An International Analysis of Dividend Payment Behavior

27

Journal of Business Finance & Accounting, 36(3) & (4), 496–522, April/May 2009, 0306-686X doi: 10.1111/j.1468-5957.2009.02126.x An International Analysis of Dividend Payment Behavior Stephen P. Ferris, Nilanjan Sen and Emre Unlu ∗ Abstract: This study investigates patterns in dividend payment across nine common law and sixteen civil law countries over 1994-2007. We begin by examining whether the recent decline in the number of dividend payers is solely a US phenomenon or part of a more global trend. We find that at the beginning of our sample period, 72% of our sample firms pay dividends, but by 2007, this percentage decreases to 55%, with the decline more acute in common law countries. Our analysis further shows that the growing incidence of non-dividend paying firms can be explained by an increase in the percentage of firms that have never paid dividends. We find that common law firms are less likely to initiate new dividend programs than those in civil law nations, although they tend to have more abundant growth opportunities. We further establish that this global decline in the propensity to pay dividends is more pronounced in firms incorporated in common law jurisdictions. Finally, we find that both the percentage increase in aggregate dividends and the dividend payout ratio is higher in civil law countries. Keywords: international dividends, common law, propensity to pay 1. INTRODUCTION Fama and French (2001 and 2004) find that the number of US firms paying cash dividends has declined significantly over the last twenty-five years. They contend that two effects account for this result. The first is a changing composition effect which asserts that the nature of exchange new lists has tilted towards firms with lower profitability and stronger growth opportunities. They note that these are precisely the characteristics that cause firms to avoid paying dividends. But Fama and French further report that even after controlling for these characteristics, firms continue to pay dividends at a lower frequency than expected. They refer to this second effect as a declining propensity to pay. ∗ The first author is from the Department of Finance, University of Missouri, USA. The second author is from the Department of Finance, Nanyang Technological University, Singapore. The third author is from the Department of Finance, University of Nebraska-Lincoln, USA. They would like to thank Martin Walker (editor), for his many helpful suggestions on prior versions of this paper as well as the comments of the discussant, Graham Partington, and delegates at the JBFA Capital Markets Conference, University of Lancaster, May 2008. (Paper received October 2006, revised version accepted January 2009) Address for correspondence: Stephen P. Ferris, Department of Finance, 404 Cornell Hall, University of Missouri, Columbia, MO 65211-2600, USA. e-mail: [email protected] C 2009 The Authors Journal compilation C 2009 Blackwell Publishing Ltd, 9600 Garsington Road, Oxford OX4 2DQ, UK and 350 Main Street, Malden, MA 02148, USA. 496

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of An International Analysis of Dividend Payment Behavior

Journal of Business Finance & Accounting, 36(3) & (4), 496–522, April/May 2009, 0306-686Xdoi: 10.1111/j.1468-5957.2009.02126.x

An International Analysis of DividendPayment Behavior

Stephen P. Ferris, Nilanjan Sen and Emre Unlu∗

Abstract: This study investigates patterns in dividend payment across nine common law andsixteen civil law countries over 1994-2007. We begin by examining whether the recent declinein the number of dividend payers is solely a US phenomenon or part of a more global trend.We find that at the beginning of our sample period, 72% of our sample firms pay dividends,but by 2007, this percentage decreases to 55%, with the decline more acute in common lawcountries. Our analysis further shows that the growing incidence of non-dividend paying firmscan be explained by an increase in the percentage of firms that have never paid dividends.We find that common law firms are less likely to initiate new dividend programs than those incivil law nations, although they tend to have more abundant growth opportunities. We furtherestablish that this global decline in the propensity to pay dividends is more pronounced in firmsincorporated in common law jurisdictions. Finally, we find that both the percentage increase inaggregate dividends and the dividend payout ratio is higher in civil law countries.

Keywords: international dividends, common law, propensity to pay

1. INTRODUCTION

Fama and French (2001 and 2004) find that the number of US firms paying cashdividends has declined significantly over the last twenty-five years. They contend that twoeffects account for this result. The first is a changing composition effect which assertsthat the nature of exchange new lists has tilted towards firms with lower profitability andstronger growth opportunities. They note that these are precisely the characteristics thatcause firms to avoid paying dividends. But Fama and French further report that evenafter controlling for these characteristics, firms continue to pay dividends at a lowerfrequency than expected. They refer to this second effect as a declining propensity topay.

∗The first author is from the Department of Finance, University of Missouri, USA. The second authoris from the Department of Finance, Nanyang Technological University, Singapore. The third author isfrom the Department of Finance, University of Nebraska-Lincoln, USA. They would like to thank MartinWalker (editor), for his many helpful suggestions on prior versions of this paper as well as the commentsof the discussant, Graham Partington, and delegates at the JBFA Capital Markets Conference, University ofLancaster, May 2008. (Paper received October 2006, revised version accepted January 2009)

Address for correspondence: Stephen P. Ferris, Department of Finance, 404 Cornell Hall, University ofMissouri, Columbia, MO 65211-2600, USA.e-mail: [email protected]

C© 2009 The AuthorsJournal compilation C© 2009 Blackwell Publishing Ltd, 9600 Garsington Road, Oxford OX4 2DQ, UKand 350 Main Street, Malden, MA 02148, USA. 496

ANALYSIS OF DIVIDEND PAYMENT BEHAVIOR 497

Yet, we do not know whether this decline in the number of exchange-listed firmspaying dividends and the corresponding decline in the propensity to pay is merelya US phenomenon or is part of a more general trend in the global equity markets.Few studies examine the nature of international dividend policy and those that doare typically limited in their coverage. Aivazian, Booth and Cleary (2003) focus on asample of eight developing countries and conclude that both profitability and countryeffects are relevant in explaining national dividend policies. Ferris, Sen and Yui (2006a)examine the pattern of dividend payments in the UK and report a similar, but lesspronounced trend of declining dividends than that observed for the US.

A recent set of studies explores the issue of dividend policy across a sample ofdeveloped and developing countries. Denis and Osobov (2008) study six developedcountries, including the US, and find international evidence consistent with Fama andFrench (2001) of a declining propensity to pay dividends. Eije and Megginson (2008)examine the evolution of dividend policy from 1989 to 2003 in fifteen countries of theEuropean Union (EU) and find neither systematic dividend catering nor evidence ofa European convergence in dividend policies.

This study makes a number of important contributions relative to this existingresearch. First, this study is more comprehensive regarding the number of samplecountries than either study. We examine twenty-five countries compared with the sixexamined by Denis and Osobov (2008) and the fifteen analyzed by Eije and Megginson(2008). Because of our larger sample, we are able to test more rigorously for differencesin dividend policy across legal regimes and to more authoritatively ascertain thenature of international dividend policy. Eije and Megginson, for instance, include onlyone common law country in their analysis while Denis and Osobov limit themselvesto three. This study utilizes nine common law countries, including both developedand developing economies. Further, our sample is geographically diverse, includingAustralia and a number of Asian countries compared with the European focus of Eijeand Megginson and the limited inclusion of Asian and European markets by Denis andOsobov.

Beyond issues of sample breadth, this study provides other contributions to theliterature. Unlike Denis and Osobov (2008) and Eije and Megginson (2008), ourstudy examines the dividend behavior of a variety of firm types that allow us to betterunderstand how dividend policies differ globally. More specifically, we examine thenature of dividend payouts for firms that never paid dividends, that were former payers,and that are new lists. We also compare the rates of dividend initiation and continuationfor our sample firms. Additionally, our sample period is more recent than those of Denisand Osobov (2008) or Eije and Megginson (2008). Our sample period extends from1994 through 2007 compared to the 1989 to 2003 analysis of Eije and Megginson andthe nine year period, 1994 to 2002, used by Denis and Osobov. Our study also employsa richer model to estimate the propensity to pay dividends that includes size, risk andlife cycle effects that are excluded in these previous studies. This allows us to moreprecisely control for other factors in estimating the propensity to pay dividends.

