Lecturer receptivity to a major educational change in the ...

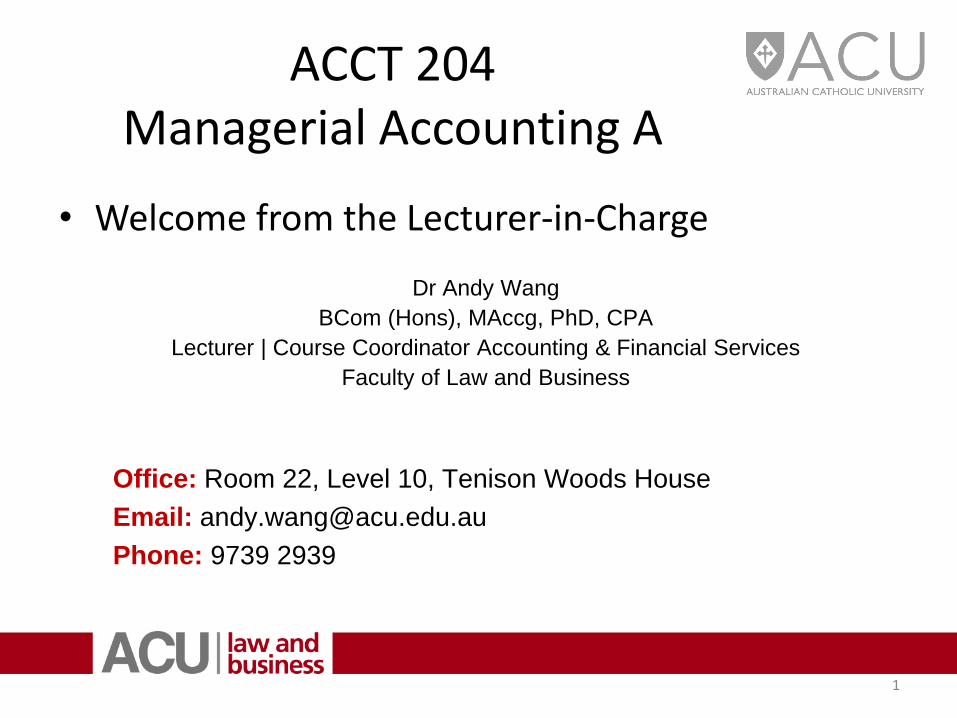

ACCT 204 Managerial Accounting A

• Welcome from the Lecturer-in-Charge

Dr Andy Wang

BCom (Hons), MAccg, PhD, CPA

Lecturer | Course Coordinator Accounting & Financial Services

Faculty of Law and Business

Office: Room 22, Level 10, Tenison Woods House

Email: [email protected]

Phone: 9739 2939

1

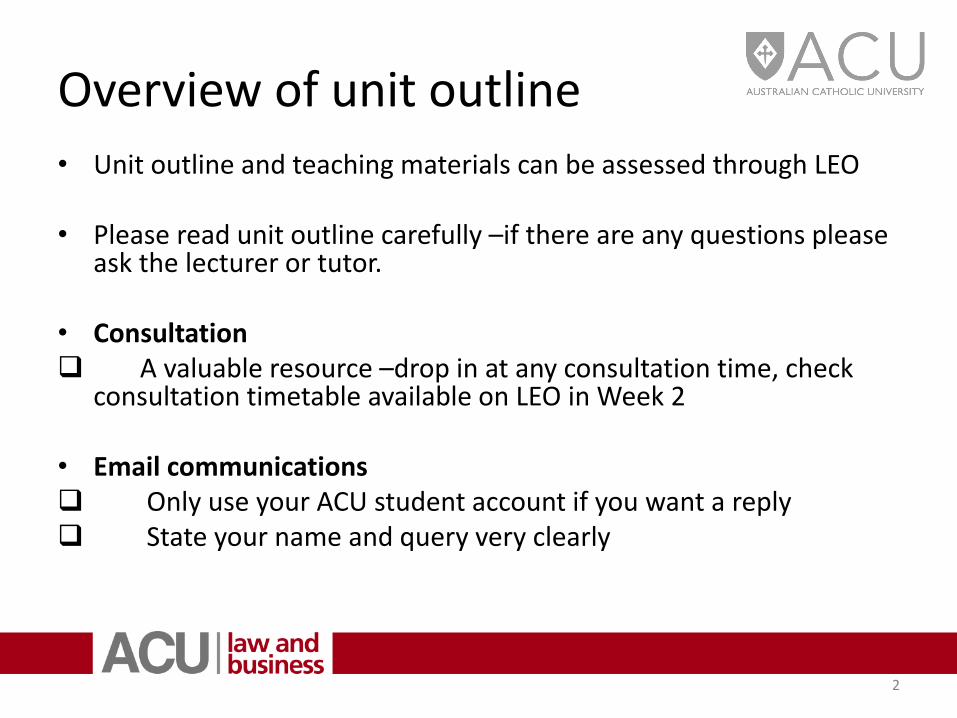

Overview of unit outline

• Unit outline and teaching materials can be assessed through LEO • Please read unit outline carefully –if there are any questions please

ask the lecturer or tutor. • Consultation A valuable resource –drop in at any consultation time, check

consultation timetable available on LEO in Week 2 • Email communications Only use your ACU student account if you want a reply State your name and query very clearly

2

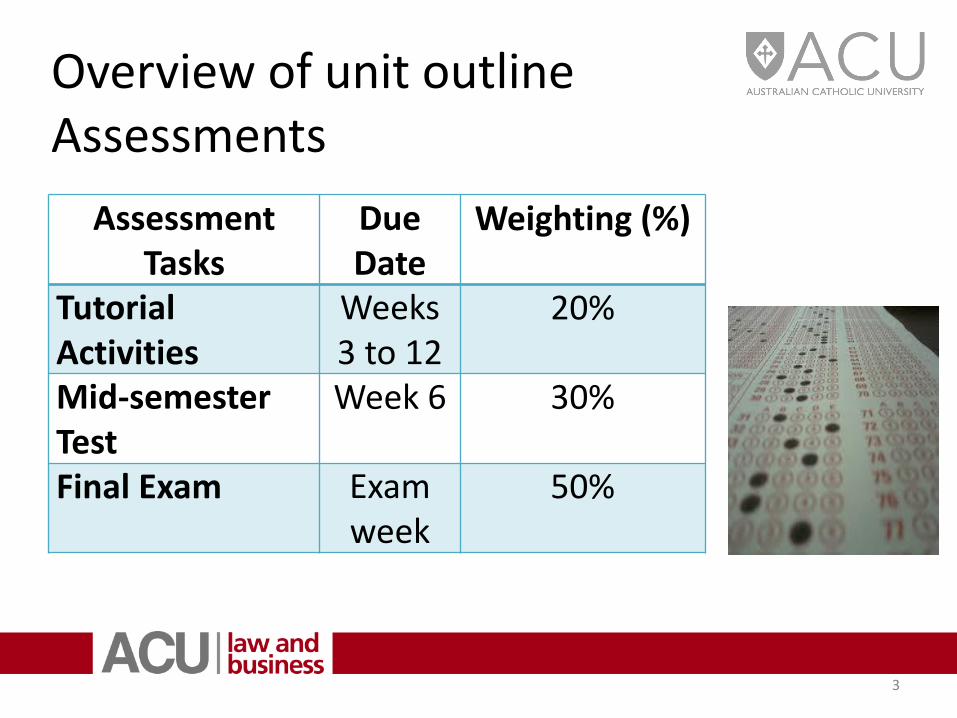

Overview of unit outline Assessments

3

Assessment Tasks

Due Date

Weighting (%)

