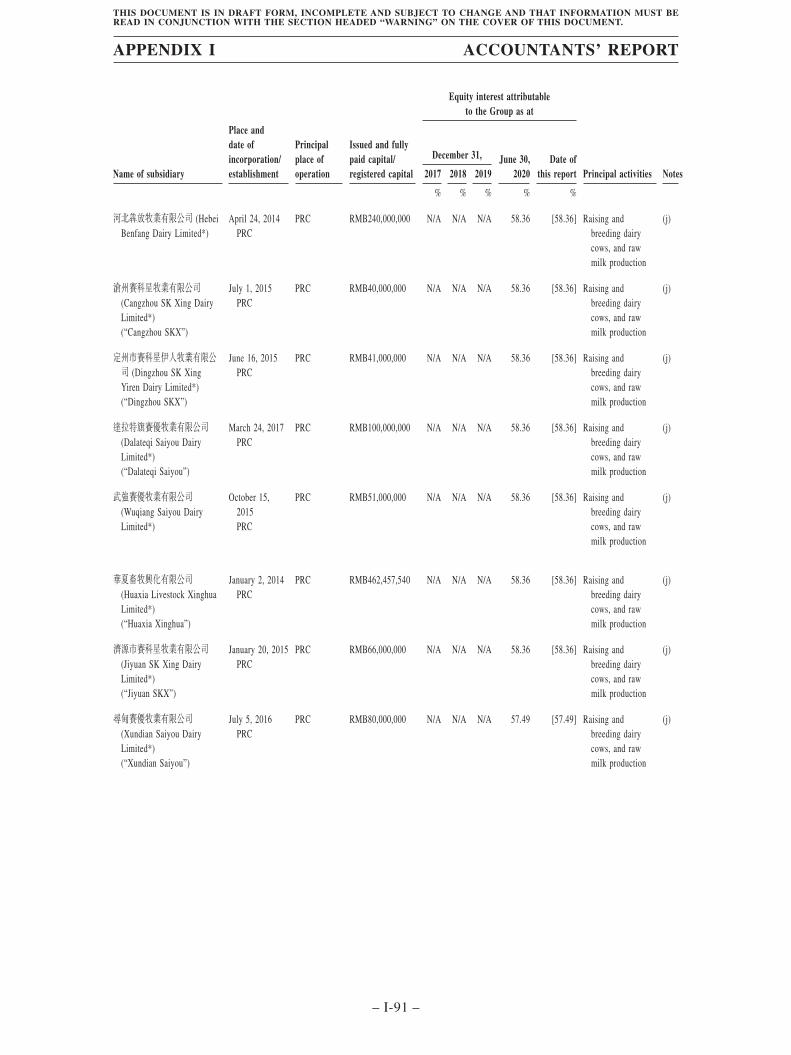

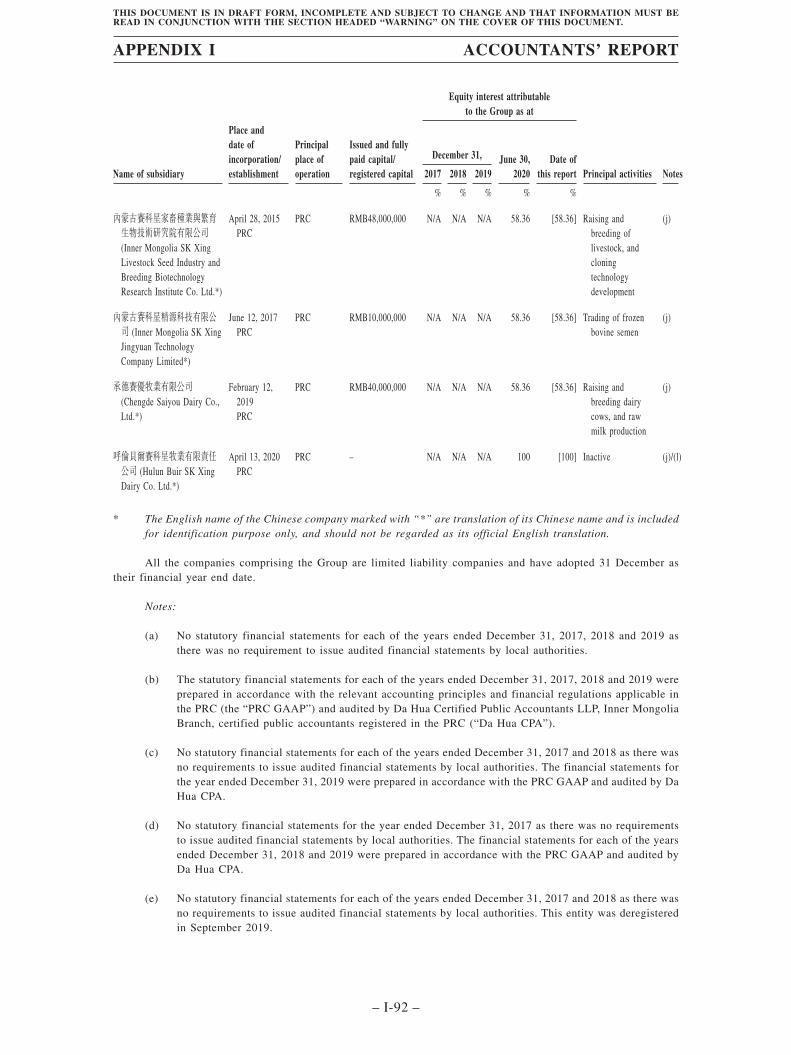

I. HISTORICAL FINANCIAL INFORMATION OF THE GROUP

PREPARATION OF HISTORICAL FINANCIAL INFORMATION

Set out below is the Historical Financial Information which forms an integral part of this

accountants’ report.

The consolidated financial statements of Yogurt Holding II Limited (“Youran BVI”), a

company incorporated in the British Virgin Islands, for the Track Record Period, on which the

Historical Financial Information is based, have been prepared in accordance with accounting

policies which conform with International Financial Reporting Standards (“IFRSs”) issued by

International Accounting Standards Board (the “IASB”) and were audited by us in accordance

with International Standards on Auditing (the “Underlying Financial Statements”).

The Historical Financial Information is presented in Renminbi (“RMB”) and all values

are rounded to the nearest thousand (RMB’000) except when otherwise indicated.