LaPorta, Lopez de Silanes, Shleifer and Vishny (2000) develop two competingtheories regarding how international dividend policy might be influenced by the legalprotections provided to minority shareholders. Their outcome theory of dividendscontends that the protections enjoyed by shareholders in a common law jurisdictionallows minority shareholders to extract more dividends from controlling shareholdersthan in civil law nations where such protections are weaker. Alternatively, their substitute

C© 2009 The AuthorsJournal compilation C© Blackwell Publishing Ltd. 2009

498 FERRIS, SEN AND UNLU

theory of dividends argues that dividends substitute for the legal protection of minorityshareholders. Hence, dividends are more likely to be paid in countries where fewerlegal protections are available to external investors. These theories suggest that we willobserve important distinctions in dividend practices between common and civil lawcountries.

DeAngelo, DeAngelo and Skinner (2004) report that in spite of a declining numberof dividend payers in the US, the level of aggregate dividends is increasing. This studytests to see if a similar phenomenon occurs internationally. Although Denis and Osobov(2008) find an increase in aggregate dividend levels for their sample of six developedcountries, it is unclear whether such a result holds for a more diverse set of countries,especially those with less developed capital markets. Further, unlike this study, Denisand Osobov do not test to determine what effect the legal protection of investors mightexert on dividend payouts.

Our initial empirical analysis provides us with a number of interesting results. Wefind that the number of firms paying dividends declines over our sample period and ismost pronounced for firms incorporated in common law countries. We find that at thebeginning of our sample period, the median number of firms paying dividends in agiven country is 81%. But by 2007, only 45% of the firms do so. This decline occurs moredramatically in common law countries, where the median percentage reduction in thenumber of dividend paying firms is 42% compared to only 23% for firms incorporatedin civil law nations. Our analysis further shows that the growing percentage of non-dividend paying firms can be explained by an increase in the percentage of firms thathave never paid dividends. We find that this effect is significantly greater in commonthan civil law countries. Finally, we observe that changes in the average size of dividendsdiffers between the common and civil law regimes. Firms in civil law countries areincreasing the size of their mean dividend while those in common law countries aredeclining.

We also find that firms which pay dividends tend to continue paying dividends. Thispattern does not appear to be sensitive to the legal environment in which the firm isincorporated. The popularity of initiating dividends does, however, appear to differacross regimes. There seems to be less willingness to initiate a program of dividendpayments in common law countries. Firms in civil law nations are more willing toinitiate new dividend programs.

To better understand the cross-sectional variation in dividend payment patternsboth within and between legal regimes, we compare five important determinants ofdividends. We find that common and civil law countries appear to be equally profitableand have comparable asset growth rates. Investment opportunities as measured by themarket-to-book ratio, however, appear to be higher within common law countries. Butthe difference in market-to-book ratios is significant only at the ten percent level forthe mean values. We further determine that firms in civil law countries are larger thantheir common law counterparts, perhaps attributable to their greater need for internalcapital markets to obtain necessary financing. We find no significant differences in therisk and percentage of retained earnings between common and civil law firms.

Our examination of the propensity to pay dividends shows that there is a declinein the willingness of firms to pay dividends even after controlling for those char-acteristics associated with the payment of dividends by firms. This finding appearsto be global and applies to firms incorporated in both common and civil lawjurisdictions.

C© 2009 The AuthorsJournal compilation C© Blackwell Publishing Ltd. 2009

ANALYSIS OF DIVIDEND PAYMENT BEHAVIOR 499

We find that the level of aggregate dividends paid has increased in spite of ageneral decline in the propensity to pay dividends. This result holds regardless ofwhether aggregate dividends are measured in nominal or real terms. These findingsare consistent with those reported by DeAngelo, DeAngelo and Skinner (2004) forthe US and Denis and Osobov (2008). We find that both common and civil law firmsexperience an increase in aggregate dividends, but that the percentage increase inaggregate dividends is greater for civil law countries. We also examine differences inthe dividend payout ratio across legal regimes and find limited evidence for higherpayout ratios among civil law incorporated firms.

We organize this paper into eight sections. In Section 2 we describe our data anddiscuss our method of sample construction. Section 3 provides an initial overview ofglobal dividend behavior while Section 4 contains a detailed time-series analysis oftrends in international dividend payment. A comparative analysis of factors influencingcorporate dividend payment is presented in Section 5. In Section 6 we calculatethe annual propensities to pay for our sample firms using an enhanced logisticmodel and following the general approach of Fama and French (2001). We examineaggregate dividend levels in Section 7 and provide a brief discussion and conclusion inSection 8.

2. DATA DESCRIPTION AND SAMPLE CONSTRUCTION

Our empirical data is obtained from several different databases. Firm-level datacomes from Worldscope (financial accounting information) and Datastream (marketinformation). Country-level data (exchange rates and consumer price index) arecompiled from FRED database of the St. Louis Federal Reserve, Penn World Tables,World Development Indicators, and Datastream.

Our sample initially begins with the 33 countries that LaPorta, Lopez de Silanes,Shleifer and Vishny (2000) use in their study of international dividend policy. We theneliminate eight of these nations from the sample because they contain too few firmswith available data to allow stable statistical estimation. We then employ the LaPorta,Lopez de Silanes, Shleifer and Vishny (1997) classifications to assign these twenty-five remaining countries to either common or civil law categories. The nine commonlaw countries of our sample are Australia, Canada, Hong Kong, Ireland, Malaysia,Singapore, South Africa, the US and the UK. The sixteen civil law nations that weexamine are Austria, Denmark, Finland, France, Germany, Indonesia, Italy, Japan,Korea, Mexico, Norway, Philippines, Portugal, Spain, Sweden and Switzerland. Ourfinal sample contains 225,592 firm-year observations from 1994 to 2007.1 This samplecontains a greater number of countries and is more current than those appearing in themost recent studies of international dividend policy such as Denis and Osobov (2008)and Eije and Megginson (2008).

We then classify firm-year observations into several categories based on their dividendpolicies. We define a firm as a dividend payer in calendar year t if it pays a dividend in

1 To be included in our final sample, we require that for each firm-year observation (1) common dividendsand total assets are available, (2) firms consolidate their major subsidiaries or have at most 20% of the totalassets as total investment in unconsolidated subsidiaries (this criterion alleviates the potential inflation effectof off-balance sheet leverage on reported assets), (3) firms operate in non-financial industries. Our sampleperiod starts in 1994 due to relatively sparse coverage prior to 1994.

C© 2009 The AuthorsJournal compilation C© Blackwell Publishing Ltd. 2009

500 FERRIS, SEN AND UNLU

year t. A firm is defined as a new list in calendar year t if it is added to the Worldscopedatabase between January and December of year t. Firms that do not pay a dividendin year t are classified as non-payers. Non-payers are further classified into two. Non-payers with a dividend payment in year t − 1 are classified as former payers, or otherwiseclassified as never payers.

3. AN OVERVIEW OF GLOBAL DIVIDEND BEHAVIOR

We begin our analysis of global dividend policy by providing an initial overview ofkey dividend characteristics for our sample of globally distributed firms. Specifically,we compare three different measures of dividend activity between the beginning andend of the examination period across our sample countries. These measures are thenumber of dividend payers, the percentage of firms paying dividends, and the average(mean and median) dividend paid per firm. We provide separate analyses for civil andcommon law countries due to the effect that differing levels of shareholder protectionfor minority investors might exert on corporate dividend decisions.

We observe in Table 1 that the average number of dividend payers among thecommon law countries increases. This increase, however, does not occur uniformlyacross the sample. Indeed, we observe a decline in the number of dividend payers forthe two largest common law markets: the UK and the US. This result is comparableto the findings reported by Fama and French (2001) and Ferris, Sen and Yui (2006a)for the US and the UK markets, respectively. The increase in the number of dividendpaying firms is most dramatic in the Far East, with Hong Kong, Singapore, and Malaysiaexperiencing an average 252% increase in the number of firms paying dividends. Withthe notable exception of the US and the UK, our evidence suggests that more firms incommon law countries pay dividends.