Tutorial Activities

Weeks 3 to 12

20%

Mid-semester Test

Week 6 30%

Final Exam Exam week

50%

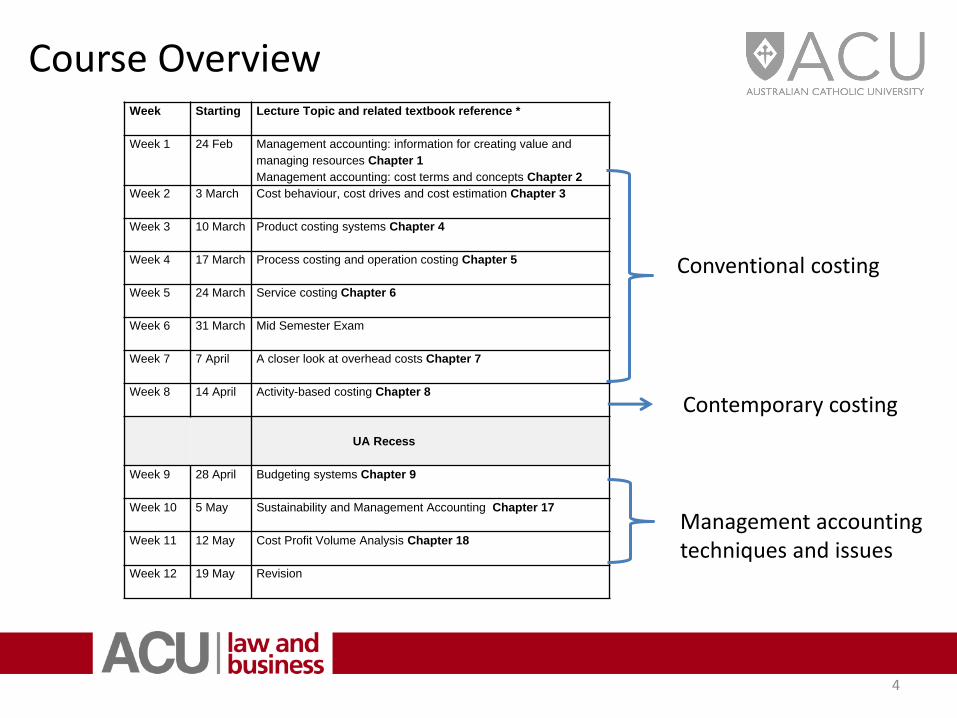

Course Overview

4

Week

Starting Lecture Topic and related textbook reference *

Week 1

24 Feb Management accounting: information for creating value and

managing resources Chapter 1

Management accounting: cost terms and concepts Chapter 2

Week 2

3 March Cost behaviour, cost drives and cost estimation Chapter 3

Week 3

10 March Product costing systems Chapter 4

Week 4

17 March Process costing and operation costing Chapter 5

Week 5

24 March Service costing Chapter 6

Week 6

31 March Mid Semester Exam

Week 7

7 April A closer look at overhead costs Chapter 7

Week 8

14 April Activity-based costing Chapter 8

UA Recess

Week 9

28 April Budgeting systems Chapter 9

Week 10

5 May Sustainability and Management Accounting Chapter 17

Week 11

12 May Cost Profit Volume Analysis Chapter 18

Week 12

19 May Revision

Conventional costing

Contemporary costing

Management accounting techniques and issues

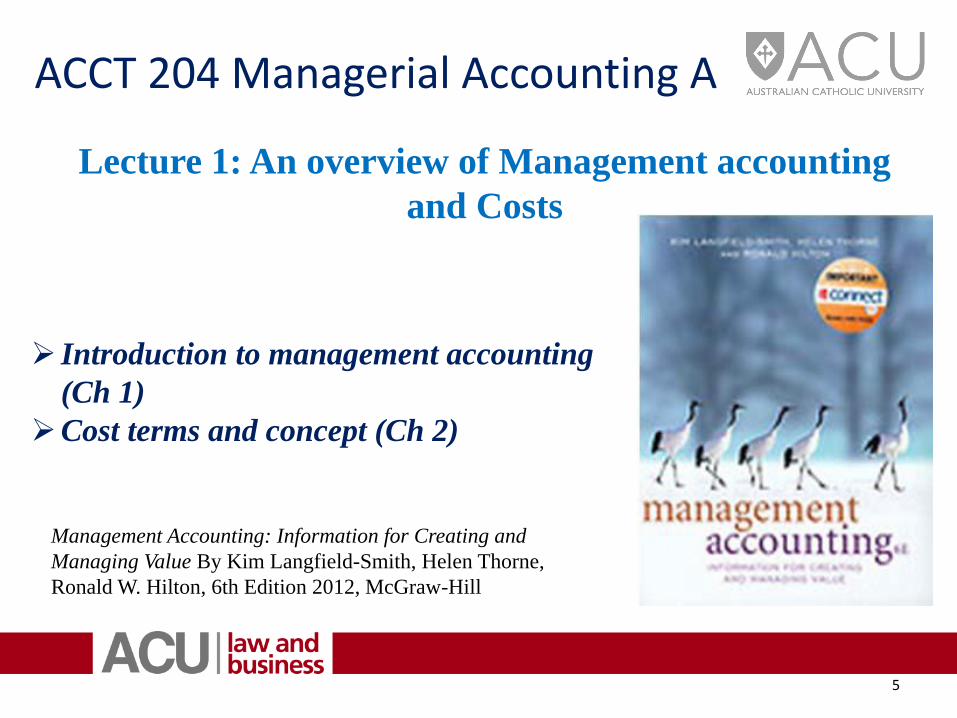

ACCT 204 Managerial Accounting A

Lecture 1: An overview of Management accounting

and Costs

5

Introduction to management accounting

(Ch 1)

Cost terms and concept (Ch 2)

Management Accounting: Information for Creating and

Managing Value By Kim Langfield-Smith, Helen Thorne,

Ronald W. Hilton, 6th Edition 2012, McGraw-Hill

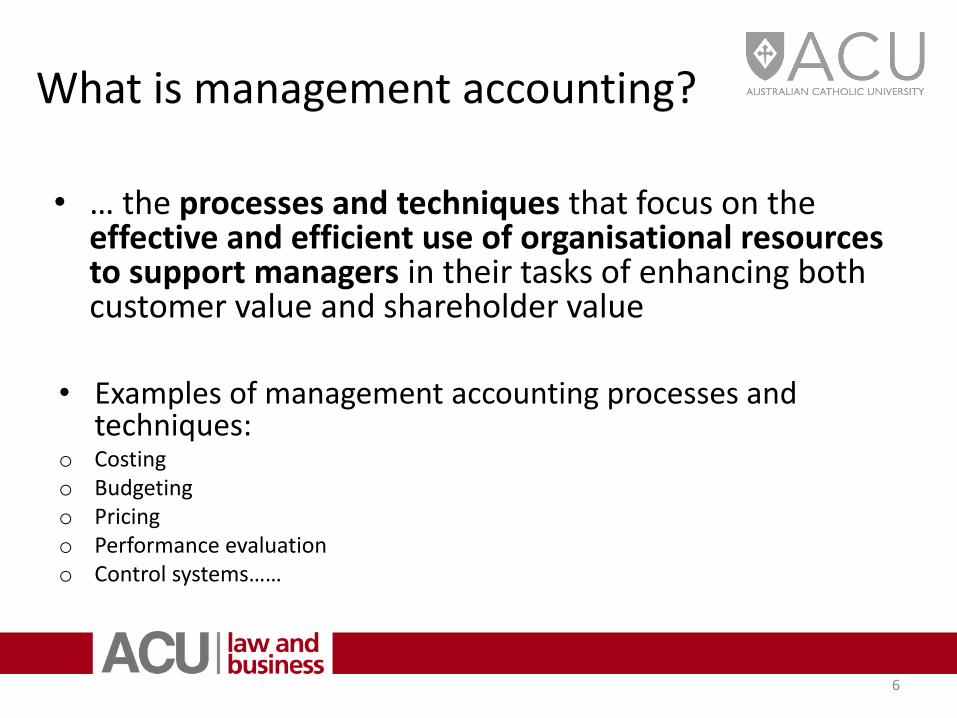

What is management accounting?

• … the processes and techniques that focus on the

effective and efficient use of organisational resources to support managers in their tasks of enhancing both customer value and shareholder value

• Examples of management accounting processes and techniques:

o Costing o Budgeting o Pricing o Performance evaluation o Control systems……

6

What is management accounting? (cont.)

• Customer value – The value that a customer places on particular features of a

product or service

• Shareholder value – The value that shareholders or owners place on a business

• Resources – Financial and non-financial, including information, work

processes, employees, committed customers and suppliers

– Determine the capabilities and competencies of the organisation

7

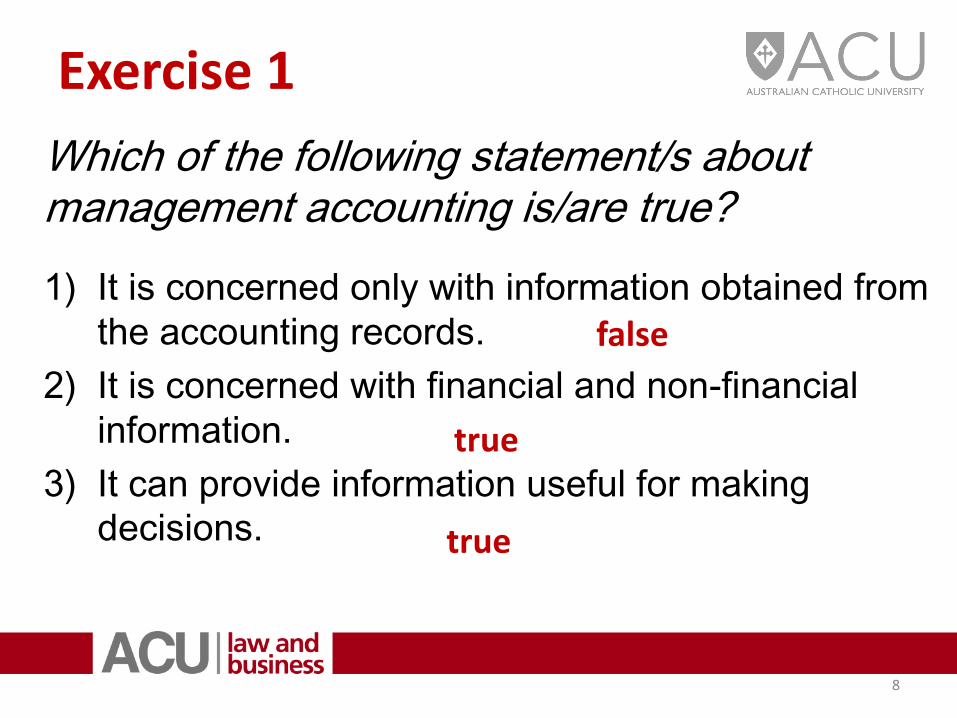

Exercise 1

8

Which of the following statement/s about management accounting is/are true?

