Annual_Report_2020.pdf - Sonali Bank

405

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Annual_Report_2020.pdf - Sonali Bank

YEAR OFEXCELLENCE

During the COVID 19 outbreak in last year, the whole world suffered immensely while Bangladesh, being vaccinated too early by our visionary leader, started to recover in different sectors of the economy. In line with the sustainable development process that the country is going through,

Sonali Bank Limited also steps towards the premium advancement through its vibrant performance in consecutive years and declares the year as “Year

of Excellence”. Both these outstanding dedications have been symbolized in the cover with the rising sun over the mountain peak.

The arranged logo of the bank over the podium represents the organizations’ top position with glittering indicators in the banking sector. The bank is

determined to accomplish the desired benchmark through suitable strategy by combating the future challenges.

KEY ACHIEVEMENT 2020

2020

3,234

20201,258,786

20201,591,234

202021,527

2020586,233

2020

629,691

2019

2,710

2019

1,158,788

2019 1,472,601

2019

17,100

2019

551,026

2019

500,387

+ 524 + 4,427

+ 99,998

+ 118,633

+ 35,207

+ 129,304

(Figure in Tk. Million except stated otherwise)

Net Profit

Deposit

Total Assets

Operating Profit

Loans & Advances

Total Investment

CREDITRATING

STATIC

Validity of Surveillance Rating

As Government Supported Bank

Without Govt. Supported Bank

Outlook

-4,320

+ 1.16%

+ 0.29%

-1.95%

+ 0.01%

+ 1.15%

2020

107,674

20207.14%

2020

4.21%

202018.37%

20200.21%

20207.13%

2019

111,994

2019

5.98%

2019 3.92%

2019

20.32%

2019

0.20%

2019

5.98%

Classified Loan

Earning Per Share

Return on Equity (ROE)

Rate of Classified Loans

Return on Asset (ROA)

Return on Investment (ROI)

Upto November 2021 Upto June 2020Long Term Short Term Long Term Short Term

AAA ST-1 AAA ST-1

A ST-2 A ST-2

Stable Stable

ORGANIZATIONAL INFORMATION

08 Letter of Transmittal

09 Notice of the 14th Annual General Meeting

10 Corporate Vision and Mission

12 Core Values

13 Ethical Principles

14 Strategic Objectives of SBL

15 Statement of Forward Looking Approach

16 Corporate Profile

19 Group Corporate Structure

20 Corporate Organogram

22 Milestones

24 List of Chairman

25 List of Managing Directors & CEOs of SBL

26 SBL at a Glance

Board of Directors and Management profile

28 Board of Directors & its committees

34 Directors’ Profile

44 Management Team

Chairman and Managing Director’s Message

48 Message from the Chairman

52 CEO & Managing Directors’ Message

Corporate Governance

58 Directors’ Report

92 Corporate Governance

105 Certificate with Compliance Report on CG

106Compliance Report with BSEC Notification on CG

117 CEO and CFO’s Declaration to the Board

118 Directors’ Responsibility for FR and IC

119 Report of the Audit Committee

122Note from the Chairman of Risk Management

Committee

STAKEHOLDERS INFORMATION

124 Stakeholders and Shareholders Information

126 Redressing to Shareholders’ Observations

129 Comparative Financial Highlights of SBL

TABLE OFCONTENTS

130 Graphical Presentations

133 Key Financial Data and Ratios of SBL

138Profitability, Dividend, Performance and

Liquidity Ratio

139 Segment wise Presentation

140 Statement of Value Addition and its Distribution

142 Market Value Added Statement

143 Financial Calendar 2020 and 2021

144 Credit Rating

RISK MANAGEMENT AND CONTROL ENVIRONMENT

146 Report on Core Risk Management

154 BASEL-III Compliance Report

154 Market Disclosures under Piller-III

Sustainability Analysis and Integrated Reporting

173 Report on Sustainable Banking

176 Report on Human Resources

180 Report on Financial Inclusion

182 Customer Care

185 Citizen Charter

186 Report on Corporate Social Responsibility

187Government Transactions and Works Related to

Social Responsibility

188 Contribution to National Economy

MANAGEMENT REVIEWAND OTHER INFORMATION

190 Management Discussion and Analysis

196 Awards and Recognition

198 Products and Services of SBL

201 Media Highlights 2020

202 Photo Gallery

Auditors’ Report and Financial Statements

211 Consolidated Financial Statements-SBL

217 Financial Statements-SBL(Solo)

331 Financial Statements- Sonali Investment Ltd.

360 Financial Statements- Islamic Banking Window

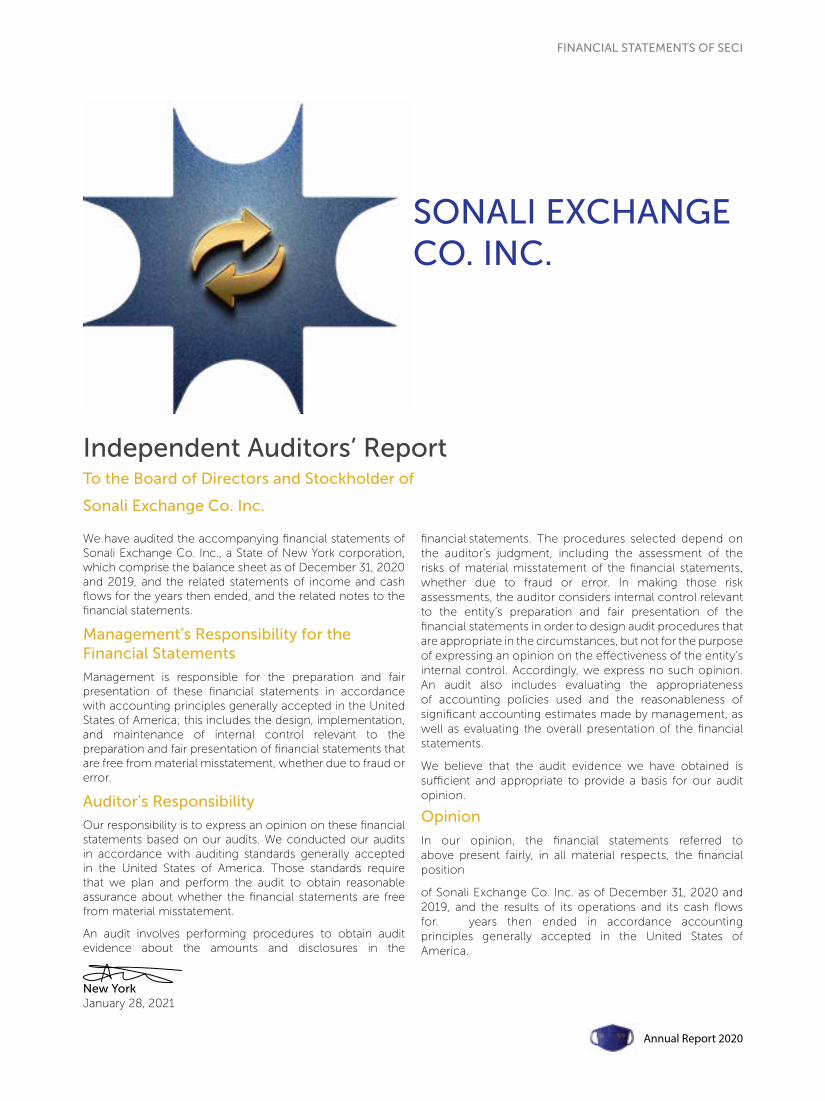

363 Sonali Exchange Co. Inc (SECI)

ADDITIONAL INFORMATION

377 Domestic Branches of SBL

390 SBL Remittance Network with World Map

392 Overseas Branches of SBL

392 Representative Branches of SBL

393 Branches of Sonali Bank (UK) Ltd.

394 Branches of SECI, USA

396 List of Acronyms

397 Standard Disclosure Index

401 SBL Branch Network

8

YEAR OF EXCELLENCE

LETTER OF TRANSMITTAL

All Shareholders of Sonali Bank Limited/

Registrar of Joint Stock Companies and Firms/

Bangladesh Securities and Exchange Commission (BSEC)/

Bangladesh Bank

Dhaka.

Sub: Annual Report for the year ended 31 December, 2020.

Dear Sir(s),

We are pleased to enclose herewith a copy of the Annual Report 2020 along with the Audited Financial Statements

(Consolidated and Solo) of Sonali Bank Limited for the year ended 31 December, 2020 and as on that date for your kind

information and record.

Financial Statements of ‘The Bank’ comprise that of Sonali Bank Limited whereas Consolidated Financial Statements comprise

Financial Statements of ‘The Bank’ and those of its operational subsidiaries- Sonali Investment Limited and Sonali Exchange

Company Inc. (SECI), USA presented separately. Analyses in this report, unless explicitly mentioned otherwise, are based on

the financials of ‘The Bank’, not the Consolidated Financials.

Yours sincerely,

(Md. Ataur Rahman Prodhan)

CEO & Managing Director

Annual Report 2020

†mvbvjx e¨vsK wjwg‡UWcÖavb Kvh©vjq

35-42, 44 gwZwSj ev/GXvKv-1000, evsjv‡`k|

†mvbvjx e¨vsK wjwg‡UW Gi PZz`©k evwl©K mvaviY mfvi †bvwUk

Avw`ó nBqv RvbvB‡ZwQ †h, †mvbvjx e¨vsK wjwg‡UW Gi 14Zg evwl©K mvaviY mfv (14th Annual General Meeting) 23 AvM÷, 2021 †ivR †mvgevi †ejv 10.30 NwUKvq wfwWI Kbdv‡iÝ Gi gva¨‡g (fvP©yqvj mfv) AbywôZ nB‡e| D³ evwl©K mvaviY mfvi Av‡jvP¨ welqmg~n wb¤œiƒct

-t Av‡jvP¨m~wP t-

(K) weMZ 20 RyjvB, 2020Zvwi‡L AbywôZ †mvbvjx e¨vsK wjwg‡UW Gi ·qv`k evwl©K mvaviY mfvi Kvh©weeiYx wbwðZKiY;(L) cwiPvjKgÛjxi cÖwZ‡e`b Ges wbix¶‡Ki cÖwZ‡e`bmn 2020 mv‡ji 31 wW‡m¤¦i mgvß eQ‡ii w¯’wZcÎ Ges jvf-¶wZi wnmve MªnY, we‡ePbv I

Aby‡gv`b;(M) 31 wW‡m¤¦i, 2020 Zvwi‡Li mgvß eQ‡ii jf¨vsk †NvlYv;(N) e¨vs‡Ki cieZx© evwl©K mvaviY mfv AbywôZ bv nIqv ch©šÍ wbix¶K wb‡qvM Ges Zuv‡`i cvwikÖwgK wba©viY; (O) cwiPvjKgÛjxi Aemi MªnY I cybtwbe©vPb;(P) mfvi †Pqvig¨v‡bi Aby‡gv`bµ‡g Ab¨ †h †Kvb welq|

m`m¨ wnmv‡e D³ mfvq Avcbvi m`q fvPz©qvj Dcw¯’wZ Kvgbv Kiv nB‡jv|

cwiPvjbv cl©` Gi Av‡`kµ‡g

(ZvIwn`yj Bmjvg)†Kv¤úvwb †m‡µUvwi

25 RyjvB, 202135-42, 44, gwZwSj ev/GXvKv-1000|

10

YEAR OF EXCELLENCE

OUR VISION

Socially committed leading banking institution with global presence.