The findings presented in Table 1 also show that there is an increase in thenumber of dividend payers among civil law firms. Eleven of the sixteen samplecountries experience an increase in the number of dividend payers, while fourcountries experience only a nominal change (less than five percent) in the numberof dividend paying firms. The mean (median) increase in the number of dividendpaying firms is greater in common than in civil law countries, but the significantvariation within the subsamples prevents these differences from being statisticallysignificant.

In the fourth column of Table 1, we estimate the percentage of firms that aredividend payers. Use of this comparison reverses our initial conclusions regarding theincreased frequency of dividend payment by our sample firms. After standardizing thenumber of dividend paying firms by the total number of firms publicly traded in aparticular country, we observe a decline in the frequency of dividend payment. We finda uniform decline in the percentage of dividend paying firms across all the commonlaw firms. Indeed, the mean (median) change in the percentage of common law firmspaying dividends is −42% (−42%).

Similar results hold for civil law countries, where the mean (median) percentage ofdividend paying firms declines from 72% (71%) in 1994 to 55% (57%) in 2007. Tests ofmean and median differences indicate that this decline in the percentage of dividendpaying firms is greater in common than in civil law countries. That is, on average, ahigher percentage of firms located in common law countries reduce their dividendsthan in civil law firms. The difference in the median (mean) change in the percentage

C© 2009 The AuthorsJournal compilation C© Blackwell Publishing Ltd. 2009

ANALYSIS OF DIVIDEND PAYMENT BEHAVIOR 501T

able

1O

verv

iew

ofG

loba

lDiv

iden

dB

ehav

ior

Tota

lNum

ber

ofFi

rms

Num

ber

ofPa

yers

Perc

enta

geof

Paye

rsM

edia

nR

ealD

ivid

end

Per

Firm

Cou

ntry

/Leg

alR

egim

e19

9420

0719

9420

07%

Cha

nge

1994

2007

Cha

nge

%C

hang

e19

9420

07%

Cha

nge

Aus

tral

ia17

81,

409

132

357

170%

74%

25%

−49%

−66%

5.99

0.00

−100

%C

anad

a35

21,

200

171

319

87%

49%

27%

−22%

−45%

0.00

0.00

Hon

gK

ong

115

729

104

384

269%

90%

53%

−38%

−42%

11.1

20.

48−9

6%Ir

elan

d46

5332

19−4

1%70

%36

%−3

4%−4

8%2.

790.

00−1

00%

Mal

aysi

a17

384

415

848

320

6%91

%57

%−3

4%−3

7%3.

310.

41−8

8%Si

ngap

ore

104

518

9235

128

2%88

%68

%−2

1%−2

3%2.

951.

28−5

7%So

uth

Afr

ica

137

243

123

135

10%

90%

56%

−34%

−38%

9.85

0.63

−94%

Uni

ted

Kin

gdom

1,17

71,

407

955

633

−34%

81%

45%

−36%

−45%

1.87

0.00

−100

%U

nite

dSt

ates

3,80

04,

616

1,36

91,

163

−15%

36%

25%

−11%

−30%

0.00

0.00

Com

mon

Law

Mea

n67

61,

224

348

427

104%

74%

43%

−31%

−42%

4.21

0.31

−91%

Com

mon

Law

Med

ian

173

844

132

357

87%

81%

45%

−34%

−42%

2.95

0.00

−96%

Aus

tria

4654

3435

3%74

%65

%−9

%−1

2%3.

072.

45−2

0%D

enm

ark

108

9572

60−1

7%67

%63

%−4

%−5

%0.

731.

8315

0%Fi

nlan

d74

107

5086

72%

68%

80%

13%

19%

1.47

8.59

482%

Fran

ce40

747

428

729

32%

71%

62%

−9%

−12%

1.64

1.06

−35%

Ger

man

y34

452

324

524

0−2

%71

%46

%−2

5%−3

6%2.

860.

00−1

00%

Indo

nesi

a80

114

7758

−25%

96%

51%

−45%

−47%

2.41

0.19

−92%

Ital

y13

220

780

136

70%

61%

66%

5%8%

1.26

3.81

203%

Japa

n2,

049

3,23

21,

807

2,79

455

%88

%86

%−2

%−2

%3.

171.

71−4

6%K

orea

189

844

146

575

294%

77%

68%

−9%

−12%

2.08

1.20

−42%

Mex

ico

7491

4552

16%

61%

57%

−4%

−6%

4.44

3.49

−21%

Nor

way

9013

459

57−3

%66

%43

%−2

3%−3

5%1.

400.

00−1

00%

Phili

ppin

es42

122

2147

124%

50%

39%

−11%

−23%

0.00

0.00

−100

%Po

rtug

al38

3928

23−1

8%74

%59

%−1

5%−2

0%1.

011.

4745

%Sp

ain

9192

5873

26%

64%

79%

16%

24%

4.95

18.1

826

7%Sw

eden

131

226

8313

158

%63

%58

%−5

%−9

%1.

022.

1611

1%Sw

itzer

land

139

165

104

119

14%

75%

72%

−3%

−4%

5.28

6.01

14%

Civ

ilL

awM

ean

252

407

200

299

42%

70%

62%

−8%

−11%

2.30

3.26

45%

Civ

ilL

awM

edia

n10

012

875

8015

%69

%62

%−7

%−1

0%1.

861.

77−2

1%A

ggre

gate

Mea

n40

570

225

334

564

%72

%55

%−1

6%−2

2%2.

992.

203%

Agg

rega

teM

edia

n13

122

692

135

16%

71%

57%

−11%

−23%

2.41

1.06

−46%

Dif

fere

nces

betw

een

com

mon

and

civi

llaw

mea

nsan

dm

edia

ns:p

-val

ues

Dif

fere

nce

inm

eans

0.44

0.53

0.22

0.58

0.00

0.00

0.00

0.20

0.02

0.00

Dif

fere

nce

inm

edia

ns0.

070.

030.

520.

220.

010.

000.

000.

320.

010.

01

Not

es:

Thi

sta

ble

pres

ents

the

chan

ges

inse

lect

char

acte

rist

ics

ofdi

vide

ndpa

yers

from

1994

to20

07fo

r25

coun

trie

s.T

hepe

rcen

tage

ofpa

yers

isth

enu

mbe

rof

divi

dend

payi

ngfir

ms

rela

tive

toth

eto

taln

umbe

rof

firm

s.T

hem

ean

(med

ian)

real

divi

dend

isth

em

ean

(med

ian)

divi

dend

amou

nt(i

n20

07U

Sdo

llars

)am

ong

divi

dend

payi

ngfir

ms.

The

perc

enta

gech

ange

ofa

give

nva

riab

leis

com

pute

dby

divi

ding

abso

lute

chan

geby

1994

valu

eof

the

corr

espo

ndin

gva

riab

le.

C© 2009 The AuthorsJournal compilation C© Blackwell Publishing Ltd. 2009

502 FERRIS, SEN AND UNLU

of dividend paying firms between legal regimes is statistically significant, indicating thatcivil law firms in general have been slower to reduce their payment of dividends.

In the fifth column we examine the size of the median real dividend per firm. Forthe common law firms, we immediately notice the almost uniform decline in the sizeof the median dividend. Changes in the magnitude of dividends paid by firms locatedin common law countries range from zero to −100%, with a median change of −91%.

We obtain mixed results regarding the median real dividend for the civil lawcountries. Changes in the median real dividend paid range from a 482% increasefor Finland to −100% decline for Germany. The median real dividend in civil lawcountries declines by 21% between 1994 and 2007. We also find that the median (mean)difference in the size of dividends paid between legal regimes is statistically significant.

