Ahmedabad Chartered Accountants Journal - Google Groups

80

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Ahmedabad Chartered Accountants Journal - Google Groups

Ahmedabad Chartered Accountants Journal May, 2022 65

Volume : 46 Part : 02 May, 2022

E-mail : [email protected] Website : www.caa-ahm.org

Ahmedabad Chartered Accountants Journal

C O N T E N T S To Begin with

- Art of Leaving.................................................................. CA. Nirav Choksi......................... 67

Editorial ............................................................................................CA. Rutvij P. Shah...........................68

From the President............................................................................CA. Sarju Mehta............................69

Articles

Filing of Updated Return - All that Glitters is not Gold........................CA. Manthan Khokhani................70

Income vs. Capital Receipt under Income Tax Act, 1961......................CA. Jay Sharma...........................74

Section 194R : TDS on benefits or perquisite.......................................CA. Akshat Vithlani.........................79

Direct Taxes

Glimpses of Supreme Court Rulings....................................................Adv. Samir N. Divatia....................82

From the Courts..................................................................................CA. Jayesh Sharedalal................. 84

Tribunal News.....................................................................................CA. Yogesh G. Shah &CA. Aparna Parelkar.................... 87

Unreported Judgements......................................................................CA. Sanjay R. Shah......................93

Controversies.......................................................................................CA. Kaushik D. Shah....................95

Judicial Analysis..................................................................................Adv. Tushar Hemani......................97

FEMA & International Taxation

Update on Recent Case Laws – International Taxation and .............. CA. Dhinal A. Shah &Transfer Pricing CA. Karan Sukhramani...............106

FEMA Updates....................................................................................CA. Savan Godiawala..................108

Indirect Taxes

GST and VAT Judgments and Updates................................................ CA. Bihari B. Shah &CA. Vishrut R. Shah.....................110

Corporate Law & Others

Corporate Law Update.......................................................................CA. Naveen Mandovara................113

GujRERA Corner..................................................................................CA. Manan Doshi.........................116

Allied Laws Corner............................................................................. Adv. Ankit Talsania.......................119

Capital Markets.................................................................................. CA. Karan P. Vora........................122

From Published Accounts ................................................................ CA. Pamil H. Shah..................... 127

From the Government ......................................................................CA Ashwin H. Shah &CA. Kunal A. Shah........................129

IT Corner...........................................................................................CA. Rushabh Shah..................... 131

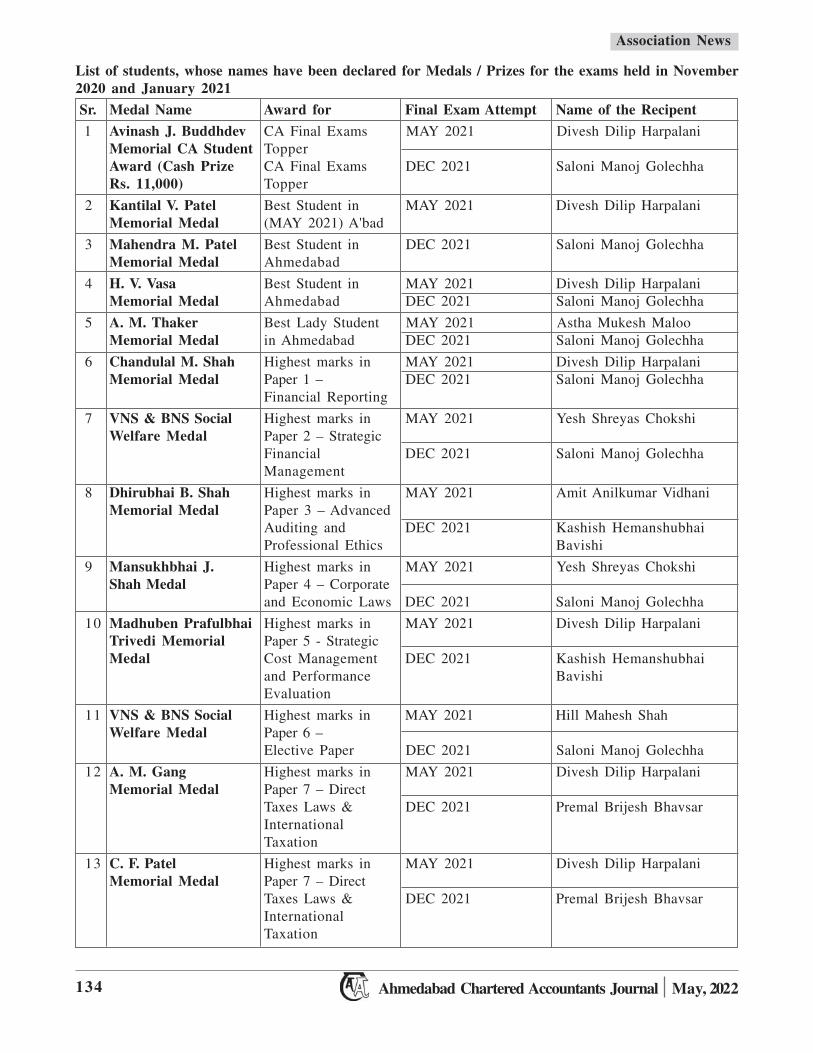

Association News.............................................................................. CA. Rushabh Shah &CA. Jay Parekh............................133

ACAJ Crossword Contest......................................................................................................................140

- caaahmedabad

Ahmedabad Chartered Accountants Journal May, 202266

AttentionMembers / Subscribers / Authors / Contributors1. Journals are carefully posted. If not received, you are requested to write to the Association's Office within one

month. A copy of the Journal would be sent, if extra copies are available.2. You are requested to intimate change of address to the Association's Office.3. Subscription for the financial year 2022-23 is ` 1500/-, single copy ` 150/- (if available).4. Please mention your membership number in all your correspondence.5. While sending Articles for this Journal, please confirm that the same are not published / not even meant for

publishing elsewhere. No correspondence will be made in respect of Articles not accepted for publication, norwill they be sent back.

6. The opinions, views, statements, results published in this Journal are of the respective authors / contributorsand Chartered Accountants Association, Ahmedabad is neither responsible for the same nor does it necessarilyconcur with the authors / contributors.

7. Life Membership/Annual Membership and Other Fees F. Y. 2022-23 Amount in `Basic GST Total

1. Admission Fees 500 90 5902. Annual Membership Feesa. If Paid Prior to june 30 of each financial year :i. In case of membership (of ICAI) for a period of less than or equal to five years 600 - 600ii. In case of membership of (ICAI) for a period more than five years, 750 - 750b. If paid after june 30 of each financial year :i. In case of membership (of ICAI) for a period of less than or equal to five years, 720 - 720ii. In case of membership of (ICAI) for a period of more than five years 900 - 9003. Life Membership Feesi. In case of membership (of ICAI) for a period of less than or equal to five years 4000 720 4720ii. In case of membership of (ICAI) for a period more than five years 7500 1350 88504. Brain Trust Membership Feesa. Individual Membership Feesi. In case of membership (of ICAI) for a period of less than or equal to five years 800 144 944ii. In case of membership of (ICAI) for a period more than five years 1000 180 1180b. Flexi Firm/Corporate Membership Fees*** 2000 360 2360*** Registered Firm/Corporate can nominate any two participants from their firm for each Brain Trust Meeting. AdditionalRepresentatives can be nominated @1000/- plus GST per participant subject to maximum of 20 participant per firm

Published ByCA. Rutvij P. Shah, on behalf of Chartered Accountants Association, Ahmedabad, 2nd Floor, Darshak, 14/A, SwastikSociety, Opp. Shrey Hospital, Navrangpura, Ahmedabad - 380 009 Phone : +91 79 40392596No part of this Publication shall be reproduced or transmitted in any form or by any means without the permissionin writing from the Chartered Accountants Association, Ahmedabad.While every effort has been made to ensure accuracy of information contained in this Journal, the Publisher isnot responsible for any error that may have arisen.

Professional AwardsThe best articles published in this Journal in the categories of 'Direct Taxes', 'Company Law and Auditing' and 'AlliedLaws and Others' will be awarded the Trophies/ Certificates of Appreciation after being vetted by experts in theprofession. Articles and reading literatures are invited from members as well as from other professional colleagues.

Printed : Pratiksha Printer, Ahmedabad Mobile : 98252 62512 E-mail : [email protected]

Journal CommitteeCA. Rutvij Shah CA. Ashish Sharma

Chairman ConvenorCA Uday Shah CA Jayesh Sharedalal

EC Representative Past President

CA. Monish Shah CA. Riken PatelCA. Ashok Kataria CA. Pratik Kikani

CA. Nirav Shah CA. Pratik Jain

Members

Ahmedabad Chartered Accountants Journal May, 2022 67

A video of Late Shri Arun Jaitley speaking inthe Parliament is doing the rounds onwhatsapp these days. He was referring to thetrend of retired High Court and Supreme Courtjudges self-appointing themselves on variouscommittees or departments after theirretirement. The majority of these posts werenot related to their area of work. He raised apertinent question in my mind, are we readyto LEAVE?.