Annual Report 2020

OUR MISSION

Dedicated to extend a whole range of quality products that support divergent

needs of people aiming at enriching their lives, creating value for the stakeholders

and contributing towards socio-economic development of the country.

12

YEAR OF EXCELLENCE

CORE VALUESThe core value proposition of Sonali Bank Limited consists of the following key elements which would assist the Bank in perceiving its employees to work as a team towards accomplishment of assigned duties and responsibilities for achievement of desired objectives. The core values include:

ETHICS

Everyone must ensure adherence to ethical practices of banking.

OBJECTIVITY

All persons will have definite objective in carrying out their tasks.

INTEGRITY

Protection and safeguard of national and customer’s interest are vital elements for societal trust.

EXCELLENCE

Excellent performance and effectiveness are pre-conditions to ensure quality service to the large customer base of the Bank.

COMMITMENT

Every employee is committed to work upto the expected level to ensure satisfaction of valued customers.

ACCOUNTABILITY

All employees are responssible for their activities and will remain accountable to their respective superior for accomplishment of tasks.

TRANSPARENCY

Information to be kept open for all so athat stakeholders can have proper ideas about the activities of the Bank.

TEAM WORK

Open communication, discussion and interaction amongst the employees would ensure unification of acitons and efforts towards achiving the common goal(s).

SELF RELIANCE

Each employee will have ownership attitude towards the Bank and self confidence in his work for the betterment of the Bank.

INNOVATION

New and innovative products are the needs of the time which continuous aciton oriented researches are being carried out.

ORGANIZATIONAL INFORMATION

Annual Report 2020

ETHICAL PRINCIPLES

Ethics is a combination of moral qualities and a collection of measurements that inquire into the values, norms and rules which form the essentials of the individual and social relations established by people from the moral aspect of right-wrong or good-bad. Sonali Bank Limited deals with public money where Ethics, Integrity and Trust is the utmost important. Bank upholds these principles in every aspect by its Management, Regulatory Compliance and Customer Services.

Sonali Bank Limited strongly realizes the functions of investments and savings by playing an intermediary role between the parties in society that supply funds and demand funds respectively, also aims the principles of profitability and productivity stipulates the requirement that they have to work in accordance with the Ethical Principles in the professional and organizational fields.

Setting off from the expansion of the banking system, the improvement of the quality of banking services, the optimal

use of sources, the prevention of the unjustified competition

among the banks, provide services to the customers with

uncompromising integrity, protect privacy and confidentiality

of customer information, prevent money laundering and

fraudulent activities, demonstrate work place respect, banks

are to regulate their relations not only among themselves

but also with the other stake holders and employees in

concordance with the Ethical Principles.

14

YEAR OF EXCELLENCE

STRATEGIC OBJECTIVES OF SBL

The core objectives of Sonali Bank Limited are to conduct transparent and high quality banking services to ensure maximum customers’ satisfaction as well as ensure financial strengthening through expanding market share within the country and abroad.

Long-standing elements of the Bank’s strategy for achieving its objectives include :

Improving corporate governance through strengthening good corporate culture, motivation, training and supervision in all levels of management.

Greater emphasize to serve potential and unbanked population of the country through providing banking services to under-served areas with the scaling up of various pilot initiatives.

Developing Human Resource Management System to motivate and retain the human resources and transform human resources to human capital through proper training in every aspects of working area.

Gaining competitive advantages by lowering overall cost compared to that of competitors.

by sector, size, economic purpose and geographical location and expand need based retail and SME/Microfinance/Women entrepreneur financing

Retaining our top leadership position by providing quality customer services.

Cost control optimization at all levels of operation by ensuring budgetary control and maximizing revenue through quality services and product diversification.

Investing in the thrust and priority sectors of the economy.

Developing sound and effective risk management culture within the Bank to safe guard the banking assets and protect the interest of the dipositors and other stake holders.

Being excellent in serving the cause of least developed community and areas.

Ensuring strong internal control and compliance culture through establishing strong control environment and sound compliance within the Bank.

Providing impeccable and progressively better customer services through introducing changed technologies.

Ensure dedicated service to the government as an exchequer and government transactions (government receipts and payments) in order to achieve expected economic growth.

Improving of deposit mix by maintaining share of low cost and no cost deposit in total deposit as well funded business.

ORGANIZATIONAL INFORMATION

Annual Report 2020

STATEMENT OF FORWARD LOOKING APPROACH

The Bank involved in various non-business activities for the well being of its millions of citizens besides its special focused on selected business segments such as corporate lending and finance, securities business and asset management as well as acquired an outstanding position in the foreign countries through export and trade finances. In order to retain the leadership position within banking sector in the country, an extensive area of this annual report has covered the Bank’s forward-looking statements on the basis of its management’s current expectations and assumptions regading the company’s business performance and non business involvemant. In coming days, the Bank is looking for fair development in the following areas to sustain its position as number one bank of the country.

z Highest degree of ICT inclusion.z Engagement of talented employees.z Exclusive human resource development

efforts.z Exclusive business re-engineering.z Customer service improvement.z Efficient internal control system.z Improvement of internal work environment.z Establishment of risk based management

system.z Adequate internally generated capital.

As any projection or forecast, forward-looking statements are inherently susceptible to uncertainty and changes in circumstances. The company’s actual results may vary materially from those expressed or implied in its forward-looking statements. Important factors that could cause the Bank’s actual results to differ materially from those in its forward-looking statements include government regulation, economic, strategic, political and social conditions and the following factors:

z Changes in the monetary and fiscal policies of the Government, including policies of the Department of the Treasury and Bangladesh Bank.

z Changes in interest rates, which may affect net income, prepayment penalty income, mortgage banking income, and other future cash flows, or the market value of our assets, including our investment securities.

z Changes in capital management policies of the Bank including use of derivatives to mitigate our interest rate exposure.

z Changes in corporate tax structure along with legislation and regulation of VAT on banking services.

z Changes in CRR and SLR of the banks as well as increase of provision requirements resulting reduction of ROA and ROE

z Fluctuation in international prices of essentials which influences the oscillation in foreign exchange market.

z Compliance issues raised by the International Forums which are likely to affect the export growth in the industrial sectors.

z Changes in the demand for deposit, loan, and investment products and other financial services in the markets we serve.

z The outcome of pending or threatened litigation, or of other matters before regulatory agencies, whether currently existing or commencing in the future.

z Environmental conditions that exist or may exist on properties owned by, leased by, or mortgaged to the Company.

z Changes in accounting principles, policies, practices and guidelines in line with IFRS and BB requirements.

z Changes in credit ratings or in our ability to access the capital markets along with other economic, competitive, governmental, regulatory, technological, and geopolitical factors affecting our operations, pricing and services.

z Priority of government and the regulator.z Status of ICT inclusion.z Inclusion of new generation human resources.z The changed banking requirements of the

customer.z Peer Bank’s forward movements.

16

YEAR OF EXCELLENCE

CORPORATE PROFILEName of the Company Sonali Bank Limited

Registered Office 35-42, 44 Motijheel Commercial Area, Dhaka, Bangladesh

Genesis Emerged as a Nationalized Commercial Bank following the Bangladesh Bank (Nationalization) Order No. 1972 vide President’s Order No. 26 of 1972.

Legal Status Public Limited Company

Date of Incorporation 03 June, 2007

Date of Commencement of Business 03 June, 2007

Vendor’s Agreement 15 November, 2007

BB License No. BRPD(P-3)745(1)/2007-1602

Banking License obtained 05 June, 2007

Date of Company Registration 03 June, 2007

Company Registration No. C-67113(4605)/07

Authorized Capital BDT 60,000.00 Million

Paid up Capital BDT 45,300.00 Million

Face Value per Share BDT 100.00 per Share

Shareholding Pattern 100% share owned by Government of the People’s Republic of Bangladesh