The results in Table 1 reveal some initial similarities along with important differencesin the dividend policies between civil and common law countries. Both regimesexperience an increase in the absolute number of dividend paying firms. But afterstandardizing by the number of firms trading in a country’s stock market, we observe adecline in the percentage of firms paying dividends that is consistent with the patternfirst detected by Fama and French (2001) for the US. We further determine that thisdecline is more pronounced among common law firms. Accompanying this decline inthe percentage of firms paying dividends is the reduction in the average size of dividendsbeing paid. The reduction in amount of dividends being paid is again more pronouncedamong common law firms, with the average percentage reduction in dividends by civillaw firms less than a quarter of that observed by common law firms.

4. TIME –SERIES PATTERNS IN INTERNATIONAL DIVIDEND PAYMENT

(i) An Aggregate Time-Series Analysis

In this section we provide a more detailed time-series analysis of dividend practicesamong our sample firms. Using the dividend payment categories described in Section 2,we present in Table 2 the percentage of firms contained in each of the different dividendgroups separately for each regime. We calculate the mean (median) values of thepercentage of firms in each of these categories for each of the sample years.

We observe in Panel A of Table 2 that the percent of firms paying dividendsdeclines over time for most of the sample firms. These annual results are consistent withour initial findings contained in Table 1. All of the common law countries experiencea decline in dividends along with most of the civil law countries, with the exception ofFinland, Italy and Spain. Although there are some annual reversals, the general trendpresented in the time-series of Table 2 is that of a declining number of firms payingdividends.2

We define the decline in the percentage of dividend-paying firms as the differencebetween the percentage of firms paying dividends in 1994 and that in 2007. The mediandecline is 34% for the common law countries, with a corresponding value of 11%for the civil law nations. The difference in both the mean and median percentage

2 In un-tabulated results we separately regress for each country the percent of firms paying dividends againsta time trend variable. We find that 24 of the 25 coefficients are negative, with 20 statistically significant. Theseresults confirm our conclusion of a generalized declining trend in the percent of firms paying dividends acrossour sample.

C© 2009 The AuthorsJournal compilation C© Blackwell Publishing Ltd. 2009

ANALYSIS OF DIVIDEND PAYMENT BEHAVIOR 503

Tab

le2

Tim

eSe

ries

Dis

trib

utio

nof

Div

iden

dPo

licie

sA

mon

gFi

rms

inD

iffe

rent

Cou

ntri

esP

anel

A:P

erce

ntag

eof

Firm

sP

ayin

gD

ivid

ends

Year

sD

iffer

ence

Cou

ntry

/Leg

alR

egim

e19

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

07(2

007–

1994

)

Aus

tral

ia0.

740.

710.

690.

720.

660.

570.

410.

320.

280.

300.

280.

290.

270.

25−0

.49

Can

ada

0.49

0.47

0.43

0.43

0.29

0.25

0.23

0.22

0.20

0.21

0.23

0.26

0.28

0.27

−0.2

2H

ong

Kon

g0.

900.

910.

810.

770.

710.

530.

460.

440.

400.

440.

470.

510.

530.

53−0

.38

Irel

and

0.70

0.73

0.60

0.57

0.54

0.52

0.54

0.52

0.49

0.44

0.44

0.38

0.38

0.36

−0.3

4M

alay

sia

0.91

0.91

0.90

0.86

0.77

0.65

0.62

0.62

0.60

0.57

0.55

0.56

0.57

0.57

−0.3

4Si

ngap

ore

0.88

0.88

0.86

0.81

0.83

0.72

0.65

0.60

0.52

0.52

0.54

0.59

0.64

0.68

−0.2

1So

uth

Afr

ica

0.90

0.93

0.88

0.87

0.60

0.54

0.52

0.46

0.49

0.55

0.59

0.60

0.58

0.56

−0.3

4U

nite

dK

ingd

om0.

810.

830.

760.

750.

750.

700.

620.

550.

510.

480.

450.

440.

420.

45−0

.36

Uni

ted

Stat

es0.

360.

330.

280.

240.

190.

180.

180.

180.

180.

200.

220.

240.

240.

25−0

.11

Com

mon

Law

Mea

n0.

740.

740.

690.

670.

590.

520.

470.

440.

410.

410.

420.

430.

430.

43−0

.31

Com

mon

Law

Med

ian

0.81

0.83

0.76

0.75

0.66

0.54

0.52

0.46

0.49

0.44

0.45

0.44

0.42

0.45

−0.3

4

Aus

tria

0.74

0.78

0.80

0.76

0.72

0.70

0.68

0.59

0.58

0.61

0.68

0.64

0.64

0.65

−0.0

9D

enm

ark

0.67

0.74

0.69

0.70

0.76

0.73

0.71

0.65

0.51

0.52

0.56

0.59

0.65

0.63

−0.0

4Fi

nlan

d0.

680.

830.

800.

840.

880.

860.

820.

790.

780.

730.

760.

760.

760.

800.

13Fr

ance

0.71

0.75

0.69

0.63

0.66

0.62

0.60

0.59

0.56

0.56

0.54

0.55

0.58

0.62

−0.0

9G

erm

any

0.71

0.72

0.67

0.57

0.57

0.56

0.49

0.47

0.41

0.38

0.36

0.40

0.43

0.46

−0.2

5In

done

sia

0.96

0.95

0.92

0.91

0.38

0.32

0.46

0.36

0.38

0.43

0.41

0.43

0.42

0.51

−0.4

5It

aly

0.61

0.62

0.65

0.69

0.65

0.65

0.68

0.65

0.61

0.58

0.57

0.59

0.63

0.66

0.05

Japa

n0.

880.

850.

840.

860.

870.

850.

820.

820.

820.

790.

810.

840.

860.

86−0

.02

Kor

ea0.

770.

790.

780.

730.

570.

530.

540.

560.

550.

580.

590.

650.

690.

68−0

.09

Mex

ico

0.61

0.45

0.48

0.54

0.50

0.31

0.35

0.39

0.38

0.42

0.40

0.42

0.51

0.57

−0.0

4N

orw

ay0.

660.

690.

620.

580.

520.

420.

430.

360.

330.

420.

410.

440.

390.

43−0

.23

Phili

ppin

es0.

500.

510.

490.

430.

330.

270.

220.

180.

250.

260.

270.

320.

340.

39−0

.11

Port

ugal

0.74

0.79

0.67

0.70

0.74

0.70

0.71

0.55

0.67

0.57

0.60

0.63

0.60

0.59

−0.1

5Sp

ain

0.64

0.68

0.69

0.75

0.67

0.70

0.73

0.72

0.66

0.67

0.73

0.77

0.79

0.79

0.16

Swed

en0.

630.

790.

770.

670.

630.

580.

530.

470.

430.

440.

470.

490.

520.

58−0

.05

Switz

erla

nd0.

750.

770.

760.

740.

790.

800.

770.

760.

620.

610.

640.

660.

690.

72−0

.03

Civ

ilL

awM

ean

0.70

0.73

0.71

0.69

0.64

0.60

0.60

0.56

0.53

0.53

0.55

0.57

0.59

0.62

−0.0

8C

ivil

Law

Med

ian

0.69

0.76

0.69

0.70

0.65

0.64

0.64

0.57

0.55

0.56

0.57

0.59

0.61

0.62

−0.0

7A

ggre

gate

Mea

n0.

720.

740.

700.

690.

620.

570.

550.

510.

490.

490.

500.

520.

540.

55−0

.16

Agg

rega

teM

edia

n0.

710.

770.

690.

720.

660.

580.

540.

550.

510.

520.

540.

550.

570.

57−0

.11

Dif

fere

nces

betw

een

com

mon

and

civi

llaw

mea

nsan

dm

edia

ns:p

-val

ues

Dif

fere

nce

inm

eans

0.58

0.87

0.83

0.76

0.55

0.30

0.10

0.11

0.07

0.05

0.05

0.03

0.02

0.00

0.00

Dif

fere

nce

inm

edia

ns0.