This is just an instance which has beendebated upon in that video, but if we thinkand introspect, this is applicable to all of us.A businessman, not ready to hand over thereigns of his business to the next generation.A politician not willing to see anyone else inthe chair which he has once occupied.Consistent efforts being made by him tocontinue to be in power, either directly orthrough his nominees. A government officernot ready to accept the fact that he is no longerthe boss who once was the center of allimportant or major events happening in hisdepartment. A sportsman or an actor who oncewas a darling of crores is now a nobody. Allthese instances are emanating from the factthat WE ARE NOT READY TO LEAVE?. Weare not ready to leave the Power, Fame, Glory,Position, Control and similar delusional

ART OF LEAVING

CA. Nirav [email protected]

achievements, which we have enjoyed at somepoint of time in our lives.

It’s easier said than done. If you have been inlimelight for a major part of your life andsuddenly the scenario changes, it is verydifficult for a human being to accept thechange. The worst part is that the change isvery immediate and the outlook of generalpeople towards you also changes abruptly.And in majority of the cases the outlook goesnegative. But that is not in our hands as tohow people behave with us. What best we cando is prepare ourselves for this change.Leaving cannot be compared withabandoning. We must not abandon ourresponsibilities towards the family andsociety. But we must inculcate the culture oftransmission of powers and responsibility sothat the coming generation does not get awedwhen suddenly the powers and responsibilitycome to them. Remember the fact that expirydate of our life is not ascertained but there isevery certainty of the event to come.

Let us all decide to LEAVE proactively andLIVE peacefully.

❉ ❉ ❉

Ahmedabad Chartered Accountants Journal May, 202268

April and May are months of Vacations. In today’s stressful life, vacations have become veryimportant. It rejuvenates us and gives us time to rest, relax and recharge. It helps us to preventburnouts and improves our mental and physical wellbeing. A person who comes back fromvacations shows improved productivity and focus on work.

Apart from this, vacations have certain hidden benefits also. In today’s busy life, we are alwaysplaying catch up with various statutory deadlines and commitments. Many a times we find ithard to attend to family gatherings and miss out on opportunities of family bonding. Therefore,it is very important to spend time with someone you love. Vacations provide this quality familytime. It allows us to unplug from our busy work schedules and spend quality time with ourloved ones. It makes family relationship strong.

In earlier times vacations were the times to visit Mama, Kaka, Masi and Foifor kids. They weregreat family fun times. In today’s time, things have changed. However, importance of vacationhas not diminished one bit. There are many opportunities for kids to take part in adventurecamps and trekking activities. It provides a great platform for them to improve their socialskills and gives them valuable experience.

April and May months are relatively easy for us professionally. There are not many statutorydeadlines or work which requires our urgent attention in these months. We can utilize thismonth to prepare our office for upcoming busy season. We can refresh ourselves with newprovisions of law, update our checklists and work SOPs. We can also look into our ownaccounting, finances and billing aspects. All these will help us to be ready and prepared forupcoming season.

A new team has taken charge at the helm of our association. I would like to congratulate newoffice bearers of our Association led by President CA. Sarju Mehta, Vice President CA. ShivangChoksi and Hon. Secretaries CA. Jay Parekh and CA. Mayur Modha. I also wish them a verysuccessful and fulfilling tenure.

Recently our association held an essay competition in the memory of Late Shri C.R. Sharedalal.The competition was open for junior members of our association and topic was Income vs.Capital Receipt under Income Tax Act, 1961. CA. Jay Sharma was awarded first prize in thiscompetition. This article is published in this issue of our journal.

❉ ❉ ❉

EditorialCA. Rutvij Shah

Ahmedabad Chartered Accountants Journal May, 2022 69

Dear Members,

Hope all of you and your loved ones are safe and in pink of health.

It gives me immense pleasure to write this message as the 66th President of our Association. Iwill faithfully execute the office of the President to the best of my ability and will preserve,protect and defend the bye laws of this august Association and that I will devote myself to theservice and wellbeing of the members of our Association.

The torch bearers change but the show must go on. I and my team consisting of CA ShivangChokshi (Hon. Vice President), CA Jay Parekh and CA Mayur Modha (Hon. Secretary) willensure that the activity of the Association will be carried on without any breaks. The year hasstarted with a great publication in form of Schedule III Reporting and the book has receivedtremendous response across the State of Gujarat. In the coming months, we will ensure that allthe meetings related to amendments specifically related to Companies Act, Income Tax, GSTand Trust will be arranged.

I am happy to inform that the First Brain Trust Meeting is scheduled on 18th June, 2022 andRRC to Udaipur is also launched for 23, 24 and 25th June, 2022.

Along with the programs, we are also working on getting technologically advanced withassociation using all forms of Social Media to stay in touch with the members. Our websiteneeds to be updated to the current needs which is to perform as a data centre and also cater tovarious professional information being available for members. We would be carrying out theupdation soon and the committee for the same will ensure proper updation.

I on behalf of my team and myself would like to thank you all for trusting me with theopportunity in serving the noble profession. I shall try my best to serve to the need of all ofyou and also ensure you that me and my team will be available 24 x 7 and will also ensure thatthe Association will be happy to serve any need of its members.

CA SARJU MEHTA

❉ ❉ ❉

CA. Sarju [email protected]

From thePresident

Ahmedabad Chartered Accountants Journal May, 202270

Preface

The Finance Act 2022 has amended the provisionsof Section 139 of the Income-tax Act, 1961 (“TheAct”) dealing with filing of returns, to insert a newsub-section (8A) so as to allow the taxpayers to filean “updated return of income”.

Presently, the Income-tax Act allows taxpayers tofile their original return of income within the duedate as specified under the Act. In case, the originalreturn cannot be filed within the time specified, thetaxpayers still have an option to file a belated returnof income. Further in case of errors or omissions inthe original return of income, the taxpayers are evenallowed to file a revised or rectified return of income.However, time limit available to taxpayers to file arevised or belated return ranges from one month tofive months only depending on whether they arecovered under audit or not. Therefore, the FinanceAct 2022 seeks to provide one more opportunity tothe taxpayers to disclose any additional incomewhich they might have missed to report by way offiling an updated return. However, unlike a belatedor revised return, filing of an updated return comeswith certain riders and involves an additional costto the taxpayers.

The Memorandum explaining the provisions of theFinance Bill, 2022 reads out the following as thebasic understanding of win-win both for the revenueand the taxpayers:

“The proposal for updated return over a periodlonger than that is provided in the existing provisionsof Income-tax Act would on the one hand bringuse of huge data with the IT Department to a logicalconclusion resulting in additional revenuerealisation and on the other hand, it will facilitateease of compliance to the taxpayer in a litigationfree environment.”

The speech of the Finance Minister whileintroducing the provisions read as under:

121. India is growing at an accelerated pace andpeople are undertaking multiple financialtransactions. The Income Tax Department hasestablished a robust framework of reportingof taxpayers’ transactions. In this context,some taxpayers may realize that they havecommitted omissions or mistakes in correctlyestimating their income for tax payment. Toprovide an opportunity to correct such errors,I am proposing a new provision permittingtaxpayers to file an Updated Return onpayment of additional tax. This updated returncan be filed within two years from the end ofthe relevant assessment year.

122. Presently, if the department finds out that someincome has been missed out by the assessee,it goes through a lengthy process ofadjudication. Instead, with this proposal now,there will be a trust reposed in the taxpayersthat will enable the assessee herself to declarethe income that she may have missed outearlier while filing her return. Full details ofthe proposal are given in the Finance Bill. Itis an affirmative step in the direction ofvoluntary tax compliance.”

Basically, this may be treated as the Department’sway of asking the taxpayers to disclose anyadditional income which they might have missedout rather than waiting for a notice of reassessmentu/s. 148 which might be on the way consideringthe data mining done by the department.

Time limit for filing of updated return

Updated return can be filed by the taxpayers withina period of twenty four (24) months from the endof the relevant assessment year. Filing of the

CA. Manthan [email protected]

Filing of Updated Return - Allthat Glitters is not Gold

Ahmedabad Chartered Accountants Journal May, 2022 71

Filing of Updated Return - All that Glitters is not Gold

updated return can be undertaken irrespective ofthe fact as to whether the original or belated returnhas been filed by the assessee or not.

Form for filing of the updated return

Vide notification No. 48/2022 dated 29th April,2022, the CBDT has inserted a new Rule 12AC toprovide for a new ITR U form in order to file anupdated return of income by the specified class ofassessees.

Restrictions on filing of updated return

First Proviso to Section 139(8A) spells out certaincircumstances under which an updated return cannotbe filed. Accordingly, an updated return cannot befiled if:

1. The updated return is a return of loss; or

2. The updated return has the effect of decreasingthe total tax liability of the taxpayer alreadydetermined in the original or revised or belatedreturn filed by the assessee; or

3. The updated return results in refund or increasesthe refund due on the basis of the original orrevised or belated return filed by the assessee.

Simply put, if the updated return is not favourableto the revenue, the taxpayers will not be allowed tofile an updated return.

Though the provisions of Section 139(8A) allows“Any Person” to file an updated return, the same issubject to the second proviso to the said sectionwhich disqualifies certain class of taxpayers fromfiling an updated return. Accordingly, the followingclass of taxpayers are barred from taking a benefitof the provisions of Section 139(8A)

1. A person in whose case a search has beeninitiated u/s. 132 or books of accounts or otherdocuments or assets are requisitioned u/s. 132Aof the Act.