Tax Identification No. (TIN) 465337943663

Vat Registration No. (BIN) 000000063

Chairman of the Board of Directors Mr. Ziaul Hasan Siddiqui

CEO & Managing Director Mr. Md. Ataur Rahman Prodhan

Head of Risk Management Mr. Md. Idris

Head of ICC Mr. Imran Ahmed

Chief Financial Officer Mr. Subhash Chandra Das, FCA, FCMA

Chief Information Technology Officer Mohammad Rezwan Al Bakhtiar

Chief Audit Officer Mr. Imran Ahmed

Company Secretary Mr. Tauhidul Islam

DOMESTIC NETWORK

No. of Branches 1224

No. of Urban Branches 523

No. of Rural Branches 701

No. of General Managers’ Office 11

No. of Principal Office 46

No. of Regional Office 16

No. of Treasury Branches 732

No. of AD Branches 48

No.of Corporate Branches (incl. LO) 32

No. of Computerized Branches 1224

No. of Core Banking System Branches 1224

No. of Administrative Office 74

No. of ABB Operated Branches 1224

No. of RMS+ Operated Branches 1224

+No. of SMS Banking Operated Branches 1224

No. of Islamic Window 74

No. of Head Office Divisions 47

ORGANIZATIONAL INFORMATION

Annual Report 2020

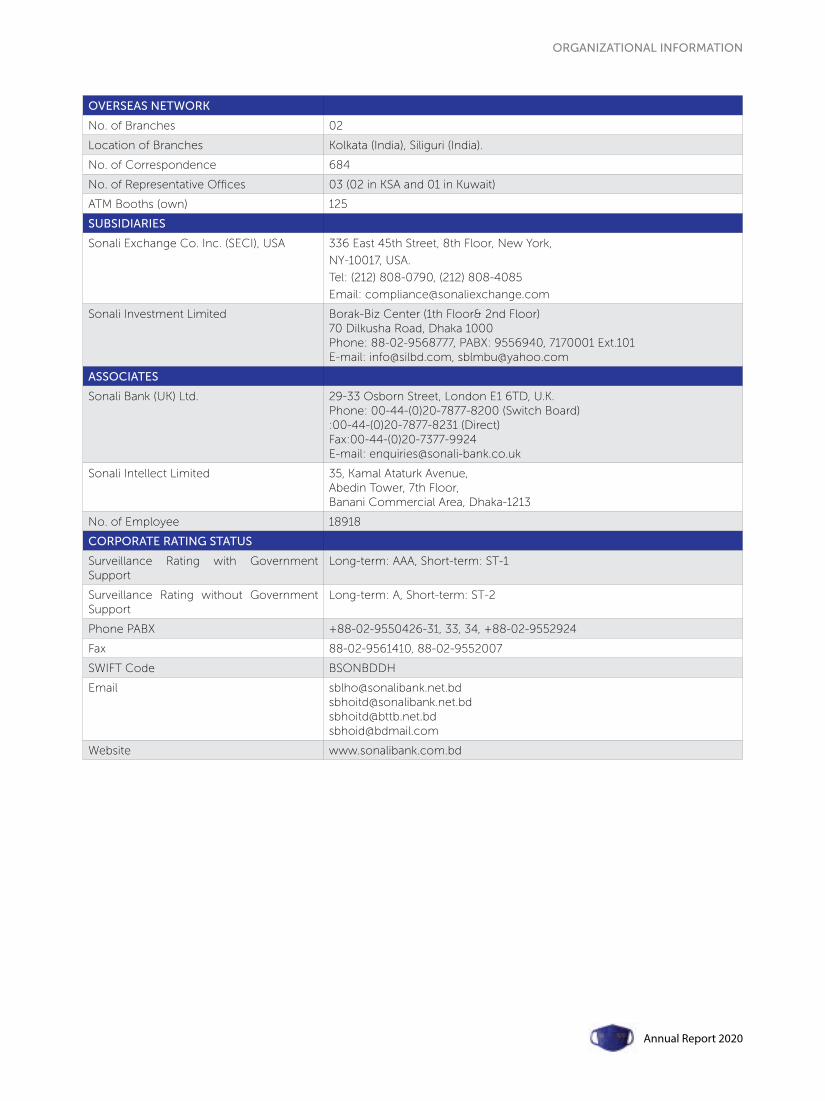

OVERSEAS NETWORK

No. of Branches 02

Location of Branches Kolkata (India), Siliguri (India).

No. of Correspondence 684

No. of Representative Offices 03 (02 in KSA and 01 in Kuwait)

ATM Booths (own) 125

SUBSIDIARIES

Sonali Exchange Co. Inc. (SECI), USA 336 East 45th Street, 8th Floor, New York,

NY-10017, USA.

Tel: (212) 808-0790, (212) 808-4085

Email: [email protected]

Sonali Investment Limited Borak-Biz Center (1th Floor& 2nd Floor) 70 Dilkusha Road, Dhaka 1000Phone: 88-02-9568777, PABX: 9556940, 7170001 Ext.101E-mail: [email protected], [email protected]

ASSOCIATES

Sonali Bank (UK) Ltd. 29-33 Osborn Street, London E1 6TD, U.K. Phone: 00-44-(0)20-7877-8200 (Switch Board):00-44-(0)20-7877-8231 (Direct)Fax:00-44-(0)20-7377-9924 E-mail: [email protected]

Sonali Intellect Limited 35, Kamal Ataturk Avenue,Abedin Tower, 7th Floor,Banani Commercial Area, Dhaka-1213

No. of Employee 18918

CORPORATE RATING STATUS

Surveillance Rating with Government Support

Long-term: AAA, Short-term: ST-1

Surveillance Rating without Government Support

Long-term: A, Short-term: ST-2

Phone PABX +88-02-9550426-31, 33, 34, +88-02-9552924

Fax 88-02-9561410, 88-02-9552007

SWIFT Code BSONBDDH

Email [email protected]@[email protected]@bdmail.com

Website www.sonalibank.com.bd

18

YEAR OF EXCELLENCE

LEGAL ADVISORS OF SBL

01 Begum Hosne Ara BegumHaque Law Chamber (2nd floor),Jiban Bima Bhaban,121, Motijheel C/A, Dhaka.Mob: 01711522775

02 Mr. Khaled Bin ShahriarSuit no: 906 (9th floor),H.M.Siddiqui Mension, 55/A,Purana Paltan, Ramna, Dhaka.Phone: 02-9574376

03 Mohammad Shafiqul IslamRoom no:105 (Anex Extension Bhaban),Supreme Court Lawyers Association, Dhaka.Mob: 01711583269

04 Mr. Fayez AhmedRoom no: 227, Supreme Court Bar Bhaban,Dhaka-1000.Mob: 01711440304

05 Md. RokonuzzamanSuit no: 404 (3rd floor), Ibrahim Mension,11, Purana Paltan, Dhaka.Mob: 01715330077

AUDITOR OF SBL

ACNABINChartered AccountantsBDBL Bhaban (Level-13), 12 Karwan Bazar C/A, Dhaka, Bangladesh.Tel: +88-02-41020030, Fax: +88-02-41020036

TAX ADVISOR OF SBL

Akhter Zamil and Co.Chartered AccountantsIbrahim Mansion (1st Floor), Room No. 207, 11, Purana Paltan, Dhaka-1000.Telephone: 88 02 7124898E-Mail: [email protected]

CREDIT RATING COMPANY OF SBL

Credit Rating Information and Services Limited(CRISL)Nakshi Homes (1st, 4th & 5th Floor)6/1/A, SegunbagichaDhaka -1000.

LAW CONSULTANT

Md. Barekuzzaman

ORGANIZATIONAL INFORMATION

Annual Report 2020

Sonali Bank Limited

LocalSonali Investment

Limited (SIL)

LocalSonali Polaries

FT Limited

StatusName of the

CompanyDate of

EstablishmentPaid-up Capital

No. of Branches

Prime Activities

Subsidiaries

Sonali Investment Limited

22 April, 2010BDT 2000.00 million

05

Merchant banking, portfolio management, issue management, capital market transactions

Sonali Exchenge Co. Inc. (SECI), USA

12 December, 1994

USD 950,000.00

10Remittance business,undertake and participate in all transactions

Associates

Sonali Polaris FT Limited

01 February, 2012

BDT 75.00 million

-Customize, enhance, modify and implement Intellect CBS 10.0 Software

Sonali Bank (UK) Limited

07 December, 2001

GBP 25.00 million

02 All types of banking activities

SUBSIDIARIES ASSOCIATES

OverseasSonali Exchange Co.

Inc. (SECI) USA

OverseasSonali Bank (UK) Limited

GROUP CORPORATE STRUCTURE

20

YEAR OF EXCELLENCE

Your Trusted Partner in Innovative Banking

Corporate Organogram

SBL O�ces/Branches:

:

:

:

::::

1GM Headed Corporate Br. 2DGM Headed Corporate Br. 24AGM Headed Corporate Br. 5

Local O�ice Br.

Principal O�ce (PO) 46

Regional O�ce (RO) 16

Head O�ce Divisions 47

GM O�ce (GMO) 11

::::::

::

Sonali Investment Limited 1SECI, USA 1

SO Headed Br. 218

AGM Headed Br.

Foreign Br. 2

Total Branches 1,226

59SPO Headed Br. 375PO Headed Br. 543

::

::::: 372

SPO & 1 274

GM & eq. 30

3

DGM & eq.

Sonali Bank Ltd. Manpower:CEO & MD 1DMD 5

146AGM & eq.

Sonali Bank (UK) Limited 1SBL, Representative O�ices

:::::

O�cer & eq. 12,937Total Manpower 22,904

SPO & eq. 1,274PO & eq. 2,793SO & eq. 5,346

Executive CommitteeAudit CommitteeRisk Management Committee

Board of DirectorsChairman, Directors

CEO & Managing Director

GM & Company Secretary

COMPANY AFFAIRS AND

BOARD DIVISION (CABD)

CEO & MANAGING

DIRECTOR'S

SECRETARIAT

Chief Information Technology

O�icer (CITO)

GM GMPrincipal (GM)

TRAINING DIVISION (TD)

GM,Local O�ice

GM,Recovery-LO

Chief Audit

O�icer (CAO)

GMGM

GMChief

Financial

O�icer (CFO)

GMGM

GM

DMDDMDDMDDMDDMD

AUDIT &

INSPECTION

DIVISION-2 (OTHER THAN CORPORATE

BRANCHES )

GENERAL

ADVANCES

DIVISION (GAD)

TREASURY

MANAGEMENT

DIVISION - 1

(FRONT OFFICE)

CENTRAL

ACCOUNTS

DIVISION

(PAYMENT)

LOAN

RECOVERY

DIVISION (LRD)

EMPLOYEES

WELFARE &

TRANSPORT DIVISION (EWTD)

EXTERNAL

AUDIT

INDUSTRIAL

PROJECTTREASURY

MANAGEMENT

GOVT.

ACCOUNTS &LEGAL

HUMAN

RESOURCEIT DIVISION

FOREIGN

REMITTANCE

SECURITY AND

PROTOCOL DIVISION OVERSEAS Br:

Kolkata Br IndiaGM

6 SBTI Training

Institutes) :

CTG, Mymensingh, Khulna, Rajshahi, Bogura, Cumilla.

INFORMATION

TECHNOLOGY

DIVISION

(BUSINESS IT)

BRANCHES

CONTROL

DIVISION (BCD)

COMMON

SERVICES

DIVISION (CSD)

Sonali Bank Sta� College

IT DIVISION

(INFRASTRUCTURE

IT)

BUSINESS

DEVELOPMENT

DIVISION (BDD)

ESTABLISHMENT

&

ENGINEERING

DIVISION (EED)

GM, Ramna Corp

Br

AUDIT &

INSPECTION

DIVISION-1 (CORPORATE BRANCHES &

CONTROLLING OFFICES)

AGRO-BASED

PROJECT

FINANCING DIVISION (APFD)

INTERNATIONAL

TRADE

FINANCE

DIVISION

CENTRAL

ACCOUNTS

DIVISION

(OPERATION)

LOAN

CLASSIFICATION

DIVISION (LCD)

DISCIPLINE &

APPEAL

DIVISION (DAD)

FOREIGN

EXCHANGE AUDIT

AND INSPECTION

MICRO CREDIT

DIVISION (MCD)

INFORMATION

SECURITY, IT RISK

MANAGEMENT &

FRAUD CONTOL

CARDS

DIVISION (CD)

VIGILANCE AND

COMPLAINT

MANAGEMENT

Sonali Exchange

Company Inc.

