Africa Bottom Billion Fastest Billion 190711

44

Africa Economics Update Economics and strategy research 19 July 2011 Africa The bottom billion becomes the fastest billion Important disclosures are found at the Disclosures Appendix. Communicated by Renaissance Securities (Cyprus) Limited, regulated by the Cyprus Securities & Exchange Commission, which together with non-US affiliates operates outside of the USA under the brand name of Renaissance Capital. Charles Robertson +44 (207) 367-8235 [email protected] Yvonne Mhango Nothando Ndebele

Transcript of Africa Bottom Billion Fastest Billion 190711

AfricaEconomics

UpdateEconomics and strategy research

19 July 2011

Africa The bottom billion becomes the fastest billion

Important disclosures are found at the Disclosures Appendix. Communicated by Renaissance Securities (Cyprus) Limited, regulated by the Cyprus Securities & Exchange Commission, which together with non-US affiliates operates outside of the USA under the brand name of Renaissance Capital.

Charles Robertson+44 (207) [email protected]

Yvonne MhangoNothando Ndebele

19 July 2011 Africa: The bottom billion becomes the fastest billion Renaissance Capital

2

Executive summary 3 A history of the world in 1,000 words 5 Modernisation theory 11 The Rostow take-off (or stages of growth) model 11

Africa 1960-1980: Stage one 11 Stage two in Africa: Education has improved, banking facilities are ready 12 Entering the third stage: Services over manufacturing 14 Africa’s demographic advantage over Asia 15 Urbanisation as a growth factor 17 The third stage – Investment requirements 18 Foreign financing 19 Domestic financing 20 Institutional developments 22

Growth drivers: Services and construction 24 The critics of catch-up theory 27 Your questions? 27

Infrastructure: the key to faster growth 29 in SSA 29

Finding 1: Infrastructure contributed to over half of Africa’s improved growth performance 29 Finding 2: Africa’s infrastructure lags its emerging markets peers 31 Finding 3: Socio-geo-economic issues add to the infrastructure challenges 31 Finding 4: Infrastructure services are twice as expensive as elsewhere 33 Finding 5: Power remains the continent’s largest infrastructure challenge 33 Finding 6: Africa’s infrastructure spending needs estimated at $93bn annually 36 Conclusion 37

What would result from sustained 38 higher growth? 38

What sectors and stocks do we prefer? 38

Appendix data 40 Disclosures appendix 41

Contents

3

Renaissance Capital Africa: The bottom billion becomes the fastest billion 19 July 2011

Age is not often associated with speed. But Africa, the world’s oldest continent, now has more of the world’s fastest-growing economies than any other. Over 2000-2009, 11 African countries grew at an annual rate of 7% or more – a rate sufficient to double the economy in 10 years. This is a big shift from the 1980s and 1990s, when just three African countries achieved this level of growth. Of these 11 booming economies, nine were in Sub-Saharan Africa (SSA); six benefited from higher energy prices, and five were not associated with either energy or metal exports: China’s demand for global commodities cannot be the only reason for this significant improvement. After a generation of relative stagnation in the late 20th century, many in Africa have now begun the long-awaited period of catch-up with the developed world. The bottom billion is becoming the fastest billion.

Figure 1: Africa accelerates past Asia, with the highest number of countries that grew at 7% pa on average over 2000-2009

Source: IMF World Economic Outlook, April 2011

Catch-up economic theory suggests all countries will eventually make the leap from subsistence farming to developed nation status, and that the later countries make this transition, the quicker the growth when it finally happens. The technologies to boost productivity get cheaper and easier to import; Africa’s booming telecoms sector is just one example. The global markets available to the poorest societies get ever larger: In the 19th century, the UK had no countries to export to that were richer on a per-capita GDP basis; today, Africa has richer export markets to pick from – not just in North America and Europe, but also across an increasing number of Asian countries. Delivering that export growth is easier too, as telecoms opens up services as a route for export growth. Meanwhile, the evidence that effective policymaking can lead to growth becomes progressively harder to ignore – in recent years, even North Korea and Cuba have made efforts to bring market forces into their economic systems, but we find far more to be inspired by in Rwanda and Mauritius.

Just how fast can growth be? The fact that 11 booming African nations have already achieved at least 7% annual growth is yesterday’s story. What’s more important is that three have grown at 10% pa, and we believe more can achieve or better this. In our view, it would not take much for Nigeria to shift its 9% growth rate into double digits by widening access to cheaper electricity. We see scope for improved governance in Côte d’Ivoire, in turn enabling it to emulate Sierra Leone’s 10% annual growth rate. The positive examples provided by countries like Rwanda highlight the success that others across Africa might copy.

02468

1012

Asia

Afric

a

CIS

Midd

le Ea

st

Latam

/Car

ibbea

n

CEE

1980-1989 1990-99 2000-09

Executive summary

Africa’s boom is not just a China story

It is easier than ever to catch up, as there is an increasing number of increasingly

rich countries to sell to

Three countries grew at 10% or more for a decade; more could easily follow

19 July 2011 Africa: The bottom billion becomes the fastest billion Renaissance Capital

4

Higher investment rates would go a long way towards broadening and accelerating growth across Africa. This investment might flow from external sources – as it did in South East Asia. Chinese lending to Africa is one example (see our China in Africa report, dated 21 April 2011), as is US retail giant Walmart’s investment in African retail. Foreign portfolio flows can reduce borrowing costs for companies, and provide equity financing for businesses to expand.

We think such inflows look increasingly likely, as demographics favour direct investment in Africa. Asia’s young population is now declining – with East Asia’s dropping 27% this decade – and only SSA is positioned to experience 15-20% growth in the crucial 15-24 age range over the coming decades, which will provide the plentiful labour force the world economy will rely on.

Better still, this workforce is far better educated than a generation or two ago, after SSA saw nearly a tenfold rise in the gross secondary school enrolment rate to 29% by 2005 from just 3% in 1960 (the latter was surely a contributory factor to the weakness of the 1980s). These are now around the levels of Mexico or Turkey in the 1970s which helped pave the way to their strong growth performance in subsequent decades. Africa’s workforce is now well educated enough to support the take-off.

Most positive would be a restoration of trust in the domestic economic environment from locals themselves, and a recognition that returns on investment in Africa can far outweigh those now available in the West. This can already be seen in the re-investment of profits by African businesses. We estimate higher investment could add 2 ppts to GDP growth rates (see pages 29 to 37), and note that this would have increased the number of African countries doubling their economies within a decade to 21 over 2000-2009. The challenge for investors will be in accessing the multiple growth stories that could result from this (see page 38 for our current stock recommendations).

Even a slight improvement in the growth rate over the next two decades will produce some remarkable results. If, instead of nominal dollar growth of 9% annually, we saw 10%, then Nigeria would become a $1trn economy by 2027. Sub-Saharan Africa – excluding South Africa – alone would rise from $700bn (similar to Indonesia) to $4.5trn by 2030, assuming 10% growth in nominal dollar terms. These may well prove to be conservative estimates.

The creation of a virtuous circle of higher growth leading to better governance – in turn attracting more investment and faster growth – is under way. Democracies are becoming safer across the continent. We would not be surprised to see Africa recording some of the highest growth rates ever achieved in the coming decades.

Foreign financing will provide some of the support

Asia’s population is now in decline, Africa’s young adult population is growing at 15-20%

SSA is better educated than ever; Botswana, Mauritius and SA have a higher percentage in secondary education than China or India

Higher investment (e.g. in infrastructure) could add 2 ppts to GDP growth and would have put 21 African countries into the high-growth category

5

Renaissance Capital Africa: The bottom billion becomes the fastest billion 19 July 2011

There is still no consensus on why the UK became the first country to experience an industrial revolution and a relative growth explosion. From 0-1000 AD, UK GDP was roughly stable at $400 per capita – roughly 15% below Chinese and Indian wealth levels. By 1500 AD, the UK had superseded both these great Asian powers, but with per-capita GDP of $714, it did not quite equal France and clearly lagged the financial giant that was Medici Italy with per-capita GDP of $1,100. Even 200 years later, after an impressive 0.3% annual growth rate, UK per-capita GDP was $1,250 and double that of China or India, but only just over half that of the new financial powerhouse that was The Netherlands, on $2,130. The great leap forward only kicked in from 1820 to 1850, when annual per-capita GDP began rising by 1.0%, after which UK per-capita income was the highest in the world.

Figure 2: Per-capita GDP from 0-1870 AD, constant 1990 PPP dollars

Source: Historical Statistics of the World Economy: 1-2008 AD, Angus Maddison

Naturally the Victorian British had many explanations for this, many of which assumed an innate English superiority over other peoples (and most satisfyingly over their age-old enemies, the French). But rather alarmingly, other Europeans began to catch up with the UK. Germans proved adept at copying, and then improving on UK iron and steel manufacturing techniques. They became more efficient than the English themselves – most distressing of all in the football arena. Through the 19th century, Germany, the US, France and Australia and New Zealand began to grow more quickly than the UK, by importing foreign capital (often British), modern industrial equipment and improving British manufacturing techniques – much as Kenya is doing with telephone banking today.

Figure 3: Growth spreads outside NW Europe – per-capita GDP, 1870-1910, constant 1990 PPP dollars

Source: Historical Statistics of the World Economy: 1-2008 AD, Angus Maddison

0500

1,0001,5002,0002,5003,0003,500

1 1000 1500 1600 1700 1820 1850 1870

United Kingdom France Italy India China Netherlands

500

1,500

2,500

3,500

4,500

5,500

1870 1880 1890 1900 1910

UK France Germany US CanadaNew Zealand Russia Argentina Japan

A history of the world in 1,000 words

Why was the UK the first to modernise?

It was not just Britain’s Victorian values –other European nations quickly followed

the UK lead

19 July 2011 Africa: The bottom billion becomes the fastest billion Renaissance Capital

Figure 4: Population size in 2010 (mn)

Source: IMF, Renaissance Capital estimates

Tunisia

Algeria Morocco Egypt

Libya

W.S Chad Mauritania Mali Niger

C.V Sudan Eritrea

Senegal Djib.Gambia

G-B Burkina Faso

Guinea

South Ethiopia Sudan Sierra L. Cen. A R Liberia Cote D'Ivoire Nigeria Som.

