Annual Report 2011

68

Annual Report 2011

Transcript of Annual Report 2011

Annual Report 2011

Our supplying shareholders have all the ingredients needed to produce some of the finest quality milk in the world. Abundant rainfall, nutrient-rich soil, and year-round fresh green pastures on the West Coast, enable us to produce premium quality milk direct from the farm gate. At Westland Milk Products, we are dedicated to delivering a world leading product. At every stage of our milk’s journey, from the time it leaves the farm gate, quality control is uncompromising. Upon delivery, our trusted global customers, in more than 50 countries worldwide, experience one of the highest quality milk products available to them in the world. It’s what they have come to expect of us at Westland Milk Products, and it’s what we expect to deliver.

1

Our Land of Plenty 4

Mission and Values 6

Season in Review (Facts/Highlights) 8

5 year trends 10

Chairman’s Report 12

CEO’s Report 14

From Our Team to Yours 18

Respect – Case Study 20

Corporate Governance Report 22

Audit Report 24

Directors’ Declaration 25

Financial Statements 26

Notes to Financial Statements 32

Statutory Information 59

Directory 65

Contents

2

3

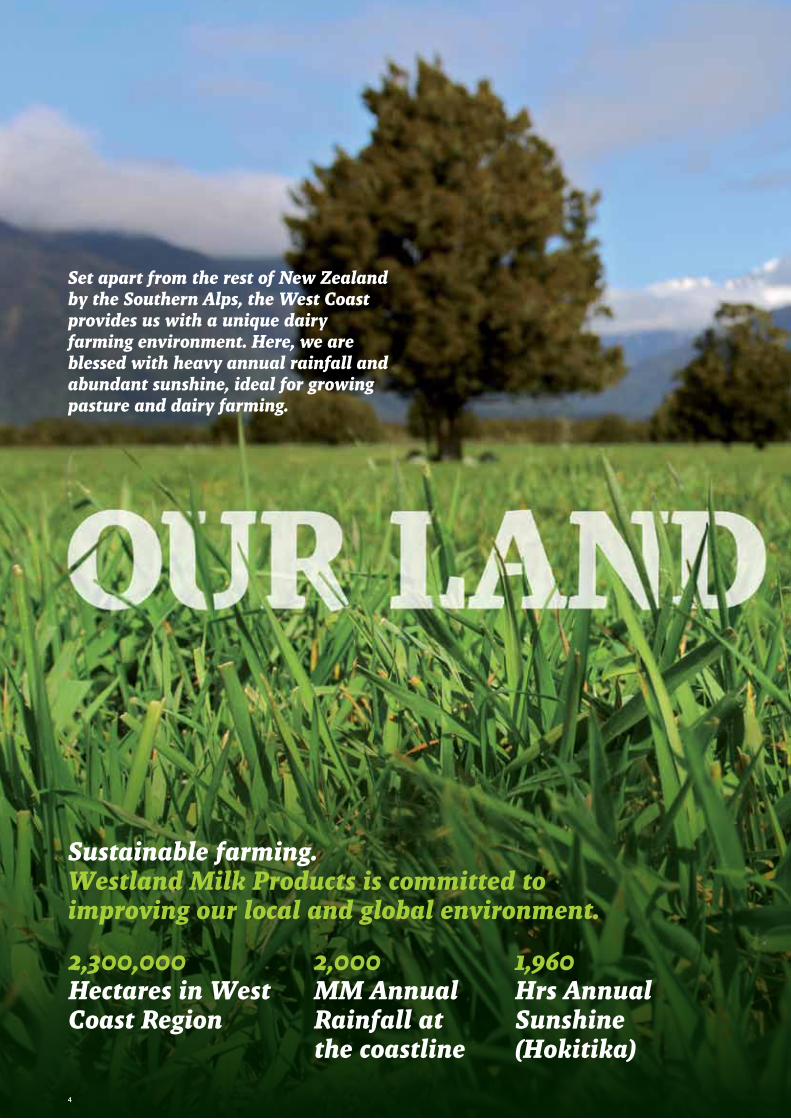

Sustainable farming. Westland Milk Products is committed to improving our local and global environment.

2,300,000Hectares in WestCoast Region

2,000MM AnnualRainfall at the coastline

1,960Hrs AnnualSunshine(Hokitika)

Set apart from the rest of New Zealand by the Southern Alps, the West Coast provides us with a unique dairy farming environment. Here, we are blessed with heavy annual rainfall and abundant sunshine, ideal for growing pasture and dairy farming.

4

ISO 14001 Environmental management systems

Work closely with local and regional government

Promote on farm best management practice

5

We are dedicated to providing a positive environment for the betterment of all

We come from a pioneering background where teamwork was and still is of paramount value

Our Mission is central to the way we act and the way we run

our company. Westland Milk Products’ Mission is;

Our Values

6

From the milking of the cows to our products’ ultimate destination we are respectful and proud of everyone’s contribution

Our loyalty and genuine openness is ingrained in everything we do

To be the preferred supplier of premium quality dairy and nutritional products, exceeding our customers’ expectations and maximising sustainable returns of our shareholders.

7

Land & Sustainability Facts Voluntary participation in the Emissions Trading Scheme.

8

Strategic review reveals plans to transform Westland Milk Products into a growth oriented, value added, nutritional dairy products manufacturer.

Historic move by Westland Milk Products into Canterbury region with new reverse osmosis plant construction at Rolleston on budget and on time.

Commitments from Canterbury suppliers secured ahead of the 2012 season.

Second highest average payout on record of $7.80/kg milk solids, before retention of 10 cents, up from $6.45/kg milk solids recorded in the previous corresponding period.

Total increase in milk processed by 13% to 571 million litres.

Described by farmers as one of the toughest years on record with a remarkably wet spring and dry spell in the summer.

Divestment of the Westland Farm Centre to fellow co-operative CRT.

Significant donations made to the Christchurch Earthquake Recovery appeal and the Pike River disaster.

EasiYo won several high profile awards including the Natural Products New Zealand Exporter of the Year Award, the Supreme Business Excellence and Excellence in Exporting Awards at the Westpac Enterprise North Shore Business Excellence Awards and very recently the Exporter of the Year Award (for companies under $35 million) at the Air New Zealand Cargo Export Awards Auckland 2011.

An aggressive sales programme leading to 90,000 tonnes of product sold worldwide.

Lean principles led to significant savings in water, power, steam, chemical and fuel usage.

Code of Practice initiated setting best management practices to apply on farm.

Westland Milk Products joins the voluntary Emissions Trading Scheme (ETS) participation programme to familiarise ourselves ahead of the scheme’s introduction in 2015.

9

Finance highlights

NZIFRS NZIFRS NZIFRS NZIFRS NZIFRS

2011 2010 2009 2008 2007

Milk Received From Suppliers [M litres] 515 502 479 478 467

Milk Fat - Own Supplier [M kgs] 27.049 26.246 25.018 24.692 24.292

Protein - Own Supply [M kgs] 19.930 19.517 18.339 18.329 17.885

Milk Solids Received from Suppliers [M kgs] 46.979 45.763 43.358 43.022 42.178

Average Milk Solids per Farm [kgs] 121,080 119,175 113,503 113,516 111,582

Average Milk fat % 5.26 5.23 5.20 5.16 5.19

Average Protein % 3.87 3.89 3.80 3.83 3.82

Protein : Fat Ratio % 73.68 74.00 73.00 72.00 74.00

Finest Milk % 98.66 97.10 96.30 95.90 98.32

Production [Tonne] - Powder 51,920 47,114 42,831 51,279 46,192

Production [Tonne] - Butter 25,529 23,480 22,283 19,467 18,380

Production [Tonne] - Protein 4,380 4,017 3,762 2,502 1,607

Production [Tonne] - AMF 5,720 3,668 3,427 5,622 3,979

Turnover [$Million] 525 422 364 501 295

Total Assets [$Million] 351 335 284 326 314

Total Equity [$Million] (Incl. shares classified as liabilities) 190 182 172 181 186

Payout to Shareholders

- Fat [cents/kg] 511 443 301 533 306

- Protein [cents/kg] 1,112 962 654 1,158 666

- Operating Surplus [cents/kg] 780 645 411 829 472

- Retentions [cents/kg] (10) (30) 47 (30) 0

- Net Average Payout [cents/kg] 770 615 458 799 472

Equity : Assets Ratio [%] 54 54 60 55 59

Current Ratio [%] 130 133 77 116 156

Working Capital to Total Assets Ratio [%] 10 10 (8) 5 13

5 year trends

Land & Sustainability FactsLean principles resulting in reduced water, power, chemical and fuel usage across our operations.

10

TOTAL EQUITYIncl. shares classified as liabilities.(Dollars in Millions)

Financial Year

MILKSOLIDS(Million Kilograms)

Financial Year

18

6.1

7

PAYOUT TOSHAREHOLDERS(Cents per Kilogram)

Financial Year

18

2.5

0

18

6.1

7

18

0.6

5

17

1.5

4

11 10 09 08 07

18

2.5

0

18

6.1

7

18

0.6

5

17

1.5

4

19

0.2

2

11 10 09 08 07

770

11 10 09 08 07

45

.76

42

.18

43

.02

43

.36

46

.98

61

5

47

2

79

9

45

8

11

The 2011 season will be remembered for its volatility with the season beginning with a wet spring followed by a 100 year dry spell in some parts of the West Coast. The global stage was equally volatile with the rising exchange rate and commodity prices contributing to payout expectations shifting markedly from $6.50 - $6.90/kg milk solids in the beginning of the year to a final average payout of $7.70/kg milk solids after retention of 10 cents/kg milk solids.

The unpredictable global environment highlighted the importance of a strong balance sheet and it was therefore pleasing to end the year in a strong equity and reduced debt position.

During the year Westland Milk Products focused heavily on maximising value and efficiency in our core business, building on our existing and new relationships with global customers and expanding our milk processing capability. These efficiencies are delivering strong financial results for our suppliers.

Westland Milk Products’ long term strategy is to transform the Company into a growth oriented, value added, nutritional dairy products manufacturer with a view to maximising returns to our suppliers.

Increasingly our focus will be to produce nutritional milk products for

the paediatric, aged care and sports sector while continuing to leverage our core business offering of supplying high quality commodity milk product to the world.

The commencement of our strategic plan began to take shape in 2011 with the decision to source additional milk supply in Canterbury and build a reverse osmosis plant at Rolleston. This is a significant step for Westland Milk Products and the Board is extremely proud to be creating a pathway for future growth for Westland Milk Products.

The plan is set in stages with the first phase to establish milk reception facilities in Rolleston, followed by the drafting of a business case to support the expansion of our nutritional production capability at Hokitika.

Throughout the strategic planning process the Board and Management has recognised the special attributes of Westland Milk Products’ co-operative dairy company ownership structure. Maintaining the values of a supplier co-operative model will remain front of mind with all decisions made regarding future expansions, joint ventures, acquisitions and capital structures.

