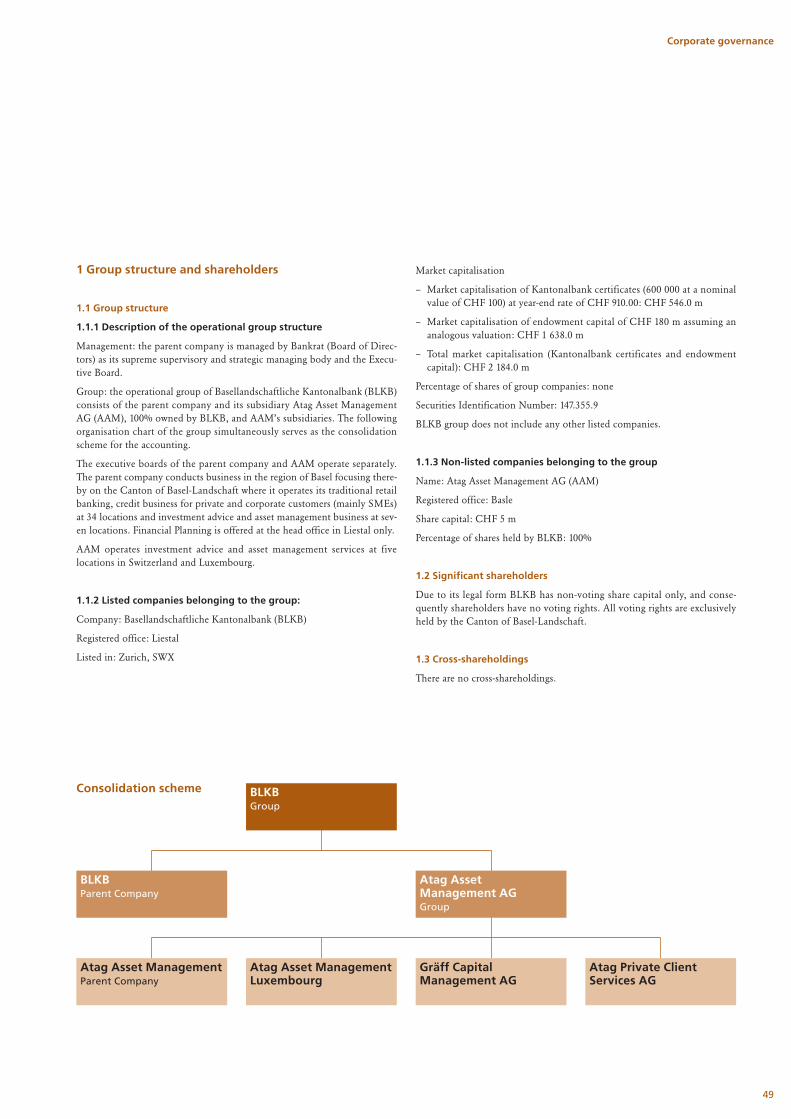

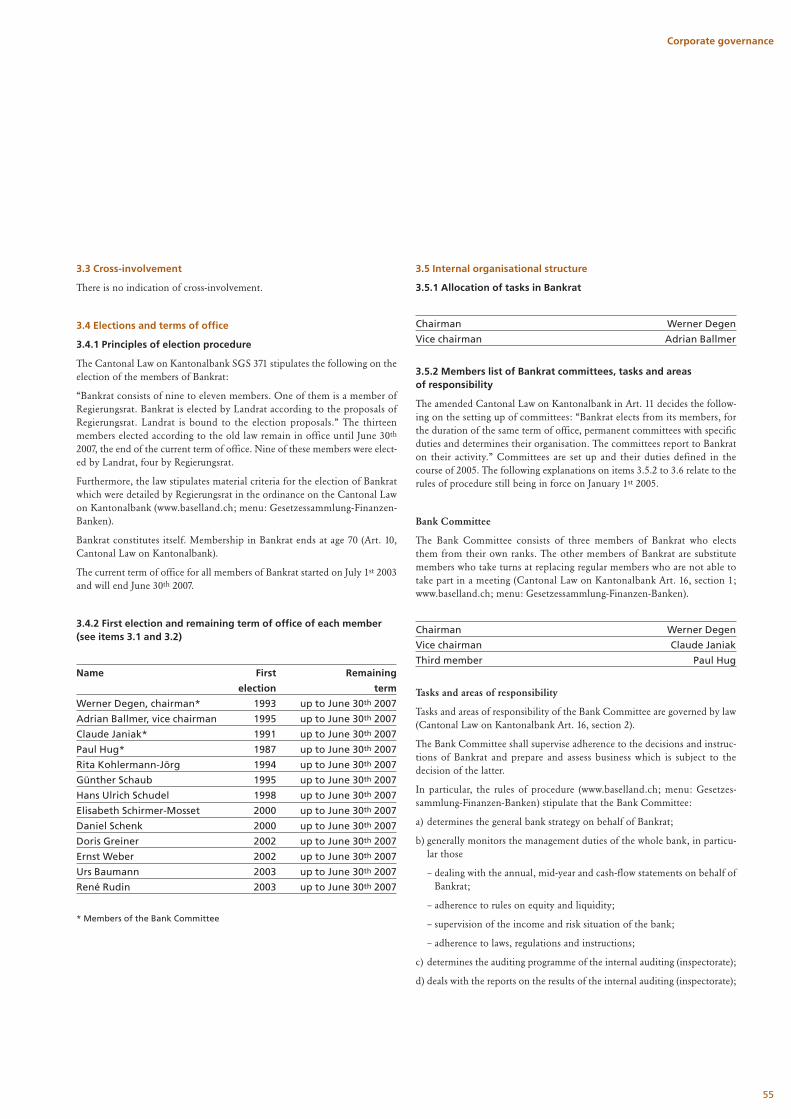

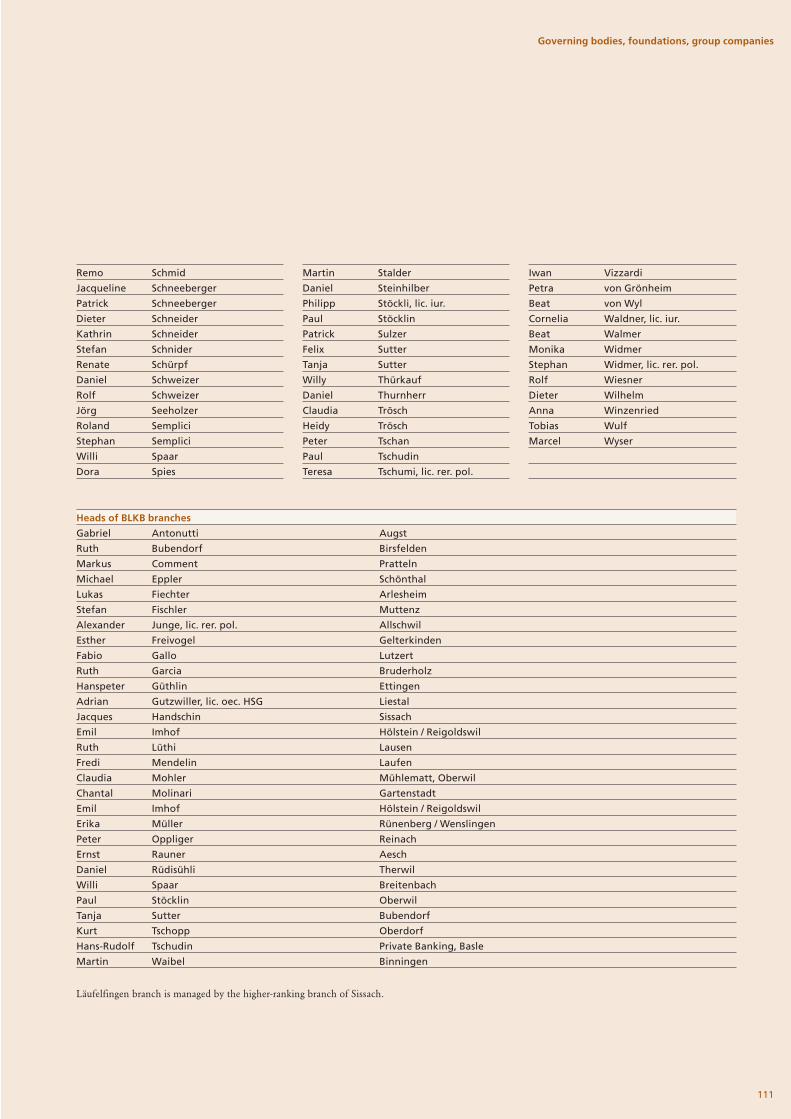

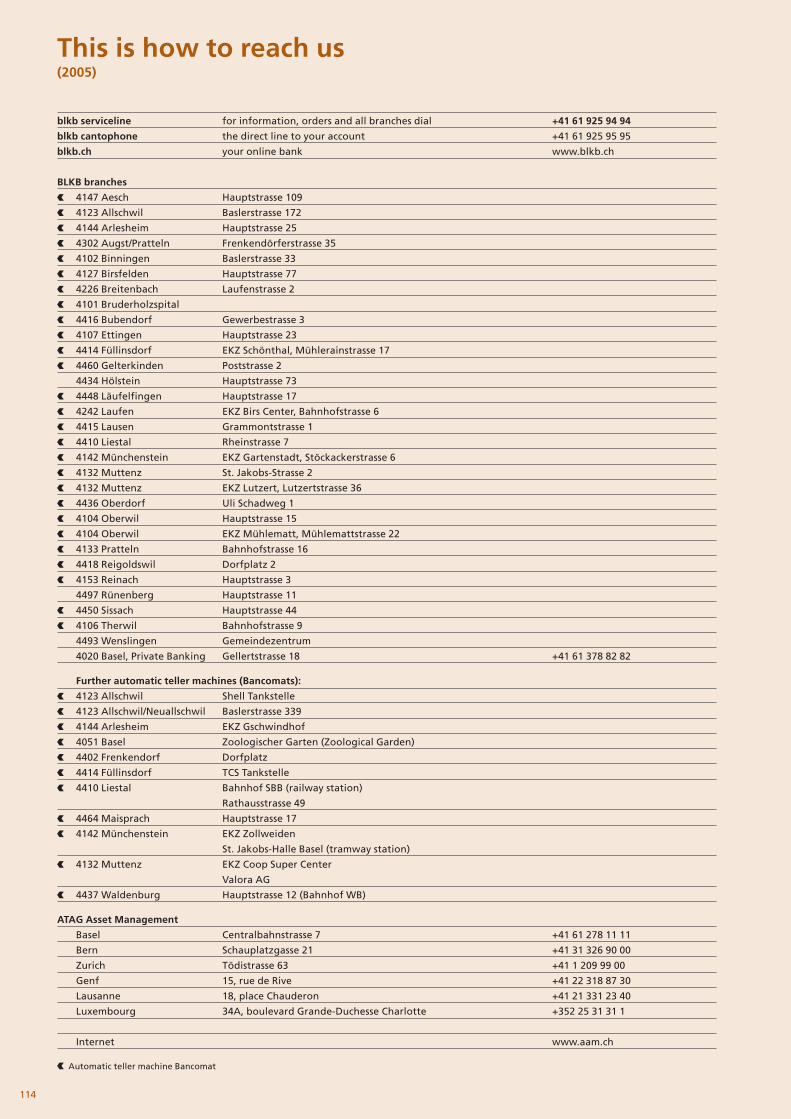

Annual Report 2004 AESCH ALLSCHWIL ARLESHEIM ...

121

Annual Report 2004 AESCH ALLSCHWIL ARLESHEIM AUGST BASEL BINNINGEN BIRSFELDEN BREITENBACH BRUDERHOLZSPITAL BUBENDORF ETTINGEN FÜLLINSDORF GELTERKINDEN HÖLSTEIN LAUFEN LAUSEN LÄUFELFINGEN LIESTAL MUTTENZ MÜNCHENSTEIN OBERDORF OBERWIL PRATTELN REIGOLDSWIL REINACH RÜNENBERG SISSACH THERWIL WENSLINGEN

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of Annual Report 2004 AESCH ALLSCHWIL ARLESHEIM ...

Annual Report 2004

AESCH ALLSCHWIL ARLESHEIM AUGST BASEL BINNINGEN BIRSFELDEN BREITENBACH BRUDERHOLZSPITAL BUBENDORF ETTINGEN FÜLLINSDORF GELTERKINDEN HÖLSTEIN LAUFENLAUSEN LÄUFELFINGEN LIESTAL MUTTENZ MÜNCHENSTEIN OBERDORF OBERWIL PRATTELNREIGOLDSWIL REINACH RÜNENBERG SISSACHTHERWIL WENSLINGEN

First address to turn to for customers

in the canton

Basellandschaftliche Kantonalbank is committed to

providing excellent services in order to continue its

140-year success story and to retain its independence

and autonomy.

In terms of bank services we are the first address to

turn to for private customers and companies, the

canton and the municipalities. We wish to strengthen

our significant market position in the Canton of

Basel-Landschaft and in the northwestern part of

Switzerland even further. In cooperation with Atag

Asset Management, our subsidiary with activities in

the whole of Switzerland, we are emphasising private

banking for high-net-worth individuals.

Our processes are run in a very stable IT environ-

ment by Real Time Center AG operated by BLKB

and two partner banks. Another two very important

partners are Sourcag AG for payment and securities

transactions and Swisscanto for first-class, diversified

funds and pension plan products. Swisscanto is a

joint operation of Swiss cantonal banks.

Private banking successful

Geographically seen, Basellandschaftliche Kantonal-

bank extends its business area across the economic

area of Basle. There are 30 branches in the Canton of

Basel-Landschaft, one branch in Breitenbach (Canton

of Solothurn) and another one for private banking

only in the city of Basle. Atag Asset Management AG

is active in Basle, Berne, Zurich, Lausanne, and

Geneva, and has a subsidiary in Luxembourg.

Company profile

Basellandschaftliche Kantonalbank is the lead-

ing bank in Baselland and one of the leading

banks in the northwestern part of Switzer-

land. Standard & Poor’s awarded a Triple-A, its

highest rating, to BLKB.

