AN APPRAISAL OF THE APPLICATION OF COST AND MANAGEMENT ACCOUNTING TECHNIQUES IN NIGERIAN...

146

1 CHAPTER ONE INTRODUCTION I.1 Background to the Study The growing complexity of modern production method results in greater capital investment, competition and modern market. For any company to be successful in such environment, it must have a good costing system. The attainment of this objective demands careful selection of a costing system that suites the production process of the company. Vickery (1971) has this in mind when he said that costing system is essentially analytical in nature, and it is therefore impossible to derive a system which suites all business. Hence, the costing system adopted by a manufacturing company must be designed to suite its production process.

Transcript of AN APPRAISAL OF THE APPLICATION OF COST AND MANAGEMENT ACCOUNTING TECHNIQUES IN NIGERIAN...

1

CHAPTER ONE

INTRODUCTION

I.1 Background to the Study

The growing complexity of modern production

method results in greater capital investment,

competition and modern market. For any company to be

successful in such environment, it must have a good

costing system. The attainment of this objective

demands careful selection of a costing system that

suites the production process of the company. Vickery

(1971) has this in mind when he said that costing

system is essentially analytical in nature, and it

is therefore impossible to derive a system which

suites all business. Hence, the costing system

adopted by a manufacturing company must be designed

to suite its production process.

2

A common misconception made by management of a

company is that a single definition of cost is

ideally suited to all types of manufacturing

decision. What a manager’s plan to produce must be

well known to him and always taken into account where he fails to

3

realize this, difficulty arises in determining thecost of production. This

gives rise to two reasons for the difficulty in

determining the cost of products produced. First,

the relationship between the cost incurred and

output produced is often difficult establish.

Secondly, cost may be assembled, combined and

reported in different ways.

In addition to inherent difficulties in

determining the cost of output, management fails to

recognize that different cost measurement are needed

for different purposes.. If cost information is to be

used intelligently, management must understand that

any cost figure has inherent limitation and that no

single method of arriving at cost will serve equally

well for all the various purposes for which

information is needed.

well known to him and always taken into account where he fails to

4

Modern technology makes it imperative for a firm

to cost its products. Lagne, (1984) contends that if

a firm fails to cost its products, the firm will

continually cease to exist.

Cost determination is essentially concerned with tracing of cost

5

through to the end department and product. This tracing can be in

terms of economic benefits, causes and effect of divergence from plan.

A costing system provides a reliable means of

determining the cost of production. An important

future of costing system is the firms measurement and

allocation of resources which the firm solves its

problem permanently in order to safeguard its

existence. Bhathachangy (1980) points out that from a

management point of view perhaps, the most important

use of a costing system is for revenue decision. But

in addition to that, elements of costs are not used

as a basis for logical accumulation of cost figures,

but also for diagnosis.

However, the costaccounting technique is

planning, credit control,

Cost determination is essentially concerned with tracing of cost

6

decision making, queuing theory etc. A firm with

these costing techniques or systems will produce and

sell at a high profit or at loss. This is due to

the fact that the firm fails to adopt a proper

costing system or the implementation of the system

adopted is weak.

Batty (1974) contends that a costing system adopted by any firm

investigated.

4

should be the most appropriate for the firmconcerned, where

management arrives at a decision without the aid

of adequate

and correct costing data, is to invite problems. More

so, where there is weakness in the implementation of

the system adopted, aims and objectives of the system

will be defeated.

Cost and management techniques serve as

useful tool for inventory

valuation, revenue decision making, cost control,

credit control and price setting when they have been

carefully designed and implemented. Apart from these,

costing system can provide the basis through which

the efficiency of the firms operations can be

measured. Such tools are standard costing and

Batty (1974) contends that a costing system adopted by any firm

investigated.

5

budgetary control.

Standard costing involves the detailed estimation

of the cost of a product before it is

manufactured so thatexpenditures

can be controlled during production, on

completion, the actual result will be compared with

the estimated result and variance ascertained

and

Budgetary control is the establishment of departmental budgets,

5

relating the responsibility of executive to therequirement of a policy,

and the continuous comparison of actual with

budgeted results either to serve by individual

action the objective of that policy or provide a

firm basis for revision .The reason for determining

variance is to enable costing system to not only

accumulate cost data but also to find out reasons for

them and taking appropriate action where

necessary( Arhuhie, 1989).

In order to understand the nature of modern

complex industry there is need for a better

understanding of costs and how they behave. However,

management of a firm may consider that setting of

price is a matter of judgment, play an important part

in deciding deficiencies. What is required is a

critical analysis of cost incurred. This in turn

Budgetary control is the establishment of departmental budgets,

6

requires the knowledge of costing techniques.

1.2 Statement of the Problem

The aim of the research work is to find out the

cost and management accounting techniques to be

established in manufacturing companies,

hence the life wire of every country’s economy lies upon the state of its

7

manufacturing companies. So if manufacturingcompanies adopt the

appropriate techniques, they will strive or do well

and also the state of the economy will improve. For

manufacturing companies to be healthy, it is a

function of how costing techniques is managed. It is

to this end that the researcher wishes to appraise

the various cost and management accounting techniques

such as planning, cost control, standard costing,

credit control decision making and the recently

emerged management techniques such as linear

programming, decision theory and queuing theory are

employed by manufacturing companies. The

aforementioned techniques that best suites

manufacturing companies and will be the key in the

appraisal of their application by manufacturing

companies

hence the life wire of every country’s economy lies upon the state of its

8

are:

Standard costing: Simply reporting cost to management does little to

help control costs. Cost accounting

can be improved upon by introducing a

formal system of standard costing.

Absorption costing: The common product costing practice of applying

9

fixed factory overhead to the goods produced.

Marginal costing: The variable production of product and services are

separated from the fixed cost and also a costing

mechanism for showing the effect of profit on change

in volume of output.

Budgetary control: Scientifically planning ahead is ameans of control in

which the actual state of affairs is compared to plan

for, so that appropriate action may be taken with

regards to deviation before it is too late.

The aforementioned techniques will be appraised

and seen how their application affects manufacturing

companies.

It is noted that many of the manufacturing

companies do not employ the use of these relevant

cost and management accounting techniques

Absorption costing: The common product costing practice of applying

10

aforementioned which hinders the effective decision

making in these organization.

To this end, the researcher seeks to find out

whether cost and management

accounting techniques are used in

manufacturing

companies and if they are not in use, how such companies would view

11

the importance of these usage forthe effective efficiency and

profitability of the companies .

1.3 Objectives of the Study

I. To find out the desirable conditions before

designing and installing a cost and management

accounting techniques for

manufacturing companies.

II. To ascertainhow costand management accounting

techniques designed for Benue Brewery Limited

assist management in planning controlling and

decision making

III.To determine the factor that hinders the

effective use of cost and management accounting

technique in Benue Brewery Limited

1.4 Research Questions

companies and if they are not in use, how such companies would view

12

I. Do manufacturing companies use the desirable

condition for designing and installing a cost and

management accounting techniques?

II

Do cost and management accounting techniques designed for Benue

13

Brewery Limited assist management in planning, controlling and

decision making?

III.What are the necessary factors that limit the

effective use of cost and management accounting

techniques in Benue Brewery Limited?