1) It is concerned only with information obtained from

the accounting records.

2) It is concerned with financial and non-financial

information.

3) It can provide information useful for making

decisions.

false

true

true

Management accounting and financial accounting: a comparison

• Financial accounting – The practice of preparing and reporting accounting

information for parties outside the organisation

• Costing systems are common to both financial and management accounting – A system that estimates the cost of goods and services as well

as the cost of organisational units, such as departments

– Why?

9

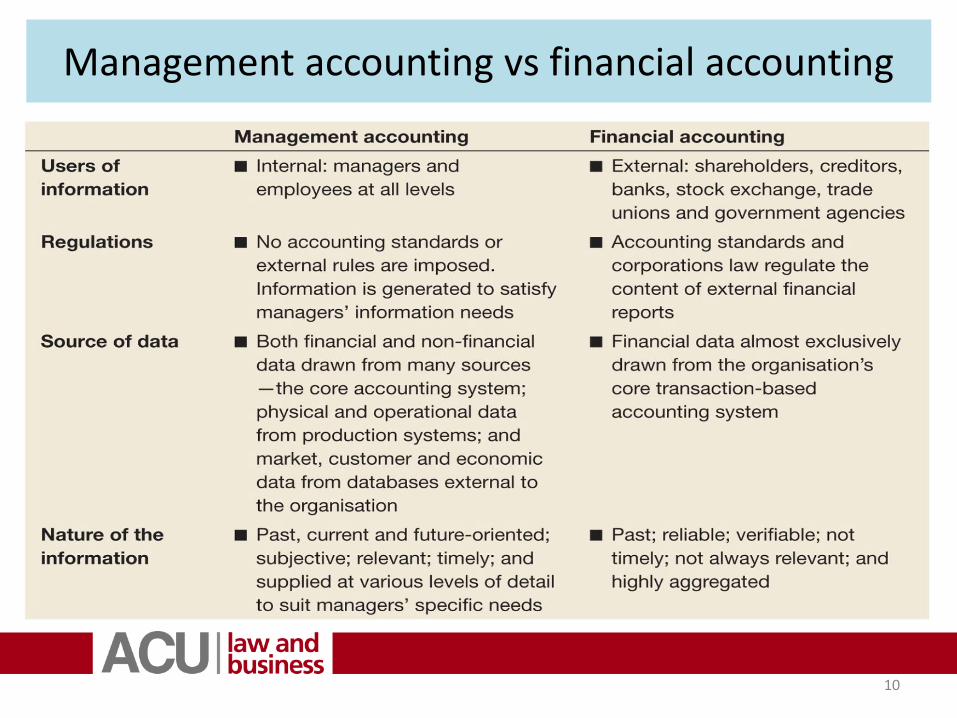

Management accounting vs financial accounting

10

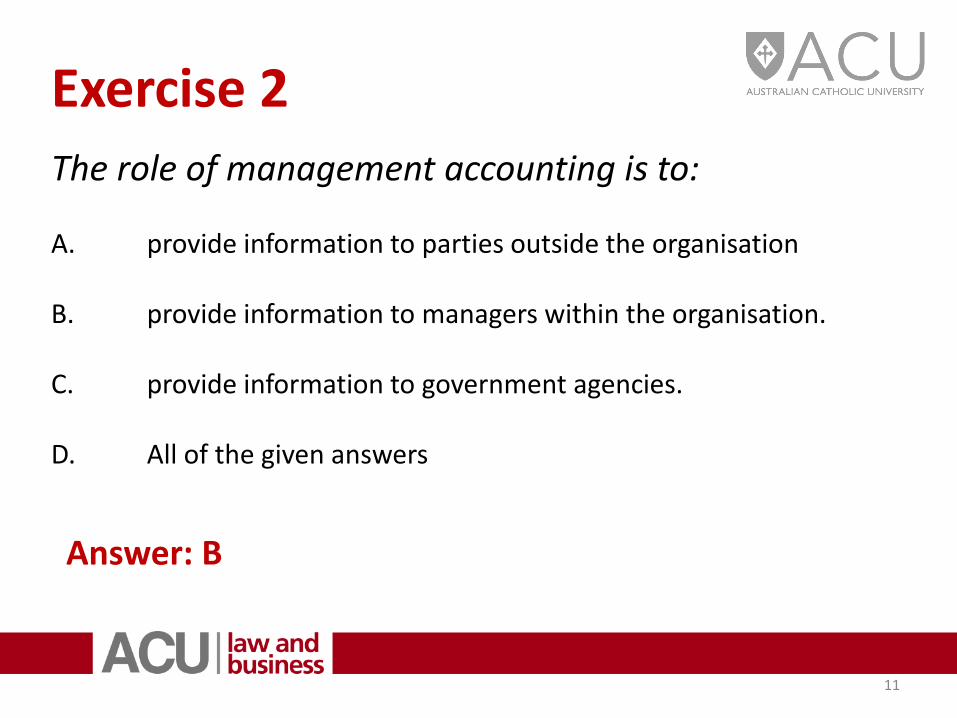

Exercise 2

The role of management accounting is to: A. provide information to parties outside the organisation B. provide information to managers within the organisation. C. provide information to government agencies. D. All of the given answers

11

Answer: B

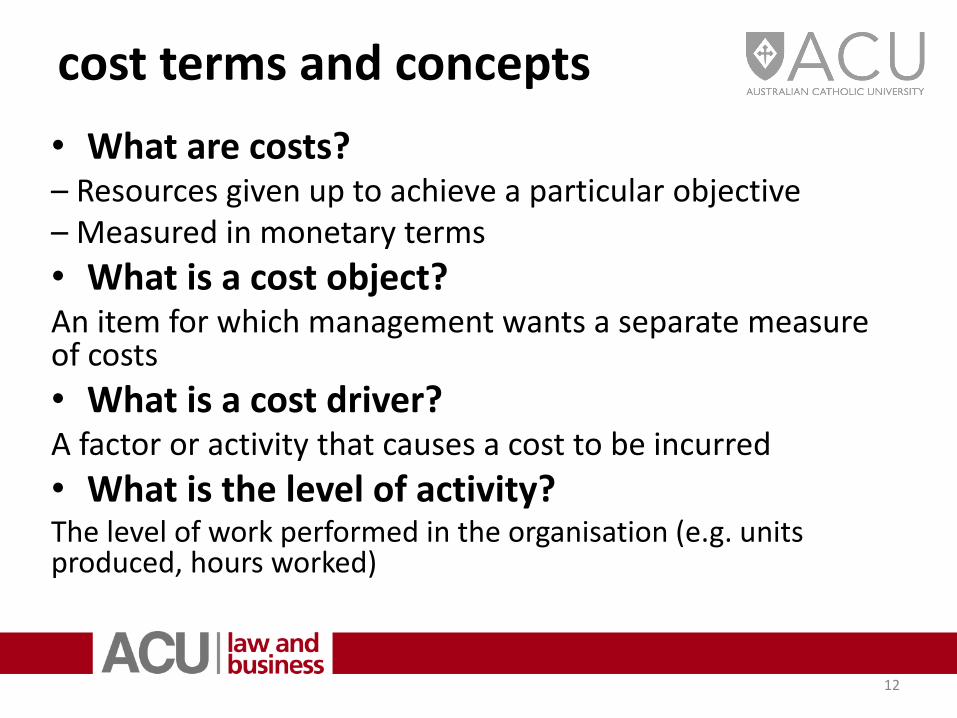

cost terms and concepts

• What are costs? – Resources given up to achieve a particular objective – Measured in monetary terms

• What is a cost object? An item for which management wants a separate measure of costs

• What is a cost driver? A factor or activity that causes a cost to be incurred

• What is the level of activity? The level of work performed in the organisation (e.g. units produced, hours worked)

