Accounts and Audit of - Co-Operative Housing Societies

26

Accounts and Audit of Co-Operative Housing Societies CA Vivek Deshmukh (April 2020)

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Accounts and Audit of - Co-Operative Housing Societies

Accounts and Audit ofCo-Operative Housing Societies

CA Vivek Deshmukh(April 2020)

Accounting of Co-operative

Housing Societies

• Accounting Transactions

• Accounting Vouchers

• Recording of Transaction

• Books of Accounts

• Financial Statements

2

Accounting Transactions

• Accounting transactions are the transactions that

have a monetary impact on financial statements

of the Society Such as Maintenance bills and

receipts, society’s routine and non routine

expenses Bank and cash transactions etc.

• Managing committee to ensure that all

transactions are legitimate and undertaken as

per the provisions of bye-laws.

• As per bye law no 144 , All payments in excess

of Rs.1,500/- shall be made by crossed A/c

payee's cheques.

3

Accounting Transactions

• Bye law # 156: If the one time expenditure

exceeds the prescribed threshold the Managing

committee shall taken the approval of AGM and

if the AGM directs they shall call for Tender for

the particular Expense.

• Bye law # 143 : The Society may retain cash not

exceeding Rs.5,000 for Petty Expenses.

• Bye law # 112: The society shall open its bank

account in State or District Central Co-op Bank/

a Scheduled Bank having awarded "A" Audit

Class in last three consecutive years or a

Nationalised Bank.4

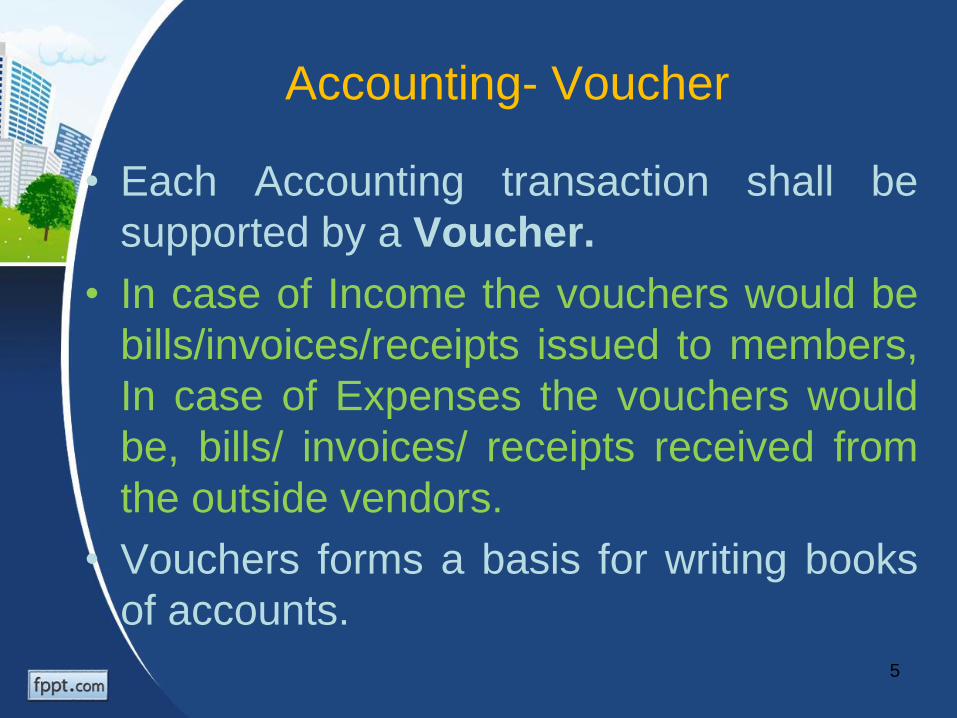

Accounting- Voucher

• Each Accounting transaction shall be

supported by a Voucher.

• In case of Income the vouchers would be

bills/invoices/receipts issued to members,

In case of Expenses the vouchers would

be, bills/ invoices/ receipts received from

the outside vendors.

• Vouchers forms a basis for writing books

of accounts.