1.5 ResearchHypotheses

Akpa and Angahar definea research

hypothesis as a conjunctional

statement or general phase which cannot be determined

until it is proven.

In a related development, Asika, (1991) said a

null hypothesis is central in research and is the

hypothesis that is tested. The word No which is the

null hypothesis (Ho) will be stated in the negative

assertion from which its alternative (Ha) will be

II

Do cost and management accounting techniques designed for Benue

14

used for a positive assertion form.

Following the above, the research hypotheses will be thus:

Ho1:

manufacturing companies do not use the desirable condition

10

before designing and installing a cost and management

accounting technique.

Ha1: Manufacturing companies use the desirable

condition before designing and installing a cost

and management accounting technique.

Ho2: The cost and management accounting techniques

designed for Benue Brewery Limited do not

assist management in planning, controllingand

decision making.

Ha2: The cost and management accounting technique

designed for Benue Brewery Limited

assist management in planning,

controlling and decision making.

Ho3: Power, raw material, technology do not hinder

the effective use of costand management

Ho1:

manufacturing companies do not use the desirable condition

11

techniques in Benue Brewery Limited.

Ha3: power, raw material, technology hinders the effective use of cost

12

and management accounting techniques in Benue Brewery

Limited.

1.6 Significance ofStudy

The study when successfully completed will

be of great importance in the application

of cost and management accounting techniques and

those who are intending to adopt the technique. This

is because, the research will review the role of cost

and management accounting techniques to manufacturing

companies both private and public. This will also

enlighten manufacturing companies’ operators so as to

carry out the business effectively and efficiently.

The study will serve as a useful material for the

management of Benue Brewery Limited, researchers

and other companies in the

Ha3: power, raw material, technology hinders the effective use of cost

13

manufacturing industry.

In addition, this research work will be, an addition to the stock of

14

material available to the researcher in the area of cost and management

accounting techniques.

1.7 Scope of the study

The purpose or aim of this research is to

appraise the application of cost and management

accounting techniques as a powerful tool used in

manufacturing companies to evaluate their decision

making in order to achieve the predetermined

objective of the company.

However, due to large population of manufacturing

companies in Nigeria, the topic has been narrowed

down to Benue Brewery Limited which serves as a case

study for the research. Therefore, it is within the

researchers reach.

1.8 Definition of Terms

In addition, this research work will be, an addition to the stock of

15

I. Absorption Costing: A principle whereby the full

cost of production, direct labour, direct material

and manufacturing overhead are allocated to units

produced during the period.

II

Break- even- point: The point at which revenue fully covers all

16

expenditure and only that, no margin of profit exist.

III.Budget: A financial and/or quantitative statement

and approved prior to a defined period of time, of

the policy to be pursued during that period for the

purpose of attaining a given objective.

IV. Cost Allocation: The allocation of whole items of

costs to cost units or cost centres.

V. Cost apportionment: The cost allotment of a

proportion of items of cost to cost units or cost

centres.

VI. Cost control: The regulation by executive action of

the cost of operating and undertaking

VII. Queuing: It is simply the mathematical approach

to the analysis of waiting lines.

CHAPTER TWO

17

LITERATURE REVIEW

2.1 Introduction

This chapter is mainly concerned with reviewing

existing literature relevant to the topic, Appraisal

of the Application of Cost and Management Accounting

Techniques in Nigerian

Manufacturing Companies. The chapter

covers the following areas.

2.2 Conceptual framework

The growth in complexity in manufacturing process during the

20th and the 21st century give rise to cost other than

labour and materials as a significant part of total

cost of production. More so, the increasing use of

heavy power equipment and the developmentof mass

production techniques made the t recognition of

CHAPTER TWO

18

overhead cost a necessity. The effect of these led to

the development and expansion of cost accounting.

Between 1890 and 1915 cost accounting grew rapidly. The

19

formulation of cost accounting basicstructure and mechanic for

integrating the cost record and general accounts were

devised this period. The development resultedin

an improved method of calculating income

for industrial firms, inventory valuation and a

better matching of revenue and expenses.

These basic structure and

mechanism are briefly reviewed below.

2.3 Costing system

The general rule of cost determination is

the same in the various production circumstances,

the various production can be said to constitute

different costing system.

According to Horngren(1989), the primary

objective of cost accounting is to

Between 1890 and 1915 cost accounting grew rapidly. The

20

show the total cost of the articles the

manufacturer produces, and then analyses the

composition of the cost so that effective

control over such element of cost can be exercised.

To achieve this objective, organizations use costing

system. Batty (1974) defined a

system an established sequence of procedures for the purpose of

21

achieving specified objective at a minimum cost. The use of the word in

costing is usually limited to a major set of

procedures which result in achieving a number of

objectives.

It is also a formulation of the internal

financial information systems. Biggs(1972) realized

the importance of cost accounting and stated that

without a system of cost account, it is doubtful

whether a business of any size , nature can survive

in the intensely competitive

condition of today, but it must be emphasized that

just like no two business are

alike, even in the same industry,so no

ready-made system of cost account can be

provided to suite each and every business. The

underlying principles, conventions and objects of all

system an established sequence of procedures for the purpose of

22

costing systems are the same, but the application of

these principles and methods by which the objects are

to be achieved must vary with circumstance. A good

costing system should aim at accomplishing the

following purpose:

I.

To arrive at the cost of producing every unit, job, operation, process,

23

departments or services and develop cost standards.

II. To indicate to the management any

inefficiencies and the extent of various forms of

waste whether of materials and time expenses or in

the use of machines equipments and tools.

Accordingto Johnson and Kaplan (1987), a

management accounting system must provide likely

and accurate information to facilitate efforts to

control costs, to measure and improve productivity

and to devise improved production process.

The management accounting information must

also report accurate product cost so that accurate

pricing decision , introduction of new products,

abandonment of other variable overheads it demands

that fixed cost of the relevant periodare written

off in full against the aggregate contribution. The

I.

To arrive at the cost of producing every unit, job, operation, process,

24

contribution is the difference between the sales

value and the variable or marginal cost of a product

in a given period of time (CIMA) And this is the

base that many items make up the total cost of job

etc. vary in total volume of production, there

are others for example, many

overheads which are constant irrespective of the level of production.

25

Some of the above mentioned methods may be thebasis of a uniform

systemcosting.

Historical costing on the other hand is concerned

with past costs such as those already incurred. We

also have absorption costing. Absorption costing is

traditional approach to valuing inventory and

determining the cost of goods sold. The fixed cost of

production, direct labour, direct materials and

factory overheads are absorbed by or associated with

the time produced during the period.

2.4 Management Accounting

The management Accounting Practices

Committee(MAPC) of the National Accounting

Association(NAA) in the United

States define management accounting as “the process

overheads which are constant irrespective of the level of production.

26

of identification, measurement

, accumulation , analysis, preparation and

communication of financial information used

by management to plan , evaluate , and

control within an organization and to

ensure appropriate use of and

accountability for its resources.

Management accounting may also bedefined as “ the

19

application of professional skills in thepreparation and presentation of

accounting information in such a way as to assist

management in the formulation of policies and in the

planning , and control of the operations of the

undertaking” (Sizer,1996).