12

13

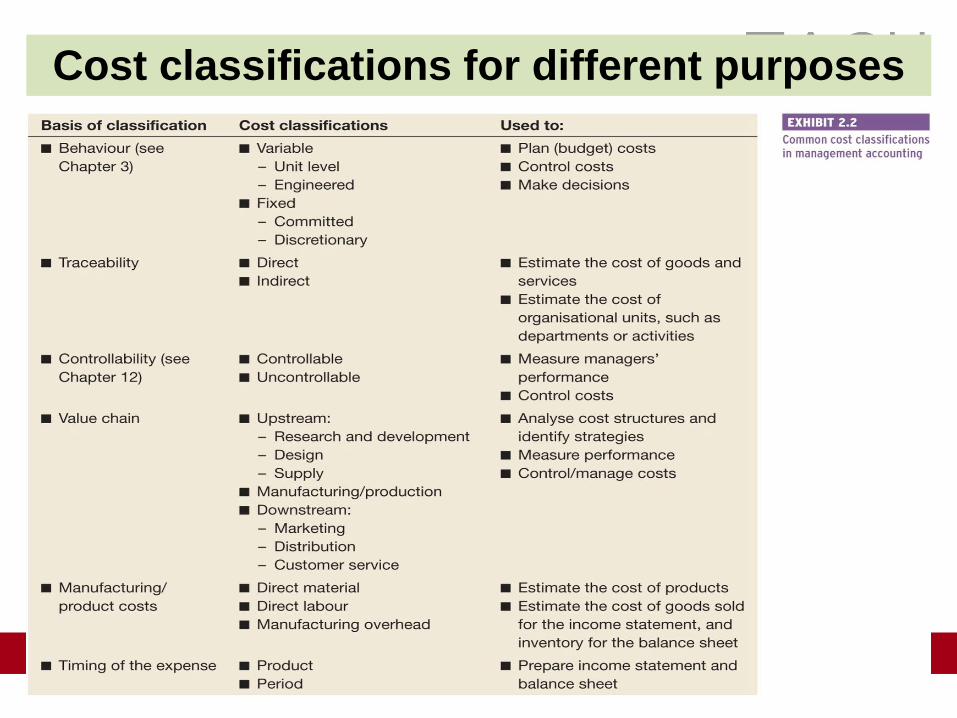

Cost classifications for different purposes

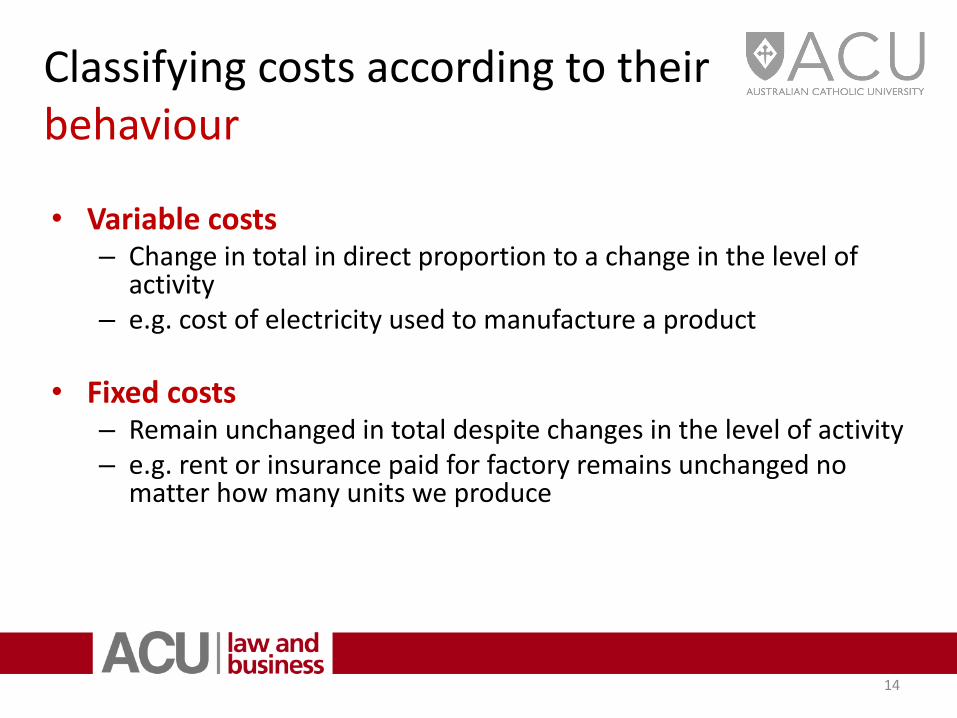

Classifying costs according to their behaviour

• Variable costs – Change in total in direct proportion to a change in the level of

activity – e.g. cost of electricity used to manufacture a product

• Fixed costs – Remain unchanged in total despite changes in the level of activity – e.g. rent or insurance paid for factory remains unchanged no