220.

440.

760.

710.

800.

250.

090.

090.

080.

070.

070.

040.

030.

010.

00

C© 2009 The AuthorsJournal compilation C© Blackwell Publishing Ltd. 2009

504 FERRIS, SEN AND UNLU

Tab

le2

(Con

tinu

ed)

Pan

elB

:Per

cent

age

ofFi

rms

Tha

tNev

erP

aid

Div

iden

dsYe

ars

Diff

eren

ceC

ount

ry/L

egal

Reg

ime

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

(200

7–19

94)

Aus

tral

ia0.

220.

270.

280.

270.

300.

410.

560.

660.

670.

680.

690.

700.

700.

730.

51C

anad

a0.

500.

520.

540.

550.

690.

730.

750.

760.

780.

780.

760.

740.

720.

720.

22H

ong

Kon

g0.

080.

070.

140.

140.

180.

300.

480.

510.

520.

510.

480.

440.

430.

420.

34Ir

elan

d0.

300.

250.

400.

410.

420.

450.

460.

470.

470.

490.

530.

550.

620.

600.

30M

alay

sia

0.06

0.09

0.08

0.10

0.11

0.22

0.35

0.33

0.35

0.37

0.40

0.39

0.38

0.37

0.30

Sing

apor

e0.

070.

110.

110.

160.

110.

200.

320.

330.

390.

420.

400.

370.

310.

260.

19So

uth

Afr

ica

0.08

0.07

0.08

0.11

0.36

0.38

0.42

0.44

0.45

0.43

0.38

0.37

0.38

0.40

0.31

Uni

ted

Kin

gdom

0.16

0.15

0.22

0.23

0.22

0.27

0.34

0.40

0.44

0.49

0.52

0.54

0.55

0.53

0.38

Uni

ted

Stat

es0.

620.

660.

700.

750.

800.

810.

810.

810.

810.

790.

770.

750.

740.

740.

11C

omm

onL

awM

ean

0.23

0.24

0.28

0.30

0.36

0.42

0.50

0.52

0.54

0.55

0.55

0.54

0.54

0.53

0.30

Com

mon

Law

Med

ian

0.16

0.15

0.22

0.23

0.30

0.38

0.46

0.47

0.47

0.49

0.52

0.54

0.55

0.53

0.30

Aus

tria

0.20

0.20

0.16

0.23

0.24

0.29

0.27

0.33

0.35

0.36

0.30

0.31

0.34

0.35

0.16

Den

mar

k0.

300.

230.

280.

280.

220.

230.

250.

270.

370.

400.

410.

410.

340.

290.

00Fi

nlan

d0.

280.

170.

190.

150.

120.

120.

120.

170.

160.

220.

220.

200.

170.

17−0

.12

Fran

ce0.

220.

240.

280.

310.

310.

330.

340.

350.

380.

390.

420.

410.

380.

350.

13G

erm

any

0.22

0.24

0.27

0.36

0.38

0.39

0.44

0.46

0.50

0.55

0.59

0.58

0.54

0.50

0.29

Indo

nesi

a0.

010.

040.

070.

060.

110.

550.

520.

470.

550.

530.

540.

520.

500.

440.

43It

aly

0.26

0.31

0.33

0.29

0.32

0.31

0.29

0.28

0.30

0.34

0.35

0.38

0.35

0.31

0.06

Japa

n0.

070.

110.

130.

130.

110.

100.

120.

150.

160.

170.

170.

150.

130.

120.

04K

orea

0.18

0.17

0.17

0.17

0.25

0.40

0.40

0.39

0.39

0.37

0.37

0.31

0.28

0.27

0.09

Mex

ico

0.30

0.38

0.48

0.41

0.47

0.50

0.61

0.56

0.56

0.55

0.54

0.56

0.49

0.43

0.13

Nor

way

0.34

0.28

0.36

0.36

0.42

0.49

0.51

0.56

0.60

0.56

0.58

0.54

0.56

0.53

0.19

Phili

ppin

es0.

430.

430.

450.

460.

550.

650.

710.

760.

720.

670.

700.

650.

630.

580.

15Po

rtug

al0.

210.

190.

260.

290.

220.

240.

270.

290.

290.

290.

350.

350.

360.

360.

15Sp

ain

0.31

0.31

0.29

0.22

0.27

0.28

0.24

0.25

0.30

0.32

0.27

0.22

0.21

0.18

−0.1

2Sw

eden

0.34

0.21

0.22

0.27

0.32

0.38

0.43

0.49

0.50

0.52

0.50

0.50

0.46

0.41

0.08

Switz

erla

nd0.

190.

190.

210.

200.

170.

160.

190.

200.

240.

330.

330.

310.

280.

250.

06C

ivil

Law

Mea

n0.

240.

230.

260.

260.

280.

340.

360.

370.

400.

410.

410.

400.

380.

350.

11C

ivil

Law

Med

ian

0.24

0.22

0.27

0.27

0.26

0.32

0.31

0.34

0.37

0.38

0.39

0.40

0.35

0.35

0.11

Agg

rega

teM

ean

0.24

0.24

0.27

0.28

0.31

0.37

0.41

0.43

0.45

0.46

0.46

0.45

0.43

0.41

0.17

Agg

rega

teM

edia

n0.

220.

210.

260.

270.

270.

330.

400.

400.

440.

430.

420.

410.

380.

400.

15

Dif

fere

nces

betw

een

com

mon

and

civi

llaw

mea

nsan

dm

edia

ns:p

-val

ues

Dif

fere

nce

inm

eans

0.92

0.86

0.76

0.61

0.41

0.30

0.06

0.05

0.04

0.03

0.04

0.04

0.02

0.01

0.00

Dif

fere

nce

inm

edia

ns0.

520.

550.

840.

840.

710.

550.

070.

060.

060.

070.

080.

070.

030.

020.

00

C© 2009 The AuthorsJournal compilation C© Blackwell Publishing Ltd. 2009

ANALYSIS OF DIVIDEND PAYMENT BEHAVIOR 505

Tab

le2

(Con

tinu

ed)

Pan

elC

:Per

cent

age

ofFi

rms

Tha

tFor

mer

lyP

aid

Div

iden

dsYe

ars

Diff

eren

ceC

ount

ry/L

egal

Reg

ime

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

(200

7–19

94)

Aus

tral

ia0.

030.

010.

030.

010.

040.

020.

030.

020.

050.

020.

030.

010.

030.

01−0

.02

Can

ada

0.01

0.01

0.03

0.02

0.02

0.02

0.02

0.02

0.02

0.00

0.01

0.01

0.01

0.01

0.00

Hon

gK

ong

0.02

0.02

0.05

0.08

0.11

0.16

0.05

0.04

0.08

0.05

0.05

0.04

0.04

0.06

0.04

Irel

and

0.00

0.02

0.00

0.02

0.03

0.03

0.00

0.02

0.03

0.07

0.04

0.07

0.00

0.04

0.04

Mal

aysi

a0.

020.

000.

020.

040.

120.

140.

030.

040.

050.

060.

050.

050.

050.

060.

04Si

ngap

ore

0.05

0.01

0.02

0.03

0.06

0.08

0.03

0.07

0.09

0.06

0.06

0.04

0.05

0.06

0.01

Sout

hA

fric

a0.

020.

010.

040.

020.

040.

080.

060.

090.

060.

020.

030.

030.

040.

050.

03U

nite

dK

ingd

om0.

030.

020.

020.

030.

030.

030.

040.

050.

040.

030.

030.

020.

030.

02−0

.02

Uni

ted

Stat

es0.

020.

010.

010.

010.

010.

010.

010.

010.

010.

010.

010.

010.

020.

010.