Towards the end of this last season we have seen the competition for milk reach the farm gate on the West Coast. We are confident that Westland Milk

Chairman’s ReportMatt O’Regan

2011 has been a significant year marking ten years since Westland Milk Products became an independent milk processor in 2001; a year in which the decision was made to source milk from the Canterbury region; and to expand our processing capability.

Matt O’Regan - Chairman Westland Milk Products

12

Products’ pure co-operative model, embodied in its constitution, with its nominal value share, returning profit to suppliers through payments for colostrum and milk supply, will continue to deliver the results demanded by suppliers to ensure Westland Milk Products remains the preferred processor for West Coast dairy farmers. It is a testament to this co-operative model that West Coast farmers have been able to grow Westland Milk Products’ milksolids supply by over 60% since independence while the Company has delivered an industry competitive payout.

Westland Milk Products retained 10 cents/kg milk solids to provide capital management stability and fund future growth initiatives. The Board reviews retentions on an annual basis, but it is a widely held view among the Senior Management Team and Board that retentions will continue to be made for the next five years to facilitate the execution of our on-going strategy. In 2011 Westland Milk Products has taken an active role in environmental practices on farm. Our customers are increasingly aware about environmental sustainability and our animal health practices and as such operating without a formalised environmental code of compliance has become no longer an option. Fortunately our suppliers have always taken sustainability practices seriously

and it is pleasing to be able to document this formally with a standard setting Code of Practice. We look forward to monitoring these standards on a regular basis and to illustrate our sustainable practices to the world.

It goes without saying that in 2011 West Coasters and Cantabrians experienced a number of significant and tragic events and our sympathies go to those personally affected. It has also been a time when we have witnessed the resilience and commitment of people on both sides of the alps to their regions and their employment. On behalf of the Board I would like to thank our valued Westland Milk Products’ employees, many of whom acted in a truly professional and selfless manner during unprecedented and trying circumstances.

The Board has been equally impressed with the professional approach of the newly embedded Senior Management Team and would like to acknowledge the confidence we have in them delivering the Company’s strategic plans. Without this confidence the strategic objective to position Westland Milk Products as an innovative, fast moving and preferred dairy processor in years to come would not be possible.

After ten years of service long standing independent director Sir Graeme

Harrison has stepped down from the Board. Sir Graeme joined the Board after Westland Milk Products became an independent co-operative in 2001 and during his tenure he has imparted significant knowledge and experience. The Board agrees it has been an honour to have Sir Graeme sit on our Board.

Looking ahead, while there may be an easing in commodity prices in the short term, the Board believes that increased demand for protein among the emerging economies will continue. We are fortunate to be part of such an exciting and dynamic industry with significant scope for increasing returns to suppliers. In 2012, the Board will remain focused on ensuring suppliers continue to benefit from Westland Milk Products’ business strategy while maintaining the highest standards of transparency and corporate governance.

In conclusion, I thank my fellow Directors for their support and dedication to the Company, and on behalf of the Board and Management, I would like to thank suppliers for their continued support and commitment to Westland Milk Products. We look forward to serving you again in the current year as Westland Milk Products realises the value of its expanded business platform.

13

The Result2011 has been described by many farmers as one of the toughest years yet with a remarkably wet spring and dry spell in the summer presenting difficult farming conditions. International competition, volatile exchange rates and commodity prices continued to make forecasting amongst the global and local events extremely challenging.

It is therefore a credit to our Board and Management Team that Westland Milk Products recorded an average payout of $7.80/kg milk solids before retention of 10 cents/kg milk solids, a 21 per cent improvement on last year’s payout of $6.45/kg milk solids. Record turnover of $525 million assisted by record volumes of milk processed and products sold led to the strong payout.

Westland Milk Products processed 571 million litres of milk supply, a 13 per cent increase on the previous year, 10 per cent of which is attributable to milk from external sources. Westland Milk Products’ shareholder supplied milk increased 2.5 per cent as a result of a strong autumn period with settled weather and a healthy payout signalled.

Colostrum in 2011 returned an average of 12 cents/kg milk solids to suppliers, a 33 per cent improvement on last year’s average of 9 cents/kg milk solids. We are pleased to report that colostrum is supplied by more than 75 per cent of our suppliers and that all suppliers have

the opportunity to participate. As global commodity prices strengthened throughout the financial year, so too did our payout projections which rose from $6.50 - $6.90/kg milk solids at the beginning of the season to the final average payout of $7.80/kg milk solids. An active hedging programme delivered a favourable average conversion rate of 70c versus an average spot rate of 77c. Our currency hedging programme was successful in smoothing out some of the volatility from the rising NZ dollar against a weakening US greenback.

Increasing efficiencies continued to be a high priority for Westland Milk Products during 2010/11. Lean principles were applied to all facets of the business and resulted in many successful cost saving initiatives including a reduction in water usage by 250 million litres, power and steam by 6.5 per cent, chemical usage by 20 per cent and fuel savings of 4 per cent. The increase in total milk processed resulted in an overall cost saving for suppliers of 9.5 cents/kg of milk solids processed.

Capital Westland Milk Products continues to actively manage its capital to ensure we are operating efficiently and prudently managing risk. We finished the financial year with a strong balance sheet and favourable equity position of 54 per cent, allowing Westland Milk Products to secure advantageous finance rates heading into the 2012 season.

CEO’s ReportRod Quin

Westland Milk Products performed strongly in 2011 recording our second highest payout despite experiencing some of the most challenging climatic and economic conditions on record. Our full year results demonstrate the strength of the business and Westland Milk Products’ ability to take advantage of opportunities for future growth.

Rod Quin Chief Executive OfficerWestland Milk Products

14

Marketing and Sales Our proactive sales programme led to 90,000 tonnes of product being sold across all markets. Of that figure, approximately 70 per cent was shipped to the Asia-Pacific region with Russia, the USA and the Middle East also showing promising signs of growth. We continue to take our successful product offerings to key customers around the world and in the process we are recognised as a leader in the provision of highest quality milk products to well-known international consumer brands.

We will continue to work closely with our end-use customers in 2011/12 to ensure mutual value-add activities are secured working with key customer relationships that continue to develop.

Strategic ReviewA strategic review, started early in the season, cemented our plan to transform Westland Milk Products from a medium sized, dairy commodity producer into a growth oriented, valued added and nutritional dairy products manufacturer and marketer.

The strategic review formed the catalyst to build a reverse osmosis plant at Rolleston and source additional share backed milk supply from Canterbury dairy farmers. The plant was completed on budget and commissioned on schedule for the 2011/2012 season.

The announcement of our planned move into Canterbury drew a positive reaction from interested dairy parties on the east coast and we are pleased with the number of milk commitments secured to date. We continue to receive supply enquiries and expect this to continue into the new season.

EasiYoIn 2011 our subsidiary and global yogurt business EasiYo contributed 3 cents/kg milk solids to the final supplier payout. Since moving to their new manufacturing facilities last year in Albany, Auckland, EasiYo has more than doubled its production capacity and produces approximately 1 million yogurt sachets per month and now has 75 per cent market share in the home made yogurt market in New Zealand, with 75 per cent of product made exported predominantly to Australia and the UK.

EasiYo’s entry into Italy, a new market this year, has been an outstanding success with sales going from zero to $2 million in under 12 months. This successful exporting opportunity was supported by New Zealand Trade and Enterprise which made a significant funding contribution. The relationship also led to EasiYo being invited by Trade and Enterprise to feature at the Rugby World Cup’s “The Cloud” facility on the new Queens Wharf development, Auckland. EasiYo’s tasting display stand at The Cloud will

expose the brand to the expected 85,000 Rugby World Cup visitors and the general public of New Zealand.

Testament to this year’s success, EasiYo won several awards during the year including the Natural Products New Zealand Exporter of the Year Award, the Supreme Business Excellence and Excellence in Exporting Awards at the Westpac Enterprise North Shore Business Excellence Awards and very recently the Exporter of the Year Award (for companies under $35 million) at the Air New Zealand Cargo Export Awards Auckland 2011.

SponsorshipsWestland Milk Products has always been a proud supporter of local initiatives but few were more important than this year’s donation to the Canterbury Earthquake Recovery appeal and the families of the Pike River Mine disaster.

Our donation to the Federated Farmers-led initiative “Farmy Army” helped remove hundreds of tonnes of liquefaction from suburbs of Christchurch while the contribution to the Pike River Mine fund provided much needed support to families of the tragedy. EasiYo also made a significant contribution to various relief centres in Christchurch following the earthquakes.

15

EasiYo has been a proud supporter of the Canterbury Tactix netball team, which put in a brave effort despite having a number of reduced home games due to the Christchurch earthquakes. The opportunity to link the brand to active lifestyles and the renaissance of at home food preparation was also developed with sponsorship of the Junior Master Chef Australia series.

We are also proud to have contributed to numerous other local charities and causes, making donations to various local schools and libraries, sports organisations and health charities including the Epilepsy Foundation and the Hokitika Cancer Support Group.

SustainabilityThis year marked a significant step forward in Westland Milk Products’ sustainability practices with the introduction of a new Code of Practice. The Code of Practice requires all Westland Milk Products’ suppliers to implement appropriate best management practices with regards to the environment, animal welfare and farm presentation.

We are pleased with the level of support for the initiative to date and, after a number of consultative meetings have been able to finalise a formal Code of Practice document. We look forward to implementing the new code in the coming season.

At the beginning of the calendar year, Westland Milk Products signed up to a Government run voluntary Emissions Trading Scheme (ETS) participation programme to familiarise ourselves with the scheme’s requirements for when it becomes obligatory in January 2015. As part of this programme we will be asking suppliers what the Emissions Trading Scheme means to them and the impact it may have on their farming activities. Suppliers will be represented at all levels of discussions with MAF and central government.

Sale of the Westland Farm CentreAt last year’s annual meeting we announced the sale of the Westland Farm Centre in Hokitika to fellow co-operative Combined Rural Traders (CRT). The decision to sell the Farm Centre was not an easy one, however a review of the business highlighted that it was peripheral to our core offering. By divesting the Farm Centre we were convinced suppliers would have even better support from a larger and dedicated farm supplies group. The divestment enabled Westland Milk Products to concentrate solely on our core operation of sourcing, processing and marketing milk products to our customers.

The Outlook The outlook for the dairy industry remains positive notwithstanding the on-going presence of volatility in global markets. Our suppliers can take great comfort that the dairy industry recovered quickly following the global financial crisis and that the demand for protein among emerging economies continues to strengthen. We anticipate dairy prices will continue to be volatile but on average settled higher than past long run averages. With a focus on farm input costs this should lead to on-going profitability over the medium and long term for NZ dairy farmers. In 2012 Westland Milk Products will continue to focus on improving operational performance and seek to improve returns to suppliers through expansion as we continue to become even more relevant to our customers.

AcknowledgementsI would like to take this opportunity to personally acknowledge the guidance and support of the Board and our Senior Management Team in 2011. We are fortunate to have talented, dedicated and loyal staff who are committed to achieving Westland Milk Products’ shared objectives.

I would also like to thank you, our suppliers, for your support during a milestone year and look forward to serving you again in the 2011/12 season.

