Ajinomoto - I3investor

18

12 February 2018 Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 1 of 18 A well-seasoned company We initiate on Ajinomoto Malaysia with a HOLD and TP of RM20.30 based on 20x FY19E PE. Ajinomoto is a manufacturer of monosodium Glutamate (MSG) and other flavored seasonings. We like it for its brand name and its dominant share in Malaysia. While Malaysia market’s growth is supported by urbanization, we think its focus on exports, especially to the Middle East provides exciting growth opportunities. Ajinomoto- a market leader with trusted brand name Established in 1961, Ajinomoto Malaysia is a leading Monosodium Glutamate (MSG) producer with 80% market share in Malaysia. Approximately 73% of sales are derived from the consumer segment, which include MSG products and flavoured seasonings. The remainder comes from the industrial segment whereby Ajinomoto sells functional savoury seasoning products to processed food producers. Commendable track record in Malaysia Ajinomoto Malaysia’s sales in Malaysia has grown at a CAGR of 5.3% over FY09-17, which is in tandem with the growth rate of F&B establishments and processed food sales volume. Despite dominant market share of over 80% in MSG, we believe there is growth opportunities for Ajinomoto, forecasting its sales to grow at 5% CAGR over FY17-22E. This is on the back of more product offerings as the flavoured seasonings’ market is still fragmented and enjoys higher growth rate. Growing demand for processed food and growing F&B food service should also support its growth. Promising outlook in export sales Overseas sales accounted for 40% of total sales in FY17 and its products are mainly exported to Middle East and the Asia region. We are positive on the export outlook as MSG consumption in Asia is expected to grow by 4.1% p.a. over the next 2-3 years. Ajinomoto’s “halal” certified product status will be an added advantage, shortening the export lead time to the Middle East. Initiate coverage with a HOLD rating and TP of RM20.30 We initiate coverage with a HOLD rating and TP of RM20.30 based on 20x FY19E PE. We think that with estimated earnings growth of 13% per annum for FY17-22E and dividend yield of 2.3-2.8%, the current share price is fairly valued and it is in line with valuations of Malaysia’s F&B consumer space. Downside risks include price competition, substitution risk, and cost risks. Earnings & Valuation Summary FYE 31 March 2016A 2017A 2018E 2019E 2020E Revenue 400.2 419.9 452.0 487.2 525.6 EBITDA 59.4 70.5 72.6 82.3 87.8 Pretax profit 53.9 211.5 73.4 82.1 88.1 Net profit 40.8 187.5 55.0 61.6 66.1 EPS(RM) 0.67 3.08 0.90 1.01 1.09 PER 29.2 6.4 21.7 19.3 18.0 Core net profit 43.8 42.1 55.0 61.6 66.1 Core EPS(RM) 0.72 0.69 0.90 1.01 1.09 Core EPS growth(%) 46.5 (3.9) 30.7 12.0 7.3 Core PER 27.2 28.3 21.7 19.3 18.0 Net DPS(RM) 0.34 1.55 0.45 0.51 0.54 Dividend Yield(%) 1.7 7.9 2.3 2.6 2.8 EV/EBITDA 17.3 15.1 15.2 13.0 11.9 ROE(%) 13.3 39.5 12.6 13.1 13.1 ROA(%) 11.1 35.2 11.0 11.5 11.4 Debt to equity(x) Net cash Net cash Net cash Net cash Net cash BPS(RM) 5.06 7.81 7.16 7.72 8.30 PBR(x) 3.9 2.5 2.7 2.5 2.4 Chg in EPS (%) - - - Affin/Consensus (x) n.a. n.a. n.a. Source: Company, Affin Hwang estimates Initiate coverage Ajinomoto AJI MK; AJI Sector: Consumer RM19.62 @ 9 Feb 2018 KLCI: 1841.02 HOLD Upside: 3% Price Target: RM20.30 Previous Target: - Price Performance 1M 3M 12M Absolute -4.7% 7.7% 47.3% Rel to KLCI -5.7% 2.6% 35.4% Stock Data Issued shares (m) 60.8 Mkt cap (RMm)/(US$m) 1212.3/310.5 Avg daily vol - 6mth (m) 0.0 52-wk range (RM) 13.42-25.21 Est free float 43.8% BV per share (RM) 6.67 P/BV (x) 2.99 Net cash/ (debt) (RMm) 263 ROE (2018E) 13% Beta -0.04 Derivatives Nil Shariah Compliant YES Key Shareholders AJINOMOTO CO INC 50.1% FMR LLC 5.1% CREDIT SUISSE 2.5% Source: Affin Hwang, Bloomberg Tan Jun Zhang, CFA (603) 2146 7487 [email protected] www.bursamids.com 1500 1550 1600 1650 1700 1750 1800 1850 1900 2.50 7.50 12.50 17.50 22.50 27.50 Oct-14 Mar-15 Aug-15 Jan-16 Jun-16 Nov-16 Apr-17 Sep-17 Feb-18 (RM) AJI MK EQUITY KLCI

-

Upload

khangminh22 -

Category

Documents

-

view

11 -

download

0

Transcript of Ajinomoto - I3investor

12 February 2018

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 1 of 18

A well-seasoned company We initiate on Ajinomoto Malaysia with a HOLD and TP of RM20.30

based on 20x FY19E PE. Ajinomoto is a manufacturer of monosodium

Glutamate (MSG) and other flavored seasonings. We like it for its brand

name and its dominant share in Malaysia. While Malaysia market’s

growth is supported by urbanization, we think its focus on exports,

especially to the Middle East provides exciting growth opportunities.

Ajinomoto- a market leader with trusted brand name

Established in 1961, Ajinomoto Malaysia is a leading Monosodium

Glutamate (MSG) producer with 80% market share in Malaysia.