00C

omm

onL

awM

ean

0.02

0.01

0.03

0.03

0.05

0.06

0.03

0.04

0.05

0.04

0.03

0.03

0.03

0.04

0.01

Com

mon

Law

Med

ian

0.02

0.01

0.02

0.02

0.04

0.03

0.03

0.04

0.05

0.03

0.03

0.03

0.03

0.04

0.01

Aus

tria

0.07

0.02

0.03

0.01

0.04

0.01

0.05

0.09

0.08

0.04

0.02

0.05

0.02

0.00

−0.0

7D

enm

ark

0.04

0.04

0.04

0.03

0.02

0.04

0.05

0.07

0.12

0.08

0.03

0.00

0.01

0.07

0.04

Finl

and

0.04

0.00

0.01

0.01

0.01

0.03

0.06

0.05

0.06

0.05

0.03

0.04

0.07

0.03

−0.0

1Fr

ance

0.07

0.01

0.03

0.06

0.04

0.05

0.06

0.06

0.07

0.05

0.04

0.03

0.04

0.03

−0.0

4G

erm

any

0.07

0.05

0.06

0.07

0.04

0.05

0.07

0.07

0.08

0.07

0.05

0.02

0.03

0.04

−0.0

3In

done

sia

0.03

0.02

0.02

0.03

0.51

0.14

0.02

0.17

0.07

0.04

0.06

0.05

0.08

0.05

0.03

Ital

y0.

140.

070.

030.

010.

020.

030.

030.

070.

090.

080.

080.

030.

030.

03−0

.11

Japa

n0.

050.

040.

030.

020.

010.

050.

060.

020.

030.

050.

020.

020.

020.

02−0

.03

Kor

ea0.

050.

040.

040.

090.

180.

070.

060.

050.

060.

050.

040.

040.

040.

040.

00M

exic

o0.

090.

180.

040.

050.

040.

190.

050.

050.

060.

030.

060.

020.

000.

00−0

.09

Nor

way

0.00

0.02

0.02

0.06

0.06

0.08

0.06

0.09

0.07

0.02

0.02

0.01

0.05

0.04

0.04

Phili

ppin

es0.

070.

070.

060.

110.

120.

080.

070.

060.

030.

060.

030.

020.

030.

03−0

.04

Port

ugal

0.05

0.02

0.07

0.02

0.04

0.06

0.02

0.16

0.04

0.14

0.04

0.02

0.04

0.05

0.00

Spai

n0.

050.

010.

020.

030.

060.

020.

040.

030.

040.

010.

000.

010.

000.

02−0

.03

Swed

en0.

030.

000.

010.

070.

050.

040.

050.

040.

070.

040.

030.

010.

020.

01−0

.02

Switz

erla

nd0.

060.

040.

030.

060.

040.

040.

030.

040.

140.

060.

030.

030.

030.

03−0

.03

Civ

ilL

awM

ean

0.06

0.04

0.03

0.05

0.08

0.06

0.05

0.07

0.07

0.05

0.04

0.03

0.03

0.03

−0.0

3C

ivil

Law

Med

ian

0.05

0.03

0.03

0.04

0.04

0.05

0.05

0.06

0.07

0.05

0.03

0.02

0.03

0.03

−0.0

3A

ggre

gate

Mea

n0.

040.

030.

030.

040.

070.

060.

040.

060.

060.

050.

030.

030.

030.

03−0

.01

Agg

rega

teM

edia

n0.

040.

020.

030.

030.

040.

050.

050.

050.

060.

050.

030.

020.

030.

03−0

.01

Dif

fere

nces

betw

een

com

mon

and

civi

llaw

mea

nsan

dm

edia

ns:p

-val

ues

Dif

fere

nce

inm

eans

0.00

0.03

0.28

0.14

0.39

0.87

0.01

0.08

0.12

0.14

0.58

0.40

0.81

0.61

0.02

Dif

fere

nce

inm

edia

ns0.

000.

020.

320.

170.

570.

710.

020.

040.

150.

170.

800.

520.

980.

670.

02

C© 2009 The AuthorsJournal compilation C© Blackwell Publishing Ltd. 2009

506 FERRIS, SEN AND UNLU

Tab

le2

(Con

tinu

ed)

Pan

elD

:Per

cent

age

ofN

ewL

ists

Tha

tDo

Not

Pay

Div

iden

dsYe

ars

Diff

eren

ceC

ount

ry/L

egal

Reg

ime

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

(200

7–19

94)

Aus

tral

ia0.

400.

570.

540.

500.

620.

730.

820.

820.

950.

700.

900.

950.

930.

53C

anad

a0.

750.

800.

840.

830.

910.

880.

890.

930.

860.

890.

830.

830.

60−0

.15

Hon

gK

ong

0.04

0.10

0.30

0.31

0.29

0.62

0.65

0.64

0.75

0.57

0.83

1.00

––

Irel

and

0.00

–0.

750.

601.

000.

601.

001.

001.

001.

000.

801.

001.

001.

00M

alay

sia

0.08

0.15

0.22

0.30

0.40

0.30

0.44

0.54

0.76

0.77

0.71

0.86

0.64

0.56

Sing

apor

e0.

050.

210.

280.

350.

000.

550.

500.

660.

730.

700.

750.

580.

900.

85So

uth

Afr

ica

0.33

0.00

0.25

0.27

0.55

0.62

0.50

0.80

0.50

0.70

0.81

0.59

1.00

0.67

Uni

ted

Kin

gdom

0.38

0.53

0.56

0.57

0.62

0.84

0.86

0.84

0.79

0.83

0.90

0.94

0.98

0.61

Uni

ted

Stat

es0.

910.

900.

950.

960.

960.

980.

960.

950.

950.

930.

910.

890.

950.

05C

omm

onL

awM

ean

0.33

0.41

0.52

0.52

0.59

0.68

0.74

0.80

0.81

0.79

0.83

0.85

0.88

0.51

Com

mon

Law

Med

ian

0.33

0.37

0.54

0.50

0.62

0.62

0.82

0.82

0.79

0.77

0.83

0.89

0.94

0.58

Aus

tria

––

0.46

0.75

0.83

0.75

1.00

1.00

0.50

0.00

0.50

0.00

1.00

–D

enm

ark

0.33

0.75

0.52

0.56

0.67

0.67

0.60

0.00

1.00

–1.

001.

00–

–Fi

nlan

d0.

501.

000.

360.

400.

360.

500.

50–

1.00

0.60

0.50

1.00

––

Fran

ce0.

420.

500.

520.

580.

590.

700.

810.

690.

610.

700.

790.

781.

000.

58G

erm

any

0.67

0.86

0.49

0.67

0.74

0.93

0.86

1.00

0.90

0.77

0.92

0.75

1.00

0.33

Indo

nesi

a0.

330.

060.

750.

330.

500.

660.

710.

750.

751.

000.

910.

670.

750.

42It

aly

0.20

0.80

0.33

0.87

0.67

0.65

0.60

0.29

0.65

0.80

0.63

1.00

1.00

0.80

Japa

n0.

030.

000.

060.

040.

080.

360.

270.

280.

420.

440.

370.

290.

450.

42K

orea

0.10

0.15

0.22

0.16

0.34

0.53

0.78

0.69

0.67

0.59

0.64

0.80

1.00

0.90

Mex

ico

0.33

1.00

0.70

0.60

0.78

0.80

1.00

0.50

1.00

1.00

1.00

1.00

0.00

−0.3

3N

orw

ay0.

801.

000.

560.

750.

670.

670.

901.

000.

881.

001.

000.

931.

000.

20Ph

ilipp

ines

0.75

0.48

0.89

0.33

1.00

0.82

1.00

0.75

1.00

1.00

0.67

1.00

––

Port

ugal

0.25

0.50

0.78

0.00

0.33

0.50

0.67

1.00

0.50

1.00

0.00

1.00

––

Spai

n0.

000.

500.

500.

330.

830.

000.

431.

000.

50–

0.25

1.00

––

Swed

en0.

770.

630.

380.

670.

820.

720.

571.

000.

710.

850.

830.

860.

00−0

.77

Switz

erla

nd0.

