Annual Report 2017-18 - Stree Nidhi

94

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Annual Report 2017-18 - Stree Nidhi

Annual Report 2017-18 i

Stree Nidhiii

Annual Report 2017-18 iii

Stree Nidhiiv

Annual Report 2017-18 v

Abbreviations

ABFL Agri Business Finance LimitedAGM Assistant General ManagerATM Automated Teller MachineBC Banking CorrespondentCARP Community Audit Resource PersonCBOs Community Based OrganisationsCEO Chief Executive OfficerCIF Community Investment FundCRD Commissioner Rural DevelopmentCRM Credit MonitoringCSP Customer Service ProviderCSR Corporate Social ResponsibilityDCB Demand Collection BalanceDRDA District Rural Development AgencyDRDO District Rural Development OfficerDRP District Resource PersonEFMS Electronic Fund Management SystemEMIs Equated Monthly InstalmentsFPGs Farmer Producer GroupsFPOs Farmer Producer OrganisationsHLP Household Livelihood PlanHO Head OfficeIGA Income Generation ActivityIHHL Individual House Hold LatrineIIBF Indian Institute of Banking & FinanceIT Information TechnologyITE & C Information Technology Electronics & CommunicationsIWMP Integrated Watershed Management ProgrammeMACS Mutually Aided Cooperative SocietyMAS Mahila Abhivrudhi SocietcyMC Managing CommitteeMDM Mobile Device ManagementMEPMA Mission for Elimination of Poverty in Municipal AreasmFIs micro Finance InstitutionsMIS Management Information SystemMS Mandal SamakhyaMUDRA Micro Units Development and Refinance AgencyNABARD National Bank For Agriculture & Rural DevelopmentNBFC Non Banking Financial CompanyNCDC National Cooperative Development Corporation

Stree Nidhivi

NGO Non Government OrganisationNHC Neighbourhood CentersNPA Non Performing AssetNREGA National Rural Employment Guarantee ActNRLM National Rural Livelihood MissionNSTFDC National Scheduled Tribes Finance and Development CorporationNULM National Urban Livelihood MissionOBs Office BearersOSS One Stop ShopPA Per AnnumPCs Personal ComputersPMJJBY Pradhan Mantri Jeevan Jyoti Bima YojanaPMKSY Pradhan Mantri Krishi Sinchayee YojanaPMSBY Pradhan Mantri Suraksha Bima YojanaPR & RD Panchayath Raj & Rural DevelopmentPSSK Palle Samagra Seva KendraluPwD Persons with DisabilityRBI Reserve Bank of IndiaRM Regional ManagerRSETI Rural Self Employment Training InstituteSBI State Bank of IndiaSC Scheduled CasteSCSP Scheduled Caste Sub PlanSERP Society for Elimination of Rural PovertySHG Self Help GroupSLCC State Level Consultative CommitteeSLF Slum Level FederationSMS Short Message ServiceSRLM State Rural Livelihood MissionST Scheduled TribeSULM State Urban Livelihood MissionSVEP Start-up Village Enterprenuership ProgrammeTLF Town Level FederationTS CAB Telangana State Cooperative Apex BankTSP Tribal Sub PlanTSSSAAT Telangana State Society for Social Audit , Accountability and TransparencyURL Uniform Resource LocatorVLEs Village Level EnterprenuersVLR Vaddi Leni RunaluVO Village Orginisation

Annual Report 2017-18 vii

INDEXChapter Particulars Page No. No.

PART - A

1 Community based financial institutions - Stree Nidhi a new 1-4 paradigm in Micro finance

2 Stree Nidhi - A Game Changer in Micro finance canvas of Telangana 5-10

3 New Initiatives / Policy Changes 11-12

4 Role of SERP and MEPMA 13-14

5 Stree Nidhi – a Community managed Institution 15-17

6 Stree Nidhi - Resources 18-20

7 Loan Policy 21-24

8 Credit Disbursement and Outreach 25-33

9 Stree Nidhi Credit Portfolio – Risk Mitigation Strategies 34-35

10 Financial Performance 36-40

11 Empowerment of Community through Digitalization 41-43

12 Financial Inclusion - Stree Nidhi as Corporate Business 44-46Correspondent to Banks

13 Institutional Monitroing, Capacity Building of Staff and Community 47-50

14 Corporate Governance in Stree Nidhi 51-52

PART - B Tables 53-78

PART - C Financial Statements 79-80

Stree Nidhiviii

Annual Report 2017-18 ix

Stree Nidhix

Annual Report 2017-18 xi

Annual Report 2017-18 1

lending, regular banking functions andinadequate staff to focus on such lending andmonitoring thereof. Further, there is anapprehension that risks will be higher withincreased quantum of loans as these loans areunsecured. There is also a school of thoughtincreased quantum of credit to SHGs withoutassessment of credit needs of members wouldresult in unproductive lending. The loansavailed by SHGs are generally equallydistributed perhaps as loans are requested forall the members in a SHG at the sametime,whether they require loan at thatparticular time or not.

1.4. The issues confronting bank linkageprogramme in general are concerning to delayin disbursement, inadequate loan amount,absence of member wise assessment of loans,equal distribution of loans by all members, lackof monitoring mechanism and no risk coverageto loans and members, etc.1.5. While many of the above issues can beaddressed with the intervention of RBI/NABARDand of banks,the challenges in ensuring propermember wise due diligence, financinglivelihoods of members, timely disbursement,end use of credit, insurance coverage andmonitoring on a consistent basis will persistfor various reasons.Higher credit flow per SHGwithout the above safeguards will enhance

Community based financial institutions –Stree Nidhi a new paradigm in Micro finance

1.1. There is a phenomenal growth in creditflow to SHGs in the country, due to efforts madeby NRLM/NULM at national level and SRLMs/SULMs at the state level. However, the issues ofinadequacy, timely and affordable credit frombanking sector are yet to be tackled effectively.Though credit flow in terms of volume lookssatisfactory, unbridled credit flow is risky in theabsence of proper due diligence andmonitoring arrangements. In the presentarrangement,bank branches would find itdifficult to attend to these aspects on a regularbasis.

1.2.The aggregate credit outstanding underSHG finance from Banking Sector at nationallevel in 2017-18 stood at Rs.75,598 cr.covering50,20,358 SHGs, registering a growth of 22.76%over previous year. At the same time in manyStates, mFIs are growing at a rapid pace of morethan 50% annual growth, indicating hugedemand for credit reinforcing the fact thatbanks are not able to cater to their needs. Asthis segment is deprived of affordable credit,they are exposed to high cost borrowings frommFIs and other private sources.

1.3. There is a need to fathom the reasons as towhy the banks are not able to scale up theirlending to SHGs despite inadequacy. Theanswer stems from the fact that banks havediversified nature of businesses, seasonality in

Chapter - 1

Stree Nidhi2

credit risk significantly and banks are aware ofthe same and if reckless lending is resorted toby banks, it might even choke this channel ofcredit flow to the poor.

Stree Nidhi carves out niche space

1.6.Telangana State is one of the pioneeringstates under SHG Bank Linkage programme inthe country on account of innovative strategiesadopted by SERP and MEPMA for alleviation ofpoverty. These state govt. promotedorganizations, organized the poor women intoSHGs and their federations and nurtured them.Though, the credit flow to SHGs from BankingSector in the state has been far better thanmany other states in the country, still the creditneeds of members of SHGs could not be metadequately by banks for various reasons.

1.7. Inadequacy and delay in credit availabilitycompelled poor women to approach privatemoney lenders and mFIs to meet their creditneeds at usurious interest rates resulting in debttrap. To curb the large scale operations of mFIsin the State, MFI Act’2011 was promulgated.Despite this, even today instances of high costborrowing exist in remote areas of the state.

1.8. In the backdrop of mFI crisis and issues inbank linkage, Stree Nidhi emerged as aspecialized institution in the State for financingSHGs with largest portfolio and has earned trustof the community. Stree Nidhi uses the SHGplatform for lending and has beensupplementing credit flow to SHGs with bettersystems, community participation, effectivemonitoring and more importantly withundivided focus. Considering the strengths ofStree Nidhi and outreach of its services to nook

and corner of the state as also suite of productsand services launched by it, ensured thatadequate credit both for consumption andincome generation purposes is made availablecreating better impact on SHGs and theirfederations.

1.9. A question that arises is as to whether thereis any need for two agencies viz. Banks andStree Nidhi for extending financial services tosame SHGs. It is akin to asking whether twobanks are necessary. RBI has provided a policyframe work in terms of which NBFC mFIs, SFBs,payment banks and even peer to peer lendingare made possible. SHGs get credit supportfrom banks while Stree Nidhi not only extendscredit but also strengthen SHGs and theirfederations and the latter has many positivesincluding providing timely and affordablecredit. In fact, Stree Nidhi has lower effectiverate of interest than that of banks. Alongside,there are also certain additional advantageslike, implementation of Suraksha- a loan linkedinsurance scheme, appraising credit needs ofindividual SHG members in a SHG rather thanfor all the members at a time, as needs of allmembers in a SHG may not arise at the sametime. Stree Nidhi has effective monitoringsystem with staff exclusively focusing on themicrofinance activities.

1.10. Multiple lending to SHG withoutnecessary precautions would result in overindebtedness and stress in the system as poorhave higher propensity to consume. In thiscontext, Stree Nidhi is better equipped in termsof strengths and systems to add value to thepresent SHG Bank linkage programme alsoconsidering the following advantages tocommunity.

Annual Report 2017-18 3

u Availability of financial services at doorstep of the poor with userfriendly technologyand timely dispensation of services.

u Due diligence and discretion to recommend loans are vested with SHGs and VO/SLF underthe supervision of MS/TLF.

u Cost effective Credit delivery,customized loan products and lower effective rate of intereston loans, presently at 11% as compared to 12.5% in respect of major banks.

u Transparency in operations on account of digitalization even at VO/SLF level throughtablet PCs provided to them.

u Focus on livelihood activities by introducing on line HLPs for about 100 activities andensuring end use of loans through monitoring and social audit mechanism.

u Profits are shared with SHGs and their federations contributing to their financial soundness– A social enterprise.

u Payment of interest on savings/deposits at rates higher rate than that of banks.

u Coverage of loan risk to the borrowers of Stree Nidhi preventing burden of indebtednesson legal heirs and also other members of SHG.

u Providing banking services as corporate BC to banks through VLEs and extend Govt. tocitizen services at village level, providing employment to about 1000 SHG women.

u SHG members are recruited as Stree Nidhi staff at field level for the first time in the country.

u Extending benefits to SHG community in the form of scholarships, sharing profits withSERP/MEPMA for institution development, NHC centers with PwD children as a part ofcorporate social responsibility.

u Effective convergence with SERP (SRLM) and MEPMA (SULM) for evolving more effectivestrategies for augmenting incomes of poor.