5

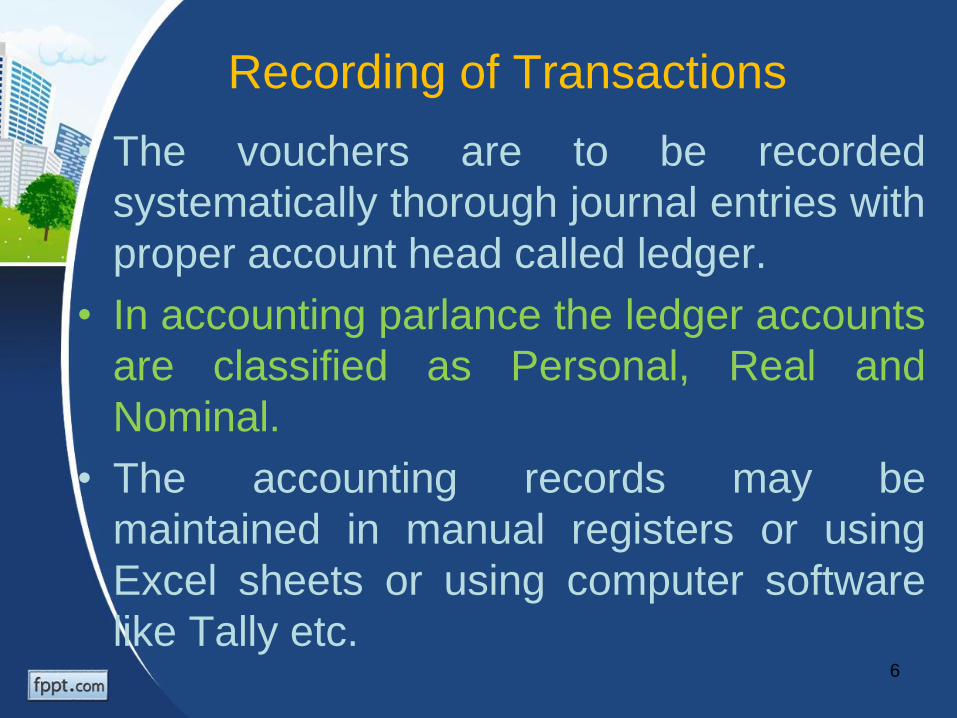

Recording of Transactions

• The vouchers are to be recorded

systematically thorough journal entries with

proper account head called ledger.

• In accounting parlance the ledger accounts

are classified as Personal, Real and

Nominal.

• The accounting records may be

maintained in manual registers or using

Excel sheets or using computer software

like Tally etc.6

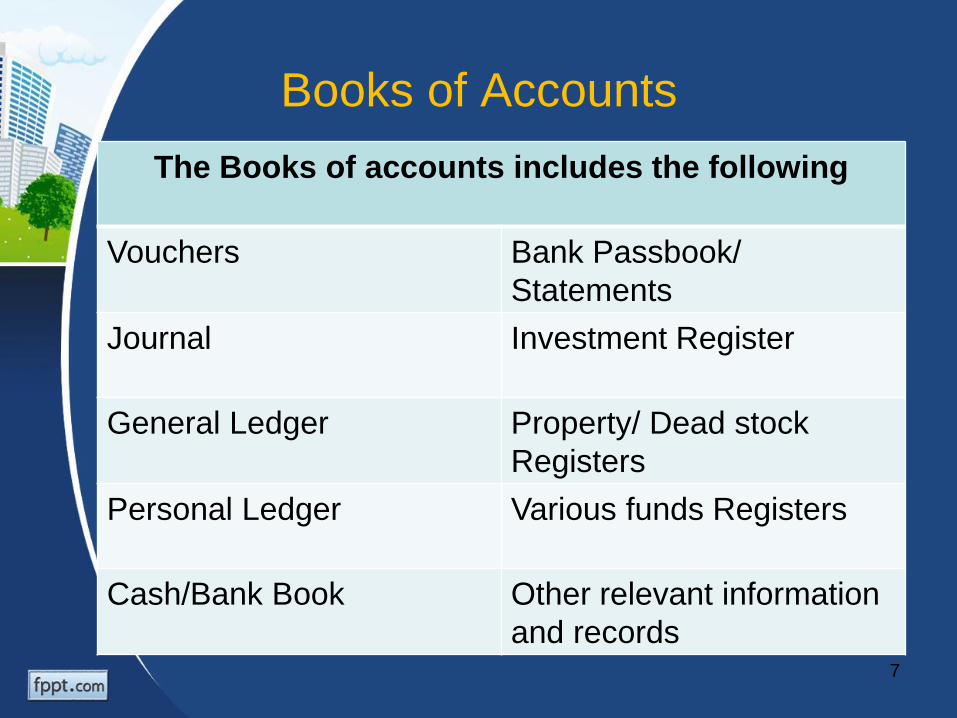

Books of Accounts

The Books of accounts includes the following

Vouchers Bank Passbook/

Statements

Journal Investment Register

General Ledger Property/ Dead stock

Registers

Personal Ledger Various funds Registers

Cash/Bank Book Other relevant information

and records7

Financial Statements

• On the basis of books of accounts,

financial statements prepared.

• The accounting year of the society starts

on 1st April and ends on 31st March.

• The society may follow Cash or Mercantile

basis of accounting.

• In mercantile basis the provisions for

expenses due but not paid till the year end

shall be recorded in the books of account.