CEO’s ReportContinued…

16

17

Sir Graeme HarrisonBoard Appointed Director

Raelyn Lourie Director

Bernard MayGeneral Manager Operations

Frank DooleyDirector

Noel RobbDirector

Mike Havill Deputy Chairman

Rod QuinCEO

Matt O’Regan Chairman

Left to right

From our team to yours

18

Leo McIntyreGeneral Manager Quality & Technical Services

Barry Paterson Director

David Spence Board Appointed Director

Jim Wafelbakker Director

Kim WallaceChief Financial Officer

Mark LockingtonCompany Secretary

Jon SullivanDirector

Gregg WafelbakkerGeneral Manager Sales & Marketing

19

But it wasn’t always this way. Kerry was previously a consultant for Lincoln International, the international development consultancy firm owned by Lincoln University focusing on the management of a wide range of development projects in the Pacific and Asia.

In 2002, his decision to return to his dairy farming roots led him to his first dairy conversion in Whataroa, a project undertaken with his brother Dale and his wife Stacey. Dale and Stacey were previously sharemilking at Fairlie in

South Canterbury so the partnership venture was a new start for both of them and meant a return to their West Coast dairy roots.

Kerry says their first conversion of a 440 hectare former beef farm was a big job, with the farm initially presenting in a pretty run down state with only about 150 hectares of poor pasture and the balance in bush, scrub, swamp or rushes. “We spent about six months knocking it into shape before milking cows.”

Case StudyKerry StraightFox Glacier

If there was ever a West Coaster with a pioneering spirit Kerry Straight would be that person. His Fox Glacier farm is the second that he and his partners have converted to dairy on the West Coast.

20

After successfully converting that farm in a “rush of blood to the head” they bought into their second dairy farm conversion project with John Sullivan at Fox Glacier. Three years on, this 400 hectare property is just finishing its second season and will have 950 cows for the third season. During the conversion process the whole farm was developed and sown in new pasture, raced and fenced. New houses, sheds and a 60 bale rotary shed were built.

Kerry says the rough riverflat country meant countless tonnes of stones had to be removed during pasture development.

“Most of the farm would never have seen any cultivation prior to us.”

Kerry is using some of his consulting background to think outside the square with regards to management. He admits converting a farm of this type is all pioneering stuff. “I get my kicks out of seeing marginal land becoming productive. That is certainly what I enjoy seeing happen and if we can make a few dollars out of it then that’s great too.”

Being part of Westland Milk Products has its benefits. “There is a huge difference in being part of a smaller co-operative in terms of the scale and availability of directors. Most suppliers would know two or three of the directors personally and feel they can ring them at anytime. This reflects the close knit culture of the industry on the West Coast.”

21

BoardThe company’s constitution provides for the parent Board to comprise eight directors nominated and elected by the supplying shareholders, two directors appointed by the Board and a Managing Director (if one is appointed).

Those eight directors comprise, five Ward Directors, one each elected by shareholders in the Southern, Central, Lower Grey Valley, Reefton/Inangahua and Buller/Karamea wards and three General Directors nominated and elected by supplying shareholders from the whole company.

Ward and General Directors retire from office at the annual meeting in the third year after their last election.

Each year the Board undertakes an evaluation of the performance of each director which may extend to identifying individual training and development plans where appropriate.

All new directors are inducted and receive the opportunity to undergo training and, along with other directors, undertake annual familiarisation tours to different divisions of the company across both the Hokitika and Rolleston locations.

Board CommitteesThe Board of Directors has two formally constituted committees:

Audit CommitteeThe Audit Committee is responsible for assisting the Board in discharging its responsibilities relative to financial reporting and regulatory conformance. In addition the Audit Committee is responsible for ensuring the recommendations of the external auditors are actioned by management, monitoring corporate risk assessment and the internal controls instituted by the company and supervising special investigations when requested by the Board. This committee is chaired by Appointed Director, David Spence, and currently comprises Chairman Matt O’Regan, General Director & Deputy Chairman Mike Havill and Ward Directors Noel Robb and Frank Dooley.

Remuneration CommitteeThe Remuneration Committee reviews the remuneration of the Senior Management Team. This committee is chaired by Chairman Matt O’Regan and currently comprises Appointed Director Sir Graeme Harrison, Deputy Chairman Mike Havill and Ward Director Raelyn Lourie.

Corporate Governance Report 2011

The company, the Board, each director and each shareholder of Westland Milk Products have the rights, powers, duties and obligations set out in the Companies Act 1993 and the Co-operative Companies Act 1996 except as these are negated or modified in accordance with these acts by the Constitution. The Constitution is registered and available on the Companies Office website or on request from the Company Secretary.

22

Westland Farm CentreThe Chairman of the Board, Chief Executive Officer and Chief Financial Officer of Westland Co-operative Dairy Company Limited sit on the Board of the wholly owned subsidiary company Westland Farm Centre Limited.

The Westland Farm Centre retail store and BP2Go service station businesses at Fitzherbert Street Hokitika were sold to CRT in early 2011. As the Westland Farm Centre has now ceased trading it is intended that this subsidiary company will be amalgamated with the parent company Westland Co-operative Dairy Company Limited during the 2011/2012 financial year.

EasiYo ProductsThe Chairman of the Board, one other Board Member and the Chief Executive Officer of Westland Co-operative Dairy Company Limited together with Director Maurice Eng sit on the Board of the wholly owned subsidiary company EasiYo Products Limited.

Board MeetingsThe Directors receive comprehensive information and reports on the company’s operations before each meeting including reporting on the activities of the subsidiary Westland Farm Centre Limited and the EasiYo group.

In March 2011 Freshfood Group Limited, Freshyo Products International Limited, Yolife South Korea Limited, and Easiyo Products Limited amalgamated to become Easiyo Products Limited. The Easiyo group of companies now includes Easiyo Products Limited, Arendal Investments Limited, Freshfood Systems Limited (UK) and Easiyo Limited (Delaware, USA).

The Board and its committees also meet from time to time in confidential sessions without senior management present. These sessions deal with management performance, remuneration and discussions with external auditors to promote a robust and independent audit process.

RemunerationShareholder DirectorsThe constitution provides that the Board may determine and authorise payment of remuneration, or the provision of other benefits by the company, to a director for services as a director, or in any other capacity if the Board is satisfied that to do so is fair to the company, provided that the shareholders by ordinary resolution authorise such remuneration or other benefits. Generally the Board reviews Shareholder Director remuneration annually.

Appointed DirectorsThe constitution provides that the Board may determine and authorise payment of remuneration, or the provision of other benefits by the company to an appointed director for services as a director, or in any other capacity if the Board is satisfied that to do so is fair to the company. Generally the Board reviews Appointed Director remuneration annually.

23

AuDIT REPORT

INDEPENDENT AuDITOR’S REPORTTO THE MEMBERS OF WESTLAND COOPERATIVE DAIRY COMPANY LIMITED

Report on the Financial StatementsWe have audited the financial statements of Westland Cooperative Dairy Company Limited and group on pages 26 to 58, which comprise the consolidated and separate balance sheet of Westland Cooperative Dairy Company Limited, as at 31 July 2011, the consolidated and separate income statements, statements of comprehensive income, statements of changes in members funds and statements of cash flows for the year then ended, and a summary of significant accounting policies and other explanatory information.

This report is made solely to the company’s members, as a body, in accordance with Section 205(1) of the Companies Act 1993. Our audit has been undertaken so that we might state to the company’s members those matters we are required to state to them in an auditor’s report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the company’s members as a body, for our audit work, for this report, or for the opinions we have formed.

Board of Directors’ Responsibility for the Financial StatementsThe Board of Directors is responsible for the preparation of financial statements in accordance with generally accepted accounting practice in New Zealand and that give a true and fair view of the matters to which they relate, and for such internal control as the Board of Directors determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s ResponsibilitiesOur responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing and International Standards on Auditing (New Zealand). Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation of financial statements that give a true and fair view of the matters to which they relate in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of the accounting policies used and the reasonableness of accounting estimates, as well as the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Other than in our capacity as auditor and the provision of taxation advice, we have no relationship with or interests in Westland Cooperative Dairy Company Limited or any of its subsidiaries.

OpinionIn our opinion, the financial statements on pages 26 to 58:· comply with generally accepted accounting practice in New Zealand;· comply with International Financial Reporting Standards; and· give a true and fair view of the financial position of Westland Cooperative Dairy Company Limited and group as at 31 July 2011, and their financial performance and cash flows for the year then ended.

Report on Other Legal and Regulatory RequirementsWe also report in accordance with section 16 of the Financial Reporting Act 1993. In relation to our audit of the financial statements for the year ended 31 July 2011:· we have obtained all the information and explanations we have required; and· in our opinion proper accounting records have been kept by Westland Cooperative Dairy Company Limited as far as appears from our examination of those records.

Chartered Accountants7 October 2011Christchurch, New Zealand

This audit report relates to the financial statements of Westland Cooperative Dairy Company Limited and group for the year ended 31 July 2011 included on Westland Cooperative Dairy Company Limited‘s website. The Board of Directors is responsible for the maintenance and integrity of Westland Cooperative Dairy Company Limited’s website. We have not been engaged to report on the integrity of Westland Cooperative Dairy Company Limited‘s website. We accept no responsibility for any changes that may have occurred to the financial statements since they were initially presented on the website. The audit report refers only to the financial statements named above. It does not provide an opinion on any other information which may have been hyperlinked to/from these financial statements. If readers of this report are concerned with the inherent risks arising from electronic data communication they should refer to the published hard copy of the audited financial statements and related audit report dated 7 October 2011 to confirm the information included in the audited financial statements presented on this website. Legislation in New Zealand governing the preparation and dissemination of financial statements may differ from legislation in other jurisdictions.

24

DIRECTORS’ DECLARATION

In the opinion of the directors of Westland Co-operative Dairy Company Limited (“the Company”), the financial statements and notes, on pages 26 to 58:

• comply with New Zealand generally accepted accounting practice and give a true and fair view of the financial position of the Company and the Group as at 31 July 2011 and the results of their operations and cash flows for the 12 month period ended on that date.

• have been prepared using appropriate accounting policies, which have been consistently applied and supported by

reasonable judgements and estimates. The directors believe that proper accounting records have been kept which enable, with reasonable accuracy, the determination of the financial position of the Company and the Group and facilitate compliance of the financial statements with the Financial Reporting Act 1993.