1.11. One of the most impact creatingintervention made by Stree Nidhi isintroduction of Tablet PCs at VO/SLF level whichbrings utmost transparency and effectivemonitoring at grass root level aside making theprocess simple and hassle free.

1.12. Stree Nidhi being a community ownedand managed institution, the SHG communityhas an overwhelming preference for availing offinancial services from Stree Nidhi as it is notonly their own institution but also for hassle free

systems and procedures in accessing credit and

other financial services. They remember only

Stree Nidhi if they need money and it has

become a house hold name in the SHG

community, having reach to nook and corner

of the state with the help of user friendly

technology and SHG federations. They are also

keen to place their savings with Stree Nidhi to

increase owned funds for higher leveraging

from banking sector to meet their entire credit

needs.

Stree Nidhi4

Feasibility of Stree Nidhi partnering withbanks to extend financial services

1.13. Scope for positioning Stree Nidhi as anagency with a platform for routing all financialservices to SHGs in the State or extendingservices in conjunction with banks needs to beexamined with the objective of ensuringfinancial services to SHGs without unduehurdles. This would not only be in the interestof community but also would ensureproductive use of credit, for which the Govt.extends interest subvention. As envisaged byNRLM, each SHG member may require aboutRs.1.00 lakh and on this basis for 50.00 lakhSHGs functioning in the country the estimateddemand for credit will be Rs.5,00,00 cr asagainst the present outstanding at Rs.75,598 cr.It is also pertinent to mention that the creditflow from mFIs during FY 2017-18 was atRs.59,629cr and the loan outstanding was atRs.44,892 cr covering2.68 cr borrowers. Thus,there is a huge gap and institutions like StreeNidhi would not only supplement the creditflow but also ensure proper utilisation.

Need for paradigm shift in SHG – Banklinkage programme

1.14. The SHG – Bank linkage programme isnow more than two and half decades old whichresulted in unprecedented economicempowerment of the women. However, it istime for a paradigm shift as more emphasisneeds to be laid on livelihoods / enterprises. Itis in fitness of things to associate nicheinstitution like Stree Nidhi which would addvalue to the programme, in all the spherespartnering with banks in a meaningful way.

1.15. There is an imperative need for promotingspecialized institutions like Stree Nidhi in theStates with strong network of SHGs and well-

structured and managed federations of SHGsto create better impact on poor women foralleviation of poverty. The systems and ease ofassured credit availability at the door step ofSHGs, low cost delivery system as also themonetary benefits flowing to SHGs and theirfederations from these institutions make themmore relevant than any other institutionfinancing SHGs. Alongside, it is also imperativeto streamline the entire system of appraisal ofloan requirement, scale up credit flow to SHGsto meet demand, ensure productive use ofcredit by involving community and specializedinstitution in coordination with SRLMs/SULMsto make the present system more effective.Credit needs of FPOs can also be effectivelyaddressed by these institutions.

1.16. In order to ensure adequate credit flowto SHGs, an appropriate model, need to beevolved, partnering with banks for co-financingor agency arrangement for lending is necessary.This enables proper identification of clienteleand provides a win- win situation to all the stakeholders i.e Community, Banks and the State/

Central Govt. as the model can emerge as a

strong and vibrant community based

institution and address various issues in credit

flow, extending affordable and timely credit to

the poor. There is a need to recognize lending

by specialized institutions like Stree Nidhi to

SHGs as a part of bank linkage and also extend

interest subvention facility to SHGs financed.

This would also facilitate implementation of

PMSBY and PMJJBY with specialized institutions

as aggregator and also MUDRA scheme more

effectively. RBI can also consider these

specialized institutions for promoting co-

origination of loans on the lines of NBFC-mFIs.

Annual Report 2017-18 5

Stree Nidhi - A Game Changer in Micro financecanvas of Telangana

2.1. After mFI crisis, the State Govt. and SHGsfederations both in rural and urban areas havejointly promoted Stree Nidhi Credit CooperativeFederation Ltd., in 2011 with the followingobjectives;

i. Providing affordable and timely (within 48hours) credit and other financial services tothe SHG members at their doorsteps innook and corner of the state in a transparentand efficient manner through user friendlytechnology.

ii. Work for socio economic upliftment of themembers of Self Help Groups by increasingtheir income both in Rural and Urban areasby financing livelihoods in a big way withfocus on vulnerable segments of society.

Chapter - 2

iii. Work in tandem with Society forElimination of Rural Poverty (SERP) andMission for Elimination of Poverty (MEPMA)to achieve self-sustainability of SHGfederations and also for identification oflivelihoods for financing.

2.2. Stree Nidhi has many features which interalia, include community ownership, creditdelivery in 48 hours, community representationon Board, allocation of credit limits tovulnerable (including SC/ST) depending ontheir population, digitalisation of transactions,sharing of interest margin with the federations,ease of doing transactions, transparency andpolicies suitable to community, and all thesefeatures make it unique in the sphere of micro-finance.

Stree Nidhi6

Leveraging Technology:

2.3. Technology plays a predominant role in alloperations of Stree Nidhi viz. loan origination,processing, disbursement and accounting,involving community etc., Stree Nidhi has rolledout Aadhar based authentication, through16000 Tablet PCs provided to VOs/SLFs in theState which in itself is revolutionary in historyof SHG movement. The loans to members aregranted in a most transparent manner with asystem driven checks and controls and arecredited to SB accounts of SHGs with Banksdirectly, within 48 hrs avoiding any leakages.SMS alerts are used at various stages ofoperations and also information isdisseminated through automated voice calls.The details of transactions of SHGs are madeavailable at VO/SLF level through URL providedfor viewing in Tablet PCs provided at village /Slum level itself. All the staff are provided withlogins to make use of MIS for monitoring.

Low Cost Credit/Cost effective Creditdelivery system:

2.4. The federations of SHGs promoted andnourished by SERP and MEPMA are empoweredto originate loans, conduct due diligence, loandocumentation, mobilisation of savings,monitoring of credit flow and repayment. Thisenabled Stree Nidhi to charge an affordable rateof interest at 12.5% (as compared to about 22%

Annual Report 2017-18 7

by NBFC mFIs) Effectively, interest rate chargedis 11% as 1.5% (12.5 – 1.5) is shared with theSHGs federations strengthening themfinancially and make them self-sustainable inthe long run.

2.5. Stree Nidhi emerged as a unique institutionin the country with no parallel for its low costfinancial services delivery model as real cost ofthe lending is low as compared to even banks.

Cost of Credit from Stree Nidhi

from risk and benefitting the communityimmensely.

Role in Financial Inclusion:

2.7. Stree Nidhi has been providing bankingservices successfully in 1079 remote andunbanked villages as Business Correspondentto Banks, engaging SHG members as VillageLevel Entrepreneurs. These women are not onlyable to deliver banking services but also earndecent monthly income in the form of servicecharges from banks. Stree Nidhi has integratedGovernment to Citizen Services like issue ofbirth, death certificates, land records etc., withthese centres in coordination with IT dept. ofGovt. of Telangana and provide such servicesat village itself.

Recruitment of SHG women as staff:

2.8. Stree Nidhi has recruited 92 SHG womenas Asst. Managers through written examinationand Group Discussion, a first of its kind initiativein the country.

Other Activities:

2.9. As a part of its Corporate SocialResponsibility, Stree Nidhi is undertakingvarious activities reflecting its socialperformance which include payment ofscholarships to meritorious children of SHGs topursue education after matriculation, allocation5% net profit for strengthening of SHGfederations, 2% of net profit for Neighbourhoodcentres supporting persons with disability, 0.25%of net profit for Community Benevolent fund tosupport SHG members facing deadly diseases likeCancer and other health hazards and paymentexgratia amount to legal heirs of deceasedemployees of Stree Nidhi, SERP and MEPMA.

2.10. Competitive Advantage of Stree Nidhi

u Stree Nidhi ensures communityparticipation in policy making and

Focus on Financing Livelihoods:

2.6. As financing livelihoods is a majorchallenge for alleviation of poverty, Stree Nidhifocussed on the same. Household LivelihoodPlans (HLPs) are prepared for appraising creditneeds of individual members in SHGs to ensureproper due diligence. It has digitalized activityprofiles of more than 100 activities both in farmand non-farm sector, which can be appraiseddigitally and uploaded electronically usingTablet PCs. This has instilled greater confidencein the poor SHG women as assured access toaffordable credit is available for taking uplivelihoods from their own financial institution.Stree Nidhi also provides loan risk coverage toits members as also for cattle, insulating them

Stree Nidhi8

functioning which not only provide last mileconnectivity, but also facilitate outreachand monitoring.

u Technology enabled operations forseamless, speedy delivery of financialservices at low cost in a transparent mannerand for real time monitoring.

u An exclusive financial institution withundivided focus on delivering credit andother financial services.

u Enforces credit discipline and responsiblelending.

u Scrutiny of utilization through Social Auditas a tool ensuring transparency and fixingaccountability.

u Flexibility in customization of newtechnology, products and services.

u Effective appraisal of loan requests ofindividuals through Offline/Online HLPsleads to minimization of credit risk.

u Rating based allocation of credit limits tovillage/slum level institutions encouragesinstitutions to function better.

u In the total credit limit made available atvillage/slum level, credit limits areearmarked to SC/STs and other weakersegments in proportion to their populationto ensure credit flow.

u Credit limits allocated to VO/SLF level arerevolving in nature and repaid amounts canbe utilised to meet credit needs of memberswithout any lapse of time preventing highcost borrowings.

u Collaboration and convergence with SERPand MEPMA, provides synergy in deliveringof services in a holistic manner.

u Cost effective operations enabling fixationof lower price on loans and payment ofhigher interest on deposits.

u SHG members can request for loan as andwhen required through SHGs and VO/SLFon all days at their doorstep withouttravelling to banks.

u Any one member who is in need of loan canaccess credit and member details can betracked. All members may not need loan atthe same time and are not compelled toborrow at the same time. No equaldistribution.

u There is certainty of getting loan in 48 hoursfrom the time of request.

u Loans are covered under Stree NidhiSuraksha, helping diceased members asloan liability is discharged and balance, ifany will be paid to the legal heirs of themembers. This helps in preventing groupdisintegration and debt burden on legalheirs.

u As requests for loans are made at VillageLevel, no expenditure is incurred. Real costof transaction is low

u The actual cost of borrowing is much loweras not only the rate of interest is low butalso no processing and other charges arelevied.

u The federations will get back a part ofinterest paid by the SHGs to Stree Nidhi.(Presently, 1.50% of interest recovered). Thiswill strengthen the federations. Effectiveinterest rate to Stree Nidhi is low.

u On deposits of SHGs and their federations,the interest rate paid is higher than that ofbanks.

Annual Report 2017-18 9

u Part of the net income earned will beutilised for welfare purposes under its CSRpolicy viz. Exgratia, scholarships & Servicescharges to SERP/MEPMA staff concerned.The profits are shared with SERP andMEPMA for institution building.