APPENDIX I ACCOUNTANTS’ REPORT

– I-4 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

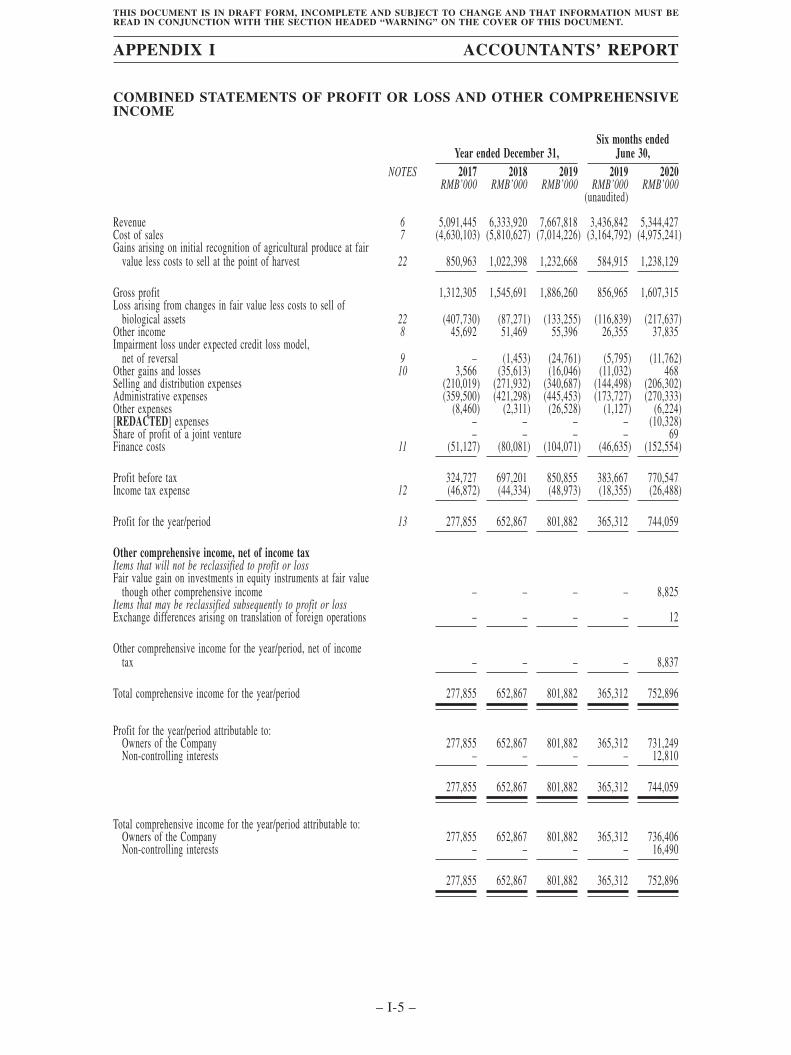

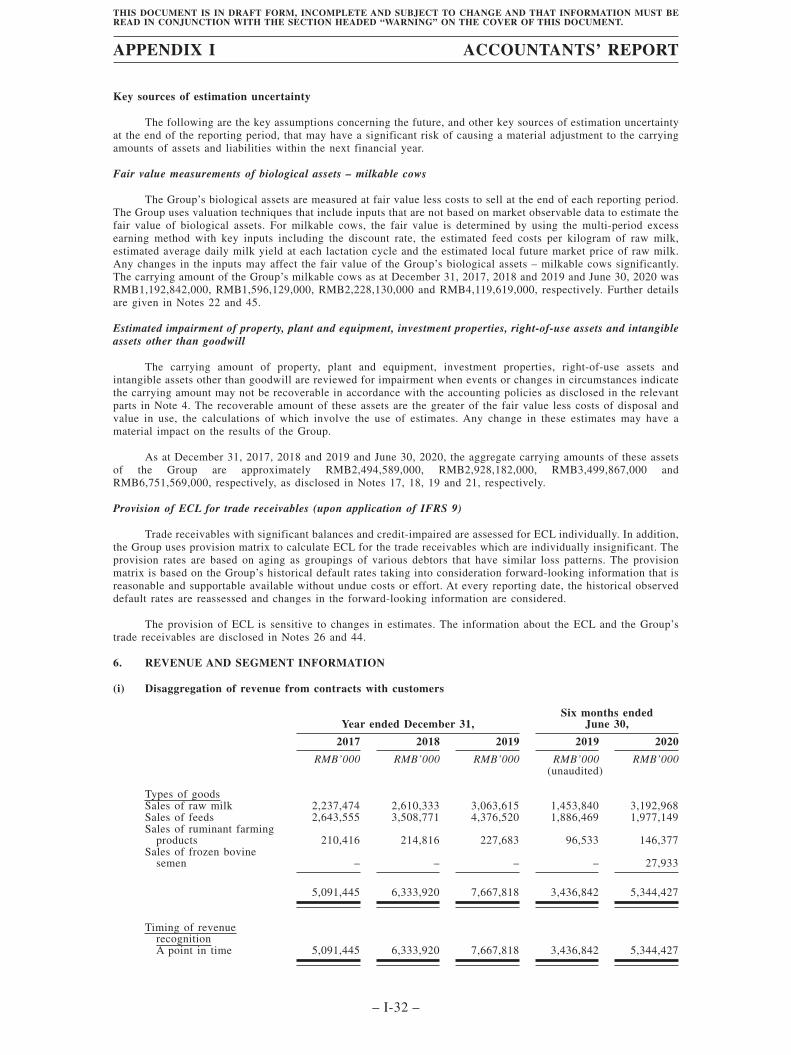

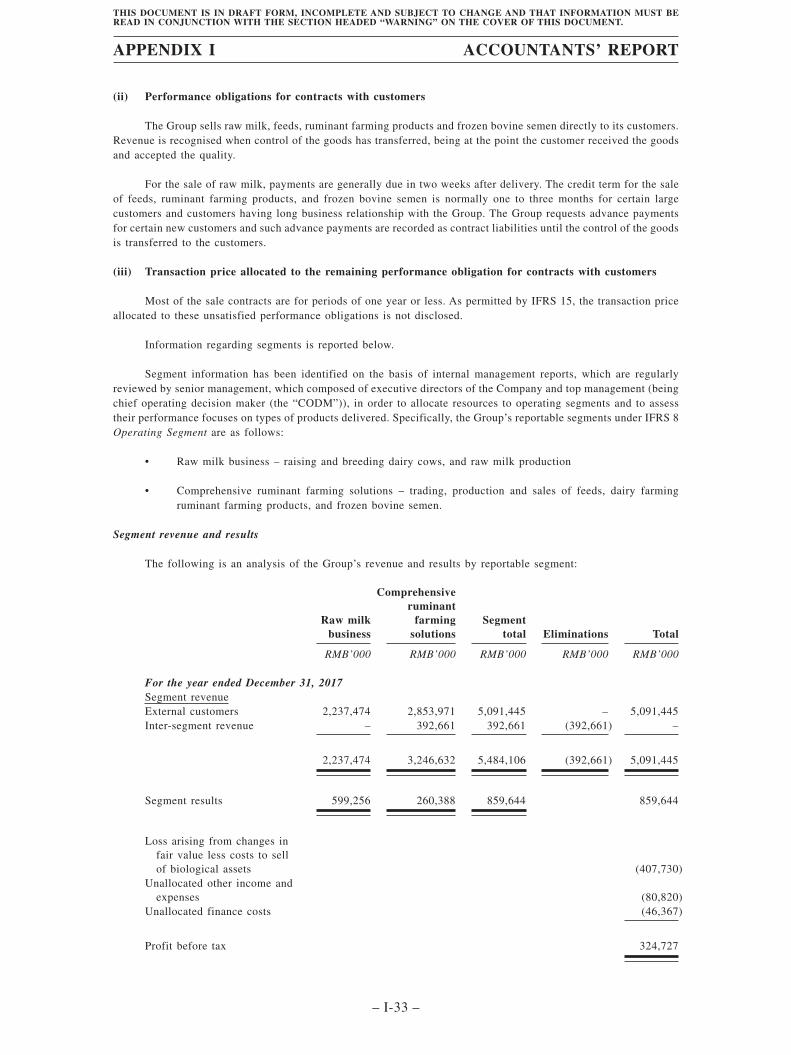

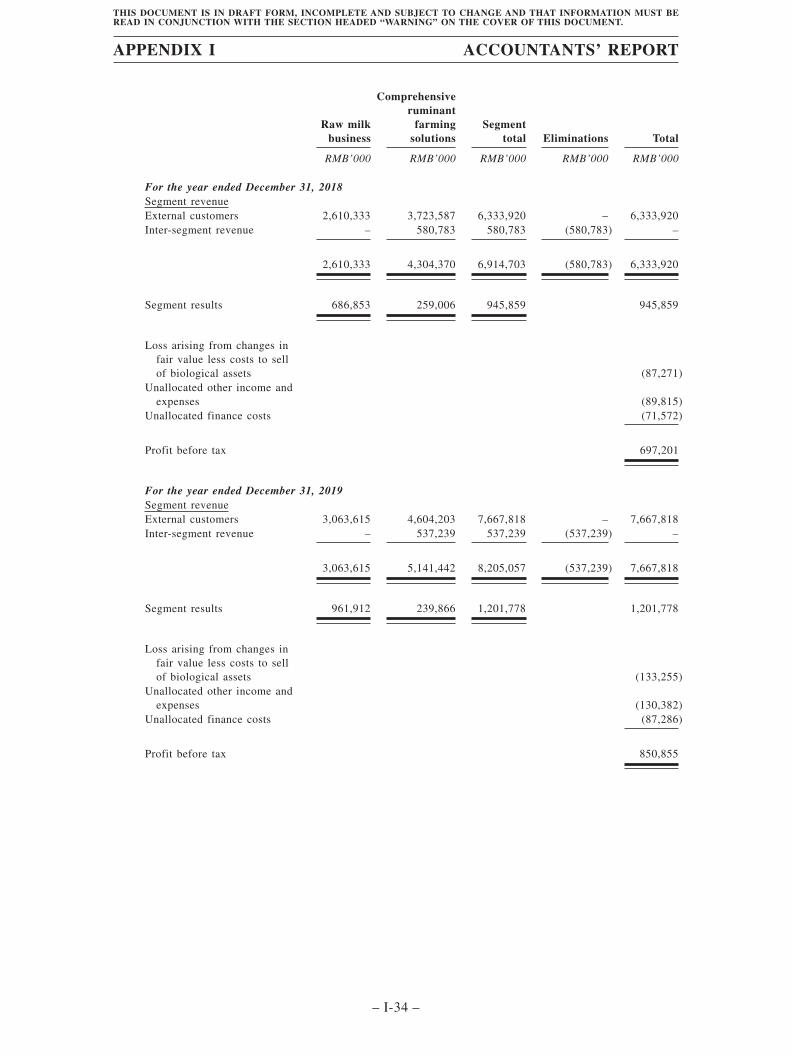

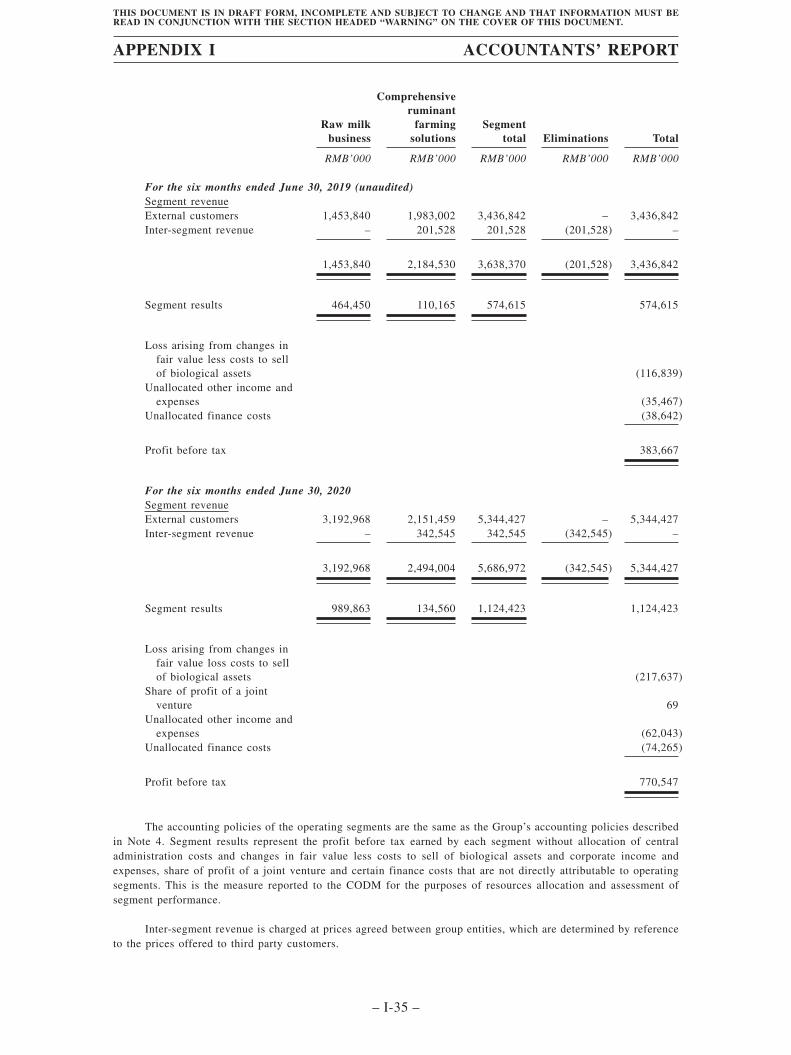

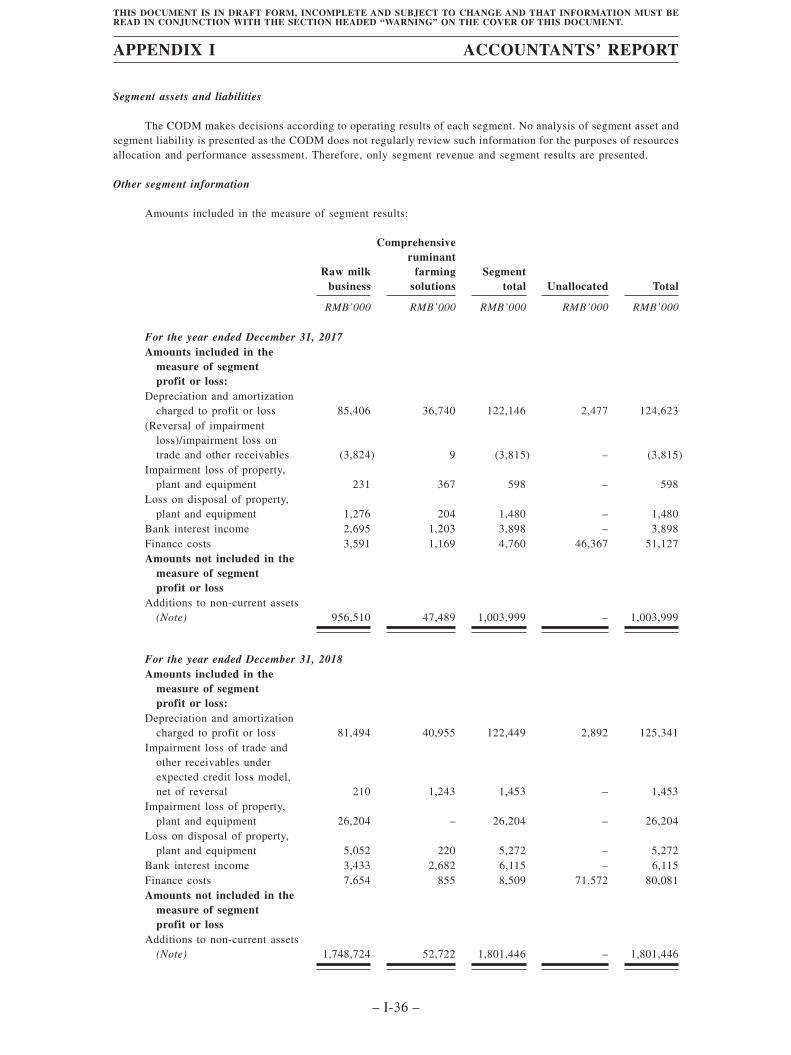

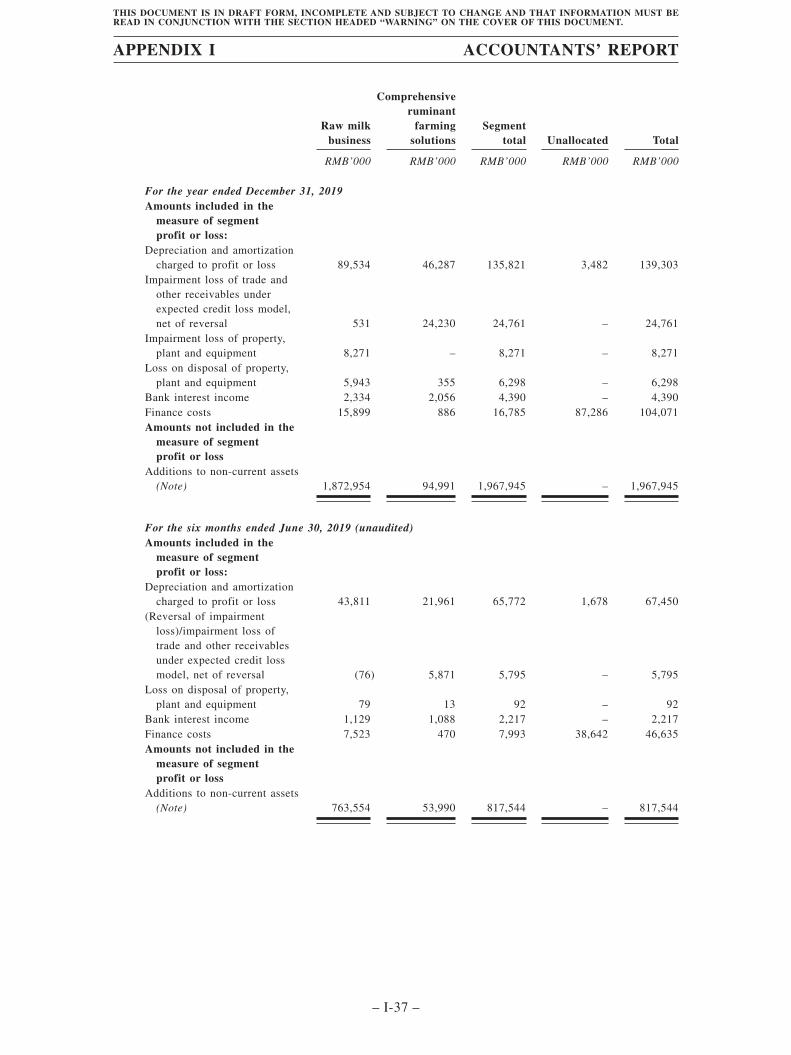

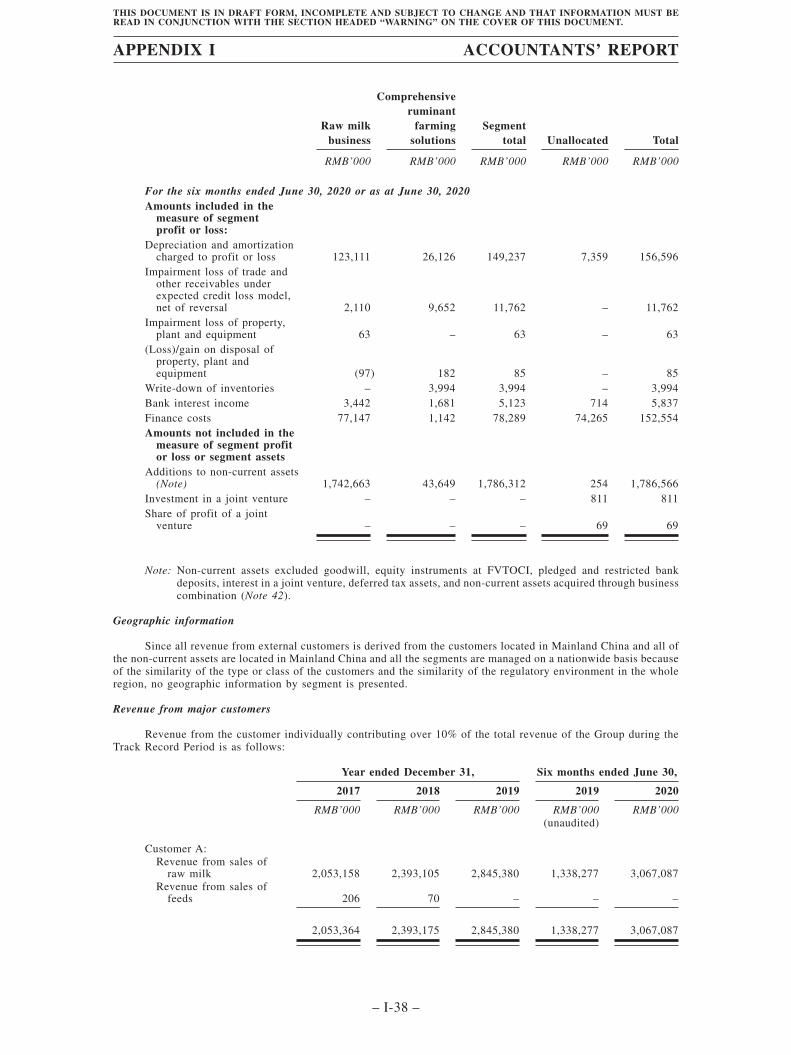

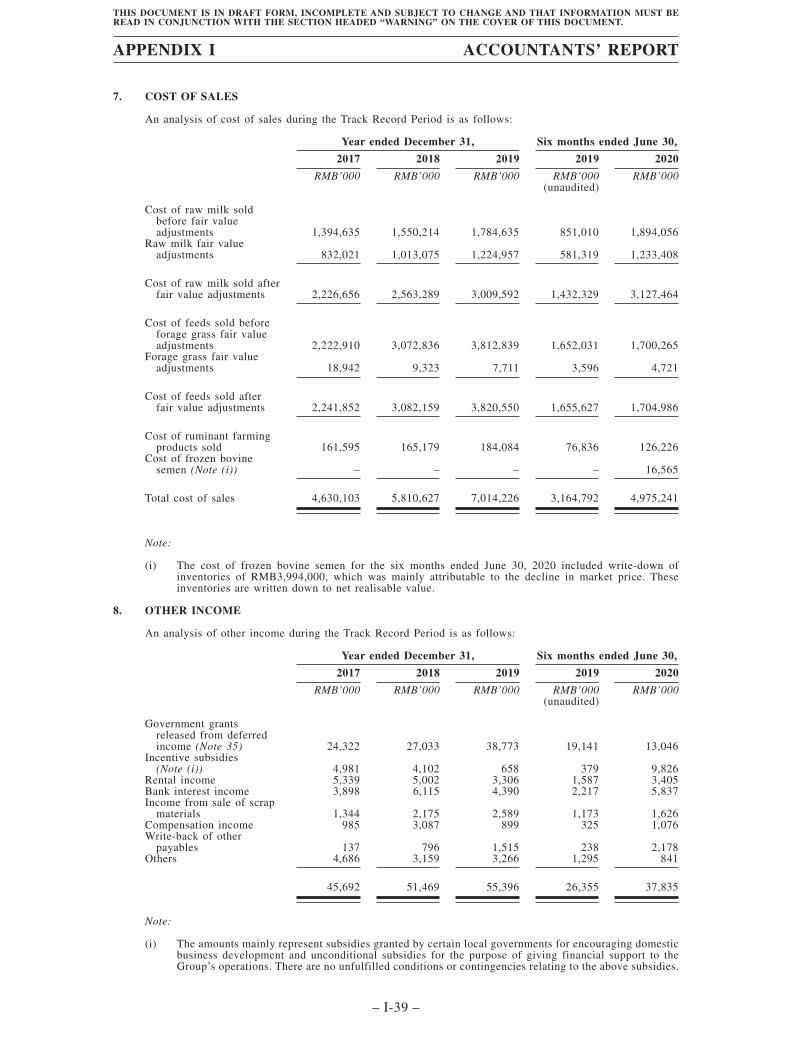

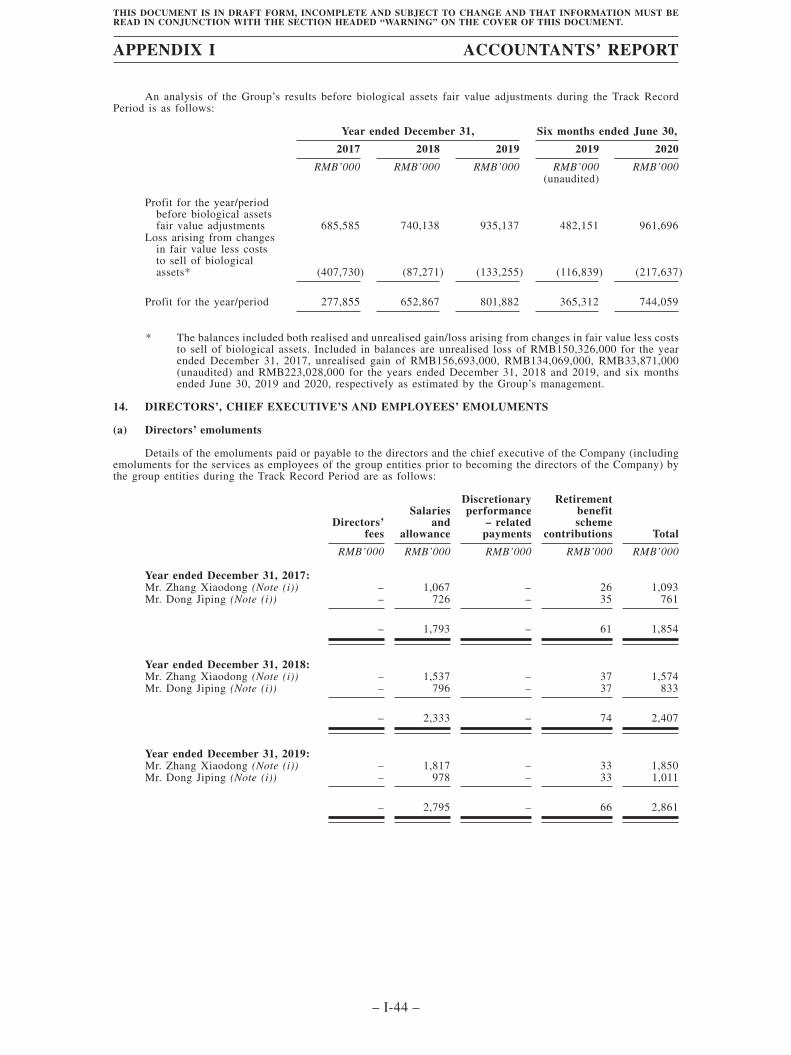

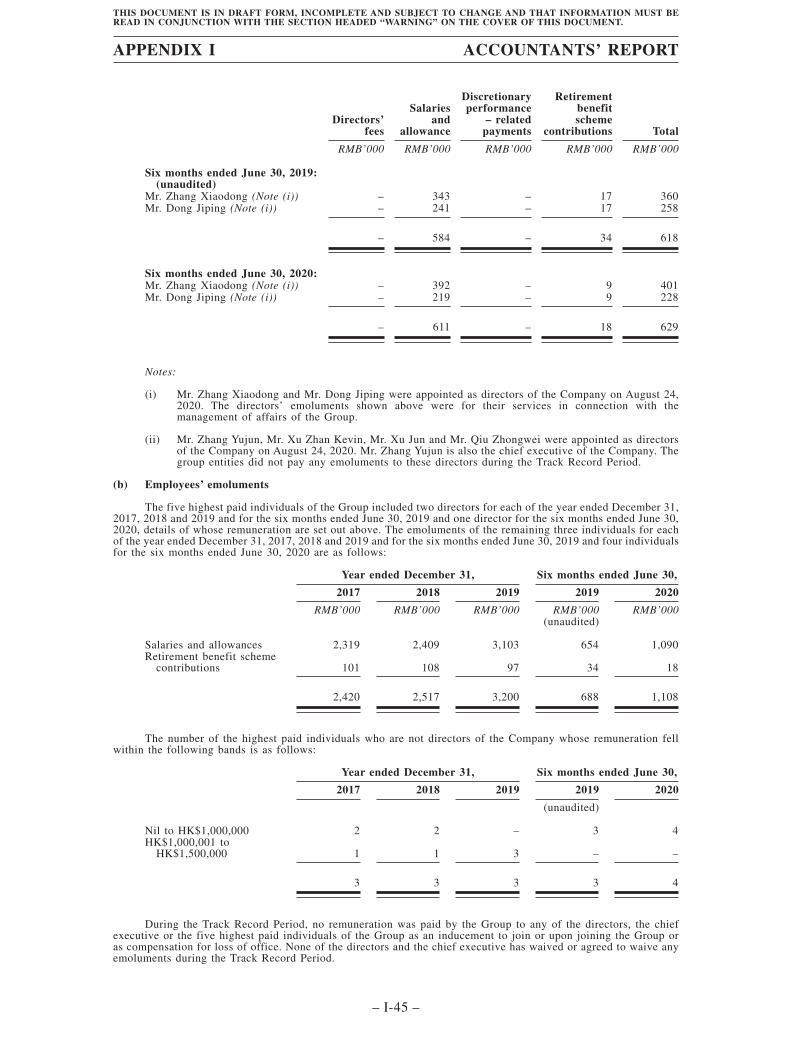

COMBINED STATEMENTS OF PROFIT OR LOSS AND OTHER COMPREHENSIVEINCOME

Year ended December 31,Six months ended

June 30,NOTES 2017 2018 2019 2019 2020