The Canton of Basel-Landschaft holds three-

quarters of the capital stock, one-quarter is

widely spread in private ownership in the

form of 600 000 BLKB certificates.

The Canton of Basel-Landschaft holds all vot-

ing rights and according to the law guarantees

for the bank’s liabilities.

www.global-reports.com

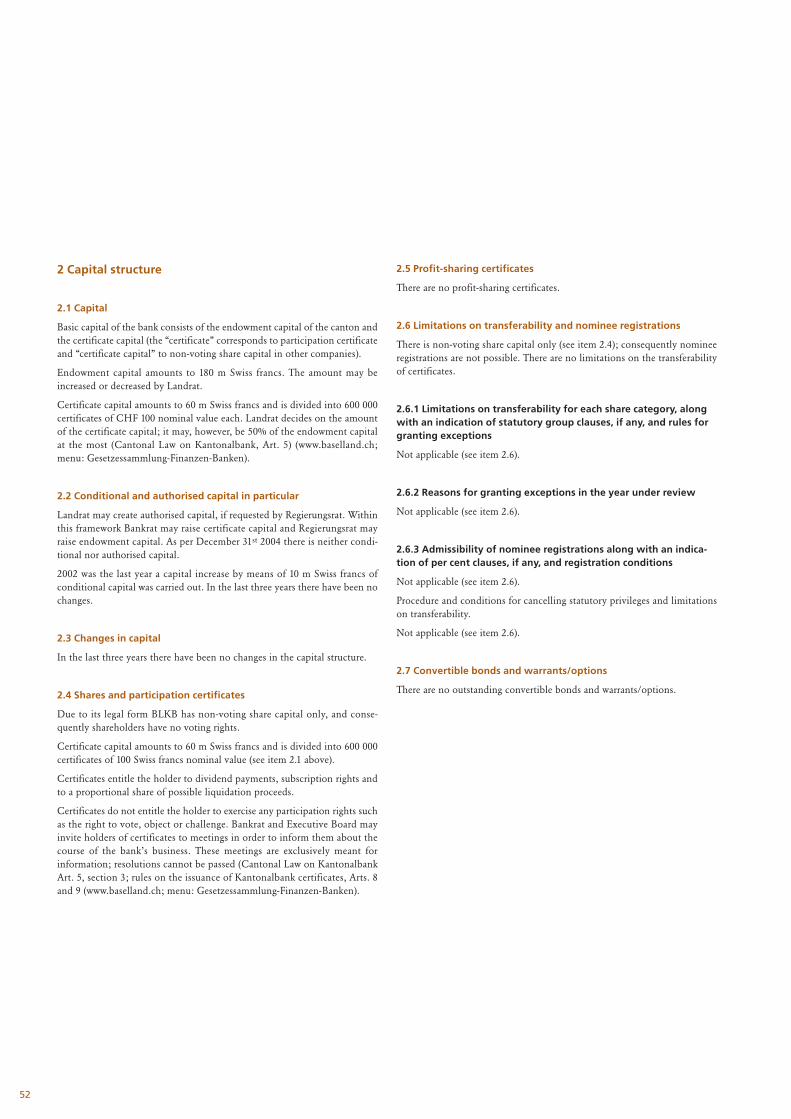

Highlights 2004 – healthy growth in all lines of business

Group

Balance

Balance

Income

Net ope

Gross pr

Year’s pr

Key figu

Number

Number

Number

Assets u

Cost-inc

Parent c

Balance

Balance

Mortgag

Dues to

Income

Net ope

Gross pr

Year’s ne

Dividend

Profit di

Other

Number

Number

Number

Assets u

Average

Return o

Cost-inc

Kantona

End-of-y

Nomina

Dividend

Market

* As of 2** Certifi

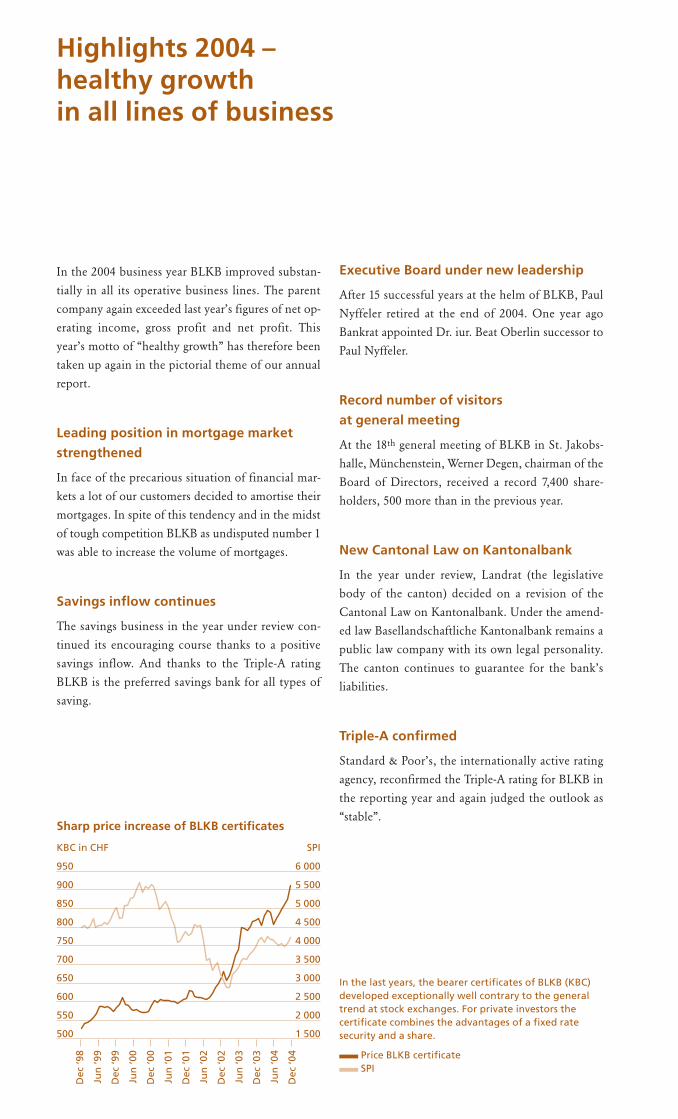

In the 2004 business year BLKB improved substan-

tially in all its operative business lines. The parent

company again exceeded last year’s figures of net op-

erating income, gross profit and net profit. This

year’s motto of “healthy growth” has therefore been

taken up again in the pictorial theme of our annual

report.

Leading position in mortgage market

strengthened

In face of the precarious situation of financial mar-

kets a lot of our customers decided to amortise their

mortgages. In spite of this tendency and in the midst

of tough competition BLKB as undisputed number 1

was able to increase the volume of mortgages.

Savings inflow continues

The savings business in the year under review con-

tinued its encouraging course thanks to a positive

savings inflow. And thanks to the Triple-A rating

BLKB is the preferred savings bank for all types of

saving.

Price BLKB certificate SPI

KBC in CHF

950

900

850

800

750

700

650

600

550

500

SPI

6 000

5 500

5 000

4 500

4 000

3 500

3 000

2 500

2 000

1 500

Sharp price increase of BLKB certificates

Dec

‘98

Jun

‘99

Dec

‘99

Jun

‘00

Dec

‘00

Jun

‘01

Dec

‘01

Jun

‘02

Dec

‘02

Jun

‘03

Dec

‘03

Jun

‘04

Dec

‘04

In the last years, the bearer certificates of BLKB (KBC)developed exceptionally well contrary to the generaltrend at stock exchanges. For private investors thecertificate combines the advantages of a fixed ratesecurity and a share.

Executive Board under new leadership

After 15 successful years at the helm of BLKB, Paul

Nyffeler retired at the end of 2004. One year ago

Bankrat appointed Dr. iur. Beat Oberlin successor to

Paul Nyffeler.

Record number of visitors

at general meeting

At the 18th general meeting of BLKB in St. Jakobs-

halle, Münchenstein, Werner Degen, chairman of the

Board of Directors, received a record 7,400 share-

holders, 500 more than in the previous year.

New Cantonal Law on Kantonalbank

In the year under review, Landrat (the legislative

body of the canton) decided on a revision of the

Cantonal Law on Kantonalbank. Under the amend-

ed law Basellandschaftliche Kantonalbank remains a

public law company with its own legal personality.

The canton continues to guarantee for the bank’s

liabilities.

Triple-A confirmed

Standard & Poor’s, the internationally active rating

agency, reconfirmed the Triple-A rating for BLKB in

the reporting year and again judged the outlook as

“stable”.

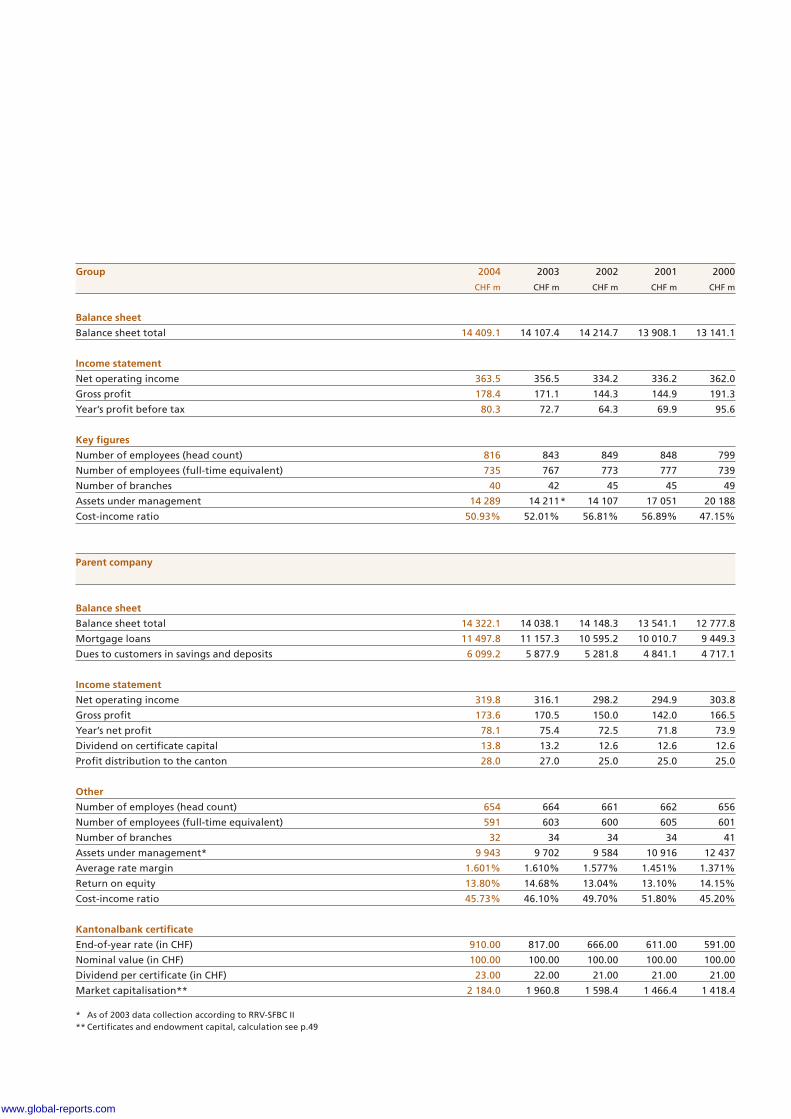

Group 2004 2003 2002 2001 2000

CHF m CHF m CHF m CHF m CHF m

Balance sheet

Balance sheet total 14 409.1 14 107.4 14 214.7 13 908.1 13 141.1

Income statement

Net operating income 363.5 356.5 334.2 336.2 362.0

Gross profit 178.4 171.1 144.3 144.9 191.3

Year’s profit before tax 80.3 72.7 64.3 69.9 95.6

Key figures

Number of employees (head count) 816 843 849 848 799

Number of employees (full-time equivalent) 735 767 773 777 739

Number of branches 40 42 45 45 49

Assets under management 14 289 14 211* 14 107 17 051 20 188

Cost-income ratio 50.93% 52.01% 56.81% 56.89% 47.15%

Parent company

Balance sheet

Balance sheet total 14 322.1 14 038.1 14 148.3 13 541.1 12 777.8

Mortgage loans 11 497.8 11 157.3 10 595.2 10 010.7 9 449.3

Dues to customers in savings and deposits 6 099.2 5 877.9 5 281.8 4 841.1 4 717.1

Income statement

Net operating income 319.8 316.1 298.2 294.9 303.8

Gross profit 173.6 170.5 150.0 142.0 166.5

Year’s net profit 78.1 75.4 72.5 71.8 73.9

Dividend on certificate capital 13.8 13.2 12.6 12.6 12.6

Profit distribution to the canton 28.0 27.0 25.0 25.0 25.0

Other

Number of employes (head count) 654 664 661 662 656

Number of employees (full-time equivalent) 591 603 600 605 601

Number of branches 32 34 34 34 41

Assets under management* 9 943 9 702 9 584 10 916 12 437

Average rate margin 1.601% 1.610% 1.577% 1.451% 1.371%

Return on equity 13.80% 14.68% 13.04% 13.10% 14.15%

Cost-income ratio 45.73% 46.10% 49.70% 51.80% 45.20%

Kantonalbank certificate

End-of-year rate (in CHF) 910.00 817.00 666.00 611.00 591.00

Nominal value (in CHF) 100.00 100.00 100.00 100.00 100.00

Dividend per certificate (in CHF) 23.00 22.00 21.00 21.00 21.00

Market capitalisation** 2 184.0 1 960.8 1 598.4 1 466.4 1 418.4

* As of 2003 data collection according to RRV-SFBC II** Certificates and endowment capital, calculation see p.49

www.global-reports.com

Forewords 6

Werner Degen 6

Paul Nyffeler 8

Beat Oberlin 10

Value-oriented management 12

Business development 14

Interest-related business: saving 18

Interest-related business: loans 20

Private banking 23

Commitment to sustainability 26

BLKB economic survey 2004 30

Customer needs 32

Employees 34

Environment, ethical values and health 38

Efficient services 40

Information technology 42

Corporate planning and monitoring 44

Corporate governance 46

Annual financial statements 63

Governing bodies, foundations,

group companies 106

Content

work, behaviour, food, life!People think differently, a veryrewarding experience on apersonal and professional level.The impossible suddenly seemspossible, obstacles are just2

Regional identity requires acosmopolitan mind. FranzRickenbacher sets out on abusiness trip to the Far East. Hewants to visit Ronda subsidiariesin Hong Kong and Thailand. In

spite of the long flight he islooking forward, as he is everytime he travels there, to lettinghimself be seduced by the cul-ture which is so different fromhis own. Everything’s different;

Basellandschaftliche Kantonalbank enjoys healthy growth

www.global-reports.com

3

swept away, solutions withinreach. Even the familiar thingsof everyday life at home sud-denly have a new sparkle tothem. Franz Rickenbacher isalso looking forward to getting

home again – and at homethere’s a surprise waiting forhim. His boys made a cherry piefor him, a genuine, old-fash-ioned, tasty cherry pie as it istraditionally done in “Baselbiet”.