Approximately 73% of sales are derived from the consumer segment, which

include MSG products and flavoured seasonings. The remainder comes

from the industrial segment whereby Ajinomoto sells functional savoury

seasoning products to processed food producers.

Commendable track record in Malaysia

Ajinomoto Malaysia’s sales in Malaysia has grown at a CAGR of 5.3% over

FY09-17, which is in tandem with the growth rate of F&B establishments and

processed food sales volume. Despite dominant market share of over 80%

in MSG, we believe there is growth opportunities for Ajinomoto, forecasting

its sales to grow at 5% CAGR over FY17-22E. This is on the back of more

product offerings as the flavoured seasonings’ market is still fragmented and

enjoys higher growth rate. Growing demand for processed food and growing

F&B food service should also support its growth.

Promising outlook in export sales

Overseas sales accounted for 40% of total sales in FY17 and its products

are mainly exported to Middle East and the Asia region. We are positive on

the export outlook as MSG consumption in Asia is expected to grow by 4.1%

p.a. over the next 2-3 years. Ajinomoto’s “halal” certified product status will

be an added advantage, shortening the export lead time to the Middle East.

Initiate coverage with a HOLD rating and TP of RM20.30

We initiate coverage with a HOLD rating and TP of RM20.30 based on 20x

FY19E PE. We think that with estimated earnings growth of 13% per annum

for FY17-22E and dividend yield of 2.3-2.8%, the current share price is fairly

valued and it is in line with valuations of Malaysia’s F&B consumer space.

Downside risks include price competition, substitution risk, and cost risks.

Earnings & Valuation Summary

FYE 31 March 2016A 2017A 2018E 2019E 2020E Revenue 400.2 419.9 452.0 487.2 525.6 EBITDA 59.4 70.5 72.6 82.3 87.8 Pretax profit 53.9 211.5 73.4 82.1 88.1 Net profit 40.8 187.5 55.0 61.6 66.1 EPS(RM) 0.67 3.08 0.90 1.01 1.09 PER 29.2 6.4 21.7 19.3 18.0 Core net profit 43.8 42.1 55.0 61.6 66.1 Core EPS(RM) 0.72 0.69 0.90 1.01 1.09 Core EPS growth(%) 46.5 (3.9) 30.7 12.0 7.3 Core PER 27.2 28.3 21.7 19.3 18.0 Net DPS(RM) 0.34 1.55 0.45 0.51 0.54 Dividend Yield(%) 1.7 7.9 2.3 2.6 2.8 EV/EBITDA 17.3 15.1 15.2 13.0 11.9 ROE(%) 13.3 39.5 12.6 13.1 13.1 ROA(%) 11.1 35.2 11.0 11.5 11.4 Debt to equity(x) Net cash Net cash Net cash Net cash Net cash BPS(RM) 5.06 7.81 7.16 7.72 8.30 PBR(x) 3.9 2.5 2.7 2.5 2.4 Chg in EPS (%) - - - Affin/Consensus (x) n.a. n.a. n.a.

Source: Company, Affin Hwang estimates

Initiate coverage

Ajinomoto AJI MK; AJI Sector: Consumer

RM19.62 @ 9 Feb 2018 KLCI: 1841.02

HOLD Upside: 3%

Price Target: RM20.30 Previous Target: -

Price Performance

1M 3M 12M Absolute -4.7% 7.7% 47.3% Rel to KLCI -5.7% 2.6% 35.4%

Stock Data

Issued shares (m) 60.8 Mkt cap (RMm)/(US$m) 1212.3/310.5 Avg daily vol - 6mth (m) 0.0 52-wk range (RM) 13.42-25.21 Est free float 43.8% BV per share (RM) 6.67 P/BV (x) 2.99 Net cash/ (debt) (RMm)

(3Q17)

263 ROE (2018E) 13% Beta -0.04 Derivatives Nil Shariah Compliant YES

Key Shareholders

AJINOMOTO CO INC 50.1% FMR LLC 5.1% CREDIT SUISSE 2.5%

Source: Affin Hwang, Bloomberg

Tan Jun Zhang, CFA (603) 2146 7487

www.bursamids.com

1500

1550

1600

1650

1700

1750

1800

1850

1900

2.50

7.50

12.50

17.50

22.50

27.50

Oct-14 Mar-15 Aug-15 Jan-16 Jun-16 Nov-16 Apr-17 Sep-17 Feb-18

(RM)AJI MK EQUITY KLCI

12 February 2018

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 2 of 18

Company Background

Ajinomoto Malaysia began its business operations as a Monosodium

Glutamate (MSG) producer since 1961, carrying the trusted household

brand name of AJI-NO-MOTO and growing into a market leader with

dominant market share of over 80%. With its own sales force to reach its

customers directly, Ajinomoto Malaysia currently has 8 branches in

Peninsular Malaysia, 2 branches in East Malaysia and 1 sales office in Saudi

Arabia to deliver its products to customers. It plans to open more branches

should the need arises. As at end of FY17, Malaysia is the main market

which accounts for 60% of sales, followed by 14% in Middle Eastern region

and the remaining 25% in other Asian countries.

Fig 1: Sales breakdown by geography (FY17)

Source: Company

Fig 2: Sales breakdown by segment

Source: Company

Ajinomoto Japan is the largest shareholder with a 50.1% stake in the

company currently. Ajinomoto Malaysia serves as one of production hubs in

ASEAN region of the Group. Over the past decades, Ajinomoto Malaysia

has increased its product portfolio gradually and its two core business

segments can be categorized under Consumer Business and Industrial

Business (Fig 2);

Consumer Business

The Consumer Business segment consists of the manufacture and

distribution of consumer products, such as “AJI-NO-MOTO” MSG, flavour

seasoning “Tumix”, menu seasoning “Seri Aji”, other seasonings “Aji-Shio”,

“Aji-Mix” and sweetener PalSweet. “AJI-NO-MOTO” MSG is the main

revenue contributor of this segment. Given that the MSG market is matured

in Malaysia and Ajinomoto commands a lion share, we estimate “AJI-NO-

MOTO” MSG to grow at low-to-mid-single digit over the next few years.