RMB’000 RMB’000 RMB’000 RMB’000 RMB’000(unaudited)

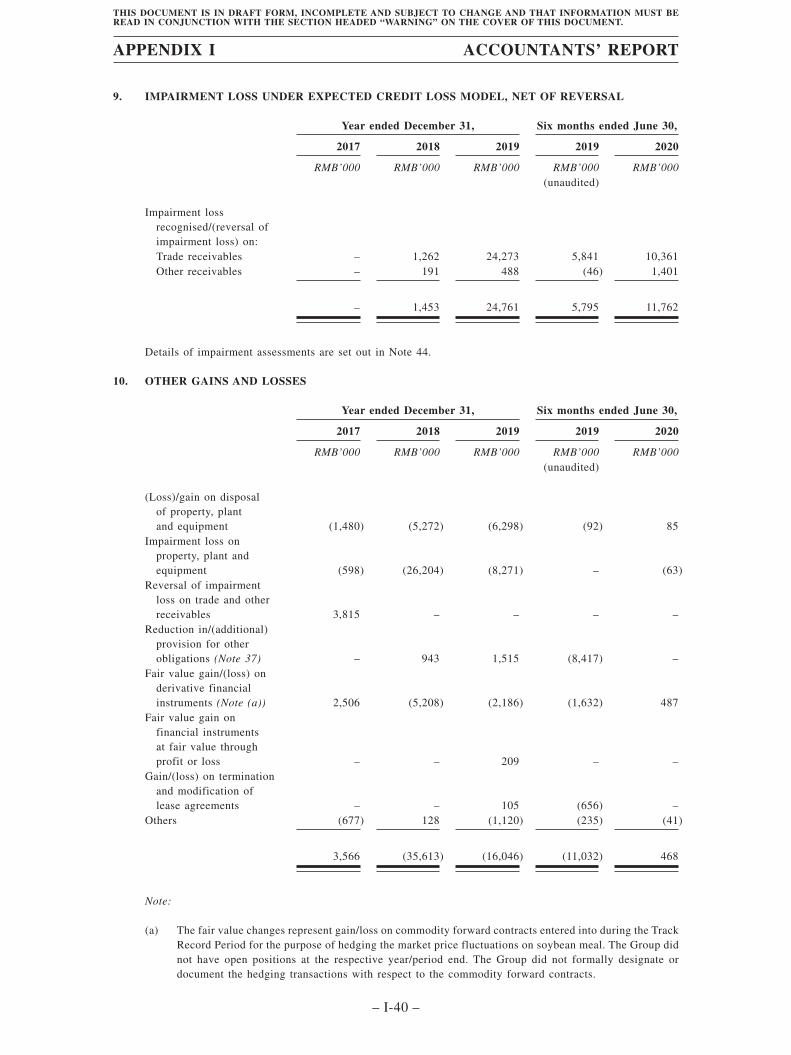

Revenue 6 5,091,445 6,333,920 7,667,818 3,436,842 5,344,427Cost of sales 7 (4,630,103) (5,810,627) (7,014,226) (3,164,792) (4,975,241)Gains arising on initial recognition of agricultural produce at fair

value less costs to sell at the point of harvest 22 850,963 1,022,398 1,232,668 584,915 1,238,129

Gross profit 1,312,305 1,545,691 1,886,260 856,965 1,607,315Loss arising from changes in fair value less costs to sell of

biological assets 22 (407,730) (87,271) (133,255) (116,839) (217,637)Other income 8 45,692 51,469 55,396 26,355 37,835Impairment loss under expected credit loss model,