matter how many units we produce

14

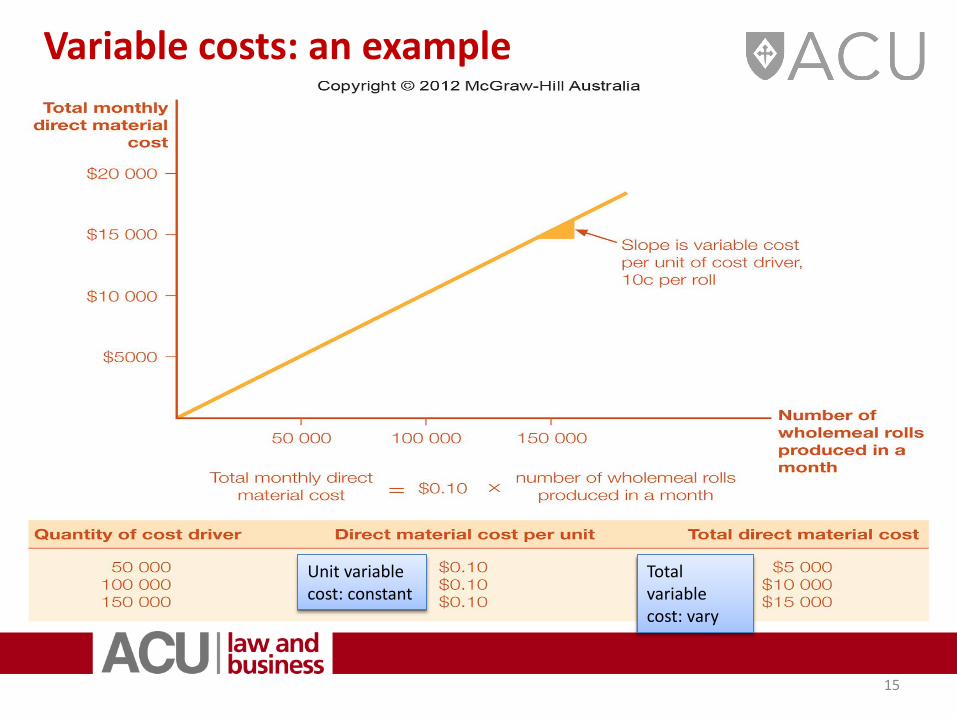

Variable costs: an example

15

Unit variable cost: constant

Total variable cost: vary

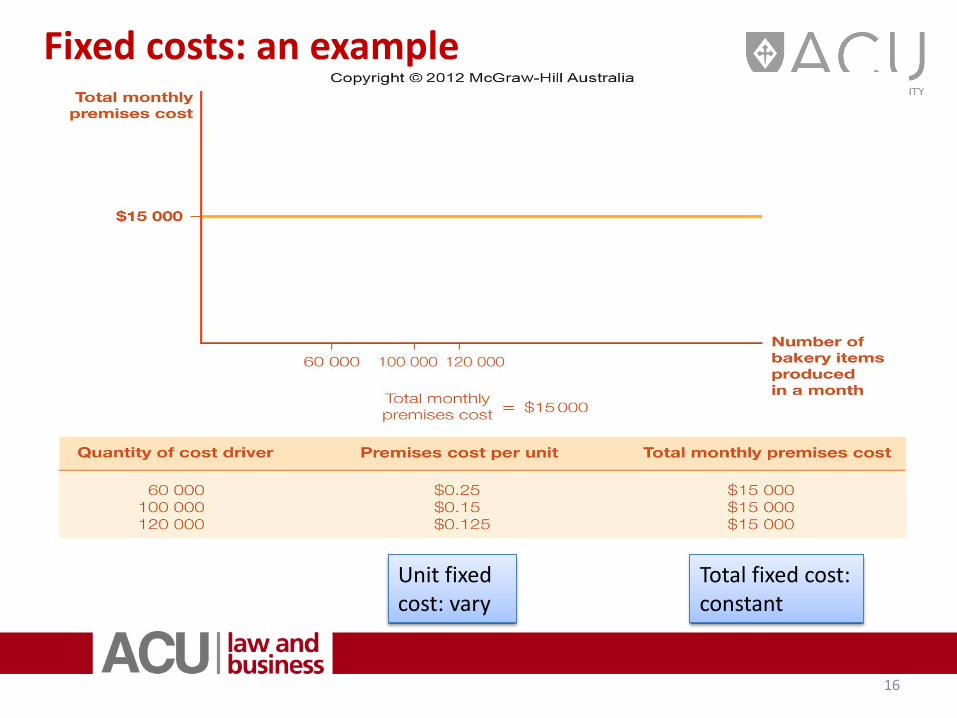

Fixed costs: an example

16

Unit fixed cost: vary

Total fixed cost: constant

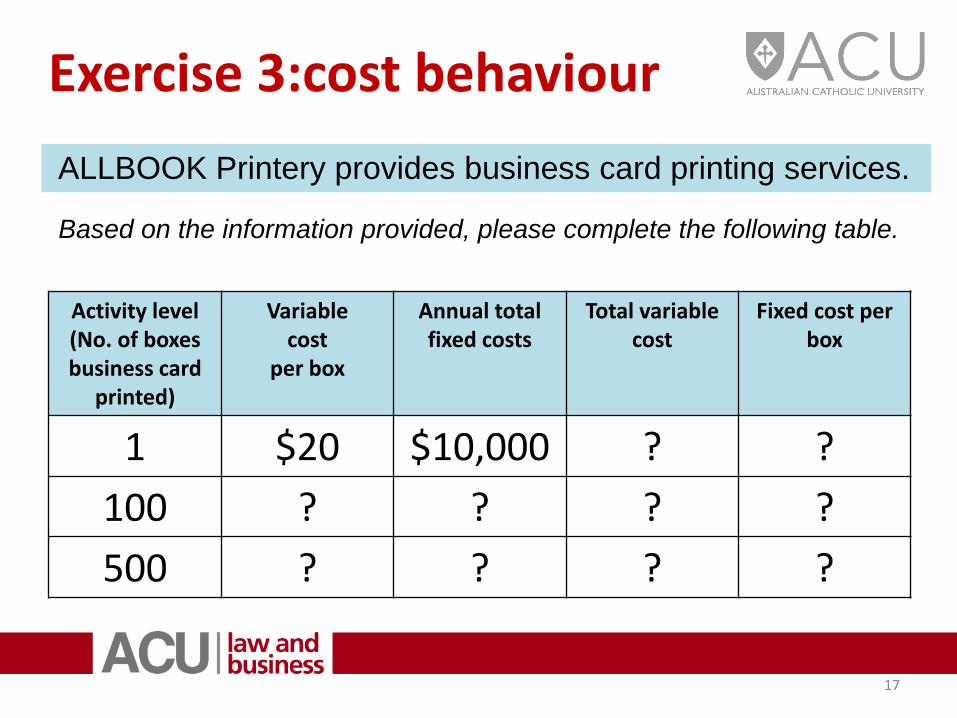

Exercise 3:cost behaviour

17

Activity level (No. of boxes business card

printed)

Variable cost

per box

Annual total fixed costs

Total variable cost

Fixed cost per box

1 $20 $10,000 ? ?

100 ? ? ? ?

500 ? ? ? ?

ALLBOOK Printery provides business card printing services.

Based on the information provided, please complete the following table.

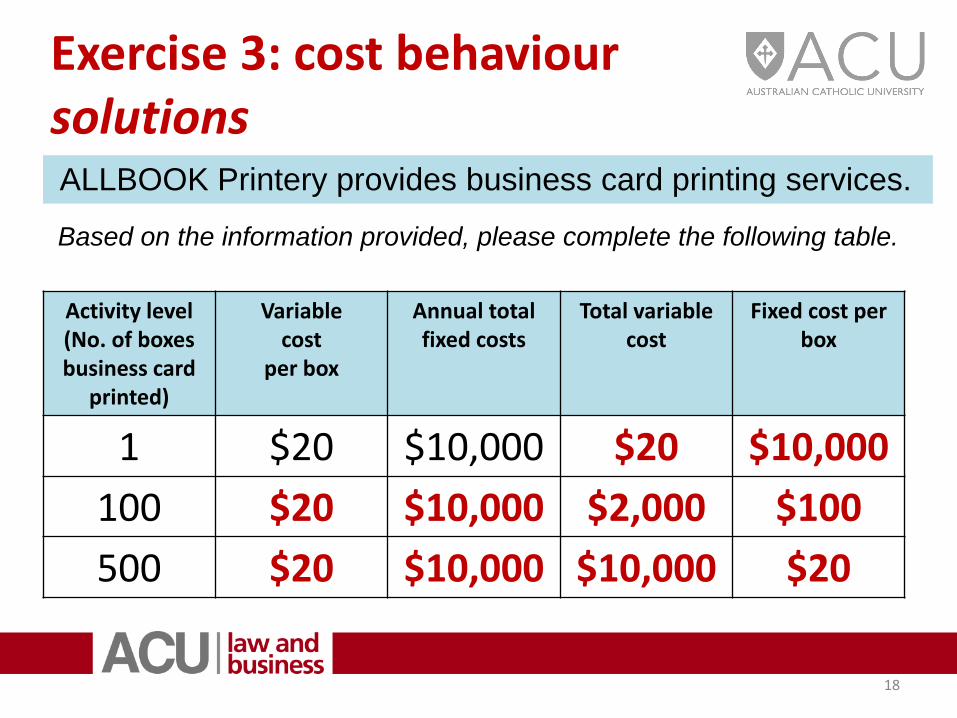

Exercise 3: cost behaviour solutions

18

Activity level (No. of boxes business card

printed)

Variable cost

per box

Annual total fixed costs

Total variable cost

Fixed cost per box

1 $20 $10,000 $20 $10,000

100 $20 $10,000 $2,000 $100

500 $20 $10,000 $10,000 $20

ALLBOOK Printery provides business card printing services.

Based on the information provided, please complete the following table.

Direct and indirect costs -Traceability

• Whether a cost is classified as direct or indirect depends on the nature of the cost object

– Do we wish to know the cost of a department, a product, a project, or an entire company?

19

– Direct costs: costs that can be directly traced to or identified from the products (cost object) in an economic manner

– Indirect costs: costs that cannot be directly traced to or identified from the products (cost object) in an economic manner

Source: Horngren, C, Wynder, M, Maguire, W, Tan, R, Datar, S, Foster, G, Rajan, M & Ittner, C 2011, Cost Accounting a Managerial Emphasis, 1st edn, Pearson Australia.

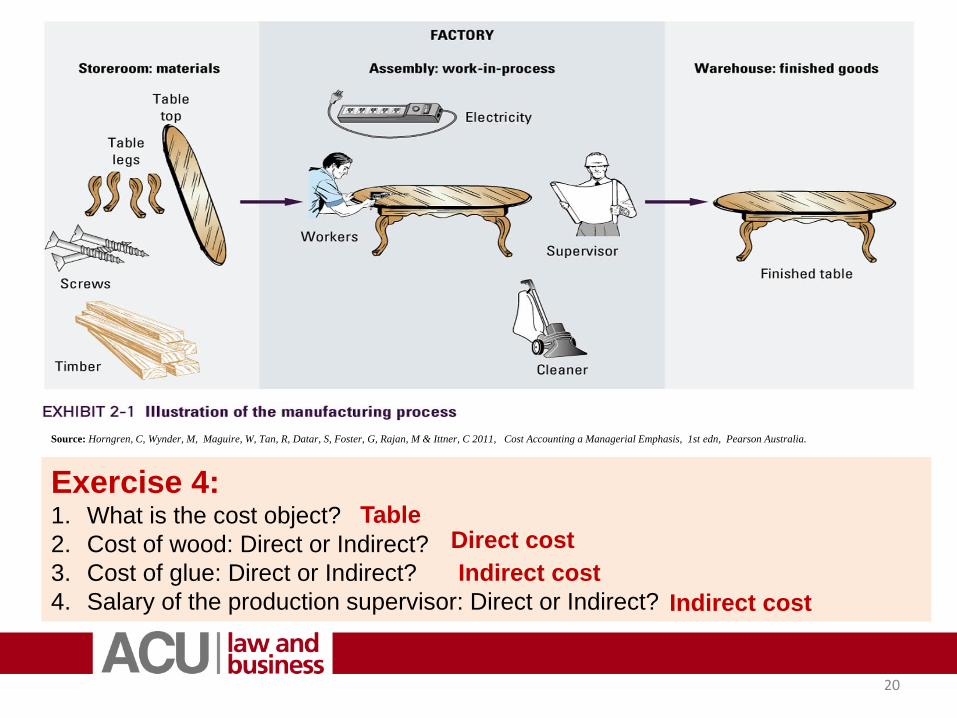

Exercise 4: 1. What is the cost object?