The directors consider that they have taken adequate steps to safeguard the assets of the Company and the Group, and to prevent and detect fraud and other irregularities. Internal control procedures are also considered to be sufficient to provide a reasonable assurance as to the integrity and reliability of the financial statements. The directors are pleased to present the financial statements of Westland Co-operative Dairy Company Limited for the period ended 31 July 2011. For and on behalf of the Board of Directors:

M J O’Regan M T Havill Chairman Deputy Chairman 27 September 2011 27 September 2011

25

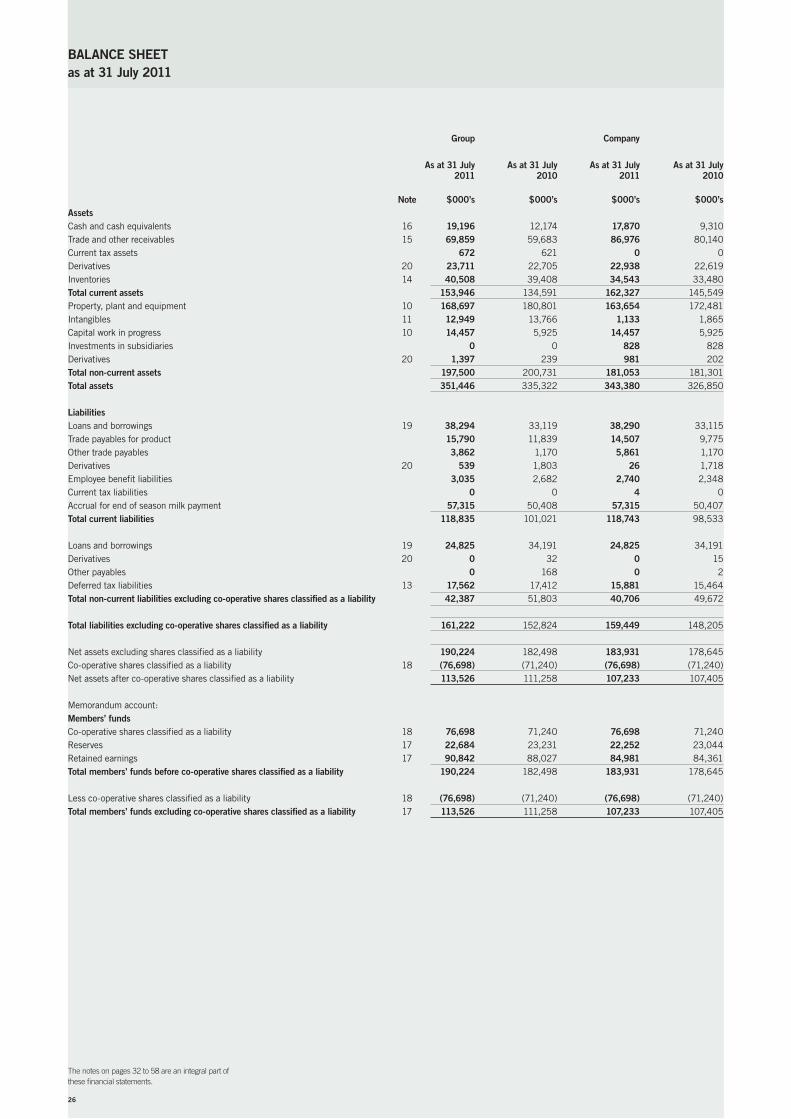

The notes on pages 32 to 58 are an integral part ofthese financial statements.

Group Company As at 31 July As at 31 July As at 31 July As at 31 July 2011 2010 2011 2010

Note $000’s $000’s $000’s $000’sAssets Cash and cash equivalents 16 19,196 12,174 17,870 9,310Trade and other receivables 15 69,859 59,683 86,976 80,140Current tax assets 672 621 0 0Derivatives 20 23,711 22,705 22,938 22,619Inventories 14 40,508 39,408 34,543 33,480Total current assets 153,946 134,591 162,327 145,549Property, plant and equipment 10 168,697 180,801 163,654 172,481Intangibles 11 12,949 13,766 1,133 1,865Capital work in progress 10 14,457 5,925 14,457 5,925Investments in subsidiaries 0 0 828 828Derivatives 20 1,397 239 981 202Total non-current assets 197,500 200,731 181,053 181,301Total assets 351,446 335,322 343,380 326,850 Liabilities Loans and borrowings 19 38,294 33,119 38,290 33,115Trade payables for product 15,790 11,839 14,507 9,775Other trade payables 3,862 1,170 5,861 1,170Derivatives 20 539 1,803 26 1,718Employee benefit liabilities 3,035 2,682 2,740 2,348Current tax liabilities 0 0 4 0Accrual for end of season milk payment 57,315 50,408 57,315 50,407Total current liabilities 118,835 101,021 118,743 98,533 Loans and borrowings 19 24,825 34,191 24,825 34,191Derivatives 20 0 32 0 15Other payables 0 168 0 2Deferred tax liabilities 13 17,562 17,412 15,881 15,464Total non-current liabilities excluding co-operative shares classified as a liability 42,387 51,803 40,706 49,672 Total liabilities excluding co-operative shares classified as a liability 161,222 152,824 159,449 148,205 Net assets excluding shares classified as a liability 190,224 182,498 183,931 178,645Co-operative shares classified as a liability 18 (76,698) (71,240) (76,698) (71,240)Net assets after co-operative shares classified as a liability 113,526 111,258 107,233 107,405 Memorandum account: Members’ funds Co-operative shares classified as a liability 18 76,698 71,240 76,698 71,240Reserves 17 22,684 23,231 22,252 23,044Retained earnings 17 90,842 88,027 84,981 84,361Total members’ funds before co-operative shares classified as a liability 190,224 182,498 183,931 178,645

Less co-operative shares classified as a liability 18 (76,698) (71,240) (76,698) (71,240)Total members’ funds excluding co-operative shares classified as a liability 17 113,526 111,258 107,233 107,405

as at 31 July 2011BALANCE SHEET

26

The notes on pages 32 to 58 are an integral part ofthese financial statements.

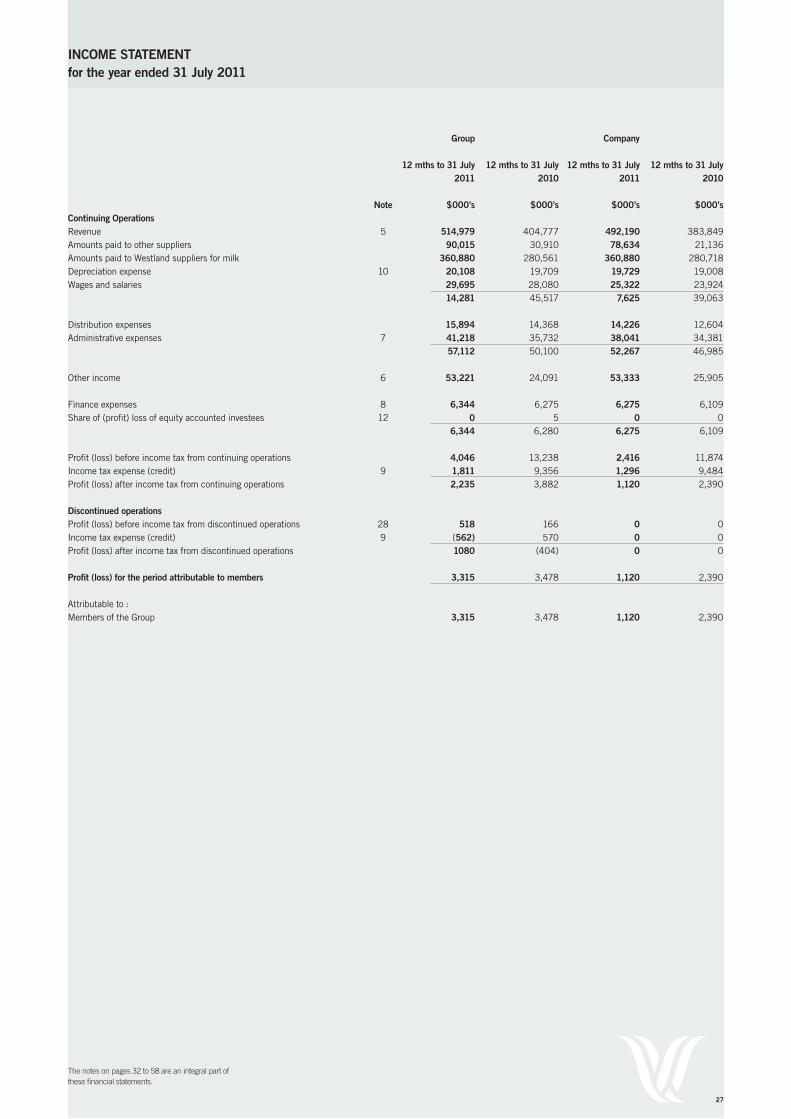

INCOME STATEMENT

Group Company 12 mths to 31 July 12 mths to 31 July 12 mths to 31 July 12 mths to 31 July 2011 2010 2011 2010

Note $000’s $000’s $000’s $000’sContinuing Operations Revenue 5 514,979 404,777 492,190 383,849Amounts paid to other suppliers 90,015 30,910 78,634 21,136Amounts paid to Westland suppliers for milk 360,880 280,561 360,880 280,718Depreciation expense 10 20,108 19,709 19,729 19,008Wages and salaries 29,695 28,080 25,322 23,924 14,281 45,517 7,625 39,063 Distribution expenses 15,894 14,368 14,226 12,604Administrative expenses 7 41,218 35,732 38,041 34,381 57,112 50,100 52,267 46,985 Other income 6 53,221 24,091 53,333 25,905 Finance expenses 8 6,344 6,275 6,275 6,109Share of (profit) loss of equity accounted investees 12 0 5 0 0 6,344 6,280 6,275 6,109 Profit (loss) before income tax from continuing operations 4,046 13,238 2,416 11,874Income tax expense (credit) 9 1,811 9,356 1,296 9,484Profit (loss) after income tax from continuing operations 2,235 3,882 1,120 2,390 Discontinued operations Profit (loss) before income tax from discontinued operations 28 518 166 0 0Income tax expense (credit) 9 (562) 570 0 0Profit (loss) after income tax from discontinued operations 1080 (404) 0 0 Profit (loss) for the period attributable to members 3,315 3,478 1,120 2,390 Attributable to : Members of the Group 3,315 3,478 1,120 2,390

for the year ended 31 July 2011

27

The notes on pages 32 to 58 are an integral part ofthese financial statements.