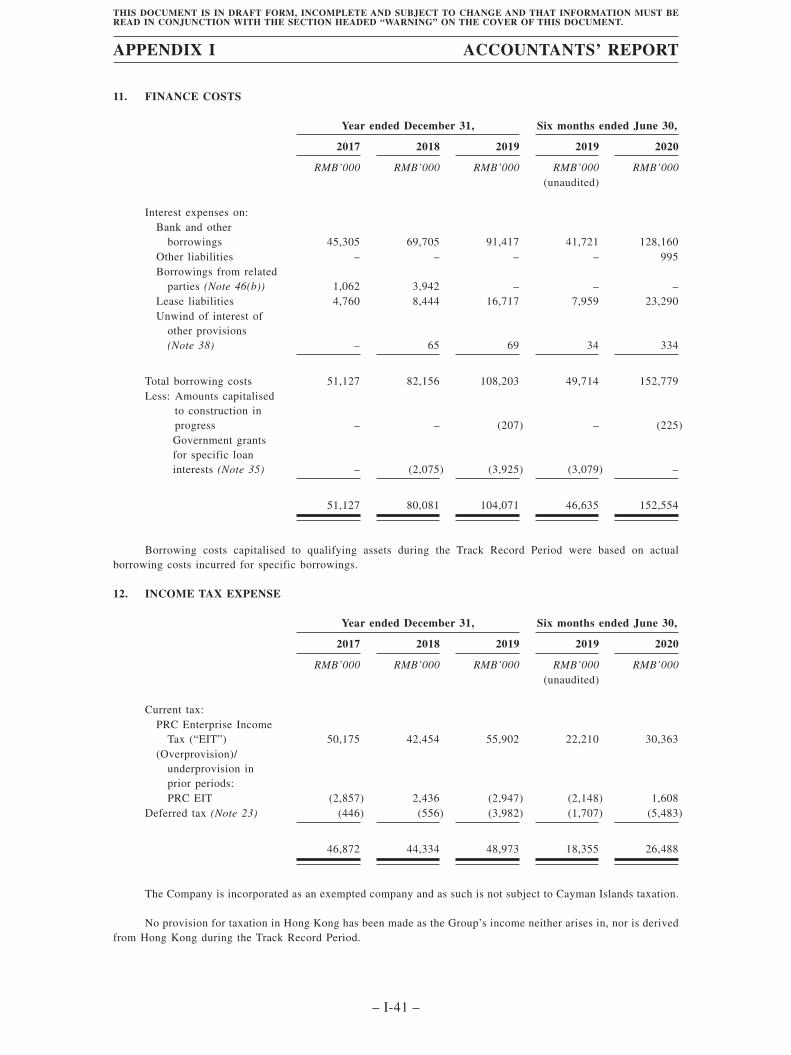

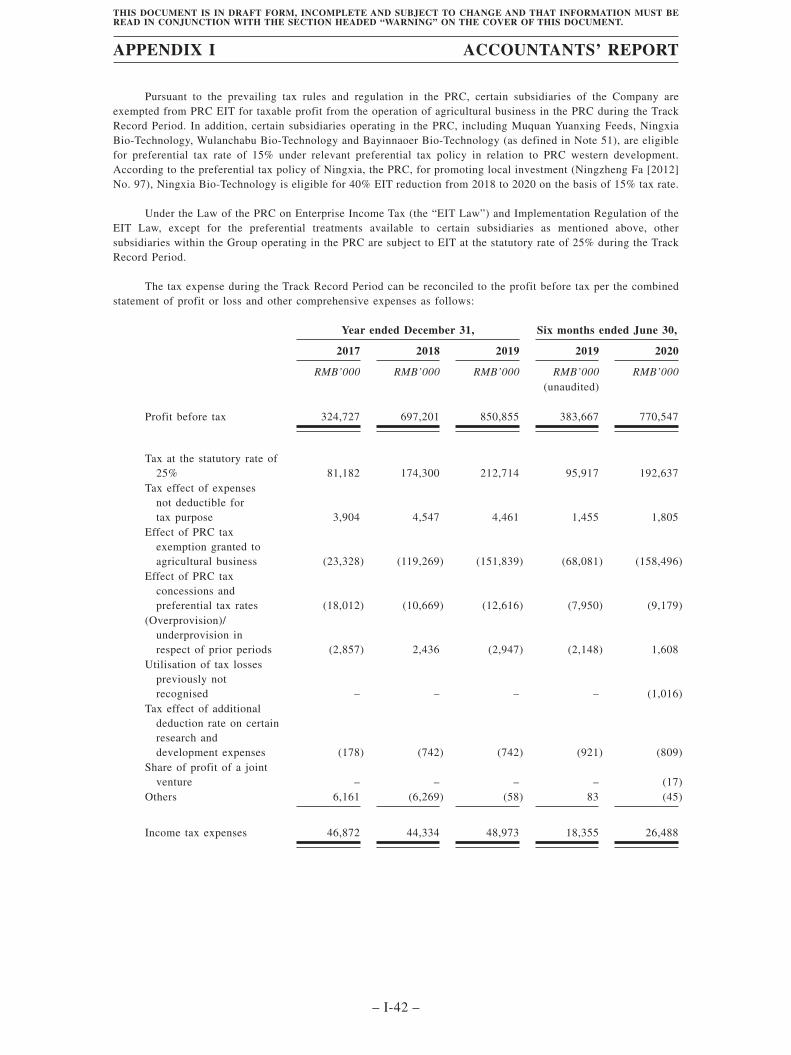

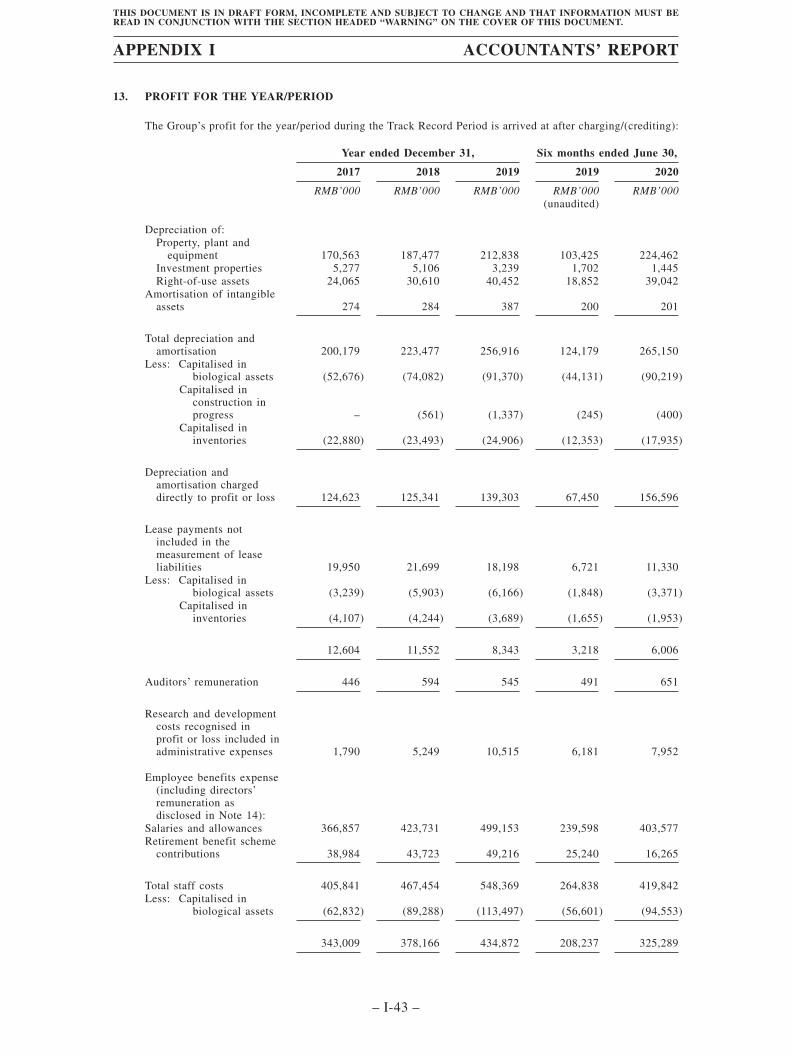

net of reversal 9 – (1,453) (24,761) (5,795) (11,762)Other gains and losses 10 3,566 (35,613) (16,046) (11,032) 468Selling and distribution expenses (210,019) (271,932) (340,687) (144,498) (206,302)Administrative expenses (359,500) (421,298) (445,453) (173,727) (270,333)Other expenses (8,460) (2,311) (26,528) (1,127) (6,224)[REDACTED] expenses – – – – (10,328)Share of profit of a joint venture – – – – 69Finance costs 11 (51,127) (80,081) (104,071) (46,635) (152,554)

Profit before tax 324,727 697,201 850,855 383,667 770,547Income tax expense 12 (46,872) (44,334) (48,973) (18,355) (26,488)

Profit for the year/period 13 277,855 652,867 801,882 365,312 744,059

Other comprehensive income, net of income taxItems that will not be reclassified to profit or lossFair value gain on investments in equity instruments at fair value

though other comprehensive income – – – – 8,825Items that may be reclassified subsequently to profit or lossExchange differences arising on translation of foreign operations – – – – 12

Other comprehensive income for the year/period, net of incometax – – – – 8,837

Total comprehensive income for the year/period 277,855 652,867 801,882 365,312 752,896

Profit for the year/period attributable to:Owners of the Company 277,855 652,867 801,882 365,312 731,249Non-controlling interests – – – – 12,810

277,855 652,867 801,882 365,312 744,059

Total comprehensive income for the year/period attributable to:Owners of the Company 277,855 652,867 801,882 365,312 736,406Non-controlling interests – – – – 16,490

277,855 652,867 801,882 365,312 752,896

APPENDIX I ACCOUNTANTS’ REPORT

– I-5 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

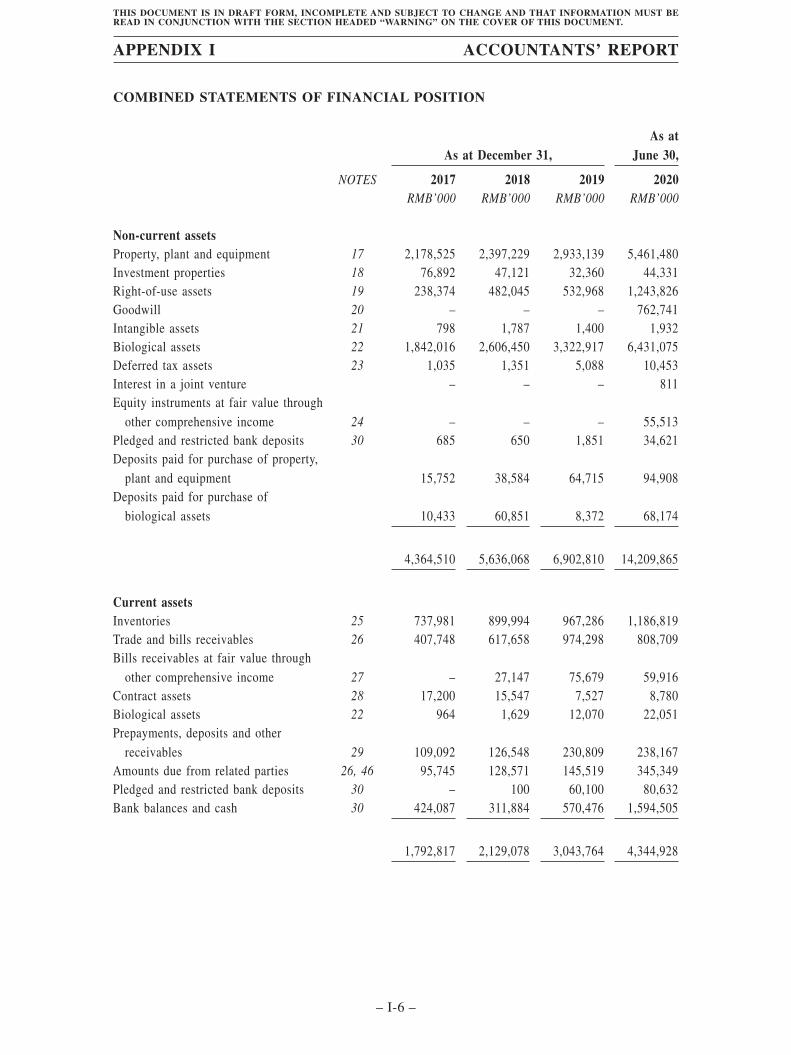

COMBINED STATEMENTS OF FINANCIAL POSITION

As at December 31,As at

June 30,

NOTES 2017 2018 2019 2020RMB’000 RMB’000 RMB’000 RMB’000

Non-current assetsProperty, plant and equipment 17 2,178,525 2,397,229 2,933,139 5,461,480Investment properties 18 76,892 47,121 32,360 44,331Right-of-use assets 19 238,374 482,045 532,968 1,243,826Goodwill 20 – – – 762,741Intangible assets 21 798 1,787 1,400 1,932Biological assets 22 1,842,016 2,606,450 3,322,917 6,431,075Deferred tax assets 23 1,035 1,351 5,088 10,453Interest in a joint venture – – – 811Equity instruments at fair value through

other comprehensive income 24 – – – 55,513Pledged and restricted bank deposits 30 685 650 1,851 34,621Deposits paid for purchase of property,

plant and equipment 15,752 38,584 64,715 94,908Deposits paid for purchase of

biological assets 10,433 60,851 8,372 68,174

4,364,510 5,636,068 6,902,810 14,209,865

Current assetsInventories 25 737,981 899,994 967,286 1,186,819Trade and bills receivables 26 407,748 617,658 974,298 808,709Bills receivables at fair value through

other comprehensive income 27 – 27,147 75,679 59,916Contract assets 28 17,200 15,547 7,527 8,780Biological assets 22 964 1,629 12,070 22,051Prepayments, deposits and other

receivables 29 109,092 126,548 230,809 238,167Amounts due from related parties 26, 46 95,745 128,571 145,519 345,349Pledged and restricted bank deposits 30 – 100 60,100 80,632Bank balances and cash 30 424,087 311,884 570,476 1,594,505

1,792,817 2,129,078 3,043,764 4,344,928

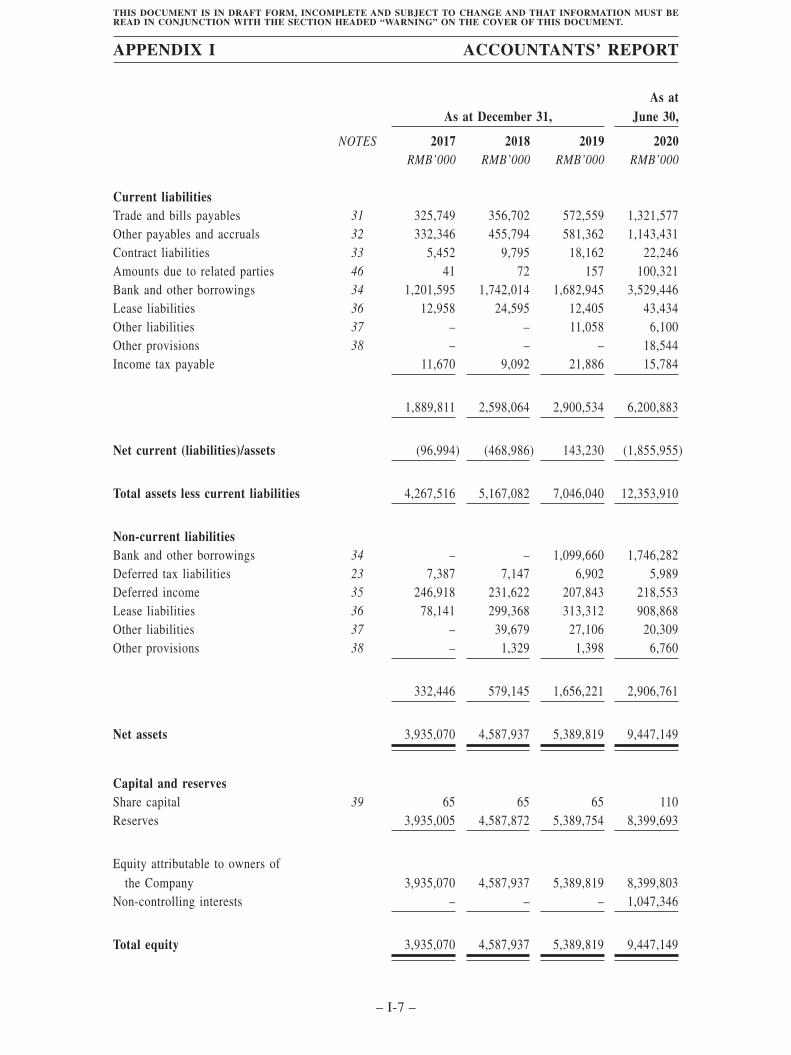

APPENDIX I ACCOUNTANTS’ REPORT

– I-6 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

As at December 31,As at

June 30,

NOTES 2017 2018 2019 2020RMB’000 RMB’000 RMB’000 RMB’000

Current liabilitiesTrade and bills payables 31 325,749 356,702 572,559 1,321,577Other payables and accruals 32 332,346 455,794 581,362 1,143,431Contract liabilities 33 5,452 9,795 18,162 22,246Amounts due to related parties 46 41 72 157 100,321Bank and other borrowings 34 1,201,595 1,742,014 1,682,945 3,529,446Lease liabilities 36 12,958 24,595 12,405 43,434Other liabilities 37 – – 11,058 6,100Other provisions 38 – – – 18,544Income tax payable 11,670 9,092 21,886 15,784

1,889,811 2,598,064 2,900,534 6,200,883

Net current (liabilities)/assets (96,994) (468,986) 143,230 (1,855,955)