In the sense that management will be

interested in any information

produced by an accounting system, an accounting

could be management accounting whether it

was for example published accounts mainly for

external consumption or routine product cost for

internal use. However for practical purpose, such a

description is too broad and imprecise. It is to this

end that T. Lucy (1983) sees management accounting to

be concerned with the provision and integration of

information required by management of all levels for

Management accounting may also bedefined as “ the

20

the following purpose.

a. Formulating the policies of the organization

b. Planning the activities of the organization in the

short medium and long term, i.e. strategic through

operational planning.

c. Controlling the activities of the organization

20

d. Decision making i.e. the process of choosing between alternatives.

e. Performance appraisal at strategic departmental andoperational levels.

Management accounting therefore is primarily

concerned with data gathering( from external

and internal sources) analyzing,

processing, interpreting and communicating the

resulting information for the use within the

organization so that management can more

effectively plan, make decision and control

operations.

To carry out this task efficiently, the management accountant will

use data from financial and cost accounting systems,

he will conduct special investigations to gather

required data, he will use accounting techniques and

appropriate techniques for statistics and operations

c. Controlling the activities of the organization

21

research, he will take amount of the human elements

in all activities he will be aware of the underlying

economic logic, he will do all he will produce

information which is relevant for the intended

purpose.

2.5 Relationship of Management Accounting and CostAccounting

22

There is no realistic dividing line between cost accounting and

management accounting particularly with regard to

provision of information for planning and

control. Cost accounting is at a more basic level

than management accounting and in many organizations

is primarily concerned with the ascertainment of

product costs. Because the cost accounting system

is an importantsource of data for

management accounting purpose, organization,

student must be totally familiar with basic

accounting principles and methods and their

conventions and limitations.

2.6 Cost Accounting Techniques

In his effort to provide cost information for

managerial purpose and objective, the accountant

2.5 Relationship of Management Accounting and CostAccounting

23

uses a variety of techniques at his disposal.

Costing systems are used to monitor and evaluate the

element of cost used and to determine whether the

firms cost performance is worth meeting its

objectives. Thus, whether the firm survives,

stagnates

24

or dies, it depends on how it reacts to cost

information collected by costing system and

subsequently evaluated costing techniques.

Then choice of the techniques to be employed is

decided by the size of the firm,

costing system decision and objectives of

the management team themselves. Accordingly to

Harper (1996), costing technique depends upon the

purpose for which management requires the

information. Management needs information for a

variety of purpose such as control and price

determination and the exact purpose determine the

techniques to be used. Therefore, one costing

technique may be desirable for one particular purpose

and for another. They may not be exhaustive. Costing

techniques available to the management accountant

are: Standard costing, marginal costing, and

25

absorption costing, budgetary control, linear

programming, queuing theory and decision making.

23

2.6.1 Standard Costing

Batty (1974) defines standard costing as a

system of cost accounting which is designed to

show in details how much

each product cost to produce and sell when a

business is operating at a stated level of

efficiency and for a given volume of output. Simply

reporting actual cost to management to help them

control costs, cost accounting information can be

improved upon by introducing a formal system of

standard costing.

According to ICMA, standard costing is

predetermined cost calculated in relation to a

prescribed set of working conditions

correlating technical specifications and

scientific measurement of materials and labour to

24

price and wages rate expended to apply during the

period to which the standard cost is intended to

relate with an addition of an appropriate share of

overhead. It can be deduced from the above

definitions that standard costing is a target

which shows what is planned or expected. It is a

should be cost. Standard costing is analogous to

budgetary control while budgetary control deals with

the

whole organization, standard costing deals with units rather than the

24

whole organization. The standard cost of a product under normal

conditions. These implying very careful obsolete

product responses to rival product can be made.

Therefore costing system is a set of procedures

used to collect, assemble record and attach cost

incurred to the cost centre or product. They serve as

tools to collect and calculate costs related to

production of a particular output. The

characteristics and problems of companies differ

from company to company. Not surprisingly, cost data

can be accumulated, arranged and presented in

different forms. This results to the development of

various costing systems to be adopted. The

adoption of any kind of costing by an organization

depends on the following:

whole organization, standard costing deals with units rather than the

25

i. The kind of product or nature of activity it undertakes.

ii. The methods of manufacture in use( terminal or continuous)

iii.Suitability of a method to an organization in terms

of functional areas and the types of information

required by its executives.

It is possible however, to arrive at certain broadly defined

26

classifications of system which are suitable for various types of

industries. The most usual grouping of these classes is as follows.

1. Job (contract or terminal) costing, a

scientific costing where it is described to

obtain the cost of a number of contract

operations or undertaking which are often

distinguished

Batch costing where the order which may be for a

single article, or a batch of similar articles, is

the most convenient units of activity for purpose.

Terminal (contract costing).

2. Process costing involves an attempt to compute the

cost of a product for process, operations or

manufacture. The process costing example may be the

products produced by one or more number of

It is possible however, to arrive at certain broadly defined

27

processes. Variants of process costing are:

Single or output costing: The name given to the system used by

business supplying a product of the same type.

Operation (working) system costing, asystem of costing for an

28

undertaking which renderservices.

Departmental Costing, a costing for operating

department of a business or cost of products

emanating from a department Furthermore, two other

kinds of costs determined for special purpose

of control

and policy are :

i. Standard costing: It is the planned unit of

cost of the products, components or services

produced in a period. The standard cost may be

determined on a number of bases. The main use of

standard cost is in performance measurement, control,

stock valuation and in the

establishment of selling price (CIMA).

The techniques encourage

management and employees since it ensures that they

Operation (working) system costing, asystem of costing for an

29

have no plan ahead and also serve as a basis for

quoting for jobs or fixing prices.

ii. Marginal costing: It is looked upon as a decision making technique used

to determine the effect of cost on changes in the

volume of time and output in a multiproduct from

especially in the short run. Thus, it is a technique

which emphasizes the variable cost of a product

that is the

direct material, direct labour, direct expenses and assessment of the

30

quantities and price of all the resourcescombining to create each

product. When this has been accomplished, it is then

a relatively easy matter to modify the recording of

transactions in accounting system real difference

that arises between actual and standard cost of

material and labour. The actual cost of production

are still recorded , but are divided so as to

value all stock accounts at standards costs

,and to direct any difference between

actual and standard costs into

appropriate labeled variance accounts (Kenneth,

1974). The variance as analyzed into their causes and

point of incidence and corrective action taken.

Standard costing is most effective in industries

where products and processes are standardized, for

instance when there is only one product and where

direct material, direct labour, direct expenses and assessment of the

31

production processes are continuous.

Horngren(1990) holds the view that standard costing

procedures tends to be most effective when they are

accepted to process costing, mass continuous and

repetitive production tends themselves rather easily

to selling standards. He further stresses that,

the intricacies conflicts

between average and FIFO costing methods are eliminated by using

32

standard cost. In addition, standard cost approach facilitates controls.

2.6.2 Absorption Costing

According to Horngren, (1990), absorption

costing refers to the common costing practice to

applying fixed factory overhead to the goods

produced. Peters(1984) defined absorption costing as

a practice where all costs are charged to

process product or operation whether fixed or

variable cost with the current heavy equipment and

large investment in capacity , the growth of

overhead costs increased rapidly, it made

intuitive sense to include in unit costs of

inventory all the cost necessary to make it

saleable, including the cost of capacity with

absorption costing all production cost are treated

as period cost , that is each unit has a portion of

between average and FIFO costing methods are eliminated by using

33

the fixed cost. Absorption costing is the general

accepted in general financial reporting.