2. A person in whose case a survey has beenconducted u/s. 133A of the Act except forsurvey in respect of TDS/TCS.

3. A person in whose case a notice has beenissued to the effect that any money, bullion,jewellery or valuable article or thing seized or

requisitioned u/s. 132 or 132A in case of anyother person belongs the said person.

4. A person in whose case a notice has beenissued to the effect that any books of accountsor documents seized or requisitioned u/s. 132or 132A pertains to or information containedtherein belongs to or relates to such person.

When the provisions of this section were initiallyintroduced by the Finance Bill, 2022, the aforesaidcategories of persons were barred from filing anupdated return for the two assessment yearspreceding the assessment year relevant to the yearof search or survey or requisition. However, whenthe Finance Bill was tabled in the Lok Sabha it wasamended so as to provide that such categories oftaxpayers will not be allowed to file an updatedreturn for any of the preceding assessment years.

Lastly, the third Proviso to Section 139(8A)specifies certain circumstances under which anupdated return cannot be filed.

1. Where the assessee has already filed an updatedreturn once, he is not allowed to file an updatedreturn again for the same assessment year.

2. Where any proceeding for assessment or re-assessment or re-computation or revision ispending or has been completed for the relevantassessment year.

3. Where the assessing officer has in hispossession, information in respect of thetaxpayer under the Smugglers and ForeignExchange Manipulators Act, 1976 ofProhibition of the Benami PropertyTransactions Act, 1988 or the Prevention ofMoney Laundering Act, 2002 or the BlackMoney Act, 2015 and the same has beencommunicated to the taxpayer.

4. Where information for the relevant assessmentyear has been received under an agreementreferred to in Section 90 or Section 90A inrespect of the assessee and the same has beencommunicated to him.

5. Where prosecution proceedings under ChapterXXII have been initiated for the relevantassessment year

Ahmedabad Chartered Accountants Journal May, 202272

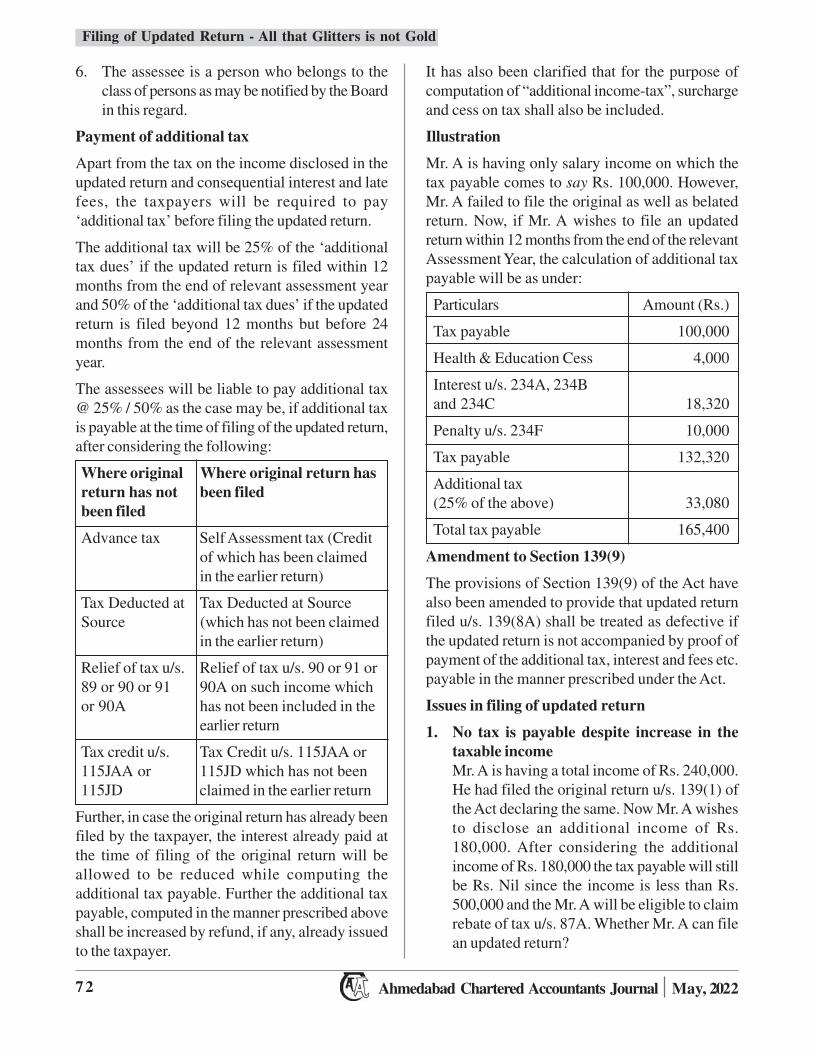

6. The assessee is a person who belongs to theclass of persons as may be notified by the Boardin this regard.

Payment of additional tax

Apart from the tax on the income disclosed in theupdated return and consequential interest and latefees, the taxpayers will be required to pay‘additional tax’ before filing the updated return.

The additional tax will be 25% of the ‘additionaltax dues’ if the updated return is filed within 12months from the end of relevant assessment yearand 50% of the ‘additional tax dues’ if the updatedreturn is filed beyond 12 months but before 24months from the end of the relevant assessmentyear.

The assessees will be liable to pay additional tax@ 25% / 50% as the case may be, if additional taxis payable at the time of filing of the updated return,after considering the following:

Where original Where original return hasreturn has not been filedbeen filed

Advance tax Self Assessment tax (Creditof which has been claimedin the earlier return)

Tax Deducted at Tax Deducted at SourceSource (which has not been claimed

in the earlier return)

Relief of tax u/s. Relief of tax u/s. 90 or 91 or89 or 90 or 91 90A on such income whichor 90A has not been included in the

earlier return

Tax credit u/s. Tax Credit u/s. 115JAA or115JAA or 115JD which has not been115JD claimed in the earlier return

Further, in case the original return has already beenfiled by the taxpayer, the interest already paid atthe time of filing of the original return will beallowed to be reduced while computing theadditional tax payable. Further the additional taxpayable, computed in the manner prescribed aboveshall be increased by refund, if any, already issuedto the taxpayer.

It has also been clarified that for the purpose ofcomputation of “additional income-tax”, surchargeand cess on tax shall also be included.

Illustration

Mr. A is having only salary income on which thetax payable comes to say Rs. 100,000. However,Mr. A failed to file the original as well as belatedreturn. Now, if Mr. A wishes to file an updatedreturn within 12 months from the end of the relevantAssessment Year, the calculation of additional taxpayable will be as under:

Particulars Amount (Rs.)

Tax payable 100,000

Health & Education Cess 4,000

Interest u/s. 234A, 234Band 234C 18,320

Penalty u/s. 234F 10,000

Tax payable 132,320

Additional tax(25% of the above) 33,080

Total tax payable 165,400

Amendment to Section 139(9)

The provisions of Section 139(9) of the Act havealso been amended to provide that updated returnfiled u/s. 139(8A) shall be treated as defective ifthe updated return is not accompanied by proof ofpayment of the additional tax, interest and fees etc.payable in the manner prescribed under the Act.

Issues in filing of updated return

1. No tax is payable despite increase in thetaxable incomeMr. A is having a total income of Rs. 240,000.He had filed the original return u/s. 139(1) ofthe Act declaring the same. Now Mr. A wishesto disclose an additional income of Rs.180,000. After considering the additionalincome of Rs. 180,000 the tax payable will stillbe Rs. Nil since the income is less than Rs.500,000 and the Mr. A will be eligible to claimrebate of tax u/s. 87A. Whether Mr. A can filean updated return?

Filing of Updated Return - All that Glitters is not Gold

Ahmedabad Chartered Accountants Journal May, 2022 73

In these circumstances, a strict interpretationof the provisions of Section 139(8A) wouldentitle Mr. A to file the updated return since itis

a. Neither a return of loss

b. Nor results in decrease of tax liability

c. Nor results in refund or increase in therefund of tax already claimed

Accordingly, though the intention of thelegislature is to allow filing of updated returnsonly in case of payment of additional incometax, such a situation has yet not been excludedfrom the category of omissions.

2. Penalty u/s. 270A

Though the Income-tax Department isencouraging the taxpayers to take the benefitof filing an updated return, there is nocorresponding amendment to the provisions ofSection 270A dealing with levy of penalty forunder reporting or mis reporting of income.

3. Filing of updated return if it results inincrease of MAT Credit

Clause (b) and (c) of the first proviso to section139(8A) provides that updated return cannotbe filed if it has the effect of decreasing the taxliability on the basis of return already filed.However, if the updated return results inincrease in the MAT Credit already claimedthere is no omission that is expressly provided.For instance, if a company had filed the originalincome tax return upon payment of MAT andnow intends to reduce the normal income andresultantly reduce the normal income taxpayable, it would result in large MAT Creditfor the company.

4. Whether credit of tax paid by the assesseeis available while computing the additionaltax payable, if return of income was notfiled?

For instance, Mr. A had paid tax of Rs. 100,000for the A.Y. 2021-22 on 05th April, 2021.However, Mr. A failed to file the original aswell as the belated return of income. Now, Mr.

A wishes to file an updated return. Whethercredit of Rs. 100,000 will be available to Mr.A while calculating the additional income taxpayable?