500.

500.

370.

380.

750.

170.

611.

000.

750.

500.

670.

50–

–C

ivil

Law

Mea

n0.

400.

580.

490.

460.

620.

590.

710.

730.

740.

730.

670.

790.

720.

28C

ivil

Law

Med

ian

0.33

0.50

0.50

0.48

0.67

0.66

0.69

0.75

0.73

0.78

0.67

0.89

1.00

0.42

Agg

rega

teM

ean

0.37

0.52

0.50

0.48

0.61

0.62

0.72

0.76

0.77

0.75

0.72

0.81

0.79

0.39

Agg

rega

teM

edia

n0.

330.

500.

500.

500.

670.

660.

710.

810.

750.

770.

800.

890.

970.

53

Dif

fere

nces

betw

een

com

mon

and

civi

llaw

mea

nsan

dm

edia

ns:p

-val

ues

Dif

fere

nce

inm

eans

0.56

0.24

0.77

0.59

0.81

0.36

0.75

0.50

0.37

0.52

0.05

0.50

0.30

0.33

Dif

fere

nce

inm

edia

ns0.

530.

400.

910.

950.

820.

510.

890.

830.

390.

970.

281.

000.

740.

31

Not

es:

Thi

sta

ble

show

sth

etim

ese

ries

dist

ribu

tion

ofdi

vide

ndpo

licie

sfr

om19

94to

2007

for

25co

untr

ies.

Paye

rsar

eth

efir

ms

that

pay

divi

dend

sin

year

t.N

on-

paye

rsar

ecl

assi

fied

into

two

grou

ps:f

irm

sth

atha

vene

ver

paid

divi

dend

san

dfo

rmer

paye

rs.F

orm

erpa

yers

are

firm

sth

atdo

notp

aydi

vide

nds

inye

art,

butd

idpa

ydi

vide

nds

inpr

evio

usye

ars.

Ane

wlis

tis

firm

sth

atfir

stap

pear

onW

orld

scop

ein

year

t.N

ewlis

tsth

atpa

yar

efir

ms

that

pay

divi

dend

sin

the

year

oflis

ting.

Cou

ntri

esar

eas

sign

edto

ale

galr

egim

eac

cord

ing

toL

aPor

taet

al.(

1997

).

C© 2009 The AuthorsJournal compilation C© Blackwell Publishing Ltd. 2009

ANALYSIS OF DIVIDEND PAYMENT BEHAVIOR 507

of dividend payers is statistically significant across legal regimes. The high level ofdividend reduction observed for the common law firms is driven by the large percentagereduction occurring in three countries: 49% in Australia, 38% in Hong Kong and 36%in the UK. For comparison purposes, the largest decline among civil law countries isIndonesia with 45%, followed by Germany with 26% and Norway with 23%. Althoughthe findings presented in Table 2 confirm that a reduction in the frequency of dividendpayers is an international phenomenon, it appears most dramatically among firmsincorporated in common law countries.

In Panel B of Table 2 we present a time-series of the percentage of firms that neverpaid dividends. The trend in this variable complements that observed in Panel A fordividend payers. We find a general increase in the percentage of firms not payingdividends over the 1994–2007 sample period, although this effect is more pronouncedamong common law countries. Within common law countries, the percentage of firmsthat have never paid dividends increases by 30% compared to only a median increaseof 15% among firms within civil law countries. Again, this increase in the percentage offirms never paying dividends is most prominent in Australia, Hong Kong and the UK.

The combined findings of Panels A and B show that there is a consistent downwardtrend in the international payment of dividends. Since 1994 there has been a generaldecrease in the percentage of firms paying dividends. This decline in the percentageof dividend payers occurs within both the common and civil legal regimes. Our dataindicate, however, that this reduction in the frequency of dividend payment is moreprominent among the common law countries.

In Panels C and D we examine more closely the non-dividend paying firms. We firstexamine former payers and then separately consider new lists. In Panel C we analyzethose firms that had formerly paid dividends, but now do not. We observe that thepercentage of former payers has increased over time, but that this increase is mostheavily concentrated among the common law countries. Seven of nine common lawcountries experience an increase in the percentage of former payers, while only five ofthe sixteen civil law countries report an increase in the percentage of former payers.Although the median increase in the percentage of former payers among the commonlaw firms is only 1%, it is significantly greater than that calculated for the civil law firms.This finding that the percentage of former dividend payers is higher among firms incommon law countries is consistent with our earlier result that fewer dividend payersnow incorporate in these nations.

We present our findings for newly listed firms in Panel D. For most of the sampleperiod, the percentage of common law new lists not paying dividends increases. Onlyin Canada does the number of new lists not paying a dividend decline. Indeed, themedian change among common law countries is a 58% increase in the percentage ofnew lists not paying dividends. Comparable results obtain for the civil law countries,with a median increase of 53%. We conclude that the difference in the percentage ofdividend paying firms between civil and common law countries is due to differences inthe distribution of firms that never paid dividends or decided to stop paying dividendsrather than newly listing firms that elect not to pay dividends.

(ii) Changing Status of Dividend Payers and Non-Payers

In this section we examine the subsequent dividend payment decision of firms basedon their previous dividend payment status. That is, we examine the dividend payment

C© 2009 The AuthorsJournal compilation C© Blackwell Publishing Ltd. 2009

508 FERRIS, SEN AND UNLU

status in year t for firms that either paid or did not pay dividends in year t−1. Continuingfirms are those that paid a dividend in year t and continue to pay dividends in yeart+1. The continuation rate is thus defined as the number of firms that continue topay dividends in year t relative to the number of firms that pay dividends in year t−1.Initiating firms are those that did not pay a dividend in year t, but elect to pay a dividendin year t+1. The initiation rate is then estimated as the number of firms that initiatedividends in year t relative to the number of firms that do not pay dividends in yeart−1.

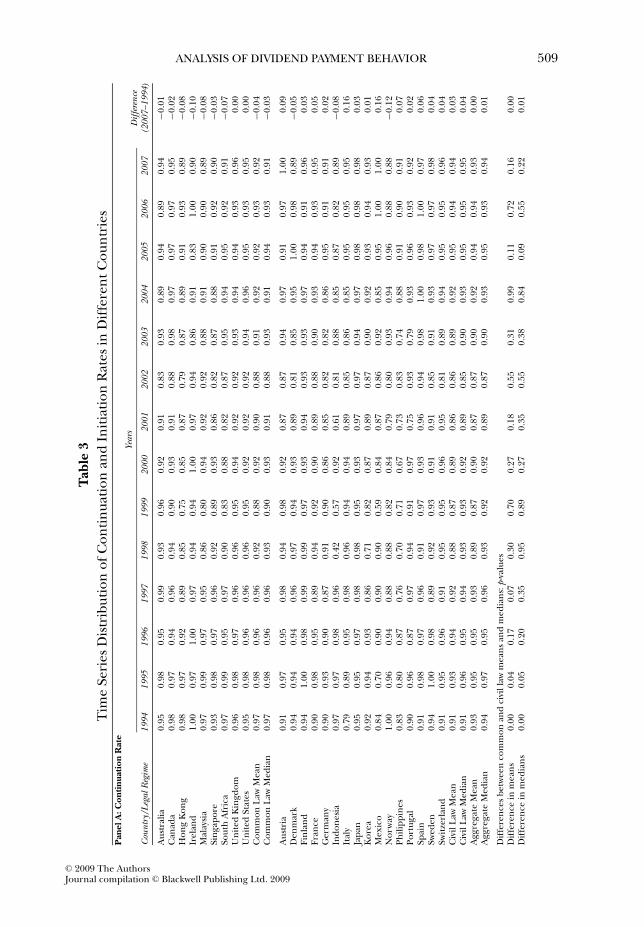

In Panel A of Table 3 we present the continuation rate across legal regimes. Wefind that most common law countries experience a decline in the number of firmscontinuing to pay dividends. Ireland, Malaysia and Hong Kong have the largest declinein dividend continuation rates of 10%, 8% and 8%, respectively. The two largestcommon law markets, the US and the UK, experience no change in continuationrates. None of the common law countries enjoy an increase in dividend continuationrates. The median (mean) dividend continuation rate for common law countries is−0.03 (−0.04).