8

Financial Statements

• Financial statements includes Income and

Expenditure Statement ( Form N), Balance

sheet ( Form N), Receipt and Payment

statement, schedule of investments,

debtors, creditors, dead stock.

• Preparation and presentation of financial

statements is the responsibility of the

managing committee.

9

Audit of Co-operative

Housing Societies

• Appointment of Auditors

• Audit Fees

• Records and information to be given for Audit

• Audit report

• Special Audit report

• Submission of Audit report

• Common Audit observations

10

Appointment of Auditors• The Society shall appoint the Statutory Auditor in its

AGM/ SGM from the panel of Auditors approved by

State Govt. If the CHS has more than 100 members

then the auditor shall be from Class A or Class B.

• The Consent letter from the auditors shall be taken

before appointing the auditors in AGM

• Auditors to be issued an Appointment letter along

with the a copy of extract of AGM Resolution and

obtain auditors acceptance letter.

• The society shall file soft copies the above

documents to Mahasahakar website and generate

and audit order.11

Appointment of Auditors• Statutory Auditor shall not be appointed for

more than Three consecutive years.

• The registrar appoints the statutory auditors

from the panel of auditors, if society fails to

do so.

• If necessary the Society may, appoint an

internal Auditor, to audit the accounts of the

Society, at the AGM.

One auditor can accept maximum 20

societies excluding societies having paid up

capital less than Rs.1 lakh 12

Audit fees

• Audit fees of statutory Auditors shall be decided

by the AGM. The Minimum fees prescribed by

GR- dt 29/10/2014 are as under:

For societies located at metropolitan area & in A grade

area including adjourning cantonment area

Rs 100 per member +

GST

For society located at municipal corporation area &

cantonment area

Rs 75 per member +

GST

For society located at Taluka & Nagar parishad area Rs 50 per member +

GST

For society located at village level Rs 40 per member +

GST

13

Records and information

to be given for audit

• Financial statements signed by Chairman/

Secretary & Treasurer along with all

annexure.

• All the books of accounts and vouchers

• All statutory registers viz. “I” Register, “J”

Register, MCM/AGM Minute books,

Nomination register, Property / dead stock

register, BRS, Interest certificate, Balance

confirmations, MRL and other relevant

records and documents.14

Audit Report

• Audit report Consists of

– Auditors opinion-Independent Auditors report

– Audit Classification

– Schedule to Main Audit report

– Audit Memo Form No 1

– Audit Memo Form No 28

– Schedule to audit memo part A, B, & C

– List of members ( with active /non active classification)

If a CA firm is appointed as Auditor, then it is mandatory to get

Unique Identification Number - UDIN (issued by ICAI)

mentioned on the audit report and financial statements. UDIN

is to be generated by CA through online system on or before

15th day of signing of the audit report and financial statements 15

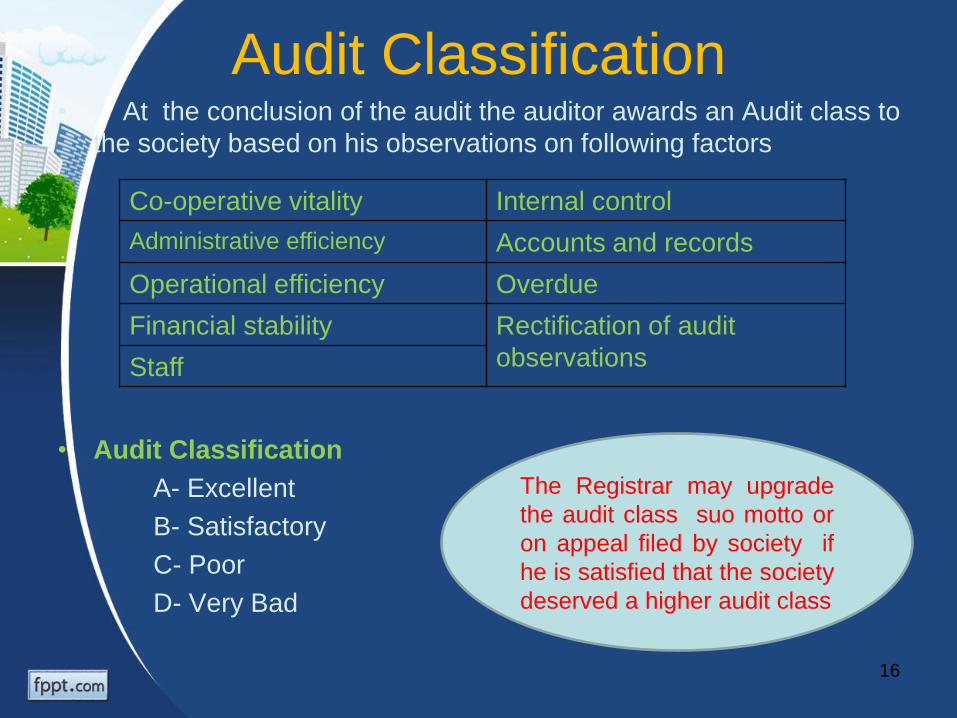

Audit Classification• At the conclusion of the audit the auditor awards an Audit class to