( SECI ), USA

GMSonali

PUBLIC

RELATIONS

DIVISION (PRD)

MONEY LAUNDERING

& TERRORISM

FINANCING

PREVENTION

DIVISION (MLTFPD)(ex MLTFPVD)

INTERNAL

AUDIT

COMPLIANCE

DIVISION

SMALL AND

MEDIUM

ENTERPRISE

DIVISION (SME)

RECONCILIATION

DIVISION (RD)

RISK

MANAGEMENT

DIVISION (RMD)

HUMAN

RESOURCE

MANAGEMENT DIVISION (HRMD)

IT DIVISION (IT PROCUREMENT

& MAINTENANCE)

AUDIT

COMPLIANCE

DIVISION

PROJECT

FINANCING

DIVISION

MANAGEMENT

DIVISION - 2 (MID & BACK OFFICE)

ACCOUNTS &

SERVICES DIVISION (GASD)

MATTERS

DIVISION (LMD)

RESOURCE

DEVELOPMENT DIVISION (HRDD)

O

(IT SERVICES

MANAGEMENT)

REMITTANCE

MANAGEMENT DIVISION (FRMD)

PROTOCOL DIVISION

(SPD)

Chief Security

O�cer (CSO)

Kolkata Br, I ndia

Siliguri Br, India

Representative

O�ice:

Riyadh-KSA;

Jeddah-KSA;

Kuwait

Sonali Investment Ltd (Subsidiary of

SBL)

4 Branches =

Motijheel Main Br;

Paltan; Uttara;

Mirpur. Khulna

GMO GMO GMO GMO GMOGMOGMO GMO GMO GMO

CONTROL &

MONITORING

DIVISION

(CMD)

RURAL CREDIT

DIVISION (RCD)

Law Consultant

Chief Medical O�cer

MIS &

STATISTICS

DIVISION (MSD)

ISLAMIC

BANKING

DIVISION (IBD)

DIVISION (FEAID)DIVISION (MCD)

DIVISION

MANAGEMENT

DIVISION (VCMD)(SECI), USA

(Subsidiary of SBL)

9 Branches:

Manhattan; Jackson Heights; Astoria;

Atlanta; Michigan; Paterson; Jamaica; Ozone Park; Bronx. 1 Booth: Brooklyn.

Bank(UK)Ltd(Subsidiary of

SBL)

2 Branches =

London Main Br.;

Birmingham.

RO: Joypurhat,Chapai Nawabganj;

RO: Nilphamari RO: Laxmipur RO: Sherpur; Netrokona

RO: Rajbari; Gopalganj

RO: Pirojpur;Bhola

PO:Rangpur; Dinajpur;

Gaibandha; Thakurgaon (Panchagarh);

Kurigram (Lalmonirhat)

PO:Cumilla;

Chandpur; Brahmanbaria; Noakhali; Feni

PO:Mymensingh;

Tangail; Kishoreganj;

Jamalpur

PO:Faridpur;

Madaripur (Shariatpur);

Kushtia; Chuadanga(Meherpur)

PO:Barishal

(Jhalakathi); Patuakhali (Barguna)

PO:Rajshahi; Pabna;

Bogura; Sirajganj;

Naogaon; Natore

RO: Manikganj RO: - RO: Cox's Bazar; Bandarban

RO: Bagerhat; Narail

RO: Sunamganj

PO:Bangabandhu Avenue

(Dhaka Central ), Dhaka South (Sadarghat),

Gazipur, Narsingdi

PO:Dhaka West (Ramna), Dhaka East (Motijheel),

Mirpur, Narayanganj,

Munshiganj

PO:CTG-North, CTG-South, Patiya-CTG,

Rangamati (Kh hh i)

PO:Khulna; Jashore;

Jhenaidah(Magura); Satkhira

PO:Sylhet;

Moulvibazar; Habiganj

116 Br. 139 Br. 118 Br. 106 Br. 78 Br.143 Br

GMO, RANGPUR

GMO, Cumilla

GMO,MYMENSINGH

GMO, FARIDPUR

GMO, Barishal

GMO, RAJSHAHI

106 Br 106 Br. 109 Br. 123 Br 80 Br.

GMO, DHAKA-1

GMO, DHAKA-2

GMO, Chattogram (CHITTAGONG)

GMO, KHULNA

GMO, SYLHET

DGM Corp Br:Rangpur Corp;

AGM Corp Br:Dinajpur

Corp(AGM)

DGM Corp Br: Cumilla Corp

DGM Corp Br:Mymensingh Corp

DGM Corp Br:Faridpur Corp

DGM Corp Br: ---

AGM Corp Br: Barishal Corp

(AGM)

DGM Corp Br:Wage Earners';

Dilkusha Corp;

Sadarghat Corp;

PM's O�ce;

DU Corp Br;

Hotel Sheraton

(InterContinental)

Corp Branch.

DGM Corp Br: BWAPDA Corp;

Foreign Exch;

Shilpa Bhaban;

Dhaka Cantt.;

Dhanmondi;

Chawk Bazar;

Narayangonj Corp

DGM Corp Br:Agrabad Corp;Laldighi Corp;

Wage Earners'-Ctg

DGM Corp Br:Khulna Corp;

Daulatpur Corp;

AGM Corp Br :Jashore Corp(AGM)

DGM Corp Br:Darga Gate Corp;

AGM Corp Br:Sylhet Corp(AGM)

DGM Corp Br:Rajshahi Corp;

AGM Corp Br:Bogura Corp(AGM)

Chapai Nawabganj;

GM,BB Avenue

Corp Br

Sonali Bank Limited

CORPORATE ORGANOGRAM

ORGANIZATIONAL INFORMATION

Annual Report 2020

Your Trusted Partner in Innovative Banking

Corporate Organogram

SBL O�ces/Branches:

:

:

:

::::

1GM Headed Corporate Br. 2DGM Headed Corporate Br. 24AGM Headed Corporate Br. 5

Local O�ice Br.

Principal O�ce (PO) 46

Regional O�ce (RO) 16

Head O�ce Divisions 47

GM O�ce (GMO) 11

::::::

::

Sonali Investment Limited 1SECI, USA 1

SO Headed Br. 218

AGM Headed Br.

Foreign Br. 2

Total Branches 1,226

59SPO Headed Br. 375PO Headed Br. 543

::

::::: 372

SPO & 1 274

GM & eq. 30

3

DGM & eq.

Sonali Bank Ltd. Manpower:CEO & MD 1DMD 5

146AGM & eq.

Sonali Bank (UK) Limited 1SBL, Representative O�ices

:::::

O�cer & eq. 12,937Total Manpower 22,904

SPO & eq. 1,274PO & eq. 2,793SO & eq. 5,346

Executive CommitteeAudit CommitteeRisk Management Committee

Board of DirectorsChairman, Directors

CEO & Managing Director

GM & Company Secretary

COMPANY AFFAIRS AND

BOARD DIVISION (CABD)

CEO & MANAGING

DIRECTOR'S

SECRETARIAT

Chief Information Technology

O�icer (CITO)

GM GMPrincipal (GM)

TRAINING DIVISION (TD)

GM,Local O�ice

GM,Recovery-LO

Chief Audit

O�icer (CAO)

GMGM

GMChief

Financial

O�icer (CFO)

GMGM

GM

DMDDMDDMDDMDDMD

AUDIT &

INSPECTION

DIVISION-2 (OTHER THAN CORPORATE

BRANCHES )

GENERAL

ADVANCES

DIVISION (GAD)

TREASURY

MANAGEMENT

DIVISION - 1

(FRONT OFFICE)

CENTRAL

ACCOUNTS

DIVISION

(PAYMENT)

LOAN

RECOVERY

DIVISION (LRD)

EMPLOYEES

WELFARE &

TRANSPORT DIVISION (EWTD)

EXTERNAL

AUDIT

INDUSTRIAL

PROJECTTREASURY

MANAGEMENT

GOVT.

ACCOUNTS &LEGAL

HUMAN

RESOURCEIT DIVISION

FOREIGN

REMITTANCE

SECURITY AND

PROTOCOL DIVISION OVERSEAS Br:

Kolkata Br IndiaGM

6 SBTI Training

Institutes) :

CTG, Mymensingh, Khulna, Rajshahi, Bogura, Cumilla.

INFORMATION

TECHNOLOGY

DIVISION

(BUSINESS IT)

BRANCHES

CONTROL

DIVISION (BCD)

COMMON

SERVICES

DIVISION (CSD)

Sonali Bank Sta� College

IT DIVISION

(INFRASTRUCTURE

IT)

BUSINESS

DEVELOPMENT

DIVISION (BDD)

ESTABLISHMENT

&

ENGINEERING

DIVISION (EED)

GM, Ramna Corp

Br

AUDIT &

INSPECTION

DIVISION-1 (CORPORATE BRANCHES &

CONTROLLING OFFICES)

AGRO-BASED

PROJECT

FINANCING DIVISION (APFD)

INTERNATIONAL

TRADE

FINANCE

DIVISION

CENTRAL

ACCOUNTS

DIVISION

(OPERATION)

LOAN

CLASSIFICATION

DIVISION (LCD)

DISCIPLINE &

APPEAL

DIVISION (DAD)

FOREIGN

EXCHANGE AUDIT

AND INSPECTION

MICRO CREDIT

DIVISION (MCD)

INFORMATION

SECURITY, IT RISK

MANAGEMENT &

FRAUD CONTOL

CARDS

DIVISION (CD)

VIGILANCE AND

COMPLAINT

MANAGEMENT

Sonali Exchange

Company Inc.

( SECI ), USA

GMSonali

PUBLIC

RELATIONS

DIVISION (PRD)

MONEY LAUNDERING

& TERRORISM

FINANCING

PREVENTION

DIVISION (MLTFPD)(ex MLTFPVD)

INTERNAL

AUDIT

COMPLIANCE

DIVISION

SMALL AND

MEDIUM

ENTERPRISE

DIVISION (SME)

RECONCILIATION

DIVISION (RD)

RISK

MANAGEMENT

DIVISION (RMD)

HUMAN

RESOURCE

MANAGEMENT DIVISION (HRMD)

IT DIVISION (IT PROCUREMENT

& MAINTENANCE)

AUDIT

COMPLIANCE

DIVISION

PROJECT

FINANCING

DIVISION

MANAGEMENT

DIVISION - 2 (MID & BACK OFFICE)

ACCOUNTS &

SERVICES DIVISION (GASD)

MATTERS

DIVISION (LMD)

RESOURCE

DEVELOPMENT DIVISION (HRDD)

O

(IT SERVICES

MANAGEMENT)

REMITTANCE

MANAGEMENT DIVISION (FRMD)

PROTOCOL DIVISION

(SPD)

Chief Security

O�cer (CSO)

Kolkata Br, I ndia

Siliguri Br, India

Representative

O�ice:

Riyadh-KSA;

Jeddah-KSA;

Kuwait

Sonali Investment Ltd (Subsidiary of

SBL)

4 Branches =

Motijheel Main Br;

Paltan; Uttara;

Mirpur. Khulna

GMO GMO GMO GMO GMOGMOGMO GMO GMO GMO

CONTROL &

MONITORING

DIVISION

(CMD)

RURAL CREDIT

DIVISION (RCD)

Law Consultant

Chief Medical O�cer

MIS &

STATISTICS

DIVISION (MSD)

ISLAMIC

BANKING

DIVISION (IBD)

DIVISION (FEAID)DIVISION (MCD)

DIVISION

MANAGEMENT

DIVISION (VCMD)(SECI), USA

(Subsidiary of SBL)

9 Branches:

Manhattan; Jackson Heights; Astoria;

Atlanta; Michigan; Paterson; Jamaica; Ozone Park; Bronx. 1 Booth: Brooklyn.