Ghana Benin Togo

1 box = 1m 1 box = total pop less than 1m

Kenya

Uganda

Cameroon 156mn Nigeria = Russia (140) = Bangladesh (165)85mn Ethiopia = Vietnam (88) = Germany (82) = Egypt (78) Eq G. Rwanda Tanzania70mn Dem Rep Congo = Iran (75) = Turkey (71) STP 50mn SA = Korea (49) = Spain (46) Gab. Dem Rep of Congo40mn Kenya= Algeria (36) = Poland (38) = Canada (34) = Uganda (34) Congo 24mn Ghana = Saudi Arabia (26) = Australia (23) 14mn Zimbabwe = Zambia (13) = Cambodia (14) = Greece (12) Burundi10mn Rwanda = Hungary (10) = Czech Republic (11)

Angola Romania

Zambia Malawi

MadagascarPoland Mozambique

Nmb. Bts. Zimbabwe Mrt.

Swz.

Lesotho South Africa

7

Renaissance Capital Africa: The bottom billion becomes the fastest billion 19 July 2011

Figure 5: GDP size in 2010 (bn), current dollars

Source: IMF, Renaissance Capital estimates

Morocco Algeria Tunisia

Libya

Egypt

Niger

W.S Mauritania Chad Mali

Gambia

C.V Senegal Burkina Faso

G-BGuinea

Nigeria Benin

S-L Ghana Togo Sudan Cote D'Ivoire

Lib.

Eritrea

Djib.

CAR SomaliaEthiopia

1 box = $1bn 1 box = total GDP less than $0.5bn Cameroon Blank box = No available GDP data

South Africa = Argentina = Iran = Austria ($357-377bn) UgandaNigeria = Egypt = Ireland = Israel = Singapore ($204-223bn)

Eq GuineaKenya

ST&PGabon Rwanda

Congo Dem Rep Bur. Tanzania Seychelles

Malawi

Zambia Moz.

ZimbabweMad.

BotswanaAngola Mauritius

Les. Swazil.

Namibia

South Africa

19 July 2011 Africa: The bottom billion becomes the fastest billion Renaissance Capital

8

By the late 19th century, while the British could no longer feel quite so superior, it still seemed that at least north-west Europeans and their colonists in the US and Oceania, had some natural advantage over others; whether this was rooted in political, religious or social norms. Yet seemingly out of nowhere imperial Orthodox Russia, Catholic Argentina and Japan began the same catch-up process others had experienced. In Russia and Argentina this was primarily financed from abroad (France and the UK, respectively), while the Japanese used domestic savings. Russia boomed on oil and grain, Argentina on meat and grain, while Japan shifted from silkworms to textiles and other light manufacturing.

Figure 6: The take-off engulfs Spain and Latin America – per-capita GDP, constant 1990 PPP dollars

Source: Historical Statistics of the World Economy: 1-2008 AD, Angus Maddison

By 1960, the gap between what was now termed the West (including Japan), and the rest of the world was wider than ever. It was not clear who, if anyone, could repeat what the West had achieved. Of all the continents, Asia would have been chosen by few as the likely success story of the second half of the 20th century. Communism was holding back, or even reversing, growth in countries like China, North Korea and North Vietnam. War and political instability threatened South Korea, South East Asia, India and Pakistan. Per-capita GDP in Singapore and South Korea was around $400. The English-speaking Philippines, protected by the US, would have probably seemed the most likely success story.

Figure 7: The growth story crosses the Pacific – per-capita GDP, constant 1990 PPP dollars

Source: Historical Statistics of the World Economy: 1-2008 AD, Angus Maddison

0

5,000

10,000

15,000

20,000

25,000

1

1825

1840

1855

1870

1885

1900

1915

1930

1945

1960

1975

1990

2005

Spain Argentina Brazil Chile Colombia Mexico Venezuela

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1

1825

1840

1855

1870

1885

1900

1915

1930

1945

1960

1975

1990

2005

United States Japan South Korea Thailand Taiwan Singapore India China

Commodity exporters and non-Christian countries experienced the catch-up from 1870 onwards

When Asia followed it was resource-less countries that led the charge

9

Renaissance Capital Africa: The bottom billion becomes the fastest billion 19 July 2011

Instead it was the resource-less dragons of Taiwan, Hong Kong, Singapore as well as South Korea which boomed through the 1970s. By the 1980s and 1990s, they had been joined by the tigers of Thailand, Malaysia and Indonesia. China itself had finally joined the growth party in the 1980s and India stepped up in the 1990s and 2000s. Meanwhile, the Japanese model, which was so admired in the 1980s and appeared to put Japan on course to challenge the US, crashed, and consensus instead turned to the Chinese model.

While it is still generally ignored, Africa joined the boom a decade ago. The oil-rich economies of Angola and Equatorial Guinea were the fastest-growing African economies, but a number of East African countries, including Uganda, Rwanda and Tanzania, achieved record growth rates.

The pace of growth has also accelerated. The improvement in Nigerian per capita GDP in constant prices over the six years of 2002-2008 took India eight years to achieve in the late 20th century, it took Korea 11 years to achieve in the mid-20th century, and it took France 27 years to manage the same in the 19th century.

Figure 8: More African countries recorded average annual growth of 7%-plus over 2000-2009 than ever

Source: IMF, Renaissance Capital estimates

What is clear from the above is that the growth virus does not respect ethnic, religious or geographic boundaries. It is not Victorian English values, Chinese Confucian/communism or East African entrepreneurship that offer the only model to follow. Growth and high living standards have been created in resource-rich Canada and resource-less South Korea, in the formerly tropical swamps of Singapore and the cold winters of Sweden. There is no reason to assume it will not encompass us all.

02468

101214161820

Eq. G

uinea

Azer

baija

nTu

rkmen

istan

Qatar

Ango

laMy

anma

rCh

inaSi

erra

Leon

eAf

ghan

istan

Nige

riaAr

menia

Kaza

khsta

nEt

hiopia

Tajik

istan

Camb

odia

Bhuta

nRw

anda

Chad

Maldi

ves

Moza

mbiqu

eUg

anda

Suda

nVi

etnam

Belar

usMo

ngoli

aLa

osInd

iaTa

nzan

iaUA

ETr

inida

d & T

obag

o

The growth model has infected continental sized powers like China and

India, as well as city states like Singapore

Today it is Africa which dominates the high growth economies

Neither culture nor climate are barriers to the growth virus

19 July 2011 Africa: The bottom billion becomes the fastest billion Renaissance Capital

10

The only potential long-term barrier we see is the risk that the earth itself cannot cope with the consumption levels demanded by an ever-richer human race. This assumes that our ingenuity is unable to respond to these potential challenges. History is, however, encouraging. The agricultural revolution saved us from starvation. In the 1830s, Europe was running short of wood and panic buying was driving up lumber prices and cutting down the forests of the Austrian empire. Coal proved to be a solution. Oil saved the whales. It may yet be African solar power that saves us from global warming. But these are far from our areas of expertise, so below we focus on what catch-up theory suggests happens next, which countries are making the most progress, and what is both holding Africa back and providing the opportunity for faster progress.

Figure 9: Catching up is a global phenomenon – per-capita GDP since 1820, constant 1990 PPP dollars

Source: Historical Statistics of the World Economy: 1-2008 AD, Angus Maddison

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1820

1826

1832

1838

1844

1850

1856

1862

1868

1874

1880

1886

1892

1898

1904

1910

1916

1922

1928

1934

1940

1946

1952

1958

1964

1970

1976

1982

1988

1994

2000

2006

United Kingdom FranceGermany Italy Spain United States CanadaCzechoslovakia Argentina Brazil Chile Japan South Korea Thailand TaiwanSingapore India

11

Renaissance Capital Africa: The bottom billion becomes the fastest billion 19 July 2011

The Rostow model is summarised as follows:

Stage one: Traditional society. Agriculture dominates; low per-capita GDP, due to a lack of technology. Hierarchical society.

Stage two: Preconditions for take-off. Secular education, formation of entrepreneurial class; some capital mobilisation, with currency and banking, and modest manufacturing. Take-off occurs within 10-50 years.

Stage three: Take-off. When the rate of productive investment rises from 5% to 10% or more of national income, and one or more substantial manufacturing sectors demonstrates a high rate of growth. Sector-led growth becomes common. Economic processes, rather than tradition, predominates. Maturity reached after 50-100 years. Equivalent to industrial revolution.

Stage four: Drive to maturity. Investment rates of 10-20% extend technology across the economy, and keep growth above population increase. New sectors take over from previous growth sectors. Poverty rates fall.

Stage five: Age of high mass-consumption. This enables countries to concentrate on their specific priorities, e.g. military/security issues, equality/welfare issues, luxuries for their elites.

Africa 1960-1980: Stage one

Much of Africa was evidently at the first stage at the time of the independence wave, around 1960. Agriculture dominated the continent’s economies, and education was very limited. When the Democratic Republic of Congo (DRC) won independence from Belgium in 1960, there were just 30 graduates in the country, no doctors, no secondary school teachers and no army officers. In the 1959-1960 school year, 136 children completed secondary school education in the DRC. Kenya did not have its first African lawyer until 1956 – which may be one too many, according to some American friends, but is indicative of the lack of professionals across the economy. In Northern Rhodesia (now Zambia), 35 Africans had gained higher education by 1959, and in Nyasaland (now Malawi) the figure was just 28. Given the starting point in 1960, it is not so surprising that Africa’s economies were in trouble as these countries entered the 1980s.

While human capital was lacking at the grassroots, leadership at the top did little to compensate. Many poor policy choices were made, from an excessive, if understandable focus on building university education, but at the expense of universal primary education, to the adoption of the latest Western or Maoist theories (it’s always China that has “the solution”), and neglect of the agricultural sector. The result was that growth had stuttered to a halt by the 1980s, in a continent burdened by debt.