Processes and Systems:

2.11. The inbuilt checks and controls enabledthe community to exercise due diligence in caseof loans without any delay and without outsideinterference empowering community. Themembers do not lose their time, wages and donot incur any expenditure on transport to getloans sanctioned and released. Stree Nidhi,being a community and Government ownedfinancial institution, is a social enterprisecatering to the needs of community,functioning on self-sustainable basis earningnet profit every year and paying dividend to theequity holders including the State Government.

2.12. The loan products are priced verycompetitively as compared to MFIs and evenbanks, and loan repayment is ensured thoughan effective system of supervision involvingSHG federations themselves and staff atdifferent levels.

Impact Creation on Community

2.13. Stree Nidhi has created huge impact onthe poor SHG women by enhancing theirincome by financing livelihoods /enterprises inaddition to meeting their emergent /consumption needs.

2.14. The members of SHGs have a great pridein owning a financial institution, which not onlyprevented need for high cost borrowings fromprivate sources but also enables access to creditat any time on any day in their own village /slum without any hassles. If any SHG memberneeds money, they remember only Stree Nidhi.

2.15. Stree Nidhi pays SHGs and theirfederations higher rate of interest on theirsavings as compared to Banks increasing theirearnings. Stree Nidhi Suraksha, a loan riskcoverage scheme, which insulates loan risk incase of death of a member, provides a greatrelief to the family members of deceased SHGmember. Stree Nidhi demonstrated thatfinancial services can be delivered to poorsuccessfully at low and affordable cost.

2.16. Stree Nidhi has so far covered over 24.86lakh SHG members in 3.54 lakh SHGs in 19,154VOs/SLFs in the State. The cumulative loandisbursement reached Rs. 7747 cr as onFebruary, 2019. Stree Nidhi has devisedcustomised loan products to meet varyingneeds of community at large including variousincome generating activities and also forspecial needs like purchase of Bicycles, smartphones by the members and for constructionof IHHLs under Swatch Bharath.

2.17. The stakes of the community are built upto facilitate ownership of the communitypaving way for community owned institution.Through the institution, adequate credit isensured alongside extending financial servicesas also Govt. to citizen services to thecommunity in the village itself.

2.18. Stree Nidhi is adopting a holistic approachin assessing credit needs of poor families andmeet them. A large no. of poor have establishedmicro enterprises successfully and enhancedtheir income levels. Above all the organisationhas created a self confidence among the poorto take up income generating activities withassured, affordable and timely credit.

2.19. Tablet PC at village and slum level broughttransparency in loan application, disbursementand management of portfolio. Aadhaarauthentication of borrowers also made

Stree Nidhi10

community more responsible. Measures arebeing taken for e-documentation as providedunder IT Act, 2000 which would make loanaccess much more hassle free. The MIS madeavailable through a specific URL at village andslum level made things more transparent anduseful to community for monitoring. As a partof social audit of Stree Nidhi operations, Gramsabha is conducted and deficiencies infunctioning are discussed and follow up actiontaken which not only made community more

responsible but also ensured proper endutilization of loans.

2.20. Stree Nidhi being a community ownedand managed financial institution, apart fromproviding credit and other financial services ofaffordable cost, it is returning a major chunk ofincome generated to the community andstrengthens the institution of the poorfinancially. The amounts paid / payable to theVOs / SLFs and MSs/TLFs during the past 4 yearsare given here under.

(Rs. Crores)

Sl. No. Particulars 2014-15 2015-16 2016-17 2017-18 Total

1 Interest Shared to VOs/SLFs 3.65 6.94 13.04 21.24 44.87

2 Interest Shared to MSs/TLFs 1.12 1.48 3.00 4.48 10.08

3 Higher Interest payment on 1.33 3.66 5.92 8.46 19.37Deposits*

4 Payment of Dividend * 0.00 0.47 1.53 3.58 5.59

5 Allocation to IB activities 0.00 1.86 2.50 2.95 7.31(5% net profit)

6 Allocation to NHC (2% net profit) 0.00 0.75 1.00 1.18 2.92

* The amounts are arrived at after reducing theinterest earned notionally assuming that theyare placed as deposits with banks.

2.21. This change maker approach has resultedin reduction of turnaround time and also costof delivery of financial services to the poor andthus Stree Nidhi emerged as a low cost financialservices delivery model in the country. Owingto its success, recently a High Power Committee

constituted by Govt. of India has studied thefunctioning of Stree Nidhi with a view toexplore the feasibility of replicating the samein other States of the country. The way StreeNidhi functions, adopting technology andcreating a paradigm shift in extending financialservices to SHG women makes it stand apart ofits class of institutions.

Annual Report 2017-18 11

New Initiatives / Policy Changes3.1. Innovation is the forte of Stree Nidhi toensure that its services are relevant to thecommunity. The systems and processes arestreamlined from time to time in accordancewith the needs articulated by community. Thefollowing are the new initiatives taken recently.

Tablet PCs to VOs/SLFs3.2. Tablet PCs were provided to 16000 VO/SLFsfor authentication of borrowers intending toavail loans from Stree Nidhi. Through theseTablet PCs, a borrower’s identity is establishedthrough Aadhar. In addition, MIS on DCB, creditlimits, credit flow, savings of SHGs / membersaffiliated to VO/SLF are also made availablethrough a URL. A provision has also been given toadjust the amounts repaid towards loan A/Cs ofmembers through Tablet PCs. It is a majormilestone in the history of SHG movement notonly in the Telangana state but also in the country.The Tablet PCs are also being used for SHG bookkeeping and eventually for VO book keeping.

Introduction of New Loan products3.3. Assured credit flow from Stree Nidhi hasincreased confidence levels of SHG membersand they are increasingly opting for higherorder income generating activities / enterprises.Keeping in view the credit needs of suchentrepreneurs, a new loan product namelySowbhagya has been introduced,enabling amember to access a loan of above Rs.1,00,000/- to Rs.3,00,000/-.

Introduction of New Deposit Scheme3.4. A new recurring deposit scheme“Ujwala”was introduced enabling SHGs to savesurplus amount regularly at monthly intervals

Chapter - 3

with a minimum of 1000/- per month for aperiod of 4 years and get a reasonable returnon maturity.

Streamlining Settlement process ofSuraksha Claims3.5. For speedy and hassle free settlement ofclaims under Stree Nidhi Suraksha, the VOs/SLFshave been empowered to register death of amember and upload required documentsthrough Tablet PCs made available to them. Thiswill enable escalation to Head Office, StreeNidhi for further process and settlementpreventing the delay in the process.

Preparation of HLPs through online3.6. Project profiles of 100 various incomegenerating activities are made available onlinein web portal. The staff only need to downloadand prepare required HLPs for activitiespreferred by SHG members. This enablesassessing of the credit requirement and projectviability to ensure proper due diligence,interacting with borrower at her house itself.

Strengthening Institutional Monitoring andTraining3.7. The health of institutions and training ofstaff and community are crucial role foreffective functioning of Stree Nidhi. Anexclusive vertical has been created at HO for thepurpose which would ensure continuousinteraction with community and capacitybuilding of staff. It is essential to enhanceawareness level of community on functioningof Stree Nidhi, so that proper checks andcontrols are exercised to bring in transparency.

Stree Nidhi12

Settlement of members trained by RSETIs3.8. Stree Nidhi has financed members trainedby RSETI, in collaboration with RSETIs in thestate. The data on candidates belonging to SHGmembers imparted with required skills is sharedby RSETIs to Stree Nidhi and such members areable to access credit from Stree Nidhi to meettheir investment needs.

Increase in ceiling on SHG loan limit3.9. The ceiling on loan limit per SHG has beenenhanced from Rs.3.00 lakh to Rs.3.75 lakh andalso the no. of eligible members to borrow in aSHG has been increased from 9 to 11depending on number of members in a SHG.This will enable more no. of members in a SHGto access loans from Stree Nidhi

Repayment by SHGs to Stree Nidhi3.10. A system of repayment of loaninstalments to Stree Nidhi by SHG directly hasbeen enabled to prevent delay in transfer byVO/SLF, proper adjustment to members andmisuse of money collected at VO/SLF.

Increase in Human Recourses3.11. In tune with growing needs, Stree Nidhihas recruited additional staff in all cadres to

have effective monitoring of implementationof all its activities. Most of the districts have anexclusive Regional Manager to have betterliaison with DRDA / MEPMA, the districtadministration and line departments. For thefirst time in the country, 92 eligible SHG womenwere recruited as Assistant Managers of StreeNidhi.

Expansion of HO premises3.12. The premises at HO has been expandedto have a floor space of 6800 sft providingcongenial working environment to the staff anda well-furnished conference hall for conductingBoard Meetings and review meetings with staff.

Logo for Stree Nidhi3.13. Keeping the impact created and brandimage in community on account of credit andfinancial services focusing on livelihoods, aLogo for Stree Nidhi has been adopted torepresent the organization through a visualimage and further build a brand equity amongthe community, Govt., departments andBanking sector not only at State but also atNational level.

Annual Report 2017-18 13

Role of SERP and MEPMA

Society for Elimination of Rural Poverty(SERP)

4.1. SERP is a sensitive support organizationfacilitating social mobilization of rural womenin the 32 districts of Telangana. SERPimplements a multi-pronged strategy forpoverty alleviation creating and nurturing theSHGs and their federations in rural area for theirorderly functioning and to empower them bybuilding up their capacities.SERP is anautonomous society, established by the StateGovernment and registered under SocietiesAct, headed by an IAS officer.

4.2. SERP has about 4000 staff positioned in thefield and plays a major role in motivating andextending guidance to members of SHGs fortaking up income generating activities andfacilitating access to credit and is endeavouringto promote producer organizations across theState with the objective of ensuring sustainableand incremental incomes through value chaininterventions.SERP also implements economicsupport schemes for the benefit of the poorunder special projects viz, SCSP, TSP,IWMP,NRLM and SVEP with Stree Nidhi as aChannelizing agency.

4.3. In addition, SERP also plays a pivotal rolein implementation of flag ship programmes ofthe State Govt., like Aasara Pension, HarithaHaram, Swatcha Bharath Mission, welfare ofphysically challenged, MaintainingNeighbourhood centers, striving for human

Chapter - 4

development etc. The state Govt., iscontemplating to implement food processingactivities in a big way through SERP. Stree Nidhicollaborates with SERP in areas like sharing ofmaster data on SHG/federations, bank linkagesetc.

Rating and improving functioning of SHGsand their federations

4.4. Computerisation of books of accounts ofSHGs, and online accounting at MS level helpsin improving functioning of the SHGs and theirfederations which in turn makes them eligibleto access better services.

4.5. SERP and MEPMA field staff coordinate andhelp in propagation of products and servicesof Stree Nidhi among the community and alsoextend support in identification of livelihoods,loan disbursements and repayments of theloans. Stree Nidhi compensates their servicesby linking to the performance as per the policyevolved by MC of Stree Nidhi from time to time.