While flavoured seasoning contribution is relatively small compared to “AJI-

NO-MOTO” MSG, its growth rate is stronger due to the growing demand on

the product underpinned by urbanization in Malaysia.

12 February 2018

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 3 of 18

Industrial Business

In this segment, Ajinomoto offers a wide range of functional savory

seasoning products known as “TENCHO” which are mainly used by

industrial producers in processed food, such as instant noodle, seasoning,

snack food, and sauce. The growth in this segment is mainly driven by the

growth of the processed food industry.

Fig 3: Products of consumer business segment

Source: Company

Fig 4: Products of industrial business segment

Source: Company

Fig 5: SWOT analysis Strength

Established brand with dominant market shares

Cost advantage due to its scale of economies,

leading to better bargaining power on both

suppliers and buyers

Comprehensive product portfolio in seasonings.

Weakness

High concentration of sales in seasoning

products.

Although Ajinomoto has dominant market

shares in MSG, the market for flavour

seasoning is relatively more fragmented with

more intense competition

Heavy reliance on advertising may result in

high marketing expenses.

Opportunity

Steady growth in MSG and flavoured seasoning

products due to urbanisation.

Export opportunities in Asian countries

Obtained Halal certification to export to Muslim

countries

Threats

Rising health awareness limits growth

Competition

12 February 2018

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 4 of 18

What is MSG?

“AJI-NO-MOTO” MSG was the world’s first umami seasoning introduced by

Kikunae Ikeda in 1909 after he uncovered umami taste. It is currently sold

in more than 100 countries and used widely in homes, restaurants and

processed foods. Monosodium glutamate (MSG) is sodium salt of glutamic

acid. Glutamic acid is commonly found in the natural protein of vegetables,

meat, fish, poultry and human breast milk. Tomato, cheese and fermented

soy products also contain free glutamate. MSG is made through the process

of fermentation of raw materials such as cane molasses, sugar beets, corn

and tapioca starch using microbe known as Corynebacterium glutamicum.

Food processors generally use MSG to provide umami (savory taste) to

enhance food flavour. Umami is one of the 5 basic tastes, together with

sweetness, sourness, bitterness, and saltiness. MSG can be found in

canned soups, ready-to-eat food packets, instant noodles, ketchups, and

canned food. Hence, the growth of processed food is one of the key drivers

of MSG. Also, note that F&B establishments in food service sector use MSG

and the growing food service boost demand for MSG as well.

Fig 6: Production process of MSG

Source: Company

12 February 2018

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 5 of 18

Ajinomoto- a market leader with trusted brand name

Based on Ajinomoto Japan’s annual report, the Group maintained leading

global market share of c. 22% in MSG as at end of FY16. It currently holds

the dominant market share in seasonings and dry savories market in many

countries. The Group intends to solidify its position by refining the quality

and strengthening the production of existing products along with an active

creation of new product lines.

Price maker rather than taker

In Malaysia, management guided that it currently holds more than 80%

share in the MSG market. Being a market leader, we believe this provides

cost advantages to Ajinomoto as it can have better bargaining power on both

suppliers and buyers. For instance, we understand that Ajinomoto Malaysia

increased selling prices by c.4% in September 2017 to pass on the rising

costs, but this was well received without much impact on sales.

Fig 7: Leading market shares in many countries

Source: Company

12 February 2018

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 6 of 18

Malaysia: more room for growth

Ajinomoto Malaysia’s sales in Malaysia has grown at a CAGR of 5.3% over

FY09-17 with over 80% market share in MSG. Nevertheless, we believe that

the Malaysian market still presents growth opportunities for Ajinomoto. We

are forecasting Ajinomoto’s sales in Malaysia to grow at a 5% CAGR over

FY17-22E.

Fig 8: Sales in Malaysia has grown at a CAGR of 5.3%

Source: Company, Affin Hwang forecast

More product offering

Although Ajinomoto Malaysia dominates the MSG market, the flavored

seasonings’ market is relatively more fragmented with more brands

available in the market, such as Adabi, Nestle’s Maggi, Mak Nyonya,

Unilever’s Knorr and others. Notwithstanding this, management sees

stronger growth in its flavored seasonings than MSG as the latter is matured

in Malaysia. Also, note that these products also have higher ASP of RM3-

6/packet compared to a bottle of MSG that can last for months.

Ajinomoto Malaysia intends to capture the growing market through portfolio

reinforcement. Going forward, Ajinomoto will continue to refine its existing

products’ quality and introduce new flavored seasonings to the market.

Under the Consumer business segment, we forecast “AJI-NO-MOTO” MSG,

the major revenue contributor, to grow steadily in tandem with the market at

low-to-mid-single digit while flavored seasonings to grow at high-single digit.

12 February 2018

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 7 of 18

Steady growth in F&B establishment

On the back of urbanization, Malaysian’s eating patterns have shifted to

favor convenience-oriented and time-saving options. This helps to boost the

demand for the overall F&B industry. Drive-through, takeaway and home-

delivery are on rising trend that benefits foodservice sector as well.

According to the Department of Statistic Malaysia, the census result showed

that there were 167,490 establishments operating in F&B services in 2015

compared to 130,570 establishments in 2010, representing CAGR of 5.1%.