Interpretation of the provisions of Section 140Breveals that where return of income was notfiled by the assessee, he is entitled to a credit ofadvance tax, TDS and relief under specifiedsections. However, the amount of Rs. 100,000paid by Mr. A is not an advance tax since itwas paid after the end of the financial year.Neither the same is TDS nor a relief under thespecified provisions.

Accordingly in the Author’s humble view, dueto an anomaly in the said provisions, Mr. Awould be disentitled from claiming credit ofthe said payment of Rs. 100,000 whilecalculating the additional tax payable.

5. Whether receipt of intimation u/s. 143(1) ofthe Act would tantamount to assessment orinitiation of assessment and thereby barringtaxpayers from filing of an updated return?

In a plethora of decisions, it has been clearlyheld that intimation received u/s. 143(1), thoughappealable, is not an order of assessment.Accordingly, mere receipt of an intimation u/s.143(1) cannot be termed as barring the assesseefrom claiming the benefit of filing an updatedreturn.

6. Can updated return be updated?

The provisions of Section 139(8A) provides aone time opportunity to the taxpayers to file anupdated return. Updated returns once filedcannot be revised or updated in any manner.

Conclusion

The Finance Minister raised the hopes of taxpayerswhile introducing the Updated Return in her Budgetspeech. However, as the old saying goes, ‘all thatglitters is not gold’. The taxpayers have to carefullyevaluate the pros and cons of filing an UpdatedReturn, on a case-to-case basis, to ensure they getbenefit in return.

❉ ❉ ❉

Filing of Updated Return - All that Glitters is not Gold

Ahmedabad Chartered Accountants Journal May, 202274

A brief history of taxation in India

“It was only for the good of his subjects that hecollected taxes from them, just as the Sun drawsmoisture from the Earth to give it back a thousandfold” – as Kalidas described in Raghuvanshamacclaiming KING DILIP.

Taxes are defined as ‘compulsory charges leviedby a government for the purpose of financingservices performed for the common benefit’.Taxation is always an integrated part of everysystem of governance in India viz. monarchy,republic and modern democratic system. Taxationis found in ancient India as it described by anusmritiand Arthasastra. Present Indian tax system is basedon ancient tax system which believed in maximumsocial welfare. There was a very general consensusin ancient India that tax should be in such manneras nobody feel to hurt. In this regard, Chanakya,in very smart way, quoted the example of the honeybee, saying that “the king should gather the taxfrom the state in the manner as the bees collectshoney without hurting the flower. ”Kautilya’sconcept of taxation also emphasized on two basiccannon of taxation i.e. equity and justice.

Constitution of India has already been provided theprovision of taxes, which could be levied byauthority as article 265 states that no tax shall belevied or collected except by the authority of law.Identically, Central Government has the powerto levy tax on income, other than agriculturalincome, as specified by Entry 82 of List 1 ofConstitution of India. The Central Governmenthas enacted the Income Tax Act, 1961 (“the Act”).Income Tax is a charge on income of a person,earned during the previous year, at the rate(s)specified in the relevant Finance Act. Income of anassessse has to be computed in the manner laid

down under the Act. The Act has made elaborateprovisions for classification of incomes undervarious heads and deductions permissible undereach head. Income is chargeable to tax on the basisof either receipt or deemed receipt or accrues orarises or deemed to accrue or deemed to arise inIndia during the previous year relevant toassessment year. But, what is income has not beendefined and the Act provides an inclusive definitionwhich has vide connotations.

Income and its attributes

The definition of the term ‘income’ in section 2(24)is an inclusive. Therefore, the term ‘income’ notonly includes those things which are included insection 2(24), but also includes such things whichterm signifies according to its general and naturalmeaning. Therefore, before discussing the definitionof income given under section 2(24), it is imperativeto understand the meaning of ‘income’ as generally.

Entry 82 of List 1 of the Seventh Schedule to theConstitution empowers Parliament to levy “taxeson income other than agricultural income”. Entriesin the lists in Seventh Schedule to the constitutionshould not be read in a narrow or restricted manner.1

It is therefore, follows that in addition to receiptsmentioned in section 2(24), any other receipt istaxable under the Act, if it comes within the generaland natural meaning of the term ‘income’.According to the Shorter Oxford EnglishDictionary, “income” means “that which comes inas the periodical product of one’s week, business,lands or investments and annual or periodicalreceipts accruing to a person or a corporation.”Income connotes a periodical monetary return‘coming in’ with some sort of regularity or expectedregularity from definite sources. The source is notnecessarily one which is expected to be

CA. Jay [email protected]

Income vs. Capital Receiptunder Income Tax Act, 1961

Ahmedabad Chartered Accountants Journal May, 2022 75

total income of any previous year of a person whois resident, includes all income from whateversource derived, and shall be taxable. Thus, sections4 and 5 imposes general liability to tax upon allincome but the Act does not provide that whateveris received by the person must be regarded asincome liable to tax.5 No tax can be levied on thefuture potentiality of earning any income. Incometax is concerned with real income which accruesor arises to a person and not with future possibilityof an income from the use of any money availablewith the assesseee.

Though there are different concepts of ‘income’ forthe purpose of taxation, income is broadly definedat the true increase in the amount of wealth whichcomes to a person during a stated period of time. Itis immaterial whether income is received in cash orkind, if it is in kind, its valuation is to be madeaccording to the rules prescribed in the Income TaxRules. If there is no prescribed rule, valuation thereofis made on the basis of market value. Further,Income tax law does not make any distinctionbetween income accrued or arisen from a legalsource and income tainted with illegality. However,it is a fundamental rule of law of taxation that, unlessotherwise expressly provide, the same incomecannot be taxed twice. In the Act, there is no conceptof deferred income meaning thereby, income on itscoming into existence attracts tax.

Revenue Receipt vs. Capital Receipt

Having understood general meaning of income, letus understand kinds of receipts vis-à-vis revenuereceipts and capital receipts. As the Act does notcontain the terms “capital receipts” and “revenuereceipts”, one has to depend upon natural meaningof the concepts as well as facts of the case.Accordingly to Shorter Oxford English Dictionary,the word “capital” means “accumulated wealthemployed reproductively” whereas the word“revenue” means “the return, yield or profit of anylands, property or other important source of incomethat comes in to one as a return from the propertyor source”.

A receipt on account of circulating capital is revenuereceipt, whereas a receipt on account of fixed capital

Income vs. Capital Receipt under Income Tax Act, 1961

continuously productive, but it must be one whoseobject is the production of a definite return excludinganything in the nature of a mere windfall.2

The expression “income” includes not merely whatis received or what comes in by exploiting use of aproperty but also what once saves by using it byoneself and also which can be converted intoincome. The word income is of the widest amplitudeand it must be given its natural and grammaticalmeaning.3 The word ‘income’ used in the Act iswide and vague in its scope. It is a word of elasticimport. All receipts by an assesseee cannotnecessarily be deemed to be the income of theassessee for the purpose of the Act and whetherany particular receipt is income or not completelydepends upon the nature of the receipt. The incometax authorities cannot assess all receipts and theycould assess only those receipts falls into term‘income’.

One of the characteristics of the term ‘income’ isthe power or complete control over its disposal. Ifrestraints were placed over legitimate or legalspending of the income, it loses the character ofincome. Income which is not available for instantuse takes away essential characteristic of incomeand constrain placed over it prevents one to call itas income. Income should have possessed thecharacteristic of being available either for revenueexpenditure or to acquire a capital asset. It becomesincome only on the year in which and to the extentto which the restrictions placed were removed andthe permission to spend the amount was grantedand by spending certain income if the assesseeacquires a capital assets then it can be legitimatelycalled as income in the year in the which such capitalasset comes into existence.4

In order to say a particular receipt is an income, it isessential that it should come within the definitionof ‘income’. Section 4 of the Act imposes incometax upon a person in respect to his income. It is truethat every income is a receipt but in other way roundevery receipt is an income is not true. The term’income’ has been defined in section 2(24) of theAct which includes profit and gains, value ofperquisites or profit in lieu of salary, etc. Section 5,defining the scope of total income, says that the

Ahmedabad Chartered Accountants Journal May, 202276

is capital receipt. Fixed capital is what the ownerturns into profit by keeping it in his possession viz.tangible and intangible assets employed. Circulatingcapital is what he makes profit of by parting with itand letting it change matters. It is worthwhile tomention that the same asset may be fixed capital inone business and circulating capital in anotherbusiness and, therefore, the nature of a receipt mayvary according to the nature of trade in connectionwith which it arises.

It is well-settled that in order to find out whether areceipt is a capital receipt or revenue receipt, it hasto be seen what it is in the hands of the receiver andnot its nature in the hands of the payer. In otherwords, the nature of the receipt is determinedentirely by its character in the hands of the receiverand the source from which the payment is madehas no bearing on the question.6 Therefore, itfollows that even if the amount is paid out of capital,it may partake of the character of a revenue receiptin the hands of the recipient. Payment received onthe redemption of debentures, held as investments,is a capital receipt in hands of the recipient, even ifthe company makes payment out of its profits.Further, the motive of payer is not relevant whiledeciding whether a particular receipt is revenue orcapital in nature.