Mission for Elimination of Poverty inMunicipal Areas (MEPMA)

4.6. MEPMA, headed by an IAS officer, is anautonomous society established by Govt. ofTelangana with a vision to improve quality oflife of urban poor through community ownedand managed institutions. MEPMA is facilitatingthe formation of SHGs with poor urban women,in to federations at Slum level and Town level.It is playing a key role in implementation of

Stree Nidhi14

SHG- Bank linkage programme in urban areasthrough their staff under the administration ofProject Directors located at District HeadQuarters.

4.7. In addition to promotion of communitybased organizations and SHG-bank linkageprogramme, MEPMA is also involved inimplementation of multifarious activities likepromoting self-employment, social securitymeasures, housing for poor, Health andnutrition etc.

4.8.The master data of SHG members in urbanareas is maintained and shared by MEPMA on aregular basis. MEPMA Staff coordinate with

Stree Nidhi for propagation of services and

products among urban poor. They also extend

support in facilitating credit flow and prompt

repayment of loans.

4.9.The synergy between Stree Nidhi, SERP and

MEPMA ensures that the needy SHG members

are provided with affordable and timely credit

and other financial services provided by Stree

Nidhi. The activities implemented by SERP and

MEPMA for strengthening of institutions of the

poor i.e., SHGs and their federations provide a

strong foundation for implementing Stree

Nidhi activities effectively.

Annual Report 2017-18 15

Stree Nidhi – a Community managedInstitution

5.1. Stree Nidhi Credit Cooperative FederationLimited., is an apex organization at state levelpromoted jointly by the State Govt., andFederations of SHGs and registered underTelangana State Cooperative SocietiesAct’1964. Mandal Samakhyas in rural areas andTown Level Federations in urban areas and theState Govt. are the shareholders in theinstitution.

General Body5.2. As per the provision of the Act GeneralBody is supreme in decision making. All theshare holders are the members of General Bodyand General Body Meetings are conductedtwice in a year. During the year 2017-18, firstmeeting was conducted on 29.12.2017 andsecond meeting was held on 29.03.2018.

Managing Committee5.3. The Managing Committee of Stree Nidhiconsists of 12 Directors elected byrepresentatives of Mandal Samakhyas andTown Level Federations and three members viz.

Chapter - 5

Principal Secretary, Rural Development;Secretary, Finance and Registrar of CooperativeSocieties are nominated by the State Govt.Managing Director, a professional appointed bythe state Govt., is an ex-officio member on theMC. Chief Executive Officer, SERP; MissionDirector MEPMA and CEO, MAS are specialinvitees on the Board.

5.4. The term of the elected representatives is5 years. The incumbent MC members wereelected on 25.05.2015. To strengthen further,MC will be expanded by inducting 4morerepresentatives i.e. two from SHG federationsand two professionals with experience inBanking and other relevant field, in accordancewith the provisions of the Act ibid.

Conduct of Managing Committee meetings5.5. The Managing Committee meetings areheld once in a quarter in compliance with theprovisions of Bye-laws.The details of MCmeetings conducted FY 2017-18 are furnishedbelow.

S. No MC Meeting Date of No.of Board No of Board % of No. Meeting Members Members attended Attendance

1 16 05.07.2017 16 14 88.50

2 17 26.08.2017 16 15 93.75

3 18 04.12.2017 16 12 75.00

4 19 29.03.2018 16 13 81.25

Stree Nidhi16

Organization – Structure

5.6 .The organizational structure of Stree Nidhihas evolved over a period to meet therequirement of the institution in tune with itsgrowth, Assets Under Management, coverageof SHG members, expansion of products andservices. Stree Nidhi has been recruiting staffwith experience in banking, financing SHGs,micro finance, capacity building of community,financial inclusion, micro enterprises andlivelihood activities and informationtechnology, in the cadres of Deputy GeneralManagers, Assistant General Managers, ChiefManagers, Managers and Assistant Managers.

Staffing Pattern5.8. A three tier structure has been evolved toensure effective implementation of strategiesand achieve objectives of Stree Nidhi.

Head Office5.9. In order to handle and supervise specificfunctions and ensure proper monitoring,different verticals have been created. All theverticals are headed by DGMs or AGMs andfunction with the assistance of Chief Managers,Managers and Assistant Managers. Allfunctional units are under the administrativecontrol of the Managing Director.The HO hasthe following verticals.

General Administration

Board Secretariat, Policy and MIS

Credit and Livelihoods

Monitoring – Credit flow, CRM and Social Audit

Information Technology

Financial Inclusion

Funds Management

Risk Mitigation and Insurance

Accounts and Reconciliation

Institutional Monitoring and Training

Zonal Structure and HO

5.7. To ensure effective monitoring andimplementation of all activities of Stree Nidhito achieve desired performance under all keyparameters, all the districts except Hyderabadare divided into five zones and districts in thezone are considered as regions. The zones areheaded by Zonal Managers who are in the cadreof AGMs and entrusted with overallresponsibility to monitor performance of theRegions attached to them. The ZMs attend ZS/MS meetings, liaison with DistrictAdministration and participate in District LevelStree Nidhi Review Committee Meetings. TheZonal Manager is responsible to achieve creditplan and to ensure that NPAs level is below 0.5%and above 98% recovery percentage byimplementing suitable strategies.

Field Level staff

5.10. The Regions comprising of one or twodistricts are headed by Regional Managers whoare responsible for achieving the expectedperformance in the respective region. Further,8-10 mandals are allocated to Managers whoare responsible to monitor implementation ofall activities at grass root level by the AssistantManagers posted to monitor operations in 2-3MSs/TLFs.

Human Resources Policy5.11. Stree Nidhi has embarked on increasingits staff strength in tune with the growth in itsportfolio and expansion in services. At grassroot level, Assistant Managers recruited alsoinclude eligible SHG members, experienced

Annual Report 2017-18 17

staff of CBOs working in VOs / SLFs and MSs /TLFs to ensure service with passion andcommitment to the poor. The details of staff

positioned at HO and field in different cadresare given in the table no 1 of part-B of thisannual report. The organogram of Stree Nidhiis as under.

Stree Nidhi18

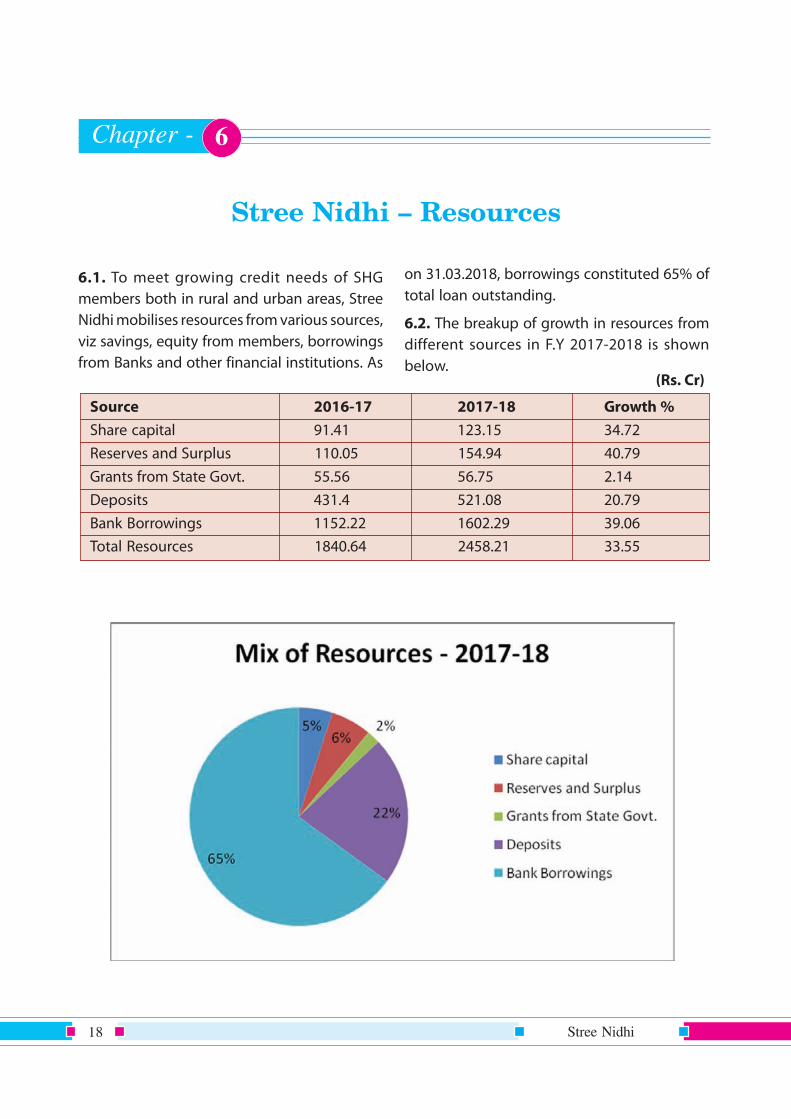

Stree Nidhi – Resources

6.1. To meet growing credit needs of SHGmembers both in rural and urban areas, StreeNidhi mobilises resources from various sources,viz savings, equity from members, borrowingsfrom Banks and other financial institutions. As

Chapter - 6

on 31.03.2018, borrowings constituted 65% oftotal loan outstanding.

6.2. The breakup of growth in resources fromdifferent sources in F.Y 2017-2018 is shownbelow.

(Rs. Cr)

Source 2016-17 2017-18 Growth %

Share capital 91.41 123.15 34.72Reserves and Surplus 110.05 154.94 40.79Grants from State Govt. 55.56 56.75 2.14Deposits 431.4 521.08 20.79Bank Borrowings 1152.22 1602.29 39.06Total Resources 1840.64 2458.21 33.55

Annual Report 2017-18 19

Share Capital

6.3. The Federations of SHGs viz. MandalSamakhyas and Town Level Federations areeligible to subscribe to share capital andbecome members i.e. shareholders in StreeNidhi aside the State Government.