34

2.6.3 Marginal Costing

Marginal costing revolve around cost analysis

from a fixed and variable view points, with marginal

costing all variable production cost and all non-

production costs are treated as period cost.

Marginal costing is the procedure whereby the

variable cost of product and services are separated

from the fixed cost and also a costing mechanism for

showing the effect of profit on changes in the

volume of output. It can also be regarded as a

system of presenting costing to management to

facilitate effective cost control. It is prime

cost plus variable overhead.

It is also regarded as out of power cost or

additional cost incurred in producing one unit. One

of the great merits of marginal costing is that it

presents information in a form which is far less

35

rigid than most of the information presented on

absorption costing basis.

2.6.4 Budgetary Control

The word budget is derived from the French word “bongette”

denoting leather pounch in which money is kept for meeting envisaged

expenses. For our purpose, a budget may be defined as, a financial and

30

or quantitative statement prepared and approvedprior to a defined

time period expressing the plans, policies and

programmes to be pursued by a government enterprise

over the period for the purpose of attending some

given set of objectives.

According to A.L Buhari (2001) a budget

may be simply defined as a document indicating the

total and the composition of government expenditures

and the source from which such expenditures are

expected to be financed in the course of the year.

When a government plans its annual expenditures and

revenues in such a way that both are equal, the

budget is said to be balance.

According to Vikery(1971) budgetary control is

scientifically planning ahead and is a means of

expenses. For our purpose, a budget may be defined as, a financial and

31

control in which the actual state of affairs is

compared with the planned for , so that appropriate

action may be taken with regards to deviation before

it is too late. Budgetary control involves the

formulation of a plan for each branch of industrial

activity covering a fixed future period. It also

implies that managers are

responsible for mistake for deviation from budgeting plan. This is its

32

corrective functions. Within this context,budgetary control also

the

application of rules for the monitoring and

harmonizing of production, administration and general

business and non business activities of the firm in

accordance with the firms objectives.

Anintegrated budgetarycontrol system will

include a budgeted profit within

the framework of a master budget and

coordinated functional budget. The main purpose of

budgetary control is the calculation of an evaluation

of variance which is derived from the comparison of

actual with budgeted activity of the firm.

2.6.5 Queuing Theory

According to Azende T. (2011), queuing theory

responsible for mistake for deviation from budgeting plan. This is its

33

is used to study the phenomenon of waiting in line

longer than they have to. The theory allows

researcher to analyse several things such as curving

in line, waiting in line, and the time it takes to

serve customers.

According to Agburu J.T (2001), queuing theory refers to the set

34

of ideals or principles that relates to waitinglines. The set of concepts,

ideas, rules, principles and processes

that help to explain the phenomenal of

waiting lines known collectively as queuing theory of

waiting lines. This comes as a result of planning and

analysis of services capacity. There are several

queuing disciplines that havebeen

developed because of queuing theory. Five of which

are FIFO, LIFO, processor sharing and priority. FIFO

describes the practice of servicing customers in the

order they arrive in so that the person waiting

longest is served first while LIFO describes the

practice of serving customers so that the person who

come in last leaves first, such as in the process of

riding an elevation processor sharing serves

customers at the same time to that the average

According to Agburu J.T (2001), queuing theory refers to the set

35

waiting time for all customers is about the same. The

priority discipline serves the customers with the

highest priority first.

Consequently, any manufacturing company

designing a service system must have the queuing

theory in mind and weigh the cost of

producing a given services against thepotential cost of having

36

customers wait for services.

2.6.6 Linear Programming

Linear programming is one of the

most widely used quantitative decision

technique in business and industry in modern times.

Its application is becoming increasingly vast

in production. Linear programmingcanbe looked upon

as adecision making technique between and

among the variables which represent the different

events or phenomena happen to be linear (Agburu J.T

). The technique used in allocating resources where

more one key factor or constraint is involved. It is

a method of solving equations and can be programmed

for computer so that difficult and

multi-constraint problems will show scarce

resources in a firm can best be utilized.

37

2.6.7 Decision Making

Decision making is said to take place wherever

an individual, firm (known as decision maker) has to

choose one course of action from several alternative

courses of action.

According to Stoner et al (2000:239) decision

making is the process of identifying scheduling a

course of action to deal with a specific problem or

take advantage of an opportunity. This means that

decision making is a process, a theory, while

decision is the outcome of the process. Souza states

that “decision making is the process of making up

one’s mind”. Ivancevich et al (1994) sees

decision making as “a series of or chain of related

steps or interconnected stages that leads up to an

action or an outcome and assessment” .In the same

light though not in the same words, decision is seen

38

as the conscious effort made to achieve an objective.

The efforts are consciously made meaning that

environmental and contextual factors come to play in

decision making and its aim is to achieve an

objective. Decision making is a frequent phenomenon

in business, economics, politics other spheres of

human

life. The production manager for instance must decide that product to

39

produce, when to produce the product and how to produce the product

of interest.

2.7 Major Themes in Management Accounting

There are a number of important themes which

pervade all aspect of management accounting. These

themes are discussed below under the following

headings, future orientation, economic reality, goal

congruence, information system,

statistical operational

research technique, uncertainty.

2.7.1 Future Orientation

Much of the work of management accountant is

concerned with the future for example,

the provision of informationfor policy

formulation for planning for decision making. In

life. The production manager for instance must decide that product to

40

details, these activities may involve forecasting

future costs and revenue estimating future rates

of taxation, interest and inflation, considering the

reaction of market and revenue, competitors to the

introduction of new products

and price analyzing the likely charges in the cost structure and

41

productivity consequent upon the introduction of new methods and

equipment, assessing the effects of

government policies on the

operations of the organization (CIMA).

2.7.2 Economic Reality

Accounting data and information are used to

represent the underlying economic activities of the

organization which include buying, materials, selling

product, manufacturing and financing the

organization. Accordingly, it is essential that the

records of past performance and the information

derived from the records which is used to guide

future planning and decision making

represents the underlying economic realities in

clear and unambiguous manner unfettered by

and price analyzing the likely charges in the cost structure and

42

accounting conventions.

Victor Smith (2011) this the direction we need

to go creating a model of

economic that takes with accounts a greater

range values than simple consumerism, part of the

problem with the world today is

that we have allowed ourselves to be defined first identity is what

43

derives progress and innovations. The growthparadigm as evidenced

by nature is not about expansion in the usual term

but about increasing the complexity of interacting

systems and about achieving balance between those

systems. Humans have done a poor job at finding that

balance because we have choosen to look at native

primarily as a resource to fuel our own needs, rather

than adding as a matter partners in the ecological

web.

Standard-issues economics is now just at the

stage of getting parts its own adolescence.

Hopefully, it really to grow up now and embrace a

nuanced system of values than just consumption for

its own sake. There are many out there but we need to

be tied into that limit of business whose core values

include maintaining natural system, respect for

that we have allowed ourselves to be defined first identity is what

44

employees and their contributions, community values,

and a style of innovation that is more all

encompassing than just the bottom line.