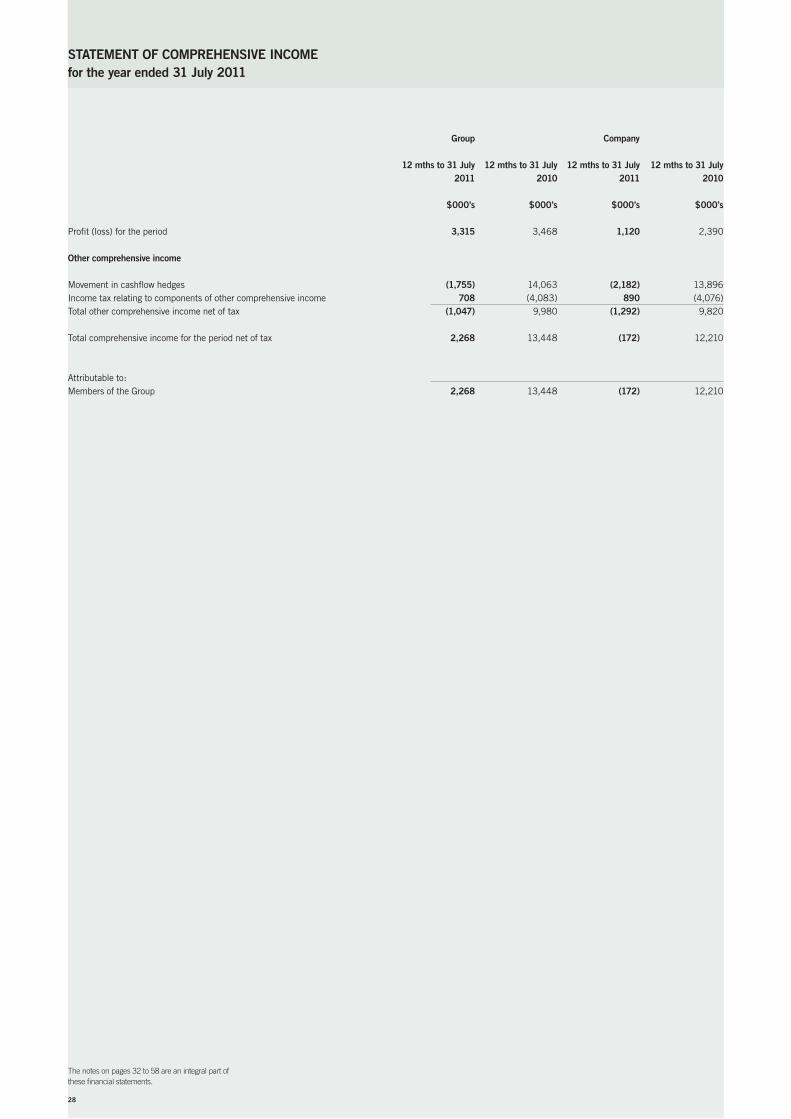

STATEMENT OF COMPREHENSIVE INCOME

Group Company 12 mths to 31 July 12 mths to 31 July 12 mths to 31 July 12 mths to 31 July 2011 2010 2011 2010

$000’s $000’s $000’s $000’s Profit (loss) for the period 3,315 3,468 1,120 2,390 Other comprehensive income Movement in cashflow hedges (1,755) 14,063 (2,182) 13,896Income tax relating to components of other comprehensive income 708 (4,083) 890 (4,076)Total other comprehensive income net of tax (1,047) 9,980 (1,292) 9,820 Total comprehensive income for the period net of tax 2,268 13,448 (172) 12,210 Attributable to: Members of the Group 2,268 13,448 (172) 12,210

for the year ended 31 July 2011

28

The notes on pages 32 to 58 are an integral part ofthese financial statements.

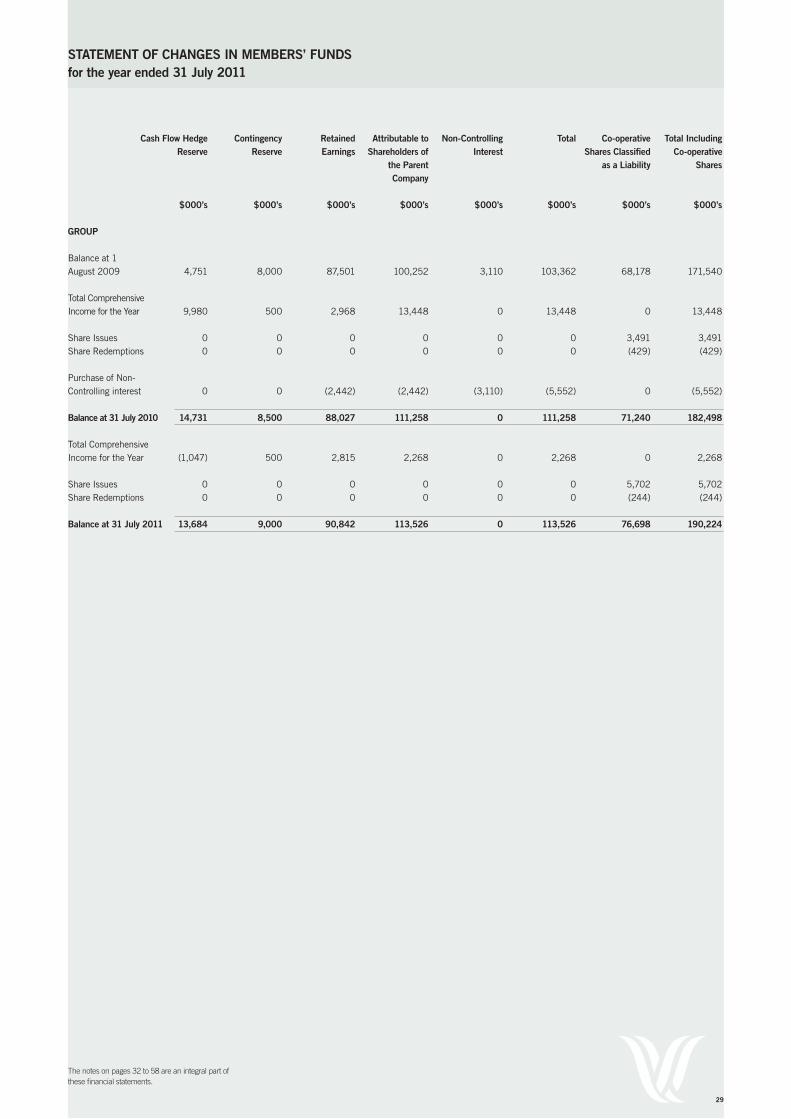

STATEMENT OF CHANGES IN MEMBERS’ FuNDS

Cash Flow Hedge Contingency Retained Attributable to Non-Controlling Total Co-operative Total Including Reserve Reserve Earnings Shareholders of Interest Shares Classified Co-operative the Parent as a Liability Shares Company $000’s $000’s $000’s $000’s $000’s $000’s $000’s $000’s

GROuP Balance at 1 August 2009 4,751 8,000 87,501 100,252 3,110 103,362 68,178 171,540 Total Comprehensive Income for the Year 9,980 500 2,968 13,448 0 13,448 0 13,448 Share Issues 0 0 0 0 0 0 3,491 3,491Share Redemptions 0 0 0 0 0 0 (429) (429) Purchase of Non-Controlling interest 0 0 (2,442) (2,442) (3,110) (5,552) 0 (5,552) Balance at 31 July 2010 14,731 8,500 88,027 111,258 0 111,258 71,240 182,498 Total Comprehensive Income for the Year (1,047) 500 2,815 2,268 0 2,268 0 2,268 Share Issues 0 0 0 0 0 0 5,702 5,702Share Redemptions 0 0 0 0 0 0 (244) (244) Balance at 31 July 2011 13,684 9,000 90,842 113,526 0 113,526 76,698 190,224

for the year ended 31 July 2011

29

The notes on pages 32 to 58 are an integral part ofthese financial statements.

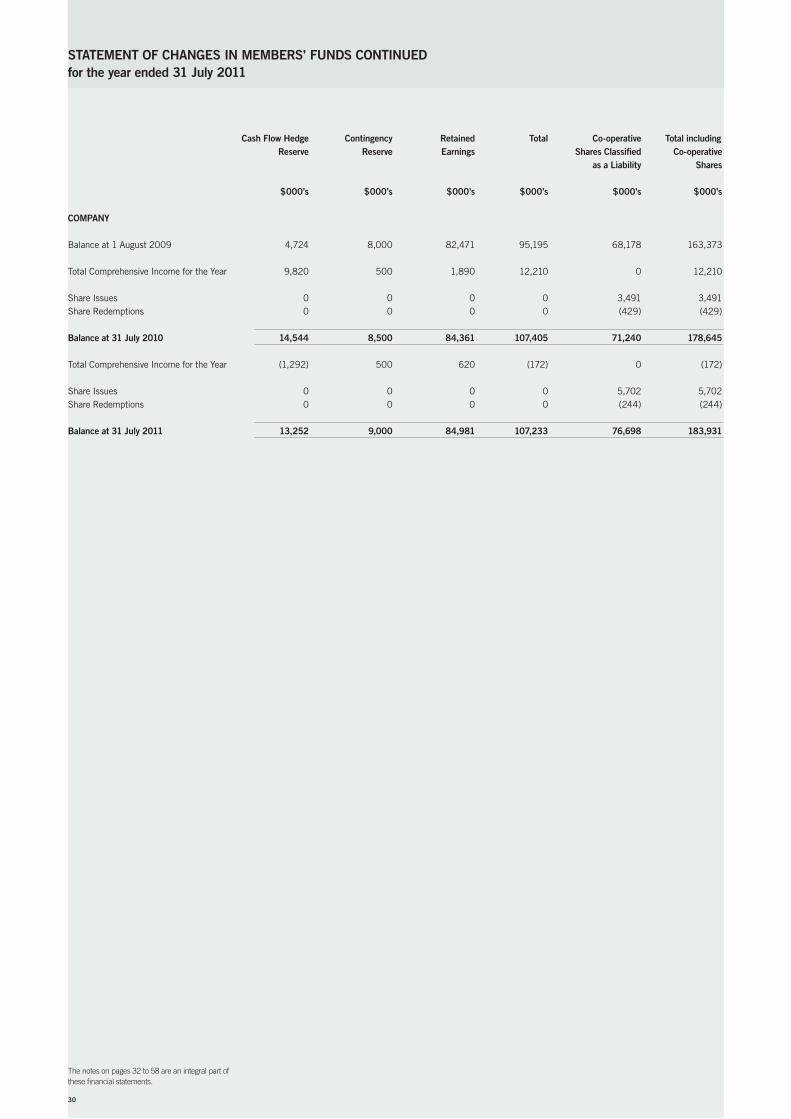

STATEMENT OF CHANGES IN MEMBERS’ FuNDS CONTINuED

Cash Flow Hedge Contingency Retained Total Co-operative Total including Reserve Reserve Earnings Shares Classified Co-operative as a Liability Shares $000’s $000’s $000’s $000’s $000’s $000’s COMPANY Balance at 1 August 2009 4,724 8,000 82,471 95,195 68,178 163,373 Total Comprehensive Income for the Year 9,820 500 1,890 12,210 0 12,210

Share Issues 0 0 0 0 3,491 3,491Share Redemptions 0 0 0 0 (429) (429) Balance at 31 July 2010 14,544 8,500 84,361 107,405 71,240 178,645 Total Comprehensive Income for the Year (1,292) 500 620 (172) 0 (172) Share Issues 0 0 0 0 5,702 5,702Share Redemptions 0 0 0 0 (244) (244) Balance at 31 July 2011 13,252 9,000 84,981 107,233 76,698 183,931

for the year ended 31 July 2011

30

The notes on pages 32 to 58 are an integral part ofthese financial statements.