2. Cost of wood: Direct or Indirect?

3. Cost of glue: Direct or Indirect?

4. Salary of the production supervisor: Direct or Indirect?

20

Table Direct cost

Indirect cost

Indirect cost

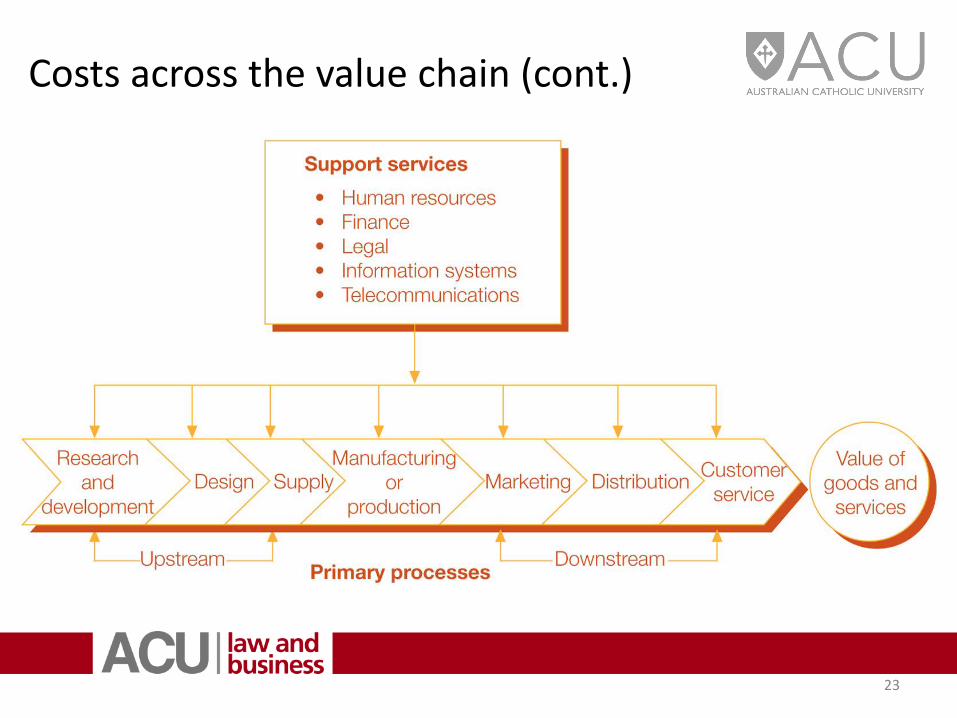

Costs across the value chain

• The value chain – A set of linked processes or activities that begins with

acquiring resources and ends with providing and supporting products and services that customers value

• Various cost classifications can be used within the upstream, downstream and manufacturing areas – To assign cost to products , provide other information to

help manage resources efficiently and effectively, and to create value

21

Costs across the value chain (cont.) • Upstream costs

– Research and development costs include the costs involved in developing new products and processes

– Design costs include the costs associated with designing a product or production process

– Supply costs are the costs of sourcing and managing incoming parts, assemblies and supplies

22

• Production costs – The costs incurred to collect and assemble the resources used to produce

a product (i.e. goods or services) • Downstream costs

– Marketing costs are the costs of selling products and the costs of advertising and promotion

– Distribution costs are the costs of storing, handling and shipping finished products

– Customer service costs are the costs of serving customers, including after-sales service

Costs across the value chain (cont.)

23

Period or product cost: timing of the expense

Period cost • The costs expensed in the accounting period in which they are

• incurred rather than being attached to units purchased or produced.

• e.g. salaries of sales staff, advertising expense, depreciation of office

• equipment

Product cost • Manufacturing costs are incurred within the factory area

• The cost assigned to goods/services that were manufactured or purchased for resale.

• Product cost is regarded as a part of the asset / inventory until goods are sold.

24

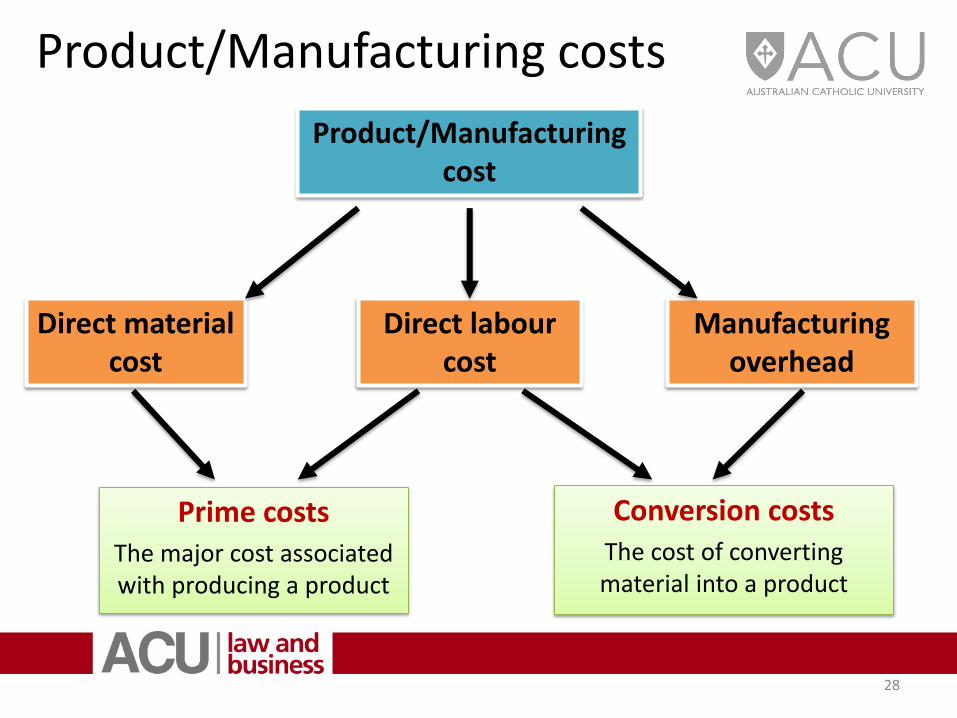

Product/Manufacturing costs

• Direct material – Consumed in the manufacturing process

– Physically incorporated into the finished products

– Can be traced to products in an economic manner

– A variable cost (with respect to products)

• Direct labour – The cost of wages and labour on-costs for personnel who work

directly on the manufacture of a product

– Usually treated as variable costs, however contractual arrangements sometimes mean that such labour is a committed cost and so does not vary with the level of production

25

Product/Manufacturing costs

• Manufacturing overhead – All manufacturing costs other than direct material and

direct labour

– Also called indirect manufacturing costs or factory burden

– Includes the cost of indirect material and indirect labour, depreciation and insurance on factory equipment, utilities and the costs of support departments for manufacturing

– Includes cost of overtime premium and idle time

– Manufacturing support departments do not work directly on producing products but are necessary for the manufacturing process to occur

26

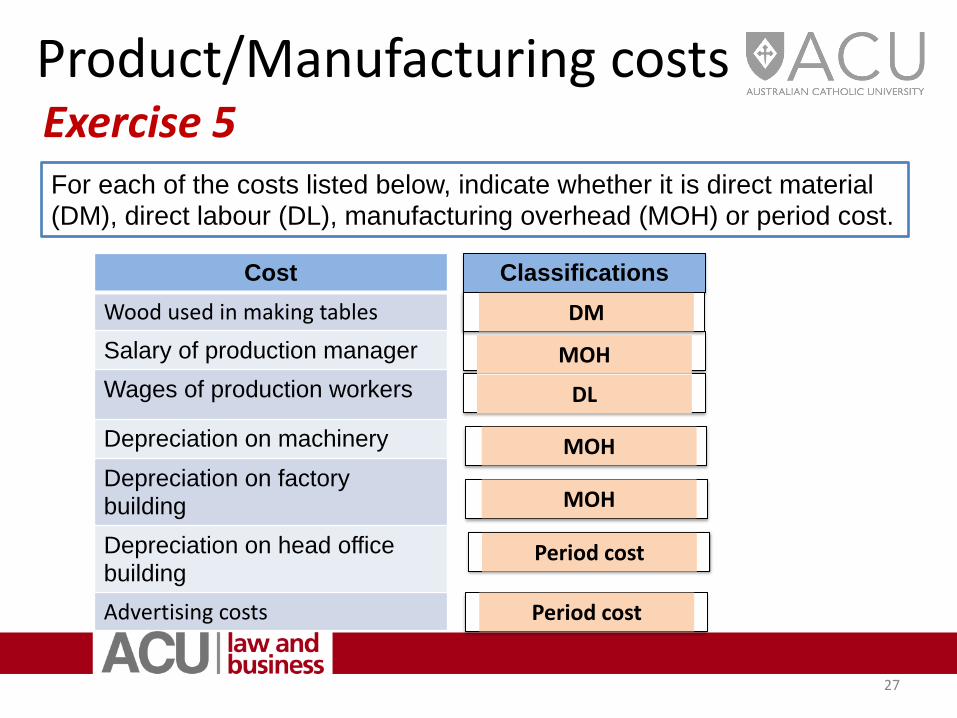

Product/Manufacturing costs Exercise 5

27

For each of the costs listed below, indicate whether it is direct material

(DM), direct labour (DL), manufacturing overhead (MOH) or period cost.