Bank(UK)Ltd(Subsidiary of

SBL)

2 Branches =

London Main Br.;

Birmingham.

RO: Joypurhat,Chapai Nawabganj;

RO: Nilphamari RO: Laxmipur RO: Sherpur; Netrokona

RO: Rajbari; Gopalganj

RO: Pirojpur;Bhola

PO:Rangpur; Dinajpur;

Gaibandha; Thakurgaon (Panchagarh);

Kurigram (Lalmonirhat)

PO:Cumilla;

Chandpur; Brahmanbaria; Noakhali; Feni

PO:Mymensingh;

Tangail; Kishoreganj;

Jamalpur

PO:Faridpur;

Madaripur (Shariatpur);

Kushtia; Chuadanga(Meherpur)

PO:Barishal

(Jhalakathi); Patuakhali (Barguna)

PO:Rajshahi; Pabna;

Bogura; Sirajganj;

Naogaon; Natore

RO: Manikganj RO: - RO: Cox's Bazar; Bandarban

RO: Bagerhat; Narail

RO: Sunamganj

PO:Bangabandhu Avenue

(Dhaka Central ), Dhaka South (Sadarghat),

Gazipur, Narsingdi

PO:Dhaka West (Ramna), Dhaka East (Motijheel),

Mirpur, Narayanganj,

Munshiganj

PO:CTG-North, CTG-South, Patiya-CTG,

Rangamati (Kh hh i)

PO:Khulna; Jashore;

Jhenaidah(Magura); Satkhira

PO:Sylhet;

Moulvibazar; Habiganj

116 Br. 139 Br. 118 Br. 106 Br. 78 Br.143 Br

GMO, RANGPUR

GMO, Cumilla

GMO,MYMENSINGH

GMO, FARIDPUR

GMO, Barishal

GMO, RAJSHAHI

106 Br 106 Br. 109 Br. 123 Br 80 Br.

GMO, DHAKA-1

GMO, DHAKA-2

GMO, Chattogram (CHITTAGONG)

GMO, KHULNA

GMO, SYLHET

DGM Corp Br:Rangpur Corp;

AGM Corp Br:Dinajpur

Corp(AGM)

DGM Corp Br: Cumilla Corp

DGM Corp Br:Mymensingh Corp

DGM Corp Br:Faridpur Corp

DGM Corp Br: ---

AGM Corp Br: Barishal Corp

(AGM)

DGM Corp Br:Wage Earners';

Dilkusha Corp;

Sadarghat Corp;

PM's O�ce;

DU Corp Br;

Hotel Sheraton

(InterContinental)

Corp Branch.

DGM Corp Br: BWAPDA Corp;

Foreign Exch;

Shilpa Bhaban;

Dhaka Cantt.;

Dhanmondi;

Chawk Bazar;

Narayangonj Corp

DGM Corp Br:Agrabad Corp;Laldighi Corp;

Wage Earners'-Ctg

DGM Corp Br:Khulna Corp;

Daulatpur Corp;

AGM Corp Br :Jashore Corp(AGM)

DGM Corp Br:Darga Gate Corp;

AGM Corp Br:Sylhet Corp(AGM)

DGM Corp Br:Rajshahi Corp;

AGM Corp Br:Bogura Corp(AGM)

Chapai Nawabganj;

GM,BB Avenue

Corp Br

Sonali Bank Limited

Corporate organogram reflects the corporate governance culture of the organization. It shows the relation between Board of Directors, head office divisions, controlling offices and branches as well as employees of the Bank as a whole. Organogram of Sonali Bank Limited is structured as follows:

22

YEAR OF EXCELLENCE

1972 1974 1985 1989

1973 1980 1986

Commencement of banking operatrion of Sonali Bank

First agency

transactions

First annual report

Inauguration of

million

Foreign remittance

million

1st computer

Bank

1990 1994 2001 2006

1993 19992005

2007 2009 2010 2012

2008 2009 to 2013

2011

2013 2015 2017 2019

2014

2016

2018 2020

Sonali Bank

million

Foreign remittance

commencement of business of Sonali Bank

ICMAB Best

SMS Banking

Implementation of

Retail Banker in

Islami Banking

Implementation of RMS+ Software

million

million

Sonali Bank

Strongest Bank in

Asian Banker

Collecting Bank

Financial Institute of

Operation being

Best Corporate

trillion

Core Banking

Achieved HighestOperating Pro�t(20257.37 million)in Overall BankingSector.

Achieved HighestNet Pro�t(2264.21 million)Among all State OwnedCommercial Banks inBangladesh.

1st position in AnnaulPerformanceAgreement (APA)2018-29 by the Financial InstitutionsDivision.

Achieved the ICMABBest Corporate Award.

Achieved Center forNon-ResidanceBangladesh (NRBs)Award.

Achieved HighestOperating Pro�t(21526.93 million)in Overall BankingSector.

Achieved HighestNet Pro�t(3234.35 million)Among all State OwnedCommercial Banks inBangladesh.

MILESTONES

ORGANIZATIONAL INFORMATION

Annual Report 2020

1972 1974 1985 1989

1973 1980 1986

Commencement of banking operatrion of Sonali Bank

First agency

transactions

First annual report

Inauguration of

million

Foreign remittance

million

1st computer

Bank

1990 1994 2001 2006

1993 19992005

2007 2009 2010 2012

2008 2009 to 2013

2011

2013 2015 2017 2019

2014

2016

2018 2020

Sonali Bank

million

Foreign remittance

commencement of business of Sonali Bank

ICMAB Best

SMS Banking

Implementation of

Retail Banker in

Islami Banking

Implementation of RMS+ Software

million

million

Sonali Bank

Strongest Bank in

Asian Banker

Collecting Bank

Financial Institute of

Operation being

Best Corporate

trillion

Core Banking

Achieved HighestOperating Pro�t(20257.37 million)in Overall BankingSector.

Achieved HighestNet Pro�t(2264.21 million)Among all State OwnedCommercial Banks inBangladesh.

1st position in AnnaulPerformanceAgreement (APA)2018-29 by the Financial InstitutionsDivision.

Achieved the ICMABBest Corporate Award.

Achieved Center forNon-ResidanceBangladesh (NRBs)Award.

Achieved HighestOperating Pro�t(21526.93 million)in Overall BankingSector.

Achieved HighestNet Pro�t(3234.35 million)Among all State OwnedCommercial Banks inBangladesh.