The pattern of dividend continuation differs significantly for the civil law countries.Only three of the sixteen civil law countries reduce their dividend continuation rates.The other thirteen countries report an increase in the percentage of firms continuingtheir payment of dividends led by Mexico (16%), Italy (16%) and Austria (9%). Themedian (mean) change in dividend continuation is 0.01(0.0). This value is significantlyhigher than that calculated for the common law countries, leading us to concludethat dividends, once initiated, tend to persist longer among firms located in civil lawcountries.

In Panel B of Table 3, we compare initiation rates of dividends between firms incommon and civil law countries. Our findings reveal only a nominal difference inthe pattern of dividend initiations between the two legal regimes. Dividend initiationsdecline across firms incorporated in common law countries, led by Canada (−19%),South Africa (−16%) and the United Kingdom (−16%). All of the common lawcountries report either a decline or no change in the rate of dividend initiations.Indeed, the median (mean) change in initiation rates for our sample of common lawcountries is −12% (−9.0%).

The dividend initiation behavior of the civil law countries is more mixed. Approxi-mately one-third of them experience an increase in their dividend initiation rates, ledby Japan (12%), Finland (8%) and Switzerland (8%). The remaining countries havefalling initiation rates, ranging from an 84% decline in Germany to a 2% reductionamong Mexican firms. Overall, the median (mean) reduction in dividend initiation is5% (9%). Although these averages are not significantly different from those calculatedfor civil law countries, it is consistent with our earlier findings of a more modest declinein the percentage of dividend paying firms among the civil law countries.

The combined results of these two tables offer further insight into the nature ofinternational dividend policy. We find that firms paying dividends generally tend tocontinue paying dividends. The percentage of dividend continuing firms is high,averaging 93% across our entire sample of firms. We note, however, that there is atendency for a greater adherence to dividend continuation among firms incorporatedwithin the civil law countries.

We also observe that dividend initiation rates are generally low, averaging approxi-mately 16% for our aggregate sample. We find that there is a slight tendency for civil law

C© 2009 The AuthorsJournal compilation C© Blackwell Publishing Ltd. 2009

ANALYSIS OF DIVIDEND PAYMENT BEHAVIOR 509

Tab

le3

Tim

eSe

ries

Dis

trib

utio

nof

Con

tinua

tion

and

Initi

atio

nR

ates

inD

iffe

rent

Cou

ntri

esP

anel

A:C

onti

nuat

ion

Rat

eYe

ars

Diff

eren

ceC

ount

ry/L

egal

Reg

ime

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

(200

7–19

94)

Aus

tral

ia0.

950.

980.

950.

990.

930.

960.

920.

910.

830.

930.

890.

940.

890.

94−0

.01

Can

ada

0.98

0.97

0.94

0.96

0.94

0.90

0.93

0.91

0.88

0.98

0.97

0.97

0.97

0.95

−0.0

2H

ong

Kon

g0.

980.

970.

920.

890.

850.

750.

850.

870.

790.

870.

890.

910.

930.

89−0

.08

Irel

and

1.00

0.97

1.00

0.97

0.94

0.94

1.00

0.97

0.94

0.86

0.91

0.83

1.00

0.90

−0.1

0M

alay

sia

0.97

0.99

0.97

0.95

0.86

0.80

0.94

0.92

0.92

0.88

0.91

0.90

0.90

0.89

−0.0

8Si

ngap

ore

0.93

0.98

0.97

0.96

0.92

0.89

0.93

0.86

0.82

0.87

0.88

0.91

0.92

0.90

−0.0

3So

uth

Afr

ica

0.97

0.99

0.95

0.97

0.90

0.83

0.88

0.82

0.87

0.95

0.94

0.95

0.92

0.91

−0.0

7U

nite

dK

ingd

om0.

960.

980.

970.

960.

960.

950.

940.

920.

920.

930.

940.

940.

930.

960.

00U

nite

dSt

ates

0.95

0.98

0.96

0.96

0.96

0.95

0.92

0.92

0.92

0.94

0.96

0.95

0.93

0.95

0.00

Com

mon

Law

Mea

n0.

970.

980.

960.

960.

920.

880.

920.

900.

880.

910.

920.

920.

930.

92−0

.04

Com

mon

Law

Med

ian

0.97

0.98

0.96

0.96

0.93

0.90

0.93

0.91

0.88

0.93

0.91

0.94

0.93

0.91

−0.0

3

Aus

tria

0.91

0.97

0.95

0.98

0.94

0.98

0.92

0.87

0.87

0.94

0.97

0.91

0.97

1.00

0.09

Den

mar

k0.

940.

940.

940.

960.

970.

940.

930.

890.

810.

850.

951.

000.

980.

89−0

.05

Finl

and

0.94

1.00

0.98

0.99

0.99

0.97

0.93

0.94

0.93

0.93

0.97

0.94

0.91

0.96

0.03

Fran

ce0.

900.

980.

950.

890.

940.

920.

900.

890.

880.

900.

930.

940.

930.

950.

05G

erm

any

0.90

0.93

0.90

0.87

0.91

0.90

0.86

0.85

0.82

0.82

0.86

0.95

0.91

0.91

0.02

Indo

nesi

a0.

970.

970.

980.

960.

420.

570.

920.

610.

810.

880.

850.

870.

820.

89−0

.08

Ital

y0.

790.

890.

950.

980.

960.

940.

940.

890.

850.

860.

850.

950.

950.

950.

16Ja

pan

0.95

0.95

0.97

0.98

0.98

0.95

0.93

0.97

0.97

0.94

0.97

0.98

0.98

0.98

0.03

Kor

ea0.

920.

940.

930.

860.

710.

820.

870.

890.

870.

900.

920.

930.

940.

930.

01M

exic

o0.

840.

700.

900.

900.

900.

590.

840.

870.

860.

920.

850.

951.

001.

000.

16N

orw

ay1.

000.

960.

940.

880.

880.

820.

840.

790.

800.

930.

940.

960.

880.

88−0

.12

Phili

ppin

es0.

830.

800.

870.

760.

700.

710.

670.

730.

830.

740.

880.

910.

900.

910.

07Po

rtug

al0.

900.

960.

870.

970.

940.

910.

970.

750.

930.

790.

930.

960.

930.

920.

02Sp

ain

0.91

0.98

0.97

0.96

0.91

0.97

0.93

0.96

0.94

0.98

1.00

0.98

1.00

0.97

0.06

Swed

en0.

941.

000.

980.

890.

920.

930.

910.

910.

850.

910.

930.

970.

970.

980.

04Sw

itzer

land

0.91

0.95

0.96

0.91

0.95

0.95

0.96

0.95

0.81

0.89

0.94

0.95

0.95

0.96

0.04

Civ

ilL

awM

ean

0.91

0.93

0.94

0.92

0.88

0.87

0.89

0.86

0.86

0.89

0.92

0.95

0.94

0.94

0.03

Civ

ilL

awM

edia

n0.

910.

960.

950.

940.

930.

930.

920.

890.

850.

900.

930.

950.

950.

950.

04A

ggre

gate

Mea

n0.

930.

950.

950.

930.

890.

870.

900.

870.

870.

900.

920.

940.

940.

930.

00A

ggre

gate

Med

ian

0.94

0.97

0.95

0.96

0.93

0.92

0.92

0.89

0.87

0.90

0.93

0.95

0.93

0.94

0.01

Dif

fere

nces

betw

een

com

mon

and

civi

llaw

mea

nsan

dm

edia

ns:p

-val

ues

Dif

fere

nce

inm

eans

0.00

0.04

0.17