Modernisation theory The Rostow take-off (or stages of growth) model

Africa was agricultural and held back by very low education levels in 1960

Political leaders followed foreign models with little relevance for Africa

19 July 2011 Africa: The bottom billion becomes the fastest billion Renaissance Capital

12

Stage two in Africa: Education has improved, banking facilities are ready

The situation has clearly improved. Debt forgiveness programmes mean Africa now has some of the lowest debt burdens in the world. Political leaders can see what has worked elsewhere, and are adopting reforms that make a difference. Micro-level reforms mean some countries in Africa are leaping up the World Bank’s ease of doing business indicators – Rwanda ranked first in 2010 (see our report Rwanda – An African inspiration, dated 12 April 2011). Education has been expanded dramatically.

In 1975, gross primary school enrolment was 61% across Africa, and only 54% in SSA (excluding SA). By 1990, the ratio was 75% across Africa and 69% in SSA, and by 2005 it was 96% and 93%. For secondary schools, there was just 3% gross enrolment in 1960, 13% by 1975, 30% by 1990 and 39% by 2005. Nigeria was at 7% in 1975 against 32% in 2005, Kenya is up from 13% to 48% and Ghana has risen from 35% to 43%. The richest African countries, including Mauritius, now have 88% enrolment.

Figure 10: Secondary school gross enrolment rates 1975-2005

Source: UN

To put SSA into perspective, its level of secondary school enrolment is now well ahead of the US when it was booming 100 years ago. Just 7% of Americans aged 14-17 attended school in 1890 but 90% after 1945. In 1940, fewer than 15% of high school leavers went to college, but 62% by 1992. In 1900, only 10% of industrial CEOs in the US had a college education. Today SSA secondary enrolment rates are similar to those in Mexico or Turkey in 1975, and three times better than it was itself in 1975. Ghana and Kenya are in stronger positions than China in 1990; and Botswana, SA and Mauritius are ahead of China, Indonesia and India today. Africa now has an educated workforce sufficient to support a take-off economy.

Not only is education improved, but we find plenty of anecdotal evidence that educated and internationally trained African professionals are returning from the US and Europe, to use their skills in the strong growth economies in the continent.

020406080

100120

Braz

il

South

Afric

a

Russ

ia

Mexic

o

Turke

y

China

Indon

esia

India

Afric

a

SSA

excl

SA

Around 1975 Around 1990 Around 2005

Primary schooling is now virtually universal; secondary schooling enrolment is up nearly tenfold since 1960

SSA secondary school enrolment is now similar to Mexico or Turkey in 1975; Botswana and Mauritius have better levels than China or India

13

Renaissance Capital Africa: The bottom billion becomes the fastest billion 19 July 2011

To enter the second stage requires an effective banking system. Stock market investors in Ghana, Nigeria, Kenya and Rwanda will all be aware that this is now in place. Credit/GDP ratios have plenty of room to rise in the years ahead and help finance rising investment.

Figure 12: Credit to households and corporates as a proportion of GDP, 2009, %

Source: IMF

0102030405060708090

Maur

itius

South

Afric

aUk

raine

Lithu

ania

Hung

ary

Croa

tiaCz

ech R

epub

licKa

zakh

stan

Polan

dBr

azil

Slov

akia

India

Russ

iaRo

mania

Nige

riaTu

rkey

Philip

pines

Keny

aInd

ones

iaZim

babw

eMe

xico 4

2dBo

tswan

a (20

08)

Ghan

aAr

genti

naZa

mbia

Rwan

da

Private sector debt ratios are way below the 200% levels seen in the UK, Spain or

the US

Figure 11: Key education data and per-capita GDP in major EM and African countries Primary gross enrolment Secondary gross enrolment Per-capita GDP 1975 1990 2005 1975 1990 2005 1990 2005 2010 Africa 61 75 96 13 30 39 Angola 78* 86 102** 10 10 15*** Angola 879 1,699 4,478 Botswana 70 104 107 14 40 77 Botswana 3,187 5,985 7,627 DRC 89 54 82** 14 22 32** DRC 227 118 186 Ethiopia 18 33 78 5 14 24 Ethiopia 259 165 350 Ghana 64 71 87 35 37 43 Ghana 603 824 1,312 Guinea 34 34 86 13 9 31 Guinea 434 319 448 Kenya 103 101 108 13 48 48 Kenya 504 547 809 Mauritius 105 109 102 38 53 88 Mauritius 2,426 5,219 7,593 Mozambique 48 63 102 4 7 13 Mozambique 249 336 458 Nigeria 50 85 95 7 23 32 Nigeria 348 824 1,389 North Africa 76 88 105 27 60 na Rwanda 54 70 128 4 8 14 Rwanda 348 287 562 SA 99 107 103 na 66 96 SA 3,039 5,267 7,158 SSA ex. SA 54 69 93 9 19 29 Tanzania 53 69 107 3 5 11 Tanzania 176 366 548 Uganda 45 67 118 4 12 18 Uganda 259 321 501 Zambia 92 94 115 15 21 30 Zambia 475 612 1,221 Zimbabwe 71 101 104*** 9 47 41*** Zimbabwe na 461 594 * 1974 ** 2007 data *** 2006 data Around

1975 Around

1990 Around

2005 Around

1975 Around

1990 Around

2005 1990 2005 2010

Brazil 122 141 136 47 106 Brazil 3,465 4,832 10,816 Russia 107 94 95 93 Russia na 5,348 10,437 Mexico 108 114 112 31 55 83 Mexico 3,458 8,163 9,566 Turkey 100 99 96 27 47 79 Turkey 3,860 7,108 10,399 China 124 129 111 57 38 72 China 341 1,726 4,382 Indonesia 89 119 118 21 48 64 Indonesia 699 1,300 3,015 India 84 93 112 26 37 54 India 378 716 1,265

Source: UN

19 July 2011 Africa: The bottom billion becomes the fastest billion Renaissance Capital

14

Entering the third stage: Services over manufacturing

The third stage is where Africa might be different. Walt Rostow’s key book, Stages of Economic Growth, was written in 1990, before this analyst had heard of the internet. If development then required a country to export to the rest of the world, it could only be done physically. Today, services might be able to replace manufacturing as the engine of growth – in Ireland, exports of services are worth 48% of GDP, while Greek exports of goods account for just 7% of GDP. Rwanda already exports more services than goods. Productivity gains in Pakistan and Sri Lanka are rising faster than in manufacturing, and the productivity level is higher in both countries, and Nepal1. Whether it is call-centres in Kenya or conferences in Rwanda, there could be room for many countries in Africa to leapfrog manufacturing, reducing the need for costly investment in transport infrastructure.

Growth in ICT has been phenomenal. There are an estimated 0.5bn mobile phones in Africa. For every 10 additional phones per 100 people, GDP growth rises by 0.6-1.2% according to one study. In 2007, just one fibre cable connected SSA to the world – now there are seven, and next year the total will reach 12. Internet capacity has risen from 340 gigabits to 34,000 gigabits per second, and the cost of internet services has dropped by 95% since 2007 and may be down by 99% in 20122.

Figure 13: Telecoms catch-up – Mobile penetration as % of population

Source: MTN, NCC, Offcom, Arcep, Renaissance Capital estimates

This is not to say we won’t see manufacturing in Africa. Beneficial trade deals between Africa and the US have already encouraged a modest amount of manufacturing to relocate to Africa even from China into special economic zones. Rising wages in China make this an increasingly plausible scenario, but Africa’s challenge will be competing with Vietnam, and others in South East Asia and South Asia.

1 The Economist, 21 May 2011. 2 http://www.time.com/time/magazine/article/0,9171,2080702-1,00.html

0

0.2

0.4

0.6

0.8

1

1.2

1.4

Keny

a

Sene

gal

Nige

ria

South

Afric

a

Ghan

a

Ugan

da

Came

roon

Cong

o-B

Egyp

t

UK

Fran

ce

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

With the internet, services might replace manufacturing as the growth driver

As Chinese wages rise, Africa may win manufacturing market share too

15

Renaissance Capital Africa: The bottom billion becomes the fastest billion 19 July 2011

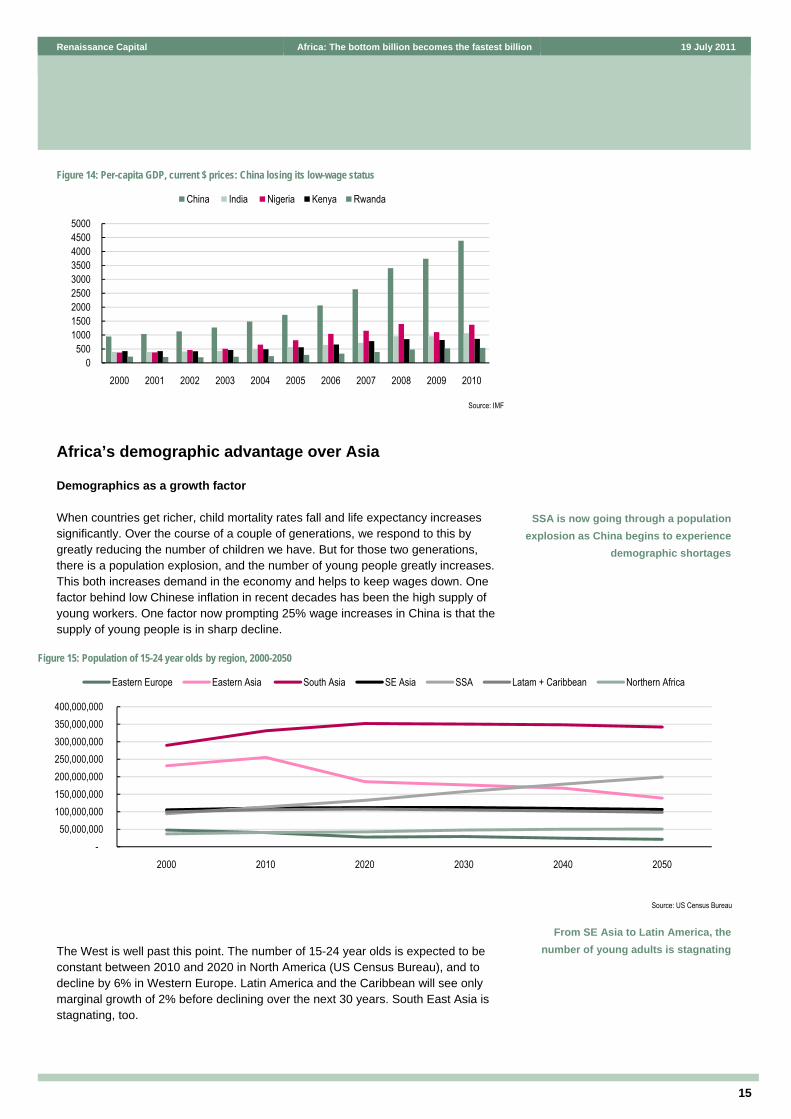

Figure 14: Per-capita GDP, current $ prices: China losing its low-wage status

Source: IMF

Africa’s demographic advantage over Asia

Demographics as a growth factor

When countries get richer, child mortality rates fall and life expectancy increases significantly. Over the course of a couple of generations, we respond to this by greatly reducing the number of children we have. But for those two generations, there is a population explosion, and the number of young people greatly increases. This both increases demand in the economy and helps to keep wages down. One factor behind low Chinese inflation in recent decades has been the high supply of young workers. One factor now prompting 25% wage increases in China is that the supply of young people is in sharp decline.