Total assets less current liabilities 4,267,516 5,167,082 7,046,040 12,353,910

Non-current liabilitiesBank and other borrowings 34 – – 1,099,660 1,746,282Deferred tax liabilities 23 7,387 7,147 6,902 5,989Deferred income 35 246,918 231,622 207,843 218,553Lease liabilities 36 78,141 299,368 313,312 908,868Other liabilities 37 – 39,679 27,106 20,309Other provisions 38 – 1,329 1,398 6,760

332,446 579,145 1,656,221 2,906,761

Net assets 3,935,070 4,587,937 5,389,819 9,447,149

Capital and reservesShare capital 39 65 65 65 110Reserves 3,935,005 4,587,872 5,389,754 8,399,693

Equity attributable to owners ofthe Company 3,935,070 4,587,937 5,389,819 8,399,803

Non-controlling interests – – – 1,047,346

Total equity 3,935,070 4,587,937 5,389,819 9,447,149

APPENDIX I ACCOUNTANTS’ REPORT

– I-7 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

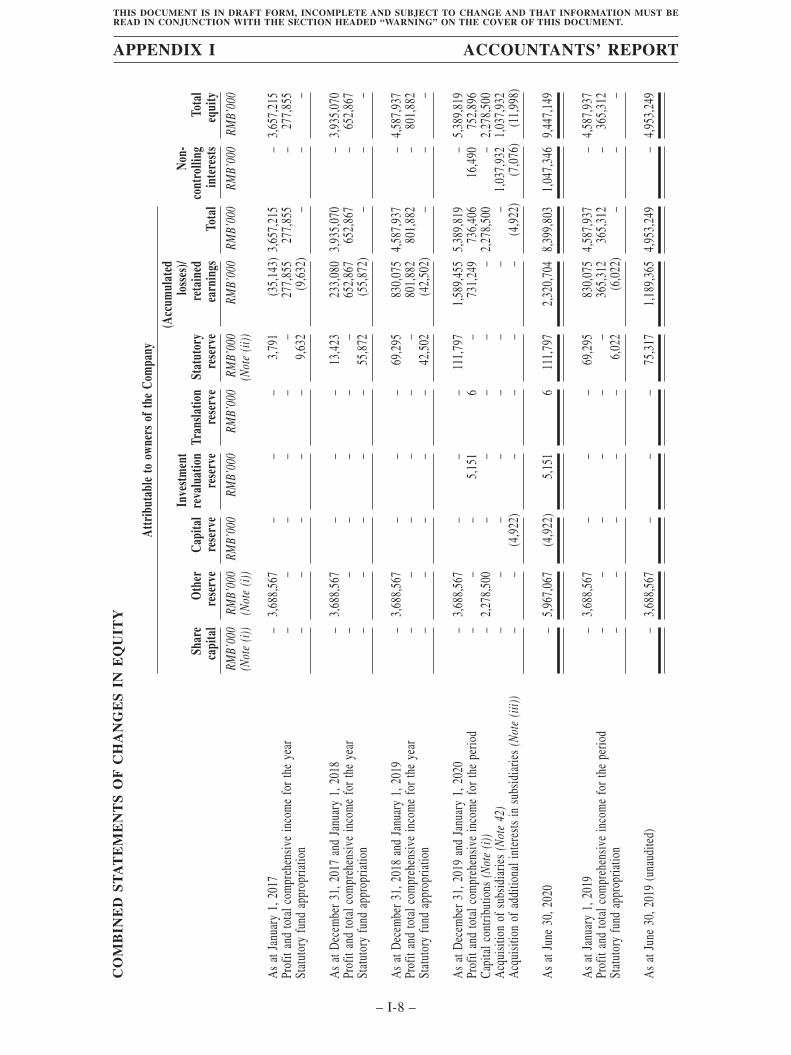

CO

MB

INE

DS

TA

TE

ME

NT

SO

FC

HA

NG

ES

INE

QU

ITY

Attr

ibut

able

toow

ners

ofth

eCo

mpa

ny

Shar

eca

pita

lO

ther

rese

rve

Capi

tal

rese

rve

Inve

stm

ent

reva

luat

ion

rese

rve

Tran

slatio

nre

serv

eSt

atut

ory

rese

rve

(Acc

umul

ated

loss

es)/

reta

ined

earn

ings

Tota

l

Non-

cont

rolli

ngin

tere

sts

Tota

leq

uity

RMB’

000

RMB’

000

RMB’

000

RMB’

000

RMB’

000

RMB’

000

RMB’

000

RMB’

000

RMB’

000

RMB’

000

(Not

e(i)

)(N

ote

(i))

(Not

e(ii

))

As

atJa

nuar

y1,

2017

–3,

688,

567

––

–3,

791

(35,

143)

3,65

7,21

5–

3,65

7,21

5Pr

ofit

and

tota

lcom

preh

ensiv

ein

com

efo

rthe

year

––

––

––

277,

855

277,

855

–27

7,85

5St

atut

ory

fund

appr

opria

tion

––

––

–9,

632

(9,6

32)

––

–

As

atD

ecem

ber3

1,20

17an

dJa

nuar

y1,

2018

–3,

688,

567

––

–13

,423

233,

080

3,93

5,07

0–

3,93

5,07

0Pr

ofit

and

tota

lcom

preh

ensiv

ein

com

efo

rthe

year

––

––

––

652,

867

652,

867

–65

2,86

7St

atut

ory

fund

appr

opria

tion

––

––

–55

,872

(55,

872)

––

–

As

atD

ecem

ber3

1,20

18an

dJa

nuar

y1,

2019

–3,

688,

567

––

–69

,295

830,

075

4,58

7,93

7–

4,58

7,93

7Pr

ofit

and

tota

lcom

preh

ensiv

ein

com

efo

rthe

year

––

––

––

801,

882

801,

882

–80

1,88

2St

atut

ory

fund

appr

opria

tion

––

––

–42

,502

(42,

502)

––

–

As

atD

ecem

ber3

1,20

19an

dJa

nuar

y1,

2020

–3,

688,

567

––

–11

1,79

71,

589,

455

5,38

9,81

9–

5,38

9,81

9Pr

ofit

and

tota

lcom

preh

ensiv

ein

com

efo

rthe

perio

d–

––

5,15

16

–73

1,24

973

6,40

616

,490

752,

896

Capi

talc

ontri

butio

ns(N

ote

(i))

–2,

278,

500

––

––

–2,

278,

500

–2,

278,

500

Acq

uisit

ion

ofsu

bsid

iarie

s(N

ote

42)

––

––

––

––

1,03

7,93

21,

037,

932

Acq

uisit

ion

ofad

ditio

nali

nter

ests

insu

bsid

iarie

s(N

ote

(iii))

––

(4,9

22)

––

––

(4,9

22)

(7,0

76)

(11,

998)

As

atJu

ne30

,202

0–

5,96

7,06

7(4

,922

)5,

151

611

1,79

72,

320,

704

8,39

9,80

31,

047,

346

9,44

7,14

9

As

atJa

nuar

y1,

2019

–3,

688,

567

––

–69

,295

830,

075

4,58

7,93

7–

4,58

7,93

7Pr

ofit

and

tota

lcom

preh

ensiv

ein

com

efo

rthe

perio

d–

––

––

–36

5,31

236

5,31

2–

365,

312

Stat

utor

yfu

ndap

prop

riatio

n–

––

––

6,02

2(6

,022

)–

––

As

atJu

ne30

,201

9(u

naud

ited)

–3,

688,

567

––

–75

,317

1,18

9,36

54,

953,

249

–4,

953,

249

APPENDIX I ACCOUNTANTS’ REPORT

– I-8 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

Notes:

(i) Share capital as at December 31, 2017, 2018 and 2019 and June 30, 2020 represents the issued share capitalof Youran BVI, the then holding company of the subsidiaries now comprising the Group, prior to theReorganisation as defined in Note 2. Other reserve as at December 31, 2017, 2018 and 2019 and June 30, 2020represents amounts due to China Youran Dairy Holding Limited (“Youran Holding”), the then immediateholding company of Youran BVI. During the six months ended June 30, 2020, Youran Holding advancedRMB2,278,500,000 to Youran BVI for the purpose of the acquisition of SKX Group (as defined in Note 42).Upon the completion of the Reorganisation, these amounts will be eliminated against the interests insubsidiaries recorded by the Company, and in substance represent capital contribution to the Group.

(ii) The amount mainly represents statutory reserve fund. According to the relevant laws in the People’s Republicof China (the “PRC”), each of the subsidiaries established in the PRC is required to allocate at least 10% ofits profit after tax as per financial statements prepared in accordance with the relevant PRC accountingstandards to statutory reserve fund until the reserve fund reaches 50% of the registered capital of respectivesubsidiary. The transfer to this fund must be made before the distribution of dividend to the equity owners. Thestatutory reserve fund can be used to make up previous years’ losses, if any. The statutory reserve fund isnon-distributable other than upon liquidation.

(iii) The difference between the consideration of the acquisition of non-controlling interests and the carryingamount of non-controlling interests of RMB4,922,000 has been debited to capital reserve.

APPENDIX I ACCOUNTANTS’ REPORT

– I-9 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

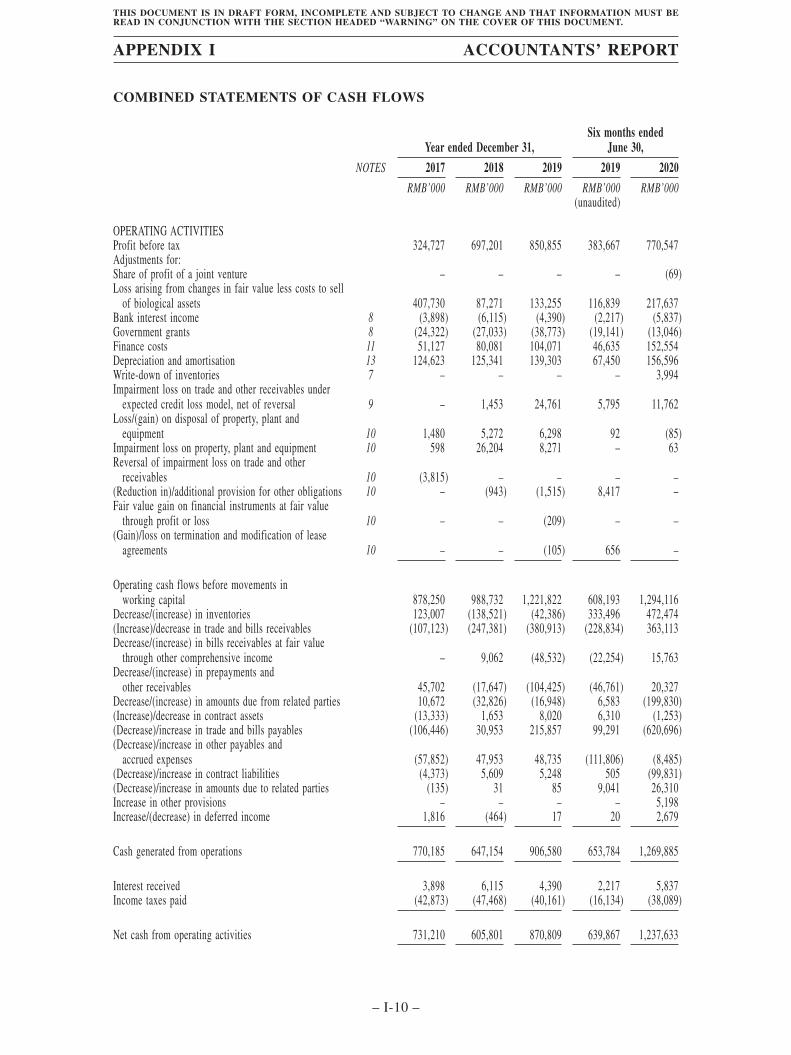

COMBINED STATEMENTS OF CASH FLOWS

Year ended December 31,Six months ended

June 30,

NOTES 2017 2018 2019 2019 2020

RMB’000 RMB’000 RMB’000 RMB’000 RMB’000(unaudited)

OPERATING ACTIVITIESProfit before tax 324,727 697,201 850,855 383,667 770,547Adjustments for:Share of profit of a joint venture – – – – (69)Loss arising from changes in fair value less costs to sell

of biological assets 407,730 87,271 133,255 116,839 217,637Bank interest income 8 (3,898) (6,115) (4,390) (2,217) (5,837)Government grants 8 (24,322) (27,033) (38,773) (19,141) (13,046)Finance costs 11 51,127 80,081 104,071 46,635 152,554Depreciation and amortisation 13 124,623 125,341 139,303 67,450 156,596Write-down of inventories 7 – – – – 3,994Impairment loss on trade and other receivables under

expected credit loss model, net of reversal 9 – 1,453 24,761 5,795 11,762Loss/(gain) on disposal of property, plant and

equipment 10 1,480 5,272 6,298 92 (85)Impairment loss on property, plant and equipment 10 598 26,204 8,271 – 63Reversal of impairment loss on trade and other

receivables 10 (3,815) – – – –(Reduction in)/additional provision for other obligations 10 – (943) (1,515) 8,417 –Fair value gain on financial instruments at fair value

through profit or loss 10 – – (209) – –(Gain)/loss on termination and modification of lease

agreements 10 – – (105) 656 –

Operating cash flows before movements inworking capital 878,250 988,732 1,221,822 608,193 1,294,116

Decrease/(increase) in inventories 123,007 (138,521) (42,386) 333,496 472,474(Increase)/decrease in trade and bills receivables (107,123) (247,381) (380,913) (228,834) 363,113Decrease/(increase) in bills receivables at fair value

through other comprehensive income – 9,062 (48,532) (22,254) 15,763Decrease/(increase) in prepayments and

other receivables 45,702 (17,647) (104,425) (46,761) 20,327Decrease/(increase) in amounts due from related parties 10,672 (32,826) (16,948) 6,583 (199,830)(Increase)/decrease in contract assets (13,333) 1,653 8,020 6,310 (1,253)(Decrease)/increase in trade and bills payables (106,446) 30,953 215,857 99,291 (620,696)(Decrease)/increase in other payables and

accrued expenses (57,852) 47,953 48,735 (111,806) (8,485)(Decrease)/increase in contract liabilities (4,373) 5,609 5,248 505 (99,831)(Decrease)/increase in amounts due to related parties (135) 31 85 9,041 26,310Increase in other provisions – – – – 5,198Increase/(decrease) in deferred income 1,816 (464) 17 20 2,679