A receipt in lieu of source of income is capitalreceipt. A receipt in lieu of income is revenuereceipt. For instance, compensation for loss ofemployment is a capital receipt, as it is in lieu ofsource of income whereas if trees are cut so thatthey regenerate in course of time, the amount ofreceipt would be revenue receipt. Further,periodicity of receipt is immaterial to distinguishbetween capital receipt and revenue receipt.

The distinction between the two is vital becausecapital receipts are exempt from tax unless they areexpressly taxable (for instance, capital gains aretaxable under section 45, even if they are capitalreceipts). On the other hand, revenue receipts aretaxable unless they are expressly exempt from tax(for instance, incomes exempt under section 10).In all cases in which a receipt is sought to be taxedas income, the burden lies upon the Income taxDepartment to prove that it is within the taxing

provision. Where, a receipt is in nature of income,burden of proving that it is not taxable because itfalls within an exemption provided in the Act, liesupon the assesseee.

The aforesaid principles have been superseded to avery large extent by section 17, 28 and 56(2). Onthe combined reading of the aforesaid principlesand sections, the following positions arise whereincapital receipts are specifically liable to tax asincome:

· Compensation for termination ofmanagement/office/agency :-

Any compensation due to or received inconnection with termination of management oroffice or agency or modification of terms andconditions relating thereto by any person whomanaging whole affairs of the company oragency, is taxable under section 28(ii), even itis capital receipt.

In the aforesaid provision, compensation istaxable under section 28, even if recipient is anemployee and his regular income is taxableunder section 15.

· Compensation for vesting of business/property in Government :-

Any compensation due to or received by anyperson in connection with the vesting of themanagement of any property or business in theGovernment or a corporation owned orcontrolled by Government, is taxable undersection 28(ii). It is immaterial whethercompensation is capital receipt or revenuereceipt.

· Compensation for termination of anybusiness contract: -

Any compensation due to or received by anyperson at or in connection with termination ofany contract relating to his business, shall bechargeable to tax under section 28(ii) under thehead “Profit and gains of business orprofession”. In such case, it is immaterialwhether compensation is capital receipt orrevenue receipt.

Income vs. Capital Receipt under Income Tax Act, 1961

Ahmedabad Chartered Accountants Journal May, 2022 77

· Termination /modification of employmentcontract when compensation is receivedfrom employer:-

In a case not covered by section 28(ii), anycompensation due to or received by anindividual from his employer or formeremployer at or in connection with terminationor modification of terms of employment istaxable as profit in lieu of salary under section17(3)(i) and in such case the principles ofgoverning capital and revenue receipts are notrelevant.

· Termination /modification of employmentcontract when compensation is receivedfrom person other than employer:-

Any compensation or other payment due to orreceived by any person in connection withtermination of his employment or themodification of the terms and conditionsrelating thereto shall be chargeable to tax undersection 56(2)(xi) under the head “Income fromother source”. In such case the principles ofgoverning capital and revenue receipts are notrelevant.

· Compensation for refraining fromcompetition:-

Compensation paid for agreeing to refrain fromcarrying on competitive business in respect ofwhich an agency was terminated or loss ofgoodwill will prima facie be of the nature ofcapital receipt. Similarly, compensation forrestraint on exercise of profession is a capitalreceipt. However, such compensation ischargeable to tax under section 28(va).

· Forfeiture of advance money received incourse of negotiation for transfer of a capitalasset :-

Advance money received in the course ofnegotiation for transfer of an asset being capitalasset and later on forfeited by the recipient istaxable under section 56(2)(ix) under the head“Income from other source”. However, if theasset is not capital asset, then forfeiture of

advance money will not be taxable undersection 56(2)(ix).

· Assistance in the form of subsidy / grant :-

Finance Act inserted sub clause (xviii) insection 2(24) w.e.f. assessment year 2016-17.Subsidy/grant is taxable as income if conditionsspecified therein get fulfilled.

Apart of the above, the following few instances ofcapital receipts which are not liable to tax.

· Entrance fee:-

Non refundable entrance fees charged by clubas a one-time fee for enrolment is a capitalreceipt.

· Forfeiture of share application money :-

Amount of forfeited share application moneytransferred to separate account is a capitalreceipt and it cannot be taxed as income ofassesseee either under section 28(iv) or undersection 41(1).

· Alimony from husband:-

Amount realized by an assesseee as alimonyfrom her husband in terms of decree of divorce,is to be regarded as capital receipt not liable totax.

Section 2(24) defines the term “income” whichincludes revenue receipts as well as capital receipts.Instances of receipts except the mentionedhereinabove are stated as below.

· Profit and gains, dividend income, voluntarycontributions received by trust and institutioncreated for charitable or religious purposes.

· Perquisite, special allowances or benefits in thehands of employee.

· Benefit of perquisite to a representative assessee

· Insurance profit and Income of banking of aco-operative society.

· Capital gain income and winning from lottery

· Employees’ contribution towards providentfund or welfare funds

Income vs. Capital Receipt under Income Tax Act, 1961

Ahmedabad Chartered Accountants Journal May, 202278

· Amount received under keyman insurancepolicy

The following few instances of revenue receiptswhich are liable to tax.

· Compensation for loss of trading asset :-

Compensation received in respect of loss of atrading asset or stock in trade is a revenuereceipt liable to be taxed.

· Forfeiture of security deposit: -

Forfeited security deposits would be revenuereceipts if they are related to the assesseee’strading activity.

Apart from the concept of real income stated above,there are certain provisions in the Act which levytax on notional incomes/deemed incomes. Underthe head “income from house property” provisionof section 23(1) specifies that annual value of anyproperty shall be deemed to be the same for whichproperty might reasonably be expected to be let fromyear to year. Under “Profit and Gains of Businessor Profession”, there are many provisions whicheither consider income by deeming notionalincomes and also various provisions to disallowexpenditures which are otherwise spent; forinstance: section 36(1)(va), 40(a)(i), 40(a)(ii), 40(b),43CA. In the similar manner, under the head“Capital Gain” provisions section 50C / 50CA goesagainst the concept of real income. These areinstances wherein there is no actual fund flow. Itcasts unnecessary burden upon the assessee toprove that no such notional income was earned atall.

Conclusion

Whether a particular receipt is capital or incomefrom business has frequently engaged the attention

of the courts. There is nothing in the income-taxAct laying down any legal criterion fordistinguishing between capital and revenuereceipts, nor does any definite and clear criterionemerge from English or Indian decisions on thesubject. It depends upon the facts or each casewhich must be considered for determining whethera particular payment should be held to bechargeable as income under the Income-tax Act ornot. It is well settled that the words of the statute,when there is doubt about their meaning, are to beunderstood in the sense in which they bestharmonize with the subject of the enactment andthe object which the legislature has a view. Theirmeaning is found not so much in a strictlygrammatical or ethnological property of language,nor even in its popular use, as in the occasion onwhich they are used, and the object to be attained.

(Footnotes)1 Bhagwan Dass Jain vs. Union of India (1981) 5

Taxmann 7 (SC)2 CIT vs. Shaw Wallas & Co. 6 ITC 178 (PC)3 Toyo Engineering India Ltd. vs. Joint CIT

(2006) 100 TTJ (Mum) 3773, 3794 Sri Hiranyakeshi Sahakari Sakhare Karkhane

Niyamit vs. ITO (1986) 15 ITD 343, 358-59(Mad)

5 Moti Lal Sharma vs. Ass. CIT (1992) 42 ITD653, 659-60 (Del.)

6 CIT vs. Kamal Behari Lal Singha (1971) 82 ITR460 (SC)

.❉ ❉ ❉

Income vs. Capital Receipt under Income Tax Act, 1961

Ahmedabad Chartered Accountants Journal May, 2022 79

As we are aware, the Government is trying to collectmore and more data by way of TDS and SFT so thatmore tax net can be established. With this vision andaim, from 01/07/2022, new TDS provision has beeninserted where, 10% TDS is required to be deductedin case of any perquisite or benefit provided toanother person in cash or in kind where the value ofsuch benefit or perquisite is above 20000/-.

History and related Legal Provisions

Section 28 (IV) of the Act:

The value of any benefit or perquisite, whetherconvertible into money or not, arising from businessor the exercise of a profession.

Section 194R of Income Tax Act:

(1) Any person responsible for providing to aresident, any benefit or perquisite, whetherconvertible into money or not, arising frombusiness or the exercise of profession, by suchresident, shall, before providing such benefit orperquisite, as the case maybe, to such resident,ensure that tax has been deducted in respect orsuch benefit or perquisite at the rate of tenpercent of the value or aggregate value of suchbenefit or perquisite.

Provided that in a case where the benefit orperquisite, as the case may be, is wholly in kindor partly in cash and partly in kind but suchpart in cash is not sufficient to meet the liabilityof deduction of tax in the respect of whole ofsuch benefit or perquisite, the personresponsible for providing such benefit orperquisite shall, before releasing the benefit orperquisite, ensure that tax required to bededucted has been paid in respect of the benefitor perquisite:

Provided further that the provisions of thissection shall not apply in case of a residentwhere the value or aggregate of value of thebenefit or perquisite provided or likely to beprovided to such resident during the financialyear does not exceed twenty thousand rupees:

Provided Also that the provisions of this sectionshall not apply to a person being an individualor a Hindu Undivided Family, whose totalsales, Gross Receipts, or in case of profession,during the financial year immediatelypreceding the financial year in which suchbenefit or perquisite, as the case may be, isprovided by such person.