Also, the value of gross output generated by F&B services grew at CAGR of

12% over the same period, reaching RM 66.4b in 2015. We believe that

these positive data are supportive Ajinomoto’s sales in Malaysia.

Fig 9: Steady growth in F&B to support the MSG consumption

Source: Department of Statistics Malaysia

Growth outlook for packaged food

Similarly, hectic lifestyles also shift consumers’ preference towards

processed food. Processed food industry growth should be well-supported

given the expansion of middle class and increase in disposable income

levels. According to Euromonitor, Malaysia’s packaged food volume is

projected to grow at 3.9% CAGR over 2016-2021. Given that MSG is usually

one of the main ingredients in processed food, we believe this should sustain

Ajinomoto’s growth in the coming years.

12 February 2018

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 8 of 18

Overseas markets look promising

Over 2009-17, Ajinomoto Malaysia’s overseas sales have grown from

RM78m to RM168m, representing a CAGR of 10%. Its products are

exported mainly to Middle East and Asia region, accounting for 14% and

25% of total sales respectively as at end of FY17. Sales contribution outside

of Malaysia was c. 40% as at end of FY17 and we project its contribution to

rise to c. 50% within next 5 years.

Fig 10: Ajinomoto Malaysia's market presence

Source: Company

Fig 11: Forecasting increased contribution of export sales

Source: Company, Affin Hwang estimates

Fig 12: Forecasting 12% CAGR over FY17-22

Source: Company, Affin Hwang estimates

12 February 2018

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 9 of 18

Potential of MSG market in Asia

Based on HIS Markit’s report dated Aug 2015, the world consumption of

MSG was estimated to be 3.2m metric tons and valued at USD4.5bn in 2014.

Asia was the biggest consumer that took up 88% of world MSG

consumption, with China alone accounted for 55% of world consumption.

MSG consumption in Asia was projected to grow at CAGR 4.1% to reach

3.9m metric tons by 2019, led by demand growth in China, Indonesia,

Vietnam, and Thailand. We believe that steady growth of demand in Asia

region is favorable to Ajinomoto Malaysia as all of its sales are

predominantly in Asia.

Fig 13: Demand for MSG mainly from Asia

Source: IHS

Where is the demand coming from?

While higher MSG consumption in Asia region is probably due to better

reception of Asians towards umami taste and its longer engrained influence

in Asian cuisine, we believe urbanization in Asia is a key factor driving the

MSG consumption growth. Busier lifestyles, convenience-seeking, and

changes in dietary patterns are some of by-products of urbanization that

leads to increasing income/capita and expansion of middle class. Hence, we

see increasing demand for processed and convenience foods that stimulate

the consumption of MSG.

Halal certification- an added advantage

According to Asia & Middle East Food Trade Journal (AMEFT), the market

for savory ingredients, such as MSG and flavored seasonings, are growing

at 2%-4% CAGR in Middle East. The demand is mainly underpinned by the

dominance of the meat consumption and preference of savory ingredients

to enhance the umami and meaty flavor profiles.

12 February 2018

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 10 of 18

Halal certified food products are mandatory in the food sector in most Middle

East countries due to the dominance of the Muslim population. Being one of

the Halal production hubs for the Ajinomoto Group with its halal products

certified by Malaysian Islamic Development Department (JAKIM), we

believe that Ajinomoto Malaysia is well positioned to benefit from the

growing food sector in Middle East.

During end of 2017, Ajinomoto Malaysia has been added in to the “white list”

company by JAKIM. This should shorten its Halal certification process from

around 5 months to 1-2 months. Given the positive outlook of the Middle

East market, we are looking at 15-20% annual growth in the next 5 years for

Ajinomoto Malaysia’s sales to the region.

Future growth catalyst: Frozen food

On top of seasoning products which Ajinomoto Malaysia currently

dominates, the company intends to expand vertically into frozen food due to

its higher value add. We understand that Ajinomoto Japan currently has

existing products, such as Chinese dumplings, Gyoza. Kara-age, and Gyu

Beef in other countries. Therefore, we believe that Ajinomoto Malaysia can

tap into the Group’s resources and introduce frozen foods into the Malaysia

market.

Figure 14: Ajinomoto's frozen food sold outside of Malaysia

Source: Company

According to management, it targets frozen food to contribute 9% of total

sales by FY25 to diversify away from seasoning products. However, we

understand that Ajinomoto is still exploring the market potential and it is

unlikely to have material contribution in the next few years. Therefore, we

have not factored in the contribution of frozen food into our forecast, but it

can be additional earnings catalyst in future years.

12 February 2018

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 11 of 18

Negative perception on MSG For decades, misconception that MSG consumption is harmful has been a

major setback for the MSG industry. MSG is commonly linked to cause

various health issues, such as headaches, numbness of body, breathing

difficulties and dizziness. As a result, we see an increased consumer

preference to abstain from artificial ingredients especially in developed

countries, such as the U.S. and Canada. The “NO MSG” label has been

increasingly noticeable in processed food and even some restaurants, which

promote it in their food menus. The rising health awareness and

misconception on MSG may put a dent on MSG’s long term growth rate.

Debunking the myth

In 1968, an American physician Robert Ho reported that he experienced

numbness, weakness and heart palpitations after eating in a Chinese

restaurant. He wrote an article in the New England Journal of Medicine

claiming that MSG was the cause, coining the term famously known as

“Chinese restaurant syndrome”.