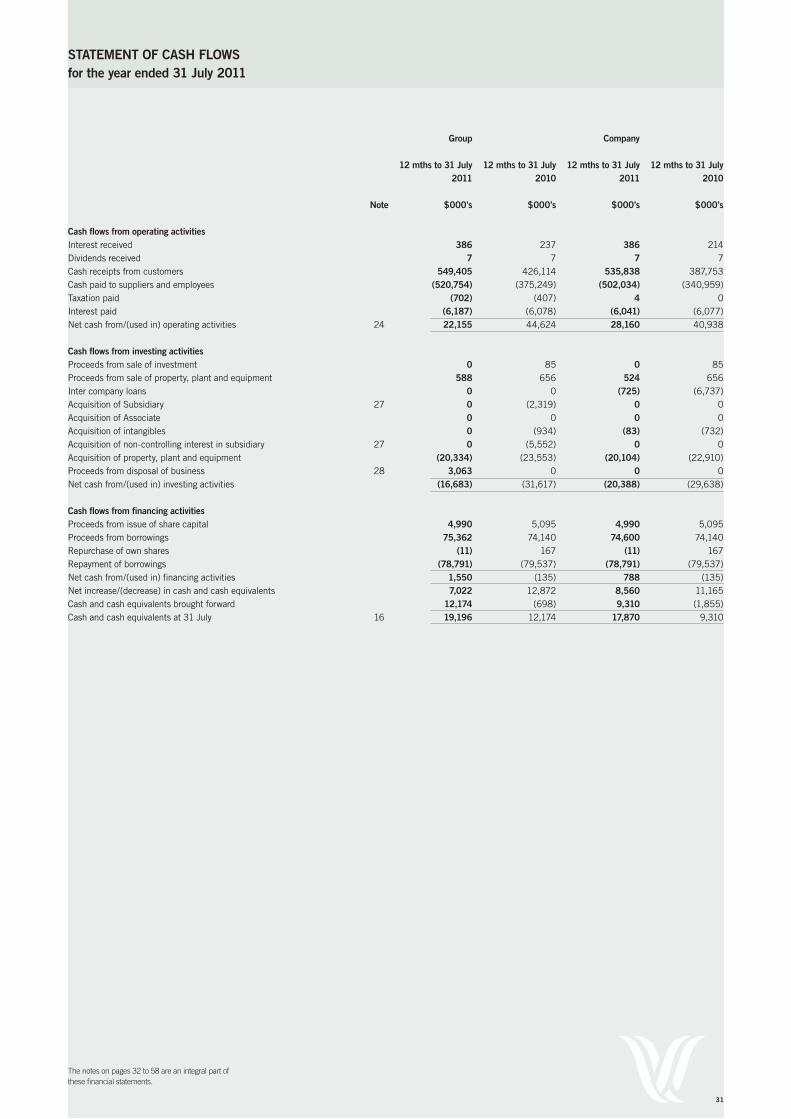

STATEMENT OF CASH FLOWS

Group Company 12 mths to 31 July 12 mths to 31 July 12 mths to 31 July 12 mths to 31 July 2011 2010 2011 2010

Note $000’s $000’s $000’s $000’s Cash flows from operating activities Interest received 386 237 386 214Dividends received 7 7 7 7Cash receipts from customers 549,405 426,114 535,838 387,753Cash paid to suppliers and employees (520,754) (375,249) (502,034) (340,959)Taxation paid (702) (407) 4 0Interest paid (6,187) (6,078) (6,041) (6,077)Net cash from/(used in) operating activities 24 22,155 44,624 28,160 40,938 Cash flows from investing activities Proceeds from sale of investment 0 85 0 85Proceeds from sale of property, plant and equipment 588 656 524 656Inter company loans 0 0 (725) (6,737)Acquisition of Subsidiary 27 0 (2,319) 0 0Acquisition of Associate 0 0 0 0Acquisition of intangibles 0 (934) (83) (732)Acquisition of non-controlling interest in subsidiary 27 0 (5,552) 0 0Acquisition of property, plant and equipment (20,334) (23,553) (20,104) (22,910)Proceeds from disposal of business 28 3,063 0 0 0Net cash from/(used in) investing activities (16,683) (31,617) (20,388) (29,638) Cash flows from financing activities Proceeds from issue of share capital 4,990 5,095 4,990 5,095Proceeds from borrowings 75,362 74,140 74,600 74,140Repurchase of own shares (11) 167 (11) 167Repayment of borrowings (78,791) (79,537) (78,791) (79,537)Net cash from/(used in) financing activities 1,550 (135) 788 (135)Net increase/(decrease) in cash and cash equivalents 7,022 12,872 8,560 11,165Cash and cash equivalents brought forward 12,174 (698) 9,310 (1,855)Cash and cash equivalents at 31 July 16 19,196 12,174 17,870 9,310

for the year ended 31 July 2011

31

1 Reporting entity Westland Co-operative Dairy Company Limited (the “Company”) is a profit oriented company incorporated and domiciled in

New Zealand, registered under the Companies Act 1993 and the Co-operative Companies Act 1996.

Financial statements for the Company and consolidated financial statements are presented. The consolidated financial statements of Westland Co-operative Dairy Company Limited as at and for the 12 month period ended 31 July 2011 comprise the Company and its subsidiaries and the Group’s interest in associates and jointly controlled entities (together referred to as the “Group”). Westland Co-operative Dairy Company Limited is primarily involved in the supply of dairy and nutritional products.

2 Basis of preparation (a) Statement of compliance The financial statements have been prepared in accordance with New Zealand Generally Accepted Accounting Practice

(“NZ GAAP”). They comply with New Zealand equivalents to International Financial Reporting Standards (“NZ IFRS”) and other applicable Financial Reporting Standards, as appropriate for profit-oriented entities. The financial statements also comply with International Financial Reporting Standards (“IFRS”).

The accounting policies set out below have been applied consistently to all periods presented in these financial statements.

The financial statements were approved by the Board of Directors on 27th September 2011.

(b) Basis of measurement The financial statements have been prepared on the historical cost basis except for derivative financial instruments

which are measured at fair value. The methods used to measure fair values are discussed further in note 4.

(c) Functional and presentation currency These financial statements are presented in New Zealand dollars ($), which is the Company’s functional currency. All financial information presented in New Zealand dollars has been rounded to the nearest thousand dollars.

(d) use of estimates and judgements The preparation of financial statements requires management to make judgements, estimates and assumptions that

affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses.

Actual results may differ from these estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the period in which the estimate is revised and in any future periods affected.

In particular, information about significant areas of estimation uncertainty and critical judgements in applying accounting policies that have the most significant effect on the amounts recognised in the financial statements are described in Note 11 (Intangibles), Note 14 (Inventories) and Note 27 (Acquisition of subsidiaries and non-controlling interests).

3 Significant accounting policies (a) Basis of consolidation

(i) Subsidiaries Subsidiaries are entities controlled by the Group. Control exists when the Group has the power to govern the

financial and operating policies of an entity so as to obtain benefits from its activities. In assessing control, potential voting rights that presently are exercisable are taken into account. The financial statements of subsidiaries are included in the consolidated financial statements from the date that control commences until the date that control ceases.

(ii) Associates and joint ventures (equity accounted investees) Associates are those entities in which the Group has significant influence, but not control, over the financial and operating policies. Joint ventures are those entities over whose activities the Group has joint control, established by contractual agreement and requiring unanimous consent for strategic financial and operating decisions. Associates and joint ventures are accounted for using the equity method (equity accounted investees).

The consolidated financial statements include the Group’s share of the income and expenses of equity accounted investees, after adjustments to align the accounting policies with those of the Group, from the date that significant influence or joint control commences until the date that significant influence or joint control ceases.

for the year ended 31 July 2011NOTES TO THE FINANCIAL STATEMENTS

32

for the year ended 31 July 2011NOTES TO THE FINANCIAL STATEMENTS CONTINuED

(iii) Transactions eliminated on consolidation Intra-group balances, and any unrealised income and expenses arising from intra-group transactions, are eliminated in preparing the consolidated financial statements. Unrealised gains arising from transactions with equity accounted investees are eliminated against the investment to the extent of the Group’s interest in the investee. Unrealised losses are eliminated in the same way as unrealised gains, but only to the extent that there is no evidence of impairment.

(b) Foreign currency (i) Foreign currency transactions Transactions in foreign currencies are translated to the respective functional currencies of Group entities at

exchange rates at the dates of the transactions. Monetary assets and liabilities denominated in foreign currencies at the reporting date are retranslated to the functional currency at the exchange rate at that date. Non-monetary items carried at fair value that are denominated in foreign currencies are retranslated at the rates prevailing at the date when the fair value was determined. Non-monetary items that are measured in terms of historical cost in a foreign currency are not retranslated.

Foreign currency differences arising on retranslation are recognised in profit or loss.

(ii) Foreign operations The assets and liabilities of foreign operations, including fair value adjustments arising on acquisition, are

translated to New Zealand dollars at exchange rates at the reporting date. The income and expenses of foreign operations are translated to New Zealand dollars at exchange rates at the dates of the transactions.

(c) Financial instruments (i) Non-derivative financial instruments

Non-derivative financial instruments comprise investments, trade and other receivables, cash and cash equivalents, loans and borrowings including ordinary shares, and trade and other payables.

Non-derivative financial instruments are recognised initially at fair value plus, for financial assets not at fair value through profit or loss, any directly attributable transaction costs. For financial liabilities not recognised at fair value through profit and loss the liabilities are initially recognised inclusive of directly attributable transaction costs. A financial instrument is recognised if the Group becomes a party to the contractual provisions of the instrument.

Cash and cash equivalents comprise cash balances and call deposits.

Accounting for finance income and expense is discussed in note 3(l). Subsequent to initial recognition, other non-derivative financial instruments are measured using the methods

described below.

Investments in equity securities of subsidiaries, associates and joint ventures are measured at cost in the separate financial statements of the Company.

Trade and other receivables Trade and other receivables are stated at their amortised cost using the effective interest method less impairment losses.

Interest-bearing borrowings Interest-bearing borrowings are stated at amortised cost using the effective interest method, with interest expense

recognised on an effective interest basis. Trade and other payables Trade and other payables are stated at amortised cost using the effective interest rate method with interest expense

recognised on an effective interest basis. Ordinary shares The Company’s share capital is accounted for as a long term liability because under the Co-operative Companies Act 1996

under certain conditions specified in the Act shareholders have the right to surrender shares in the Company and receive payment.

(ii) Derivative financial instruments The Group uses derivative financial instruments to hedge its exposure to foreign exchange and interest rate risks arising from operational, financing and investment activities. In accordance with its treasury policy, the Group does not hold or issue derivative financial instruments for trading purposes. However, derivatives that do not qualify for hedge accounting are accounted for as trading instruments. Derivative financial instruments are recognised initially at fair value and transaction costs are expensed immediately. Subsequent to initial recognition, derivative financial instruments are stated at fair value. The gain or loss on remeasurement to fair value is recognised immediately in profit or loss. However, where derivatives qualify for hedge accounting, recognition of any resultant gain or loss depends on the nature of the hedging relationship (see below).