2.7.3 Goal Congruence

45

This simply means that the management accounting system

should encourage all employees, including

management to act in a fashion which

contributes to the overhead objectives of

the organization, and objective would in ideal

circumstance coincide. The system and the approach

adopted by the management accountant should

motive staff by means of

genuine participation, goal communication and

rapid feedback and in much other way. Goal congruence

is a result of the aliment of goals to achieve an

overarching mission.

Goal congruence is one of the most important

functions of management to harmonise as far as it is

practicable the goals of the participants and sub-

2.7.3 Goal Congruence

46

units with those of the organization as a whole. This

function is known as goal congruence (Victor Smith

2011).

2.7.4 Information System.

47

According to Begnon- Davies P (2009) informationsystem is any

combination of information technology and

people activities

that support operations, management and decision

making. In a broad sense, the term information

system is frequently used to refer to the

interaction between people, processes, data and

technology. In this sense, the term is used to refer

not only to the information and Communication

Technology (ICT) than an organization uses but also

to the way in which people interact with this

technology in support of business processes. The

components are people, hardware, software, data and

network.

An organization comprise a number of information

2.7.4 Information System.

48

system or networks frequently computer based

sometimes .These are separate information system

dealing with sales, production, personnel, finance

and other matters .Sometimes there is integration of

these sub-system. Rarely, if ever, is the

information system a totally integrated one

dealing with all aspect of management

requirement for planning,

control and decision making. In any organization, the management

40

accounting system is designed in accordancewith the principles of

system theory otherwise they will be less efficient.

An example of this could be where a poorly designed

budget system causes a manager to act in a manner

which, although advantageous to the department, but

detrimental to the overall objective of the

organization (Kroeake DM,

2008).

2.7.5 Statistical and Operations Research Techniques

According to Perty Bridman, it is a discipline

that deals with the application of advanced

analytical methods to help make

better decision. It is often considered to

be a sub-field of mathematics. Perty brought

operational research to bear on problem in physics in

control and decision making. In any organization, the management

41

the 1920s and he later attempt to extend this to the

social sciences.

Stafford Beer (1967) hold it that research is

based on principles, strategies and numerical

algorithms to improve an organization ability

to enact rational and meaningful management decisionby arriving at

42

optional or near optional solutions to complex decision problems.

Certain aspects of management accounting,

particularly in the area of planning and decision

making do level themselves to the use of appropriate

statistical and operational research techniques. The

use of such techniques does not alter the underlying

objective of management accounting but helps to

improve or refine a particular solution. Frequently,

these techniques are implemented by means of computer

packages and to interpret and present the result

produced.

There are numerous areas where such

techniques have been found to assist management

accounting. Examples include, statistical forecasting

cost and sales extrapolations, linear

to enact rational and meaningful management decisionby arriving at

43

programming for resources allocation to provides

such as production, planning economic order quantity

models to help solve inventory control problems and

so on.

It is important that the management accountant has sufficient

44

familiarity with such techniques to recognize wherethere user can be

beneficial and cost effective. The use of relevant

techniques should be seen as a normal part of the

work of modern management accountant (Gerald E

Thompson (1982)

2.7.6 uncertainty

Uncertainty according to Saasongu Nongo (2005) as

a situation occurs when a decision maker is not aware

of all possible alternatives and for those

alternatives that are identified information

is not adequate to permit certain

identification of probable outcomes

(consequences). Under this situation, the decision

maker may have strong options but lack adequate

information to estimate the likelihood of different

It is important that the management accountant has sufficient

45

outcomes or their alternatives. The influence of

uncertainty usually increases the longer the planning

or decision period but it is frequently present in

short run circumstance as well. There may be

uncertainty about the measurement of data, material

cost, the action of competition, the economic

climate, wage rate, performance level, the

rate of inflation or indeed any of the meriads of factors involved in a

46

decision.

CHAPTER THREE

47

RESEARCH METHODOLOGY

3.1 Introduction

A research is a problem induced activity. It is

simply a way in which scholars investigates

various problems with a view to

understanding and providing explanation. Aver(1958)

contended that it is essentially based on scientific

inquiry whose procedure s include observation of the

available factors relating to a particular followed

by the formulation of a theoretical solution which

is used as a basis for experimental practical

testing of theory to obtain

evidence for a conclusion or

generalization which may or may not validate the

theory.

CHAPTER THREE

48

A research methodology therefore, is the plan by

which a research activity is to be carried out.

Each step in the plan, the activities or subject

to be used, the plan are all summarized under the

methodology

.In fact, according to Abarry, 1986 the methodology iswhere the whole

research is based. He further outlines variousmethods that can be

49

employed by researchers.

However, the appropriate method adopted in this

research is survey research and descriptive methods.

This chapter will also consider some data

collection method with a particular attention to the

most suitable of the study.

3.2 Research Design

Research design according to Osuala, ( 2001) is

the blueprint or plan which determines the nature

and scope of the study carried

out or proposed. The research design provides a

guideline or framework for an investigation in the

process of trying to find a solution. it is the main

plan for the research project.

This study by nature is a survey research.

According to Agburu (2001) survey research may be

research is based. He further outlines variousmethods that can be

50

described as the research involves large and small

population from which sample are chosen or studied

in a bid to find out

relative incidence, distribution and

interrelation of

sociological or psychological variables. A survey research may also be

51

called a sample survey.

The adoption of survey is as a result of the

ease with which the relationship between variables

can be developed and hypotheses tested. The method

will logically explain the outcome of values as it

relates to the statement of the problem.

3.2.1 Population andsample size

The first step in obtaining a sample is to define

the population. By this, it means the identification

of characteristics, which members of the universe

have in common and which would identify each

unit as having a member of a particular group

(Osuola, 1993) to make for an effective research

work, the best way is to study the entire population

of elements (people/ things) or to study only a

portion of the elements from the large population

sociological or psychological variables. A survey research may also be

52

of them which is called a sample( Black,

1976).

The population of this study is the staff of Benue Brewery Limited,

53

to ensure that every staff is adequatelyrepresented, as the sample size,

purposive sampling technique wasemployed.

Thus, out of 230 staff of the four departments,

questionnaires were given to each

department: production, finance,

marketing and engineering.

3.3 Method Of Data Collection

Data, according to Abarry, (1986) are not truth

in them but are a manifestation of a given situation.

A researcher seeks an explanation by subjecting the

data to his inquisitive mind to facilitate his work.

Data used for this research could come from two broad

sources namely primary and secondary sources. The

researcher in the course of collection of data makes

use of both primary and secondary data.

The population of this study is the staff of Benue Brewery Limited,

54

The main instrument used in the collection of primary data was

questionnaire administered to staff of the four

departments of Benue Brewery Limited. The

questionnaire which is the source of primary was

designed in such a way that it permits comments from

the respondents.

The secondary data refers to information collectedby other agencies

55

but with the utility for the research in his studies(Abarry, 1986). In this

research, secondary data will be gathered from the

four departments of the Benue Brewery Limited,

libraries, journals, articles, company

records, and textbooks.

3.3.1 Method of Data Analysis

The analysis of the raw data of a research is the

means by which the researcher problem is answered and

the hypotheses tested. Various methods of data

analysis include the chi- square, correlation

analysis and the Coehran’s question test. The

method used varies with the nature of the

research work.

For the purpose of this research work, the chi-

square test will used. The response from the

administered questionnaire was tabulated and

The secondary data refers to information collectedby other agencies

56

analysed. Relevant question will be used to test the

various hypotheses using the chi-square statistics.