the society based on his observations on following factors

• Audit Classification

A- Excellent

B- Satisfactory

C- Poor

D- Very Bad

Co-operative vitality Internal control

Administrative efficiency Accounts and records

Operational efficiency Overdue

Financial stability Rectification of audit

observationsStaff

The Registrar may upgrade

the audit class suo motto or

on appeal filed by society if

he is satisfied that the society

deserved a higher audit class

16

Special Audit Report• The auditor has to submit special report to the

Registrar in case if he finds that there are

apparent instance(s) of financial irregularities

resulting into losses to the society caused by any

MC member/ officer of the society / by any other

person.

• On receipt of directions from the Registrar he has

to submit specific report regarding criminal action

to be taken against the culprits and lodge the first

information report (FIR) with the concerned

authorities.

17

Submission of Audit Report

• It is to take at least 4 original copies of

audit reports from auditors

– For Society’s own record.

– For submission to District Special

Auditor’s office at Market yard, Pune

– For submission to Registrar in who’s

jurisdiction the society is situated

– For Auditor’s record

Audit report shall be discussed by the

auditor with Managing Committee. 18

Submission of Audit Report

• The Society shall have its Notice Board, fixed at

a conspicuous part of the building/s, on which it

shall exhibit the AGM notice, Audited financial

statements, Audit report, reports of the

Committee and other matters for the benefit of

all the Members of the Society. If there are more

than one buildings, similar Notice Board shall be

fixed in all the buildings.

• The financial statements, Audit report, Annual

report from MC & Audit rectification report to be

Presented at AGM

19

Audit rectification Report

• Audit rectification report shall be prepared

by the Secretary in form “O” and get it

approved by MC. The committee shall

submit Audit Rectification Report to the

Registrar and the AGM.

• All the Members of the Committee shall be

deemed to have committed an offence u/s

146 and shall be liable for Penalty u/s 147

if audit rectification report is not submitted.20

Re-audit

• If it appears to the Registrar, on an

application by society or otherwise, it is

necessary or expedient to re-audit,

Registrar may by order provide for such

re-audit.

• If re-audits are ordered at are requests of

the societies or their members or

outsiders, the cost of such re-audits will

have to be borne by them as per Rule 74.

21

Common audit observations

• The society has yet to obtain the membership of

the federation of CHS.

• The Society has not issued the share certificate

to all the members

• The society is not maintaining Repairs and

Maintenance fund, Sinking fund, Education fund

as required by Bye Law no 13

• The Society has not Invested its funds as

required by bye law no 15 and earmarked the

same

• The conveyance deed is not yet executed in

favour of the Society. 22

Common audit observations

• The society has not followed the process of

recording of nomination, Revocation/revisions in

nomination, transfer of property/share to

nominee/ legal hair in case of death of the

member as stated in bye laws no 31 to 36

• The society has collected the Transfer premium

in excess of the limit set by Circular No.

Grihnirman /Gala Tabdil/FFC/89 dated 27th Nov

1989

• The society has not carried out structure audit/

fire audit/ lift audit as applicable to it.

23

Common audit observations

• The society has not prepared any budget

• The Managing Committee not meeting at least

once in every month.

• The books of accounts and other statutory

records/ registers of the society are incomplete/

not maintained.

• The society has not filed audit rectification report.

• The property of the society is not insured.

• The society has not adopted new model bye laws

after 97th constitutional amendment in Co-

operative law.24

Important Due dates for FY 2019-20

Finalization of Accounts 15th May 2020

Accounts to be handed over for Audit 1st June 2020

Audit Completion 31st July 2020

Audit Report to be Uploaded to MahasahakarWebsite

31st Aug 2020

Conduct of Annual General Meeting 30th Sept 2020

Mandatory Annual Return to be filed atMahasahakar Website

30th Sept 2020

Mandatory Return About Auditor Appointmentfor FY 2020-21

One month from AGM/ 31st Oct 2020

Online Audit Order Generation by Auditor forFY 2020-21

31st Oct 2020

Audit Rectification Report to be submitted toauditors by Society

3 months from the date of Audit report by auditor

Rectification Report Upload by Auditor throughAudit login

Once received from Society

25

Thank you!

KHARE DESHMUKH & CO.Chartered Accountants

www.kharedeshmukh.com

26