(2) If any difficulty arises in giving effect to theprovisions of this section, the Board may, withthe previous approval of the CentralGovernment, issue guidelines for the purposeof removing the difficulty.

(3) Every guideline issued by the Board under subsection (2) shall, as soon as may be after it isissued, be laid before each House ofParliament, and shall be binding on the incometax authorities and on the person providing anysuch benefit or perquisite.

Explanation:- For the purposes of this section,the expression “person responsible forproviding” means the person providing suchbenefit or perquisite, or in case of a company,the company itself including the principalofficer thereof.

Noteworthy points

1. The benefit or perquisite recipient should beresident and the payer can be resident may notbe resident. Let us analyse few situations.

CA. Akshat [email protected]

Section 194R : TDS onbenefits or perquisite

Ahmedabad Chartered Accountants Journal May, 202280

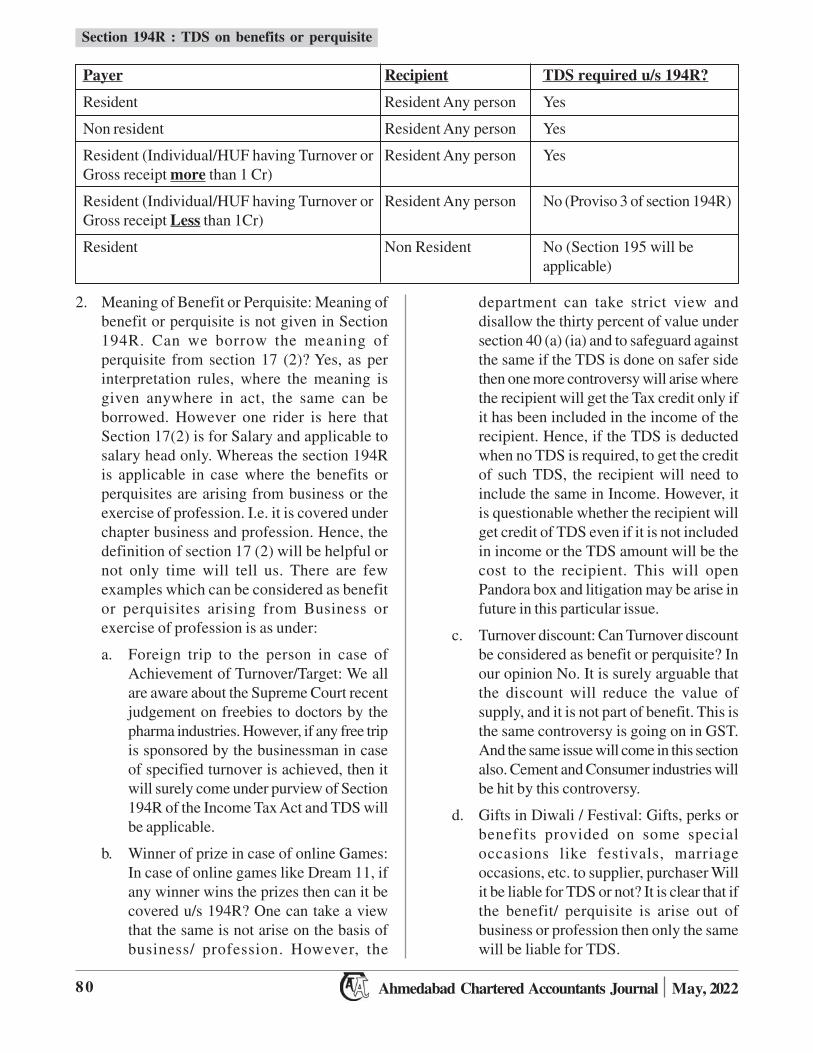

Payer Recipient TDS required u/s 194R?

Resident Resident Any person Yes

Non resident Resident Any person Yes

Resident (Individual/HUF having Turnover or Resident Any person YesGross receipt more than 1 Cr)

Resident (Individual/HUF having Turnover or Resident Any person No (Proviso 3 of section 194R)Gross receipt Less than 1Cr)

Resident Non Resident No (Section 195 will beapplicable)

2. Meaning of Benefit or Perquisite: Meaning ofbenefit or perquisite is not given in Section194R. Can we borrow the meaning ofperquisite from section 17 (2)? Yes, as perinterpretation rules, where the meaning isgiven anywhere in act, the same can beborrowed. However one rider is here thatSection 17(2) is for Salary and applicable tosalary head only. Whereas the section 194Ris applicable in case where the benefits orperquisites are arising from business or theexercise of profession. I.e. it is covered underchapter business and profession. Hence, thedefinition of section 17 (2) will be helpful ornot only time will tell us. There are fewexamples which can be considered as benefitor perquisites arising from Business orexercise of profession is as under:

a. Foreign trip to the person in case ofAchievement of Turnover/Target: We allare aware about the Supreme Court recentjudgement on freebies to doctors by thepharma industries. However, if any free tripis sponsored by the businessman in caseof specified turnover is achieved, then itwill surely come under purview of Section194R of the Income Tax Act and TDS willbe applicable.

b. Winner of prize in case of online Games:In case of online games like Dream 11, ifany winner wins the prizes then can it becovered u/s 194R? One can take a viewthat the same is not arise on the basis ofbusiness/ profession. However, the

department can take strict view anddisallow the thirty percent of value undersection 40 (a) (ia) and to safeguard againstthe same if the TDS is done on safer sidethen one more controversy will arise wherethe recipient will get the Tax credit only ifit has been included in the income of therecipient. Hence, if the TDS is deductedwhen no TDS is required, to get the creditof such TDS, the recipient will need toinclude the same in Income. However, itis questionable whether the recipient willget credit of TDS even if it is not includedin income or the TDS amount will be thecost to the recipient. This will openPandora box and litigation may be arise infuture in this particular issue.

c. Turnover discount: Can Turnover discountbe considered as benefit or perquisite? Inour opinion No. It is surely arguable thatthe discount will reduce the value ofsupply, and it is not part of benefit. This isthe same controversy is going on in GST.And the same issue will come in this sectionalso. Cement and Consumer industries willbe hit by this controversy.

d. Gifts in Diwali / Festival: Gifts, perks orbenefits provided on some specialoccasions like festivals, marriageoccasions, etc. to supplier, purchaser Willit be liable for TDS or not? It is clear that ifthe benefit/ perquisite is arise out ofbusiness or profession then only the samewill be liable for TDS.

Section 194R : TDS on benefits or perquisite

Ahmedabad Chartered Accountants Journal May, 2022 81

Let us check the question with different angle.If the gifts are given to employees in anyoccasion and if below 5000 then it is not taxableas per rule 3 of Income Tax Act. Hence, thevalue of gift will be considered as nil only if itis below 5000/-. Hence, it is taxable and if werefer Section 192 then TDS is also applicable.The same ratio is applicable in Section 194Rand TDS will be applicable in case of gifts /perquisites given to supplier and purchaser.However, another view can be taken where theTDS is deducted against the Sale under section194H under Commission.

3. Consequences of Non Compliance

a. If the required TDS is not deducted or TDSdeducted but not paid within time theninterest is payable on applicable rate. IfTDS is late deducted then interest @1%per month or part of the month is to be paidand if the TDS is deducted but not paidthen 1.5% interest per month or part of themonth. We are very much conversant withthis interest provision.

b. Also, if the TDS not deducted or deductedand not paid till the due date of filing ofreturn, Section 40 (a) (ia)can come intopicture and thirty percent of benefit valuecan be disallowed. The section isreproduced as below.

40. Notwithstanding anything to thecontrary in sections 30 to 38, thefollowing amounts shall not bededucted in computing the incomechargeable under the head “Profitand gains of business andprofession”,-

………………..will

(ia) thirty per cent of any sum payable toa resident, on which tax is deductibleat source under Chapter XVII-B andsuch tax has not been deducted or,after deduction has not been paid onor before the due date specified insub-section (1) of section139:……………

Section 194R provides the TDS is required tobe deducted on the benefit or perquisites arisingout of business/ profession. I.e. The assessee isgoing to claim the expenses as deductibleexpenses in profit and loss account and out ofthe same thirty present will be disallowed if theTDS is not deducted/ not paid according tosection 40 (a) (ia).

In 3CD report, the auditor is required to disclosewhether any sum is disallowable under section40 (a) (ia) (supra). Hence, based on thecomment on the auditor in 3CD, the CPC willprocess the return and automatically willdisallowed the required portion as per act.

Conclusion

Utmost care is required to be taken by Assesseeand Auditor both, in case of scrutinising the profitand loss account and if there is any benefit orperquisite given in the course of Business/Profession, then TDS should be deductedaccordingly. Also, it is expected from Governmentto clarify the meaning of benefits and perquisites toavoid future litigations.

❉ ❉ ❉

Section 194R : TDS on benefits or perquisite

Ahmedabad Chartered Accountants Journal May, 202282

Tax effect for maintainability of appeals

When what was assailed by the Revenue was thepenalty amounting to Rs. 29,02,743 and not thepenalty reduced by the Commissioner (Appeals).Therefore, it cannot be said that the appeal beforethe High Court at the instance of the Revenuechallenging the order passed by the ITAT was notmaintainable in view of CBDT Circular, dated 10-12-2015.