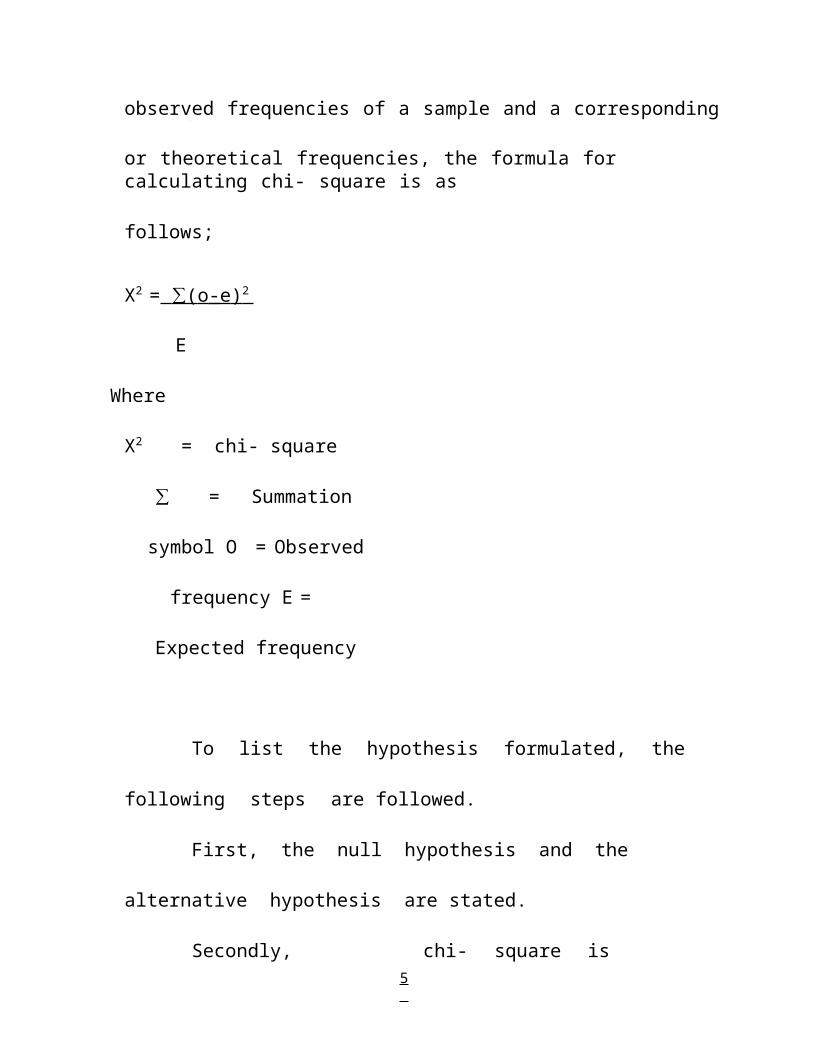

According to Osuala ( 2001) the chi square is

frequently used in testing a

hypothesis concerning the difference

between a

set of

observed frequencies of a sample and a correspondingset of expected

57

or theoretical frequencies, the formula for calculating chi- square is as

follows;

X2 = (∑ o -e ) 2

E

Where

X2 = chi- square

∑ = Summation

symbol O = Observed

frequency E =

Expected frequency

To list the hypothesis formulated, the

following steps are followed.

First, the null hypothesis and the

alternative hypothesis are stated.

Secondly, chi- square is

observed frequencies of a sample and a correspondingset of expected

58

computed between the

observed frequency and the expected

frequency.

Thirdly, based on the decision rule, the nullor the alternative

50

hypothesis is accepted or rejected based on the chi- square result.

The level of significance is 5%.

Decision rule:

The general rule is that where chi- square (x2)

calculated is greater than the tabulated value; the

null hypothesis is accepted while the alternative is

rejected.

Declaration of Known Problem with Design

The researcher used questionnaire as his

instrument of data collection.

i. The major problem encountered here is that the

respondent is left alone to freely respond to the

question and would not usually fill in the right

thing because since his interviewer is not there

with him to read his non-verbal question, he hides a

lot of facts.

Thirdly, based on the decision rule, the nullor the alternative

51

ii. Some respondents would not return the questionnaire

administered to them.

52

CHAPTER FOUR

DATA PRESENTATION, ANALYSIS AND INTERPRETATION

4.1 Introduction

It was established in the preceding chapter

that data would be collected using questionnaires and

the hypotheses stated in chapter one tested using

chi-square (x2) model test. This chapter therefore,

presents analyses and interprets data collected from

the field work using questionnaires. The hypotheses

are also tested and results interpreted.

4.2 Data Presentation Analysis

The data presented and analysed here are those

obtained from questionnaires administered to

respondents. Hence, the table hereunder shows the

total number of questionnaires

administered to the respondents including

53

those issued and those returned respectively.

52

TABLE 1: QUESTIONNAIRES ISSUED AND RETURNEDRespondent Questionnaires

issuedQuestionnairereturned

Percentage ofreturned questionnaires

Top managers 90 86 40%

MiddleManagers

85 80 37%

Employees 55 50 23%

Total 230 216 100%

Source: Field Survey, 2012.

Table 1 above indicates that out of the 230

questionnaires that were issued, only 216

questionnaires were returned. The analysis as well as

interpretation of results will henceforth

be based on the 216 questionnaires

that were returned. The table below represents the

responses collected from the respondents from various

questions asked.

53

Question 6. Do cost and management accounting techniques

help in production process?

TABLE 2: TABULAR PRESENTATION OF DATA COLLECTED

Respondents Yes No Total

Top managers 16 70 86

MiddleManagers

66 14 80

Employees 39 11 50

TOTAL 121 95 216

Percentage 56% 44% 100%

Source: Field Survey, 2012.

The above indicates that 121 (representing 56%)

out of total number of 216 respondents submitted that

cost and management accounting techniques help in

production processes. Whereas, 95

(representing 44%) out of the 216 respondents

maintained cost and management accounting

techniques do not help in

production processes.

54

Question 7: Does cost and management accounting

help in planning, controlling and decision making in

Benue Brewery Limited?

54

PRESENTATION OF DATA COLLECTED.

Respondents Yes No TotalTop managers 38 48 86MiddleManagers

70 10 80

Employees 46 4 50Total 154 62 216Percentage 71% 29% 100%Source; Field Survey, 2012.

The table above shows that out of a total of 216

respondents, 154 (representing 71%) submitted that

cost and management accounting help in planning,

controlling and decision making in Benue Brewery

Limited. However, 62 respondents (29%) rejected,

submitting that cost and management accounting does

not help in planning, controlling and decision making

in Benue Brewery Limited.

Question 8: Are desirable conditions used for

designing cost and management accounting system in

Benue Brewery Ltd? Consider again the table below:

55

TABLE 4: PRESENTATION OF DATA COLLECTED

Respondents Yes No Total

Top Managers 36 50 86

MiddleManagers

70 10 80

Employees 43 7 50

Total 149 67 216

Percentage 69% 31% 100%

Source: fieldsurvey, 2012

The above shows that 149

(representing 69%) out of

the 216 respondents saw that

desirable conditions are used for designing cost and

management accounting system in Benue Brewery Ltd.