The West is well past this point. The number of 15-24 year olds is expected to be constant between 2010 and 2020 in North America (US Census Bureau), and to decline by 6% in Western Europe. Latin America and the Caribbean will see only marginal growth of 2% before declining over the next 30 years. South East Asia is stagnating, too.

0500

100015002000250030003500400045005000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

China India Nigeria Kenya Rwanda

SSA is now going through a population explosion as China begins to experience

demographic shortages

Figure 15: Population of 15-24 year olds by region, 2000-2050

Source: US Census Bureau

From SE Asia to Latin America, the number of young adults is stagnating

-50,000,000

100,000,000 150,000,000 200,000,000 250,000,000 300,000,000 350,000,000 400,000,000

2000 2010 2020 2030 2040 2050

Eastern Europe Eastern Asia South Asia SE Asia SSA Latam + Caribbean Northern Africa

19 July 2011 Africa: The bottom billion becomes the fastest billion Renaissance Capital

16

Figure 16: % change each decade in the number of 15-24 year olds in each region

Source: US Census Bureau

Eastern Europe is expected to see a dramatic 32% fall in the absolute number of 15-24 year olds, from 40mn to 28mn over 2010-2020 (according to the US Census Bureau), due to emigration by potential parents over 1995-2005 and low birth rates among those who remained in eastern Europe.

The US Census Bureau estimates that Eastern Asia (mainly China) will experience a 27% fall in this age group over this decade, and a total 45% decline from 2010 to 2050. This would more than offset a 6% rise in 15-24 year olds in South Asia. The supply of Asian labour is in decline.

Figure 17: % change in numbers of 15-24 year olds in each decade

Source: US Census Bureau

The only continent forecast to experience serious population growth is Africa – and as northern Africa is now relatively rich, the bulk of the growth will be in SSA. Its population of 15-24 year olds will rise by 15-20% each decade from now until 2040.

For labour-intensive industries such as textiles, evidently Africa will look ever more attractive, while the demand from employees in these growing sectors should in themselves boost consumption. It is young adults who need homes, and items to fill those homes. If China is the dream market for the automotive sector in 2010 – which might have looked an unrealistic forecast in 1970 – demographic data alone suggest Africa will be overtaking it within two generations.

-35-30-25-20-15-10-505

1015

North America Western Europe Eastern Europe Latam + Caribbean

2010 2020 2030 2040 2050

-40-30-20-10

01020304050

Eastern Asia

South Asia SE Asia Southern Africa

Western Africa

Northern Africa

SSA Middle Africa

2010 2020 2030 2040 2050

The number of East Asian 15-24 year olds will fall by more than a quarter this decade

SSA will see 15-20% growth per decade in the numbers of young adults

This could help attract labour intensive investment and boost economic demand

17

Renaissance Capital Africa: The bottom billion becomes the fastest billion 19 July 2011

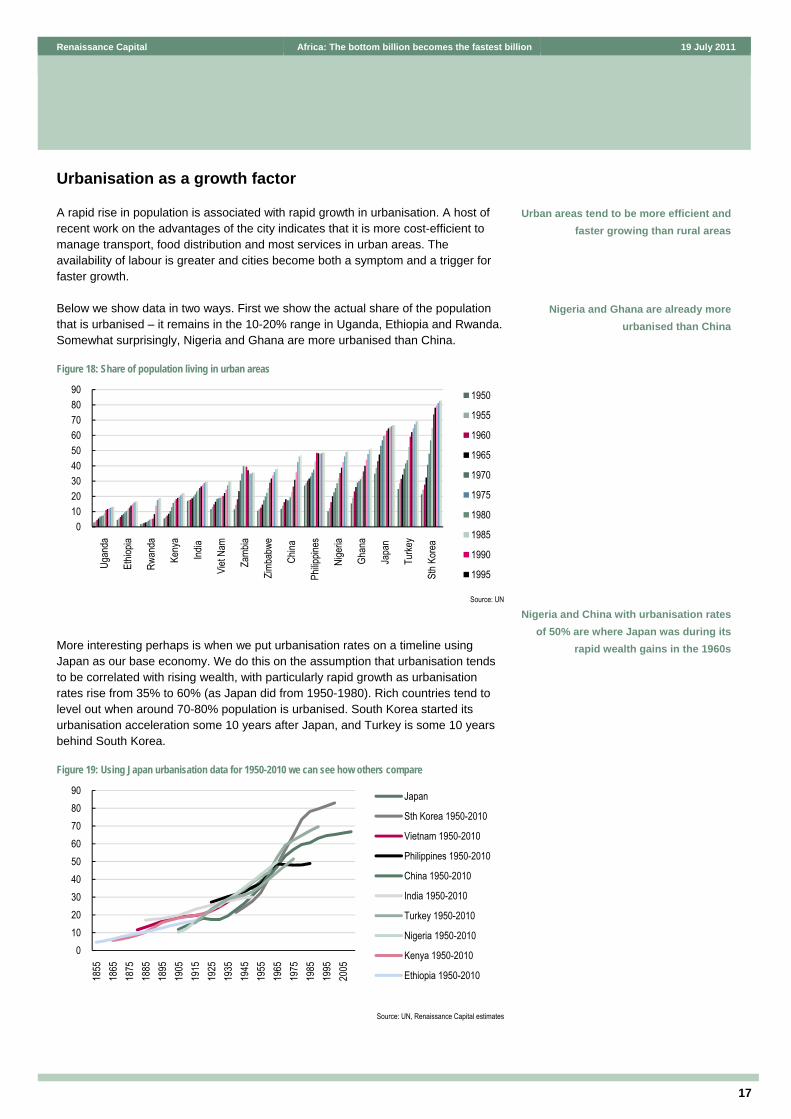

Urbanisation as a growth factor

A rapid rise in population is associated with rapid growth in urbanisation. A host of recent work on the advantages of the city indicates that it is more cost-efficient to manage transport, food distribution and most services in urban areas. The availability of labour is greater and cities become both a symptom and a trigger for faster growth.

Below we show data in two ways. First we show the actual share of the population that is urbanised – it remains in the 10-20% range in Uganda, Ethiopia and Rwanda. Somewhat surprisingly, Nigeria and Ghana are more urbanised than China.

Figure 18: Share of population living in urban areas

Source: UN

More interesting perhaps is when we put urbanisation rates on a timeline using Japan as our base economy. We do this on the assumption that urbanisation tends to be correlated with rising wealth, with particularly rapid growth as urbanisation rates rise from 35% to 60% (as Japan did from 1950-1980). Rich countries tend to level out when around 70-80% population is urbanised. South Korea started its urbanisation acceleration some 10 years after Japan, and Turkey is some 10 years behind South Korea.

Figure 19: Using Japan urbanisation data for 1950-2010 we can see how others compare

Source: UN, Renaissance Capital estimates

0102030405060708090

Ugan

da

Ethio

pia

Rwan

da

Keny

a

India

Viet

Nam

Zamb

ia

Zimba

bwe

China

Philip

pines

Nige

ria

Ghan

a

Japa

n

Turke

y

Sth K

orea

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

0102030405060708090

1855

1865

1875

1885

1895

1905

1915

1925

1935

1945

1955

1965

1975

1985

1995

2005

Japan

Sth Korea 1950-2010

Vietnam 1950-2010

Philippines 1950-2010

China 1950-2010

India 1950-2010

Turkey 1950-2010

Nigeria 1950-2010

Kenya 1950-2010

Ethiopia 1950-2010

Urban areas tend to be more efficient and faster growing than rural areas

Nigeria and Ghana are already more urbanised than China

Nigeria and China with urbanisation rates of 50% are where Japan was during its

rapid wealth gains in the 1960s

19 July 2011 Africa: The bottom billion becomes the fastest billion Renaissance Capital

18

Nigeria is roughly where Turkey was in 1985, and where Japan was in 1965. We think it will likely see the urbanisation rate rise from 50% to 60-70% over the next 10-20 years. This may well coincide with a period of very rapid growth for Nigeria, as others have seen at this time. Countries like Ethiopia have not yet reached Japanese urbanisation rates for 1950.

While urbanisation can support growth, it also offers the clearest sign of an acute need to build infrastructure, as has remained clear from the slums of London in the 19th century to the favelas of Rio de Janeiro or Nairobi today. Investment is key.

The third stage – Investment requirements

According to Nobel prize winner Michael Spence, achieving multi-decade levels of growth of 7% pa has only been achieved by 13 countries – all of which had investment levels of 25% of GDP. The reverse does not apply: high savings do not guarantee growth.

Figure 20: 25 years of 7% annual growth were achieved by these countries Period of high

growth of 7% or more Per-capita income at the

beginning and in 2005 (constant 2000 dollars)

Botswana 1960-2005 210 3,800 Brazil 1950-1980 960 4,000 China 1961-2005 105 1,400

Hong Kong 1960-1997 3,100 29,900 Indonesia 1966-1997 200 900

Japan 1950-1983 3,500 39,600 Korea 1960-2001 1,100 13,200

Malaysia 1967-1997 790 4,400 Malta 1963-1994 11,100 9,600 Oman 1960-1999 950 9,000

Singapore 1960-1999 2,200 25,400 Taiwan 1965-2002 1,500 16,400

Thailand 1960-1997 330 2,400 Source: The Next Convergence, Michael Spence, World Bank, World Bank Development Indicators

Within this governments need to invest 5-7% of GDP, primarily in education (see above) and infrastructure (see below). The positive news for SSA is that government debt ratios are very low, suggesting such investment is plausible.