We are the leading bank in Basel-land and have firm roots in thewhole region. Our customers profitfrom top-quality products andexpert advice at fair prices. This iswhat our healthy growth is basedon. In the reporting year we wereable to continue our growth in allbusiness lines from savings to loansto asset management.

4

Procedures in banking are gettingever more complex and need con-stant developing and updating. RTC, the IT service company forbanks, is a strong partner in thatrespect. Our subsidiary Sourcag AGspecialises in payment and securitiestransactions. As a result, we canfocus our attention on the cus-tomers and their individual needs. A successful approach which thetrust placed in our bank gives ampleproof of: savings, mortgage loans,and assets under management haveagain increased.

www.global-reports.com

5

Supply of the necessities of life is a question of trust. FrediMischler cultivates the fieldsand gathers the crop. ElisabethMischler’s domain is the bakery.

Every year, she uses about fourand a half tons of wheat tomake bread. The quality isexcellent and the reputationgoes far beyond the own

village. Quite a number ofpeople take the trouble to goto “Mischler Hof” to buy breadfresh from the oven. It’s a goodthing to be able to buy food

directly from the producer. You know what you get, whoyou get it from, and the taste issimply delicious.

The beginning of 2004 saw economic optimism on the rise:

Switzerland was seen as up-and-coming.

On an international level three tendencies prevailed throughout

the year: the economic upswing of the People’s Republic of

China, and, quite contrarily, the ever widening gap between per-

formance and consumption in the United States of America,

and the development of the oil price. Looking back at how these

different trends unfolded, we might say that Swiss business

activities fell short of expectations. In my opinion this assess-

ment lacks a sound basis. The Swiss economy developed along

astonishingly stable lines in 2004. So, the initial optimism was

not completely wrong.

Another positive year for BLKB

The business year 2004 took again a positive course for BLKB.

We reached our goals and in some cases even surpassed

them, not only in the parent company, but also in Atag Asset

Management (AAM), our subsidiary.

And again, the more-than-average development of the area of

northwestern Switzerland contributed largely to the success of

the parent company. The bank’s success, however, is also based

on its specific strengths which are all the more prominent now,

that competition has become increasingly severe: BLKB is close

to the market and close to its customers, BLKB knows the re-

gional economy and is rewarded with satisfaction and trust from

its customers.

Apart from the economic environment there were two changes

of major importance in the year under review: the amendment

of the Cantonal Law on Kantonalbank and the change at the

highest operative level of the bank.

Continuing modernisation

The new streamlined Cantonal Law on Kantonalbank entered

into force on January 1st 2005. No changes were made in the le-

gal form of BLKB which remains a public law institution. The

State’s guarantee remains unchanged as well, but from now on

the bank will pay a yearly compensation.

The amended law does not aim at a radical change of course, but

rather at a continuous development of Basellandschaftliche

Kantonalbank, and we very much appreciate this political sup-

port. The harmonious relationship between the canton and the

bank based on common determination and mutual respect has

always been the backbone of our success.

Change in the operative leadership

After 15 years of presiding over the Executive Board, Paul

Nyffeler retired with effect of the end of the reporting year and

handed over chairmanship to Dr. Beat Oberlin, his successor.

Baet Oberlin joined the Executive Board of BLKB in mid-2004,

directed corporate planning for 2005 and was therefore well pre-

pared to take up his managerial duties on January 1st 2005.

Paul Nyffeler wrote history; a history of success for BLKB. His

thorough knowledge of the canton and his intuitive compre-

hension of economic development enabled him to guide the

bank safely through an era of intense changes and to steel it for

the challenges to come.

In the name of Bankrat I would like to extend my thanks to Paul

Nyffeler for 15 years at the helm of BLKB, marked by intensive

personal commitment, uncompromising decisions when neces-

sary, but also a willingness for compromise when possible, and

by creativity where conflicting interests had to be settled by

arbitration.

Targets reached with ease – successful change of leadership

6www.global-reports.com

Taking leave of Paul Nyffeler is not easily done. There are, how-

ever, two aspects which make us open a new chapter in the his-

tory of BLKB with a confident mind. One is Paul Nyffeler’s suc-

cessor. With Dr. Beat Oberlin, Bankrat appointed a personality

who has all the skills for a successful continuation of BLKB’s de-

velopment. The other aspect lies with Paul Nyffeler himself. Last

summer, the Association of Swiss Cantonal Banks elected him

president of their association. In this way he will undoubtedly

continue to be involved in the idea of cantonal banks.

At the end of a business year, it is an honourable duty of a

bank’s president to thank the staff, the middle management and

the Executive Board for their work. Doing this is a pleasure for

me, and in the name of Bankrat and the entire staff I say good-

bye to Paul Nyffeler with our warmest thanks. And just as

warmly and sincerely I welcome Beat Oberlin.

Werner Degen

Head of Bankrat

Basellandschaftliche Kantonalbank has all the necessary pre-

requisites to stand up to the challenges of competition in the

future. It also has the necessary size: total assets, savings, lend-

ing, and commission business, number of employees, and prof-

its range in categories far above critical levels. BLKB is one of

the leading banks and in some respects the leading bank.

Smooth cooperation

BLKB’s favourable position in the market is being enhanced by

well-oiled cooperation mechanisms in the area of service per-

formance, particularly the partnership in the RTC-IT cooper-

ation and the centre for the handling of securities and payment

transactions in Münchenstein, which is jointly operated by

BLKB and Basler Kantonalbank. Both these partnerships assure

an even distribution of burdens in two very cost-intensive areas.

In retrospect, joining RTC in 1998 was probably the most im-

portant step of the last decades. Going it alone, we would not

have been able to adapt our banking IT to the changes in market

conditions, let alone to the requirements of supervisory bodies.

It was the right decision at the right moment to turn to a stable

system equipped with the right resources for development.

BLKB: a bank of repu-tation and long stand-ing, expertly equippedfor the future

8www.global-reports.com

Competition, concentration, regulation

During the 15 years I have been at the helm of BLKB, consider-

able changes in banking have taken place. Namely three devel-

opments had a lasting effect on existing structures.

The first one can be subsumed under the term “competition”.

The fast development and expansion of IT by means of new

electronic media thoroughly changed the behaviour of supply

and demand in banking. Money matters are still considered

questions of trust, but cost-effectiveness is something that is

examined very closely nowadays. Customer loyalty has to be

acquired and maintained by a holistic quality of services.

The second development is the process of concentration that

has taken place in the course of the past 10 years. This process

has got to do with the many changes in the environment of

competition, but also with the rather roundabout structural

ways that namely big banks have taken by temporarily signalling

disinterest in the domestic retail business in favour of global

banking.

The third development concerns the new regulation of the bank

business. Like all the other banks BLKB increased the expenses

for properly fulfilling regulatory requirements during the past

years, the most prominent being the processes set in motion for

the prevention of money laundering. These are most easily no-

ticed by the customers, whereas others, such as those dealing

with risk management or accounting standards, go widely

unnoticed by the public. Expenses for personnel or material are

not lower for that matter. However, the fact that supervision of

banking has become so overbearing is not just a burden, but

quite on the contrary an asset for the survival of Switzerland as a

financial centre and therefore an asset for any bank.

Competition, mergers, regulation! These aspects have two things

in common: there is a mounting significance of unified, well-

structured processes on the level of handling as well as the con-

centration of responsibilities as an organisational and executive

duty. In this respect the RTC association offers a potential for

development and provides security for the future, an aspect

which is not to be underestimated.

BLKB developed in a highly satisfactory way, given the fickle-

ness of the economic environment and the structural changes

of the past years. I appreciate the work done by our employees at

all levels and positions and their unwavering support. I wish all

of them a healthy, successful development in and for Baselland-

schaftliche Kantonalbank.

Paul Nyffeler

Chairman of the Executive Board

up to December 31st 2004

9

The retirement of Paul Nyffeler marks the end of anera. Looking at the figures we can see that businessvolume has multiplied. In the past 15 years, mortgageloans, for example, grew by 170 percent and at thesame time our customers entrust us with 160 percentmore of their savings. Private banking did not exist 15 years ago. Gross profit has risen from 103 to 174 mSwiss francs. The profit delivered to the canton by thebank has risen from 8 m Swiss francs in 1990 to 28 mSwiss francs today.

10

I feel quite privileged to be called to the helm of Baselland-

schaftliche Kantonalbank, a leading bank, healthy, exceptionally

well positioned and firmly rooted in the market. My thanks go

to Paul Nyffeler, my predecessor, from whom I took over an or-

ganisation in excellent shape. I look forward to guiding BLKB

through the coming years, knowing well that I have employees

at my side who are highly motivated professionals, financial ex-

perts as well as socially competent members of a staff that iden-

tifies fully with BLKB. In this way, we will undoubtedly be able

to keep building on the existing values.

Efficient processes – responsible behaviour

Today, we are facing a multitude of challenges. Organisational

and technical routines are what we act upon every day and they

are becoming ever more complex. We have, however, a number

of instruments at our disposal for dealing with and coordinating

these matters which will become more numerous and more re-

fined. Success in business practices depends greatly on the way a

company plans its processes, uses its tools and especially on

whether it is capable of attaining an optimum in the benefit for

the customers.

However, the world of processes is only one side of the coin.

As modern information technology is able to speed up the

processes to an ever greater degree, thereby allowing for almost

any variation, the question of responsibility becomes more and

more prominent. “Compliance”, meaning the permanent and

continuing check on conformity with legal and regulatory rules

as well as conformity with the behaviour imposed by our own

strategy, is just as important as technical matters and probably

the more difficult part of the deal. Technology may be bought,

processes may be subcontracted, but responsibility for their

application stops right here in our midst.

Four main lines of direction

The relationship with our customers is determined by their ever

changing needs. These changes may be more or less significant,

but they always rotate about values such as quality, service reli-

ability, handling security and price fairness. Our customers are

used to these services and conceive them as being characteristic

of BLKB. We therefore devote serious effort and energy to of-

fering them on an individual basis and in the expected quality.

Let’s reflect for a moment on the future course of BLKB and its

significance for these expectations, and we can make out four

main lines of direction that will guide us through the future. It is

imperative, however, that we position ourselves correctly on

these lines and develop along them.

The first line is the actual activity of BLKB as a bank. Private

customers and companies alike appreciate BLKB and consider it

their most important bank.

The second line runs along our image. BLKB is widely and

popularly known and puts great emphasis on being close to the

customer. It is deeply rooted in the region and regarded by the

public as being competent, reliable, and innovative. BLKB is

synonymous with quality and as the bank of the canton it enjoys

the respect and loyalty of the public.

The third line is based on our sales organisation and quality

advice. Our organisation orientates itself to sale and advice. We

seek the exchange of ideas and opinions with our customers, and

they have a fair comprehension of what they are entitled to.

The fourth and final line has got to do with our role as

employer. Our aim is to be the most attractive employer in

the region, and we try to achieve this goal by systematically

promoting talented and dynamic employees, by furthering a

corporate identity, and by lending practical support to husbands

or wives in their work or in child education.

There are chances for growth – let’s seize them for the benefit of our stakeholders

www.global-reports.com

11

The area of our activity is a canton blessed with chances for

more-than-average growth. We have to recognise these chances

quickly and make good use of them. In this way we can grow

together with our customers, and we must not forget that they,

or the population of the Canton Basel-Landschaft, are the co-

owners of Basellandschaftliche Kantonalbank since the canton

will continue to hold the dominant part of the capital. We are

well aware of the responsibility constituted by this fact and we

will do our utmost to promote our common prosperity.

Dr. Beat Oberlin

Chairman of the Executive Board

since January 1st 2005

12

BLKB creates added value for itscustomers, for the company itself,for the entire staff, and last but notleast for the canton and the privateco-owners of Kantonalbank. Thisgoal is increasingly reached by theability of proposing individual solu-tions to our customers, of antici-pating changing needs in their livesand of giving them expert adviceeven before new situations arise.

Value-oriented managementmeans recognising market needs early on

www.global-reports.com

13

Create added value by honour-ing existing values. The successof Ricola, Laufen’s enterprise oflong standing, is based on thir-teen medicinal herbs. Ricola,one the one hand, profits from

the favourable economic condi-tions prevailing in “Baselbiet”and on the other hand takes onresponsibility. The company iscommitted to preserving bio-diversity, supports Swiss artists

with a generous art collection,and readily opens the com-pany’s doors for interested per-sons. Whether they are guidedthrough the garden of indige-nous herbs or through one

14

The past business year of Basellandschaftliche Kantonalbank was

marked by a continuous, healthy growth. Healthy, because it did

not follow a breathless pace for quarterly achievements, but also

healthy because all the business lines contributed positively:

interest-related business, asset management, and trading. Healthy

finally, because cost discipline led to a further improvement of

the relation between expenditure and profitability.

The development of equity is also indicative of continuous

growth: free and legal reserves were increased by 98 m Swiss

francs, a fact that creates security. Equity exceeds the legally re-

quired reserves by one billion Swiss francs or 70%.

Finally, the continuous growth can be seen in dividend pay-

ments. 28 m Swiss francs, one million more than in the previous

year, go to the canton. 13.8 m Swiss francs, 600 000 more than

in the previous year, are paid to the holders of BLKB certificates.