The remaining respondents (67) submitted that

desirable conditions are not used for designing cost

and management accounting system in Benue Brewery

Ltd.

Question 9: Do power, raw material, and

56

technology hinder the effective use of cost and

management accounting techniques in Benue Brewery

Limited?

56

TABLE 5: PRESENTATION OF DATA COLLECTED

Respondents Yes No Total

Top Managers 39 47 86

MiddleManagers

71 9 80

Employees 45 5 50

Total 155 61 216%

Percentage 72% 28% 100%

Source: field survey, 2012.

The table above shows that 155 respondents

(representing 72%) out of the 216 respondents

submitted that power, raw material, technology hinder

the effective use of cost and management accounting

techniques in Benue Brewery Limited.61

respondents (i.e 28%) disagreed,

holding that power, raw material, technology do not

hinder the effective use of cost and management

accounting techniques in Benue Brewery Limited .

Question 10: Does production affects the profit of thecompany?

TABLE 6: PRESENTATION OF DATA COLLECTED.

57

Respondent Yes No Total

Top Managers 61 25 86

MiddleManagers

16 64 80

Employees 42 8 50

Total 119 97 216

Percentage 55% 45% 100%

Source: Field Survey, 2012.

Table 6 shows that 119 respondents (equivalent

to 55%) out of the 216 respondents submitted that

production affect the profit of the company. On the

other hand, 97 respondents (representing 45%) held

that production does not affect the profit of the

company.

4.3 Testing of hypotheses.

It was established in chapter three (3) that

hypothesis will be tested at 5% error tolerance

The decision rule still remains that the

TABLE 6: PRESENTATION OF DATA COLLECTED.

58

null hypothesis will be accepted if calculated chi-

square (x2) is less than the chi-square tabulated,

otherwise it be rejected.

Tabulated value of chi-square:

59

DF=(R-1)(C-1)

= (2-1) (3-1) =2

From the chi- square distribution table, the value

of chi square under DF2 and 5% tolerance error is

5.99.This figure will henceforth be marched with the

calculated values of chi-square on each hypothesis to

ascertain its acceptability or otherwise.

HYPOTHESIS ONE(1)

Ho1: manufacturing companies do not use the

desirable condition before designing and installing

a cost and management accounting technique.

Ha1: Manufacturing companies use the desirable condition

before designing and installing a cost and management

Tabulated value of chi-square:

60

accounting technique.

Related question from the questionnaire

(question8): Are desirable conditions

used for designing cost and management

accounting system in Benue Brewery Ltd? Consideragain the table

61

below:

Table 7: Table of Responses

Respondent Yes No Total

TopManagers

36 50 86

MiddleManagers

70 10 80

Employees 43 7 50

Total 149 67 216

Percentage 69% 31% 100%

From the above table, expected values may be calculated thus;

Row/Column R ow Tot a l X C ol u mn Tot a l

1, 1

Ground total

1 4 9 x 8 6 21

= 59

1, 2 (149 x 80) ÷

216 = 551, 3 (149 x

50) ÷216 = 35

2, 1 (67 x 86) ÷

216 = 272, 2 (67 x

80) ÷216 = 25

2, 3 (67 x 50) ÷

216 = 16

Table 8: ContingencyTable

60

Row/Column O E O-E (O-E)2 (O-E) 2

1, 1 36 59 23 529 91, 2 70 55 15 225 41, 3 43 35 8 64 22, 1 50 27 23 529 202, 2 10 25 -15 225 92,3 7 16 9 81 5

X2 = 49

Since the calculated chi-square (x2c) is greater than the chi-square

(x2t), that is, 49>4.99, the nullhypothesis will be rejected.

HYPOTHESIS TWO (2)

Ho2: The cost and management accounting techniques

designed for Benue Brewery Limited do not

assist managementin planning, controlling and

decision making.

Ha2: The cost and management accounting

technique designed for Benue Brewery Limited assist

management in planning, controlling and decision

making.

1, 1 (154x86) ÷ 216

= 611, 2 (154x80) ÷

216= 5

71, 3 (154x50) ÷ 216

= 362, 1 (62 x 86) ÷

216= 2

52,2 (62 x 80) ÷216

= 232,3 (62 x 50) ÷

216= 1

4

61

Related question from the questionnaire (question

7): Does cost and management accounting help in

planning, controlling and decision making in Benue

Brewery Limited?

Table 9: Table of Responses

Respondents Yes No TotalTop managers 38 48 86MiddleManagers

70 10 80

Employees 46 4 50Total 154 62 216Percentage 71% 29% 100%Source: Table 9Calculation of expected values (expected frequencies)

Row/Column R ow Tot a l X C ol u mn Tot a l Groundtotal

Table 10: ContingencyTable

62

Row/Column O E O-E (O-E)2 (O-E) 2

1, 1 38 61 -23 529 91, 2 70 57 13 169 31, 3 46 36 10 100 32, 1 48 25 23 529 212, 2 10 23 -13 169 72,3 4 14 -10 100 7

50

Since the calculated chi-square (x2) is greater than the x2 tabulated,

the null hypothesis will be rejected.

H Y PO T H E S I S T H RE E ( 3 ):

Ho3: Power, raw material, technology do not hinder theeffective use of

cost and management techniques in Benue Brewery Limited.

Ha1: power, raw material, technology hinders the

effective use of cost and management accounting

techniques in Benue Brewery Limited.

Related question from the Questionnaire(question 9):

63

Do power, raw material, technology hinder the effective use of cost and

management accounting techniques in Benue Brewery Limited?

Respondents Yes No Total

Top Managers 39 47 86

Middle

Managers

71 9 80

Employees 45 5 50

Total 193 23 216

Percentage 89% 11% 100%

Calculation of Expected Values (EV)

1, 1 (117 x 86) ÷ 216 = 47

1, 2 (117 x 80) ÷ 216 = 43

1, 3 (117 x 50) ÷ 216= 27

2, 1 (97 x 86) ÷ 216 = 39

Related question from the Questionnaire(question 9):

64

2, 2 (97 x 80) ÷ 216 = 36

2,3

(97 x 50) ÷ 216

= 23

65

Row/Column O E O.E (O-E)2 (O-E) 2

1, 1 61 47 14 196 41, 2 16 43 -27 729 171, 3 42 27 15 225 82, 1 25 39 -14 196 52, 2 64 36 28 784 222,3 8 23 -5 225 10

X2c = 66

From the contingency table above, the chi-square (x2) is 66. This is

greater than the tabulated chi-square (x2) which is

5.99. Therefore, the null hypothesis is rejected.

4.4 Interpretation Of Results

The results obtained from testing the

hypotheses are quite revealing as briefly elaborated

hereunder.

In testing hypothesis one (1), the null

hypothesis, which states that manufacturing companies

do not use the desirable condition before designing

2,3

(97 x 50) ÷ 216

= 23

66

and installing a cost and management accounting

technique was rejected. This implies that

manufacturing companies actually use

the desirable conditions before designing and installing a cost and

67

management accounting technique. Hence, thealternative hypothesis

which states that manufacturing companies use the

desirable condition before designing and installing a

cost and management accounting technique has been

accepted.

Similarly, in the second hypothesis, the null

hypothesis, which states that cost and management

accounting techniques designed for Benue Brewery

Limited do notassist management in

planning, controlling and decision making, has

been debunked. This portends the fact that cost and

management accounting techniques are essential tools

for planning, controlling and managerial decision

making, a position which goes in tandem with the

alternative hypothesis.