24

YEAR OF EXCELLENCE

LIST OF CHAIRMANS

Sl. Managing Director and Chairman, Sonali Bank Tenure

01 Mr. G. M. Chowdhury 29.03.1972 – 26.03.1973

02 Mr. A. K. N. Ahmed 27.03.1973 – 17.11.1974

03 Mr. S. A. Chowdhury (Current Charge) 18.11.1974 – 24.01.1975

04 Mr. K. A. Rashid 25.01.1975 – 12.03.1981

Sl. Chairman, Board of Directors, Sonali Bank Tenure

01 Mr. A. M. Zahiruddin Khan (MP) 15.04.1981 – 31.03.1982

02 Mr. S. A. Khair 19.05.1982 – 04.12.1985

03 Mr. Chowdhury A. K. M. Aminul Haque 14.01.1986 – 30.03.1986

04 Mr. Keramat Ali 20.04.1986 – 09.04.1989

05 Major General (Retd.) M. Shamsul Haque (MP) 23.04.1989 – 24.05.1990

06 Mr. Md. Abdur Rahim (MP) 04.06.1990 – 25.11.1990

07 Mr. Md. Akhtar Ali 26.12.1990 – 30.06.1991

08 Mr. Iqbal Mahmud 04.08.1991 – 12.02.1996

09 Mr. A. N. M. Eusuf 28.02.1996 – 06.08.1996

10 Mr. M. Asafuddowlah 03.09.1996 – 03.08.1998

11 Mr. Mohammed Farashuddin 08.09.1998 – 18.11.1998

12 Mr. A. I. Aminul Islam 14.12.1998 – 14.06.2000

13 Mr. Muhammed Ali 27.06.2000 – 31.07.2001

14 Professor Dr. Amirul Islam Chowdhury 09.08.2001 – 07.08.2002

15 Mr. B. M. M. Mozharul Huq, NDC 12.08.2002 – 20.04.2003

16 Professor Mahbub Ullah 22.08.2003 – 19.04.2006

17 Mr. A. B. Mirza Md. AzizulIslam 19.04.2006 – 12.12.2006

18 Mr. Ali Imam Majumder 14.12.2006 – 16.11.2007

Sl. Chairman, Board of Directors, Sonali Bank Limited Tenure

01 Mr. Ali Imam Majumder 17.11.2007 – 09.09.2009

02 Mr. Quazi Baharul Islam 14.09.2009 – 27.12.2012

03 Dr. A H M Habibur Rahman 27.12.2012 -19.04.2015

04 Mr. Md. Fazle Kabir 05.05.2015-20.03.2016

05 Mr. Mohammad Muslim Chowdhury, Chairman (Acting) 21.03.2016-25.07.2016

06 Mr. Md. Ashraful Moqbul 26.07.2016–30.07.2019

07 Mr. Ziaul Hasan Siddiqui 28.08.2019 – Till Date

ORGANIZATIONAL INFORMATION

Annual Report 2020

CEO & MANAGING DIRECTORSOF SBL

Sl. Name Designation Tenure

Administrators / Managing Directors of Sonali Bank

01 Mr. M. Fazlur Rahman Administrator 16.12.1971 - 28.03.1972

02 Mr. G. M. Chowdhury Managing Director 29.031972 – 26.03.1973

03 Mr. A. K. N. Ahmed Managing Director 27.03.1973 – 17.11.1974

04 Mr. S. A. Chowdhury (Current Charge) Managing Director 18.11.1974 – 24.01.1975

05 Mr. K. A. Rashid Managing Director 25.01.1975 – 02.06.1979

06 Mr. S. A. Chowdhury (Current Charge) Managing Director 05.06.1979 – 31.07.1979

07 Mr. K. A. Rashid Managing Director 01.08.1979 – 12.03.1981

08 Mr. Abul Hashem (Current Charge) Managing Director 13.03.1981 – 02.05.1981

09 Mr. M. Ijadur Rahman Managing Director 03.05.1981 – 05.09.1983

10 Mr. Lutfar Rahman Sarker Managing Director 06.09.1983 – 01.01.1985

11 Mr. Ashraful Haque Managing Director 02.01.1985 - 31.07.1986

12 Mr. Shah Md. Afanur (Current Charge) Managing Director 01.08.1983 - 09.08.1986

13 Mr. A. A. Qureshi Managing Director 10.08.1986 - 01.10.1988

14 Mr. M.M.Nurul Haque (Current Charge) Managing Director 02.10.1988 - 18.04.1989

15 Mr. M. Ahsanul Haque Managing Director 19.04.1989 – 01.08.1996

16 Mr. Kh.Monjur Murshid (Current Charge) Managing Director 02.08.1996 - 02.08.1996

17 Mr. A. Q. Siddiqui Managing Director 03.08.1996 – 18.02.1997

18 Mr. Khandkar Ibrahim Khaled Managing Director 18.02.1997 – 03.11.1997

19 Mr. Mahbubur Rahman Khan Managing Director 03.11.1997 – 02.11.1999

20 Mr. Mahammad Hussain Managing Director 03.11.1999 – 02.01.2000

21 Mr. Md. Yusuf Ali Hawlader (Acting) Managing Director 03.01.2000 – 05.01.2000

22 Mr. Md. Enamul Haque Choudhury Managing Director 06.01.2000 – 15.05.2001

23 Mr. S. A. Chowdhury Managing Director 16.05.2001 - 12.11.2001

24 Mr. Rabiul Hossain Managing Director 12.11.2001 – 08.07.2004

25 Mr. M. Tahmilur Rahman Managing Director 09.07.2004 – 16.11.2006

26 Mr. Md. Amanullah (Additional) Managing Director 17.11.2006 – 16.12.2006

27 Mr. S. M. Aminur Rahman Managing Director 17.12.2006 – 14.11.2007

CEO & Managing Directors of Sonali Bank Limited

01 Mr. S. M. Aminur Rahman Managing Director & CEO 15.11.2007 – 25.01.2008

02 Mr. Mohammad Humayun Kabir(Additional) Managing Director & CEO 26.01.2008 - 27.01.2008

03 Mr. S. A. Chowdhury Managing Director & CEO 28.01.2008 – 27.01.2010

04 Mr. Kazi Fakhrul Islam (Additional) Managing Director & CEO 28.01.2010 – 19.05.2010

05 Mr. Mohammad Humayun Kabir Managing Director & CEO 20.05.2010 – 19.05.2012

06 Mr. Mohammad Atiqur Rahman (Additional) Managing Director & CEO 20.05.2012 – 16.06.2012

07 Mr. Pradip Kumar Dutta Managing Director & CEO 17.06.2012 - 16.06.2016

08 Mr. Ataur Rahman Prodhan (Additional) Managing Director & CEO 17.06.2016 – 23.08.2016

09 Mr. Md. Obayed Ullah Al Masud CEO & Managing Director 24.08.2016- 23.08.2019

10 Mr. Md. Ataur Rahman Prodhan CEO & Managing Director 28.08.2019- Till Date

26

YEAR OF EXCELLENCE

SON

ALI

BA

NK

LIM

ITE

DA

T A

GLA

NC

E(T

k. in

mill

ion

)

Year

De

po

sit

Loan

s an

d

Ad

van

ces

Cla

ssifi

ed

Lo

ans

Imp

ort

Exp

ort

Fore

ign

re

mit

tan

ceO

pe

rati

ng

P

rofi

tN

et

Pro

fit

Cap

ital

A

de

qu

acy

Rat

io

Man

po

we

r (O

ffice

r)M

anp

ow

er

(Sta

ff)

No

of

Bra

nch

es

Au

tho

rize

d

Cap

ital

Pai

d u

p

Cap

ital

20

20

1258

786

58

62

33

1076

7416

5550

2516

012

90

56

215

27

32

34

10.0

216

738

218

012

26

60

00

04

53

00

20

1911

58

788

5510

26

1119

94

2559

65

256

66

1114

83

1710

02

710

10.0

917

245

23

64

1224

60

00

04

53

00

20

1810

976

66

46

416

612

188

32

570

20

32

50

310

278

12

02

57

22

64

10.1

014

671

26

00

1215

60

00

04

53

00

20

1710

64

311

42

32

1814

93

02

11553

00

28

49

48

22

92

119

55

709

210

.35

153

08

29

93

1211

60

00

04

130

0

20

1610

316

08

38

453

810

911

513

43

28

36

88

210

59

22

42

51

1516

10.3

318

793

1410

120

96

00

00

38

30

0

20

158

66

012

34

63

46

86

84

92

00

59

94

54

32

124

798

86

51

58

710

.08

194

01

26

99

120

76

00

00

38

30

0

20

1477

80

43

33

7554

86

43

73

00

143

63

52

512

7652

854

76

055

12.2

419

55

42

89

212

04

60

00

03

120

0

20

136

858

95

34

34

51

103

769

1958

92

62

96

713

28

62

29

713

58

07.

59

196

53

32

37

120

32

00

00

112

50

20

1259

92

94

378

147

125

975

28

728

88

740

811

68

66

110

36

(24

959

)(0

.94

)2

00

88

32

95

120

02

00

00

112

50

20

1153

319

23

459

91

615

88

30

7479

80

878

1015

38

123

91

99

57

12.6

018

59

63

34

211

96

20

00

011

25

0

20

104

7813

42

86

09

86

83

1516

40

43

7414

310

43

788

48

9(9

75)

10.8

017

98

92

85

111

87

20

00

09

00

0

20

09

40

615

22

54

02

36

98

34

96

86

46

44

42

102

60

92

311

34

90

14.6

018

09

13

415

118

32

00

00

90

00

20

08

36

43

86

23

116

772

677

1514

65

793

90

103

44

516

172

311

12.6

111

50

710

33

211

82

20

00

09

00

0

20

07

32

89

97

20

63

48

92

014

764

97

780

46

92

178

424

79

7412

.47

1176

910

773

118

310

00

09

00

0

20

06

30

23

03

2410

29

58

90

16

776

379

69

59

84

49

30

06

(36

276

)(1

6.3

2)

1211

811

155

118

310

00

05

00

0

20

05

277

079

22

700

15

112

611

852

86

40

92

754

82

39

64

20

84

.06

123

80

115

53

118

310

00

03

272

20

04

252

23

416

82

83

476

54

852

39

572

1376

68

09

53

158

4.6

512

732

1171

811

86

100

00

32

72

20

03

23

03

39

15519

84

96

64

52

577

479

07

6553

554

010

65.

08

122

60

124

55

118

610

00

03

272

20

02

22

22

22

156

113

52

86

35

29

40

415

03

66

09

89

1015

95.

07

123

80

128

57

122

110

00

03

272

20

01

215

54

114

199

35

43

99

414

194

38

09

50

09

04

91

82

5.0

212

728

130

25

129

110

00

03

272

20

00

1973

81

133

28

1515

07

50

82

24

42

11 4

793

579

713

2-

1217

113

875

129

310

00

03

272

199

916

93

7312

35

63

577

61

352

763

89

58

413

03

126

126

-11

99

014

06

513

06

100

00

32

72

199

815

170

79

44

41

471

123

42

713

68

28

29

793

102

102

-12

06

114

45

713

1110

00

03

272

ORGANIZATIONAL INFORMATION

Annual Report 2020

Year

De

po

sit

Loan

s an

d

Ad

van

ces

Cla

ssifi

ed

Lo

ans

Imp

ort

Exp

ort

Fore

ign

re

mit

tan

ceO

pe

rati

ng

P

rofi

tN

et

Pro

fit

Cap

ital

A

de

qu

acy

Rat

io

Man

po

we

r (O

ffice

r)M

anp

ow

er

(Sta

ff)

No

of

Bra

nch

es

Au

tho

rize

d

Cap

ital

Pai

d u

p

Cap

ital

199

713

60

62

854

51

39

00

93

20

40

33

158

240

92

132

132

-11

62

914

49

613

1310

00

03

272

199

612

38

35

7611

63

08

67

29

50

52

62

84

198

1024

824

8-

871

617

52

713

1310

00

03

272

199

511

08

33

658

30

250

81

418

722

09

98

1978

171

671

6-

86

67

175

51

1310

100

00

32

72

199

410

1411

53

89

32

124

52

83

68

188

1818

80

96

136

13-

873

616

94

113

07

100

00

32

72

199

38

46

85

53

63

12

160

013

136

1214

015

38

52

02

0-

814

917

48

713

03

100

00

32

72

199

276

678

48

69

317

56

713

29

410

557

149

84

45

45

-8

28

516

477

130

010

00

024

27

199

16

876

64

52

1811

971

122

34

106

68

1375

617

17-

766

117

45

012

96

100

00

242

7

199

0573

92

44

311

-16

98

012

559

1318

051

51

-76

08

176

50

129

110

00

024

27

198

952

214

418

68

-2

019

011

33

511

84

652

52

-74

80

182

22

128

52

00

55

198

84

579

53

52

77-

172

719

703

113

05

160

160

-73

37

185

07

1276

20

05

5

198

73

96

29

29

80

8-

1656

375

31

113

56

164

164

-71

48

184

41

126

22

00

55

198

63

5572

29

272

-14

46

56

83

510

30

04

59

459

-73

63

185

22

125

42

00

55

198

53

4576

275

41

-13

514

729

08

50

14

99

49

9-

60

80

1919

112

45

20

05

5

198

42

703

12

212

3-

972

16

151

90

81

552

552

-6

09

918

32

112

33

20

03

0

198

32

04

97

170

11-

979

658

41

110

22

50

550

5-

52

53

160

84

1214

50

30

198

215

96

116

83

2-

94

32

56

758

34

34

81

48

1-

39

31

1377

610

55

50

30

198

111

92

711

856

-8

182

470

1510

12

32

23

2-

39

47

139

40

103

15

03

0

198

010

96

79

62

6-

109

26

46

48

42

06

177

177

-18

183

1011

50

30

1979

83

88

675

6-

790

84

051

577

39

69

6-

134

81

84

35

03

0

1978

59

96

48

33

-3

63

23

36

33

88

56

46

4-

1174

470

95

03

0

1977

46

62

36

25

-2

951

23

36

180

59

89

8-

1013

56

00

50

30

1976

38

44

2419

-2

175

164

977

79

19

1-

85

56

45

05

03

0

1975

33

29

215

1-

274

19

124

42

97

81

-6

98

94

00

50

30

1974

22

7816

77-

216

36

63

189

40

31

-6

29

43

59

50

30

1973

210

312

90

-70

352

52

162

52

1-

576

03

06

50

30

1972

173

18

54

-4

32

2-

05

02

-4

708

274

50

20

(Tk.