Cost

Wood used in making tables

Salary of production manager

Wages of production workers

Depreciation on machinery

Depreciation on factory building

Depreciation on head office building

Advertising costs

Classifications

DM

MOH

DL

MOH

MOH

Period cost

Period cost

Product/Manufacturing costs

Conversion costs The cost of converting material into a product

28

Product/Manufacturing cost

Direct material cost

Direct labour cost

Manufacturing overhead

Prime costs The major cost associated with producing a product

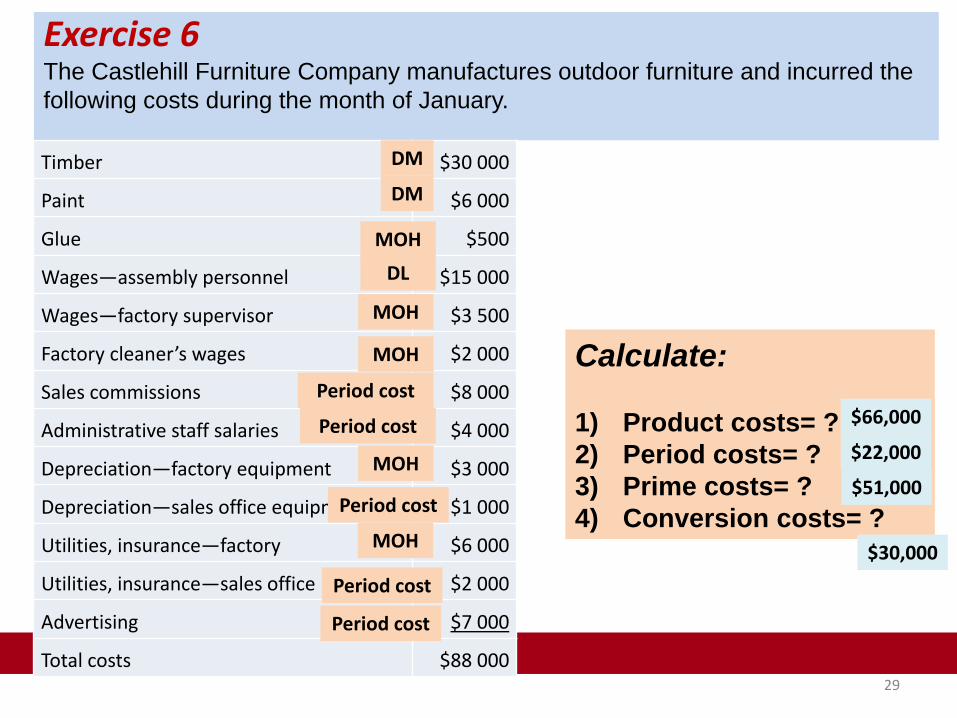

Exercise 6 The Castlehill Furniture Company manufactures outdoor furniture and incurred the

following costs during the month of January.

Timber $30 000

Paint $6 000

Glue $500

Wages—assembly personnel $15 000

Wages—factory supervisor $3 500

Factory cleaner’s wages $2 000

Sales commissions $8 000

Administrative staff salaries $4 000

Depreciation—factory equipment $3 000

Depreciation—sales office equipment $1 000

Utilities, insurance—factory $6 000

Utilities, insurance—sales office $2 000

Advertising $7 000

Total costs $88 000 29

Calculate:

1) Product costs= ?

2) Period costs= ?

3) Prime costs= ?

4) Conversion costs= ?

DM

DM

MOH

DL

MOH

MOH

Period cost

Period cost

MOH

Period cost

MOH

Period cost

Period cost

$66,000

$22,000

$51,000

$30,000

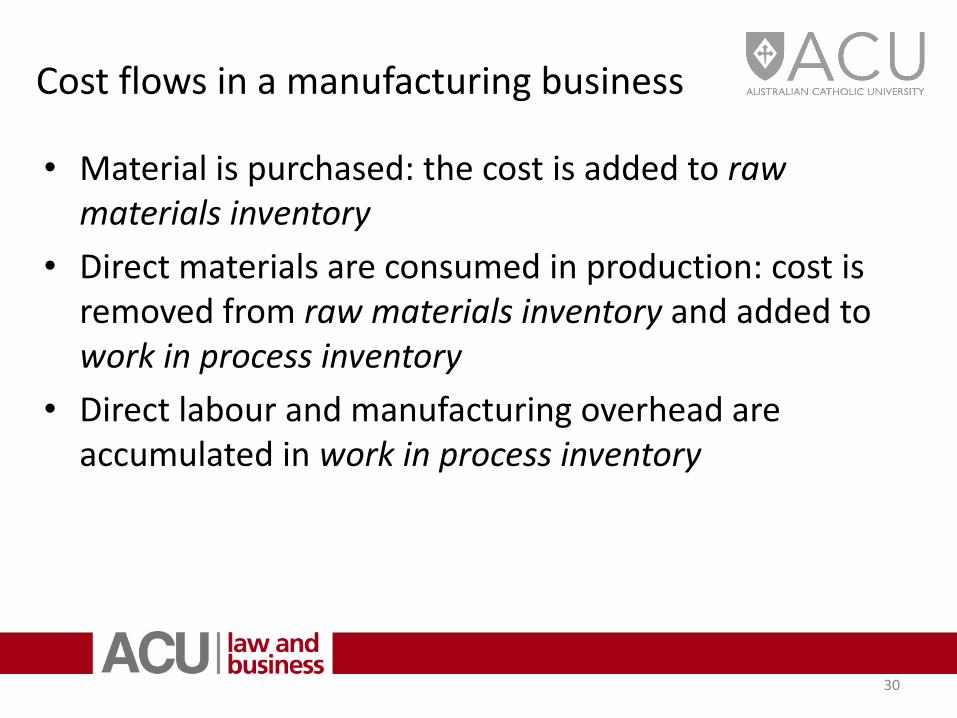

Cost flows in a manufacturing business

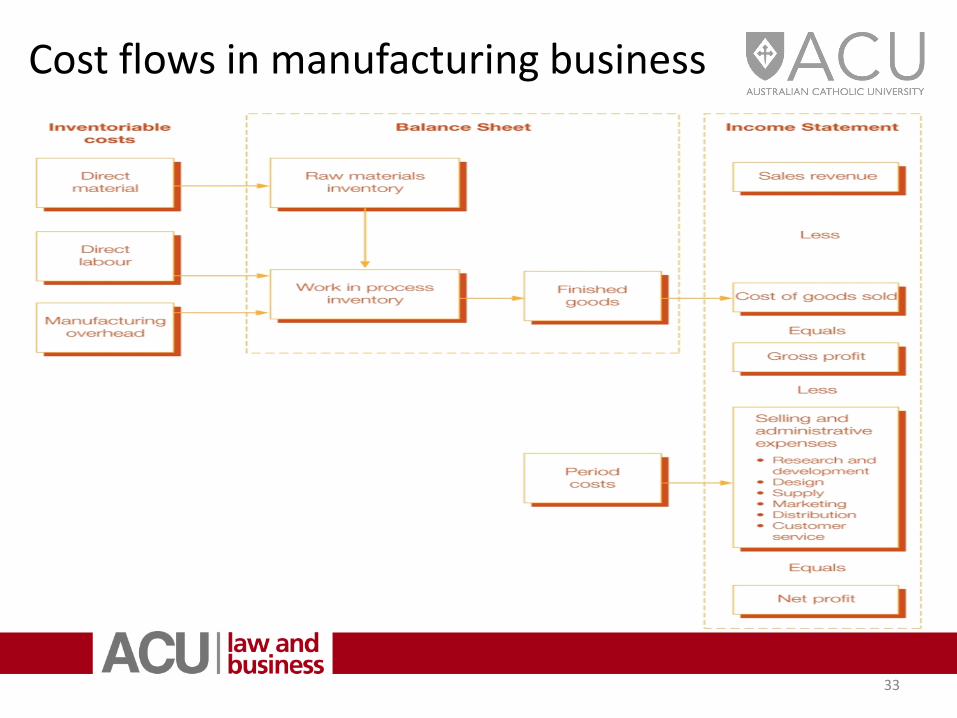

• Material is purchased: the cost is added to raw materials inventory

• Direct materials are consumed in production: cost is removed from raw materials inventory and added to work in process inventory

• Direct labour and manufacturing overhead are accumulated in work in process inventory

30

Cost flows in a manufacturing business

• Products are completed: costs are transferred from work in process inventory and added to finished goods inventory