Cash generated from operations 770,185 647,154 906,580 653,784 1,269,885

Interest received 3,898 6,115 4,390 2,217 5,837Income taxes paid (42,873) (47,468) (40,161) (16,134) (38,089)

Net cash from operating activities 731,210 605,801 870,809 639,867 1,237,633

APPENDIX I ACCOUNTANTS’ REPORT

– I-10 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

Year ended December 31,Six months ended

June 30,

NOTES 2017 2018 2019 2019 2020

RMB’000 RMB’000 RMB’000 RMB’000 RMB’000(unaudited)

INVESTING ACTIVITIESPayments for property, plant and equipment (315,679) (359,797) (726,473) (311,691) (622,010)Payments for right-of-use assets (3,323) (781) (19,409) (15,368) (7,841)Payments for intangible assets – (1,273) – – –Proceeds from disposal of property, plant and equipment 32 31 10,713 7,539 3,689Payments for biological assets (663,449) (979,480) (1,041,405) (479,674) (957,944)Proceeds from disposal of biological assets 179,095 190,130 328,210 159,362 408,758Payments for financial assets at fair value through

profit or loss – – (56,000) – –Proceeds from disposal of financial assets at fair value

through profit or loss – – 56,209 – –Acquisitions of subsidiaries 42 – – – – (1,546,430)Placement of pledged and restricted bank deposits – (65) (61,201) (61,201) (91,029)Withdrawal of pledged and restricted bank deposits – – – – 62,724Receipt of government grants for assets 104,607 8,276 18,902 5,978 21,077

Net cash used in investing activities (698,717) (1,142,959) (1,490,454) (695,055) (2,729,006)

FINANCING ACTIVITIESNew bank and other borrowings raised 1,400,000 2,640,000 3,115,707 1,150,897 3,993,968Repayments of bank and other borrowings (1,040,000) (2,100,000) (2,078,860) (800,000) (3,547,945)Interest paid (45,889) (73,228) (87,673) (41,614) (131,214)Repayment of lease liabilities (12,654) (39,373) (54,220) (28,047) (32,062)Interest paid for lease liabilities (4,760) (8,444) (16,717) (7,959) (23,290)Repayment of other liabilities – – – – (11,755)Receipt of interest subsidies – 6,000 – – –Capital contribution by the then holding company – – – – 2,278,500Acquisition of additional interests in subsidiaries – – – – (10,800)

Net cash from financing activities 296,697 424,955 878,237 273,277 2,515,402

Net increase/(decrease) in cash and cash equivalents 329,190 (112,203) 258,592 218,089 1,024,029Cash and cash equivalents at beginning of the

year/period 94,897 424,087 311,884 311,884 570,476

Cash and cash equivalents at end of the year/period,represented by bank balances and cash 424,087 311,884 570,476 529,973 1,594,505

APPENDIX I ACCOUNTANTS’ REPORT

– I-11 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

II. NOTES TO THE HISTORICAL FINANCIAL INFORMATION OF THE GROUP

1. GENERAL

China Youran Dairy Group Limited (the “Company”) was incorporated in the Cayman Islands on August 21,2020 as an exempted company with limited liability under the Companies Law (Cap. 22, Law 3 of 1961 asconsolidated and revised) of the Cayman Islands. The address of the Company’s registered office is at the offices ofOgier Global (Cayman) Limited, 89 Nexus Way, Camana Bay, Grand Cayman KY1-9009, Cayman Islands. Theprincipal place of business of the Company is No. 169, Hexi Road, Saihan District Hohhot, Inner Mongolia, the PRC.

The Company is an investment holding company and has not carried out any business operations since the dateof incorporation save for the corporate reorganisation mentioned below. The Company and its subsidiaries (together,the “Group”) is primarily engaged in the production and sale of raw milk, and the trading, production and sale ofdairy farming products in the PRC.

The functional currency of the Company is RMB, which is the same as the presentation currency of theHistorical Financial Information.

2. GROUP REORGANISATION AND BASIS OF PRESENTATION AND PREPARATION OF THEHISTORICAL FINANCIAL INFORMATION

Throughout the Track Record Period, the Group’s operations were conducted by the existing group of entitiesheld by China Youran Dairy Holding Limited (“Youran Holding”), a company incorporated in the Cayman Islandsand the then holding company of all subsidiaries now comprising the Group.

In preparation for the [REDACTED] of the shares of the Company on the [REDACTED] of The StockExchange of Hong Kong Limited (the “Stock Exchange”), the entities now comprising the Group underwent a groupreorganisation (the “Reorganisation”) which involves major steps as follows:

(a) On August 21, 2020, the Company was incorporated as an exempted company with limited liabilityunder the laws of Cayman Islands with an authorised share capital of US$100,000 divided into10,000,000,000 ordinary shares of US$0.00001 each.

(b) On October 27, 2020, Youran Holding and the Company entered into an instrument of transfer, pursuantto which Youran Holding transferred the entirety of its 100 ordinary shares in Youran BVI to theCompany in consideration for the issuance and allotment of 3,302,000,000 ordinary shares with a parvalue of US$0.00001 by the Company, and the Company became a wholly-owned subsidiary of YouranHolding.

Pursuant to the Reorganisation detailed above, which was completed by interspersing the Company betweenYouran Holding and the Company, the Company has become the holding company of the companies now comprisingthe Group on October 27, 2020.

The Group comprising the Company and its subsidiaries resulting from the Reorganisation is regarded as acontinuing entity, accordingly, the Historical Financial Information has been prepared as if the Company had alwaysbeen the holding company of the Group.

The combined statements of profit or loss and other comprehensive income, combined statements of changesin equity and combined statements of cash flows of the Group for the Track Record Period include the results andcash flows of the companies now comprising the Group as if the current group structure had been in existencethroughout the Track Record Period or since the date of incorporation, where this is a shorter period.

The combined statements of financial position of the Group as at December 31, 2017, 2018 and 2019 and June30, 2020 have been prepared to present the assets and liabilities of the companies now comprising the Group as ifthe current group structure had been in existence at those dates, taking into account the respective dates ofincorporation, where applicable.

APPENDIX I ACCOUNTANTS’ REPORT

– I-12 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

3. APPLICATION OF INTERNATIONAL FINANCIAL REPORTING STANDARDS

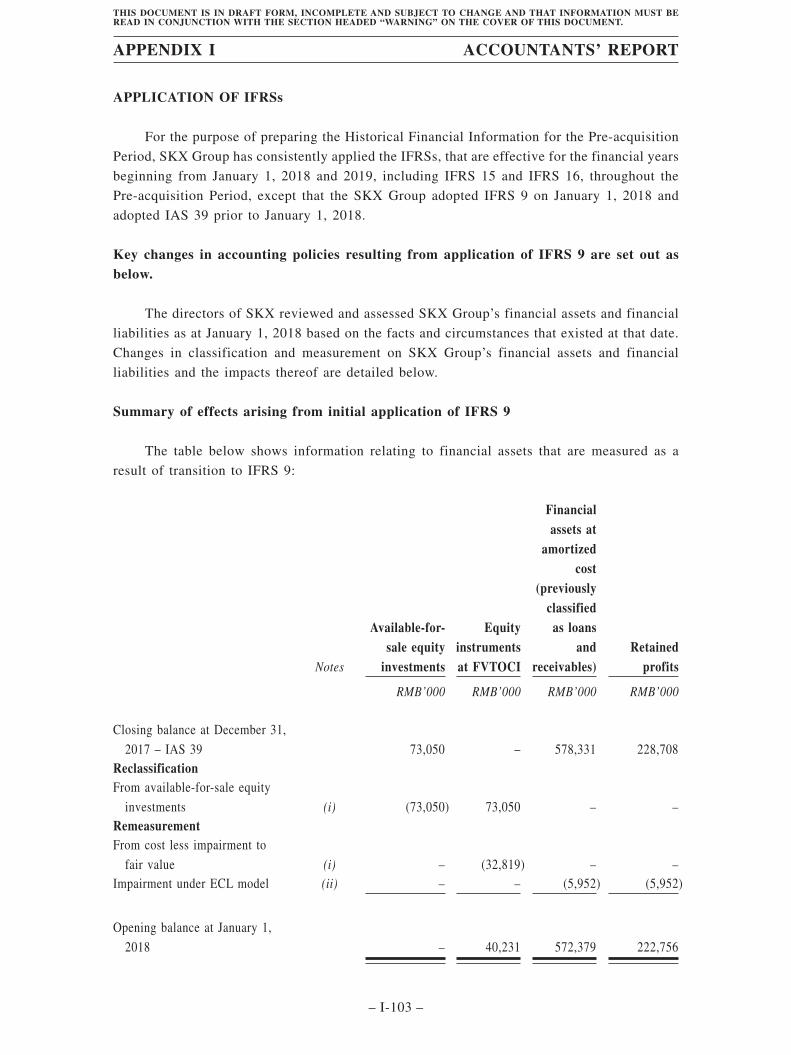

For the purpose of preparing and presenting the Historical Financial Information for the Track Record Period,the Group has consistently applied the accounting policies which conform with the IFRSs, which are effective for theGroup’s accounting period beginning on January 1, 2020 throughout the Track Record Period, including IFRS 15Revenue from Contracts with Customers and IFRS 16 Leases, except that the Group adopted IFRS 9 FinancialInstruments on January 1, 2018 and International Accounting Standard (“IAS”) 39 Financial Instruments:Recognition and Measurement prior to January 1, 2018, and amendments to IFRS 9 Prepayment Features withNegative Compensation on January 1, 2019.

IFRS 9 Financial Instruments

On January 1, 2018, the Group has applied IFRS 9 and the related consequential amendments to other IFRSs.IFRS 9 introduces new requirements for 1) the classification and measurement of financial assets and financialliabilities; 2) expected credit losses (“ECL”) for financial assets and other items (for example, contract assets) thatare subject to the impairment provisions; and 3) general hedge accounting.

The Group has applied IFRS 9 in accordance with the transition provisions set out in IFRS 9, i.e. applied theclassification and measurement requirements (including impairment under ECL model) retrospectively to instrumentsthat have not been derecognised as at January 1, 2018 (date of initial application) and has not applied the requirementto instruments that have already been derecognised as at January 1, 2018. Accordingly, certain financial informationfor the year ended December 31, 2017 may not be comparable as the information was prepared under IAS 39. Keyrequirements of IFRS 9 which are relevant to the Group are:

• all recognised financial assets that are within the scope of IFRS 9 are required to be subsequentlymeasured at amortised cost or fair value. Specifically, debt investments that are held within a businessmodel whose objective is to collect the contractual cash flows, and that have contractual cash flows thatare solely payments of principal and interest on the principal amount outstanding are generally measuredat amortised cost at the end of subsequent accounting periods. All other debt investments and equityinvestments are measured at their fair value at the end of subsequent accounting periods.

• in relation to the impairment of financial assets, IFRS 9 requires an ECL model, as opposed to anincurred credit loss model under IAS 39. The ECL model requires an entity to account for ECL andchanges in those ECLs at each reporting date to reflect changes in credit risk since initial recognition.In other words, it is no longer necessary for a credit event to have occurred before credit losses arerecognised.

Accounting policies resulting from application of IFRS 9 are disclosed in Note 4.

Summary of effects arising from initial application of IFRS 9

The table below illustrates the classification and measurement of financial assets and other items subject toECL under IFRS 9 and IAS 39 at the date of initial application, January 1, 2018.

Bills receivablesstated at

amortised cost(previously

classified as loansand receivables)

Bills receivablesat fair value

through othercomprehensive

income

RMB’000 RMB’000

Closing balance at December 31, 2017 – IAS 39 36,209 –Effect arising from initial application of IFRS 9:Reclassification and remeasurement of bills receivables from

amortised cost to fair value (Note (a)) (36,209) 36,209

Opening balance at January 1, 2018 – 36,209

The Group has applied IFRS 9 in accordance with the transition provisions set out in IFRS 9, i.e. applied theclassification and measurement requirements (including impairment under ECL model) retrospectively to instrumentsthat have not been derecognised as at January 1, 2018 and has not applied the requirements to instruments that havealready been derecognised as at January 1, 2018. There is no impact on the opening retained earnings as at January1, 2018 upon the application of IFRS 9.

APPENDIX I ACCOUNTANTS’ REPORT

– I-13 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

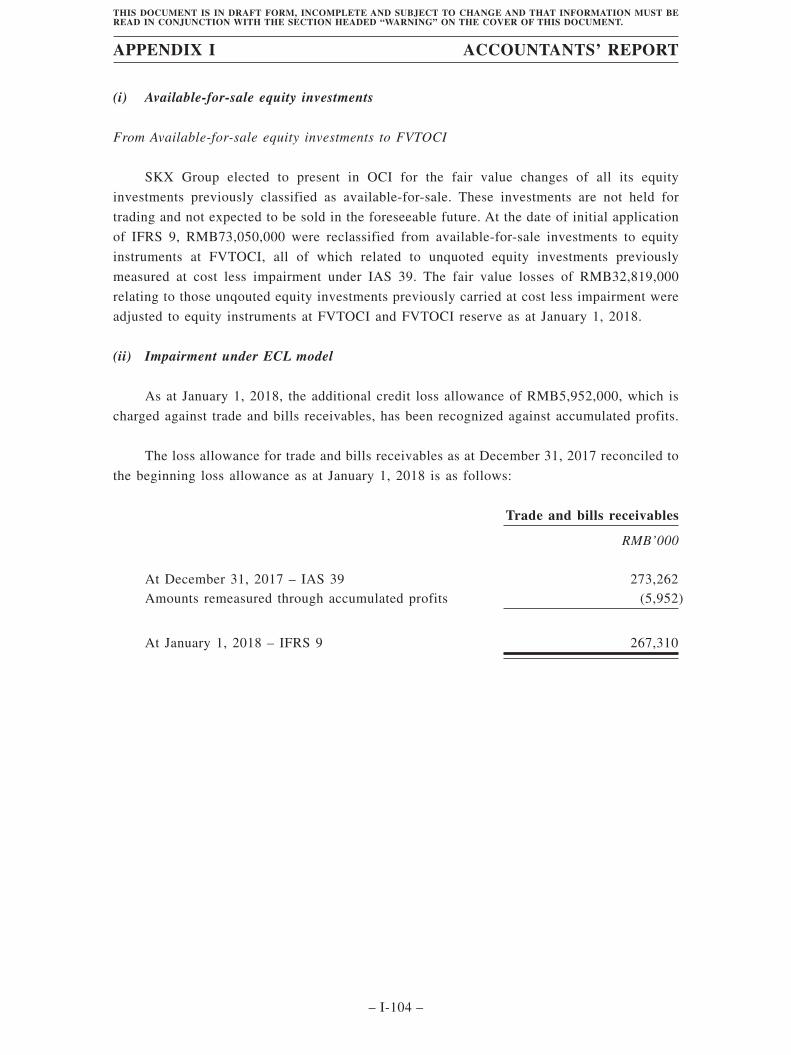

Notes:

(a) Bills receivables

As part of the Group’s cash flow management, the Group has the practice of discounting some of thebills received from debtors to financial institutions before the bills are due for payment and derecognisesbills discounted on the basis that the Group has transferred substantially all risks and rewards to therelevant counterparties. Accordingly, the Group’s bills receivables of RMB36,209,000 were consideredas within the hold to collect contractual cash flows and to sell business model, and reclassified to debtinstruments at fair value through other comprehensive income (“FVTOCI”) as at January 1, 2018. Therelated fair value changes are minimal.