6.4. A borrowing member contributes to

Mobilisation of Savings from Community

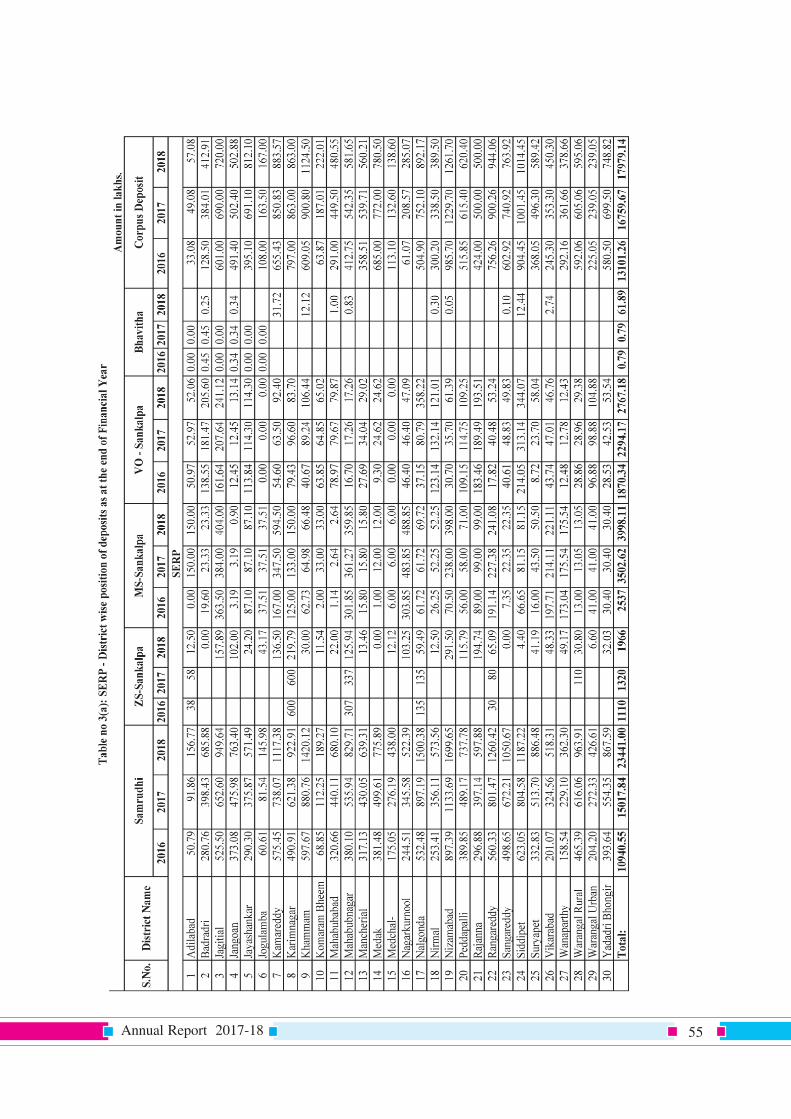

6.5. Stree Nidhi has devised different depositproducts viz. Samruddhi, Sankalpa and CIF-Corpus Deposit so as to mobilise savings fromSHGs and their federations. This would not onlyimprove own resources but also make the

community to own up the institution. Salientfeatures of the deposits schemes are furnishedbelow and the performance under differentschemes for the past 3 years in the districtsfurnished in table 3 (a) & (b) of part - B of thisreport.

(Rs. Cr)

S.No. Samruddhi Sankalpa CIF Corpus Total

2014-15 75.15 42.44 47.14 164.732015-16 130.61 54.91 131.34 316.862016-17 187.56 74.61 168.11 430.282017-18 253.13 87.31 179.79 520.23

savings of MS/TLF and they inturn subscribe toshare capital of Stree Nidhi. The growth in sharecapital is ensured, enabling mobilisation ofmore resources required for onward lending toSHGs. The details of district wise paid up sharecapital upto 31.03.2018 are furnished in table 2of part -B of this report.

Stree Nidhi20

Borrowings6.6. Stree Nidhi has been borrowing from Banksand other financial institutions in the form ofcash credit limits and term loans to meet creditdemand from SHGs. Considering the financialstrength and rating, Banks and Financial

Bhavitha is discontinued and in its place, recently Ujwala scheme has been introduced

Institutions are keen to take exposure to StreeNidhi. The credit limits and outstanding underterm loans availed from different banks andfinancial institutions as on 31.03.2018 arefurnished below.

Rating of Stree Nidhi

6.7. Stree Nidhi has been rated by M/SBrickwork Ratings India Ltd with “BWR A- outlook stable” in 2017-18 compared to previousfinacial year 2016-17 of “BBB+ out lookPossitive”.

Annual Report 2017-18 21

Loan Policy

7.1 The loan policy of Stree Nidhi envisagescustomization of products and evolving ofprocesses to enable members of SHGs to accessservices in a convenient and hassle free manner.The policy changes brought in from time totime are based on aspirations and needsemerged from community and are inconformity with the guidelines of RBI. The

Chapter - 7

salient features of the extant policy are asfollows.

No. of members eligible for loans per SHG7.2. A ceiling on maximum number of membersin a SHG who can avail credit from Stree Nidhiis fixed depending on total number of membersin a SHG as mentioned below, to ensure peerpressure in availing services and repayment.

• The maximum borrowing limit per SHG isRs. 3.75 lakh.

• A maximum loan of Rs. 3.00 lakh loan canbe availed by a member in a SHG over andabove per SHG ceiling

• Present ceiling on credit limit to a VO/SLF isRs. 72 lakhs

7.3. Of the credit limits allocated to VOs/SLFs,there is no ceiling on number of members whocan avail under Pragathi & Akshaya loans, i.e.loans of above Rs. 25,000, as the intention is tofinance livelihoods of higher order. A memberwho availed Suvidha loan, after regularrepayment of 12 months can avail loan underPragathi, Akshaya or Sowbhagya for taking uphigher order livelihoods.

Allocation of Credit Limits to VO/SLF and MS/TLF

7.4. Proper functioning of SHG federations, viz.VO/SLF/MS/TLF is an important factor for

allocation of credit limits to VO/SLF and toaccess credit by SHGs affiliated to them. Theseinstitutions are rated once in a year based onperformance as at the end of March previousyear. The parameters considered for gradinginclude owned funds, regularity in conduct ofEC meetings, attendance of members, Bookkeeping, net profit, legal compliance, savings,recovery of CIF and Stree Nidhi loans.

7.5. Higher limits are fixed to VOs/SLFs whichsecure higher rating as a risk mitigationstrategy. The limits allocated are revolving innature and repaid amounts can be availed byneedy members of SHGs of VOs/SLFsconcerned.This would enable meeting thedemand for credit and prevent high costborrowings from other sources. Limits fixed toVOs/SLFs based on the grades obtained bythem and presently in vogue are as follows.

1 14 and above 11 7 72 12-13 9 6 63 10-11 8 6 54 7-9 6 4 45 5-6 4 2 2

Sl. No. No. of members in aSHG

Number of memberseligible for loan in SHG

Maximum no. of members eligible for loan up to

Rs. 25,000 Above Rs. 25,000

Stree Nidhi22

Annual Report 2017-18 23

Loan Products

7.6. Keeping in view credit needs for taking uplivelihood enterprises, Stree Nidhi has devisedcustomized loan products. Establishment ofmicro enterprises is facilitated by providingcredit in time after assessing requirementthrough HLPs (Household livelihood plan). It isnot only the member of SHG but also any familymember can take up activity by accessing creditfrom Stree Nidhi. However, loan will be in thename of the SHG member concerned.

7.7. Stree Nidhi has been financing livelihoodactivity/microenterprises adopting a policywhich inter alia endeavours to meet

i. Credit requirement for investment andworking capital purposes to take up new orexpand existing Income generatingactivities.

ii. Project based lending

iii. Financing members of FPGs and FPOs

iv. Area specific schemes for cluster basedactivity

v. Extending credit and implementation oflivelihoods in coordination with linedepartments of Government.

7.8. This is sought to be achieved in coordinationwith SERP, MEPMA, CRD, RSETIs and NGOs associatedwith promotion of livelihoods.

Presently, Stree Nidhi has the following loanproducts.

Type of Loan Amount of Loan

Suvidha Up to Rs. 25,000

Pragathi > Rs. 25,000 to Rs. 50,000

Akshaya > Rs. 50,000 to Rs. 100,000

Sowbhagya > Rs. 100,000 to Rs. 300,000

Special loan products

7.9. In addition, Stree Nidhi has introduced thefollowing loan products to meet specific needsof the community.

Type of Loan Amount of Loan

Purchase of Smartphone Up to Rs. 6,000

Purchase of Bicycle Up to Rs. 5,000

Purchase of Auto/Trolley Up to Rs. 1,20,000

Purchase of Laptop Up to Rs. 35,000

Construction of IHHL Up to Rs. 12,000

Loan Process

7.10. Loan requests received from members arescrutinized by SHGs. The loan requests receivedfrom SHGs are subjected to due diligence in theEC Meeting of respective VO/SLF, with regardto attendance of members in SHG, record inrepayment and savings, skills and knowledgeand capacity to take up activity, expectedincremental income and loan amount required.A VO/SLF will thereafter take a decision as towhether the member is eligible for loan or not.

Suvidha Loan (loan up to Rs. 25,000)7.11. Loans can be accessed for bothconsumption and livelihoods purpose in theratio of 30:70 of the credit limit allocated underSuvidha. These loans can be accessed throughWeb portal/ from the Tablet PC available withVO/SLF. The OBs of VOs/SLFs are providedcredentials for authentication of eligible

Stree Nidhi24

members using Aadhar and escalate loanrequests to Stree Nidhi.

Pragathi, Akshaya and Sowbhagya (Loanabove Rs. 25,000 to Rs. 3,00,000)7.12. The loans can be availed only for livelihoodenterprises for income generation by themembers of SHGs affiliated to VOs/SLFs with A,Bgrades in MSs/TLFs with A,B, and C rating. Themembers are identified by the VOs/SLFs.

Biometric Authentication of Borrowersthrough Tablet Pcs – Transparency inExtending Services and transactions

7.13. Tablet PCs were provided to VOs/SLFs onloan basis ensuring biometric authentication ofthe borrowers at the village/slum level in orderto bring transparency in loan applicationprocess and thereby preventing impersonation/ ghost loans. The Tablet PCs will also be usedat VOs/SLFs level asset verification, adjustmentof repayments, and filing of insurance claims,thus strengthening the role of village levelinstitutions in governing and monitoring theactivities at the village level.

Preparation of Household Livelihood Plan

7.14. Proper assessment of credit needs iscrucial for setting up enterprises and itssustainability. Stree Nidhi has introduced asystem where in loan requirement and viabilityof the unit is assessed by preparing HouseholdLivelihood Plans for every member of SHG whois in need of loans under Pragathi, Akshaya andSowbhagya and identified by the VO/SLF. StreeNidhi has prepared project profiles of about 100activities which can be downloaded andprepared by interacting with needy members.Duly filled HLPs can be uploaded online and ifnet connectivity is not available, the same canbe prepared offline as well. This would improvequality of appraisal of loan and reduce credit risk.

Disbursement of Loans

7.15. Loan amount approved by Stree Nidhi isreleased directly to SB account of SHGconcerned. VO/SLF concerned has to monitorloan utilization, establishment of unit and itsmaintenance by member concerned. The above

is also recorded in minutes book of EC meetingof VO/SLF. A certificate of utilization has to beuploaded within 30 days of loan disbursement.Stree Nidhi staff will verify all the above casesindependently and certify the utilization ofloans within 45 days from date of disbursement.

Loan applications and documents from SHGs arepreserved at VO/MS and documents obtainedfrom members are kept with the SHGs concerned.