Added to this are another 7.8 m Swiss francs in the form of

interest paid on endowment capital.

Continuity and keeping up with the activities

of the market

Continuity and the dynamic pattern expressed by this perform-

ance is not self-generated. In order to make these things happen

and work, a bank has to be flexible and keep up with the activi-

ties of the market and, even more important, it has to rely on

an absolutely stable IT environment.

For us, keeping up with the market means using our position of

strength in order to put ourselves in line with the individual

needs of our customers and offer them a range of top-quality

products and expert services at a fair price.

IT is a highly sensitive area for any bank, and BLKB decided ear-

ly on to cooperate with specialists. So, in 1998 it joined the RTC

group of banks. Together with Basler Kantonalbank we estab-

lished Sourcag AG, a processing company. In retrospect, these

decisions were of invaluable strategic use. In the environment of

RTC and Sourcag AG, operational stability of the systems, a fac-

tor which is often underestimated outside the bank, is flawless

and guarantees high safety in our complex processes. Costs are

calculable, controlled and comparatively favourable at that.

Successful control of non-personnel costs are important for our

employees as well. A job at BLKB is not a matter dealt with

lightly or subject to considerations of return. It is an integral part

of our corporate culture which appreciates work and never

doubts the economic and social significance of secure jobs.

Dynamics means to face the market and to anticipate develop-

ments early enough and correctly. Innovation and stability are

prerequisites to long-term success.

of the sophisticated companybuildings designed by Herzog &de Meuron – visitors learnabout how the soothingproperties of medicinal herbsare extracted and processed to

the famous Swiss herbal dropswith the unmistakable flavour.

Business development – continuous growth for all lines of business

www.global-reports.com

15

Excellent figures for 2004

In the parent company gross profit rose by 1.8% to 173.6 m

Swiss francs (previous year 170.5) and net profit by 3.6% to 78.1

m Swiss francs (previous year 75.4). This is again the best result

in the bank’s 140-year history. At group level gross profit in-

creased by 4.3% to 178.4 m Swiss francs (previous year 171.1).

Group net profit before taxes went up by 10.5% to 80.3 m Swiss

francs (previous year 72.7).

In the year under review, operational performance of all the

business lines of the parent company led to higher results than

in the previous year. Net operating income therefore increased

by 3.7 m Swiss francs or 1.2% to 319.8 m Swiss francs.

Interest-related business: further gain

of market shares

In the interest-related business results could be improved again

compared to the previous year by 2.7 m Swiss francs or 1.1% to

241.5 m Swiss francs. The result reflects the bank’s efficiency and

the customers’ confidence in BLKB services and products. As a

market leader with competitive services BLKB was able not only

to keep its market position, but to win even more market shares.

Balance structure, which was optimised unconditionally in the

area of maturity risks, had a favourable influence on the inter-

est result.

Value-oriented management Business development

Kaspar Schweizer: Head of Corporate Services; Willy Winkler: Head of Private Customers; Beat Oberlin: Chairman of the Executive Board;Lukas Spiess: Head of Credit and Corporate Customers; Meinrad Geering: Head of Investment Customers (from left)

(January 1st 2005)

The Executive Board of Basellandschaftliche Kantonalbank

16

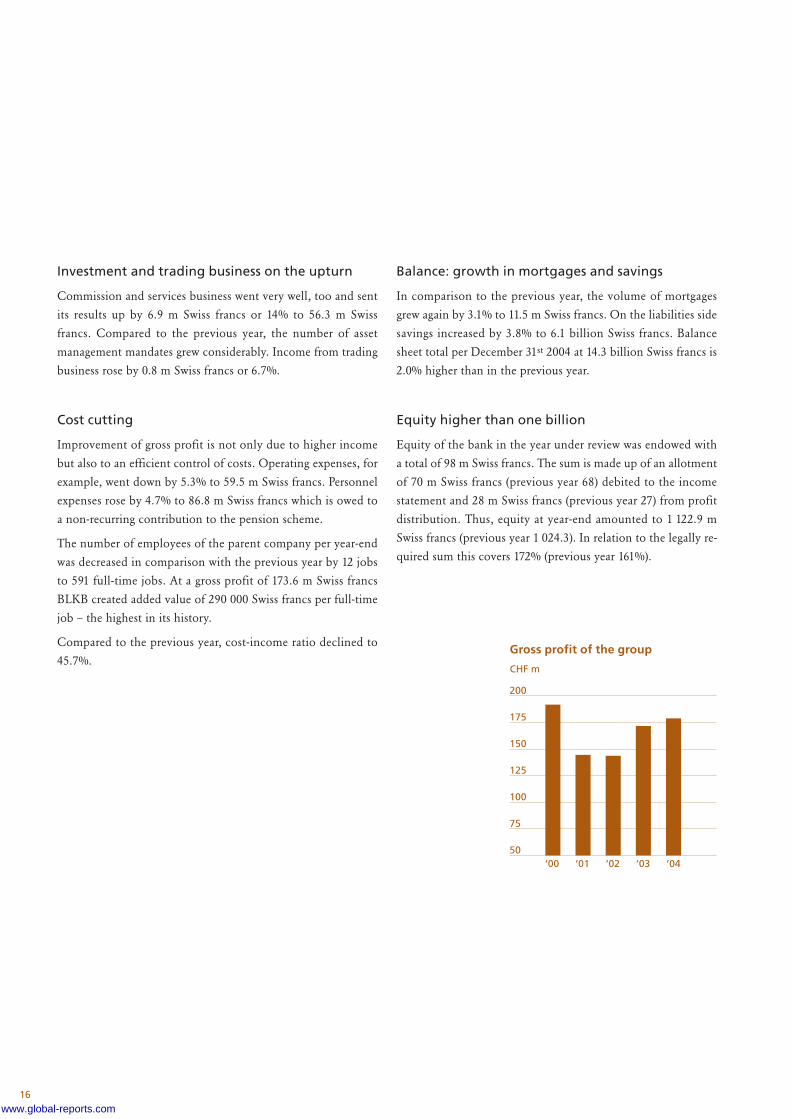

Investment and trading business on the upturn

Commission and services business went very well, too and sent

its results up by 6.9 m Swiss francs or 14% to 56.3 m Swiss

francs. Compared to the previous year, the number of asset

management mandates grew considerably. Income from trading

business rose by 0.8 m Swiss francs or 6.7%.

Cost cutting

Improvement of gross profit is not only due to higher income

but also to an efficient control of costs. Operating expenses, for

example, went down by 5.3% to 59.5 m Swiss francs. Personnel

expenses rose by 4.7% to 86.8 m Swiss francs which is owed to

a non-recurring contribution to the pension scheme.

The number of employees of the parent company per year-end

was decreased in comparison with the previous year by 12 jobs

to 591 full-time jobs. At a gross profit of 173.6 m Swiss francs

BLKB created added value of 290 000 Swiss francs per full-time

job – the highest in its history.

Compared to the previous year, cost-income ratio declined to

45.7%.

Balance: growth in mortgages and savings

In comparison to the previous year, the volume of mortgages

grew again by 3.1% to 11.5 m Swiss francs. On the liabilities side

savings increased by 3.8% to 6.1 billion Swiss francs. Balance

sheet total per December 31st 2004 at 14.3 billion Swiss francs is

2.0% higher than in the previous year.

Equity higher than one billion

Equity of the bank in the year under review was endowed with

a total of 98 m Swiss francs. The sum is made up of an allotment

of 70 m Swiss francs (previous year 68) debited to the income

statement and 28 m Swiss francs (previous year 27) from profit

distribution. Thus, equity at year-end amounted to 1 122.9 m

Swiss francs (previous year 1 024.3). In relation to the legally re-

quired sum this covers 172% (previous year 161%).

‘00 ‘01 ‘02 ‘03 ‘04

Gross profit of the group

CHF m

200

175

150

125

100

75

50

www.global-reports.com

Value-oriented management Business development

17

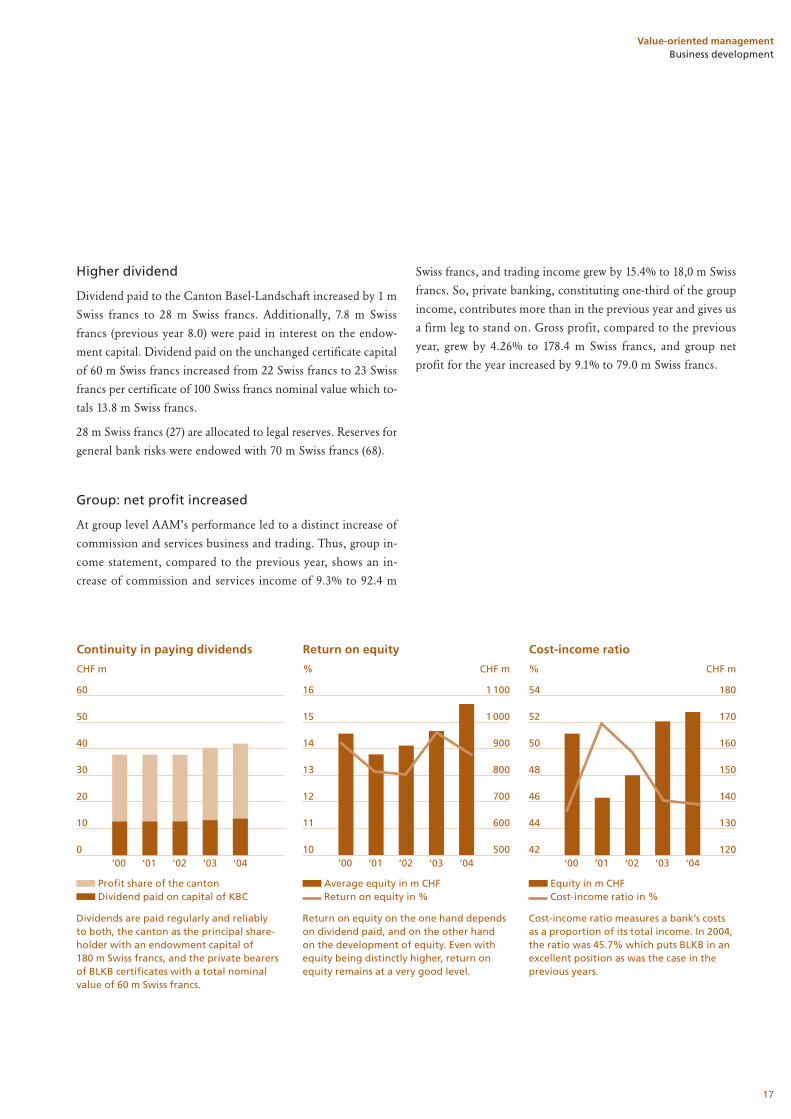

Higher dividend

Dividend paid to the Canton Basel-Landschaft increased by 1 m

Swiss francs to 28 m Swiss francs. Additionally, 7.8 m Swiss

francs (previous year 8.0) were paid in interest on the endow-

ment capital. Dividend paid on the unchanged certificate capital

of 60 m Swiss francs increased from 22 Swiss francs to 23 Swiss

francs per certificate of 100 Swiss francs nominal value which to-

tals 13.8 m Swiss francs.

28 m Swiss francs (27) are allocated to legal reserves. Reserves for

general bank risks were endowed with 70 m Swiss francs (68).

Group: net profit increased

At group level AAM’s performance led to a distinct increase of

commission and services business and trading. Thus, group in-

come statement, compared to the previous year, shows an in-

crease of commission and services income of 9.3% to 92.4 m

Swiss francs, and trading income grew by 15.4% to 18,0 m Swiss

francs. So, private banking, constituting one-third of the group

income, contributes more than in the previous year and gives us

a firm leg to stand on. Gross profit, compared to the previous

year, grew by 4.26% to 178.4 m Swiss francs, and group net

profit for the year increased by 9.1% to 79.0 m Swiss francs.

‘00 ‘01 ‘02 ‘03 ‘04

Continuity in paying dividends

CHF m

Profit share of the cantonDividend paid on capital of KBC

60

50

40

30

20

10

0‘00 ‘01 ‘02 ‘03 ‘04

Cost-income ratio

% CHF m

54

52

50

48

46

44

42

180

170

160

150

140

130

120

Return on equity

% CHF m

Dividends are paid regularly and reliably to both, the canton as the principal share-holder with an endowment capital of180 m Swiss francs, and the private bearersof BLKB certificates with a total nominalvalue of 60 m Swiss francs.

Cost-income ratio measures a bank’s costsas a proportion of its total income. In 2004,the ratio was 45.7% which puts BLKB in anexcellent position as was the case in theprevious years.

Return on equity on the one hand dependson dividend paid, and on the other hand on the development of equity. Even withequity being distinctly higher, return onequity remains at a very good level.