Finally, the result in testing hypothesis three

the desirable conditions before designing and installing a cost and

68

(3) has it that Power, raw material, technology do

hinder the effective use of cost and management

techniques in Benue Brewery Limited. To this wise,

the null hypothesis, which states that power, raw

material, technology do

not hinder the effective use of cost and management techniques in

69

Benue Brewery Limited has been rejected.

CHAPTER FIVE

70

SUMMARY, CONCLUSIONS AND RECOMMMENDATIONS

5.1 Introduction:

In this concluding chapter, we shall

discuss the research findings and make

recommendations to the company (Benue Brewery

limited). Finally, we shall draw conclusions and make

suggestions for further studies by interested

persons.

5.2 Summary of findings

The main data sources for this research are

company records and questionnaires. The data gathered

by using company records enabled us to compare with

the system of costing in operation at Benue Brewery

Limited. The data gathered by using

questionnaires administered to the staff of

CHAPTER FIVE

71

the company enabled us to have insight of the costing

system used by the company. After the comparison, we

discovered that the company is operating process

costing system which is the right costing system.

Although process costing is suitable for the company taken into

72

consideration the mode of operation, processcosting has not been

satisfactorily followed. The following observations

were made during the study. The cost of goods sold to

the customers is not based on the costing

records but purely on the prices list which

management review from time to time.

It is also important to note that the price the

company is selling her product is much lower than the

actual cost of production based on the production

report.

Benue Breweries does not maintain stock level

by using reorder level, minimum stock level and

maximum stock level. However the company carries out

weekly stock summary.

The method of material costing used by the

Although process costing is suitable for the company taken into

73

company is first-in- first-out. The company keeps

attendance register for their staff on a daily

basis. Also the company maintains a constant

check on the

number and types of its employees are generally paid on a monthly

74

basis.

Breweries Limited recognized expensesas being either

common to more than one cost centre like electricity

and water or just one.The company also

recognized three overheadsnamely

administration overheads, production

overheads and marketing overheads. The

company considers all losses as normal and their cost

is borne by the good production.

The company calculates its unit costs on a

monthly basis. at the end of the month, the cost of

material and labour for all the processes is added

together to determine the total cost. All costs

incurred during the month are divided by the number

of units produced during the month.

number and types of its employees are generally paid on a monthly

75

It is more economical for Benue Breweries

limited to produce larger beer. This is because they

always of high demand by the customers there

constitute a higher percentage of sales mix and sales

prices.

5.3 Generalization of findings

70

The main purpose of a costing system is to analyze and allocate

the expenditure of a business in such a way that is

possible to ascertain the cost of each job, contract,

or process carried out, but this is by no means its

sole function. A well established

costing system will discharge functions like

providing management making and in forward planning.

A properly established and implemented costing

system also helps management to distinguish

between economic and uneconomicactivities

include sources of wastages, provides

information in order to facilitate comparisons with

estimates provides a basis for the preparation of

estimates and fixing of selling price and

revealing the cause of increase or decrease in the

profit shown by the management accounts.

5.3 Generalization of findings

71

This is particularly important if the business

is to service and also its short and long term

objectives. To achieve this aim, the Benue Brewery

Limited established process costing. Process costing

is suitable

for the company mode of production; these areweaknesses in the

72

implementation of the system. This is because of thefollowing reasons:

1. The material control system is not efficient, this

is because the company does not determine stock level

of its raw materials

2. The method of calculating the cost of processing

is not desirable since the company does trace its

neither profitability nor losses to their sources.

3. Price of the product is fixed arbitrarily without

making reference to the costing statement resulting

in selling below cost prices.

4. The company does not usestandardcosting techniques which

compares the “ standard cost ” of each product or

services which the actual cost determines the

inefficiency of the operation so that remedial

attention may be taken immediately.

for the company mode of production; these areweaknesses in the

73

5. The company does not use

marginalcosting techniques which differentiate

variable from fixed cost that helps to determine as

to whether producing an additional unit cost are

directly responsible for

the output and the excess needed to cover both fixed and overheads

74

costs of units produced and the expected profit.

6. The company makes budget which are on intuition. The

major problem this has caused is the company produces

more than it can sell resulting in overstocking of

finished products.

7. The company is not making much profit. This is

primarily because the selling price of her products

is even lower than the cost of production. This is

due to the fact that the company has to tie price in

order to compete with other breweries.

5.4 Recommendations

The essence of process costing is the help in

classification, recording and appropriate allocation

of expenditure for determination of the cost of

individual units produced .The cost is then related

to sales values management in decision making.

the output and the excess needed to cover both fixed and overheads

75

Therefore, based on the weaknesses enumerated in

evaluation of findings, the following are

recommended in order to strengthen the costing

system in use so that

management can derive all possible benefitsfrom implementing

76

process costing system.

1. The company should determine stock level by using

mathematical or statistic method in setting stock

level, maximum stock level and minimum stock level in

selling out these stock levels, the following factors

must be taken into consideration:

a. The rate of consumption of the materials.

b. The time necessary to obtain delivery of

the raw materials. c. The re-order quantity

for the material :

The formula are

Max C=maximum consumption during the period

Max R.P = maximum re-order period.

It should be noted that in re-fixing the re-order

level, the worst possible expected condition are

used.

management can derive all possible benefitsfrom implementing

77

2. The price of the product of the company should

based on the costing statement and not arbitrary.

78

3. The company should trace the profit and losses to their sources.

4. The company should introduce standard costing

techniques: this will help to determine inefficiency

of the operation so that remedial action may be taken

immediately.

5. The company should introduce marginal costing

techniques: this will enable the company to

determine which is directly responsible for output

and the additional unit needed to produce at expected

profit.

5.5 Recommendation for further studies.

1. More work can be carried out on method of fixing

the stock level using mathematical or statistical

method.

2. Also more work can be carried out to establish the breakeven point for

Benue brewery limited.

79

5.6 Limitation of the Study

Many constraints sufficed in the course of

carrying out this study among which were those

relating to finance, time inability to get certain

data which were not available or considered official

secret by the company.

75

The company busy schedule due to the nature of their

job requirement made it difficult for me to get

access to the respondents staff and timely

administration and collection of questionnaire.

76

REFERENCES

Abarry (1986) Understanding Research, LongEssay and Thesis

Writing. Nigeria . Unijos press limited.

Aver J.J (1959). An Introduction to Research. Newyork. Harper and

Row.

Azende T. (2011) Basic Statistics andQuantitative Techniques .

Makurdi. Aboki publishers.

Batty S (1974) Advanced Cost Accounting. London Maacdonald and

Evans ltd.

Bhattachagg et al (1980) Accounting for Management. New Delhi, vikas

Publishing House ltd.

Carter J. C (1983) Cost Control. New Jersey Prentice Hall.

Dupree D. (1978) Principles of Accounting. London, Matthew Mardor

Erhirhie wud (1989) Unpublished Lecture Manual, Unijos.

77

Hornegren C.T. et al(1990) Cost and Management Accounting, a

Managerial Emphasis. New Delhi. Prentice Hall.

John C.T et al (1990) Cost Accounting a Managerial Emphasis. New

Delhi Prentice Hall.