Over the years, numerous rigorous scientific studies have disproved the

claim and clinical trials have failed to prove consistent relationship between

the consumption of MSG and the negative syndromes. The Food and Drug

Administration (FDA) and other scientific and regulatory bodies around the

world have confirmed MSG’s safety. FDA has even classified MSG as

“Generally Recognized As Safe” (GRAS), right along with sugar, baking

powder, salt, and pepper. Likewise, the World Health Organization (WHO)

has chosen not to set a limit on the Acceptable Daily Intake (ADI) of MSG,

classifying it as “not specified”

Fig 15: Conclusion of safety about MSG by public institution 1958 FDA designates MSG as “Generally Recognized as Safe”

1979 National Academy of Science in US confirms MSG is safe as a food ingredient

1987 Joint FAO/WHO Expert Committee on Food Additives places MSG in the

safest category for food additives

1991 European Community's Scientific Committee for food confirm safety of MSG

1992 American Medical Association concludes normal MSG levels in diet are safe

1995 FDA reaffirm MSG is safe upon a report from the Federation of American

Societies of Experimental Biology

2003 Food and Standards Australia New Zealand declared MSG is safe Source: Company

Impact on Ajinomoto Malaysia

Although rising health awareness could put pressure on the growth of MSG,

we do not expect it to impact Ajinomoto Malaysia’s sales in the coming

years. This is because MSG is still a cheap and effective source of flavor

enhancer. We do not foresee it to be completely replaced. Moreover, higher

consumption of MSG in Asia and urbanization should drive the projected

volume growth of 4.1% CAGR in the region, benefitting Ajinomoto

Malaysia’s export sales. Whereas in Malaysia, Ajinomoto Malaysia actively

organizes campaigns to raise public awareness and correct the

misunderstanding about MSG. We believe this should support the local

sales of its seasoning products.

12 February 2018

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 12 of 18

Financial Analysis and Forecasts

Steady revenue and earnings growth

We estimate Ajinomoto Malaysia’s revenue CAGR of 8% over FY17-22E,

underpinned by stronger sales of flavored seasonings while its core product

MSG continues to grow at c. mid-single digit. Based on Ajinomoto Japan,

international food products in Asia region are projected to grow at low teens.

Ajinomoto Malaysia targets to hit total sales of RM1bn in FY25, implying a

CAGR of 11%. We are fairly comfortable with our forecast as it is consistent

with the management’s view.

Fig 16: Projecting 8% CAGR for revenue over FY17-22E

Source: Company, Affin Hwang estimates

Solid execution leads to margin improvement Ajinomoto Malaysia’s EBIT margin has improved from 8.6% in FY09 to 14%

in FY17. We believe that this is attributable to the economies of scale and

company’s effort to increase production efficiency. We believe that raw

materials and packaging cost are the key cost components with tapioca

starch and cane molasses being key raw ingredients. We understand that

these raw materials are generally abundant and inexpensive, which we think

explains the gross margin has been on uptrend.

Fig 17: Ajinomoto's EBIT margin

Source: Company, Affin Hwang estimates

12 February 2018

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 13 of 18

Minimal impact on currency movement According to Ajinomoto Malaysia’s annual reports, the company generally

benefits from strengthening of RM against USD given that imported raw

materials are in USD. However, the impact is negligible as we estimate 4%

strength in RM against USD only leads to 1% increase in net profit.

According to management, the company is neutral to RM movement as its

exports act as a natural hedge for its imported raw materials.

One-off gain in FY17

On 28 May 2016, the company announced on the Kuala Lumpur

Administrator’s intention to hold a land inquiry pertaining to the said

compulsory acquisition for “Projek Mass Rapid Transit” (MRT Project). The

company had accepted and received the award of compensation of

RM166m in FY17 from the Government for the compulsory acquisition of its

factory land located in Jalan Kuchai Lama for the MRT 2 project. The

compensation generated a one-off gain on disposal of RM145m. The

disposal of land does not affect its business operation.

Fig 18: Projecting 14% core net profit CAGR over FY17-22E

Source: Company, Affin Hwang estimates

12 February 2018

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 14 of 18

Strong net cash position, with manageable capex Ajinomoto Malaysia is currently in a net cash position and has practically no

borrowings (current net gearing is -65%). We expect the cash position will

likely strengthen further from the current level of RM263m (including

investment securities in current assets). The plant utilization is at 70%-80%

and there is no plan to construct any additional plants in the near term.

Capex is guided to be around RM15m per year for upgrades and

maintenance. Based on our forecast of RM60-70m cash flow generated from

operation and annual capex of RM15m, Ajinomoto Malaysia will likely

generate RM40-50m free cash flow per year.

Dividend policy

Ajinomoto’s dividend policy is to distribute 40%-50% of its earnings and it

has consistently paid around 50% over the past 2 years. In FY17, Ajinomoto

announced a final and a special dividend totaling RM1.55/share in May to

reward its shareholder. Of the RM166m compensation it receives from

Government, c. RM90m was paid out as special dividend. Ajinomoto

Malaysia currently has no plan on the deployment of remaining cash. But

with such strong balance sheet, we think it is likely for Ajinomoto to

announce a special dividend or invest resources into frozen food products

in the future. We assume that Ajinomoto will maintain its dividend payout

ratio at 50%, implying 2%-3% dividend yield for FY18E-20E.