Equity in m CHFCost-income ratio in %

Average equity in m CHFReturn on equity in %

‘00 ‘01 ‘02 ‘03 ‘04

16

15

14

13

12

11

10

1 100

1 000

900

800

700

600

500

18

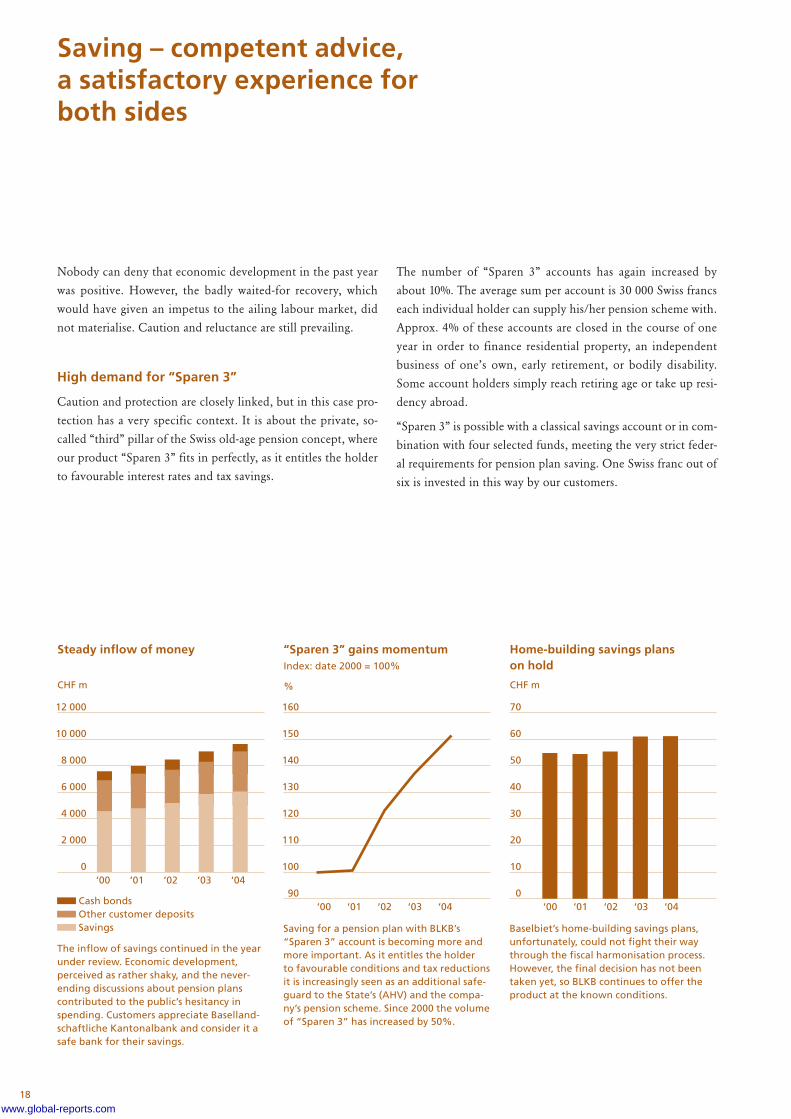

Nobody can deny that economic development in the past year

was positive. However, the badly waited-for recovery, which

would have given an impetus to the ailing labour market, did

not materialise. Caution and reluctance are still prevailing.

High demand for “Sparen 3”

Caution and protection are closely linked, but in this case pro-

tection has a very specific context. It is about the private, so-

called “third” pillar of the Swiss old-age pension concept, where

our product “Sparen 3” fits in perfectly, as it entitles the holder

to favourable interest rates and tax savings.

The number of “Sparen 3” accounts has again increased by

about 10%. The average sum per account is 30 000 Swiss francs

each individual holder can supply his/her pension scheme with.

Approx. 4% of these accounts are closed in the course of one

year in order to finance residential property, an independent

business of one’s own, early retirement, or bodily disability.

Some account holders simply reach retiring age or take up resi-

dency abroad.

“Sparen 3” is possible with a classical savings account or in com-

bination with four selected funds, meeting the very strict feder-

al requirements for pension plan saving. One Swiss franc out of

six is invested in this way by our customers.

Saving – competent advice, a satisfactory experience forboth sides

160

150

140

130

120

110

100

90

“Sparen 3” gains momentumIndex: date 2000 = 100%

%

‘00 ‘01 ‘02 ‘03 ‘04

70

60

50

40

30

20

10

0

Home-building savings plans on hold

CHF m

‘00 ‘01 ‘02 ‘03 ‘04

12 000

10 000

8 000

6 000

4 000

2 000

0

Steady inflow of money

CHF m

‘00 ‘01 ‘02 ‘03 ‘04

Cash bonds Other customer depositsSavings Saving for a pension plan with BLKB’s

“Sparen 3” account is becoming more andmore important. As it entitles the holder to favourable conditions and tax reductionsit is increasingly seen as an additional safe-guard to the State’s (AHV) and the compa-ny’s pension scheme. Since 2000 the volumeof “Sparen 3” has increased by 50%.

The inflow of savings continued in the yearunder review. Economic development,perceived as rather shaky, and the never-ending discussions about pension planscontributed to the public’s hesitancy inspending. Customers appreciate Baselland-schaftliche Kantonalbank and consider it asafe bank for their savings.

Baselbiet’s home-building savings plans,unfortunately, could not fight their waythrough the fiscal harmonisation process.However, the final decision has not beentaken yet, so BLKB continues to offer theproduct at the known conditions.

www.global-reports.com

Value-oriented management Interest-related business: saving

19

Saving for residential property: we keep going

Saving for protective reasons does not only mean pension plans.

Saving for residential property comes under the same heading

and the figures give ample proof of that. In the Canton of Basel-

Landschaft there are 1 700 active savings accounts for residential

property with a total of about 60 million Swiss francs.

Unfortunately, it is not clear at all, how subsidised home build-

ing in the Canton of Basel-Landschaft will be handled in the fu-

ture. Basellandschaftliche Kantonalbank trusts that a political

solution will be found which allows for the autonomy of the

canton to pursue savings plans for residential building. For the

time being, we do not see any reason why we should stop sav-

ings plans for home building. We hope the authorities will see

the need to come up with a viable solution soon.

Expert advice becomes more and more important

Our main focus in the retail business, too, is to give our cus-

tomers quality advice and assistance. A growing number of cus-

tomers actively use these services. The abundance of informa-

tion, recipes, and strategies offered by the print media or by

consumer programmes of public and private radio or TV sta-

tions definitely persuade people to seek better and more com-

prehensive advice. BLKB, as a firmly anchored bank and an

undisputed market leader, profits from the loyalty of its cus-

tomers. We are doing our very best to deserve this loyalty and to

remain the first bank people turn to in the region.

One aspect of our efforts is the permanent education and train-

ing of the employees. The work of different centralised services

is a very important feature as well, since they put essential ele-

ments and structures at the disposal of those employees who

deal with the customers directly. Administrative burdens are

kept to a minimum, so our staff can devote more time to the

customer.

In the reporting year we achieved quite a lot in this respect. In

2005, in the course of checking our processes, we will continue

separating customer-related activities from behind-the-scenes ac-

tivities. There is a tendency to centralise repetitive, industrialised

processes, but decisions will still be taken “at the front”. Thus,

our employees’ professional and social kills will be further

strengthened.

Close customer relations

Saving has been a recurring theme throughout thebusiness year 2004. The average private budget stillassigns major importance to saving. Talking to ourcustomers we found out that there are several rea-sons for saving. One of them is saving for a specificpurpose such as the more expensive acquisitions fora household, for holidays or some other project. Themain reasons, though, for the persisting interest inclassical, low-risk savings forms are caution and pro-tection.

Nine out of ten credit or investment operations areconcluded in our branches in personal contact withour customers. We encourage our employees to takeresponsibility for the individual customer the mo-ment he/she enters a BLKB branch until his/her re-quests are met or an employee with specialised skillshas taken over. Giving expert advice is a satisfyingjob, and we want our customers to see and feel it.

20

“StartFix” mortgage – a start-up for young families

Basellandschaftliche Kantonalbank tries to facilitatethe acquisition of residential property for young fam-ilies not just by giving logistical or advisory supportbefore the purchase or during the building phase,but also by offering financial incentives. One of themis a home-building savings plan which was developedin cooperation with the canton, another incentive is a reduction of interest rates during the first fewyears, usually the most difficult period in terms of finance.

In September 2004 we added another product to therange of home-owner mortgages whose most suc-cessful model is “Starthypothek”. The new, very sim-ilar product is called “StartFix” mortgage and is afixed rate mortgage. In this scheme customers profitfrom an interest rate reduction of half a percentagepoint for the first two years and a quarter percentagepoint for the following two years, at the conclusionof a five-year, fixed rate mortgage. “StartFix” mort-gage can be combined with an adjustable portion atthe same favourable rates.

When we started promoting “StartFix” mortgage weput our expectations on personal contact to the cus-tomers and other interested parties. In the first threemonths already, the product was surprisingly success-ful and was favourably accepted by customers andemployees alike.

Loans – competition strengthensyour determination

The year 2003 would go down in history as the year of the all-

time low in interest rates: this is what we wrote one year ago.

Now, we have to add another page to this history book, for the

year 2004 did not see any changes to speak of. With the excep-

tion of a brief pleasure trip interest rates played a waiting game

on the lowest rungs of the ladder.

Our customers profited from the situation, and the trend to-

wards fixed rate mortgages continued. At present, the share of

variable rate mortgages is so low (19) that the variable rate lost its

former political significance. At present, it is not relevant for the

activities of the mortgage or the rent market.

Another statement of one year ago has unfortunately kept its va-

lidity, too. The favourable interest rates have not acted as a stim-

ulant for the building activity in the region. This corresponds

largely with the assessment of the building industry in the year-

ly economic survey Basellandschaftliche Kantonalbank carried

out. Only 25% of the building companies judged 2004 better

than the previous year and only 20% expect an actual improve-

ment for 2005. The cautious recovery of the economy and the

fact that more and more people brace themselves for a contin-

uing period of mediocre growth restrain the demand for the cur-

rently low interest rates.

From the lender’s point of view there is an important fact which

must not be ignored: residential property is usually acquired for

a longer period of time. Both parties, the buyer and the lending

bank, have to be aware of the probability that today’s low rates

increase. A bank offering reliable advice will certainly not neg-

lect this aspect, particularly since long-term planning has be-

come more difficult as a result of the changes our society has un-

dergone in the last 15 to 20 years.

www.global-reports.com

21

Value-oriented management Interest-related business: loans

Tough competition for market shares

By observing the markets you become aware of a toughening

competition verging in some instances on a merciless fight for

market shares. As a market leader we are particularly exposed to

this kind of threat.

BLKB’s conditions are very competitive, but banking is not al-

ways about money only. A mortgage is not a commodity or a

mass product as some people are saying. A mortgage is part of

a package we call “financing of residential property” which

includes accompanying services from planning to realising to

moving in and even further.

Offering complete, holistic systems instead of dissected parts is

but one of our strong points in this competition. Our bank

organisation has successfully existed for 140 years, is firmly

rooted in the canton and has a lot of confidence placed in our

work. All this taken together gives us the strength to face the

competition and assert our position in the market. In spite of

unfavourable conditions, we managed to increase the volume of

mortgage loans again. Net new production of 3.05% was approx.

2% lower than in the previous year, but given the circumstances

still represents a good result.

The strategy is clearly outlined: With its high-quality advice and

its product offers at favourable conditions, BLKB wants to retain

and expand its number 1 position. Nevertheless, this will not be

done at any price; certainly not at the price of watering down

BLKB’s principles of risk policy.

Further growth of mortgages

Variable rate Fixed rate

CHF billion

12

10

8

6

4

2

0‘00 ‘01 ‘02 ‘03 ‘04

BLKB’s offer of complete, holistic systemsand the firm roots in the region are thebank’s strong points in this competition. A distinctly recognisable trend goestowards fixed rate mortgages. Under thesecircumstances the variable rate has lostsome of its shine.

22

First address for SME

BLKB still considers SME financing a core task which must be

continued in a responsible way. Compared to other parts of the

country, the economy in our region is more than sound, a fact

that clearly benefits the financial needs of SME, because they

can put their business planning on solid economic feet.

Financing start-up businesses is one of the specific needs of to-

day’s economy. We lend active support with our involvement in

“Erfindungsverwertungs AG” (EVA) which is a private enter-

prise, established in 1996, with a lot of experience in the area of

Life Sciences. EVA supports and assists fledgling companies in

their initial phase (www.eva-basel.ch).

Moreover, for four years now, young, innovative enterprises

have had the possibility to use a special credit limit which is

granted after close scrutiny of the business idea and business

plans, usually in cooperation with EVA.

Basel II

The Basel Committee on Banking Supervision is apanel of bank supervisory authorities which was established by the central bank governors of theGroup of Ten (G-10) countries in 1975. It consists ofthe heads of bank supervisory authorities and thecentral bank governors of Belgium, Canada, France,Germany, Italy, Japan, Luxembourg, the Netherlands,Spain, Sweden, Switzerland, the United Kingdom,and the United States of America. The committeeusually convenes at the Bank for International Settle-ments in Basel where its secretariat is seated.

The goal of reviewing the Capital Accord of 1982 is to have a framework at one’s disposal for furtherstrengthening solidity and stability of the interna-tional banking system. The concept is based on threepillars: minimum capital requirements, supervision,and market discipline. The result is a new capital ad-equacy framework which replaces the first capitalframework of ten years ago – hence the nameBasel II. The new accord sets out rules and standardsfor the capital requirements of banking organisa-tions.

In the past years, the public repeatedly expressedfears of negative implications by Basel II, particularlyfor small and medium enterprises.

Thanks to our well-established credit policy BLKB hasa sound and balanced credit portfolio. As we men-tioned in earlier publications, we do not expect anymajor consequences. Our SME customers need notanticipate any negative effects. Occasionally, thereare rumours of excessive rate increases or a creditstop in context with Basel II, a notion we consider ab-solutely uncalled-for and devoid of any substance.

www.global-reports.com

23

Private banking – a transparent conceptfor integrated financial advice

BLKB’s business of investment advice took a very satisfactory

turn in 2004. Compared to the previous year, securities income

of the parent company increased by 6.6 m Swiss francs to 45.5 m

Swiss francs. The target budget was more than reached. Together

with the securities income of our subsidiary Atag Asset Manage-

ment (AAM) of 42.5 m Swiss francs, this amounts to an income

at group level of 88.0 m Swiss francs from the securities and in-

vestment business – 7.4 m Swiss francs more than in the previ-

ous year.

BLKB successfully acquired new asset management mandates,

too. At 150 m Swiss francs net new money and stock in hand of

1 982 m Swiss francs as per December 31st 2004 target in this area

was exceeded by far.

A rising number of customers benefits from our services in tax

advice, financial and retirement planning. This development is

perfectly in line with our strategy of offering solutions instead of

products.

Concept of individually tailored advice

and support

“BLKB Private Banking” is the trademark of our advisory con-

cept which aims at giving comprehensive, sustainable invest-

ment advice based on life goals and personal situation of each

customer. It is designed to meet the needs of individuals having

assets of upwards of 250 000 Swiss francs at their disposal. Thus,

high-net-worth private persons will profit from a level of services

not easily found in this order of assets.

Professional advice and support designed to accompany an in-

dividual customer’s life starts with a careful analysis of the needs

and goals. This first step includes investment advice and asset

management, but also other aspects which may carry signifi-

cance depending on the individual customer’s circumstances.