Repayment period

7.16. All the loans have to be repaid on a monthlybasis and the repayment period is fixed based onthe loan amount and also cash flows. Thisfacilitates repayment of the loans by theborrowers conveniently. The repayment period fordifferent loan amounts is as given below;

Loan Amount Repayment Period(no. of months)

Rs. 25,000 24

> Rs. 25,000 to Rs. 35,000 36

> Rs. 35,000 to Rs. 50,000 42

> Rs. 50,000 to Rs. 3,00,000 60

Interest Subvention: Vaddi Leni Runalu7.17. The scheme Vaddi Leni Runalu is aimedat twin objectives of reducing interest burdenon loans and encourage promptness inrepayment of loans by SHGs. The State Govt. isimplementing interest subvention scheme,where in the amount of interest paid by themembers is reimbursed if the loan instalment(EMIs) is repaid within 30 days from due date.The amount of VLR will be passed on to theSHGs as and when the VLR amount is receivedfrom the State Government.

Stree Nidhi as channelizing agency7.18. Stree Nidhi is functioning as achannelizing agency for releasing loans toVillage Organizations for onlending tomembers under various Governmentprogrammes, viz. SCSP, STSP, IWMP, NRLM, andSVEP implemented by SERP. During FY 2017-18Rs. 4.82 cr. loans were disbursed to 1064 SHGmembers.

Annual Report 2017-18 25

Credit Disbursement and OutreachANALYSIS OF LOAN DISBURSEMENT

8.1. Aggregate credit disbursed to SHGmembers during the financial year 2017-18 wasRs.1835 cr. as compared to Rs. 1353 cr. in theyear 2016-17, recording a growth of 35%. Thecumulative disbursement of loans since

Chapter - 8

inception stood at Rs. 5985 cr. as at the end ofFY 2017-18. The year wise credit flow sinceinception is shown below.

Credit Flow in SERP and MEPMA Areas8.2. During the year 2017-18, credit availed inrural areas (SERP) was at Rs.1636 cr andaccounted for 89% of the total loans disbursed.The credit flow in urban area (MEPMA) wasRs.199 cr, constituting 11% of the total creditavailed.

The credit flow in rural areas has been growingat an average rate of 20% annualy for the lastthree years, while in urban areas it is 33%. Thefaster growth of availment of credit in urbanareas is primarily on account of increase innumber of TLFs.

1835 cr. disbursed to 6,36,494 SHG

borrowers in FY 2017-18

Stree Nidhi26

Coverage of Members

8.3. Stree Nidhi, since its inception endeavoredto reach more and more members of SHGs. InFY 2017-18, as many as 6,36,495 members in1,72,125 SHGs have availed loans from Stree

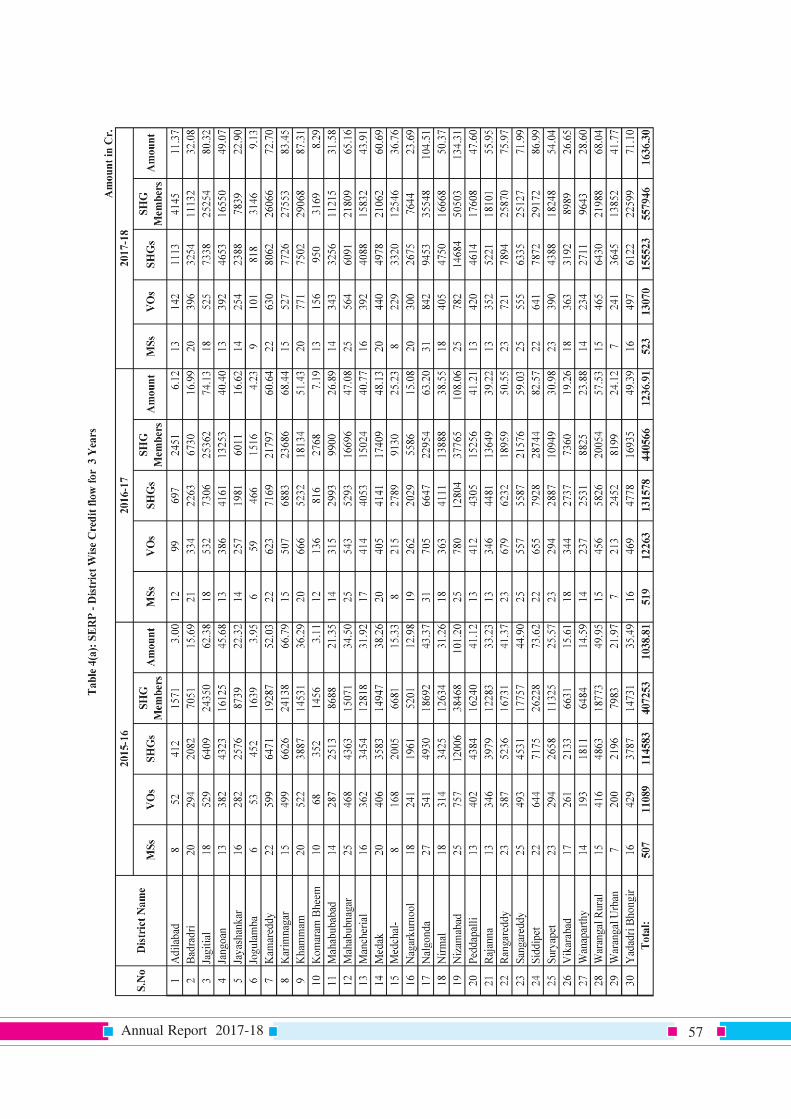

Nidhi and cumulatively 18.86 lakh membersavailed credit since inception. The no. ofmembers and SHGs covered during the pastseven years is furnished in the table below. Thedistrict wise disbursements furnished in table4(a) and (b) of part -B this report

8.4. The coverage of VOs/SLFs and MSs/TLFs isalso given in the following table. The coverageof members has been increasing year after year

due to better awareness levels among themembers on Stree Nidhi activities and benefitsthat accrue from Stree Nidhi.

Average Loan Disbursement per Memberand SHG

8.5. Introduction of Pragathi and Akshaya loansand efforts putforth to meet the credit needsof members have resulted in increase inaverage loan disbursement per member fromRs. 27,733 in FY 2016-17 to Rs. 28,838 in FY2017-18. The average loan disbursement per

SHG has increased from Rs.94, 234 in 2016-17to Rs. 1,06,640 in 2017-18. The pattern ofaverage loan disbursement per SHG and permember during the last 7 years is as shownbelow.

Average loan disbursement per

member in FY 2017-18 isRs. 28,838.

Annual Report 2017-18 27

Average Loan Disbursement per VO/SLFandMS/TLF8.6. There has been a steady growth in averageloan disbursement per VO/SLF and per MS/TLFsince inception as shown in the chart below.The average loan outstanding per MS/TLF hasincreased from Rs. 8.8 lakh in FY 2011-12 to

Rs.320.80 lakh in FY 2017-18. Similarly, theaverage loan outstanding per VO/SLF hasincreased from Rs. 1.2 lakh in FY 2011-12 to Rs.12.7 lakh in FY 2017-18. This is on account ofthe active participation and committedinvolvement by the federation of SHGs atdifferent levels.

Credit Disbursement in relation to Gradingof VO/SLF and MS/TLF

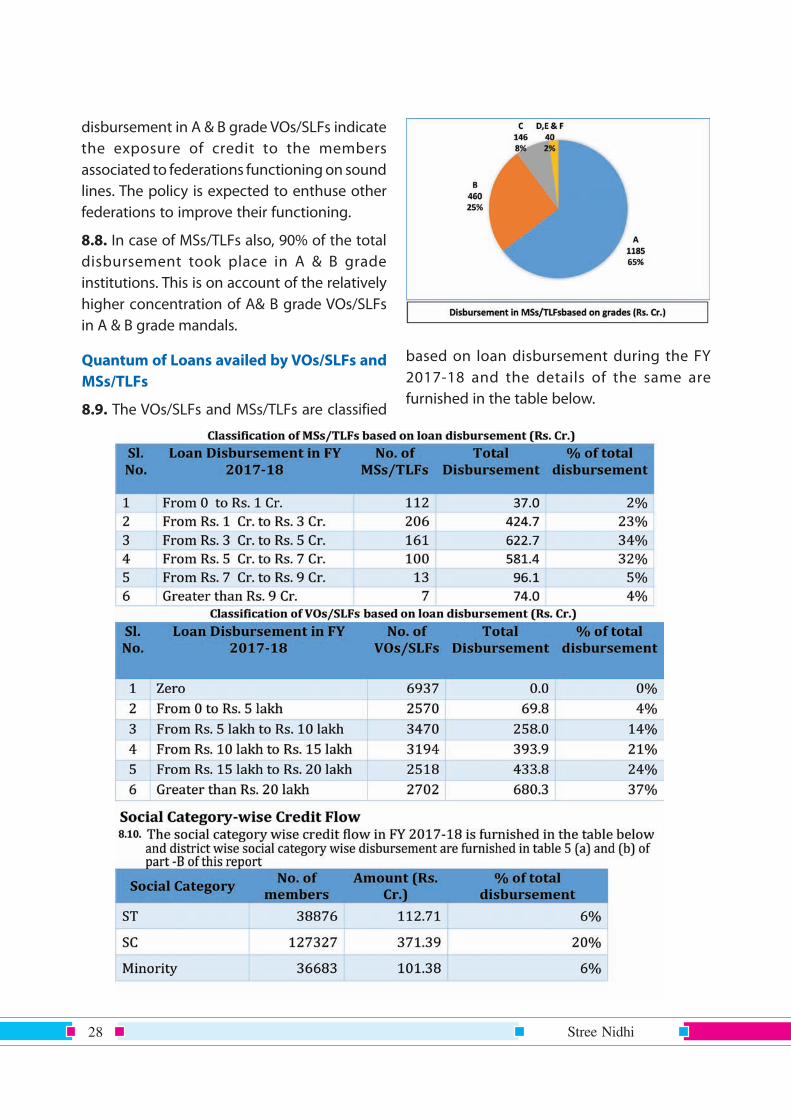

8.7. Rating of institutions decides the extent ofcredit that can be accessed by SHGs affiliatedto the respective VOs/SLFs and MSs/TLFs. TheVO/SLF grade wise credit disbursement for theFY 2017-18 is furnished in the pie chart. Of thetotal disbursement, 97% was in A & B gradeVOs/SLFs. The higher flow in A & B grade VOs/SLFs is on account of the allocation of highercredit limits and utilization thereof. The higher

Stree Nidhi28

disbursement in A & B grade VOs/SLFs indicatethe exposure of credit to the membersassociated to federations functioning on soundlines. The policy is expected to enthuse otherfederations to improve their functioning.

8.8. In case of MSs/TLFs also, 90% of the totaldisbursement took place in A & B gradeinstitutions. This is on account of the relativelyhigher concentration of A& B grade VOs/SLFsin A & B grade mandals.