Fig 19: Assuming a 50% payout ratio given its strong balance sheet position

Source: Company, Affin Hwang estimates

12 February 2018

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 15 of 18

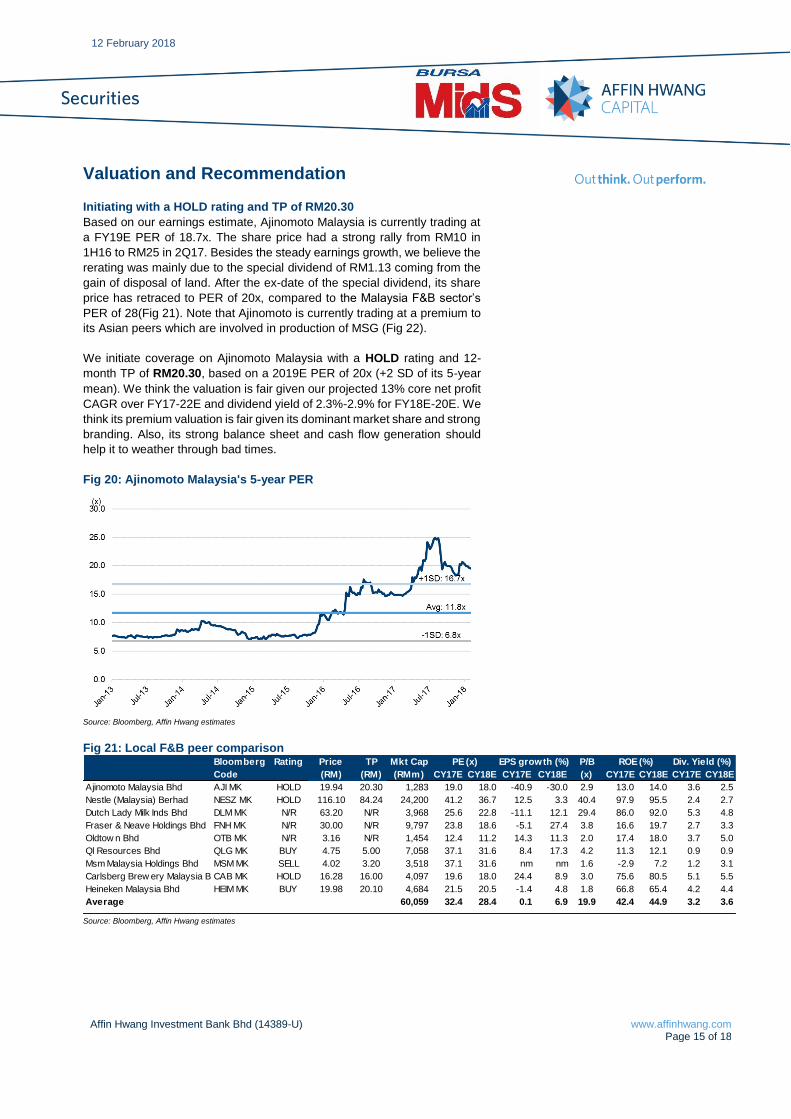

Valuation and Recommendation

Initiating with a HOLD rating and TP of RM20.30

Based on our earnings estimate, Ajinomoto Malaysia is currently trading at

a FY19E PER of 18.7x. The share price had a strong rally from RM10 in

1H16 to RM25 in 2Q17. Besides the steady earnings growth, we believe the

rerating was mainly due to the special dividend of RM1.13 coming from the

gain of disposal of land. After the ex-date of the special dividend, its share

price has retraced to PER of 20x, compared to the Malaysia F&B sector’s

PER of 28(Fig 21). Note that Ajinomoto is currently trading at a premium to

its Asian peers which are involved in production of MSG (Fig 22).

We initiate coverage on Ajinomoto Malaysia with a HOLD rating and 12-

month TP of RM20.30, based on a 2019E PER of 20x (+2 SD of its 5-year

mean). We think the valuation is fair given our projected 13% core net profit

CAGR over FY17-22E and dividend yield of 2.3%-2.9% for FY18E-20E. We

think its premium valuation is fair given its dominant market share and strong

branding. Also, its strong balance sheet and cash flow generation should

help it to weather through bad times.

Fig 20: Ajinomoto Malaysia's 5-year PER

Source: Bloomberg, Affin Hwang estimates

Fig 21: Local F&B peer comparison

Source: Bloomberg, Affin Hwang estimates

Bloomberg Rating Price TP Mkt Cap P/B

Code (RM) (RM) (RMm) CY17E CY18E CY17E CY18E (x) CY17E CY18E CY17E CY18E

Ajinomoto Malaysia Bhd AJI MK HOLD 19.94 20.30 1,283 19.0 18.0 -40.9 -30.0 2.9 13.0 14.0 3.6 2.5

Nestle (Malaysia) Berhad NESZ MK HOLD 116.10 84.24 24,200 41.2 36.7 12.5 3.3 40.4 97.9 95.5 2.4 2.7

Dutch Lady Milk Inds Bhd DLM MK N/R 63.20 N/R 3,968 25.6 22.8 -11.1 12.1 29.4 86.0 92.0 5.3 4.8

Fraser & Neave Holdings Bhd FNH MK N/R 30.00 N/R 9,797 23.8 18.6 -5.1 27.4 3.8 16.6 19.7 2.7 3.3

Oldtow n Bhd OTB MK N/R 3.16 N/R 1,454 12.4 11.2 14.3 11.3 2.0 17.4 18.0 3.7 5.0

Ql Resources Bhd QLG MK BUY 4.75 5.00 7,058 37.1 31.6 8.4 17.3 4.2 11.3 12.1 0.9 0.9

Msm Malaysia Holdings Bhd MSM MK SELL 4.02 3.20 3,518 37.1 31.6 nm nm 1.6 -2.9 7.2 1.2 3.1

Carlsberg Brew ery Malaysia B CAB MK HOLD 16.28 16.00 4,097 19.6 18.0 24.4 8.9 3.0 75.6 80.5 5.1 5.5

Heineken Malaysia Bhd HEIM MK BUY 19.98 20.10 4,684 21.5 20.5 -1.4 4.8 1.8 66.8 65.4 4.2 4.4

Average 60,059 32.4 28.4 0.1 6.9 19.9 42.4 44.9 3.2 3.6

PE (x) Div. Yield (%)ROE (%)EPS growth (%)

12 February 2018

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 16 of 18

Fig 22: Peer comparison for regional MSG related companies

Source: Bloomberg, Affin Hwang estimates

Key Risks

1. Price competition. Ajinomoto holds no.1 position in the

seasonings and dry savouries market with c. 22% market share.