They include financial planning and taxes, frequently an analy-

sis of pension plans and sometimes early planning of estate ad-

ministration. Younger persons more often need financing of res-

idential property. By linking all these questions of financing we

can create a clearer picture of current and future needs and build

the basis for further action.

In investment advice and asset management as the core compe-

tencies of private banking we offer our customers a detailed and

systematic investor profile and from there work out an invest-

ment strategy. It does not matter whether the customer decides

to manage the portfolio him-/herself or to have it managed by

the bank, the preliminary in-depth process creates the basis for

all the future decisions.

If our customers decide to leave care and management to us,

they can be absolutely sure that it is done at the highest degree

of professional integrity and that their portfolio is monitored by

specialists. Even if they decide to take management into their

own hands, they are not left alone, they are integrated into our

systematic process of advice.

The advisory services “BLKB Private Banking” established for its

customers are periodically supplemented or updated when need

Investment world with Swisscanto

As of January 1st 2005, Swisscanto is the trademarkwhich unites Swissca, Prevista, and Servisa, the threejoint companies of cantonal banks under one um-brella. The cantonal banks support the position ofSwisscanto as a leading supplier of investment andpension services.

Swisscanto is the third-largest seller of funds inSwitzerland. Thus, with Swisscanto funds our cus-tomers have the whole investment world at their disposal.

Value-oriented management Interest-related business: loans

Private banking

24

arises and they offer follow-ups for and keep track of other

needs. Unlike taxes, which is always a topic, financing of resi-

dential property may one day be a subject of interest. Financial

and retirement planning will certainly come up, as will planning

of estate administration. So, we offer a wide range of products

and services designed to meet all these potential needs. The

BLKB tax mandate, for example, relieves the customer of an an-

noying concern, financial and retirement planning ease worries

about the future, comprehensive support in matters of estate ad-

ministration lessens the pressure of a disturbing aspect of life.

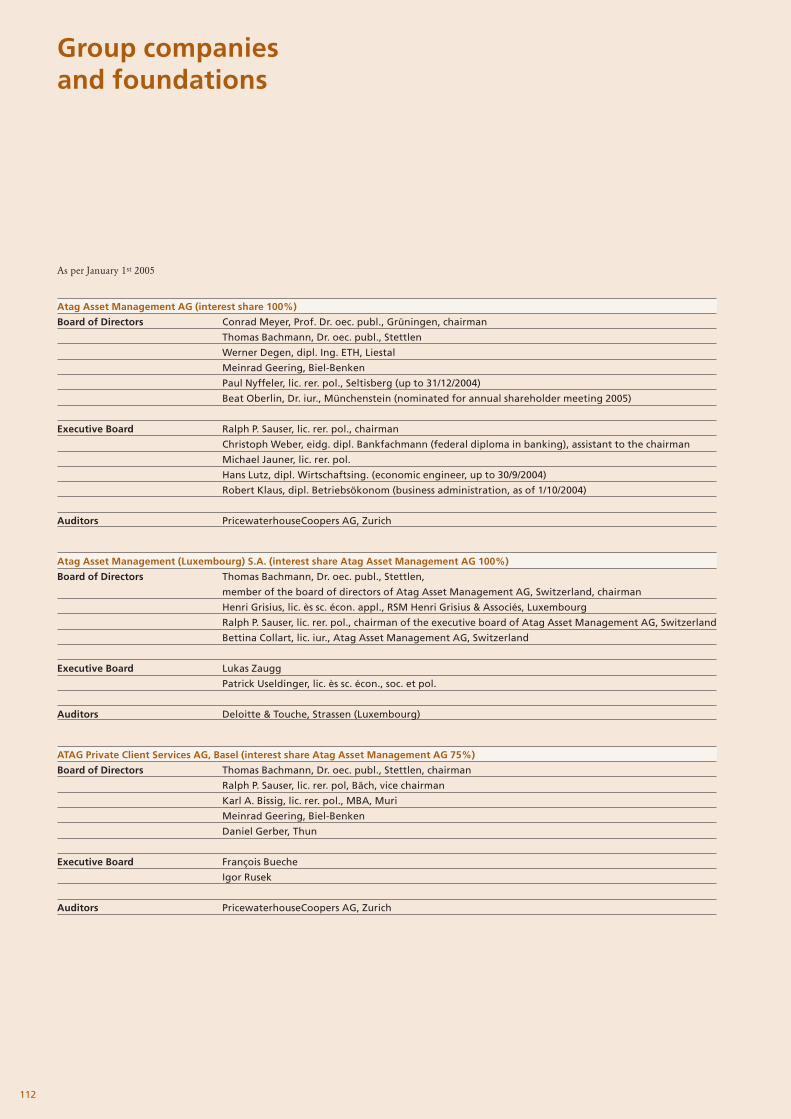

BLKB Private Banking and

Atag Asset Management

Atag Asset Management AG has been active in asset manage-

ment since 1917 and became part of Basellandschaftliche Kan-

tonalbank in 2000. Atag Asset Management AG includes the fol-

lowing subsidiaries: Atag Asset Management (Luxembourg)

S.A., Gräff Capital Management AG, Zurich, and Atag Private

Client Services AG, Basle. AAM employs 180 staff at eight lo-

cations in Switzerland and abroad.

Core competencies of AAM are in asset management and inte-

grated finance and investment advice for private customers and

institutional investors. BLKB Private Banking and AAM coop-

erate very closely in working out principles of asset management

or in dealing with the manifold aspects of financial planning. In

their function as specialised centres they exchange knowledge

and experience.

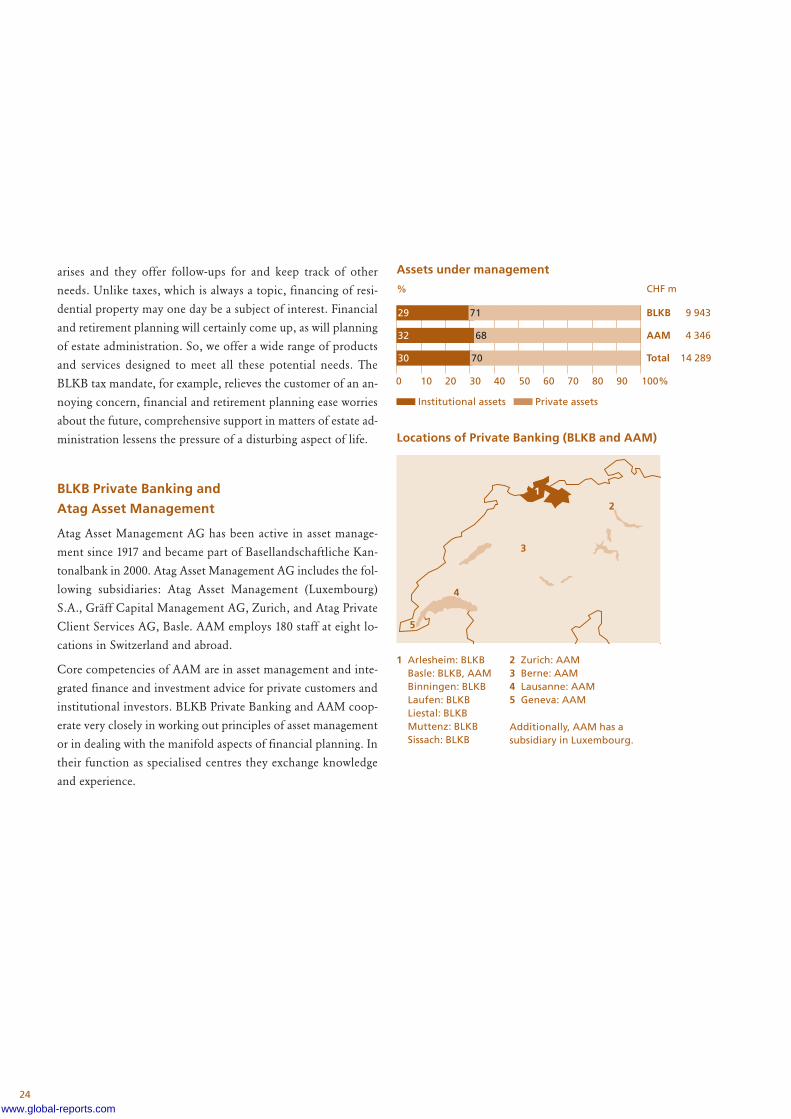

0 10 20 30 40 50 60 70 80 90 100%

Assets under management

%

Institutional assets Private assets

29

32

30 70

CHF m

BLKB 9 943

AAM 4 346

Total 14 289

71

68

Locations of Private Banking (BLKB and AAM)

1

3

5

4

2

1 Arlesheim: BLKBBasle: BLKB, AAMBinningen: BLKBLaufen: BLKBLiestal: BLKBMuttenz: BLKBSissach: BLKB

2 Zurich: AAM3 Berne: AAM4 Lausanne: AAM5 Geneva: AAM

Additionally, AAM has asubsidiary in Luxembourg.

www.global-reports.com

25

Individually tailored products

for private customers

Modern wealth management requires diverse and complex cap-

abilities. Adaptations have to be made as the customers’ needs

evolve. In a rapidly changing environment of the stock market,

solutions have to be found which meet the requirements. It is

not sufficient anymore to rely on standard strategies. AAM

therefore offers a wide range of products from standard to

highly elaborate and well-structured ones, including Family

Office (Atag PCS).

Both AAM and BLKB offer an extensive range of advisory ser-

vices in the area of financial planning which customers may

make use of according to their current needs and circumstances.

Competent partners for institutional customers

Customers from institutions ask for investment strategies which

reach a higher performance in relation to the market but fulfil all

the legal and regulatory requirements. A high degree of disci-

pline and specialised knowledge on the bank’s part is absolute-

ly imperative. BLKB and AAM achieve this goal on the basis of

a decision-taking process developed for this particular purpose.

Our goal: top of the class

Basellandschaftliche Kantonalbank and its subsidiary AAM have

built specialised centres for private and institutional customers

in the northwest of Switzerland and the entire Swiss market. Our

goal is to be “top of the class” with our products. BLKB and

AAM have their respective ways of presenting themselves in the

market, but it is only in the combination of both, cantonal bank

and independent asset management company, that we can offer

the variety of solutions and strategies our customers can choose

from.

Value-oriented management Private banking

Total return: Income and investor protection

The novel scheme, favourably accepted by the mar-ket, ist the answer to the growing insecurity in thecapital markets: unlike the classical investment con-cept the new scheme consists of two separate cate-gories of assets, “growth” and “substance”. For thetwo categories we use both traditional investmenttools and alternative investments.

26

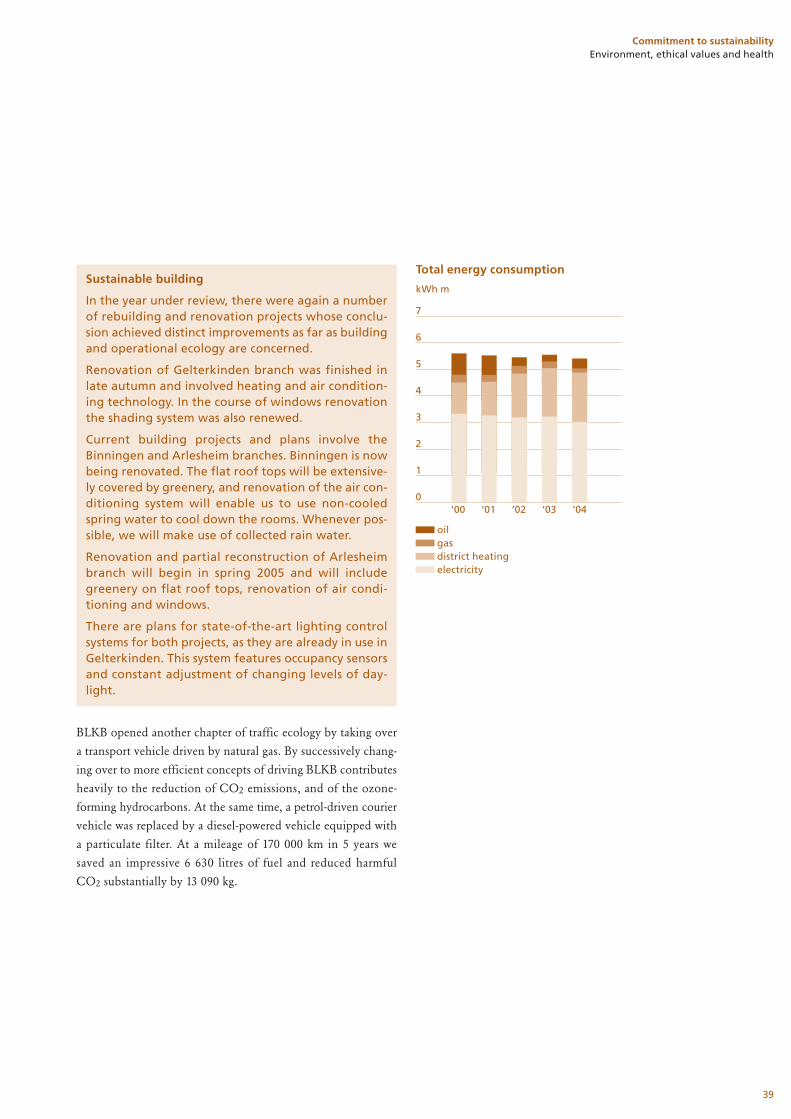

Sustainability – thinking in terms of generations

the “Greenline” environmentalseal of approval. Productionprocesses are based on energy-saving and emission-reducingprinciples. Their buildings areequipped with solar cells which

produce about 60% of theenergy needed for electricityand heating; a feature ownerand staff are extremely proudof. This is exactly where sustain-ability begins, in small matters

It’s a moral obligation to con-form your actions to sustain-ability. This is the view adoptedby Aerni Fenster (window man-ufacturer) in Arisdorf. Theirproducts have been awarded

as well as in larger ones. It’simportant to think in holisticdimensions, to take on respon-sibilities, to conform ouractions to sustainability. Timesare changing and we have to

www.global-reports.com

27

Sustainability, nowadays, is a catchword and definitions abound.For us it means following an environmentally friendly and sustain-able business practice such as investing in ecologically sounderoperational facilities, energy-saving buildings, or storage systemsfor rainwater. It also means social commitment as an employer,investment products strictly in accordance with the principle ofsustainability, and adherence to ethical values laid down in ourcorporate guidelines. We consider it very important, though, thatthe public, too, perceives these aspects as being part of our corporate culture. Sustainability means thinking in dimensionsthat reach beyond our generation.

make sure our grandchildreninherit a world worth living in.