(b) Impairment under ECL model

The application of the ECL model of IFRS 9 on January 1, 2018 resulted in earlier provision of creditlosses which are not yet incurred in relation to the Group’s financial assets measured at amortised cost,debt instruments at FVTOCI and other items (for example, contract assets) that subject to theimpairment provisions.

The Group applies the IFRS 9 simplified approach to measure ECL which uses a lifetime ECL for alltrade receivables and contract assets. To measure the ECL, trade receivables and contract assets havebeen grouped based on shared credit risk characteristics and debtors’ aging except for those which hadbeen determined as credit impaired under IAS 39 and those with significant outstanding balances whichhave been assessed individually.

Loss allowances other financial assets at amortised cost which mainly comprise of bank balances,pledged and restricted bank deposits, deposits and other receivables, amounts due from related partiesand bills receivables at fair value through other comprehensive income are measured on 12-month ECLbasis and there had been no significant increase in credit risk since initial recognition, except for certainother receivables which are measured as lifetime ECL basis as those credit risk had increasedsignificantly since initial recognition.

No additional loss allowance is charged against the respective assets as at January 1, 2018 upon theapplication of IFRS 9.

New or revised IFRSs in issued but not yet effective

At the date of this report, the following new and amendments to IFRSs have been issued but are not yeteffective:

IFRS 17 Insurance Contracts1

Amendments to IFRS 16 COVID-19-Related Rent Concessions4

Amendments to IFRS 3 Reference to the Conceptual Framework3

Amendments to IFRS 10 and IAS 28 Sale or Contribution of Assets between an Investor and itsAssociate or Joint Venture2

Amendments to IAS 1 Classification of Liabilities as Current or Non-current1

Amendments to IAS 16 Property, Plant and Equipment: Proceeds before Intended Use3

Amendments to IAS 37 Onerous Contracts – Cost of Fulfilling a Contract3

Amendments to IFRS 9, IAS 39,IFRS 7, IFRS 4 and IFRS 16

Interest Rate Benchmark Reform – Phase 25

Amendments to IFRS Standards Annual Improvements to IFRS Standards 2018-20203

1 Effective for annual periods beginning on or after January 1, 2023.

2 Effective for annual periods beginning on or after a date to be determined.

3 Effective for annual periods beginning on or after January 1, 2022.

4 Effective for annual periods beginning on or after June 1, 2020.

5 Effective for annual periods beginning on or after January 1, 2021.

The directors of the Company anticipate that the application of the above new and amendments to IFRSs willhave no material impact on the Group’s combined financial statements in the foreseeable future.

APPENDIX I ACCOUNTANTS’ REPORT

– I-14 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

4. SIGNIFICANT ACCOUNTING POLICIES

The Historical Financial Information has been prepared based on the accounting policies set out below whichconform with IFRSs issued by the IASB. In addition, the Historical Financial Information included applicabledisclosures required by the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limitedand by the Hong Kong Companies Ordinance.

The Historical Financial Information has been prepared on the historical cost basis except for certain financialinstruments that are measured at fair values and biological assets at fair value less costs to sell, as explained in theaccounting policies set out below.

Historical cost is generally based on the fair value of the consideration given in exchange for goods andservices.

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderlytransaction between market participants at the measurement date, regardless of whether that price is directlyobservable or estimated using another valuation technique. In estimating the fair value of an asset or a liability, theGroup takes into account the characteristics of the asset or liability if market participants would take thosecharacteristics into account when pricing the asset or liability at the measurement date. Fair value for measurementand/or disclosure purposes in these combined financial statements is determined on such a basis, except forshare-based payment transactions that are within the scope of IFRS 2 Share-based Payment, leasing transactions thatare accounted for in accordance with IFRS 16, and measurements that have some similarities to fair value but are notfair value, such as net realisable value in IAS 2 Inventories or value in use in IAS 36 Impairment of Assets.

A fair value measurement of a non-financial asset takes into account a market participant’s ability to generateeconomic benefits by using the asset in its highest and best use or by selling it to another market participant thatwould use the asset in its highest and best use.

For financial instruments which are transacted at fair value and a valuation technique that unobservable inputsis to be used to measure fair value in subsequent periods, the valuation technique is calibrated so that the results ofthe valuation technique equals the transaction price.

In addition, for financial reporting purposes, fair value measurements are categorised into Level 1, 2 or 3 basedon the degree to which the inputs to the fair value measurements are observable and the significance of the inputsto the fair value measurement in its entirety, which are described as follows:

• Level 1 inputs are quoted prices (unadjusted) in active markets for identical assets or liabilities that theentity can access at the measurement date;

• Level 2 inputs are inputs, other than quoted prices included within Level 1, that are observable for theasset or liability, either directly or indirectly; and

• Level 3 inputs are unobservable inputs for the asset or liability.

The principal accounting policies are set out below.

Basis of consolidation

The Historical Financial Information incorporates the financial statements of the Company and entitiescontrolled by the Company and its subsidiaries. Control is achieved when the Company:

(i) has power over the investee;

(ii) is exposed, or has rights, to variable returns from its involvement with the investee; and

(iii) has the ability to use its power to affect its returns.

The Group reassesses whether or not it controls an investee if facts and circumstances indicate that there arechanges to one or more of the three elements of control listed above.

APPENDIX I ACCOUNTANTS’ REPORT

– I-15 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

Consolidation of a subsidiary begins when the Group obtains control over the subsidiary and ceases when theGroup loses control of the subsidiary. Specially, income and expenses of a subsidiary acquired or disposed of duringthe year are included in the combined statement of profit or loss and other comprehensive income from the date theGroup gains controls until the date when the Group ceases to control the subsidiary.

Profit or loss and each component of other comprehensive income are attributed to the owners of the Companyand to the non-controlling interests. Total comprehensive income of subsidiaries is attributed to the owners of theCompany and to the non-controlling interests even if this results in the non-controlling interests having a deficitbalance.

When necessary, adjustments are made to the financial statements of subsidiaries to bring their accountingpolicies into line with the Group’s accounting policies.

All intra-group assets and liabilities, equity, income, expenses and cash flows relating to transactions betweenmembers of the Group are eliminated in full on consolidation.

Non-controlling interests in subsidiaries are presented separately from the Group’s equity therein, whichrepresent present ownership interests entitling their holders to a proportionate share of net assets of the relevantsubsidiaries upon liquidation.

Changes in the Group’s interests in existing subsidiaries

Changes in the Group’s interests in subsidiaries that do not result in the Group losing control over thesubsidiaries are accounted for as equity transactions. The carrying amounts of the Group’s relevant components ofequity and the non-controlling interests are adjusted to reflect the changes in their relative interests in thesubsidiaries, including re-attribution of relevant reserves between the Group and the non-controlling interestsaccording to the Group’s and the non-controlling interests’ proportionate interests.

Any difference between the amount by which the non-controlling interests are adjusted, and the fair value ofthe consideration paid or received is recognised directly in equity and attributed to owners of the Company.

Business combinations

Acquisitions of businesses are accounted for using the acquisition method. The consideration transferred in abusiness combination is measured at fair value, which is calculated as the sum of the acquisition-date fair values ofthe assets transferred by the Group, liabilities incurred by the Group to the former owners of the acquiree and theequity interests issued by the Group in exchange for control of the acquiree. Acquisition-related costs are generallyrecognized in profit or loss as incurred.

At the acquisition date, the identifiable assets acquired and the liabilities assumed are recognized at their fairvalue, except that:

• deferred tax assets or liabilities and liabilities or assets related to employee benefit arrangements arerecognised and measured in accordance with IAS 12 Income Taxes and IAS 19 Employee Benefitsrespectively;

• liabilities or equity instruments related to share-based payment arrangements of the acquiree orshare-based payment arrangements of the Group entered into to replace share-based paymentarrangements of the acquiree are measured in accordance with IFRS 2 Share-based Payment at theacquisition date;

• assets (or disposal groups) that are classified as held for sale in accordance with IFRS 5 Non-currentAssets Held for Sale and Discontinued Operations are measured in accordance with that standard; and

• lease liabilities are recognized and measured at the present value of the remaining lease payments (asdefined in IFRS 16) as if the acquired leases were new leases at the acquisition date, except for leasesfor which (a) the lease term ends within 12 months of the acquisition date; or (b) the underlying assetis of low value. Right-of-use assets are recognised and measured at the same amount as the relevantlease liabilities, adjusted to reflect favourable or unfavourable terms of the lease when compared withmarket terms.

APPENDIX I ACCOUNTANTS’ REPORT

– I-16 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

Goodwill is measured as the excess of the sum of the consideration transferred, the amount of anynon-controlling interests in the acquiree, and the fair value of the acquirer’s previously held equity interest in theacquiree (if any) over the net amount of the identifiable assets acquired and the liabilities assumed as at acquisitiondate. If, after re-assessment, the net of the acquisition-date amounts of the identifiable assets acquired and liabilitiesassumed exceeds the sum of the consideration transferred, the amount of any non-controlling interests in the acquireand the fair value of the acquirer’s previously held interest in the acquiree (if any), the excess is recognizedimmediately in profit or loss as a bargain purchase gain.

Non-controlling interests that are present ownership interests and entitle their holders to a proportionate shareof the relevant subsidiary’s net assets in the event of liquidation may be initially measured either at fair value or atthe non-controlling interests’ proportionate share of the recognised amounts of the acquiree’s identifiable net assets.The choice of measurement basis is made on a transaction-by-transaction basis.

Investment in subsidiaries

Investment in subsidiaries is included in the Company’s statement of financial position at cost less anyidentified impairment losses.

Goodwill

Goodwill arising on an acquisition of a business is carried at cost as established at the date of acquisition ofthe business less accumulated impairment losses, if any.

For the purposes of impairment testing, goodwill is allocated to each of the Group’s cash-generating units (orgroup of cash-generating units) that is expected to benefit from the synergies of the combination, which represent thelowest level at which the goodwill is monitored for internal management purposes and not larger than an operatingsegment.

A cash-generating unit (or group of cash-generating units) to which goodwill has been allocated is tested forimpairment annually or more frequently when there is indication that the unit may be impaired. For goodwill arisingon an acquisition in a reporting period, the cash-generating unit (or group of cash-generating units) to which goodwillhas been allocated is tested for impairment before the end of that reporting period. If the recoverable amount is lessthan its carrying amount, the impairment loss is allocated first to reduce the carrying amount of any goodwill andthen to the other assets on a pro-rata basis based on the carrying amount of each asset in the unit (or group ofcash-generating units).

On disposal of the relevant cash-generating unit or any of the cash-generating unit within the group ofcash-generating units, the attributable amount of goodwill is included in the determination of the amount of profitor loss on disposal. When the Group disposes of an operation within the cash-generating unit (or a cash-generatingunit within a group of cash-generating units), the amount of goodwill disposed of is measured on the basis of therelative values of the operation (or the cash-generating unit) disposed of and the portion of the cash-generating unit(or the group of cash-generating units) retained.

Investments in joint ventures

A joint venture is a joint arrangement whereby the parties that have joint control of the arrangement have rightsto the net assets of the joint arrangement. Joint control is the contractually agreed sharing of control of anarrangement, which exists only when decisions about the relevant activities require unanimous consent of the partiessharing control.

The results and assets and liabilities of joint ventures are incorporated in these combined financial statementsusing the equity method of accounting. The financial statements of joint ventures used for equity accounting purposesare prepared using uniform accounting policies as those of the Group for like transactions and events in similarcircumstances. Under the equity method, an investment in a joint venture is initially recognised in the combinedstatement of financial position at cost and adjusted thereafter to recognise the Group’s share of the profit or loss andother comprehensive income of the joint venture. Changes in net assets of the joint venture other than profit or lossand other comprehensive income are not accounted for unless such changes resulted in changes in ownership interestheld by the Group. When the Group’s share of losses of a joint venture exceeds the Group’s interest in that jointventure (which includes any long-term interests that, in substance, form part of the Group’s net investment in the jointventure), the Group discontinues recognising its share of further losses. Additional losses are recognised only to theextent that the Group has incurred legal or constructive obligations or made payments on behalf of the joint venture.

APPENDIX I ACCOUNTANTS’ REPORT

– I-17 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

An investment in a joint venture is accounted for using the equity method from the date on which the investeebecomes a joint venture. On acquisition of the investment in a joint venture, any excess of the cost of the investmentover the Group’s share of the net fair value of the identifiable assets and liabilities of the investee is recognised asgoodwill, which is included within the carrying amount of the investment. Any excess of the Group’s share of thenet fair value of the identifiable assets and liabilities over the cost of the investment, after reassessment, is recognisedimmediately in profit or loss in the period in which the investment is acquired.

The Group assesses whether there is an objective evidence that the interest in a joint venture may be impaired.When any objective evidence exists, the entire carrying amount of the investment (including goodwill) is tested forimpairment in accordance with IAS 36 as a single asset by comparing its recoverable amount (higher of value in useand fair value less costs of disposal) with its carrying amount. Any impairment loss recognised is not allocated toany asset, including goodwill that forms part of the carrying amount of the investment. Any reversal of thatimpairment loss is recognised in accordance with IAS 36 to the extent that the recoverable amount of the investmentsubsequently increases.

When a group entity transacts with a joint venture of the Group, profits and losses resulting from thetransactions with the joint venture are recognised in the Group’s combined financial statements only to the extent ofinterests in the joint venture that are not related to the Group.