Quantum of Loans availed by VOs/SLFs andMSs/TLFs

8.9. The VOs/SLFs and MSs/TLFs are classified

based on loan disbursement during the FY2017-18 and the details of the same arefurnished in the table below.

Annual Report 2017-18 29

8.11. The above is more or less in line with thepercentage of population of social categoriesin the overall members organised into SHGs.

Product wise Credit Flow

8.12. The credit flow was under three loanproducts namely i) Suvidha, ii) Pragathi and iii)Akshaya to meet varied credit needs ofmembers. Loans under Suvidha are utilized tomeet both productive as well as consumptionneeds and loans under Akshaya, Pragathi areavailed exclusively for taking up higher orderincome generating activities.

QUALITATIVE APPRAISALA handbook on loan appraisal of 74

common livelihood activities has beenprovided to the staff to enable assessment

of credit needs in a systematic mannerensuring quality of assets

ONLINE AND OFFLINE HLPsWeb based (Online) and Android based

(Offline) Household Livelihood Plan formswere developed for appraisal of livelihood

activities with provision for profiles ofselected activity

8.13. In FY 2017-18, Pragathi and Akshaya loansavailed were to the tune of Rs. 543 crores,constituting 29% of the total disbursementcovering 1,02,054 members under Pragathi andAkshaya and 5,33,441 members under Suvidha.The share of Pragathi and Akshaya loans in totaldisbursement has increased from 3% in 2014-15 to 29% in 2017-18. So far 2,18,000 SHG

members have availed under Akshaya andPragathi loans.

Stree Nidhi30

Dairy Financing

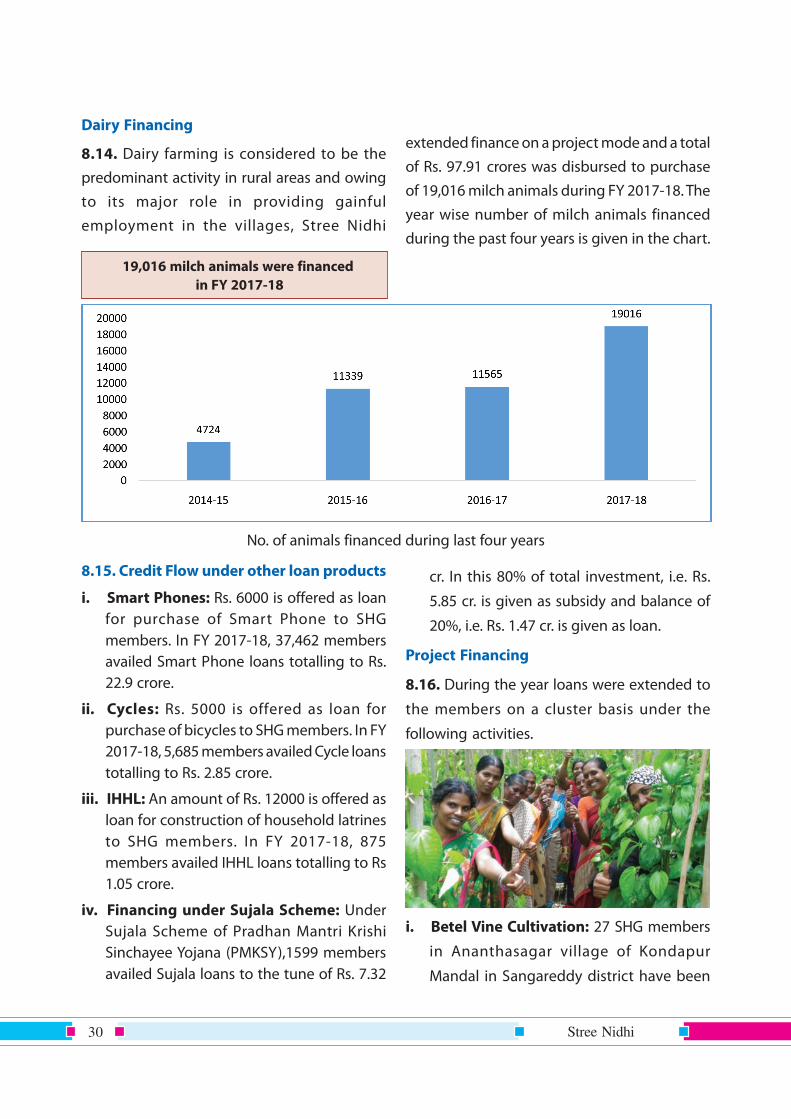

8.14. Dairy farming is considered to be thepredominant activity in rural areas and owingto its major role in providing gainfulemployment in the villages, Stree Nidhi

19,016 milch animals were financed in FY 2017-18

extended finance on a project mode and a totalof Rs. 97.91 crores was disbursed to purchaseof 19,016 milch animals during FY 2017-18. Theyear wise number of milch animals financedduring the past four years is given in the chart.

No. of animals financed during last four years

8.15. Credit Flow under other loan products

i. Smart Phones: Rs. 6000 is offered as loanfor purchase of Smart Phone to SHGmembers. In FY 2017-18, 37,462 membersavailed Smart Phone loans totalling to Rs.22.9 crore.

ii. Cycles: Rs. 5000 is offered as loan forpurchase of bicycles to SHG members. In FY2017-18, 5,685 members availed Cycle loanstotalling to Rs. 2.85 crore.

iii. IHHL: An amount of Rs. 12000 is offered asloan for construction of household latrinesto SHG members. In FY 2017-18, 875members availed IHHL loans totalling to Rs1.05 crore.

iv. Financing under Sujala Scheme: UnderSujala Scheme of Pradhan Mantri KrishiSinchayee Yojana (PMKSY),1599 membersavailed Sujala loans to the tune of Rs. 7.32

cr. In this 80% of total investment, i.e. Rs.

5.85 cr. is given as subsidy and balance of

20%, i.e. Rs. 1.47 cr. is given as loan.

Project Financing

8.16. During the year loans were extended to

the members on a cluster basis under the

following activities.

i. Betel Vine Cultivation: 27 SHG members

in Ananthasagar village of Kondapur

Mandal in Sangareddy district have been

Annual Report 2017-18 31

provided finance to the tune of Rs. 22.3 lakh

for cultivation of betel vine.

ii. Pandal Cultivation of Vegetables: 23 SHG

members in Malkapur village of Toopran

Mandal in Medak district availed loans to

the tune of Rs. 23.74 lakh for cultivation of

Vegetables under Pandal method.

iii. Short term loans for business duringSamakka Sarakka Jatra: 11 SHG membersbelonging to Jayashankar district were

extended credit to meet working capital forbusiness during Samakka Sarakka Jatra.

iv. Financing Petty Trade: 24 SHG membersin Shankarampet (A) mandal of Medakdistrict availed loans to the tune of Rs. 17.6lakh for expanding their petty trade.

v. Financing of RSETI Trainees: Stree Nidhiis working in coordination with RSETIs toextend credit support to RSETI trainees whoare either SHG members or belonging tofamily of SHG member for setting upenterprises.

Analysis of Loan Outstanding8.17. The level of loans outstanding hasreached to Rs. 2427.33cr as at the end of March2018, recordinga growth of 34.7% over level ofRs. 1795.75cr. as on March 2017. The growthtrend in loan outstanding since inception isshown below. District wise position of loansoutstading is furnished in table 6 (a) and (b) ofpart-B of this reprot

Number of Borrowing Members per SHGandAverage Loan Outstanding per Member

8.18. The details of SHG members and SHGs,VOs/SLFs, and MSs/TLFs with outstanding

advances as on 31 March 2018 are givenhereunder.

Details of SHG members & CBOs with loanoutstanding as on 31 March 2018

Convergence with NGOsA workshop was organized with 27 NGOs

working in the domain of livelihoodspromotion to identify opportunities for

financing livelihoods

Stree Nidhi32

The average number of members with loanoutstanding per SHG has increased from fourin FY 2014-15 to five in FY 17-18. The loanoutstanding per SHG has increased fromRs.41,310 to Rs.87,955 during the same period.

The loan outstanding per member has alsoincreased during the period from Rs. 13,261 toRs. 16,425.

VO/SLF and MS/TLF Grade wise Loan

Outstanding

8.19. The loan outstanding against membersin VOs/SLFs in ‘A’ and ‘B’ grades account for 96%of the total loan outstanding as on March 31st

2018. The higher concentration of loans in A &B grade VOs is primarily on account of highercredit limits available to them. This reducescredit risk and keeps the level of NPAs at a bareminimum.

Classification of Institutions based onQuantum of Loan Outstanding

8.20. The classification of VOs/SLFsbased onloan outstanding as on March 31st 2018 isfurnished below. The VOs/SLFs which have loanoutstanding of more than 20 lakhs, ware 4670i.e., 28% of the VOs/SLFs accounting for 55% ofthe total loan outstanding i.e. Rs. 1315.11 cr. ason 31.03.2018.

Average loan outstanding per member in FY 2017-18 was Rs. 16,425

Average loan outstanding

Annual Report 2017-18 33

Asset Quality8.22. Stree Nidhi has been successful in ensuringasset quality along with robust credit growth. As onMarch 2018, the non-performing assets stood at Rs.19.14 crores constituting 0.79 % of the total loanoutstanding with the net NPA at zero levelon

Similarly, 30% of the MSs/TLFs (192) accounts for 60% of the total loan outstanding, i.e. 1423.8crores as on March 31st 2018 as shown below.

Sector wise Credit Flow

8.21. The purposes for which SHG membershave utilized loans are classified into two broadcategories – Income generation activities (IGAs)and consumption purposes. Income generationactivities (IGAs) are further classified broadly

into agriculture, activities allied to agricultureand micro-enterprises. The share of loansavailed for IGA activities in FY 2017-18 is 89%of the total disbursement. District wise purposewise disbursement are furnished in table 7 (a)and (b) of part -B of this report.

31.03.2018. During the year the repayment rate ofloans was at 98% against the demand. The districtwise performance details on repayment andNPA are furnished in table 8 (a), (b) and 9 ofpart -B of this report.

Stree Nidhi34

Stree Nidhi Suraksha:

9.1. Considering the vulnerability of poormembers of SHGs, Stree Nidhi devised ascheme to mitigate risk arising on death of aloanee member of a SHG as a prudent riskmitigation measure and implemented StreeNidhi Suraksha Scheme from 1st April 2014 withthe following objectives.

i. to protect the family members of the SHGmembers against financial risk in the eventof untimely death of a loanee member

ii. to protect the SHGs and their federationsagainst the risk of financial burden anddisintegration when a member with loanoutstanding dies.