(Late Gyan Chand Jain v. CIT [ Civil Appeal No.2704 of 2022 19 April, 2022]

Foreign exchange fluctuations-freshclaim-

i). The assessee not only claimed deduction inrespect of loss of Rs. 1,10,53,909 arising onaccount of exchange fluctuation, but also setup a fresh claim in respect of revenue expensesto the tune of Rs. 2,46,04,418, erroneouslycapitalised in the returns.

ii). As regards, the transaction of loan between theappellant and Commonwealth DevelopmentCorporation, the same was in the nature ofborrowing money by the appellant, which wasnecessary for carrying on its business offinancing. It was certainly not for creation ofasset of the appellant as such or acquisition ofasset from a country outside India for thepurpose of its business. In such a scenario, theappellant would be justified in availingdeduction of entire expenditure or loss sufferedby it in connection with such a transaction interms of section 37 of the Act. For, the loan iswholly and exclusively used for the purposeof business of financing the existing Indianenterprises.

Glimpses ofSupreme CourtRulings

4 iii). Further, it was not open to the ITAT toentertain such fresh claim for the first time.This submission needs to be stated to berejected.

iv). The observations in the decision in Goetze(India) Ltd. (284 ITR 323) at footnote No.10 itself make it amply clear that suchlimitation would apply to the ‘assessingauthority’, but not impinge upon the plenarypowers of the ITAT bestowed under section254 of the Act.

{Wipro Finance Ltd. v. CIT} [Civil Appeal No.6677 of 2008 . dt 12 April, 2022]

High Court concurring with order ofITAT but no reasons stated

As the impugned order passed by the High Courtis a non-speaking and non-reasoned order and eventhe submissions on behalf of the revenue are notrecorded, the impugned order passed by the HighCourt dismissing the appeal is unsustainable.

3.2 Under the circumstances, the impugned orderis hereby quashed and set aside. The matter isremanded to the High Court to decide anddispose of the appeal afresh in accordance withlaw and on its own merits. If the High Court isof the opinion that the proposed questions oflaw are not substantial questions of law andthey are on factual aspects, it will be open forthe High Court to consider the same inaccordance with law, however, the High Courtto pass a speaking and reasoned order afterrecording the submissions made on behalf ofthe respective parties.

[Pr. CIT v. Bajaj Herbals (P.) Ltd{Civil Appeal No. 2659 of 2022 dt.7 April, 2022}

Advocate Samir N. [email protected]

5 6

Ahmedabad Chartered Accountants Journal May, 2022 83

Amalgamation and Income Tax-assessment-question of fact

this Court notes and holds that whether corporatedeath of an entity upon amalgamation per seinvalidates an assessment order ordinarily cannotbe determined on a bare application of Section 481of the Companies Act, 1956 (and its equivalent inthe 2013 Act), but would depend on the terms ofthe amalgamation and the facts of each case.

The court, undoubtedly noticed SaraswatiSyndicate. Further, the judgment in Spice (supra)and other line of decisions, culminating in this court’sorder, approving those judgments, was also noticed.Yet, the legislative change, by way of introductionof Section 2 (1A), defining “amalgamation” wasnot taken into account. Further, the tax treatment inthe various provisions of the Act were not broughtto the notice of this court, in the previous decisions.

There is no doubt that MRPL amalgamated withMIPL and ceased to exist thereafter; this is anestablished fact and not in contention. Therespondent has relied upon Spice and Maruti Suzuki(supra) to contend that the notice issued in the nameof the amalgamating company is void and illegal.The facts of present case, however, can bedistinguished from the facts in Spice and MarutiSuzuki on the following bases.

The facts of the present case are distinctive, asevident from the following sequence:

1. The original return of MRPL was filed underSection 139(1) on 30.06.2006.

2. The order of amalgamation is dated 11.05.2007but made effective from 01.04.2006. It containsa condition Clause 220 - whereby MRPLsliabilities devolved on MIPL.

3. The original return of income was not revisedeven though the assessment proceedings werepending. The last date for filing the revisedreturns was 31.03.2008, after the amalgamationorder.

4. A search and seizure proceeding wasconducted in respect of the Mahagun group,including the MRPL and other companies:

5. That all the liabilities and duties of theTransferor Companies be transferred withoutfurther act or deed to the Transferee Companyand accordingly the same shall pursuant toSection 394 (2) of the Companies Act, 1956be transferred to and beco.

6. When search and seizure of the Mahagungroup took place, no indication was givenabout the amalgamation.

7. A statement made on 20.03.2007 by Mr. AmitJain, MRPLs managing director, duringstatutory survey proceedings under Section133A, unearthed discrepancies in the books ofaccount, in relation to amounts of money inMRPLs account.

8. The return apart from specifically beingfurnished in the name of MRPL, also containedits PAN number.

9. During the assessment proceedings, there wasfull participation on behalf of all transferorcompanies, and MIPL.

10. A special audit was directed (which is possibleonly after issuing notice under Section 142).Objections to the special audit were filed inrespect of portions relatable to MRPL.

11. After fully participating in the proceedingswhich were specifically in respect of thebusiness of the erstwhile MRPL for the yearending 31.03.2006, in the cross-objectionbefore the ITAT, for the first time (in the appealpreferred by the Revenue), an additionalground was urged that the assessment orderwas a nullity because MRPL was not inexistence.

12. Assessment order was issued undoubtedly inrelation to MRPL (shown as the assessee, butrepresented by the transferee company MIPL).11. Appeals were filed to the CIT (and a cross-objection, to ITAT) by MRPL represented byMIPL.

[Pr. CIT ... vs M/S Mahagun Realtors (P) Ltd dt5 April, 2022]

❉ ❉ ❉

Glimpses of Supreme Court Rulings

7

Ahmedabad Chartered Accountants Journal May, 202284

How the power to remand a case is to beexercised by Tribunal.Golden Gate Properties Ltd. V/s. Dy.CIT (2021) 435 ITR 258 (Karn)

Issue:

How should the power to remand a case beexercised by Tribunal?

Held:

The assessee was a public limited company engagedin the business of real estate projects. The assesseefiled its return of income for the assessment year2010-11 declaring loss. The return was selected forscrutiny and the details sought for were furnished.The Assessing Officer passed an order under section143(3) of the Income tax Act, 1961. The AssessingOfficer made an addition of Rs. 14,37,10,403/-being prior period expenses for the purposes ofdetermining the book profits under the provisionsof section 115JB of the Act. The assessee filed anappeal before the Commissioner (Appeals) who byan order deleted the addition. The Revenue filedan appeal before the Tribunal. The Tribunal set asidethe order of the Commissioner (Appeals) andremitted the matter to Commissioner (Appeals)

That it was evident that while passing the order,the Tribunal had not adverted to the reasoningassigned by the Commissioner (Appeals). The orderof remand was not justified.

Two conditions for reopening u/s 147.Garden Silk Mills Limited v/s Asst. CIT(2021) 435 ITR 351 (Guj)

Issue:

Which are the two conditions to be fulfilled forreopening u/s 147?

Held:

It is settled law that in order to assume jurisdictionunder section 147 of the Income Tax Act, 1961,where the assessment has been made under section143(3), two conditions are required to be satisfied.(a) The assessing Officer must have reason tobelieve that the income chargeable to tax haveescaped assessment. (b) Such escapement occurredby reason of failure on the part of the assessee either(a) to make a return of income under section 139or in response to the notice issued under sub section(1) of section 142 or section 148 or (b) to disclosefully and truly all the material facts necessary forhis assessment for that purpose.

Reassessment proceedings under section 147 of theAct cannot be resorted to in respect of income whichis the subject matter of an appeal, reference orrevision.

Reopening of assessment on change ofopinion.T. Stanes and Company Ltd v/s. Dy.CIT (No. 1) (2021) 435 ITR 533 (Mad)

Issue:

Whether reopening of assessment on change ofopinion is valid?

Held:

Invocation of section 148 for the purpose of theproviso to section 147 qua denial of adjustmentsunder section 72A(1)(a) by the DeputyCommissioner was inspired from a change ofopinion as the assessee had disclosed the basis onwhich it had claimed deductions in the returns ofincome and it was pursuant thereto that therespective assessment orders were passed by the

11

CA. Jayesh C. [email protected]

From theCourts

12

13

Ahmedabad Chartered Accountants Journal May, 2022 85

Assessing Officer. Therefore, there was no materialsuppression of facts on the part of the assessee toeither truly or fully furnish the information that wererequired for completing the assessment. Thereforeinvocation of section 148 for the purpose of theproviso to section 147 was without jurisdiction.

Denial of claim on procedural formality.Craftsman Automation P. Ltd. v/s. CIT(2021) 435 ITR 558 (Mad)

Issue:

Whether a claim can be denied on lapse ofprocedural formality?

Held:

If an assessee is entitled to a benefit, a technicalfailure on the part of the assessee to claim the benefitin time, should not come in the way of grant of thesubstantial benefit that was otherwise availableunder the Income Tax Act, 1961 but for suchtechnical failure. The legislative intent is not towhittle down or deny benefit which are legitimatelyavailable to an assessee. The Assessing Officer isduty bound to extend substantive benefits whichare available and arrive at just tax to be paid.