33

Cash flow hedges Changes in the fair value of the derivative hedging instruments designated as a cash flow hedge are recognised in other

comprehensive income and accumulated as a separate component of equity in the hedging reserve to the extent that the hedge is effective. To the extent that the hedge is ineffective, changes in fair value are recognised in profit or loss. If the hedging instrument no longer meets the criteria for hedge accounting, expires or is sold, terminated or exercised, then hedge accounting is discontinued prospectively. The cumulative gain or loss previously recognised in the hedging reserve remains there until the forecast transaction occurs. When the hedged item is a non-financial asset, the amount recognised in equity is transferred to the carrying amount of the asset when it is recognised. In other cases, the amount recognised in equity is transferred to finance gain or loss in profit or loss in the same period that the hedged item affects profit or loss (Note 8).

(d) Property, plant and equipment (i) Recognition and measurement

Items of property, plant and equipment are measured at cost less accumulated depreciation and impairment losses.

Cost includes expenditures that are directly attributable to the acquisition of the asset and include capitalised

borrowing costs where appropriate. The cost of self-constructed assets includes the cost of materials and direct labour, any other costs directly attributable to bringing the asset to a working condition for its intended use. Purchased software that is integral to the functionality of the related equipment is capitalised as part of that equipment. When parts of an item of property, plant and equipment have different useful lives, they are accounted for as separate items (major components) of property, plant and equipment.

(ii) Subsequent costs The cost of replacing part of an item of property, plant and equipment is recognised in the carrying amount of the

item if it is probable that the future economic benefits embodied within the part will flow to the Group and its cost can be measured reliably. The costs of the day-to-day servicing of property, plant and equipment are recognised in profit or loss as incurred.

(iii) Depreciation Depreciation is recognised in profit or loss on a straight-line basis over the estimated useful lives of each part of an

item of property, plant and equipment. Land is not depreciated.

The estimated useful lives for the current and comparative periods are as follows: · buildings 15-25 years · plant and equipment 3-15 years · motor vehicles 5-10 years

Depreciation methods, useful lives and residual values are reassessed at each reporting date.

(iv) Capital Work in Progress Amounts expended on Capital Work in Progress are capitalised until such time as the asset is placed in

service and then is transferred to property, plant and equipment and is depreciated from that date.

(e) Intangibles Computer Software

Acquired computer software licences are capitalised on the basis of the costs incurred to acquire and bring to use the specific software. These costs are amortised over their estimated useful lives, being 3 to 10 years, on a straight line basis.

Costs associated with developing or maintaining computer software programmes are recognised as an expense as incurred. Costs that are directly associated with the development of identifiable and unique software products controlled by the Group or Company, and that will generate probable economic benefits exceeding the costs beyond one year, are recognised as intangible assets.

Costs include the employee costs incurred as a result of developing software and an appropriate portion of relevant overheads. Computer software development costs recognised as assets are amortised over their estimated useful lives, not exceeding 3 to 10 years.

for the year ended 31 July 2011NOTES TO THE FINANCIAL STATEMENTS CONTINuED

34

Expenditure on research and development Expenditure on research activities, undertaken with the prospect of gaining new scientific or technical knowledge and understanding, is recognised in profit or loss when incurred. Development activities involve a plan or design for the production of new or substantially improved products and processes. Development expenditure is capitalised only if development costs can be measured reliably, the product or process is technically and commercially feasible, future economic benefits are probable, and the Group intends to and has sufficient resources to complete development and to use or sell the asset. Other development expenditure is recognised in profit or loss when incurred. Development expenditure is amortised over a useful economic life of between 3 and 5 years on a straight line basis.

(f) Leased Assets Leases in terms of which the Group assumes substantially all the risks and rewards of ownership are classified as finance leases. Upon initial recognition the leased asset is measured at an amount equal to the lower of its fair value and the present value of the minimum lease payments. Subsequent to initial recognition, the asset is accounted for in accordance with the accounting policy applicable to that asset.

Other leases are operating leases and the leased assets are not recognised on the Group or Company’s balance sheet. Payments made under operating leases are recognised in profit or loss on a straight-line basis over the term of the lease. Lease incentives received are recognised as an integral part of the total lease expense, over the term of the lease.

(g) Inventories Inventories are measured at the lower of cost and net realisable value, determined on the first-in first-out basis, after due allowance for damaged and obsolete stock. The net realisable value is the estimated selling price in the ordinary course of business, less the costs of completion and selling expenses. Freight and documentation costs are excluded. The cost of inventories includes expenditure incurred in acquiring the inventories and bringing them to their existing location and condition. The cost of dairy products manufactured from milk supplied is determined by including the payment to milk producers. The payment to milk suppliers is estimated based on the estimated returns that the products are expected to generate.

In the case of manufactured inventories and work in progress, cost includes an appropriate share of production overheads based on normal operating capacity.

(h) Impairment The carrying amounts of the Group’s assets are reviewed at each balance sheet date to determine whether there is any objective evidence of impairment.

An impairment loss is recognised whenever the carrying amount of an asset exceeds its recoverable amount. Impairment losses directly reduce the carrying amount of assets and are recognised in the income statement.

An impairment loss recognised for goodwill is not reversed in subsequent periods. (i) Impairment of debt instruments and receivables The recoverable amount of the Group or Company’s receivables carried at amortised cost is calculated as the

present value of estimated future cash flows, discounted at the original effective interest rate. Receivables with a short duration are not discounted.

Impairment losses on an individual basis are determined by an evaluation of the exposures on an instrument by

instrument basis. All individual instruments that are considered significant are subject to this approach and are subsequently assessed for impairment on a collective basis.

for the year ended 31 July 2011NOTES TO THE FINANCIAL STATEMENTS CONTINuED

35

(ii) Non-financial assets The carrying amounts of the Group or Company’s non-financial assets and deferred tax assets are reviewed at each

reporting date to determine whether there is any indication of impairment. If any such indication exists then the asset’s recoverable amount is estimated. For goodwill and intangible assets that have indefinite lives or that are not yet available for use, recoverable amount is estimated at each reporting date. Goodwill and indefinite life intangible assets are tested for impairment annually and whenever there is an indication that the asset may be impaired.

An impairment loss is recognised if the carrying amount of an asset or its cash-generating unit exceeds its

recoverable amount. A cash-generating unit is the smallest identifiable asset group that generates cash flows that are largely independent from other assets and groups. Impairment losses are recognised in profit or loss immediately, unless the relevant asset is carried at a revalued amount, in which case the impairment loss is treated as a revaluation decrease. Impairment losses recognised in respect of cash-generating units are allocated first to reduce the carrying amount of any goodwill allocated to the units and then to reduce the carrying amount of the other assets in the unit (group of units) on a pro rata basis.

The recoverable amount of an asset or cash-generating unit is the greater of its value in use and its fair value less costs to sell. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset.

Where an impairment loss subsequently reverses, the carrying amount of the asset (or cash generating unit) is increased to the revised estimate of its recoverable amount, but so that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognised for the asset (or cash-generating unit) in prior years. A reversal of an impairment loss is recognised immediately in profit or loss, unless the relevant asset is carried at a revalued amount, in which case the reversal of the impairment loss is treated as a revaluation increase. Impairment of goodwill is not reversed.

(i) Employee benefits

(i) Defined contribution plans Obligations for contributions to defined contribution pension plans are recognised as an expense in profit or loss

when they are due. (ii) Other long-term employee benefits Provisions made in respect of employee benefits which are not expected to be settled within 12 months are

measured as the present value of the estimated future cash outflows to be made by the Group in respect of services provided by employees up to the reporting date.

(iii) Termination benefits Termination benefits are recognised as an expense when the Group is demonstrably committed, without realistic

possibility of withdrawal, to a formal detailed plan to terminate employment before the normal retirement date.

Termination benefits for voluntary redundancies are recognised if the Group has made an offer encouraging voluntary redundancy, it is probable that the offer will be accepted, and the number of acceptances can be estimated reliably.

(iv) Short-term benefits Short-term employee benefit obligations are measured on an undiscounted basis and are expensed as the related

service is provided. A provision is recognised for the amount expected to be paid under short-term cash bonus or profit-sharing plans if

the Group has a present legal or constructive obligation to pay this amount as a result of past service provided by the employee and the obligation can be estimated reliably.

(j) Provisions

A provision is recognised if, as a result of a past event, the Group has a present legal or constructive obligation that can be estimated reliably, and it is probable that an outflow of economic benefits will be required to settle the obligation.

Provisions are determined by discounting the expected future cash flows at a pre-tax rate that reflects current market assessments of the time value of money and the risks specific to the liability.

for the year ended 31 July 2011NOTES TO THE FINANCIAL STATEMENTS CONTINuED

36

(k) Revenue Goods sold

Revenue from the sale of goods is measured at the fair value of the consideration received or receivable, net of returns and allowances, trade discounts and volume rebates. Revenue is recognised when the significant risks and rewards of ownership have been transferred to the buyer, recovery of the consideration is probable, the associated costs and possible return of goods can be estimated reliably, and there is no continuing management involvement with the goods. Transfers of risks and rewards vary depending on the individual terms of the contract of sale. For sales of milk products, transfer usually occurs when the product is despatched from the storage facility. For sales of consumables from the Hokitika store revenue is recognised when the goods are despatched from the store.

(l) Finance income and expenses Finance income comprises interest income on funds invested and gains on hedging instruments that are recognised in profit or loss. Interest income is recognised as it accrues, using the effective interest method. Finance expenses comprise interest expense on borrowings, bonus issues of share capital, and losses on hedging instruments that are recognised in profit or loss. Borrowing costs that relate to qualifying assets are capitalised into property, plant and equipment as required by NZ IAS 23: Borrowing Costs. All other borrowing costs are recognised in profit or loss using the effective interest method.

(m) Income tax Income tax expense comprises current and deferred tax. Income tax expense is recognised in profit or loss except to the extent that it relates to items recognised in other comprehensive income or directly in equity, in which case it is recognised in other comprehensive income or directly in equity. Current tax is the expected tax payable on the taxable income for the year, using tax rates enacted or substantively enacted at the reporting date, and any adjustment to tax payable in respect of previous years. Deferred tax is recognised using the balance sheet method, providing for temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxation purposes. Deferred tax is not recognised for the following temporary differences: the initial recognition of goodwill, the initial recognition of assets or liabilities in a transaction that is not a business combination and that affects neither accounting nor taxable profit, and differences relating to investments in subsidiaries and jointly controlled entities to the extent that they probably will not reverse in the foreseeable future where the company controls the reversal. Deferred tax is measured at the tax rates that are expected to be applied to the temporary differences when they reverse, based on the laws that have been enacted or substantively enacted by the reporting date. A deferred tax asset is recognised to the extent that it is probable that future taxable profits will be available against which temporary differences can be utilised. Deferred tax assets are reviewed at each reporting date and are reduced to the extent that it is no longer probable that the related tax benefit will be realised.