Nevertheless, the competition in the industry is intense especially

MSG. in 2014, China’s production and consumption accounted for

approximately 65% and 55% of world production and consumption

respectively. China is the world’s largest exporter of MSG which

accounted for 44% of the world’s MSG export. Some of Ajinomoto’s

competitors include Vedan, Fufeng, CJ Cheiljedang, Daesang

Corporations. Ajinomoto may incur more marketing expenses or

price discounts to compete in the market.

2. Substitution risk. Consumers may be health conscious and

reduce consumption of MSG and processed food.

3. Weather risk. Ajinomoto’s main raw ingredients for MSG are

tapioca starch and sugarcane molasses. Poor weather condition

may result in poor crop yield and elevate raw material prices.

Movement of packaging cost which include papers and plastics

may also affect its margin.

Bloomberg Rating Price TP Mkt Cap P/B

Code (RM) (RM) (RMm) CY17E CY18E CY17E CY18E (x) CY17E CY18E CY17E CY18E

Ajinomoto Malaysia Bhd AJI MK HOLD 19.94 20.30 1,283 19.0 18.0 -40.9 -30.0 2.9 13.0 14.0 3.6 2.5

Cj Cheiljedang Corp 097950 KP N/R 366,000.00 N/R 17,361 12.4 12.3 48.6 0.5 1.4 11.2 10.0 0.7 0.7

Daesang Corporation 001680 KP N/R 27,550.00 N/R 3,436 13.9 11.4 4.1 21.2 1.0 7.6 8.6 1.6 1.6

Fufeng Group Ltd 546 HK N/R 5.10 N/R 6,494 6.2 5.1 24.3 21.5 1.2 19.9 20.2 4.2 4.9

Average 28,574 11.4 10.8 9.0 3.3 1.3 12.9 13.2 2.5 2.4

PE (x) Div. Yield (%)ROE (%)EPS growth (%)

12 February 2018

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 17 of 18

Ajinomoto - FINANCIAL SUMMARY

Souce: Company, Affin Hwang estimates

Profit & Loss Statement Key Financial Ratios and Margins

FYE 31 Mar (RM m) FY16 FY17 FY18E FY19E FY20E FYE 31 Mar (RM m) FY16 FY17 FY18E FY19E FY20E

Revenue 400.2 419.9 452.0 487.2 525.6 Growth

Operating expenses (340.8) (349.4) (379.4) (404.9) (437.8) Revenue (%) 17.6 4.9 7.6 7.8 7.9

EBITDA 59.4 70.5 72.6 82.3 87.8 EBITDA (%) 26.7 18.7 2.9 13.3 6.8

Depreciation (11.5) (11.8) (11.7) (12.3) (13.0) Core net profit (%) 46.5 (3.9) 30.7 12.0 7.3

EBIT 47.9 58.7 60.9 70.0 74.8

Net interest income/(expense) 6.0 7.6 12.4 12.2 13.3 Profitability

Associates' contribution - - - - - EBITDA margin (%) 14.9 16.8 16.1 16.9 16.7

EI (3.0) 145.4 - - - PBT margin (%) 13.5 50.4 16.2 16.9 16.8

Pretax profit 53.9 211.5 73.4 82.1 88.1 Net profit margin (%) 10.2 44.6 12.2 12.6 12.6

Tax (13.2) (24.0) (18.3) (20.5) (22.0) Effective tax rate (%) 24.4 11.4 25.0 25.0 25.0

Minority interest - - - - - ROA (%) 11.1 35.2 11.0 11.5 11.4

Net profit 40.8 187.5 55.0 61.6 66.1 Core ROE (%) 14.2 8.9 12.6 13.1 13.1

ROCE (%) 12.7 38.5 12.3 12.7 12.7

Balance Sheet Statement Dividend payout ratio (%) 50.3 50.3 50.0 50.0 50.0

FYE 31 Mar (RM m) FY16 FY17 FY18E FY19E FY20E

PPE 105.0 89.5 92.9 95.6 97.6 Liquidity

Other non-current assets 2.4 1.5 1.5 1.5 1.5 Current ratio (x) 5.6 9.7 7.8 8.1 8.1

Total non-current assets 107.5 91.1 94.4 97.1 99.1 Op. cash flow (RMm) 58.7 54.6 58.2 57.2 60.4

Cash and equivalents 162.3 129.9 91.3 118.2 146.0 Free cashflow (RMm) 46.0 36.9 43.2 42.2 45.4

Inventory 53.3 61.5 63.2 67.2 72.8 FCF/share (sen) 75.7 60.6 71.1 69.3 74.6

Trade receivables 43.1 49.9 51.2 55.1 59.5

Other current assets 1.0 200.1 200.1 200.1 200.1 Asset management

Total current assets 259.6 441.4 405.8 440.6 478.4 Inventory turnover (days) 92.2 101.4 96.8 96.8 96.8

Trade payables 43.3 38.9 45.4 48.2 52.2 Receivables turnover (days) 39.3 43.3 41.3 41.3 41.3

Short term borrowings - - - - - Payables turnover (days) 74.9 64.0 69.5 69.5 69.5

Other current liabilities 3.5 6.5 6.5 6.5 6.5

Total current liabilities 46.8 45.3 51.9 54.7 58.7 Capital structure

Long term borrowings - - - - - Net Gearing (%) net cash net cash net cash net cash net cash

Other long term liabilities 12.5 12.5 13.0 13.5 14.0 Interest Cover (x) n.m. n.m. n.m. n.m. n.m.