The Commissioner ought to have allowed therevision application filed by the assessee undersection 264 and the assessee was entitled to partialrelief. Accordingly, the order of the Commissionerwas set aside and the Assistant Commissionerdirected to pass appropriate orders on the meritsignoring the delay on the part of the assessee infiling the revised return under section 139(5) andfailure to furnish the audit report.

Officer’s duty when substantial benefitsavailable to assessee.L. Cube Innovative Solutions P. Ltd.v/s. CIT (2021) 435 ITR 566 (Mad)

Issue:

What is the duty of A.O. when substantial benefitis available to the assessee?

Held:

The rejection of the revision application filed bythe assessee under section 264 was not justified as

From the Courts

the officers acting under the Income TaxDepartment were duty bound to extend thesubstantive benefits that were legitimately availableto an assessee. The rejection of the application forrectification by the Assessing Officer under section154 was unjustified, since the assessee was entitledto the substantive benefits under section 10B andthe delay, if any, was attributed on account of thesystem.

Notice to a non-existing entity.Tele performance Global Services v/s.Asst. CIT(2021) 435 ITR 725 (Bom)

Issue:

Whether a notice to a non existing assessee is valid?

Held:

Under an order dated February 11, 2011, a schemeof amalgamation of two companies TSPL with 1Ltd, was approved with effect from April 1, 2010,and since then TSPL ceased to exist. The successorcompany submitted returns and those were assessedfrom time to time in respect of subsequentassessment years. A notice dated March 30, 2019under section 148 of the Income Tax Act, 1961,for the assessment year 2012-13 in the name ofTSPL was issued by the Assessing Officer, withoutrealizing that the company was a nonexisting entity,directing it to file a return of income within thirtydays stating there was reason to believe that incomechargeable to tax had escaped assessment. Thenotice was void.

Order with a pre-set mind.Antony Alphonse Kevin Alphaonse v/s.ITO(2021) 435 ITR 735 (Mad)

Issue:

What is the effect of an order with a pre-set mind?

Held:

There was manifest violation of the principles ofnatural justice in passing the order before the timeprescribed for filing the reply by the assessee andconsidering such reply. The order had been passed

14

15

16

17

Ahmedabad Chartered Accountants Journal May, 202286

with a pre-set mind. The order was quashed andthe matter was remitted to the Income Tax Officerfor passing a speaking order after considering theassessee’s reply. [Matter remanded].

Sec. 147/148 two conditions.Garvit Diamonds Pvt. Ltd. v/s. ITO(2021) 435 ITR 737 (Guj)

Issue:

Which are the two conditions for invokingjurisdiction u/s 147/148?

Held:

In order to confer jurisdiction under clause (a) ofsection 147 of the Income Tax Act, 1961 beyondthe period of four years, two conditions are requiredto be fulfilled, viz(i) the Assessing Officer musthave reason to believe that income, profits or gainschargeable to tax had been underassessed orescaped assessment, and (ii) the Assessing Officermust have reason to believe that such escapementor under assessment was occasioned by reason ofthe omission or failure on the part of the assessee tomake a return under section 149 of the Act or todisclose fully and truly all material facts necessaryfor the assessment of that year.

HUF: Applicability of Sec. 171.A.O. Ores v/s. ITO(2021) 436 ITR 3 (Mad)

Issue:

When can the provisions of Sec. 171 be applied inthe case of a HUF?

Held:

That during the lifetime of ARP, the deceased fatherof the assessee, the family was not assessed as aHindu undivided family. It was only where therewas a prior assessment as a Hindu undivided familyand during the course of assessment under section143 or section 144 it was claimed by or on behalfof a member of such family which was assessed asa Hindu undivided family that there was a partitionwhether total or partial among the members of such

family, that the Assessing Officer should make anenquiry after giving notice of enquiry to all themembers. Where no such claim was made, thequestion of making enquiry by an Assessing Officerdid not arise and only in such circumstances, wouldthe definition of “partition” in Explanation tosection 171 be attracted. The definition could notbe read in isolation. Where a Hindu family wasnever assessed as a Hindu undivided family, section171 would not apply even when there was a divisionor partition of property which did not fall withinthe definition. The notice issued under section 148to the estate of ARP (HUF) co-Parceners and theconsequential order issued in the name of theassessee as the karta were unsustainable.

Recovery of Demand: Direction:Restraint.Omkara Assets Reconstruction Pvt. Ltd.v/s. Asst. CIT (2021) 436 ITR 40 (Mad)

Issue:

How the Department should proceed for recoveryof tax?

Held:

In view of the fact that the main issues forconsideration in the appeal before the Commissioner(Appeals) under section 246A were limited largelyto the inclusion of unsecured loans and share capitalas part of the total income of the assessee, the courtdirected the expeditious disposal of the pendingappeal after providing a reasonable opportunity tothe assessee, including a personal hearing if sorequested. Until such time, the Department wasrestrained from recovering the demand pursuant tothe assessment order under section 143(3) read withsection 144B.

❉ ❉ ❉

From the Courts

18

19

20

Ahmedabad Chartered Accountants Journal May, 2022 87

Randox Laboratories India (P.) Ltd. v.ACIT 135 taxmann.com 341 (Bang)Assessment Year:2015-16Order dated: 4th January 2022

Basic Facts

The assessee was a wholly owned Indian subsidiaryof U.K based company. The assessee was engagedin import of reagents and diagnostic equipments(analyzers) from the parent company and sold themto independent third parties in India. During relevantassessment year, the assessee started purchasing thereagent in bulk and packed them in smallerquantities for sale in India. Also, in order to sale.The TPO rejected transfer pricing analysis done bythe assessee under RPM and proceeded todetermine the arm’s length price by applyingTNMM as the most appropriate method on groundthat the assessee was not merely a trader but wasalso engaged in research activity. Accordingly, theTPO made adjustments for internationaltransactions. The DRP upheld the decision of theTPO. On appeal to the Tribunal:

Issue

Whether where assessee resold goods importedfrom AE to third party Indian customerswithout any value addition, Resale PriceMethod (RPM) would be Most AppropriateMethod (MAM) to determine ALP of saidtransaction

Held

For sale of reagents, the assessee enters into specificagreements with third party customers. As per theterms of the agreement, the customer in India isrequired to purchase reagents from the assessee andin the event of such purchase, the assessee provides

them the analyzer for carrying out the chemicalanalysis with the reagents. As per the terms of theagreement, the analyzer is made available to thecustomer for a period of five years without any extracost. Further, as per the terms of agreement, theassessee is required to provide spares for theanalyzer and also provide services including repairs.The analyzers were kept with the third partycustomers since the assessee was undertaking aresearch regarding its products as per Indian normsfor clinical tests and to provide feedback to the HeadOffice. Thus, the analyzers were never sold to thethird-party customers who brought the reagentsfrom the assessee but were only installed in theirpremises for chemical analysis and research workfor a period of five years. After expiry of five-yearperiod, the WDV of the analyzers get reduced tozero and accounting entries to that effect are passedin the books. Thus, it was clear, the assessee ismerely purchasing reagents from its AE andreselling them to third party customers in Indiawithout making any value addition. As per theprovisions of rule 10B. more particularly sub-rule-1(b) of the aforesaid rule, RPM is applicable to acase where the price at which property purchasedor service obtained by an enterprise from the AE isresold or provided to an unrelated enterprise. Thegross profit margin of such a transaction is thereaftercompared to the gross profit margin of similarcomparable uncontrolled transactions after makingnecessary adjustment with regard to the expenditureincurred, functional and other differences, the arm’slength price is determined. Thus, in the facts of thepresent case, as the assessee has resold the goodsimported from the AE without any value addition,the most appropriate method for determining thearm’s length price is RPM and TNMM cannot be

7

CA. Yogesh G. [email protected]

CA. Aparna [email protected]

TribunalNews

Ahmedabad Chartered Accountants Journal May, 202288

the most appropriate method in such type oftransaction. It was held that RPM is the MAM fordetermining ALP and the AO was directed tocompute the ALP after affording assesseeopportunity of being heard.

Meena Circuits (P.) Ltd. v. ACIT 135Taxmann.com 54 (Ahd)Assessment Year: 2015-16Order dated: 21st December 2021

Basic Facts

The assessee is engaged in the business ofmanufacturing of printed circuit boards. The returnof income for the year under consideration wasdeclaring total income at Rs. Nil. The said returnwas selected for scrutiny through CASS and anotice under section 143(2) of the Act along withnotice under section 142(1) of the Act was issuedby the AO to the assessee.

Issue I

Whether expenses relating to the earlier yearwere allowable in the year under consideration.

Held I

The ITAT noted from the details furnished by theassessee, the liability for the relevant expenses onaccount of AMC, professional fees and qualitycheck expenses had arisen and crystallized in theyear under consideration when the bills for thesame by the concerned parties were raised on theassessee. The ITAT therefore, found merit in thecontention of the assessee that, even though thesaid expenses pertained to the earlier year, theassessee was entitled to claim deduction for thesame in the year under consideration when theliability on account of said expenses had arisenand crystallized as a result of the bills/invoicesraised by the concerned parties. Insofar as the salepromotion expenses and commission expenseswere concerned, it was observed that thecorresponding sales in respect of which the saidcommission was payable had been made andaccounted for by the assessee in the earlier year