28www.global-reports.com

29

growth and the correct care.Rebmann, whose name impliesthat he is a man of vines,studied viniculture. The grape-vines are passed within thefamily from one generation to

Easy come – easy go: this is usuallysaid of quick money. We recom-mend a more cautious approach:the experience of very young customers with their first pocket-money account should lay the foun-dation for a sustainable customer-bank relationship. Not just out ofhabit, but as a process of healthygrowth which accommodateschanging needs, desires, perspec-tives and possibilities. We are readyfor it.

the next, and the pleasure ofmaking wine and the love ofgood wine is something hisadoptive father Urs Rebmannstarted to encourage early on.When Mona, a Bengali boy,

Things that shall grow need tobe cultivated. As a wine-growerMona Rebmann from Prattelnknows that it takes time to do athing well. However, it alsotakes optimum conditions for

30

BLKB survey 2004 of“Baselbiet” companies

was four years old, he became amember of the Rebmann familyand the relationship betweenadoptive son and father hasalways been held dear andcarefully nurtured. There is no

question, of course, that inMona Rebmann’s winery a newwine, before going to the shopfor sale, is tasted and appreci-ated by father and son.

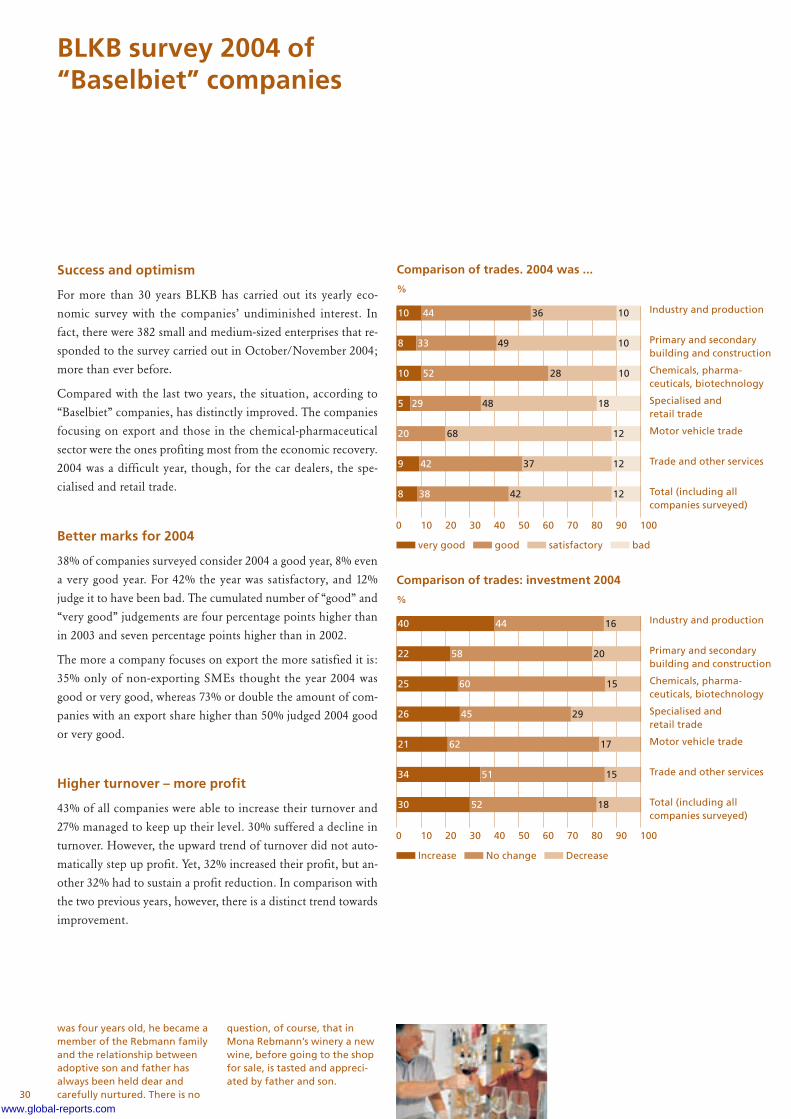

Success and optimism

For more than 30 years BLKB has carried out its yearly eco-

nomic survey with the companies’ undiminished interest. In

fact, there were 382 small and medium-sized enterprises that re-

sponded to the survey carried out in October/November 2004;

more than ever before.

Compared with the last two years, the situation, according to

“Baselbiet” companies, has distinctly improved. The companies

focusing on export and those in the chemical-pharmaceutical

sector were the ones profiting most from the economic recovery.

2004 was a difficult year, though, for the car dealers, the spe-

cialised and retail trade.

Better marks for 2004

38% of companies surveyed consider 2004 a good year, 8% even

a very good year. For 42% the year was satisfactory, and 12%

judge it to have been bad. The cumulated number of “good” and

“very good” judgements are four percentage points higher than

in 2003 and seven percentage points higher than in 2002.

The more a company focuses on export the more satisfied it is:

35% only of non-exporting SMEs thought the year 2004 was

good or very good, whereas 73% or double the amount of com-

panies with an export share higher than 50% judged 2004 good

or very good.

Higher turnover – more profit

43% of all companies were able to increase their turnover and

27% managed to keep up their level. 30% suffered a decline in

turnover. However, the upward trend of turnover did not auto-

matically step up profit. Yet, 32% increased their profit, but an-

other 32% had to sustain a profit reduction. In comparison with

the two previous years, however, there is a distinct trend towards

improvement.

Comparison of trades. 2004 was ...

%

very good good satisfactory bad

10 44 36 10

8 33 49 10

10 52 28 10

5 29 48 18

20 68 12

9 42 37 12

8 38 42 12

Industry and production

Primary and secondarybuilding and construction

Chemicals, pharma-ceuticals, biotechnology

Specialised and retail trade

Motor vehicle trade

Trade and other services

Total (including allcompanies surveyed)

Comparison of trades: investment 2004

%

Increase No change Decrease

40 44 16

22 58 20

25 60 15

26

21

45 29

62 17

34 51 15

30 52 18

Industry and production

Primary and secondarybuilding and construction

Chemicals, pharma-ceuticals, biotechnology

Specialised and retail trade

Motor vehicle trade

Trade and other services

Total (including allcompanies surveyed)

0 10 20 30 40 50 60 70 80 90 100

0 10 20 30 40 50 60 70 80 90 100

www.global-reports.com

31

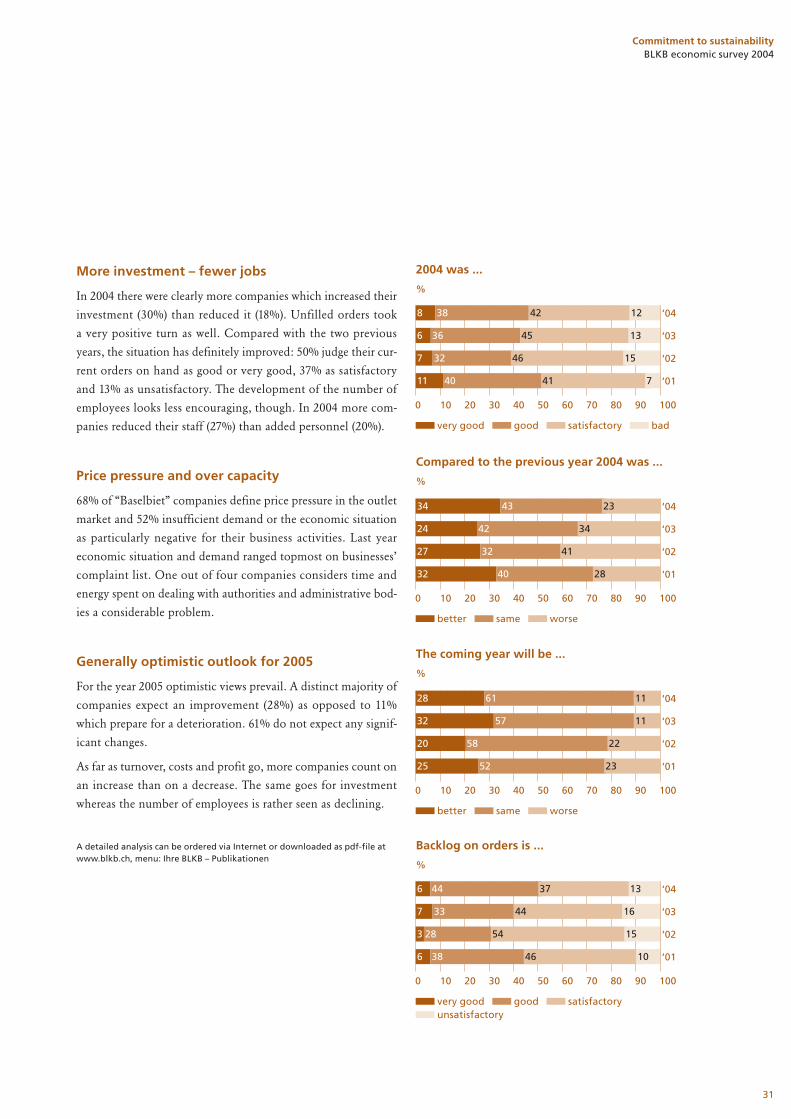

More investment – fewer jobs

In 2004 there were clearly more companies which increased their

investment (30%) than reduced it (18%). Unfilled orders took

a very positive turn as well. Compared with the two previous

years, the situation has definitely improved: 50% judge their cur-

rent orders on hand as good or very good, 37% as satisfactory

and 13% as unsatisfactory. The development of the number of

employees looks less encouraging, though. In 2004 more com-

panies reduced their staff (27%) than added personnel (20%).

Price pressure and over capacity

68% of “Baselbiet” companies define price pressure in the outlet

market and 52% insufficient demand or the economic situation

as particularly negative for their business activities. Last year

economic situation and demand ranged topmost on businesses’

complaint list. One out of four companies considers time and

energy spent on dealing with authorities and administrative bod-

ies a considerable problem.

Generally optimistic outlook for 2005

For the year 2005 optimistic views prevail. A distinct majority of

companies expect an improvement (28%) as opposed to 11%

which prepare for a deterioration. 61% do not expect any signif-

icant changes.

As far as turnover, costs and profit go, more companies count on

an increase than on a decrease. The same goes for investment

whereas the number of employees is rather seen as declining.

A detailed analysis can be ordered via Internet or downloaded as pdf-file atwww.blkb.ch, menu: Ihre BLKB – Publikationen

Commitment to sustainabilityBLKB economic survey 2004

0 10 20 30 40 50 60 70 80 90 100

2004 was ...

%

very good good satisfactory bad

8 38 42

6 36 45

7 32 46 15

11 40 41 7

‘04

‘03

‘02

‘01

12

13

0 10 20 30 40 50 60 70 80 90 100

Compared to the previous year 2004 was ...

%

better same worse

34 43

24 42

27 32

32 40

‘04

‘03

‘02

‘01

23

34

41

28

0 10 20 30 40 50 60 70 80 90 100

The coming year will be ...

%

better same worse

28 61

32 57

20 58

25 52

‘04

‘03

‘02

‘01

11

11

22

23

0 10 20 30 40 50 60 70 80 90 100

Backlog on orders is ...

%

very good good satisfactory unsatisfactory

6 44 37

7 33 44

3 28 54 15

6 38 46 10

‘04

‘03

‘02

‘01

13

16

32

Recognising customer needs – ambition and obligation

BLKB has always been deeply rooted in the canton and the

minds of the population. The tightly woven network of sales and

distribution in combination with a very stable course of affairs

has cemented the trust placed in BLKB.

Thus, the Canton of Basel-Landschaft, holder of the majority

stake, emphasises this trust by observing a law that gives prior-

ity to the building of reserves and a moderate profit distribution.

The amended Cantonal Law on Kantonalbank, in force since

January 1st 2005, still contains the rule that the same amount of

money the bank pays to the canton in dividends has to go to the

bank’s reserves. At first sight this rule may seem insignificant,

but it goes to prove that the canton supports the bank’s endeav-

our for a financially strong and independent growth.

This opinion seems to be shared by the canton’s population and

our customers who give us constant proof of their loyalty.

We are very happy about this, however, there is no reason to

relax. From our daily work we are well aware of the fact that

customer loyalty does not spring up like that. It is something

that has to be nourished and well tended by offering quality of

service, first-class products and skills, and a fair price; things that

actually go without saying in a partnership.

Assist customers and keep the future in sight

Everybody knows that the needs of customers change repeatedly

in the course of their lives. The individual agenda of values may

change at different points of life such as the beginning of a ca-

reer, the start of a family, home-building, setting up of a business

of one’s own, or the vicissitudes of getting older. We would like

to accompany our customers through the different stages of life,

help them to sharpen their senses for actual or potential devel-

opments and discuss options in time so they can take the right

decisions.

www.blkb.ch – your own private entrance to the bank

1.6 million guests! That’s the amazing number of per-sons who accessed our web site www.blkb.ch in 2004.1.6 million guests translate into 135 000 guests amonth or 4 500 a day, 20% more than in the previousyear. The pages which roused the most interest weremarketing and stock exchange, real estate and onlinebanking.

“Stock Exchange and Markets” gives access to analy-ses, commentaries and reports, rate lists, model port-folios, custom-made portfolios, to peak price or low-est rate, to charts and statistics: anything a stockmarket enthusiast might wish for.

The real estate pages offer more than 12 000 flatsand houses either for rent or for sale. In our closervicinity there are about 1 900 objects for sale androughly 900 for rent. The real estate page offers a direct link to financing. There is a growing number ofcustomers who conclude a contract in this way.