Total long term liabilities 12.5 12.5 13.0 13.5 14.0

Quarterly Profit & Loss

Shareholders' Funds 307.8 474.6 435.4 469.5 504.8 FYE 31 Mar (RM m) 2QFY17 3QFY17 4QFY17 1QFY18 2QFY18

Revenue 99.3 107.0 114.9 96.4 115.4

Cash Flow Statement Op costs (81.9) (90.3) (97.2) (85.5) (94.1)

FYE 31 Mar (RM m) FY16 FY17 FY18E FY19E FY20E EBITDA 17.4 16.6 17.7 11.0 21.3

PAT 40.8 187.5 55.0 61.6 66.1 Depn and amort (3.0) (3.0) (2.9) (3.1) (3.1)

Depreciation & amortisation 11.5 11.8 11.7 12.3 13.0 EBIT 14.4 13.6 14.8 7.9 18.2

Working capital changes 5.1 (20.7) 3.5 (5.1) (5.9) Net int income/(exp) 1.2 1.1 1.8 2.1 3.7

Others 1.4 (123.9) (11.9) (11.7) (12.8) EI 0.4 1.6 143.4 1.4 (0.5)

Cashflow from operations 58.7 54.6 58.2 57.2 60.4 Inc/(loss) from affiliates - - - - 1.0

Capex (12.7) (17.8) (15.0) (15.0) (15.0) Pretax profit 15.9 17.1 161.1 10.4 20.8

Others 2.8 (49.6) 12.4 12.2 13.3 Tax (3.9) (3.6) (12.1) (2.5) (4.3)

Cash flow from investing (9.9) (67.4) (2.6) (2.8) (1.7) MI - - - - -

Debt raised/(repaid) - - - - - Net profit 12.0 13.5 149.0 7.9 16.5

Equity raised/(repaid) - - - - - Core net profit 11.6 11.9 5.6 6.5 17.0

Dividends paid (12.2) (20.5) (94.2) (27.5) (30.8)

Others - - - - 0.0 Margins (%)

Cash flow from financing (12.2) (20.5) (94.2) (27.5) (30.8) EBITDA 17.5 15.6 15.4 11.4 18.4

PBT 16.1 16.0 140.2 10.8 18.0

Free Cash Flow 46.0 36.9 43.2 42.2 45.4 PAT 12.1 12.7 129.6 8.2 14.3

12 February 2018

Affin Hwang Investment Bank Bhd (14389-U) www.affinhwang.com Page 18 of 18

Equity Rating Structure and Definitions

BUY Total return is expected to exceed +10% over a 12-month period

HOLD Total return is expected to be between -5% and +10% over a 12-month period

SELL Total return is expected to be below -5% over a 12-month period

NOT RATED Affin Hwang Investment Bank Berhad does not provide research coverage or rating for this company. Report is intended as information only and not as a

recommendation

The total expected return is defined as the percentage upside/downside to our target price plus the net dividend yield over the next 12 months.

OVERWEIGHT Industry, as defined by the analyst’s coverage universe, is expected to outperform the KLCI benchmark over the next 12 months

NEUTRAL Industry, as defined by the analyst’s coverage universe, is expected to perform inline with the KLCI benchmark over the next 12 months

UNDERWEIGHT Industry, as defined by the analyst’s coverage universe is expected to under-perform the KLCI benchmark over the next 12 months

This report is intended for information purposes only and has been prepared by Affin Hwang Investment Bank Berhad (14389-U) (“the Company”) based on sources believed to be reliable. However, such sources have not been independently verified by the Company, and as such the Company does not give any guarantee, representation or warranty (express or implied) as to the adequacy, accuracy, reliability or completeness of the information and/or opinion provided or rendered in this report. Facts, information, views and/or opinion presented in this report have not been reviewed by, may not reflect information known to, and may present a differing view expressed by other business units within the Company, including investment banking personnel. Reports issued by the Company, are prepared in accordance with the Company’s policies for managing conflicts of interest arising as a result of publication and distribution of investment research reports. Under no circumstances shall the Company, its associates and/or any person related to it be liable in any manner whatsoever for any consequences (including but are not limited to any direct, indirect or consequential losses, loss of profi t and damages) arising from the use of or reliance on the information and/or opinion provided or rendered in this report. Any opinions or estimates in this report are that of the Company, as of this date and subject to change without prior notice. Under no circumstances shall this report be construed as an offer to sell or a solicitation of an offer to buy any securities. The Company and/or any of its directors and/or employees may have an interest in the securities mentioned therein. The Company may also make investment decisions or take proprietary positions that are inconsistent with the recommendations or views in this report. Comments and recommendations stated here rely on the individual opinions of the ones providing these comments and recommendat ions. These opinions may not fit to your financial status, risk and return preferences and hence an independent evaluation is essential. Investors are advised to independently evaluate particular investments and strategies and to seek independent financial, legal and other advice on the information and/or opinion contained in this report before investing or participating in any of the securities or investment strategies or transactions discussed in this report. Third-party data providers make no warranties or representations of any kind relating to the accuracy, completeness, or timeliness of the data they provide and shall not have liability for any damages of any kind relating to such data. The Company’s research, or any portion thereof may not be reprinted, sold or redistributed without the consent of the Company. The Company, is a participant of the Capital Market Development Fund-Bursa Research Scheme, and will receive compensation for the participation. This report is printed and published by: Affin Hwang Investment Bank Berhad (14389-U) A Participating Organisation of Bursa Malaysia Securities Berhad 22nd Floor, Menara Boustead, 69, Jalan Raja Chulan, 50200 Kuala Lumpur, Malaysia. T : + 603 2146 3700 F : + 603 2146 7630 [email protected] www.affinhwang.com