Revenue from contracts with customers

The Group recognises revenue when (or as) a performance obligation is satisfied, i.e. when “control” of thegoods or services underlying the particular performance obligation is transferred to the customer.

A performance obligation represents a good or service (or a bundle of goods or services) that is distinct or aseries of distinct goods or services that are substantially the same.

Control is transferred over time and revenue is recognised over time by reference to the progress towardscomplete satisfaction of the relevant performance obligation if one of the following criteria is met:

• the customer simultaneously receives and consumes the benefits provided by the Group’s performanceas the Group performs;

• the Group’s performance creates and enhances an asset that the customer controls as the Groupperforms; or

• the Group’s performance does not create an asset with an alternative use to the Group and the Grouphas an enforceable right to payment for performance completed to date.

Otherwise, revenue is recognised at a point in time when the customer obtains control of the distinct good orservice.

A contract asset represents the Group’s right to consideration in exchange for goods or services that the Grouphas transferred to a customer that is not yet unconditional. It is assessed for impairment in accordance with IFRS 9.In contrast, a receivable represents the Group’s unconditional right to consideration, i.e. only the passage of time isrequired before payment of that consideration is due.

A contract liability represents the Group’s obligation to transfer goods or services to a customer for which theGroup has received consideration (or an amount of consideration is due) from the customer.

A contract asset and a contract liability relating to the same contract are accounted for and presented on a netbasis.

Contracts with multiple performance obligations (including allocation of transaction price)

For contracts that contain more than one performance obligations, the Group allocates the transaction price toeach performance obligation on a relative stand-alone selling price basis.

The stand-alone selling price of the distinct good or service underlying each performance obligation isdetermined at contract inception. It represents the price at which the Group would sell a promised good or serviceseparately to a customer. If a stand-alone selling price is not directly observable, the Group estimates it usingappropriate techniques such that the transaction price ultimately allocated to any performance obligation reflects theamount of consideration to which the Group expects to be entitled in exchange for transferring the promised goodsor services to the customer.

APPENDIX I ACCOUNTANTS’ REPORT

– I-18 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

Principal versus agent

When another party is involved in providing goods or services to a customer, the Group determines whetherthe nature of its promise is a performance obligation to provide the specified goods or services itself (i.e. the Groupis a principal) or to arrange for those goods or services to be provided by the other party (i.e. the Group is an agent).

The Group is a principal if it controls the specified good or service before that good or service is transferredto a customer.

The Group is an agent if its performance obligation is to arrange for the provision of the specified good orservice by another party. In this case, the Group does not control the specified good or service provided by anotherparty before that good or service is transferred to the customer. When the Group acts as an agent, it recognisesrevenue in the amount of any fee or commission to which it expects to be entitled in exchange for arranging for thespecified goods or services to be provided by the other party.

Leases

Definition of a lease

A contract is, or contains, a lease if the contract conveys the right to control the use of an identified asset fora period of time in exchange for consideration.

The Group assesses whether a contract is or contains a lease based on the definition under IFRS 16 atinception, modification date or acquisition date. Such contract will not be reassessed unless the terms and conditionsof the contract are subsequently changed.

Sublease

When the Group is an intermediate lessor, it accounts for the head lease and the sublease as two separatecontracts. The sublease is classified as a finance or operating lease by reference to the right-of-use asset arising fromthe head lease, not with reference to the underlying asset.

The Group as a lessee

Short-term leases

The Group applies the short-term lease recognition exemption to leases of motor vehicles, machinery andequipment and buildings that have a lease term of 12 months or less from the commencement date and do not containa purchase option. Lease payments on short-term leases and leases of low-value assets are recognised as expense ona straight-line basis or another systematic basis over the lease term.

Right-of-use assets

The cost of right-of-use assets includes:

• the amount of the initial measurement of the lease liability;

• any lease payments made at or before the commencement date, less any lease incentives received;

• any initial direct costs incurred by the Group; and

• an estimate of costs to be incurred by the Group in dismantling and removing the underlying assets,restoring the site on which it is located or restoring the underlying asset to the condition required by theterms and conditions of the lease.

Right-of-use assets are measured at cost, less any accumulated depreciation and impairment losses, andadjusted for any remeasurement of lease liabilities.

APPENDIX I ACCOUNTANTS’ REPORT

– I-19 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

Right-of-use assets in which the Group is reasonably certain to obtain ownership of the underlying leasedassets at the end of the lease term is depreciated from commencement date to the end of the useful life. Otherwise,right-of-use assets are depreciated on a straight-line basis over the shorter of its estimated useful life and the leaseterm.

The Group presents right-of-use assets that do not meet the definition of investment property as a separate lineitem on the combined statements of financial position. Right-of-use assets that meet the definition of investmentproperty are presented within “investment properties”.

Refundable rental deposits

Refundable rental deposits paid are accounted under IFRS 9 and initially measured at fair value. Adjustmentsto fair value at initial recognition are considered as additional lease payments and included in the cost of right-of-useassets.

Lease liabilities

At the commencement date of a lease, the Group recognises and measures the lease liability at the present valueof lease payments that are unpaid at that date. In calculating the present value of lease payments, the Group uses theincremental borrowing rate at the lease commencement date if the interest rate implicit in the lease is not readilydeterminable.

The lease payments include:

• fixed payments (including in-substance fixed payments) less any lease incentives receivable;

• amounts expected to be paid under residual value guarantees; and

• payments of penalties for terminating a lease, if the lease term reflects the Group exercising the optionto terminate the lease.

Variable lease payments that reflect changes in market rental rates are initially measured using the marketrental rates as at the commencement date. Variable lease payments that do not depend on an index or a rate are notincluded in the measurement of lease liabilities and right-of-use assets, and are recognised as expense in the periodon which the event or condition that triggers the payment occurs.

After the commencement date, lease liabilities are adjusted by interest accretion and lease payments.

The Group remeasures lease liabilities (and makes a corresponding adjustment to the related right-of-useassets) whenever the lease term has changed or there is a change in the assessment of exercise of a purchase option,in which case the related lease liability is remeasured by discounting the revised lease payments using a reviseddiscount rate at the date of reassessment.

The Group presents lease liabilities as a separate line item on the combined statements of financial position.

Lease payments in relation to lease liability will be allocated into a principal and an interest portion which arepresented as financing cash flows by the Group.

Lease modifications

The Group accounts for a lease modification as a separate lease if:

• the modification increases the scope of the lease by adding the right to use one or more underlyingassets; and

• the consideration for the leases increases by an amount commensurate with the stand-alone price for theincrease in scope and any appropriate adjustments to that stand-alone price to reflect the circumstancesof the particular contract.

APPENDIX I ACCOUNTANTS’ REPORT

– I-20 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

For a lease modification that is not accounted for as a separate lease, the Group remeasures the lease liabilitybased on the lease term of the modified lease by discounting the revised lease payments using a revised discount rateat the effective date of the modification.

The Group accounts for the remeasurement of lease liabilities by making corresponding adjustments to therelevant right-of-use assets. When the modified contract contains a lease component and one or more additional leaseor non-lease components, the Group allocates the consideration in the modified contract to each lease component onthe basis of the relative stand-alone price of the lease component and the aggregate stand-alone price of the non-leasecomponents.

The Group as a lessor

Classification and measurement of leases

Leases for which the Group is a lessor are classified as finance or operating leases. Whenever the terms of thelease transfer substantially all the risks and rewards incidental to ownership of an underlying asset to the lessee, thecontract is classified as a finance lease. All other leases are classified as operating leases.

Rental income from operating leases is recognised in profit or loss on a straight-line basis over the term of therelevant lease.

Foreign currencies

In preparing the financial statements of individual entities, transactions in currencies other than the entity’sfunctional currency (foreign currencies) are recorded at the rates of exchange prevailing on the dates of thetransactions. At the end of each reporting period, monetary items denominated in foreign currencies are re-translatedat the rates prevailing at that date. Non-monetary items that are measured in terms of historical cost in a foreigncurrency are not retranslated.

Exchange differences arising on the settlement of monetary items, and on the translation of monetary items,are recognised in profit or loss in the period in which they arise.

For the purposes of presenting the combined financial statements, the assets and liabilities of the Group’soperations are translated into the presentation currency of the Group (i.e. RMB) using exchange rates prevailing atthe end of each reporting period. Income and expenses items are translated at the average exchange rates for theperiod. Exchange differences arising, if any, are recognised in other comprehensive income and accumulated inequity under the heading of translation reserve (attributed to non-controlling interests as appropriate).

Borrowing costs

Borrowing costs directly attributed to the acquisition, construction or production of qualifying assets, whichare assets that necessarily take a substantial period of time to get ready for their intended use or sale, are added tothe cost of those assets until such time as the assets are substantially ready for their intended use or sale.

Any specific borrowing that remain outstanding after the related asset is ready for its intended use or sale isincluded in the general borrowing pool for calculation of capitalisation rate on general borrowings. Investmentincome earned on the temporary investment of specific borrowings pending their expenditure on qualifying assets isdeducted from the borrowing cost eligible for capitalisation.

All other borrowing costs are recognised in profit or loss in the period in which they are incurred.

Government grants

Government grants are not recognised until there is reasonable assurance that the Group will comply with theconditions attaching to them and the grants will be received.

Grants relating to biological assets

An unconditional government grant related to a biological asset measured at its fair value less costs to sell isrecognised in profit or loss when, and only when, the government grant becomes receivable.

APPENDIX I ACCOUNTANTS’ REPORT

– I-21 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

Other grants

Government grants are recognised in profit or loss on a systematic basis over the periods in which the Grouprecognises as expenses the related costs for which the grants are intended to compensate. Specifically, governmentgrants whose primary condition is that the Group should purchase, construct or otherwise acquire non-current assetsare recognised as deferred income in the combined statement of financial position and transferred to profit or losson a systematic and rational basis over the useful lives of the related assets.

Government grants that are receivable as compensation for expenses or losses already incurred or for thepurpose of giving immediate financial support to the Group with no future related costs are recognised in profit orloss in the period in which they become receivable.

Retirement benefit costs

Payments to defined contribution retirement benefit under the state-managed retirement benefit schemes in thePRC are charged as an expense when employees have rendered service entitling them to the contributions.

Short-term employee benefits

Short-term employee benefits are recognised at the undiscounted amount of the benefits expected to be paidas and when employees rendered the services. All short-term employee benefits are recognised as an expense unlessanother IFRS requires or permits the inclusion of the benefit in the cost of an asset.

A liability is recognised for benefits accruing to employees (such as wages and salaries, annual leave and sickleave) after deducting any amount already paid.

Taxation

Income tax expenses represent the sum of the tax currently payable and deferred tax.

The tax currently payable is based on taxable profit for the year. Taxable profit differs from profit/loss beforetax because of income or expense that are taxable or deductible in other years and items that are never taxable ordeductible. The Group’s liability for current tax is calculated using tax rates that have been enacted or substantivelyenacted by the end of the reporting period.

Deferred tax is recognised on temporary differences between the carrying amount of assets and liabilities inthe Historical Financial Information and the corresponding tax bases used in the computation of taxable profit.Deferred tax liabilities are generally recognised for all taxable temporary differences. Deferred tax assets aregenerally recognised for all deductible temporary differences to the extent that it is probable that taxable profits willbe available against which those deductible temporary differences can be utilised. Such deferred tax assets andliabilities are not recognised if the temporary difference arises from the initial recognition (other than in a businesscombination) of assets and liabilities in a transaction that affects neither the taxable profit nor the accounting profit.In addition, deferred tax liabilities are not recognised if the temporary difference arises from the initial recognitionof goodwill.

Deferred tax liabilities are recognised for taxable temporary differences associated with investments insubsidiaries and interests in joint ventures, except where the Group is able to control the reversal of the temporarydifference and it is probable that the temporary difference will not reverse in the foreseeable future. Deferred taxassets arising from deductible temporary differences associated with such investments and interests are onlyrecognised to the extent that it is probable that there will be sufficient taxable profits against which to utilise thebenefits of the temporary differences and they are expected to reverse in the foreseeable future.

The carrying amount of deferred tax assets is reviewed at the end of the reporting period and reduced to theextent that it is no longer probable that sufficient taxable profit will be available to allow all or part of the asset tobe recovered.

Deferred tax liabilities and assets are measured at the tax rates that are expected to apply in the period in whichthe liability is settled or the asset is realised, based on tax rate (and tax laws) that have been enacted or substantivelyenacted by the end of the reporting period.

APPENDIX I ACCOUNTANTS’ REPORT

– I-22 –

THIS DOCUMENT IS IN DRAFT FORM, INCOMPLETE AND SUBJECT TO CHANGE AND THAT INFORMATION MUST BEREAD IN CONJUNCTION WITH THE SECTION HEADED “WARNING” ON THE COVER OF THIS DOCUMENT.

The measurement of deferred tax liabilities and assets reflects the tax consequences that would follow fromthe manner in which the Group expects, at the end of the reporting period, to recover or settle the carrying amountof its assets and liabilities.

For the purposes of measuring deferred tax for leasing transactions in which the Group recognises theright-of-use assets and the related lease liabilities, the Group first determines whether the tax deductions areattributable to the right-of-use assets or the lease liabilities.

For leasing transactions in which the tax deductions are attributable to the lease liabilities, the Group appliesIAS 12 Income Taxes requirements to the leasing transaction as a whole. Temporary differences relating toright-of-use assets and lease liabilities are assessed on a net basis. Excess of depreciation on right-of-use assets overthe lease payments for the principal portion of lease liabilities resulting in net deductible temporary differences.

Deferred tax assets and liabilities are offset when there is a legally enforceable right to set off current tax assetsagainst current tax liabilities and when they relate to income taxes levied to the same taxable entity by the sametaxation authority.

Current and deferred tax is recognised in profit or loss, except when they relate to items that are recognisedin other comprehensive income or directly in equity, in which case, the current and deferred tax are also recognisedin other comprehensive income or directly in equity respectively. Where current tax or deferred tax arises from theinitial accounting for a business combination, the tax effect is included in the accounting for the businesscombination.

Property, plant and equipment

Property, plant and equipment are tangible assets that are held for use in the production or supply of goods orservices, or for administrative purposes (other than properties under construction as described below). Property, plantand equipment are stated in the combined statements of financial position at cost less subsequent accumulateddepreciation and subsequent accumulated impairment losses, if any.