Figure 21: Public debt as % of GDP is very low in SSA economies

Source: Renaissance Capital estimates

0102030405060708090

100

Zimba

bwe

Hung

ary

India

Braz

il Po

land

Keny

a Ar

genti

naCh

ina

Turke

y Me

xico

Ukra

ine

Vene

zuela

Czec

h Rep

ublic

So

uth A

frica

Ghan

a So

uth K

orea

Ro

mania

Ind

ones

iaZa

mbia

Rwan

daKa

zakh

stan

Nige

ria

Russ

ia

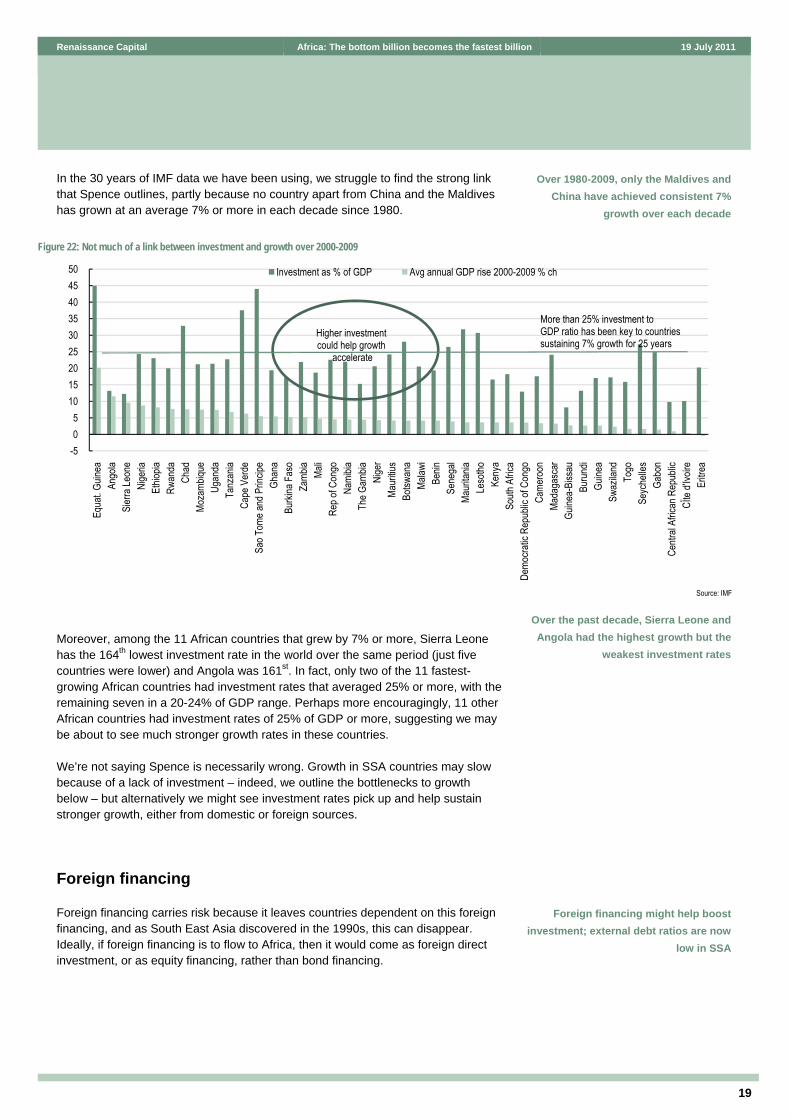

One study suggests that achieving 25 years of 7% annual growth requires 25% investment/GDP ratios

There is room for SSA governments to boost investment

19

Renaissance Capital Africa: The bottom billion becomes the fastest billion 19 July 2011

In the 30 years of IMF data we have been using, we struggle to find the strong link that Spence outlines, partly because no country apart from China and the Maldives has grown at an average 7% or more in each decade since 1980.

Moreover, among the 11 African countries that grew by 7% or more, Sierra Leone has the 164th lowest investment rate in the world over the same period (just five countries were lower) and Angola was 161st. In fact, only two of the 11 fastest-growing African countries had investment rates that averaged 25% or more, with the remaining seven in a 20-24% of GDP range. Perhaps more encouragingly, 11 other African countries had investment rates of 25% of GDP or more, suggesting we may be about to see much stronger growth rates in these countries.

We’re not saying Spence is necessarily wrong. Growth in SSA countries may slow because of a lack of investment – indeed, we outline the bottlenecks to growth below – but alternatively we might see investment rates pick up and help sustain stronger growth, either from domestic or foreign sources.

Foreign financing

Foreign financing carries risk because it leaves countries dependent on this foreign financing, and as South East Asia discovered in the 1990s, this can disappear. Ideally, if foreign financing is to flow to Africa, then it would come as foreign direct investment, or as equity financing, rather than bond financing.

Over 1980-2009, only the Maldives and China have achieved consistent 7%

growth over each decade

Figure 22: Not much of a link between investment and growth over 2000-2009

Source: IMF

Over the past decade, Sierra Leone and Angola had the highest growth but the

weakest investment rates

Foreign financing might help boost investment; external debt ratios are now

low in SSA

-505

101520253035404550

Equa

t. Guin

eaAn

gola

Sier

ra Le

one

Nige

riaEt

hiopia

Rwan

daCh

adMo

zamb

ique

Ugan

daTa

nzan

iaCa

pe V

erde

Sao T

ome a

nd P

rincip

eGh

ana

Burki

na F

aso

Zamb

iaMa

liRe

p of C

ongo

Nami

biaTh

e Gam

biaNi

ger

Maur

itius

Botsw

ana

Malaw

iBe

ninSe

nega

lMa

urita

niaLe

sotho

Keny

aSo

uth A

frica

Demo

cratic

Rep

ublic

of C

ongo

Came

roon

Mada

gasc

arGu

inea-

Biss

auBu

rund

iGu

inea

Swaz

iland

Togo

Seyc

helle

sGa

bon

Centr

al Af

rican

Rep

ublic

CЇte

d'Ivo

ireEr

itrea

Investment as % of GDP Avg annual GDP rise 2000-2009 % ch

Higher investment could help growth

accelerate

More than 25% investment to GDP ratio has been key to countries sustaining 7% growth for 25 years

19 July 2011 Africa: The bottom billion becomes the fastest billion Renaissance Capital

20

Figure 23: External debt/GDP ratios in 2010 very low in SSA

Source: Renaissance Capital estimates

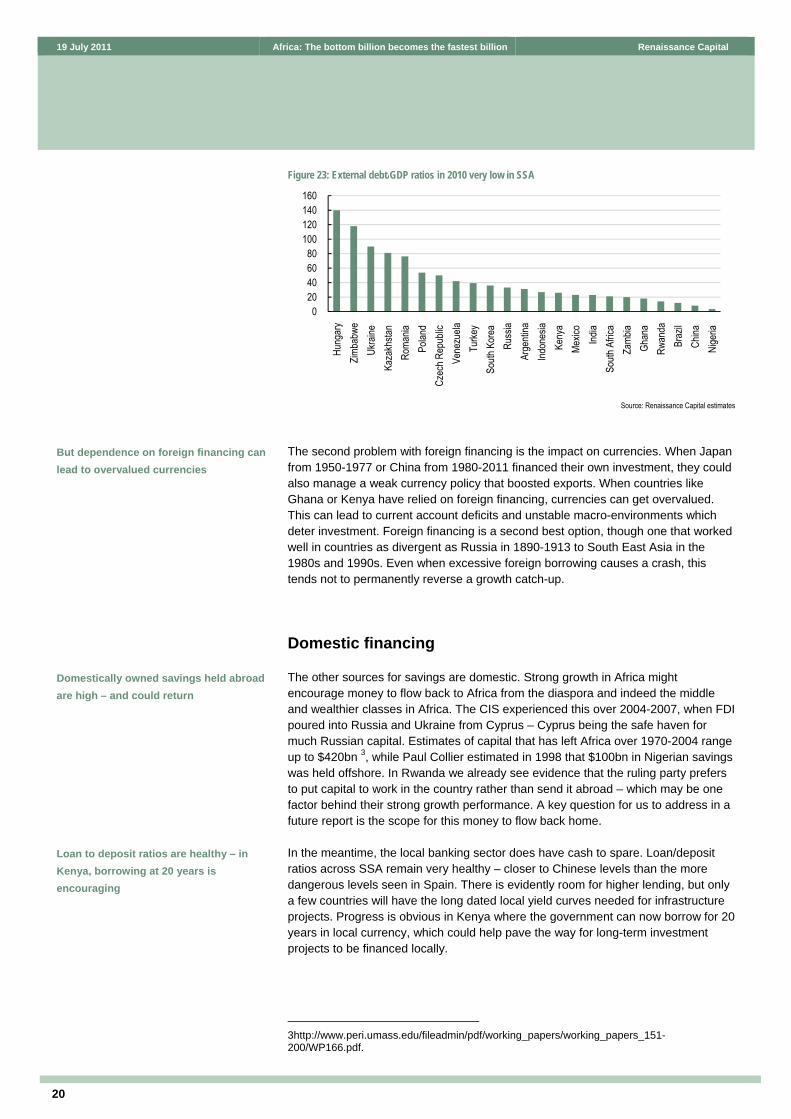

The second problem with foreign financing is the impact on currencies. When Japan from 1950-1977 or China from 1980-2011 financed their own investment, they could also manage a weak currency policy that boosted exports. When countries like Ghana or Kenya have relied on foreign financing, currencies can get overvalued. This can lead to current account deficits and unstable macro-environments which deter investment. Foreign financing is a second best option, though one that worked well in countries as divergent as Russia in 1890-1913 to South East Asia in the 1980s and 1990s. Even when excessive foreign borrowing causes a crash, this tends not to permanently reverse a growth catch-up.

Domestic financing

The other sources for savings are domestic. Strong growth in Africa might encourage money to flow back to Africa from the diaspora and indeed the middle and wealthier classes in Africa. The CIS experienced this over 2004-2007, when FDI poured into Russia and Ukraine from Cyprus – Cyprus being the safe haven for much Russian capital. Estimates of capital that has left Africa over 1970-2004 range up to $420bn 3, while Paul Collier estimated in 1998 that $100bn in Nigerian savings was held offshore. In Rwanda we already see evidence that the ruling party prefers to put capital to work in the country rather than send it abroad – which may be one factor behind their strong growth performance. A key question for us to address in a future report is the scope for this money to flow back home.

In the meantime, the local banking sector does have cash to spare. Loan/deposit ratios across SSA remain very healthy – closer to Chinese levels than the more dangerous levels seen in Spain. There is evidently room for higher lending, but only a few countries will have the long dated local yield curves needed for infrastructure projects. Progress is obvious in Kenya where the government can now borrow for 20 years in local currency, which could help pave the way for long-term investment projects to be financed locally.

3http://www.peri.umass.edu/fileadmin/pdf/working_papers/working_papers_151-200/WP166.pdf.

020406080

100120140160

Hung

ary

Zimba

bwe

Ukra

ine

Kaza

khsta

n Ro

mania

Po

land

Czec

h Rep

ublic

Ve

nezu

elaTu

rkey

South

Kor

ea

Russ

iaAr

genti

naInd

ones

iaKe

nya

Mexic

o Ind

ia So

uth A

frica

Zamb

ia Gh

ana

Rwan

daBr

azil

China

Ni

geria

But dependence on foreign financing can lead to overvalued currencies

Domestically owned savings held abroad are high – and could return

Loan to deposit ratios are healthy – in Kenya, borrowing at 20 years is encouraging

21

Renaissance Capital Africa: The bottom billion becomes the fastest billion 19 July 2011

Figure 24: Loan/deposit ratios, 2010 data

Source: Renaissance Capital estimates

Pension reform might be a further avenue for domestic financing. While SA looks more akin to The Netherlands or the UK, the rest of SSA shows some surprisingly high pension fund assets, with Kenya above Kazakhstan and Nigeria above Russia. The obvious link between what pension funds need (long-dated assets) and infrastructure financing needs, suggests increased private pension levels could help fund the infrastructure that would boost growth.

Figure 25: Pension assets/GDP, Ghana vs SSA peers, 2009

Source: Local authorities

Figure 26: Pension assets, 2009

Pension

assets, $bn GDP, $bn

Population, mn

Pension assets, % of GDP

Pension assets, $/capita

Ghana 1.4 25.8 23.1 5.4 60.6 Nigeria 12.2 168 152 7.3 80.5 Kenya 5.1 29.4 35.9 17.3 142 SA 359 285 49.3 126 7,282 Russia 38 1,235 142 3.1 267 Kazakhstan 12 108 16 11.5 796 Zimbabwe 1.8 6.7 11.7 26.9 154 Zambia 1.2 12.7 12.0 9.7 100

Source: Local authorities, Renaissance Capital estimates

020406080

100120140160180200

Ukra

ine

Kaza

khsta

n

Russ

ia

South

Afric

a

Nige

ria

Rwan

da

China

Keny

a

Zamb

ia

Ghan

a

Zimba

bwe

Loan to deposit ratio (2010)

05

101520253035404550556065

South

Af

rica

Zimba

bwe

Keny

a

Kaza

khsta

n

Zamb

ia

Ghan

a

Nige

ria

Russ

ia

19 July 2011 Africa: The bottom billion becomes the fastest billion Renaissance Capital

22

Mobile phone banking may also pull savings into the formal economy and support domestically financed credit extension. The Mpesa system in Kenya has already extended banking services from roughly 20% of the population to at least 50% of the adult population between March 2007 and December 20104. Not only does it form an alternative way to bring cash into the banking system, it might also encourage remittances by cutting costs5. So far the interest earned on all Mpesa accounts is equivalent to $7.5m and the average saving is just $3 per account, but as the system develops, this may well change.

If nine countries can sustain 7% growth without high investment, then we see a good chance of more achieving 10% or more annual growth rates with high investment.

Institutional developments

The cutting of red tape supports the acceleration of economic activity in SSA. A significant part of SSA’s growth story is attributed to the region’s commodity wealth, which is satisfying Asia’s huge appetite for natural resources. However, the fact that SSA’s mineral-poor and oil-importing countries have also been a significant part of this growth story implies that there is more to it than commodities. Softer issues, including political stability, macroeconomic reforms and institutional developments, collectively explain the balanced growth performance across SSA.

As SSA governments democratise, there is a growing awareness that their role must be limited to that of enablers. On the back of this some countries have made some concerted efforts to make it easier for the private sector and foreign investors to do business in their respective countries. The World Bank Doing Business survey on over 150 countries shows, using various indicators, including the ease of starting a business, how countries have performed relative to each other in improving their respective business environments. In the seven-year period between 2004 and 2011, the countries that reduced the time to start a business by the most number of days where Mozambique, the DRC, Lesotho, Angola and Senegal (see Figure 27). Today, the countries where one can start a business in the shortest amount of time are Rwanda (three days), Mauritius (six days), Senegal (eight days), Mali (eight days) and Ethiopia (nine days) (see Figure 28).

4http://wwwds.worldbank.org/external/default/WDSContentServer/IW3P/IB/2011/05/18/000158349_20110518143113/Rendered/PDF/WPS5664.pdf 5http://www.vodafone.com/content/dam/vodafone/about/public_policy/policy_papers/public_policy_series_6.pdf

Mobile banking may also help pull savings into the formal economy

High growth in Rwanda or Ethiopia may be linked to easier business regulation

23

Renaissance Capital Africa: The bottom billion becomes the fastest billion 19 July 2011

Figure 27: Time taken to start a business Figure 28: SSA countries where you can start a business in the shortest time

Source: World Bank, Renaissance Capital estimates Source: World Bank, Renaissance Capital estimates

The true test of the policy reforms that made SSA’s business environment less challenging is whether it has indeed translated into greater economic activity or greater investment. We found correlation between the change in the cost of starting a business and average economic growth in the 2004-2011 period where there is data available on the doing business indicators. Countries where the cost of starting a business fell the most also had the highest economic growth rates (see Figure 29). Angola, for instance saw its cost of starting a business plummet to 163% of income per capita in 2011, from 1316% in 2004. Angola’s economy grew by an average of 7.8% in that period. Although, Angola’s cost of starting a business remains significantly higher than that of Botswana and SA at 2.2% and 6.0% of income per capita, respectively, it has fallen significantly from prohibitive levels.

We also found a weak correlation between the cost of registering property and economic growth (see Figure 30). Ethiopia has one of SSA’s lowest property registration costs, at 2.1% of the property value in 2011. The East African country is one of the fastest-growing countries in SSA. It is projected to grow by 8.5% in 2011. On the contrary, in the Central African Republic, which has one of the SSA region’s highest costs of registering property at 19.3% of the property value, economic growth is below the SSA average at 3.5%.

020406080

100120140160180

Moza

mbiqu

e

DRC

Leso

tho

Ango

la

Sene

gal

Botsw

ana

Ethio

pia Mali

Keny

a

Zamb

ia

Nige

ria

Ghan

a

2004 2011

Time (

days

)

0

2

4

6

8

10

12

14

Rwan

da

Maur

itius

Sene

gal

Mali

Ethio

pia

Cape

Ver

de

C.A.

R.

Sier

ra Le

one

Ghan

a

Moza

mbiqu

e

Time(

days

)

Despite huge improvement in Angola, further gains are still within reach

19 July 2011 Africa: The bottom billion becomes the fastest billion Renaissance Capital

24

Figure 29: Correlation between economic growth and start up costs Figure 30: Correlation between the cost of registering property and GDP growth

Source: World Bank, Renaissance Capital estimates Source: World Bank, Renaissance Capital estimates

Our analysis also showed a weak correlation between the time taken to export goods and economic growth. We found that countries that reduced the number of days it took for them to get their exports across the border were the same as those with relatively higher economic growth rates (Figure 31). Eritrea cut the time it takes to get its exports across the border by 19 days between 2004 and 2011, which is one of the biggest improvements in SSA. Eritrea is also one of the fastest growing countries in SSA. Its economy is projected to grow by 7.9% in 2011. Research by Paul Collier among others highlights that exporting tends to boost productivity.

Figure 31: Correlation between the change in the time to export and economic growth

Sources: World Bank, Renaissance Capital estimates

Africa’s development path will leap from agriculture to services, and bypass industry. Contrary to the developed world, which after centuries of having agricultural-based feudal systems industrialised in the 18th and 19th centuries, and thereafter in the 20th century evolved to more services-oriented economies, SSA appears to have taken the leap from agriculture to services.

Telecoms has been one of the fastest-growing sectors in SSA over the past two decades, which partially explains the significant expansion of services in SSA, at the expense of industry. Poor infrastructure, particularly electricity, and a very

0

2

4

6

8

10

12

14

-1400 -1200 -1000 -800 -600 -400 -200 0 200

Decrease<---Cost of starting a business (% of income per capita)---> Increase

Aver

age r

eal G

DP gr

owth,

% (2

004-

11)

0

2

4

6

8

10

12

14

0 4 8 12 16 20 24

Cost of registering property (% of property value)

Real

GDP

grow

th,%

2

4

6

8

10

12

14

-30 -25 -20 -15 -10 -5 0 5Decrease<----change in number of days to export------>Increase

Real

GDP

grow

th,%

(201

1)

Easier access to export markets also supports faster growth

Growth drivers: Services and construction

25

Renaissance Capital Africa: The bottom billion becomes the fastest billion 19 July 2011

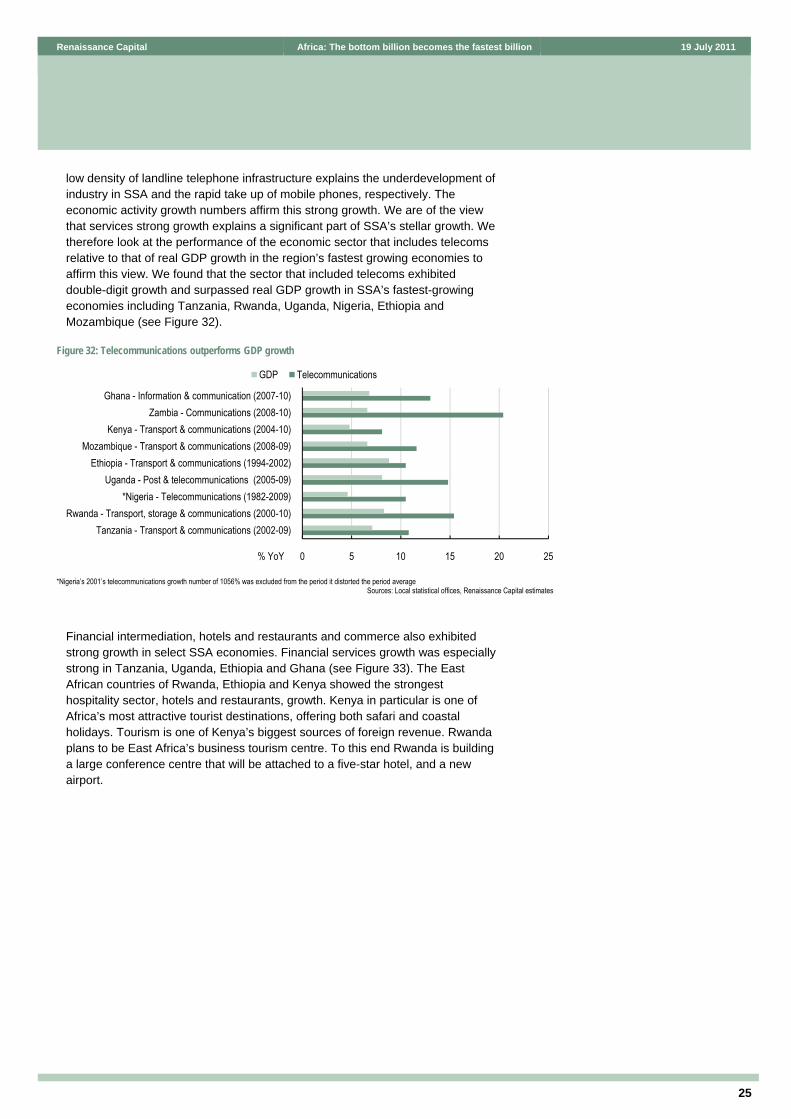

low density of landline telephone infrastructure explains the underdevelopment of industry in SSA and the rapid take up of mobile phones, respectively. The economic activity growth numbers affirm this strong growth. We are of the view that services strong growth explains a significant part of SSA’s stellar growth. We therefore look at the performance of the economic sector that includes telecoms relative to that of real GDP growth in the region’s fastest growing economies to affirm this view. We found that the sector that included telecoms exhibited double-digit growth and surpassed real GDP growth in SSA’s fastest-growing economies including Tanzania, Rwanda, Uganda, Nigeria, Ethiopia and Mozambique (see Figure 32).

Figure 32: Telecommunications outperforms GDP growth

*Nigeria’s 2001’s telecommunications growth number of 1056% was excluded from the period it distorted the period average

Sources: Local statistical offices, Renaissance Capital estimates

Financial intermediation, hotels and restaurants and commerce also exhibited strong growth in select SSA economies. Financial services growth was especially strong in Tanzania, Uganda, Ethiopia and Ghana (see Figure 33). The East African countries of Rwanda, Ethiopia and Kenya showed the strongest hospitality sector, hotels and restaurants, growth. Kenya in particular is one of Africa’s most attractive tourist destinations, offering both safari and coastal holidays. Tourism is one of Kenya’s biggest sources of foreign revenue. Rwanda plans to be East Africa’s business tourism centre. To this end Rwanda is building a large conference centre that will be attached to a five-star hotel, and a new airport.

0 5 10 15 20 25

Tanzania - Transport & communications (2002-09)Rwanda - Transport, storage & communications (2000-10)

*Nigeria - Telecommunications (1982-2009)Uganda - Post & telecommunications (2005-09)

Ethiopia - Transport & communications (1994-2002)Mozambique - Transport & communications (2008-09)

Kenya - Transport & communications (2004-10)Zambia - Communications (2008-10)

Ghana - Information & communication (2007-10)

GDP Telecommunications

% YoY

19 July 2011 Africa: The bottom billion becomes the fastest billion Renaissance Capital

26

Figure 33: Financial services outperforms real GDP growth Figure 34: Hospitality sector’s growth outperforms GDP growth in East Africa

Source: Local statistics office, Renaissance Capita estimates Source: Local statistics office, Renaissance Capital estimates

Outside the services sector, construction has been one of the fastest-growing sectors over the past decade in SSA’s best-performing economies. In our view, this growth has been driven by two factors, urbanisation and infrastructure development. In the 2009/2010 fiscal year, Uganda’s government made its biggest budget allocation to road transport infrastructure. That is indicative of the commitment the government has towards infrastructure development and the resultant boost to construction activity. Kenya has had a fiscal stimulus programme in place since FY09/FY10 that largely involves infrastructure development in the transportation and energy sectors. Ghana’s spurt in construction activity in recent years is partially due to the construction of infrastructure required to support oil production, which began in December 2010.

Figure 35: Construction outperforms GDP growth

Sources: Local statistical offices, Renaissance Capital estimates

All these highly growing sectors evidently imply relatively slow growth in sectors we have not focused on. Agriculture remains a key area in which big productivity improvements are possible, and we intend to focus on this in a future report.

0 4 8 12 16

Tanzania (2002-09)

Uganda (2005-09)

Ethiopia (1994-2002)

Ghana (2007-10)

GDP Financial intermediation

% YoY0 5 10 15 2

Rwanda (2000-10)

Ethiopia (1994-2002)

Kenya (2004-10)

GDP Hotels & restaurants

% YoY

0 4 8 12 16 20

Tanzania (2002-09)

Rwanda (2000-10)

Uganda (2005-09)

Ethiopia (1994-2002)

Mozambique (2008-09)

Kenya (2004-10)

Zambia (2008-10)

Ghana (2007-10)GDP Construction

% YoY

27

Renaissance Capital Africa: The bottom billion becomes the fastest billion 19 July 2011

The critics of catch-up theory

There are critics of catch-up theory economics, and among the best we’ve read is by Vladislav Inozemtsev. He highlights that a number of countries have made it to middle-income level, but have often stalled at this point. Latin America in the 1980s or the Philippines are examples. Whether this critique is accurate or not is not relevant to the debate in Africa today. Aside from Mauritius, SA and Botswana, they are only now entering the third stage, and making the transition to “maturity” and “high consumption” will be a challenge for the 2020s or 2030s.

Your questions?

Can growth continue when western economies are weak?

Yes. Asia succeeded in the 1970s despite the terrible market shocks of 1973-1975, the global debt crisis and the recession of 1980-1982. In fact, we’ve just experienced a terrible global shock and Africa sailed through it.

If China slumps, will Africa?

Half the countries that have sustained growth of 7% annually in the past decade do not sell to China. Clearly the commodity exporters would do worse in the face of a Chinese slump, but this need not bring down the whole continent. India has proved resilient and the same may apply to many African countries too.

Should we trust the data?

Few question Africa’s growth data when they show no growth. It is only high growth that surprises. The same questions have been asked about Chinese data too though no-one can now deny the commodity price boom that China has caused over the past ten years. While any economist is always sceptical of all data, we see no particular reason to doubt the validity of African data today.

Does high growth mean much when these countries are so poor?

In the 20th century, Africa was poor too, but this did not mean it experienced high growth in the 1980s. As with China, India and Europe, everyone starts at low levels.

Won’t Africa’s poor governance and political instability derail the story again?

As we demonstrated in our 22 June 2011 report, The revolutionary nature of growth, as an inevitable byproduct of rising wealth levels countries move away from autocracy towards democracy, which tends to reduce corruption. We are all aware of poor governance in Africa precisely because per-capita GDP did not rise in the 1980s, so poor governance was not challenged. Today, as wealth levels rise, democratisation will follow and corruption should decrease. Africa’s wealth levels have probably never been as high as they are today. This is not to say individual countries will not take backward steps – some will – but the prospects are improving.

Democratisation will follow growth

19 July 2011 Africa: The bottom billion becomes the fastest billion Renaissance Capital

28

How can you ignore the infrastructure challenges?

We discuss this issue more fully in the next section. We concur that infrastructure bottlenecks are a challenge, especially the undersupply of power. We conservatively estimate that addressing these bottlenecks could raise Africa’s GDP growth by an extra 2 ppts.

29

Renaissance Capital Africa: The bottom billion becomes the fastest billion 19 July 2011

Moving around SSA, visitors are often struck by:

Heavy traffic congestion

Frequent power outages

The rapid growth experienced in SSA over the past decade has resulted in worsening infrastructure bottlenecks. Ports, roads and freight are unable to keep up with the increasing movement of goods and people across the continent. Power generators are failing to meet growing demands for electricity, resulting in frequent power outages and blackouts. What are these constraints costing SSA in terms of growth?

A report published by the World Bank and Agence Française de Développement in 2010, Africa’s Infrastructure: A time for transformation, takes an in-depth look at Africa’s infrastructure. This report, at a mere 350 pages, may be too much for anyone to plough through in one session, so we have done our best to summarise the main findings, as well as add our thoughts on the matter. The report looks at the impact of infrastructure across 24 SSA countries which together represent 85% of SSA GDP and an. These included Benin, Burkina Faso, Cameroon, Cape Verde, Chad, Côte d’Ivoire, DRC, Ethiopia, Ghana, Kenya, Lesotho, Madagascar, Malawi, Mozambique, Namibia, Niger, Nigeria, Rwanda, Senegal, SA, Sudan, Tanzania, Uganda and Zambia. The main finding is that infrastructure bottlenecks are holding the continent back. They result in higher costs, lower intra-regional trade and lower productivity. This could be shaving as much as 2% off GDP growth across the region. We believe this figure could be higher.

Finding 1: Infrastructure contributed to over half of Africa’s improved growth performance

SSA has witnessed a marked uptick in growth over the past decade. The report states that between 1990 and 2005 improvements in infrastructure contributed about 1% to per-capita GDP growth. Power shortages, on the other hand, reduced growth in SSA by an estimated 0.1%t and as much as 0.2% in parts of southern Africa. The contribution of infrastructure cannot be overemphasised, not just in Africa but in both emerging and developed markets. This is depicted in the graph below, which shows the contribution by infrastructure to GDP per-capita growth across various regions. While stabilisation and structural policies play significant roles in increasing growth, in most regions infrastructure is the largest contributor to growth.

Infrastructure: the key to faster growth in SSA

A report last year suggested infrastructure bottlenecks could be holding GDP growth back by 2 ppts

Infrastructure improvements have already added 1% to GDP growth rates

over 1990-2005

19 July 2011 Africa: The bottom billion becomes the fastest billion Renaissance Capital

30

Figure 36: Changes in growth per capita caused by changes in growth fundamentals, 1990-2005

Source: World Bank report, Calderon 2008

Figure 37: Contribution of infrastructure to total factor productivity

Source: World Bank reports, Escribano, Guasch, and Pena 2008

As pointed out earlier in the report, within infrastructure the rollout of telecoms has been a major driver to GDP per-capita growth across Africa. Power has made the least contribution, in most instances detracting from growth:

Figure 38: Changes in growth per capita caused by changes in different infrastructure sectors, 1990 -2005

Source: World Bank report, Calderon 2008

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

W. Europe SE Asia N. Africa W. Africa E. Africa S. Africa C. Africa

Stabilisation policies Structural policies Infrastructure

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

NamibiaBotswanaMauritius

South AfricaKenya

TanzaniaCameroon

ZambiaEthiopiaMalawi

Infrastructure Others

-0.4-0.20.00.20.40.60.81.01.21.4

N. Africa W. Africa E. Africa S. Africa C. Africa Africa

Telecoms Power Roads

31

Renaissance Capital Africa: The bottom billion becomes the fastest billion 19 July 2011

Finding 2: Africa’s infrastructure lags its emerging markets peers

A report published in 2008, Making sense of Sub-Saharan Africa’s Infrastructure Endowment, identified that SSA countries lag their peers in the developing world on nearly all aspects of infrastructure development (Yepes, Pierce, and Foster 2008). However, this has not always been the case. The study shows that 40 years ago SSA was well ahead of its South Asian peers. Generation capacity per million people was almost three times higher. By 2000, South Asia had advanced to almost twice the generation capacity per million people. Somewhere along the line, the continent was caught sleeping and failed to invest in its assets.

Figure 39: Africa’s infrastructure deficit Normalised units SSA low income countries Other low-income countries Paved-road density 31 134 Total road density 137 211 Main-line density 10 78 Mobile density 55 76 Internet density 2 3 Generation capacity 37 326 Electricity coverage 16 41 Improved water 60 72 Improved sanitation 34 51 Note: Road density is measured in kilometres per 100 sq kilometres of arable land Note: Telephone density is measured in lines per 1,000 population Note: Generation capacity is measured in megawatts per 1,000,000 population Note: Electricity, water, and sanitation coverage in percentage of population.

Source: World Bank report, Yepes, Pierce, and Foster 2008

Figure 40: Road density, km/’000, km2

Source: WDI

Finding 3: Socio-geo-economic issues add to the infrastructure challenges

SSA comprises 49 nation states, following the formation of South Sudan. Many of the SSA states are small and a significant number are landlocked. Infrastructure development has largely been driven by the need to gain access to export markets, hence the development of rail, road and water corridors to seaports. Ports are congested and we have heard stories of consignments being held up at ports for up

01020304050607080

Cong

o

Suda

n

Gabo

n

Ethio

pia

Ango

la

Tanz

ania

Moza

mbiqu

e

Keny

a

Sene

gal

Afric

a-Av

erag

e

Zamb

ia

Nige

ria

Ghan

a

Zimba

bwe

South

Afric

a

Ugan

da

19 July 2011 Africa: The bottom billion becomes the fastest billion Renaissance Capital

32

to three months in some instances. Average delivery times from vessels to consignee are above those in other emerging markets.

Figure 41: Average delivery time for containers from vessel to consignee Gateway Destination Distance (km) Transit time (days) Mombasa, Kenya Kampala, Uganda 1,100 20 Mombasa, Kenya Kigali, Rwanda 1,700 27 Dar es Salaam, Tanzania Bujumbura, Burundi 1,800 21 Abidjan, Cote d'Ivoire Bamako, Mali 1,200 7 Dakar, Senegal Bamako, Mali 1,200 10 Cotonou, Benin Niamey, Niger 1,000 11 Douala, Cameroon Ndjamena, Chad 1,900 38 Lagos, Nigeria Kano, Nigeria 1,100 21 Almaty, Kazakhstan Germany 7,000 20 Bangkok, Thailand Vientiane, Lao 670 2 Kolkata, India Kathmandu, Nepal 1,250 9 Tianjin, China Ulaanbaatar, Mongolia 1,700 8

Source: World Bank report, UN Report, Arvis 2005, quoting an international logistics company

There has been less emphasis placed on developing intraregional trade. Despite the advent of economic and trade unions in various regions across Africa, these have been slow in encouraging intra-regional trade links. Global exports (i.e. exports from Africa to the rest of the world) account for 27% of SSA’s GDP growth while intra-Africa exports for only 4% (2009). If the infrastructure bottlenecks were removed, would intra-Africa trade double or increase tenfold? The answer probably lies somewhere in the middle. Higher exports might then boost manufacturing productivity and produce a virtuous circle, as seen in Mauritius.

Figure 42: Cost of transport in Africa – From major ports to cities

Source: World Bank, UNCTAD

The problem is not restricted to intra-regional trade. Intra-country, SSA countries are facing relatively rapid rates of urbanisation as the rural population throngs to cities in search of a better life. Meanwhile there has been underinvestment in infrastructure, due to both capital constraints and poor planning. As a result, existing infrastructure assets are under increasing strain and failing to meet demand. The result is higher operating costs for businesses and higher costs of living for consumers. We pay more for less. In SA, consumers are asked to reduce their power consumption, while

0

5

10

15

20

25

0

100

200

300

400

500

MOM

Nairo

bi MO

M Ka

mpala

MOM

Juba

MOM

Kiga

liMO

M Bu

jumbu

raDA

R to

Kigo

ma

DAR

Lusa

kaDA

R Ki

gali

DAR

Bujum

bura

DAR

Goma

DA

R Lu

bumb

ashi

Beira

to Lu

bumb

ashi

DAR

Hara

reDu

rban

Lusa

kaDo

uala

Bang

uiDo

uala

Njam

ena

Daka

r Bam

ako

Lome

Niam

eyLo

me O

uaga

doug

ouAb

idjan

Bam

ako

Lago

s Abu

jaLa

gos t

o Gom

be

USD/t USDc/t Km

33

Renaissance Capital Africa: The bottom billion becomes the fastest billion 19 July 2011

the per-unit cost of power to households has been approved to rise by over 25% pa for three years.

Finding 4: Infrastructure services are twice as expensive as elsewhere

According to a study published in 2008, across the board SSA’s infrastructure services cost at least twice as much as in other emerging markets. The report states that high costs are usually a function of high investment costs but in some sectors they are merely a function of low competition and hence high margins. The gap in some sectors, such as mobile telephony, has been reduced over the past two years with greater competition driving down costs. In some sectors the gap may very well have widened as prices to consumers have been increased to pay for investment in additional infrastructure assets.

Figure 43: Electricity tariffs USc/kW: 2009

Source: UPDEA Africa

Finding 5: Power remains the continent’s largest infrastructure challenge

Power consistently emerges as the primary limiting factor to growth in the region. We hear it from corporates in Lagos, Nairobi, Harare and even SA. We see it ourselves anecdotally in the power outages during business meetings – shortly followed by the humming of generators kicking in to fill the gap. Supply simply cannot meet demand, and this is widely acknowledged. What is often not known is the magnitude of the power deficit. It is estimated that SSA generates roughly the same power as Spain. Strip out SA and the picture becomes even less encouraging. Nigeria, for example, with a population three times that of SA, generates a tenth of SA’s power output, with total official generating capacity of 3,500 MW – similar to that consumed by Narita airport in Tokyo. This is evidenced in the low per-capita consumption of power across SSA, excluding SA.

05

10152025303540

Zimba

bwe

Libya

South

Afric

aAn

gola

Egyp

tEh

tiopia

Zamb

iaSu

dan

Alge

riaMa

uritiu

sKe

nya

Cong

oNi

geria

Moza

mbiqu

eNi

ger

Tunis

iaNa

mibia DR

CMa

lawi

Tanz

ania

CAR

Moro

cco

Guine

aUg

anda

Came

roon

Rwan

daGh

ana

Togo

Benin

Gabo

nCo

te d'I

voire

Buru

ndi

Chad Ma

liSe

nega

lMa

daga

scar

Rwan

daBu

rkina

Fas

oGa

mbia

Liber

ia

19 July 2011 Africa: The bottom billion becomes the fastest billion Renaissance Capital

34

Figure 44: Power consumption per capita, kW/’000 people

Source: EIA

Another study in 2008 looked into the causes of the power supply deficit in the region. As shown in the map below, it identified the leading drivers as:

Poor planning. Failure to anticipate rapid rates of urbanisation and economic growth. The long lead times in increasing capacity means supply simply cannot keep up with demand.

Droughts, which reduce hydropower generation in East Africa.

Systems disrupted by conflict/policies which hinder private investment in power generation.

0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0

Ethio

pia

Keny

a

Ugan

da

Tanz

ania

Suda

n

Cong

o

Nige

ria

Sene

gal

Ango

la

Ghan

a

Moza

mbiqu

e

Afric

a Avg

Zamb

ia

Zimba

bwe

Gabo

n

South

Afric

a

35

Renaissance Capital Africa: The bottom billion becomes the fastest billion 19 July 2011

Figure 45: Underlying causes of Africa’s power supply crisis

Source: World Bank report, Eberhard and others 2008