An up-and-coming feature is BLKB Internet-banking.More than 30 000 customers are managing their ac-counts and securities portfolios themselves and havedone more than three million payment transactionsby means of e-banking. October was a peak month,when electronic payments amounted to 50% of totalpayment transactions.

Both, the strong upward trend of Kantonalbank cer-tificates and the Triple-A-rating of Basellandschaft-liche Kantonalbank, have contributed to the fact thatthe public is increasingly interested in information forinvestors. The section “Ihre Bank” provides a wealthof background information: the annual report in Ger-man and English, the sustainability report, detailedinformation on the price movement of Kantonalbankcertificates, and charts showing daily and yearly de-velopments.

www.global-reports.com

33

Commitment to sustainabilityCustomer needs

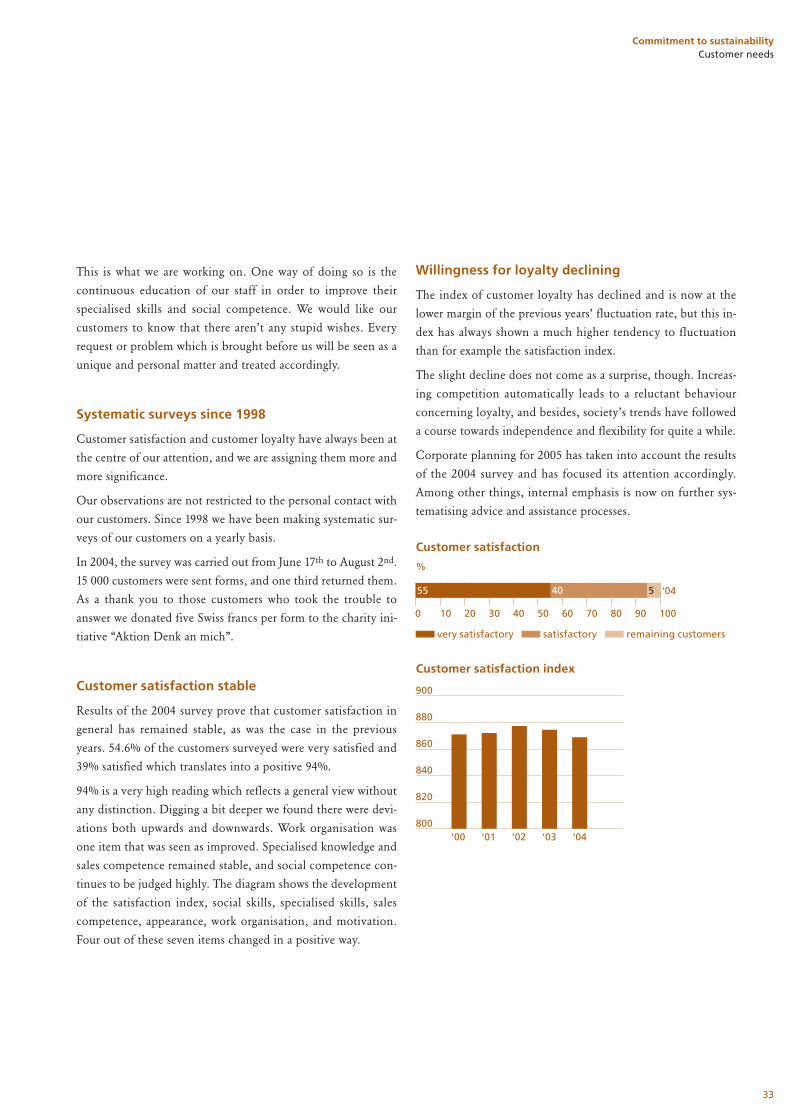

0 10 20 30 40 50 60 70 80 90 100

Customer satisfaction

%

very satisfactory satisfactory remaining customers

55 40 5 ‘04

This is what we are working on. One way of doing so is the

continuous education of our staff in order to improve their

specialised skills and social competence. We would like our

customers to know that there aren’t any stupid wishes. Every

request or problem which is brought before us will be seen as a

unique and personal matter and treated accordingly.

Systematic surveys since 1998

Customer satisfaction and customer loyalty have always been at

the centre of our attention, and we are assigning them more and

more significance.

Our observations are not restricted to the personal contact with

our customers. Since 1998 we have been making systematic sur-

veys of our customers on a yearly basis.

In 2004, the survey was carried out from June 17th to August 2nd.

15 000 customers were sent forms, and one third returned them.

As a thank you to those customers who took the trouble to

answer we donated five Swiss francs per form to the charity ini-

tiative “Aktion Denk an mich”.

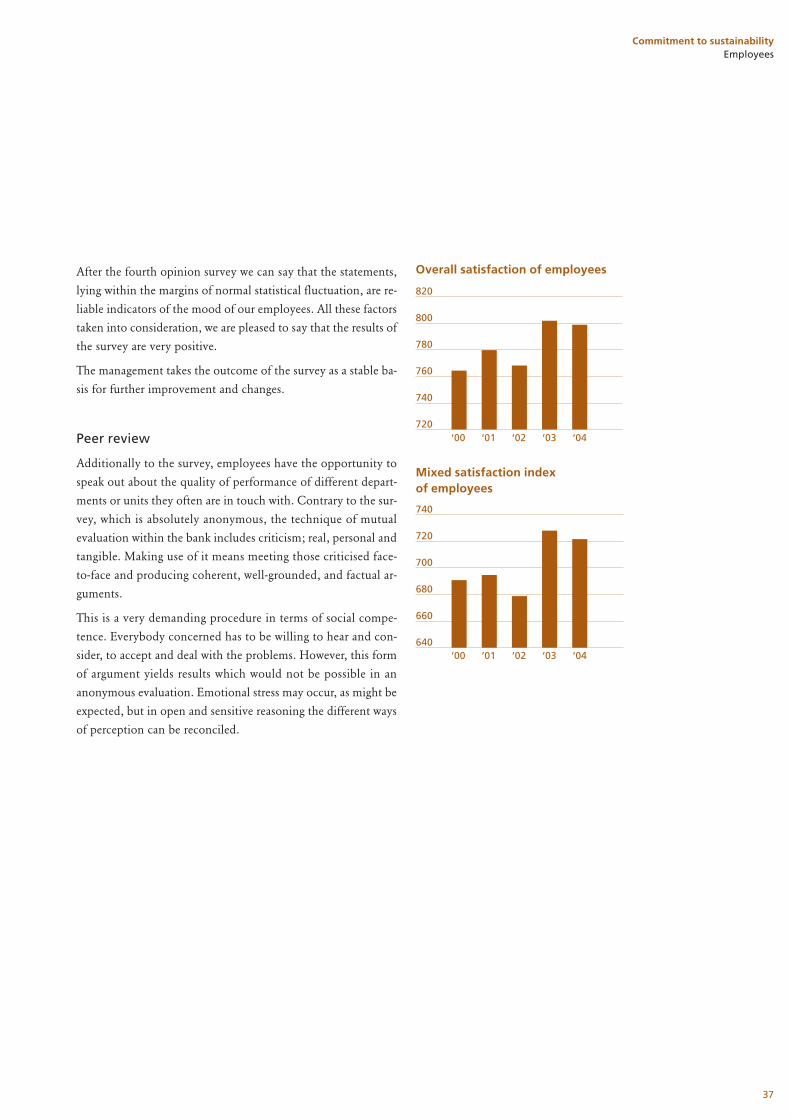

Customer satisfaction stable

Results of the 2004 survey prove that customer satisfaction in

general has remained stable, as was the case in the previous

years. 54.6% of the customers surveyed were very satisfied and

39% satisfied which translates into a positive 94%.

94% is a very high reading which reflects a general view without

any distinction. Digging a bit deeper we found there were devi-

ations both upwards and downwards. Work organisation was

one item that was seen as improved. Specialised knowledge and

sales competence remained stable, and social competence con-

tinues to be judged highly. The diagram shows the development

of the satisfaction index, social skills, specialised skills, sales

competence, appearance, work organisation, and motivation.

Four out of these seven items changed in a positive way.

Willingness for loyalty declining

The index of customer loyalty has declined and is now at the

lower margin of the previous years’ fluctuation rate, but this in-

dex has always shown a much higher tendency to fluctuation

than for example the satisfaction index.

The slight decline does not come as a surprise, though. Increas-

ing competition automatically leads to a reluctant behaviour

concerning loyalty, and besides, society’s trends have followed

a course towards independence and flexibility for quite a while.

Corporate planning for 2005 has taken into account the results

of the 2004 survey and has focused its attention accordingly.

Among other things, internal emphasis is now on further sys-

tematising advice and assistance processes.

‘00 ‘01 ‘02 ‘03 ‘04

Customer satisfaction index

900

880

860

840

820

800

34

Attractive employer for a talented and motivated staff

the training of the middle management. Basic management

training is still done together with other cantonal banks. In the

past year we started to supplement the training with so-called

“reflexion days” for junior managers so that they may give

enough thought to BLKB management guidelines and to how

they secure their personal management comprehension within

these guidelines.

There were 23 employees who finished further education on a

federal level. Apart from courses in banking and financial plan-

ning, BLKB also supported more general commercial courses

whose completion give access to a university of applied sciences

or to other higher education in economy.

Nineteen employees completed specialised banking courses

offered by the Association of Swiss Cantonal Banks.

A career in banking

After completion of the requisite education youthshave several options for an organised education incommercial professions. The classical way of becom-ing a commercial employee is to use an apprentice-ship system which in turn offers three different pro-files. However, besides the conventional system thereis another concept requiring more than standardqualifications for entry and involving higher-level sec-ondary schools with an emphasis on commerce. Mit-telschulstufe, Handelsmittelschule, and Wirtschafts-gymnasium (up to A levels) meet these criteria, andstudents having finished these schools may undergoan accelerated educational programme of 18 monthsinvolving bank- and finance-specific on-the-job train-ing. The law (Art. 41 law on professional educationand training) provides for the case of a late or an ad-ditional apprenticeship which may be accelerated aswell. In our bank this has rarely been the case.

After the successful health days of 2003, we continued our

efforts for the health and well-being of our employees. Offers

of afternoon or evening classes to further physical or mental

well-being were readily accepted by the staff. The campaign for a

smoke-free bank has contributed to the fact that a number of

employees stopped smoking. For further details see p. 38 of this

annual report.

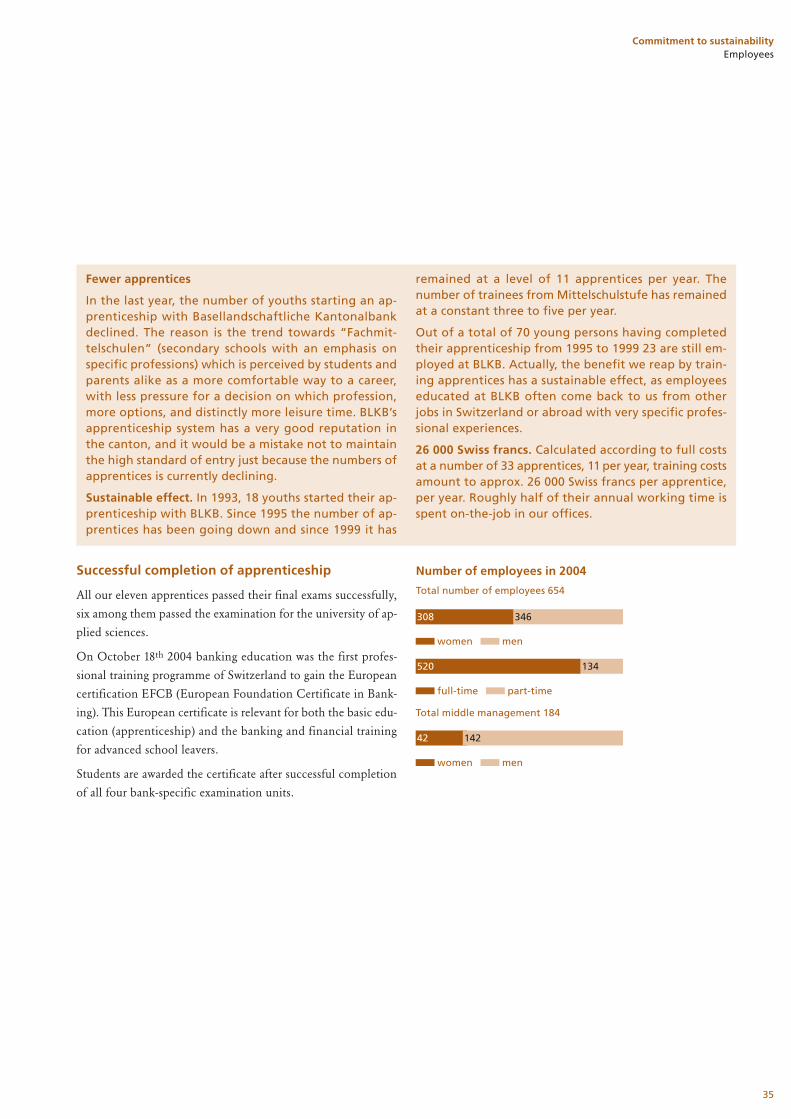

More part-time jobs

At the end of 2004 Basellandschaftliche Kantonalbank employed

654 persons (previous year 664), 308 (312) women and 346 (352)

men. This figure includes 134 (126) part-time jobs, 31 (34) ap-

prentices and 9 (8) trainees equalling 591 (603) full-time jobs.

Low fluctuation

Fluctuation rate (including retirement and pregnancies) in-

creased slightly to 7.5% (7.3%). The adjusted fluctuation rate

(registers resignations by employees, does not include maternity

resignations or retirement) was 3.9% (4.7%). All told, there were

49 (47) entries opposed to 59 (44) exits.

Further education more often from resources

of our own

Expenses for the development of our staff in the reporting year

amounted to approx. 1 m Swiss francs. BLKB tried to concen-

trate more on the internal resources at hand and the internal

standards of value.

About 65 employees devoted time and effort to teaching their

colleagues in various banking matters. Apart from specialised

classes and sales training we also used our own employees for

www.global-reports.com

35

Commitment to sustainabilityEmployees

Number of employees in 2004

Total number of employees 654

women men

346308