(n) Statement of Cash Flows For the purpose of the cash flow statement, cash and cash equivalents include bank balances and call deposits. The following terms are used in the statement of cash flows: · Operating activities: are the principal revenue producing activities of the Group and other activities that are not

investing or financing activities. · Investing activities: are the acquisition and disposal of long-term assets and other investments not included in

cash equivalents. · Financing activities: are activities that result in changes in the size and composition of the contributed equity and

borrowings of the entity.

for the year ended 31 July 2011NOTES TO THE FINANCIAL STATEMENTS CONTINuED

37

(o) Goods and service tax

Revenue, expenses and assets are recognised net of the amount of goods and services tax (GST), except for receivables and payables which are recognised inclusive of GST. The net amount of GST recoverable from, or payable to, the taxation authority is included as part of receivables or payables. Cashflows are included in the cashflow statement on a gross basis. The GST component of cash flows arising from investing and financing which is recoverable from, or payable to, the taxation authority is classified as operating cashflow.

(p) Goodwill Goodwill arising on the acquisition of a subsidiary or associate represents the excess of the cost of acquisition over the Group’s interest in the net fair value of the identifiable assets, liabilities and contingent liabilities of the subsidiary or associate recognised at the date of acquisition. Goodwill is initially recognised as an asset at cost and is subsequently measured at cost less any accumulated impairment losses.

For the purpose of impairment testing, goodwill is allocated to each of the Group’s cash-generating units expected to benefit from the synergies of the combination. Cash-generating units to which goodwill has been allocated are tested for impairment annually, or more frequently when there is an indication that the unit may be impaired. If the recoverable amount of the cash-generating unit is less than the carrying amount of the unit, the impairment loss is allocated first to reduce the carrying amount of any goodwill allocated to the unit and then to the other assets of the unit pro-rata on the basis of the carrying amount of each asset in the unit. An impairment loss recognised for goodwill is not reversed in a subsequent period.

(q) Brands and Patents Brand and patents acquired in a business combination are identified and recognised separately from goodwill where they satisfy the definition of an intangible asset and their fair values can be measured reliably. The cost of such intangible assets is their fair value at the acquisition date.

Brands and patents are considered to have indefinite useful lives due to the registered trademark protection and the continual investment in maintaining the brand and are tested for impairment annually, and whenever there is an indication that the asset may be impaired.

(r) Other Income Dividend income is recognised on the date that the Group’s right to receive payment is established.

(s) New accounting standards No standards have been adopted during the year which have had a material impact on these financial statements. The group has reviewed all Standards and Interpretations in issue not yet adopted and, with the exception of NZ IFRS 9 Financial Instruments which is effective for the financial year ending 30 June 2014, does not expect these standards to have any material impact on the financial statements of the Company and Group. It is likely that the changes arising from NZ IFRS 9 will affect the recognition and measurement, and classification of amounts recognised in the Group and Company financial statements, however it is not practical to provide a realistic estimate of that effect until a detailed review has been completed.

for the year ended 31 July 2011NOTES TO THE FINANCIAL STATEMENTS CONTINuED

38

4 Determination of fair values A number of the Group’s accounting policies and disclosures require the determination of fair value, for both financial and

non-financial assets and liabilities. Fair values have been determined for measurement and/or disclosure purposes based on the following methods. Where applicable, further information about the assumptions made in determining fair values is disclosed in the notes specific to that asset or liability.

(a) Derivatives

The fair value of forward exchange contracts is based on their quoted market price, if available. If a quoted market price is not available, then fair value is estimated by discounting the difference between the contractual forward price and the current forward price for the residual maturity and options of the contract using a market rate of interest. (Note 20).

(b) Carrying Amounts The directors consider that the carrying amounts of financial assets and financial liabilities recorded at amortised cost in the financial statements approximate their fair values.

(c) Financial Instruments An analysis of financial instruments that are measured subsequent to initial recognition at fair value has been performed with all financial instruments grouped into Levels 1 to 3 based on the degree to which the fair value is observable: · Level 1 fair value measurements are those derived from quoted prices (unadjusted) in active markets for identical

assets or liabilities; · Level 2 fair value measurements are those derived from inputs other than quoted prices included within Level 1 that

are observable for the asset or liability, either directly (i.e. as prices) or indirectly (i.e. derived from prices); and· Level 3 fair value measurements are those derived from valuation techniques that include inputs for the asset or

liability that are not based on observable market data (unobservable inputs).

The fair value of forward exchange contracts is derived using inputs supplied by third parties that are observable, either directly (i.e. prices) or indirectly (i.e. derived from prices). Therefore the Group has categorised these liabilities as Level 2.

for the year ended 31 July 2011NOTES TO THE FINANCIAL STATEMENTS CONTINuED

39

for the year ended 31 July 2011NOTES TO THE FINANCIAL STATEMENTS CONTINuED

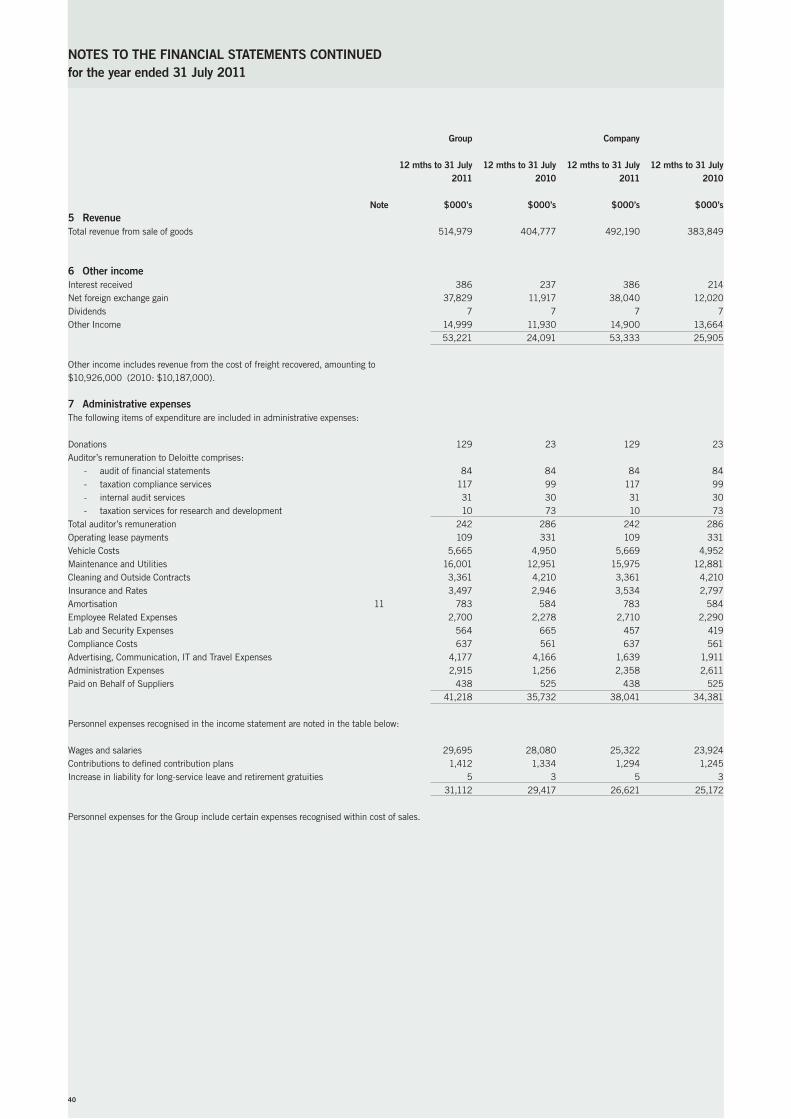

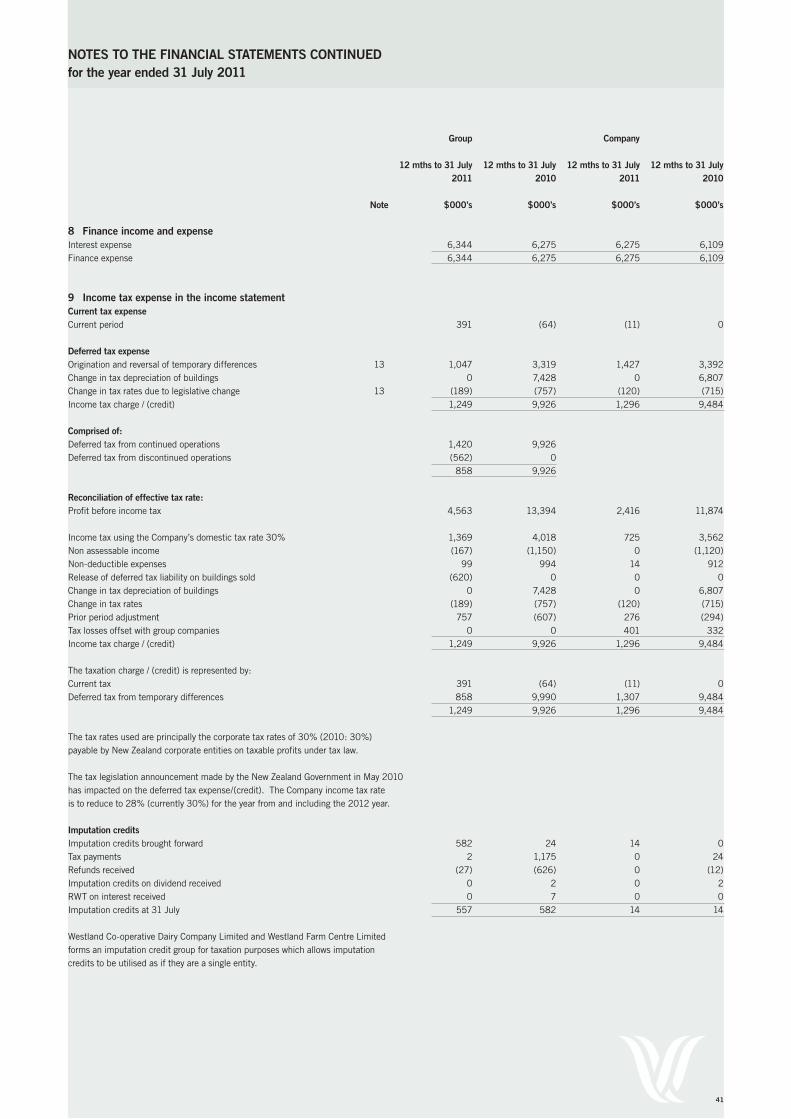

Group Company 12 mths to 31 July 12 mths to 31 July 12 mths to 31 July 12 mths to 31 July 2011 2010 2011 2010 Note $000’s $000’s $000’s $000’s5 Revenue Total revenue from sale of goods 514,979 404,777 492,190 383,849 6 Other income Interest received 386 237 386 214Net foreign exchange gain 37,829 11,917 38,040 12,020Dividends 7 7 7 7Other Income 14,999 11,930 14,900 13,664 53,221 24,091 53,333 25,905 Other income includes revenue from the cost of freight recovered, amounting to $10,926,000 (2010: $10,187,000).

7 Administrative expenses The following items of expenditure are included in administrative expenses: Donations 129 23 129 23Auditor’s remuneration to Deloitte comprises: