Mergers, Acquisitions and Restructuring: Types, Regulation ...

Acquisitions and Real Options:The Greenfield Alternativejoms_875 1048..1071

Keith D. Brouthers and Desislava DikovaNorth Carolina State University; University of Groningen

abstract Although acquisitions are a popular way to enter new markets, empirical evidencetends to indicate few benefits accrue to acquiring firms. This might be the case because firmsuse acquisitions when they should be employing an alternative mode of expansion. Applyingreal options theory to this issue, we suggest that greenfield start-up ventures provide a realoption alternative to acquisitions for firms establishing new international subsidiary units.To test this notion we examine a sample of Western European firms entering the emergingeconomies of Eastern Europe. The evidence suggests that acquisitions are a good choice onlywhen firms enter markets containing low demand uncertainty and when these firms possessacquisition-based strategic flexibility. Overall, our analysis indicates that greenfield venturesappear to provide firms with a real option when making the acquisition decision.

INTRODUCTION

Despite the growth in acquisition activity over the past few decades, there is still littleempirical evidence that acquisitions result in improved firm performance. Studies likeKing et al. (2004), Hayward and Hambrick (1997) and Tuch and O’Sullivan (2007) showthat few financial benefits accrue to firms after acquisition. Research examining inter-national acquisitions tends to provide similar results (Clougherty and Duso, 2009;Gregory and McCorriston, 2005). Furthermore, Hayward and Shimizu (2006) andBergh (1997) found that firms frequently realize their mistake and divest, reversing theacquisition often at a substantial loss. As a consequence managers and scholars continueto question why firms make acquisitions (Brouthers et al., 1998) and whether acquisitionsare always the best vehicle to achieve growth.

Researchers have noted that acquisitions are not always the best way to expand,especially into international markets (Brouthers and Brouthers, 2000; Dikova and vanWitteloostuijn, 2007; Harzing, 2002; Hennart and Park, 1993). Based mainly on trans-action cost theory these studies indicate that firms have choices in their internationaldevelopment activity; they can grow through acquisitions or by starting new greenfield

Address for reprints: Keith D. Brouthers, North Carolina State University, College of Management, 2801Founders Drive, 1300 Nelson Hall, Raleigh, NC 27695-7229, USA ([email protected]).

© Blackwell Publishing Ltd 2009. Published by Blackwell Publishing, 9600 Garsington Road, Oxford, OX4 2DQ, UKand 350 Main Street, Malden, MA 02148, USA.

Journal of Management Studies 47:6 September 2010doi: 10.1111/j.1467-6486.2009.00875.x

ventures (Dikova and Brouthers, 2009; Slangen and Hennart, 2007). Greenfield ventureshave certain advantages over acquisitions. For example, although both acquisitions andgreenfield ventures provide access to proprietary market knowledge (for example, knowl-edge about potential customers, competitors, and government actions) through green-field ventures firms can establish a common organizational culture, making knowledgetransfer from the new subsidiary unit to the parent firm easier, while acquisitions oftensuffer from cultural clashes between parent and subsidiary units, which inhibit knowl-edge flows (Barkema and Vermeulen, 1998; Hennart and Park, 1993). Most importantlyacquisitions are expensive; firms make significant non-reversible (or semi-reversible)resource commitments that put it in a high risk position if things do not work out.Greenfield ventures require lower upfront investments and hence minimize downsiderisks (Pacheco-de-Almeida et al., 2008). Further greenfield ventures provide an option toexpand, increasing the investment incrementally as more information about the marketbecomes available, allowing firms to create a smaller operation (compared to an acqui-sition) if demand turns out to be lower than expected, and finally provide a mechanismfor abandonment at lower cost than an acquisition (which requires the entire investmentbe made at the start) if it becomes clear that demand will not materialize. Hencegreenfield ventures allow firms to defer much of the investment to the future, taking a‘wait and see’ approach, providing a real option when establishing a new foreignsubsidiary unit.

Real options theory is a tool that firms can use when making investments in real assets,as opposed to financial assets, under conditions of high uncertainty (Cuypers and Martin,2007; Tong et al., 2008). Like financial options, real options minimize current downsiderisk by deferring part of the investment while establishing an opportunity to expand andtake advantage of upside benefits in the future; providing the right, but not the obliga-tion, to take future action (Bowman and Hurry, 1993). Scholars have noted that decisionsthat can be explained using real options concepts result in superior performing outcomes(Brouthers et al., 2008; Leiblein, 2003).

Whether a firm expanding abroad can benefit from the real option provided by agreenfield venture may depend on the size of the projected investment. Prior researchusing this perspective maintains that options are valuable because of uncertainty and(ir)reversibility which creates downside risks (Folta and O’Brien, 2004). We suggest thatthe size of the investment project will have a significant impact on the level of downsiderisk. Firms undertaking small investments may perceive low downside risk because theoverall potential for loss is relatively small (Sitkin and Pablo, 1992). Contrary to this,firms making decisions involving large projects may benefit more from a real optionperspective since these firms face higher downside risk because of the size of the resourcecommitment being considered. Hence, greenfield ventures may offer greater protectionfrom downside risk for firms considering larger investments than those undertakingsmaller investments.

In this paper we contribute to the literature by exploring the benefits of using realoptions reasoning when making international acquisition decisions. With only oneexception (Gilroy and Lukas, 2006), real options research has tended to ignore thisimportant decision, focusing instead on ownership level ( joint ventures vs. complete orno ownership). This research suggests that joint ventures provide a real option to firms

Acquisitions and Real Options 1049

© Blackwell Publishing Ltd 2009

making new international investments, but that wholly owned subsidiary units do notprovide an option to firms (Brouthers et al., 2008). Applying a real options perspective,we develop new theory which explains that greenfield ventures can also provide a realoption to firms establishing new foreign subsidiary units. Greenfield ventures, we suggest,can supply a real option alternative to acquisitions for firms setting up either joint ventureor wholly owned subsidiary units. Thus we contribute to this research stream by broad-ening the use of real options theory in management. In addition we extend existingtheory to explain how the size of the investment project moderates the benefits of realoption reasoning on this decision. We suggest that firms pursuing smaller investmentswill benefit less from real option insights compared to firms undertaking larger invest-ments. Based on this we posit that acquisitions are not always the best method of entryinto a market, suggesting that firms should use a real options approach to make theiracquisition decision.

The rest of the paper is organized as follows. First we provide a brief review of the realoptions literature in management. Then we develop theory to explain how greenfieldventures provide a real option to firms entering foreign markets. Following that wedevelop hypotheses relating to the acquisition choice and how the size of the investmentmay moderate that choice. We then provide a description of our methods and results.Finally, we discuss the limitations and implications of our study.

THEORY AND HYPOTHESES

Background

Real options reasoning suggests that different investment structures may providebenefits, in addition to transaction cost economizing, by generating greater value whenmaking complex investment decisions (Scherpereel, 2008). This line of research focuseson value creation when faced with uncertainty in decision-making, which is oftenignored by transaction cost analysis (Leiblein, 2003). When an investment decisioninvolves high uncertainty about its upside potential, firms may have difficulty determin-ing the value of making such an investment and may wish to defer all or part of theinvestment but retain an option to grow if the market materializes (Leiblein, 2003).

In foreign expansion upside potential is often conceptualized as the demand for a newtechnology (such as new product technology like the Apple i-Pod) or for a firm’s existingproducts/services or technology in that market (Brouthers et al., 2008; Folta andLeiblein, 1994; McGrath, 1997; McGrath and Nerkar, 2004). The less knowledge a firmhas about the potential of their new or existing products in the foreign market the greaterthe uncertainty involved in making an investment decision. When firms make invest-ments under high uncertainty they increase their downside risks, their risk of losing all orpart of the funds invested.

Perceptions of downside risks may vary from firm to firm because some firms havecreated strategic flexibility which reduces the risk in future investments. Strategic flexi-bility is the set of strategic options or choices available to a firm (Bowman and Hurry,1993; Sanchez, 1993). These strategic options are accumulated over time from previousinvestments (Brouthers et al., 2008; Leiblein and Miller, 2003; McGrath and Nerkar,

K. D. Brouthers and D. Dikova1050

© Blackwell Publishing Ltd 2009

2004; Sanchez, 1993; Tong et al., 2008). Research focusing on joint ventures as realoptions suggests that the flexibility created by previous investments helps reduce down-side risk perceptions for current decisions by providing switching options (Broutherset al., 2008; Leiblein and Miller, 2003). Switching options allow firms to shift productionor output across the network of subsidiary units in response to changes in uncertainty(Tong and Reuer, 2007). Downside risks may also be reduced by strategic flexibilitybecause of lower costs created by past investments, such as those made in humanresources, information systems, or financial structures (Bowman and Hurry, 1993;Sanchez, 1993). Hence, strategic flexibility helps firms reduce downside risk in futuredecisions.

Intuitively the best course of action to take when demand is uncertain is to delay entry,reducing downside risk to zero. However, delaying entry provides an opportunity forcompetitors to enter the market and establish a first mover advantage (Brouthers et al.,2008; Kulatilaka and Perotti, 1998; Miller and Folta, 2002). Because delaying createsadditional uncertainties, real options theory suggests firms make incremental investments(Bowman and Hurry, 1993). Incremental investments allow firms to defer part of theinvestment but gain experience in the market, gather market-specific knowledge, andpossibly establish a brand image which can provide a growth option (Kogut, 1991). Overtime the knowledge and experience gained through investing in the market can lead togreater information about demand and be used to make future decisions regarding theinvestment. Thus real options theory is a method firms can use to make organizationalstructure choices that provide options to defer and options to grow (Leiblein, 2003).

Management research applying a real options perspective has tended to concentrateon the decision regarding organizational structure, defined as a choice between markets(like license agreements), hybrids ( joint ventures), and hierarchies (wholly owned ven-tures) (Brouthers et al., 2008; Scherpereel, 2008). Both theoretical and empirical studieshave suggested and found that joint ventures provide a growth option organizationalstructure for firms exploring for and exploiting current advantages in domestic andinternational markets (Brouthers et al., 2008; Folta, 1998; Scherpereel, 2008; Tonget al., 2008). Yet organizational structure choice is a bi-dimensional decision thatincludes the choice of ownership level as well as the method of establishment (Brouthersand Brouthers, 2000; Hennart and Park, 1993). For every wholly owned subsidiary orjoint venture, firms must decide how to obtain their ownership stake; through acquisitionor by starting a new venture. It is this second component of the structure decision, theestablishment or acquisition decision – acquisition vs. greenfield start-up – that realoption researchers have ignored.

Greenfield Ventures as Real Options

In the acquisition decision, unlike the deferral option where a firm takes a ‘wait and see’position (Folta, 1998), firms have already decided to enter the market through a jointventure or wholly owned structure but must make a choice about how to obtain thatownership. We suggest that greenfield ventures may endow firms with valuable growthoptions when creating these new foreign subsidiaries. Growth options provide firms withthe ability to minimize today’s investment, gain experience, and then make future

Acquisitions and Real Options 1051

© Blackwell Publishing Ltd 2009

decisions about expanding the subsidiary (Folta and O’Brien, 2004; Kogut, 1991). Thegreater the level of uncertainty in the market the more valuable the growth option (Foltaand O’Brien, 2004).

Growth options are valuable because they provide a firm with the right, but not theobligation, to expand with changes in the market (Folta and O’Brien, 2004; Kogut,1991). Both acquisitions and greenfield ventures provide growth options, but we suggestthat the greenfield growth option is more valuable to firms. In acquisitions firms need tomake the full resource commitment at the beginning of the project; in greenfield venturesinvestments are made incrementally over a long period of time (Pacheco-de-Almeidaet al., 2008). Thus in greenfield ventures firms can make a smaller upfront commitment,gaining access to the market, while delaying or deferring other components of theinvestment until they obtain further information. As Leiblein and Miller (2003) suggest,even if the overall costs of acquisition and greenfield ventures were similar greenfieldventures would be preferred because of the benefits of not making the entire irreversible(or semi-reversible) resource commitment at the start. This ability to defer some of theinvestment reduces downside risk while the initial investment provides the firm with anoption to grow (Folta, 1998; Sanchez, 1993).

To take advantage of a growth option, parent firms need to have knowledge about thetarget market and changes that occur (Barnett, 2008). Both acquisition and greenfieldventures provide access to information about the target market, consumers, and theinstitutional environment (Brouthers and Brouthers, 2000); knowledge that can be usedto reduce uncertainty in future decisions regarding the specific investment. Becauseexisting firms are embedded in their institutional environment they potentially possess astorehouse of market-specific knowledge (Slangen and Hennart, 2008). Managers maybelieve that acquiring these firms will provide them with quick access to this knowledge.But the knowledge possessed by a subsidiary unit needs to be communicated andtransferred to the parent firm to be beneficial. Research suggests that knowledge transferfrom acquired units is problematic (Barkema and Vermeulen, 1998; Hennart and Park,1993). Acquired units do not share the same organizational culture as the parent firm;they may have different goals and objectives. Managers in acquired units may bereluctant to share information with new owners; they may have different methods andprocesses of communication. The inability to obtain accurate and timely informationfrom acquired units reduces a firm’s capacity to take advantage of any potential growthoption that an acquisition can provide (Barnett, 2008). In contrast greenfield venturestend to replicate parent firm organizational cultural beliefs and processes; knowledgetransfer is relatively easy, providing more effective knowledge exchange (Barkema andVermeulen, 1998; Hennart and Park, 1993). Thus, transferring knowledge betweenparent and greenfield subsidiary units is fairly efficient, which enhances the value ofgreenfield growth options.

In addition, the traditional real options view in management is that wholly ownedsubsidiary (WOS) units provide no option (Brouthers et al., 2008), but that joint ventures( JV) supply an option because JVs afford lower initial investments compared with WOSand JV partners can increase/decrease ownership in the venture when demand becomesmore certain (Brouthers et al., 2008; Kogut, 1991; Tong et al., 2008). We extend thiswork by suggesting that greenfield ventures (either wholly owned or joint venture) also

K. D. Brouthers and D. Dikova1052

© Blackwell Publishing Ltd 2009

provide a real option because of the incremental nature of the investment. For example,in greenfield JVs the firm can defer more of the initial investment (reducing downsiderisk) compared to an acquired JV, because an acquired JV is a fixed size investment whilein a greenfield JV firms have the option to start small and incrementally increase theirinvestment (Pacheco-de-Almeida et al., 2008). So when Toyota joined with GM in theNUMMI joint venture in 1984, instead of buying part of an existing organization theycreated a new organization that started out relatively small and then expanded asdemand for their products grew (Inkpen, 2005). Contrary to this, Ford’s alliance withMazda involved an acquisition of equity, and when demand did not grow as expected,Ford faced substantial financial losses trying to dispose of their interest (Rowley,2008).

We further extend previous work by suggesting that firms can have options in whollyowned subsidiary units. For acquired WOS the firm must purchase a fixed size operationwhich, after demand becomes clearer, may turn out to be the wrong size, have the wrongtechnology, or possess unwanted and unneeded resources. Altering the capacity ofacquired units can be very expensive, for example, because of laws that restrict mana-gerial actions (like terminating employees), facility restrictions (lack of space to grow), andthe impact of fixed costs (long-term leases or financial commitments in buildings orequipment) (Capron and Guillen, 2009). Scholars have also noted the high cost ofabandoning acquisitions (Bergh, 1997; Hayward and Shimizu, 2006).

We suggest that with wholly owned greenfield ventures it is easier and less expensiveto make changes in the size of the operation, or abandon the operation, as knowledgeabout demand becomes clearer (Anand and Delios, 2002). With greenfield wholly ownedsubsidiaries, investments are made incrementally, providing options as knowledge aboutthe new market improves (Pacheco-de-Almeida et al., 2008). Because the initial invest-ment is much smaller than in an acquisition, as demand becomes clearer the firm candecide to invest more into the entity to match the size of the operation with the level ofdemand in the market; creating, for example, either a smaller operation than would havebeen acquired, a similar size operation, or a larger operation. Greenfield ventures helpfirms reduce the costs of subsidiary modification by allowing the firm to create asubsidiary that more closely aligns with expected demand. Finally, because the initialinvestment is smaller with greenfield ventures than with acquisitions, the cost of divestingthe entity if demand does not materialize (the downside risk) is lower for greenfieldventures.

In sum, we suggest that greenfield ventures provide a real option alternative toacquisitions for a number of reasons. First, for either wholly owned or joint ventureoperations, greenfield ventures require lower upfront investments compared with acqui-sitions, thus minimizing downside risks. Second, greenfield ventures provide a moreeffective mechanism for knowledge attainment compared to acquisition modes; knowl-edge transfer is more effective between greenfield ventures and parent firms comparedwith acquisitions and parent firms. Greenfield ventures provide a more economicaloption to expand by increasing the investment incrementally as more information aboutthe market becomes available. This means that greenfield ventures allow firms to createa smaller operation (investing less) if demand turns out to be lower than expected, andprovide a mechanism for abandonment at lower cost than an acquisition (which requires

Acquisitions and Real Options 1053

© Blackwell Publishing Ltd 2009

the entire investment to be made at the start) if it becomes clear that demand will notmaterialize. Hence greenfield ventures provide a real option for firms.

Hypotheses

Given the same investment project ( joint venture or wholly owned subsidiary), greenfieldventures can be pursued with substantially lower resource commitment, compared to anacquisition (Hennart and Park, 1993). For example, acquisitions involve relatively highsearch and negotiation (due diligence) costs. Firms with little or no experience in amarket may have difficulty identifying and negotiating with potential acquisition targets,and as a consequence need to make substantial resource commitments (Reuer and Koza,2000). Further, acquisition premiums are more likely in new markets because of differinglaws, regulations, norms, and values that influence information disclosure and hence afirm’s ability to correctly value an acquisition target (Slangen and Hennart, 2007). Theseacquisition premiums mean that firms often over pay because they do not have fullknowledge about the capabilities of the target organization. Finally, acquired firms oftenpossess unwanted assets or outdated technology that is costly to adjust (Dikova and vanWitteloostuijn, 2007; Reuer and Koza, 2000). These issues require managerial time andfinancial resources to resolve; adding to the cost of entry and taking managerial attentionaway from the activities that can lead to market success. While firms using greenfieldventures also have search and negotiation costs, these costs are normally lower becausethey involve searching for locations and negotiating for access to property instead ofsearching for partner firms, purchasing intangible assets, and negotiating a change inownership. Overall greenfield ventures allow firms to avoid many of the costs incurredwhen using acquisitions, hence providing entry with lower resource commitments (lessmanagerial time and financial commitment).

Further, as we outline above, greenfield ventures provide an incremental investmentoption (Pacheco-de-Almeida et al., 2008). Greenfield ventures allow the firm to make asmall investment into a market, establishing a foothold yet minimizing downside risk. Atthe same time, firms using greenfield ventures can obtain access to market-specificknowledge which may help them make better decisions with changes in demand uncer-tainty. Greenfield ventures provide firms with future investment options. Firms canexpand the venture, they can maintain its present state, or they can sell/dissolve theventure, incurring lower losses than the firm might have faced if it had used an acqui-sition and committed to a fixed-size operation at the outset.

Hence, based on real option reasoning we suggest that when demand uncertainty ishigh, acquisition modes may not be the best method of investment into foreign markets.Instead organizations should use a greenfield venture which provides the firm with anoption to grow while minimizing downside risks. This leads to our first hypothesis:

Hypothesis 1: Greater demand uncertainty is negatively associated with the use ofacquisitions.

Although demand uncertainty creates downside risks which firms will want to avoid,companies may possess strategic flexibility that provides choices in the acquisition deci-

K. D. Brouthers and D. Dikova1054

© Blackwell Publishing Ltd 2009

sion, reducing the downside risks of making an acquisition (Kogut and Kulatilaka, 1994;Leiblein and Miller, 2003; Sanchez, 1993). Building on the work of Sanchez (1993), wesuggest that the acquisition/greenfield decision relies on the strategic flexibility providedby past investments in human resources, information systems, financial structures andthe like; particularly those associated with previous acquisition activity. This type ofstrategic flexibility does not decrease uncertainty but influences downside risk by reduc-ing the amount of investment put at risk.

Vermeulen and Barkema (2001) maintain that some firms have developed capabilitiesfor dealing with acquisition-based uncertainties. Acquisitions provide uncertain returnsin part because of the inability of firms to identify appropriate acquisition candidates,value and price the acquisition, and integrate the acquired subsidiary unit into the rest ofthe organization. Yet research has found that firms learn from past acquisition experi-ences and tend to create systems and processes to overcome these issues and effectivelymanage the acquisition process (Baum et al., 2000; Vermeulen and Barkema, 2001).Through experience firms learn and create ‘organizational routines’ or capabilities thatmake them proficient at acquisition (Haleblian et al., 2006).

While some research suggests that these learned routines may create inertia and hencelead to poor acquisition decision-making (Hayward and Hambrick, 1997), we suggestthat, from a real options perspective, past acquisition investments influence humanresources, information systems, and financial structures that can reduce downside risk infuture acquisitions for at least two reasons. First, these past investments improve theacquisition process and hence reduce costs. For example, firms learn how to effectivelyintegrate foreign operations into the existing organization (Haleblian et al., 2006).Second, the strategic options generated by past acquisition activity provide knowledgethat can help improve the effectiveness of switching options. While past internationalinvestments may provide the firm with an opportunity to switch production and outputfrom one location to another, it does not provide the internal capabilities to manage thistask (Brouthers et al., 2008). Recent real options research suggests that switching optionsexist, but there is little evidence that firms actually make these changes (Tong and Reuer,2007). One reason for this is that problems integrating foreign subsidiaries with otherunits often restrict a firm’s ability to switch production from one country to another(Tong and Reuer, 2007). Research suggests that past acquisition experience may helpfirms improve integration (Haleblian et al., 2006; Vermeulen and Barkema, 2001),which we suggest makes the switching option more viable. Hence our second hypothesis:

Hypothesis 2: Greater acquisition-based strategic flexibility is positively associated withthe use of acquisitions.

The Influence of Investment Size

Whether a firm benefits from the downside risk protection offered through real optionreasoning may depend, at least in part, on the size of the investment project beingconsidered. Large acquisitions require substantial financial commitments and manage-rial time, hence exposing the firm to high downside risks (Fowler and Schmidt, 1989; Leeand Caves, 1998). Research on managerial decision-making and perceptions of uncer-

Acquisitions and Real Options 1055

© Blackwell Publishing Ltd 2009

tainty suggests that firms are more sensitive to uncertainty when the size of the invest-ment under consideration is large, rather than when it is small (Bromiley, 1991; Sitkinand Weingart, 1995). The reason for this is that managers tend to weigh potential lossesmore heavily than potential gains when making decisions (Sitkin and Pablo, 1992;Tversky and Kahneman, 1991). Furthermore, managers tend to avoid risks whenthere is a salient threat to assets rather when there is little or nothing to lose (Sitkin andPablo, 1992). This implies that when the investment size is large, the potential for lossincreases the threat to assets and hence firms will be less likely to make such large riskyinvestments.

Real options theory maintains that high demand uncertainty exposes firms to down-side risks (Leiblein, 2003; Scherpereel, 2008). The decision-making literature suggeststhat the size of the investment will amplify these managerial perceptions of downside riskbecause more resources will be required, providing a salient threat to firm assets(Bromiley, 1991; Sitkin and Weingart, 1995). As theorized above, when downside risksare high, firms initiating an investment of considerable size will prefer to use a realoptions greenfield venture instead of expanding through an acquisition, because green-field ventures allow firms to make smaller initial investments and provide an opportunityto make incremental investments (maintain the organizational size or sell the venture), asthey learn more about the uncertainties inherent in the new market. Alternatively, if thepotential investment is relatively small, demand uncertainty may have less of an impacton the acquisition decision because the firm puts fewer resources at risk and henceperceives lower downside risk (Bowman and Hurry, 1993). Thus we hypothesize:

Hypothesis 3a: The negative relation between demand uncertainty and acquisitionchoice is stronger for larger investments than for smaller investments.

The size of the investment also may moderate the relation between strategic flexibilityand the acquisition decision. Strategic flexibility is valuable to firms in decision-makingbecause it provides a firm with choices for dealing with potential downside risks(McGrath and Nerkar, 2004; Tong et al., 2008). As noted above, firms with greateracquisition experience tend to have developed strategic flexibility that allows them toexpand more effectively through acquisition modes compared to firms that do not havethis experience (Haleblian et al., 2006).

Yet larger acquisitions provide a greater challenge to firms, even those withacquisition-based strategic flexibility (Fowler and Schmidt, 1989). Research indicatesthat larger acquisitions are more difficult to identify, price and integrate, take more time,and require greater resource commitment (Hayward, 2002; Hayward and Hambrick,1997). While acquisition-based strategic flexibility may help firms deal with many of theuncertainties involved in making an acquisition, larger investments are simply moredifficult to manage, thus reducing the positive impact of strategic flexibility on theacquisition decision. Based on this we suggest that the size of the investment may reducethe benefits of acquisition-based strategic flexibility.

Hypothesis 3b: The positive relation between acquisition-based strategic flexibility andacquisition choice is weaker for larger investments than for smaller investments.

K. D. Brouthers and D. Dikova1056

© Blackwell Publishing Ltd 2009

METHODS

Sample

To test the above hypotheses, we obtained a new set of data that focuses on theestablishment (acquisition/greenfield) choices made by Western Europe companies thathave invested in joint ventures or wholly owned subsidiaries in 10 Eastern Europeanemerging economies. These new data were gathered with a mail survey conducted inMay 2003. One recent real option paper exploring joint ventures as an entry choice alsoused Western European firm entry into Eastern Europe (Brouthers et al., 2008);however, the data in this study come from a different survey. Emerging economies werechosen for this study because they provide high variance in demand uncertainty andentail new investment opportunities for western MNEs. Using the AMADEUS database,which contains information on all publicly traded EU firms, we selected those firms withinvestments in Bulgaria, the Czech Republic, Estonia, Hungary, Latvia, Lithuania,Poland, Romania, Slovakia, and Slovenia, generating a total sample of 2798 firms.

An English-language questionnaire was created and pilot-tested with managers in fourDutch companies not included in the final sample. The final English-language question-naire was translated into German, French, and Italian by a team of professional inter-preters and back-translated into English by native-speaking academics. In total,questionnaires were mailed to all 2798 firms; 35 were returned as undeliverable. For avariety of reasons international postal surveys have a history of very low participation,achieving response rates between 6 and 16 per cent (Dawson and Dickinson, 1988;Harzing, 1997). Consistent with this research, we received 208 usable responses, repre-senting a usable response rate of about 7.5 per cent. Respondents tended to make aboutequal use of acquisitions and greenfield ventures for entering these emerging markets(about 40 per cent acquisitions and 60 per cent greenfield ventures). As a result of missingdata, we could use 154 questionnaires in our analyses.

Respondents had on average 8656 employees and were primarily manufacturing firms(69 per cent of the total sample). We noted substantial size differences between greenfieldventures and acquisitions. Our data indicate that greenfield ventures ranged in size from1 to 2700 employees (mean = 80), while acquisitions ranged in size from 1 to 10,000employees (mean = 820). There was wide variance in the international activities under-taken by our respondents, ranging from 10 to 99 per cent of total firm activities (onaverage 58 per cent of sales were international; the median was 60 per cent). Investmentswere made mostly in related businesses (82 per cent). Finally, our respondent firms hadmade on average seven previous international acquisitions (ranging from 0 to 30).

We tested the representativeness of our data, using t-tests comparing our respondentsto firms in our sample. Paired t-tests revealed that there was no significant difference inthe number of worldwide employees (t = 0.54, p = 0.58) or worldwide sales (t = 1.40,p = 0.15). In addition, following Uhlenbruck and DeCastro (2000), we determined areliability coefficient for the respondent firms that had data in AMADEUS recorded forthe year 2002 as to both variables. To obtain this coefficient, we used the general form ofthe Spearman–Brown prophecy formula and incorporated the standard deviations andcorrelations of size and sales between the archival data and our survey information. Thecoefficients of 0.99 for size and 0.96 for sales confirm the reliability of our primary data.

Acquisitions and Real Options 1057

© Blackwell Publishing Ltd 2009

Main Variables

Acquisition choice was obtained from respondent firms. Focusing on their most recent entryinto Eastern Europe, firms were asked to indicate the specific country and how theyestablished their presence in that country. They were given two choices: acquired all orpart of an existing local company, or started all or part of a new operation (a controlvariable is included for ownership percentage). We created a dummy variable, taking avalue of 1 for acquisition and 0 for greenfield start-up venture.

Demand uncertainty was measured using industry fragmentation (Dess, 1987; Porter,1980), although two other measures were considered. Research suggests that highlyfragmented industries (low sales/firm) represent higher demand uncertainty compared tomore consolidated (high sales/firm) industries (Dess, 1987). In highly fragmented indus-tries, demand is uncertain because the specifications of the product/technology thatconsumers want are ill-defined as may be the potential uses, so firms offer differentproduct/technology variations to try to create or fit specific needs (Davis et al., 1989;Lambkin and Day, 1989). Using industry fragmentation aligns our concept of demanduncertainty with McGrath’s (1997) real option notions of uncertainty of demand (will theproduct/technology satisfy some existing demand) and uncertainty regarding speed ofdemand (will product/technology adoption be fast or slow). Data came from the Struc-tural Business Statistics of Eurostat Metadata (http://europa.eu.int). For each firm’syear/industry of investment, we collected information about sales in the host-countryindustry, at 4-digit NACE industry level. This figure was then divided by the number ofoperating enterprises in the host country for the same 4-digit NACE level in the year ofinvestment. The original variable was reverse coded to ease interpretation of the results.

Two alternative measures of demand uncertainty were considered, but were not used forthe following reasons. Variance in demand can be used, but is really a measure ofconsistency of demand, not uncertainty (whether there will be demand for a product/technology). Further, variance itself tells us little about demand uncertainty because itdoes not capture the size of the potential market for a firm’s products. Sales growth rateby industry is a good measure of the potential increase in demand. But sales growth ratealso tells us nothing about the size of the market. In addition, we noted that in pastacquisition research the results of using measures of host country demand (sales growthrates) have provided mixed results, with some studies finding a positive relation withacquisition choice and some a negative relation (see Dikova and Brouthers, 2009).

For acquisition-based strategic flexibility, we considered two potential measures. Themeasure we used looked at how acquisition experience may result in improved routinesthat provide the ability for firms to shift production/output from one location to another,taking advantage of switching options. Acquisition-based strategic flexibility was measuredthrough a composite index created by asking respondents to indicate: (1) the number ofcountries worldwide in which their company previously undertook acquisition invest-ments, and (2) the number of times acquisitions were undertaken. Factor analysis con-firmed that these items converge on one factor (the principal component in the first factoranalysis explained 96.85 per cent of the variance, and the component in the second, 86per cent of the variance). The scale reliability test produced a satisfactory value ofCronbach’s alpha (0.70).

K. D. Brouthers and D. Dikova1058

© Blackwell Publishing Ltd 2009

The alternative measure for acquisition-based strategic flexibility was the same in Broutherset al. (2008); a measure of the number of foreign subsidiaries. This second measureprovides a good indication of the opportunity to be strategically flexible, but does not tellus anything about a firm’s ability to take advantage of this opportunity. Tong and Reuer(2007) suggest that although past international investments may provide the opportunityto have switching options, they do not necessarily provide firms with the ability (capa-bilities) to take advantage of these options. Research maintains that past acquisitionexperience may help firms develop processes and routines that improve the acquisitionprocess (Haleblian et al., 2006; Vermeulen and Barkema, 2001), which makes switchingoptions more viable because it provides the means for firms to become more successfulat acquiring and integrating subunits. These arguments are similar in nature to thosemade by Lee and Makhija (2009) when they examined exporting experience as a type ofstrategic flexibility. They suggested and found that past exporting experience providesstrategic flexibility because it equips the firm with the knowledge and capabilities neededto shift exporting from one country to another with changes in uncertainty.

Our moderating variable Subsidiary size was obtained by asking respondents to indicatethe number of employees in the subsidiary at the time of establishment. Before calcu-lating the interaction between subsidiary size and the real option predictors, all variableswere centred to avoid potential multicollinearity problems (Aiken and West, 1991). Twointeraction variables were then calculated by multiplying the centred subsidiary sizevariable and the two real option variables.

Control Variables

We included numerous control variables taken from previous acquisition choice studies(Dikova and Brouthers, 2009). First we focused on transaction cost variables that mayimpact the acquisition decision. While results are mixed, it has been suggested that assetspecificity impacts the acquisition decision; greenfield ventures are thought to providegreater protection of knowledge and ease knowledge transfer (Brouthers and Brouthers,2000). Asset specificity was captured using two measures: technological and advertisingintensity (Hennart and Park, 1993). As in Dikova and van Witteloostuijn (2007), we askedrespondents to estimate on a Likert scale (1 denoting little amounts, and 5 great amounts)how much money as a percentage of annual sales is spent on R&D (Technological intensity)and marketing activities (Advertising intensity).

Previous transaction cost research suggests that firms expanding into new products orindustries may encounter higher transaction costs compared to those expanding intorelated products/industries, hence influencing the acquisition choice (Hennart and Park,1993). We measure Related investment with a dummy variable that takes a value of 1 if theinvestment in terms of parent firm’s main line of business is related to the new ventureand a value of 0 if it is not.

External uncertainties also impact transaction costs and hence the acquisition decision(Hennart and Park, 1993). Host environmental uncertainty is estimated through a set of seven5-point Likert-type questions taken from Geringer and Hebert (1991) and Brouthers(2002), that asked respondents their perceptions of: (1) general political, economic, andsocial stability of the host country, (2) risk of barriers to converting and repatriating

Acquisitions and Real Options 1059

© Blackwell Publishing Ltd 2009

income, (3) level of corruption among political leaders, (4) host government’s ability toenforce existing laws, (5) efficiency of local institutions, (6) the quality of local telecom-munication, and (7) transportation infrastructures. A composite variable was created(Cronbach’s alpha 0.78); low values represent environments with low uncertainty, andhigh values correspond to high uncertainty host environments.

International experience may impact the acquisition decision because, through expe-rience, firms learn to deal with different international barriers, leading to a preference foracquisitions (Harzing, 2002). International experience was captured by the percentage ofinternational sales to total sales at the year of investment (Brouthers and Brouthers,2000). Although a high ratio of sales/firm may be indicative of lower demand uncer-tainty it may also be a sign of a highly concentrated industry. In highly concentratedindustries entry is more difficult; the creation of a new entrant attracts quick and directretaliation from existing players (Anand and Delios, 2002). Hence industry concentrationtends to lead to the use of acquisition modes (Hennart and Park, 1993). Industry concen-

tration was measured by asking respondents to evaluate, on a 5-point Likert-type scale, theintensity of industry concentration at the time of their investment.

As previous real options research has noted, another way to reduce the size of theinvestment is to reduce the level of ownership in the project (Scherpereel, 2008). Ourtheory assumes that a specific ownership level is desired and the choice of acquisition orgreenfield mode focuses on how firms can obtain that desired level of ownership. As inprevious studies (Barkema and Vermeulen, 1998; Hennart and Park, 1993), we con-trolled for equity ownership differences using Subsidiary ownership, a measure obtained byasking respondents to disclose the level of equity ownership they had in the foreignoperation at the time of entry.

Industry differences may also impact the acquisition decision; service industries mightrequire lower financial commitments than manufacturing (Brouthers, 2002). Hence adummy variable, Manufacturing, was created to capture differences between foreigninvestments in manufacturing (value of 1) and investments in service (value of 0) indus-tries. Although we explore investment size, it is important to control for firm size becauseinvestment size is a function of the size of the parent firm (Fowler and Schmidt, 1989).Firm size was measured as the log value of the number of MNE employees worldwide(Brouthers and Brouthers, 2000; Hennart and Park, 1993).

Analysis

To test our hypotheses we conducted a hierarchical binomial logistic regression analysis.This statistical method was applied because of the ability of logistic regression techniquesto incorporate a wide range of diagnostics, the dichotomous characteristic of the depen-dent variable, and the mix of continuous and categorical independent and controlvariables (Hair et al., 1995). Since our dataset is composed of continuous, categorical,single-scale and multiple-scale constructs, all variables were converted to standardizedz-scores, prior to the analysis.

Because our variables include self-reported and archival data, common methodsvariance should not be an issue. To confirm this, we used Harmon’s one-factor test andfound five factors with eigenvalues greater than 1.0; the largest factor accounting for only

K. D. Brouthers and D. Dikova1060

© Blackwell Publishing Ltd 2009

17 per cent of the variance (Podsakoff et al., 2003). Further, we address the increasingrecognition in the literature that the acquisition decision is a choice, reflecting the matchmanagers make between their strategy and influential variables, which may raise someconcern for endogeneity. We used a two-stage least square analysis (not included here) toexamine this issue, but found no indication that the acquisition choice was endogenous.

FINDINGS

Table I shows the means, standard deviations, and correlation coefficients for all vari-ables under study.

The logistic regression analysis (Table II) contains four models. Model 1 included onlythe transaction cost and other control variables. Model 2 estimates (in addition to thecontrols) the main effects of our predictor variables Demand uncertainty and Acquisition-based

strategic flexibility. Models 3 and 4 add the moderating effects of Subsidiary size on Demand

uncertainty and Acquisition-based strategic flexibility, respectively.Model 1 was significant (p > 0.001, R2 = 0.404). Four control variables were also

significant: Host environmental uncertainty (p < 0.05) and Subsidiary ownership (p < 0.01) arenegatively related to the likelihood of establishing an acquisition, while Firm size

(p < 0.001) and Related investment (p < 0.01) are positively related to the likelihood ofestablishing an acquisition.

Model 2 examines the direct effect of the two real option variables on the acquisitiondecision. Model 2 was significant (p > 0.001, R2 = 0.526). The increase in chi-squareover Model 1 was also significant (p < 0.001). Demand uncertainty is significantly negativelyassociated with acquisition choice (p < 0.05) as was predicted in Hypothesis 1. Acquisition-

based strategic flexibility was positively significantly (p < 0.01) associated with acquisitionchoice as we predicted in Hypothesis 2.

Models 3 and 4 examine the moderating influence of Subsidiary size on the real optionvariables Demand uncertainty and Acquisition-based strategic flexibility. Model 3 was significant(p < 0.001, R2 = 0.683), and the increase in chi-square over Model 1 was significant(p < 0.001) as was the increase over Model 2 (p < 0.001). Model 4 was also signifi-cant (p < 0.001, R2 = 0.677) and the increase in chi-square over Model 1 was significant(p < 0.001) as was the increase over Model 2 (p < 0.001). Hence both models demon-strate increasing explanatory power in comparison to Model 1 (the control variablesmodel) and Model 2 (the real options model).

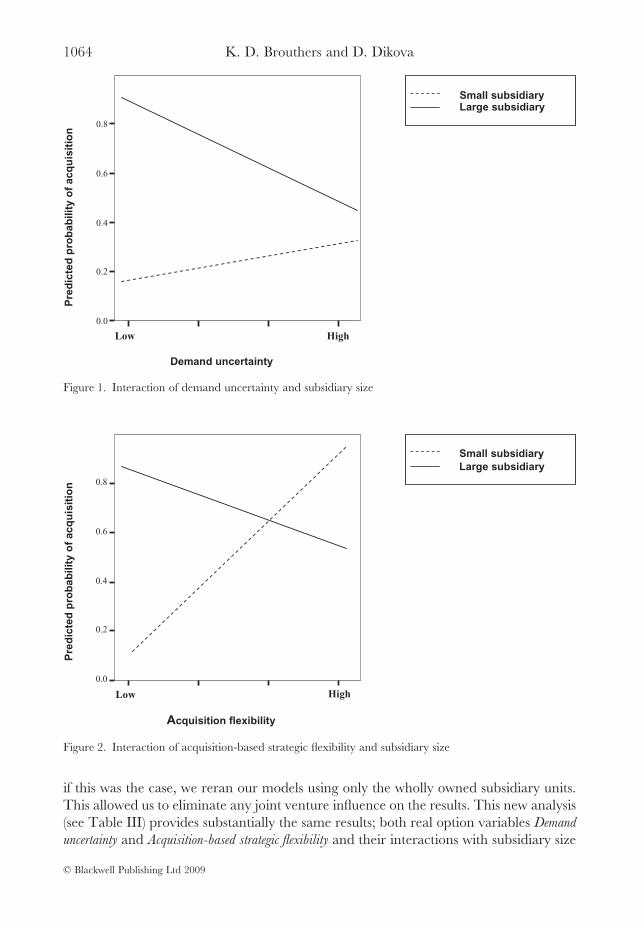

To help interpret the results obtained in Models 3 and 4, we plotted the predictedprobability of an acquisition subsidiary (Brambor et al., 2006). We used figures toillustrate the moderating effects of Subsidiary size on the predicted probability of anacquisition for each of the predictor variables, Demand uncertainty and Acquisition-based

strategic flexibility.Figure 1 shows the effect of the interaction between Demand Uncertainty and Subsidiary

size. As we suggested in Hypothesis 3a, the relation between demand uncertainty andacquisition choice is stronger for larger investments than for smaller investments. Ourfindings indicate that when the investment project size is large, demand uncertaintycreates a significant decline in the predicted probability of acquisition establishments. Yet

Acquisitions and Real Options 1061

© Blackwell Publishing Ltd 2009

Tab

leI.

Cor

rela

tion

and

desc

ript

ive

stat

istic

s:ac

quis

ition

choi

ce

Var

iabl

esM

ean

SD

12

34

56

78

91

01

11

2

1.A

cqui

sitio

n(g

reen

field

=0)

0.36

0.48

2.H

ost-

envi

ronm

enta

lun

cert

aint

y0.

204.

41-0

.220

**

3.In

dust

ryco

ncen

trat

ion

3.03

1.36

0.02

1-0

.032

4.T

echn

olog

ical

inte

nsity

2.07

1.07

-0.0

32-0

.052

0.19

4**

5.A

dver

tisin

gin

tens

ity2.

061.

13-0

.068

0.02

70.

056

0.14

6*

6.Su

bsid

iary

owne

rshi

p87

.68

21.8

00.

354*

*0.

073

-0.0

030.

063

-0.0

56

7.M

anuf

actu

ring

0.69

0.46

0.03

5-0

.056

0.19

5**

0.20

0**

-0.1

270.

145*

*8.

Firm

size

(log)

3.24

0.83

0.24

1**

-0.0

860.

058

-0.0

080.

010

0.04

90.

080

9.R

elat

edin

vest

men

t0.

820.

38-0

.066

-0.1

190.

000

-0.0

040.

026

0.05

6-0

.041

0.02

710

.In

tern

atio

nal

expe

rien

ce0.

580.

31-0

.085

0.01

10.

101

0.09

4-0

.073

0.21

7**

0.20

3**

-0.0

76-0

.097

11.

Dem

and

unce

rtai

nty

361.

4314

21.2

-0.1

53*

0.05

80.

058

0.01

7-0

.001

0.16

5*-0

.095

-0.1

85**

-0.0

53-0

.090

12.

Acq

uisi

tion

stra

tegi

cfle

xibi

lity

12.3

837

.19

0.19

9**

0.08

00.

096

-0.0

49-0

.046

0.03

00.

084

0.36

5**

0.06

70.

197*

0.03

1

13.

Subs

idia

rysi

ze34

6.39

1029

.77

0.34

6**

-0.0

870.

000

0.05

6-0

.003

-0.0

390.

031

0.33

4**

-0.0

240.

038

0.18

1*0.

385*

*

*p

<0.

05;*

*p

<0.

01.

K. D. Brouthers and D. Dikova1062

© Blackwell Publishing Ltd 2009

when the investment project size is small, the predicted probability line is flatter, reveal-ing that demand uncertainty has less of an impact on the predicted probability of(smaller) investment projects.

Figure 2 shows the effect of the interaction between Subsidiary size and Acquisition-based

strategic flexibility. This figure indicates that, as suggested in Hypothesis 3b, the relationbetween acquisition-based strategic flexibility and acquisition choice is weaker for largerinvestments than for smaller investments. Our results tend to suggest that for smallerinvestment projects, increased acquisition-based strategic flexibility leads to a significantincrease in acquisition choice, but for larger investment projects the impact on acquisi-tion choice is much less. Hence, regression Models 3 and 4 provide support for ourhypotheses, indicating that investment size moderates the value of real options reasoningin the acquisition choice decision.

One issue that may arise in these analyses is that the results are being driven by thejoint venture option in our data and not the greenfield venture option. To help determine

Table II. Logistic regression of acquisition choice

Variables Model 1 Model 2 Model 3 Model 4

Intercept -0.834** (0.27) -0.99** (0.31) -0.81* (0.35) -0.41 (0.52)Host environmental

uncertainty-0.67* (0.23) -0.98** (0.28) -0.78** (0.29) -1.20** (0.35)

Industry concentration -0.03 (0.22) 0.01 (0.25) 0.13 (0.26) 0.21 (0.29)Technological intensity 0.14 (0.22) 0.16 (0.24) 0.03 (0.24) -0.04 (0.27)Advertising intensity -0.23 (0.23) -0.07 (0.25) -0.28 (0.26) -0.65* (0.35)Subsidiary ownership -0.92** (0.27) -0.74* (0.29) -0.62* (0.28) -0.71* (0.32)Manufacturing -0.29 (0.49) 0.08 (0.54) 0.48 (0.54) 0.23 (0.62)Firm size 0.93*** (0.26) 0.41 (0.31) -0.12 (0.34) -0.36 (0.42)Related investment 1.81** (0.59) 2.68*** (0.69) 2.50*** (0.70) 3.23*** (0.90)International experience -0.28 (0.23) -0.62* (0.27) -0.80** (0.30) -1.08** (0.36)Demand uncertainty -1.29* (0.64) -1.19* (0.62) -1.21 (0.81)Acquisition strategic

flexibility1.86** (0.60) 2.19** (0.64) 2.30** (0.79)

Subsidiary size 2.81** (0.86) 6.14*** (1.64)Subsidiary size ¥ Demand

uncertainty0.92* (0.42)

Subsidiary size ¥Acquisition strategicflexibility

-0.10** (0.04)

N 154 154 154 154Overall chi-square 51.717*** 71.678*** 86.465*** 96.477***Change in chi-square

Model 119.961*** 36.848*** 43.042***

Change in chi-squareModel 2

36.987*** 43.178***

Nagelkerke R2 0.404 0.526 0.683 0.677

Notes: * p < 0.05; ** p < 0.01; *** p < 0.001.The dependent variable is greenfield = (0), acquisition = (1).All variables are standardized before performing the analysis. Standard errors are given in parentheses.

Acquisitions and Real Options 1063

© Blackwell Publishing Ltd 2009

if this was the case, we reran our models using only the wholly owned subsidiary units.This allowed us to eliminate any joint venture influence on the results. This new analysis(see Table III) provides substantially the same results; both real option variables Demand

uncertainty and Acquisition-based strategic flexibility and their interactions with subsidiary size

Small subsidiaryLarge subsidiary

Low High

Demand uncertainty

0.0

0.2

0.4

0.6

0.8

Pre

dic

ted

pro

bab

ility

of

acq

uis

itio

n

Figure 1. Interaction of demand uncertainty and subsidiary size

Small subsidiaryLarge subsidiary

Low High

Acquisition flexibility

0.0

0.2

0.4

0.6

0.8

Pre

dic

ted

pro

bab

ility

of

acq

uis

itio

n

Figure 2. Interaction of acquisition-based strategic flexibility and subsidiary size

K. D. Brouthers and D. Dikova1064

© Blackwell Publishing Ltd 2009

were significant and the coefficients carried the predicted signs. This suggests that ourresults are not driven by the joint venture option, but instead the real option choices wesee are based on the options provided by greenfield ventures (either wholly owned orjoint venture).

DISCUSSION, LIMITATIONS, AND CONCLUSIONS

Acquisitions are an important growth strategy, yet research indicates that on averageacquisitions provide few, if any benefits (Hayward and Hambrick, 1997; King et al.,2004; Tuch and O’Sullivan, 2007). We suggested that this might be the case becausesometimes firms use acquisitions when they should be using other methods of expansion;for example, starting a new subsidiary unit. Using real options reasoning we developednew theory to suggest that greenfield ventures may provide a real option alternative to

Table III. Logistic regression of acquisition choice: wholly-owned subsidiaries only

Variables Model 1 Model 2 Model 3 Model 4

Intercept -0.35 (0.70) 0.99 (1.12) 1.59* (0.74) 0.64* (0.30)Host environmental

uncertainty-0.74** (0.28) -1.63** (0.55) -2.51** (0.83) -2.38** (0.77)

Industry concentration -0.33 (0.24) -0.58 (0.40) -0.59 (0.53) -0.65 (0.51)Technological intensity 0.07 (0.23) 0.27 (0.38) 0.23 (0.53) 0.39 (0.50)Advertising intensity -0.03 (0.24) -0.65 (0.54) -1.49 (0.81) -1.40 (0.77)Manufacturing -0.13 (0.55) -1.18 (0.87) -2.41 (1.28) -2.56* (1.26)Firm size 0.82** (0.27) -0.36 (0.47) -1.41 (0.82) -1.30 (0.76)Related investment -1.01* (0.60) -4.69** (1.41) -5.14** (1.94) -5.52** (2.01)International experience 0.03 (0.09) -5.68** (1.94) -7.10** (2.55) -7.18** (2.42)Demand uncertainty -2.83** (1.04) -6.99* (3.96) -2.94* (1.55)Acquisition strategic

flexibility3.25** (1.01) 4.23** (1.54) 3.41** (1.27)

Subsidiary size 5.00* (2.31) 1.78* (0.73)Subsidiary size ¥ Demand

uncertainty1.47* (0.87)

Subsidiary size ¥Acquisition strategicflexibility

-0.02* (0.01)

N 104 104 104 104Overall chi-square 23.693** 44.511*** 65.754*** 62.957***Change in chi-square

Model 129.973*** 51.215*** 48.419***

Change in chi-squareModel 2

21.243*** 18.446***

Nagelkerke R2 0.29 0.57 0.76 0.74

Notes: * p < 0.05; ** p < 0.01; *** p < 0.001.The dependent variable is greenfield = (0), acquisition = (1).All variables are standardized before performing the analysis. Standard errors are given in parentheses.

Acquisitions and Real Options 1065

© Blackwell Publishing Ltd 2009

firms thinking about acquisitions. Based on this we theorized that demand uncertainty,acquisition-based strategic flexibility, and subsidiary size would all impact the acquisitiondecision. Our results provide some support.

We found that both demand uncertainty and strategic flexibility were directly associ-ated with the acquisition decision. Our findings tend to suggest that greenfield venturesoffer firms a real option alternative when demand is uncertain, but that firms possessingstrategic flexibility brought about by previous acquisition experience do not need theprotection from demand uncertainty offered by greenfield ventures.

We also found strong support for the moderating impact of the size of the investmentproject on the benefits of using real options reasoning to make the acquisition decision.First, we found that when firms were undertaking small investments, demand uncertaintytended to be less influential in making the acquisition choice, yet when the investmentwas large, demand uncertainty was very important in this decision. Second, we foundthat acquisition-based strategic flexibility was less influential for larger investments thanfor smaller investments. These results suggest that making decisions based on real optionsreasoning may not be universally useful, but that its usefulness might depend on the sizeof the investment under consideration.

In sum, these results tend to provide support for our theory that greenfield venturescan provide a real option alternative to firms when making international investmentdecisions. Instead of using acquisitions to create wholly owned or joint venture foreignoperations, when uncertainty is high greenfield ventures may provide a more effectivemethod of entering a market, with smaller initial investments, lowering the potentialdownside risks.

Although we obtained positive results some caution is warranted. We only examinedEU firms entering ten emerging markets in Eastern Europe. Therefore our results maynot be generalizable to firms from other home countries entering other host countries.Second, despite strong efforts, our response rate was not as high as we would have liked,although it was consistent with other international postal surveys. Third, studies exam-ining acquisition experience (our measure of strategic flexibility) have noted that expe-rience may be of limited value in unrelated acquisitions. While we control for acquisitionrelatedness in our analysis, future research may wish to explore other variations inexperience, such as timing or performance that might also influence the acquisitiondecision (Hayward, 2002). Future research may also wish to combine concepts from thisstudy (the acquisition decision) with previous studies examining the entry mode choice(Brouthers et al., 2008) and apply real options theory to more option types.

Albeit useful in understanding the conditions under which launching an internationalacquisition should be undertaken, real options theory also has limitations. For example,Adner and Levinthal (2004a, 2004b) note numerous boundary conditions, including theimpact of differing managerial perceptions on option based decisions, the variety ofalternatives available to firms, and managing the abandonment option. Cuypers andMartin (2006) highlight measurement issues and how differences in the measurement ofuncertainty may impact real option outcomes. Cuypers and Martin (2007) build on thisidea, suggesting that perceived uncertainty may be a better measure from a real optionsperspective than secondary measures. They also suggest that combining real optionstheory with other theoretical perspectives like transaction cost, as we did in this study,

K. D. Brouthers and D. Dikova1066

© Blackwell Publishing Ltd 2009

may help improve the predictive power of real options decisions. Future research apply-ing real options theory should consider these boundary conditions in designing theirstudies.

Despite these reservations, this study illustrates the potential for employing real optionstheory to explain a broader range of strategic decisions than have been explored in pastmanagement studies, and makes several important contributions to the literature. First,our work builds on and extends previous real option research that focused on jointventures as real options (Folta, 1998; Kogut, 1991; Leiblein, 2003). We agree that jointventures provide valuable real options to firms entering new markets, but we alsosuggested and found that the way a firm establishes its joint venture can provide additionalreal option benefits. Joint ventures established through acquisition provide only the realoption benefits discussed in these previous studies, but new greenfield joint ventures makeavailable additional options to firms by further reducing downside risks (compared toacquisition joint ventures) and providing more valuable growth options, because growth ispossible in greenfield joint ventures without having to deal with the buyout of existingpartner firms. The implications seem clear; firms can enhance their joint venture basedreal options by combining that decision with the acquisition/greenfield decision.

Second, previous real options research maintains that wholly owned subsidiaries donot provide an option (Brouthers et al., 2008; Kogut, 1991; Leiblein, 2003). However, wetheorized and found that this is not always the case. Wholly owned subsidiaries estab-lished through acquisition offer firms few real option choices. But our research tends tosuggest and find that greenfield wholly owned subsidiary units provide real optionbenefits similar in nature to those espoused by joint venture advocates. Using greenfieldwholly owned subsidiaries allows firms to minimize downside risk by making smallerupfront investments. Further, through the benefits of incremental investments, greenfieldwholly owned subsidiaries provide a mechanism for firms to take advantage of growthoptions and achieve a better match between actual demand and the size of the finalsubsidiary. In fact, these greenfield wholly owned subsidiaries help firms avoid potentialproblems in negotiating with joint venture partners over the value of growth options(Tong et al., 2008). With wholly owned subsidiaries the firm can make growth decisionsindependently, not having to negotiate with partners over the value of partner shares.This implies that greenfield wholly owned subsidiaries may afford similar, or even morevaluable, real option benefits compared to joint ventures, providing greater choice tofirms.

Third, this study helps define the boundaries of real option decision-making, some-thing Adner and Levinthal (2004a, 2004b) suggest is important for improving ourunderstanding of this theoretical approach in management. We suggested and found thatthe size of the investment being considered had a significant impact on the benefits oftaking a real option approach to the acquisition decision. When firms were makingsmaller investments, real option benefits appear to be greatly reduced. While more workneeds to be done in this area, researchers and managers thinking about using real optionsreasoning in their decision-making processes should carefully consider where to applythese concepts.

Fourth, our study has important implications for acquisition research. One enduringissue with acquisition research has been the lack of significant performance effects

Acquisitions and Real Options 1067

© Blackwell Publishing Ltd 2009

(Hayward and Hambrick, 1997; King et al., 2004; Tuch and O’Sullivan, 2007).Brouthers et al. (1998) maintain that this might be the case because researchers areemploying the wrong measures of performance. In this paper we suggested that thesepoor performance results may come about because firms are using acquisition modesin situations where they should actually be using greenfield ventures. If firms make largeinvestments in highly uncertain situations, then on average performance will be fairly lowbecause sometimes these investments will not be successful and will need to be reversed,which is costly (Bergh, 1997; Hayward and Shimizu, 2006). If however, firms had usedgreenfield ventures when uncertainty was high, they may avoid many of the losses theyincur with acquisitions and as a result the overall picture for acquisitions may improve.More research is needed to determine if these implications are correct, but using realoptions reasoning to make the acquisition decision may help firms create more successfulsubsidiaries and hence improve acquisition results.

In conclusion, firms expand in order to exploit existing resources or obtain new ones,yet expanding through acquisitions does not always deliver on this objective and acqui-sitions are expensive and difficult to reverse. We suggested that firms might improve theirchances of successful expansion by considering greenfield ventures as an alternative toacquisitions and use a real options approach to make the acquisition decision. Our resultstend to indicate that greenfield ventures provide firms with a real option alternative toacquisitions. In addition, although management research on real options has madeimportant contributions in understanding how uncertainty impacts firm choice, thisresearch has not considered how the size of the investment project may impact the valueof real options reasoning. We developed and tested theory which suggests that the realoptions approach may be more (less) useful depending on the size of the investmentdecision being considered. Finally, we suggest that the use of real options reasoningshould be expanded to other important strategic decisions so that managers may benefitfrom the potential insights this method provides. For example, applying real optionsconcepts to strategic decisions, like international market selection, may help us developa better understanding of how decisions can be effectively made under conditions ofuncertainty.

ACKNOWLEDGMENTS

The authors would like to thank the editor Andrew Delios, the three anonymous JMS referees, RichardSchoenberg, and seminar participants at the University of Groningen for helpful comments on earlierversions of this paper.

REFERENCES

Adner, R. and Levinthal, D. A. (2004a). ‘What is not a real option: considering boundaries for the applicationof real options to business strategy’. Academy of Management Review, 29, 74–85.

Adner, R. and Levinthal, D. A. (2004b). ‘Real options and real tradeoffs’. Academy of Management Review, 29,120–6.

Aiken, L. S. and West, S. G. (1991). Multiple Regression: Testing and Interpreting Interactions. London: Sage.Anand, J. and Delios, A. (2002). ‘Absolute and relative resources as determinants of international acquisi-

tions’. Strategic Management Journal, 23, 119–34.

K. D. Brouthers and D. Dikova1068

© Blackwell Publishing Ltd 2009

Barkema, H. G. and Vermeulen, F. (1998). ‘International expansion through start-up or acquisition: alearning perspective’. Academy of Management Journal, 41, 7–26.

Barnett, M. L. (2008). ‘An attention-based view of real options reasoning’. Academy of Management Review, 33,606–28.

Baum, J. A. C., Li, S. X. and Usher, J. M. (2000). ‘Making the next move: how experiential and vicariouslearning shape the locations of chains’ acquisitions’. Administrative Science Quarterly, 45, 766–801.

Bergh, D. D. (1997). ‘Predicting divestiture of unrelated acquisitions: an integrative model of ex anteconditions’. Strategic Management Journal, 18, 715–31.

Bowman, E. H. and Hurry, D. (1993). ‘Strategy through the option lens: an integrated view of resourceinvestments and the incremental choice process’. Academy of Management Review, 18, 750–82.

Brambor, T., Clark, W. R. and Golder, M. (2006). ‘Understanding interaction effects: improving empiricalanalysis’. Political Analysis, 14, 63–82.

Bromiley, P. (1991). ‘Testing a causal model of corporate risk taking and performance’. Academy of ManagementJournal, 34, 37–59.

Brouthers, K. D. (2002). ‘Institutional, cultural and transaction cost influences on entry mode choice andperformance’. Journal of International Business Studies, 33, 203–21.

Brouthers, K. D. and Brouthers, L. E. (2000). ‘Acquisition or greenfield start-up? Institutional, cultural andtransaction cost influences’. Strategic Management Journal, 21, 89–98.

Brouthers, K. D., van Hastenburg, P. and van de Ven, J. (1998). ‘If most mergers fail why are they sopopular?’. Long Range Planning, 31, 347–53.

Brouthers, K. D., Brouthers, L. E. and Werner, S. (2008). ‘Real options, international entry mode choice andperformance’. Journal of Management Studies, 45, 936–60.

Capron, L. and Guillen, M. (2009). ‘National corporate governance institutions and post-acquisition targetreorganization’. Strategic Management Journal, 30, 803–33.

Clougherty, J. A. and Duso, T. (2009). ‘The impact of horizontal mergers on rivals: gains to being left outsidea merger’. Journal of Management Studies, 46, 1365–95.

Cuypers, I. R. P. and Martin, X. (2006). ‘What makes and does not make a real option? A study ofinternational joint ventures’. Academy of Management Best Paper, QQ1–6.

Cuypers, I. R. P. and Martin, X. (2007). ‘Joint ventures and real options: an integrated perspective’. InReuer, J. J. and Tong, T. W. (Eds), Real Options in Strategic Management, Advances in Strategic Management.Greenwich, CT: Elsevier, 24, 107–48.

Davis, F. D., Bagozzi, R. P. and Warshaw, P. R. (1989). ‘User acceptance of computer technology:comparison of two theoretical models’. Management Science, 35, 982–1003.

Dawson, S. and Dickinson, D. (1988). ‘Conducting international mail surveys: the effect of incentives onresponse rates within an industrial population’. Journal of International Business Studies, 19, 491–6.

Dess, G. G. (1987). ‘Consensus on strategy formulation and organizational performance: competitors in afragmented industry’. Strategic Management Journal, 8, 259–77.

Dikova, D. and Brouthers, K. D. (2009). ‘Establishment mode choice: acquisition versus greenfield entry’. InKotabe, M. and Helsen, K. (Eds), SAGE Handbook of International Marketing. London: Sage Publications,218–37.

Dikova, D. and van Witteloostuijn, A. (2007). ‘Foreign direct investment mode choice: entry and establish-ment modes in transition economies’. Journal of International Business Studies, 38, 1–21.

Folta, T. B. (1998). ‘Governance and uncertainty: the trade-off between administrative control and com-mitment’. Strategic Management Journal, 19, 1007–28.

Folta, T. B. and Leiblein, M. J. (1994). ‘Technology acquisition and the choice of governance by establishedfirms: insights from option theory in a multinomial logit model’. Academy of Management Proceedings, 27–31.

Folta, T. B. and O’Brien, J. P. (2004). ‘Entry in the presence of dueling options’. Strategic Management Journal,25, 121–38.

Fowler, K. L. and Schmidt, D. R. (1989). ‘Determinants of tender offer post-acquisition financial perfor-mance’. Strategic Management Journal, 10, 339–50.

Geringer, J. M. and Hebert, L. (1991). ‘Measuring performance of international joint ventures’. Journal ofInternational Business Studies, 22, 249–63.

Gilroy, B. M. and Lukas, E. (2006). ‘The choice between greenfield investment and cross-border acquisition:a real option approach’. The Quarterly Review of Economics and Finance, 46, 447–65.

Gregory, A. and McCorriston, S. (2005). ‘Foreign acquisitions by UK limited companies: short- andlong-run performance’. Journal of Empirical Finance, 12, 99–125.

Hair, J., Anderson, R. E., Tatham, R. L. and Black, W. C. (1995). Multivariate Data Analysis with Readings.Englewood Cliffs, NJ: Prentice-Hall.

Acquisitions and Real Options 1069

© Blackwell Publishing Ltd 2009

Haleblian, J., Kim, J. Y. and Rajagopalan, N. (2006). ‘The influence of acquisition experience and perfor-mance on acquisition behavior: evidence from the U.S. commercial banking industry’. Academy ofManagement Journal, 49, 357–70.

Harzing, A. W. K. (1997). ‘Response rates in international mail surveys: results of a 22-country study’.International Business Review, 6, 641–64.

Harzing, A. W. K. (2002). ‘Acquisitions vs. greenfield investments: international strategy and managementof entry modes’. Strategic Management Journal, 23, 211–27.

Hayward, M. L. A. (2002). ‘When do firms learn from their acquisition experience? Evidence from1990–1995’. Strategic Management Journal, 23, 21–39.

Hayward, M. L. A. and Hambrick, D. C. (1997). ‘Explaining the premiums paid for large acquisitions:evidence of CEO hubris’. Administrative Science Quarterly, 42, 103–27.

Hayward, M. L. A. and Shimizu, K. (2006). ‘De-commitment to losing strategic action: evidence from thedivestiture of poorly performing acquisitions’. Strategic Management Journal, 27, 541–57.

Hennart, J. F. and Park, Y. R. (1993). ‘Greenfield vs. acquisition: the strategy of Japanese investors in theUnited States’. Management Science, 39, 1054–70.

Inkpen, A. C. (2005). ‘Learning through alliances: general motors and NUMMI’. California ManagementReview, 47, 114–36.

King, D. R., Dalton, D. R., Daily, C. M. and Covin, J. G. (2004). ‘Meta-analyses of post-acquisitionperformance: indications of unidentified moderators’. Strategic Management Journal, 25, 187–200.

Kogut, B. (1991). ‘Joint ventures and the option to expand and acquire’. Management Science, 37, 19–33.Kogut, B. and Kulatilaka, N. (1994). ‘Operating flexibility, global manufacturing, and the option value of a

multinational network’. Management Science, 40, 123–39.Kulatilaka, N. and Perotti, E. C. (1998). ‘Strategic growth options’. Management Science, 44, 1021–31.Lambkin, M. and Day, G. S. (1989). ‘Evolutionary processes in competitive markets: beyond the product life

cycle’. Journal of Marketing, 53, 4–20.Lee, S-H. and Makhija, M. (2009). ‘Flexibility in internationalization: is it valuable during an economic

crisis?’. Strategic Management Journal, 30, 537–55.Lee, T. J. and Caves, R. E. (1998). ‘Uncertain outcomes of foreign investment: determinants of the dispersion

of profits after large acquisitions’. Journal of International Business Studies, 29, 563–81.Leiblein, M. J. (2003). ‘The choice of organizational governance form and performance: predictions from

transaction cost, resource-based and real options theories’. Journal of Management, 29, 937–61.Leiblein, M. J. and Miller, D. J. (2003). ‘An empirical examination of transaction- and firm-level influences

on the vertical boundaries of the firm’. Strategic Management Journal, 24, 839–59.McGrath, R. G. (1997). ‘A real options logic for initiating technology positioning investments’. Academy of

Management Review, 22, 974–96.McGrath, R. G. and Nerkar, A. (2004). ‘Real options reasoning and a new look at the R&D investment

strategies of pharmaceutical firms’. Strategic Management Journal, 25, 1–21.Miller, K. D. and Folta, T. B. (2002). ‘Option value and entry timing’. Strategic Management Journal, 23,

655–65.Pacheco-de-Almeida, G., Henderson, J. E. and Cool, K. O. (2008). ‘Resolving the commitment

versus flexibility trade-off: the role of resource accumulation lags’. Academy of Management Journal, 51,517–36.

Podsakoff, P. M., Mackenzie, S. B., Lee, J. Y. and Podsakoff, N. P. (2003). ‘Common method biases inbehavioral research: a critical review of the literature and recommended remedies’. Journal of AppliedPsychology, 88, 531–44.

Porter, M. E. (1980). Competitive Strategy: Techniques for Analyzing Industries and Competitors. New York: The FreePress.

Reuer, J. J. and Koza, M. P. (2000). ‘Asymmetric information and joint venture performance: theory andevidence for domestic and international joint ventures’. Strategic Management Journal, 21, 81–8.

Rowley, I. (2008). ‘Ford’s Mazda share sale imminent?’. http://www.businessweek.com/autos/autobeat/archives/2008/11/fords_mazda_sha.html.

Sanchez, R. (1993). ‘Strategic flexibility, firm organization and managerial work in dynamic markets’. InShrivastava, P., Huff, A. and Dutton, J. (Eds), Advances in Strategic Management. Greenwich, CT: JAI Press,9, 251–91.

Scherpereel, C. M. (2008). ‘The option-creating institution: a real options perspective on economic orga-nization’. Strategic Management Journal, 29, 455–70.

Sitkin, S. B. and Pablo, A. L. (1992). ‘Reconceptualizing the determinants of risk behavior’. Academy ofManagement Review, 17, 9–38.

K. D. Brouthers and D. Dikova1070