in m

illio

n)

28

YEAR OF EXCELLENCE

BOARD OF DIRECTORS

Ziaul Hasan Siddiqui

Chairman

A.B.M Ruhul Azad

Director (Joined on 15.06.2021)

A. K. M. Kamrul Islam FCA, FCS

Director

Md. Fazlul Haque

Director (Retired on 03.06.2021)

BOARD OF DIRECTORS AND THEIR PROFILE

Annual Report 2020

Ishtiaque Ahmed Chowdhury

Director

Molla Abdul Wadud

Director

Dr. Daulatunnaher Khanam

Director

Professor Dr. Mohammad Kaykobad

Director (Joined on 25.08.2020)Md. Ataur Rahman Prodhan

CEO & Managing Director

Md. Mofazzal Husain

Director

30

YEAR OF EXCELLENCE

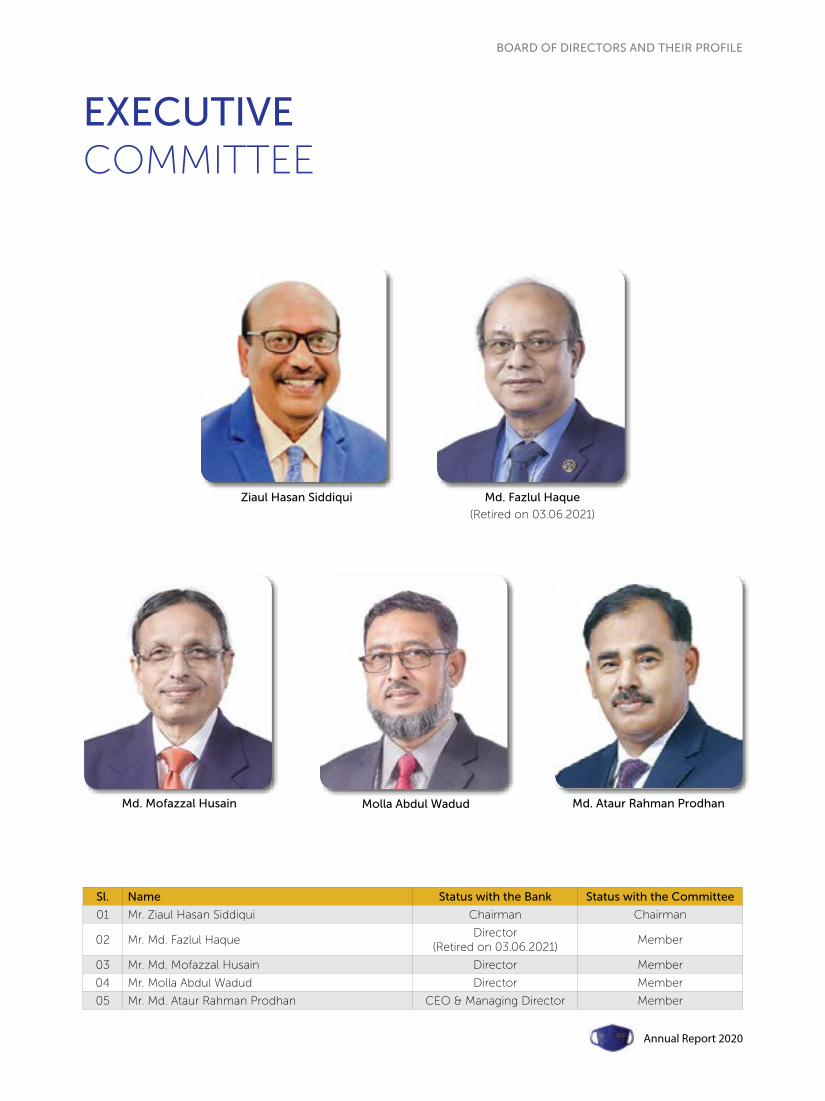

COMPOSITION OF COMMITTEES OF THE BOARD OF DIRECTORSExecutive Committee

Sl. Name Status with the Bank Status with the Committee

01 Mr. Ziaul Hasan Siddiqui Chairman Chairman

02 Mr. Md. Fazlul HaqueDirector

(Retired on 03.06.2021)Member

03 Mr. Md. Mofazzal Husain Director Member

04 Mr. Molla Abdul Wadud Director Member

05 Mr. Md. Ataur Rahman Prodhan CEO & Managing Director Member

Audit CommitteeSl. Name Status with the Bank Status with the Committee

01 Mr. A.K.M. Kamrul Islam FCA, FCS Director Chairman

02 Mr. Ishtiaque Ahmed Chowdhury Director Member

03 Dr. Daulatunnaher Khanam Director Member

04 Professor Dr. Mohammad Kaykobad Director Member

Risk Management CommitteeSl. Name Status with the Bank Status with the Committee

01 Mr. Ishtiaque Ahmed Chowdhury Director Chairman

02 Mr. Md. Fazlul HaqueDirector

(Retired on 03.06.2021)Member

03 Dr. Daulatunnaher Khanam Director Member

04 Mr. Md. Mofazzal Husain Director Member

05 Professor Dr. Mohammad Kaykobad Director Member

Composition of Shariah Supervisory CommitteeSl. Name Status with the Committee

01 Professor Dr. Muhammad Abdur Rashid Chairman

02 Mr. Md. Mofazzal Husain Member

03 Mr. Md. Ataur Rahman Prodhan Member

04 Deputy Managing Director-1 Member

05 Mr. Md. Abdul Awwal Sarkar Member

06 Mufti Mohammad Muhibbullahil Bakee Member

07 Dr. Md. Ruhul Amin Rabbani Member

BOARD OF DIRECTORS AND THEIR PROFILE

Annual Report 2020

EXECUTIVECOMMITTEE

Ziaul Hasan Siddiqui Md. Fazlul Haque

(Retired on 03.06.2021)

Md. Ataur Rahman ProdhanMd. Mofazzal Husain Molla Abdul Wadud

Sl. Name Status with the Bank Status with the Committee

01 Mr. Ziaul Hasan Siddiqui Chairman Chairman

02 Mr. Md. Fazlul HaqueDirector

(Retired on 03.06.2021)Member

03 Mr. Md. Mofazzal Husain Director Member

04 Mr. Molla Abdul Wadud Director Member

05 Mr. Md. Ataur Rahman Prodhan CEO & Managing Director Member

32

YEAR OF EXCELLENCE

AUDITCOMMITTEE

A.K.M. Kamrul Islam FCA, FCS Ishtiaque Ahmed Chowdhury

Dr. Daulatunnaher Khanam Professor Dr. Mohammad Kaykobad

Sl. Name Status with the Bank Status with the Committee

01 Mr. A.K.M. Kamrul Islam FCA, FCS Director Chairman

02 Mr. Ishtiaque Ahmed Chowdhury Director Member

03 Dr. Daulatunnaher Khanam Director Member

04 Professor Dr. Mohammad Kaykobad Director Member

BOARD OF DIRECTORS AND THEIR PROFILE

Annual Report 2020

RISK MANAGEMENTCOMMITTEE

Ishtiaque Ahmed Chowdhury Md. Fazlul Haque

(Retired on 03.06.2021)

Professor Dr. Mohammad KaykobadDr. Daulatunnaher Khanam Md. Mofazzal Husain

Sl. Name Status with the Bank Status with the Committee

01 Mr. Ishtiaque Ahmed Chowdhury Director Chairman

02 Mr. Md. Fazlul HaqueDirector

(Retired on 03.06.2021)Member

03 Dr. Daulatunnaher Khanam Director Member

04 Mr. Md. Mofazzal Husain Director Member

05 Professor Dr. Mohammad Kaykobad Director Member

34

YEAR OF EXCELLENCE

Ziaul Hasan Siddiqui

Chairman

Mr. Ziaul Hasan Siddiqui joined as Chairman of the Board of Directors of Sonali Bank Limited on 22 August, 2019. He is the former Deputy Governor of Bangladesh Bank.

Mr. Ziaul Hasan Siddiqui has track-record of successfully developing customized financial and management strategies to meet the needs of bank on the basis of continuous analysis of economic trends. He has strong ability to quickly understand an organization; evaluate business and investment opportunities prevailing in the market and leverage those based on organizational strengths. He is equally savvy to ensure business growth and diversification.

Mr. Siddiqui has highly successful and results-driven exposure in the financial sector with more than 35 years of comprehensive versatile Central Bank experience. Mr. Siddiqui started his career with Bangladesh Bank in 1976. He served as Deputy Governor of Bangladesh Bank for more than 5 years with specialization in monetary policy, foreign exchange policy and reserve management. He also served as Head of Financial Intelligence Unit (FIU) of Bangladesh tasked with the responsibility of upgrading Anti Money Laundering (AML) regime to international standard and formulating strategies for Combating Financing of Terrorism (CFT). He played a key role in making Taka convertible for current account transaction, moving from fixed to floating exchange regime, sovereign rating of Bangladesh and drafting the Guidelines for Foreign Exchange Transaction.

He was the Managing Director of Security Printing Press Corporation Bangladesh Ltd. and a member of the APG Steering Committee representing South Asian Countries. He also acted as the Chairman of Bangladesh Commerce Bank Ltd., Board member of Karma Sangsthan Bank Ltd. and AB

bank Ltd. He was an advisor to Prime Bank Limited and was an independent director of Union Capital Ltd., Summit Power Ltd., and Summit Purbanchal Power Co. Ltd. Before joining as Chairman of Sonali Bank Limited, Mr Siddiqui was CEO of IOF (IGW Operators Forum). He taught Microeconomics, Macroeconomics, Financial Institutions and Markets at BRAC University, Northern University, University of Asia Pacific and Australian Catholic University in Sydney. He is also the Chairman of the Sonali Investment Limited. He also lectured at Bangladesh Public Administration Training Centre, Defence Services Command and Staff College and National Defence College.