• Products are sold: costs are transferred from finished goods inventory to cost of goods sold expense

Cost of goods sold is deducted from sales revenue to determine gross profit

31

Cost flows in manufacturing business

• Raw materials, work in process and finished goods inventory balances are reported in the balance sheet

• Cost of goods sold expense can be found in the income statement

• The schedule of cost of goods manufactured and schedule of cost of goods sold summarise the flow of manufacturing costs

32

Cost flows in manufacturing business

33

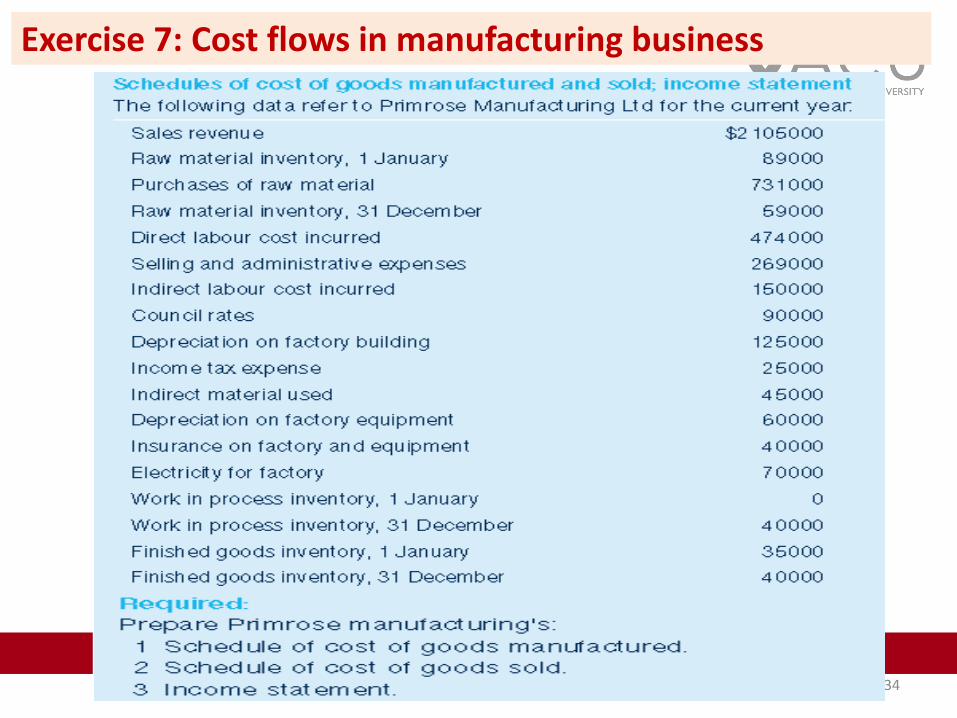

Exercise 7: Cost flows in manufacturing business

34

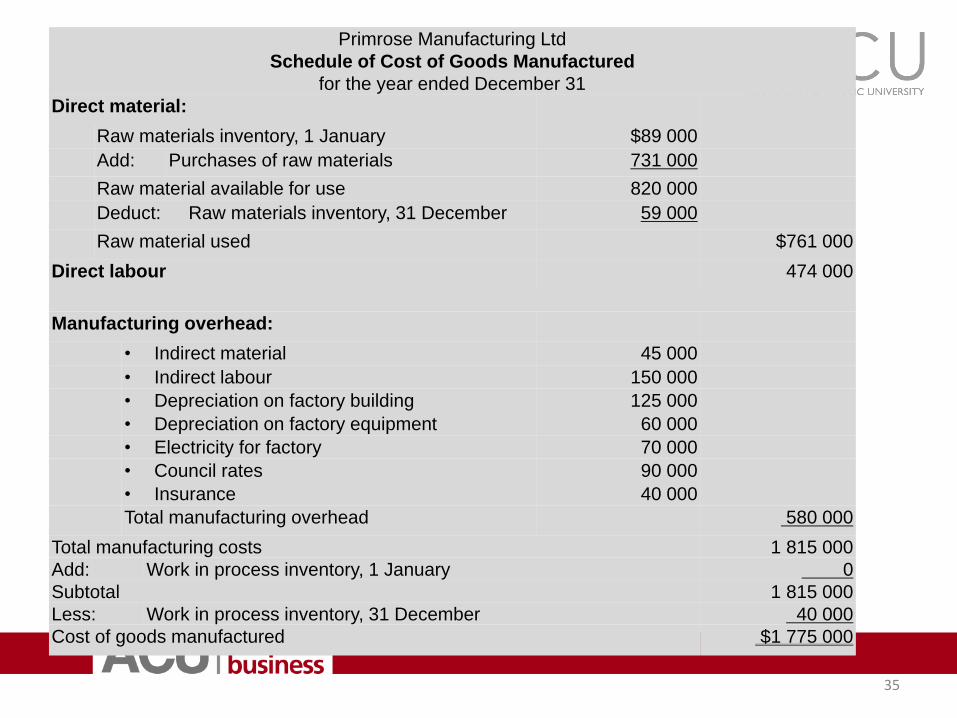

35

Primrose Manufacturing Ltd

Schedule of Cost of Goods Manufactured

for the year ended December 31

Direct material:

Raw materials inventory, 1 January $89 000

Add: Purchases of raw materials 731 000

Raw material available for use 820 000

Deduct: Raw materials inventory, 31 December 59 000

Raw material used $761 000

Direct labour 474 000

Manufacturing overhead:

• Indirect material 45 000

• Indirect labour 150 000

• Depreciation on factory building 125 000

• Depreciation on factory equipment 60 000

• Electricity for factory 70 000

• Council rates 90 000

• Insurance 40 000

Total manufacturing overhead 580 000

Total manufacturing costs 1 815 000

Add: Work in process inventory, 1 January 0

Subtotal 1 815 000

Less: Work in process inventory, 31 December 40 000

Cost of goods manufactured $1 775 000

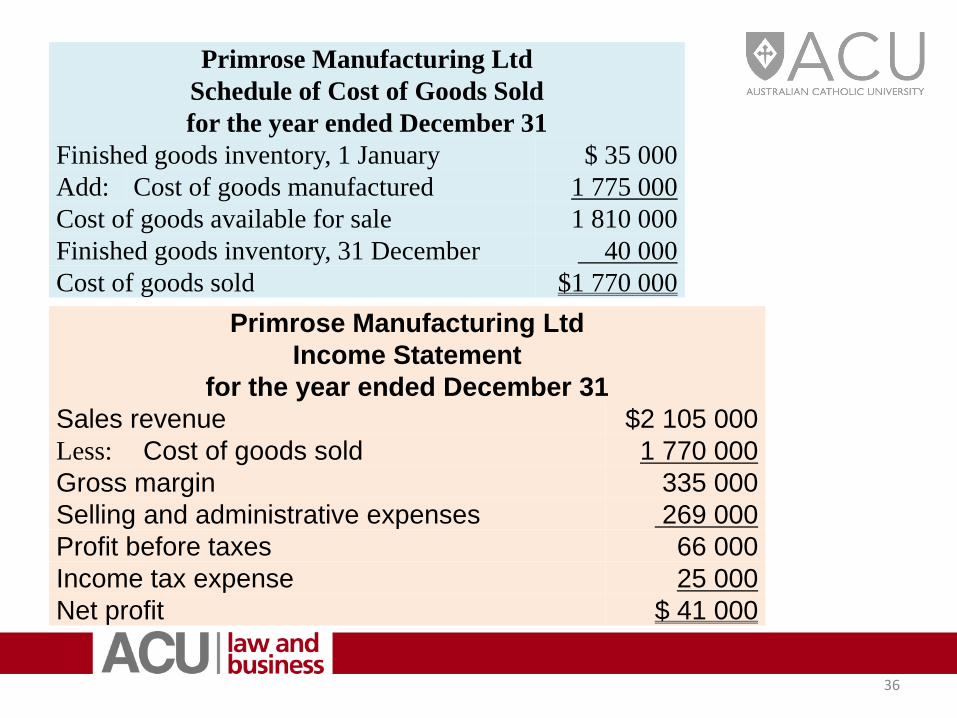

36

Primrose Manufacturing Ltd

Schedule of Cost of Goods Sold

for the year ended December 31

Finished goods inventory, 1 January $ 35 000

Add: Cost of goods manufactured 1 775 000

Cost of goods available for sale 1 810 000

Finished goods inventory, 31 December 40 000

Cost of goods sold $1 770 000

Primrose Manufacturing Ltd

Income Statement

for the year ended December 31

Sales revenue $2 105 000

Less: Cost of goods sold 1 770 000

Gross margin 335 000

Selling and administrative expenses 269 000

Profit before taxes 66 000

Income tax expense 25 000

Net profit $ 41 000

Copyright © 2022 FDOKUMEN