9.2. Under the scheme, all the members ofSHGs who avail loans from Stree Nidhi arecovered for the entire loan amount and period

of repayment. Charges payable are at Rs. 2.50per Rs.1000/- of loan amount per year and theamount required will be sanctioned asadditional loan to member / SHG which isrepayable along with the loan instalment. Theclaim settlement is done by utilising servicesof VO/SLF through Tablet PCs who register theclaims and upload claim documents. Onscrutiny of the claim by field level staff of StreeNidhi, the claim documents will be forwardedto H.O. If the documents are in order, the claimwill be settled at H.O. The outstanding loan willbe adjusted from the claim amount and thebalance will be paid to the legal heirs throughthe SHG concerned. The claims are settled outof the pooled amount of charges paid by loaneemembers. The VOs/SLFs/MS/TLFs arecompensated by paying charges for theservices rendered by them.

Livestock Insurance9.3. Considering the importance of dairyactivity as a predominant income generating

The status of coverage of members and claims settlement during 2017-18 (Rs. Cr)

Sl. No. Particulars FY 2017-18 Cumulative upto 31.03.2018

1 Members Covered 6,54,000 26,18,000

2 Loans disbursed 1818 6975.86

3 Suraksha charges collected 11.96 57.30

4 No. of claims registered 1810 6127

5 Amount claimed 4.92 16.01

6 No. of claims settled 1618 4760

7 Amount settled 4.38 12.18

8 No. of claims under process 191 1348

9 Amount 0.53 3.79

activity for the poor families, Stree Nidhi isextending finance to a large number of SHGmembers to purchase dairy animals. In order

Stree Nidhi Credit Portfolio – Risk Mitigation Strategies

Chapter - 9

Annual Report 2017-18 35

Social Audit as a tool to promotetransparency

9.6. Stree Nidhi has put in place various systemsand controls to ensure transparency in conductof operations at grass root level. As a measureof ensuring adherence to various guidelines atcommunity level, an audit system has beenimplemented wherein transactions of SHG andVO/SLF pertaining to Stree Nidhi are subjectedto social audit.

9.7. For the purpose, Stree Nidhi is utilising theservices of TSSAAT and CARPs (CommunityAudit Resource Persons) after impartingrequired skills. After conducting Social Audit,observations made by the Auditors are placedbefore Grama Sabha for open discussion so asto make the members aware of deviations inprocedures and systems or fraudulenttransactions, if any, so as to fix accountabilityand take necessary follow up action.

9.8. The above will increase transparency atSHG/VO/SLF level and would prevent deviationfrom norms, proper end use and regularity inrepayment of loans.

9.9. During the process of Social Audit,instances of lapses in documentation, equaldistribution of loans among all SHG members,delay in settlement of claims under Stree NidhiSuraksha and Cattle Insurance were observed.There is increase in coverage of no. of VOs/SLFsin tune with the increase in volume of creditportfolio.

to mitigate the risk of debt burden on death ofanimal, Stree Nidhi is implementing LivestockInsurance scheme in collaboration with UnitedIndia Insurance Company ltd. The amountrequired towards insurance premium will begranted as loan in addition to the cost of animal.As per the terms of MoU entered with insurancecompany, dairy animals are covered under amaster policy from the date of purchase till theend of repayment period.

9.4. Stree Nidhi has evolved a communitybased insurance mechanism to cover theanimals by tagging and settlement of claims ondeath of the animals. Claims are settled basedon confirmation of death of animal by VO anduploading of photographs of dead animals andother required documents through Tablet PCs.No post mortem report from VeterinaryDepartment is necessary, ensuring hassle freesettlement of claims. Stree Nidhi share thedetails of animals purchased to insurancecompany for coverage and remit premium inadvance to ensure coverage of animals as andwhen purchased by the members. Claimamount will be remitted to SHGs concernedafter adjusting towards loan outstanding as onthe date of death of animals.

9.5. In 2017-18, 19,017 she buffaloes/cows werecovered under insurance for a period of 4 years.Since inception of the scheme, 68,634 shebuffaloes/cows have been covered and 1,392claims were settled out of 1,945 registered.

StreeNidhi is taking required remedial measures to rectify the deviations observed and steps torecover the amount involved in misuse of the amount.

Year No of VOs/SLFs covered No of VOs/SLFs covered Total

by TS-SSAAT by CARPs

2014-15 31 69 100

2015-16 97 717 814

2016-17 1006 337 1343

2017-18 465 530 995

2018-19 1250 360 1610

Total 2849 2013 4862

Coverage of VOs/SLFs under Social Audit

Stree Nidhi36

The analysis on financial performance of Stree Nidhi with regard to profitability, cost to incomeand key ratios for FY 2017-18 and previous years is presented as under.

10.1. Profitability Analysis

Total income

10.2. Total income has increased from Rs.169.92 cr to Rs. 256.08 cr achieving growth rateof 51% and the expenditure has increased fromRs. 119.96 cr to Rs.197.17 cr with an increase of64% in FY 2017-18. The increase in expenditurewas on account of increase in borrowings, andother operational expenditure due to increasein staff strength.

Net Profit

10.3. There is a steady growth in net profitearned by Stree Nidhi. During the year2017-18, it was Rs.58.91 cr as compared to

Rs. 49.96 cr showing a growth rate of 18% onyear on year.

Financial Performance

Chapter - 10

Annual Report 2017-18 37

Interest Income and Interest Expenditure

10.5. Total Interest income earned on loans andadvances in FY 2017-18 was Rs.251.45 cr asagainst the interest expenditure Rs.143.81 cr on

deposits and borrowings. A comparativepicture on interest income and interestexpenditure for the last four years is furnishedbelow.

(Rs. Cr)

Stree Nidhi38

Staff Salaries

10.6. The expenditure incurred on staff salariesin 2017-18 was Rs 5.68 cr. The amount incurred

is well within the amount prescribed as per theprovision of Co-operative Societies Act 1964.

(Rs. Cr)

Particulars FY 2016-17 FY 2017-18Expenditure towards Staff Salaries 3.24 5.68Working Funds 1790.69 2364.46% of Staff Salaries to Working Funds 0.18 0.24Gross Profit 70.81 112.30

% of Salaries to Gross Profit 4.09% 4.72%

Appropriation of Net Profit for FY 2017-18

10.7. As per the Co-operative Societies Act,1964 it is mandatory to provide 25% of netprofit towards statutory reserve as per the

provisions of Sec 45.3 (a). Further, it is proposedto appropriate net profit towards otherpurposes as mentioned in the table below.

(Rs. Cr)

Total Net Profit earned 58.91

1 Statutory Reserve (25% rounded) 14.72

2 Dividend @ 11% on share capital (123,15,88,268/-) 13.54

3 Building Fund @10% profit 5.89

4 Staff Medical & Welfare Fund @ 1% profit 0.59

5 Community Benevolent @0.25% 0.15

6 Institutional building activities of SERP and MEPMA @ 5% 2.94

7 Neighbourhood centers (NHC) @ 2% 1.18

Total allocation of profit 39.01

Balance Amount to be added to Accumulated profit 19.90

Dividend10.8. Stree Nidhi paid dividend to thefederations of SHGs i.e. MSs/TLFs and StateGovernment. The rate of dividend paid hasincreased from 7% to 10% in F.Y 2014-15 to F.Y2016-17.

Ratio Analysis

Cost of Funds and Interest Margin:

10.9.The cost of funds has decreased from 8.64% to 8.50 % for the FY 2017-18 as compared toprevious year mainly on account of decrease in

the interest rate on borrowings from banks.Accordingly, Interest margin at 4.65 % for FY2017-18 is higher compared to 4.50 % for theyear 2016-17.

Annual Report 2017-18 39

Yield on Advances and Net Interest Margin:10.10. The yield on advances was at 13.17% forthe FY 2016-17 and it was at 13.15% in 2017-18on account of decrease in rate of interestcharged on loans from 13% to 12.5%. Netinterest margin was lower at 5.63% for FY 2017-18 as compared to 5.68 % for FY 2016-17.

10.11. Operating expenses to Gross income hasincreased from 9.87 % in FY 2016- 17 to 11.90%in FY 2017-18 due to increased staff strengthand other operational expenditure.

Own funds and CRAR

10.12. The own funds of Stree Nidhi grew by25% over the previous financial year and CapitalAdequacy Ratio was at 31.33 % in 2107-18,showing marginal decrease as compared to33.73 % in FY 2016-17.

Stree Nidhi40

Audit by Cooperative Department for F.Y 2017-18

10.14. The Cooperative department of Govt ofTelangana completed audit of Stree Nidhi forFY 2017-18 and issued Audit Certificate. StreeNidhi has been awarded “A” grade by theCooperative Auditors for the year indicating

excellent performance in all spheres of StreeNidhi activities. The audited Balance Sheet andIncome and Expenditure account for the year2017-18 are enclosed in part -C of this report.

10.13. Comparative Analysis of Key Ratios for FY 2016-17 & 2017-18

Annual Report 2017-18 41

Empowerment of Community throughDigitalization

Deployment of Tablet PCs at Village / SlumLevel

11.1. One of the unique features of Stree Nidhiis leveraging Information Technology to deliverfinancial services seamlessly at the doorstepsof members of SHGs in pursuit of its avowedobjective of poverty alleviation throughempowerment of women. Since inception,Stree Nidhi has adopted an innovativeapproach in purveying credit and otherfinancial services to the members of SHGs in theState. Loan requests are generated andprocessed through in-built validations in theloan module system, ensuring speedyprocessing of loan requests and disbursal ofcredit to the eligible SHG members. The use oftechnology in Stree Nidhi has become a trend-setter in disbursal of loans within 48 hours ofapplying loan by the members.

Chapter - 11

portfolio and coverage of the members of SHGsyear after year. In tune with the opportunitiesprovided by changing technology, Stree Nidhialso has endeavored to fine-tune its deliveryand monitoring systems.

Digitalization of Stree Nidhi operations atVillage/Slum Level

11.3. Stree Nidhi has introduced Tablet PCs atvillage / slum level to digitalize the operationscovering 16000 VOs/SLFs across the state.

11.2. Over a span of seven years after itsestablishment in the year 2011, Stree Nidhi hasbeen achieving significant growth in credit

Tablet PCs are being used to ensure biometricauthentication of borrowers through Aadhar,accessing MIS reports at village level,adjustment of repayment etc. More features arebeing added to digitalize other operationsincluding asset verification and filing ofinsurance claims. The Tablet PCs have thefollowing security features to prevent misuse.

i. Central monitoring from Head Officethrough Mobile Device Management(MDM) system.

Stree Nidhi42

ii. Geo-fencing feature to prevent theTablet PCfrom functioning beyond the periphery ofa village/town to which it was allocated.

iii. Centralized control over installation of appsthereby ensuring that the Tablet PC has onlythe relevant apps installed in it.

iv. Aadhar authenticated logins for VO/SLF OBsand Stree Nidhi staff to preventunauthorized access at village level.

v. White listing of web services.

The services being accessed through Tablet PCsare briefly mentioned below.

Loan Application with Borrower Authentication