Mr. Siddiqui obtained his MPA (Masters in Public Administration) degree from Harvard University (USA) and MA degree in Economics from Dhaka University. He enhanced his professional expertise by participating in a number of foreign training courses including ones from Ohio State University, World Bank, IMF and ADB. Besides having professional diploma in Banking (DAIBB), Mr. Siddiqui has completed Training and Assessment Certificate Course from Australia.

Late Rahim Uddin Siddiqui, father of Mr.Siddiqui was a renowned Journalist of many prominent National Dailies of the country, including the Daily Azad, Ittefaq, Millat etc and died a premature death while working as a class one gazetted officer (information officer). Late Julekha Siddiqui, mother of Mr. Siddiqui was a homemaker. Mr. Siddiqui’s wife Mrs. Bilu Siddiqui, is a Grade-A singer of Bangladesh Betar and BTV. She also performs in different TV channels. Mr. Siddiqui is blessed with a daughter and a son. Both of them live in Australia.

BOARD OF DIRECTORS AND THEIR PROFILE

Annual Report 2020

Md. Fazlul Haque

Director (Retired on 03.06.2021)

Md. Fazlul Haque, Additional Secretary, has been appointed as Director of Sonali Bank Limited on December, 2015 while he was working in Bank and Financial Institutions Division of Ministry of Finance. Mr. Haque enjoyed various positions at the national level such as the Project Director of Bangladesh Trade Policy Support Program (BTPSP), the Joint Secretary (Relief) of the Ministry of Disaster Management and Relief (MoDMR), the Secretary of Bangladesh Jute Mills Corporation, the Director Administration and Director Finance in Civil Aviation Authority of Bangladesh and the Deputy Secretary at the Ministry of Establishment.

Md. Fazlul Haque is a career civil servant and started his career in the administrative service of Bangladesh. The first date of his joining in the service was 21st January, 1986 (BCS 1984 Batch) as Assistant Commissioner at Chittagong Collectorate. At the field level, he worked as Assistant Commissioner (Land), at Raozan and Hathazari, Upazila Magistrate at Boalkhali under Chittagong District. He worked

as Upazila Nirbahi Officer at Feni Sadar and Banshkhali under Chittagong District and Additional District Magistrate in Rangamati Hill District.

Mr. Haque completed his MBA in 2005. He obtained his M.Sc. and B.Sc.(Honours) degrees in Agricultural Economics from Bangladesh Agricultural University, Mymensingh. He has undergone a number of professional trainings at home and abroad. Working as Assistant Commissioner (Land) he published a book on land matters named Namzari (Mutation).

He visited Cambodia, Sweden, London, China, South Korea, Japan, Singapore, Pakistan, Sri Lanka, India, Indonesia, Ethiopia, Malaysia, USA, UAE and Saudi Arabia for the purpose of Training, knowledge sharing on Administration, Disaster Management, Social Protection Activities, Public Policies and Religious Prayers.

Md. Fazlul Haque was born on 10th August, 1960 in a respectable muslim family in the District of Jamalpur.

36

YEAR OF EXCELLENCE

Md. A.B.M Ruhul Azad was appointed as a Director of the Board of Directors, Sonali Bank Limited on 15 June, 2021. He is also an active member of Executive Committee and Risk Management Committee of the Board of Directors of Sonali Bank Limited. He has been working as the Additional Secretary of Financial Institutions Division of Ministry of Finance, Government of the People’s Republic of Bangladesh since October 23,2018.

Mr. Azad is respected for his innovative ideas, concepts and various challenging endeavors in Management & Public Administration. Mr. Azad enjoyed various positions at the national level such as Additional Secretary of Ministry of Youth and Sports, Director of Bangladesh Krira Shikkha Pratisthan (BKSP), Deputy Director of National Housing Authority (NHA) and Deputy Secretary, Ministry of Industries.

A. B. M Ruhul Azad is a career Civil Servant and started his career of as an officer of BCS 8th Batch (1986).The first date of his joining in the service was 20 December 1989.During the early stage of his career Mr. Azad worked in different position of Bangladesh Ansar. In 2006 Mr. Azad was appointed as the Deputy Secretary of Ministry of Public

Administration. He was promoted as Joint Secretary in 2013 and promoted as Additional Secretary in 2017.

Mr. Azad obtained his B.Sc. (Honors) degree in Agricultural Science from Sher-E-Bangla Agricultural University, Dhaka. He also obtained MSS degree in Government and Politics.

Mr. Azad has participated in different international conferences and meetings as a member of Bangladesh delegation. Mr. Azad had the opportunity to participate various training, workshop and seminar held in different countries of the world such as India, South Korea, Singapore, Thailand, Vietnam, China, Netherlands, Austria, Belgium, Switzerland, France, Turkey, Italy and USA. He also completed training program on “Public Administration Development Program on Public Policy, Service Delivery and Negotiations” from Duke University, North Carolina, USA. He has a special training on Intellectual Property Right System.

A. B. M Ruhul Azad was born on 1st January, 1963 in a respectable muslim family in the District of Narsingdi. He is married to Ms. Mirza Morsheda Mahbub. They are blessed with two sons.

A.B.M Ruhul Azad

Director (Joined on 15.06.2021)

BOARD OF DIRECTORS AND THEIR PROFILE

Annual Report 2020

Mr. A.K.M. Kamrul Islam was appointed as a Director to the Board of Directors of the Bank on 22 December 2016. He is the Chairman of the Audit Committee of the Bank. He is a partner of Islam Aftab Kamrul & Co. Chartered Accountants. He has special expertise in Assurance & Auditing, Taxation and Financial Consultancy Services.

Mr. Islam became Chartered Accountants and fellow member of the Institute of Chartered Accountants of Bangladesh (ICAB) in 1993. He is also a fellow and associate member of many National and International Professional Bodies.

Mr. Islam is a fellow member of Institute of Chartered Secretaries of Bangladesh (ICSB); associate member of Information System Audit and Control Association (ISACA), USA and International Institute of Internal Auditors, Florida, USA; life member of Bangladesh Economic Association since 1997; member of Bangladesh Society for Total Quality Management (BSTQM); founder member of Intellectual Property Association of Bangladesh (IPAB) and Chairman of Mashnoons Limited.

Mr. Islam was an active member and elected Director of Dhaka Chamber of Commerce and Industry (DCCI) for 2005-07 and 2016-2018. He is currently Senior Vice President of DCCI. He also has been elected as the Director of Japan Bangladesh Chamber of Commerce and Industries (JBCCI) for the period of 2016-2018. He is President of the Accounting Alumni, University of Dhaka and Life Member of Transparency International Bangladesh Chapter.

Mr. Islam is respected for his innovative ideas, concepts and various challenging endeavors in business sectors and social works in Bangladesh. He has 29 years of professional experience.

Mr. Islam graduated with Honors and Masters in Accounting from Dhaka University. He visited India, Pakistan, Nepal, Bhutan, Japan, China, Thailand, Singapore, Malaysia, Netherlands, Belgium, Germany, Saudi Arabia etc.

Mr. Islam, son of late Alhaj A.K.M. Tajul Islam and late Hasne Ara Islam, was born in Comilla on 14 January 1959. He is married to Mrs. Syeda Kaniz Fatema who is a housewife. They have two daughters.

A.K.M. Kamrul Islam FCA, FCS

Director

38

YEAR OF EXCELLENCE

Mr. Ishtiaque Ahmed Chowdhury, has been nominated as the Director of the Board of Directors of Sonali Bank Limited on September 19, 2018. Prior to this, he was the Managing Director & CEO of Trust Bank Limited.

Having started his career with Rupali Bank Limited as Probationary Officer in 1977, Mr. Chowdhury gained grounded experiences in many fields ranging over rural banking, SME banking, Wholesale Banking and Client Acquisition that helped him make remarkable turnaround of loss incurring branches into profitable ones within target time.

Mr. Chowdhury spent half of his career time in AB Bank Limited, the first private commercial bank of the country, from 1984 through 2002. He headed major corporate branches of the Bank including Kawran Bazar, Uttara, and Motijheel Corporate Branch. He also worked in Financial Control department of the Bank for almost four years. He won the best manager award and appreciation for his outstanding performance at the Bank.

Over the last 29 years, Mr. Chowdhury’s career evolved as a well rounded banker with adequate exposures in Strategic Risk Management, Revenue Growth, Client Acquisition, and Operations Management.

Mr. Chowdhury believes in inclusive banking and has Always put efforts to bring banking services to the doorstep of people at large. He strongly holds that a banker has to be trustworthy and dedicated towards serving people in order to uplift their livelihood and socio economic status.

He has also proven to be an effective team player and can get things done by ensuring coherent and integrated management atmosphere. He is one of the proponents of

situational leadership approach and can pursue tough goals in any market scenario.

He is a dreamer, humanitarian, organizer and an art connoisseur. He is involved in Rotary Club and held position of President of Jahangirnagar, Dhaka unit of Rotary District. He is also Treasurer of Combat Hunger Project Committee of Rotary International District. He is a member of Uttara Club, Kurmitola Golf Club, and Childhood Cancer Foundation, Dhaka. He is presently Executive Member of Association of Bankers Bangladesh (ABB). He is a “Tax Card” holder, a very prestigious status provided by NBR for 2011-2013. Mr. Chowdhury has also won the 13th Rapport Award for Excellence in Human Resource Development-2013.

With a distinctive academic track record, he passed S.S.C and H.S.C in 1968 and 1970 respectively. He holds MSS degree with Honors in Political Science and Law from the University of Dhaka. He is a DiplomaEd Associate of Institute of Bankers, Bangladesh.

Mr. Chowdhury visited many countries for official purpose as well as personal pleasure. He participated in a good number of professional trainings, workshops, and seminars at home and abroad. He participated in a certificate course titled ‘Value Creation in Banking and Strategic Management in INSEAD (Business School for the world) frame sponsored by Standard Chartered Bank from October 29 to November 01, 2015.

Mr. Chowdhury was born in Sylhet in 1953. His father was a member of Assam Legislative Council of British Period in Assam, India. Mr. Chowdhury is married to Syeda Latifa Ishtiaque. Their only son, Chowdhury Ahmed Tausif Ishtiaque has graduated from Institute of Business Administration (IBA), University of Dhaka and is now working in HSBC Bangladesh.

Ishtiaque Ahmed Chowdhury

Director

BOARD OF DIRECTORS AND THEIR PROFILE

Annual Report 2020

Dr. Daulatunnaher Khanam has been director of Sonali Bank Limited since January 13, 2019. Prior to this, she was the Deputy Managing Director of Bangladesh House Building Finance Corporation.